Embed Size (px)

Citation preview

Factor Models

Riccardo Colacito

Foundations of Financial Markets 2

Diversification and Portfolio Risk

• Market risk– Systematic or Nondiversifiable

• Firm-specific risk– Diversifiable or nonsystematic

Foundations of Financial Markets 3

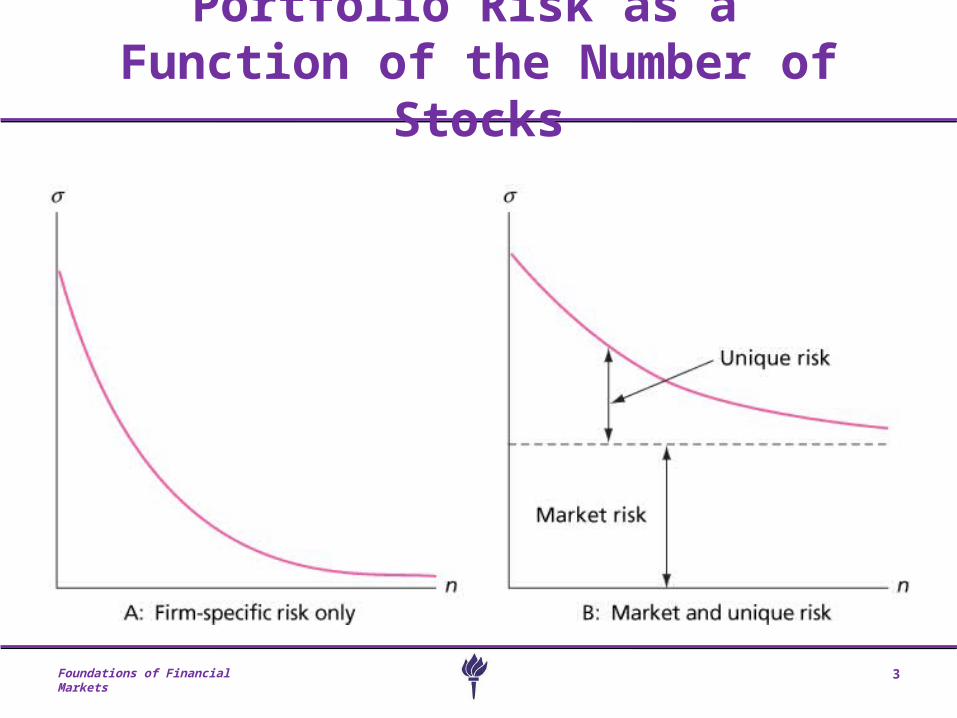

Portfolio Risk as a Function of the Number of Stocks

Foundations of Financial Markets 4

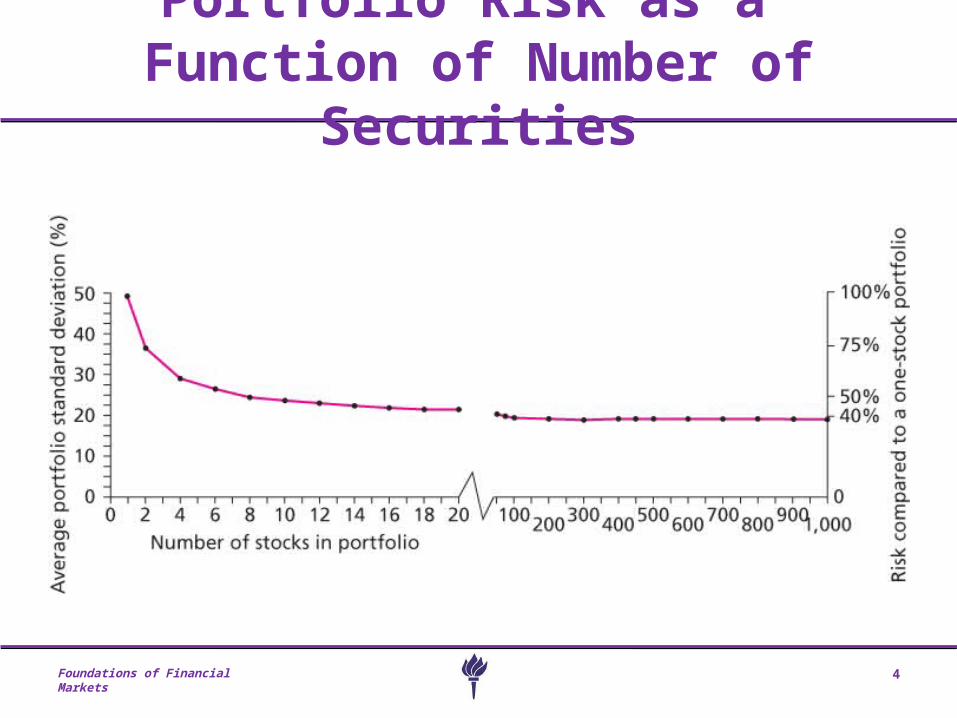

Portfolio Risk as a Function of Number of Securities

Foundations of Financial Markets 5

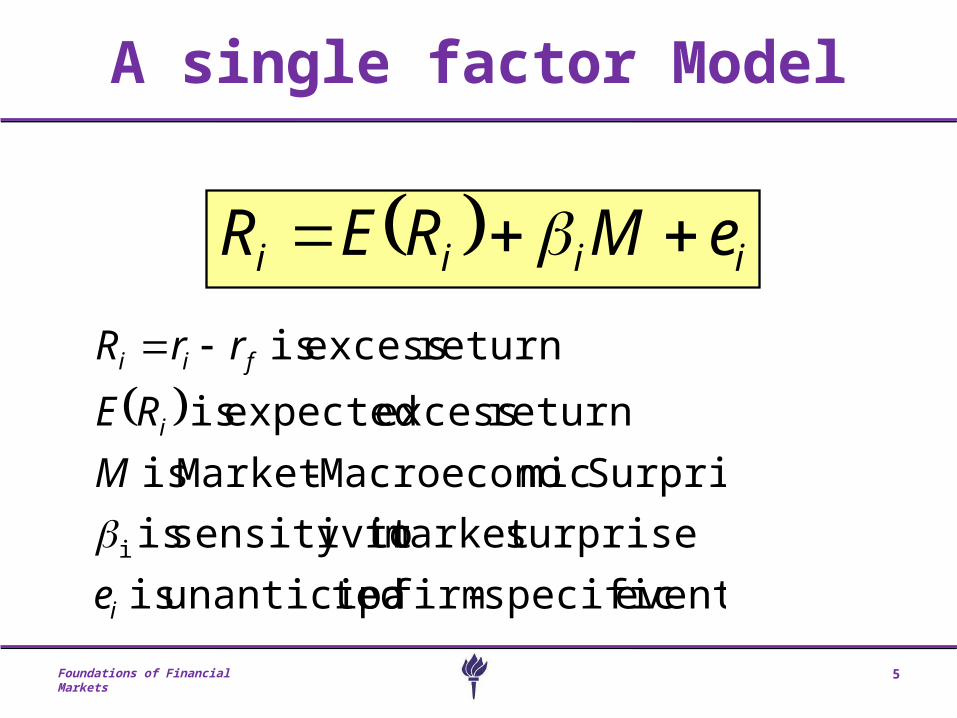

A single factor Model

iiii eMRER

event specific-firm tedunanticipa is

surprisemarket y tosensitivit is

Surprise micMacroecono-Market is

return excess expected is

return excess is

i

i

i

fii

e

M

RE

rrR

Foundations of Financial Markets 6

What is M?

• Anything that can be regarded as a proxy for macroeconomic risk

• Commonly used factor: a broad market index like the S&P500

• Call it Rm

Foundations of Financial Markets 7

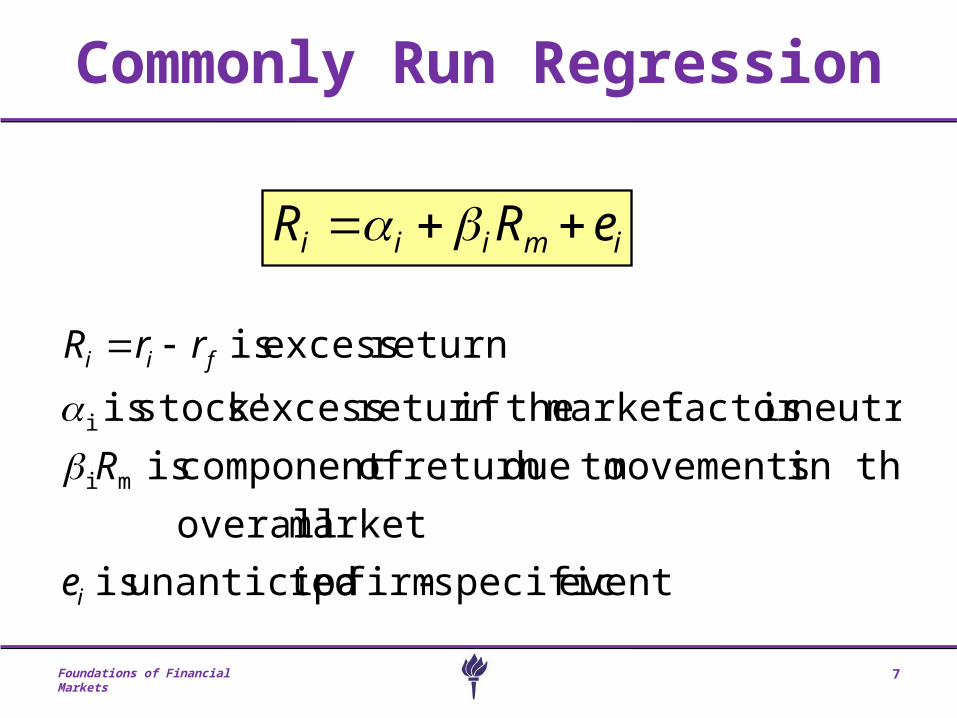

Commonly Run Regression

imiii eRR

event specific-firm tedunanticipa is

market overall

in the movements toduereturn ofcomponent is

neutral isfactor market theifreturn excess sstock' is

return excess is

mi

i

i

fii

e

R

rrR

Foundations of Financial Markets 8

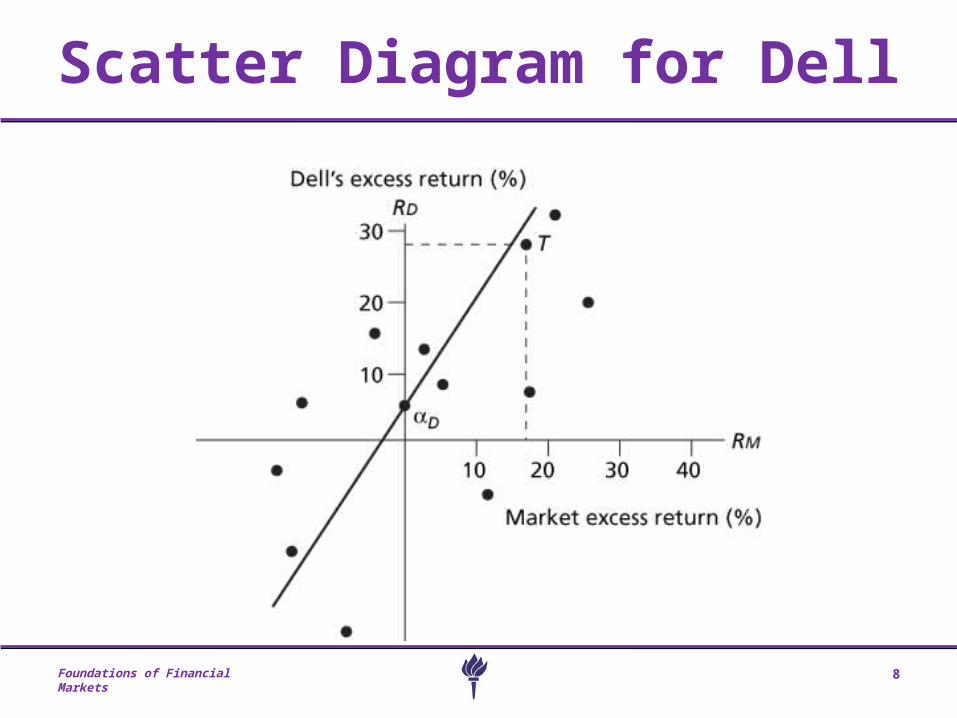

Scatter Diagram for Dell

Foundations of Financial Markets 9

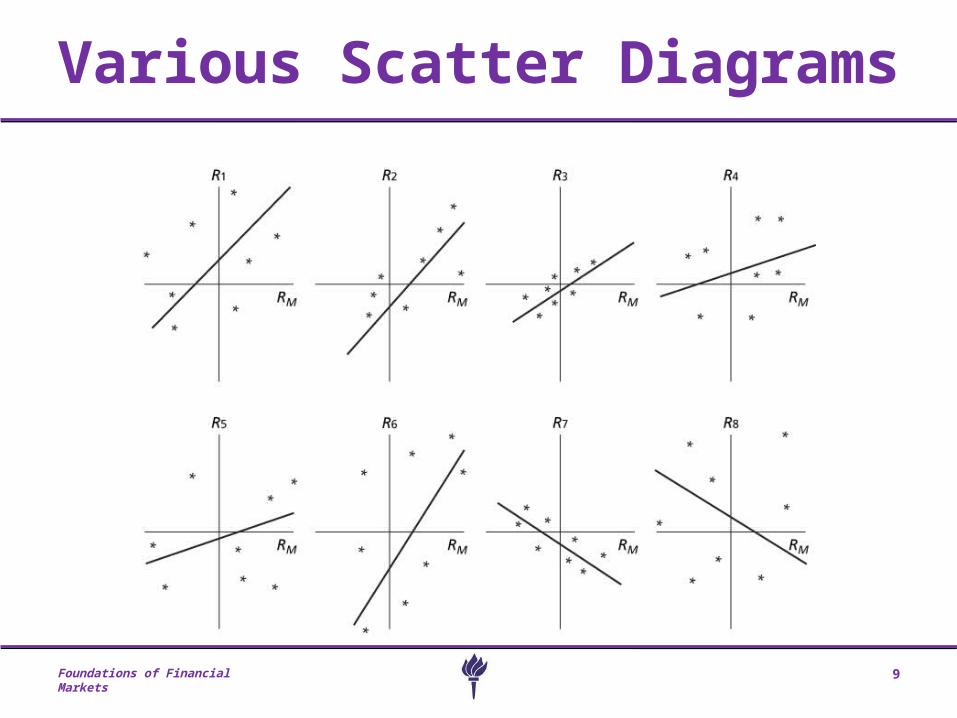

Various Scatter Diagrams

Foundations of Financial Markets 10

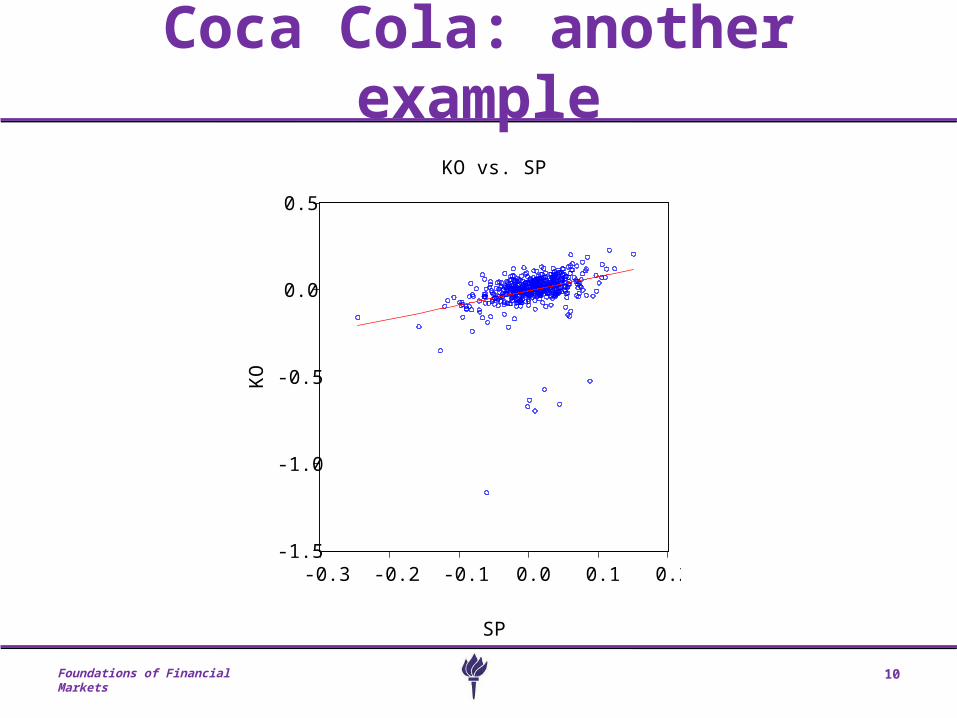

Coca Cola: another example

-1.5

-1.0

-0.5

0.0

0.5

-0.3 -0.2 -0.1 0.0 0.1 0.2

SP

KO

KO vs. SP

Foundations of Financial Markets 11

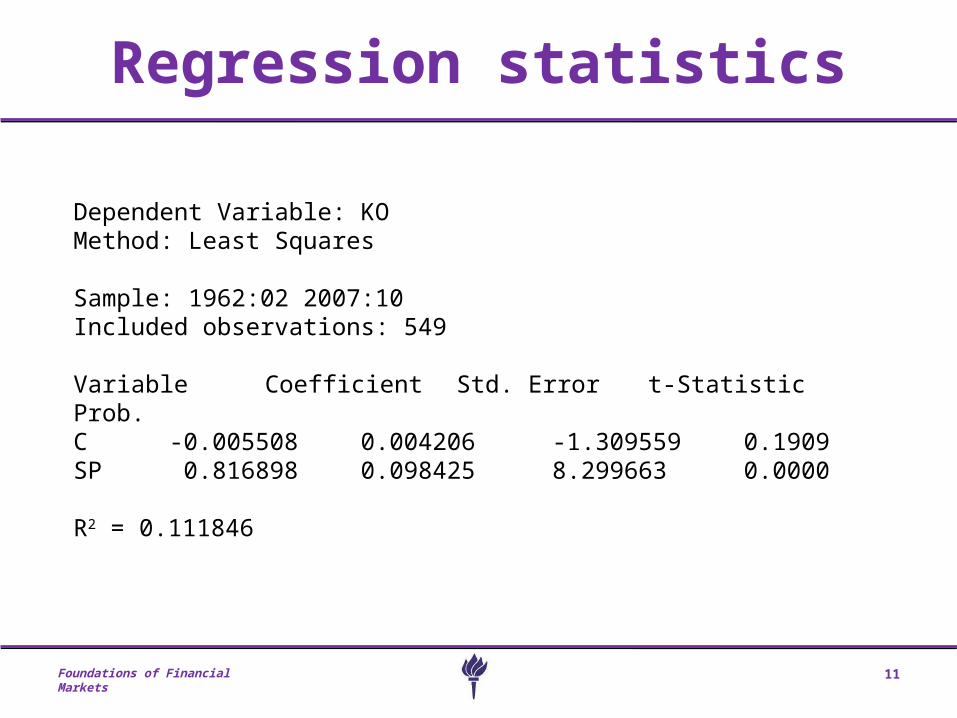

Regression statistics

Dependent Variable: KOMethod: Least SquaresSample: 1962:02 2007:10Included observations: 549

Variable Coefficient Std. Error t-Statistic Prob. C -0.005508 0.004206 -1.309559 0.1909SP 0.816898 0.098425 8.299663 0.0000

R2 = 0.111846

Foundations of Financial Markets 12

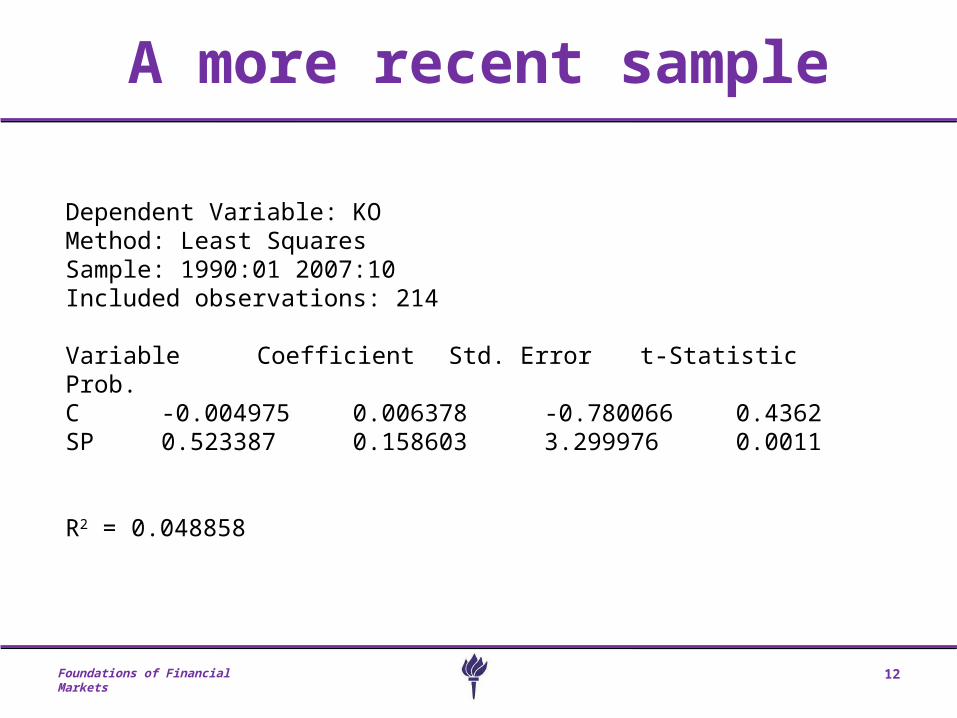

A more recent sample

Dependent Variable: KOMethod: Least SquaresSample: 1990:01 2007:10Included observations: 214

Variable Coefficient Std. Error t-Statistic Prob. C -0.004975 0.006378 -0.780066 0.4362SP 0.523387 0.158603 3.299976 0.0011

R2 = 0.048858

Foundations of Financial Markets 13

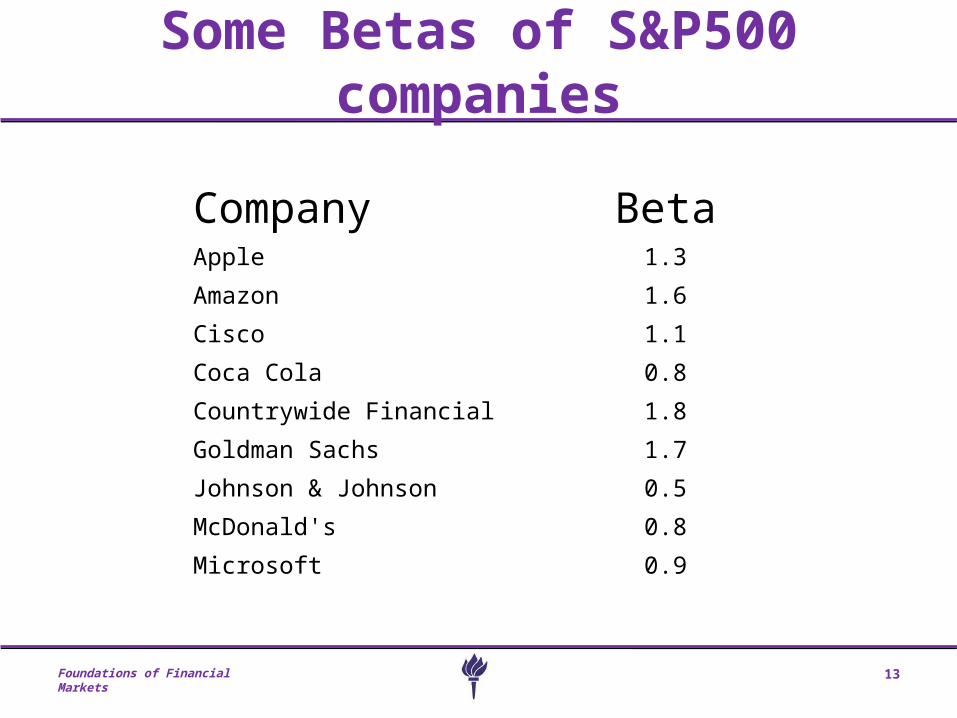

Some Betas of S&P500 companies

Company BetaApple 1.3

Amazon 1.6

Cisco 1.1

Coca Cola 0.8

Countrywide Financial 1.8

Goldman Sachs 1.7

Johnson & Johnson 0.5

McDonald's 0.8

Microsoft 0.9

Foundations of Financial Markets 14

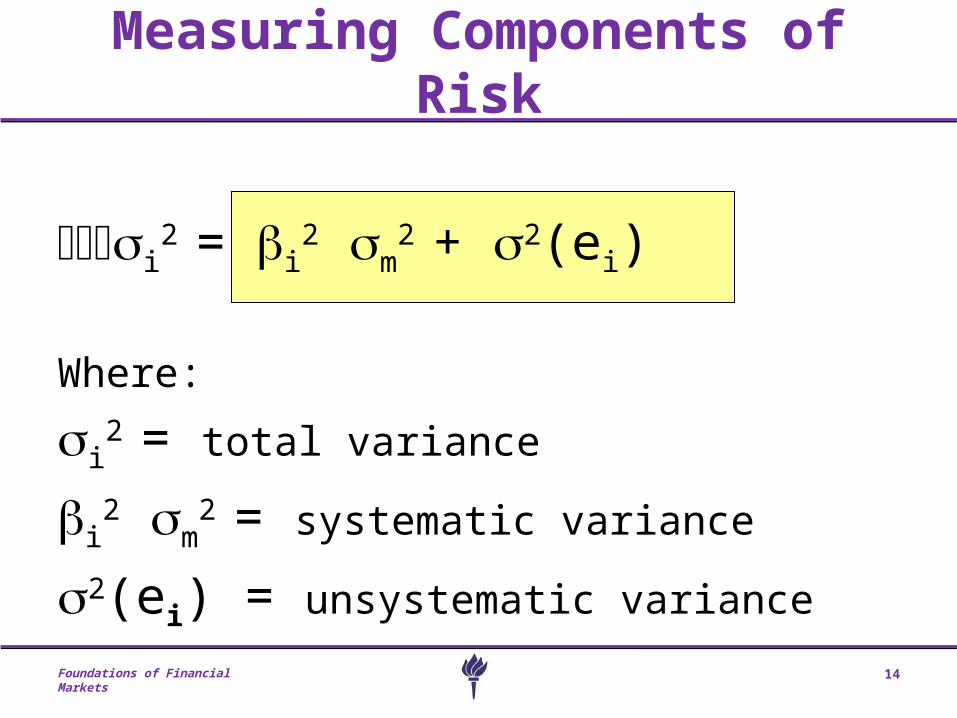

Measuring Components of Risk

i2 = i

2 m2 + 2(ei)

Where:

i2 = total variance

i2 m

2 = systematic variance

2(ei) = unsystematic variance

Foundations of Financial Markets 15

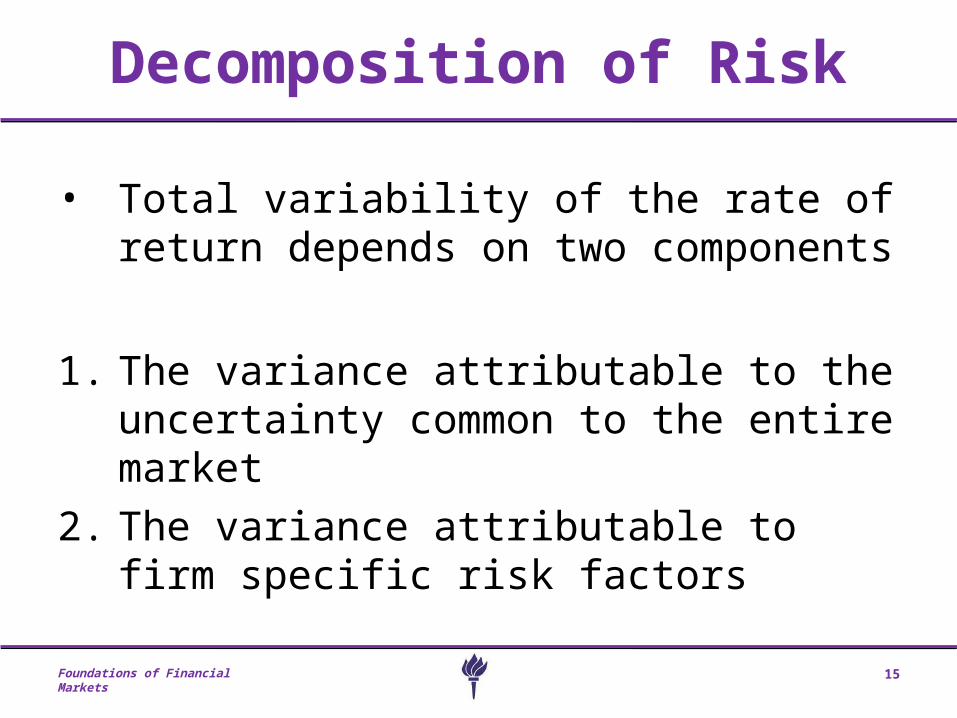

Decomposition of Risk

• Total variability of the rate of return depends on two components

1. The variance attributable to the uncertainty common to the entire market

2. The variance attributable to firm specific risk factors

Foundations of Financial Markets 16

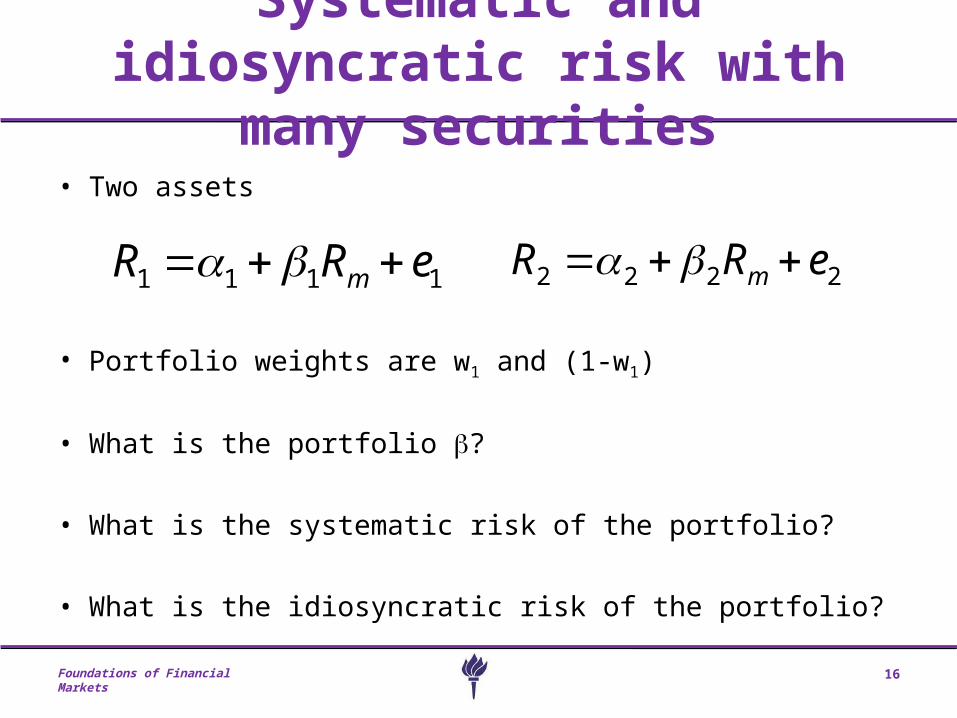

Systematic and idiosyncratic risk with many securities

• Two assets

• Portfolio weights are w1 and (1-w1)

• What is the portfolio ?

• What is the systematic risk of the portfolio?

• What is the idiosyncratic risk of the portfolio?

1111 eRR m 2222 eRR m

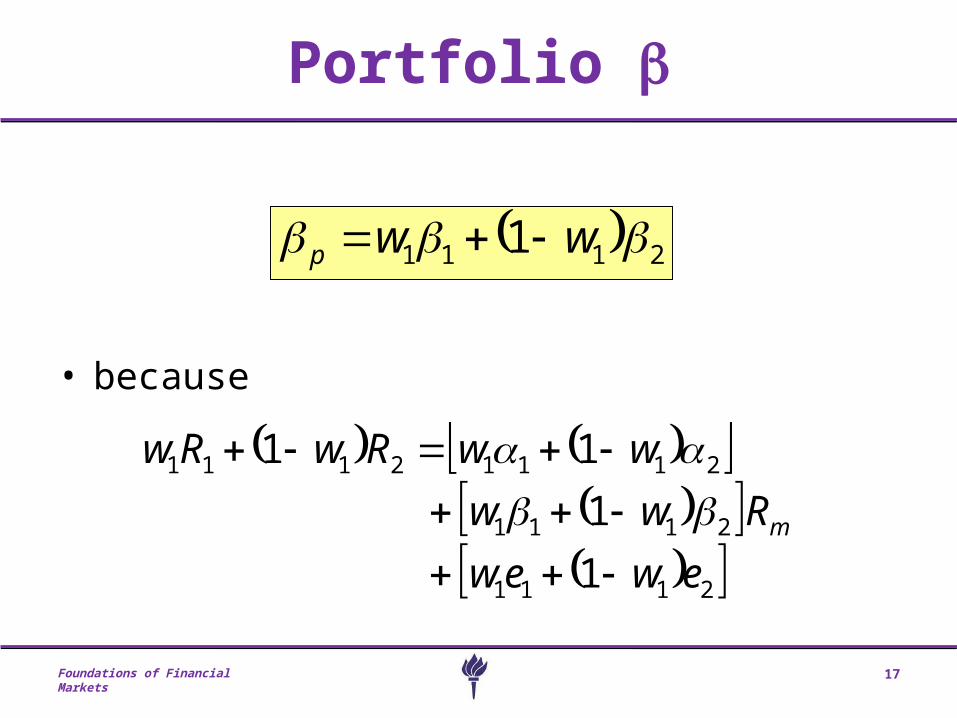

Foundations of Financial Markets 17

Portfolio

• because

2111

2111

21112111

1

1

11

ewew

Rww

wwRwRw

m

2111 1 wwp

Foundations of Financial Markets 18

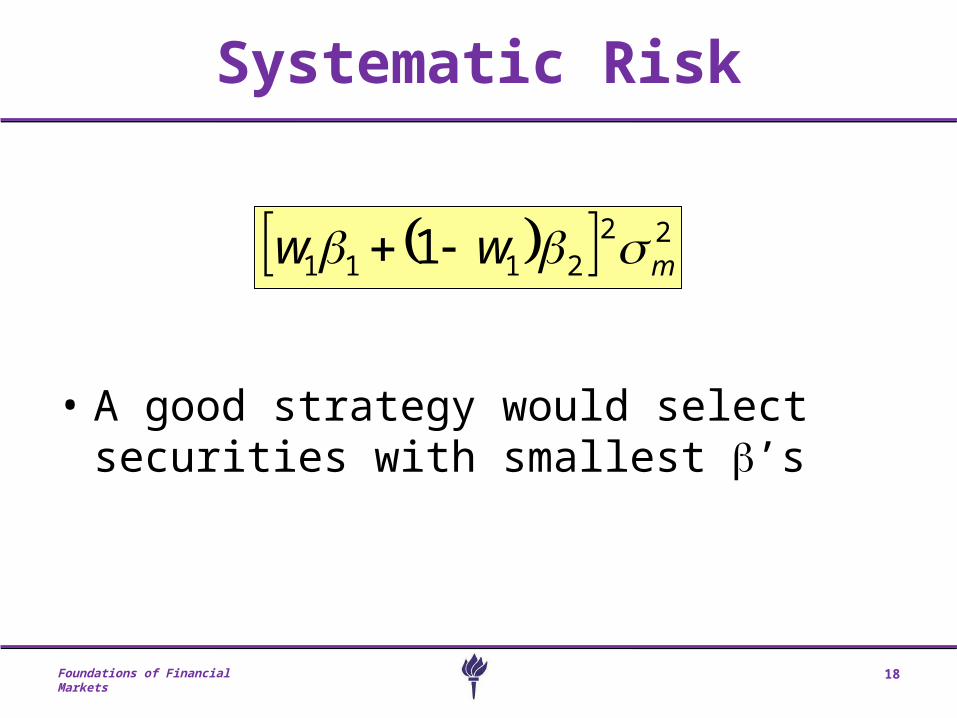

Systematic Risk

• A good strategy would select securities with smallest ’s

222111 1 mww

Foundations of Financial Markets 19

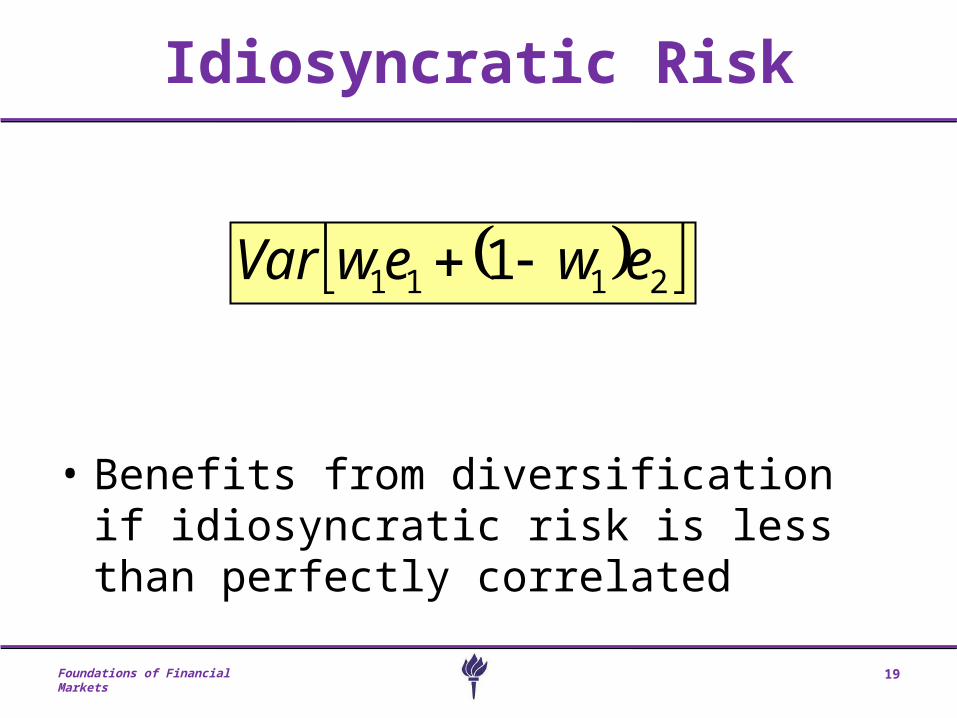

Idiosyncratic Risk

• Benefits from diversification if idiosyncratic risk is less than perfectly correlated

2111 1 ewewVar

Foundations of Financial Markets 20

Advantages of the Single Index Model

• Reduces the number of inputs for diversification

• Easier for security analysts to specialize

Foundations of Financial Markets 21

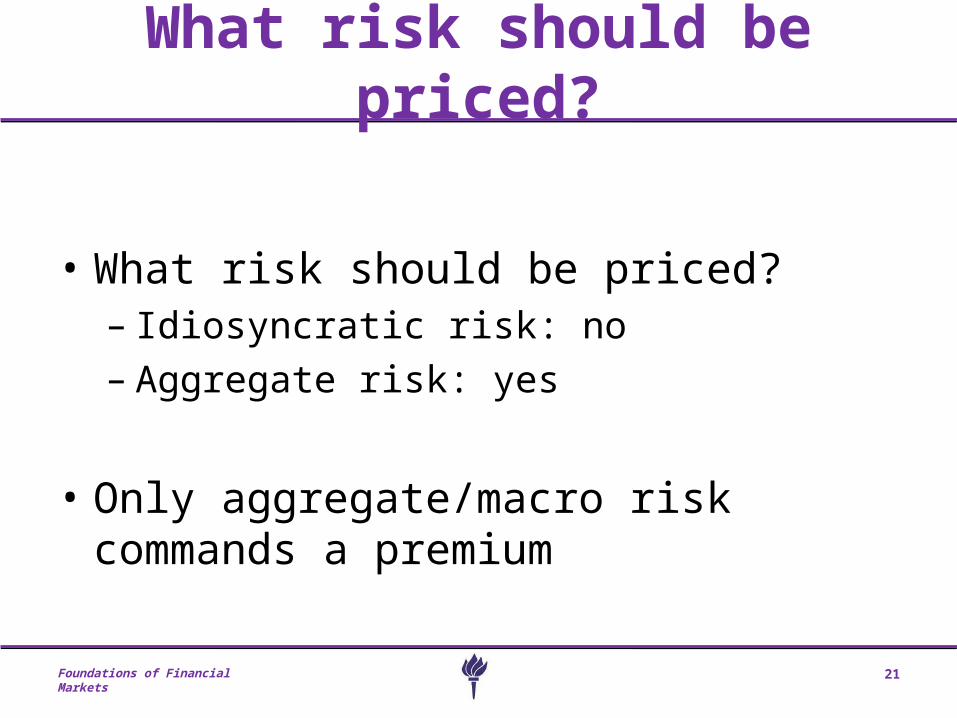

What risk should be priced?

• What risk should be priced?– Idiosyncratic risk: no– Aggregate risk: yes

• Only aggregate/macro risk commands a premium

Foundations of Financial Markets 22

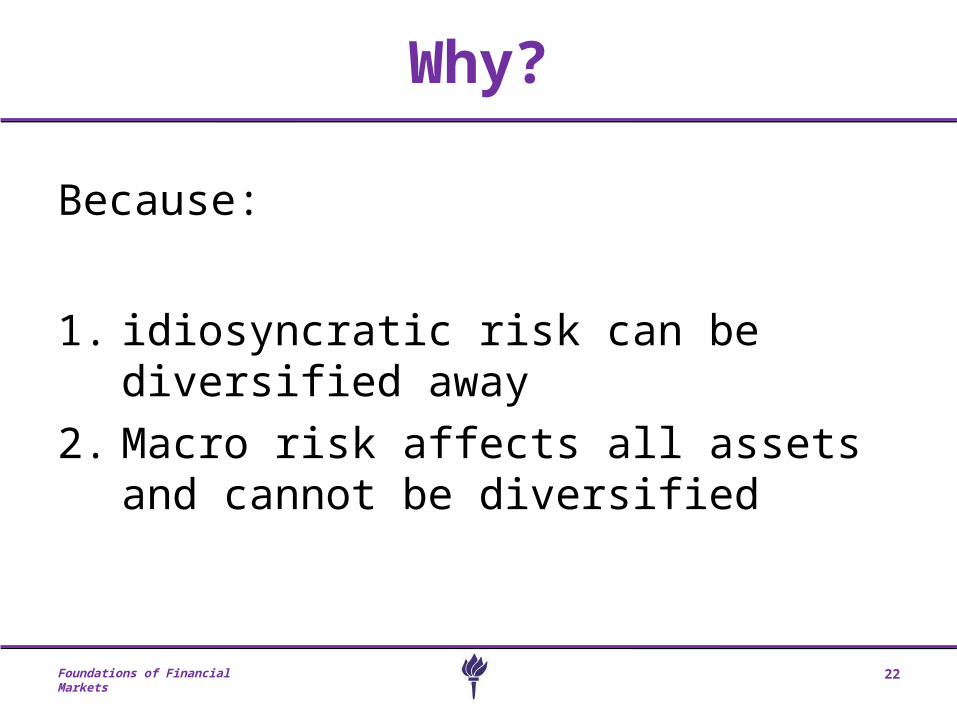

Why?

Because:

1. idiosyncratic risk can be diversified away

2. Macro risk affects all assets and cannot be diversified

Foundations of Financial Markets 23

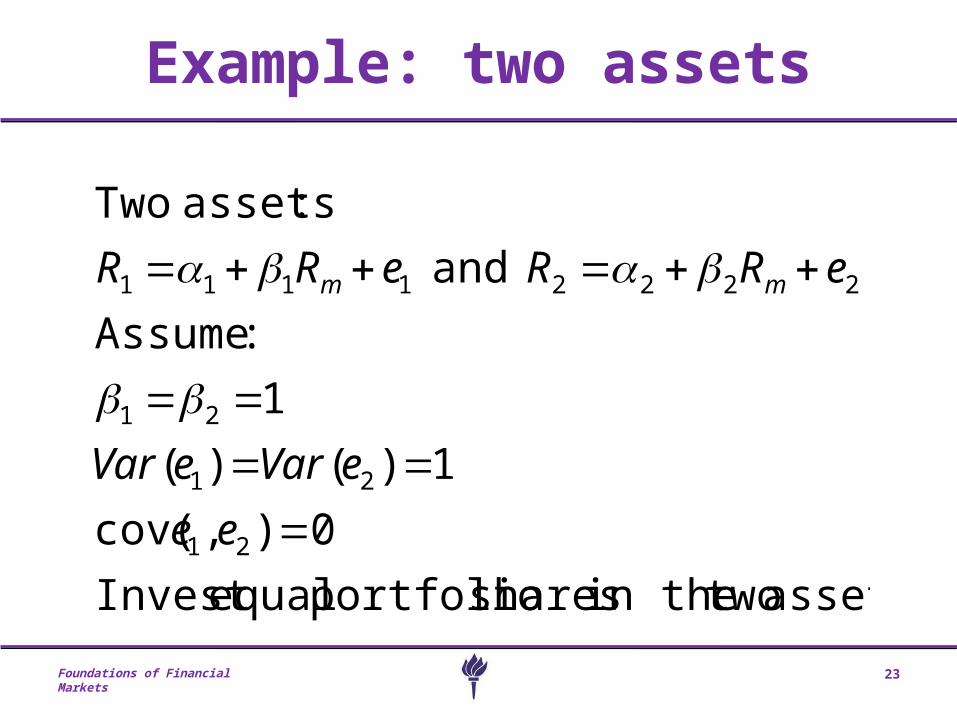

Example: two assets

assets twoin the shares portfolio equalInvest

0),cov(

1)()(

1

:Assume

and

:assets Two

21

21

21

22221111

ee

eVareVar

eRReRR mm

Foundations of Financial Markets 24

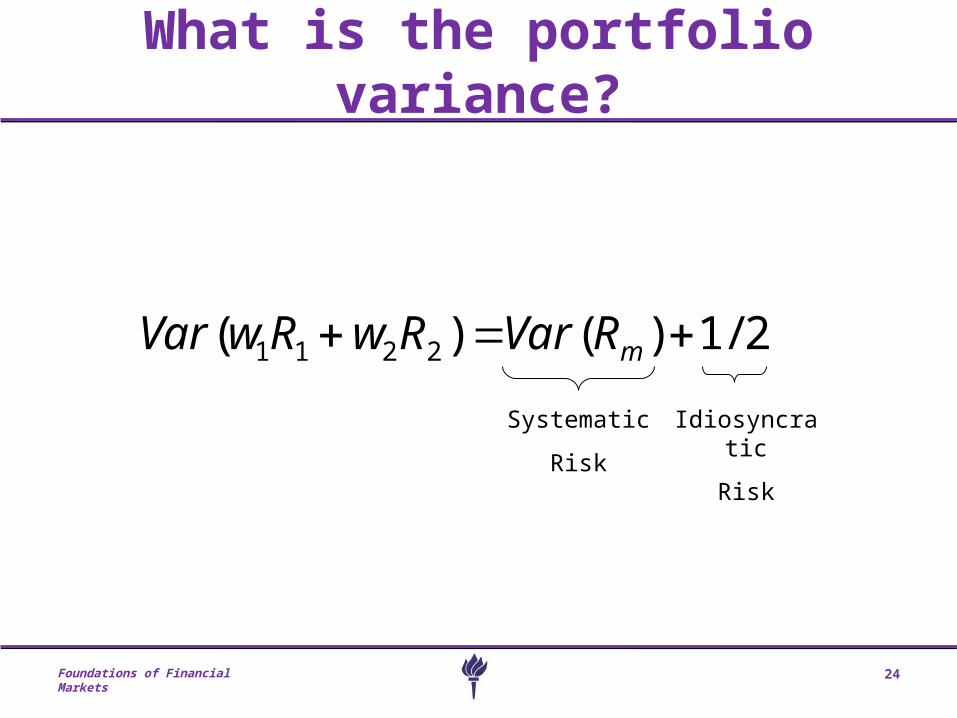

What is the portfolio variance?

2/1)()( 2211 mRVarRwRwVar

Systematic

Risk

Idiosyncratic

Risk

Foundations of Financial Markets 25

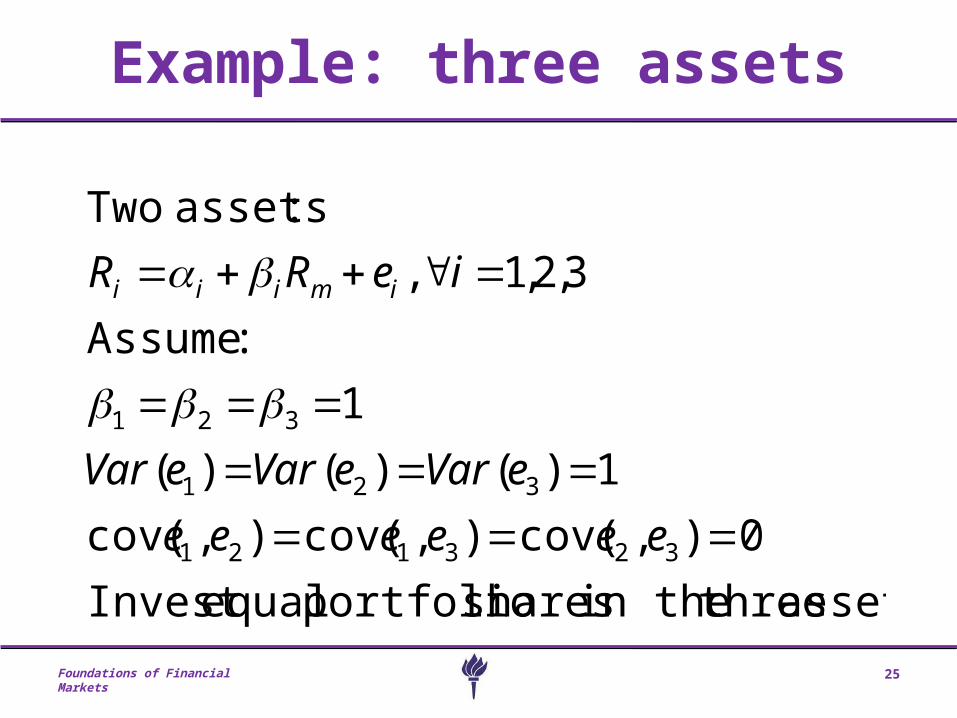

Example: three assets

assets threein the shares portfolio equalInvest

0),cov(),cov(),cov(

1)()()(

1

:Assume

3,2,1 ,

:assets Two

323121

321

321

eeeeee

eVareVareVar

ieRR imiii

Foundations of Financial Markets 26

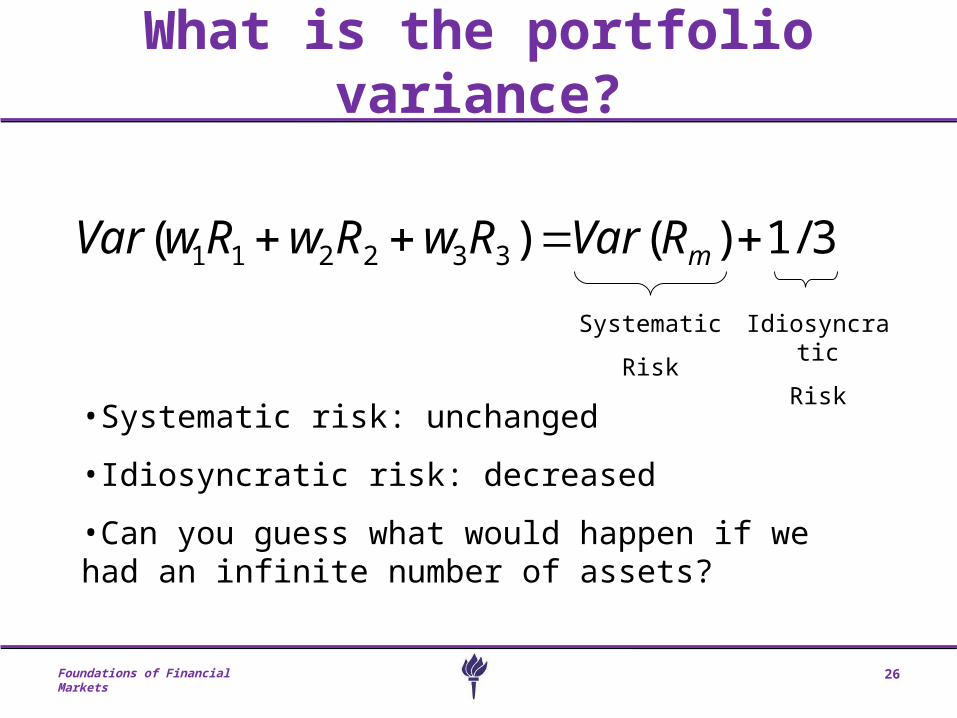

What is the portfolio variance?

3/1)()( 332211 mRVarRwRwRwVar

Systematic

Risk

Idiosyncratic

Risk

•Systematic risk: unchanged

•Idiosyncratic risk: decreased

•Can you guess what would happen if we had an infinite number of assets?

Foundations of Financial Markets 27

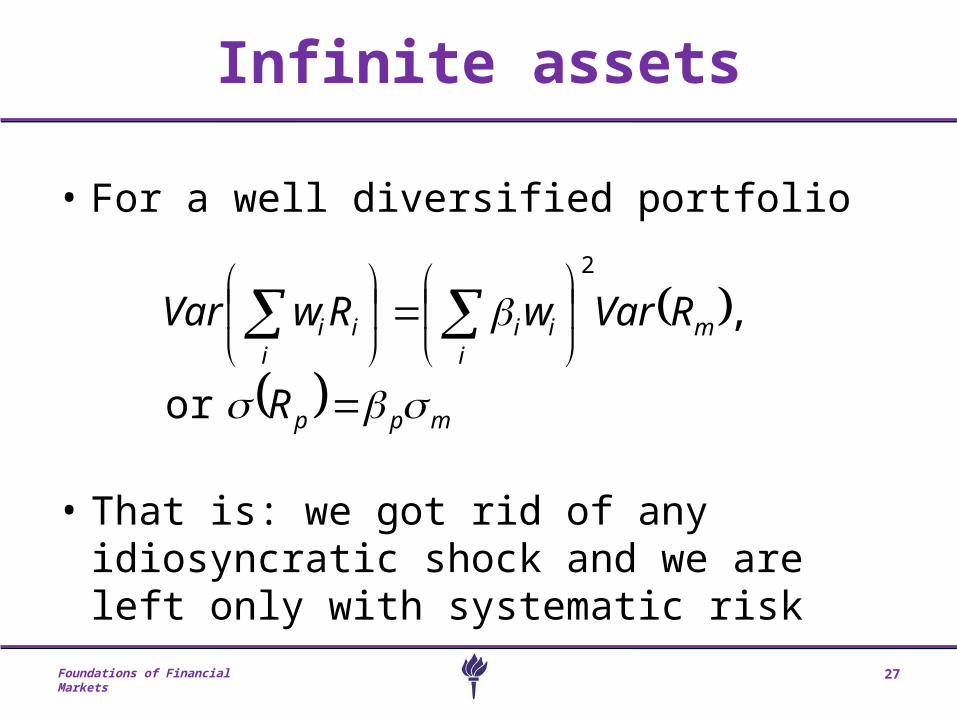

Infinite assets

• For a well diversified portfolio

• That is: we got rid of any idiosyncratic shock and we are left only with systematic risk

mpp

mi

iii

ii

R

RVarwRwVar

or

,2

Foundations of Financial Markets 28

What lesson did we learn?

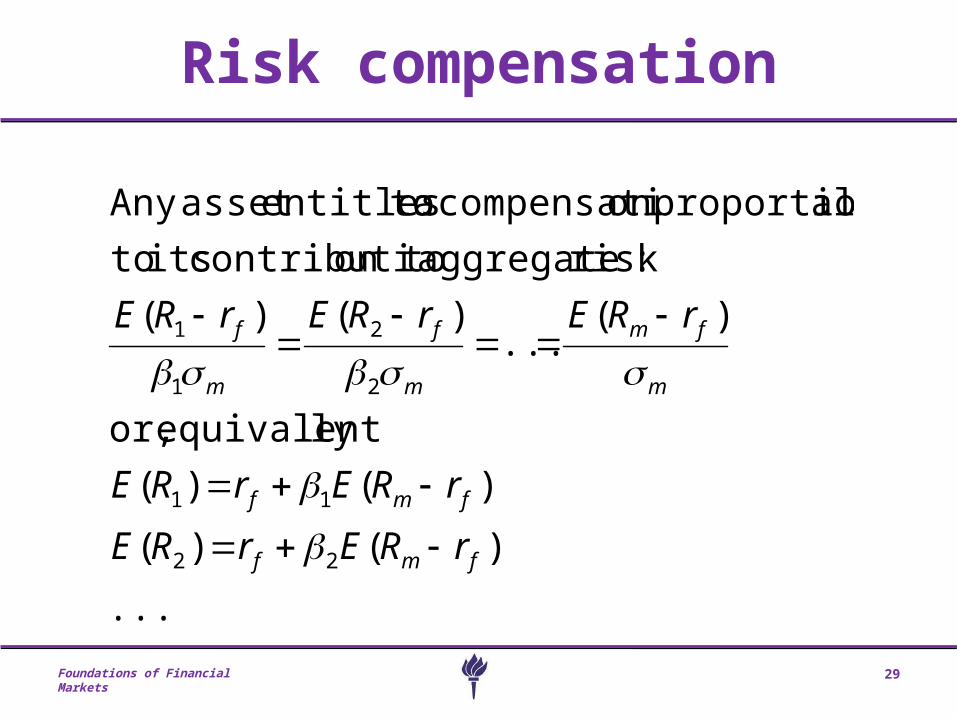

• The only source of risk that we are entitled to ask a compensation for is aggregate risk.

• Idiosyncratic risk does not entitle to any compensation because it can be diversified away.

Foundations of Financial Markets 29

Risk compensation

...

)()(

)()(

lyequivalent or,

)(...

)()(

:risk aggregate on tocontributi its to

alproportionon compensati a toentitlesasset Any

22

11

2

2

1

1

fmf

fmf

m

fm

m

f

m

f

rRErRE

rRErRE

rRErRErRE

Foundations of Financial Markets 30

This opens up to our next topic

• The Capital Asset Pricing model!