Embed Size (px)

Citation preview

Agricultural & Applied Economics Association

Exchange Rate Effects on the Relationship between FDI and Trade in the U.S. Food ProcessingIndustryAuthor(s): Munisamy Gopinath, Daniel Pick and Utpal VasavadaReviewed work(s):Source: American Journal of Agricultural Economics, Vol. 80, No. 5, Proceedings Issue (Dec.,1998), pp. 1073-1079Published by: Oxford University Press on behalf of the Agricultural & Applied Economics AssociationStable URL: http://www.jstor.org/stable/1244207 .

Accessed: 05/03/2013 02:03

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Agricultural & Applied Economics Association and Oxford University Press are collaborating with JSTOR todigitize, preserve and extend access to American Journal of Agricultural Economics.

http://www.jstor.org

This content downloaded on Tue, 5 Mar 2013 02:03:17 AMAll use subject to JSTOR Terms and Conditions

EXCHANGE RATE EFFECTS ON THE RELATIONSHIP

BETWEEN FDI AND TRADE IN THE U.S. FOOD PROCESSING INDUSTRY

MUNISAMY GOPINATH, DANIEL PICK, AND UTPAL VASAVADA

The effect of exchange rates on international trade and, more specifically, on agricultural trade flows has been documented by several studies.' Most studies agree that an appreci- ation (depreciation) in the value of the U.S. dollar hurts (helps) U.S. agricultural exports. An appreciation of the U.S. dollar raises the cost of U.S. products to foreign buyers and reduces their purchases.2 Although neglected early on, the effect of exchange rate risk as measured by its volatility on trade flows was also found to be negative (Arize, Pick).

Parallel to this literature were the devel- opment and testing of theories on the rela- tionship between exchange rates and foreign direct investment (FDI). Using an imperfect- capital-market approach, Froot and Stein demonstrated that exchange rate movements affect the relative-wealth positions of coun- tries and thus have a systematic effect on FDI.3 To the extent that foreigners own their wealth in non-dollar-denominated forms, a depreciation of the dollar increases the wealth position of foreigners relative to domestic agents. This lowers foreigners' relative cost of capital and allows them to bid more ag- gressively for domestic assets (Froot and Stein, p. 1194). While the empirical results of Froot and Stein have been questioned (Ste-

vens), a majority of studies support the neg- ative relationship between the dollar value and FDI inflows into the United States (Caves, Cushman 1985).

The juxtaposition of these two strands of literature suggests that as the value of the dol- lar declines, exports increase and FDI out- flows decrease. Effectively, FDI and trade may be substitutes and exchange rate move- ments can cause this substitution.4 In this ar- ticle, the exchange-rate-induced substitution hypothesis is tested for the U.S. food pro- cessing industry, which presents an interest- ing case study. The composition of global ag- ricultural trade has shifted toward high-value processed food products, which account for two-thirds of the $381 billion global trade in agricultural products and commodities (Hen- derson and Handy). The U.S. share in global agricultural trade has fallen from 22% to less than 15%, and processed foods account for less than 40% of total U.S. agricultural ex- ports for the period 1962-94 (Gehlhar and Vollrath). However, the United States ac- counted for six out of ten of the world's largest food-processing (multinational) firms. In ad- dition, sales by U.S.-owned food-processing foreign affiliates are estimated to have reached $103 billion in 1994 (Neff et al.). Declining export shares and the increasing role of U.S.- owned multinational corporations (MNCs) suggest some degree of substitution in the food processing industry. This has been tested at the aggregate level and at the firm level. For instance, Gopinath, Pick, and Vasavada found that exports and foreign sales by U.S.- based multinational firms are substitutes.

The purpose of this study is to test for the effects of the real exchange rate and its vol- atility on exports, outward FDI, and foreign

Munisamy Gopinath is an assistant professor in the Department of Agricultural and Resource Economics, Oregon State University. Daniel Pick is an economist in the Markets and Trade Economics Division, Economic Research Service, U.S. Department of Agricul- ture. Utpal Vasavada is an economist in the Resource Economics Division, Economic Research Service, U.S. Department of Agricul- ture.

Thanks to Andy Jerardo, Mark Gehlhar, and Alisa Livensperger for their help in compiling the data. The authors benefited from helpful comments by John Beghin, Bruce Blonigen, and Tom Worth.

1'Some studies focused on nominal exchange rate effects (e.g., Chambers and Just), while others looked at real exchange rate effects (e.g., Cushman 1983, Batten and Belongia).

2 As Schuh notes, a rise in the dollar value not only discourages exports, but also exerts pressure on the domestic import-competing industries (automobile, textile, and others).

3 See Cushman (1985) and Caves for other studies on exchange rate effects on FDI.

4 Lipsey provides a useful discussion on the effects of outward FDI on the broader economy.

Amer. J. Agr. Econ. 80 (Number 5, 1998): 1073-1079 Copyright 1998 American Agricultural Economics Association

This content downloaded on Tue, 5 Mar 2013 02:03:17 AMAll use subject to JSTOR Terms and Conditions

1074 Number 5, 1998 Amer. J. Agr. Econ.

affiliate sales by the U.S. food-processing in- dustry. The relevant question is whether the appreciation (depreciation) of the U.S. dollar and its volatility has contributed to the ob- served relationship between FDI and trade in this industry. Besides underscoring the im- portance of the level and stability of exchange rates for trade and foreign investment, this research has implications for policy, since ex- panding trade and/or foreign investment can bring about changes in the distribution of in- come to those engaged in food processing in the United States.

A Test of Exchange Rate Effects

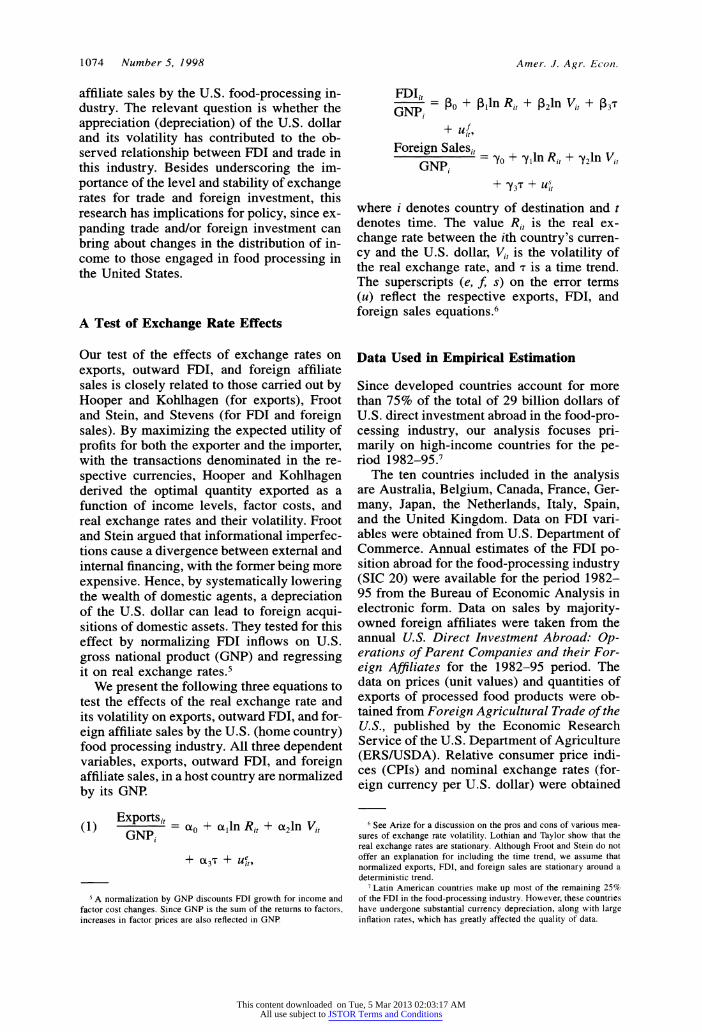

Our test of the effects of exchange rates on exports, outward FDI, and foreign affiliate sales is closely related to those carried out by Hooper and Kohlhagen (for exports), Froot and Stein, and Stevens (for FDI and foreign sales). By maximizing the expected utility of profits for both the exporter and the importer, with the transactions denominated in the re- spective currencies, Hooper and Kohlhagen derived the optimal quantity exported as a function of income levels, factor costs, and real exchange rates and their volatility. Froot and Stein argued that informational imperfec- tions cause a divergence between external and internal financing, with the former being more expensive. Hence, by systematically lowering the wealth of domestic agents, a depreciation of the U.S. dollar can lead to foreign acqui- sitions of domestic assets. They tested for this effect by normalizing FDI inflows on U.S. gross national product (GNP) and regressing it on real exchange rates.5

We present the following three equations to test the effects of the real exchange rate and its volatility on exports, outward FDI, and for- eign affiliate sales by the U.S. (home country) food processing industry. All three dependent variables, exports, outward FDI, and foreign affiliate sales, in a host country are normalized by its GNP.

Exportsi, (1) = ao0 + aln R, + a21n Vi, GNP,

+ (37 + Ui,

FDI, GNP -

o + P3ln Ri, + 321n Vi, + P33 GNPj

Foreign Salesi, = + ylln R, + y2ln Vi

GNP, + Y"3 +

Uit

where i denotes country of destination and t denotes time. The value Rit, is the real ex- change rate between the ith country's curren- cy and the U.S. dollar, Vi, is the volatility of the real exchange rate, and 7 is a time trend. The superscripts (e, f s) on the error terms (u) reflect the respective exports, FDI, and foreign sales equations.6

Data Used in Empirical Estimation

Since developed countries account for more than 75% of the total of 29 billion dollars of U.S. direct investment abroad in the food-pro- cessing industry, our analysis focuses pri- marily on high-income countries for the pe- riod 1982-95.7

The ten countries included in the analysis are Australia, Belgium, Canada, France, Ger- many, Japan, the Netherlands, Italy, Spain, and the United Kingdom. Data on FDI vari- ables were obtained from U.S. Department of Commerce. Annual estimates of the FDI po- sition abroad for the food-processing industry (SIC 20) were available for the period 1982- 95 from the Bureau of Economic Analysis in electronic form. Data on sales by majority- owned foreign affiliates were taken from the annual U.S. Direct Investment Abroad: Op- erations of Parent Companies and their For- eign Affiliates for the 1982-95 period. The data on prices (unit values) and quantities of exports of processed food products were ob- tained from Foreign Agricultural Trade of the U.S., published by the Economic Research Service of the U.S. Department of Agriculture (ERS/USDA). Relative consumer price indi- ces (CPIs) and nominal exchange rates (for- eign currency per U.S. dollar) were obtained

I A normalization by GNP discounts FDI growth for income and factor cost changes. Since GNP is the sum of the returns to factors, increases in factor prices are also reflected in GNP.

6 See Arize for a discussion on the pros and cons of various mea- sures of exchange rate volatility. Lothian and Taylor show that the real exchange rates are stationary. Although Froot and Stein do not offer an explanation for including the time trend, we assume that normalized exports, FDI, and foreign sales are stationary around a deterministic trend.

7 Latin American countries make up most of the remaining 25% of the FDI in the food-processing industry. However, these countries have undergone substantial currency depreciation, along with large inflation rates, which has greatly affected the quality of data.

This content downloaded on Tue, 5 Mar 2013 02:03:17 AMAll use subject to JSTOR Terms and Conditions

Gopinath, Pick, and Vasavada Exchange Rate Effects 1075

Table 1. Pooled Regression Results on Exchange Rate Effects

Real Exchange Volatility

Equation Constant Rate Measure Trend R2 d.f.

Export/GNP 0.00014a -0.000136a -0.00003a 0.000004 0.89 136 (31.1) (-15.2) (-4.11) (0.31)

Foreign Sales/GNP 0.0050a 0.00029a -0.00189a 0.00018a 0.17 136 (2.72) (4.27) (9.15) (3.40)

FDI/GNP -0.00196a 0.00116a - 0.00092a 0.00008a 0.27 136 (-3.30) (8.18) (-29.6) (2.38)

Note: Numbers in parentheses are t-values. a Significant at the 5% level.

Table 2. Effect of Exchange Rates on (Normalized) U.S. Exports Real

Exchange Volatility Countries Constant Rate Measure Trend DWa R2 d.f.

Australia 0.0008 -0.0006b 0.00003 -0.00001 1.83 0.22 9 (6.09) (-2.32) (0.83) (-1.90)

Belgium 0.0054 -0.0012b 0.00006 -0.00003 1.59 0.55 9 (2.63) (-2.16) (0.41) (-1.56)

Canada -0.0026 0.01558b -0.0003b 0.0002 1.82 0.88 9 (- 1.14) (2.30) (-1.49) (1.64)

France 0.0007 -0.0003b 0.00001 -0.00001 1.81 0.72 9 (3.57) (-1.99) (0.22) (-5.05)

Germany 0.0004 -0.00001 0.00003 -0.00001 1.78 0.35 9 (1.48) (-0.04) (0.43) (-1.44)

Italy 0.0013 -0.00014b -0.00004b 0.00006 1.37 0.18 9 (3.05) (-2.51) (-2.44) (1.82)

Japan 0.0005 0.0001 -0.00002 -0.00001 2.60 0.37 9 (1.01) (1.09) (-0.78) (-0.71)

The Netherlands 0.0017 0.0048b -0.00005 -0.00023 1.79 0.94 9 (1.16) (4.36) (-0.13) (-7.28)

Spain 0.0012 -0.0002 -0.0001 0.00001 1.18 0.67 9 (1.48) (-0.95) (-0.97) (1.00)

United Kingdom -0.0002 0.00014 -0.00015b 0.00004 2.12 0.60 9 (-0.88) (0.31) (-1.91) (1.64)

Note: Numbers in parentheses are t-values. a Durbin-Watson statistic after correcting for serial correlation. " Significant at the 5% level.

SSignificant at the 10% level.

from the International Monetary Fund to de- rive the real exchange rates between the cur- rencies of the ten countries listed above and the U.S. dollar. A moving twelve-month stan- dard deviation of the relative changes in the real exchange rate was used to represent its volatility.

Estimation and Results

Table 1 presents the results from the pooled time series and cross-section models, while the results for individual countries are re-

ported in tables 2-4. Recall that by normal- izing on GNP, we account for both income effects and, possibly, changes in factor costs in exports, outward FDI, and foreign affiliate sales.8

Both Ri, and Vi, were replaced with their one-period lags, Ri,_1 and Vi,,_-, respectively,

8 Overall, the U.S. dollar experienced lows as well as highs during the sample period. Beginning in the early 1980s, the value of the dollar appreciated until 1985-86. The late 1980s and early 1990s saw the dollar fall in value. This pattern changed just after 1992, and since then, the value of the dollar has increased relative to most other currencies.

This content downloaded on Tue, 5 Mar 2013 02:03:17 AMAll use subject to JSTOR Terms and Conditions

1076 Number 5, 1998 Amer. J. Agr. Econ.

Table 3. Effect of Exchange Rates on (Normalized) Outward FDI by U.S. Multinationals

Real Exchange Volatility

Countries Constant Rate Measure Trend DWa R2 d.f.

Australia 0.0025 0.0121b -0.0014c -0.0002 1.96 0.21 9 (0.76) (3.71) (-1.54) (-1.99)

Belgium -0.0292 0.01008b -0.0031b 0.0005 2.80 0.96 9 (-3.17) (3.89) (-4.47) (5.51)

Canada 0.0106 0.0197b -0.0007b -0.0004 3.01 0.93 9 (3.92) (3.24) (-2.12) (-3.94)

France -0.0049 0.0040c 0.0002 0.00027 2.26 0.29 9 (-0.88) (1.56) (0.25) (3.22)

Germany -0.0020 0.0034b -0.0008c 0.0003 2.40 0.77 9 (-0.88) (2.01) (-1.49) (5.40)

Italy -0.0098 0.0016c 0.00011 -0.00004 1.96 0.42 9 (-1.47) (1.62) (0.37) (-0.18)

Japan -0.0023 0.0005 -0.00004 0.00007 1.89 0.54 9 (-0.97) (1.16) (-0.41) (2.31)

The Netherlands 0.0136 0.0029 -0.0003 0.0007 1.57 0.43 9 (1.35) (0.29) (-0.18) (2.07)

Spain -0.0210 0.0044b 0.0012 0.0004 1.95 0.67 9 (-1.73) (1.93) (1.38) (2.93)

United Kingdom 0.0066 0.0062c -0.0014b -0.0001 2.66 0.75 9 (2.57) (1.63) (-2.56) (-0.14)

Note: Numbers in parentheses are t-values. a Durbin-Watson statistic after correcting for serial correlation. 1 Significant at the 5% level. c Significant at the 10% level.

Table 4. Effect of Exchange Rates on (Normalized) Foreign Affiliate Sales by U.S. Multinationals

Real Exchange Volatility

Countries Constant Rate Measure Trend DWa R2 d.f.

Australia 0.0017 0.0041b -0.0001 -0.00008 1.99 0.35 9 (1.08) (1.66) (-0.25) (-1.24)

Belgium 0.035 -0.0006 -0.0005c 0.00013 2.61 0.81 9 (1.07) (-0.63) (-2.82) (2.88)

Canada 0.00043 0.0126c -0.0004b 0.00002 2.59 0.73 9 (0.23) (3.04) (-1.43) (0.35)

France -0.0020 0.00114c -0.00021 0.0001 2.08 0.79 9 (-1.18) (1.83) (-1.19) (1.91)

Germany 0.0002 0.00027 -0.00004 0.00004 2.17 0.79 9 (0.59) (0.83) (-0.43) (2.97)

Italy -0.00033 0.00002 0.00008b 0.00012 1.90 0.59 8 (-0.25) (0.10) (1.78) (1.99)

Japan 0.00001 0.00003 -0.00003 0.00001 1.89 0.55 9 (0.02) (0.32) (-1.02) (2.01)

The Netherlands -0.0044 0.0092c -0.0003 0.0001 2.26 0.42 9 (-0.80) (1.89) (-0.35) (0.71)

Spain -0.0009 0.00053 -0.00022 0.00004 1.95 0.05 9 (-0.41) (1.16) (-0.79) (1.52)

United Kingdom -0.0007 0.0057c -0.0012c 0.00020 2.37 0.86 9 (-0.63) (2.93) (-4.23) (0.77)

Note: Numbers in parentheses are t-values. a Durbin-Watson statistic after correcting for serial correlation. h Significant at the 10% level. c Significant at the 5% level.

This content downloaded on Tue, 5 Mar 2013 02:03:17 AMAll use subject to JSTOR Terms and Conditions

Gopinath, Pick, and Vasavada Exchange Rate Effects 1077

in order to account for the expectations as- sociated with exchange rates and their vola- tility. In the pooled model, we accounted for serial correlation, contemporaneous correla- tion between cross sections and heteroske- dasticity by using two types of error struc- tures. The Parks method specifies errors as:

(2) Uit = piUi,t1 + Eit.

This model assumes a first-order autoregres- sive error structure with contemporaneous correlation between cross sections and was used to estimate the export equations. How- ever, we used the Da Silva method for the foreign affiliate sales and FDI equation, which specifies errors as:

(3) uit = ai + b, + eit,

where

ei = oE, + J1E,1 - . . + Et-m.

This procedure is used to estimate a mixed- variance-component moving average process for the errors. The moving average process of order m for ei, should satisfy m - T - 1, where T is the total number of observations over time. The order m was chosen to be three, although the results did not vary much for m ranging from three to eight. This moving av- erage process was chosen in addition to an error-component specification to account for the possible lag involved in the FDI process leading to foreign affiliate sales. In the indi- vidual country analysis, an OLS procedure was used to estimate the parameters of all three equations after accounting for serial cor- relation.

Most of the parameter estimates of equation (1) reported in table 1 are significant at the 1% level. The R2 for the export equation was 0.89, while that for the foreign sales and FDI equations were 0.17 and 0.27, respectively, and similar in magnitude to those reported by Froot and Stein.9 The negative sign on the real exchange rate in the normalized export equa- tion confirms the importance of real exchange rates in determining agricultural trade flows (Batten and Beiongia, Pick). Moreover, the negative effect of exchange rate volatility on exports is consistent with previous studies as well. These results illustrate the importance

of the real exchange rate and its stability for agricultural trade flows.

Real exchange rates have a positive effect on outward FDI and foreign sales by U.S. majority-owned multinational food compa- nies. That is, an appreciation of the U.S. dollar leads to an increase in outward FDI and the resulting foreign affiliate sales. Our reasoning, which is in accord with Froot and Stein, is that an appreciation in the U.S. dollar increas- es the wealth of U.S. food processors relative to foreigners and allows them to bid aggres- sively for foreign assets through FDI. As other studies have documented, the volatility in real exchange rates has a negative effect on both outward FDI and foreign sales. Consistent with our hypothesis, these results suggest that dollar appreciation has been a causal factor in the observed substitutability between FDI and trade in the U.S. food-processing industry (Gopinath, Pick, and Vasavada).

The magnitudes of the above-mentioned ef- fects are also important. Note that the right- hand side variables in the equations are in logarithms, while the left-hand side variables are shares in GNP of exports, outward FDI, and foreign sales for each country. By divid- ing the parameter estimates in table 1 by an average of these shares (over all countries), we obtain a measure of share elasticity. A 1% rise in the real value of the U.S. dollar causes a fall of 0.13% for normalized exports. In oth- er words, exports as a share of GNP fell by 0.13% for every 1% rise in the real value of U.S. dollar. Outward FDI and foreign sales as shares of GDP expanded by 0.54% and 0.04%, respectively, in response to a 1% in- crease in the real value of the U.S. dollar. The negative effect of the real exchange rate on U.S. processed food exports is accompanied by the rise in the foreign affiliate sales of U.S. majority-owned MNCs.

Tables 2-4 report the parameter estimates for the normalized export, FDI, and foreign sales equations for each of the ten countries. This estimation, similar to that of Froot and Stein, was constrained by the available de- grees of freedom given the annual time series data for 1982-95. However, these results con- firm earlier results from the pooled regres- sions.

The effect of the real exchange rate on ex- ports was negative and significant for five of the ten countries investigated (table 2). Of the rest, only one had a positive and significant coefficient (Canada). Three countries showed significant negative effects of real exchange

9 As FDI and foreign sales are often outcomes of intangibles (knowledge capital, including trade secrets and brand names), it is not surprising that exchange rates alone do not account for all of the variation in these variables.

This content downloaded on Tue, 5 Mar 2013 02:03:17 AMAll use subject to JSTOR Terms and Conditions

1078 Number 5, 1998 Amer. J. Agr. Econ.

rate volatility on exports, while this effect was insignificant for the other countries.

Table 3 shows that in eight out of ten coun- tries, the effect of the real exchange rate on foreign affiliate sales was positive and sig- nificant, as expected. In most countries, for- eign affiliate sales were negatively affected by the volatility of exchange rates. However, this effect was significant for only five coun- tries. Similarly, the effect of the real exchange rate and its volatility on outward FDI was positive and significant for about half of the sampled countries (table 4). The results of the country-wise analysis, given the degrees of freedom constraint, provide some support for our pooled regression results (table 1).

Issues and Implications for Future Research

The relationship between FDI and trade has been addressed theoretically and empirically. Researchers agree on a substitution relation- ship along direct product lines. However, con- ceptual and empirical studies have shown that a complementary relationship exists for sev- eral reasons. First, foreign opportunities/mar- kets are not fixed. Second, exports of the same product may fall, but more intermediate inputs may be exported from the home country. Fi- nally, if the technology is different between home and host countries, it is possible for both FDI and trade to expand together.

In the U.S. food-processing industry, a sub- stitution relationship between FDI and trade has been identified previously by Gopinath, Pick, and Vasavada. In this study, real ex- change rates have been shown to be a causal factor in this apparent substitution between FDI and trade. That is, the adverse effects of real exchange rates on processed food exports are accompanied by a rise in foreign affiliate sales by U.S. majority-owned MNCs.

A key issue for the future is to test for the relationship between FDI and trade at a more disaggregated level for the U.S. food-pro- cessing industry by including the possibility that farm and other product (intermediate) ex- ports may compensate for the substitution at the aggregate level. Many other factors may potentially affect exports, FDI, and foreign affiliate sales. For example, outward FDI may be affected by a host of factors. These include, but are not limited to, classical sources of competitiveness such as wage rates, tax rates, market size, and transport costs. While the

focus of the current research is on the impact of real exchange rates, it may be interesting to incorporate these measures into future stud- ies at a more disaggregated level.

Nontraditional variables affecting FDI in- clude environmental policy variables, mea- sures of degree of openness, and measures of riskiness of investment. For example, factors such as the quality of the legal system, cor- ruption, presence of import restrictions, and currency convertibility may affect the deci- sion to invest abroad and sales by foreign af- filiates (Wheeler and Mody).

References

Arize, A.C. "Conditional Exchange Rate Vola- tility and the Volume of Foreign Trade: Ev- idence from Seven Industrialized Coun- tries." S. Econ. J. 64(July 1997):235-54.

Batten, D.S., and M.T. Belongia. "Monetary Pol- icy, Real Exchange Rates and U.S. Agricul- tural Exports." Amer. J. Agr. Econ. 68(May 1986):422-27.

Caves, R.E. "Exchange Rate Movements and Foreign Direct Investment in the United States." The Internationalization of the U.S. Markets, D.R. Audretsch and M.P. Claudon, ed. pp. 199-229. New York: New York Uni- versity Press, 1990.

Chambers, R.G., and R.E. Just. "Effects of Ex- change Rate Changes on U.S. Agriculture: A Dynamic Analysis." Amer. J. Agr. Econ. 63(February 1981):32-46.

Cushman, D.O. "The Effects of Exchange Rate Risk on International Trade." J. Int. Econ. 15(1983):45-63. . "Real Exchange Rate Risk, Expectations, and the Level of Foreign Direct Investment." Rev. Econ. and Statist. 67(1985):297-308.

Da Silva, J.G.C. "The Analysis of Cross-Sec- tional Time Series Data." PhD dissertation, Department of Statistics, North Carolina State University, 1975.

Froot, K.A., and J.C. Stein. "Exchange Rates and Foreign Direct Investment: An Imperfect Capital Markets Approach." Quart. J. Econ. 106(November 1991):1191-217.

Gehlhar, M.J., and T. Vollrath. "U.S. Agricultural Trade Competitiveness in Foreign Markets." Washington DC: U.S. Department of Agri- culture, ERS Tech. Pap. No. 1854, 1997.

Gopinath, M., D. Pick, and U. Vasavada. "The Economics of Foreign Direct Investment and Trade with an Application to the U.S. Food Processing Industry." Amer. J. Agr. Econ.,

This content downloaded on Tue, 5 Mar 2013 02:03:17 AMAll use subject to JSTOR Terms and Conditions

Gopinath, Pick, and Vasavada Exchange Rate Effects 1079

International Agricultural Trade Research Consortium, University of Minnesota, forth-

coming, 1998. Henderson, D.R., and C. Handy. "International

Dimensions of the Food Marketing System." Food and Agricultural Markets: The Quiet Revolution. L.P. Schertz and L.M. Daft, eds.

pp. 166-95, Washington DC: National Plan-

ning Association, 1994.

Hooper, P, and S.W. Kohlhagen. "The Effects of

Exchange Rate Risk and Uncertainty on the Prices and Volume of Trade." J. Int. Econ. 8(1978):483-511.

International Monetary Fund. International Fi- nancial Statistics. Washington DC. 1982- 1995.

Lipsey, R.E. "Outward Direct Investment and U.S. Economy." Working Paper No. 4691, National Bureau of Economic Research, Cambridge MA, 1994.

Lothian, J.R., and M.P. Taylor. "Real Exchange Rate Behavior: The Recent Float from the

Perspective of the Past Two Centuries." J. Polit. Econ. 104(June 1996):488-509.

Neff, S., M. Harris, M. Malonoski, and E Ruppel. "U.S. Trade in Processed Foods." Global- ization of the Processed Food Markets. D.R.

Henderson, C.R. Handy, and S.A. Neff, eds., pp. 25-65 Washington DC: U.S. Department of Agriculture, ERS AER No. 742, 1996.

Parks, R.W. "Efficient Estimation of a System of

Regression Equations when Disturbances are both Serially and Contemporaneously Cor- related." J. Amer. Statist. Assoc. 62(1967): 500-9.

Pick, D.H. "Exchange Rate Risk and U.S. Ag- ricultural Trade Flows." Amer. J. Agr. Econ.

72(August 1990):694-99. Schuh, E. G. "The Exchange Rate and U.S. Ag-

riculture." Amer J. Agr. Econ. 56(February 1974):1-13.

Stevens, G.V.G. "Exchange Rates and Foreign Direct Investment: A Note." J. Policy Mod. 20(June 1998):393-401.

U.S. Department of Agriculture, Economic Re- search Service. Foreign Agriculture Trade of the United States, 1982-1995.

U.S. Department of Commerce, Bureau of Eco- nomic Analysis. U.S. Direct Investment Abroad, Operations of Parent Companies and Their Affiliates, 1982-1995.

Wheeler, D., and A. Mody. "International In- vestment Location Decisions." J. Int. Econ. 33(August 1992):57-76.

This content downloaded on Tue, 5 Mar 2013 02:03:17 AMAll use subject to JSTOR Terms and Conditions