Embed Size (px)

Citation preview

Europe in the World Economy: An Economic HistoryThe Great Depression

Slides by Karl Gunnar Persson and Paul Sharp

Left-overs from last lecture: Who killed Bretton Woods?

The rest of the world did not want US to dictate monetary policy and inflation targets.

Capital controls which were meant to give member states some autonomy over monetary policy were outsmarted by currency traders.

In the end US monetary policy dominated rest of the world, but in particular Germany, Switzerland and Japan, had lower inflation targets.

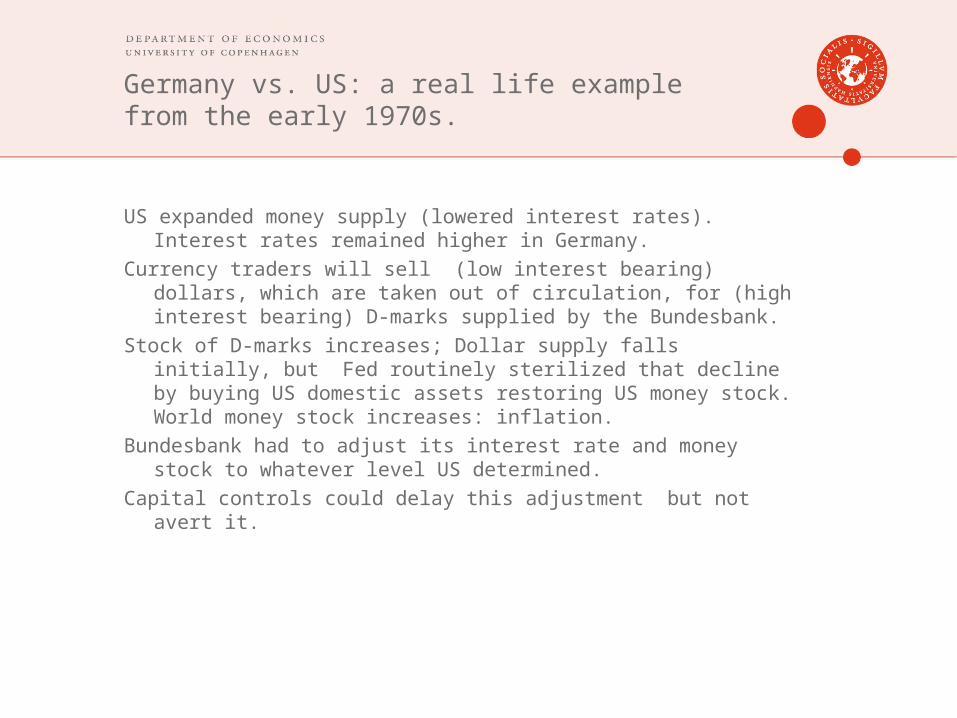

Germany vs. US: a real life example from the early 1970s.

US expanded money supply (lowered interest rates). Interest rates remained higher in Germany.

Currency traders will sell (low interest bearing) dollars, which are taken out of circulation, for (high interest bearing) D-marks supplied by the Bundesbank.

Stock of D-marks increases; Dollar supply falls initially, but Fed routinely sterilized that decline by buying US domestic assets restoring US money stock. World money stock increases: inflation.

Bundesbank had to adjust its interest rate and money stock to whatever level US determined.

Capital controls could delay this adjustment but not avert it.

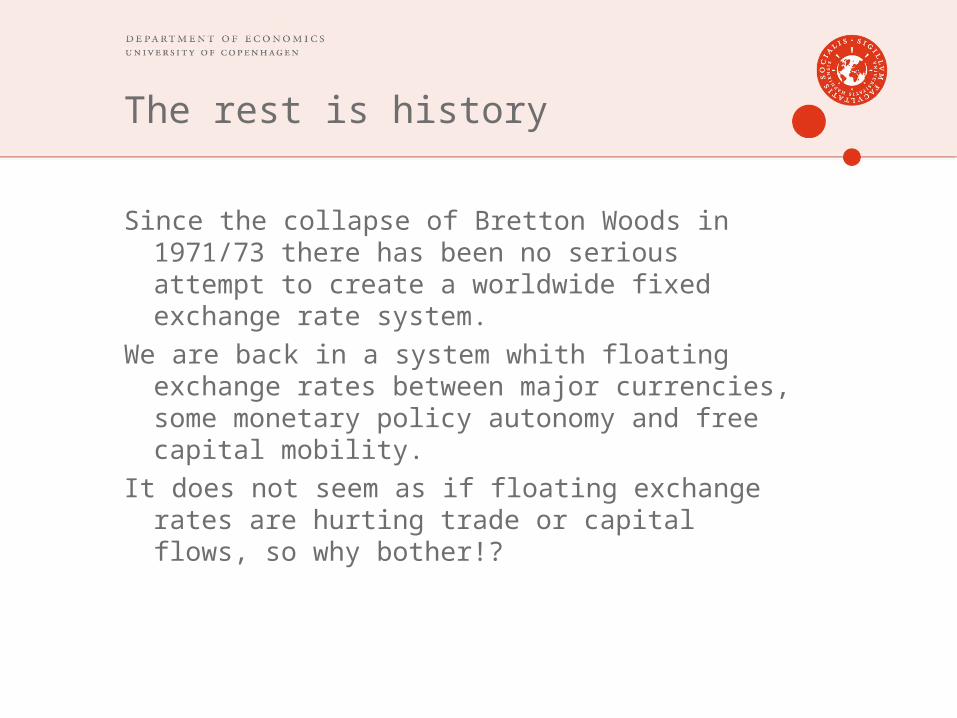

The rest is history

Since the collapse of Bretton Woods in 1971/73 there has been no serious attempt to create a worldwide fixed exchange rate system.

We are back in a system whith floating exchange rates between major currencies, some monetary policy autonomy and free capital mobility.

It does not seem as if floating exchange rates are hurting trade or capital flows, so why bother!?

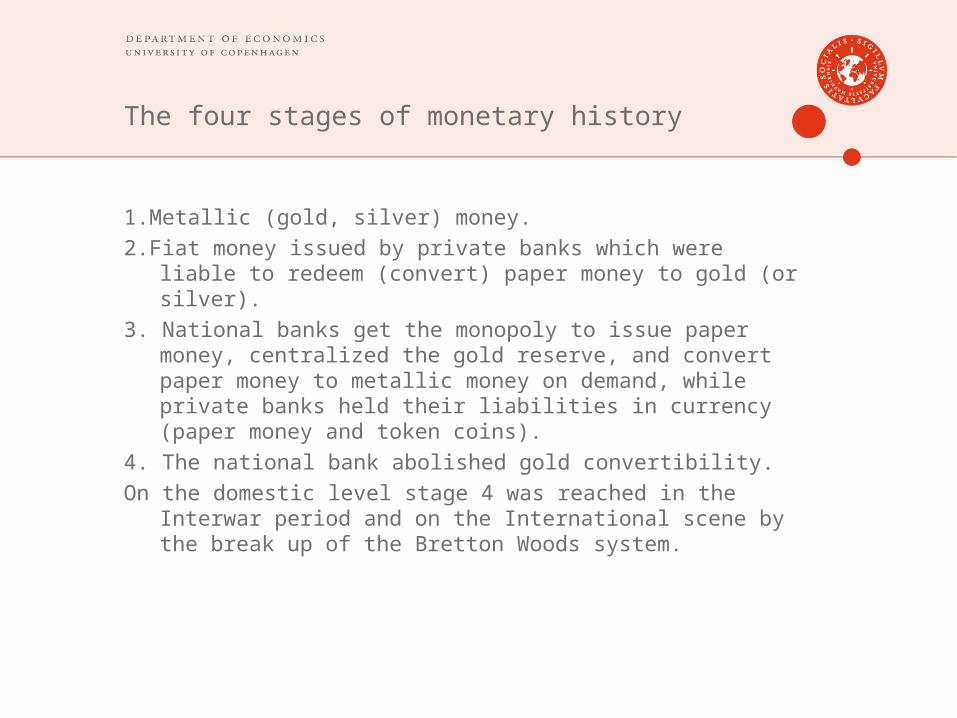

The four stages of monetary history

1.Metallic (gold, silver) money.2.Fiat money issued by private banks which were liable to

redeem (convert) paper money to gold (or silver).3. National banks get the monopoly to issue paper money,

centralized the gold reserve, and convert paper money to metallic money on demand, while private banks held their liabilities in currency (paper money and token coins).

4. The national bank abolished gold convertibility.On the domestic level stage 4 was reached in the Interwar

period and on the International scene by the break up of the Bretton Woods system.

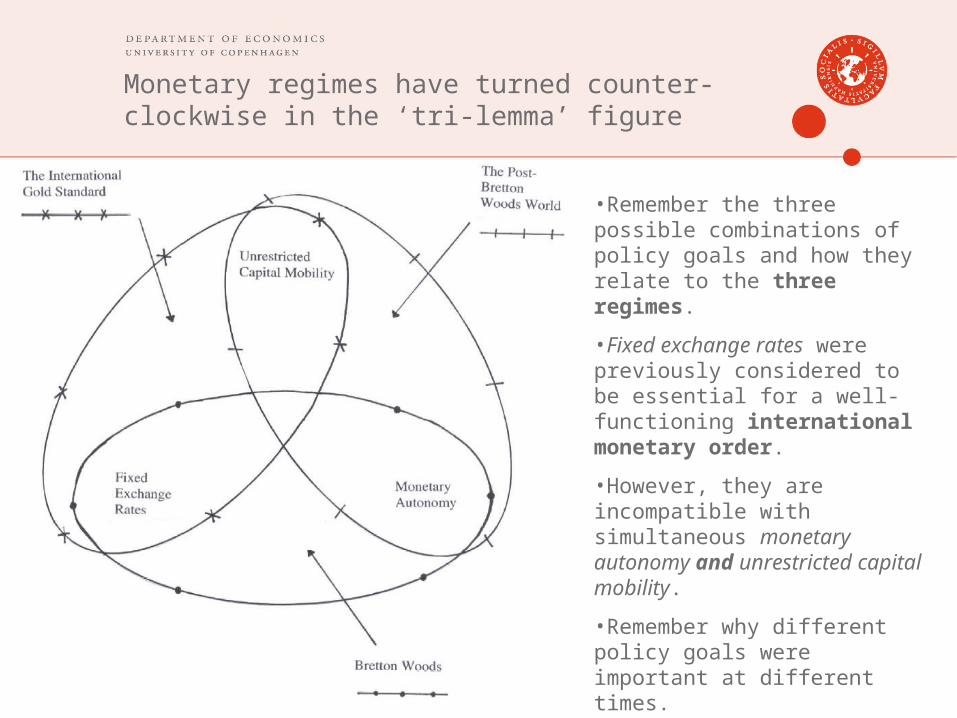

Monetary regimes have turned counter-clockwise in the ‘tri-lemma’ figure

•Remember the three possible combinations of policy goals and how they relate to the three regimes.

•Fixed exchange rates were previously considered to be essential for a well-functioning international monetary order.

•However, they are incompatible with simultaneous monetary autonomy and unrestricted capital mobility.

•Remember why different policy goals were important at different times.

Why the Great Depression is important

To understand the Great Depression is the Holy Grail of macroeconomics. Not only did the Depression give birth to macroeconomics as a distinct field of study, but also… the experience of the 1930s continues to influence macroeconomists’ beliefs, policy recommendations, and research agendas. And, practicalities aside, finding an explanation for the worldwide economic collapse of the 1930s remains a fascinating intellectual challenge.

- Ben Bernanke (2000), Essays on the Great Depression Economics Professor at Princeton and presently Chairman

of the US National Bank, the Federal Reserve. He is a self-professed ‘Depression buff’.

If you want to become Director of a National Bank do study economic history, as Ben did.

Ben Bernanke’s understanding of the Great Depression is that money had great impact on the real economy.

The decline in money supply in the Great Depression was not a passive response to the decline in output and prices but to a large extent the causality went from money to real output.

It is possible to interpret the present activist money supply management of the Fed under Chairman Ben as guided by the principle: Do not repeat the mistakes in the Great Depression.

From Roaring Twenties to Great Depression

• Considered to be a time of prosperity in the United States.

• Actually unbalanced: Agricultural prices were falling while industrial incomes increased.

• Hoover won Presidential election on March 4, 1929, after declaring “We in America today are nearer to the final triumph over poverty than ever before in the history of any land.”

• Good times came to an end in 1929.• Period after this became known as the Great

Depression.

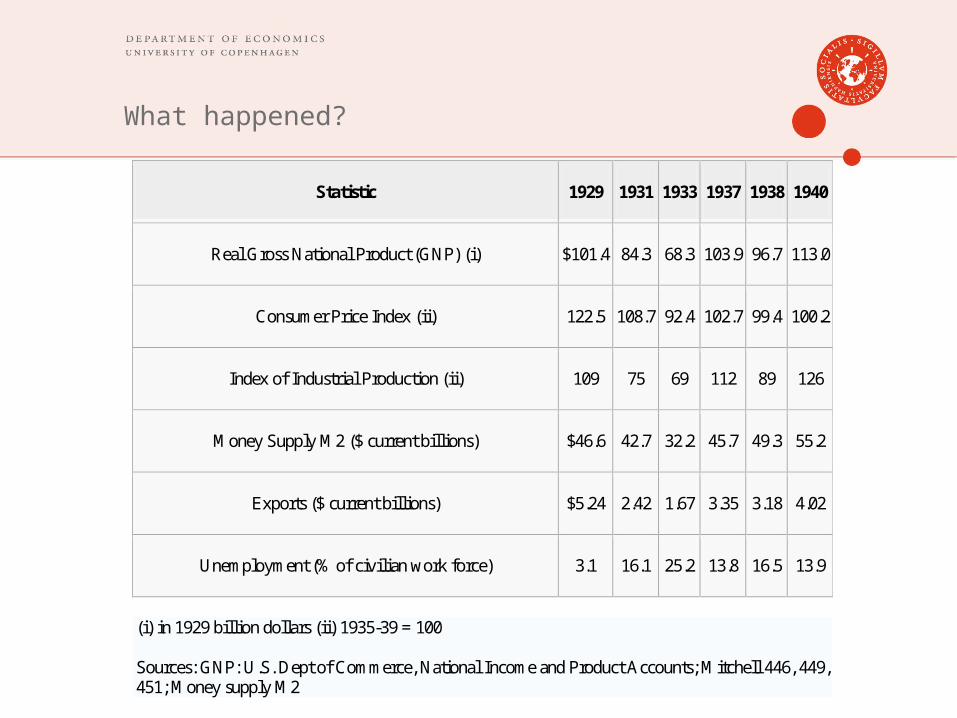

What happened?

Statistic 1929 1931 1933 1937 1938 1940

Real Gross National Product (GNP) (i) $101.4 84.3 68.3 103.9 96.7 113.0

Consumer Price Index (ii) 122.5 108.7 92.4 102.7 99.4 100.2

Index of Industrial Production (ii) 109 75 69 112 89 126

Money Supply M2 ($ current billions) $46.6 42.7 32.2 45.7 49.3 55.2

Exports ($ current billions) $5.24 2.42 1.67 3.35 3.18 4.02

Unemployment (% of civilian work force) 3.1 16.1 25.2 13.8 16.5 13.9

(i) in 1929 billion dollars (ii) 1935-39 = 100

Sources: GNP: U.S. Dept of Commerce, National Income and Product Accounts; Mitchell 446, 449, 451; Money supply M2

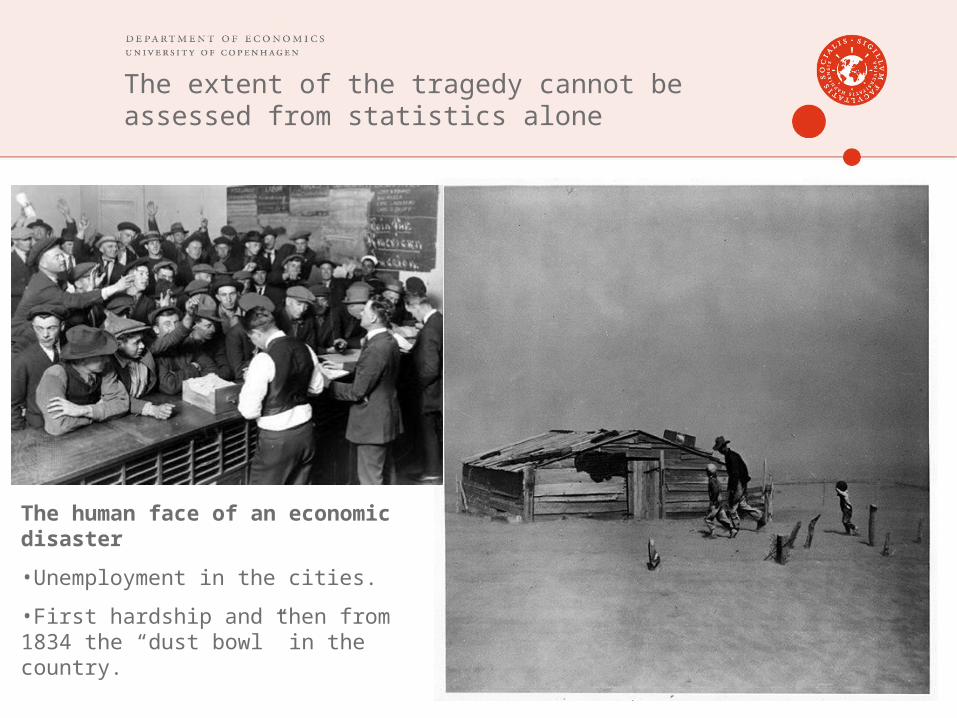

The extent of the tragedy cannot be assessed from statistics alone

The human face of an economic disaster

•Unemployment in the cities.

•First hardship and then from 1834 the “dust bowl” in the country.

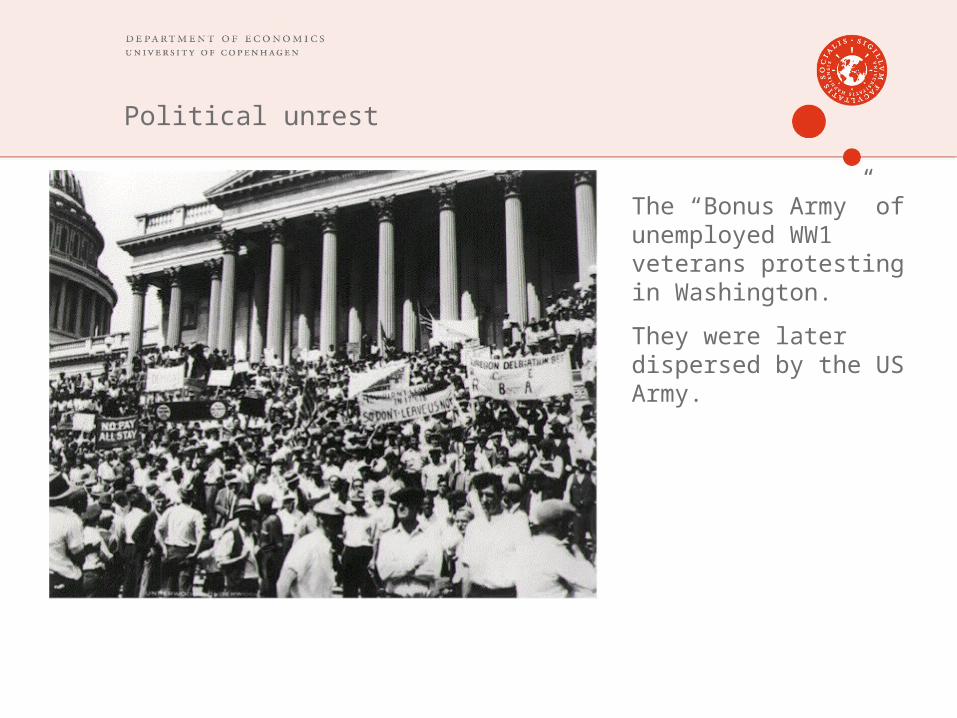

Political unrest

The “Bonus Army” of unemployed WW1 veterans protesting in Washington.

They were later dispersed by the US Army.

California during the Great Depression

I saw and approached the hungry and desperate mother, as if drawn by a magnet. I do not remember how I explained my presence or my camera to her… I did not ask her name or her history. She told me her age, that she was thirty-two. She said that they had been living on frozen vegetables from the surrounding fields, and birds that the children killed. She had just sold the tires from her car to buy food. There she sat in that lean- to tent with her children huddled around her, and seemed to know that my pictures might help her, and so she helped me. There was a sort of equality about it.

- Dorothea Lange

Early developments

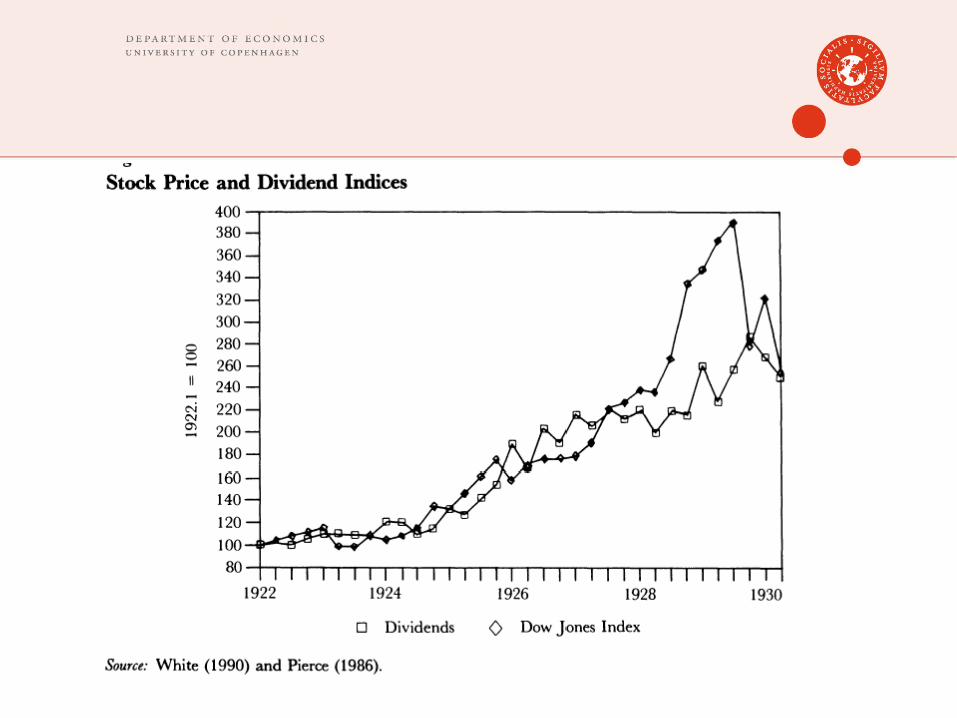

• Strong growth during 1920s.• Led to stock market speculation and rising prices.• Federal Reserve attempted to dampen this by selling bonds

and raising interest rates.• Money supply grows by just 0.6% per year from 1928-9.• Stock market peaks on September 7, 1929 with revelations

of fraud on London stock exchange. Drifts slowly downwards.

• Industrial production started to fall in second half of 1929.• Fed responds by relaxing monetary policy.• Early October: Stocks rally.• Irving Fisher: would be “a good deal higher… within a few

months”.

1929 Wall Street Crash

• Symbolic start to the Great Depression.

• Oct. 24: “Black Thursday”: 13 million shares sold. Technology overwhelmed.

• Banks attempt to sure up the market. But more bad news.

• Oct. 28-29: “Black Tuesday and Wednesday”: 16 million shares sold. Major corporations also hit.

• Panic spread to London, Paris, Berlin, Tokyo.

• But don’t overestimate the impact of the Wall Street Crash!

Source: about.com

Value of a $100 investment on December 31, 1925

The six cents rule

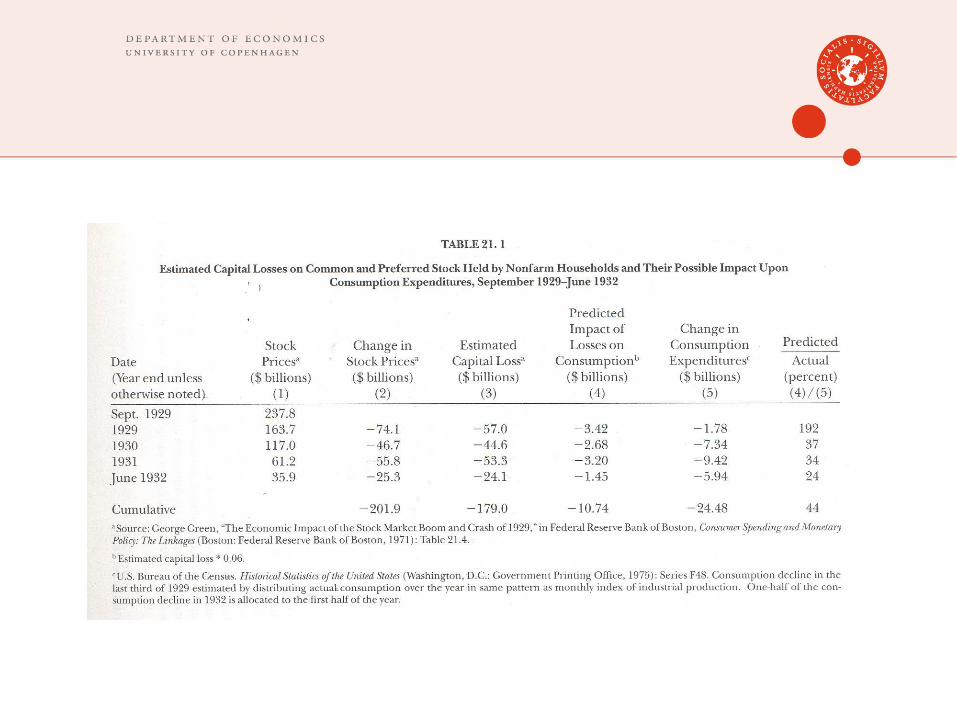

Estimates of the effect on consumption of changes in wealth such as stocks (equities,shares) vary between 5 and 10 per cent.

For the Great Depression the consensus estimate is six per cent.

The six cents rule means that a 1$ decline in wealth leads to a 6 cents decline in consumption.

Initially conumption declined far less than predicted from changes in wealth but later in Depression far more, see columns 4-6.

Explanations for the Great Depression

•The original 1930s debate was between Keynes and Hayek.

•Keynes blamed a loss of business confidence that undermined investment.

•Hayek argued that the Federal Reserve inhibited the free market’s adjustment to a new equilibrium.

•Hayek lost the debate and became a philosopher.

•That is why you learn about Keynes in Mankiw and not Hayek!

Later explanations

• Friedman & Schwartz: Criticized the Federal Reserve for doing too little too late.

• Peter Temin: Argued for impact of an unanticipated and unexplained decline in consumer expenditures.

• Others: Role of international trade and finance.

• We will go for a combination of the above!

• Today we concentrate on aggregate demand-based explanations of the outbreak of the Depression and next time we look at how monetary policy affected the different paths of recovery.

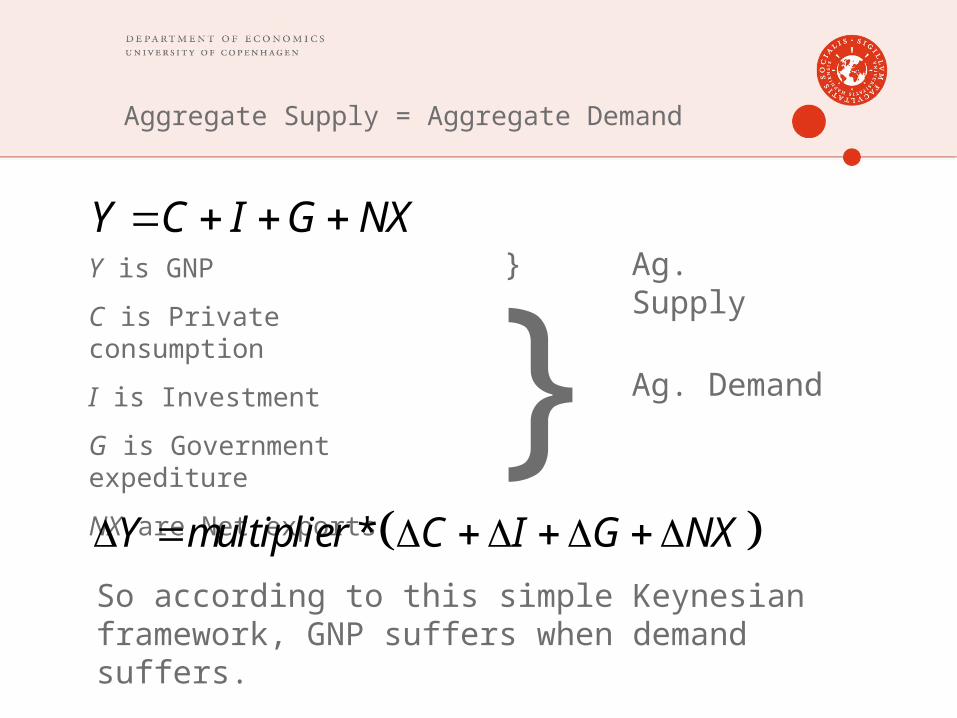

Y is GNP

C is Private consumption

I is Investment

G is Government expediture

NX are Net exports

Aggregate Supply = Aggregate Demand

Y C I G NX

}} Ag. Supply

Ag. Demand

*Y multiplier C I G NX So according to this simple Keynesian framework, GNP suffers when demand suffers.

C, Private consumption

• Real consumption fell 23% between 1929 and 1933.• Consumption depends on (expected) wealth and income.• Table 21.1 shows that the Wall Street Crash explains about

1/3 of the decline in consumption.• Few owned stocks.• But influence on expectations.

• Good harvests caused agricultural prices to fall from all time high during WWI.

• Reduced agricultural income and consumption.• Offset by rising real income of rest of population!

• With deflation, debtors saw the real value of their liabilities increase.

• Temin: Inexplicably large drop in consumption. Might be due to expectation of permanent drop in income.

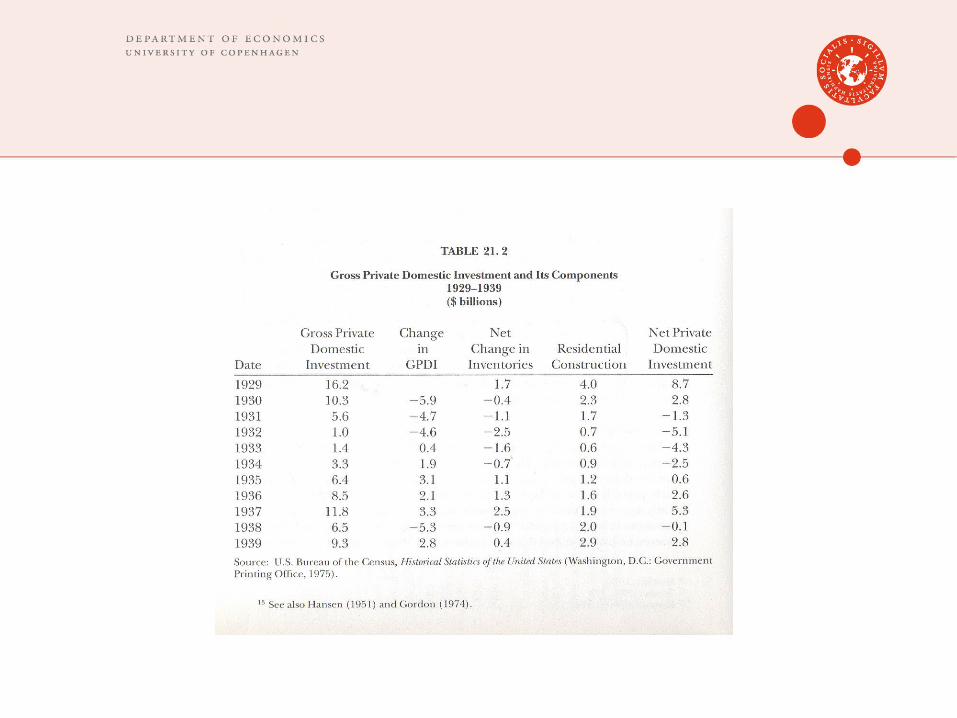

I, Private domestic investment

• Keynes’ explanation.• 1929-33 saw disinvestment!• Gross investment fell from 15% of GNP to under 1%.• Depreciating capacity was not replaced.• Residential investment falling before 1929 due to

immigration restrictions.• Stock price uncertainty.• Big problem again deflation:

• Debtors have highest propensity to invest (and consume).

• High real interest rates (real interest rate = nominal interest - inflation) harmed investment.

• But real wages increased for those with a job!

G, Government consumption

• Keynesians would argue that the government should have increased expenditure – it did in the beginning!

• Early on government ran (unintended) budget deficits.

• Tax increase in 1932 made policy pro-cyclical.

• But this was after the Depression had started and it made things worse.

NX, Net exports

• 1928: Net exports of $1 billion.• 1936: Net exports of $33 million. Trade volume

halved.• Rise in US interest rates made it expensive to

borrow. Debtor nations thus reduced imports.• Primary producers particularly hardly hit. Prices

falling on their exports. Unable to borrow so limited imports.

• US introduced Smoot-Hawley tariffs in 1930s.• Other countries followed suit.• World trade collapses.

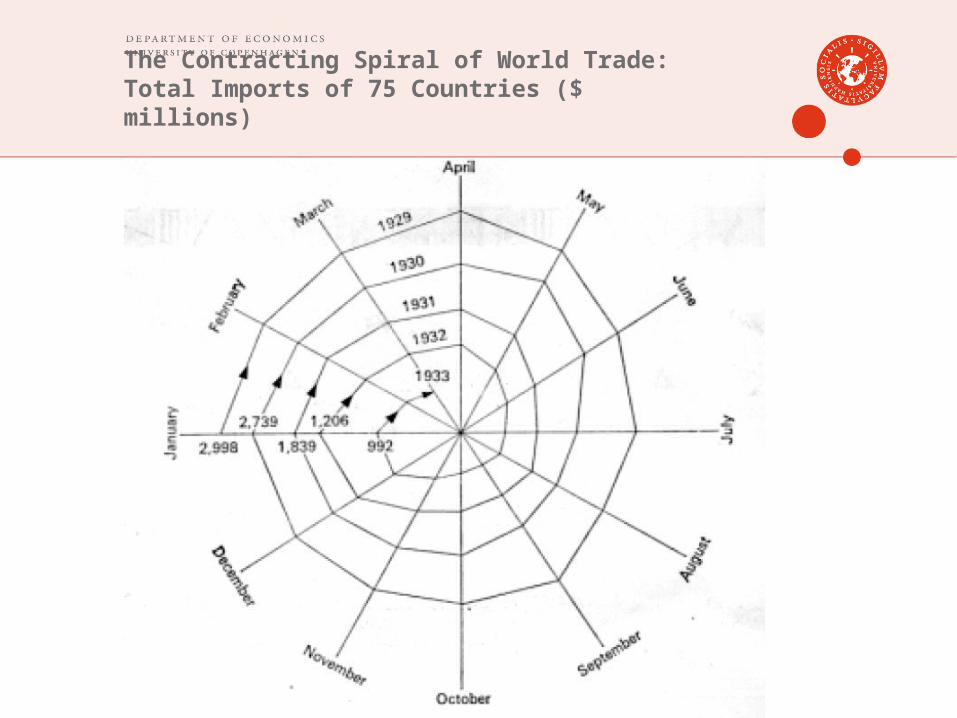

The Contracting Spiral of World Trade:Total Imports of 75 Countries ($ millions)

Monetary factors

• Many banks had a high proportion of “bad” loans.• Banks in agricultural areas particularly badly hit.• Federal Reserve could have acted as “lender of last resort”.• But Fed limited by commitment to the gold standard.• Money supply decreased because of mistrust of banks

(remember fractional reserve principle, lecture 5)• Banks cautious about lending that is they increased the ratio of

reserves to deposits.• Customers preferred to hold cash (currency) rather than

deposit their money• Both factors limited the money creation job of banks

On Monday

• We will look at the varying national responses to the Great Depression.

• In particular, we will answer: Why did the speed of recovery differ between countries?

• And I will return to the role of the Gold Standard

References

Pictures from:http://www.english.uiuc.edu/maps/depression/photoessay.htmMankiw, N.G. (2004) Principles of Economics.And of course the following is compulsory reading!Attack & Passel, pp. 583-603