Embed Size (px)

Citation preview

Rückblick 2012 – Ausblick 2013 Der Pharmamarkt in ZahlenPMCA-Pharma Marketing Club Austria

Erika Sander

February 2013

1

Agenda

• Global and regional trends

• Europe versus the world

• The challenge

• Austrian trends

• Market Overview

• Hospital

• Retail

2

• OTC

• Go to market strategy

− Fundamentals

− Payer/ regulator

− Physicians

− Patients

− Winning

• Conclusions

The pharmaceutical market - Erika Sander, 18.02.2013© 2012, IMS HEALTH

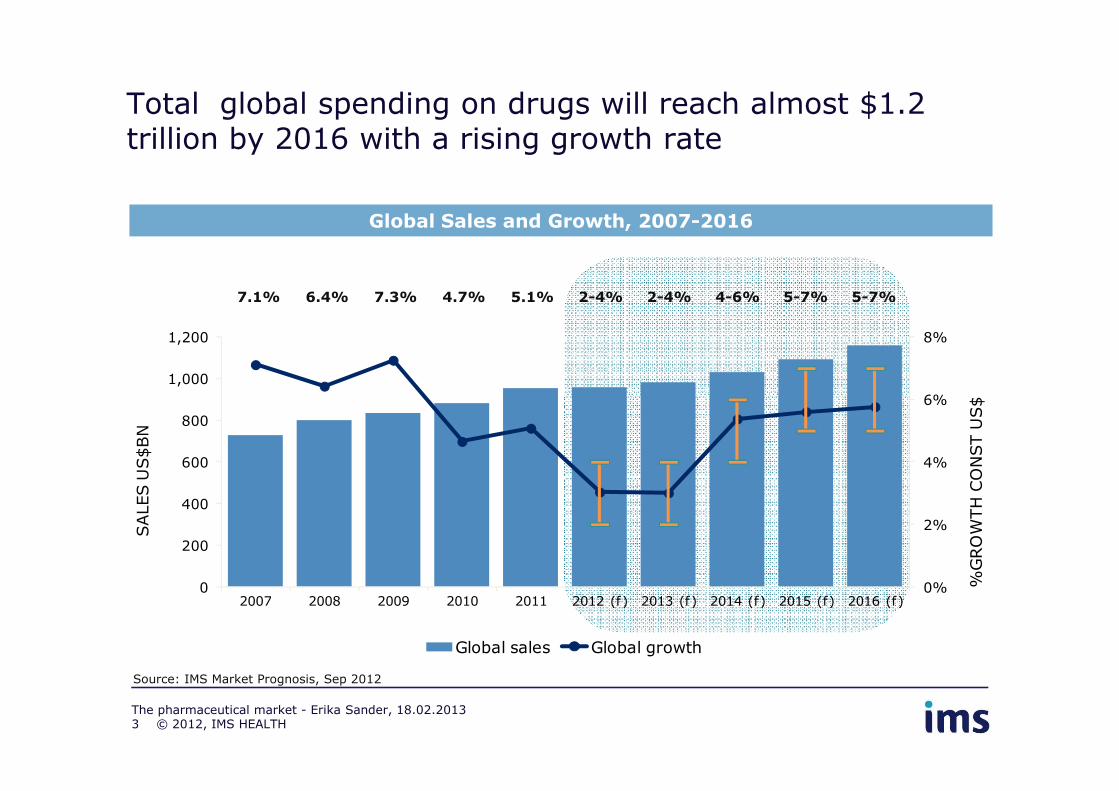

7.1% 6.4% 7.3% 4.7% 5.1% 2-4% 2-4% 4-6% 5-7% 5-7%

6%

8%

1,000

1,200

Total global spending on drugs will reach almost $1.2 trillion by 2016 with a rising growth rate

Global Sales and Growth, 2007-2016

$728 $799 $832 $881 $953 $960-970 $995-1,005$1,040-1,060

$1,105-$1,125

$1,175-$1,205

0%

2%

4%

6%

0

200

400

600

800

2007 2008 2009 2010 2011 2012 (f) 2013 (f) 2014 (f) 2015 (f) 2016 (f)

%G

RO

WTH

CO

NST U

S$

SALES U

S$BN

Global sales Global growth

Source: IMS Market Prognosis, Sep 2012

The pharmaceutical market - Erika Sander, 18.02.2013© 2012, IMS HEALTH3

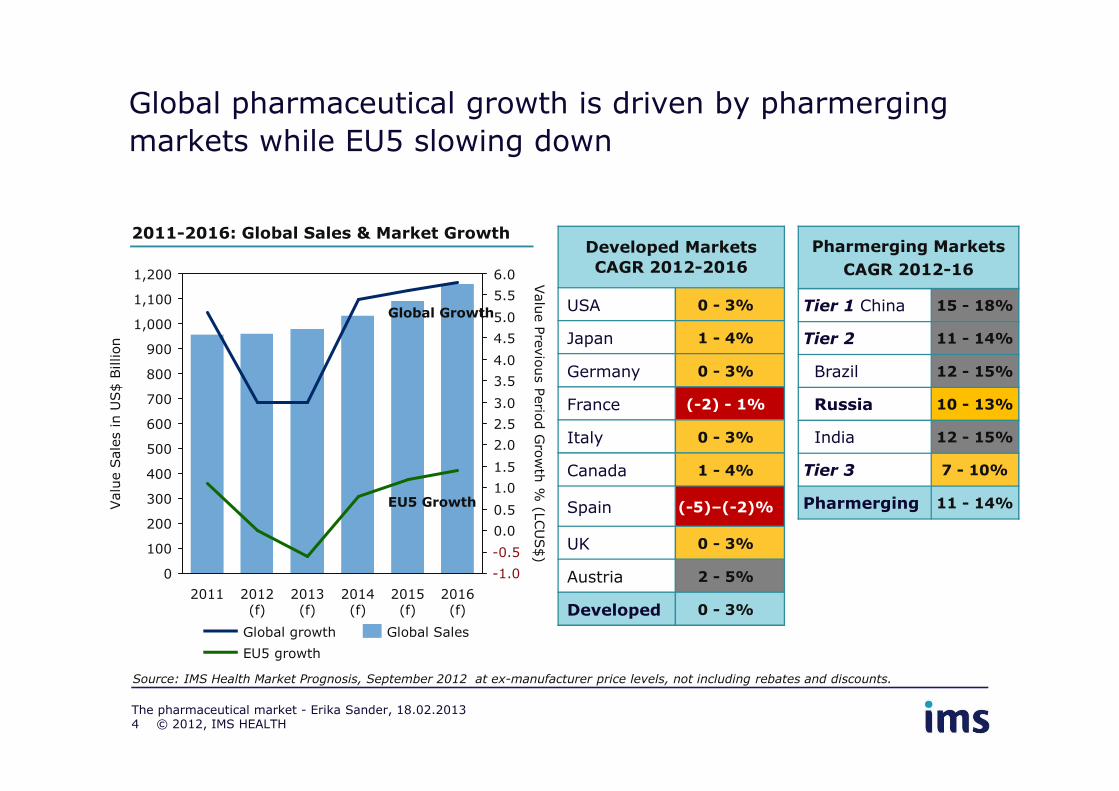

Global pharmaceutical growth is driven by pharmerging

markets while EU5 slowing down

2011-2016: Global Sales & Market GrowthDeveloped Markets

CAGR 2012-2016

USA 0 - 3%

Japan 1 - 4%

Germany 0 - 3%

France (-2) - 1%

Pharmerging Markets

CAGR 2012-16

Tier 1 China 15 - 18%

Tier 2 11 - 14%

Brazil 12 - 15%

Russia 10 - 13%

6.0

5.5

5.0

4.5

4.0

3.5

3.0

1,200

1,100

1,000

900

800

700

Valu

e S

ale

s in U

S$ B

illion

Valu

e P

revio

us P

erio

d G

row

th %

(LCU

S$)

Global Growth

France (-2) - 1%

Italy 0 - 3%

Canada 1 - 4%

Spain (-5)–(-2)%

UK 0 - 3%

Austria 2 - 5%

Developed 0 - 3%

Russia 10 - 13%

India 12 - 15%

Tier 3 7 - 10%

Pharmerging 11 - 14%

3.0

2.5

2.0

1.5

1.0

0.5

0.0

-0.5

-1.00

700

600

500

400

300

200

100

Valu

e S

ale

s in U

S$ B

illion

2016 (f)

2015 (f)

2014 (f)

2013 (f)

2012 (f)

2011Valu

e P

revio

us P

erio

d G

row

th %

(LCU

S$)

Source: IMS Health Market Prognosis, September 2012 at ex-manufacturer price levels, not including rebates and discounts.

Global Sales

EU5 growth

Global growth

EU5 Growth

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.2013

-0.5

-1.0

4

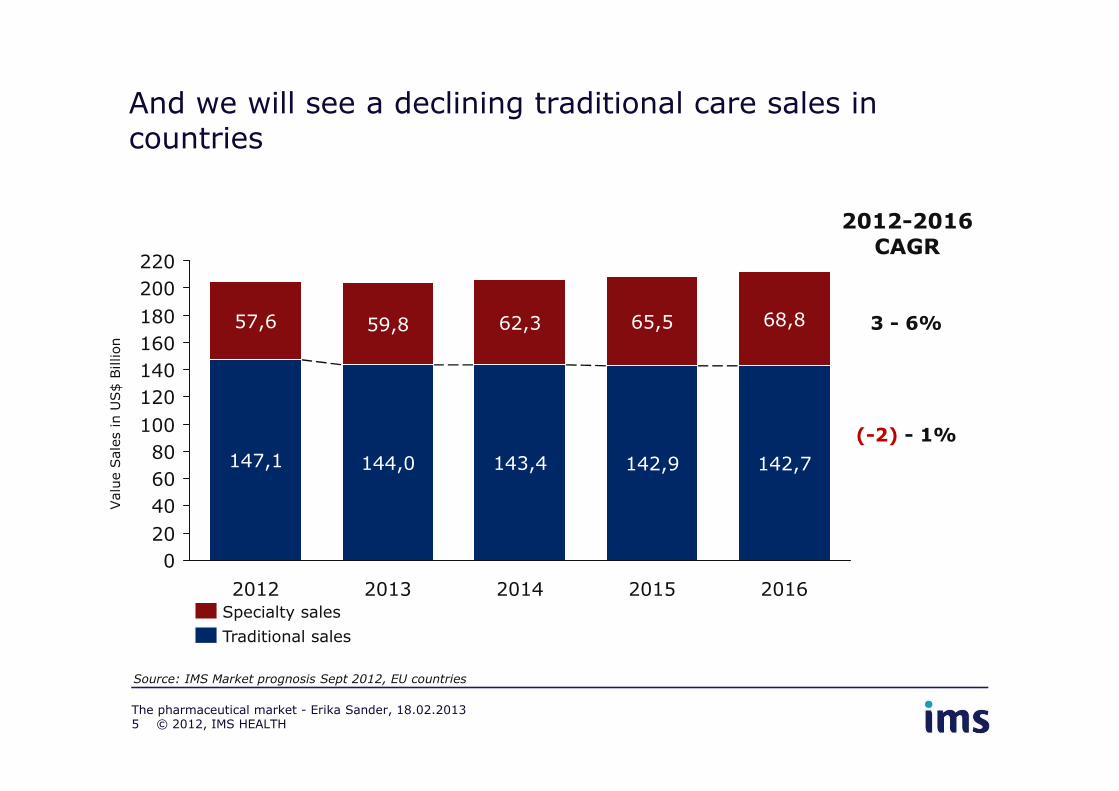

And we will see a declining traditional care sales in countries

220

120

160

140

57,6 59,8

200

68,865,562,3180 3 - 6%

2012-2016CAGR

Valu

e S

ale

s in U

S$ B

illion

© 2012, IMS HEALTH

40

20

60

80

120

2012

147,1

100

0

2016

142,7

2015

142,9

2014

143,4

2013

144,0

(-2) - 1%

Traditional sales

Specialty sales

Source: IMS Market prognosis Sept 2012, EU countries

The pharmaceutical market - Erika Sander, 18.02.20135

Valu

e S

ale

s in U

S$ B

illion

Antidiabetics

Asthma/COPD

Autoimmune

HIV Antivirals

Vaccines

Multiple Sclerosis

ADHD50Bn

5Bn

25Bn

15%

20%

SPEN

DIN

G C

AG

R 2

007-2

011

Spending and Growth in Leading Therapy Areas

But some key Therapy Areas will continue to see strong growth Specialty outpacing traditional

Immuno-suppressants

Specialty

Traditional

OncologicsAsthma/COPD

Lipid Regulators

Angiotensin IIAntipsychotics

Anti-Ulcerants Anti-Epileptics

Platelet Aggr Inhibitors

Contraceptives

Cephalosporins

Antivirals excl HIV

Anticoagulants

-5%

0%

5%

10%

-10% -5% 0% 5% 10% 15%

SPEN

DIN

G C

AG

R 2

007

SPENDING CAGR 2012-2016Source: IMS Institute for Healthcare Informatics, May 2012

Global market CAGR 2007-2011: 6%

Global market CAGR 2012-2016: 3-6%

Immuno-stimulants

Narcotic Analgesics

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.20136

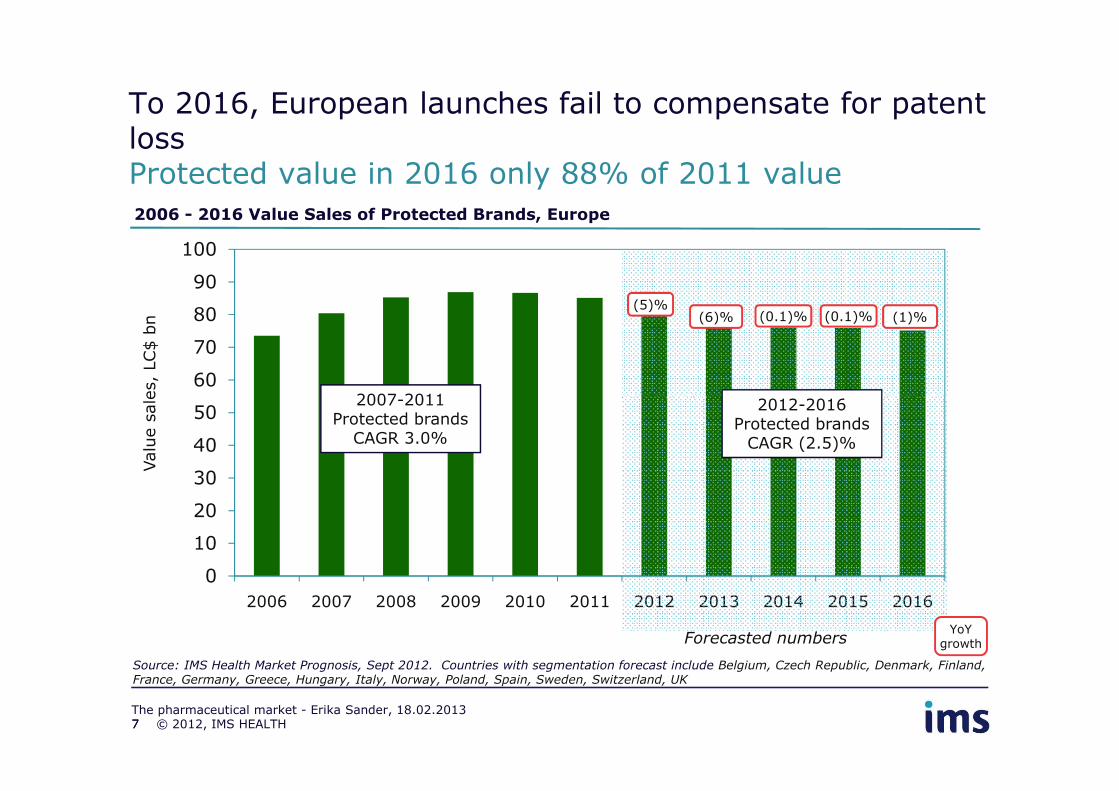

60

70

80

90

100

2006 - 2016 Value Sales of Protected Brands, Europe

2012-2016 2007-2011

Valu

e s

ale

s,

LC$ b

n

To 2016, European launches fail to compensate for patent lossProtected value in 2016 only 88% of 2011 value

(5)%(6)% (0.1)% (1)%(0.1)%

0

10

20

30

40

50

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Source: IMS Health Market Prognosis, Sept 2012. Countries with segmentation forecast include Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Italy, Norway, Poland, Spain, Sweden, Switzerland, UK

2012-2016 Protected brands

CAGR (2.5)%

2007-2011 Protected brands

CAGR 3.0%

Valu

e s

ale

s,

LC$ b

n

Forecasted numbers

7

YoY growth

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.20137

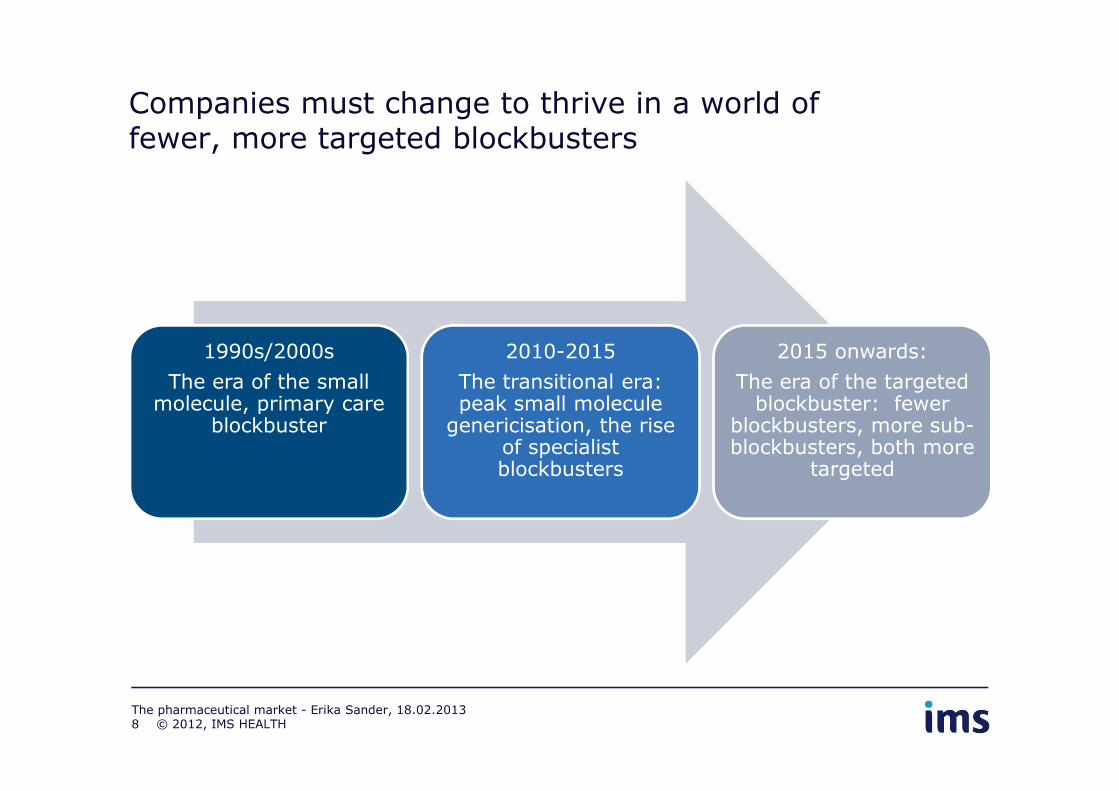

Companies must change to thrive in a world of fewer, more targeted blockbusters

1990s/2000s

The era of the small molecule, primary care

2010-2015

The transitional era: peak small molecule

2015 onwards:

The era of the targeted blockbuster: fewer molecule, primary care

blockbusterpeak small molecule

genericisation, the rise of specialist blockbusters

blockbuster: fewer blockbusters, more sub-blockbusters, both more

targeted

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.20138

Austrian Pharma market 2012-2016 will show higher growth than European average

Valu

e S

ale

s in M

io.

USD

4,2%3,9%

3,5%3,1%

Specialty sales

3,0

2,5

3,5

5,0

4,0

4,5

The total pharmaceutical market is forecasted to grow at a CAGR

of 2-5% over the period

The total pharmaceutical market is forecasted to grow at a CAGR

of 2-5% over the period

5 - 8%

Valu

e S

ale

s

0,0

1,5

0,5

1,0

20162015201420132012

Traditional sales

2,0

2,5of 2-5% over the period

2012-2016.of 2-5% over the period

2012-2016.

The pharmaceutical market - Erika Sander, 18.02.2013

Source: IMS Health Market Prognosis, Sept 2012 (*) at ex-manufacturer price levels, not including rebates and discounts

© 2012, IMS HEALTH9

1 - 4%

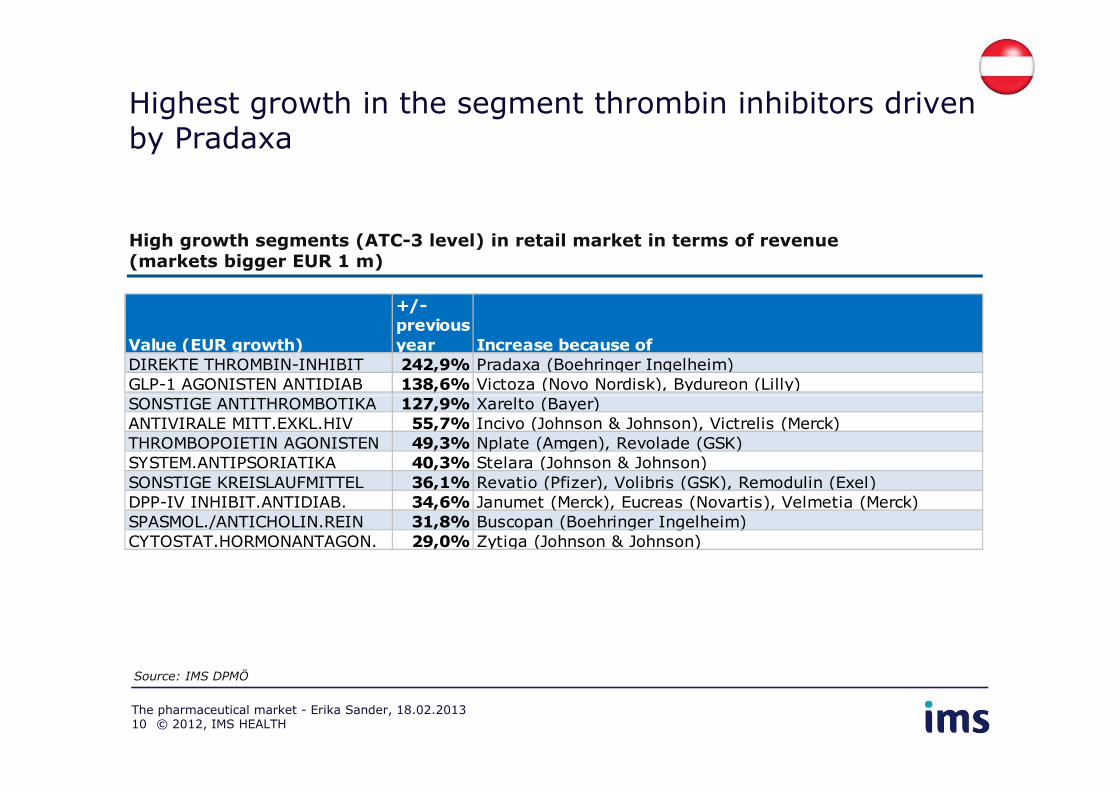

Highest growth in the segment thrombin inhibitors drivenby Pradaxa

High growth segments (ATC-3 level) in retail market in terms of revenue(markets bigger EUR 1 m)

Value (EUR growth)

+/-

previous

year Increase because of

DIREKTE THROMBIN-INHIBIT 242,9% Pradaxa (Boehringer Ingelheim)

GLP-1 AGONISTEN ANTIDIAB 138,6% Victoza (Novo Nordisk), Bydureon (Lilly)

SONSTIGE ANTITHROMBOTIKA 127,9% Xarelto (Bayer)

Source: IMS DPMÖ

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201310

SONSTIGE ANTITHROMBOTIKA 127,9% Xarelto (Bayer)

ANTIVIRALE MITT.EXKL.HIV 55,7% Incivo (Johnson & Johnson), Victrelis (Merck)

THROMBOPOIETIN AGONISTEN 49,3% Nplate (Amgen), Revolade (GSK)

SYSTEM.ANTIPSORIATIKA 40,3% Stelara (Johnson & Johnson)

SONSTIGE KREISLAUFMITTEL 36,1% Revatio (Pfizer), Volibris (GSK), Remodulin (Exel)

DPP-IV INHIBIT.ANTIDIAB. 34,6% Janumet (Merck), Eucreas (Novartis), Velmetia (Merck)

SPASMOL./ANTICHOLIN.REIN 31,8% Buscopan (Boehringer Ingelheim)

CYTOSTAT.HORMONANTAGON. 29,0% Zytiga (Johnson & Johnson)

Highest revenue growth in the segment Ophthalm. Corticosteroids driven by Ozurdek

High growth segments (ATC-3 level) in hospital market in terms of revenue(markets bigger EUR 1 m)

Value (EUR growth)

+/-

previous

year Increase because of

OPHTHALM.CORTICOSTEROIDE 169,8% Ozurdek (Allergan)

HAEMATOPOETIKA MIT EISEN 76,2% Ferinject (Galenica), Monofer (Pharmacosmos)

OPIATENTWOEHNUNGSMITTEL 49,7% L-Polamidon (Sanofi)

Source: IMS DPMÖ

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201311

OPIATENTWOEHNUNGSMITTEL 49,7% L-Polamidon (Sanofi)

LEBERSCH+LIPOTROPE PRAEP 33,3% Hepamerz (Merz), Legalon (Rotta)

THROMBOPOIETIN AGONISTEN 27,0% Nplate (Amgen), Revolade (GSK)

EINFACH - IMPFSTOFFE 25,8% FSME-Immun (Baxter), Gardasil (Merck, Sanofi)

ANTIRHEUMATIKA,SPEZIF. 22,8% Roactempra (Roche)

ALKYLIERENDE CYTOSTATIKA 21,3% Levact (Temmler), Busilvex (Pierre Fabre), Ovastat (Medac)

VIT.A+D INCL.EINF.KOMB. 19,8% Mimpara (Amgen), Zemplar (Abbott)

LAXANTIEN 17,0% Picoprep (Ferring), Moviprep (Norgine)

There are several key products which will lose exclusivity in Austria going forward to 2016

Austrian LoE going forwards

Product Therapy Area 2012 Sales, EUR

2013

Seretide Respiratory 27.6 m

Zometa Bisphosphonates 10.0 m

Singulair Receptor antagonist 9.7 m

Aclasta Osteoporosis 6.1 m

Xeloda Chemotherapy 5.9 m

Viagra Erectile Dysfunction 5.2 m

2014

Cipralex Anti-Depressants 19.5 m

Abilify Antipsychotics 15.7 m

Avelox Antibacterial agent 8.0 m

Ebixa Alzheimer 6.4 m

2015

Spiriva Respiratory 28.7 m

Copaxone Immunostimulants 21.1 m

Alimta Oncology 12.1 m

Cymbalta Anti-Depressants 12.6 m

Tarceva Oncology 8.4 m

2016Glivec Oncology 30.6 m

Zyvoxid Antibiotic 9.9 m

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201312

Total Market growth 2012 slowing down against 2011

in %

6,8

7,5

3,84,3

Volume

Value

Source: IMS DPMÖ, DPMÖK, Q4 2012

1,5

2,4

0,9

2,6

-0,2

0,7

-0,3

2,3

3,8

20082007 2009 2010 2011 2012

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201313

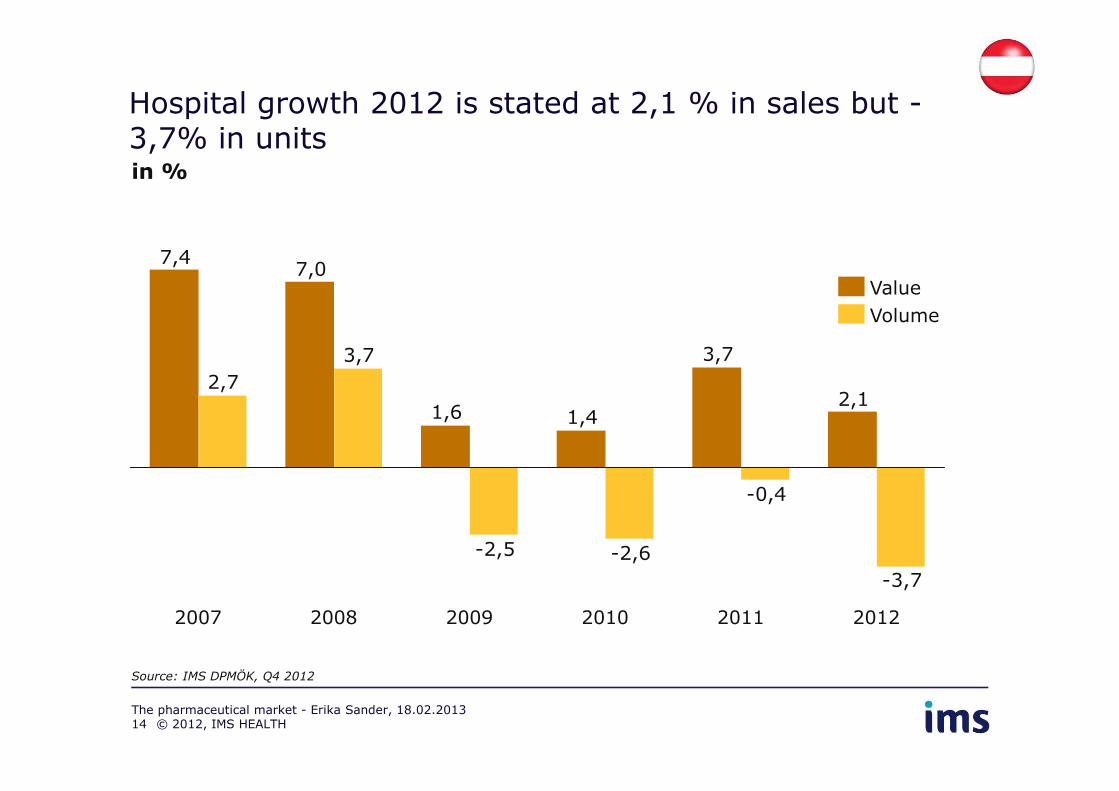

Hospital growth 2012 is stated at 2,1 % in sales but -3,7% in unitsin %

2,1

7,07,4

3,73,7

2,7

Volume

Value

Source: IMS DPMÖK, Q4 2012

2,11,41,6

-3,7

-0,4

-2,6-2,5

20082007 2009 2010 2011 2012

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201314

Imported products account for 5.8% of the total hospitalmarket (value)

5.8%

Parallel Import

0.3%

Parallel Import

Value [%] Volume [%]

Parallel Import in hospital market

Remarks

• Value share higher thanvolume share

• Expensive products are

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201315

94.2% 99.7%

• Expensive products aremore often affected byparallel trade (e.g. Avastin: EUR 1,338; Mabthera: EUR 1,516)

Source: IMS DPMÖK

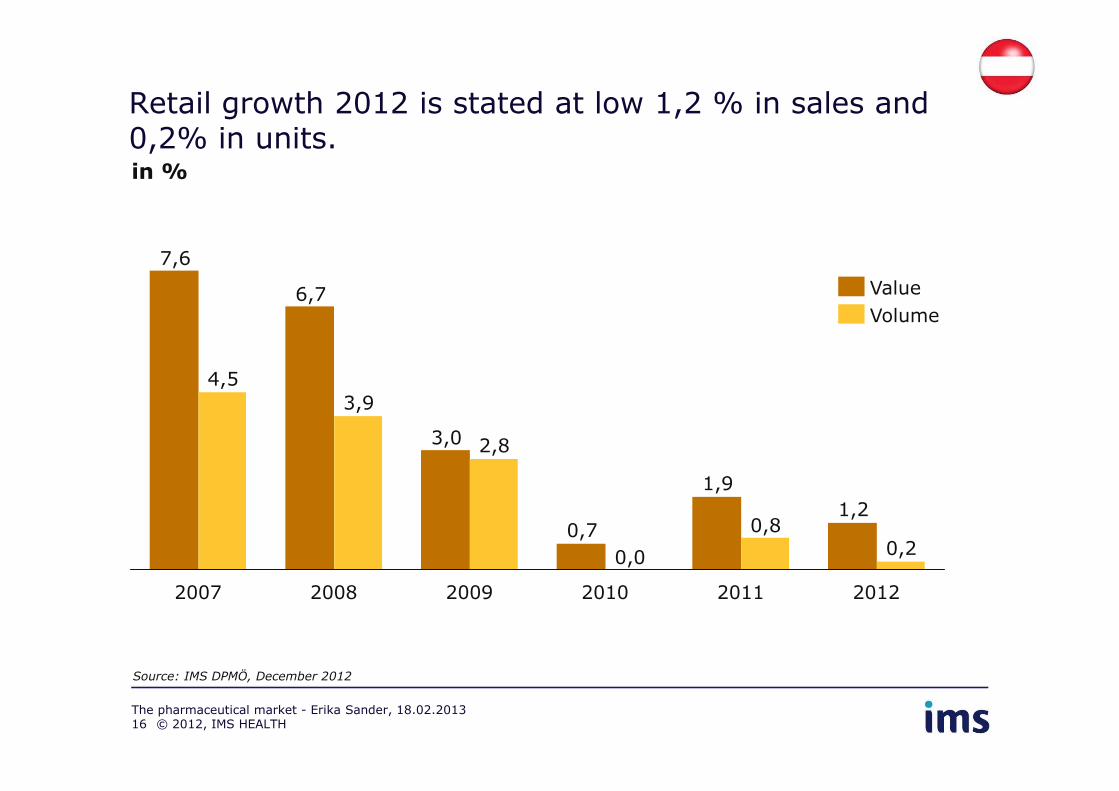

Retail growth 2012 is stated at low 1,2 % in sales and 0,2% in units.in %

6,7

7,6

3,9

4,5

Value

Volume

1,2

1,9

0,7

3,0

0,20,0

2,8

3,9

0,8

201220112010200920082007

Source: IMS DPMÖ, December 2012

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201316

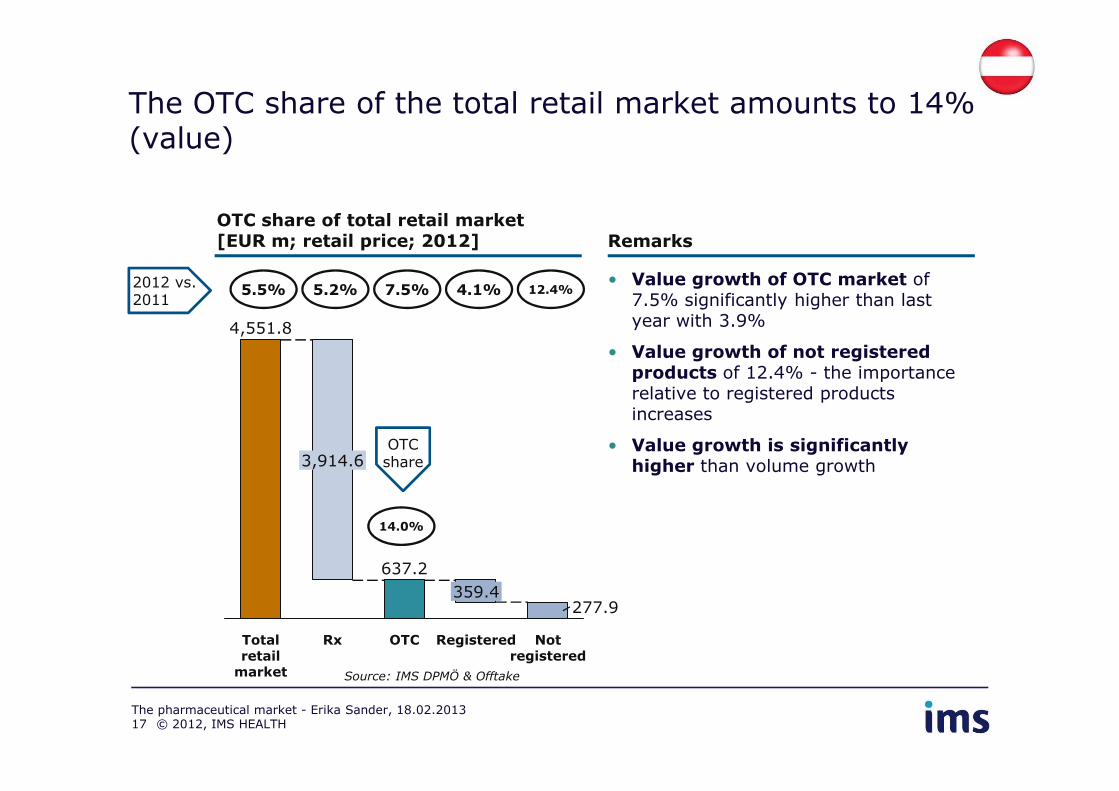

The OTC share of the total retail market amounts to 14% (value)

OTC share of total retail market[EUR m; retail price; 2012]

4,551.8

Remarks

5.5% 5.2% 7.5% 12.4%4.1%2012 vs. 2011

• Value growth of OTC market of7.5% significantly higher than last year with 3.9%

• Value growth of not registered products of 12.4% - the importancerelative to registered products

Not registered

277.9

Registered

359.4

OTC

637.2

Rx

3,914.6

Total retail market

relative to registered productsincreases

• Value growth is significantlyhigher than volume growth

14.0%

OTC share

Source: IMS DPMÖ & Offtake

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201317

The OTC share of the total retail market amounts to 28% (volume)

OTC share of total retail market[´000 units; 2012]

237,891

3.4% 3.6% 3.0% 8.8%0.8%2012 vs. 2011

Remarks

• Volume growth of OTC market of3%

• Volume growth of not registered products of 8.8% significantly higherthan increase of registered products(0.8%)OTC

Not registered

19,971

Registered

47,537

OTC

67,508

Rx

170,383

Total retail market

(0.8%)

• Share of OTC market (28%) demonstrates the relative importanceof the OTC market

28,4%

OTC share

Source: IMS DPMÖ & Offtake

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201318

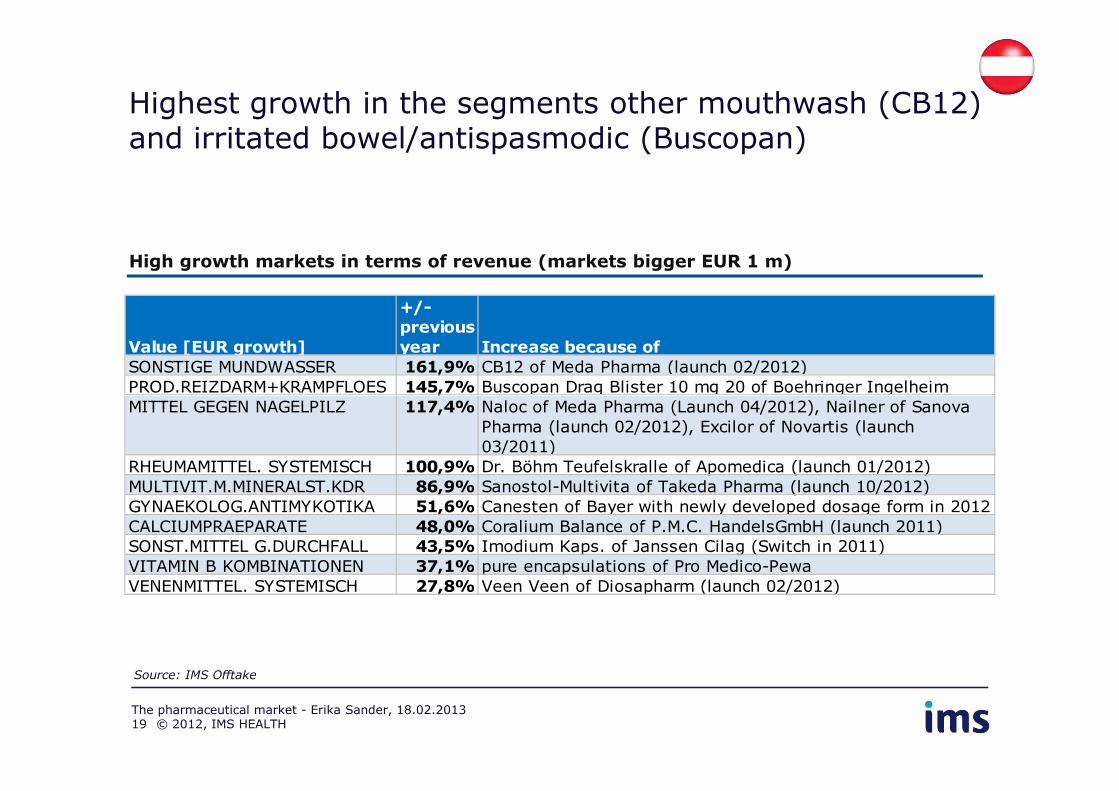

Highest growth in the segments other mouthwash (CB12) and irritated bowel/antispasmodic (Buscopan)

High growth markets in terms of revenue (markets bigger EUR 1 m)

Value [EUR growth]

+/-

previous

year Increase because of

SONSTIGE MUNDWASSER 161,9% CB12 of Meda Pharma (launch 02/2012)

PROD.REIZDARM+KRAMPFLOES 145,7% Buscopan Drag Blister 10 mg 20 of Boehringer Ingelheim

Source: IMS Offtake

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201319

PROD.REIZDARM+KRAMPFLOES 145,7%

MITTEL GEGEN NAGELPILZ 117,4% Naloc of Meda Pharma (Launch 04/2012), Nailner of Sanova

Pharma (launch 02/2012), Excilor of Novartis (launch

03/2011)

RHEUMAMITTEL. SYSTEMISCH 100,9% Dr. Böhm Teufelskralle of Apomedica (launch 01/2012)

MULTIVIT.M.MINERALST.KDR 86,9% Sanostol-Multivita of Takeda Pharma (launch 10/2012)

GYNAEKOLOG.ANTIMYKOTIKA 51,6% Canesten of Bayer with newly developed dosage form in 2012

CALCIUMPRAEPARATE 48,0% Coralium Balance of P.M.C. HandelsGmbH (launch 2011)

SONST.MITTEL G.DURCHFALL 43,5% Imodium Kaps. of Janssen Cilag (Switch in 2011)

VITAMIN B KOMBINATIONEN 37,1% pure encapsulations of Pro Medico-Pewa

VENENMITTEL. SYSTEMISCH 27,8% Veen Veen of Diosapharm (launch 02/2012)

Highest growth for 2013 expected for not registered products in OTC segment

4,5

Estimated growth rate in 2013 [%]

10

Remarks

• Estimated growth in hospital higher than in retail

• Highest growth expectedin OTC segment

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201320

1,5

2,0

OTCHospitalRetail

0

Not registered

Registered

in OTC segment

• Only not registered products are expected togrow in OTC sgement

Source: IMS Experts

The promotional environment is changing rapidly

Company

Yesterday

• 4-6 major brands

• 1-2 launches/year

• Mature markets focus

Today

• Larger number of smaller brands, many multi-indication

• 4-6 launches/year (new products and new indications)

• Focus split between Pharmerging and Mature markets

Tomorrow?

• Genetic profiling and biomarkers segment brands further

• RWE extends the launch across the lifecycle

• Mixture of highly segmented specialist and primary care marketsC

ompany

Market • Prescribers the key

stakeholder

• Distribution channels simple

• Competition simple: other branded on patent agents

• Primary care focus

• Payers increasingly dominant

• Distribution channels increasingly complex

• Competition against generics as well as other brands

• Specialist care focus

• Patients become significant stake-holders

• Health economic and outcome measures crucial

• RWE and lifetime pricing accelerates competition complexity

markets

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201321

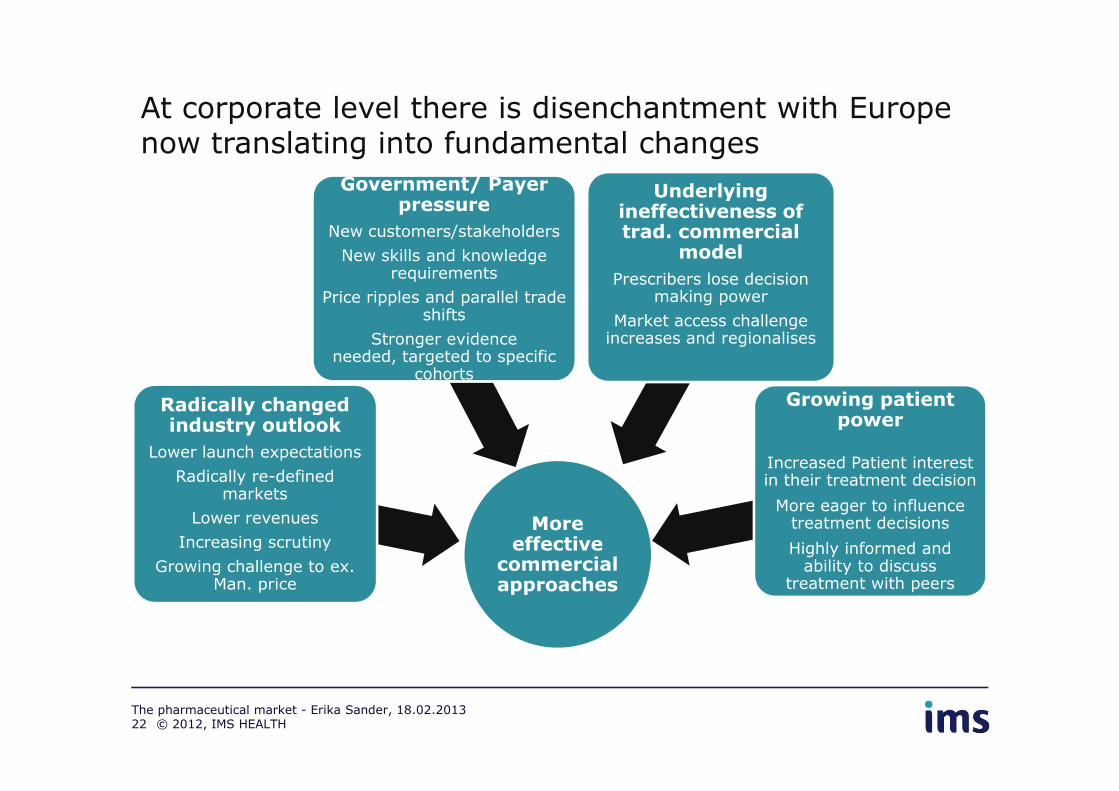

Radically changed

Government/ Payer pressure

New customers/stakeholders

New skills and knowledge requirements

Price ripples and parallel trade shifts

Stronger evidence needed, targeted to specific

cohorts

Underlying ineffectiveness of trad. commercial

model

Prescribers lose decision making power

Market access challenge increases and regionalises

Growing patient

At corporate level there is disenchantment with Europe now translating into fundamental changes

More effective

commercial approaches

Radically changed industry outlook

Lower launch expectations

Radically re-defined markets

Lower revenues

Increasing scrutiny

Growing challenge to ex. Man. price

Growing patient power

Increased Patient interest in their treatment decision

More eager to influence treatment decisions

Highly informed and ability to discuss

treatment with peers

22 © 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.2013

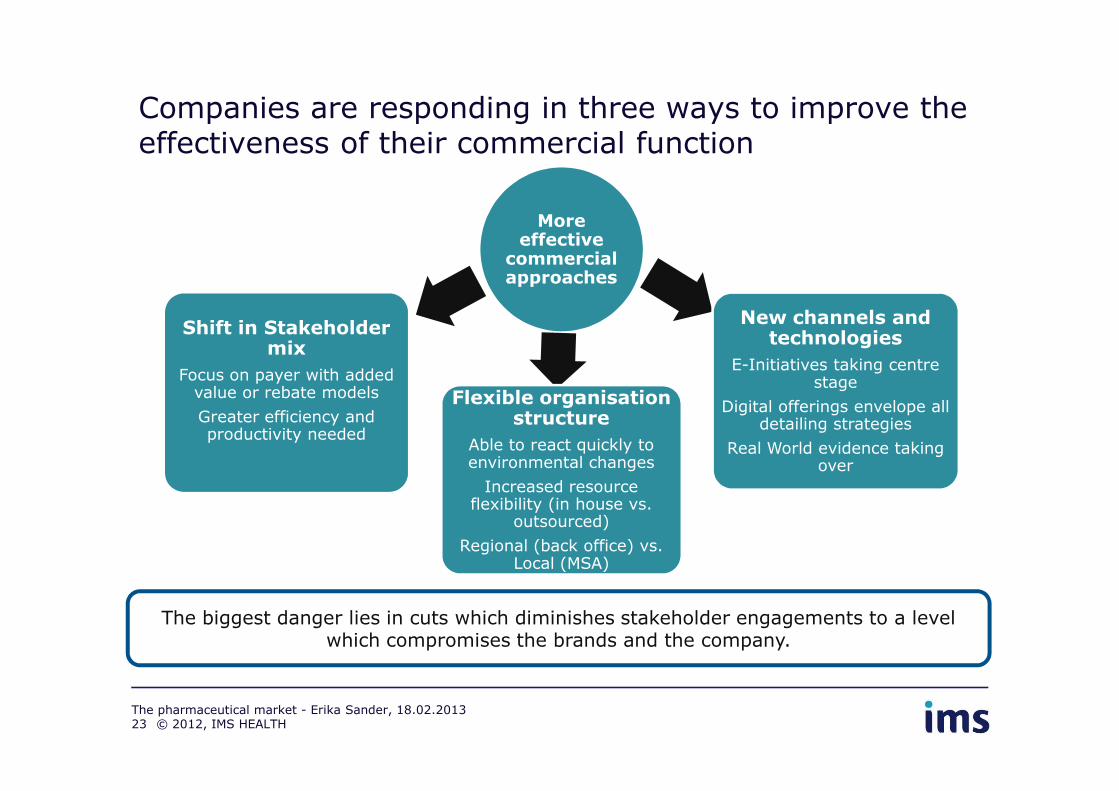

More effective

commercial approaches

Shift in Stakeholder mix

Focus on payer with added value or rebate models Flexible organisation

New channels and technologies

E-Initiatives taking centre stage

Companies are responding in three ways to improve the effectiveness of their commercial function

value or rebate models

Greater efficiency and productivity needed

Flexible organisation structure

Able to react quickly to environmental changes

Increased resource flexibility (in house vs.

outsourced)

Regional (back office) vs. Local (MSA)

Digital offerings envelope all detailing strategies

Real World evidence taking over

23

The biggest danger lies in cuts which diminishes stakeholder engagements to a level which compromises the brands and the company.

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.2013

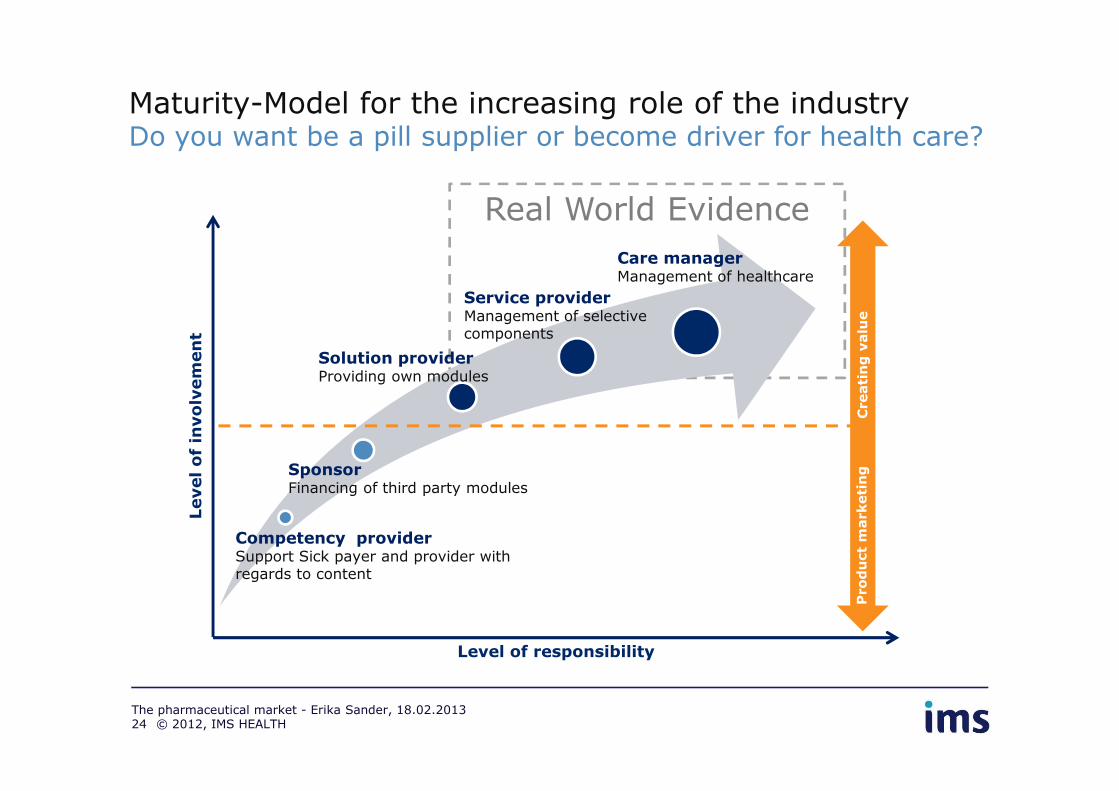

Real World Evidence

Maturity-Model for the increasing role of the industryDo you want be a pill supplier or become driver for health care?

Solution providerProviding own modules

Service providerManagement of selective components

Care managerManagement of healthcare

Level of involvement

Creating value

SponsorFinancing of third party modules

Competency providerSupport Sick payer and provider with regards to content

Level of responsibility

Level of involvement

Product marketing

Creating value

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201324

Pharma moving away from Dr centric models mostly in response to market dynamics

Physician-centric model(rep-led)

B2B-model(cross-functional)

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201325

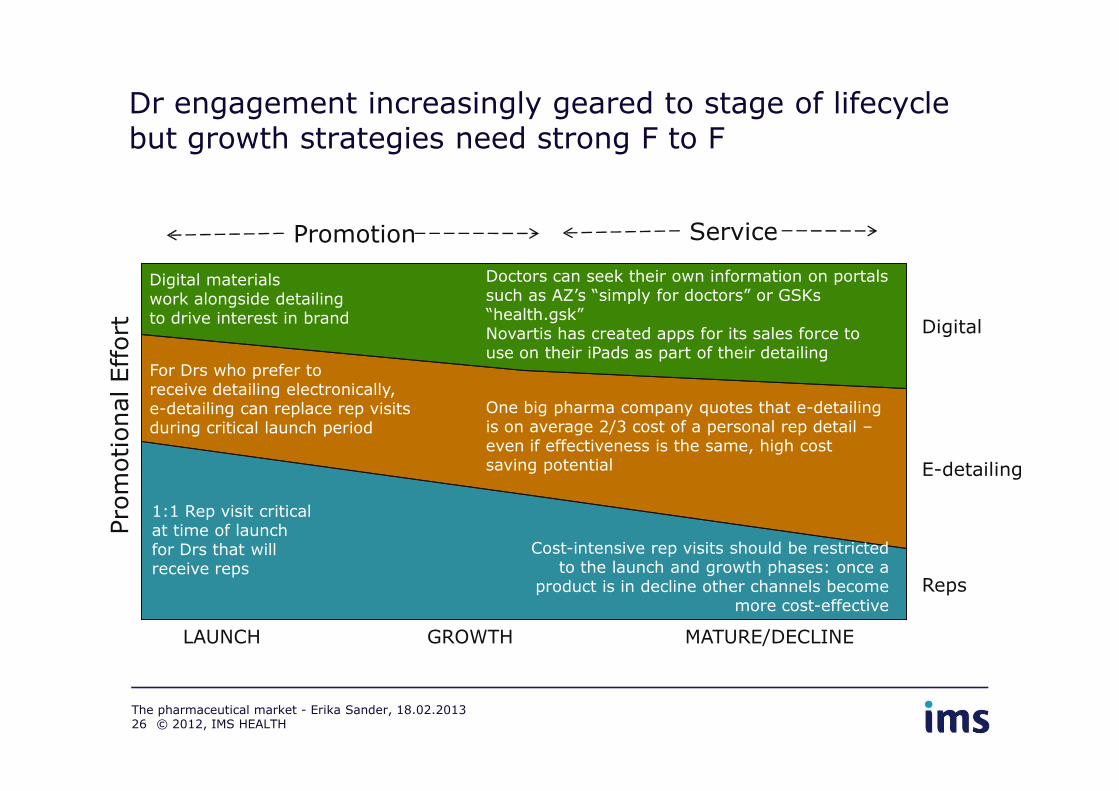

Dr engagement increasingly geared to stage of lifecycle but growth strategies need strong F to F

Digital

Pro

motional Eff

ort

Promotion Service

For Drs who prefer to receive detailing electronically,

Digital materials work alongside detailing to drive interest in brand

Doctors can seek their own information on portals such as AZ’s “simply for doctors” or GSKs “health.gsk” Novartis has created apps for its sales force to use on their iPads as part of their detailing

E-detailing

Reps

LAUNCH GROWTH MATURE/DECLINE

Pro

motional Eff

ort

1:1 Rep visit critical at time of launch for Drs that will receive reps

receive detailing electronically, e-detailing can replace rep visits during critical launch period

Cost-intensive rep visits should be restricted to the launch and growth phases: once a

product is in decline other channels become more cost-effective

One big pharma company quotes that e-detailing is on average 2/3 cost of a personal rep detail –even if effectiveness is the same, high cost saving potential

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201326

Although you need a more integrated, combined cross functional approach

Marketing Medical Sales

Rep visitFace to face

seminareDetailing

© 2012, IMS HEALTH

Customer centre contact

Rep visit

eCME seminarPhysical detailing

Website

The pharmaceutical market - Erika Sander, 18.02.201327

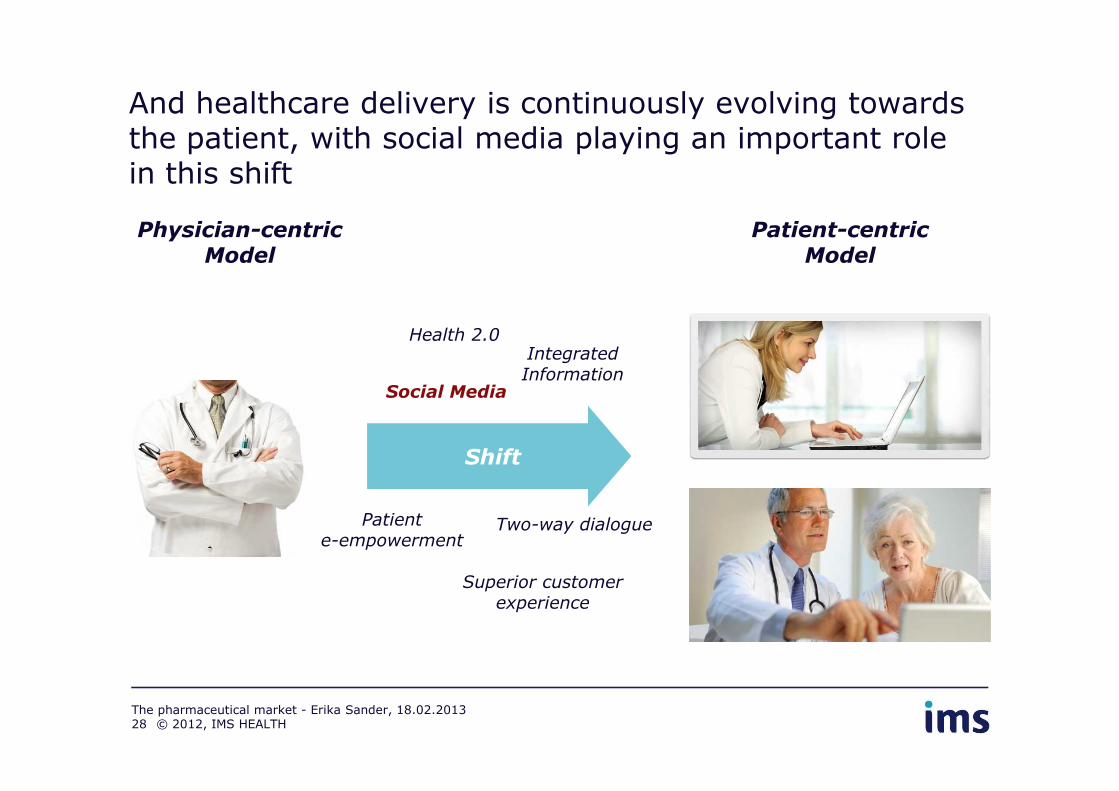

And healthcare delivery is continuously evolving towards the patient, with social media playing an important role in this shift

Physician-centric Model

Patient-centric Model

Health 2.0

Social Media

Integrated Information

Patiente-empowerment

Two-way dialogue

Social Media

Shift

Superior customer experience

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201328

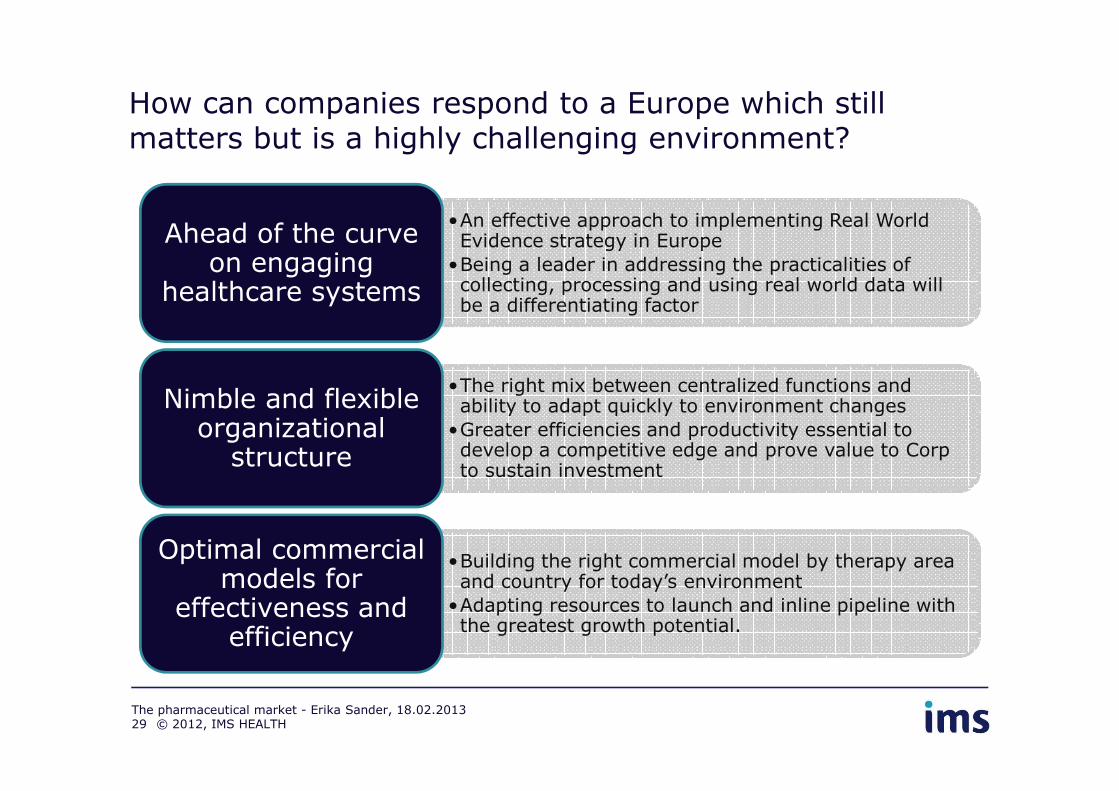

How can companies respond to a Europe which still matters but is a highly challenging environment?

•An effective approach to implementing Real World Evidence strategy in Europe

•Being a leader in addressing the practicalities of collecting, processing and using real world data will be a differentiating factor

Ahead of the curve on engaging

healthcare systems

•The right mix between centralized functions and ability to adapt quickly to environment changesNimble and flexible

•The right mix between centralized functions and ability to adapt quickly to environment changes

•Greater efficiencies and productivity essential to develop a competitive edge and prove value to Corp to sustain investment

Nimble and flexible organizational

structure

•Building the right commercial model by therapy area and country for today’s environment

•Adapting resources to launch and inline pipeline with the greatest growth potential.

Optimal commercial models for

effectiveness and efficiency

© 2012, IMS HEALTHThe pharmaceutical market - Erika Sander, 18.02.201329

Mag. Erika Sander

Senior Manager Commercial, Austria

Prokurist

Phone: +43 1 78 002 11Mobile: +43 664 80 002 110Email: [email protected]<http://www.imshealth.com/>

© 2012, IMS HEALTH GmbH & Co. OHG

Alle Rechte vorbehalten. Die Informationen dürfen weder ganz noch teilweise ohne vorherige ausdrückliche Erlaubnis vonIMS HEALTH GmbH & Co. OHG vervielfältigt, gespeichert, weiterverarbeitet und in keiner Weise zugänglich gemacht werden.

30

IMS HEALTH GmbH & Co. OHG vervielfältigt, gespeichert, weiterverarbeitet und in keiner Weise zugänglich gemacht werden.

IMS stellt durch den Einsatz modernster Technologien und Verfahren sicher, dass seine Dienstleistungen, unabhängig davonwie die Daten untereinander verknüpft werden, den Datenschutzbestimmungen entsprechen.