Embed Size (px)

Citation preview

EMEA TMC clientconferenceCountry-by-countryreporting

1

The Crystal, London9-10 June 2015

PBC – Provided by client

LTP – Local tax provision

CITR – Corporate income tax return

DTi – Deloitte Tax Insight

DOL – Deloitte Online

Acronyms

2© 2015 For information, contact Deloitte Touche Tohmatsu Limited

• Introduction

• The tax function

• Base Erosion Profit Shifting (BEPS)

• The program

• Country-by-country reporting

• Country-by-country reporting tool - screenshots

Agenda

3© 2015 For information, contact Deloitte Touche Tohmatsu Limited

4

Introduction

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

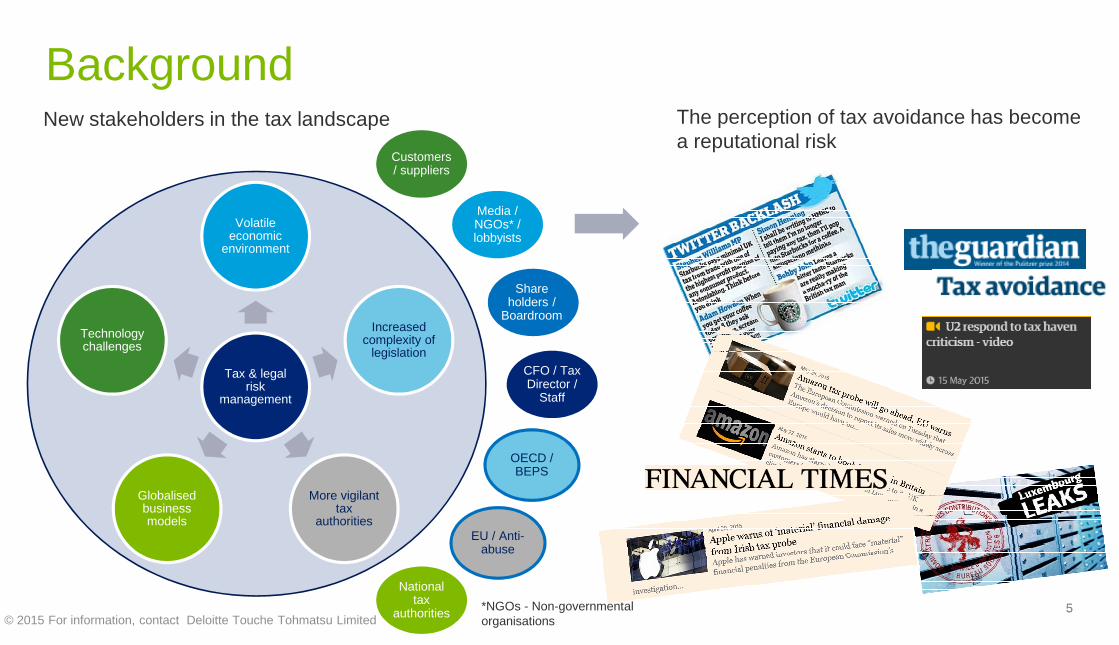

Background

5

Tax & legalrisk

management

Volatileeconomic

environment

Increasedcomplexity of

legislation

More vigilanttax

authorities

Globalisedbusinessmodels

Technologychallenges

Customers/ suppliers

Media /NGOs* /lobbyists

OECD /BEPS

EU / Anti-abuse

Nationaltax

authorities

Shareholders /

Boardroom

CFO / TaxDirector /

Staff

New stakeholders in the tax landscape The perception of tax avoidance has becomea reputational risk

*NGOs - Non-governmentalorganisations© 2015 For information, contact Deloitte Touche Tohmatsu Limited

5

6

Tax function

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

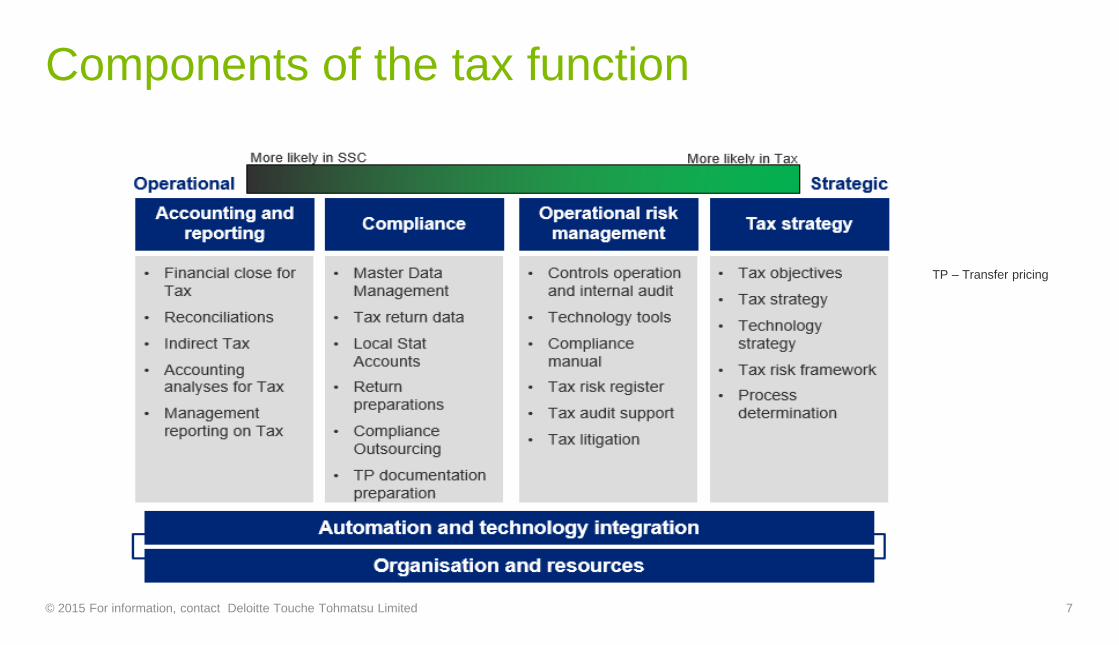

Components of the tax function

7

TP – Transfer pricing

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

8

BEPSProgram

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

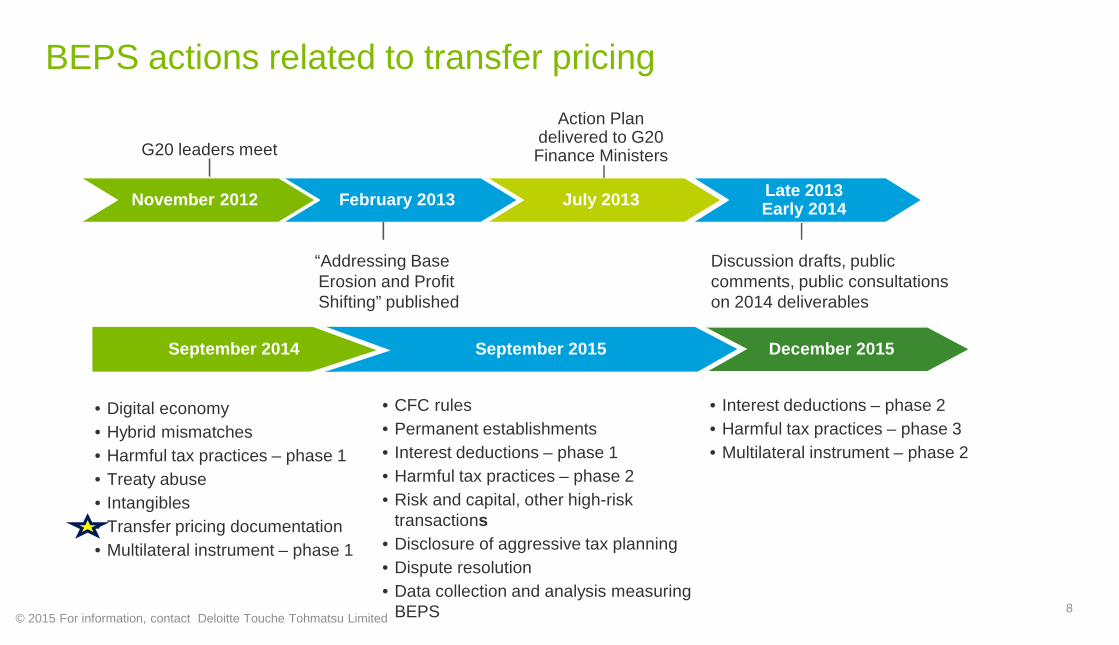

BEPS actions related to transfer pricing

February 2013 July 2013

G20 leaders meet

“Addressing BaseErosion and ProfitShifting” published

• Digital economy

• Hybrid mismatches

• Harmful tax practices – phase 1

• Treaty abuse

• Intangibles

• Transfer pricing documentation

• Multilateral instrument – phase 1

• CFC rules

• Permanent establishments

• Interest deductions – phase 1

• Harmful tax practices – phase 2

• Risk and capital, other high-risktransactions

• Disclosure of aggressive tax planning

• Dispute resolution

• Data collection and analysis measuringBEPS

• Interest deductions – phase 2

• Harmful tax practices – phase 3

• Multilateral instrument – phase 2

September 2014 September 2015 December 2015

Late 2013Early 2014

Discussion drafts, publiccomments, public consultationson 2014 deliverables

Action Plandelivered to G20Finance Ministers

November 2012

8© 2015 For information, contact Deloitte Touche Tohmatsu Limited

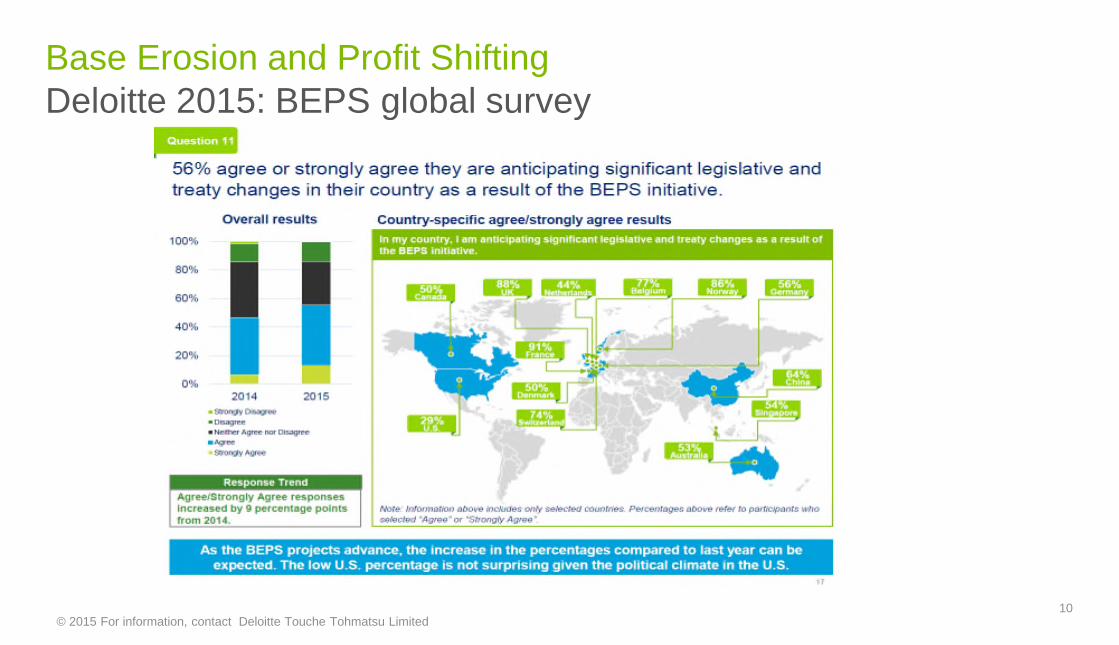

Deloitte 2015: BEPS global surveyBase Erosion and Profit Shifting

10© 2015 For information, contact Deloitte Touche Tohmatsu Limited

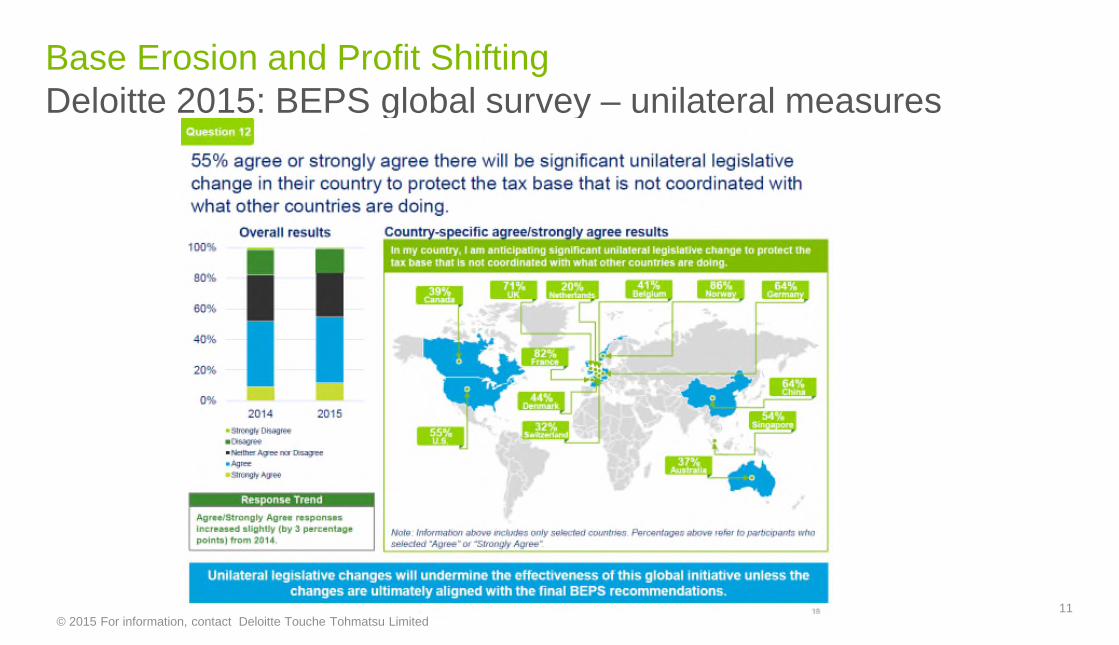

Base Erosion and Profit ShiftingDeloitte 2015: BEPS global survey – unilateral measures

11© 2015 For information, contact Deloitte Touche Tohmatsu Limited

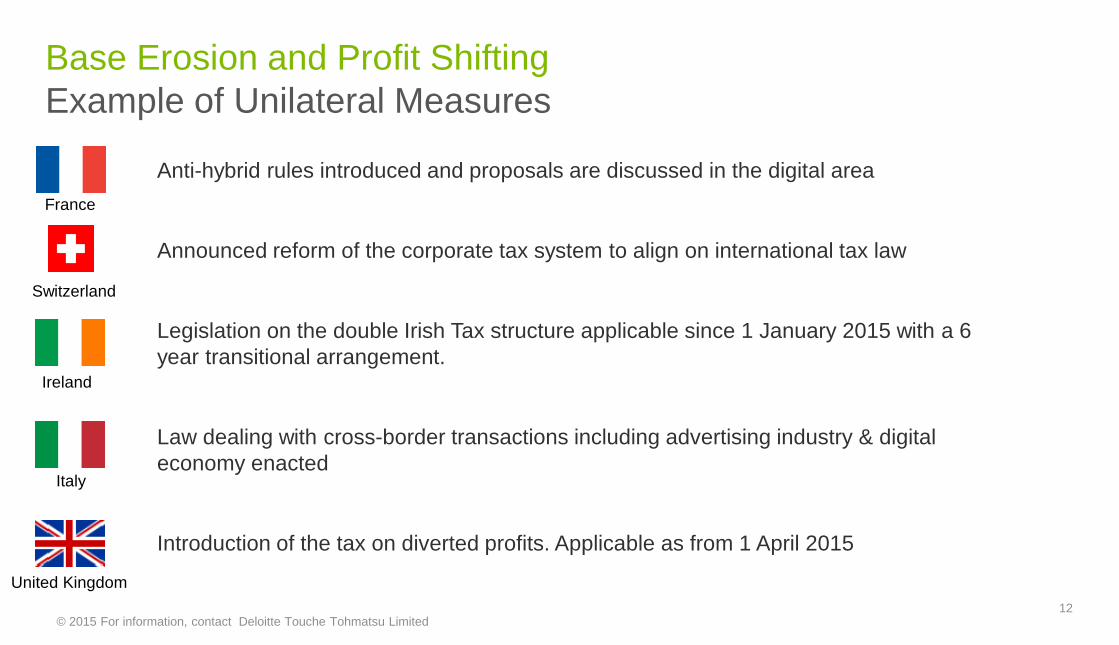

Base Erosion and Profit ShiftingExample of Unilateral Measures

Anti-hybrid rules introduced and proposals are discussed in the digital area

Announced reform of the corporate tax system to align on international tax law

Legislation on the double Irish Tax structure applicable since 1 January 2015 with a 6year transitional arrangement.

Law dealing with cross-border transactions including advertising industry & digitaleconomy enacted

Introduction of the tax on diverted profits. Applicable as from 1 April 2015

12

France

Switzerland

Ireland

Italy

United Kingdom

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

13

BEPSCountry-by-country

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

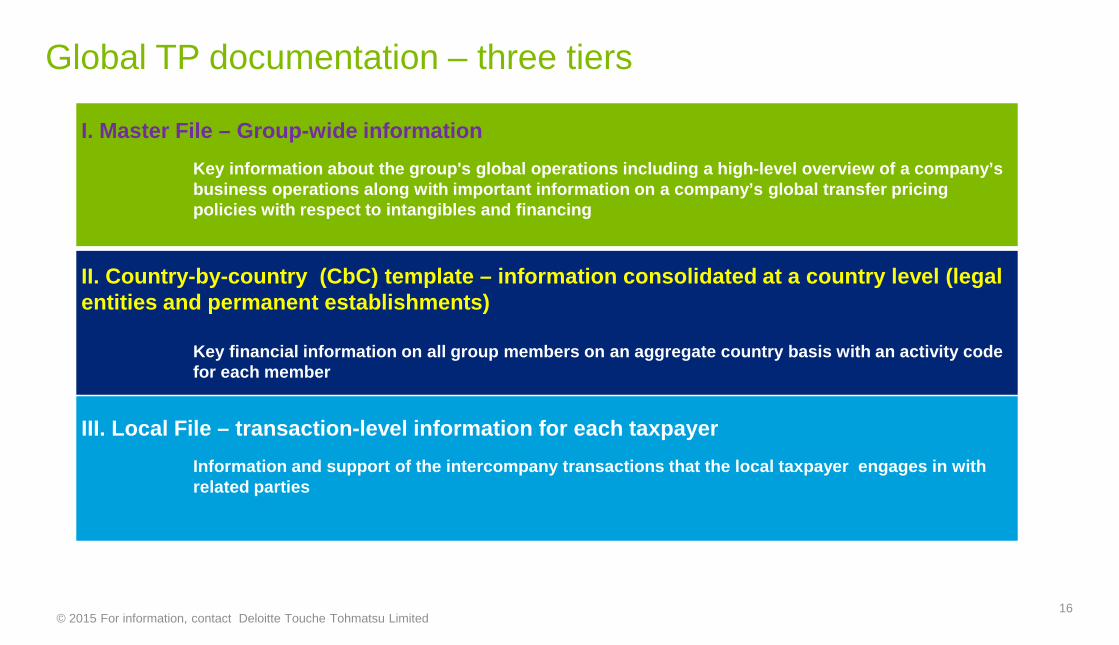

Global TP documentation – three tiers

I. Master File – Group-wide information

Key information about the group's global operations including a high-level overview of a company’sbusiness operations along with important information on a company’s global transfer pricingpolicies with respect to intangibles and financing

II. Country-by-country (CbC) template – information consolidated at a country level (legalentities and permanent establishments)

Key financial information on all group members on an aggregate country basis with an activity codefor each member

III. Local File – transaction-level information for each taxpayer

Information and support of the intercompany transactions that the local taxpayer engages in withrelated parties

16© 2015 For information, contact Deloitte Touche Tohmatsu Limited

Country-by-countryWhat’s new?

15© 2015 For information, contact Deloitte Touche Tohmatsu Limited

Source: http://www.oecd.org/

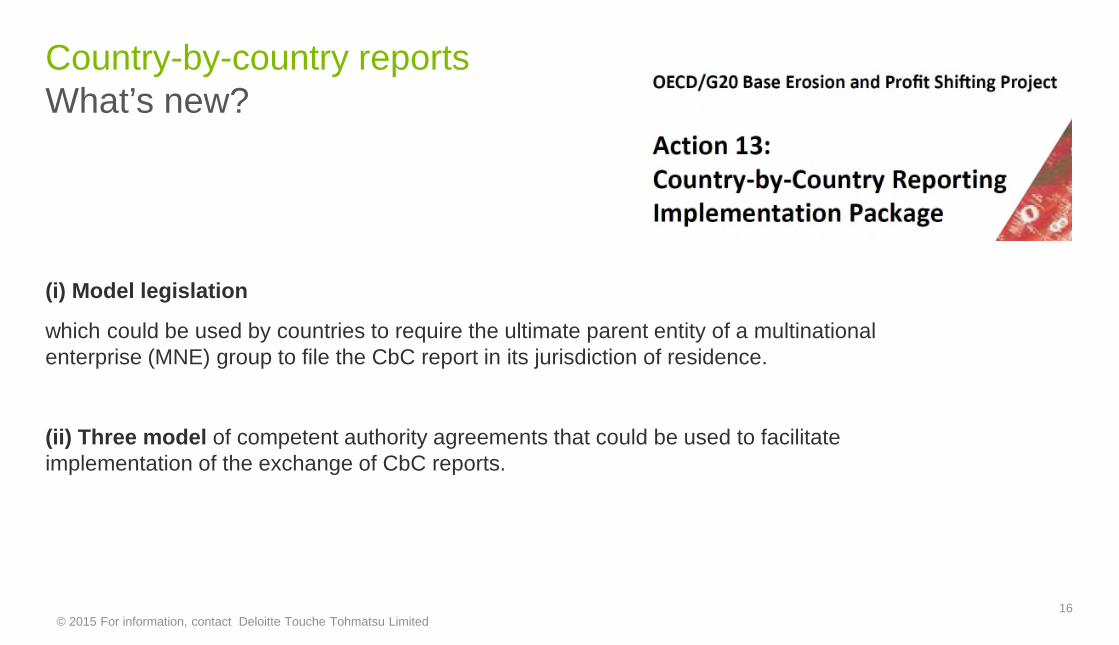

Country-by-country reportsWhat’s new?

16

(i) Model legislation

which could be used by countries to require the ultimate parent entity of a multinationalenterprise (MNE) group to file the CbC report in its jurisdiction of residence.

(ii) Three model of competent authority agreements that could be used to facilitateimplementation of the exchange of CbC reports.

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

Country-by-country reports

Article 6 of the proposed model legislation

Country tax administrations should use the report to:

- Assess high level transfer pricing risks where “effective risk assessment becomes an essentialprerequisite for a focused and resource-efficient tax audit”

- Assess other Base Erosion and Profit Shifting risks in country

Transfer pricing adjustments imposed by country tax administration shall not be based on CbCreports: “Country-by-country report on its own does not constitute conclusive evidence thattransfer pricings are or are not appropriate”

17© 2015 For information, contact Deloitte Touche Tohmatsu Limited

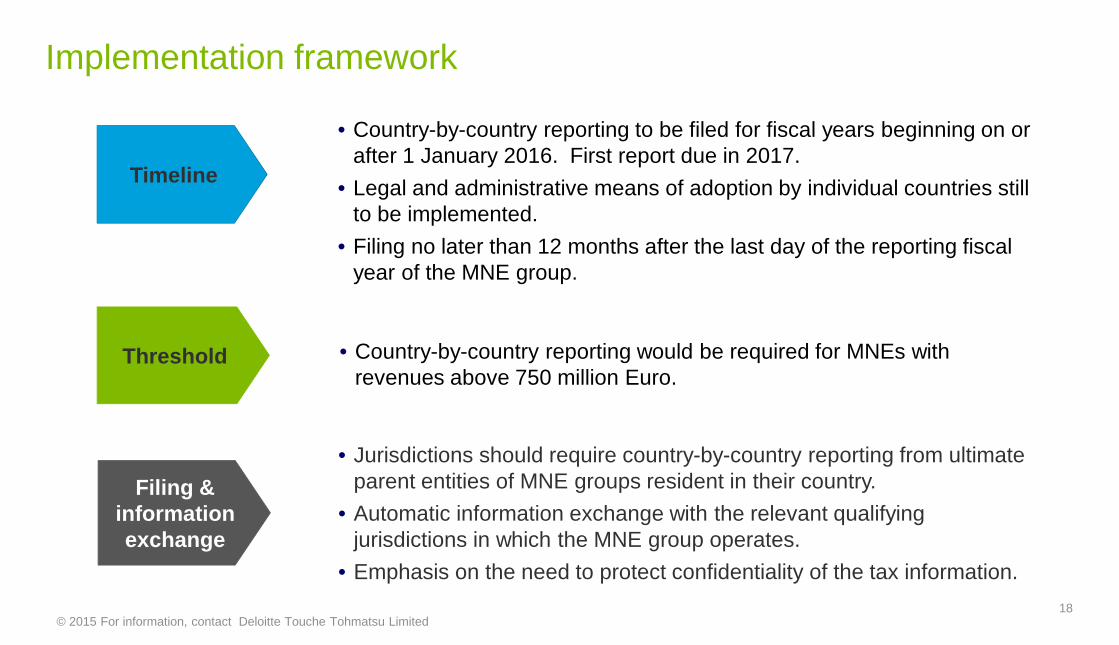

Implementation framework

Timeline

Threshold

• Country-by-country reporting to be filed for fiscal years beginning on orafter 1 January 2016. First report due in 2017.

• Legal and administrative means of adoption by individual countries stillto be implemented.

• Filing no later than 12 months after the last day of the reporting fiscalyear of the MNE group.

• Country-by-country reporting would be required for MNEs withrevenues above 750 million Euro.

Filing &informationexchange

• Jurisdictions should require country-by-country reporting from ultimateparent entities of MNE groups resident in their country.

• Automatic information exchange with the relevant qualifyingjurisdictions in which the MNE group operates.

• Emphasis on the need to protect confidentiality of the tax information.

18© 2015 For information, contact Deloitte Touche Tohmatsu Limited

Implementation framework

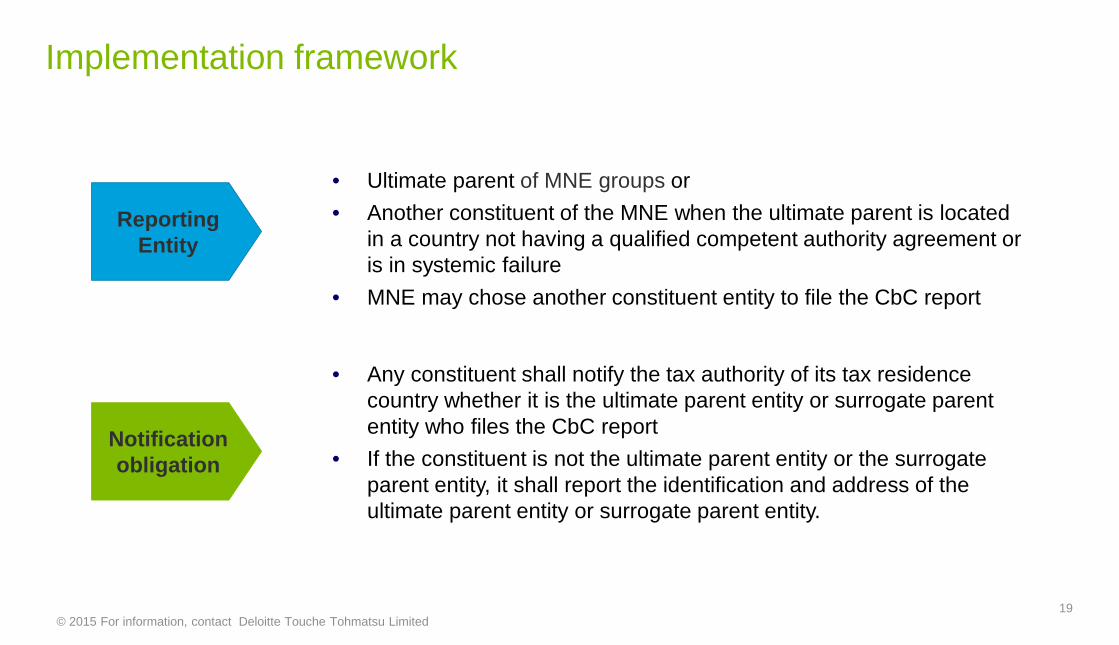

Notificationobligation

• Any constituent shall notify the tax authority of its tax residencecountry whether it is the ultimate parent entity or surrogate parententity who files the CbC report

• If the constituent is not the ultimate parent entity or the surrogateparent entity, it shall report the identification and address of theultimate parent entity or surrogate parent entity.

ReportingEntity

• Ultimate parent of MNE groups or

• Another constituent of the MNE when the ultimate parent is locatedin a country not having a qualified competent authority agreement oris in systemic failure

• MNE may chose another constituent entity to file the CbC report

19© 2015 For information, contact Deloitte Touche Tohmatsu Limited

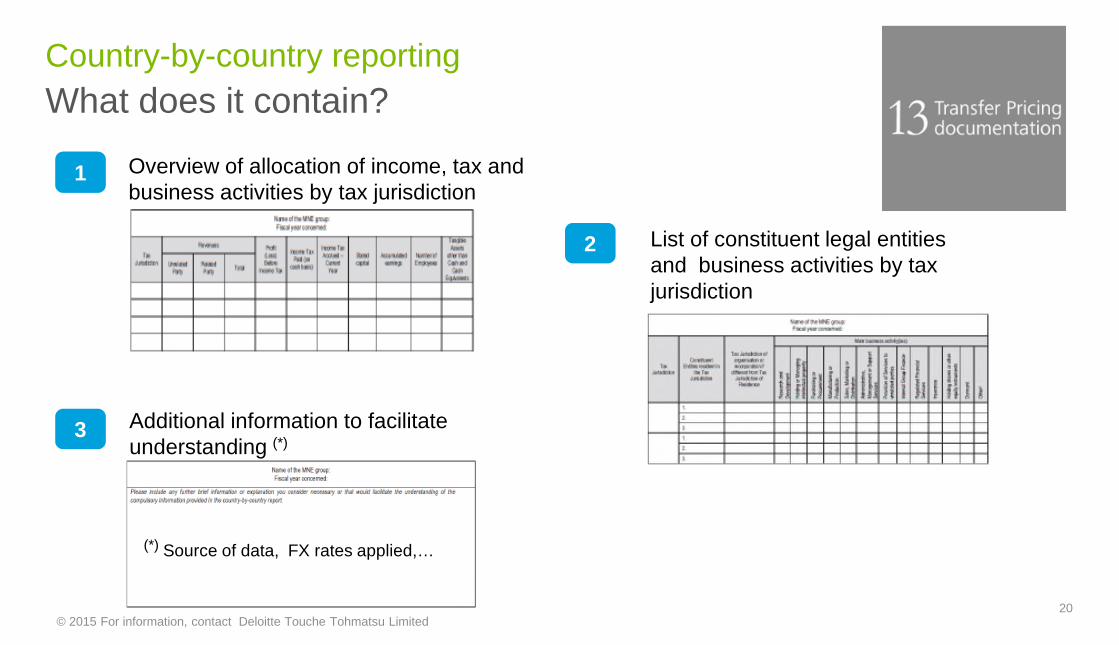

Country-by-country reporting

What does it contain?

20

Overview of allocation of income, tax andbusiness activities by tax jurisdiction

List of constituent legal entitiesand business activities by taxjurisdiction

Additional information to facilitateunderstanding (*)

1

2

3

(*) Source of data, FX rates applied,…

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

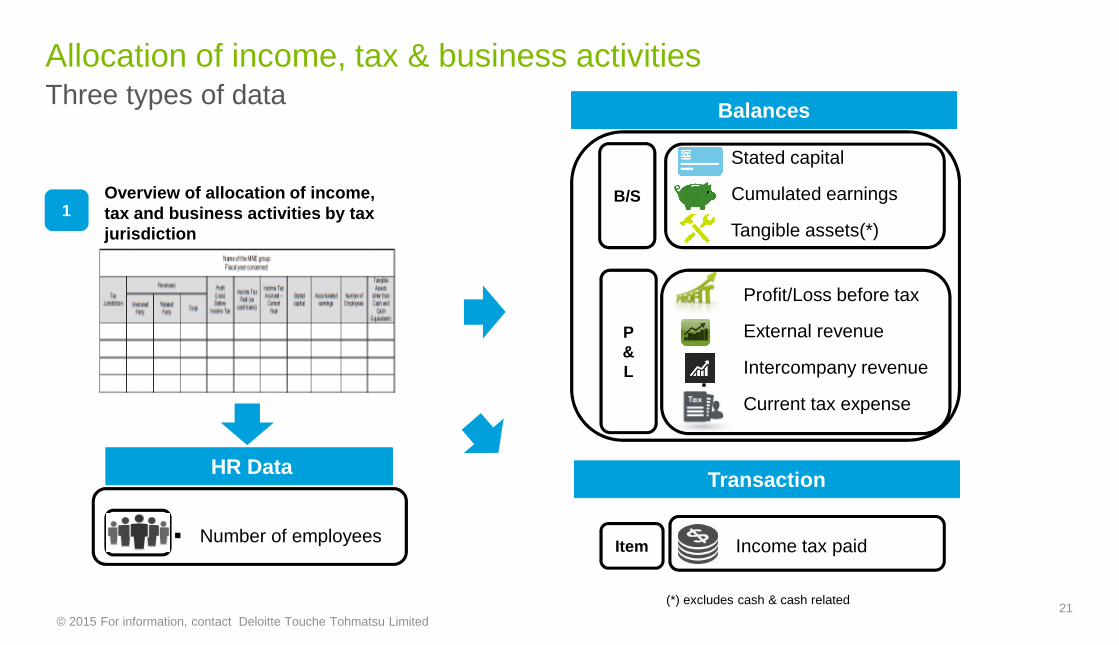

Allocation of income, tax & business activitiesThree types of data

Overview of allocation of income,tax and business activities by taxjurisdiction

1

Balances

Stated capital

Cumulated earnings

Tangible assets(*)

B/S

P&L

Profit/Loss before tax

External revenue

Intercompany revenue

Current tax expense

Item Income tax paid

(*) excludes cash & cash related

#

HR Data

Number of employees

Transaction

21© 2015 For information, contact Deloitte Touche Tohmatsu Limited

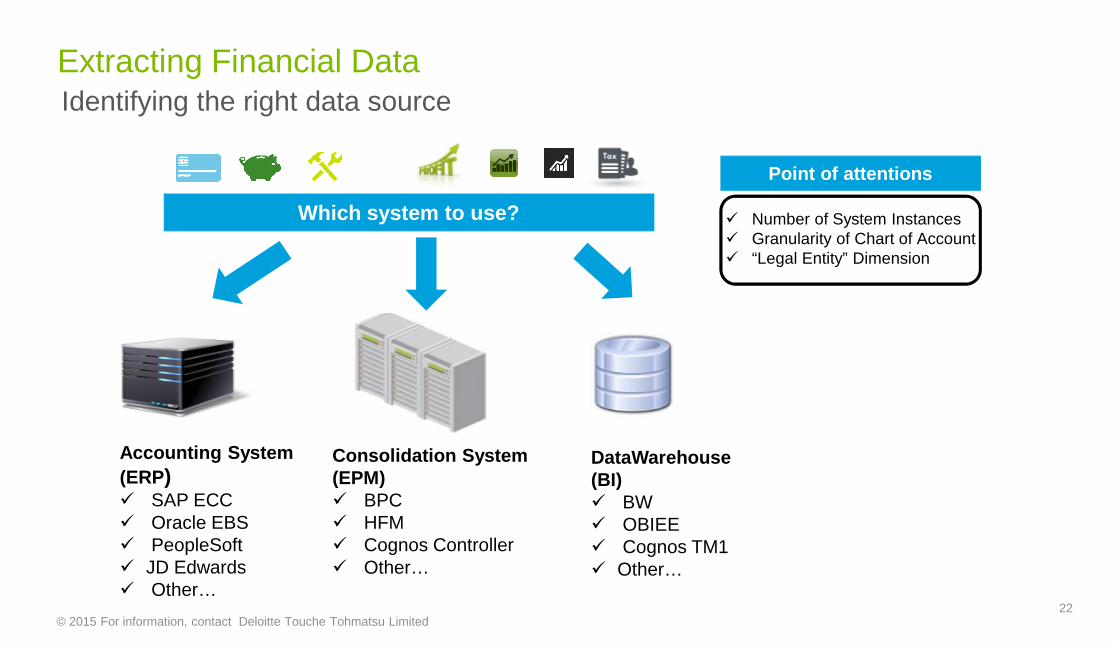

Extracting Financial DataIdentifying the right data source

Which system to use?

Accounting System

(ERP) SAP ECC Oracle EBS PeopleSoft JD Edwards Other…

Consolidation System(EPM) BPC HFM Cognos Controller Other…

DataWarehouse(BI) BW OBIEE Cognos TM1 Other…

Number of System Instances Granularity of Chart of Account “Legal Entity” Dimension

Point of attentions

22© 2015 For information, contact Deloitte Touche Tohmatsu Limited

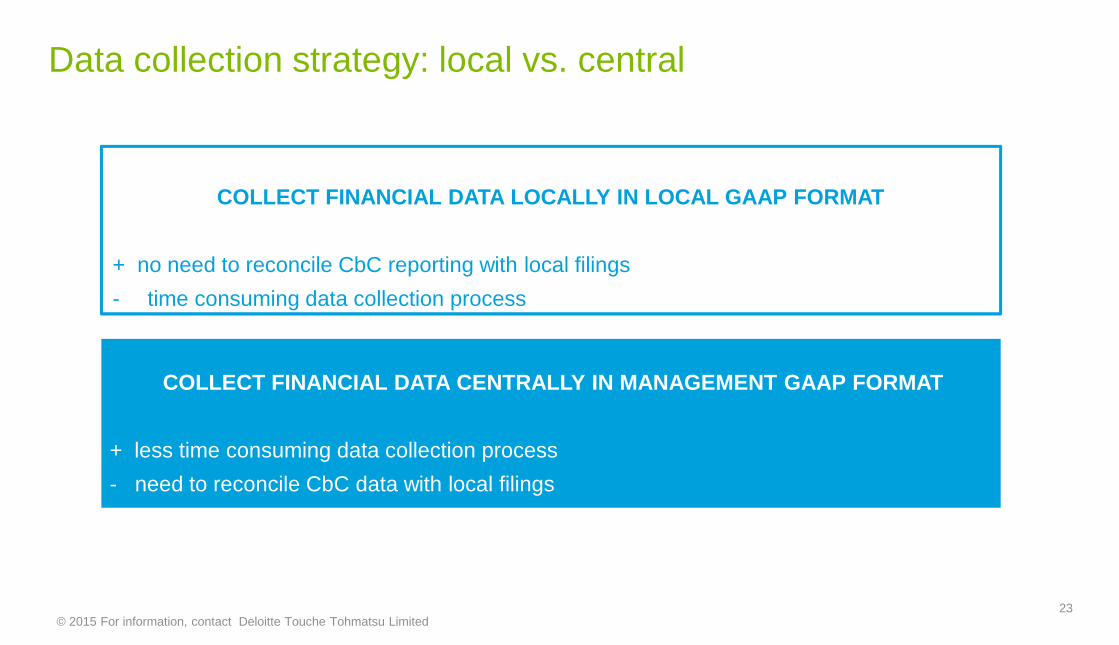

COLLECT FINANCIAL DATA CENTRALLY IN MANAGEMENT GAAP FORMAT

+ less time consuming data collection process

- need to reconcile CbC data with local filings

Data collection strategy: local vs. central

COLLECT FINANCIAL DATA LOCALLY IN LOCAL GAAP FORMAT

+ no need to reconcile CbC reporting with local filings

- time consuming data collection process

23© 2015 For information, contact Deloitte Touche Tohmatsu Limited

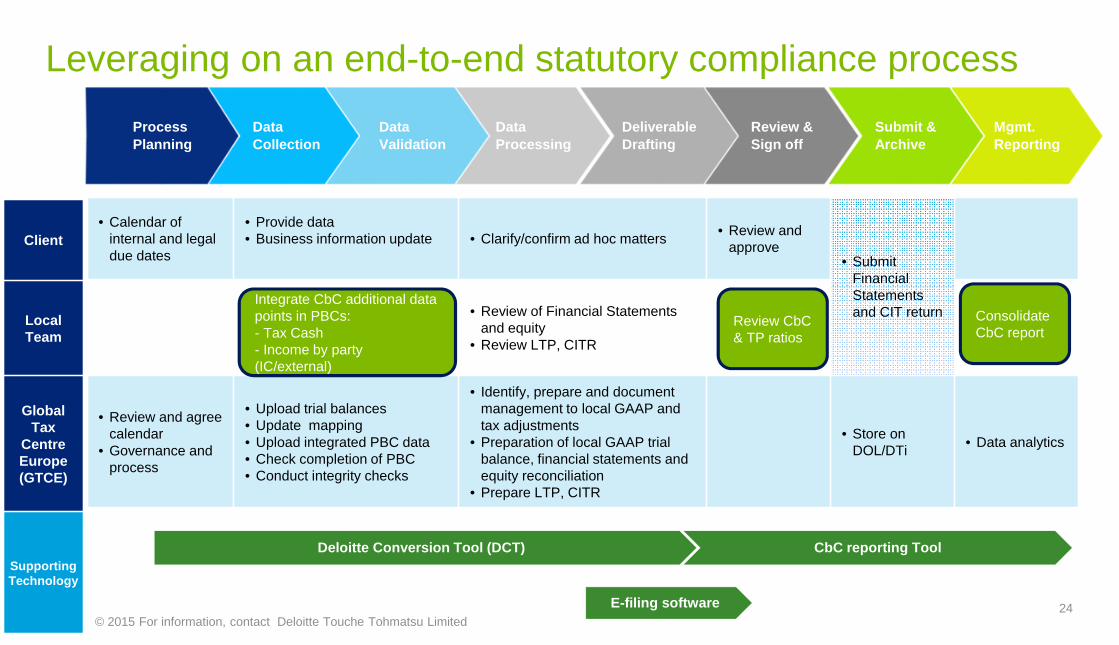

Leveraging on an end-to-end statutory compliance process

• Calendar ofinternal and legaldue dates

• Provide data• Business information update • Clarify/confirm ad hoc matters

• Review andapprove

• SubmitFinancialStatementsand CIT return• Review of Financial Statements

and equity• Review LTP, CITR

• Review and agreecalendar

• Governance andprocess

• Upload trial balances• Update mapping• Upload integrated PBC data• Check completion of PBC• Conduct integrity checks

• Identify, prepare and documentmanagement to local GAAP andtax adjustments

• Preparation of local GAAP trialbalance, financial statements andequity reconciliation

• Prepare LTP, CITR

• Store onDOL/DTi

• Data analytics

Client

LocalTeam

GlobalTax

CentreEurope(GTCE)

SupportingTechnology

Deloitte Conversion Tool (DCT)

E-filing software

Data

Collection

Data

Validation

Data

Processing

Deliverable

Drafting

Review &

Sign off

Submit &

Archive

Mgmt.

Reporting

Process

Planning

CbC reporting Tool

Integrate CbC additional datapoints in PBCs:- Tax Cash- Income by party(IC/external)

Review CbC& TP ratios

ConsolidateCbC report

24© 2015 For information, contact Deloitte Touche Tohmatsu Limited

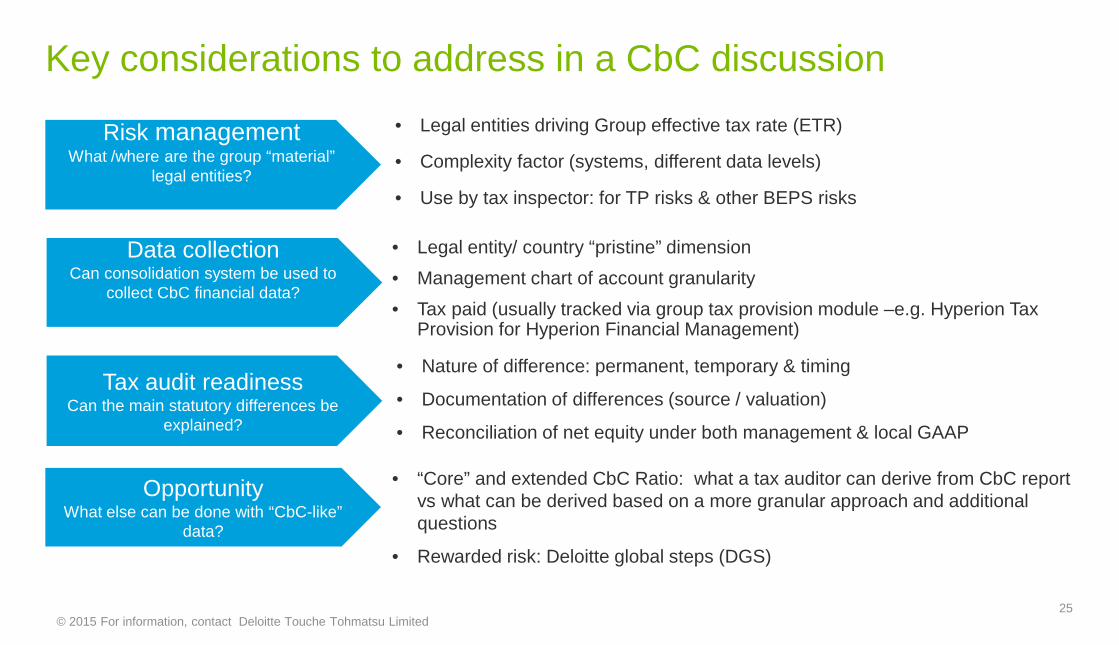

Key considerations to address in a CbC discussion

• Legal entities driving Group effective tax rate (ETR)

• Complexity factor (systems, different data levels)

• Use by tax inspector: for TP risks & other BEPS risks

Risk managementWhat /where are the group “material”

legal entities?

• Legal entity/ country “pristine” dimension

• Management chart of account granularity

• Tax paid (usually tracked via group tax provision module –e.g. Hyperion TaxProvision for Hyperion Financial Management)

Data collectionCan consolidation system be used to

collect CbC financial data?

• Nature of difference: permanent, temporary & timing

• Documentation of differences (source / valuation)

• Reconciliation of net equity under both management & local GAAP

Tax audit readinessCan the main statutory differences be

explained?

OpportunityWhat else can be done with “CbC-like”

data?

• “Core” and extended CbC Ratio: what a tax auditor can derive from CbC reportvs what can be derived based on a more granular approach and additionalquestions

• Rewarded risk: Deloitte global steps (DGS)

25© 2015 For information, contact Deloitte Touche Tohmatsu Limited

26

CbCAppendix

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

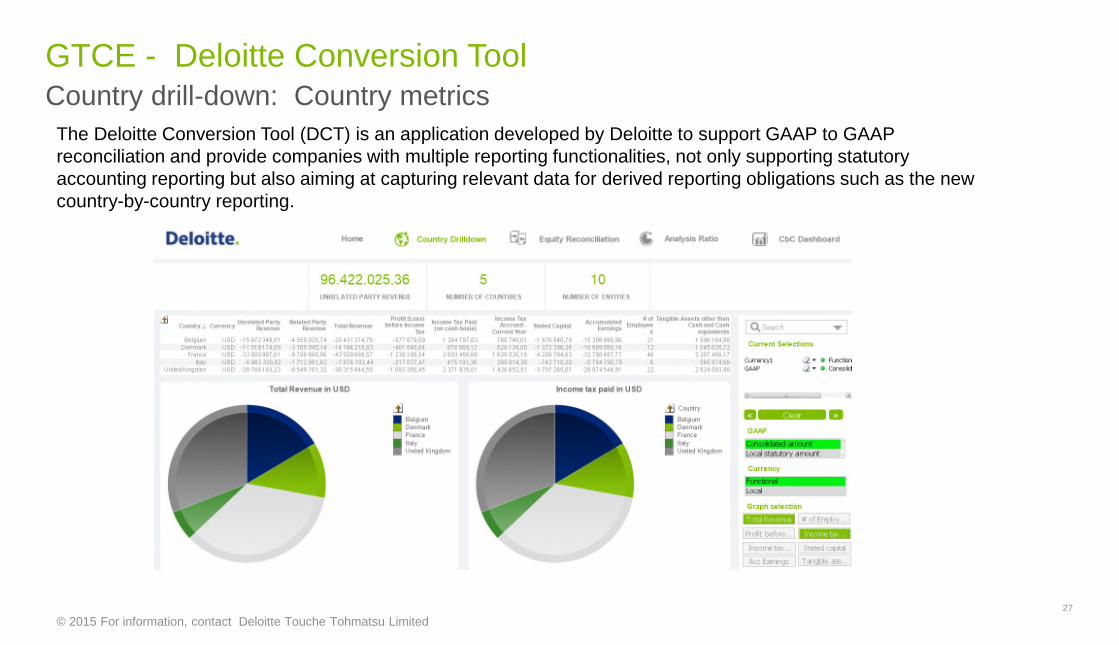

GTCE - Deloitte Conversion ToolCountry drill-down: Country metrics

27

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

The Deloitte Conversion Tool (DCT) is an application developed by Deloitte to support GAAP to GAAPreconciliation and provide companies with multiple reporting functionalities, not only supporting statutoryaccounting reporting but also aiming at capturing relevant data for derived reporting obligations such as the newcountry-by-country reporting.

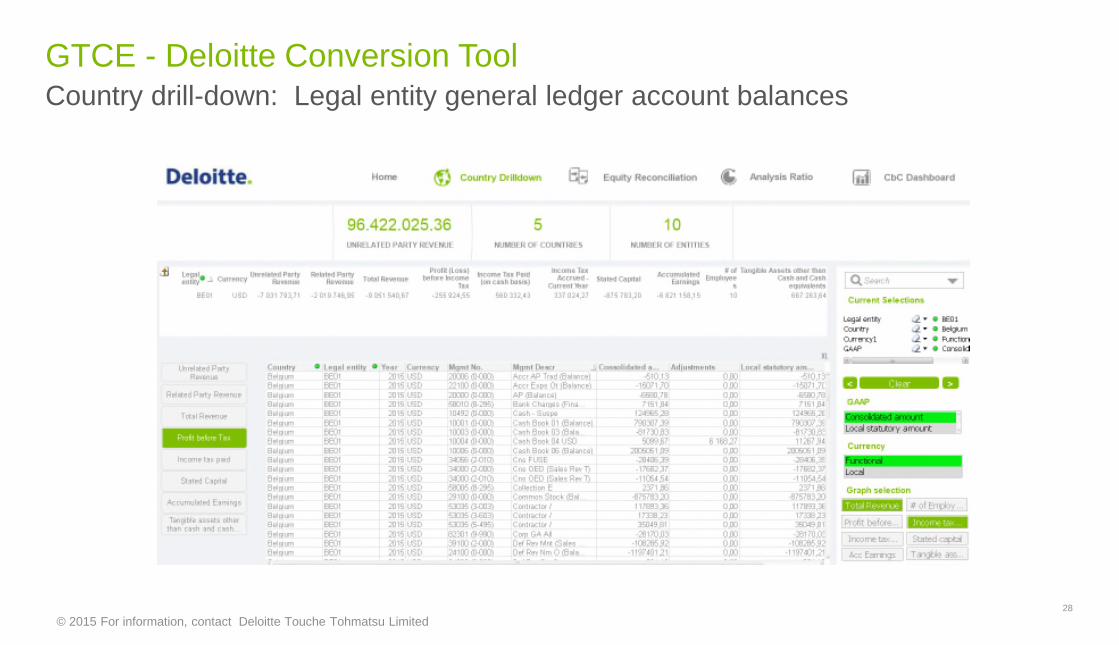

GTCE - Deloitte Conversion ToolCountry drill-down: Legal entity general ledger account balances

28

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

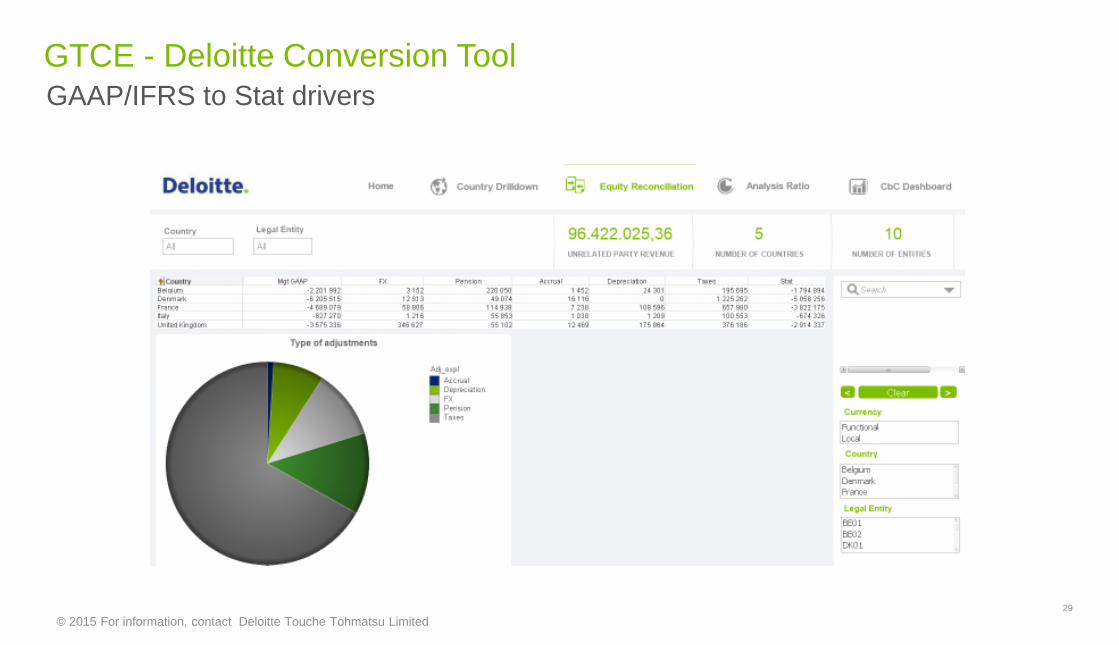

GTCE - Deloitte Conversion ToolGAAP/IFRS to Stat drivers

29

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

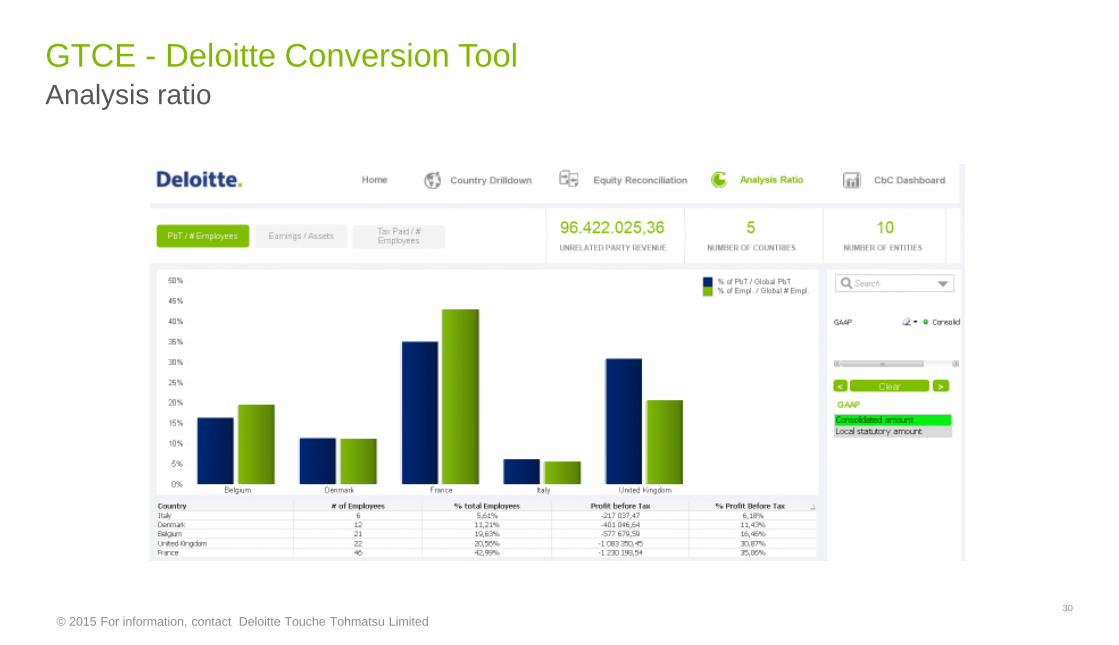

GTCE - Deloitte Conversion ToolAnalysis ratio

30

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

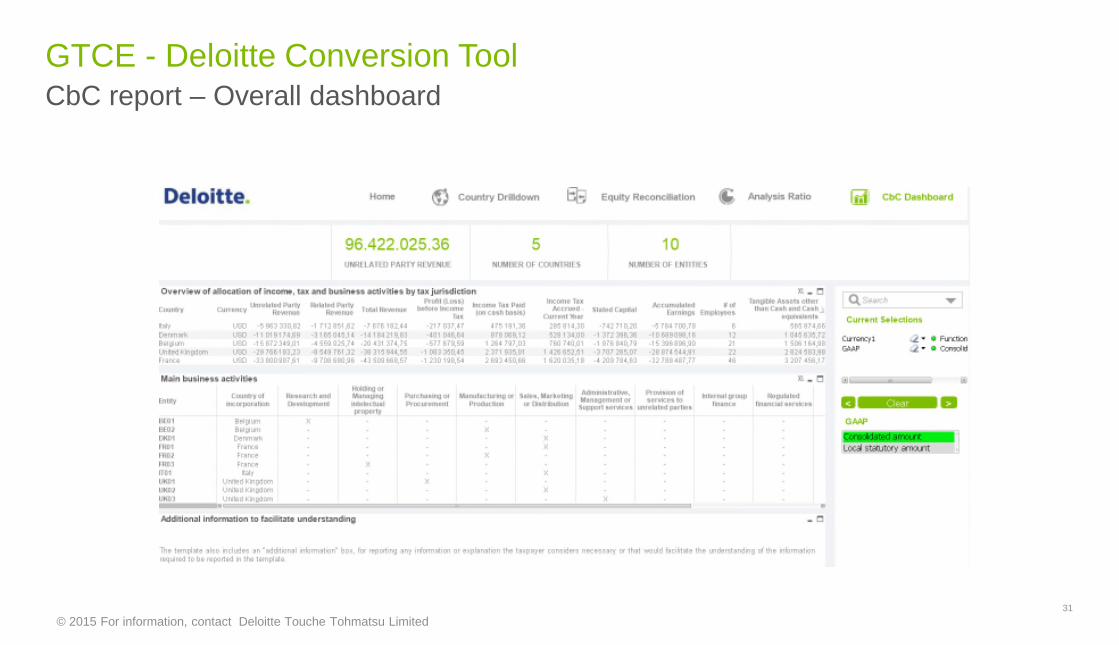

GTCE - Deloitte Conversion ToolCbC report – Overall dashboard

31

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

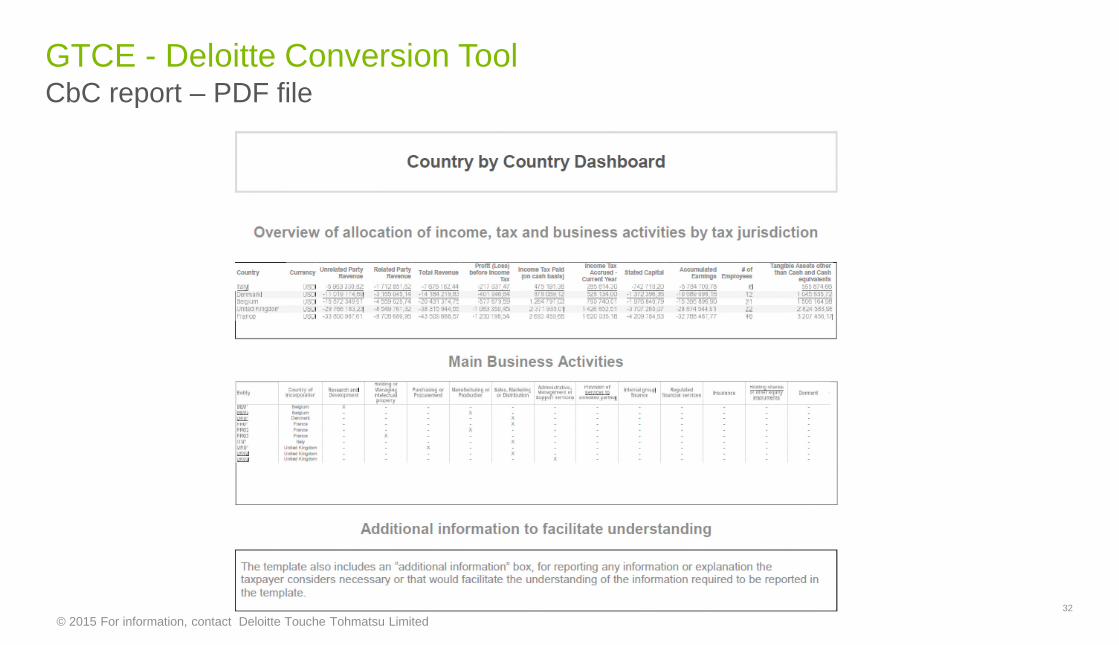

GTCE - Deloitte Conversion ToolCbC report – PDF file

32

© 2015 For information, contact Deloitte Touche Tohmatsu Limited

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please seewww.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a globallyconnected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insightsthey need to address their most complex business challenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “DeloitteNetwork”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustainedby any person who relies on this communication.

© 2015. For information, contact Deloitte Touche Tohmatsu Limited. 33