Embed Size (px)

Citation preview

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 1/52

OUTBOUND PROPERTY TRANSFERSUNDER

§367(a)(5)Panel Discussion

Foreign Activities of U.S. Taxpayers

ABA May MeetingMay 10, 2013

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 2/52

Panelists

• Joseph Calianno, Grant Thornton LLP

• Robert Williams, Internal Revenue Service

• Brenda Zent, Department of Treasury

• Giovanna T. Sparagna, Sutherland (moderator)

2

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 3/52

Agenda

• Recently released final and temporary regulations in

TD 9614 and TD 9615 – §367(a)(5) regulations proposed in August 2008

which were substantially adopted

– §367(a) temporary regulations on coordinationrules

– §367(b) final regulations

– §1248(f) regulations to provide an elective

exception to gain on the distribution of CFC stock*All examples herein assume §7874 is N/A

3

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 4/52

§367 Background

• Function of §367(a)

– Overlay on Subchapter C non-recognitionprovisions

– Primarily prevents US persons from using

Subchapter C non-recognition provisions totransfer appreciated assets outside US taxing

jurisdiction

4

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 5/52

5

§367 Background

• Outbound Transfers Subject to Tax Unless an

Exception Applies – §367(a)(1) general rule – foreign acquiring

corporation denied corporate status indetermining extent to which gain recognized

– Generally results in US person recognizing gain on eachitem of appreciated property transferred

– Transaction continues to otherwise qualify for tax-freetreatment

• Character and source of gain determined as if propertydisposed of in taxable transaction

• Appropriate adjustments to basis, E&P, and other items

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 6/52

§367 Background

• §367(a) Exception for Certain Outbound Asset Transfers

– Exceptions for certain stock transfers and certain assets usedor held for use in a foreign trade or business

– §367(a) Exception limited where

• Certain subsequent dispositions of transferred property(Reg. §1.367(a)-2T)

• Outbound §368 asset reorganization (§367(a)(5))

• “Tainted” assets (Reg. §1.367(a)-4T, 5T)

• Depreciation recapture (Reg. §1.367(a)-4T)

• Branch loss recapture (Reg. §1.367(a)-6T)

6

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 7/52

§367 Background

• Further Limitation of Active Foreign Trade or Business

Exception – Active Foreign Trade or Business Exception not generally

available for

• Stock transfers (separate rules apply)

• Transfers described in §367(a)(5)

• Transfers of §367(d) property (intangibles)

7

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 8/52

§367 Background

• §367 Exception for Outbound Transfer of Foreign

Corporation Stock or Securities – Reg. §1.367(a)-3(b) – except as provided in §367(a)(5), gain

not recognized if

– US transferor is less than 5% shareholder oftransferee foreign corporation, or

– US transferor is 5% shareholder of transferee

foreign corporation and enters into GRA

– Must also consider the provisions of §367(b) in certain

situations (Reg. §1.367(b)-4)

8

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 9/52

§367 Background

• §367 Exception for Outbound Transfer of Domestic

Stock or Securities (assuming §7874 does not treat foreignacquiring as a domestic corporation)

– Gain recognized unless substantive and reporting

requirements satisfied

• US transferors receive no more than 50% (by vote or

value) of stock of transferee foreign corporation in the

transaction

• US persons who are either officers or directors of UStarget, or 5% shareholders of US target own,

immediately after transfer, no more than 50% (by vote

or value) of stock of transferee foreign corporation

(cont’d) 9

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 10/52

§367 Background

• §367 Exception for Outbound Transfer of Domestic

Stock or Securities – Gain recognized unless substantive and reporting

requirements satisfied

• Transferee foreign corporation active trade or business requirement – 36-month foreign active trade or business

– Substantiality requirement – FMV of transferee foreign

corporation greater than or equal to FMV of transferred

domestic corporation – No intention to dispose of or discontinue trade or business

– GRA requirement – US person must file GRA if 5%

transferee shareholder10

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 11/52

11

§367 Background

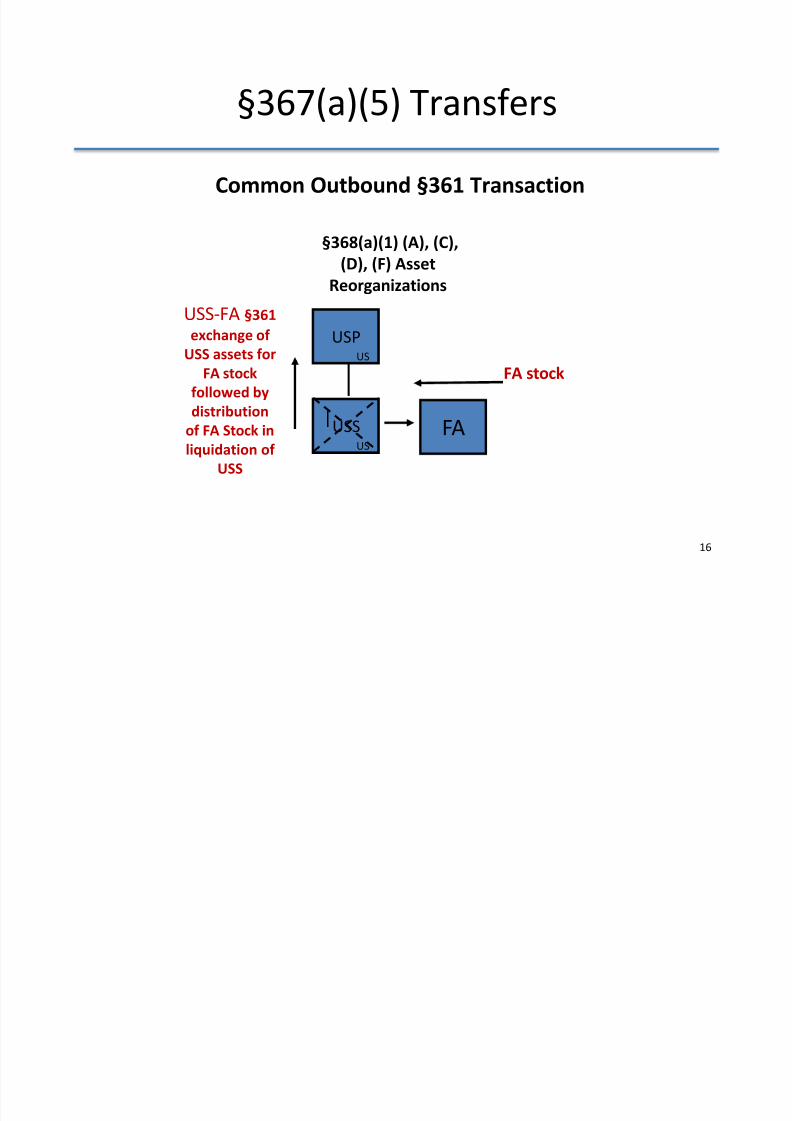

• Outbound §361 Transfers

– §367(a)(5) generally requires US target to recognize gainon outbound §361(a) or (b) transfer of property by

disallowing exceptions that might otherwise apply

• Statute contemplates regulatory exception – US target corporation controlled (§368(c)) by five or fewer

domestic corporate shareholders

– Subject to basis adjustment and other conditions provided

in regulations

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 12/52

§367(a)(5) PROPOSED REGULATIONS

MODIFIED IN FINAL REGULATIONS (T.D.9614)

12

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 13/52

§367(a)(5) Guidance History

• Pre-August 2008

– Limited guidance provided by IRS regarding the

application of §367(a)(5) prior to the proposed

regulations. See e.g., Reg. § 1.367(a)-3(e)(1), Notice

2008-10, and PLRs 9731039 and 9533005.• Proposed regulations issued August 2008

– Proposed regulations implemented §367(a)(5) through

an “Elective Exception” regime. – Proposed regulations could be relied upon until effective

date of any final regulations

13

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 14/52

§367(a)(5) Guidance History

• TD 9614

• Final regulations adopt, in substantial part, the August

2008 Proposed regulation (changes discussed below).

• However, there are many significant modifications and

some favorable modifications to the proposedregulations (including certain modifications to the

§367(b) and §1248(f) proposed regulations).

• Generally effective April 18th (some special effectivedates).

14

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 15/52

15

Taxation of §367(a)(5) Transfers• §367(a)(5)

– Generally requires US target to recognize gain on outbound§361 transfer of property by disallowing exceptions that mightotherwise apply UNLESS

• US target corporation controlled (§368(c)) by five or fewerdomestic corporate shareholders, and

• Subject to basis adjustment and other conditions provided inregulations

• Objective of statutory/regulatory exception where

– Preserve U.S. taxation of the “inside gain” inherent in the UStransferor’s transferred assets (post-repeal of General Utilities).

– U.S. taxation preserved through adjustments to the basis of theforeign acquiring’s stock basis received in the reorganization bythe US target’s domestic corporate shareholders

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 16/52

§367(a)(5) Transfers

USP

USS FA

USS-FA §361

exchange of

USS assets for

FA stock

followed by

distribution

of FA Stock inliquidation of

USS

US

US

§368(a)(1) (A), (C),

(D), (F) Asset

Reorganizations

Common Outbound §361 Transaction

FA stock

16

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 17/52

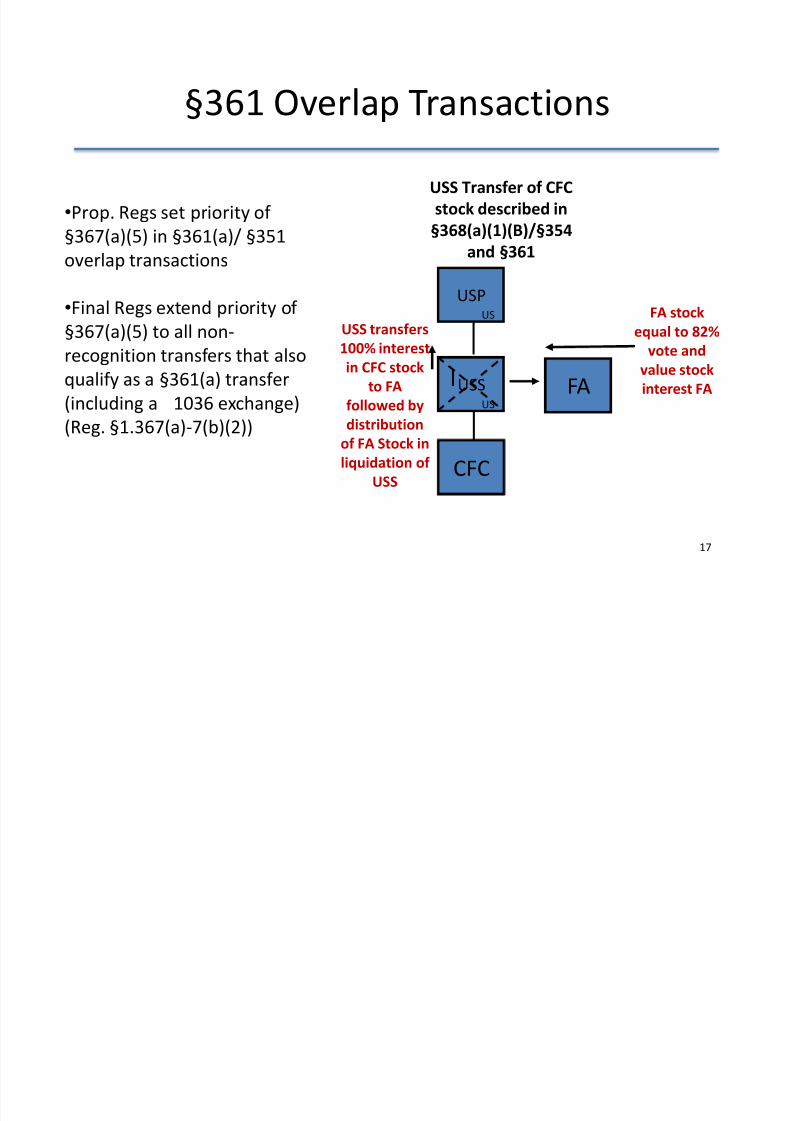

§361 Overlap Transactions

17

USP

USS FA

USS transfers100% interest

in CFC stock

to FA

followed by

distributionof FA Stock in

liquidation of

USS

US

US

USS Transfer of CFC

stock described in§368(a)(1)(B)/§354

and §361

FA stock

equal to 82%

vote and

value stock

interest FA

•Prop. Regs set priority of§367(a)(5) in §361(a)/ §351

overlap transactions

•Final Regs extend priority of

§367(a)(5) to all non-recognition transfers that also

qualify as a §361(a) transfer

(including a 1036 exchange)

(Reg. §1.367(a)-7(b)(2))

CFC

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 18/52

Property Subject to §367(a)(5)

• Final Regs Define Section 367(a) Property

– Final Regs limit the application of §367(a)(5) to the transfer of“section 367(a) property”

• Section 367(a) property is defined in Reg. §1.367(a)-7(f)(10) as any

property other than “section 367(d) property”

• Section 367(d) property is “clarified” in Reg. §1.367(a)-7(f)(11) asany property described in §936(h)(3)(b)

• As will be seen below, the valuation of intangibles will significantly

impact §367(a)(5) compliance

• A correct valuation will be critical

18

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 19/52

§367(a) Property

Treatment of Foreign Goodwill

• §367 Treatment of Foreign Goodwill and Going Concern

– Preamble to final regulations indicates that the reference to§936(h)(3)(B) is a clarification for purposes of defining §367(d)

property.

– IRS has taken the position that goodwill/going concern is a

§936(h)(3)(B) intangible.

– President Obama’s budget proposals have included a proposal

“clarifying” that goodwill/going concern is a §936(h)(3)(B) intangible.

19

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 20/52

§367(a) Property

Treatment of Foreign Goodwill• Assuming that foreign goodwill/going concern is a §936(h)(3)(B)

intangible, does a domestic corporation’s §361 transfer of foreign

goodwill/going concern escape taxation under §367(a)?

• Compare

– Reg. § 1.367(d)-1T(b) provides that §367(d) does not apply to the

transfer of foreign goodwill or going concern value.

• Does legislative history support position that no tax should result on the transfer offoreign goodwill/going concern? See 1984 Senate Report, 1984 House Report and

1984 Blue Book.

– Reg. § 1.367(d)-1T(b) provides that foreign goodwill/going concern will

be included for the purpose of determining branch loss recapture

under Reg. § 1.367(a)-6T.

• Does this language as it relates to branch loss recapture under §367(a) imply that

foreign goodwill/going concern otherwise would not be subject to any of the

367(a) rule?

20

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 21/52

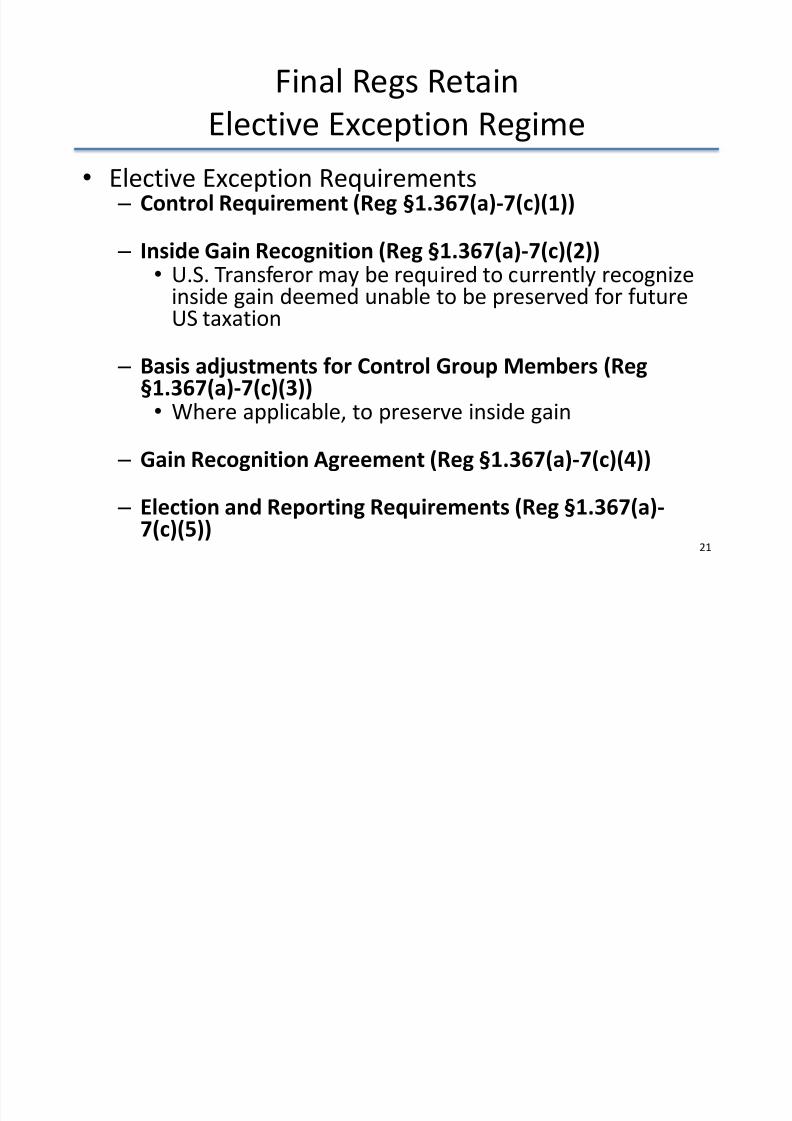

Final Regs Retain

Elective Exception Regime

• Elective Exception Requirements – Control Requirement (Reg §1.367(a)-7(c)(1))

– Inside Gain Recognition (Reg §1.367(a)-7(c)(2))• U.S. Transferor may be required to currently recognize

inside gain deemed unable to be preserved for future

US taxation

– Basis adjustments for Control Group Members (Reg§1.367(a)-7(c)(3))

• Where applicable, to preserve inside gain

– Gain Recognition Agreement (Reg §1.367(a)-7(c)(4))

– Election and Reporting Requirements (Reg §1.367(a)-

7(c)(5)) 21

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 22/52

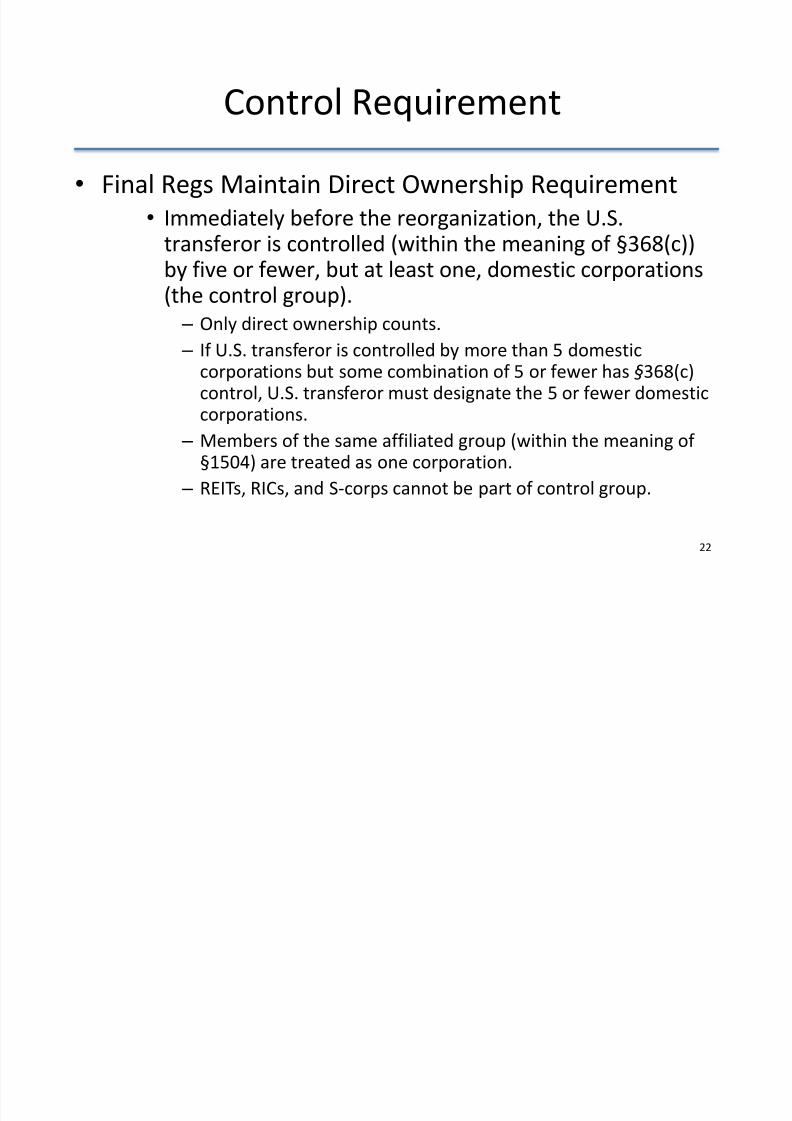

Control Requirement

• Final Regs Maintain Direct Ownership Requirement

• Immediately before the reorganization, the U.S.transferor is controlled (within the meaning of §368(c))by five or fewer, but at least one, domestic corporations(the control group).

– Only direct ownership counts. – If U.S. transferor is controlled by more than 5 domestic

corporations but some combination of 5 or fewer has §368(c)control, U.S. transferor must designate the 5 or fewer domesticcorporations.

– Members of the same affiliated group (within the meaning of§1504) are treated as one corporation.

– REITs, RICs, and S-corps cannot be part of control group.

22

8/13/2019 Faust 367a5 Slides

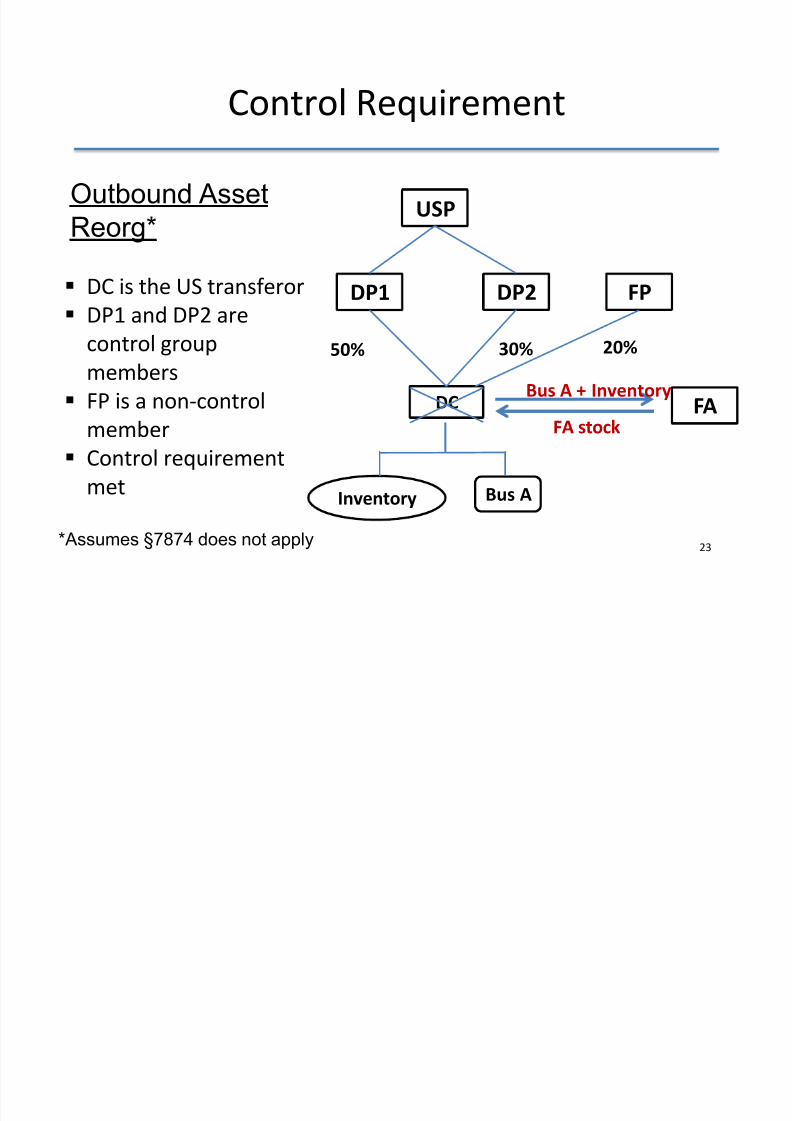

http://slidepdf.com/reader/full/faust-367a5-slides 23/52

DP1

Inventory

FPDP2

DC

Bus A

50% 20%30%

FABus A + Inventory

FA stock

DC is the US transferor

DP1 and DP2 arecontrol group

members

FP is a non-control

member Control requirement

met

Outbound Asset

Reorg*

Control Requirement

USP

23*Assumes §7874 does not apply

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 24/52

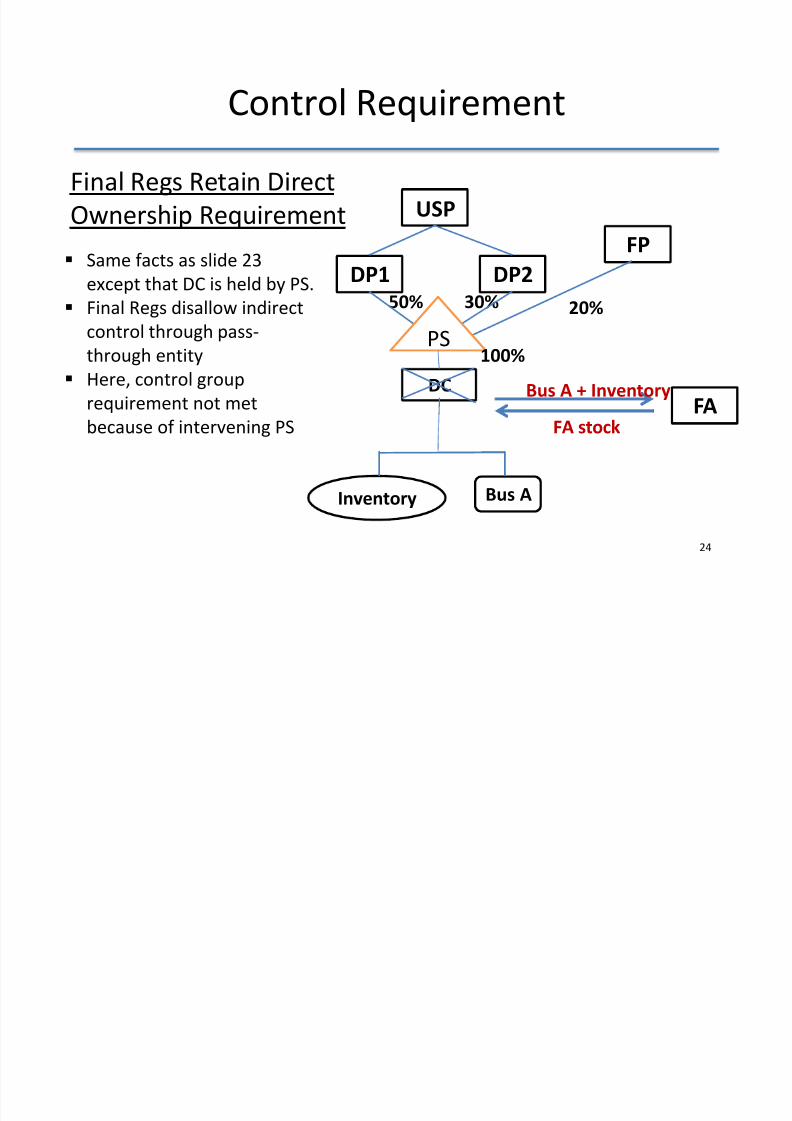

DP1

Inventory

FP

DP2

DC

Bus A

50% 20%30%

FABus A + Inventory

FA stock

Same facts as slide 23

except that DC is held by PS.

Final Regs disallow indirect

control through pass-through entity

Here, control group

requirement not met

because of intervening PS

Final Regs Retain Direct

Ownership Requirement

Control Requirement

USP

PS100%

24

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 25/52

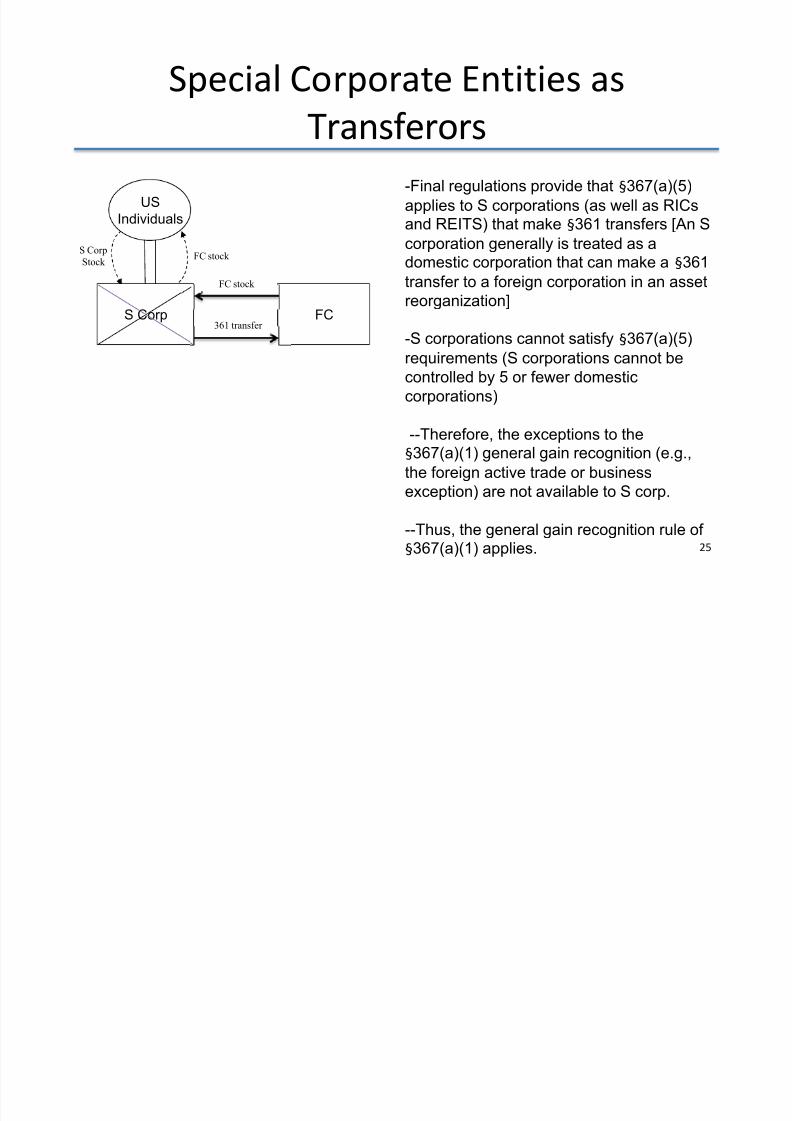

S Corp

Stock FC stock

US

Individuals

FC

-Final regulations provide that §367(a)(5)

applies to S corporations (as well as RICs

and REITS) that make §361 transfers [An Scorporation generally is treated as adomestic corporation that can make a §361

transfer to a foreign corporation in an asset

reorganization]

-S corporations cannot satisfy §367(a)(5)

requirements (S corporations cannot be

controlled by 5 or fewer domestic

corporations)

--Therefore, the exceptions to the§367(a)(1) general gain recognition (e.g.,

the foreign active trade or business

exception) are not available to S corp.

--Thus, the general gain recognition rule of

§367(a)(1) applies.

S Corp361 transfer

FC stock

Special Corporate Entities as

Transferors

25

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 26/52

S Corp

Stock FC stock

US

Individuals

FC

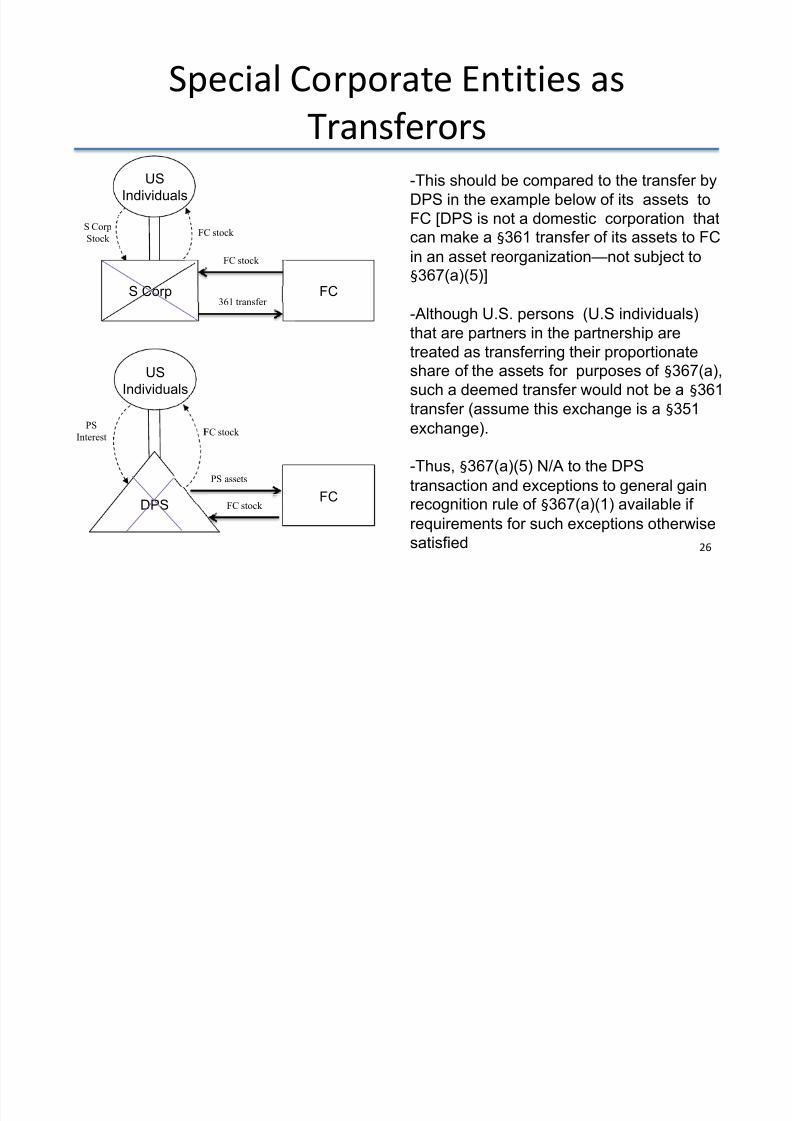

-This should be compared to the transfer by

DPS in the example below of its assets to

FC [DPS is not a domestic corporation thatcan make a §361 transfer of its assets to FC

in an asset reorganization—not subject to

§367(a)(5)]

-Although U.S. persons (U.S individuals)

that are partners in the partnership are

treated as transferring their proportionate

share of the assets for purposes of §367(a),

such a deemed transfer would not be a §361

transfer (assume this exchange is a §351

exchange).

-Thus, §367(a)(5) N/A to the DPS

transaction and exceptions to general gainrecognition rule of §367(a)(1) available if

requirements for such exceptions otherwise

satisfied

S Corp361 transfer

FC stock

US

Individuals

FC stock

PS

Interest

DPS

PS assets

FC stock FC

Special Corporate Entities as

Transferors

26

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 27/52

S Corp

Stock FC stock

US

Individuals

FC

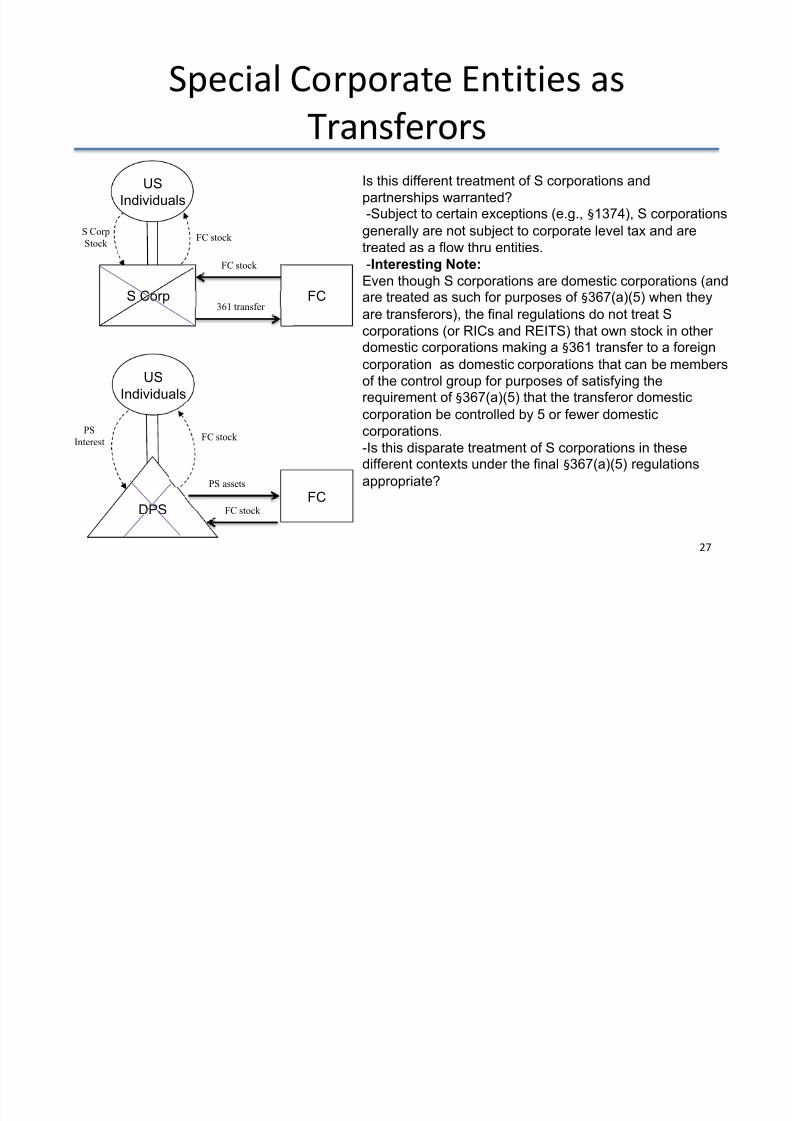

Is this different treatment of S corporations and

partnerships warranted?

-Subject to certain exceptions (e.g., §1374), S corporationsgenerally are not subject to corporate level tax and are

treated as a flow thru entities.

-Interesting Note:

Even though S corporations are domestic corporations (andare treated as such for purposes of §367(a)(5) when they

are transferors), the final regulations do not treat S

corporations (or RICs and REITS) that own stock in otherdomestic corporations making a §361 transfer to a foreign

corporation as domestic corporations that can be members

of the control group for purposes of satisfying therequirement of §367(a)(5) that the transferor domestic

corporation be controlled by 5 or fewer domestic

corporations.-Is this disparate treatment of S corporations in thesedifferent contexts under the final §367(a)(5) regulations

appropriate?

S Corp361 transfer

FC stock

US

Individuals

FC stock PSInterest

DPS

PS assets

FC stock

FC

Special Corporate Entities as

Transferors

27

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 28/52

Inside Gain Recognition

• Final Regs Adopt Inside Gain Recognition Rules of

Proposed Regs• US Transferor’s Gain

– The US transferor must currently recognize inside gainin certain property (§367(a) property) transferred by

the U.S. transferor in the 361 exchange andattributable to non-control group members andattributable to control group members where unableto preserve gain

28

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 29/52

Inside Gain Recognition• Inside Gain Computation

• Generally speaking, the inside gain is the aggregate fairmarket value of the §367(a) property transferred by theU.S. transferor in a 361 exchange over the aggregateadjusted bases in such property plus a proportionateamount of any liabilities of the U.S. transferor assumed in

the 361 exchange or satisfied in the reorganizationpursuant to 361(c)(3), but only to the extent thepayment of such liability would give rise to a deduction.

– Special adjustments to basis if gain recognized by U.S.transferor on transfer.

– Special rules and definitions apply.

29

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 30/52

Inside Gain Recognition

• Final Regs Modify Deductible LiabilitiesThat Reduce Inside Gain – When computing inside gain, the Prop. Regs took

into account liabilities assumed by the foreigntransferee and liabilities satisfied in the exchange if

such liability gave rise to a deduction when paid. – Final regs limit deductible liabilities to those assumed

by the foreign transferee on the theory that the UStransferor does not receive a benefit for the liability.

Why not take into account other tax attributes such asnet operating losses and foreign tax credits for whichthe US transferor has not received a benefit?

30

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 31/52

Basis Adjustment Requirement• Final Regs Clarify the Basis Adjustment Rules

• Control Group Basis Adjustments

• Each control group member's basis in the stock received in thetransaction as determined under §358 and the regulations underthat section (§358 basis) that is allocable to the §367(a) propertytransferred by the U.S. transferor in the §361 exchange is reduced to

the extent necessary to preserve the control group member's shareof inside gain.

– Only the basis of stock received by the control group memberthat is attributable to §367(a) property transferred in the §361exchange is reduced (for example, the basis of stock attributable

to §367(d) property is not reduced).

• Final Regulations clarify that group members are treated as a singletaxpayer solely for computing the ownership threshold and the basis of foreign acquiring stock received in the reorganization is adjusted.

31

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 32/52

Basis Adjustment Requirement

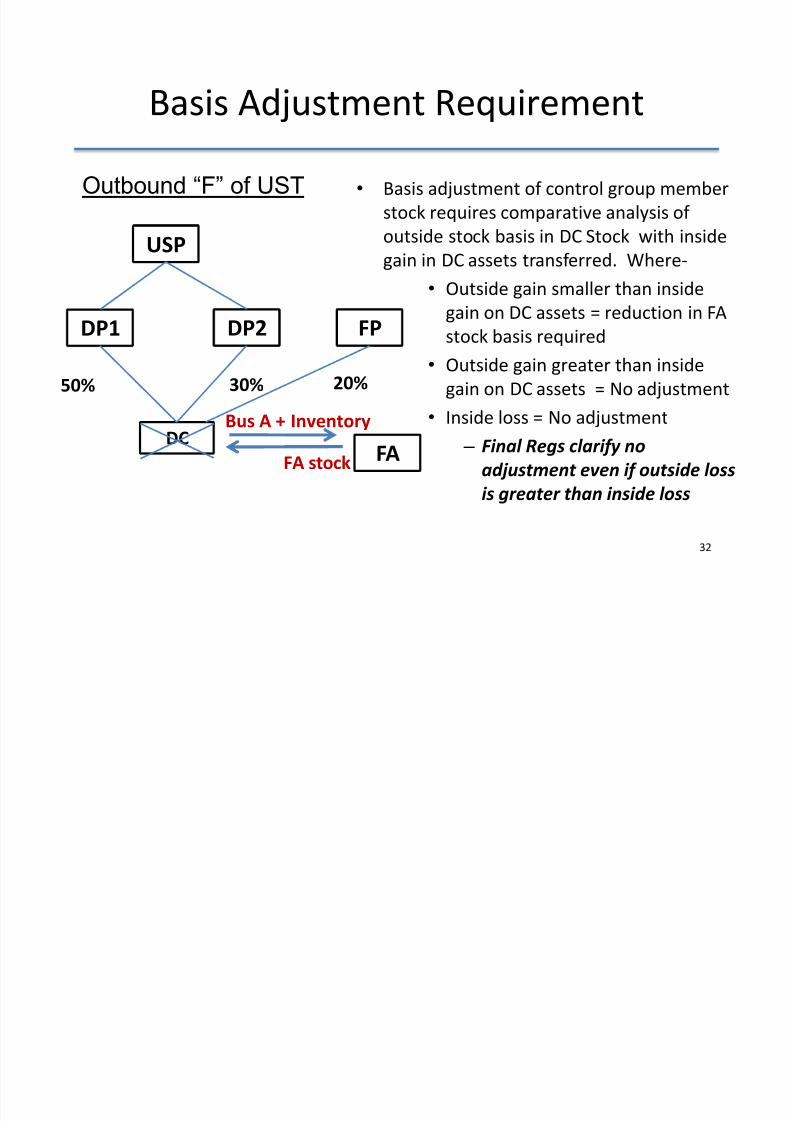

• Basis adjustment of control group member

stock requires comparative analysis ofoutside stock basis in DC Stock with inside

gain in DC assets transferred. Where-

• Outside gain smaller than inside

gain on DC assets = reduction in FA

stock basis required

• Outside gain greater than inside

gain on DC assets = No adjustment

• Inside loss = No adjustment

– Final Regs clarify no

adjustment even if outside loss

is greater than inside loss

32

Outbound “F” of UST

DP1 FPDP2

DC

50% 20%30%

FA

Bus A + Inventory

FA stock

USP

8/13/2019 Faust 367a5 Slides

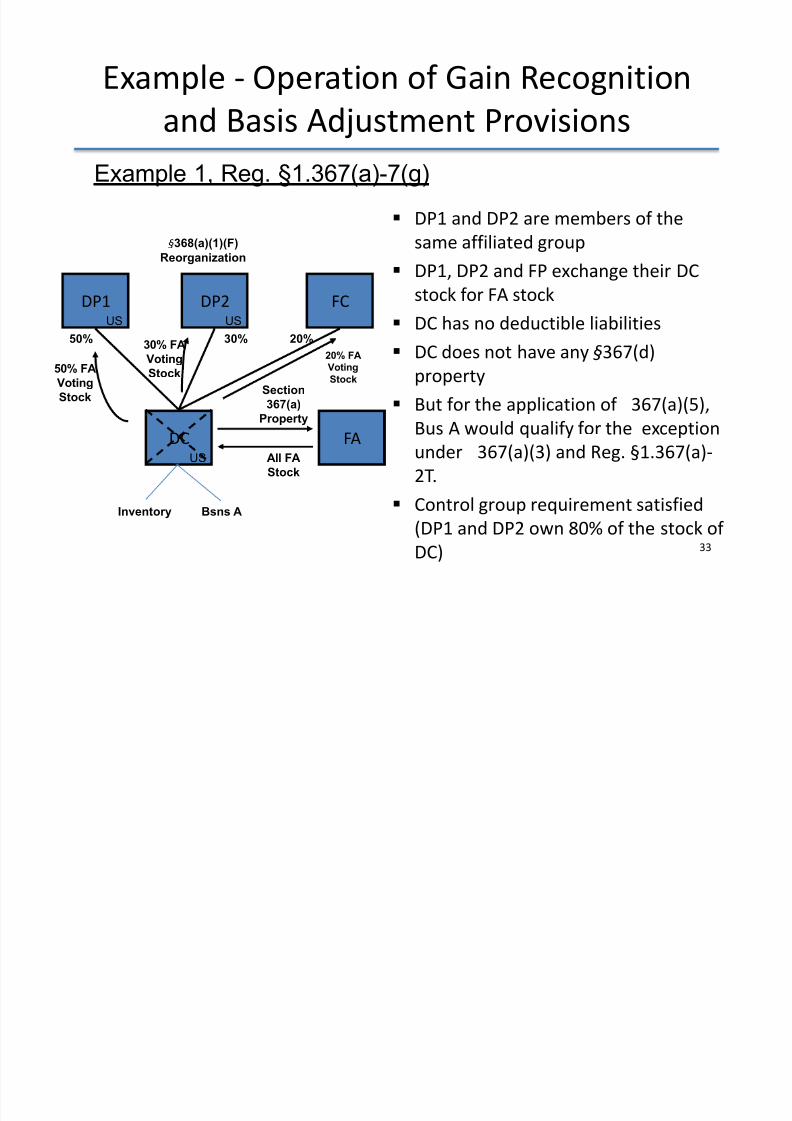

http://slidepdf.com/reader/full/faust-367a5-slides 33/52

Example - Operation of Gain Recognition

and Basis Adjustment Provisions

DP1 and DP2 are members of thesame affiliated group

DP1, DP2 and FP exchange their DC

stock for FA stock

DC has no deductible liabilities DC does not have any §367(d)

property

But for the application of 367(a)(5),

Bus A would qualify for the exceptionunder 367(a)(3) and Reg. §1.367(a)-

2T.

Control group requirement satisfied

(DP1 and DP2 own 80% of the stock of

DC)

Section

367(a)

Property

All FA

Stock

DP1

DC FA

DP2US US

US

50%

50% FA

Voting

Stock

30% FA

Voting

Stock

FC

30% 20%

20% FA

Voting

Stock

§368(a)(1)(F)

Reorganization

33

Example 1, Reg. §1.367(a)-7(g)

Inventory Bsns A

8/13/2019 Faust 367a5 Slides

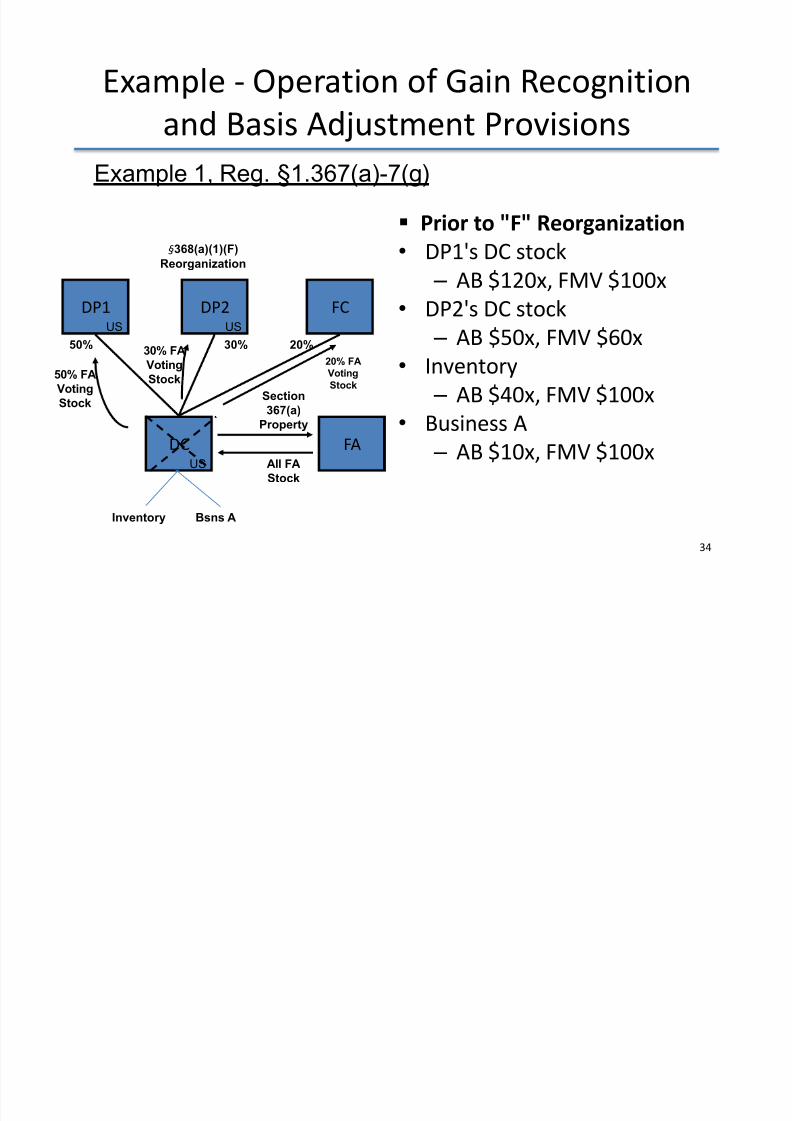

http://slidepdf.com/reader/full/faust-367a5-slides 34/52

Prior to "F" Reorganization• DP1's DC stock

– AB $120x, FMV $100x

• DP2's DC stock

– AB $50x, FMV $60x• Inventory

– AB $40x, FMV $100x

•Business A

– AB $10x, FMV $100x

34

Example - Operation of Gain Recognition

and Basis Adjustment Provisions

Section

367(a)

Property

All FA

Stock

DP1

DC FA

DP2

US US

US

50%

50% FA

Voting

Stock

30% FA

Voting

Stock

FC

30% 20%

20% FA

Voting

Stock

§368(a)(1)(F)

Reorganization

Inventory Bsns A

Example 1, Reg. §1.367(a)-7(g)

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 35/52

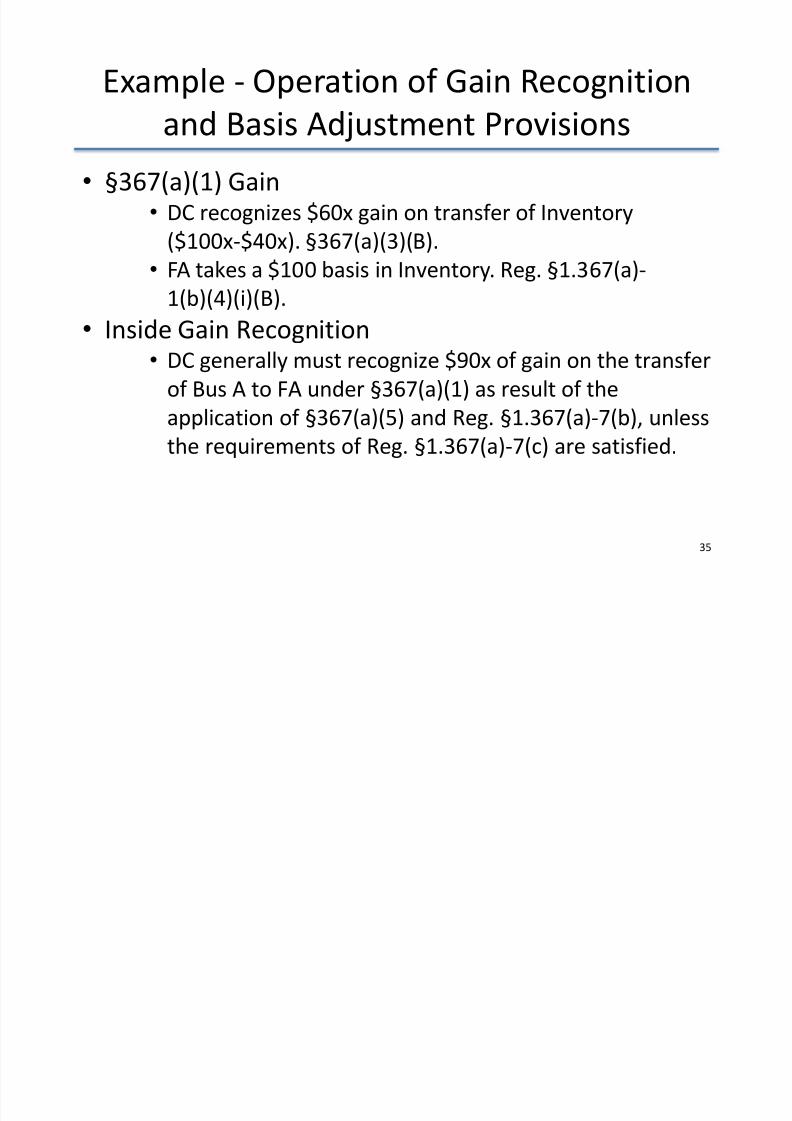

Example - Operation of Gain Recognition

and Basis Adjustment Provisions

• §367(a)(1) Gain

• DC recognizes $60x gain on transfer of Inventory($100x-$40x). §367(a)(3)(B).

• FA takes a $100 basis in Inventory. Reg. §1.367(a)-

1(b)(4)(i)(B).

• Inside Gain Recognition• DC generally must recognize $90x of gain on the transfer

of Bus A to FA under §367(a)(1) as result of the

application of §367(a)(5) and Reg. §1.367(a)-7(b), unless

the requirements of Reg. §1.367(a)-7(c) are satisfied.

35

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 36/52

• Gain Recognition Requirement Inside gain is $90x

– The amount by which the aggregate FMV ($200x) of section367(a) property exceeds $110x (the sum of inside basis of

$110x [ $50x basis of §367(a) property plus $60x gain

recognized by DC] and the product of the 367(a) percentage

(100%) multiplied by the deductible liabilities of DC ($0x))

Gain attributable to non-control group member

– DC must recognize $18x on transfer of Bus A (inside gain

attributable to FP)--$90x multiplied by 20%

– Gain treated as recognized with respect to Bus A

– FA increases its basis in Bus A by $18x Control group member gain fully preserved through basis

adjustments (see below)

But result can be different if boot was received or liabilities

were assumed

Example - Operation of Gain Recognition

and Basis Adjustment Provisions

36

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 37/52

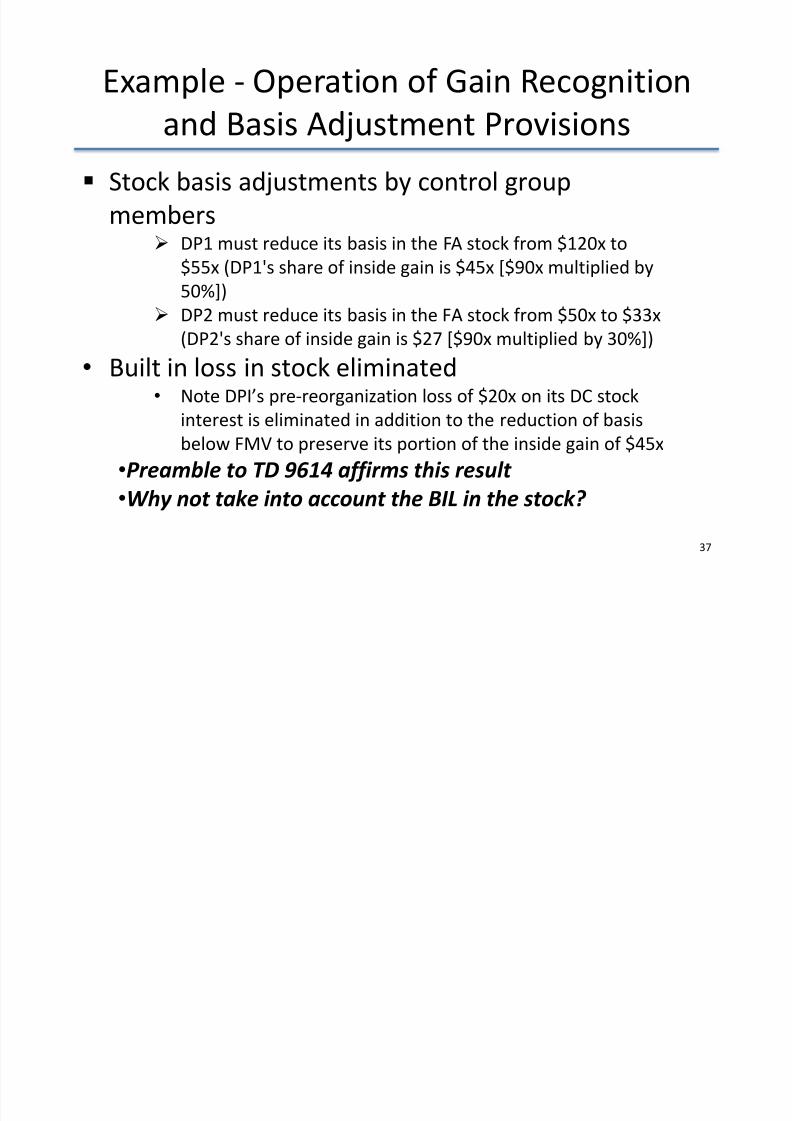

Stock basis adjustments by control group

members DP1 must reduce its basis in the FA stock from $120x to

$55x (DP1's share of inside gain is $45x [$90x multiplied by

50%])

DP2 must reduce its basis in the FA stock from $50x to $33x

(DP2's share of inside gain is $27 [$90x multiplied by 30%])

• Built in loss in stock eliminated• Note DPI’s pre-reorganization loss of $20x on its DC stock

interest is eliminated in addition to the reduction of basis

below FMV to preserve its portion of the inside gain of $45x

•Preamble to TD 9614 affirms this result

•Why not take into account the BIL in the stock?

Example - Operation of Gain Recognition

and Basis Adjustment Provisions

37

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 38/52

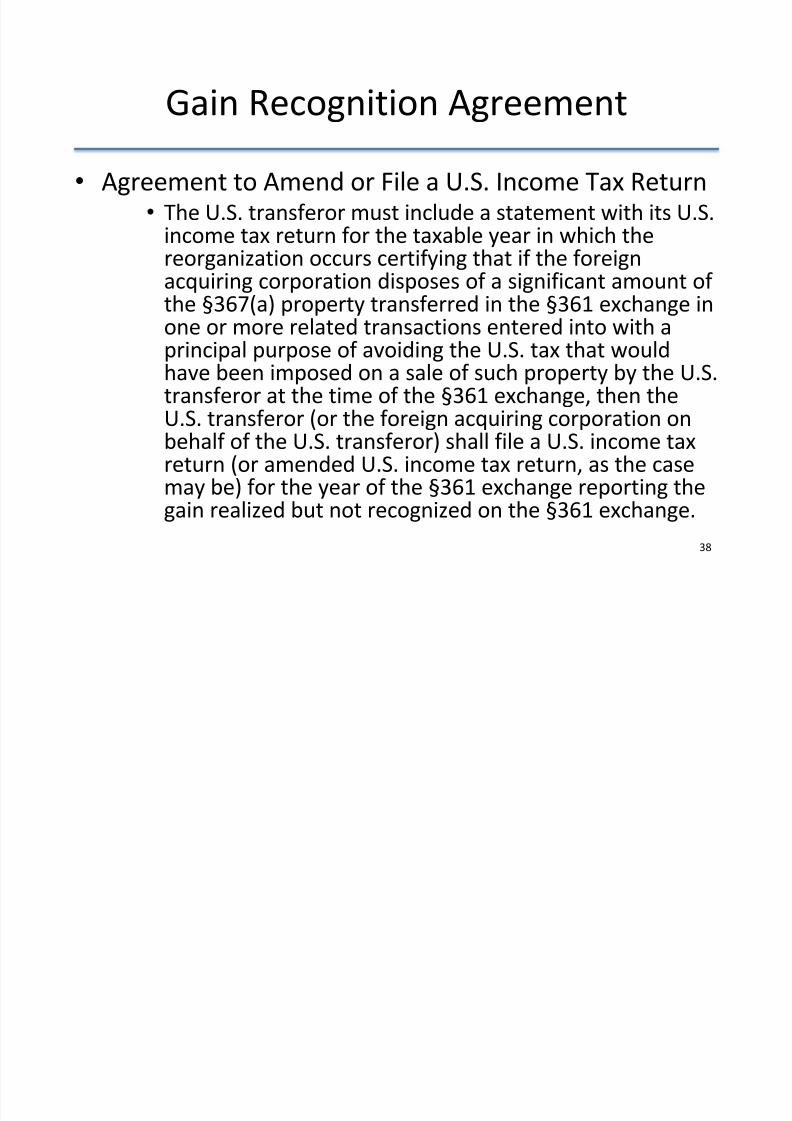

Gain Recognition Agreement• Agreement to Amend or File a U.S. Income Tax Return

• The U.S. transferor must include a statement with its U.S.income tax return for the taxable year in which thereorganization occurs certifying that if the foreignacquiring corporation disposes of a significant amount ofthe §367(a) property transferred in the §361 exchange in

one or more related transactions entered into with aprincipal purpose of avoiding the U.S. tax that wouldhave been imposed on a sale of such property by the U.S.transferor at the time of the §361 exchange, then theU.S. transferor (or the foreign acquiring corporation on

behalf of the U.S. transferor) shall file a U.S. income taxreturn (or amended U.S. income tax return, as the casemay be) for the year of the §361 exchange reporting thegain realized but not recognized on the §361 exchange.

38

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 39/52

Gain Recognition Agreement

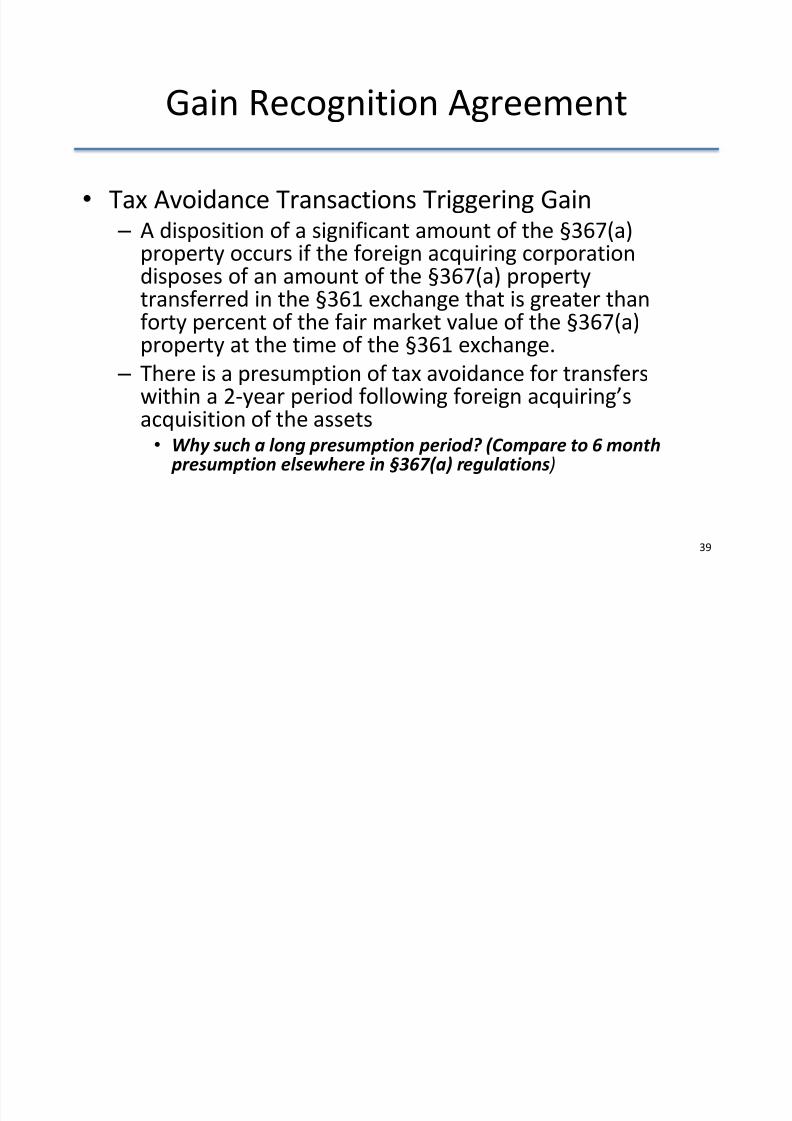

• Tax Avoidance Transactions Triggering Gain

– A disposition of a significant amount of the §367(a)property occurs if the foreign acquiring corporationdisposes of an amount of the §367(a) propertytransferred in the §361 exchange that is greater than

forty percent of the fair market value of the §367(a)property at the time of the §361 exchange.

– There is a presumption of tax avoidance for transferswithin a 2-year period following foreign acquiring’sacquisition of the assets

• Why such a long presumption period? (Compare to 6 month presumption elsewhere in §367(a) regulations )

39

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 40/52

Gain Recognition Agreement

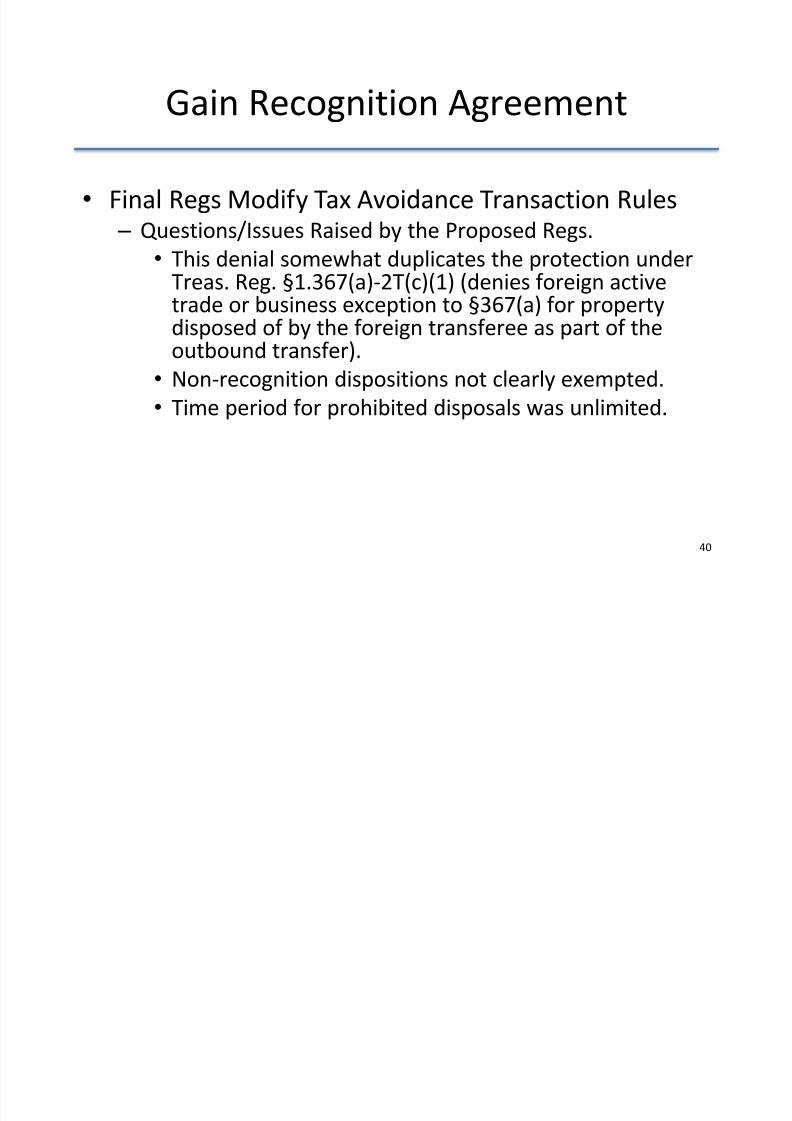

• Final Regs Modify Tax Avoidance Transaction Rules

– Questions/Issues Raised by the Proposed Regs.• This denial somewhat duplicates the protection under

Treas. Reg. §1.367(a)-2T(c)(1) (denies foreign activetrade or business exception to §367(a) for property

disposed of by the foreign transferee as part of theoutbound transfer).

• Non-recognition dispositions not clearly exempted.

• Time period for prohibited disposals was unlimited.

40

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 41/52

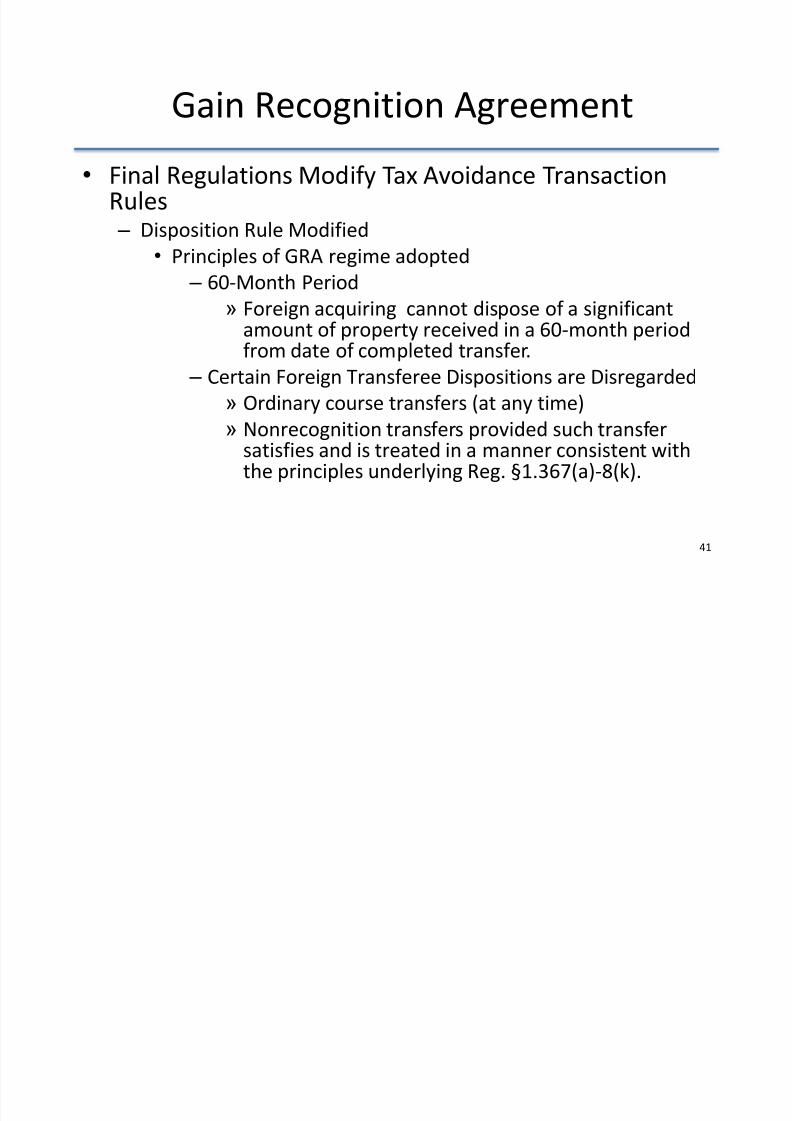

Gain Recognition Agreement• Final Regulations Modify Tax Avoidance Transaction

Rules – Disposition Rule Modified

• Principles of GRA regime adopted

– 60-Month Period

» Foreign acquiring cannot dispose of a significant

amount of property received in a 60-month periodfrom date of completed transfer.

– Certain Foreign Transferee Dispositions are Disregarded

» Ordinary course transfers (at any time)

» Nonrecognition transfers provided such transfersatisfies and is treated in a manner consistent withthe principles underlying Reg. §1.367(a)-8(k).

41

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 42/52

MODIFICATIONS TO OTHER §367(a)

REGULATIONS IN T.D. 9615

42

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 43/52

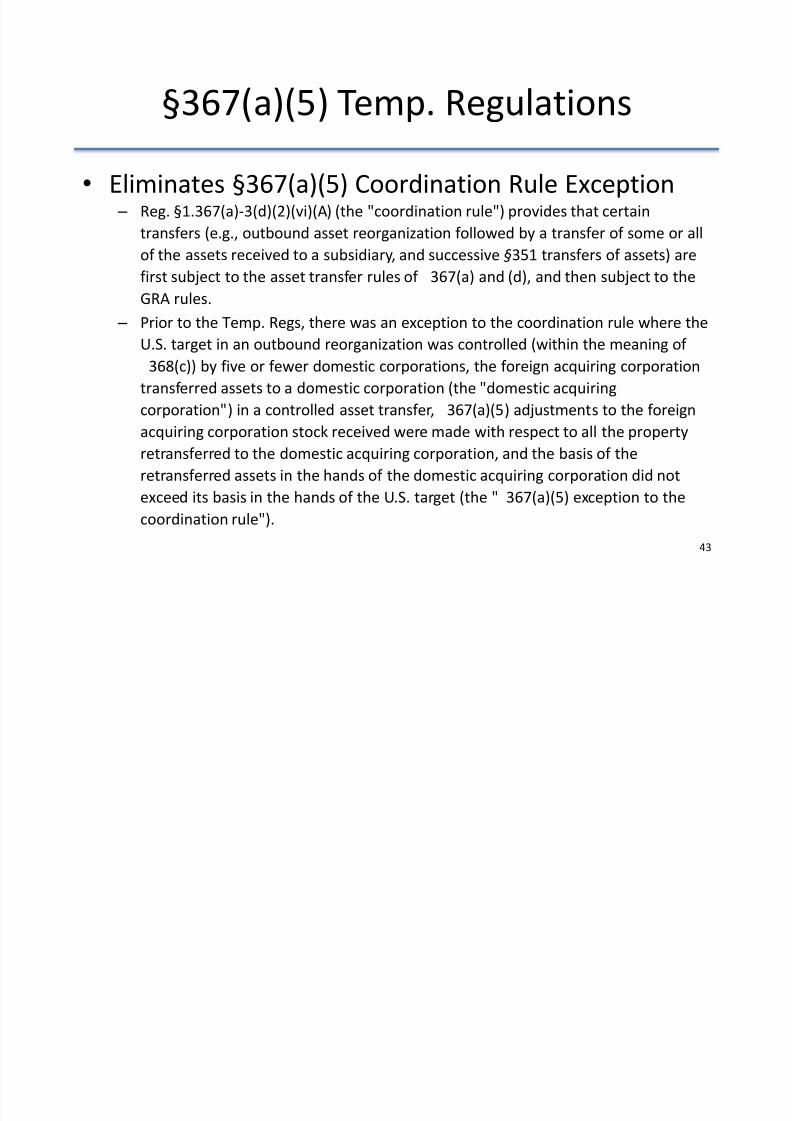

§367(a)(5) Temp. Regulations• Eliminates §367(a)(5) Coordination Rule Exception

– Reg. §1.367(a)-3(d)(2)(vi)(A) (the "coordination rule") provides that certain

transfers (e.g., outbound asset reorganization followed by a transfer of some or all

of the assets received to a subsidiary, and successive §351 transfers of assets) are

first subject to the asset transfer rules of 367(a) and (d), and then subject to the

GRA rules.

–Prior to the Temp. Regs, there was an exception to the coordination rule where the

U.S. target in an outbound reorganization was controlled (within the meaning of

368(c)) by five or fewer domestic corporations, the foreign acquiring corporation

transferred assets to a domestic corporation (the "domestic acquiring

corporation") in a controlled asset transfer, 367(a)(5) adjustments to the foreign

acquiring corporation stock received were made with respect to all the propertyretransferred to the domestic acquiring corporation, and the basis of the

retransferred assets in the hands of the domestic acquiring corporation did not

exceed its basis in the hands of the U.S. target (the " 367(a)(5) exception to the

coordination rule").

43

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 44/52

MODIFICATIONS TO §367(b)

REGULATIONS IN T.D. 9614

44

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 45/52

Background on §367(b)• §367(b)(1) provides that in the case of any exchange described in §§332,

351, 354, 355, 356, or 361 in connection with which there is no transfer of

property described in §367(a)(1), a foreign corporation shall be consideredto be a corporation except to the extent provided in regulations prescribed

by the Secretary which are necessary or appropriate to prevent the

avoidance of Federal income taxes.

• A fundamental policy of §367(b) is to preserve the potential application of§1248 following certain §367(b) exchanges.

• For example, the inclusion in income of the §1248 amount is required if

the §367(b) exchange results in the loss of §1248 shareholder status or if

the foreign acquired corporation or foreign acquiring corporation is not aCFC immediately after the §367(b) exchange. See Reg. §1.367(b)-4(b)(1)(i).

45

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 46/52

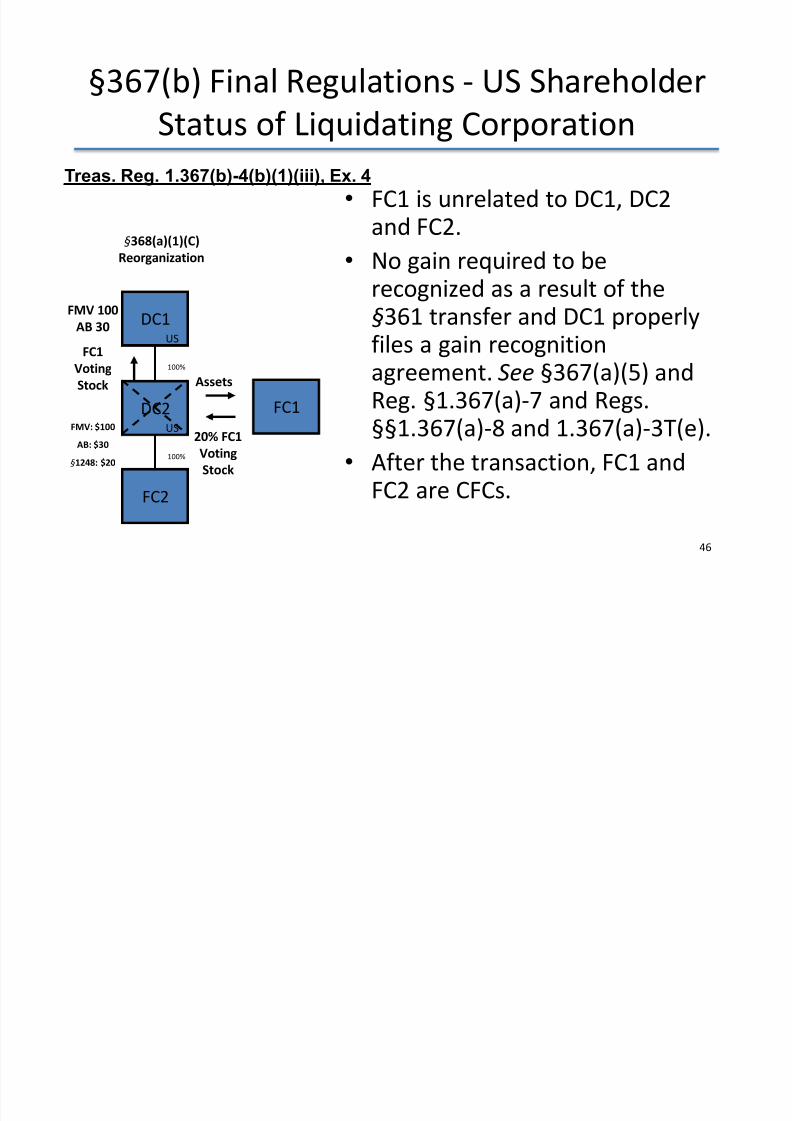

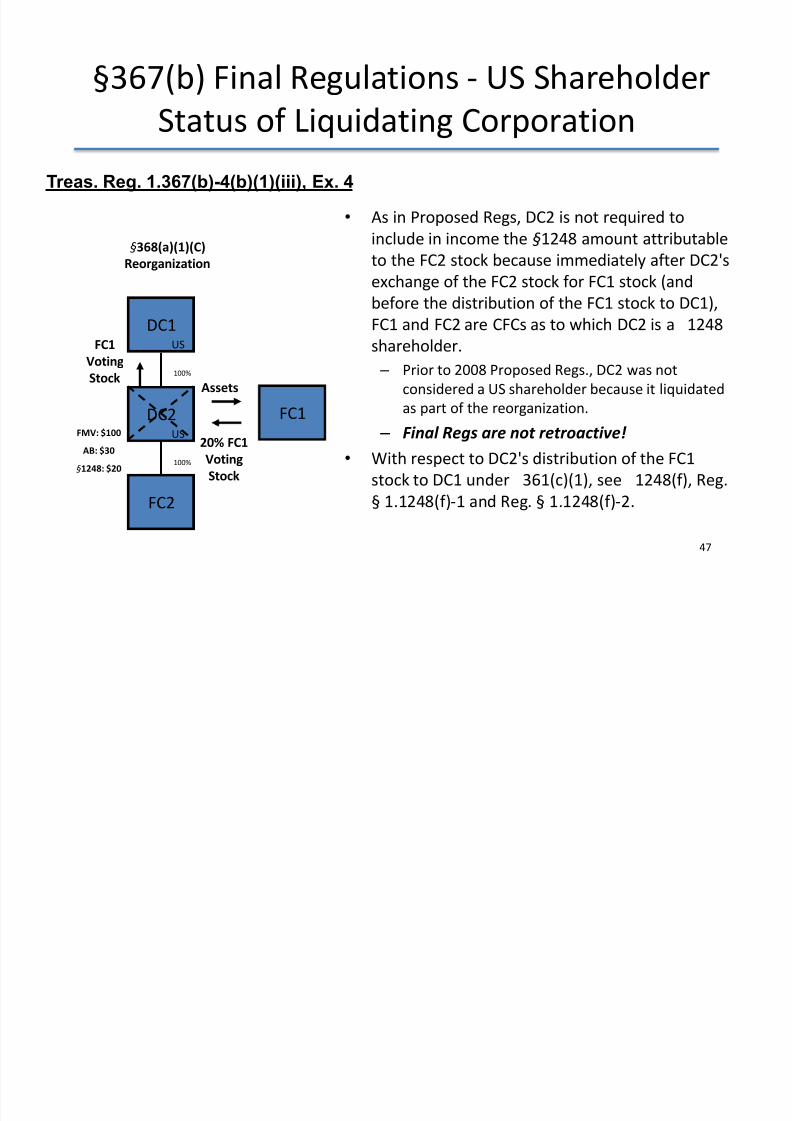

§367(b) Final Regulations - US Shareholder

Status of Liquidating Corporation

• FC1 is unrelated to DC1, DC2

and FC2.• No gain required to be

recognized as a result of the§361 transfer and DC1 properlyfiles a gain recognitionagreement. See §367(a)(5) andReg. §1.367(a)-7 and Regs.

§§1.367(a)-8 and 1.367(a)-3T(e).• After the transaction, FC1 and

FC2 are CFCs.

Assets

20% FC1Voting

Stock

DC1

DC2 FC1

FC2

FMV 100

AB 30FC1

Voting

Stock

US

US

100%

100%

FMV: $100

AB: $30

§1248: $20

§368(a)(1)(C)

Reorganization

46

Treas. Reg. 1.367(b)-4(b)(1)(iii), Ex. 4

§367(b) Fi l R l ti US Sh h ld

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 47/52

• As in Proposed Regs, DC2 is not required toinclude in income the §1248 amount attributable

to the FC2 stock because immediately after DC2's

exchange of the FC2 stock for FC1 stock (and

before the distribution of the FC1 stock to DC1),

FC1 and FC2 are CFCs as to which DC2 is a 1248shareholder.

– Prior to 2008 Proposed Regs., DC2 was not

considered a US shareholder because it liquidated

as part of the reorganization.

– Final Regs are not retroactive! • With respect to DC2's distribution of the FC1

stock to DC1 under 361(c)(1), see 1248(f), Reg.

§ 1.1248(f)-1 and Reg. § 1.1248(f)-2.

Assets

20% FC1Voting

Stock

DC1

DC2 FC1

FC2

FC1

Voting

Stock

US

US

100%

100%

FMV: $100

AB: $30

§1248: $20

§368(a)(1)(C)

Reorganization

§367(b) Final Regulations - US Shareholder

Status of Liquidating Corporation

47

Treas. Reg. 1.367(b)-4(b)(1)(iii), Ex. 4

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 48/52

MODIFICATION TO §1248 REGULATIONS

(T.D. 9614)

48

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 49/52

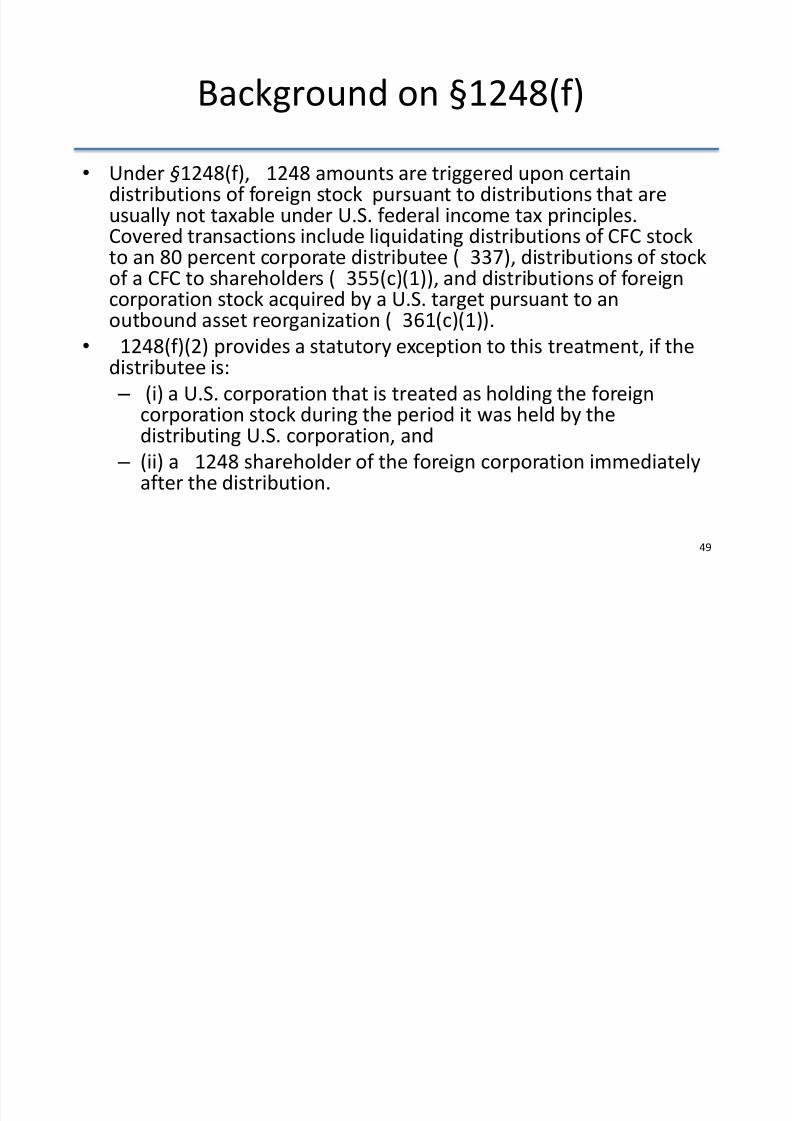

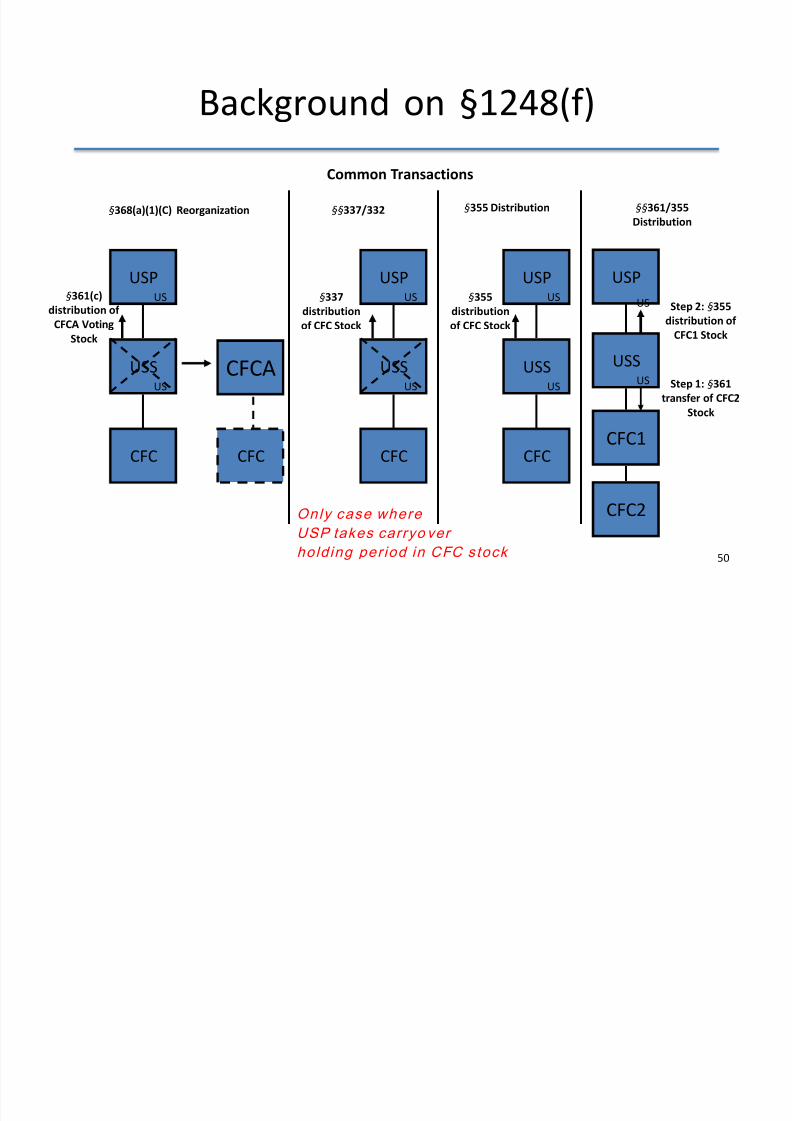

• Under §1248(f), 1248 amounts are triggered upon certaindistributions of foreign stock pursuant to distributions that areusually not taxable under U.S. federal income tax principles.Covered transactions include liquidating distributions of CFC stockto an 80 percent corporate distributee ( 337), distributions of stockof a CFC to shareholders ( 355(c)(1)), and distributions of foreigncorporation stock acquired by a U.S. target pursuant to anoutbound asset reorganization ( 361(c)(1)).

• 1248(f)(2) provides a statutory exception to this treatment, if thedistributee is:

– (i) a U.S. corporation that is treated as holding the foreigncorporation stock during the period it was held by the

distributing U.S. corporation, and – (ii) a 1248 shareholder of the foreign corporation immediately

after the distribution.

Background on §1248(f)

49

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 50/52

Background on §1248(f)

USP

USS CFCA

CFC

§361(c)

distribution of

CFCA Voting

Stock

US

US

§368(a)(1)(C) Reorganization

CFC

USP

USS

CFC

§337

distribution

of CFC Stock

US

US

§§337/332

USP

USS

CFC

§355

distribution

of CFC Stock

US

US

§355 Distribution

USP

USS

CFC1

US

US

§§361/355

Distribution

CFC2

Common Transactions

Step 1: §361

transfer of CFC2

Stock

Step 2: §355

distribution of

CFC1 Stock

50

Only case where

USP takes carryo ver

holding period in CFC stock

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 51/52

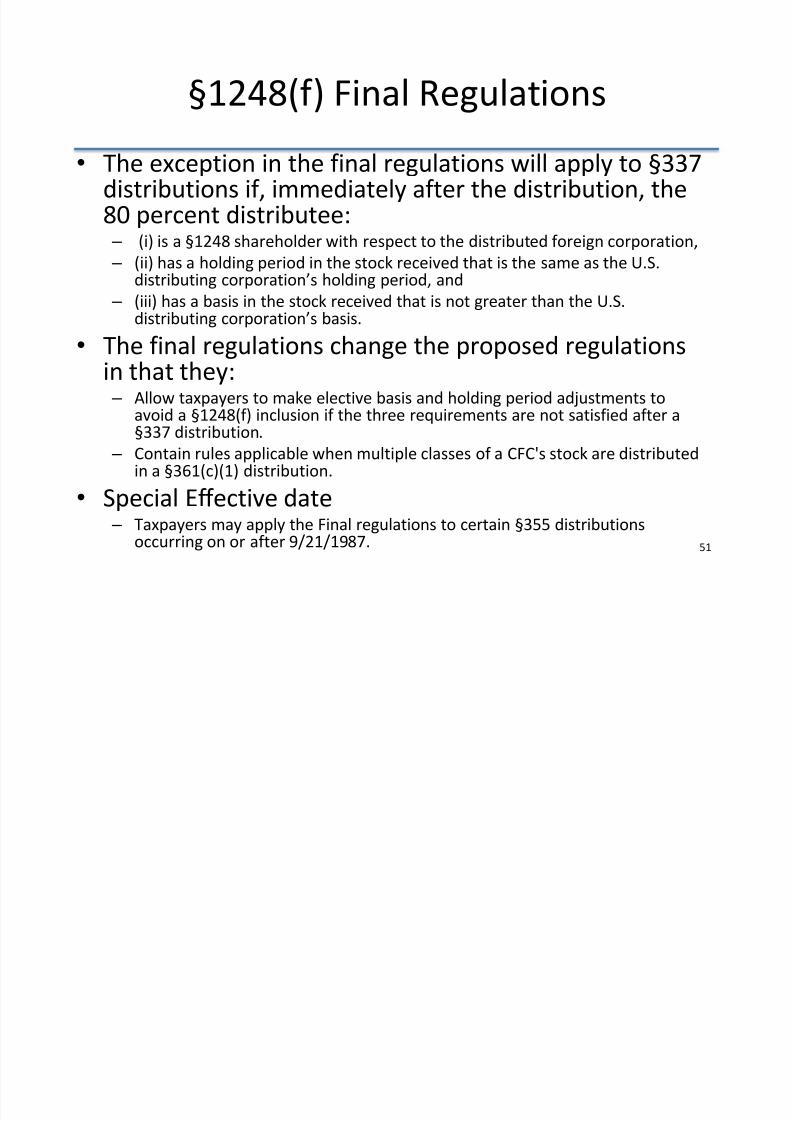

• The exception in the final regulations will apply to §337distributions if, immediately after the distribution, the

80 percent distributee: – (i) is a §1248 shareholder with respect to the distributed foreign corporation,

– (ii) has a holding period in the stock received that is the same as the U.S.distributing corporation’s holding period, and

– (iii) has a basis in the stock received that is not greater than the U.S.distributing corporation’s basis.

• The final regulations change the proposed regulationsin that they: – Allow taxpayers to make elective basis and holding period adjustments to

avoid a §1248(f) inclusion if the three requirements are not satisfied after a

§337 distribution. – Contain rules applicable when multiple classes of a CFC's stock are distributedin a §361(c)(1) distribution.

• Special Effective date – Taxpayers may apply the Final regulations to certain §355 distributions

occurring on or after 9/21/1987.

§1248(f) Final Regulations

51

8/13/2019 Faust 367a5 Slides

http://slidepdf.com/reader/full/faust-367a5-slides 52/52

This document is for general guidance only, and does not constitute

the provision of legal advice, accounting services, or written tax

advice under Circular 230. The information provided herein should not

be used as a substitute for consultation with professional tax,

accounting, legal or other competent advisers. Before making any

decision or taking any action, you should consult with a professional

adviser who has been provided with all pertinent facts relevant to your

particular situation.

![[Bill Faust, Michael Faust] Pitch Yourself Stando(BookFi.org)](https://img.pdfslide.us/doc/110x75/55cf8f5d550346703b9b9f46/bill-faust-michael-faust-pitch-yourself-standobookfiorg.jpg)