Embed Size (px)

Citation preview

FDI in the Retail Sector:

Some Implications for Host Countries

Beata Javorcik

Professor of Economics

University of Oxford

Outline

Introductory remarks

Implications for the retail sector

Implications for the supplying industries

Two case studies

Wal-Mart in Mexico

Romania

Opening of retail sector to FDI has led to emergence of global retail chains

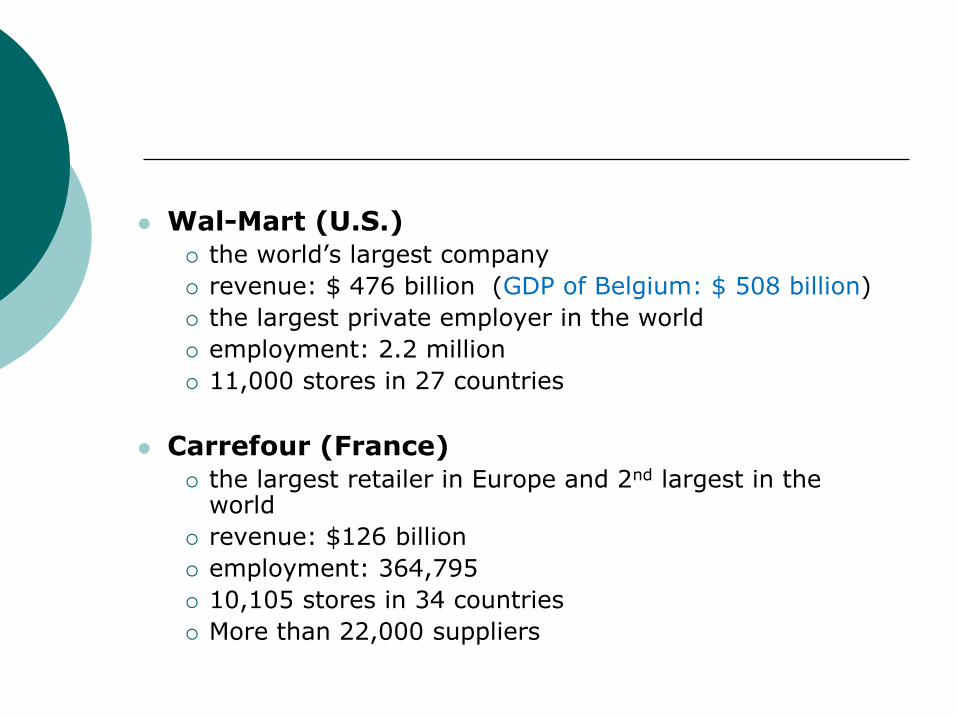

Wal-Mart (U.S.) the world’s largest company

revenue: $ 476 billion (GDP of Belgium: $ 508 billion)

the largest private employer in the world

employment: 2.2 million

11,000 stores in 27 countries

Carrefour (France) the largest retailer in Europe and 2nd largest in the

world

revenue: $126 billion

employment: 364,795

10,105 stores in 34 countries

More than 22,000 suppliers

Tesco (UK)

3rd largest retailer in the world

revenue: $ 113 billion

employment: 500,000

6,784 stores

present in 12 countries

Metro (Germany)

5th largest retailer in the world

revenue: $84 billion

employment: 244,601

present in 32 countries

Global Retailers Are Special

Global retail chains are characterized by

Large scale

Advanced technology

Modern management strategies

Global sourcing networks

Their presence may lead to a transformation of the retail sector in their own country or a host country

Increased competition

Modernization

Concentration

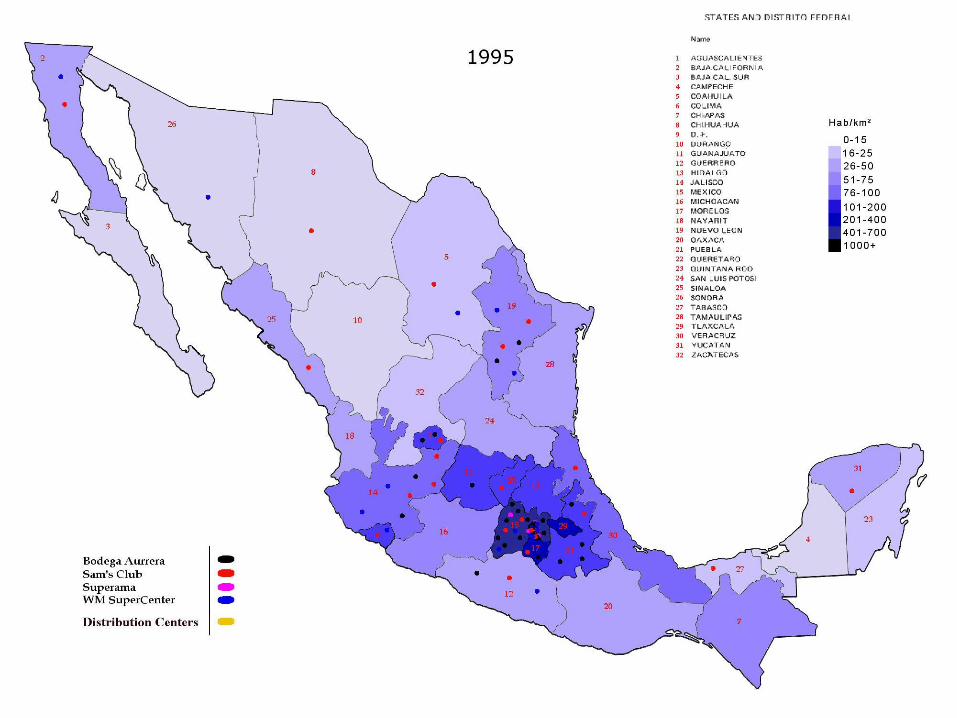

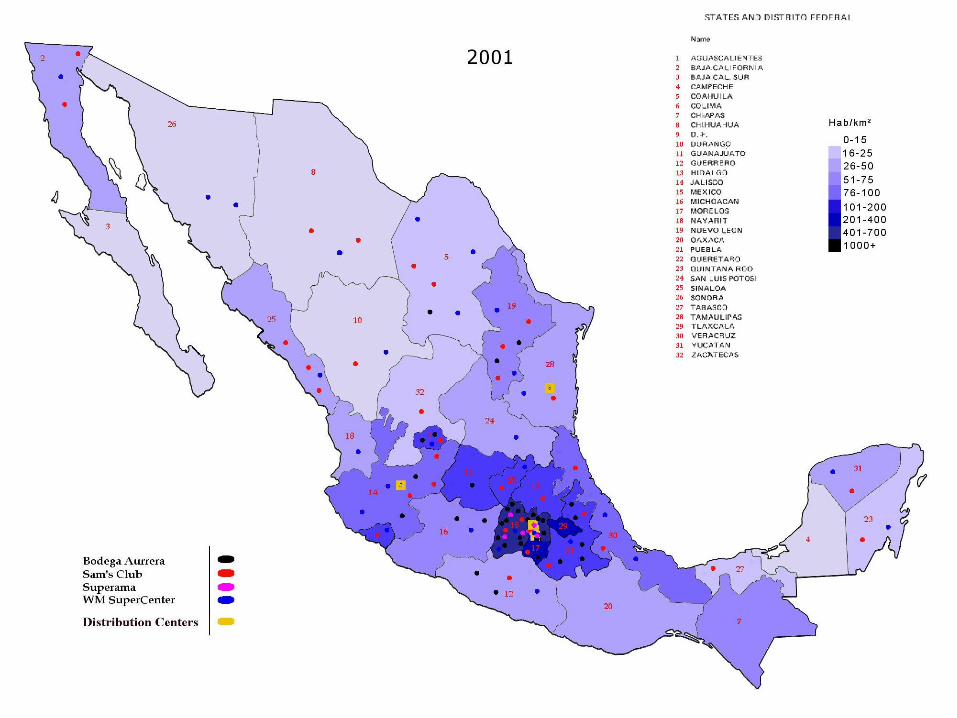

Expansion may happen very fast:

Wal-Mart in Mexico

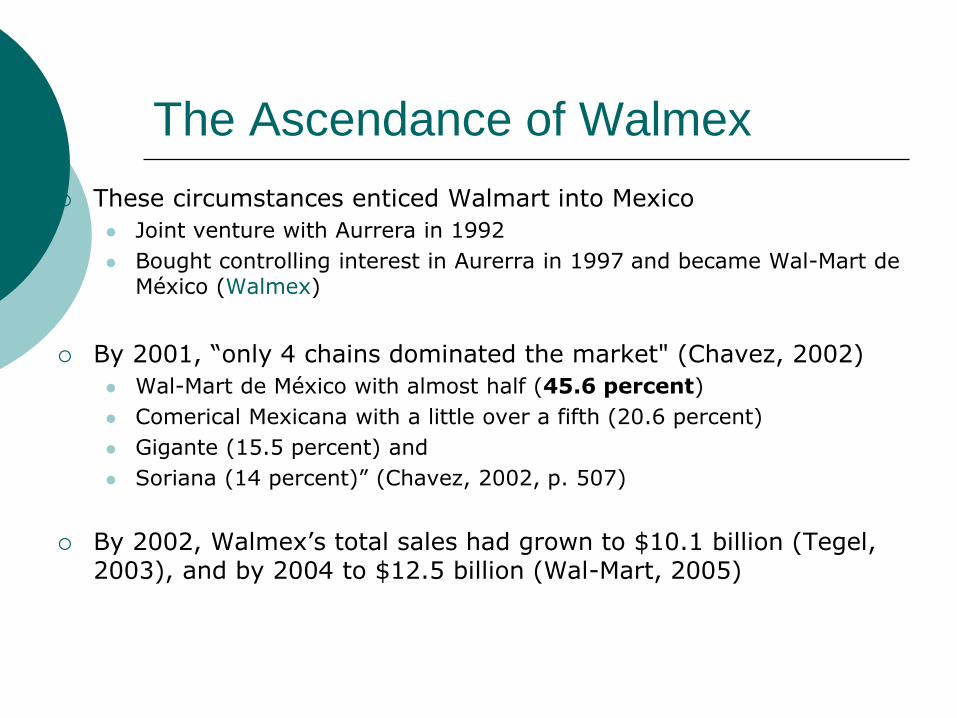

The Ascendance of Walmex

Three decades ago, Mexico committed itself to greater integration with the global economy

Joined the GATT in 1985 (lower tariffs on consumer goods)

Signed NAFTA in 1992 (national treatment to foreign investors)

At the same time, the Mexican economy was becoming more attractive to foreign retailers for other reasons

Big, with a growing middle class

Increasingly urbanized population

The Ascendance of Walmex

These circumstances enticed Walmart into Mexico

Joint venture with Aurrera in 1992

Bought controlling interest in Aurerra in 1997 and became Wal-Mart de México (Walmex)

By 2001, “only 4 chains dominated the market" (Chavez, 2002)

Wal-Mart de México with almost half (45.6 percent)

Comerical Mexicana with a little over a fifth (20.6 percent)

Gigante (15.5 percent) and

Soriana (14 percent)” (Chavez, 2002, p. 507)

By 2002, Walmex’s total sales had grown to $10.1 billion (Tegel, 2003), and by 2004 to $12.5 billion (Wal-Mart, 2005)

The Ascendance of Walmex

A variety of retailers now operate under the Walmex umbrella

Bodega Aurrera (lower end grocery chain)

Superama (basic big box store, without food)

Walmex Supercenters (big box store, plus grocery store)

Sam’s Club (bulk version of Supercenter)

VIPs (restaurants)

Suburbia (clothing)

Entry of global retail chains

can shake up the retail sector

Walmex Business Practices

Innovative warehousing, distribution, and inventory management

Channels deliveries from suppliers through centralized warehouses

Requires delivery trucks to have appointments and drivers to carry standard identification cards

Shipments must be on standardized palettes (rentable from Walmex), shrink-wrapped with corner protectors, subject to third-party quality audits

Stimulated diffusion of modern retail technology

Javorcik, Keller and Tybout (2006)

Durand (2007)

Evidence from Industrialized Countries

Wal-Mart’s expansion in the US from the late 1980s to the late 1990s explains about 40-50% of the net change in the number of small discount retailers and a similar percentage for all other discount stores (Jia, 2008)

A study by Basker (2005a) estimating the effect of Wal-Mart’s expansion on retail employment at the US county level produces mixed results

Wal-Mart’s entry into US regions has been associated with lower retail prices of various consumer goods. The magnitude of the effects ranges from 1.5–3% in the short run to four times as much in the long run (Basker, 2005b)

Effect on Non-industrialized

Countries Likely to Be Larger

Walmex policy of “everyday low prices” is estimated to have led to lower average prices by about 14% in Mexico (Tegel, 2003)

Global retail chains and their effect on the supplying sectors

Potential Implications of the Expansion of

Global Retail Chains for the Supplying Sectors

Increased competitive pressure thanks to the threat of

imports and greater bargaining power due to the high volume of orders may force suppliers to increase their productivity improve their products to meet certain quality requirements

Lower distribution costs thanks to dealing with larger buyers may increase the observed productivity of suppliers

Dealing with retail chains may stimulate economies of scale

Detailed information on changes in demand may help suppliers utilize their capacity better (and thus lead to higher observed productivity)

Anecdotal Evidence

Wal-Mart provides its suppliers with full and free access to real-time data on how their products are selling, store by store. Suppliers can plan production runs earlier and offer better prices. (Economist, 12/06/2001)

Retailers, for instance Tesco, use their insights into consumer behavior and have been able to out-innovate markers of branded consumer good. They can also test and adapt innovations from their private-label suppliers quicker than branded producers can by using their store network and evaluating real-time sale data. (The Boston Consulting Group, 2007)

Walmex Business Practices

Hard-nosed style of negotiation with its suppliers

Wal-Mart keeps negotiations with its suppliers as stark as possibleboth the bargaining environment and the number of negotiable contract features (price, quality, quantity)

Often makes a take-or-leave-it offer

Expects product innovation or annual price concessions

Uses store brands to create competition

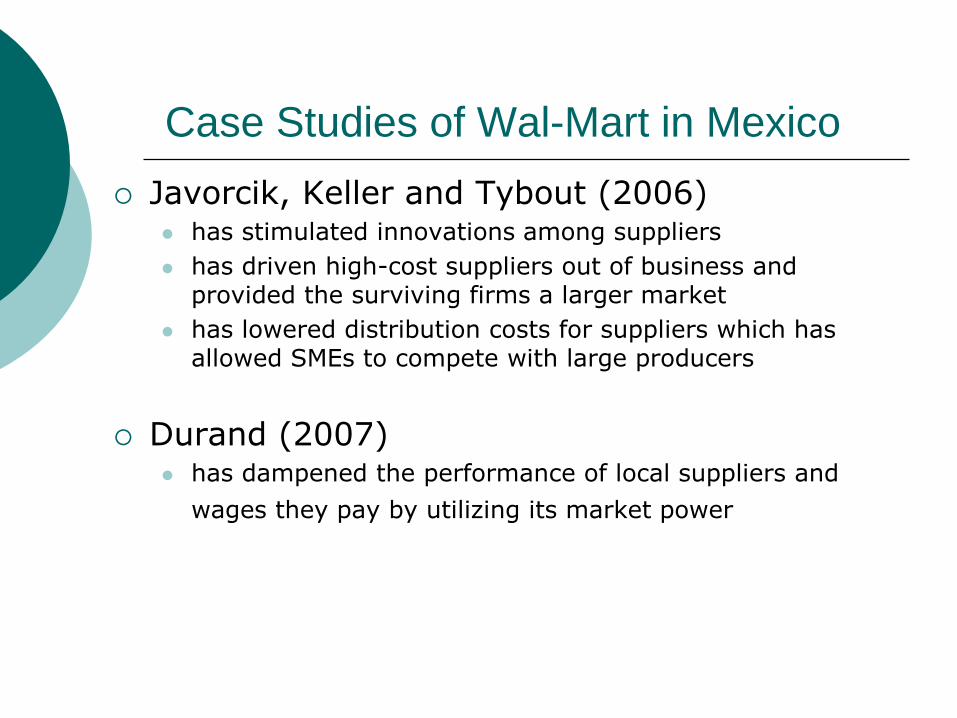

Case Studies of Wal-Mart in Mexico

Javorcik, Keller and Tybout (2006) has stimulated innovations among suppliers

has driven high-cost suppliers out of business and provided the surviving firms a larger market

has lowered distribution costs for suppliers which has allowed SMEs to compete with large producers

Durand (2007) has dampened the performance of local suppliers and

wages they pay by utilizing its market power

Evidence from Romania

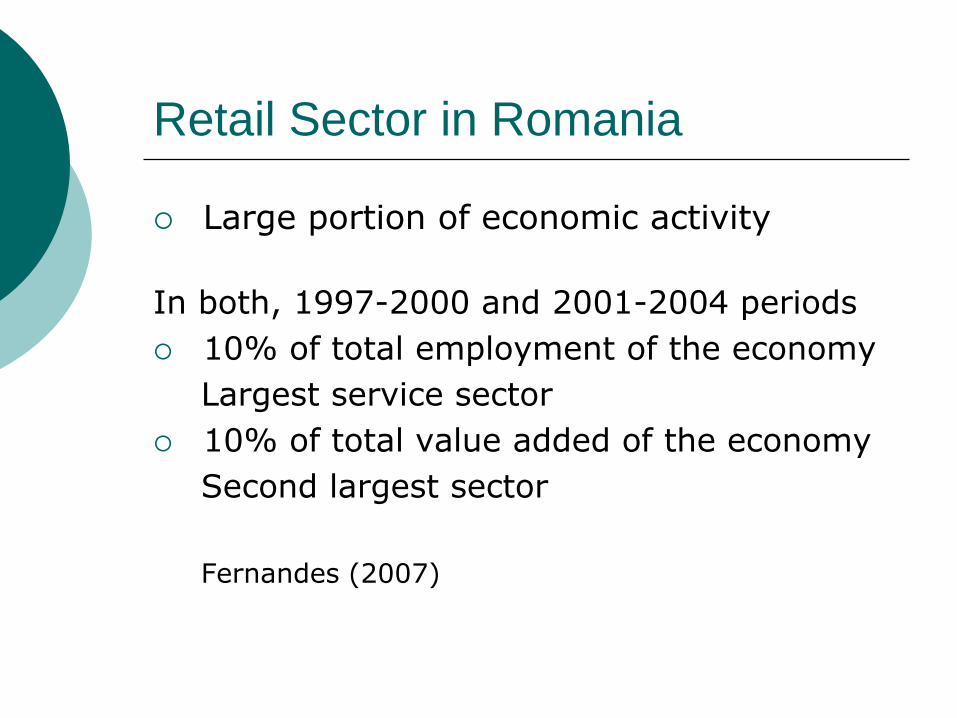

Retail Sector in Romania

Large portion of economic activity

In both, 1997-2000 and 2001-2004 periods

10% of total employment of the economy

Largest service sector

10% of total value added of the economy

Second largest sector

Fernandes (2007)

Global Retail Chains in Romania

Romanian subsidiary parent

company country of

origin year of entry

METRO CASH & CARRY

ROMANIA SRL Metro Germany 1997

BILLA ROMANIA SRL Rewe Germany 1999

MEGA IMAGE SA* Delhaize Belgium 2000

PROFI ROM FOOD SRL Louis Delhaize Belgium 2000

SELGROS CASH & CARRY SRL Rewe Germany 2001

HIPROMA SA Carrefour France 2001

REWE (ROMANIA) SRL Rewe Germany 2001

ROMANIA HYPERMARCHE SA Louis Delhaize Belgium 2003

KAUFLAND ROMANIA SCS* Kaufland Germany 2005

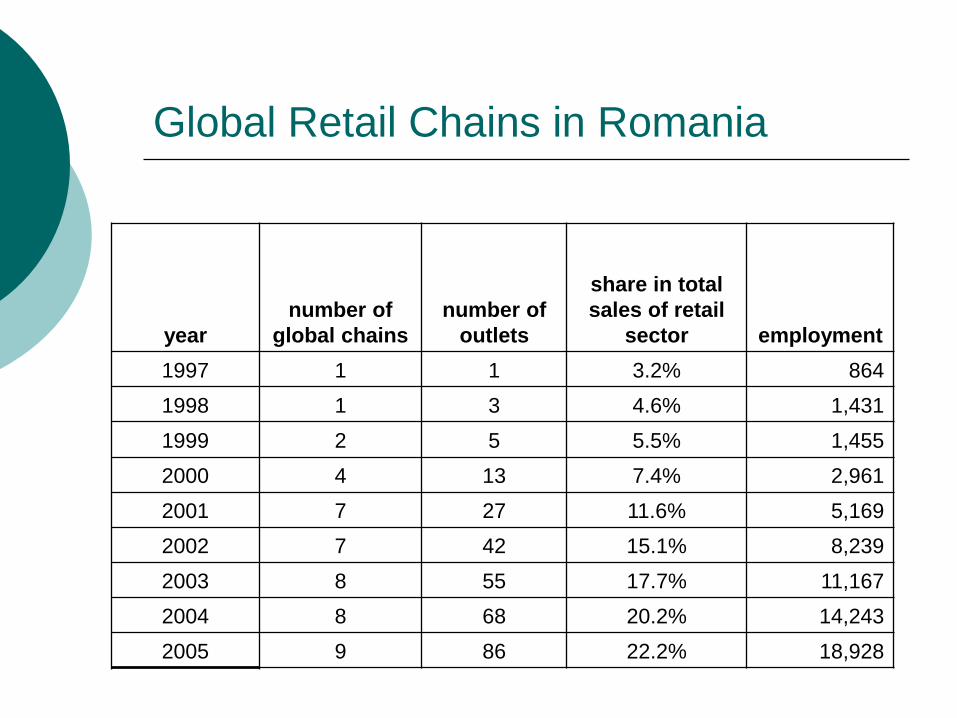

Global Retail Chains in Romania

year

number of

global chains number of

outlets

share in total

sales of retail

sector employment

1997 1 1 3.2% 864

1998 1 3 4.6% 1,431

1999 2 5 5.5% 1,455

2000 4 13 7.4% 2,961

2001 7 27 11.6% 5,169

2002 7 42 15.1% 8,239

2003 8 55 17.7% 11,167

2004 8 68 20.2% 14,243

2005 9 86 22.2% 18,928

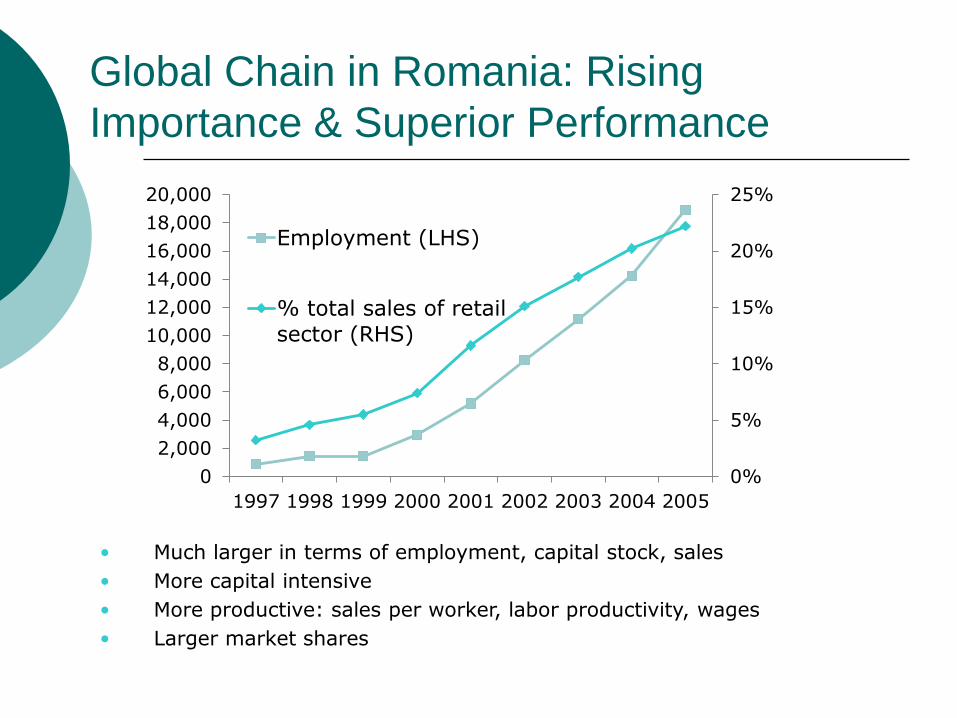

Global Chain in Romania: Rising

Importance & Superior Performance

0%

5%

10%

15%

20%

25%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1997 1998 1999 2000 2001 2002 2003 2004 2005

Employment (LHS)

% total sales of retail

sector (RHS)

Much larger in terms of employment, capital stock, sales

More capital intensive

More productive: sales per worker, labor productivity, wages

Larger market shares

1

Distribution of Global Chain in Romania, 1997

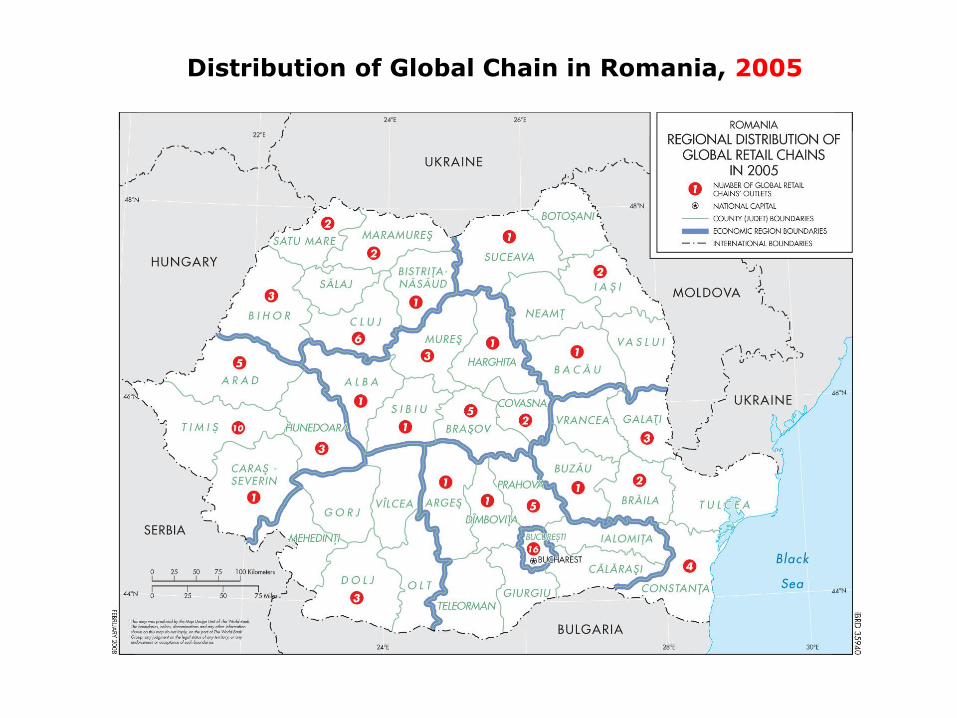

Distribution of Global Chain in Romania, 2005

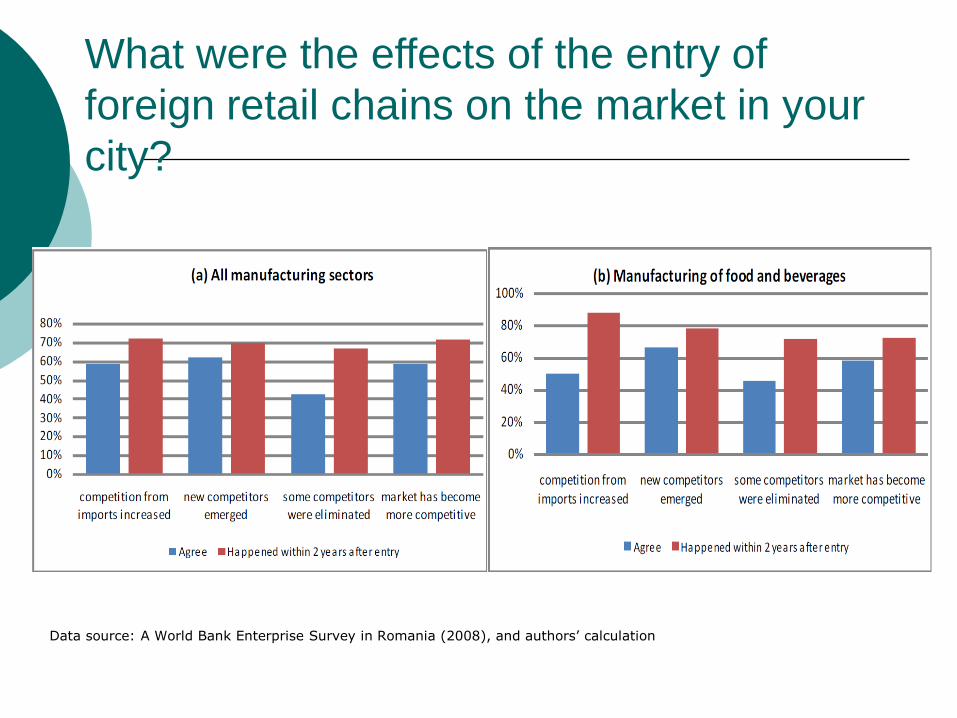

Data source: A World Bank Enterprise Survey in Romania (2008), and authors’ calculation

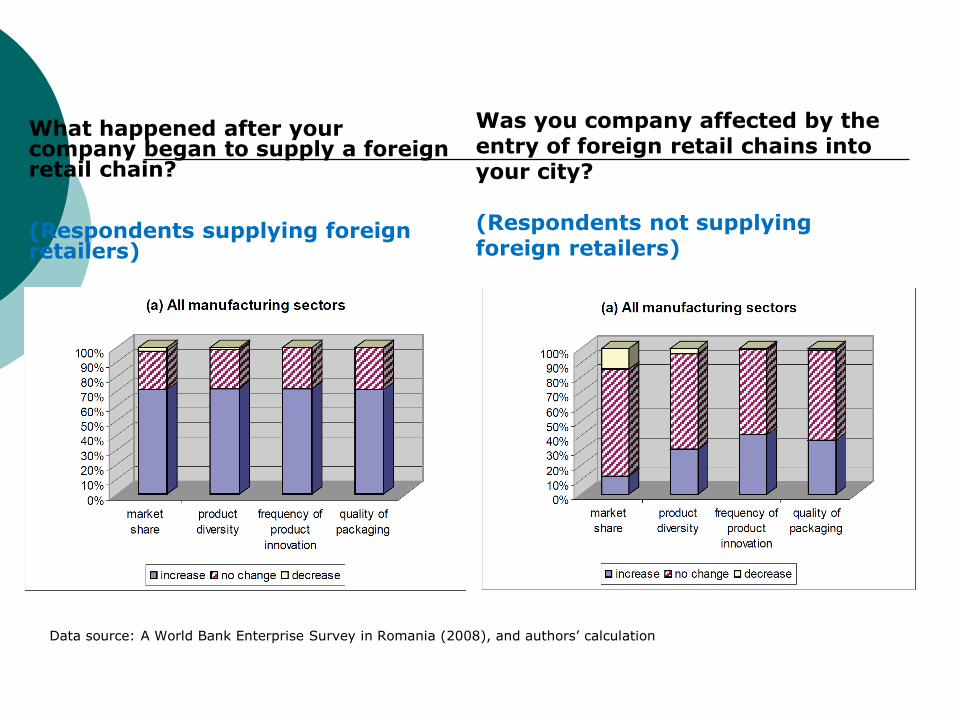

What were the effects of the entry of

foreign retail chains on the market in your

city?

What happened after your company began to supply a foreign retail chain? (Respondents supplying foreign retailers)

Data source: A World Bank Enterprise Survey in Romania (2008), and authors’ calculation

Was you company affected by the entry of foreign retail chains into your city? (Respondents not supplying foreign retailers)

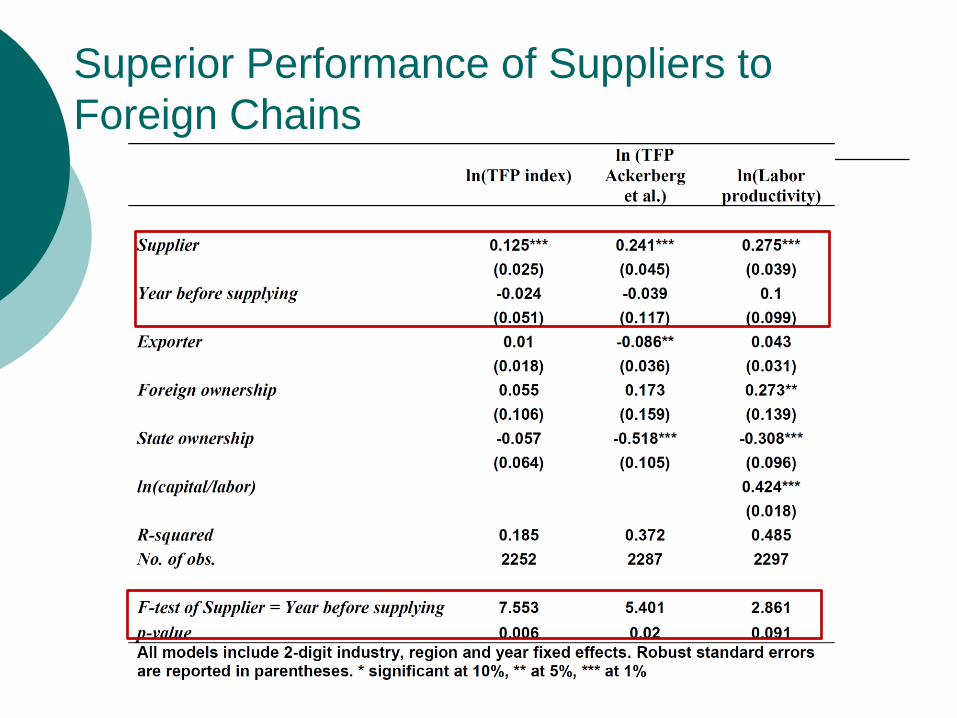

Superior Performance of Suppliers to

Foreign Chains

Some Econometric Evidence

Javorcik and Li (2013, 2014)

How does the presence of global retail chains affect the performance of firms in the supplying industries in Romania?

Why focus on Romania?

Comprehensive high quality data: 50k+ manufacturing firms operating in Romania

during 1997-2005

firms of all sizes, including SMEs

Timing of the entry of foreign retailers data cover the pre- and post-entry period

Large country the third largest country in Eastern Europe

population over 22 million

238,391 km2

48

Empirical Strategy

Difference-in-differences approach

Compare the performance of

food sectors before and after entry of global chains into their region

to the performance of non-food sectors

during the same period

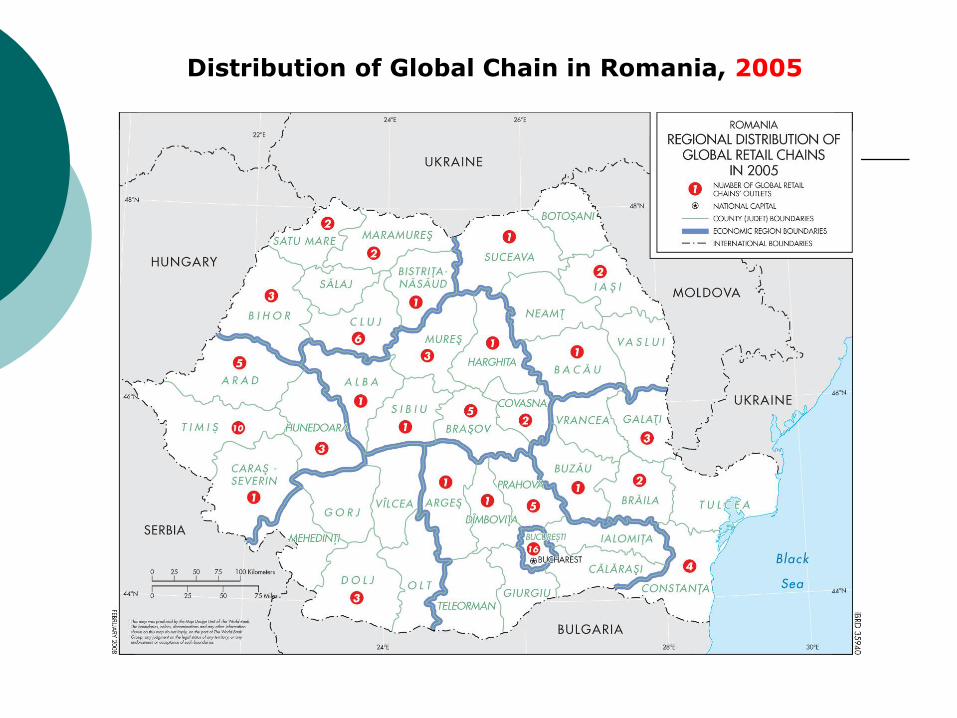

Distribution of Global Chain in Romania, 2005

Focus on Food and Beverage Industries

NACE industry description

151 Production, processing and preserving of meat and meat products

153 Processing and preserving of fruit and vegetables

155 Manufacture of dairy products

156 Manufacture of grain mill products, starches and starch products

158 Manufacture of other food products

159 Manufacture of beverages

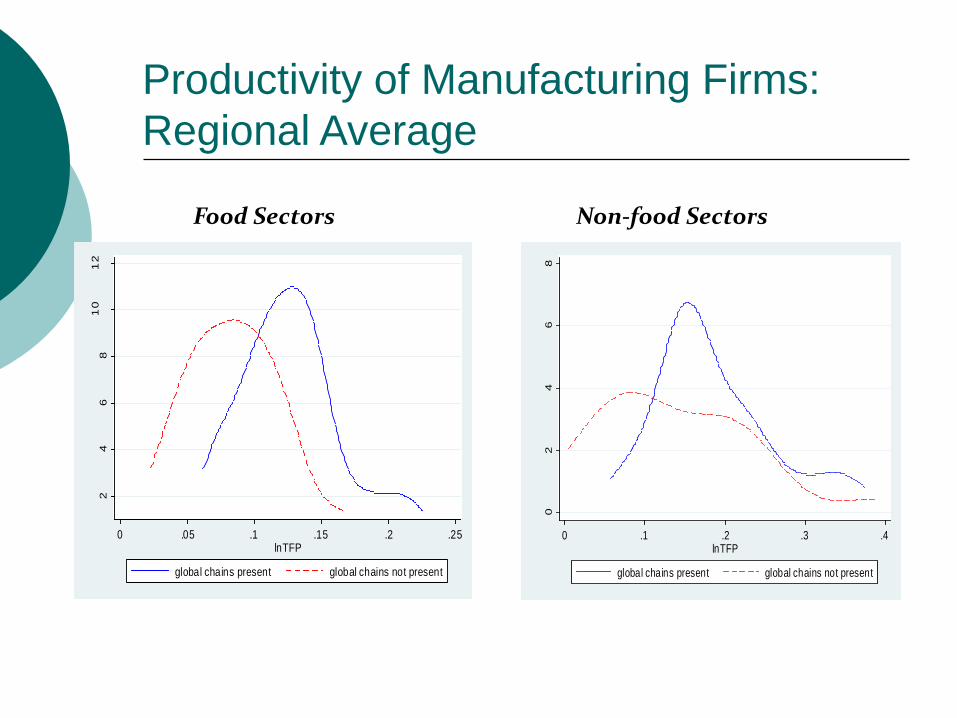

Food Sectors Non-food Sectors

24

68

10

12

de

nsity

0 .05 .1 .15 .2 .25lnTFP

global chains present global chains not present

02

46

8

de

nsity

0 .1 .2 .3 .4lnTFP

global chains present global chains not present

Productivity of Manufacturing Firms:

Regional Average

Measuring Chains’ Presence

Regional presence of global chains measured at 2 digit NUTS level

Indicator variable capturing whether global chains are present in region r at time t

Number of chain stores operating in region r at time t

Selling space of global chains operating in region r at time t

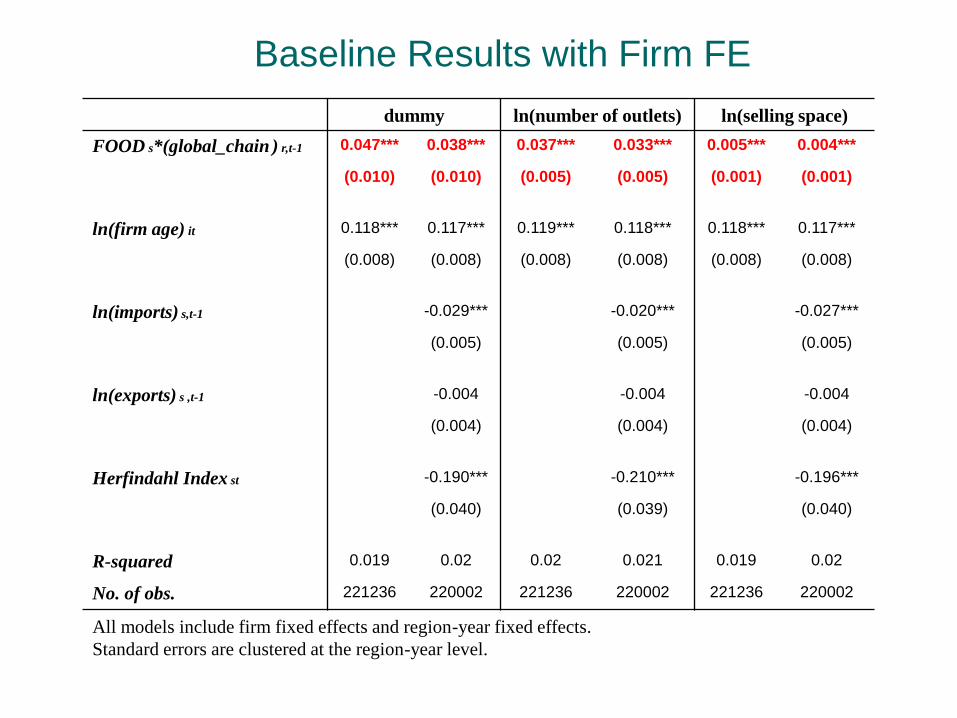

Baseline Results with Firm FE

dummy ln(number of outlets) ln(selling space)

FOOD s*(global_chain ) r,t-1 0.047*** 0.038*** 0.037*** 0.033*** 0.005*** 0.004***

(0.010) (0.010) (0.005) (0.005) (0.001) (0.001)

ln(firm age) it 0.118*** 0.117*** 0.119*** 0.118*** 0.118*** 0.117***

(0.008) (0.008) (0.008) (0.008) (0.008) (0.008)

ln(imports) s,t-1 -0.029*** -0.020*** -0.027***

(0.005) (0.005) (0.005)

ln(exports) s ,t-1 -0.004 -0.004 -0.004

(0.004) (0.004) (0.004)

Herfindahl Index st -0.190*** -0.210*** -0.196***

(0.040) (0.039) (0.040)

R-squared 0.019 0.02 0.02 0.021 0.019 0.02

No. of obs. 221236 220002 221236 220002 221236 220002

All models include firm fixed effects and region-year fixed effects.

Standard errors are clustered at the region-year level.

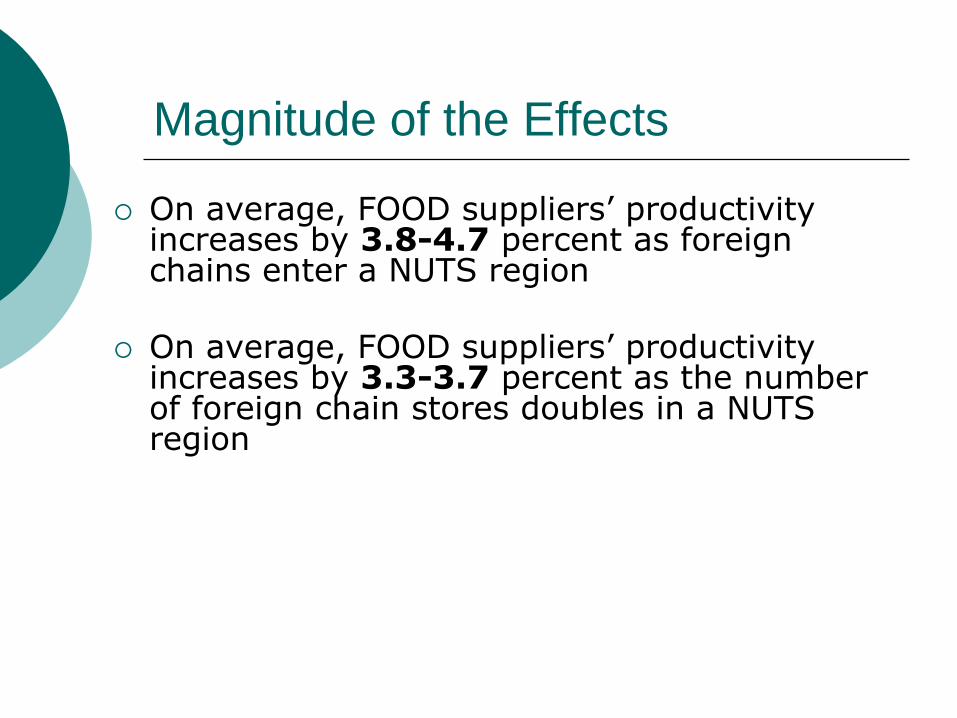

Magnitude of the Effects

On average, FOOD suppliers’ productivity increases by 3.8-4.7 percent as foreign chains enter a NUTS region

On average, FOOD suppliers’ productivity increases by 3.3-3.7 percent as the number of foreign chain stores doubles in a NUTS region

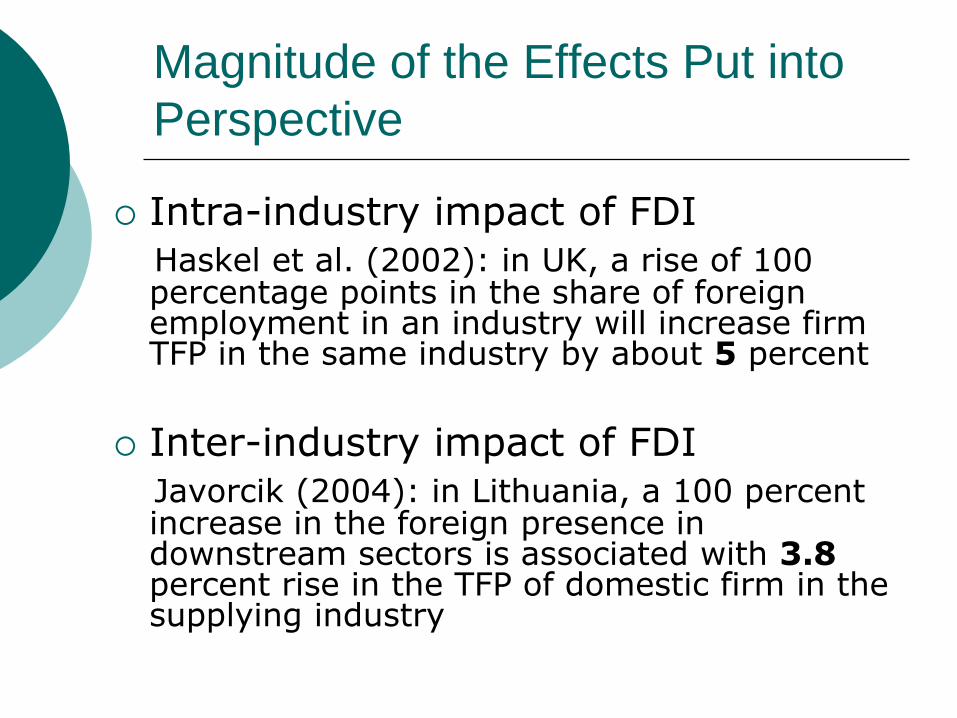

Magnitude of the Effects Put into

Perspective

Intra-industry impact of FDI Haskel et al. (2002): in UK, a rise of 100

percentage points in the share of foreign employment in an industry will increase firm TFP in the same industry by about 5 percent

Inter-industry impact of FDI Javorcik (2004): in Lithuania, a 100 percent

increase in the foreign presence in downstream sectors is associated with 3.8 percent rise in the TFP of domestic firm in the supplying industry

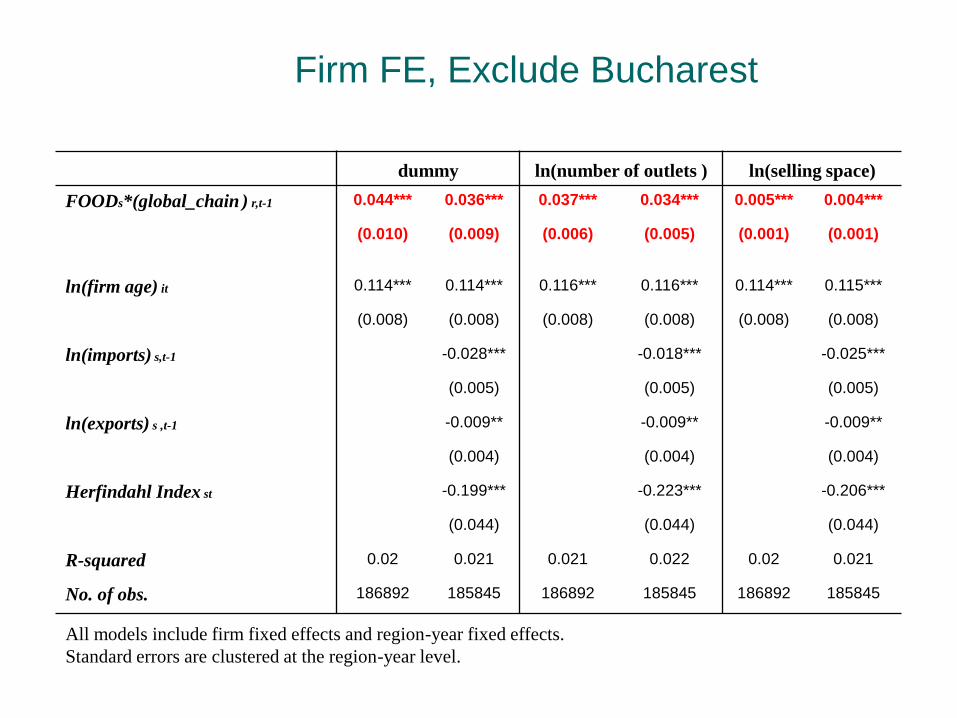

Firm FE, Exclude Bucharest

dummy ln(number of outlets ) ln(selling space)

FOODs*(global_chain ) r,t-1 0.044*** 0.036*** 0.037*** 0.034*** 0.005*** 0.004***

(0.010) (0.009) (0.006) (0.005) (0.001) (0.001)

ln(firm age) it 0.114*** 0.114*** 0.116*** 0.116*** 0.114*** 0.115***

(0.008) (0.008) (0.008) (0.008) (0.008) (0.008)

ln(imports) s,t-1 -0.028*** -0.018*** -0.025***

(0.005) (0.005) (0.005)

ln(exports) s ,t-1 -0.009** -0.009** -0.009**

(0.004) (0.004) (0.004)

Herfindahl Index st -0.199*** -0.223*** -0.206***

(0.044) (0.044) (0.044)

R-squared 0.02 0.021 0.021 0.022 0.02 0.021

No. of obs. 186892 185845 186892 185845 186892 185845

All models include firm fixed effects and region-year fixed effects.

Standard errors are clustered at the region-year level.

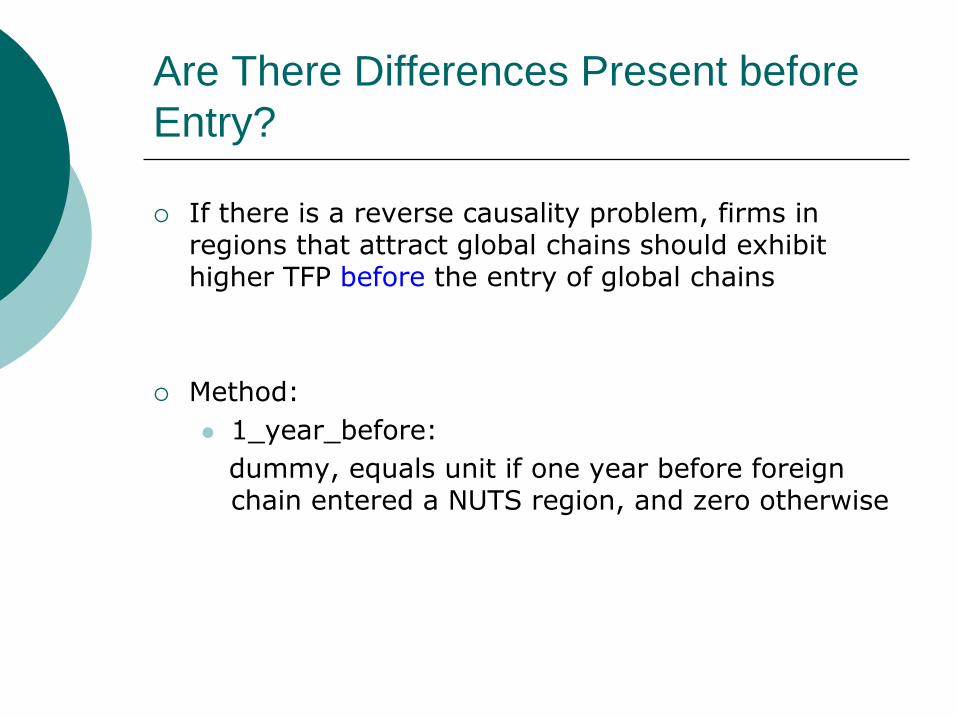

Are There Differences Present before

Entry?

If there is a reverse causality problem, firms in regions that attract global chains should exhibit higher TFP before the entry of global chains

Method:

1_year_before:

dummy, equals unit if one year before foreign chain entered a NUTS region, and zero otherwise

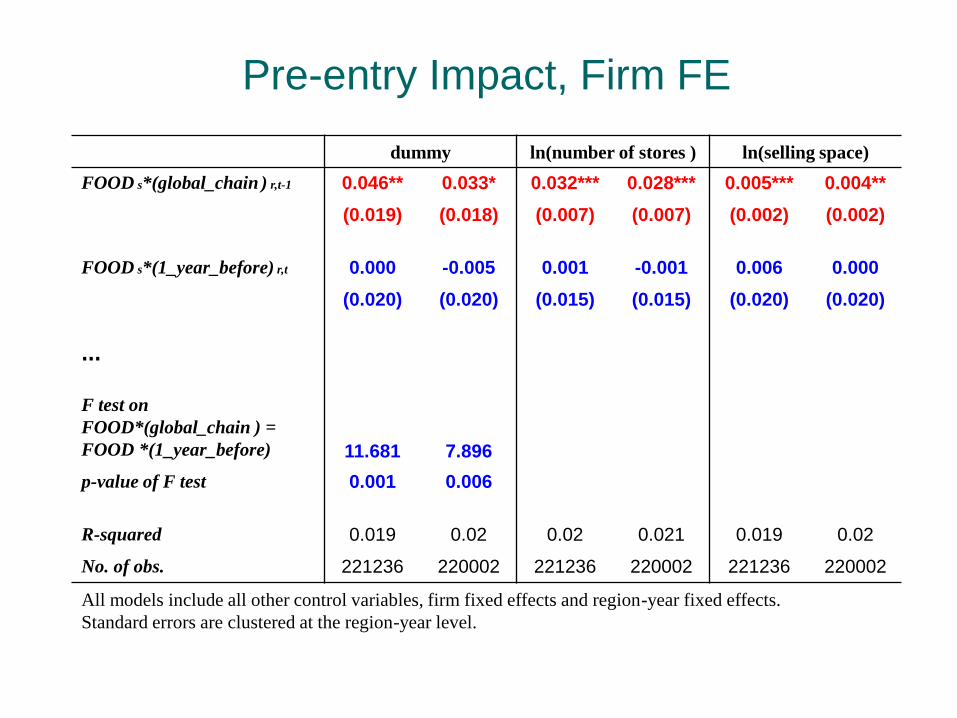

Pre-entry Impact, Firm FE

dummy ln(number of stores ) ln(selling space)

FOOD s*(global_chain ) r,t-1 0.046** 0.033* 0.032*** 0.028*** 0.005*** 0.004**

(0.019) (0.018) (0.007) (0.007) (0.002) (0.002)

FOOD s*(1_year_before) r,t 0.000 -0.005 0.001 -0.001 0.006 0.000

(0.020) (0.020) (0.015) (0.015) (0.020) (0.020)

…

F test on

FOOD*(global_chain ) =

FOOD *(1_year_before) 11.681 7.896

p-value of F test 0.001 0.006

R-squared 0.019 0.02 0.02 0.021 0.019 0.02

No. of obs. 221236 220002 221236 220002 221236 220002

All models include all other control variables, firm fixed effects and region-year fixed effects.

Standard errors are clustered at the region-year level.

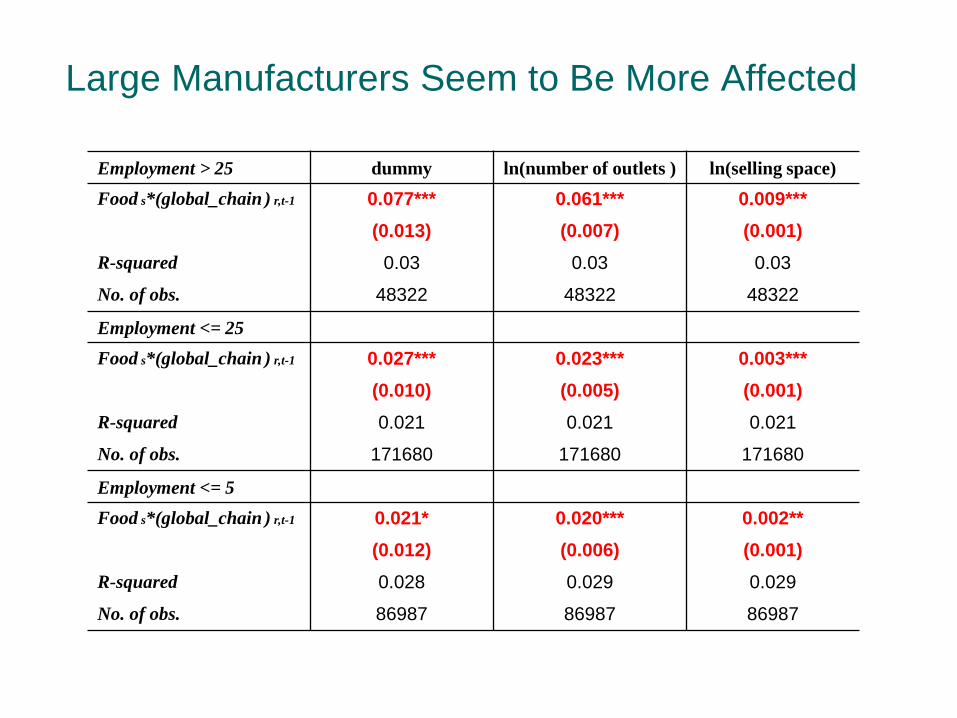

Large Manufacturers Seem to Be More Affected

Employment > 25 dummy ln(number of outlets ) ln(selling space)

Food s*(global_chain ) r,t-1 0.077*** 0.061*** 0.009***

(0.013) (0.007) (0.001)

R-squared 0.03 0.03 0.03

No. of obs. 48322 48322 48322

Employment <= 25

Food s*(global_chain ) r,t-1 0.027*** 0.023*** 0.003***

(0.010) (0.005) (0.001)

R-squared 0.021 0.021 0.021

No. of obs. 171680 171680 171680

Employment <= 5

Food s*(global_chain ) r,t-1 0.021* 0.020*** 0.002**

(0.012) (0.006) (0.001)

R-squared 0.028 0.029 0.029

No. of obs. 86987 86987 86987

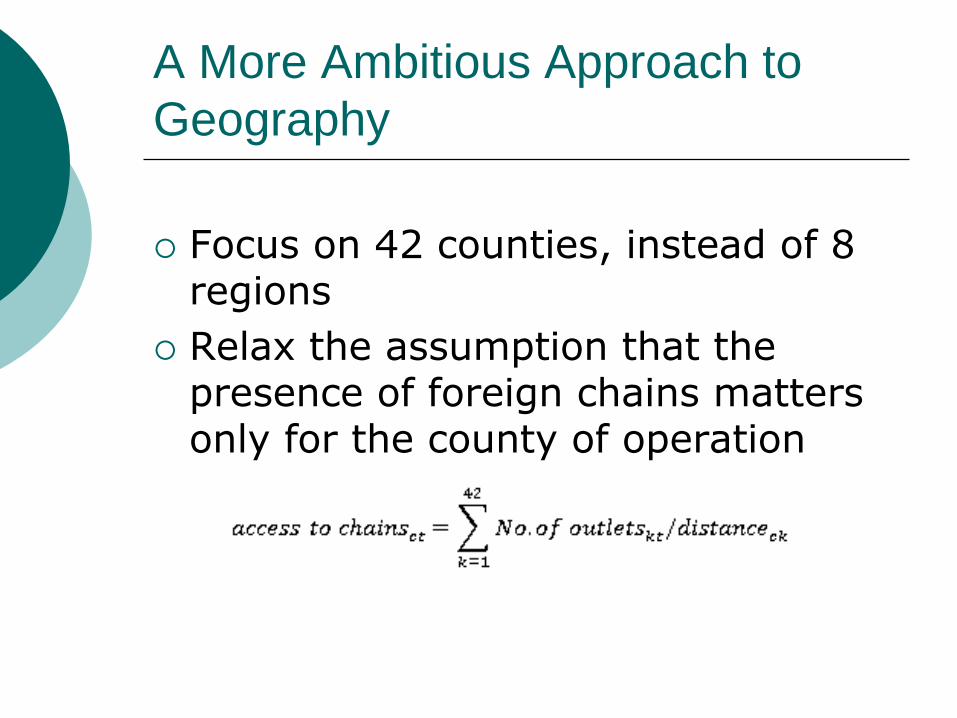

A More Ambitious Approach to

Geography

Focus on 42 counties, instead of 8 regions

Relax the assumption that the presence of foreign chains matters only for the county of operation

Distribution of Global Chain in Romania, 2005

A More Ambitious Approach to

Geography

Focus on 42 counties, instead of 8 regions

Relax the assumption that the presence of foreign chains matters only for the county of operation

Our conclusions are robust to this change

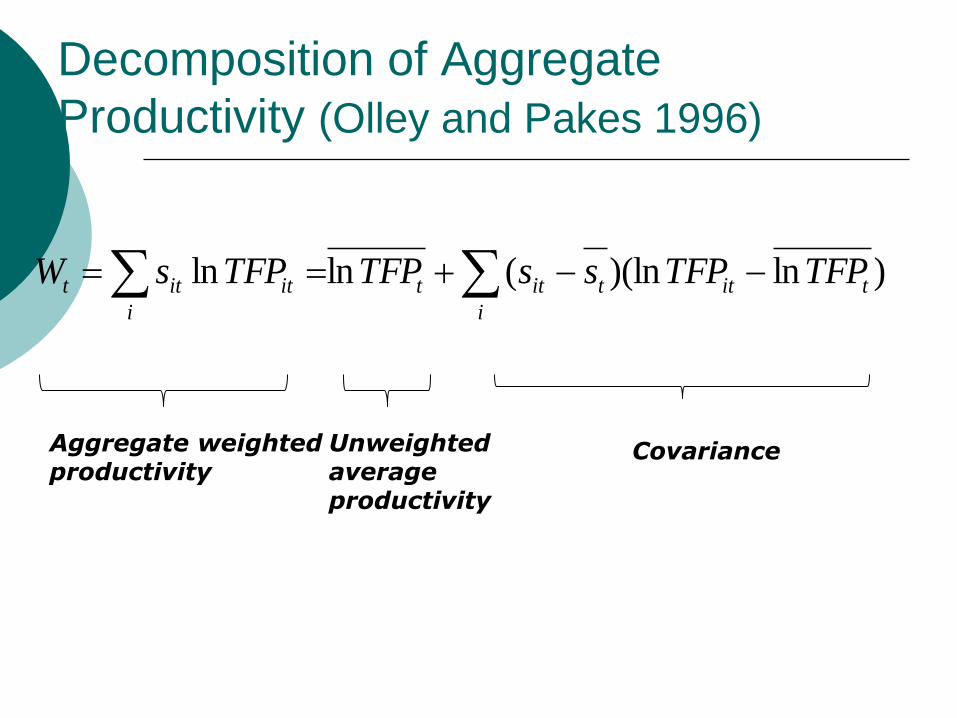

Decomposition of Aggregate

Productivity (Olley and Pakes 1996)

i

tittitt

i

ititt TFPTFPssTFPTFPsW )ln)(ln(lnln

Aggregate weighted productivity

Unweighted average productivity

Covariance

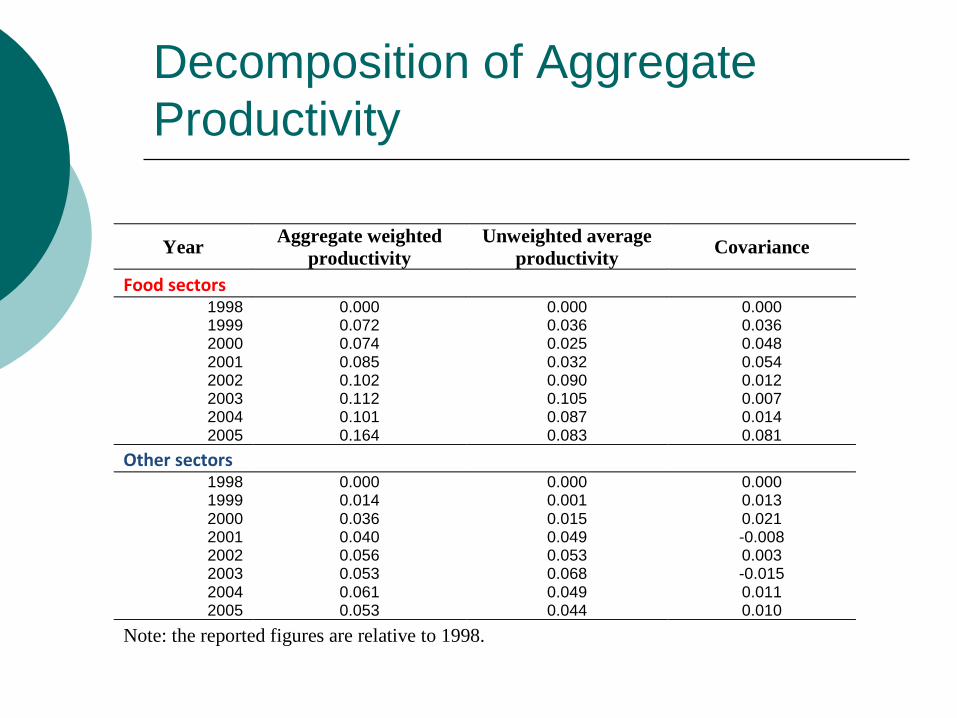

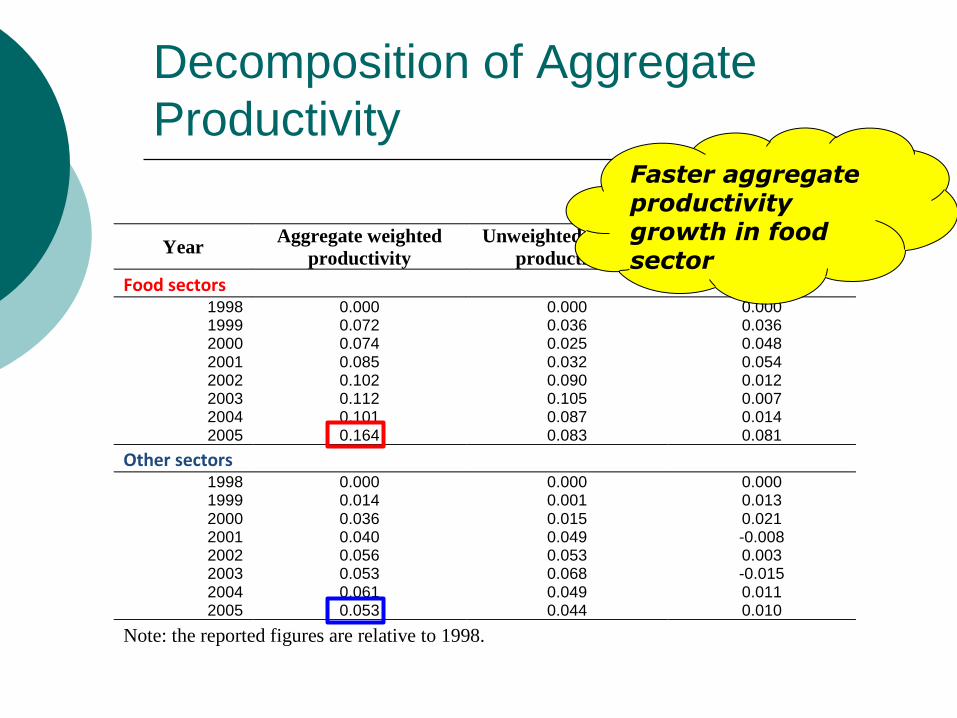

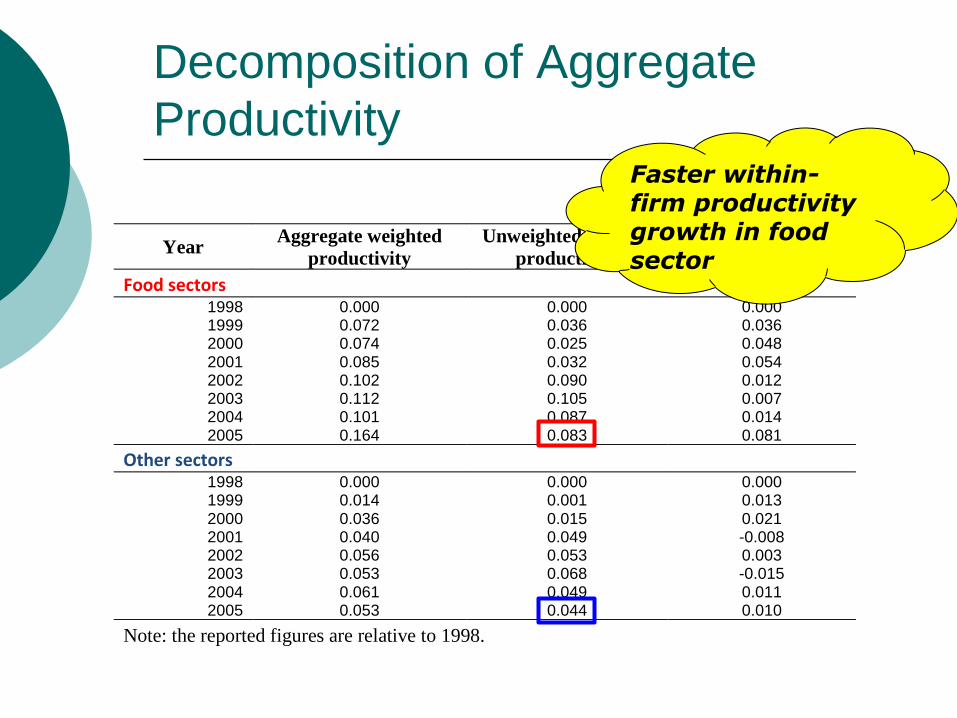

Decomposition of Aggregate

Productivity

Year

Aggregate weighted

productivity Unweighted average

productivity Covariance

Food sectors 1998 0.000 0.000 0.000 1999 0.072 0.036 0.036 2000 0.074 0.025 0.048 2001 0.085 0.032 0.054 2002 0.102 0.090 0.012 2003 0.112 0.105 0.007 2004 0.101 0.087 0.014 2005 0.164 0.083 0.081

Other sectors 1998 0.000 0.000 0.000

1999 0.014 0.001 0.013 2000 0.036 0.015 0.021 2001 0.040 0.049 -0.008 2002 0.056 0.053 0.003 2003 0.053 0.068 -0.015 2004 0.061 0.049 0.011 2005 0.053 0.044 0.010

Note: the reported figures are relative to 1998.

Decomposition of Aggregate

Productivity

Year

Aggregate weighted

productivity Unweighted average

productivity Covariance

Food sectors 1998 0.000 0.000 0.000

1999 0.072 0.036 0.036 2000 0.074 0.025 0.048 2001 0.085 0.032 0.054 2002 0.102 0.090 0.012 2003 0.112 0.105 0.007 2004 0.101 0.087 0.014 2005 0.164 0.083 0.081

Other sectors 1998 0.000 0.000 0.000

1999 0.014 0.001 0.013 2000 0.036 0.015 0.021 2001 0.040 0.049 -0.008 2002 0.056 0.053 0.003 2003 0.053 0.068 -0.015 2004 0.061 0.049 0.011 2005 0.053 0.044 0.010

Note: the reported figures are relative to 1998.

Changes expressed relative to 1998

Decomposition of Aggregate

Productivity

Year

Aggregate weighted

productivity Unweighted average

productivity Covariance

Food sectors 1998 0.000 0.000 0.000 1999 0.072 0.036 0.036 2000 0.074 0.025 0.048 2001 0.085 0.032 0.054 2002 0.102 0.090 0.012 2003 0.112 0.105 0.007 2004 0.101 0.087 0.014 2005 0.164 0.083 0.081

Other sectors 1998 0.000 0.000 0.000

1999 0.014 0.001 0.013 2000 0.036 0.015 0.021 2001 0.040 0.049 -0.008 2002 0.056 0.053 0.003 2003 0.053 0.068 -0.015 2004 0.061 0.049 0.011 2005 0.053 0.044 0.010

Note: the reported figures are relative to 1998.

Faster aggregate productivity growth in food sector

Decomposition of Aggregate

Productivity

Year

Aggregate weighted

productivity Unweighted average

productivity Covariance

Food sectors 1998 0.000 0.000 0.000 1999 0.072 0.036 0.036 2000 0.074 0.025 0.048 2001 0.085 0.032 0.054 2002 0.102 0.090 0.012 2003 0.112 0.105 0.007 2004 0.101 0.087 0.014 2005 0.164 0.083 0.081

Other sectors 1998 0.000 0.000 0.000

1999 0.014 0.001 0.013 2000 0.036 0.015 0.021 2001 0.040 0.049 -0.008 2002 0.056 0.053 0.003 2003 0.053 0.068 -0.015 2004 0.061 0.049 0.011 2005 0.053 0.044 0.010

Note: the reported figures are relative to 1998.

Faster within-firm productivity growth in food sector

Decomposition of Aggregate

Productivity

Year

Aggregate weighted

productivity Unweighted average

productivity Covariance

Food sectors 1998 0.000 0.000 0.000 1999 0.072 0.036 0.036 2000 0.074 0.025 0.048 2001 0.085 0.032 0.054 2002 0.102 0.090 0.012 2003 0.112 0.105 0.007 2004 0.101 0.087 0.014 2005 0.164 0.083 0.081

Other sectors 1998 0.000 0.000 0.000

1999 0.014 0.001 0.013 2000 0.036 0.015 0.021 2001 0.040 0.049 -0.008 2002 0.056 0.053 0.003 2003 0.053 0.068 -0.015 2004 0.061 0.049 0.011 2005 0.053 0.044 0.010

Note: the reported figures are relative to 1998.

Reallocation played a greater role in food sector

Decomposition of Aggregate

Productivity

Econometric analysis confirms that both within-firm productivity growth and reallocation of market shares toward more productive producers have been stimulated by entry of foreign retail chains

Summary

Global retail chains are larger in terms of employment and capital investment, more capital intensive, and display higher labor productivity

Expansion of global retail chains leads to an improved performance in the supplying industries

Large firms seem to be affected more than SMEs

Entry of global retail chains stimulates both within-firm productivity growth as well as reallocation of market shares towards more productive suppliers

Another piece of evidence in favor of services liberalization

References

Basker, Emek (2005a) Job Creation or Destruction? Labor-Market Effects of Wal-Mart Expansion. Review of Economics and Statistics 87(1): 174-183

Basker, Emek (2005b). Selling a Cheaper Mousetrap: Wal-Mart's Effect on Retail Prices. Journal of Urban Economics 58(2): 203-229

Chavez, Manuel (2002) The Transformation of Mexican Retailing with NAFTA. Development Policy Review, 20(4): 503-13

Durand, Cedric (2007). Externalities from Foreign Direct Investment in the Mexican Retailing Sector. Cambridge Journal of Economics 31 (3): 393-411

Haskel, Jonathan E., Sonia C. Pereira, and Matthew J. Slaughter (2007). Does Inward Foreign Direct Investment Boost the Productivity of Domestic Firms? Review of Economics and Statistics, 89(2)

Javorcik, Beata S. (2004). Does Foreign Direct Investment Increase the Productivity of Domestic Firms? In Search of Spillovers through Backward Linkages. American Economic Review 94(3): 605-627

References

Javorcik, Beata S. and Yue Li (2013) Do the Biggest Aisles Serve a Brighter Future? Global Retail Chains and Their Implications for Romania. Journal of International Economics, 90(2): 348–363

Javorcik, Beata S. and Yue Li (2014) Global Retail Chains and the Supplying Industries: Evidence from Romania CESifo Economic Studies 60 (1): 107-134

Javorcik, Beata S., Wolfgang Keller and James R.Tybout (2008). Openness and Industrial Response in a Wal-Mart World: A Case Study of Mexican Soaps, Detergents and Surfactant Producers. The World Economy, 31(12)

Jia, Panle (2008) What Happens when Wal-Mart comes to Town? An Empirical Analysis of the Discount Retailing Industry," Econometrica 76(6): 1263-1316

Tegel, S. (2003) Every Day Higher Sales: Wal-Mart Wunderkind Walmex shows them how it’s done in a down economy: The Giant 24, Latin Trade (August) Downloaded February 15, 2006 from http://www..ndarticles.com/p/articles/mi_m0BEK/is_8_11/ai_106860473