Embed Size (px)

Citation preview

Message From The Chair, STEP Toronto

The STEP Toronto Executive invites any members who are interested in becoming more involved in STEP to make their interest known to the nominating committee. Involvement at the executive level or otherwise as an ex officio committee member involved in developing membership, education, professional development programming, student affairs and other initiatives are all

great ways to contribute . A call for nominations for the 2015-2016 executive is open at this time.

This month, I will be chairing the program to be held on February 11, 2015, entitled: “Pilfering the Community Chest: High Stakes Monopoly for Seniors – Financial Abuse: Detection and Intervention.”

We will have the privilege of participating in a panel presentation from Douglas Melville who is the Ombudsman and CEO, Ombudsman Banking Services and Investments (OBSI) and Fiona Crean, who is Office of the Ombudsman, City of Toronto, as well as Laura Watts, of Elder Concepts. This panel promises to be a lively discussion of some pressing issues and concerns our society is now facing given our aging demographics.

We continue to consider articles for publication in our Newsletter. Please submit articles to one of our Newsletter Editors: Ted Polci at: [email protected]; Paul Keul at: [email protected]; Elaine Blades at: [email protected]; Marina Panourgias at: [email protected]; or Joan Jung at: [email protected].

As ever, should you wish to share any ideas or initiatives with your STEP Executive, please contact myself or a member of your Executive. Finally, we are finalizing our passport program for 2015-2016 at this time so if you would like to share any thoughts with us, please do so as soon as possible.

With Warm Wishes,

Kimberly A. Whaley, CS, TEP, LLM

Whaley Estate Litigation, Chair STEP Toronto Executive

Message From the ChairSTEP Toronto Presents...In Case You Missed It... Other Upcoming EventsRequest for Nominations: STEP Canada, Toronto Regional BranchSTEP Executive ProfilesArticle: Case Update: Leibel v. Leibel: Blended Costs AwardArticle: Business Succession Planning: What Every Business Owner Needs To Know (Part 3 of 3)Article: Beware of 2016 Tax Measures for Estates and TrustsAbout Connection

February 2015 - Vol. 2 No. 2

In this Newsletter

Kimberly Whaley, Branch ChairGreg McNally, Branch Past ChairBrian Cohen, Treasurer & Secretary David Stevens, Governance Liaison Paul Keul, Member Services Officer Marina Panourgias Student Liaison OfficerTed Polci, Sponsorship Officer & Newsletter OfficerCraig Vander Zee, Program OfficerMembers at Large:Elaine BladesRachel BlumenfeldChris DelaneyDaniel DochyloJeff HalpernElena HoffsteinHarris JonesJoan JungGillian MuskCorina Weigl

STEP Toronto Executive

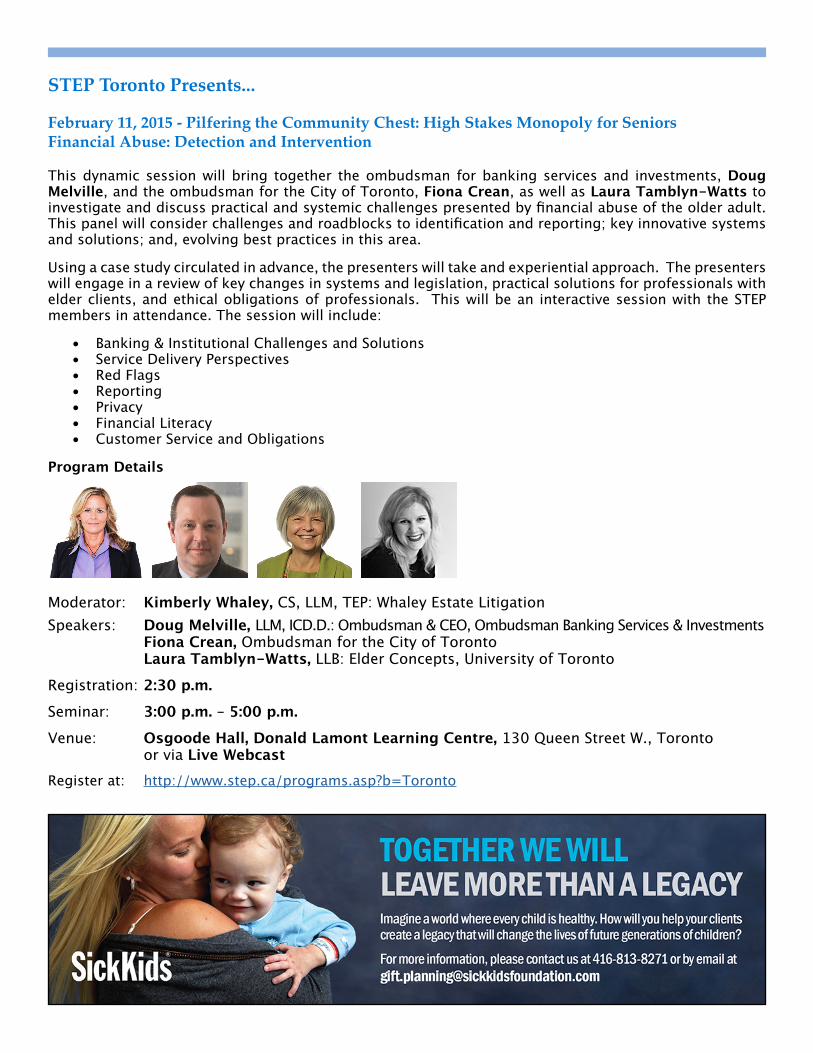

STEP Toronto Presents...

February 11, 2015 - Pilfering the Community Chest: High Stakes Monopoly for SeniorsFinancial Abuse: Detection and Intervention

This dynamic session will bring together the ombudsman for banking services and investments, Doug Melville, and the ombudsman for the City of Toronto, Fiona Crean, as well as Laura Tamblyn-Watts to investigate and discuss practical and systemic challenges presented by financial abuse of the older adult. This panel will consider challenges and roadblocks to identification and reporting; key innovative systems and solutions; and, evolving best practices in this area.

Using a case study circulated in advance, the presenters will take and experiential approach. The presenters will engage in a review of key changes in systems and legislation, practical solutions for professionals with elder clients, and ethical obligations of professionals. This will be an interactive session with the STEP members in attendance. The session will include:

• Banking & Institutional Challenges and Solutions• Service Delivery Perspectives• Red Flags• Reporting• Privacy• Financial Literacy• Customer Service and Obligations

Program Details

Moderator: Kimberly Whaley, CS, LLM, TEP: Whaley Estate LitigationSpeakers: Doug Melville, LLM, ICD.D.: Ombudsman & CEO, Ombudsman Banking Services & Investments Fiona Crean, Ombudsman for the City of Toronto Laura Tamblyn-Watts, LLB: Elder Concepts, University of TorontoRegistration: 2:30 p.m.Seminar: 3:00 p.m. – 5:00 p.m.Venue: Osgoode Hall, Donald Lamont Learning Centre, 130 Queen Street W., Toronto or via Live WebcastRegister at: http://www.step.ca/programs.asp?b=Toronto

In case you missed it…

Guardianships: Dealing with Minors and Adults under Disability

On January 14, 2015, Steve Adams, Superior Court of Justice, Kenneth Goodman, The Public Guardian and Trustee, Linda Waxman, Office of the Children’s Lawyer and Kimberly Whaley, Whaley Estate Litigation, discussed guardianship respecting minors and adults under disability as well as the jurisdiction and role of the Public Guardian and Trustee, the Children’s Lawyer, and the Accountant of the Ontario Superior Court of Justice. See some of the interesting discussion in the question period (links to archived webcast): Question 1

Question 2

London and Southwestern Ontario Chapter: Value Creation & Business Succession for Small Business and Farms

The London and Southwestern Ontario Chapter of STEP enjoyed a shared event with the Estate Planners Council of London on January 19 at the Highland Golf & Country Club. The theme for the evening was value creation in business and farm succession planning. This region of Ontario has seen dramatic rises in land values over the last three years which made the farm element especially pressing for clients. The sixty-seven attendees enjoyed a presentation from lawyer and author John Mill. John recently published “Hire Your Buyer: A Philosophy of Value Creation”. He shared concepts from his book with the audience which expanded on methods of enhancing business valuation multiples by engaging key employees with a trust model. Local accountants Mike Bossy and Mike Bondy then participated in a round table with John wherein they shared best practices on business transition including Kolbe analysis and integration of the well-known Three Circle Model.

L to R: John Mill, Mike Bondy, Mike Bossy

Other Upcoming Events

2014/2015 VALUE PASSPORT:

April 15, 2015 – The Transfer of Wealth including the Family CottageSeminar: 3:00 p.m. – 4:45 p.m.

May 13, 2015 – Elder Care: A Practical ApproachSeminar: 3:00 p.m. - 5:00 p.m.

Request for Nominations: STEP Canada, Toronto Regional Branch

A REQUEST for nominations is hereby made for the following Branch Officers of the Society of Trust and Estate Practitioners (Canada), Toronto Regional Branch:

• Chair

• Deputy Chair

• Secretary

• Treasurer

If you wish to be considered for either a position as a Branch Officer or Member at Large, please send in a brief CV detailing your suitability for the position such as participation in the branch, e.g. program presenter, or evidence of leadership in your local professional/trusts & estates community.

Nominations should be communicated to the Branch Nominations Committee c/o Kimberly Whaley at [email protected] no later than April 12th, 2015.

STEP Executive Profiles

Brian Cohen is Treasurer/Secretary of STEP Toronto Branch. Brian is the Canadian co-lead of Dentons’ Trust, Estates and Wealth Preservation practice focusing in the area of estate and succession planning, trusts and personal taxation for high net worth clients. For more, please visit www.dentons.com/en/brian-cohen

Kimberly A. Whaley is Chair of STEP Toronto Branch and serves on the STEP national board. She is the principal of Whaley Estate Litigation, a Toronto based boutique estate litigation firm offering clients a legal team, experienced in the resolution of estate, trust, capacity, guardianship, attorney, fiduciary and other related disputes. For more information please visit: www.whaleyestatelitigation.com

Elena Hoffstein, MA, LLB, TEP, is Education and Student Liaison Officer for the Toronto STEP Branch. Elena is engaged in personal tax and estate planning, family business succession planning, wills and trusts, corporate reorganizations, marriage contracts and charities and not for profit law. Elena also represents clients in estate litigation matters including will challenges, mental capacity matters, applications for advice and direction of the court and passing of fiduciary accounts. For more, please visit http://www.fasken.com

Case Update: Leibel v. Leibel: Blended Costs Award

By Kimberly A. Whaley, Principal, Whaley Estate Litigation

The costs decision in Leibel v. Leibel was recently released, in which the Court made a blended costs award in favour of the successful respondents/moving parties in a motion to dismiss a Will challenge claim as being statute-barred. 1 The applicant was required to pay the majority of the costs personally and the remainder of the moving parties’ costs were ordered to be paid out of the Estate.2

As a reminder, this case involved a motion to strike a claim in which Justice Greer (as she then was) found that a son’s challenge against his mother’s estate was barred pursuant to s.4 and 5 of the Limitations Act, as he did not bring his claim until two years after his mother’s death. Justice Greer also found his Will challenge claim was barred by the equitable doctrines of estoppel by convention and estoppel by representation.3

The Parties’ Positions on Costs

The successful moving parties were made up of two groups represented by separate counsel, as they had different allegations to respond to in the son’s claim and represented separate interests. Justice Greer referred to them as the “Lewis Parties” and the “Leibel Parties”. Both the Lewis and Leibel Parties sought their costs on a substantial indemnity basis from the applicant son personally.

The son argued that both his costs and the costs of the moving parties should be paid out of the Estate; arguing that it was the Leibel and Lewis Parties who brought the motion to strike his claim and it was reasonable that he oppose it and that it raised novel issues of law. He also argued that the costs sought were inflated as there was a duplication of efforts between the two sets of parties.

The Court’s Ruling

Justice Greer found that the son was personally liable for the costs of the moving parties:

In my view, this is not a case where there was a drafting error in the testator’s Will that needed correcting. In that case, the Costs would properly be paid out of the Estate. I adopt the reasoning in McDougald Estate, that Costs in estate litigation are subject to the general civil regime that the losing party should bear the Costs if there are no public policy considerations otherwise present…In addition, I found it unreasonable for [the son] to try to bring on a Will challenge at this late date in the administration of the Estate, and given that he had already benefited. . .I find that [the son] as the losing party on the Motion, should bear and pay the Costs of both sets of Respondents, as the moving parties. [. . .] I am satisfied that this is not a case where the Costs of the moving parties, which were divided into 2 groups, namely the Lewis parties

1 2014 ONSC 6482. 2 2014 ONSC 6482.3 2014 ONSC 4516.

Enhance your estate planning and litigation advice with our legal expertise.

Together, we make sure your clients get the best hand.

follow us on:Call Lori Duffy at 416.947.5009, visit www.weirfoulds.com or

Hold all the .

and the Leibel parties, should only be awarded a lump sum to be divided between them as they may agree. There were good reasons why these 2 groups required separate representation.4

In deciding on the quantum of the costs award Justice Greer referred to the serious allegations of misconduct that the son made, as well as to the complexity of the Estate and the amounts involved. Justice Greer did not find that the case warranted substantial indemnity costs, as “[a]lthough the Motion was difficult and contentious; [the son] had a right to oppose it. I do not see this as a case where there should be an award of Costs on anything other than a Partial Indemnity scale”.5 The son was ordered to pay costs on a partial indemnity basis of $108,000.00 for the Lewis Parties and $77,000.00 for the Leibel Parties.

However, Justice Greer went on to find that “the balance of the Costs of the Lewis parties and the Leibel parties shall be paid to them on a Substantial Indemnity basis out of the residue of the Estate, based on the Costs principles set out in Sawdon Estate v. Sawdon, 2014 ONCA 101”.6 Sawdon held that “blended” costs awards (where partial indemnity costs are paid by the losing party and the balance of the costs are paid by the Estate) are available in estate litigation. Such blended costs awards “respect public policy considerations” and “maintain the discipline” needed in costs in estate litigation.7

4 2014 ONSC 6482 at paras.28-30 &33.5 2014 ONSC 6482 at para.37.6 2014 ONSC 6482 at para.43.7 Sawdon Estate v. Sawdon, 2014 ONCA 101 at para. 96-97.

Business Succession Planning: What Every Business Owner Needs To Know Jeffrey Halpern, CPA, CA, TEP, Business Succession Advisor with TD Wealth. This is part three of a three part article.

In Parts 1 and 2, we examined why Business Succession Planning has become such an important topic in Canada, and what needs to be considered as part of a well thought out succession plan. In this final part, we will look at transition timing issues.

When is the Right Time to Plan an Exit?

There is no “one” right time to exit a business, but planning an exit must be done in advance of external factors that may adversely influence the decision (for example, poor health or declining market conditions).

It is possible for a business owner to wait too long to exit. Take the case of Phil and Mark Hall, two brothers who were in business for four decades until disaster struck. Phil and Mark had grown their business more than 10 fold over their business partnership.

Phil had 2 daughters. Mark had 2 sons and 1 daughter. Unfortunately, Phil’s two daughters never wanted to join the business. Mark’s 2 sons and son-in-law joined the business 15 years ago, and have worked hard to help the business flourish.

Owing to their long and trusting relationship as brothers, Phil and Mark never thought they needed a shareholders’ agreement, so they never put one in place.

Last year, Phil’s nephews boldly made him a “take it or leave it offer’ to buy his shares for what Phil found to be a lowball price. They told him it was time for him to go, and that if he refused, they would start a new business next door and take all the customers with them.

Phil had no choice but to accept their offer. But he was heartbroken. Feeling cheated, Phil, his wife and children stopped speaking to Uncle Mark and his family, and a family division arose as a result of the lack of a succession plan. Yes, Uncle Phil should have seen this coming, given what was happening in the business, but sometimes we are blind to the obvious until it is too late.

A comprehensive business succession review would have told Phil there was a problem looming, and could have recommended corrective action including a shareholders’ agreement and non-compete agreements with his nephews.

How can a Business Succession Advisor Help?

Business succession planning is a relatively new specialty advice area, whose time has definitely come.

Implementation of a succession plan ordinarily relies on experts including Chartered Business Valuators, lawyers and accountants, insurance specialists, M&A advisors and business brokers, family mediators, bankers and investment professionals whose normal charges would apply.

Business succession planning, while a relatively new specialty advice area, can be expected to expand and flourish in the years to come.

Beware of 2016 Tax Measures for Estates and TrustsPamela Liang, WeirFoulds LLPOn October 23, 2014, the Department of Finance released Bill C-43 to implement the federal budget measures that were tabled on February 11, 2014. Starting in 2016, grandfathered inter vivos trusts (prior to June 18, 1971) and testamentary trusts and estates that have existed for more than 36 months will be taxed at the highest marginal rate, and will be subject to a calendar taxation year end. The only exceptions are graduated rate estates and qualified disability trusts.

A qualifying graduated rate estate (GRE) will be taxed at graduated rates for up to 36 months and may continue to have a non-calendar taxation year end, provided the estate meets the following conditions:

- the estate arose on and as a consequence of an individual’s death;

- no more than 36 months have passed from the date of death;

- the estate is a testamentary trust;

- the deceased individual’s Social Insurance Number (SIN) is provided in the estate’s tax return;

- the estate designates itself as the deceased’s GRE in its T3 for its first taxation year; and

- no other estate has been designated as a GRE of the deceased in its tax return.

It is important to note that only one estate can be designated as a GRE.

A qualified disability trust (QDT) will also continue to be taxed at graduated rates, but only one trust may be designated as a QDT provided the following conditions are met:

- the trust is a testamentary trust;

- the trust is resident in Canada;

- one or more beneficiaries qualify for the disability tax credit (DTC);

- the trust has elected jointly with an “electing beneficiary” to be a QDT and includes the electing beneficiary’s SIN in its tax return for the year; and

- the electing beneficiary has not made an election in respect of any other trust.

QDT’s disability tax credit restriction excludes individuals who do not meet its narrow eligibility requirements but are still a dependent of another individual because of a mental or physical infirmity. The proposals also provide for a recovery of tax in respect of a previous year under certain circumstances.

The proposals can result in many inequities, timing issues and increased litigation risks. Designations to have distributed income taxed in the trust will be invalidated if the trust has taxable income after the designation. Deemed dispositions and income in life interest trusts (spousal, alter ego and joint partner) will be deemed paid out to the deceased so the resultant tax falls on the deceased’s terminal return, with the trust being jointly and severally liable. One positive development is the introduction of more flexibility in the use of donation tax credits (DTC). However, these flexible provisions have not been extended to life interest trusts.

In summation, current estate plans should be revisited to prepare for the incoming changes.

About ConnectionPlease note that each advertiser is linked to their web page (as are our program sponsors on the last page). Please click through to their web pages to learn more about each of our sponsors and advertisers.STEP Toronto publishes ‘Connection’ for our membership 6-7 times per year between August and May. We welcome your feedback. Please send any comments or inquiries to Ted Polci, [email protected]. Interested advertisers are also encouraged to contact Ted Polci to inquire about advertising rates and terms.

Letters, announcements, opinions, comments from membersIf you have an article or an idea that would be of interest to other members of STEP, please send them to [email protected] for inclusion in our next edition of the STEP Toronto Connection.STEP continues to grow and a number of new members have recently been added to the Toronto branch. We extend a hearty welcome to all of the new members, and look forward to seeing you at upcoming programs and events. The process for the Experienced Practitioner route to membership has recently been changed, to ensure we maintain the high quality of our membership. If you know anyone who would be a good candidate for STEP membership, and who has the requisite experience to qualify under the Experienced Practitioner route, please direct them to the STEP Canada website.

Connection Newsletter ContactsTed Polci – Newsletter Officer, co-ordination, advertising - [email protected] Blades – content, articles, proofing - [email protected] Keul – content, articles, proofing - [email protected] Panourgias – program/events information - [email protected] Jung – reports, STEP Branch news - [email protected]

Connection STEP Toronto Newsletter - February 2015, Vol. 2 No. 2

Program Sponsors

PREMIER SPONSORS

EVENT SPONSORS

SUPPORTING SPONSORS de VRIES LITIGATION, PPI Advisory, Thorsteinssons LLP