Embed Size (px)

Citation preview

Emerging Trends in Corporate Contributions

and Employee EngagementOctober 13, 2014

Michael StroikManager, Research and Analytics

CECP

2

About CECP

2

“I helped to start CECP with the belief that corporate

America could be a force for good in society.”

- Paul Newman

Today’s Presentation

2013 Research Headlines

• Most Generous Companies Gave 1.95% of Profits or More

• Giving and Business Performance Rise Together

• Grantmaking Evolves in Post-Recession Era

• Employees Take Center Stage in CSR

Measuring the Value

• Program Evaluation in Corporate Contributions

• Case Studies

3

Parenting and CSR – Not so Different!

1. ‘Problem Definition’ is

a lot easier said than

done.

4

2. Understanding impact

is difficult to assess in

the short-term.

5

2013 Industry Giving Comparisons – Median Giving

as a % of Pre-Tax Profit

1.23%

1.06%

0.98%

0.76%

1.58%

0.96%

0.76%

1.12%

1.25%

1.10%

Utilities (n=18)

Technology (n=25)

Materials (n=16)

Industrials (n=25)

Health Care (n=24)

Financials (n=48)

Energy (n=11)

Consumer Staples (n=20)

Consumer Discretionary (n=26)

Communications (n=10)

6

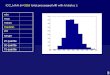

Identifying the Most Generous Companies of 2013

Median:

$18.5M

Top

Quartile

Cutoff:

$53.8M

Bottom

Quartile

Cutoff:

$7.5M Bottom 25%

of Companies

Top 25%

of Companies

Middle

50% of

Companies

7

Identifying the Most Generous Companies of 2013

using a Diverse Range of Metrics

Total Giving

(N=261)

Cash Giving

(N=261)

Total Giving

as a % of

Revenue

(N=241)

Total Giving

as a % of

Pre-Tax

Profit

(N=224)

Top 25%

(75th Percentile)$53.8 Million $35.5 Million 0.22% 1.95%

Bottom 25%

(25th Percentile)$7.5 Million $5.5 Million 0.06% 0.60%

Note: The Top 25% is the top quartile: the value of the data point below which three-quarters of the data lie when ranked in

ascending order. The Bottom 25% is the bottom quartile: the value of the data point below which one-quarter of the data lie when

ranked in ascending order.

8

Pop Quiz: Identifying How Much Cash it Takes to be

Among the Most Generous Companies

Which U.S. Census Bureau region (West, Midwest, Northeast, or South) required

the highest cash contribution to be included in the top quartile?

U.S. Midwest-Based Companies (n=61):

$34.7 million

U.S. Northeast-Based Companies

(n=76): $33.7 million

U.S. South-Based Companies (n=60):

$32.5 million

U.S. West-Based Companies (n=43):

$22.0 million

Which U.S. state required the highest cash contribution to be included in the top

quartile (only includes states with at least 8 companies participating in the Giving

in Numbers Survey: CA, CT, IL, MN, NJ, NY, TX, VA)?

State Top Quartile

MN (n=14) $63.6 Million

CA (n=32) $54.9 Million

IL (n=11) $46.2 Million

NJ (n=9) $42.6 Million

NY (n=39) $40.2 Million

VA (n=9) $38.1 Million

TX (n=17) $28.8 Million

CT (n=11) $25.3 Million

Education Continues to be the Most Popular Program

Area Supported by Corporations

9

Civic & Public Affairs, 5% Community &

Economic Development,

14%

Culture & Arts, 5%

Disaster Relief, 3%Education,

Higher, 12%

Education, K-12, 16%

Environment, 3%

Health & Social Services, 27%

Other, 15%

Note: Average Percentages, N=181.

Giving and Business Rise Together

Distribution of Companies by Changes in

Total Giving Between 2010 and 2013

Note: Inflation-Adjusted, N=144.

64% of Companies Increased Giving from 2010 to 2013

“Community

Investors”

13

Non-Cash Giving Drove Aggregate Increases

from 2010 to 2013

“Community

Investors”

(N=75)

All Other

Companies

(N=69)

Aggregate Total Giving +47% -16%

Total Direct Corporate Cash

Giving+29% -14%

Total Foundation Cash Giving +4% -7%

Total Non-Cash Giving +66% -20%

Median Giving as a % of

Revenue+0.05pp -0.02pp

Median Revenue +11% -3%

12

Non-Cash Contributions Growing for

Service Companies

13

14.95% 15.14% 15.20%

17.74%

29.12%28.83%

28.11%

25.47%

2010 2011 2012 2013

Service Companies (n=82) Manufacturing Companies (n=62)

Non-Cash Giving as a Percentage of Total Giving

Note: Matched-Set Data.

Nearly all Consumer Staples Companies Increased

Giving from 2010 to 2013, Driven by Non-Cash Gifts

14

2010 to 2013

Industry% of Companies

Increasing Giving

Median % Change

in Revenues

Consumer Staples (N=12) 92% +14%

Industrials (N=11) 73% +19%

Health Care (N=21) 71% +5%

Materials (N=6) 67% +5%

Energy (N=8) 63% -19%

Financials (N=35) 63% +3%

Technology (N=19) 58% +26%

Consumer Discretionary

(N=17)53% +2%

Communications (N=6) 50% +13%

Utilities (N=9) 44% -2%

“Excess

non-cash

resources.”

“Business

performance

is projected

to continue

improving.”

“Increasing

focus in

strategic

areas…thus,

moving away

from certain

categories.”

Giving Expansion Slowed in 2013

15

Companies Giving at

least 10% More in 2013

Than 2010 (n=75)

Median

Giving

% Change

from Prior

Year

2010$22.1

Million

2011$26.8

Million+21%

2012$31.3

Million+17%

2013$33.1

Million+6%

The year 2013 saw the largest marginal change by companies that decreased

giving and the smallest marginal change by companies that increased giving.

All Other

Companies

(n=69)

Median

Giving

% Change

from Prior

Year

$26.6

Million

$25.4

Million-5%

$25.2

Million-1%

$23.8

Million-6%

66% of Companies Increased Giving as a Percentage

of Revenue from 2010 to 2013

16Note: Inflation-Adjusted, Matched Set, N=138.

7.2% Growth3.0% Growth

2.2% Growth

Grantmaking Evolves in Post-

Recession Era

Grant Sizes are Growing while the Number of

Recipients Per Grantmaker Declined from 2010 to 2013

18Note: Medians, Inflation-Adjusted, N=38.

19

Note: N=63

1000 975

744701

2010 2011 2012 2013

Median # of Grants by Year

See Program Type Sheet ‘Prog Type –Grants Decreasers’

Giving Changes Among Companies

Decreasing # of Grants from 2010 to 2013

Program Type

% Change in

Average Giving

Level

Higher Education +69%

Community & Economic

Development+56%

K-12 Education -16%

Civic & Public Affairs -18%

Environment -19%

Disaster Relief -32%

Culture & Arts -40%

Note: N=29

Approved Grants Decline from 2010 to 2013; Culture &

Arts Hit Hardest by Changing Strategies

Community & Economic Development, up 34% from

2010, is the Fastest-Growing Program Area

20

$0

$200

$400

$600

$800

$1,000

$1,200

2010 2011 2012 2013

Mill

ion

s

Non-Cash

Foundation Cash

Corporate DirectCash

Note: Total Corporate Funding for Community & Economic Development, Inflation-Adjusted, Matched Set, N=80.

Arts Support Has Been Declining Each Year Since

the Global Recession

21

$0

$50

$100

$150

$200

$250

2010 2011 2012 2013

Mill

ion

s

Non-Cash

Foundation Cash

Corporate DirectCash

Note: Total Corporate Funding for Culture & Arts, Inflation-Adjusted, Matched Set, N=80.

.

Despite Decline in Grants Approved, Team Sizes Have

Mostly Increased Since 2010

22

2.0

4.0

11.0

8.5

19.0

25.5

3.5

5.0

10.0 10.0

21.0

26.0

3.5

5.0

10.0 10.0

24.0

22.0

3.5

5.5

9.010.0

24.0

28.5

Cash Giving Under $5Million (n=14)

Cash Giving Between $5+and $15 Million (n=20)

Cash Giving Between $15+and $25 Million (n =14)

Cash Giving Between $25+and $50 Million (n=18)

Cash Giving Between $50and $100 Million (n=14)

Cash Giving Over $100Million (n=10)

Team Size (Contributions FTEs) by Giving Tier, 2010 to 2013, Medians

2010 2011 2012 2013

Among Companies Making Global Contributions in

2013, International Giving Has Grown Since 2010

23 Note: Inflation-Adjusted, Matched Set, N=58.

$3.11

$3.61

$3.98

$4.88

16.93%17.15%

17.44%

18.16%

15.00%

16.00%

17.00%

18.00%

19.00%

20.00%

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

2010 2011 2012 2013

Median International Giving International Giving as a % of Total Giving

Companies Support a Variety of Geographic Regions,

Driven by Operational Footprint and Disaster Support

24Note: 2013 Data. Average Percentages, Includes only contributions from U.S.-based companies to end-

recipients outside of North America (i.e., Giving to U.S. and Canada excluded).

10%

13%

33%

21%

16%

22%

21%

20%

15%

4%

5%

20%

Manufacturing (n=48)

Service (n=49)

Global (Not region-specific) Asia & the Pacific Europe

Latin America & the Caribbean Middle East & Africa Breakdown Unavailable

Budget Management Statistics from 2010 to 2013

25

Corporate

Community

Affairs

(Avg. %)

Corporate

Foundation

(Avg. %)

All Other

Groups

(Avg. %)

2010 42.5% 33.7% 23.8%

2011 42.9% 33.7% 23.4%

2012 42.4% 33.5% 24.2%

2013 43.9% 32.2% 24.3%

Centralized

Corporate

Cash:

+28%

Decentralized

Corporate

Cash: +10%

Foundation

Cash: +2%

Average Contribution % Change from 2010 to 2013

Note: Matched Set. N=84.

Pass-Through Foundation Structures Were Most

Common Everywhere but the U.S. Northeast

26

25%

17%

19%

15%

9%

17%

19%

9%

5%

3%

9%

7%

6%

14%

35%

13%

20%

20%

25%

52%

30%

59%

54%

45%

25%

8%

11%

10%

8%

11%

International (n=16)

Midwest (n=58)

Northeast (n=57)

South (n=39)

West (n=35)

All Companies (N=205)

Hybrid Operating Predominately Endowed Predominately Pass-Through Other

Percentage of Companies by Corporate Foundation Structures

Discussion Questions

• Which trends surprised you?

• How do your company’s giving practices

compare to global trends?

• What do you think will be the main trend CECP

identifies next year (examining 2014 giving

information)?

Employees Take Center Stage in

Corporate Social Responsibility

CEOs at CECP’s Board of Boards Conference Identified

Employees as the Most Influential Stakeholder

29

Poll Question at February’s Board of Boards Conference:

Encouragement from which stakeholder group would matter

most in a decision to expand your company’s investment in the

community?

• Employees: 36%

• Customers: 22%

• Board of Directors: 22%

• Shareholders: 14%

• Nonprofit/Community Leaders: 3%

• Media: 3%

• Government: 0%

Employee Time and Contributions Account for 23% of

the Value Created by the Average Company

30

66%

11%

14%

9%

Cash Contributions

In-Kind Contributions

Employee Gifts

Employee Time

Note: Average Percentages, N=46. Value of Employee Time = $22.55, Source: Independent Sector (unless value is

provided by company).

Chief Giving Officers at Leading Companies Identify

Paid-Release-Time as Most Engaging Program

31

Poll Question at May’s CECP Summit: Which tactic do you

believe is the most effective for increasing employee satisfaction

with your company?

1. Volunteer Time Off: 47%

2. Ongoing (Year-Round) Matching Gifts: 22%

3. Communicating (internally) about Signature

Programs or Large Grants: 21%

4. Matching Gifts Events (like United Way): 9%

Note: N=135.

More Companies Gave Time Off for Volunteering

in 2013

32 Note: Matched Set, N=100.

Percentage of Companies Offering

Domestic Service Programs by Year

34% 33%

44%

50%51%53% 54%

59%

2010 2011 2012 2013

Pro Bono Service Paid-Release Time

Employees Are Taking Advantage of Generous

Volunteer Opportunities

33

45,21147,506

55,623

61,938

31.97%

33.53%

35.31%

36.56%

25.00%

28.00%

31.00%

34.00%

37.00%

40.00%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2010 2011 2012 2013

Median # of Hours Volunteered On Company Time (N=28)

Average Percentage of Employees Volunteering At Least 1 Hour On Company Time (N=36)

Paid-Release-Time Volunteer Programs are Most Common

in the Financials and Cons. Discretionary Industries

34

33%

33%

38%

39%

45%

55%

60%

60%

68%

74%

Materials, n=15

Utilities, n=15

Consumer Staples, n=16

Industrials, n=18

Technology, n=20

Communications, n=11

Energy, n=10

Health Care, n=25

Consumer Discretionary, n=28

Financials, n=46

Percentage of Companies Offering

Volunteer Time Off in 2013

86% of Companies Encourage Employee Contributions by

Offering At Least One of the Following Matching-Gift Policies

35

66%

56% 54%

42%

A Year-Round MatchingGift Policy

A Workplace GivingCampaign

A Dollars-for-DoersMatching Policy

A Disaster ReliefMatching Gift Policy

Percentage of Companies Offering…

Across All Companies, Employee Participation Grew

for Year-Round Matching Policies

36

Year-Round Policy

Workplace Giving Campaigns

Note: Not Matched-Set Data.

2011 2012 2013

Participation Rate (Average Percentage) 46% 43% 34%

Number of Companies (Sample Size) 20 28 38

2011 2012 2013

Participation Rate (Average Percentage) 8% 10% 14%

Number of Companies (Sample Size) 17 16 36

Corporations Evaluate the Social

Value of Contributions

A Majority of Companies are Measuring the Societal

Value of their Contributions

38

18%

35%

47%

Very Experienced(5 Years or More)

ModeratelyExperienced(3-4 Years)

Slightly Experienced(2 Years or Less)

76% Measure

Outcomes

and/or

Impacts

24% Do Not

Measure

Outcomes

and/or

Impacts

Note: N=160. Note: N=119.

A Majority of Companies are Measuring the Societal

Value of their Contributions

39

24% Do Not

Measure

Outcomes

and/or

Impacts

Note: N=121.

Note: N=81. Only includes companies that

provided specific method.

77% Focus

Impact

Evaluation on

Specific Grants

24%

17%

47%

12%

Methods for Focusing Impact Evaluation

23% Evaluate

All Grants

Only grants to a specific

cause area

Only grants made for a

strategic philanthropic

program

Only grants larger than a

threshold AND to a

specific cause area

Only grants larger than a

specific threshold

Best Practice Case Studies – Learning from

Industry Leaders

40

23% Evaluate

All Grants

Tiered Evaluation Approach

1. Developmental Evaluation

2. Formative Evaluation

3. Summative Evaluation

Building a Measurement Culture

1. Incorporating Impact Measures

into Annual Reviews

2. Transparency: CSR Scorecard

3. Building Programs with ‘Scale’

in Mind

The Most Generous Companies in 2010 Realized

Strong Business Returns from 2010 to 2013

41

24% Do Not

Measure

Outcomes

and/or

Impacts

23% Evaluate

All Grants

Change in Revenues

from 2010 to 2013

Change in Pre-Tax Profits

from 2010 to 2013

2010 Most Generous

Companies

(75th Percentile)+3% +4%

2010 Least Generous

Companies

(25th Percentile)-3% +1%

“A high-quality measurement process is a critical input for good

management and demonstrates that a company recognizes how its

philanthropic strategies can be successful in creating long-term

business value” (p. 62).

—Terence Lim, Measuring the Value of Corporate Philanthropy, 2010

Note: Company generosity established by quartiles. The Top Quartile is the value of the data point below which three-quarters of the

data lie when ranked in ascending order (using Giving as a % of Total Revenue). The Bottom Quartile is the value of the data point

below which one-quarter of the data lie when ranked in ascending order (using Giving as a % of Total Revenue). N=68.

Questions / Comments

42

43

Giving in Numbers Participant List

Communications (n=11) Consumer Discretionary (n=34) Consumer Staples (n=25)

AOL (2) ADT Corporation (1) Altria Group, Inc. (12)

AT&T Inc. (3) Amway Global (2) Anheuser-Busch InBev (3)

DIRECTV, LLC (7) Apollo Education Group (3) BJ’s Wholesale Club, Inc. (1)

Discovery Communications, Inc. (2) Best Buy Co., Inc. (8) Brasil Foods (1)

Ogilvy & Mather (8) Carlson (12) Cargill (9)

Pearson plc (9) CarMax, Inc. (1) The Clorox Company (2)

Sprint Corporation (8) Darden Restaurants, Inc. (4) The Coca-Cola Company (12)

Time Warner Inc. (13) eBay Inc. (4) Colgate-Palmolive Company (7)

Verizon Communications Inc. (11) Ecolab Inc. (3) CVS Caremark Corporation (10)

Vodafone Group Plc (4) Gap Inc. (11) FEMSA (1)

The Walt Disney Company (9) General Motors Company (2) General Mills, Inc. (9)

Hasbro, Inc. (13) The Hershey Company (10)

The Home Depot, Inc. (12) The Hillshire Brands Company (2)

Honda North America (3) Kellogg Company (2)

J. C. Penney Company, Inc. (8) Kimberly-Clark Corporation (8)

JM Family Enterprises, Inc. (4) The Kroger Co. (2)

Johnson Controls, Inc. (5) Land O'Lakes, Inc. (1)

KPMG LLP (11) McCormick & Company, Incorporated (4)

Macy’s, Inc. (8) Newman’s Own (2)

Marriott International, Inc. (3) PepsiCo (9)

Masco Corporation (4) Philip Morris International (5)

Mattel, Inc. (10) Procter & Gamble Company (5)

MGM Resorts International (1) S.C. Johnson & Son, Inc. (2)

Mitsubishi Corporation (Americas) (9) Target (12)

Newell Rubbermaid Inc. (4) Wal-Mart Stores, Inc. (10)

PricewaterhouseCoopers LLP (4)

Sabre Holdings (5)

Southwest Airlines Co. (3)

Starbucks Coffee Company (4)

Starwood Hotels & Resorts Worldwide, Inc. (6)

Toyota Motor North America, Inc. (12)

Under Armour, Inc. (1)

United Stationers Inc. (1)

Yum! Brands, Inc. (3)

Note: Number in parenthesis is the number of years the company completed the Giving in Numbers Survey. Bolded

companies are part of the 4-year matched set.

44

Giving in Numbers Participant List

Energy (n=14) Financials (n=55) Financials (Continued)

Chesapeake Energy Corporation (4) Allstate Insurance Company (9) MetLife, Inc. (10)

Chevron Corporation (13) American Express (9) Morgan Stanley (12)

CITGO Petroleum Corporation (4) Ameriprise Financial, Inc. (3) Mutual of Omaha Insurance Company (1)

ConocoPhillips (8) AXA Equitable (6) Nationwide Insurance (3)

Devon Energy Corporation (1) Banco Bilbao Vizcaya Argentaria, S.A. (6) Neuberger Berman (3)

Exxon Mobil Corporation (8) Bank of America Corporation (13) New York Life Insurance Company (6)

Halliburton (8) Barclays (4) Northern Trust Corporation (2)

Hess Corporation (7) BNY Mellon (9) Northwestern Mutual (4)

Peabody Energy Corporation (5) Capital One Financial Corporation (6) NYSE (9)

Phillips 66 (1) The Charles Schwab Corporation (2) PIMCO (1)

Shell Oil Company (11) Citigroup Inc. (11) The PNC Financial Services Group, Inc. (9)

Spectra Energy (2) Citizens Bank (8) Popular, Inc. (5)

Total S.A. (2) Credit Suisse (3) Principal Financial Group (8)

TransCanada Corporation (2) CSAA Insurance Group (2) Prudential Financial, Inc. (10)

Deutsche Bank (9) Royal Bank of Canada (4)

First Niagara Financial Group, Inc. (2) State Farm Mutual Automobile Insurance Company (10)

Genworth Financial, Inc. (7) Thrivent Financial for Lutherans (1)

The Goldman Sachs Group, Inc. (11) The Travelers Companies, Inc. (8)

The Guardian Life Insurance Company of America (5) U.S. Bancorp (3)

The Hartford (7) UBS (7)

HSBC Bank USA, N.A. (10) Unum Group (1)

JPMorgan Chase & Co. (13) Vanguard (2)

KeyCorp (3) Visa Inc. (1)

Lincoln Financial Group (3) Voya Financial, Inc. (7)

Macquarie Group (3) Wells Fargo & Company (12)

Marsh & McLennan Companies, Inc. (4) The Western Union Company (8)

Massachusetts Mutual Life Insurance Company (6) Weyerhaeuser Company (3)

MasterCard Worldwide (9)

Note: Number in parenthesis is the number of years the company completed the Giving in Numbers Survey. Bolded

companies are part of the 4-year matched set.

45

Giving in Numbers Participant List

Health Care (n=26) Industrials (n=26) Materials (n=18)

Abbott (8) BAE Systems, Inc. (2) 3M (10)

Aetna Inc. (12) The Boeing Company (7) Alcoa Inc. (9)

Agilent Technologies, Inc. (10) Caterpillar Inc. (6) Ashland Inc. (4)

Amgen Inc. (4) CH2M Hill Companies, Ltd. (1) Bemis Company, Inc. (2)

BD (8) Crane Co. (10) The Dow Chemical Company (10)

Boston Scientific Corporation (3) CSX Corporation (5) DuPont (6)

Bristol-Myers Squibb Company (13) Cummins Inc. (3) FMC Corporation (5)

Cardinal Health, Inc. (7) Eaton Corporation (5) Gerdau (2)

CIGNA (5) Emerson Electric Co. (9) International Paper Company (2)

DaVita Inc. (5) FedEx Corporation (6) MeadWestvaco Corporation (3)

Eli Lilly and Company (13) Fluor Corporation (2) Monsanto Company (2)

Express Scripts, Inc. (5) General Electric Company (12) The Mosaic Company (5)

GSK (12) Itron (1) Novelis, Inc. (1)

HCA Inc. (9) John Deere (4) Owens Corning (3)

Humana Inc. (5) Lockheed Martin Corporation (7) Praxair, Inc. (5)

Johnson & Johnson (11) Meritor, Inc. (8) The Sherwin-Williams Company (2)

Kaiser Permanente (3) Northrop Grumman Corporation (7) Vale (3)

McKesson Corporation (10) PACCAR Inc (4) Vulcan Materials Company (4)

Medtronic, Inc. (5) Raytheon Company (4)

Merck (10) Rockwell Automation, Inc. (3)

Novo Nordisk A/S (2) Rockwell Collins, Inc. (4)

Pfizer Inc (11) Union Pacific Corporation (4)

Quest Diagnostics Incorporated (5) United Technologies Corporation (11)

Sabin (1) UPS (3)

UnitedHealth Group (8) Votorantim Group (2)

WellPoint, Inc. (8) Xylem (3)

Note: Number in parenthesis is the number of years the company completed the Giving in Numbers Survey. Bolded

companies are part of the 4-year matched set.

46

Giving in Numbers Participant List

Technology (n=31) Utilities (n=21)

Accenture (9) Ameren Corporation (1)

Adobe (7) American Electric Power Company, Inc. (4)

Alcatel-Lucent (1) Arizona Public Service Company (3)

Applied Materials, Inc. (5) CenterPoint Energy, Inc. (1)

Autodesk, Inc. (2) Consolidated Edison, Inc. (13)

BMC Software (10) Dominion Resources, Inc. (4)

Booz Allen Hamilton Inc. (1) DTE Energy Company (2)

CA Technologies (7) Duke Energy Corporation (9)

Cisco Systems (13) Entergy Corporation (9)

Corning Incorporated (3) Exelon Corporation (7)

Dell Inc. (8) FirstEnergy (5)

EMC Corporation (4) NRG Energy (1)

Google Inc. (4) Pepco Holdings, Inc. (2)

IBM Corporation (13) PG&E Corporation (9)

IHS Inc. (1) PNM Resources, Inc. (7)

Intel Corporation (7) PPL Corporation (2)

McGraw Hill Financial (12) Public Service Enterprise Group Incorporated (6)

Microsoft Corporation (7) Sempra Energy (8)

Moody’s Corporation (9) Southern California Edison (9)

Motorola Solutions, Inc. (2) Southern Company (3)

NVIDIA Corporation (2) TECO Energy, Inc. (5)

Pitney Bowes Inc. (7)

Qualcomm Incorporated (8)

salesforce.com (9)

Samsung Electronics America, Inc. (4)

SAP AG (2)

Symantec Corporation (5)

Synopsys, Inc. (2)

Texas Instruments Incorporated (6)

Toshiba America, Inc. (2)

Xerox Corporation (9)

Note: Number in parenthesis is the number of years the company completed the Giving in Numbers Survey. Bolded

companies are part of the 4-year matched set.