Embed Size (px)

DESCRIPTION

Second issue of Norway's student-run journal in economics and finance

Citation preview

Magazine

The euro crisis Why being a turkey before

thanksgiving is not a good idea Financial leverage and capital structure Managing emerging markets Careers in Norges Bank

Second IssueSpring 2013A new target?

The future of monetary policy

[ 2 ]

EditorAmaar [email protected]

WritersAlexander AlbertLouisa BrandtMorten FylkesnesEven Comfort HvindenFabian HarangFarzad KhoshnoudPetter KongslieAmaar MalikKjetil Stiansen

Layout & graphicsLasse André [email protected]

ONLINEequilibriummagazine.no

PublisherEquilibrium Magazine FLIc/o Økonomisk instituttPostboks 1095 Blindern0317 Oslo

Cover photoAdam Fagen

Colophone

M ACRONominal issues 4The euro crisis 8Guest article: Misconceptions of wages and unemployment 10

FI NA NCEWhy being a turkey before thanksgiving is not a good idea 15Financial leverage and capital structure 18Financial derivatives 22Alternative marketplaces 25

I NTER NATIONA L E X PER I ENCEManaging emerging markets 29

Ca r eer sNorges Bank 32

''Inflation, if anything, is a little bit too low.'' – Ben Bernanke Photo: Federal Reserve

[ 3 ]

It is with great excitement our editorial staff is releasing the second issue of Equilibrium Magazine. We are delighted to currently be distributing at nine universities and colleges in Norway as well as attracting readers from eight additional countries on three continents. We are looking forward to contribute with more ideas, views and theories in this issue as we seek to inspire the broader student community to take the economic and financial debate outside the lecture halls.

When we established this magazine, our main goal was to carry out high-quality economic and financial research as well as creating a platform for students from all over the world to come together and participate in the debate. Bearing in mind our goals, we have omitted interviews with academics and industry practitioners in this issue as we have received numerous appli-cations from students who want to contribute with editorial content. Hence, we have focused on gathering students together to write about highly relevant economic and financial topics that we believe will influence economic policy-making in the time to come. This issue consists of discussions on macroeconomic topics such as monetary policy and economic challenges in the

euro-area while also highlighting financial top-ics covering financial risk management, corpo-rate finance and alternative marketplaces.

Our academically founded views on these topics encompass theories ranging from neo-Keynesian economics to Austrian perspec-tives as we aim to enable students to critically assess economic and financial theories. We also want to encourage you to perceive this magazine as active learning. Please do not only read, but do also digest and anal-yse the content as well as ultimately partici-pating in the economic and financial debate by writing a guest column.

In this ubiquitous economic environment that is characterised by new unorthodox policymaking and changing regulations, we hope you enjoy our analysis of both the current situation and the key opportu-nities going forward.

Amaar Malik, Editor-in-ChiefBA Economics, University of Oslo

Continuing tobuild on our success

Digest and analyse the content as well as ultimately participating

in the economic and financial de-bate by writing a guest column

[ 4 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

Replacing the inflation target?Central bankers have become super-

stars. As the financial crisis and Europe’s debt crisis unfolded, central banks took the stage, using conventional and uncon-ventional means to stave off disaster and return the world to prosperity. While the influence and power of central banks have expanded rapidly, they are still subject to rules. The rules come in the form of mon-etary policy regimes, given by politicians, which govern what central banks are al-lowed to do and which economic variables they should be targeting.

Inflation targeting, which is the mone-tary policy regime adopted by most cen-tral banks in the developed world, has succeeded in bringing stable inflation and stable growth for several years. However, during the crisis, it has increasingly shown itself to be a distraction, diverting fo-

cus from returning the economy to full employment, giving inflation an unwar-ranted amount of attention, as if by de-fault. Rather than looking at the economy through the lens of inflation, countries might be better served with a central bank that targets the level of economic output directly. The time may have come for re-placing the inflation target with a target for nominal GDP.

What is NGDP-targeting,monetary policy targets?

Governments leave the issue of con-trolling monetary policy to an independent central bank due to issues of time incon-sistency. According to standard macro-economic theory, there exists a trade-off between inflation and unemployment in the short run but not in the long run. A democratically elected government will

have problems taking the long-term view, essentially because it faces re-election and will thus have incentives to pursue an ex-pansionary policy, sacrificing price stabil-ity (which is regarded as a good thing) for temporary low unemployment. In other words, the short term preference of lower unemployment is inconsistent with long term preferences for price stability.

As long as unemployment is kept below its equilibrium rate (also known as the natural rate, the rate at which inflation is constant), inflation will rise as people re-vise their inflation expectations. In the end the government will have to accept a rise in unemployment back to the equilibrium rate to avoid inflation skyrocketing. Thus the economy has been saddled with higher inflation without any permanent gain in lower unemployment. Giving an indepen-dent central bank the responsibility of

Nominal issues✎ Kjetil Stiansen

Photo: U.S. Department of the Treasury

[ 5 ]

keeping inflation at a predetermined target, which is the essence of inflation targeting, should thus anchor inflation expectations and keep unemployment at its equilibrium level.

Targeting nominal GDP (NGDP-targeting) means that the central bank picks a “normal year” with unemployment at its equilibrium rate and sets a target for the growth path of nominal GDP (GDP not adjusted for inflation). For example, if trend growth is projected at 3 %, and the favoured inflation rate is 2 %, then a NGDP-target would be 5 % growth per year. Also, since the central bank is targeting a growth path, lower than expected NGDP growth one year, e.g. at 4 %, would mean it should target NGDP growth of 6 % the next year, to catch up.

Managing expectationsThe current economic climate is best

characterised by the standard Keynesian liquidity trap. In the liquidity trap, produc-tion has fallen due to a powerful negative demand shock, such as a large increase in desired private savings, with a correspond-ing increase in unemployment. To coun-teract this, the central bank has lowered rates all the way to zero as a way to expand the economy. However, even a zero inter-est rate policy is insufficient to return the economy to full employment. Because the rate is already at zero, cutting it further is not an option, as people would rather hold cash than pay banks to hold their money. Thus, the central bank is unable to affect the economy through changes in the inter-est rate; the trap is sprung.

In the liquidity trap, the main weapon of the central bank becomes expectations

management, but the inflation target could make this more difficult. Consider the cur-rent US Federal Reserve policy of keeping monetary policy accommodative until the unemployment rate falls below 6.5 per-cent or inflation exceeds 2.5 percent. The goal of this policy is to influence people’s expectations about future growth: people and firms should be certain that the Fed won’t move to choke off the recovery, and should thus be more optimistic about their future income. This should in turn make them more willing to spend and invest to-day, feeling less of a need to save in order to sustain themselves in the coming years. However, in the current situation, the in-flation target acts as an unhelpful distrac-tion. Unemployment at 6,5 percent is still well above the equilibrium rate, which is estimated to be between 5 and 6 percent, and there is virtually no reason to expect inflation to run wild with unemployment above its equilibrium rate. Also, the appar-ent unwillingness to allow inflation to run temporarily above 2.5 percent creates un-necessary uncertainty: would the Federal Reserve for instance move to tighten pol-icy in the face of a supply side inflation shock such as an oil price surge? It prob-ably wouldn’t, but it would come under political pressure to do so, and the uncer-tainty is unnecessary. In an economic envi-ronment where focus should be directed at returning the economy to full employment the current monetary policy regime may grant inflation an undeserved amount of attention.

NGDP-targeting would provide a better paradigm for expectations management. A central bank with an NGDP target would not be forced to evaluate all its actions in

light of an inflation target, which could help make promises of accommodative policy more credible and easier to under-stand. Currently, GDP (nominal as well as real) is well below the level it would have been at if the economy had continued growing along the trend it was on before the financial crisis. An NGDP mandate would in this situation call for substantive catch up growth to return the economy to its target growth path. Following such a mandate, the central bank would commit to keeping monetary policy accommoda-tive for as long as necessary to return the economy to the growth path. The message in this scenario is simple and lacks the res-ervations and contradictions of the cur-rent messages from central banks in both Europe and the US.

More inflatingFar from dangerous, moderate inflation

would be helpful in the current economic environment by reducing long term real rates. With high levels of private debt, and with interest rates pressed against the zero lower bound, standard macroeconomic theory points to moderate inflation as be-ing helpful. Moderately higher inflation would help in two main ways: most obvi-ously it would help erode the real value of debt. Also, in a country that issues debt in its own currency, such as the US, long term interest rates will basically be an average of expected future short term rates. As such, higher expected inflation decreases real long term interest rates, something which should help boost economic activity today.

The Japanese experience provides a case in point here. The Japanese economy has been stuck in the liquidity trap for

NGDP-targeting would provide a better paradigm for expectations management

[ 6 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

over a decade, with nominal interest rates essentially at zero. Long term interest rates have, however, been positive, as they are an average of expected short rates, which can only go up, being already at zero. The recent message from Japanese policy mak-ers has been one of targeting higher infla-tion, and markets seem to have responded. Expected inflation (which can be mea-sured by looking at so called breakeven rates, which are the spread between nom-inal and inflation indexed bond yields) have increased, with no increase in interest rates; in other words long term real inter-est rates have fallen. Lower long term real interest rates means higher future real in-come and lower costs of managing new debt (as real interest payments would be lower). This should make households more willing to spend, and firms more willing to invest today, expecting higher income and demand, respectively, in the future.

It’s (still) the politics, stupid!In principle, there is nothing preventing

policy makers from pursuing the policies outlined above within the framework of an inflation target, but the politics are dif-ferent. First of all: people tend to dislike inflation, and policies that are perceived to increase inflation tend to be unpopu-lar. Completely rational agents shouldn’t be too concerned with this, as prices nor-mally move in response to wages, leaving most people no worse off. However, peo-ple arguably judge the benefits of inflation in relation to their current, nominal in-come, perceiving inflation as something that erodes their standard of living. As such, announcements by the central bank calling for higher inflation are unlikely

to gain much traction. By the same token, raising the inflation target to, for instance, 4 %, while economically sound, is probably politically unfeasible. This makes it diffi-cult for the central bank to alter inflation expectations: the central bank often finds itself under pressure from politicians and the public when the inflation exceeds the target, but rarely when it dips below. It thus

becomes hard to make promises (or threats, depending on your position) of higher in-flation credible. (In econspeak: inflation expectations are too well anchored.)

The politics of NGDP-targeting would be substantially simpler, as well as easier to understand. In response to a slump, poli-cymakers would not have to sell a message of targeting higher inflation explicitly, but

rather reaffirm their commitment to bring nominal income back on track. As long as nominal income remained below its tar-get path, the central bank would be un-der pressure to get it back on track, rather than have their every policy decision scrutinised in light of the inflation target. Even under a regime such as that of the US, where there is a double mandate to target both unemployment and inflation, policy has arguably been biased towards moderat-ing inflation. Either way, the inflation tar-get acts as an anchor in the debate, and in an environment such as now, the distrac-tion it creates is damaging.

A fittingly imperfect policy “Monetary policy is not a panacea”.

The US Federal Reserve Chairman, Ben Bernanke’s warning to US policy makers goes for all forms of monetary policy mea-sures and its regimes, including NGDP tar-geting. However, as Christina and David Romer of Berkeley argue in a recent paper, being overly pessimistic about the power of monetary policy, even in the face of ma-jor challenges, can be dangerous, having resulted in limited and slow response to both the current and past crises. A good monetary policy regime is one that en-ables the central bank to credibly commit to whichever policy it deems appropriate for the current situation. An NGDP target could help enhance central bank credibil-ity, even in instances when what is needed is a dose of monetary recklessness. While politicians remain hard at work squabbling over structural reforms, budget deficits and other “real issues”, there may be some-thing to gain by considering the nominal ones.

Inflation expectations are too well anchored

Advertisement

Join the international debateInterested in economics, finance, politics or current affairs?

• Write a guest column• Share your opinions• Participate in the international debate

Send us your contribution before September 15th 2013 [email protected]

Find out more atwww.equilibriummagazine.no

[ 8 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

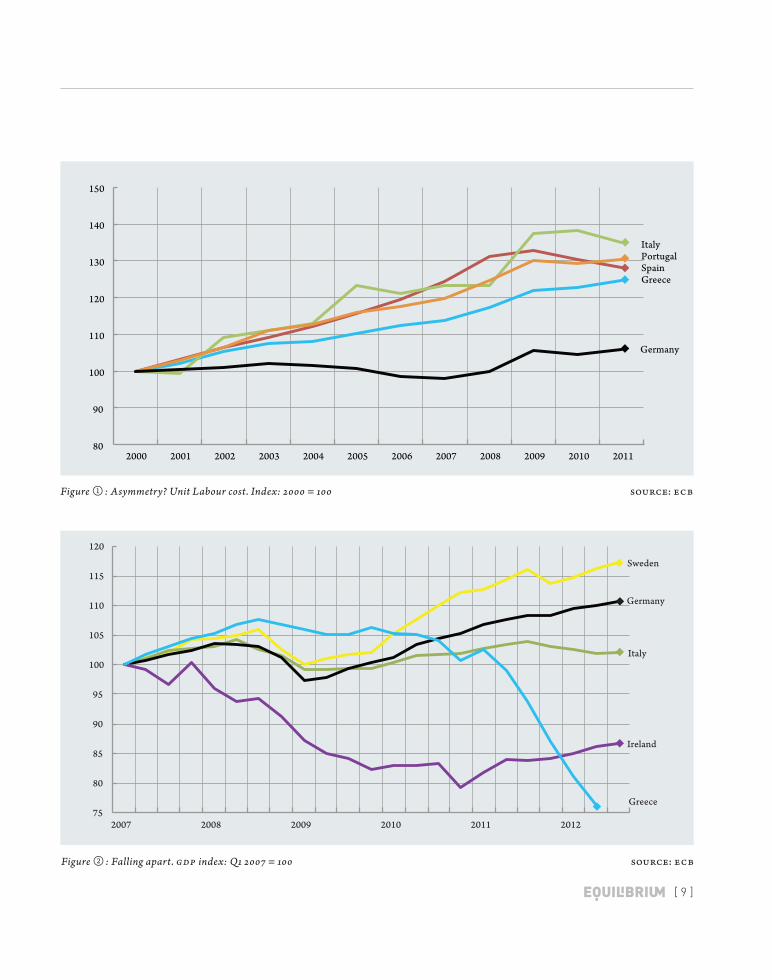

The medium term prospects for a successful resolution are be-coming bleaker as the ongoing crisis exacerbates the between country asymmetries that form part of the euro’s Original Sin.

Much can be said about flaws and perverse incentives in the construction of the common currency and its institutions. One of these is the issue of asymmetry, understood as the economic in-compatibility of the constituent nations in forming the common currency area.

The countries comprising the euro zone differ fundamentally in the structure, scope, scales and composition of their econo-mies, explaining differences in competitiveness and productivity and ultimately the countries' real income level. When asymme-try (figure ❶) is represented as differences in macro indicators such as GDP per capita and the current account balance they ul-timately reflect these relative fundamentals. At the same time, a common currency, free flows of capital and trade, and a central bank with an inflation targeting regime ensures that there is one rate of interest and one exchange rate. If the fundamentals of the euro zone countries differ, what are the consequences of the one-size-fits-all solution?

Writing on optimal currency areas, R .A Mundell (1961) stated that “[…] a region is an economic unit while a currency domain is partly an expression of national sovereignty […] the argument for a common currency area works best if each nation (and currency) has internal factor mobility and external factor immobility.”

Given that the euro zone is characterised by low internal fac-tor-mobility, describing the semi-rigid Bretton Woods system, R. A. Mundell is ironically prophetic when stating “[it] is patently obvious that periodic balance-of-payments will remain an integral

feature of the economic system as long as fixed exchange rates and rigid wage and price levels prevent the terms of trade from fulfilling a natural role in the adjustment process.”

Two alternatives thus exist for the euro zone one-size-fits-all-currency to work. One is convergence, which requires Greeks to become more like Germans. The second is a transfer union: German taxpayers treating the Greeks as if they were German. With the latter option being politically impossible, the creation of the euro was based on the assumption that the former would hold. Thus, the Maastricht Treaty stipulated a number of convergence criteria, goals for macro indicators such as inflation, deficits and debt to GDP ratios that individual countries had to fulfill to be eligible for euro zone membership. And indeed, during the 1990s, convergence appeared to happen.

There are two problems with the Maastricht criteria. Firstly, they are at best proxies for convergence as they do not contain in-formation on fundamentals. Second, the numbers were achieved for a short time period and with national currencies. Therefore the actual medium term feasibility of convergence would be tested after the creation of the currency area (figure ❷).

The traditional strategy of currency devaluation followed by export growth is explicitly impossible under the current policy scheme and is aggravated by the fact that the euro zone countries trade mostly with each other. Prolonged high unemployment is guaranteed as peripheral countries deleverage their debts with low domestic demand.

Meanwhile, the damage being wrought on the peripheral econ-omies reduces their medium to long term potential and the euro zone becomes ever more suboptimal as a currency area.

Far from over✎ Even Comfort Hvinden

THE Euro CrISIS:

[ 9 ]

Figure ② : Falling apart. GDP index: Q1 2007 = 100 Source: ECB

Figure ① : Asymmetry? Unit Labour cost. Index: 2000 = 100 Source: ECB

80

90

100

110

120

130

140

150

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

SpainGreece

ItalyPortugal

Germany

75

80

85

90

95

100

105

110

115

120

2007 2008 2009 2010 2011 2012

Sweden

Italy

Germany

Ireland

Greece

[ 10 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

In the aftermath of the last decade’s economic crisis, most western nations are struggling with massive problems. One of the most urgent problems, especially in the majority of European nations, is un-employment. Governments, politicians and economists are proposing solutions. Underpinning their policies is that they advocate increased government control and regulation, in order to create oppor-tunities. Do the problems we are facing require such policies, or could there be a much simpler answer? Could the solution be found in the complete opposite direc-tion; less state intervention? In this article, I will discuss wages and unemployment. I will try to establish a solid understanding of what factors are causing unemployment. I will not be technical, but rather I will ask simple questions. At the end, I will discuss the future and what to expect.

What are wages?Common opinion seems to be that

workers are paid too little and executives too much. People also tend to think of wages as something “sacred”. Most people think of their jobs as one of the most im-portant parts of their lives. We depend on it to survive, thus personal feelings have a tendency to blur discussions about wages. Is it so, that wages are any different from other prices?

Labour is a scarce factor of production. Hence, it is bought and sold on the market

like any other commodity. It is unfortu-nate that wages should be differentiated from other prices in the language of eco-nomics. The price of labour is simply just a price. In addition to the fact that labour is a factor of production, it is also the source of disutility. Workers do not value work only in regards to the immediate satisfaction received in the form of a pay check, they must also take into consider-ation the cost of forgone leisure. Workers may, however, overcome this disutility in several ways. They could justify the disut-ility with working for a higher power, for the “common good”, or simply because it might make their minds and bodies strong. As stated above, a wage is noth-ing more than a price, the price for which workers are willing to sell their precious time and skills. Both workers and employ-ers engage in voluntary mutual beneficial trade, trading value for value. People work for the sole reason that they want to reap the fruits of labour.

Determination of wagesThe most obvious and easy way for work-

ers to compete is by the price they charge for their labour. Furthermore, workers can compete on efficiency or other attri-butes. Ultimately, all relates to the price paid. Based on the continuous competi-tion between workers and employers, mar-kets will ultimately determine the correct price. Each individual is special in its own sense and therefore employers will value each individual differently. It is the abun-dance of a certain skill or attributes, that plays the most important part in the deter-mination of wage rates. Consider the sim-ple example of a film production; the actor obviously adds more value to the overall production than the cameraman, as cam-eramen are more common than high qual-ity actors. The sum of the prices an em-ployer pays for the factors of production, must therefore at least equal the price of the product he sells. There are several fac-tors which affect how this process works, and markets will determine the correct price. Important factors for capitalists are specialisation and division of labour. Specialised workers will lead to more ef-ficient firms, and ultimately increase the overall wealth of society.

Wage earners make up the majority of people in a society. It is ultimately wage earners who will determine the prices of goods and services. Wages in the respec-tive industries will be determined

Misconceptions of wages and unemployment

✎ Alexander Albert (Guest Writer)

A wage is nothing more than

a price

[ 11 ]

by the consumer. In a free market, wages across industries will tend to equal over time. Businessmen are under the neces-sity of producing what consumers ask for, and of selling goods at prices the consum-ers can afford and are willing to pay. It is human action working at its finest. This is one of the most important economic prin-ciples. This principle is, sadly enough, con-stantly violated by highly ranked econo-mists.

When the market determines wage rates it also sets the ceiling of wages. The ceiling of wages will be determined at the instant labour being bought and sold. It also rest on prices of all other complemen-tary factors of production. In a changing economy, there are several factors affect-ing such relationships of prices. We have to take into consideration employers and workers time-preferences, and also their outlooks for the future. In addition, wages depend on the workers ability and motiva-tion for moving, acquiring new set of skills, gaining education and their personal value of leisure.

Unemployment and what it meansFollowing the principle of supply and

demand, unemployment tells us that the supply is greater than the demand. The de-mand for a commodity is usually low when the price is unsatisfactory. A producer would usually lower the price on his prod-ucts if he observes that the demand for his

products is decreasing. The same princi-ple holds for workers, it works, however, in the opposite direction. Workers would offer their labour at a lower price in order to attract employers to demand their ser-vices.

The truth about unemploymentAs the chart above shows, unemploy-

ment rates vary from 4.5 % to as high as 27 %. The situation is quite bleak and utterly disturbing. The implications such levels of unemployment have on Europe, and soci-eties in general, are disastrous. Moreover, all income that is derived from taxation

and used in the public sector should be regarded as extremely non-productive for society. The reason is simple: The public sector is detached from the pri-vate sector's requirement of profitability. Therefore, the public sector leads to large inefficiencies. This will lead to a waste of society`s resources. To measure real un-employment one only needs to examine who are the producers in the economy and subtract the number of people who are able and willing to produce but who are not employed. Hence, current official unemployment rates deceive the real situ-ation in the labour markets.

What could cause unemploy-ment to reach such levels?

If we assume that people need to work to be able to live and prosper, every per-son able and willing to work would be employed in a free market. Hence, real un-employment rates would tend to get close to zero. The current situation tells us that something is not working properly. The root to the problem can be traced back to several features in the economy. The main one is regulation of labour markets. We start by looking at the most popular of them all: Minimum wage laws. A good in-tended policy with outcomes opposite of their intentions.

A minimum wage law is essentially a law making it illegal to hire someone at a rate lower than what is set by the

The public sector is detached from the

private sector's require-ment of profitability. Therefore, the public sector leads to large

inefficiencies

ã Unemployment. (*September 2012, **October 2012, ***Q 3 2012) Source: EUROSTAT

5% 5% 5% 6% 7% 7% 7% 7% 8% 8% 8% 8%10% 10% 11% 11% 11% 11% 11% 12% 12% 13%

14% 14% 15% 16% 16%

26% 27%

0%

5%

10%

15%

20%

25%

30%

AT LU DE NLRO M

T BE CZUK*

DK FI SEEE** SI FR PL

EU27HU** IT

EA17BG LT CY

LV*** SK IE PTEL* ES

[ 12 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

government. The worst part of such laws is that it can deprive man of the ability to work. Most importantly, it hurts the group of people the minimum wage law is intended to help, namely the unskilled and the young. The main sources of ac-quiring important and highly valuable skills are by getting work experience. This will allow workers to gain highly valuable skills, making them more attractive for fu-ture employers. If minimum wages are set above the unhampered market rate, unem-ployment will follow.

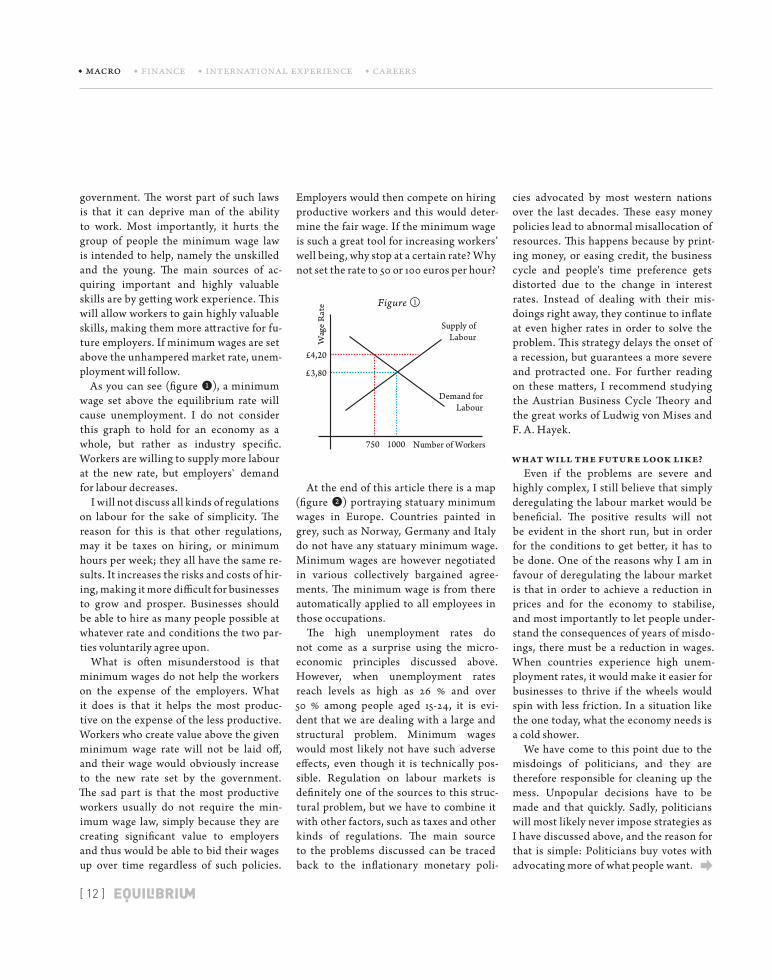

As you can see (figure ❶), a minimum wage set above the equilibrium rate will cause unemployment. I do not consider this graph to hold for an economy as a whole, but rather as industry specific. Workers are willing to supply more labour at the new rate, but employers demand for labour decreases.

I will not discuss all kinds of regulations on labour for the sake of simplicity. The reason for this is that other regulations, may it be taxes on hiring, or minimum hours per week; they all have the same re-sults. It increases the risks and costs of hir-ing, making it more difficult for businesses to grow and prosper. Businesses should be able to hire as many people possible at whatever rate and conditions the two par-ties voluntarily agree upon.

What is often misunderstood is that minimum wages do not help the workers on the expense of the employers. What it does is that it helps the most produc-tive on the expense of the less productive. Workers who create value above the given minimum wage rate will not be laid off, and their wage would obviously increase to the new rate set by the government. The sad part is that the most productive workers usually do not require the min-imum wage law, simply because they are creating significant value to employers and thus would be able to bid their wages up over time regardless of such policies.

Employers would then compete on hiring productive workers and this would deter-mine the fair wage. If the minimum wage is such a great tool for increasing workers’ well being, why stop at a certain rate? Why not set the rate to 50 or 100 euros per hour?

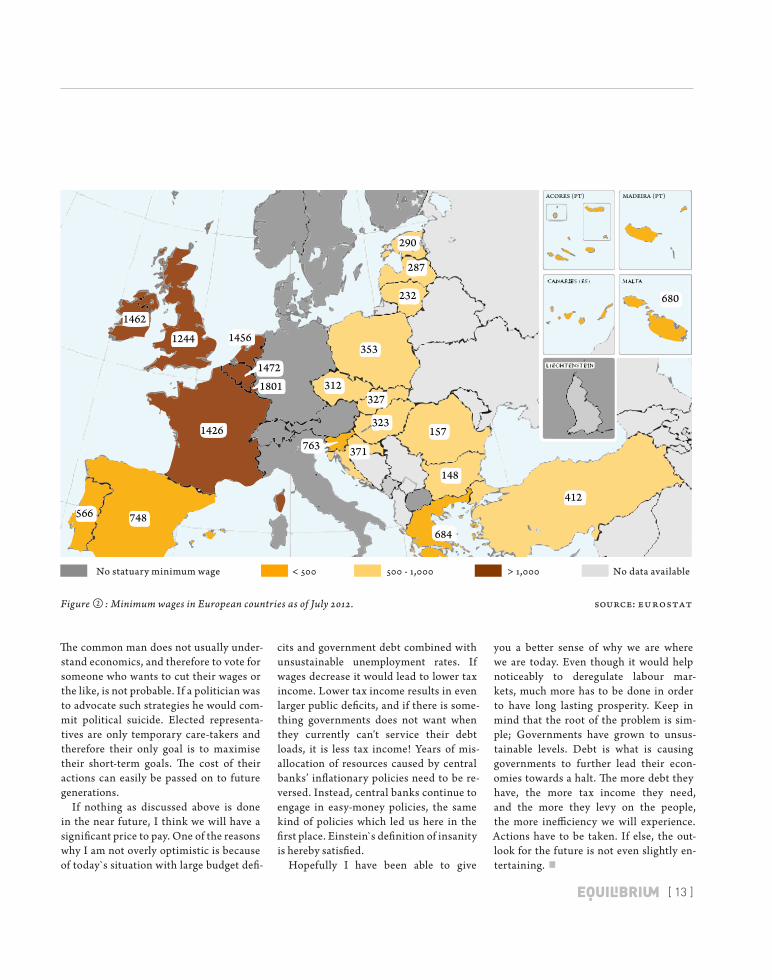

At the end of this article there is a map (figure ❷) portraying statuary minimum wages in Europe. Countries painted in grey, such as Norway, Germany and Italy do not have any statuary minimum wage. Minimum wages are however negotiated in various collectively bargained agree-ments. The minimum wage is from there automatically applied to all employees in those occupations.

The high unemployment rates do not come as a surprise using the micro-economic principles discussed above. However, when unemployment rates reach levels as high as 26 % and over 50 % among people aged 15-24, it is evi-dent that we are dealing with a large and structural problem. Minimum wages would most likely not have such adverse effects, even though it is technically pos-sible. Regulation on labour markets is definitely one of the sources to this struc-tural problem, but we have to combine it with other factors, such as taxes and other kinds of regulations. The main source to the problems discussed can be traced back to the inflationary monetary poli-

cies advocated by most western nations over the last decades. These easy money policies lead to abnormal misallocation of resources. This happens because by print-ing money, or easing credit, the business cycle and people's time preference gets distorted due to the change in interest rates. Instead of dealing with their mis-doings right away, they continue to inflate at even higher rates in order to solve the problem. This strategy delays the onset of a recession, but guarantees a more severe and protracted one. For further reading on these matters, I recommend studying the Austrian Business Cycle Theory and the great works of Ludwig von Mises and F. A. Hayek.

What will the future look like?Even if the problems are severe and

highly complex, I still believe that simply deregulating the labour market would be beneficial. The positive results will not be evident in the short run, but in order for the conditions to get better, it has to be done. One of the reasons why I am in favour of deregulating the labour market is that in order to achieve a reduction in prices and for the economy to stabilise, and most importantly to let people under-stand the consequences of years of misdo-ings, there must be a reduction in wages. When countries experience high unem-ployment rates, it would make it easier for businesses to thrive if the wheels would spin with less friction. In a situation like the one today, what the economy needs is a cold shower.

We have come to this point due to the misdoings of politicians, and they are therefore responsible for cleaning up the mess. Unpopular decisions have to be made and that quickly. Sadly, politicians will most likely never impose strategies as I have discussed above, and the reason for that is simple: Politicians buy votes with advocating more of what people want.

Supply ofLabour

Demand forLabour

Number of Workers750

£3,80

£4,20

1000

Wag

e R

ate Figure ①

[ 13 ]

No statuary minimum wage < 500 500 - 1,000 > 1,000 No data available

The common man does not usually under-stand economics, and therefore to vote for someone who wants to cut their wages or the like, is not probable. If a politician was to advocate such strategies he would com-mit political suicide. Elected representa-tives are only temporary care-takers and therefore their only goal is to maximise their short-term goals. The cost of their actions can easily be passed on to future generations.

If nothing as discussed above is done in the near future, I think we will have a significant price to pay. One of the reasons why I am not overly optimistic is because of today`s situation with large budget defi-

cits and government debt combined with unsustainable unemployment rates. If wages decrease it would lead to lower tax income. Lower tax income results in even larger public deficits, and if there is some-thing governments does not want when they currently can't service their debt loads, it is less tax income! Years of mis-allocation of resources caused by central banks’ inflationary policies need to be re-versed. Instead, central banks continue to engage in easy-money policies, the same kind of policies which led us here in the first place. Einstein s definition of insanity is hereby satisfied.

Hopefully I have been able to give

you a better sense of why we are where we are today. Even though it would help noticeably to deregulate labour mar-kets, much more has to be done in order to have long lasting prosperity. Keep in mind that the root of the problem is sim-ple; Governments have grown to unsus-tainable levels. Debt is what is causing governments to further lead their econ-omies towards a halt. The more debt they have, the more tax income they need, and the more they levy on the people, the more inefficiency we will experience. Actions have to be taken. If else, the out-look for the future is not even slightly en-tertaining.

Figure ② : Minimum wages in European countries as of July 2012. Source: EUROSTAT

1462

1244 1456

1472

1801

1426

748566

763

312327

353

232

287

290

323157

680

148

684

412

371

Advertisement

BenefitsOur members can get great bank- and insur-ance deals with DnB, including free computer insurance, as well as a telephone based advi-sory service (tlf 04700 or see www.medlems-radgiveren.no). You get a free subscription to our scientific journal, Samfunnsøkonomen, as well as the opportunity to attend our highly regarded conferences at a reduced price.

signing a contract? The Norwegian Association of Economists is on hand to give you tips and advice before you sign your first contract.

Wondering aBout Wages?The Norwegian Association of Economists’ yearly wage statistics is a useful tool when you’re negotiating wages with your employer. We have a network of work place represen-tatives in the public sector that can help you negotiate your wages. The Norwegian Associa-tion of Economists is part of The Federation of Norwegian Professional Associations (Aka-demikerne), which is the primary Norwegian organisation dedicated to improving salary and working conditions for professionals with a higher education. For more information about Akademikerne, please read up on their website: www.akademikerne.no.

conferencesThe Norwegian Association of Economists holds several conferences and seminars throughout the year, including the well-known Monetary Policy Symposium (Valutaseminaret) and The Researchers’ Annual Meeting (Forsker-møtet). These conferences are a great oppor-tunity to meet working economists, who may give you the inspiration you need to focus on a special area of interest.

“Kandidattreffet”Perhaps the most important reason you should join our organisation is the chance to attend the Students’ Annual Recruitment Meeting. This is a one-day meeting and includes lectures, case working and speed interviews with poten-tial employers. Several of our student members have been offered jobs after attending speed interviews. We have an established student network and are present at several Norwegian universities, including the University of Bergen (UiB), The University of Oslo (UiO), The Nor-wegian University of Science and Technology (NTNU), and The University of Life Sciences (UMB).

so what are you waiting for? Join us today!

are you an economics student? If so, you may want to consider joining The Norwegian Association of Economists (Sam-

funnsøkonomene), a professional membership association organising people with a higher degree in economics (Masters degree or higher), as well as students of economics. We can help you

throughout your study period, student membership is only 300NOK!

[ 15 ]

Currently Apple Inc., the world’s largest listed company by market capitalisation, has 54 analysts tracking their performance.

Ever since the late mastermind Steve Jobs introduced the i-products to the market, analysts’ estimates for the company performance have gone higher every quarter, without looking down. Until recently. For the last five months the share price has seen a near 40% collapse since its 52-week high, just south of $700. Apple still continue to bleed from its “bombshell” quarterly re-sults, just below market expectations. The last time Apple missed their estimate for a second successive quarter was ten years ago, in 2003. Yet, with a growth estimate of around 60% last year such a high price (relative to earnings) could be considered reason-able. However, what has happened over the autumn and winter is a classic play of market irrationality or humans behaving like hu-mans. By mid-August last year, analysts had slashed their growth estimates for this year’s EPS growth by two-thirds. Nonetheless, while the price was tumbling over the next nine weeks in a row, all you could hear on Bloomberg, FT or any other financial re-lated news-provider was analysts literally every day telling us how cheap Apple was at 650, then 600, then 550 and so on. So, one might wonder why the guys who actually makes the estimates in the first place, after cutting the growth rates from 60% to 20%, were on T V telling you to keep buying the stock?

One does not need a Harvard degree to work out the relation-ship between a decline in growth and what is going to happen to the share price of a company, yet today there are still 39 analysts recommending buying A APL shares. Whereas the analysts are watching Apple more carefully than ever, this article is going to turn the tables and direct its attention on the market and to the analyst themselves. As introduced above, understanding why you should be very critical about any estimate or forecast is rather es-sential to any investment-related action. Furthermore, in the fol-lowing sections, several human behaviour phenomena are intro-

duced, hopefully offering some mind-tinkering revelations that should be helpful to anyone investing capital in the markets.

Why we suck at probabilities

A rather fair assumption in the wake of the late 2008 crisis is that the financial sphere includes a population who, indeed, has a lot of confidence in their own abilities. Alas (and perhaps more surprisingly) in the same population, a somewhat innumeracy is also rather common. Suppose the weather forecaster on T V pre-dicts (say, with 80% probability) a clear sky tomorrow because of little wind and increased pressure (air density). The next morning you arrive at work soaking wet, cursing a certain anchor-man’s in-competence for not suggesting taking the umbrella. Concluding that the forecaster is unreliable based on a single instance is the

“data beats your lying eyes”-fallacy; forgetting that an 80% proba-bility of something happening also implies a 20% chance of it not happening, i.e. no reason to feel surprised by rain, unfortunately. Similarly, as will be introduced throughout this article, the hu-man mind prefer heuristics or comprehensible stories, and are (es-pecially) prone to overlooking logic when it comes to probabili-ties and decision-making with stakes (risks) included. It turns out that even if you are the CEO of a Fortune 500 company, an elite equity analyst or a graduate trading your precious savings, when faced with choices and assessments involving risk and probabili-ties, your decisions will often be based on heuristics, and not the

“rational optimal choice”. Heuristics are everyday simple men-tal “shortcuts”, possibly deviating from logic, which people base (complex) decisions on. In an economic framework, the most promising ideas come from what is called prospect theory, intro-duced in the late 1970’s by Daniel Kahneman and Amos Tversky. Their seminal work on behavioural finance, also later awarded the Nobel Memorial Prize in Economic Science (2002), offers some interesting contrasts from the conventional textbook alter-

Why being a turkey before Thanksgiving is

not a good idea✎ Morten Fylkesnes

[ 16 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

native; expected utility theory – where the rational agent operates regardless of the reference point. (E.g. with a 98% probability to win, would you bet $10 to win $100? What if it was $1,000,000 to win $10,000,000? If you are indifferent between the two bets, you are likely either very rich or poor with numbers, possibly both).

Another phenomenon, particularly found in social science and fields with unexpected and ambiguous events occurring, is the

“narrative fallacy”; a preference for stories to data. Events does not always go down the road as we had anticipated in the first place. Therefore, we are often trying to explain history by evolving a story around what happened or fitting history neatly into a predetermined story (cherry picking) – or both. However, the financial market is an organic creature by humans and not an exact pre-dictable science. For that reason, dealing effectively within such a context requires the acceptance of randomness and its influence (which cannot a-priori be in-cluded in a story).

Irrespective of model and theory, beating the market has never been easy. As introduced in the previous passage, most investors prefer coun-selling analysts, online forums, bankers, Google search engine, etc. rather than looking at the facts (empirically) when making investment decisions. Even if you do not believe in technical analysis (forecasting price levels by charting), why argue with the market? Don’t listen to the analyst (or anyone) on Bloomberg telling you to buy Apple when the price, P/E, EPS and so on is telling you otherwise. Let the market tell you the direction. In 99 out of a 100 cases, an analyst (even if he works for Goldman Sachs) does not know something the market doesn’t know. Don’t play the sucker’s game, at least get the odds in your favour: the trend is your friend, until it bends.

Curb your enthusiasmFor many market participants, certainly agents relying on fore-

cast models, uncertainty and volatility means bad news. In the smooth linear narrative world, surprises are usually on the down-side, e.g. when things are not “in line with consensus or expec-tations”. Such a system is very fragile and must be handled with care.

Let’s turn back to our 54 Apple analysts. The earnings game is all about accuracy, right? Analysts generally make a living of fore-casting company earnings four times a year, plus recommending some market over-performers in-between. The delinquent part

however, is the incentive to not be worse than the other analysts and not hurting the overhead-business (i.e. banking and mergers and acquisitions activity with the respective company), rather than being correct. Specifically, it hurts an analyst a lot more to be completely off (blowing his reputation and possibly being replaced), then it yields him credibility to be in line with oth-ers (keeps the job). Why take the risk? One of the killer trades last decade would have been shorting Lehman Brothers in 2008. Surely, someone following the financial sector and in particular Lehman would spotted some forthcoming gloom and doom, and

recommend a sell? Turns out, in the beginning of the year, there were 17 analysts covering Lehman. The break-

down was nine had "hold," five at "buy" and two had "strong buy" and by headcount, only one

had sell (although, this recommendation came not of fear of collapse but because it

was seen as overvalued). In fact, a paper by Pablo Fernández López, and Javier Aguirreamalloa Arízaga published last year, confirms the herd mentality,

“Indeed, only one out of a total of 106 (emphasis mine) reports issued

by analysts between January and September of that year recommended

selling Lehman stock.”

Another human behaviour effect enlightened by prospect theory is anchoring – When estimating a num-

ber (say, a distance, a percentage, a stock index level or a share price) people tend to start from an offered (but not necessarily applicable) available number. I.e. is the kilometres of road in the U.S more or less than 150,000,000 km? By the same fallacy, when dealing with confidence intervals, say, asked to estimate a 98% range, people still miss the correct answer 30-40% of the time, lacking enough deviation around their best estimate. (Try make a 98% upper and lower boundary for the question in italic above. The answer is found at the bottom of this page).

Forecasts and estimates may give you a ball park clue of where a particular stock or index could be heading, but even if being a his-torical, statistical or educated estimate, it is still just an estimate, if the market disagrees, you’re in trouble. Again, and sadly for investors, the same anomaly described above applies to brokers

“hot stock” or best picks of the year, those usually covering finan-cial front pages in January. A short backtesting done by The Wall Street Journal in 2011, looked at the performance of the 10 most cherished (with most buy recommendations) and most loathed stocks of Wall Street analysts for the impending year. For

(Correct answer, U.S .road length 6,550,030.08 kilometres or 4.07 million miles.)

Photo: Dennis Skley

[ 17 ]

2010 and 2009 the favourite 10 returned 24% (13%) and 22% (26%) percent respectively, with the index return in parenthesis. Not bad, but here’s the caveat, including the -10- most hated stocks in your portfolio had yielded you 32% and 70% (!) over the same two years (going back to the crisis year 2008, the numbers are about equal for all three portfolios).

The lessons here is that as humans we are comfortable being al-most right most of the time, forgetting about those 5% - 2% prob-ability of, say, rain, missing an earnings estimate, or a Greek de-fault. The issue is easily transferable to other domains that might help for amplification. Consider a doctor or surgeon. Even if he has the remedies for your everyday ailments (infections, head-ache, allergies, stitching, cosmetic surgery etc.), his usefulness ultimately comes down to detecting (and curing) the low-prob-ability but high impact illnesses, (think cancer, heart diseases or other complex/emergency interventions). Same applies to driv-ing, most of the time driving without a seatbelt would not harm you, except that one time. These are areas where the downside is typically very large (perhaps the largest) and upside is limited (status quo). Fortunately, in financial markets, we have the same asymmetrical options, but also to the upside. The final section of-fers a primer in unpredictability and how uncertainty and shocks plays an underappreciated important role in our lives.

The Black Swan theory and the turkey500 years ago, an elite called Renaissance Men were the go-to

guys for pretty much anything challenging. Boasting expertise in several different subjects, gentlemen such as Newton, Galilei, Da Vinci, Leibniz, were the so-called polymaths (leading experts in many scientific fields). And in 16th century, there were still many unsolved mysteries (spherical Earth, algebra, exploration and so on). Some questions and happenings where thought of as not fea-sible or impossible, even for polymaths, and sometimes coined as black swans, something that was yet to be seen in the Old World (Europe) at that time. However, since the Dutch explorer Willem de Vlamingh discovered black swans in Australia in the 17th century, the term has been used with regards to falsification of a proposition and debunking alleged beliefs (via negativa). In 2004 Nassim Nicholas Taleb introduced the Black Swan Theory in his book, Fooled by Randomness. Taleb, a senior derivatives trader turned scholar, applied this metaphor to the financial domain and extended it to other areas in his 2007 book The Black Swan. Despite presented with two books on the subject, people are still struggling to understand the fundamental idea behind it. A 2007 assertion from Taleb in the New York Times may very well serve as illumination for our purpose too,

"What we call here a Black Swan (and capitalise it) is an event with the following three attributes. First, it is an outlier, as it lies outside the realm of regular expectations, because nothing in the past can convincingly point to its possibility. Second, it carries an extreme 'impact'. Third, in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it ex-plainable and predictable."

"I stop and summarise the triplet: rarity, extreme 'impact', and retrospective (though not prospective) predictability. A small number of Black Swans explains almost everything in our world, from the success of ideas and religions, to the dy-namics of historical events, to elements of our own personal lives."

Pay close attention here, by definition we are not able to pre-dict or model these Black Swans (the first attribute) or their im-pact (second), but we often think otherwise (third, particularly applies for finance and especially equity analysts in January). But as humans and with heuristics as our decision-making tool, a neat story, some nice charts and an analyst (or two) on the phone claiming that Apple has not failed on earnings in the last 10 years, often convince us to think that it’s not going to happen this time either and commit capital accordingly.

Many turkeys currently residing in (but not restricted to) North America are fed by their butcher every day. And each day the butcher comes over handing them nourishment, the turkeys become more and more convinced that all is well and the butcher is just being nice, giving them a free lunch (although this should ring a bell). After a thousand days, say, the morning of November 24 (a.k.a. T-2), the butcher comes over for a special occasion, Thanksgiving. The turkey’s statistical assurance that the butcher was never going to hurt him, was hit by a Black Swan Event (from the turkey’s point of view).

Throughout this article we have been acquainted with several heuristics and fallacies that humans often have a habit of using. Although these are part of our natural behaviour as humans and can often be both precise and effective, it turns out they are not particularly fruitful for investing purposes. The key take-away lesson is, a narrative cause and effect approach, be it as an analyst, investor or a turkey, is often unjustified and ill-advised (possibly dangerous), especially in a capital market setting. As Taleb puts it,

“You are worse off relying on misleading information than on not having any information at all. If you give a pilot an altimeter that is sometimes defective he will crash the plane. Give him nothing and he will look out the window.”

[ 18 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

In aftermath of the Lehman Brothers collapse and the subse-quent economic turmoil, the economic environment has been characterised by ongoing challenges and changing regula-tions. On the one hand, the Basel III requirements, which advocate for stronger equity ratios and lower levels of debt financing, have been implemented. On the other hand, ma-jor investment banks such as Goldman Sachs are currently advising their clients to ‘’borrow as much as they can for as long as they can.’’ Thus, the problem many banks are facing today is measuring the risk trade-off between equity and debt financing as they seek to find an optimal capital structure in an environment with excess liquidity and low interest rates.

Recent market developmentsFirms that want to raise capital have three main choices. They

can issue shares, take on debt (issue bonds and take out bank loans) or retain a bigger portion of their profits (increasing the plowback ratio). Most companies’ capital structure consists of a mix of debt (20 %), equity (10 %) and plowback (70 %). After the financial meltdown of 2008, however, the following economic tur-moil in Europe triggered activity in the corporate bond markets. As interest rates were historically low, investor demand for corpo-rate bonds had increased due to low government bond yields. In 2013, continued accommodative monetary policy, higher equity valuations, a pickup in inflation expectations and stronger M&A activity have led to a reversal of this trend as equity inflows for the first time since 2008 have surpassed fixed-income inflows.

Equity versus debt financingConventional thought among regulators and policymakers to

date has been that lowering the level of debt financing reduces a firm’s exposure to risk. Hence, policymakers have for the last five years been urging entities to raise more capital, improve equity ratios and deleverage balance sheets. According to the OECD the global GDP will shrink by .15-.5 % when the Basel III require-ments kick in as banks will reduce lending in order to strengthen their capital buffers. This process has already started as equity and reserves as a percentage of assets in the euro zone banking sector has risen since last summer.

The question as to whether the benefits of this industry restruc-turing outweigh the potential costs on global GDP is worth an-alysing. In corporate finance, the management’s main goal is to maximise their shareholders value by creating rates of return that exceed their cost of capital. The restraint is to maximise the share price while also designing an effective capital structure to sup-port the corporation’s strategy and minimise the risk of financial distress.

Assume a world without taxes, transaction costs, bankruptcy risks and differences in borrowing costs. There are two firms whereas one of them is unlevered (i.e. financed by equity only) and the other one is levered. Both firms deliver the same operat-ing income. The investor can adopt an investing strategy that is as follows: buy 10 % of the shares of the unlevered firm, and be entitled to 10 % of the firm’s profits. For the leveraged firm the in-vestor can buy the exact same fraction of both the debt and

Financial leverage and capital structure

✎ Amaar Malik

[ 19 ]

equity. The payoff will be the same for both firms. Given efficient markets where both strategies yield the same pay off, they must also have the same cost. Thus, given perfect markets where every-body can borrow at the same interest rate, investors can cancel out the effect of changes in a firm’s capital structure. This is the main argument in the Modigliani and Miller theorem that states that the market value of any firm is independent of its capital structure.

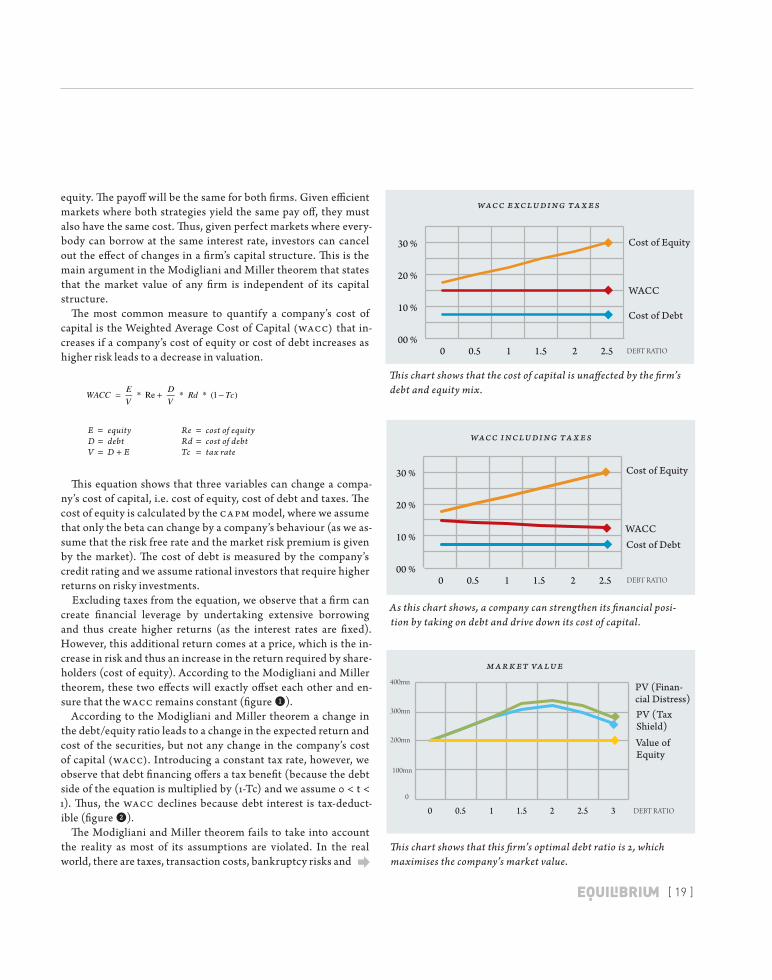

The most common measure to quantify a company’s cost of capital is the Weighted Average Cost of Capital (WACC) that in-creases if a company’s cost of equity or cost of debt increases as higher risk leads to a decrease in valuation.

This equation shows that three variables can change a compa-ny’s cost of capital, i.e. cost of equity, cost of debt and taxes. The cost of equity is calculated by the CAPM model, where we assume that only the beta can change by a company’s behaviour (as we as-sume that the risk free rate and the market risk premium is given by the market). The cost of debt is measured by the company’s credit rating and we assume rational investors that require higher returns on risky investments.

Excluding taxes from the equation, we observe that a firm can create financial leverage by undertaking extensive borrowing and thus create higher returns (as the interest rates are fixed). However, this additional return comes at a price, which is the in-crease in risk and thus an increase in the return required by share-holders (cost of equity). According to the Modigliani and Miller theorem, these two effects will exactly offset each other and en-sure that the WACC remains constant (figure ❶).

According to the Modigliani and Miller theorem a change in the debt/equity ratio leads to a change in the expected return and cost of the securities, but not any change in the company’s cost of capital (WACC). Introducing a constant tax rate, however, we observe that debt financing offers a tax benefit (because the debt side of the equation is multiplied by (1-Tc) and we assume 0 < t < 1). Thus, the WACC declines because debt interest is tax-deduct-ible (figure ❷).

The Modigliani and Miller theorem fails to take into account the reality as most of its assumptions are violated. In the real world, there are taxes, transaction costs, bankruptcy risks and

This chart shows that the cost of capital is unaffected by the firm’s debt and equity mix.

As this chart shows, a company can strengthen its financial posi-tion by taking on debt and drive down its cost of capital.

This chart shows that this firm’s optimal debt ratio is 2, which maximises the company’s market value.

E = equityD = debtV = D + E

Re = cost of equityRd = cost of debtTc = tax rate

00 %

10 %

20 %

30 %

0 0.5 1 1.5 2 2.5

00 %

10 %

20 %

30 %

0 0.5 1 1.5 2 2.5

0 0.5 1 1.5 2 2.5 3

WACC EXCLUDING TA X ES

WACC INCLUDING TA X ES

MAR K ET VA LUE

Cost of Equity

Cost of Debt

WACC

Cost of Equity

Cost of DebtWACC

PV (Finan-cial Distress)PV (Tax Shield)Value of Equity

Debt Ratio

Debt Ratio

100mn

200mn

300mn

400mn

0

Debt Ratio

= + −WACC EV

DV

Rd Tc* Re * * (1 )

[ 20 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

differences in borrowing costs. Gathering all of those variables in the parameter PV (Financial Distress) the value of the firm can be broken into the sum of three parts (figure ❸):

Although, the cost of financial distress varies heavily from firm to firm, and is difficult to estimate, the theoretical simplification provides some valuable insight. Given that the Modigliani and Miller theorem’s assumptions do not hold, the main point is that the cost of debt is not linear. As a firm's debt level increases, the costs connected to financial distress and the total cost of capital increases too. The optimal debt ratio is given at the level of the present value of the tax shield of further borrowing is exactly off-set by the increase in the present value of the cost of financial dis-tress. Hence, a firm can find its optimal capital structure, and can maximise its market value by choosing an optimal debt/equity mix.

A vital point is that the debt/equity ratio differs from firm to firm. Companies with tangible assets and a large amount of tax-able income, such as ExxonMobil, usually have high debt ratios. Companies like Facebook, which are characterised by risky and intangible assets have lower debt ratios and rely more on equity financing. As the banks’ main assets are financial assets such as government bonds, and they also generate a large taxable income to shield, banks generally benefit from higher debt ratios than other firms.

Implications of new regulationIntroducing new capital requirements such as the Basel III

might lead to a deviation from the banks’ optimal capital struc-tures. This can lead to further mispricing in a market where Goldman Sachs, JPMorgan Chase, Morgan Stanley, Credit Suisse and Deutsche Bank all have price/book ratios that are be-low one (which implies that the market prices their assets lower than their accountants). Furthermore, introducing one-size-fits-all capital requirements, which the Basel III requirements aim to

do, might squeeze out the smaller players in the banking sector in a time regulators are trying to reduce the systemic risk by break-ing up the ‘’too big to fail’’ institutions. Thus, smaller players will suffer as their profitability takes a hit (as lending out becomes rel-atively more expensive) and they face the risk of being acquired by the bigger banks.

Implementing such reforms in an environment where banks’ profitability has been slashed and the industry is characterised by job cuts, bonus stops and smaller shareholder returns has histori-cally led to banks engaging in risk-taking in their search for yield as they are under pressure to generate a return on equity that exceed their cost of capital (WACC). Moreover, there are indica-tions of the re-emergence of shadow-banking and risky off bal-ance sheet activities as banks look to cut how much it sets aside to cover defaults, while also keeping assets such as loans on their balance sheets. Ultimately, what we already are seeing is that banks are announcing to specialise in only their niche areas and thus undermine their economies of scale benefit, which has been described as the only advantage of ‘’too big to fail’’ institutions by economists such as Paul Krugman.

SummaryDebt financing enables banks to leverage their balance sheets

and create higher returns on equity as the WACC declines. As banks hold a limited number of intangible assets and generate a large taxable income to shield, banks generally benefit from higher debt ratios than other firms. Although, borrowing seems beneficial in this environment with record-low interest rates, banks might not be able to take advantage of it as they are adapt-ing to new regulations and building capital strength. Thus, policy-makers have to ensure they do not become too aggressive imple-menting new capital requirements as banks might be tempted to engage in risk-taking in their search for yield. As banks are seek-ing to generate a return on capital that exceeds the cost of capital (WACC), capital restraints may force significant deviations from the banks’ optimal capital structures.

Banks generally benefit from higher debt ratios than other firms

Value = Equity + PV (Tax shield) + PV (Cost of financial distress)

Advertisement

Magazine

?Next issue: Autumn 2013

www.equilibriummagazine.no

Follow us on: www.fb.com/equilibriummagazine

[ 22 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

Derivatives are mystified instruments, which combined with their central role in the financial crisis of 2008, have resulted in massive attention. Some people endorse them, while others hate them. Warren Buffett referred to them as ''Financial weapons of mass destruction'' in his annual report for Berkshire Hathaway in 2002. There is now a debate going on as to whether derivatives are beneficial for the economy as a whole or not. This article will give a historical perspective on derivatives, as well as explaining some basic concepts.

The general definition of a derivative from Wikipedia is: “A de-rivative is a term that refers to a wide variety of financial instru-ments or contract whose value is derived from the performance of underlying market factors, such as market securities or indices, interest rates, currency exchange rates, and commodity, credit, and equity prices.”

One of the most basic derivatives is called a forward contract. A forward contract is an agreement to buy a certain good (com-modities, equities, interest rates etc.), at an agreed price, at some time in the future. One example could be a farmer selling the grain he will harvest in six months, today. The advantage of such a contract is that the seller of a forward contract secures his future income, and the buyer secures his future payment, at an agreed price. Another important feature with forward contracts, and most derivatives, is that the contract itself can be traded in the secondary market. This is probably one of the main reasons why such contracts occurred in the first place, as we will examine later on.

Another very important derivative is the option contract. An option is a contract where the buyer pays an amount for the right,

but not the obligation, to sell an underlying asset at an agreed price, at some agreed time in the future. Today, there exist numer-ous types of options with the two most common types being the European option and the American option. The European may only be exercised on expiration of the contract, but the American option can be exercised at any time until expiration.

Some highlights from the history of derivatives. In the book of genesis, chapter 29, Jacob was interested in mar-

rying Laban's daughter, Rachel. He agreed with Laban to work for seven years to get the right to marry Rachel. This can be seen as the first purchase of an option. The option premium being the seven years of labor, and the underlying good being Laban’s daughter, to which Jacob received the right, but was not obliged, to marry. The seller of the option was Rachel’s father Laban. This incident, which apparently took place around 1700 BC, is not only seen as the first option like agreement that we know of, but also the first default on such. At settlement date, Laban required Jacob to marry his older daughter Leah, as it was custom to give away the youngest daughter first. Jacob did marry Leah, but be-cause he still loved Rachel, he bought another option to marry Rachel, again, costing him seven years of labor. As bigamy was allowed at the time, Jacob ended up with two wives, and twelve sons. The debate among finance academics still goes on whether the contract Jacob purchased from Laban was a forward contract or an option; whether he was obliged to marry the daughter or if he had a choice, after working for seven years.

Another interesting story is from the first book of ''Politics'' by Aristotle in 350 BC. In par XI he tells about Thales of Miletus.

Financial derivatives:A historical perspective

✎ Fabian Harang

[ 23 ]

Thales was a poor man that was skilled in reading the stars. One winter he saw that there would be a great harvest of olives in the upcoming summer. Having little money, he gave deposits for the use of the olive-presses in Chios and Miletus. As no one bid against him, he won the auction at a bargain. When harvest time came, and many people wanted to use the presses, he could rent them out for any rate he wanted. Thales made a lot of money by in-vesting in something that could give a payoff in the future, a sort of a forward contract.

If you look closely in the history books you can probably find many stories like this, people agreeing on exchanging goods at some fixed “price” at some time in the future.

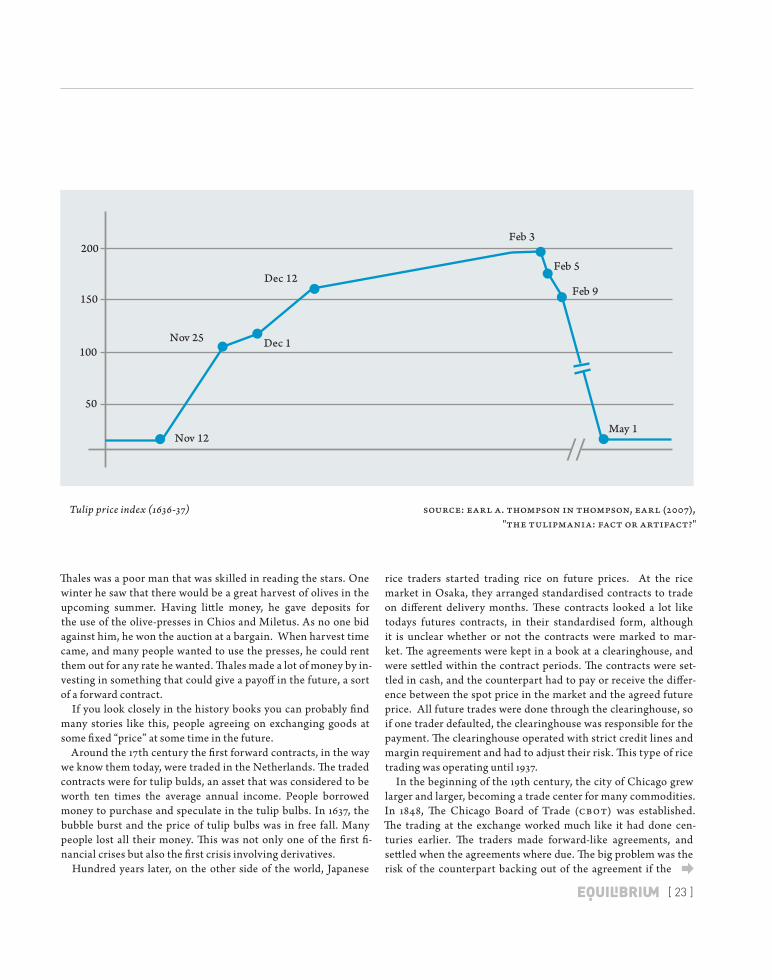

Around the 17th century the first forward contracts, in the way we know them today, were traded in the Netherlands. The traded contracts were for tulip bulds, an asset that was considered to be worth ten times the average annual income. People borrowed money to purchase and speculate in the tulip bulbs. In 1637, the bubble burst and the price of tulip bulbs was in free fall. Many people lost all their money. This was not only one of the first fi-nancial crises but also the first crisis involving derivatives.

Hundred years later, on the other side of the world, Japanese

rice traders started trading rice on future prices. At the rice market in Osaka, they arranged standardised contracts to trade on different delivery months. These contracts looked a lot like todays futures contracts, in their standardised form, although it is unclear whether or not the contracts were marked to mar-ket. The agreements were kept in a book at a clearinghouse, and were settled within the contract periods. The contracts were set-tled in cash, and the counterpart had to pay or receive the differ-ence between the spot price in the market and the agreed future price. All future trades were done through the clearinghouse, so if one trader defaulted, the clearinghouse was responsible for the payment. The clearinghouse operated with strict credit lines and margin requirement and had to adjust their risk. This type of rice trading was operating until 1937.

In the beginning of the 19th century, the city of Chicago grew larger and larger, becoming a trade center for many commodities. In 1848, The Chicago Board of Trade (CBOT) was established. The trading at the exchange worked much like it had done cen-turies earlier. The traders made forward-like agreements, and settled when the agreements where due. The big problem was the risk of the counterpart backing out of the agreement if the

ã Tulip price index (1636-37) Source: Earl A. Thompson in Thompson, Earl (2007), "The tulipmania: Fact or artifact?"

Dec 12

Nov 25

50

200

150

Nov 12

Dec 1

May 1

Feb 3

Feb 5

Feb 9

100

[ 24 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

prices moved too much. CBOT lacked a very important ingredient to make the trading efficient and secure to investors; the clearing-house. The reformation of CBOT came in 1864. Over 50 different standardised forward contracts were made with the exchange as counterpart to transfer the counterpart risk from investors to the exchange. This was very similar to what the Japanese did over 100 years earlier. In 1919, the Chicago butter and egg board, a spin-off of the CBOT, changed its name to Chicago Mercantile Exchange (CME) and allowed members to trade fu-tures. CME and CBOT have been the lead-ing exchanges for derivatives and com-modities to this day.

The Midas formulaThe next evolution in derivatives trad-

ing came through mathematics. The big question was, how can you set a price on a right, but not an obligation to buy something in the future? The first per-son to find a sensible answer to this question was the French mahematician Louis Bachelier. In his Ph.D. thesis, “The theory of speculation” published in year 1900, he used stochastic processes and Brownian motion to model random be-haviour in the markets. The theory was not well received in academia at that time. In the 1950’s, economist Paul Samuelson, a highly influen-tial economist, discovered Bachelier’s work. The word spread, and in a couple of years, everyone was using geometric Brownian mo-tion in their models on stock prices. Many people tried to calcu-late the value of the option by looking at the expected discounted pay-off, all of them using different discount rates. Often the dis-count rate was non observable, and would not serve well in real market situations. In 1973, Fischer Black and Myron Scholes de-rived what has been one of the most influential formulas in finan-cial history, the Black-Scholes model. By using stochastic calcu-lus, they derived a formula only dependent on actual observable data. The formula was based on the idea of perfectly hedging the option by buying or selling the underlying asset and a bond in the

right way to eliminate risk and replicate an option's pay-off. The model changed the financial world. It was easy to use, and seemed to give accurate prices. The traders endorsed the formula immedi-ately, and the volume in options trading took off. In 2008, the no-tional amount of all outstanding positions in the futures and op-tions market traded at an exchange was $81 trillion according to the Bank of International Settlements (BIS). The notional value of the over-the-counter derivatives was $615tn in 2009 according

to BIS.Now, 40 years after Black-Scholes,

we recently had a financial crisis that many say was caused by financial deriv-atives, in particular credit derivatives. Collateralised-debt-obligations (CDO) and Credit-default-swaps (CDS) are both seen as heavy contributors to the recent crisis. Derivatives often have complex features that are hard to understand and thus difficult to price right. The models can be misleading, and the skepticism among politician, regulators, investors and common people to these instruments is profound. Still the benefit that compa-nies and individuals achieve from using these instruments is huge. One thing his-tory has shown is the importance of the ability to store future value and hedge un-

wanted risk. In 2010 the Dodd-Frank act was signed by President Barack Obama. This act is the most significant change in financial regulation, since the great depression of the 1930s. It was legis-lated to enhance consumer protection, transparency and market efficiency. Still some people argue that the regulation can cause inefficiency in some market places because of its complicated na-ture and uncertainty. Financial regulation will increase financial innovation, and financial innovation will increase financial regu-lation. This spiral will certainly go in to the future. What we will see in the future is highly uncertain, but it will hopefully bring more transparency and efficiency while we get more instruments that are tailored for different purposes.

The benefit that companies and

individuals achieve from using

derivatives is huge

[ 25 ]

Approximately a quarter of all stock trading in Norwegian shares is now through alternative marketplaces. Cost, efficiency, infrastructure, latency and ano-nymity are the main advantages of trading through such marketplaces. The increas-ingly competitive nature of the market-place has contributed to a higher degree of fragmentation in trading. A typical agent may trade the same security on many dif-ferent platforms as she seeks to avoid mov-ing markets when carrying out big volume transactions.

Regulatory authorities are losing track of financial markets as markets are becom-ing fragmented. Traditionally, big volume transactions were carried out under regu-lated and transparent terms. Proliferation of alternative trading markets, however, has impaired market efficiency and raised issues concerned with transparency. In re-cent years, less than half of the total trad-ing in Norwegian equities have been car-ried out on the Oslo Stock Exchange, while as much as 25 % of the trades have been carried out in the dark. "Technological de-velopment and new regulations have been

the main drivers of the growth in alterna-tive marketplaces we have seen in recent years. It had not been basis for all the new platforms without a rapid development in technology" says Per Eikrem, a press con-tact and senior vice president of corporate communications at Oslo Stock Exchange.

Algorithmic tradingAlgorithmic trading is carried out by

the usage of computers in order to place orders on stocks and other securities. The software's settings dictate the circum-stances that must be present for an order to be executed. These settings may include absolute values that refer to time, price, or quantity. Once this pre-programmed cri-terion is fulfilled, the algorithm will place the order automatically. Due to the tech-nological development, the increase in use of algorithms has been a natural develop-ment in the global markets.

The European Markets in Financial Instruments Directive (MIFID) was im-plemented in 2007 and lead to increased competition in securities trading. As a result, a number of establishments of new

electronic marketplaces were created. The shares of the largest and most liquid com-panies on the Oslo Stock Exchange are now traded on several markets in Europe, most of which are located in London. This internationalisation has enabled al-gorithms to function simultaneously on multiple marketplaces, and thus take ad-vantage of time delays and mispricing on different marketplaces for the same secu-rity.

There are many reasons why algorith-mic trading has become more widespread. The most important ones, however, is the mathematical accuracy and cost-efficiency such pre-programmed algorithms offer. Furthermore, this service also offers in-vestors more options in terms of risk di-versification of trades. Some people argue that the rise in pre-programmed algorith-mic trading is a natural development as the increased sophistication in computer softwares has led to automation in several other industries as well. Furthermore, sup-porters of algorithmic trading have also highlighted the fact that their presence promotes efficiency by exploiting

alternative marketplaces

✎ Petter Kongslie

[ 26 ]

◆ Macro ◆ Finance ◆ International Experience ◆ Careers

market imperfections and short-term fluc-tuations in valuation.

"It is also challenging for firms to offer best execution for their customers as this requires that they must have lightning fast technology that can follow the order books (algorithms) of multiple markets si-multaneously. This has resulted in signifi-cant investments in networks and technol-ogy, while the revenues have been under pressure due to increased competition" is Eikrem`s verdict on the current situation.

High Frequency Trading (HFT) dif-fer from traditional algorithmic trading as these algorithms perform a very large number of orders and transactions in a short time. There may be several thousand orders, changes and transactions within seconds. These algorithms’ main goal is to make small low-risk profits several thou-sand times a day.

"Even the exchanges' revenues have de-clined as a result of the increased compe-tition and lower volumes in the markets after the financial crisis of 2008," says Eikrem.

OTCOver-the-Counter (OTC) market is an

alternative to stock trading as it encom-passes trading in unlisted companies. Trade is conducted among investors who meet directly for trading. This market has five players: companies, investors, bro-