Embed Size (px)

Citation preview

1

European Property IndicatorsQuarter 3 2010 : Issue 7

Market recovery exhibits north-south divide

• Recovery continues but sentiment remainsfragile.

• Office rents in London and Paris rising, whileelsewhereinEuroperentsarestabilising.

• Prime yields expected to remain stable in theshorttermuntiloccupiermarketpicksup.

Economic Outlook

Economic growth expected to flatten out. Overrecentmonths,globaldemandhascontinuedtorecover,butuncertaintyaboutthefuturehasalsorisen.EurozoneGDPclimbedbyahealthy1%duringQ2 2010, though this concealed awide range ofnationaloutcomes,withaclearnorth-southdivide.Germanoutputjumpedby2.2%,drivenbybuoyantexportdemand.Francewaswellbehind(at+0.6%),however,whileactivitywasevenmoremarginalinSpainandItaly,albeitstillpositive.

Europe is central to ongoing concerns about theshort-termglobaloutlook,withthesovereigndebtcrisisdraggingon into theautumn.Largesupportpackages have not allayed fears about prospectsin the most vulnerable economies. Greece hasevaded default, but without convincing marketsthatitisclearofdanger.Bondspreadsarebacktoall-timehighsinIrelandandPortugalaswell.Spainalonehasbeenfavourablyre-evaluated,aftertakingthenecessaryfiscalstepstoreassureinvestors.

With theUS recovery faltering, prospects for therest of this year and into next are for growth toflattenout.Asaresult,EurozoneGDPisforecasttodipslightlynextyearto1.4%comparedto1.5%thisyear,withnoaccelerationpredicteduntilinto2012.Therearealsodownside riskswithanysovereigndefaultlikelytohitEurope’sfragilebanksandchokeoffthesupplyofcreditfortherecovery.

Fortunes remain mixed across the EU. Germanyis expected to lead GDP growth in 2010, butfails to sustain this next year. France has amoreconsistent, but slower, upturn, with Italy laggingfurtherbehind.Spain,Ireland,PortugalandGreeceare forecast toexperience fallingoutput this year

and,atbest,mutedrevival in2011.ProspectsarestrongeroutsidetheEurozone,withtheUKthetopperformer of the larger western economies after2010. Central and eastern European economiesarelikelytoreturntotheirpost-crisisgrowthratesby2012.Currently,Polandoutperforms itscentralEuropeanneighbours.

Office Markets

London and Paris lead recoveryMost office markets across Europe experiencedstablelevelsofoccupieractivityinQ32010.WhileLondon andParis registered strong rental growthon thebackof improvingoccupiersentiment, therestofEuropeshowsamoremixedpicture.

London continues to performwellwithQ3officetakeupintheWestEndroughlyonaparwithQ2andasignificantboost inactivityregisteredintheCity.WhilerentsremainedstableintheWestEnd,theCityrecordedgrowthforthefourthconsecutivequarter. PrimeCity rentsnowstandat£52.50/ft²(€656/m²), up around23.5%on the year. Furtherrentalgrowthisexpectedinthenextsixmonthsasthepause indevelopmentstartsduring2008and2009hastightenednewofficesupplyconsiderably.

The Paris office market experienced sustainedlevelsofdemand,pushinguprentsforthesecondconsecutive quarter to €750/m². The 7% rentalgrowth seen in Paris was the highest in EuropeduringQ32010.Elsewhere,rentsalsoincreasedinLuxembourgandStockholm.

Frankfurt and Athens fared less well with primerents coming under further pressure. Athensregisteredthesharpestrentaldecline,witha6.7%fallto€336/m².FurtherrentaldeclineinQ4islikelyascompetitionbetweenlandlordsremainsfierce.

Subdued demand for office space across CEEcontinuestoputdownwardpressureonrentsinanumberof locations.SofiasawasharpcorrectioninQ3 2010,with rents down by around 5.3% tostandat€216/m².Rents inPragueandBucharesteased to€240/m² and€246/m² respectively. Formost of the cities surveyed, rents should remainstable until the end of 2010. The twoexceptions

Economic forecasts: Oxford Economics (July 2010) Rent and yield data as at end September 2010

2

King Sturge: European Property Indicators Quarter 3 2010 : Issue 7

areMoscowandIstanbul,whereagradualincreaseinoccupierdemand,combinedwithatighteningofGradeAsupply,shouldsupportfurtherrentaluplifts.

Office investmentactivitycontinuedapaceacrossEurope in Q3. According to preliminary figuresfromRealCapitalAnalytics(RCA),totalinvestmentvolumescameto€8.3bninQ3.Whilstthisis7.5%downon thepreviousquarter it still represents a12.6%increaseonthesameperiodlastyear.

The office investment upturn is strongest inWestern Europe and more specifically LondonandParis. Both centres saw somemarginal yieldcompressioninQ3.ElsewhereintheWest,marketsgenerallyremainedstablewithnoyieldchangeonQ2.Withyieldsnowclosetotheirhistoricaverages,theoutlookformostWesternEuropeanmarketsisstableoverthenextquarter.

InCentralEuropemostsurveyedcitiesrecordedafurtherinwardyieldshift.InWarsawyieldsseemtohavestabilisedsomewhatafter threeconsecutivequartersofhardening.Theprimeofficeyieldnowstands at 6.35%, 65bp less then a year ago. InEastern Europe, most centres saw no change inQ3 2010. Prime yields are likely to remain stableintheshorttermunlessinvestorinterestpicksupconsiderably.

Industrial Markets

Investment activity slows in Q3. European occupier markets in the industrial andlogistics sectors paint a mixed picture. Some oftheunderlyingdemanddriversareimproving,withoveralleconomicactivitygenerallyexpanding,worldtrade sharply up on last year (when it contractedby around 12%) and container volumes throughEurope’slargest10containerportsup12%inthefirsthalfoftheyearcomparedwithH12009.Thatsaid,theeconomicrecoveryremainsfragileinmanypartsofEuropeandmanufacturingactivityremainsvolatile.

IntheUK,demandforlogisticspropertyhaspickedup during 2010with take-up on an upward trend

sinceQ12009.Recently,enquirieshavepickeduparoundHeathrowAirport but rents in thismarketremainedstableat£13/ft²(€162/m²)inQ3,andareexpectedtodosointheshortterm.Ingeneral,rentfreeperiodsandotherincentives,whichhaverisensignificantly over the last two years,will need tocomedownfurtherbeforeanyupwardmovementinheadlinerentscanbeexpected.

Dublin and Milan registered a sharp fall in rentsas demand for logistics space continues to slow.ElsewhereinEurope,rentallevelsremainedbroadlystablewiththeexceptionofMoscow,whererentsmovedup over the quarter. Given the decline inthe availability of new speculative product andthe tentative improvement in demand, headlinelogistics rentsshould remain largelystableacrossEuropeduringtherestof2010.Followingastrongfirsthalfoftheyear,investmenttransaction volumes in the industrial sector fell inQ3. According to preliminary figures from RCA,around€1.3bnwastransacted inthequarter, justover 20% down on the same period last year.Pricing has now stabilised across most parts ofEurope,withyieldscomingdownfromtheirhighsofearly2009,andwithlimitedrentalgrowthexpectedintheshorttermtheindustrialsectorhaslostsomeofitsattraction.Inaddition,therearestillconcernsaboutthefragilestateoftheoccupiermarket.

Therecoveryof industrial investmentactivityoverthelast12monthswaslargelyledbystrongactivityin the UK. This picture was somewhat differentduring Q3 with core markets such as Germany,France and the Netherlands, but also some oftheNordics,accountingforan increasingshareoftransactions.Primeyieldssawsomefurther,marginal,downwardmovementinanumberofmarkets,whileinDublinandAthensprimeyieldssoftenedinQ3.Ingeneral,primeyieldsarelikelytoremainfairlystableattheircurrent level towardstheendof theyear inmostmarkets, although certainCEEmarkets could stillseesomeyieldcompression.

Research contacts:Alexander Colpaert, European Research 44 (0) 20 7087 5511 [email protected]

3

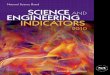

Office: rents (€/m²/annum)quoted refer toheadline rents inhighqualitybuildingssituated inprime locationsandareassumed tobeover500m².Investmentyield(%)quotedrefertoavaluationofofficepropertyletatfullmarketvalueandwhichisofthebestphysicalquality,intheprimelocation,andwiththebesttenant’scovenantandcontemporaryleaseterms.Generally,abenchmarkwithwhichtocompareotherproperties.Warehouse:rents(€/m²/annum)quotedrefertoheadlinerentsinhighqualitybuildingssituatedinprimelocationsandareassumedtobeover5,000m².Investmentyield(%)quotedrefertoavaluationoflogisticspropertyletatfullmarketvalueandwhichisofthebestphysicalquality,intheprimelocation,andwiththebesttenant’scovenantandcontemporaryleaseterms.Generally,abenchmarkwithwhichtocompareotherproperties.

UNITED KINGDOM

CROATIA

HUNGARY

BELGIUM

NETHERLANDS

DENMARK

NORWAY

SWEDEN

FINLAND

RUSSIA

POLAND

CZECH REP.

SLOVAKIA

ROMANIA

BULGARIA

TURKEY

GREECE

SERBIA

GERMANY

FRANCE

SPAIN

IRELANDDublin ●

Paris ●

● Madrid

● Frankfurt ● Prague●

Luxembourg

● Moscow

● Bratislava

● Budapest

● Belgrade

● Istanbul

● Warsaw

Bucharest ●

London ●

City

West End

Brussels ●

Amsterdam ●

● Copenhagen

Stockholm ●

Helsinki ●● Oslo

Zagreb ●

Vienna ●

● Sofia

364 : 6.00125 : 7.00

285 : 5.85104 : 7.90

656 : 5.25

440 : 6.00

875 : 4.50162 : 6.25

260 : 6.2548 : 7.25

375 : 7.0065 : 8.50 300 : 6.50

65 : 7.75

360 : 5.7578 : 8.25

208 : 5.0070 : 7.25

276 : 6.3540 : 8.00

168 : 7.1548 : 8.25

216 : 9.0060 : 10.50

353 : 7.7557 : 9.00

336 : 7.5060 : 8.75

450 : 5.0048 : 7.25

246 : 9.5045 : 10.50

180 : 9.5048 : 10.50

599 : 10.5081 : 12.50

240 : 6.7554 : 8.50

216 : 7.7542 : 9.50

● Geneva

903 : 4.25120 : 6.00

192 : 8.5072 : 9.25

265 : 5.50102 : 7.00

750 : 5.1050 : 7.25

378 : 5.2566 : 7.25

409 : 5.0085 : 7.25

Rent (€/m2/annum) : Yield (%)Rent (€/m2/annum) : Yield (%)

OfficeWarehouse

ITALY

Milan ●

Athens ●

4

King Sturge: European Property Indicators Quarter 3 2010 : Issue 7

AlldatacontainedinthisreporthasbeencompiledbyKingSturgeLLPandispublishedforgeneralinformationpurposesonly.Whileeveryefforthasbeenmadetoensuretheaccuracyofthedataandothermaterialcontainedinthisreport,KingSturgeLLPdoesnotacceptanyliability(whetherincontract,tortorotherwise)toanypersonforanylossordamagesufferedasaresultofanyerrorsoromissions.Theinformation,opinionsandforecastssetoutinthereportshouldnotbereliedupontoreplaceprofessionaladviceonspecificmatters,andnoresponsibilityforlossoccasionedtoanypersonacting,orrefrainingfromacting,asaresultofanymaterialinthispublicationcanbeacceptedbyKingSturgeLLP.©KingSturgeLLPOctober2010

Chart 1: European prime office rents and yields

0

100

200

300

400

500

600

700

800

900

1,000

Bra

tisla

va

Bel

grad

e

Zagr

eb

Cop

enha

gen

Sof

ia

Bud

apes

t

Pra

gue

Buc

hare

st

Bru

ssel

s

Vie

nna

War

saw

Hel

sink

i

Am

ster

dam

Ath

ens

Ista

nbul

Mad

rid

Osl

o

Dub

lin

Fran

kfur

t

Sto

ckho

lm

Luxe

mbo

urg

Mila

n

Mos

cow

Par

is

Lond

on

Gen

eva

Prime rent Prime yield

Ren

t €

/m2 /

annu

m

Yiel

d %

0

2

4

6

8

10

12

14

Source: King Sturge (September 2010)

Chart 2: European prime industrial rents and yields (units >5,000m2)

0

20

40

60

80

100

120

140

160

180

War

saw

Bud

apes

t

Buc

hare

st

Bel

grad

e

Bra

tisla

va

Mila

n

Bru

ssel

s

Par

is

Pra

gue

Ista

nbul

Sof

ia

Ath

ens

Am

ster

dam

Dub

lin

Fran

kfur

t

Cop

enha

gen

Zagr

eb

Mad

rid

Mos

cow

Sto

ckho

lm

Vie

nna

Hel

sink

i

Gen

eva

Osl

o

Lond

on

Prime rent Prime yield

Ren

t €

/m2 /

annu

m

Yiel

d %

0

2

4

6

8

10

12

14

Source: King Sturge (September 2010)