Embed Size (px)

DESCRIPTION

http://cmimarseille.org/_src/EW2_wk1/EW2_wk1_JordanFinalReport.pdf

Citation preview

JORDAN WATER DEMAND MANAGEMENT STUDY

December, 2011

Prepared for the Ministry of Water and Irrigation of Jordan (MWI), supported and funded by

the French Development Agency (AFD / FDA)

i

About this report

This report is the synthesis of a series of reports on aspects of water demand management,

which were prepared for the Jordanian Ministry of Water and Irrigation under a funding

scheme of the French Development Agency by consultants from ATEEC and QUASIR between

July, 2010 and November 2011.

The five reports provide detailed and in‐depth information on the considered topics and are

available at the Ministry of Water and Irrigation and the French Development Agency:

Diagnostic report – compiles information on the current water situation, its future trends

and an assessment of impacts from selected programs in Jordanian water demand

management

Valuation report – comprises calculations and explanations about the values of water in

Jordan’s different sectors of water demand

Intermediary report – describes potential scenarios of water demand development until

2025

Scenario Impact Analysis – gives an overview on the major consequences under the

developed scenarios.

Pre‐conditions for Successful Implementation – comments on the results from the scenario

impact analyses in the framework of Jordan's Water Strategy and Action Plan.

www.quasir.de

ii

Context of the study

The Declaration of the Euro‐Mediterranean Ministerial Conference on Water, adopted by

Ministers and Heads of Delegations participating in the Euro‐Mediterranean Conference on

Water held in Jordan on 22 December 2008 has launched the preparation of a strategy for

water in the Mediterranean. One of the two focuses of this strategy is “the balance between

the quantity of water used and the quantity of water available, including mitigating and

preventing the consequences of droughts and water scarcity”.

In this context, the French Development Agency (AFD) and Blue Plan have proposed, within

the framework of the new Marseille Centre for Mediterranean Integration, to launch a

regional programme on water demand management (WDM), whose main objective is to

make the concept of WDM more operational for decision makers by: 1) building on existing

projects in agriculture optimisation, 2) bringing economic analysis into national strategies

and 3) organising share of experience between high level decision makers.

This Programme is complementary to other regional initiatives related to water demand

management in Mediterranean that provide training and capacity building. It is based on

pilot studies that illustrate how this cost‐effectiveness approach can be a tool for water

decision makers. The present “JORDAN WATER DEMAND MANAGEMENT STUDY” is one of these

case‐studies on Middle Eastern, North African and Balkan Mediterranean countries.

The study was conducted under the auspices and guidance of H.E. Maysoun Zoubi, Secretary

General of the Ministry of Water and Irrigation, with direct supervision from Eng. Ali Subah.

The Steering Committee chaired by Eng. Ali Subah (MWI consisted of Serge Perrin (AFD),

Qais Owais and Nayef Seder (JVA), Khair Hadidi (WAJ), Tobias El‐Fahem (BGR) and Johannes

Stork (MWI‐CIM). Information and data were provided by the MWI, WAJ, JVA, the

Department of Statistics (DoS), other relevant Ministries and the University of Jordan (UoJ).

The scenario development relied on a series of “Story & Simulation (SAS)” workshops hosted

by the MWI between October 2010 and April 2011.

Additional, extensive support was provided by:

MWI – Nisreen Haddad and her team from the Water Demand Management Unit at the MWI

WAJ ‐ F. Al‐Azzam, A. Ulimat, J. Hijazi and B.Saleh

JVA ‐ Y. Hassan and F. Ejeilat

AFD – Frédéric Maurel and Lise Breuil

iii

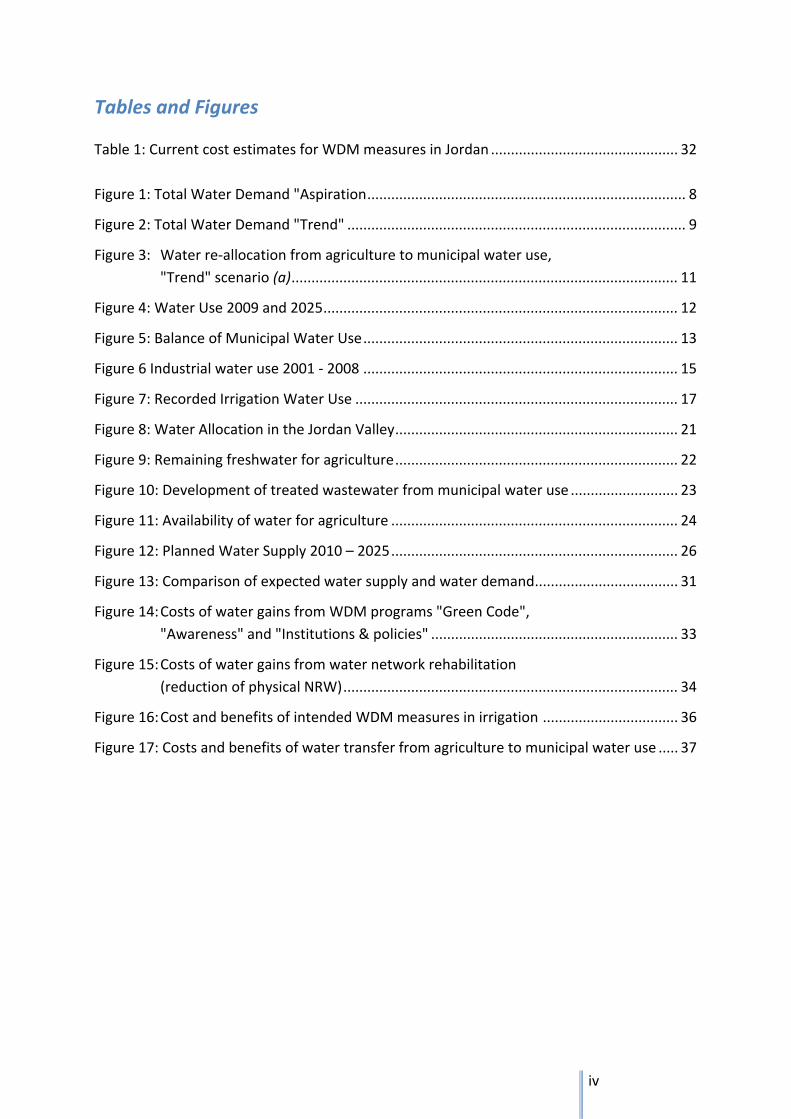

Table of contents

Context of the study ...................................................................................... ii

Table of contents .......................................................................................... iii

Tables and Figures ........................................................................................ iv

List of Abbreviations ...................................................................................... v

Key findings ................................................................................................... 1

Introduction ................................................................................................... 4

Chapter 1: Prospective water demands of Jordan ......................................... 6

Chapter 2: Water demand by sectors ..........................................................12

Chapter 3: Water resources .........................................................................26

Chapter 4: Economic considerations ............................................................32

Conclusion ...................................................................................................41

References ...................................................................................................42

Appendix 1: Water Demand ............................................................................................. 43

Appendix 2: Water Supply ................................................................................................ 47

Appendix 3: Water Demand Scenarios ............................................................................. 50

Appendix 4: Water Values ................................................................................................ 59

Appendix 5: Cost Benefit Analyses of WDM measures .................................................... 65

Appendix 6: Strategies, policies and legislations ............................................................. 71

iv

Tables and Figures

Table 1: Current cost estimates for WDM measures in Jordan ............................................... 32

Figure 1: Total Water Demand "Aspiration ................................................................................ 8

Figure 2: Total Water Demand "Trend" ..................................................................................... 9

Figure 3: Water re‐allocation from agriculture to municipal water use,

"Trend" scenario (a) ................................................................................................. 11

Figure 4: Water Use 2009 and 2025 ......................................................................................... 12

Figure 5: Balance of Municipal Water Use ............................................................................... 13

Figure 6 Industrial water use 2001 ‐ 2008 ............................................................................... 15

Figure 7: Recorded Irrigation Water Use ................................................................................. 17

Figure 8: Water Allocation in the Jordan Valley ....................................................................... 21

Figure 9: Remaining freshwater for agriculture ....................................................................... 22

Figure 10: Development of treated wastewater from municipal water use ........................... 23

Figure 11: Availability of water for agriculture ........................................................................ 24

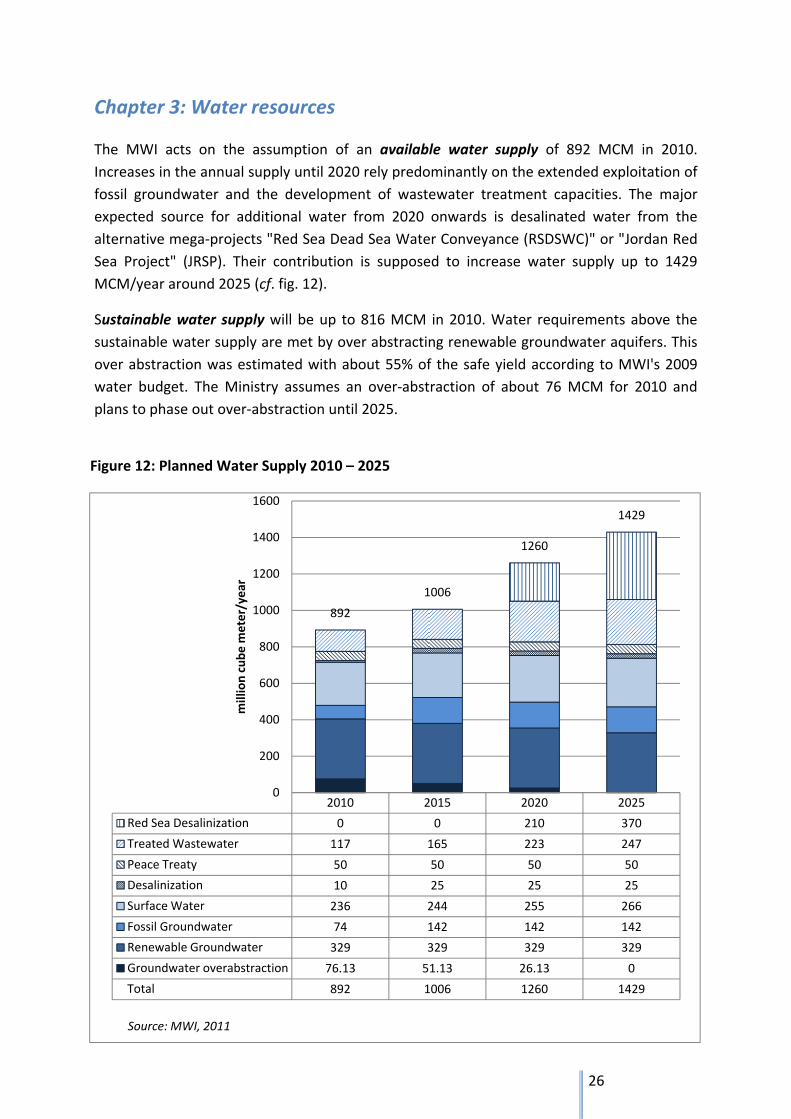

Figure 12: Planned Water Supply 2010 – 2025 ........................................................................ 26

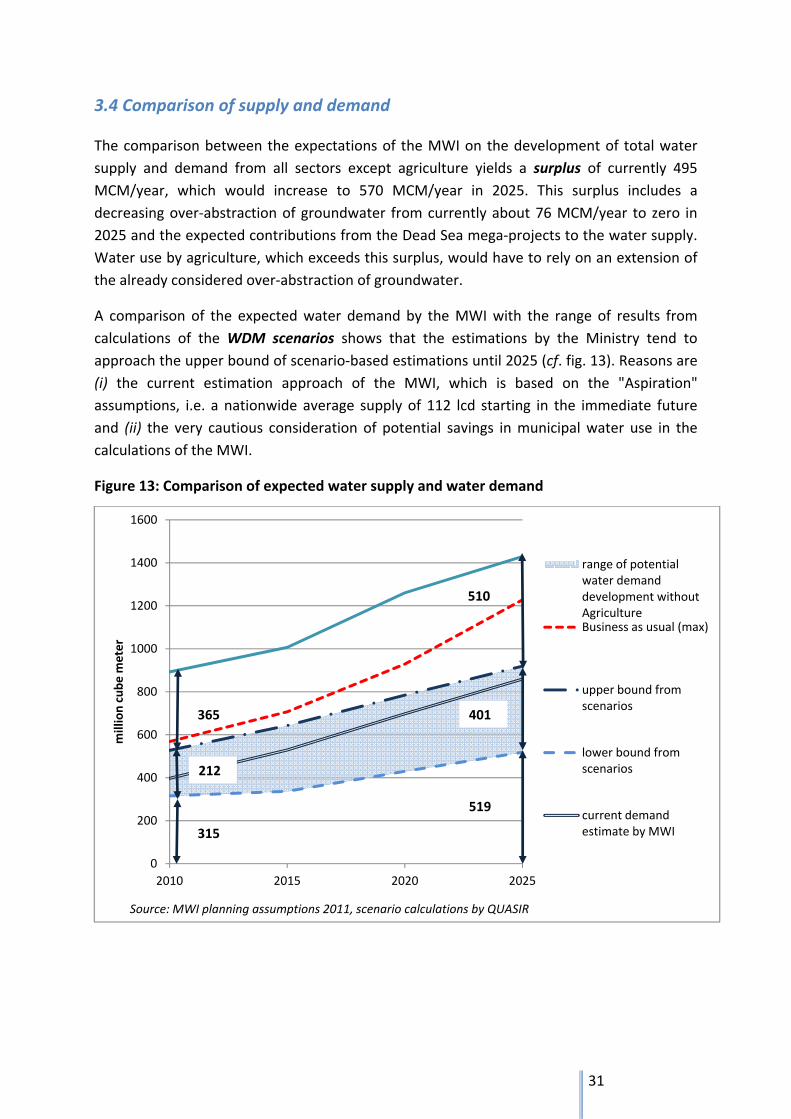

Figure 13: Comparison of expected water supply and water demand .................................... 31

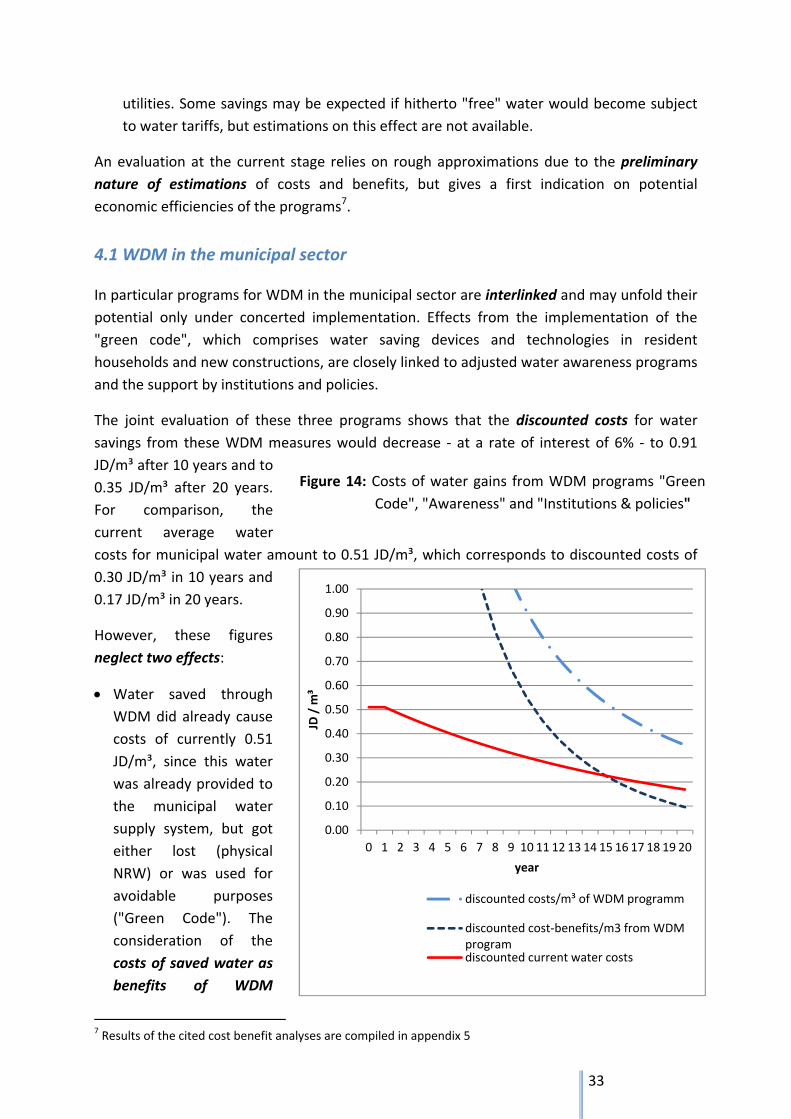

Figure 14: Costs of water gains from WDM programs "Green Code",

"Awareness" and "Institutions & policies" .............................................................. 33

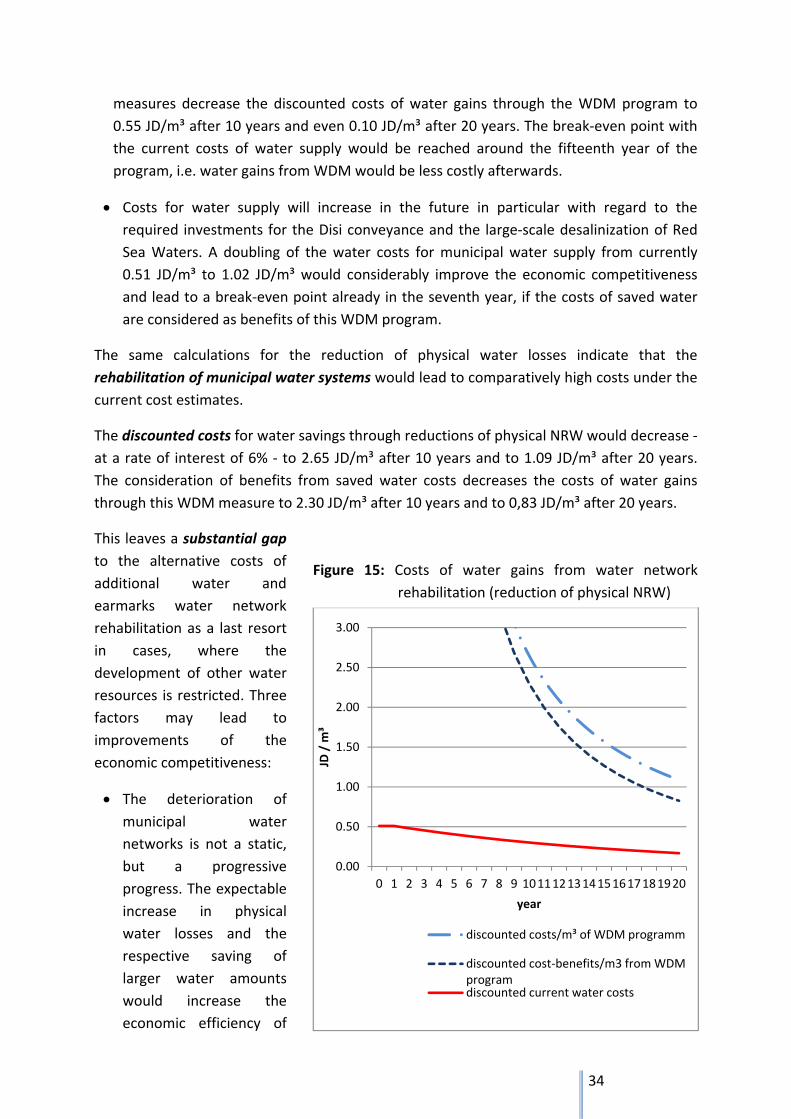

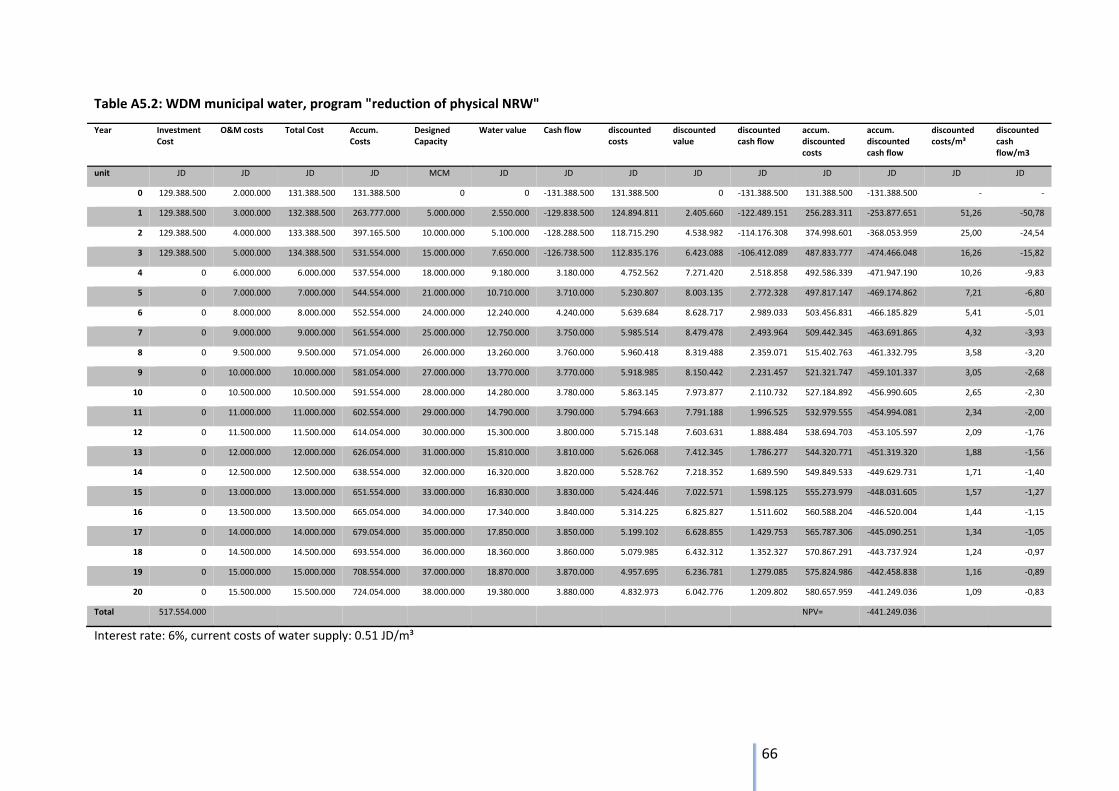

Figure 15: Costs of water gains from water network rehabilitation

(reduction of physical NRW) .................................................................................... 34

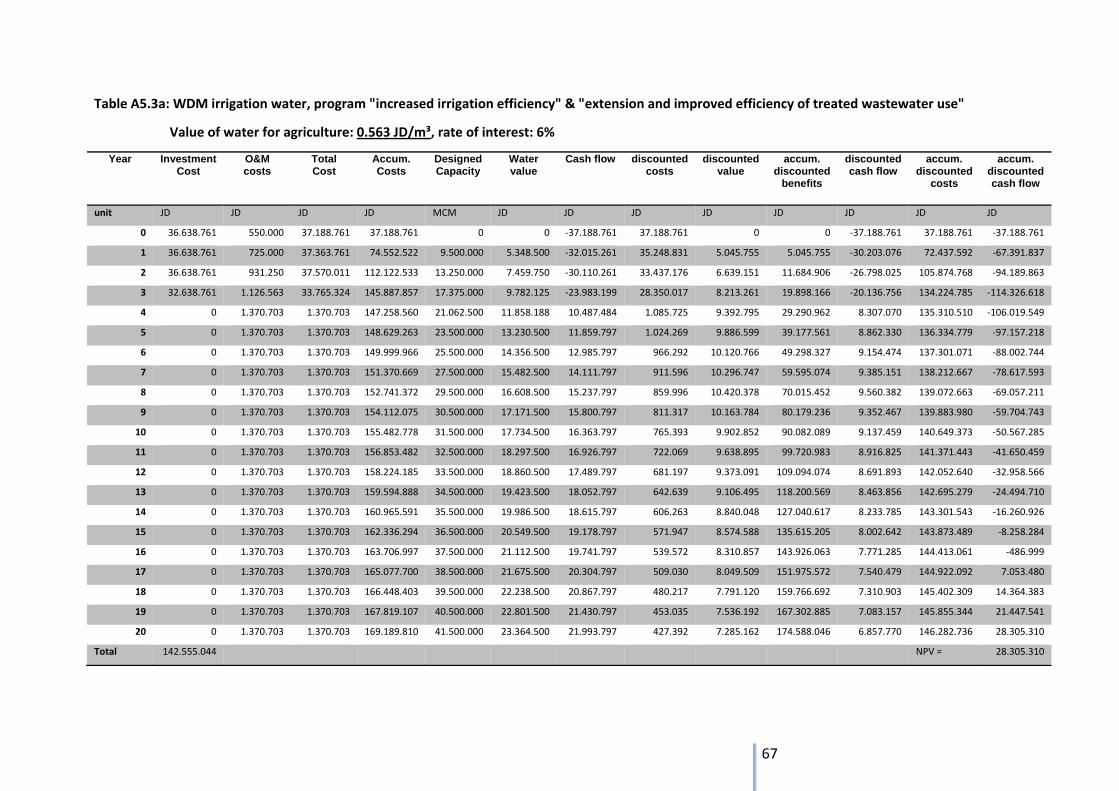

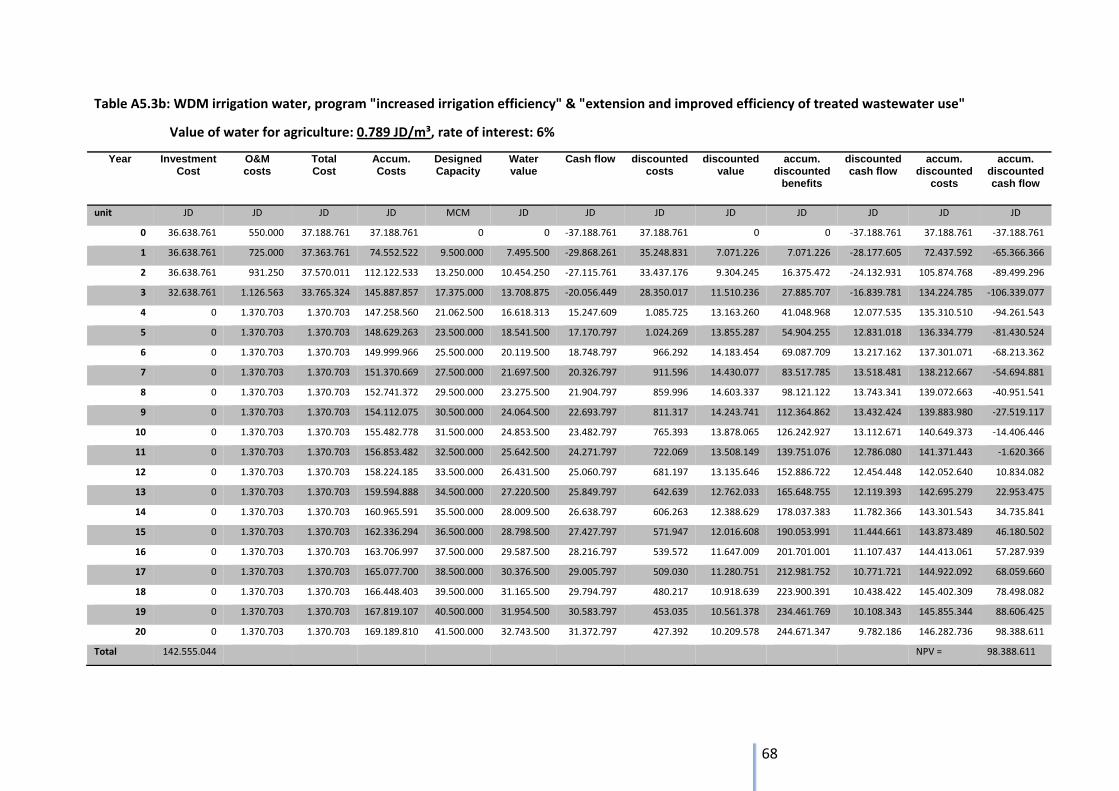

Figure 16: Cost and benefits of intended WDM measures in irrigation .................................. 36

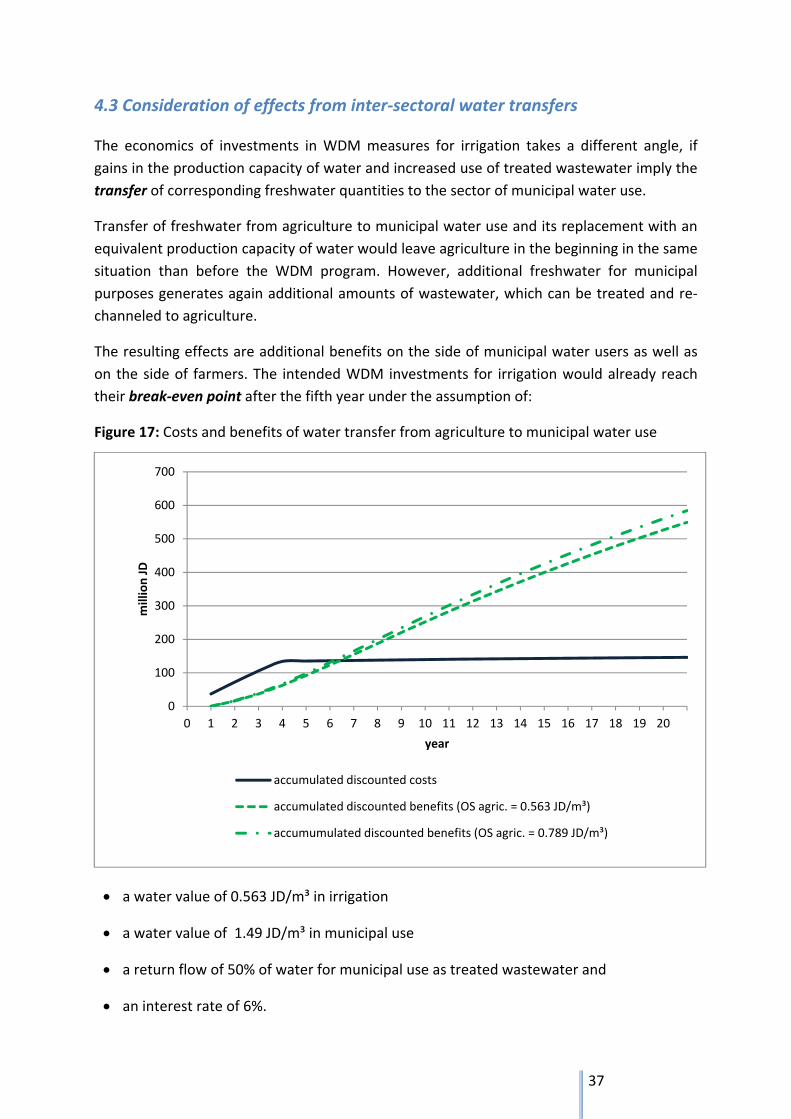

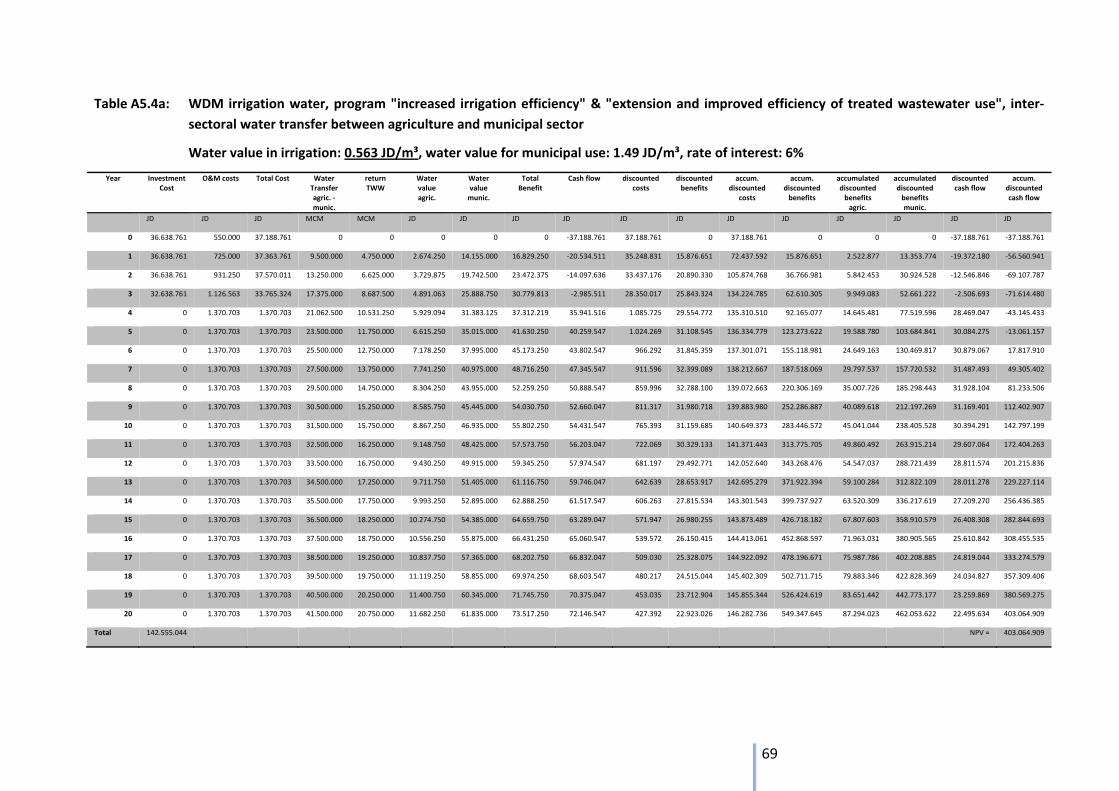

Figure 17: Costs and benefits of water transfer from agriculture to municipal water use ..... 37

v

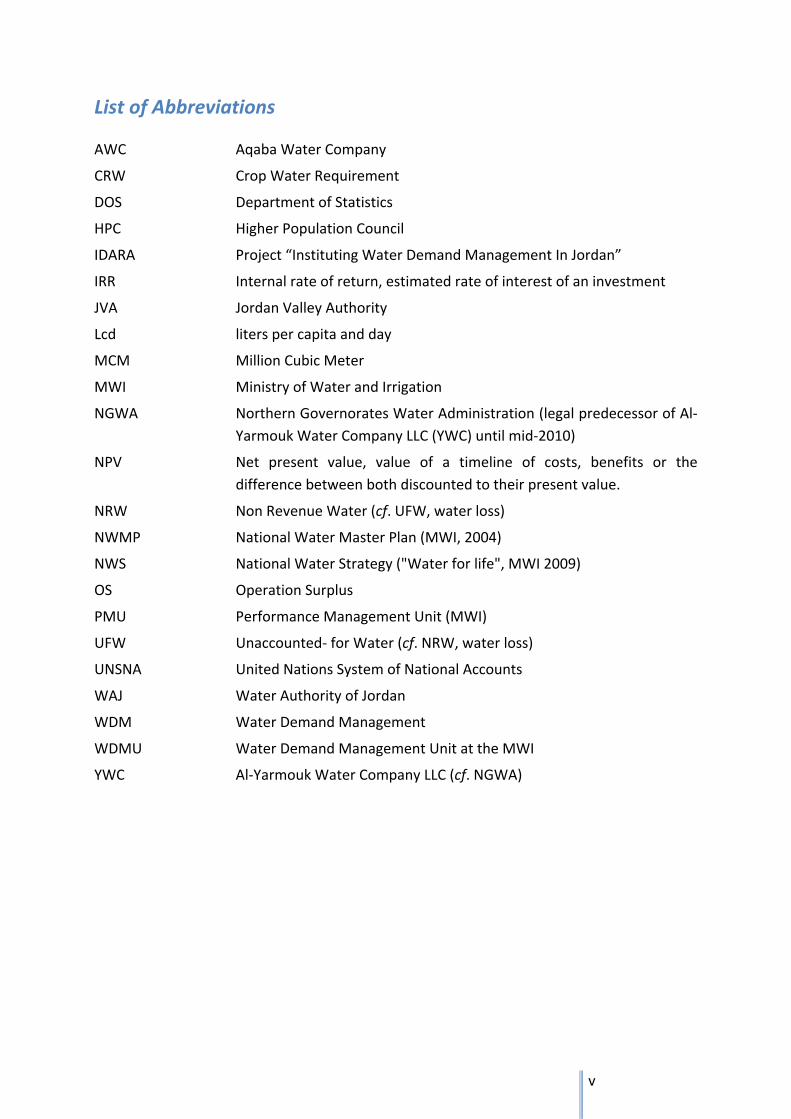

List of Abbreviations

AWC Aqaba Water Company

CRW Crop Water Requirement

DOS Department of Statistics

HPC Higher Population Council

IDARA Project “Instituting Water Demand Management In Jordan”

IRR Internal rate of return, estimated rate of interest of an investment

JVA Jordan Valley Authority

Lcd liters per capita and day

MCM Million Cubic Meter

MWI Ministry of Water and Irrigation

NGWA Northern Governorates Water Administration (legal predecessor of Al‐

Yarmouk Water Company LLC (YWC) until mid‐2010)

NPV Net present value, value of a timeline of costs, benefits or the

difference between both discounted to their present value.

NRW Non Revenue Water (cf. UFW, water loss)

NWMP National Water Master Plan (MWI, 2004)

NWS National Water Strategy ("Water for life", MWI 2009)

OS Operation Surplus

PMU Performance Management Unit (MWI)

UFW Unaccounted‐ for Water (cf. NRW, water loss)

UNSNA United Nations System of National Accounts

WAJ Water Authority of Jordan

WDM Water Demand Management

WDMU Water Demand Management Unit at the MWI

YWC Al‐Yarmouk Water Company LLC (cf. NGWA)

1

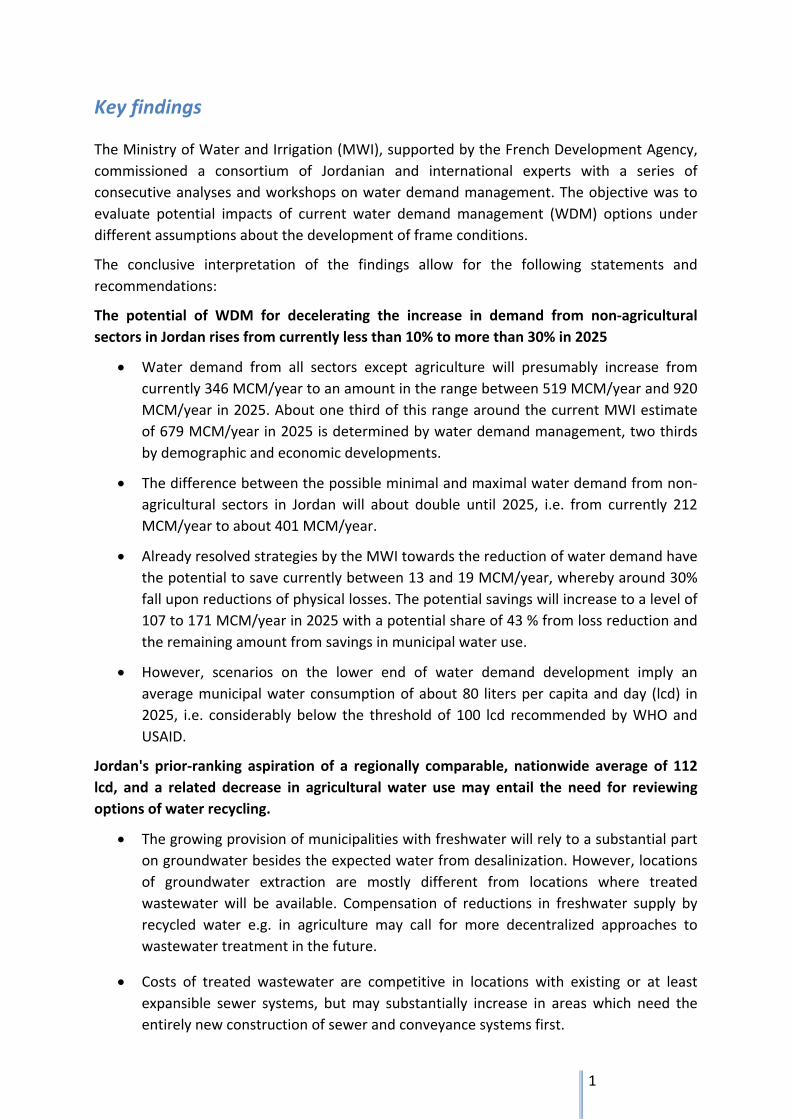

Key findings

The Ministry of Water and Irrigation (MWI), supported by the French Development Agency,

commissioned a consortium of Jordanian and international experts with a series of

consecutive analyses and workshops on water demand management. The objective was to

evaluate potential impacts of current water demand management (WDM) options under

different assumptions about the development of frame conditions.

The conclusive interpretation of the findings allow for the following statements and

recommendations:

The potential of WDM for decelerating the increase in demand from non‐agricultural

sectors in Jordan rises from currently less than 10% to more than 30% in 2025

Water demand from all sectors except agriculture will presumably increase from

currently 346 MCM/year to an amount in the range between 519 MCM/year and 920

MCM/year in 2025. About one third of this range around the current MWI estimate

of 679 MCM/year in 2025 is determined by water demand management, two thirds

by demographic and economic developments.

The difference between the possible minimal and maximal water demand from non‐

agricultural sectors in Jordan will about double until 2025, i.e. from currently 212

MCM/year to about 401 MCM/year.

Already resolved strategies by the MWI towards the reduction of water demand have

the potential to save currently between 13 and 19 MCM/year, whereby around 30%

fall upon reductions of physical losses. The potential savings will increase to a level of

107 to 171 MCM/year in 2025 with a potential share of 43 % from loss reduction and

the remaining amount from savings in municipal water use.

However, scenarios on the lower end of water demand development imply an

average municipal water consumption of about 80 liters per capita and day (lcd) in

2025, i.e. considerably below the threshold of 100 lcd recommended by WHO and

USAID.

Jordan's prior‐ranking aspiration of a regionally comparable, nationwide average of 112

lcd, and a related decrease in agricultural water use may entail the need for reviewing

options of water recycling.

The growing provision of municipalities with freshwater will rely to a substantial part

on groundwater besides the expected water from desalinization. However, locations

of groundwater extraction are mostly different from locations where treated

wastewater will be available. Compensation of reductions in freshwater supply by

recycled water e.g. in agriculture may call for more decentralized approaches to

wastewater treatment in the future.

Costs of treated wastewater are competitive in locations with existing or at least

expansible sewer systems, but may substantially increase in areas which need the

entirely new construction of sewer and conveyance systems first.

2

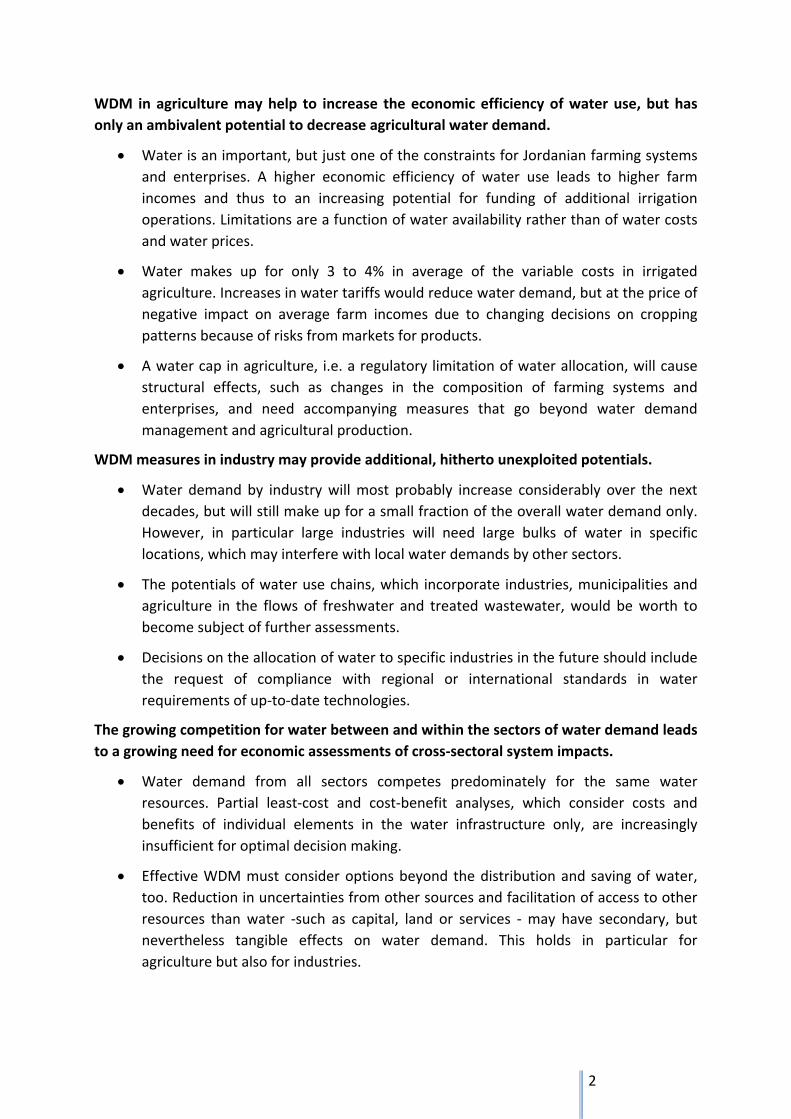

WDM in agriculture may help to increase the economic efficiency of water use, but has

only an ambivalent potential to decrease agricultural water demand.

Water is an important, but just one of the constraints for Jordanian farming systems

and enterprises. A higher economic efficiency of water use leads to higher farm

incomes and thus to an increasing potential for funding of additional irrigation

operations. Limitations are a function of water availability rather than of water costs

and water prices.

Water makes up for only 3 to 4% in average of the variable costs in irrigated

agriculture. Increases in water tariffs would reduce water demand, but at the price of

negative impact on average farm incomes due to changing decisions on cropping

patterns because of risks from markets for products.

A water cap in agriculture, i.e. a regulatory limitation of water allocation, will cause

structural effects, such as changes in the composition of farming systems and

enterprises, and need accompanying measures that go beyond water demand

management and agricultural production.

WDM measures in industry may provide additional, hitherto unexploited potentials.

Water demand by industry will most probably increase considerably over the next

decades, but will still make up for a small fraction of the overall water demand only.

However, in particular large industries will need large bulks of water in specific

locations, which may interfere with local water demands by other sectors.

The potentials of water use chains, which incorporate industries, municipalities and

agriculture in the flows of freshwater and treated wastewater, would be worth to

become subject of further assessments.

Decisions on the allocation of water to specific industries in the future should include

the request of compliance with regional or international standards in water

requirements of up‐to‐date technologies.

The growing competition for water between and within the sectors of water demand leads

to a growing need for economic assessments of cross‐sectoral system impacts.

Water demand from all sectors competes predominately for the same water

resources. Partial least‐cost and cost‐benefit analyses, which consider costs and

benefits of individual elements in the water infrastructure only, are increasingly

insufficient for optimal decision making.

Effective WDM must consider options beyond the distribution and saving of water,

too. Reduction in uncertainties from other sources and facilitation of access to other

resources than water ‐such as capital, land or services ‐ may have secondary, but

nevertheless tangible effects on water demand. This holds in particular for

agriculture but also for industries.

3

The findings recommend the following five focal points for an efficient WDM policy:

Coordinate water demand policies with Jordan's overall goals and sectorial

objectives. Gains in the economic efficiency of water use may – and do often ‐stand

against development goals and economic efficiencies of other resources and in other

sectors. This requires (1) the reduction of overlaps in mandates and the improvement

of cooperation between water authorities as well as between ministries and (2)

quantified social and economic assessments of policies with regard to the overall

goals rather than with regard to water economics alone. The Ministry of Water and

Irrigation, Ministry of Municipalities, Ministry of Agriculture, and Ministry of

Environment should formulate a joint policy.

Prioritize the stability of a continuous water supply. A low risk in water supply in

times of water demand reduces water use by the insurance rate, i.e. water stocked or

overused in order to minimize risks from sudden interruption of supply. This holds for

over‐irrigation in agriculture as well as for excessive stocking of water from water

tankers by resident households. Possible actions in this regard range from recharge

of the groundwater aquifers as "natural buffer capacities", other decentralized water

storage capacities and the continued reclamation of wastewater up to the respective

planning of storage elements in the intended mega‐projects.

Support resident households in their efforts for water savings and water recycling.

Potential gains from water demand management result mostly from lower expansion

rates of water use per capita. Increasing benefits from water use without

proportional increases in water consumption, e.g. by measures from Jordan's "green

code", requires investments which may not be shouldered by families or property

owners alone. The same holds for installations in urban rainwater harvesting,

greywater use and sewerage.

Address the question on water for agriculture from the focus of rural area

development. Decisions on water distribution and caps in water for irrigation must

take into account (1) the specific functions of land use systems, (2) the economic and

operational fundamentals of the different types of farming systems, (3) the desired

objectives towards modernization and structural adjustments in the agricultural

sector and (4) the livelihood and environmental structures that Jordan wants to

preserve. The central technical challenges and opportunities are the control of

groundwater over‐abstraction and the continuous expansion of water recycling.

Develop the Water Information System (WIS) into a Water Management

Information System (MIS). The Jordanian water administrations and utilities already

run extensive systems of data collection and partial analyses. The resulting data and

information bases are fragmented and scattered in several sub‐units of the

authorities and the MWI, which is an obstacle with regard to quick and reliable

information for the Ministry's decision makers. There is an urgent need for

consolidation and transformation into a Management Information System with

defined workflows and specifications that include economic performance indicators.

4

Introduction

Jordan’s economic opportunities, social necessities and aspirations entail a significant

growth in water demand over the last decades and will continue to do so in the future. This

coincides with a situation where the exploitation of renewable natural water resources

already exceeds a sustainable level and the reclamation of non‐conventional water

resources requires considerable investments. The resulting increase in water costs and

values amplifies the role of economic reflections in decision making on water resource

management as well as on the allocation and use of water in the different sectors of water

consumption.

Jordan’s water management in the past has been dominated by the necessity to supply

water. Initial approaches to the management of water demand focused in particular on

agriculture in the Jordan Valley through operations on water‐distribution by the Jordan

Valley Authority (JVA). Water demand management (WDM) in other sectors than agriculture

gained momentum with the establishment of a Water Demand Management Unit (WDMU)

at the Ministry of Water and Irrigation (MWI) in 2002. More recent activities of the Unit

include the USAID‐funded IDARA project (2007‐2011), which supported the build‐up of

institutional capacities, and a close cooperation with Jordan’s private utilities in planning and

prognoses of future water requirements.

The MWI defined WDM as one of the pillars in its strategy of a “rational water resources

management consistent with overall national socio‐economic development objectives”.

Tentative milestones of this strategy formulation are Jordan’s National Water Master Plan

(NWMP, 2004) and its National Water Strategy 2008‐2022 (“Water for Life”, NWS, 2009),

which are subject to continuous updates and enhancements. This indicates that WDM in

Jordan intends to go beyond the economic pricing of water and partial criteria of water use

efficiency, such as water productivities in different sectors of water consumption.

The present study inserts itself into the development of an efficient strategy by contributing

analyses and projections about the framework, results and economic consequences of

options in Water Demand Management. It builds on information from the broad data bases

provided by the MWI, JVA, Water Authority of Jordan (WAJ), Department of Statistics (DOS),

Water and Environmental Research and Study Centre (WERSC, University of Jordan) and

other Jordanian organizations, current research results on water in Jordan as well as on the

results from four workshops and numerous interviews with Jordanian professionals from

different fields of expertise.

The main objectives of the study were

to bring economic analysis into Jordan water policy and help prioritizing actions

according to their cost‐effectiveness

to propose a cost‐effectiveness analysis of these different actions, and to

5

enhance ownership of the activities proposed under the Jordan National Water

Strategy by ensuring the involvement of key stakeholders and authorities.

Work steps towards the fulfillment of these objectives included:

A review and analysis of current water politics and the status of water resources

an assessment of future trends in water resources, available water supply, water

demand, water pollution and of the impact from selected existing WDM programs in

Jordan,

the calculation of economic values of water in the different sectors of water demand,

the workshop‐based development and impact assessment of alternative scenarios on

the development of water demand in Jordan and

the identification of pre‐conditions for the successful implementation of each

scenario.

This report summarizes and integrates information from the more detailed reports on each

of the work steps.

6

Chapter 1: Prospective water demands of Jordan

Jordan's water requirements started to exceed its natural water resources already in the

1970s (1). The Jordanian government undertook substantial efforts over the last decades to

alleviate this deficit through the mobilization of additional water resources, which included

surface water, water recycling, desalination and extractions from non‐renewable aquifers.

However, the gap between sustainable water supply and water consumption still increases

until today. Demographic and economic growth as well as the intended developments in

mining and new energies will magnify the

speed of growth in water demand.

The recorded total water use in 2009

amounted to 883 MCM/year (2), which

may be less than the factual water use due

to partially uncontrolled abstraction of

groundwater in particular by agricultural

enterprises and farming systems.

Prognoses of the total water use in 2025 by

the MWI vary around 1,500 and 1,600

MCM/year, but are subject to a number of

potential variations and assumptions about

the development of determining factors

(see Box 1).

These prognoses already contain assumed

effects of current decisions on water

demand management by the MWI. The

"business‐as‐usual" scenario, i.e. the

continuation of water use under the

current conditions without interventions of

the MWI would end up with about 1.998

MCM/year in 2025.

Results from scenario‐based planning1, i.e.

the comparison of situations with different

sets of developments in drivers and

decisions, indicate a range between 1,219 MCM and 1,620 MCM in 2025. This holds under

the assumption of a cap in water for agriculture at a level of 700 MCM/year.

Today, about 90% of the difference between minimum and maximum are a function of the

variations in demographic and economic growth, i.e. drivers, which hardly can be influenced

by decision making on water demand management. This proportion will shrink to about 70%

1 For detailed scenario assumptions and results see appendix 3

Box 1: Insecurities in Water Demand

predictions until 2025

Drivers:

Demographic Growth: may vary between 2.1

and 2.6% per year

Economic Growth: growth in industrial water

demand may vary between 1.3 and 3.9

% per year

Decisions:

Municipal Water Demand: will increase to

93 lcd according to trend, but socio‐

political target is about 112 lcd

Non‐Revenue Water: aspired reduction from

43% today down to 24% in 2025, but

35% in 2025 may be more realistic

according to the utilities

Urban Water Demand Management:

theoretical potentials for savings in

domestic water use amount to 21.4%

in 2025, but viability is disputable

Water for agriculture: a water cap is

decided, but the level is still under

discussion.

7

until 2025. The remaining 30%, which equal about 120 MCM in 2025, depend on water

demand management and the development of water use per capita.

The considered components of this water demand management include the success in

reducing water losses (NRW) and in the implementation of water saving measures in

municipal water use, which includes domestic water use as well as water for tourism,

commerce, education, health, governmental offices, worship and other urban infrastructure.

1.1 Aspiration – 112 lcd in average nationwide

The current domestic water use in Jordan is, with a national average of about 70 lcd,

considerably lower than the 100 lcd, which were proposed by the WHO as the lower bound

of an optimal water access (3). The factual, nationwide average municipal water demand,

which includes besides domestic water also water for commerce, education, health,

governmental offices, worship and other urban infrastructure, is estimated to be up to 112

lcd. Variances within the country range from 102 lcd in Karak up to 138 lcd in Amman.

Jordan's water strategy (4) formulates the goal to increase the nationwide municipal water

supply to a nationwide average of 120 lcd in 2022. However, the current planning by the

MWI calculates with the mentioned 112 lcd (without water losses), but aspires to achieve

this goal already in the immediate future. This is still below the regional target value of 120

to 150 l/c/d but marks a substantial improvement to the past.

Water demand management measures, which are supposed to alleviate the sharply

growing water demand under this scenario, are the reduction of water losses (NRW) and the

implementation of household water

saving measures. Both approaches are

still in the stage of planning and early

implementation, so there is still

insecurity about the size of their factual

success in the future.

A comparison between scenario (a),

where NRW reduction achieves only a

level of 35% and water savings in

households have nearly no effects, and

the scenario (b), where NRW reduction

succeeds in achieving the intended level

of 24% and water saving measures allow

for a reduction of domestic water needs

by 21.4%, indicates that

The difference in total water demand

between both scenarios would

Box 2: Non‐Revenue Water

NRW, which is called Unaccounted‐for

Water (UFW) in the National Water Master

Plan, consists out of:

Administrative losses: this water is part of

the water use, but does not yield

revenues for the utility.

Physical losses: Losses due to leakages and

other inefficiencies in conveyance

systems.

The working assumption of the MWI

assumes an equal share of both types of

losses in the current 43% NRW in municipal

water supply. Assumed reductions in the

scenario calculations consider physical losses

only.

8

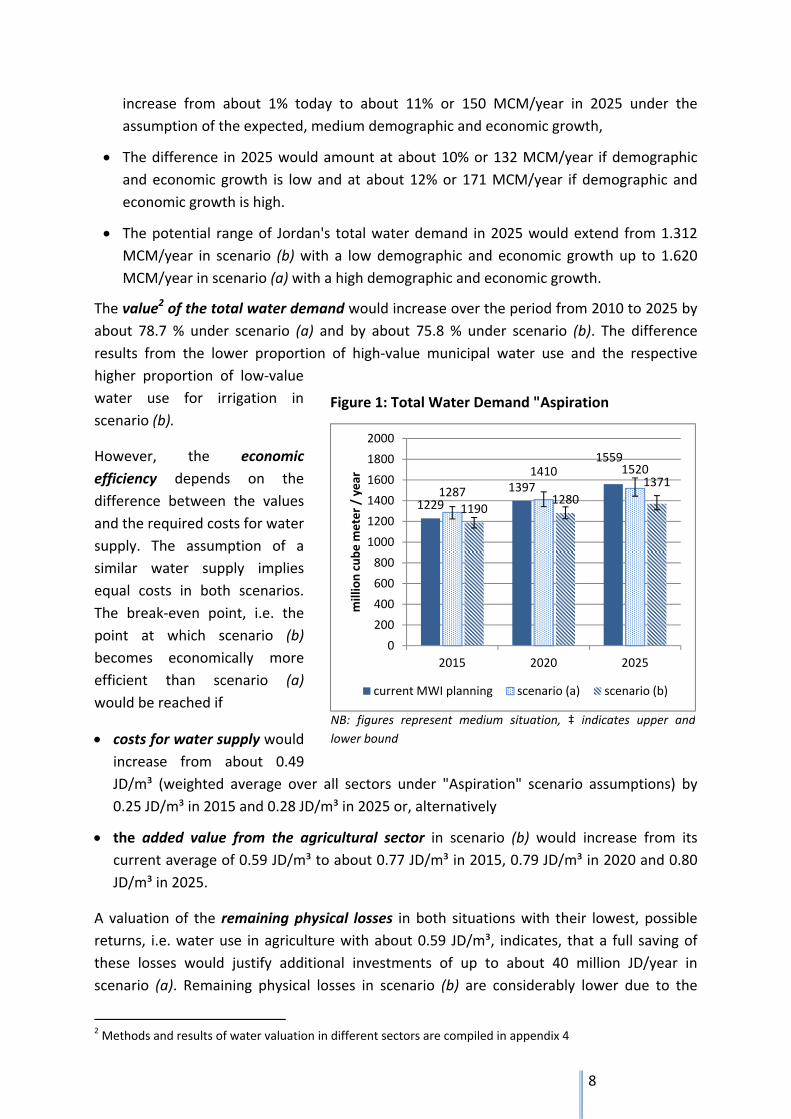

increase from about 1% today to about 11% or 150 MCM/year in 2025 under the

assumption of the expected, medium demographic and economic growth,

The difference in 2025 would amount at about 10% or 132 MCM/year if demographic

and economic growth is low and at about 12% or 171 MCM/year if demographic and

economic growth is high.

The potential range of Jordan's total water demand in 2025 would extend from 1.312

MCM/year in scenario (b) with a low demographic and economic growth up to 1.620

MCM/year in scenario (a) with a high demographic and economic growth.

The value2 of the total water demand would increase over the period from 2010 to 2025 by

about 78.7 % under scenario (a) and by about 75.8 % under scenario (b). The difference

results from the lower proportion of high‐value municipal water use and the respective

higher proportion of low‐value

water use for irrigation in

scenario (b).

However, the economic

efficiency depends on the

difference between the values

and the required costs for water

supply. The assumption of a

similar water supply implies

equal costs in both scenarios.

The break‐even point, i.e. the

point at which scenario (b)

becomes economically more

efficient than scenario (a)

would be reached if

costs for water supply would

increase from about 0.49

JD/m³ (weighted average over all sectors under "Aspiration" scenario assumptions) by

0.25 JD/m³ in 2015 and 0.28 JD/m³ in 2025 or, alternatively

the added value from the agricultural sector in scenario (b) would increase from its

current average of 0.59 JD/m³ to about 0.77 JD/m³ in 2015, 0.79 JD/m³ in 2020 and 0.80

JD/m³ in 2025.

A valuation of the remaining physical losses in both situations with their lowest, possible

returns, i.e. water use in agriculture with about 0.59 JD/m³, indicates, that a full saving of

these losses would justify additional investments of up to about 40 million JD/year in

scenario (a). Remaining physical losses in scenario (b) are considerably lower due to the

2 Methods and results of water valuation in different sectors are compiled in appendix 4

Figure 1: Total Water Demand "Aspiration

NB: figures represent medium situation, ‡ indicates upper and

lower bound

1229

1397

1559

1287

1410 1520

11901280

1371

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2015 2020 2025

million cube m

eter / year

current MWI planning scenario (a) scenario (b)

9

assumed higher efficiency in NRW reduction and would justify additional investments of 14

million JD/year in 2025.

1.2 Trend – continuation of past developments in water demand

A continuation of the trends over the last decades would lead to a nationwide average of 88

lcd of domestic water use in 2025 plus an additional 5 lcd for other municipal water

demands. The differences in municipal water demand within the country would vary

between 68 lcd in the governorate of Ajloun and about 110 lcd in Amman and Aqaba,

whereby the population in all governorates except for these both would receive less than

100 lcd in 2025. т‡

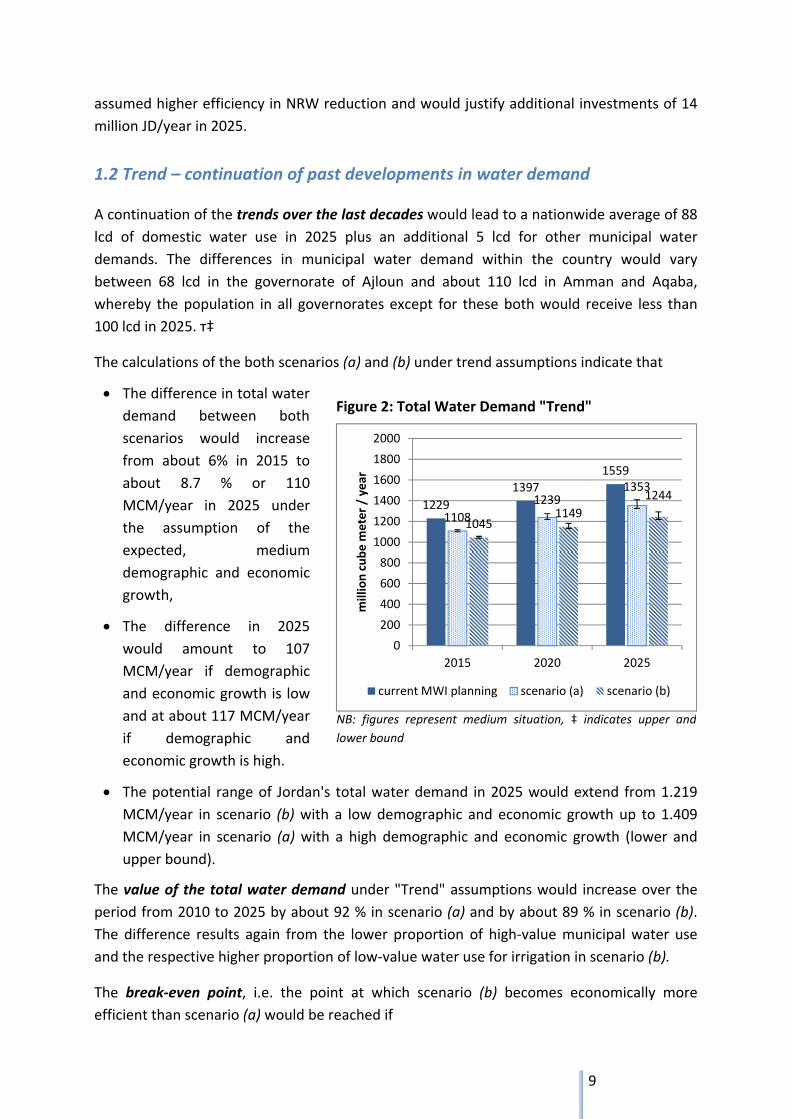

The calculations of the both scenarios (a) and (b) under trend assumptions indicate that

The difference in total water

demand between both

scenarios would increase

from about 6% in 2015 to

about 8.7 % or 110

MCM/year in 2025 under

the assumption of the

expected, medium

demographic and economic

growth,

The difference in 2025

would amount to 107

MCM/year if demographic

and economic growth is low

and at about 117 MCM/year

if demographic and

economic growth is high.

The potential range of Jordan's total water demand in 2025 would extend from 1.219

MCM/year in scenario (b) with a low demographic and economic growth up to 1.409

MCM/year in scenario (a) with a high demographic and economic growth (lower and

upper bound).

The value of the total water demand under "Trend" assumptions would increase over the

period from 2010 to 2025 by about 92 % in scenario (a) and by about 89 % in scenario (b).

The difference results again from the lower proportion of high‐value municipal water use

and the respective higher proportion of low‐value water use for irrigation in scenario (b).

The break‐even point, i.e. the point at which scenario (b) becomes economically more

efficient than scenario (a) would be reached if

Figure 2: Total Water Demand "Trend"

NB: figures represent medium situation, ‡ indicates upper and

lower bound

1229

1397

1559

1108

12391353

10451149

1244

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2015 2020 2025

million cube m

eter / year

current MWI planning scenario (a) scenario (b)

10

costs for water supply would increase from the currently about 0.43 JD/m³ (weighted

average over all sectors under "Trend" assumptions) by 0.19 JD/m³ in 2015 and 0.21

JD/m³ in 2025 or, alternatively

the added value from the agricultural sector in scenario (b) would increase from its

current average of 0.59 JD/m³ to about 0.68 JD/m³ in 2015, 0.70 JD/m³ in 2020 and 0.72

JD/m³ in 2025.

A valuation of the remaining physical losses in both situations with their lowest, possible

returns, i.e. water use in agriculture with about 0.59 JD/m³, indicates, that a full saving of

these losses would justify additional investments of up to about 25.7 million JD/year in

scenario (a). Remaining physical losses in scenario (b) are considerably lower due to the

assumed higher efficiency in NRW reduction and would justify additional investments of 11

million JD/year in 2025.

1.3 Major differences between "Aspiration" and "Trend"

Increasing the municipal water use of Jordanians from trend extrapolations to a regionally

comparable level of 112 lcd would require an additional amount of 180 MCM of water in

2015 and of 167 MCM in 2025. This holds under the assumption of medium developments in

demography and economy.

Low growth in demography and economy would decrease the additionally required water to

124 MCM in 2015 and 118 MCM in 2025. High growth in both drivers would increase the

additionally required water to 224 MCM in 2015 and 211 MCM in 2025. The decreasing

difference between 2015 and 2025 is in all cases due to the steady increase of daily water

use under "Trend" assumptions over the observed period.

Changes in demographic and economic developments have considerably stronger effects on

the total water demand under "Aspiration" assumptions than under "Trend" assumptions.

Consequences for planning under "Aspiration" assumptions include the necessity for a more

diligent consideration of contingency plans for potential disproportionate increases in water

requirements as well as the related higher investment costs in water supply and storage

infrastructure.

Investments in water savings under "Trend" assumptions become already cost‐effective at a

lower level of increases in water costs or with lower increases in water use efficiency in

agriculture. This effect originates from the higher value of municipal water compared to

water for agriculture and the higher proportion of the former in the total water use under

"Aspiration" assumptions. It is correct from an economic point of view, but disregards the

fact that the value of water for municipal purposes is, amongst others, a function of water

costs. This emphasizes the difference between financial budget calculations of the

government, which may come to different results, and economic evaluations, which focus on

the value added of the whole national economy only.

11

1.4 Intersectoral re‐allocation

One option for achieving the aspired 112 lcd without additional pressure on Jordan's already

stressed water balance is the transfer of freshwater from the agricultural to the municipal

sector of water demand. The analysis of effects from such transfers was based on the

"Trend" scenario (a), i.e. the situation where NRW are reduced to 35% in 2025 and water

savings in households have nearly no effects.

The initial municipal water use amounts to 74 MCM/year and increases under the scenario

on water re‐allocation continuously to 112 lcd in 2020. The cap on water for agriculture was

assumed at 700 MCM in the initial year and required water for covering the increasing

municipal water needs was

taken from this amount in

the following years.

The additional require‐

ments of municipal water

demand would cause a

reallocation from

agriculture of about 70

MCM/year already in 2015.

This amount more than

doubles to 149 MCM/year

until 2020, the year when

municipal water demands

would be adjusted to a

regionally comparative

level. A low demographic

and economic growth

would lead to an about

1.2% lower increase, a high

developments in these drivers to a 7.4% higher increase in municipal water demand.

However, recycling of wastewater from municipal water use and decreasing physical NRW

would lessen the impact on water re‐allocation for agriculture already by 5 MCM in 2015.

The combined effects would exceed the required water withdrawal for agriculture from

around 2020 and lead to a slight recovery of water availability for agriculture until 2025,

assuming that treated wastewater amounts to 50% of municipal water use.

The higher value of water use in the municipal sector compared to the water value in

agriculture leads to an increase of the total value of water use by about 1 %. However, losses

in agricultural net returns (operation surplus) would amount to about 36 million JD/year in

2015, 83 million JD/year around 2020 and 79 million JD/year in 2025.

2010 2015 2020 2025

Nuclear Power 0 0 50 100

Touristic 6 10 18 19

Industrial 52 78 91 100

Municipal 258 385 527 573

Agriculture 700 635 552 560

0

200

400

600

800

1000

1200

1400

1600

million cube m

eter

Agriculture Municipal Industrial

Touristic Nuclear Power

Figure 3: Water re‐allocation from agriculture to municipal

water use, "Trend" scenario (a)

12

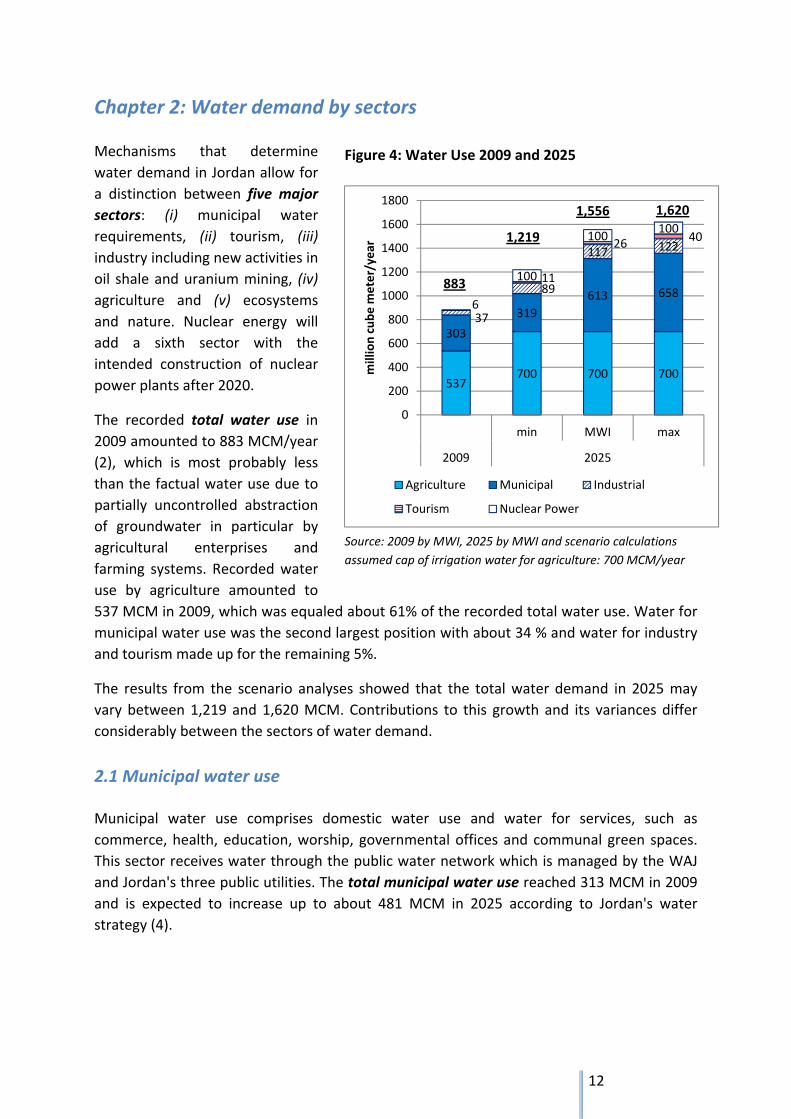

Chapter 2: Water demand by sectors

Mechanisms that determine

water demand in Jordan allow for

a distinction between five major

sectors: (i) municipal water

requirements, (ii) tourism, (iii)

industry including new activities in

oil shale and uranium mining, (iv)

agriculture and (v) ecosystems

and nature. Nuclear energy will

add a sixth sector with the

intended construction of nuclear

power plants after 2020.

The recorded total water use in

2009 amounted to 883 MCM/year

(2), which is most probably less

than the factual water use due to

partially uncontrolled abstraction

of groundwater in particular by

agricultural enterprises and

farming systems. Recorded water

use by agriculture amounted to

537 MCM in 2009, which was equaled about 61% of the recorded total water use. Water for

municipal water use was the second largest position with about 34 % and water for industry

and tourism made up for the remaining 5%.

The results from the scenario analyses showed that the total water demand in 2025 may

vary between 1,219 and 1,620 MCM. Contributions to this growth and its variances differ

considerably between the sectors of water demand.

2.1 Municipal water use

Municipal water use comprises domestic water use and water for services, such as

commerce, health, education, worship, governmental offices and communal green spaces.

This sector receives water through the public water network which is managed by the WAJ

and Jordan's three public utilities. The total municipal water use reached 313 MCM in 2009

and is expected to increase up to about 481 MCM in 2025 according to Jordan's water

strategy (4).

Figure 4: Water Use 2009 and 2025

537700 700 700

303

319

613 658

37

89

117 122

6

11

2640

100

100100

0

200

400

600

800

1000

1200

1400

1600

1800

min MWI max

2009 2025

million cube m

eter/year

Agriculture Municipal Industrial

Tourism Nuclear Power

883

1,219

1,556 1,620

Source: 2009 by MWI, 2025 by MWI and scenario calculations

assumed cap of irrigation water for agriculture: 700 MCM/year

13

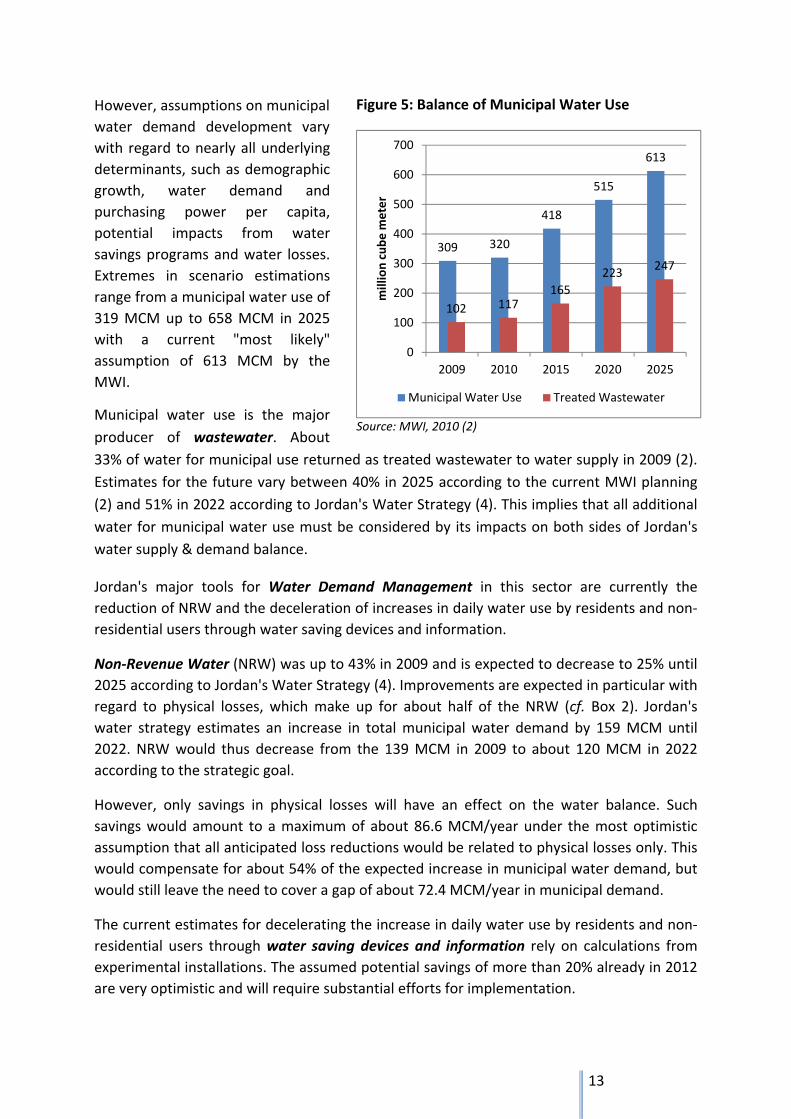

However, assumptions on municipal

water demand development vary

with regard to nearly all underlying

determinants, such as demographic

growth, water demand and

purchasing power per capita,

potential impacts from water

savings programs and water losses.

Extremes in scenario estimations

range from a municipal water use of

319 MCM up to 658 MCM in 2025

with a current "most likely"

assumption of 613 MCM by the

MWI.

Municipal water use is the major

producer of wastewater. About

33% of water for municipal use returned as treated wastewater to water supply in 2009 (2).

Estimates for the future vary between 40% in 2025 according to the current MWI planning

(2) and 51% in 2022 according to Jordan's Water Strategy (4). This implies that all additional

water for municipal water use must be considered by its impacts on both sides of Jordan's

water supply & demand balance.

Jordan's major tools for Water Demand Management in this sector are currently the

reduction of NRW and the deceleration of increases in daily water use by residents and non‐

residential users through water saving devices and information.

Non‐Revenue Water (NRW) was up to 43% in 2009 and is expected to decrease to 25% until

2025 according to Jordan's Water Strategy (4). Improvements are expected in particular with

regard to physical losses, which make up for about half of the NRW (cf. Box 2). Jordan's

water strategy estimates an increase in total municipal water demand by 159 MCM until

2022. NRW would thus decrease from the 139 MCM in 2009 to about 120 MCM in 2022

according to the strategic goal.

However, only savings in physical losses will have an effect on the water balance. Such

savings would amount to a maximum of about 86.6 MCM/year under the most optimistic

assumption that all anticipated loss reductions would be related to physical losses only. This

would compensate for about 54% of the expected increase in municipal water demand, but

would still leave the need to cover a gap of about 72.4 MCM/year in municipal demand.

The current estimates for decelerating the increase in daily water use by residents and non‐

residential users through water saving devices and information rely on calculations from

experimental installations. The assumed potential savings of more than 20% already in 2012

are very optimistic and will require substantial efforts for implementation.

Source: MWI, 2010 (2)

309 320

418

515

613

102 117165

223247

0

100

200

300

400

500

600

700

2009 2010 2015 2020 2025million cube m

eter

Municipal Water Use Treated Wastewater

Figure 5: Balance of Municipal Water Use

14

However, the minimum water use in the municipal sector of 319 MCM in 2025 relies on the

assumption that municipal water use does not grow faster than its trend in the past and that

all of these expected water savings can be achieved. The average water supply would then

amount to 69 liters per capita and day only, which is in the area of the current water

provision level and articulately below regionally comparable standards.

The costs of water supply via public networks vary between 0.50 JD/m³ and 0.61 JD/m³.

However, the apportionment of these costs on billed water only increases the costs per m³

to a range from 0.8 and 0.9 JD/m³ in Amman, Aqaba, and the northern regions and up to

1.20 JD/m³ in the rest of Jordan. Current

average water tariffs for residential

customers cover with 0.42 JD/m³ only a

part of the full costs. Non‐residents, e.g.

commerce and offices, pay 1 JD/m³.

Wastewater discharge adds to both tariffs

with another 0.39 JD/m³ and 0.59 JD/m³,

respectively.

Costs of water provision will increase in

the future due to the additionally required

water from new investment projects, such

as the Disi water conveyance, water

network rehabilitation, Jordan Read Sea

Conveyance or its alternative, the Red‐Sea‐

Dead‐Sea Project. As an example,

estimated costs of Disi water supply are up

to about 0.8 JD/m³. Adding distribution

cost and accounting for NRW at the

current level would bring the costs of

delivering Disi water to customers up to

around 1.5 JD/m³.

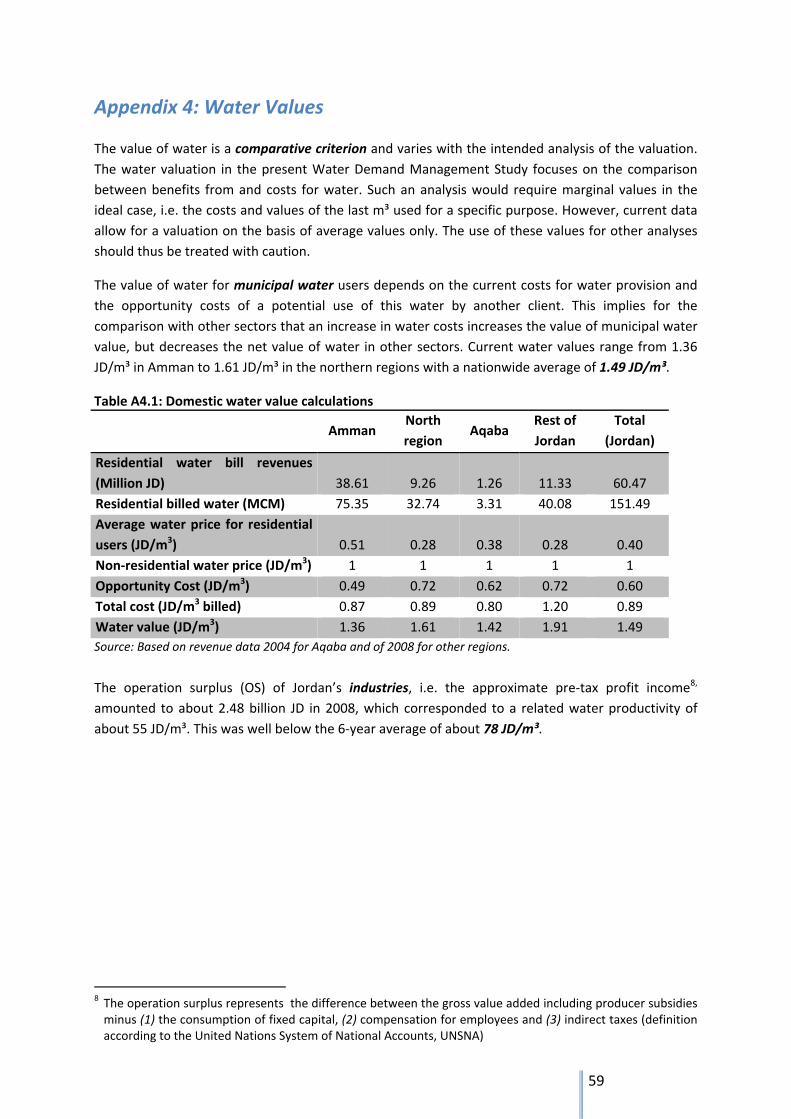

The value of water3 for municipal water

users depends on the current costs for water provision and the opportunity costs of a

potential use of this water by another client. This implies for the comparison with other

sectors that an increase in water costs increases the value of municipal water value, but

decreases the net value of water in other sectors. Current water values range from 1.36

JD/m³ in Amman to 1.61 JD/m³ in the northern regions with a nationwide average of 1.49

JD/m³.

3 On methods and results for water valuation see appendix 4

Box 3: Definitions

Water demand = requested water for

(monetary and non‐monetary) beneficial

use

Water requirement = water required for

sustaining living standards (households),

operations (industry, tourism,

agriculture) and functionality (e.g.

nature, agriculture)

Water use = water demand covered by water

supply

Water consumption = water use minus return

flows

Water supply = water provision from developed

water resources

Water allocation = determined amount of

water supply for a specific purpose or

region

15

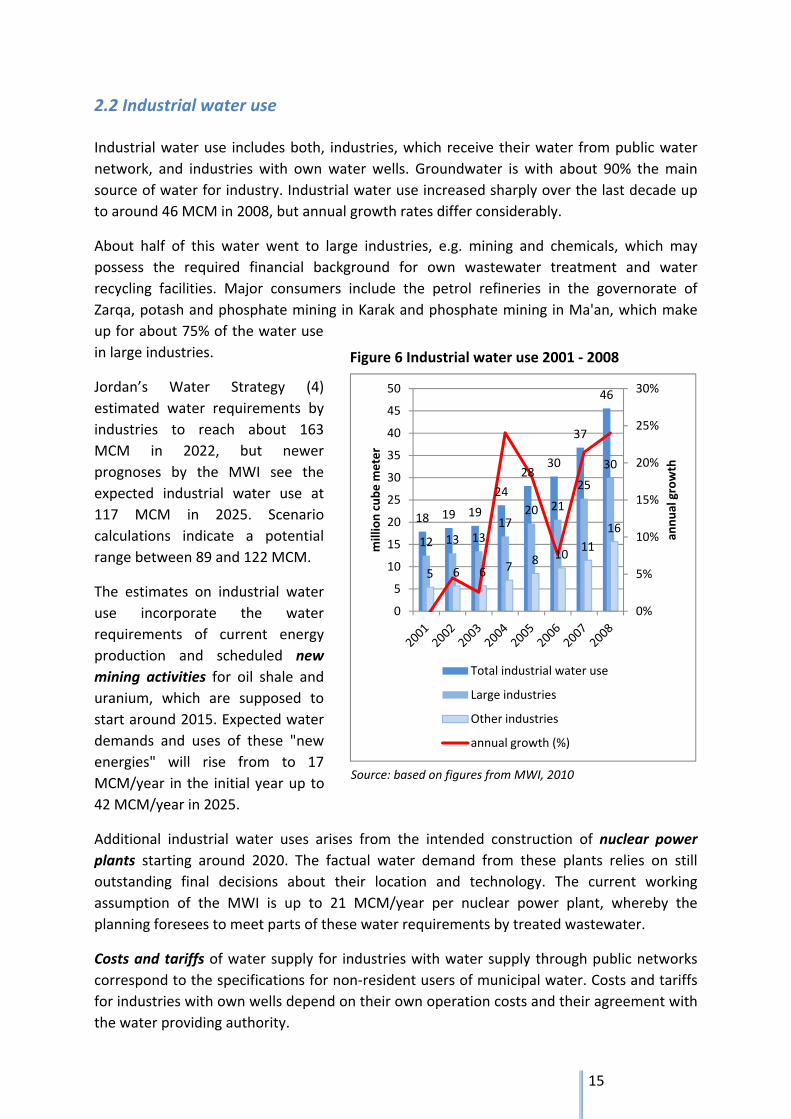

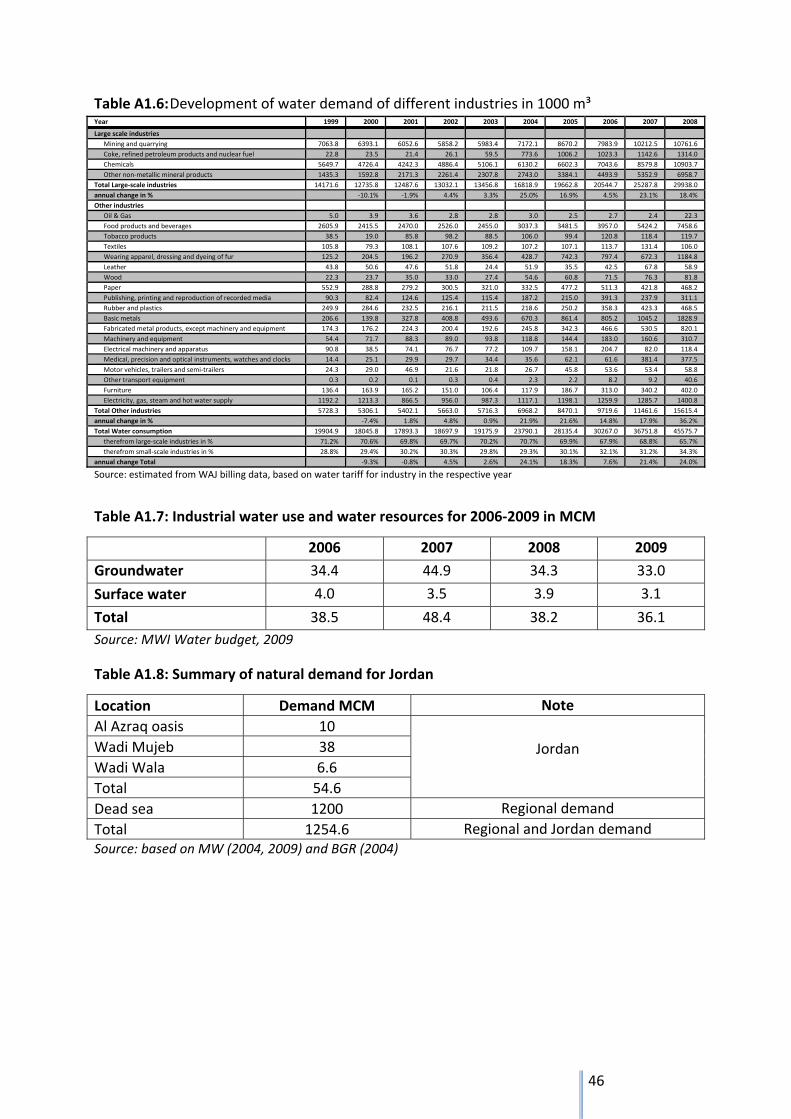

2.2 Industrial water use

Industrial water use includes both, industries, which receive their water from public water

network, and industries with own water wells. Groundwater is with about 90% the main

source of water for industry. Industrial water use increased sharply over the last decade up

to around 46 MCM in 2008, but annual growth rates differ considerably.

About half of this water went to large industries, e.g. mining and chemicals, which may

possess the required financial background for own wastewater treatment and water

recycling facilities. Major consumers include the petrol refineries in the governorate of

Zarqa, potash and phosphate mining in Karak and phosphate mining in Ma'an, which make

up for about 75% of the water use

in large industries.

Jordan’s Water Strategy (4)

estimated water requirements by

industries to reach about 163

MCM in 2022, but newer

prognoses by the MWI see the

expected industrial water use at

117 MCM in 2025. Scenario

calculations indicate a potential

range between 89 and 122 MCM.

The estimates on industrial water

use incorporate the water

requirements of current energy

production and scheduled new

mining activities for oil shale and

uranium, which are supposed to

start around 2015. Expected water

demands and uses of these "new

energies" will rise from to 17

MCM/year in the initial year up to

42 MCM/year in 2025.

Additional industrial water uses arises from the intended construction of nuclear power

plants starting around 2020. The factual water demand from these plants relies on still

outstanding final decisions about their location and technology. The current working

assumption of the MWI is up to 21 MCM/year per nuclear power plant, whereby the

planning foresees to meet parts of these water requirements by treated wastewater.

Costs and tariffs of water supply for industries with water supply through public networks

correspond to the specifications for non‐resident users of municipal water. Costs and tariffs

for industries with own wells depend on their own operation costs and their agreement with

the water providing authority.

Figure 6 Industrial water use 2001 ‐ 2008

Source: based on figures from MWI, 2010

18 19 19

24

2830

37

46

12 13 1317

20 21

25

30

5 6 6 7 8 1011

16

0%

5%

10%

15%

20%

25%

30%

0

5

10

15

20

25

30

35

40

45

50

annual growth

million cube m

eter

Total industrial water use

Large industries

Other industries

annual growth (%)

16

Applied and foreseen Water Demand Management tools for the industrial sector focus on

wastewater treatment, i.e. the reduction of water consumption instead of water use. All

major industries and mines are supposed to be connected or equipped with wastewater

treatment plants until 2022, which would make up for 45 to 61 MCM/year of treated

wastewater under the assumption of a recycling rate of 50%.

However, Jordan's Water Strategy (4) foresees only 27 MCM of treated wastewater for

industrial use in 2022, which would leave some leeway for water chain management, i.e. the

use of recycled water from industries in agriculture or for environmental purposes. Recycling

of water from Nuclear Power Plants for use in other sectors is currently not regarded as an

option.

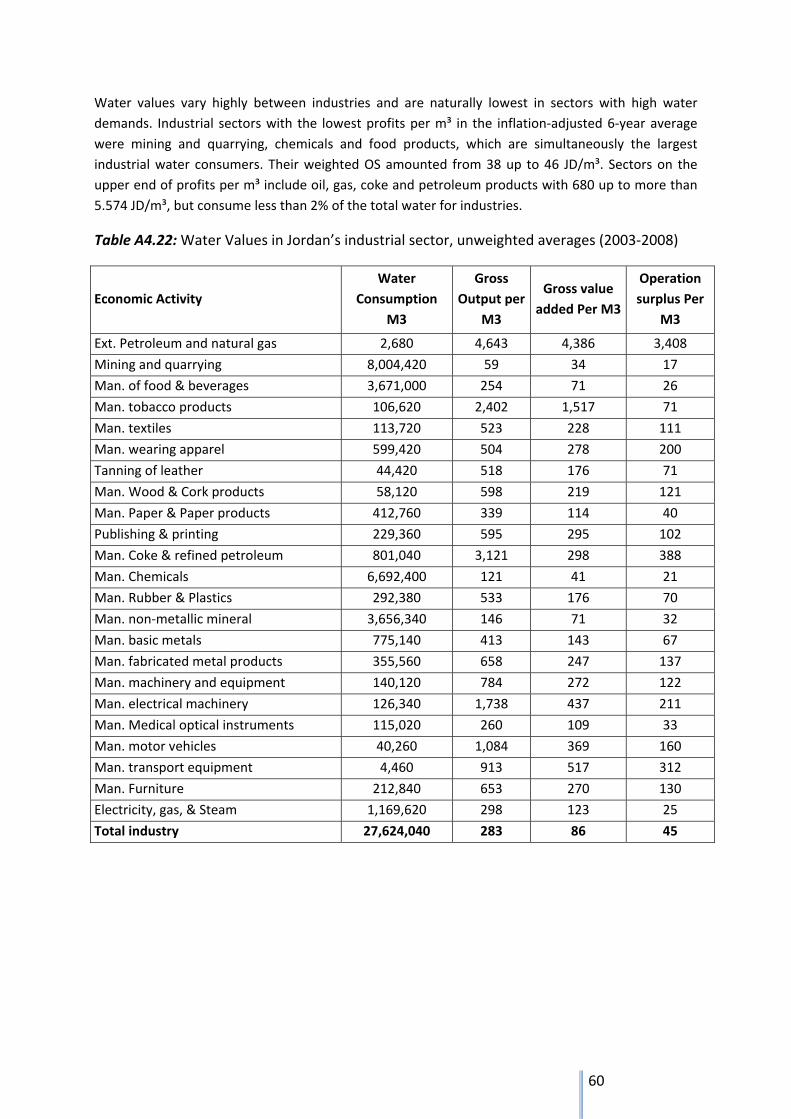

Water values vary highly between industries and are naturally lowest in sectors with high

water demands. Industrial sectors with the lowest profits per m³ in the inflation‐adjusted 6‐

year average were mining and quarrying, chemicals and food products, which are

simultaneously the largest industrial water consumers. Their weighted operation surplus, i.e.

the approximate pre‐tax profit income4, amounted from 38 up to 46 JD/m³. Sectors on the

upper end of profits per m³ include oil, gas, coke and petroleum products with 680 up to

more than 5.574 JD/m³, but consume less than 2% of the total water for industries.

The total operation surplus of Jordan’s industries, amounted to about 2.48 billion JD in 2008,

which corresponded to an average operation surplus of about 55 JD/m³. This was well below

the 6‐year average of about 78 JD/m³.

2.3 Water use by tourism

Water use by tourism includes water for hotels, restaurants and other tourist services and

facilities. Water to this sector is supplied by WAJ and the utilities via the domestic water

network and is considered administratively as part of the municipal water supply. Touristic

water use reached around 10 MCM in 2007 and is expected to reach 29 MCM by year 2025

(NWS, 2009). Scenario calculations set the range for 2025 between 11 and 40 MCM.

The majority of water use in tourism arises in the three touristic centers Amman, Aqaba and

the hotel resorts along the eastern shore of the Dead Sea. Applied and foreseen Water

Demand Management tools comprise amongst others greywater and water recycling.

International studies show that water saving techniques allow for a decrease of water use in

hotels by about 20% without affecting standards or clients' satisfaction. However, these

studies were conducted in countries with moderate climates and experiences in Jordan are

still outstanding.

4 The operation surplus represents the difference between the gross value added including producer subsidies minus (1) the consumption of fixed capital, (2) compensation for employees and (3) indirect taxes (definition according to the United Nations System of National Accounts, UNSNA)

17

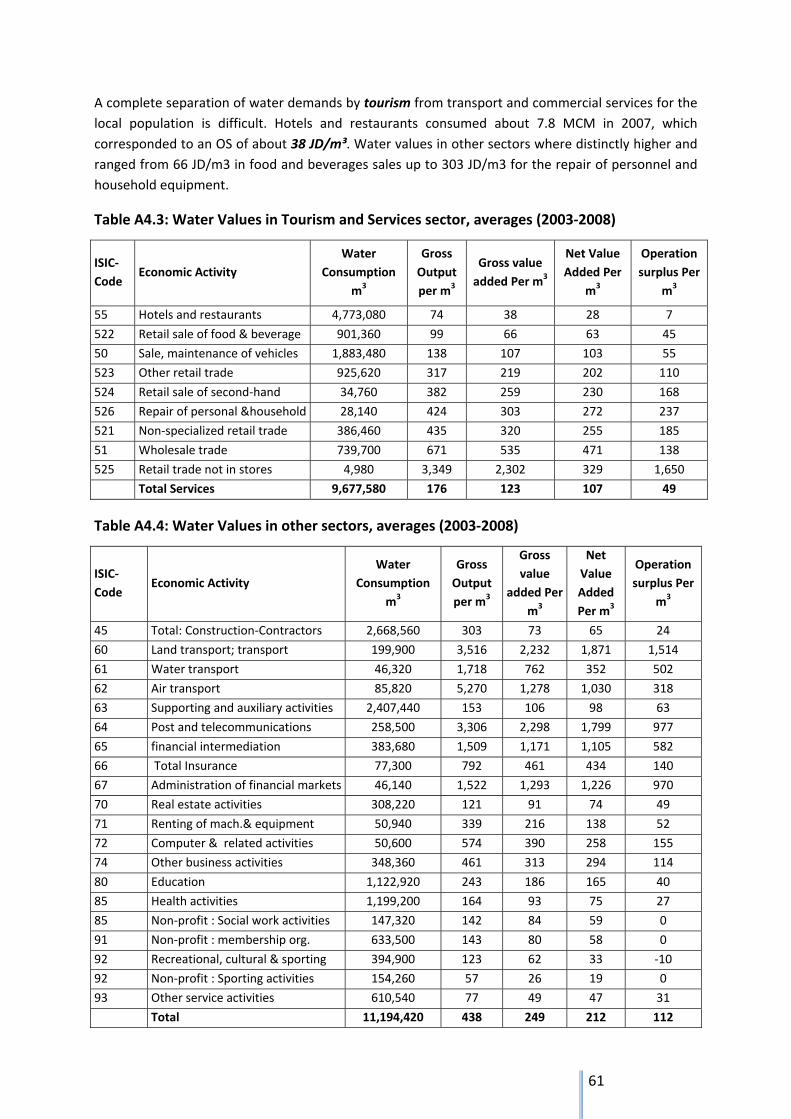

A complete separation of water demands by tourism from transport and commercial

services for the local population is difficult. Hotels and restaurants consumed about 7.8

MCM in 2007, which corresponded to an operation surplus of about 38 JD/m³. Water values

in other sectors where distinctly higher and ranged from 66 JD/m3 in food and beverages

sales up to 303 JD/m3 for the repair of personnel and household equipment (cf. appendix 4).

2.4 Agricultural water use

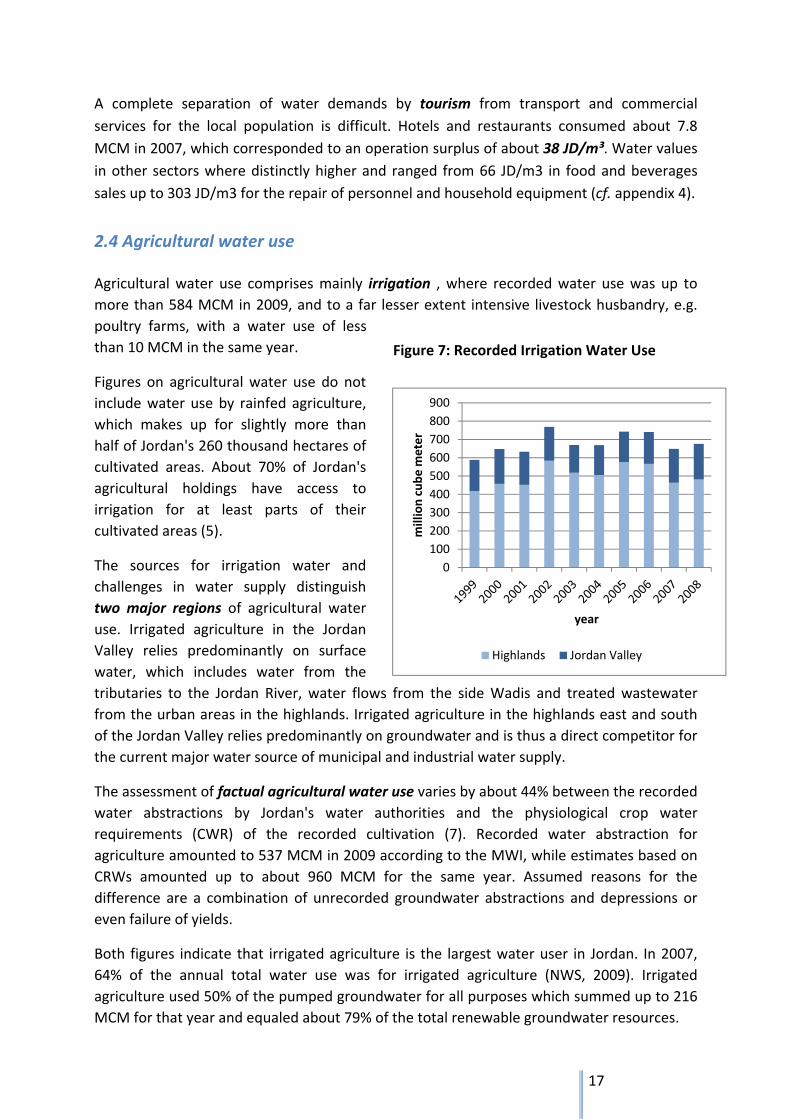

Agricultural water use comprises mainly irrigation , where recorded water use was up to

more than 584 MCM in 2009, and to a far lesser extent intensive livestock husbandry, e.g.

poultry farms, with a water use of less

than 10 MCM in the same year.

Figures on agricultural water use do not

include water use by rainfed agriculture,

which makes up for slightly more than

half of Jordan's 260 thousand hectares of

cultivated areas. About 70% of Jordan's

agricultural holdings have access to

irrigation for at least parts of their

cultivated areas (5).

The sources for irrigation water and

challenges in water supply distinguish

two major regions of agricultural water

use. Irrigated agriculture in the Jordan

Valley relies predominantly on surface

water, which includes water from the

tributaries to the Jordan River, water flows from the side Wadis and treated wastewater

from the urban areas in the highlands. Irrigated agriculture in the highlands east and south

of the Jordan Valley relies predominantly on groundwater and is thus a direct competitor for

the current major water source of municipal and industrial water supply.

The assessment of factual agricultural water use varies by about 44% between the recorded

water abstractions by Jordan's water authorities and the physiological crop water

requirements (CWR) of the recorded cultivation (7). Recorded water abstraction for

agriculture amounted to 537 MCM in 2009 according to the MWI, while estimates based on

CRWs amounted up to about 960 MCM for the same year. Assumed reasons for the

difference are a combination of unrecorded groundwater abstractions and depressions or

even failure of yields.

Both figures indicate that irrigated agriculture is the largest water user in Jordan. In 2007,

64% of the annual total water use was for irrigated agriculture (NWS, 2009). Irrigated

agriculture used 50% of the pumped groundwater for all purposes which summed up to 216

MCM for that year and equaled about 79% of the total renewable groundwater resources.

Source: based on figures from MWI, 2010

0

100

200

300

400

500

600

700

800

900million cube m

eter

year

Highlands Jordan Valley

Figure 7: Recorded Irrigation Water Use

18

Agricultural production contributes only about 3.6% to Jordan's GDP and employs 2% of its

labor force, but 30% of Jordan's population lives in rural areas. Arguments for water supply

to agriculture do thus not only rely on production values but also on functions of agriculture

in the preservation and development of rural systems and areas.

The Jordanian government decided to approach future water allocation to agriculture by a

combined strategy of control of hitherto unrecorded groundwater abstractions and a

simultaneous cap of water for this sector. The intended level of the cap is still under

discussion. Current ideas range between 700 and 1,000 MCM/year, which would put the

water allocation somewhere between half and the upper limit of the estimated physiological

water demand for the current cropping pattern on Jordan's cultivated areas. Most of the

increased control of groundwater wells and the water cap will affect agriculture in the

highlands, which use currently about 70% of the recorded total irrigation water.

Applied and foreseen Water Demand Management tools in agriculture focus in particular

on increases in irrigation efficiency, water tariffing and water caps. Increases in water

efficiency include technical as well as managerial improvements, e.g. the promotion of water

users associations and participatory irrigation management (PIM). The evaluation of first

experiences with PIM in the Jordan Valley yielded promising results with regard to cost

reduction in water supply and increases in economic water use efficiency. However, all

measures which focus on irrigation efficiency and water productivity promoted the

extension of the now even more profitable agricultural activities and increased rather than

decreased water demands.

The Jordan Valley Authority uses blocked tariffs with increasing prices for higher water

quotas already since the 1990s. The experience shows that this also did not lead to

decreases in water demand, which is a function of land tenureship, rental agreements,

resource endowment of different types of farming systems and the situation of alternative

incomes for farming families.

Water quotas and charges for over‐abstraction of wells in the highlands, as stipulated in the

Underground Water Control By‐Law no. 85 (2002) and its amendments (2003, 2004, 2007),

did not solve the problem of unsustainable groundwater withdrawal either.

Jordan's water strategy foresees a cap for water use in agriculture and an enforced control

of groundwater abstraction from currently private wells and boreholes. The consequences

and secondary effects of these measures will highly depend on the conditions of these

regulatory measures.

Costs of water for irrigation depend on the source of water and vary widely. The Jordan

Valley Authority (JVA) applies a block tariff structure and charges about 0,02 JD/m³ for water

from the pressurized irrigation water system, which covers approximately 40% percent of

the costs for operation and maintenance (O&M) and 10% of the full costs. However,

irrigation in the Jordan Valley also uses treated and blended wastewater, which would be of

less use otherwise without additional and expensive steps for purification.

19

Costs of water for irrigation in the highlands depend in the first place on the investments

and O&M costs for the private well operators. Tariffs by the water authorities are up to

0.025 JD/m³ for non‐licensed wells and increase stepwise with the amount of water

extraction. Owners of licensed wells pay this tariff only for over‐abstraction, i.e. above

150.000 m³/year.

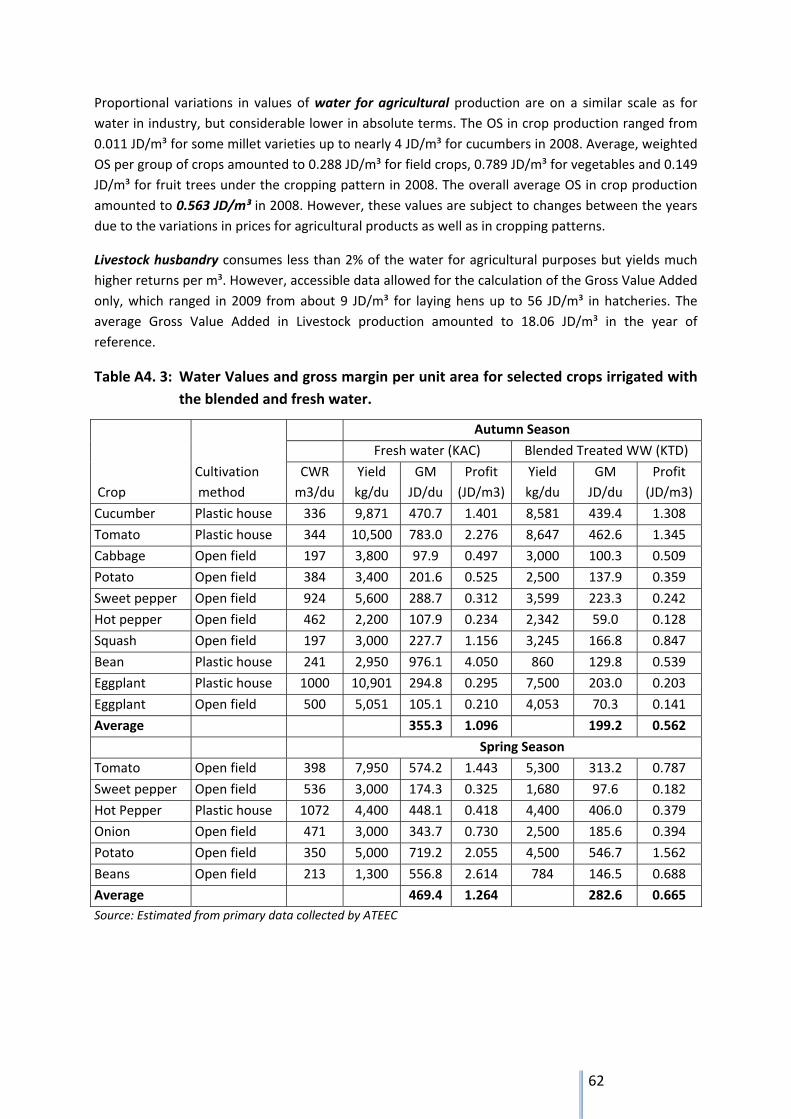

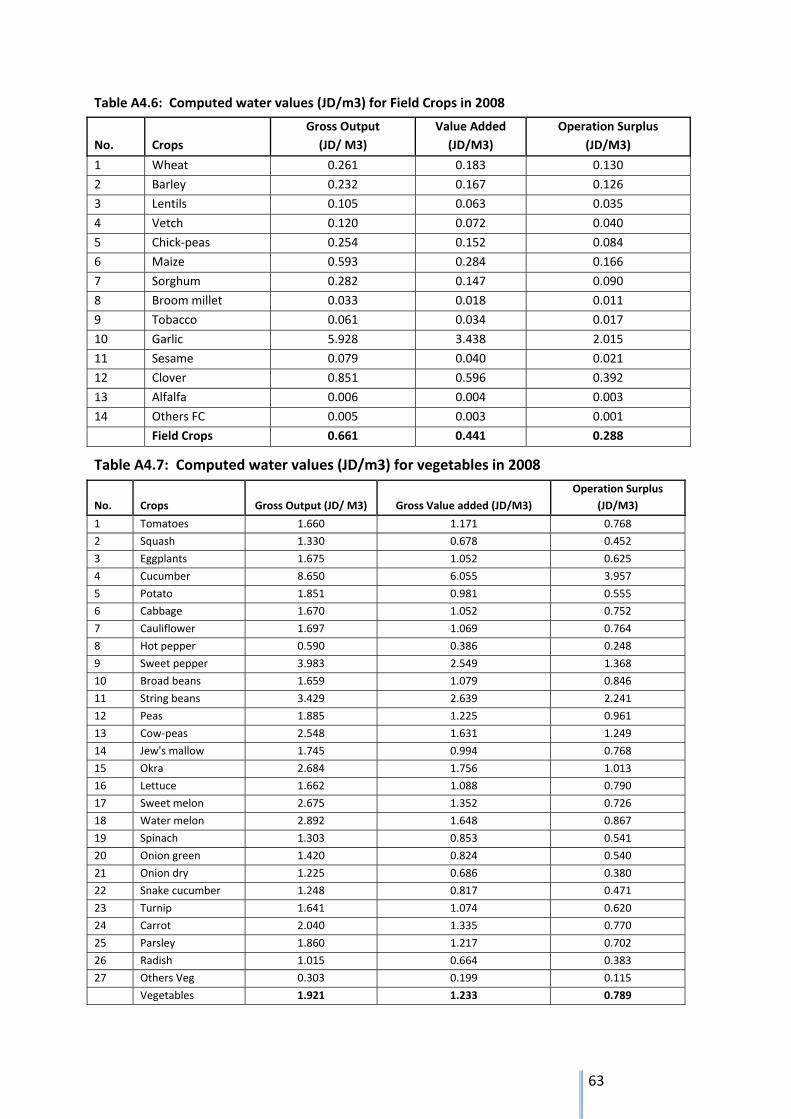

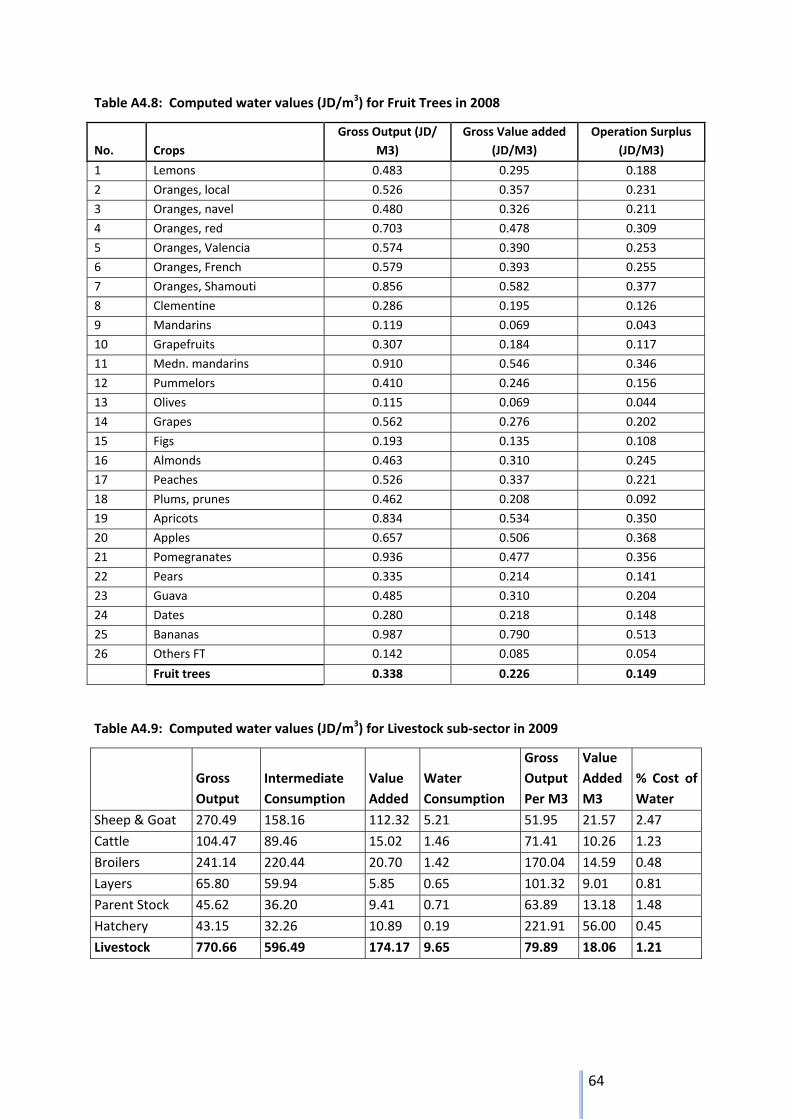

Proportional variations in the value of water for agricultural production are on a similar

scale as for water in industry, but considerable lower in absolute terms. The operation

surplus in crop production ranged from 0.011 JD/m³ for some millet varieties up to nearly 4

JD/m³ for cucumbers in 2008. The average, weighted operation surplus per group of crops

amounted to 0.288 JD/m³ for field crops, 0.789 JD/m³ for vegetables and 0.149 JD/m³ for

fruit trees under the cropping pattern in 2008. The overall average operation surplus in crop

production amounted to 0.563 JD/m³ in 2008. However, these values are subject to changes

between the years due to the variations in prices for agricultural products as well as in

cropping patterns.

Livestock husbandry consumes less than 2% of the water for agricultural purposes but yields

much higher returns per m³. However, accessible data allowed for the calculation of the

Gross Value Added only, which ranged in 2009 from about 9 JD/m³ for laying hens up to 56

JD/m³ in hatcheries. The average Gross Value Added in Livestock production amounted to

18.06 JD/m³ in the year of reference.

2.4.1 Starting points for WDM in the agricultural sector

Agriculture is the only sector of water demand where an intra‐sectoral reallocation of water

is likely. But even in this sector reallocation of water would be restricted to exchanges within

a given location. A mere transfer of water to more water‐efficient crops would benefit

already specialized rich farmers, but discriminates against poorer farmers, who depend on

diversification in order to minimize risk and do not possess the required capacities, e.g.

capital, for the required adjustments of production and marketing structures.

Expectable consequences from an unidirectional focus on economic water use efficiency

alone would include in the first place:

a structural change in Jordanian farming systems towards larger enterprises and a

decline in smaller family farms and traditional farming and

an increase in agricultural water demand due to the improved economics of irrigation

water use in combination with farming enterprises, which possess the required

endowment in land and capital for enhancing their farming business.

Suitable policies and instruments to curtail agricultural water demand without undesired

consequences will depend on the identification of the specific functions of land use systems,

the economic and operational fundamentals of the different types of farming systems, the

desired objectives towards modernization and structural adjustments in the agricultural

sector and the livelihood and environmental structures that Jordan wants to preserve.

20

The central technical challenge is the improvement of farmers' access to irrigation

techniques and training under the simultaneous consideration of

an equitable provision of services to all farmers, which may require additional

adjustments in the economic frame conditions , e.g. access to capital, for farms with

low resource endowment and the respective harmonization in the planning of local

rural development,

the control of groundwater abstraction, which allows for its reduction to a

sustainable level, and

the further expansion of water recycling, i.e. treated wastewater use, which provides

the major alternative water resource.

Data for the required farming systems analyses, which have to include the socio‐economic

situation of concerned farming families, exist in part for the Jordan Valley, even if these data

from 2003 are somewhat outdated. Respective information on farming systems in the

highlands may be hidden in the extensive data bases of Jordan's agricultural surveys, but

would require a comprehensive re‐structuring and analysis of these data.

However, some known bottlenecks for farmers offer first suggestions for starting points of WDM

measures, which may have the double potential of improving the situation of farmers without

simultaneous incentives for more water use.

Timing of water supply: Gaps between the formation of water quantities and the need

for water in agriculture require storage facilities and an outflow management, which

correspond to water requirements in agriculture. A better balance of the management of

water storage systems with water needs in agriculture would improve water use

efficiency in agriculture even without changes in the current cropping patterns.

Groundwater for irrigation is basically available “on demand”. Water from treatment

facilities and other sources provide a more or less constant flow, which requires storage

until relevant irrigation periods. The implementation of storage facilities leads not only to

additional demands to capital for the investments but also requires additional space. The

latter may become a substantial factor in particular when those storage facilities are

placed on land of farming systems with comparatively low land endowment and/or high

potential returns per dunum.

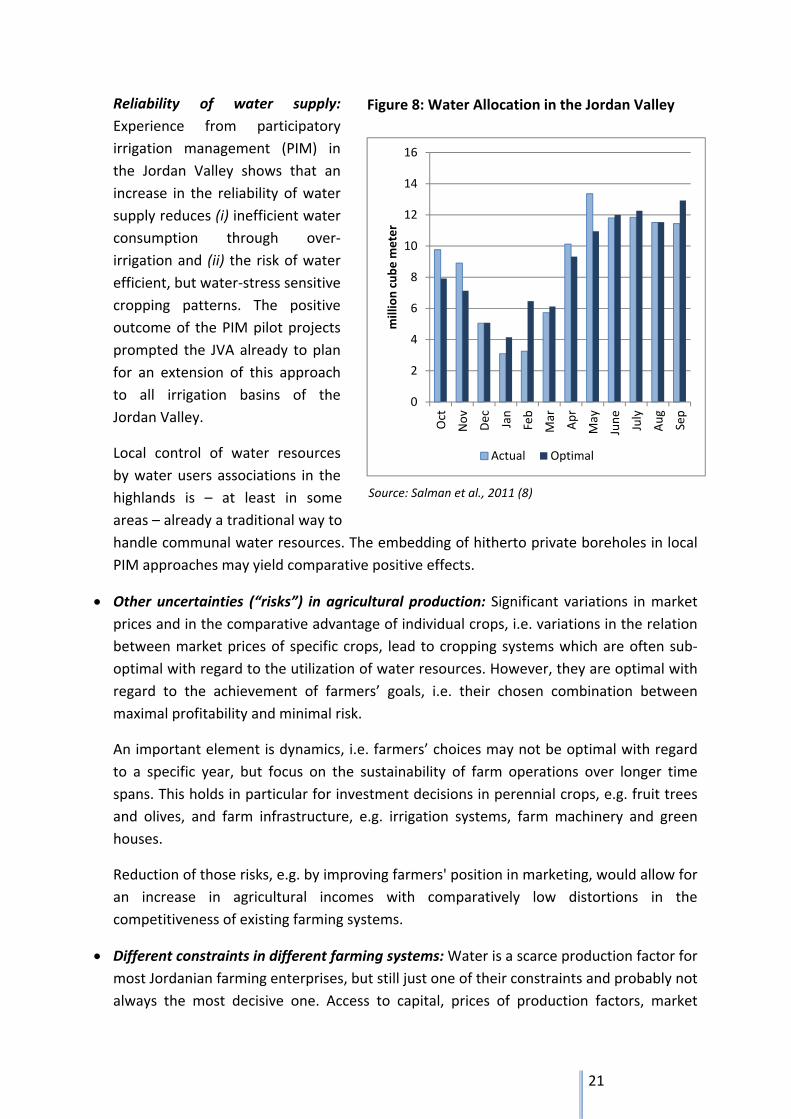

Central storage facilities for larger amounts of water are mostly available in the Jordan

Valley and adjacent side valley (wadis). Timing of water distribution via the conveyance

system connected to King Abdullah Canal (KAC) has to respond to a multitude of

combinations of farmers’ individual objectives, amongst which maximum profits and

minimal risk may be the most important. The comparison between JVA’s intra‐annual

water distribution, the optimal water distribution for attaining maximum profits and the

respective distribution for minimizing risk indicates the difficulty in managing centrally

stored water resources (cf. fig. 8).

21

Reliability of water supply:

Experience from participatory

irrigation management (PIM) in

the Jordan Valley shows that an

increase in the reliability of water

supply reduces (i) inefficient water

consumption through over‐

irrigation and (ii) the risk of water

efficient, but water‐stress sensitive

cropping patterns. The positive

outcome of the PIM pilot projects

prompted the JVA already to plan

for an extension of this approach

to all irrigation basins of the

Jordan Valley.

Local control of water resources

by water users associations in the

highlands is – at least in some

areas – already a traditional way to

handle communal water resources. The embedding of hitherto private boreholes in local

PIM approaches may yield comparative positive effects.

Other uncertainties (“risks”) in agricultural production: Significant variations in market

prices and in the comparative advantage of individual crops, i.e. variations in the relation

between market prices of specific crops, lead to cropping systems which are often sub‐

optimal with regard to the utilization of water resources. However, they are optimal with

regard to the achievement of farmers’ goals, i.e. their chosen combination between

maximal profitability and minimal risk.

An important element is dynamics, i.e. farmers’ choices may not be optimal with regard

to a specific year, but focus on the sustainability of farm operations over longer time

spans. This holds in particular for investment decisions in perennial crops, e.g. fruit trees

and olives, and farm infrastructure, e.g. irrigation systems, farm machinery and green

houses.

Reduction of those risks, e.g. by improving farmers' position in marketing, would allow for

an increase in agricultural incomes with comparatively low distortions in the

competitiveness of existing farming systems.

Different constraints in different farming systems: Water is a scarce production factor for

most Jordanian farming enterprises, but still just one of their constraints and probably not

always the most decisive one. Access to capital, prices of production factors, market

Source: Salman et al., 2011 (8)

Figure 8: Water Allocation in the Jordan Valley

0

2

4

6

8

10

12

14

16

Oct

Nov

Dec Jan

Feb

Mar

Apr

May

June

July

Aug

Sep

million cube m

eter

Actual Optimal

22

access and competition for resources of farming families by alternative employments in

off‐farm sectors often play an at least equally important role.

The consequences of changes in water availability and quality depend much more on the

interrelationships between these constraints in individual farming systems (i.e. systems

that determine farmers’ overall economic success and livelihood) than on agricultural

systems (i.e. cropping systems and the combination of agricultural uses of natural

resources).

The type, amount and complexity of required support for transforming existing farming

systems into sustainable enterprises under changed conditions in water supply depends

on their resource endowment and socio‐economic situation. The formulation of effective

policies for specific farming systems will require further investigations .

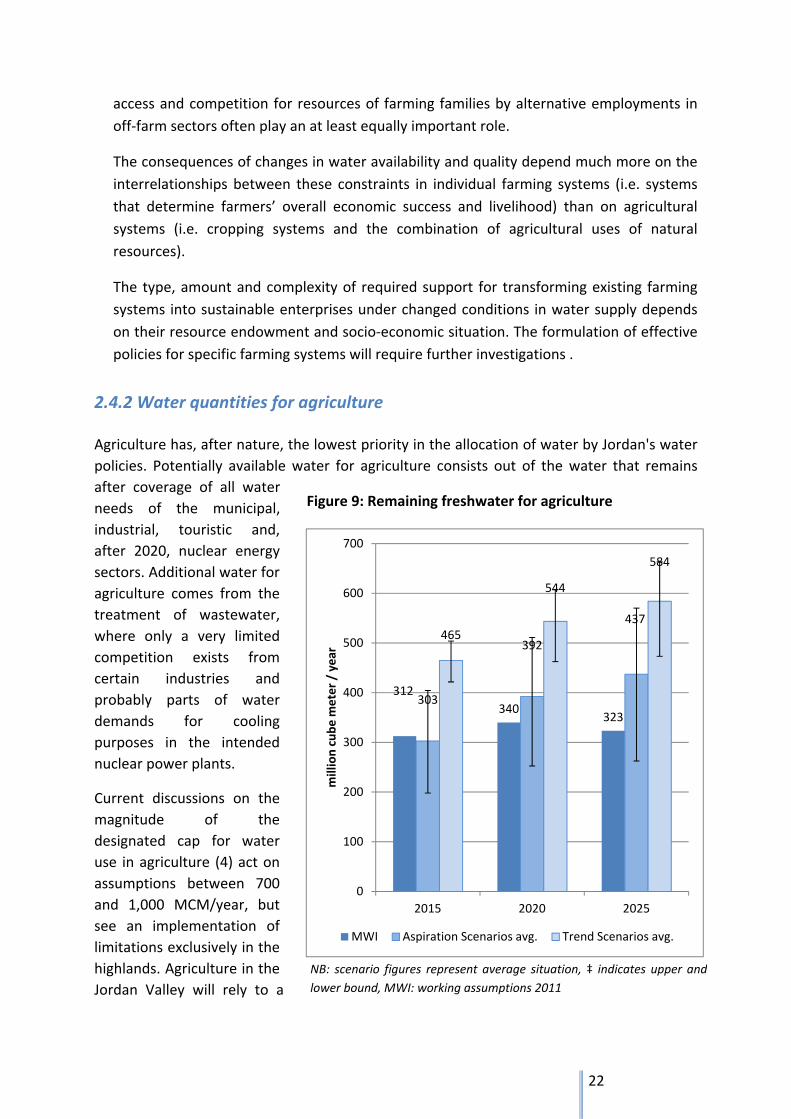

2.4.2 Water quantities for agriculture

Agriculture has, after nature, the lowest priority in the allocation of water by Jordan's water

policies. Potentially available water for agriculture consists out of the water that remains

after coverage of all water

needs of the municipal,

industrial, touristic and,

after 2020, nuclear energy

sectors. Additional water for

agriculture comes from the

treatment of wastewater,

where only a very limited

competition exists from

certain industries and

probably parts of water

demands for cooling

purposes in the intended

nuclear power plants.

Current discussions on the

magnitude of the

designated cap for water

use in agriculture (4) act on

assumptions between 700

and 1,000 MCM/year, but

see an implementation of

limitations exclusively in the

highlands. Agriculture in the

Jordan Valley will rely to a

NB: scenario figures represent average situation, ‡ indicates upper and

lower bound, MWI: working assumptions 2011

Figure 9: Remaining freshwater for agriculture

312

340323

303

392

437465

544

584

0

100

200

300

400

500

600

700

2015 2020 2025

million cube m

eter / year

MWI Aspiration Scenarios avg. Trend Scenarios avg.

23

growing extend on the provision with treated wastewater, which increasingly replaces

freshwater from the tributaries to the Jordan River. This freshwater will be diverted to an

increasing degree to the urban areas in the highland for municipal water supply.

The current calculations by the MWI assume that remaining amounts of freshwater, i.e.

annually available freshwater resources5 minus demands from all other sectors, will amount

to between 312 and 340 MCM/year in the period from 2015 to 2025. The estimations from

the scenario analyses indicate that this amount may vary between far less than 303 MCM in

2015 up to more than 600 MCM in 2025, depending on (i) the factual developments in

demographic and economic growth and (ii) the effects from loss reductions and water

savings.

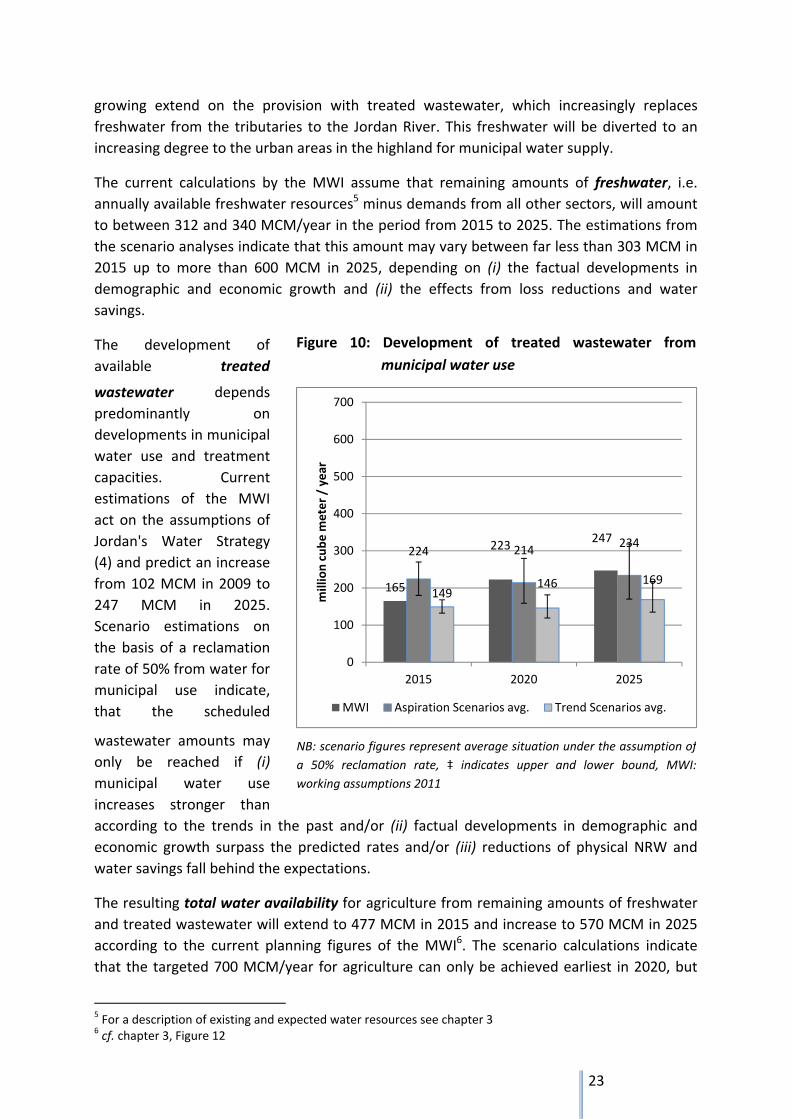

The development of

available treated

wastewater depends

predominantly on

developments in municipal

water use and treatment

capacities. Current

estimations of the MWI

act on the assumptions of

Jordan's Water Strategy

(4) and predict an increase

from 102 MCM in 2009 to

247 MCM in 2025.

Scenario estimations on

the basis of a reclamation

rate of 50% from water for

municipal use indicate,

that the scheduled

wastewater amounts may

only be reached if (i)

municipal water use

increases stronger than

according to the trends in the past and/or (ii) factual developments in demographic and

economic growth surpass the predicted rates and/or (iii) reductions of physical NRW and

water savings fall behind the expectations.

The resulting total water availability for agriculture from remaining amounts of freshwater

and treated wastewater will extend to 477 MCM in 2015 and increase to 570 MCM in 2025

according to the current planning figures of the MWI6. The scenario calculations indicate

that the targeted 700 MCM/year for agriculture can only be achieved earliest in 2020, but

5 For a description of existing and expected water resources see chapter 3 6 cf. chapter 3, Figure 12

NB: scenario figures represent average situation under the assumption of

a 50% reclamation rate, ‡ indicates upper and lower bound, MWI:

working assumptions 2011

165

223247

224 214234

149146 169

0

100

200

300

400

500

600

700

2015 2020 2025

million cube m

eter / year

MWI Aspiration Scenarios avg. Trend Scenarios avg.

Figure 10: Development of treated wastewater from

municipal water use

24

even then only under the assumption of (i) an increase in municipal water use according to

the trends, i.e. a considerably lower water use per capita than 100 lcd and (ii) factual

developments in demographic and economic growth that surpass the predicted rates.

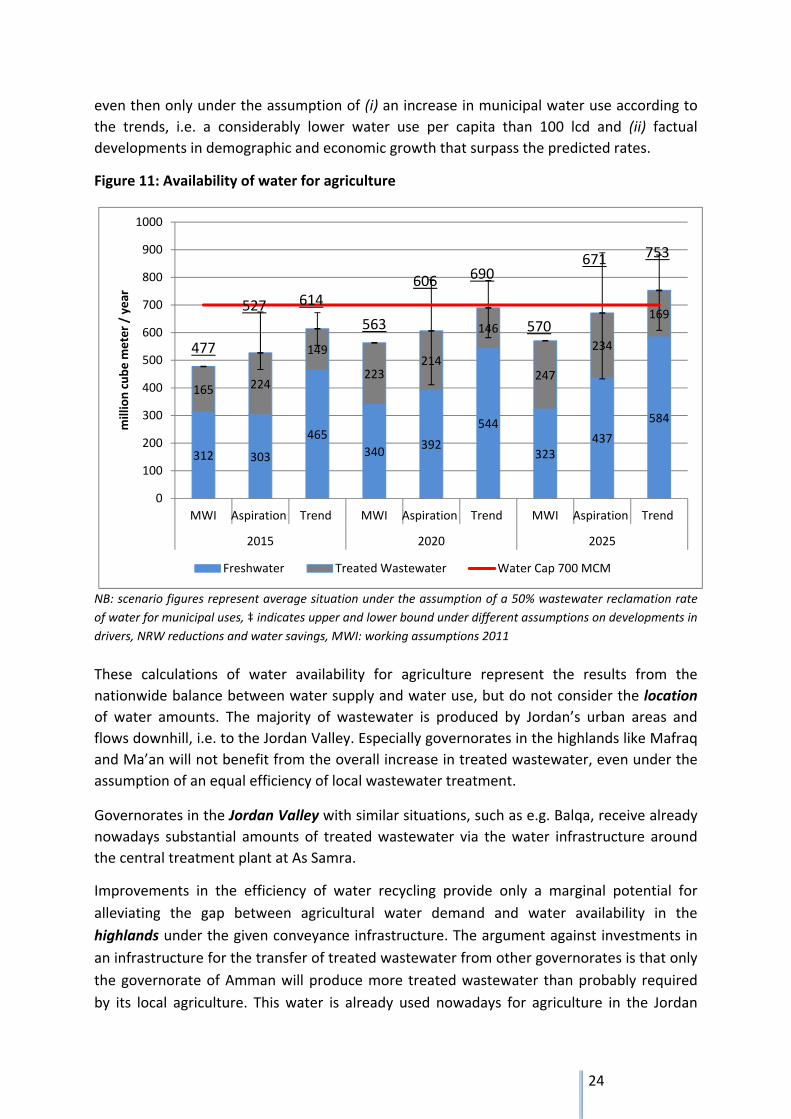

Figure 11: Availability of water for agriculture

NB: scenario figures represent average situation under the assumption of a 50% wastewater reclamation rate

of water for municipal uses, ‡ indicates upper and lower bound under different assumptions on developments in

drivers, NRW reductions and water savings, MWI: working assumptions 2011

These calculations of water availability for agriculture represent the results from the

nationwide balance between water supply and water use, but do not consider the location

of water amounts. The majority of wastewater is produced by Jordan’s urban areas and

flows downhill, i.e. to the Jordan Valley. Especially governorates in the highlands like Mafraq

and Ma’an will not benefit from the overall increase in treated wastewater, even under the

assumption of an equal efficiency of local wastewater treatment.

Governorates in the Jordan Valley with similar situations, such as e.g. Balqa, receive already

nowadays substantial amounts of treated wastewater via the water infrastructure around

the central treatment plant at As Samra.

Improvements in the efficiency of water recycling provide only a marginal potential for

alleviating the gap between agricultural water demand and water availability in the

highlands under the given conveyance infrastructure. The argument against investments in

an infrastructure for the transfer of treated wastewater from other governorates is that only

the governorate of Amman will produce more treated wastewater than probably required

by its local agriculture. This water is already used nowadays for agriculture in the Jordan

312 303

465

340392

544

323437

584

165 224

149

223214

146

247

234

169

477

527 614

563

606 690

570

671 753

0

100

200

300

400

500

600

700

800

900

1000

MWI Aspiration Trend MWI Aspiration Trend MWI Aspiration Trend

2015 2020 2025

million cube m

eter / year

Freshwater Treated Wastewater Water Cap 700 MCM

25

Valley, which has the advantages of an already existing conveyance system and lower

conveyance costs due to the difference in altitude.

2.5 Water demand by Nature

The assessment of water requirements by nature focuses on the major natural reserves and

unique ecosystems in Jordan, whereby the Dead Sea takes a special position due to its cross‐

border location.

The deficit between the historical inflow and the current inflow to the Dead Sea amounts to

about 1.20 billion MCM/year, which led to a decline of its sea level by about 1 m per year

over the last decades. Jordan's part in this deficit consists mainly out of the diversion of

about 70 MCM/year from the Yarmouk River to King Abdulla Canal for domestic supply to

west Amman and for agricultural use in the Jordan Valley. One proposed solutions to restore

the Dead Sea level is the Red Sea Dead Sea Canal project, which is expected to bring about

850 million cubic meter of brine to the sea.

Other major natural areas endangered by water stress comprise the Al Azraq Oasis, Wadi

Mujib and Wadi Wala. Estimates of the total water demand for these areas amount to 55

MCM /year, but significant return flows of this water can be and are used by other sectors,

such as in the case of Wadi Mujib and Wadi Wala. This water demand is assumed to be the

minimum amount required to save these ecosystems and regarded as a long‐term constant.