Embed Size (px)

Citation preview

Q1 2015 Healthcare IT Funding and M&A Executive Summary

1 Copyright 2010-2015 | Mercom Capital Group, llc | www.mercomcapital.com | [email protected]

Executive Summary

Healthcare IT Funding and M&A 2015 First Quarter Report

Funding and merger & acquisition activity for the

Healthcare IT / Digital Health sector

http://www.mercomcapital.com

Q1 2015 Healthcare IT Funding and M&A Executive Summary

2 Copyright 2010-2015 | Mercom Capital Group, llc | www.mercomcapital.com | [email protected]

About Mercom’s Healthcare IT Funding and M&A Report

Mercom was one of the first research firms to track funding and M&A activity in the Healthcare IT

sector, starting in 2010. We refer to the industry as “Healthcare IT” while others use terms such

as digital health or ehealth, among others.

Here is how our report is different: Our report includes deals of all sizes globally to present a

complete picture of Healthcare IT funding and technology trends. As an independent research

firm, we have no conflicts of interest with companies covered in this report.

This is the most comprehensive report covering funding and M&A deals of all sizes,

globally. The trends revealed in this report give a more complete picture of the industry.

This report does not cover bioinformatics and medical devices.

All charts, graphs and trends are clearly categorized and defined by technology and sub-

technology groups.

This report includes concise deal information for every transaction.

This report covers historical trends.

As the industry evolves, our report evolves with it and we continuously improve the

information, analysis, charts and trends covered every quarter.

Our subscribers include companies and executives from venture capital, private equity,

investment banking, healthcare, healthcare IT (aka digital health and eHealth), insurance,

healthcare associations, universities, tech firms and more.

Audience Why they like our reports

Venture Capital/Private Equity leads from early-stage deals, technology trends

Investment bankers leads for funding and M&A deals, investor leads

Healthcare IT, digital health sector trends, investor targets (by funding behavior, including

technology, technology partnership targets, and more)

Insurance companies acquisition leads, investment leads, technology partnerships

Large healthcare & Tech firms acquisition leads, R&D partnerships, investment leads

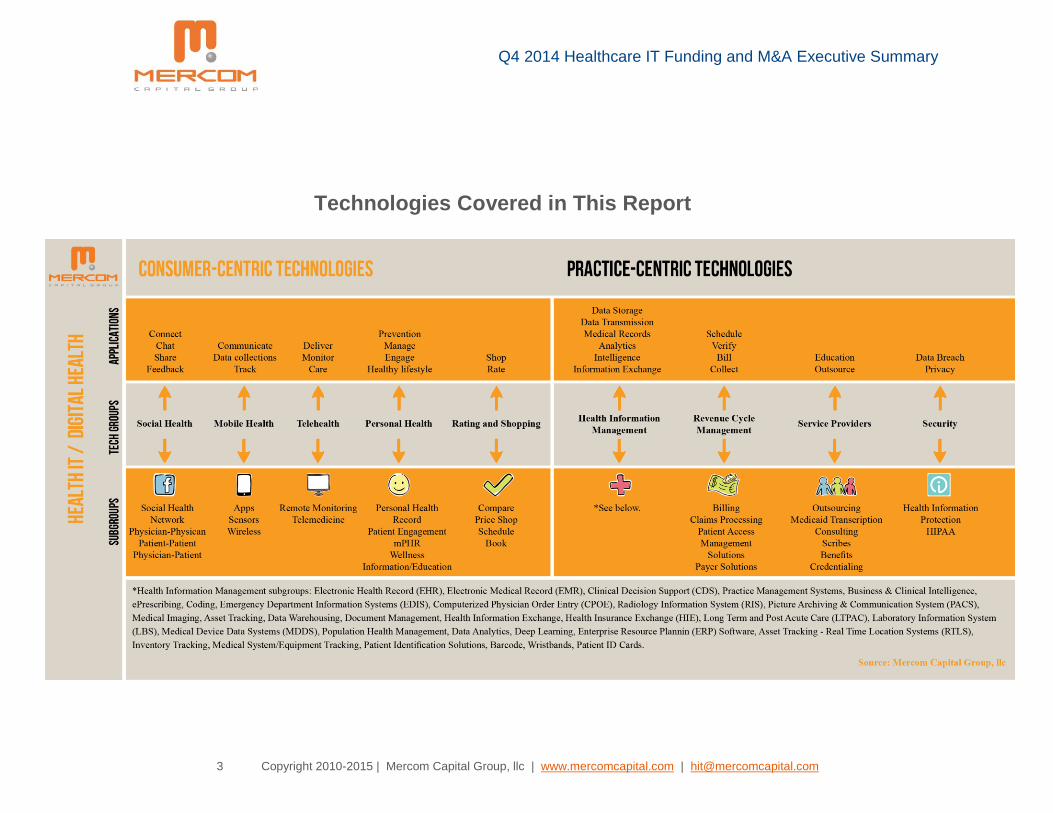

The report covers the technologies listed below and the sub-technologies under them.

Q4 2014 Healthcare IT Funding and M&A Executive Summary

3 Copyright 2010-2015 | Mercom Capital Group, llc | www.mercomcapital.com | [email protected]

Technologies Covered in This Report

Q1 2015 Healthcare IT Funding and M&A Executive Summary

4 Copyright 2010-2015 | Mercom Capital Group, llc | www.mercomcapital.com |

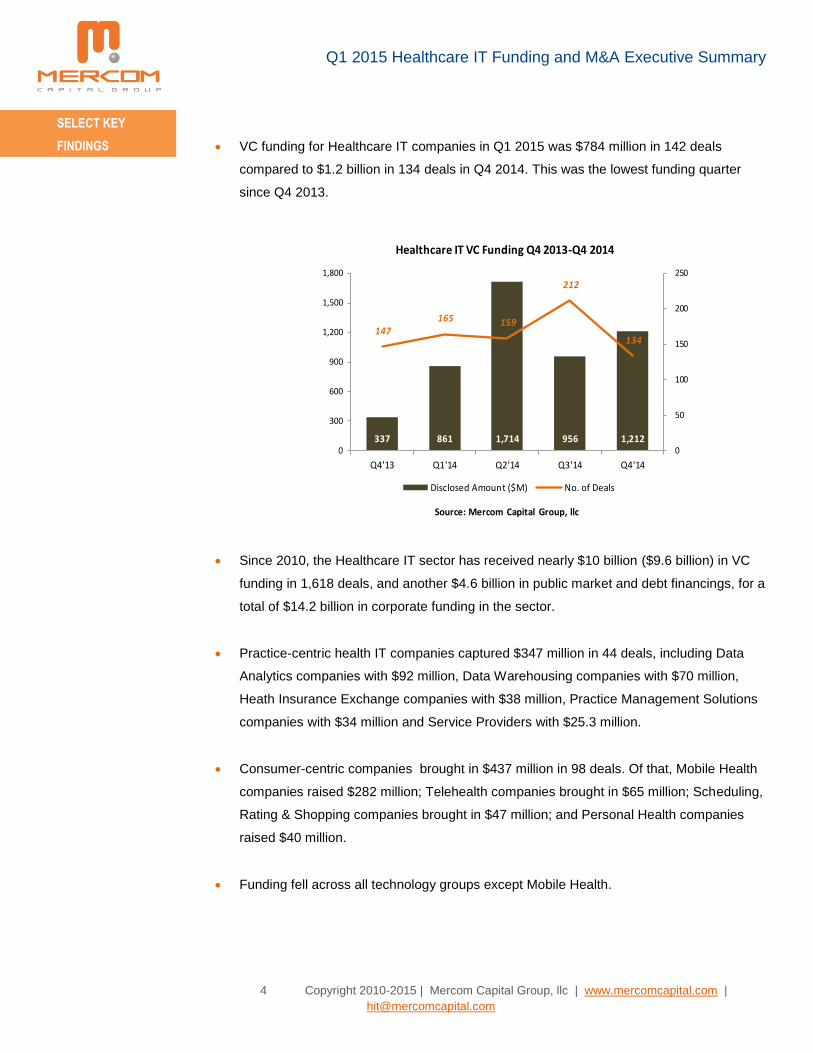

VC funding for Healthcare IT companies in Q1 2015 was $784 million in 142 deals

compared to $1.2 billion in 134 deals in Q4 2014. This was the lowest funding quarter

since Q4 2013.

337 861 1,714 956 1,212

147 165 159

212

134

0

50

100

150

200

250

0

300

600

900

1,200

1,500

1,800

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

Source: Mercom Capital Group, llc

Healthcare IT VC Funding Q4 2013-Q4 2014

Disclosed Amount ($M) No. of Deals

Since 2010, the Healthcare IT sector has received nearly $10 billion ($9.6 billion) in VC

funding in 1,618 deals, and another $4.6 billion in public market and debt financings, for a

total of $14.2 billion in corporate funding in the sector.

Practice-centric health IT companies captured $347 million in 44 deals, including Data

Analytics companies with $92 million, Data Warehousing companies with $70 million,

Heath Insurance Exchange companies with $38 million, Practice Management Solutions

companies with $34 million and Service Providers with $25.3 million.

Consumer-centric companies brought in $437 million in 98 deals. Of that, Mobile Health

companies raised $282 million; Telehealth companies brought in $65 million; Scheduling,

Rating & Shopping companies brought in $47 million; and Personal Health companies

raised $40 million.

Funding fell across all technology groups except Mobile Health.

SELECT KEY

FINDINGS

Q1 2015 Healthcare IT Funding and M&A Executive Summary

5 Copyright 2010-2015 | Mercom Capital Group, llc | www.mercomcapital.com | [email protected]

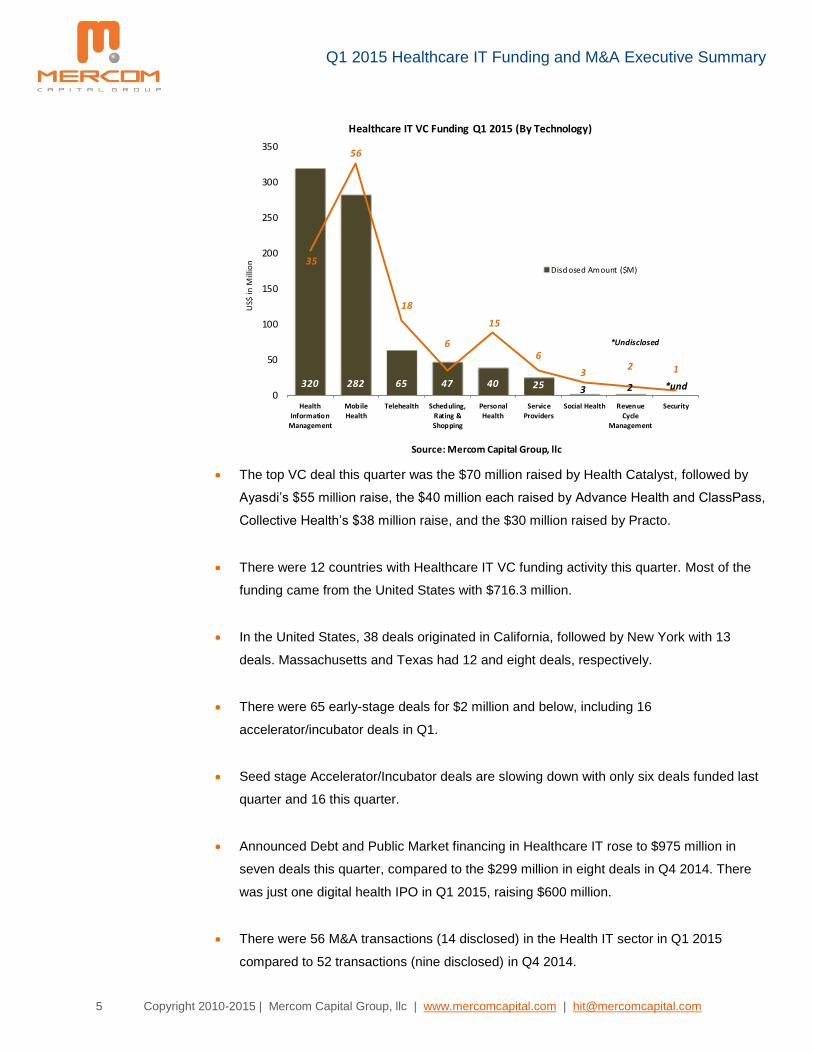

The top VC deal this quarter was the $70 million raised by Health Catalyst, followed by

Ayasdi’s $55 million raise, the $40 million each raised by Advance Health and ClassPass,

Collective Health’s $38 million raise, and the $30 million raised by Practo.

There were 12 countries with Healthcare IT VC funding activity this quarter. Most of the

funding came from the United States with $716.3 million.

In the United States, 38 deals originated in California, followed by New York with 13

deals. Massachusetts and Texas had 12 and eight deals, respectively.

There were 65 early-stage deals for $2 million and below, including 16

accelerator/incubator deals in Q1.

Seed stage Accelerator/Incubator deals are slowing down with only six deals funded last

quarter and 16 this quarter.

Announced Debt and Public Market financing in Healthcare IT rose to $975 million in

seven deals this quarter, compared to the $299 million in eight deals in Q4 2014. There

was just one digital health IPO in Q1 2015, raising $600 million.

There were 56 M&A transactions (14 disclosed) in the Health IT sector in Q1 2015

compared to 52 transactions (nine disclosed) in Q4 2014.

320 282 65 47 40 25 3 2 *und

35

56

18

6

15

6

32 1

0

10

20

30

40

50

60

0

50

100

150

200

250

300

350

Health

Information

Management

Mobile

Health

Telehealth Scheduling,

Rating &

Shopping

Personal

Health

Service

Providers

Social Health Revenue

Cycle

Management

Security

US$

in M

illio

n

Source: Mercom Capital Group, llc

Healthcare IT VC Funding Q1 2015 (By Technology)

Disclosed Amount ($M)

*Undisclosed

Q1 2015 Healthcare IT Funding and M&A Executive Summary

6 Copyright 2010-2015 | Mercom Capital Group, llc | www.mercomcapital.com | [email protected]

Introduction……………………………………………………………………….……...………. 3

Key Findings ……………………………….…………………………….……………… 4

2015 Healthcare IT Funding and M&A ……………………………….………………. 8

VC Funding 2010-2015 YTD…………………………………………………….……………… 8

VC Funding by Quarter …………………………………………………………………..….…. 9

VC Funding by Technology……………………………………………………………. 10

Health Information Management……….…………………….……..………. 12

Mobile Health…….…………….…………….………………………..………. 17

Telehealth…….…….………….…………….………………………..………. 25

Scheduling, Rating and Shopping………….……………..………..………. 28

Personal Health….…………….…………….………………...……..………. 29

Social Health…….…………….…………….………………………..………. 31

VC Funding by Stage……………..………………………………….….….…………. 32

VC Activity by Country…………..…………………………………………….……….. 33

VC Activity by U.S. States……………………………………………………………… 34

Trends in VC Funding Large vs Smaller Deals…………………………………….. 36

Top VC Funding Deals………..…………………… …………………………........... 37

Top VC Investors………..………………………………………………….................. 38

Accelerators/Incubators………..…………………………………………………......... 40

VC Deals………………………..………………………………….……………………. 53

VC Investors…….……………………..……………………………..…………........... 55

Debt and Public Market Financing….………………………………………………………… 65

Debt and Public Market Financing Activity ...…………..……………………………. 66

Debt and Public Market Financing Investors…………………………….................. 66

Initial Public Offering (IPO) ……………………………........................................... 67

Mergers and Acquisitions (M&A)………………………….…………………………………. 68

M&A by Technology………..…………………………………………..……….……… 69

M&A by Sub-Technology…..……..…..………………..………………………..…….. 69

Multiple Acquirers………..…………………………………………..……….………… 70

Top Five M&A Transactions……………………………………………..…………….. 71

Disclosed M&A Transactions…………................................................................... 72

M&A Transactions by Country…………................................................................... 73

M&A Transactions……….…………………………………………………….……….. 74

TABLE of

CONTENTS

Q1 2015 Healthcare IT Funding and M&A Executive Summary

7 Copyright 2010-2015 | Mercom Capital Group, llc | www.mercomcapital.com | [email protected]

Interested in Reading More?

Click here to purchase

Mercom’s Q1 2015 Healthcare IT

Funding and M&A Report.

Subscribe to Mercom’s weekly

Healthcare IT market intelligence report.

Visit:

MercomCapital.com

to purchase past reports

DISCLAIMER: © 2015 by Mercom Capital Group, llc. All rights reserved. Mercom hereby grants user a personal, non-exclusive, non-refundable, non-transferable license to use the Report for research purposes only. Mercom retains exclusive and sole ownership of all its Reports. When quoting from this report, please cite “Mercom Capital Group, llc”. Information contained in this publication is derived from carefully selected sources we believe to be reliable. Mercom its employees, affiliates, agents, and licensors do not warrant the accuracy, completeness, currentness, non-infringement, merchantability, or fitness for a particular purpose of this report. Nothing in this report constitutes or should be taken as investment advice. For information about this document, please contact us at 512-215-4452 or via email at: [email protected].