Embed Size (px)

Citation preview

English for Tax Administration IV

General info

Lecturer: Dr. sc. Marijana Javornik Čubrić

Classes: Tuesday 11:30-12:30 Office hours: Tuesday 10:00 –

11:00, Room No. 6 Contact:

Coursebook

M. Javornik Čubrić, English for Tax Administration Study, Društveno veleučilište u Zagrebu, 2009.

Units 6-9

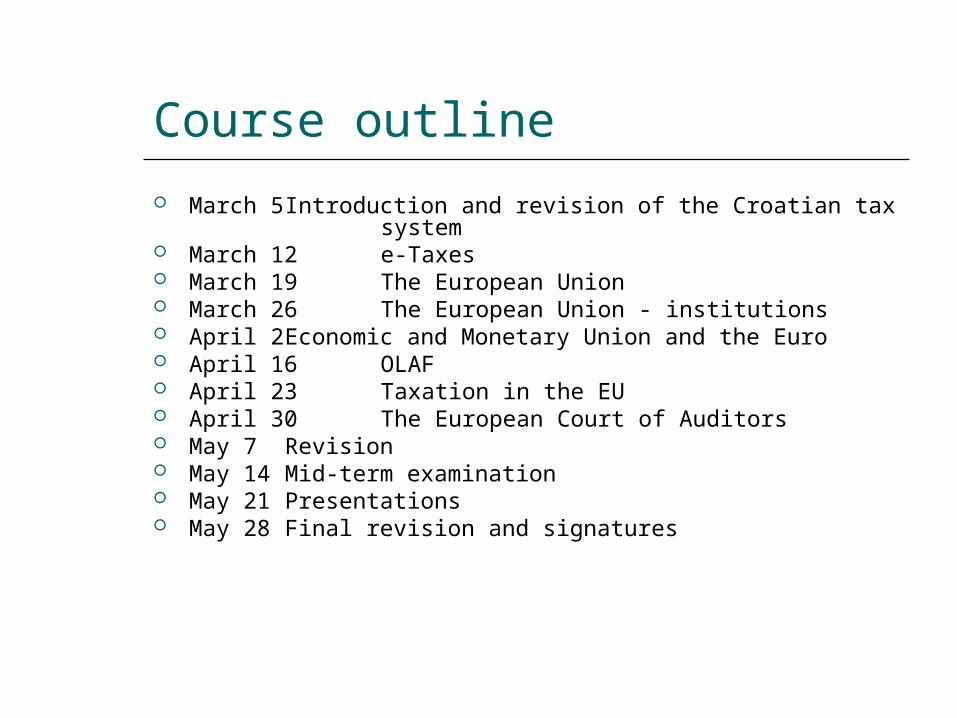

Course outline

March 5 Introduction and revision of the Croatian tax system

March 12 e-Taxes March 19 The European Union March 26 The European Union - institutions April 2 Economic and Monetary Union and the Euro April 16 OLAF April 23 Taxation in the EU April 30 The European Court of Auditors May 7 Revision May 14 Mid-term examination May 21 Presentations May 28 Final revision and signatures

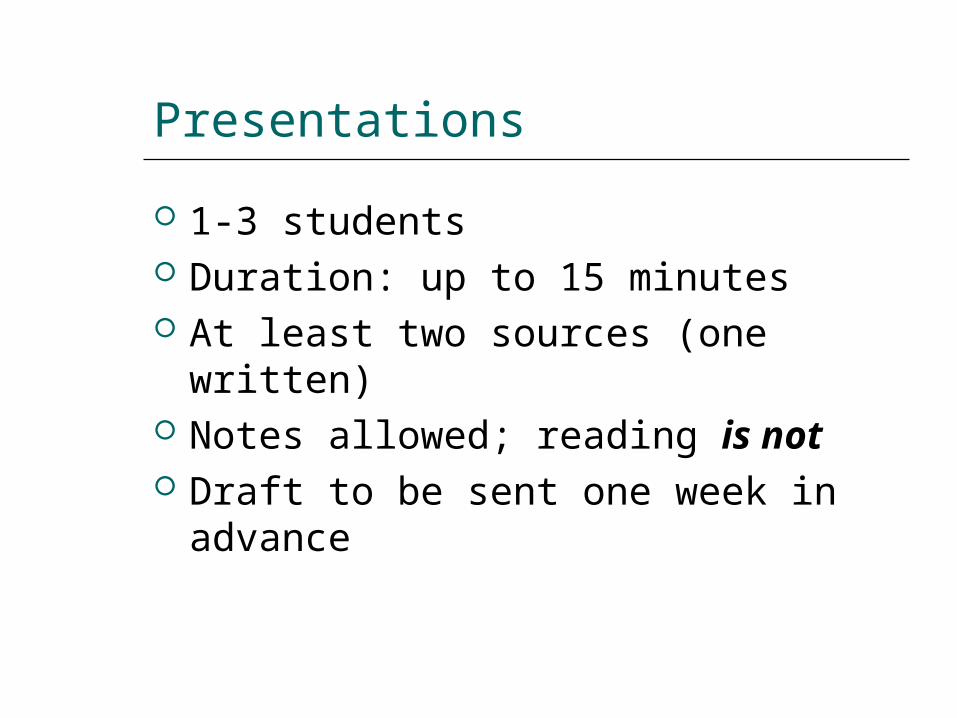

Presentations

1-3 students Duration: up to 15 minutes At least two sources (one written) Notes allowed; reading is not Draft to be sent one week in

advance

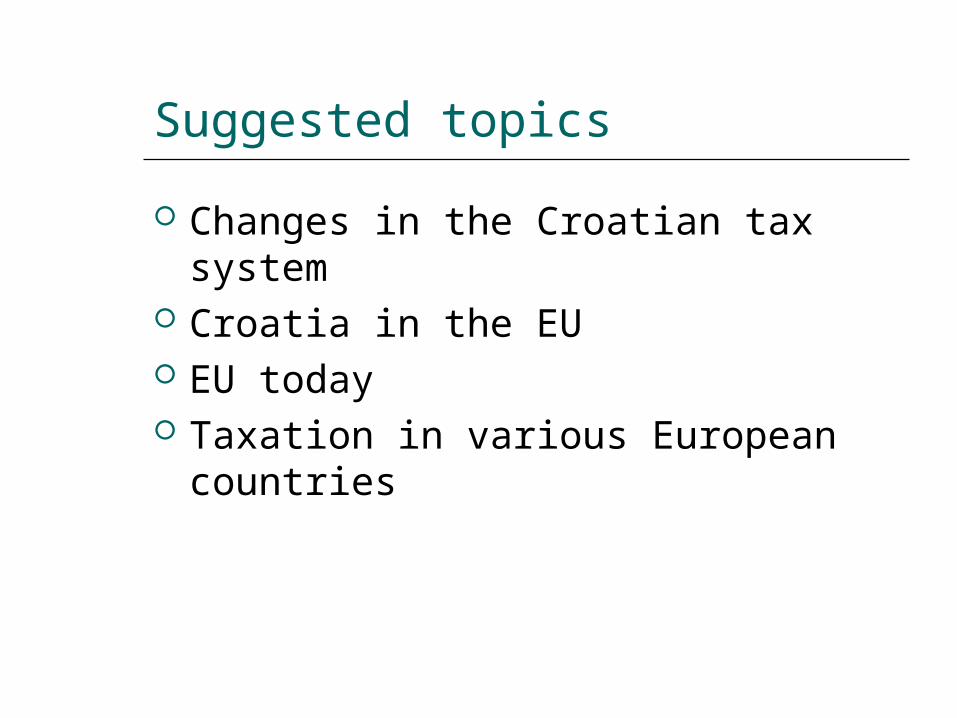

Suggested topics

Changes in the Croatian tax system Croatia in the EU EU today Taxation in various European

countries

Revision

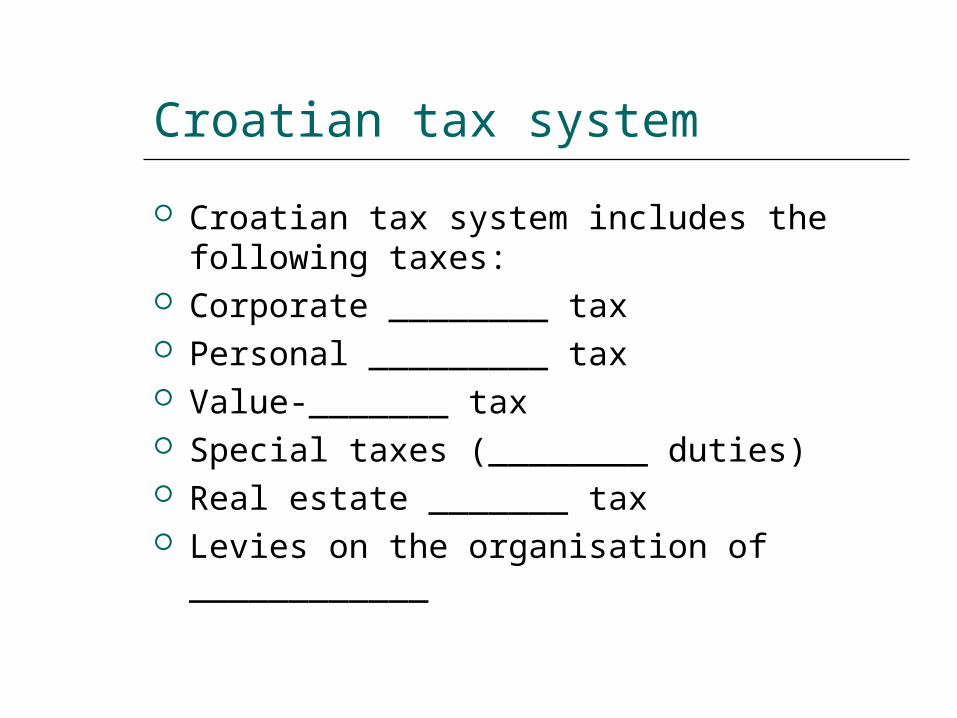

Croatian tax system

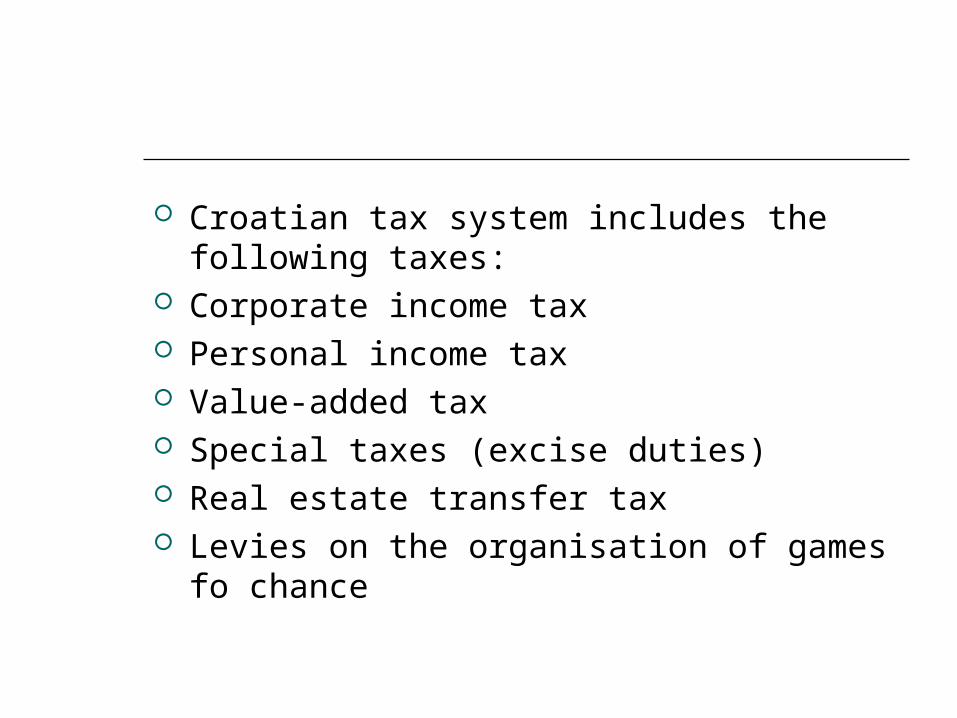

Croatian tax system includes the following taxes:

Corporate ________ tax Personal _________ tax Value-_______ tax Special taxes (________ duties) Real estate _______ tax Levies on the organisation of ____________

Croatian tax system includes the following taxes:

Corporate income tax Personal income tax Value-added tax Special taxes (excise duties) Real estate transfer tax Levies on the organisation of games fo

chance

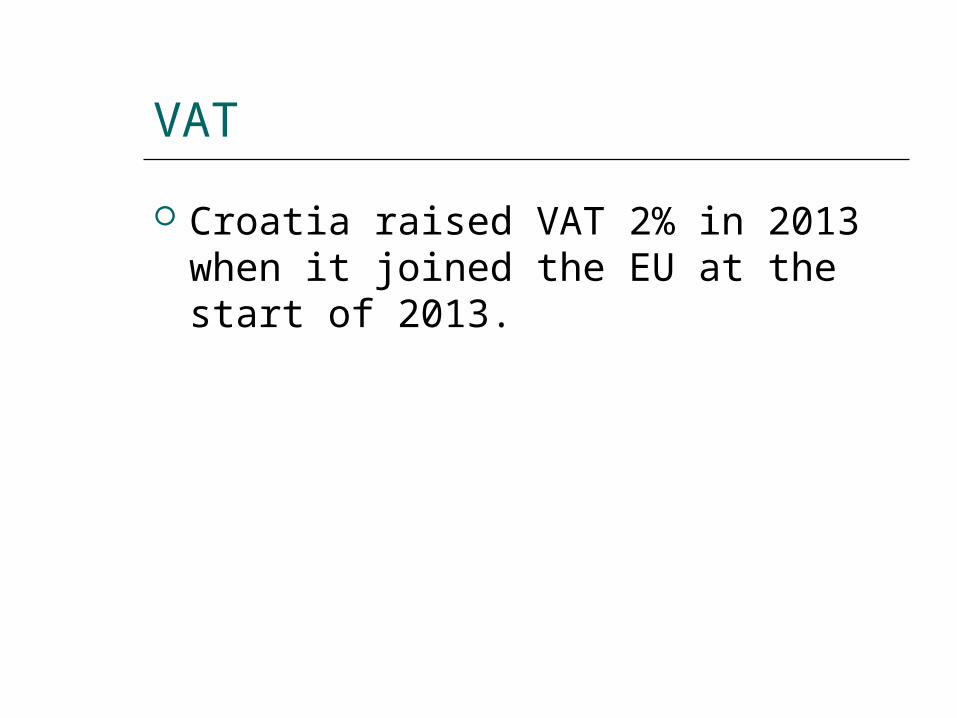

VAT

Croatia raised VAT 2% in 2013 when it joined the EU at the start of 2013.

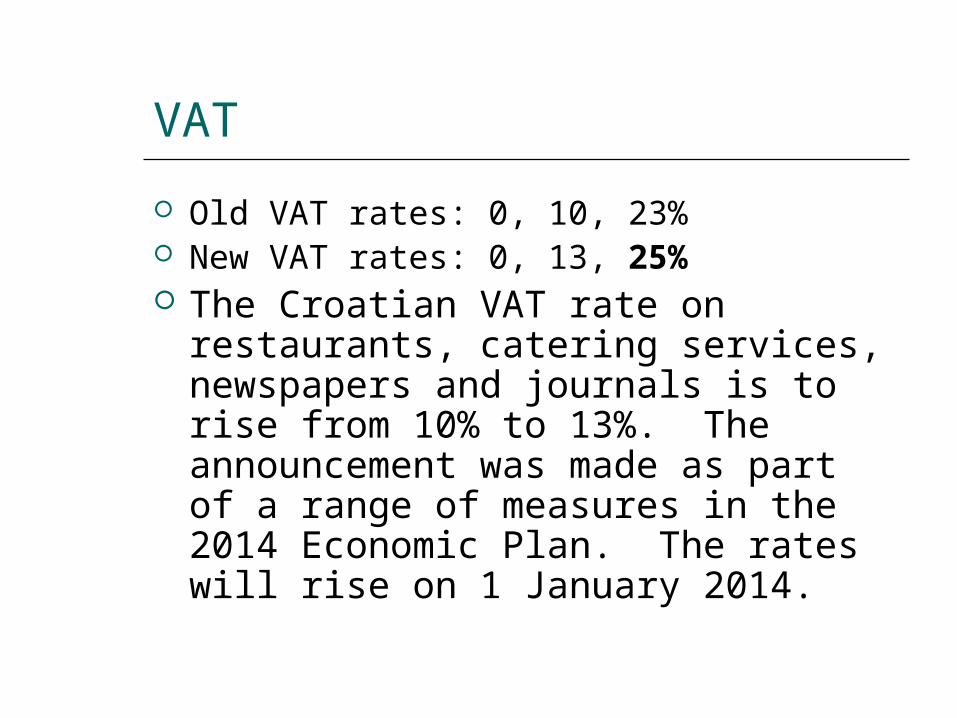

VAT

Old VAT rates: 0, 10, 23% New VAT rates: 0, 13, 25% The Croatian VAT rate on restaurants,

catering services, newspapers and journals is to rise from 10% to 13%. The announcement was made as part of a range of measures in the 2014 Economic Plan. The rates will rise on 1 January 2014.

PIT

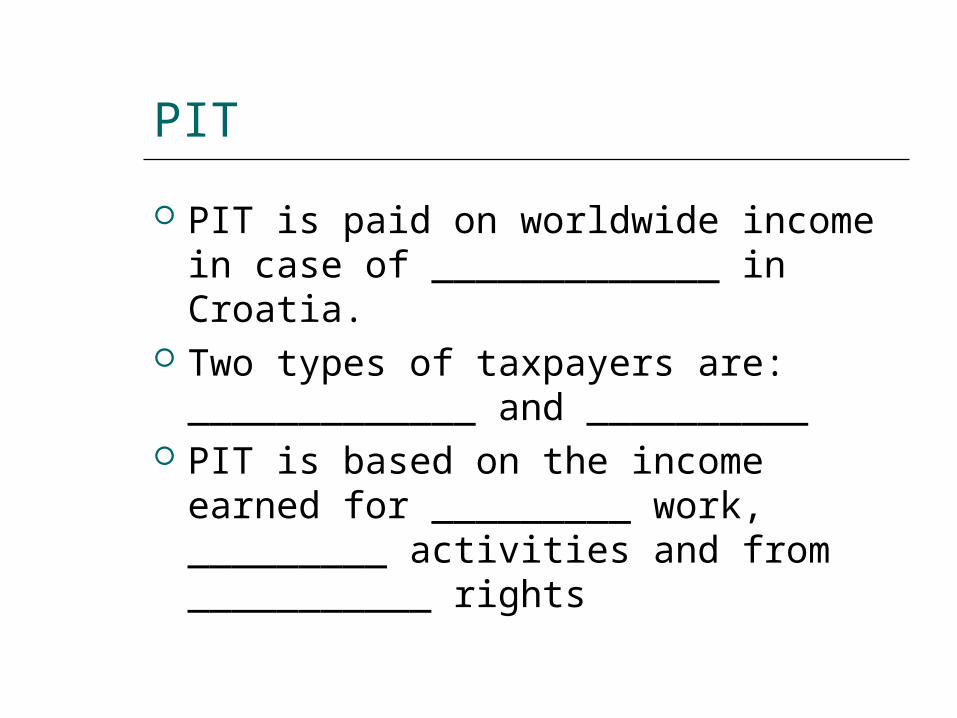

PIT is paid on worldwide income in case of _____________ in Croatia.

Two types of taxpayers are: _____________ and __________

PIT is based on the income earned for _________ work, _________ activities and from ___________ rights

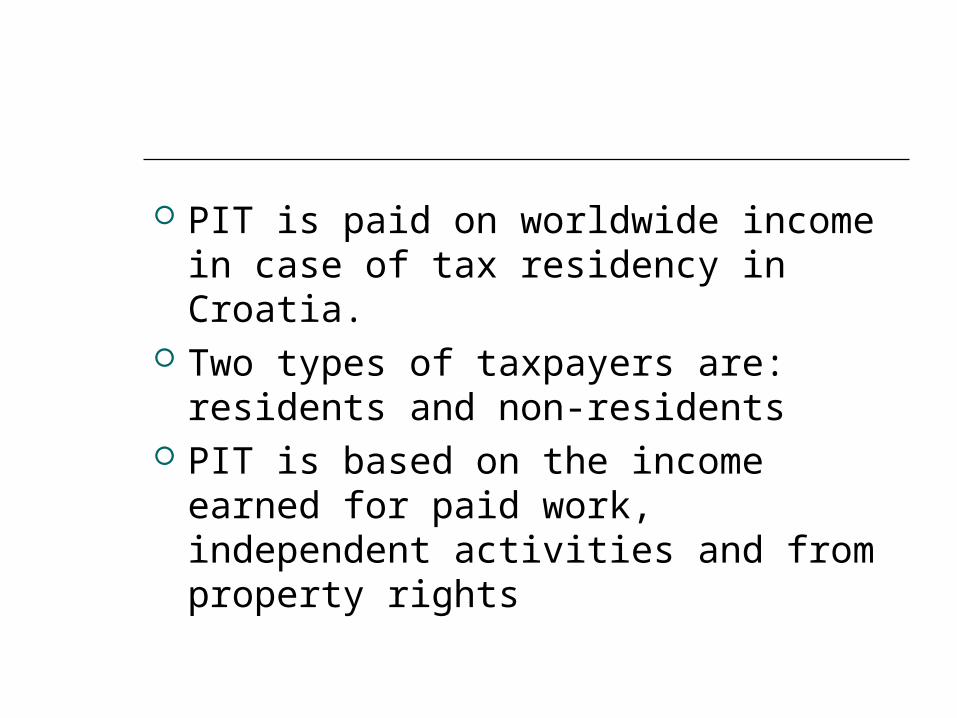

PIT is paid on worldwide income in case of tax residency in Croatia.

Two types of taxpayers are: residents and non-residents

PIT is based on the income earned for paid work, independent activities and from property rights

Excise duties

Excise duties are paid on certain products, such as….

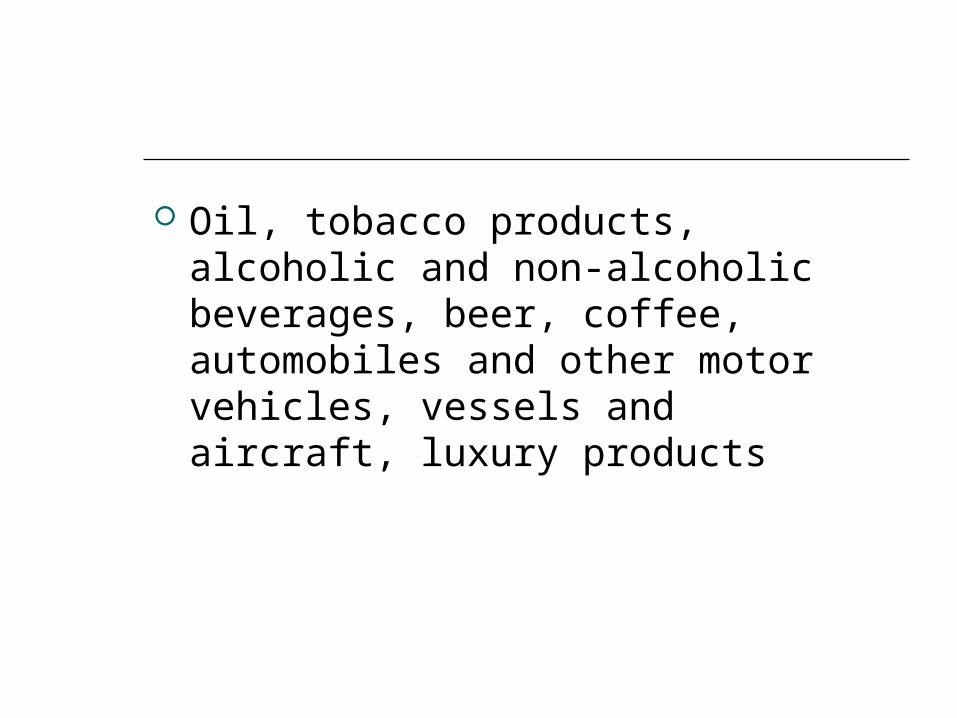

Oil, tobacco products, alcoholic and non-alcoholic beverages, beer, coffee, automobiles and other motor vehicles, vessels and aircraft, luxury products

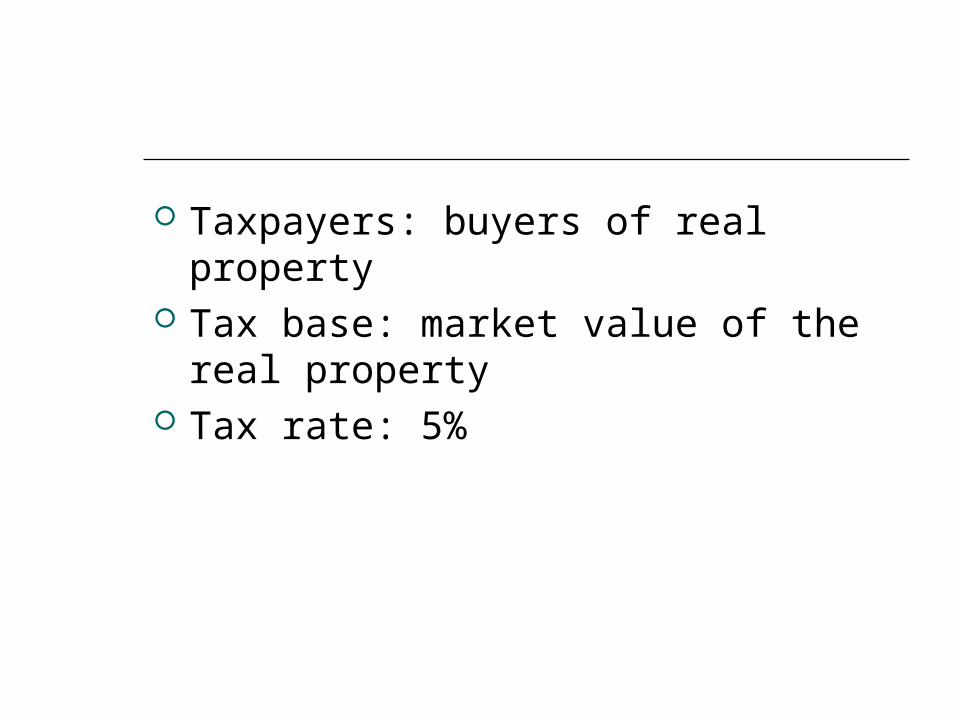

Real estate transfer tax

Taxpayers: Tax base: Tax rate:

Taxpayers: buyers of real property Tax base: market value of the real

property Tax rate: 5%

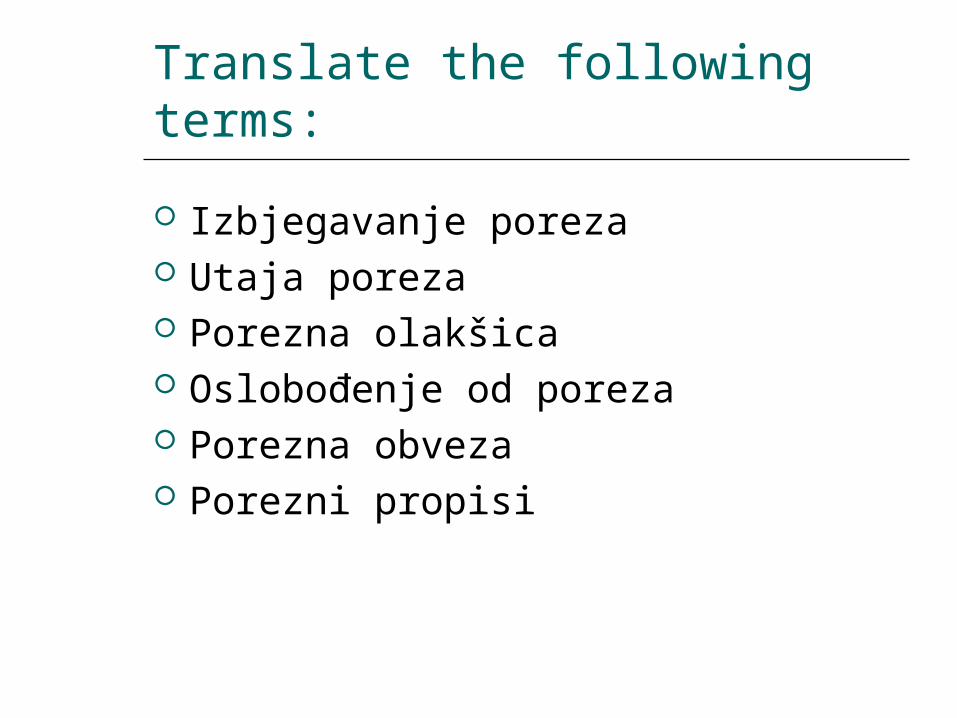

Translate the following terms:

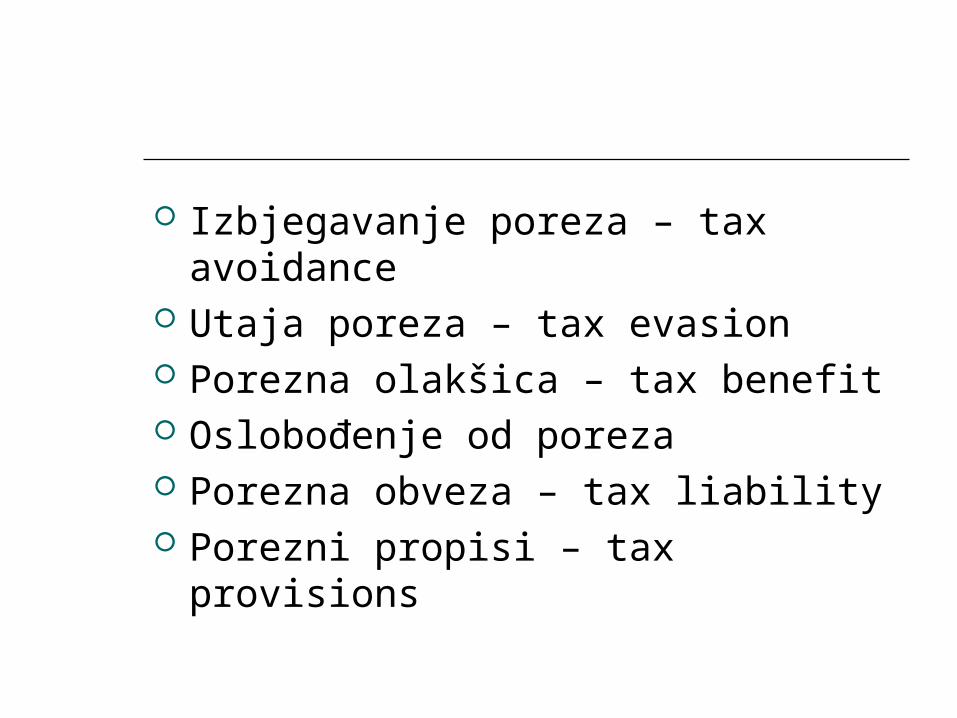

Izbjegavanje poreza Utaja poreza Porezna olakšica Oslobođenje od poreza Porezna obveza Porezni propisi

Izbjegavanje poreza – tax avoidance Utaja poreza – tax evasion Porezna olakšica – tax benefit Oslobođenje od poreza Porezna obveza – tax liability Porezni propisi – tax provisions

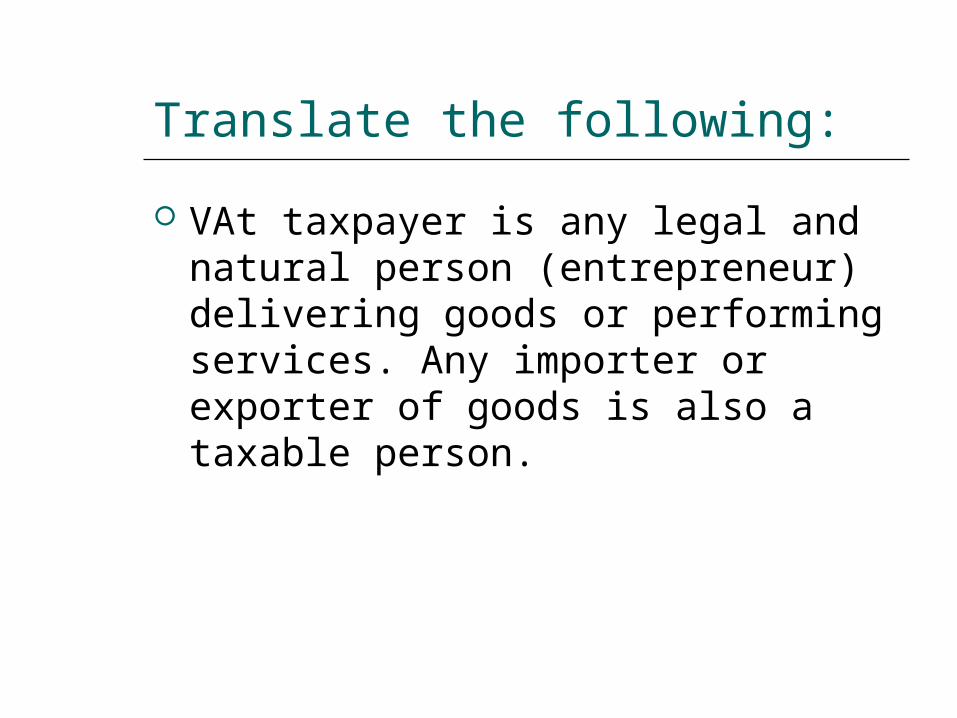

Translate the following:

VAt taxpayer is any legal and natural person (entrepreneur) delivering goods or performing services. Any importer or exporter of goods is also a taxable person.

Thank you for your attention!