Embed Size (px)

Citation preview

Equity

Investment Philosophy & Process

September 2019

Content

2

Investment Philosophy

Team & Structure

Investment Process

Risk Management

Product Offerings

Equity – Investment Philosophy

3

Active Fund Management

▪ Our core investment premise is that equity markets are not fully efficient

▪ A well organized and thorough research effort combined with a disciplined portfolio

management approach will enable out-performance of the market index over time

Being True to Mandate

▪ The fund’s investment objective is paramount

▪ Stock selection, Industry and Asset allocation flow from the fund’s objective

▪ No Style ideology; use stock appropriate measures

Equity Team – Structure

4

Figures for Industry experience and Firm tenure may be rounded off. Please also refer slide ‘Fund Management Responsibility. 1Includes 3 dealers. Industry experience numbers as on

September 30, 2019

12 member team1 with 174 years of collective experience

Name RoleIndustry experience

(years)

Tenure with the

Firm

(years)

Taher Badshah Chief Investment Officer - Equities 24 2

Amit Nigam Fund Manager - PMS 18 1

Amit Ganatra Fund Manager 16 12

Pranav Gokhale Fund Manager 17 10

Neelesh Dhamnaskar

Fund Manager

Sectors – Auto & Auto Ancillaries, Real Estate,

Telecommunication Services

14 9

Nitin Gosar

Fund Manager

Sectors – Consumer Discretionary, Consumer Staples,

Healthcare

14 8

Dhimant KothariFund Manager

Sectors – Energy, Materials, Utilities, Financials14 8

Hiten Jain Sectors – Financials, Information Technology 10 3

Rita Tahilramani Sector – Industrials 5 1

Rajeev Bhardwaj Equity Dealer 14 10

Kuber Mannadi Equity Dealer 14 8

Pratik Sanghvi Equity Dealer- PMS 14 4

Equity Team – Coverage

5

Comprehensive in-house coverage of Indian equities

▪ 302 companies currently in the universe1 (5 Benchmark Indices + Select Bottom-up ideas)

▪ Total market cap of the universe - approximately $1.81 trillion1

▪ Approximately 93.7% of total market cap of stocks listed on BSE5001

340 company interactions during April 19 – September 19 (FY19-20)

▪ 164 meetings

▪ 176 conference calls

Meetings with companies, sell side analysts, economists, strategists, industry

experts & policy makers on a regular basis

1Data as on September 2019

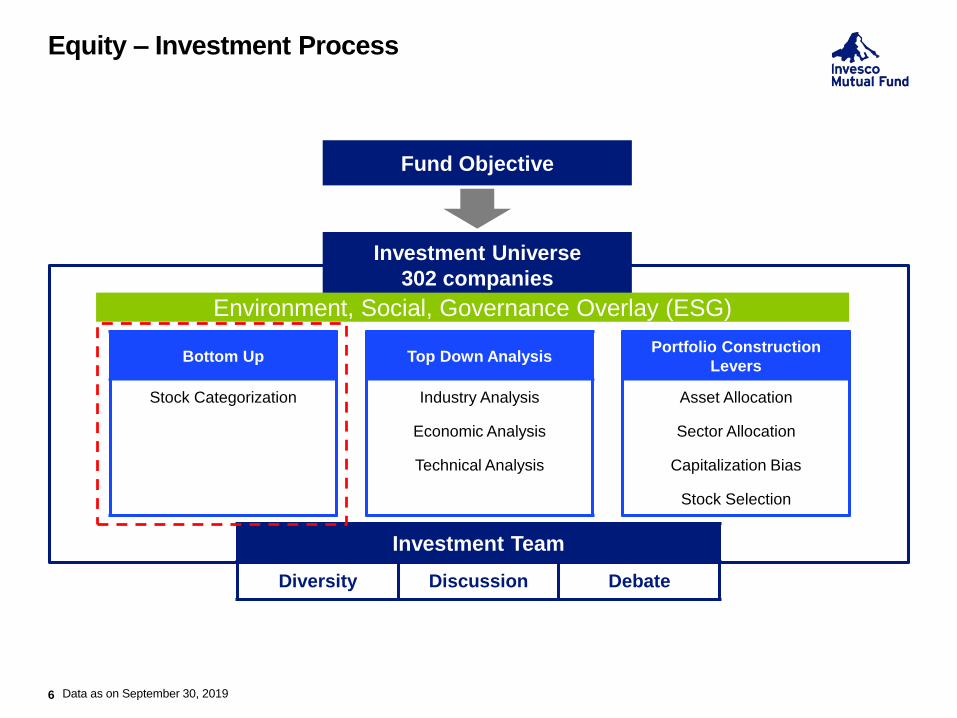

Equity – Investment Process

6

Fund Objective

Investment Universe

302 companies

Bottom Up Top Down AnalysisPortfolio Construction

Levers

Stock Categorization Industry Analysis Asset Allocation

Economic Analysis Sector Allocation

Technical Analysis Capitalization Bias

Stock Selection

Investment Team

Diversity Discussion Debate

Data as on September 30, 2019

Environment, Social, Governance Overlay (ESG)

Stock Categorization Framework

7

P2P: Path to Profit; ROE: Return on Equity

The Stock Categorization Framework is for Internal reference purposes only.

Stock Category

Descriptions

(e.g.)

Growth

Prospects

(e.g.)

Company Attribute

(e.g.)

Financial

Parameter

(e.g.)

Leader Established companies In line with or

better than

industry

Track record of leadership,

globally competitive

Industry leading

margin/ROE

Warrior Young/established

companies

Better than

industry

Unique proposition and/or right

place, right time

Margin & ROE

Expansion

Star Young companies High growth Entrepreneur vision, scalability Operating Leverage

Diamond Company with

valuable assets

Low growth Management intent to

unlock value

Value of

asset/business

Frog Prince Company in a

turnaround situation

Back to growth Intrinsic strengths in

core business

P2P, ROE

expansion

Shotgun Opportunistic

investment

Positive surprise Corporate event, restructuring,

earnings news

Event visibility

Commodities Call on the cycle

is paramount

Positive Integration, cost efficiency,

globally competitive

Profit leverage

The categorization framework enables us to filter the universe and identify the best investment

opportunities

Growth

Value

Event

Leader

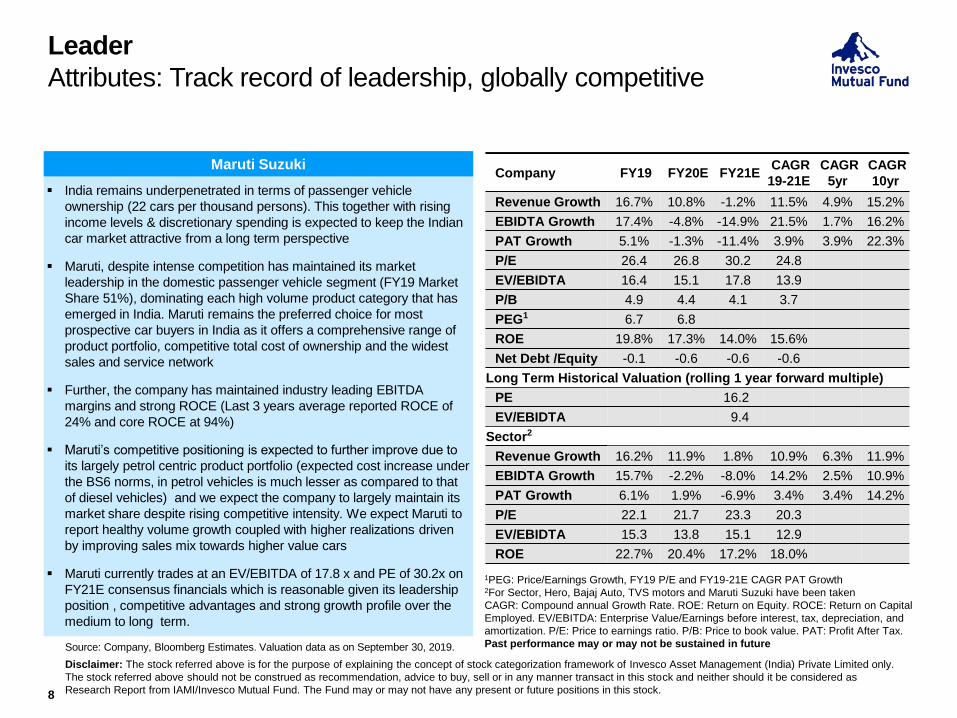

Attributes: Track record of leadership, globally competitive

8

Source: Company, Bloomberg Estimates. Valuation data as on September 30, 2019.

▪ India remains underpenetrated in terms of passenger vehicle

ownership (22 cars per thousand persons). This together with rising

income levels & discretionary spending is expected to keep the Indian

car market attractive from a long term perspective

▪ Maruti, despite intense competition has maintained its market

leadership in the domestic passenger vehicle segment (FY19 Market

Share 51%), dominating each high volume product category that has

emerged in India. Maruti remains the preferred choice for most

prospective car buyers in India as it offers a comprehensive range of

product portfolio, competitive total cost of ownership and the widest

sales and service network

▪ Further, the company has maintained industry leading EBITDA

margins and strong ROCE (Last 3 years average reported ROCE of

24% and core ROCE at 94%)

▪ Maruti’s competitive positioning is expected to further improve due to

its largely petrol centric product portfolio (expected cost increase under

the BS6 norms, in petrol vehicles is much lesser as compared to that

of diesel vehicles) and we expect the company to largely maintain its

market share despite rising competitive intensity. We expect Maruti to

report healthy volume growth coupled with higher realizations driven

by improving sales mix towards higher value cars

▪ Maruti currently trades at an EV/EBITDA of 17.8 x and PE of 30.2x on

FY21E consensus financials which is reasonable given its leadership

position , competitive advantages and strong growth profile over the

medium to long term.

Company FY19 FY20E FY21ECAGR

19-21E

CAGR

5yr

CAGR

10yr

Revenue Growth 16.7% 10.8% -1.2% 11.5% 4.9% 15.2%

EBIDTA Growth 17.4% -4.8% -14.9% 21.5% 1.7% 16.2%

PAT Growth 5.1% -1.3% -11.4% 3.9% 3.9% 22.3%

P/E 26.4 26.8 30.2 24.8

EV/EBIDTA 16.4 15.1 17.8 13.9

P/B 4.9 4.4 4.1 3.7

PEG1 6.7 6.8

ROE 19.8% 17.3% 14.0% 15.6%

Net Debt /Equity -0.1 -0.6 -0.6 -0.6

Long Term Historical Valuation (rolling 1 year forward multiple)

PE 16.2

EV/EBIDTA 9.4

Sector2

Revenue Growth 16.2% 11.9% 1.8% 10.9% 6.3% 11.9%

EBIDTA Growth 15.7% -2.2% -8.0% 14.2% 2.5% 10.9%

PAT Growth 6.1% 1.9% -6.9% 3.4% 3.4% 14.2%

P/E 22.1 21.7 23.3 20.3

EV/EBIDTA 15.3 13.8 15.1 12.9

ROE 22.7% 20.4% 17.2% 18.0%

1PEG: Price/Earnings Growth, FY19 P/E and FY19-21E CAGR PAT Growth2For Sector, Hero, Bajaj Auto, TVS motors and Maruti Suzuki have been taken

CAGR: Compound annual Growth Rate. ROE: Return on Equity. ROCE: Return on Capital

Employed. EV/EBITDA: Enterprise Value/Earnings before interest, tax, depreciation, and

amortization. P/E: Price to earnings ratio. P/B: Price to book value. PAT: Profit After Tax.

Past performance may or may not be sustained in future

Maruti Suzuki

Disclaimer: The stock referred above is for the purpose of explaining the concept of stock categorization framework of Invesco Asset Management (India) Private Limited only.

The stock referred above should not be construed as recommendation, advice to buy, sell or in any manner transact in this stock and neither should it be considered as

Research Report from IAMI/Invesco Mutual Fund. The Fund may or may not have any present or future positions in this stock.

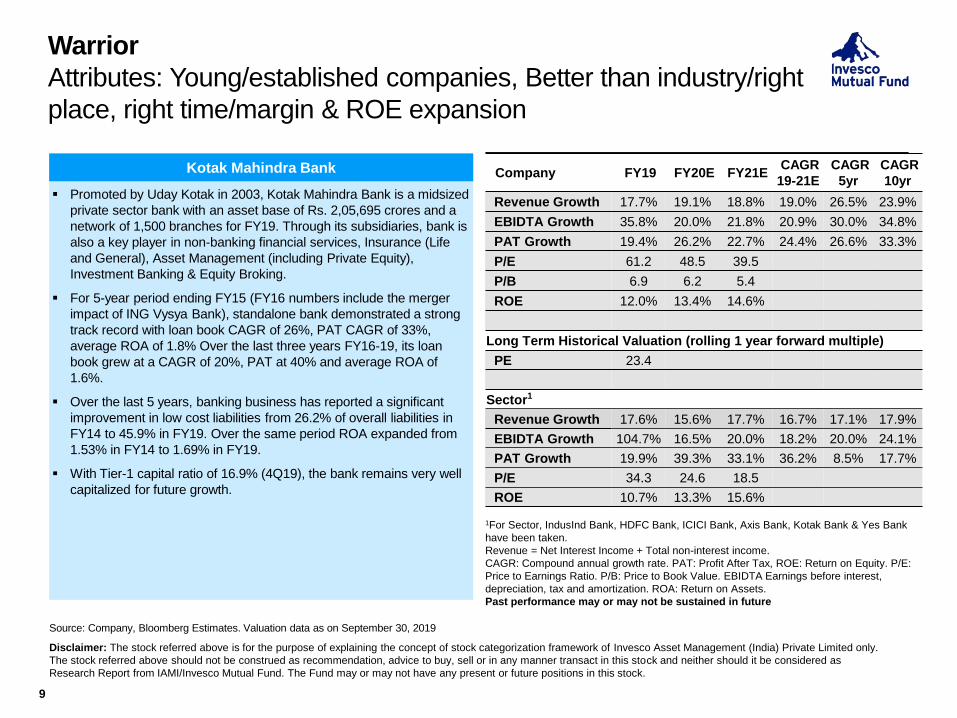

Warrior

Attributes: Young/established companies, Better than industry/right

place, right time/margin & ROE expansion

9

Source: Company, Bloomberg Estimates. Valuation data as on September 30, 2019

Supreme Industries (SIL)

▪ Promoted by Uday Kotak in 2003, Kotak Mahindra Bank is a midsized

private sector bank with an asset base of Rs. 2,05,695 crores and a

network of 1,500 branches for FY19. Through its subsidiaries, bank is

also a key player in non-banking financial services, Insurance (Life

and General), Asset Management (including Private Equity),

Investment Banking & Equity Broking.

▪ For 5-year period ending FY15 (FY16 numbers include the merger

impact of ING Vysya Bank), standalone bank demonstrated a strong

track record with loan book CAGR of 26%, PAT CAGR of 33%,

average ROA of 1.8% Over the last three years FY16-19, its loan

book grew at a CAGR of 20%, PAT at 40% and average ROA of

1.6%.

▪ Over the last 5 years, banking business has reported a significant

improvement in low cost liabilities from 26.2% of overall liabilities in

FY14 to 45.9% in FY19. Over the same period ROA expanded from

1.53% in FY14 to 1.69% in FY19.

▪ With Tier-1 capital ratio of 16.9% (4Q19), the bank remains very well

capitalized for future growth.

1For Sector, IndusInd Bank, HDFC Bank, ICICI Bank, Axis Bank, Kotak Bank & Yes Bank

have been taken.

Revenue = Net Interest Income + Total non-interest income.

CAGR: Compound annual growth rate. PAT: Profit After Tax, ROE: Return on Equity. P/E:

Price to Earnings Ratio. P/B: Price to Book Value. EBIDTA Earnings before interest,

depreciation, tax and amortization. ROA: Return on Assets.

Past performance may or may not be sustained in future

Kotak Mahindra Bank

Disclaimer: The stock referred above is for the purpose of explaining the concept of stock categorization framework of Invesco Asset Management (India) Private Limited only.

The stock referred above should not be construed as recommendation, advice to buy, sell or in any manner transact in this stock and neither should it be considered as

Research Report from IAMI/Invesco Mutual Fund. The Fund may or may not have any present or future positions in this stock.

Company FY19 FY20E FY21ECAGR

19-21E

CAGR

5yr

CAGR

10yr

Revenue Growth 17.7% 19.1% 18.8% 19.0% 26.5% 23.9%

EBIDTA Growth 35.8% 20.0% 21.8% 20.9% 30.0% 34.8%

PAT Growth 19.4% 26.2% 22.7% 24.4% 26.6% 33.3%

P/E 61.2 48.5 39.5

P/B 6.9 6.2 5.4

ROE 12.0% 13.4% 14.6%

Long Term Historical Valuation (rolling 1 year forward multiple)

PE 23.4

Sector1

Revenue Growth 17.6% 15.6% 17.7% 16.7% 17.1% 17.9%

EBIDTA Growth 104.7% 16.5% 20.0% 18.2% 20.0% 24.1%

PAT Growth 19.9% 39.3% 33.1% 36.2% 8.5% 17.7%

P/E 34.3 24.6 18.5

ROE 10.7% 13.3% 15.6%

Star

Attributes: Young companies/high growth/Entrepreneur vision,

scalability/operating leverage

10

Source: Company, Bloomberg Estimates. Valuation data as on September 30, 2019

Gujarat State Petronet (GSPL)

▪ India is becoming a favorable destination for electronics

manufacturing driven by increasing cost of labor in China, favorable

policies of Indian government and levy of import duties, most of the

brands prefer domestic sourcing of their consumer products.

▪ In manufacturing, Dixon Technologies India ltd. (DTIL) has leading

market share in three core sub-segments (Television, Lighting &

Washing Machines), rising prominence of original design

manufacturer (ODM) model and a diversified business profile.

▪ An asset-light balance sheet with strong return ratios and low working

capital cycle coupled with availability of adequate capacity.

▪ Rising share of ODM model where product development and

designing is done in-house has scope to structurally improve the

company margins apart from operating leverage.

▪ DTIL’s new manufacturing facility at Tirupati will enable it to diversify

into TV, CCTV cameras and DVRs as part of further diversification.

Dixon Technologies

Disclaimer: The stock referred above is for the purpose of explaining the concept of stock categorization framework of Invesco Asset Management (India) Private Limited only.

The stock referred above should not be construed as recommendation, advice to buy, sell or in any manner transact in this stock and neither should it be considered as

Research Report from IAMI/Invesco Mutual Fund. The Fund may or may not have any present or future positions in this stock.

1PEG: Price/Earnings Growth, FY18 P/E and FY19-21 CAGR PAT Growth2For Sector, Voltas, Amber and Hitachi have been taken.

Revenue = Net Interest Income + Total Non-Interest Income

CAGR: Compound annual Growth Rate. PAT: Profit After Tax, ROE: Return on Equity.

P/E: Price to Earnings Ratio. P/B: Price to Book Value. EBIDTA: Earnings before interest,

tax, depreciation, and amortization.

Past performance may or may not be sustained in future

Company FY19 FY20E FY21ECAGR

19-21E

CAGR

5yr

CAGR

10yr

Revenue Growth 5.8% 43.2% 17.5% 29.8% 22.4% Na

EBIDTA Growth 7.5% 44.3% 17.9% 30.4% 39.1% Na

PAT Growth 12.2% 44.1% 31.6% 31.6% 38.3% Na

P/E 49.0 34.0 28.3

EV/EBIDTA 24.8 17.3 15.4

P/B 8.8 7.2 5.8

PEG1 1.6

ROE 19.7% 23.2% 22.6%

Long Term Historical Valuation (rolling 1 year forward multiple)

PE 32

EV/EBITA 16

Sector2

Revenue Growth 12.8% 22.4% 14.1% 18.2% 14.7% 11.8%

EBIDTA Growth 18.8% 27.4% 16.6% 21.9% 26.1% 14.5%

PAT Growth 3.0% 26.2% 22.9% 22.9% 23.1% 12.8%

P/E 51.7 41.0 34.2

EV/EBIDTA 33.3 26.2 21.3

ROE 14.8% 16.7% 17.5%

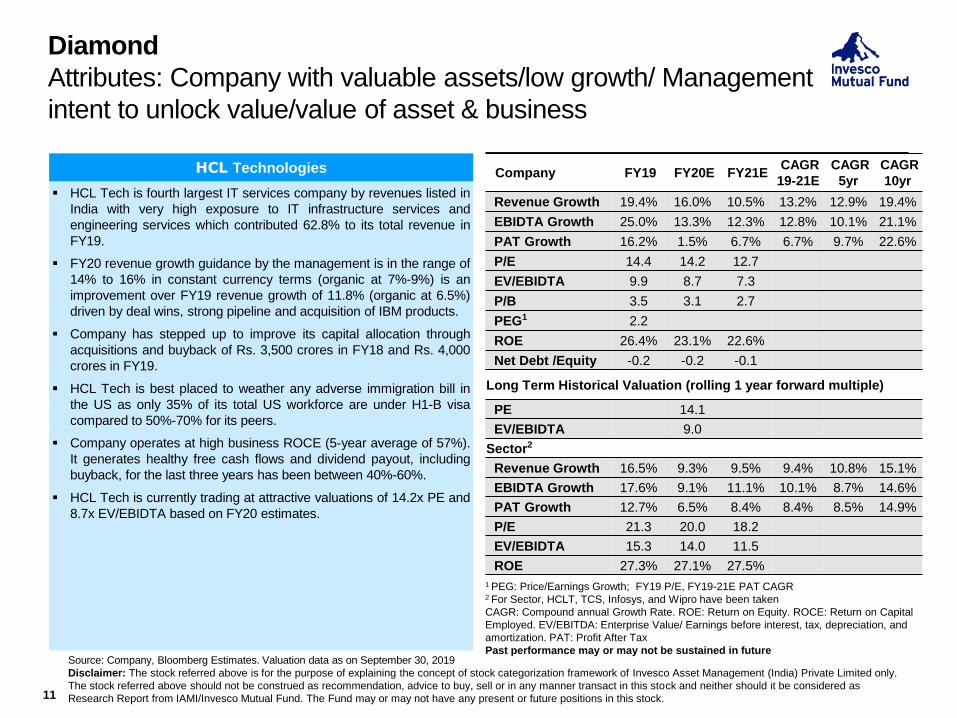

Diamond

Attributes: Company with valuable assets/low growth/ Management

intent to unlock value/value of asset & business

11

Source: Company, Bloomberg Estimates. Valuation data as on September 30, 2019

Gujarat State Petronet (GSPL)

▪ HCL Tech is fourth largest IT services company by revenues listed in

India with very high exposure to IT infrastructure services and

engineering services which contributed 62.8% to its total revenue in

FY19.

▪ FY20 revenue growth guidance by the management is in the range of

14% to 16% in constant currency terms (organic at 7%-9%) is an

improvement over FY19 revenue growth of 11.8% (organic at 6.5%)

driven by deal wins, strong pipeline and acquisition of IBM products.

▪ Company has stepped up to improve its capital allocation through

acquisitions and buyback of Rs. 3,500 crores in FY18 and Rs. 4,000

crores in FY19.

▪ HCL Tech is best placed to weather any adverse immigration bill in

the US as only 35% of its total US workforce are under H1-B visa

compared to 50%-70% for its peers.

▪ Company operates at high business ROCE (5-year average of 57%).

It generates healthy free cash flows and dividend payout, including

buyback, for the last three years has been between 40%-60%.

▪ HCL Tech is currently trading at attractive valuations of 14.2x PE and

8.7x EV/EBIDTA based on FY20 estimates.

HCL Technologies

Disclaimer: The stock referred above is for the purpose of explaining the concept of stock categorization framework of Invesco Asset Management (India) Private Limited only.

The stock referred above should not be construed as recommendation, advice to buy, sell or in any manner transact in this stock and neither should it be considered as

Research Report from IAMI/Invesco Mutual Fund. The Fund may or may not have any present or future positions in this stock.

1 PEG: Price/Earnings Growth; FY19 P/E, FY19-21E PAT CAGR2 For Sector, HCLT, TCS, Infosys, and Wipro have been taken

CAGR: Compound annual Growth Rate. ROE: Return on Equity. ROCE: Return on Capital

Employed. EV/EBITDA: Enterprise Value/ Earnings before interest, tax, depreciation, and

amortization. PAT: Profit After Tax

Past performance may or may not be sustained in future

Company FY19 FY20E FY21ECAGR

19-21E

CAGR

5yr

CAGR

10yr

Revenue Growth 19.4% 16.0% 10.5% 13.2% 12.9% 19.4%

EBIDTA Growth 25.0% 13.3% 12.3% 12.8% 10.1% 21.1%

PAT Growth 16.2% 1.5% 6.7% 6.7% 9.7% 22.6%

P/E 14.4 14.2 12.7

EV/EBIDTA 9.9 8.7 7.3

P/B 3.5 3.1 2.7

PEG1 2.2

ROE 26.4% 23.1% 22.6%

Net Debt /Equity -0.2 -0.2 -0.1

Long Term Historical Valuation (rolling 1 year forward multiple)

PE 14.1

EV/EBIDTA 9.0

Sector2

Revenue Growth 16.5% 9.3% 9.5% 9.4% 10.8% 15.1%

EBIDTA Growth 17.6% 9.1% 11.1% 10.1% 8.7% 14.6%

PAT Growth 12.7% 6.5% 8.4% 8.4% 8.5% 14.9%

P/E 21.3 20.0 18.2

EV/EBIDTA 15.3 14.0 11.5

ROE 27.3% 27.1% 27.5%

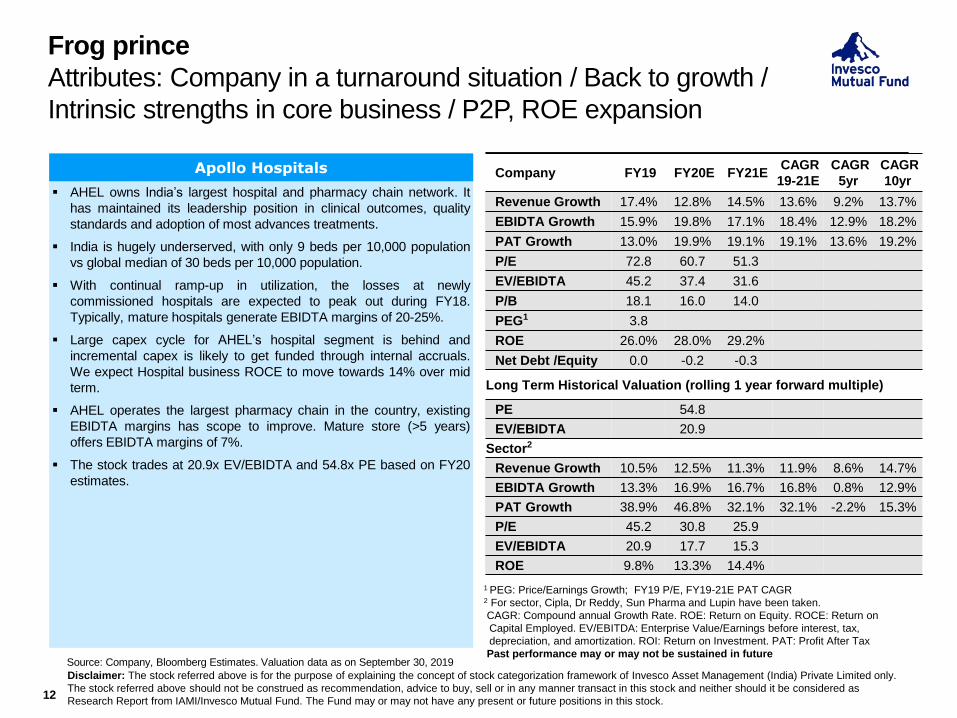

Frog prince

Attributes: Company in a turnaround situation / Back to growth /

Intrinsic strengths in core business / P2P, ROE expansion

12

Source: Company, Bloomberg Estimates. Valuation data as on September 30, 2019

Cipl

▪ AHEL owns India’s largest hospital and pharmacy chain network. It

has maintained its leadership position in clinical outcomes, quality

standards and adoption of most advances treatments.

▪ India is hugely underserved, with only 9 beds per 10,000 population

vs global median of 30 beds per 10,000 population.

▪ With continual ramp-up in utilization, the losses at newly

commissioned hospitals are expected to peak out during FY18.

Typically, mature hospitals generate EBIDTA margins of 20-25%.

▪ Large capex cycle for AHEL’s hospital segment is behind and

incremental capex is likely to get funded through internal accruals.

We expect Hospital business ROCE to move towards 14% over mid

term.

▪ AHEL operates the largest pharmacy chain in the country, existing

EBIDTA margins has scope to improve. Mature store (>5 years)

offers EBIDTA margins of 7%.

▪ The stock trades at 20.9x EV/EBIDTA and 54.8x PE based on FY20

estimates.

1 PEG: Price/Earnings Growth; FY19 P/E, FY19-21E PAT CAGR2 For sector, Cipla, Dr Reddy, Sun Pharma and Lupin have been taken.

CAGR: Compound annual Growth Rate. ROE: Return on Equity. ROCE: Return on

Capital Employed. EV/EBITDA: Enterprise Value/Earnings before interest, tax,

depreciation, and amortization. ROI: Return on Investment. PAT: Profit After Tax

Past performance may or may not be sustained in future

Company FY19 FY20E FY21ECAGR

19-21E

CAGR

5yr

CAGR

10yr

Revenue Growth 17.4% 12.8% 14.5% 13.6% 9.2% 13.7%

EBIDTA Growth 15.9% 19.8% 17.1% 18.4% 12.9% 18.2%

PAT Growth 13.0% 19.9% 19.1% 19.1% 13.6% 19.2%

P/E 72.8 60.7 51.3

EV/EBIDTA 45.2 37.4 31.6

P/B 18.1 16.0 14.0

PEG1 3.8

ROE 26.0% 28.0% 29.2%

Net Debt /Equity 0.0 -0.2 -0.3

Long Term Historical Valuation (rolling 1 year forward multiple)

PE 54.8

EV/EBIDTA 20.9

Sector2

Revenue Growth 10.5% 12.5% 11.3% 11.9% 8.6% 14.7%

EBIDTA Growth 13.3% 16.9% 16.7% 16.8% 0.8% 12.9%

PAT Growth 38.9% 46.8% 32.1% 32.1% -2.2% 15.3%

P/E 45.2 30.8 25.9

EV/EBIDTA 20.9 17.7 15.3

ROE 9.8% 13.3% 14.4%

Apollo Hospitals

Disclaimer: The stock referred above is for the purpose of explaining the concept of stock categorization framework of Invesco Asset Management (India) Private Limited only.

The stock referred above should not be construed as recommendation, advice to buy, sell or in any manner transact in this stock and neither should it be considered as

Research Report from IAMI/Invesco Mutual Fund. The Fund may or may not have any present or future positions in this stock.

CommoditiesAttributes: Call on the cycle is paramount/positive growth

prospects/integration, cost efficiency, globally competitive/profit leverage

13

Source: Company, Bloomberg Estimates. Valuation data as on September 30, 2019. Mtpa: Million tons per annum.

Gujarat State Petronet (GSPL)

▪ Ramco Cements is one of largest cement manufacturers in South

India. It has integrated cement capacity of 12.5 mtpa, with additional 6

mtpa of split grinding units.

▪ Company operates at utilization of ~70% on integrated capacity, with

huge scope for operating leverage.

▪ The South Indian region has witnessed subdued demand in last 4–5

years due to varied reasons including division of the states of Andhra

Pradesh and Telangana, political uncertainty, natural calamities, etc.

besides general economic weakness in India.

▪ Despite low utilization levels, company’s cement EBITDA per tonne

has been above industry average in last five years, which is function

of better realization (reward for strong brand) and its cost efficiencies.

▪ Even at 70% utilization and weak realization scenario in FY19,

company’s RoE stood at 12%, as against low single digit RoE

reported by many regional focused players.

▪ The company has meaningfully deleveraged itself (without dilution),

with net debt to equity at 0.3x as on March 2019 as against 1.2x as on

march 2014.

1 PEG: Price/Earnings Growth; FY19 P/E, FY19-21E PAT CAGR2 For Sector, Ramco, Ultratech, JK Cement, JK Lakshmi & Shree Cement have been taken.

CAGR: Compound annual Growth Rate. ROE: Return on Equity.

ROCE: Return on Capital Employed. EV/EBITDA: Enterprise Value/Earnings before

interest, tax, depreciation and amortization. PAT: Profit After Tax

Past performance may or may not be sustained in future

Company FY19 FY20E FY21ECAGR

19-21E

CAGR

5yr

CAGR

10yr

Revenue Growth 16.8% 11.8% 15.1% 13.4% 6.9% 8.1%

EBIDTA Growth -5.7% 30.5% 13.9% 21.9% 12.3% 2.9%

PAT Growth -9.0% 37.4% 15.4% 25.9% 29.7% 3.4%

P/E 32.8 23.9 20.7

EV/EBIDTA 17.2 13.7 12.1

P/B 3.7 3.3 2.9

PEG1 1.3

ROE 11.9% 14.6% 15.0%

Net Debt /Equity 0.3 0.4 0.4

Long Term Historical Valuation (rolling 1 year forward multiple)

PE 21.6

EV/EBIDTA 14.2

Sector1

Revenue Growth 18.5% 17.3% 12.7% 15.0% 12.0% 15.7%

EBIDTA Growth 7.8% 37.8% 12.3% 24.4% 12.1% 10.5%

PAT Growth -6.1% 58.8% 20.1% 38.1% 5.8% 6.8%

P/E 46.1 29.0 24.2

EV/EBIDTA 19.5 14.0 12.2

ROE 9.7% 13.7% 14.3%

Ramco Cements

Disclaimer: The stock referred above is for the purpose of explaining the concept of stock categorization framework of Invesco Asset Management (India) Private Limited only.

The stock referred above should not be construed as recommendation, advice to buy, sell or in any manner transact in this stock and neither should it be considered as

Research Report from IAMI/Invesco Mutual Fund. The Fund may or may not have any present or future positions in this stock.

Stock Categorization Financial Ratios

14

Data as on September 30, 2019 and relate to FY20/CY19 Estimates.

Source: Internal/Consensus/Bloomberg. Ratios based on Bloomberg consensus mean estimates for FY20/CY19.

Negative values have been removed from valuation measures where required to prevent distortion.

P/B: Price to Book Ratio, P/E: Price to Earnings Ratio. PEG: Price/Earnings To Growth Ratio, EBITDA: Earnings Before Interest, Taxes, Depreciation and Amortization,

EV/ Sales: Enterprise-Value-To-Sales Ratio, EV/EBITDA: Enterprise Value/Earnings Before Interest, Taxes, Depreciation and Amortization or Enterprise Multiple, Div Yield: Dividend

Yield. Revenue growth, EV/EBITDA and EV/Sales are for non-financial companies.

For PEG, FY19E/CY18E P/E and FY20E/CY19E growth is considered.

Disclaimer: The categorisation is as per the stock categorisation framework given on slide “Categorization Framework”. The categorisation does not in any manner reflect the quality of

the portfolio or its future performance/ returns. Invesco Asset Management (India) Private Limited/Invesco Mutual Fund is not guaranteeing or promising or forecasting any returns.

Investment universe: 302 companies, 131 categorized.

101 Unique companies across 11 active portfolios

Stock Category

No. of

Stocks % of Stock

Revenue

Growth

EBITDA

Growth

Profit

Growth RoE P/BV P/E PEG

EV/

EBITDA

EV/

Sales

Div

Yield

Growth

Leader 44 33.6% 10.0% 10.2% 6.7% 21.1% 5.3 26.3 3.9 16.7 3.5 1.09%

Star 2 1.5% 36.8% 37.7% 15.7% 19.5% 7.1 39.8 2.5 17.7 1.1 0.09%

Warrior 30 22.9% 9.9% 9.4% 20.8% 16.7% 3.9 25.7 1.2 15.0 2.5 0.80%

ValueDiamond 23 17.6% 3.8% 7.6% 59.1% 12.0% 1.4 12.3 0.2 6.8 1.1 2.00%

Frog Prince 14 10.7% 7.6% 16.7% 52.3% 7.1% 2.3 34.6 0.7 10.6 2.3 0.44%

Event Commodities 16 12.2% 1.8% 1.4% 1.3% 14.1% 1.5 11.8 8.8 7.4 0.9 4.05%

NA Shotgun 2 1.5% 14.0% 34.2% 24.2% 12.4% 17.1 139.6 5.8 0.0 0.0 2.09%

Total 131 100.0% 4.4% 6.4% 14.2% 15.0% 2.8 19.5 1.4 10.6 1.6 1.50%

Past performance may or may not be sustained in future.

Benefits of Stock Categorization

15

Focuses on the source of risk & return

▪ By identifying the key fundamental attributes of the company & drivers of stock price

performance

Stock appropriate valuation methodology

▪ Valuation attractiveness judged in the context of the category

▪ Provides a framework in which we can judge both under & overvaluation

Consistency across sectors and team members

Portfolio level clustering can be monitored

20

88

63

56

46

29

0

10

20

30

40

50

60

70

80

90

100

0 1-10 11-20 21-30 31-40 40+N

o.

of C

om

panie

s

No. of Analysts (Coverage by Sell-Side Analysts)

Invesco Asset Management (India) - Universe

Wide Research Coverage An Advantage

16

Source: Bloomberg. Data as on September 30, 2019

▪ Invesco Asset Management (India) has an

in-depth research coverage universe of

302 stocks

▪ Our unique research coverage is

underscored by the fact that ~36% of the

companies in the Invesco Asset

Management (India)’s investment universe

are under the research coverage of not

more than 10 sell-side analysts

Equity – Investment Process

17

Fund Objective

Investment Universe

Bottom Up Top Down AnalysisPortfolio Construction

Levers

Stock Categorization Industry Analysis Asset Allocation

Economic Analysis Sector Allocation

Technical Analysis Capitalization Bias

Stock Selection

Investment Team

Diversity Discussion Debate

Environment, Social, Governance Overlay (ESG)

Top Down Analysis

18

Industry/Economic Analysis

▪ View on the economy

▪ Implications for industries & companies

▪ Meetings with external sources – sell side analysts, economists, strategists, industry

experts & policy makers

Technical Analysis

▪ Industry & asset allocation decisions-where relevant

▪ Fine tuning of execution strategy-where relevant

▪ Idea generation

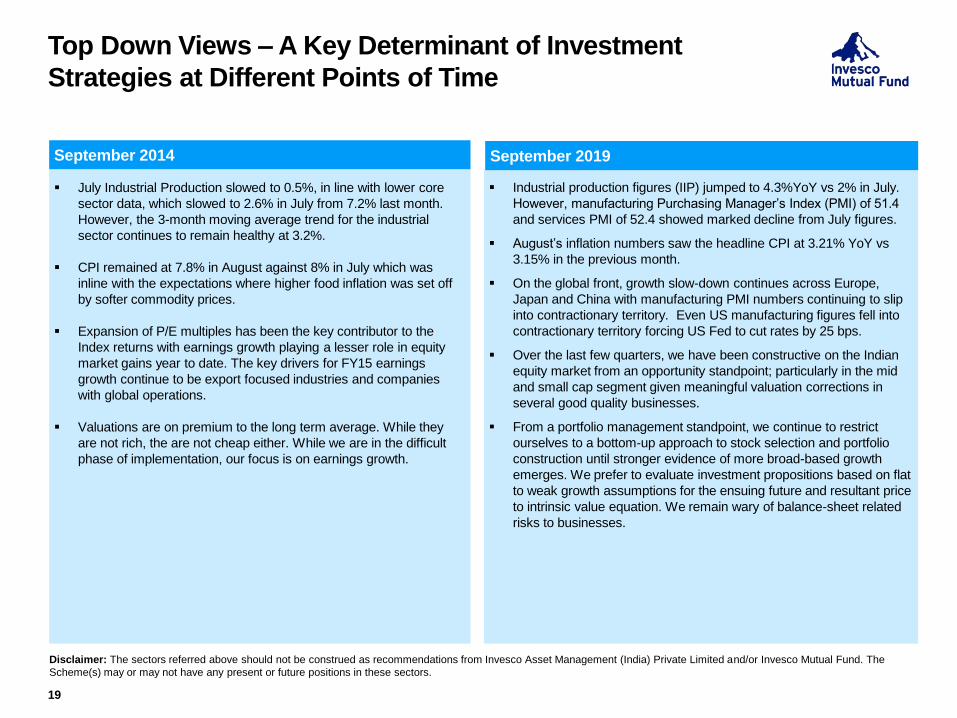

▪ July Industrial Production slowed to 0.5%, in line with lower core

sector data, which slowed to 2.6% in July from 7.2% last month.

However, the 3-month moving average trend for the industrial

sector continues to remain healthy at 3.2%.

▪ CPI remained at 7.8% in August against 8% in July which was

inline with the expectations where higher food inflation was set off

by softer commodity prices.

▪ Expansion of P/E multiples has been the key contributor to the

Index returns with earnings growth playing a lesser role in equity

market gains year to date. The key drivers for FY15 earnings

growth continue to be export focused industries and companies

with global operations.

▪ Valuations are on premium to the long term average. While they

are not rich, the are not cheap either. While we are in the difficult

phase of implementation, our focus is on earnings growth.

▪ Industrial production figures (IIP) jumped to 4.3%YoY vs 2% in July.

However, manufacturing Purchasing Manager’s Index (PMI) of 51.4

and services PMI of 52.4 showed marked decline from July figures.

▪ August’s inflation numbers saw the headline CPI at 3.21% YoY vs

3.15% in the previous month.

▪ On the global front, growth slow-down continues across Europe,

Japan and China with manufacturing PMI numbers continuing to slip

into contractionary territory. Even US manufacturing figures fell into

contractionary territory forcing US Fed to cut rates by 25 bps.

▪ Over the last few quarters, we have been constructive on the Indian

equity market from an opportunity standpoint; particularly in the mid

and small cap segment given meaningful valuation corrections in

several good quality businesses.

▪ From a portfolio management standpoint, we continue to restrict

ourselves to a bottom-up approach to stock selection and portfolio

construction until stronger evidence of more broad-based growth

emerges. We prefer to evaluate investment propositions based on flat

to weak growth assumptions for the ensuing future and resultant price

to intrinsic value equation. We remain wary of balance-sheet related

risks to businesses.

Top Down Views –A Key Determinant of Investment

Strategies at Different Points of Time

19

September 2014 September 2019

Disclaimer: The sectors referred above should not be construed as recommendations from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. The

Scheme(s) may or may not have any present or future positions in these sectors.

Equity – Investment Process

20

Fund Objective

Investment Universe

Bottom Up Top Down AnalysisPortfolio Construction

Levers

Stock Categorization Industry Analysis Asset Allocation

Economic Analysis Sector Allocation

Technical Analysis Capitalization Bias

Stock Selection

Investment Team

Diversity Discussion Debate

Environment, Social, Governance Overlay (ESG)

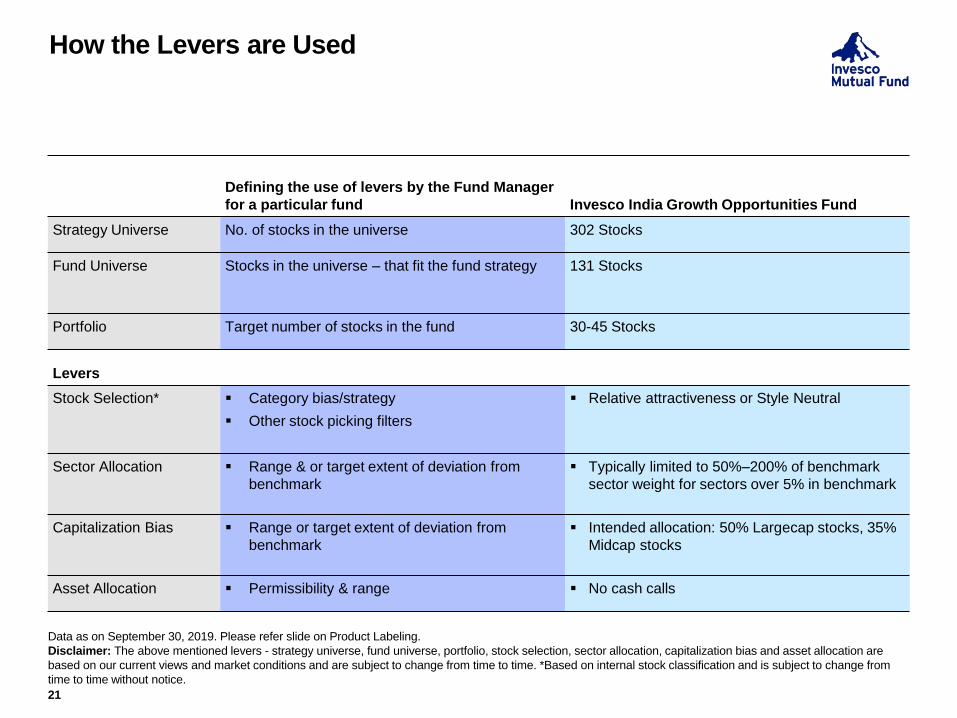

How the Levers are Used

21

Data as on September 30, 2019. Please refer slide on Product Labeling.

Disclaimer: The above mentioned levers - strategy universe, fund universe, portfolio, stock selection, sector allocation, capitalization bias and asset allocation are

based on our current views and market conditions and are subject to change from time to time. *Based on internal stock classification and is subject to change from

time to time without notice.

Defining the use of levers by the Fund Manager

for a particular fund Invesco India Growth Opportunities Fund

Strategy Universe No. of stocks in the universe 302 Stocks

Fund Universe Stocks in the universe – that fit the fund strategy 131 Stocks

Portfolio Target number of stocks in the fund 30-45 Stocks

Levers

Stock Selection* ▪ Category bias/strategy

▪ Other stock picking filters

▪ Relative attractiveness or Style Neutral

Sector Allocation ▪ Range & or target extent of deviation from

benchmark

▪ Typically limited to 50%–200% of benchmark

sector weight for sectors over 5% in benchmark

Capitalization Bias ▪ Range or target extent of deviation from

benchmark

▪ Intended allocation: 50% Largecap stocks, 35%

Midcap stocks

Asset Allocation ▪ Permissibility & range ▪ No cash calls

How the Levers are Used (CONTINUED)

22

Data as on September 30, 2019. Please refer slide on Product Labeling.

Disclaimer: The above mentioned levers - strategy universe, fund universe, portfolio, stock selection, sector allocation, capitalization bias and asset allocation are

based on our current views and market conditions and are subject to change from time to time. *Based on internal stock classification and is subject to change from

time to time without notice.

Invesco India

Multicap Fund

Invesco India

Tax Plan

Invesco India

Contra Fund

Strategy Universe (No.

of Companies)

302 Stocks 302 Stocks 302 Stocks

Fund Universe

(No. of Companies)

131 Stocks 131 Stocks 131 Stocks

Portfolio

(No. of Holdings)

30–50 Stocks 30-40 Stocks 35-50 Stocks

Levers

Stock Selection* ▪ All categories, growth biased ▪ All categories, growth biased ▪ Value bias

▪ At least 60% invested in Frog

Prince, Diamond,

Commodities, and in de-

rated companies from other

categories

Sector Allocation ▪ Significant deviations from

benchmark due to bottom up

approach

▪ Significant deviations from

benchmark

▪ No limits

Capitalization Bias ▪ Intended allocation: 50% -

70% allocation towards

midcap and smallcap stocks

▪ Significant deviations from the

benchmark

▪ Significant deviations from

benchmark

Asset Allocation ▪ No cash calls ▪ No cash calls ▪ No cash calls

How the Levers are Used (CONTINUED)

23

Data as on September 30, 2019. Please refer slide on Product Labeling.

Disclaimer: The above mentioned levers - strategy universe, fund universe, portfolio, stock selection, sector allocation, capitalization bias and asset allocation are

based on our current views and market conditions and are subject to change from time to time. *Based on internal stock classification and is subject to change from

time to time without notice.

Invesco India

Dynamic Equity Fund

Invesco India

Midcap Fund

Invesco India

Largecap Fund

Strategy Universe (No. of

Companies)

302 Stocks 302 Stocks 302 Stocks

Fund Universe

(No. of Companies)

131 Stocks 131 Stocks 131 Stocks

Portfolio

(No. of Holdings)

15–30 Stocks 30-50 Stocks 20-30 Stocks

Levers

Stock Selection* ▪ Relative attractiveness

▪ Earnings & Price momentum

▪ Growth bias ▪ 75–100% in leaders, warriors

including commodities

▪ Growth bias

Sector Allocation ▪ Significant deviation from

benchmark

▪ Significant deviations from

benchmark due to bottom up

approach

▪ Deviations from benchmark

Capitalization Bias ▪ Intended allocation:

Predominantly largecap

stocks

▪ Significant deviation from

benchmark

▪ Minimum 65% investment in

midcap stocks due to strategy

▪ Minimum 80% investment in

largecap stocks due to

strategy

Asset Allocation ▪ Active cash calls/hedges ▪ No cash calls ▪ No cash calls

How the Levers are Used (CONTINUED)

24

Data as on September 30, 2019. Please refer slide on Product Labeling.

Disclaimer: The above mentioned levers - strategy universe, fund universe, portfolio, stock selection, sector allocation, capitalization bias and asset allocation are

based on our current views and market conditions and are subject to change from time to time. *Based on internal stock classification and is subject to change from

time to time without notice.

Invesco India

Smallcap Fund

Invesco India

Financial Services

Fund

Invesco India

Infrastructure Fund

Invesco India

PSU Equity Fund

Strategy Universe (No.

of Companies)

302 Stocks 65 Stocks 180 Stocks 64 Stocks

Fund Universe

(No. of Companies)

131 Stocks 21 Stocks 84 Stocks 20 Stocks

Portfolio

(No. of Holdings)

30-50 Stocks 15–30 Stocks 20-40 Stocks 15–30 Stocks

Levers

Stock Selection* ▪ Growth bias ▪ Relative

attractiveness in

financial sector

▪ Relative attractiveness

in infrastructure

oriented companies

▪ Relative

attractiveness in

PSU’s

Sector Allocation ▪ Significant deviations

from benchmark due

to bottom up

approach

▪ NA ▪ Significant deviations

from the benchmark

▪ No limits

Capitalization Bias ▪ Minimum 65%

investment in

smallcap stocks due

to strategy

▪ Flexible ▪ Flexible ▪ Flexible

Asset Allocation ▪ No Cash calls ▪ No cash calls ▪ No cash calls ▪ No cash calls

Benefits of Portfolio Levers

25

▪ The levers follow on from the fund’s objective

▪ The levers provide the framework, the flexibility and the limits, which the fund manager

must adhere to in order to create alpha

▪ Enables monitoring of fund manager drift

▪ The levers are key to monitoring and delivering on our promise of running our funds “True

to Mandate”

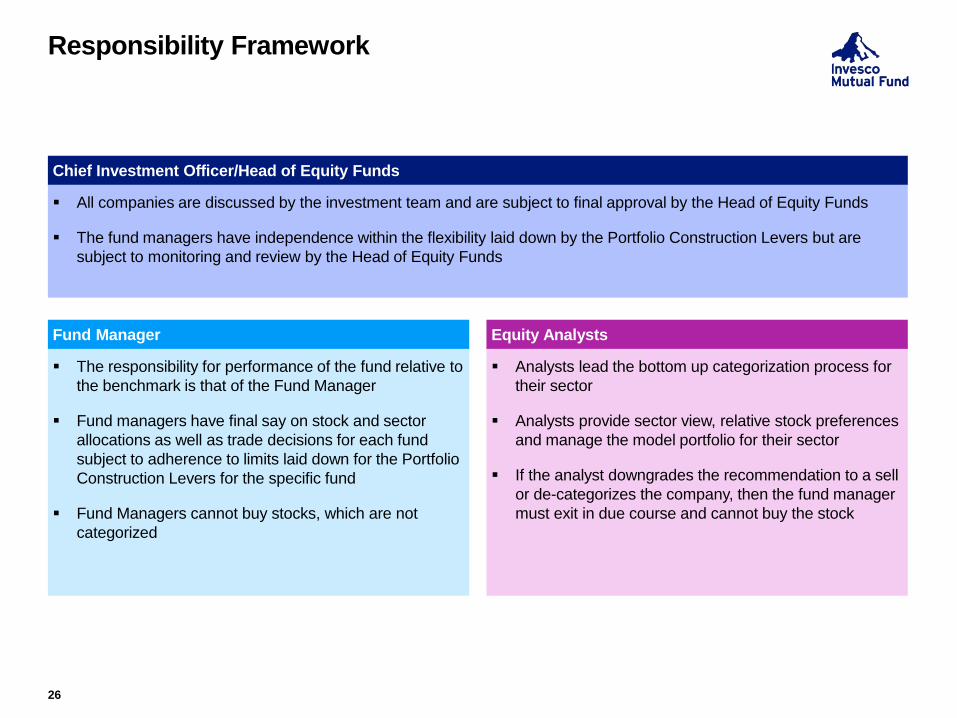

▪ All companies are discussed by the investment team and are subject to final approval by the Head of Equity Funds

▪ The fund managers have independence within the flexibility laid down by the Portfolio Construction Levers but are

subject to monitoring and review by the Head of Equity Funds

Responsibility Framework

26

Chief Investment Officer/Head of Equity Funds

▪ The responsibility for performance of the fund relative to

the benchmark is that of the Fund Manager

▪ Fund managers have final say on stock and sector

allocations as well as trade decisions for each fund

subject to adherence to limits laid down for the Portfolio

Construction Levers for the specific fund

▪ Fund Managers cannot buy stocks, which are not

categorized

Fund Manager

▪ Analysts lead the bottom up categorization process for

their sector

▪ Analysts provide sector view, relative stock preferences

and manage the model portfolio for their sector

▪ If the analyst downgrades the recommendation to a sell

or de-categorizes the company, then the fund manager

must exit in due course and cannot buy the stock

Equity Analysts

Risk Management

27

Dealing

▪ Separate team for Debt &

Equity

▪ Best Execution

▪ Compliance & Regulatory

checks

Review & Compliance

▪ Investment committee

▪ Consistency review

▪ Independent auditors

Investment Guidelines

▪ Absolute exposure limits

▪ Pre & post-trade checking

▪ Risk allocation

Portfolio Risk

▪ Bloomberg

Management of

Risk

Risk Management – The Process

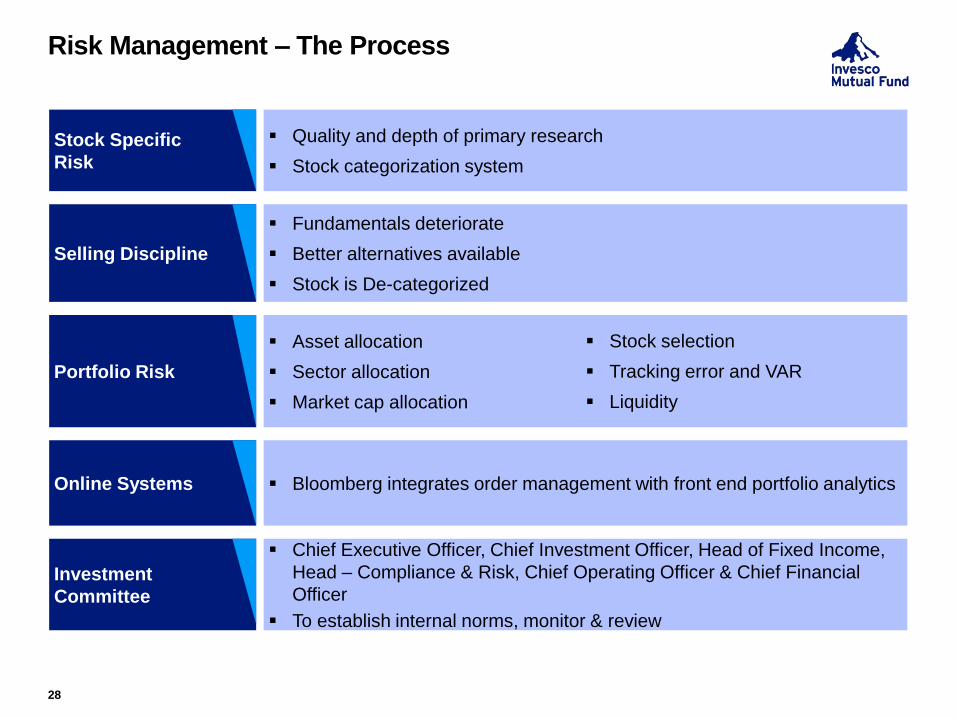

28

Stock Specific

Risk

▪ Quality and depth of primary research

▪ Stock categorization system

Selling Discipline

▪ Fundamentals deteriorate

▪ Better alternatives available

▪ Stock is De-categorized

Portfolio Risk

▪ Asset allocation

▪ Sector allocation

▪ Market cap allocation

▪ Stock selection

▪ Tracking error and VAR

▪ Liquidity

Online Systems ▪ Bloomberg integrates order management with front end portfolio analytics

Investment

Committee

▪ Chief Executive Officer, Chief Investment Officer, Head of Fixed Income,

Head – Compliance & Risk, Chief Operating Officer & Chief Financial

Officer

▪ To establish internal norms, monitor & review

Risk Management Details

29

▪ Committees to review AMC activities

– Investment Committee of Executives of Invesco Asset Management (India) Private

Limited

– Audit Committee of Board of Directors of Invesco Asset Management (India) Private

Limited

▪ Policy for Prohibition of Insider Trading

Audit Committee

30

▪ Review of financial statements, portfolio statements, financial reporting to unit holders

▪ Review compliance procedures, processes and reports, discuss with Compliance Officer

about the compliance framework and to monitor compliance and governance issues

▪ Review Risk Management framework

▪ Review the internal audit systems and internal and statutory audit reports

▪ Recommend appointment of auditors

Broad Product Portfolio

31

Note: Please refer slide on Product Labeling1 An open ended equity linked saving scheme with a statutory lock-in of 3 years and tax benefit.2 The investor will bear the recurring expenses of the scheme, in addition to the expenses of underlying scheme

Equity (10)

▪ Invesco India Tax Plan1

▪ Invesco India Growth

Opportunities Fund

▪ Invesco India Midcap Fund

▪ Invesco India Multicap Fund

▪ Invesco India

Infrastructure Fund

▪ Invesco India Contra Fund

▪ Invesco India Largecap

Fund

▪ Invesco India Financial

Services Fund

▪ Invesco India PSU Equity

Fund

▪ Invesco India Smallcap

Fund

Hybrid/ETFs/

Alternatives (7)

▪ Invesco India Arbitrage

Fund

▪ Invesco India Dynamic

Equity Fund

▪ Invesco India Equity & Bond

Fund

▪ Invesco India Equity

Savings Fund

▪ Invesco India Nifty ETF

▪ Invesco India Gold ETF

▪ Invesco India Gold FoF2

Fund of Funds (2)

(Investing Overseas)

▪ Invesco India Feeder –

Invesco Pan European

Equity Fund2

▪ Invesco India Feeder –

Invesco Global Equity

Income Fund2

Fixed Income (10)

▪ Invesco India Liquid Fund

▪ Invesco India Ultra Short

Term Fund

▪ Invesco India Short Term

Fund

▪ Invesco India Treasury

Advantage Fund

▪ Invesco India Corporate

Bond Fund

▪ Invesco India Money Market

Fund

▪ Invesco India Gilt Fund

▪ Invesco India Banking &

PSU Debt Fund

▪ Invesco India Credit Risk

Fund

▪ Fixed Maturity Plans of

various maturities

Fund Management Responsibility

32

Funds Managed Inception date Fund Manager/ Managing since Jointly Managed By/ Managing since

Invesco India Tax Plan December 29, 2006Amit Ganatra

Managing since (March 29, 2018)

Dhimant Kothari

Managing since (March 29, 2018)

Invesco India Contra Fund April 11, 2007Taher Badshah

Managing since (January 13, 2017)

Amit Ganatra

Managing since (August 14, 2012)

Invesco India Midcap Fund April 19, 2007Pranav Gokhale

Managing since (March 29, 2018)

Neelesh Dhamnaskar

Managing since (July 18, 2018)

Invesco India Arbitrage Fund April 30, 2007Pranav Gokhale

Managing since (April 1, 2011)-

Invesco India Growth Opportunities Fund August 9, 2007Taher Badshah

Managing since (January 13, 2017)

Amit Ganatra

Managing since (June 23, 2014)

Invesco India Dynamic Equity Fund October 4, 2007Taher Badshah

Managing since (January 13, 2017)

Pranav Gokhale

Managing since (June 1, 2018)

Invesco India Infrastructure Fund November 21, 2007Pranav Gokhale

Managing since (August 14, 2012)

Neelesh Dhamnaskar

Managing since (June 1, 2018)

Invesco India Multicap Fund March 17, 2008Taher Badshah

Managing since (March 29, 2018)

Pranav Gokhale

Managing since (March 29, 2018)

Invesco India Financial Services Fund July 14, 2008Amit Ganatra

(Managing since November 9, 2010)

Dhimant Kothari

Managing since (June 1, 2018)

Invesco India Largecap Fund August 21, 2009Amit Ganatra

Managing since (March 29, 2018)

Nitin Gosar

Managing since (March 29, 2018)

Invesco India PSU Equity Fund November 18, 2009Pranav Gokhale

Managing since (September 28, 2015)

Nitin Gosar

Managing since (June 1, 2018)

Invesco India Nifty ETF June 13, 2011Pranav Gokhale

Managing since (June 13, 2011)-

Invesco India Equity & Bond Fund1 June 30, 2018Taher Badshah(Equity Portion)

Managing since (June 30, 2018)

Amit Ganatra(Equity Portion)

Managing since (June 30, 2018)

Invesco India Small Cap Fund October 30, 2018Taher Badshah

Managing since (October 30, 2018)

Pranav Gokhale

Managing since (March 1, 2019)

Invesco India Equity Savings Fund2 March 7, 2019Taher Badshah (Equity Portion)

Managing since (March 7, 2019)

Amit Ganatra (Equity Portion)

Managing since (March 7, 2019)

1. Debt portion of the scheme is managed by Krishna Cheemalapati since June 30, 2018. 2. Debt potion of the scheme is managed by Krishna Cheemalapati since March 7, 2019.

Product LabellingSuitable for investors who are seeking* (CONTINUED)

33

Invesco India Tax Plan(an open-ended Equity Linked Saving Scheme with a statutory lock-in of 3 years and tax benefit)▪ capital appreciation over long-term▪ investment in equity and equity-related

instruments

Invesco India Growth Opportunities Fund(Large & Mid cap Fund - An open ended equity scheme investing in both large cap and mid cap stocks)▪ capital appreciation over long-term▪ investments predominantly in equity and

equity-related instruments of large and midcap companies

Invesco India Dynamic Equity Fund(an open ended dynamic asset allocation fund)▪ capital appreciation over long-term▪ investments in equity and debt securities

which are managed dynamically

Invesco India Contra Fund(an open ended equity scheme following contrarian investment strategy)▪ capital appreciation over long-term▪ investments predominantly in equity and equity

related instruments through contrarian investing

Invesco India Midcap Fund(Mid Cap Fund - An open ended equity scheme predominantly investing in mid cap stocks)▪ capital appreciation over long-term▪ investments predominantly in equity and

equity-related instruments of Midcap companies

Invesco India Multicap Fund

(Multi Cap Fund - An open ended equity scheme investing

across large cap, mid cap, small cap stocks)▪ capital appreciation over long-term▪ investments in equity and equity related instruments

across market capitalization

Invesco India Largecap Fund(Large Cap Fund - An open ended equity scheme predominantly investing in large cap stocks)▪ capital appreciation over long-term▪ investments predominantly in equity and equity-related

instruments of largecap companies

Invesco India Nifty Exchange Traded Fund(an open ended scheme replicating Nifty 50 Index)▪ capital appreciation over long term▪ generate returns that closely correspond to the returns

generated by the securities represented by the Nifty 50, subject to tracking error, if any

Invesco India Gold Fund1

(an open ended fund of fund scheme investing in Invesco India Gold Exchange Traded Fund)▪ regular income and capital appreciation over medium to

long term▪ investment in units of Invesco India Gold Exchange

Traded Fund, which in turn invests in physical gold

Invesco India Gold Exchange Traded Fund (an open ended scheme tracking returns provided by investment in physical gold)▪ capital appreciation over long-term▪ generate returns that closely correspond to the returns

provided by investment in physical gold in the domestic market, subject to tracking error

Invesco India Equity Savings Fund

(An open ended scheme investing in equity, arbitrage and debt)

▪ capital appreciation and current income

▪ Investments in equity and equity related instruments, arbitrage

opportunities and fixed income instruments (including debt,

government securities and money market instruments)

Invesco India Infrastructure Fund

(an open ended equity scheme following

Infrastructure theme)

▪ capital appreciation over long-term

▪ investments predominantly in equity and equity-

related instruments of infrastructure companies

Invesco India Feeder - Invesco Global Equity

Income Fund1

(an open ended fund of fund scheme investing in

Invesco Global Equity Income Fund)

▪ capital appreciation and/or income over long-

term

▪ investment in units of Invesco Global Equity

Income Fund, an overseas equity fund

Invesco India Financial Services Fund

(an open ended equity scheme investing in financial

services sector)

▪ capital appreciation over long-term

▪ investment predominantly in equity and equity-related

instruments of companies engaged in the business of

banking and financial services

Invesco India PSU Equity Fund

(an open ended equity scheme following PSU theme)

▪ capital appreciation over long-term

▪ investment in predominantly equity and equity-related

instruments of Government companies (PSU’s)

Invesco India Feeder - Invesco Pan

European Equity Fund1

(an open ended fund of fund scheme

investing in Invesco Pan European Equity

Fund)

▪ capital appreciation over long-term

▪ investment in units of Invesco Pan

European Equity Fund, an overseas equity

fund

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them1 The investor will bear the recurring expenses of the scheme, in addition to expenses of the underlying scheme

LOW HIGH

Investors understand that their principal will be at

moderately high risk

RISKOMETER

LOW HIGH

Investors understand that their principal will be at

high risk

RISKOMETER

Invesco India Equity & Bond Fund

(an open ended hybrid scheme investing predominantly

in equity and equity related instruments)

▪ capital appreciation and current income over medium to long term

▪ investments in equity and equity related instruments and fixed

income securities

Invesco India Smallcap Fund

(Small Cap Fund – An open-ended equity

scheme predominantly investing in small cap

stocks)

• capital Appreciation over long term

• investments predominantly in equity and

equity-related instruments of Smallcap

companies

Product Labelling

Suitable for investors who are seeking*

34

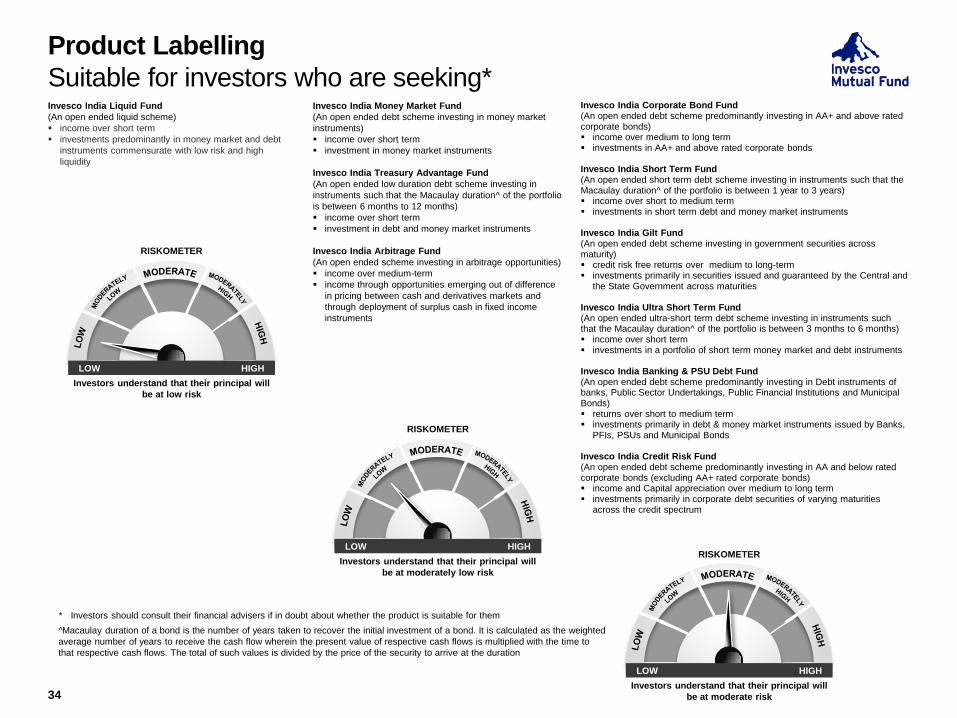

Invesco India Liquid Fund

(An open ended liquid scheme)

▪ income over short term

▪ investments predominantly in money market and debt

instruments commensurate with low risk and high

liquidity

Invesco India Money Market Fund

(An open ended debt scheme investing in money market

instruments)

▪ income over short term

▪ investment in money market instruments

Invesco India Treasury Advantage Fund

(An open ended low duration debt scheme investing in

instruments such that the Macaulay duration ̂of the portfolio

is between 6 months to 12 months)

▪ income over short term

▪ investment in debt and money market instruments

Invesco India Arbitrage Fund

(An open ended scheme investing in arbitrage opportunities)

▪ income over medium-term

▪ income through opportunities emerging out of difference

in pricing between cash and derivatives markets and

through deployment of surplus cash in fixed income

instruments

Invesco India Corporate Bond Fund(An open ended debt scheme predominantly investing in AA+ and above rated corporate bonds)▪ income over medium to long term▪ investments in AA+ and above rated corporate bonds

Invesco India Short Term Fund(An open ended short term debt scheme investing in instruments such that the Macaulay duration ̂of the portfolio is between 1 year to 3 years)▪ income over short to medium term▪ investments in short term debt and money market instruments

Invesco India Gilt Fund (An open ended debt scheme investing in government securities across maturity)▪ credit risk free returns over medium to long-term▪ investments primarily in securities issued and guaranteed by the Central and

the State Government across maturities

Invesco India Ultra Short Term Fund(An open ended ultra-short term debt scheme investing in instruments such that the Macaulay duration ̂of the portfolio is between 3 months to 6 months)▪ income over short term▪ investments in a portfolio of short term money market and debt instruments

Invesco India Banking & PSU Debt Fund(An open ended debt scheme predominantly investing in Debt instruments of banks, Public Sector Undertakings, Public Financial Institutions and Municipal Bonds)▪ returns over short to medium term▪ investments primarily in debt & money market instruments issued by Banks,

PFIs, PSUs and Municipal Bonds

Invesco India Credit Risk Fund(An open ended debt scheme predominantly investing in AA and below rated corporate bonds (excluding AA+ rated corporate bonds)▪ income and Capital appreciation over medium to long term▪ investments primarily in corporate debt securities of varying maturities

across the credit spectrum

LOW HIGH

Investors understand that their principal will

be at low risk

RISKOMETER

LOW HIGH

Investors understand that their principal will

be at moderately low risk

RISKOMETER

LOW HIGH

Investors understand that their principal will

be at moderate risk

RISKOMETER

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them

^Macaulay duration of a bond is the number of years taken to recover the initial investment of a bond. It is calculated as the weighted

average number of years to receive the cash flow wherein the present value of respective cash flows is multiplied with the time to

that respective cash flows. The total of such values is divided by the price of the security to arrive at the duration

Disclaimer

35

Disclaimer: This presentation is for information purposes only and is not an offer to sell or a solicitation to buy any mutual fund units/securities. The

content of this document is confidential and intended solely for the use of the addressee. If you are not the addressee, or the person responsible for

delivering it to the addressee, any disclosure, copying, distribution or any action taken or omitted to be taken in reliance on it is prohibited and may be

unlawful. The views/ information alone are not sufficient and shouldn’t be used for the development or implementation of an investment strategy. It

should not be construed as investment advice to any party. All opinions, figures, charts/graphs, estimates and data included in this document are as

on date and are subject to change without notice. The statements contained herein may include statements of future expectations and other forward

looking statements that are based on our current views and assumptions and involve known and unknown risks and uncertainties that could cause

actual results, performance or events to differ materially from those expressed or implied in such statements. The data used in this material is

obtained by Invesco Asset Management (India) Private Limited from the sources which it considers reliable. While utmost care has been exercised

while preparing the presentation, Invesco Asset Management (India) Private Limited does not warrant the completeness or accuracy of the information

and disclaims all liabilities, losses and damages arising out of the use of this information. Neither Invesco Asset Management (India) Private Limited

nor any person connected with it accepts any liability arising from the use of this information. The recipient(s) before acting on any information herein

should make his/their own investigation and seek appropriate professional advice.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Get in Touch

Corporate Office:

Invesco Asset Management (India) Pvt Ltd.

Unit No: 2101 A, 21st floor, A – Wing,

Marathon Futurex, N. M. Joshi Marg,

Lower Parel, Mumbai – 400 013

T +91 22 67310000 F +91 22 23019422

To invest:

Call 1800-209-0007 ∆ sms ‘Invest’ to 56677

Invest Online www.invescomutualfund.com

Follow us on