Embed Size (px)

Citation preview

EE

Electricity generation major projects

November 2015

Department of Industry, Innovation and Science (2015), Electricity generation major projects,

Canberra, November.

Further information

For more information or to comment on this publication please contact:

Allison Ball

Manager, Energy Statistics

Office of the Chief Economist

Department of Industry, Innovation and Science

GPO Box 9839

CANBERRA ACT 2601

Email: [email protected]

Web: www.industry.gov.au/oce

Project Team

Caitlin McCluskey

Christian Tisdell

Acknowledgements

The authors would like to express their appreciation for the assistance and support provided by

colleagues in the Department of Industry, Innovation and Science, the Clean Energy Regulator,

representatives from various state and territory government agencies, and the companies involved in

the projects listed in this report.

The views expressed in this publication are those of the authors and do not necessarily reflect those

of the Australian Government or the Department of Industry, Innovation and Science.

© Commonwealth of Australia 2015

ISSN (Online): 2204-2172

This work is copyright. Apart from use under Copyright Act 1968, no part may be reproduced or

altered by any process without prior written permission from the Australian Government. Requests

and inquiries concerning reproduction and rights should be addressed to

[email protected]. For more information on Office of the Chief Economist publications

please access the Department’s website at: www.industry.gov.au/OCE

Creative Commons Licence

With the exception of the Coat of Arms, this publication is licensed under a Creative Commons

Attribution 3.0 Australia Licence.

Creative Commons Attribution 3.0 Australia Licence is a standard form license agreement that

allows you to copy, distribute, transmit and adapt this publication provided that you attribute the

work. A summary of the licence terms is available from

http://creativecommons.org/licenses/by/3.0/au/deed.en. The full licence terms are available from

http://creativecommons.org/licenses/by/3.0/au/legalcode.

The Commonwealth’s preference is that you attribute this publication (and any material sourced from

it) using the following wording:

Source: Licensed from the Commonwealth of Australia under a Creative Commons Attribution 3.0

Australia Licence. The Commonwealth of Australia does not necessarily endorse the content of this

publication.

Electricity generation major projects November 2015

2

Foreword

This annual publication provides a summary of electricity generation projects

under consideration or development in Australia.

Investment in new electricity generation capacity is constrained by the current

overcapacity in the market and weak expectations for demand growth in

electricity from the grid. In the medium term demand is expected to remain

subdued, and some existing capacity to be decommissioned. Projects under

development are mainly being driven by the need to refurbish or replace existing

plants, local demand, and government incentives to drive innovation and

decarbonise the electricity market.

Project proponents surveyed noted renewed optimism and increased certainty in

the sector, compared with this time last year, following recent announcements

confirming the target for the Renewable Energy Target (RET).

As of 31 October 2015, there are 18 committed projects around Australia, all

using renewable energy sources. The additional planned capacity of these

projects totals 3 747 megawatts, equivalent to 6 per cent of existing installed

capacity in Australia, with an estimated capital expenditure of $5.5 billion. The

proposed new generation capacity is likely to be sufficient to meet requirements

going forward.

Mark Cully

Chief Economist

Department of Industry, Innovation and Science

November 2015

Electricity generation major projects November 2015

3

Contents

Foreword 2

Figures 4

Tables 4

1. Executive summary 6

1.1 Factors affecting investment 6

1.2 Current investment pipeline 6

2. About the Electricity Generation Major Projects Report 9

2.1 Project classification 10

3. Investment in electricity generation in Australia 12

3.1 Current electricity generation and investment trends 12

3.2 Factors affecting decisions to invest 16

Electricity demand 16

Surplus capacity 18

Electricity prices 19

Power purchase agreements 20

Government policies 20

Emerging technologies 21

4. Projects at the Completed Stage 22

5. Projects at the Committed Stage 23

5.1 Solar Projects 26

5.2 Wind Projects 26

5.3 Hydro projects 26

6. Projects at the Feasibility Stage 27

6.1 Non-renewable electricity projects 28

6.2 Renewable electricity projects 29

7. Projects at the Publicly Announced Stage 30

7.1 Non-renewable electricity projects 30

7.2 Renewable electricity projects 31

References 32

Electricity generation major projects November 2015

4

Figures

Figure 1.1: Investment pipeline for new capacity, by fuel type and by year of expected start

up, as at October 2015 7

Figure 1.2: Number and nominal value of projects at the Committed Stage 7

Figure 2.1: The stages of the investment pipeline 10

Figure 3.1: Electricity generation, by fuel type 13

Figure 3.2: Electricity generation by fuel type, and by state and territory, 2013–14 14

Figure 3.3: Cumulative solar PV installations 14

Figure 3.4: Annual investment in registered capacity 15

Figure 3.5: Australia’s electricity consumption, by region 17

Figure 5.1: Electricity generation projects, Committed Stage, October 2015 25

Figure 5.2: Additional capacity by location and by energy source, Committed Stage, as at

October 2015 25

Figure 6.1: Additional capacity by location and by energy source, Feasibility Stage, as at

October 2015 28

Figure 7.1: Additional capacity by location and by energy source, Publicly Announced Stage,

as at October 2015 31

Tables

Table 1.1: Summary of projects in the investment pipeline, as at October 2015 8

Table 3.1: Australia’s electricity consumption, by region 18

Table 4.1: Major electricity projects, Completed Stage, as at October 2015 22

Table 5.1: Major electricity projects, Committed Stage, as at October 2015 23

Table 5.2: Major electricity projects investment pipeline, by region, as at October 2015 24

Table 6.1: Major electricity projects, Feasibility Stage, as at October 2015 27

Table 7.1: Major electricity projects, Publicly Announced Stage, as at October 2015 30

Electricity generation major projects November 2015

5

Major Projects List

The major projects list in Excel format is located on the Department of Industry,

Innovation and Science website, http://www.industry.gov.au/Office-of-the-Chief-

Economist/Publications/Pages/Major-electricity-generation-projects.aspx

Abbreviations and acronyms

ACCC Australian Competition and Consumer Commission

AEMO Australian Energy Market Operator

AES Australian Energy Statistics

ARENA Australian Renewable Energy Agency

CER Clean Energy Regulator

ESAA Energy Supply Association of Australia

ESOO Electricity Statement of Opportunities

FID Final Investment Decision

IMOWA Independent Market Operator of Western Australia

MW Megawatts

NEM National Electricity Market

NWIS North-West Interconnected System

PPA Power Purchase Agreement

PV Photovoltaic

RET Renewable Energy Target

SWIS South-West Interconnected System

WEM Wholesale Energy Market, Western Australia

Electricity generation major projects November 2015

6

1. Executive summary

1.1 Factors affecting investment

Since 2010–11 demand for electricity has fallen, resulting in overcapacity in

the market, lower wholesale electricity prices, and less ability to finance

projects. Growth in distributed generation, particularly rooftop solar

photovoltaics (PV), plant closures by large scale industrial users, and

energy efficiency improvements have contributed to this aggregated

demand decrease.

Anecdotal evidence suggests that there is difficulty in securing long term

PPAs, affecting the ability of project proponents to have certainty in the

return on their investments.

Maximum demand for electricity is projected to increase, helping to drive

some demand for electricity generation, particularly peaking plants.

Policy incentives such as the Renewable Energy Target (RET), funding

from the Australian Renewable Energy Agency (ARENA), and some state

schemes continue to drive some investment in this subdued climate.

Project proponents surveyed reported that government announcements

confirming the target for the RET earlier this year had improved the

environment for investment.

1.2 Current investment pipeline

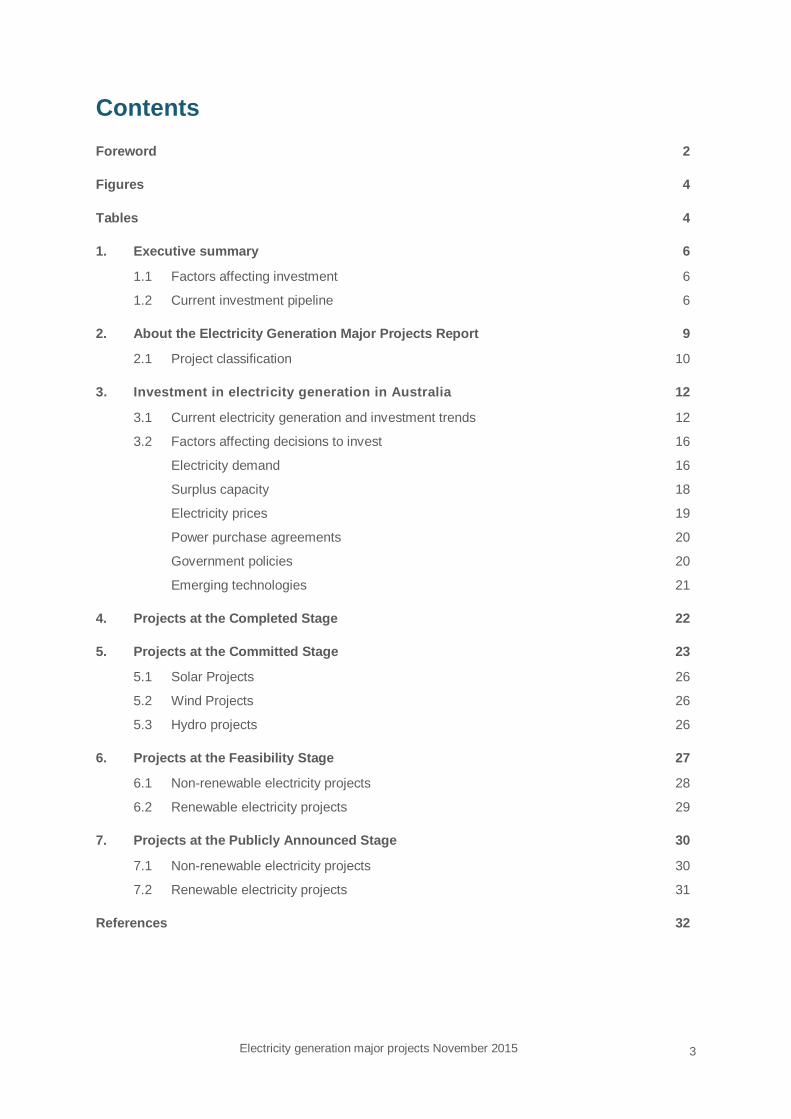

There are 133 projects in the investment pipeline, including those

completed since October 2014, with a combined disclosed value of

$42 billion and 28 968 megawatts of planned capacity (Figure 1.1, Table

1.1).

This is expected to be sufficient to meet requirements when investment

conditions become more favourable and extra capacity is required.

The portfolio of new capacity in the investment pipeline, as reported by

project proponents and gathered from publicly available sources, includes:

- three projects at the Completed Stage worth $936 million with

320 megawatts of additional capacity;

- 18 projects at the Committed Stage worth $5.5 billion with

3 747 megawatts of planned capacity (Figure 1.2);

- 85 projects at the Feasibility Stage that have a combined disclosed

value of $29.7 billion and 20 107 megawatts of planned capacity; and

- 27 projects at the Publicly Announced Stage that have a combined

disclosed value of $5.7 billion and 4 794 megawatts of planned capacity.

There are seven fewer projects than in last year’s report, and fewer projects

at each stage in the investment pipeline, except for committed projects.

All committed projects are currently renewable energy generation projects.

Their combined capacity (3 747 megawatts) is equal to six per cent of

Australia’s currently installed capacity.

Electricity generation major projects November 2015

7

Renewable projects constitute 78 per cent of proposed new capacity in the

investment pipeline, and 88 per cent of capital expenditure. Wind accounts

for half of total planned capacity and 59 per cent of total capital expenditure.

Figure 1.1: Investment pipeline for new capacity, by fuel type and by year of expected start up, as at October 2015

Notes: Projects with undisclosed timelines are presented as post 2020.

Source: Department of Inudstry, Innovation and Science (2015)

Figure 1.2: Number and nominal value of projects at the Committed Stage

Source: Department of Inudstry, Innovation and Science (2015)

Electricity generation major projects November 2015

8

Table 1.1: Summary of projects in the investment pipeline, as at October 2015

Publicly Announced * Feasibility Stage ** Committed *** Completed Total

Energy source No. Capacity

MW Value

$m No.

Capacity MW

Value $m

No. Capacity

MW Value

$m No.

Capacity MW

Value $m

No. Capacity

MW Value

$m

Non-renewable 5 1 830 1 060 11 4 438 3 955

16 6 268 5 015

Gas 5 1 830 1 060 9 3 688 2 855

14 5 518 3 915

Brown coal gasification

1 600 1 100 1 600 1 100

Black coal

1 150 na 1 150 na

Renewable 22 2 964 4 593 74 15 669 25 695 18 3 747 5 525 3 320 936 117 22 700 36 749

Wind 17 2 610 3 968 49 10 938 17 642 9 1 194 2 495 2 220 636 77 14 962 24 741

Hydro 1 30 na 2 367 330 2 40 20

5 437 350

Solar 2 240 625 17 3 014 6 543 7 2513 3010 1 100 300 27 5 867 10 478

Biomass

3 160 1030

3 160 1 030

Geothermal 1 50 na 2 740 150

3 790 150

Ocean 1 34 na 1 450 na

2 484 na

Total 27 4 794 5 653 85 20 107 29 650 18 3 747 5 525 3 320 936 133 28 968 41 764

Notes: * Capital expenditure data for project costs is undisclosed for 9 of the 27 projects in the Publicly Annouched Stage

** Capital expenditure data for project costs is undisclosed for 21 of the 85 projects in the Feasability Stage

*** Capital expenditure data for project costs is undisclosed for 1 of the 18 projects and capacity is undisclosed for 1 of the 18 projects in the Committed Stage

Source: Department of Industry, Innovation and Science (2015)

Electricity generation major projects November 2015 9

2. About the Electricity Generation Major Projects Report

The annual Electricity generation major projects report provides an update on

electricity generation investment and additions to Australia’s installed capacity.

The list of major projects covers all fuel types, including black and brown coal,

oil, natural gas, solar, wind, hydro, bioenergy, geothermal and ocean. The

information draws on publicly available sources and information provided directly

by companies. The list that accompanies this report is provided as a Microsoft

Excel workbook. Projects are shown on separate worksheets based on the fuel

type used in generation.

Power plants of 30 megawatts or more are defined as major projects in this

report. This threshold is consistent with the requirement in the National

Electricity Rules for plants to be scheduled to the National Electricity Market

(NEM). Therefore, many smaller scale projects are not represented on the list,

including small-scale solar and bioenergy facilities. While these generation units

have an important role to play in Australia’s electricity supply, it is not feasible to

obtain a comprehensive list of all these projects.

As of 31 October 2015, the major electricity generation projects list contains

information on 133 projects, with the following details, where available:

project name

proponent company or joint venture

state

location

type — expansion or new project

estimated start up

project status — publicly announced, feasibility, committed, or completed

additional new capacity

fuel type

capital cost of the project in nominal terms

employment at the construction and operating stages.

Electricity generation major projects November 2015 10

2.1 Project classification

The report classifies projects into four stages of development that represent the

investment pipeline as reported by proponents (see Figure 2.1).

Figure 2.1: The stages of the investment pipeline

Source: Department of Industry, Innovation and Science (2015)

The four stages of the pipeline are:

1. Publicly Announced Stage. Projects at this stage are either at a very early

stage of planning or have stalled in their feasibility studies and may have an

unclear development path. Reflecting this, not all projects will progress from

this stage to become operational facilities. Preliminary information on project

schedule, planned capacity or cost is generally publicly available at this

stage.

2. Feasibility Stage. In this stage of development initial feasibility studies have

been completed and the results support further development. Further

studies are generally undertaken to finalise project scope and engineering

designs, assess environmental impacts and develop commercial plans.

Projects are classified as at the Feasibility Stage until a Final Investment

Decision (FID) is made. Typically, information can be gathered about at

least the cost, schedule and planned capacity of projects, as these have

been defined in the completed pre-feasibility study. Though more certain

than projects at the Publicly Announced Stage, these projects are not

guaranteed to progress further as evaluations of commercial prospects and

approvals have not yet been finalised.

3. Committed Stage. Projects at this stage of the development cycle have

received or are expected to recieve a positive FID from the owner and a

PPA is typically in place. These projects are either under construction or

preparing to commence construction. Cost estimates, schedules and plant

capacities are typically well defined and often publicly released. However,

plans are changeable due to schedule delays, scope changes and cost

overruns even after construction has commenced.

4. Completed Stage. Projects are moved to the completed list when

construction is substantially finished to the point where initial production can

commence, however work may still be continuing to bring full capacity

online.

Electricity generation major projects November 2015 11

There are earlier stages in developing projects, such as concept and

pre-development activities, which are not included in this report. These earlier

stages are important for the commercial development of an electricity generation

project but it is beyond the scope of this report to report these on a per project

basis.

Electricity generation major projects November 2015 12

3. Investment in electricity generation in Australia

3.1 Current electricity generation and investment trends

In 2013–14, total electricity generation in Australia declined by 0.6 per cent to

248 terawatt hours (Figure 3.1). This continues the downward trend since 2010–

11, in response to lower demand for electricity in the National Electricity Market

(NEM), which declined by 2 per cent in 2013-14. In contrast, generation

continued to grow in Western Australia (8 per cent growth) and the Northern

Territory (5 per cent growth). This is largely attributed to continued expansion in

off-grid generation, particularly to support the mining sector, which accounted for

an estimated 12 per cent of total generation in 2013–14.

Coal remained the major fuel source for electricity generation in 2013–14,

however the share of coal in the fuel mix fell to 61 per cent, down from 79 per

cent a decade ago. Coal’s dominant share is due to it providing continuous

base-load power and having relatively low cost input fuels (Figure 3.2).

Gas is Australia’s second largest source of electricity generation, accounting for

22 per cent of generation in 2013–14. Generation from natural gas increased

overall in the past two years, with increases in Western Australia, Queensland

and New South Wales in 2013–14. However, wholesale gas prices in the

eastern gas market have increased due to the transition to LNG exporting,

making gas a less attractive fuel for base and intermediate load electricity

generation.

Generation from renewable fuels contributed nearly 15 per cent of Australia’s

electricity generation in 2013–14, with hydro, wind and solar being the

predominant energy sources. Although hydro generation retains the largest

share of renewable electricity generation, it has dropped to below 50 per cent for

the first time in 2013–14, while wind and solar have continued to grow strongly.

Distributed rooftop solar PV, both residential and commercial, has grown

particularly strongly, which has replaced demand for electricity from the network

and reduced the need for new capacity. To date, around 15 per cent of

Australian households have installed solar PV, one of the highest penetrations in

the world,1 with the most installations occurring in Queensland (Figure 3.3).

Tasmania produces the largest amount of renewable energy in Australia,

followed by New South Wales. The largest shares of renewable generation in

the electricity generation mix occurred in Tasmania (93 per cent share,

predominantly hydro) and South Australia (38 per cent, predominantly wind) in

2013–14. Decisions to invest in renewables are largely driven by government

incentive schemes.

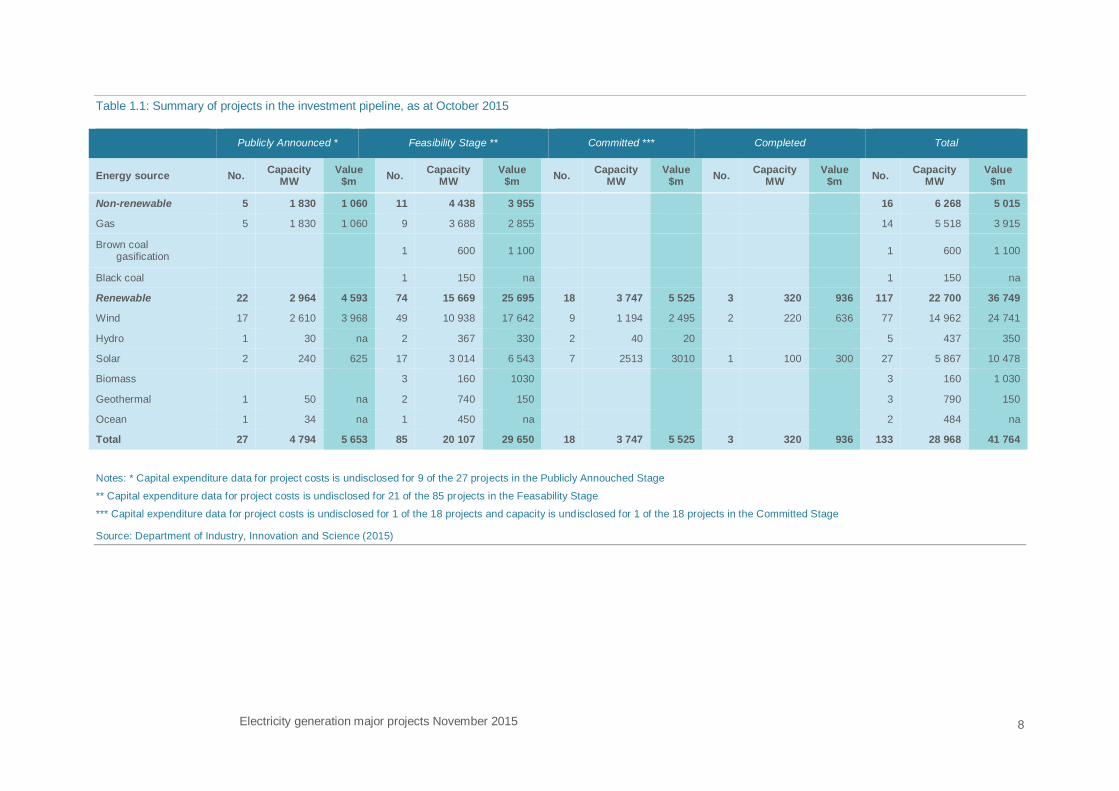

The profile of annual investment in registered capacity differs from year to year.

In 2014, gas and wind accounted for all of the new capacity in Australia, with

588 megawatts of new gas coming online and 567 megawatts of wind, spread

across all states except Tasmania (Figure 3.4). In 2013, there was strong uptake

1 Energy Supply Association Australia (ESAA) (2015) Electricity Gas Australia 2015, p. 4

Electricity generation major projects November 2015 13

of wind generation, with some black coal, and in 2012 a mixture of largely coal

and gas. From 2011 onwards, there is a considerable reduction in new capacity

additions.

Figure 3.1: Electricity generation, by fuel type

Source: Department of Industry and Science (2015) Australian Energy Statistics, Table O

Electricity generation major projects November 2015 14

Figure 3.2: Electricity generation by fuel type, and by state and territory, 2013–14

Notes: New South Wales includes the Australian Capital Territory.

Source: Department of Industry and Science (2015) Australian Energy Statistics, Table O

Figure 3.3: Cumulative solar PV installations

Notes: New South Wales includes the Australian Capital Territory.

Source: Clean Energy Regulator (2015) Postcode Data for Small-Scale Installations

Electricity generation major projects November 2015 15

Figure 3.4: Annual investment in registered capacity

Notes: Q = Queensland; N = New South Wales; V = Victoria; S = South Australia; T= Tasmania; W = Western Australia; NT = Northern Territory. The timing of the reported investment in additional capacity

reflects the time of registration rather than when the plant was commissioned or operating at full capacity. In the NEM region, market capacity data is either 1) summer rating for scheduled/semi-scheduled

generators, or 2) registered capacity for all non-scheduled generating units

Source: Department of Industry, Innovation and Science (2014) Electricity Generation Major Projects

Electricity Generation Major Projects November 2015 16

3.2 Factors affecting decisions to invest

There are many interconnected factors that influence decisions to invest in the

electricity generation sector in Australia. The most common reasons cited by

project proponents surveyed for this report were related to the ability to finance

projects, particularly whether there was demand for electricity in an oversupplied

market, wholesale electricity prices, and the ability to secure PPAs. Other

interrelated factors affecting whether a project goes forward include: regional

considerations, cost of fuel inputs, consideration of state or federal government

policies, incentives and loans, and the perceived risk of investing in new or

emerging technologies.

In 2015, a significant proportion of publicly announced projects across all fuel

types have continued to be put on hold or shelved, and projects at the feasibility

stage have had the expected commencement delayed.

Electricity demand

Electricity consumption in the NEM Region accounts for the majority of electricity

consumption in Australia (84 per cent in 2013–14) (Figure 3.5). Electricity

consumption in the NEM Region has declined by 1 per cent per year on average

since 2009–10, while it has continued to increase in Western Australia (6 per

cent) and the Northern Territory (1 per cent) as a result of increasing end-use

activity, largely in the mining sectors (Table 3.1).

Since 2010–11, milder weather across much of Australia, energy efficiency

improvements in residential and non-residential sectors, consumer responses to

higher retail electricity prices, and declines in the petroleum refining, non-ferrous

metals, and food, beverage and tobacco manufacturing industries, have

combined to cause a decline in electricity demand. Energy efficiency

improvements have occurred in appliances, such as refrigeration and air

conditioning, and energy efficiency requirements in the Building Code of

Australia. Electricity consumption fell by 4 per cent in the residential sector in

2013–14 and by 3 per cent in the manufacturing sector which, together with the

commercial and services sector which remained fairly flat, are the largest users

of electricity.

However, while aggregate demand has declined, maximum demand is projected

to increase. This is particularly true in Queensland, where high electricity

consumption from LNG plants is expected to increase maximum demand in the

short term. Population growth is expected to drive up maximum demand in the

medium to long term, particularly in New South Wales, Victoria and South

Australia.2 This means that extra investment may be needed in generation to

meet maximum demand.

2 Australian Energy Market Operator (AEMO) (2015) 2015 Electricity Statement of Opportunities,

p. 4

Electricity Generation Major Projects November 2015 17

Figure 3.5: Australia’s electricity consumption, by region

Notes: New South Wales Includes the Australian Capital Territory

Source: Department of Industry and Science (2015) Australian Energy Statistics, Table L

Electricity Generation Major Projects November 2015 18

Table 3.1: Australia’s electricity consumption, by region

Notes: NEM States include New South Wales, Victoria, Queensland, South Australia, Tasmania and

the Australian Capital Territory

Source: Department of Industry and Science (2015) Australian Energy Statistics, Table L

Surplus capacity

The unexpected plateauing and subsequent fall in demand around 2009–10 has

contributed to excess capacity in the NEM. Figure 3.6 shows two indexes

summarising relative changes in installed generating capacity and electricity

demand in the NEM.

Figure 3.6: Growth in installed generating capacity in the NEM region and demand for electricity

Source: Energy Supply Association of Australia (2015) Electricity Gas Australia; Global Roam, NEM Review database

The Electricity Statement of Opportunities (ESOO), published by the Australian

Energy Market Operator (AEMO), concludes that there is currently surplus

2013–14

Average annual growth

TWh Share

(per cent)

2013–14 (per cent)

10 years (per cent)

National Electricity Market (NEM) states

208.1 83.8

-2.0 0.2

Western Australia 36.7 14.8 8.4 6.4

Northern Territory 3.5 1.4 5.0 4.2

Total 248.3 100.0 -0.5 0.9

Electricity Generation Major Projects November 2015 19

capacity in the NEM. However, scheduled withdrawal of capacity from the NEM

(as a response to surplus capacity), and the projected continued increase in

maximum demand, means that over the next 10 years some additional capacity

is expected to be required to maintain the reliability standard and to meet

requirements under the RET. This is particularly true in New South Wales and

South Australia where projected withdrawals from the NEM exceed projected

surplus capacity. Additionally, withdrawal of capacity from South Australia will

lead to an increasingly high penetration of renewables in South Australia, and

possible effects on reliability of supply due to the intermittent nature of renewable

generation.

The Independent Market Operator (IMO) of Western Australia publishes the

ESOO for Western Australia. The IMO conclude that existing and committed

capacity should be sufficient to meet demand until 2024–25 and that no new

generation will be required in the South West Interconnected System (SWIS) for

this period. This is result of lower than expected demand due to consumer

responses to electricity prices, energy efficiency measures, and the impact of

distributed generation. However, the SWIS only covers a small portion of

Western Australia, and new capacity may be required elsewhere, particularly in

off-grid and mini-grid systems in remote mining regions.

The Power System Review is published by the Utilities Commission of the

Northern Territory that reports on the need for investment in further generation

capacity in each of the Alice Springs, Darwin-Katherine, and Tennant creek

regulated systems. The report concludes that in the Darwin-Katherine region

there is sufficient capacity to meet demand over the next ten years. In Alice

Springs and Tennant Creek regions there is almost enough capacity to meet

demand with good management over the ten year outlook period.

Electricity prices

Wholesale electricity purchase prices, as well as contract prices, have a strong

effect on decisions to invest in electricity generation, as these prices represent a

large part of the return that generators will receive on their investments. In the

NEM, generators are paid only for energy sent out, and wholesale prices provide

incentives to invest in generation according to demand for electricity.

There are notable differences in the wholesale energy purchase costs across

states in the NEM which partly reflect actual differences in wholesale prices

faced by retailers in each state as network capacity constraints limit the amount

of electricity transmitted across state borders. Figure 3.7 shows the spread

between average monthly wholesale prices in the NEM states.

In the early 2000s, relatively high wholesale electricity prices, combined with

robust demand growth, provided strong signals for investment in generation.

The cost of purchasing energy rose sharply between 2006 and 2009, as drought

conditions limited hydro-electric generation and reduced the availability of water

resources for cooling in the operation of thermal generation plants. This required

generation from other sources to make up for the shortfall. The effect of the

carbon pricing mechanism contributed to higher dispatch prices in 2012–13 and

2013–14, but there is, overall, a declining trend in wholesale prices, reflecting

weak demand and the oversupply of electricity generation in the NEM.

Electricity Generation Major Projects November 2015 20

Power purchase agreements

PPAs are contracts where an electricity generator contracts to sell power to a

purchaser (typically an electricity provider) for a set price. This can protect the

generator from market volatility. The continued oversupply of electricity in the

NEM, and, up until recently, uncertainty surrounding government renewable

energy policies, has created little appetite for energy providers to sign PPAs with

electricity generators. Anecdotal evidence suggests that companies are

unwilling to sign long term PPAs in the current investment climate, leaving

project developers with uncertainty over the viability of proceeding with projects.

However, recent announcements concerning the RET have led to greater

certainty in the sector and may lead to more willingness to sign PPAs going

forward.

Figure 3.7: Spread of monthly average real spot prices across states in the NEM region compared to the average

NEM spot price

Notes: Wholesale prices reported for the Snowy Scheme are excluded as well as the price spike in 2005 which may be associated

with high prices in Tasmania at the time that state joined the NEM

Source: Global Roam, NEM Review database; ABS (2015) Producer Price Indexes, cat. no. 6427.0

Government policies

Legislation to amend the RET was agreed to by the Australian Parliament in

June 2015. This included the new target for large-scale generation of 33,000

GWh in 2020. This is expected to be equivalent to around 23.5 per cent of

Australia’s electricity generation in 2020 being sourced from renewable energy.

Electricity Generation Major Projects November 2015 21

Queensland introduced Solar 60, an initiative committed to supporting up to 60

megawatts of solar power generation. Queensland retailer, Ergon Energy,

commenced a 150 megawatt tender for large scale renewable projects to be

added to its regional grid.

The ACT held two reverse auctions through 2015 to develop and encourage

more renewable electricity generation to reach its 90 per cent renewable energy

target by 2020. The ACT Government developed a legislated feed-in tariff

mechanism and reverse auction process that aims to provide a higher degree of

investment certainty for project developers and financiers.3

Nationwide, federally funded ARENA’s $100 million grants round has attracted

high interest as well as the Clean Energy Finance Corporations $250 million

financing opportunities.

Emerging technologies

A potentially disruptive emerging technology, and one that will need to be

considered going forward when investing in utility scale electricity generation, is

the potential for home storage options for solar rooftop PV generation. When

uptake of this technology combined with solar rooftop PV becomes cost

competitive it will further reduce demand from the electricity grid, including a

potential reduction in peak demand.4

3 ACT Government (2015) Renewable Energy Local Investment Framework. Accessed: November

2015 http://www.environment.act.gov.au

4 Parkinson G (2014) UBS: Australian Households Could Go Off-Grid by 2018, Reneweconomy,

May. Accessed: November 2015 http://reneweconomy.com.au/2014/ubs-australian-households-go-

grid-2018

Electricity Generation Major Projects November 2015 22

4. Projects at the Completed Stage

In the twelve months to October 2015, three electricity generation projects were

completed (Table 4.1), all of which were renewable energy projects. This

compares with seven completed in the year to October 2014 and the four

completed in the year to October 2013. The 2015 completed projects have a

total generation capacity of 320 megawatts and a total disclosed capital cost of

around $936 million.

Table 4.1: Major electricity projects, Completed Stage, as at October 2015

Energy source

Project Location Company Capacity MW

Value $m

Wind Boco Rock Wind Farm NSW EGCO 113 361

Wind Taralga Wind Farm NSW Banco Santander SA/BlueNRGY

107 275

Solar Nyngan Solar Farm NSW AGL Energy 100 300

Total 320 936

Source: Department of Industry, Innovation and Science (2015)

The largest renewable electricity project was the Boco Rock Wind Farm, owned

by EGCO and operated by CWP Renewables. Boco Rock was completed in

February 2015 and has a total capacity of 113 megawatts at a cost of $361

million.

Taralga Wind Farm was commissioned in July 2015, by Banco Santander SA

and BlueNRGY. Taralga’s 51 turbines, valued at $275 million, add capacity of

107 megawatts in the southern tablelands of NSW.

AGL’s Nyngan Solar Farm in western New South Wales is now the largest

operating solar project in Australia, adding 100 megawatts of power from

1.3 million solar panels. The $300 million project commenced operation in July

2015.

Electricity Generation Major Projects November 2015 23

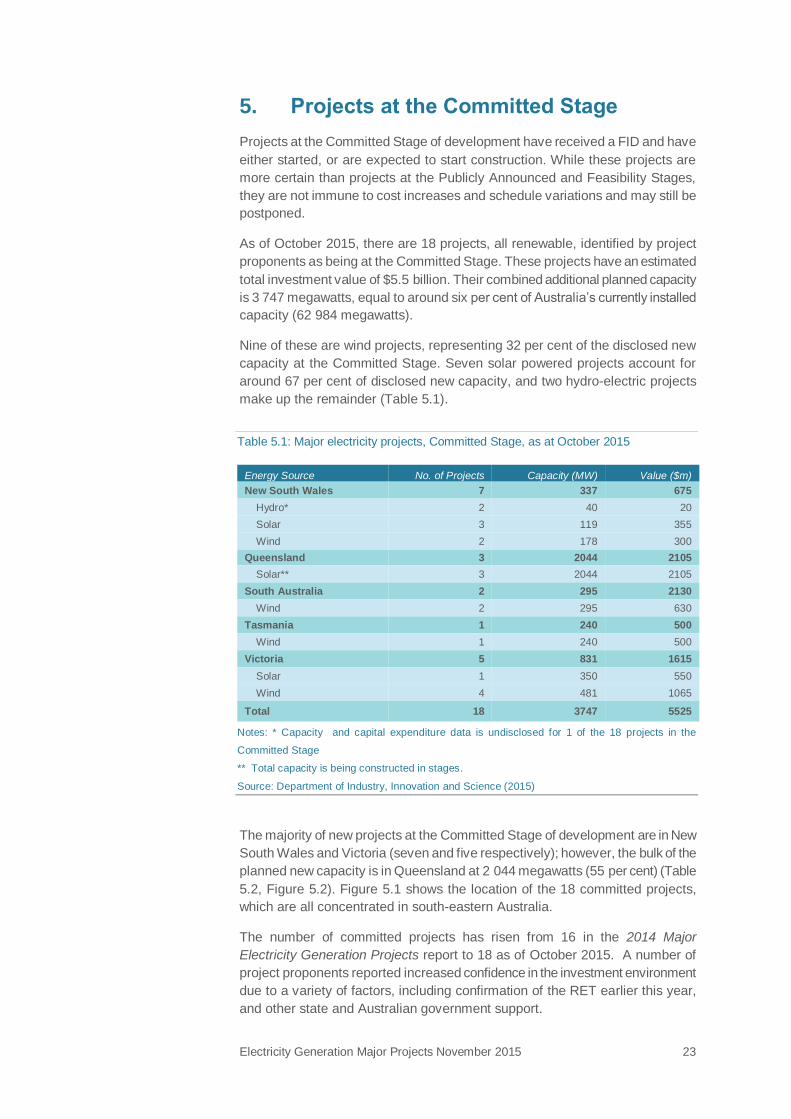

5. Projects at the Committed Stage

Projects at the Committed Stage of development have received a FID and have

either started, or are expected to start construction. While these projects are

more certain than projects at the Publicly Announced and Feasibility Stages,

they are not immune to cost increases and schedule variations and may still be

postponed.

As of October 2015, there are 18 projects, all renewable, identified by project

proponents as being at the Committed Stage. These projects have an estimated

total investment value of $5.5 billion. Their combined additional planned capacity

is 3 747 megawatts, equal to around six per cent of Australia’s currently installed

capacity (62 984 megawatts).

Nine of these are wind projects, representing 32 per cent of the disclosed new

capacity at the Committed Stage. Seven solar powered projects account for

around 67 per cent of disclosed new capacity, and two hydro-electric projects

make up the remainder (Table 5.1).

Table 5.1: Major electricity projects, Committed Stage, as at October 2015

Energy Source No. of Projects Capacity (MW) Value ($m)

New South Wales 7 337 675

Hydro* 2 40 20

Solar 3 119 355

Wind 2 178 300

Queensland 3 2044 2105

Solar** 3 2044 2105

South Australia 2 295 2130

Wind 2 295 630

Tasmania 1 240 500

Wind 1 240 500

Victoria 5 831 1615

Solar 1 350 550

Wind 4 481 1065

Total 18 3747 5525

Notes: * Capacity and capital expenditure data is undisclosed for 1 of the 18 projects in the

Committed Stage

** Total capacity is being constructed in stages.

Source: Department of Industry, Innovation and Science (2015)

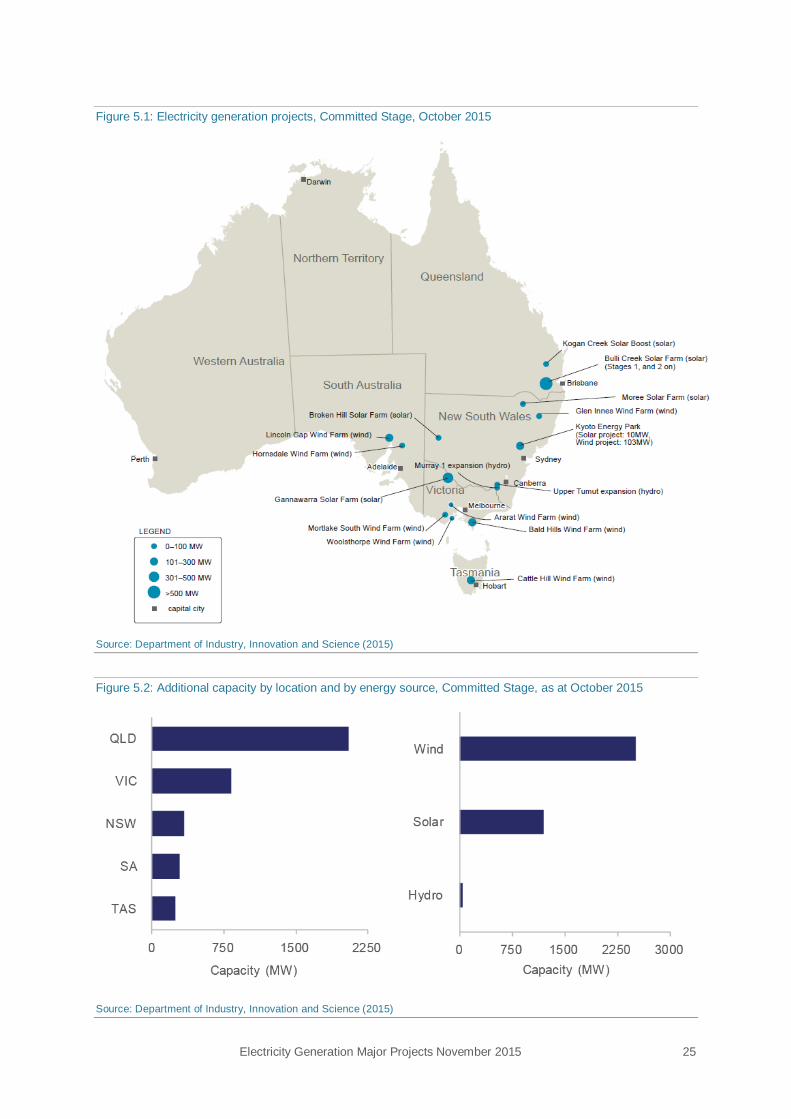

The majority of new projects at the Committed Stage of development are in New

South Wales and Victoria (seven and five respectively); however, the bulk of the

planned new capacity is in Queensland at 2 044 megawatts (55 per cent) (Table

5.2, Figure 5.2). Figure 5.1 shows the location of the 18 committed projects,

which are all concentrated in south-eastern Australia.

The number of committed projects has risen from 16 in the 2014 Major

Electricity Generation Projects report to 18 as of October 2015. A number of

project proponents reported increased confidence in the investment environment

due to a variety of factors, including confirmation of the RET earlier this year,

and other state and Australian government support.

Electricity Generation Major Projects November 2015 24

Table 5.2: Major electricity projects investment pipeline, by region, as at October 2015

Publicly Announced * Feasibility Stage ** Committed *** Completed Total

Region No. Capacity

MW Value

$m No.

Capacity MW

Value $m

No. Capacity

MW Value

$m No.

Capacity MW

Value $m

No. Capacity

MW Value

$m

New South Wales 8 1834 1677 22 5848 5925 7 337 675 3 319.8 936 40 8 339 9 213

Northern Territory

1 450

1 450

Queensland 4 770 625 18 3927 8855 3 2044 2105

25 6 741 11 585

South Australia 5 680 1160 12 3604 3530 2 295 630

19 4 579 5 320

Tasmania

2 539 1400 1 240 500

3 779 1 900

Victoria 9 1360 1621 17 4003 6390 5 830.5 1615

31 6 194 9 626

Western Australia 1 150 570 13 1736.4 3550

14 1 886 4 120

Total 27 4 794 5 653 85 20 107 29 650 18 3 747 5 525 3 320 936 133 28 968 41 764

Notes: * Capital expenditure data for project costs is undisclosed for 9 of the 27 projects

** Capital expenditure data for project costs is undisclosed for 21 of the 85 projects

*** Capacity and capital expenditure data for project costs is undisclosed for 1 of the 18 projects

Source: Department of Industry, Innovation and Science (2015)

Electricity Generation Major Projects November 2015 25

Figure 5.1: Electricity generation projects, Committed Stage, October 2015

Source: Department of Industry, Innovation and Science (2015)

Figure 5.2: Additional capacity by location and by energy source, Committed Stage, as at October 2015

Source: Department of Industry, Innovation and Science (2015)

Electricity Generation Major Projects November 2015 26

5.1 Solar Projects

Australia’s abundance of space, climate conditions and investment in

renewables R&D makes it an attractive location for large scale solar projects.

Solar projects dominate the Committed Stage of project development,

representing 67 per cent of total planned capacity (2 513 megawatts) and

$3 billion. While there are seven solar projects across Australia, most capacity is

from the two gigawatt Bulli Creek mega solar project in south Queensland.

The $2 billion Bulli Creek Solar Farm, owned by Solar Choice, co-developed

with Sun Edison, will be the world’s largest solar farm once fully developed. The

project is set for staged deployment over eight years and will be 20 times the

capacity of Australia’s current largest solar farm when completed. Solar Choice

is also undertaking staged development of the 350 megawatt Gannawarra Solar

Farm in north-western Victoria.

CS Energy is developing the 44 megawatt Kogan Creek Solar Boost project.

The solar boost project is a hybrid between renewable solar thermal power and

the existing coal powered Kogan Creek Power Station and will be completed in

2016.

5.2 Wind Projects

Wind is a well-established and competitive renewable energy source, and

accounted for 4 per cent of Australia’s electricity generation in 2013–14. Wind

projects represent 32 per cent (1 194 megawatts) of new capacity in the

Committed Stage at a total value of $2.5 billion.

Victoria has the highest new capacity of wind at 481 megawatts, followed by

South Australia at 295 megawatts, and Tasmania at 240 megawatts.

OneWind owns (or is a subsidiary in) three of the four largest wind projects in

the Committed Stage of development: Tasmania’s 240 megawatt Cattle Hill

Wind Farm; South Australia’s 195 megawatt Lincoln Gap Wind Farm; and the

75 megawatt Glenn Innes Wind Farm in New South Wales.

The largest project in Victoria is RES Australia’s Ararat Windfarm in Ararat. The

project is scheduled for completion in 2017 at a capital cost of $450 million, and

is planned to add 240 megawatts to existing capacity.

5.3 Hydro projects

Hydro projects make up 40 megawatts of disclosed capacity at the Committed

Stage. There are no new identified hydro projects, with new capacity coming

from the expansion of two Snowy Hydro facilities.

The Upper Tumut project is being developed as part of Snowy Hydro’s $400

million Scheme Modernisation project and is planned to expand capacity by 40

megawatts at a capital cost of $20 million and be completed in 2015. Snowy

Hydro has also committed to the development of the Murray 1 project with the

proposed expansion of hydro-electricity capacity at the plant.

Electricity Generation Major Projects November 2015 27

6. Projects at the Feasibility Stage

Projects at this stage have completed initial feasibility studies into their

commercial viability and have an announced development path ahead of them.

There is uncertainty over the number of projects that are likely to receive a

positive FID in the short to medium term, and not all of potential investment will

become committed. Consequently, the value of projects at the Feasibility Stage

is not directly comparable to the value of the more certain projects at the

Committed Stage.

There are 85 projects identified as at the Feasibility Stage with combined

capacity of 20 107 megawatts and total disclosed capital expenditure of

$29.7 billion (Table 6.1). The location of projects is widespread, with at least one

project in each jurisdiction (Figure 6.1).

Table 6.1: Major electricity projects, Feasibility Stage, as at October 2015

Energy Source No. of Projects Capacity (MW) Value ($m)*

New South Wales 22 5848 5925

Gas 5 1950 1350

Solar 3 130 378

Wind 14 3768 4197

Northern Territory 1 450 na

Ocean 1 450 na

Queensland 18 3927 8855

Black coal 1 150 na

Biomass 1 85 500

Hydro 2 367 330

Solar 6 2369 4925

Wind 8 956 3100

South Australia 12 3604 3530

Gas 2 1020 800

Geothermal 1 600 75

Solar 1 50 na

Wind 8 1934 2655

Tasmania 2 539 1400

Wind 2 539 1400

Victoria 17 4003 6390

Brown coal gasification 1 600 1100

Gas 1 550 525

Geothermal 1 140 75

Solar 2 180 na

Wind 12 2533 4690

Western Australia 13 1736 3550

Gas 1 168 180

Biomass 2 75 530

Solar 5 285 1240

Wind 5 1208 1600

Total 85 20107 29650

Notes: *Capital expenditure data for project costs is undisclosed for 21 of the 85 projects.

Source: Department of Industry, Innovation and Science (2015)

Electricity Generation Major Projects November 2015 28

Figure 6.1: Additional capacity by location and by energy source, Feasibility Stage, as at October 2015

Source: Department of Industry, Innovation and Science (2015)

6.1 Non-renewable electricity projects

Non-renewable electricity generation projects accounted for 11 of the

85 projects at the Feasibility Stage, and 22 per cent (4 438 megawatts) of

disclosed new capacity. The majority of these non-renewable projects — nine of

11 — are gas-fired projects, as well one black coal-fired power station and one

brown coal gasification station.

Most of the gas projects are currently on hold, awaiting positive investment

signals and approvals. The transition from Feasibility Stage to Committed Stage

for gas projects seems unlikely and unprofitable at this point in time, with

domestic gas prices expected to rise in the next few years.

The coal-fired project currently in the Feasibility Stage is the Moray Power

station (150 megawatts), run by Moray Power. It is proposed as the main power

supply to Adani’s Carmichael coal mine in the Galilee Basin, Central

Queensland. The Carmichael mine has encountered approval barriers including

environmental concerns and public backlash. Moray Power’s operations will

coincide with decisions made on the mine.

Electricity Generation Major Projects November 2015 29

6.2 Renewable electricity projects

There are 74 renewable electricity generation projects at the Feasibility Stage,

totalling 15 669 megawatts of capacity at a value of $25.7 billion.

Forty-nine of these projects are wind (compared to 51 in 2014), representing 54

per cent of the disclosed renewable capacity at the Feasibility Stage (10 938

megawatts). Wind projects are spread throughout Australia in all jurisdictions but

the Northern Territory and the ACT, with particular concentration in New South

Wales and Victoria.

Solar projects rose to 17 projects from nine in 2014. They currently account for

around 15 per cent of total planned new capacity at the Feasibility Stage with

capital expenditure of $6.5 billion.

There are two geothermal projects (740 megawatts) as well as two hydro-

electric plants (367 megawatts). The three bioenergy generation facilities have a

planned capacity of 160 megawatts, and one ocean powered project is

proposed for development with planned capacity of 450 megawatts.

Electricity Generation Major Projects November 2015 30

7. Projects at the Publicly Announced Stage

Projects at this stage include those for which concept and pre-development

activities are completed, but which have not yet completed an initial form of

feasibility study to fully assess the commercial viability of the project. During this

development phase project costs and market conditions may prevent the project

from going ahead or change the initial publicly announced project proposal. In

some cases this progression through to the Feasibility Stage and further can

take several years.

As of October 2015, 27 projects at the Publicly Announced Stage have been

identified, with a total capacity of 4 794 megawatts and total disclosed

investment value of $5.7 billion (Table 7.1). These projects are mostly wind and

gas-fired generation (Figure 7.1).

Table 7.1: Major electricity projects, Publicly Announced Stage, as at October 2015

Energy Source No. of Projects Capacity (MW) Value ($m)*

New South Wales 7 1834 1677

Gas 2 730 490

Wind 6 1104 1187

Queensland 4 770 625

Gas 1 500 na

Hydro 1 30 na

Solar 2 240 625

South Australia 5 680 1160

Wind 5 680 1160

Victoria 9 1360 1621

Gas 1 450 na

Geothermal 1 50 na

Ocean 1 34 na

Wind 6 826 1621

Western Australia 1 150 570

Gas 1 150 570

Grand Total 27 4794 5653

Notes: * Capital expenditure data for project costs is undisclosed for 9 of the 27 projects

Source: Department of Industry, Innovation and Science (2015)

7.1 Non-renewable electricity projects

Non-renewable electricity generation projects accounted for five of the

27 projects at the Publicly Announced Stage, and around 38 per cent

(1 830 megawatts) of disclosed new capacity. All of these non-renewable

projects are gas-fired projects with total disclosed value of $1 billion.

The largest non-renewable project at the Publicly Announced stage of

development is the $450 million Marulan power station in New South Wales.

Electricity Generation Major Projects November 2015 31

The proposed 700 megawatt gas-fired power station is planned as a peaking

plant to supply the Southern Tablelands region, but is currently on hold due to

reduced electricity demand.

Figure 7.1: Additional capacity by location and by energy source, Publicly Announced Stage, as at October 2015

Source: Department of Industry, Innovation and Science (2015)

7.2 Renewable electricity projects

There are 22 renewable electricity generation projects accounting for around 62

per cent (2 964 megawatts) of new capacity with a disclosed value of

$4.6 billion. 17 of these projects are wind-powered, representing 54 per cent of

the disclosed new capacity.

EPYC’s Jupiter Wind Farm in New South Wales is the largest wind project at the

Publicly Announced Stage in terms of capacity and capital expenditure. The

project has a planned capacity of up to 350 megawatts and an estimated capital

cost of $400 million.

The two large-scale solar farms at the Publicly Announced Stage are both in

Queensland and account for 240 megawatts of new capacity and $625 million of

capital expenditure. The projects, Clare Solar Farm and Lilyvale Solar Farm, are

owned by FRV.

Electricity generation major projects 32

References

ACT Government (2015) Renewable Energy Local Investment Framework.

Accessed: November 2015 http://www.environment.act.gov.au

Australian Energy Market Operator (AEMO) (2015) 2015 Electricity Statement of

Opportunities, August. Accessed: November 2015

http://www.aemo.com.au/Electricity/Planning/~/media/Files/Electricity/Planning/

Reports/ESOO/2015/2015%20ESOO%20Exec%20Summary.ashx

Australian Energy Market Operator (AEMO) (2015) 2015 National Electricity

Forecasting Report, June. Accessed: November 2015

http://www.aemo.com.au/Electricity/Planning/Forecasting/National-Electricity-

Forecasting-Report

Australian Bureau of Statistics (ABS) (2015) Producer Price Indexes, Australia,

cat. no. 6427.0, September. Accessed: November 2015

http://www.abs.gov.au/ausstats/[email protected]/mf/6427.0

Australian Energy Market Operator (AEMO) 2015 2015 Gas Statement of

Opportunities, April. Accessed: November 2015

http://www.aemo.com.au/Gas/Planning/Gas-Statement-of-Opportunities

Clean Energy Regulator (CER) (2015) Postcode Data for Small-Scale

Installations, March

Clean Energy Council (2015) Clean Energy Australia Report 2014, Melbourne,

June

Department of Industry and Science (2015) Australian Energy Statistics,

Canberra, August

Energy Supply Association Australia (ESAA) (2015) Electricity Gas Australia

2015, Melbourne, July

Global-Roam, NEM Review database

Independent Market Operator (IMO) of Western Australia (2015) 2014 Electricity

Statement of Opportunities, June

Parkinson G (2014) UBS: Australian Households Could Go Off-Grid by 2018,

Reneweconomy, May. Accessed: November 2015

http://reneweconomy.com.au/2014/ubs-australian-households-go-grid-2018

Queensland Government (2015) Solar 60 — Queensland's large-scale solar

investment program. Accessed: November 2015

http://www.business.qld.gov.au/industry/energy/renewable-energy/solar-60,

Utilities Commission (2015) Power System Review 2013–14, Northern Territory

Government, May