Embed Size (px)

Citation preview

11

Emerging Markets in FocusFIDELITY QUARTERLY INTERNATIONAL UPDATE

Presented byMatt GodfreyVice President, Investment Product

Jake WeinsteinSenior Analyst, Asset Allocation Research

Heather KnightRegional Brokerage Consultant, Personal Investing

September 2016

22

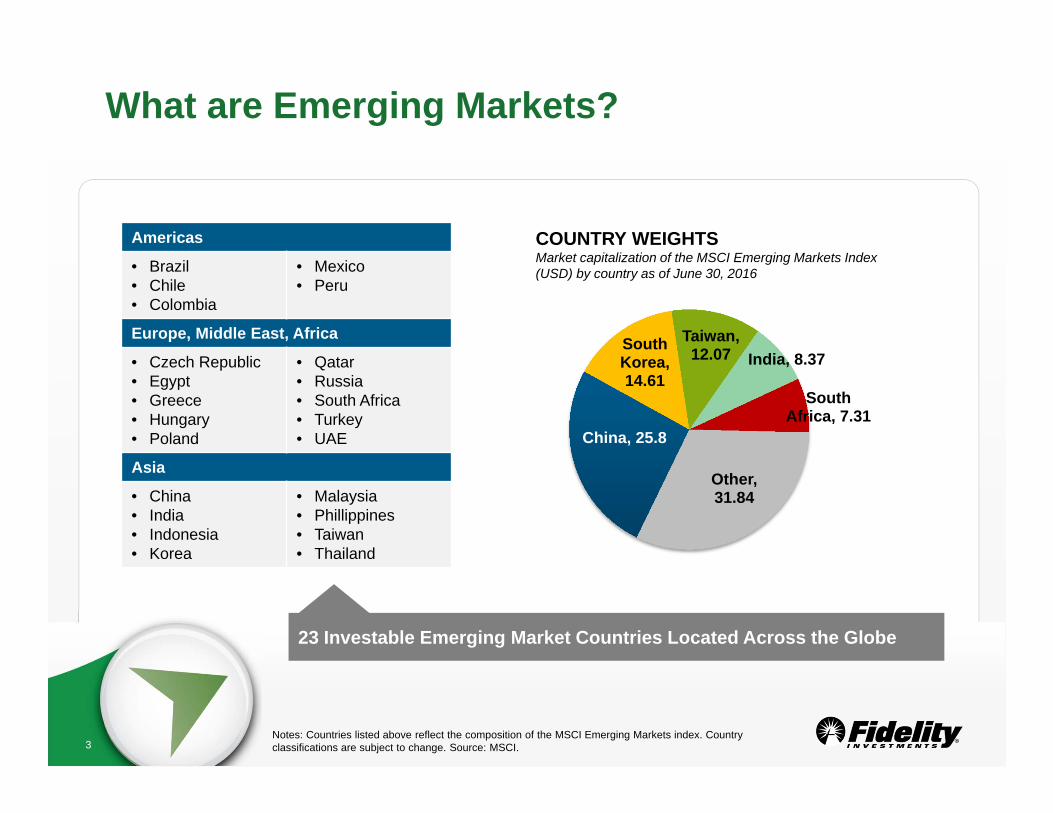

What are Emerging Markets?

Japan, France, United Kingdom

• Established economies• Industrialized• Robust infrastructure• Higher GDP

Developed International

Markets

Brazil, Russia, India, China

• Rapid growth and industrialization• Formalization of industries• Increasing middle class, urbanization• Higher GDP growth

Emerging Markets

33

What are Emerging Markets?

China, 25.8

South Korea, 14.61

Taiwan, 12.07 India, 8.37

South Africa, 7.31

Other, 31.84

Americas

• Brazil• Chile• Colombia

• Mexico• Peru

Europe, Middle East, Africa

• Czech Republic• Egypt• Greece• Hungary• Poland

• Qatar• Russia• South Africa• Turkey• UAE

Asia

• China• India• Indonesia• Korea

• Malaysia• Phillippines• Taiwan• Thailand

COUNTRY WEIGHTSMarket capitalization of the MSCI Emerging Markets Index (USD) by country as of June 30, 2016

Notes: Countries listed above reflect the composition of the MSCI Emerging Markets index. Country classifications are subject to change. Source: MSCI.

23 Investable Emerging Market Countries Located Across the Globe

44

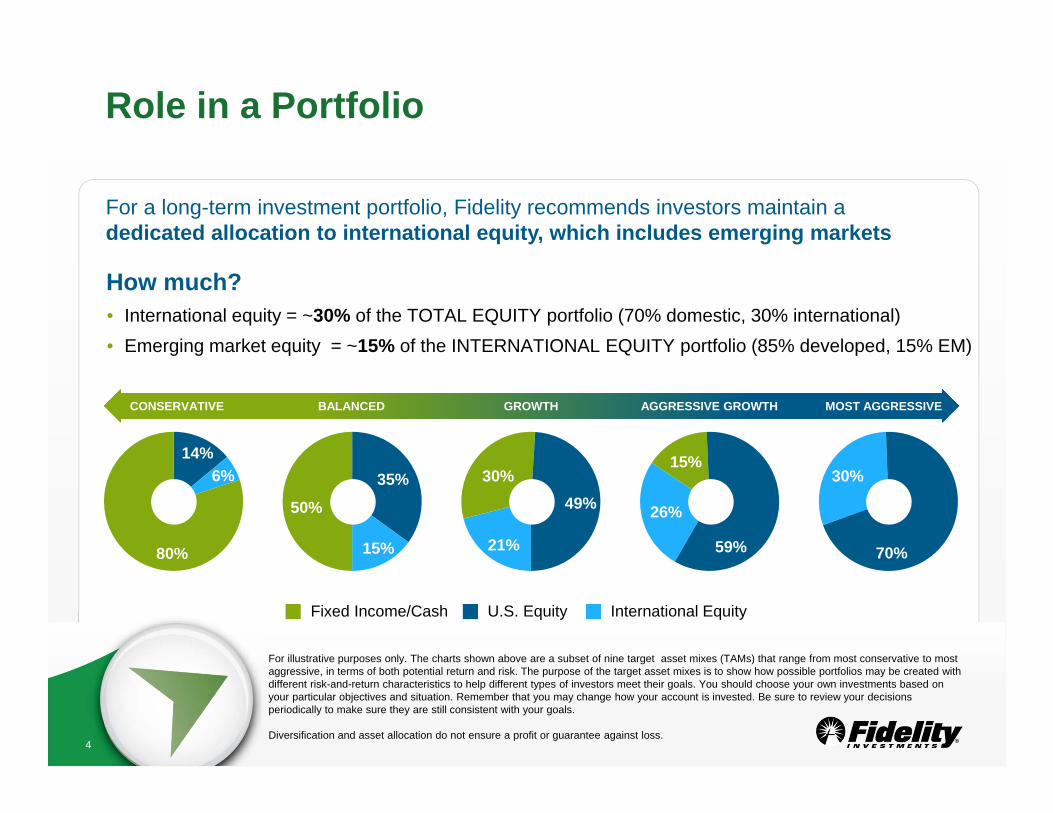

Role in a Portfolio

For illustrative purposes only. The charts shown above are a subset of nine target asset mixes (TAMs) that range from most conservative to most aggressive, in terms of both potential return and risk. The purpose of the target asset mixes is to show how possible portfolios may be created with different risk-and-return characteristics to help different types of investors meet their goals. You should choose your own investments based on your particular objectives and situation. Remember that you may change how your account is invested. Be sure to review your decisions periodically to make sure they are still consistent with your goals.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

For a long-term investment portfolio, Fidelity recommends investors maintain a dedicated allocation to international equity, which includes emerging markets

How much? • International equity = ~30% of the TOTAL EQUITY portfolio (70% domestic, 30% international)• Emerging market equity = ~15% of the INTERNATIONAL EQUITY portfolio (85% developed, 15% EM)

U.S. Equity International Equity

35%

15%

50%

21%

30%49% 26%

15%

59%

30%

70%

14%6%

80%

CONSERVATIVE BALANCED GROWTH AGGRESSIVE GROWTH MOST AGGRESSIVE

Fixed Income/Cash

55

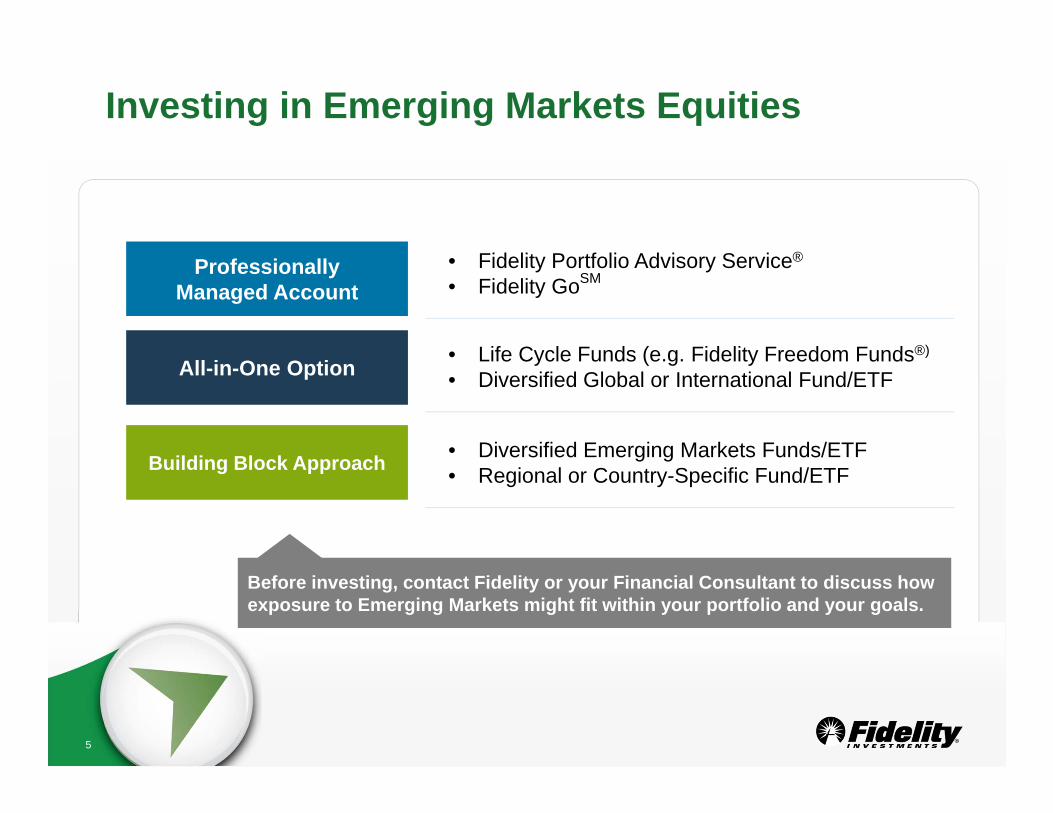

Investing in Emerging Markets Equities

• Fidelity Portfolio Advisory Service®

• Fidelity GoSMProfessionally Managed Account

Before investing, contact Fidelity or your Financial Consultant to discuss how exposure to Emerging Markets might fit within your portfolio and your goals.

• Life Cycle Funds (e.g. Fidelity Freedom Funds®)

• Diversified Global or International Fund/ETFAll-in-One Option

• Diversified Emerging Markets Funds/ETF• Regional or Country-Specific Fund/ETFBuilding Block Approach

66

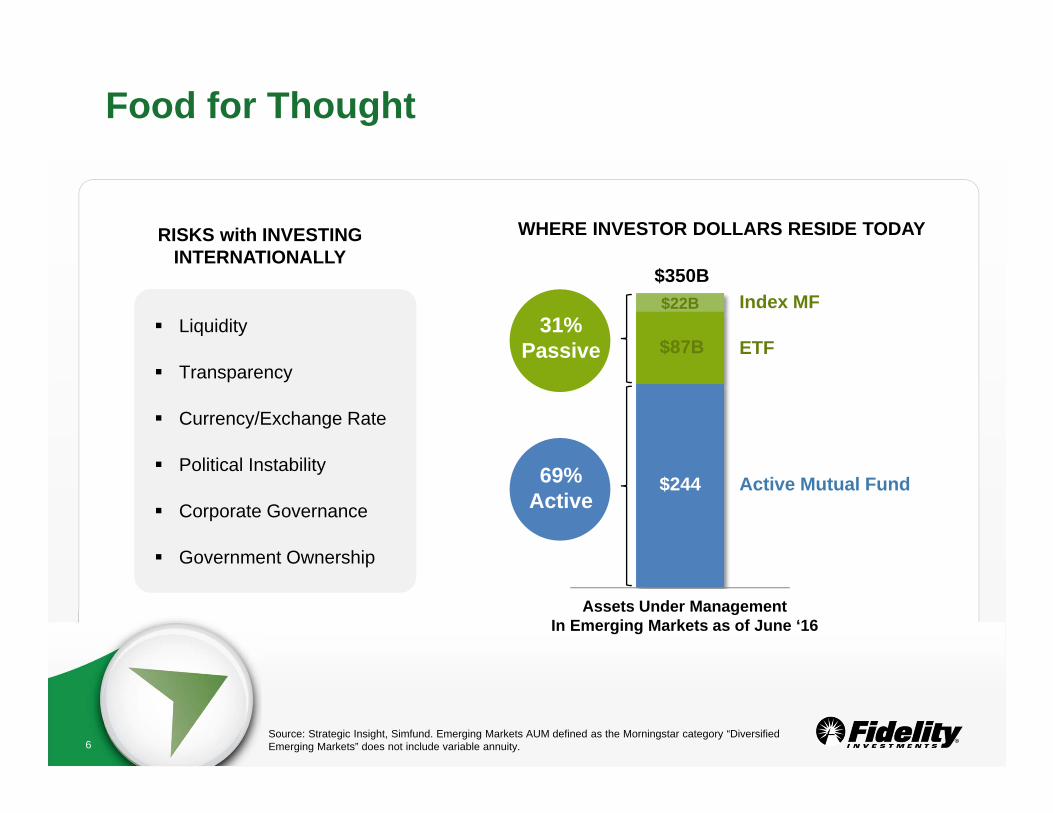

Food for Thought

Liquidity

Transparency

Currency/Exchange Rate

Political Instability

Corporate Governance

Government Ownership

Liquidity

Transparency

Currency/Exchange Rate

Political Instability

Corporate Governance

Government Ownership

RISKS with INVESTING INTERNATIONALLY

WHERE INVESTOR DOLLARS RESIDE TODAY

Assets Under ManagementIn Emerging Markets as of June ‘16

$350BIndex MF

31% Passive ETF

Active Mutual Fund69% Active

Source: Strategic Insight, Simfund. Emerging Markets AUM defined as the Morningstar category “Diversified Emerging Markets” does not include variable annuity.

$87B

$22B

$244

7

Emerging Markets: Improved Cyclical Trends After a Long Dry SpellJake WeinsteinSenior Analyst, Asset Allocation Research

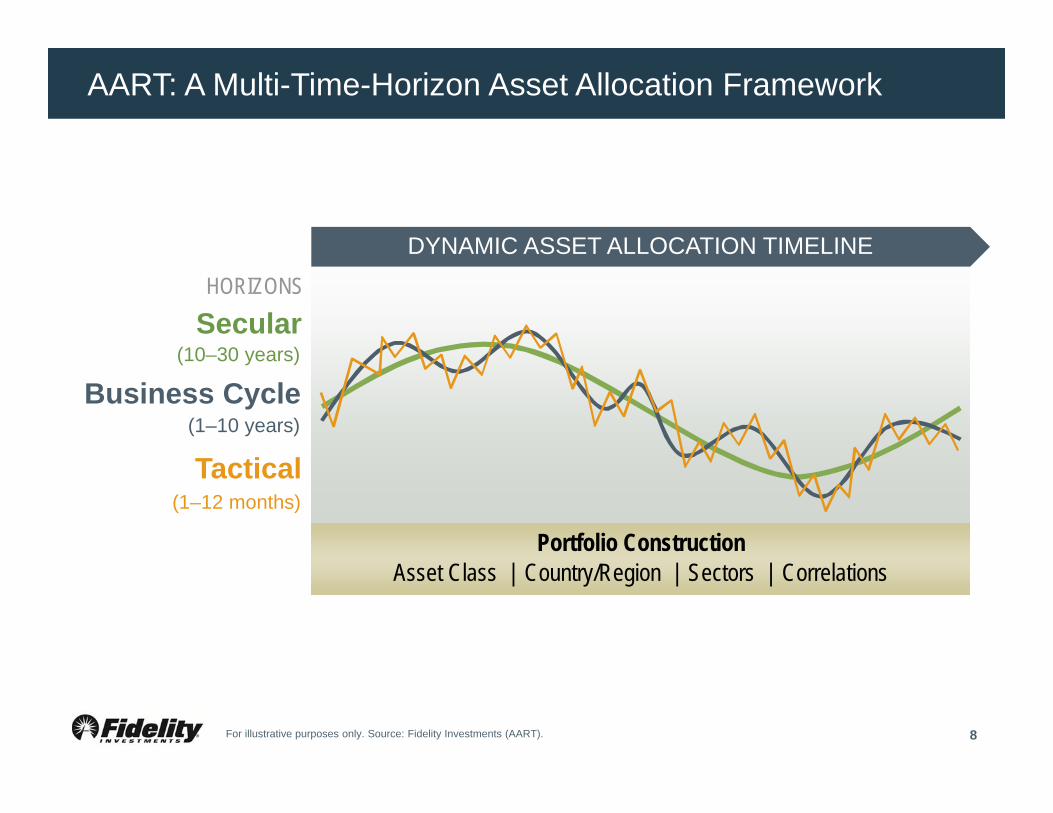

AART: A Multi-Time-Horizon Asset Allocation Framework

8

DYNAMIC ASSET ALLOCATION TIMELINE

Business Cycle(10–30 years)

SecularHORIZONS

(1–10 years)

Tactical(1–12 months)

Portfolio ConstructionAsset Class | Country/Region | Sectors | Correlations

For illustrative purposes only. Source: Fidelity Investments (AART).

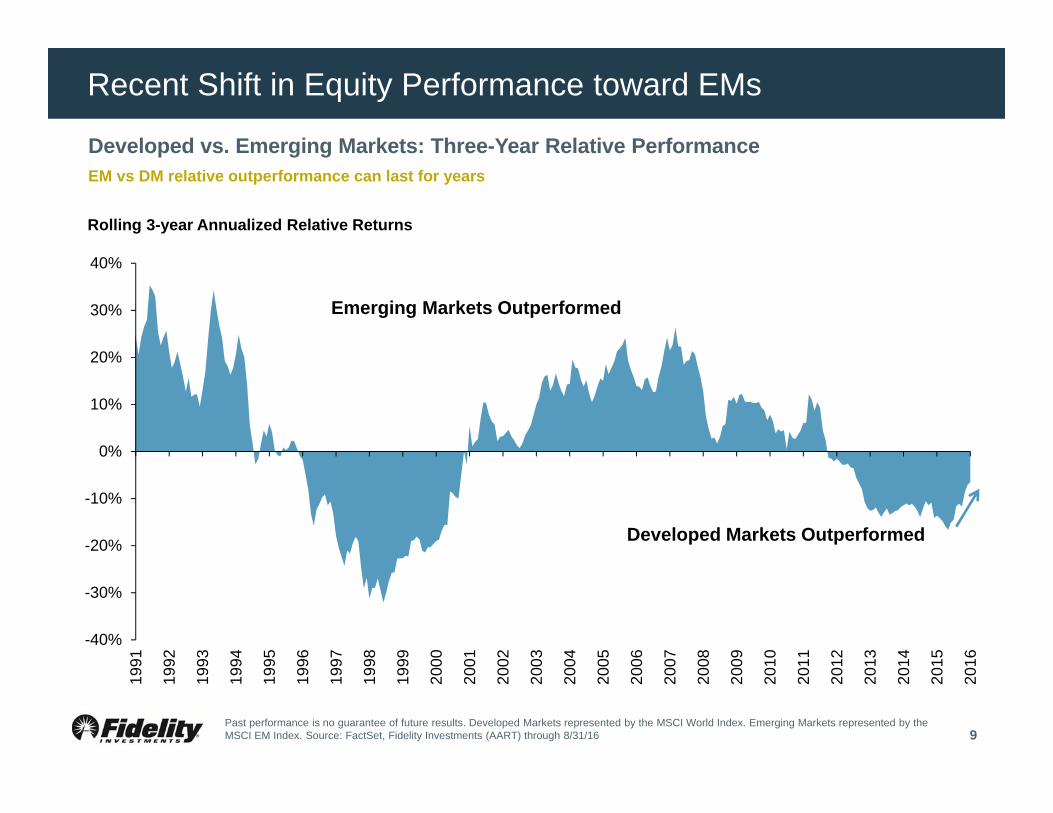

Recent Shift in Equity Performance toward EMs

9

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Developed Markets Outperformed

Emerging Markets Outperformed

Developed vs. Emerging Markets: Three-Year Relative Performance

Rolling 3-year Annualized Relative Returns

Past performance is no guarantee of future results. Developed Markets represented by the MSCI World Index. Emerging Markets represented by the MSCI EM Index. Source: FactSet, Fidelity Investments (AART) through 8/31/16

EM vs DM relative outperformance can last for years

Keys to Emerging Market Performance

10

• China’s stabilization

• Positive “base effect” of global stabilization

• Improved cyclical outlook

• Easier financial conditions – currency, rates, credit spreads, equity prices

• Long-term secular trends

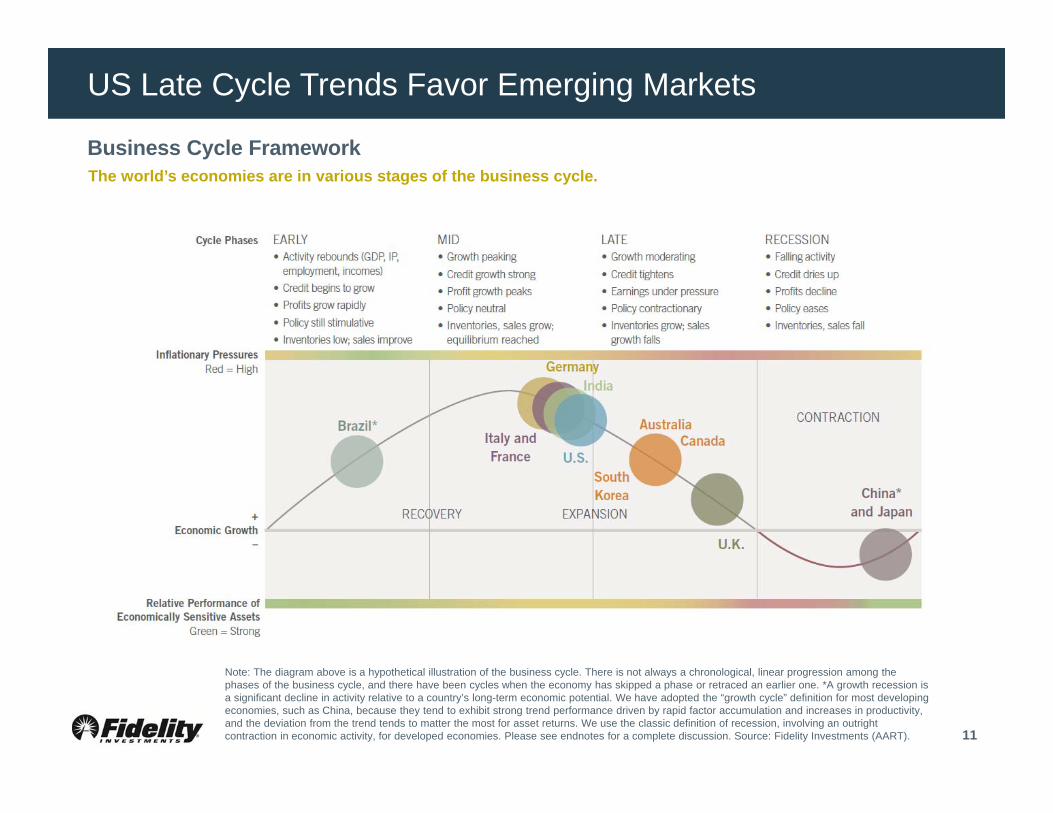

US Late Cycle Trends Favor Emerging Markets

11

Business Cycle FrameworkThe world’s economies are in various stages of the business cycle.

Note: The diagram above is a hypothetical illustration of the business cycle. There is not always a chronological, linear progression among the phases of the business cycle, and there have been cycles when the economy has skipped a phase or retraced an earlier one. *A growth recession is a significant decline in activity relative to a country’s long-term economic potential. We have adopted the “growth cycle” definition for most developing economies, such as China, because they tend to exhibit strong trend performance driven by rapid factor accumulation and increases in productivity, and the deviation from the trend tends to matter the most for asset returns. We use the classic definition of recession, involving an outright contraction in economic activity, for developed economies. Please see endnotes for a complete discussion. Source: Fidelity Investments (AART).

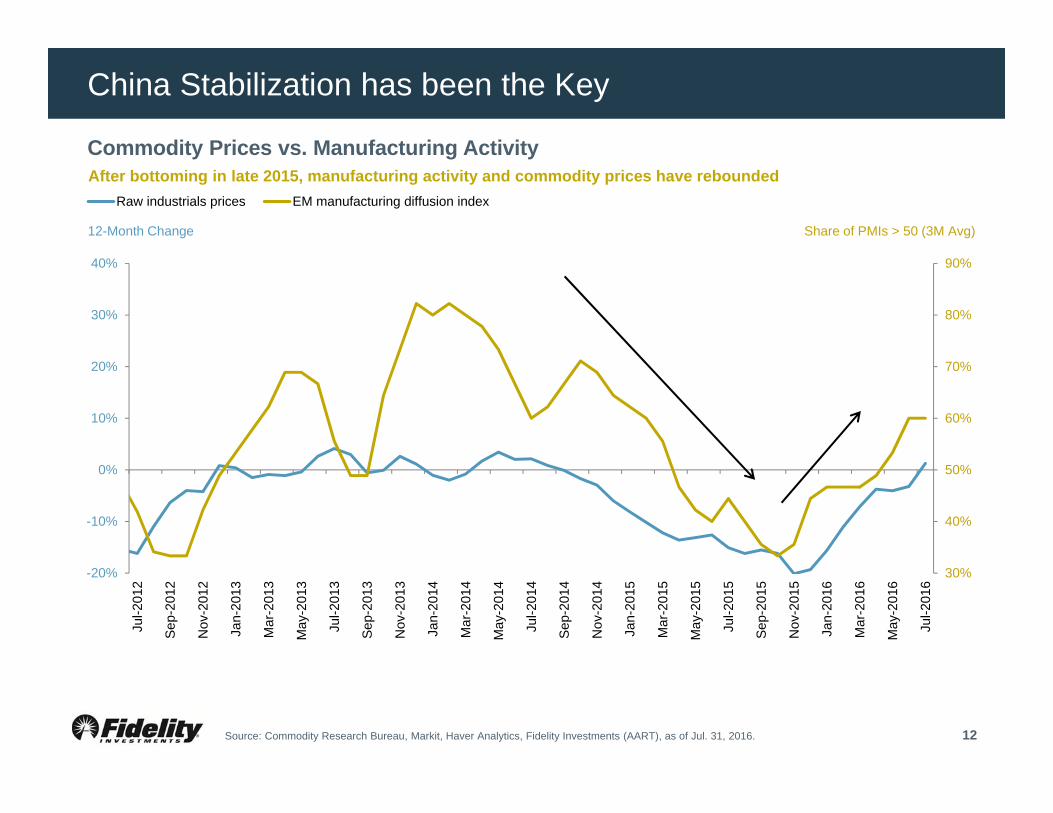

China Stabilization has been the Key

12

Commodity Prices vs. Manufacturing Activity

Source: Commodity Research Bureau, Markit, Haver Analytics, Fidelity Investments (AART), as of Jul. 31, 2016.

After bottoming in late 2015, manufacturing activity and commodity prices have rebounded

12-Month Change Share of PMIs > 50 (3M Avg)

30%

40%

50%

60%

70%

80%

90%

-20%

-10%

0%

10%

20%

30%

40%

Jul-2

012

Sep

-201

2

Nov

-201

2

Jan-

2013

Mar

-201

3

May

-201

3

Jul-2

013

Sep

-201

3

Nov

-201

3

Jan-

2014

Mar

-201

4

May

-201

4

Jul-2

014

Sep

-201

4

Nov

-201

4

Jan-

2015

Mar

-201

5

May

-201

5

Jul-2

015

Sep

-201

5

Nov

-201

5

Jan-

2016

Mar

-201

6

May

-201

6

Jul-2

016

Raw industrials prices EM manufacturing diffusion index

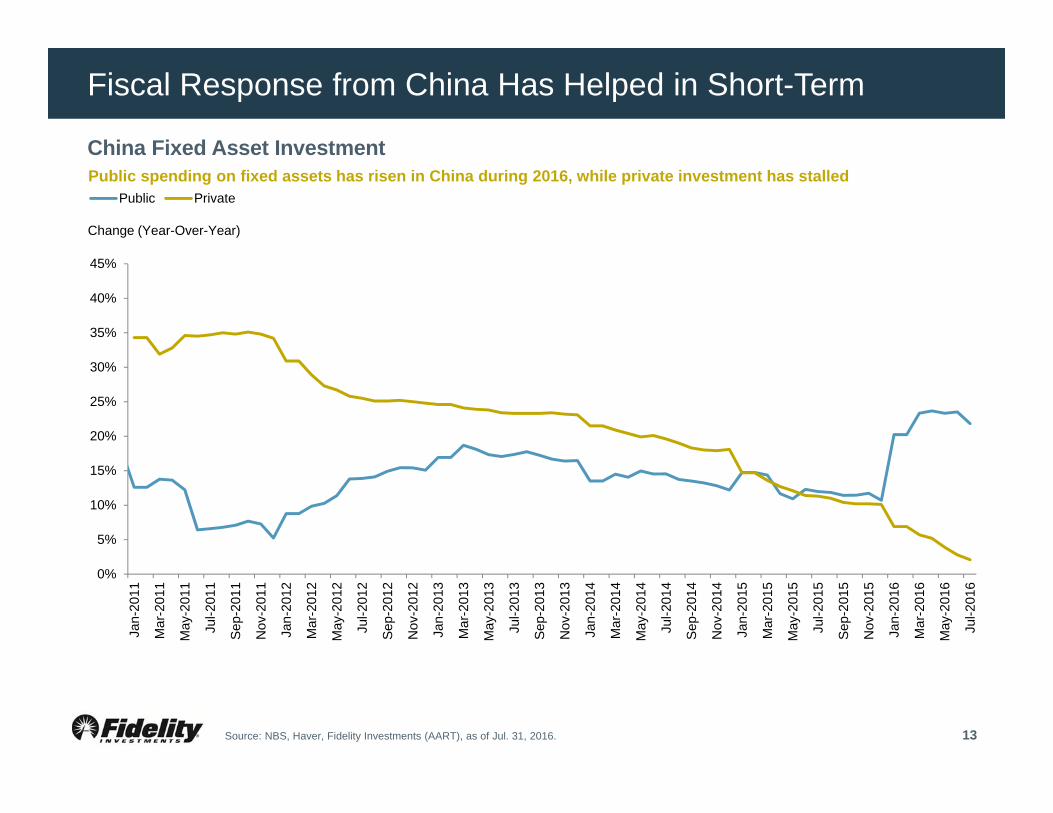

Fiscal Response from China Has Helped in Short-Term

13

China Fixed Asset Investment

Source: NBS, Haver, Fidelity Investments (AART), as of Jul. 31, 2016.

Public spending on fixed assets has risen in China during 2016, while private investment has stalled

Change (Year-Over-Year)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Jan-

2011

Mar

-201

1

May

-201

1

Jul-2

011

Sep

-201

1

Nov

-201

1

Jan-

2012

Mar

-201

2

May

-201

2

Jul-2

012

Sep

-201

2

Nov

-201

2

Jan-

2013

Mar

-201

3

May

-201

3

Jul-2

013

Sep

-201

3

Nov

-201

3

Jan-

2014

Mar

-201

4

May

-201

4

Jul-2

014

Sep

-201

4

Nov

-201

4

Jan-

2015

Mar

-201

5

May

-201

5

Jul-2

015

Sep

-201

5

Nov

-201

5

Jan-

2016

Mar

-201

6

May

-201

6

Jul-2

016

Public Private

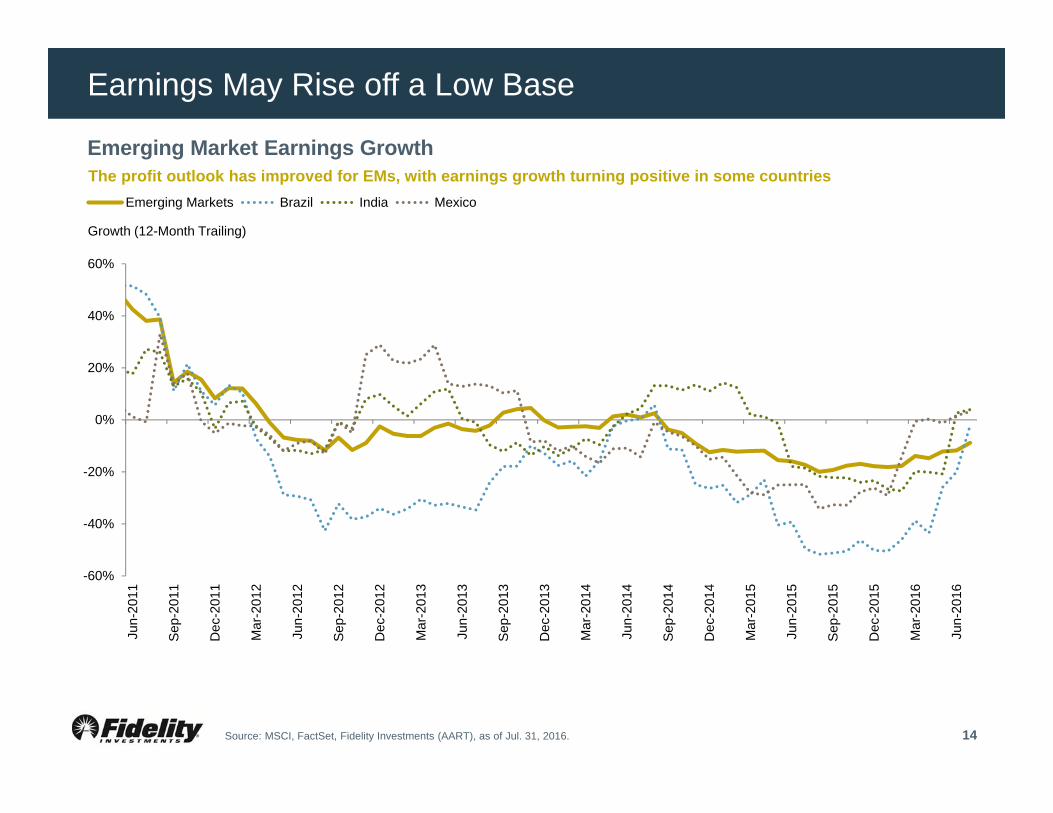

Earnings May Rise off a Low Base

14

Emerging Market Earnings Growth

Source: MSCI, FactSet, Fidelity Investments (AART), as of Jul. 31, 2016.

The profit outlook has improved for EMs, with earnings growth turning positive in some countries

Growth (12-Month Trailing)

-60%

-40%

-20%

0%

20%

40%

60%

Jun-

2011

Sep

-201

1

Dec

-201

1

Mar

-201

2

Jun-

2012

Sep

-201

2

Dec

-201

2

Mar

-201

3

Jun-

2013

Sep

-201

3

Dec

-201

3

Mar

-201

4

Jun-

2014

Sep

-201

4

Dec

-201

4

Mar

-201

5

Jun-

2015

Sep

-201

5

Dec

-201

5

Mar

-201

6

Jun-

2016

Emerging Markets Brazil India Mexico

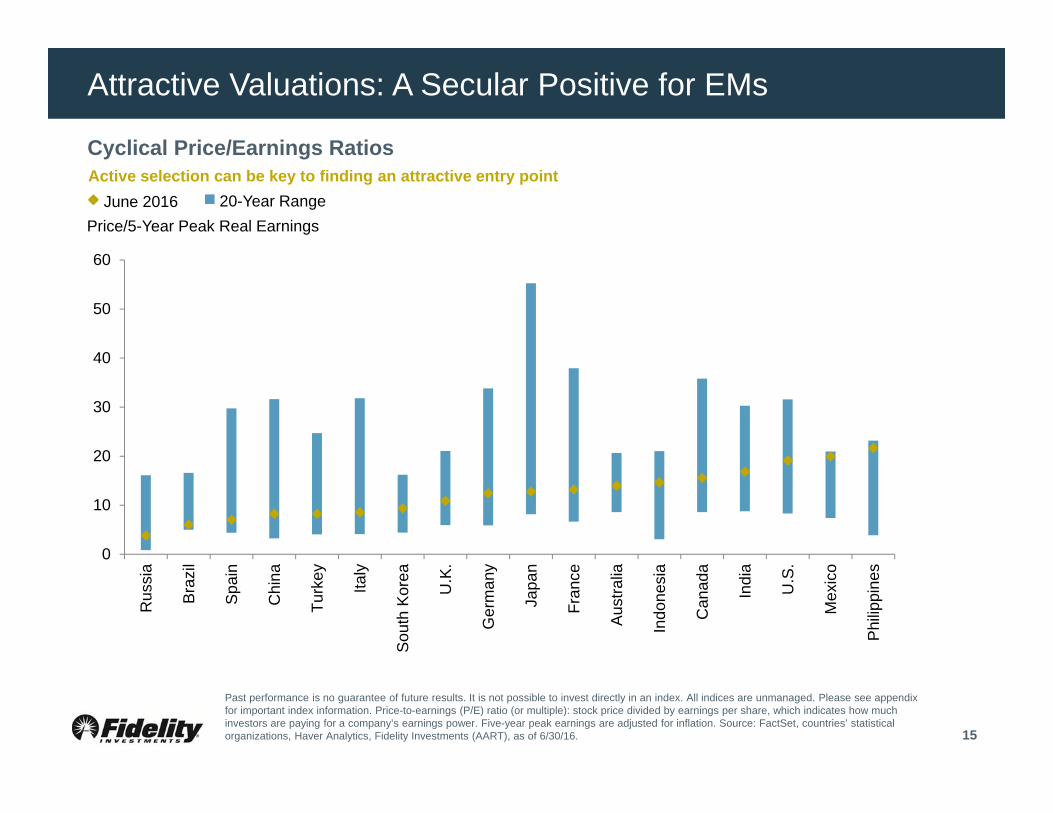

Attractive Valuations: A Secular Positive for EMs

15

0

10

20

30

40

50

60

Rus

sia

Bra

zil

Spai

n

Chi

na

Turk

ey

Italy

Sou

th K

orea

U.K

.

Ger

man

y

Japa

n

Fran

ce

Aus

tralia

Indo

nesi

a

Can

ada

Indi

a

U.S

.

Mex

ico

Phi

lippi

nes

Cyclical Price/Earnings Ratios

Price/5-Year Peak Real EarningsJune 2016 20-Year Range

Past performance is no guarantee of future results. It is not possible to invest directly in an index. All indices are unmanaged. Please see appendix for important index information. Price-to-earnings (P/E) ratio (or multiple): stock price divided by earnings per share, which indicates how much investors are paying for a company’s earnings power. Five-year peak earnings are adjusted for inflation. Source: FactSet, countries’ statistical organizations, Haver Analytics, Fidelity Investments (AART), as of 6/30/16.

Active selection can be key to finding an attractive entry point

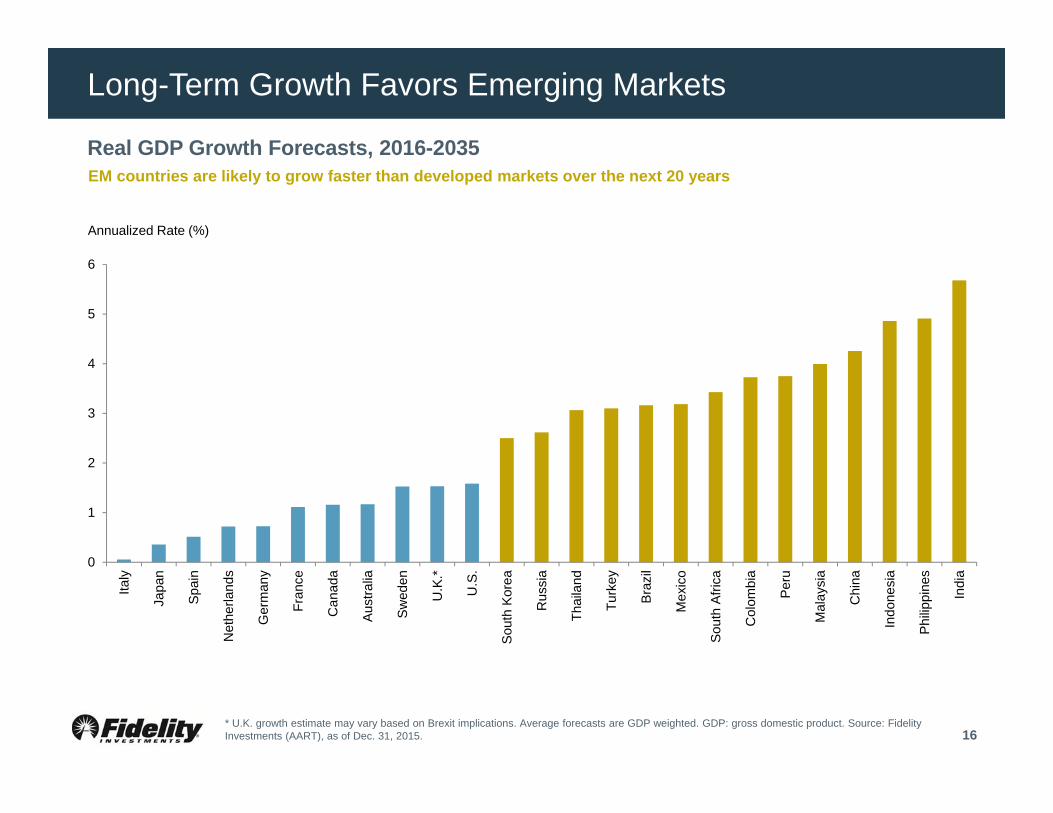

Long-Term Growth Favors Emerging Markets

16

Real GDP Growth Forecasts, 2016-2035

* U.K. growth estimate may vary based on Brexit implications. Average forecasts are GDP weighted. GDP: gross domestic product. Source: FidelityInvestments (AART), as of Dec. 31, 2015.

EM countries are likely to grow faster than developed markets over the next 20 years

Annualized Rate (%)

0

1

2

3

4

5

6

Italy

Japa

n

Spa

in

Net

herla

nds

Ger

man

y

Fran

ce

Can

ada

Aus

tralia

Sw

eden

U.K

.*

U.S

.

Sou

th K

orea

Rus

sia

Thai

land

Turk

ey

Braz

il

Mex

ico

Sou

th A

frica

Col

ombi

a

Peru

Mal

aysi

a

Chi

na

Indo

nesi

a

Phi

lippi

nes

Indi

a

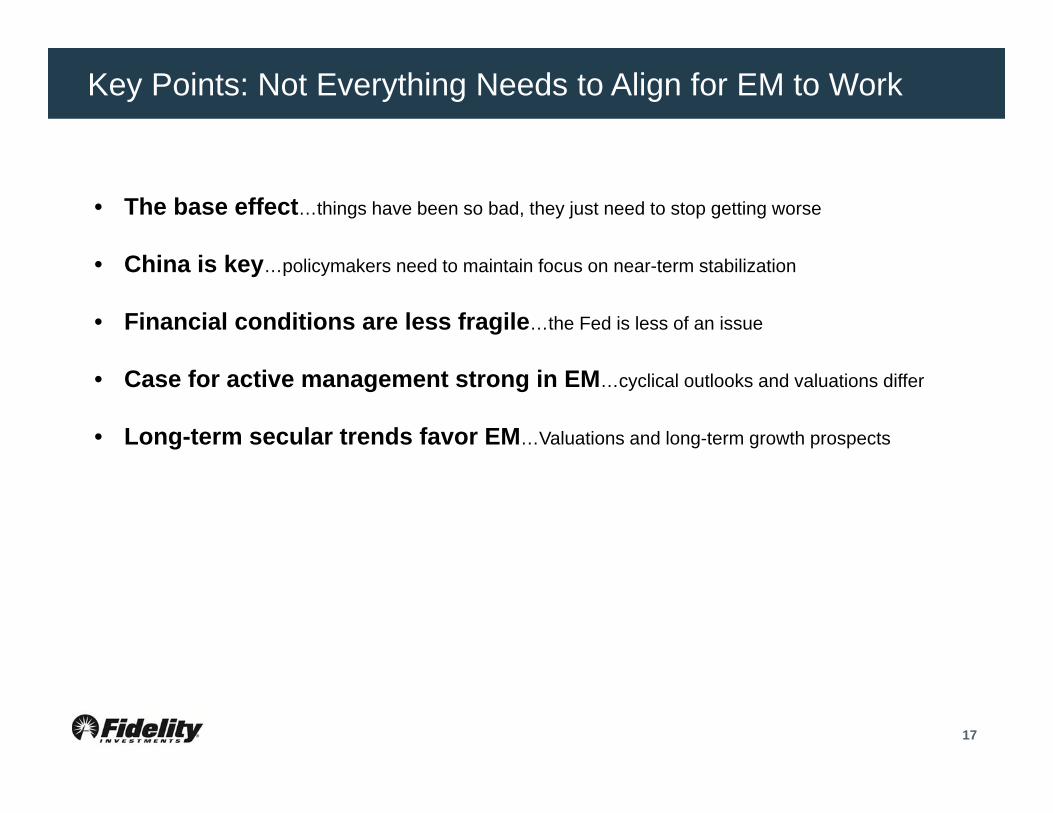

Key Points: Not Everything Needs to Align for EM to Work

17

• The base effect…things have been so bad, they just need to stop getting worse

• China is key…policymakers need to maintain focus on near-term stabilization

• Financial conditions are less fragile…the Fed is less of an issue

• Case for active management strong in EM…cyclical outlooks and valuations differ

• Long-term secular trends favor EM…Valuations and long-term growth prospects

18

Fidelity Tools & ResourcesHeather KnightRegional Brokerage Consultant, Personal Investing

1919

Q&AQ&A

20 20

Diversification does not ensure a profit or guarantee against loss.

Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Foreign securities are subject to interest rate, currency exchange rate, economic, and political risks, all of which are magnified in emerging markets. The risks are particularly significant for funds that focus on a single country or region. Foreign investments, especially those in emerging markets, involve greater risk and may offer greater potential returns than U.S. investments. This risk includes political and economic uncertainties of foreign countries, as well as the risk of currency fluctuation. Investments in smaller companies may involve greater risks than those in larger, more well known companies.

Before investing in any mutual fund or exchange-traded fund, you should consider its investment objectives, risks, charges, and expenses. Contact Fidelity for a prospectus, offering circular, or, if available, a summary prospectus containing this information.Read it carefully.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917

© 2016 FMR LLC. All rights reserved.

774276.1.0

Important Information