Embed Size (px)

Citation preview

Growing Beyond

Entrepreneurs speak outA call to action for G20 governments

The Nice Côte d’Azur 2011 Entrepreneurship Barometer

Produced for the G20 Young Entrepreneur Summit, October 2011

Country digestArgentinaAustralia•BrazilCanadaChinaFranceGermanyIndiaIndonesiaItalyJapanMexicoRussiaSaudi ArabiaSouth AfricaSouth KoreaTurkeyUnited KingdomUnited StatesEuropean Union

ViewpointAlexandre Costa Chairman, Cacau Show, Brazil

The seed for Brazilian chocolate retailer Cacau Show was sown in 1988, when founder Alexandre Costa was just 17 years old. He opened his

first franchise in 2001, and today the company has almost 1,100 franchises in Brazil and produces 14,000 tons of chocolate a year.

“People in Brazil are increasingly looking to entrepreneurs for inspiration, but this has not always been the case; it is a fairly recent development. In the past, young people wanted to work for big corporations and major multinational companies. Now, entrepreneurs are showing the younger generation that they can achieve their dreams.

“The Government understands that it is important and has taken some steps toward developing entrepreneurial behavior and reinforcing this message. There are various initiatives already in schools and various sponsorship programs to help young people through education. A further step could be for the Government to provide some funding for budding entrepreneurs. However, the message needs to be one of encouragement rather than just financial support. This would help foster a culture of entrepreneurship in Brazil.

“Simplifying the tax system to encourage entrepreneurship would also have a positive impact. Politicians frequently talk about tax reform, but we have not seen any concrete changes yet.”

TendencyWeighted score:

higher quartileWeighted score: lower quartile

++–––

+

Dete

riorated

Improved

The perception barometerThis study focuses on the entrepreneurship environment of G20 countries through the lens of five fundamental enablers: entrepreneurship culture; education and training; access to funding; regulation and taxation; and coordinated support.

Through these enablers, we explore the climate for entrepreneurs in the G20 countries and the likely direction things will take.

Our original approach is based on:

• Quantitative economic indicators• The opinions of entrepreneurs on the progress and impact of

specificenablers

Our perception barometer sums up progress as evaluated by more than 1,000 entrepreneurs during the last five years, using four score ranges.

The analysis of these indicators and opinions also highlights how entrepreneurs’ perceptions may differ from the latest economic figures; a divergence that may be due to cultural bias, derivative ideas or lack of information. Red tape can also present challenges when it comes to accessing sources of funding.

These gaps in perception raise a call to action for governments to tackle these specific issues.

1Entrepreneurs speak out The Nice Côte d’Azur 2011 Entrepreneurship Barometer | Brazil digest

Strengths• Access to tertiary education is increasing sharply• Brazilian culture is becoming more favorable for

entrepreneurs • Private equity (PE)‑backed IPOs accounted for almost

30% of all IPOs in 2006 and 2007

Weaknesses• The legal system is still very complex and bureaucratic• Starting a new business is a cumbersome task• High tax rates and the complexity of the tax system are

asignificantdisadvantage• Average PE deals are quite small• High interest rates compared with other markets

Opportunities• Economic growth has increased the size of the domestic

market, generating more business opportunities• Increases in R&D spending and in the number of

researchersarelikelytoleadtomorepatentsbeingfiledin Brazil than has been the case thus far

• High demand for infrastructure investments • Highly fragmented market in many sectors, with

consolidation opportunities• Small capital markets and a local preference for

government bond investment is an important opportunity for development of the local capital markets

Threats• The degree of ease involved in starting a business has

not improved quickly enough in Brazil given the extent ofthecurrentdifficulties

• A complex and bureaucratic tax system threatens Brazil’s competitiveness

• Highlaborcostsandaninflexiblelaborregulatoryenvironment threatens growth and innovation

• A strong exchange rate undermines the international competitiveness of Brazilian SMEs

• Higher competition for deals in certain industries has increased asset prices

The Nice Côte d’Azur 2011 Entrepreneurship Barometer by Ernst & Young

Generalandspecificfactorsinfluencingtheentrepreneurship environment

Brazil High potentials and strong growthStrong economic growth, coupled with great policy improvements, make Brazil one of the most attractive countries for young entrepreneurs. On the G20 scale, Brazil scores third best country among the G20 in offering young entrepreneurs the most favorable environment. Brazil comes after the United States (24%) and China (8%), and slightly above Germany and Canada (6%). Among young Brazilian entrepreneurs, 58% believe their country is the best in the G20 for business.

Creationofnewbusinessesconfirmstheoptimismaboutthecountry, having risen from 243,643 in 2005 to 315,066 in 2008 — a 29.3% jump, which compares favorably with average increases of 11.8% for the G20 and 5.3% for rapid‑growth markets in the group.Reflectingthis,thecountry’snewbusinessdensity, which measures new registrations per 1,000 people aged 15–64, increased from 1.9 to 2.4 in the same period, all but closing the gap with the G20 average (2.5) and well above the average rapid‑growth market (1.3). Moreover, 80% of jobs being created in Brazil are through small and medium enterprises (SMEs).

Yet challenges still abound for young entrepreneurs in Brazil. For example, access to funding has improved in recent years, butremainsdifficult,moresothanintheG20asawhole. Starting a new business requires much more time and many more procedures than in the group’s average and, despite recent progress, the country still lags behind the G20 average in terms of university education and research and development (R&D).

New businesses registeredBrazil compared to G20 and rapid-growth market average

Source: World Bank. Data not available for US, China and Saudi Arabia.

0

100,000

200,000

300,000

400,000

2005 2006 2007 2008 2009

Brazil Rapid-growth market averageG20 average

2 Entrepreneurs speak out The Nice Côte d’Azur 2011 Entrepreneurship Barometer | Brazil digest

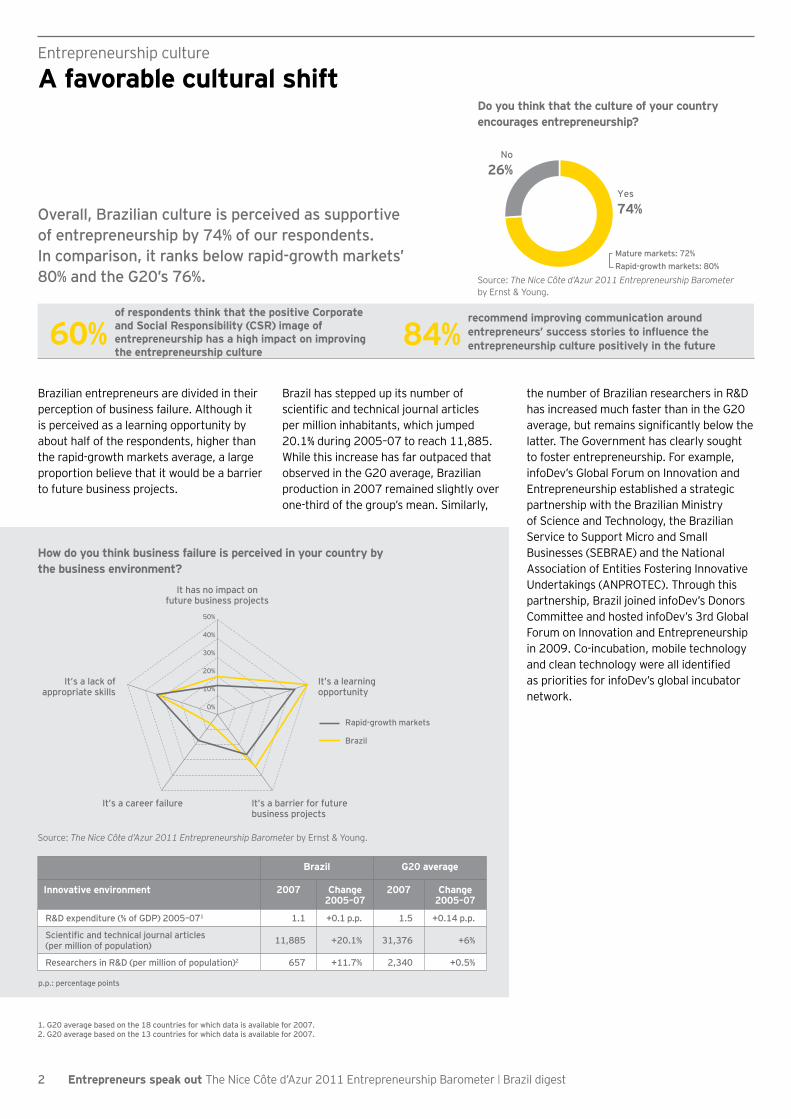

Overall, Brazilian culture is perceived as supportive of entrepreneurship by 74% of our respondents. In comparison, it ranks below rapid‑growth markets’ 80% and the G20’s 76%.

Entrepreneurship culture A favorable cultural shift

Brazilian entrepreneurs are divided in their perception of business failure. Although it is perceived as a learning opportunity by about half of the respondents, higher than the rapid-growth markets average, a large proportion believe that it would be a barrier to future business projects.

Brazil has stepped up its number of scientific and technical journal articles per million inhabitants, which jumped 20.1% during 2005–07 to reach 11,885. While this increase has far outpaced that observed in the G20 average, Brazilian production in 2007 remained slightly over one-third of the group’s mean. Similarly,

the number of Brazilian researchers in R&D has increased much faster than in the G20 average, but remains significantly below the latter. The Government has clearly sought to foster entrepreneurship. For example, infoDev’s Global Forum on Innovation and Entrepreneurship established a strategic partnership with the Brazilian Ministry of Science and Technology, the Brazilian Service to Support Micro and Small Businesses (SEBRAE) and the National Association of Entities Fostering Innovative Undertakings (ANPROTEC). Through this partnership, Brazil joined infoDev’s Donors Committee and hosted infoDev’s 3rd Global Forum on Innovation and Entrepreneurship in 2009. Co-incubation, mobile technology and clean technology were all identified as priorities for infoDev’s global incubator network.

Do you think that the culture of your country encourages entrepreneurship?

Source: The Nice Côte d’Azur 2011 Entrepreneurship Barometer by Ernst & Young.

Yes

74%

No

26%

Mature markets: 72%Rapid-growth markets: 80%

1. G20 average based on the 18 countries for which data is available for 2007.2. G20 average based on the 13 countries for which data is available for 2007.

84%recommend improving communication around entrepreneurs’successstoriestoinfluencetheentrepreneurship culture positively in the future60%

of respondents think that the positive Corporate and Social Responsibility (CSR) image of entrepreneurship has a high impact on improving the entrepreneurship culture

Brazil G20 average

Innovative environment 2007 Change 2005–07

2007 Change 2005–07

R&D expenditure (% of GDP) 2005–071 1.1 +0.1 p.p. 1.5 +0.14 p.p.

Scientificandtechnicaljournalarticles (per million of population) 11,885 +20.1% 31,376 +6%

Researchers in R&D (per million of population)2 657 +11.7% 2,340 +0.5%

How do you think business failure is perceived in your country by the business environment?

Source: The Nice Côte d’Azur 2011 Entrepreneurship Barometer by Ernst & Young.

0%

10%

20%

30%

40%

50%

It has no impact onfuture business projects

It’s a learningopportunity

It’s a barrier for futurebusiness projects

It’s a career failure

It’s a lack of appropriate skills

Rapid-growth markets

Brazil

p.p.: percentage points

3Entrepreneurs speak out The Nice Côte d’Azur 2011 Entrepreneurship Barometer | Brazil digest

Education and training Specifictrainingmakesbetterentrepreneurs

The majority of respondents described recent improvements in college and school programs, coaching sessions for entrepreneurs, conferences, seminars and dedicated chairs at universities. Brazil’s efforts in relation to the development of education on a wider scale are patent. The Government invests a higher share of its GDP (5.1%) on it than the average of other G20 countries (4.8%). The increase in its rate scored a record in the group.

The gross enrollment ratio in secondary education, above 100%3 until recently, illustrates this catch-up process. A corresponding figure of 34.4% for enrollment in tertiary education, against 53.5% for the G20, reveals the country lags behind in this area.

The Brazilian national telecentre.org Academy, run by the Telecentre Information and Business Association (ATN), pays

special attention to establishing courses in the areas of telecenter management and digital entrepreneurship. All of the 356 telecenter operators that registered for the first pilot were supported in their efforts to promote more options for their social enterprise, and to become centers of digital inclusion.

Regarding business education, 66% of Brazilian entrepreneursbelievespecifictrainingmakesbetterentrepreneurs. And many expressed satisfaction with the quality of that offered in Brazil.

Brazil G20 average

2008 Change 2005-08

2008 Change 2005-08

Public spending on education, total (% of GDP) 20074 5.1 +0.6 p.p. 4.8 +0.3 p.p.

School enrollment, secondary (% gross) 100.8 ‑4.8 p.p. 95.9 +1.6 p.p.

School enrollment, tertiary (% gross) 34.4 +9 p.p. 53.5 +1 p.p.

3.Percentageabove100%reflectsthat100%oftheofficialagegroupisreceivingthatlevelofeducationinadditiontopeopleofotheragegroups.4. Figure for 2007, the latest year for which data is available. Change based on 2005–07 data.

Do you think that students need to follow specific training to become entrepreneurs?

Source: The Nice Côte d’Azur 2011 Entrepreneurship Barometer by Ernst & Young.

Yes

66%No

32%

Can’t say

2%

Mature markets: 59%Rapid-growth markets: 80%

80% 96%of respondents acknowledge better entrepreneurship conferences and seminars

viewspecificprogramsatuniversitiesandbusinessschools as a key priority to boost student favorability of entrepreneurship as a career option

p.p.: percentage points

4 Entrepreneurs speak out The Nice Côte d’Azur 2011 Entrepreneurship Barometer | Brazil digest

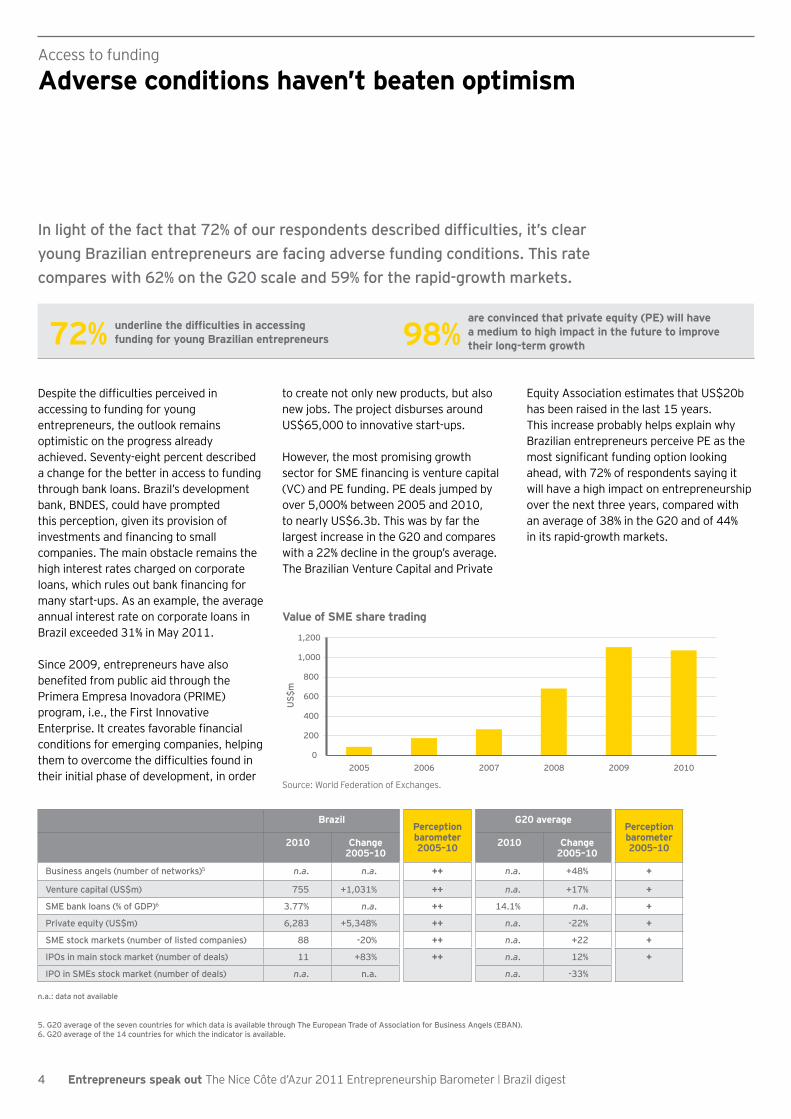

Despite the difficulties perceived in accessing to funding for young entrepreneurs, the outlook remains optimistic on the progress already achieved. Seventy-eight percent described a change for the better in access to funding through bank loans. Brazil’s development bank, BNDES, could have prompted this perception, given its provision of investments and financing to small companies. The main obstacle remains the high interest rates charged on corporate loans, which rules out bank financing for many start-ups. As an example, the average annual interest rate on corporate loans in Brazil exceeded 31% in May 2011.

Since 2009, entrepreneurs have also benefited from public aid through the Primera Empresa Inovadora (PRIME) program, i.e., the First Innovative Enterprise. It creates favorable financial conditions for emerging companies, helping them to overcome the difficulties found in their initial phase of development, in order

to create not only new products, but also new jobs. The project disburses around US$65,000 to innovative start-ups.

However, the most promising growth sector for SME financing is venture capital (VC) and PE funding. PE deals jumped by over 5,000% between 2005 and 2010, to nearly US$6.3b. This was by far the largest increase in the G20 and compares with a 22% decline in the group’s average. The Brazilian Venture Capital and Private

Equity Association estimates that US$20b has been raised in the last 15 years. This increase probably helps explain why Brazilian entrepreneurs perceive PE as the most significant funding option looking ahead, with 72% of respondents saying it will have a high impact on entrepreneurship over the next three years, compared with an average of 38% in the G20 and of 44% in its rapid-growth markets.

BrazilPerception barometer 2005–10

G20 averagePerception barometer 2005–102010 Change

2005–102010 Change

2005–10

Business angels (number of networks)5 n.a. n.a. ++ n.a. +48% +

Venture capital (US$m) 755 +1,031% ++ n.a. +17% +

SME bank loans (% of GDP)6 3.77% n.a. ++ 14.1% n.a. +

Private equity (US$m) 6,283 +5,348% ++ n.a. ‑22% +

SME stock markets (number of listed companies) 88 ‑20% ++ n.a. +22 +

IPOs in main stock market (number of deals) 11 +83% ++ n.a. 12% +

IPO in SMEs stock market (number of deals) n.a. n.a. n.a. ‑33%

Inlightofthefactthat72%ofourrespondentsdescribeddifficulties,it’sclearyoung Brazilian entrepreneurs are facing adverse funding conditions. This rate compares with 62% on the G20 scale and 59% for the rapid‑growth markets.

Access to funding Adverse conditions haven’t beaten optimism

Value of SME share trading

Source: World Federation of Exchanges.

0

200

400

600

800

1,000

1,200

2005 2006 2007 2008 2009 2010

US$

m

n.a.: data not available

5. G20 average of the seven countries for which data is available through The European Trade of Association for Business Angels (EBAN).6. G20 average of the 14 countries for which the indicator is available.

98%are convinced that private equity (PE) will have a medium to high impact in the future to improve their long-term growth72% underlinethedifficultiesinaccessing

funding for young Brazilian entrepreneurs

5Entrepreneurs speak out The Nice Côte d’Azur 2011 Entrepreneurship Barometer | Brazil digest

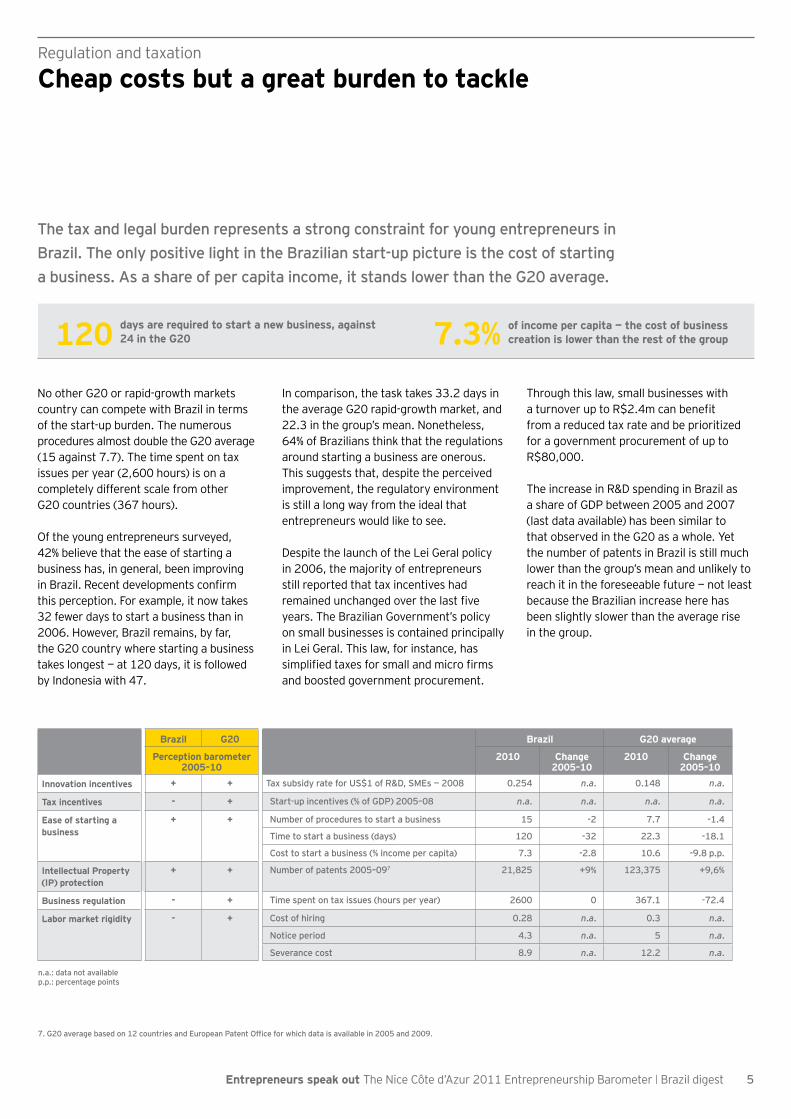

No other G20 or rapid-growth markets country can compete with Brazil in terms of the start-up burden. The numerous procedures almost double the G20 average (15 against 7.7). The time spent on tax issues per year (2,600 hours) is on a completely different scale from other G20 countries (367 hours).

Of the young entrepreneurs surveyed, 42% believe that the ease of starting a business has, in general, been improving in Brazil. Recent developments confirm this perception. For example, it now takes 32 fewer days to start a business than in 2006. However, Brazil remains, by far, the G20 country where starting a business takes longest — at 120 days, it is followed by Indonesia with 47.

In comparison, the task takes 33.2 days in the average G20 rapid-growth market, and 22.3 in the group’s mean. Nonetheless, 64% of Brazilians think that the regulations around starting a business are onerous. This suggests that, despite the perceived improvement, the regulatory environment is still a long way from the ideal that entrepreneurs would like to see.

Despite the launch of the Lei Geral policy in 2006, the majority of entrepreneurs still reported that tax incentives had remained unchanged over the last five years. The Brazilian Government’s policy on small businesses is contained principally in Lei Geral. This law, for instance, has simplified taxes for small and micro firms and boosted government procurement.

Through this law, small businesses with a turnover up to R$2.4m can benefit from a reduced tax rate and be prioritized for a government procurement of up to R$80,000.

The increase in R&D spending in Brazil as a share of GDP between 2005 and 2007 (last data available) has been similar to that observed in the G20 as a whole. Yet the number of patents in Brazil is still much lower than the group’s mean and unlikely to reach it in the foreseeable future — not least because the Brazilian increase here has been slightly slower than the average rise in the group.

Brazil G20 Brazil G20 average

Perception barometer 2005–10

2010 Change 2005–10

2010 Change 2005–10

Innovation incentives + + Tax subsidy rate for US$1 of R&D, SMEs — 2008 0.254 n.a. 0.148 n.a.

Tax incentives - + Start‑up incentives (% of GDP) 2005–08 n.a. n.a. n.a. n.a.

Ease of starting a business

+ + Number of procedures to start a business 15 ‑2 7.7 ‑1.4

Time to start a business (days) 120 ‑32 22.3 ‑18.1

Cost to start a business (% income per capita) 7.3 ‑2.8 10.6 ‑9.8 p.p.

Intellectual Property (IP) protection

+ + Number of patents 2005–097 21,825 +9% 123,375 +9,6%

Business regulation - + Time spent on tax issues (hours per year) 2600 0 367.1 ‑72.4

Labor market rigidity - + Cost of hiring 0.28 n.a. 0.3 n.a.

Notice period 4.3 n.a. 5 n.a.

Severance cost 8.9 n.a. 12.2 n.a.

n.a.: data not availablep.p.: percentage points

7.G20averagebasedon12countriesandEuropeanPatentOfficeforwhichdataisavailablein2005and2009.

The tax and legal burden represents a strong constraint for young entrepreneurs in Brazil. The only positive light in the Brazilian start‑up picture is the cost of starting a business. As a share of per capita income, it stands lower than the G20 average.

Regulation and taxation Cheap costs but a great burden to tackle

120 days are required to start a new business, against 24 in the G20 7.3% of income per capita — the cost of business

creation is lower than the rest of the group

6 Entrepreneurs speak out The Nice Côte d’Azur 2011 Entrepreneurship Barometer | Brazil digest

Coordinated support Impactful and improving

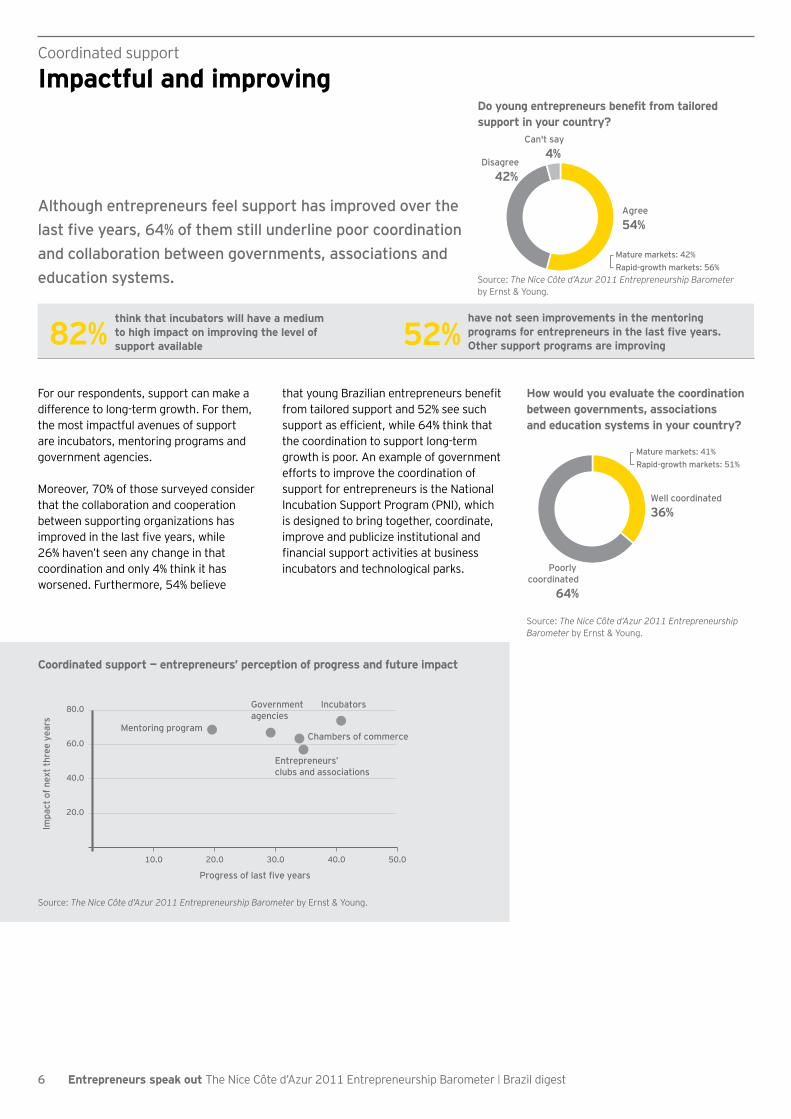

Although entrepreneurs feel support has improved over the lastfiveyears,64%ofthemstillunderlinepoorcoordinationand collaboration between governments, associations and education systems.

For our respondents, support can make a difference to long-term growth. For them, the most impactful avenues of support are incubators, mentoring programs and government agencies.

Moreover, 70% of those surveyed consider that the collaboration and cooperation between supporting organizations has improved in the last five years, while 26% haven’t seen any change in that coordination and only 4% think it has worsened. Furthermore, 54% believe

that young Brazilian entrepreneurs benefit from tailored support and 52% see such support as efficient, while 64% think that the coordination to support long-term growth is poor. An example of government efforts to improve the coordination of support for entrepreneurs is the National Incubation Support Program (PNI), which is designed to bring together, coordinate, improve and publicize institutional and financial support activities at business incubators and technological parks.

Coordinated support — entrepreneurs’ perception of progress and future impact

Source: The Nice Côte d’Azur 2011 Entrepreneurship Barometer by Ernst & Young.

Chambers of commerce

Government agencies

Incubators

Mentoring program

20.0

40.0

60.0

80.0

10.0 20.0 30.0 40.0 50.0

Entrepreneurs’ clubs and associations

Impa

ct o

f nex

t thr

ee y

ears

Progress of last five years

52%have not seen improvements in the mentoring programsforentrepreneursinthelastfiveyears.Other support programs are improving82%

think that incubators will have a medium to high impact on improving the level of support available

Do young entrepreneurs benefit from tailored support in your country?

Source: The Nice Côte d’Azur 2011 Entrepreneurship Barometer by Ernst & Young.

Agree54%

Disagree 42%

Can't say4%

Mature markets: 42%Rapid-growth markets: 56%

How would you evaluate the coordination between governments, associationsand education systems in your country?

Source: The Nice Côte d’Azur 2011 Entrepreneurship Barometer by Ernst & Young.

Well coordinated 36%

Poorly coordinated

64%

Mature markets: 41%Rapid-growth markets: 51%

7Entrepreneurs speak out The Nice Côte d’Azur 2011 Entrepreneurship Barometer | Brazil digest

Launch date Main application area

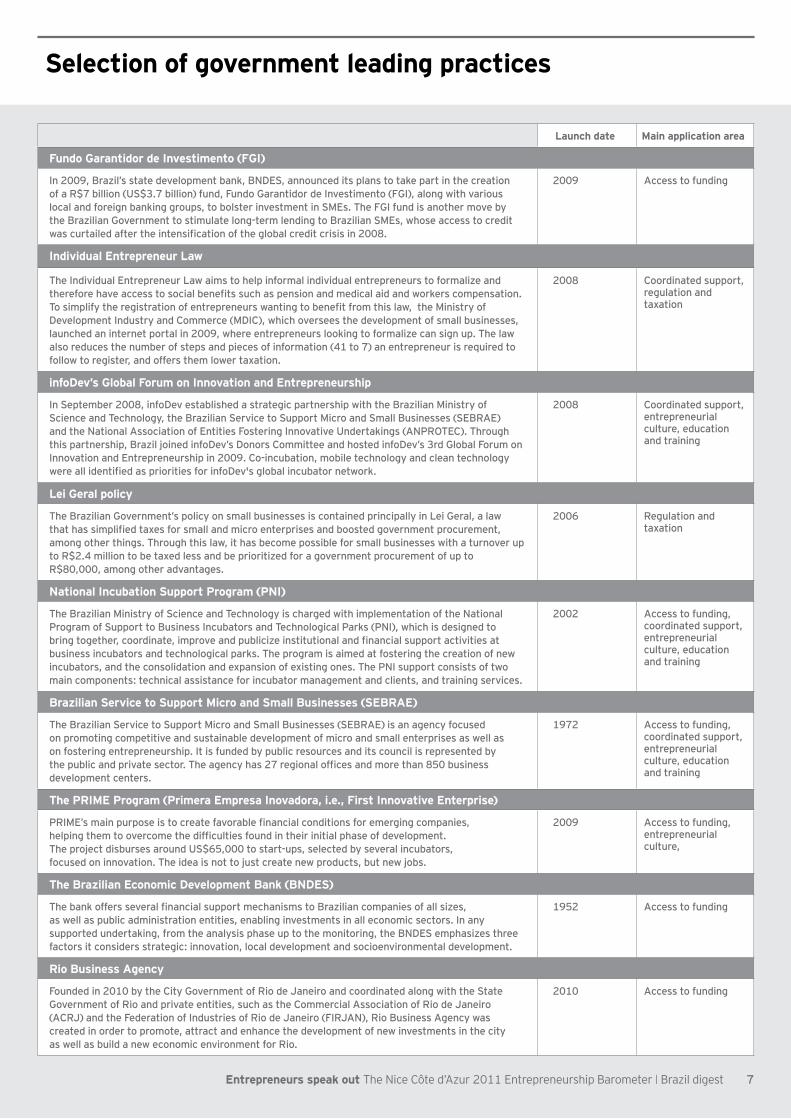

Fundo Garantidor de Investimento (FGI)

In 2009, Brazil’s state development bank, BNDES, announced its plans to take part in the creation of a R$7 billion (US$3.7 billion) fund, Fundo Garantidor de Investimento (FGI), along with various local and foreign banking groups, to bolster investment in SMEs. The FGI fund is another move by the Brazilian Government to stimulate long‑term lending to Brazilian SMEs, whose access to credit wascurtailedaftertheintensificationoftheglobalcreditcrisisin2008.

2009 Access to funding

Individual Entrepreneur Law

The Individual Entrepreneur Law aims to help informal individual entrepreneurs to formalize and thereforehaveaccesstosocialbenefitssuchaspensionandmedicalaidandworkerscompensation.Tosimplifytheregistrationofentrepreneurswantingtobenefitfromthislaw,theMinistryofDevelopment Industry and Commerce (MDIC), which oversees the development of small businesses, launched an internet portal in 2009, where entrepreneurs looking to formalize can sign up. The law also reduces the number of steps and pieces of information (41 to 7) an entrepreneur is required to follow to register, and offers them lower taxation.

2008 Coordinated support, regulation and taxation

infoDev’s Global Forum on Innovation and Entrepreneurship

In September 2008, infoDev established a strategic partnership with the Brazilian Ministry of Science and Technology, the Brazilian Service to Support Micro and Small Businesses (SEBRAE) and the National Association of Entities Fostering Innovative Undertakings (ANPROTEC). Through this partnership, Brazil joined infoDev’s Donors Committee and hosted infoDev’s 3rd Global Forum on Innovation and Entrepreneurship in 2009. Co‑incubation, mobile technology and clean technology wereallidentifiedasprioritiesforinfoDev'sglobalincubatornetwork.

2008 Coordinated support, entrepreneurial culture, education and training

Lei Geral policy

The Brazilian Government’s policy on small businesses is contained principally in Lei Geral, a law thathassimplifiedtaxesforsmallandmicroenterprisesandboostedgovernmentprocurement,among other things. Through this law, it has become possible for small businesses with a turnover up to R$2.4 million to be taxed less and be prioritized for a government procurement of up to R$80,000, among other advantages.

2006 Regulation and taxation

National Incubation Support Program (PNI)

The Brazilian Ministry of Science and Technology is charged with implementation of the National Program of Support to Business Incubators and Technological Parks (PNI), which is designed to bringtogether,coordinate,improveandpublicizeinstitutionalandfinancialsupportactivitiesatbusiness incubators and technological parks. The program is aimed at fostering the creation of new incubators, and the consolidation and expansion of existing ones. The PNI support consists of two main components: technical assistance for incubator management and clients, and training services.

2002 Access to funding, coordinated support, entrepreneurial culture, education and training

Brazilian Service to Support Micro and Small Businesses (SEBRAE)

The Brazilian Service to Support Micro and Small Businesses (SEBRAE) is an agency focused on promoting competitive and sustainable development of micro and small enterprises as well as on fostering entrepreneurship. It is funded by public resources and its council is represented by thepublicandprivatesector.Theagencyhas27regionalofficesandmorethan850businessdevelopment centers.

1972 Access to funding, coordinated support, entrepreneurial culture, education and training

The PRIME Program (Primera Empresa Inovadora, i.e., First Innovative Enterprise)

PRIME’smainpurposeistocreatefavorablefinancialconditionsforemergingcompanies, helpingthemtoovercomethedifficultiesfoundintheirinitialphaseofdevelopment. The project disburses around US$65,000 to start‑ups, selected by several incubators, focused on innovation. The idea is not to just create new products, but new jobs.

2009 Access to funding, entrepreneurial culture,

The Brazilian Economic Development Bank (BNDES)

ThebankoffersseveralfinancialsupportmechanismstoBraziliancompaniesofallsizes, as well as public administration entities, enabling investments in all economic sectors. In any supported undertaking, from the analysis phase up to the monitoring, the BNDES emphasizes three factors it considers strategic: innovation, local development and socioenvironmental development.

1952 Access to funding

Rio Business Agency

Founded in 2010 by the City Government of Rio de Janeiro and coordinated along with the State Government of Rio and private entities, such as the Commercial Association of Rio de Janeiro (ACRJ) and the Federation of Industries of Rio de Janeiro (FIRJAN), Rio Business Agency was created in order to promote, attract and enhance the development of new investments in the city as well as build a new economic environment for Rio.

2010 Access to funding

Selection of government leading practices

8 Entrepreneurs speak out The Nice Côte d’Azur 2011 Entrepreneurship Barometer | Brazil digest

Methodology

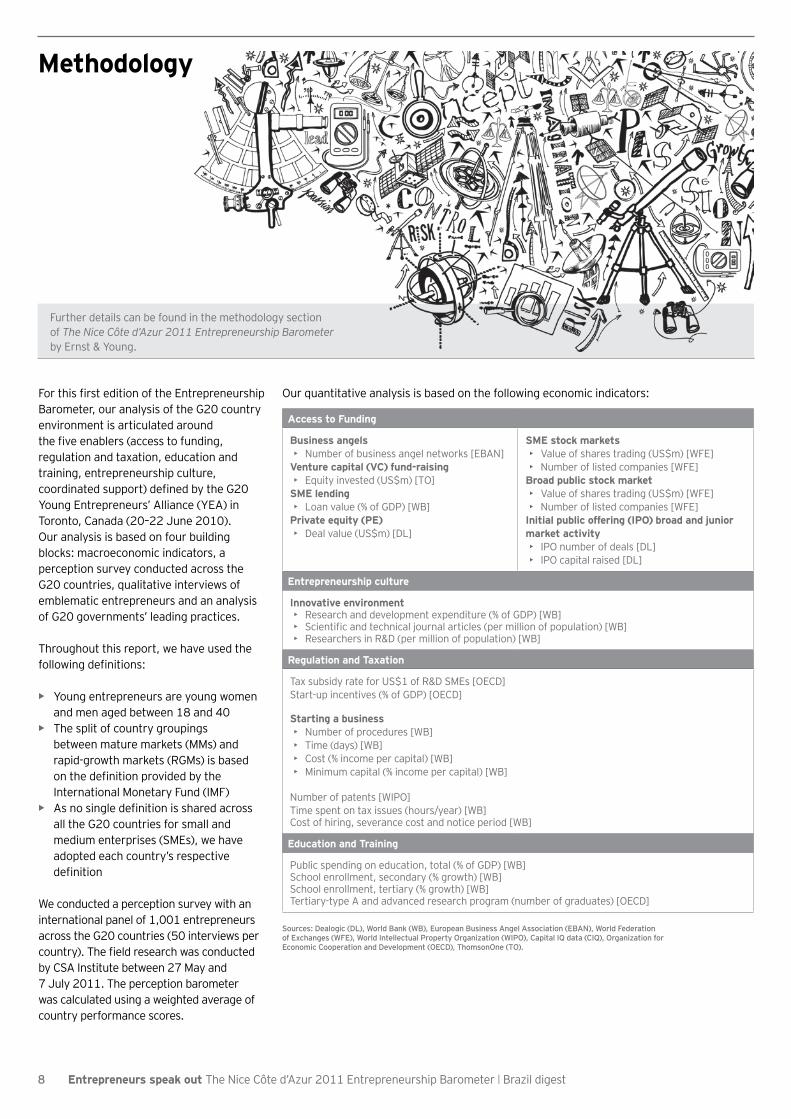

For this first edition of the Entrepreneurship Barometer, our analysis of the G20 country environment is articulated around the five enablers (access to funding, regulation and taxation, education and training, entrepreneurship culture, coordinated support) defined by the G20 Young Entrepreneurs’ Alliance (YEA) in Toronto, Canada (20–22 June 2010). Our analysis is based on four building blocks: macroeconomic indicators, a perception survey conducted across the G20 countries, qualitative interviews of emblematic entrepreneurs and an analysis of G20 governments’ leading practices.

Throughout this report, we have used the following definitions:

• Young entrepreneurs are young women and men aged between 18 and 40

• The split of country groupings between mature markets (MMs) and rapid-growth markets (RGMs) is based on the definition provided by the International Monetary Fund (IMF)

• As no single definition is shared across all the G20 countries for small and medium enterprises (SMEs), we have adopted each country’s respective definition

We conducted a perception survey with an international panel of 1,001 entrepreneurs across the G20 countries (50 interviews per country). The field research was conducted by CSA Institute between 27 May and 7 July 2011. The perception barometer was calculated using a weighted average of country performance scores.

Our quantitative analysis is based on the following economic indicators:

Access to Funding

Business angels• Number of business angel networks [EBAN]

Venture capital (VC) fund-raising• Equity invested (US$m) [TO]

SME lending• Loan value (% of GDP) [WB]

Private equity (PE)• Deal value (US$m) [DL]

SME stock markets• Value of shares trading (US$m) [WFE]• Number of listed companies [WFE]

Broad public stock market • Value of shares trading (US$m) [WFE]• Number of listed companies [WFE]

Initial public offering (IPO) broad and junior market activity• IPO number of deals [DL]• IPO capital raised [DL]

Entrepreneurship culture

Innovative environment • Research and development expenditure (% of GDP) [WB]• Scientific and technical journal articles (per million of population) [WB]• Researchers in R&D (per million of population) [WB]

Regulation and Taxation

Tax subsidy rate for US$1 of R&D SMEs [OECD]Start-up incentives (% of GDP) [OECD]

Starting a business• Number of procedures [WB]• Time (days) [WB]• Cost (% income per capital) [WB]• Minimum capital (% income per capital) [WB]

Number of patents [WIPO]Time spent on tax issues (hours/year) [WB]Cost of hiring, severance cost and notice period [WB]

Education and Training

Public spending on education, total (% of GDP) [WB]School enrollment, secondary (% growth) [WB]School enrollment, tertiary (% growth) [WB] Tertiary-type A and advanced research program (number of graduates) [OECD]

Sources: Dealogic (DL), World Bank (WB), European Business Angel Association (EBAN), World Federation of Exchanges (WFE), World Intellectual Property Organization (WIPO), Capital IQ data (CIQ), Organization for Economic Cooperation and Development (OECD), ThomsonOne (TO).

Further details can be found in the methodology section of The Nice Côte d’Azur 2011 Entrepreneurship Barometer by Ernst & Young.

1 Throughfivekeyenablers,theEntrepreneurshipBarometeranalyzesentrepreneurs’ perception as well as government leading practices in

order to provide key recommendations to governments and entrepreneurs.

2 Thecountryprofilesexplorethenationalspecificitiesofentrepreneurshipenvironment to provide a better understanding to entrepreneurs

considering international expansion.

3 Highlighting the main conclusions of the report, the Barometer website provides further government leading practices and entrepreneurs’

success stories. • www.ey.com/entrepreneurship-barometer

Entrepreneurs speak outA call to action for G20 governments

Ernst & Young

Assurance | Tax | Transactions | Advisory

About Ernst & Young

Ernst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 152,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

© 2011 EYGM Limited. All Rights Reserved.

EYG No. CY0189

In line with Ernst & Young’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

The opinions of third parties set out in this publication are not necessarily the opinions of the global Ernst & Young organization or its member firms. Moreover, they should be seen in the context of the time they were expressed.

Contact

Andre FerreiraBrazil Strategic Growth Markets LeaderTel: +55 11 3054 0007Email: [email protected]

Leandro SanchesBrazil Entrepreneur Of The Year Co-LeaderTel: +55 11 2573 5050Email: [email protected]

Leonardo DonatoBrazil Entrepreneur Of The Year Co-LeaderTel: +55 11 2573 3245Email: [email protected]

Growing Beyond

In these challenging economic times, opportunities still exist for growth. In Growing Beyond, we’re exploring how companies can best exploit these opportunities — by expanding into new markets, finding new ways to innovate and taking new approaches to talent. You’ll gain practical insights into what you need to do to grow. Join the debate at www.ey.com/growingbeyond.

This report has been produced in collaboration with Oxford Analytica (www.oxan.com), an independent consultancy that has for over 35 years provided authoritative analysis of the macro environment.

![Southampton Open Wireless Network. Talk outline Aims of SOWN Technical Outline Campus nodes Servers SOWN[at]HOME nodes What would I have](https://img.pdfslide.us/doc/110x75/56649eff5503460f94c14f3f/southampton-open-wireless-network-wwwsownorguk-talk-outline-aims-of-sown.jpg)