Embed Size (px)

Citation preview

EY Canada Independence Policy CA-P1101

December 2014

1 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

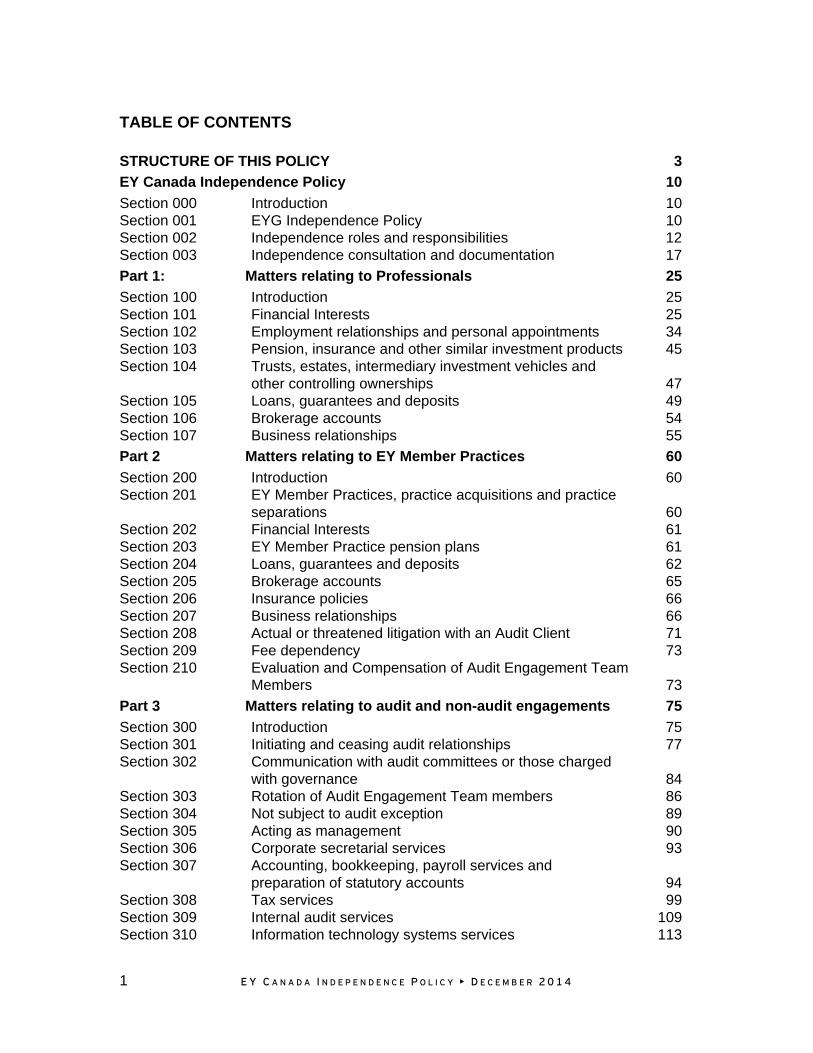

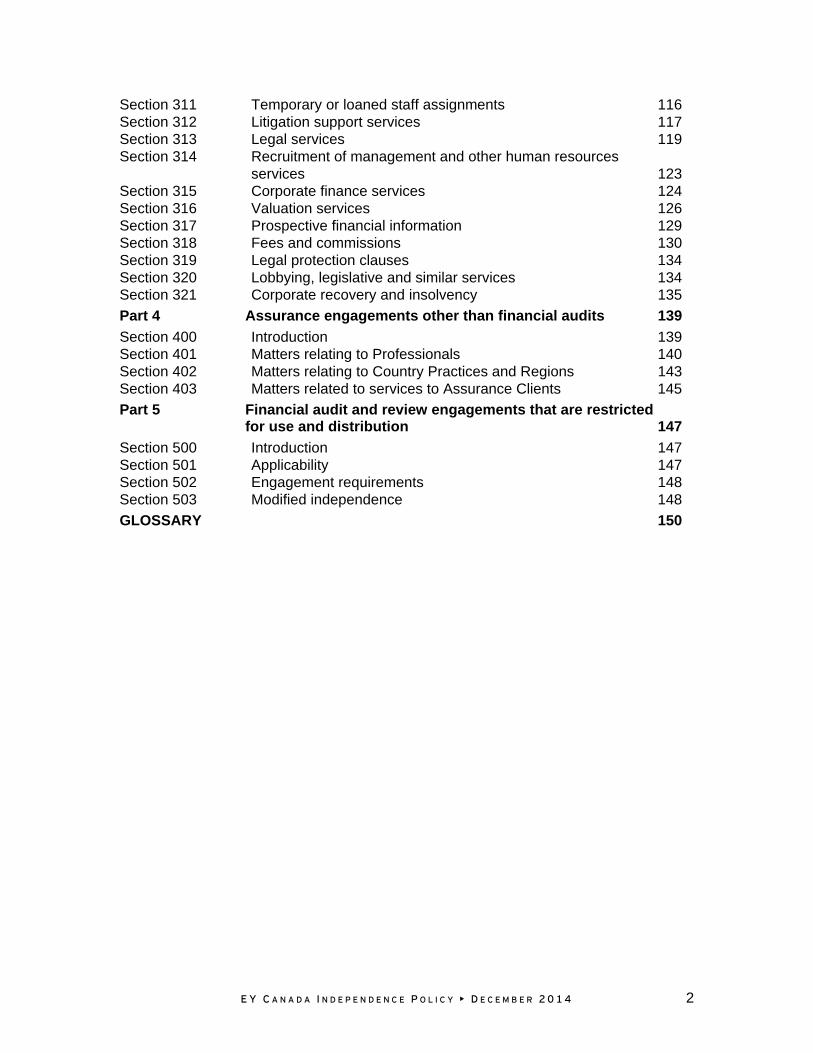

TABLE OF CONTENTS

STRUCTURE OF THIS POLICY 3

EY Canada Independence Policy 10

Section 000 Introduction 10 Section 001 EYG Independence Policy 10 Section 002 Independence roles and responsibilities 12 Section 003 Independence consultation and documentation 17

Part 1: Matters relating to Professionals 25

Section 100 Introduction 25 Section 101 Financial Interests 25 Section 102 Employment relationships and personal appointments 34 Section 103 Pension, insurance and other similar investment products 45 Section 104 Trusts, estates, intermediary investment vehicles and

other controlling ownerships 47 Section 105 Loans, guarantees and deposits 49 Section 106 Brokerage accounts 54 Section 107 Business relationships 55

Part 2 Matters relating to EY Member Practices 60

Section 200 Introduction 60 Section 201 EY Member Practices, practice acquisitions and practice

separations 60 Section 202 Financial Interests 61 Section 203 EY Member Practice pension plans 61 Section 204 Loans, guarantees and deposits 62 Section 205 Brokerage accounts 65 Section 206 Insurance policies 66 Section 207 Business relationships 66 Section 208 Actual or threatened litigation with an Audit Client 71 Section 209 Fee dependency 73 Section 210 Evaluation and Compensation of Audit Engagement Team

Members 73

Part 3 Matters relating to audit and non-audit engagements 75

Section 300 Introduction 75 Section 301 Initiating and ceasing audit relationships 77 Section 302 Communication with audit committees or those charged

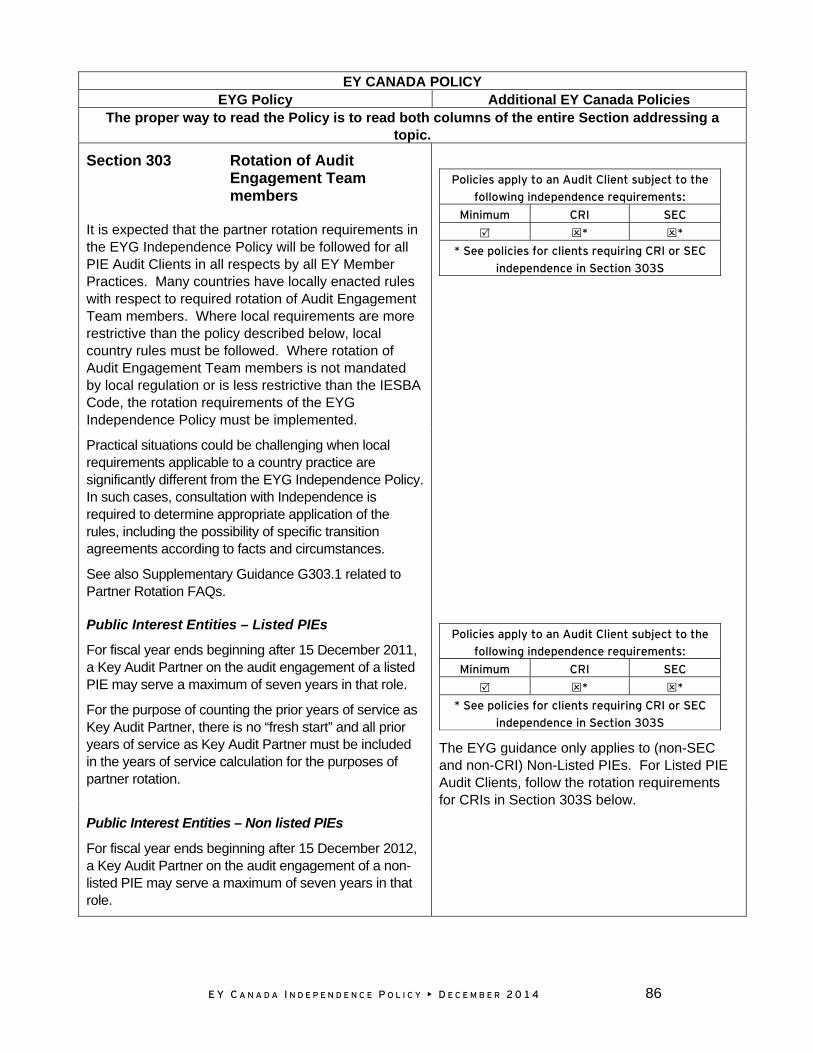

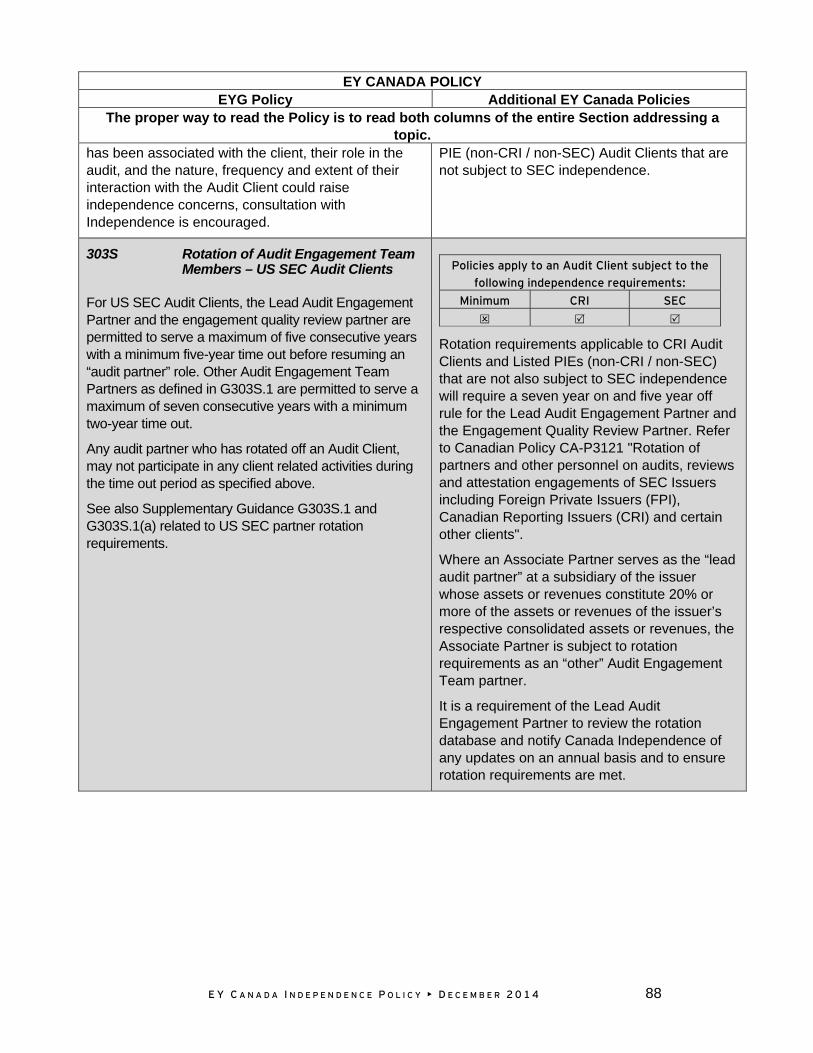

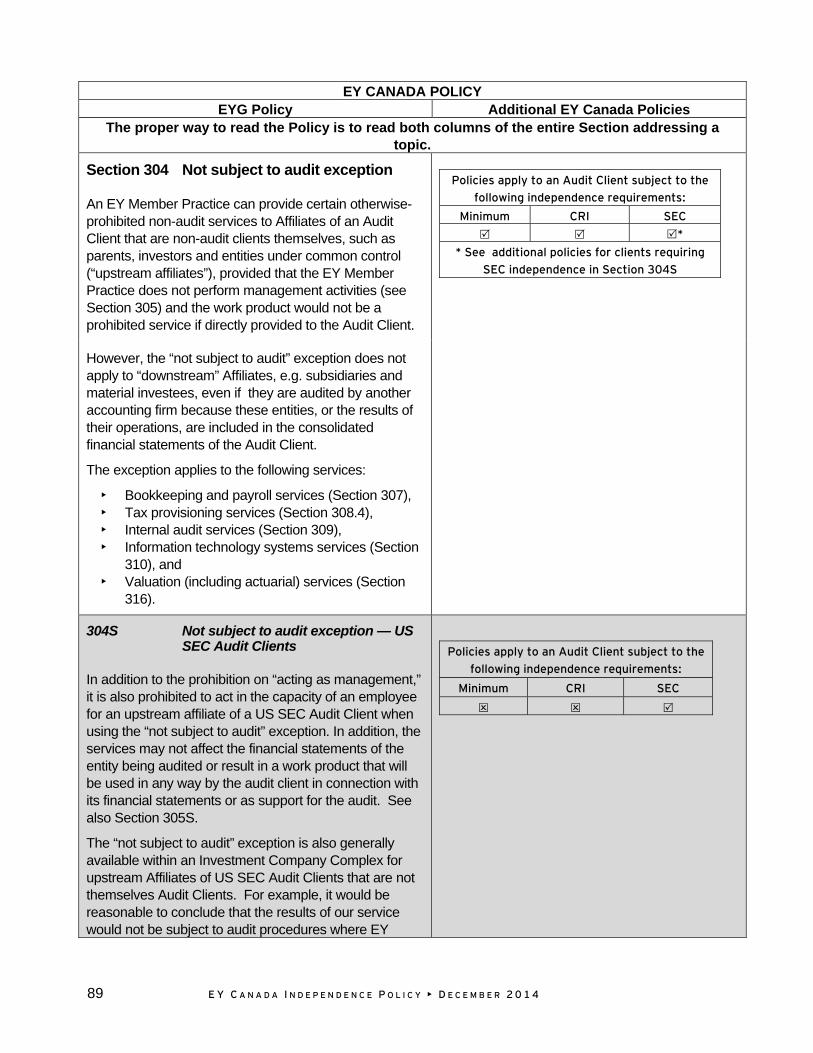

with governance 84 Section 303 Rotation of Audit Engagement Team members 86 Section 304 Not subject to audit exception 89 Section 305 Acting as management 90 Section 306 Corporate secretarial services 93 Section 307 Accounting, bookkeeping, payroll services and

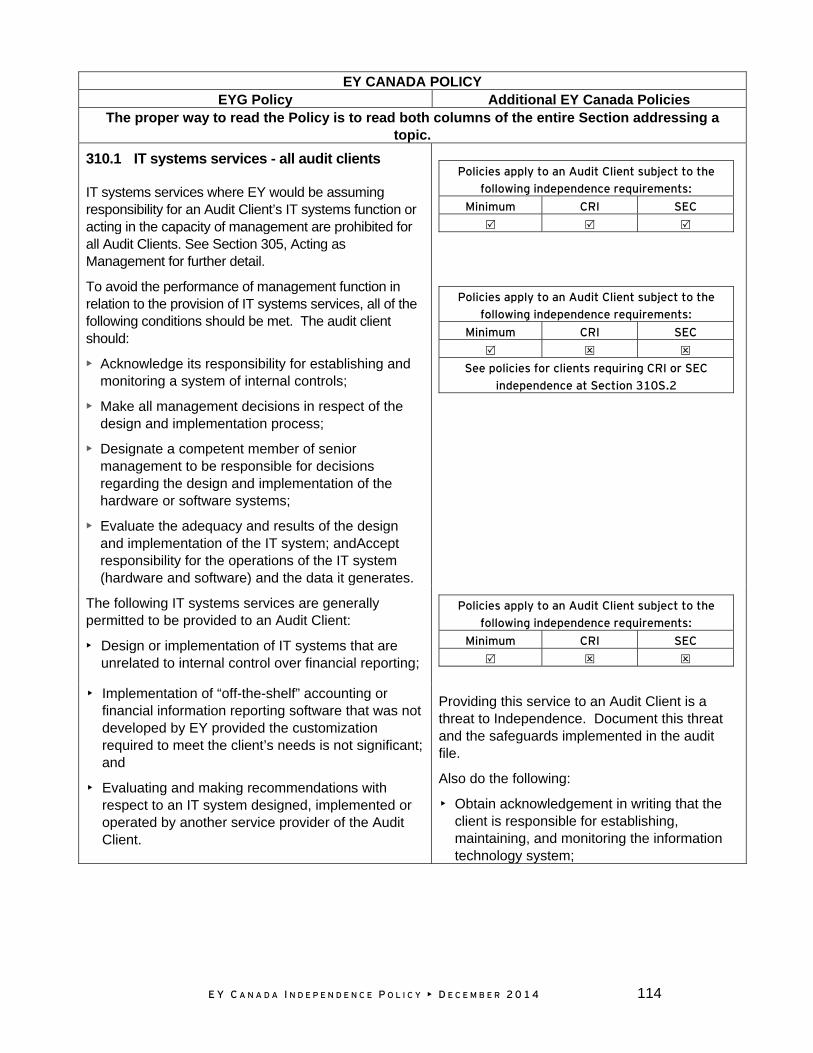

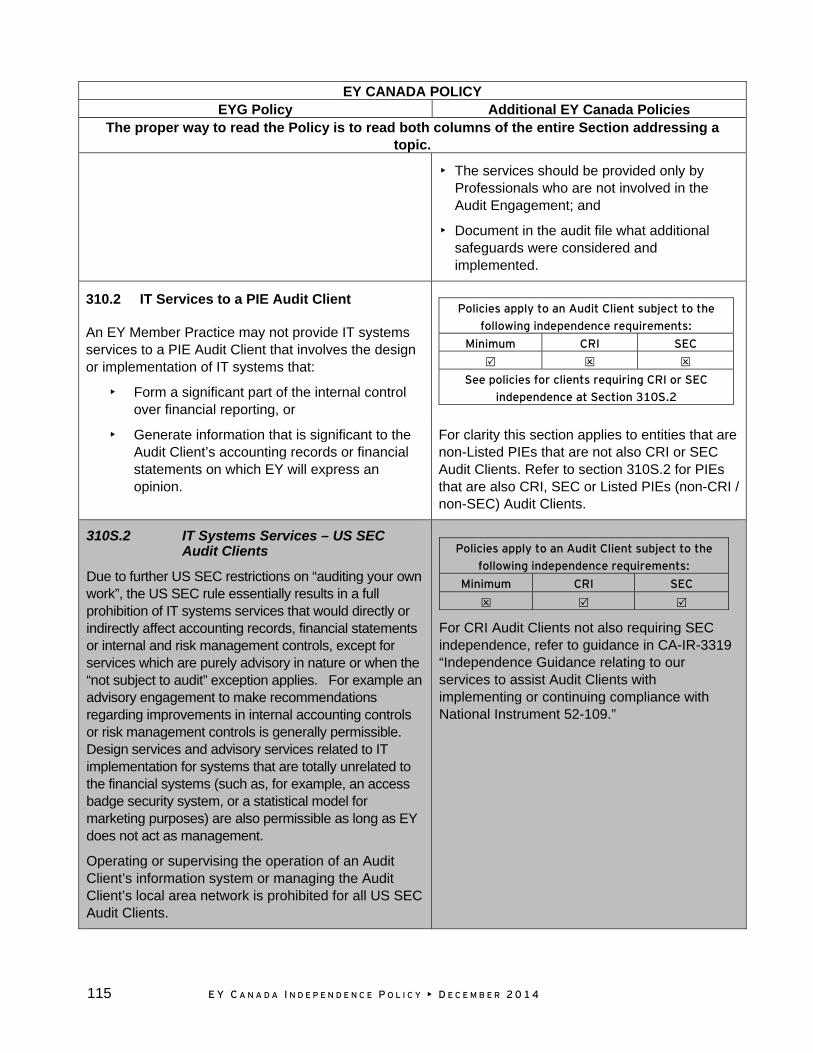

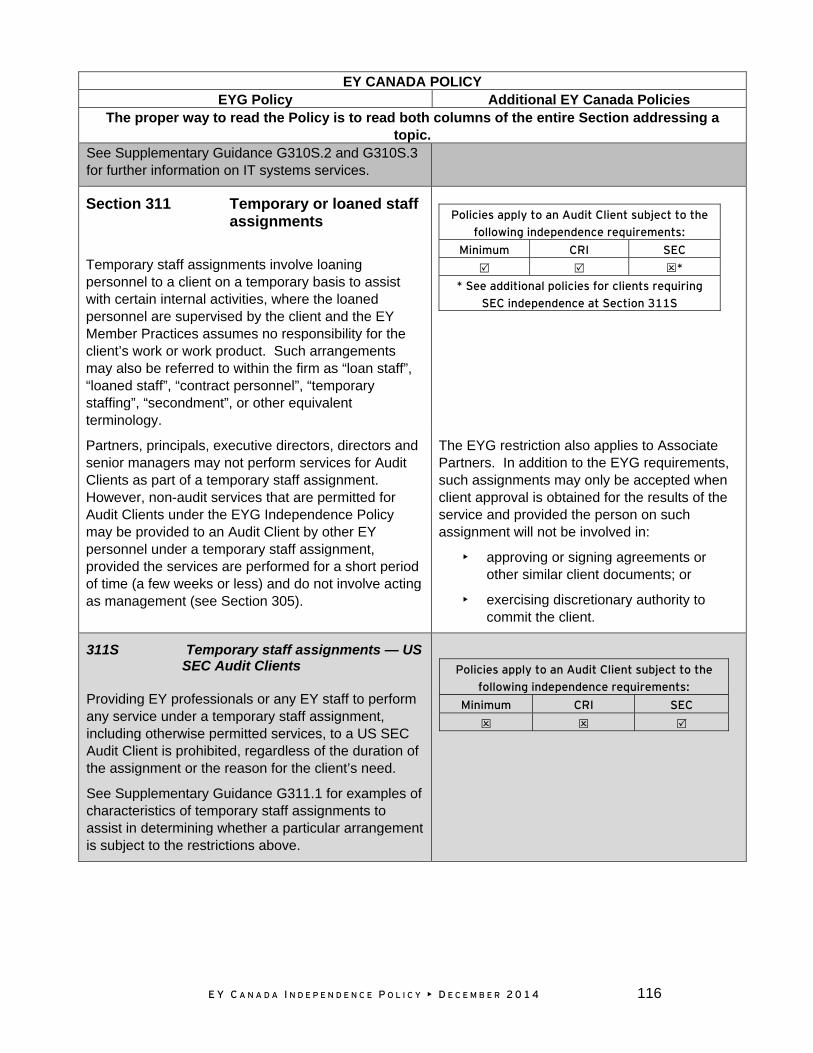

preparation of statutory accounts 94 Section 308 Tax services 99 Section 309 Internal audit services 109 Section 310 Information technology systems services 113

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 2

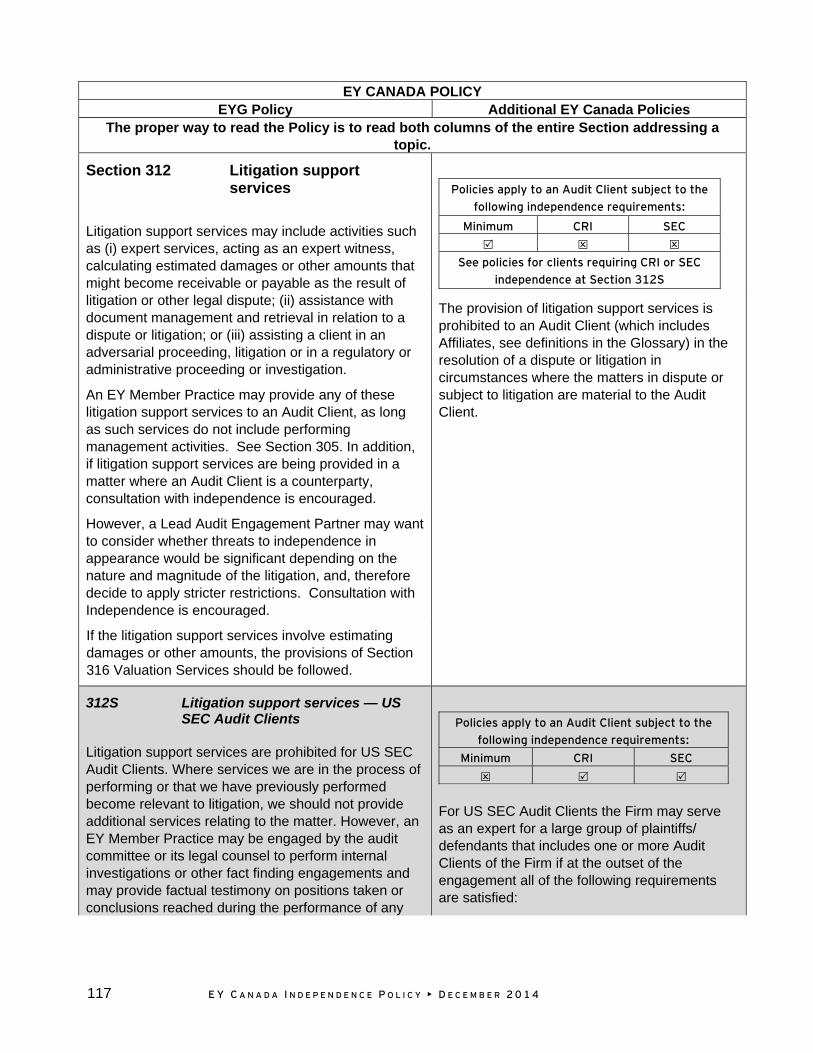

Section 311 Temporary or loaned staff assignments 116 Section 312 Litigation support services 117 Section 313 Legal services 119 Section 314 Recruitment of management and other human resources

services 123 Section 315 Corporate finance services 124 Section 316 Valuation services 126 Section 317 Prospective financial information 129 Section 318 Fees and commissions 130 Section 319 Legal protection clauses 134 Section 320 Lobbying, legislative and similar services 134 Section 321 Corporate recovery and insolvency 135

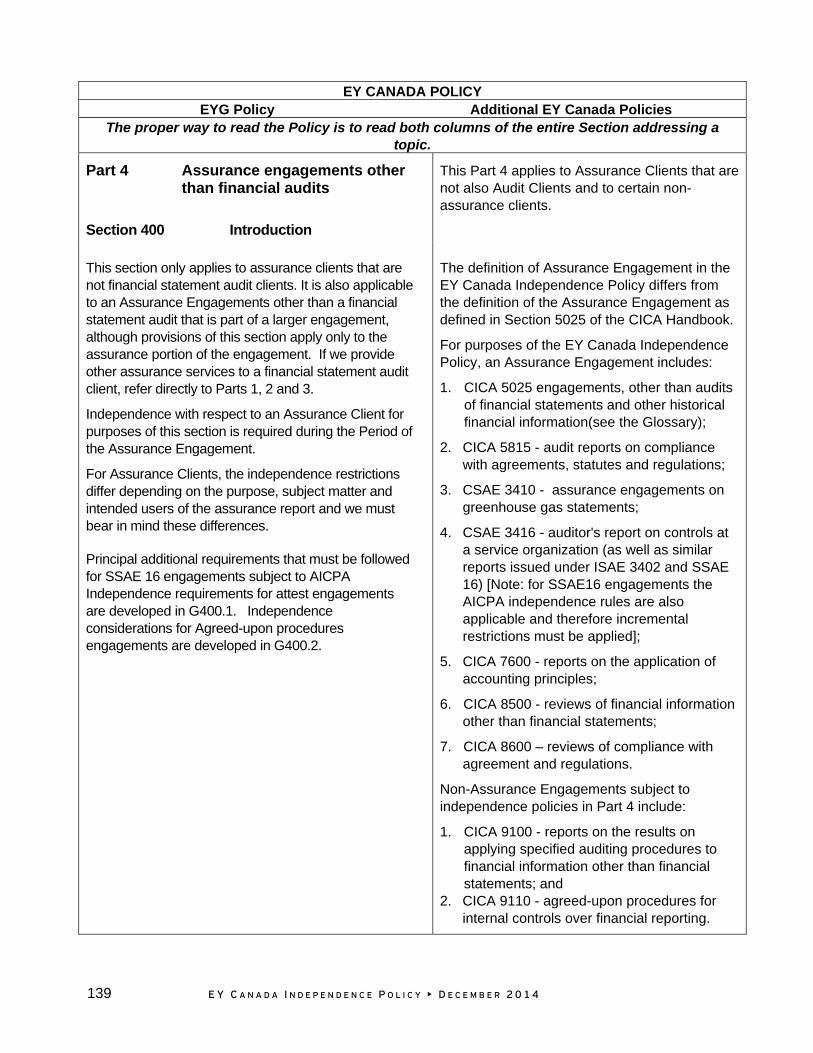

Part 4 Assurance engagements other than financial audits 139

Section 400 Introduction 139 Section 401 Matters relating to Professionals 140 Section 402 Matters relating to Country Practices and Regions 143 Section 403 Matters related to services to Assurance Clients 145

Part 5 Financial audit and review engagements that are restricted for use and distribution 147

Section 500 Introduction 147 Section 501 Applicability 147 Section 502 Engagement requirements 148 Section 503 Modified independence 148

GLOSSARY 150

3 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

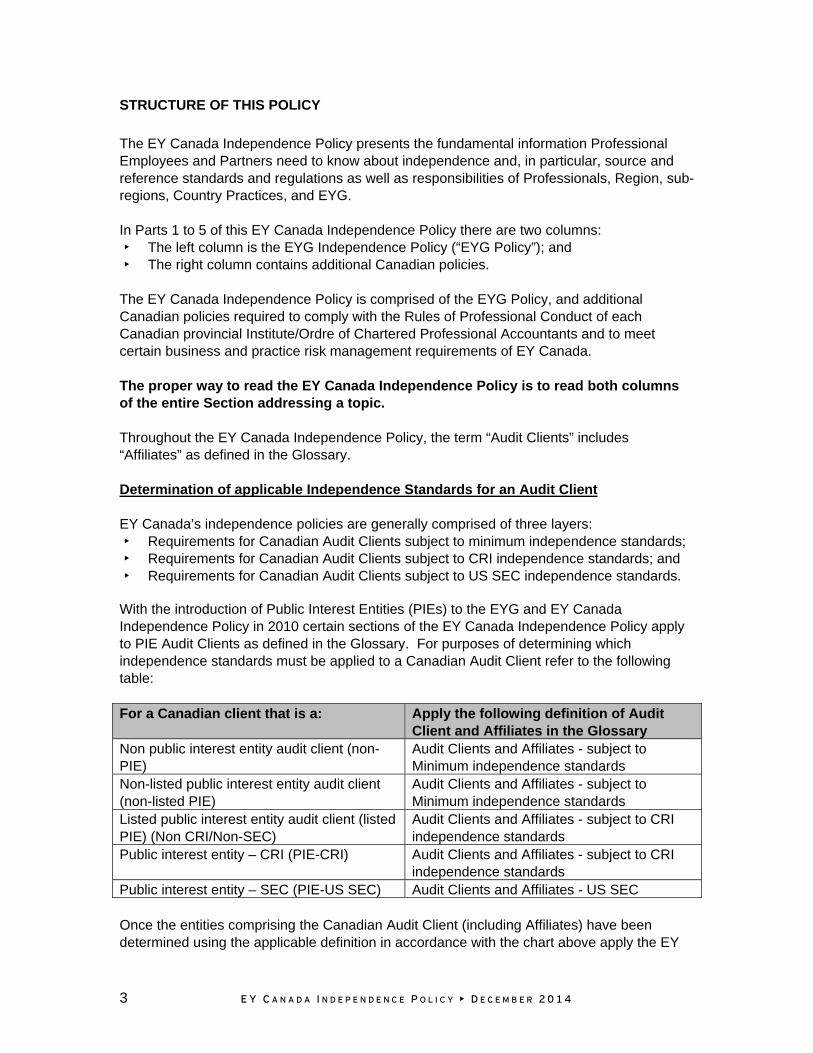

STRUCTURE OF THIS POLICY

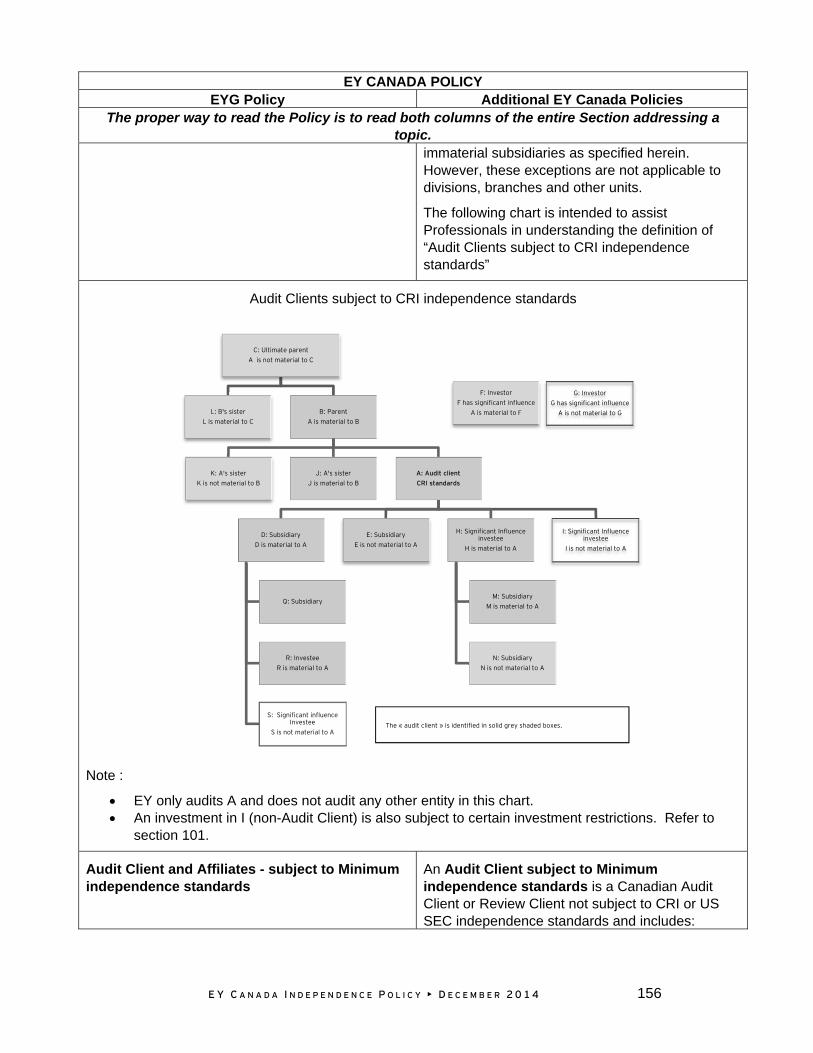

The EY Canada Independence Policy presents the fundamental information Professional Employees and Partners need to know about independence and, in particular, source and reference standards and regulations as well as responsibilities of Professionals, Region, sub-regions, Country Practices, and EYG. In Parts 1 to 5 of this EY Canada Independence Policy there are two columns: • The left column is the EYG Independence Policy (“EYG Policy”); and • The right column contains additional Canadian policies.

The EY Canada Independence Policy is comprised of the EYG Policy, and additional Canadian policies required to comply with the Rules of Professional Conduct of each Canadian provincial Institute/Ordre of Chartered Professional Accountants and to meet certain business and practice risk management requirements of EY Canada. The proper way to read the EY Canada Independence Policy is to read both columns of the entire Section addressing a topic. Throughout the EY Canada Independence Policy, the term “Audit Clients” includes “Affiliates” as defined in the Glossary. Determination of applicable Independence Standards for an Audit Client EY Canada’s independence policies are generally comprised of three layers: • Requirements for Canadian Audit Clients subject to minimum independence standards; • Requirements for Canadian Audit Clients subject to CRI independence standards; and • Requirements for Canadian Audit Clients subject to US SEC independence standards.

With the introduction of Public Interest Entities (PIEs) to the EYG and EY Canada Independence Policy in 2010 certain sections of the EY Canada Independence Policy apply to PIE Audit Clients as defined in the Glossary. For purposes of determining which independence standards must be applied to a Canadian Audit Client refer to the following table: For a Canadian client that is a: Apply the following definition of Audit

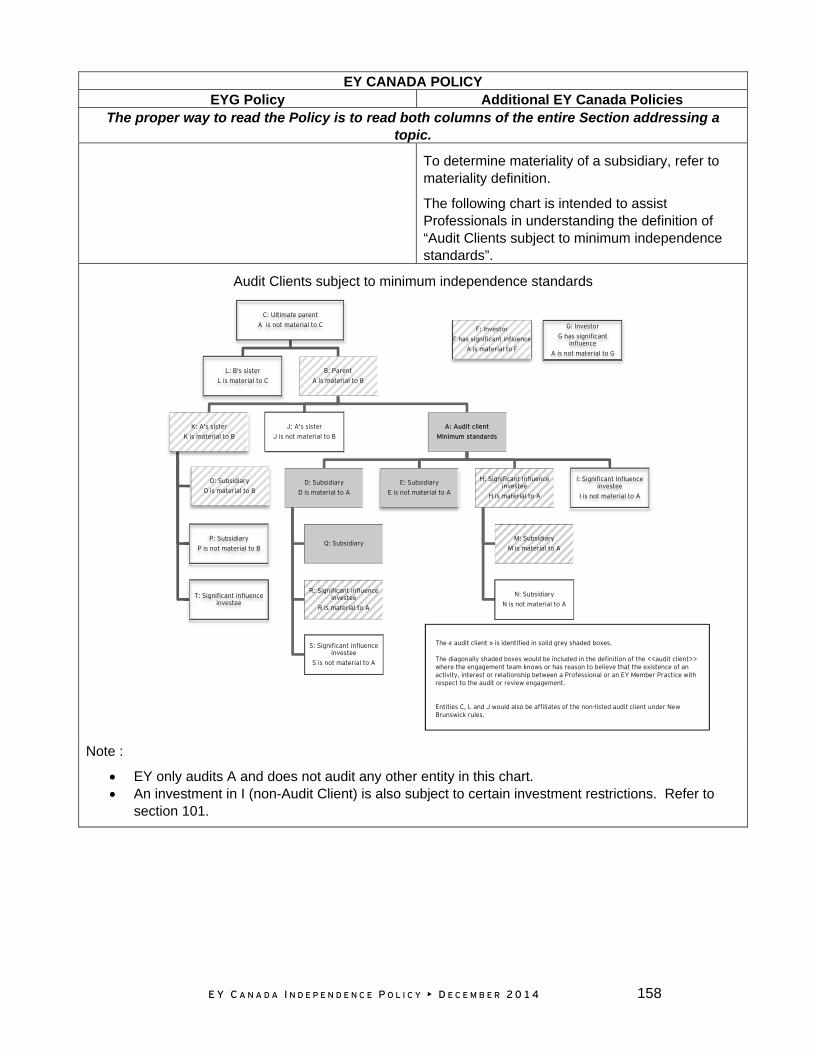

Client and Affiliates in the Glossary Non public interest entity audit client (non-PIE)

Audit Clients and Affiliates - subject to Minimum independence standards

Non-listed public interest entity audit client (non-listed PIE)

Audit Clients and Affiliates - subject to Minimum independence standards

Listed public interest entity audit client (listed PIE) (Non CRI/Non-SEC)

Audit Clients and Affiliates - subject to CRI independence standards

Public interest entity – CRI (PIE-CRI) Audit Clients and Affiliates - subject to CRI independence standards

Public interest entity – SEC (PIE-US SEC) Audit Clients and Affiliates - US SEC Once the entities comprising the Canadian Audit Client (including Affiliates) have been determined using the applicable definition in accordance with the chart above apply the EY

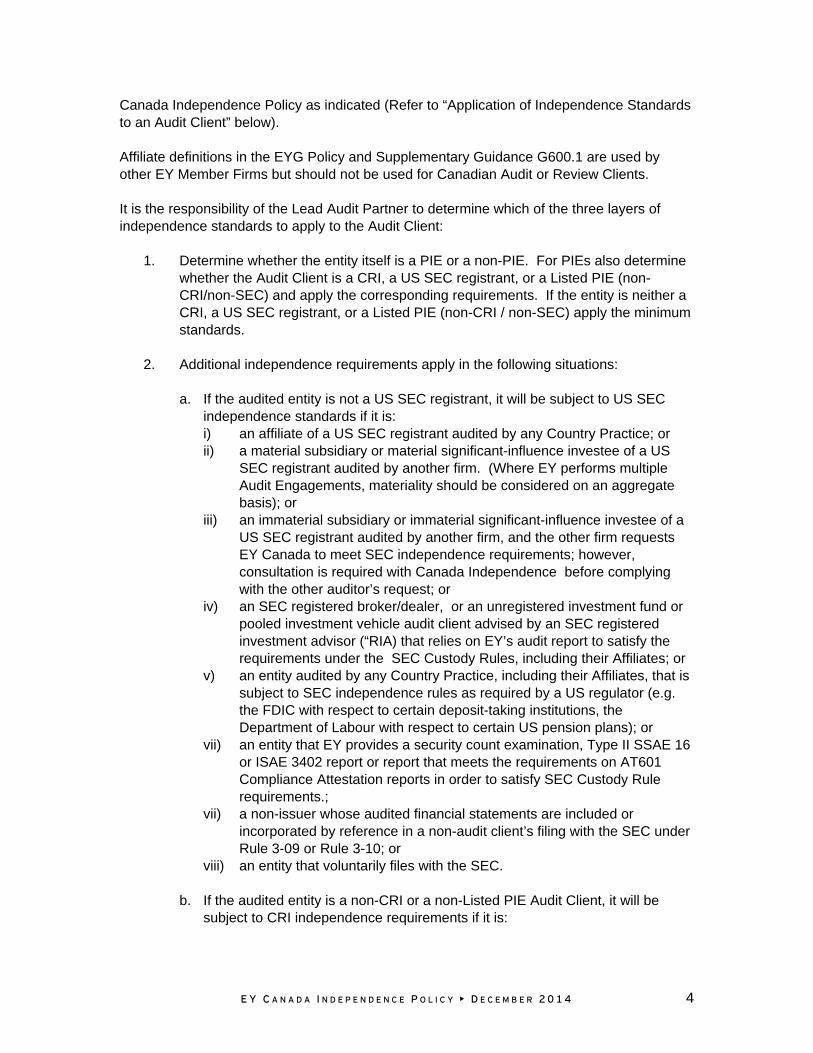

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 4

Canada Independence Policy as indicated (Refer to “Application of Independence Standards to an Audit Client” below). Affiliate definitions in the EYG Policy and Supplementary Guidance G600.1 are used by other EY Member Firms but should not be used for Canadian Audit or Review Clients. It is the responsibility of the Lead Audit Partner to determine which of the three layers of independence standards to apply to the Audit Client:

1. Determine whether the entity itself is a PIE or a non-PIE. For PIEs also determine whether the Audit Client is a CRI, a US SEC registrant, or a Listed PIE (non-CRI/non-SEC) and apply the corresponding requirements. If the entity is neither a CRI, a US SEC registrant, or a Listed PIE (non-CRI / non-SEC) apply the minimum standards.

2. Additional independence requirements apply in the following situations:

a. If the audited entity is not a US SEC registrant, it will be subject to US SEC

independence standards if it is: i) an affiliate of a US SEC registrant audited by any Country Practice; or ii) a material subsidiary or material significant-influence investee of a US

SEC registrant audited by another firm. (Where EY performs multiple Audit Engagements, materiality should be considered on an aggregate basis); or

iii) an immaterial subsidiary or immaterial significant-influence investee of a US SEC registrant audited by another firm, and the other firm requests EY Canada to meet SEC independence requirements; however, consultation is required with Canada Independence before complying with the other auditor’s request; or

iv) an SEC registered broker/dealer, or an unregistered investment fund or pooled investment vehicle audit client advised by an SEC registered investment advisor (“RIA) that relies on EY’s audit report to satisfy the requirements under the SEC Custody Rules, including their Affiliates; or

v) an entity audited by any Country Practice, including their Affiliates, that is subject to SEC independence rules as required by a US regulator (e.g. the FDIC with respect to certain deposit-taking institutions, the Department of Labour with respect to certain US pension plans); or

vii) an entity that EY provides a security count examination, Type II SSAE 16 or ISAE 3402 report or report that meets the requirements on AT601 Compliance Attestation reports in order to satisfy SEC Custody Rule requirements.;

vii) a non-issuer whose audited financial statements are included or incorporated by reference in a non-audit client’s filing with the SEC under Rule 3-09 or Rule 3-10; or

viii) an entity that voluntarily files with the SEC.

b. If the audited entity is a non-CRI or a non-Listed PIE Audit Client, it will be subject to CRI independence requirements if it is:

5 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

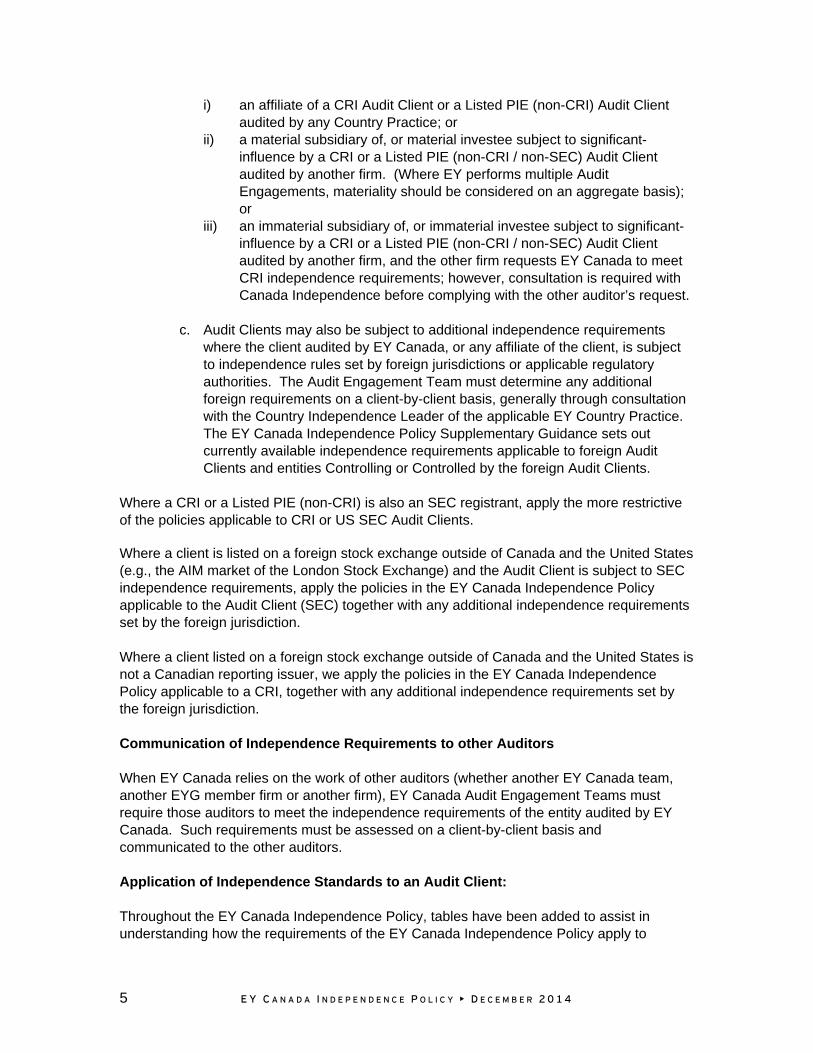

i) an affiliate of a CRI Audit Client or a Listed PIE (non-CRI) Audit Client audited by any Country Practice; or

ii) a material subsidiary of, or material investee subject to significant-influence by a CRI or a Listed PIE (non-CRI / non-SEC) Audit Client audited by another firm. (Where EY performs multiple Audit Engagements, materiality should be considered on an aggregate basis); or

iii) an immaterial subsidiary of, or immaterial investee subject to significant-influence by a CRI or a Listed PIE (non-CRI / non-SEC) Audit Client audited by another firm, and the other firm requests EY Canada to meet CRI independence requirements; however, consultation is required with Canada Independence before complying with the other auditor’s request.

c. Audit Clients may also be subject to additional independence requirements

where the client audited by EY Canada, or any affiliate of the client, is subject to independence rules set by foreign jurisdictions or applicable regulatory authorities. The Audit Engagement Team must determine any additional foreign requirements on a client-by-client basis, generally through consultation with the Country Independence Leader of the applicable EY Country Practice. The EY Canada Independence Policy Supplementary Guidance sets out currently available independence requirements applicable to foreign Audit Clients and entities Controlling or Controlled by the foreign Audit Clients.

Where a CRI or a Listed PIE (non-CRI) is also an SEC registrant, apply the more restrictive of the policies applicable to CRI or US SEC Audit Clients.

Where a client is listed on a foreign stock exchange outside of Canada and the United States (e.g., the AIM market of the London Stock Exchange) and the Audit Client is subject to SEC independence requirements, apply the policies in the EY Canada Independence Policy applicable to the Audit Client (SEC) together with any additional independence requirements set by the foreign jurisdiction. Where a client listed on a foreign stock exchange outside of Canada and the United States is not a Canadian reporting issuer, we apply the policies in the EY Canada Independence Policy applicable to a CRI, together with any additional independence requirements set by the foreign jurisdiction. Communication of Independence Requirements to other Auditors When EY Canada relies on the work of other auditors (whether another EY Canada team, another EYG member firm or another firm), EY Canada Audit Engagement Teams must require those auditors to meet the independence requirements of the entity audited by EY Canada. Such requirements must be assessed on a client-by-client basis and communicated to the other auditors. Application of Independence Standards to an Audit Client: Throughout the EY Canada Independence Policy, tables have been added to assist in understanding how the requirements of the EY Canada Independence Policy apply to

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 6

different types of Audit Clients. For example, if the policy section is applicable to an Audit Client subject to minimum standards and also applicable to an Audit Client subject to CRI independence standards, but is not applicable to an Audit Client subject to SEC independence, the table indicates the following:

Policies apply to an Audit Client subject to

the following independence requirements:

Minimum CRI SEC

See policies for clients requiring SEC

independence in XXXS

In some areas of the policy there may be additional policies on a specific topic that are applicable to the Audit Client. For example, if a section of the policy is applicable to an Audit Client requiring all three layers of independence standards (Minimum, CRI and SEC) and there are additional policies which apply to Audit Clients subject to SEC independence standards, the table indicates the following:

Policies apply to an Audit Client subject to

the following independence requirements:

Minimum CRI SEC *

* See additional policies for clients

requiring SEC independence in XXXS

Certain sections throughout the policy are applicable to all PIE Audit Clients. These sections are not separately indicated in the tables but restrictions for PIEs are contained in the policy text for applicable sections. If there is any uncertainty in how these restrictions apply, consultation with Canada Independence is encouraged.

7 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

Overview of the EY Canada Independence Policy The EY Canada Independence Policy includes the Introduction, Parts 1 to 5 and the Glossary.

EY Canada Independence Policy

The Introduction presents the fundamental information you need to know about independence, and particular source and reference standards and regulations as well as responsibilities of Professionals, Areas, Sub-Areas, Country Practices and EYG. Parts 1, 2, and 3 of the EY Canada Independence Policy provide for independence policy requirements for Professionals and EY Member practices, and also restrictions with respect to audit and non-audit services provided to Audit and Review Clients. Some paragraphs are presented in bold letters to add emphasis to significant independence requirements or prohibitions. Additional independence requirements that must be followed for Audit Clients that are US SEC registrants or subsidiaries, divisions or Affiliates of US SEC registrants are developed in each section of this policy in subsections marked with an “S”. These subsections are also presented in grey shading for easier access. For instance, US SEC considerations in relation to the topic developed in Section 101 is numbered Section 101S. When applying the independence rules to Audit Clients subject to SEC independence, the appropriate way to read the Policy is to read the applicable primary policy section in addition to the same section denoted with an “S”, to ensure all requirements are captured. The requirements in the section marked with an “S” are often incremental to the primary section and by no means comprehensive on a standalone basis. Where such SEC requirements apply to non-SEC Canadian clients, this is indicated in the “Additional Canadian Policies” column, usually through use of a table as discussed above. Part 4 provides for independence policy requirements in relation to Assurance Engagements other than Audit or Review Engagements with clients that are not also Audit or Review Clients. Refer to the definition of Assurance Engagement in the Glossary as certain Non-Assurance Engagements are, for purposes of the EY Canada Independence Policy, included in the Assurance Engagement definition and therefore such Clients are subject to the independence requirements of Part 4.

Part 5 provides for the EY Global independence policy requirements in relation to financial Audit and Review Engagements that are restricted for use and distribution. However, this section is not applicable in Canada as the requirements of Part 1 to 3 must be applied for such clients/engagements for all Canadian Audit or Review Clients.

The Glossary provides definitions of independence words and concepts consistently used within the EY Canada Independence Policy in an alphabetical order. Defined terms are generally capitalized throughout the EY Canada Independence Policy. Where the Canadian definitions are more rigorous than the EYG definition (usually to meet the requirements of the Rules of Professional Conduct of each Canadian provincial Institute/Ordre of Chartered Professional Accountants), use the Additional Canadian Policies definitions and guidance.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 8

Supplementary Guidance EY Canada has adopted the Supplementary Guidance of the EYG Independence Policy which can be found through the Risk Management CHS. Although the EYG Supplementary Guidance is applicable to EY Canada, the EYG Independence Policy itself should NOT be used for Canadian Audit or Assurance Clients. The EY Canada Independence Policy should continue to be applied instead as it not only incorporates the EYG Independence policy but also contains additional Canadian policies required to comply with the Rules of Professional Conduct of each Canadian provincial Institute of Chartered Professional Accountants and to meet certain business and practice risk management requirements of EY Canada.

A table of concordance that indicates how the EYG Supplementary Guidance applies to Canadian Audit Clients and Assurance Clients subject to minimum, CRI or SEC independence requirements is available in the Americas Area Policies and Practices Repository. Professionals should refer to this document when applying the EYG Supplementary Guidance to Canadian Audit Clients and Assurance Clients. The EY Canada Independence Policy does not address additional independence requirements for non-SEC companies that EY Canada audits using US generally accepted auditing standards. For this information, see the EY US Independence Policy (Score CA7528). The following independence resources are available for service line consultation: Tax: Karen Nixon (403-206-5326, EY Comm: 1656496): TAS: Carolyn Kerr (416-943-5486, EY Comm: 1625379); Advisory: Paul O’Donnell (416-943-3651, EY Comm: 1676036) Petar Nikolic (416-943-3114, EY Comm: 1676459); and Audit Engagement Team/Partner Rotation Matters: Gord Briggs (416-943-3257, EY Comm: 8624673). Throughout the EY Canada Independence Policy, there may be references to consult with the Regional Independence Leader, Rich Huesken (Cleveland Office: 216-583-2400, EY Comm:2574837). Before contacting the Area Independence Leader, contact the Canada Independence Leader, Ross Pearman (416-943-3176, EY Comm: 8677677).

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 9

EY Canada Independence Policy CA-P1101

December 2014

Parts 1 to 5

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 10

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

EY Canada Independence Policy

Parts 1 to 5

Section 000 Introduction

Independence is a concept fundamental to the audit profession and is pervasive in all dealings between EY Member Practices and their Audit and Assurance Clients. Independence means that EY Member Practices and their Professionals should be (in fact) and should appear to be (in appearance) free from interests that might be regarded as being incompatible with objectivity, integrity, and impartiality.

Independence therefore requires:

• independence of mind—the ability to provide an opinion without being affected by influences that compromise professional judgment, to act with integrity, and to exercise objectivity and professional scepticism; and

• independence in appearance—the avoidance of facts and circumstances that would lead a reasonable and informed third party to conclude that the integrity, objectivity or professional scepticism of a EY Member Practice or their Professionals had been compromised.

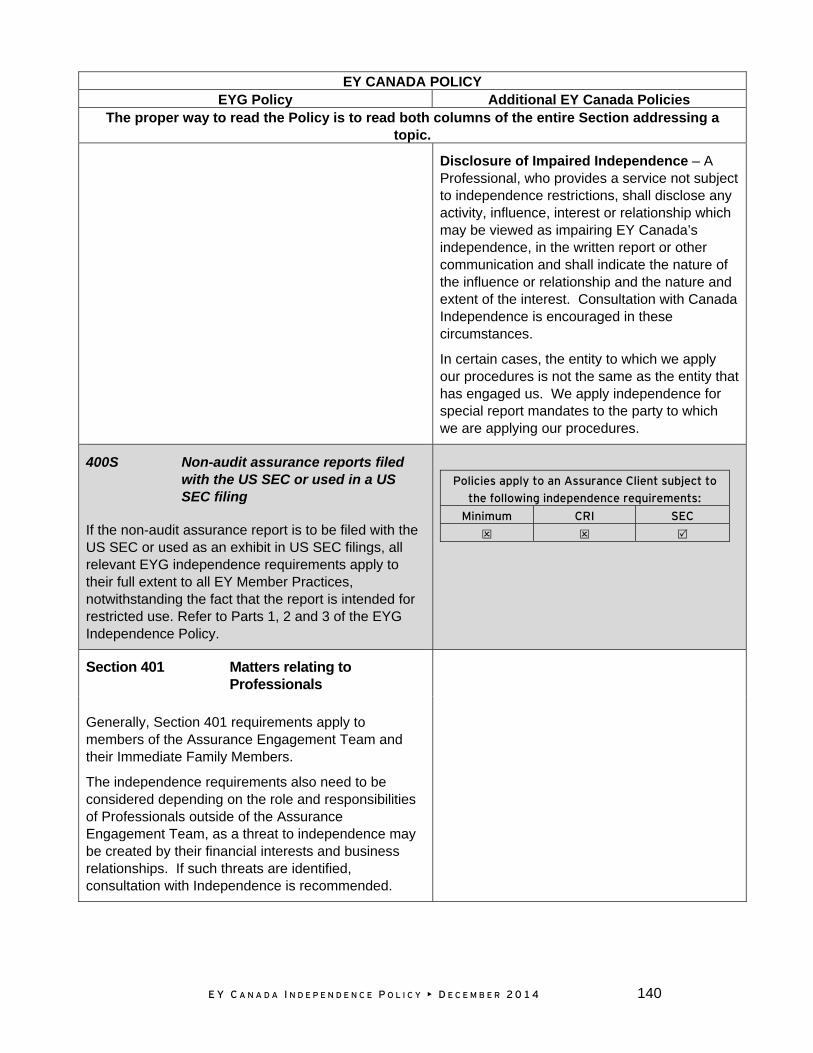

Assurance Engagements include specified auditing procedures engagements. See Part 4 in this Policy.

Section 001 EYG Independence Policy

The EYG Independence Policy establishes mandatory requirements and prohibitions with respect to the most common independence matters related to EY Member Practices and their Professionals.

The EYG Independence Policy is designed to comply with the elements of the International Ethics Standards Board for Accountants Code of Ethics for Professional Accountants (the IESBA Code) that deal with independence, objectivity and integrity.

This column in the EY Canada Independence Policy indicates additional requirements to comply with the Rules of Professional Conduct of each Canadian provincial Institute/Ordre of Chartered Professional Accountants and to meet certain business and practice risk management requirements of EY Canada.

11 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

In addition, US SEC independence requirements must be followed with respect to Audit Clients and entities that are subject to US SEC and PCAOB independence rules globally. Because of the extraterritorial reach of the US SEC requirements and the risk associated with non-compliance, the additional US SEC requirements are included where applicable and should be considered part of EYG Independence Policy.

More stringent independence rules than those contained in this policy may be required by country regulatory or standard-setting bodies. EY Member Practices sometimes adopt country independence policies that are more stringent than the EYG Independence Policy in order to align to local regulatory requirements and to efficiently communicate those requirements to their personnel. If an EY Member Practice adopts stricter policy requirements than those contained in this policy or required by local regulation, the Member Practice will inform the Region Independence leader, the Region and Area Risk Management Leaders and the Global Vice Chair – Independence of such requirements.

To be independent pursuant to the Canadian independence rules, Audit Engagement Teams must identify threats to independence, evaluate the significance of those threats and, if the threats are other than clearly insignificant, identify and apply safeguards to reduce them to an acceptable level.

Independence is potentially affected by self-interest, self-review, advocacy, familiarity, and intimidation threats. Safeguards fall into three broad categories: (i) safeguards created by the profession, legislation, or regulator, (ii) safeguards within the client entity and (iii) safeguards within EY Canada’s own systems and procedures.

Where safeguards are not available to reduce threats to an acceptable level, Audit Engagement Teams must eliminate the activity, interest, or relationship creating the threats or refuse to accept, or continue, the engagement. Consult with Canada Independence if such threats are identified or if the assessment of the adequacy of safeguards requires significant judgment. It is the responsibility of the Lead Audit Engagement Partner to make this determination and to ensure threats and safeguards are adequately documented for each engagement in the engagement file. See documentation requirements throughout the EY Canada Independence Policy and in Section 003.4.

When any EY Canada Audit Engagement Team is relying on the work of other auditors, (whether another EY Canada team, EYG member firm or another firm) that conduct other than an insignificant part of the audit of an Audit Client (which includes Affiliates, see definitions in the Glossary):

the EY Canada Audit Engagement Team is required to communicate its independence requirements to the other auditors; and

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 12

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

the EY Canada Audit Engagement Team is required to obtain written confirmation of independence from any other EYG member firm or any other audit firm.

An overview of the Canadian independence requirements is provided in the Country Supplement CA001.

Throughout this policy subsections marked with an “S” may also apply to Canadian Audit Clients, other than US SEC Audit Clients. Refer to the tables throughout the Canadian column of this policy to determine to which clients the subsections marked with an “S” apply.

Section 002 Independence roles and responsibilities

002.1 Responsibilities of Regions and Country Practices

Each EY Member Practice shall operate within and conduct engagements in accordance with that country’s professional standards, the EYG Independence Policy, all local/national independence requirements, and independence rules required by another country’s professional standards where applicable.

Accordingly, Regions and Country Practices are required to put in place appropriate resources and procedures to accomplish the following. Within a Region, these responsibilities can be assigned as appropriate between the Region and its Country Practices:

• Appoint qualified Region and Country Practice independence leaders;

13 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

• Comply with the EYG Independence Policy and any stricter local requirements and make the independence policies available to Professionals;

• Provide independence training to Professionals, including globally deployed independence training, and monitor compliance therewith;

• Implement appropriate disciplinary actions based on the global Risk Management guidance in relation to violations of professional/regulatory rules and the EYG Independence Policy (and any stricter Country Practice independence requirements);

• Record regulatory independence violations and breaches of the IESBA Code of Ethics and local professional standards in the Global Independence Incident Reporting System;

• Use the Global Monitoring System (or equivalent) and Global Independence List for verifying permitted investments and for reporting Financial Interests of the Region and Country Practice including all associated entities;

• Maintain current entity and affiliate information in the Global Independence System;

• Require Partners and other Professionals to use the Global Monitoring System (or equivalent) and Global Independence List for verifying permitted investments, reporting Financial Interests and periodic confirmation purposes according to their rank and individual requirements;

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 14

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

• Enable compliance with applicable partner rotation requirements in collaboration with the Assurance Practice;

• Implement required global independence processes, including PCIPs, BRET requirements, and GIS family tree maintenance and validation;

• Carry out the EY Global Personal Independence Compliance Testing program in accordance with instructions distributed by the Independence Executive;

• Maintain a process for evaluating independence matters, including financial relationships and employment relationships with Audit Clients, related to new employees at the executive level or new admissions (direct or internal) to partnership within the EY Member Practice, prior to hiring the individual as a Professional Employee or admitting the individual as a Partner;

• Provide Professionals with appropriate independence resources for consultations, and request support for such consultations from the Independence Executive as needed;

• Respond timely to specific requests from the Independence Executive; and

• Monitor that the above requirements are complied with and annually provide an independence confirmation for the Region or Country Practice to the Independence Executive.

15 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

002.2 Responsibilities of Professionals

Professionals are required to:

• Be knowledgeable of the EYG Independence Policy and applicable local independence requirements;

• Comply fully with EYG Independence Policy and applicable local independence requirements, including discussion or consultation where necessary and appropriate;

• Complete independence training provided by the Independence Executive in addition to any EY Member Practice provided training;

• Use the Global Independence System to check clients’ status with respect to independence requirements;

• Use the Global Monitoring System (or equivalent) and Global Independence List for verifying permitted investments, reporting Financial Interests and periodic confirmation purposes, according to their rank and individual requirements;

• Comply with the EY Global Personal Independence Compliance testing program; and

• Monitor applicable partner rotation requirements.

Professionals are also required to comply with the documentation requirements in Section 003.4

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 16

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

002.3 Responsibilities of the Independence Executive

The Independence Executive shall:

• Develop, maintain and communicate the EYG Independence Policy and Supplementary Guidance;

• Maintain global processes for monitoring and compliance with independence requirements, including BRET, PCIP, GIS and monitoring systems;

• Provide global independence training material;

• Manage the EY Global Personal Independence Compliance Testing program and maintain and deploy associated work programs;

• Engage the Global Internal Audit function to perform the independence compliance testing program;

• Provide infrastructure and resources for independence systems;

• Advise Regions and Country Practices of significant independence changes and developments as appropriate;

• Inform the Risk Management Executive Committee and, as appropriate, the Global Executive of any significant independence matters and their resolution;

• Support Region and Country Practice independence consultations; and

• Perform periodic reviews of the efficiency and effectiveness of the Independence function as it operates in the Regions, and provide recommendations for improvement.

17 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

Section 003 Independence consultation and documentation

It is impossible to define every situation that creates threats to independence and specify the appropriate mitigating action that should be taken. EY Member Practices and their Professionals should, therefore, be alert to identify, evaluate, address and document threats to independence not covered by these policies and procedures in accordance with the framework set out in the IESBA Code. Independence consultation or discussion is encouraged for these situations.

003.1 Independence Consultation

Every EY professional is responsible for being knowledgeable of and compliant with applicable independence policies, including the requirement to consult when necessary, and to implement the conclusions reached as a result of the independence consultation process described herein. Consultation on matters of independence is an essential element of providing quality services to our clients. The organizational structure of EY Independence consists of a distributed network of independence professionals assigned to the Executive, Regions and country practices.

The Lead Audit Engagement Partner has the ultimate responsibility for determining that the appropriate conclusions are reached and the proper course of action is taken with respect to engagement related independence matters, including consulting with Independence when necessary. Engagement Partners performing non-audit services are also responsible for discussing independence matters with the Lead Audit Engagement Partner and for consulting with Independence when appropriate.

Refer also to Section 003.4 regarding documentation requirements for independence matters, including consultations.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 18

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

A consultation between an engagement team or other Professionals and Independence is intended to reach an appropriate conclusion on independence matters. Depending on the matter, informal interaction between Professionals or engagement team and Independence or other relevant resources could be sufficient. Other independence matters that are complex, difficult, sensitive or contentious typically require a formal consultation process.

A consultation process is deemed “formal” when:

• Consultation with Independence on a specific matter is explicitly required under the EYG Independence Policy or advance approval from Independence is required in SORT;

• Independence documentation is required (see section on Documentation);

• The consultation involves the resolution of a difference of professional opinions within the engagement team or with those consulted

• The independence matter is intended to be discussed with regulators; or

• Request for a waiver or exemption to the EYG Independence Policy is granted.

Differences of professional opinion among the engagement partner, engagement personnel or other professionals, and members of Independence are resolved by elevating the matter to the Leader of the Global IFAC Independence Center or Global SEC Independence Center as appropriate. After giving appropriate consideration to all relevant facts and circumstances and discussing the differing views with those involved in the consultation, the Center Leader will evaluate relevant facts and develop a recommendation. In circumstances where differences of professional opinion remain unresolved after consultation with the Center Leader, those involved may consult with Global Vice Chair,

19 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

Independence, who will involve others as appropriate to resolve the matter.

Independence consultants who currently serve or in the last 24 month period have served as a member of the engagement team or an engagement quality reviewer for an audit client must recuse themselves from participating in a consultation with respect to that same client. See PPS 13-03 Recusal protocol: Consultation and risk management duties and responsibilities.

003S.1 Independence consultation – US SEC audit clients

Formal consultations relating to US SEC independence matters should involve Global SEC Independence Center consultants.

In addition, a Global SEC independence center consultant who currently is, or within the last seven years has been, an Audit Engagement Team member or an Engagement Quality Reviewer for a US SEC Audit Client cannot provide concurrence or approval on US SEC independence matters with respect to that US SEC Audit Client.

003.2 Exemptions

When an EY Member Practice or Professional believes that compliance with one or more provisions of the EYG Independence Policy which are not mandated by any regulatory requirement would create undue hardship, an exemption may be requested from the Region Independence Leader and may be granted with concurrence of the Global Vice Chair – Independence. The Global Vice Chair – Independence will evaluate the request and determine the appropriate course of action, which may include further consultation with Risk Management and other leadership.

When compliance with one or more provisions of the EY Canada Independence Policy that is more restrictive than both the EYG Policy and applicable external independence rules would create undue hardship, the Canada Independence Leader may grant an exemption from the EY Canada Independence Policy.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 20

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

003.3 EYG Independence Policy Violations

Any violations of the EYG Independence Policy by Professionals, other than violations that are inadvertent and are timely reported and corrected, can have severe consequences to the Professional, including dismissal without notice or payment in lieu of notice.

Violations of the EY Canada Independence Policy have the same consequences as violations of the EYG Policy.

When EYG Independence Policy violations are identified, consultation with independence is required to determine whether the matter is also a breach of the IESBA Code of Ethics, or of local independence regulations or professional standards, in which case it is subject to the communication requirements of Section 302. See also Supplementary Guidance G302.1.

Refer to Section 003.4 for independence reporting requirements including addressing and reporting independence violations.

003.4 Documentation

Conclusions of formal independence consultations and discussion supporting those conclusions should be documented.

Independence documentation is also required for all of the following situations:

• All independence violations;

• All situations when it is concluded that specific action steps and safeguards need to be implemented to address the independence issue;

• All situations where threats to independence require significant analysis and interaction to reach the conclusion, even if ultimately it is concluded that there is no independence issue or that no safeguard or action is necessary.

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

Consultations regarding independence with Canada Independence or the service line Quality Leaders are to be documented in writing. It is the responsibility of the individual, who initiates the consultation, to document the consultation. That individual should forward a copy of the consultation memo to the Lead Audit Engagement Partner, as well as the individual in Canada Independence consulted. Documentation of the threats and safeguards is to be maintained in the related engagement file.

The documentation should include a description of all relevant facts and circumstances including the applicable independence policies and regulations, the substance of the analysis, the action steps and safeguards to be implemented, if any, the conclusion reached and the confirmation that EY Independence agrees with the conclusion. Independence documentation

1. Analysis of threats and safeguards:

Where EY Canada has identified a threat to independence that is not clearly insignificant, documentation is required supporting the decision to accept or continue the engagement affected by the threat to independence.

21 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

can be achieved through any written material, including emails, but preferably in the format of an independence memorandum or an entry in a documentation database when available.

When a formal consultation with Independence is initiated, it is the responsibility of the team or individual initiating the consultation to document the issue, with the support of Independence.

However, the absence of documentation is not a determinant of whether a particular matter was considered or whether independence has been impaired.

The following documentation is required in each particular engagement file, in addition to any matters discussed elsewhere in the EY Canada Independence Policy:

a description of the nature of the engagement;

the threat identified;

the safeguard(s) identified and applied to eliminate the threat or reduce it to an acceptable level; and

an explanation of how the safeguard(s) eliminate the threat or reduce it to an acceptable level.

A threat to independence that is not clearly insignificant is to be documented in writing, and communicated to the Lead Audit Engagement Partner. The Lead Audit Engagement Partner has the responsibility to ensure that the file includes appropriate documentation.

For clients requiring audit committee pre-approval, only after the proper audit committee pre-approval has been obtained, and the Lead Audit Engagement Partner or his/her designee confirms audit committee pre-approval has been obtained may the engagement proceed. A best practice would be to obtain written confirmation or an email from the Lead Audit Engagement Partner that audit committee approval has been obtained.

Independence considerations for Audit Clients are required to be documented at least annually in accordance with Canadian Policy CA-P3119 Public Company Independence Procedures Policy and Practice Statement.

2. Consultation with Canada Independence:

Refer to section 003.1 and above noted requirements.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 22

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

3. Independence reporting requirements:

a. Identifying and reporting violations of EY Canada Independence Policy:

There are two sources to identify independence threats and violations:

(i) The results of independence procedures carried out by the engagement team, including the procedures required by Canadian Policy CA-P3119 Public Company Independence Procedures Policy and Practice Statement.

(ii) Matters reported in EY Canada’s centralized independence databases such as GMS (primarily personal independence matters) and GIIRS.

Any threat to independence that is not “clearly insignificant” must be communicated to the Lead Audit Engagement Partner.

Immediately upon discovery, Professionals must report:

All known violations of the EY Canada Independence Policy for personal independence requirements in GMS; and

All other known violations of the EY Canada Independence Policy to the Lead Audit Engagement Partner of the entity to which such infraction occurred, as well as the parent of such entity, in writing, and copy Canada Independence.

b. Reporting Financial Interests – GMS

All Partners through managers must update their Publicly Available Financial Interests in GMS within 10 business days of the purchase, inheritance, sale or acquisition/disposition by any other means, of any Financial Interest of the Professional or their Immediate Family Members, including securities over which the

23 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

professional or their Immediate Family Members act as trustee or executor, or act under a power of attorney. The GMS website address is https://gms.iweb.ey.com.

Professional Employees below manager are to report a Financial Interest held by the Professional Employee or their Immediate Family Member in an Audit Client or any proscribed entity as a general exception in GMS.

c. Confirming compliance with the EY Canada Independence Policy

New hire Professionals must document compliance with EY Canada’s independence policy as part of the orientation process.

At least annually, all Professionals must electronically sign their independence confirmation of compliance with EY Canada’s independence policies.

Managers and above must also sign quarterly independence confirmations.

d. Reporting Relationships with Audit Clients

All Professionals must document and report the nature of family relationships with persons associated with Audit Clients (which includes Affiliates, see definitions in the Glossary) as described in Section 102.5, Family members of Professionals accepting employment with an Audit client.

All Professionals who have been assigned to an engagement team for an Audit Engagement or Assurance Engagement shall advise the Lead Audit Engagement Partner and Canada Independence in writing of any interest, relationship or activity that would, under the EY Canada Independence Policy, preclude that person from being on the engagement team.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 24

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

e. Updating Audit Client family trees – GIS

It is the responsibility of the Lead Audit Engagement Partner to:

Ensure GIS accurately and completely reflects the Audit Client and its Affiliates and the GIS markups are correct.

Ensure the GIL includes all Audit Clients and Affiliates of Audit Clients with Publicly Available Financial Interests.

It is the responsibility of the Global Client Service Partner, or his/her designated audit executive, to re-approve the GIS family tree for each of their clients, at a minimum, on an annual basis.

003.5 Materials containing Independence guidance

It is expected that documents and materials containing authoritative independence guidance or considerations, such as policies, information releases, service line guidance, training or other materials, will be discussed with Independence for review, evaluation, and approval prior to issuance.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 25

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

Part 1: Matters relating to Professionals

Section 100 Introduction

These policies set out the independence requirements applicable to Partners and Professional Employees (collectively referred to as “Professionals”). These requirements, as they relate to Audit Clients, apply throughout the Audit and Professional Engagement Period. The Independence requirements vary among differing categories of Professionals, so it is important that all Professionals carefully read the policies to determine which of the requirements apply to them. In some EY Member Practices these policies may be supplemented by additional local independence requirements. Professionals have a responsibility to determine what additional local requirements, if any, are in place.

Use definitions of Partners and Professional Employees in the Glossary.

Professionals are also to comply with the documentation requirements in Section 003.4. Additional requirements are also outlined throughout Section 000, Introduction.

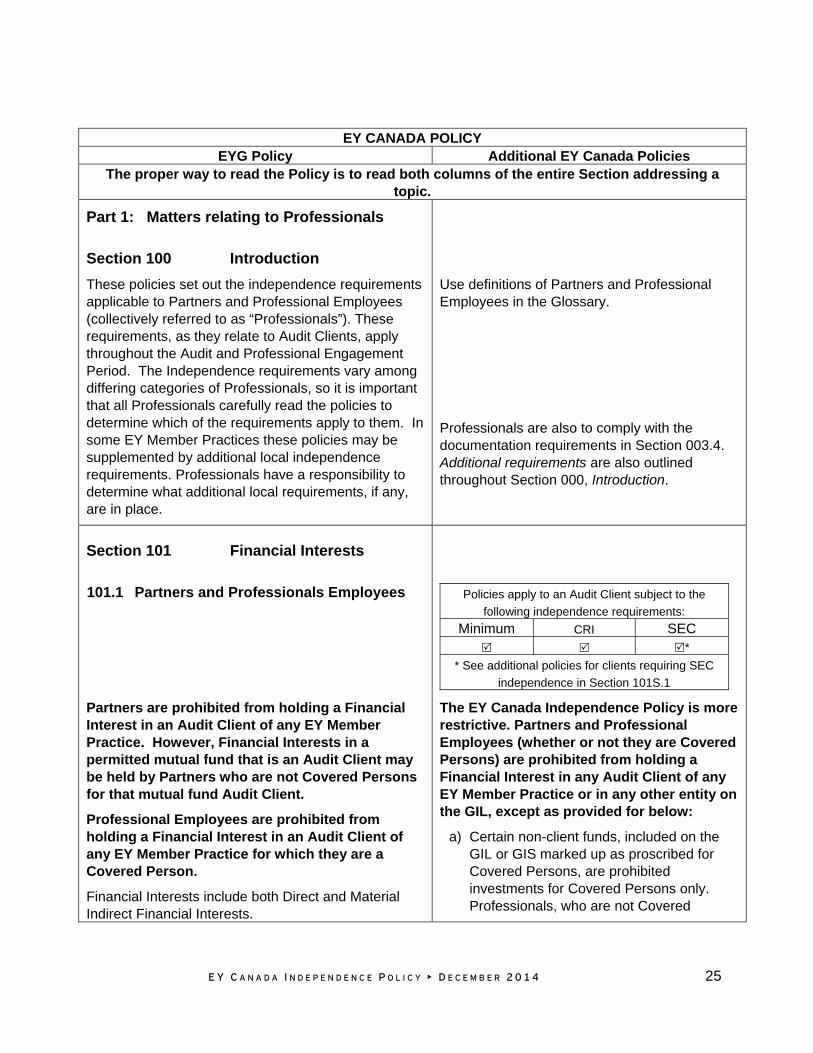

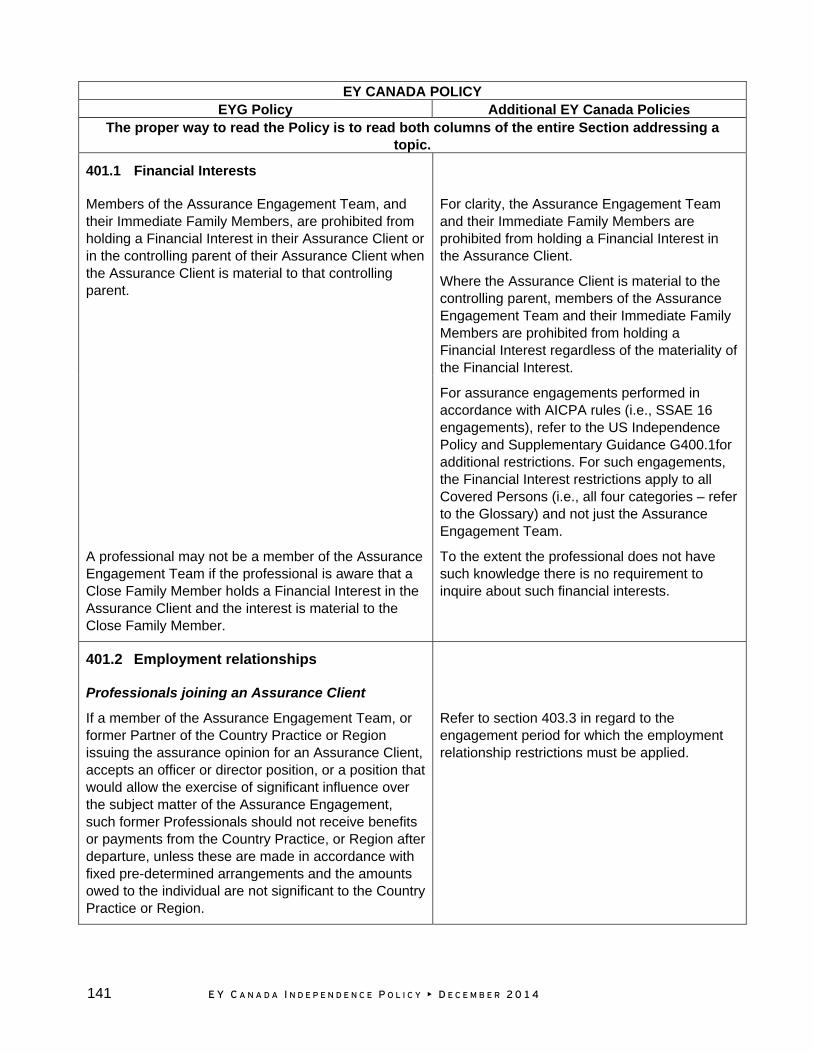

Section 101 Financial Interests

101.1 Partners and Professionals Employees

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC *

* See additional policies for clients requiring SEC

independence in Section 101S.1

Partners are prohibited from holding a Financial Interest in an Audit Client of any EY Member Practice. However, Financial Interests in a permitted mutual fund that is an Audit Client may be held by Partners who are not Covered Persons for that mutual fund Audit Client.

Professional Employees are prohibited from holding a Financial Interest in an Audit Client of any EY Member Practice for which they are a Covered Person.

Financial Interests include both Direct and Material Indirect Financial Interests.

The EY Canada Independence Policy is more restrictive. Partners and Professional Employees (whether or not they are Covered Persons) are prohibited from holding a Financial Interest in any Audit Client of any EY Member Practice or in any other entity on the GIL, except as provided for below:

a) Certain non-client funds, included on the GIL or GIS marked up as proscribed for Covered Persons, are prohibited investments for Covered Persons only. Professionals, who are not Covered

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 26

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

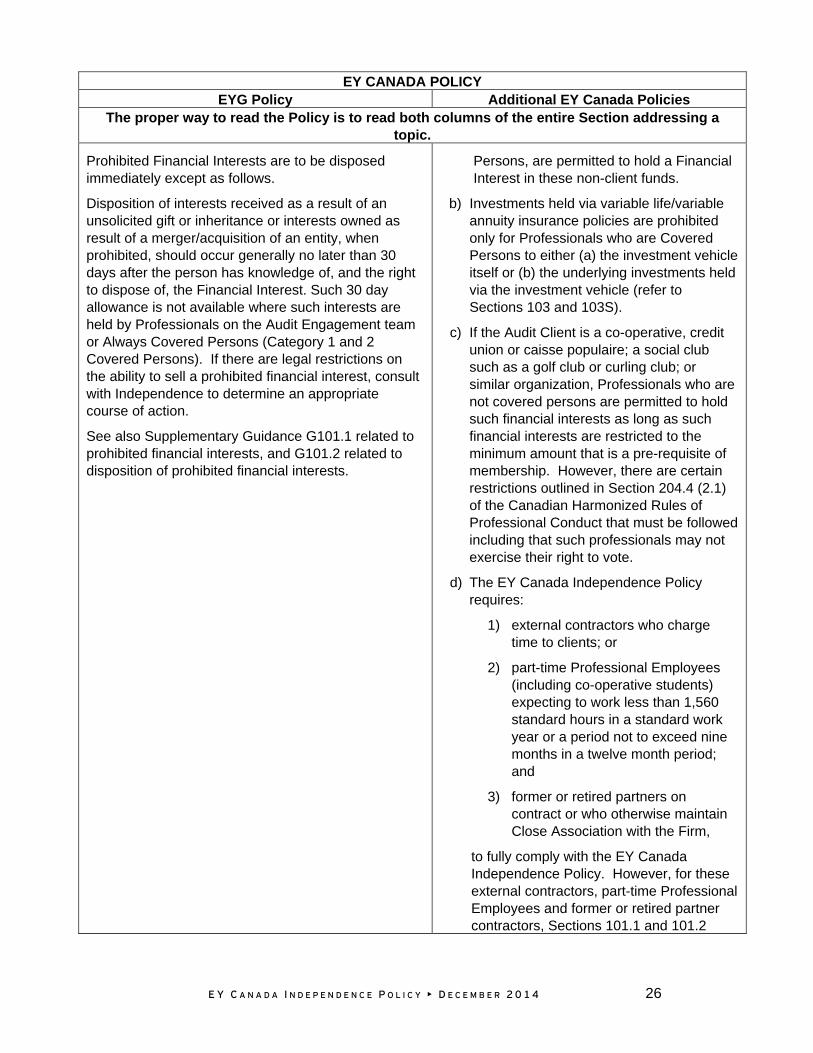

Prohibited Financial Interests are to be disposed immediately except as follows.

Disposition of interests received as a result of an unsolicited gift or inheritance or interests owned as result of a merger/acquisition of an entity, when prohibited, should occur generally no later than 30 days after the person has knowledge of, and the right to dispose of, the Financial Interest. Such 30 day allowance is not available where such interests are held by Professionals on the Audit Engagement team or Always Covered Persons (Category 1 and 2 Covered Persons). If there are legal restrictions on the ability to sell a prohibited financial interest, consult with Independence to determine an appropriate course of action.

See also Supplementary Guidance G101.1 related to prohibited financial interests, and G101.2 related to disposition of prohibited financial interests.

Persons, are permitted to hold a Financial Interest in these non-client funds.

b) Investments held via variable life/variable annuity insurance policies are prohibited only for Professionals who are Covered Persons to either (a) the investment vehicle itself or (b) the underlying investments held via the investment vehicle (refer to Sections 103 and 103S).

c) If the Audit Client is a co-operative, credit union or caisse populaire; a social club such as a golf club or curling club; or similar organization, Professionals who are not covered persons are permitted to hold such financial interests as long as such financial interests are restricted to the minimum amount that is a pre-requisite of membership. However, there are certain restrictions outlined in Section 204.4 (2.1) of the Canadian Harmonized Rules of Professional Conduct that must be followed including that such professionals may not exercise their right to vote.

d) The EY Canada Independence Policy requires:

1) external contractors who charge time to clients; or

2) part-time Professional Employees (including co-operative students) expecting to work less than 1,560 standard hours in a standard work year or a period not to exceed nine months in a twelve month period; and

3) former or retired partners on contract or who otherwise maintain Close Association with the Firm,

to fully comply with the EY Canada Independence Policy. However, for these external contractors, part-time Professional Employees and former or retired partner contractors, Sections 101.1 and 101.2

27 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

apply only where they are a Covered Person.

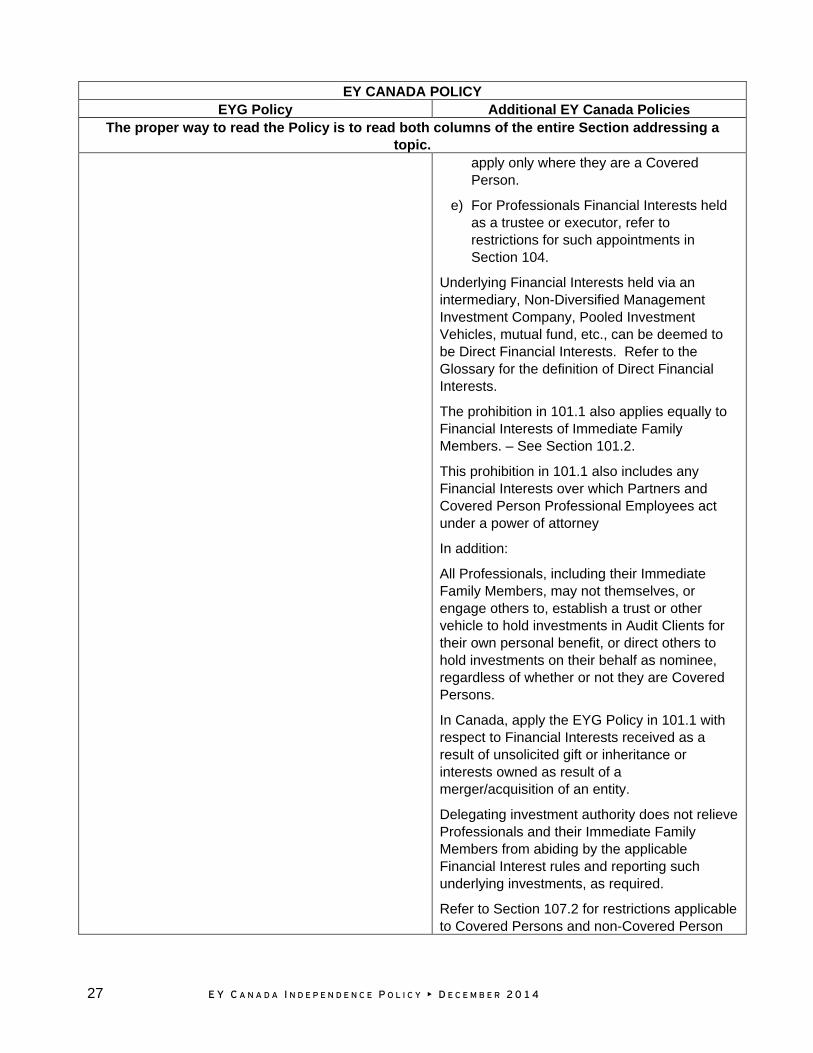

e) For Professionals Financial Interests held as a trustee or executor, refer to restrictions for such appointments in Section 104.

Underlying Financial Interests held via an intermediary, Non-Diversified Management Investment Company, Pooled Investment Vehicles, mutual fund, etc., can be deemed to be Direct Financial Interests. Refer to the Glossary for the definition of Direct Financial Interests.

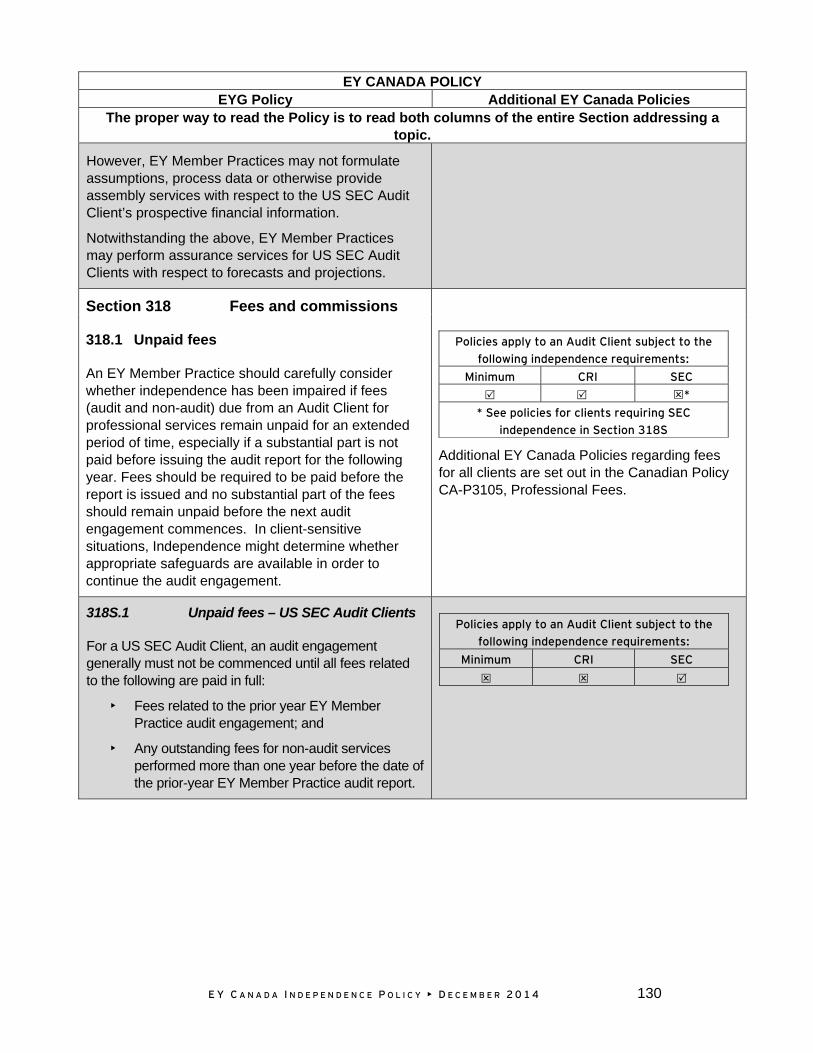

The prohibition in 101.1 also applies equally to Financial Interests of Immediate Family Members. – See Section 101.2.

This prohibition in 101.1 also includes any Financial Interests over which Partners and Covered Person Professional Employees act under a power of attorney

In addition:

All Professionals, including their Immediate Family Members, may not themselves, or engage others to, establish a trust or other vehicle to hold investments in Audit Clients for their own personal benefit, or direct others to hold investments on their behalf as nominee, regardless of whether or not they are Covered Persons.

In Canada, apply the EYG Policy in 101.1 with respect to Financial Interests received as a result of unsolicited gift or inheritance or interests owned as result of a merger/acquisition of an entity.

Delegating investment authority does not relieve Professionals and their Immediate Family Members from abiding by the applicable Financial Interest rules and reporting such underlying investments, as required.

Refer to Section 107.2 for restrictions applicable to Covered Persons and non-Covered Person

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 28

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

Partners with respect to joint investments and alliances.

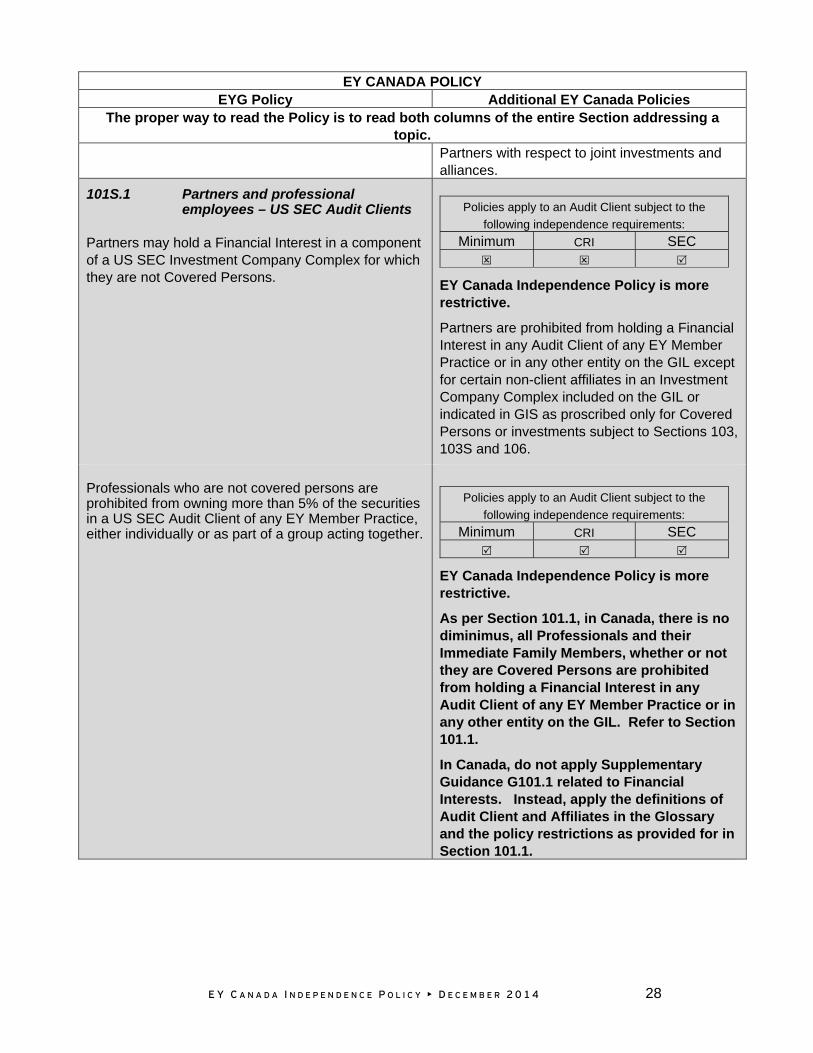

101S.1 Partners and professional employees – US SEC Audit Clients

Partners may hold a Financial Interest in a component of a US SEC Investment Company Complex for which they are not Covered Persons.

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

EY Canada Independence Policy is more restrictive.

Partners are prohibited from holding a Financial Interest in any Audit Client of any EY Member Practice or in any other entity on the GIL except for certain non-client affiliates in an Investment Company Complex included on the GIL or indicated in GIS as proscribed only for Covered Persons or investments subject to Sections 103, 103S and 106.

Professionals who are not covered persons are prohibited from owning more than 5% of the securities in a US SEC Audit Client of any EY Member Practice, either individually or as part of a group acting together.

EY Canada Independence Policy is more restrictive.

As per Section 101.1, in Canada, there is no diminimus, all Professionals and their Immediate Family Members, whether or not they are Covered Persons are prohibited from holding a Financial Interest in any Audit Client of any EY Member Practice or in any other entity on the GIL. Refer to Section 101.1.

In Canada, do not apply Supplementary Guidance G101.1 related to Financial Interests. Instead, apply the definitions of Audit Client and Affiliates in the Glossary and the policy restrictions as provided for in Section 101.1.

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

29 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

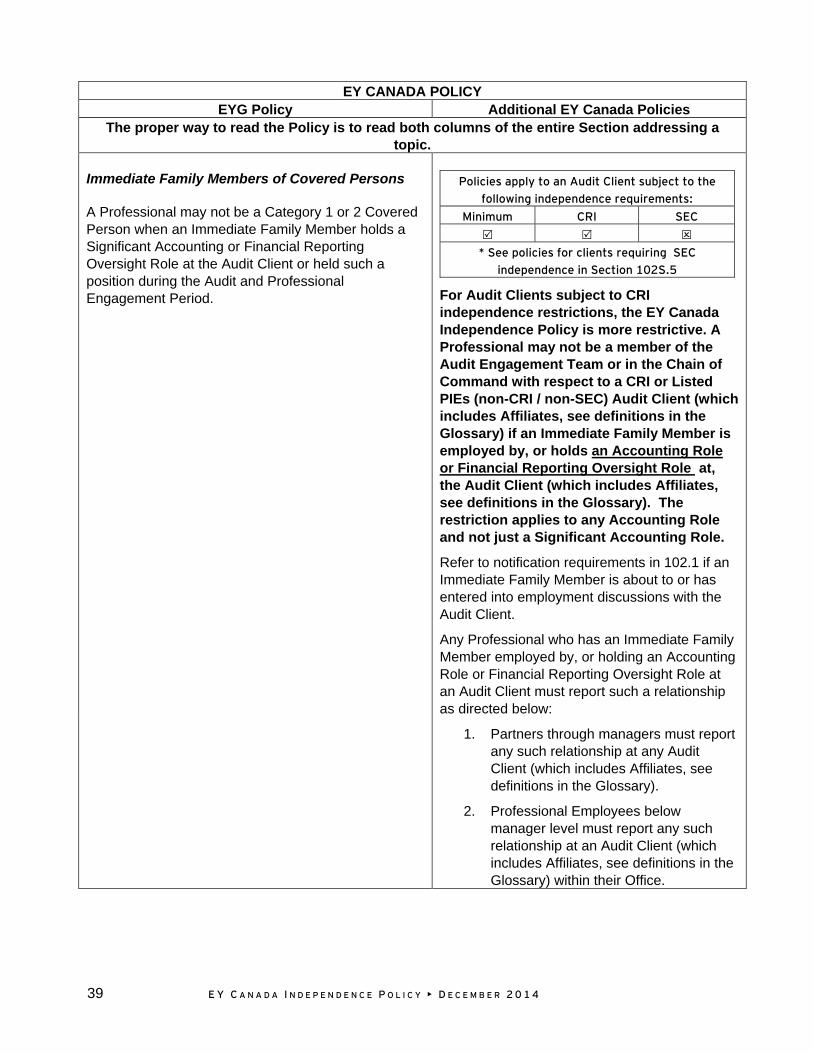

101.2 Immediate Family – Partners and Professional Employees

All provisions and exceptions in Section 101.1, which cover Partners and Professional Employees, also extend to their Immediate Family Members.

However, Immediate Family Members of Partners who are not Covered Persons may hold an employment related Financial Interest in an Audit Client for as long as they remain employed by the Audit Client. The interest must be disposed once employment has ended, as soon as there is the ability to sell.

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

The EY Canada Independence Policy is more restrictive than the EYG Independence Policy. Immediate Family Members of Partners and Professional Employees (regardless of whether they are a Covered Person) are prohibited from holding a Financial Interest in any Audit Client of any EY Member Practice or any other entity on the GIL, with the exception only for certain employment-related Financial Interests as described below and other exceptions specifically provided for as referenced in Section 101.1.

Under no circumstance can an Immediate Family Member hold an employment-related Financial Interest in an Audit Client for which the Professional is a Category 1 or Category 2 Covered Person.

Immediate Family Members of Partners and Professional Employees who are Covered Persons

Immediate Family Members of Category 3 or Category 4 Covered Persons may also hold an employment related Financial Interest in an Audit Client, but must dispose of the interest as soon as they have the ability to sell, even if they are still employed by the Audit Client. When the Immediate Family Member has the possibility to select investment options within an employment benefit plan, they should select investment options for which the Professional is not a Covered Person whenever available.

Where there are legal or similar restrictions on an Immediate Family Member’s right to dispose of a Financial Interest, the Immediate Family Member need not dispose of the interest until the restrictions have lapsed.

Policies apply to a Financial Interest in an Audit

Client offered through the employer of an Immediate Family Member, and that Audit Client

is subject to the following independence requirements:

Minimum CRI SEC

Apply the EYG restrictions in Canada.

For clarity, this section applies to Professionals who are Category 3 or Category 4 Covered Persons with respect to the investment selection offered by the employer of their Immediate Family Member whether or not the employer is an Audit Client.

If the employment-related benefit plan offers the Immediate Family Member a selection of investments that includes Audit Clients the Immediate Family Member is not permitted to

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 30

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

select an investment for which the Professional is a Covered Person. However, if the investment alternatives available to the Immediate Family Member consist entirely of investments for which the Professional is a Covered Person, the Immediate Family Member is permitted to select the alternatives for which the Professional is a Category 3 or Category 4 Covered Person. Under no circumstances can an Immediate Family Member hold a Financial Interest in an Audit Client for which the Professional is a Category 1 or Category 2 Covered Person.

Immediate Family Members of Partners who are not Covered Persons

Policies apply to a Financial Interest in an Audit

Client offered through the employer of an Immediate Family Member, and that Audit Client

is subject to the following independence requirements:

Minimum CRI SEC

Immediate Family Members of Partners who are not Covered Persons may hold an employment-related Financial Interest in an Audit Client for as long as they remain employed by the Audit Client. The interest must be disposed once employment has ended, as soon as there is the ability to sell.

This exception applies whether or not the Immediate Family Member is employed at an Audit Client.

For clarity, if the employment-related benefit plan offers the Immediate Family Member a selection of investments that includes Audit Clients, then the Immediate Family Member is permitted to select any investment for which the Partner is not a Covered Person.

Once employment has ended such employment-related Financial Interests must be sold as soon as there is the ability to sell.

31 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

Immediate Family Members of Professional Employees who are not Covered Persons

Policies apply to a Financial Interest in an Audit

Client offered through the employer of an Immediate Family Member, and that Audit Client

is subject to the following independence requirements:

Minimum CRI SEC

The following exception regarding an employment-related Financial Interest applies whether or not the Immediate Family Member is employed at an Audit Client.

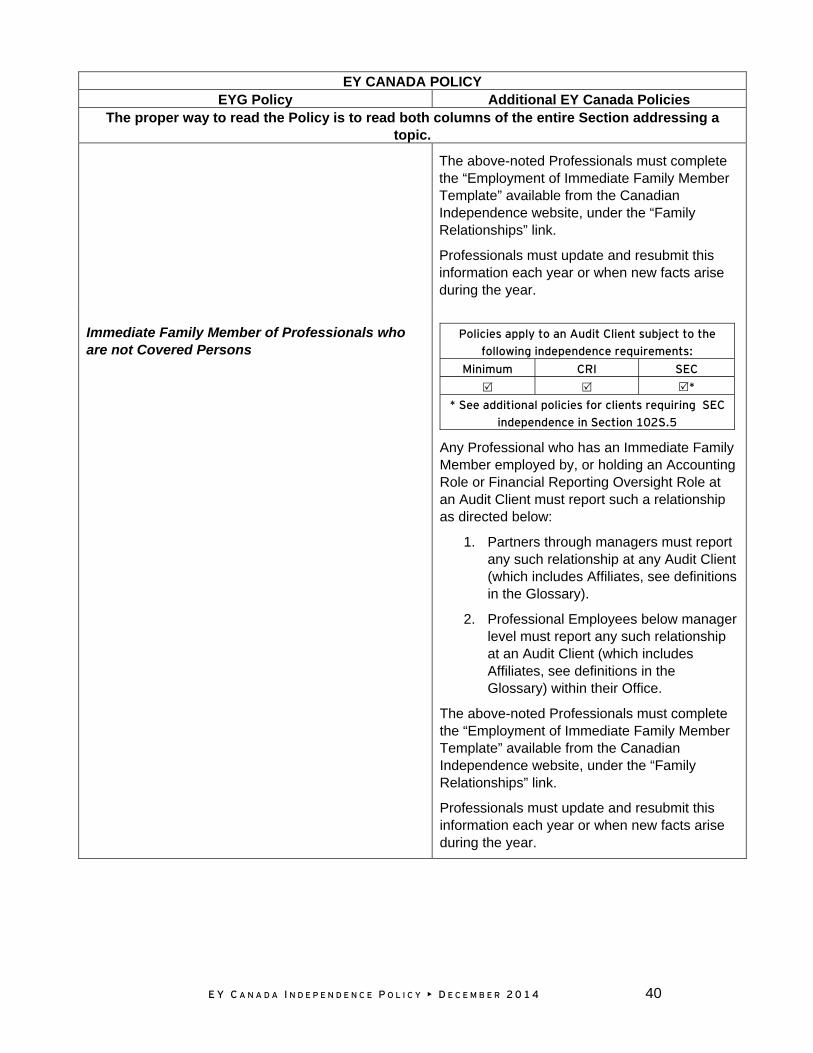

Immediate Family Members of Professional Employees who are not Covered Persons may hold an employment-related Financial Interest in an Audit Client (which includes Affiliates, see definitions in the Glossary) (e.g., participate in stock options, stock purchase programs, stock compensation plans and employer-sponsored retirement plans) for as long as they remain employed with that employer. Once employment has ended, such employment-related Financial Interests must be sold as soon as there is the ability to sell.

For clarity, if the employment-related benefit plan offers the Immediate Family Member a selection of investments that includes Audit Clients, then the Immediate Family Member is permitted to select any investment for which the Professional Employee is not a Covered Person. Where the Professional Employee is a Covered Person for that investment selection, the guidance with respect to Covered Persons in the Section above is applicable. The following chart is intended to assist Professionals in understanding the requirements of Sections 101.2 as applicable.

Can a Financial Interest in an Audit Client be held by an Immediate Family Member?

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 32

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

Covered Persons with respect to the

employment-related Financial Interest

Immediate Family

Member of:

Engag-ement Team

Chain of

Com-mand

≥10 Hrs. Non

Audit Services

Office of Lead Audit

Engagement Partner Others

Partners No No Yes 1, Yes 1, Yes 2 Professional Employees

No No Yes 1, N/A Yes 2

1 Only if the Financial Interest was obtained as a result of employment rights. However, such Financial Interests must be disposed as soon as they have the right/ability to sell, even if they are still employed by the entity. If the employment-related benefit plan offers a selection of investments that includes Audit Clients, the Immediate Family Member cannot select an investment for which the Professional is a Covered Person. However, if the only available investments consist entirely of investments for which the Professional is a Covered Person, then the Immediate Family Member can select those investments for which the Professional is a Category 3 or Category 4 Covered Person.

2 Only if obtained as a result of employment rights. Once employment ends, the Financial Interest must be sold as soon as there is an ability to sell.

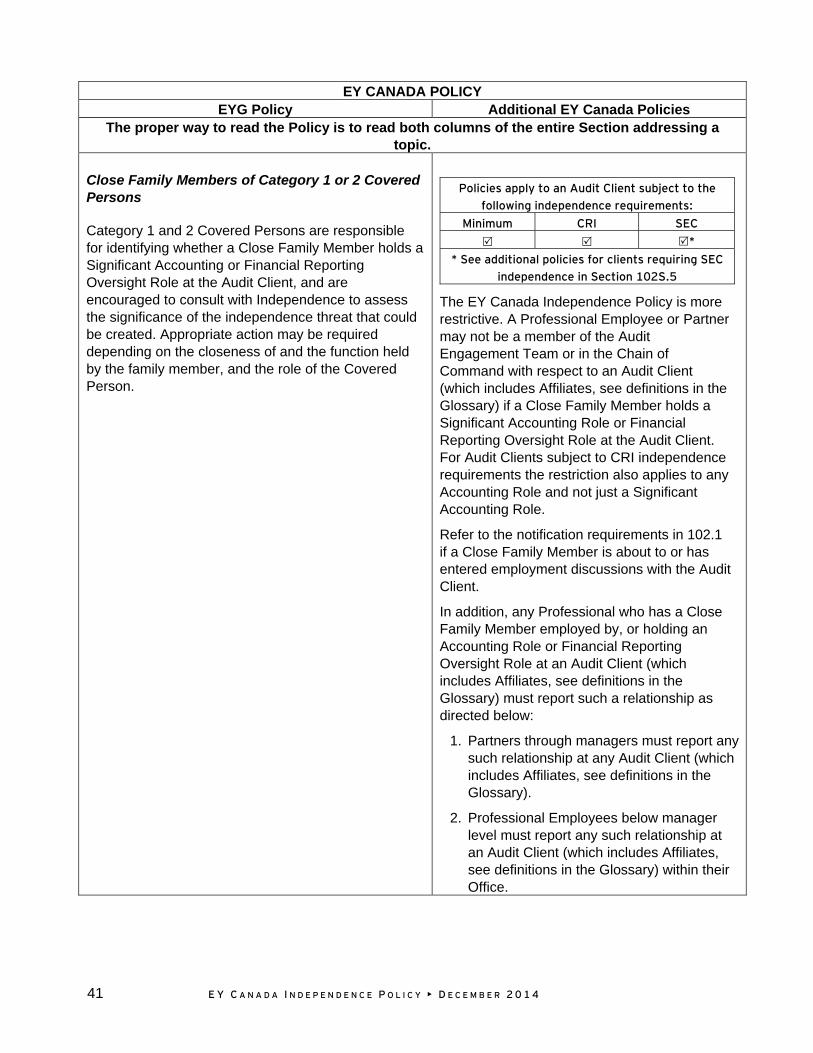

101.3 Close family – Partners and Professional Employees

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

A Professional may not be a member of the Audit Engagement Team if the Professional has knowledge that a Close Family Member holds a Material Financial Interest in the Audit Client.

EY Canada Independence Policy is more restrictive. A Professional Employee or Partner may not be a Category 1 Covered Person or in the Chain of Command with respect to an Audit Client (which includes Affiliates, see definitions in the Glossary) if the Professional has knowledge that the Close Family Member holds a Material Financial Interest in the Audit Client.

To the extent the Professional does not have such knowledge there is no requirement to inquire about such Financial Interests.

33 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

101S.3 Close family - Partners and Professional Employees - US SEC Audit Clients

• Close Family Members of any Partner, including those Partners who are not Covered Persons, may not have control over a US SEC Audit Client. (For SEC purposes, control means the possession, direct or indirect, of the power to direct or cause the direction of the management and policies of a person or entity, whether through the ownership of voting shares, by contract or otherwise.)

• Partners and Professionals may not be Covered Persons with respect to a US SEC Audit Client if they have knowledge that a Close Family Member owns (or has beneficial ownership of) more than 5% of the securities in (or otherwise controls) the US SEC Audit Client, either individually or as part of a group acting together.

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

To the extent the Professional does not have such knowledge there is no requirement to inquire about such Financial Interests.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 34

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

Section 102 Employment relationships and personal appointments

102.1 Employment discussions with an Audit Client

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

*

* See additional policies for clients requiring SEC independence in Section 102S.1

A member of the Audit Engagement Team (Category 1 Covered Person) who enters into employment discussions with the Audit Client must notify the Lead Audit Engagement Partner (or the EY Member Practice PPD if the individual is the Lead Audit Engagement Partner), and should not have any further involvement with or participate in further audit work for the client until the employment discussion is resolved.

For clarity, submitting a resume or making an application intended for any position at the Audit Client is considered to be “entering into employment discussions”.

In such cases, the Lead Audit Engagement Partner (or EY Member Practice PPD) should give consideration as to whether it is necessary or appropriate to adjust any aspects of the audit plan for any actual or perceived risk arising from the employment discussions, and may apply additional safeguards, such as a review of the individual’s work. The nature and extent of the procedures to be undertaken will vary depending on the individual’s role in the firm, the position being considered with the Audit Client and the timing of the decision to leave the EY Member Practice.

The positions that may be taken by members of the Audit Engagement Team joining either a CRI, SEC, or Listed PIE (non-CRI / non-SEC) Audit Client (which includes Affiliates, see definitions in the Glossary) are limited by the cooling off rules as discussed in Section 102.2.

An Area, Region or Country Practice Managing Partner may not enter into employment discussions for a Significant Accounting or Financial Reporting Oversight Role with a Public Interest Entity Audit Client from their own Area, Region or Country Practice, respectively, while functioning as an Area, Region or Country Practice Managing Partner.

In Canada, the restrictions applicable to the Country Managing Partner extend to discussions related to any Accounting Role.

If a Professional becomes aware that an Immediate Family Member is about to or has entered into employment negotiations concerning a Significant Accounting or Financial Reporting Oversight Role with an Audit Client for which the Professional is a member

In Canada, the notification requirements apply equally to Immediate and Close Family Members and include employment negotiations concerning any Accounting Role.

35 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

of the Audit Engagement Team, the Professional should notify the Lead Audit Engagement Partner (or EY Member Practice PPD).

102S.1 Employment discussions with an Audit Client - US SEC Audit Clients

The notification requirement above extends to all Partners and all Covered Persons and applies to both Immediate and Close Family Members, when the family member is considering joining a US SEC Audit Client as a director or as an employee in an Accounting Role or Financial Reporting Oversight Role.

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

102.2 Cooling-off period prior to accepting employment with an Audit Client

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

* *

* See additional policies for clients requiring CRI or SEC independence in Section 102S.2

A Key Audit Partner may not join his/her PIE Audit Client in a Significant Accounting or Financial Reporting Oversight Role until, subsequent to the partner ceasing to be a Key Audit Partner, the EY Member Practice has completed an audit covering a period of at least 12 months, and the Partner was not involved in any capacity with respect to the audit of those financial statements.

Area, Region and Country Managing Partners may not join a PIE Audit Client from their own Area, Region and Country Practice, respectively, in a Significant Accounting or Financial Reporting Oversight Role until 12 months have elapsed since leaving the EY Member Practice or ceasing to be a Managing Partner.

For clarity, the Global Policy in this section does not apply to non-PIEs.

If either a Key Audit Partner or an Area, Region or Country Practice Managing Partner joins a PIE Audit Client in a Significant Accounting or Financial Reporting Oversight Role before the respective specified periods above have elapsed, the Country Practice must resign from the Audit Engagement.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 36

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

See also Supplementary Guidance G102.1 related to Retired Partners and employing Retired Partners.

In Canada, refer also to CA-P3113 Retired Partners and employing Retired Partners.

102S.2 Cooling-off period prior to accepting employment with an audit client - US SEC Audit Clients

The cooling off requirement above extends to all members of the Audit Engagement Team who are joining an US SEC Issuer Audit Client in a Financial Reporting Oversight Role. It applies to all Professionals who participated in the audit, during the last annual reporting period preceding the commencement of the audit period started after joining the client. The one-year “cooling off” starts on the first day after the US SEC Issuer Audit Client files its periodic report and ends when the US SEC Issuer Audit Client files its next annual report. The cooling off period calculation can be complex and could be up to a two-year period.

See also Supplementary Guidance G102S.1.

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

For clarity, cooling-off rules also apply to all Professionals who provide audit, review or attest services to a US SEC Audit Client whether or not those services are related to the audit of the financial statements. For CRI and Listed PIEs (non-CRI / non-SEC) Audit Clients the cooling-off rules only apply to members of the Audit Engagement Team.

The CRI independence rules are similar to the SEC independence rules in this area and therefore the guidance in G102S.1 applies to CRI Audit Clients (which includes Affiliates, see definitions in the Glossary), except that the “cooling off period” for CRI and Listed PIEs (non-CRI / non-SEC) Audit Clients ends one year after the financial statements were filed with the relevant securities regulator.

102.3 Other Independence considerations upon accepting employment with an Audit Client

In all cases, where a Partner, former Partner or member of the Audit Engagement Team accepts a Significant Accounting or Financial Reporting Oversight Role at an Audit Client, such former Professionals should not receive benefits or payments from an EY Member Practice unless these are made in accordance with fixed pre-determined arrangements and the amounts owed to the individual are not significant to the EY Member Practice. In addition, once joining an Audit Client, the former Professional may not retain any other business or professional relationship with the EY Member Practice that would be prohibited under the requirements related to Business Relationships.

Policies apply to an Audit Client subject to the following independence requirements:

Minimum CRI SEC

*

* See policies for clients requiring SEC independence in Section 102S.3

For clarity, a former Partner may not have a Close Association with the Firm if the individual is in an Accounting Role or Financial Reporting Oversight Role.

In addition, a former Partner or Professional cannot continue to participate or appear to participate in the Firm’s business or professional activities if the individual is in a Significant

37 E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

See also Section 107 related to Business Relationships.

Accounting or Financial Reporting Oversight Role at an Audit Client.

102S.3 Other independence considerations upon accepting employment with an audit client - US SEC Audit Client

Any former Professional who joins a US SEC Audit Client in an Accounting Role or Financial Reporting Oversight Role must sever or re-structure certain financial relationships with, and cease any other relationships or influence over, any EY Member Practice. See also Supplementary Guidance G102S.2.

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

In addition to the EYG Policy requirements, any former Partner in an employment relationship with a US SEC Audit Client (which includes Affiliates, see definitions in the Glossary) may not maintain Close Association with the Firm.

102.4 Professionals previously employed by an Audit Client

A Professional previously employed in a Significant Accounting or Financial Reporting Oversight Role at an Audit Client may not be assigned to the Audit Engagement Team for the audit of the financial

Policies apply to an Audit Client subject to the

following independence requirements:

Minimum CRI SEC

*

* See policies for clients requiring SEC independence in Section 102S.4

statements covering any period during which they were employed at or associated with the Audit Client.

For those Professionals who were previously employed by an Audit Client prior to joining EY Canada, arrangements must be made to dispose of any financial interests held in the former employer audit client (e.g., stock, stock options, restricted stock units, carried interests must be sold, and retirement plan investments must be rolled into another plan with allowable investment alternatives). All financial interests that can be disposed of would be required to be disposed prior to starting at the EY Member Practice. If certain benefits cannot be divested of (e.g., defined benefit plan that is not portable) the Professional may not become an Audit Engagement Team member or be in the Chain of Command for the Audit Client unless these benefits are first forfeited.

E Y C A N A D A I N D E P E N D E N C E P O L I C Y • D E C E M B E R 2 0 1 4 38

EY CANADA POLICY EYG Policy Additional EY Canada Policies

The proper way to read the Policy is to read both columns of the entire Section addressing a topic.

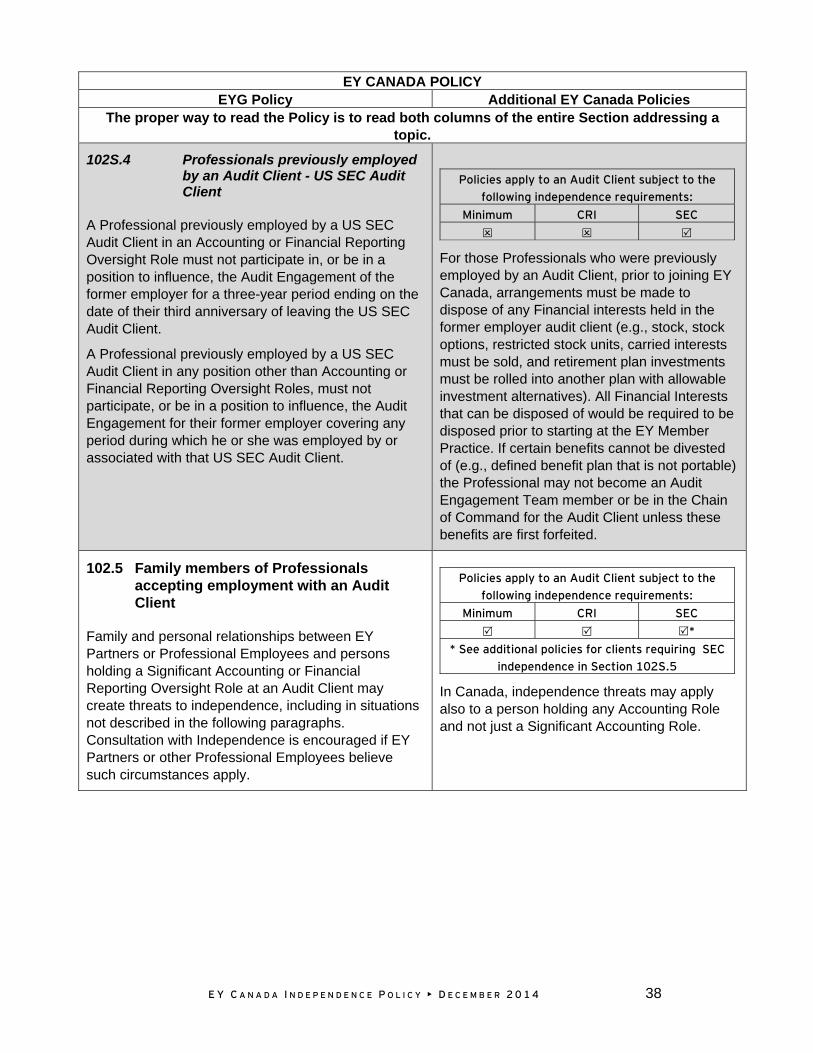

102S.4 Professionals previously employed by an Audit Client - US SEC Audit Client

A Professional previously employed by a US SEC Audit Client in an Accounting or Financial Reporting Oversight Role must not participate in, or be in a position to influence, the Audit Engagement of the former employer for a three-year period ending on the date of their third anniversary of leaving the US SEC Audit Client.