Embed Size (px)

Citation preview

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Essentials of Management

Chapter 15Essentials of Control

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Controlling and Other Management FunctionsControlling is known as terminal management

function because it takes place after other management functions are completed.

Controls help evaluate whether other functions have been carried out properly.

Control function can also be used to measure the effectiveness of the control system.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Time Element of ControlsPreventive controls take place prior to the

performance of an activity, as when quality standards are applied.

Concurrent controls monitor activities while they are being carried out, such as a computerized supervisory system.

Feedback controls evaluate an activity after it is carried out, as with financial statement.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

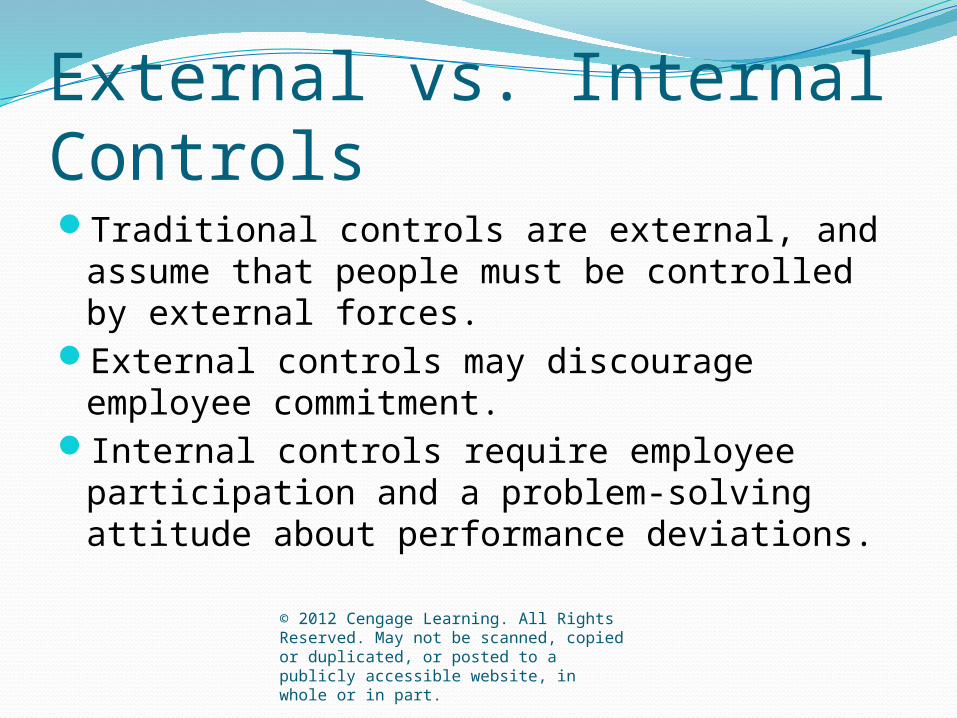

External vs. Internal ControlsTraditional controls are external, and assume

that people must be controlled by external forces.

External controls may discourage employee commitment.

Internal controls require employee participation and a problem-solving attitude about performance deviations.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Steps in Control Process1. Setting appropriate performance standards

(should be realistic and acceptable to people involved)

2. Measuring actual performance (managers should agree on aspects of performance to be measured)

3. Comparing actual performance to standards (deviation indicates size of discrepancy)

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Steps in Control Process, continued4. Taking corrective action a. Do nothing if things are proceeding

according to plan.b. Solve the problem (the big payoff from

controls).c. Revise the standard (important if standard

was unrealistically difficult or easy).

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Nonbudgetary Control TechniquesQualitative control techniques are based on

human judgment about performance.Result in verbal, not numerical evaluation.Quantitative control techniques based on

numerical measures of performance. Controls widely used to keep costs at an

acceptable level (focus on variable costs). Audits should be made independently.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Types of BudgetsBudgets can be fixed or variable.Fixed budget allows for expenditures based on

one-time allocation of resources.Flexible budget allows for variation in use of

resources based on activity.Budget types include (1) master, (2) cash, (3)

cash flow, (4) revenue-and-expense, (5) materials purchase, (6) human-resource, and (7) capital expenditure.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Suggestions for Preparing a Budget Judgment and political tactics enter into

budget preparation.1. Leave wiggle room.2. Research the competition.3. Embrace reality (such as studying facts, and

taking historical perspective).4. Do not neglect intuition.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

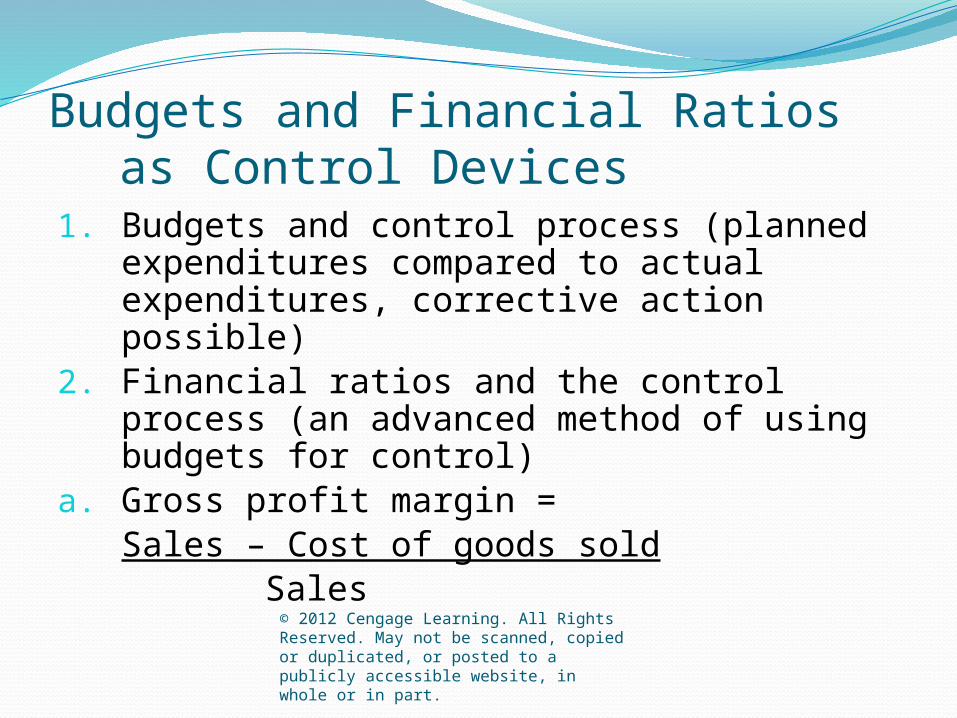

Budgets and Financial Ratios as Control Devices

1. Budgets and control process (planned expenditures compared to actual expenditures, corrective action possible)

2. Financial ratios and the control process (an advanced method of using budgets for control)

a. Gross profit margin = Sales – Cost of goods sold

Sales

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

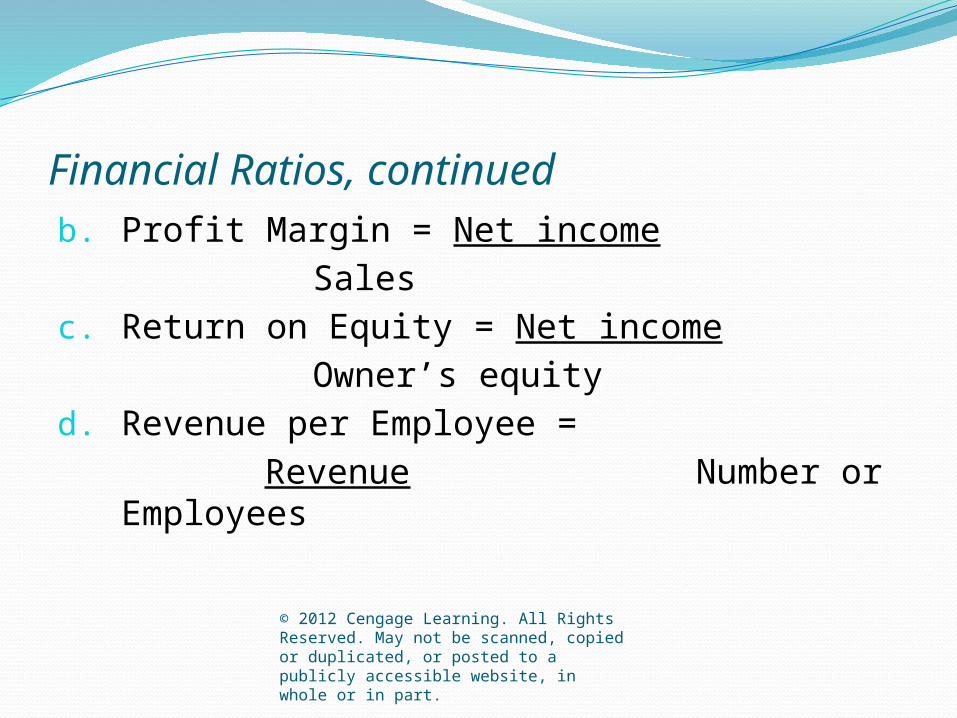

Financial Ratios, continuedb. Profit Margin = Net income

Salesc. Return on Equity = Net income

Owner’s equityd. Revenue per Employee =

RevenueNumber or Employees

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

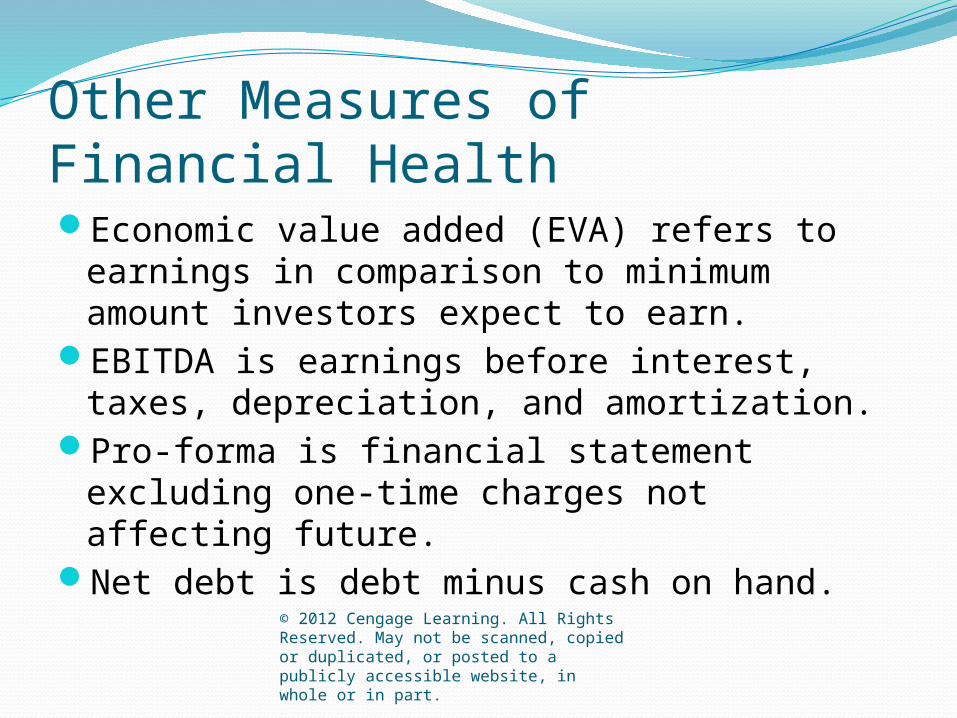

Other Measures of Financial HealthEconomic value added (EVA) refers to

earnings in comparison to minimum amount investors expect to earn.

EBITDA is earnings before interest, taxes, depreciation, and amortization.

Pro-forma is financial statement excluding one-time charges not affecting future.

Net debt is debt minus cash on hand.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

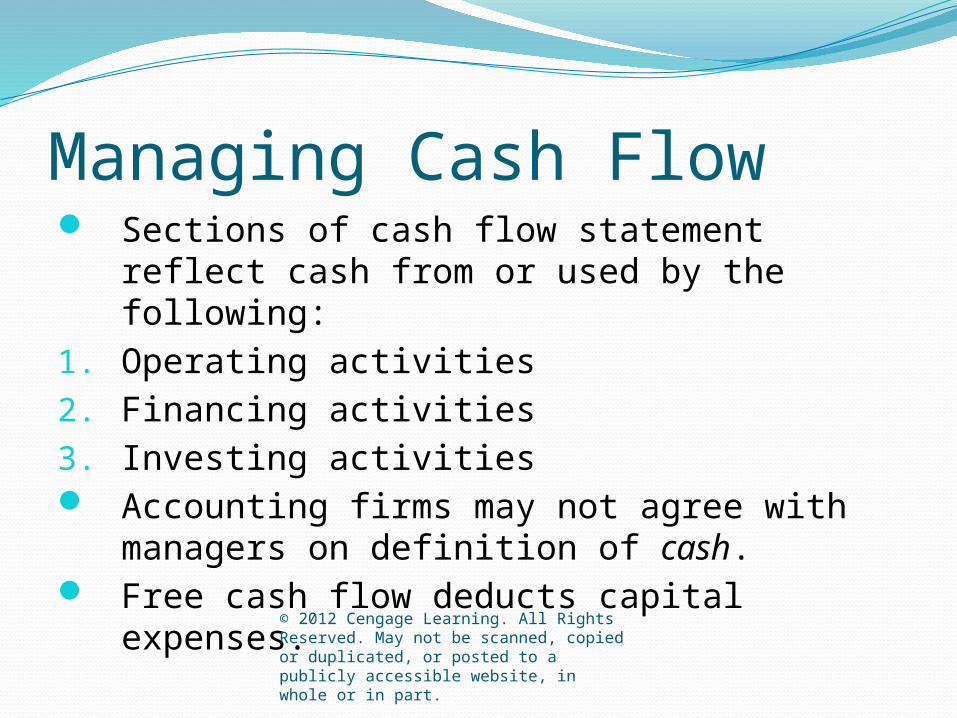

Managing Cash Flow Sections of cash flow statement reflect cash

from or used by the following:1. Operating activities2. Financing activities3. Investing activities Accounting firms may not agree with

managers on definition of cash. Free cash flow deducts capital expenses.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Investing in Positive Approaches to Cost Reduction Investing money in right process or

equipment often leads to useful cost reductions.

a. Video conferencing equipment can help reduce travel expenses.

b. Automation in general is a positive investment that reduces costs, such as self-service counters in supermarket.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Potential Hazards of Cost Reduction Can lead to low morale, lower quality goods

and services, and foster image of being a cheap company.

a. Some of Toyota’s recall problems were attributed to heavy cost cutting.

b. Fatal blowout of Deepwater Horizon oil rig in Gulf of Mexico (2010) was attributed in part to cost cutting.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Balanced ScorecardAlternative to exclusive reliance on financial

measures of health of company.Enables organizations to clarify vision and

strategy and translate into action.Sets goals and measures performance from

the perspectives of (1) learning and growth, (2) business processes, (3) customer satisfaction, (4) financial health.

Widens horizons about success.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Activity-Based Costing (ABC)Allocates cost of production to all the

activities performed and resources used.Leads to understanding of true costs involved

in production and getting product or service off to market.

Some ABC systems rank activities by degree to which they add value to organization or its outputs.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Measurement of Intellectual CapitalEmployee brainpower is major contributor to

wealth of an organization.Intellectual capital is value of useful ideas and

the people who generate them.Investing in intangible assets like research

and development and training might yield a return eight times greater than equal investment in new plants and equipment.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Relative Standing Against the CompetitionComparing company’s performance against

the competition can be more meaningful than comparison with own previous performance.

Measuring performance in terms of anticipated market share is valuable performance metric.

Asking customers can yields this metric.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Information Systems and ControlProvides management with information useful

or necessary for making decisions.Information from information system (IS) or

management information system (MIS) well suited for control purposes.

Control information generated by information system is virtually unlimited. (Convenience store example would be tracking sales by time of day or weather.)

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Computer-Aided Monitoring of WorkUses computer-based system to monitor work

habits and productivity of workers.Can also uncover leaks of sensitive

information including trade secrets.Provides constant worker surveillance.Helps monitor work of remote workers.Electronic evidence may be important in any

lawsuits against workers.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Workers Most Likely to Be MonitoredOffice workers, including those in frequent

telephone contact with customersWorkers who could be involved in information

leaks, such as in healthcare, law, product development, and marketing

Monitoring works best with workers who performed discrete, measurable tasks during prescribed hours, such as call center employees.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Concerns about Electronic Monitoring SystemsCritics say that system invades employee

privacy and violates their dignity.Executives are not monitored.Results of monitoring systems often used to

take harsh action against rule violators.Advance notice of system may lead to more

positive attitude about monitoring.Good to have policy about acceptable use of

company resources before monitoring.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Characteristics of Effective Controls1. Accepted by employees.2. Appropriate and meaningful.3. Provides diagnostic information.4. Allows for self-feedback and self-control.5. Provides timely information.6. Allows employees control over results

measured.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Characteristics of Effective Controls, continued7. Not contradict itself (such as setting high

quantity and quality standards)8. Allows for random deviation from standard9. Cost-effective (control system does not cost

more than its savings)10. Not limit innovation (such as too much

emphasis on short-term profit vs. long-term investment)