Embed Size (px)

Citation preview

Risk management for asset managementEY EMEIA survey 2013

Contents

Introduction 1

Executive summary 4

‘Top 10’ action list to achieve better risk management 10

Survey findings 14

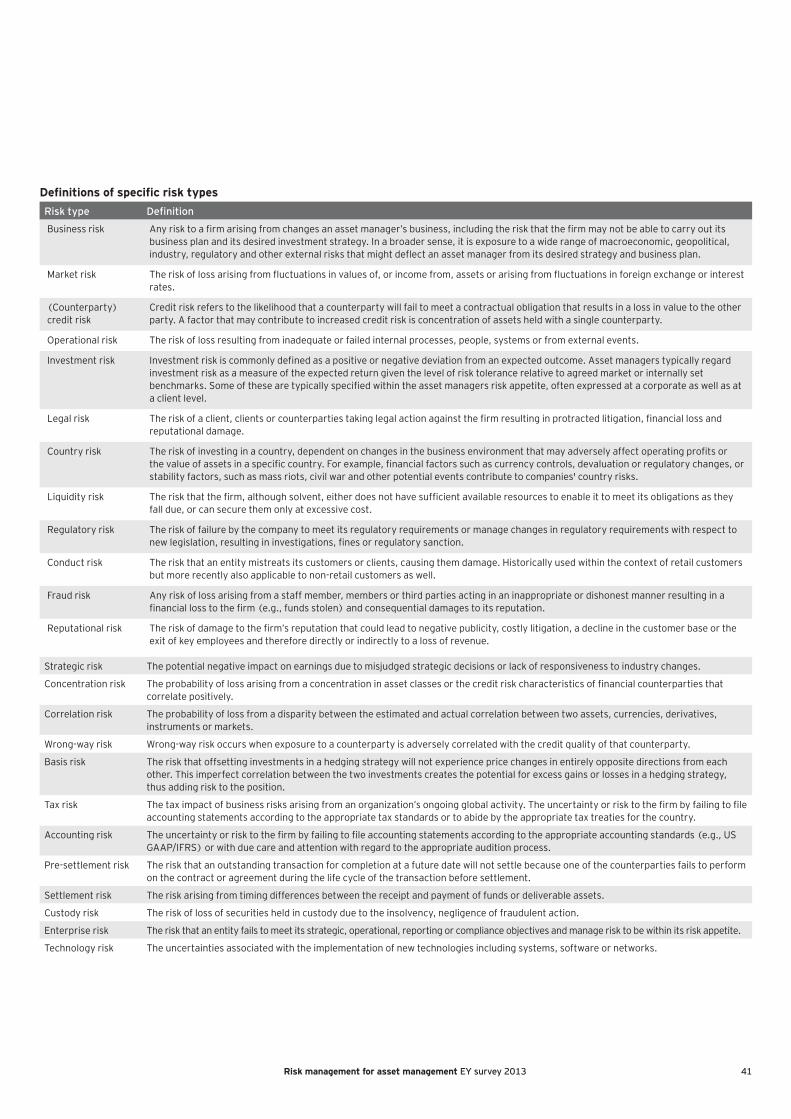

Summary of findings — 2013 survey vs. 2012 survey 40

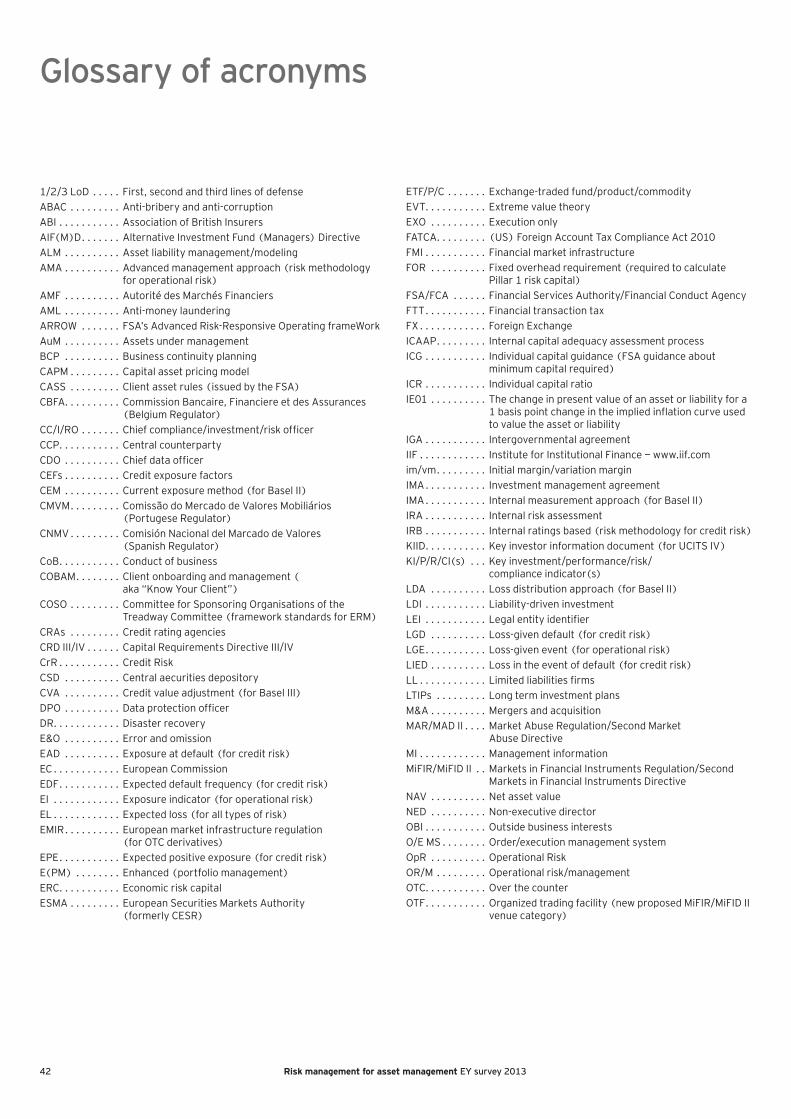

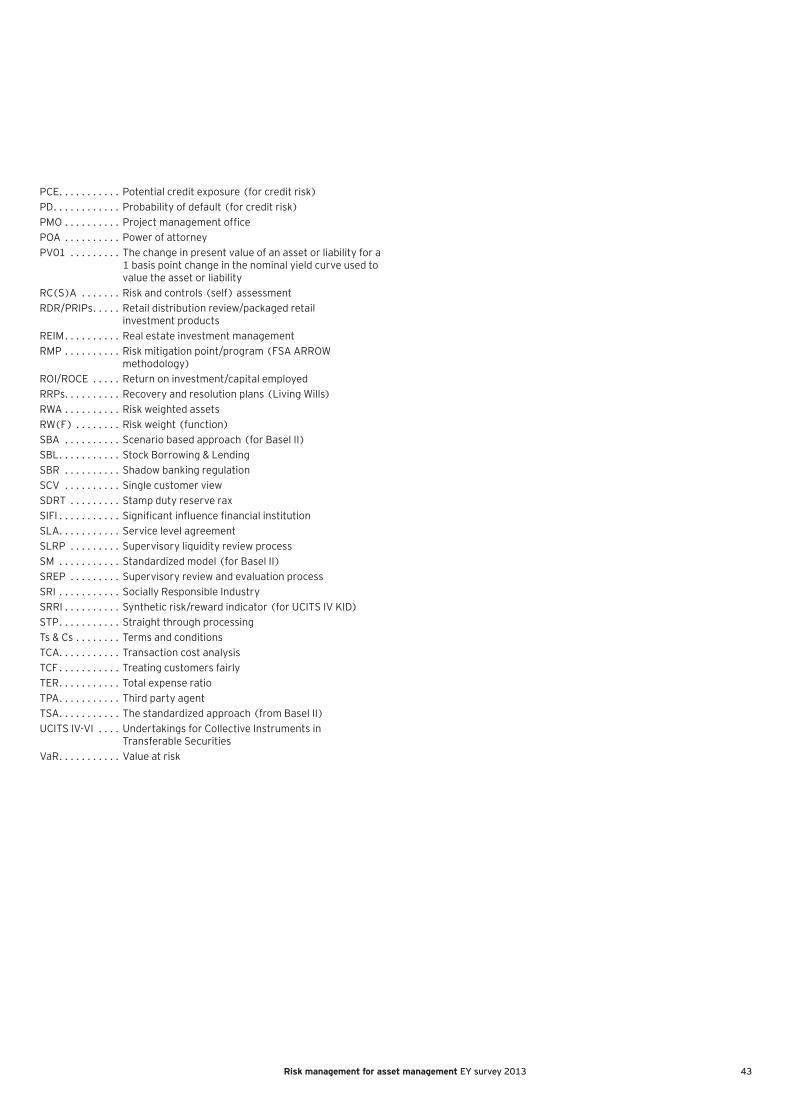

Glossary of acronyms 42

Contacts 44

1Risk management for asset management EY survey 2013

Introduction

The cycle of cost growth, fee competition, squeezed margins and the need for greater scale was a feature over 2012, and the trend was set to accelerate during 2013, challenging asset managers to innovate to safeguard sustainable profits. Innovation among European asset managers and asset servicers was becoming increasingly complex, often driven by specialized entrants from the US. The asset management industry was also ripe for consolidation, with smaller players the most likely targets. As change was constant, the need for proportionate risk management — in the form of appropriate governance, risk appetite, embedded procedures and effective use of risk management frameworks/KRIs — was never greater in the current business climate.

Examples of innovation seen in the survey consisted of loan ETFs, post-RDR share classes, portable alpha, LDI-variant and smart beta strategies. Given that successful innovators stood to gain first-mover advantage, higher fees and greater customer loyalty, innovation coupled with effective risk mitigation was seen as a vital source of differentiation and/or a compelling route to direct market entry. In addition asset managers and asset servicers were being impacted by a plethora of regulations with varying effects, some significant and others contradictory. What these regulations had in common, however, was a tendency to push up costs. The most successful firms proved to be those that managed to keep their cost/income (C/I) ratio in the range 55–65 in this environment.

For example, at a macro-prudential level, approaches were proposed to address the need for provisioning high-quality capital to mitigate pro-cyclicality, particularly for significant influence financial institutions (SIFIs), to reform risk management, to bolster compensation practices and to strengthen crisis management procedures. Regulators in the UK and Germany in particular were more keen to see evidence of advanced, externally validated capital modeling and reverse stress testing (RST). In response, firms recognized that extra capital provisioning and shoring up procedures would not come free, and costs would inevitably need to be passed on to end investors.

At a macro conduct level, European asset managers remained keen to expand globally, but as yet, there was no consensus on how to overcome the problem of fragmented product regulations despite high-level agreements from G20 governments on the critical issues to be tackled. Most argued the case that their interests were auto-aligned with the interests of their clients, but to little avail. As the G20 deadline of 31 December 2012 expired, asset managers seemed challenged to handle more complexities than ever before against a backdrop of competing regulatory approaches and desires for greater transparency. The latter were anything but convergent.

Several respondents commented that if this process was left unmanaged moving forward, competing regulatory changes could limit the industry’s innovative zeal. Recent topical examples included the use of substituted compliance involving entity- and transaction-level tests (employed by the US regulators), third-country equivalence tests/mutual recognition (employed by the EC/Trilogue processes), use of regulatory colleges (in Europe, typically used when evaluating CCPs), and finally thematic reviews undertaken by individual competent authorities such as the AMF or CNMV (for managing conflicts in France and Spain, respectively) or CMVM for sale of complex products ahead of MiFID II in Portugal.

“The biggest difference from 2012 is that the tidal wave of regulation is even higher, and more tentative,

meaning that the impact of the regulations is even bigger while

the detail is less clear. We expect this firm to be caught with the full force of Dodd-Frank — registration,

Volcker Rule on covered funds and OTC derivative measures — while the precise rulemaking is

still work in progress.”

“There is a big focus to ensure that products should be priced appropriately, and if we cannot

rely on the safety and soundness of our intermediaries, this will

have a radical effect on our business models.”

“The regulators are pushing for the asset management

industry to become unviable at a time when returns are falling. Some are asking whether fees

levied should be reflective of performance or risk. Others are

pushing for firms to be penalized if the expected outcome is

not delivered.”

2 Risk management for asset management EY survey 2013

As the investment management industry was maturing, tax was equally becoming an increasingly complex issue, both in terms of reporting and at an investment portfolio level. The proposed introduction of a financial transaction tax (FTT), in the potential form of a directive spooked many asset managers this year, who were not at all clear on the intended impacts, much less the unintended ones. There were several factors at work, not least because FTT was presented as a tax information sharing scheme (like FATCA) but also because the FTT would seemingly apply to cases involving a “riskless principal” transaction (where the current understanding is that both parties to the transaction will be liable to pay the FTT, giving rise to a cascade effect). Scenario modeling will be key.

It was clear that running a successful asset management business was equally about the need for sound risk management and innovation as sound returns and profitability. Regulators had migrated from the mindset of “tick-box” compliance per the rulebooks to feature two additional mindsets: a) firms to demonstrate that the products or services offered did not lead to customer detriment under various market conditions, and b) firms to provide evidence of the value-add per the fees being charged.

Given the open-ended and ongoing nature of these “asks” above, respondents in 2013 wanted to know how much is enough allocating FTE numbers and assessing the quality of expertise required to keep pace with complex and shifting rules. There was a significant desire for benchmarking effectiveness, fitness for purpose and market “best practices.” Indeed counting resources, noting where they were located and measuring how they would respond to a crisis became a functional pastime this year. Where some firms saw challenges given the pace of innovation and regulatory impact, a top quartile of firms expressed excitement at new opportunities, designing asset management solutions to win share of mind and market.

Moving forward, we believe that careful thought about future developments and possible improvements in risk management should be extremely valuable for firms of all sizes and locations, covering active, passive, quantitative, alternative/hedge fund, real estate, investment trust, LDI, SRI, ETF or other styles of managing assets. We also believe that third parties, such as asset servicers, fund administrators, outsourcing providers, transfer agents, platform providers and prime brokers who service asset managers, could greatly benefit from this knowledge and thus serve their clients better.

“The lack of decent-quality collateral is our primary concern.

We are doing a lot of work around SBL, repo and collateral because

we are worried about the position of the banks, and the amount of collateral shortfall runs into the

trillions of dollars.”

“Risk officers will need to do a lot more than act as the

boundary between Portfolio Risk management and Internal Audit.”

3Risk management for asset management EY survey 2013

In conducting this survey, we interviewed 54 heads of risk and chief risk officers representing a selection of large, medium and small traditional and alternative investment management firms (by AuM) operating in the UK/Ireland, France, Germany, Luxembourg, The Netherlands, Switzerland and Italy. The survey built on the results recorded during the four previous risk management for asset management surveys, which were conducted from 2009 to 2012. Our interviews covered strategy, horizon risk, risk appetite and governance, themed risk areas, such as investment risk, product/conduct risk, prudential risk, counterparty credit risk, operational risk, tax (FATCA/FTT) risk and reputational risk. The survey also covered practical areas, such as resourcing, prioritization, risk monitoring, systems and controls, and data/management information. Interviews gave respondents the scope to offer their full opinions under conditions of anonymity. Once again, we are most grateful to them for their continued patience and considerable support behind this endeavour.

We have also added EY’s view of the “Top 10” actions that we believe will help firms to improve their risk management processes still further. Critical conclusions are featured in the executive summary for ready reference by seniors, particularly from the boards, non-executive directors (NEDs) or the business. This survey complements the Compliance Management for Asset Management 2012 survey.

We hope that you and your colleagues enjoy reading this report and that you find it constructive and thought-provoking in helping your firm raise its game against your peers and mitigate risks effectively to innovate, offering new products and services without fear of reputational damage.

As ever, we welcome your comments, feedback and continued dialogue. If you would like to discuss any aspect of the survey, please get in touch using the contact details at the back of the report.

“The direction of travel of regulators and policy-makers is that they work on the assumption that the markets don’t function efficiently. What concerns me is that regulation is becoming more frequent, more evidence-based, and it is insufficient that a firm demonstrates lack of customer detriment. Regulators want to see that value was added, but then our buyers are looking for strong performance asset management.”

“Pay and bonuses are all a red herring. This is about demonstrating the value of intermediation to the regulator. The current focus on sell-side commissions, paying for company visits or the margins of the FX business all arise from the same suspicion.”

Risk management for asset management EY survey 20134

Executive summaryEY’s risk management for asset management 2013 survey offers a revealing insight into the unique set of challenges currently confronting our industry’s risk management professionals. In comparing the views of more than 54 heads of risk and chief risk officers at many of the most recognized traditional and alternative asset managers in the UK and continental Europe, the survey provides indications about the future development of the continued evolution and strategic importance of the risk function for asset management firms.

5Risk management for asset management EY survey 2013

Executive summary

1. Given the tsunami of new directives and regulatory measures at global, regional and local levels, the gap between risk management and regulatory management is narrowing; both the regulators and NEDs were becoming critical drivers.

Running a successful asset management business is equally about the need for forward-facing, sound risk management and innovation as sound returns and profitability. Respondents in this year’s survey commented how regulatory risk was now considered to be the number one risk. Nearly every firm mentioned challenges that their firms are facing by trying to comply with a torrent of global, regional and local/thematic prudential and conduct regulations, applied in the form of rule-making, principles and recommendations, sometimes over varying timelines and sometimes expressed at citizens or entities located cross-border (extraterritorially). As a result, we noted how the gap between risk and compliance functions was narrowing, with more risk professionals involving themselves in regulatory reform and compliance issues.

Another new feature in the survey was the interest of NEDs in the top horizon risks impacting firms, arising from macroeconomic factors, geopolitical changes to regulations at a local or regional level, or tax legislation changes. Leading firms were able to route horizon risk outputs directly into their decisioning through their analysts and desk-heads. Intrusive regulations and legal risks were the top two horizon risks on the radar, with the AIFMD and UCITS V/VI measures representing regulatory implementations with the highest priority and impact for asset managers in general. Satisfying the needs of NEDs for guidance and challenge at board level was certainly a primary motivation behind firms in the UK raising their game in this way.

2. Proving that investment risk was ring-fenced from bias and conviction became a badge of honor in 2013. Responses were varied when it came to the management of certain strands of investment risk, e.g., risk budgeting, single portfolio views, advanced risk metrics, sensitivity analyses and management of model risks.

Investment risk arises from the promise of performance, which remains undelivered. A key element of the overall investment risk framework is the clear identification, documentation and communication of the client’s risk appetite, as explained above. However, the governance of the investment risk function is a critical component of this framework, taking into account the different criteria that are used across different styles of asset managers. Many of the larger firms claimed that their investment risk function was truly independent, but this was in evidence only if there was qualified headcount located in the second line of defense (2LD) able to provide effect challenge against bias and conviction decisioning on the part of the portfolio managers. By contrast, many smaller firms still provided investment risk monitoring from within the front office teams.

The top quartile of respondents in this regard featured dedicated investment risk individuals with 1) the skillsets to analyze and support portfolio managers, and 2) the personalities to challenge the business robustly and evidentially when called to do so. Given the competition for this skillset, we discovered that many of the individuals might need to be on remuneration packages more aligned to front office or banking. The leading firms provided deep technical analysis into investment risk issues, developing investment risk parameters for products; conducting independent reviews and analysis of investment risk within products, models and portfolios; and developing the reporting and risk analytics capability to support portfolio managers. Respondents also commented on the need to derive quality management information from interlinked systems (allowing a “single portfolio view” to be drawn) — a critical differentiator between firms in the survey.

“The sheer volume of current regulations is the problem.

More research is needed on how dangerous this situation is

becoming, given that regulation comes from a huge political

agenda. In the UK, we are losing the notion of a relationship with the regulator. Given the spate of thematic reviews, the narrative

remains ‘be afraid, be very afraid’ under the FCA.”

“The world has moved on from the historic view of OpR as

pertaining to people, processes and systems; today, OpR can span

anything from counterparty CrR oversight to business risk, which

we would see as strategy risk.”

“Previous FSA visits had focused on governance, platforms, ICAAP

and client assets/s166 client money. This time around, the

3LD was hammered owing to a lack of evidence of meaningful

challenge in existence and a need for a stronger risk management

framework. The Business Risk team was a particular focus

because the business had of late de-emphasized the need for

business champions working with the risk team.”

6 Risk management for asset management EY survey 2013

Executive summary

“Having prepared well in advance for Solvency II and seen the

deadline pushed back a couple of years, we are now in search

of last mover advantage. We feel that some capital modeling

benefits to be gained from Solvency II, but we also need to

answer a lot of questions around whether the money could have

been spent differently.”

“We don’t do things in Risk and Compliance for the sake

of regulators, actually. We do things because they make sound

commercial sense, and that reputation attracts and retains

our clients.”

“We have thought about the AIFM/MiFID firm separation and

have decided for now to keep the entities separate because we don’t think that dual registration

will be a constraint, but the capital costs are a nuisance.”

3. Regulatory approaches showed signs of divergence. In the US, there is the prospect of extraterritorial impacts. In France and Luxembourg, competent authorities are focusing on liability. In the UK, there is the prospect of more thematic approaches — for example, assessing the risk from asset management firms outsourcing operational activities to external service providers as part of complex international banking groups.

Many of the larger asset managers and entities that outsourced material functions to third-party agents (TPAs) were considering the implications of outsourcing to external suppliers, while deliberating on the activities they performed and deciding which ones they would be able to continue in the event of the failure of a bank to which they subcontracted. As a majority of the respondents depended on an outsourcer, transfer agent or prime broker/fund administrator for conducting a critical operation, this hardly came as a surprise. The results of this year’s survey showed that 56% of the respondents were concerned about managing regulatory expectations around outsourcing risk in particular, and despite the recent focus on living wills, majority of the respondents were aware that their outsourcing agents maintained recovery and resolution plans without having an opportunity to study the same.

There was widespread skepticism as to whether the failure of an outsourcing agent per se was a realistic outcome, given that the failure of an investment or retail banking entity would be the more realistic possibility, creating significant potential for banking contagion. In view of last year’s scenario of modeling and contingency planning around failures developing in the Eurozone, many respondents commented that they felt prepared. Most had already devised adequate contingency plans that they felt to be viable, robust and realistic in the event of a termination of outsourced activity under any circumstances, including stressed market conditions. Responses were much more tentative concerning the determination of risk under normal and stressed market conditions, the commercials around “step-in” or “warm second provider” arrangements, or the direction of travel that global custodians were taking to evaluate the liability arrangements to cover cases of fraud and/or insolvency of any end agents, such as sub-custodians.

7Risk management for asset management EY survey 2013

4. Respondents commented on how they dealt with reputational risks in different ways, some exercising management through cross-functional and multidisciplinary approaches, while others treated reputational risk more monochromatically, either driven by events or powered by corporate communication.

Reputation risk for an asset manager can arise from a variety of contributions, ranging from market risk, counterparty risk, operational risk, regulatory risk, fiduciary risk or fraud. True reputational failures in asset management are hardly numerous — Morgan Grenfell, Long-Term Capital Management, Gartmore and New Star are some of the few that come to mind. Reputation is a fragile asset, as much about perception as it is about fact — which means that a reputation can be gained over a considerable period of time and lost in considerably less time. Reputation is a wider concept than brand alone, impacting ethics, trust, relationships and, above all, the ethos of a firm — by way of its culture, values, integrity and its confidence behind how these concepts are communicated to clients and regulators.

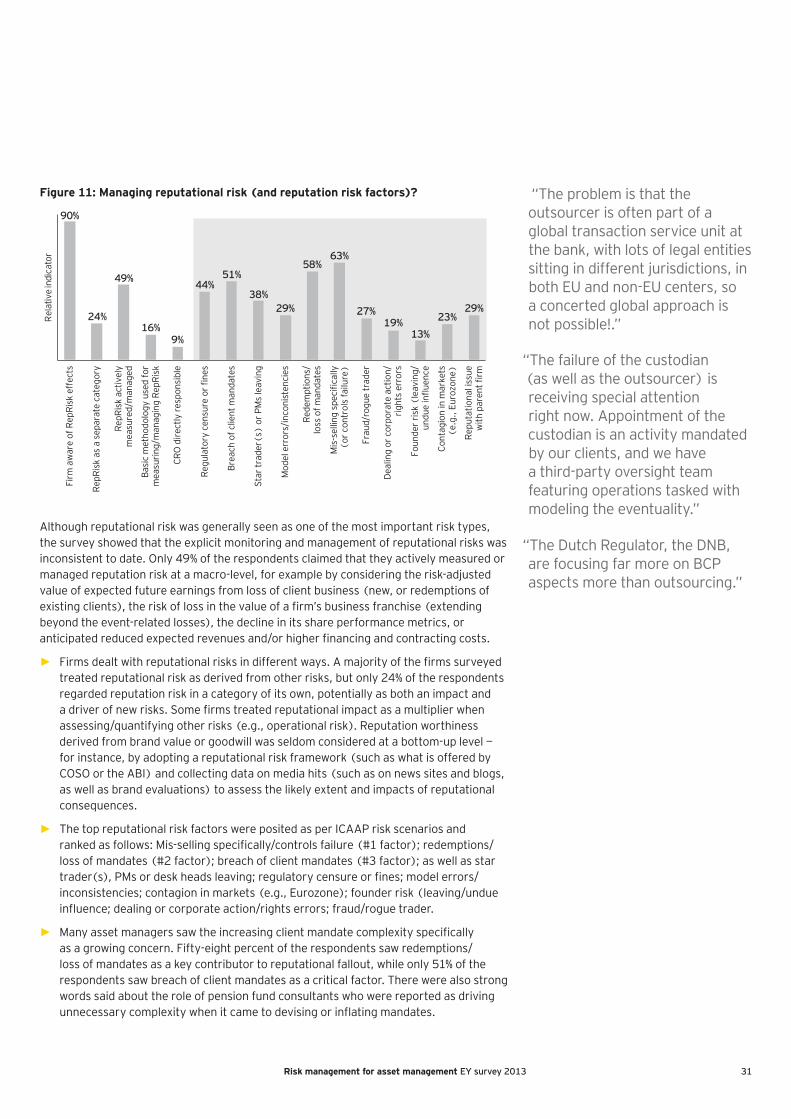

Although reputational risk was generally seen as one of the most important risk types, the survey showed that the explicit monitoring and management of reputational risks were inconsistent to date. We found that reputational risk is usually “owned” by either the CEO, the board, or both, but the processes were often driven and managed by risk. This sometimes created a disconnect that impacted the effectiveness of managing reputational risk. For example, many firms remained reactive to events, and only 24% of respondents regarded reputation risk in a category of its own, potentially as both an impact and a driver of new risks. Reputation worthiness derived from brand value or goodwill was seldom considered at a bottom-up level — for instance, by adopting a reputational risk framework (such as what is offered by COSO or the ABI) and collecting data on media hits (such as on news sites and blogs, as well as brand evaluations) to assess the likely extent and impacts of reputational consequences. All of which left scope for exposure and room for remediation.

“HR are involved and leading the discussions on remuneration in the wake of AIFMD. This is the first directive I can recall that involves pretty much all the functions within a company.”

“Remuneration is a huge focus — struggling to see where the agreement lies between Dodd-Frank (disclosure, transparency, clawback), CRD/AIFMD prescriptions, FSA approaches, and bonus caps recommended by MEPs, for example.”

“There are too many options for remuneration — FSA, AIFMD, CRD, UCITS V — necessitating too many systems. Conflicts will arise from managers with personal interest to be paid on performance not linked to funds.”

8 Risk management for asset management EY survey 2013

Executive summary

5. The tail risk of FATCA-like measures in the US (and potentially elsewhere), coupled with the political will to impose a financial transaction tax across Europe, has buoyed senior management to ensure that “tax risk” is managed effectively.

A majority of the respondents indicated that they thought tax risk was a key horizon risk, although most thought that there would no longer be a high impact on their business and operating models through the introduction of either FATCA or a Euro-FATCA on account of the intergovernmental agreements (IGAs) in place. While firms in the main were relatively well-advanced by way of preparations for FATCA, the general level of understanding and preparation to manage risks arising from the potential introduction of the FTT vs. the introduction of local FTT measures in individual countries, such as France or Italy, was comparatively low. Even if their CEOs or boards remained unconvinced, many CROs believed the prospect of an FTT Directive to be a potential game changer to their business model.

Most respondents were perturbed by the prospect of the introduction of the FTT. As currently proposed, the FTT would apply to secondary market transactions in equities, bonds, fund units, and repos and stock loans, as well as entry into derivatives transactions. There would be no exemptions for items such as intra-group transactions, intermediaries/market-makers, stock loan or repo transactions. One of the biggest concerns for respondents would be a “cascade effect,” whereby multiple charges would bite where a number of brokers act in transferring securities between two counterparties. Although it was envisaged under the draft Directive that the EU Member States would transpose the relevant rules expressed under COM(2013)71 into their national law, with the tax having a “go live” date potentially as early as 1 January 2014, only one respondent was of the view that this would actually happen by that effective date.

“We see opportunities arising from regulation and are building a stockbroking capability offered

to clients who are prepared to pay a premium — which

could result in ‘channel conflict’ between products offered via

brokers vs. direct (e.g., platform/stockbroking) if left unmanaged.”

“The founder is very blasé about the FTT, saying it’ll never happen, but I am very concerned because

of its potential to shift models if it does.”

“Value may be added, but questions remain legally as to

when guidance become advice. For example, investment guidance

is treated differently in Germany. This is particularly relevant

when differentiating the offer of our badged funds vs.

third-party funds.”

9Risk management for asset management EY survey 2013

6. Risk management is all about access to the right data. In 2013 risk management is increasingly about guarding your data too.

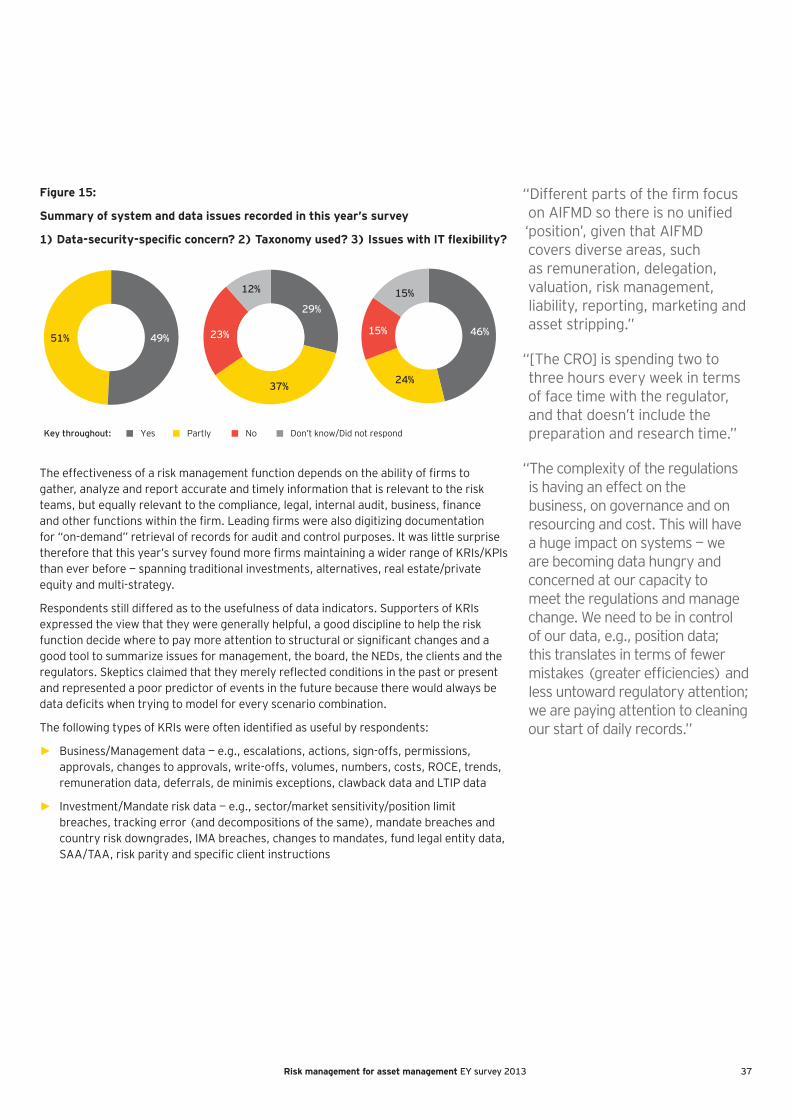

In 2013, we saw a shift toward more focus on data security and cyber risk. There was increasing awareness among risk professionals of the importance of “big data,” particularly from the point of view of innovation opportunity, of safeguarding data, or of generating the supporting data to enable firms to conduct back-testing. Respondents still differed as to the usefulness of data indicators. Supporters of KRIs expressed the view that they were generally helpful, a good discipline to help the risk function decide where to pay more attention to structural or significant changes and a good tool to summarize issues for management, the board, the NEDs, the clients and the regulators. Managing data was no longer an issue of merely managing static (reference) data or filtering stale data, but as equal to the lifeblood of innovation and therefore the golden source of economic value for the business.

Further, data security (whether concerning the firm, data warehouse, outsourcer or surrounding hacking, impersonations or cybersecurity) was a new concern as reported by 49% of the respondents. Historically, the focus was on the quality, robustness and completeness of data. However, the percentage of firms experiencing issues with flexibility/IT change requests remained quite high this year at 46%. “Top-quartile” asset managers (by way of automated risk prevention) were able link their portfolio management systems (PMS), order management systems (OMS) and general ledger systems (GL) into a seamless system architecture, enabling them to perform “what if” scenarios according to model, product or portfolio criteria. The leading firms were also digitizing documentation for “on-demand” retrieval of records for audit and control purposes. It was little surprise, therefore, that this year’s survey found more firms maintaining a wider range of KRIs/KPIs than ever before — spanning traditional investments, alternatives, real estate/private equity and multi-strategy.

Overcoming these challenges to be able to provide a holistic approach to risk management that is so vitally needed is now of foremost concern — and the rationale for running this survey.

“Consultants are a real nuisance as they introduce mandate risk into the mix because of inflating the expectations of plan sponsors, pension funds and SWFs!”

“For the part of reputation risk that is seen as impact/consequence, it is the function responsible for the specific risks. For the other, more isolated, externally driven reputation risk, it is at board level. A good, very recent example was negative publicity because of IT problems within the bank.”

“Reputational risk is considered very important … because it is the only thing you have.”

“Recruiting skilled and knowledgeable risk professionals is quite difficult. [The functions] need specialists without management ambition. Remuneration and image can be an issue.”

10 Risk management for asset management EY survey 2013

“Top 10” action list to achieve better risk management

1 With more than 38 regulatory measures currently in process in the EU alone, the quantity, types and intrusiveness of regulations have become a critical issue for respondents. More firms should ensure that horizon risk outputs are linked not only to control functions but to the business (and particularly portfolio managers and analysts) to reinforce a “one risk” approach.

All respondents mentioned challenges that their firms were facing in trying to comply with a torrent of global, regional and local/thematic prudential and conduct regulations, applied in the form of rule-making, principles and recommendations, sometimes over varying timelines and expressed at citizens or entities located cross-border (extraterritorially). Most firms acknowledged the particular importance of managing so-called “third-country” issues (i.e., measures that are dependent on private placement regimes, requiring mutual cooperation agreements, arising from the function of “regulatory colleges” or the consequences of extraterritoriality).

When the risk management for ssset management surveys started in 2009, risk managers functioned in an environment of one significant regulatory change per year, and the notion of a “regulatory reform” function to help determine horizon risks was rare. Now, as firms are confronted with incremental regulatory changes every month, it is vital. In 2013, most firms had already taken the steps to create and reinforce a “one-risk” culture across group/business unit and regional structures, ensuring that risk management should align with how clients had been sold products. When it came to managing the “horizon risk” radar, a “best practice” idea consisted of routing the outputs not just to the control functions (2LD/3LD) but to the portfolio managers and analysts to educate and inform the business of the impacts of regulatory changes in parallel.

2 The profile and scope of the risk management function has been raised and broadened, with the debate around remuneration coming to the fore. Firms should revisit tolerances, limits and how they apply the use test in practice.

A robust model for corporate governance and ethics goes hand in hand with sound hygiene around effective risk management. The corollary is true too — good risk management reflects a good governance culture, and this is increasingly evident to end investors and regulators alike. There was greater evidence of the risk function being treated even more seriously this year. Not only was the skillset broadening out from operational risk to feature investment risk and regulation risk management, but there was more solid evidence of the use test being applied in all its facets, particularly as far as scenario modeling (e.g., Eurozone, FTT) or reputation risk modeling was concerned.

There was also more awareness in general (particularly among hedge funds) regarding firms articulating their risk appetites effectively to allocate technical resources to where they were needed (e.g., partitioned between the firm/outsourcing agents) or to avoid shocks to future earnings. The CRO was continuing to offer challenge to the 1LD as a “critical friend” but, equally, the CRO was aware of when to apply judgments to tolerances (discrimination as per “hard” or “soft” risk limits) and to intervene more forcefully when needed. This was amply demonstrated in the product arena (see later, with earlier involvement of the CRO in the manufacturing cycle or demonstrating their veto), but a minority of firms indicated CRO involvements in strategic planning, M&A and setting budgets or remuneration, a notable departure from the 2012 survey.

On the basis of the results of the survey and the experience of our own EY practice professionals, we have identified the “top 10” actions to help firms better manage the risks they face. This list is not a definitive action plan, but we hope it will offer a useful starting point for identifying the steps that would most benefit your firm.

“The tone from the top percolates the business — to do the right

thing for clients. We survey every client on a rolling three-year

basis, and our code of ethics is imbued within our partnership culture. The measures are tied

into the risk appetite and six TCF outcomes, and we feature

mentoring for the business and control functions, and adopt a

partnership liability approach to risk as appropriate.”

“We are a midsize firm with a simplified structure and we are

not looking to separate our UCITS from our AIF or MiFID business.”

“We’ve spent the last year embedding the risk culture

between teams. We are much more proactive than previously — our current focus is 75-25 forward-

looking to backward-looking, which is a huge change. We started the

other way one year ago.”

“The regulators are forcing us to think more about what is

appropriate for the end client.”

“I am really not happy about the direction that the UK regulator is

taking during the FSA’s fishing trips. Conduct risk is a high priority and firms don’t just

have to evidence that they are preventing customer detriment; they also need to evidence that they are adding value and also

paying attention to the needs of their clients’ clients.”

11Risk management for asset management EY survey 2013

3 Given the greater potential risks from product mis-selling and regulatory intervention, it is even more important to involve both risk and other control functions at the beginning of the product development cycle and to focus on conduct risk, devising appropriate conduct risk frameworks that focus on ethics and behaviors to complement traditional approaches.

Effective risk management should align with the strategic objectives of the firm and the manner in which investors have been sold products. In this year’s survey, respondents confirmed that some European Member States were showing signs of adopting non-convergent courses concerning product regulation and that they could no longer be certain of a consistent direction of travel. The FSA/FCA were touting a product intervention approach. The AMF in France and the CBFA in Belgium were pushing for prescriptive pre-screening, mainly in relation to product intervention around simple/complex products and execution-only (EXO) business. Other EU Member States had introduced product safety warnings (e.g., color coding in Portugal or risk indicator measures in Denmark and Luxembourg).

Moving forward, with the spotlight increasingly turning to the customer, it seems as if short-term national responses will need to be managed against the backdrop of regional regulation. Given recent fines levied for mis-selling of products claiming to be “guaranteed,” “absolute return,” “leveraged,” or “structured” to retail-classified investors, the notion of conduct risk — the risk that an entity mistreats its customers or clients, causing them detriment — has come to the fore. It is clear that business and operating models may need to accommodate multiple ways of conducting business across Europe over the next three years at least. It makes sense for firms to revise their taxonomies and compile product characteristics, while shoring up suitability and appropriateness procedures provide the neccessary evidence to regulators if called to do so.

4 More firms are becoming independent by ensuring that investment risk is ring-fenced from bias and conviction on the part of fund managers or founders. There is still scope for performance improvement among the non top-quartile firms when applying risk budgeting, single portfolio views, risk metrics, performance attribution, liquidity management and treatment of model risks.

Performance is the promise that is not always delivered. Many firms claim that their investment risk function is independent, but this is evidence only if qualified headcount located in the second line of defense (2LD) is able to provide effective challenge against bias and conviction decisioning on the part of the portfolio managers, particularly if their decisioning contravenes regulations or the firms’ stated risk appetite, or both. Firms should ensure that they can derive quality management information from interlinked systems (allowing “single portfolio views” to be drawn) — a critical differentiator between firms in the survey. It is also advisable to populate the 2LD control function with FTEs familiar with the terminology of the portfolio managers (e.g., tracking error, TAA, expected beta, CAPM, Sharpe ratio and sensitivity indicators DV01/IE01). Additionally, the appropriate level of remuneration should be an important consideration when attracting (and retaining) appropriate technical skillsets to perform the investment risk function effectively.

5 The treatment of individual capital guidance (ICG) and capital allocation as per the ICAAP is a perennial focal point. The optimization of capital and evaluation of insurance benefits is a key differentiator between asset managers and a barometer of regulatory standing.

As greater capital charges often correlate with constraining the budget for innovation, it is vital that asset managers take steps to optimize their capital provision, including seed capital provision. This year’s survey recorded a similar “new normal” of 135% to 175% across 40 firms for ICG uplift scores relative to Pillars I and II capital and unwinding effectiveness/charges (the latter sometimes spanning over 12 months). Firms should benchmark themselves to evaluate whether they should take advantage of waivers, such as consolidation (diversification) benefit and the quality of insurance. Although effective optimization is far from trivial, leading asset managers are already looking to compare themselves through capability maturity modeling on what other firms are doing as part of their ICAAP/SREP processes, bearing in mind the type and combination of style factors that might give the regulator cause for setting elevated ICG uplifts.

Regulators in the UK and Germany are in particular more keen to see evidence of advanced, externally validated capital modeling and reverse stress testing (RST) procedures made specific to firms (not just proportionate to market conditions). Firms should be aware of the need to model for regulatory sensitivities; legal entity restructuring, joint ventures, material outsourcing of critical functions at a corporate level; qualifying NEDs or control function representatives from a governance perspective; managing client assets and money, especially those carrying products targeted at retail-classified consumers from a conduct perspective; or firms manufacturing complex, illiquid or non-fungible products or offering “guaranteed” or “absolute return” products to clients.

12 Risk management for asset management EY survey 2013

“Top 10” action list to achieve better risk management

“Our RCSA represents the risks to the firm, linked to the prudential risk; conduct risk models risks to the client. Prudential regulators are becoming more focused on

the former — conduct regulators such as the FCA on the latter.

We believe that ‘vetter controls make better client outcomes,’ but need to persuade regulators that

our interests are aligned with their clients.”

“InvR sits in the second line of defense and the focus varies according to the 1LD and the

quality of people providing quant support; remuneration (such as paying for FTEs with PM or quant skills or both) is

not a problem given the parent compensation structure.”

“The measurement and monitoring of risk occurs both at the

aggregate level and at the factor level. This is done for all active

asset types (EQ, FI, LDI) but not done for index — measurement

and risk monitoring is done daily.”

“Managing outsourcing risk is our top risk priority, partly driven by where the FSA was going,

although this hasn’t been mirrored by the SEC or BaFIN, which are equally critical regulators for us.

We are at the stage of kicking the DR tyres of our outsourcing

provider although really we should be deconstructing their recovery and resolution plan, aided by the

regulator. Asking us to evolve step-in processes is ridiculous, and we

are consulting the IMA on that.”

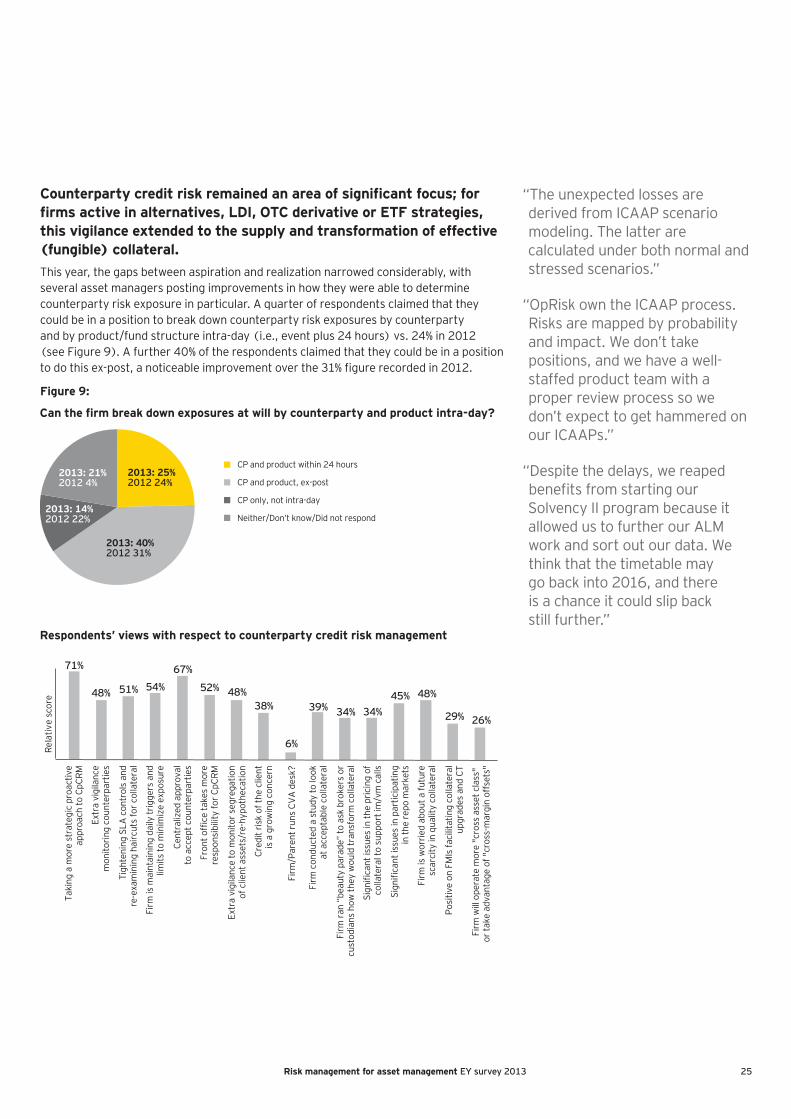

6 Improved credit risk was a key focus in 2013, with more firms upgrading risk systems to enable them to determine counterparty risk exposure by using CDS spreads as well as CRAs. More firms should run “beauty parades” to help assess the quality of their counterparties under normal and stressed market conditions when it comes to collateral management, repo or clearing.

The gaps between aspiration and realization have narrowed considerably this year, with several asset managers posting improvements in how they were able to determine both intra-day and ex-post counterparty risk exposure. Firms should continue to adopt a more proactive approach to counterparty risk management by increasing the level of monitoring and close scrutiny per credit rating, CDS spreads, tier-1 banking ratios, price movements, etc. There was welcome evidence of more CROs than ever before involving front office colleagues taking responsibility for counterparty risk management. Given the prospect of ad hoc political or legal changes imposed at a local level (e.g., Cyprus), the credit risk of the client should not be relegated to a negligible concern.

It is recommended that firms that are expanding or are contemplating expanding their footprint in alternatives, LDI, OTC derivative or synthetic ETF strategies should conduct a study to look at acceptable forms of collateral if they are yet to do so. The study should focus on the likely factors impacting the supply and demand of quality, fungible collateral, and how asset classes might be priced to support the demands for initial and variation margin by CCPs. Firms worried about any “pinch points” should consult with custodian banks and financial market infrastructure facilitators (such as Euroclear or Clearstream) as to the pacing of infrastructural reform and contemplate whether to run benchmarking exercises such as a “beauty parade” of their brokers and custodian banks to assess the quality and appropriateness of collateral management, execution and prime services.

7 Firms had strengthened the robustness of their operational risk frameworks and the effectiveness of their outsourcing arrangements under normal and stressed market conditions last year but needed to respond to regulators during thematic reviews this year.

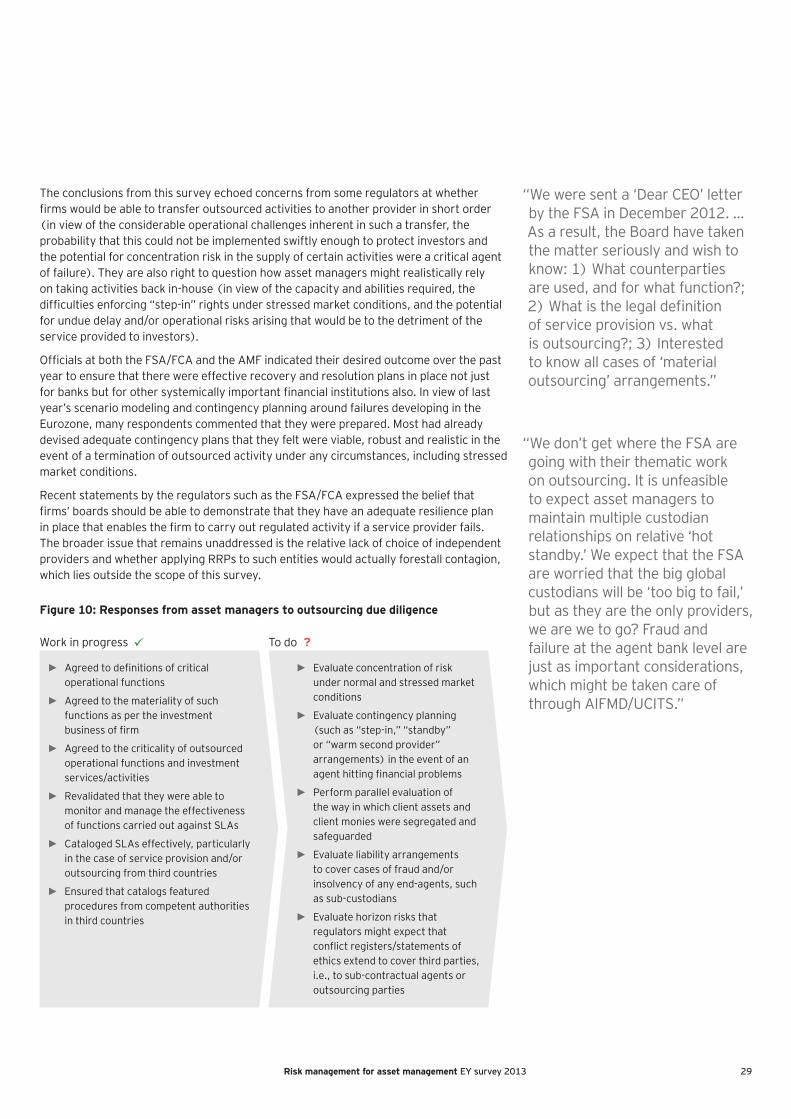

Most firms had already devised adequate contingency plans that they felt were viable, robust and realistic in the event of a termination of outsourced activity under any circumstances, including stressed market conditions. Many respondents mentioned for the most part that they had i) agreed to definitions of critical operational functions, ii) agreed to the materiality of such functions per the investment business of firm, iii) agreed to the criticality of outsourced operational functions as per and investment services/activities, iv) revalidated that they were able to monitor and manage the effectiveness of functions carried out against SLAs, v) catalogued SLAs effectively, particularly in the case of service provision and/or outsourcing from third countries, and vi) ensured that catalogs featured procedures from competent authorities in third countries.

Recent statements by the regulators, such as the FSA, expressed the belief that firms’ boards should be able to demonstrate that they have in place an adequate resilience plan that enables the firm to carry out IFCA-regulated activity if a service provider fails. It is recommended that firms should: i) evaluate concentration of risk under normal and stressed market conditions, ii) evaluate contingency planning (such as “step-in” or “standby” arrangements) in the event of an agent hitting financial problems, iii) perform parallel evaluation of the way in which client assets and client monies were segregated and safeguarded, iv) evaluate liability arrangements to cover cases of fraud and/or insolvency of any end agents, such as sub-custodians, v) evaluate horizon risks that regulators might expect that conflict registers/statements of ethics extend to cover third parties, i.e., to sub-contractual agents or outsourcing parties.

13Risk management for asset management EY survey 2013

8 Compliance measures involving tax, such as, the FTT should be treated concurrently with regulations, and appropriate care and attention needs to be dedicated to client onboarding to ensure that correct and appropriate treatments are applied.

Tax risk1 management came of age two years ago with the introduction of the FATCA, impacting risk and operations departments just as much as tax professionals. While most felt comfortable with the scope of the IGA measures in place catering for country-per-country assessments, managing the ongoing BAU operational tax landscape for funds/fund managers was at least as important as the big headline issues. Tax risk was cited as a current issue by 38% firms (up from 27% last year), which suggested that some tax teams were not ensuring that tax risk was understood and embedded within the business or a lack of knowledge on the part of the CROs. Operational tax risk — covering the SLA relationships with service providers on a technical level, managing the plethora of tax rates applying to investments (and CGT in particular, which could impact performance) — proved key. From the data angle, firms should re-examine legal entity identifier (LEI) indications to differentiate US financial institutions (USFIs) from foreign financial institutions (FFIs) in case of the need to prepare for an EU-FATCA.

While firms in the survey were relatively well-advanced by way of preparation for FATCA, respondents seemed far more uncertain as to the scope of local vs. EU FTT measures. Firms would be wise to apply the “issuance,” “establishment” and “materiality” tests and model the known “worst case” impacts on equities, bonds, fund units, and repos and stock loans, as well as entry into derivatives transactions. Firms should be on the alert for modeling intra-group transactions, transactions involving intermediaries and stock loan or repo transactions on a “what if” basis. Scenario modeling will be particularly important in cases involving a “riskless principal” transaction, where the current understanding is that both parties to the transaction could be liable to pay the FTT, giving rise to a cascade effect.

9 Resourcing should be weighted according to the scope of investment style of the firm, and quality of that resourcing is paramount. Firms should be able to evidence and justify how resources are allocated and why, when called to do so by regulators.

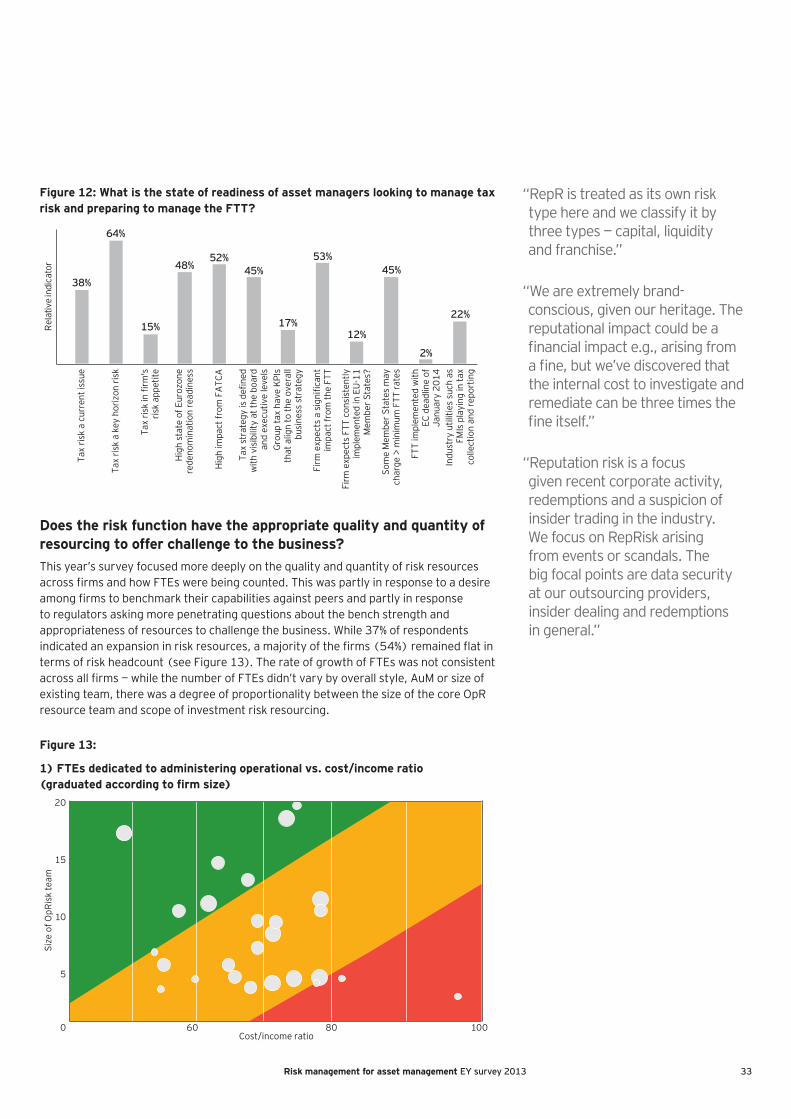

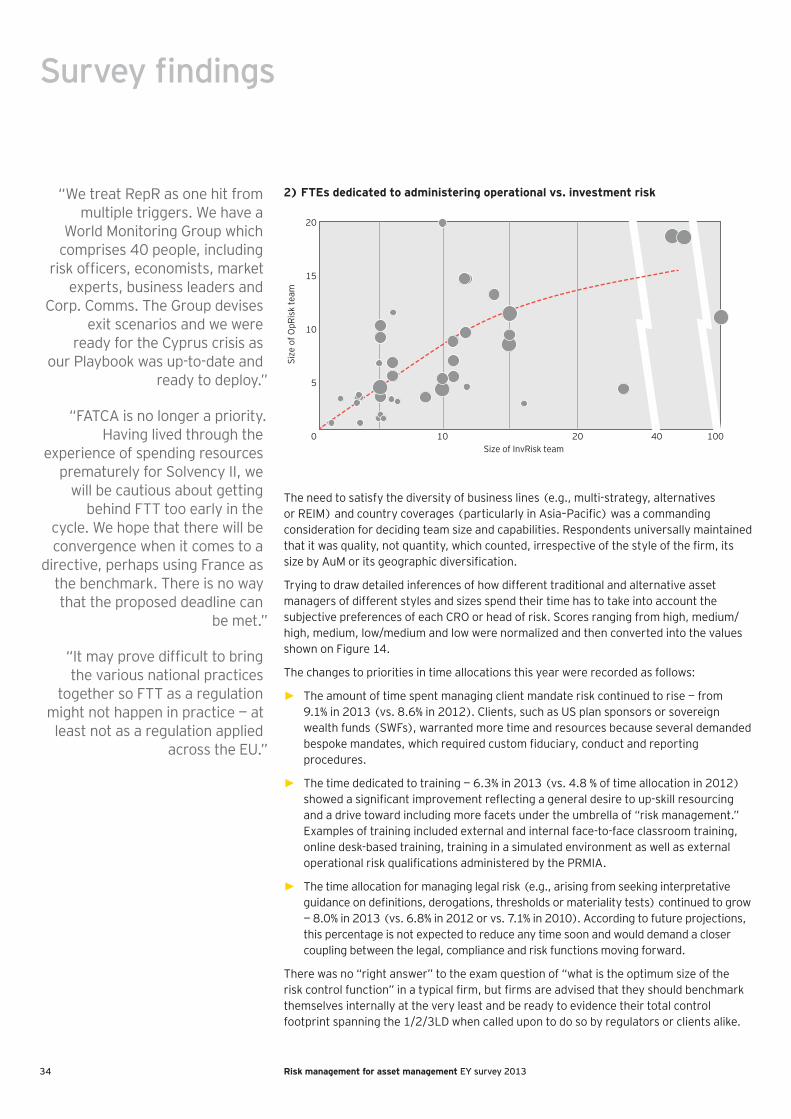

This year’s survey focused more deeply on the balance of risk resources across firms and how those resources were being counted, partly in response to regulators posing deeper questions about skillsets and bench strength to cover all the countries where a firm did business. While 37% of the respondents indicated an expansion in risk resources, majority of the firms (54%) remained flat in terms of risk headcount, and the rate of growth of FTEs was not consistent across all firms. The number of FTEs didn’t vary by overall style, AuM, or size of existing team, and there was a degree of proportionality between the size of the core OpR resource team and scope of investment risk resourcing (see Figure 13 on page 33). Diverse business lines (e.g., multi-strategy, alternatives or REIM) and country coverages (particularly in Asia-Pacific) were considerations for deciding team size and capabilities.

10 Data security is paramount. More firms than ever before recognize that collecting, retrieving and evidencing quality data is a differentiator, not just in terms of ensuring good regulatory compliance but also in terms of innovating service offerings and improving client service.

More firms than ever before made reference to the importance of the risk function overseeing BCP (business continuity planning), a task normally consigned to operations or IT. Indeed, the flexibility and resilience of the latter proved once again to be a major dependency when delivering a sustainable risk infrastructure to respond to the challenges of regulation and demanding client mandates. “Top-quartile” asset managers were either installing “state of the art” system components (such as Aladdin, mentioned by several respondents) or able to link their PMS, OMS and GL into a seamless system architecture, enabling them to perform “what if” scenarios according to model, product or portfolio criteria. They were also digitizing documentation for “on-demand” retrieval of records for audit and control purposes.

This year was also the year of “big data,” particularly from the point of view of either safeguarding data or generating supporting data to enable firms to conduct back-testing or reverse stress testing. Several firms indicated that cybersecurity was an important and growing theme for the risk function, not merely an IT issue. Opinions still varied considerably as to the usefulness of data indicators, such as KRIs or risk data types — such as business, investment risk, credit risk, operational risk, regulatory data or (especially) customer indications. The latter included status-type information (e.g., used to qualify US persons or FTT establishment criteria) as well as taxpayer indications, and were cited as particularly important components of legal entity identification (LEI) this year. Asset managers are advised to design data taxonomies2 for their LEIs in particular and develop master golden copy records that feature “a single version of the truth,” allying more closely with collaborators, such as asset servicers and prime service providers, if need be. Legal permissioning around data privacy will become increasingly important next year.

1 Tax risk management can be thought of as the identification of business risks arising from an organization’s tax-related activity (across all taxes and all jurisdictions) and its effective management and control of those risks.

2 Firm-wide consistent nomenclatures behind specifying unique instrument or legal entity identifiers of parent/child relationships concerning corporate entities or fund structures

14 Risk management for asset management EY survey 2013

Survey findings

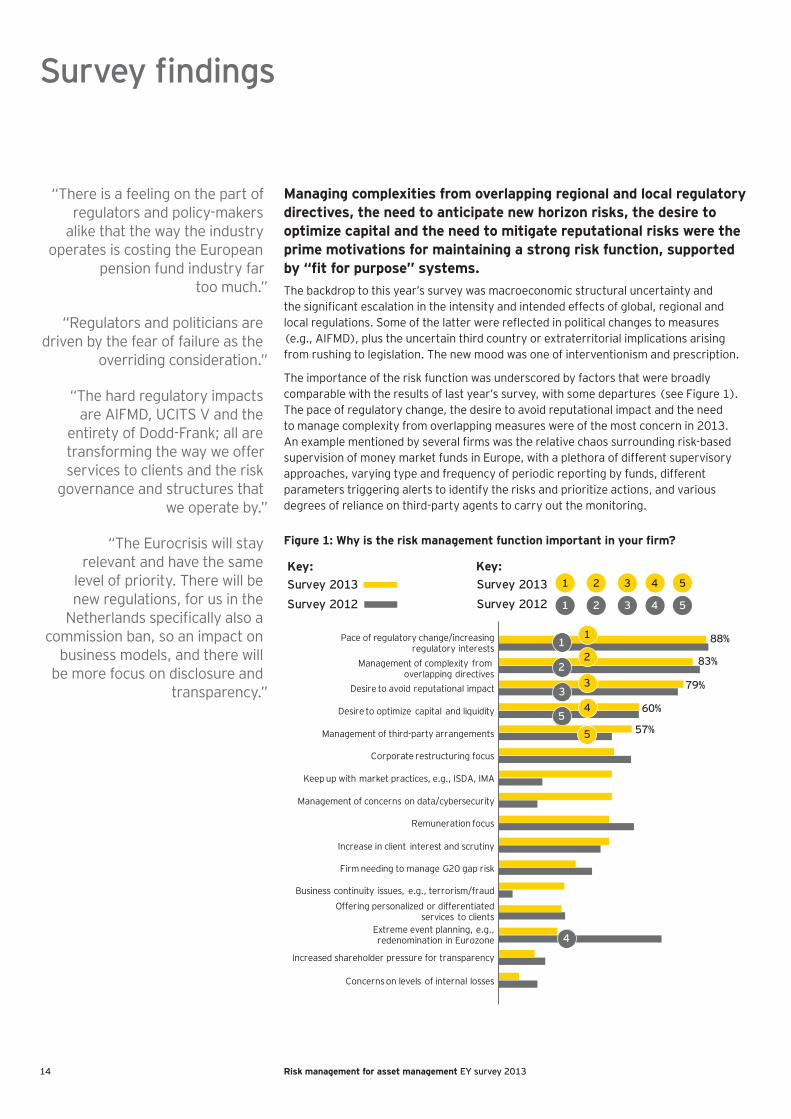

Managing complexities from overlapping regional and local regulatory directives, the need to anticipate new horizon risks, the desire to optimize capital and the need to mitigate reputational risks were the prime motivations for maintaining a strong risk function, supported by “fit for purpose” systems.The backdrop to this year’s survey was macroeconomic structural uncertainty and the significant escalation in the intensity and intended effects of global, regional and local regulations. Some of the latter were reflected in political changes to measures (e.g., AIFMD), plus the uncertain third country or extraterritorial implications arising from rushing to legislation. The new mood was one of interventionism and prescription.

The importance of the risk function was underscored by factors that were broadly comparable with the results of last year’s survey, with some departures (see Figure 1). The pace of regulatory change, the desire to avoid reputational impact and the need to manage complexity from overlapping measures were of the most concern in 2013. An example mentioned by several firms was the relative chaos surrounding risk-based supervision of money market funds in Europe, with a plethora of different supervisory approaches, varying type and frequency of periodic reporting by funds, different parameters triggering alerts to identify the risks and prioritize actions, and various degrees of reliance on third-party agents to carry out the monitoring.

Figure 1: Why is the risk management function important in your firm?

Key: Survey 2013Survey 2012

Key: Survey 2013Survey 2012

1 2 3

1 2 3

4

4

5

5

Desire to optimize capital and liquidity

Increased shareholder pressure for transparency

Concerns on levels of internal losses

Increase in client interest and scrutiny

Management of third-party arrangements

Pace of regulatory change/increasingregulatory interests

Business continuity issues, e.g., terrorism/fraud

Keep up with market practices, e.g., ISDA, IMA

Desire to avoid reputational impact

Management of complexity from overlapping directives

Corporate restructuring focus

Firm needing to manage G20 gap risk

Extreme event planning, e.g.,redenomination in Eurozone

Offering personalized or differentiatedservices to clients

88%

83%

60%

57%

Remuneration focus

1

2

5

3

43

2

1

4

5

Management of concerns on data/cybersecurity

79%

“There is a feeling on the part of regulators and policy-makers

alike that the way the industry operates is costing the European

pension fund industry far too much.”

“Regulators and politicians are driven by the fear of failure as the

overriding consideration.”

“The hard regulatory impacts are AIFMD, UCITS V and the

entirety of Dodd-Frank; all are transforming the way we offer services to clients and the risk

governance and structures that we operate by.”

“The Eurocrisis will stay relevant and have the same

level of priority. There will be new regulations, for us in the

Netherlands specifically also a commission ban, so an impact on

business models, and there will be more focus on disclosure and

transparency.”

15Risk management for asset management EY survey 2013

“In 2012–13, we were involved in the calibration of bonus amounts but at the end of the cycle. In 2013–14, we’ll be involved much earlier in the cycle. Remuneration will be a meld of Dodd-Frank’s ‘Say on Pay’ and CRD/AIFMD/FSA regs.”

“Regulatory change/reform is a significant focus. Dodd-Frank is a big issue; AIFMD is a big issue; we have more AIFMD trusts (including investment trusts) than UCITS. We apply a US person screen — there are complications with tentative versions, aggravated following two acquisitions affecting PE and bonds.”

Growing motivations for risk management included the firm (or parent) impacted by a fine/regulatory sanction, the need to manage expectations around administering remuneration, and business continuity issues (e.g., terrorism/fraud). The pattern was broadly comparable with the results from 2012, with the need to manage extreme event risk (such as events in the Eurozone) decreasing in relative importance.

As mentioned above, remuneration was a particular focus in 2013. Respondents felt that there was too much complexity from different and changing models in circulation — Dodd-Frank, CRD, Art. 107 AIFMD and FSA approaches. Respondents felt that the prospect of moving from deferrals/LTIPs to capping bonus ratios to base salary could have widespread impacts on economics of current models — affecting incentives, domiciles of employees, severance/mobility issues and FOR calculations by way of holding more capital.

Besides the traditional operational and counterparty credit risks, the top risk categories of major concern to CROs were regulatory, mandate, conduct and liquidity risks, with market and investment risks not far behind.The “top 20” risk categories receiving special attention from CROs and their risk teams were ranked as shown in Figure 2 according to the percentage of respondents making reference to them. Regulatory risk — the risk of failure by the company to meet its regulatory requirements or manage changes in regulatory requirements with respect to new legislation, resulting in investigations, fines or regulatory sanctions — occupied the top spot for the first time (up from 67% in 2012):

Figure 2: Top risk categories mentioned by respondents

Regulatory risk

Counterparty/credit risk

(Pure) operational risk

Conduct/mis-selling risk

Investment risk

Liquidity risk

Outsourcing risk

Mandate risk

Business model risk

Reputational risk

Market risk

Tech — data risk

Tax risk

Country risk

Legal risk

Correlation risk

Misc. risk

Fiduciary risk

Tech — systems risk

(Other) fraud risk

76% vs. 67% in 2012

73%73% vs. 82% in 2012

56% vs. 24% in 2012

64%

61%

52% vs. 40% in 2012

44% vs. 50% in 2012

32%22%

17%

12%10%

63% vs. 36% in 2012

47% vs. 24% in 2012

48%

12%

21%

38% 38%

16 Risk management for asset management EY survey 2013

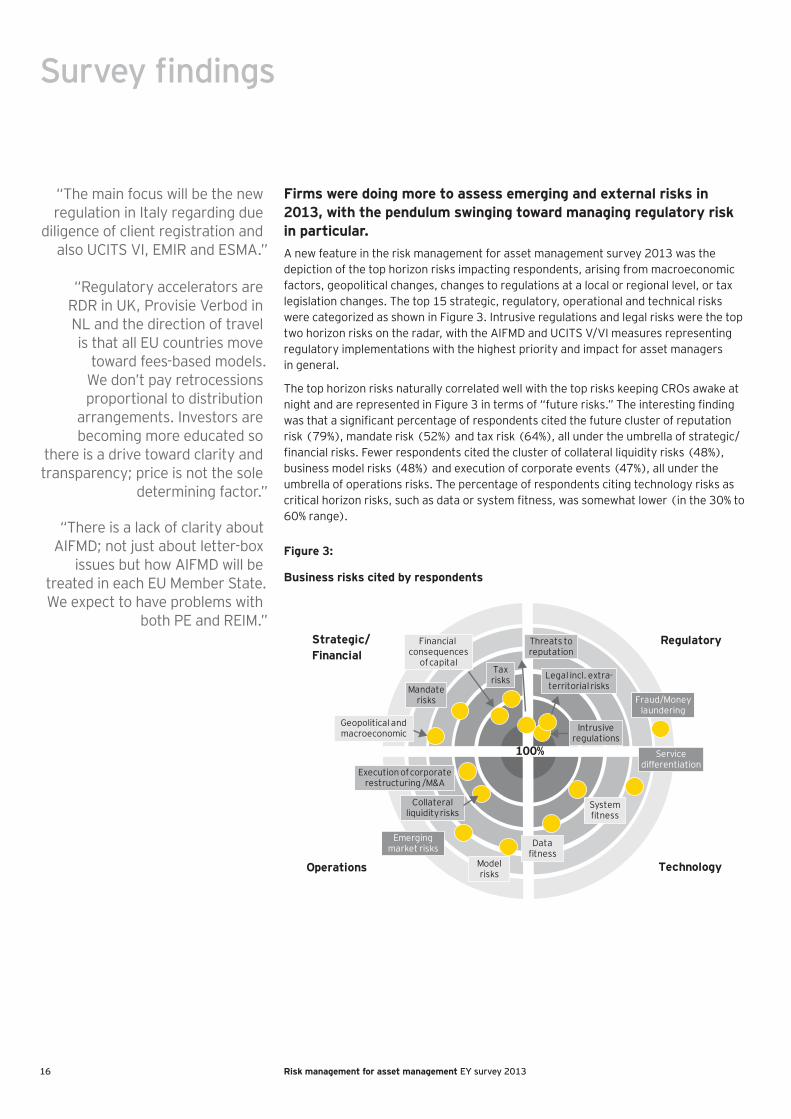

Firms were doing more to assess emerging and external risks in 2013, with the pendulum swinging toward managing regulatory risk in particular.A new feature in the risk management for asset management survey 2013 was the depiction of the top horizon risks impacting respondents, arising from macroeconomic factors, geopolitical changes, changes to regulations at a local or regional level, or tax legislation changes. The top 15 strategic, regulatory, operational and technical risks were categorized as shown in Figure 3. Intrusive regulations and legal risks were the top two horizon risks on the radar, with the AIFMD and UCITS V/VI measures representing regulatory implementations with the highest priority and impact for asset managers in general.

The top horizon risks naturally correlated well with the top risks keeping CROs awake at night and are represented in Figure 3 in terms of “future risks.” The interesting finding was that a significant percentage of respondents cited the future cluster of reputation risk (79%), mandate risk (52%) and tax risk (64%), all under the umbrella of strategic/financial risks. Fewer respondents cited the cluster of collateral liquidity risks (48%), business model risks (48%) and execution of corporate events (47%), all under the umbrella of operations risks. The percentage of respondents citing technology risks as critical horizon risks, such as data or system fitness, was somewhat lower (in the 30% to 60% range).

Figure 3:

Survey findings

Strategic/ Financial

Regulatory

Operations Technology

Geopolitical andmacroeconomic

Financial consequences

of capital

Threats toreputation

Modelrisks

Systemfitness

Emergingmarket risks

Legal incl. extra-territorial risks

Datafitness

Servicedifferentiation

Fraud/Moneylaundering

Collateralliquidity risks

Mandaterisks

Taxrisks

100%

Execution of corporaterestructuring /M&A

Intrusiveregulations

Business risks cited by respondents

“The main focus will be the new regulation in Italy regarding due

diligence of client registration and also UCITS VI, EMIR and ESMA.”

“Regulatory accelerators are RDR in UK, Provisie Verbod in NL and the direction of travel is that all EU countries move

toward fees-based models. We don’t pay retrocessions proportional to distribution

arrangements. Investors are becoming more educated so

there is a drive toward clarity and transparency; price is not the sole

determining factor.”

“There is a lack of clarity about AIFMD; not just about letter-box

issues but how AIFMD will be treated in each EU Member State. We expect to have problems with

both PE and REIM.”

17Risk management for asset management EY survey 2013

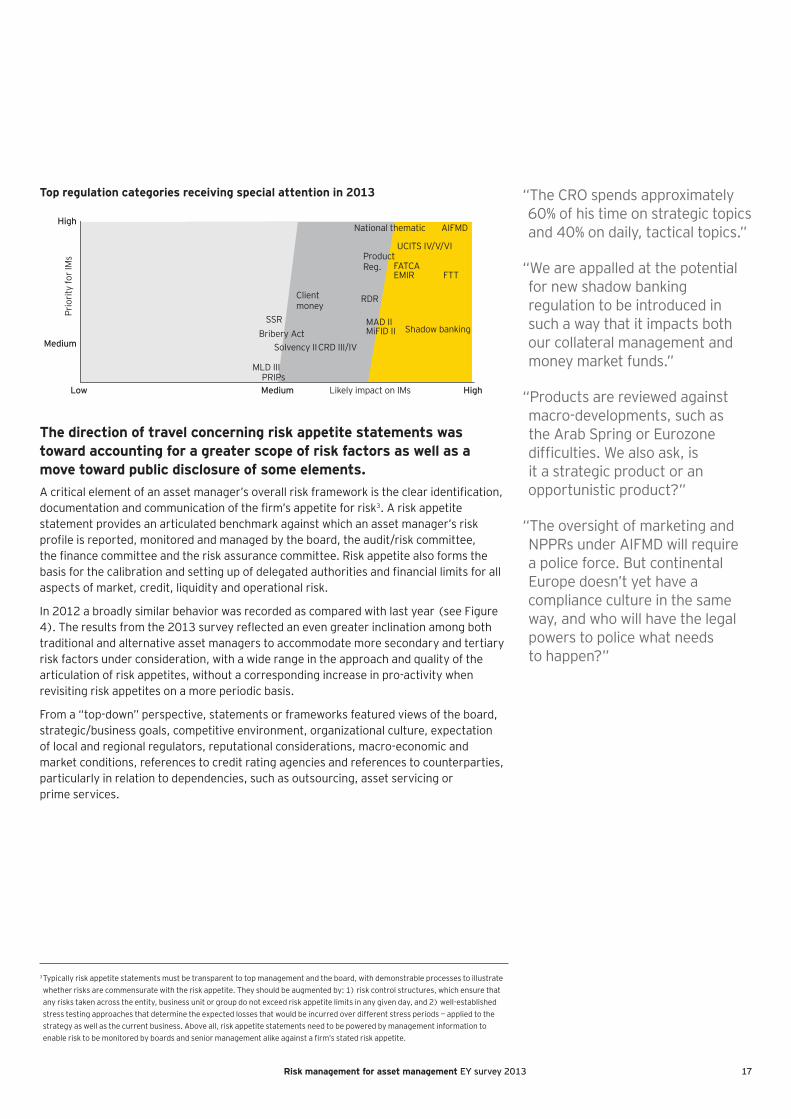

The direction of travel concerning risk appetite statements was toward accounting for a greater scope of risk factors as well as a move toward public disclosure of some elements.A critical element of an asset manager’s overall risk framework is the clear identification, documentation and communication of the firm’s appetite for risk3. A risk appetite statement provides an articulated benchmark against which an asset manager’s risk profile is reported, monitored and managed by the board, the audit/risk committee, the finance committee and the risk assurance committee. Risk appetite also forms the basis for the calibration and setting up of delegated authorities and financial limits for all aspects of market, credit, liquidity and operational risk.

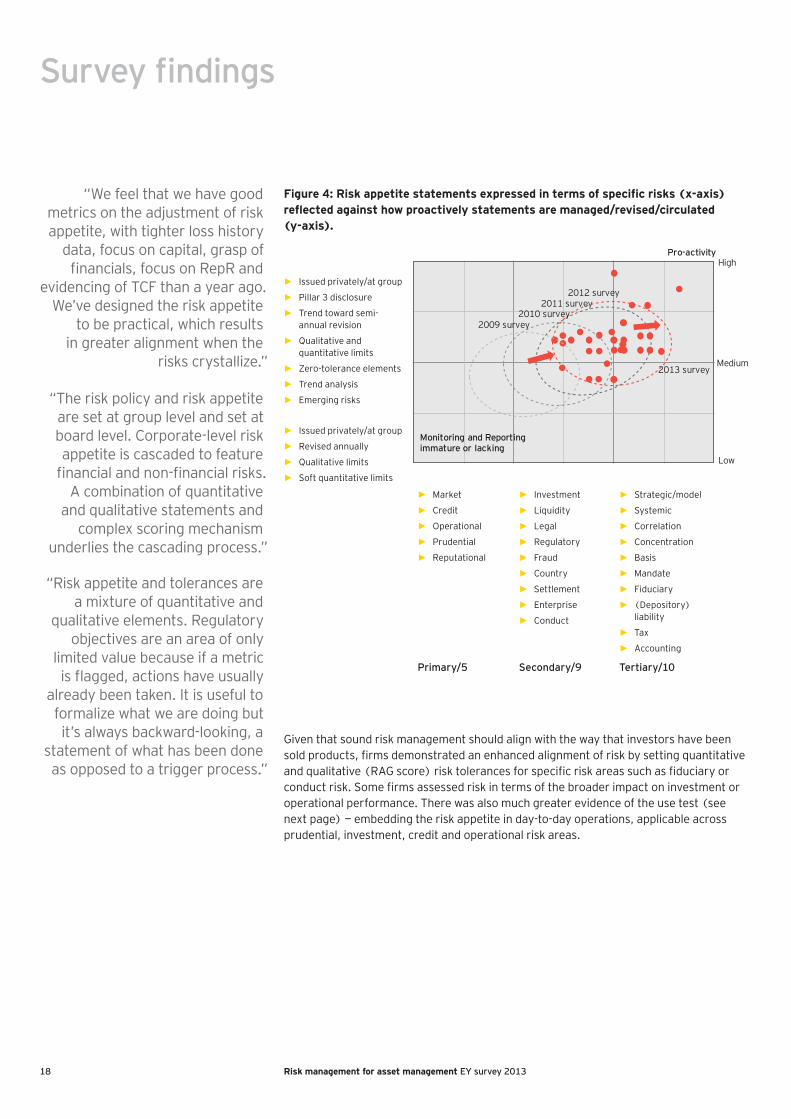

In 2012 a broadly similar behavior was recorded as compared with last year (see Figure 4). The results from the 2013 survey reflected an even greater inclination among both traditional and alternative asset managers to accommodate more secondary and tertiary risk factors under consideration, with a wide range in the approach and quality of the articulation of risk appetites, without a corresponding increase in pro-activity when revisiting risk appetites on a more periodic basis.

From a “top-down” perspective, statements or frameworks featured views of the board, strategic/business goals, competitive environment, organizational culture, expectation of local and regional regulators, reputational considerations, macro-economic and market conditions, references to credit rating agencies and references to counterparties, particularly in relation to dependencies, such as outsourcing, asset servicing or prime services.

3 Typically risk appetite statements must be transparent to top management and the board, with demonstrable processes to illustrate whether risks are commensurate with the risk appetite. They should be augmented by: 1) risk control structures, which ensure that any risks taken across the entity, business unit or group do not exceed risk appetite limits in any given day, and 2) well-established stress testing approaches that determine the expected losses that would be incurred over different stress periods — applied to the strategy as well as the current business. Above all, risk appetite statements need to be powered by management information to enable risk to be monitored by boards and senior management alike against a firm’s stated risk appetite.

Low Medium

Bribery Act

MLD IIIPRIPs

Clientmoney

SSR

Solvency IICRD III/IV

MAD IIMiFID II Shadow banking

FTT

AIFMD

FATCAEMIR

RDR

UCITS IV/V/VI

National thematic

ProductReg.

Medium

High

High

Likely impact on IMs

Prio

rity

for I

Ms

Top regulation categories receiving special attention in 2013 “The CRO spends approximately 60% of his time on strategic topics and 40% on daily, tactical topics.”

“We are appalled at the potential for new shadow banking regulation to be introduced in such a way that it impacts both our collateral management and money market funds.”

“Products are reviewed against macro-developments, such as the Arab Spring or Eurozone difficulties. We also ask, is it a strategic product or an opportunistic product?”

“The oversight of marketing and NPPRs under AIFMD will require a police force. But continental Europe doesn’t yet have a compliance culture in the same way, and who will have the legal powers to police what needs to happen?”

18 Risk management for asset management EY survey 2013

Figure 4: Risk appetite statements expressed in terms of specific risks (x-axis) reflected against how proactively statements are managed/revised/circulated (y-axis).

Medium

Monitoring and Reportingimmature or lacking

Low

HighPro-activity

2013 survey

2009 survey2010 survey

2011 survey2012 survey

Given that sound risk management should align with the way that investors have been sold products, firms demonstrated an enhanced alignment of risk by setting quantitative and qualitative (RAG score) risk tolerances for specific risk areas such as fiduciary or conduct risk. Some firms assessed risk in terms of the broader impact on investment or operational performance. There was also much greater evidence of the use test (see next page) — embedding the risk appetite in day-to-day operations, applicable across prudential, investment, credit and operational risk areas.

Survey findings

“We feel that we have good metrics on the adjustment of risk appetite, with tighter loss history

data, focus on capital, grasp of financials, focus on RepR and

evidencing of TCF than a year ago. We’ve designed the risk appetite

to be practical, which results in greater alignment when the

risks crystallize.”

“The risk policy and risk appetite are set at group level and set at board level. Corporate-level risk appetite is cascaded to feature

financial and non-financial risks. A combination of quantitative

and qualitative statements and complex scoring mechanism

underlies the cascading process.”

“Risk appetite and tolerances are a mixture of quantitative and

qualitative elements. Regulatory objectives are an area of only

limited value because if a metric is flagged, actions have usually

already been taken. It is useful to formalize what we are doing but it’s always backward-looking, a

statement of what has been done as opposed to a trigger process.”

► Issued privately/at group

► Pillar 3 disclosure

► Trend toward semi-annual revision

► Qualitative and quantitative limits

► Zero-tolerance elements

► Trend analysis

► Emerging risks

► Market

► Credit

► Operational

► Prudential

► Reputational

► Investment

► Liquidity

► Legal

► Regulatory

► Fraud

► Country

► Settlement

► Enterprise

► Conduct

► Strategic/model

► Systemic

► Correlation

► Concentration

► Basis

► Mandate

► Fiduciary

► (Depository) liability

► Tax

► Accounting

► Issued privately/at group

► Revised annually

► Qualitative limits

► Soft quantitative limits

Primary/5 Secondary/9 Tertiary/10

19Risk management for asset management EY survey 2013

The use test was a focal point this year, with firms showing a wide variance in involvement of the risk function in key decisions and how tolerances and limits were defined.The more advanced firms in the survey provided ample evidence of deploying risk parameter frameworks for portfolio (investment) risk, consisting of allowable ranges for the applicable risk measures, calibrated for each model type, product or portfolio depending on asset class. Every client portfolio could be mapped to the appropriate model type/product and therefore managed in line with the appropriate risk framework, with some exceptions — such as real estate investment management (REIM) or private equity. The management of counterparty credit risk saw a divergence between those firms with hard limits on exposure and rating versus a softer limit/monitoring type approach where action was ad hoc in order to take into account the market dynamics at the time. Operational risk appetite still appeared to be the most difficult to articulate and embed due to its limited quantitative data and, therefore, heavy reliance on qualitative aspects.

There was also more awareness in general (particularly among hedge funds) of firms articulating their risk appetites effectively to allocate technical resources to where they were needed (e.g., partitioned between the firm/outsourcing agents) or to avoid shocks to future earnings. The CRO was continuing to challenge 1LD as a “critical friend,” but the CRO was equally aware of when to apply judgments to tolerances (discrimination as per “hard” or “soft” risk limits) and to intervene more forcefully when needed. This was amply demonstrated in the product arena (see below, with earlier involvement of CROs in the manufacturing cycle or demonstrating their veto), but a minority of firms indicated CRO involvements in strategic planning, M&A, setting budgets or remuneration or client onboarding (see Figure 5).

Figure 5: Comparison of use test components

Key: Survey 2013

Rel

ativ

e in

dica

tor

Out

sour

cing

dec

isio

ns

78%

49% 54%

31%38%

71%61% 63%

24%

58%69%

30%

46%

Stra

tegi

c pl

anni

ng

Acqu

isiti

on/D

ivest

iture

New

pro

duct

app

rova

l

Post

-impl

emen

tatio

n re

view

s

Budg

et-s

ettin

g pr

oces

ses

Appr

aisa

ls/R

emun

erat

ion-

sett

ing

Clie

nt o

nboa

rdin

g

Bein

g in

form

ed o

f dec

isio

n

Prov

idin

g op

inio

nto

dec

isio

n-m

aker

s

Key

cont

ribu

tor

tode

cisio

n-m

akin

g pr

oces

s

Exer

cisi

ng a

righ

t of v

eto

Form

al ri

sk a

sses

smen

t co

nduc

ted

as p

art o

f thi

s pro

cess

with

as

sess

men

t of i

mpa

ct o

n th

e fir

m’s

risk

app

etite

Risk involved in the following decision-making processes Involvement includes

“We are keen not to apply a risk appetite for investment risk. A risk appetite is all about governance — do we have the triggers going outside the normal limits and expectations? For example, private equity is a low OpR because each PE deal is structured and each of the PMs do their own RCSA.”

“We spend time discussing the appropriateness of the products

— under various market, product and client conditions — and take a TCF view as to ‘can this product be mis-sold?’ For example, there is huge investor appetite for high-yield products, and investors don’t always understand the heightened risks. Regulators will always focus on outcomes, so we have to be prudent.”

“The use test is very helpful — several regulators are emphasizing its use. The right values are paramount — governance and stress testing must be appropriate, and an easy escalation process must be in evidence.”

20 Risk management for asset management EY survey 2013

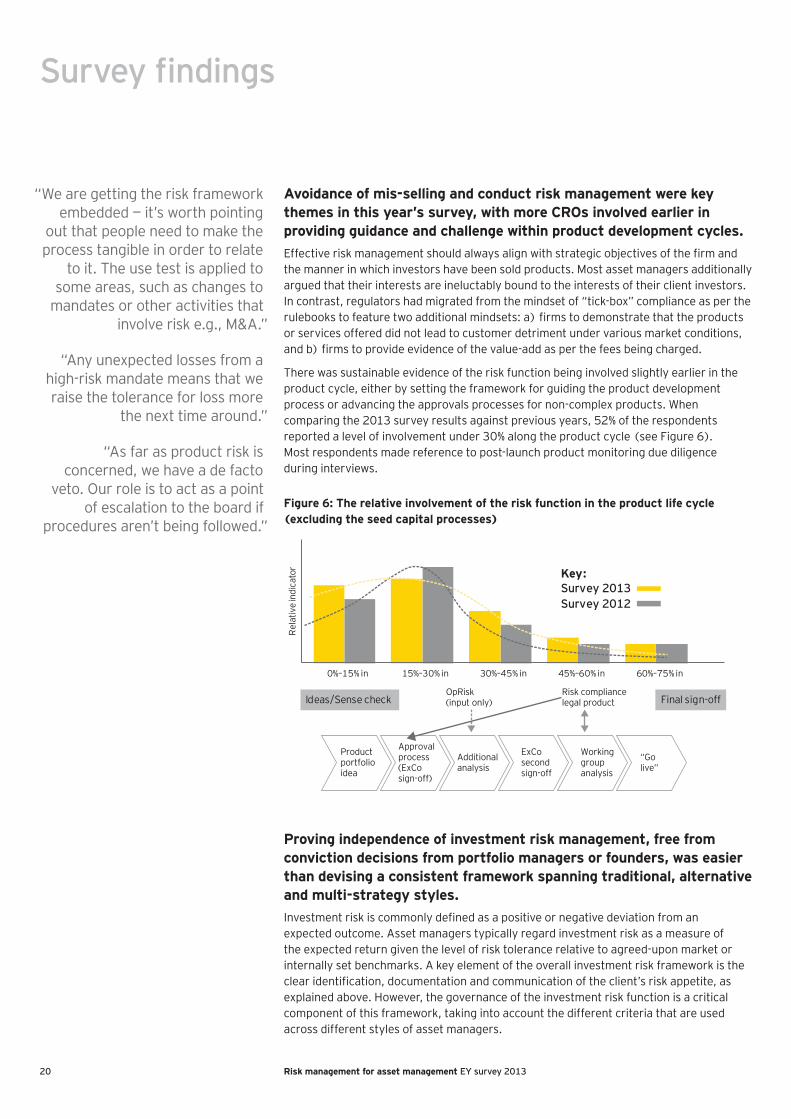

Avoidance of mis-selling and conduct risk management were key themes in this year’s survey, with more CROs involved earlier in providing guidance and challenge within product development cycles.Effective risk management should always align with strategic objectives of the firm and the manner in which investors have been sold products. Most asset managers additionally argued that their interests are ineluctably bound to the interests of their client investors. In contrast, regulators had migrated from the mindset of “tick-box” compliance as per the rulebooks to feature two additional mindsets: a) firms to demonstrate that the products or services offered did not lead to customer detriment under various market conditions, and b) firms to provide evidence of the value-add as per the fees being charged.

There was sustainable evidence of the risk function being involved slightly earlier in the product cycle, either by setting the framework for guiding the product development process or advancing the approvals processes for non-complex products. When comparing the 2013 survey results against previous years, 52% of the respondents reported a level of involvement under 30% along the product cycle (see Figure 6). Most respondents made reference to post-launch product monitoring due diligence during interviews.

Figure 6: The relative involvement of the risk function in the product life cycle (excluding the seed capital processes)

Final sign-off

Rel

ativ

e in

dica

tor

0%–15% in 15%–30% in 30%–45% in 45%–60% in 60%–75% in

Key: Survey 2013Survey 2012

Ideas/Sense checkOpRisk(input only)

Risk compliancelegal product

Product portfolio idea

Approvalprocess(ExCo sign-off)

Additionalanalysis

ExCosecondsign-off

Workinggroupanalysis

“Golive”

Proving independence of investment risk management, free from conviction decisions from portfolio managers or founders, was easier than devising a consistent framework spanning traditional, alternative and multi-strategy styles.Investment risk is commonly defined as a positive or negative deviation from an expected outcome. Asset managers typically regard investment risk as a measure of the expected return given the level of risk tolerance relative to agreed-upon market or internally set benchmarks. A key element of the overall investment risk framework is the clear identification, documentation and communication of the client’s risk appetite, as explained above. However, the governance of the investment risk function is a critical component of this framework, taking into account the different criteria that are used across different styles of asset managers.

Survey findings

“We are getting the risk framework embedded — it’s worth pointing

out that people need to make the process tangible in order to relate

to it. The use test is applied to some areas, such as changes to

mandates or other activities that involve risk e.g., M&A.”

“Any unexpected losses from a high-risk mandate means that we raise the tolerance for loss more

the next time around.”

“As far as product risk is concerned, we have a de facto

veto. Our role is to act as a point of escalation to the board if

procedures aren’t being followed.”

21Risk management for asset management EY survey 2013

Most survey respondents commented that fund managers were tasked with reviewing each portfolio on a daily basis as part of the ongoing investment management process. The portfolio manager would often have the ability to review the outliers in cash instruments, such as equities and bonds against the investment risk parameter frameworks — a particular focus for French firms. Exception reports highlighting portfolios that had moved outside their designated investment risk parameters were usually generated on a daily basis for the most automated firms, allowing the heads of desk to review the exceptions for cash instruments each day, and the exceptions for more illiquid instruments, such as OTC instruments to be reviewed on a monthly basis (or quarterly in the case of real-estate assets).

Many firms also claimed that their investment risk function was independent, but this was in evidence only if there were qualified headcount located in the 2LD able to provide effective challenge against bias and conviction decisioning on the part of the portfolio managers, (particularly if their decisioning contravened regulations and/or the firms’ stated risk appetite). Client expectations could be managed by demonstrating that risk management arrangements were free from conflicts of interest or conviction decisioning on the part of founders, portfolio managers or desk heads. Of the respondents in 2013, 51% could attest the independence of the investment risk function (see Figure 7), and the figures were notably higher in the UK compared with some continental European centers.

Other points to note concern the large disparities in the way firms managed investment risk. To a large extent, these were driven by the underlying investment style of the firm. For example, 56% of the respondents demonstrated ready access to quant skills in product engineering. Only 40% of the respondents demonstrated an advanced process for risk budgeting (the process of decomposing the aggregate risk of a portfolio into its risk factor constituents, using quantitative risk measures to allocate assets). Sixty one percent of firms could demonstrate the measurement and monitoring of risk at both an aggregate and a factor level, while 47% could demonstrate dynamic modeling (e.g., hedging portfolios in near or real time).

Some firms followed a direction of travel that enabled them to task a dedicated investment risk and analytics team to support and enhance the investment risk framework through a number of roles that included:

► Providing technical analysis into investment risk issues, covering portfolios, markets and investment risk models

► Further developing investment risk parameters for products, models and portfolios for the various asset classes (traditional, alternative, cash, derivatives, multi-asset, PE/RE, etc.)

► Conducting independent reviews and analysis of investment risk within products, models and portfolios

► Developing the reporting and risk analytics capability to support professionals in managing the investment risk within their portfolios

“Investment objectives are laid out in the prospectuses and linked to ‘hard’ limits; there is a specific focus in UK around preventing product mis-selling and client assets/money. Both hard and soft limits are used by both the business and the Risk function; Liquidity funding limits are encouraged, there is a particular motivation by UCITS and a similar logic will be applied with AIFMD in mind.”

“Investment risk is taken seriously in Germany; it is the third most important risk priority behind outsourcing risk and data security here. We have portfolio risk management skills in the 2LD able to provide challenge to the 1LD. The job of InvR in the 1LD is to maximize risk adjusted returns for our portfolios. The job of InvR in the 2LD is to mitigate unwanted InvR outside the firm’s regular risk appetite.”

22 Risk management for asset management EY survey 2013