Embed Size (px)

Citation preview

EXECUTIVE FRINGE BENEFITS

BRIAN L. CUMBERLAND, Dallas Alvarez & Marsal

STEVEN W. MILTON, Irving

Kimberly-Clark Corporation

State Bar of Texas

EXECUTIVE COMPENSATION COURSE May 2, 2008

Dallas

CHAPTER 3

Brian L. Cumberland Alvarez & Marsal Taxand, LLC

2001 Ross Ave, Suite 1400 Dallas, Texas 75201

214-438-1013 Fax: 214-438-1001

BIOGRAPHICAL INFORMATION

EDUCATION

• BBA in Finance, the University of Texas. • Juris Doctorate, St. Mary’s School of Law. • LL.M - Taxation from the University of Denver.

PROFESSIONAL ACTIVITIES

• National Managing Director - Compensation and Benefits, Alvarez & Marsal Taxand, Dallas, Texas.

• Member of the State Bar of Texas • Member of American Bar Association (ABA) • Member of Southwest Benefits Association

LAW RELATED PUBLICATIONS, ACADEMIC APPOINTMENT Recent Articles / Publications

• “IRS Drops 162(m) Bomb,” Tax Advisor Weekly Newsletter, February 2008 • 2006 and 2007 “Change in Control Report,” by Brian L. Cumberland • “There’re Here: 409A Final Deferred Compensation Regulations,” Tax Advisor Weekly

Newsletter, June 2007 • “What Every Tax Director Needs to Know Regarding Benefit Plan Tax Issues,” Tax Advisor

Weekly, August 2006 • “SEC Proposes to Broaden Disclosure of Golden Parachute Payments,” by Brian Cumberland

and JD Ivy, Executive’s Tax & Management Report, July 2006 • “Expensing Stock Options: Income Tax Consequences,” by Brian L. Cumberland and J.D. Ivy,

Financial Reporting Watch, July 2006 • “Backdating Stock Options: Tax Ramifications,” by Brian L. Cumberland and J.D. Ivy, Tax

Analysts, June 2006 • “SEC Proposed Changes to Executive Pay Disclosure Requirements – What Companies may not

have Focused on,” Tax Advisor Weekly Newsletter, April 2006 Recent Speeches • Speaker for Southwest Benefits Association on Section 409A Final Regulations (May 2007) • Speaker for the Tax Executive Institute (TEI) for the Dallas (May 2006 & May 2007), Houston

(June 2007), Fort Worth (April 2007), South Florida (June 2007), Tulsa (September 2007), Carolina (December 2007) and San Jose (November 2006) Chapters on Executive Compensation Issues

• Speaker for Lorman Education Services on Executive Compensation Issues (November 2007).

Steve W. Milton Steve Milton joined Kimberly-Clark Corporation in August 2007 as Assistant Corporate Secretary and Counsel. Steve has significant expertise in corporate governance issues as well as related corporate and securities law matters. Steve’s responsibilities include providing oversight regarding corporate governance issues and working with business teams to ensure a coordinated approach to the management of governance issues. His duties also include preparation of Kimberly-Clark’s annual proxy statement. Steve formerly served as Assistant Corporate Secretary and Senior Counsel for RadioShack Corporation, headquartered in Fort Worth. Prior to this position, Steve was an associate with the law firm of Haynes and Boone, LLP, where he specialized in corporate, securities, mergers and acquisition, and general business law. Steve graduated with a Bachelor of Business Administration in Accounting from the University of Texas. He also has a Juris Doctor degree from the University of Texas School of Law. Steve, his wife and two children reside in Fort Worth, Texas.

1

Perquisite Treatment:

L E A D E R S H I P P R O B L E M SO L V I N G V A L U E C R E A T I O N

Perquisite Treatment: SEC Disclosure vs. Taxable Income

May 2, 2008

Brian L C mberland Ste e W MiltonBrian L. CumberlandNational Managing Director, Compensation and [email protected]

Steve W. MiltonCounsel and Assistant SecretaryKimberly-Clark [email protected]

Copyright 2007. Alvarez & Marsal Taxand, LLC. All Rights Reserved.

Executive Fringe Benefits Chapter 8

2

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OFANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF

(I) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR

(II) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the

Copyright 2007. Alvarez & Marsal Taxand, LLC. All Rights Reserved. 1

there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Executive Fringe Benefits Chapter 8

3

Agenda

• Identifying Perquisites

• SEC Requirements Overview• SEC Requirements – Overview

• Tax Treatment – Overview

• Personal Use of Corporate Aircraft

Th F t f P i it• The Future of Perquisites

Copyright 2007. Alvarez & Marsal. All Rights Reserved.2

Executive Fringe Benefits Chapter 8

4

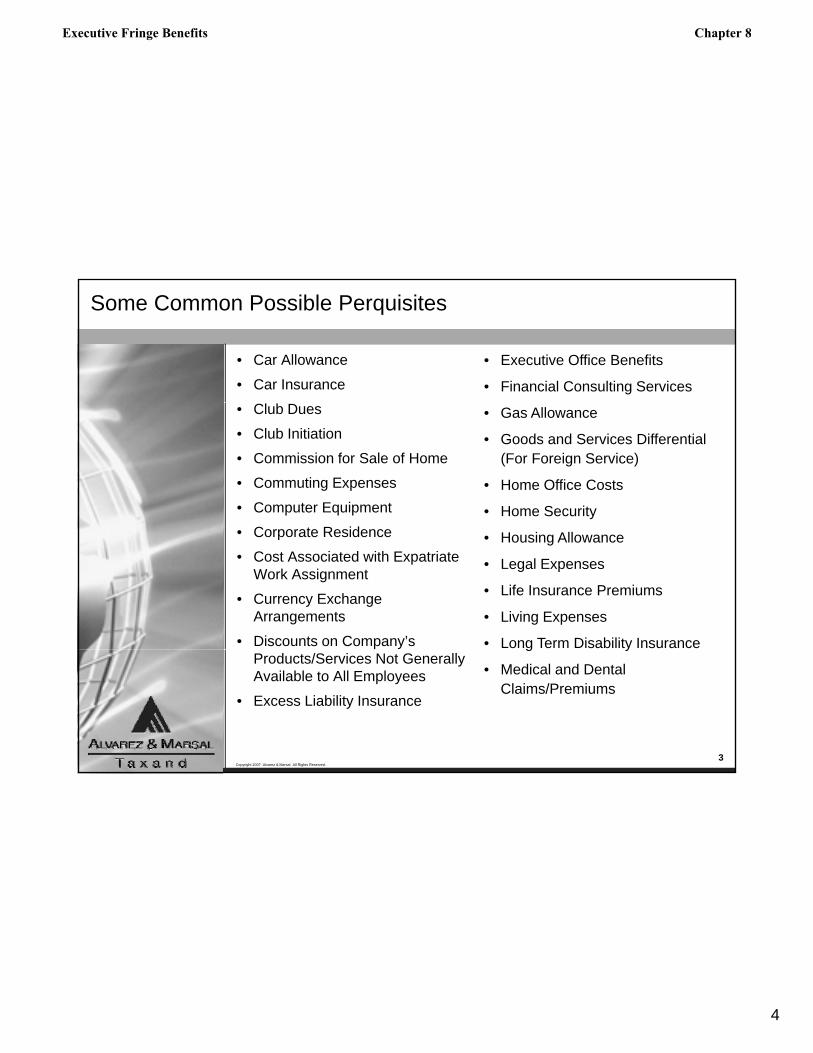

Some Common Possible Perquisites

• Car Allowance

• Car Insurance• Executive Office Benefits

• Financial Consulting Services• Club Dues

• Club Initiation

• Commission for Sale of Home

• Commuting Expenses

• Computer Equipment

• Gas Allowance

• Goods and Services Differential (For Foreign Service)

• Home Office Costs

• Home Security• Corporate Residence

• Cost Associated with Expatriate Work Assignment

• Currency Exchange Arrangements

• Discounts on Company’s

• Housing Allowance

• Legal Expenses

• Life Insurance Premiums

• Living Expenses

• Long Term Disability Insurance

Copyright 2007. Alvarez & Marsal. All Rights Reserved.3

Products/Services Not Generally Available to All Employees

• Excess Liability Insurance

g y

• Medical and Dental Claims/Premiums

Executive Fringe Benefits Chapter 8

5

Some Common Possible Perquisites (continued)

• Parking Fees

• Personal Liability Insurance

• Stipend for Effective Company Representation in the Community

S l t l A id t l D th• Personal Travel on Corporate Aircraft

• Personal Use of Company Provided Admin. Support

• Physical Exam/Voluntary Health Screening

• Supplemental Accidental Death and Dismemberment Insurance

• Tax Equalization Payments

• Tax Gross ups

• Telephone Services

T i A d d t T S lScreening

• Relocation Allowance

• School Tuition

• Secured Parking

• Security Concerning Fraudulent Data Access

• Trips Awarded to Top Sales Performers

• Use of Corporate Travel Agency for Personal Travel

• Use of Executive Dinning Room

• Wellness Reimbursement (For

Copyright 2007. Alvarez & Marsal. All Rights Reserved.4

Data Access

• Spouse/Family Member Tag Along on Business Travel

• Wellness Reimbursement (For Fitness Related Activities)

• Wireless Network for Computer Use

Executive Fringe Benefits Chapter 8

6

. . . And Some Not-So-Common Ones

• Beer for personal use• Beer for personal use

• Use of company barber shop

• Free theme park tickets

• Vehicle “evaluation” program

Copyright 2007. Alvarez & Marsal. All Rights Reserved.5

Executive Fringe Benefits Chapter 8

7

SEC RequirementsSEC Requirements

Copyright 2007. Alvarez & Marsal. All Rights Reserved.6

Executive Fringe Benefits Chapter 8

8

SEC Requirements – Two-Prong Perquisites Test

1. Is the item “integrally and directly related” to performance of executive’s duties?

o If so not a perk and no need to disclose incremental costo If so, not a perk and no need to disclose incremental cost

o Does the executive need the item to do his or her job?

– Does not cover items that merely facilitate job performance

– Fact that there is a less expensive alternative does not make item a perk

o Examples of items that may not be perks:

– Blackberry or laptop

– Bigger office

– Additional administrative support (for business reasons)

– Business trips on corporate aircraft

– Business accommodations

– Security service provided during business travel

Copyright 2007. Alvarez & Marsal. All Rights Reserved.7

Executive Fringe Benefits Chapter 8

9

SEC Requirements - Two-Prong Perquisites Test

2. Does the item “confer a direct or indirect benefit that has a personal aspect”?

o If so it is a perk unless it is generally available on a non discriminatory basiso If so, it is a perk, unless it is generally available on a non-discriminatory basis to all employees

o Determination that an item is an ordinary and necessary business expense for federal income tax purposes does not resolve whether it is a perk

o Examples of perks (per SEC):

– Club membership not used excessively for business entertainment

Personal use of company auto airplane and housing– Personal use of company auto, airplane and housing

– Security provided at personal residence

– Administrative assistance for personal matters

– Personal finance or tax advice

– Housing or other living expenses

Copyright 2007. Alvarez & Marsal. All Rights Reserved.8

Executive Fringe Benefits Chapter 8

10

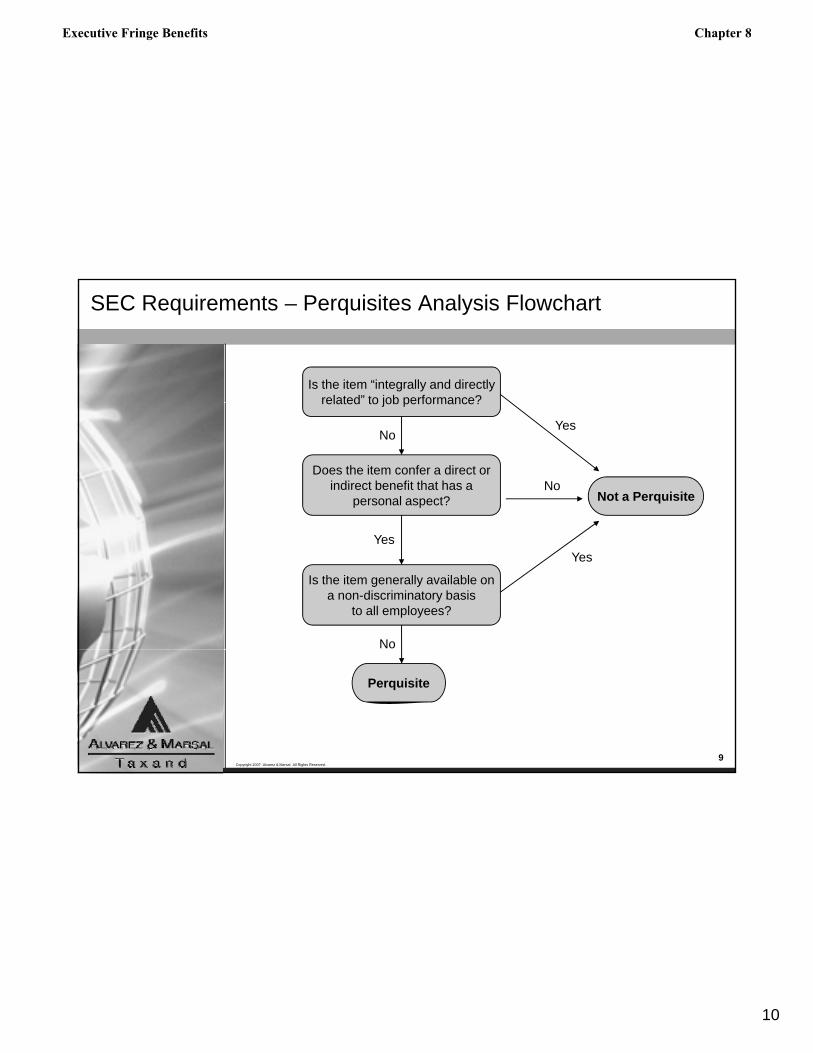

SEC Requirements – Perquisites Analysis Flowchart

Is the item “integrally and directlyrelated” to job performance?related to job performance?

Does the item confer a direct orindirect benefit that has a

personal aspect? Not a Perquisite

NoYes

No

Is the item generally available ona non-discriminatory basis

to all employees?

Yes

No

Yes

Copyright 2007. Alvarez & Marsal. All Rights Reserved.9

Perquisite

Executive Fringe Benefits Chapter 8

11

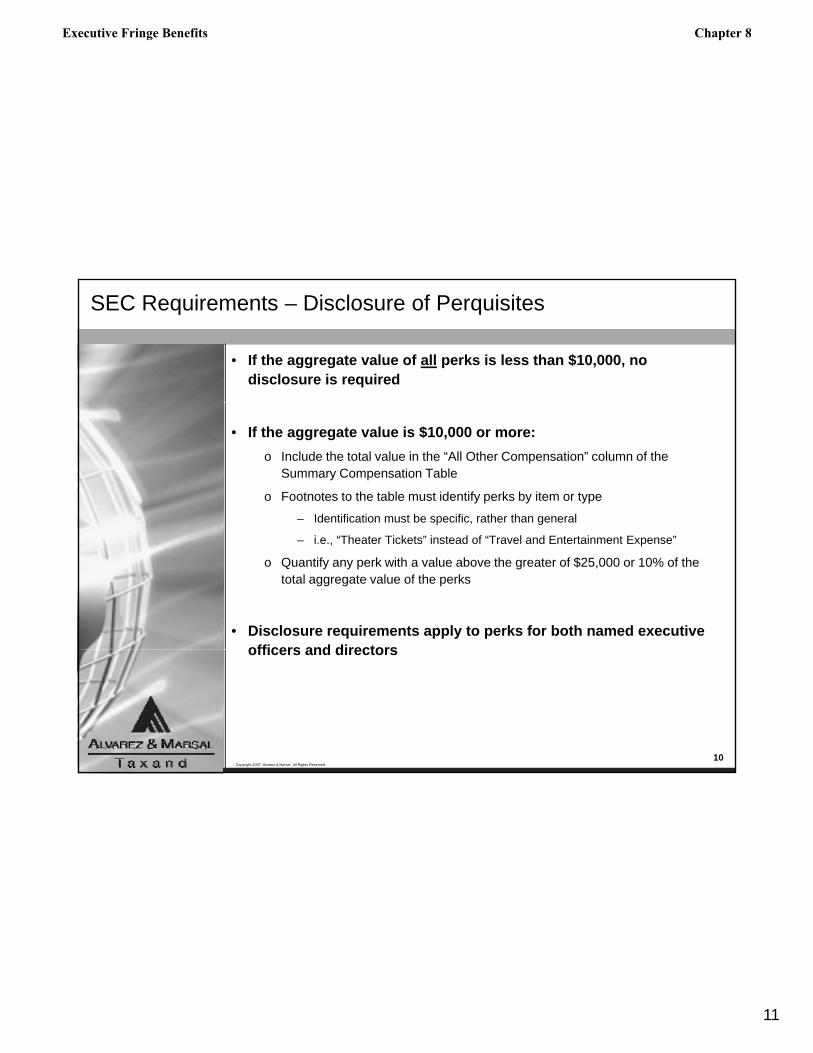

SEC Requirements – Disclosure of Perquisites

• If the aggregate value of all perks is less than $10,000, no disclosure is required

• If the aggregate value is $10,000 or more:o Include the total value in the “All Other Compensation” column of the

Summary Compensation Table

o Footnotes to the table must identify perks by item or type

– Identification must be specific, rather than general

– i.e., “Theater Tickets” instead of “Travel and Entertainment Expense”

o Quantify any perk with a value above the greater of $25,000 or 10% of the total aggregate value of the perks

• Disclosure requirements apply to perks for both named executive officers and directors

Copyright 2007. Alvarez & Marsal. All Rights Reserved.10

officers and directors

Executive Fringe Benefits Chapter 8

12

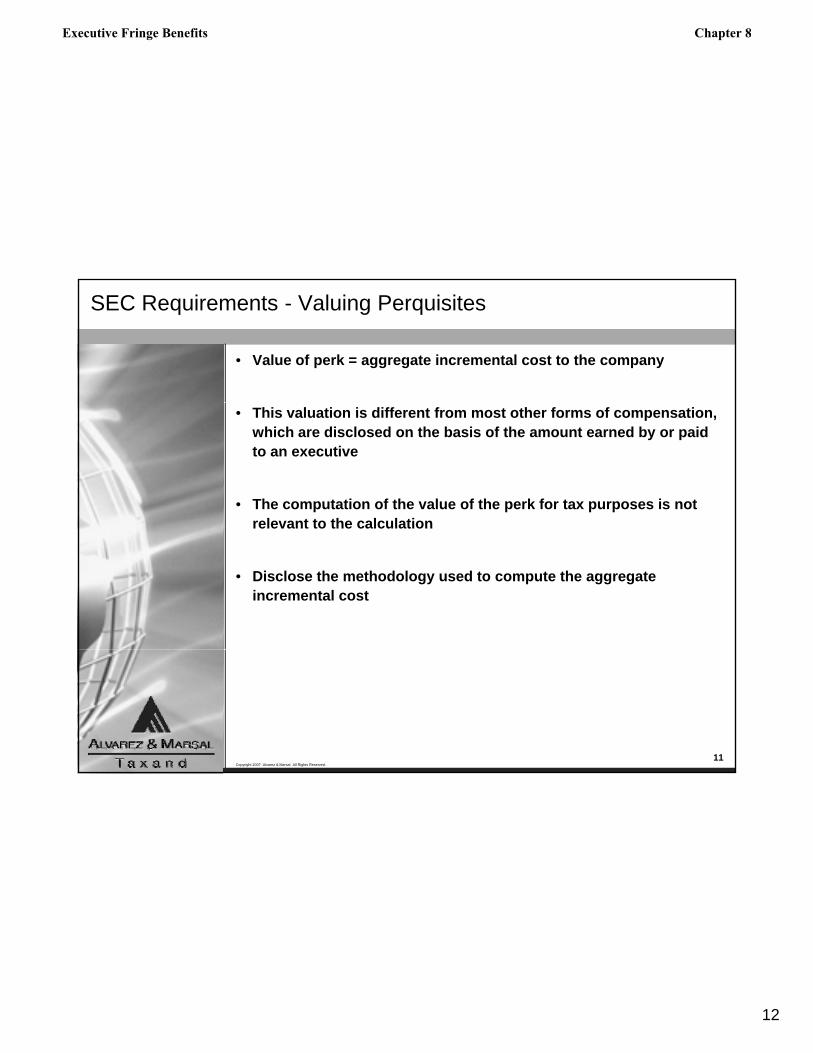

SEC Requirements - Valuing Perquisites

• Value of perk = aggregate incremental cost to the company

• This valuation is different from most other forms of compensation, which are disclosed on the basis of the amount earned by or paid to an executive

• The computation of the value of the perk for tax purposes is not relevant to the calculationrelevant to the calculation

• Disclose the methodology used to compute the aggregate incremental cost

Copyright 2007. Alvarez & Marsal. All Rights Reserved.11

Executive Fringe Benefits Chapter 8

13

Tax TreatmentTax Treatment

Copyright 2007. Alvarez & Marsal. All Rights Reserved.12

Executive Fringe Benefits Chapter 8

14

Fringe Benefit Background

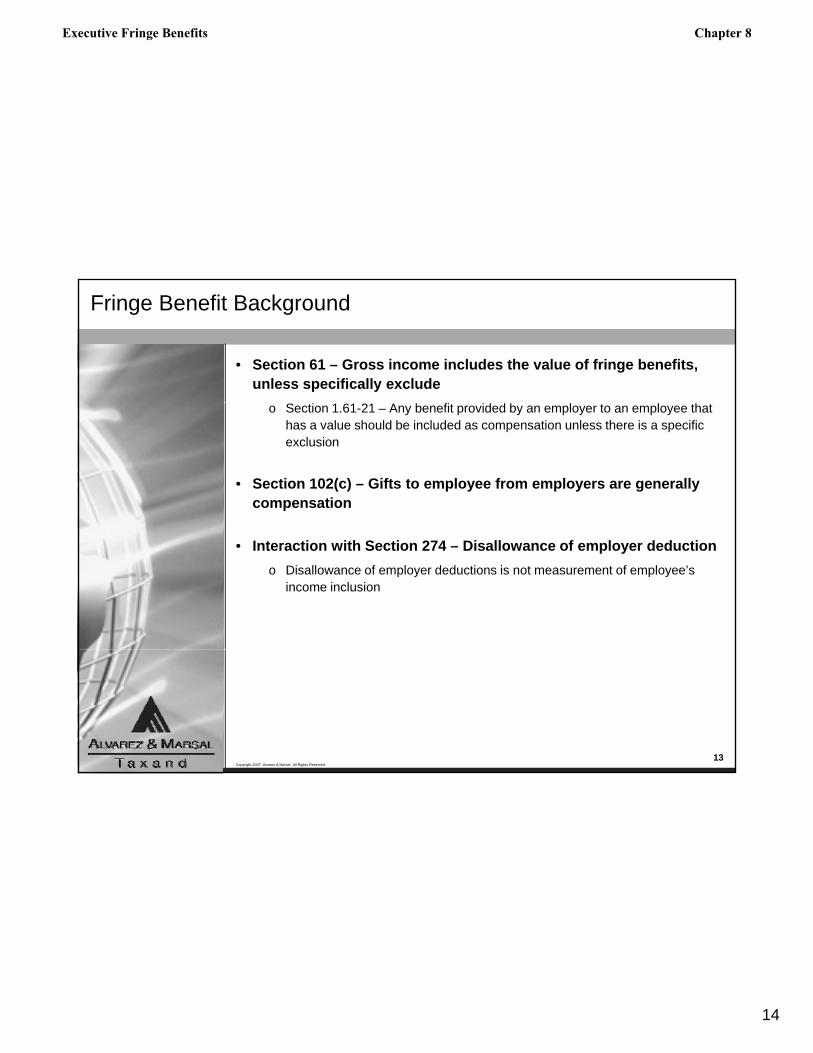

• Section 61 – Gross income includes the value of fringe benefits, unless specifically exclude

o Section 1.61-21 – Any benefit provided by an employer to an employee that has a value should be included as compensation unless there is a specific exclusion

• Section 102(c) – Gifts to employee from employers are generally compensation

• Interaction with Section 274 – Disallowance of employer deductiono Disallowance of employer deductions is not measurement of employee’s

income inclusion

Copyright 2007. Alvarez & Marsal. All Rights Reserved.13

Executive Fringe Benefits Chapter 8

15

Excludible Fringe Benefits

• Section 132 – Excludible Fringe Benefitso De minimis fringe benefits

o Working condition

o On premise gym

o Employee discounts

o Transportation fringe/parking

o No additional cost benefit

o Line of business ruleso Line of business rules

o Discrimination rules

Copyright 2007. Alvarez & Marsal. All Rights Reserved.14

Executive Fringe Benefits Chapter 8

16

Fair Market Value

• General Valuation Ruleso What the employee would have to pay for the benefit in an arms length

t ti ( ith f ti )transaction (with a few exceptions)

• Special Valuation Ruleso Regulation Section 1.61-21 has special exceptions

− Automobiles

− Airplane Use

Copyright 2007. Alvarez & Marsal. All Rights Reserved.15

Executive Fringe Benefits Chapter 8

17

IRS Initiative on Executive Compensation

• IRS Program started in 2003 to review executive compensation and benefit reporting and withholding

• One of the focus items is fringe benefits

• Currently included on IRS Information Data Requests (IDRs)

• IRS has stated that as part of the corporate audit, executives that returns will be reviewed

• Failure to report perks may result in:o Corporate Exposure

o Amendments to executive’s tax returns

Copyright 2007. Alvarez & Marsal. All Rights Reserved.16

Executive Fringe Benefits Chapter 8

18

Payroll Tax Rules

• Taxable fringe benefits for employees and former employees must be reported on Form W-2 (From 1099- MISC for directors or independent contractors)independent contractors)

• Treat like other compensation – FICA and FIT withholding apply

• Announcement 85-113 gives employer choice of when to withholdo Quarterly, semi annually, or annually

o Often done in last pay period

Copyright 2007. Alvarez & Marsal. All Rights Reserved.17

Executive Fringe Benefits Chapter 8

19

Personal Use of Corporate Aircraftp

Copyright 2007. Alvarez & Marsal. All Rights Reserved.18

Executive Fringe Benefits Chapter 8

20

Airplanes - SEC Disclosure

• How should “incremental cost” to the company be calculated?o Practice varies among companies

o Note: SIFL rates are not incremental costs

• Valuation should be based on variable flight costso Personal use is typically such a low portion of overall aircraft use that fixed

costs (e.g., insurance, hangar, etc.) can typically be excluded

• What variable costs should be included?o More obvious ones:

– Fuel, landing fees, catering service

o Gray areas:– Major maintenance

– Dead-head (repositioning)

Copyright 2007. Alvarez & Marsal. All Rights Reserved.19

Dead head (repositioning)

– Disallowed deductions

• Footnote should describe methodology used to calculate incremental costs

Executive Fringe Benefits Chapter 8

21

Airplanes – Tax Treatment

• Valuation Methodso General Rule - Fair Market Value Method

A ’ l th t t h t bl fli ht ith ll ti– Arm’s length cost to charter comparable flights, with allocation among executives on flight

o Standard Industry Fare Level Formula (“SIFL”) Method

– Formulaic formula

Number of miles x SIFL cents/mile rate

x Control employee multiple

Control employee 400% vs. non-control employee 31.3%

x size of plane multiple

+ terminal charge

– Security Concern Exception

If the bona-fide business security concern exception is satisfied, personal trip valued at 200%, rather than 400%

Copyright 2007. Alvarez & Marsal. All Rights Reserved.20

Executive Fringe Benefits Chapter 8

22

Airplanes – Tax Treatment

• Combination purpose – Trip has business and personal purposeo Impute income if primarily personal purpose

o If trip has multiple destinations with some personal and some business:

– If primarily for business, actual value of total trip less value of hypo trip to business destinations

– If primarily for personal, hypo value of trip only of personal destinations

Copyright 2007. Alvarez & Marsal. All Rights Reserved.21

Executive Fringe Benefits Chapter 8

23

Airplanes – Tax Treatment

• If control person is not correctly identified, or if SIFL rates are not properly applied, general rules apply

• Guests on boardo Allocate to all employees on flight, or

o Allocate to the control employee on flight (person exercising control over the flight)

o Usually shareholder, director, family member of control employee

o If allocate to control employee, use control SIFL calculation

• 50% seating capacity ruleo Regular seating capacity

o 50% of more business flyers

o If rule satisfied guests fly free

Copyright 2007. Alvarez & Marsal. All Rights Reserved.22

o If rule satisfied, guests fly free

Executive Fringe Benefits Chapter 8

24

Airplanes – Tax Treatment

• Reimbursement of personal use of corporate aircrafto Reimbursement is generally not feasible under FAA regulations, though

lt ti t t b il bl th t it i b talternative structures may be available that permit reimbursement– Reimbursement of aircraft expenses may require registration of issuer with

FAA

Copyright 2007. Alvarez & Marsal. All Rights Reserved.23

Executive Fringe Benefits Chapter 8

25

The Future of Perquisites

• Looking at the bottom line: do the “benefits” outweigh the costs?

Eli i t th f ill• Eliminate the frillso Can it be done?

– Jet use is actually rising

– Recruitment tool

– Status symbol

• Perquisite Allowanceso A significant number of companies maintain perk allowance programs,

generally offering to reimburse executives for certain expenses

Copyright 2007. Alvarez & Marsal. All Rights Reserved.24

Executive Fringe Benefits Chapter 8

26

Copyright 2007. Alvarez & Marsal. All Rights Reserved.25

www.alvarezandmarsal.com

NORTH AMERICA • EUROPE • LATIN AMERICA • ASIA

Executive Fringe Benefits Chapter 8