Embed Size (px)

Citation preview

EMERGING MARKETS

OUTLOOK Q4 2021FLIPPERS AND FLOPPERS

LOCAL EYES FOR A GLOBAL VIEW

Please refer to important information at the end of the report and MAR disclosures

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

1E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

KEY MESSAGES• In emerging markets, we see policy ‘flippers’ and ‘floppers’.

• In most of the West (Latam and CEEMEA), robust recovery has come with higher inflation,

forcing central banks to flip to rate hikes. In turn, growth in these regions is set to moderate

next year.

• In emerging Asia, by contrast, sluggish growth and low inflation allow central banks to keep

interest rates floppy, at low levels. Along with loose fiscal policy, low rates should support a

bounce back.

• We expect EM fiscal consolidation will be gradual, due to little appetite for austerity. Politics

bears watching, especially in countries with elections.

• We believe comfortable current account positions will be sustained across most EM,

especially where commodity prices help.

• We think the outlook for EM asset prices remains broadly benign, especially if EM

decouples from concerns on China.

• Still, differentiation favours relative value trades and being more selective.

Emerging Market outlook: Flippers and floppers

EMERGING MARKETS RESEARCH

Emerging Markets 360 team

EM ECONOMICS | EM STRATEGY

TABLE OF CONTENTS

Macro overview ….. 2

EM strategy ….. 3

GDP growth outlook …. 4

Inflation and policy rates.… 5

External accounts ….. 6

Fiscal policy ….. 7

Key dates ….. 8

Overviews: EM Asia/Latam... 9

Overviews: CEEMEA... 10

Central bank cheatsheet..... 11

BNPP forecasts table..... 12

Our team ..... 13

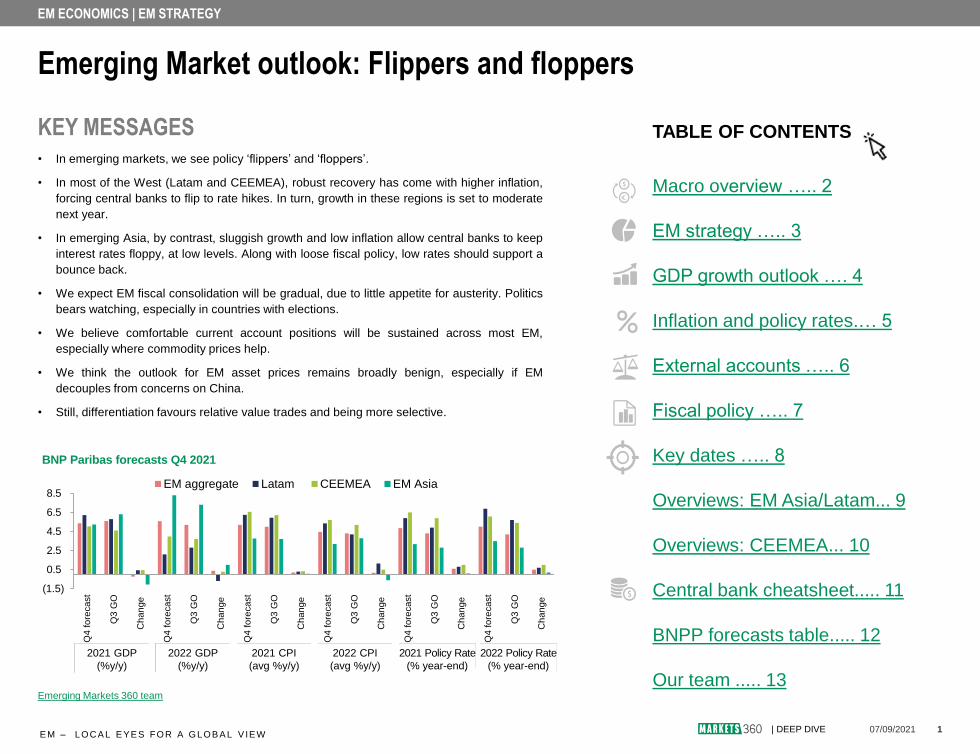

BNP Paribas forecasts Q4 2021

(1.5)

0.5

2.5

4.5

6.5

8.5

Q4

fo

recast

Q3

GO

Ch

an

ge

Q4

fo

recast

Q3

GO

Ch

an

ge

Q4

fo

recast

Q3

GO

Ch

an

ge

Q4

fo

recast

Q3

GO

Ch

an

ge

Q4

fo

recast

Q3

GO

Ch

an

ge

Q4

fo

recast

Q3

GO

Ch

an

ge

EM aggregate Latam CEEMEA EM Asia

2021 GDP

(%y/y)

2022 GDP

(%y/y)

2021 CPI

(avg %y/y)

2022 CPI

(avg %y/y)

2021 Policy Rate

(% year-end)

2022 Policy Rate

(% year-end)

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

2E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

Market concerns on growth downturn look overdone

We have seen two significant developments in recent months: the spread of the

Covid-19 Delta variant (and associated supply constraints), and a slowdown in

China on the back of new restrictions and a regulatory shift. However, we think

market concerns about the growth impact of these developments have been

exaggerated (see Global Outlook Q4 2021, dated 7 September).

In our opinion, progress in vaccinations will continue to weaken the link between

the pandemic and its economic impact, while upcoming Chinese stimulus is likely

to support China’s growth. In addition, commodity prices, a key driver for many

emerging markets, are increasingly supported by global growth trends rather than

Chinese growth alone.

That said, we worry that lingering supply-chain disruptions, along with continued

de-globalisation and nearshoring trends, could work as a negative supply-side

shock putting upward pressure on inflation. In fact, we are concerned that EM

inflation could peak higher and persist for longer than many assume.

Global outlook supportive for EM, if less than before

Despite a near-term speed bump, our view on underlying global growth remains

positive: global liquidity conditions remain abundant, prospects for commodity

prices still look encouraging (supporting EM current account balances) and we

continue to expect a fairly tantrum-less taper by the US Fed. That said, the

prospective rise in real yields in advanced economies suggests less support than

before for EM asset prices. We therefore prefer relative value trades in EM, rather

than outright bullish positions.

Local conditions indicate different paths among EM regions

Beyond global factors, local conditions suggest differing paths ahead for EM

regions. In Latam and most of CEEMEA, growth remains fairly robust, although

inflation concerns are forcing more central banks to hike interest rates, from Brazil

and Chile to Russia and Central Europe. In turn, with a lag, we expect cumulative

monetary tightening to cool growth in these regions next year.

In contrast, especially in countries where Covid-19 has continued to be a

concern, growth in emerging Asia remains sluggish compared to its otherwise

speedy long-term trend, entailing a more protracted recovery path. Facing smaller

macroeconomic imbalances and less inflation pressure than other regions, most

central banks in Southeast Asia seem in no rush to hike. As a result, we see room

for growth to gain traction in emerging Asia into next year.

Policy flippers and floppers

Virtually every country eased policy in the initial aftermath of the pandemic shock.

However, we now see increasing policy differentiation across the globe, including

within EM. Fiscal balances in EM are likely to take time to recover their pre-

pandemic levels, as fiscal consolidation will probably prove to be gradual. While

such a broad description remains true for EM overall, the specifics vary from

country to country.

We think the monetary policy response so far falls roughly into two main

categories: flippers and floppers. Flippers are the policymakers who are facing

increasing inflation pressure and cannot afford to stay in denial for too long, so

are embarking on a tightening cycle. They have either been hiking rates already

or we think they will start soon. That includes almost every central bank in Latam

(Brazil, Mexico, Chile, Colombia), and many in CEEMEA (Russia, Hungary,

Czech Republic, Poland, South Africa).

In contrast, floppers are the policymakers who are keen to keep policy in

accommodative territory for longer. In some cases, this is because they are not

yet facing any major inflationary pressure (most countries in EM Asia) or are even

considering some additional easing (Japan). Alternatively, they explicitly prefer to

stay behind the curve on purpose, under their recently altered monetary policy

regimes (the Fed and the ECB).

All things considered, while global factors remain broadly supportive (if less so

than before), varying local conditions look set to bring increased differentiation

within EM in the months ahead, in our view.

.

Macro overview: Flippers and floppers

EMERGING MARKETS RESEARCH

Marcelo Carvalho, Global Head of Emerging Markets Research | BNP Paribas London branch

EM ECONOMICS | EM STRATEGY

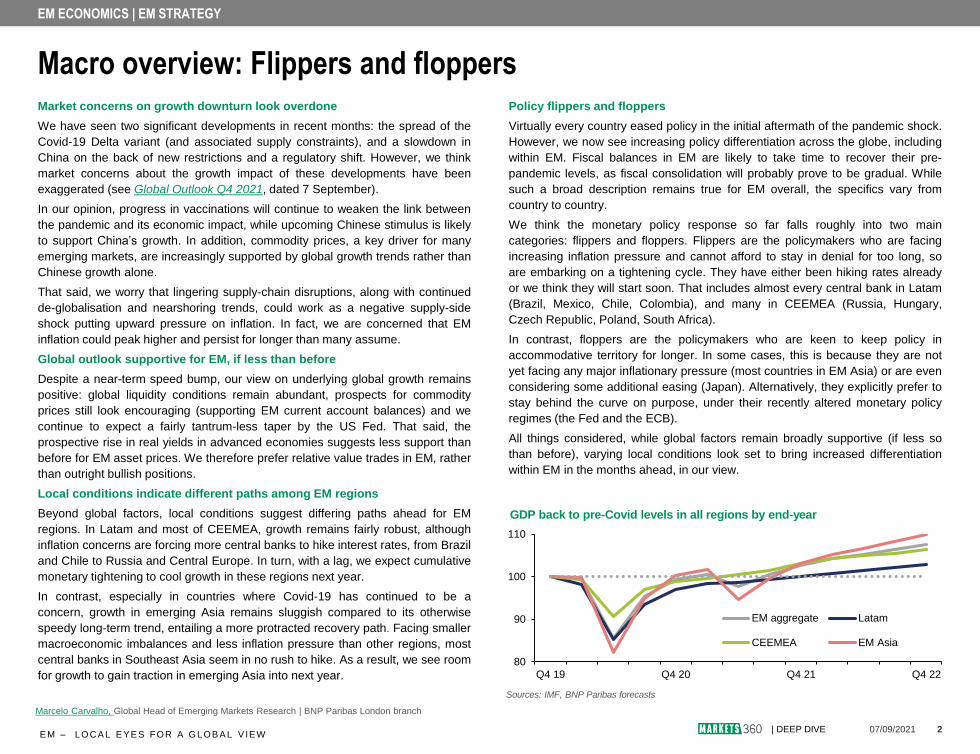

Sources: IMF, BNP Paribas forecasts

80

90

100

110

Q4 19 Q4 20 Q4 21 Q4 22

EM aggregate Latam

CEEMEA EM Asia

GDP back to pre-Covid levels in all regions by end-year

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

3E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

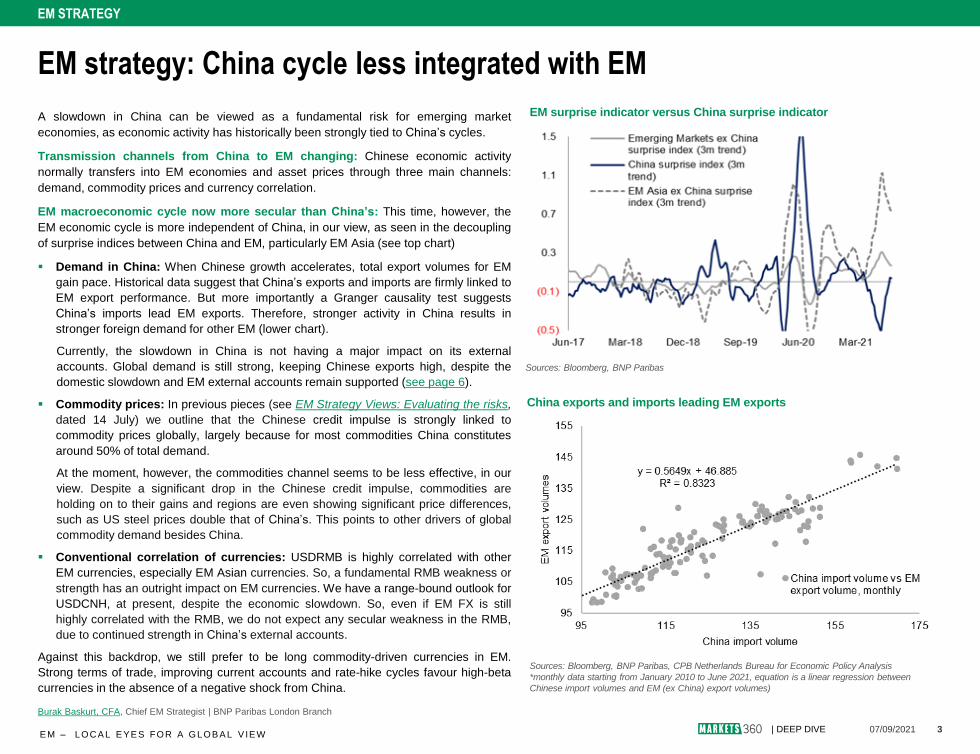

A slowdown in China can be viewed as a fundamental risk for emerging market

economies, as economic activity has historically been strongly tied to China’s cycles.

Transmission channels from China to EM changing: Chinese economic activity

normally transfers into EM economies and asset prices through three main channels:

demand, commodity prices and currency correlation.

EM macroeconomic cycle now more secular than China’s: This time, however, the

EM economic cycle is more independent of China, in our view, as seen in the decoupling

of surprise indices between China and EM, particularly EM Asia (see top chart)

Demand in China: When Chinese growth accelerates, total export volumes for EM

gain pace. Historical data suggest that China’s exports and imports are firmly linked to

EM export performance. But more importantly a Granger causality test suggests

China’s imports lead EM exports. Therefore, stronger activity in China results in

stronger foreign demand for other EM (lower chart).

Currently, the slowdown in China is not having a major impact on its external

accounts. Global demand is still strong, keeping Chinese exports high, despite the

domestic slowdown and EM external accounts remain supported (see page 6).

Commodity prices: In previous pieces (see EM Strategy Views: Evaluating the risks,

dated 14 July) we outline that the Chinese credit impulse is strongly linked to

commodity prices globally, largely because for most commodities China constitutes

around 50% of total demand.

At the moment, however, the commodities channel seems to be less effective, in our

view. Despite a significant drop in the Chinese credit impulse, commodities are

holding on to their gains and regions are even showing significant price differences,

such as US steel prices double that of China’s. This points to other drivers of global

commodity demand besides China.

Conventional correlation of currencies: USDRMB is highly correlated with other

EM currencies, especially EM Asian currencies. So, a fundamental RMB weakness or

strength has an outright impact on EM currencies. We have a range-bound outlook for

USDCNH, at present, despite the economic slowdown. So, even if EM FX is still

highly correlated with the RMB, we do not expect any secular weakness in the RMB,

due to continued strength in China’s external accounts.

Against this backdrop, we still prefer to be long commodity-driven currencies in EM.

Strong terms of trade, improving current accounts and rate-hike cycles favour high-beta

currencies in the absence of a negative shock from China.

EM strategy: China cycle less integrated with EM

Sources: Bloomberg, BNP Paribas

EM ECONOMICS | EM STRATEGY | MARKET ECONOMICS

EM surprise indicator versus China surprise indicator

Burak Baskurt, CFA, Chief EM Strategist | BNP Paribas London Branch

Sources: Bloomberg, BNP Paribas, CPB Netherlands Bureau for Economic Policy Analysis

*monthly data starting from January 2010 to June 2021, equation is a linear regression between

Chinese import volumes and EM (ex China) export volumes)

China exports and imports leading EM exports

EM STRATEGY

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

4E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

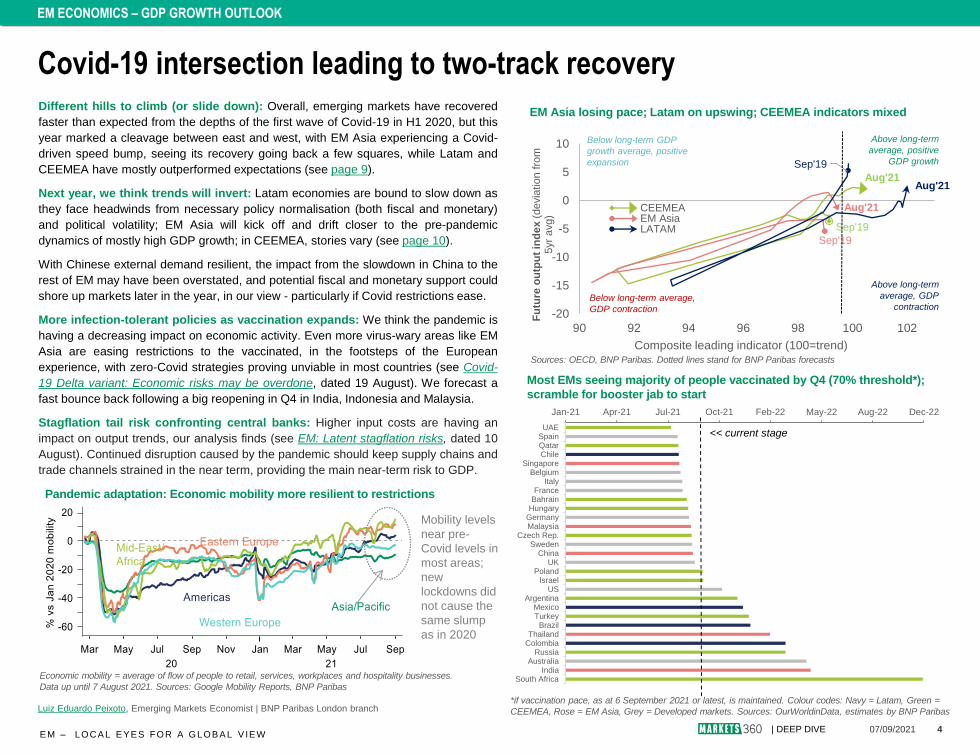

Jan-21 Apr-21 Jul-21 Oct-21 Feb-22 May-22 Aug-22 Dec-22

UAESpainQatarChile

SingaporeBelgium

ItalyFrance

BahrainHungary

GermanyMalaysia

Czech Rep.Sweden

ChinaUK

PolandIsrael

USArgentina

MexicoTurkeyBrazil

ThailandColombia

RussiaAustralia

IndiaSouth Africa

Sep'19

Aug'21

Sep'19

Aug'21

Sep'19

Aug'21

-20

-15

-10

-5

0

5

10

90 92 94 96 98 100 102

Fu

ture

ou

tpu

t in

de

x (

devia

tio

n f

rom

5yr

avg)

Composite leading indicator (100=trend)

CEEMEAEM AsiaLATAM

Above long-term

average, positive

GDP growth

Below long-term GDP

growth average, positive

expansion

Below long-term average,

GDP contraction

Above long-term

average, GDP

contraction

Different hills to climb (or slide down): Overall, emerging markets have recovered

faster than expected from the depths of the first wave of Covid-19 in H1 2020, but this

year marked a cleavage between east and west, with EM Asia experiencing a Covid-

driven speed bump, seeing its recovery going back a few squares, while Latam and

CEEMEA have mostly outperformed expectations (see page 9).

Next year, we think trends will invert: Latam economies are bound to slow down as

they face headwinds from necessary policy normalisation (both fiscal and monetary)

and political volatility; EM Asia will kick off and drift closer to the pre-pandemic

dynamics of mostly high GDP growth; in CEEMEA, stories vary (see page 10).

With Chinese external demand resilient, the impact from the slowdown in China to the

rest of EM may have been overstated, and potential fiscal and monetary support could

shore up markets later in the year, in our view - particularly if Covid restrictions ease.

More infection-tolerant policies as vaccination expands: We think the pandemic is

having a decreasing impact on economic activity. Even more virus-wary areas like EM

Asia are easing restrictions to the vaccinated, in the footsteps of the European

experience, with zero-Covid strategies proving unviable in most countries (see Covid-

19 Delta variant: Economic risks may be overdone, dated 19 August). We forecast a

fast bounce back following a big reopening in Q4 in India, Indonesia and Malaysia.

Stagflation tail risk confronting central banks: Higher input costs are having an

impact on output trends, our analysis finds (see EM: Latent stagflation risks, dated 10

August). Continued disruption caused by the pandemic should keep supply chains and

trade channels strained in the near term, providing the main near-term risk to GDP.

Covid-19 intersection leading to two-track recovery

Sources: OECD, BNP Paribas. Dotted lines stand for BNP Paribas forecasts

EM ECONOMICS | EM STRATEGY | MARKET ECONOMICS

EM Asia losing pace; Latam on upswing; CEEMEA indicators mixed

*if vaccination pace, as at 6 September 2021 or latest, is maintained. Colour codes: Navy = Latam, Green =

CEEMEA, Rose = EM Asia, Grey = Developed markets. Sources: OurWorldinData, estimates by BNP ParibasLuiz Eduardo Peixoto, Emerging Markets Economist | BNP Paribas London branch

EM ECONOMICS | EM STRATEGY

Most EMs seeing majority of people vaccinated by Q4 (70% threshold*);

scramble for booster jab to start

Economic mobility = average of flow of people to retail, services, workplaces and hospitality businesses.

Data up until 7 August 2021. Sources: Google Mobility Reports, BNP Paribas

<< current stage

Mobility levels

near pre-

Covid levels in

most areas;

new

lockdowns did

not cause the

same slump

as in 2020

Pandemic adaptation: Economic mobility more resilient to restrictions

EM ECONOMICS – GDP GROWTH OUTLOOK

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

5E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

CBRT

CBE

BI

PBoCBNMBoT

BNR

RBI

NBPBoK

SARB

NBH

Banxico CNB

BCCh

BanRep

CBR

BCB

-1

-0.5

0

0.5

1

1.5

2

2.5

-3 -2 -1 0 1 2 3 4

Po

licy r

ate

ch

an

ge e

xp

ecte

d

(Sep to D

ec 2

021)

Dove–Hawk scale (3=more hawkish)

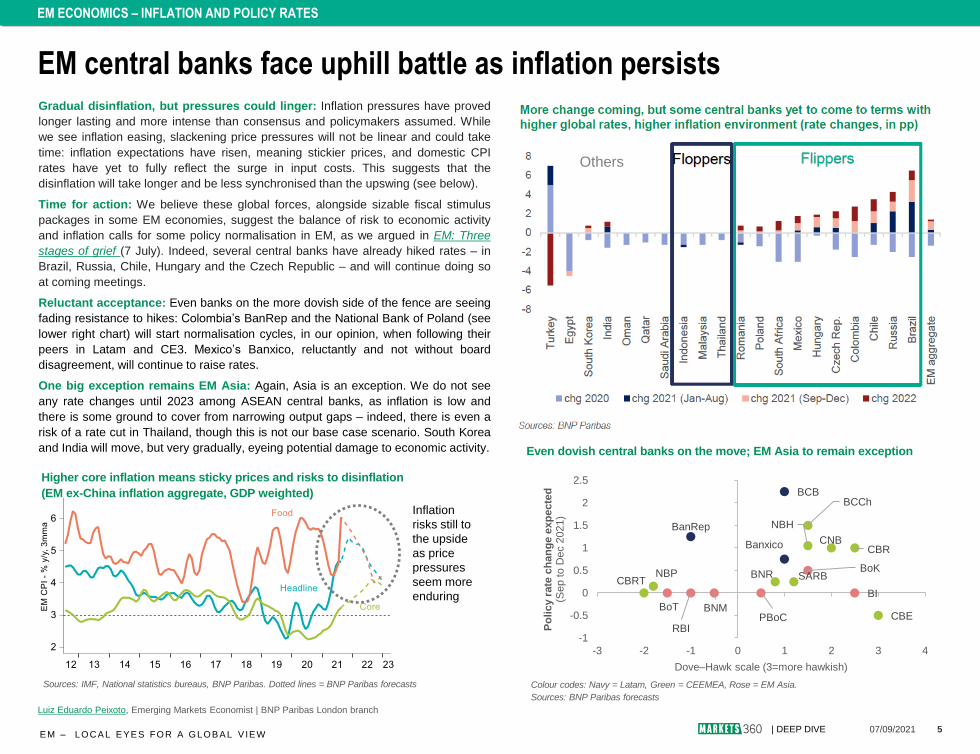

Gradual disinflation, but pressures could linger: Inflation pressures have proved

longer lasting and more intense than consensus and policymakers assumed. While

we see inflation easing, slackening price pressures will not be linear and could take

time: inflation expectations have risen, meaning stickier prices, and domestic CPI

rates have yet to fully reflect the surge in input costs. This suggests that the

disinflation will take longer and be less synchronised than the upswing (see below).

Time for action: We believe these global forces, alongside sizable fiscal stimulus

packages in some EM economies, suggest the balance of risk to economic activity

and inflation calls for some policy normalisation in EM, as we argued in EM: Three

stages of grief (7 July). Indeed, several central banks have already hiked rates – in

Brazil, Russia, Chile, Hungary and the Czech Republic – and will continue doing so

at coming meetings.

Reluctant acceptance: Even banks on the more dovish side of the fence are seeing

fading resistance to hikes: Colombia’s BanRep and the National Bank of Poland (see

lower right chart) will start normalisation cycles, in our opinion, when following their

peers in Latam and CE3. Mexico’s Banxico, reluctantly and not without board

disagreement, will continue to raise rates.

One big exception remains EM Asia: Again, Asia is an exception. We do not see

any rate changes until 2023 among ASEAN central banks, as inflation is low and

there is some ground to cover from narrowing output gaps – indeed, there is even a

risk of a rate cut in Thailand, though this is not our base case scenario. South Korea

and India will move, but very gradually, eyeing potential damage to economic activity.

EM central banks face uphill battle as inflation persists

EM ECONOMICS | EM STRATEGY | MARKET ECONOMICS

Sources: BNP Paribas

Even dovish central banks on the move; EM Asia to remain exception

EM ECONOMICS | EM STRATEGY

Colour codes: Navy = Latam, Green = CEEMEA, Rose = EM Asia.

Sources: BNP Paribas forecasts

More change coming, but some central banks yet to come to terms with

higher global rates (pp)

Sources: IMF, National statistics bureaus, BNP Paribas. Dotted lines = BNP Paribas forecasts

Higher core inflation means sticky prices and risks to disinflation

(EM ex-China inflation aggregate, GDP weighted)

Luiz Eduardo Peixoto, Emerging Markets Economist | BNP Paribas London branch

FlippersFloppersFloppersOthers

Inflation

risks still to

the upside

as price

pressures

seem more

enduring

EM ECONOMICS – INFLATION AND POLICY RATES

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

6E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

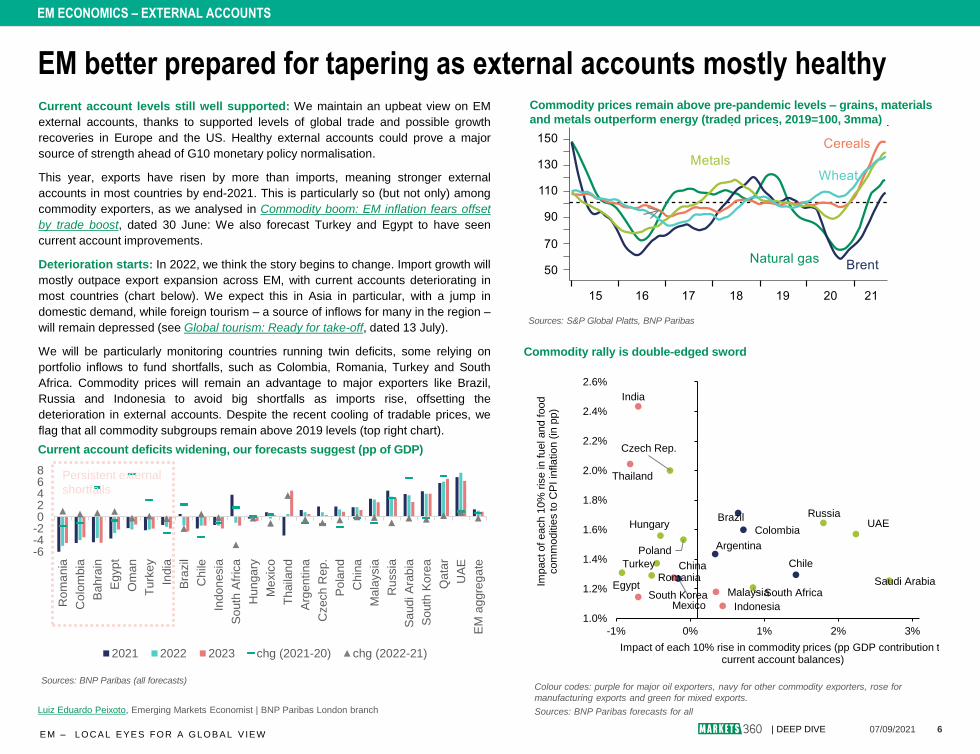

Current account levels still well supported: We maintain an upbeat view on EM

external accounts, thanks to supported levels of global trade and possible growth

recoveries in Europe and the US. Healthy external accounts could prove a major

source of strength ahead of G10 monetary policy normalisation.

This year, exports have risen by more than imports, meaning stronger external

accounts in most countries by end-2021. This is particularly so (but not only) among

commodity exporters, as we analysed in Commodity boom: EM inflation fears offset

by trade boost, dated 30 June: We also forecast Turkey and Egypt to have seen

current account improvements.

Deterioration starts: In 2022, we think the story begins to change. Import growth will

mostly outpace export expansion across EM, with current accounts deteriorating in

most countries (chart below). We expect this in Asia in particular, with a jump in

domestic demand, while foreign tourism – a source of inflows for many in the region –

will remain depressed (see Global tourism: Ready for take-off, dated 13 July).

We will be particularly monitoring countries running twin deficits, some relying on

portfolio inflows to fund shortfalls, such as Colombia, Romania, Turkey and South

Africa. Commodity prices will remain an advantage to major exporters like Brazil,

Russia and Indonesia to avoid big shortfalls as imports rise, offsetting the

deterioration in external accounts. Despite the recent cooling of tradable prices, we

flag that all commodity subgroups remain above 2019 levels (top right chart).

EM better prepared for tapering as external accounts mostly healthy

Sources: S&P Global Platts, BNP Paribas

EM ECONOMICS | EM STRATEGY | MARKET ECONOMICS

Commodity prices remain above pre-pandemic levels – grains, materials

and metals outperform energy (traded prices, 2019=100, 3mma)

Sources: BNP Paribas (all forecasts)

Current account deficits widening, our forecasts suggest (pp of GDP)

EM ECONOMICS | EM STRATEGY

Colour codes: purple for major oil exporters, navy for other commodity exporters, rose for

manufacturing exports and green for mixed exports.

Sources: BNP Paribas forecasts for all

Commodity rally is double-edged sword

Luiz Eduardo Peixoto, Emerging Markets Economist | BNP Paribas London branch

-6-4-202468

Rom

an

ia

Colo

mbia

Ba

hra

in

Eg

yp

t

Om

an

Tu

rke

y

India

Bra

zil

Chile

Indo

nesia

So

uth

Afr

ica

Hun

ga

ry

Me

xic

o

Th

aila

nd

Arg

en

tina

Czech

Rep

.

Po

lan

d

Chin

a

Ma

laysia

Ru

ssia

Sa

ud

i A

rab

ia

So

uth

Ko

rea

Qa

tar

UA

E

EM

ag

gre

ga

te

2021 2022 2023 chg (2021-20) chg (2022-21)

Persistent external

shortfalls

Argentina

Brazil

Chile

Colombia

Mexico

Czech Rep.

Hungary

Poland

Romania

Russia

South Africa

Turkey

Saudi ArabiaEgypt

UAE

China

India

Indonesia

MalaysiaSouth Korea

Thailand

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

2.6%

-1% 0% 1% 2% 3%

Impact of each 1

0%

ris

e in

fuel and f

ood

com

mo

ditie

s to C

PI in

fla

tio

n (

in p

p)

Impact of each 10% rise in commodity prices (pp GDP contribution to current account balances)

EM ECONOMICS – EXTERNAL ACCOUNTS

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

7E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

-12

-10

-8

-6

-4

-2

0

2019 2020 2021 2022

EM aggregate LATAM CEEMEA EM Asia

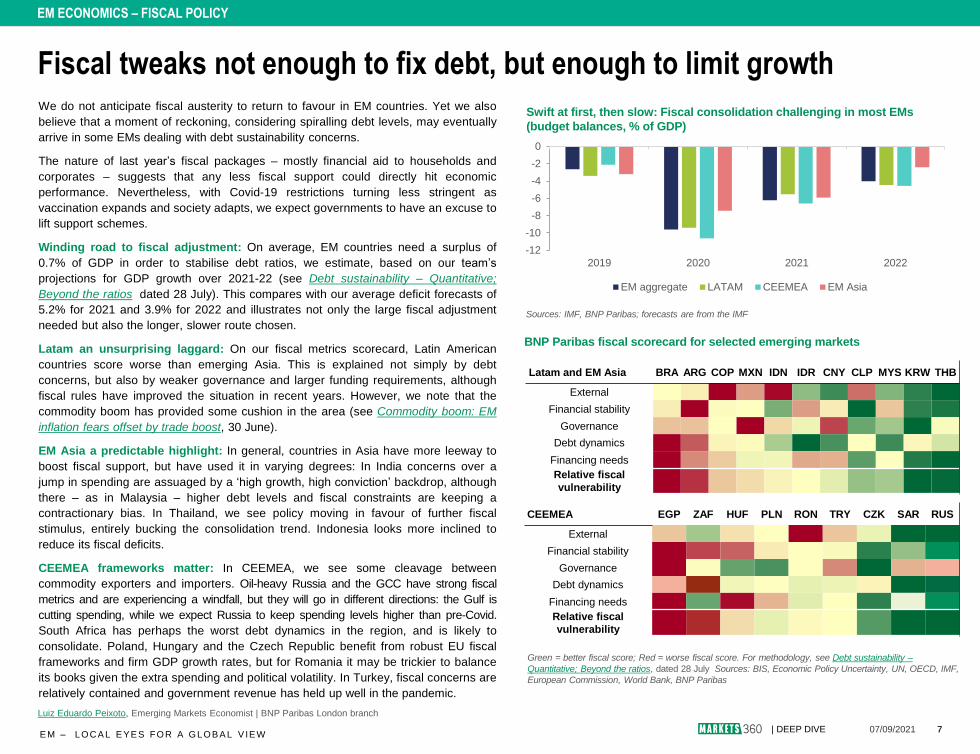

We do not anticipate fiscal austerity to return to favour in EM countries. Yet we also

believe that a moment of reckoning, considering spiralling debt levels, may eventually

arrive in some EMs dealing with debt sustainability concerns.

The nature of last year’s fiscal packages – mostly financial aid to households and

corporates – suggests that any less fiscal support could directly hit economic

performance. Nevertheless, with Covid-19 restrictions turning less stringent as

vaccination expands and society adapts, we expect governments to have an excuse to

lift support schemes.

Winding road to fiscal adjustment: On average, EM countries need a surplus of

0.7% of GDP in order to stabilise debt ratios, we estimate, based on our team’s

projections for GDP growth over 2021-22 (see Debt sustainability – Quantitative;

Beyond the ratios, dated 28 July). This compares with our average deficit forecasts of

5.2% for 2021 and 3.9% for 2022 and illustrates not only the large fiscal adjustment

needed but also the longer, slower route chosen.

Latam an unsurprising laggard: On our fiscal metrics scorecard, Latin American

countries score worse than emerging Asia. This is explained not simply by debt

concerns, but also by weaker governance and larger funding requirements, although

fiscal rules have improved the situation in recent years. However, we note that the

commodity boom has provided some cushion in the area (see Commodity boom: EM

inflation fears offset by trade boost, 30 June).

EM Asia a predictable highlight: In general, countries in Asia have more leeway to

boost fiscal support, but have used it in varying degrees: In India concerns over a

jump in spending are assuaged by a ‘high growth, high conviction’ backdrop, although

there – as in Malaysia – higher debt levels and fiscal constraints are keeping a

contractionary bias. In Thailand, we see policy moving in favour of further fiscal

stimulus, entirely bucking the consolidation trend. Indonesia looks more inclined to

reduce its fiscal deficits.

CEEMEA frameworks matter: In CEEMEA, we see some cleavage between

commodity exporters and importers. Oil-heavy Russia and the GCC have strong fiscal

metrics and are experiencing a windfall, but they will go in different directions: the Gulf is

cutting spending, while we expect Russia to keep spending levels higher than pre-Covid.

South Africa has perhaps the worst debt dynamics in the region, and is likely to

consolidate. Poland, Hungary and the Czech Republic benefit from robust EU fiscal

frameworks and firm GDP growth rates, but for Romania it may be trickier to balance

its books given the extra spending and political volatility. In Turkey, fiscal concerns are

relatively contained and government revenue has held up well in the pandemic.

Fiscal tweaks not enough to fix debt, but enough to limit growth

EM ECONOMICS | EM STRATEGY | MARKET ECONOMICS

Green = better fiscal score; Red = worse fiscal score. For methodology, see Debt sustainability –

Quantitative; Beyond the ratios, dated 28 July Sources: BIS, Economic Policy Uncertainty, UN, OECD, IMF,

European Commission, World Bank, BNP Paribas

EM ECONOMICS | EM STRATEGY

Swift at first, then slow: Fiscal consolidation challenging in most EMs

(budget balances, % of GDP)

Sources: IMF, BNP Paribas; forecasts are from the IMF

BNP Paribas fiscal scorecard for selected emerging markets

CEEMEA EGP ZAF HUF PLN RON TRY CZK SAR RUS

External

Financial stability

Governance

Debt dynamics

Financing needs

Relative fiscal

vulnerability

Latam and EM Asia BRA ARG COP MXN IDN IDR CNY CLP MYS KRW THB

External

Financial stability

Governance

Debt dynamics

Financing needs

Relative fiscal

vulnerability

Luiz Eduardo Peixoto, Emerging Markets Economist | BNP Paribas London branch

EM ECONOMICS – FISCAL POLICY

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

8E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

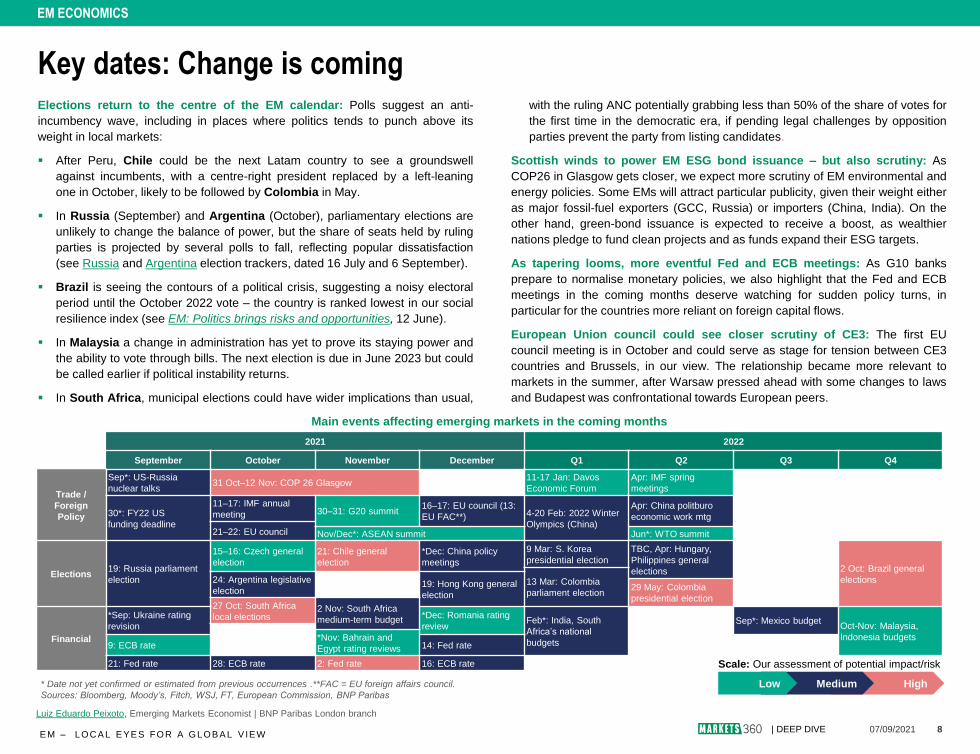

Key dates: Change is coming

EM ECONOMICS | EM STRATEGY | MARKET ECONOMICSEM ECONOMICS | EM STRATEGY

Luiz Eduardo Peixoto, Emerging Markets Economist | BNP Paribas London branch

Elections return to the centre of the EM calendar: Polls suggest an anti-

incumbency wave, including in places where politics tends to punch above its

weight in local markets:

After Peru, Chile could be the next Latam country to see a groundswell

against incumbents, with a centre-right president replaced by a left-leaning

one in October, likely to be followed by Colombia in May.

In Russia (September) and Argentina (October), parliamentary elections are

unlikely to change the balance of power, but the share of seats held by ruling

parties is projected by several polls to fall, reflecting popular dissatisfaction

(see Russia and Argentina election trackers, dated 16 July and 6 September).

Brazil is seeing the contours of a political crisis, suggesting a noisy electoral

period until the October 2022 vote – the country is ranked lowest in our social

resilience index (see EM: Politics brings risks and opportunities, 12 June).

In Malaysia a change in administration has yet to prove its staying power and

the ability to vote through bills. The next election is due in June 2023 but could

be called earlier if political instability returns.

In South Africa, municipal elections could have wider implications than usual,

with the ruling ANC potentially grabbing less than 50% of the share of votes for

the first time in the democratic era, if pending legal challenges by opposition

parties prevent the party from listing candidates.

Scottish winds to power EM ESG bond issuance – but also scrutiny: As

COP26 in Glasgow gets closer, we expect more scrutiny of EM environmental and

energy policies. Some EMs will attract particular publicity, given their weight either

as major fossil-fuel exporters (GCC, Russia) or importers (China, India). On the

other hand, green-bond issuance is expected to receive a boost, as wealthier

nations pledge to fund clean projects and as funds expand their ESG targets.

As tapering looms, more eventful Fed and ECB meetings: As G10 banks

prepare to normalise monetary policies, we also highlight that the Fed and ECB

meetings in the coming months deserve watching for sudden policy turns, in

particular for the countries more reliant on foreign capital flows.

European Union council could see closer scrutiny of CE3: The first EU

council meeting is in October and could serve as stage for tension between CE3

countries and Brussels, in our view. The relationship became more relevant to

markets in the summer, after Warsaw pressed ahead with some changes to laws

and Budapest was confrontational towards European peers.

Main events affecting emerging markets in the coming months

2021 2022

September October November December Q1 Q2 Q3 Q4

Trade /

Foreign

Policy

Sep*: US-Russia

nuclear talks31 Oct–12 Nov: COP 26 Glasgow

11-17 Jan: Davos

Economic Forum

Apr: IMF spring

meetings

30*: FY22 US

funding deadline

11–17: IMF annual

meeting 30–31: G20 summit16–17: EU council (13:

EU FAC**) 4-20 Feb: 2022 Winter

Olympics (China)

Apr: China politburo

economic work mtg

21–22: EU council Nov/Dec*: ASEAN summit Jun*: WTO summit

Elections19: Russia parliament

election

15–16: Czech general

election

21: Chile general

election

*Dec: China policy

meetings

9 Mar: S. Korea

presidential election

TBC, Apr: Hungary,

Philippines general

elections 2 Oct: Brazil general

elections13 Mar: Colombia

parliament election

24: Argentina legislative

election2 N 19: Hong Kong general

election29 May: Colombia

presidential election27 Oct: South Africa

local elections2 Nov: South Africa

medium-term budget

Financial

*Sep: Ukraine rating

revision

*Dec: Romania rating

reviewFeb*: India, South

Africa’s national

budgets

Sep*: Mexico budgetOct-Nov: Malaysia,

Indonesia budgets*Nov: Bahrain and

Egypt rating reviews9: ECB rate 14: Fed rate

21: Fed rate 28: ECB rate 2: Fed rate 16: ECB rate

HighMediumLow

Scale: Our assessment of potential impact/risk

* Date not yet confirmed or estimated from previous occurrences .**FAC = EU foreign affairs council.

Sources: Bloomberg, Moody’s, Fitch, WSJ, FT, European Commission, BNP Paribas

EM ECONOMICS

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

9E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

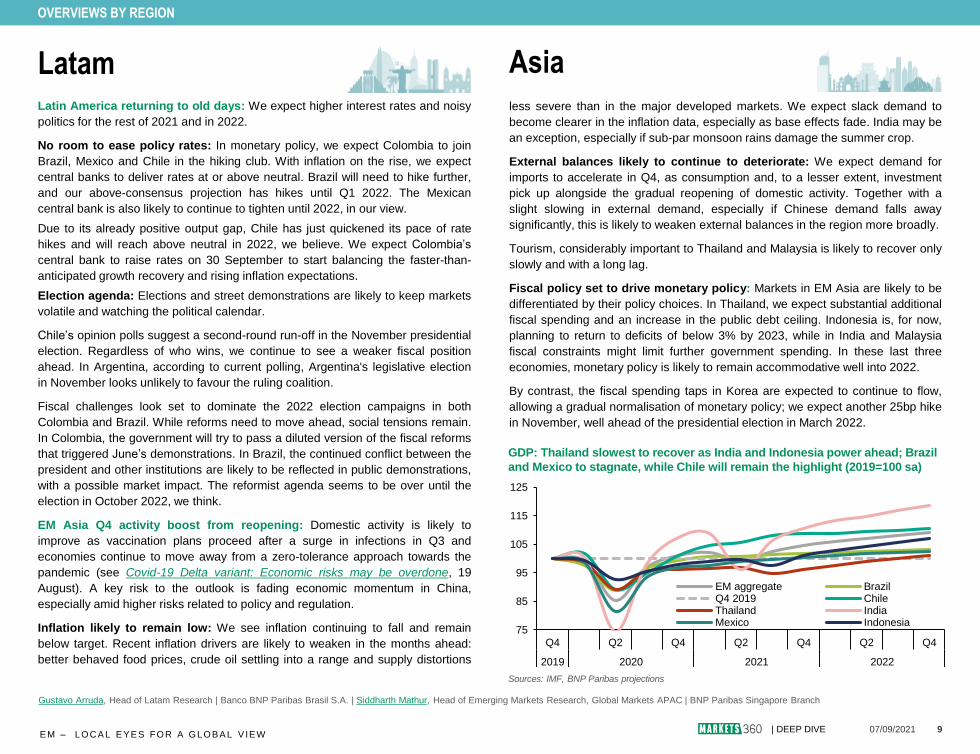

Latam

ECONOMICS

Gustavo Arruda, Head of Latam Research | Banco BNP Paribas Brasil S.A. | Siddharth Mathur, Head of Emerging Markets Research, Global Markets APAC | BNP Paribas Singapore Branch

OVERVIEWS BY REGION

Latin America returning to old days: We expect higher interest rates and noisy

politics for the rest of 2021 and in 2022.

No room to ease policy rates: In monetary policy, we expect Colombia to join

Brazil, Mexico and Chile in the hiking club. With inflation on the rise, we expect

central banks to deliver rates at or above neutral. Brazil will need to hike further,

and our above-consensus projection has hikes until Q1 2022. The Mexican

central bank is also likely to continue to tighten until 2022, in our view.

Due to its already positive output gap, Chile has just quickened its pace of rate

hikes and will reach above neutral in 2022, we believe. We expect Colombia’s

central bank to raise rates on 30 September to start balancing the faster-than-

anticipated growth recovery and rising inflation expectations.

Election agenda: Elections and street demonstrations are likely to keep markets

volatile and watching the political calendar.

Chile’s opinion polls suggest a second-round run-off in the November presidential

election. Regardless of who wins, we continue to see a weaker fiscal position

ahead. In Argentina, according to current polling, Argentina's legislative election

in November looks unlikely to favour the ruling coalition.

Fiscal challenges look set to dominate the 2022 election campaigns in both

Colombia and Brazil. While reforms need to move ahead, social tensions remain.

In Colombia, the government will try to pass a diluted version of the fiscal reforms

that triggered June’s demonstrations. In Brazil, the continued conflict between the

president and other institutions are likely to be reflected in public demonstrations,

with a possible market impact. The reformist agenda seems to be over until the

election in October 2022, we think.

EM Asia Q4 activity boost from reopening: Domestic activity is likely to

improve as vaccination plans proceed after a surge in infections in Q3 and

economies continue to move away from a zero-tolerance approach towards the

pandemic (see Covid-19 Delta variant: Economic risks may be overdone, 19

August). A key risk to the outlook is fading economic momentum in China,

especially amid higher risks related to policy and regulation.

Inflation likely to remain low: We see inflation continuing to fall and remain

below target. Recent inflation drivers are likely to weaken in the months ahead:

better behaved food prices, crude oil settling into a range and supply distortions

less severe than in the major developed markets. We expect slack demand to

become clearer in the inflation data, especially as base effects fade. India may be

an exception, especially if sub-par monsoon rains damage the summer crop.

External balances likely to continue to deteriorate: We expect demand for

imports to accelerate in Q4, as consumption and, to a lesser extent, investment

pick up alongside the gradual reopening of domestic activity. Together with a

slight slowing in external demand, especially if Chinese demand falls away

significantly, this is likely to weaken external balances in the region more broadly.

Tourism, considerably important to Thailand and Malaysia is likely to recover only

slowly and with a long lag.

Fiscal policy set to drive monetary policy: Markets in EM Asia are likely to be

differentiated by their policy choices. In Thailand, we expect substantial additional

fiscal spending and an increase in the public debt ceiling. Indonesia is, for now,

planning to return to deficits of below 3% by 2023, while in India and Malaysia

fiscal constraints might limit further government spending. In these last three

economies, monetary policy is likely to remain accommodative well into 2022.

By contrast, the fiscal spending taps in Korea are expected to continue to flow,

allowing a gradual normalisation of monetary policy; we expect another 25bp hike

in November, well ahead of the presidential election in March 2022.

Asia

75

85

95

105

115

125

Q4 Q2 Q4 Q2 Q4 Q2 Q4

2019 2020 2021 2022

EM aggregate BrazilQ4 2019 ChileThailand IndiaMexico Indonesia

Sources: IMF, BNP Paribas projections

GDP: Thailand slowest to recover as India and Indonesia power ahead; Brazil

and Mexico to stagnate, while Chile will remain the highlight (2019=100 sa)

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

10E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

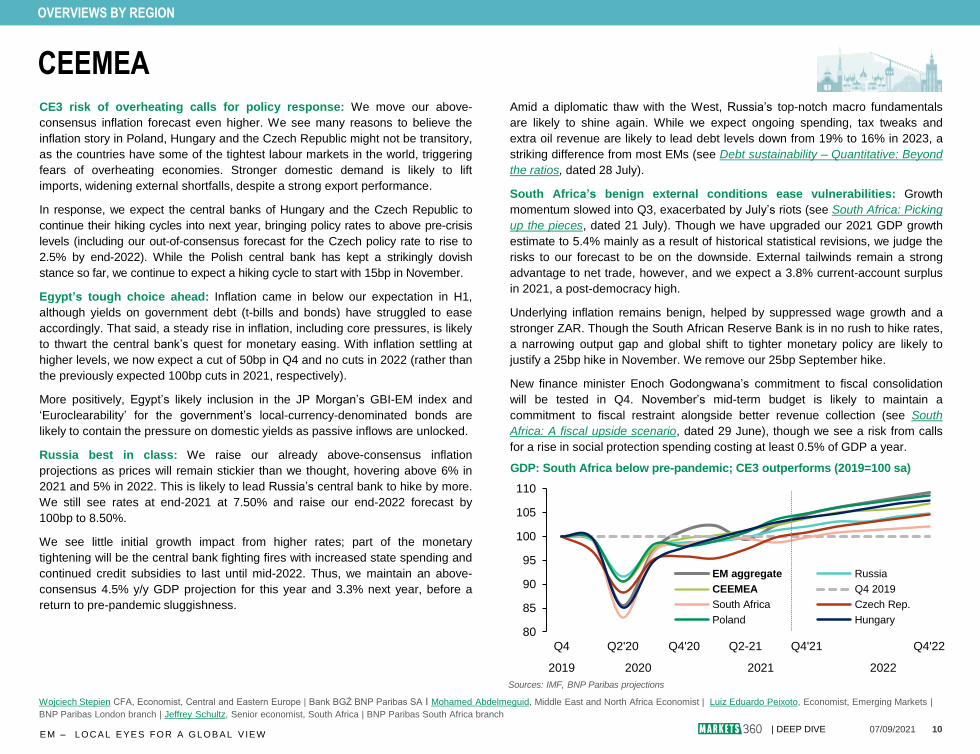

CE3 risk of overheating calls for policy response: We move our above-

consensus inflation forecast even higher. We see many reasons to believe the

inflation story in Poland, Hungary and the Czech Republic might not be transitory,

as the countries have some of the tightest labour markets in the world, triggering

fears of overheating economies. Stronger domestic demand is likely to lift

imports, widening external shortfalls, despite a strong export performance.

In response, we expect the central banks of Hungary and the Czech Republic to

continue their hiking cycles into next year, bringing policy rates to above pre-crisis

levels (including our out-of-consensus forecast for the Czech policy rate to rise to

2.5% by end-2022). While the Polish central bank has kept a strikingly dovish

stance so far, we continue to expect a hiking cycle to start with 15bp in November.

Egypt’s tough choice ahead: Inflation came in below our expectation in H1,

although yields on government debt (t-bills and bonds) have struggled to ease

accordingly. That said, a steady rise in inflation, including core pressures, is likely

to thwart the central bank’s quest for monetary easing. With inflation settling at

higher levels, we now expect a cut of 50bp in Q4 and no cuts in 2022 (rather than

the previously expected 100bp cuts in 2021, respectively).

More positively, Egypt’s likely inclusion in the JP Morgan’s GBI-EM index and

‘Euroclearability’ for the government’s local-currency-denominated bonds are

likely to contain the pressure on domestic yields as passive inflows are unlocked.

Russia best in class: We raise our already above-consensus inflation

projections as prices will remain stickier than we thought, hovering above 6% in

2021 and 5% in 2022. This is likely to lead Russia’s central bank to hike by more.

We still see rates at end-2021 at 7.50% and raise our end-2022 forecast by

100bp to 8.50%.

We see little initial growth impact from higher rates; part of the monetary

tightening will be the central bank fighting fires with increased state spending and

continued credit subsidies to last until mid-2022. Thus, we maintain an above-

consensus 4.5% y/y GDP projection for this year and 3.3% next year, before a

return to pre-pandemic sluggishness.

Amid a diplomatic thaw with the West, Russia’s top-notch macro fundamentals

are likely to shine again. While we expect ongoing spending, tax tweaks and

extra oil revenue are likely to lead debt levels down from 19% to 16% in 2023, a

striking difference from most EMs (see Debt sustainability – Quantitative: Beyond

the ratios, dated 28 July).

South Africa’s benign external conditions ease vulnerabilities: Growth

momentum slowed into Q3, exacerbated by July’s riots (see South Africa: Picking

up the pieces, dated 21 July). Though we have upgraded our 2021 GDP growth

estimate to 5.4% mainly as a result of historical statistical revisions, we judge the

risks to our forecast to be on the downside. External tailwinds remain a strong

advantage to net trade, however, and we expect a 3.8% current-account surplus

in 2021, a post-democracy high.

Underlying inflation remains benign, helped by suppressed wage growth and a

stronger ZAR. Though the South African Reserve Bank is in no rush to hike rates,

a narrowing output gap and global shift to tighter monetary policy are likely to

justify a 25bp hike in November. We remove our 25bp September hike.

New finance minister Enoch Godongwana’s commitment to fiscal consolidation

will be tested in Q4. November’s mid-term budget is likely to maintain a

commitment to fiscal restraint alongside better revenue collection (see South

Africa: A fiscal upside scenario, dated 29 June), though we see a risk from calls

for a rise in social protection spending costing at least 0.5% of GDP a year.

CEEMEA

ECONOMICS

Sources: IMF, BNP Paribas projections

Wojciech Stepien CFA, Economist, Central and Eastern Europe | Bank BGŻ BNP Paribas SA I Mohamed Abdelmeguid, Middle East and North Africa Economist | Luiz Eduardo Peixoto, Economist, Emerging Markets |

BNP Paribas London branch | Jeffrey Schultz, Senior economist, South Africa | BNP Paribas South Africa branch

GDP: South Africa below pre-pandemic; CE3 outperforms (2019=100 sa)

OVERVIEWS BY REGION

80

85

90

95

100

105

110

Q4 Q2'20 Q4'20 Q2-21 Q4'21 Q4'22

2019 2020 2021 2022

EM aggregate Russia

CEEMEA Q4 2019

South Africa Czech Rep.

Poland Hungary

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

11E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

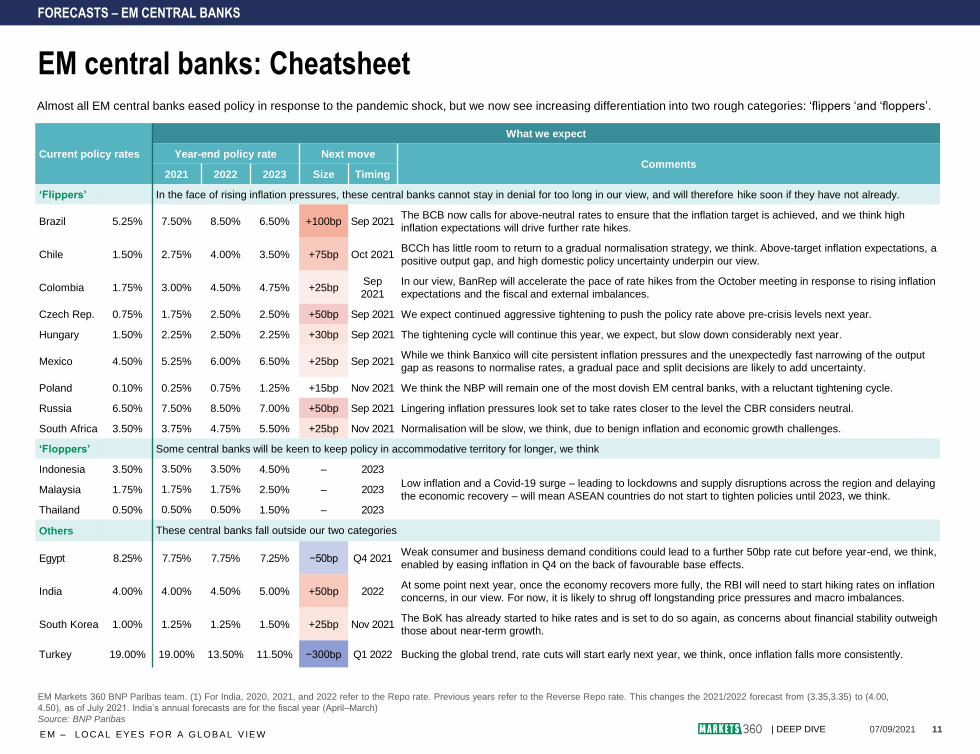

EM central banks: Cheatsheet

EM Markets 360 BNP Paribas team. (1) For India, 2020, 2021, and 2022 refer to the Repo rate. Previous years refer to the Reverse Repo rate. This changes the 2021/2022 forecast from (3.35,3.35) to (4.00,

4.50), as of July 2021. India’s annual forecasts are for the fiscal year (April–March)

Source: BNP Paribas

Almost all EM central banks eased policy in response to the pandemic shock, but we now see increasing differentiation into two rough categories: ‘flippers ‘and ‘floppers’.

Outlook for selected EM central banks

FORECASTS – EM CENTRAL BANKS

Current policy rates

What we expect

Year-end policy rate Next moveComments

2021 2022 2023 Size Timing

‘Flippers’ In the face of rising inflation pressures, these central banks cannot stay in denial for too long in our view, and will therefore hike soon if they have not already.

Brazil 5.25% 7.50% 8.50% 6.50% +100bp Sep 2021The BCB now calls for above-neutral rates to ensure that the inflation target is achieved, and we think high

inflation expectations will drive further rate hikes.

Chile 1.50% 2.75% 4.00% 3.50% +75bp Oct 2021BCCh has little room to return to a gradual normalisation strategy, we think. Above-target inflation expectations, a

positive output gap, and high domestic policy uncertainty underpin our view.

Colombia 1.75% 3.00% 4.50% 4.75% +25bpSep

2021

In our view, BanRep will accelerate the pace of rate hikes from the October meeting in response to rising inflation

expectations and the fiscal and external imbalances.

Czech Rep. 0.75% 1.75% 2.50% 2.50% +50bp Sep 2021 We expect continued aggressive tightening to push the policy rate above pre-crisis levels next year.

Hungary 1.50% 2.25% 2.50% 2.25% +30bp Sep 2021 The tightening cycle will continue this year, we expect, but slow down considerably next year.

Mexico 4.50% 5.25% 6.00% 6.50% +25bp Sep 2021While we think Banxico will cite persistent inflation pressures and the unexpectedly fast narrowing of the output

gap as reasons to normalise rates, a gradual pace and split decisions are likely to add uncertainty.

Poland 0.10% 0.25% 0.75% 1.25% +15bp Nov 2021 We think the NBP will remain one of the most dovish EM central banks, with a reluctant tightening cycle.

Russia 6.50% 7.50% 8.50% 7.00% +50bp Sep 2021 Lingering inflation pressures look set to take rates closer to the level the CBR considers neutral.

South Africa 3.50% 3.75% 4.75% 5.50% +25bp Nov 2021 Normalisation will be slow, we think, due to benign inflation and economic growth challenges.

‘Floppers’ Some central banks will be keen to keep policy in accommodative territory for longer, we think

Indonesia 3.50% 3.50% 3.50% 4.50% – 2023

Low inflation and a Covid-19 surge – leading to lockdowns and supply disruptions across the region and delaying

the economic recovery – will mean ASEAN countries do not start to tighten policies until 2023, we think.Malaysia 1.75% 1.75% 1.75% 2.50% – 2023

Thailand 0.50% 0.50% 0.50% 1.50% – 2023

Others These central banks fall outside our two categories

Egypt 8.25% 7.75% 7.75% 7.25% −50bp Q4 2021Weak consumer and business demand conditions could lead to a further 50bp rate cut before year-end, we think,

enabled by easing inflation in Q4 on the back of favourable base effects.

India 4.00% 4.00% 4.50% 5.00% +50bp 2022At some point next year, once the economy recovers more fully, the RBI will need to start hiking rates on inflation

concerns, in our view. For now, it is likely to shrug off longstanding price pressures and macro imbalances.

South Korea 1.00% 1.25% 1.25% 1.50% +25bp Nov 2021The BoK has already started to hike rates and is set to do so again, as concerns about financial stability outweigh

those about near-term growth.

Turkey 19.00% 19.00% 13.50% 11.50% −300bp Q1 2022 Bucking the global trend, rate cuts will start early next year, we think, once inflation falls more consistently.

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

12E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

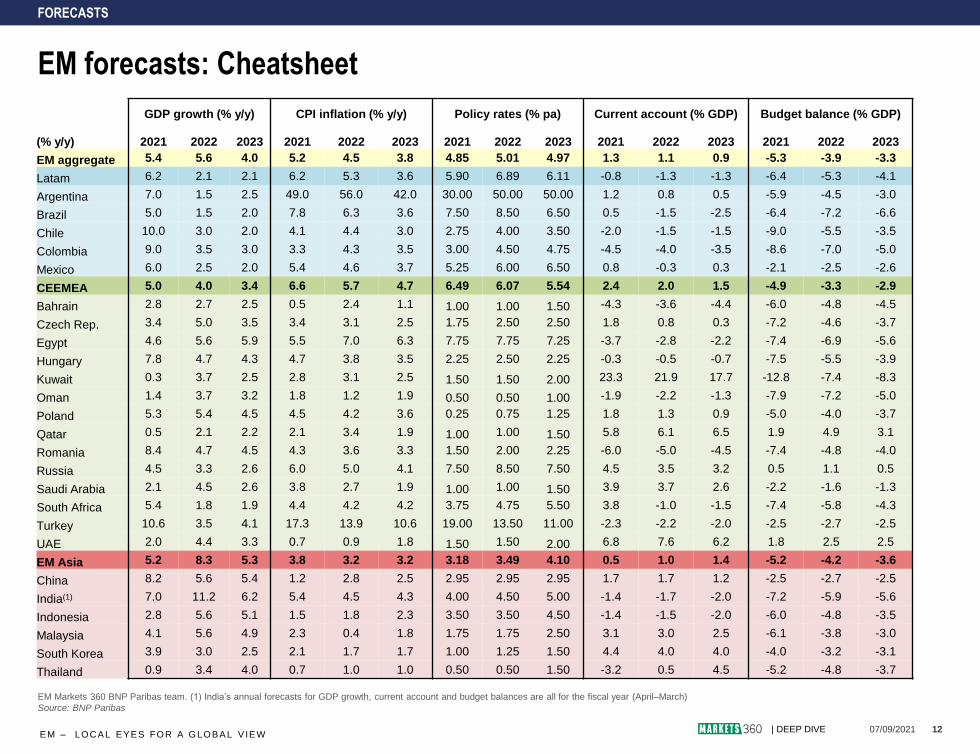

EM forecasts: Cheatsheet

EM Markets 360 BNP Paribas team. (1) India’s annual forecasts for GDP growth, current account and budget balances are all for the fiscal year (April–March)

Source: BNP Paribas

FORECASTS

GDP growth (% y/y) CPI inflation (% y/y) Policy rates (% pa) Current account (% GDP) Budget balance (% GDP)

(% y/y) 2021 2022 2023 2021 2022 2023 2021 2022 2023 2021 2022 2023 2021 2022 2023

EM aggregate 5.4 5.6 4.0 5.2 4.5 3.8 4.85 5.01 4.97 1.3 1.1 0.9 -5.3 -3.9 -3.3

Latam 6.2 2.1 2.1 6.2 5.3 3.6 5.90 6.89 6.11 -0.8 -1.3 -1.3 -6.4 -5.3 -4.1

Argentina 7.0 1.5 2.5 49.0 56.0 42.0 30.00 50.00 50.00 1.2 0.8 0.5 -5.9 -4.5 -3.0

Brazil 5.0 1.5 2.0 7.8 6.3 3.6 7.50 8.50 6.50 0.5 -1.5 -2.5 -6.4 -7.2 -6.6

Chile 10.0 3.0 2.0 4.1 4.4 3.0 2.75 4.00 3.50 -2.0 -1.5 -1.5 -9.0 -5.5 -3.5

Colombia 9.0 3.5 3.0 3.3 4.3 3.5 3.00 4.50 4.75 -4.5 -4.0 -3.5 -8.6 -7.0 -5.0

Mexico 6.0 2.5 2.0 5.4 4.6 3.7 5.25 6.00 6.50 0.8 -0.3 0.3 -2.1 -2.5 -2.6

CEEMEA 5.0 4.0 3.4 6.6 5.7 4.7 6.49 6.07 5.54 2.4 2.0 1.5 -4.9 -3.3 -2.9

Bahrain 2.8 2.7 2.5 0.5 2.4 1.1 1.00 1.00 1.50 -4.3 -3.6 -4.4 -6.0 -4.8 -4.5

Czech Rep. 3.4 5.0 3.5 3.4 3.1 2.5 1.75 2.50 2.50 1.8 0.8 0.3 -7.2 -4.6 -3.7

Egypt 4.6 5.6 5.9 5.5 7.0 6.3 7.75 7.75 7.25 -3.7 -2.8 -2.2 -7.4 -6.9 -5.6

Hungary 7.8 4.7 4.3 4.7 3.8 3.5 2.25 2.50 2.25 -0.3 -0.5 -0.7 -7.5 -5.5 -3.9

Kuwait 0.3 3.7 2.5 2.8 3.1 2.5 1.50 1.50 2.00 23.3 21.9 17.7 -12.8 -7.4 -8.3

Oman 1.4 3.7 3.2 1.8 1.2 1.9 0.50 0.50 1.00 -1.9 -2.2 -1.3 -7.9 -7.2 -5.0

Poland 5.3 5.4 4.5 4.5 4.2 3.6 0.25 0.75 1.25 1.8 1.3 0.9 -5.0 -4.0 -3.7

Qatar 0.5 2.1 2.2 2.1 3.4 1.9 1.00 1.00 1.50 5.8 6.1 6.5 1.9 4.9 3.1

Romania 8.4 4.7 4.5 4.3 3.6 3.3 1.50 2.00 2.25 -6.0 -5.0 -4.5 -7.4 -4.8 -4.0

Russia 4.5 3.3 2.6 6.0 5.0 4.1 7.50 8.50 7.50 4.5 3.5 3.2 0.5 1.1 0.5

Saudi Arabia 2.1 4.5 2.6 3.8 2.7 1.9 1.00 1.00 1.50 3.9 3.7 2.6 -2.2 -1.6 -1.3

South Africa 5.4 1.8 1.9 4.4 4.2 4.2 3.75 4.75 5.50 3.8 -1.0 -1.5 -7.4 -5.8 -4.3

Turkey 10.6 3.5 4.1 17.3 13.9 10.6 19.00 13.50 11.00 -2.3 -2.2 -2.0 -2.5 -2.7 -2.5

UAE 2.0 4.4 3.3 0.7 0.9 1.8 1.50 1.50 2.00 6.8 7.6 6.2 1.8 2.5 2.5

EM Asia 5.2 8.3 5.3 3.8 3.2 3.2 3.18 3.49 4.10 0.5 1.0 1.4 -5.2 -4.2 -3.6

China 8.2 5.6 5.4 1.2 2.8 2.5 2.95 2.95 2.95 1.7 1.7 1.2 -2.5 -2.7 -2.5

India(1) 7.0 11.2 6.2 5.4 4.5 4.3 4.00 4.50 5.00 -1.4 -1.7 -2.0 -7.2 -5.9 -5.6

Indonesia 2.8 5.6 5.1 1.5 1.8 2.3 3.50 3.50 4.50 -1.4 -1.5 -2.0 -6.0 -4.8 -3.5

Malaysia 4.1 5.6 4.9 2.3 0.4 1.8 1.75 1.75 2.50 3.1 3.0 2.5 -6.1 -3.8 -3.0

South Korea 3.9 3.0 2.5 2.1 1.7 1.7 1.00 1.25 1.50 4.4 4.0 4.0 -4.0 -3.2 -3.1

Thailand 0.9 3.4 4.0 0.7 1.0 1.0 0.50 0.50 1.50 -3.2 0.5 4.5 -5.2 -4.8 -3.7

07/09/2021

EMERGING MARKETS RESEARCH | COMMODITIES | G10FX | CROSS-ASSET | EQUITY DERIVATIVES | G10 INTEREST RATES | EMERGING MARKETS | MACRO QUANT & DERIVATIVES |

CREDIT

13E M – LOCA L E YE S FOR A GLOB A L V IE W

| DEEP DIVE

MARCELO CARVALHO *

Head of Emerging Markets ResearchBNP Paribas London Branch

LATAM APAC

Burak BaskurtChief EM Strategist

BNP Paribas London Branch

Luiz Eduardo PeixotoEconomist, Emerging MarketsBNP Paribas London Branch

Mohamed AbdelmeguidEconomist, MENABNP Paribas London Branch

Tatiana TchembarovaCEEMEA Credit AnalystBNP Paribas London Branch

Mikhail LiluashviliStrategist, CEEMEABNP Paribas London Branch

Jeffrey SchultzSenior Economist, South AfricaBNP Paribas South Africa Branch

Nic BorainPolitics Analyst, South AfricaBNP Paribas South Africa Branch

Michal DybulaChief Economist, Central

and Eastern EuropeBank BGŻ BNP Paribas SA

Wojciech Stepien CFAEconomist, Central and

Eastern EuropeBank BGŻ BNP Paribas SA

Hakan AklarChief Economist, TurkeyTürk Ekonomi Bankasi A.S.

Okan ErtemSenior Economist, TurkeyTürk Ekonomi Bankasi A.S.

Yasemin BasygitEconomist, TurkeyTürk Ekonomi Bankasi A.S.

Florencia VazquezEconomist, ArgentinaBNP Paribas Sucursal Buenos Aires

Felipe KleinEconomist, Colombia, ChileBNP Paribas Sucursal Buenos Aires

Pamela Diaz LoubetEconomist, MexicoBNP Paribas Securities Corp

Thais TeixeiraLatam Economics AssistantBanco BNP Paribas Brasil S.A.

Luca MaiaFX and Rates Strategist,

EM/LatamBanco BNP Paribas Brasil S.A.

Michelle HwangFX and Rates Strategist,

EM/LatamBanco BNP Paribas Brasil S.A.

Andre DigiacomoFX and Rates Strategist,

EM/LatamBanco BNP Paribas Brasil S.A.

Luryê BindaLatam Strategy AssistantBanco BNP Paribas Brasil S.A.

Siddharth Mathur

Head of Emerging Markets Research, Global

Markets APACBNP Paribas Singapore Branch

Arup RahaHead of ASEAN EconomicsBNP Paribas Singapore Branch

Michael LohEM Asia FX & Rates

StrategistBNP Paribas Singapore Branch

Hiroshi ShiraishiSenior Economist, South Korea & JapanBNP Paribas Securities (Japan) Limited

* reporting to Global Head of Markets 360

Gustavo ArrudaHead of Latam Research

Banco BNP Paribas Brasil S.A.

CEEMEA

OUR TEAM

07/09/2021

LEGAL NOTICEThis document or where relevant the document/communication to which this notice relates (all references in this notice to a document or communication shall be construed as referring to this document or such

document/communication related to this notice, as appropriate) has been written by our Strategist and Economist teams within the BNP Paribas group of companies (collectively “BNPP”); it does not purport to be an

exhaustive analysis, and may be subject to conflicts of interest resulting from their interaction with sales and trading which could affect the objectivity of this report. This document is non-independent research for the

purpose of the UK Financial Conduct Authority rules. For the purposes of the recast Markets in Financial Instruments Directive (2014/65/EU) (MiFID II), non-independent research constitutes a marketing communication. This

document is not investment research for the purposes of MiFID II. It has not been prepared in accordance with legal requirements designed to provide the independence of investment research, and is not subject to any

prohibition on dealing ahead of the dissemination of investment research.

The content in this document/communication may also contain “Research” as defined under the MiFID II unbundling rules. If the document/communication contains Research, it is intended for those firms who are either in

scope of the MiFID II unbundling rules and have signed up to one of the BNPP Global Markets Research packages, or firms that are out of scope of the MiFID II unbundling rules and therefore not required to pay for Research

under MiFID II. Please note that it is your firm’s responsibility to ensure that you do not view or use the Research content in this document if your firm has not signed up to one of the BNPP Global Markets Research

packages, except where your firm is out of scope of the MiFID II unbundling rules.

Please note any reference to EU legislation or requirements herein or in the document should be read as a reference to the relevant EU legislation or requirement and/or its UK equivalent legislation or requirement, as

appropriate, where applicable, and as the context requires. For example references to “MiFID II” means Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments

and amending Directive 2002/92/EC and Directive 2011/61/EU. and/or such directive as implemented in UK law through the relevant UK legislation and PRA and FCA rules as may give effect to Directive 2014/65/EU, as

appropriate, where applicable, and as the context requires.

STEER™ is a trade mark of BNPP.

MARKETS 360 is a trade mark of BNP Paribas

This document constitutes a marketing communication and has been prepared by BNPP for, and is directed at, (a) Professional Clients and Eligible Counterparties as defined by the recast Markets in Financial Instruments Directive

(2014/65/EU) (MiFID II), and (b) where relevant, persons who have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, and at

other persons to whom it may lawfully be communicated (together “Relevant Persons”) under the regulations of any relevant jurisdiction. Any investment or investment activity to which this document relates is available only to and will be

engaged in only with Relevant Persons. Any person who is not a Relevant Person should not act or rely on this document or its content.

Securities described herein or in the document may not be eligible for sale in all jurisdictions or to certain categories of investors.

The information and opinions contained in this document have been obtained from, or are based on, public sources believed to be reliable, but there is no guarantee of the accuracy, completeness or fitness for any particular purpose of such

information and such information may not have been independently verified by BNPP or by any person. None of BNPP, any of its subsidiary undertakings or affiliates or its members, directors, officers, agents or employees accepts any

responsibility or liability whatsoever or makes any representation or warranty, express or implied, as to the accuracy and completeness of the information or any opinions based thereon and contained in this document and it should not be

relied upon as such.

This document does not constitute or form any part of any offer to sell or issue and is not a solicitation of any offer to purchase any financial instrument, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on,

in connection with any contract or investment decision. To the extent that any transaction is subsequently entered into between the recipient and BNPP, such transaction will be entered into upon such terms as may be agreed by the parties in

the relevant documentation.

Information and opinions contained in this document are published for the information of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient, are subject to change

without notice and not intended to provide the sole basis of any evaluation of the instruments discussed herein or in the document. In providing this document, BNPP does not offer investment, financial, legal, tax or any other type of advice to,

nor has any fiduciary duties towards, recipients. Any reference to past performance is not indicative of future performance, which may be better or worse than prior results. Any hypothetical, past performance simulations are the result of

estimates made by BNPP, as of a given moment, on the basis of parameters, market conditions, and historical data selected by BNPP, and should not be used as guidance, in any way, of future performance. To the fullest extent permitted by

law, no BNPP group company accepts any liability whatsoever (including in negligence) for any direct or consequential loss arising from any use of or reliance on material contained in this document even where advised of the possibility of

such losses. All estimates and opinions included in this document are made as of the date of this document. Unless otherwise indicated in this document there is no intention to update this document.

BNPP may make a market in, or may, as principal or agent, buy or sell securities of any issuer or person mentioned in this document or derivatives thereon. Prices, yields and other similar information included in this document are included for

information purposes however numerous factors will affect market pricing at any particular time, such information may be subject to rapid change and there is no certainty that transactions could be executed at any specified price.

BNPP may have a financial interest in any issuer or person mentioned in this document, including a long or short position in their securities and/or options, futures or other derivative instruments based thereon, or vice versa. BNPP, including

its officers and employees may serve or have served as an officer, director or in an advisory capacity for any person mentioned in this document. BNPP may, from time to time, solicit, perform or have performed investment banking,

underwriting or other services (including acting as adviser, manager, underwriter or lender) within the last 12 months for any person referred to in this document. BNPP may be a party to an agreement with any person relating to the

production of this document. BNPP may to the extent permitted by law, have acted upon or used the information contained herein or in the document, or the analysis on which it was based, before the document was published. BNPP may

receive or intend to seek compensation for investment banking services in the next three months from or in relation to any person mentioned in this document. Any person mentioned in this document may have been provided with relevant

sections of this document prior to its publication in order to verify its factual accuracy.

This document is for information purposes only and there is no assurance that a transaction(s) will be entered into on such indicative terms. Any indicative price(s) contained herein or in the document have been prepared in good faith in

accordance with BNPP’s own internal models and calculation methods and/or are based on or use available price sources where considered relevant. Indicative price(s) based on different models or assumptions may yield different results.

Numerous factors may affect the price(s), which may or may not be taken into account. Therefore, these indicative price(s) may vary significantly from indicative price(s) obtained from other sources or market participants. BNPP expressly

disclaims any responsibility for the accuracy or completeness of its own internal models or calculation methods, the accuracy or reliability of any price sources used, any errors or omissions in computing or disseminating these indicative

price(s), and for any use you make of the price(s) provided. The indicative price(s) do not represent (i) the actual terms on which a new transaction could be entered into, (ii) the actual terms on which any existing transactions could be

unwound, (iii) the calculation or estimate of an amount that would be payable following an early termination of the transactions or (iv) the price(s) given to the transactions by BNPP in its own books of account for financial reporting, credit or

risk management purposes. As an investment bank with a wide range of activities, BNPP may face conflicts of interest, which are resolved under applicable legal provisions and internal guidelines. You should be aware, however, that BNPP

may engage in transactions in a manner inconsistent with the views expressed in this document, either for its own account or for the account of its clients.

This document may contain certain performance data based on back-testing, i.e. simulations of performance of a strategy, index or assets as if it had actually existed during a defined period of time. To the extent any such performance data is

included, the scenarios, simulations, development expectations and forecasts contained in this document are for illustrative purposes only. All estimates and opinions included in this document constitute the judgment of BNPP and its affiliates

as of the date of the document and may be subject to change without notice. This type of information has inherent limitations which recipients must consider carefully. While the information has been prepared in good faith in accordance with

BNPP’s own internal models and other relevant sources, an analysis based on different models or assumptions may yield different results. Unlike actual performance records, simulated performance returns or scenarios may not necessarily

reflect certain market factors such as liquidity constraints, fees and transactions costs. Actual historical or back tested past performance does not constitute an indication of future results or performance.

This document is only intended to generate discussion regarding particular products and investments and is subject to change or may be discontinued. We are willing to discuss it with you on the understanding that you have sufficient

knowledge, experience and professional advice to understand and make your own independent evaluation of the merits and risk of the information and any proposed structures. The information contained herein or in the document is not and

under no circumstances is to be construed as, a prospectus, an advertisement, a public offering, an offer to sell securities described herein or in the document, or solicitation of an offer to buy securities described herein or in the document, in

Canada, the U.S. or any other province or territory nor shall it be deemed to provide investment, tax, accounting or other advice. Transactions involving the product(s) described in this document may involve a high degree of risk and the value

of such transactions may be highly volatile. Such risks include, without limitation, risk of adverse or unanticipated market developments, risk of counterparty or issuer default, risk of adverse events involving any underlying reference obligation

or entity and risk of illiquidity. In certain transactions, counterparties may lose their entire investment or incur an unlimited loss.

07/09/2021

LEGAL NOTICEThe information relating to performance contained in this document is illustrative and no assurance is given that any indicated returns, performance or results will be achieved. Moreover, past performance is not indicative of future results.

Information herein or in the document is believed reliable but BNPP and its affiliates do not warrant or guarantee its completeness or accuracy. All information, terms and pricing set forth herein or in the document reflect our judgment at the

date and time hereof and are subject to change without notice. In the event that we were to enter into a transaction with you, we will do so as principal (and not as agent or in any other capacity, including, without limitation, as your fiduciary,

advisor or otherwise). Only in the event of a potential transaction will an offering document be prepared, in which case, you should refer to the prospectus or offering document relating to the above potential transaction which includes

important information, including risk factors that relate to an investment in the product(s) described herein or in the document.

Prior to transacting, you should ensure that you fully understand (either on your own or through the use of independent expert advisors) the terms of the transaction and any legal, tax and accounting considerations applicable to them. You

should also consult with independent advisors and consultants (including, without limitation, legal counsel) to determine whether entering into any securities transactions contemplated herein or in the document would be contrary to local

laws. Unless the information contained herein or document/communication to which this notice relates is made publicly available by BNPP, it is provided to you on a strictly confidential basis and where it is provided to you on a strictly

confidential basis you agree that it may not be copied, reproduced or otherwise distributed by you, whether in whole or in part (other than to your professional advisers), without our prior written consent.. Neither we, nor any of our affiliates,

nor any of their respective directors, partners, officers, employees or representatives accepts any liability whatsoever for any direct or consequential loss arising from any use of this document or its content; and any of the foregoing may from

time to time act as manager, co-manager or underwriter of a public offering or otherwise, in the capacity of principal or agent, deal in, hold or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to

the securities or related derivatives that are discussed herein or in the document. BNPP and its affiliates may (or may in the future) hold a position or act as a market maker in the financial instruments discussed, or act as an advisor, manager,

underwriter or lender to such issuer. In no circumstances shall BNPP or its affiliates be obliged to disclose any information that it has received on a confidential basis or to disclose the existence thereof.

The information presented herein or in the document does not comprise a prospectus of securities for the purposes of EU Regulation (EU) 2017/1129 (as amended from time to time).

This document was produced by a BNPP group company. This document is for the use of intended recipients and may not be reproduced (in whole or in part) or delivered or transmitted to any other person without the prior written consent of

BNPP. By accepting or accessing this document you agree to this.

For country- specific disclaimers (United States, Canada, United Kingdom, France, Germany, Belgium, Ireland, Italy, Netherlands, Portugal, Spain, Switzerland, Brazil, Turkey, Israel, Bahrain, South Africa, Australia, China, Hong Kong,

India, Indonesia, Japan, Malaysia, Singapore, South Korea, Taiwan, Thailand, Vietnam) please type the following URL to access our legal notices:

https://globalmarkets.bnpparibas.com/gm/home/Markets_360_Country_Specific_Notices.pdf

Some or all of the information contained in this document may already have been published on MARKETS 360TM Portal

© BNPP (2021). All rights reserved.

IMPORTANT DISCLOSURES by producers and disseminators of investment recommendations for the purposes of the Market Abuse Regulation:

Although the disclosures provided herein or in the document have been prepared on the basis of information we believe to be accurate, we do not guarantee the accuracy, completeness or reasonableness of any such disclosures. The

disclosures provided herein or in the document have been prepared in good faith and are based on internal calculations, which may include, without limitation, rounding and approximations.

BNPP and/or its affiliates may be a market maker or liquidity provider in financial instruments of the issuer mentioned in the recommendation.

BNPP and/or its affiliates may provide such services as described in Sections A and B of Annex I of MiFID II (Directive 2014/65/EU), to the Issuer to which this investment recommendation relates. However, BNPP is unable to disclose

specific relationships/agreements due to client confidentiality obligations.

Section A and B services include A. Investment services and activities: (1) Reception and transmission of orders in relation to one or more financial instruments; (2) Execution of orders on behalf of clients; (3) Dealing on own account; (4)

Portfolio management; (5) Investment advice; (6) Underwriting of financial instruments and/or placing of financial instruments on a firm commitment basis; (7) Placing of financial instruments without a firm commitment basis; (8) Operation of

an MTF; and (9) Operation of an OTF. B. Ancillary services: (1) Safekeeping and administration of financial instruments for the account of clients, including custodianship and related services such as cash/collateral management and

excluding maintaining securities accounts at the top tier level; (2) Granting credits or loans to an investor to allow him to carry out a transaction in one or more financial instruments, where the firm granting the credit or loan is involved in the

transaction; (3) Advice to undertakings on capital structure, industrial strategy and related matters and advice and services relating to mergers and the purchase of undertakings; (4) Foreign exchange services where these are connected to

the provision of investment services; (5) Investment research and financial analysis or other forms of general recommendation relating to transactions in financial instruments; (6) Services related to underwriting; and (7) Investment services

and activities as well as ancillary services of the type included under Section A or B of Annex 1 related to the underlying of the derivatives included under points (5), (6), (7) and (10) of Section C (detailing the MiFID II Financial Instruments)

where these are connected to the provision of investment or ancillary services.

BNPP and/or its affiliates do not, as a matter of policy, permit pre-arrangements with issuers to produce recommendations. BNPP and/or its affiliates as a matter of policy do not permit issuers to review or see unpublished recommendations.

BNPP and/or its affiliates acknowledge the importance of conflicts of interest prevention and have established robust policies and procedures and maintain effective organisational structure to prevent and avoid conflicts of interest that could

impair the objectivity of this recommendation including, but not limited to, information barriers, personal account dealing restrictions and management of inside information.

BNPP and/or its affiliates understand the importance of protecting confidential information and maintain a “need to know” approach when dealing with any confidential information. Information barriers are a key arrangement we have in place

in this regard. Such arrangements, along with embedded policies and procedures, provide that information held in the course of carrying on one part of its business to be withheld from and not to be used in the course of carrying on another

part of its business. It is a way of managing conflicts of interest whereby the business of the bank is separated by physical and non-physical information barriers. The Control Room manages this information flow between different areas of the

bank where confidential information including inside information and proprietary information is safeguarded. There is also a conflict clearance process before getting involved in a deal or transaction.

In addition, there is a mitigation measure to manage conflicts of interest for each transaction with controls put in place to restrict the information flow, involvement of personnel and handling of client relations between each transaction in such

a way that the different interests are appropriately protected. Gifts and Entertainment policy is to monitor physical gifts, benefits and invitation to events that is in line with the firm policy and Anti-Bribery regulations. BNPP maintains several

policies with respect to conflicts of interest including our Personal Account Dealing and Outside Business Interests policies which sit alongside our general Conflicts of Interest Policy, along with several policies that the firm has in place to

prevent and avoid conflicts of interest.

The remuneration of the individual producer of the investment recommendation may be linked to trading or any other fees in relation to their global business line received by BNPP and/or affiliates.

IMPORTANT DISCLOSURES by disseminators of investment recommendations for the purposes of the Market Abuse Regulation:

Where relevant, the BNPP disseminator of the investment recommendation is identified in the document/communication including information regarding the relevant competent authorities which regulate the disseminator. The name of the

individual producer within BNPP or an affiliate and the legal entity the individual producer is associated with is identified where relevant, in the document/communication. The date and time of the first dissemination of this investment

recommendation by BNPP or an affiliate is addressed where relevant, in the document/communication. Where this investment recommendation is communicated by Bloomberg chat or by email by an individual within BNPP or an affiliate, the

date and time of the dissemination by the relevant individual is contained, where relevant, in the communication by that individual disseminator.

The disseminator and producer of the investment recommendations are part of the same group, i.e. the BNPP group. The relevant Market Abuse Regulation disclosures required to be made by producers and disseminators of investment

recommendations are provided by the producer for and on behalf of the BNPP Group legal entities disseminating those recommendations and the same disclosures also apply to the disseminator.

If an investment recommendation is disseminated by an individual within BNPP or an affiliate via Bloomberg chat or email, the disseminator’s job title is available in their Bloomberg profile or bio. If an investment recommendation is

disseminated by an individual within BNPP or an affiliate via email, the individual disseminator’s job title is available in their email signature.

For further details on the basis of recommendation specific disclosures available at this link (e.g. valuations or methodologies, and the underlying assumptions, used to evaluate financial instruments or issuers, interests or conflicts that could

impair objectivity recommendations or to 12 month history of recommendations history) are available at MARKETS 360TM Portal. If you are unable to access the website please contact your BNPP representative for a copy of this document.