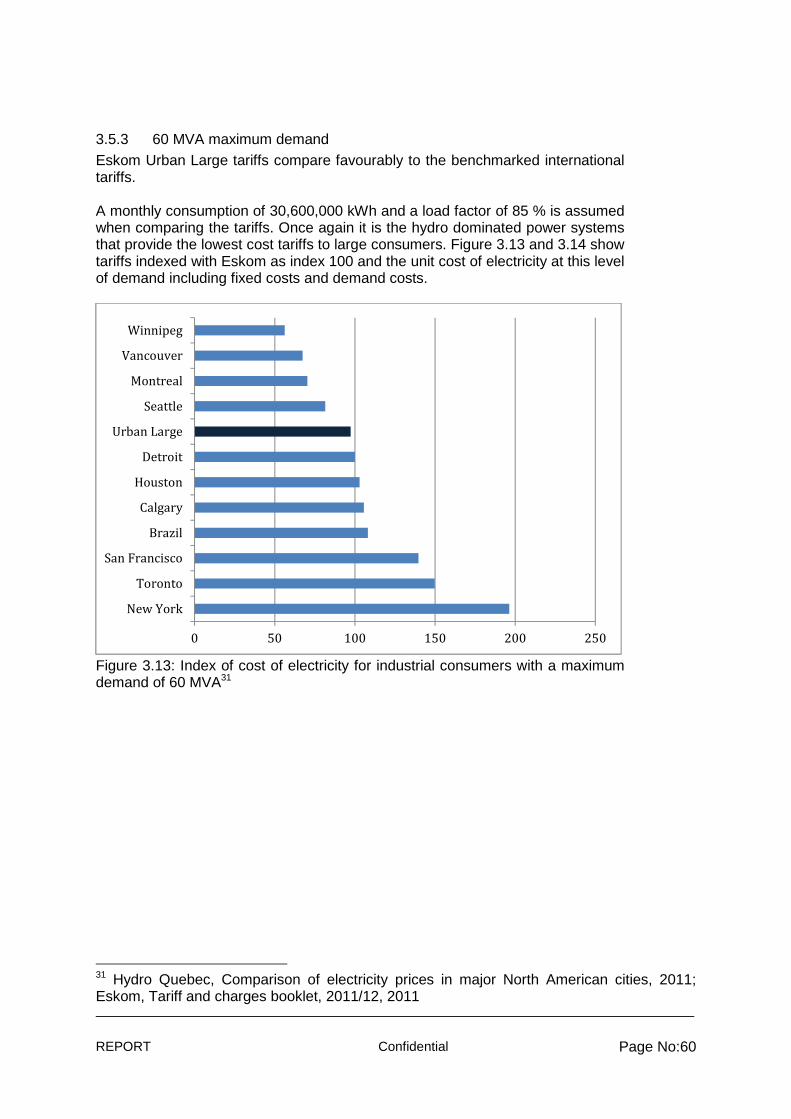

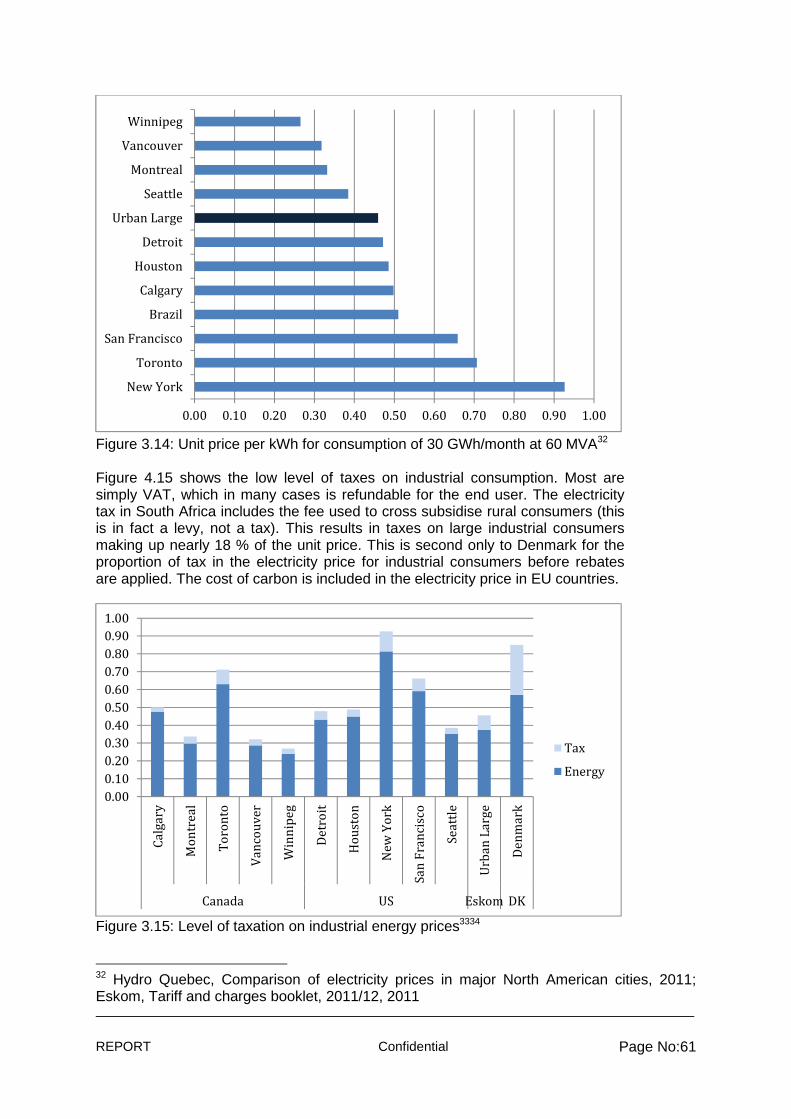

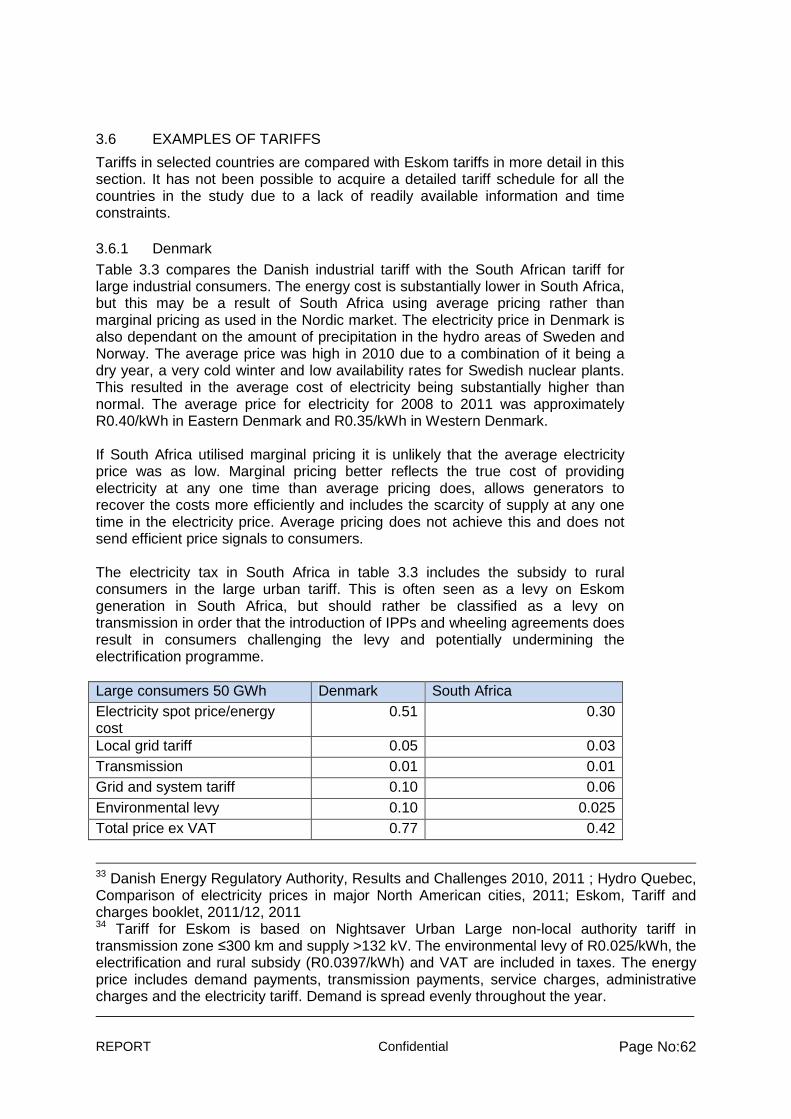

Embed Size (px)

Citation preview

COPYRIGHT © ESKOM HOLDINGS LIMITED NO PUBLICATION OR DISSEMINATION OF ITS CONTENTS IS ALLOWED WITHOUT

WRITTEN PERMISSION

ESKOM

RESEARCH REPORT

INTERNATIONAL BENCHMARKING OF ELECTRICITY TARIFFS

AUTHOR(S) : LTE Energy in association with EA Energy

Analysis, Denmark ORGANISATION : LTE

REPORT Confidential Page No:1

RESEARCH REPORT

INTERNATIONAL BENCHMARKING OF ELECTRICITY TARIFFS

REPORT Confidential Page No:2

EXECUTIVE SUMMARY

INTERNATIONAL BENCHMARKING OF ELECTRICITY TARIFFS

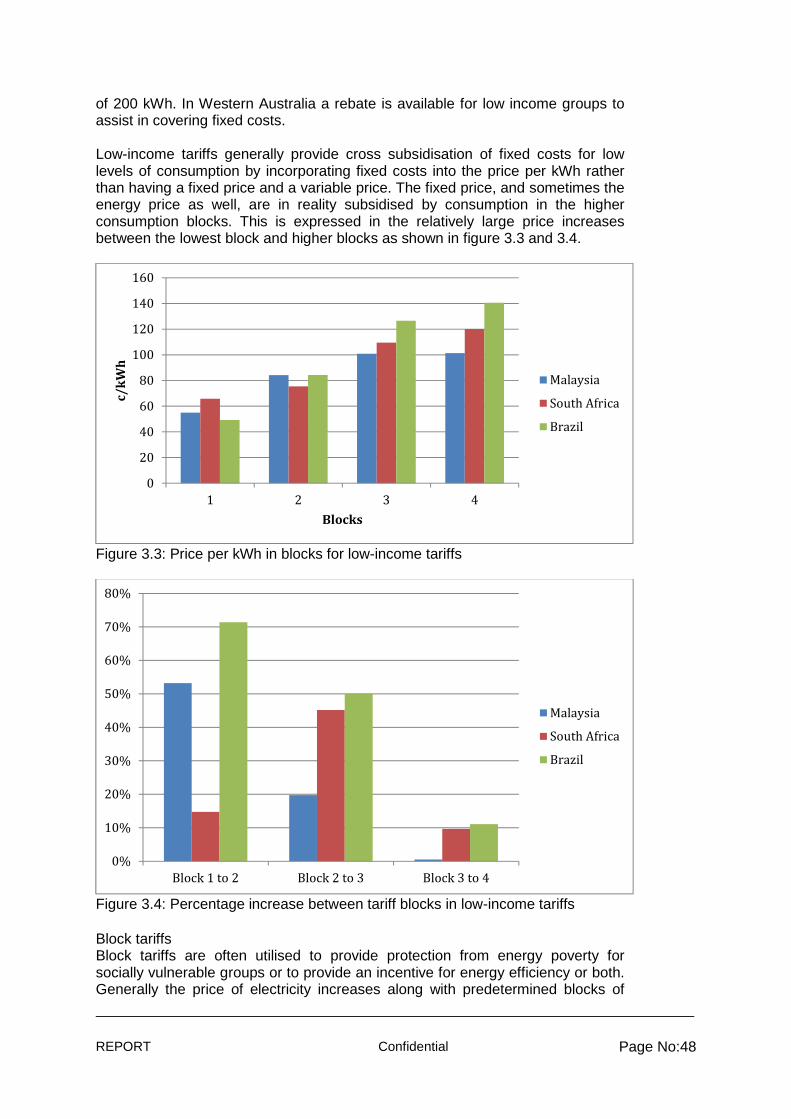

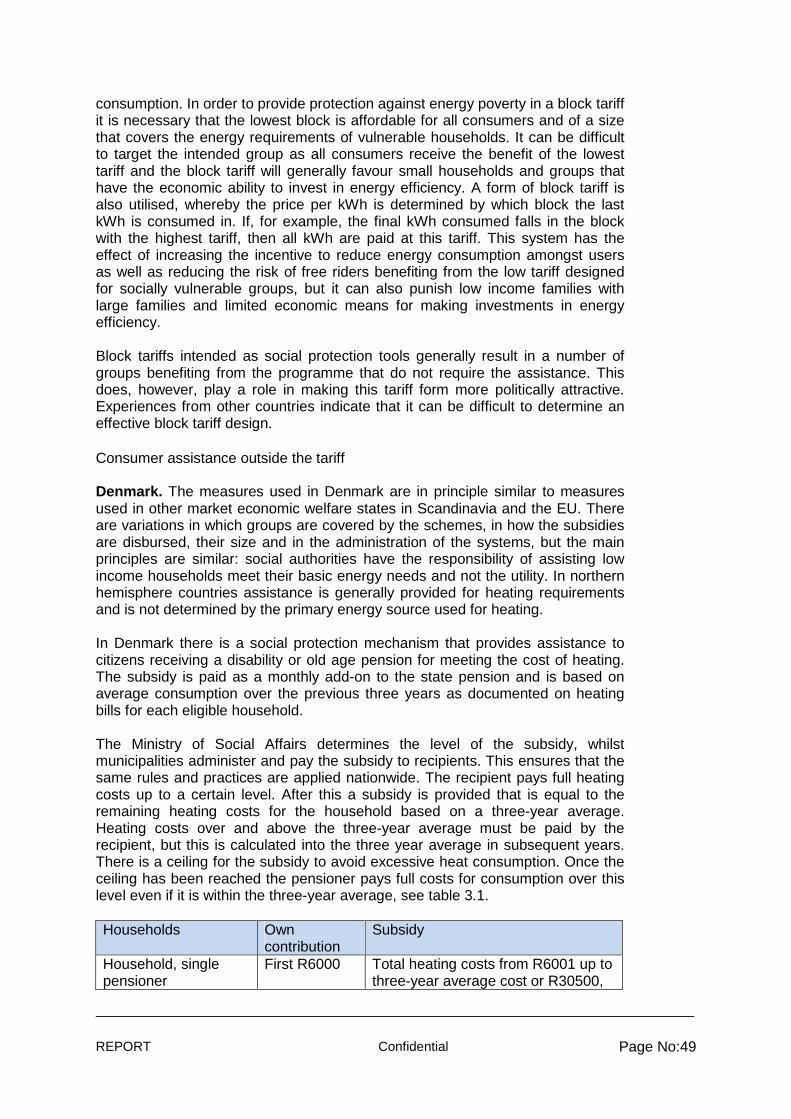

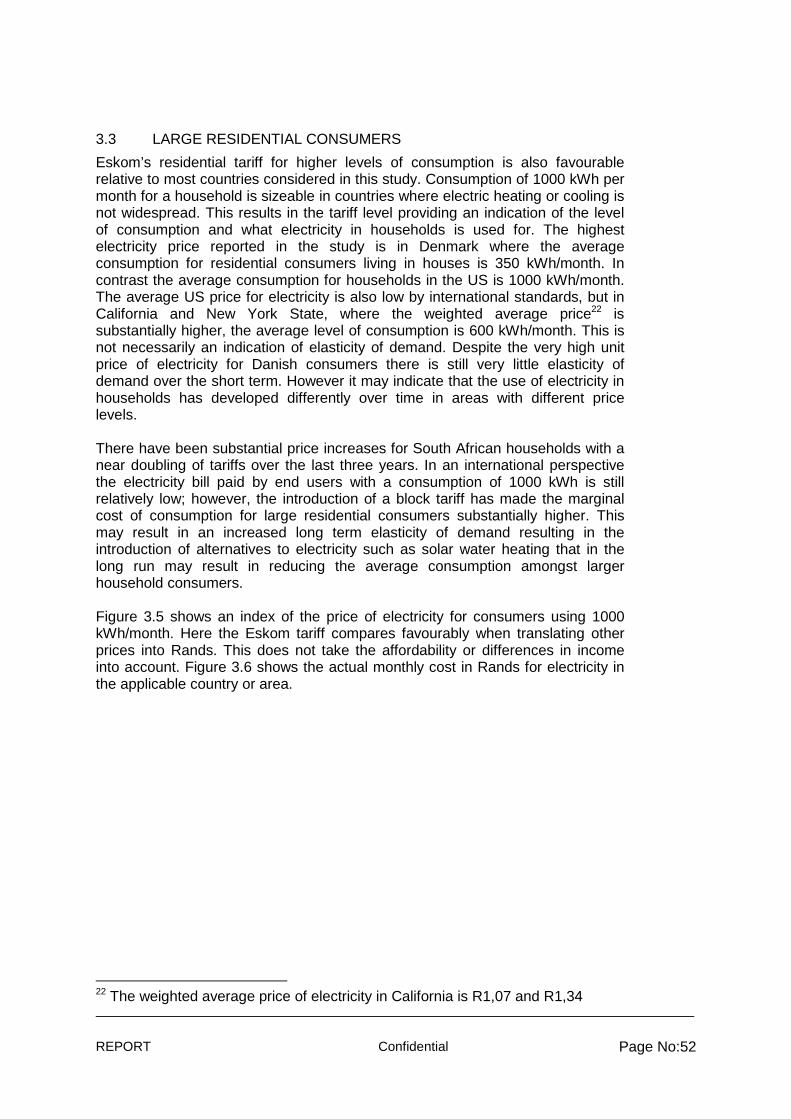

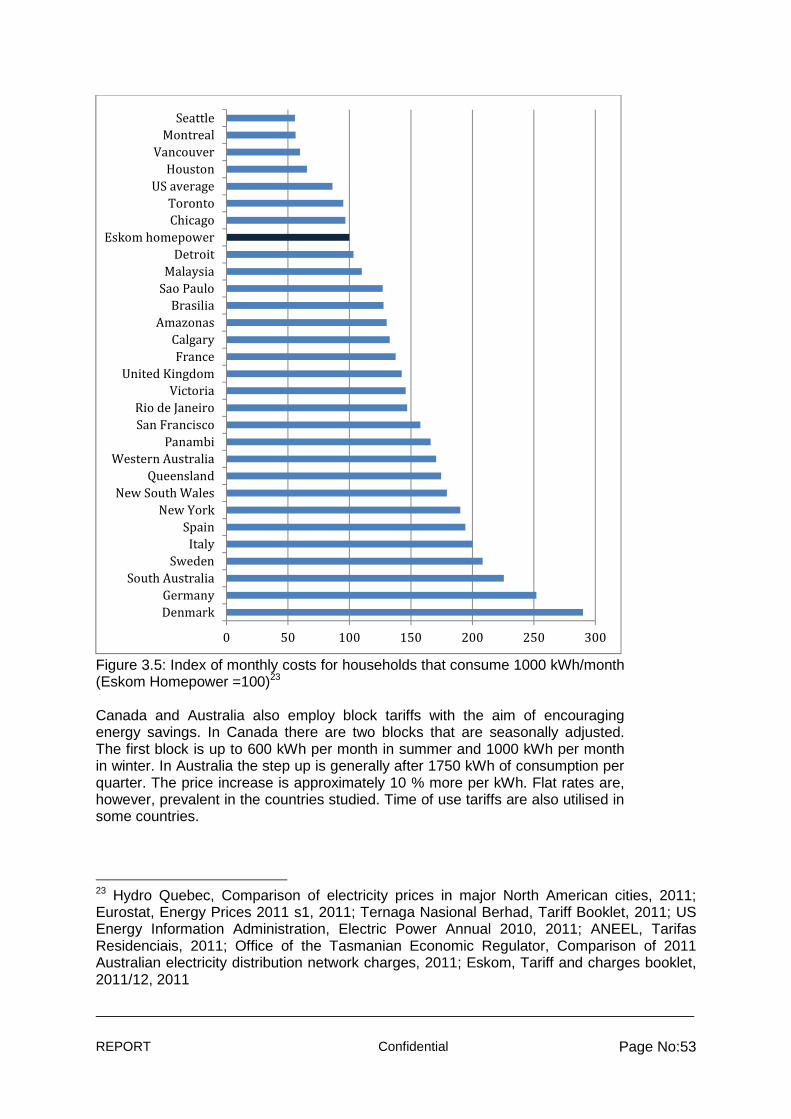

OVERVIEW In the recent past Eskom has implemented a framework of pricing and tariff methodologies guided by the Strategic Pricing Direction for Tariffs documents whose objective in a broad sense is to promote economic efficiency and sustainability, ensure revenue recovery and promote fairness and equity. The current Eskom Tariff Methodology seeks to allocate the costs of its different divisions in a cost reflective manner as well as in conjunction with other parameters essential to each division so as to arrive at a tariff per customer category and account for subsidies in a way such that each cost per division and its tariff component does not affect revenue neutrality. It is with this background, the need arise for an international tariff benchmarking review. With the international benchmarking tariff study, Eskom wishes to contribute to the continued development and refinement of the tariff levels and structures in South Africa. BACKGROUND In the recent past Eskom has implemented a framework of pricing and tariff methodologies guided by the Strategic Pricing Direction for Tariffs documents whose objective in a broad sense is to promote economic efficiency and sustainability, ensure revenue recovery and promote fairness and equity. The utility’s divisions have been unbundled, financially ring-fenced and regulated separately. This allows for the real costs per division to be known and adequately accounted for, and that the tariffs for each division can reflect cost levels and ensure revenue neutrality. This means that the sum of all tariff components is not more than the NERSA approved revenue requirement. The current Eskom Tariff Methodology seeks to allocate the costs of its different divisions in a cost reflective manner as well as in conjunction with other parameters essential to each division so as to arrive at a tariff per customer category and account for subsidies in a way such that each cost per division and its tariff component does not affect revenue neutrality. OBJECTIVES It is with this background, the need arise for an international tariff benchmarking review, which comes at a time of sustained volatility in a number of cost drivers for energy utilities. Increasingly, tariff structures seek to provide an incentive for reducing peak demand, reward customers for lowering their energy us and reduce the need for capacity expansion. To achieve these ends, utilities are increasingly considering alternative tariff structures, which include but are not limited to inclining block tariffs, time-of-use tariffs and controlled load tariffs. With the international benchmarking tariff study, Eskom wishes to contribute to the continued development and refinement of the tariff levels and structures in South Africa. One important aspect is continued comparisons and lessons learned from other countries around the world. It shall be noted that the report primarily provides a 2010 ‘snapshot’ comparison. APPROACH

REPORT Confidential Page No:3

The study covers the following three areas: Comparison of average tariff levels, comparison of tariff structure for selected customer groups, and comparison of tariff setting methodologies. The study compares tariffs in South Africa with a selected group of countries. The study is divided in three parts with the following issues to be included. Part A: Benchmarking of Eskom total average price against a selected group of countries with focus on an apples-versus-apples comparison of Eskom total average tariff (total regulated revenue divided by total sales volume) with that of other similar utilities in selected countries. The overall tariff comparison is provided in chapter 2.1. The following systemic sense-making factors qualify the comparative understanding of the total average tariff levels and have been provided for in chapter 2.2: (i) The trend of the total average tariff, (ii) the contribution of the average tariff to creating sustainable utilities, and (iii) the historical developments in exchange rates. Part B: Benchmarking of Eskom customer tariff categories against regional, developed and developing countries with focus on a comparison of customer categories tariff levels on average: municipality, large and medium industrial, residential, domestic etc. Each charge component comparisons include the consumers’ total average electricity unit cost by assuming typical customer profiles and assumptions. In order to compare price differences for different consumption volumes, typical standard consumers are defined for households and large and small industrial consumers. This is provided for in Chapter 3. Part C: Detailed comparison and discussion of tariff methodologies with a particular focus on a comparison and discussion of different tariff methodologies for a number of selected countries and utilities, see Chapter 4. This part carries out an analysis of selected countries in order to compare the tariff methodologies employed in these countries, the overriding factors in determining tariffs and how the choice of tariff methodology influences consumption for different consumer groups. RESULTS The Eskom tariff benchmarking study has provided a number of interesting findings and results. Of key results, discussions, cautions and lessons learned can the following be highlighted. For Part A the following general results can be noted:

• The benchmarking study of average tariffs is based on comparison of key national energy utilities total revenue and sales (Gwh). The ranking in column three is based on a simple exchange rate conversion of the resulting tariff per kWh in each utility. The benchmarking shows that South Africa (Eskom) is ranked fourth cheapest average tariff of the 15 countries utilities included in the survey. The last four countries (South Africa, India, Australia and China), however, only have marginally different average tariffs (+/- 2 SA cent). Then there is 10-20 SA-cent up to the next group of countries (Argentina, Canada, US, Denmark, South Korea, Thailand, Kenya). The highest average tariffs can be found in Malaysia, Spain and UK

• South Africa (Eskom) is the third largest utility included in the benchmarking based on sales only smaller than the German and South

REPORT Confidential Page No:4

Korean utilities. The smallest utilities included are the utilities from Kenya Argentina and Australia. The ranking show poor relation between sales and revenue

• South Africa (Eskom) is ranked as having the second largest inflation corrected tariff increase of the benchmarked countries during the last 8 years. UK had the biggest average tariff increase, while South Korea, Denmark and Canada had the lowest average increase. None of the countries included had a negative tariff to inflation increase rate over the last 8 years

• South Africa (Eskom) is has the third lowest RoA of the utilities included in the benchmarking. Denmark’s DONG has by far the highest RoA, followed by utilities in India, Spain, Thailand, Germany, UK and Kenya. Only the Chinese and Argentina utilities have lower RoA than Eskom. No correlation between RoA and credit ratings can be seen

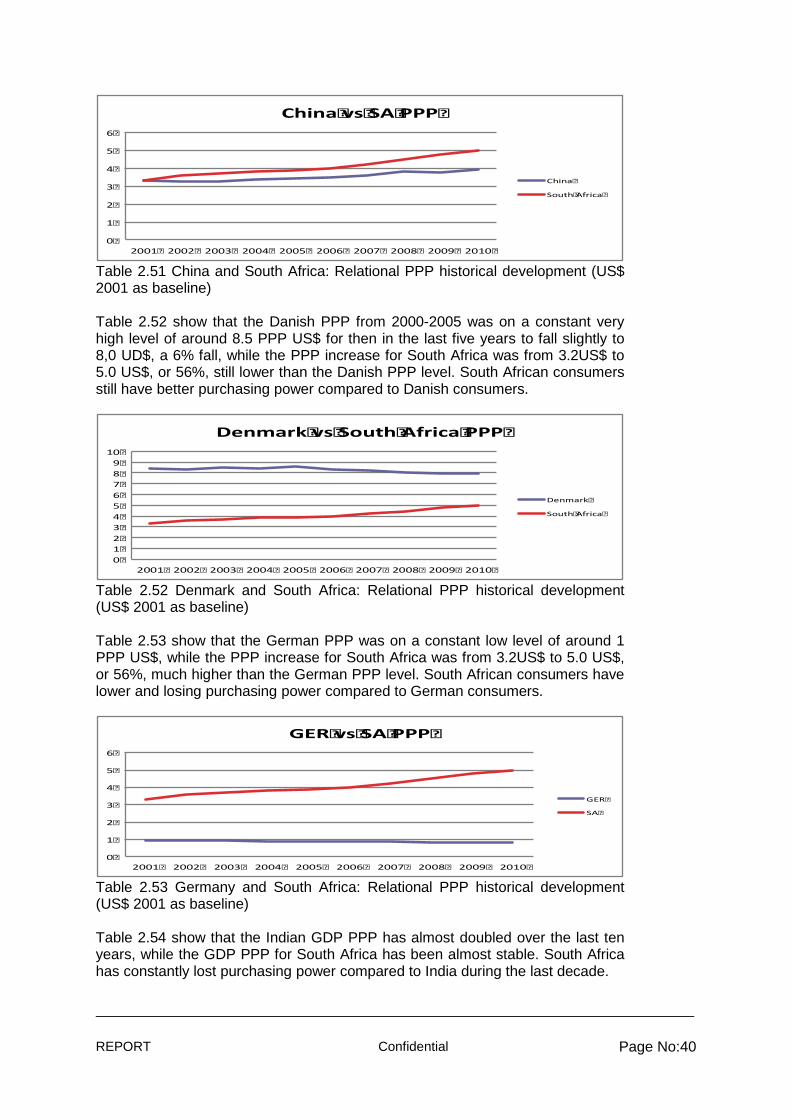

• The PPP results show that there is no correlation of the total average tariffs (based on exchange rate calculations) to the corresponding international PPP benchmarking of the national utilities including in the study. The PPP results also show markedly large changes in rankings for some countries, e.g. South Africa. Based on these findings it is found that the interpretation of the PPP results has to be undertaken with care, and it is suggested that further investigations into the use and practicability of the PPP comparison technique for power utilities.

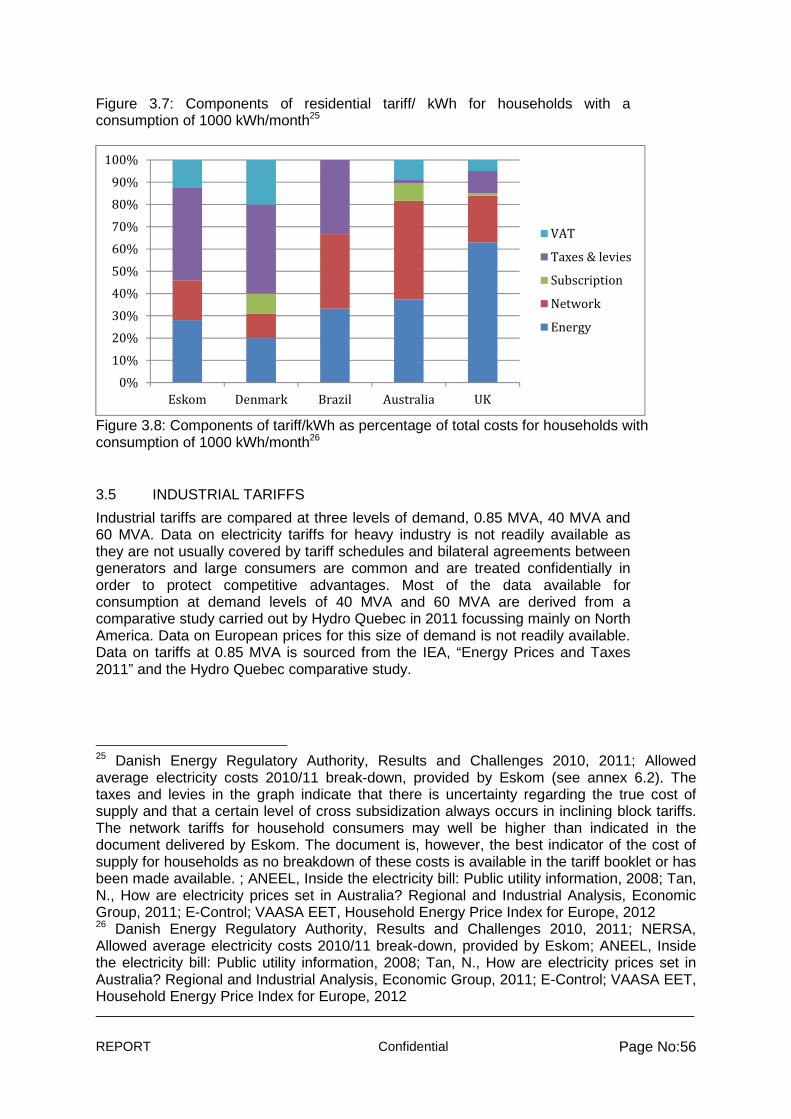

For Part B the following general results can be noted:

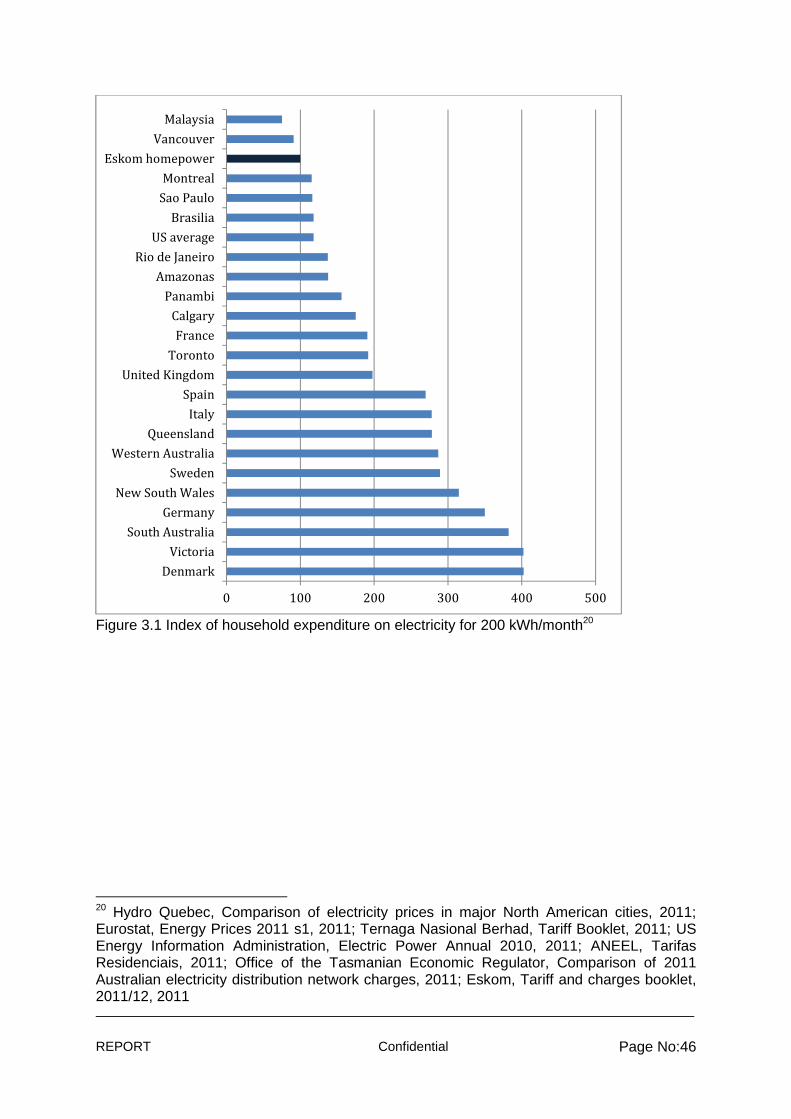

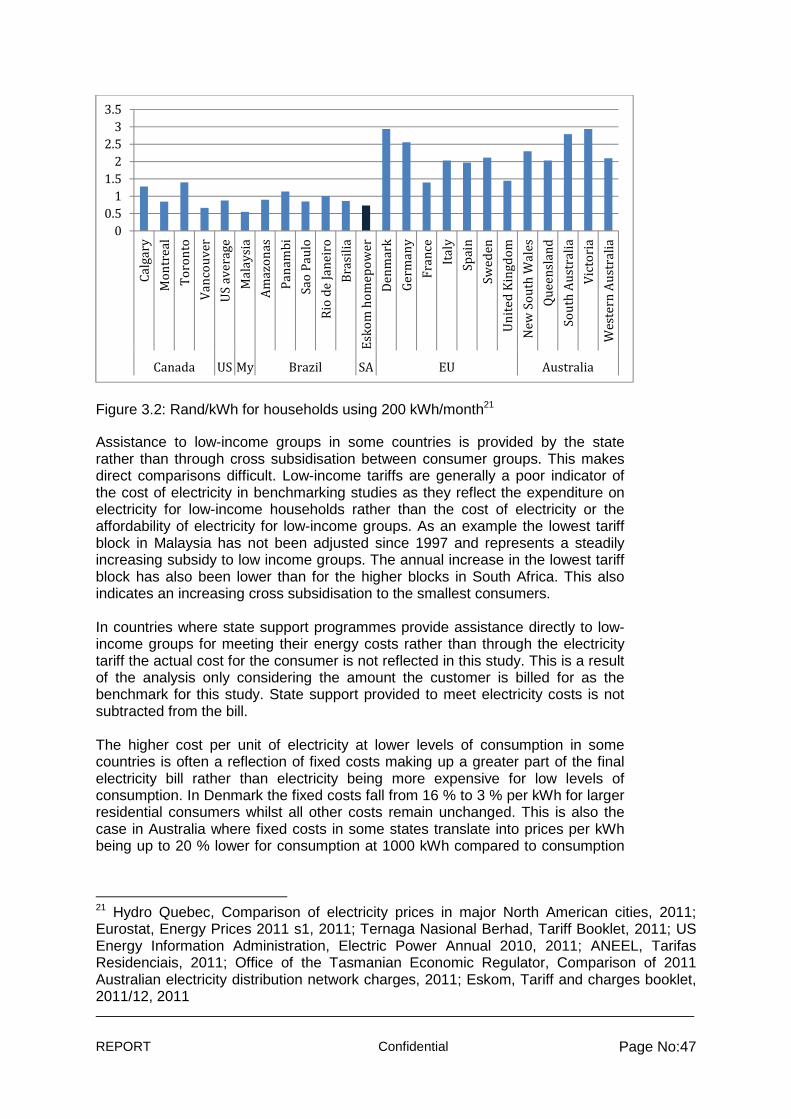

• Eskom’s tariffs generally compare favourably with many other countries when considered as a price only comparison. The tariffs were not compared on an affordability basis. Eskom has the third lowest tariff for consumers using 200 kWh/month. Malaysia has the lowest tariff at this level. Tariffs in Vancouver are also lower than in South Africa. Still, the study showed that reducing the amount of kWh in the lowest tariff block or only providing the lowest tariff to households with single phase connections or prepaid meters etc. could be considered for improved financial feasibility and better international market match

• The marginal cost of electricity for South African consumers in the highest tariff block is on a par with tariffs in Australia and the lower European tariffs. The European tariffs generally include high energy taxes

• The average cost per unit for consumption of 1000 kWh/month under the Eskom block tariff is generally higher than tariffs in North America, but lower than in Europe, Australia, Malaysia and Brazil. Most countries have a flat rate tariff for consumers at this level so they do not benefit from the low-income block tariff as consumers do in South Africa

• Malaysia and Brazil have block tariffs that are aimed at assisting low-income households. In Malaysia this is done with a number of small

REPORT Confidential Page No:5

blocks, whilst in Brazil qualification for lifeline tariffs is based on the size of the connection

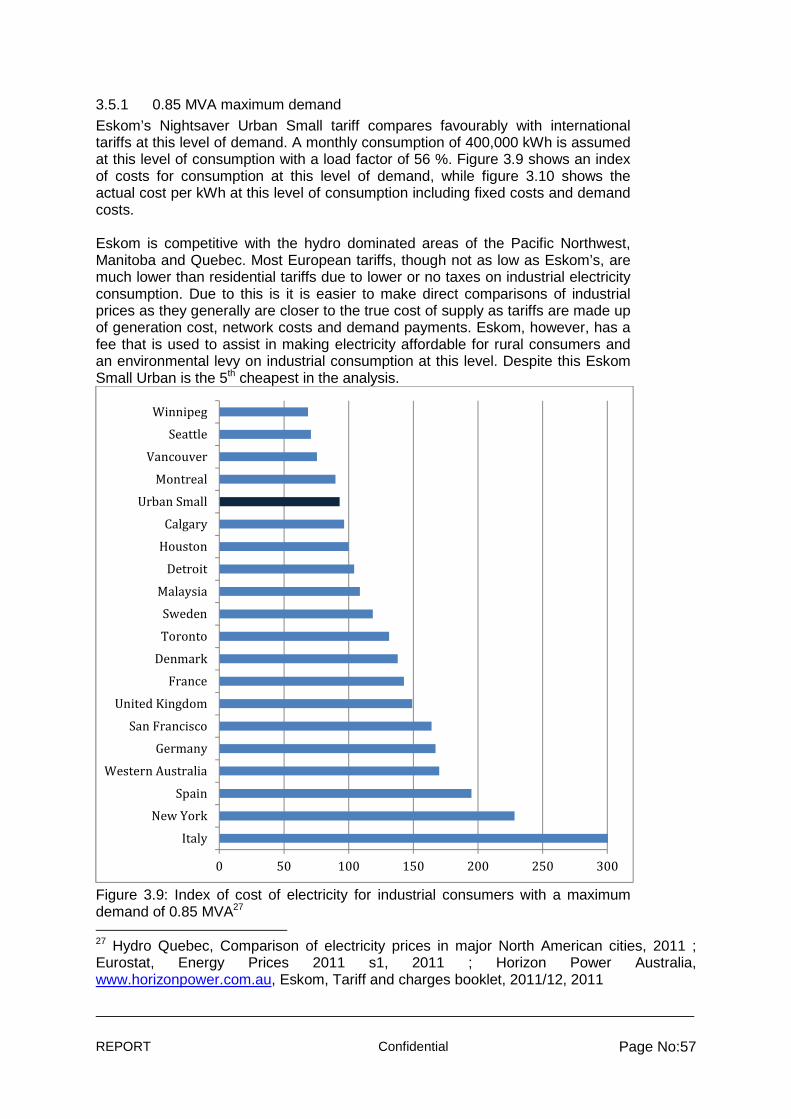

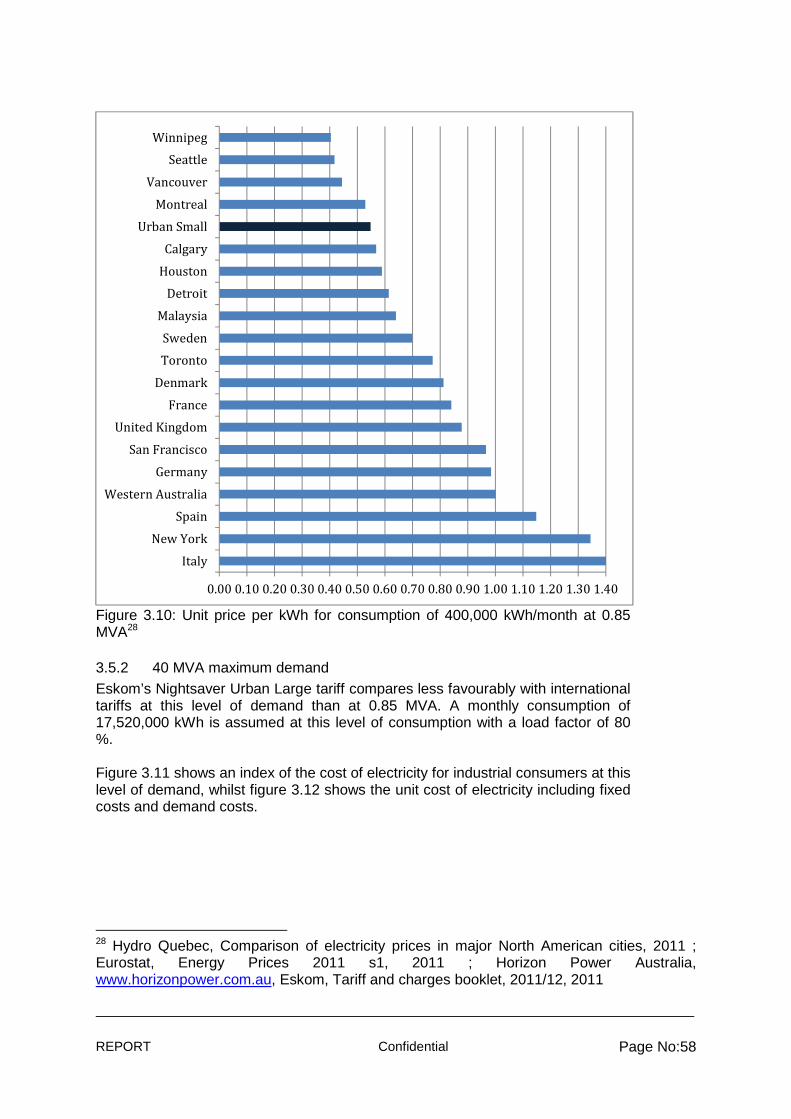

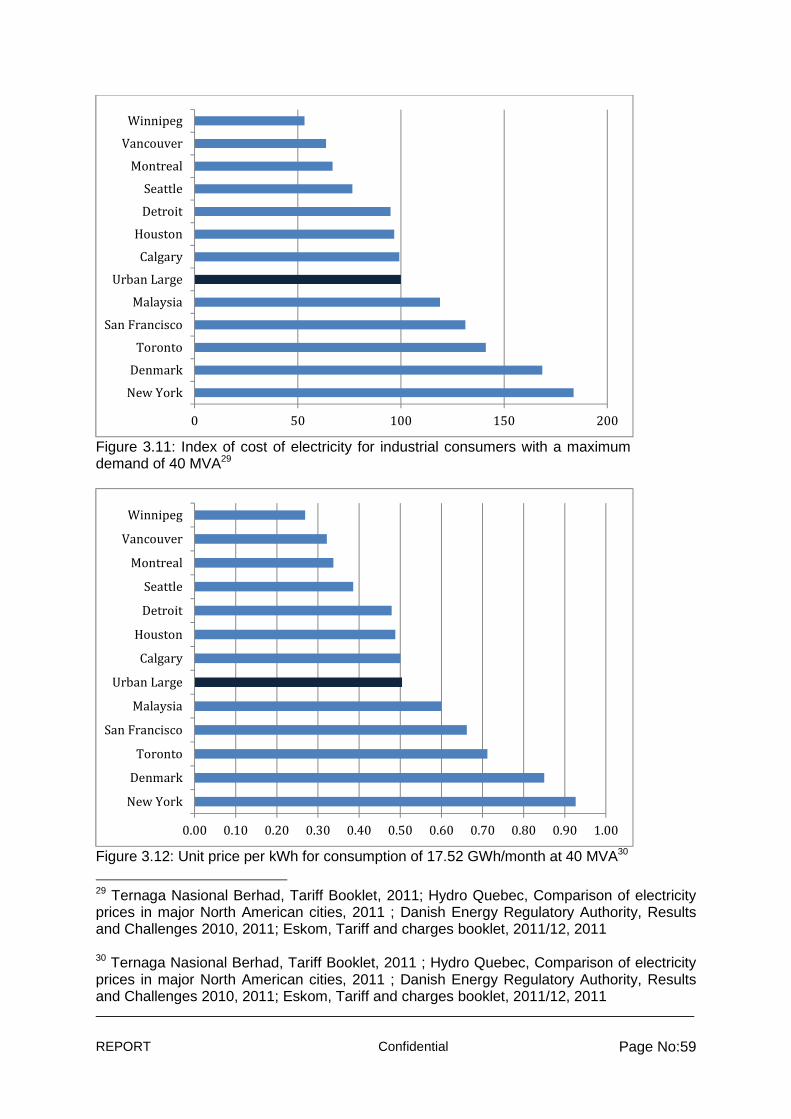

• Industrial tariffs in South Africa are generally more expensive than tariffs in North America. The South African tariffs are, however, listed prices. Very large industrial consumers in South Africa may well have negotiated their own contracts at a lower rate than those listed

• Cross subsidisation of rural consumers through industrial tariffs should be defined as a levy on transmission in order that wheeling agreements or the introduction of other pricing mechanisms do not circumvent or undermine the rural electrification programme.

For Part C the following general results can be noted:

• There is low transparency in the tariff breakdown for residential consumers in South Africa

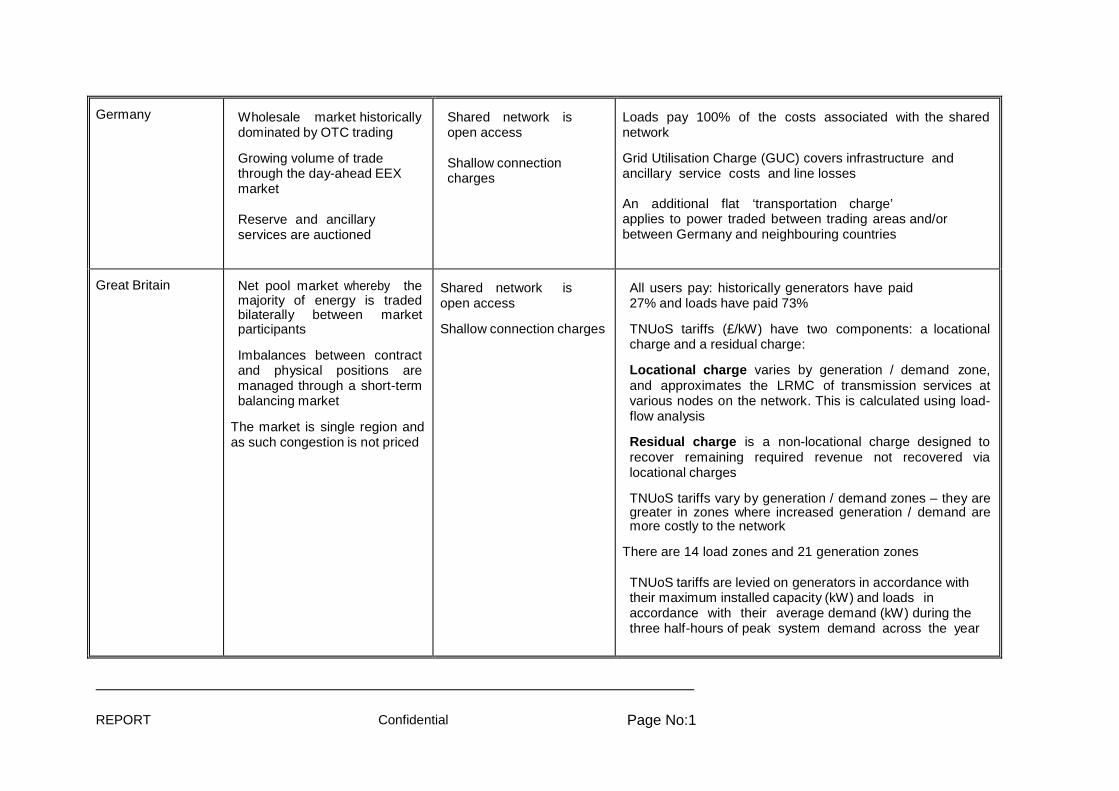

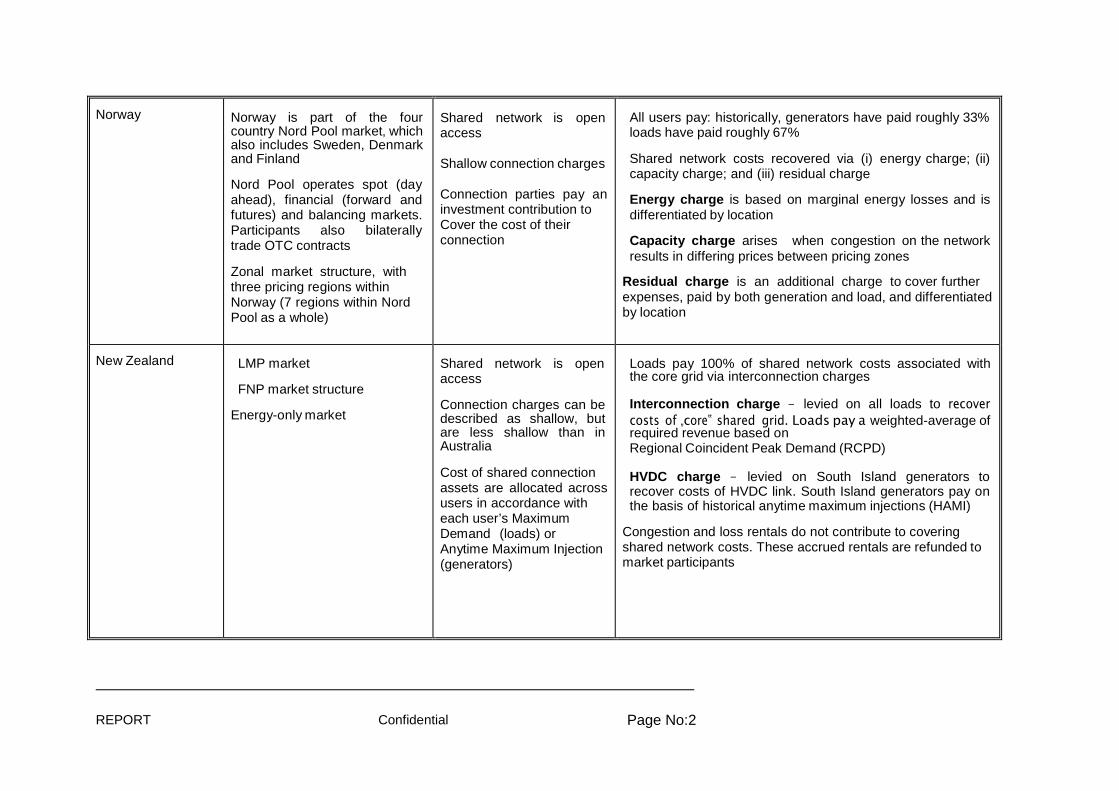

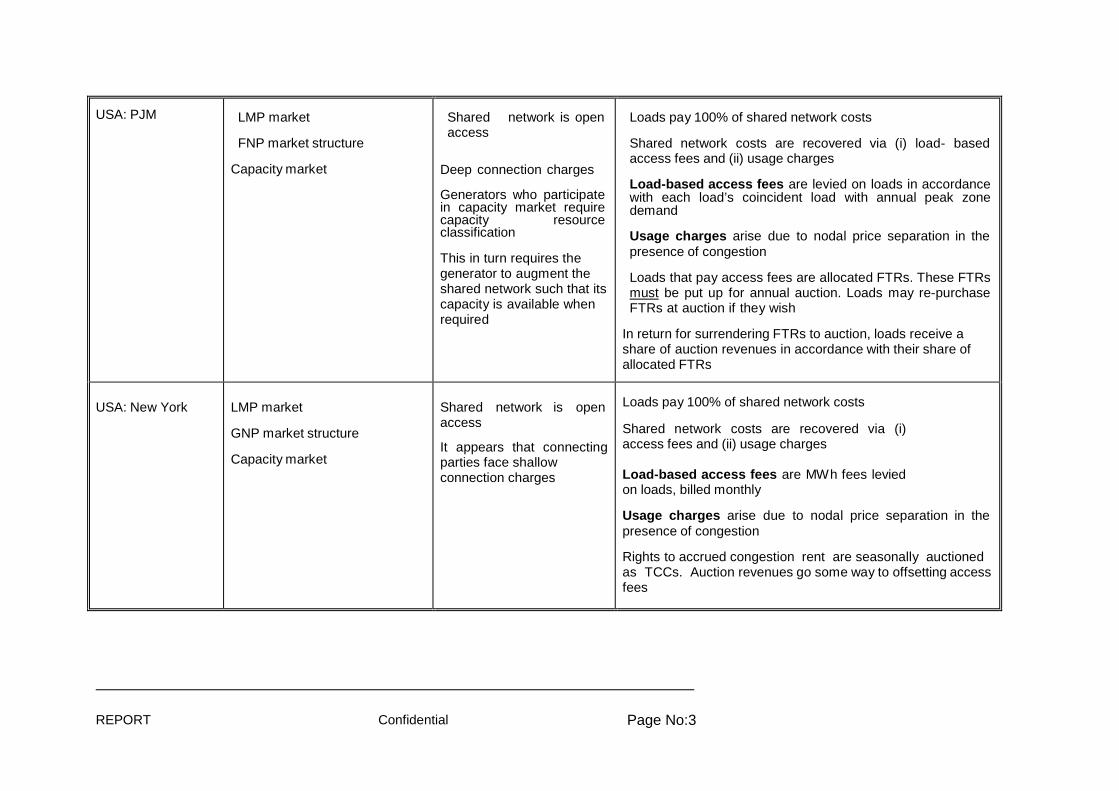

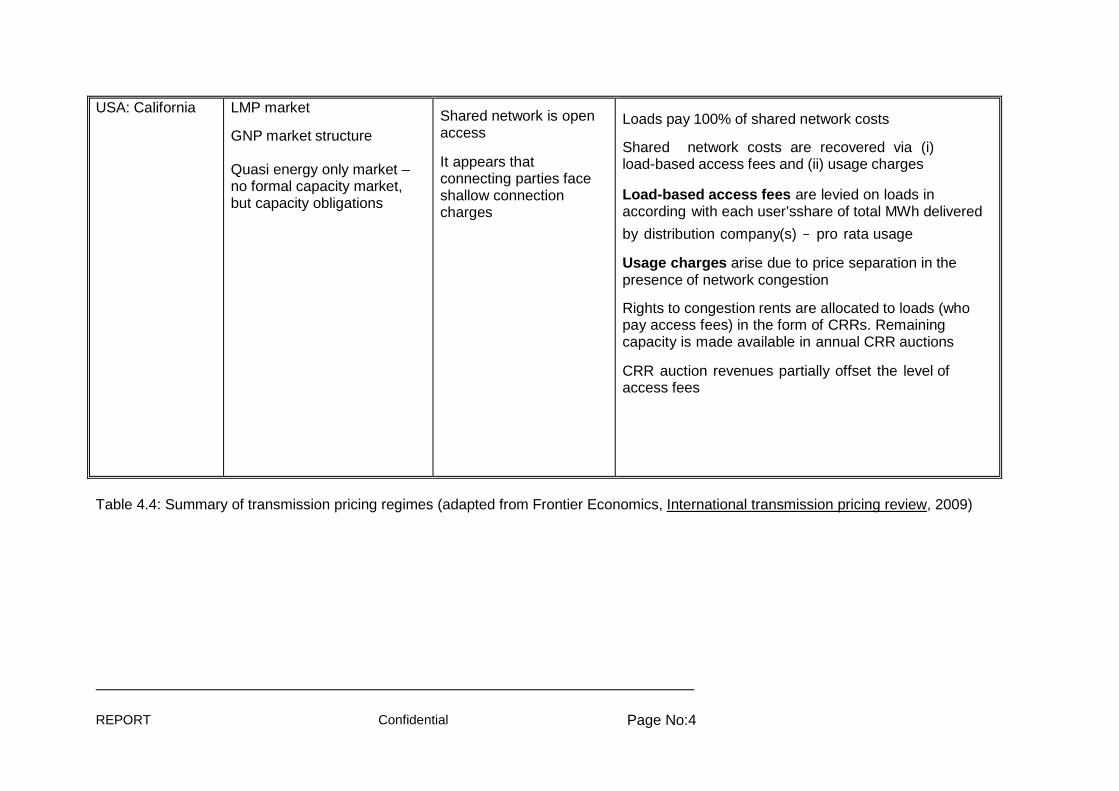

• Tariff methodologies are generally most transparent in countries with market systems and regulated monopolies in the transmission and distribution sectors. Generation is not regulated and determined by market economics whilst transmission and distribution is regulated using revenues caps or cost plus methodologies. In parts of the US and some Canadian provinces generation is also regulated through cost plus methodologies

• Important parts of the electricity system have been liberalized in many countries and competition has been introduced. To create the framework for the competitive part of the sector more rules and laws are needed for monopolies. A substantial part of the electricity sector in most countries is still regulated as monopolies. The regulation of monopolies is therefore still very important, also after the introduction of competition. This is so, not only because of the part of the consumer’s prices that are payment to the monopolies, but also because the linkages between the competitive sector and the monopolies are very strong.

CONCLUSIONS As almost always with international benchmarking studies, they raise more questions than they answer (which normally is good, as international benchmarking stimulate innovations, questions business as usual, contribute to competition and improvements). Some of the interesting hypothesis and trends that is raised by the general results for Part A, include amongst others:

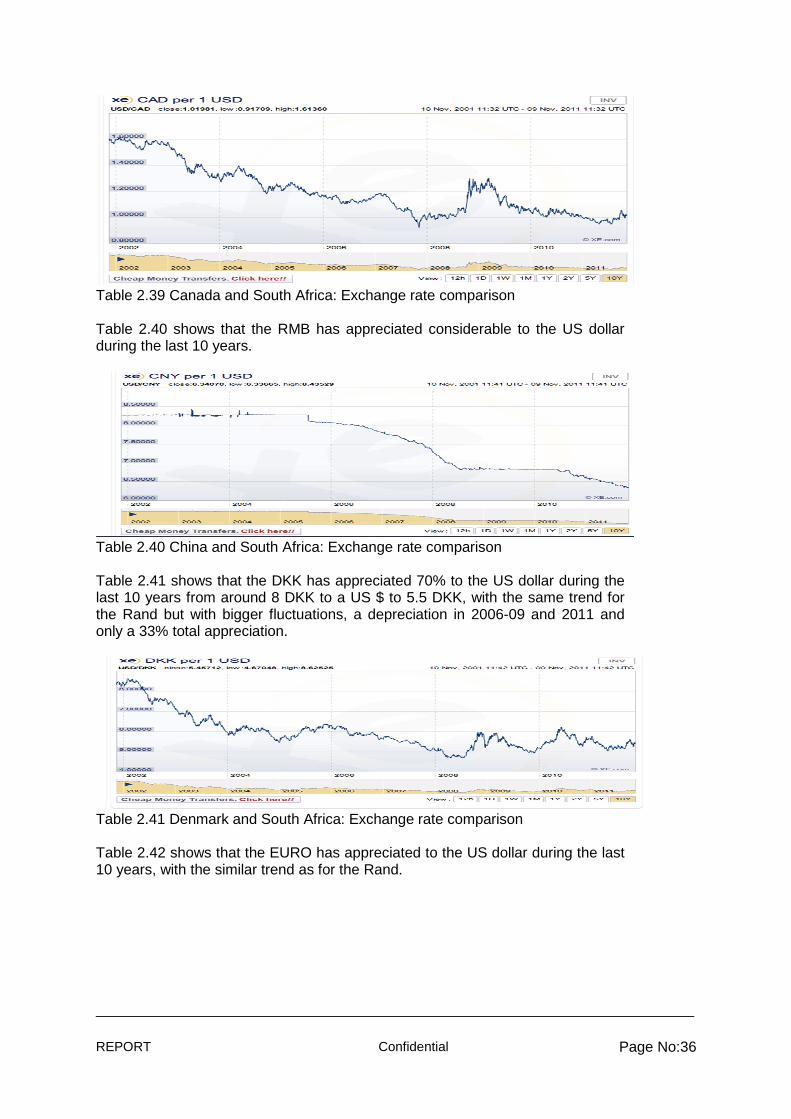

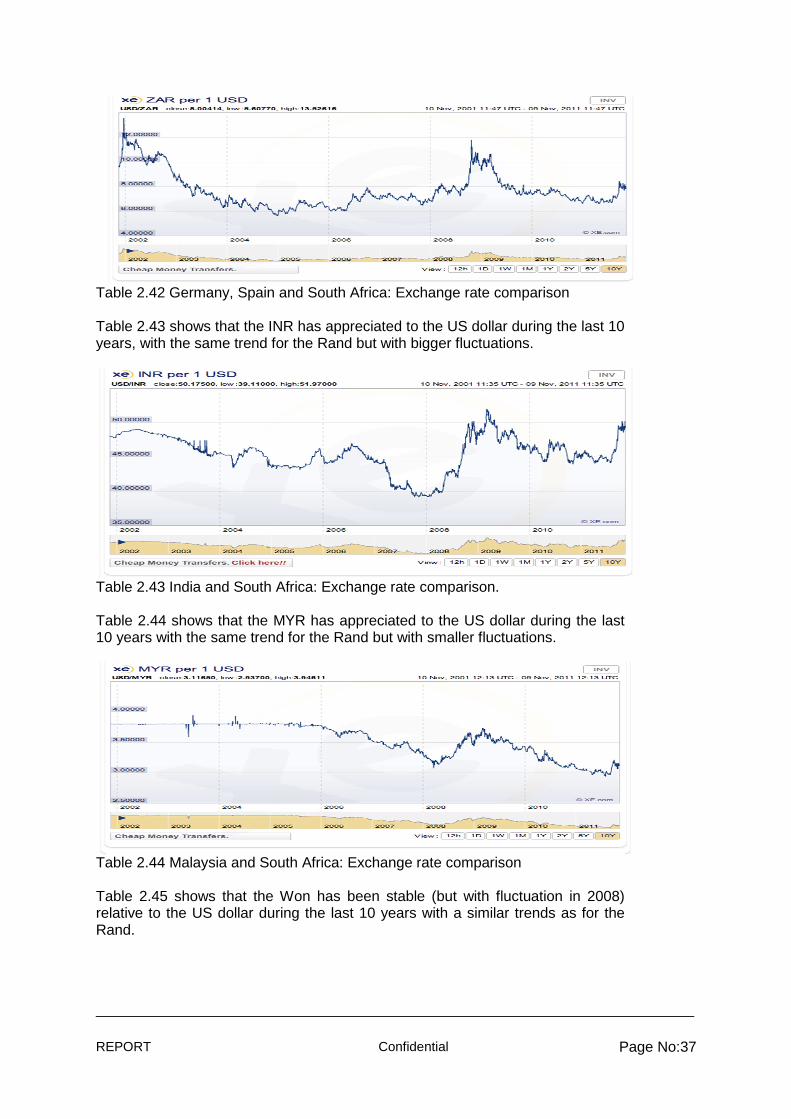

• It seems like South Africa has a low average tariff (simple exchange rate) compared to other countries, while the opposite is the case for the PPP comparison. The consequences and implications of this for e.g. tariff setting need to be better understood

REPORT Confidential Page No:6

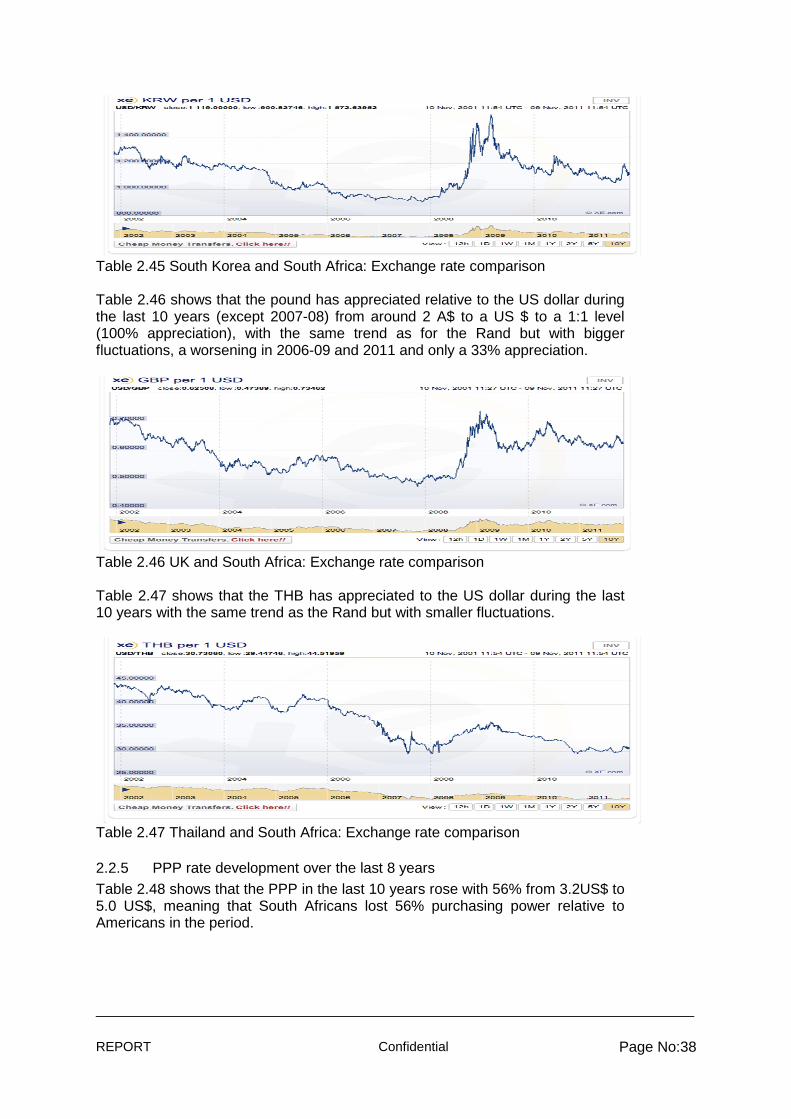

• It seems like South Africa in relation to PPP ranking is in a middle situation with a number of lower GDP income countries above, and higher GDP income countries below. The implications of this grouping also needs to be better understood

• It seems like there is an uncorrelated relation with utilities key parameters (e.g. sales, revenue, etc) and RoA (Return on Assests). Likewise it seems like there is no correlation between RoA and credit ratings. What are the underlying reasons for these non-correlations?

For Part B the following general conclusions can be made:

• The affordability of electricity in South Africa is a key issue due to the prevalence of energy poverty in many households. A better understanding of the affordability of electricity will provide useful information in designing a lifeline tariff that is directed towards the target group rather than benefitting all consumers. This could lower the cost of supply for the utility and provide greater incentive for energy efficiency in households that can afford these measures

• The lowest block of 200 kWh per month is a high level of consumption. If the intention is to target low-income households then Eskom should consider re-evaluating the size of the first tariff block or attaching a requirement along the line of the size of connection. This would reduce cross subsidisation to those that do not require assistance and bring residential tariffs closer to reflecting the true cost of supply for those that can afford it. It may also allow for the lifeline tariff to be reduced if the affordability of electricity for low-income households is low

• The pricing of industrial tariffs could be based more closely on marginal pricing in order to send the correct price signals to large consumers and provide greater incentives for them to plan consumption according to the cost of supply at the time of consumption. This would provide a more nuanced pricing mechanism and allow for unforeseen system events to influence the electricity price for short periods as required. This could be done in association with offering fixed prices at a premium rather than at a discount as is the tradition in South Africa. Fixed prices should be seen as an insurance against high prices rather than an assurance of low prices. Fixed price contracts place the pricing risk on the utility and the utility should therefore be compensated for this. Variable price contracts place the price risk on the consumer and they are rewarded through low prices in off peak periods. This could be considered for consumers where time interval metering is possible and with a sufficient level of consumption.

For Part C the following general conclusions can be made:

• Rules and regulations for transmission system, access to transmission system, wheeling and system operation should be assessed to find simple yet robust model for transmission pricing and wheeling rules

REPORT Confidential Page No:7

• Greater transparency in the breakdown of costs could be considered for consumers. This will also provide the opportunity for benchmarking distribution companies in South Africa with each other and internationally and should provide incentives to increase efficiency through regulation

• Differentiating between generation, transmission and distribution costs is an important part of unbundling utilities. Eskom is currently in the process of ring fencing generation, transmission and distribution. As in some other countries, this could be reflected in the tariff breakdown

• Transmission and distribution tariffs should represent grid investments that help reduce the overall cost of supply for the end user. The way investments are included in tariffs should be assessed and justified using the principle of least-cost-supply rather than least-cost-investment on a project-by-project basis.

RECOMMENDATIONS Results, hypothesis and cautions leads to a number of key lessons learned and recommendations for the present international benchmarking study, including:

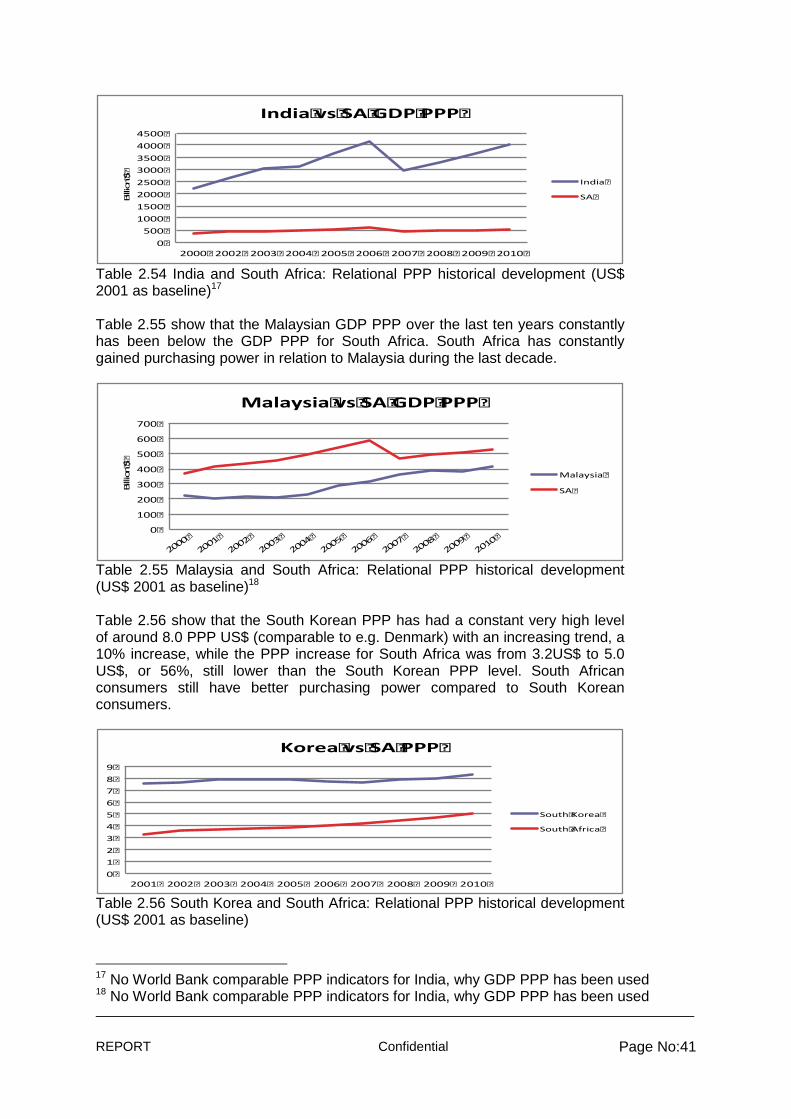

• The market share of the utilities included for each country should be increased to at least 50-60% of the national energy market to improve reliability in comparisons

• The utilities either need to be unbundled in Generation, Transmission, Distribution and Retail or other methodologies needs to be developed to further improve the apple-to-apple comparison. This also include a greater focus on generation technologies for comparisons

• Data collection should be complemented by direct data collection from included utilities. E.g. was China not included in the study due to lack of Annual Report data. China should (of many reasons) be included in the next study and other avenues of getting data from Chinese utilities should be used

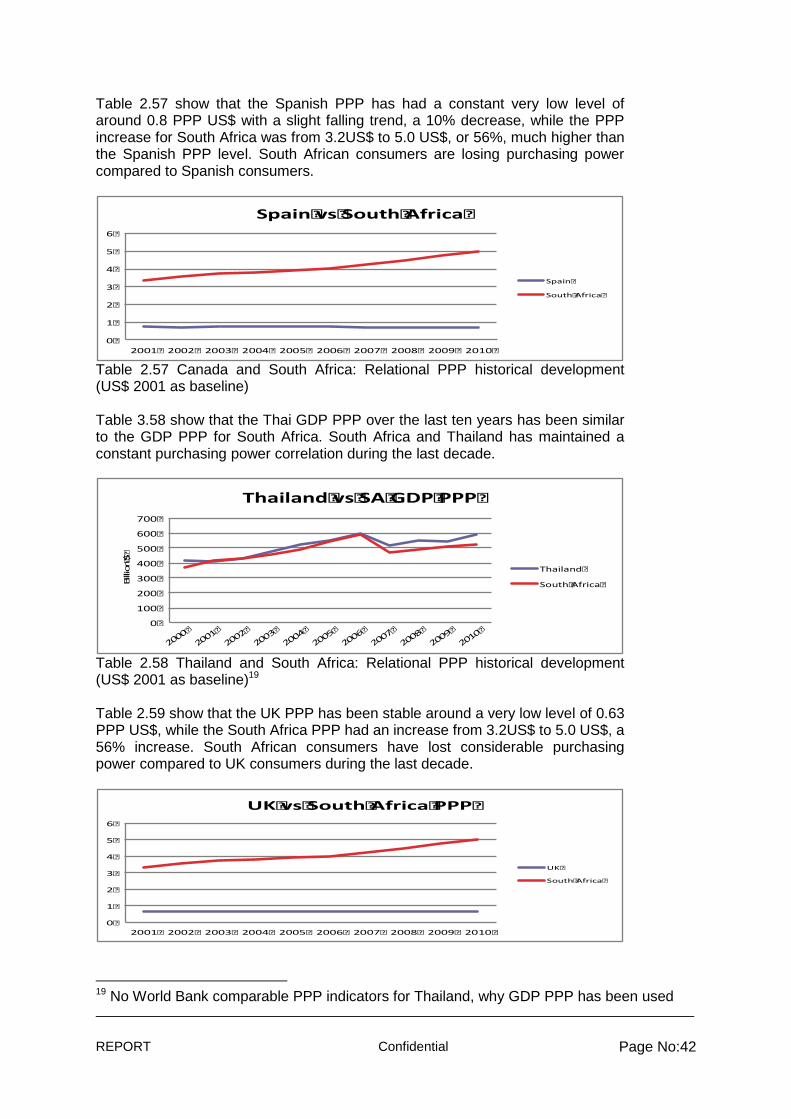

• Detailed studies of the hypothesis’ of the study e.g. the use of PPP or the differences between different customer group tariffs, should be initiated to gain further lessons of the international benchmarking study

• A study should be made into the effect of reducing the number of kWh in the lowest tariff block and how this would affect the tariff in other blocks. This is in reality an alternative to large tariff increases. 200 kWh can be considered to be a high level of consumption for a low income household. There are most likely a number of free riders in this programme. A study could be carried out to assess this issue

• A study should be carried out to determine the marginal price of electricity in South Africa hour for hour for the last couple of years and scenarios for future years. This would provide the basis for determining a more nuanced pricing structure for large industrial consumers

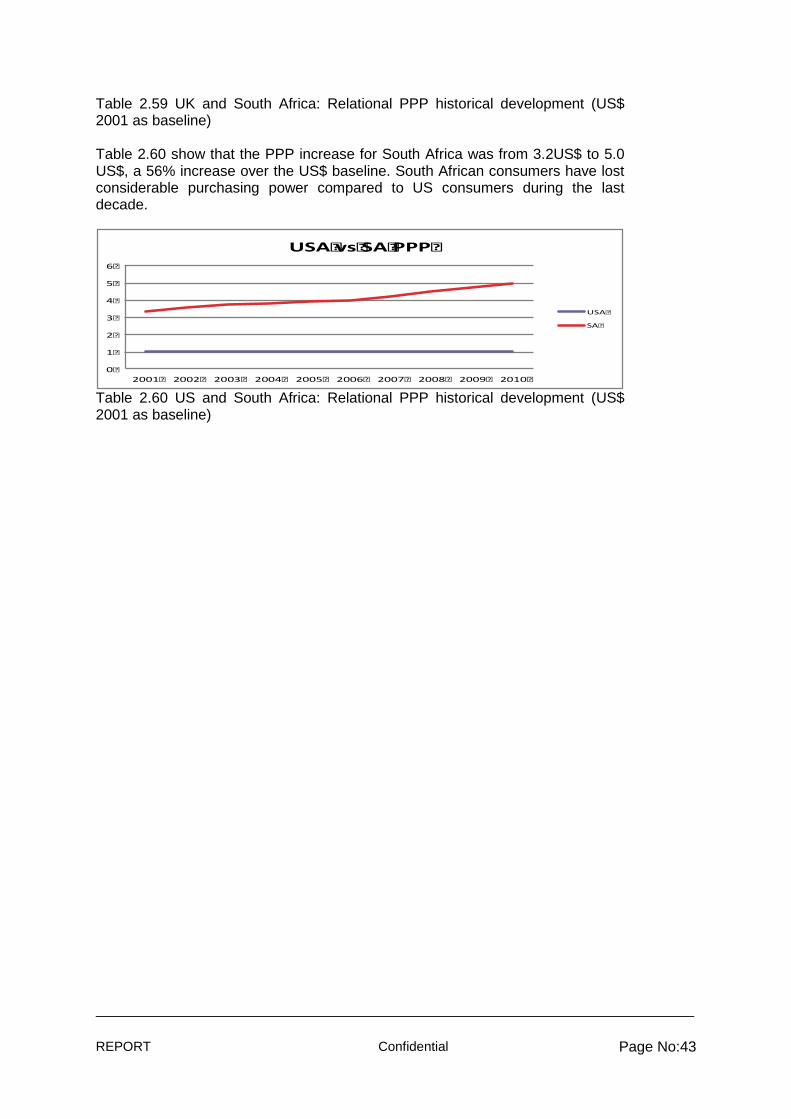

REPORT Confidential Page No:8

• Development of a methodology for determining the value of investments for transmission and distribution and how these investments will influence the overall cost of electricity for the end user. This could also be applied for generation, but is best suited for grid companies

• Assess the needs of the market and determine how wheeling should be handled and develop market rules for use of transmission system.

The above would constitute key component in a Terms of Reference for a possible new and expanded international tariff benchmarking study.

INDUSTRY PERSPECTIVE As always with international benchmarking studies, numerous cautions and clarifications is needed in order not to make over-interpretations of the results. In this benchmarking studies attention should be made towards:

• The use of selected national power utilities as base for the international benchmarking. This has provided new results, but also showed the difficulties and need for further detailing of such studies: The different structuring of Annual Reports, the difficulties in separating Generation, Transmission, Distribution and Retail in the figures provided in the Annual Reports, lack of clarity in most Annual Report on what revenue contains, e.g. exploration, market sales, transmission sales delinked from own generation, etc (the lack of correlation between sales and revenues in table 2.3 is an indicator hereof)

• The use of simple exchange and PPP rates contributes to increased nuances in interpretations, but also decreased clarity

• The study attempted to unbundle the utilities in Generation, Transmission, Distribution and Retail costs. This proved to be an almost impossible task based on the information available for the desk study, which was based on Annual Report 2010. This contributes in some instances to difficulties in interpretation of the benchmarking results, e.g. the companies from Australia and Canada are pure generation companies, others are full GTDR companies, others again is even much more than that, e.g. oil exploration etc. as in the case of Germany and Denmark

• Data availability and specificity therefore has to noted as a serious limiting factor in providing ‘bullet-proof’ apple-versus- apple comparisons. One reason for this can be related to the ownership structure of the utilities. There is no doubt that the government-owned companies, like e.g. South Africa, Malaysia and Thailand, provide clearer and more transparent data than private-owned companies that compete on a competitive energy market, e.g. UK, Germany and Spain

• South Africa and Eskom, of the countries and utilities included in the study, provide, with Denmark’s DONG, the most transparent and easy data to analyze. This conclusion is based on the detailed analysis of Annual Reports 2010 published by the Utilities.

REPORT Confidential Page No:9

KEYWORDS Average tariffs Benchmarking Consumer tariffs Data comparisons Exchange rates Industrial tariffs International Power Purchase Parity Power Utilities Tariffs Tariff methodologies Trends FUTURE REVIEW It is recommended that the present study is further detailed and extended whereby Eskom can contribute constructively to the trend and increased effort of international benchmarking of tariffs between power utilities.

REPORT Confidential Page No:10

1 INTRODUCTION

In the recent past Eskom has implemented a framework of pricing and tariff methodologies guided by the Strategic Pricing Direction for Tariffs documents whose objective in a broad sense is to promote economic efficiency and sustainability, ensure revenue recovery and promote fairness and equity. The utility’s divisions have been unbundled, financially ring-fenced and regulated separately. This allows for the real costs per division to be known and adequately accounted for, and that the tariffs for each division can reflect cost levels and ensure revenue neutrality. This means that the sum of all tariff components is not more than the NERSA approved revenue requirement. The current Eskom Tariff Methodology seeks to allocate the costs of its different divisions in a cost reflective manner as well as in conjunction with other parameters essential to each division so as to arrive at a tariff per customer category and account for subsidies in a way such that each cost per division and its tariff component does not affect revenue neutrality. It is with this background, the need arise for an international tariff benchmarking review, which comes at a time of sustained volatility in a number of cost drivers for energy utilities. Increasingly, tariff structures seek to provide an incentive for reducing peak demand, reward customers for lowering their energy us and reduce the need for capacity expansion. To achieve these ends, utilities are increasingly considering alternative tariff structures, which include but are not limited to inclining block tariffs, time-of-use tariffs and controlled load tariffs. With the international benchmarking tariff study, Eskom wishes to contribute to the continued development and refinement of the tariff levels and structures in South Africa. One important aspect is continued comparisons and lessons learned from other countries around the world.

1.1 KEY ISSUES ADDRESSED AND METHODOLOGY UTILISED

The study covers the following three areas: Comparison of average tariff levels, comparison of tariff structure for selected customer groups, and comparison of tariff setting methodologies. The study compares tariffs in South Africa with a selected group of countries. The study is divided in three parts with the following issues to be included. Part A Benchmarking of Eskom total average price ag ainst a selected group of countries with focus on an apples-versus-apples comparison of Eskom total average tariff (total regulated revenue divided by total sales volume) with that of other similar utilities in selected countries. The key overall results of the international benchmarking of average tariffs is presented followed by an outline of trends and hypothesis that can be drawn for these results, cautions and

REPORT Confidential Page No:11

clarifications, and finally, by lessons learned and recommendations for the international average benchmarking study. The overall tariff comparison is provided in chapter 2.1. The following systemic sense-making factors qualify the comparative understanding of the total average tariff levels and have been provided for in country-to-country comparisons in chapter 2.2: (i) The trend of the total average tariff. Has the tariff increased or decreased relatively to inflation during the last decade? What is the expected trend for the tariff the next 3 years? (ii) the contribution of the average tariff to creating sustainable utilities, (iii) the historical developments in exchange rates, and (iv) the historical development of the power purchase parity (PPP). These four contextual sense-making background factors provide a systemic approach to understanding the average total tariff levels and making relevant comparisons between the selected countries and utilities. Part A of the study has been carried out as a desk top study using statistical data available from mainly the selected utilities annual reports (chapter 2.1), International Energy Agency, United Nations, European Union and other relevant national and international authorities (chapter 322). These data make it possible to compare total average utility tariffs in South Africa with utilities in selected countries. The study, besides a number of more well-known comparisons parameters, utilises Power Purchase Parity and Credit Ratings for comparisons purposes. Part B Benchmarking of Eskom customer tariff categories against regional, developed and developing countries with focus on a comparison of customer categories tariff levels on average: municipality, large and medium industrial, residential, domestic etc. Each charge component comparisons include the consumers’ total average electricity unit cost by assuming typical customer profiles and assumptions. In order to compare price differences for different consumption volumes, typical standard consumers are defined for households and large and small industrial consumers. The standard consumers used are based on the standard consumers used by EU Statistics for comparing tariffs between member countries. This is provided for in Chapter 3. Part C Detailed comparison and discussion of tariff methodologies with a particular focus on a comparison and discussion of different tariff methodologies for a number of selected countries and utilities, see Chapter 4. This part carries out an analysis of selected countries in order to compare the tariff methodologies employed in these countries, the overriding factors in determining tariffs and how the choice of tariff methodology influences consumption for different consumer groups. Correct pricing is essential in the electricity sector in order to ensure an efficient allocation of new capacity and reduced demand. Tariffs should send the correct price signals to consumers, but remain practical for utilities and consumers. An appropriate or effective electricity tariff is not in itself capable of stimulating investment in the electricity sector, however, a poorly conceived pricing structure is often sufficient to depress investments. There are four criteria that should be met to achieve an effective tariff: Marginal costs are reflected in the tariff; Recovery of total costs; Ease of computation and transparency; and Fairness. Chapter 5 includes conclusion and a discussion of the findings, while chapter 6 include references.

REPORT Confidential Page No:12

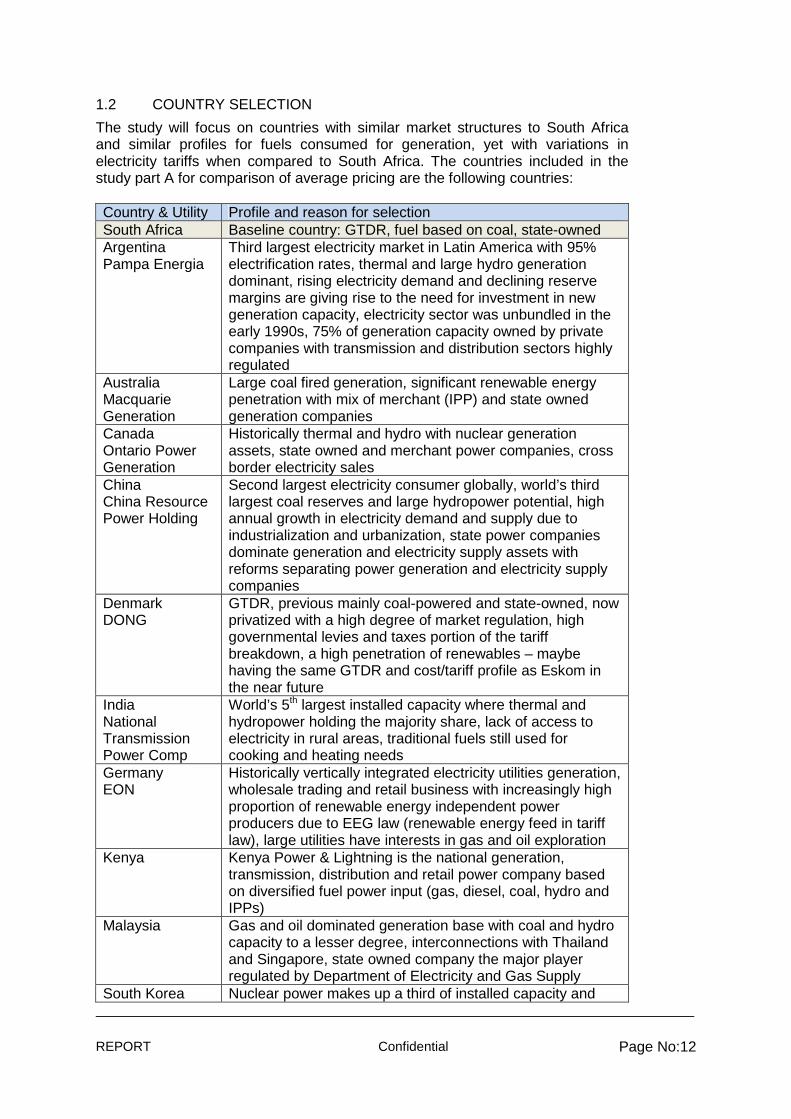

1.2 COUNTRY SELECTION

The study will focus on countries with similar market structures to South Africa and similar profiles for fuels consumed for generation, yet with variations in electricity tariffs when compared to South Africa. The countries included in the study part A for comparison of average pricing are the following countries: Country & Utility Profile and reason for selection South Africa Baseline country: GTDR, fuel based on coal, state-owned Argentina Pampa Energia

Third largest electricity market in Latin America with 95% electrification rates, thermal and large hydro generation dominant, rising electricity demand and declining reserve margins are giving rise to the need for investment in new generation capacity, electricity sector was unbundled in the early 1990s, 75% of generation capacity owned by private companies with transmission and distribution sectors highly regulated

Australia Macquarie Generation

Large coal fired generation, significant renewable energy penetration with mix of merchant (IPP) and state owned generation companies

Canada Ontario Power Generation

Historically thermal and hydro with nuclear generation assets, state owned and merchant power companies, cross border electricity sales

China China Resource Power Holding

Second largest electricity consumer globally, world’s third largest coal reserves and large hydropower potential, high annual growth in electricity demand and supply due to industrialization and urbanization, state power companies dominate generation and electricity supply assets with reforms separating power generation and electricity supply companies

Denmark DONG

GTDR, previous mainly coal-powered and state-owned, now privatized with a high degree of market regulation, high governmental levies and taxes portion of the tariff breakdown, a high penetration of renewables – maybe having the same GTDR and cost/tariff profile as Eskom in the near future

India National Transmission Power Comp

World’s 5th largest installed capacity where thermal and hydropower holding the majority share, lack of access to electricity in rural areas, traditional fuels still used for cooking and heating needs

Germany EON

Historically vertically integrated electricity utilities generation, wholesale trading and retail business with increasingly high proportion of renewable energy independent power producers due to EEG law (renewable energy feed in tariff law), large utilities have interests in gas and oil exploration

Kenya Kenya Power & Lightning is the national generation, transmission, distribution and retail power company based on diversified fuel power input (gas, diesel, coal, hydro and IPPs)

Malaysia Gas and oil dominated generation base with coal and hydro capacity to a lesser degree, interconnections with Thailand and Singapore, state owned company the major player regulated by Department of Electricity and Gas Supply

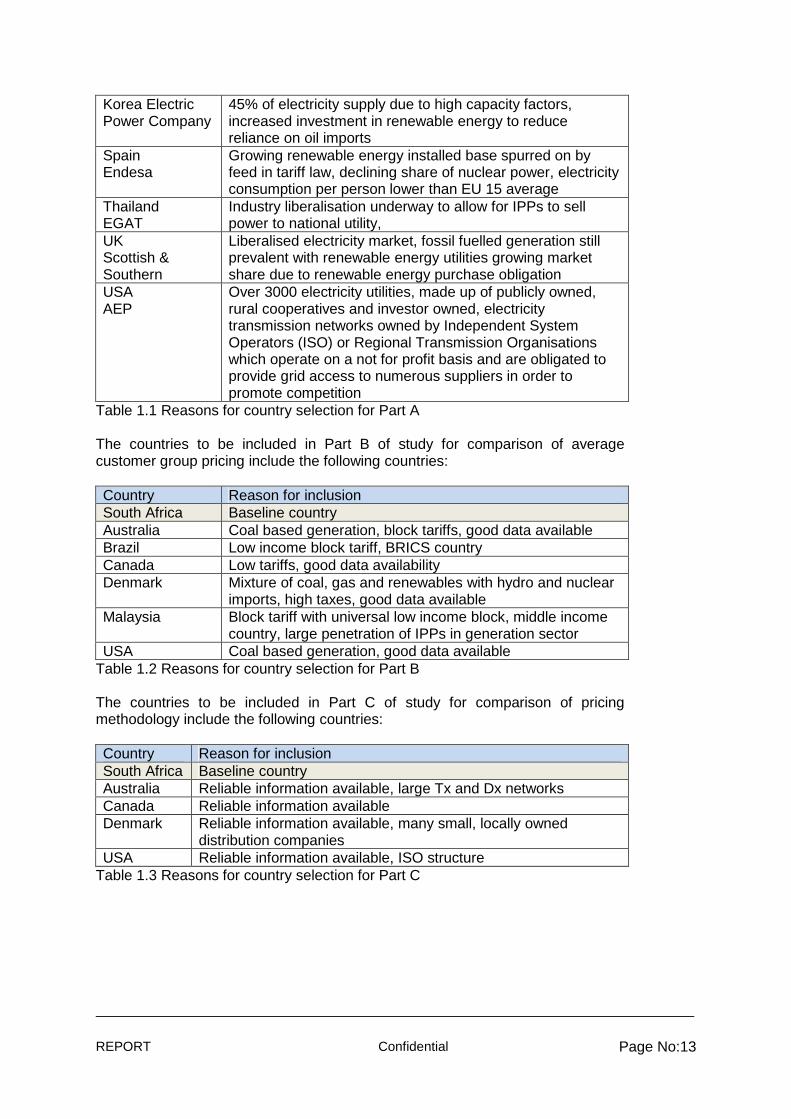

South Korea Nuclear power makes up a third of installed capacity and

REPORT Confidential Page No:13

Korea Electric Power Company

45% of electricity supply due to high capacity factors, increased investment in renewable energy to reduce reliance on oil imports

Spain Endesa

Growing renewable energy installed base spurred on by feed in tariff law, declining share of nuclear power, electricity consumption per person lower than EU 15 average

Thailand EGAT

Industry liberalisation underway to allow for IPPs to sell power to national utility,

UK Scottish & Southern

Liberalised electricity market, fossil fuelled generation still prevalent with renewable energy utilities growing market share due to renewable energy purchase obligation

USA AEP

Over 3000 electricity utilities, made up of publicly owned, rural cooperatives and investor owned, electricity transmission networks owned by Independent System Operators (ISO) or Regional Transmission Organisations which operate on a not for profit basis and are obligated to provide grid access to numerous suppliers in order to promote competition

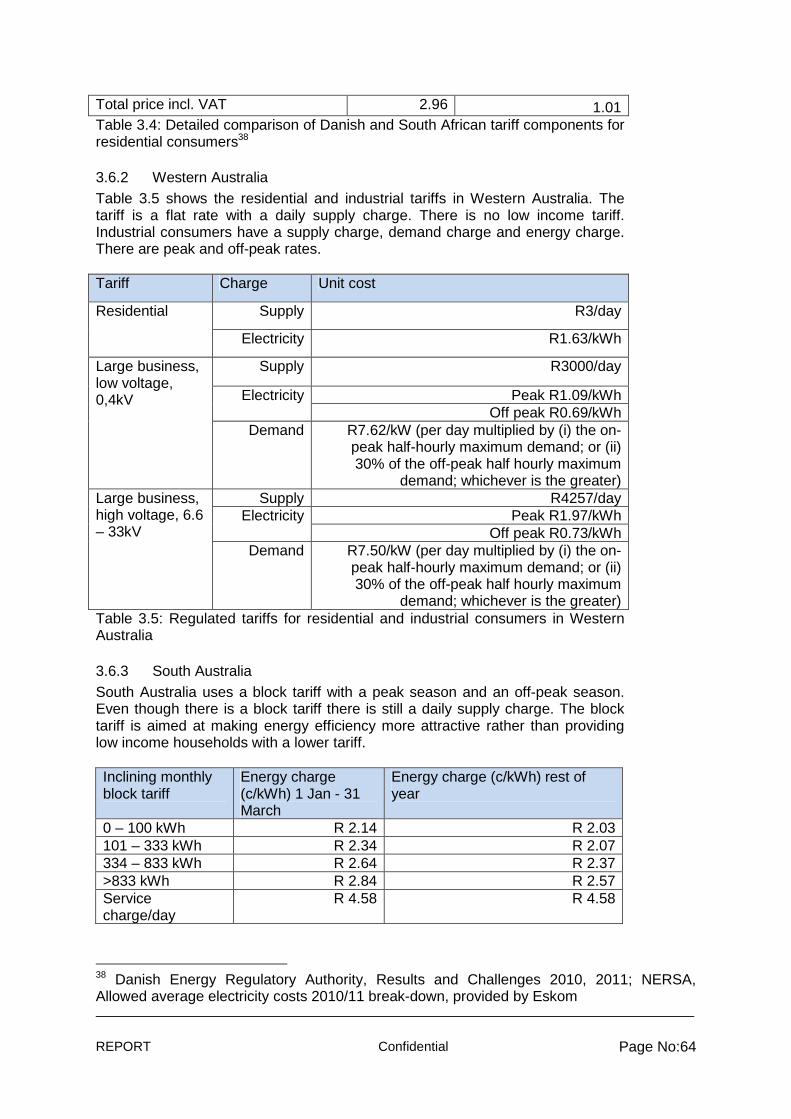

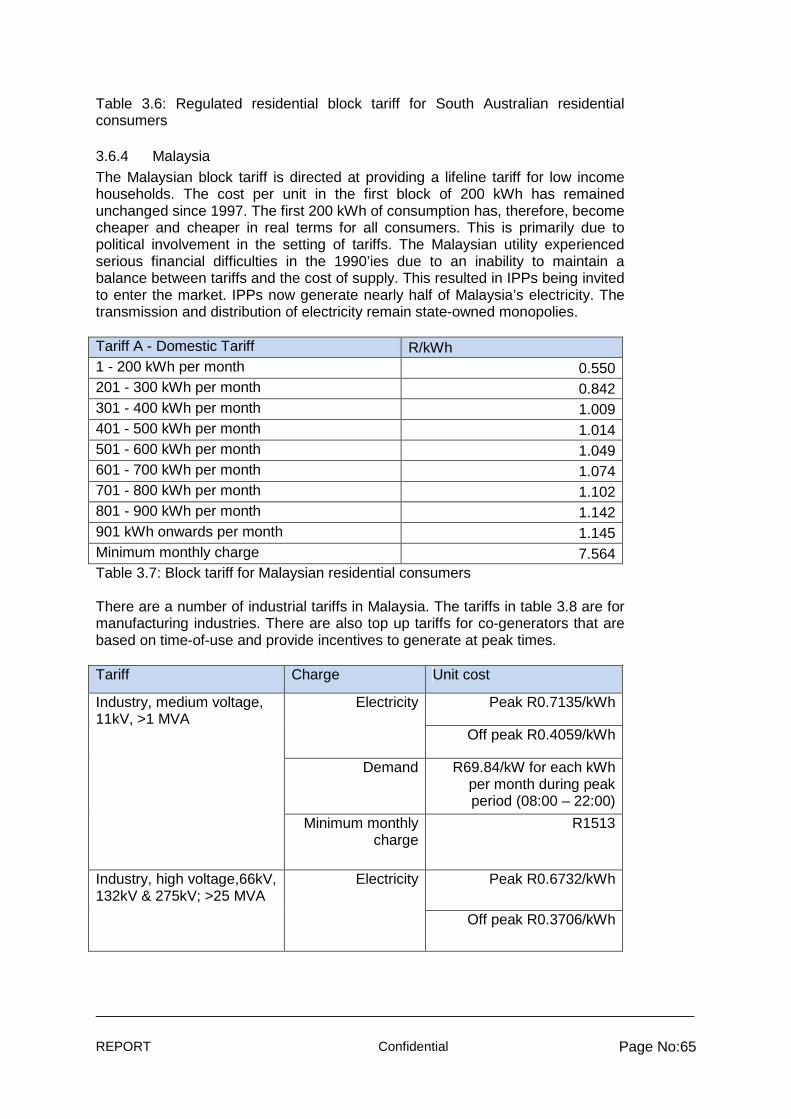

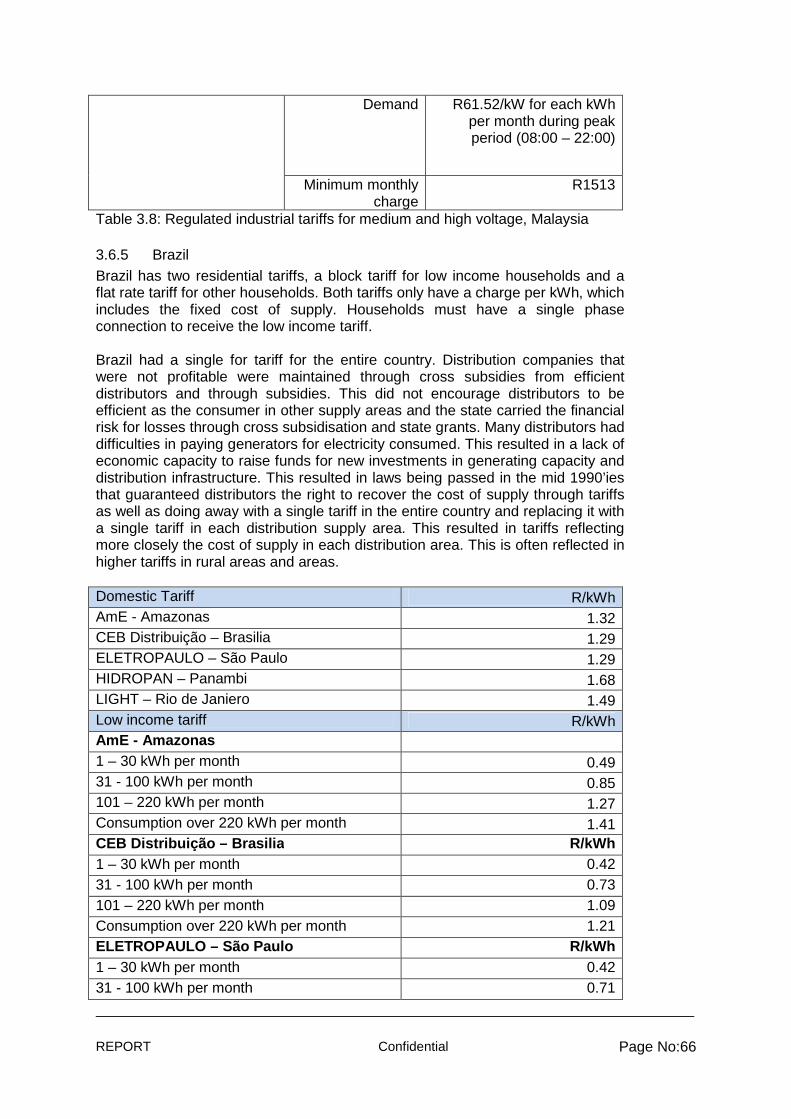

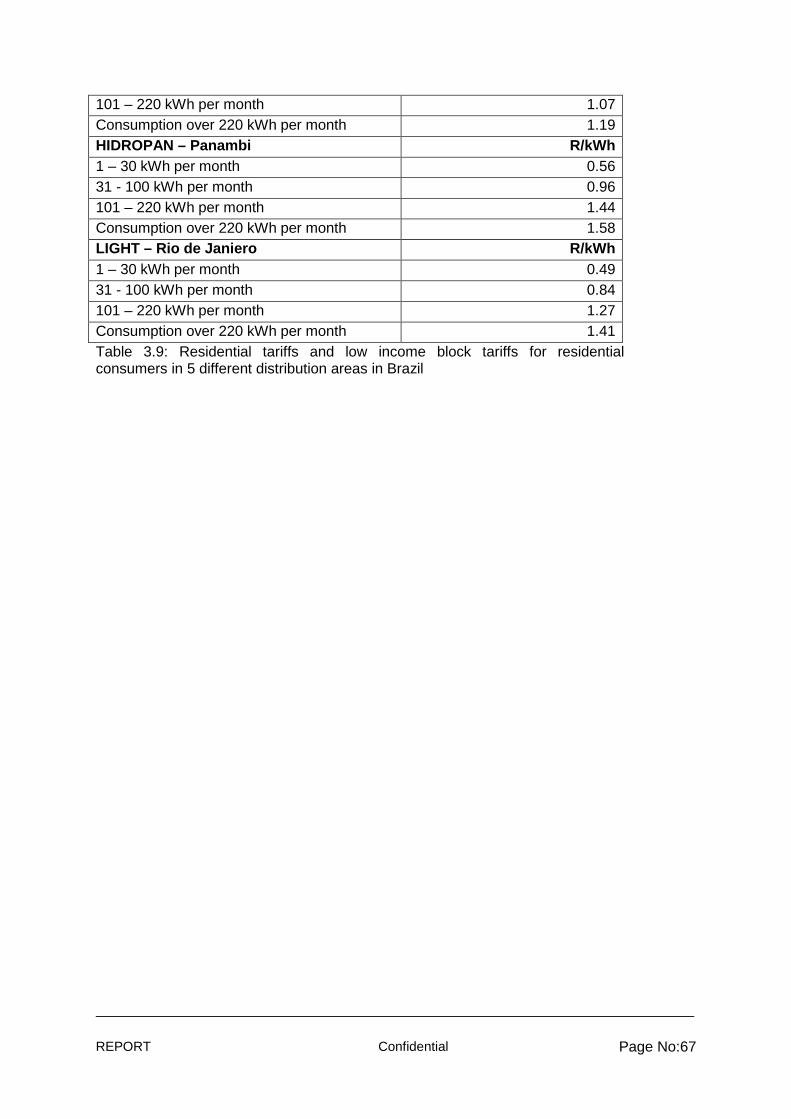

Table 1.1 Reasons for country selection for Part A The countries to be included in Part B of study for comparison of average customer group pricing include the following countries: Country Reason for inclusion South Africa Baseline country Australia Coal based generation, block tariffs, good data available Brazil Low income block tariff, BRICS country Canada Low tariffs, good data availability Denmark Mixture of coal, gas and renewables with hydro and nuclear

imports, high taxes, good data available Malaysia Block tariff with universal low income block, middle income

country, large penetration of IPPs in generation sector USA Coal based generation, good data available

Table 1.2 Reasons for country selection for Part B The countries to be included in Part C of study for comparison of pricing methodology include the following countries: Country Reason for inclusion South Africa Baseline country Australia Reliable information available, large Tx and Dx networks Canada Reliable information available Denmark Reliable information available, many small, locally owned

distribution companies USA Reliable information available, ISO structure

Table 1.3 Reasons for country selection for Part C

REPORT Confidential Page No:14

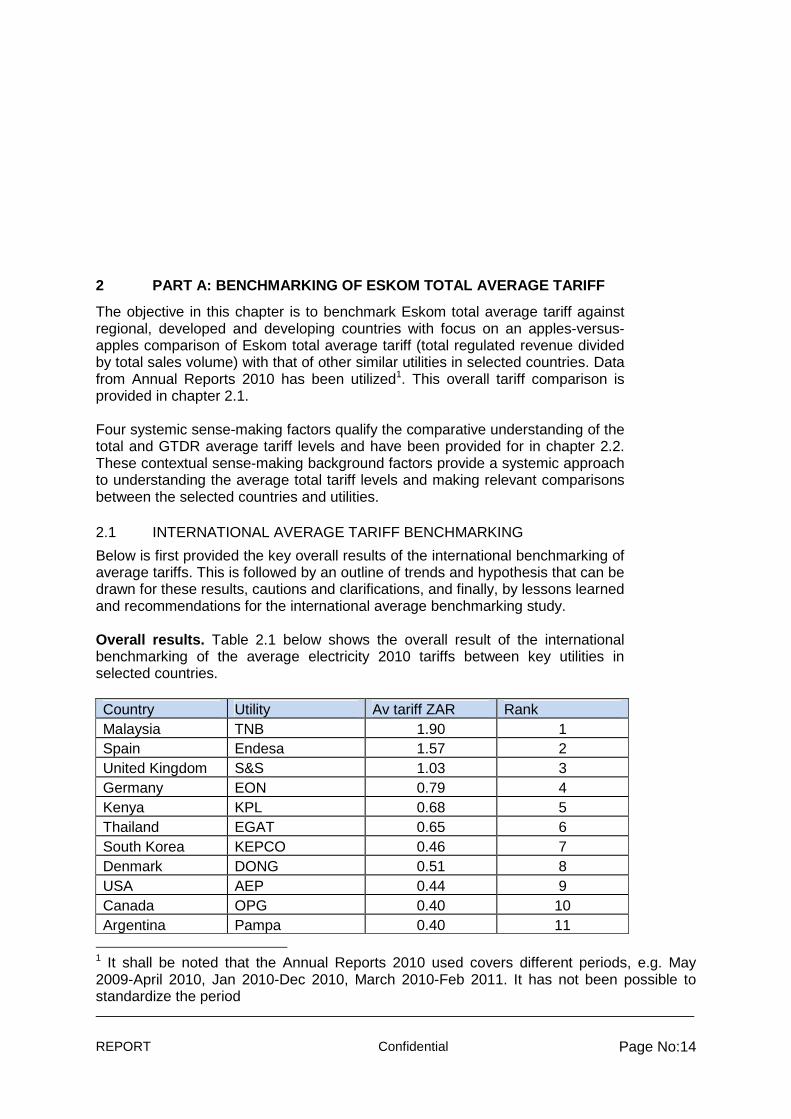

2 PART A: BENCHMARKING OF ESKOM TOTAL AVERAGE TARIF F

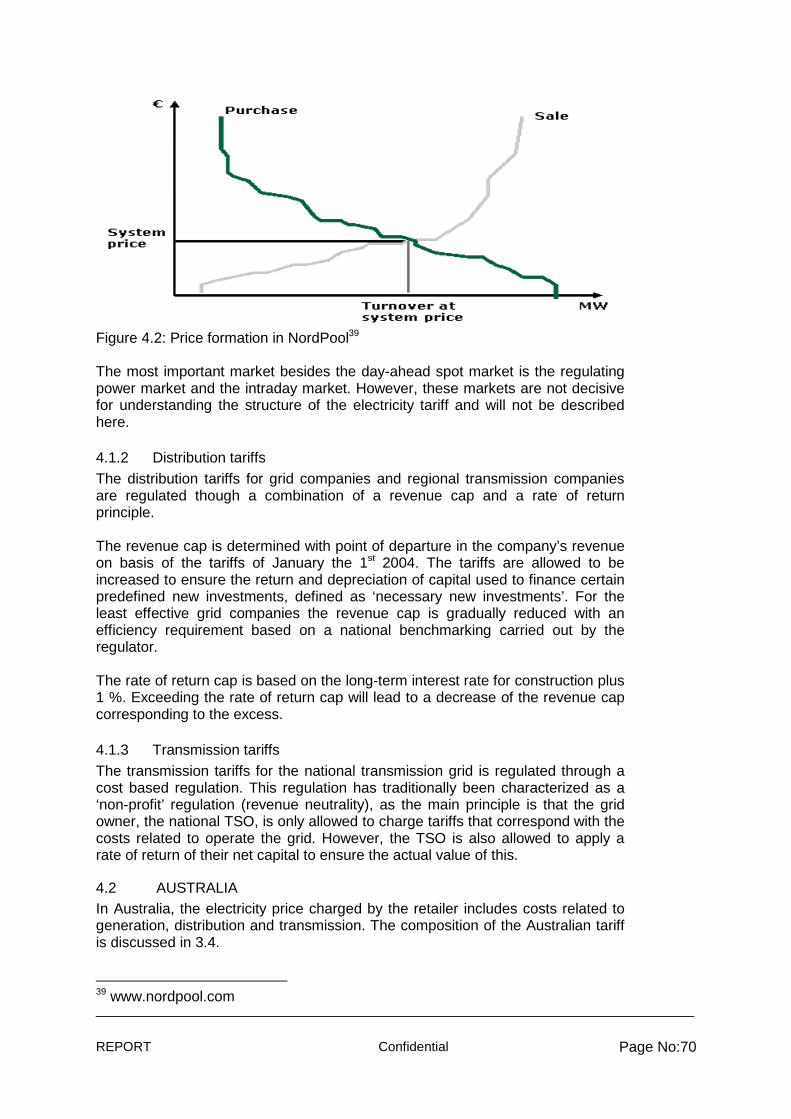

The objective in this chapter is to benchmark Eskom total average tariff against regional, developed and developing countries with focus on an apples-versus-apples comparison of Eskom total average tariff (total regulated revenue divided by total sales volume) with that of other similar utilities in selected countries. Data from Annual Reports 2010 has been utilized1. This overall tariff comparison is provided in chapter 2.1. Four systemic sense-making factors qualify the comparative understanding of the total and GTDR average tariff levels and have been provided for in chapter 2.2. These contextual sense-making background factors provide a systemic approach to understanding the average total tariff levels and making relevant comparisons between the selected countries and utilities.

2.1 INTERNATIONAL AVERAGE TARIFF BENCHMARKING

Below is first provided the key overall results of the international benchmarking of average tariffs. This is followed by an outline of trends and hypothesis that can be drawn for these results, cautions and clarifications, and finally, by lessons learned and recommendations for the international average benchmarking study. Overall results. Table 2.1 below shows the overall result of the international benchmarking of the average electricity 2010 tariffs between key utilities in selected countries. Country Utility Av tariff ZAR Rank Malaysia TNB 1.90 1 Spain Endesa 1.57 2 United Kingdom S&S 1.03 3 Germany EON 0.79 4 Kenya KPL 0.68 5 Thailand EGAT 0.65 6 South Korea KEPCO 0.46 7 Denmark DONG 0.51 8 USA AEP 0.44 9 Canada OPG 0.40 10 Argentina Pampa 0.40 11

1 It shall be noted that the Annual Reports 2010 used covers different periods, e.g. May 2009-April 2010, Jan 2010-Dec 2010, March 2010-Feb 2011. It has not been possible to standardize the period

REPORT Confidential Page No:15

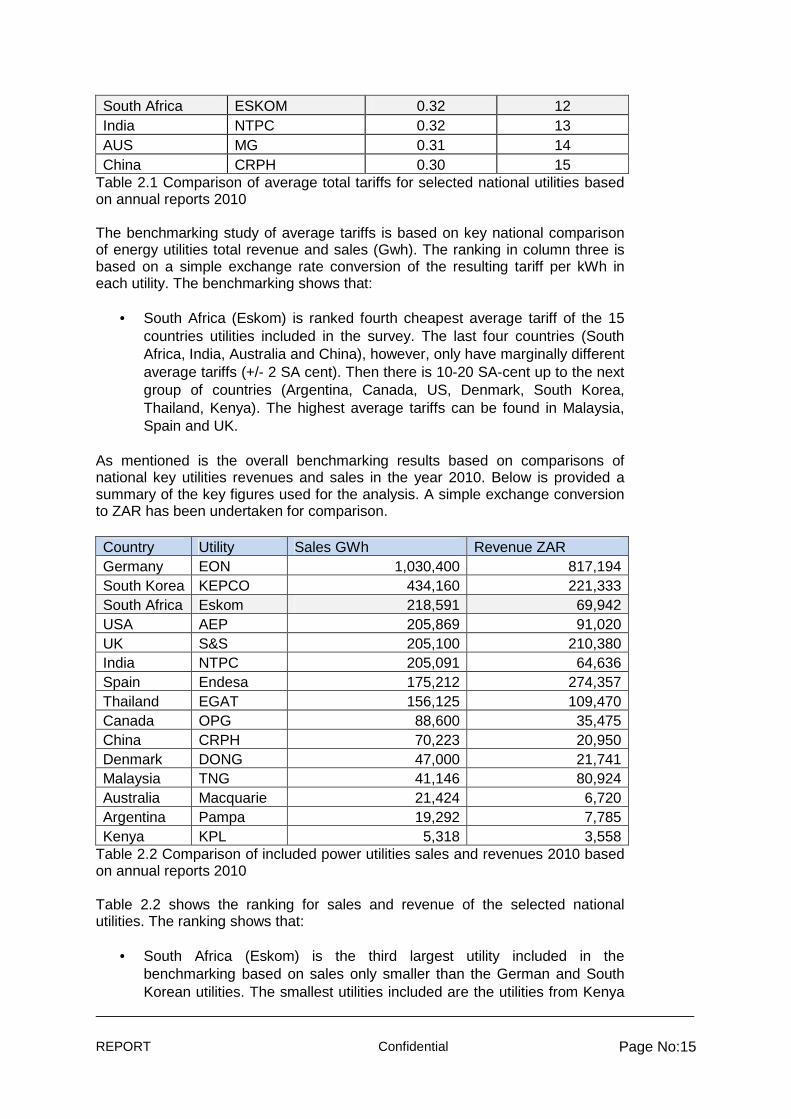

South Africa ESKOM 0.32 12 India NTPC 0.32 13 AUS MG 0.31 14 China CRPH 0.30 15

Table 2.1 Comparison of average total tariffs for selected national utilities based on annual reports 2010 The benchmarking study of average tariffs is based on key national comparison of energy utilities total revenue and sales (Gwh). The ranking in column three is based on a simple exchange rate conversion of the resulting tariff per kWh in each utility. The benchmarking shows that:

• South Africa (Eskom) is ranked fourth cheapest average tariff of the 15 countries utilities included in the survey. The last four countries (South Africa, India, Australia and China), however, only have marginally different average tariffs (+/- 2 SA cent). Then there is 10-20 SA-cent up to the next group of countries (Argentina, Canada, US, Denmark, South Korea, Thailand, Kenya). The highest average tariffs can be found in Malaysia, Spain and UK.

As mentioned is the overall benchmarking results based on comparisons of national key utilities revenues and sales in the year 2010. Below is provided a summary of the key figures used for the analysis. A simple exchange conversion to ZAR has been undertaken for comparison. Country Utility Sales GWh Revenue ZAR Germany EON 1,030,400 817,194 South Korea KEPCO 434,160 221,333 South Africa Eskom 218,591 69,942 USA AEP 205,869 91,020 UK S&S 205,100 210,380 India NTPC 205,091 64,636 Spain Endesa 175,212 274,357 Thailand EGAT 156,125 109,470 Canada OPG 88,600 35,475 China CRPH 70,223 20,950 Denmark DONG 47,000 21,741 Malaysia TNG 41,146 80,924 Australia Macquarie 21,424 6,720 Argentina Pampa 19,292 7,785 Kenya KPL 5,318 3,558

Table 2.2 Comparison of included power utilities sales and revenues 2010 based on annual reports 2010 Table 2.2 shows the ranking for sales and revenue of the selected national utilities. The ranking shows that:

• South Africa (Eskom) is the third largest utility included in the benchmarking based on sales only smaller than the German and South Korean utilities. The smallest utilities included are the utilities from Kenya

REPORT Confidential Page No:16

Argentina and Australia. The ranking show poor relation between sales and revenue

• South Africa’s sales / revenue factor is around 3, while most of the remaining have a factor 2 or even (much) lower.

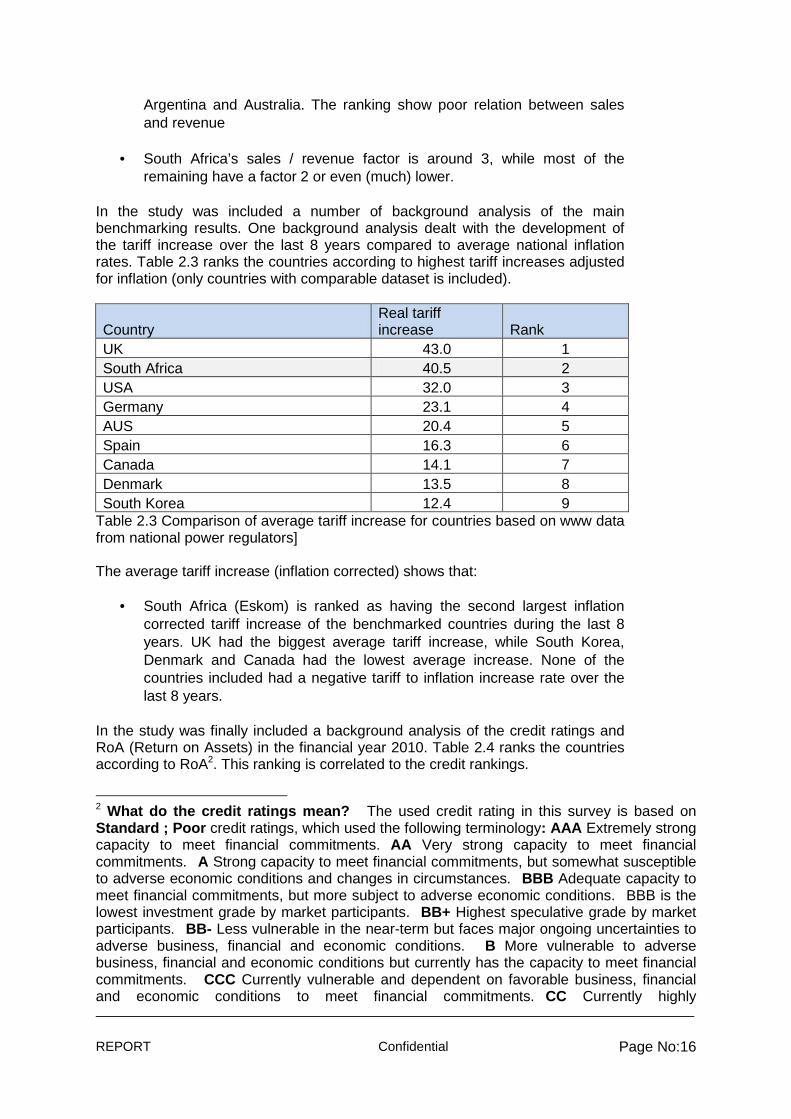

In the study was included a number of background analysis of the main benchmarking results. One background analysis dealt with the development of the tariff increase over the last 8 years compared to average national inflation rates. Table 2.3 ranks the countries according to highest tariff increases adjusted for inflation (only countries with comparable dataset is included).

Country Real tariff increase Rank

UK 43.0 1 South Africa 40.5 2 USA 32.0 3 Germany 23.1 4 AUS 20.4 5 Spain 16.3 6 Canada 14.1 7 Denmark 13.5 8 South Korea 12.4 9

Table 2.3 Comparison of average tariff increase for countries based on www data from national power regulators] The average tariff increase (inflation corrected) shows that:

• South Africa (Eskom) is ranked as having the second largest inflation corrected tariff increase of the benchmarked countries during the last 8 years. UK had the biggest average tariff increase, while South Korea, Denmark and Canada had the lowest average increase. None of the countries included had a negative tariff to inflation increase rate over the last 8 years.

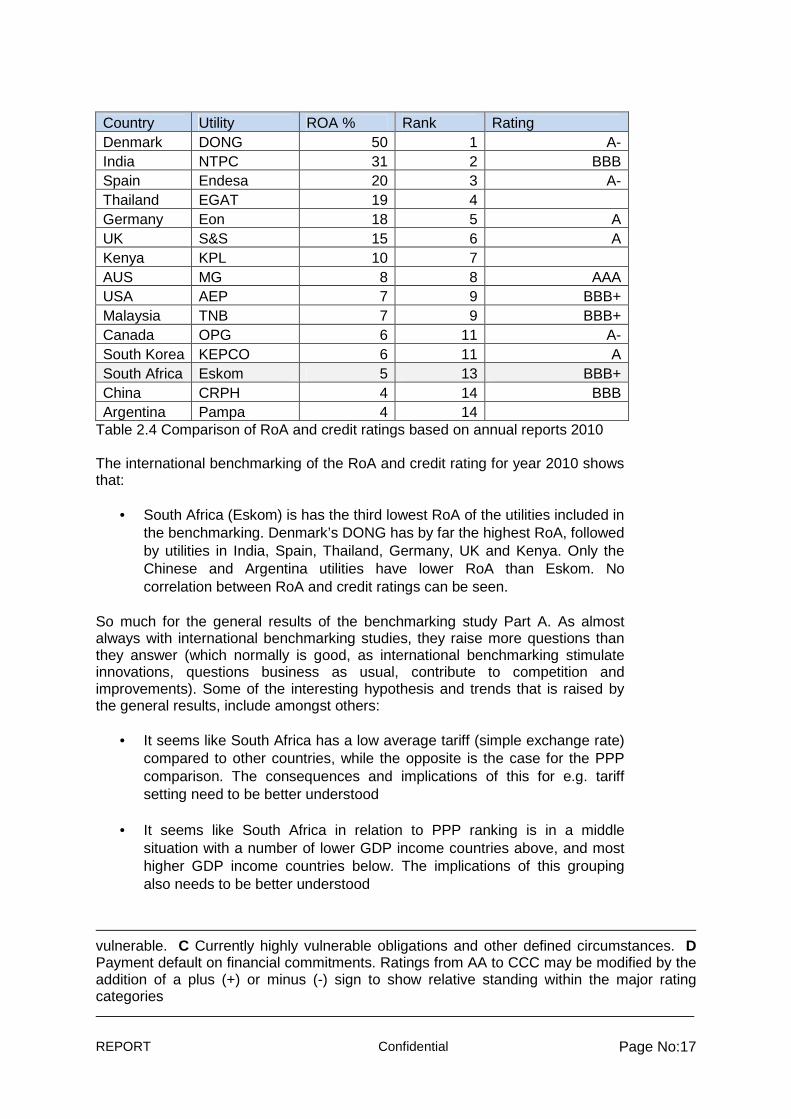

In the study was finally included a background analysis of the credit ratings and RoA (Return on Assets) in the financial year 2010. Table 2.4 ranks the countries according to RoA2. This ranking is correlated to the credit rankings.

2 What do the credit ratings mean? �The used credit rating in this survey is based on Standard ; Poor credit ratings, which used the following terminology: AAA Extremely strong capacity to meet financial commitments. AA Very strong capacity to meet financial commitments.�A Strong capacity to meet financial commitments, but somewhat susceptible to adverse economic conditions and changes in circumstances.�BBB Adequate capacity to meet financial commitments, but more subject to adverse economic conditions.�BBB is the lowest investment grade by market participants.�BB+ Highest speculative grade by market participants.�BB- Less vulnerable in the near-term but faces major ongoing uncertainties to adverse business, financial and economic conditions. �B More vulnerable to adverse business, financial and economic conditions but currently has the capacity to meet financial commitments. �CCC Currently vulnerable and dependent on favorable business, financial and economic conditions to meet financial commitments.�CC Currently highly

REPORT Confidential Page No:17

Country Utility ROA % Rank Rating Denmark DONG 50 1 A- India NTPC 31 2 BBB Spain Endesa 20 3 A- Thailand EGAT 19 4 Germany Eon 18 5 A UK S&S 15 6 A Kenya KPL 10 7 AUS MG 8 8 AAA USA AEP 7 9 BBB+ Malaysia TNB 7 9 BBB+ Canada OPG 6 11 A- South Korea KEPCO 6 11 A South Africa Eskom 5 13 BBB+ China CRPH 4 14 BBB Argentina Pampa 4 14

Table 2.4 Comparison of RoA and credit ratings based on annual reports 2010 The international benchmarking of the RoA and credit rating for year 2010 shows that:

• South Africa (Eskom) is has the third lowest RoA of the utilities included in the benchmarking. Denmark’s DONG has by far the highest RoA, followed by utilities in India, Spain, Thailand, Germany, UK and Kenya. Only the Chinese and Argentina utilities have lower RoA than Eskom. No correlation between RoA and credit ratings can be seen.

So much for the general results of the benchmarking study Part A. As almost always with international benchmarking studies, they raise more questions than they answer (which normally is good, as international benchmarking stimulate innovations, questions business as usual, contribute to competition and improvements). Some of the interesting hypothesis and trends that is raised by the general results, include amongst others:

• It seems like South Africa has a low average tariff (simple exchange rate) compared to other countries, while the opposite is the case for the PPP comparison. The consequences and implications of this for e.g. tariff setting need to be better understood

• It seems like South Africa in relation to PPP ranking is in a middle situation with a number of lower GDP income countries above, and most higher GDP income countries below. The implications of this grouping also needs to be better understood

vulnerable.�C Currently highly vulnerable obligations and other defined circumstances.�D Payment default on financial commitments. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories

REPORT Confidential Page No:18

• It seems like there is an uncorrelated relation with utilities key parameters (e.g. sales, revenue, etc) and RoA. Likewise it seems like there is no correlation between RoA and credit ratings. What are the underlying reasons for these non-correlations?

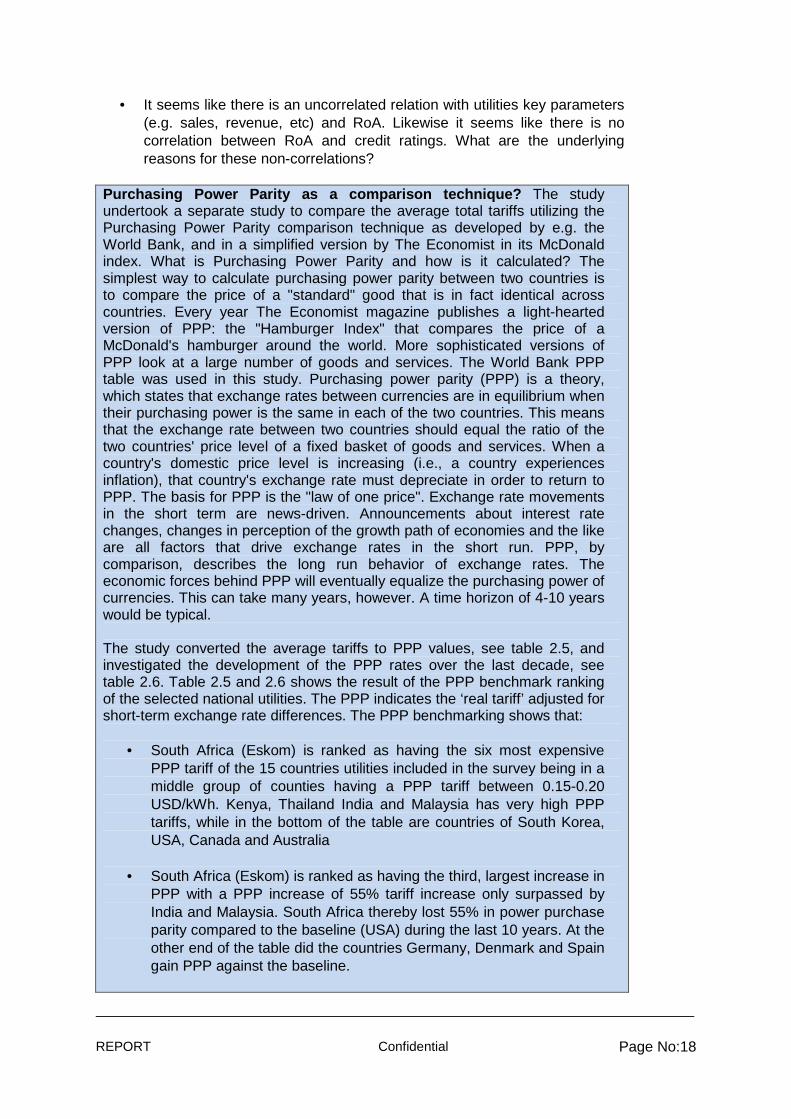

Purchasing Power Parity as a comparison technique? The study undertook a separate study to compare the average total tariffs utilizing the Purchasing Power Parity comparison technique as developed by e.g. the World Bank, and in a simplified version by The Economist in its McDonald index. What is Purchasing Power Parity and how is it calculated? The simplest way to calculate purchasing power parity between two countries is to compare the price of a "standard" good that is in fact identical across countries. Every year The Economist magazine publishes a light-hearted version of PPP: the "Hamburger Index" that compares the price of a McDonald's hamburger around the world. More sophisticated versions of PPP look at a large number of goods and services. The World Bank PPP table was used in this study. Purchasing power parity (PPP) is a theory, which states that exchange rates between currencies are in equilibrium when their purchasing power is the same in each of the two countries. This means that the exchange rate between two countries should equal the ratio of the two countries' price level of a fixed basket of goods and services. When a country's domestic price level is increasing (i.e., a country experiences inflation), that country's exchange rate must depreciate in order to return to PPP. The basis for PPP is the "law of one price". Exchange rate movements in the short term are news-driven. Announcements about interest rate changes, changes in perception of the growth path of economies and the like are all factors that drive exchange rates in the short run. PPP, by comparison, describes the long run behavior of exchange rates. The economic forces behind PPP will eventually equalize the purchasing power of currencies. This can take many years, however. A time horizon of 4-10 years would be typical. The study converted the average tariffs to PPP values, see table 2.5, and investigated the development of the PPP rates over the last decade, see table 2.6. Table 2.5 and 2.6 shows the result of the PPP benchmark ranking of the selected national utilities. The PPP indicates the ‘real tariff’ adjusted for short-term exchange rate differences. The PPP benchmarking shows that:

• South Africa (Eskom) is ranked as having the six most expensive PPP tariff of the 15 countries utilities included in the survey being in a middle group of counties having a PPP tariff between 0.15-0.20 USD/kWh. Kenya, Thailand India and Malaysia has very high PPP tariffs, while in the bottom of the table are countries of South Korea, USA, Canada and Australia

• South Africa (Eskom) is ranked as having the third, largest increase in PPP with a PPP increase of 55% tariff increase only surpassed by India and Malaysia. South Africa thereby lost 55% in power purchase parity compared to the baseline (USA) during the last 10 years. At the other end of the table did the countries Germany, Denmark and Spain gain PPP against the baseline.

REPORT Confidential Page No:19

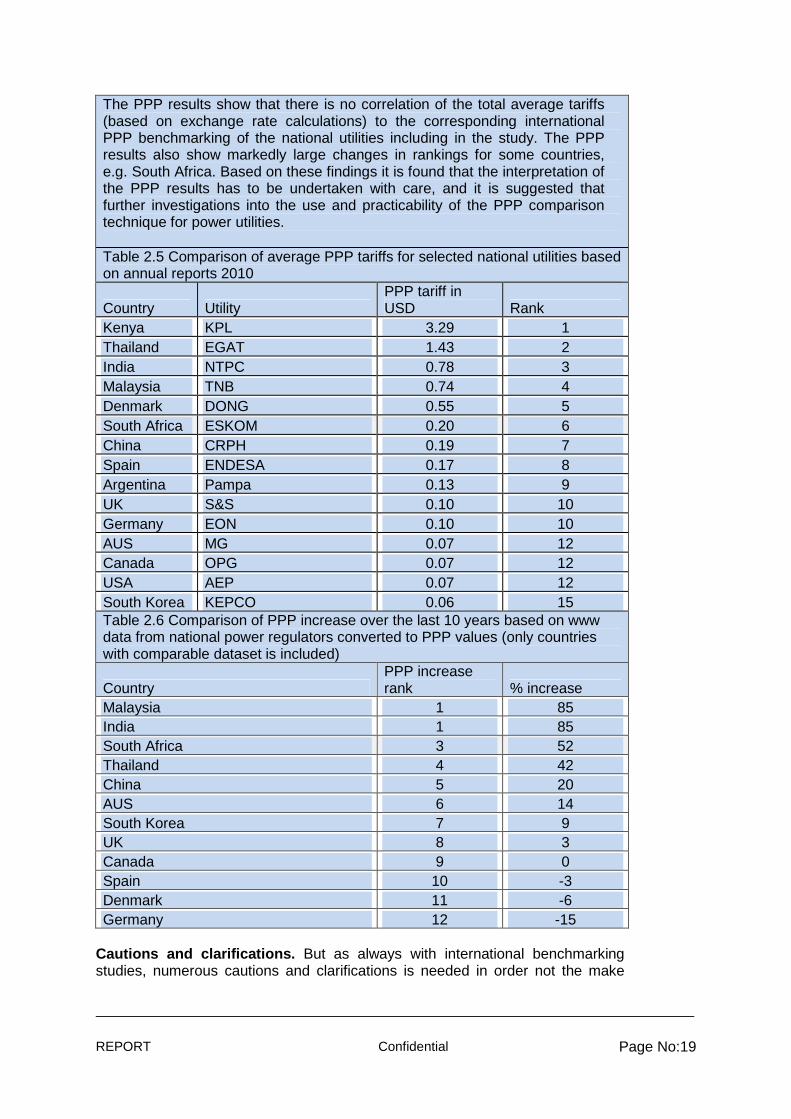

The PPP results show that there is no correlation of the total average tariffs (based on exchange rate calculations) to the corresponding international PPP benchmarking of the national utilities including in the study. The PPP results also show markedly large changes in rankings for some countries, e.g. South Africa. Based on these findings it is found that the interpretation of the PPP results has to be undertaken with care, and it is suggested that further investigations into the use and practicability of the PPP comparison technique for power utilities. Table 2.5 Comparison of average PPP tariffs for selected national utilities based on annual reports 2010

Country Utility PPP tariff in USD Rank

Kenya KPL 3.29 1 Thailand EGAT 1.43 2 India NTPC 0.78 3 Malaysia TNB 0.74 4 Denmark DONG 0.55 5 South Africa ESKOM 0.20 6 China CRPH 0.19 7 Spain ENDESA 0.17 8 Argentina Pampa 0.13 9 UK S&S 0.10 10 Germany EON 0.10 10 AUS MG 0.07 12 Canada OPG 0.07 12 USA AEP 0.07 12 South Korea KEPCO 0.06 15 Table 2.6 Comparison of PPP increase over the last 10 years based on www data from national power regulators converted to PPP values (only countries with comparable dataset is included)

Country PPP increase rank % increase

Malaysia 1 85 India 1 85 South Africa 3 52 Thailand 4 42 China 5 20 AUS 6 14 South Korea 7 9 UK 8 3 Canada 9 0 Spain 10 -3 Denmark 11 -6 Germany 12 -15

Cautions and clarifications. But as always with international benchmarking studies, numerous cautions and clarifications is needed in order not the make

REPORT Confidential Page No:20

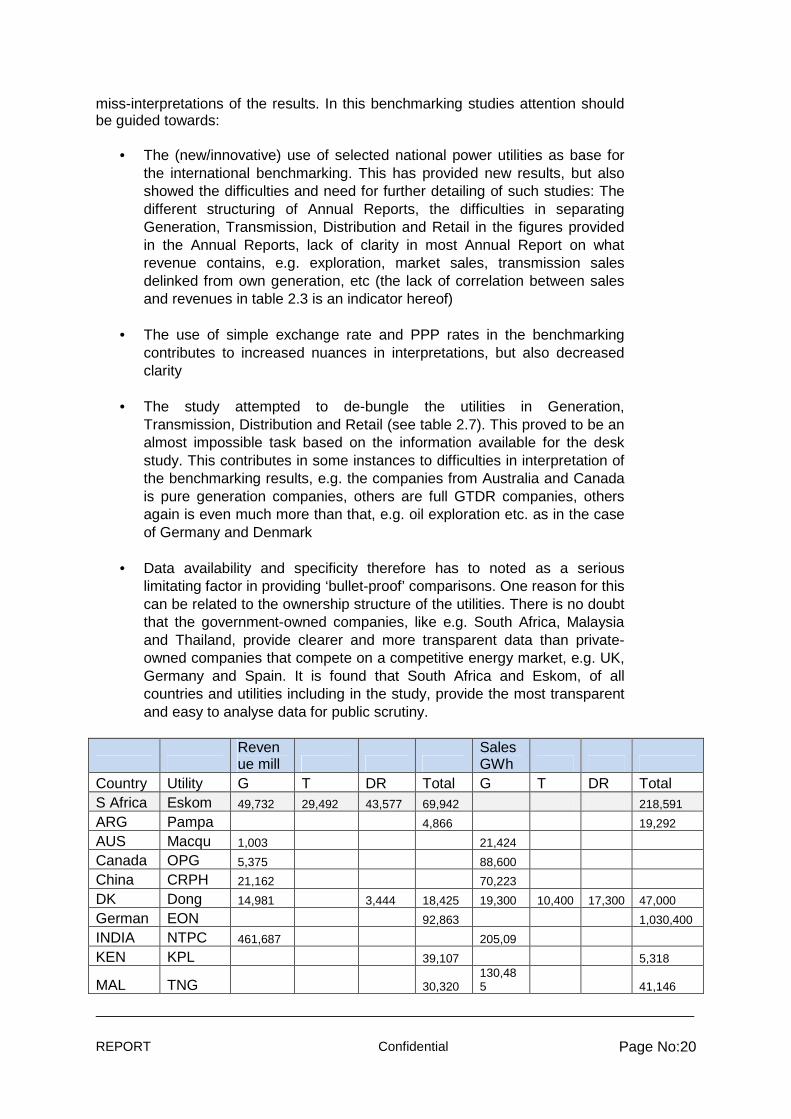

miss-interpretations of the results. In this benchmarking studies attention should be guided towards:

• The (new/innovative) use of selected national power utilities as base for the international benchmarking. This has provided new results, but also showed the difficulties and need for further detailing of such studies: The different structuring of Annual Reports, the difficulties in separating Generation, Transmission, Distribution and Retail in the figures provided in the Annual Reports, lack of clarity in most Annual Report on what revenue contains, e.g. exploration, market sales, transmission sales delinked from own generation, etc (the lack of correlation between sales and revenues in table 2.3 is an indicator hereof)

• The use of simple exchange rate and PPP rates in the benchmarking contributes to increased nuances in interpretations, but also decreased clarity

• The study attempted to de-bungle the utilities in Generation, Transmission, Distribution and Retail (see table 2.7). This proved to be an almost impossible task based on the information available for the desk study. This contributes in some instances to difficulties in interpretation of the benchmarking results, e.g. the companies from Australia and Canada is pure generation companies, others are full GTDR companies, others again is even much more than that, e.g. oil exploration etc. as in the case of Germany and Denmark

• Data availability and specificity therefore has to noted as a serious limitating factor in providing ‘bullet-proof’ comparisons. One reason for this can be related to the ownership structure of the utilities. There is no doubt that the government-owned companies, like e.g. South Africa, Malaysia and Thailand, provide clearer and more transparent data than private-owned companies that compete on a competitive energy market, e.g. UK, Germany and Spain. It is found that South Africa and Eskom, of all countries and utilities including in the study, provide the most transparent and easy to analyse data for public scrutiny.

Revenue mill

Sales GWh

Country Utility G T DR Total G T DR Total S Africa Eskom 49,732 29,492 43,577 69,942 218,591

ARG Pampa 4,866 19,292

AUS Macqu 1,003 21,424

Canada OPG 5,375 88,600

China CRPH 21,162 70,223

DK Dong 14,981 3,444 18,425 19,300 10,400 17,300 47,000

German EON 92,863 1,030,400

INDIA NTPC 461,687 205,09

KEN KPL 39,107 5,318

MAL TNG 30,320 130,485 41,146

REPORT Confidential Page No:21

S Korea KEPCO 38,161 434,160

Spain Endesa 31,177 175,212

Thai EGAT 405,445 71,205 156125

UK S&S 20,465 205,100

USA AEP 13,791 205,869 Table 2.7 Indicative table for comparison of GTDR between utilities Lessons learned and recommendations. Results, hypothesis and cautions, as outlined above, leads to a number of key lessons learned and recommendations for the present international benchmarking study of average tariffs. These include:

• The market share of the utilities included for each country should be increased to at least 50-60% of the national energy market to improve reliability in comparisons

• The utilities either needs to be de-bungled in Generation, Transmission, Distribution and Retail or other methodologies needs to be developed to further improve the apple-to-apple comparison. Greater focus also has to be placed on the different generation technologies and fuel sources

• Detailed studies of the hypotheses outlined above, e.g. should be initiated to gain further lessons of the international benchmarking study.

Below is provided background data for each country and utility included in the international benchmarking study. The background data for each country and utility is compared to South Africa and Eskom.

2.2 BACKGROUND DATA

Below is provided background data for the findings presented in chapter 3.1. Background data include brief data and descriptions of the included utilities, followed by data on the four sense-making factors included in the study.

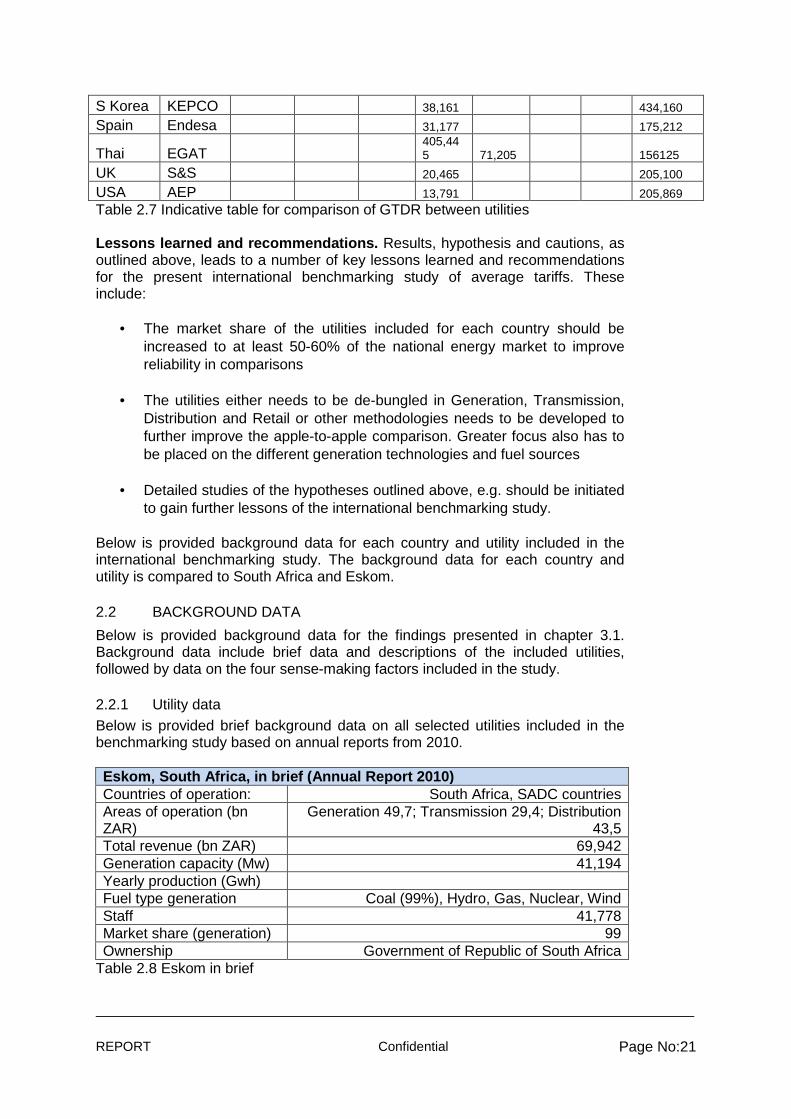

2.2.1 Utility data Below is provided brief background data on all selected utilities included in the benchmarking study based on annual reports from 2010. Eskom, South Africa, in brief (Annual Report 2010) Countries of operation: South Africa, SADC countries Areas of operation (bn ZAR)

Generation 49,7; Transmission 29,4; Distribution 43,5

Total revenue (bn ZAR) 69,942 Generation capacity (Mw) 41,194 Yearly production (Gwh) Fuel type generation Coal (99%), Hydro, Gas, Nuclear, Wind Staff 41,778 Market share (generation) 99 Ownership Government of Republic of South Africa

Table 2.8 Eskom in brief

REPORT Confidential Page No:22

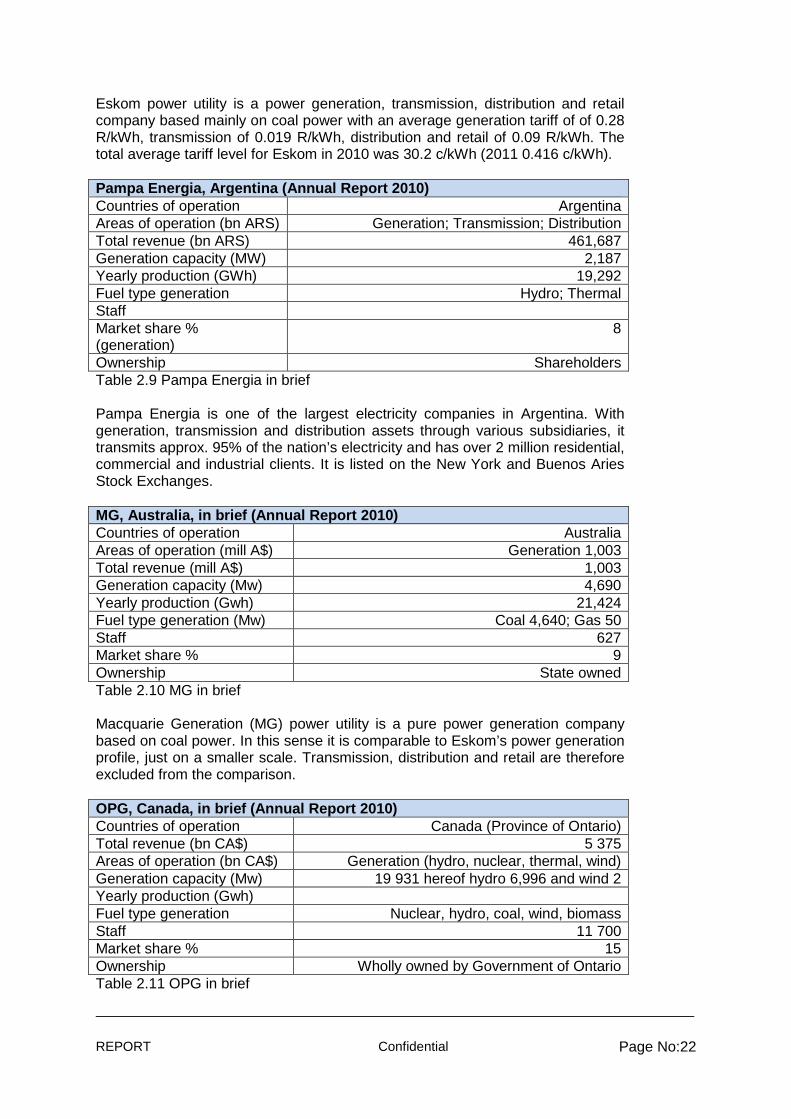

Eskom power utility is a power generation, transmission, distribution and retail company based mainly on coal power with an average generation tariff of of 0.28 R/kWh, transmission of 0.019 R/kWh, distribution and retail of 0.09 R/kWh. The total average tariff level for Eskom in 2010 was 30.2 c/kWh (2011 0.416 c/kWh). Pampa Energia, Argentina (Annual Report 2010) Countries of operation Argentina Areas of operation (bn ARS) Generation; Transmission; Distribution Total revenue (bn ARS) 461,687 Generation capacity (MW) 2,187 Yearly production (GWh) 19,292 Fuel type generation Hydro; Thermal Staff Market share % (generation)

8

Ownership Shareholders Table 2.9 Pampa Energia in brief Pampa Energia is one of the largest electricity companies in Argentina. With generation, transmission and distribution assets through various subsidiaries, it transmits approx. 95% of the nation’s electricity and has over 2 million residential, commercial and industrial clients. It is listed on the New York and Buenos Aries Stock Exchanges. MG, Australia, in brief (Annual Report 2010) Countries of operation Australia Areas of operation (mill A$) Generation 1,003 Total revenue (mill A$) 1,003 Generation capacity (Mw) 4,690 Yearly production (Gwh) 21,424 Fuel type generation (Mw) Coal 4,640; Gas 50 Staff 627 Market share % 9 Ownership State owned Table 2.10 MG in brief Macquarie Generation (MG) power utility is a pure power generation company based on coal power. In this sense it is comparable to Eskom’s power generation profile, just on a smaller scale. Transmission, distribution and retail are therefore excluded from the comparison. OPG, Canada, in brief (Annual Report 2010) Countries of operation Canada (Province of Ontario) Total revenue (bn CA$) 5 375 Areas of operation (bn CA$) Generation (hydro, nuclear, thermal, wind) Generation capacity (Mw) 19 931 hereof hydro 6,996 and wind 2 Yearly production (Gwh) Fuel type generation Nuclear, hydro, coal, wind, biomass Staff 11 700 Market share % 15 Ownership Wholly owned by Government of Ontario Table 2.11 OPG in brief

REPORT Confidential Page No:23

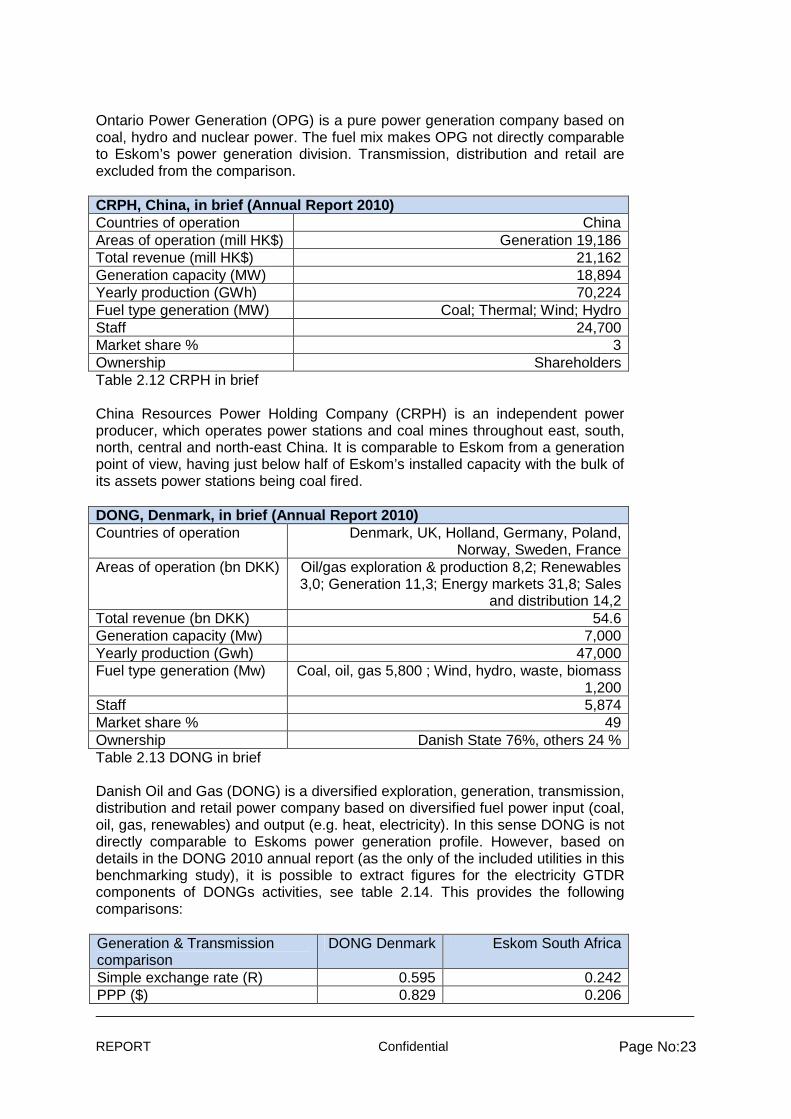

Ontario Power Generation (OPG) is a pure power generation company based on coal, hydro and nuclear power. The fuel mix makes OPG not directly comparable to Eskom’s power generation division. Transmission, distribution and retail are excluded from the comparison. CRPH, China, in brief (Annual Report 2010) Countries of operation China Areas of operation (mill HK$) Generation 19,186 Total revenue (mill HK$) 21,162 Generation capacity (MW) 18,894 Yearly production (GWh) 70,224 Fuel type generation (MW) Coal; Thermal; Wind; Hydro Staff 24,700 Market share % 3 Ownership Shareholders Table 2.12 CRPH in brief China Resources Power Holding Company (CRPH) is an independent power producer, which operates power stations and coal mines throughout east, south, north, central and north-east China. It is comparable to Eskom from a generation point of view, having just below half of Eskom’s installed capacity with the bulk of its assets power stations being coal fired. DONG, Denmark, in brief (Annual Report 2010) Countries of operation Denmark, UK, Holland, Germany, Poland,

Norway, Sweden, France Areas of operation (bn DKK) Oil/gas exploration & production 8,2; Renewables

3,0; Generation 11,3; Energy markets 31,8; Sales and distribution 14,2

Total revenue (bn DKK) 54.6 Generation capacity (Mw) 7,000 Yearly production (Gwh) 47,000 Fuel type generation (Mw) Coal, oil, gas 5,800 ; Wind, hydro, waste, biomass

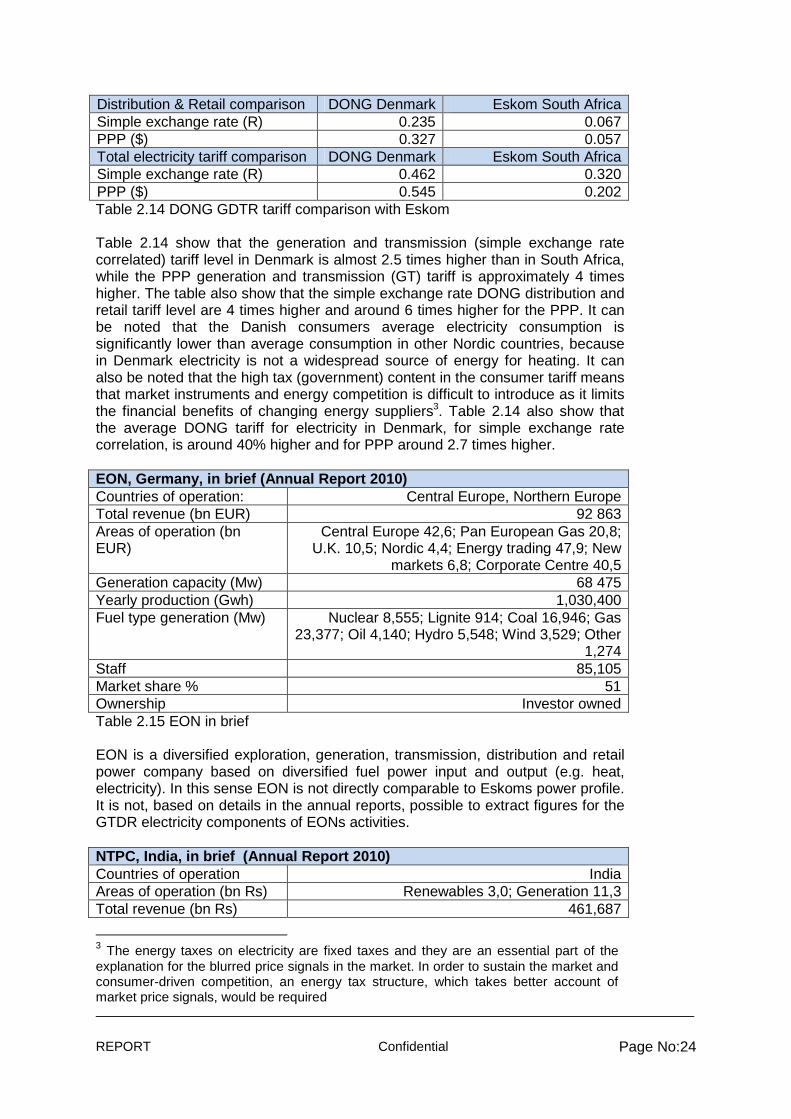

1,200 Staff 5,874 Market share % 49 Ownership Danish State 76%, others 24 % Table 2.13 DONG in brief Danish Oil and Gas (DONG) is a diversified exploration, generation, transmission, distribution and retail power company based on diversified fuel power input (coal, oil, gas, renewables) and output (e.g. heat, electricity). In this sense DONG is not directly comparable to Eskoms power generation profile. However, based on details in the DONG 2010 annual report (as the only of the included utilities in this benchmarking study), it is possible to extract figures for the electricity GTDR components of DONGs activities, see table 2.14. This provides the following comparisons: Generation & Transmission comparison

DONG Denmark Eskom South Africa

Simple exchange rate (R) 0.595 0.242 PPP ($) 0.829 0.206

REPORT Confidential Page No:24

Distribution & Retail comparison DONG Denmark Eskom South Africa Simple exchange rate (R) 0.235 0.067 PPP ($) 0.327 0.057 Total electricity tariff comparison DONG Denmark Eskom South Africa Simple exchange rate (R) 0.462 0.320 PPP ($) 0.545 0.202 Table 2.14 DONG GDTR tariff comparison with Eskom Table 2.14 show that the generation and transmission (simple exchange rate correlated) tariff level in Denmark is almost 2.5 times higher than in South Africa, while the PPP generation and transmission (GT) tariff is approximately 4 times higher. The table also show that the simple exchange rate DONG distribution and retail tariff level are 4 times higher and around 6 times higher for the PPP. It can be noted that the Danish consumers average electricity consumption is significantly lower than average consumption in other Nordic countries, because in Denmark electricity is not a widespread source of energy for heating. It can also be noted that the high tax (government) content in the consumer tariff means that market instruments and energy competition is difficult to introduce as it limits the financial benefits of changing energy suppliers3. Table 2.14 also show that the average DONG tariff for electricity in Denmark, for simple exchange rate correlation, is around 40% higher and for PPP around 2.7 times higher. EON, Germany, in brief (Annual Report 2010) Countries of operation: Central Europe, Northern Europe Total revenue (bn EUR) 92 863 Areas of operation (bn EUR)

Central Europe 42,6; Pan European Gas 20,8; U.K. 10,5; Nordic 4,4; Energy trading 47,9; New

markets 6,8; Corporate Centre 40,5 Generation capacity (Mw) 68 475 Yearly production (Gwh) 1,030,400 Fuel type generation (Mw) Nuclear 8,555; Lignite 914; Coal 16,946; Gas

23,377; Oil 4,140; Hydro 5,548; Wind 3,529; Other 1,274

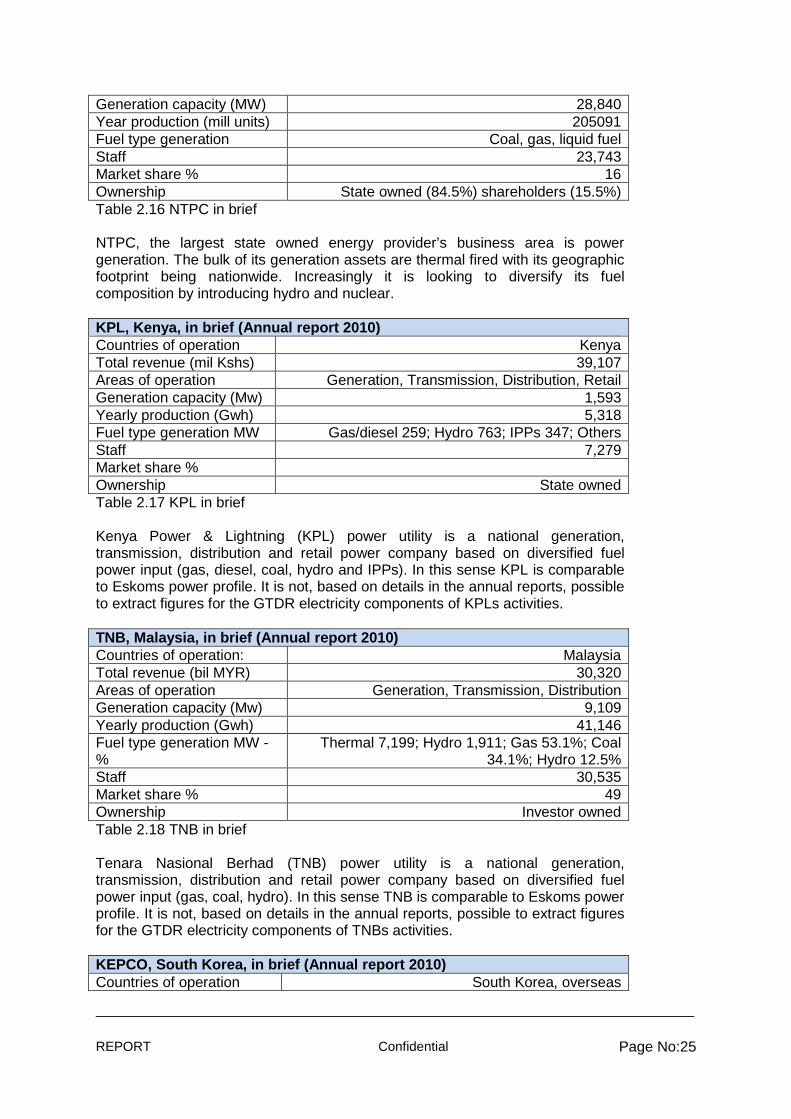

Staff 85,105 Market share % 51 Ownership Investor owned Table 2.15 EON in brief EON is a diversified exploration, generation, transmission, distribution and retail power company based on diversified fuel power input and output (e.g. heat, electricity). In this sense EON is not directly comparable to Eskoms power profile. It is not, based on details in the annual reports, possible to extract figures for the GTDR electricity components of EONs activities. NTPC, India, in brief (Annual Report 2010) Countries of operation India Areas of operation (bn Rs) Renewables 3,0; Generation 11,3 Total revenue (bn Rs) 461,687

3 The energy taxes on electricity are fixed taxes and they are an essential part of the explanation for the blurred price signals in the market. In order to sustain the market and consumer-driven competition, an energy tax structure, which takes better account of market price signals, would be required

REPORT Confidential Page No:25

Generation capacity (MW) 28,840 Year production (mill units) 205091 Fuel type generation Coal, gas, liquid fuel Staff 23,743 Market share % 16 Ownership State owned (84.5%) shareholders (15.5%) Table 2.16 NTPC in brief NTPC, the largest state owned energy provider’s business area is power generation. The bulk of its generation assets are thermal fired with its geographic footprint being nationwide. Increasingly it is looking to diversify its fuel composition by introducing hydro and nuclear. KPL, Kenya, in brief (Annual report 2010) Countries of operation Kenya Total revenue (mil Kshs) 39,107 Areas of operation Generation, Transmission, Distribution, Retail Generation capacity (Mw) 1,593 Yearly production (Gwh) 5,318 Fuel type generation MW Gas/diesel 259; Hydro 763; IPPs 347; Others Staff 7,279 Market share % Ownership State owned Table 2.17 KPL in brief Kenya Power & Lightning (KPL) power utility is a national generation, transmission, distribution and retail power company based on diversified fuel power input (gas, diesel, coal, hydro and IPPs). In this sense KPL is comparable to Eskoms power profile. It is not, based on details in the annual reports, possible to extract figures for the GTDR electricity components of KPLs activities. TNB, Malaysia, in brief (Annual report 2010) Countries of operation: Malaysia Total revenue (bil MYR) 30,320 Areas of operation Generation, Transmission, Distribution Generation capacity (Mw) 9,109 Yearly production (Gwh) 41,146 Fuel type generation MW - %

Thermal 7,199; Hydro 1,911; Gas 53.1%; Coal 34.1%; Hydro 12.5%

Staff 30,535 Market share % 49 Ownership Investor owned Table 2.18 TNB in brief Tenara Nasional Berhad (TNB) power utility is a national generation, transmission, distribution and retail power company based on diversified fuel power input (gas, coal, hydro). In this sense TNB is comparable to Eskoms power profile. It is not, based on details in the annual reports, possible to extract figures for the GTDR electricity components of TNBs activities. KEPCO, South Korea, in brief (Annual report 2 010) Countries of operation South Korea, overseas

REPORT Confidential Page No:26

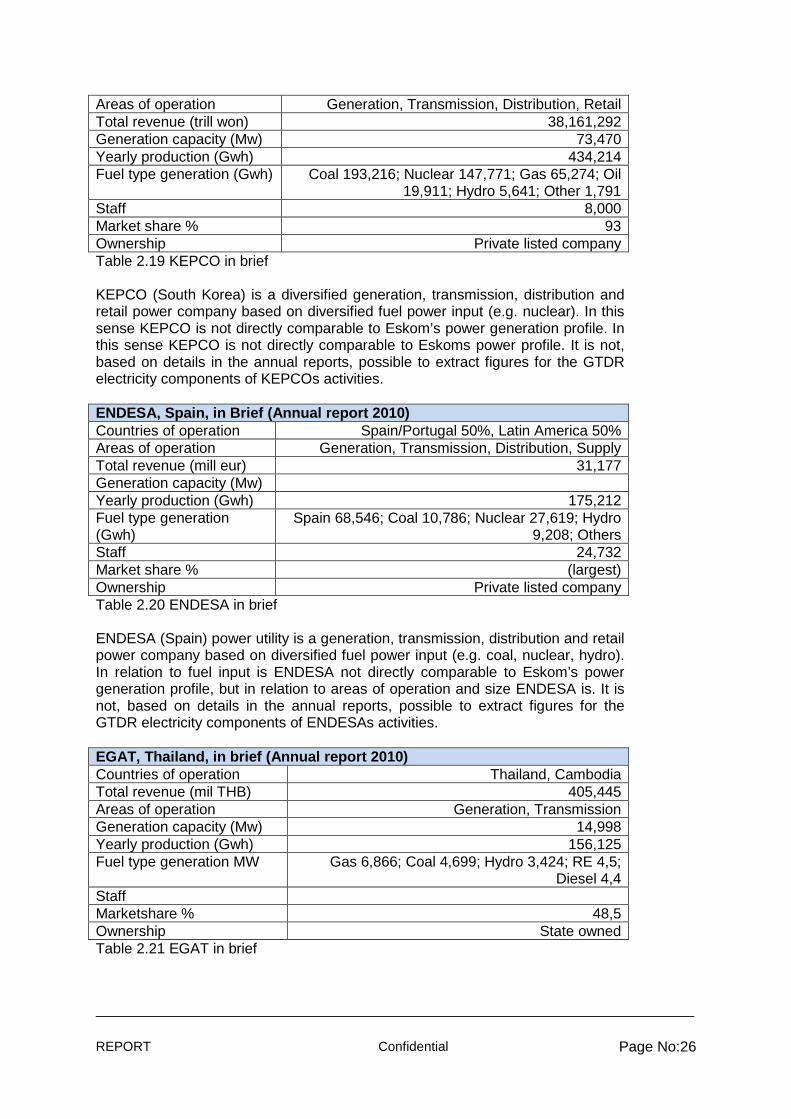

Areas of operation Generation, Transmission, Distribution, Retail Total revenue (trill won) 38,161,292 Generation capacity (Mw) 73,470 Yearly production (Gwh) 434,214 Fuel type generation (Gwh) Coal 193,216; Nuclear 147,771; Gas 65,274; Oil

19,911; Hydro 5,641; Other 1,791 Staff 8,000 Market share % 93 Ownership Private listed company Table 2.19 KEPCO in brief KEPCO (South Korea) is a diversified generation, transmission, distribution and retail power company based on diversified fuel power input (e.g. nuclear). In this sense KEPCO is not directly comparable to Eskom’s power generation profile. In this sense KEPCO is not directly comparable to Eskoms power profile. It is not, based on details in the annual reports, possible to extract figures for the GTDR electricity components of KEPCOs activities. ENDESA, Spain, in Brief (Annual report 2010) Countries of operation Spain/Portugal 50%, Latin America 50% Areas of operation Generation, Transmission, Distribution, Supply Total revenue (mill eur) 31,177 Generation capacity (Mw) Yearly production (Gwh) 175,212 Fuel type generation (Gwh)

Spain 68,546; Coal 10,786; Nuclear 27,619; Hydro 9,208; Others

Staff 24,732 Market share % (largest) Ownership Private listed company Table 2.20 ENDESA in brief ENDESA (Spain) power utility is a generation, transmission, distribution and retail power company based on diversified fuel power input (e.g. coal, nuclear, hydro). In relation to fuel input is ENDESA not directly comparable to Eskom’s power generation profile, but in relation to areas of operation and size ENDESA is. It is not, based on details in the annual reports, possible to extract figures for the GTDR electricity components of ENDESAs activities. EGAT, Thailand, in brief (Annual report 2010) Countries of operation Thailand, Cambodia Total revenue (mil THB) 405,445 Areas of operation Generation, Transmission Generation capacity (Mw) 14,998 Yearly production (Gwh) 156,125 Fuel type generation MW Gas 6,866; Coal 4,699; Hydro 3,424; RE 4,5;

Diesel 4,4 Staff Marketshare % 48,5 Ownership State owned Table 2.21 EGAT in brief

REPORT Confidential Page No:27

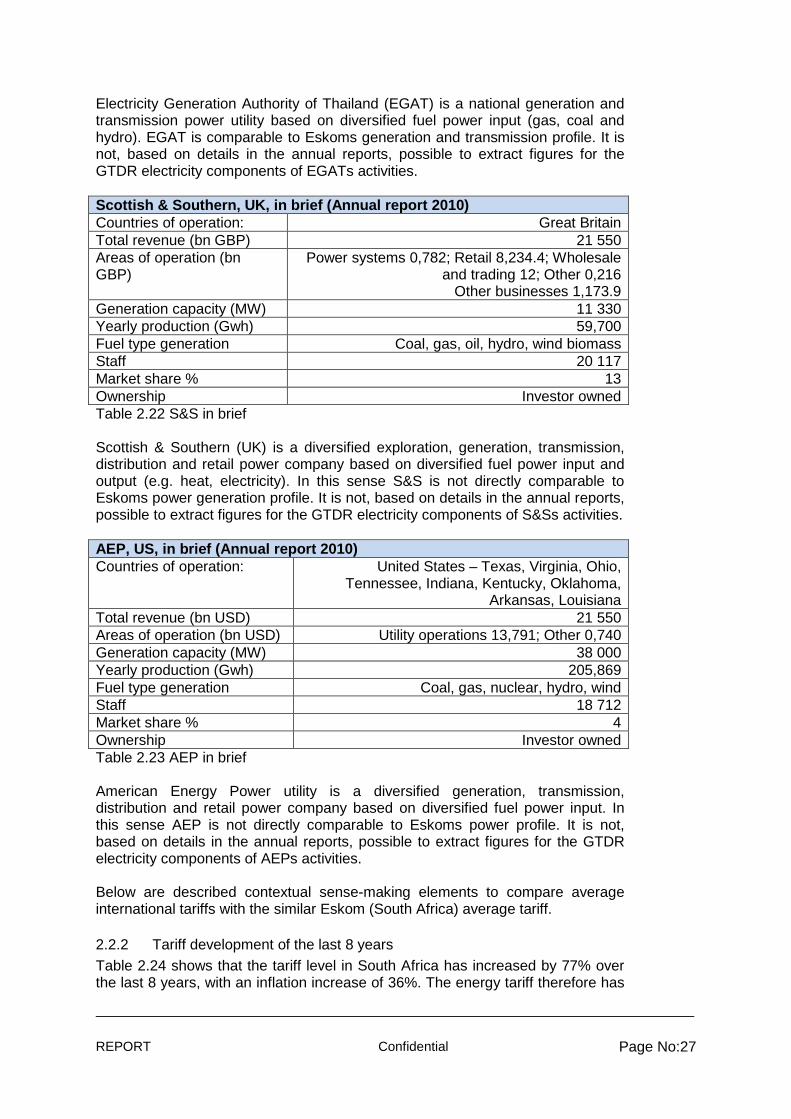

Electricity Generation Authority of Thailand (EGAT) is a national generation and transmission power utility based on diversified fuel power input (gas, coal and hydro). EGAT is comparable to Eskoms generation and transmission profile. It is not, based on details in the annual reports, possible to extract figures for the GTDR electricity components of EGATs activities. Scottish & Southern, UK, in brief (Annual report 20 10) Countries of operation: Great Britain Total revenue (bn GBP) 21 550 Areas of operation (bn GBP)

Power systems 0,782; Retail 8,234.4; Wholesale and trading 12; Other 0,216

Other businesses 1,173.9 Generation capacity (MW) 11 330 Yearly production (Gwh) 59,700 Fuel type generation Coal, gas, oil, hydro, wind biomass Staff 20 117 Market share % 13 Ownership Investor owned Table 2.22 S&S in brief Scottish & Southern (UK) is a diversified exploration, generation, transmission, distribution and retail power company based on diversified fuel power input and output (e.g. heat, electricity). In this sense S&S is not directly comparable to Eskoms power generation profile. It is not, based on details in the annual reports, possible to extract figures for the GTDR electricity components of S&Ss activities. AEP, US, in brief (Annual report 2010) Countries of operation: United States – Texas, Virginia, Ohio,

Tennessee, Indiana, Kentucky, Oklahoma, Arkansas, Louisiana

Total revenue (bn USD) 21 550 Areas of operation (bn USD) Utility operations 13,791; Other 0,740 Generation capacity (MW) 38 000 Yearly production (Gwh) 205,869 Fuel type generation Coal, gas, nuclear, hydro, wind Staff 18 712 Market share % 4 Ownership Investor owned Table 2.23 AEP in brief American Energy Power utility is a diversified generation, transmission, distribution and retail power company based on diversified fuel power input. In this sense AEP is not directly comparable to Eskoms power profile. It is not, based on details in the annual reports, possible to extract figures for the GTDR electricity components of AEPs activities. Below are described contextual sense-making elements to compare average international tariffs with the similar Eskom (South Africa) average tariff.

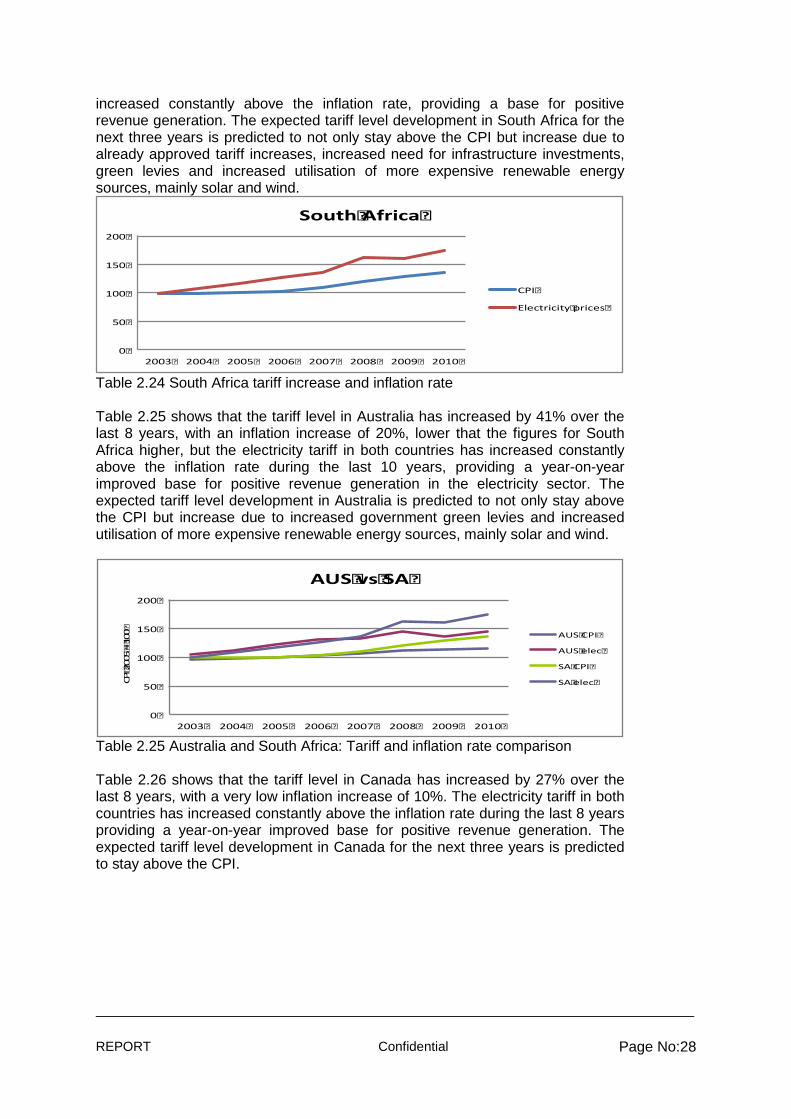

2.2.2 Tariff development of the last 8 years Table 2.24 shows that the tariff level in South Africa has increased by 77% over the last 8 years, with an inflation increase of 36%. The energy tariff therefore has

REPORT Confidential Page No:28

increased constantly above the inflation rate, providing a base for positive revenue generation. The expected tariff level development in South Africa for the next three years is predicted to not only stay above the CPI but increase due to already approved tariff increases, increased need for infrastructure investments, green levies and increased utilisation of more expensive renewable energy sources, mainly solar and wind.

Table 2.24 South Africa tariff increase and inflation rate Table 2.25 shows that the tariff level in Australia has increased by 41% over the last 8 years, with an inflation increase of 20%, lower that the figures for South Africa higher, but the electricity tariff in both countries has increased constantly above the inflation rate during the last 10 years, providing a year-on-year improved base for positive revenue generation in the electricity sector. The expected tariff level development in Australia is predicted to not only stay above the CPI but increase due to increased government green levies and increased utilisation of more expensive renewable energy sources, mainly solar and wind.

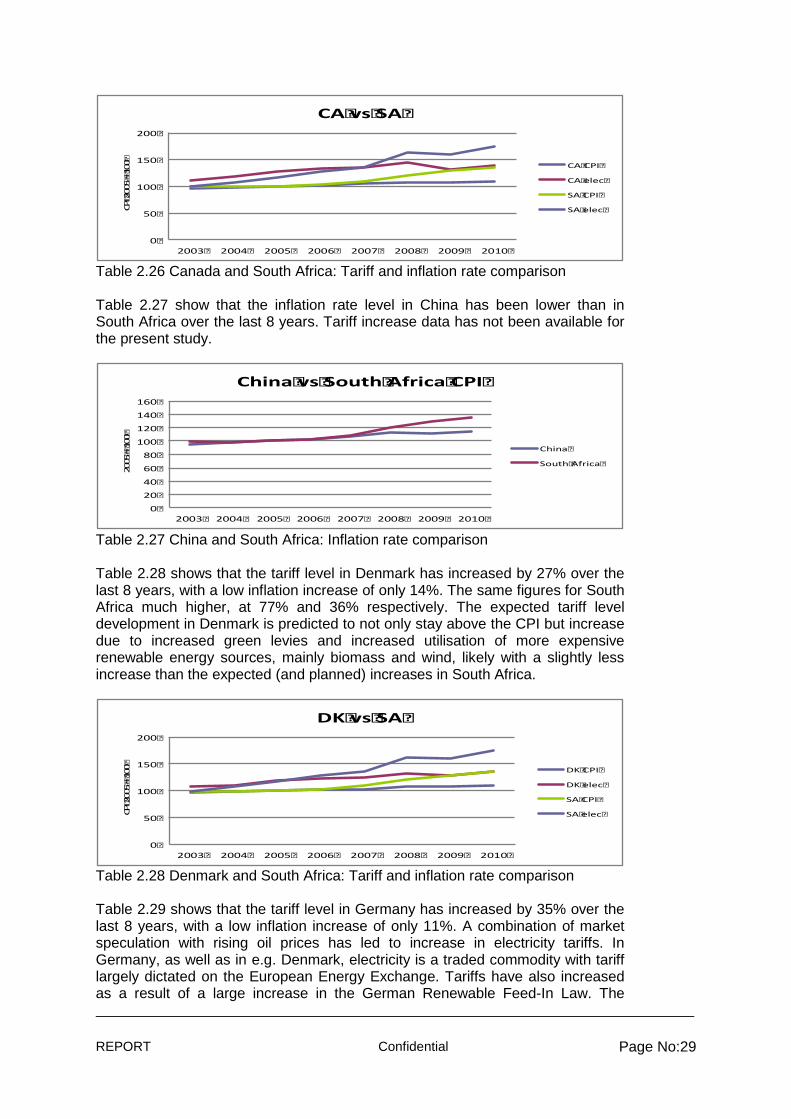

Table 2.25 Australia and South Africa: Tariff and inflation rate comparison Table 2.26 shows that the tariff level in Canada has increased by 27% over the last 8 years, with a very low inflation increase of 10%. The electricity tariff in both countries has increased constantly above the inflation rate during the last 8 years providing a year-on-year improved base for positive revenue generation. The expected tariff level development in Canada for the next three years is predicted to stay above the CPI.

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

SouthAfrica

CPI

Electricityprices

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

CPI2005=

100

AUSvsSA

AUSCPI

AUSelec

SACPI

SAelec

REPORT Confidential Page No:29

Table 2.26 Canada and South Africa: Tariff and inflation rate comparison Table 2.27 show that the inflation rate level in China has been lower than in South Africa over the last 8 years. Tariff increase data has not been available for the present study.

Table 2.27 China and South Africa: Inflation rate comparison Table 2.28 shows that the tariff level in Denmark has increased by 27% over the last 8 years, with a low inflation increase of only 14%. The same figures for South Africa much higher, at 77% and 36% respectively. The expected tariff level development in Denmark is predicted to not only stay above the CPI but increase due to increased green levies and increased utilisation of more expensive renewable energy sources, mainly biomass and wind, likely with a slightly less increase than the expected (and planned) increases in South Africa.

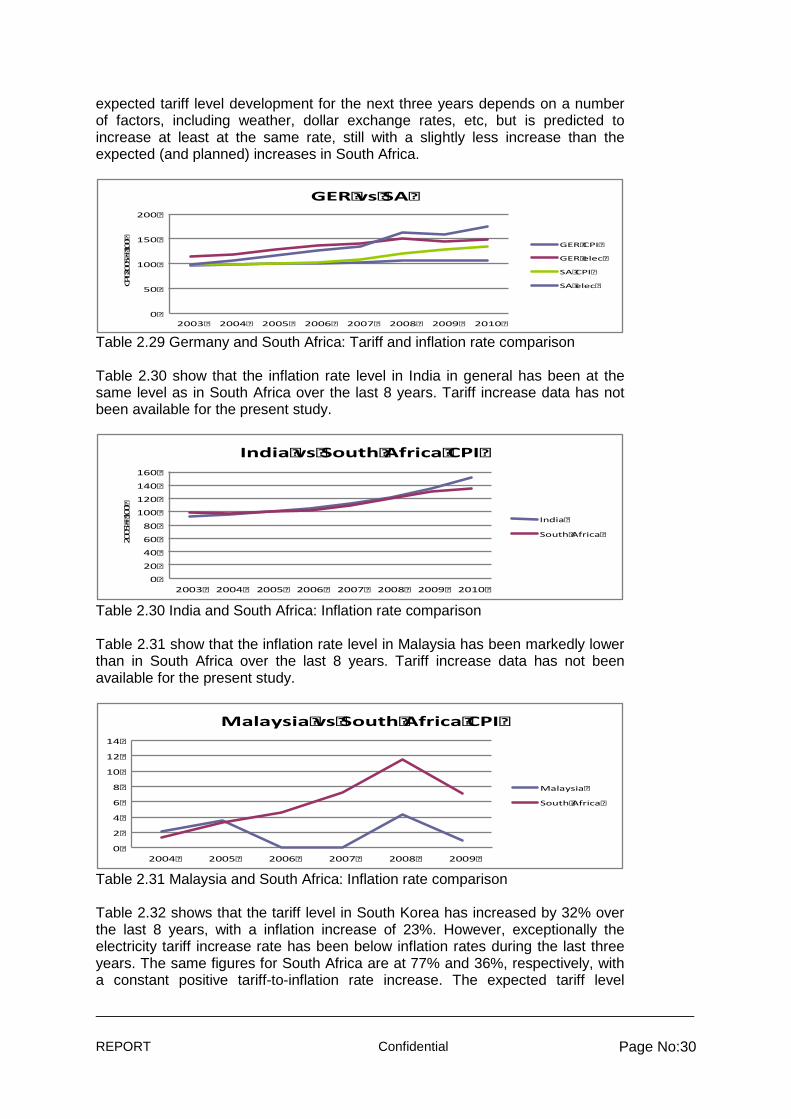

Table 2.28 Denmark and South Africa: Tariff and inflation rate comparison Table 2.29 shows that the tariff level in Germany has increased by 35% over the last 8 years, with a low inflation increase of only 11%. A combination of market speculation with rising oil prices has led to increase in electricity tariffs. In Germany, as well as in e.g. Denmark, electricity is a traded commodity with tariff largely dictated on the European Energy Exchange. Tariffs have also increased as a result of a large increase in the German Renewable Feed-In Law. The

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

CPI2005=1

00

CAvsSA

CACPI

CAelec

SACPI

SAelec

0

20

40

60

80

100

120

140

160

2003 2004 2005 2006 2007 2008 2009 2010

2005=1

00

ChinavsSouthAfricaCPI

China

SouthAfrica

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

CPI2005=1

00

DKvsSA

DKCPI

DKelec

SACPI

SAelec

REPORT Confidential Page No:30

expected tariff level development for the next three years depends on a number of factors, including weather, dollar exchange rates, etc, but is predicted to increase at least at the same rate, still with a slightly less increase than the expected (and planned) increases in South Africa.

Table 2.29 Germany and South Africa: Tariff and inflation rate comparison Table 2.30 show that the inflation rate level in India in general has been at the same level as in South Africa over the last 8 years. Tariff increase data has not been available for the present study.

Table 2.30 India and South Africa: Inflation rate comparison Table 2.31 show that the inflation rate level in Malaysia has been markedly lower than in South Africa over the last 8 years. Tariff increase data has not been available for the present study.

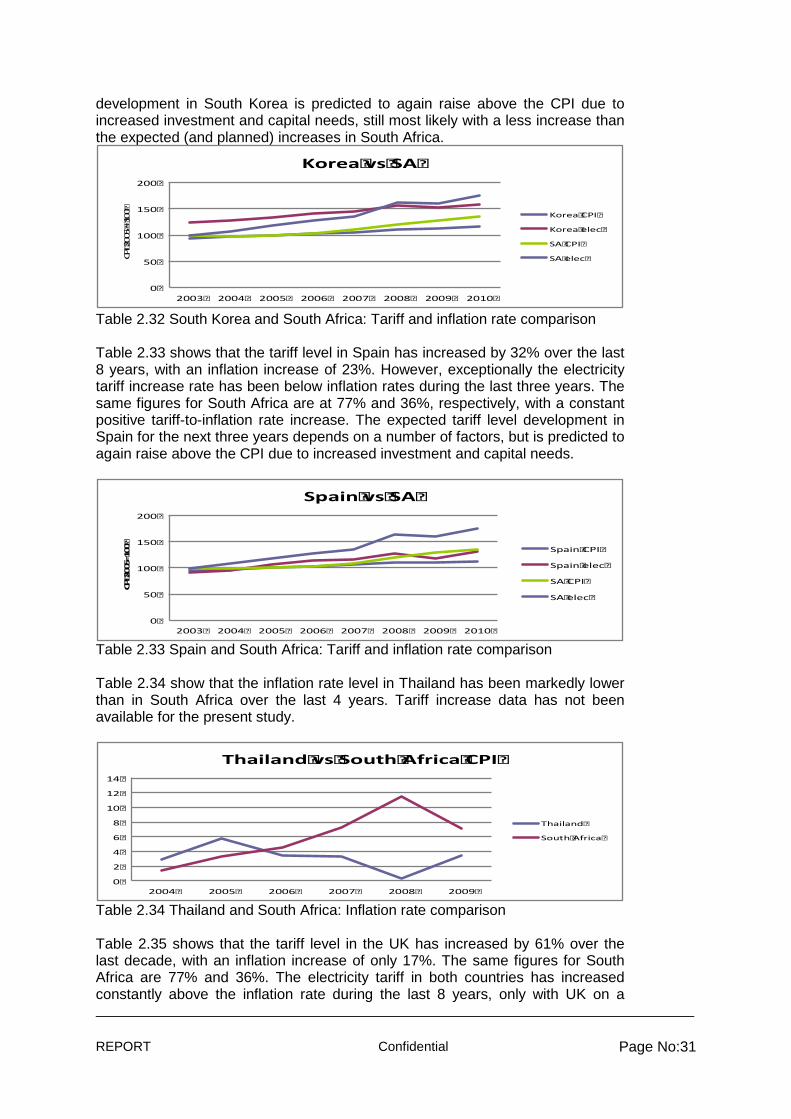

Table 2.31 Malaysia and South Africa: Inflation rate comparison Table 2.32 shows that the tariff level in South Korea has increased by 32% over the last 8 years, with a inflation increase of 23%. However, exceptionally the electricity tariff increase rate has been below inflation rates during the last three years. The same figures for South Africa are at 77% and 36%, respectively, with a constant positive tariff-to-inflation rate increase. The expected tariff level

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

CPI2005=100

GERvsSA

GERCPI

GERelec

SACPI

SAelec

0

20

40

60

80

100

120

140

160

2003 2004 2005 2006 2007 2008 2009 2010

2005=1

00

IndiavsSouthAfricaCPI

India

SouthAfrica

0

2

4

6

8

10

12

14

2004 2005 2006 2007 2008 2009

MalaysiavsSouthAfricaCPI

Malaysia

SouthAfrica

REPORT Confidential Page No:31

development in South Korea is predicted to again raise above the CPI due to increased investment and capital needs, still most likely with a less increase than the expected (and planned) increases in South Africa.

Table 2.32 South Korea and South Africa: Tariff and inflation rate comparison Table 2.33 shows that the tariff level in Spain has increased by 32% over the last 8 years, with an inflation increase of 23%. However, exceptionally the electricity tariff increase rate has been below inflation rates during the last three years. The same figures for South Africa are at 77% and 36%, respectively, with a constant positive tariff-to-inflation rate increase. The expected tariff level development in Spain for the next three years depends on a number of factors, but is predicted to again raise above the CPI due to increased investment and capital needs.

Table 2.33 Spain and South Africa: Tariff and inflation rate comparison Table 2.34 show that the inflation rate level in Thailand has been markedly lower than in South Africa over the last 4 years. Tariff increase data has not been available for the present study.

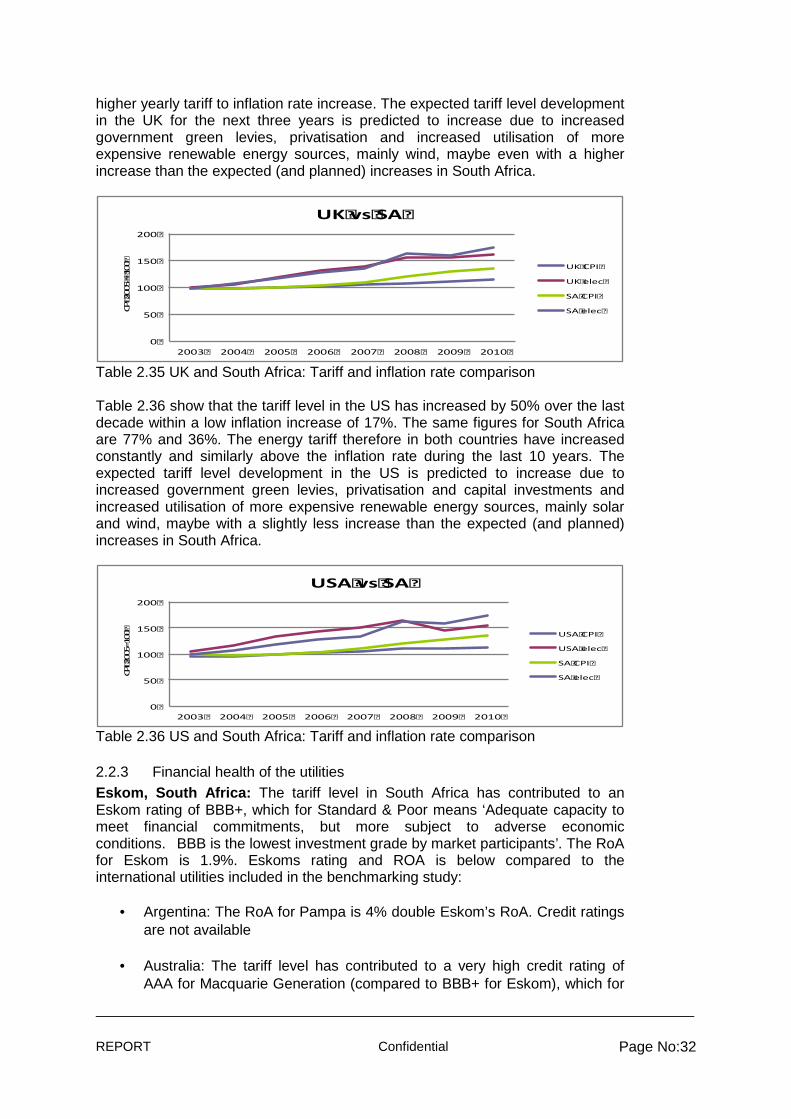

Table 2.34 Thailand and South Africa: Inflation rate comparison Table 2.35 shows that the tariff level in the UK has increased by 61% over the last decade, with an inflation increase of only 17%. The same figures for South Africa are 77% and 36%. The electricity tariff in both countries has increased constantly above the inflation rate during the last 8 years, only with UK on a

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

CPI2005=100

KoreavsSA

KoreaCPI

Koreaelec

SACPI

SAelec

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

CPI2005=100

SpainvsSA

SpainCPI

Spainelec

SACPI

SAelec

0

2

4

6

8

10

12

14

2004 2005 2006 2007 2008 2009

ThailandvsSouthAfricaCPI

Thailand

SouthAfrica

REPORT Confidential Page No:32

higher yearly tariff to inflation rate increase. The expected tariff level development in the UK for the next three years is predicted to increase due to increased government green levies, privatisation and increased utilisation of more expensive renewable energy sources, mainly wind, maybe even with a higher increase than the expected (and planned) increases in South Africa.

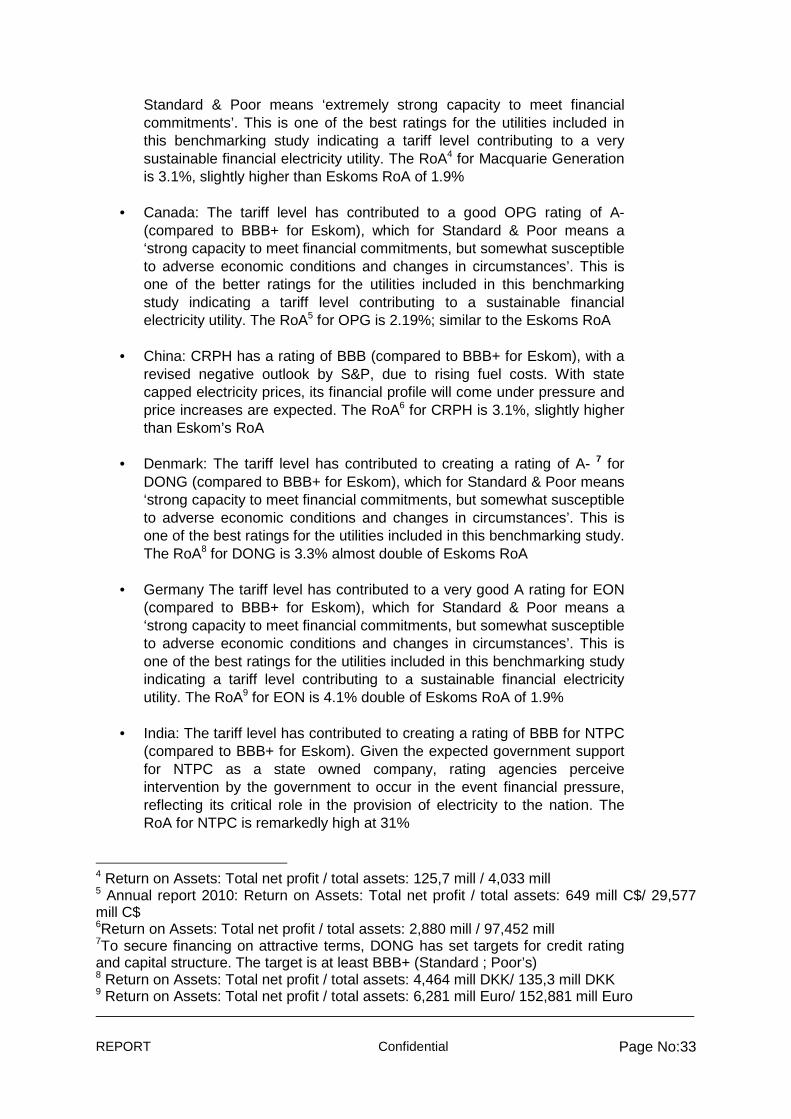

Table 2.35 UK and South Africa: Tariff and inflation rate comparison Table 2.36 show that the tariff level in the US has increased by 50% over the last decade within a low inflation increase of 17%. The same figures for South Africa are 77% and 36%. The energy tariff therefore in both countries have increased constantly and similarly above the inflation rate during the last 10 years. The expected tariff level development in the US is predicted to increase due to increased government green levies, privatisation and capital investments and increased utilisation of more expensive renewable energy sources, mainly solar and wind, maybe with a slightly less increase than the expected (and planned) increases in South Africa.

Table 2.36 US and South Africa: Tariff and inflation rate comparison

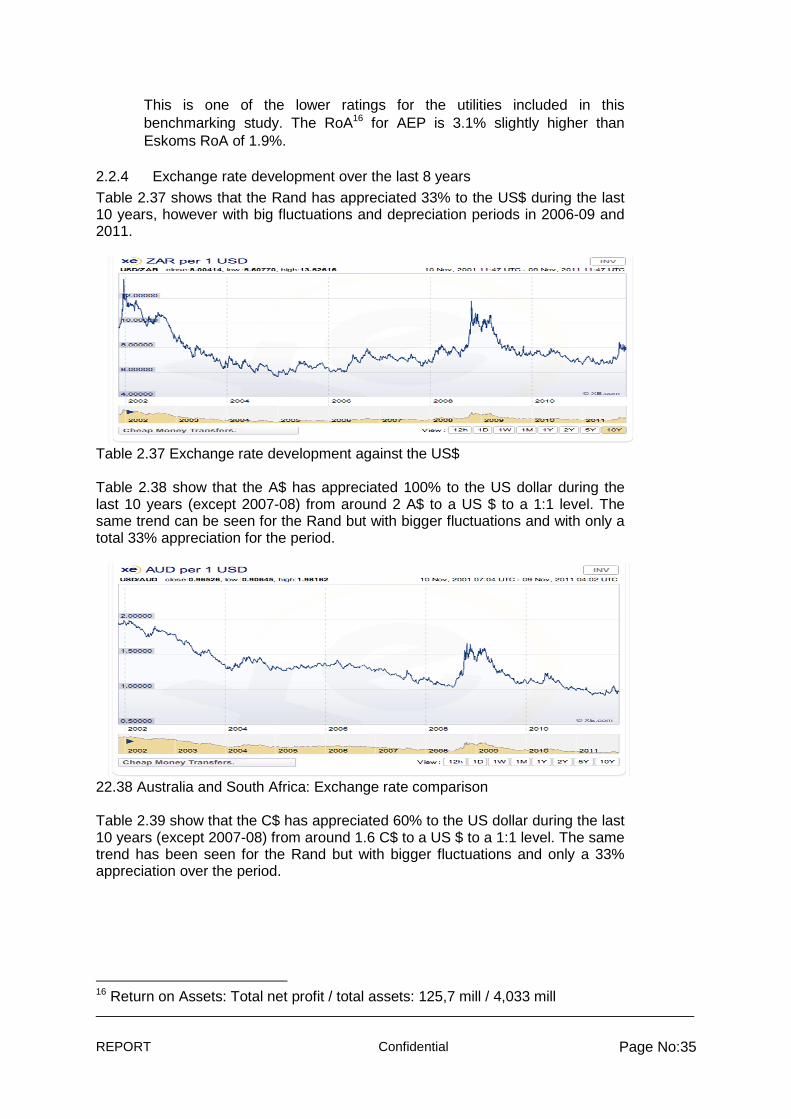

2.2.3 Financial health of the utilities Eskom, South Africa: The tariff level in South Africa has contributed to an Eskom rating of BBB+, which for Standard & Poor means ‘Adequate capacity to meet financial commitments, but more subject to adverse economic conditions.�BBB is the lowest investment grade by market participants’. The RoA for Eskom is 1.9%. Eskoms rating and ROA is below compared to the international utilities included in the benchmarking study:

• Argentina: The RoA for Pampa is 4% double Eskom’s RoA. Credit ratings are not available

• Australia: The tariff level has contributed to a very high credit rating of AAA for Macquarie Generation (compared to BBB+ for Eskom), which for

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

CPI2005=1

00

UKvsSA

UKCPI

UKelec

SACPI

SAelec

0

50

100

150

200

2003 2004 2005 2006 2007 2008 2009 2010

CPI2005=100

USAvsSA

USACPI

USAelec

SACPI

SAelec

REPORT Confidential Page No:33

Standard & Poor means ‘extremely strong capacity to meet financial commitments’. This is one of the best ratings for the utilities included in this benchmarking study indicating a tariff level contributing to a very sustainable financial electricity utility. The RoA4 for Macquarie Generation is 3.1%, slightly higher than Eskoms RoA of 1.9%

• Canada: The tariff level has contributed to a good OPG rating of A- (compared to BBB+ for Eskom), which for Standard & Poor means a ‘strong capacity to meet financial commitments, but somewhat susceptible to adverse economic conditions and changes in circumstances’. This is one of the better ratings for the utilities included in this benchmarking study indicating a tariff level contributing to a sustainable financial electricity utility. The RoA5 for OPG is 2.19%; similar to the Eskoms RoA

• China: CRPH has a rating of BBB (compared to BBB+ for Eskom), with a revised negative outlook by S&P, due to rising fuel costs. With state capped electricity prices, its financial profile will come under pressure and price increases are expected. The RoA6 for CRPH is 3.1%, slightly higher than Eskom’s RoA

• Denmark: The tariff level has contributed to creating a rating of A- 7 for DONG (compared to BBB+ for Eskom), which for Standard & Poor means ‘strong capacity to meet financial commitments, but somewhat susceptible to adverse economic conditions and changes in circumstances’. This is one of the best ratings for the utilities included in this benchmarking study. The RoA8 for DONG is 3.3% almost double of Eskoms RoA

• Germany The tariff level has contributed to a very good A rating for EON (compared to BBB+ for Eskom), which for Standard & Poor means a ‘strong capacity to meet financial commitments, but somewhat susceptible to adverse economic conditions and changes in circumstances’. This is one of the best ratings for the utilities included in this benchmarking study indicating a tariff level contributing to a sustainable financial electricity utility. The RoA9 for EON is 4.1% double of Eskoms RoA of 1.9%

• India: The tariff level has contributed to creating a rating of BBB for NTPC (compared to BBB+ for Eskom). Given the expected government support for NTPC as a state owned company, rating agencies perceive intervention by the government to occur in the event financial pressure, reflecting its critical role in the provision of electricity to the nation. The RoA for NTPC is remarkedly high at 31%

4 Return on Assets: Total net profit / total assets: 125,7 mill / 4,033 mill 5 Annual report 2010: Return on Assets: Total net profit / total assets: 649 mill C$/ 29,577 mill C$ 6Return on Assets: Total net profit / total assets: 2,880 mill / 97,452 mill 7To secure financing on attractive terms, DONG has set targets for credit rating and capital structure. The target is at least BBB+ (Standard ; Poor’s) 8 Return on Assets: Total net profit / total assets: 4,464 mill DKK/ 135,3 mill DKK 9 Return on Assets: Total net profit / total assets: 6,281 mill Euro/ 152,881 mill Euro

REPORT Confidential Page No:34

• Kenya: No credit rating is available for KPL. The RoA10 for KPL is 4.3% double Eskoms RoA of 1.9%

• Malaysia: The tariff level has contributed to a rating a TNB rating of BBB+ (similar to Eskoms BBB+). This is one of the lower ratings for the utilities included in this benchmarking study indicating a tariff level contributing to a medium sustainable financial electricity utility. However, the RoA11 for TNB is 4.7% more than double of Eskoms RoA of 1.9%