Embed Size (px)

Citation preview

Investing in your Future

*

Equality for Women Measure (EWM)

2010-2013

Programme Guidelines

4th

Edition

January 2015

The Equality for Women Measure is funded by the European Social Fund (ESF) through the

Human Capital Investment Operational Programme 2007-2013 and the Department of Justice and Equality

EWM Programme Guidelines _____________________________________________________________________________________________________

Page ii

Table of Contents

Section 1: Introduction and Background .......................................................................... 1

Section 2: Project Implementation ..................................................................................... 3

2.1 Project Timeframes ......................................................................................................... 3

2.2 Project Plan ..................................................................................................................... 3

2.3 Changes to your Project Plan .......................................................................................... 3

2.4 EWM Project Participants ................................................................................................ 3

2.5 Participant Data for the European Commission ............................................................... 3

2.6 Pobal Supports ............................................................................................................... 4

Section 3: Monitoring & Non-Financial Reporting Requirements ................................... 5

3.1 Project Monitoring & Reporting Requirements ...................................................................... 5

3.2 End of Year Project Report ...................................................................................................... 5

3.3 ESF/HCIOP Annual Progress Report ..................................................................................... 5

3.4 Evaluation ................................................................................................................................... 6

Section 4: Information and Publicity ................................................................................. 7

4.1 Purpose ....................................................................................................................................... 7

4.2 Use of Logos .............................................................................................................................. 7

4.3 Acknowledgment of Funding/Text ........................................................................................... 9

4.4 Publications ................................................................................................................................ 9

4.5 Press Releases/Articles ............................................................................................................ 9

4.6 Protocol for Publicity Activities and Events ............................................................................ 9

4.7 Publicity Reporting ................................................................................................................... 10

Section 5: Recruitment and Employment for EWM funded positions ........................... 11

5.1 Recruitment & Selection ......................................................................................................... 11

5.2 Record Management ............................................................................................................... 11

Section 6: Approved Budget ............................................................................................ 13

6.1 Approval of Budget by Pobal ................................................................................................. 13

6.2 Key issues in compiling and monitoring Budgets ............................................................... 13

6.3 Changes to Budget and other Project Changes. ................................................................ 13

Section 7: Payment Process and Expenditure Returns ................................................. 15

7.1 Payment of Grant and Threshold Spend ............................................................................. 15

7.2 Tax Clearance Certificate ....................................................................................................... 15

7.3 Eligibility of Expenditure ......................................................................................................... 16

7.4 Financial Expenditure Returns .............................................................................................. 17

7.5 Interim (Exceptional) Drawdowns ......................................................................................... 19

Section 8: Categories of Eligible and Ineligible Costs ................................................... 20

8.1 Direct and Indirect Costs ........................................................................................................ 20

8.2 Salary and Wages Costs ........................................................................................................ 21

EWM Programme Guidelines _____________________________________________________________________________________________________

Page iii

8.3 Administration Costs ............................................................................................................... 21

8.4 Programme Costs ..................................................................................................... 21

8.5 Travel and Subsistence .......................................................................................................... 22

8.6 Participant Expenses .............................................................................................................. 22

8.7 Childcare costs......................................................................................................................... 23

8.8 Equipment ................................................................................................................................. 23

8.9 General Payments ................................................................................................................... 23

8.10 Ineligible Costs....................................................................................................................... 23

8.11 Revenue/Income/Receipts ................................................................................................... 24

8.12 Fraud ....................................................................................................................................... 24

Section 9: Public Procurement Procedures .................................................................... 26

9.1 Public Procurement Procedures............................................................................................ 26

Section 10: Apportionment of Costs ............................................................................... 28

Section 11: Books and Records....................................................................................... 31

11.1 Books and Records ............................................................................................................... 31

11.2 Retention of Records ............................................................................................................ 32

11.3 Receipts Book ........................................................................................................................ 32

11.4 Payments Journal .................................................................................................................. 32

11.5 Bank Reconciliation ............................................................................................................... 33

11.6 Petty Cash .............................................................................................................................. 33

11.7 Reconciliation of Income and Expenditure ........................................................................ 33

Section 12: Contract Conclusion ..................................................................................... 35

Section 13: Corporate Governance – Your Board of Directors ...................................... 36

Section 14: Audit and Verification Visits ......................................................................... 38

Section 15: Data Protection .............................................................................................. 40

Section 16: Freedom of Information ................................................................................ 41

Appendices: Appendix 1 Return Template Appendix 2 Drawdown Request Template Appendix 3 Receipts and Lodgements Template Appendix 4 Payments Journal Appendix 5 Outstanding Cheques and Lodgements Template Appendix 6 Sample Pobal Reconciliation from Financial statements to Returns Appendix 7 Sample Apportionment Policy Appendix 8 ‘Questionnaire to Gather Participant Data for the European Commission’ (Template G) Appendix 9 Public Procurement Review Report Appendix 10 ESF Information and Publicity Guidelines [see enclosed booklet] Appendix 11 ESF Certifying Authority Eligibility Rules Circular 1/2012 Here is the link to all 11 EWM Appendices.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page iv

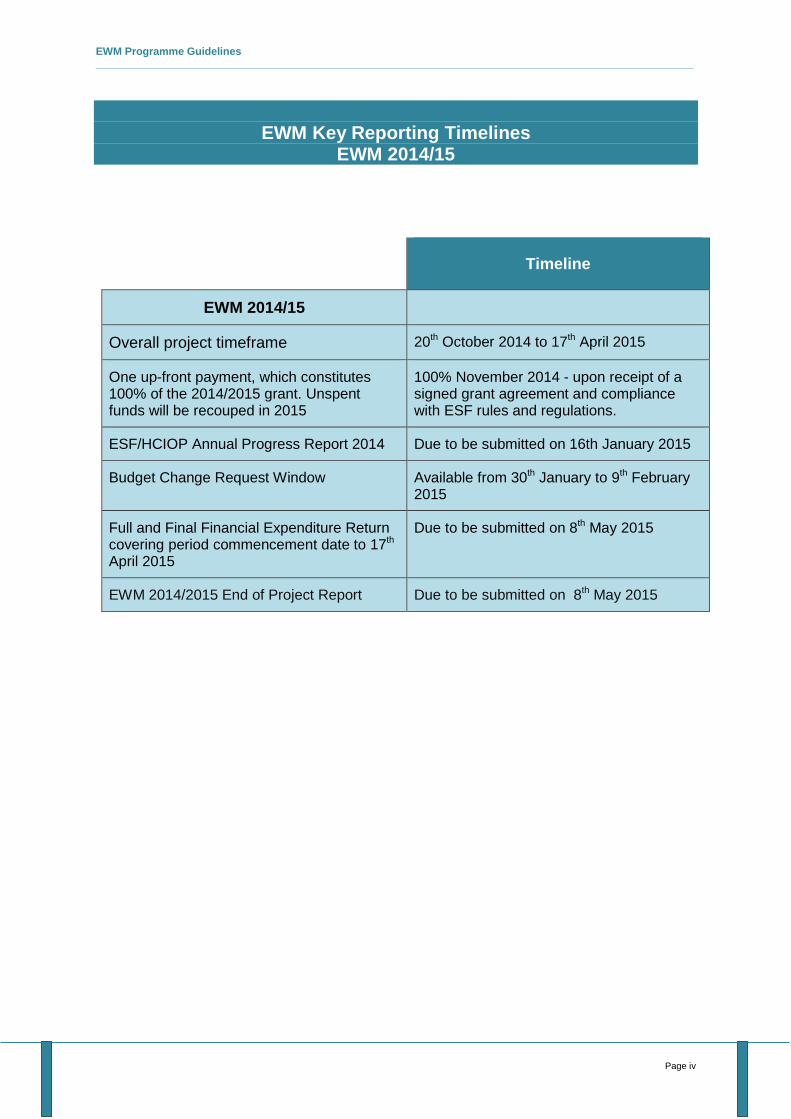

EWM Key Reporting Timelines

EWM 2014/15

Timeline

EWM 2014/15

Overall project timeframe 20th October 2014 to 17th April 2015

One up-front payment, which constitutes 100% of the 2014/2015 grant. Unspent funds will be recouped in 2015

100% November 2014 - upon receipt of a signed grant agreement and compliance with ESF rules and regulations.

ESF/HCIOP Annual Progress Report 2014 Due to be submitted on 16th January 2015

Budget Change Request Window Available from 30th January to 9th February 2015

Full and Final Financial Expenditure Return covering period commencement date to 17th April 2015

Due to be submitted on 8th May 2015

EWM 2014/2015 End of Project Report Due to be submitted on 8th May 2015

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 1

Section 1: Introduction and Background

The Equality for Women Measure (EWM) Programme Guidelines have been developed to provide information to grantees on the key requirements, policies and procedures relating to the administration and management of funding under EWM 2010-2013, which is co-funded by the European Social Fund (ESF) and the Department of Justice and Equality.

The content of the guidelines is informed by a combination of rules and regulations as stipulated by the ESF in relation to the administration and management of the Human Capital Investment Operational Programme (HCIOP), and the requirements of Pobal, who administers EWM on behalf of the Department of Justice and Equality.

The guidelines will be updated as and when the rules governing EWM or the policies and procedures change/update during the lifetime of the grant. The guidelines are divided into 16 sections. This is the 3rd edition of the guidelines with effect from October 2014.

Aims and Objectives of the Equality for Women Measure 2010-2013

EWM is a positive action programme for women, which aims to foster gender equality in accordance with the National Women’s Strategy 2007–2016. The strategic aim of the Measure is to “advance the role of women in the Irish economy and in decision making at all levels in accordance with the National Women’s Strategy 2007-2016.”

The objectives of EWM are to make funding available to support positive actions which:

Improve women’s access to education, training and personal development in preparation for employment

Support women who are undertaking entrepreneurial activity

Support women’s advancement in their employment including into decision-making roles in the organization.

The EWM is an initiative of the Department of Justice and Equality and is managed collaboratively between the Department and Pobal. The Measure is part-financed by the ESF under the Human Capital Investment Operational Programme 2007 – 2013.

EWM is organised around three separate strands, each with their own thematic focus, which are outlined below:

Strand 1: Access to Employment Aim: To provide women who are currently outside the labour market with the social skills, and/or education, and/or training to enable them to enter or return to the labour market.

Strand 2: Developing Female Entrepreneurship Aim: To support the development of women who are or want to become entrepreneurs.

Strand 3: Career Development for Women in Employment Aim: To support the provision of training and other developmental mechanisms to enable women who are in employment to advance their careers.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 2

EWM Funding 2010-2013 EWM Year 1 Under ‘EWM Year 1’, initial funding of up to €50,000, was awarded to 42 targeted projects which foster gender equality through the delivery of practical, customised, developmental supports. Projects were operational from autumn 2010 up until 30th June 2011. The projects supported a wide range of initiatives aimed at addressing areas of inequality within the labour force, or decision-making roles within the work-place and to support women undertaking entrepreneurial activity. When broken down according to strand, a total of 31 projects were funded under Strand 1 (Access to Employment), 10 projects under Strand 2 (Female Entrepreneurship) and 1 project for Strand 3 (Career Development for Women in Employment).

EWM Year 2 A total of 40 projects were successful in being awarded funding under ‘EWM Year 2’, to continue existing projects in line with original proposals. Year 2 covered the period from 1st July 2011 to 30th April 2012. A total of 29 projects were funded under Strand 1 (Access to Employment), 10 projects under Strand 2 (Female Entrepreneurship) and 1 project for Strand 3 (Career Development for Women in Employment).

Following on from this a total of 34 EWM projects were awarded funding under the ‘Year 2 Extension Phase,’ which ran from 01st May 2012 to 30th November 2012. The breakdown of the projects is as follows: EWM Strand 1 (25), EWM Strand 2 (8) and EWM Strand 3 (1). EWM 2013/2014 A total of 23 projects were successful in being awarded funding under ‘EWM 2013/2014,’ which is scheduled to run from July 2013 to 30th April 2014. Due to overall budgetary reductions it was only possible to invite the 25 projects who had been funded under Strand 1 (Access to Employment) of EWM to apply for the further phase of funding. For details of the projects funded under EWM 2013/2014 please refer to the ‘Directory of Projects’ which is available on the Pobal website. EWM 2014/2015 The Department of Justice and Equality (DJE) confirmed the availability of additional funds for 18 projects funded under Strand 1 that were previously funded under the 2013/2014 call which ended in April 2014. Pobal wrote to groups on the 14th July 2014 inviting them to apply by submission of a project plan and budget request. Successful applicants will be expected to commence project implementation from 20th October 2014 and the contract period will continue to 17th April 2015.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 3

Section 2: Project Implementation 2.1 Project Timeframes The start and end dates for funded projects are stated in the grant agreement between Pobal and the individual grantee.

2.2 Project Plan

All EWM projects were required to submit a project plan as part of their funding application; this presents a detailed overview of the schedule of work to be completed during the respective project year/phase and provides a valuable tool for project management. Once agreed with Pobal, the project plan will form part of the grant agreement and will be used as a tool for monitoring progress and assessing impact. The project plan outlines the critical objectives and actions, as well as setting out projected outputs and impact. Projects are also required to outline a strategy for the monitoring and evaluation of their EWM project, which includes the development of an evaluation baseline. The evaluation of project outcomes, including group and external stakeholder input where relevant, should form part of normal programme activity as external evaluation costs are ineligible under EWM. 2.3 Changes to your Project Plan

Funding is provided to organisations to implement the agreed objectives and actions outlined in the project plan. As such, it is an important document that informs project implementation. One of the challenges associated with project planning is to ensure that the plan remains a relevant tool for guiding work on the ground. In some cases, there may be amendments to the project plan based on changing needs or project learning. It is important to emphasis that it is not envisaged that significant changes would take place during the lifetime of the project. Proposed changes must initially be notified in writing to your regional development co-ordinator. These will be reviewed in consultation with the finance team through the Pobal formal process. Changes must not be implemented without prior written approval from Pobal. In relation to the project budget there will also be an opportunity to request a formal budget change; the timeframe for which is outlined in the key reporting timeline (page iv). 2.4 EWM Project Participants It is an ESF requirement for groups to maintain, and keep on file, an attendance record of all EWM project participants for each individual class/session. In addition, a copy of any certificates awarded as part of the EWM project must be maintained. This information forms part of the checks undertaken by Pobal, the Department and the ESF during audit/ verification site visits. 2.5 Participant Data for the European Commission In line with ESF monitoring requirements projects are required to submit statistical data on project participants. Funded organisations must ensure that all EWM project participants complete the ‘Questionnaire to Gather Participant Data for the European Commission’ at the beginning of the project (Template G – Appendix 8). Here is the link to all 11 EWM Appendices). This should record the status of each participant against a number of variables e.g. labour market status, educational attainment, before they joined your EWM

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 4

project. The questionnaire must be completed in full by all project participants. Copies of the completed questionnaire must be retained by your organisation.

Funded groups are then required to compile and submit these statistics to Pobal on an annual basis (according to calendar year) for the ESF/HCIOP Annual Progress Report.

2.6 Pobal Supports

Pobal is re-organising its staffing structures at present and we will be in touch in due course to let you know the dedicated regional development co-ordinator for your project going forward. Pobal will try and assist projects with any queries and accessing additional supports that may be required. In order to assist funded groups with planning their work, Pobal has developed a schedule of key dates in relation to EWM 2014/15 (see page iv). This will include details of the timeframe for individual grant payments and also the submission dates for annual monitoring and financial returns and request for budget changes.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 5

Section 3: Monitoring & Non-Financial Reporting Requirements 3.1 Project Monitoring & Reporting Requirements All funded groups are required to submit the following reports to comply with monitoring requirements:

End of Project Report (project/funding year) ESF/HCIOP Annual Progress Report (calendar year)

Further information regarding each of these reports is outlined below. In addition, a number of projects are randomly selected for an audit/verification site visit, undertaken by Pobal, the Department or ESF, which includes monitoring and financial verification checks.

3.2 End of Project Report At the end of each project/funding phase groups are required to complete an End of Project Report, which includes details of completed actions/outputs, project achievements, challenges and final beneficiary targets for the respective project year. The End of Project Report for EWM 2014/15 is due to be submitted on 8th May 2015. 3.3 ESF/HCIOP Annual Progress Report It is an ESF requirement that EWM projects monitor and report on the following information on a calendar year basis:

Annual Performance Indicators (Output, Result, Impact)

ESF Participant Data: Socio/Demographic profile of all project participants

Qualitative Reporting

Projects are required to submit this information to Pobal on an annual basis, at the beginning of each calendar year for the preceding year. An online portal has been developed for projects to record the relevant data, which relates to the previous calendar year. The individual reports are then collated by Pobal and compiled for the HCIOP Annual Progress Report, which is the annual monitoring report for the ESF in relation to EWM. The ESF/HCIOP Annual Progress Report is due to be submitted to Pobal by 16th January 2015. Annual Performance Indicators The Annual Performance Indicators for EWM are pre-defined by the Department and the ESF. Projects are required to report on the Performance Indicators for the particular EWM strand they are funded under, further details of which are outlined below:

Project Outputs relate to the number of individual women who have participated in the EWM project (all EWM strands) for the respective calendar year. It is important to ensure that there is no double counting of participants i.e. each individual woman should only be counted once.

Total No. of project participants broken down according to the number of women participating in: (a) accredited and (b) non-accredited; training/initiatives aimed at labour market intervention.

Project Result (post project) is focused on the position of participants at the end of the EWM project e.g. the number of women who achieved certification and the number of women who have progressed to employment/further training.

No. of women who achieved certification/accreditation; No. of women taking up employment/ further training (Str 1)

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 6

Project Impact (1 year post project) refers to the position of participant’s one year after the EWM project. It is an ESF requirement that projects undertake a survey of participants one year after they have left/completed the project in order to measure the project ‘Impact’ e.g. the no. of women who are still in employment/education, no. still engaged in entrepreneurship and the no. who have advanced their careers. It is advisable that all participants are notified of this requirement at the beginning of the project and reminded again at the end, with a contact email/telephone number retained to facilitate the survey.

No. of women still in employment/education (Str 1); No. of women still engaged in entrepreneurship (Str 2); No. of women who have advanced their careers (Str 3).

ESF Participant Data As part of the ESF/HCIOP Annual Progress Report projects are required to compile and submit statistical information on project participants for the respective calendar year. This data is provided by participants in the ‘Questionnaire to Gather Participant Data for the European Commission’ (Template G – Appendix 8). Here is link to all 11 EWM Appendices. The information contained in the individual questionnaires is then collated by each organisation and submitted to Pobal in aggregate form. It is important to ensure that each participant completes the questionnaire in full at the beginning of the project. Qualitative Reporting Projects are also required to provide information about the more qualitative aspects of their EWM work, this largely relates to details of individual project achievements and any particular challenges at a local or programme level. In addition, projects are required to provide details of any reports/publications/studies that relate to the EWM project, which have been completed during the relevant calendar year. 3.4 Evaluation In relation to project level evaluation, external evaluation costs are ineligible under EWM. Instead organisations are required to monitor and evaluate their performance as part of normal project implementation. In the project plan organisations are required to outline an evaluation plan, which includes the development of an evaluation baseline. This facilitates reporting against indicators and targets and ensures that project objectives and outcomes are achieved. As outlined in sections 3.2 and 3.3, projects need to consider the key monitoring information that is required and how and when it will be collected, so that outputs/targets are reported on an evidence basis. In terms of project level evaluation, projects should consider what information and methodology is required to demonstrate impact and outcomes and how this will be collected and analysed. In addition, it is important that the process undertaken has been documented i.e. why and how things were done – as well as project achievements. If there have been any challenges, the reasons for these and how they were overcome should also be recorded as this can highlight important learning.

Pobal hopes to explore an approach across different funding programmes to encourage consistency in project-level monitoring based on common elements of existing reporting and evaluation approaches. It will focus on monitoring of progress, process evaluation and project-level, outputs/outcomes evaluation.

In relation to an EWM programme level evaluation, there is no budget for a monitoring and evaluation framework at programme level, to facilitate the evaluation of outcomes.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 7

Section 4: Information and Publicity 4.1 Purpose In order to create a greater awareness of the project locally and to acknowledge the funders, organisations should ensure that the EWM project is appropriately publicised. This has an important role in terms of communicating project achievements and boosting the profile of the measure. In addition, it is a requirement in the grant agreement that clear acknowledgement is given to the financial support of the ESF and the Department of Justice and Equality. Acknowledgement is required in all aspects of publicity, promotional and information dissemination activities. Please refer to your grant agreement and the ESF ‘Information and Publicity Guidelines’ (Appendix 10), which are also available from www.esf.ie and the Operational Supports section of the EWM webpage on the Pobal website. All funded groups should be aware that failure to comply with the ESF Information and Publicity Guidelines may result in the loss of funding. Compliance with ESF publicity requirements will form a key part of any verification/audit visits. From a project perspective, it is important to think strategically about how the project work can be communicated to the various stakeholders. Projects may produce information leaflets/reports relating to the EWM project as well as ensuring information is contained on the organisation website in a dedicated section. The development of a communication/media strategy is useful in highlighting project achievements to other women, key stakeholders and the wider public. Projects should consider events, press releases, photographs etc. that will communicate the value of the work. The ESF has also developed posters relating to the funds which projects must display. Each funded group has received a copy of the posters previously. 4.2 Use of Logos In order to acknowledge the funding sources for EWM the relevant logos must be used on all publicity/promotional materials and activities including;

Publications/brochures/literature; invitations; launches/awards; conference & materials; exhibition(s); advertisements; press releases; posters; annual reports; videos/ dvds; supplements; project websites; correspondence.

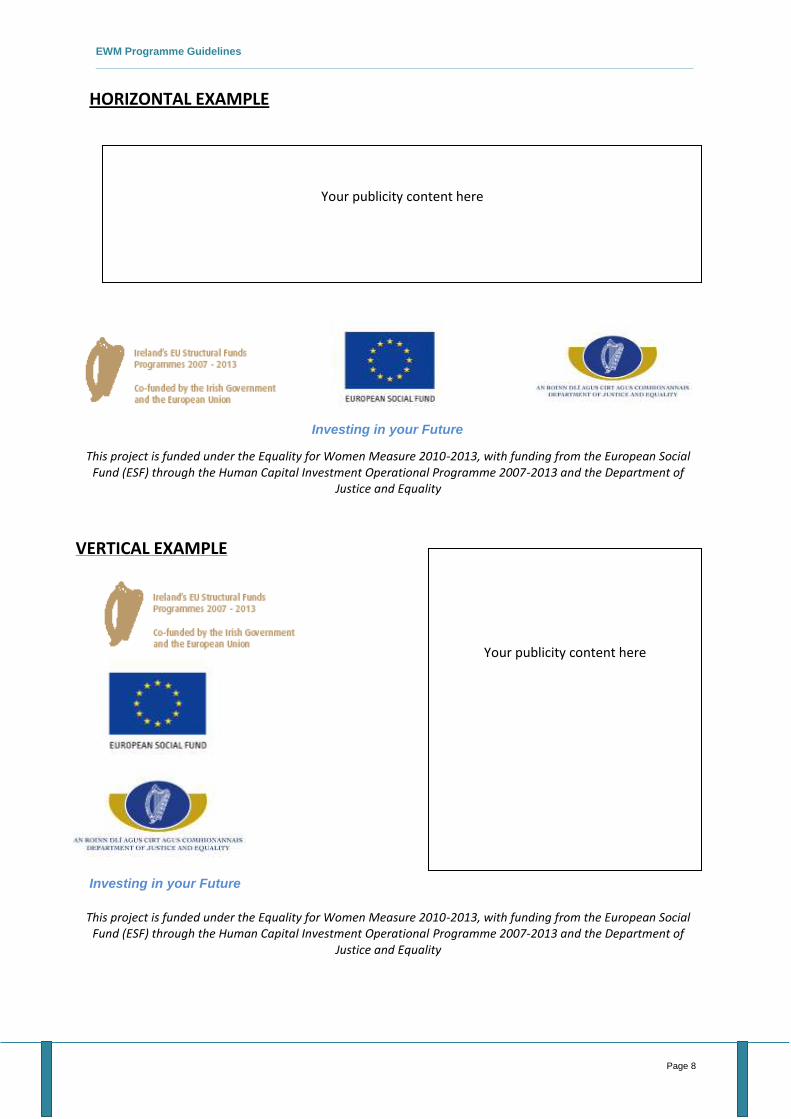

The logos must be used in the following order of priority:

I. If used horizontally, the Ireland EU Structural Funds logo should be placed on the left, followed by the ESF logo in the centre, followed by the Department of Justice and Equality logo on the right.

II. If used vertically, the Ireland EU Structural Funds logo should be placed at the top, followed by the ESF logo in the centre, followed by the Department of Justice and Equality logo on the bottom.

III. ESF tagline “Investing in your Future” should be placed beneath logos and centred.

(Please refer to the following pages for examples of logo positioning)

The relevant logos are available to download from the Operational Supports tab of the Pobal

website. Details relating to the correct use, size and positioning of the ESF logo in

promotional materials can be found in the ESF ‘Information and Publicity Guidelines.’

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 8

Investing in your Future

Investing in your Future

This project is funded under the Equality for Women Measure 2010-2013, with funding from the European Social Fund (ESF) through the Human Capital Investment Operational Programme 2007-2013 and the Department of

Justice and Equality

This project is funded under the Equality for Women Measure 2010-2013, with funding from the European Social

Fund (ESF) through the Human Capital Investment Operational Programme 2007-2013 and the Department of Justice and Equality

Your publicity content here

Your publicity content here

VERTICAL EXAMPLE

HORIZONTAL EXAMPLE

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 9

This project is funded under the Equality for Women Measure 2010-2013, with funding from the European Social Fund (ESF) through the Human Capital Investment Operational

Programme 2007-2013 and the Department of Justice and Equality

Optional Use of additional logos The following logos can be used at your own discretion and are available to download from the Pobal website. Please note that these should be placed after the Department logo. a. Gender Equality/National Women’s Strategy logo (below) has been adopted as the

thematic logo for EWM and can be used as part of the design of your publicity material.

b. Pobal logo is also available to include on any publicity material.

c. Your own organisation logo. 4.3 Acknowledgment of Funding/Text All publications and promotional literature for your EWM project (e.g. project documentation, posters, leaflets, and reports) must contain the relevant logos with the following text:

4.4 Publications All publications produced as part of your EWM project must adhere to the publicity requirements outlined in the ESF ‘Information and Publicity Guidelines’ regarding the correct use of logos on the title page and a written acknowledgement of the funders. All research and policy related publications associated with your EWM project should also include a statement that the views contained in the publication do not necessarily reflect those of the EU, the ESF, the Department or Pobal.

4.5 Press Releases/Articles It is important to emphasise that every article and/or press release relating to your EWM project must provide clear acknowledgment of the sources of funding, particularly the contribution and support of the ESF. Projects are required to liaise with journalists to ensure that the final print copy includes the appropriate acknowledgement of the funders. The text outlined in section 4.3 is useful to provide to journalists to ensure that this requirement is met. 4.6 Protocol for Publicity Activities and Events When you organise a publicity event such as a launch, conference, exhibition etc., you are encouraged to invite the relevant Minister to officiate. This is currently Minister Aodhán Ó Ríordáin - Minister of State with responsibility for New Communities, Culture and Equality.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 10

Any such invitation should be submitted in writing to the Gender Equality Division, Department of Justice and Equality, Bishop’s Square, Redmond’s Hill, Dublin 2. If the Minister is not available he/she may appoint a delegate. EWM stands/backdrops are available for seminars, ceremonies or any public event. We recommend groups avail of this offer as the stands provide an attractive background for photo opportunities. The stands are 4ft x 7ft (1200 x 2110 mm), are easy to assemble and come with their own case. To secure a stand(s) please contact your regional development co-ordinator. Requests should be emailed in advance of your event and arrangements made for the collection/return to Pobal offices in Holles St, Dublin.

4.7 Publicity Reporting Projects are required to maintain a ‘Publicity Manual’ which will be reviewed during site visits and should contain a hard copy of project publicity such as events, posters, advertisements, press releases, leaflets, press-cutting, invitations for tenders, photographs etc. In addition, projects will be required to provide details of publicity measures undertaken e.g. list of events and a hard copy of a sample of publicity materials, as part of the End of Year Project Report. This is an ESF requirement and is used to highlight activities undertaken, as well as promoting the work of individual projects to a wider audience. What events and activities should be included in a Publicity Manual / Report? Activities and events that warrant inclusion in your publicity manual and publicity report should be interpreted widely. It may include, amongst others, the following:

Conferences/Seminars Publications: Reports/Brochures/Posters Launches/Awards Ceremonies Display/Exhibition stands & signage Advertisements Press releases DVDs Website

Projects should be aware that failure to comply with the ESF publicity requirements may result in the loss of funding

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 11

Section 5: Recruitment and Employment for EWM funded positions

5.1 Recruitment & Selection

If your organisation is employing staff for the purpose of working on the EWM project, you are required to submit:

(i) a copy of the organisation’s recruitment & selection policy/procedures; (ii) Job descriptions for all EWM funded posts.

The recruitment & selection procedures must be: fully documented, open and transparent and state that the organisation is an equal opportunities employer. If the organisation does not have a recruitment & selection procedure, the following information must be submitted:

(i) An overall statement regarding the recruitment process, with confirmation that the organisation is an equal opportunities employer.

(ii) Details of the recruitment procedures for external candidates and the process for existing internal staff being recruited to EWM-funded posts.

5.2 Record Management The maintenance of employment records is a key aspect of audit/verification visits. It is a requirement that projects maintain the following records:

1) Evidence of transparency of recruitment processes; 2) Signed contract for each EWM funded employee; 3) Payroll records; 4) Timesheets i.e. evidence of hours worked signed off by the line manager.

Timesheets are an EU requirement and must be kept on site and available to audit. Open and Transparent Recruitment Pobal requires that all recruitment is open and transparent. Pobal has produced a set of Guidelines on Best Practice in Recruitment & Selection for Beneficiaries of Pobal which have been provided to each organisation and are available to download from the Pobal website. It is the responsibility of the organisation to decide on the most appropriate medium for advertising the post e.g. national/local press, Activelink and/or Intreo/Local Employment Service (LES). Please ensure that EWM and the relevant sources of funding are acknowledged in the job advert along with the required logos (see section 4). Contract of Employment A signed contract of employment must be in place for all EWM funded employees. We would advise that all EWM funded staff members have a clause inserted in their contract stating that continued employment on the project is subject to the availability of funding. Payroll Records The organisation must retain all records pertaining to EWM until 31st December 2022. After the 31st December 2022, no documents should be disposed of without the agreement of the Managing Authority. Timesheets Evidence of actual time spent on the Equality for Women project for persons working part-time on the project, through maintenance of staff time sheets, must be maintained on site and made available for inspection. This is an EU Requirement (Appendix 11, ESF Certifying Authority, Department of Education and Skills Circular 1/2012). Here is the link to Appendix 11.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 12

Timesheets should reflect 100% of the employees’ time and include a brief description of duties, be signed by the employee and reviewed and approved on a regular basis by the respective manager. The percentage of salaries claimed from the Equality for Women project will be verified against timesheets: therefore organisations should ensure that the amounts claimed in financial returns are reconciled to the hours worked on the timesheets.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 13

Section 6: Approved Budget

6.1 Approval of Budget by Pobal

Prior to entering into a grant agreement for funding under EWM a project budget must be prepared by each organisation and approved by Pobal. To ensure that Pobal is in a position to approve the budget, it is essential that budgets are reviewed pre-submission to ensure that they provide the relevant information. In particular, funded groups should ensure that all sections have been completed, descriptions are detailed, and co-funding (where applicable) is verified. Ensuring that these items have been addressed will minimise queries and delays in approving the budget. 6.2 Key issues in compiling and monitoring budgets

If project staff time is apportioned across a number of programmes, the budget must

show a clear breakdown of where staff costs are apportioned and the percentage allocated. It is required to adopt a fair and logical basis of apportioning staff members’ time.

If an employee of the project is wholly or partly assigned to and funded by EWM, the employee’s full salary should be shown on the budget details sheet under the relevant heading of direct salary or indirect salary.

Where staff time and overheads are apportioned these costs may be apportioned using only the two methods below: By reference to staff time By reference to actual recorded usage This basis should be formally agreed in writing with Pobal. You should ensure that your apportionment policy is reviewed and updated regularly so that it accurately apportions administration costs across different funding streams. Please see section 10 for further information regarding apportionment policies.

Projects must ensure that they have not received, nor do they intend to receive, another

grant for the same project from a European Institution. Double financing shall be considered a failure under the relevant articles of the grant agreement. Total recovery of the grant may be carried out in the event of double financing for the same project. It is essential to ensure that there is no overlapping of EU funds.

Once approved, the budget represents the agreed budget for the grant agreement period and should be adhered to as closely as possible. Groups should monitor their spending against the agreed budget on a continuous basis.

6.3 Changes to Budget and other Project Changes In some cases there may be amendments to your project based on changing needs or learning that emerges during project implementation. Changes may relate to reallocations across budget headings, or changes such as revision to project objectives, actions and/or outputs. A request for changes to your budget/project will be considered once during the lifetime of the grant, the timeframe for this will be February 2015. Proposed changes must be notified in

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 14

writing to the designated regional development co-ordinator and finance officers. You must not proceed with the change without prior written approval from Pobal.

A material change is considered to be greater than €500 on the ‘Programme’ costs

budget lines and €200 on the ‘Administration’ budget lines. Any proposed change to the budget greater than this requires formal approval from Pobal in advance.

If it becomes apparent throughout the funding period that spending on any of the budget lines or headings is likely to be materially at variance with the agreed budget for that particular heading, the organisation should contact Pobal immediately.

Changes to the staffing structure including changes to the amount of hours worked by

EWM project staff must be agreed in advance in writing with Pobal. Changes to your salaries budget that have not been agreed in advance and in writing by Pobal may result in the decommital of funds.

When making changes to your budget it is important to ensure that all revised costs are

eligible. Please refer to section 8.10 for further information regarding ineligible costs.

Any changes to your project action plan (project objectives, actions, outputs, timeframe)

or the beneficiary target numbers for each of the programme performance indicators must be agreed in advance with Pobal.

It is not envisaged that significant changes would take place during the lifetime of your project.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 15

Section 7: Payment Process and Expenditure Returns 7.1 Payment of Grant and Threshold Spend The following documentation must be submitted and approved by Pobal prior to the release of the payment.

Executed grant agreement (signed)

Details of dedicated bank account/cost centre approach

Signed and dated copy of budget overview template B

Evidence of compliance with all pre-payment conditions as detailed in the grant agreement

Valid tax clearance certificate. Payment of the grant is dependent on funding being made available to Pobal from the Department of Justice and Equality. The total amount of funding will be paid in one up-front instalment. It is essential to note that any unspent funds will be recouped and should any expenditure be deemed ineligible this will also be required to be refunded. Currently the position from 20th October 2014 to 17th April 2015 is as follows: Payment of 100% - paid on receipt of a signed grant agreement once any additional terms and conditions have been met. Payments are linked to satisfactory progress and the implementation of the agreed project actions and objectives. ESF funding rules and regulations must be adhered to at all times. Breaches of these regulations could result in non-payment of funds to your organisation, until the issue is resolved. Please refer to Appendix 11 for a copy of the ESF rules and regulations. Here is the link to Appendix 11. 7.2 Tax Clearance Certificate

Grant payments can only be processed where the beneficiary has submitted an up-to-date tax clearance certificate (TCC). TCC’s are granted on an annual basis by the Revenue Commissioners and your organisation must apply for a new certificate each year. No payments will be made to your organisation if Pobal does not have a copy of your current TCC. TCCs must also be obtained by your group from suppliers of goods and services to whom you have made cumulative payments in excess of €10,000 in any 12 month period. Taxpayers can now apply on-line for a tax clearance certificate at www.revenue.ie (under electronic services). While the majority of your group’s purchases will be from suppliers resident in the State, it may occasionally be necessary to purchase goods/services to a value of €10,000 or more from non-resident suppliers. Where this is the case, the non-resident supplier will not have an Irish tax clearance certificate, but must apply to the Irish Revenue Commissioners for a certificate that confirms their suitability on tax grounds to be awarded the contract. Applications for such a certificate can be made via www.revenue.ie

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 16

Note: If your organisation is registered for VAT, you are required to forward the relevant details to Pobal. 7.3 Eligibility of Expenditure Expenditure returns provide a detailed breakdown of the expenditure incurred by the funded group for six month/three month period. Expenditure is analysed across the agreed budget headings (together with co-funding where applicable). Expenditure is reported on a cash basis. Expenditure shall be eligible if it has actually been incurred and paid. No expenditure can be incurred prior to the date of approval of the grant allocation as detailed in your Grant Agreement unless written authorisation has been sought and received from Pobal prior to or at the time of expenditure. Costs must represent value for money and be related to project activity. Replacement costs and opportunity costs are not evidence/justification for real costs. All payments must be based on real identifiable costs, in particular all internal payments and all payments to related parties where proper procedures have been followed. Proof of expenditure is always required and the expenditure must be supported by receipted invoices or accounting documents of equivalent probative value which have a proven link with the projects/operations. Effectively this means any document required to support the accounting records in order to give a true and fair view of the transactions in accordance with accepted accountancy practice. The following is a list of records which meet the standard “document of equivalent probative value”.

Original invoice

Payroll records to support salaries and wages claimed. Rates of pay should be justified and certified. For staff working less than 100% of time on the project, the allocation of salaries/wages must be supported by timesheets/logs covering 100% of that staff member’s time.

Travel and subsistence claims duly authorised and in accordance with approved rates. Invoices must be provided where hotel/meal expenses are claimed in lieu of approved subsistence/per diem rates.

Documents such as purchase orders, supplier statements and delivery dockets can provide secondary support to, but do not replace, the documents listed above

Bank statements must be provided to show proof of payment. Payments by funded groups to internally administered bank accounts, including bank transfers, must only be done on a ‘needs must’ basis. Where this occurs copies of the relevant bank statements from the bank accounts must be included with the return and transactions highlighted as necessary.

• Expenditure should not be reported in the prior month/year to when it is actually incurred or issued to payees e.g. January expenditure reported as December.

• Frontloaded/advanced payments to suppliers/grantees, which relate to work/expenditure that will take place in the following year should not be reported in the current year.

• There must be no double funding / overlapping of EU aid for the same project. Co-funding must not be from an EU source.

Supporting documents, in original format, must be kept in a proper manner and available for inspection up until 31st December 2022.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 17

Expenditure returns containing total project expenditure must be submitted via email where possible along with supporting documentation as outlined below.

Expenditure Returns Process 7.4 Financial Expenditure Returns

Pobal will issue groups with Financial Expenditure Return templates for completion close to the period end dates. The templates and original supporting documentation, as listed below, are required to be submitted on or before the 8th May 2015. All financial documentation must be sent to the designated Pobal Finance Administrator within the specified timescales. See Appendix 1 for a sample Returns Template. Here is the link to all 11 EWM Appendices. Following discussions with the Department of Justice and Equality in January and as a result

of Financial Control Unit audit visits Pobal will be carrying out at 100% desk-check

verification and review of original documentation as detailed below to verify the eligibility of

the EWM expenditure.

Completed Financial Expenditure Return which shows the approved budget analysed across the agreed budget headings

Copy of Payments Journal for relevant period detailing total project expenditure reported

Please submit the following supporting original documentation with the final return (i.e.

April 2015) in order for Pobal to verify the eligibility of expenditure claimed under the Equality

for Women Measure:-

Staff costs (Direct & Indirect)

Contract / Job description for all staff working on the EWM project;

Gross to net reports / tax deduction cards for all staff;

Signed timesheets for those staff working part-time on the project;

Recruitment documentation where relevant.

P30 Revenue Declaration

Direct Non staff costs

Original invoices – all eligible items of expenditure must be supported by an

original invoice and referenced as a payment required from EWM funds.

Procurement documentation where relevant

Travel & subsistence claims and travel & subsistence policy covering both staff

and participants

Participant attendance records

Evidence of publicity

Internal Financial Procedures – this should include references to ESF rules and

regulations evidenced by copies of relevant circular being available and finance

officers aware of the content

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 18

Bank statements in respect of dedicated Bank Account for EWM (and copy of

relevant bank statement pages from for other accounts from which payments have

been made if applicable).

Evidence of authorisation levels for invoices/ Bank mandate – there should be

appropriate authorisation/approval levels in place to sanction payments, as well as

appropriate segregation of duties over the payment process. Two signatories are

required for all EWM cheque payments.

Audited Financial Statements identifying EWM as a source of funding

Income generated - any income generated as a direct result of the project should be

clearly identified and deducted from the total eligible expenditure claimed

Any expenditure deemed ineligible by Pobal will be recouped from the project on the basis of

non-compliance with the EWM rules and guidelines.

Project expenditure reported on the Expenditure Return must correspond to the expenditure reported on the payments journal for the period. A senior staff member (CEO/Finance/Project Manager) and a Board Member/Director must sign the Return Declaration. For a county council/VEC, a director of services with responsibility for the project must sign the Return Declaration. Where incorrect or incomplete documentation have been submitted grantees will be given the opportunity to submit the correct/appropriate documentation or information within 10 working days; failing receipt of such this expenditure will be categorised as ineligible and cannot be reclaimed at any other stage of the project’s life. Pobal will liaise with the grantee in order to address any queries arising from submission of expenditure returns, and will complete the desk level verification of expenditure as soon as possible, and not later than three months after receipt of claim, as required by EU Regulations. How to complete the Financial Expenditure Return

1. The expenditure return will list your budget categories and amounts as per your approved budget. All expenditure must be in line with your approved budget.

2. You are required to fill in the expenditure for the relevant reporting period in the boxes provided. The expenditure should be reported against the relevant budget headings.

3. Pobal will already have completed the cumulative boxes to the last return you submitted to Pobal. By cumulative we mean from the start of your 2014 grant and not an annualised cumulative figure.

4. The expenditure reported in your return must match the total project expenditure on

your Payments Journal.

5. An expenditure return must be completed even if you have submitted an (exceptional) drawdown request during the period.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 19

6. Information on completing the Payments Journal and Receipts and Lodgements

Journal are referenced in the ‘Books and Records’ section 11.1 of the guidelines. 7.5 Interim (Exceptional) Drawdowns A facility for an interim drawdown is only available in exceptional circumstances and will be considered on a case-by-case basis. It may also occur in circumstances where the Department have instructed that payments are to be issued within a specific timeframe. An expenditure return must be completed even if you have submitted an (exceptional) drawdown request during the period.

Documents to be submitted for interim (exceptional) drawdowns:

Request for funding to be submitted in writing detailing the reason(s) for the high level of spend during the period in question

Signed Drawdown Request. Expenditure being reported in the period from the last Half Year end date to drawdown date should be analysed over the agreed budget headings

Payments Journal from date of last expenditure return to date of drawdown request

Supporting bank statements from the end of the last reporting period to the date of the drawdown request

List of Outstanding Cheques and Outstanding Lodgements at the period end Once the drawdown request together with the supporting documentation is received by Pobal, the finance team will undertake verification and validity tests. Provided that the reported expenditure meets the eligibility requirements and that expenditure thresholds have been met, Pobal will issue a payment. See Appendix 2 for sample Drawdown Template.

Here is the link to all 11 EWM Appendices. Final Expenditure Return The final claim must be submitted within 3 weeks after the project end date. Where ineligible expenditure (See section 8.10) is identified on the final expenditure return no changes will be accepted. The amount of the ineligible expenditure will be decommitted and a cheque for the ineligible amount will need to be reimbursed to Pobal.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 20

Section 8: Categories of Eligible and Ineligible Costs The purpose of this section is to distinguish clearly between eligible and ineligible costs, and to ensure that only eligible expenditure/activity is claimed. While every effort has been made to produce clear guidance on eligibility, there remains an onus on Grantees to manage the grant responsibly in a way which is compliant with EU Regulations and Circulars. Please refer to Appendix 10 (ESF Certifying Authority Eligibility Rules Circular 1/2012) here for more detailed information. 8.1 Direct and Indirect Costs There are 3 main categories of eligible EWM expenditure:

Salaries Costs – Direct and Indirect

Administration – Overheads/indirect Costs

Programme Costs- Direct Costs The 3 main categories of costs can be broken down into direct or indirect costs. Indirect costs include Indirect Salaries and Administration costs. Direct costs include Direct Salaries and Programme costs. The definition of direct and indirect costs for the purpose of EWM is as follows: Direct Costs directly relate to the implementation of the project, where the link with the key project actions can be demonstrated. - Persons that have a direct role in the implementation of the project (i.e. Project worker and other staff directly involved in project implementation). Indirect Costs cannot be directly connected to the implementation of the EWM project. Such costs could include administrative /staff expenditure, telephone, electricity. i.e. Persons who are not directly involved in the project delivery but may provide a measurable support (i.e. administrative/management support). Please note indirect costs cannot exceed the agreed fixed % of direct costs and where possible should be kept below 15%. The eligibility of costs is based on a clear and transparent audit trail with supporting documentation. The formula below calculates the percentage:

Indirect Costs x 100 = % PERCENTAGE Direct Costs

Indirect Costs for Equality for Women to be apportioned using only the methods below:

By reference to staff time,

By reference to actual recorded usage,

Eligibility of costs will be based on a clear and transparent audit trail, with supporting documentation.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 21

8.2 Salary and Wages Costs Staffing costs and staff recruitment costs are eligible for personnel directly or indirectly engaged in a project, whether full or part time. However, it is necessary to demonstrate such full time status, details to be included in the employment contract/job description. Salary costs must be in line with the details provided in the agreed budget. Specific supporting documentation required to evidence staffing costs include job descriptions, staff contracts, timesheets for part-time staff, BACS/Payroll reports and bank statements. Claims for salary cost reimbursement must be fully supported by payroll evidence including details of employer costs which may include employers’ pension costs where there is an established pension scheme in place which applies to all staff. Where change in duties arise for staff members that directly relate to the Equality for Women Measure, there should be in place a documented decision relating to the change in duties (e.g. alteration of contractual duties, signed management agreement, and/or documentation detailing assigned tasks as per the minutes of board meetings). Notional or budgeted amounts are ineligible reporting methods against the grant. Timesheets Evidence of actual time spent on the Equality for Women project for persons working part-time and full time on the project, through the maintenance of staff time sheets, must be maintained on site and made available for inspection. This is an EU Requirement (Appendix A, ESF Certifying Authority, Department of Education and Skills Circular 1/2012). Please refer to Appendix 11 of the guidelines. Here is the link to Appendix 11. Timesheets should reflect 100% of employee’s time and include a brief description of duties, be signed by the employee and reviewed and approved on a regular basis by the respective manager. The apportioned percentage of salaries will be verified against timesheets; therefore, organisations should ensure that the amounts claimed in financial returns are reconciled to the hours worked on the timesheets. 8.3 Administration Costs Under EWM funding, all administration costs and overheads are categorised as indirect costs. Costs to be included under this heading are costs not directly connected with delivery of the project e.g. costs associated with the running of an office i.e. rent, rates, light and heat, insurance, and telephone. 8.4 Programme Costs These are costs that arise directly from the delivery of the project i.e. tutors/facilitators/trainers, publicity/advertising, childcare, venue hire/catering, course materials/ manuals etc. Organisations must ensure they are compliant with Public Procurement procedures throughout the lifetime of the project. (Section 9 Public Procurement refers). Personnel costs to be included under programme costs relate to those individuals that are not being claimed under direct salaries from the EWM grant but are involved in contract work e.g. tutors, trainers, and guest speakers.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 22

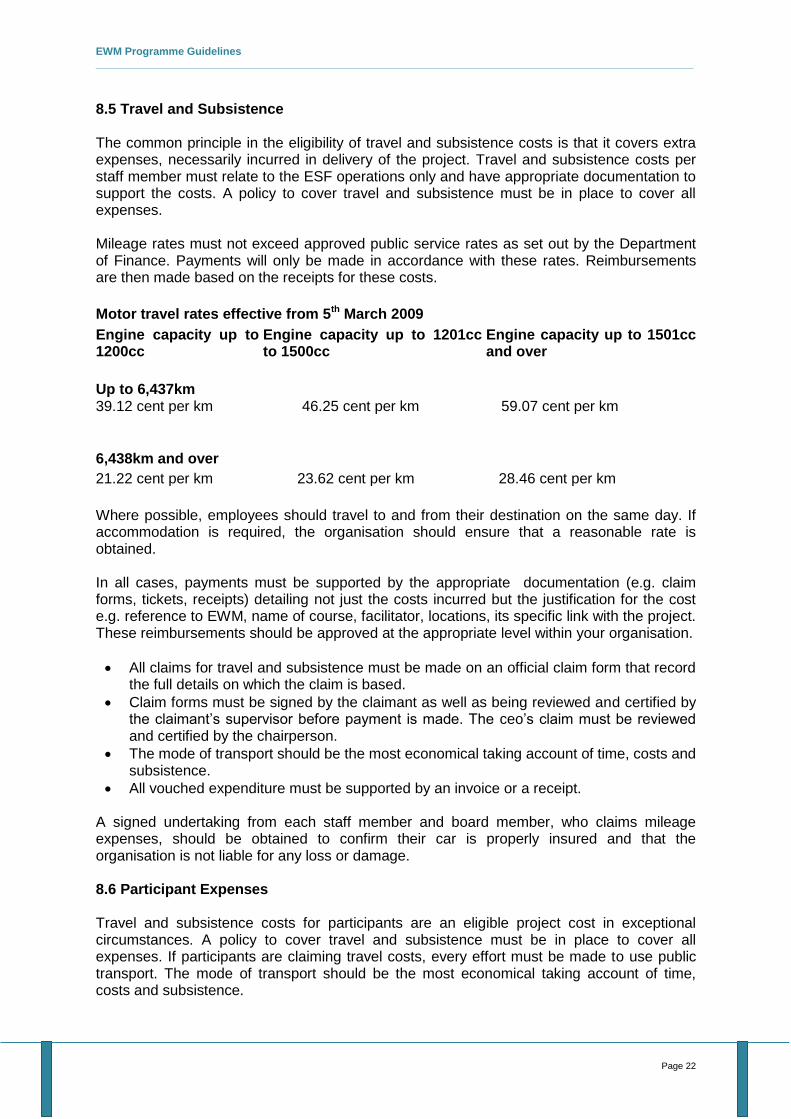

8.5 Travel and Subsistence The common principle in the eligibility of travel and subsistence costs is that it covers extra expenses, necessarily incurred in delivery of the project. Travel and subsistence costs per staff member must relate to the ESF operations only and have appropriate documentation to support the costs. A policy to cover travel and subsistence must be in place to cover all expenses. Mileage rates must not exceed approved public service rates as set out by the Department of Finance. Payments will only be made in accordance with these rates. Reimbursements are then made based on the receipts for these costs.

Motor travel rates effective from 5th March 2009

Engine capacity up to 1200cc

Engine capacity up to 1201cc to 1500cc

Engine capacity up to 1501cc and over

Up to 6,437km 39.12 cent per km

46.25 cent per km

59.07 cent per km

6,438km and over

21.22 cent per km 23.62 cent per km 28.46 cent per km

Where possible, employees should travel to and from their destination on the same day. If accommodation is required, the organisation should ensure that a reasonable rate is obtained. In all cases, payments must be supported by the appropriate documentation (e.g. claim forms, tickets, receipts) detailing not just the costs incurred but the justification for the cost e.g. reference to EWM, name of course, facilitator, locations, its specific link with the project. These reimbursements should be approved at the appropriate level within your organisation.

All claims for travel and subsistence must be made on an official claim form that record the full details on which the claim is based.

Claim forms must be signed by the claimant as well as being reviewed and certified by the claimant’s supervisor before payment is made. The ceo’s claim must be reviewed and certified by the chairperson.

The mode of transport should be the most economical taking account of time, costs and subsistence.

All vouched expenditure must be supported by an invoice or a receipt.

A signed undertaking from each staff member and board member, who claims mileage expenses, should be obtained to confirm their car is properly insured and that the organisation is not liable for any loss or damage. 8.6 Participant Expenses Travel and subsistence costs for participants are an eligible project cost in exceptional circumstances. A policy to cover travel and subsistence must be in place to cover all expenses. If participants are claiming travel costs, every effort must be made to use public transport. The mode of transport should be the most economical taking account of time, costs and subsistence.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 23

Payments to participants for subsistence can only be made on the basis of receipts for actual costs that have been incurred by the participants. Reimbursements to participants must be approved at the appropriate level within your organisation. Proof of expenditure is always required, payments must be supported by the appropriate supporting documentation (e.g. claim forms, tickets, receipts) detailing not just the costs incurred but the justification for the cost e.g. name of course, facilitator, locations, its specific link with the project. Your organisation should ensure that these receipts are maintained as part of its books and records and available for inspection. 8.7 Childcare costs In relation to childcare, only childcare costs that are paid to a HSE notified childcare provider (crèche, childcare centre or childminder if notified to the HSE) are eligible. Official invoices or receipts issued by the childcare provider must be provided to the project by the participant. The invoices and receipts must be dated and the dates correspond with the particular timeframe for courses which were attended by the participant as part of the EWM project. It is important to note that EWM costs should not constitute double-funding in cases where the child is already participating in a scheme such as Early Childhood Care & Education (ECCE) or Childcare Education & Training Support (CETS) or having his/her childcare fee subvented under Community Childcare Subvention (CCS). 8.8 Equipment Equipment costs under the Equality for Women Measure must not exceed €1,000 (including VAT) for a single item. The grantee must prepare and maintain a fixed asset register including the date of purchase, the asset description, serial number and cost, the source of funding and the asset location. Please ensure the fixed asset register is reconciled to the fixed asset details in the audited annual financial statements. Assets, whether wholly or partly purchased with grant funding, should not be disposed of during its economic life without prior written approval from Pobal.

8.9 General Payments

Grantees must date-stamp all invoices when they are received, and monitor them carefully to ensure that all are paid within 30 days in accordance with the European Communities (Late Payment in Commercial Transactions) Regulations. All paid invoices must be clearly stamped / marked paid to avoid the possibility of duplication of payments. All invoices should contain a reference to the EWM project / course. 8.10 Ineligible Costs Ineligible costs are outlined in the ESF Certifying Authority Eligibility Rules Appendix B, which is Appendix 11 of the programme guidelines. Here is the link to Appendix 11. A full copy of the rules is also available at: www.esf.ie some examples of ineligible costs are as follows:

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 24

Equipment costs in excess of €1,000 (including VAT) for a single item.

Indirect costs cannot exceed 20% of direct costs and where possible should be below this threshold.

External evaluation is not normally an eligible cost and should be discussed with your development person in Pobal.

Costs in relation to accommodation for training sessions.

Childcare costs to a childcare provider (crèche or childminder) that has not been notified to the HSE.

Bank interest payable, referral charges and legal disputes/litigation fees.

Redundancy costs.

Fines and penalties.

Recoverable VAT.

Depreciation

All notional /replacement/ opportunity costs.

In-kind contributions.

Catering costs. - In exceptional circumstances should be very modest and calculated at a rate of no more than €10 per participant.

8.11 Revenue/Income/Receipts As a general rule any revenue/income/receipts generated by an EU co-financed operation must be deducted from eligible expenditure of the operation. These amounts must be analysed separately in the receipts/lodgments book. 8.12 Fraud

Proper systems and controls reduce the risk of a fraud being perpetrated and assist in the detection of fraud. All suspected cases of fraud or corruption will be investigated. Pobal reserves the right to suspend and/or terminate the grant aid and commence legal proceedings to recover any funding at risk. Activities considered to be of a fraudulent nature may be liable to prosecution, could lead to the loss of future funding and a recovery of any previous grant paid. Fraud covers matters such as:

Receipt of income i.e. retention and misappropriation of cash;

False claims for expenses;

Misuse of the purchase and payments system for personal gain;

False wage and salary claim;

Theft of equipment and stores;

False accounting;

Suppression of documents; and

Misuse of the computer.

Types of corruption include abuse in the following areas:

Tendering and awarding of contracts;

Settlement of contractors finance accounts/claims;

Appointment and reward of consultants;

Pecuniary interest of members and officers;

Secondary employment of staff;

Hospitality: and

Disposal of assets.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 25

Pobal operate a zero-tolerance attitude to fraud and require grantees to act honestly and with integrity at all times, and to report all reasonable suspicions of fraud. Where there is any doubt as to project action required, Pobal should be contacted immediately for advice.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 26

Section 9: Public Procurement Procedures 9.1 Public Procurement Procedures Public procurement requires that all purchases must be open to fair competition from competent suppliers and that a record is maintained of how the decision to award any contract was reached (this is also the case for verbal quotes). There are a number of key points to note;

Public procurement rules applies to all expenditure for which grant aid is sought.

The EU Commission places a high priority on compliance with procurement procedures so it is essential that not only are correct procedures followed but that back up documentation to this effect is retained to verify this.

Your compliance with public procurement will be examined by Pobal; failure to comply will result in expenditure being deemed ineligible and/or financial penalties being imposed and subsequent recoupment of funds.

Any retrospective creation of documentation will automatically result in the tender competition being declared null and void, and the expenditure will be recoupable.

When determining the relevant public procurement threshold limits it is important to

note that these apply to the total value of funds paid to a particular supplier in a 12

month period. This requires funded groups to take into account any contracts entered

into with suppliers during the previous 12 months.

The grantee is responsible for compliance with the public procurement procedures and must ensure rules on procurement are strictly adhered to. Whenever purchases are made, contracts awarded or external suppliers are involved in a project, public tendering rules must be observed, including both National and EU Public Procurement thresholds. These rules are intended to ensure transparent and fair competition and to achieve value for money. Value for money should be the key consideration in purchasing goods and services – obtaining the most advantageous price available consistent with quality and fitness for purpose. A competitive process carried out in an open, objective and transparent manner can achieve best value for money in public procurement. All goods and services purchased with funding must be procured on the basis of the public procurement guidelines available at www.etenders.gov.ie. A brief synopsis is provided in the table below but it is imperative that you familiarise yourself with the full requirements of the public procurement guidelines.

Please refer to Appendix 9 a Public Procurement Review Report template to assist you when making purchases/engaging service providers. Here is the link to all 11 EWM Appendices. This report will evidence compliance with Public Procurement Procedures and ensures the correct process has been followed. Please keep a copy of the completed report on file as failure to show compliance will result in expenditure being deemed ineligible.

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 27

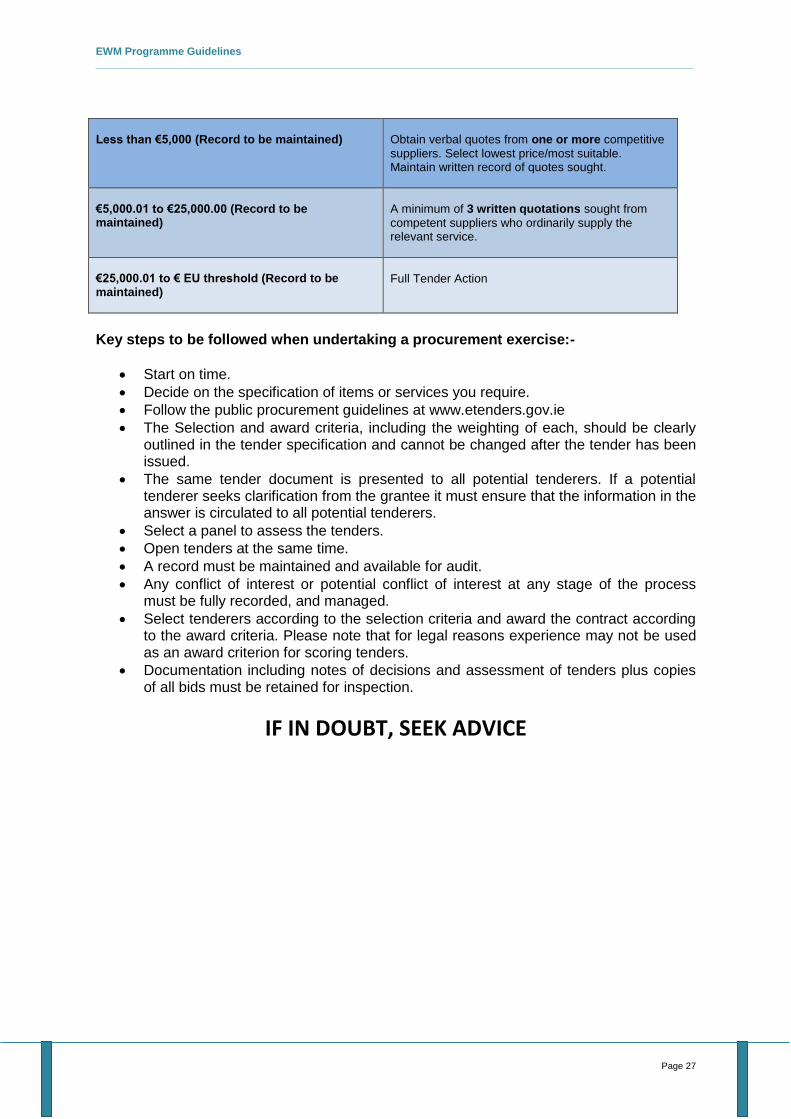

Less than €5,000 (Record to be maintained)

Obtain verbal quotes from one or more competitive

suppliers. Select lowest price/most suitable. Maintain written record of quotes sought.

€5,000.01 to €25,000.00 (Record to be maintained)

A minimum of 3 written quotations sought from

competent suppliers who ordinarily supply the relevant service.

€25,000.01 to € EU threshold (Record to be maintained)

Full Tender Action

Key steps to be followed when undertaking a procurement exercise:-

Start on time.

Decide on the specification of items or services you require.

Follow the public procurement guidelines at www.etenders.gov.ie

The Selection and award criteria, including the weighting of each, should be clearly outlined in the tender specification and cannot be changed after the tender has been issued.

The same tender document is presented to all potential tenderers. If a potential tenderer seeks clarification from the grantee it must ensure that the information in the answer is circulated to all potential tenderers.

Select a panel to assess the tenders.

Open tenders at the same time.

A record must be maintained and available for audit.

Any conflict of interest or potential conflict of interest at any stage of the process must be fully recorded, and managed.

Select tenderers according to the selection criteria and award the contract according to the award criteria. Please note that for legal reasons experience may not be used as an award criterion for scoring tenders.

Documentation including notes of decisions and assessment of tenders plus copies of all bids must be retained for inspection.

IF IN DOUBT, SEEK ADVICE

EWM Programme Guidelines _____________________________________________________________________________________________________

Page 28

Section 10: Apportionment of Costs Apportionment of Costs What is Apportionment of Costs? Apportionment of costs is the process of sharing an organisation’s expenditure among/across the individual funding streams / programmes that it implements. It relates to central costs that are applicable to more than one funding stream/programme, for example, salaries, general overheads and on-going running costs. It is important for an organisation to develop, document and implement a method/basis of apportioning costs between the various programmes it manages. When is an Apportionment Policy required to be submitted to Pobal? All organisations that have multiple sources of funding and that apply to Pobal for EWM project funding towards salary and/or overhead costs (to be incurred in the implementation of that project), are required to submit an apportionment policy to Pobal. An apportionment policy should be prepared on a per company basis i.e. each company to have one policy only, not an individual policy for each funding stream/programme. An apportionment policy is required to be submitted to Pobal as per the circumstances outlined above and:

a. on a once off basis at the application stage of a one-off Pobal grant programme (i.e. a programme that awards a specific amount of funding for a set period of time),

b. at the annual planning stage where funding is made to an organisation on an annual basis and the organisation is required to submit annual plans/project plan and

c. following a regular review of apportionment that results in a change to current policy. When apportionment of costs is not required

When the applicant organisation has applied for 100% funding towards a project and all costs in their entirety can be directly attributed to that project;

When the programmes concerned do not have an administration budget, for

example, organisations applying to Pobal for a one-off grant to fund 100% of a specific cost e.g. 100% purchase cost of a suite of computers;

When a flat rate calculation for “indirect costs” can be applied. For some larger organisations with multiple funding streams the apportionment of indirect costs is not a practical or cost effective exercise for either the organisation to implement or for Pobal to verify. Subject to this approach being eligible within the programme, e.g. the Peace 111 Programme, the applicant organisation reaches agreement at pre-contract with Pobal that indirect central admin costs can be claimed at a rate less than or up to 20% of the direct salary costs to the programme.