Embed Size (px)

Citation preview

EXXON MOBIL INVESTOR ENGAGEMENT REPORT

FOREWORD 03EXECUTIVE SUMMARY 05SECTION 01: CONTEXT 11SECTION 02: CLIMATE CHANGE, THE INVESTMENT

CHAIN & EXXON 13SECTION 03: VOTING AT THE EXXON 2016 AGM 19SECTION 04: VOTE ANALYSIS 23SECTION 05: TRANSPARENCY & ACCOUNTABILITY 27SECTION 06: CONCLUSIONS 29SECTION 07: CALL TO ACTION 31APPENDICES 33ACKNOWLEDGEMENTS 46

CONTENTS

The Asset Owners Disclosure Project is an independent not-for-profit global organisation whose objective is to protect retirement savings and other long term investments from the risks posed by climate change by improving disclosure and industry best practice.

AODP has developed the world’s leading reporting framework for institutional investors encompassing the disclosure and management of climate risk. It’s annual Global Climate 500 Index rates the world’s 500 biggest asset owners – pension funds, insurers, sovereign wealth funds, foundations and endowments – on their success at managing climate risk in their portfolios, based on direct disclosures and publicly available information.

Vote Your Pension is the world’s largest global shareholder engagement campaign. It is run by a collaboration of non-profit organisations working in the climate change corporate arena. The partners are Asset Owners Disclosure Project, SumofUs and ShareAction.

www.aodproject.net www.voteyourpension.org

ABOUT AODP

The world’s largest companies hold the key to achieving the pivot to a low carbon economy by 2025, the latest ‘safe’ date set by the UN, and fossil fuel companies have a particular responsibility. Yet in the US and UK, company law states that companies’ sole or primary obligation is to their shareholders (and in other countries, this is the de facto norm.) So the behaviour of those shareholders – both investment managers and asset owners – matters a lot.

This important report on the voting for climate resolutions at ExxonMobil’s AGM shows some leading institutional investors have stepped up to their responsibilities, but many more are in denial. Most baffling is the apparent lack of action by pension funds given their long-term responsibilities to their beneficiaries. These beneficiaries, if nothing changes, may be attempting in 40 years time to live on pensions whose value has been diminished by, inter-alia, real estate holdings under water, agricultural investments struggling with drought, insurance companies out of action and belated regulatory action slamming on the brakes on carbon emissions in an unpredictable way.

Despite pressure from public interest organisations like Vote Your Pension, and despite their membership of climate progressive organisations like CDP, Ceres and PRI – the latter having a formal commitment that members “will be active owners and incorporate ESG issues into our ownership policies and practice” – market research recently revealed that a half of the retirement/investment industry does not consider climate change material. And this is in the UK where the debate is well advanced.

That business as usual in the investment industry, even amongst those who sign up to ESG, is unfit for purpose is without doubt. One challenge is that asset owners are poorly organised to influence their managers, who channel funds from many different asset owners into companies. These asset managers have shorter time horizons, devolve voting to sector analysts and exhibit endemic commercial conflicts of interests. Yet they set the agenda.

This puts the spotlight on firms such as Blackrock and Vanguard, whose assets under management are similar in size to the GDP of Japan and the UK respectively. The #Missing60 campaign draws attention to the fact that 60% of investors who voted for carbon disclosure resolutions at Shell and BP in 2015, voted against very similar resolutions at ExxonMobil and Chevron in 2016. And this is after the substantial commitments made by governments to tackle climate change at COP21 – which ExxonMobil baldly stated that it didn’t believe would be actioned. These investors are effectively betting against governments, penalising companies leading on climate risk and backing corporate laggards.

Signatories to the #Missing60 initiative, including Sister Patricia Daly, Bob Eccles, Jean-Pierre Hellebuyck, Bob Litterman, Julian Poulter and Naomi Oreskes, are demanding that:

1 Institutional investors think, act, and vote independently of management recommendations. Inconsistency of voting on fundamentally similar 2ºC stress test / transition plan resolutions needs explanation;

2 Investors require the leadership of companies to recognise and embrace the challenges and opportunities of an energy transition to achieve a low carbon economy;

3 Investors require investee companies to provide a clear explanation of their transition plans that will result in emissions reductions consistent with achieving <2°C planetary warming.

TRANSPARENCY

FOREWORD

The good news is that there is a growing movement of investors and campaigning organisations, including AODP, seeking to use the AGM rounds to ratchet up pressure on investors to live up to these principles. They are voting for increasingly challenging resolutions – for example from disclosure to active development of transition plans to a <2ºC warming world (as happened at Southern Company in 2016, with 34% voting in favour). We now need to extend these resolutions to big users of fossil fuels as well as producers and for all of this to be happening on an industrial scale, for example with resolutions facing at least 25% of a sector (by market cap). When fossil fuel companies see that large users (for example energy utilities and autos, the latter becoming the biggest GHG emitter in the USA this year) and also influential enablers (such as insurance companies) are actively planning for a transition away from fossil fuels, their business as usual stance will become increasingly untenable.

If, as the report indicates, these measures are coupled with more assertive action by membership organisations such as CDP, Ceres/INCR and PRI to hold members to their commitments, and regulatory changes, (so that Know Your Client rules incorporate clients’ views on climate change and all investors have to report on how they vote, for example,) then eventually change is bound to come.

The only question is – how much value will have been destroyed and how much additional instability will be created while the world waits for institutional investors to live up to their fiduciary responsibilities?

This helpful but short report inevitably leaves unanswered some important questions. Who are the investors who have made positive progress this year? Do the philanthropic foundations that are concerned about climate change – both those that back Divest-Invest and those that do not – disclose their voting and are they leading this stewardship push? And which of the investors who voted for 2°C stress tests did not vote for the 2°C transition plan (Southern) resolution and why? The need for a group like AODP to monitor, on an on-going basis, the voting of all investors on all key climate resolutions is clear.

Carolyn Hayman OBE (Chair) and Raj Thamotheram (Founder & CEO), Preventable Surprises

04

EXECUTIVE SUMMARY

Climate change poses a substantive risk to global financial stability and the retirement savings of millions of people around the world. At the Paris Climate Summit world leaders pledged to limit global warming to a maximum 2ºC. Bank of England Governor and chairman of the international Financial Stability Board Mark Carney has warned that action to tackle climate change could leave fossil fuels and other high-carbon investments as worthless, stranded assets. The transition to a low-carbon economy is likely to lead to a significant reduction in the value of many companies which have powered our fossil fuel economy, with serious consequences for the pension funds, insurers and other shareholders who own them, and the ordinary people whose pensions and policies they administer.

It is against this backdrop that the Exxon 2016 AGM became a key focus for many stakeholders and provided a unique snapshot of the state of investor collaboration, the current success of company engagement as a way to mitigate climate change, the degree of resistance by the supermajors and the accountability crisis within the investment chain.

The 2016 Exxon AGM may prove to be a seminal event in climate change history. That year saw a record 94 climate change resolutions of which nine were filed at Exxon Mobil. At the Exxon AGM, 62% of shares were voted for agenda item 7, proxy access - a resolution allowing shareholders to appoint directors. This was the first shareholder proposal to be approved at Exxon since 2006. The 69 funds who pre-declared their votes was a record and has set a new precedent for investor collaboration, encouraging other funds to follow suit prior to the AGM and putting pressure on the target company to accept change.

06

Perhaps most significantly, 38% of shares were voted in favour of item 12, a resolution calling for the company to publish data about the impact on its business of the global commitment to limit climate change to 2ºC. This was a near record for a contested climate resolution but left many observers wondering why there was a 60% difference between this vote and the almost identical resolution passed by the same shareholders at the BP and Shell AGMs in 2015.

Large institutional investors’ management of their Exxon shares has become a proxy for the credibility of engagement and how well pension funds, insurers and other asset owners are managing climate risk in their portfolios.

This is the first report to analyse how investors voted at the Exxon AGM and compare it with their commitments on climate change.

This report also shows the results of one of the largest ever beneficiary campaigns run by VoteYourPension.org that saw over a thousand large Exxon shareholders contacted by their members to urge them to vote against the Exxon board and for item 12 and other climate resolutions.

REX TILLERSON, CEO EXXON-MOBIL CORPORATION

However, the world’s biggest fossil fuel companies and many of their investors are proving highly resistant to warnings about climate risk. The majority of their investors appear happy for them to continue with business as usual, although a well-established and growing group of progressive asset owners is pushing for action on climate change. Nevertheless, most of the power and voting influence resides with the asset managers, a much more consolidated and conservative grouping, dominated by the large US funds.

Exxon’s two largest shareholders BlackRock and Vanguard voted against the resolution. However, State Street, the third largest shareholder voted for the resolution. These are the three biggest asset managers in the world, and in total own 16% of Exxon shares. The BlackRock and Vanguard votes were a surprise since the CEOs of both organisations had made statements indicating possible support: BlackRock CEO Larry Fink warned in a letter to CEOs that climate change had “real and quantifiable financial impacts posing both risks and opportunities”; and Vanguard CEO Bill McNabb denounced fossil divestment in a letter to the Financial Times suggesting that the way to manage climate risk was not divestment but by good engagement.

XX

EXECUTIVE SUMMARY

08

The report finds that: Our analysis of the 2016 Exxon AGM allows us to draw a number of conclusions:

▬ Shareholder engagement as a method to drive change within companies is beginning to have real impact following many years where such efforts produced little visible results. The collaboration between investors and civil society groups created a unique level of pressure on Exxon and has also isolated the parts of the system that failed to align with these efforts.

▬ The impact of the leading asset owners is beginning to be felt in the funds management community with some large fund managers now responding to pressure by supporting these resolutions. However, this pressure is not yet sufficient to ensure that asset owner climate policies are reflected in fund manager voting patterns.

▬ There is a new and significant split amongst the giant fund managers with leading funds BlackRock and Vanguard voting against Item 12 and State Street voting most of its stock in favour.

▬ A majority of asset owners and fund managers do not seem to have capacity, processes or the will to respond to letters from their own members.

▬ There is a serious structural industry issue with a large proportion of votes being subject to a default voting option either in favour of the company, a proxy adviser who may not always think long term, or some other voting administrator. This structural deficiency was compounded in this case by some managers choosing to vote against adviser recommendations.

▬ Although many funds have signed up to Principles for Responsible Investment and similar commitments they are either not aware of how these should translate into proxy voting practice or else governance staff are not aware of the commitments they have made.

▬ There is insufficient regulation of voting disclosure to members and for public benefit.

▬ Fiduciary duty risk appears of little concern to most large investors – there has been much work done on fiduciary duty and climate change but this is not translating into proxy voting action.

▬ The FSB (Financial Stability Board) Task Force should recommend 100% voting disclosure at all levels of the investment chain

▬ All funds, owners and managers, must be required to actively vote all of their shares.

▬ Where a fund has a default voting policy (either in favour of its voting advisor or the company), it should create a mechanism where member views are incorporated.

▬ Pension fund regulators should require pension funds to pre-declare their voting intentions for key AGM’s. This could be defined as any AGM where a fund is contacted by a proportion of members.

▬ All asset owners should declare their voting policy by manager and company.

▬ All asset owners should report the degree to which asset managers adhere to their engagement policies.

▬ Proxy advisers should be pushed to declare their recommendations at least six weeks before key AGM’s. Given the volume of votes this carries in the market between ISS and Glass Lewis, asset owners should have the right to inform members of the proxy adviser recommendation.

▬ Investor groups and associations should remove signatories who do not have a credible plan for using engagement as a tool for managing risk or who are not transparent with their own members.

▬ Regulators must ensure that asset owners have a legal right to direct voting in proportion to the number of units they hold with an asset manager’s portfolio. Likewise, asset owners can lead this by making it a standard requirement of their investment manager agreements.

With such a positive vote at the 2016 AGM, progressive investors are bound to return to the Exxon AGM in 2017 supported by an even larger civil society campaign. This could lead to a successful majority for the 2 degree stress test demanded of Exxon. However, thanks to the work of Carbon Tracker and other organisations, investors already know that such a test will prove finally that Exxon must cease further exploration and commence immediate diversification or begin to return capital to shareholders. Thus resolutions requiring Exxon to produce diversification options, as Total and Statoil have, should be filed as quickly as possible to maintain momentum.

There is significant hypocrisy in the industry with many PRI members voting in breach of commitments to responsible investment: 45% of the largest shareholders that voted against the climate resolution have signed up to PRI and 25% have signed up to CDP.

There is a crisis of accountability between asset owners and managers – 29% of asset owners who responded to their members admitted to outsourcing the voting decision.

There is a crisis of accountability between members and their retirement funds of all types including pension funds, mutual funds and retail funds. Of 1069 funds in 52 countries contacted by thousands of members, only 3% responded to letters urging their funds reveal their voting intentions on the key material climate resolutions and vote against Exxon.

45%

29%

3% To address the structural issues that drive short termism in the voting context and to increase accountability through the investment chain to ensure voting better reflects the interests of retirement fund beneficiaries (the ultimate Exxon majority shareholders), AODP makes the following calls to action:

THERE IS SIGNIFICANT HYPOCRISY IN THE INDUSTRY WITH 45% OF THE LARGEST PRI SIGNATORY SHAREHOLDERS AND 25% OF THE LARGEST CDP SIGNATORY SHAREHOLDERS VOTING AGAINST THE CLIMATE RESOLUTION.

16

SECTION 01

Climate change poses a substantial risk to global financial stability and the retirement savings of millions of beneficiaries around the world. The world’s biggest polluters and many of their investors are proving resistant to warnings by leading climate experts and economists. Bank of England Governor and chairman of the international Financial Stability Board, Mark Carney, has warned that action to tackle climate change could leave fossil fuels and other high-carbon investments as worthless, stranded assets.

Carney told investors the transition to a low-carbon economy could lead to a “wholesale reassessment of prospects” that could destabilise markets. He also stated in a speech to the UN General Assembly in April 2016 that the global financial system needed to prove its resilience following the Paris agreement to limit climate change to a maximum 2ºC. These warnings are particularly relevant for long term asset owners whose funds management community is more geared to short term trading than managing long term risk. www.bankofengland.co.uk/publications/Pages/speeches/2016/897.aspx

Whilst strong regulation on climate change has been promised but not yet delivered by policymakers, the investor community, driven strongly by civil society, has moved rapidly to anticipate that regulation and has begun to mitigate climate risk for the benefit of its long term stakeholders. With much of the world’s capital residing in retirement funds, these stakeholders are mostly ordinary working people who expect their funds to act in their interests and take a long view.

It is against this backdrop that the Exxon 2016 AGM became a key focus for many stakeholders and provided a unique snapshot of the state of investor collaboration, the current success of company engagement as a way to mitigate climate change, the degree of resistance by the supermajors and the accountability crisis in the financial system, specifically the investment chain.

CONTEXT

SECTION 02

CLIMATE CHANGE, THE INVESTMENT CHAIN & EXXON

DESPITE THE URGENCY OF CLIMATE CHANGE, INVESTORS ARE HIGHLY RELUCTANT TO “ROCK THE BOAT”

14

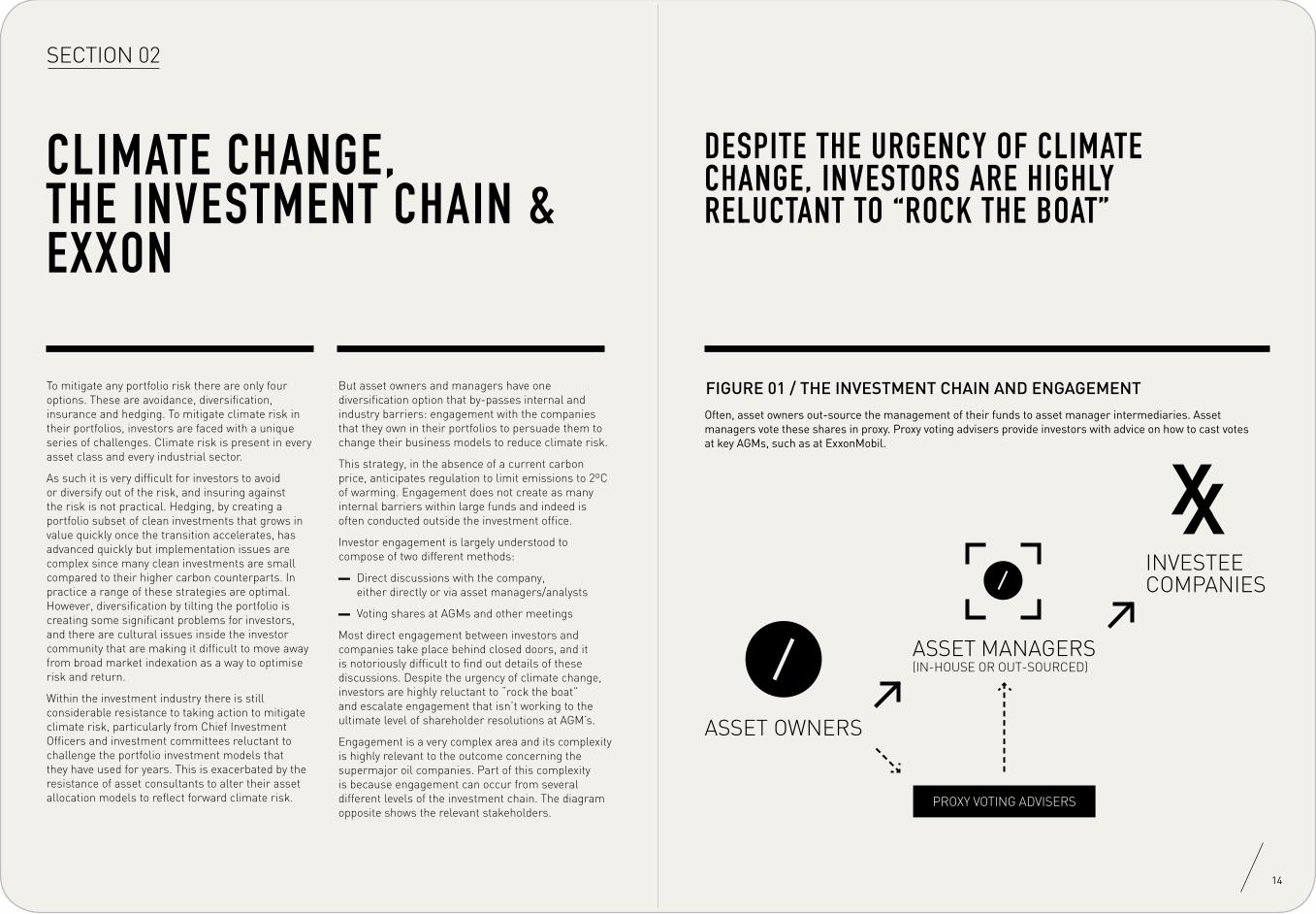

To mitigate any portfolio risk there are only four options. These are avoidance, diversification, insurance and hedging. To mitigate climate risk in their portfolios, investors are faced with a unique series of challenges. Climate risk is present in every asset class and every industrial sector.

As such it is very difficult for investors to avoid or diversify out of the risk, and insuring against the risk is not practical. Hedging, by creating a portfolio subset of clean investments that grows in value quickly once the transition accelerates, has advanced quickly but implementation issues are complex since many clean investments are small compared to their higher carbon counterparts. In practice a range of these strategies are optimal. However, diversification by tilting the portfolio is creating some significant problems for investors, and there are cultural issues inside the investor community that are making it difficult to move away from broad market indexation as a way to optimise risk and return.

Within the investment industry there is still considerable resistance to taking action to mitigate climate risk, particularly from Chief Investment Officers and investment committees reluctant to challenge the portfolio investment models that they have used for years. This is exacerbated by the resistance of asset consultants to alter their asset allocation models to reflect forward climate risk.

But asset owners and managers have one diversification option that by-passes internal and industry barriers: engagement with the companies that they own in their portfolios to persuade them to change their business models to reduce climate risk.

This strategy, in the absence of a current carbon price, anticipates regulation to limit emissions to 2ºC of warming. Engagement does not create as many internal barriers within large funds and indeed is often conducted outside the investment office.

Investor engagement is largely understood to compose of two different methods:

▬ Direct discussions with the company, either directly or via asset managers/analysts

▬ Voting shares at AGMs and other meetings

Most direct engagement between investors and companies take place behind closed doors, and it is notoriously difficult to find out details of these discussions. Despite the urgency of climate change, investors are highly reluctant to “rock the boat” and escalate engagement that isn’t working to the ultimate level of shareholder resolutions at AGM’s.

Engagement is a very complex area and its complexity is highly relevant to the outcome concerning the supermajor oil companies. Part of this complexity is because engagement can occur from several different levels of the investment chain. The diagram opposite shows the relevant stakeholders.

FIGURE 01 / THE INVESTMENT CHAIN AND ENGAGEMENTOften, asset owners out-source the management of their funds to asset manager intermediaries. Asset managers vote these shares in proxy. Proxy voting advisers provide investors with advice on how to cast votes at key AGMs, such as at ExxonMobil.

ASSET OWNERS

PROXY VOTING ADVISERS

ASSET MANAGERS (IN-HOUSE OR OUT-SOURCED)

INVESTEE COMPANIES

XX

The ultimate owners of the majority of shares in Exxon are the asset owners, consisting of the pension funds, insurance companies, sovereign wealth funds and endowments. Engagement and indeed voting can be done directly by Asset Owners but more often through their fund managers or 3rd party service manager. Through the investment chain, millions of ordinary people have a direct interest in the success or failure of Exxon because a proportion of their retirement savings will be invested in its stock. Exxon has consistently rejected claims that it is risking shareholder capital because either regulation or innovation will impact its business.

It isn’t just investment returns that should be driving long term change in the supermajors such as Exxon, there are legal drivers too. Pension funds in particular have a fiduciary duty to the long term interests of their members. Clearly a vote that sustains the Exxon business model is in conflict with that long term duty.

By implication, it is incumbent on fund trustees to ensure that, if they own shares through an asset manager, those asset managers should be held accountable forobserving the fund’s engagement policies.

In the US, the Carbon Asset Risk program run by CERES and its partners has seen many disclosure resolutions raised to drive company disclosure and in the UK a coalition of investors under the “Aiming for A” banner has raised resolutions with several large companies. Resolutions have been raised by various NGOs in Norway and the Netherlands against Statoil and Shell but the co-filing of resolutions by large investors is still rare.

In Australia where superannuation funds are perceived to be more active, not one single resolution has been raised by funds concerning climate change.

This conservatism is also particularly noticeable in the UK and much of Europe, where investors including long term asset owners take a far more conservative stance regarding the raising of shareholder resolutions. Futhermore, corporate governance laws in the US make it far easier to file shareholder resolutions than in other jurisdictions, including the UK.

Annual General Meetings are the one legislated opportunity where shareholders can exercise their rights to hold management of a company to account and ask questions.

For companies like Exxon with a history of ignoring shareholder communication, these AGMs are critical and a focal point for shareholders wanting to alter the path of one of their largest investments.

One of the problems for active shareholders is that the shareholding base of large companies like Exxon is extremely diverse with only seven shareholders owning more than 1% of the shares. This makes collaboration to challenge the company extremely difficult and is one of the main reasons that shareholders, asset owners in particular, have created associations like the PRI (Principle for Responsible Investment), INCR (Investor Network on Climate Risk) and the IIGCC (Institutional Investor Group on Climate Change) that facilitate this collaboration.

This diverse shareholder base is a great advantage to a company like Exxon looking to resist change. Furthermore, company AGMs in each of the main markets are concentrated into a very tight timeframe of only 1-2 months and it is very difficult for funds and the media to maintain pressure on any single company. Once the AGM has passed, focus on votes dissipates quickly and there is little or no accountability reported in the media for the voting patterns of shareholders.

The role of the associations is becoming increasingly relevant as more and more asset owners are demanding that their fund managers who have immediate control over their shares, also sign up to commitments like CDP and PRI.

CDP and PRI are the world’s leading investor signatory organisations. CDP (formerly known as the Carbon Disclosure Project) drives transparency amongst climate exposed companies using the power of its member base to claim authority for such transparency. The PRI (Formerly the United Nations Principles for Responsible Investment) is a broader organisation using collaboration with its investor members to advance responsible investment best practice.

In the voting context, the PRI is particularly important as it focusses on the obligations of investors.

WWW.UNPRI.ORG

16

PRINCIPLES FOR RESPONSIBLE INVESTMENT

SECTION 02

“ WE WILL BE ACTIVE OWNERS & INCORPORATE ESG ISSUES INTO OUR OWNERSHIP POLICIES & PRACTICES.”

PRINCIPLE 2

“ WE WILL EACH REPORT ON OUR ACTIVITIES & PROGRESS TOWARDS IMPLEMENTING THE PRINCIPLES.”

PRINCIPLE 6

“ WE WILL SEEK APPROPRIATE DISCLOSURE ON ESG ISSUES BY THE ENTITIES IN WHICH WE INVEST.”

PRINCIPLE 3

About PRI

PRI is the world’s leading proponent of responsible investment, and is supported by the UN. More than 1500 international members with $62 trillion of assets under management have signed up to its six Principles for Responsible Investment.

Three of these principles are particularly relevant in the context of the Exxon 2016 AGM. We would expect PRI signatories to:

A vote as per principle no 2 B support item 12 as a disclosure

resolution as per principle 3C report how they voted as per

principle 6.

About CDP

CDP investor initiatives – backed in 2015 by more than 827 institutional investors representing an excess of US$100 trillion in assets – give investors access to a global source of year-on-year information that supports long-term objective analysis. This includes evidence and insight into companies’ greenhouse gas emissions, water usage and strategies for managing climate change, water and deforestation risks.

CDP requests standardized climate change information from some of the world’s largest listed companies through annual questionnaires sent on behalf of institutional investors that endorse them as ‘CDP signatories’. These shareholder requests for information encourage companies to account for and be transparent about environmental risk. Transparency of this data throughout the global market place ensures the financial community has access to the best available corporate environmental information to help drive investment flows towards a low carbon and more sustainable economy.

SECTION 03

VOTING AT THE EXXON 2016 AGM

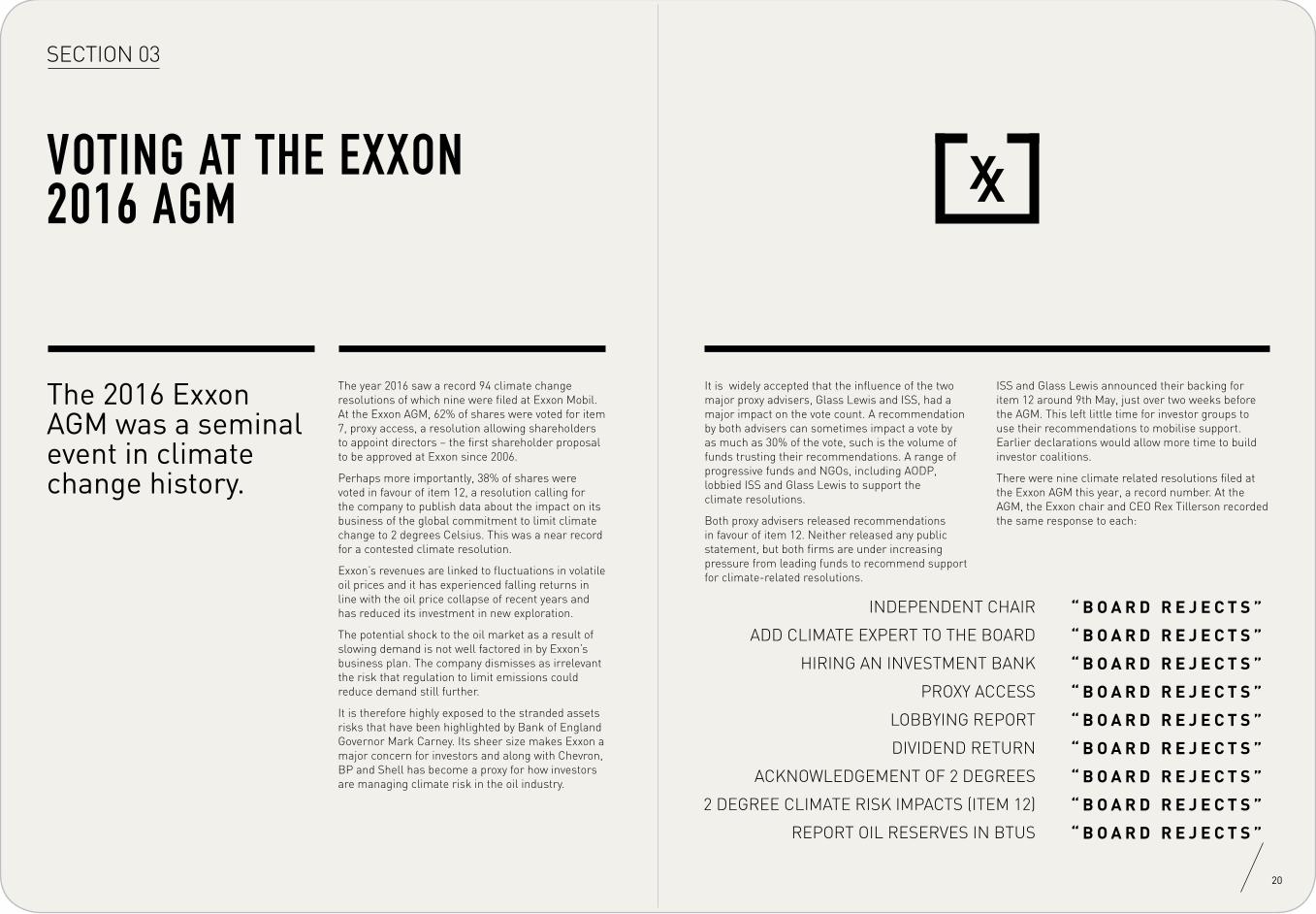

The year 2016 saw a record 94 climate change resolutions of which nine were filed at Exxon Mobil. At the Exxon AGM, 62% of shares were voted for item 7, proxy access, a resolution allowing shareholders to appoint directors – the first shareholder proposal to be approved at Exxon since 2006.

Perhaps more importantly, 38% of shares were voted in favour of item 12, a resolution calling for the company to publish data about the impact on its business of the global commitment to limit climate change to 2 degrees Celsius. This was a near record for a contested climate resolution.

Exxon’s revenues are linked to fluctuations in volatile oil prices and it has experienced falling returns in line with the oil price collapse of recent years and has reduced its investment in new exploration.

The potential shock to the oil market as a result of slowing demand is not well factored in by Exxon’s business plan. The company dismisses as irrelevant the risk that regulation to limit emissions could reduce demand still further.

It is therefore highly exposed to the stranded assets risks that have been highlighted by Bank of England Governor Mark Carney. Its sheer size makes Exxon a major concern for investors and along with Chevron, BP and Shell has become a proxy for how investors are managing climate risk in the oil industry.

The 2016 Exxon AGM was a seminal event in climate change history.

“ B O A R D R E J E C T S ”

“ B O A R D R E J E C T S ”

“ B O A R D R E J E C T S ”

“ B O A R D R E J E C T S ”

“ B O A R D R E J E C T S ”

“ B O A R D R E J E C T S ”

“ B O A R D R E J E C T S ”

“ B O A R D R E J E C T S ”

“ B O A R D R E J E C T S ”

INDEPENDENT CHAIR

ADD CLIMATE EXPERT TO THE BOARD

HIRING AN INVESTMENT BANK

PROXY ACCESS

LOBBYING REPORT

DIVIDEND RETURN

ACKNOWLEDGEMENT OF 2 DEGREES

2 DEGREE CLIMATE RISK IMPACTS (ITEM 12)

REPORT OIL RESERVES IN BTUS

It is widely accepted that the influence of the two major proxy advisers, Glass Lewis and ISS, had a major impact on the vote count. A recommendation by both advisers can sometimes impact a vote by as much as 30% of the vote, such is the volume of funds trusting their recommendations. A range of progressive funds and NGOs, including AODP, lobbied ISS and Glass Lewis to support the climate resolutions.

Both proxy advisers released recommendations in favour of item 12. Neither released any public statement, but both firms are under increasing pressure from leading funds to recommend support for climate-related resolutions.

ISS and Glass Lewis announced their backing for item 12 around 9th May, just over two weeks before the AGM. This left little time for investor groups to use their recommendations to mobilise support. Earlier declarations would allow more time to build investor coalitions.

There were nine climate related resolutions filed at the Exxon AGM this year, a record number. At the AGM, the Exxon chair and CEO Rex Tillerson recorded the same response to each:

XX

20

SECTION 03

22

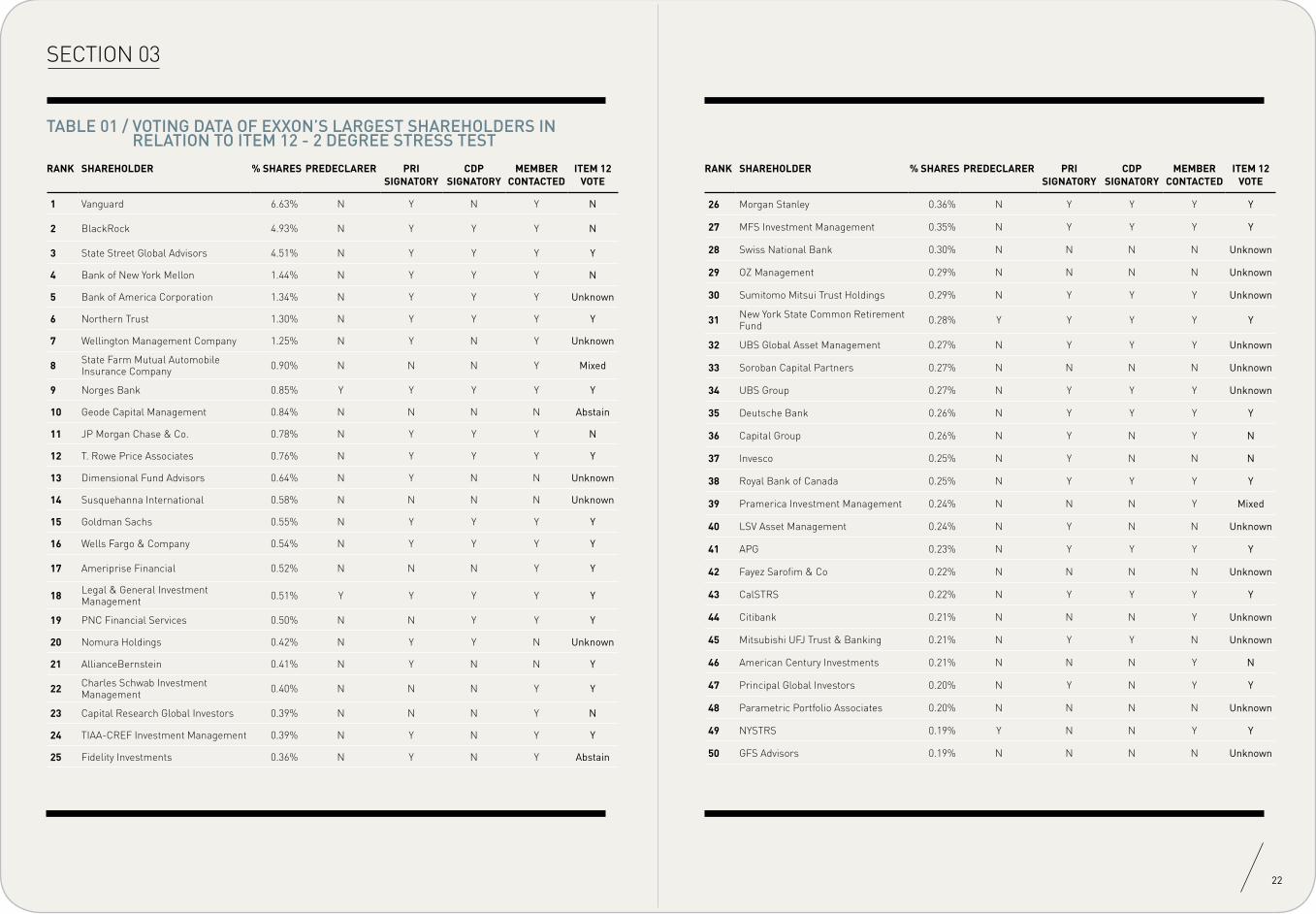

TABLE 01 / VOTING DATA OF EXXON’S LARGEST SHAREHOLDERS IN RELATION TO ITEM 12 - 2 DEGREE STRESS TEST

RANK SHAREHOLDER % SHARES PREDECLARER PRI SIGNATORY

CDP SIGNATORY

MEMBER CONTACTED

ITEM 12 VOTE

1 Vanguard 6.63% N Y N Y N

2 BlackRock 4.93% N Y Y Y N

3 State Street Global Advisors 4.51% N Y Y Y Y

4 Bank of New York Mellon 1.44% N Y Y Y N

5 Bank of America Corporation 1.34% N Y Y Y Unknown

6 Northern Trust 1.30% N Y Y Y Y

7 Wellington Management Company 1.25% N Y N Y Unknown

8 State Farm Mutual Automobile Insurance Company 0.90% N N N Y Mixed

9 Norges Bank 0.85% Y Y Y Y Y

10 Geode Capital Management 0.84% N N N N Abstain

11 JP Morgan Chase & Co. 0.78% N Y Y Y N

12 T. Rowe Price Associates 0.76% N Y Y Y Y

13 Dimensional Fund Advisors 0.64% N Y N N Unknown

14 Susquehanna International 0.58% N N N N Unknown

15 Goldman Sachs 0.55% N Y Y Y Y

16 Wells Fargo & Company 0.54% N Y Y Y Y

17 Ameriprise Financial 0.52% N N N Y Y

18 Legal & General Investment Management 0.51% Y Y Y Y Y

19 PNC Financial Services 0.50% N N Y Y Y

20 Nomura Holdings 0.42% N Y Y N Unknown

21 AllianceBernstein 0.41% N Y N N Y

22 Charles Schwab Investment Management 0.40% N N N Y Y

23 Capital Research Global Investors 0.39% N N N Y N

24 TIAA-CREF Investment Management 0.39% N Y N Y Y

25 Fidelity Investments 0.36% N Y N Y Abstain

RANK SHAREHOLDER % SHARES PREDECLARER PRI SIGNATORY

CDP SIGNATORY

MEMBER CONTACTED

ITEM 12 VOTE

26 Morgan Stanley 0.36% N Y Y Y Y

27 MFS Investment Management 0.35% N Y Y Y Y

28 Swiss National Bank 0.30% N N N N Unknown

29 OZ Management 0.29% N N N N Unknown

30 Sumitomo Mitsui Trust Holdings 0.29% N Y Y Y Unknown

31 New York State Common Retirement Fund 0.28% Y Y Y Y Y

32 UBS Global Asset Management 0.27% N Y Y Y Unknown

33 Soroban Capital Partners 0.27% N N N N Unknown

34 UBS Group 0.27% N Y Y Y Unknown

35 Deutsche Bank 0.26% N Y Y Y Y

36 Capital Group 0.26% N Y N Y N

37 Invesco 0.25% N Y N N N

38 Royal Bank of Canada 0.25% N Y Y Y Y

39 Pramerica Investment Management 0.24% N N N Y Mixed

40 LSV Asset Management 0.24% N Y N N Unknown

41 APG 0.23% N Y Y Y Y

42 Fayez Sarofim & Co 0.22% N N N N Unknown

43 CalSTRS 0.22% N Y Y Y Y

44 Citibank 0.21% N N N Y Unknown

45 Mitsubishi UFJ Trust & Banking 0.21% N Y Y N Unknown

46 American Century Investments 0.21% N N N Y N

47 Principal Global Investors 0.20% N Y N Y Y

48 Parametric Portfolio Associates 0.20% N N N N Unknown

49 NYSTRS 0.19% Y N N Y Y

50 GFS Advisors 0.19% N N N N Unknown

VOTE ANALYSIS

24

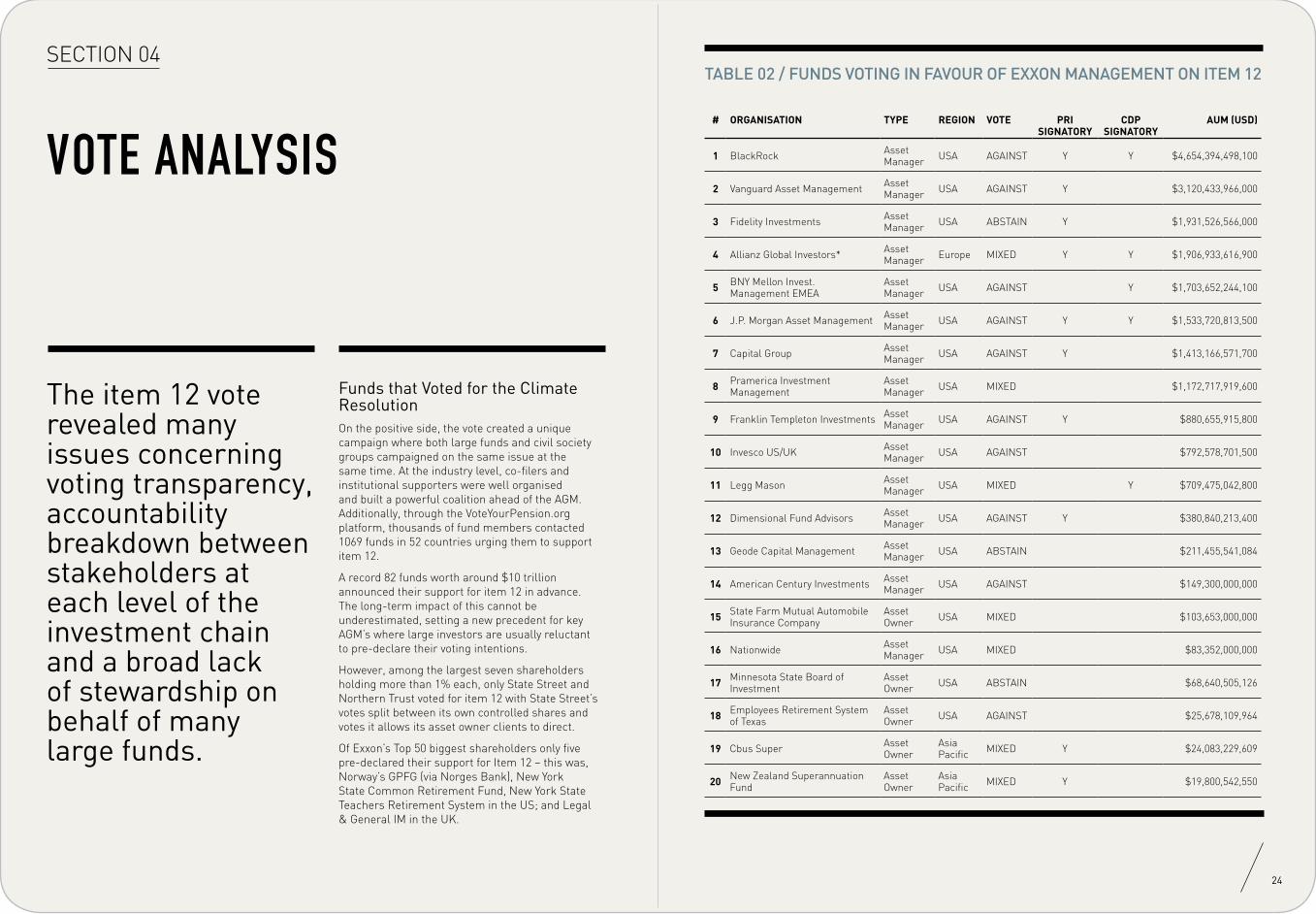

The item 12 vote revealed many issues concerning voting transparency, accountability breakdown between stakeholders at each level of the investment chain and a broad lack of stewardship on behalf of many large funds.

TABLE 02 / FUNDS VOTING IN FAVOUR OF EXXON MANAGEMENT ON ITEM 12

Funds that Voted for the Climate ResolutionOn the positive side, the vote created a unique campaign where both large funds and civil society groups campaigned on the same issue at the same time. At the industry level, co-filers and institutional supporters were well organised and built a powerful coalition ahead of the AGM. Additionally, through the VoteYourPension.org platform, thousands of fund members contacted 1069 funds in 52 countries urging them to support item 12.

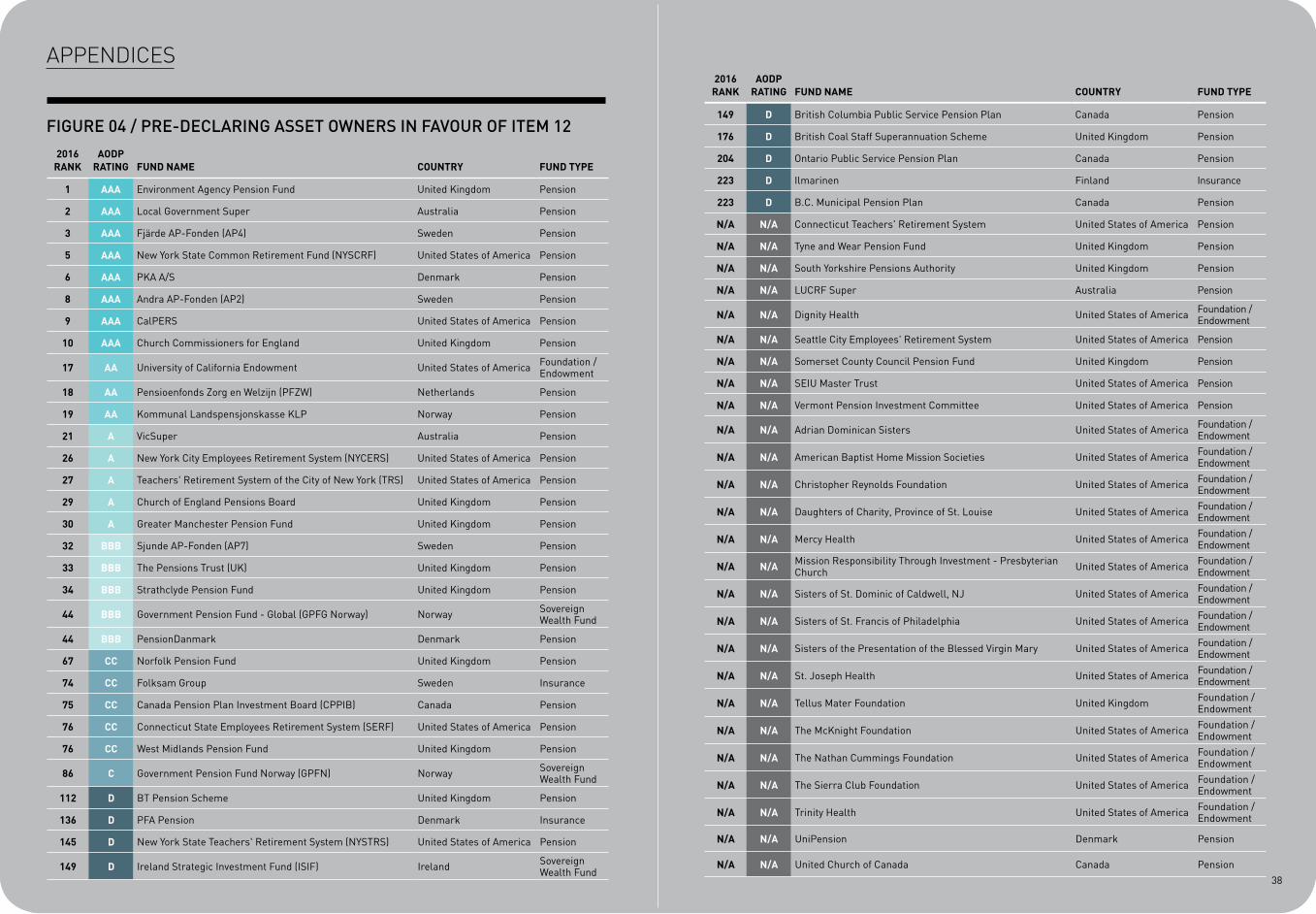

A record 82 funds worth around $10 trillion announced their support for item 12 in advance. The long-term impact of this cannot be underestimated, setting a new precedent for key AGM’s where large investors are usually reluctant to pre-declare their voting intentions.

However, among the largest seven shareholders holding more than 1% each, only State Street and Northern Trust voted for item 12 with State Street’s votes split between its own controlled shares and votes it allows its asset owner clients to direct.

Of Exxon’s Top 50 biggest shareholders only five pre-declared their support for Item 12 – this was, Norway’s GPFG (via Norges Bank), New York State Common Retirement Fund, New York State Teachers Retirement System in the US; and Legal & General IM in the UK.

# ORGANISATION TYPE REGION VOTE PRI SIGNATORY

CDP SIGNATORY

AUM (USD)

1 BlackRock Asset Manager USA AGAINST Y Y $4,654,394,498,100

2 Vanguard Asset Management Asset Manager USA AGAINST Y $3,120,433,966,000

3 Fidelity Investments Asset Manager USA ABSTAIN Y $1,931,526,566,000

4 Allianz Global Investors* Asset Manager Europe MIXED Y Y $1,906,933,616,900

5 BNY Mellon Invest. Management EMEA

Asset Manager USA AGAINST Y $1,703,652,244,100

6 J.P. Morgan Asset Management Asset Manager USA AGAINST Y Y $1,533,720,813,500

7 Capital Group Asset Manager USA AGAINST Y $1,413,166,571,700

8 Pramerica Investment Management

Asset Manager USA MIXED $1,172,717,919,600

9 Franklin Templeton Investments Asset Manager USA AGAINST Y $880,655,915,800

10 Invesco US/UK Asset Manager USA AGAINST $792,578,701,500

11 Legg Mason Asset Manager USA MIXED Y $709,475,042,800

12 Dimensional Fund Advisors Asset Manager USA AGAINST Y $380,840,213,400

13 Geode Capital Management Asset Manager USA ABSTAIN $211,455,541,084

14 American Century Investments Asset Manager USA AGAINST $149,300,000,000

15 State Farm Mutual Automobile Insurance Company

Asset Owner USA MIXED $103,653,000,000

16 Nationwide Asset Manager USA MIXED $83,352,000,000

17 Minnesota State Board of Investment

Asset Owner USA ABSTAIN $68,640,505,126

18 Employees Retirement System of Texas

Asset Owner USA AGAINST $25,678,109,964

19 Cbus Super Asset Owner

Asia Pacific MIXED Y $24,083,229,609

20 New Zealand Superannuation Fund

Asset Owner

Asia Pacific MIXED Y $19,800,542,550

SECTION 04

VOTE ANALYSIS

26

The AODP Global 500 Index database reveals that only 51 out of the largest 500 asset owners review the voting recommendations of either their fund managers, proxy advisers or the company themselves.

Asset Managers & Asset OwnersAsset owners include some of the largest public pension funds in the world, but what’s of greater significance are the voting decisions of a much smaller number of asset managers whose pooling of asset owner client capital creates larger funds with a larger shareholding in companies like Exxon.

The available voting data shows that asset owners were much more likely to vote for the climate resolutions than asset managers. Of the largest funds who have declared voting against the climate change resolution, Item 12, the vast majority are asset management firms, which manage the money for institutional clients such as pension funds.

However, while BlackRock and Vanguard voted against the resolution, State Street Global Advisers voted in favour of it. These are the three biggest asset managers in the world, and in total own 16% of Exxon shares. The fact that State Street voted in favour of this resolution might represent the beginning of a significant shift in how asset managers view the supermajors, as other investors often look to the giant trillion dollar funds for leadership in proxy voting and engagement.

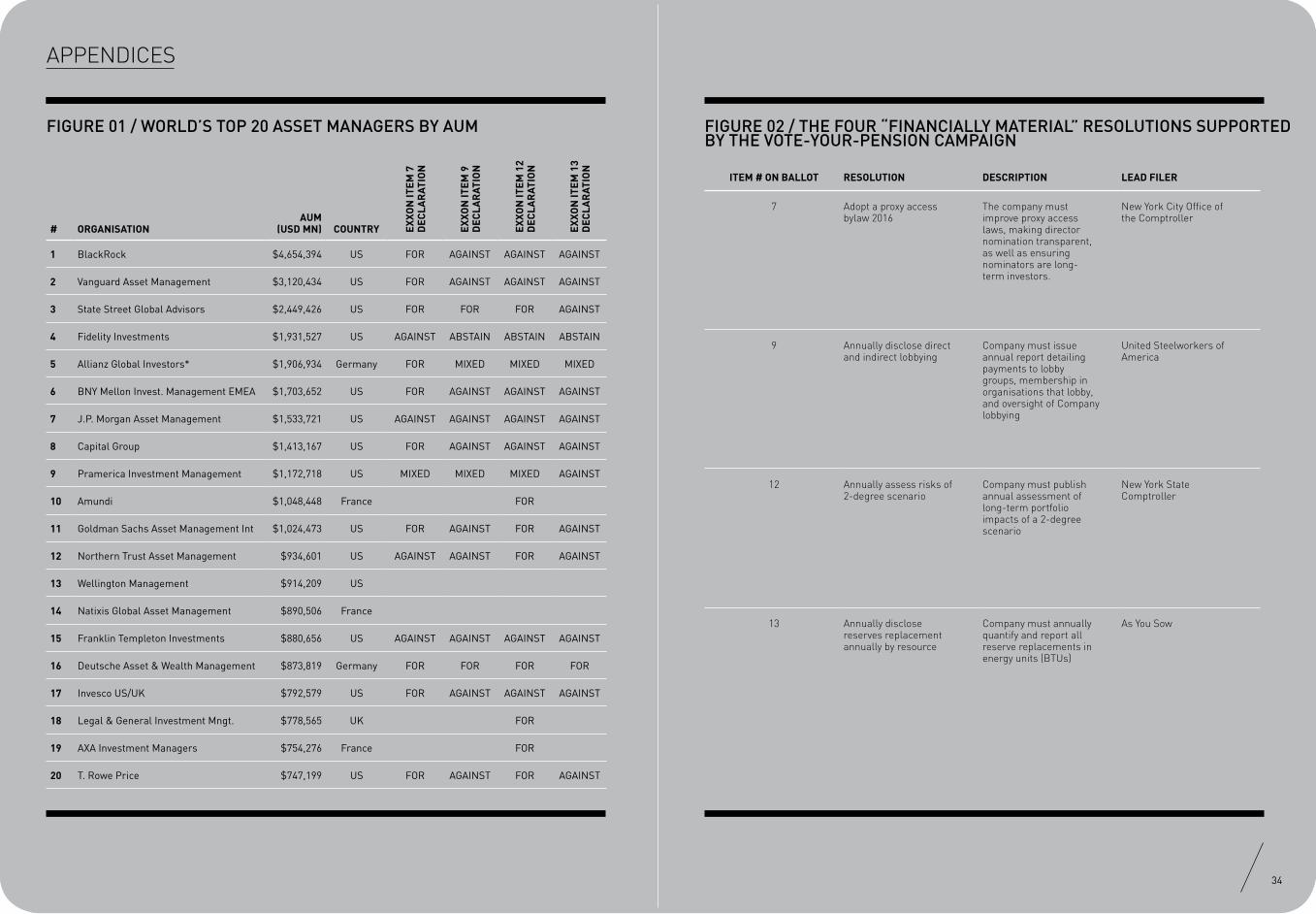

Pre-declarationsOf the top 20 asset managers in the world, only 3 pre-declared their support for Item 12: Amundi (over $1 trillion AUM), Legal & General Investment Management ($778 billion) and AXA Investment Managers ($754 billion).

Similarly, only 3 of the largest 20 Asset Owners predeclared their vote. Norway’s Government Pension Fund ($860 billion AUM), the largest US state pension fund CalPERS ($302 billion) and New York State Common Retirement Fund ($185 billion), predeclared their voting intentions.

Funds that rate highest on the AODP Global Climate 500 Index, which rates and ranks the world’s largest asset owners over their climate risk performance, are far more likely to disclose their engagement activities compared with the greater asset owner universe. 71% disclosed voting intentions on at least one resolution, compared with 9% of all funds. Tellingly, all funds who disclosed voting intentions gave information on Item 12. (Figures 6 and 7).

SECTION 04

Funds that Voted Against the Climate ResolutionNegatively, Item 12 was a near identical resolution to the two passed by a huge majority at the BP and Shell AGM’s the previous year. The question that demanded to be asked therefore was “where was the missing 60%?”.

High profile funds voting against item 12 included Blackrock, the world’s largest asset manager with $4.65 trillion under management, and Vanguard, the world’s second largest asset manager and the largest Exxon although both funds are PRI signatories and both CEOs recognise climate risk. Blackrock CEO Larry Fink warned in a letter to CEOs that climate change had “real and quantifiable financial impacts posing both risks and opportunities”; and Vanguard CEO Bill McNabb suggested in a letter to the FT that the way to manage climate risk was not divestment but by good engagement. “There is no impact to the income or balance sheet of the company. You are not sending a message to the company. You are better remaining an owner and being able to engage with the company,” he said in May 2016.

The vote also revealed a disturbing hypocrisy amongst many funds that have made commitments to transparency and active management but are simply not following those commitments. Those commitments have been made in many forums but most widely in the signing up to CDP (Carbon Disclosure Project) and the PRI (Principles for Responsible Investment).

The commitment to these organisations is supposed to be reflected in their active ownership work and it is clear that many funds are saying one thing and doing another. Several high profile PRI and CDP signatories voted against item 12 and many more refused to answer calls from their own members to support the vote with many of them failing to be transparent about their vote actions at all.

Overall, in the largest shareholders list, 20% of PRI signatories and 13% of CDP signatories voted against item 12 and in favour of Exxon, with 27% of PRI and 21% of CDP signatories as yet failing to disclose their vote. PRI signatories who voted against the resolution include Blackrock, the New Zealand Superannuation Fund ($19.9 bn in AUM), and Cbus Super of Australia ($24 bn in AUM).

Outside of the USA where voting disclosure for mutual fund managers is mandatory, only Legal and General IM and APG have disclosed their vote amongst the largest 50 shareholders.

28

TRANSPARENCY & ACCOUNTABILITY

The VoteYourPension.org campaign revealed a basic lack of accountability to pension and other retirement fund members who are entitled to understand how their funds are using engagement as a method to manage climate risk.

What is not clear from the vote analysis is the role of many asset owners in deciding and directing the vote amongst the fund management community. Many asset owners who rank highly in the AODP index declared positively well before the AGM in the hope of influencing others, showing their members they are acting and sending a message to the fund managers and proxy advisers that business as usual is not an option.

However, as appendix Figure 11 shows, a majority of asset owners have not reported either publicly or to their members how they acted. In some cases, asset owners did not contact their members either before or after the AGM, demonstrating a disturbing lack of accountability.

Whilst the number of direct responses was small due to the tight timeframe (letters were only issued three weeks before the AGM), some of the responses are insightful:

Of the funds that responded to members, the most common reason given for not divulging their plans for engaging with Exxon was the delegation of voting to their asset managers (29% of all responders).

Others told their members that they would only disclose their voting well after the AGM, and over 10% outright refused to disclose. Another declared obstacle was that asset owners only invested in Exxon indirectly, through pooled funds run by asset managers, and therefore claimed they lacked necessary voting rights.

“ Unfortunately, I am afraid to inform you that Helvetia does not disclose its financial holdings nor do we publicly communicate our voting behaviour on AGMs.“

“ To explain, shares held in our funds are the responsibility of the respective Portfolio Managers that purchased them on behalf of their clients. Their votes are cast based on their view as a shareholder with a fiduciary duty to maximize the returns of their investors. Their vote is not a reflection of Scotiabank’s view on the proxy proposal.”

The data on the Exxon AGM vote is only available in the scale reported here because of US SEC rules on such disclosures. The transparency by many other asset owners and fund managers outside the USA has been minimal.

SECTION 05

Leading asset owners have proven that all of these reasons are in fact poor excuses as many of these leaders exercise control over their fund managers, proxy adviser or company recommendations. Even smaller asset owners in the AODP Global Climate 500 Index found ways to ensure that they selected managers who would allow them to redirect their voting intentions, found ways to either drive fund managers or other service providers to engage with key companies, and responded to members regarding the vote.

Source: Vote Your Pension campaign NUMBER %

Invested through pooled funds 3 9%

Refused to disclose 4 11%

Rely on asset managers to vote 10 29%

Rely on proxy voting advisers 1 3%

Will disclose online after AGM 5 14%

TABLE 03 / FUND RESPONSES TO MEMBERS

30

CONCLUSIONS – THE STATE OF ENGAGEMENT & THE ROLE OF ACTIVE OWNERSHIP

The results of the Exxon 2016 AGM can now be seen in the context of investor engagement strategy to manage climate risk.

The following conclusions can be drawn from the voting analysis and other research:

▬ Exxon’s largest shareholder Vanguard is refusing to drive change away from fossil fuels and is perhaps the most hypocritical of all with CEO Bill McNabb having publicly criticized fossil fuel divestment arguing that engagement is a better strategy. “There is no impact to the income or balance sheet of the company. You are not sending a message to the company. You are better remaining an owner and being able to engage with the company,” he said in May 2016.

▬ Engagement as a credible method of driving climate change risk management took a major leap forward at the Exxon 2016 AGM.

▬ There is serious agency disconnect between asset owners and asset managers over climate leadership with many asset owners with progressive policies not seeing those policies reflected in the way that fund managers vote.

▬ There is a serious structural issue with a large proportion of votes being subject to a default voting option either in favour of the company, a proxy adviser who may not always think long term, or some other voting administrator.

▬ There is wide scale hypocrisy amongst funds who have made responsible investment or carbon disclosure commitments and are refusing to match those commitments with actions.

▬ There is insufficient regulation of voting disclosure to members.

▬ Fiduciary duty risk appears of little concern to most large investors – there has been much work done on fiduciary duty and climate change but this is not translating into action.

▬ There are signs of a new split in the powerful funds management community – State Street, Northern Trust and T. Rowe Price Associates were supporters of item 12 whilst BlackRock, Vanguard and JP Morgan voted against.

▬ The tight timeframes of the proxy season are preventing proper scrutiny of the roles of various agents. Driven partly by the company’s late issue of the AGM agendas, it is difficult for funds to collaborate in time, difficult for asset owners or mutual funds to respond to their members’ demands for a positive vote in time and easy for the media coverage to get lost at a time when there are many competing AGM’s competing for media coverage.

INVESTOR STRATEGY STATUS BARRIERS / NEXT STEP

Engagement via closed door discussion.

Continuing, especially in Europe. Little evidence of success.

Lack of transparency and conservative culture makes progress difficult.

Portfolio divestment of supermajor oil companies.

Rejected en masse by all leading asset owners and managers.

No change to investor position likely.

Resolutions recommending. Return of capital to shareholders in the form of dividends.

Rejected by investors – precedent set at Chevron 2015 AGM.

Diversification via disclosure. Disclosure as a first step gaining rapid support (e.g. Exxon item 12).

Disclosure resolutions now likely to pass in 2017. Unclear what investors want supermajors to do once they accept that 2 degree limitations render their business model invalid.

Diversification via direct instruction. Statoil and Total investing in significant renewables / low carbon businesses. NGO Resolution raised at Shell 2016 AGM.

Possible report preparation of diversification options by company following disclosure success? Barriers huge as company management committed to resistance. US company law places management above shareholders.

Business as usual. Positive support for the supermajor BAU business model by the majority of investors.

The build-up of climate risk, of carbon regulation and the growing body of leadership amongst key asset owners is making it more difficult for the companies and laggard funds to support this model.

SECTION 06

32

CALL TO ACTION

SECTION 07

AODP makes the following calls to action following this report:

▬ All asset owners should declare their voting policy by manager and company.

▬ All asset owners should report the degree to which asset managers adhere to their engagement policies.

▬ Proxy advisers should be pushed to declare their recommendations at least six weeks before key AGM’s. Given the volume of votes this carries in the market between ISS and Glass Lewis, asset owners should have the right to inform members of the proxy adviser recommendation.

▬ Investor groups and associations should remove signatories who do not have a credible plan for using engagement as a tool for managing risk or who are not transparent with their own members.

▬ Regulators must ensure that asset owners have a legal right to direct voting in proportion to the number of units they hold with an asset manager’s fund. Likewise, asset owners can lead this by making it a standard requirement of their investment manager agreements.

▬ The FSB Task Force www.FSB-tcfd.org, which will recommend the scope of future voting transparency in its December 2016 report, should recommend 100% voting disclosure at all levels of the investment chain

▬ All funds, owners and managers, should be forced to actively vote their shares on key votes where beneficiaries have contacted them. Where any fund’s policy is to default to a 3rd party, the majority of any members expressing an opinion on a vote should be used to inform that voting decision.

▬ Where a fund has a default voting policy (either in favour of its proxy advisor or the company), it should create a mechanism where member views are incorporated.

▬ Pension fund regulators should force pension funds to pre-declare their voting intentions for key AGM’s. This could be defined as any AGM where a fund is contacted by any member.

APPENDICES

FIGURE 01 / WORLD’S TOP 20 ASSET MANAGERS BY AUM

# ORGANISATIONAUM

(USD MN) COUNTRY EXXO

N IT

EM 7

D

ECLA

RAT

ION

EXXO

N IT

EM 9

D

ECLA

RAT

ION

EXXO

N IT

EM 1

2 D

ECLA

RAT

ION

EXXO

N IT

EM 1

3 D

ECLA

RAT

ION

1 BlackRock $4,654,394 US FOR AGAINST AGAINST AGAINST

2 Vanguard Asset Management $3,120,434 US FOR AGAINST AGAINST AGAINST

3 State Street Global Advisors $2,449,426 US FOR FOR FOR AGAINST

4 Fidelity Investments $1,931,527 US AGAINST ABSTAIN ABSTAIN ABSTAIN

5 Allianz Global Investors* $1,906,934 Germany FOR MIXED MIXED MIXED

6 BNY Mellon Invest. Management EMEA $1,703,652 US FOR AGAINST AGAINST AGAINST

7 J.P. Morgan Asset Management $1,533,721 US AGAINST AGAINST AGAINST AGAINST

8 Capital Group $1,413,167 US FOR AGAINST AGAINST AGAINST

9 Pramerica Investment Management $1,172,718 US MIXED MIXED MIXED AGAINST

10 Amundi $1,048,448 France FOR

11 Goldman Sachs Asset Management Int $1,024,473 US FOR AGAINST FOR AGAINST

12 Northern Trust Asset Management $934,601 US AGAINST AGAINST FOR AGAINST

13 Wellington Management $914,209 US

14 Natixis Global Asset Management $890,506 France

15 Franklin Templeton Investments $880,656 US AGAINST AGAINST AGAINST AGAINST

16 Deutsche Asset & Wealth Management $873,819 Germany FOR FOR FOR FOR

17 Invesco US/UK $792,579 US FOR AGAINST AGAINST AGAINST

18 Legal & General Investment Mngt. $778,565 UK FOR

19 AXA Investment Managers $754,276 France FOR

20 T. Rowe Price $747,199 US FOR AGAINST FOR AGAINST

FIGURE 02 / THE FOUR “FINANCIALLY MATERIAL” RESOLUTIONS SUPPORTED BY THE VOTE-YOUR-PENSION CAMPAIGN

ITEM # ON BALLOT RESOLUTION DESCRIPTION LEAD FILER

7 Adopt a proxy access bylaw 2016

The company must improve proxy access laws, making director nomination transparent, as well as ensuring nominators are long-term investors.

New York City Office of the Comptroller

9 Annually disclose direct and indirect lobbying

Company must issue annual report detailing payments to lobby groups, membership in organisations that lobby, and oversight of Company lobbying

United Steelworkers of America

12 Annually assess risks of 2-degree scenario

Company must publish annual assessment of long-term portfolio impacts of a 2-degree scenario

New York State Comptroller

13 Annually disclose reserves replacement annually by resource

Company must annually quantify and report all reserve replacements in energy units (BTUs)

As You Sow

34

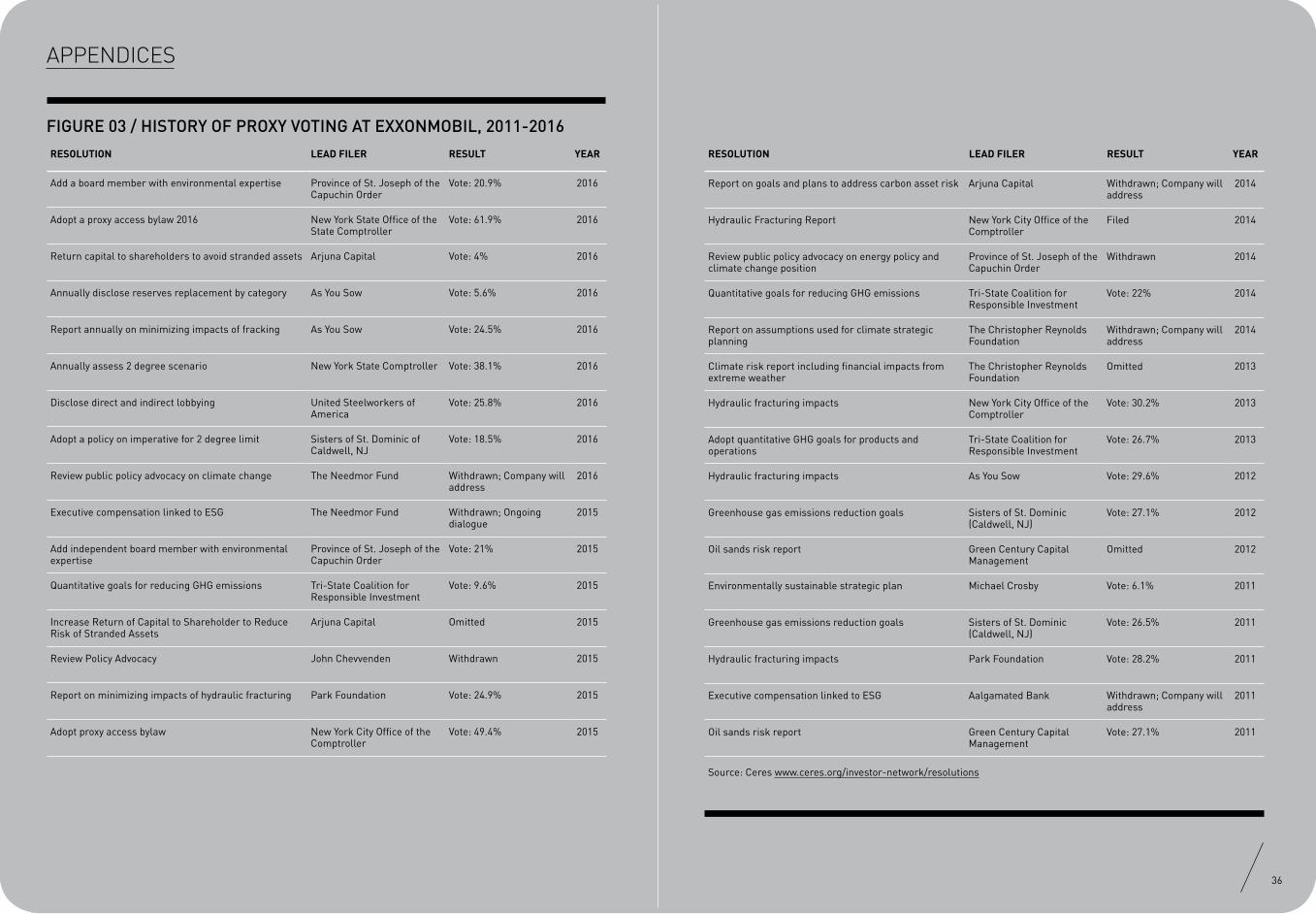

FIGURE 03 / HISTORY OF PROXY VOTING AT EXXONMOBIL, 2011-2016

36

RESOLUTION LEAD FILER RESULT YEAR

Add a board member with environmental expertise Province of St. Joseph of the Capuchin Order

Vote: 20.9% 2016

Adopt a proxy access bylaw 2016 New York State Office of the State Comptroller

Vote: 61.9% 2016

Return capital to shareholders to avoid stranded assets Arjuna Capital Vote: 4% 2016

Annually disclose reserves replacement by category As You Sow Vote: 5.6% 2016

Report annually on minimizing impacts of fracking As You Sow Vote: 24.5% 2016

Annually assess 2 degree scenario New York State Comptroller Vote: 38.1% 2016

Disclose direct and indirect lobbying United Steelworkers of America

Vote: 25.8% 2016

Adopt a policy on imperative for 2 degree limit Sisters of St. Dominic of Caldwell, NJ

Vote: 18.5% 2016

Review public policy advocacy on climate change The Needmor Fund Withdrawn; Company will address

2016

Executive compensation linked to ESG The Needmor Fund Withdrawn; Ongoing dialogue

2015

Add independent board member with environmental expertise

Province of St. Joseph of the Capuchin Order

Vote: 21% 2015

Quantitative goals for reducing GHG emissions Tri-State Coalition for Responsible Investment

Vote: 9.6% 2015

Increase Return of Capital to Shareholder to Reduce Risk of Stranded Assets

Arjuna Capital Omitted 2015

Review Policy Advocacy John Chevvenden Withdrawn 2015

Report on minimizing impacts of hydraulic fracturing Park Foundation Vote: 24.9% 2015

Adopt proxy access bylaw New York City Office of the Comptroller

Vote: 49.4% 2015

RESOLUTION LEAD FILER RESULT YEAR

Report on goals and plans to address carbon asset risk Arjuna Capital Withdrawn; Company will address

2014

Hydraulic Fracturing Report New York City Office of the Comptroller

Filed 2014

Review public policy advocacy on energy policy and climate change position

Province of St. Joseph of the Capuchin Order

Withdrawn 2014

Quantitative goals for reducing GHG emissions Tri-State Coalition for Responsible Investment

Vote: 22% 2014

Report on assumptions used for climate strategic planning

The Christopher Reynolds Foundation

Withdrawn; Company will address

2014

Climate risk report including financial impacts from extreme weather

The Christopher Reynolds Foundation

Omitted 2013

Hydraulic fracturing impacts New York City Office of the Comptroller

Vote: 30.2% 2013

Adopt quantitative GHG goals for products and operations

Tri-State Coalition for Responsible Investment

Vote: 26.7% 2013

Hydraulic fracturing impacts As You Sow Vote: 29.6% 2012

Greenhouse gas emissions reduction goals Sisters of St. Dominic (Caldwell, NJ)

Vote: 27.1% 2012

Oil sands risk report Green Century Capital Management

Omitted 2012

Environmentally sustainable strategic plan Michael Crosby Vote: 6.1% 2011

Greenhouse gas emissions reduction goals Sisters of St. Dominic (Caldwell, NJ)

Vote: 26.5% 2011

Hydraulic fracturing impacts Park Foundation Vote: 28.2% 2011

Executive compensation linked to ESG Aalgamated Bank Withdrawn; Company will address

2011

Oil sands risk report Green Century Capital Management

Vote: 27.1% 2011

Source: Ceres www.ceres.org/investor-network/resolutions

APPENDICES

FIGURE 04 / PRE-DECLARING ASSET OWNERS IN FAVOUR OF ITEM 12

38

2016 RANK

AODP RATING FUND NAME COUNTRY FUND TYPE

1 AAA Environment Agency Pension Fund United Kingdom Pension

2 AAA Local Government Super Australia Pension

3 AAA Fjärde AP-Fonden (AP4) Sweden Pension

5 AAA New York State Common Retirement Fund (NYSCRF) United States of America Pension

6 AAA PKA A/S Denmark Pension

8 AAA Andra AP-Fonden (AP2) Sweden Pension

9 AAA CalPERS United States of America Pension

10 AAA Church Commissioners for England United Kingdom Pension

17 AA University of California Endowment United States of America Foundation / Endowment

18 AA Pensioenfonds Zorg en Welzijn (PFZW) Netherlands Pension

19 AA Kommunal Landspensjonskasse KLP Norway Pension

21 A VicSuper Australia Pension

26 A New York City Employees Retirement System (NYCERS) United States of America Pension

27 A Teachers' Retirement System of the City of New York (TRS) United States of America Pension

29 A Church of England Pensions Board United Kingdom Pension

30 A Greater Manchester Pension Fund United Kingdom Pension

32 BBB Sjunde AP-Fonden (AP7) Sweden Pension

33 BBB The Pensions Trust (UK) United Kingdom Pension

34 BBB Strathclyde Pension Fund United Kingdom Pension

44 BBB Government Pension Fund - Global (GPFG Norway) Norway Sovereign Wealth Fund

44 BBB PensionDanmark Denmark Pension

67 CC Norfolk Pension Fund United Kingdom Pension

74 CC Folksam Group Sweden Insurance

75 CC Canada Pension Plan Investment Board (CPPIB) Canada Pension

76 CC Connecticut State Employees Retirement System (SERF) United States of America Pension

76 CC West Midlands Pension Fund United Kingdom Pension

86 C Government Pension Fund Norway (GPFN) Norway Sovereign Wealth Fund

112 D BT Pension Scheme United Kingdom Pension

136 D PFA Pension Denmark Insurance

145 D New York State Teachers' Retirement System (NYSTRS) United States of America Pension

149 D Ireland Strategic Investment Fund (ISIF) Ireland Sovereign Wealth Fund

149 D British Columbia Public Service Pension Plan Canada Pension

176 D British Coal Staff Superannuation Scheme United Kingdom Pension

204 D Ontario Public Service Pension Plan Canada Pension

223 D Ilmarinen Finland Insurance

223 D B.C. Municipal Pension Plan Canada Pension

N/A N/A Connecticut Teachers' Retirement System United States of America Pension

N/A N/A Tyne and Wear Pension Fund United Kingdom Pension

N/A N/A South Yorkshire Pensions Authority United Kingdom Pension

N/A N/A LUCRF Super Australia Pension

N/A N/A Dignity Health United States of America Foundation / Endowment

N/A N/A Seattle City Employees' Retirement System United States of America Pension

N/A N/A Somerset County Council Pension Fund United Kingdom Pension

N/A N/A SEIU Master Trust United States of America Pension

N/A N/A Vermont Pension Investment Committee United States of America Pension

N/A N/A Adrian Dominican Sisters United States of America Foundation / Endowment

N/A N/A American Baptist Home Mission Societies United States of America Foundation / Endowment

N/A N/A Christopher Reynolds Foundation United States of America Foundation / Endowment

N/A N/A Daughters of Charity, Province of St. Louise United States of America Foundation / Endowment

N/A N/A Mercy Health United States of America Foundation / Endowment

N/A N/A Mission Responsibility Through Investment - Presbyterian Church United States of America Foundation /

Endowment

N/A N/A Sisters of St. Dominic of Caldwell, NJ United States of America Foundation / Endowment

N/A N/A Sisters of St. Francis of Philadelphia United States of America Foundation / Endowment

N/A N/A Sisters of the Presentation of the Blessed Virgin Mary United States of America Foundation / Endowment

N/A N/A St. Joseph Health United States of America Foundation / Endowment

N/A N/A Tellus Mater Foundation United Kingdom Foundation / Endowment

N/A N/A The McKnight Foundation United States of America Foundation / Endowment

N/A N/A The Nathan Cummings Foundation United States of America Foundation / Endowment

N/A N/A The Sierra Club Foundation United States of America Foundation / Endowment

N/A N/A Trinity Health United States of America Foundation / Endowment

N/A N/A UniPension Denmark Pension

N/A N/A United Church of Canada Canada Pension

APPENDICES2016

RANKAODP

RATING FUND NAME COUNTRY FUND TYPE

FIGURE 05 / PRE-DECLARING ASSET MANAGERS IN FAVOUR OF ITEM 12 FIGURE 06 / A+ RATED FUNDS BY AODP MORE TRANSPARENT OVER ENGAGEMENT

40

COMPANY NAME COUNTRY

Amundi France

TIAA-CREF US

Legal & General Investment Management UK

AXA Investment Managers France

BNP Paribas Investment Partners France

Schroder Investment Management UK

HSBC Global Asset Management UK

Aviva Investors UK

Natixis Asset Management France

Aegon Asset Management Netherlands

CCLA UK

Dana Investment Advisors US

Pax World Management LLC US

Sonen Capital US

Walden Asset Management US

Wespath Investment Management US

Zevin Asset Management US

Mercy Investment Services US

ACTIAM Netherlands

Trillium Asset Management US

Norges Bank Investment Management (NBIM) Norway

BMO Global Asset Management Canada

British Columbia Investment Management Corporation Canada

ALL ASSET OWNERS A+ RATED FUNDS

Number of funds % of total funds Number of funds % of A-rated funds

VOTED ON AT LEAST ONE 91 9% 22 71%

Voted on #7 45 4% 16 52%

Voted on #9 43 4% 16 52%

Voted on #12 91 9% 22 71%

Voted on #13 41 4% 16 52%

SUPPORTED ALL FOUR 15 16% 8 36%

Voted on #7 42 93% 15 94%

Voted on #9 35 81% 12 75%

Voted on #12 83 91% 21 95%

Voted on #13 15 37% 8 50%

Many of the asset managers in this list, whilst laudable in their support for Item 12 at the ExxonMobil AGM, are boutique asset managers and simply do not have as much sway in capital markets as the bigger US mutual funds, who were conspicuously absent from declaring their support, or lack of, for climate change resolutions at Exxon.

Source: Vote Your Pension campaign, US Securities and Exchange Commission EDGAR database, FundVotes

Fund universe: AODP VYP Funds database; the World’s largest 50 asset managers by AUM; Exxon’s top 50 shareholders as of June 2016

Funds that rate highest on the AODP Global Climate 500 Index are far more likely to disclose their engagement activities compared with the greater asset owner universe. 71% disclosed voting intentions on at least one resolution, compared with 9% of all funds. Tellingly, all funds who disclosed voting intentions gave information on Item 12.

Whilst disclosing A+ rated funds were more than twice as likely to provide positive voting intentions on all 4 resolutions than the general asset owner universe (36% compared with 16%), there wasn’t significant delineation on individual resolutions, save more support for Item 13 (50% for top-rated funds, compared with 37%).

APPENDICES

FIGURE 07 / ASSET MANAGER SUPPORT FOR RESOLUTIONS

42

ALL ASSET MANAGERS

Number of managers % of voting asset managers

SUPPORTED ALL FOUR 1 2%

Voted on #7 26 79%

Voted on #9 12 35%

Voted on #12 41 76%

Voted on #13 2 6%

▬ Compared with asset owners, the asset management world was far more conservative in its voting record at Exxon.

▬ Only Deutsche Group’s asset management arm backed all 4 resolutions

▬ Fewer asset managers supported each individual resolution

▬ Asset managers clearly less eager to support action at Exxon than their clients.

APPENDICES

FIGURE 08 / TOP 10 FUNDS ASKED TO SUPPORT ITEM 12 BY VYP MEMBERS

VOTES FUND COUNTRY

1939 CalPERS United States of America

1399 Canada Pension Plan Canada

940 Ontario Teachers Pension Plan Canada

469 Vanguard Group United States of America

386 Fidelity Investments United States of America

329 Universities Superannuation Scheme (USS) United Kingdom

289 TIAA-CREF United States of America

251 AustralianSuper Australia

228 ABP Netherlands

212 Future Fund Australia

AGM Timeline & Shareholder CampaignsThe deadline for filing resolutions at Exxon’s AGM is the end of the calendar year. The proxy voting season really begins once investors start declaring their support for any of the resolutions. The Vote Your Pension (VYP) platform usually comes into effect to bolster this support via fund beneficiaries, around a month before the AGM. After the AGM, a post-vote analysis takes place, where Asset Owners Disclosure Project and its partners sift through the voting data and see how funds engaged with Exxon, and whether this went against their own beneficiaries’ stated preferences on VYP. This often extends up to and beyond the end of August, when US mutual funds are required to disclose their engagements to the SEC.

END OF PREVIOUS CALENDAR YEAR ABOUT A MONTH BEFORE AGM

UP TO BEGINNING OF SEPTEMBER

RESOLUTION FILING DEADLINE

INVESTORS DECIDE HOW TO VOTE AT AGMS, & PRE-DECLARATIONS ARE MADE

VOTE YOUR PENSION CAMPAIGN BEGINS

COMPANY AGMPOST-AGM VOTING ANALYSIS

FIGURE 09 / SHAREHOLDER RESOLUTION CAMPAIGN: THE DIFFERENT PHASES

FIGURE 10 / THE LARGEST 20 PENSION FUNDS, BY ASSETS UNDER MANAGEMENT (AUM), WHO VOTED FOR EXXON AGM ITEM 12

FIGURE 11 / INVESTOR ENGAGEMENT WITH EXXON, WITH MEMBERS, AND VOTING TRANSPARENCY

44

2016 AODP

RATING

ASSET OWNER NAME COUNTRY

BBB Government Pension Fund - Global (GPFG Norway) Norway

BBB TIAA-CREF - Teachers Insurance and Annuity Association of America - Col-lege Retirement Equities Fund United States of America

AAA ABP Netherlands

AAA CalPERS United States of America

CC Canada Pension Plan Investment Board (CPPIB) Canada

A California State Teachers' Retirement System (CalSTRS) United States of America

AAA New York State Common Retirement Fund (NYSCRF) United States of America

AA Pensioenfonds Zorg en Welzijn (PFZW) Netherlands

B Florida State Board Administration (SBAFLA) United States of America

BBB Florida Retirement System (FRS) United States of America

D Teacher Retirement System of Texas United States of America

CCC Ontario Teachers Pension Plan (OTPP) Canada

D New York State Teachers' Retirement System (NYSTRS) United States of America

D State of Wisconsin Investment Board (SWIB) United States of America

D Ohio Public Employees Retirement System (OPERS) United States of America

D BT Pension Scheme United Kingdom

AAA AustralianSuper Australia

D Ontario Municipal Employees Retirement System (OMERS) Canada

A Teachers' Retirement System of the City of New York (TRS) United States of America

AA Kommunal Landspensjonskasse KLP Norway

Number %

Number of Funds not responding to own members

Funds voting in favour of Exxon management

Funds without voting transparency

Funds not responding to own members

Funds voting in favour of Exxon management

Funds without voting transparency

USA 141 14 71 99% 10% 50%

Canada 25 1 17 83% 3% 57%

Europe 114 2 82 85% 1% 61%

Asia-Pacific 47 2 49 82% 4% 86%

Rest of World 13 0 14 93% 0% 100%

Asset Owners 278 6 222 89% 2% 71%

Asset Managers 63 13 11 95% 20% 17%

PRI signatories 141 12 78 87% 7% 48%

We Mean Business signatories 42 2 18 78% 4% 33%

Paris Pledge signatories 15 3 7 68% 14% 32%

ClimateWise members 7 0 7 100% 0% 100%

CDP signatories 125 7 65 88% 5% 46%

Of the 20 biggest asset owners, by AUM, who voted in favour of Item 12 at Exxon’s AGM, 8 received an A grade or more according to the AODP Global Climate 500 Index.

APPENDICES

ACKNOWLEDGEMENTS

REPORT WRITTEN AND PRODUCED BY: RAJ SINGH, JULIAN POULTER AND GREENHOUSE PR

THE ASSET OWNERS DISCLOSURE PROJECT GIVES SPECIAL THANKS TO THE FOLLOWING PEOPLE IN PRODUCING THIS REPORT:

JACKIE COOK AT FUNDVOTES, PAVEL KIRJANAS AND FABIO MICCOLI

THE ONGOING SUPPORT OF AODP’S FUNDERS IS ACKNOWLEDGED. A FULL LIST CAN BE FOUND ON OUR WEBSITE WWW.AODPROJECT.NET.

THE VIEWS IN THIS REPORT REMAIN THOSE OF AODP.

46

FUND VOTES IS AN INDEPENDENT PROJECT THAT TRACKS PROXY VOTING AND STEWARDSHIP BY LARGE ASSET MANAGERS.

WWW.AODPROJECT.NET