Embed Size (px)

Citation preview

CONFIDENTIAL

FCF and Economic Profit

ValuationGreg [email protected]+44 207 88 33 643

David [email protected]+44 207 88 33 645

CONFIDENTIAL

1

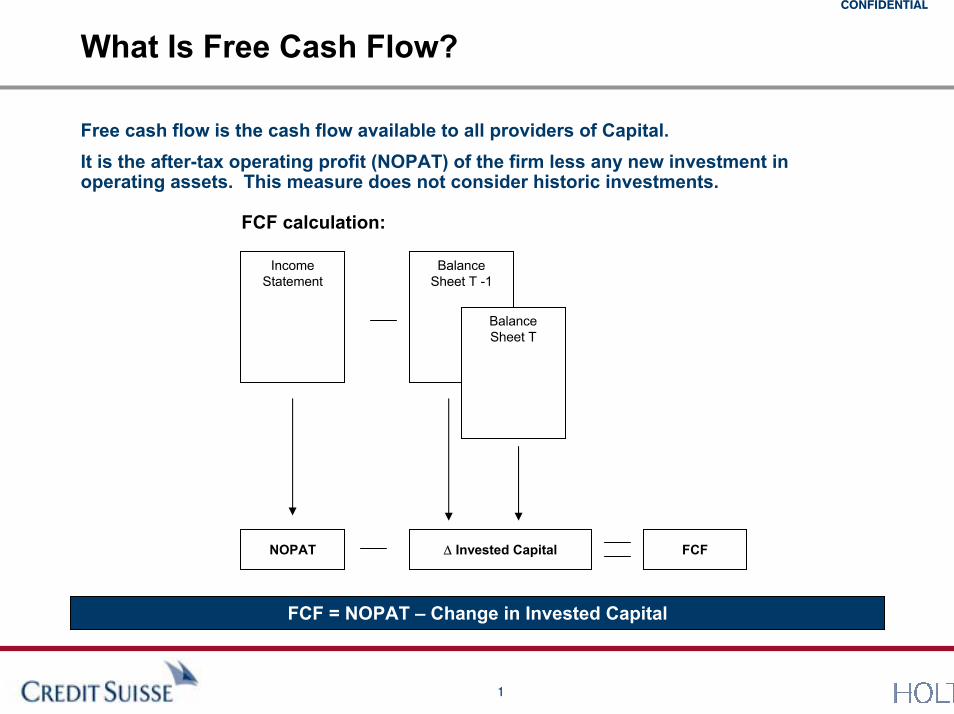

What Is Free Cash Flow?

Free cash flow is the cash flow available to all providers of Capital. It is the after-tax operating profit (NOPAT) of the firm less any new investment in operating assets. This measure does not consider historic investments.

FCF calculation:

IncomeStatement

BalanceSheet T -1

Balance Sheet T

NOPAT ∆ Invested Capital FCF

FCF = NOPAT � Change in Invested Capital

CONFIDENTIAL

2

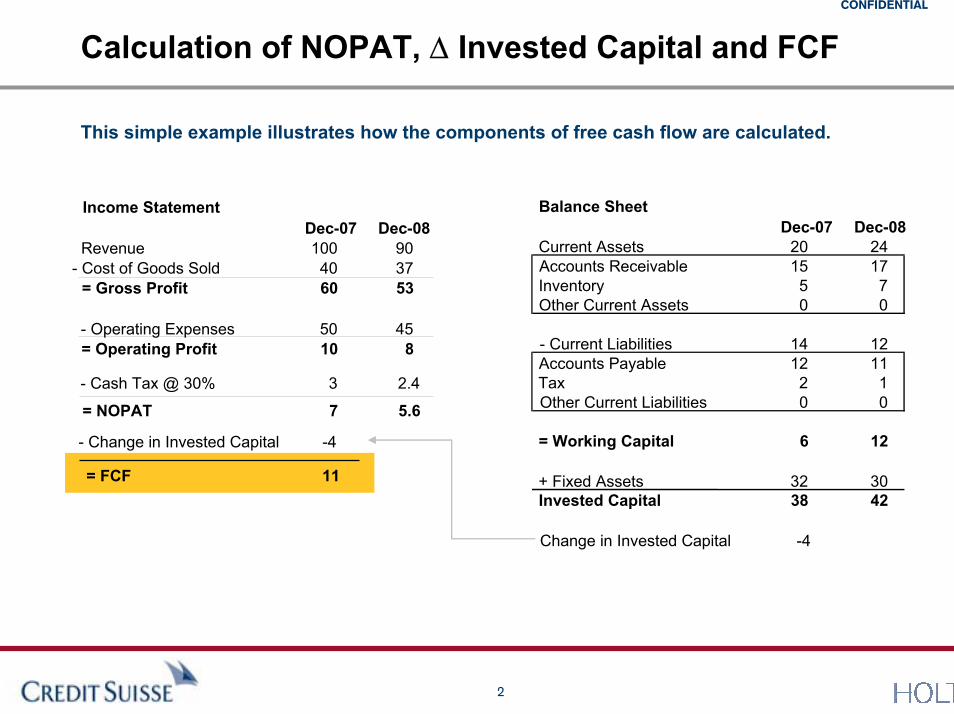

Calculation of NOPAT, ∆ Invested Capital and FCF

This simple example illustrates how the components of free cash flow are calculated.

Balance SheetDec-07 Dec-08

Current Assets 20 24Accounts Receivable 15 17Inventory 5 7Other Current Assets 0 0

Income StatementDec-071004060

Dec-08903753

Revenue- Cost of Goods Sold

= Gross Profit

- Operating Expenses= Operating Profit

5010

458

- Cash Tax @ 30% 3 2.4

= NOPAT 7 5.6

- Current Liabilities 14 12Accounts Payable 12 11Tax 2 1Other Current Liabilities 0 0

= Working Capital 6 12

+ Fixed Assets 32 30Invested Capital 38 42

Change in Invested Capital -4

= FCF 11

- Change in Invested Capital -4

CONFIDENTIAL

3

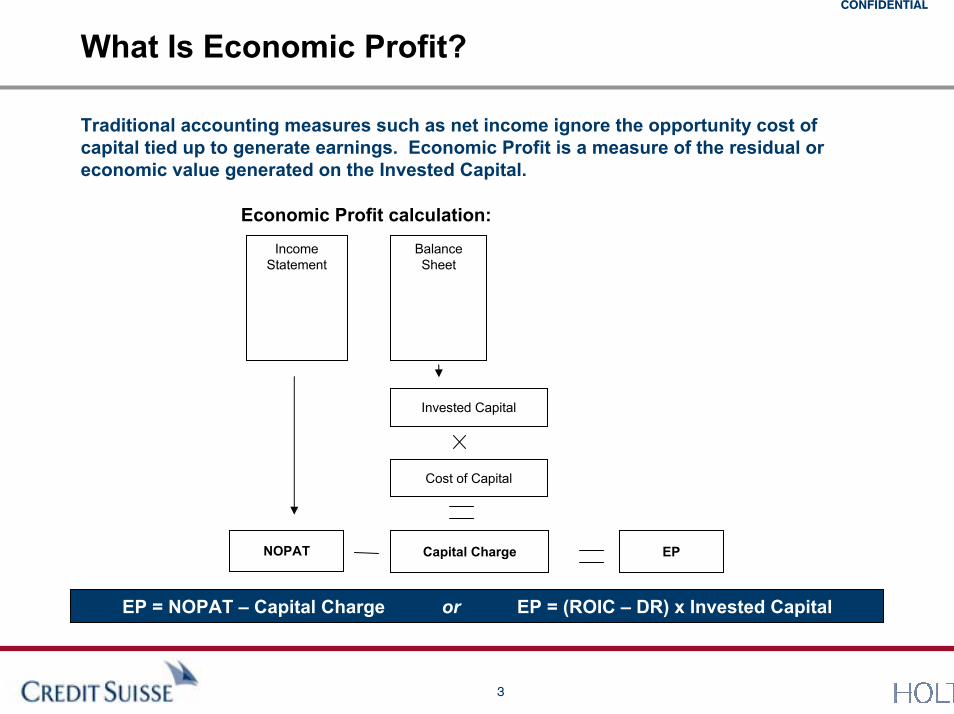

What Is Economic Profit?

Traditional accounting measures such as net income ignore the opportunity cost of capital tied up to generate earnings. Economic Profit is a measure of the residual or economic value generated on the Invested Capital.

Cost of Capital

EP

BalanceSheet

Invested Capital

IncomeStatement

NOPAT Capital Charge

Economic Profit calculation:

EP = NOPAT � Capital Charge or EP = (ROIC � DR) x Invested Capital

CONFIDENTIAL

4

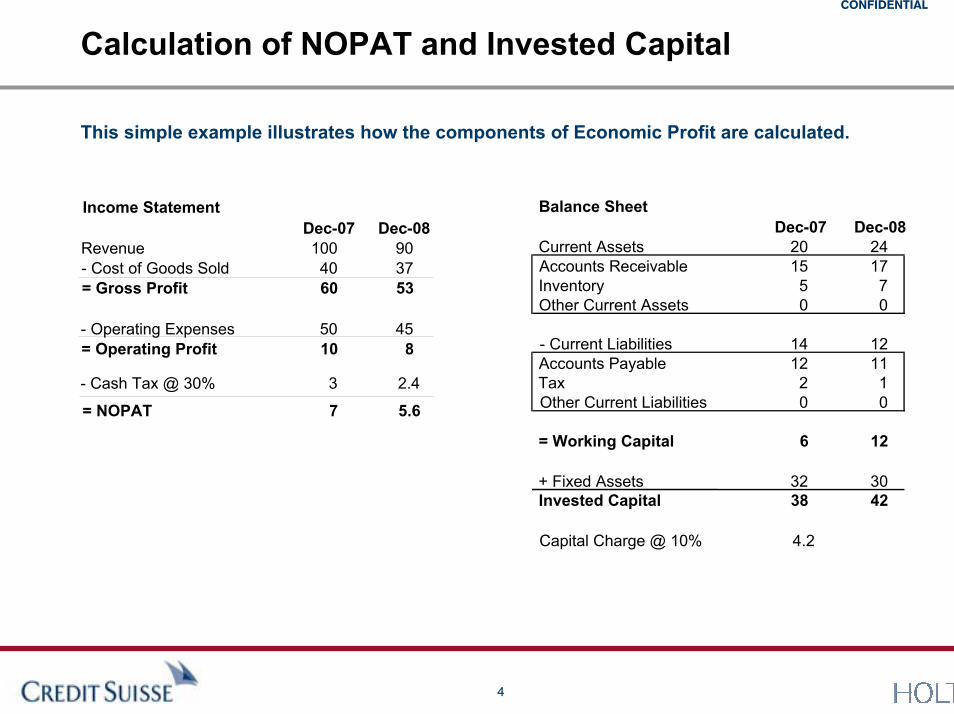

Calculation of NOPAT and Invested Capital

This simple example illustrates how the components of Economic Profit are calculated.

Balance SheetDec-07 Dec-08

Current Assets 20 24Accounts Receivable 15 17Inventory 5 7Other Current Assets 0 0

Income StatementDec-071004060

Dec-08903753

Revenue- Cost of Goods Sold= Gross Profit

- Operating Expenses= Operating Profit

5010

458

- Cash Tax @ 30% 3 2.4

= NOPAT 7 5.6

- Current Liabilities 14 12Accounts Payable 12 11Tax 2 1Other Current Liabilities 0 0

= Working Capital 6 12

+ Fixed AssetsInvested Capital

3238

3042

Capital Charge @ 10% 4.2

CONFIDENTIAL

5

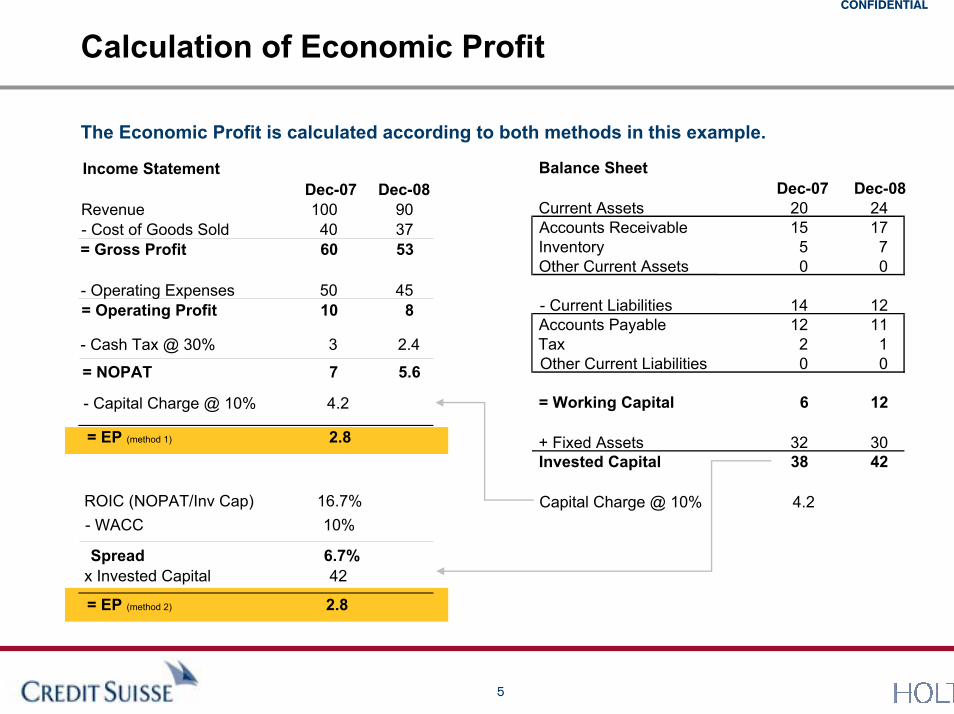

Calculation of Economic Profit

The Economic Profit is calculated according to both methods in this example.

Balance SheetDec-07 Dec-08

Current Assets 20 24Accounts Receivable 15 17Inventory 5 7Other Current Assets 0 0

Income StatementDec-071004060

Dec-08903753

Revenue- Cost of Goods Sold= Gross Profit

- Operating Expenses= Operating Profit

5010

458

- Cash Tax @ 30% 3 2.4

= NOPAT 7 5.6

- Current Liabilities 14 12Accounts Payable 12 11Tax 2 1Other Current Liabilities 0 0

= Working Capital 6 12

+ Fixed Assets 32 30Invested Capital 38 42

Capital Charge @ 10% 4.2

= EP (method 1) 2.8

- Capital Charge @ 10% 4.2

= EP (method 2)

ROIC (NOPAT/Inv Cap) 16.7%- WACC 10%

Spread 6.7%x Invested Capital 42

2.8

CONFIDENTIAL

6

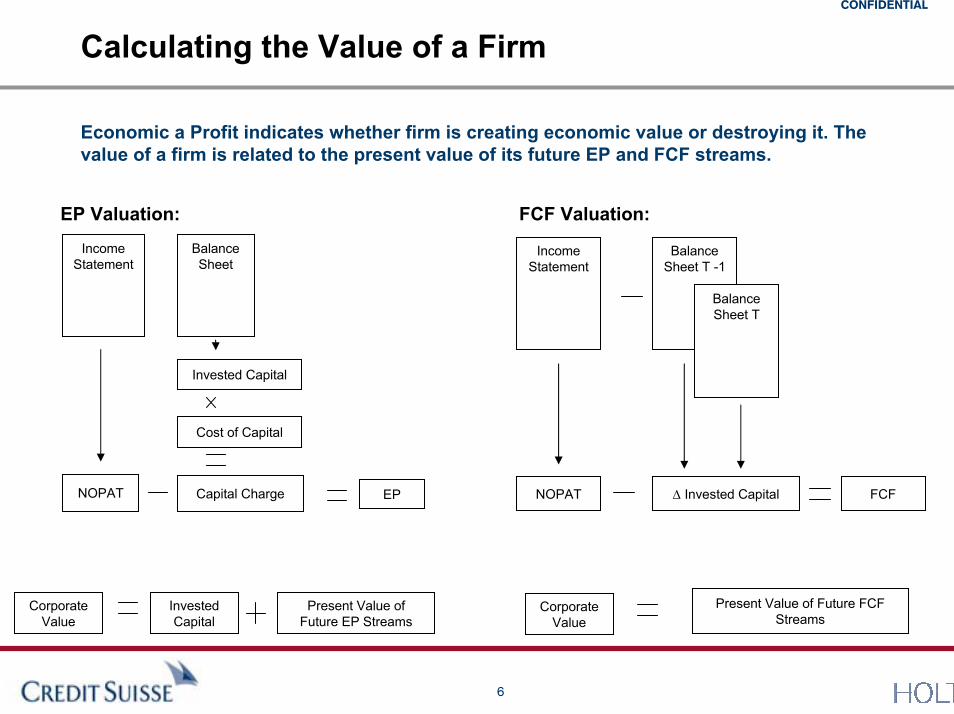

Calculating the Value of a Firm

Economic a Profit indicates whether firm is creating economic value or destroying it. The value of a firm is related to the present value of its future EP and FCF streams.

EP Valuation: FCF Valuation:

IncomeStatement

BalanceSheet

IncomeStatement

BalanceSheet T -1

Balance Sheet T

Invested Capital

Cost of Capital

NOPAT Capital Charge NOPAT ∆ Invested Capital FCFEP

Present Value of Future FCF Streams

Corporate Value

Invested Capital

Present Value of Future EP Streams

Corporate Value

CONFIDENTIAL

7

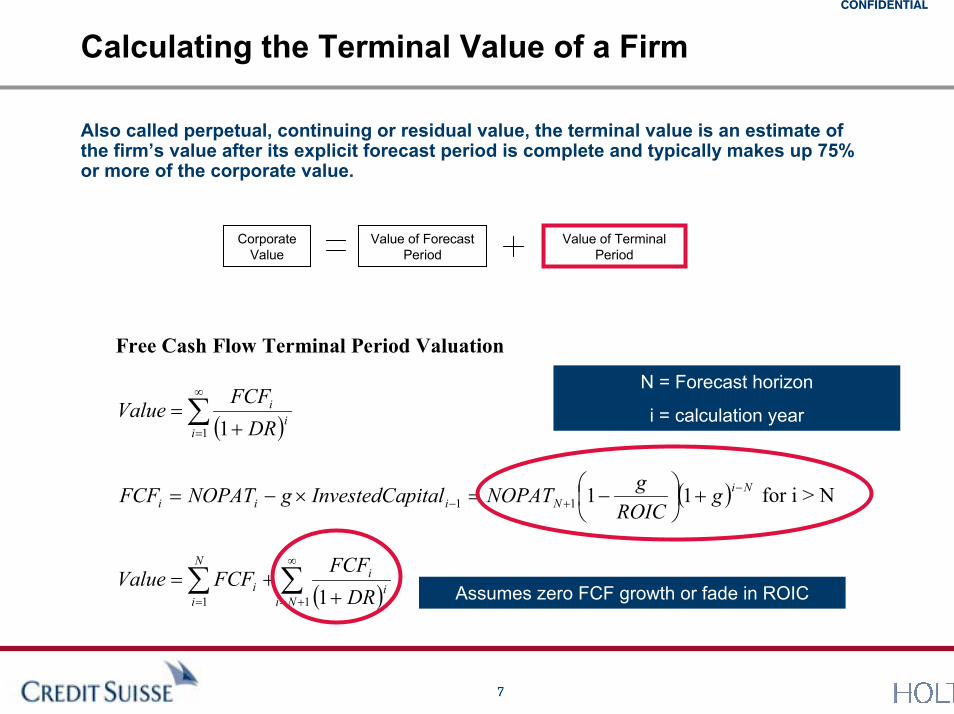

Calculating the Terminal Value of a Firm

Also called perpetual, continuing or residual value, the terminal value is an estimate of the firm�s value after its explicit forecast period is complete and typically makes up 75% or more of the corporate value.

Value of Terminal Period

Corporate Value

Value of Forecast Period

Free Cash Flow Terminal Period Valuation

( )∑∞

= +=

1 1ii

i

DRFCF

Value

( ) NiNiii g

ROICgNOPATpitalInvestedCagNOPATFCF −

+− +⎟⎠⎞

⎜⎝⎛ −=×−= 1111 for i > N

( )∑∑∞

+== ++=

11 1Nii

iN

ii DR

FCFFCFValue

Assumes zero FCF growth or fade in ROIC

N = Forecast horizon

i = calculation year

CONFIDENTIAL

8

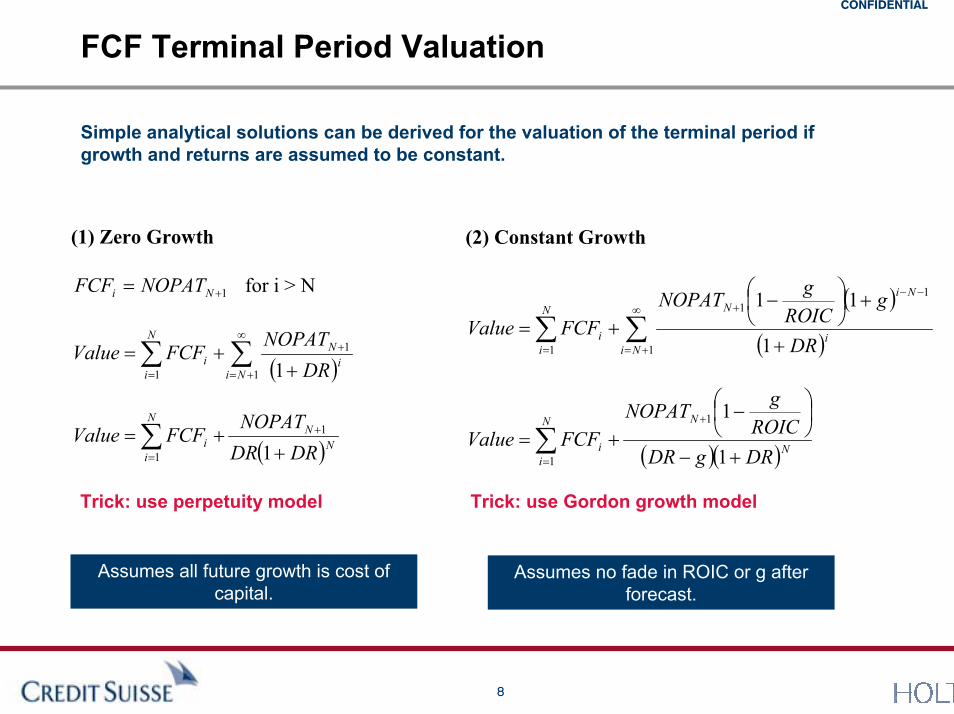

FCF Terminal Period Valuation

Simple analytical solutions can be derived for the valuation of the terminal period if growth and returns are assumed to be constant.

(1) Zero Growth

1+= Ni NOPATFCF for i > N

( )∑∑∞

+=

+

= ++=

1

1

1 1Nii

NN

ii DR

NOPATFCFValue

( )NN

N

ii DRDR

NOPATFCFValue

++= +

=∑ 1

1

1

(2) Constant Growth

( )

( )∑∑∞

+=

−−+

= +

+⎟⎠⎞

⎜⎝⎛ −

+=1

11

1 1

11

Nii

NiNN

ii DR

gROICgNOPAT

FCFValue

( )( )NNN

ii DRgDR

ROICgNOPAT

FCFValue+−

⎟⎠⎞

⎜⎝⎛ −

+=+

=∑ 1

11

1

Trick: use perpetuity model Trick: use Gordon growth model

Assumes all future growth is cost of capital.

Assumes no fade in ROIC or g after forecast.

CONFIDENTIAL

9

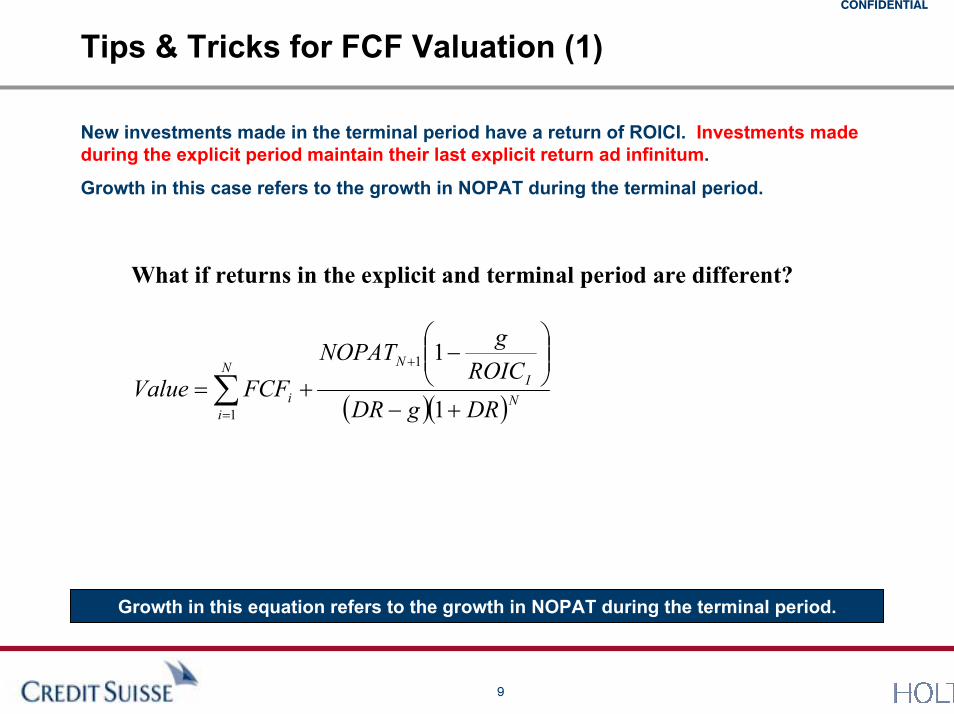

Tips & Tricks for FCF Valuation (1)

New investments made in the terminal period have a return of ROICI. Investments made during the explicit period maintain their last explicit return ad infinitum.

Growth in this case refers to the growth in NOPAT during the terminal period.

What if returns in the explicit and terminal period are different?

( )( )NI

NN

ii DRgDR

ROICgNOPAT

FCFValue+−

⎟⎟⎠

⎞⎜⎜⎝

⎛−

+=+

=∑ 1

11

1

Growth in this equation refers to the growth in NOPAT during the terminal period.

CONFIDENTIAL

10

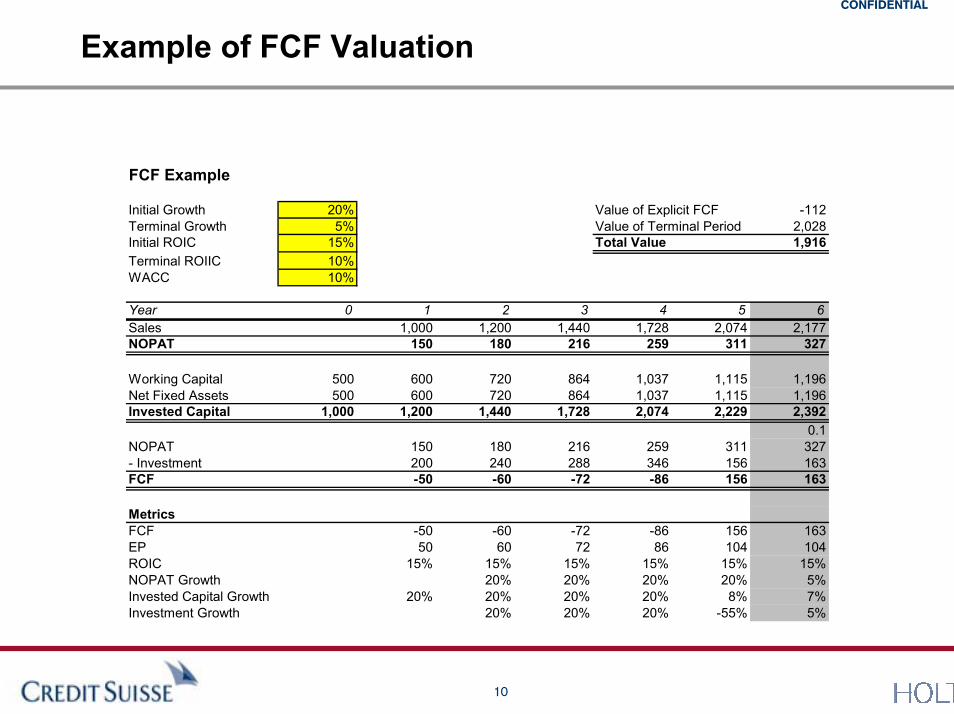

Example of FCF Valuation

FCF Example

Initial Growth 20% Value of Explicit FCF -112Terminal Growth 5% Value of Terminal Period 2,028Initial ROIC 15% Total Value 1,916Terminal ROIIC 10%WACC 10%

Year 0 1 2 3 4 5 6Sales 1,000 1,200 1,440 1,728 2,074 2,177NOPAT 150 180 216 259 311 327

Working Capital 500 600 720 864 1,037 1,115 1,196Net Fixed Assets 500 600 720 864 1,037 1,115 1,196Invested Capital 1,000 1,200 1,440 1,728 2,074 2,229 2,392

0.1NOPAT 150 180 216 259 311 327- Investment 200 240 288 346 156 163FCF -50 -60 -72 -86 156 163

MetricsFCF -50 -60 -72 -86 156 163EP 50 60 72 86 104 104ROIC 15% 15% 15% 15% 15% 15%NOPAT Growth 20% 20% 20% 20% 5%Invested Capital Growth 20% 20% 20% 20% 8% 7%Investment Growth 20% 20% 20% -55% 5%

CONFIDENTIAL

11

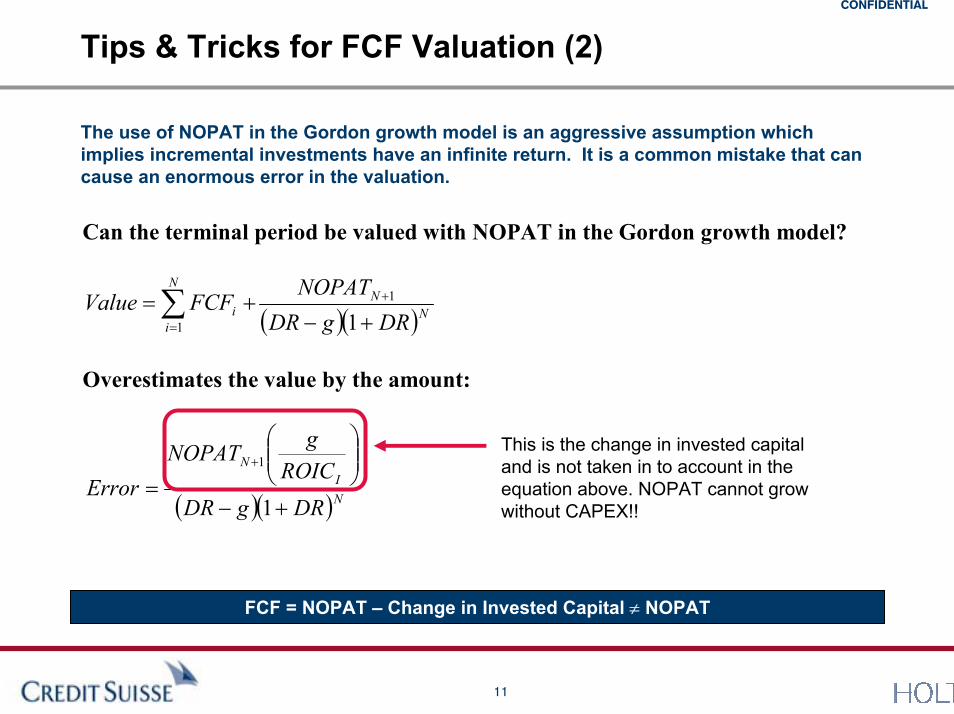

Tips & Tricks for FCF Valuation (2)

The use of NOPAT in the Gordon growth model is an aggressive assumption which implies incremental investments have an infinite return. It is a common mistake that can cause an enormous error in the valuation.

Can the terminal period be valued with NOPAT in the Gordon growth model?

( )( )NN

N

ii DRgDR

NOPATFCFValue

+−+= +

=∑ 1

1

1

Overestimates the value by the amount:

( )( )NI

N

DRgDRROICgNOPAT

Error+−

⎟⎟⎠

⎞⎜⎜⎝

⎛

=+

1

1

This is the change in invested capital and is not taken in to account in the equation above. NOPAT cannot grow without CAPEX!!

FCF = NOPAT � Change in Invested Capital ≠ NOPAT

CONFIDENTIAL

12

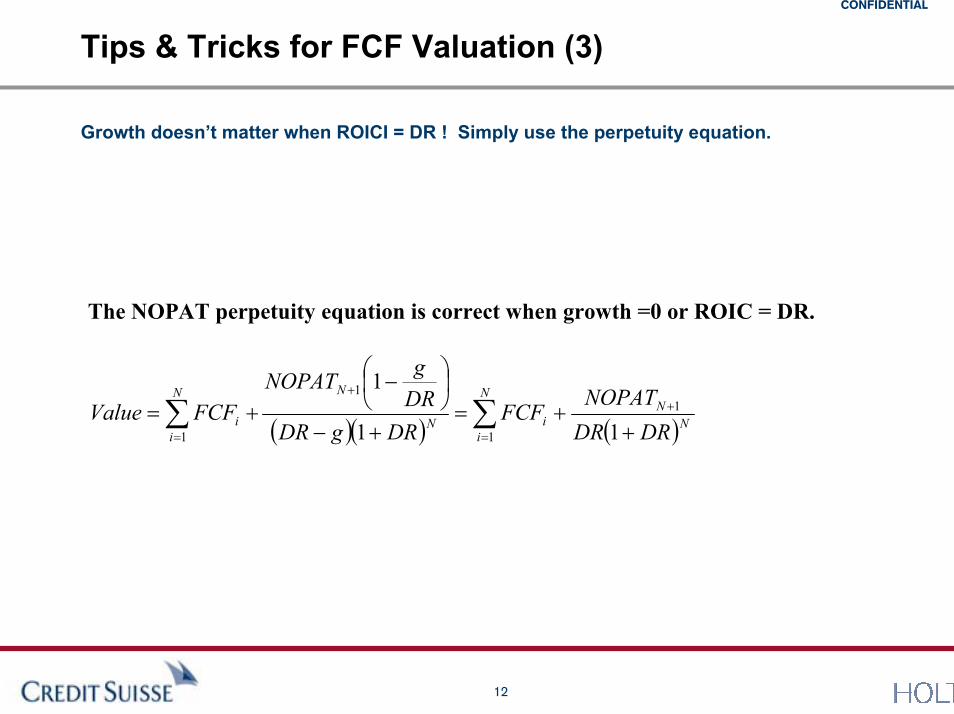

Tips & Tricks for FCF Valuation (3)

Growth doesn�t matter when ROICI = DR ! Simply use the perpetuity equation.

The NOPAT perpetuity equation is correct when growth =0 or ROIC = DR.

( )( ) ( )∑∑=

++

= ++=

+−

⎟⎠⎞

⎜⎝⎛ −

+=N

iN

NiN

NN

ii DRDR

NOPATFCF

DRgDRDRgNOPAT

FCFValue1

11

1 11

1

CONFIDENTIAL

13

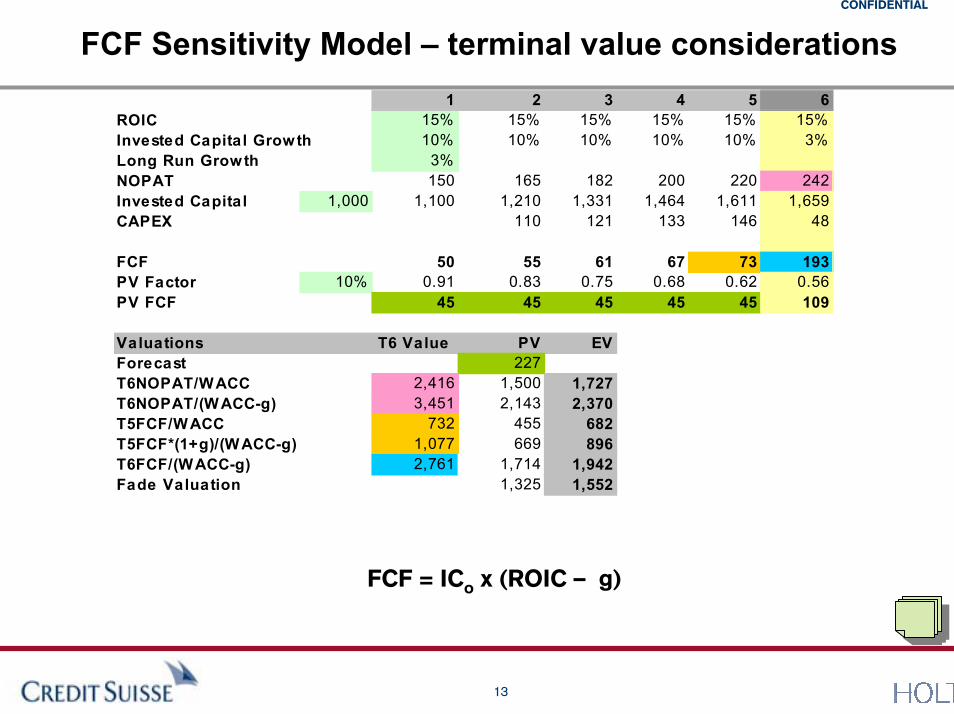

FCF Sensitivity Model � terminal value considerations1 2 3 4 5 6

ROIC 15% 15% 15% 15% 15% 15%Invested Capital Growth 10% 10% 10% 10% 10% 3%Long Run Growth 3%NOPAT 150 165 182 200 220 242Invested Capital 1,000 1,100 1,210 1,331 1,464 1,611 1,659CAPEX 110 121 133 146 48

FCF 50 55 61 67 73 193PV Factor 10% 0.91 0.83 0.75 0.68 0.62 0.56PV FCF 45 45 45 45 45 109

Valuations T6 Value PV EVForecast 227T6NOPAT/WACC 2,416 1,500 1,727T6NOPAT/(WACC-g) 3,451 2,143 2,370T5FCF/WACC 732 455 682T5FCF*(1+g)/(WACC-g) 1,077 669 896T6FCF/(WACC-g) 2,761 1,714 1,942Fade Valuation 1,325 1,552

FCF = ICo x (ROIC � g)

CONFIDENTIAL

14

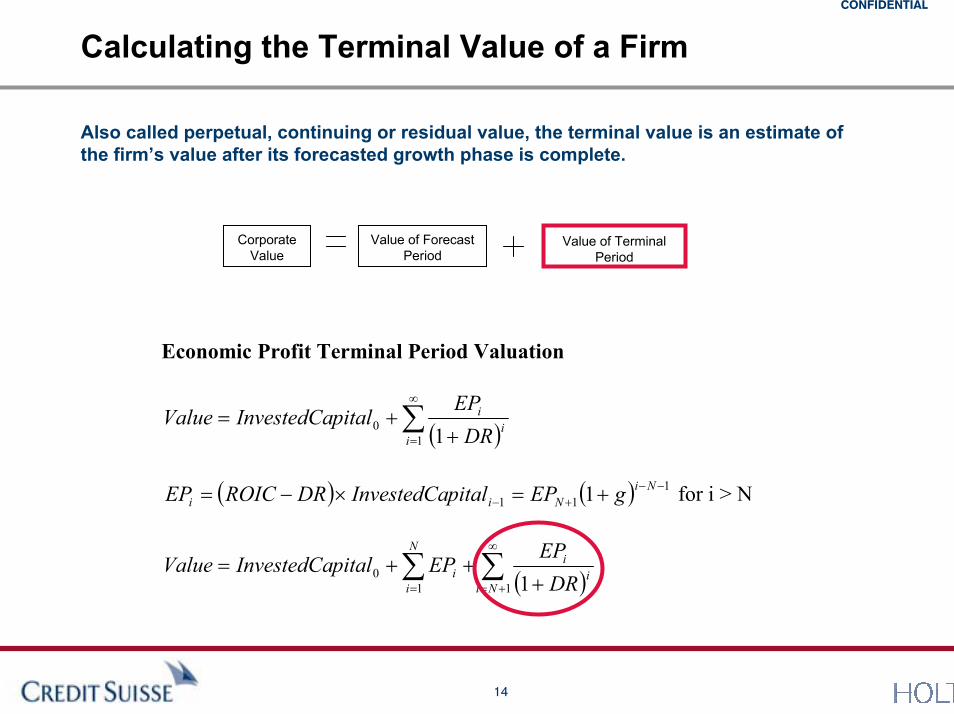

Calculating the Terminal Value of a Firm

Also called perpetual, continuing or residual value, the terminal value is an estimate of the firm�s value after its forecasted growth phase is complete.

Value of Terminal Period

Corporate Value

Value of Forecast Period

Economic Profit Terminal Period Valuation

( )∑∞

= ++=

10 1i

ii

DREP

pitalInvestedCaValue

( ) ( ) 1

11 1 −−+− +=×−= Ni

Nii gEPpitalInvestedCaDRROICEP for i > N

( )∑∑∞

+== +++=

110 1Ni

ii

N

ii DR

EPEPpitalInvestedCaValue

CONFIDENTIAL

15

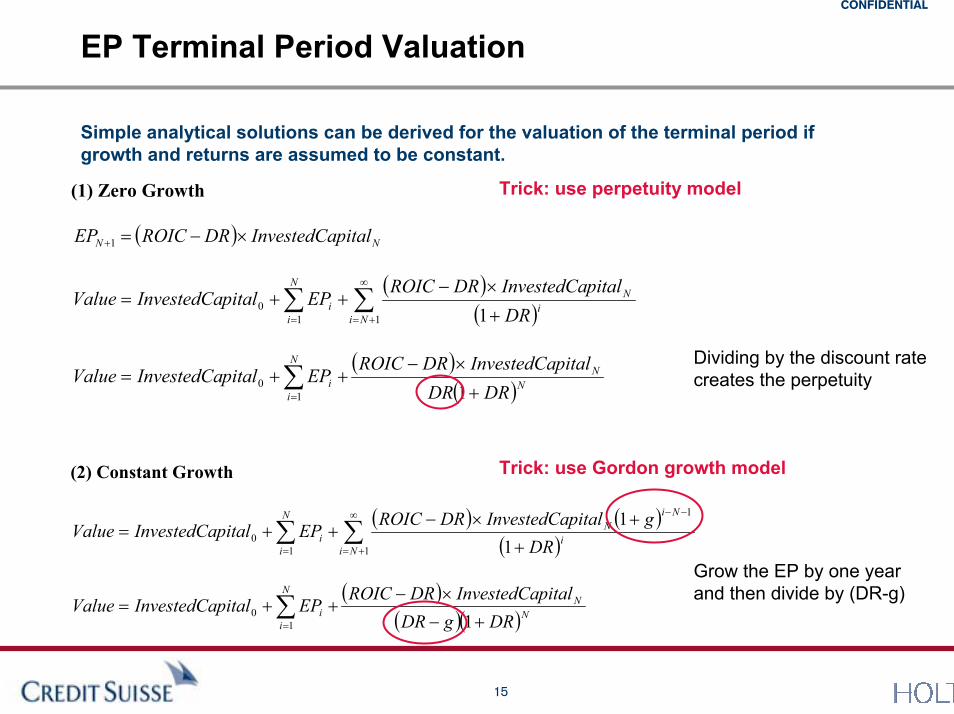

EP Terminal Period Valuation

Simple analytical solutions can be derived for the valuation of the terminal period if growth and returns are assumed to be constant.

Trick: use perpetuity model(1) Zero Growth

( ) NN pitalInvestedCaDRROICEP ×−=+1

( )( )∑∑

∞

+== +

×−++=

110 1Ni

iN

N

ii DR

pitalInvestedCaDRROICEPpitalInvestedCaValue

( )

( )NN

N

ii DRDR

pitalInvestedCaDRROICEPpitalInvestedCaValue

+

×−++= ∑

= 110

Dividing by the discount rate creates the perpetuity

Trick: use Gordon growth model(2) Constant Growth

( ) ( )( )∑∑

∞

+=

−−

= +

+×−++=

1

1

10 1

1Ni

i

NiN

N

ii DR

gpitalInvestedCaDRROICEPpitalInvestedCaValue

( )

( )( )NN

N

ii DRgDR

pitalInvestedCaDRROICEPpitalInvestedCaValue

+−

×−++= ∑

= 110

Grow the EP by one year and then divide by (DR-g)

CONFIDENTIAL

16

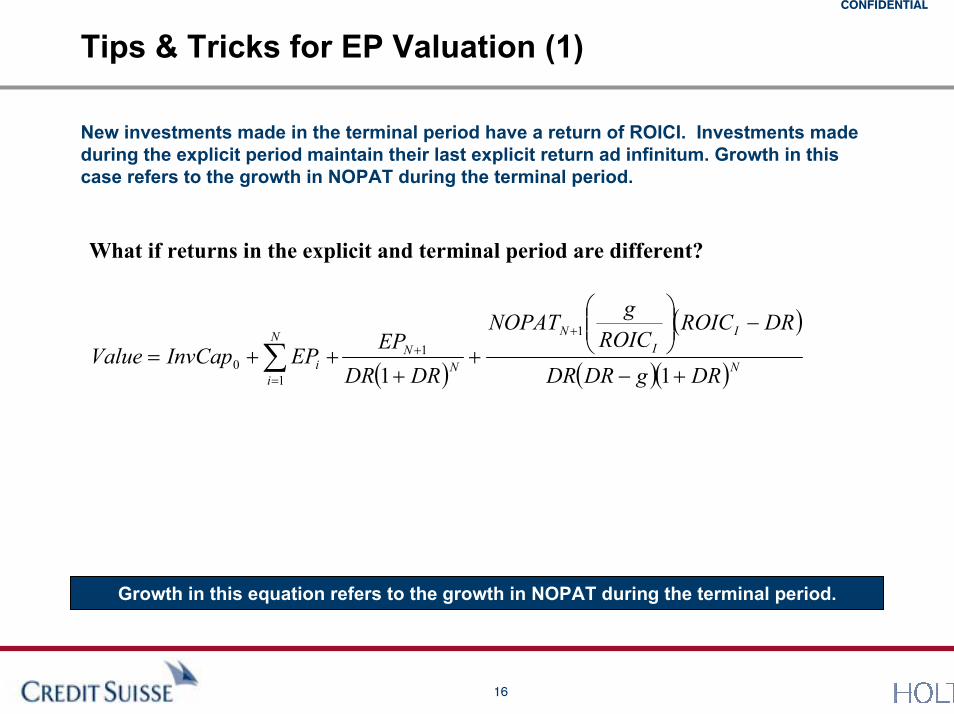

Tips & Tricks for EP Valuation (1)

New investments made in the terminal period have a return of ROICI. Investments made during the explicit period maintain their last explicit return ad infinitum. Growth in this case refers to the growth in NOPAT during the terminal period.

What if returns in the explicit and terminal period are different?

( )

( )

( )( )NI

IN

NN

N

ii DRgDRDR

DRROICROICgNOPAT

DRDREP

EPInvCapValue+−

−⎟⎟⎠

⎞⎜⎜⎝

⎛

++

++=+

+

=∑ 11

11

10

Growth in this equation refers to the growth in NOPAT during the terminal period.

CONFIDENTIAL

17

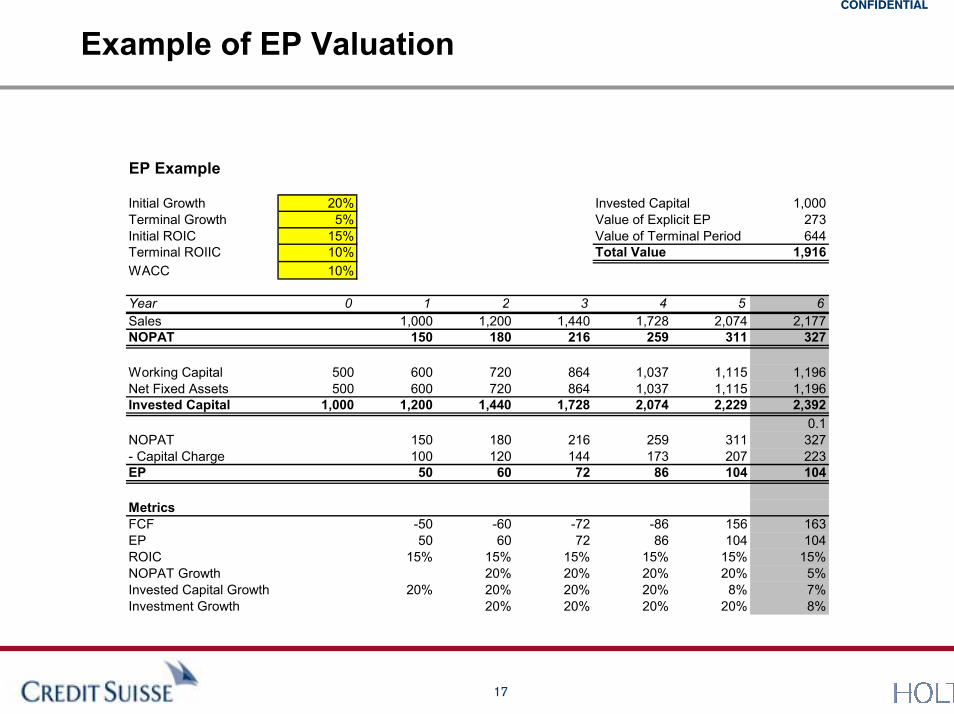

Example of EP Valuation

EP Example

Initial Growth 20% Invested Capital 1,000Terminal Growth 5% Value of Explicit EP 273Initial ROIC 15% Value of Terminal Period 644Terminal ROIIC 10% Total Value 1,916WACC 10%

Year 0 1 2 3 4 5 6Sales 1,000 1,200 1,440 1,728 2,074 2,177NOPAT 150 180 216 259 311 327

Working Capital 500 600 720 864 1,037 1,115 1,196Net Fixed Assets 500 600 720 864 1,037 1,115 1,196Invested Capital 1,000 1,200 1,440 1,728 2,074 2,229 2,392

0.1NOPAT 150 180 216 259 311 327- Capital Charge 100 120 144 173 207 223EP 50 60 72 86 104 104

MetricsFCF -50 -60 -72 -86 156 163EP 50 60 72 86 104 104ROIC 15% 15% 15% 15% 15% 15%NOPAT Growth 20% 20% 20% 20% 5%Invested Capital Growth 20% 20% 20% 20% 8% 7%Investment Growth 20% 20% 20% 20% 8%

CONFIDENTIAL

18

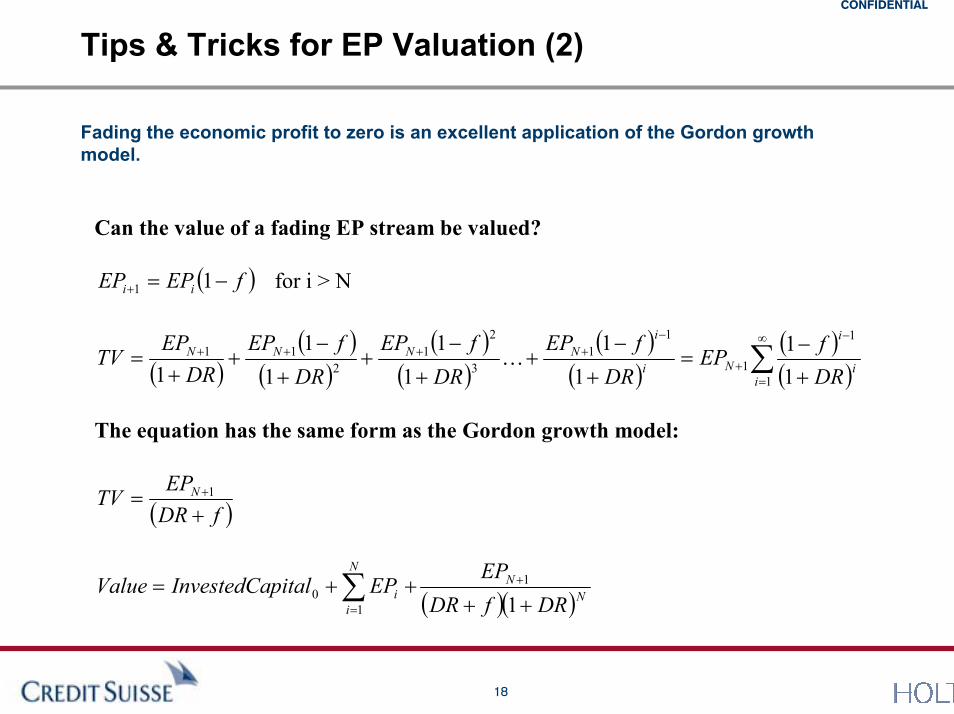

Tips & Tricks for EP Valuation (2)

Fading the economic profit to zero is an excellent application of the Gordon growth model.

Can the value of a fading EP stream be valued?

( )fEPEP ii −=+ 11 for i > N

( )( )

( )( )

( )( )

( )( )( )∑

∞

=

−

+

−++++

+−

=+

−+

+

−+

+

−+

+=

1

1

1

11

3

21

211

11

11

11

11

1 ii

i

Ni

iNNNN

DRfEP

DRfEP

DRfEP

DRfEP

DREP

TV K

The equation has the same form as the Gordon growth model:

( )fDREP

TV N

+= +1

( )( )NN

N

ii DRfDR

EPEPpitalInvestedCaValue

++++= +

=∑ 1

1

10

CONFIDENTIAL

19

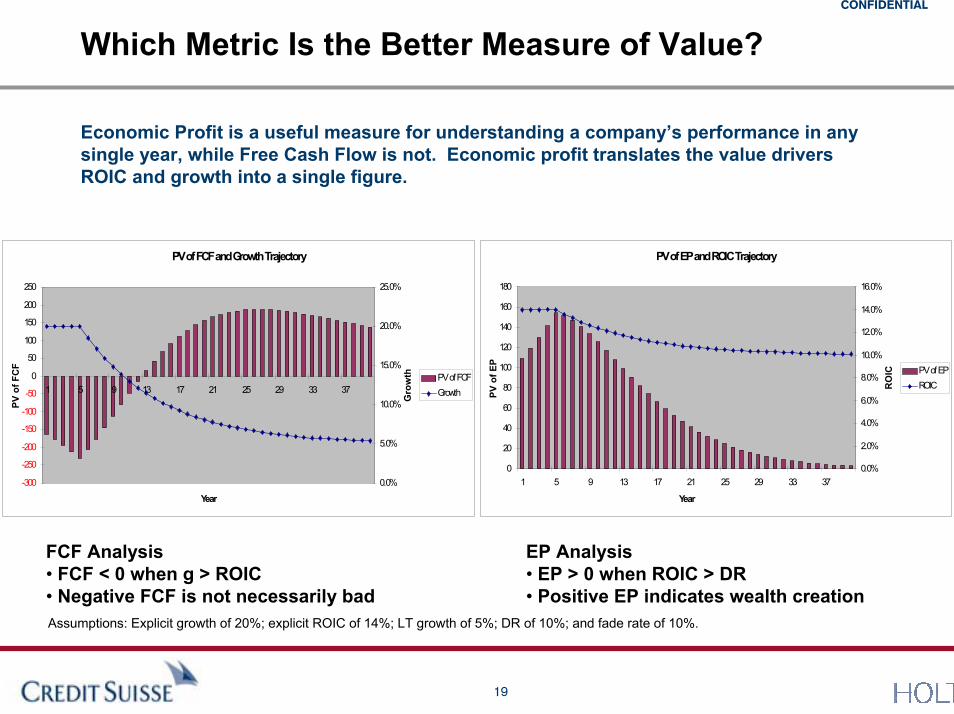

Which Metric Is the Better Measure of Value?

Economic Profit is a useful measure for understanding a company�s performance in any single year, while Free Cash Flow is not. Economic profit translates the value drivers ROIC and growth into a single figure.

PV of FCF and Growth Trajectory

-300

-250

-200

-150

-100

-50

0

50

100

150

200

250

1 5 9 13 17 21 25 29 33 37

Year

PV o

f FC

F

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Gro

wth PV of FCF

Growth

PV of EP and ROIC Trajectory

0

20

40

60

80

100

120

140

160

180

1 5 9 13 17 21 25 29 33 37

YearPV

of E

P

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

RO

IC PV of EPROIC

FCF Analysis� FCF < 0 when g > ROIC� Negative FCF is not necessarily bad

EP Analysis� EP > 0 when ROIC > DR� Positive EP indicates wealth creation

Assumptions: Explicit growth of 20%; explicit ROIC of 14%; LT growth of 5%; DR of 10%; and fade rate of 10%.

CONFIDENTIAL

20

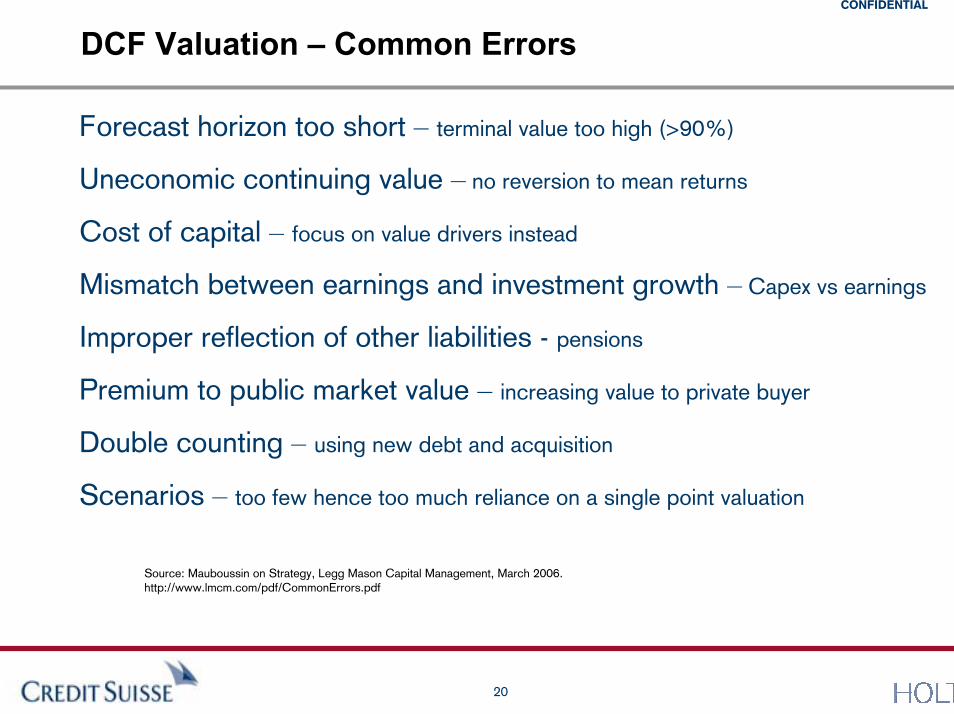

DCF Valuation � Common Errors

Forecast horizon too short � terminal value too high (>90%)

Uneconomic continuing value � no reversion to mean returns

Cost of capital � focus on value drivers instead

Mismatch between earnings and investment growth � Capex vs earnings

Improper reflection of other liabilities - pensions

Premium to public market value � increasing value to private buyer

Double counting � using new debt and acquisition

Scenarios � too few hence too much reliance on a single point valuation

Source: Mauboussin on Strategy, Legg Mason Capital Management, March 2006. http://www.lmcm.com/pdf/CommonErrors.pdf

CONFIDENTIAL

21

Disclosure and Notice

References to Credit Suisse include all of the subsidiaries and affiliates of Credit Suisse operating under its investment banking division. For more information on our structure, please follow the attached link:

http://www.creditsuisse.com/en/who_we_are/ourstructure.html

This material has been prepared by individual sales and/or trading personnel of Credit Suisse Securities (Europe) Limited or its subsidiaries or affiliates (collectively "Credit Suisse") and not by Credit Suisse's research department. It is not investment research or a research recommendation for the purposes of FSA rules as it does not constitute substantive research or analysis. All Credit Suisse research recommendations can be accessed through the following hyperlink: https://s.research-and-analytics.csfb.com/login.asp subject to the use of a suitable login. This material is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. It is intended only to provide observations and views of the said individual sales and/or trading personnel, which may be different from, or inconsistent with, the observations and views of Credit Suisse analysts or other Credit Suisse sales and/or trading personnel, or the proprietary positions of Credit Suisse. Observations and views of the salesperson or trader may change at any time without notice. Information and opinions presented in this material have beenobtained or derived from sources believed by Credit Suisse to be reliable, but Credit Suisse makes no representation as to their accuracy or completeness. Credit Suisse accepts no liability for loss arising from the use of this material. This material is directed exclusively at Credit Suisse's market professional and institutional investor customers ie market counterparties and intermediate customers as defined by the rules of the Financial Services Authority. It is not intended for private customers and such persons should not rely on this material. Moreover, any investment or service to which this material may relate, will not be made available by Credit Suisse to such private customers. All valuations are subject to Credit Suisse valuation terms. Information provided on trades executed with Credit Suisse will not constitute an official confirmation of the trade details.

FOR IMPORTANT DISCLOSURES on companies covered in Credit Suisse Investment Banking Division research reports, please see www.credit-suisse.com/researchdisclosures.

Backtested, hypothetical or simulated performance results have inherent limitations. Simulated results are achieved by the retroactive application of a backtested model itself designed with the benefit of hindsight. The backtesting of performance differs from the actual account performance because the investment strategy may be adjusted at any time, for any reason and can continue to be changed until desired or better performance results are achieved. Alternative modeling techniques or assumptions might produce significantly different results and prove to be more appropriate. Past hypothetical backtest results are neither an indicator nor a guarantee of future returns. Actual results will vary from the analysis.With respect to the analysis in this report based on the HOLT� methodology, Credit Suisse certifies that (1) the views expressed in this report accurately reflect the HOLT methodology and (2) no part of the Firm�s compensation was, is, or will be directly related to the specific views disclosed in this report. The HOLT methodology does not assign ratings to a security. It is an analytical tool that involves use of a set of proprietary quantitative algorithms and warranted value calculations, collectively called the HOLT valuation model, that are consistently applied to all the companies included in its database. Third-party data (including consensus earnings estimates) are systematically translated into a number of default variables and incorporated into the algorithms available in the HOLT valuation model. The source financial statement, pricing, and earnings data provided by outside data vendors are subject to quality control and may also be adjusted to more closely measure the underlying economics of firm performance. These adjustments provide consistency when analyzing a single company across time, or analyzing multiple companies across industries or national borders. The default scenario that is produced by the Credit Suisse HOLT valuation model establishes the baseline valuation for a security, and a userthen may adjust the default variables to produce alternative scenarios, any of which could occur. The HOLT methodology does not assign a price target to a security. The default scenario that is produced by the HOLT valuation model establishes a warranted price for a security, and as the third-party data are updated, the warranted price may also change. The default variables may also be adjusted to produce alternative warranted prices, any of which could occur. Additional information about the HOLT methodology is available on request.Credit Suisse Securities (Europe) Limited is authorised and regulated by the Financial Services Authority.

CFROI®, CFROE, HOLT, HOLTfolio, HOLTSelect, HS60, HS40, ValueSearch, AggreGator, Signal Flag and �Powered by HOLT� are trademarks or registered trademarks of Credit Suisse or itsaffiliates in the United States and other countries.HOLT is a corporate performance and valuation advisory service of Credit Suisse© 2007 Credit Suisse and its subsidiaries and affiliates. All rights reservedSeptember 1 2007