Embed Size (px)

Citation preview

Evolution of choice and innovation in the EU food sector

Key findings October 2014

1 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Objectives of the study

Analyse the evolution of choice and innovation

Identify the main potential drivers of choice and innovation (eg concentration) and measure their evolution

Determine the impact of drivers on choice and innovation

1 Scope and methodology

Assess the economic impact of modern retail on choice and innovation in the EU food sector

2 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

A comprehensive study, requiring outstanding resources

► A very broad scope to meet high expectations ► Wide scope in the EU

► Long period including pre-crisis

► Consumer standpoint: access to choice and innovation at local level in modern retail shops

► Quantitative (including econometrics) and qualitative analyses (6 case studies)

► Outstanding resources

► 2004 to 2012 (2 time periods per year)

► Selection of shops and countries based on availability of data on long period

► Data purchase / consolidation from different data sources

► Focus on local data: 343 shops, 9 Member states, 105 consumer shopping areas

► 23 product categories with a full set of information for each product

► A database of 11 million data records

1 Scope and methodology

3 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

► Validation of definitions: work process

Expert workshops and literature review

► Validation of conclusions providing a joint definition and operationalisation of key concepts

► Emphasis on differences encountered throughout the study

2nd survey round

► Validation of the first round

► Generation of consensus around choice and innovation

► Free discussion on each topic focusing on reactions and conclusions

Online focus group

► List of initial thoughts about choice and innovation

► Emphasis on drivers and operationalisation

1st survey round

1 Scope and methodology

4 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Measurement of choice ► Food choice

► Variety of products available in shops in consumer shopping areas

► Variety of packaging sizes

► Variety of prices

► Variety of suppliers

► Shop choice

► Variety of shops to which a typical consumer has access within a normal distance (consumer shopping area)

1 Scope and methodology

Expert workshops and literature review

5 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Measurement of innovation ► Need to have objective and measurable KPI, excluding subjective qualitative

qualifications

► Number of new SKUs* (excluding promotions) available for consumers at shop level

► Identification and measurement of innovation types

► New product

► Range extension

► New packaging

► New formulation

► Relaunch

* SKU = Stock keeping Unit

1 Scope and methodology

Expert workshops and literature review

6 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Innovation types (Mintel – GNPD) ► New product: assigned when a new range, line, or family of products is encountered.

This launch type is also used if a brand that already exists on GNPD, in one country, crosses over to a new sub-category

► New variety/range extension: used to document an extension to an existing range of products on the GNPD

► New packaging: determined by visually inspecting the product for changes, and also when terms like New Look, New Packaging, or New Size are written on pack.

► New formulation: determined by visually looking for key terms on pack like New Formula, Even Better, Tastier, Now Lower in Fat, New and Improved, Great New Taste..

► Relaunch: some wording indicating that the product has been relaunched on the packaging or the product does not exist on the database but there is secondary source information (such as from a press release, magazine, trade show, website or a shop display) that the product has been relaunched

1 Scope and methodology

Expert workshops and literature review

7 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

List of shops

List of new products

(EAN, type of innovation)

Socio-demographic

statistics National and NUTS3 levels

Supplier characteristics

Retails characteristics

List of EAN present on shelves for each 343 shops of the sample

Opus

DATABASE CALCULATIONS

Shop level database Shop level database Shop level database Shop level database

Output tables for descriptive statistics

Join by period

and CSA

Join by period, MS and product

category

Join by period

and EAN

Join by period

and CSA

Join by period, MS and product

category

Database of 11 millions data records processed

Trade Dimensions

1 Scope and methodology

Database construction

8 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

► Selection of shops and consumer shopping area at local level ► Identification of consumer shopping areas thanks to geolocalisation

► Consumer point of view

Geographical perimeter of each consumer

shopping area (CSA)

Travel time between the central point (city hall) and outer limit of the area 15 min travel time for large

cities 20 min travel time for

medium and small cities 25 min for a rural zone

Figure 2: Example: Consumer shopping area – Clichy-sous-Bois (FR)

1 Scope and methodology

Database construction

illustrative

9 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

► 343 shops in 105 consumer shopping areas

Sources: Eurostat, EY analysis

GDP/Capita Low Medium - Medium + High Total

Type of living Number of CSA

Number of CSA

Number of CSA

Number of CSA

Number of CSA

Predominantly Rural (PR) 8 8 3 4 23

Intermediate (INT) 13 9 13 7 42 Predominantly Urban (PU) 5 8 15 12 40

TOTAL 26 25 31 23 105

1 Scope and methodology

Database construction

25% 25% 25% 26% 25% 24%

30%

22%

Low Medium- Medium+ High

EU27

Sample

23%

35% 42%

22%

40% 38%

PR IN PU

EU27

Sample

Representativeness of sample vs EU27 population by standard and type of living categories

10 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

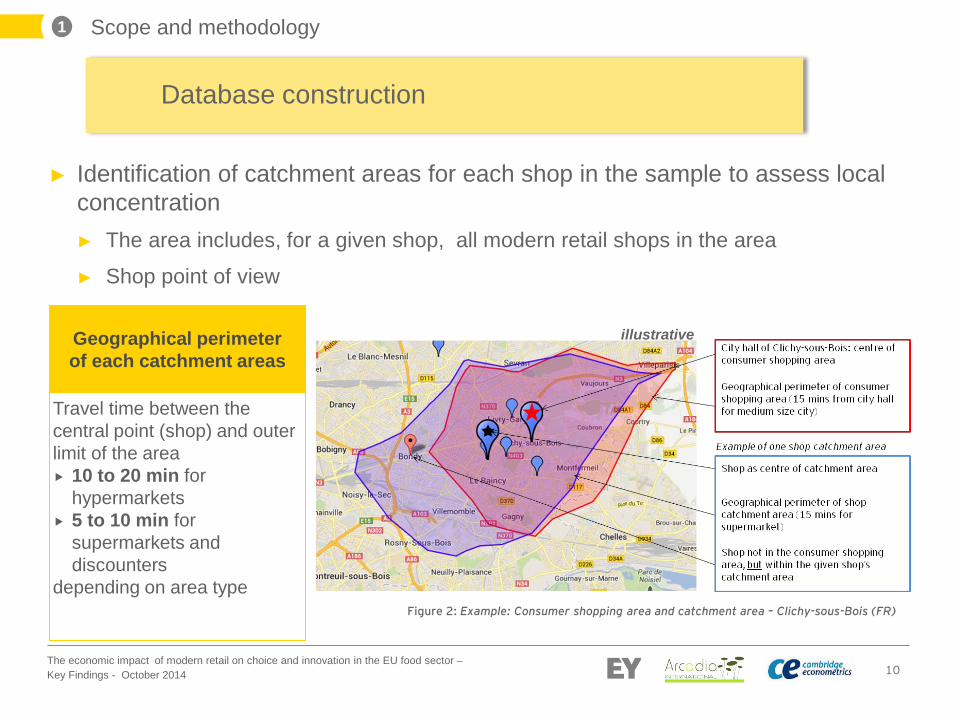

► Identification of catchment areas for each shop in the sample to assess local concentration ► The area includes, for a given shop, all modern retail shops in the area

► Shop point of view

Figure 2: Example: Consumer shopping area and catchment area – Clichy-sous-Bois (FR)

1 Scope and methodology

Database construction

Geographical perimeter of each catchment areas

Travel time between the central point (shop) and outer limit of the area 10 to 20 min for

hypermarkets 5 to 10 min for

supermarkets and discounters

depending on area type

illustrative

11 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Database of 11 millions data records processed

343 shops Hypermarkets Supermarkets Discounters

All main retail groups and banners in Europe Sh

op c

over

age

Cou

ntry

cov

erag

e

Belgium

Czech Rep.

Denmark

France

Hungary

Italy

Poland

Portugal

Spain

51% of EU pop

Prod

uct c

over

age

23 categories

Tim

e co

vera

ge

Precrisis period 2004-2008

Crisis period 2008-2012

2004-2012

105 Consumer

Shopping

Areas

CSA

cov

erag

e Frozen pizzas/starter, frozen ready cooked meals, frozen vegetables

Ice cream

Milk, cheese, yoghurt, butter/margarine, desserts

Bread, ham / delicatessen

Baby food, canned vegetables, edible oil, savoury snacks

Coffee, tea, Biscuits, cereals, chocolate

Fruit juices, mineral water, soft drinks

1 Scope and methodology

Database construction

12 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Descriptive analyses

► Aimed to distill the richness of the database into meaningful statistics ► Produced a consistent reporting pack covering choice, innovation and all

potential drivers for each member state and at consolidated level, for short and long periods

► Approach allowed comparison between CSA, countries, CSA types, shop types, identifying wider trends as well as those unique to particular markets

► Informs the econometric analysis and provides hypotheses for testing

1 Scope and methodology

13 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

► Approach ► Analyse the historical evidence for the impact of potential drivers on various

measures of choice and innovation, controlling for local and national influences

► Model the behaviour of each shop and the selection of products that it offers, with reference to various national and local drivers and shop characteristics

Econometric analyses measuring the impact of drivers on choice and innovation

1 Scope and methodology

14 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

[choice or innovation]s,p,t = f {

shop types,t

shop sizes,t

private label sharen/s,p,t

retailers' concentrationn/s,t

suppliers' concentrationn/s,p,t

[or imbalance (retailer vs supplier concentration)n/s,p,t]

socio-demographic indicatorsc,t

rural/urban categoryc or population densityc

product category turnovern,p,t

economic prosperity/macroeconomic conditionsc/n,t

Member Staten

product categoryp

yeary

seasonm

new competitor shop openings,t

}

1 Scope and methodology

Econometric analyses measuring the impact of drivers on choice and innovation

Main conclusions

16 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Main conclusions: choice

► Choice available to consumers in local shops increased in terms of the number of alternative products, the number of different brand suppliers and the number of modern retail shops

► The increase was greater during 2004-2008 than 2008-2012 ► In addition to the shop types and shop size which have an obvious impact on

choice, economic prosperity and product category turnover have been favourable factors for choice

► Competition in the form of a new shop opening in the local area improves the choice offered in existing shops

► There is no evidence that the concentrations of retailers or suppliers have been an economic driver of choice

► The impact of private labels on the evolution of choice was found to be negative but small.

17 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Main conclusions: innovation ► The presence of innovative food products at retailers’ shop level has declined in Europe

after 2008

► Innovations focused on new packaging have become considerably more common over time in most European Member States

► Innovation slowed down, particularly because of the impact of: ► Economic drivers: booming unemployment impacting the purchase power of European

households

► Increasing supplier concentration at national level

► However, the opening of new shops in the catchment areas had a positive effect on new products available to consumers, whereas greater concentration among modern retailers at a local level was associated with less innovation

► As for choice, shop type and shop size had an obvious impact on innovation available to consumers

► High share of private labels were associated with less innovation

► Evidence from the case studies suggested that, for fresh non-barcoded products, a key-driver for innovation was the organisation of the supply-chain.

Evolution of choice

19 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Choice in shops, alternative products and brand suppliers has increased in the majority of sampled MS

Type of choice Component 2004-2008 2008-2012 2004-2012 Trend

Food Choice

Choice in alternative products** 7,9% 2,4% 5,1%

Choice in packaging sizes 5,0% 2,0% 3,5%

Choice in alternative suppliers** 5,6% 1,5% 3,5%

Choice in prices per product category1 + -- -

Shop Choice

Choice in shops* 1,8% 1,3% 1,6%

+ Positive CAGR; - Negative CAGR; ++ CAGR is twice as much as average growth value; -- CAGR is twice as less as average growth value 1 : Results need to be considered with caution because of inconsistency found in data

2 Evolution of choice and innovation

20 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Choice in alternative products

Per product category

Source: EY analysis based on © Nielsen Opus, at local level - FR-IT-PT-SP-HU-BE, 2004-2012

8% 7% 7% 7% 7% 6% 6% 6% 6% 6% 5% 5% 5% 5% 5% 5% 5% 5% 4%

4% 3% 3% 3% 2%

0%1%2%3%4%5%6%7%8%9%

Annual growth of total number of EAN by product category 2004-2012

2 Evolution of choice and innovation

21 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Choice in alternative products

Per shop type

Source: EY analysis based on © Nielsen Opus - FR-IT-PT-SP-HU-BE, 23 product categories

2 Evolution of choice and innovation

8,3%

4,7%

9,3%

2,2% 2,6%

6,8%

5,2%

3,6%

8,0%

0,76 1,26 1,76 2,26 2,76 3,26 3,76

0

10000

20000

30000

40000

50000

60000

70000

0%1%2%3%4%5%6%7%8%9%

10%

Hypermarkets Supermarkets Discount Stores

Annual growth of total number of EAN by shop type

CAGR(04 - 08) CAGR(08 - 12) CAGR(04 - 12) 2004 values

Evolution of innovation

23 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Source: EY analysis based on © Nielsen Opus – BE-FR-IT-PO-PT-SP

Evolution of innovations

Innovation rate declined after 2008…

3,8%

-1,2%

-5,3% -6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Total new EANs

Evolution of the number of innovations (new EAN)

CAGR(06 - 08) CAGR(08-10) CAGR(10-12)

2 Evolution of choice and innovation

24 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

… over almost all product categories

Source: EY analysis based on © Nielsen Opus – BE-FR-IT-PO-PT-SP

Per product category

3% 2% 1% 1% 1% 0%

0% 0% 0% -1% -1% -1% -1% -1% -2% -2% -2% -3% -3% -4% -4% -4% -5%

-7% -8%

-6%

-4%

-2%

0%

2%

4%

Annual growth in number of new EAN codes by product category 2004-2012

2 Evolution of choice and innovation

25 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

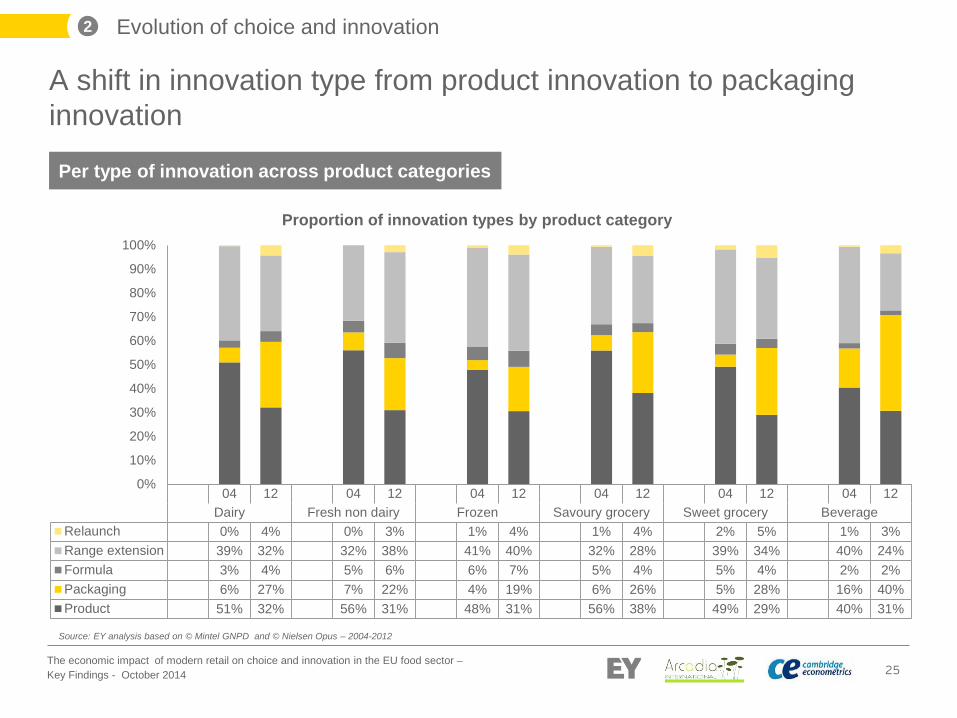

A shift in innovation type from product innovation to packaging innovation

Per type of innovation across product categories

Source: EY analysis based on © Mintel GNPD and © Nielsen Opus – 2004-2012

2 Evolution of choice and innovation

04 12 04 12 04 12 04 12 04 12 04 12Dairy Fresh non dairy Frozen Savoury grocery Sweet grocery Beverage

Relaunch 0% 4% 0% 3% 1% 4% 1% 4% 2% 5% 1% 3%Range extension 39% 32% 32% 38% 41% 40% 32% 28% 39% 34% 40% 24%Formula 3% 4% 5% 6% 6% 7% 5% 4% 5% 4% 2% 2%Packaging 6% 27% 7% 22% 4% 19% 6% 26% 5% 28% 16% 40%Product 51% 32% 56% 31% 48% 31% 56% 38% 49% 29% 40% 31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Proportion of innovation types by product category

26 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

The development of new packaging is stronger in France, Italy and Spain than in Belgium, Poland and Portugal

Belgium04

Belgium12

France04

France12 Italy 04 Italy 12 Poland

04Poland

12Portugal

04Portugal

12Spain

04Spain

12

Relaunch 0,6% 0,0% 1,0% 0,1% 0,4% 0,6% 0,6% 0,3% 0,0% 0,0% 2,4% 0,5%Range extension 45,1% 35,6% 50,6% 33,6% 30,9% 28,5% 41,4% 39,0% 33,9% 26,6% 34,9% 36,4%Formula 3,1% 3,7% 5,7% 6,2% 2,9% 2,7% 1,7% 1,8% 0,0% 2,8% 3,9% 3,0%Packaging 8,6% 9,9% 8,4% 30,8% 7,1% 33,7% 2,9% 5,8% 3,1% 8,5% 10,2% 24,1%Product 42,0% 48,7% 34,1% 24,3% 58,5% 30,3% 53,1% 52,2% 62,2% 59,6% 48,6% 33,6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Proportion of types of innovation by MS (local level)

Source: EY analysis based on © Mintel GNPD and © Nielsen Opus – 2004-2012

Per type of innovation across MS

2 Evolution of choice and innovation

27 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

New packaging development occurs across all product categories, and represents a large share of innovations for dairy products. Per type of innovation and product category

Source: EY analysis based on © Mintel GNPD and © Nielsen Opus – 2004-2012

04 12 04 12 04 12 04 12 04 12Butter/margarine Cheese Dessert Milk Yoghurt

Relaunch 0% 4% 1% 5% 0% 4% 0% 5% 1% 3%Range extension 34% 25% 35% 33% 38% 41% 33% 23% 57% 36%Formula 5% 4% 3% 2% 6% 8% 0% 2% 1% 6%Packaging 7% 31% 7% 29% 3% 19% 8% 35% 6% 23%Product 54% 35% 55% 31% 52% 28% 59% 35% 35% 32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Proportion of types of innovations: Dairy

2 Evolution of choice and innovation

28 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

New packaging share remains weaker than product innovation and range extension for fresh non dairy products

Source: EY analysis based on © Mintel GNPD and © Nielsen Opus – 2004-2012

04 12 04 12 04 12Fresh pre-packaged bread Ham/delicatessen Starters/pizzas

Relaunch 0% 2% 0% 2% 0% 5%Range extension 30% 37% 36% 41% 29% 36%Formula 3% 8% 3% 4% 9% 7%Packaging 3% 25% 8% 21% 11% 19%Product 64% 28% 53% 31% 51% 33%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Proportion of types of innovations: Fresh non dairy

2 Evolution of choice and innovation

Per type of innovation and product category

29 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

New packaging share remains weaker than product innovation and range extension for frozen products

Source: EY analysis based on © Mintel GNPD and © Nielsen Opus – 2004-2012

Per type of innovation and product category

2 Evolution of choice and innovation

04 12 04 12 04 12Frozen vegetables Ready-cooked meals Ice cream

Relaunch 0% 4% 3% 6% 0% 2%Range extension 44% 44% 44% 38% 35% 39%Formula 7% 6% 9% 10% 1% 4%Packaging 4% 21% 7% 19% 1% 15%Product 44% 25% 37% 27% 62% 40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Proportion of innovation types by category: Frozen

30 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

New packaging development occurs across all product categories for savoury grocery

Source: EY analysis based on © Mintel GNPD and © Nielsen Opus – 2004-2012

Per type of innovation and product category

04 12 04 12 04 12 04 12Baby food (ambient) Canned vegetables Edible oil Savoury snacks

Relaunch 1% 9% 0% 3% 0% 2% 1% 4%Range extension 34% 25% 21% 36% 33% 21% 41% 31%Formula 9% 8% 8% 2% 0% 1% 1% 4%Packaging 1% 27% 21% 19% 0% 31% 3% 24%Product 54% 31% 50% 39% 67% 45% 53% 38%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Proportion of types of innovations: Savoury grocery

2 Evolution of choice and innovation

31 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

New packaging development is quite strong for sweet grocery products.

Source: EY analysis based on © Mintel GNPD and © Nielsen Opus – BE-FR-IT-PO-PT-SP

Per type of innovation and product category

04 12 04 12 04 12 04 12 04 12

Biscuits Cereals Chocolate (Bar +Candies) Coffee Tea

Relaunch 1% 5% 3% 6% 1% 3% 2% 6% 3% 6%Range extension 40% 32% 26% 28% 49% 33% 38% 32% 45% 46%Formula 2% 4% 8% 7% 1% 3% 7% 2% 5% 4%Packaging 6% 27% 5% 31% 3% 26% 3% 35% 8% 21%Product 51% 33% 59% 29% 46% 36% 50% 25% 40% 22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Proportion of types of innovations: Sweet grocery

2 Evolution of choice and innovation

32 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

New packaging represents the larger share of innovation types for beverages.

Source: EY analysis based on © Mintel GNPD and © Nielsen Opus – 2004-2012

Per type of innovation and product category

04 12 04 12 04 12Fruit juices (ambient) Mineral water Soft-drinks

Relaunch 1% 5% 0% 2% 1% 3%Range extension 42% 31% 37% 14% 42% 27%Formula 1% 2% 6% 1% 0% 3%Packaging 11% 31% 26% 54% 12% 36%Product 45% 31% 31% 29% 45% 32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Proportion of types of innovations: Beverage

2 Evolution of choice and innovation

33 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Econometric results: drivers of choice and innovation

34 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Positive impacts on choice

► Product category turnover ► Economic prosperity ► Shop size ► Shop type ► New shop opening in the local area

No or low economic impact on choice

► Concentration drivers ► Private labels (-) ► Unemployment (+) ► Population density (-)

3 Econometrics results

35 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Drivers for choice Product variety Product size variety Product supplier

variety Product price

variety

impact Signif. Import. impact Signif. Import impact Signif. Import impact Signif. Import

Product category turnover ..

GDP per capita ? ..

Shop floor space ..

Shop type N.A. N.A N.A ? N.A

New shop opening in the local area ..

..

Product category turnover, economic prosperity, shop size and shop type are the most important drivers for choice

Positive impact

Negative impact

? Where the sign varies according to whether the parameter is estimated over the long or short data sets

Significant at 5% level

Significant at 1% level

Impact of more than 5%

Impact of more than 10%

-- Not statistically significant or economically important according to these thresholds

3 Econometrics results

36 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Sources: Analysis based on © Nielsen Opus and © Euromonitor International

Statistical significance ► 1% level Direction of impact ► Positive Economic importance ► Large

Product category turnover, economic prosperity, shop size and shop type are the most important drivers for choice

Product category turnover

3 Econometrics results

Choice in variety of EANS versus national product category sales turnover in 2010 period 1 in four Member States

Sources: Analysis based on © Nielsen Opus and © Euromonitor International

37 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Sources: Analysis based on © Nielsen Opus and Eurostat

Statistical significance ► 1-5% level Direction of impact ► Positive Economic importance ► Large

GDP per capita

Floorspace

Statistical significance ► 1% level Direction of impact ► Positive Economic importance ► Large

Choice in variety of EAN codes versus GDP per capita

Product category turnover, economic prosperity, shop size and shop type are the most important drivers for choice

3 Econometrics results

38 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Other drivers have no or low economic impact on choice

Drivers for choice Product variety Product size variety

Product supplier variety

Product price variety

impact Signif. Import impact Signif. Import impact Signif. Import impact Signif. Import

Retail concentration at national level .. .. .. .. .. .. .. .. ..

Retail concentration at local level .. .. .. .. .. .. .. .. .. ..

Supplier concentration at national level .. .. .. .. .. .. .. .. .. ..

Imbalance between retailers and suppliers at national level

.. .. .. ? .. .. .. .. ?

Private labels (local) .. .. .. .. Unemployment .. .. ..

Population density ..

Too few observations for conclusions to be drawn with confidence.

3 Econometrics results

39 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Sources: Analysis based on © Nielsen Opus and © Planet Retail

Very few observations from which to draw conclusions

Statistical significance ► No, except product price variety

Direction of impact ► Negative for product price variety

Economic importance ► Large for product price variety

Little indication of an impact of national retail concentration on choice

Retail concentration at national level Choice in variety of EAN codes in the sampled shops versus national retail concentration

3 Econometrics results

40 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Sources: Analysis based on © Nielsen Opus and © Euromonitor International

Statistical significance ► No (except product size variety) Direction of impact ► Positive for product size variety

Economic importance ► Small

There is no evidence that supplier concentration is an economic driver of choice

Supplier concentration at national level Choice in variety of EAN codes versus national supplier concentration by product category, 2008

3 Econometrics results

41 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Statistical significance ► Various Direction of impact ► Ambiguous for statistically significant cases Economic importance ► Moderate for product price variety

Other econometric results regarding factors driving choice

Statistical significance ► 1% level

Direction of impact ► Negative

Economic importance ► Small

Population density

Statistical significance ► Various

Direction of impact ► Positive; negative for product

price variety

Economic importance ► Small

Unemployment

Statistical significance ► 1% level

Direction of impact ► Negative

Economic importance ► Small

Private labels

Measure of imbalance between retailers and suppliers at national level

3 Econometrics results

42 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Sources: Analysis based on © Nielsen Opus and © Euromonitor International

High shares of private labels tend to be associated with less choice in hypermarkets and supermarkets

Share of private labels (in each product category) in each shop

Choice in variety of EAN codes versus private labels share, by shop type

3 Econometrics results

43 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Measured impacts on innovation

► Product category turnover (+) ► Shop size (+) ► Shop type (+) ► New shop opening in the local area (+) ► Retailers’ business expectations (+) ► Unemployment (-) ► Population density (-) ► Local retailer and supplier concentration (-) ► Private labels (-)

3 Econometrics results

44 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Drivers for innovation Opus innovations New products New packaging New

formulations New line

extensions

impact Signif. Import. impact Signif. Import impact Signif. Import impact Signif. Import impact Signif. Import

Shop size

Shop type N.A. N.A. N.A. N.A. N.A.

Retailer business expectations

?

Product category turnover

.. .. .. ? ?

Positive impact Negative impact ? Where the sign varies according to whether the parameter is estimated over the long or short data sets Significant at 5% level

Significant at 1% level Impact of more than 5% Impact of more than 10% -- Not statistically significant or economically important according to these thresholds

Shop size, shop type, retailer business expectations and product category turnover are the most important positive drivers for innovation

Too few observations for conclusions to be drawn with confidence.

3 Econometrics results

45 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Statistical significance ► 1% level Direction of impact ► Positive Economic importance ► Large

Very few observations from which to draw conclusions

Statistical significance ► 1% level Direction of impact ► Positive Economic importance ► Large

Opus innovations versus retailer business expectations

Sources: Analysis based on © Nielsen Opus and © Eurostat

Statistical significance ► 1% level Direction of impact ► Positive (larger formats offer a greater number

of innovative products) Economic importance ► Large

Shop size, shop type, retailer business expectations and product category turnover are the most important positive drivers for innovation Shop size

Shop type

Retailer business expectations

3 Econometrics results

46 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Statistical significance ► 1% level Direction of impact ► Generally positive Economic importance ► Various

Sources: Analysis based on © Nielsen Opus and © Euromonitor International

Shop size, shop type, retailer business expectations and product category turnover are the most important positive drivers for innovation Product category turnover

3 Econometrics results

New EAN codes (innovations) versus national product category sales turnover in 2010 period 1 in four Member States

47 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Other drivers have various impacts on innovation Drivers for innovation Opus innovations New products New packaging New

formulations New line

extensions

impact Signif. Import. impact Signif. Import impact Signif. Import impact Signif. Import impact Signif. Import

Retail concentration at national level

?

Retail concentration at local level

.. .. .. .. .. .. .. .. .. .. .. ..

Supplier concentration at national level

.. .. .. ?

Imbalance between retailers and suppliers at national level

?

Private labels .. .. ..

New shop opening in the local area

.. .. .. .. .. .. .. .. .. .. .. ..

Too few observations for conclusions to be drawn with confidence.

3 Econometrics results

48 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

New EAN codes (innovation) versus national retail concentration

Source: Analysis based on © Nielsen Opus and © Planet Retail

Very few observations from which to draw conclusions

Statistical significance ► 1% Direction of impact ► Positive except for new packaging (negative) and new

formulations (ambiguous) Economic importance ► Large (for modern retail measure)

Statistical significance ► No (except for new packaging) Direction of impact ► Negative Economic importance ► Large for new packaging

Greater concentration among retailers at a local level is associated with less innovation in new packaging Retailer concentration at the procurement level

Retailer concentration at the local level

3 Econometrics results

New EAN codes (innovation) versus local retail concentration in two years

Sources: Analysis based on © Nielsen Opus and © Nielsen Trade Dimensions

49 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Opus innovations versus national supplier concentration by product category, 2008

Sources: Analysis based on © Nielsen Opus and © Euromonitor International

Statistical significance ► 1% for several innovation indicators

Direction of impact ► Mostly negative

Economic importance ► Moderate to large

Greater concentration among suppliers at national level is associated with less innovation (some measures)

Supplier concentration at the national level

3 Econometrics results

50 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Sources: Analysis based on © Nielsen Opus and © Euromonitor International

The finding for supplier concentration is also reflected in the finding for retailer – supplier imbalance

Imbalance between retailers and suppliers at national level

Choice in variety of EAN codes versus imbalance between retailers and suppliers

3 Econometrics results

Statistical significance ► 1% for most innovation indicators

Direction of impact ► Positive (i.e. a greater imbalance in

favour of suppliers has a negative impact) (except new packaging where ambiguous)

► But remember that the sample does not have cases with high national retail concentration

Economic importance ► Generally large

51 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Other general economic drivers have low or negative impact on innovation

Drivers for innovation Opus innovations New products New packaging New

formulations New line

extensions

impact Signif. Import. impact Signif. Import impact Signif. Import impact Signif. Import impact Signif. Import

Unemployment .. .. ..

Population .. .. .. .. .. .. .. .. .. .. ..

Population density .. .. .. .. .. .. .. ..

3 Econometrics results

52 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

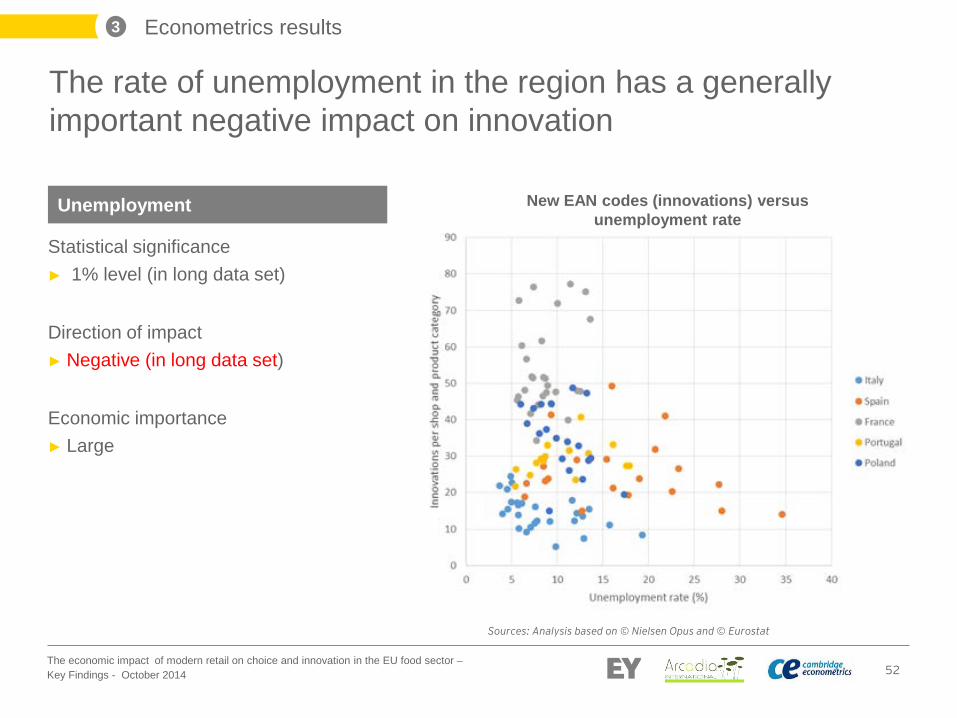

Statistical significance ► 1% level (in long data set) Direction of impact ► Negative (in long data set) Economic importance ► Large

Sources: Analysis based on © Nielsen Opus and © Eurostat

The rate of unemployment in the region has a generally important negative impact on innovation

New EAN codes (innovations) versus unemployment rate

Unemployment

3 Econometrics results

53 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

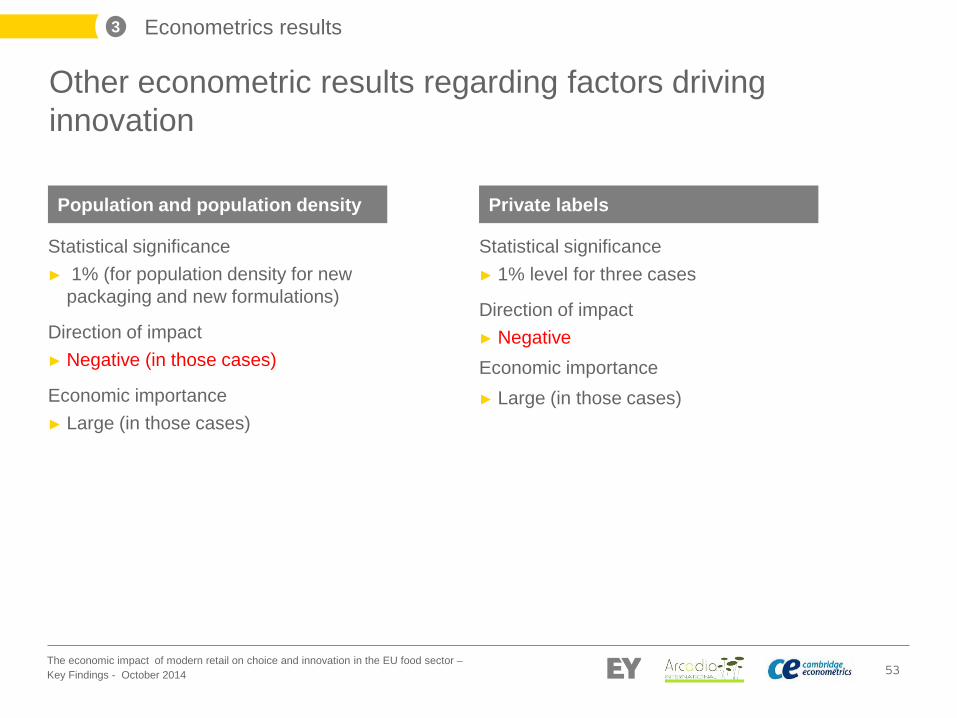

Statistical significance ► 1% (for population density for new

packaging and new formulations)

Direction of impact ► Negative (in those cases)

Economic importance ► Large (in those cases)

Statistical significance ► 1% level for three cases

Direction of impact ► Negative Economic importance ► Large (in those cases)

Other econometric results regarding factors driving innovation

Population and population density Private labels

3 Econometrics results

54 The economic impact of modern retail on choice and innovation in the EU food sector – Key Findings - October 2014

Sources: Analysis based on © Nielsen Opus and © Euromonitor International

High shares of private labels are associated with fewer innovative products in hypermarkets and supermarkets

Share of private labels (in each product category) in each shop

New EAN codes (innovations) versus private labels share, by shop type

3 Econometrics results

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization and may refer to one or more of the member firms of EY Global Limited, each of which is a separate legal entity. EY Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2014 EY Transaction Advisory Services All Rights Reserved.

ey.com/fr