Embed Size (px)

Citation preview

FDI in MULTI- BRAND Retail India

By

Dr. Rajiv Kumar

Secretary General

FICCI

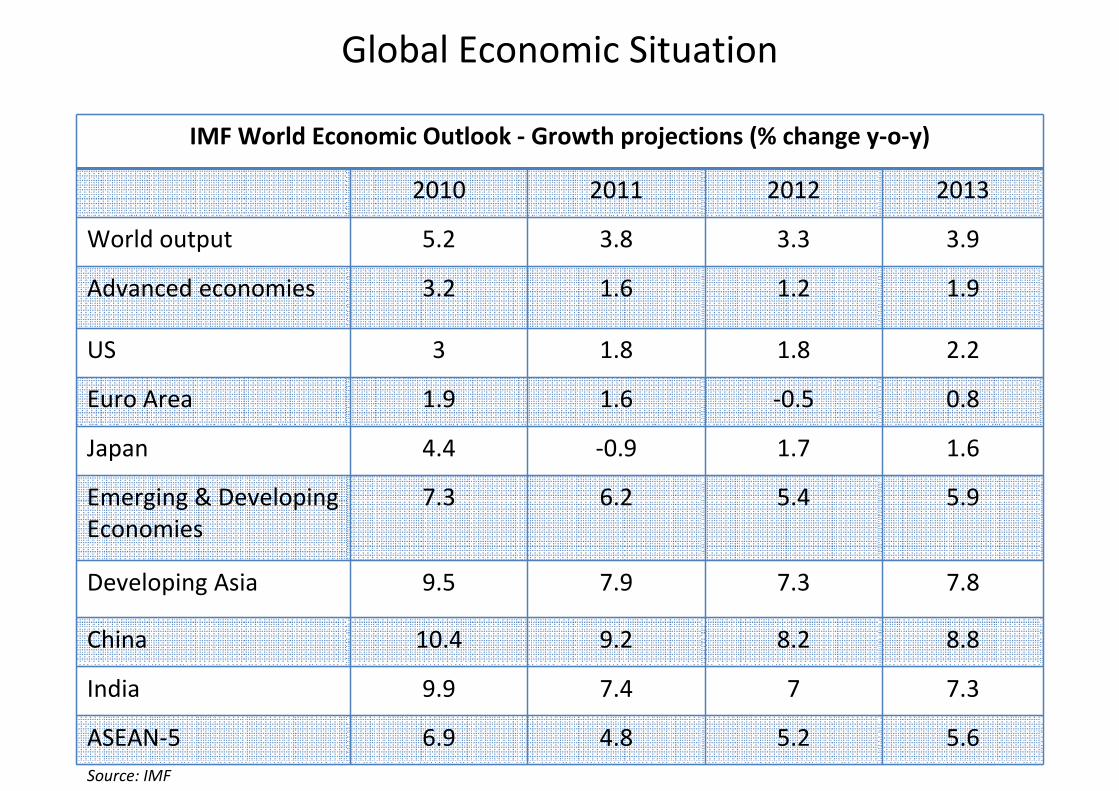

IMF World Economic Outlook - Growth projections (% change y-o-y)

2010 2011 2012 2013

World output 5.2 3.8 3.3 3.9

Advanced economies 3.2 1.6 1.2 1.9

US 3 1.8 1.8 2.2

Euro Area 1.9 1.6 -0.5 0.8

Japan 4.4 -0.9 1.7 1.6

Emerging & Developing

Economies

7.3 6.2 5.4 5.9

Developing Asia 9.5 7.9 7.3 7.8

China 10.4 9.2 8.2 8.8

India 9.9 7.4 7 7.3

ASEAN-5 6.9 4.8 5.2 5.6

Global Economic Situation

Source: IMF

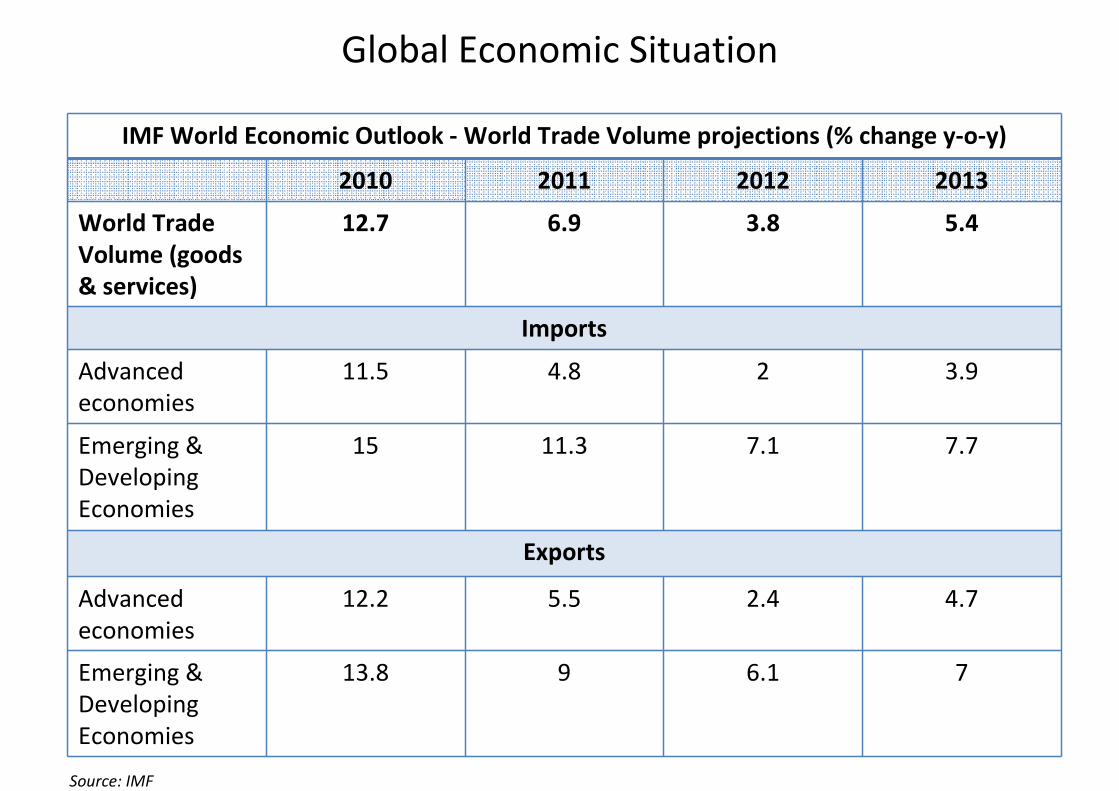

IMF World Economic Outlook - World Trade Volume projections (% change y-o-y)

2010 2011 2012 2013

World Trade

Volume (goods

& services)

12.7 6.9 3.8 5.4

Imports

Advanced

economies

11.5 4.8 2 3.9

Emerging &

Developing

Economies

15 11.3 7.1 7.7

Exports

Advanced

economies

12.2 5.5 2.4 4.7

Emerging &

Developing

Economies

13.8 9 6.1 7

Global Economic Situation

Source: IMF

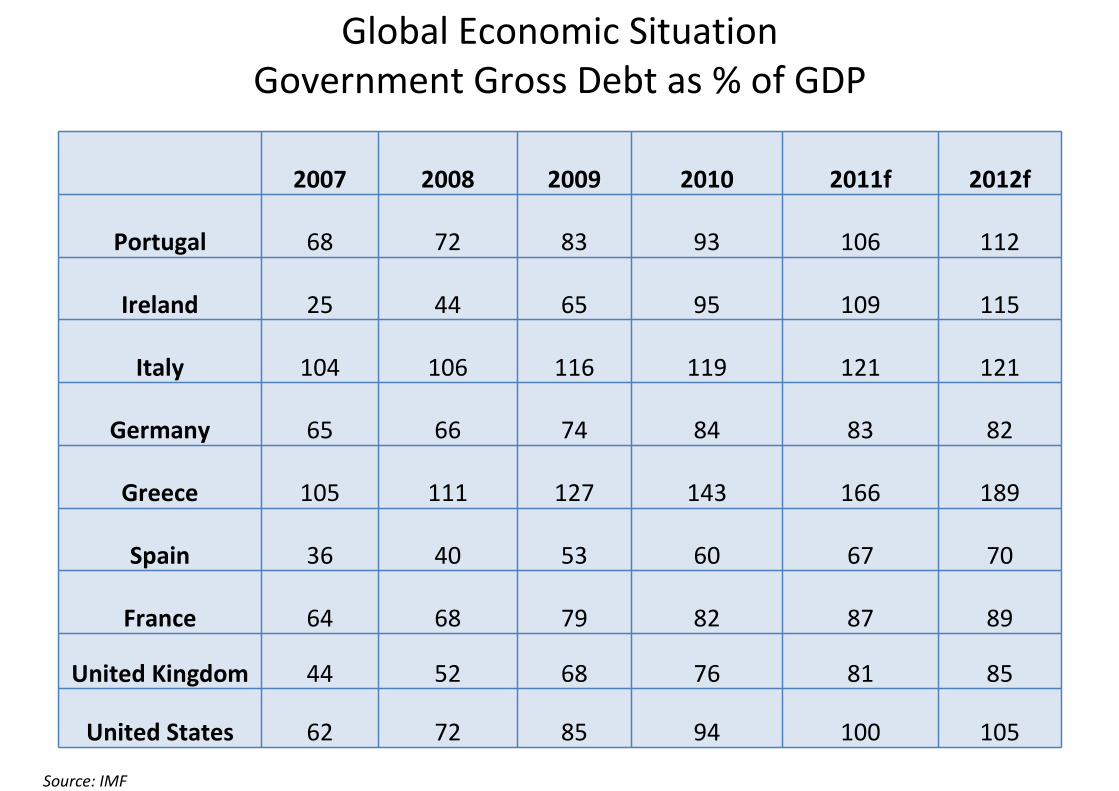

2007 2008 2009 2010 2011f 2012f

Portugal 68 72 83 93 106 112

Ireland 25 44 65 95 109 115

Italy 104 106 116 119 121 121

Germany 65 66 74 84 83 82

Greece 105 111 127 143 166 189

Spain 36 40 53 60 67 70

France 64 68 79 82 87 89

United Kingdom 44 52 68 76 81 85

United States 62 72 85 94 100 105

Source: IMF

Global Economic Situation

Government Gross Debt as % of GDP

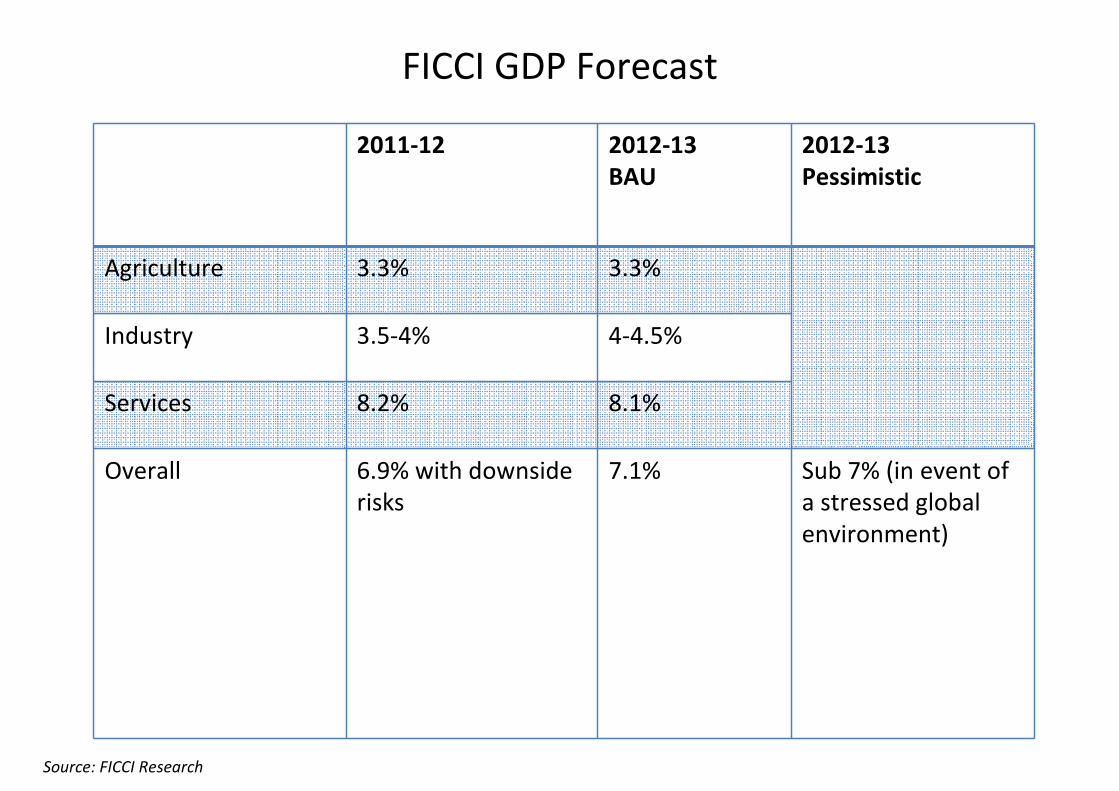

India’s Economic Situation

2011-12 2012-13

BAU

2012-13

Pessimistic

Agriculture 3.3% 3.3%

Industry 3.5-4% 4-4.5%

Services 8.2% 8.1%

Overall 6.9% with downside

risks

7.1% Sub 7% (in event of

a stressed global

environment)

FICCI GDP Forecast

Source: FICCI Research

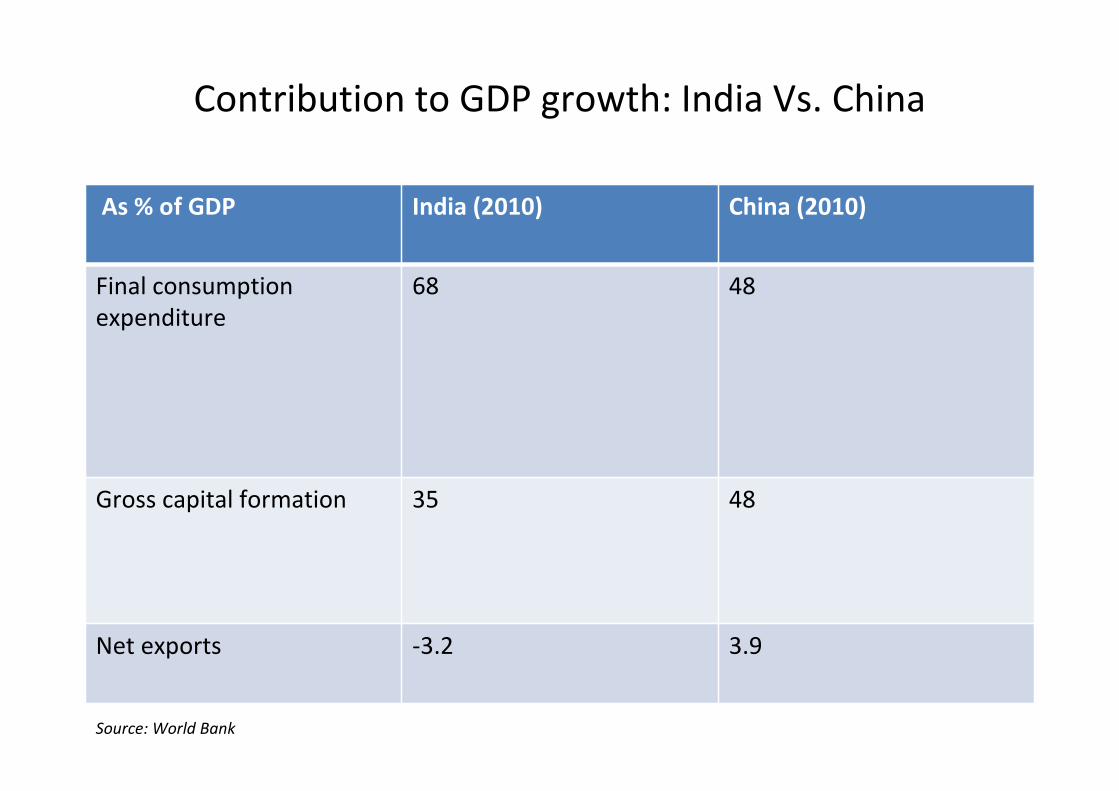

Contribution to GDP growth: India Vs. China

As % of GDP India (2010) China (2010)

Final consumption

expenditure

68 48

Gross capital formation 35 48

Net exports -3.2 3.9

Source: World Bank

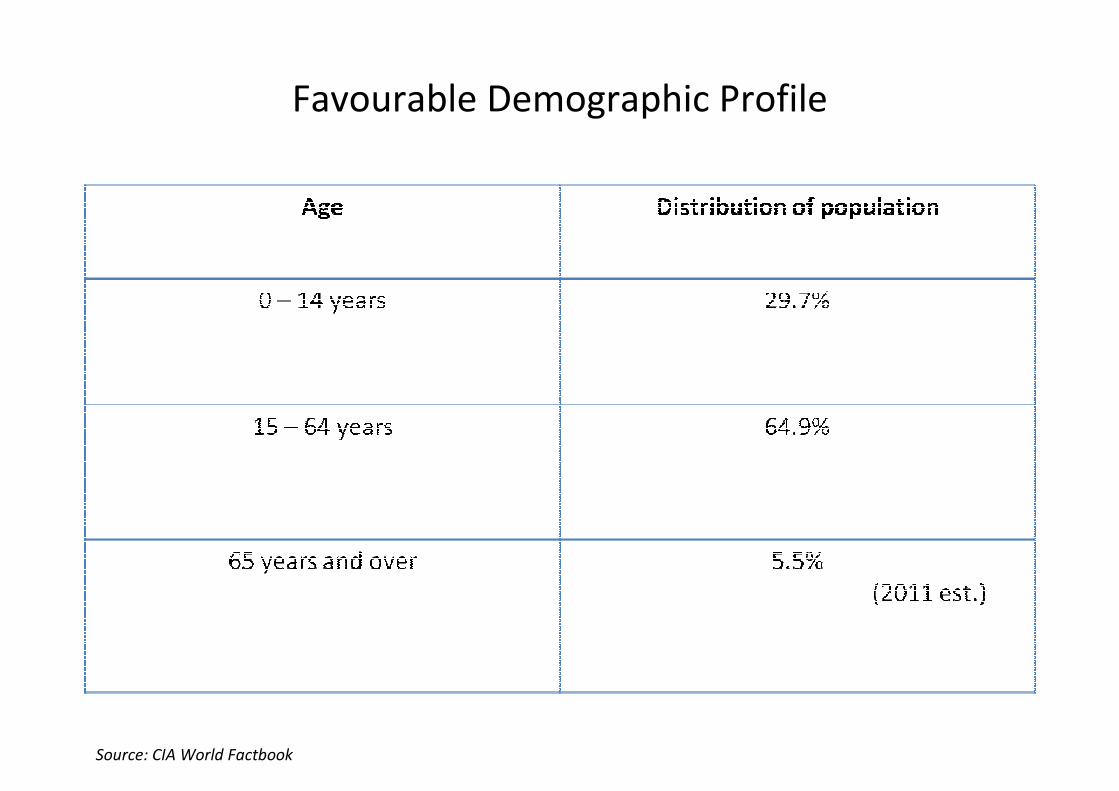

Favourable Demographic Profile

Source: CIA World Factbook

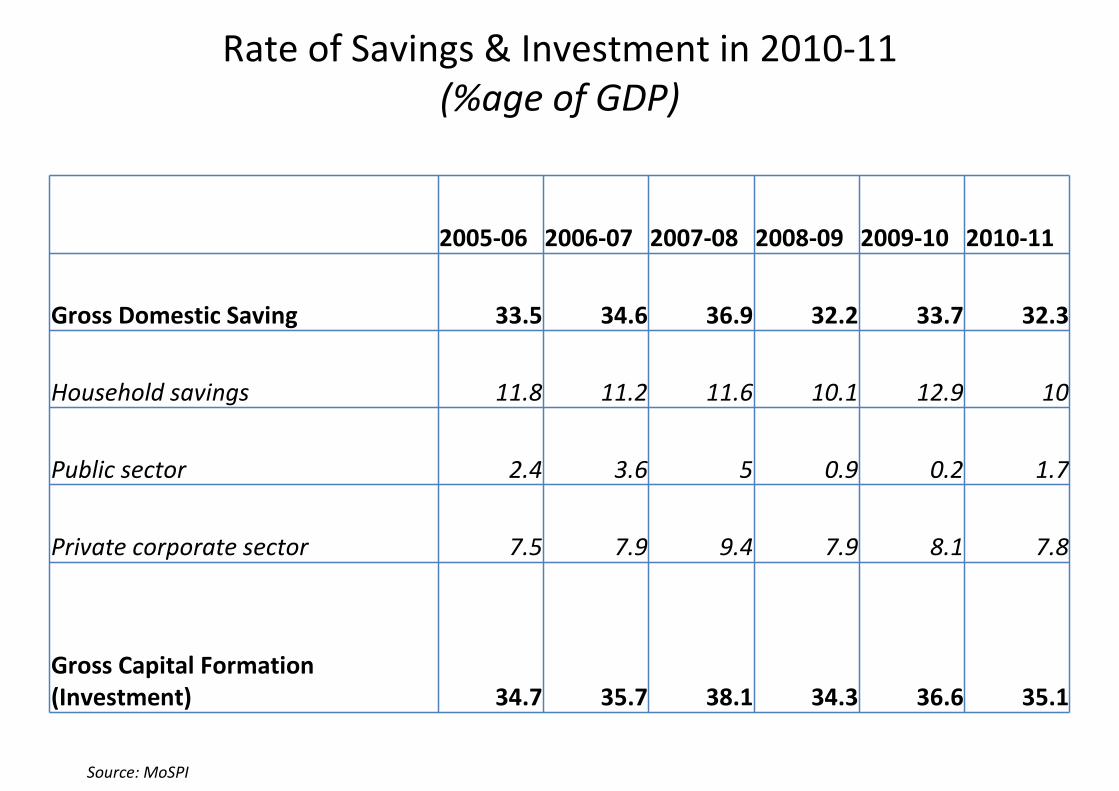

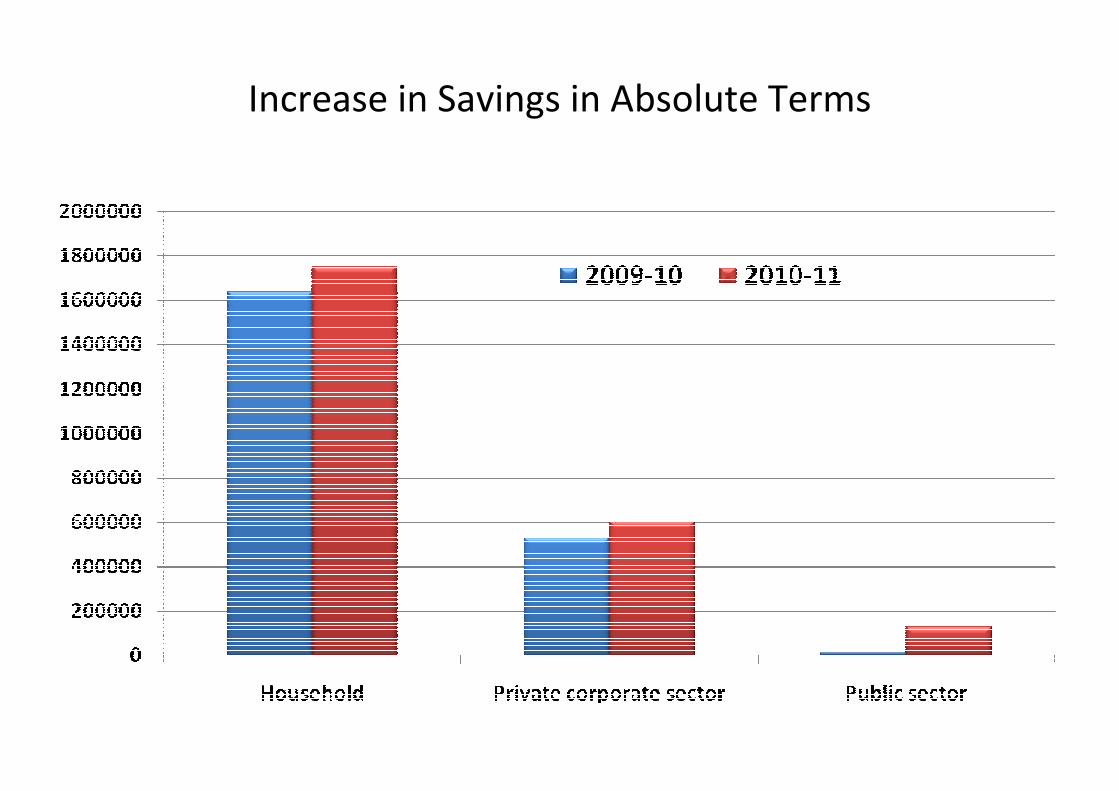

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Gross Domestic Saving 33.5 34.6 36.9 32.2 33.7 32.3

Household savings 11.8 11.2 11.6 10.1 12.9 10

Public sector 2.4 3.6 5 0.9 0.2 1.7

Private corporate sector 7.5 7.9 9.4 7.9 8.1 7.8

Gross Capital Formation

(Investment) 34.7 35.7 38.1 34.3 36.6 35.1

Rate of Savings & Investment in 2010-11

(%age of GDP)

Source: MoSPI

Increase in Savings in Absolute Terms

Rupee pull back on account of strong portfolio inflows

Forex Reserves

(USD Million)

End of

Short-term debt

residual maturity

as % of reserves

Mar-09 37

Jun-09 33.6

Mar-10 38.6

Jun-10 42.1

Mar-11 42.3

Jun-11 43.512

Forex reserves for the week ended Jan27, 2012

294 billionSource: RBI

Foreign Investments in India

Foreign Investment Inflows to India

FDI & FII

Between 2006-07 and 2010-11, the total FDI inflows crossed USD 100 billion

April-August 2011 FDI $ 21 bn FII $2.2 bn

April-August 2010 $ 11.4 bn $13.3 bn

FDI is permitted in vast majority of sectors except for a short negative list

Sector Percent of FDI Cap/Equity

Agriculture & Animal Husbandry, Mining, Petroleum &

Natural gas(Exploration Activities), Airports (Green Field

and Existing Projects), Construction Development-

Townships, Housing, Built up Infrastructure, Single

Brand Product Trading

100%

Telecommunication, Banking -Private Sector, Satellites-

Establishments & Operation

74%

Defence, Print Media 26%

Prohibited sectors - Multi brand Retailing, Lottery Business, Gambling & Betting, Chit

funds, Atomic Energy, Railway Transport

Sectoral FDI Caps

Sector wise distribution of FDI Equity Inflows

(Cumulative Percentage, between April 2000 to Feb 2011)

Share of Top Countries – FDI Equity Inflows

(Cumulative Percentage, between April 2000 to Feb 2011)

Indian Retail- Current Scenario & Future Projections

A Snapshot

2011 2016 2021 2026

India’ GDP (USD Bn) 1500 3017 4859 7825

Private Consumption (USD Bn) 870 1750 2818 4539

Share of Retail Consumption (USD Bn) 479 962 1550 2496

Modern Retail (USD Bn) 26 86 186 314

Share of Modern Retail to Total Retail (%) 5.4% 8.9% 12% 12.6%

Increase in Modern Retail (USD Bn) 60 100 128

Traditional Retail (USD Bn) 453 876 1364 2182

Share of Traditional Retail to Total Retail (%) 94.6% 91.1% 88% 87.4%

Traditional Retail Stores (Total, Million) 16 21 27 35

Annual Sales/Store (USD) 28281 41554 50557 61511

Increase in Traditional Retail Stores (Million) 5 6 8

Source: Technopak research 2011

Transition to Modern Retail in India

Emerging Trends in Retail

• Entry of big corporate houses into the sector viz Reliance, Tata, Aditya Birla

to name few

• Demand of branded goods on a large scale

• Focus shifting from low price to convenience, value and a superior shopping

experience

• Varied window display- Focus on visual merchandising

• E-retailers increasing the presence

Why Global Retailers Look Upto India

• Huge Market Size

• Increasing purchasing power - Consumer spending power increased by

75% in last 3 years.

• Evolution of new consumption class: Consumer class expected to grow

from approx 50 million at present to 583 million by 2025.

• Tax breaks, Import duty exemptions, land & power subsidies and other

incentives

• Affordable labor

• Rich and diversified natural resources

Entry Options for Foreign Players Prior to FDI policy

• Franchise Agreements: Eg: Pizza Hut, Lacoste, Mango, Nike etc. have entered

Indian marketplace by this route

• Strategic Licensing Agreements: SPAR entered into a similar agreement with

Radhakrishna Foodlands Pvt. Ltd

• Cash And Carry Wholesale Trading: Metro AG of Germany

• Manufacturing and Wholly Owned Subsidiaries: The foreign brands such as

Nike, Reebok, Adidas, etc. have wholly-owned subsidiaries in manufacturing

FDI Routes in India

FDI policy in Retail - Milestones

No FDI

100% FDI in cash & carry with prior Government approval

100% in Cash& carry under automatic route; 51% in single brand with prior Govt approval

Years

Government mulled over the idea of allowing FDI in multi-brand retail

1997 2006 2008 2011 - 12

Government proposed 51% FDI in multi-brand retail and notified increase in FDI in single brand to 100% with prior Govt approval

Existing FDI Policy - Summary

• FDI, up to 100%, permitted only in single-brand retail trading, with

Government approval, subject to conditions

• FDI not permitted in Multi-Brand Retail Trading (MBRT)

• FDI, up to 100%, permitted in cash & carry wholesale trading, under the

automatic route

FDI in Single Brand Retail

• FDI, up to 100%, permitted only in single-brand retail trading, with Government

approval, subject to conditions

• Conditions:

- Products should be sold under the same brand internationally

- ‘Single Brand’ would cover only products which are branded during manufacturing

- The foreign investor should be the owner of the brand

- Proposals involving FDI beyond 51 per cent would need to ensure mandatory

sourcing of at least 30 per cent of the value of products sold, to be done from Indian

‘small industries/village and cottage industries, artisans and craftsmen

FDI in Multi Brand Retail – Proposed Conditions

• FDI up to 51% through government approval mode

• Permitted only in cities with a population of more than 10 lakhs as per 2011 census

• Minimum investment of US $ 100 million of which at least 50% to be invested in

backend infrastructure, which would include capital expenditure on the entire

spectrum of related activities

• Mandatory sourcing of a minimum of 30% from Indian small industries with a total

investment in plant and machinery not exceeding US $ one million

• Government to have first right of procurement of agricultural products

Arguments for FDI in Multi-Brand Retail

• Need of Investments in backend infrastructure:

Rationale:

- High rates of food inflation in India

- Estimated losses due to inadequate handling facilities:

food-grains: 6 to 7%

valuable spices:10%

fruits and vegetables: 30 to 40%

- India, second largest producer of fruits and vegetables (214 million MT) , however very limited integrated cold-chain infrastructure- only 5386 stand-alone cold storages

- Estimated investment need for post harvest infrastructure for agricultural produce:

Rs 64,312 crores, during the XI Five Year Plan (2007-2012)-Planning Commission

Nearly 50% would need to come from the private sector

Source: DIPP, Ministry of Commerce

• Insignificant FDI inflow in cold-chains, though there is no restriction on FDI:

in the absence of a policy framework permitting FDI in retailing

• Indian farmers realize only one-third of the total price paid by the final

consumer:

as against two-thirds by farmers in nations with a higher share of organized

retail

• Domination of intermediaries in the value chain:

leading to non-transparent pricing

• Absence of a ‘farm-to-fork’ retail supply system:

Ultimate customers pay a premium for shortages and a charge for wastages

• Not possible for public agencies alone to address investment gaps

LEVERAGING FDI IN MULTI-BRAND RETAIL COULD BE ONE WAY OF ADDRESSING

ALL THESE ISSUES

Other Arguments

• Better choices of products for consumers

• Transfer of new and innovative retail technologies by foreign retailers -

Indian companies can access global best management practices, designs and

technological knowhow.

• Improvement in quality standards - Inflow of FDI in retail sector to pull up the

quality standards and cost-competitiveness of Indian producers in all the

segments.

• More employment opportunities

Concerns Expressed with Regard to FDI in Multi-Brand

Retail

• Indian organized retail sector is underdeveloped and should be allowed to

consolidate first

• Could lead to unfair competition and result in large scale exit of domestic

retailers

• The foreign retailers might use unethical methods to dominate the market –

Predatory pricing etc.

Implications of Recent Policy Change of FDI in

Single Brand Retail

• FDI in single brand retail increased upto 100% from 51% with prior Government

approval

Implications for India:

Consumers

• Gain from improvement in product choices and quality

• Better quality produce, not only for domestic consumers, but also for exports.

Small retailers

• Will incentivize existing traders and retail outlets to upgrade and become more

efficient

• Small retailers would continue to be able to source high quality produce, at

significantly lower prices, from wholesale cash and carry points

Small manufacturers

• Small manufacturers will benefit from the safeguard pertaining to a

minimum of 30% procurement from Indian small industries.

• Would provide the necessary scales to expand capacities in manufacturing,

thereby creating more employment and also strengthening the

manufacturing base of the country.

• Derive the benefits of technology upgradation, leading to increased

productivity and local value-addition.

• Will also enable the small enterprises to get integrated with global retail

chains, thereby enhancing their capacity to export products from India.

Future of FDI in Multi- Brand Retail

FDI in Multi- Brand Retail – Few Roadblocks but ‘Affirmative’

• Absence of political consensus led the Government to hold back

• FICCI with Government working towards garnering support and broad consensus

• FICCI Submitted representations to the Government on the positive impact of FDI in

Multi-Brand Retail on various sectors

• FICCI organized consultations with stakeholders like Farmer associations to gather views

on the subject

• FICCI Retail committee composes of all the leading retailers (physical & online formats)

with 30 member companies actively engaged in various regulations and norms:

a) Redrafting of ‘Shops & establishment act’

b) Draft norms for food safety in retail

c) Development of ‘Trustmark’ for online retailers signifying robust consumer care

processes

• FICCI to organize a mega event on Retail in June 2012 in New Delhi

Thank You

![Retail brands & brand storytelling [research]](https://img.pdfslide.us/doc/110x75/55d0fd8cbb61eb2f258b4647/retail-brands-brand-storytelling-research.jpg)