Embed Size (px)

Citation preview

Energy Analysis Department

Balancing Cost and Risk:

The Treatment of Renewable Energy in Western Utility Resource Plans

Mark Bolinger

Lawrence Berkeley National Laboratory([email protected])

NARUC Summer MeetingsSan Francisco, California

August 1, 2006

Energy Analysis Department

Integrated Resource Planning (IRP)Integrated Resource Planning (IRP)

• A formal process by which utilities analyze the costs, benefits, and risks of all resources available to them

• Goal is to identify a portfolio of resources that meets future needs at lowest cost and/or risk

• Re-emerging as an important planning process in states that are no longer exploring retail competition

Energy Analysis Department

Overview of Presentation

1) Planned RE Additions in Western Resource Plans

2) Factors that Impact Planned RE Additions

a) Candidate portfolio construction

b) RE (wind power) cost and performance assumptions

c) Treatment of natural gas price and carbon regulation risk

d) How an IRP balances cost and risk

3) Conclusions

Objective: Summarize western utility resource plan treatment of renewable energy (RE), based on compilation and analysis of resource plan assumptions and methods

Energy Analysis Department

Western Utility Resource Plans Included in Our Sample: ~50% of Western Load

Resource plans fromutilities subject to a Renewables PortfolioStandard (RPS)

Resource plans in which no regulatory requirements compel RE additions

Pacific Gas & Electric (PG&E), Southern California Edison (SCE), San Diego Gas & Electric (SDG&E), Nevada Power, Sierra Pacific

Avista, Idaho Power, NorthWestern Energy (NWE)*, Portland General Electric (PGE), PacifiCorp, Puget Sound Energy (PSE), Public Service Company of Colorado (PSCo)*

*PSCo’s and NWE’s most-recent resource plans preceded each state’s RPS

Energy Analysis Department

Western Resource Plans Could Be a Major Source of Demand for New Renewables

Non-RPS:Wind accounts for 92% of new RE capacity in 2014

RPS:Resources often unspecified

New Renewables Capacity in 2014 (MW)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Cum

ulat

ive

Nam

epla

te C

apac

ity (

MW

)

Aggregate Non-RPS

Aggregate RPS

PG&E Pacifi- Corp SCE

PSE (2005) SDG&E PSCo

Idaho Power

Nevada Power PGE

North- Western

Sierra Pacific

Avista (2005)

Non-RPS 0 1,420 0 745 115 500 450 0 195 150 0 390 RPS 2,150 NA 1,021 NA 630 NA NA 599 NA NA 154 NA

Total 2,150 1,420 1,021 745 745 500 450 599 195 150 154 390

Energy Analysis Department

Resource Plans Leading to Wind Contracts in Non-RPS States (though not always at the expected pace)

• PGE: 75 MW Klondike II (2005); in 2006, purchased development rights to Biglow Canyon (126 MW in 2007, 350-450 MW total)

• Idaho Power: 100 MW RFP reactivated in October 2005, 66 MW PPA just announced (company estimates 300 MW of wind – much of it smaller QF/PURPA contracts – on its system by end of 2007)

• Pacificorp: 41 MW Combine Hills (2003); 64.5 MW Wolverine Creek (2005); 20 MW Schwendiman project (expected 2007); reissued RFP in 2006 for 100 MW by end of 2006, more in 2007

• NorthWestern: PPA with 135 MW Judith Gap (2005)

• Avista: PPA of 35 MW from Stateline (2004); RFP for 35 aMW issued January 2006

• PSE: 150 MW Hopkins Ridge (2005) and 230 MW Wild Horse (2006)

Energy Analysis Department

Planned Renewable Energy Additions Are Affected By…

• How candidate portfolios are assembled and defined

• What assumptions are made for the cost and performance of renewable energy

• The degree to which (and how) electricity sector portfolio risks are considered

- Natural gas price risk

- Environmental compliance risk

• How tradeoffs between the expected cost and risk of different portfolios are made

Energy Analysis Department

Construction of Candidate Portfolios

• Most plans create candidate portfolios by hand, making the composition of these portfolios all the more important

• Many plans only include wind power in candidate portfolios, with other RE resources screened out at an earlier phase

• Exogenous caps limit the contribution of RE in many IRPs

- Resource plans in states with RPS obligations frequently do little to analyze the potential value of exceeding those obligations – i.e., the RPS serves as a cap, rather than floor

- Resource plans in states without RPS obligations often exogenously cap the maximum amount of wind additions, to account for concerns over integration costs, transmission constraints, resource limits, etc.

Energy Analysis Department

Exogenous Build Limits “Cap” the Amount of Wind Selected by Some Resource Plans

PSE, NWE, PSCo, and Avista all chose portfolios with wind at the cap (Sierra Pacific and Nevada Power do not report RE additions by technology, but presumably would also hit their low caps)

0

500

1,000

1,500

2,000

2,500

3,000

IdahoPower

PGE(initial)

Avista2005

PacifiCorp2003

PSE2003

PSE2005

NWE PSCoSupp.

PSCoOrig.

Avista2003

SierraPacific

NevadaPower

Win

d C

ap (

MW

nam

epla

te)

0%

5%

10%

15%

20%

25%

30%

Win

d C

ap (

% o

f P

eak

Load

)

MW (left scale)

% of Peak Load (right scale)

Utilities’ planned additions hit caps

Energy Analysis Department

Assumptions About Cost/Performance of Wind Could Be Improved in Some Cases

Busbar Costs: Capital and O&M assumptions are reasonable, but may need to be increased based on recent turbine prices

Production Tax Credit: Undervalued by some resource plans, but many plans overstate the likelihood of renewal

Transmission Costs: Plans often do not try to carefully evaluate transmission expansion needs

Integration Costs: Some plans seem to over-estimate integration costs (or set low caps on wind), but improvements are dramatic in this area

Capacity Value: Undervalued by many plans, but more recent plans more accurately evaluate capacity value

Energy Analysis Department

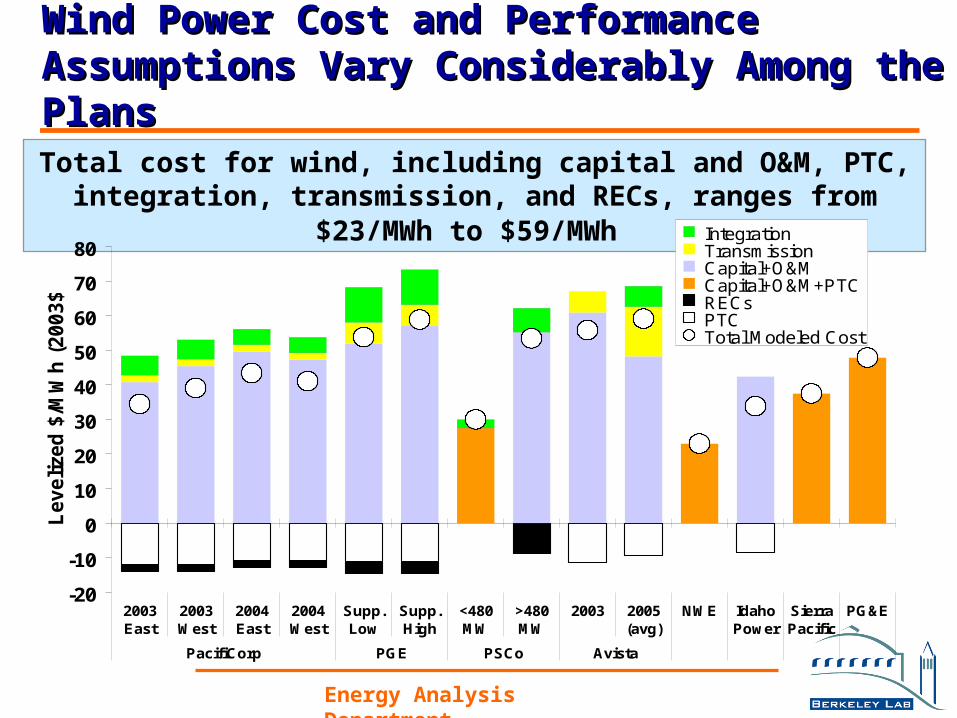

Wind Power Cost and Performance Assumptions Wind Power Cost and Performance Assumptions Vary Considerably Among the PlansVary Considerably Among the Plans

Total cost for wind, including capital and O&M, PTC, integration, transmission, and RECs, ranges from $23/MWh to $59/MWh

-20

-10

0

10

20

30

40

50

60

70

80

2003East

2003West

2004East

2004West

Supp.Low

Supp.High

<480MW

>480MW

2003 2005(avg)

NWE IdahoPower

SierraPacific

PG&E

PacifiCorp PGE PSCo Avista

Leveli

zed

$/M

Wh

(200

3$)

Integration Transmission Capital+O&M Capital+O&M+PTC RECs PTC Total Modeled Cost

Energy Analysis Department

Some Resource Plan Integration Cost Assumptions Are High Compared to Recent Literature

*PGE’s supplemental IRP estimates the cost of creating a flat, base-load block of power out of variable wind production, rather than simply the cost of integrating variable wind production. As such, its cost estimate is not directly comparable to the others.

Some resource plans set strict limits on wind penetration due to concerns about integration costs: Avista 2003 (75 MW, 4% of peak load), Nevada Power (100 MW, 2% of peak load), and Sierra Pacific (50 MW, 3% of peak load)

0

2

4

6

8

10

12

CA BPA PJM WI(We)

South-west

MN(GRE)

MN(Xcel)

PSE2005

Pacifi-Corp

PSCo Avista2005

PGE*(Supp.)

Avista2003

Win

d I

nte

gra

tio

n C

os

t ($

/MW

h)

0%

5%

10%

15%

20%

25%

30%

Win

d P

en

etr

ati

on

(%

of

peak l

oad

)

Integration Costs (left scale)

Wind Penetration (right scale)

Resource PlansIntegration Studies

to $

18/M

Wh

Energy Analysis Department

Some Resource Plan Capacity Value Assumptions Are Low Compared to Recent Literature

• Though less dependable than other resources, wind provides some capacity value• ELCC is the most widely recognized method for determining capacity value• Most utility plans did not use ELCC to calculate capacity value• Many plans assumed lower capacity value than suggested in the literature

0%

5%

10%

15%

20%

25%

30%

35%

40%

California-A California-B Colorado Minnesota New York0%

5%

10%

15%

20%

25%

30%

35%

40%

Avista 2003, PSE 2003,PacifiCorp 2003

PacifiCorp 2004,PSE 2005

PGE

Idaho Power

PSCo

Literature Estimates IRP Assumptions

Win

d P

ow

er

Ca

pa

cit

y C

red

it

Avista 2005

Energy Analysis Department

Renewable Energy as a Risk Mitigation Tool

Renewable energy may reduce at least two important risks…

- Risk of high and volatile natural gas prices

- Risk of more stringent environmental regulations

Resource plans are becoming increasingly sophisticated in analyzing both risks, but further improvements are still needed

Energy Analysis Department

Plans Increasingly Using Improved Tools to Evaluate Gas Price Risk

• Current price expectations as revealed through NYMEX futures markets suggest that higher gas-price forecasts are warranted

• IRPs using improved tools to evaluate uncertainty, but range of plausible prices may be greater than assumed in some cases

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.02003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2003 $

/MM

Btu

(H

en

ry H

ub

Eq

uiv

ale

nt)

Nevada Power 2003 NorthWestern 2003 Pacificorp 2003 PGE 2002 Pacificorp 2004 PSE 2003 SDG&E 2004 Sierra Pacific 2004 SCE 2004 Avista 2003 SCE 2005 Avista 2005 Idaho Power 2004 PG&E 2004 PSCo 2003 PG&E 2005

Energy Analysis Department

Resource Plans Are Beginning to Evaluate Carbon Regulatory Risk• 7 of 12 considered risk in latest round of resource plans

• Minimum of 10 of 12 plans will consider this risk in next round

- Two outliers: Nevada Power, Sierra Pacific

• For those utilities considering this risk, approaches vary

1) Carbon scenarios but with no probabilities attached

2) Carbon scenarios with probabilities attached

3) Included in base-case, sometimes with scenarios

• Some utilities may not be evaluating a sufficiently broad range of possible carbon regulation scenarios

• Risk of heightened environmental regulations, beyond carbon, are routinely ignored, but likely are of lesser importance to RE

Energy Analysis Department

Methods and Approach to Carbon Risk Evaluation Vary

0

10

20

30

40

50

60

70

Avista2003

PG&E PSCo(IRP)

PSE2005

Avista2005

IdahoPower

PGE(Supp.)

PacifiCorp2003

PacifiCorp2004

PSCo(Settlement)

Le

veliz

ed

$/to

n C

O2 (

200

3 $

)

Range of Scenarios

Weighted Average

Base-Case Assumption

WeightedScenarios

UnweightedScenarios

Base Case with Unweighted Scenarios

Energy Analysis Department

Balancing Cost and Risk

Ultimately, resource plans must balance portfolios that have different cost and risk characteristics; how this tradeoff occurs can effect how well renewable energy fares in IRP

• Utilities have adopted different definitions of risk (most focusing on the upper tail of the distribution), and have taken different approaches to balancing expected cost and risk

• Each electricity customer may hold different risk preferences, and utilities have been given little guidance and have conducted little research on how to best make these tradeoffs

• Utilities virtually always use WACC to discount costs: we recommend scenario analysis be conducted on a wider range of discount rates, to reflect ratepayer and/or social perspectives

Energy Analysis Department

InitialCandidate Portfolios

Stochastic /Monte Carlo

ABCDEF

EfficientFrontier

Cost / RiskTradeoff

FinalistCandidate Portfolios

ScenarioAnalysis

PreferredPortfolio

BDF

D

Natural Gas PricesElectricity PricesHydro Availability(Correlations)

CO2 RegulationsHigh/Low Gas PricesPTC ExtensionWind Capacity Value

Base-CaseScenario

AlternativeScenarios

Mean Cost

Risk

Risk Paradigm Employed By: Avista, NorthWestern, PacifiCorp, PSE (2003)

• Avista and NorthWestern assign subjective weights to cost and risk• PacifiCorp and PSE evaluate the cost/risk tradeoff more qualitatively• Some renewables portfolios “weeded out” before CO2 risk assessed!

Energy Analysis Department

Stochastic /Monte Carlo

ABCDEF

Cost / RiskTradeoff

Qualitativ

e

ADE

D

Scenario 2

InitialCandidate Portfolios

Stochastic /Monte Carlo

ABCDEF

EfficientFrontier

Cost / RiskTradeoff

FinalistCandidate Portfolios

Qualitative

PreferredPortfolio

BDF

Natural Gas PricesElectricity PricesHydro Availability(Correlations)

Scenario 1

Mean Cost

Risk

Mean Cost

Risk

Risk Paradigm Employed By PSE (2005):Each Portfolio Subjected to All Risks!

Energy Analysis Department

InitialCandidate Portfolios

ScenarioAnalysis

ABCDEF

EfficientFrontier

Cost / RiskTradeoff

PreferredPortfolio

D

CO2 RegulationsHigh/Low Gas PricesHigh/Low Power PricesPTC ExtensionWind Capacity Value

AllScenarios

Mean Cost

Risk

• PGE assigned subjective probabilities to each scenario

• PSCo, Nevada Power, and Sierra Pacific evaluate the cost/risk tradeoff more qualitatively

Risk Paradigm Employed By:PGE, PSCo, Nevada Power, Sierra Pacific

Energy Analysis Department

InitialCandidate Portfolios

ABCDEF

ScenarioAnalysis

PreferredPortfolio

D

AllScenarios

CO2 RegulationsHigh/Low Gas PricesHigh/Low Power PricesPTC ExtensionWind Capacity Value

Risk Paradigm Employed By: Idaho Power

• Idaho Power assigned a subjective probability to each scenario

• Preferred portfolio is that which has the lowest scenario-weighted expected cost, with no consideration given to the uncertainty of that cost

Energy Analysis Department

Balancing Cost and Risk:Concerns for Renewable Energy

• Plans often model RE primarily as wind power, assume a low capacity value, and/or apply low limits to wind penetration As a result, many of the hand-crafted “renewables” portfolios are weighted

heavily towards gas-fired generation, thereby exhibiting as much or more exposure to gas-price risk than other portfolios

Pushes resource selection towards coal more than renewable energy

• Fuel price risk is often analyzed quantitatively early in the modeling process, while carbon risk is typically analyzed through scenario analysis later in the process, and in a way that has less effect on portfolio choice

• Result is that RE portfolios are sometimes not considered low risk, and are sometimes “prematurely” weeded out at an early phase of the analysis, before carbon risk is considered

Energy Analysis Department

Conclusions (1)

IRP’s increasingly consider RE a serious resource option, and methodological improvements have been dramatic.

But further improvements are still possible and needed:

1) Utilities in RPS states should consider evaluating RE as an option above and beyond the level required to satisfy RPS obligations

2) Resource planners may wish to explore a broader array of RE options

3) The value of the Federal PTC, and its risk of permanent expiration, could be more consistently addressed

4) Evaluation of integration and transmission costs, and capacity value, should continue to be refined (at higher wind penetration levels)

5) Exogenous caps on wind penetration should be removed and replaced with credible analysis of the cost of higher penetrations

Energy Analysis Department

Conclusions (2)

6) Resource plans should evaluate a broad range of possible fuel costs, and subject a large number of candidate portfolios to such analysis

7) Environmental compliance risks could be more consistently and comprehensively evaluated

8) Each risk should have, as is appropriate, an opportunity to impact portfolio selection

9) Utilities and/or regulators should conduct research to evaluate ratepayer risk preferences

10) More consistent and comprehensive data presentation in resource plans would allow for far better external review

11) Wind cost assumptions may need to increase in future IRP’s, to reflect the tight turbine market

12) To ensure progress and results, ongoing benchmarking of actual procurements relative to resource plans is warranted

Energy Analysis Department

Avista 2003 vs. 2005: What a Difference Avista 2003 vs. 2005: What a Difference a Single Planning Cycle Can Make!a Single Planning Cycle Can Make!

Even with little change in assumed cost, “fixing” other related inputs can lead to vastly greater wind penetration

Avista 2003

Avista 2005

Levelized Cost of Wind (w/PTC and Transmission) (2003 $/MWh)

55.8 53.1

Capacity Value of Wind (% of nameplate)

0% 25%

Wind Integration Cost Range ($/MWh)

3-18 4.5-9

Natural Gas Price Forecast (Base-Case) (levelized 2003 $/MMBtu)

4.0 5.4

Carbon Cost Scenario Range (2003 $/ton CO2)

0-3 0-26

Exogenous Cap on Wind Allowed in Portfolio 75 MW 650 MW

Wind Included in Preferred Portfolio 75 MW 650 MW

Energy Analysis Department

For More Information...

Download the full report from:

http://eetd.lbl.gov/ea/ems/re-pubs.html

Contact the authors:

Mark Bolinger, [email protected], 603-795-4937

Ryan Wiser, [email protected], 510-486-5474