Embed Size (px)

Citation preview

Employee Treatment, Labor Investment Efficiency andFirm Performance

This version: November 30, 2017

Abstract

Using a sample of 20,583 US firm-year observations that represents more than 3,000individual firms over the period of 1995 to 2015, we investigate the link between em-ployee treatment and labor investment efficiency. We argue that firms reduce informa-tion asymmetry by signalling its ability to honor implicit claims via employee-friendlytreatment policies and predict that firms with better employee treatment performancehave a higher level of labor investment efficiency. Our empirical results confirm ourprediction. We find strong and robust evidence that firms with more employee-friendlypractices have a lower level of abnormal net hiring. Moreover, we find employee treat-ment concerns distort normal labor hiring and specifically lead to underinvestment inlabor, thus lowering firms labor investment efficiency. Finally, we find employee-friendlytreatment facilitates higher labor productivity and profitability whereas abnormal nethiring reduces labor productivity and profitability. Taken together, our findings high-light the important role of employee treatment in contributing to firms investmentbehaviour and value creation.

Keywords : Employee Treatment; Employee Welfare; Labor Investment Efficiency; Invest-ment Efficiency; Employee Governance

1. Introduction

Irrespective of the company size, employees usually are argued as a firm’s most valuable

asset and a critical source of corporate success. For example, Larry Page, the CEO of

Google, in an interview with Fortune magazine said that ‘It’s important that the company

be a family, that people feel that they’re part of the company, and that the company is like

a family to them. When you treat people that way, you get better productivity. Rather than

really caring what hours you worked, you care about output. We should continue to innovate

in our relationship with our employees and figure out the best things we can do for them.’

In today’s labor market, as the development of knowledge-based industries, firms become

more human-capital-intensive and employees are the key source of value creation. Numerous

prior studies find labor-friendly corporate practices are positively associated with better

firm performance (Edmans, 2011, 2012; Ertugrul, 2013; Faleye and Trahan, 2011). Recent

studies in employee treatment investigate how a firm’s labor-friendly corporate practices can

influence its innovation, financial policies and capital structure decisions (Bae, Kang, and

Wang, 2011; Chemmanur, Cheng, and Zhang, 2013; Chen, Chen, Hsu, and Podolski, 2016;

Ghaly, Dang, and Stathopoulos, 2015; Serfling, 2016) whereas very little is known about

the impact of employee treatment on firms’ employment decisions, and in particular labor

investment efficiency.

Finance research has long shown that agency conflicts and information asymmetry be-

tween managers and outsiders lead firms to undertake suboptimal levels of investment. A

number of recent studies have explored the factors that can mitigate such market imperfec-

tions and improve investment efficiency (Biddle and Hilary, 2006; Biddle, Hilary, and Verdi,

2009; Healy and Palepu, 2001; Lambert, Leuz, and Verrecchia, 2007).We follow this line of

research by extending capital investment efficiency to the investment efficiency in labor, an

important factor of production that has been largely overlooked by previous literature.

We posit that employee treatment help firms to lower information asymmetry and em-

ployee adverse behavior, which helps firms to maintain net hiring that is closer to a level

justified by firms underlying economics and to be less subject to the labor adjustment costs,

thus having more efficient investments in labor. An examination of the relationship between

employee treatment and labor investment efficiency is particularly interesting in this context

for two reasons. First, in today’s competitive labor market, firms become more human-

capital-intensive and maintaining high commitments to employees’ welfare in addition to

variable wage becomes more crucial for firms to obtain human capital. Echoing this trend,

numerous recent studies have increasingly paid attention to the influence of employee treat-

ment on firms’ capital structure decisions and financial policies (Bae et al., 2011; Chemmanur

1

et al., 2013; Chen et al., 2016; Ghaly et al., 2015; Serfling, 2016). Second, Benlemlih and

Bitar (2015) provide an evidence that a firms social performance can positively contribute

to its investment efficiency owing to low information asymmetry and high stakeholder sol-

idarity. However, their study looks at the investment efficiency in capital expenditure and

focuses mainly on general CSR instead of employee treatment. Despite the classical view

considers labor as a variable factor that does not involve any adjustment costs and therefore

the financing imperfections caused by information asymmetry is irrelevant for employment

decisions, a large number of labor economics studies have suggested that labor frictions not

only exist but the costs associated with labor adjustment can be substantial (Danthine and

Donaldson, 2002; Diamond, 1982; Mortensen and Pissarides, 1994; Yashiv, 2007). We follow

this line of literature and address the gap in the literature about whether the labor-relevant

dimension of social performance, namely, employee-friendly treatment policies can improve

firms’ efficiency in labor investment. In addition, we further address the economic implica-

tion of employee treatment and abnormal net hiring on firms’ value creation by investigating

the impact of employee treatment and labor investment efficiency on labor productivity and

profitability. In light of previous literature suggesting that employee-friendly policies can

positively influence value creation, we posit that firms treating their employees well enjoy

higher labor productivity and profitability whereas a high deviation from a firms employ-

ment level justified by its underlying economics deteriorate a firms labor productivity and

profitability.

In order to examine the relation between employee treatment and labor investment ef-

ficiency, we follow previous studies (Pinnuck and Lillis, 2007; Jung, Lee, and Weber, 2014)

and use firms’ net hiring (percentage change in the number of employees) to proxy for in-

vestment in labor. For our primary analyses, the expected level of net hiring is based on the

model of Pinnuck and Lillis (2007), which includes economic variables that explain normal

hiring practices, such as sales growth, liquidity, leverage, and profitability. Thus, our mea-

sure of abnormal net hiring captures the amount of net hiring not attributable to underlying

economic factors.

Our employee treatment measure is obtained from MSCI ESG Research which formerly

known as KLD database. The KLD database has been extensively employed in a large

number of previous studies in employee welfare (Bae et al., 2011; Cronqvist, Heyman, Nils-

son, Svaleryd, and Vlachos, 2009; Ertugrul, 2013; Faleye and Trahan, 2011; Ghaly et al.,

2015; Verwijmeren and Derwall, 2010). We construct our employee treatment scores by us-

ing certain KLD’s rating on ‘Employee Relations’, with a higher net scores demonstrating

better employee treatment. Our primary measure of employee treatment, EMP TREAT, is

estimated by summing identified strengths and subtracting identified concerns included in

2

‘Employee Relations’ dimensions in a given year (Faleye and Trahan, 2011; Verwijmeren and

Derwall, 2010). Following Ertugrul (2013) and Ghaly et al. (2015), we also include the

‘Work/Life Benefits’ variable from the ‘Diversity’ dimension.

Our results are consistent with the notion that employee treatment facilitates more effi-

cient investments in labor. In particular, firms’ employee treatment performance is negatively

associated with absolute abnormal net hiring. This result holds across different measures of

employee treatment and expected net hiring, and it is robust to controlling for various other

factors that might affect the efficiency of net hiring practices, including other concurrent

investments, labor power, institutional shareholdings, corporate governance and financial

reporting quality. We also provide evidence on the association between employee treatment

and specific forms of inefficiencies. In particular, we examine overinvestment (actual net

hiring greater than expected) and underinvestment (actual net hiring less than expected)

and find that each specific type of inefficiency is mitigated by employee-friendly treatment.

In addition, our results also find employee-friendly treatment facilitate higher labor produc-

tivity and profitability whereas labor investment inefficiency in form of abnormal net hiring

lowers labor productivity and profitability.

Our results contribute to the literature in several ways. First, to the best of our knowl-

edge, this is the first paper to investigate the relationship between employee treatment and

labor investment efficiency. The results of our research suggest that firms with employee-

friendly treatment policies are associated with more efficient labor investments in general.

Based on stakeholder theory and modern human capital theory of corporate governance, we

interpret our results that firms with employee-friendly treatment schemes mitigate market

friction caused by information asymmetry and mitigates employee moral hazard problems by

providing more efficient contracting with employee-friendly treatment embedded. Second,

previous literature emphasizes more on the role of financial reporting in improving invest-

ment efficiency (Biddle and Hilary, 2006; Biddle et al., 2009; Beatty and Liao, 2014; Jung

et al., 2014; Lara, Osma, and Penalva, 2016), but only few studies investigate labor invest-

ment efficiency. Jung et al. (2014) find that higher-quality financial reporting contributes

to more efficient investment in labor. Our study complements their research and suggests

that firm-level employee treatment policies also have an important implication for firm-level

employment decisions and the consideration for efficient allocation of corporate resource to

labor aspect. Third, Servaes and Tamayo (2013) suggest that employee channel of CSR can

be a fruitful area for empirical research in CSR. Our study specifically investigates one of

the integral part of CSR, employee treatment, and its impact on labor investment efficiency

and find that employee-friendly treatment positively contribute to employee productivity

whereas abnormal net hiring negatively affect employee productivity. Fourth, Benlemlih

3

and Bitar (2015) find better social performance improves corporate investment efficiency

in capital expenditure. Our analysis is different from that of Benlemlih and Bitar (2015)

from two aspects. First, we focus on employee treatment, a particular dimension of cor-

porate social performance, to examine the benefits of employee-friendly practices. Second,

unlike Benlemlih and Bitar (2015) that focuses on firms’ capital investment efficiency, our

study emphasizes on investment efficiency in labor. Hence, we contribute to this stream

of literature by extending capital investment efficiency to labor investment efficiency. Fi-

nally, our study contributes to the recent literature of employee treatment and address the

economic implication of employee treatment and labor investment efficiency for firms’ value

creation.

In the next section, we discuss the related literature and develop our hypotheses. In

Section 3, we describe our research design and empirical models and in Section 4 we present

results. In Section 5, we provide a range of robustness tests and a summary of our findings

and concluding remarks appear in Section 6.

2. Literature review and hypothesis

2.1. Market frictions and capital investment efficiency

In the frictionless capital market of Modigliani and Miller (1958) paradigm, the marginal

Q ratio is the sole drive of capital investment policy. Under the Modigliani and Miller (1958)

paradigm, firms invest until the marginal benefit of capital investment equal the marginal

costs and firms only invest in projects with positive net present value. In practice, however,

firms need to face capital market imperfections stemming from information asymmetry and

there is a possibility that firms may depart from the optimal level and either over- or under-

invest owing to the capital market frictions (Stein, 2003). Specifically, managers may invest

inefficiently by making bad investment selections in order to expropriate firms’ existing re-

sources, thus leading to overinvestment. On the contrary, firms may withdraw from projects

with positive NPV owing to costly cost of capital if they face financing constraints, thus

leading underinvestment.

Previous literature has identified the issues of moral hazard and adverse selection are the

two primary imperfections in the market that make firms depart from the optimal investment

level. First, managers may pursue certain self-serving objective to maximize their own

personal welfares and therefore may invest in projects that are not in line with the objective

of shareholder maximizations (Jensen and Meckling, 1976).Moral hazard can contribute to

either over- or underinvestment depending on the availability of capital. On one hand,

4

overinvestments are more likely to occur if firms have resource to invest. In that case,

managers have incentives to consume perquisites and engage in empire building (Jensen,

1986; Richardson, 2006).On the other hand, underinvestment occur when suppliers of capital

concern the moral hazard problem and therefore tend to ration capital ex-ante or managers

prefer to have peaceful life so that projects with positive NPV are given up (Bertrand and

Mullainathan, 2003; Lambert et al., 2007).

Adverse selection can be attributed to the existence of information asymmetry between

managers and outside suppliers of capital, which may also affect the efficiency of capital in-

vestment. If managers are better informed about the value of firms’ securities than investors,

they are more likely to time capital issuance in order to issue overpriced securities (Baker,

Stein, and Wurgler, 2003). However, investors may respond to their information disadvan-

tage by discounting new issuance of securities and charging a higher cost of capital. If

managers are reluctant to raise funds at a discounted price, projects with positive NPV

will be renounced and underinvestment occurs (Myers and Majluf, 1984). Overall, previous

literature suggests that the capital market in reality is not frictionless and capital market

imperfections stemming from information asymmetry between firms and suppliers of capital

can cause firms to deviate from the optimal level, thus leading to either overinvestment or

underinvestment.

2.2. Employee treatment and labor investment efficiency

As one of the most critical nonfinancial stakeholders and corporate assets, employees have

a significant influence on a firm’s success and recent studies have increasingly paid attention

to firms’ employee treatment schemes and its relevance to firm performance. Previous studies

shows that firms with better employee treatment schemes are usually associated with better

performance (Edmans, 2011, 2012; Ertugrul, 2013; Faleye and Trahan, 2011). For example,

Edmans (2011) finds that firms with satisfied employees exhibit considerably more positive

earnings surprises and announcement returns, showing that employee satisfaction has a pos-

itive influence on firms’ long-term stock returns. Chen et al. (2016) find that firms treating

their employees well produce more and better patents through improving employee satis-

faction and teamwork, which suggests that better employee treatment schemes are in line

with the benefits of shareholders. Recently, a number of studies also examine the impact of

employee treatment on firms’ capital structure decisions and financial policies. Specifically,

several studies test the predictions of Titman (1984) by studying the relationship between

leverage and employee treatment. For example, Chemmanur et al. (2013) find that leverage

has a positive and significant influence on average employee pay and the incremental total

5

labor expenses associated with an increase in leverage offset the incremental tax benefits of

debt, thus supporting the theoretical prediction that labor costs constrain the use of debt.

Similarly, Bae et al. (2011) find firms treating their employees well maintain low debt ratio

and suggest firms’ incentive to treat their employee well is an important determinant of

their financing policies. Moreover, Serfling (2016) finds that firms adopting state-level labor

protection laws that exogenously increase employee firing costs reduce their debt ratios. In

addition to the firm leverage, prior studies also find firms with better employee treatment

schemes and operating in industries with a higher share of skilled workers tend to hold larger

cash balances (Ghaly et al., 2015; Ghaly, Dang, and Stathopoulos, 2017). Broadly speaking,

corporate social responsibility, of which employee welfare and treatment is considered as one

of the integral parts, also has been found to reduce information asymmetry (Dhaliwal, Li,

Tsang, and Yang, 2011; Cho, Lee, and Pfeiffer, 2013), and analyst forecast error (Dhaliwal,

Radhakrishnan, Tsang, and Yang, 2012) and increase financial reporting quality (Kim, Park,

and Wier, 2012) and investment efficiency (Benlemlih and Bitar, 2015).

Prior studies on employee treatment mainly focus on the impact of employee treatment

on firms’ capital structure decisions and financial policies while previous financial literature

on market frictions and investment efficiency mainly focus on capital investment. Hence,

there is a lack of attention to market frictions and investment efficiency in labor in previous

accounting literature as well as the potential influence of employee treatment on labor in-

vestment efficiency. Jung et al. (2014) fill the gap by investigating the impact of financial

reporting quality on labor investment efficiency and find that high-quality financial reporting

improves investment efficiency in labor by lowering market frictions stemming from informa-

tion asymmetry between managers and suppliers of capital. Our study focus on employee

treatment and examines whether employee-friendly treatment helps the firm to maintain net

hiring that is close to the level justified by a firm’s underlying economics. We argue the

relation between employee treatment and firms’ net hiring likely stems from two potential

channels, information asymmetry and employees’ adverse behavior.

First, we argue one possible explanation for the connection between employee treatment

and firms’ net hiring can stem from information asymmetry. Previous literature recognizes

that friction do exist in the market and one of the most pervasive source of friction comes

from information asymmetry. In terms of labor friction, while the classical view considers

labor as a variable factor that does not involve any adjustment costs and financing because

the timing of labor costs is perfectly matched with the benefits they create, previous labor

economics studies find that despite wages can be largely treated as variable in nature, labor

frictions in fact exist in terms of search and matching (Diamond, 1982; Mortensen and

Pissarides, 1994), wage (Danthine and Donaldson, 2002) and hiring and firing (Yashiv, 2007).

6

Moreover, the existence of other fixed components in labor costs such as recruiting costs,

training costs, firing costs and disruption costs suggest that adjusting labor stock for firms

is not costless the costs associated with adjusting its labor force can be substantial (Farmer,

1985; Hamermesh, 1993). As firms become more human-capital-intensive under today’s

competitive business environment, maintaining high commitments to employees’ welfare in

addition to variable wage becomes more important for many firms to obtain human capital

as their most valuable assets (Turban and Greening, 1997; Zingales, 2000). Owing to the

existence of fixed components in labor costs, adjustment costs also apply to investments in

labor and financing labor costs is necessary for labor investments and thus labor investments

are also subject to inefficiencies caused information asymmetry between managers and the

outside suppliers of capital.

Stakeholder theory (Cornell and Shapiro, 1987) suggests that a firm need to satisfy not

only its financial stakeholders with explicit claims (e.g shareholders, bondholders) but also

its non-financial stakeholders with implicit claims. Prior literature suggests stakeholders are

more likely to increase more costly explicit claims if they doubt a firm’s ability to honor

its implicit claims and a firm’s value can be affected by its reputation for honoring implicit

claims of non-financial stakeholders (Cornell and Shapiro, 1987; Maksimovic and Titman,

1991). Zingales (2000, p. 1634) argues: ‘Once we recognize the existence of implicit contracts,

then there are other residual claimants besides equity holders who may need to be protected.

It then becomes unclear whether control should reside in the hands of shareholders, because

the pursuit of shareholder’s value maximization may lead to inefficient action, such as the

breach of value implicit contracts’. From labor perspective, a firm’s failure of achieving a

good relationship with its employees can lead to low employee morale and high employee

turnover, which can ultimately erodes the firm’s reputation in the labor market. Stuebs and

Sun (2010) find that corporate reputation is associated with improved labor efficiency and

labor productivity and therefore has important implication for corporate social activities and

initiatives. On the contrary, the adverse reputation in employee relationship is likely to make

other non-financial stakeholders cast doubt to the firm’s ability to honor their implicit claims

and lead to a reduction in the value of implicit claims sold to new stakeholders, resulting in

a reduction in future cash flows and the value of the firm (Bowen, DuCharme, and Shores,

1995; Cornell and Shapiro, 1987). Prior studies find that firms having harmonious relations

with their stakeholders enjoy higher value of implicit claims sold to its stakeholders and

its future cash flows and firm value are less likely to be adversely affected by unsatisfied

non-financial stakeholders, thus leading to a lower cost of financing (Cheng, Ioannou, and

Serafeim, 2014; Dhaliwal et al., 2011; El Ghoul, Guedhami, Kwok, and Mishra, 2011). In

this respect, firms’ employee-friendly treatment convey additional information to the market

7

about their ability to honor implicit claims, which ultimately helps firms to reduce adverse

selection problems and lower the information asymmetry between corporate managers and

market participants that creates market friction.

Moreover, current human capital theory of corporate governance emphasizes on the im-

portance of shifting from the classical agency problem between manager and shareholder

to examine human capital treatment for corporate governance (Rajan and Zingales, 1998,

2000; Zingales, 2000). For instance, Guo, Huang, Zhang, and Zhou (2015) find that employee

treatment policies are an important predictor of ineffective internal control and firms with

employee-friendly policies enjoy significantly lower propensity for employee-related material

weaknesses. From this perspective, firms with employee-friendly treatment policies are more

likely to have reliable internal control and better corporate governance from employee aspect.

By aligning the interest between firms and their employees, firms with employee-friendly

treatment mitigates moral hazard problems by enabling more effective internal monitoring,

thus contributing to lower information asymmetry.

The second potential mechanism via which employee treatment affect firms’ net hiring can

stem from employee governance. Previous literature shows that employment contracts are

generally incomplete because it is too costly to govern all aspect of labor performance (Dem-

ski and Feltham, 1978; Klein, 1980). Divergence also exists among different groups in society

regarding employee monitoring since each advocate has its own rationale for or against em-

ployee monitoring whether it be economic, legal or ethical (Martin and Freeman, 2003). In

reality, firm face various employee adverse behavior situations where the interests of em-

ployees and the firm are misaligned and employees’ motivation and effort are imperfectly

observed (Flammer and Luo, 2017). Examples of employee adverse behaviour can be those

counterproductive behaviour and disengaged behaviour, such as shirking responsibilities, on-

the-job searches for better jobs and using company resources for personal business and so on.

Flammer and Luo (2017) suggest that if employees perceive their current job to be superior

in comparison to their alternative options, they are less likely to engage in adverse behavior.

One way to lower the attractiveness of alternative options and mitigate employee adverse

behavior is to align employees with their firms’ interest. Akerlof (1982) and Akerlof and

Yellen (1986, 1990) suggest that the reciprocity in the gift exchange model makes employee

invest more effort in work because employees treat the benefits from their firms as a gift and

are assumed to respond to the benefits by reciprocating their firms with a gift of greater

effort. Moreover, employee-friendly treatment align the interests between employees and

their firms, which makes employees more likely to perceive their current employment special

and mitigate employee adverse behavior (Organ, 1997; Shapiro and Stiglitz, 1984; Akerlof

and Yellen, 1986). In addition to precuniary employee treatment, Flammer and Luo (2017)

8

find that relationship-based incentives such as CSR can be used as employee governance tool

to entail nurturing and constraining mechanism that facilitate firms to align the interests

between employees and their firms, lower the attractiveness of alternative options and di-

minish information asymmetry. In light of aforementioned literature above, we posit that

employee-friendly treatment mitigates employees’ adverse behavior and provides employees

to devote more efforts and firms with employee-friendly treatment therefore suffer less unex-

pected employment changes and are better informed of the net hiring level justified by their

underlying economics.

In light of the two channels above, we posit that firms with better employee treatment

schemes alleviate market friction caused by information asymmetry and mitigates employee

adverse behavior. Therefore, we predict that employee-friendly treatment schemes enable

firms to have employment level that is close to the level justified by their underlying eco-

nomics and therefore firm’s employee treatment is negatively associated with labor invest-

ment inefficiency. Following the above discussion, we develop the following hypothesis:

HYPOTHESIS 1: Employee treatment is negatively associated with labor investment

inefficiency.

In addition, we also examine the impact of employee treatment and abnormal net hiring

on a firms employee productivity. Numerous previous studies show that companies’ social

efforts including employee-friendly practices can facilitate higher labor productivity (Faleye

and Trahan, 2011; Sun and Stuebs, 2013; Sanchez and Benito-Hernandez, 2015; Hasan,

Kobeissi, Liu, and Wang, 2016). For instance, Sanchez and Benito-Hernandez (2015) find

that firms’ social involvements in internal aspects of the company most contribute to a short-

term increase in labor productivity. Faleye and Trahan (2011) also find that top executives

derive no pecuniary benefits from labor-friendly practices and suggest that genuine concern

for employees facilitate higher productivity and profitability, showing that employee-friendly

treatment is beneficial for both employees and shareholders. We argue that one of the

potential channels via which employee treatment and labor investment efficiency can affect

value creation is via labor productivity and therefore we examine the impact of employee

treatment and abnormal net hiring on labor productivity. Given previous literature suggests

that employee-friendly policies can positively influence value creation, we posit that firms

treating their employees well enjoy higher labor productivity. On the contrary, a larger

magnitude of abnormal net hiring suggests a higher deviation from a firms employment level

justified by its underlying economics and signals inefficient labor investment and we predict

that abnormal net hiring has negative impact on a firms employee productivity. Therefore,

we predict there is a positive relation between employee treatment and labor productivity

9

and a negative relation between abnormal net hiring and labor productivity. Following the

above discussion, we also develop the following hypothesis:

HYPOTHESIS 2: Employee treatment is positively associated with employee pro-

ductivity whereas labor investment inefficiency is negatively associated with employee pro-

ductivity.

3. Research design

3.1. Sample

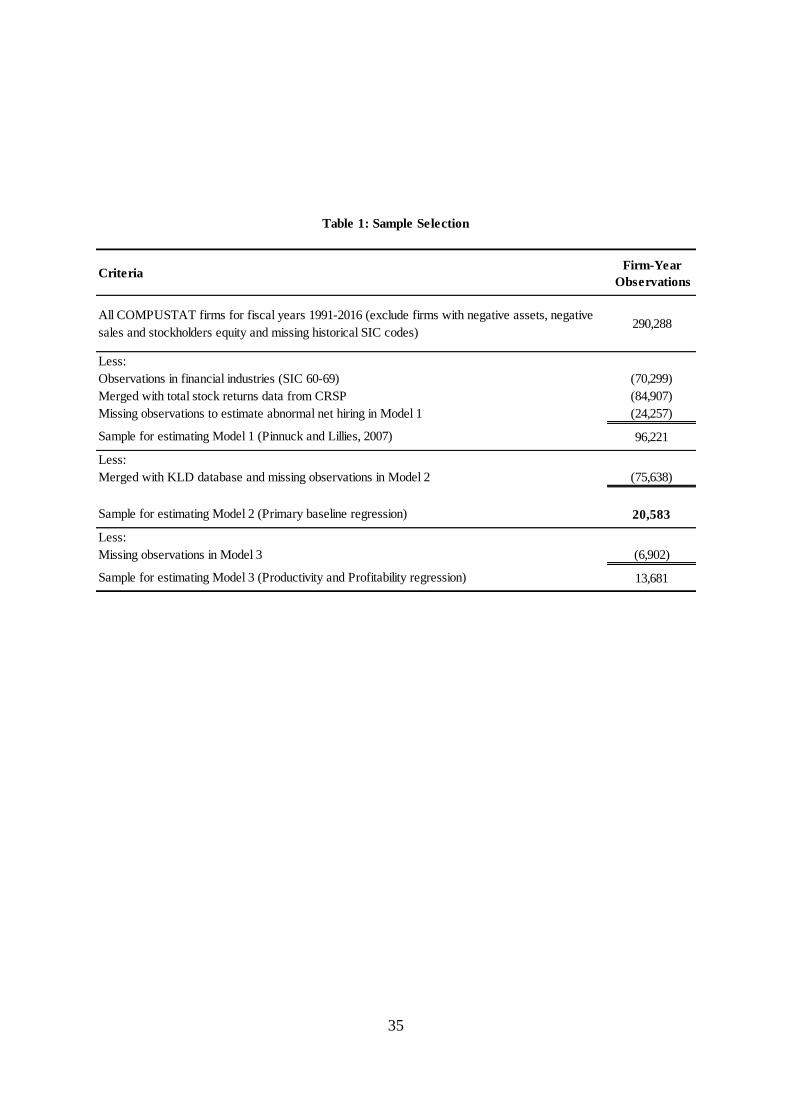

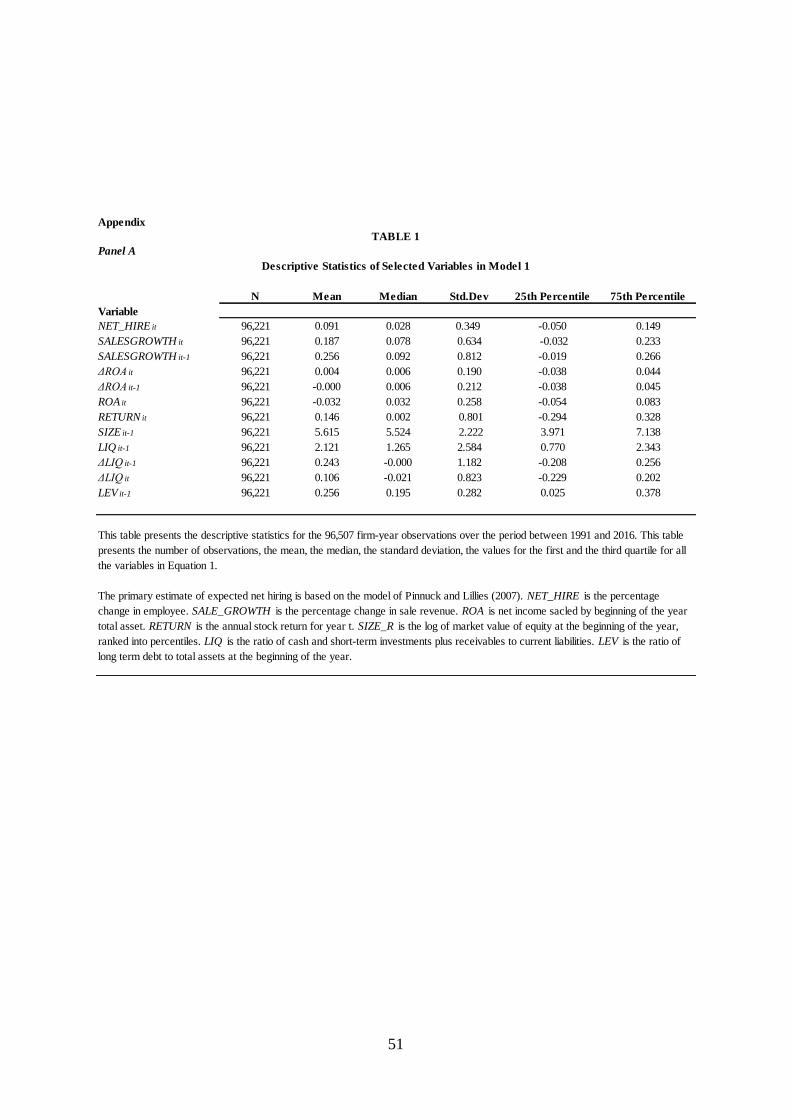

Our sample selection process is detailed in Table 1. The sample selection begins with all

COMPUSTAT firm-year between 1991-2016 with non-negative sales and asset observations

and nonmissing historical SIC codes. We merge our data with CRSP to obtain total annual

stock return and also exclude firm-year observations associated with firms in financial ser-

vices (primary two-digit SIC codes between 60-69). We further delete 24,257 firm-years with

insufficient data for use to estimate abnormal net hiring in Model 1. This leaves us with

96,221 observations to estimate our Model 1. After merged with KLD database, our sample

consists of an unbalanced panel of 20,583 firm-year observations from more than 3,000 US

firms over the period of 1995 to 2015. Our final sample for the estimation of our baseline

regression includes all firms that meet the following criteria: The firm is in the MSCI ESG

Research database, the firm is publicly traded and has financial data available from the

COMPUSTAT and security price and return information from Center for Research in Secu-

rity Prices (CRSP). We exclude firms in the financial industry (primary two-digit SIC code

between 60-69). We obtain the industry-level rate of industry unionization rate from the

website of UNIONSTATS which provides estimates of union membership and coverage data

by industry. In order to test the impact of employee treatment and abnormal net hiring on

employee productivity, we exclude 6,902 firm-years with insufficient data to compute Model

3, resulting in a test sample of 13,681 firm-years.

[Insert Table 1 near here]

3.2. Measure of labor investment efficiency

To measure labor investment, we use firms’ net hiring, as measured in the change in their

number of employees (Pinnuck and Lillis, 2007; Li, 2011). We then measure investment

10

inefficiencies using abnormal net hiring. We define abnormal net hiring as the difference

between the actual change in a firm’s labor force and the expected change based on funda-

mental economic factors and the absolute value of abnormal net hiring is the proxy for labor

investment inefficiency. A high value of abnormal net hiring indicates a high deviation of

actual labor investment from its expected value and therefore suggests a low level of labor

investment efficiency.

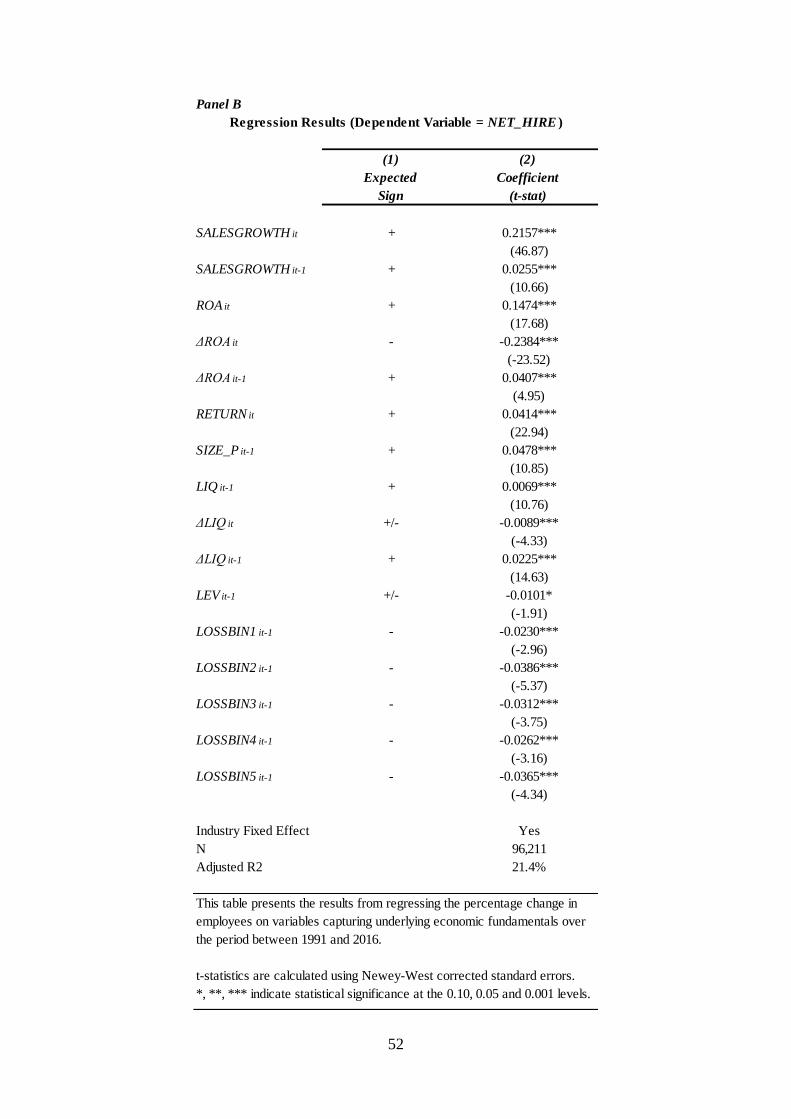

Our primary estimate of expected net hiring is based on the model of Pinnuck and Lillis

(2007), which is a regression of the percentage change in employees on several explanatory

variables capturing underlying economic fundamentals:

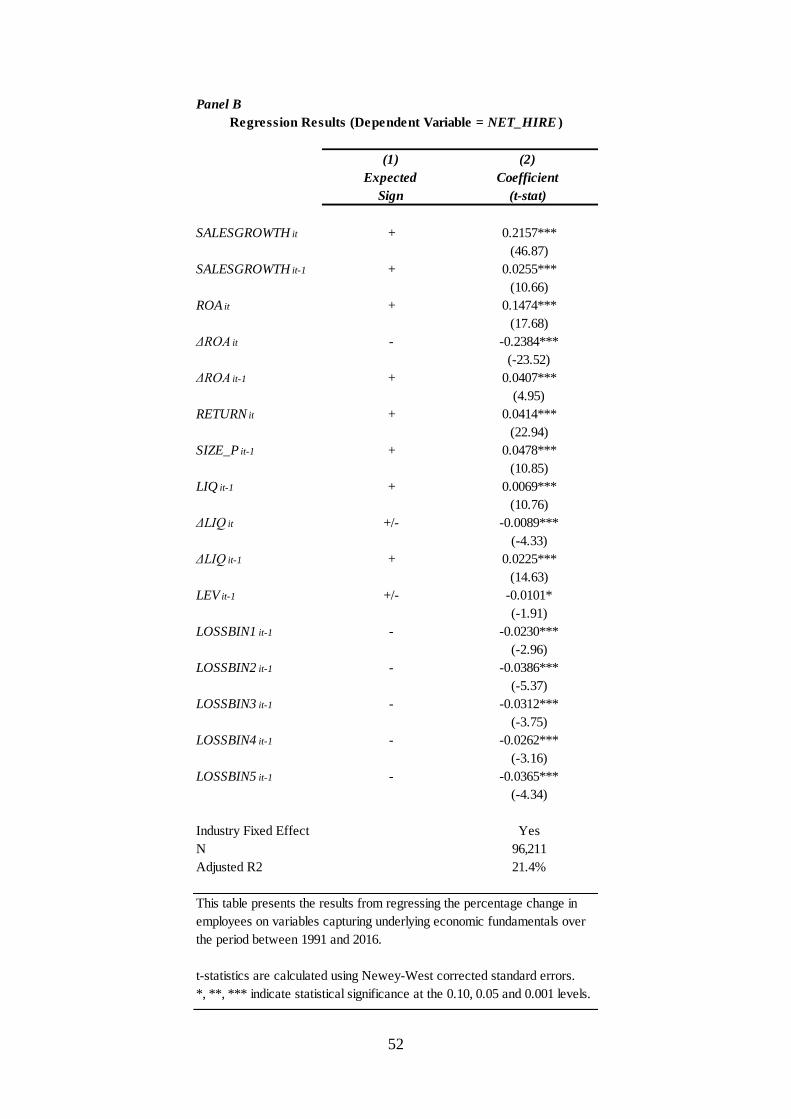

NET HIREit = β0+β1SALEGROWTHit−1+β2SALEGROWTHit+β3∆ROAit+β4∆ROAit−1

+ β5ROAit + β64RETURNit + β7SIZE Pit−1 + β8LIQit−1 + β9∆LIQit−1 + β10∆LIQit

+ β11LEVit−1 + β12LOSSBIN1it−1 + β13LOSSBIN2it−1 + β14LOSSBIN3it−1

+ β15LOSSBIN4it−1 + β16LOSSBIN5it−1 + Industry Dummies+ εit (1)

where:

NET HIRE = The percentage change in employees;

SALESGROWTH = The percentage change in sale revenue;

ROA = Net income scaled by beginning of the year total assets;

RETURN = The annual stock return for year t;

SIZE P = Log of market value of equity at the beginning of the year, ranked into per-

centiles;

LIQ = The ratio of cash and short-term investments plus receivables to current liabilities;

LEV = The ratio of long-term debt to total assets at the beginning of the year;

PROFITBIN = Indicator variables for each 0.005 interval of prior year ROA from 0 to

0.025;

LOSSBIN = Indicator variables for each 0.005 interval of prior year ROA from 0 to -0.025;

Consistent with Pinnuck and Lillis (2007) and Jung et al. (2014), we find NET HIREit is

positively associated with sale growth (SALEGROWTHit−1, SALEGROWTHit), profitability

(∆ROAit, ROAit−1), stock return (RETURNit), firm size (SIZEit−1), and liquidity (LIQit−1,

∆LIQit−1); negatively associated with current year changes in profitability (∆ROAit) and

small reported losses (LOSSBINit−1) variables; and for variables with potentially competing

effect, we find NET HIREit is negatively associated with liquidity (∆LIQit) and leverage

(LEVit−1). We report the descriptive statistics and results generated from Equation 1 in

11

Appendix.

After estimating Equation 1, we apply the estimated coefficients to each firm-year in our

sample to determine the expected level of net hiring. Our primary measure of abnormal net

hiring, AB NETHIRE, is the absolute difference between actual net hiring and the expected

level.

3.3. Measure of employee treatment

In order to assess a firm’s employee treatment, we obtain data from MSCI ESG Re-

search, which is the successor of Kinder, Lydenberg, Domini & Co. (KLD), innovest and

IRRC, which were acquired through MSCI’s acquisition of RiskMetrics. KLD specializes

in compiling rating of firms’ CSR performance and it started to track firms’ social perfor-

mance since 1991. Over time, KLD has expanded its coverage and included CSR strengths

and weaknesses for a large subset of its constituent firms. The database covers firms that

comprise the Standard & Poor’s (S&P) 500 and the Domini 400 Social Index until 2000. In

2001, it further extended its coverage to firms in the Russell 1,000 Index. Specifically, for

the period from 1991 to 2000, it includes approximately 650 companies; for the period from

2001 to 2002, 1100 companies; for the period from 2003 to 2012, 3000 companies. The KLD

database has been extensively employed in a large number of previous studies (Deng, Kang,

and Low, 2013; Servaes and Tamayo, 2013; Flammer, 2015; Khan, Serafeim, and Yoon, 2016;

Lins, Servaes, and Tamayo, 2017). The KLD database constructs a firm’s CSR performance

a wide range of sources, including company filings, government data, nongovernmental or-

ganization data, and more than 14 thousand global media sources. The database contains

seven dimensions of CSR, including community, employee relations, diversity, environment,

human rights, product quality and corporate governance. It also contains five exclusion-

ary screen classifications defined by whether a firm operate in the ’sin’ industries, including

alcohol, firearms, gambling, tobacco, nuclear power, and military contracting. For each di-

mension, the KLD is designed as a binary system and there are indicators representing a

firm’s strengths and indicators representing a firm’s concerns in certain social areas. KLD

includes a 1 indicating the presence of that criterion and a 0 indicating its absence.

Following previous studies in employee treatment and welfare (Bae et al., 2011; Cronqvist

et al., 2009; Ertugrul, 2013; Faleye and Trahan, 2011; Ghaly et al., 2015; Verwijmeren and

Derwall, 2010). we construct our employee treatment scores by using KLD’s rating on

‘Employee Relations’, with a higher net scores demonstrating better employee treatment

performance. Our primary measure of employee treatment, EMP TREAT, is estimated

by summing identified strengths and subtracting identified concerns included in ‘Employee

12

Relations’ dimensions in a given year (Faleye and Trahan, 2011; Verwijmeren and Derwall,

2010). Specifically, our employee treatment variable contains labor-relevant components

including union relations, cash profit sharing, employee involvement and retirement benefits.

Following Ertugrul (2013) and Ghaly et al. (2015), we also include the ‘Work/Life Benefits’

variable from the ‘Diversity’ dimension1.

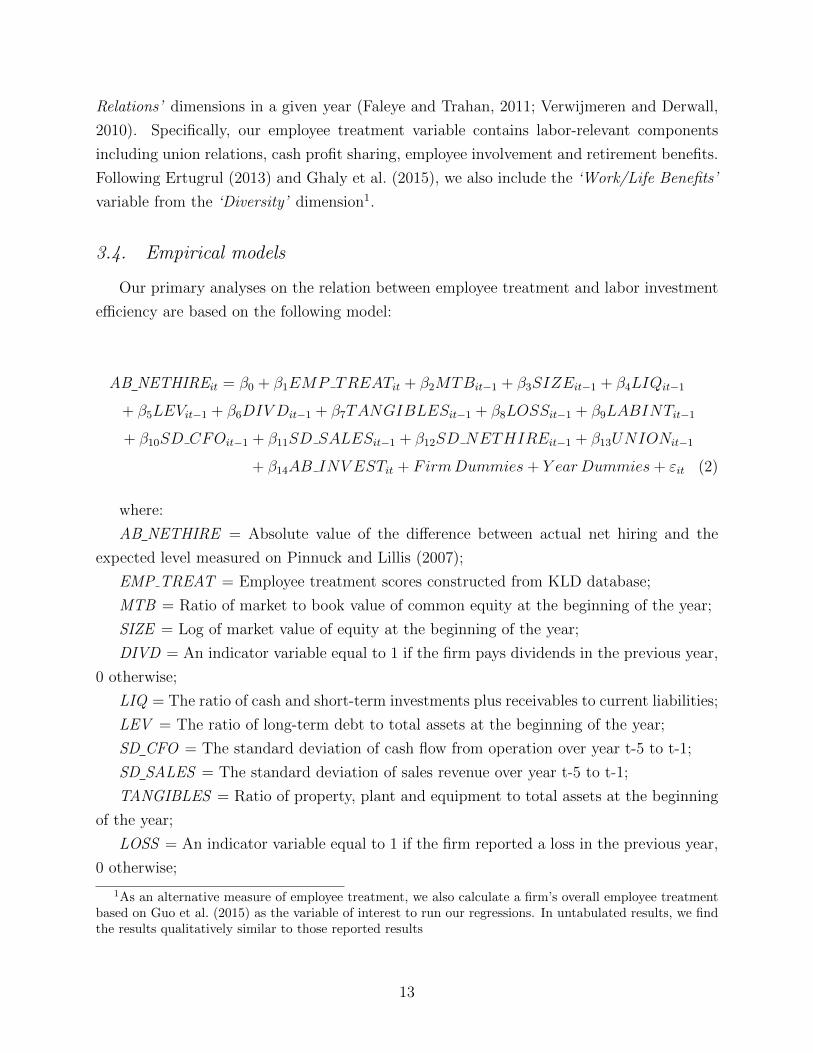

3.4. Empirical models

Our primary analyses on the relation between employee treatment and labor investment

efficiency are based on the following model:

AB NETHIREit = β0 + β1EMP TREATit + β2MTBit−1 + β3SIZEit−1 + β4LIQit−1

+ β5LEVit−1 + β6DIV Dit−1 + β7TANGIBLESit−1 + β8LOSSit−1 + β9LABINTit−1

+ β10SD CFOit−1 + β11SD SALESit−1 + β12SD NETHIREit−1 + β13UNIONit−1

+ β14AB INV ESTit + FirmDummies+ Y earDummies+ εit (2)

where:

AB NETHIRE = Absolute value of the difference between actual net hiring and the

expected level measured on Pinnuck and Lillis (2007);

EMP TREAT = Employee treatment scores constructed from KLD database;

MTB = Ratio of market to book value of common equity at the beginning of the year;

SIZE = Log of market value of equity at the beginning of the year;

DIVD = An indicator variable equal to 1 if the firm pays dividends in the previous year,

0 otherwise;

LIQ = The ratio of cash and short-term investments plus receivables to current liabilities;

LEV = The ratio of long-term debt to total assets at the beginning of the year;

SD CFO = The standard deviation of cash flow from operation over year t-5 to t-1;

SD SALES = The standard deviation of sales revenue over year t-5 to t-1;

TANGIBLES = Ratio of property, plant and equipment to total assets at the beginning

of the year;

LOSS = An indicator variable equal to 1 if the firm reported a loss in the previous year,

0 otherwise;

1As an alternative measure of employee treatment, we also calculate a firm’s overall employee treatmentbased on Guo et al. (2015) as the variable of interest to run our regressions. In untabulated results, we findthe results qualitatively similar to those reported results

13

SD NETHIRE = The standard deviation of percentage change in employees over year

t-5 to t-1;

LABINT = Ratio of employees to total assets at the beginning of the year;

UNION = The industry-level rate of labor unionization for year t-1;

AB INVEST = The absolute value of the residual from the following model:

INVESTit = β0 + β1SALEsGROWTHit−1 + εit;

Following previous literature (Biddle and Hilary, 2006; Biddle et al., 2009; Jung et al.,

2014) , we control for the following control variables that are likely to be associated with

hiring, including growth options (MTBit−1), firm size(SIZEit−1), liquidity (LIQit−1), lever-

age (LEVit−1), dividend payout (DIDVit−1), tangibility (TANGIBLEit−1), loss occurrence

(LOSSit) and labor intensity (LABINTit−1). We also consider the volatilities for three

variables, including firms’ cash flow (SD CFOit−1), sales (SD SALESit−1) and net hiring

(SD NETHIREit−1) volatilities over the period form t-1 to t-5. Moreover, we include industry-

level unionization rate control for labor protection owing to organized labor. Following pre-

vious literature in labor economics, we measure UNIONit−1 using industry-level unionization

rates to proxy for whether firms in a given industry that have a high level of labor protection.

Finally, to control for the potential effect of stemming from other non-labor investment de-

cisions on abnormal net hiring, we include AB INVESTit, which measures the magnitude of

non-labor investments deviating from their expected level. As in Biddle et al. (2009), we use

the absolute value of the residuals from the regression of non-labor investment (INVESTit)

on sales growth (SALESGROWTHit−1), where INVESTit is the sum of capital expenditures,

acquisition expenditures and research and development expenditures, less cash receipts from

the sale of property, plant and equipment, scaled by lagged total assets. We also include

firm fixed effect and year fixed effect to control for the time-invariant unobservable firm

characteristics and firm-invariant time-specific changes in economic conditions.

Our analyses on the impact of employee treatment and abnormal net hiring on employee

productivity are based on the following model:

14

EMP PRODCit = β0+β1EMP TREATit−1+β2AB NETHIRECit−1+β3SIZEit−1+β4LIQit−1

+ β5LEVit−1 + β6MTBit−1 + β7TANGIBLESit−1 + β8AB INVESTit−1 + β9LOSSit−1

+ β10HERFDit−1 + beta11SALEGROWTHit−1 + β12SALEGROWTHit

+ β13GOV ERNANCEit−1 + β14CAPXit−1 + FirmDummies+ Y earDummies+ εit

(3)

where:

EMP PRODCit = PRODC SALES, PRODC GPROFIT or PRODC NETINCOME

PRODC SALES = Employee productivity, measured as the natural logarithm of sales

divided by the number of employee;

PRODC GPROFIT = Employee productivity, measured as the natural logarithm of sales

minus cost of goods sold divided by the number of employee;

PRODC NETINCOME = Employee productivity, measured as the natural logarithm of

net income divided by the number of employee;

GOVERNANCE = Corporate governance scores from KLD database;

CAPX = The ratio of capital expenditures to total assets;

4. Results

4.1. Descriptive statistics

In order to obtain our primary measure of abnormal net hiring, we first estimate the

expected level based Equation 1. Following Pinnuck and Lillis (2007), we winsorize all con-

tinuous variable at the 1st and 99th percentiles of their respective distribution to mitigate

the influence of outliers. In untabulated results, our descriptive statistics for the percentage

change in the number of employees and other control variables are comparable to those re-

ported in Pinnuck and Lillis (2007) and Jung et al. (2014) and our results and the sign of

each variable are consistent with the results of prior studies. Our model has an adjusted R2

of approximately 21.4 percent in comparison with 24.5 percent in Pinnuck and Lillis (2007)

and 27.2 percent in Jung et al. (2014). Overall, the specification of our model is generally

consistent with prior studies and the model provides reasonable estimation for the expected

level of net hiring. The absolute difference between actual net hiring and the expected level

is our primary measure of abnormal net hiring which is the part that cannot be captured by

15

underlying economic fundamentals.

[Insert Table 1 near here]

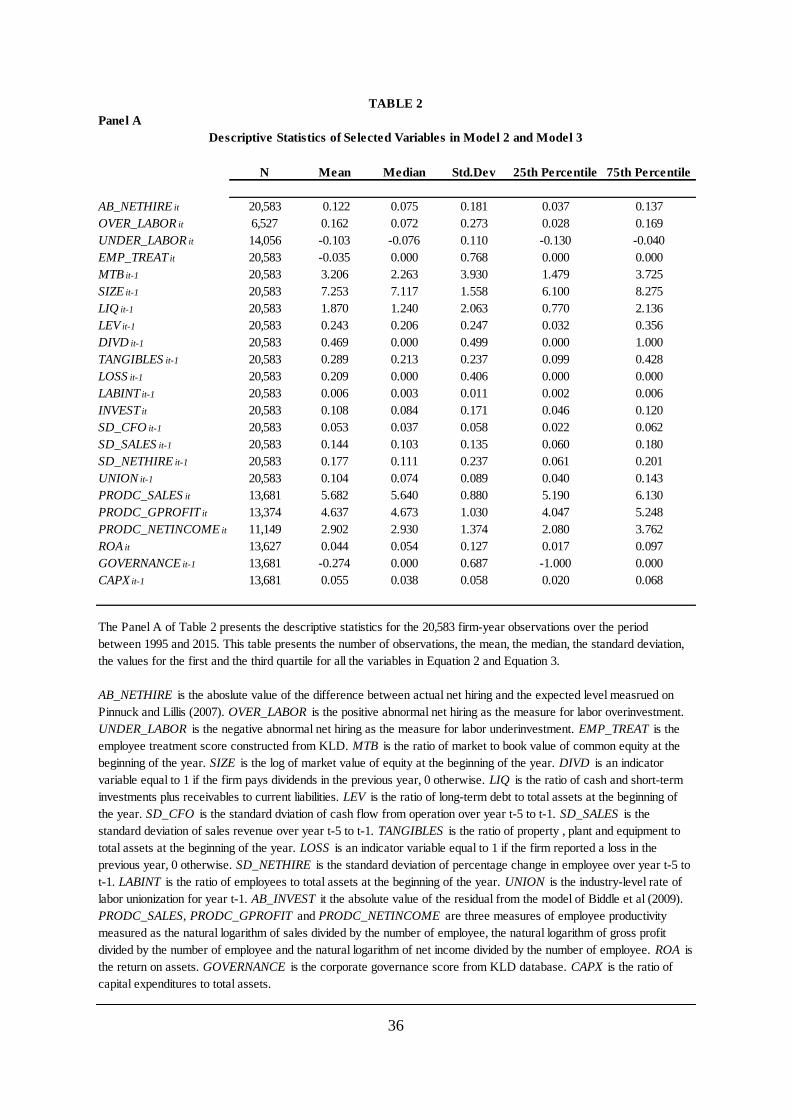

In panel A of Table 2, we present descriptive statistics for the variables in Equation 2 and

Equation 3. In terms of Equation 2, our dependent variable, AB NETHIRE, has mean of 0.12

and median of 0.08 with standard deviation of 0.19, which is close to Jung et al. (2014). that

has mean of 0.11 and median of 0.07 with standard deviation of 0.13 for abnormal net hiring.

Apart from the absolute value of abnormal net hiring as our primary measure of labor in-

vestment efficiency, we also divided the variable into two parts based on the sign of abnormal

net hiring. The positive abnormal net hiring, OVER LABOR, indicates that a firm’s actual

net hiring is greater than expected and therefore is a measure of overinvestment in labor

whereas the negative abnormal net hiring, UNDER LABOR, indicates that a firm’s actual

net hiring is less than expected and is a measure of underinvestment. Consistent with Ghaly

et al. (2015), our main variable of interest, EMP TREAT, range from -4 to 4, has a mean of

-0.04 and median of 0, suggesting that the number of firms with negative employee treatment

scores outweighs the number of firms with positive employee treatment scores. The descrip-

tive statistics of other control variables are generally consistent with Biddle et al. (2009)

and Jung et al. (2014).For Equation 3, our descriptive statistics includes three employee

productivity measures, PRODC SALES, PRODC GPROFIT and PRODC NETINCOME

and additional control variables including corporate governance (GOVERNANCEit−1) and

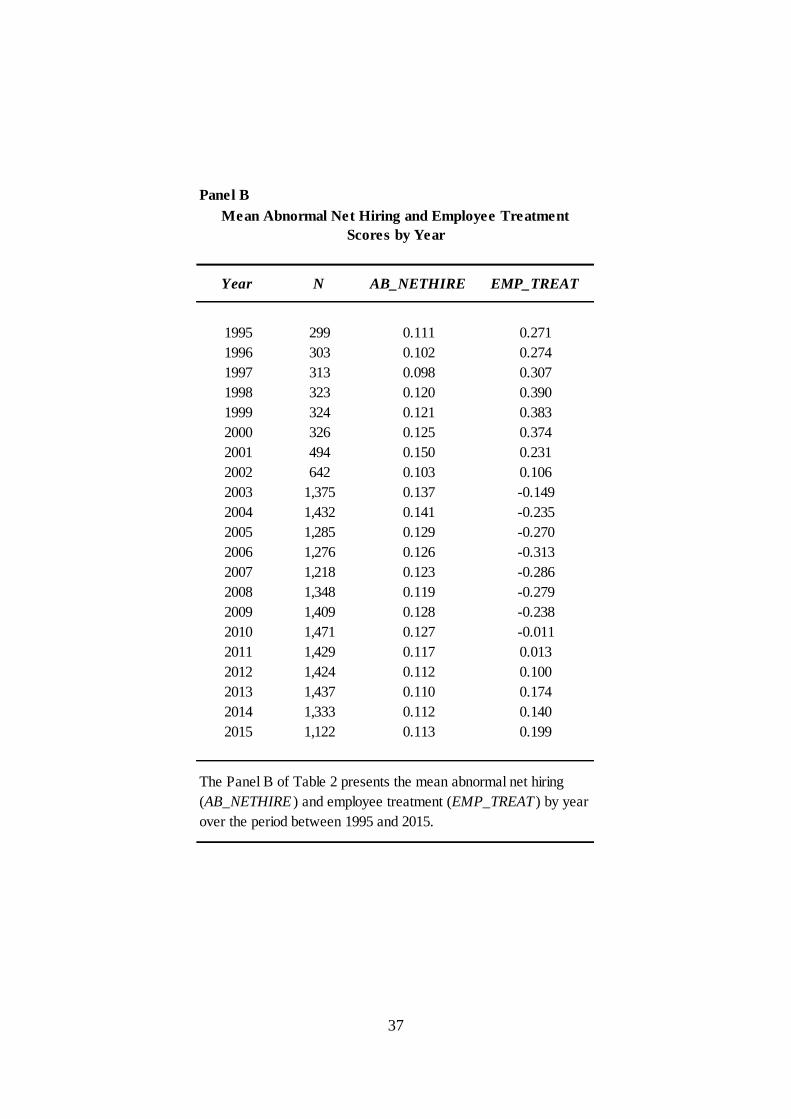

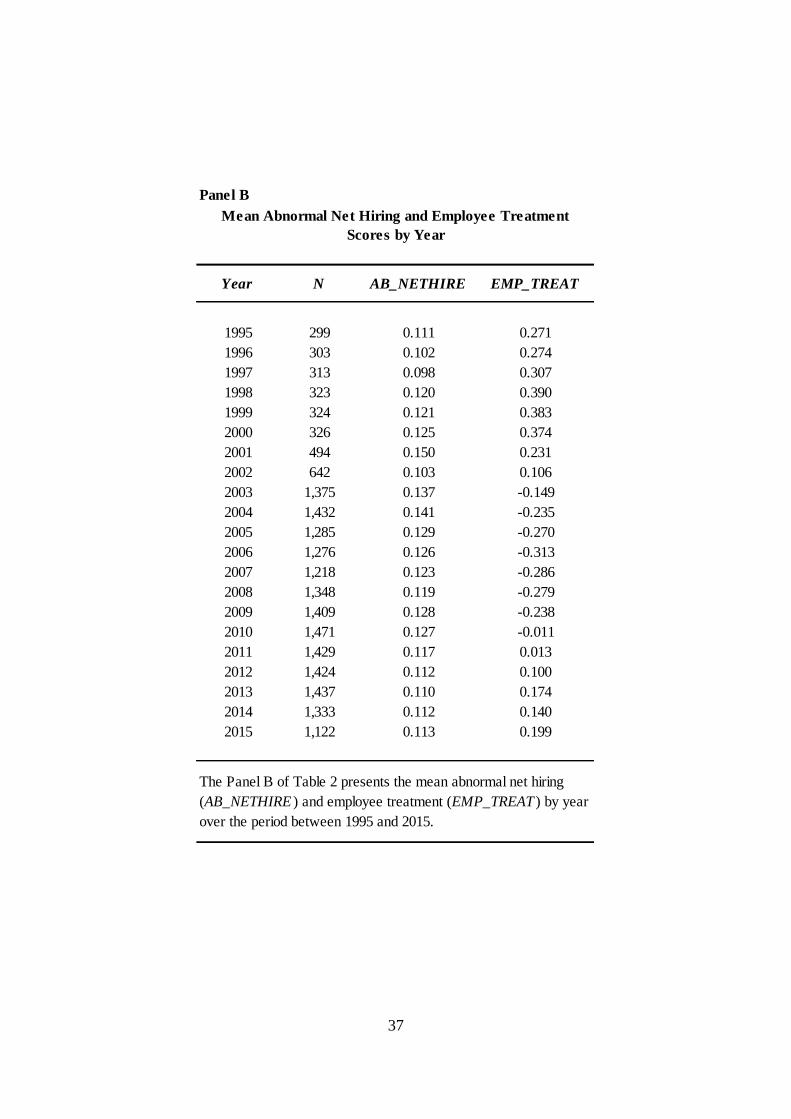

capital expenditure (CAPXit−1). In Panel B of Table 2, we report the frequency of firms

in our sample by year. Consistent with our expectation, our sample increases over time as

KLD database extends its coverage over time.

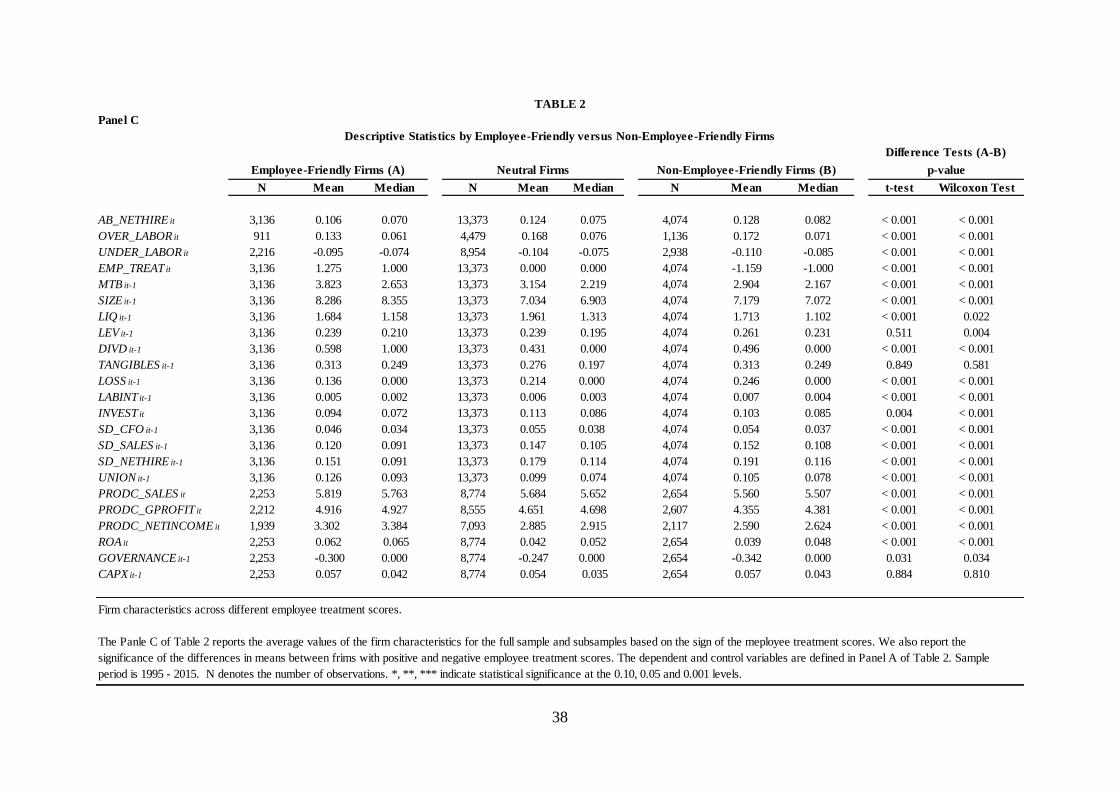

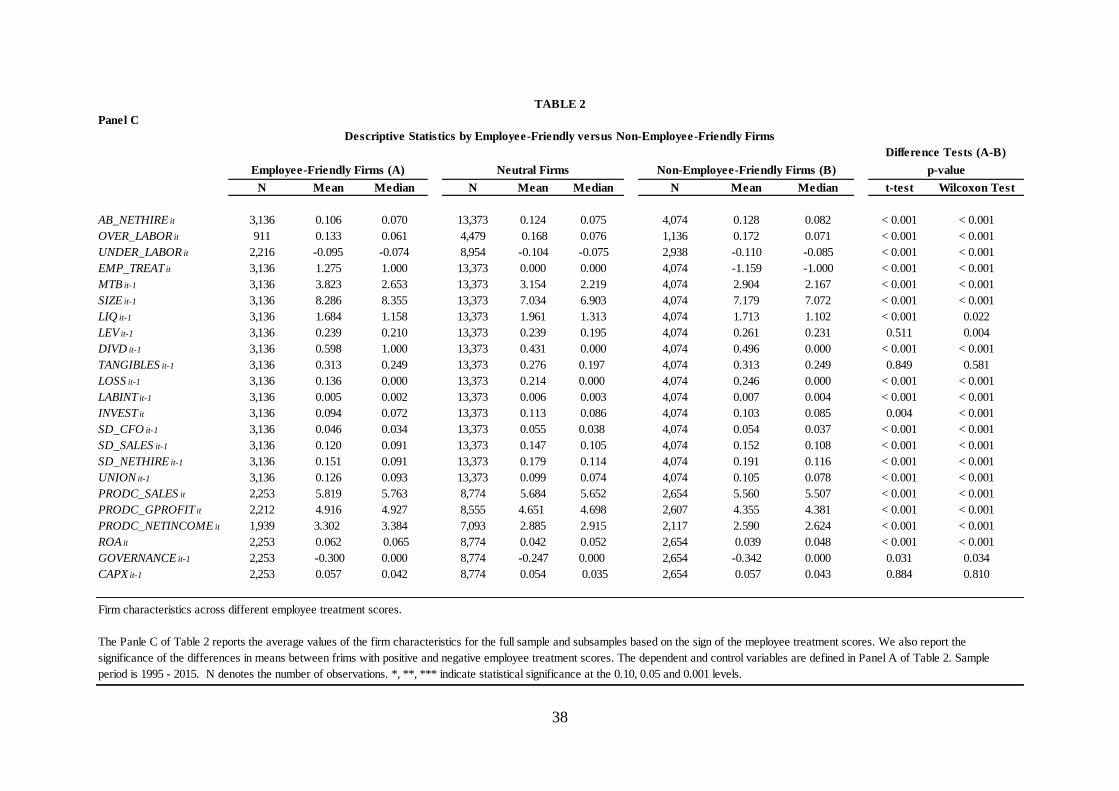

In panel C of Table 2, we define firms with positive employee treatment scores as

employee-friendly firms, and firms with negative employee treatment scores as non-employee-

friendly firms. We compare the characteristics of these two subsample groups of firms. Sec-

tion A provides the number of observations, the mean and the median of employee-friendly

firms. Section B presents the descriptive statistics for non-employee-friendly firms. Con-

sistent with prior studies in employee treatment, most observations in our sample fall into

category with neutral employee treatment subgroup, namely, EMP TREAT is equal to 0.

The comparison indicates that firms with employee-friendly treatment policies have lower

abnormal net hiring and therefore enjoy higher labor investment efficiency. Specifically, the

average abnormal net hiring is 10.6% for employee-friendly firms in comparison with 12.8%

for non-employee-friendly firms. The median comparison also indicates similar results. The

median of abnormal net hiring for employee-friendly firms is approximately 7% in comparison

16

with 8.2% for non- employee-friendly firms. The differences for mean and median compar-

ison between the two groups are all statistically significant at the 1% level and indicate

that employee-friendly treatment facilitate more efficient investment in labor. Neutral firms

generally fall in the middle between the two groups with the mean of 12.4% and median

of 7.5%. In terms of employee productivity and profitability, we find firms with employee-

friendly treatment policies have higher labor productivity and profitability in comparison

with non-employee-friendly firms and the differences for the mean and median comparison

between the two groups are statistically significant at the 1% level.

[Insert Table 2 near here]

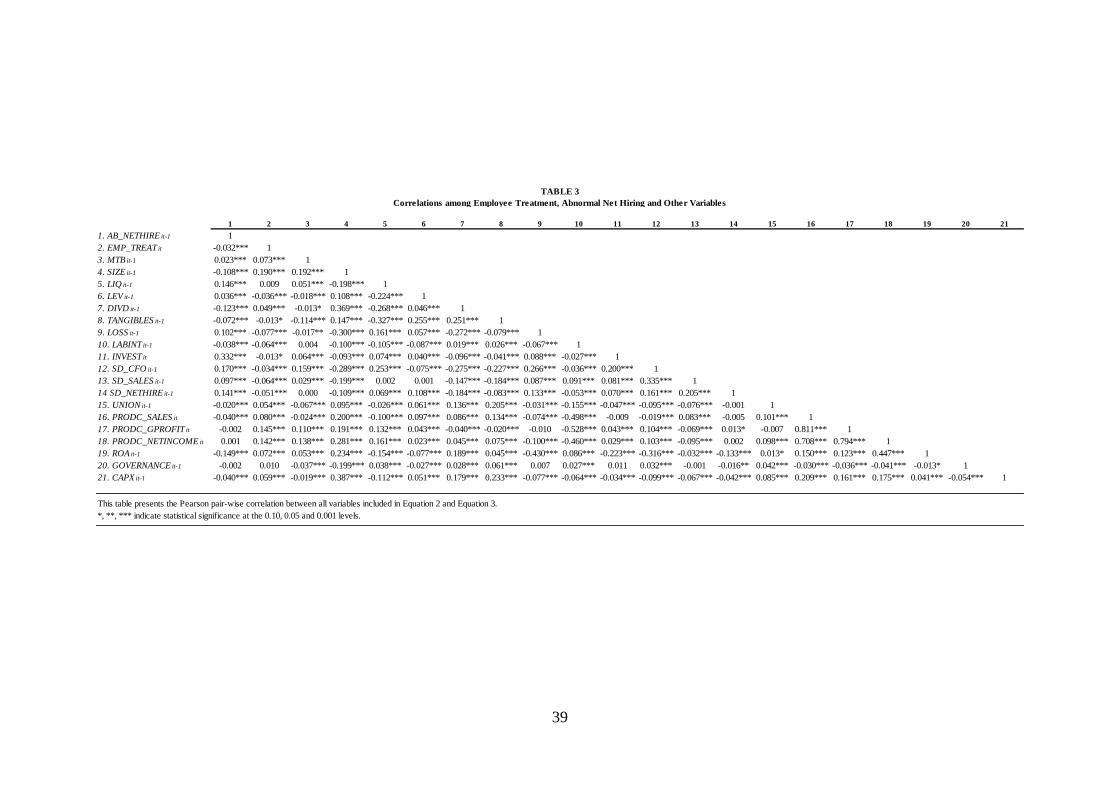

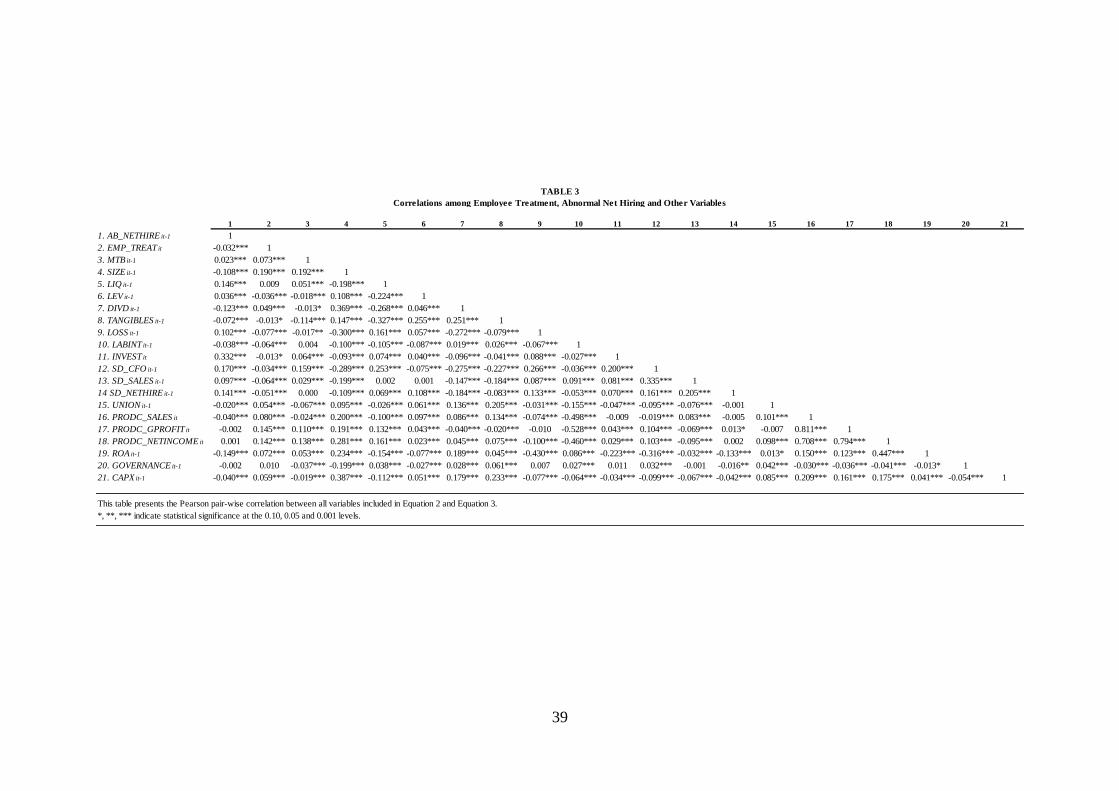

Table 3 presents Pearson correlation coefficients for all variables in Equation 2 and Equa-

tion 3. We find a negative and significant correlation between employee treatment score

(EMP TREAT ) and the level of abnormal net hiring (AB NETHIRE ), indicating that firms

with good employee treatment practices are generally associated with higher level of labor

investment efficiency. The correlations among other variables is generally consistent with our

expectations. For instance, we find firms with higher growth options, higher level of liquidity

and higher concurrent abnormal non-labor investments are more likely to have higher ab-

normal net hiring. However, larger firms, firms paying dividends in the past and firms with

higher level of tangibility are negatively associated with abnormal net hiring. In addition,

we generally find abnormal net hiring is negatively associated with labor productivity and

profitability whereas employee treatment is positively associated with labor productivity and

profitability.

[Insert Table 3 near here]

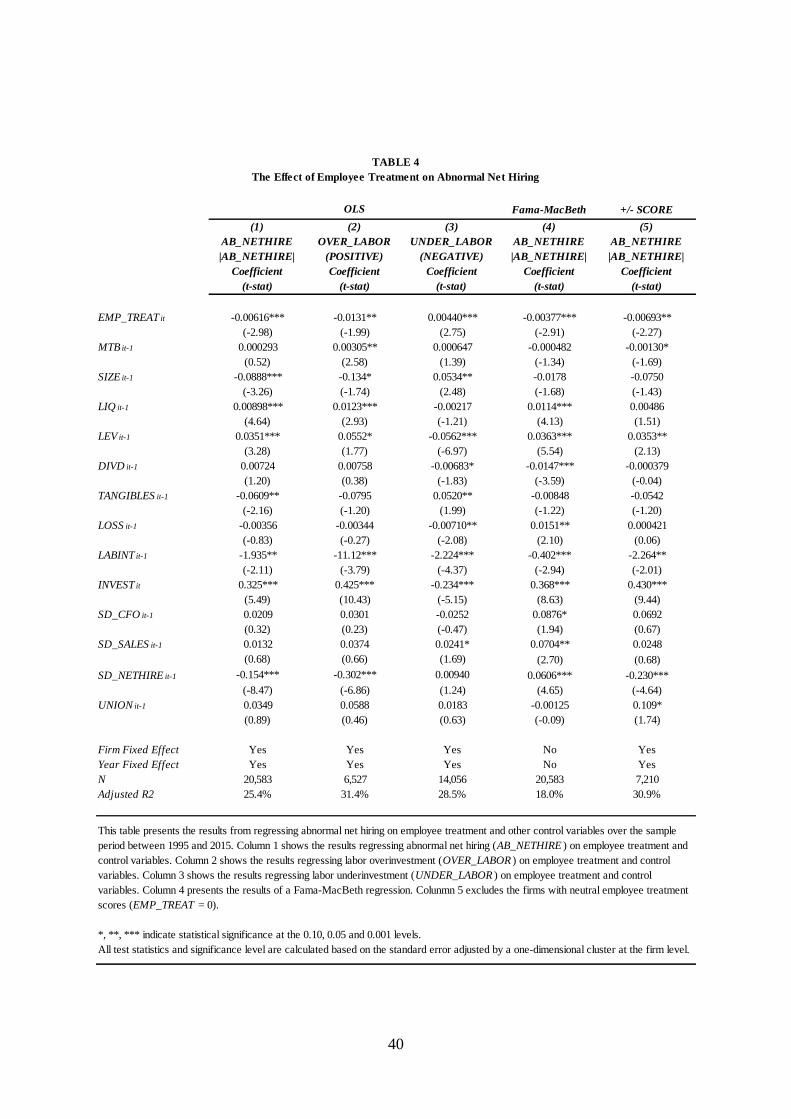

4.2. Main results

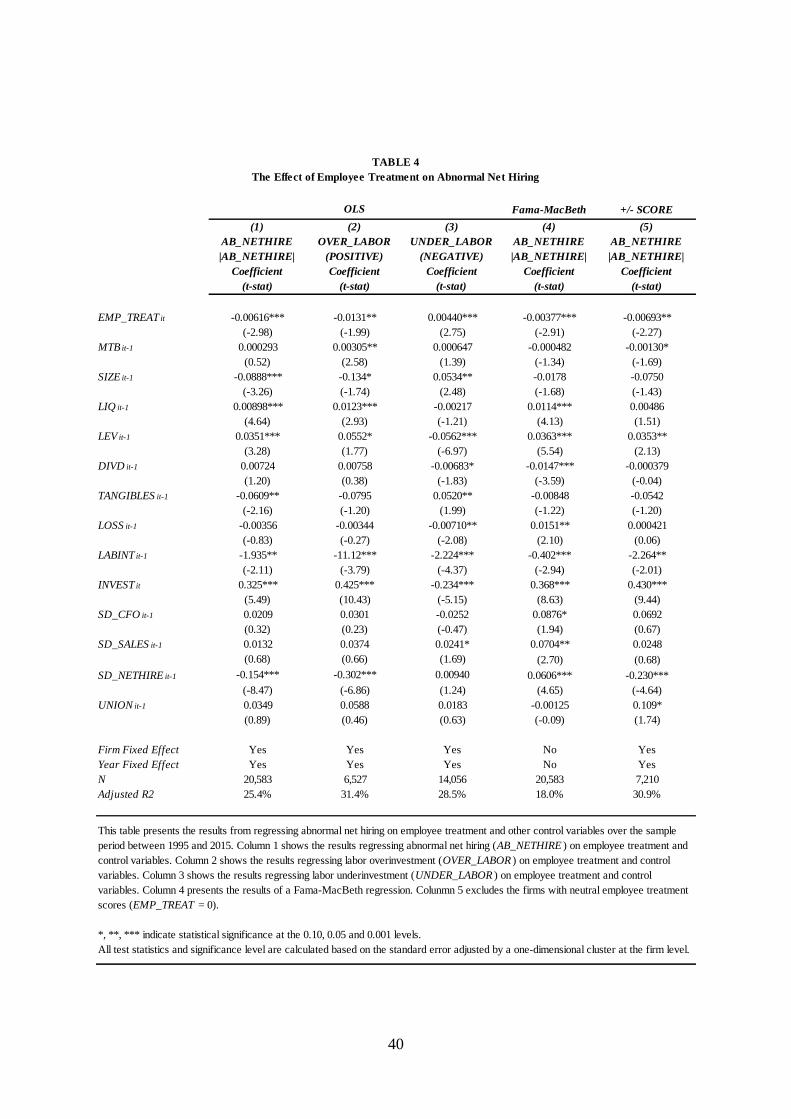

Table 4 shows the main results of multivariate regressions examining the relationship be-

tween employee treatment score (EMP TREAT ) and abnormal net hiring (AB NETHIRE ).

First, we present the results for the regression model using the absolute value of the resid-

ual, AB NETHIRE, as our primary measure of abnormal net hiring. Our main results show

that the estimated coefficient on EMP TREAT is negatively and statistically significant.

This results suggest that firms treating their employees well have smaller magnitude of ab-

normal net hiring, indicating that employee-friendly treatment facilitates more efficient net

17

hiring practices. Apart from employee treatment, we also find that larger firms and firms

with higher level of tangibility exhibit more efficient labor investments, which is consistent

with the correlation results in Table 3. On the other hand, firms with higher level of liq-

uidity, leverage and higher abnormal non-labor investments are more likely to suffer labor

investment inefficiency. Second, we further investigate the association between employee

treatment and overinvestment (OVER LABOR) and underinvestment (UNDER LABOR)

based on the sign of abnormal net hiring. In the second column of Table 4, we adopt the

positive abnormal net hiring as the measure of overinvestment in labor and estimate our

baseline model based on the subsample. Consistently, the results in column 2 suggest that

firms with better employee treatment performance tend to have less labor overinvestment

and therefore enjoy higher level of labor investment efficiency. So far, from the first two re-

gressions in Table 4, we continuously find a negative association between employee treatment

score (EMP TREAT ) and abnormal net hiring (AB NETHIRE ) and (OVER LABOR), in-

dicating that employee treatment facilitate firms to have smaller deviation between actual

and expected net hiring and more employee-friendly firms enjoy more efficient investments

in labor. In the third column, we use the negative abnormal net hiring (UNDER LABOR)

as the dependent variable to estimate our baseline model. If firms with better employee

treatment invest more efficiently in labor, we expect that there is a positive relationship

between employee treatment and labor underinvestment. Consistent with our expectation,

the results of the final regression in Table 4 show that employee treatment is positively as-

sociated with negative abnormal net hiring, showing that more employee-friendly firms have

smaller deviation between actual and expected net hiring in terms of underinvestment in

labor. In addition, in column 4, we use Fama-MacBeth to estimate our baseline regression

model and we find the results are similar to our main results in column 1. Finally, in column

5, we run our baseline regression model and exclude firms with neutral employee treat-

ment scores (EMP TREAT = 0). Again, the results in column 5 show similar results and

suggest employee-friendly treatment lowers abnormal net hiring. Overall, our main results

indicate that better employee treatment helps firms to mitigate labor investment inefficiency.

[Insert Table 4 near here]

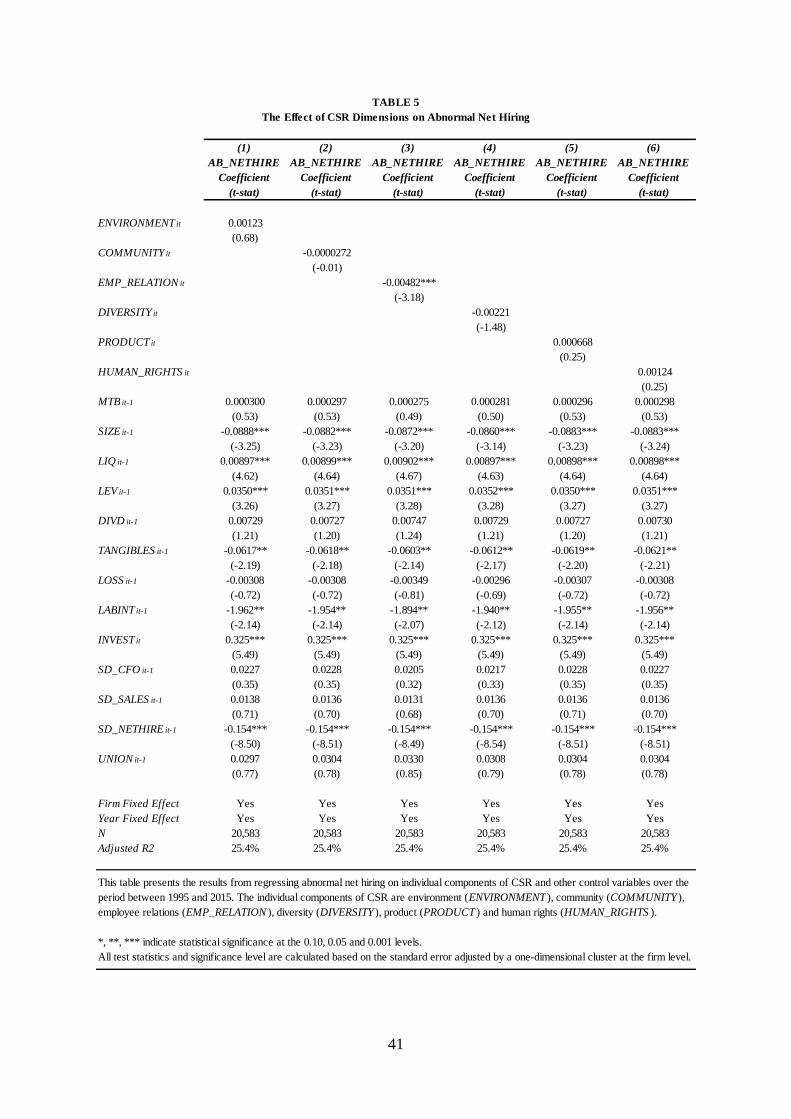

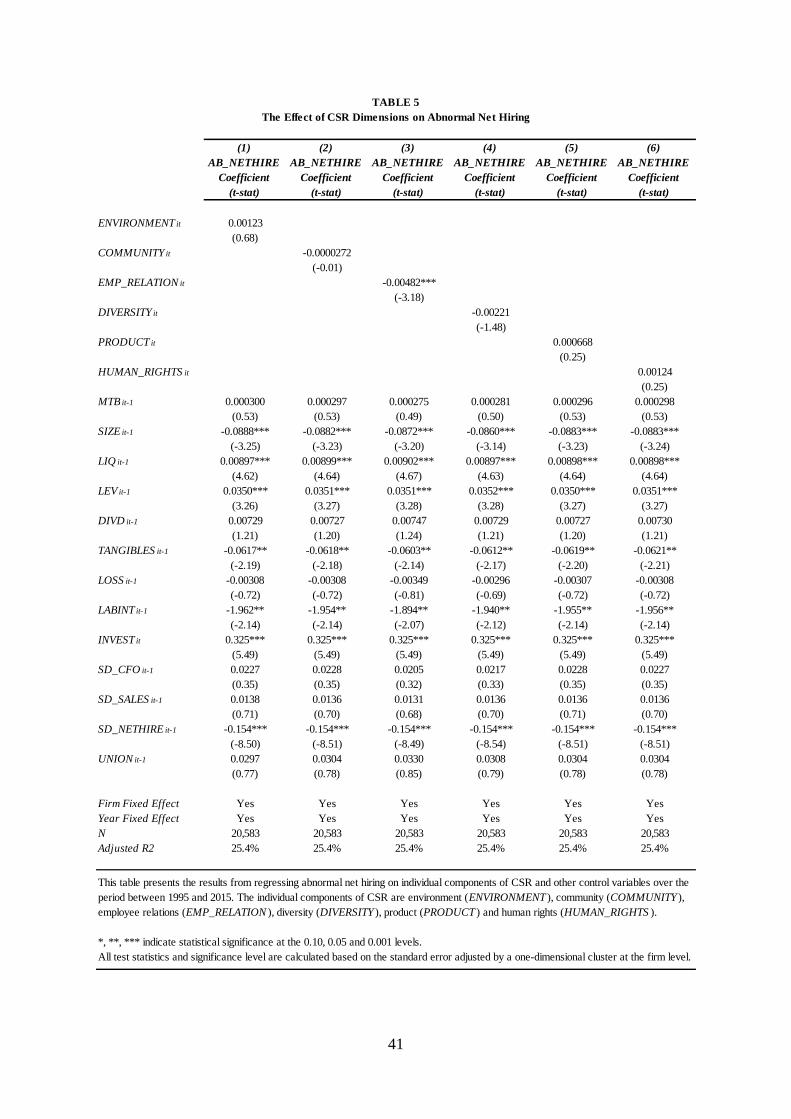

4.3. Non-labor social dimensions

Employee-friendly treatment policies potentially can be part of a firm’s CSR programme.

Given the multi-faceted nature of CSR, we further investigate the link between each indi-

vidual CSR dimension and labor investment efficiency. Bouslah, Kryzanowski, and MZali

18

(2013) point out the drawbacks associated with the use of aggregate CSR measure and ar-

gue that the aggregate CSR measure may confound the influence of each individual CSR

dimension that may not be equally relevant and therefore each individual CSR dimension

should be considered separately. One issue that can potentially mislead our interpretation

is that firms with employee-friendly treatment practices are also firms that perform well in

other non-labor social dimensions. In that case, as one of the integral parts of CSR, good

employee treatment can be merely a reflection of a firm’s social performance and the evidence

that better employee treatment increases labor investment efficiency should attribute to a

firm’s social performance instead of solely employee treatment. To rule out this possibility,

we test the impact of each dimension of CSR on abnormal net hiring, which potentially

serves as the placebo test function to indicate whether the relationship between employee

treatment and abnormal net hiring is driven by a firm’s social performance or merely em-

ployee treatment. Among the six individual social dimensions (environment, community,

employee-relations, diversity, product and human rights), the most employee-related CSR

dimension that is employee-relations (EMP RELATION ). The employee-relation dimension

(EMP RELATION ) includes employee cash profit sharing, employee involvement, employee

health & safety, human capital development, labor management relations and supply chain

issues. While other non-labor CSR dimensions may also be relevant for firms to build culture

that enforces certain social norms, the employee-relation dimension is the most labor-relevant

CSR dimensions that align employee interests with firms’ objectives and therefore more likely

to facilitate efficiency labor investments. We use individual CSR dimension and see whether

other non-labor CSR dimensions also significantly affect labor investment efficiency. If it is

the social performance that drives a firm to have higher labor investment efficiency, we will

observe significant results on the relation between abnormal net hiring and other individual

social dimensions. On the other hand, if it is employee treatment policies that drive more

efficient labor investment, we should only observe significant results between employee di-

mension and labor investment efficiency. In Table 5, our results show that only the labor

dimension of CSR (employee-relations) is significantly associated with abnormal net hiring.

Specifically, we find employee-relations scores are negatively associated with abnormal net

hiring, which is consistent with our main results and shows that firms with better employee

relations tend to have higher labor investment efficiency. On the other hand, we do not

find any significant results for other non-labor dimensions of CSR, confirming that our main

results are driven by employee treatment instead of a firm’s other non-labor social perfor-

mance.

[Insert Table 5 near here]

19

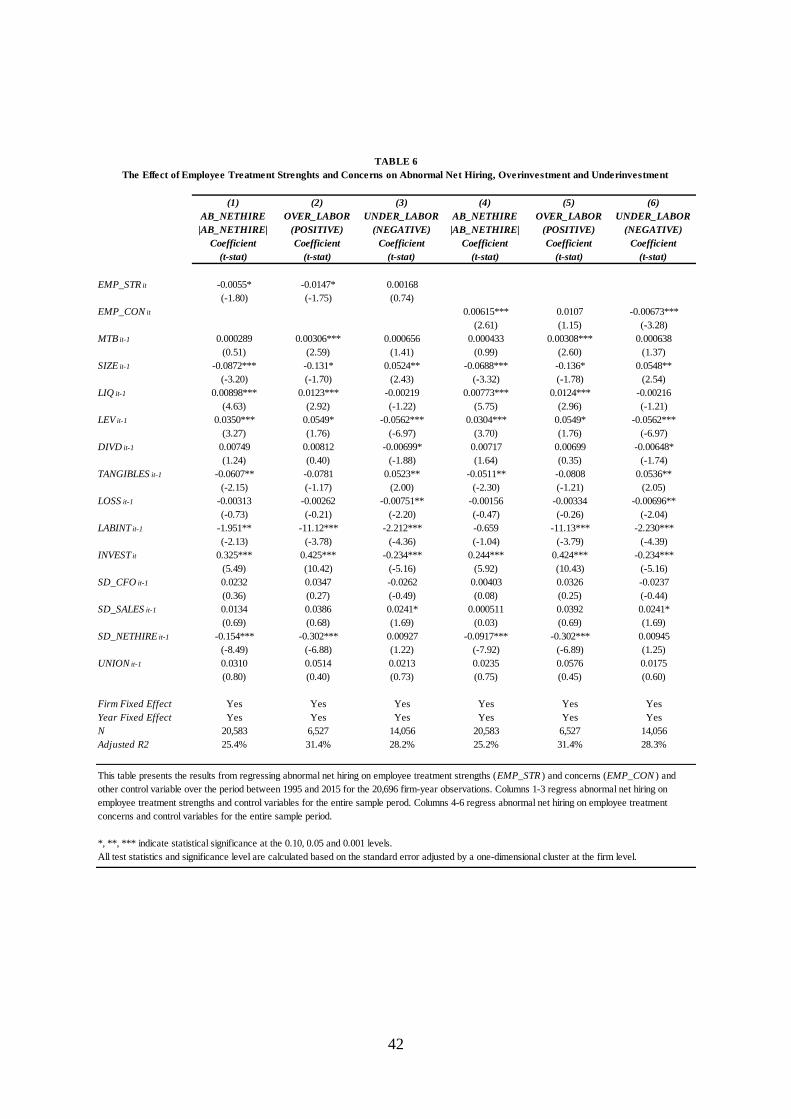

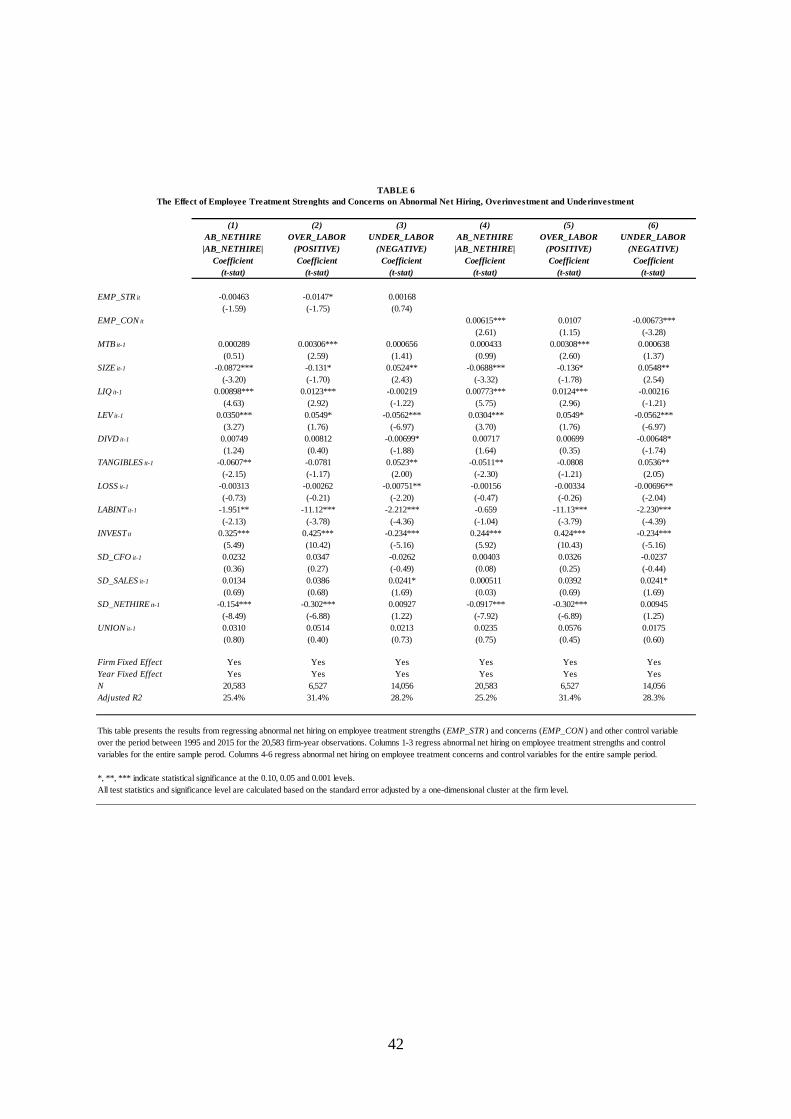

4.4. Employee treatment strengths and concerns on abnormal net hiring

Mattingly and Berman (2006) highlight the importance of distinguishing between strengths

and concerns in recent social responsibility research because they are empirically and con-

ceptually distinct constructs and there could be compensating effects. In the same spirit of

Mattingly and Berman (2006), we split the employee treatment measure into employee treat-

ment strengths (EMP STR) and employee treatment concerns (EMP CON ), which helps us

to observe how the components of the primary employee treatment (EMP TREAT ) affect

firms’ labor investment efficiency. Specifically, we predict that the strengths of employee

treatment can enhance firms’ labor investment efficiency and therefore are negatively associ-

ated with abnormal net hiring whereas the concerns of employee treatment pose a misalign-

ment between the interests of employees and a firm’s objective and signal a firm’s failure in

honoring its implicit claims and therefore are expected to lower a firm’s labor investment

efficiency.

In Table 6, we investigate the impact of employee treatment strengths (EMP STR) and

concerns (EMP CON ) on overall abnormal net hiring (AB NETHIRE ), labor overinvestment

(OVER LABOR) and labor underinvestment (UNDER LABOR). In the first three columns

in Table 6, we only find negative and relatively weak association between EMP STR and

abnormal net hiring (AB NETHIRE ) and overinvestment in labor (OVER LABOR), which

indicates that employee treatment strengths reduce labor investment inefficiency. We do

not find significant results regarding overall employee treatment strengths in reducing labor

underinvestment. On the other hand, we find employee treatment concerns, EMP CON, is

positively associated with abnormal net hiring, suggesting that firms with more employee

treatment concerns suffer more labor investment inefficiency. Moreover, we find EMP CON

variable is also negatively associated with underinvestment in labor (negative abnormal net

hiring), which suggests that firms with more employee treatment concerns are more likely to

have actual net hiring less than expected, thus leading to labor underinvestment. Overall,

we find solid evidence that employee treatment concerns can distort normal labor hiring and

lead to labor investment inefficiency and relatively weak evidence that employee treatment

strengths effectively increase labor investment efficiency.

[Insert Table 6 near here]

20

5. Sensitivity Analysis

To examine the validity of our main results indicating that corporate employee treatment

facilitates more efficient investments in labor, we conduct additional robustness tests. These

tests assess the sensitivity of our results to alternative measures of employee treatment,

investment efficiency and additional control variables.

5.1. Analysis of instrumental variable estimation

While using an extensive list of control variables that facilitate to mitigate the poten-

tial omitted variable bias in estimating the association between a firm’s employee treatment

and labor investment efficiency, we cannot rule out the possibility that our results gener-

ated from the baseline model suffer from endogeneity bias. In order to address the concerns

about endogeneity, we use several approaches by adopting the instrumental variable esti-

mation. First, as an instrument for employee treatment of firm i in year t, we use the

average employee treatment scores of firms having their headquarters located in the same

state as instrumental variable to address the endogeneity issue. Prior research shows that

geographic proximity can be an important factor for corporate policies (Pirinsky and Wang,

2010; Jiraporn, Jiraporn, Boeprasert, and Chang, 2014). As one of the integral part of a

firm’s social performance, employee welfare and treatment practices are likely to be affected

by firms’ geographic proximity as well. Firms located geographically close to each other are

more likely to be affected by the same local factors and preferences and hence tend to exhibit

similar employee treatment practices. Moreover, factors such as social connectedness, peer

effect and local competition among firms in the same geographic area may drive geographi-

cally proximate firms to adopt similar employee treatment practices. Hence, the underlying

motivation for adopting this instrument is that employee treatment tends to be correlated

among firms in a given state, but arguably the state-level employee treatment performance

is not likely to affect the labor investment efficiency of a specifically individual firm. In order

to avoid the situation where the employee treatment performance of one given firm affects

the average employee treatment score of the geographically proximate firms in a given state,

we require each state contains at least ten firm for each year 2. Thus, we mitigate a situa-

tion where a single firm’s employee treatment performance in a specific year is used as the

state-level employee treatment performance. In the same vein, firms operating in the same

industry also tend to exhibit similar employee treatment practices and we therefore use the

mean of the employee treatment score in year t of all firms belonging to firm i ’s 2-digit SIC

2To ensure robustness, we further change the minimum number of firms in each state to 5 and 15. Inuntabulated results, we find the results qualitatively unchanged.

21

code an instrument for employee treatment of firm i in year t (El Ghoul et al., 2011).

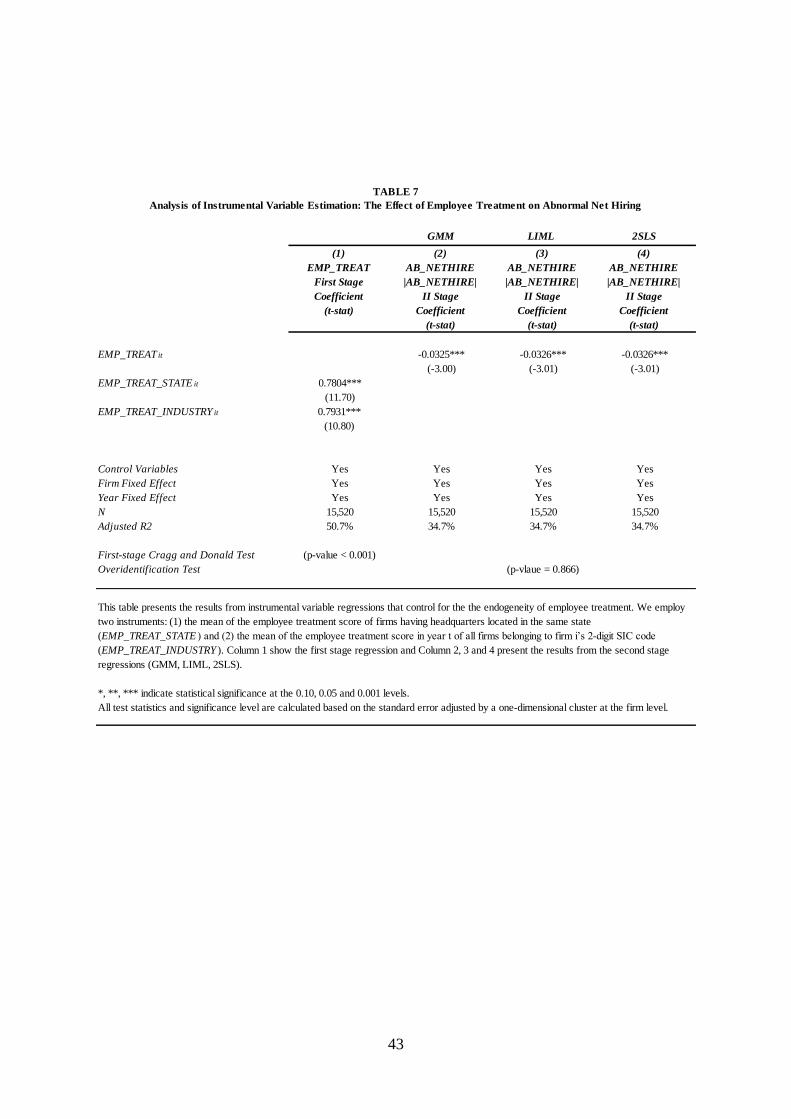

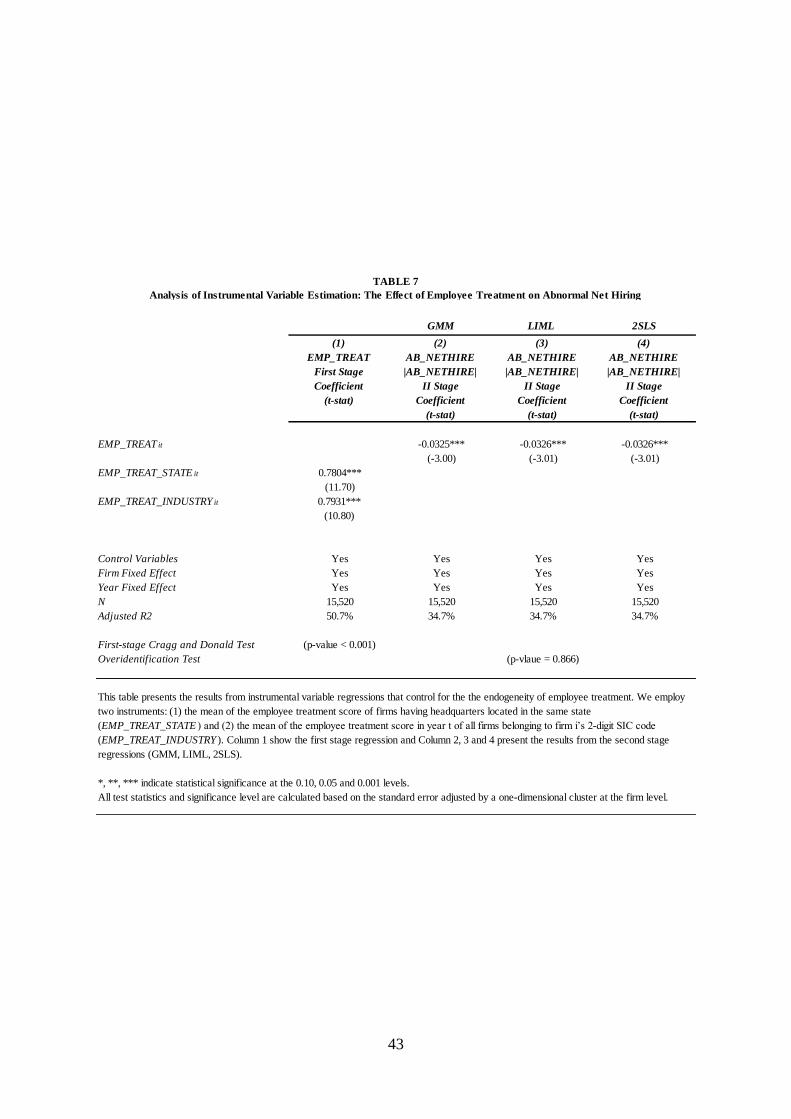

Table 7 reports results for our baseline model using instrumental variable estimation.

The first column reports estimates for the first-stage equation, indicating a strong correlation

between firm and state/industry employee treatment level. Columns 2-4 present the results

regarding the relation between employee treatment and labor investment efficiency from

the second stage regression estimated through GMM, LIML and 2SLS. The results confirm

that the negative and significant association between employee treatment and abnormal net

hiring, which is consistent with the results generated from our baseline OLS regressions. In

addition, the two instrument variables pass both the Cragg and Donald (1993) instrument

relevance test and the Sargan (1958) overidentification test.

[Insert Table 7 near here]

5.2. Alternative employee treatment: Fortune’s Best 100 List

So far, the results of our research suggest that employee-friendly treatment policies facil-

itate firms to have lower level of labor investment inefficiency as measured by abnormal net

hiring. We further show that the firms treating their employees mitigate the risk of labor

overinvestment and labor underinvestment. In order to ensure the robustness of our results,

we reestimate our main results by using the alternative employee treatment. Following prior

studies in employee treatment (Bae et al., 2011; Edmans, 2011; Faleye and Trahan, 2011;

Ghaly et al., 2015; Guo et al., 2015; Chen et al., 2016), we replace the employee treatment

scores obtained from KLD database with a dummy variable (BEST100 ) that is equal to

one if the firm is listed in Fortune magazine’s list of the ‘100 Best Companies to Work

For’ (Fortune List hereafter) between 1998 and 2012. Fortune List is created by combin-

ing employee surveys and company response and it consists of companies known for their

employee-friendly treatment policies. Since the maximum year of Fortune List we can get is

2012, our sample drops to 15,776 after we merge Fortune List with our full sample.

We report the results of regressions using the alternative employee treatment in Table

8. Our results suggest that the robustness test using BEST100 as the alternative employee

treatment yields similar results and the results are still consistent with those reported re-

sults in Table 4. Specifically, we find the estimated coefficient on BEST100 is negatively

associated with abnormal net hiring and the result suggests that better employee treatment

facilitate more efficient investment in labor. Moreover, we also divided the variable into over-

investment (OVER LABOR) and underinvestment (UNDER LABOR) based on the sign of

abnormal net hiring. Consistent with the main results in Table 4, our robustness tests using

22

BEST100 as the alternative employee treatment also indicate that employee-friendly treat-

ment policies mitigate the risk of overinvestment and underinvestment in labor. Overall,

Table 8 suggests that our findings are robust to alternative proxies of employee treatment3.

[Insert Table 8 near here]

5.3. Alternative measures of labor investment efficiency

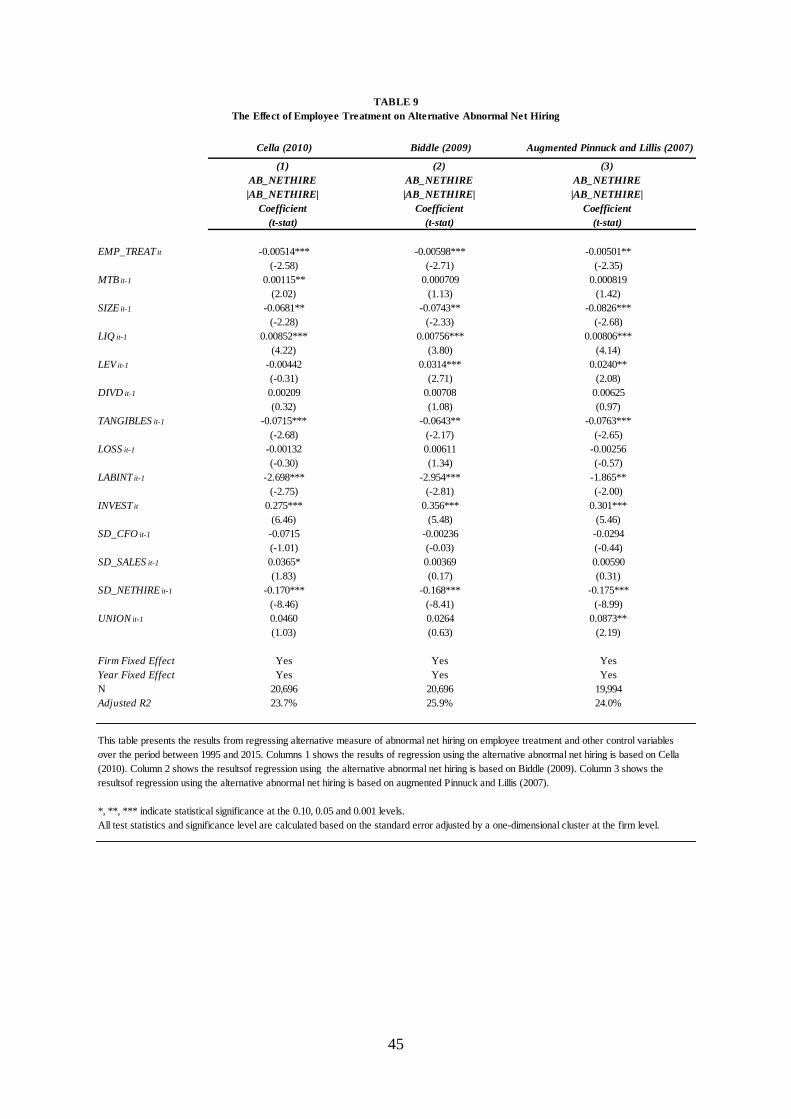

In Table 9, we adopt three alternative measures of labor investment efficiency. First,

following Cella (2009), we use a firm’s industry median level of net hiring as a proxy for its

optimal level and measure abnormal investment as the difference between a firm’s actual level

of net hiring and its industry median. Therefore, the more a firm’s net hiring deviates from

its industry peers, the larger the measure of abnormal net hiring. Second, we follow Biddle

et al. (2009) and estimate a firm-specific model of labor investment as a function of sales

growth and use the absolute value of the residuals as the proxy for deviations from expected

investment in labor. Third, we use the augmented version of Pinnuck and Lillis (2007) model.

Specifically, we augment Equation 1 with a number of additional variables, including indus-

try unionization rate, capital expenditure, research and development expenses, acquisition

expenses, lagged value of observed labor investment and logarithm of GDP per capita. We

report the results of the models using alternative measure of abnormal net hiring in Table

9. Overall, we find the results generated from the regressions using alternative abnormal net

hiring show similar results to the results of our baseline regression model. Consistent with

the results of our baseline model using the primary measure of abnormal net hiring, we find

employee treatment is negatively associated with abnormal net hiring in general across all

three alternative abnormal net hiring. For other control variables, we generally find the sign

for each control variables are consistent with the results of our baseline regression.

[Insert Table 9 near here]

3As an alternative measure of employee treatment, we also calculate a firm’s overall employee treatmentbased on Guo et al. (2015) as the variable of interest to run our regressions. In untabulated results, thealternative test yields similar results as robustness tests and the results are still consistent with those reportedresults.

23

5.4. Additional control variables

We also include various additional control variables that are not included in our baseline

model because the data requirements lead to additional sample loss. We include governance

proxies, corporate governance and institutional ownership respectively, in our baseline regres-

sion because corporate governance and the influence of institutional investor may potentially

affect investment policies and employee treatment. Moreover, Jung et al. (2014) find that

high-quality financial reporting facilitate more efficient investments in labor and show that

financial reporting quality is also one of the factors that have influential impact on labor in-

vestment efficiency. Therefore, we also use financial reporting quality as an additional control

variable in our regression to test the robustness of our results. We use discretionary accrual

as the proxy for financial reporting quality and estimate discretionary accrual by using the

performance-adjusted modified Jones model suggested in Kothari, Leone, and Wasley (2005)

given the less restrictive data requirements of cross-sectional version of modified Jones model.

The model for estimating discretionary accrual includes lagged return on assets (ROAit−1)

as a regressor to control for the effect of performance on measured discretionary accruals.

In terms of the estimation of the discretionary accruals, we estimate the model for every

industry classified by two-digit SIC code for each year. Following previous studies, we use

the absolute value of discretionary accrual (AB DISC ) as the proxy for financial report-

ing quality. The large value of the absolute value of discretionary accrual, the lower level

of financial reporting quality. We further multiply AB DISC by -1 so that large value of

AB DISC indicates higher-quality of financial reporting4. In untabulated results, the re-

gression including additional control variables yield similar results and the results are still

consistent with those reported results. Overall, the results generated from our robustness

tests show that our results are robust to additional control variables.

6. Additional Analysis

6.1. The impact of employee treatment and abnormal net hiring on labor

productivity

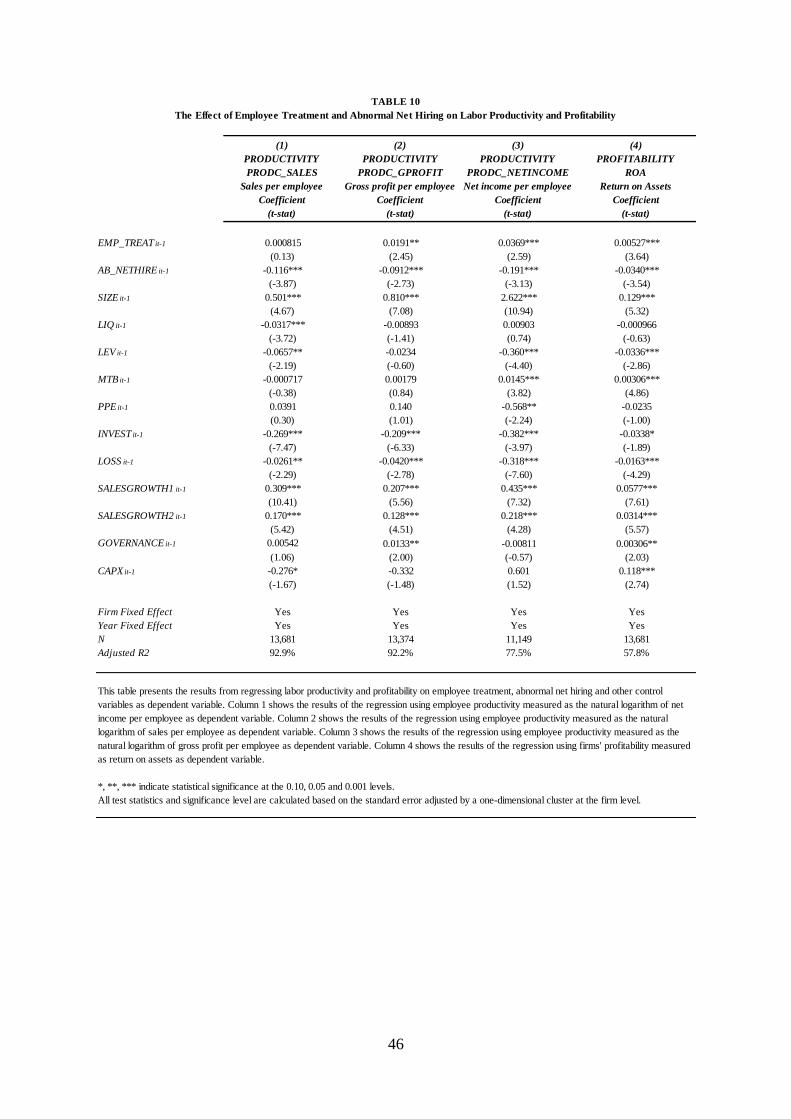

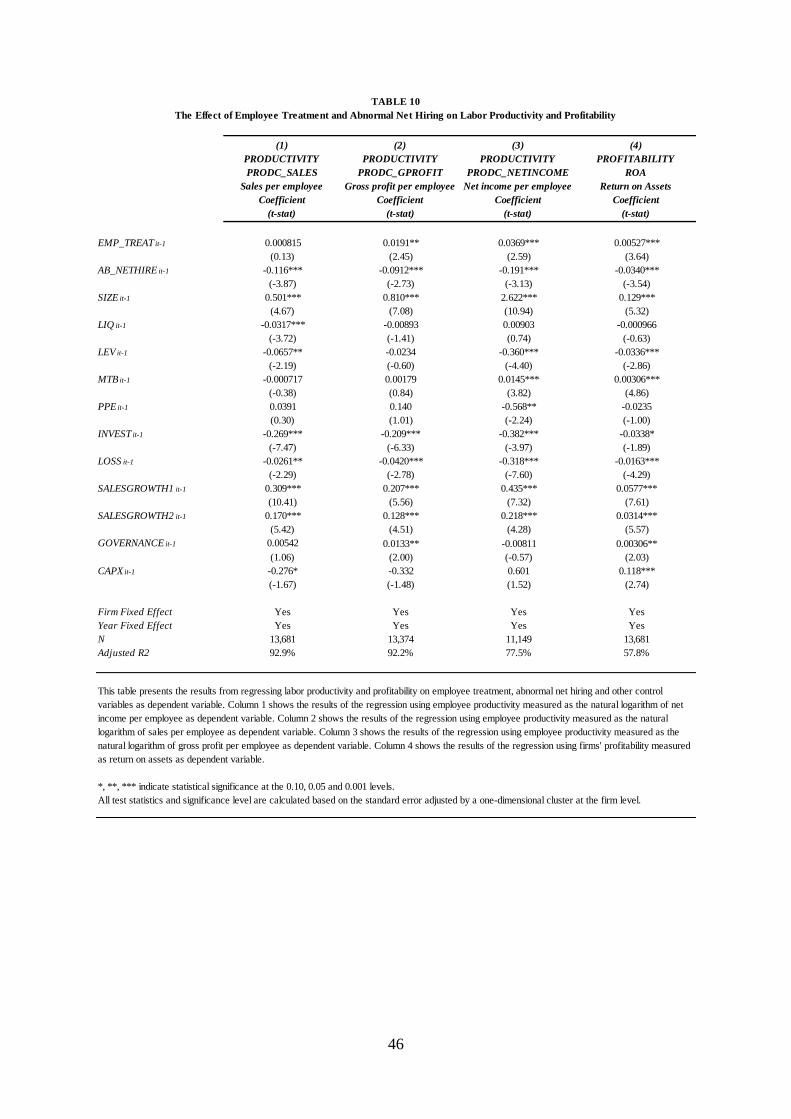

To demonstrate the economic implication of employee treatment (EMP TREAT ) and

abnormal net hiring (AB NETHIRE ), we further investigate the impact of employee treat-

4As an alternative measure of financial reporting quality, we also calculate a firm’s financial reportingquality based on Dechow and Dichev (2002) as an additional control variable to run our regressions. Theresults of financial reporting quality based on Dechow and Dichev (2002) yields similar results and are stillconsistent with those results generated from the performance-adjusted modified Jones model suggested inKothari et al. (2005).

24

ment and abnormal net hiring on labor productivity (PRODC SALES, PRODC GPROFIT

and PRODC NETINCOME ) and profitability (ROA). Numerous previous studies investi-

gate the value creation of employee-friendly treatment (Zingales, 2000; Filbeck and Preece,

2003; Edmans, 2011). We argue that one of the potential channels via which employee

treatment and labor investment efficiency can affect value creation is via labor productivity

and we examine the impact of employee treatment and abnormal net hiring on labor pro-

ductivity. Given previous literature suggests that employee-friendly policies can positively

influence value creation, we posit that firms treating their employees well enjoy higher labor

productivity and profitability. On the other hand, because abnormal net hiring deviates from

firms employment level justified by their underlying economics, we predict that abnormal

net hiring deteriorates labor productivity and profitability.

The results in Table 10 confirm our prediction. Specifically, we find the estimated coef-

ficients on employee treatment are positive and significant when gross profit per employee

(PRODC GPROFIT ), income per employee (PRODC NETINCOME ) and ROA are the

dependent variables, indicating that employee-friendly treatment positively enhances labor

productivity and firms’ profitability. On the other hand, we find the lagged abnormal net

hiring is negatively associated with labor productivity and profitability, which suggests that

abnormal net hiring deteriorates labor productivity and firms’ profitability. Overall, our

tests for the impact of employee treatment and abnormal net hiring on labor productivity

suggest that employee-friendly treatment policies enhance labor productivity whereas sub-

optimal net hiring is costly in terms of labor productivity.

[Insert Table 10 near here]

6.2. The Effect of CSR Dimensions and Abnormal Net Hiring on Labor

Productivity and Profitability

We further investigate the impact of each CSR dimension on labor productivity and prof-

itability to observe whether there are specific CSR dimensions considerably contributes to

labor productivity and profitability. In Table 11, we report the results of the tests. In terms

of profitability, we find that the estimated coefficient of employee relation is positive and

statistically significant at 1% level, showing that employee relation dimension significantly

contributes to firms profitability measured as ROA. In contrast, we generally find that other

dimensions of CSR are negatively associated with firms’ profitability. Particularly, we find

the estimated coefficient on human rights dimension is negative and statistically significant

25

at 1%, showing that investing in human right dimension of CSR is more likely to lower firms’

profitability. In terms of labor productivity, we find that the product dimension of CSR sig-

nificantly contributes to employee productivity measured as gross profit per employee and net

income per employee whereas the environment dimension of CSR lowers employee produc-

tivity measured as sales per employee. In addition, in all of our regressions, we consistently

find that the lagged abnormal net hiring is negatively associated with all measures of labor

productivity and profitability, confirming that the deviation from firms employment level

justified by underlying economics lowers firms’ labor productivity and profitability. Overall,

our results suggest that employee and product dimensions of CSR are generally beneficial

to firms’ labor productivity and profitability whereas human rights dimensions of CSR and

abnormal net hiring tend to deteriorates labor productivity and profitability.

[Insert Table 11 near here]

6.3. The Effect of Employee Treatment Strengths, Concerns and Abnormal

Net Hiring on Employee Productivity and Profitability

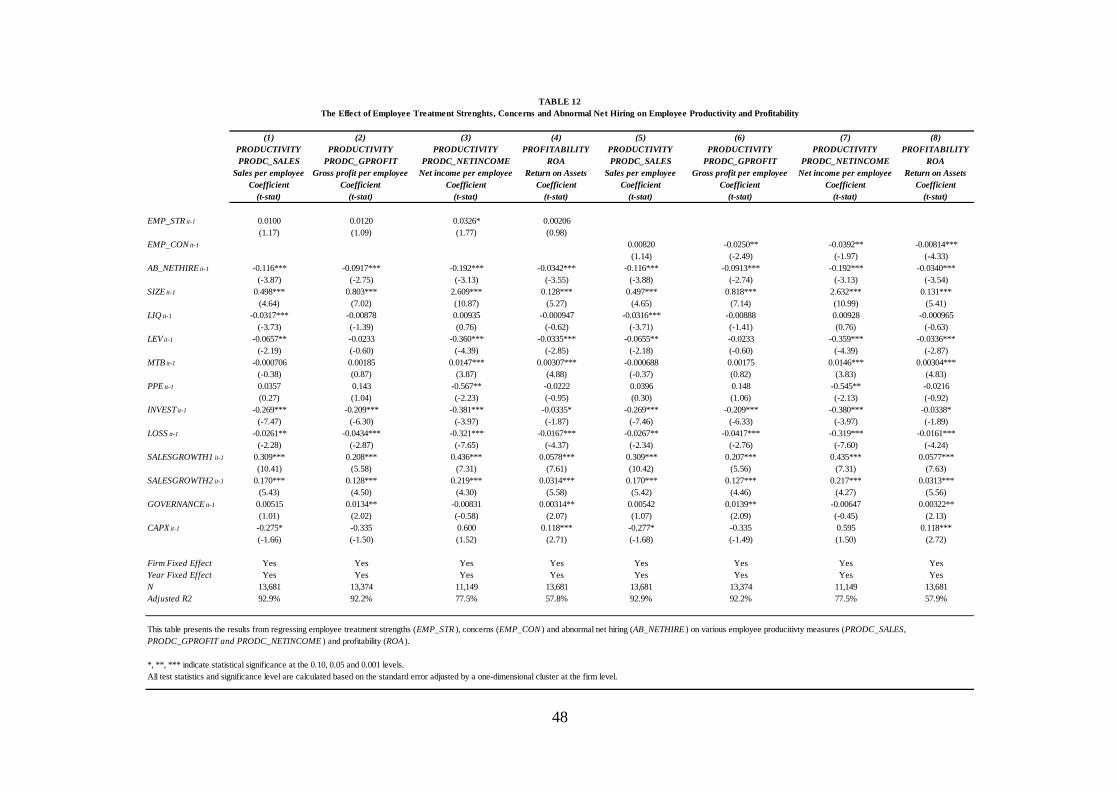

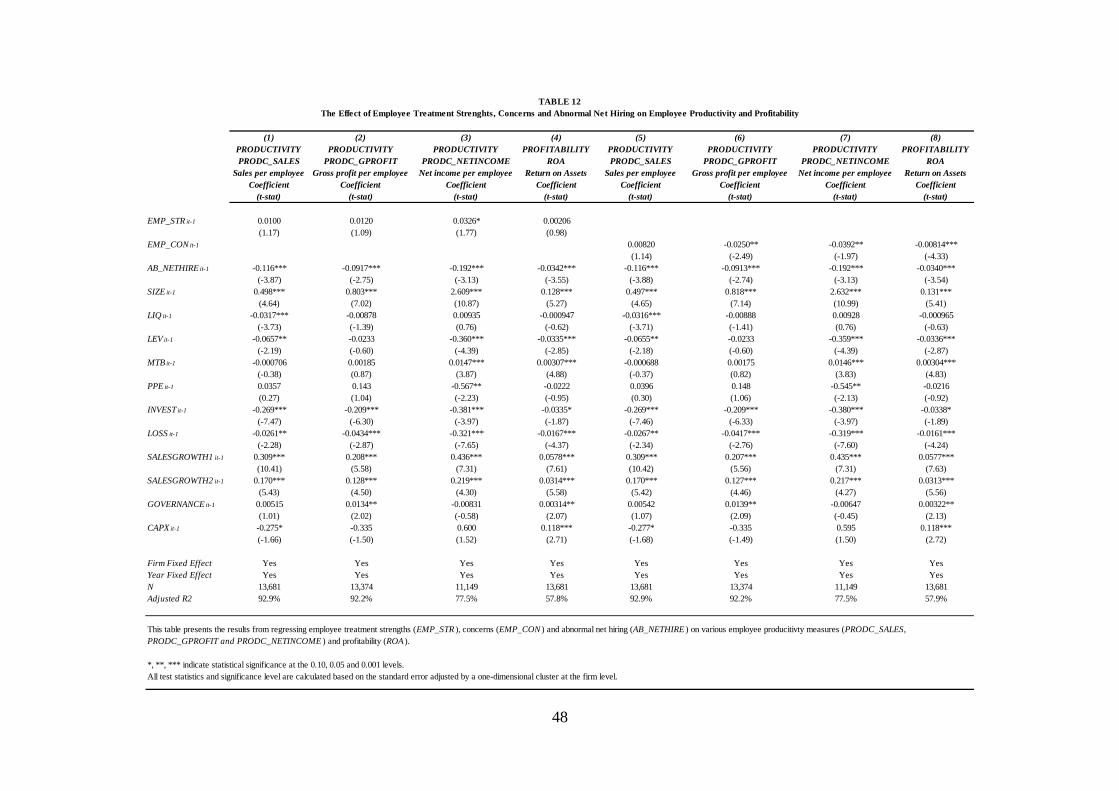

Similar to Table 6, we divide the employee treatment measure into employee treatment

strengths (EMP STR) and employee treatment concerns (EMP CON ) to observe how em-

ployee treatment strengths and concerns affect firms’ labor productivity and profitability. In

light of previous argument, we predict that the strengths of employee treatment are more

likely to enhance firms’ labor productivity and profitability and therefore are positively as-

sociated with employee productivity proxies and ROA whereas the concerns of employee

treatment pose a misalignment between the interests of employees and a firm’s objective and

therefore tend to be negatively associated with employee productivity proxies and ROA.

In Table 12, our results show a marginal significant relationship between employee strengths

and labor productivity measured as net income per employee and suggest that firms with

employee-friendly policies may have higher labor productivity. For other types of labor pro-

ductivity and profitability measures, we do not find significant results. In contrast, when

we test the impact of employee concerns on labor productivity and profitability, we find

that the estimated coefficients of labor productivity as measured by gross profit per em-

ployee (PRODC GPROFIT ) and net income per employee (PRODC NETINCOME ) and

profitability (ROA) are significant negative, suggesting that firms with employee concerns

are more likely to have lower labor productivity and profitability. Apart from above, our

results still consistently show that abnormal net hiring significantly lower firms’ labor pro-

ductivity and profitability.

26

[Insert Table 12 near here]

7. Conclusion

The capital market in reality is not frictionless and market imperfections stemming from

information asymmetry between firms and suppliers of capital can cause firms to deviate

from the optimal level, thus leading to either overinvestment or underinvestment. Previous

literature studying investment efficiency emphasizes more on the role of financial reporting

and its relation with capital investment efficiency. We follow this line of research by ex-

tending capital investment efficiency to the investment efficiency in labor and investigate the

impact of employee-treatment on labor investment efficiency. We argue employee-friendly

treatment policies facilitate firms to lower information asymmetry and employees moral haz-

ard (adverse behavior), thus helping firms to maintain net hiring that is closer to a level

justified by firms underlying economics. Instead of focusing on investment efficiency in capi-

tal expenditure, we distinguish our study from prior research and extend the line of research

by investigating investment efficiency in labor and argue that employee treatment is also a

significant determinants of labor investment efficiency. In addition, we also investigate the

impact of employee treatment and labor investment inefficiency in form of abnormal net hir-

ing on labor productivity and profitability and suggest the important economic implication

of employee treatment and abnormal net hiring on firms’ value creation.

We find that firms with employee-friendly treatment policies have lower level of abnormal

net hiring and are less likely to over or under-invest in labor, therefore investing in labor

more efficiently. When analyse employee treatment strengths and concerns, we find rela-

tively weak evidence that employee treatment strengths effectively improve labor investment