Embed Size (px)

Citation preview

EMPIRED LIMITED (ASX:EPD)

BBY TMT Conference

Russell Baskerville, Managing Director

For

per

sona

l use

onl

y

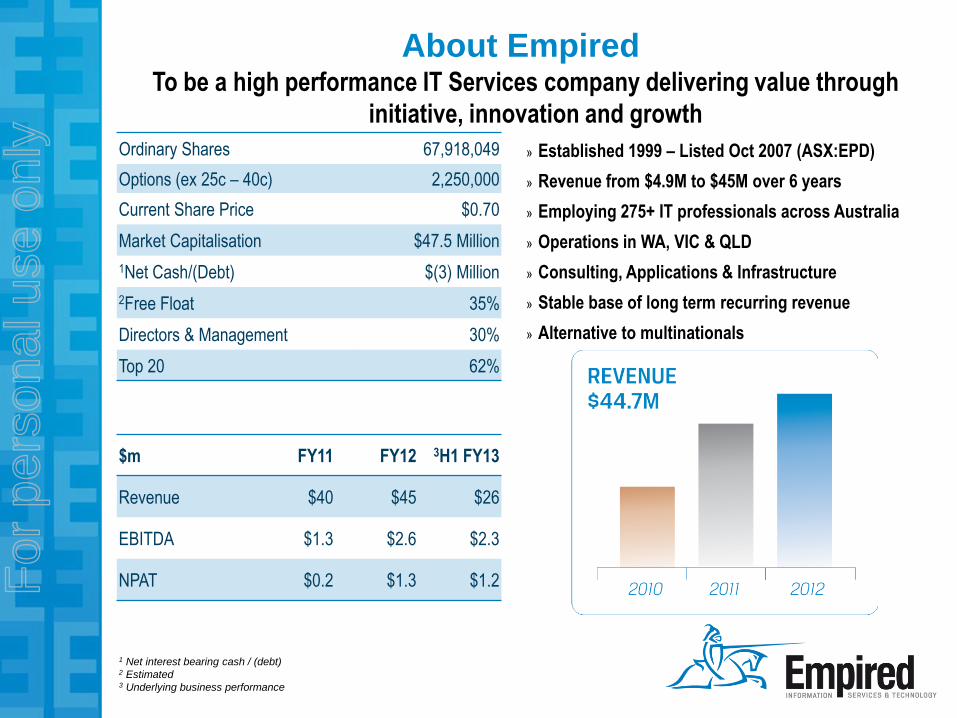

About Empired To be a high performance IT Services company delivering value through

initiative, innovation and growth

» Established 1999 – Listed Oct 2007 (ASX:EPD)

» Revenue from $4.9M to $45M over 6 years

» Employing 275+ IT professionals across Australia

» Operations in WA, VIC & QLD

» Consulting, Applications & Infrastructure

» Stable base of long term recurring revenue

» Alternative to multinationals

Ordinary Shares 67,918,049

Options (ex 25c – 40c) 2,250,000

Current Share Price $0.70

Market Capitalisation $47.5 Million

1Net Cash/(Debt) $(3) Million

2Free Float 35%

Directors & Management 30%

Top 20 62%

$m FY11 FY12 3H1 FY13

Revenue $40 $45 $26

EBITDA $1.3 $2.6 $2.3

NPAT $0.2 $1.3 $1.2

1 Net interest bearing cash / (debt) 2 Estimated 3 Underlying business performance

For

per

sona

l use

onl

y

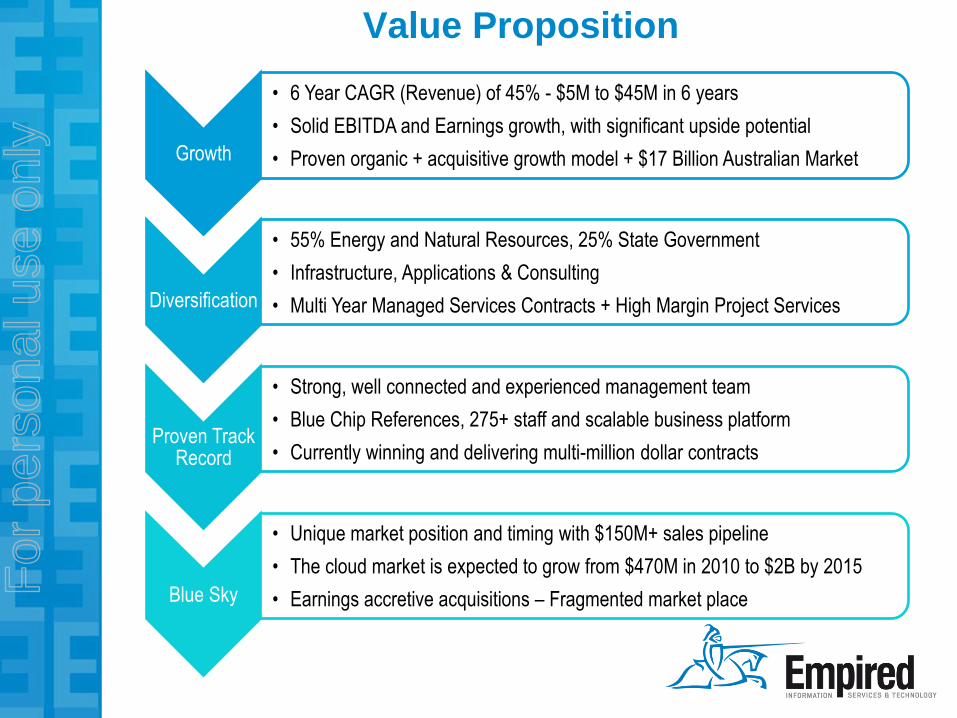

Value Proposition

Growth

• 6 Year CAGR (Revenue) of 45% - $5M to $45M in 6 years

• Solid EBITDA and Earnings growth, with significant upside potential

• Proven organic + acquisitive growth model + $17 Billion Australian Market

Diversification

• 55% Energy and Natural Resources, 25% State Government

• Infrastructure, Applications & Consulting

• Multi Year Managed Services Contracts + High Margin Project Services

Proven Track Record

• Strong, well connected and experienced management team

• Blue Chip References, 275+ staff and scalable business platform

• Currently winning and delivering multi-million dollar contracts

Blue Sky

• Unique market position and timing with $150M+ sales pipeline

• The cloud market is expected to grow from $470M in 2010 to $2B by 2015

• Earnings accretive acquisitions – Fragmented market place

For

per

sona

l use

onl

y

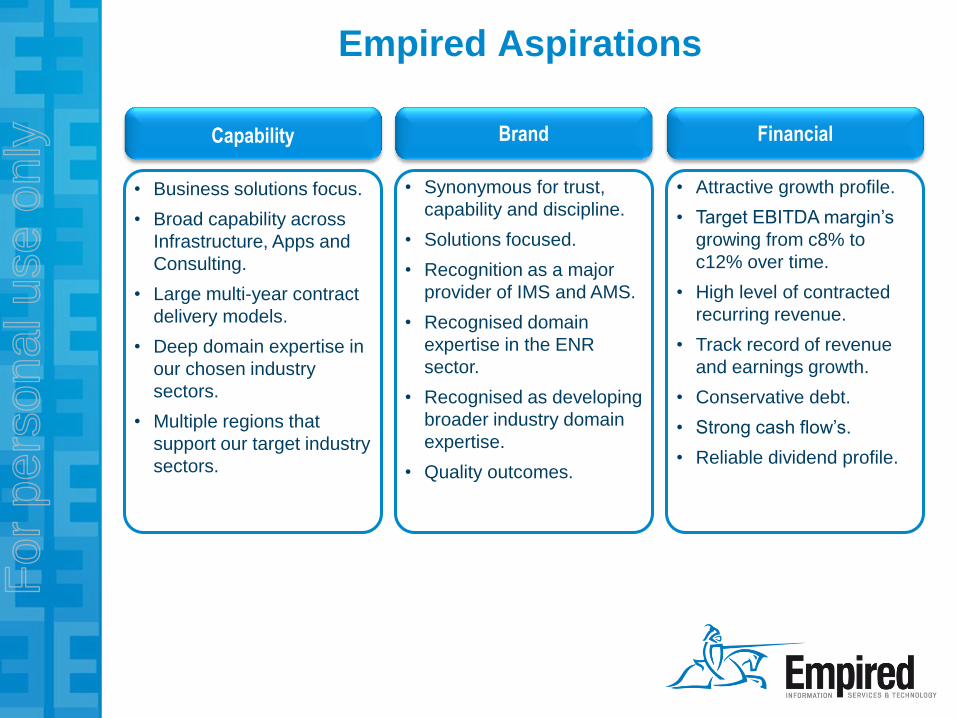

Empired Aspirations

Brand Financial

• Synonymous for trust,

capability and discipline.

• Solutions focused.

• Recognition as a major

provider of IMS and AMS.

• Recognised domain

expertise in the ENR

sector.

• Recognised as developing

broader industry domain

expertise.

• Quality outcomes.

• Attractive growth profile.

• Target EBITDA margin’s

growing from c8% to

c12% over time.

• High level of contracted

recurring revenue.

• Track record of revenue

and earnings growth.

• Conservative debt.

• Strong cash flow’s.

• Reliable dividend profile.

Capability

• Business solutions focus.

• Broad capability across

Infrastructure, Apps and

Consulting.

• Large multi-year contract

delivery models.

• Deep domain expertise in

our chosen industry

sectors.

• Multiple regions that

support our target industry

sectors.

For

per

sona

l use

onl

y

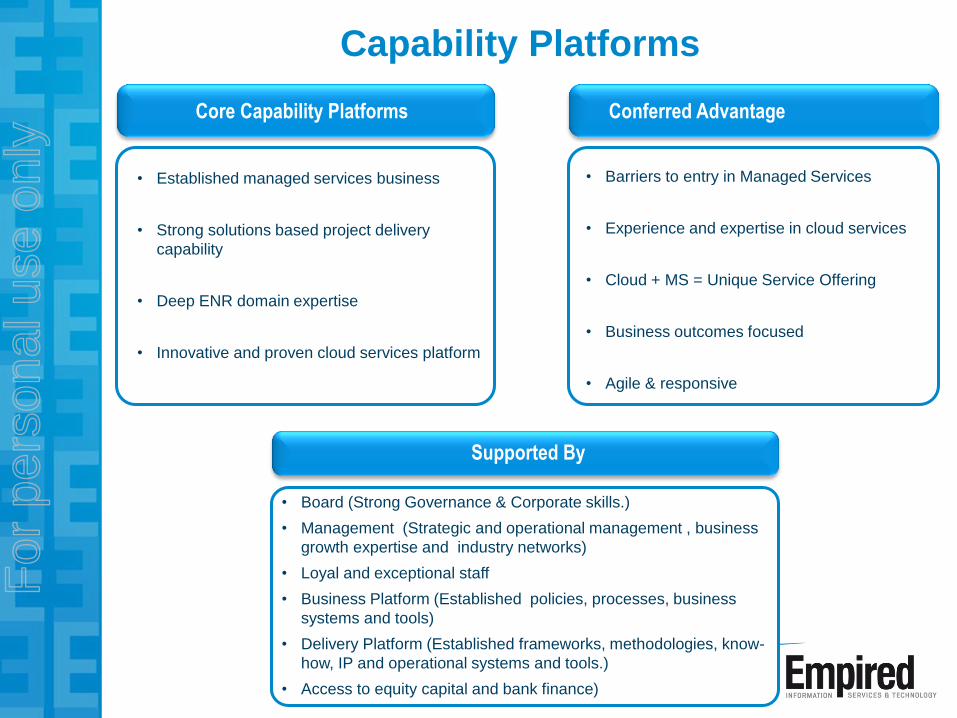

Capability Platforms

Core Capability Platforms

• Established managed services business

• Strong solutions based project delivery

capability

• Deep ENR domain expertise

• Innovative and proven cloud services platform

Conferred Advantage

Supported By

• Barriers to entry in Managed Services

• Experience and expertise in cloud services

• Cloud + MS = Unique Service Offering

• Business outcomes focused

• Agile & responsive

• Board (Strong Governance & Corporate skills.)

• Management (Strategic and operational management , business

growth expertise and industry networks)

• Loyal and exceptional staff

• Business Platform (Established policies, processes, business

systems and tools)

• Delivery Platform (Established frameworks, methodologies, know-

how, IP and operational systems and tools.)

• Access to equity capital and bank finance)

For

per

sona

l use

onl

y

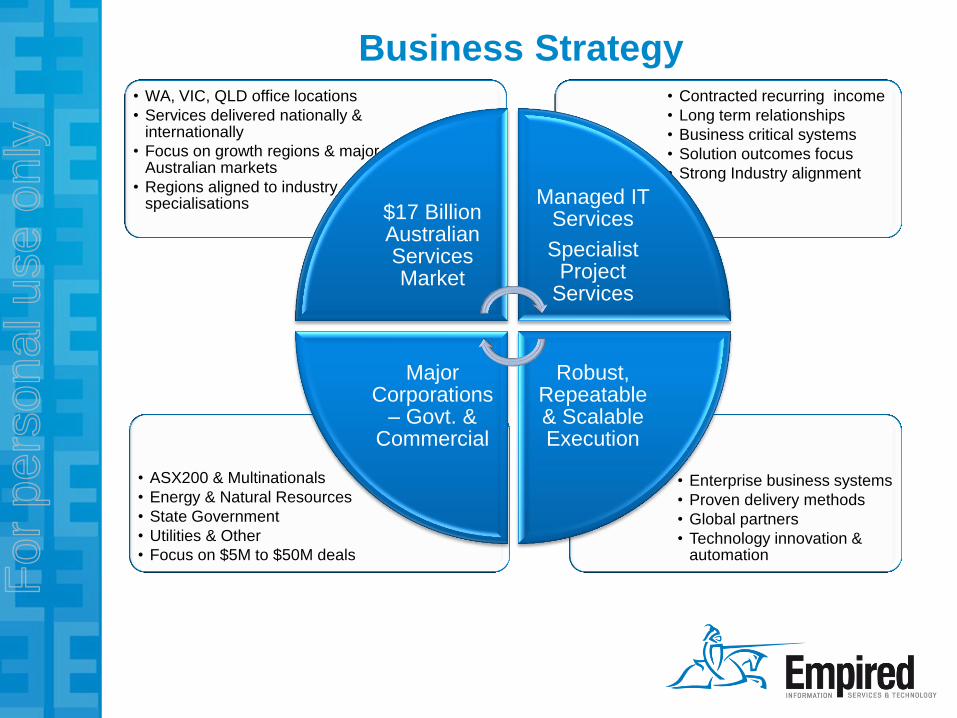

Business Strategy

• Enterprise business systems

• Proven delivery methods

• Global partners

• Technology innovation & automation

• ASX200 & Multinationals

• Energy & Natural Resources

• State Government

• Utilities & Other

• Focus on $5M to $50M deals

• Contracted recurring income

• Long term relationships

• Business critical systems

• Solution outcomes focus

• Strong Industry alignment

• WA, VIC, QLD office locations

• Services delivered nationally & internationally

• Focus on growth regions & major Australian markets

• Regions aligned to industry specialisations

$17 Billion Australian Services Market

Managed IT Services

Specialist Project

Services

Robust, Repeatable & Scalable Execution

Major Corporations

– Govt. & Commercial

For

per

sona

l use

onl

y

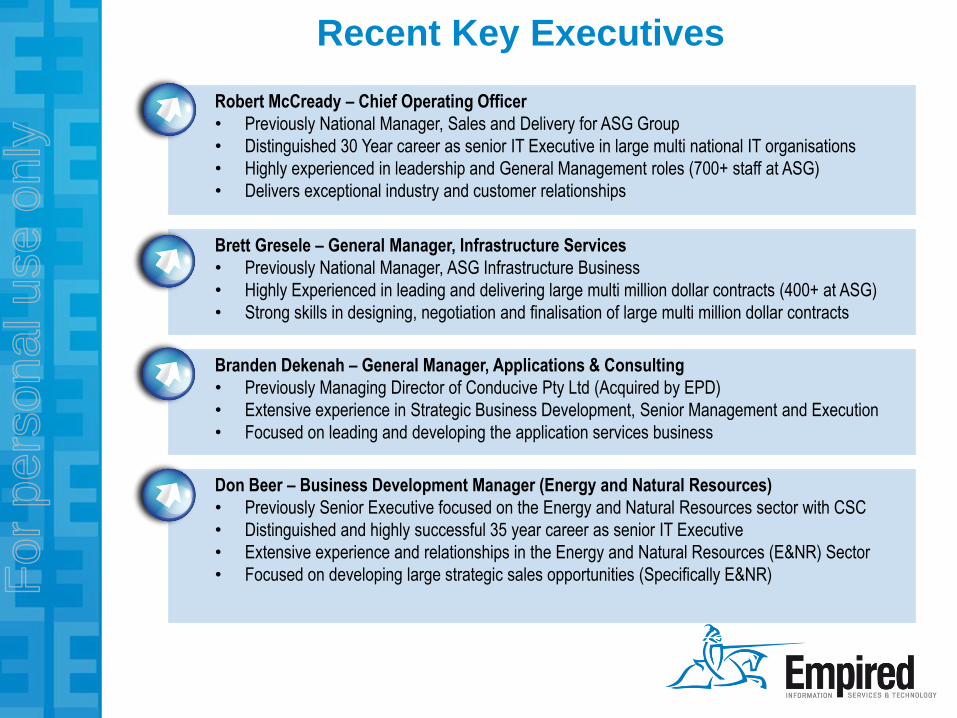

Recent Key Executives

Robert McCready – Chief Operating Officer

• Previously National Manager, Sales and Delivery for ASG Group

• Distinguished 30 Year career as senior IT Executive in large multi national IT organisations

• Highly experienced in leadership and General Management roles (700+ staff at ASG)

• Delivers exceptional industry and customer relationships

Brett Gresele – General Manager, Infrastructure Services

• Previously National Manager, ASG Infrastructure Business

• Highly Experienced in leading and delivering large multi million dollar contracts (400+ at ASG)

• Strong skills in designing, negotiation and finalisation of large multi million dollar contracts

Branden Dekenah – General Manager, Applications & Consulting

• Previously Managing Director of Conducive Pty Ltd (Acquired by EPD)

• Extensive experience in Strategic Business Development, Senior Management and Execution

• Focused on leading and developing the application services business

Don Beer – Business Development Manager (Energy and Natural Resources)

• Previously Senior Executive focused on the Energy and Natural Resources sector with CSC

• Distinguished and highly successful 35 year career as senior IT Executive

• Extensive experience and relationships in the Energy and Natural Resources (E&NR) Sector

• Focused on developing large strategic sales opportunities (Specifically E&NR)

For

per

sona

l use

onl

y

Client Snapshot F

or p

erso

nal u

se o

nly

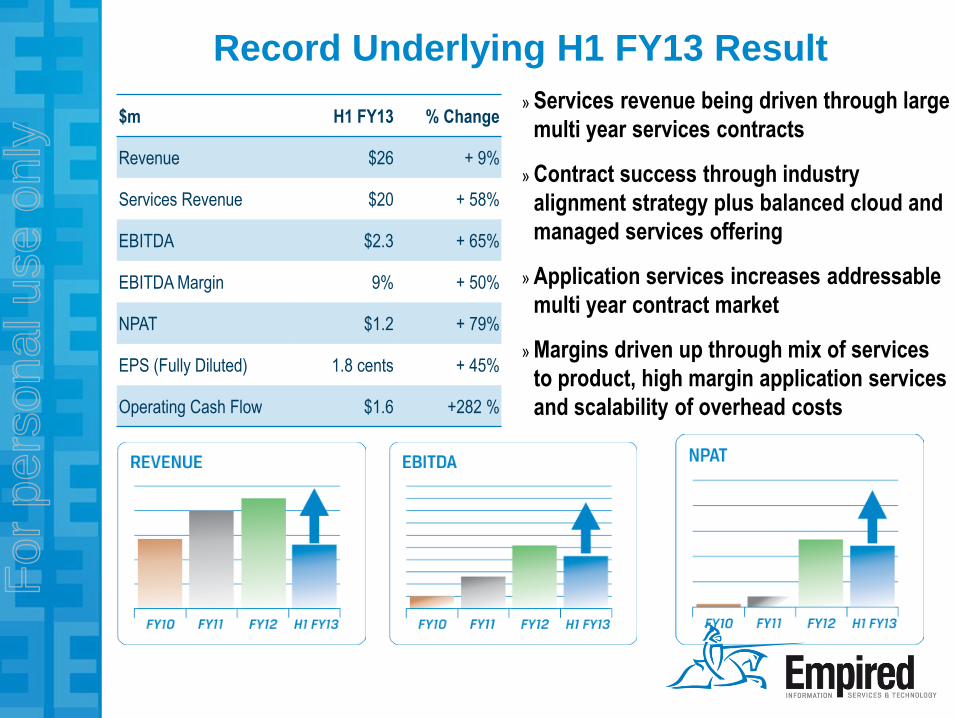

Record Underlying H1 FY13 Result

$m H1 FY13 % Change

Revenue $26 + 9%

Services Revenue $20 + 58%

EBITDA $2.3 + 65%

EBITDA Margin 9% + 50%

NPAT $1.2 + 79%

EPS (Fully Diluted) 1.8 cents + 45%

Operating Cash Flow $1.6 +282 %

» Services revenue being driven through large

multi year services contracts

» Contract success through industry

alignment strategy plus balanced cloud and

managed services offering

» Application services increases addressable

multi year contract market

» Margins driven up through mix of services

to product, high margin application services

and scalability of overhead costs

For

per

sona

l use

onl

y

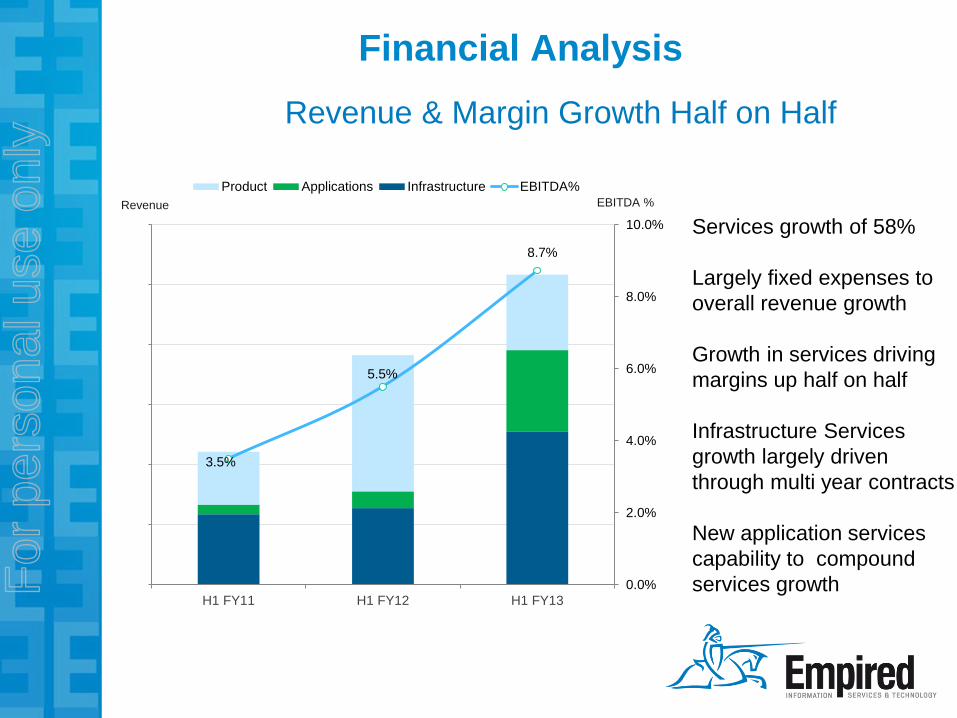

Financial Analysis

Revenue & Margin Growth Half on Half

Services growth of 58%

Largely fixed expenses to

overall revenue growth

Growth in services driving

margins up half on half

Infrastructure Services

growth largely driven

through multi year contracts

New application services

capability to compound

services growth

3.5%

5.5%

8.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

-

5,000

10,000

15,000

20,000

25,000

30,000

H1 FY11 H1 FY12 H1 FY13

Product Applications Infrastructure EBITDA%

Revenue EBITDA %

For

per

sona

l use

onl

y

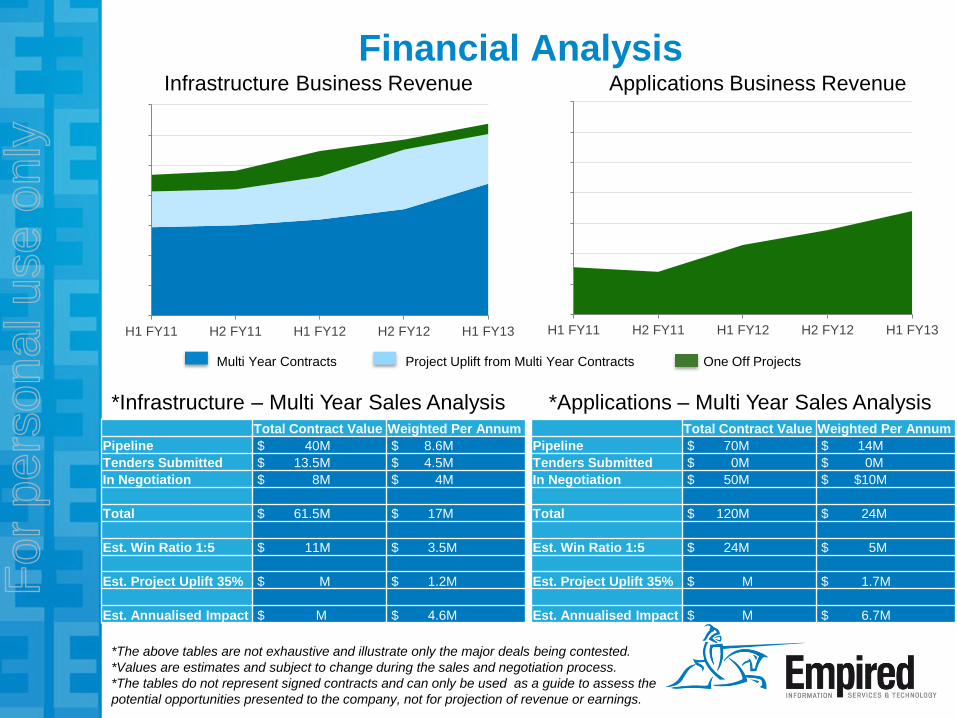

Financial Analysis

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

H1 FY11 H2 FY11 H1 FY12 H2 FY12 H1 FY13

Total Contract Value Weighted Per Annum

Pipeline $ 40M $ 8.6M

Tenders Submitted $ 13.5M $ 4.5M

In Negotiation $ 8M $ 4M

Total $ 61.5M $ 17M

Est. Win Ratio 1:5 $ 11M $ 3.5M

Est. Project Uplift 35% $ M $ 1.2M

Est. Annualised Impact $ M $ 4.6M

Total Contract Value Weighted Per Annum

Pipeline $ 70M $ 14M

Tenders Submitted $ 0M $ 0M

In Negotiation $ 50M $ $10M

Total $ 120M $ 24M

Est. Win Ratio 1:5 $ 24M $ 5M

Est. Project Uplift 35% $ M $ 1.7M

Est. Annualised Impact $ M $ 6.7M

Infrastructure Business Revenue Applications Business Revenue

*Infrastructure – Multi Year Sales Analysis *Applications – Multi Year Sales Analysis

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

H1 FY11 H2 FY11 H1 FY12 H2 FY12 H1 FY13

Multi Year Contracts Project Uplift from Multi Year Contracts One Off Projects

*The above tables are not exhaustive and illustrate only the major deals being contested.

*Values are estimates and subject to change during the sales and negotiation process.

*The tables do not represent signed contracts and can only be used as a guide to assess the

potential opportunities presented to the company, not for projection of revenue or earnings.

For

per

sona

l use

onl

y

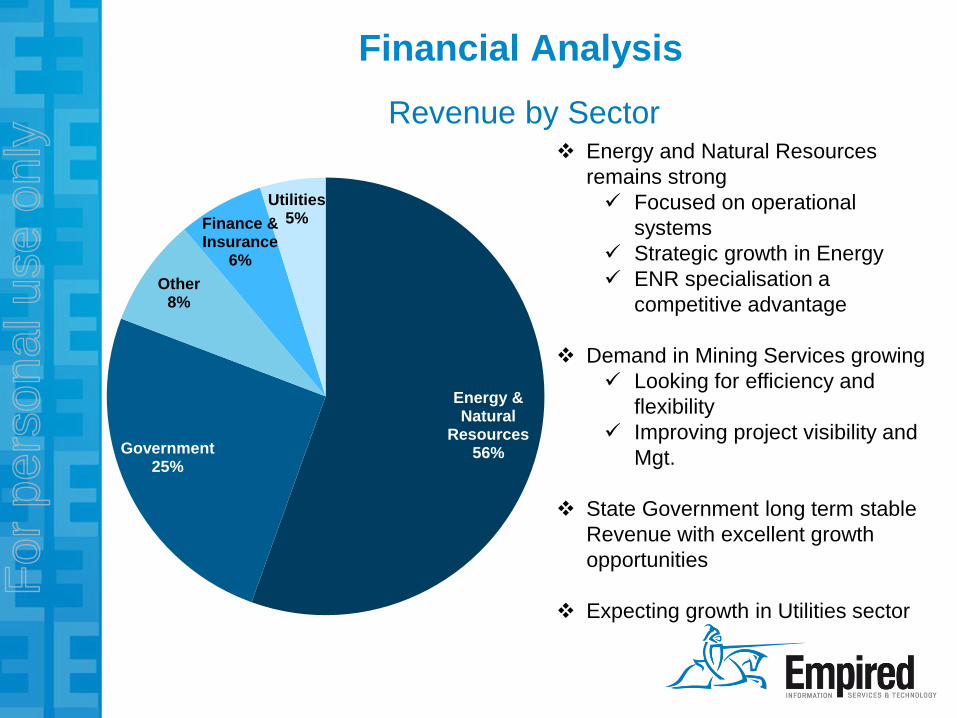

Financial Analysis

Energy & Natural

Resources 56% Government

25%

Other 8%

Finance & Insurance

6%

Utilities 5%

Revenue by Sector Energy and Natural Resources

remains strong

Focused on operational

systems

Strategic growth in Energy

ENR specialisation a

competitive advantage

Demand in Mining Services growing

Looking for efficiency and

flexibility

Improving project visibility and

Mgt.

State Government long term stable

Revenue with excellent growth

opportunities

Expecting growth in Utilities sector

For

per

sona

l use

onl

y

Key Themes

Corporate & Financial

Expecting record full year result with growth in all key financial measures in H2.

Cash flow continuing to improve following solid improvement in H1.

Increased scale & higher margin services driving margin growth at the GP, EBITDA and NPAT line.

Small debt position and fully funded for organic growth and future financial commitments.

Following successful acquisition of Conducive, targeting new acquisitions in near term.

Attracting institutional investor interest and expecting improved broker coverage.

Market & Operational

A number of recent new contracts announced driving growth in H2.

Continuing to attract the best talent.

$150M + new business pipeline for large services deals.

Scale, capability, reference-ability & management team improving new deal size and success.

State Government and ENR sectors remain robust.

Continuing to integrate Cloud and Managed Services to ensure wining solutions.

For

per

sona

l use

onl

y

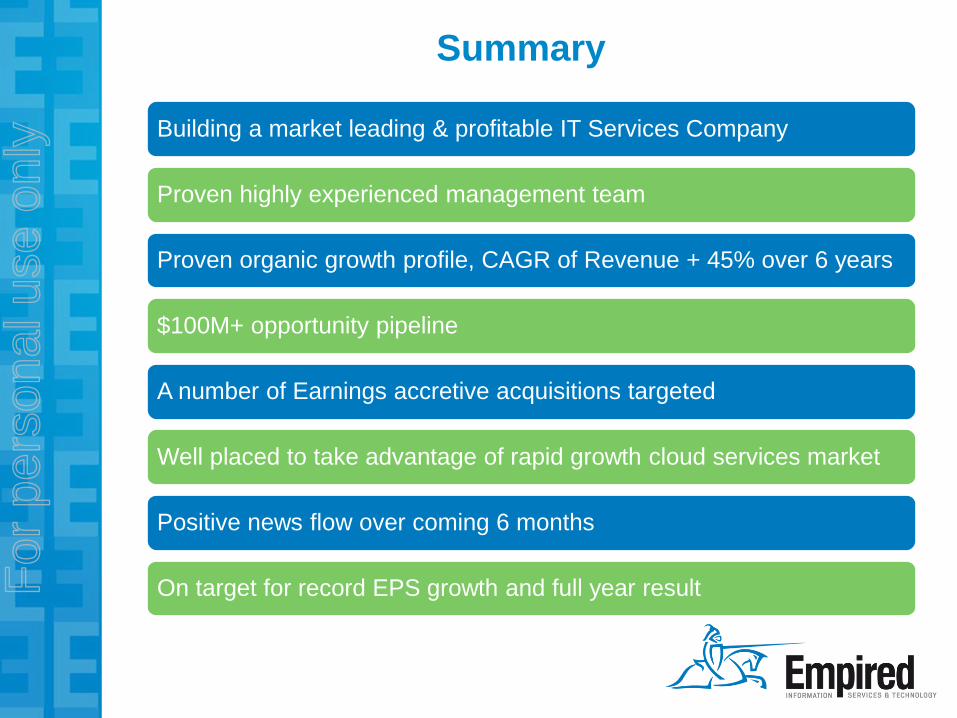

Summary

Building a market leading & profitable IT Services Company

Proven highly experienced management team

Proven organic growth profile, CAGR of Revenue + 45% over 6 years

$100M+ opportunity pipeline

A number of Earnings accretive acquisitions targeted

Well placed to take advantage of rapid growth cloud services market

Positive news flow over coming 6 months

On target for record EPS growth and full year result For

per

sona

l use

onl

y

Appendices

For

per

sona

l use

onl

y

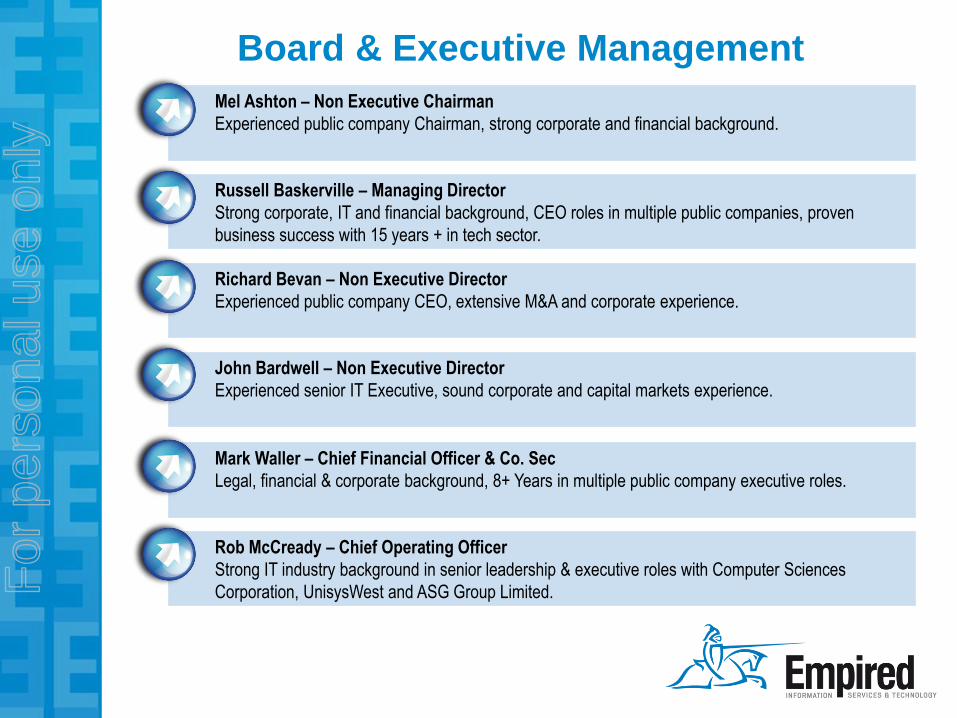

Board & Executive Management

Mel Ashton – Non Executive Chairman

Experienced public company Chairman, strong corporate and financial background.

Russell Baskerville – Managing Director

Strong corporate, IT and financial background, CEO roles in multiple public companies, proven

business success with 15 years + in tech sector.

Richard Bevan – Non Executive Director

Experienced public company CEO, extensive M&A and corporate experience.

John Bardwell – Non Executive Director

Experienced senior IT Executive, sound corporate and capital markets experience.

Mark Waller – Chief Financial Officer & Co. Sec

Legal, financial & corporate background, 8+ Years in multiple public company executive roles.

Rob McCready – Chief Operating Officer

Strong IT industry background in senior leadership & executive roles with Computer Sciences

Corporation, UnisysWest and ASG Group Limited. For

per

sona

l use

onl

y

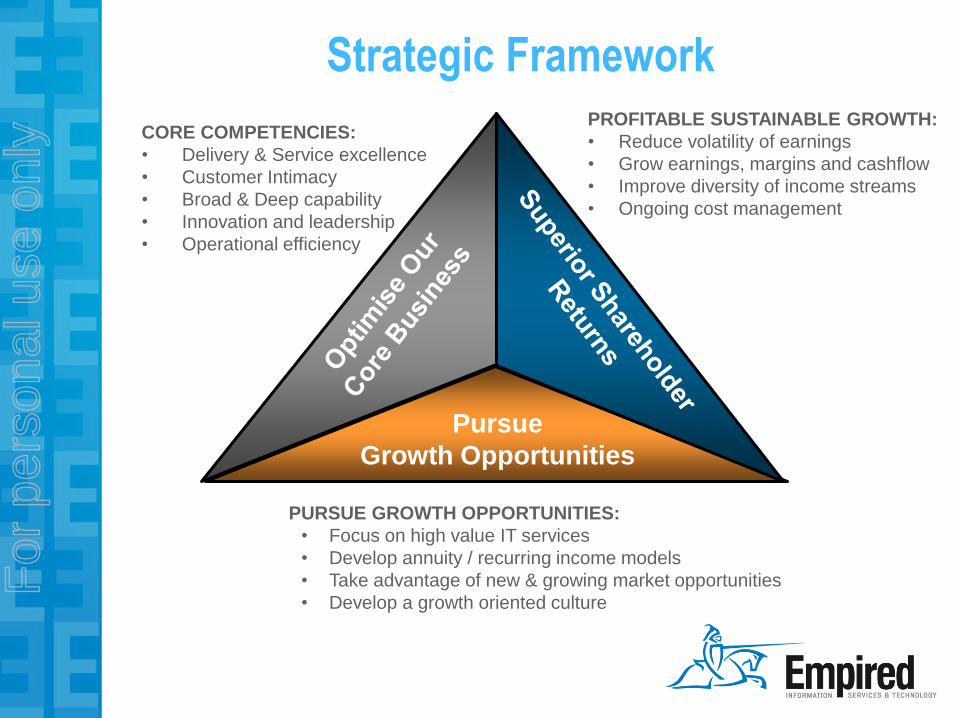

Strategic Framework

Pursue

Growth Opportunities

PURSUE GROWTH OPPORTUNITIES:

• Focus on high value IT services

• Develop annuity / recurring income models

• Take advantage of new & growing market opportunities

• Develop a growth oriented culture

CORE COMPETENCIES:

• Delivery & Service excellence

• Customer Intimacy

• Broad & Deep capability

• Innovation and leadership

• Operational efficiency

PROFITABLE SUSTAINABLE GROWTH:

• Reduce volatility of earnings

• Grow earnings, margins and cashflow

• Improve diversity of income streams

• Ongoing cost management

For

per

sona

l use

onl

y

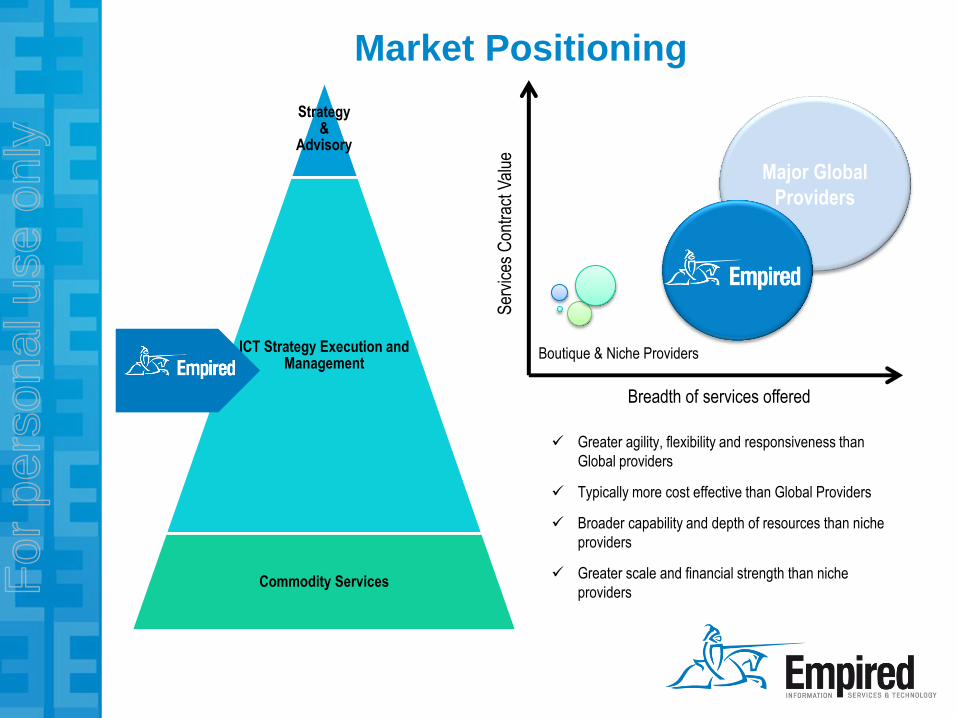

Greater agility, flexibility and responsiveness than

Global providers

Typically more cost effective than Global Providers

Broader capability and depth of resources than niche

providers

Greater scale and financial strength than niche

providers

Market Positioning

Ser

vice

s C

ontr

act V

alue

Breadth of services offered

Major Global

Providers

Boutique & Niche Providers

Strategy &

Advisory

ICT Strategy Execution and Management

Commodity Services For

per

sona

l use

onl

y

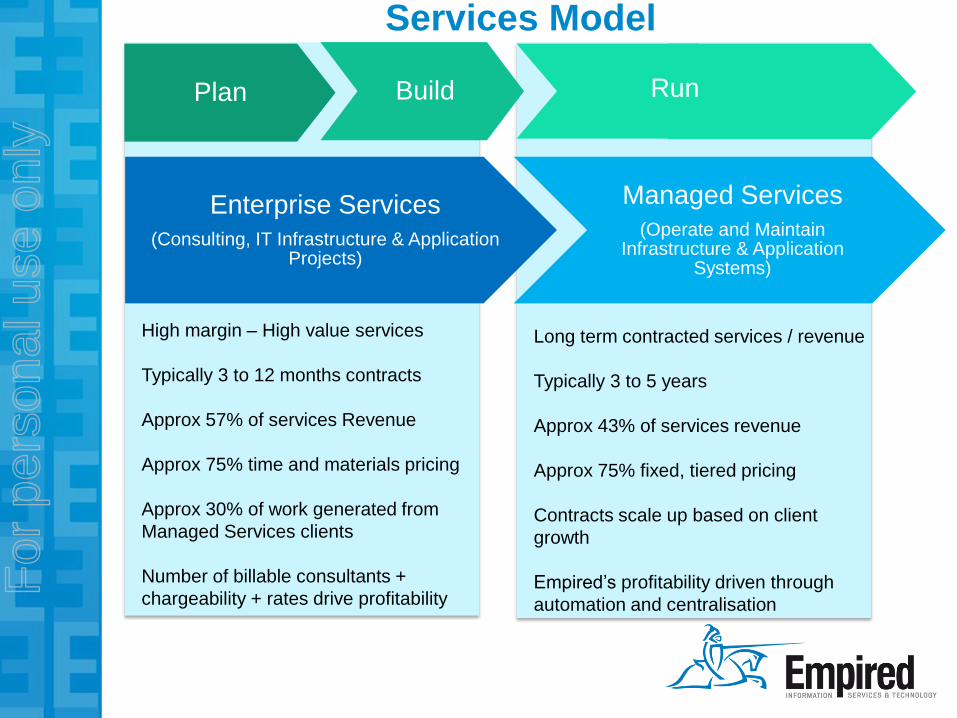

Services Model

Plan Build

Enterprise Services

(Consulting, IT Infrastructure & Application Projects)

Managed Services

(Operate and Maintain Infrastructure & Application

Systems)

Run

High margin – High value services

Typically 3 to 12 months contracts

Approx 57% of services Revenue

Approx 75% time and materials pricing

Approx 30% of work generated from

Managed Services clients

Number of billable consultants +

chargeability + rates drive profitability

Long term contracted services / revenue

Typically 3 to 5 years

Approx 43% of services revenue

Approx 75% fixed, tiered pricing

Contracts scale up based on client

growth

Empired’s profitability driven through

automation and centralisation

For

per

sona

l use

onl

y

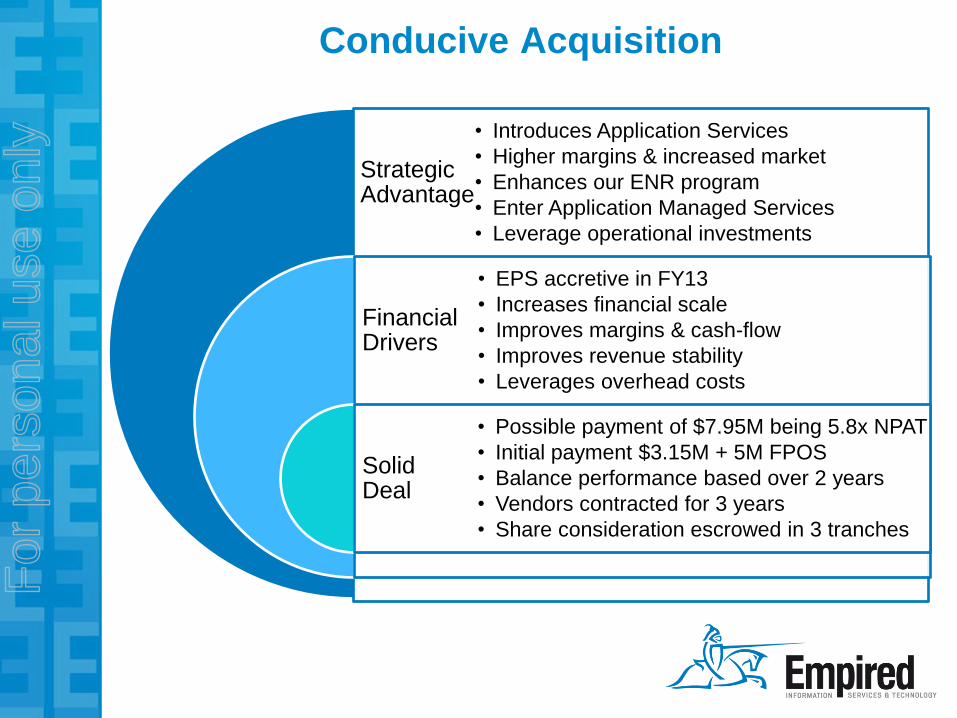

Conducive Acquisition

Strategic Advantage

Financial Drivers

Solid Deal

• Introduces Application Services

• Higher margins & increased market

• Enhances our ENR program

• Enter Application Managed Services

• Leverage operational investments

• EPS accretive in FY13

• Increases financial scale

• Improves margins & cash-flow

• Improves revenue stability

• Leverages overhead costs

• Possible payment of $7.95M being 5.8x NPAT

• Initial payment $3.15M + 5M FPOS

• Balance performance based over 2 years

• Vendors contracted for 3 years

• Share consideration escrowed in 3 tranches

For

per

sona

l use

onl

y

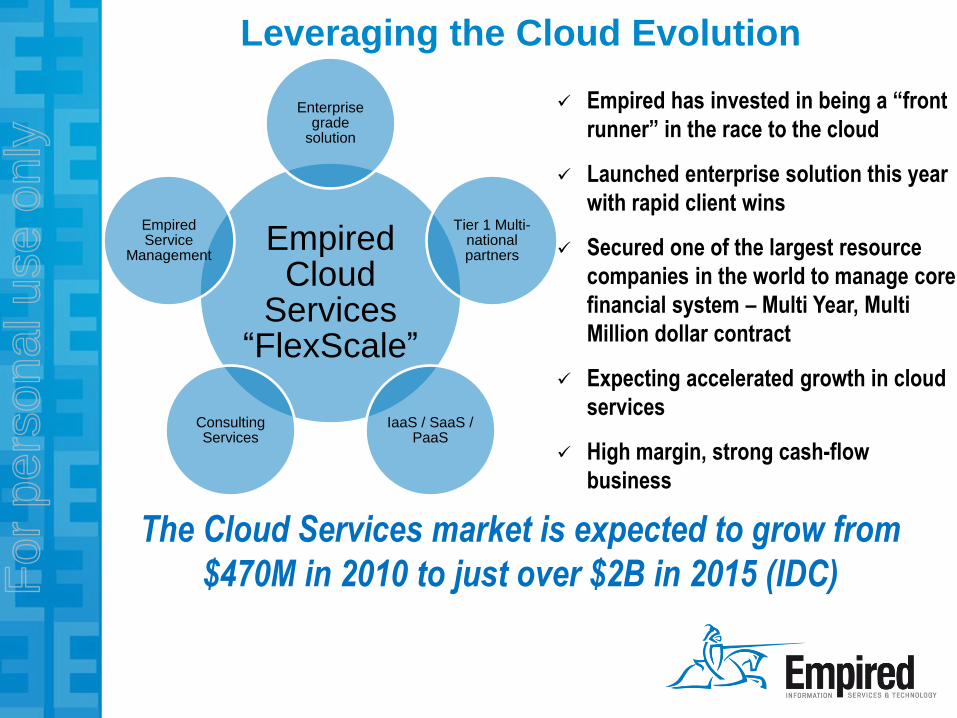

Leveraging the Cloud Evolution

Empired has invested in being a “front

runner” in the race to the cloud

Launched enterprise solution this year

with rapid client wins

Secured one of the largest resource

companies in the world to manage core

financial system – Multi Year, Multi

Million dollar contract

Expecting accelerated growth in cloud

services

High margin, strong cash-flow

business

The Cloud Services market is expected to grow from

$470M in 2010 to just over $2B in 2015 (IDC)

Empired Cloud

Services “FlexScale”

Enterprise grade

solution

Tier 1 Multi-national partners

IaaS / SaaS / PaaS

Consulting Services

Empired Service

Management

For

per

sona

l use

onl

y