Embed Size (px)

Citation preview

F-Secure CorporationInterim report 2Q 2008

July 29th, 2008

Kimmo Alkio, President and CEO

Interim Report 2Q08 – July 29th , 2008 Page 2

Q2 Highlights

• Solid revenue growth of 16% to 27.2m

• Good profitability of 4.7m, 17% of revenues

• Portfolio expansion: on-line back service for ISPs

• Vodafone: Global Frame Agreement won for Mobile security

Interim Report 2Q08 – July 29th , 2008 Page 3

Q2 Revenues

• Solid overall growth of 16% to 27.2m

• Strong ISP growth to 11.6m

• +6% quarter over quarter

• +35% from 2Q07 (YoY)

• Traditional channel sales improved

• +5% growth from 2Q07

0

5

10

15

20

25

30

Revenues

Interim Report 2Q08 – July 29th , 2008 Page 4

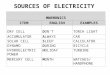

Q2 Costs

• Q2 Costs ~20.7m

• Continuously investing into future

growth

• Costs include

• Capitalization of Development costs

marginal

• Granted stock options ~0.2m

• Gross margin 91% (92%)

0

5

10

15

20

25

S&M R&D G&A write-off

Interim Report 2Q08 – July 29th , 2008 Page 5

Q2 Operating Result

• EBIT 4.7m

• 17% of revenues

• +27% EBIT growth from 2Q07

• Equity ratio strong

• Jun 30, 2008 82%

• Mar 31, 2008 71%*

• Dec 31, 2007 82%

-2

-1

0

1

2

3

4

5

6

7

Without impairment loss of Network Control* If dividends were paid in March

equity ratio 81% - was paid in April

Interim Report 2Q08 – July 29th , 2008 Page 6

Development of EBIT margin

• Continue to prioritise growth over short

term profitability

• Average EBIT has improved gradually

• The 2-4 year goal is to reach 25% EBIT

level

0 %

5 %

10 %

15 %

20 %

25 %

30 %

EBIT% Ave (4 qrts)

Graph shows EBIT without the non-recurring

impairment loss of Network Control in 4Q06

Interim Report 2Q08 – July 29th , 2008 Page 7

Q2 Cash position

• Cash flow:

• Excluding dividend 3.8m

• After dividend -7.1m

• Liquid assets 83.3m (78.1m)

• Market value on Jun 30th, 2008

50

55

60

65

70

75

80

85

90

95

100

Dividend Cash position

Dividend pay-out

Interim Report 2Q08 – July 29th , 2008 Page 8

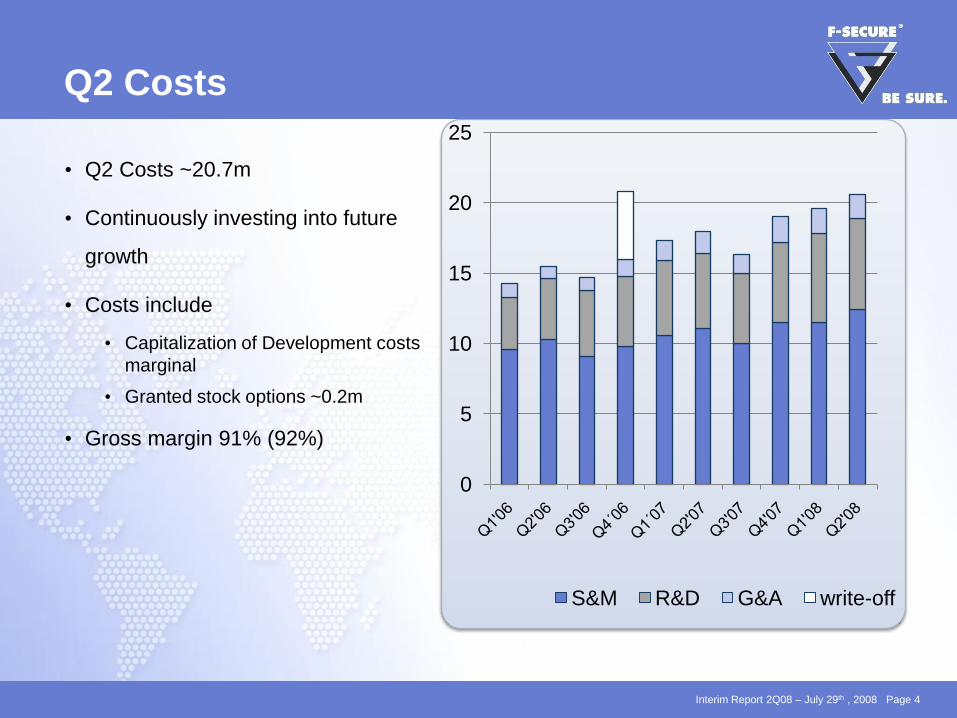

Q2 Deferred Revenues

• Deferred revenues accrued in balance

sheet

• Jun 30, 2008 33.9m

• Mar 31, 2008 33.7m

• Dec 31, 2007 31.9m

• Sep 30, 2007 29.1m

• Development following an annual pattern

10

15

20

25

30

35

Deferred Revenues

Interim Report 2Q08 – July 29th , 2008 Page 9

Regional Revenue Split

1H20071H2008

39 %

43 %

9 % 9 %

Nordic Countries RoE

North America RoW

39 %

43 %

9 %9 %

Interim Report 2Q08 – July 29th , 2008 Page 10

ISP Business – continued strong growth

• 11.6m of revenues

• 43% of total Q2 revenues

• Strong growth

• +6% from 1Q08, +35% from 2Q07

• Growth accelerating activities continued

0

2000

4000

6000

8000

10000

12000

14000

kE

UR

Interim Report 2Q08 – July 29th , 2008 Page 11

Growing number of ISP partners

• 173 partners in 39 countries

• 4 new partners in Q2

• Strong competitiveness in signing new

partners continues

• Q2 significant partner announcements

• KabelBW, Germany

• Tele2, Germany

0

20

40

60

80

100

120

140

160

180

200

Cumulative

Interim Report 2Q08 – July 29th , 2008 Page 12

F-Secure Partners’ market share of residential broadband

0 %

5 %

10 %

15 %

20 %

25 %

30 %

35 %

40 %

2006 2007 2006 2007 2006 2007

F-Secure

Partners’ market share of residential

broadband at end of 2007

• 37% (34%) in Europe

• 10% (10%) in NA

• 9% (n/a) in Asia

(estimates by Dataxis & F-Secure)

Broadband subscribers/population

• Europe (OECD): 22%

• North America: 25%

•European broadband growth +3% y/y,

with Germany +6.7% y/y

Europe

NA ASIA

Interim Report 2Q08 – July 29th , 2008 Page 13

F-Secure Service Provider partnersin the Americas

Interim Report 2Q08 – July 29th , 2008 Page 14

F-Secure Service Provider partnersin EMEA part1

Interim Report 2Q08 – July 29th , 2008 Page 15

F-Secure Service Provider partnersin EMEA part 2

Interim Report 2Q08 – July 29th , 2008 Page 16

F-Secure Service Provider partnersin APAC

Interim Report 2Q08 – July 29th , 2008 Page 17

Product announcements in Q2

• F-Secure Mobile Security for Windows

Mobile (Apr 08)

• Portfolio expansion beyond traditional

security launched to ISPs

• Online Backup

Interim Report 2Q08 – July 29th , 2008 Page 18

Q2 Mobile Security Business

• Device manufacturers

• Available for a majority of the

currently shipping or upcoming Nokia

S60 3rd edition devices

• Partnership with Sony Ericsson and Toshiba Information Systems

• Continued strong growth in trial

usage

• Slow steady growth in revenues

• Ca 3% of total revenues (Q2)

• Operators key for awareness &

availability

• T-Mobile UK & Germany

• Orange UK & Switzerland

• Swisscom

• TeliaSonera

• Elisa

• CSL (Hong Kong)

• Global Frame Agreement with

Vodafone

• Enabling offerings to Vodafone

Operating companies

• 200m subscriber base globally

Interim Report 2Q08 – July 29th , 2008 Page 19

Number of Personnel 668 at the endof the quarter

0

100

200

300

400

500

600

700

800

Q106 Q206 Q306 Q406 Q107 Q207 Q307 Q407 Q108 Q208

S&M R&D G&A

Interim Report 2Q08 – July 29th , 2008 Page 20

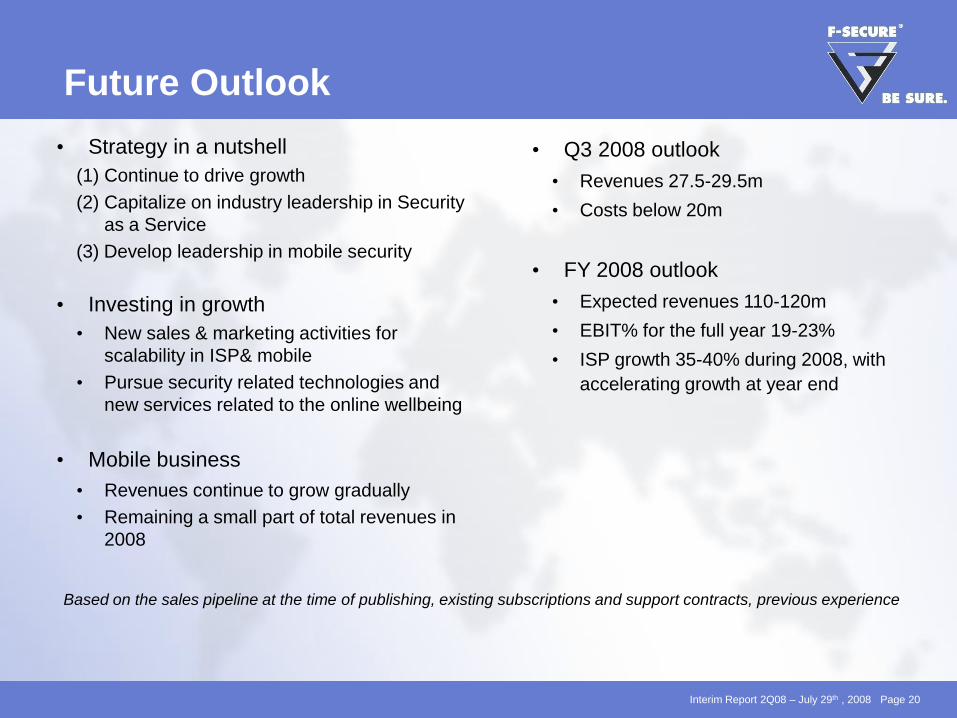

Future Outlook

• Strategy in a nutshell

(1) Continue to drive growth

(2) Capitalize on industry leadership in Security

as a Service

(3) Develop leadership in mobile security

• Investing in growth

• New sales & marketing activities for

scalability in ISP& mobile

• Pursue security related technologies and

new services related to the online wellbeing

• Mobile business

• Revenues continue to grow gradually

• Remaining a small part of total revenues in

2008

Based on the sales pipeline at the time of publishing, existing subscriptions and support contracts, previous experience

• Q3 2008 outlook

• Revenues 27.5-29.5m

• Costs below 20m

• FY 2008 outlook

• Expected revenues 110-120m

• EBIT% for the full year 19-23%

• ISP growth 35-40% during 2008, with

accelerating growth at year end