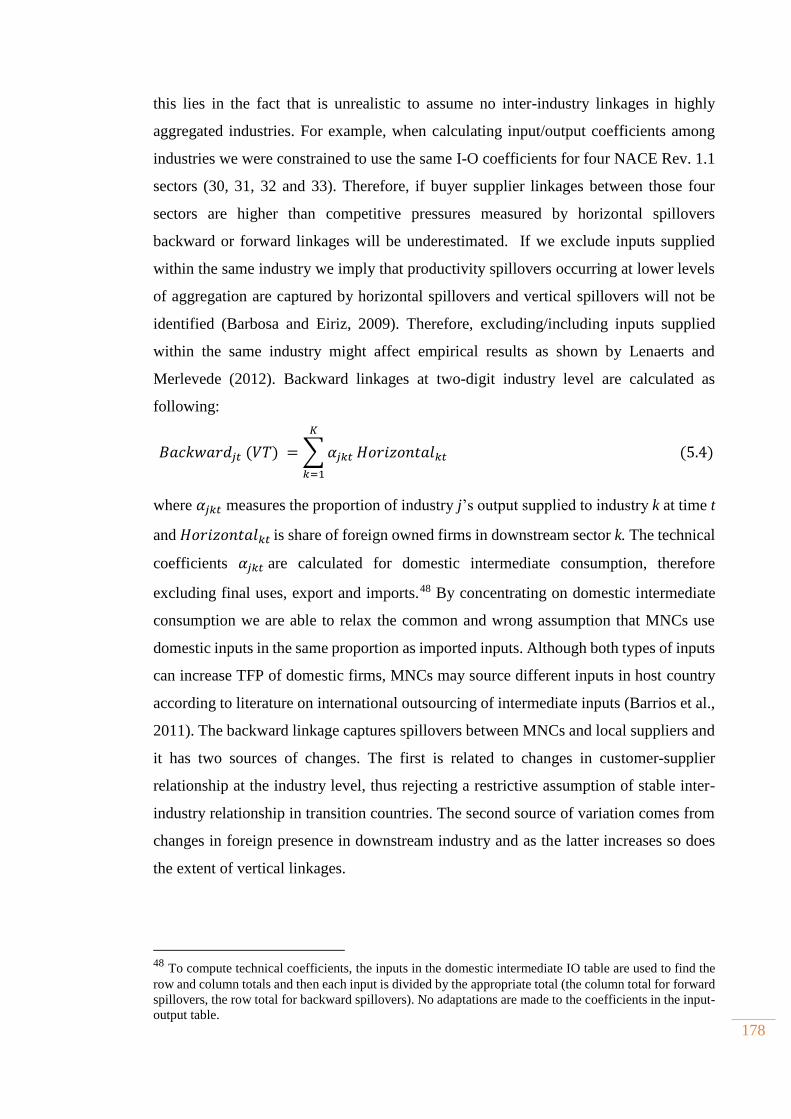

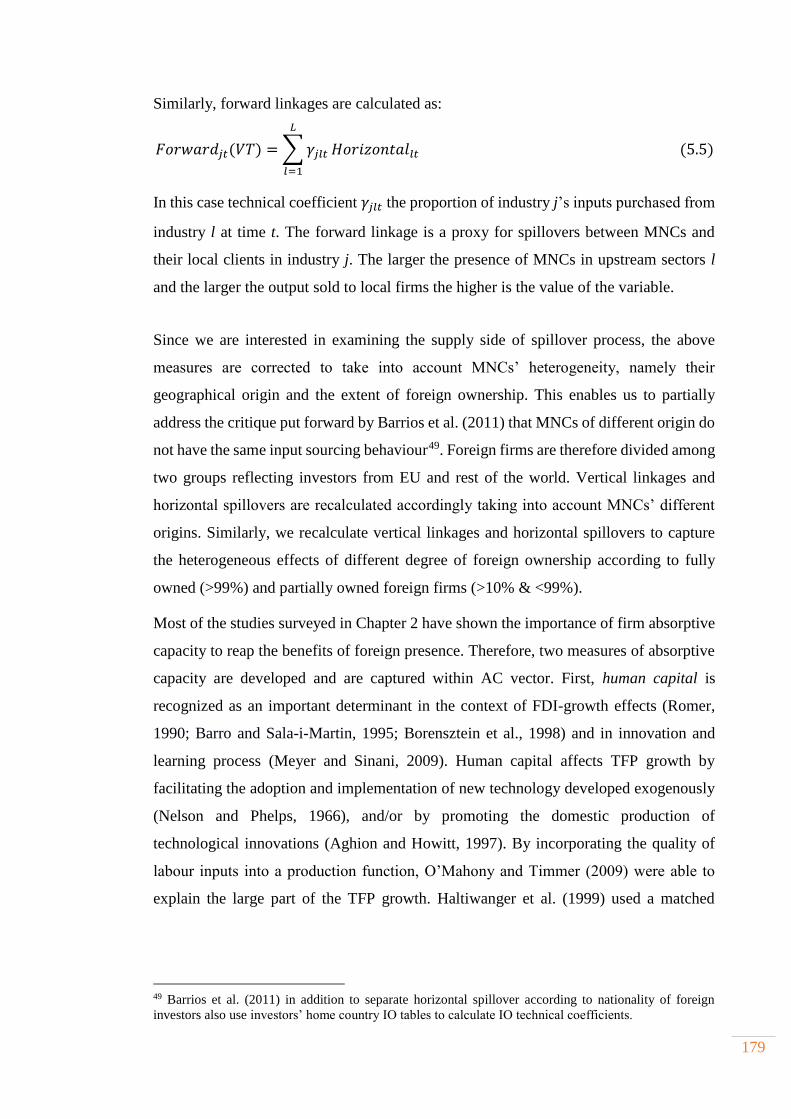

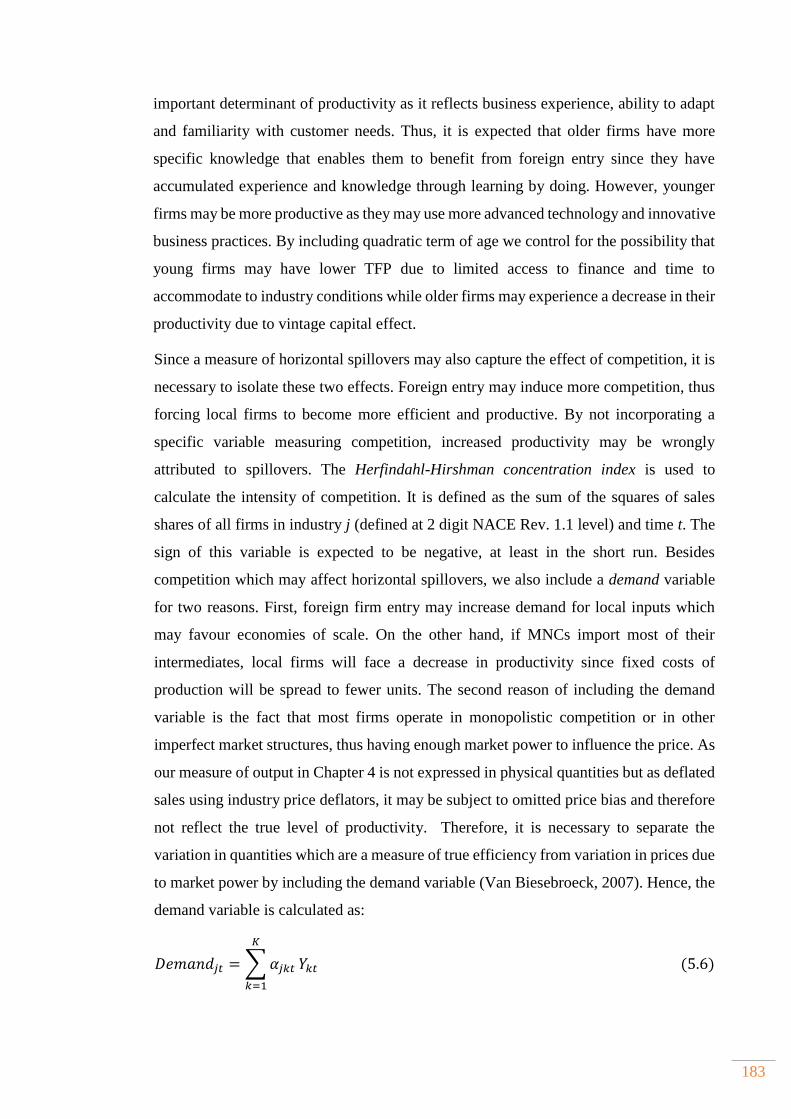

Embed Size (px)

Citation preview

Staffordshire University Faculty of Business, Education and Law

Business School

E F F E C T S O F F D I S P I L L O V E R S O N T H E P R O D U C T I V I T Y O F D O M E S T I C F I R M S

I N S E L E C T E D T R A N S I T I O N C O U N T R I E S

Edvard Orlić

A thesis submitted in partial fulfilment of the requirement of Staffordshire University for the degree of Doctor of Philosophy

March 2016

i

ABSTRACT

The transition to a market based economy in Central and East European countries

(CEECs) was characterised by deep structural and institutional reforms. These reforms,

particularly the liberalisation of trade and capital flows, played a prominent role and

enabled the entry of these countries in the “FDI market”. It was expected that the entry

of MNCs into these countries would foster firm restructuring, change the export structure

and above all generate knowledge spillovers and create linkages with indigenous firms.

Therefore, CEECs started to offer various incentives to attract FDI, hoping that some of

the technology brought by MNCs will spill over to local firms. This would enable them

to increase their productivity and achieve higher rates of growth that would result in

convergence with more advanced countries.

The aim of this thesis is to investigate productivity spillovers from FDI to local firms in

five transition countries using firm level data for the period 2002-2010. Several elements

differentiate this study from the previous analyses. We compare the effects of horizontal

spillovers and vertical linkages from FDI across countries and two main sectors

(manufacturing and services) and assess the heterogeneity of MNCs. To the best of our

knowledge this is the first study taking into account MNCs’ origin and the extent of

foreign ownership in a group of transition economies. Given the importance of FDI in

services we further disentangle vertical linkages according to sectoral source and

investigate the moderating role of firms’ absorptive capacity. Semi-parametric approach

based on control function is applied to estimate firms’ total factor productivity (TFP)

which is then used in the estimation of horizontal and vertical spillovers from FDI along

with other firm and industry level determinants. FDI spillovers are estimated using the

dynamic panel econometric technique.

Our findings indicate that local firms in the advanced stage of transition benefit from

horizontal spillovers arising mostly in service sector and from partially owned foreign

firms while the effects of MNCs’ origin are ambiguous. We also find that net effects of

FDI spillovers are driven by vertical linkages. In particular, positive effect of backward

linkages on firm productivity are found for fully owned and non-EU MNCs. However,

for a limited set of countries, these positive effects of backward linkages are in certain

ii

cases further supported or offset by negative effects of partially owned foreign firms and

EU MNCs. On the other hand, forward linkages when positive are limited to EU MNCs

while non-EU MNCs and both partially and fully owned foreign firms exhibit mostly

negative productivity effects with the exception of two countries. Furthermore, we find

that MNCs in manufacturing and service sectors generate significant productivity

spillovers to manufacturing firms which are further strengthened with higher levels of

absorptive capacity. However, in most cases these spillovers occur through different

vertical channels, namely through manufacturing backward and services forward

spillovers thus shedding new light on the increasing importance of forward linkages and

FDI in services. Human capital and investment in intangibles are found to be strong

determinants of firm productivity together with increased competition, while firms’ age

and size have U-shape and inverse U-shape effects, respectively.

This thesis shows that the effects of FDI spillovers differ among countries suggesting

that sectoral and MNCs’ heterogeneity play an important role in driving the overall

results. Therefore, based on these findings we have developed a set of policy

recommendations for policy makers and investment promotion agencies with the aim to

maximise the benefits of MNC’s entry for indigenous firms’ productivity and their

inclusion into Global Value Chains.

iii

TABLE OF CONTENTS

Abstract………….. ..................................................................................................................................................... i

Table of contents ................................................................................................................................................. iii

List of Tables…… ................................................................................................................................................ vii

List of Figures………………………….................................................................................................................. xii

List of Abbreviations ....................................................................................................................................... xiv

Acknowledgments ............................................................................................................................................. xv

Preface………………………….. ............................................................................................................................. xv

CHAPTER 1. THEORIES OF FOREIGN DIRECT INVESTMENT ................................................... 1

1.1 Introduction ............................................................................................................................................... 2

1.2 Concept of FDI – definition, measurement and types .............................................................. 4

1.3 Theories of FDI ......................................................................................................................................... 5

1.3.1 The neoclassical theory of capital movement ..................................................................... 6

1.3.2 Industrial organization theory .................................................................................................. 7

1.3.3 Macroeconomic development approach ............................................................................... 9

1.3.4 Internalisation theories .............................................................................................................. 13

1.3.5 OLI paradigm .................................................................................................................................. 16

1.3.6 Evolutionary approaches to the theory of MNC ............................................................... 19

1.3.7 New trade theory .......................................................................................................................... 22

1.4 Motives and mode of MNCs’ entry .................................................................................................. 25

1.5 Potential benefits of FDI ..................................................................................................................... 28

1.6 Conclusions .............................................................................................................................................. 31

CHAPTER 2. FDI SPILLOVERS AND LINKAGES: THEORY AND EMPIRICAL EVIDENCE………. ................................................................................................................................................. 33

2.1 Introduction ............................................................................................................................................. 34

2.2 Knowledge spillovers from FDI ....................................................................................................... 35

2.3 Intra-industry (horizontal) spillovers .......................................................................................... 38

2.3.1 Demonstration effects ................................................................................................................. 39

2.3.2 Competition effects ...................................................................................................................... 40

2.3.3 Worker mobility ............................................................................................................................ 42

2.4 Inter-industry (vertical) spillovers ................................................................................................ 44

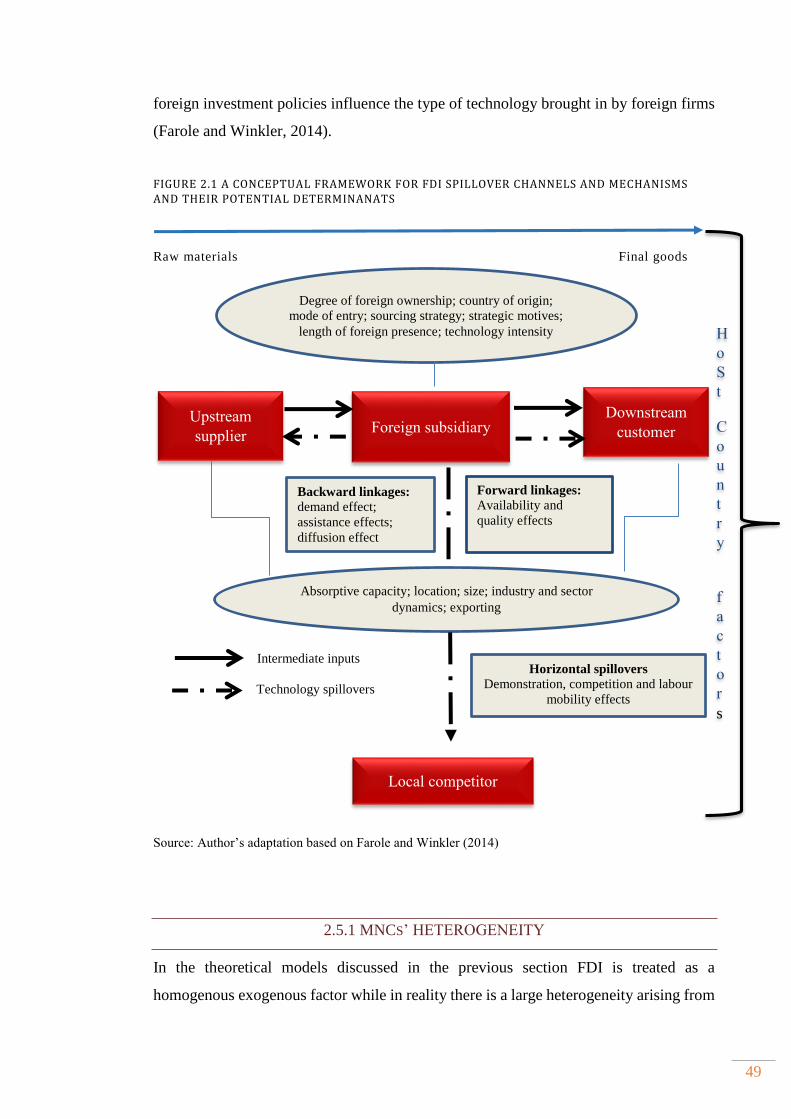

2.5 Determinants of FDI spillovers ........................................................................................................ 48

2.5.1 MNCs’ heterogeneity ................................................................................................................... 49

2.5.2 Domestic firms’ heterogeneity ................................................................................................ 54

iv

2.5.3 Other potential factors ................................................................................................................ 57

2.6 Review of the empirical literature ................................................................................................. 59

2.6.1 Empirical evidence on FDI spillovers ................................................................................... 60

2.6.2 Shortcomings of the studies on FDI spillovers in TEs ................................................... 71

2.7 Conclusions .............................................................................................................................................. 74

CHAPTER 3. CONTRIBUTION OF INWARD FDI TO NMS ECONOMIES – COUNTRY AND INDUSTRY ANALYSIS ....................................................................................................................................... 77

3.1 Introduction............................................................................................................................................ 78

3.2 The process of transition and the role of FDI ............................................................................ 79

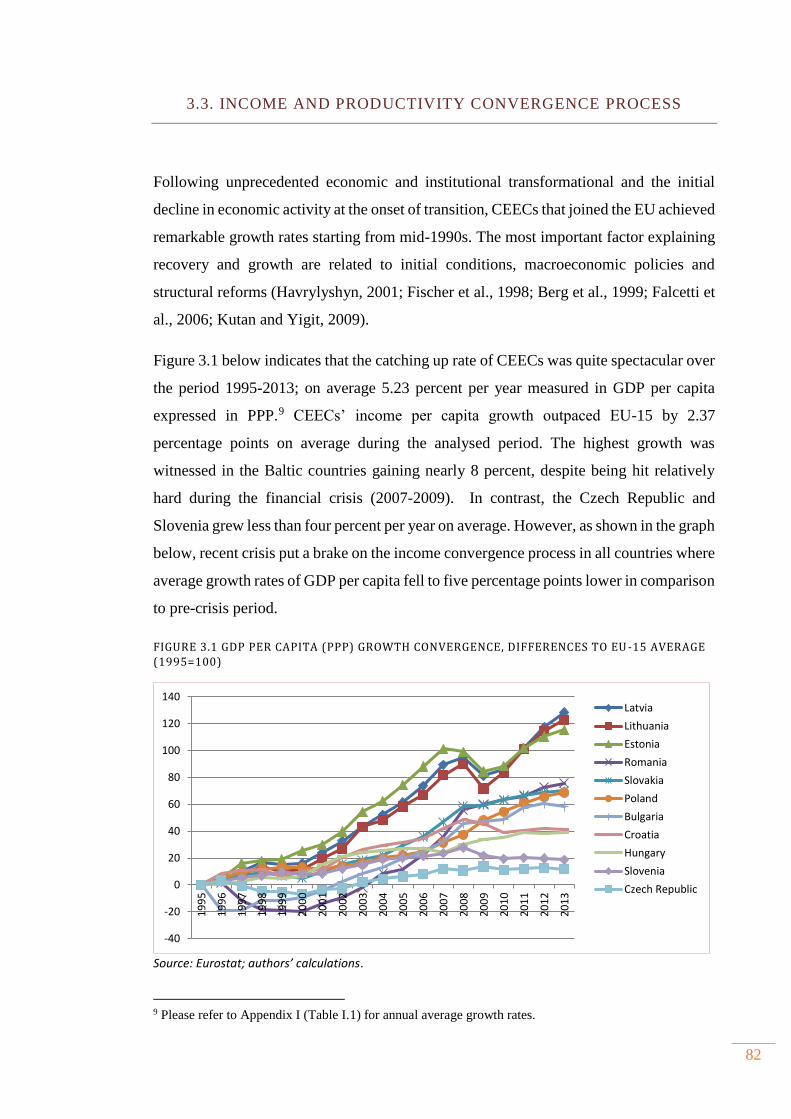

3.3. Income and productivity convergence process ....................................................................... 82

3.4 Overview of FDI in new member states ....................................................................................... 87

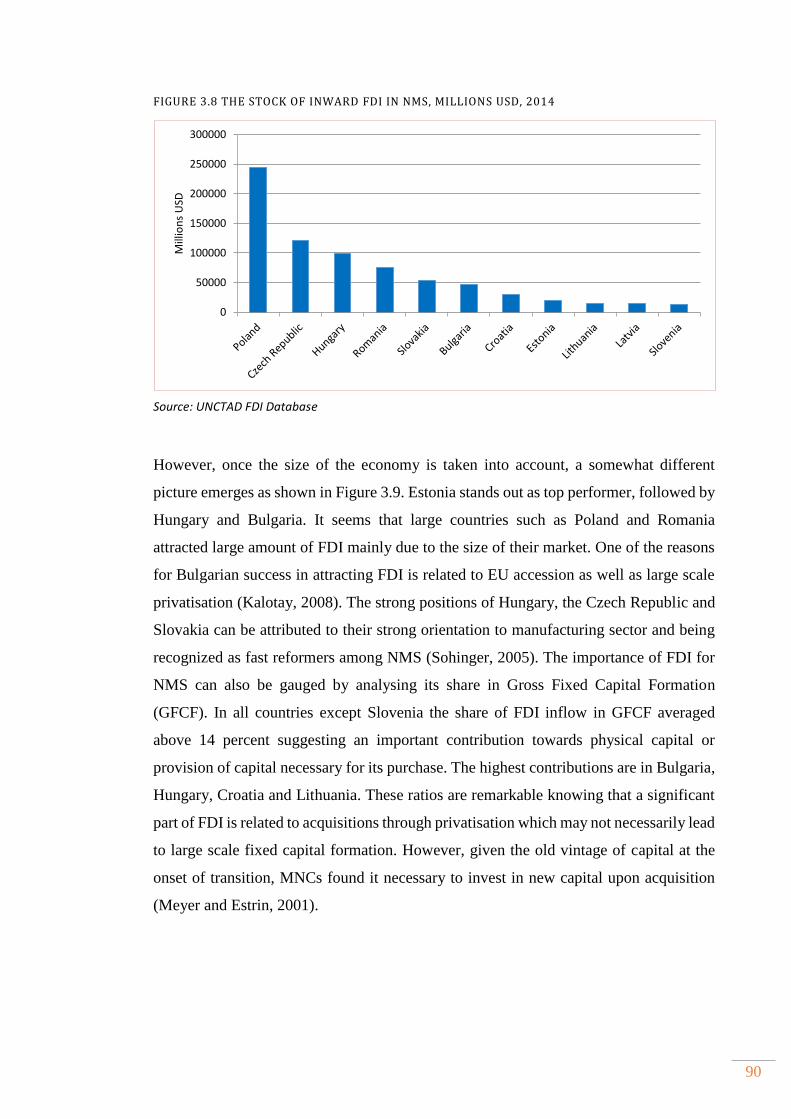

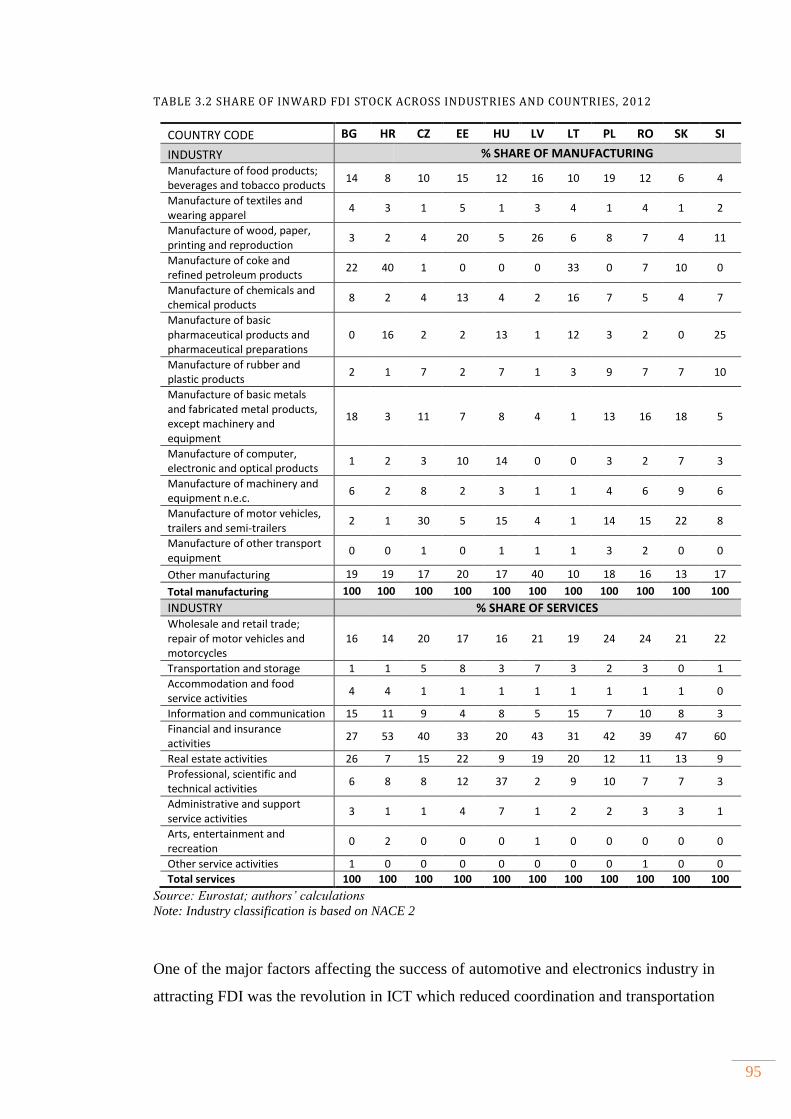

3.4.1 Country analysis of inward FDI ............................................................................................... 88

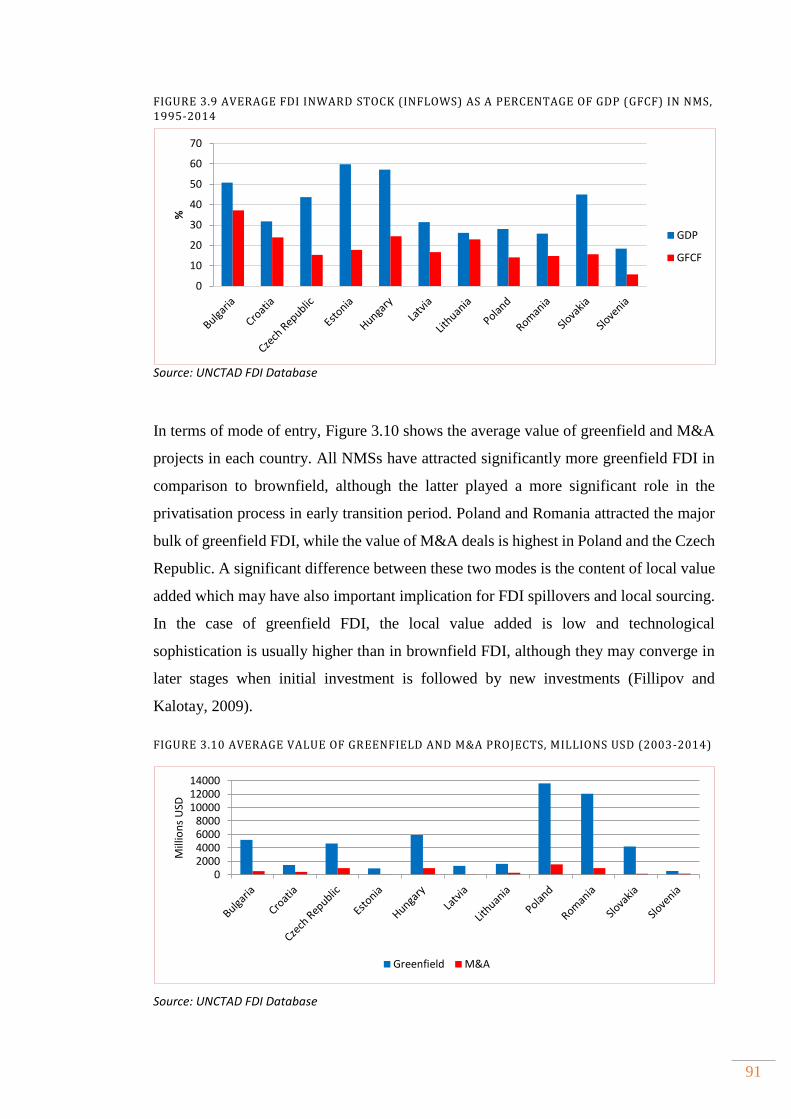

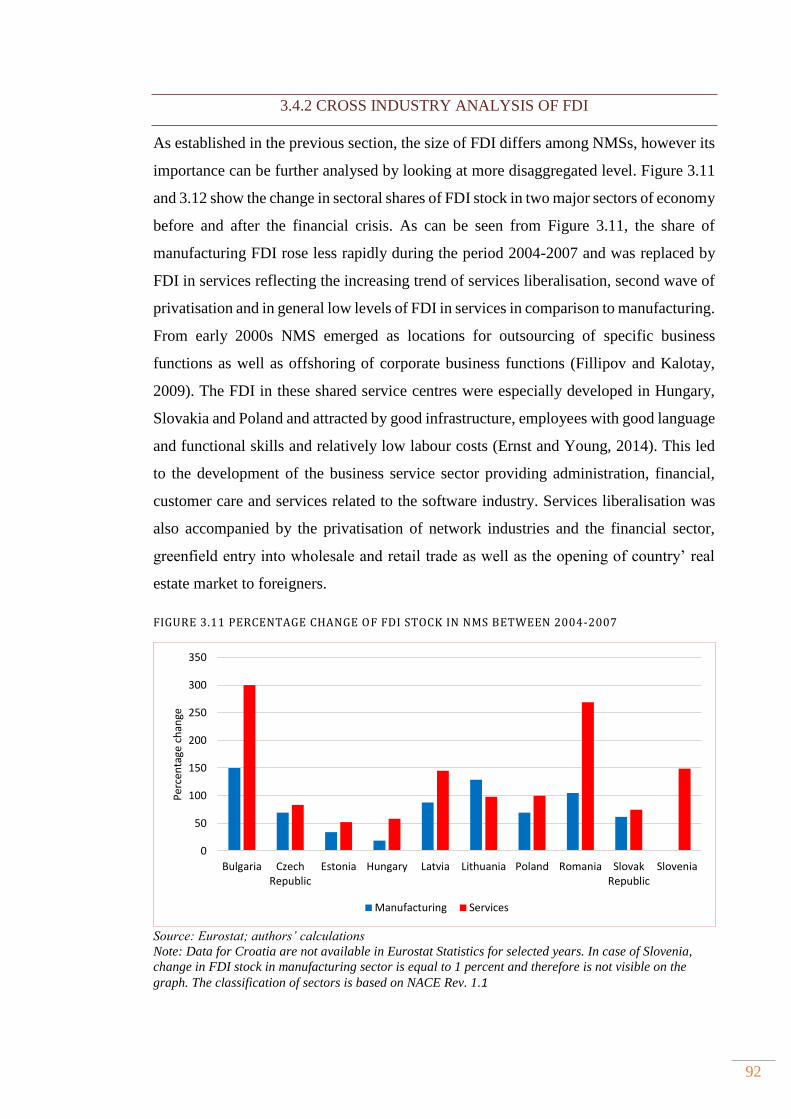

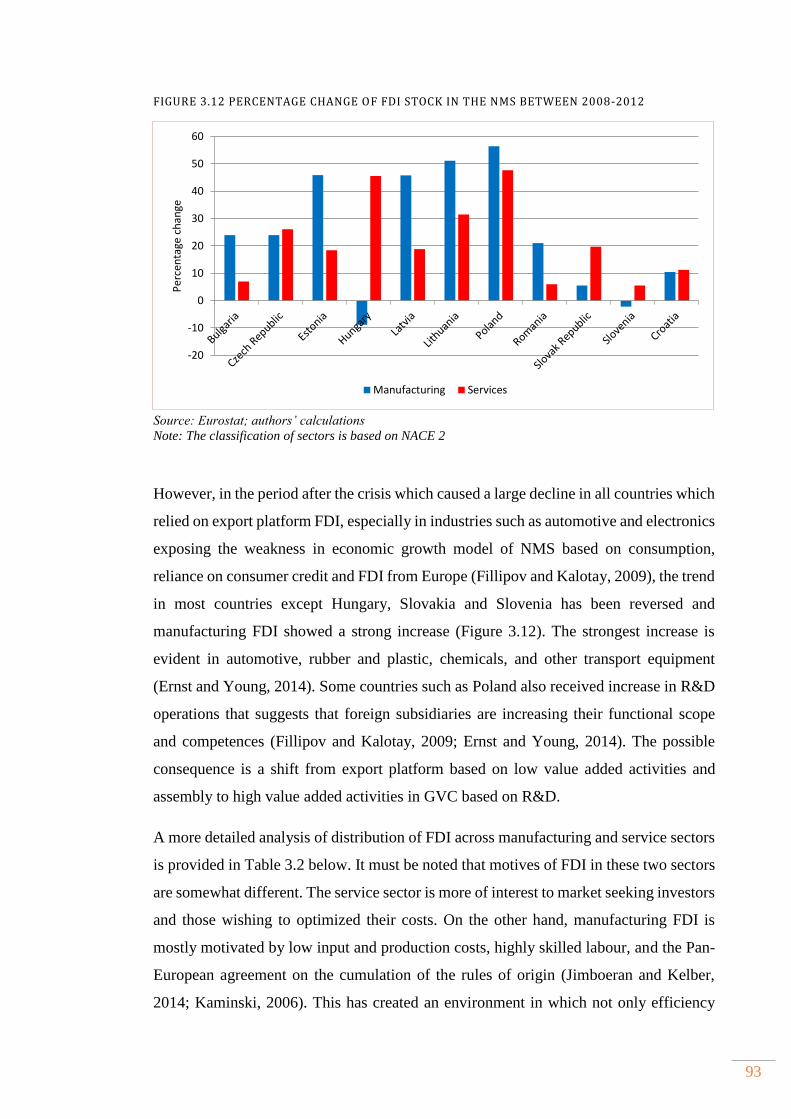

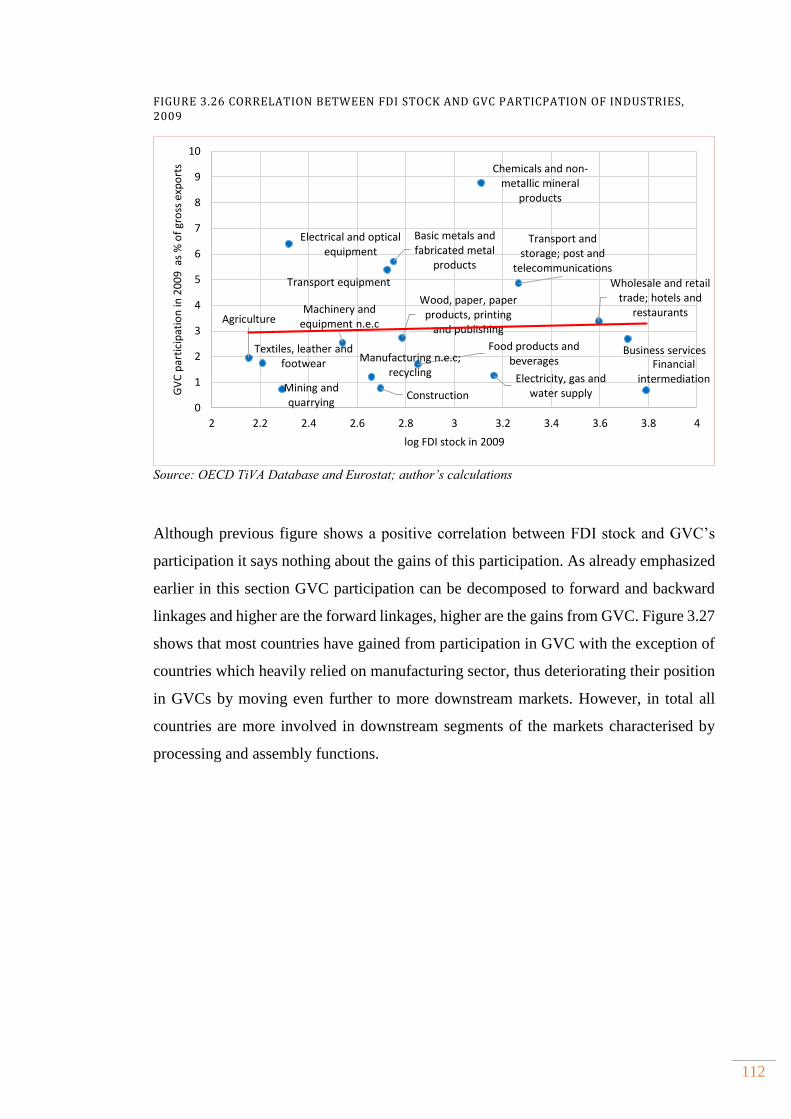

3.4.2 Cross industry analysis of FDI ................................................................................................. 92

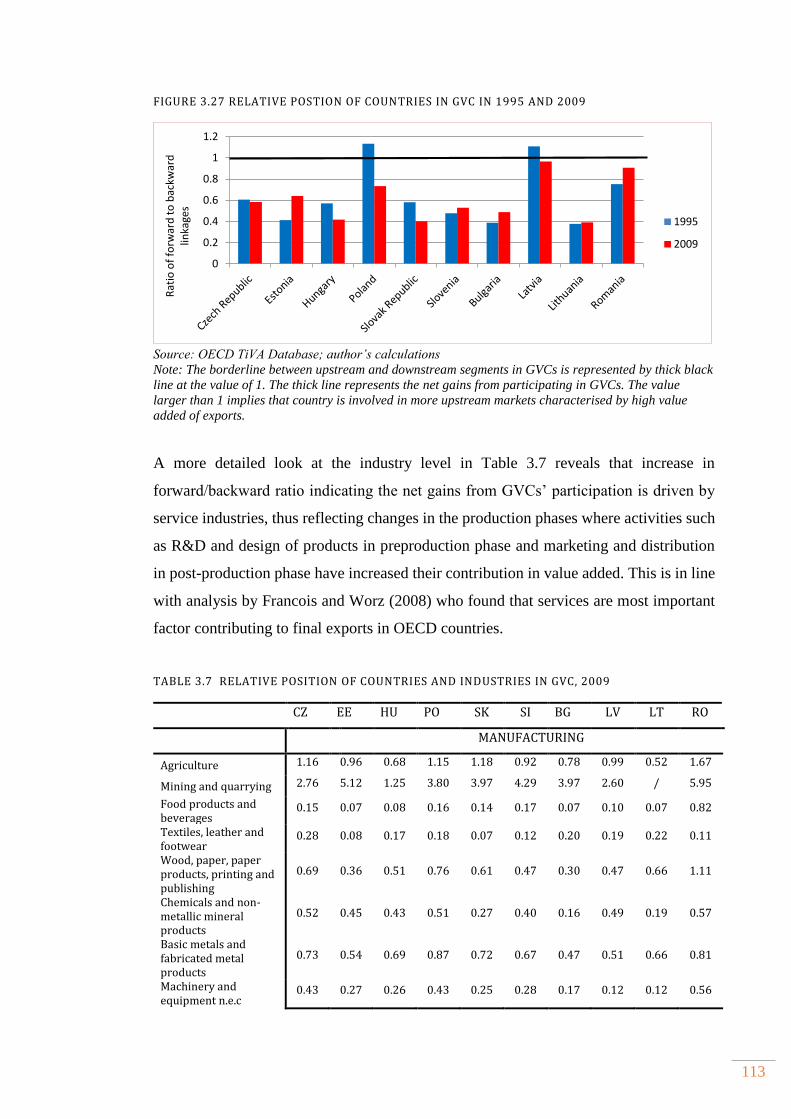

3.5 Impact of FDI on NMS Economies .................................................................................................. 96

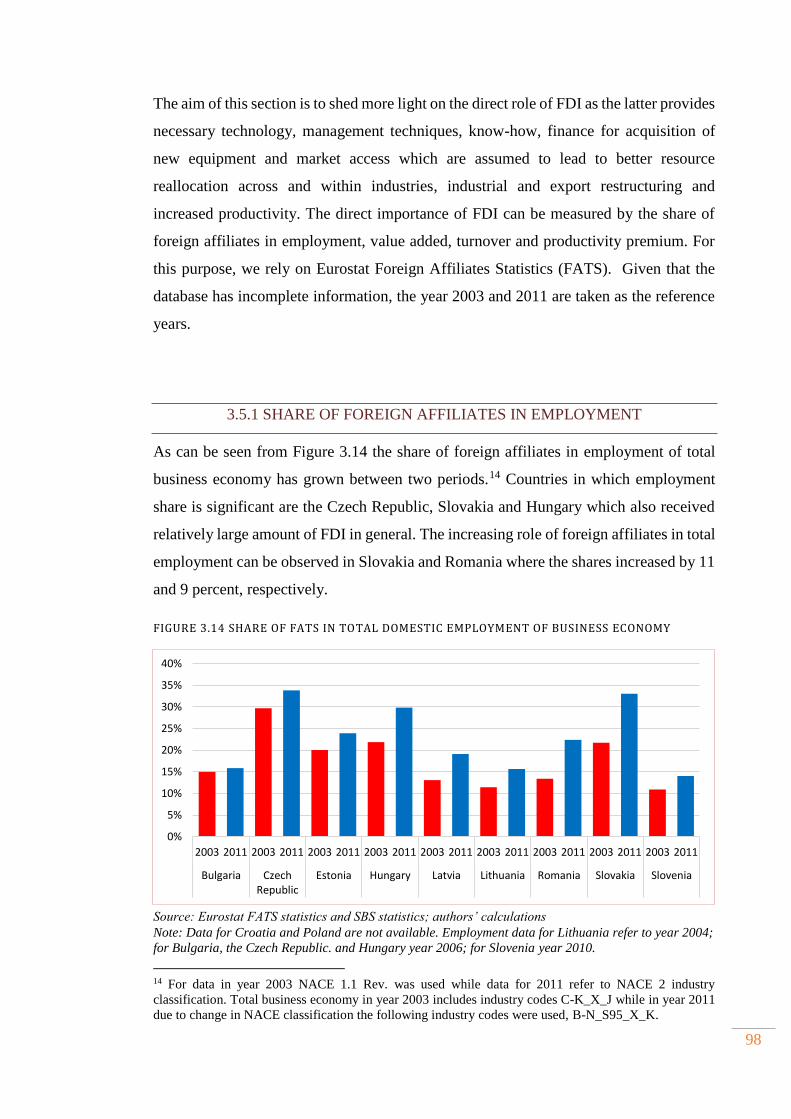

3.5.1 Share of Foreign affiliates in employment.......................................................................... 98

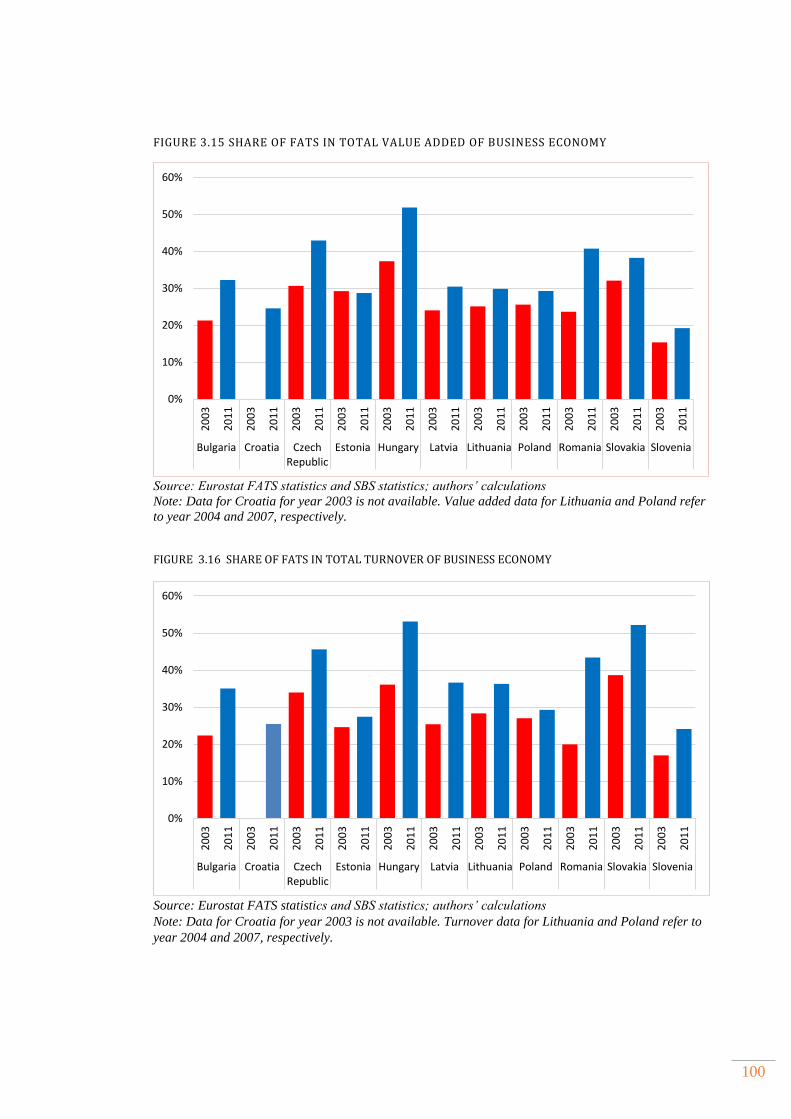

3.5.2 Share of Foreign affiliates in value added and turnover .............................................. 99

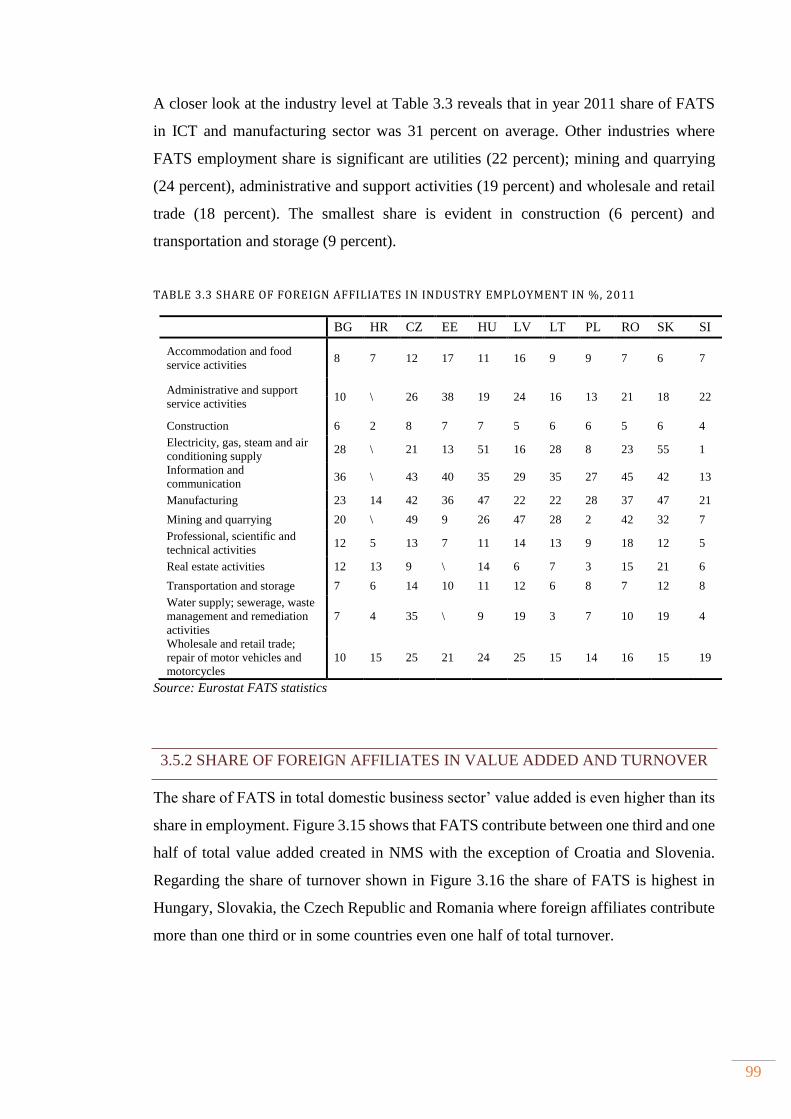

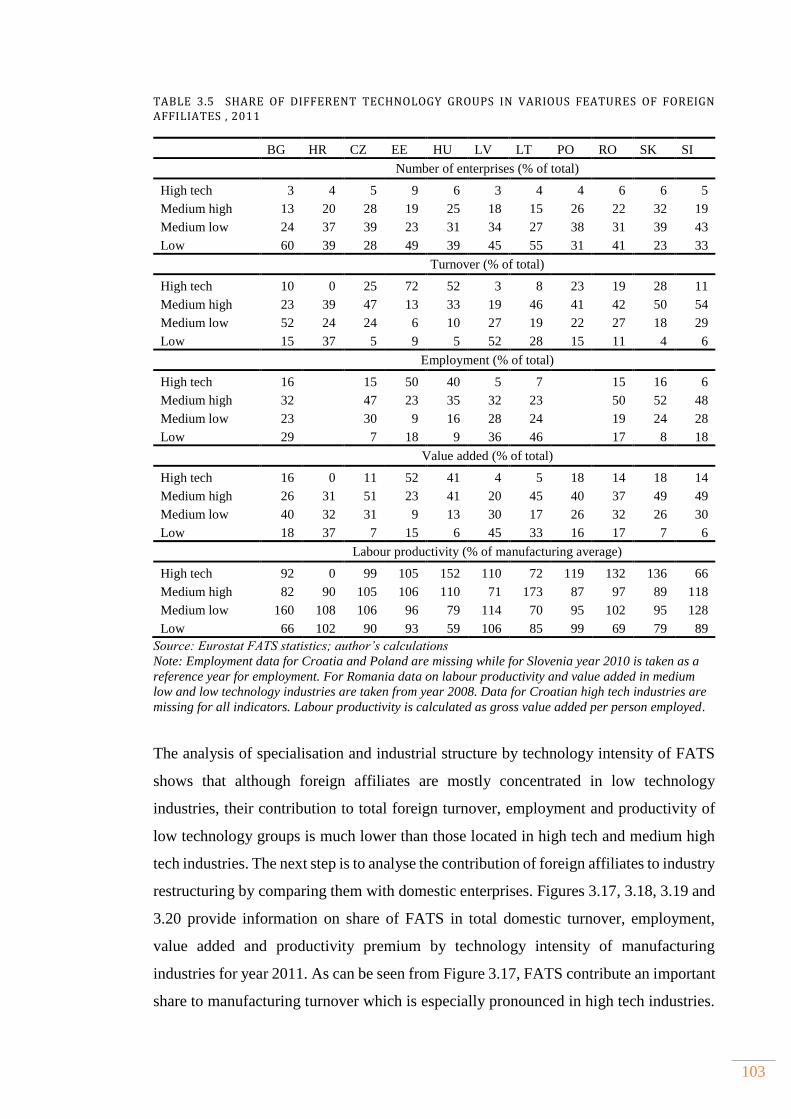

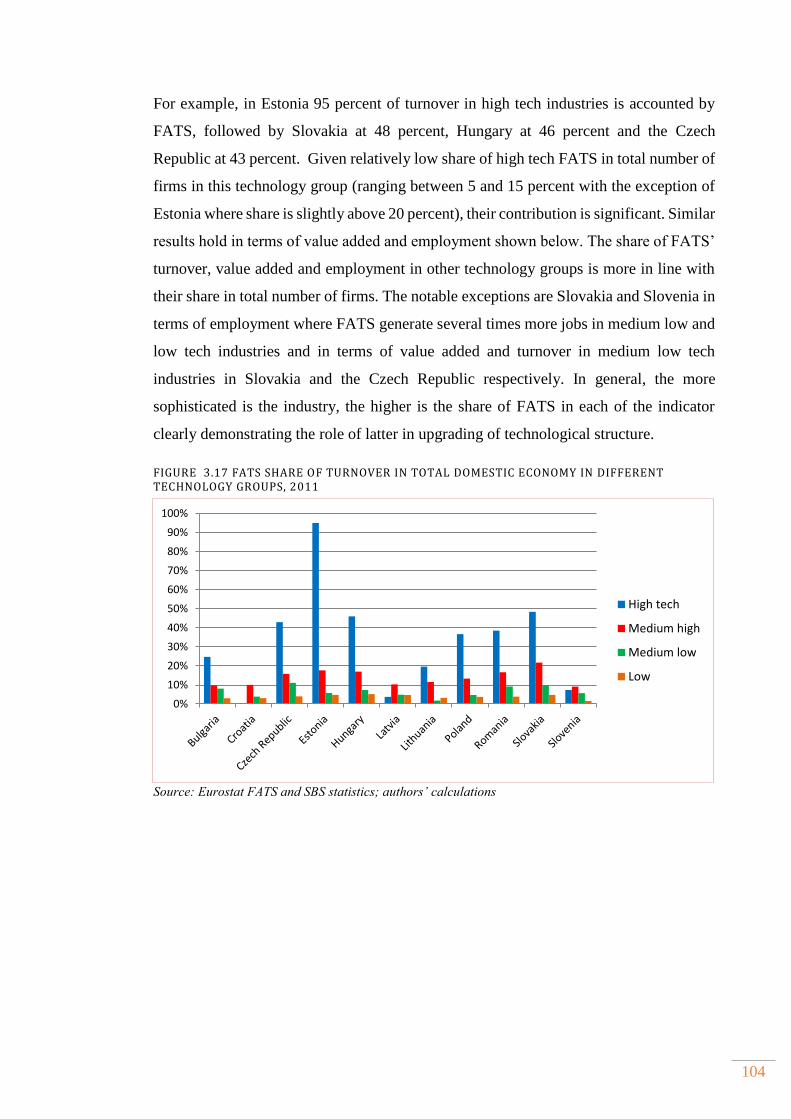

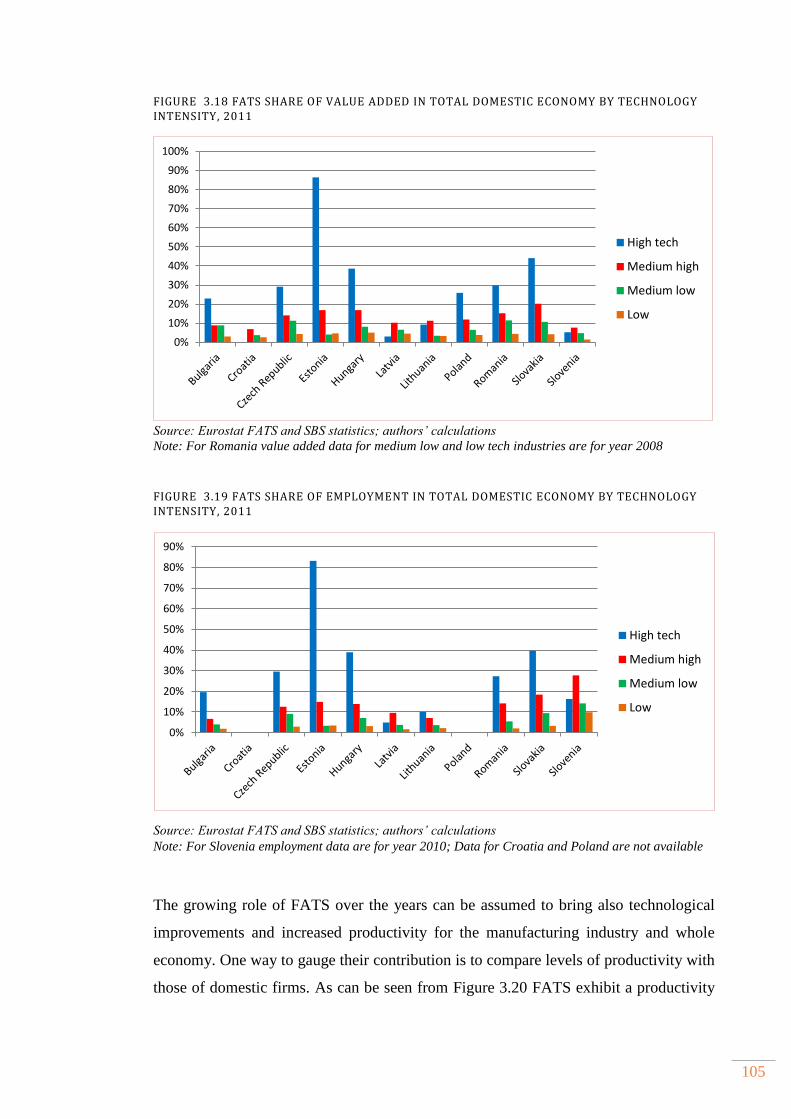

3.5.3 The role of FATS in technology upgrading and productivity improvements.... 102

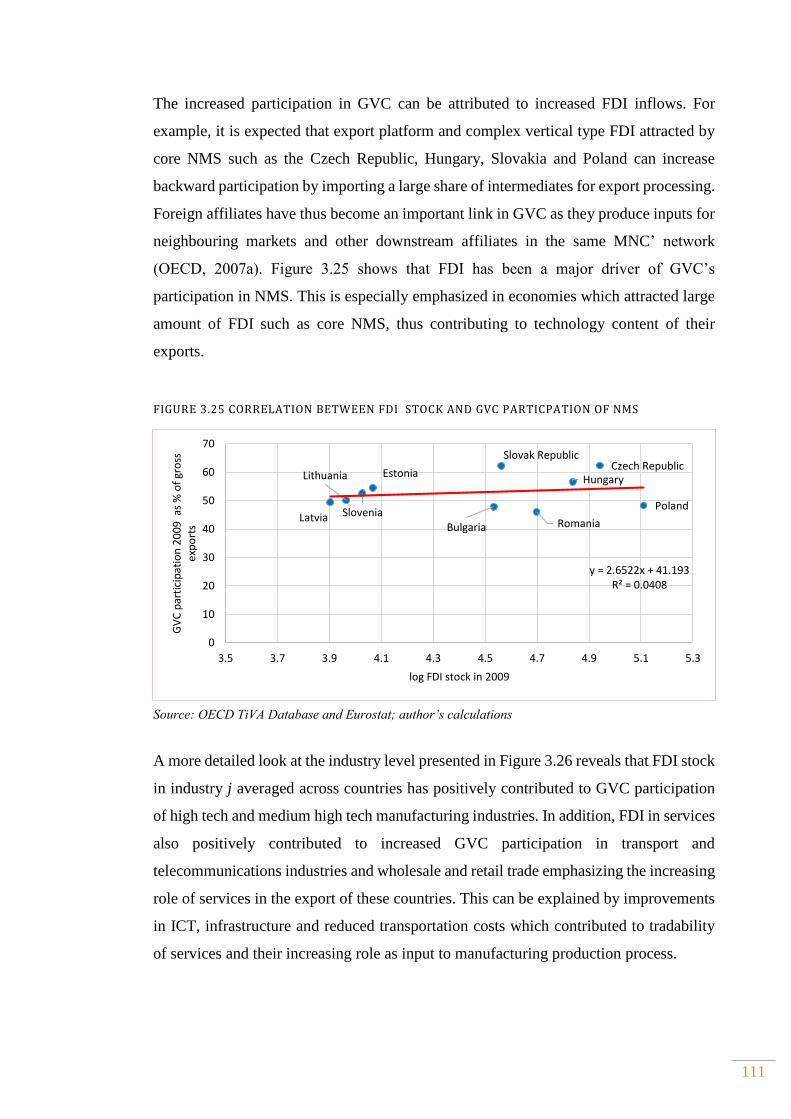

3.6 FDI and integration of NMS into GVC ......................................................................................... 108

3.7 Conclusion ............................................................................................................................................. 116

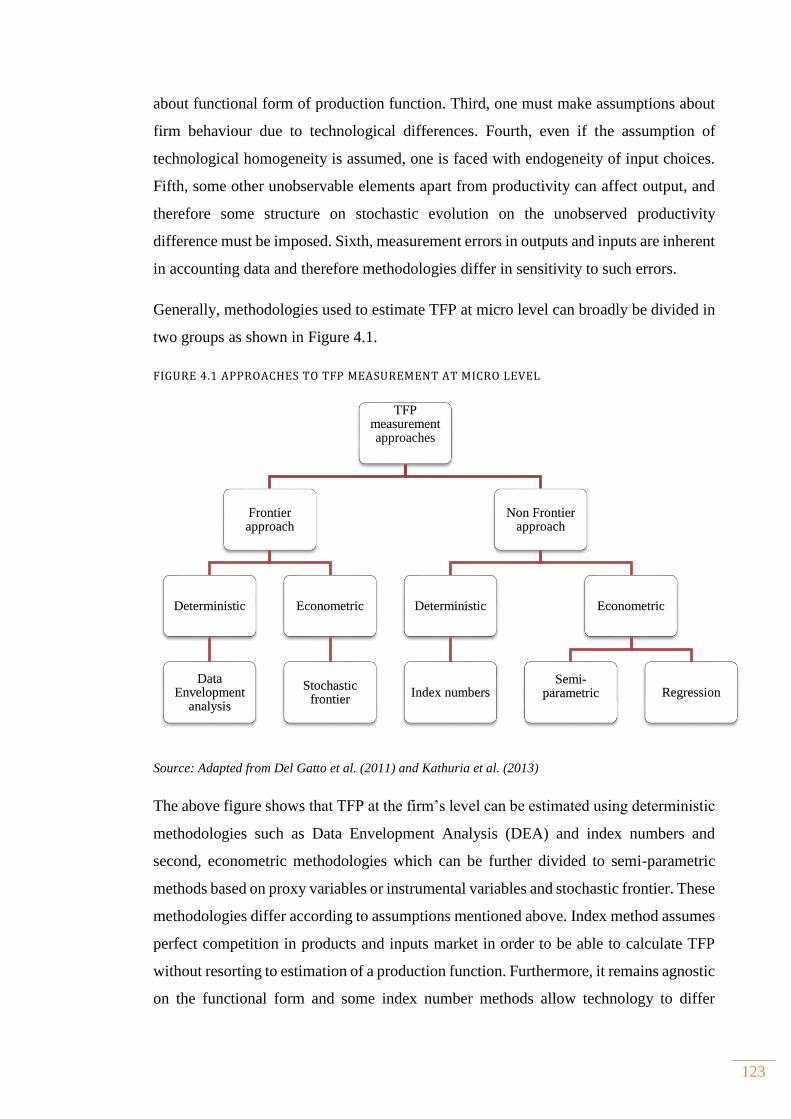

CHAPTER 4. ISSUES, METHODOLOGICAL SOLUTIONS AND ESTIMATION OF TFP AT MICRO LEVEL…… ............................................................................................................................................ 118

4.1 Introduction .......................................................................................................................................... 119

4.2 Measurement of productivity ........................................................................................................ 121

4.3 Methodological issues in estimation of TFP ............................................................................ 127

4.3.1 Simultaneity bias ........................................................................................................................ 131

4.3.2 Selection bias ............................................................................................................................... 132

4.3.3 Omitted price bias ..................................................................................................................... 132

4.3.4 Multiproduct firms ................................................................................................................... 133

4.4 Solutions to econometric problems ............................................................................................ 134

4.4.1 Traditional solutions to endogeneity of input choice ................................................. 136

4.4.2 Olley-Pakes and Levinsohn-Petrin methodology ......................................................... 137

4.4.3 Ackerberg Caves Frazer critique ......................................................................................... 142

4.4.4 Wooldridge estimator .............................................................................................................. 144

4.5 Data and descriptive statistics ...................................................................................................... 146

4.5.1 Sample Description ................................................................................................................... 147

4.5.2 Variables description and descriptive statistics ........................................................... 151

4.6 TFP estimation..................................................................................................................................... 155

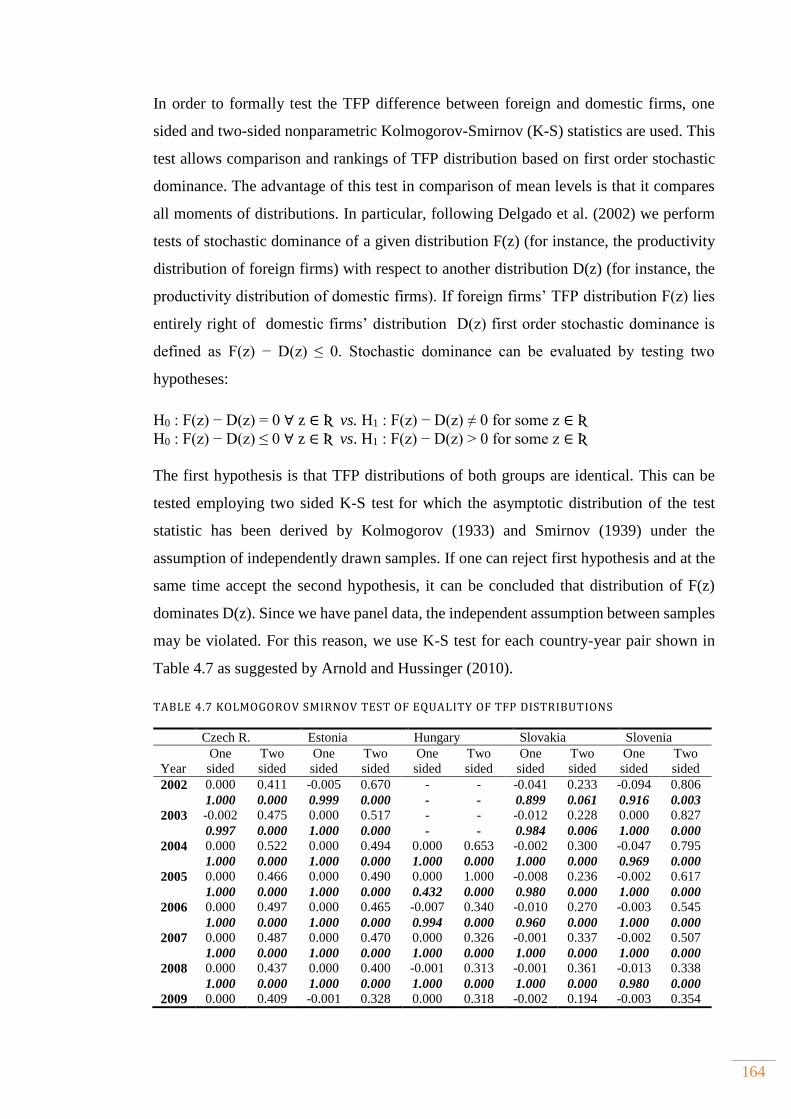

4.7 Are foreign firms more productive? ........................................................................................... 162

v

4.8 Conclusion ............................................................................................................................................. 167

CHAPTER 5. PRODUCTIVITY SPILLOVERS OF FDI IN SELECTED TRANSITION COUNTRIES – THE ROLE OF MNC’S HETEROGENEITY ............................................................. 170

5.1 Introduction .......................................................................................................................................... 171

5.2 Model specification ............................................................................................................................ 173

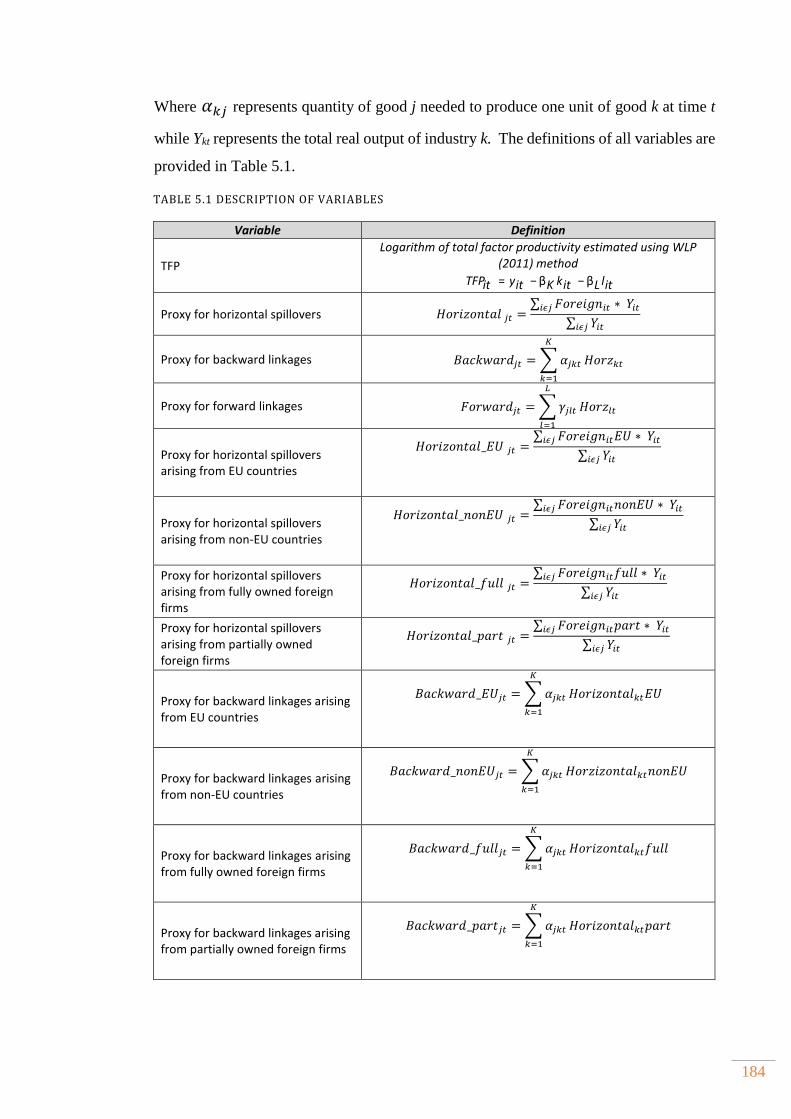

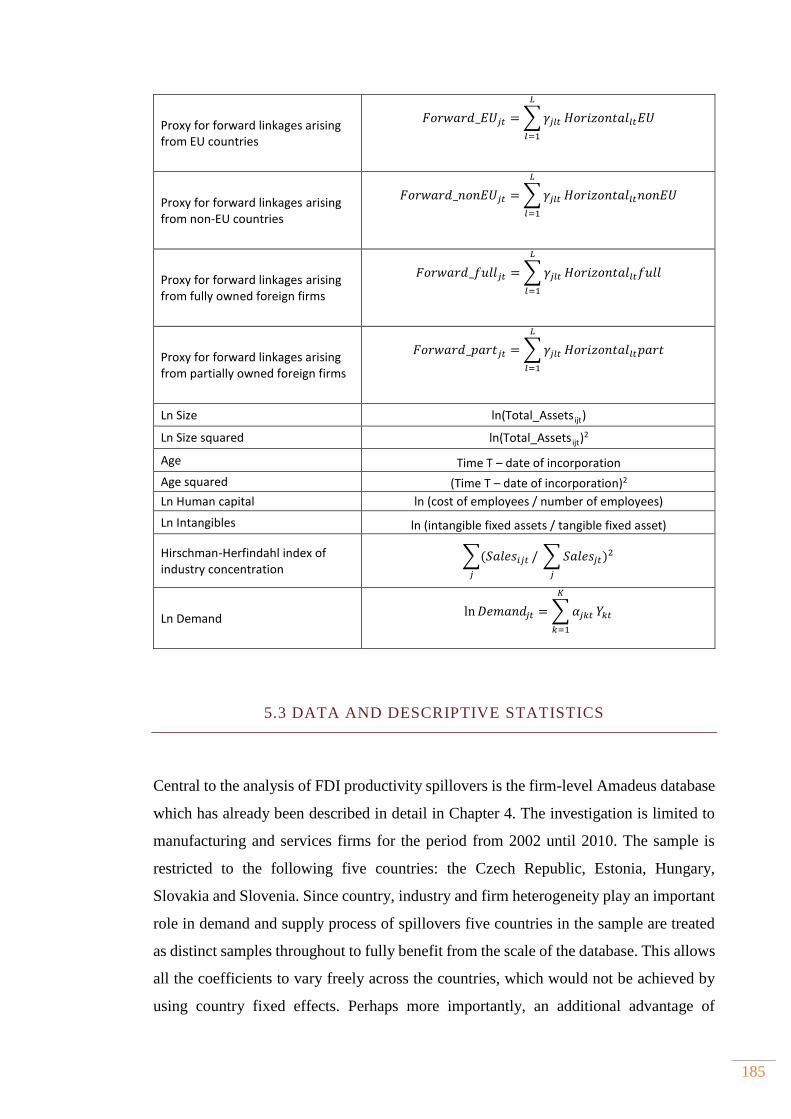

5.3 Data and descriptive statistics ...................................................................................................... 185

5.4 Methodology ......................................................................................................................................... 192

5.5 Discussion of findings ....................................................................................................................... 196

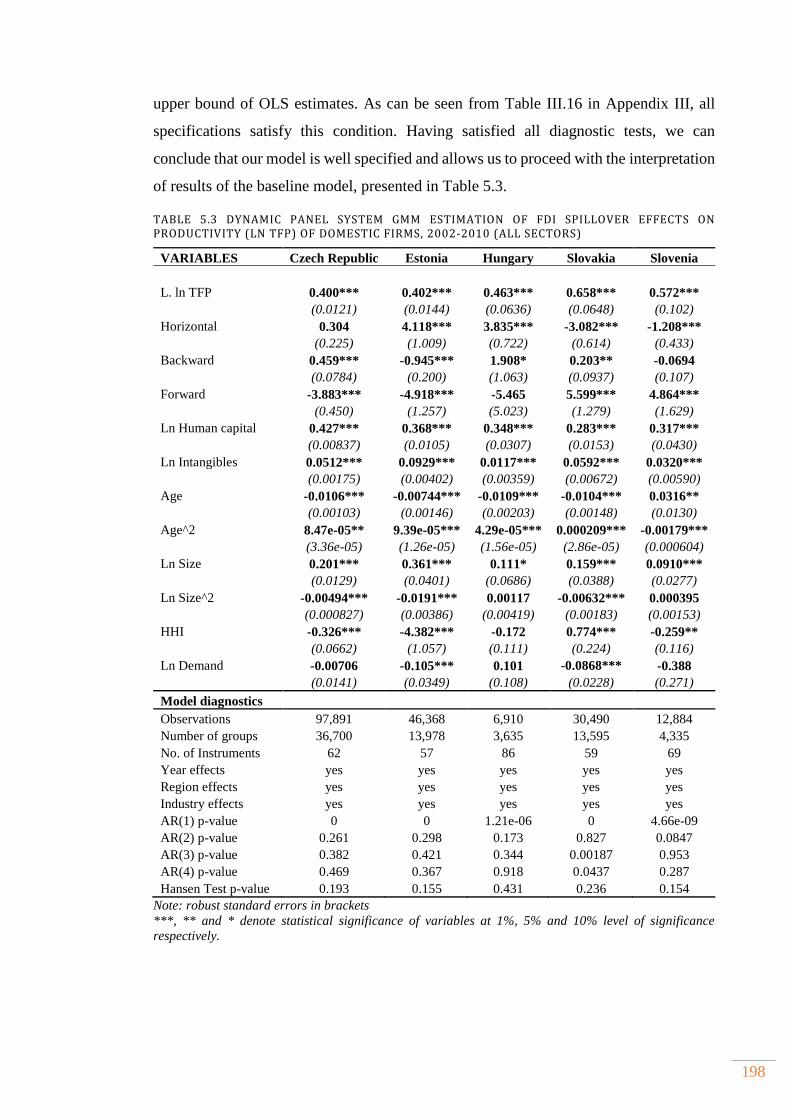

5.5.1 Results for baseline model ..................................................................................................... 197

5.5.2 The effect of ownership structure....................................................................................... 204

5.5.3 The effects of MNC’s origin .................................................................................................... 211

5.6 Conclusion ............................................................................................................................................. 219

CHAPTER 6. THE IMPACT OF SERVICES FDI ON PRODUCTIVITY OF DOWNSTREAM MANUFACTURING FIRMS ........................................................................................................................... 223

6.1 Introduction .......................................................................................................................................... 224

6.2 Conceptual framework and related research ......................................................................... 225

6.2.1 The importance of service sector and implications for MNC’s entry ................... 226

6.2.2 Interactions between services and manufacturing ..................................................... 230

6.2.3 Review of empirical literature .............................................................................................. 233

6.3 Empirical strategy .............................................................................................................................. 236

6.3.1 Empirical model and methodology .................................................................................... 237

6.3.2 Data .................................................................................................................................................. 241

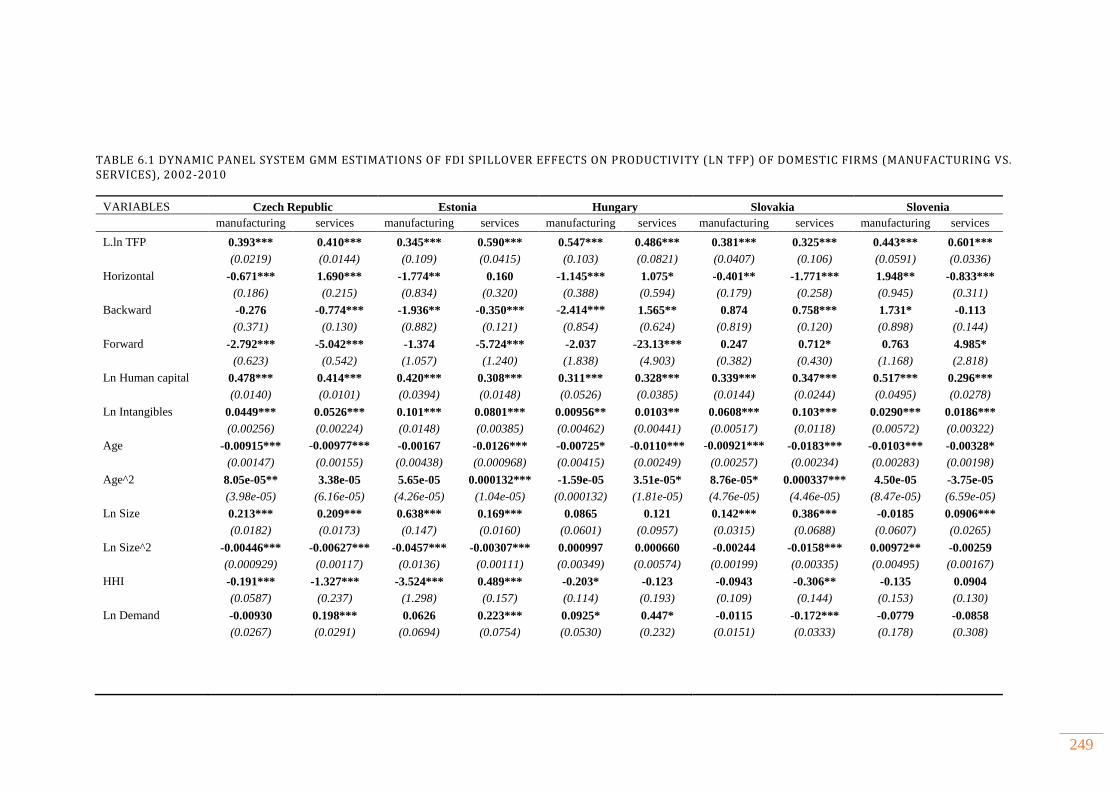

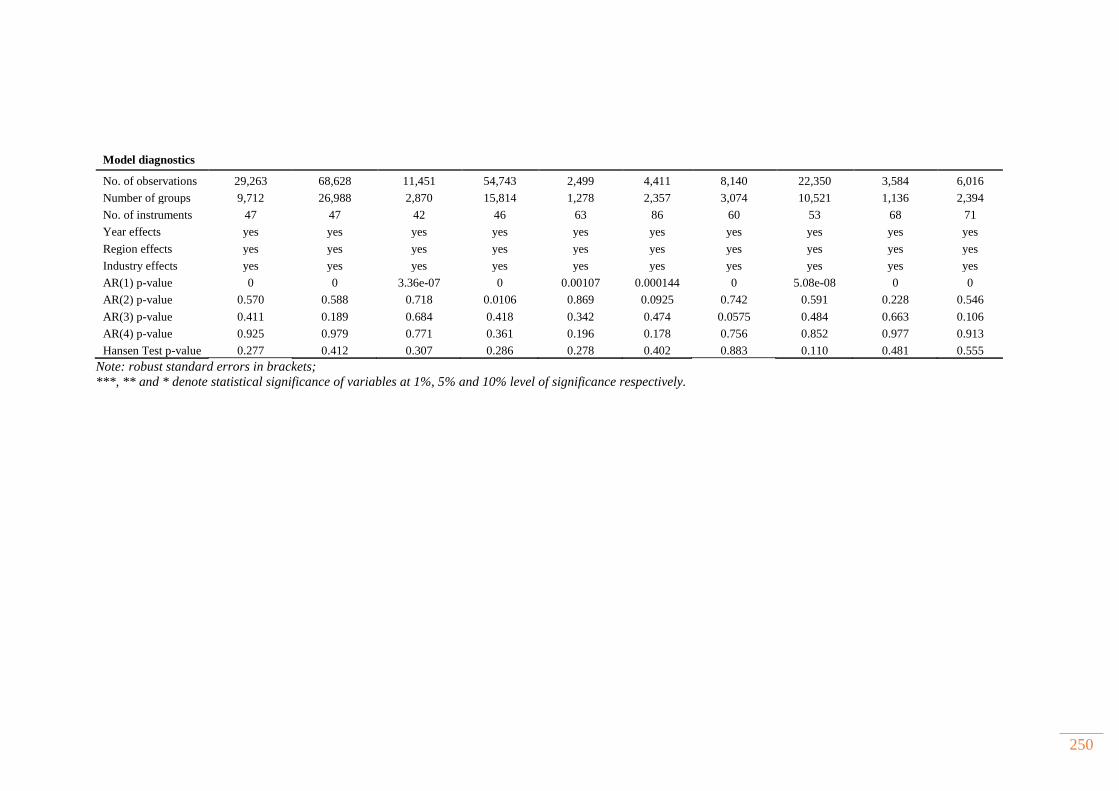

6.4 Discussion of findings ....................................................................................................................... 246

6.4.1 Results of baseline model across sectors ......................................................................... 247

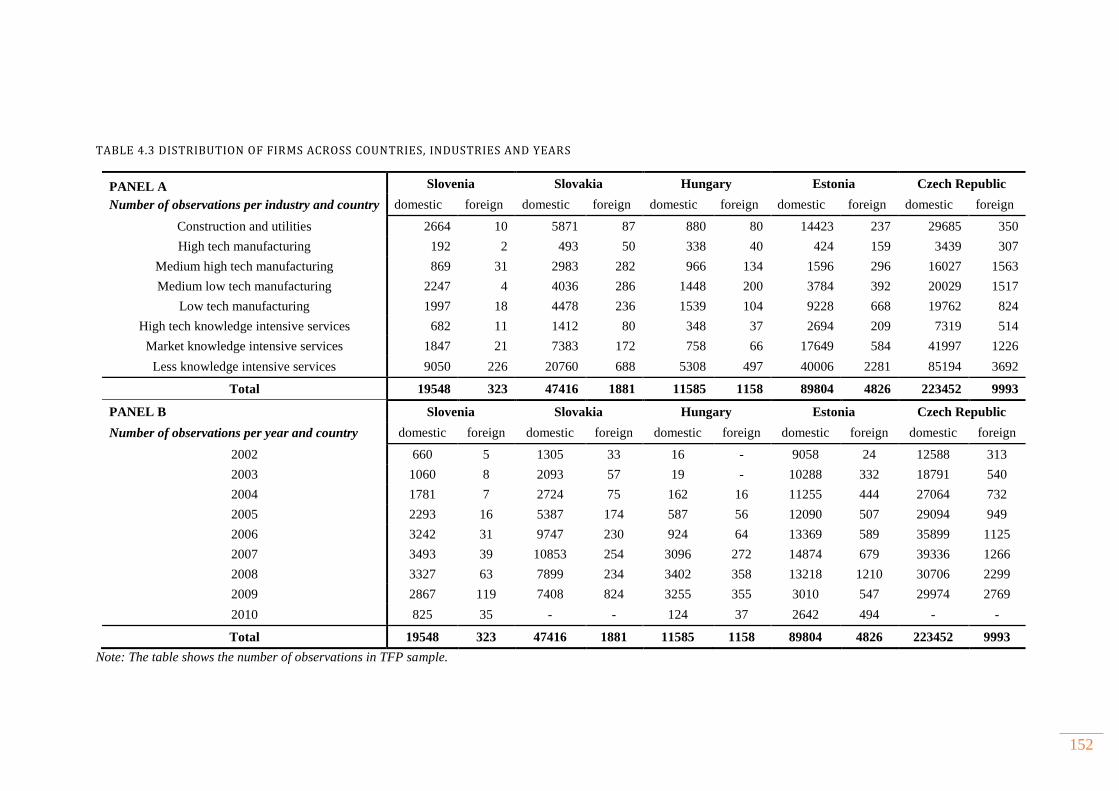

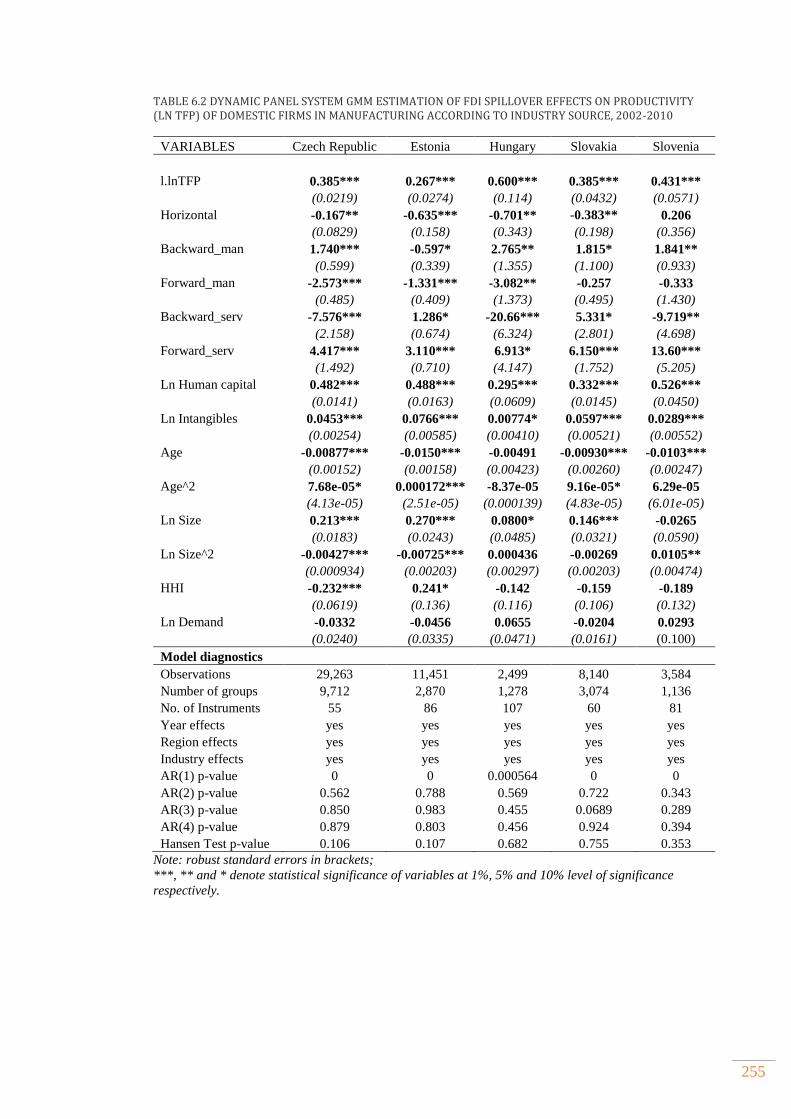

6.4.2 Effects of services fdi on downstream manufacturing firms ................................... 254

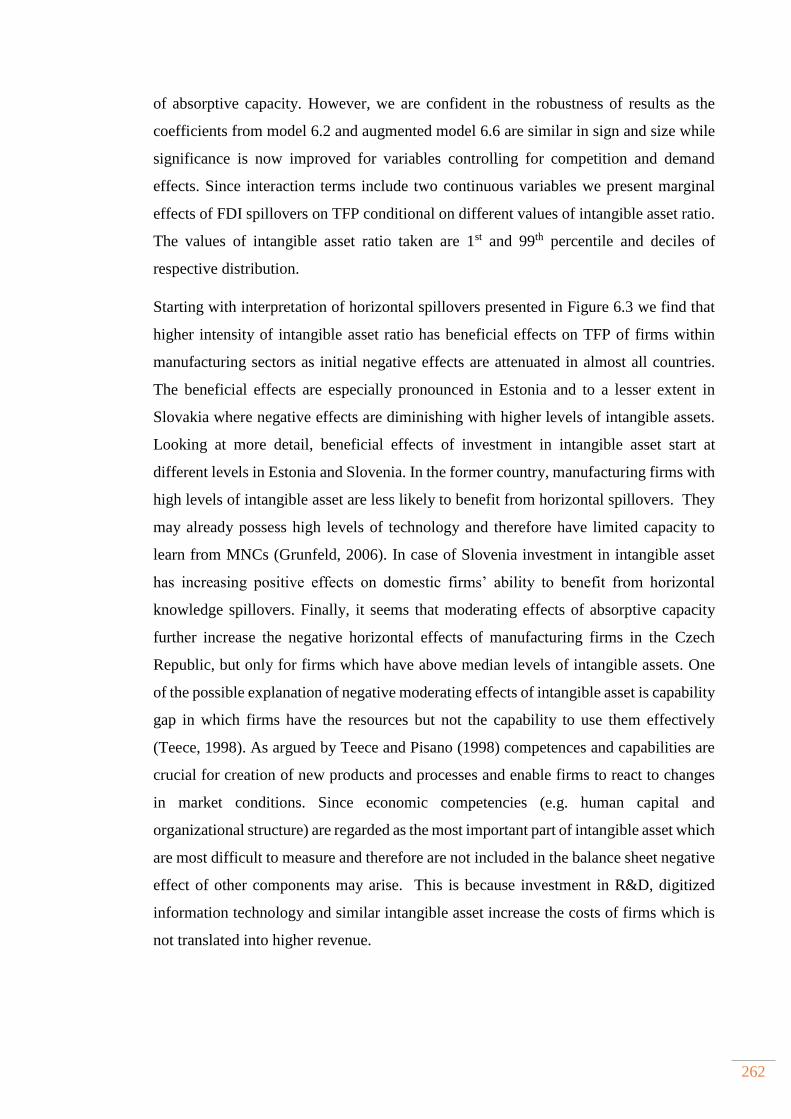

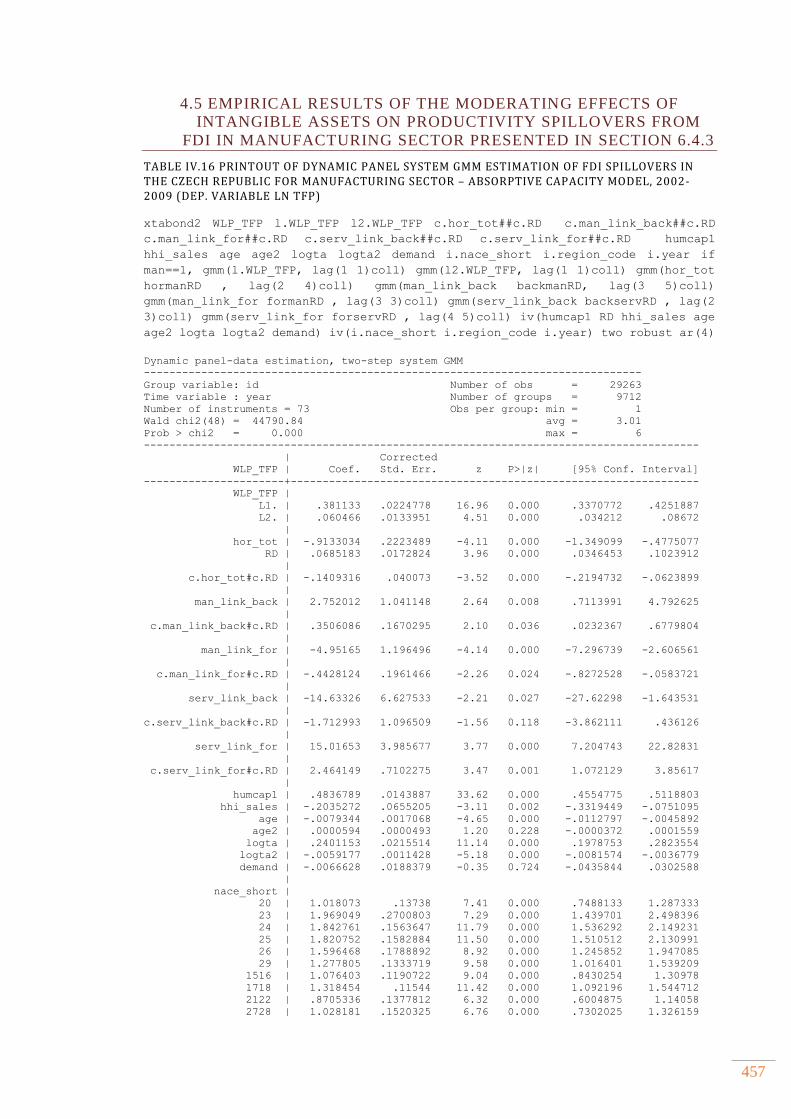

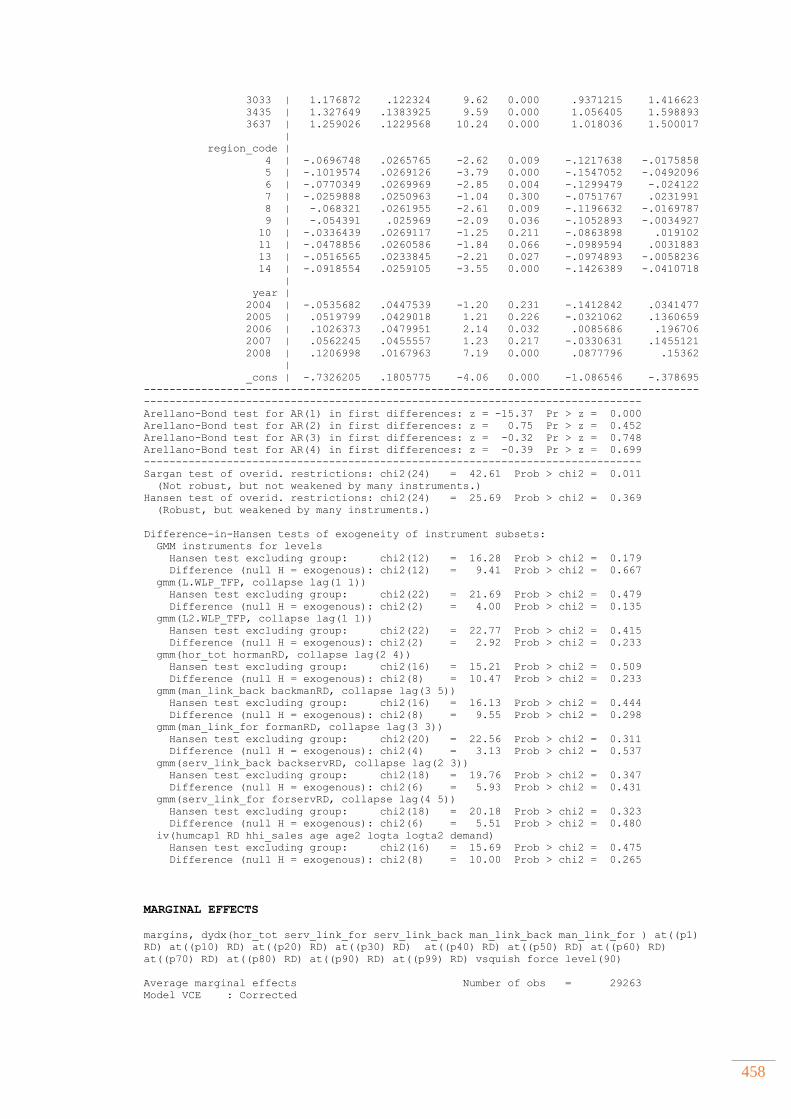

6.4.3 The moderating effects of absorptive capacity.............................................................. 259

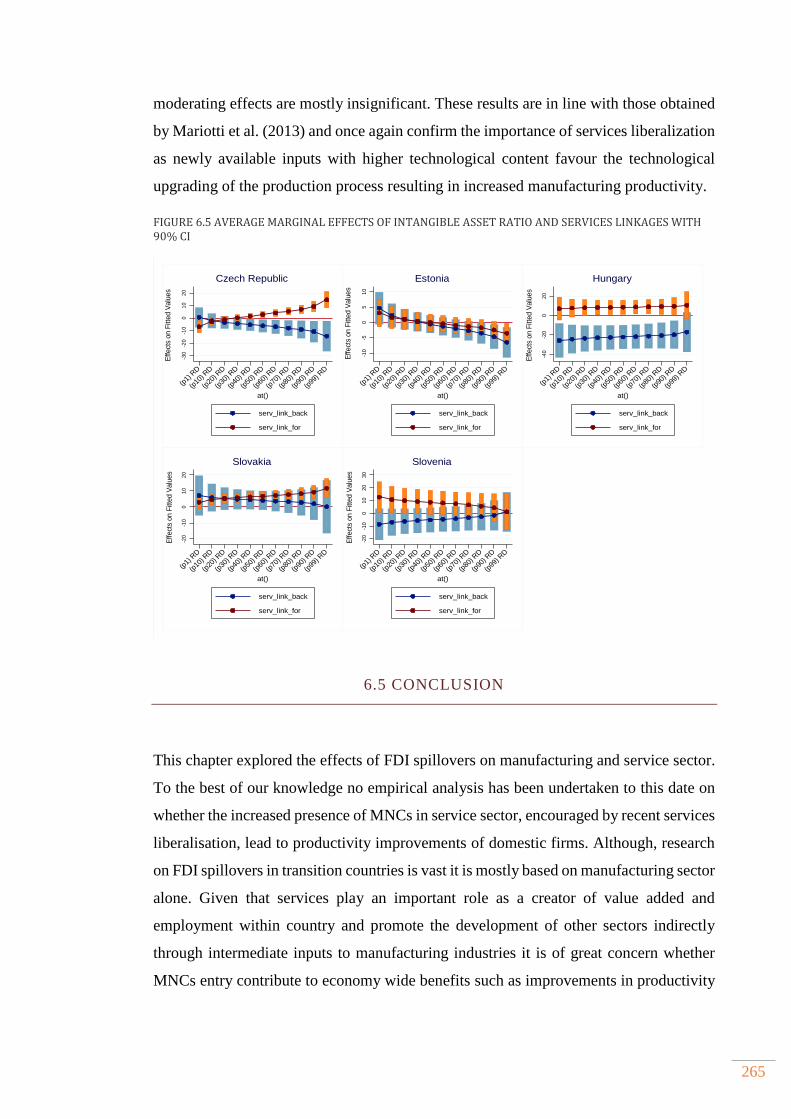

6.5 Conclusion ............................................................................................................................................. 265

CHAPTER 7. CONCLUSIONS ................................................................................................................ 268

7.1 Introduction .......................................................................................................................................... 269

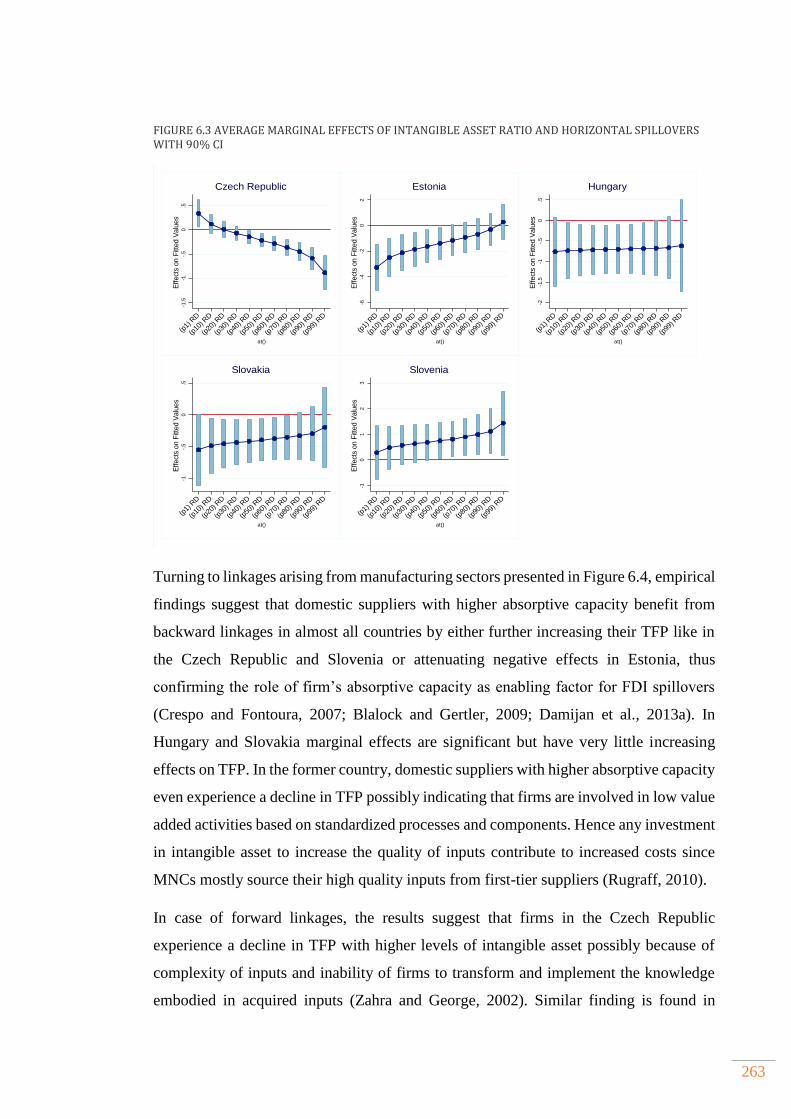

7.2 Main findings ........................................................................................................................................ 270

7.3 Contribution to knowledge ............................................................................................................ 282

7.4 Policy implications ............................................................................................................................. 285

7.4.1 Attracting the right type of foreign investors ................................................................ 286

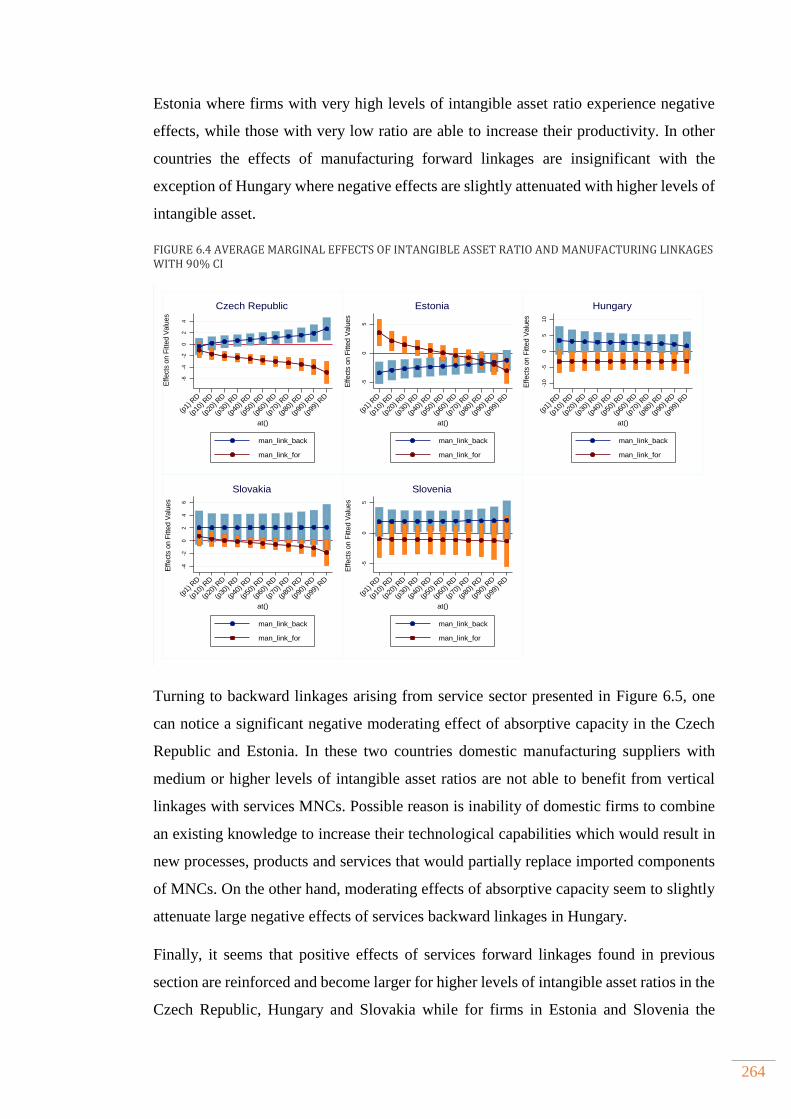

7.4.2 Promotion of linkages .............................................................................................................. 287

7.4.3 Increasing the absoprtive capacity of local firms ......................................................... 289

7.5 Limitations of research .................................................................................................................... 291

7.6 Directions for further research ..................................................................................................... 293

REFERENCES…… ............................................................................................................................................. 296

vi

Appendices……… ............................................................................................................................................. 342

APPENDIX I. SUPPLEMENT TO CHAPTER THREE ..................................................................... 342

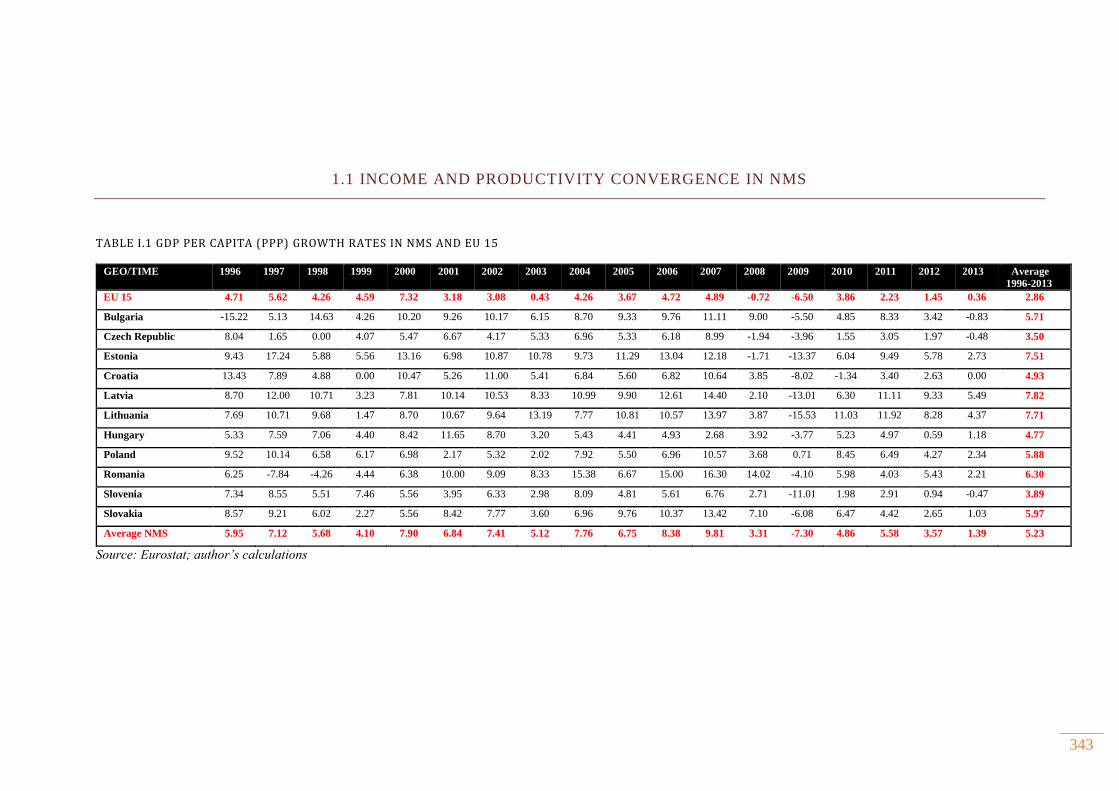

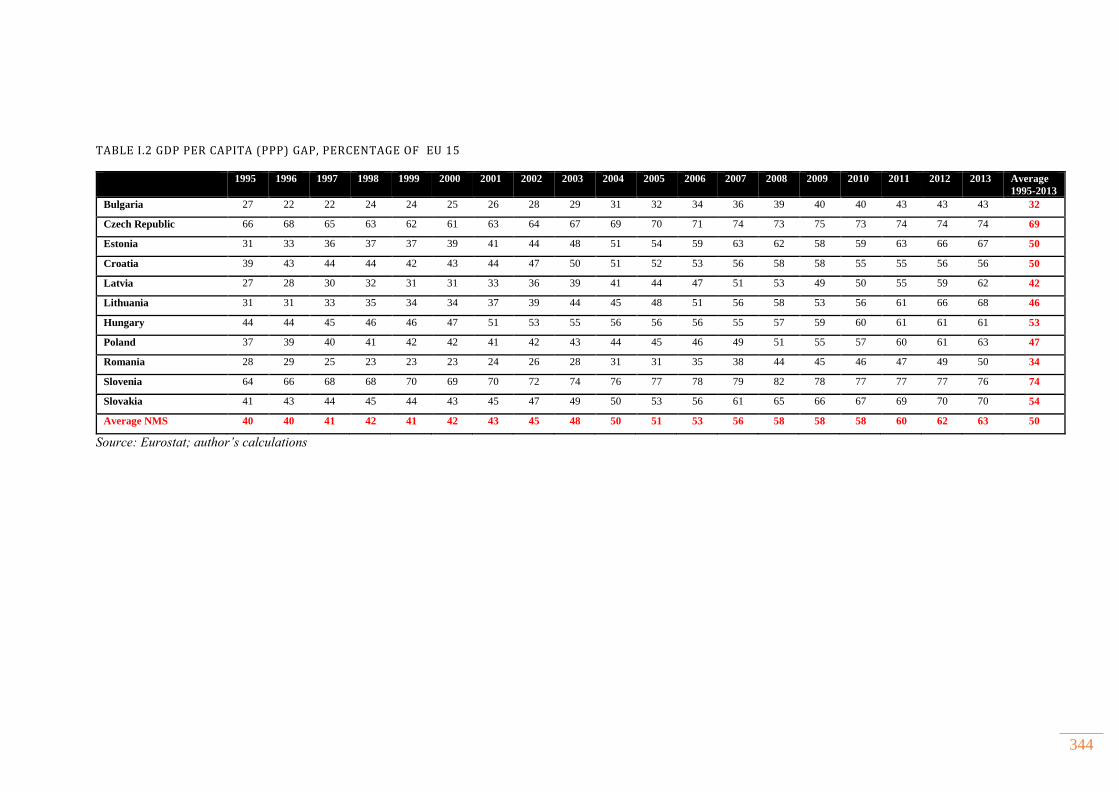

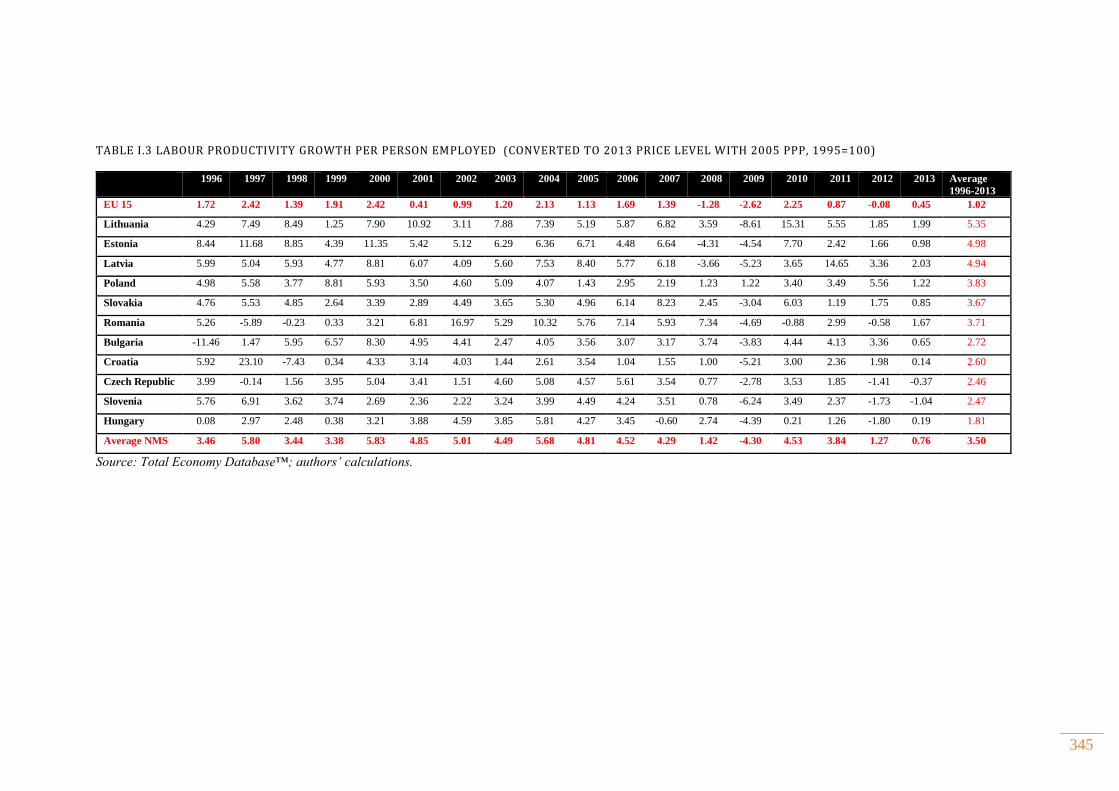

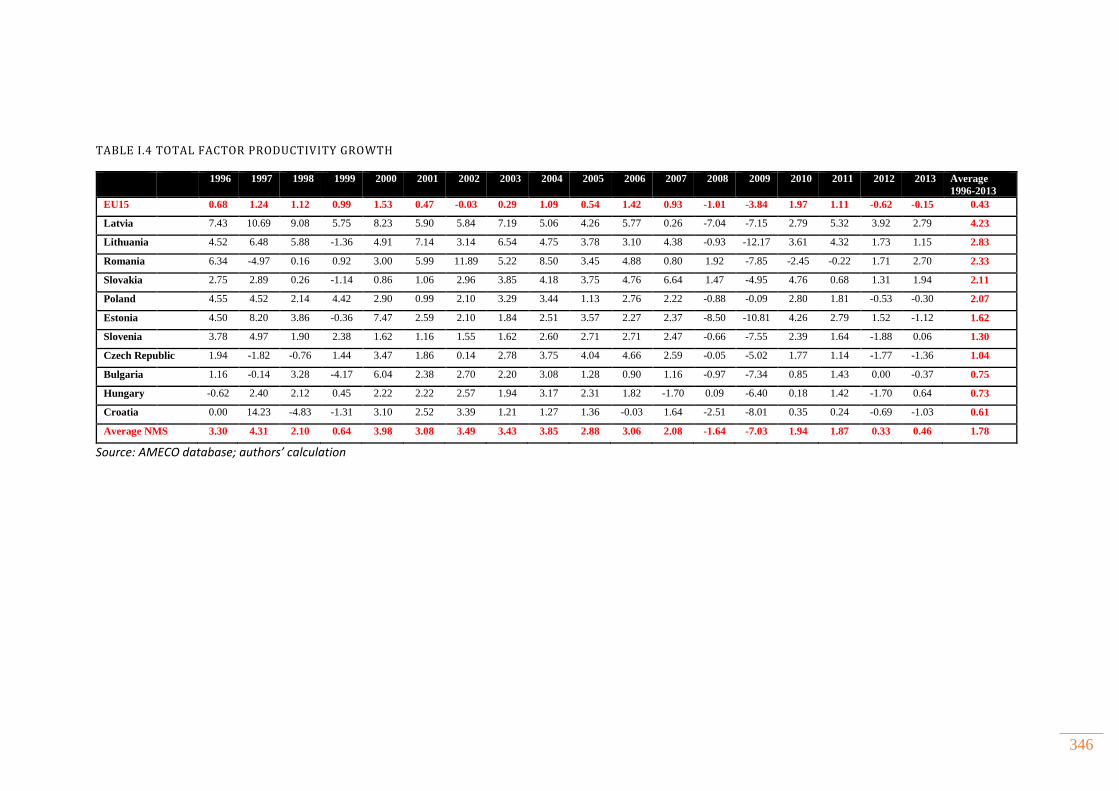

1.1 Income and productivity convergence in NMS ...................................................................... 343

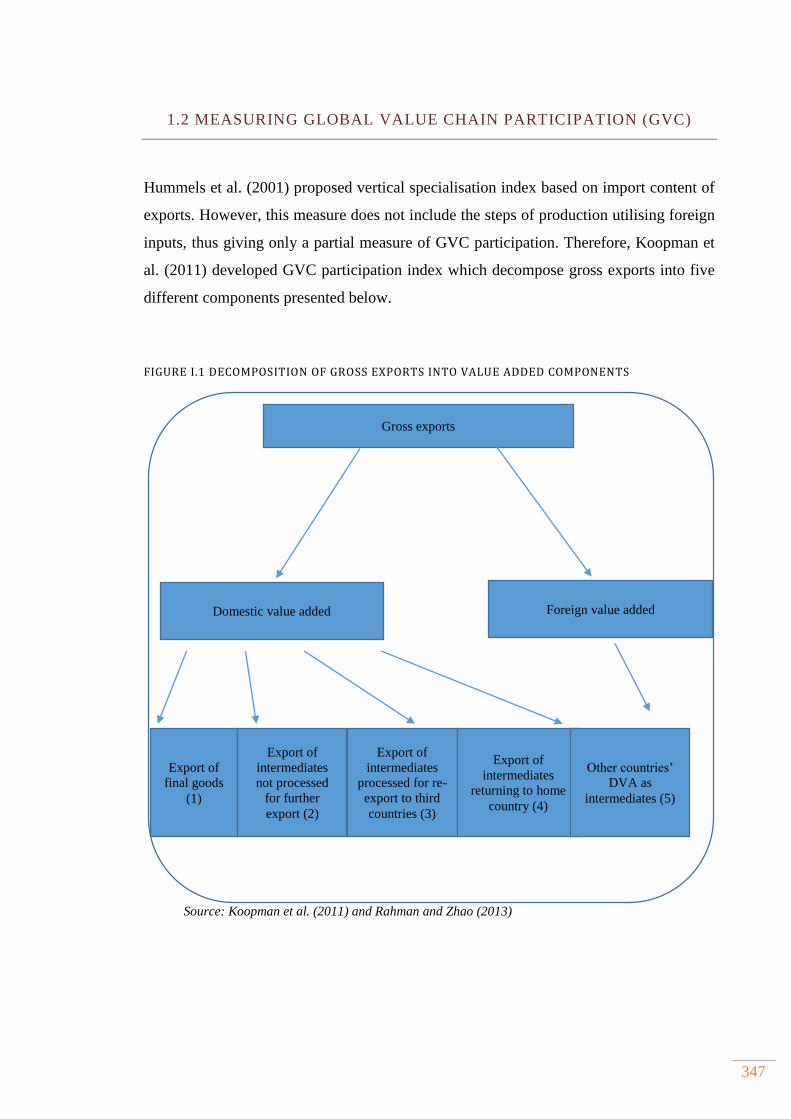

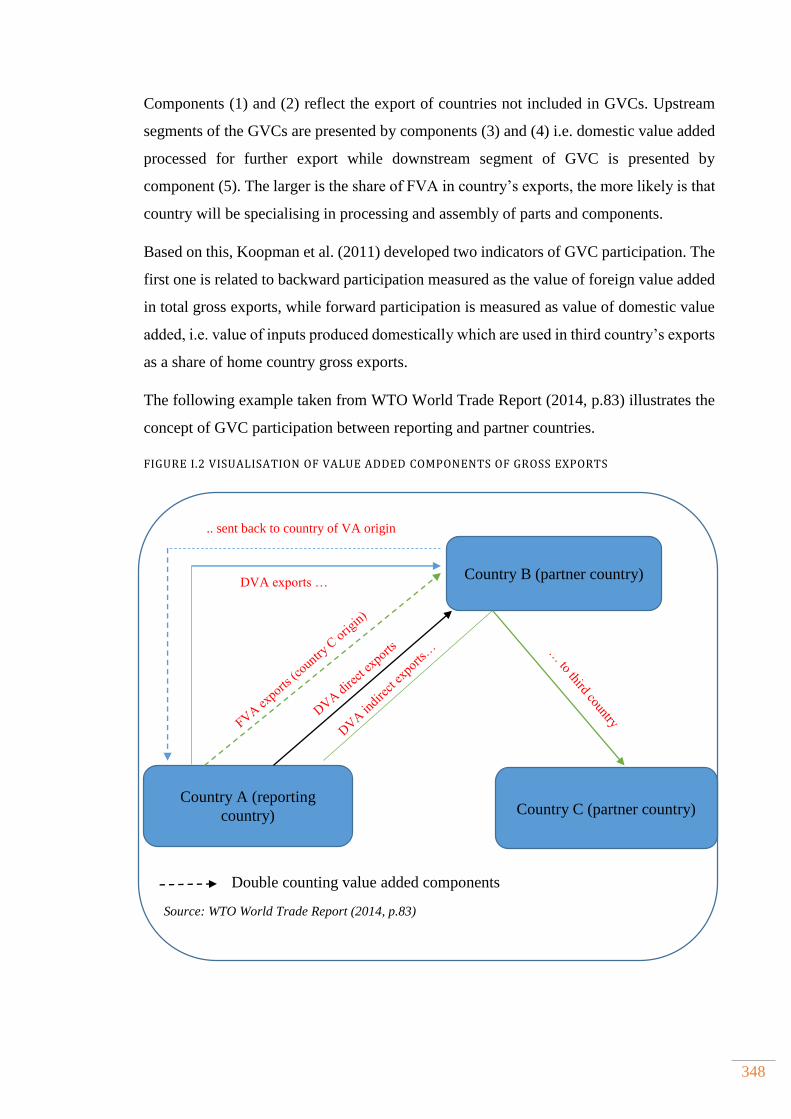

1.2 Measuring Global Value Chain participation (GVC) ............................................................. 347

1.3 Industry productivity levels and growth rates in NMS ...................................................... 349

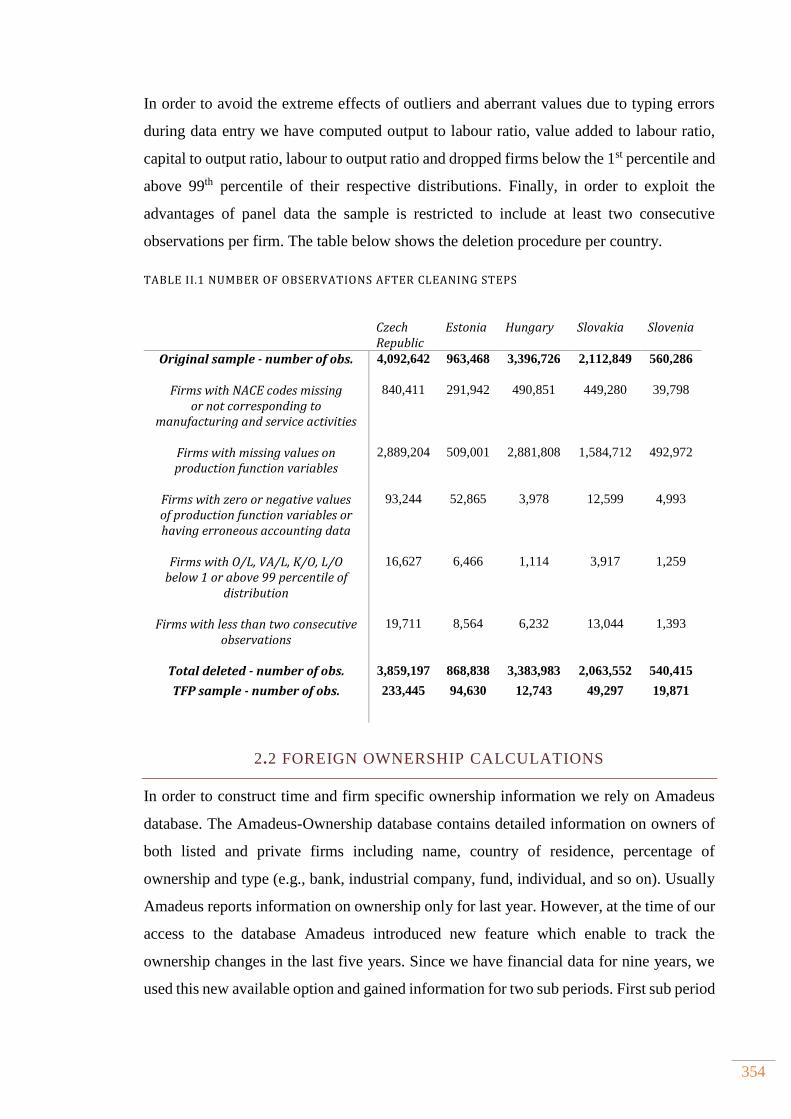

APPENDIX II. SUPPLEMENT TO CHAPTER FOUR........................................................................ 352

2.1 Cleaning procedure ........................................................................................................................... 353

2.2 Foreign ownership calculations ................................................................................................... 354

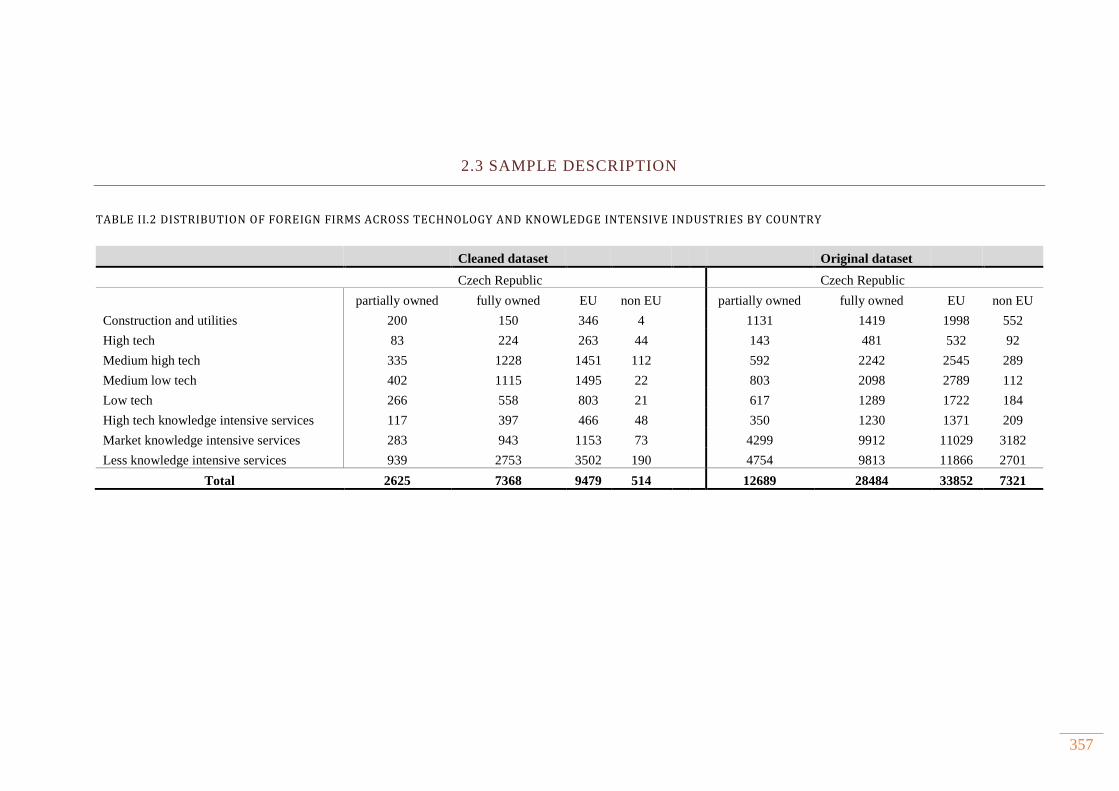

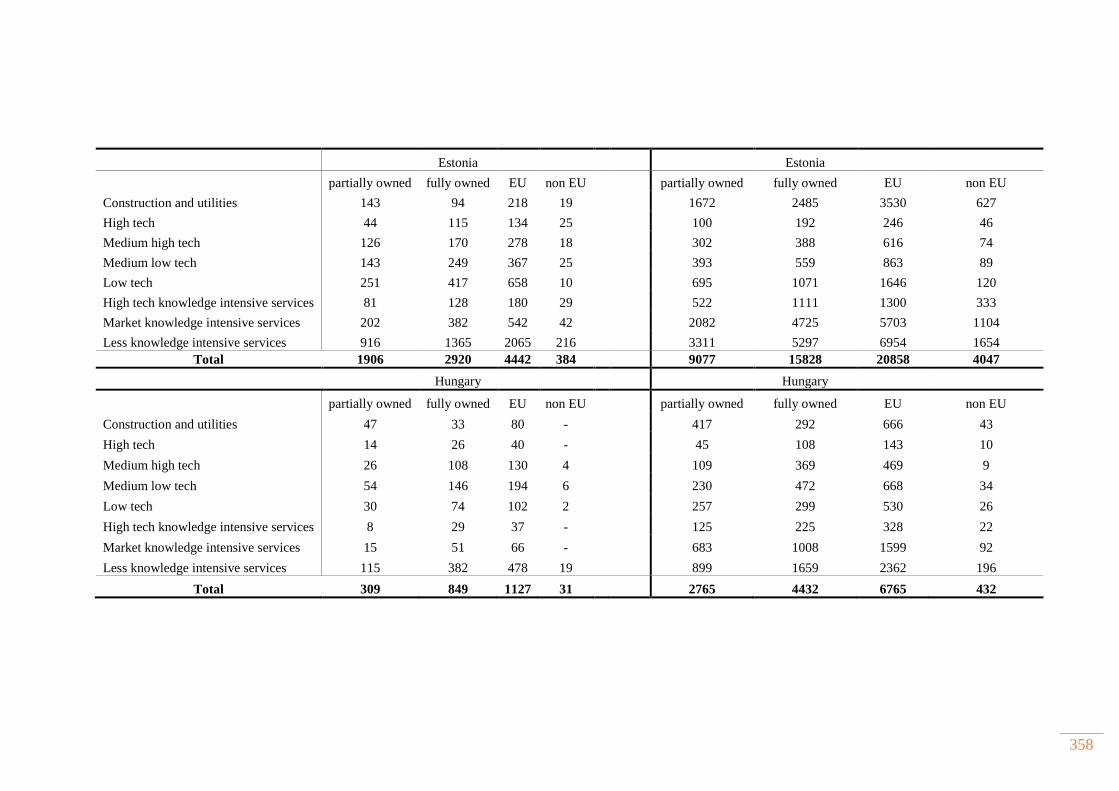

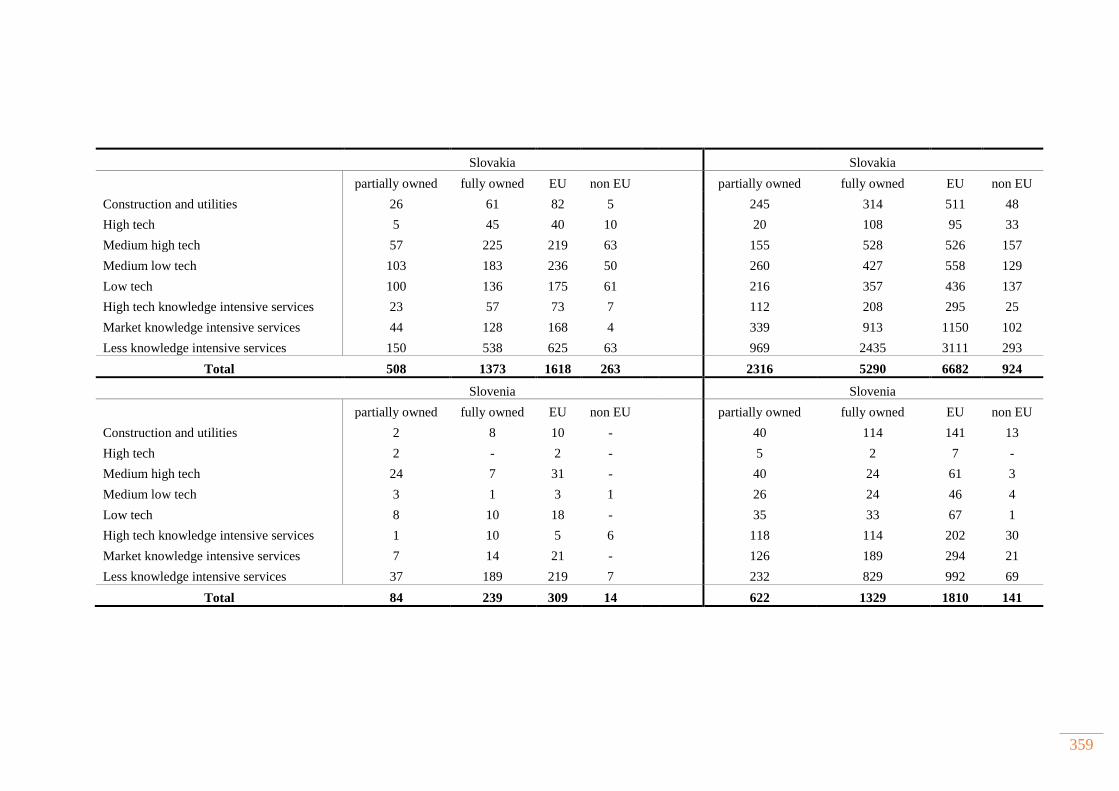

2.3 Sample description ............................................................................................................................ 357

2.4 Output of Cobb-Douglas value added production function per industry and country ........................................................................................................................................................................... 362

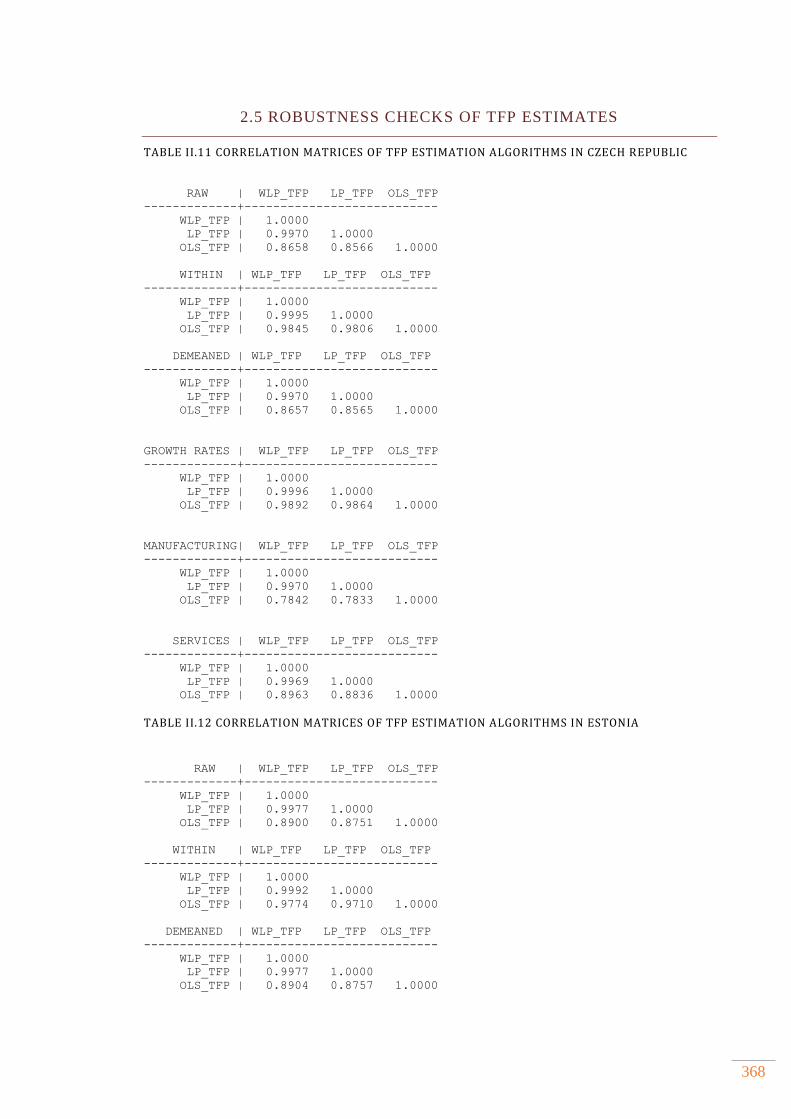

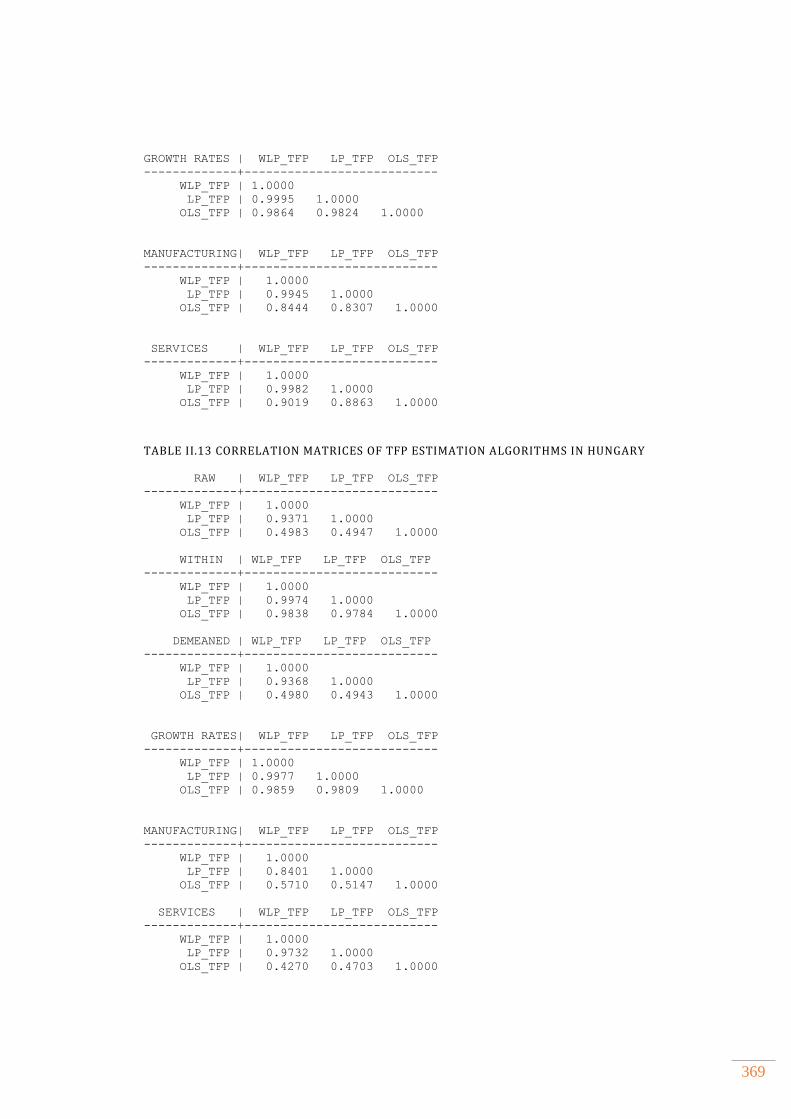

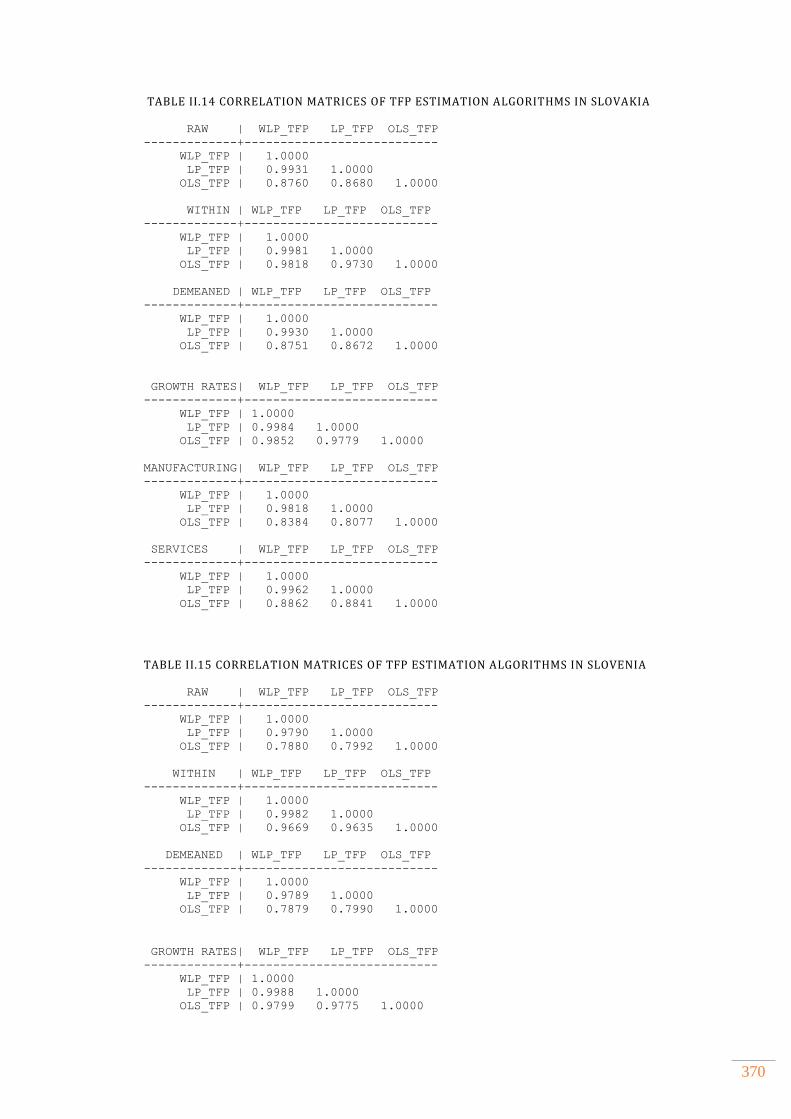

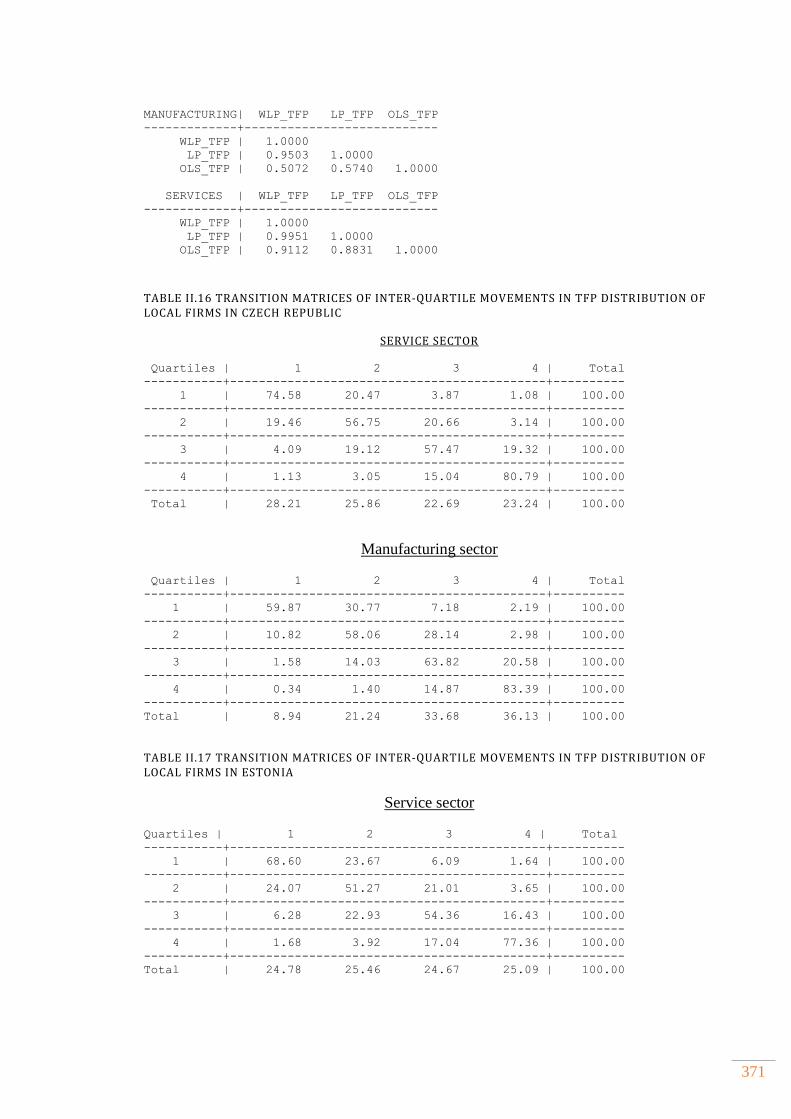

2.5 Robustness checks of TFP estimates .......................................................................................... 368

2.6 Non parametric Kolmogorov Smirnov test of foreign ownership premium ............. 374

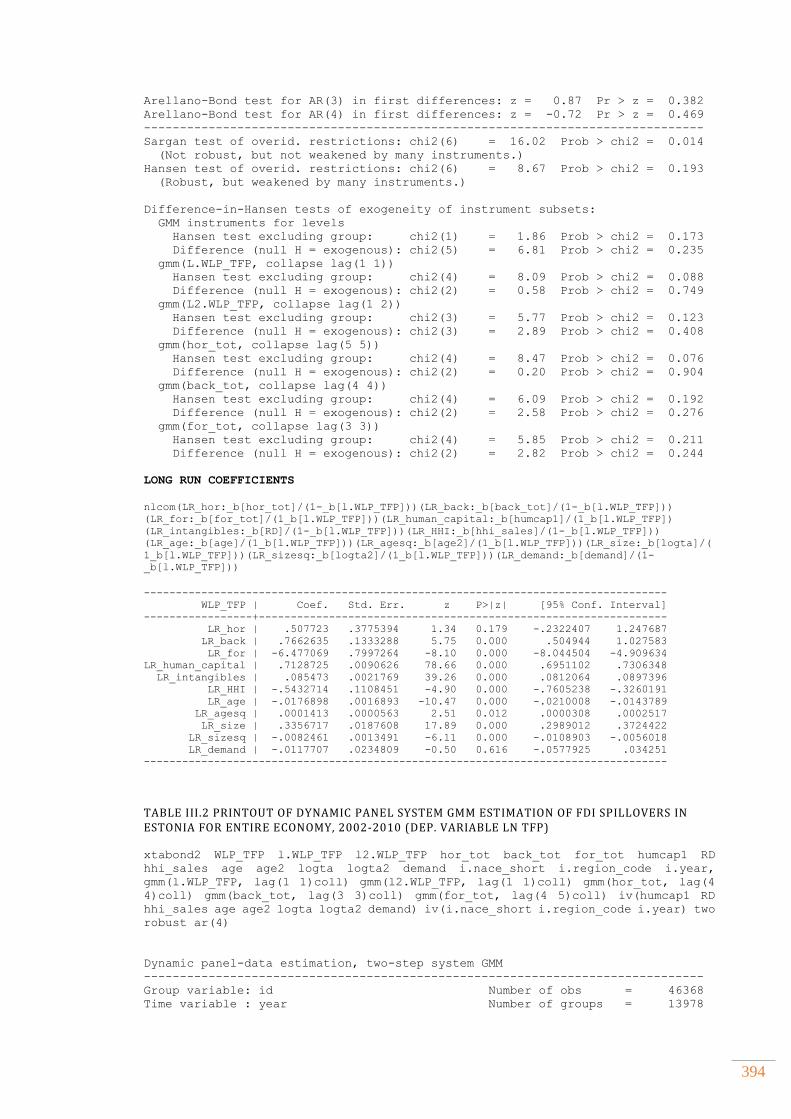

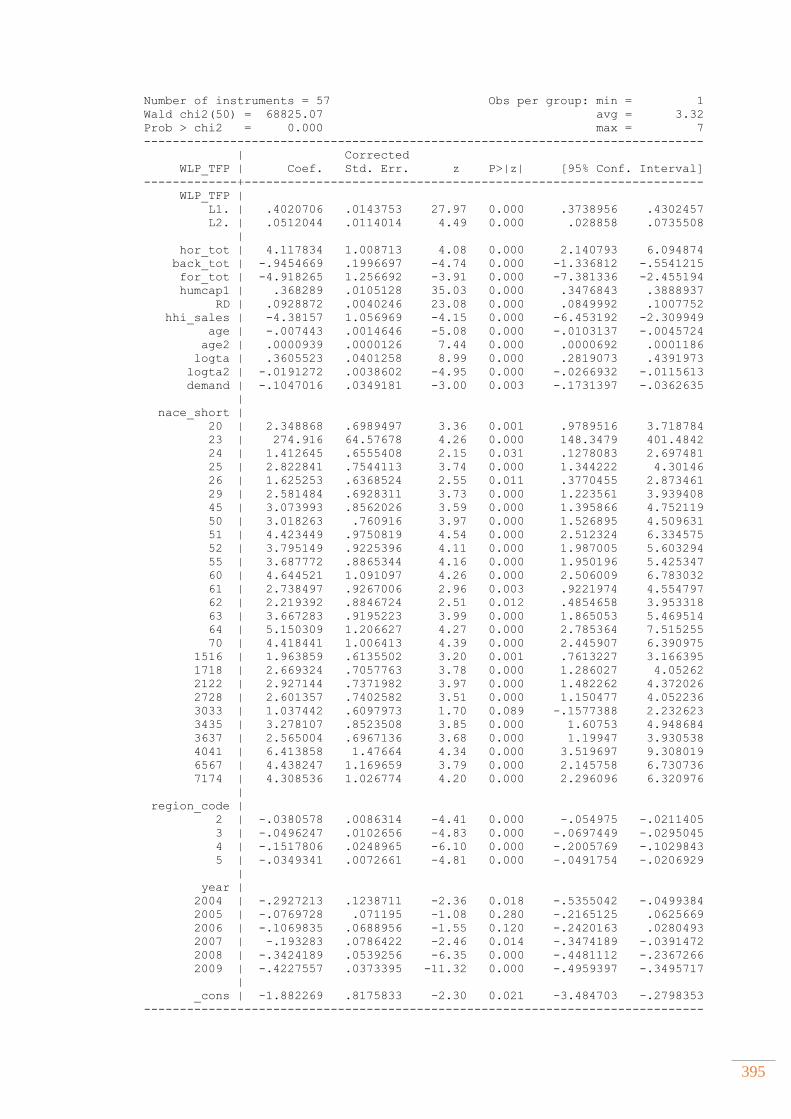

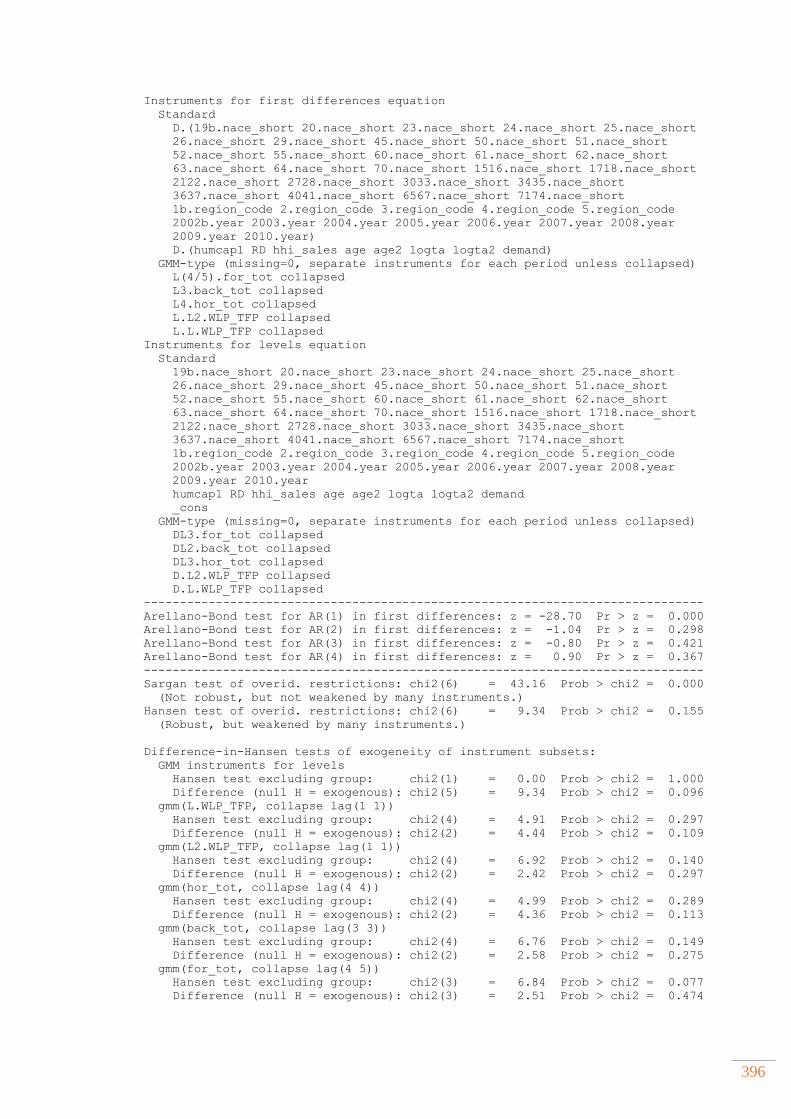

APPENDIX III. SUPPLEMENT TO CHAPTER FIVE.......................................................................... 391

3.1 Empirical results for the baseline model of productivity spillovers from FDI presented in Section 5.6.1 ...................................................................................................................... 392

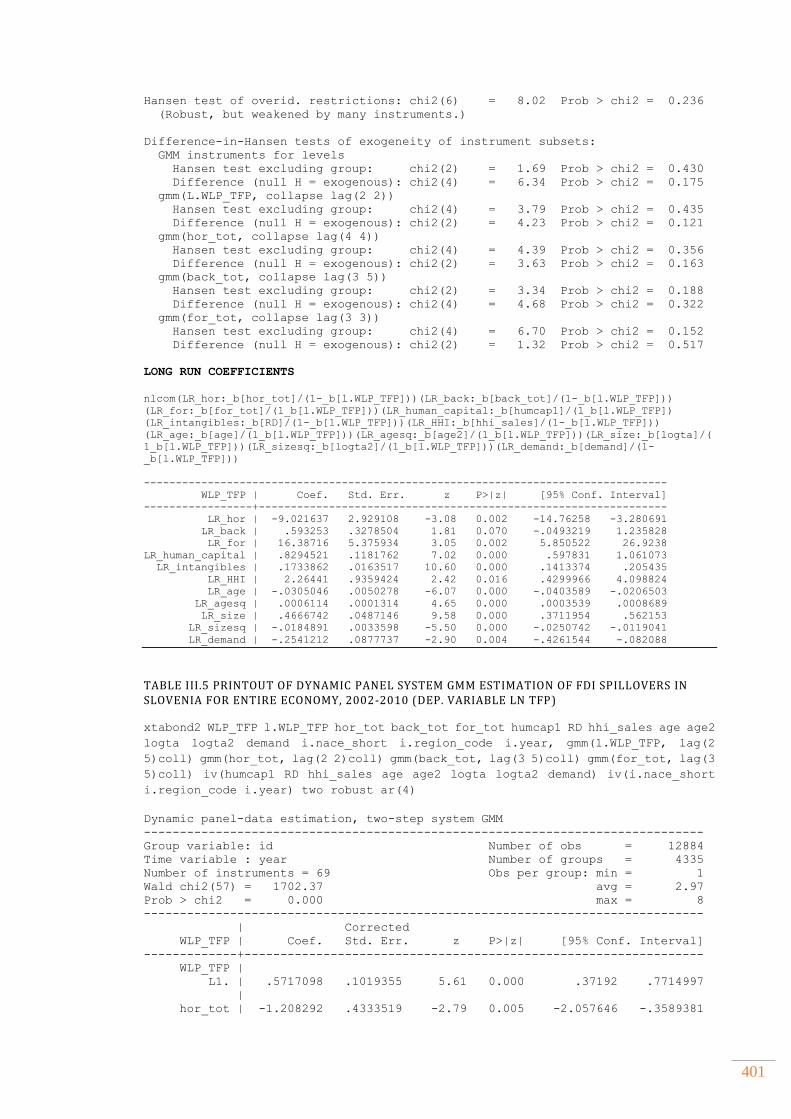

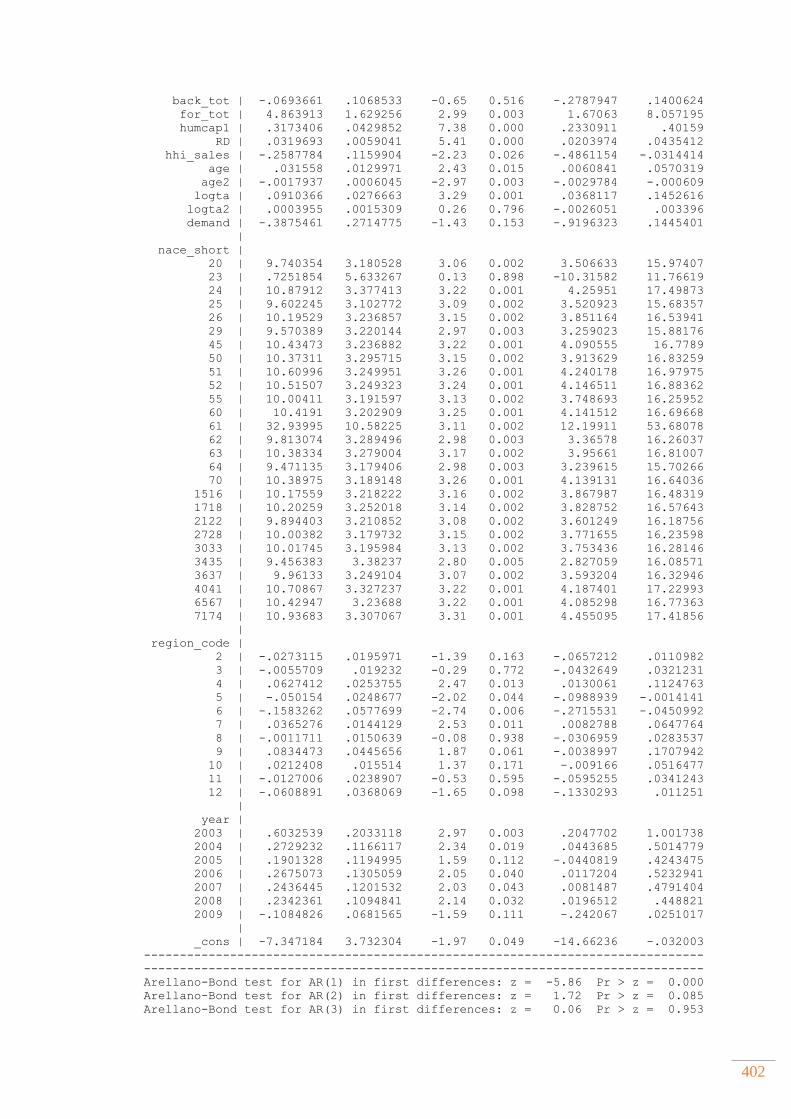

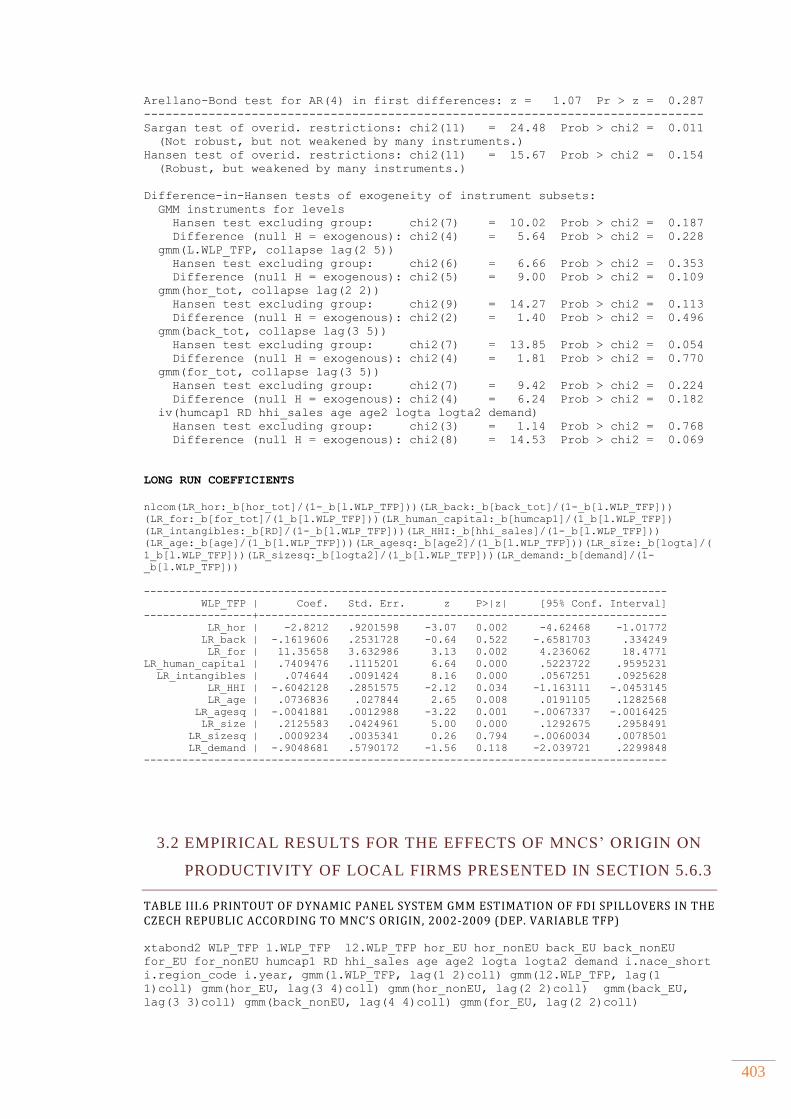

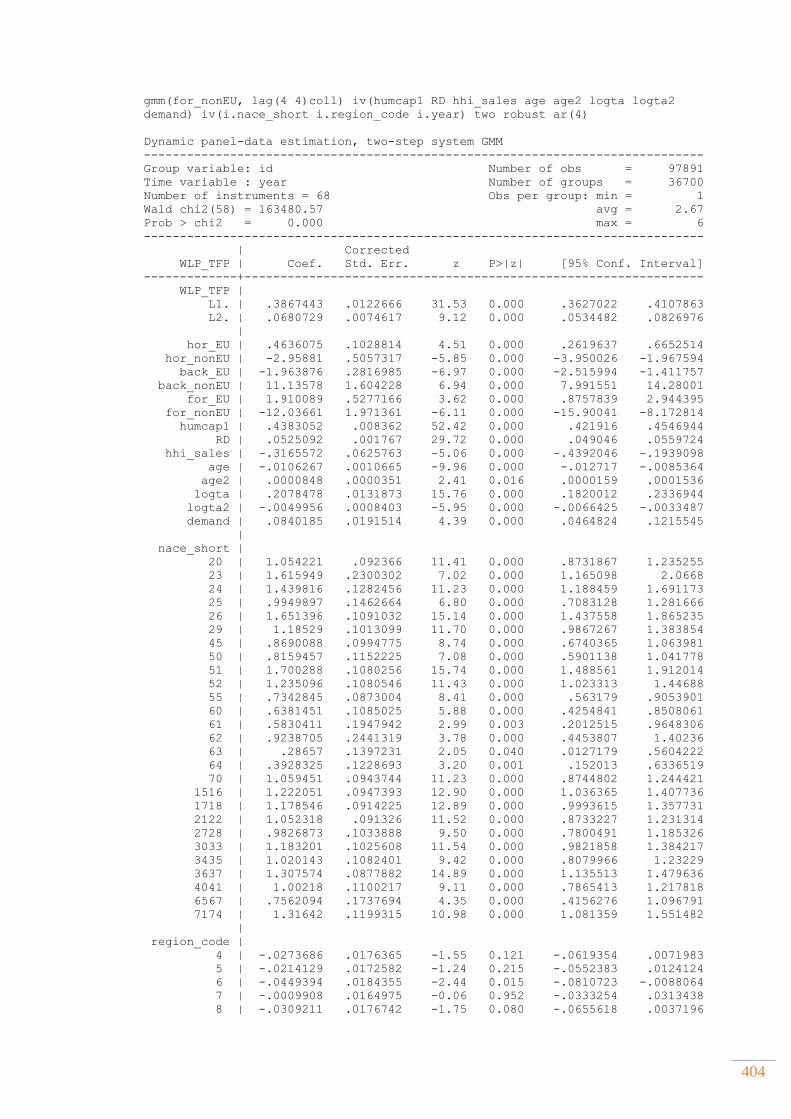

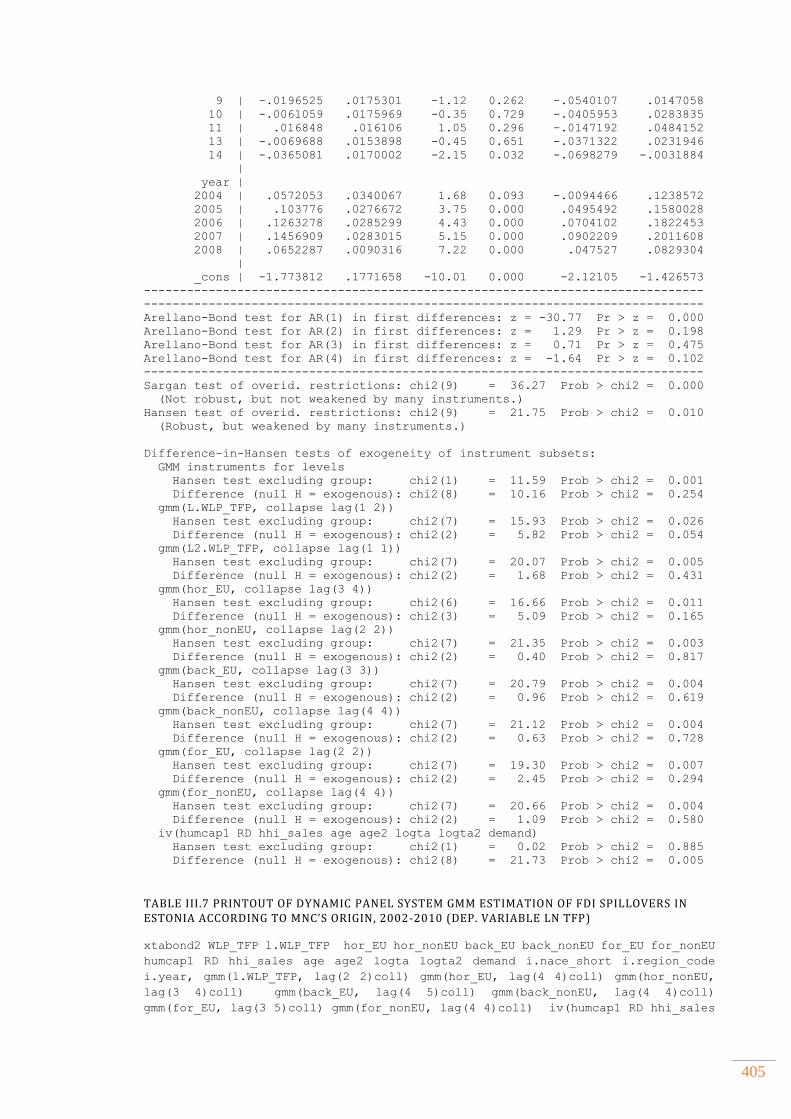

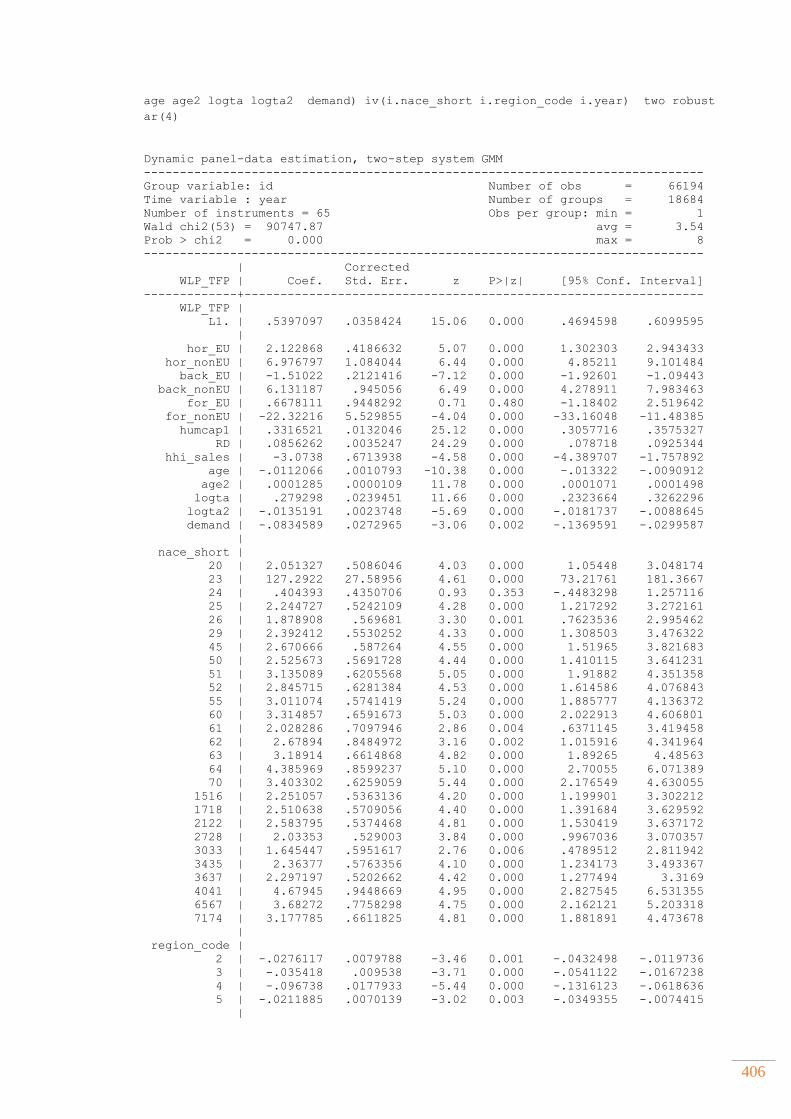

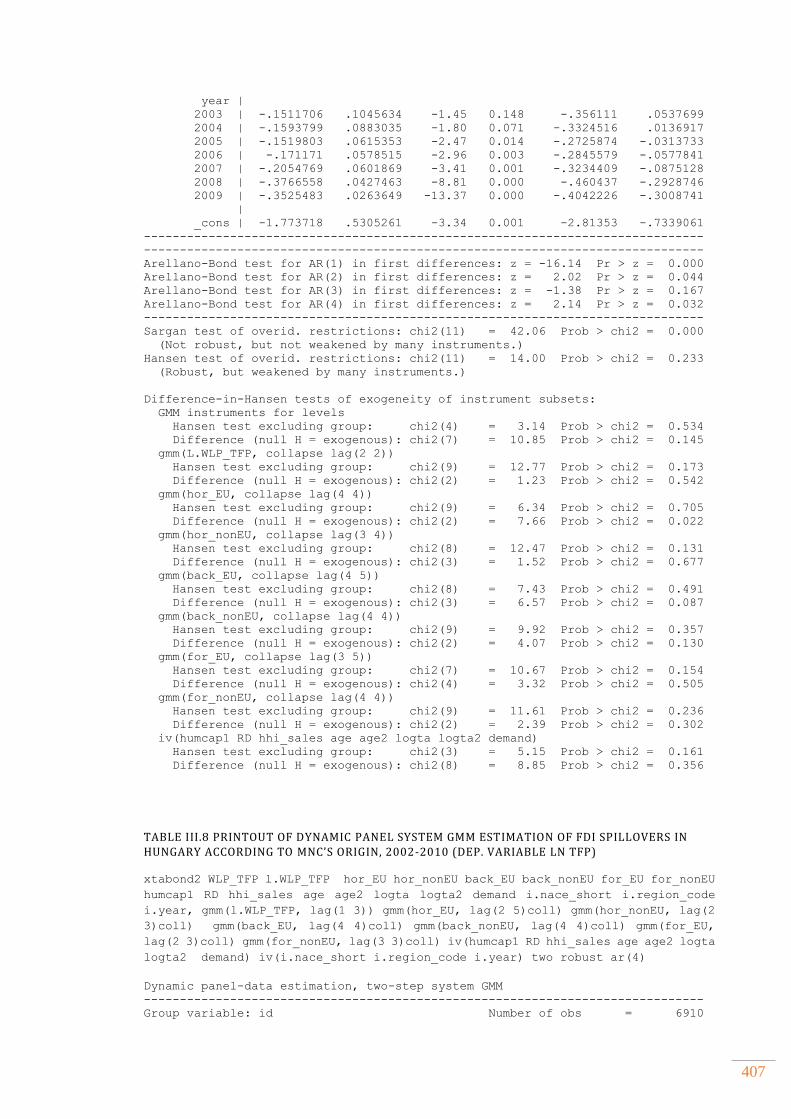

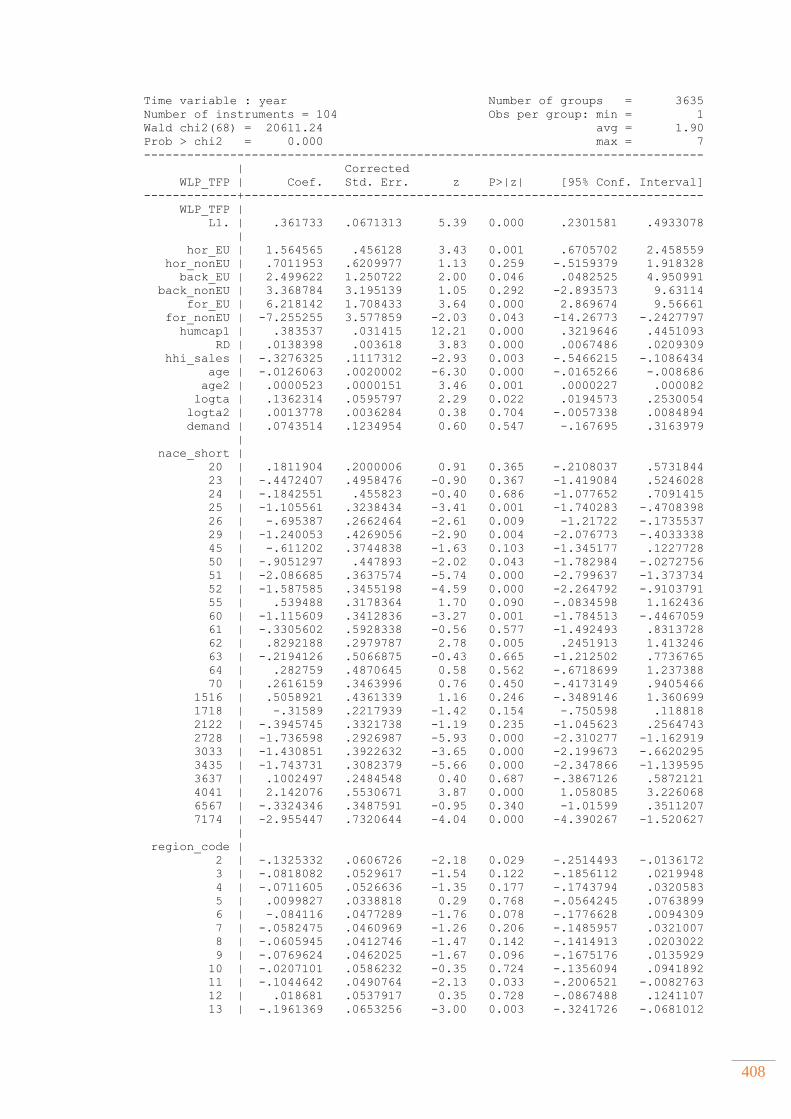

3.2 Empirical results for the effects of MNCs’ origin on productivity of local firms presented in Section 5.6.3 ...................................................................................................................... 403

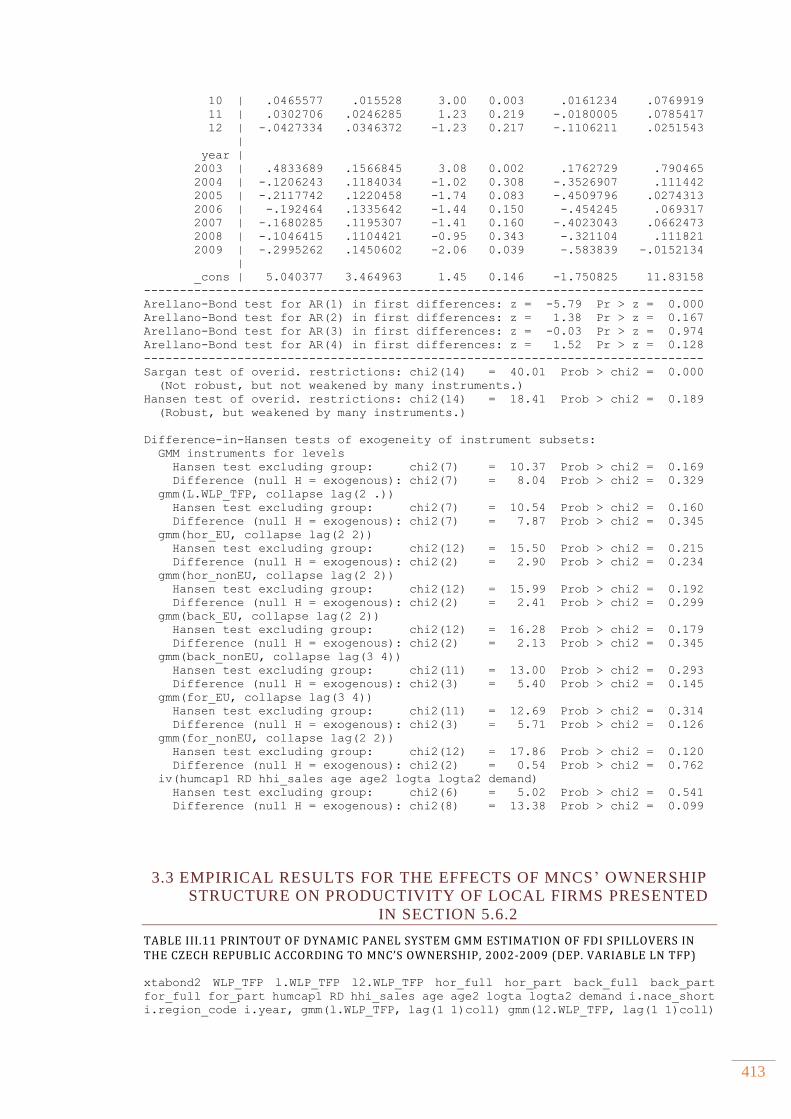

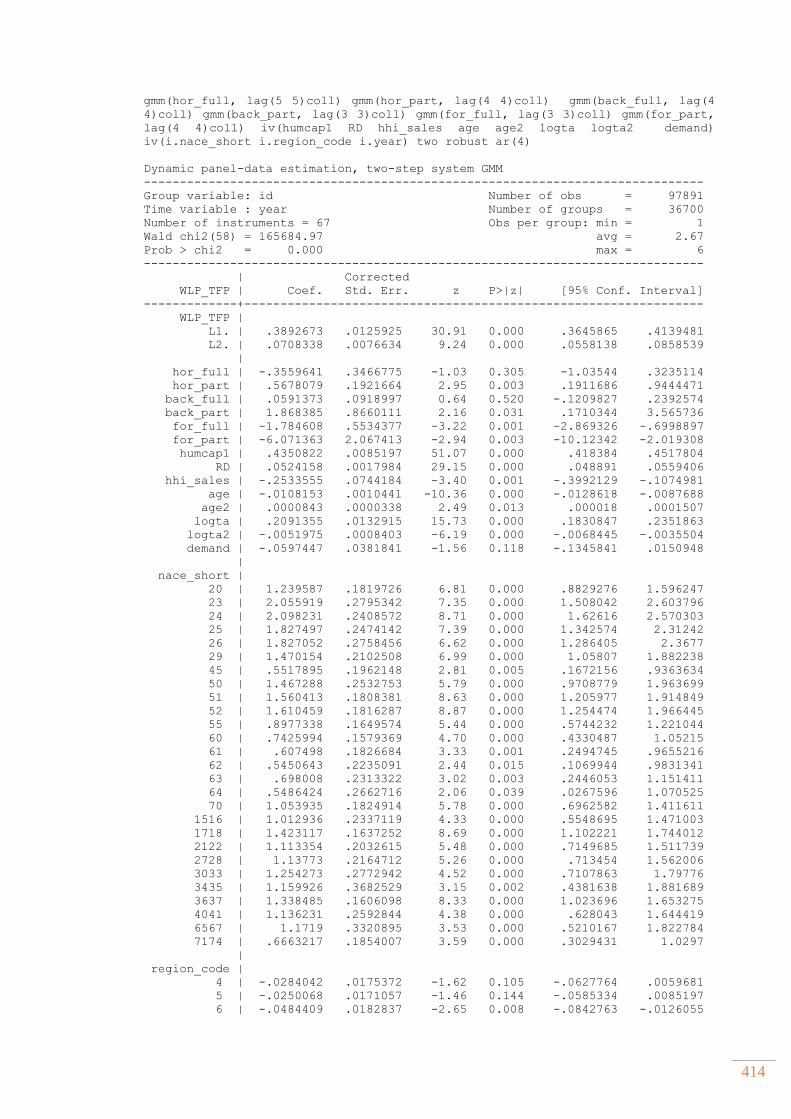

3.3 Empirical results for the effects of MNCs’ ownership structure on productivity of local firms presented in Section 5.6.2 ............................................................................................... 413

APPENDIX IV. SUPPLEMENT TO CHAPTER SIX ............................................................................. 425

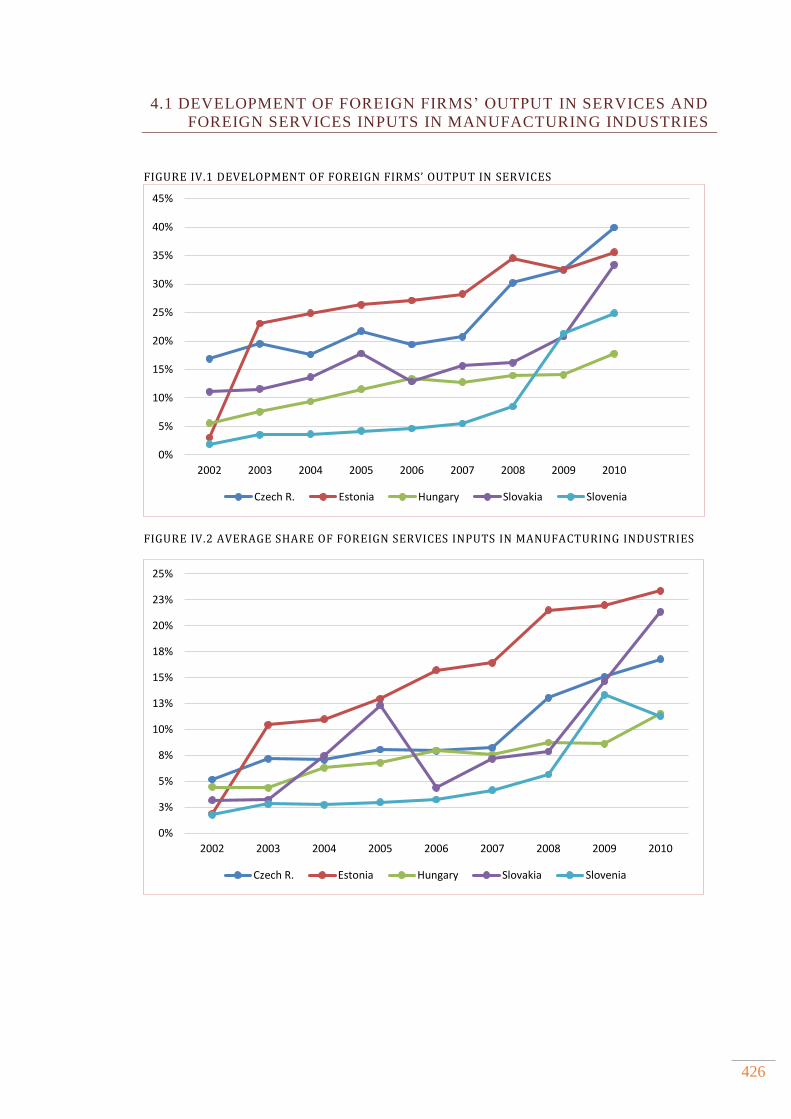

4.1 Development of foreign firms’ output in services and foreign services inputs in manufacturing industries ....................................................................................................................... 426

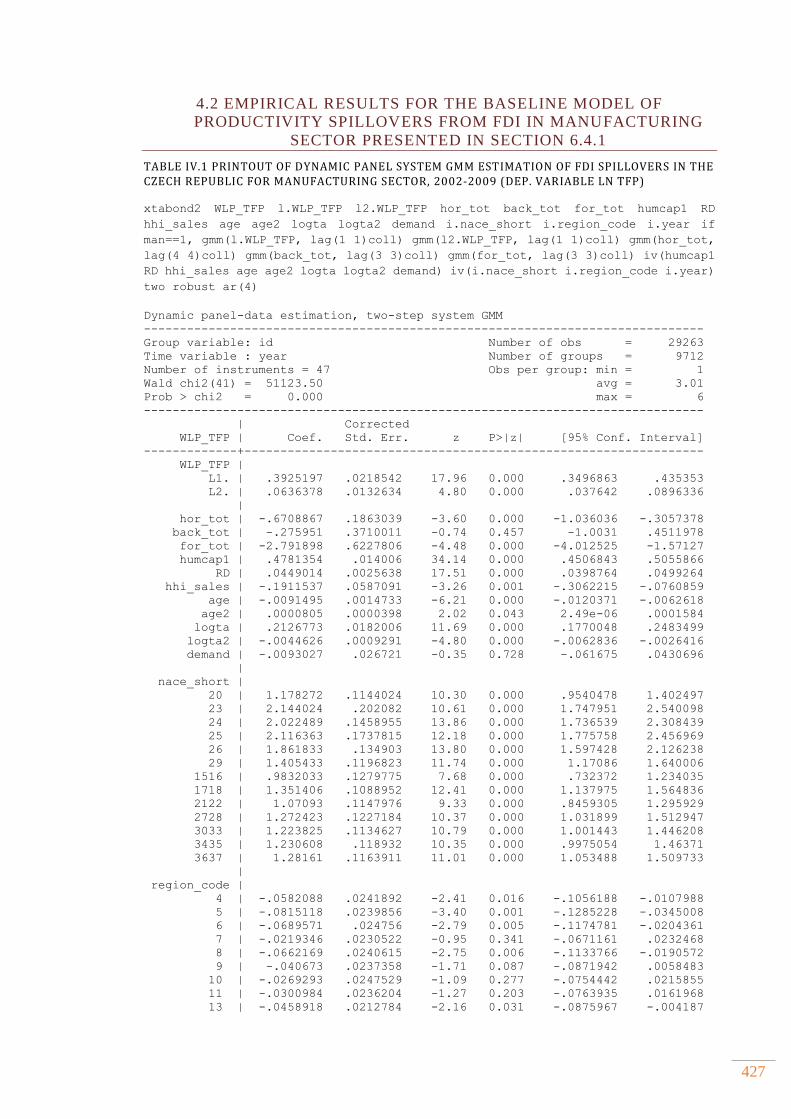

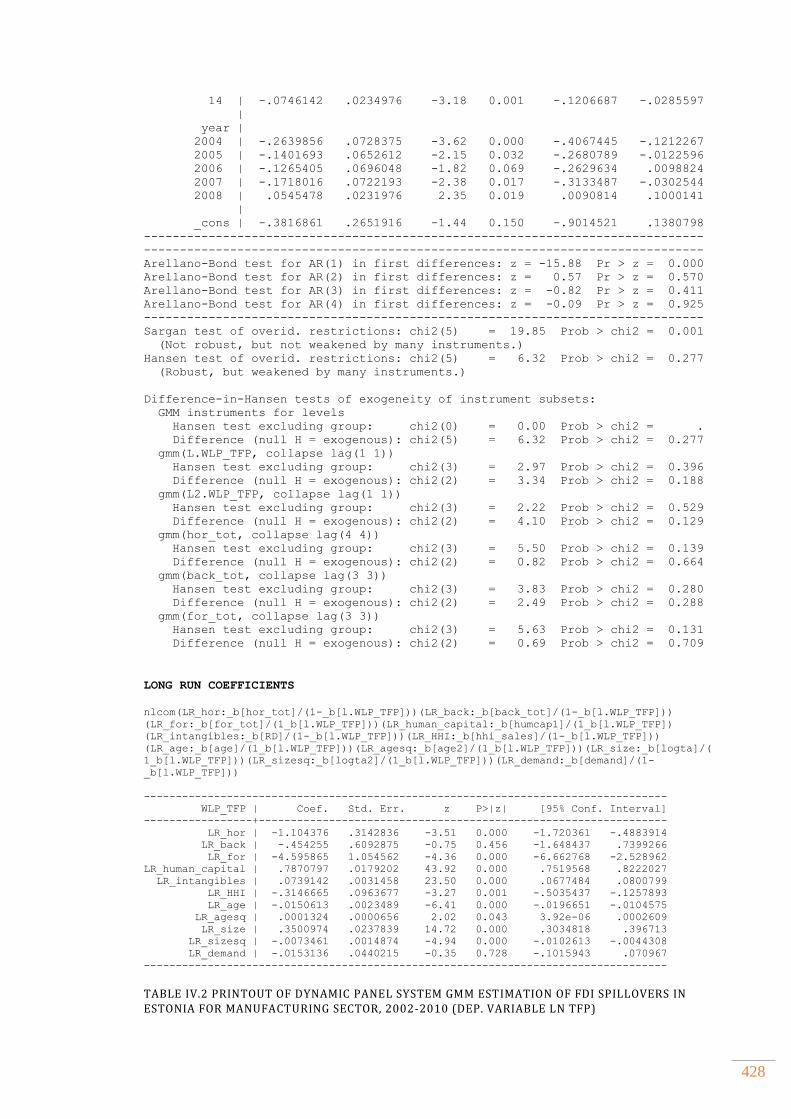

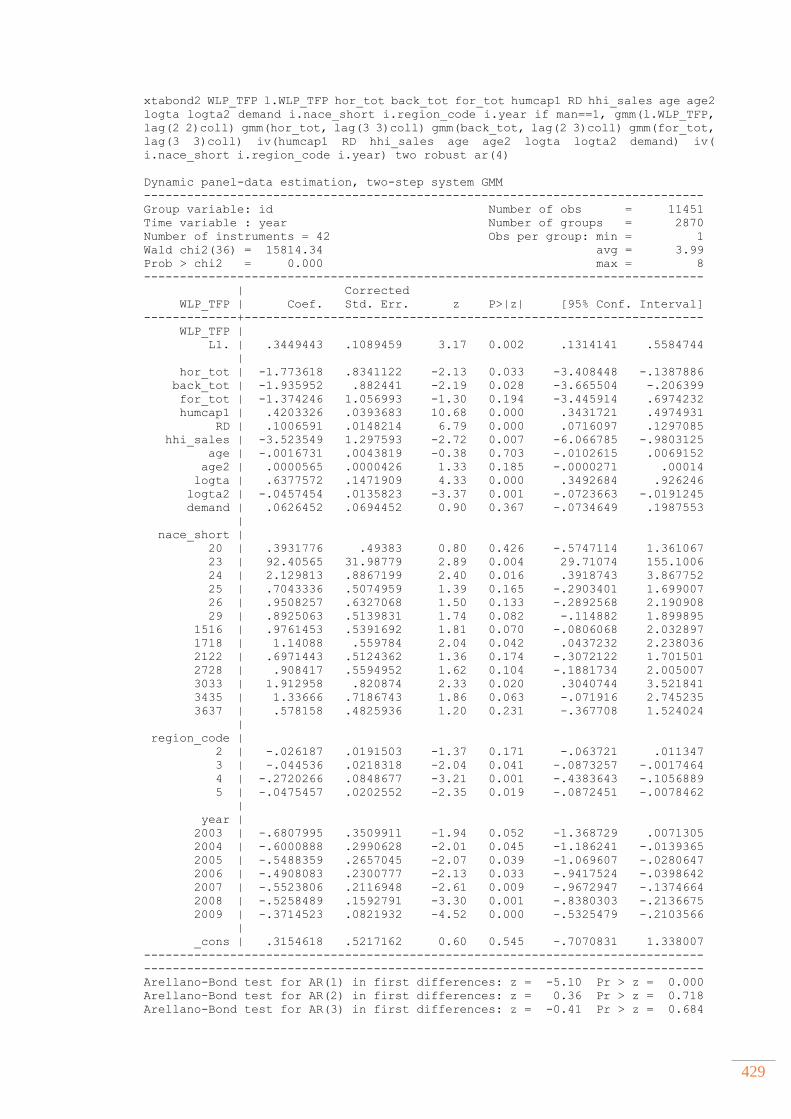

4.2 Empirical results for the baseline model of productivity spillovers from FDI in manufacturing sector presented in Section 6.4.1 ......................................................................... 427

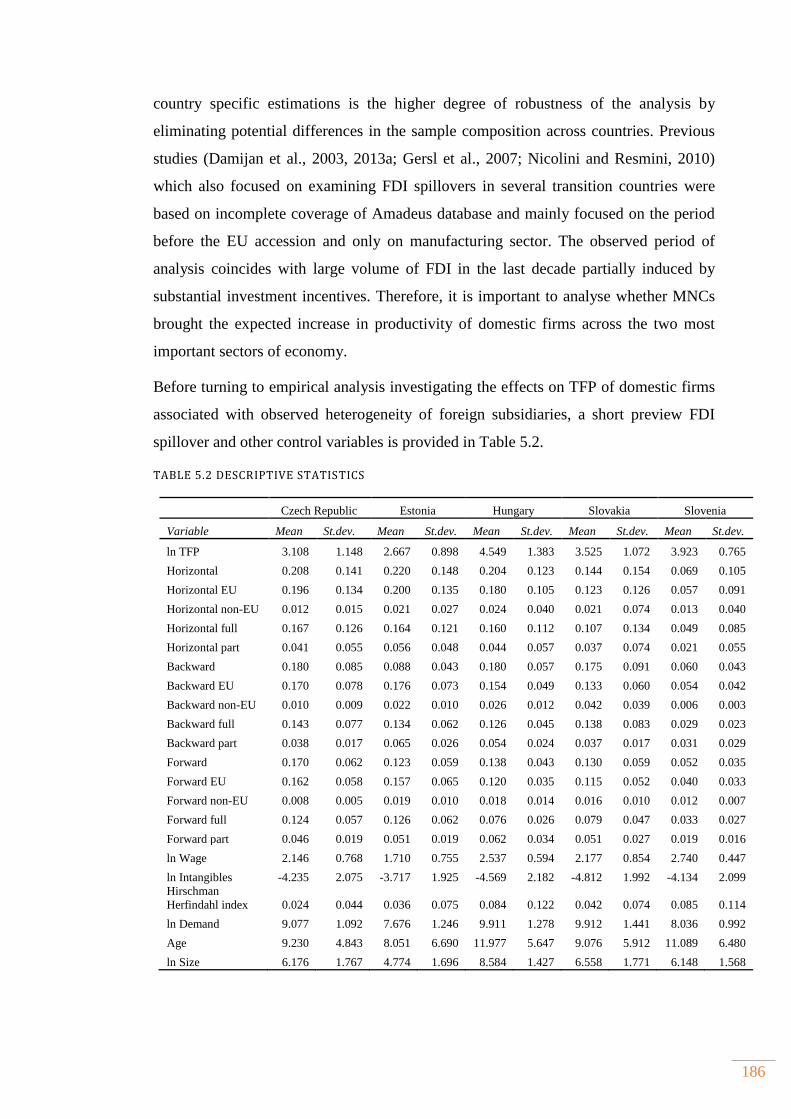

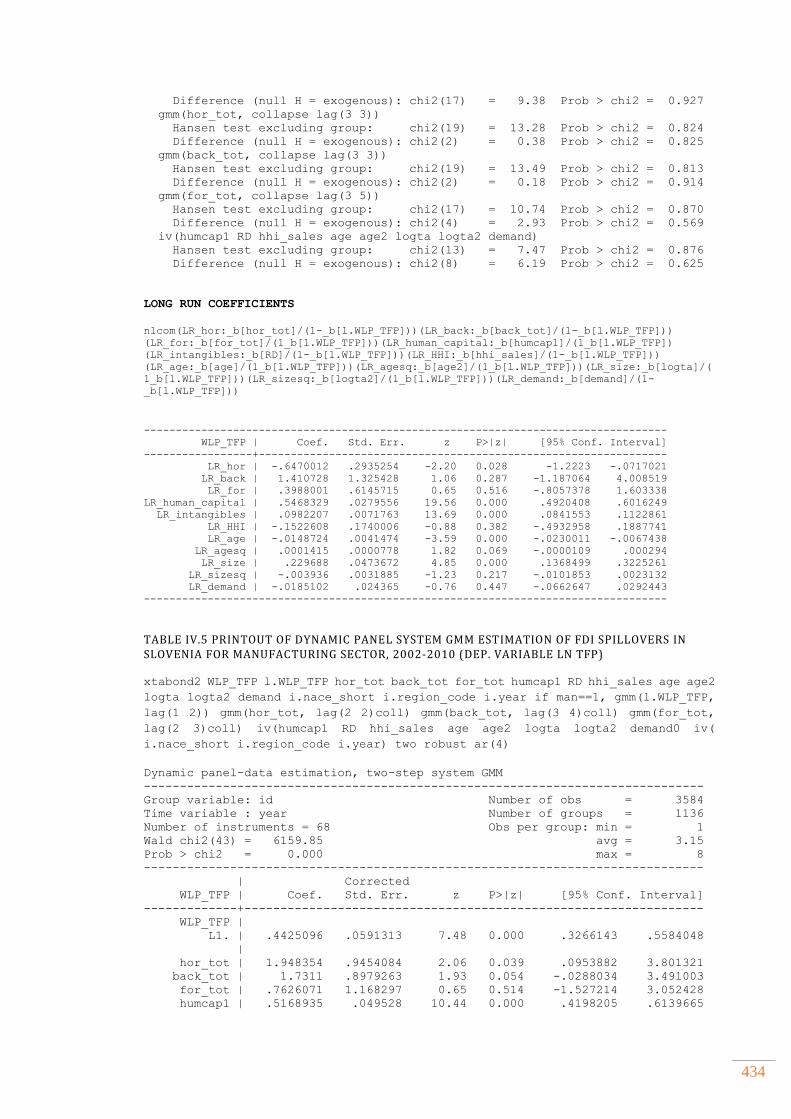

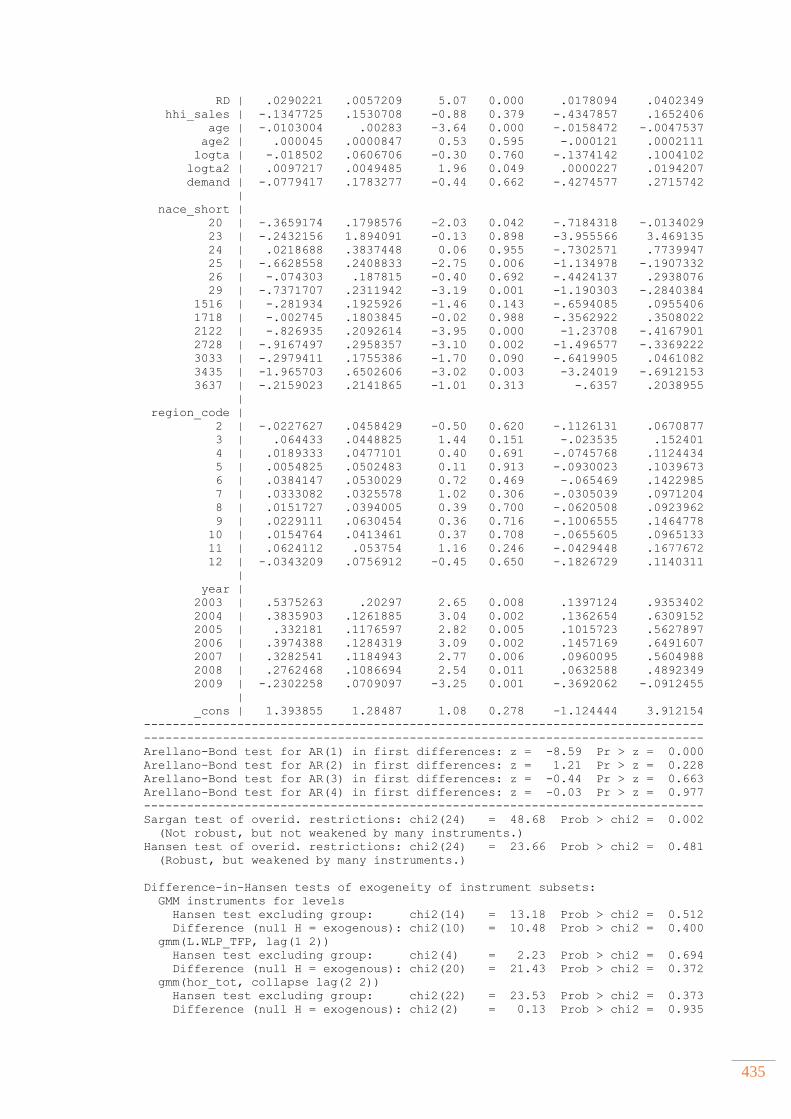

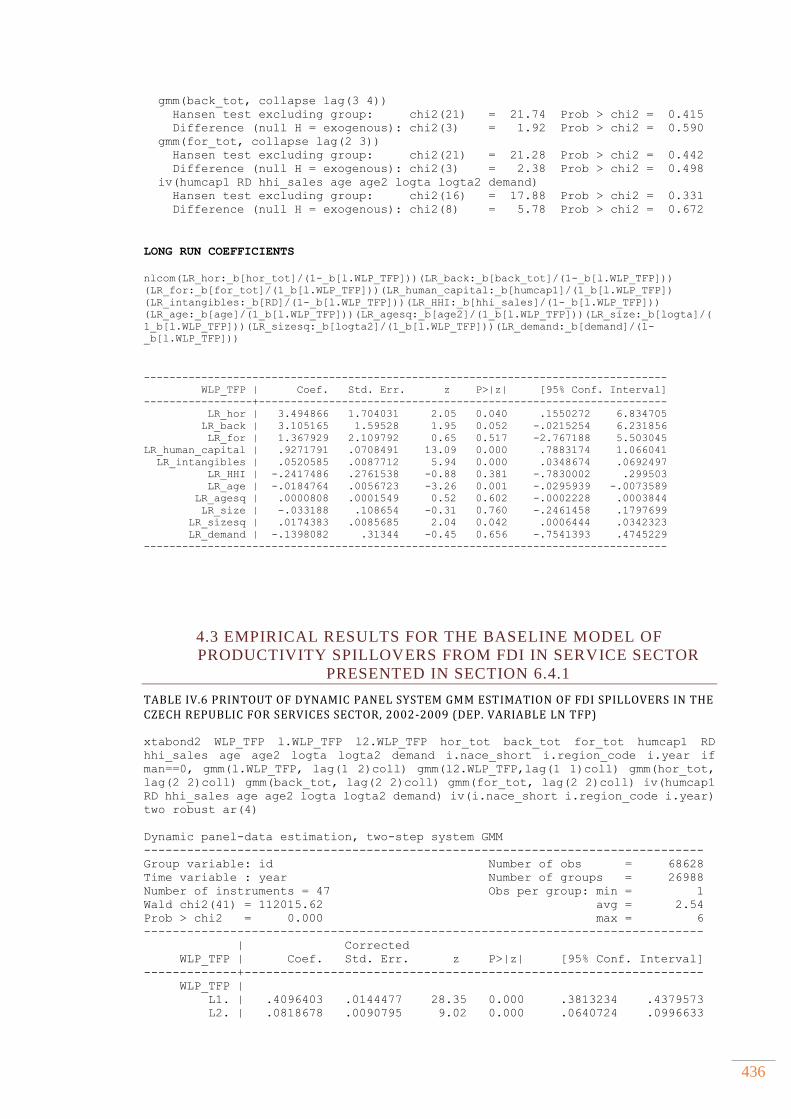

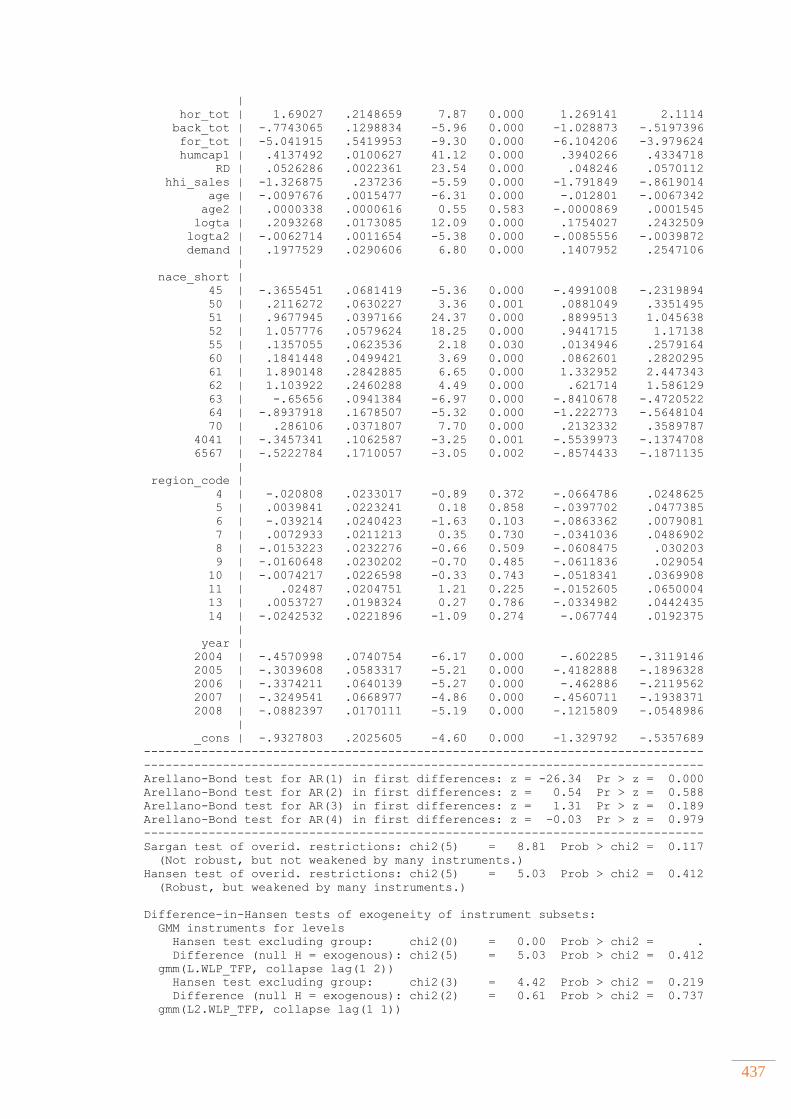

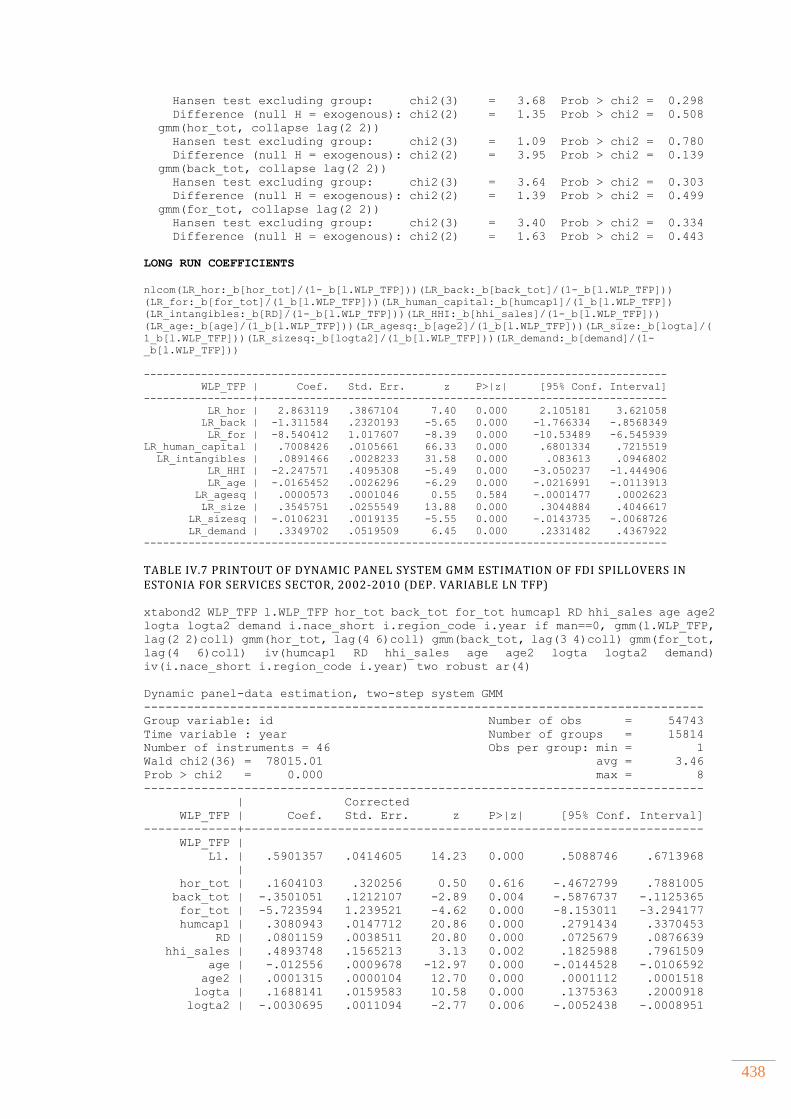

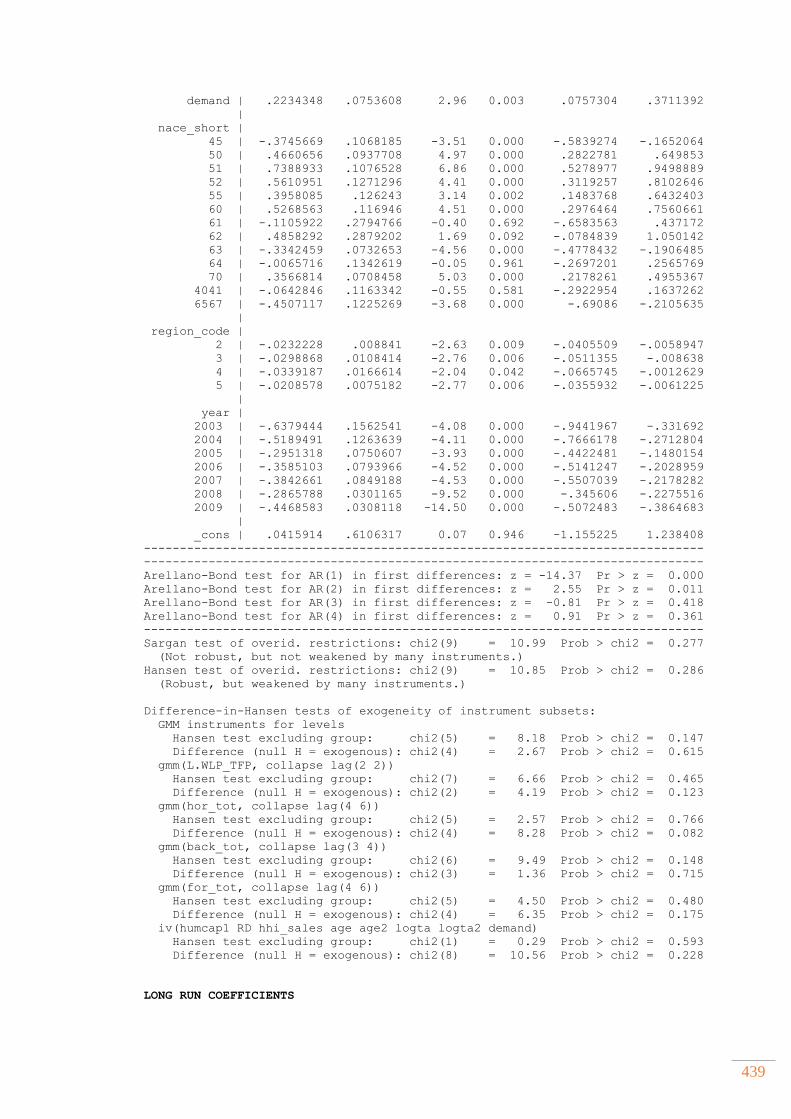

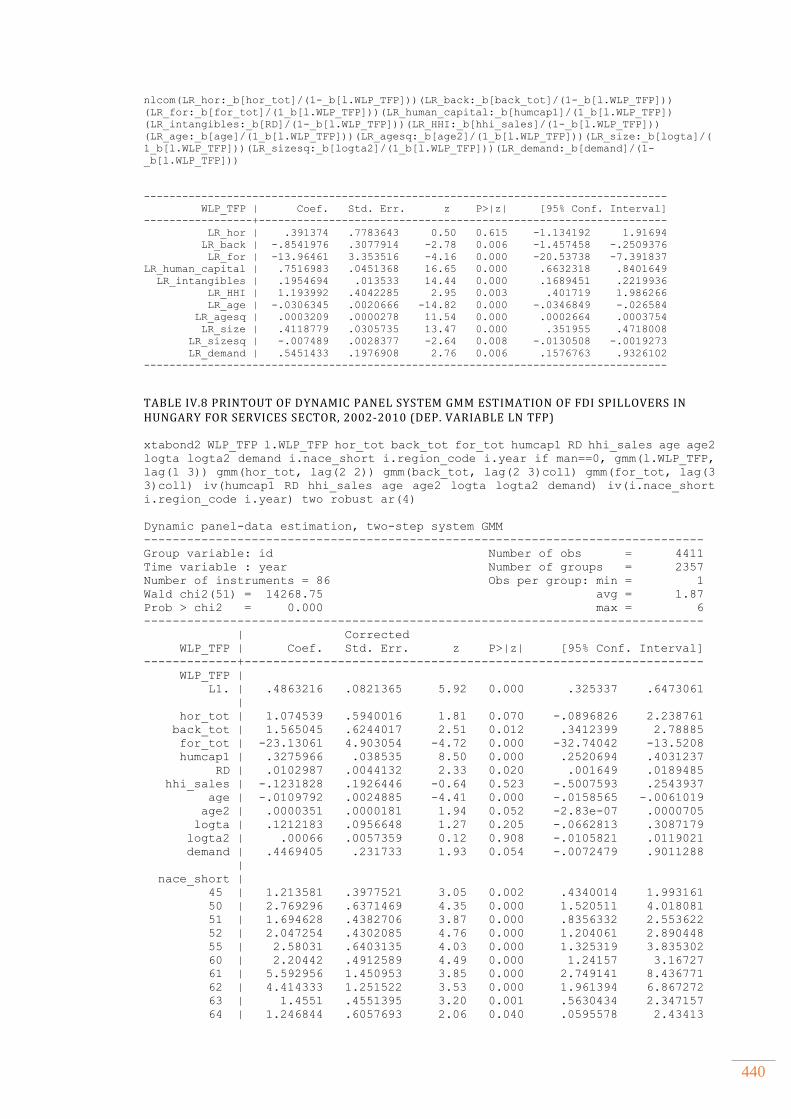

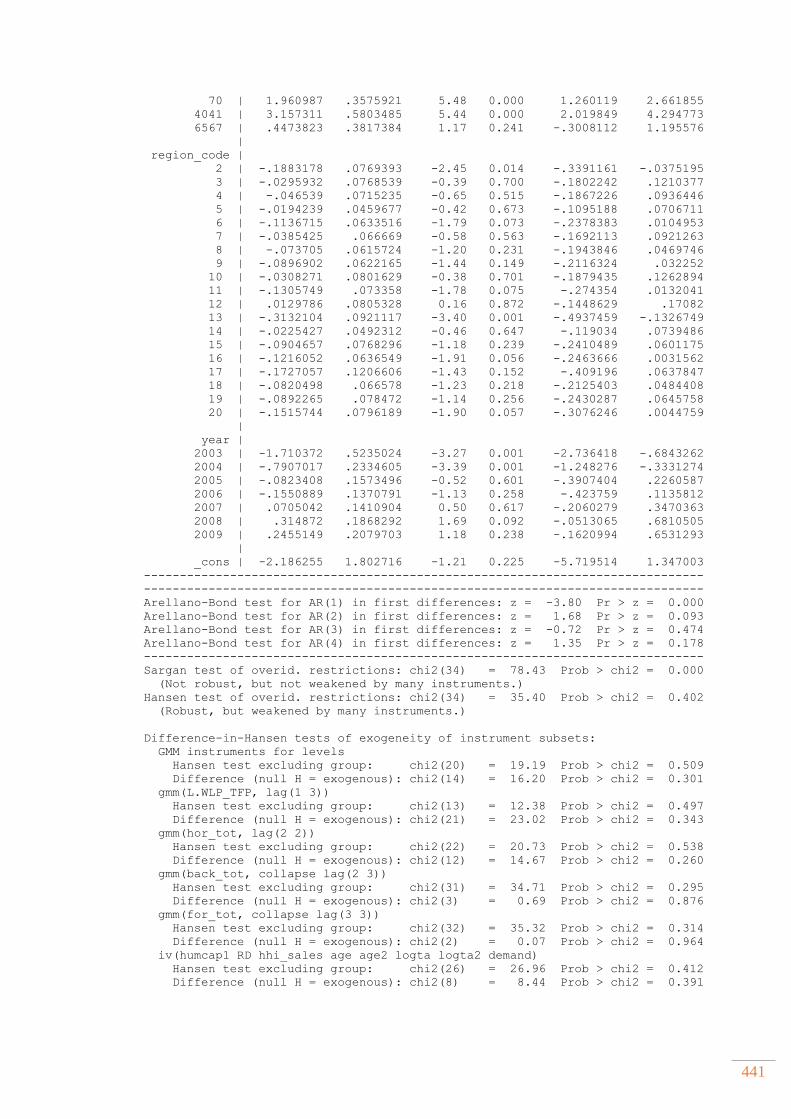

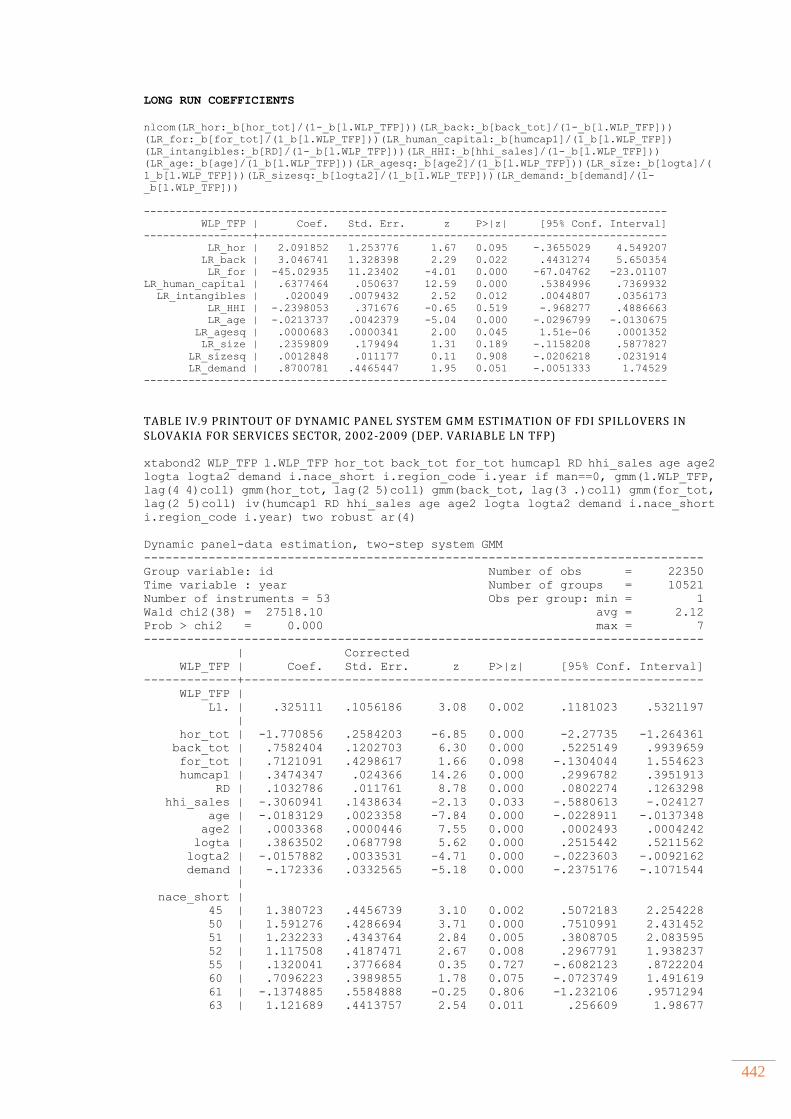

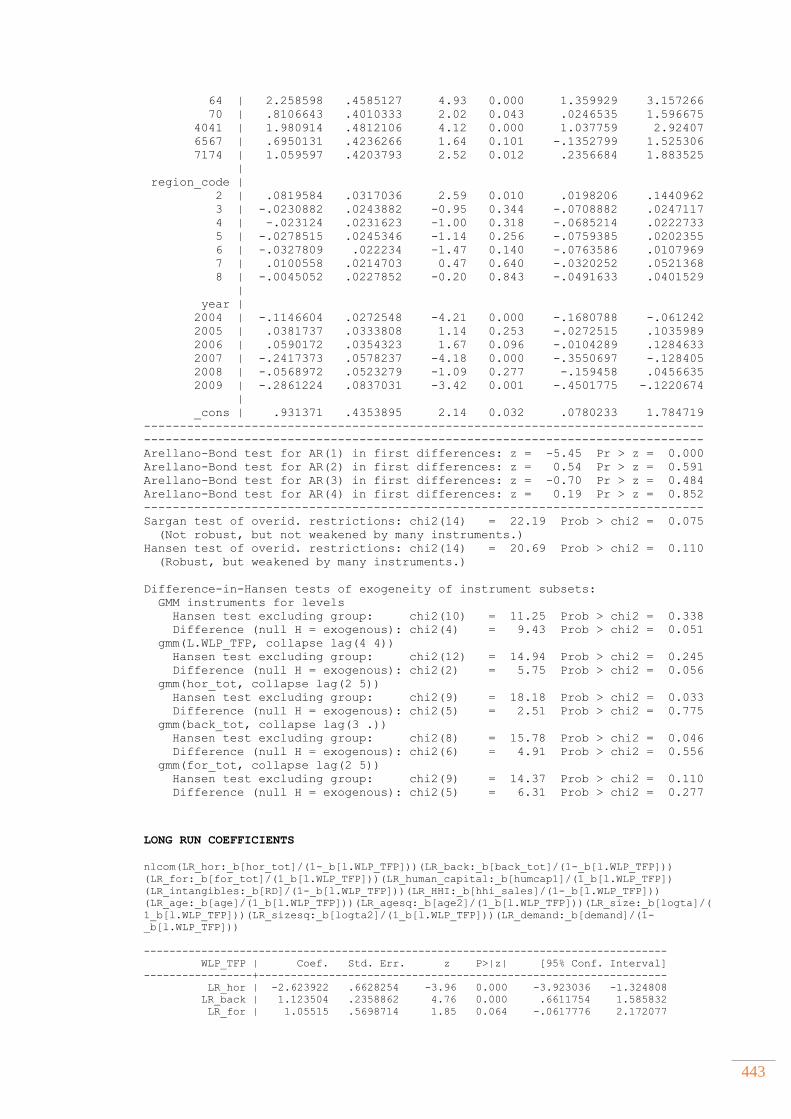

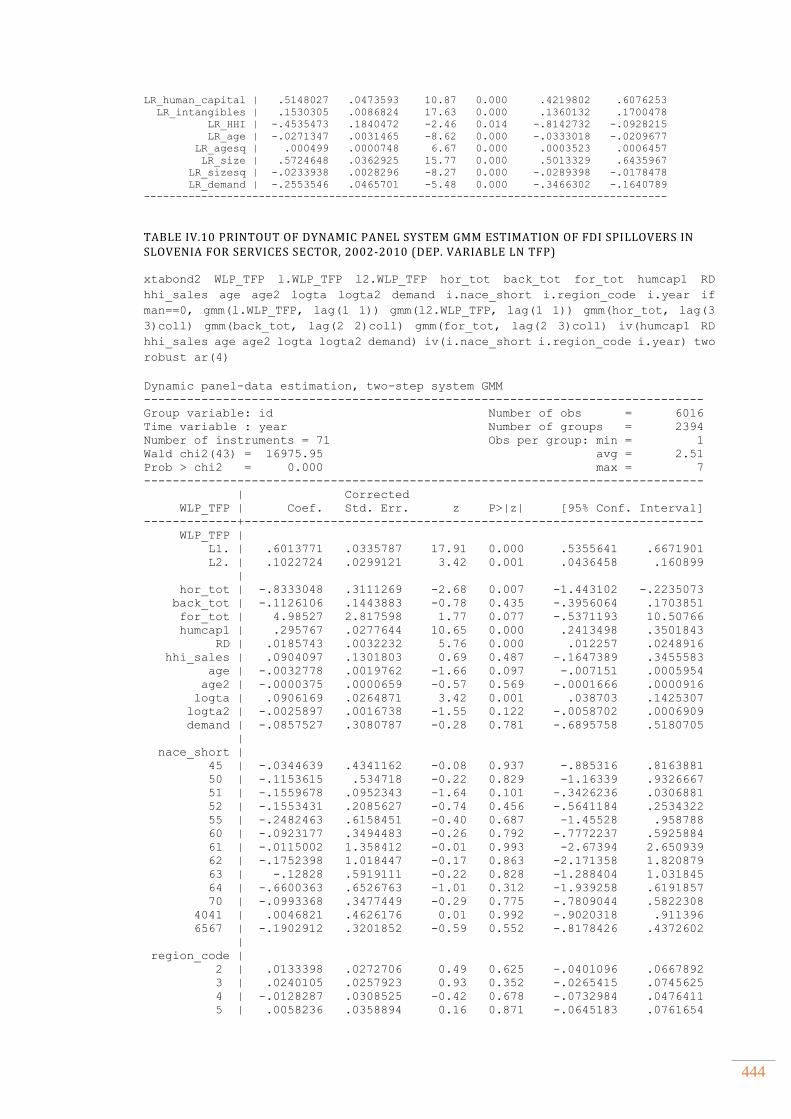

4.3 Empirical results for the baseline model of productivity spillovers from FDI in service sector presented in Section 6.4.1......................................................................................... 436

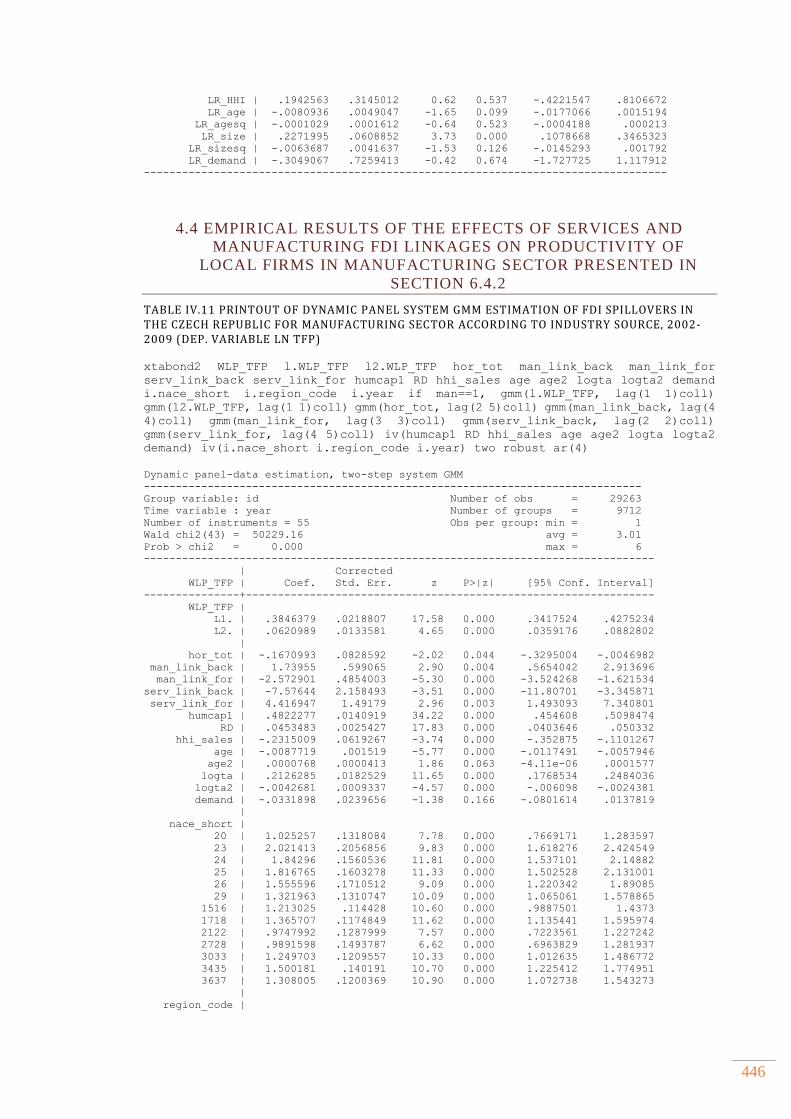

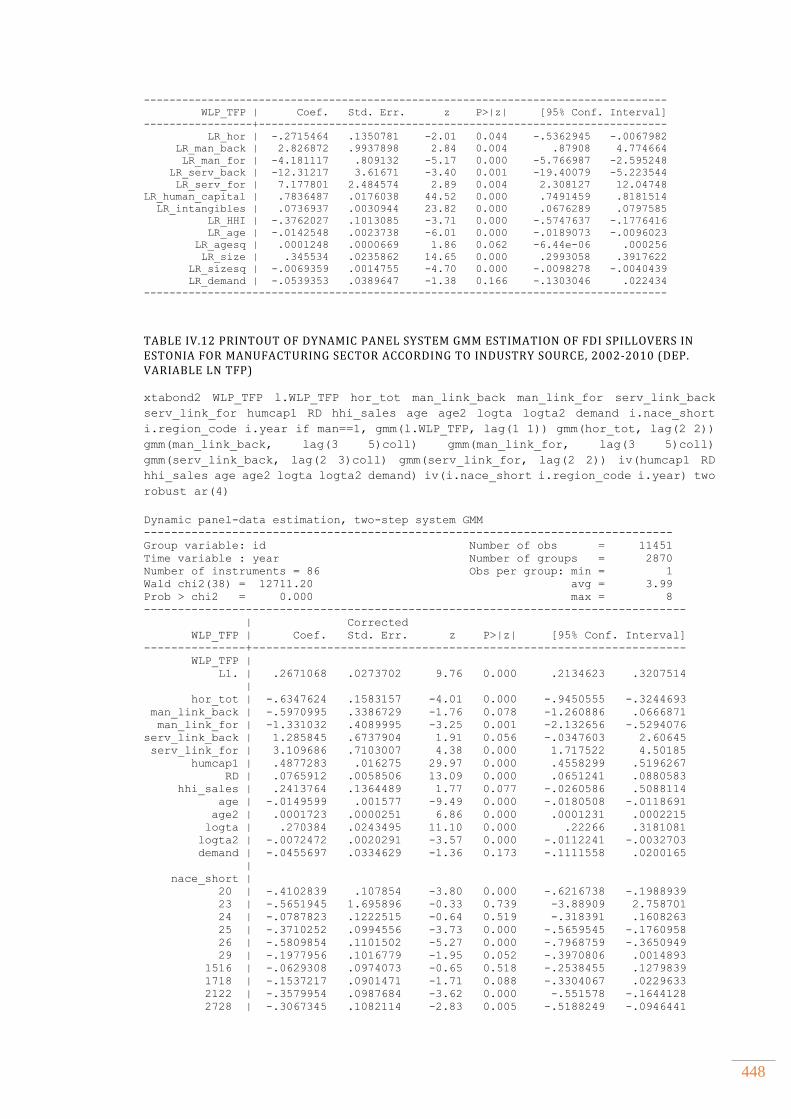

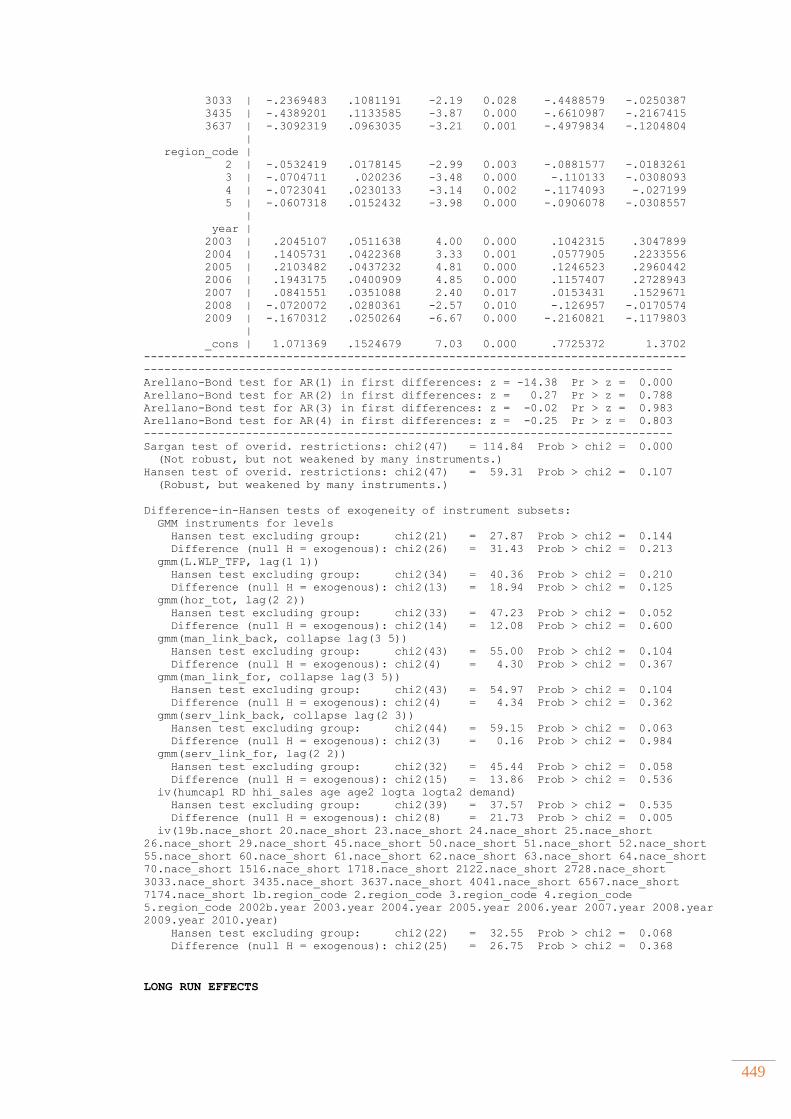

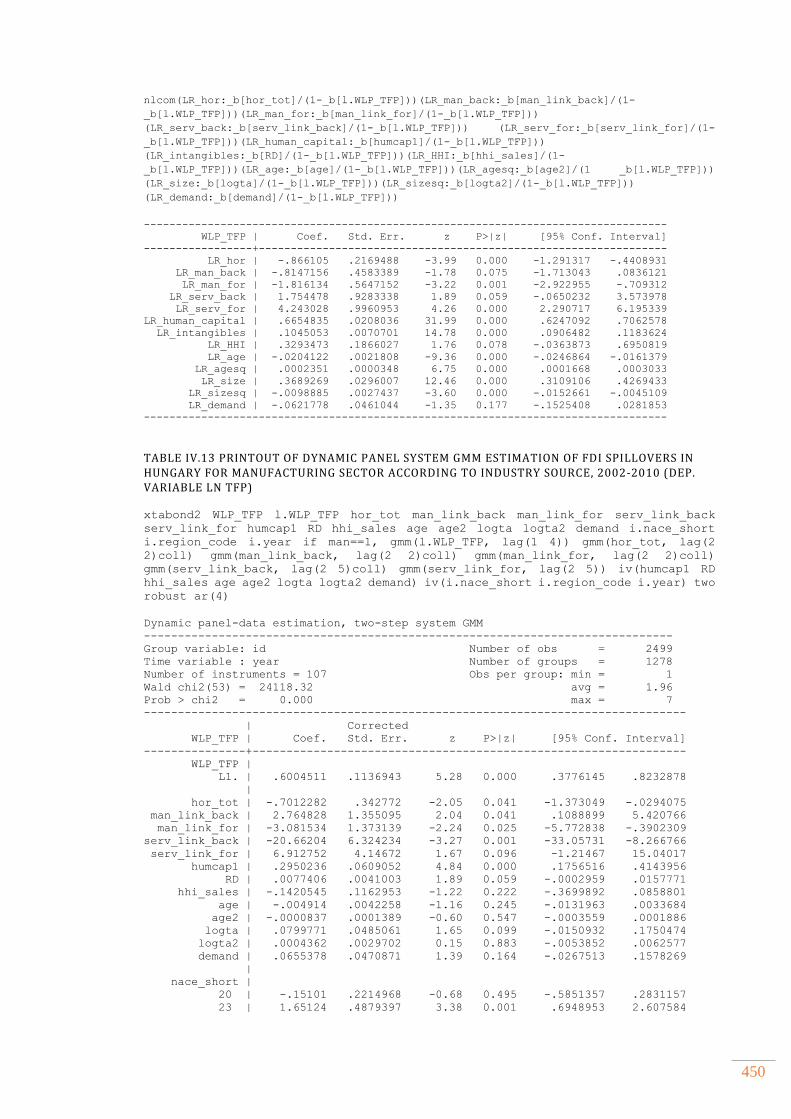

4.4 Empirical results of the effects of services and manufacturing FDI linkages on productivity of local firms in manufacturing sector presented in Section 6.4.2 ............. 446

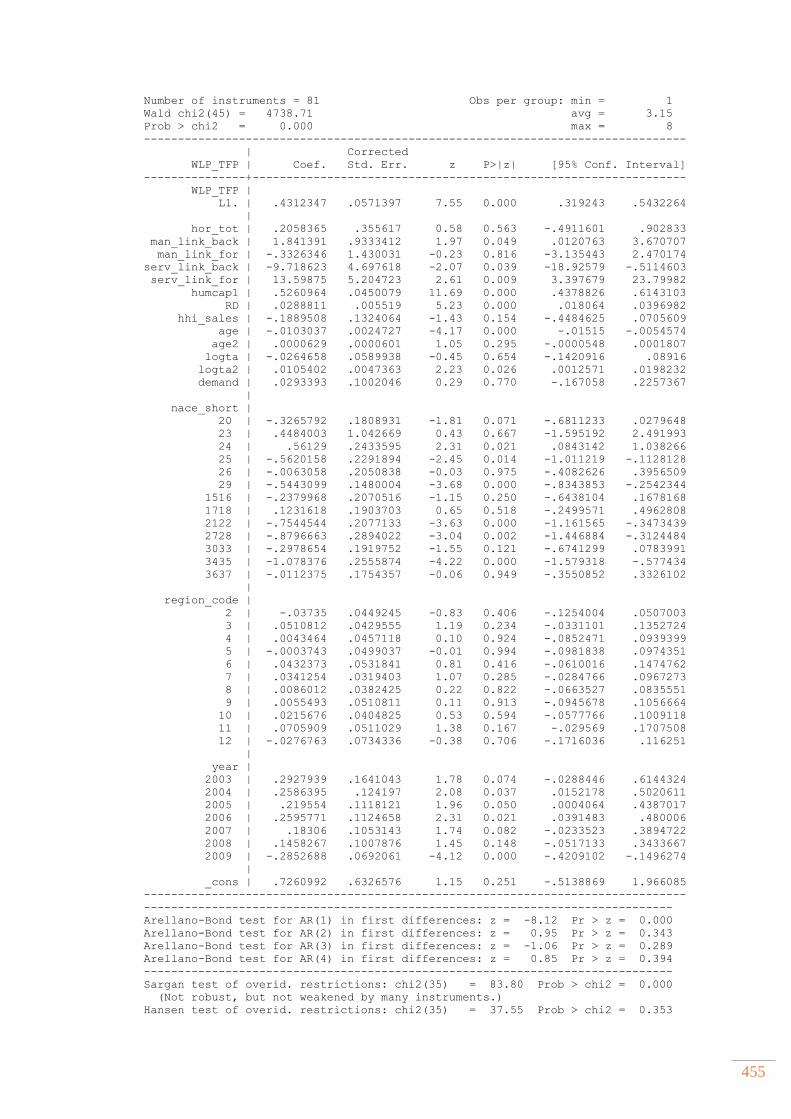

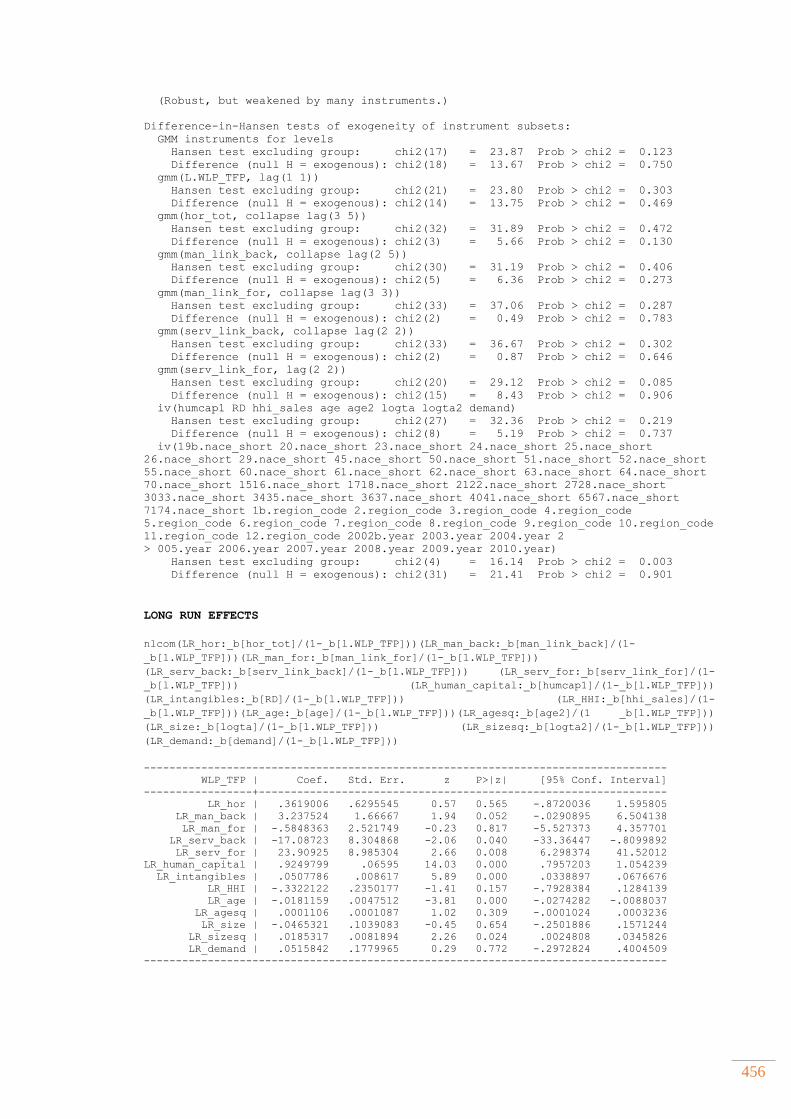

4.5 Empirical results of the moderating effects of intangible assets on productivity spillovers from FDI in manufacturing sector presented in Section 6.4.3 ........................... 457

vii

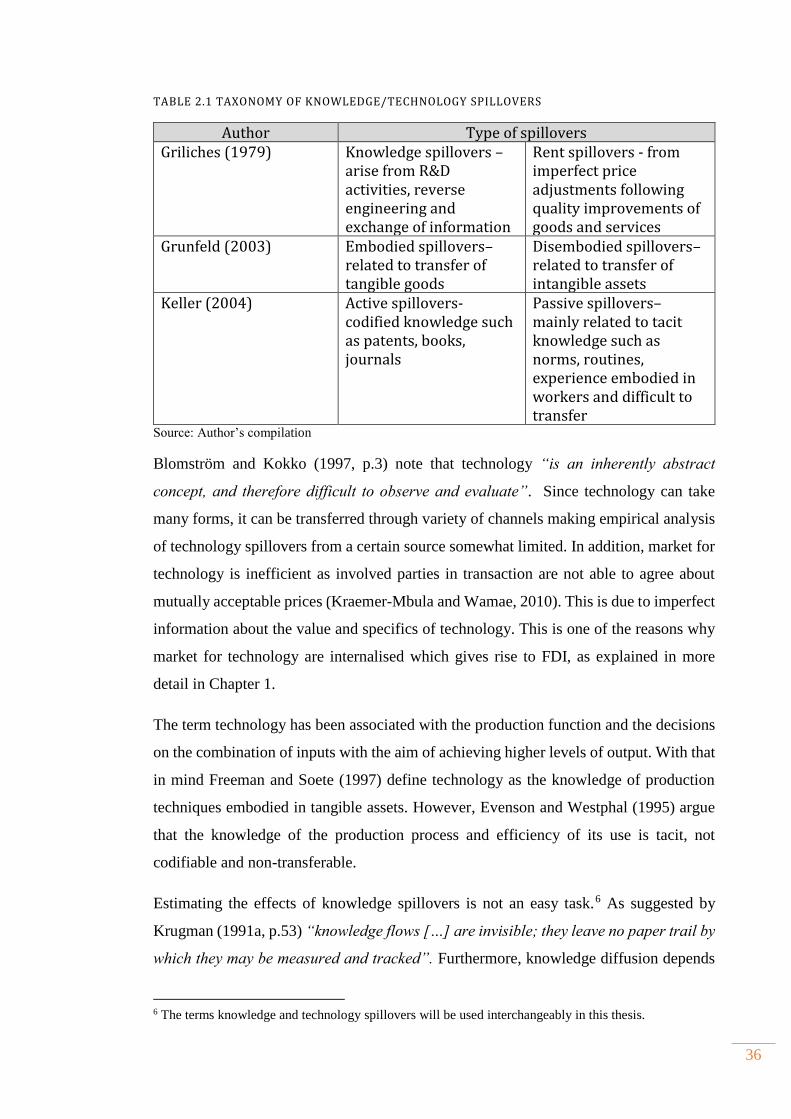

LIST OF TABLES TABLE 2.1 TAXONOMY OF KNOWLEDGE/TECHNOLOGY SPILLOVERS .................................... 36 TABLE 3.1 GROWTH CONTRIBUTIONS OF SUPPLY SIDE FACTORS IN NMS, (%) ... 87 TABLE 3.2 SHARE OF INWARD FDI STOCK ACROSS INDUSTRIES AND COUNTRIES, 2012 ....................................................................................................................................................................... 95 TABLE 3.3 SHARE OF FOREIGN AFFILIATES IN INDUSTRY EMPLOYMENT IN %, 2011 ....................................................................................................................................................................... 99 TABLE 3.4 SHARE OF FATS IN TURNOVER AT INDUSTRY LEVEL IN %, 2011 ..... 101 TABLE 3.5 SHARE OF DIFFERENT TECHNOLOGY GROUPS IN VARIOUS FEATURES OF FOREIGN AFFILIATES , 2011 ........................................................................................................ 103 TABLE 3.6 RATIO OF LABOUR PRODUCTIVITY OF FOREIGN TO DOMETIC FIRM BY INDUSTRY, 2011 .......................................................................................................................................... 107 TABLE 3.7 RELATIVE POSITION OF COUNTRIES AND INDUSTRIES IN GVC, 2009 ................................................................................................................................................................................ 113 TABLE 4.1 REPRESENTATIVENESS OF AMADEUS DATABASE VERSUS EUROSTAT SBS 150 TABLE 4.2 COMPARISON OF FIRM SIZE DISTRIBUTION BETWEEN EUROSTAT SBS AND AMADEUS DATABASE ................................................................................................................... 150 TABLE 4.3 DISTRIBUTION OF FIRMS ACROSS COUNTRIES, INDUSTRIES AND YEARS ................................................................................................................................................................. 152 TABLE 4.4 SUMMARY STATISTICS ON SELECTED INDICATORS .................................... 154 TABLE 4.5 WITHIN INDUSTRY DISPERSION OF TFP ACROSS COUNTRIES AND ESTIMATION ALGORITHMS .................................................................................................................. 160 TABLE 4.6 EFFECTS OF EXOGENOUS SHOCK ON TFP ........................................................... 162 TABLE 4.7 KOLMOGOROV SMIRNOV TEST OF EQUALITY OF TFP DISTRIBUTIONS ................................................................................................................................................................................ 164 TABLE 4.8 TFP PREMIUM OF FOREIGN OVER DOMESTIC FIRMS ................................. 165 TABLE 5.1 DESCRIPTION OF VARIABLES ..................................................................................... 184 TABLE 5.2 DESCRIPTIVE STATISTICS ............................................................................................ 186 TABLE 5.3 DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVER EFFECTS ON PRODUCTIVITY (LN TFP) OF DOMESTIC FIRMS, 2002-2010 (ALL SECTORS) ......................................................................................................................................................... 198 TABLE 5.4 DYNAMIC SYSTEM GMM ESTIMATION OF FDI SPILLOVER EFFECTS ON DOMESTIC FIRMS’ PRODUCTIVITY (LN TFP) - EXTENT OF MNC’S OWNERSHIP, 2002-2010 (ALL SECTORS) ................................................................................................................... 206 TABLE 5.5 DYNAMIC SYSTEM GMM ESTIMATION OF FDI SPILLOVER EFFECTS ON DOMESTIC FIRMS’ PRODUCTIVITY (LN TFP) – THE ROLE OF MNC’S ORIGIN, 2002-2010 (ALL SECTORS) ................................................................................................................... 215 Table 6.1 DYNAMIC PANEL SYSTEM GMM ESTIMATIONS OF FDI spillover effects on PRODUCTIVITY (LN TFP) OF DOMESTIC FIRMS (MANUFACTURING VS. SERVICES), 2002-2010 ..................................................................................................................................................................... 249 TABLE 6.2 DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVER EFFECTS ON PRODUCTIVITY (LN TFP) OF DOMESTIC FIRMS IN MANUFACTURING ACCORDING TO INDUSTRY SOURCE, 2002-2010 ............................................................................................................... 255 TABLE 7.1 SUMMARY OF FINDINGS ACROSS COUNTRIES AND EMPIRICAL MODELS .... 279 Table I.1 GDP PER CAPITA (PPP) GROWTH RATES IN NMS AND EU 15 ................................ 343 Table I.2 GDP PER CAPITA (PPP) GAP, PERCENTAGE OF EU 15 ............................................... 344 Table I.3 LABOUR PRODUCTIVITY GROWTH PER PERSON EMPLOYED (CONVERTED TO 2013 PRICE LEVEL WITH 2005 PPP, 1995=100) ............................................................................. 345 Table I.4 TOTAL FACTOR PRODUCTIVITY GROWTH ...................................................................... 346

viii

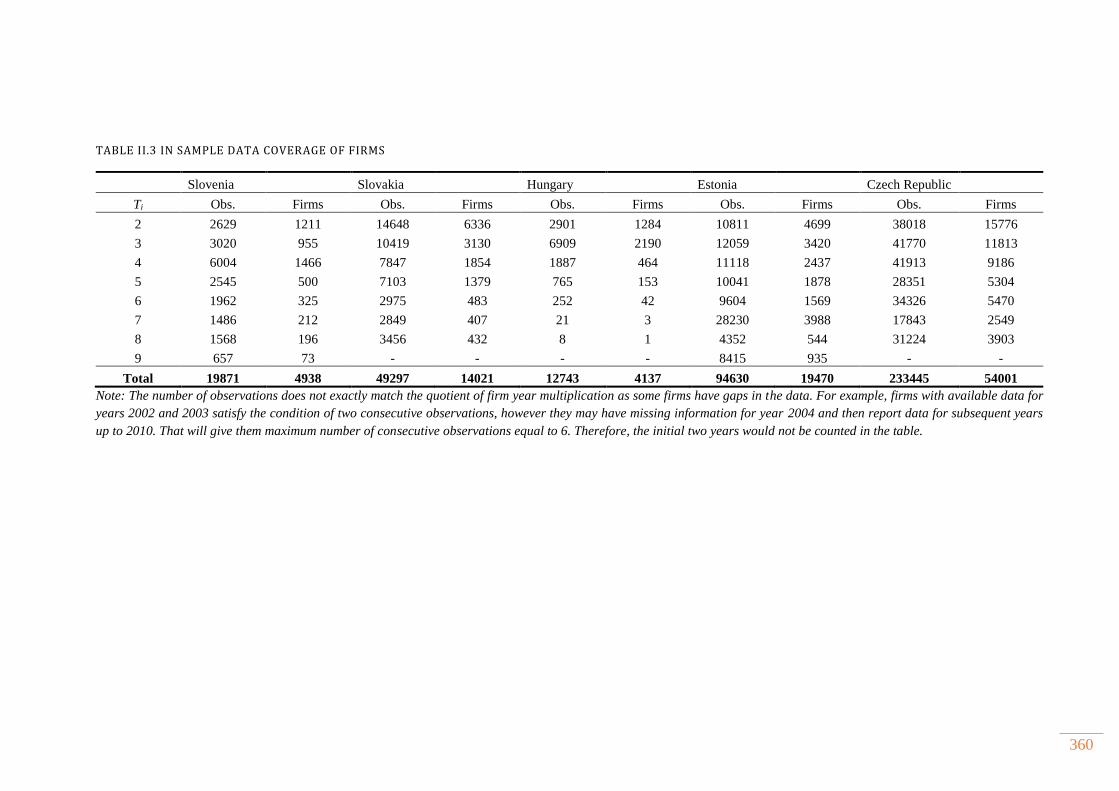

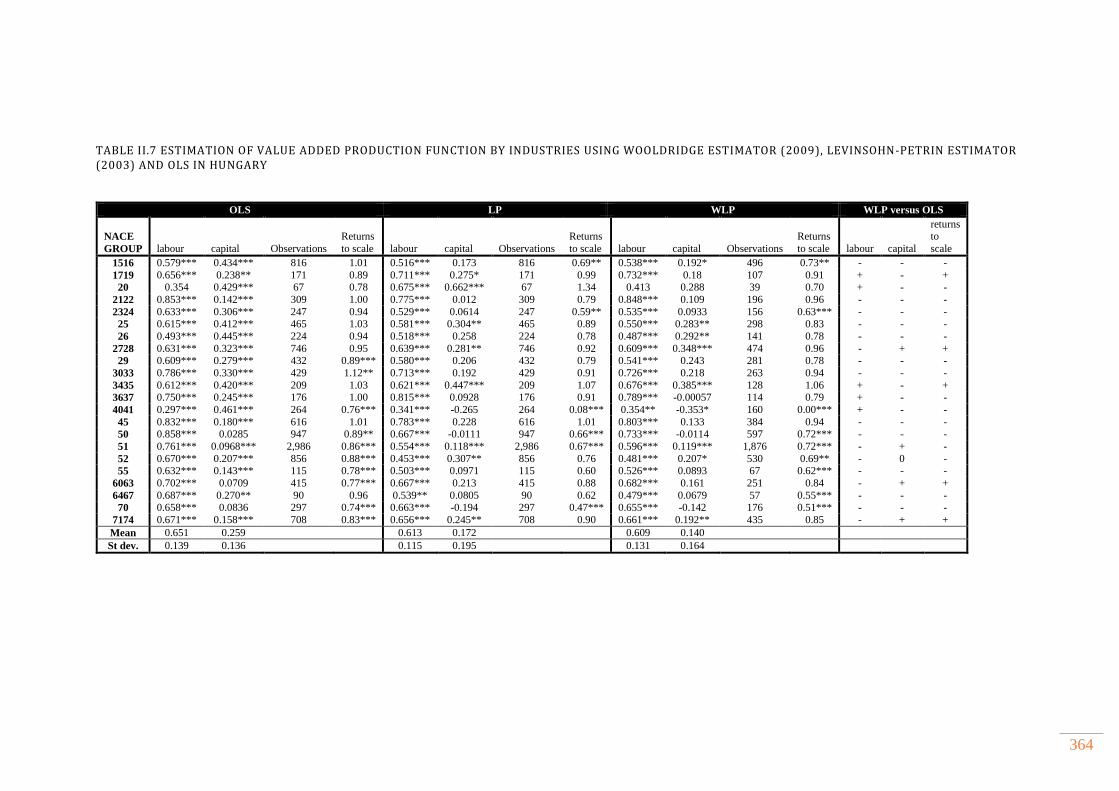

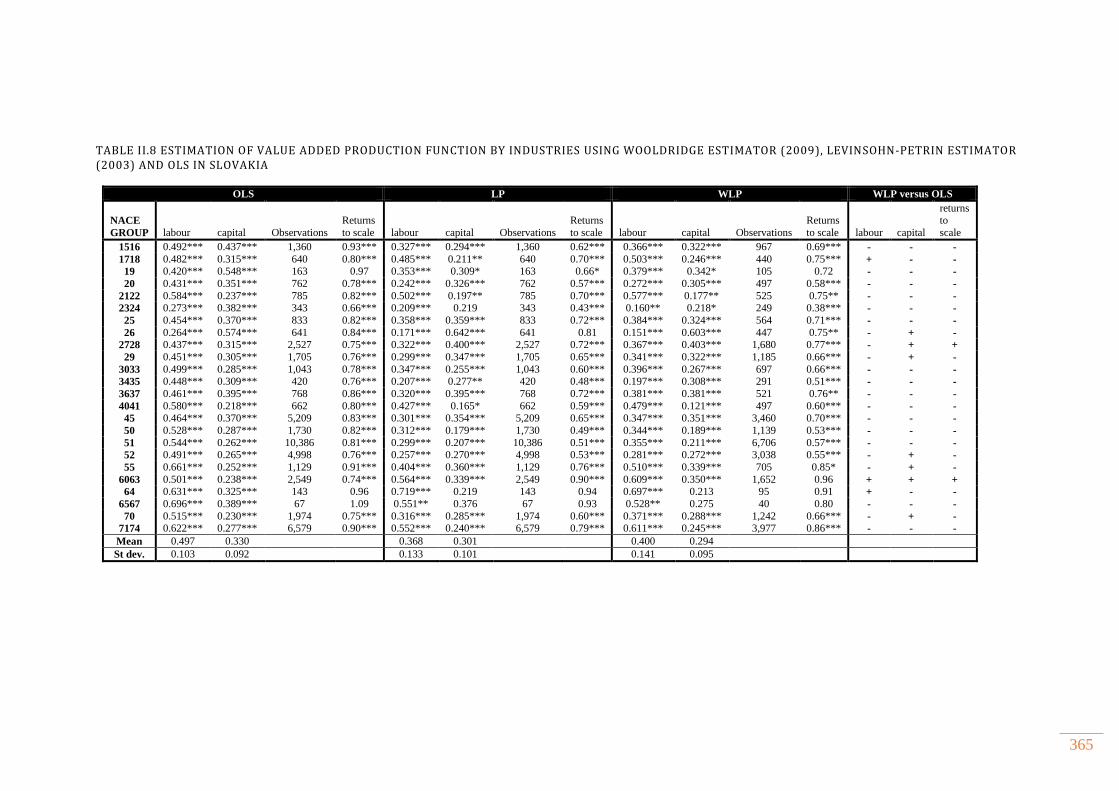

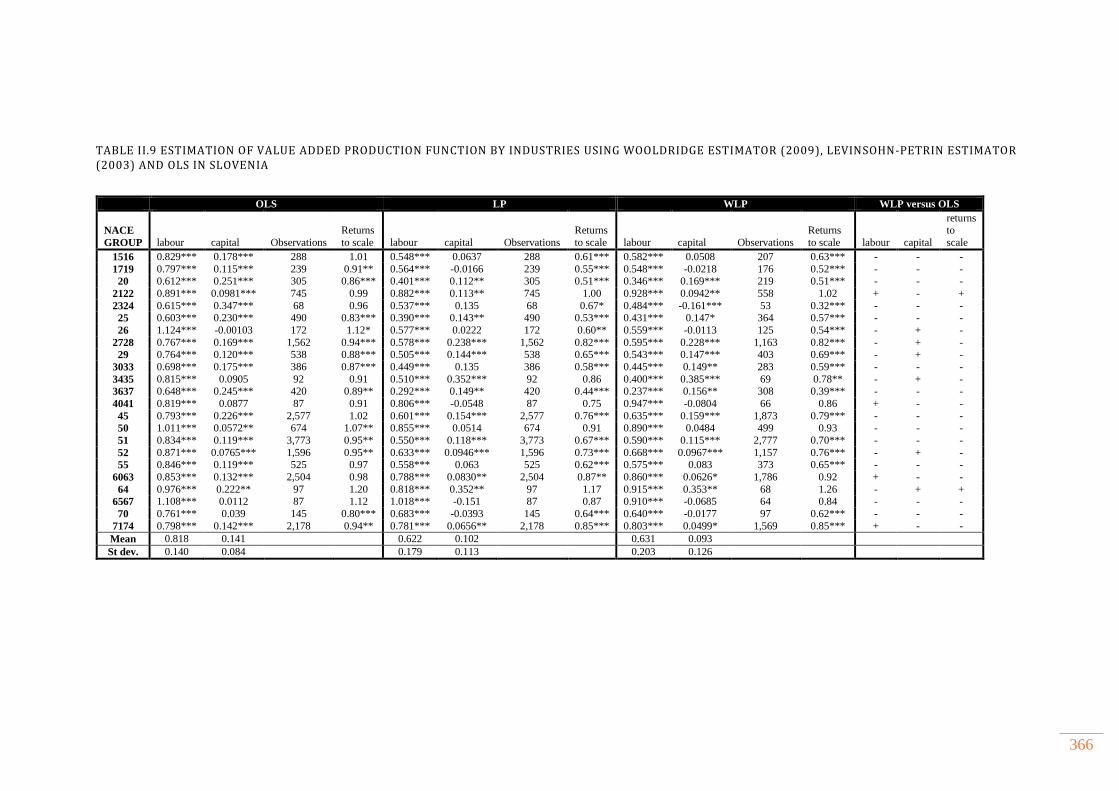

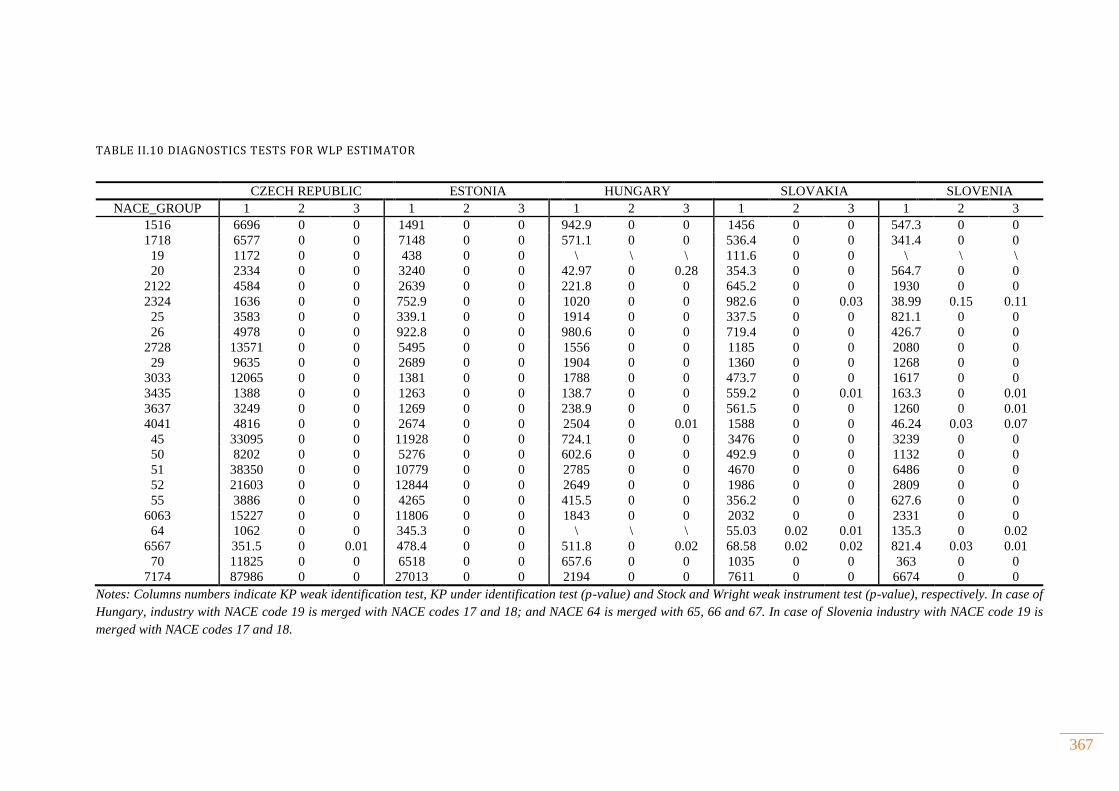

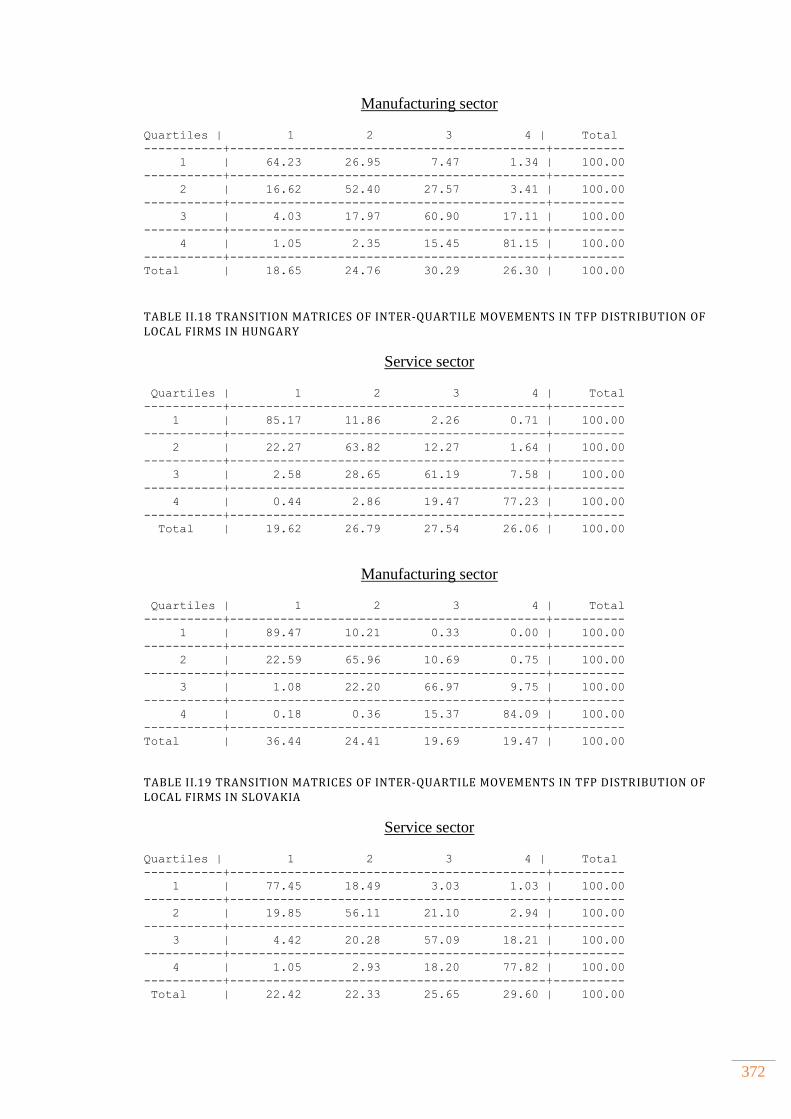

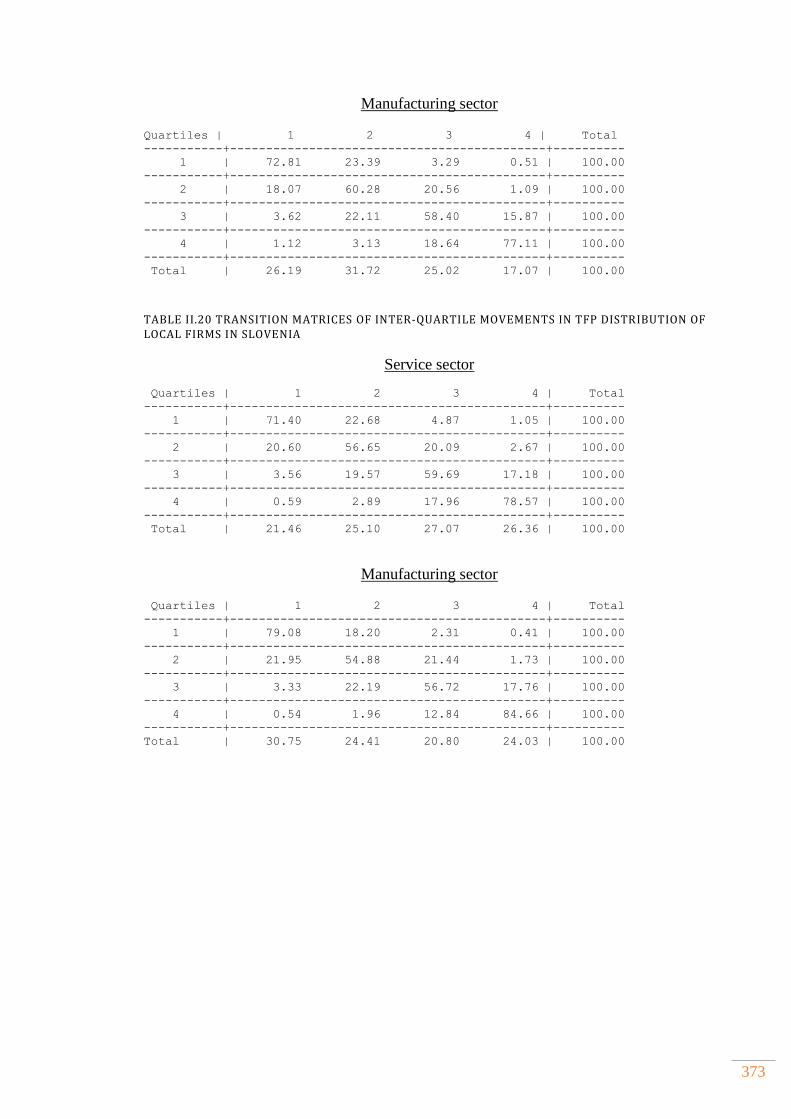

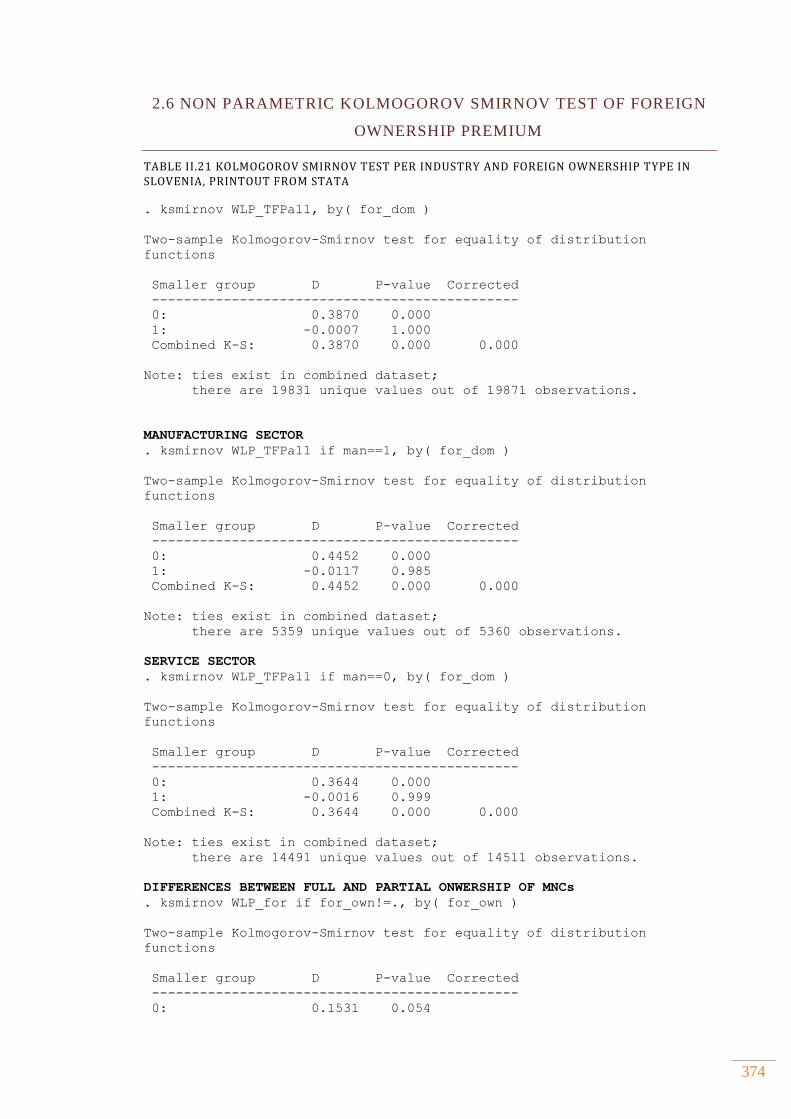

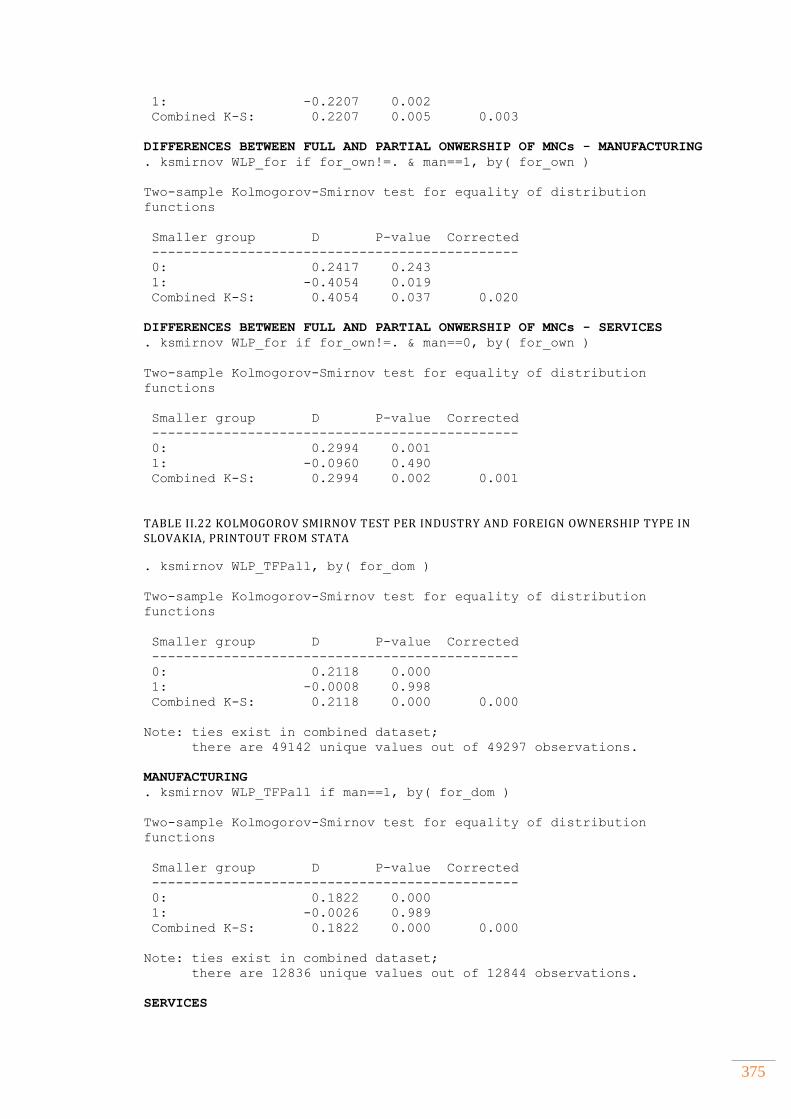

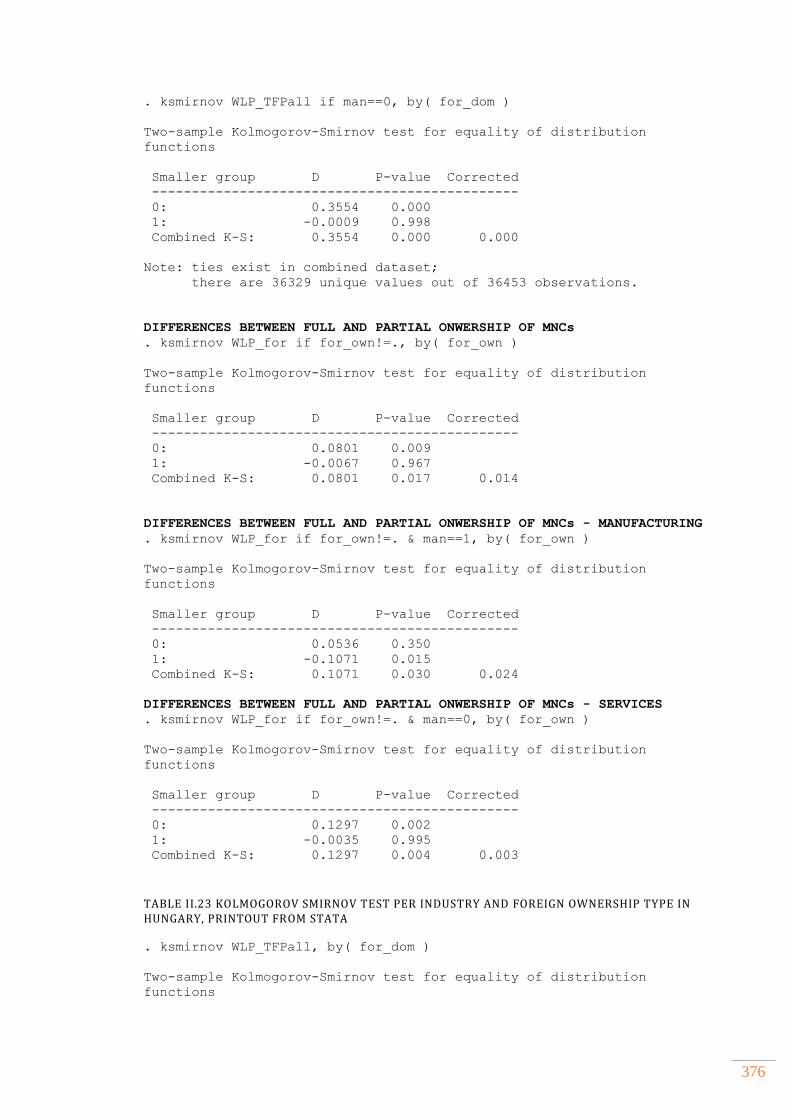

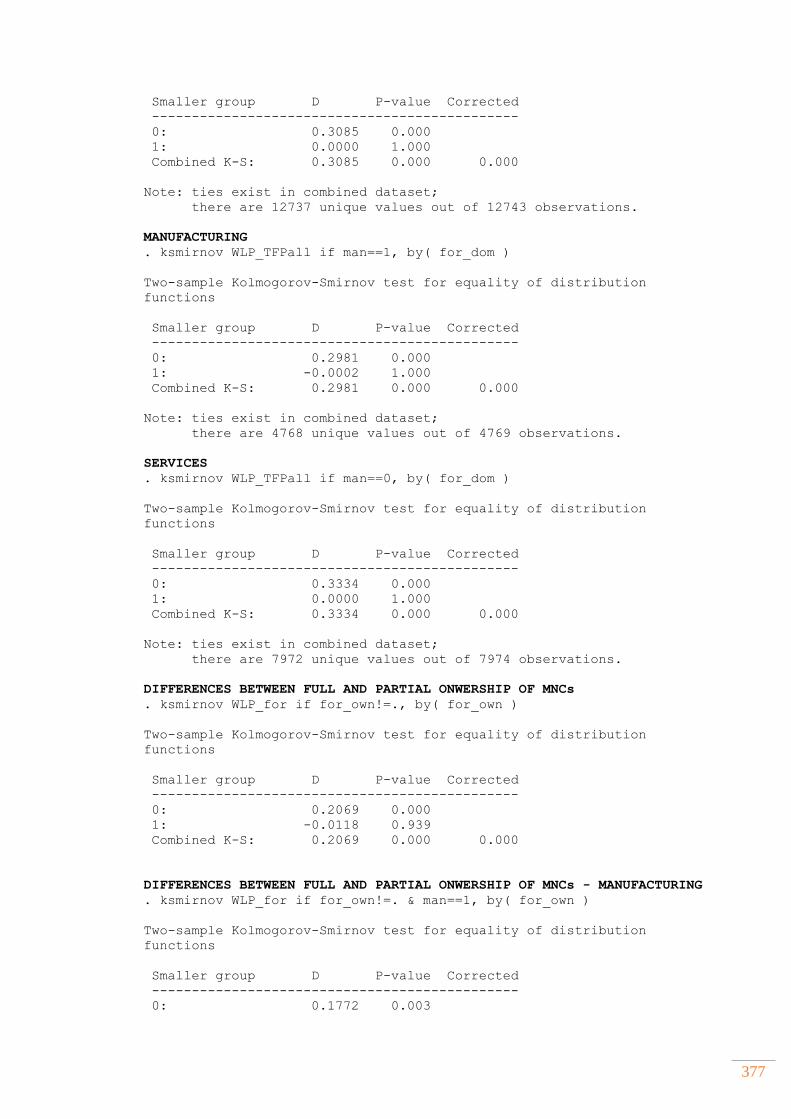

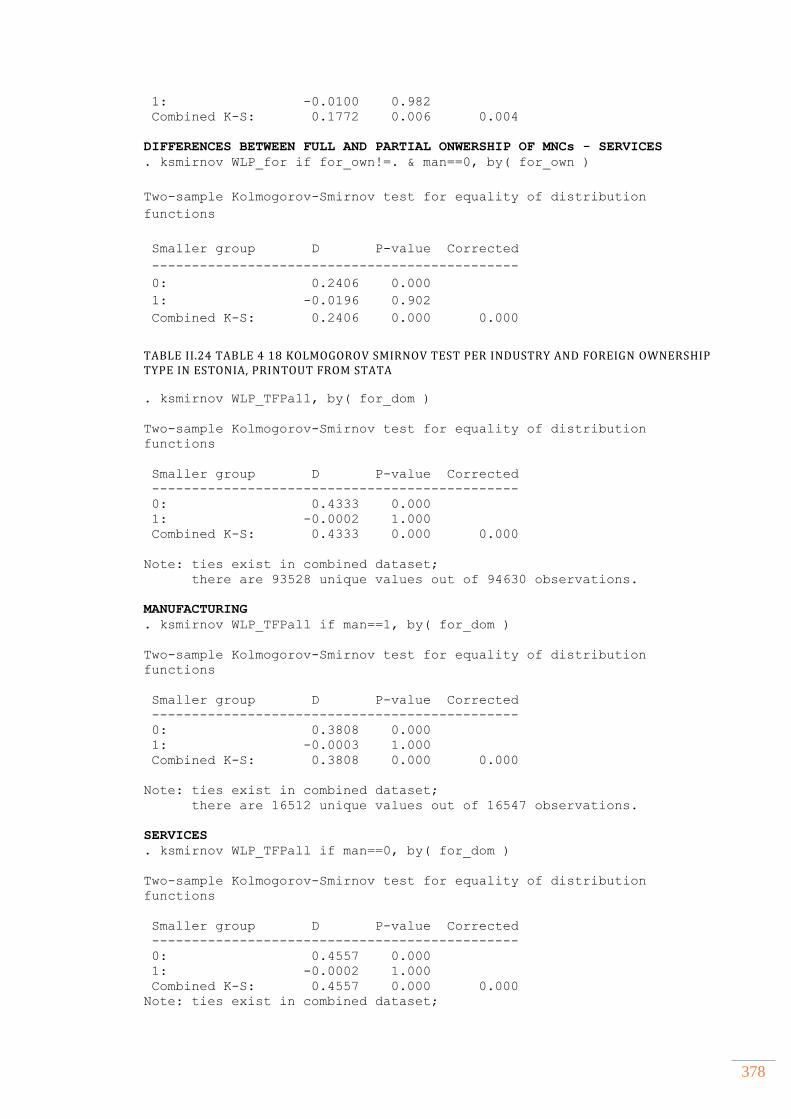

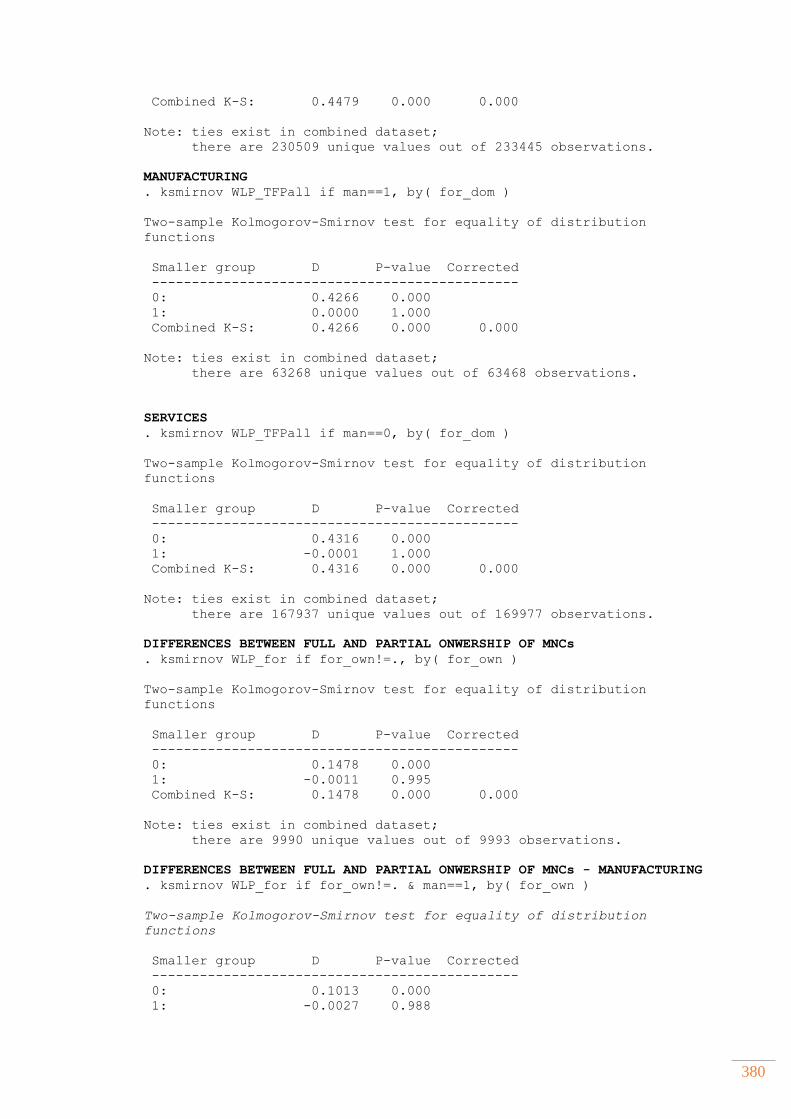

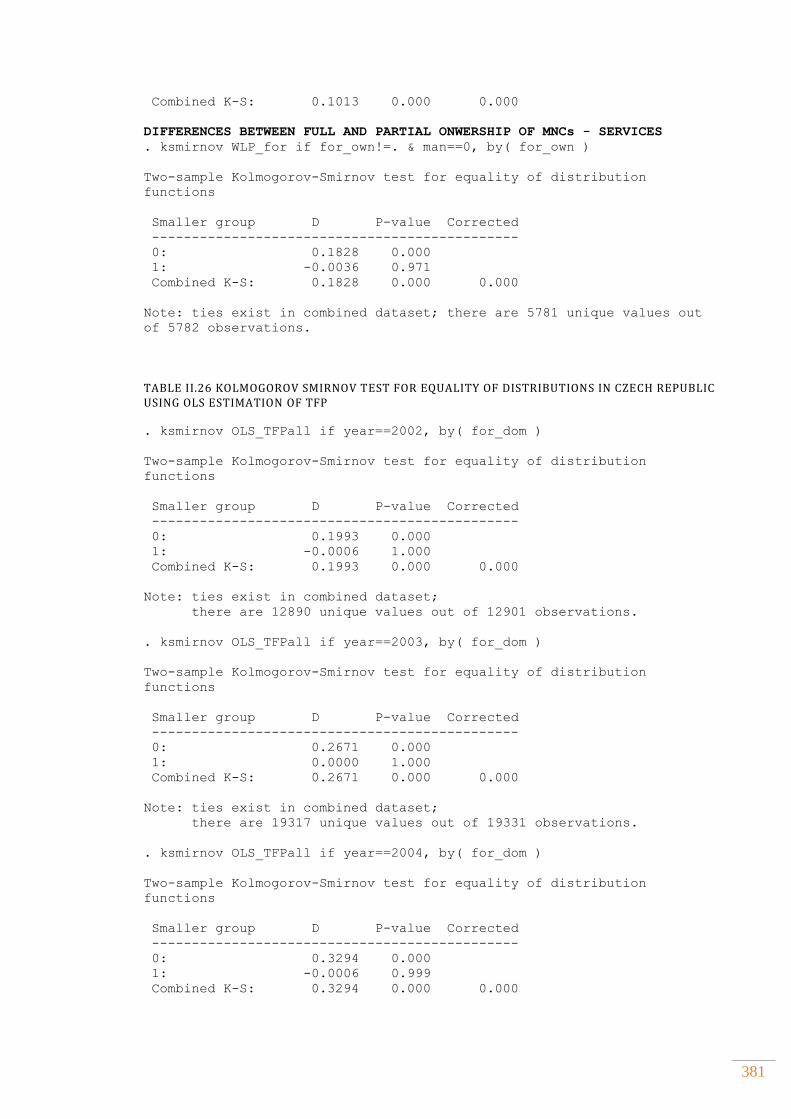

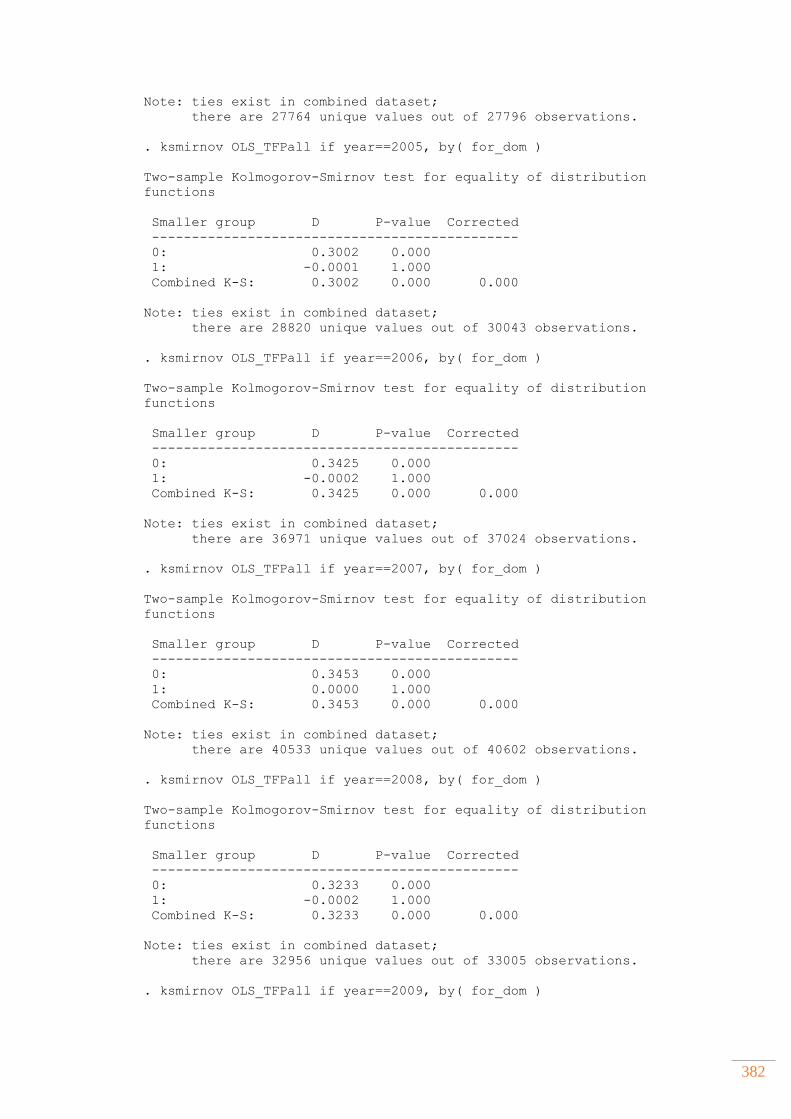

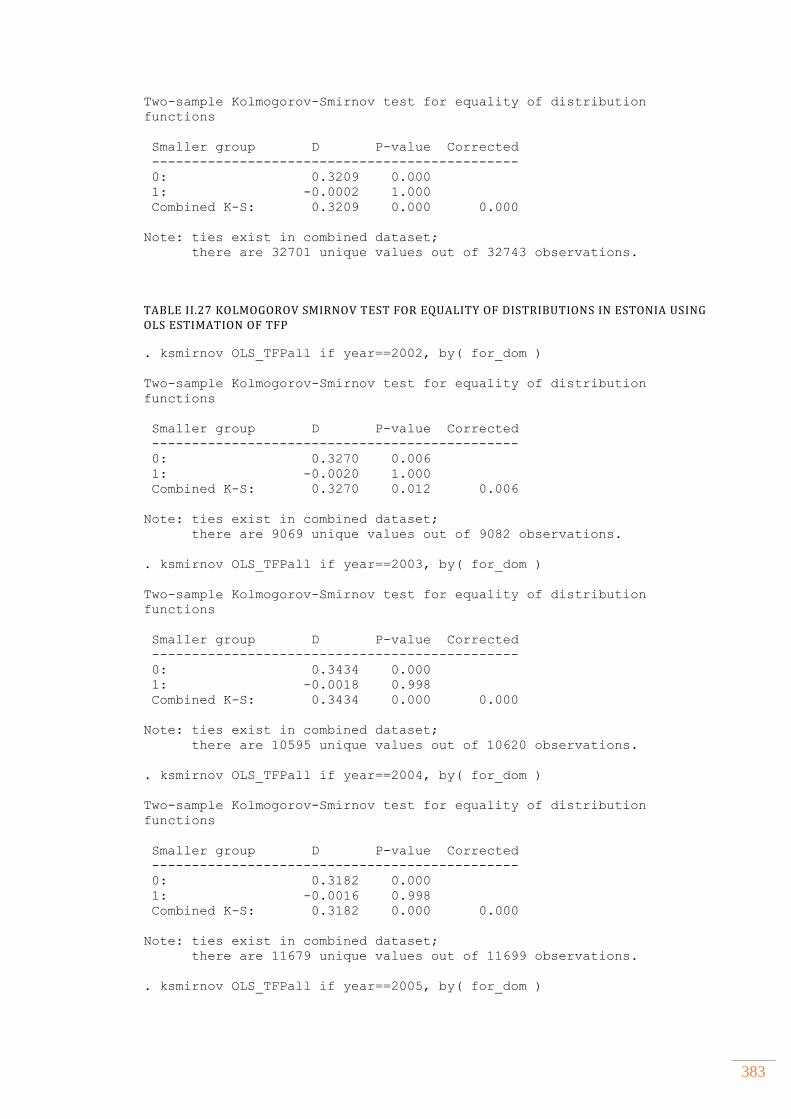

Table II.1 NUMBER OF OBSERVATIONS AFTER CLEANING STEPS .......................................... 354 Table II.2 DISTRIBUTION OF FOREIGN FIRMS ACROSS TECHNOLOGY AND KNOWLEDGE INTENSIVE INDUSTRIES BY COUNTRY ................................................................................................. 357 Table II.3 IN SAMPLE DATA COVERAGE OF FIRMS ......................................................................... 360 Table II.4 DESCRIPTIVE STATISTICS OF PRODUCTION FUNCTION VARIABLES USED IN TFP ESTIMATION OF DOMESTIC FIRMS .............................................................................................. 361 Table II.5 ESTIMATION OF VALUE ADDED PRODUCTION FUNCTION BY INDUSTRIES USING WOOLDRIDGE ESTIMATOR (2009), LEVINSOHN-PETRIN ESTIMATOR (2003) AND OLS IN CZECH REPUBLIC ............................................................................................................................ 362 Table II.6 ESTIMATION OF VALUE ADDED PRODUCTION FUNCTION BY INDUSTRIES USING WOOLDRIDGE ESTIMATOR (2009), LEVINSOHN-PETRIN ESTIMATOR (2003) AND OLS IN ESTONIA .............................................................................................................................................. 363 Table II.7 ESTIMATION OF VALUE ADDED PRODUCTION FUNCTION BY INDUSTRIES USING WOOLDRIDGE ESTIMATOR (2009), LEVINSOHN-PETRIN ESTIMATOR (2003) AND OLS IN HUNGARY ........................................................................................................................................... 364 Table II.8 ESTIMATION OF VALUE ADDED PRODUCTION FUNCTION BY INDUSTRIES USING WOOLDRIDGE ESTIMATOR (2009), LEVINSOHN-PETRIN ESTIMATOR (2003) AND OLS IN SLOVAKIA ........................................................................................................................................... 365 Table II.9 ESTIMATION OF VALUE ADDED PRODUCTION FUNCTION BY INDUSTRIES USING WOOLDRIDGE ESTIMATOR (2009), LEVINSOHN-PETRIN ESTIMATOR (2003) AND OLS IN SLOVENIA ........................................................................................................................................... 366 Table II.10 DIAGNOSTICS TESTS FOR WLP ESTIMATOR .............................................................. 367 Table II.11 CORRELATION MATRICES OF TFP ESTIMATION ALGORITHMS IN CZECH REPUBLIC........................................................................................................................................................... 368 Table II.12 CORRELATION MATRICES OF TFP ESTIMATION ALGORITHMS IN ESTONIA ................................................................................................................................................................................ 368 Table II.13 CORRELATION MATRICES OF TFP ESTIMATION ALGORITHMS IN HUNGARY ................................................................................................................................................................................ 369 Table II.14 CORRELATION MATRICES OF TFP ESTIMATION ALGORITHMS IN SLOVAKIA ................................................................................................................................................................................ 370 Table II.15 CORRELATION MATRICES OF TFP ESTIMATION ALGORITHMS IN SLOVENIA ................................................................................................................................................................................ 370 Table II.16 TRANSITION MATRICES OF INTER-QUARTILE MOVEMENTS IN TFP DISTRIBUTION OF LOCAL FIRMS IN CZECH REPUBLIC ................................................................ 371 Table II.17 TRANSITION MATRICES OF INTER-QUARTILE MOVEMENTS IN TFP DISTRIBUTION OF LOCAL FIRMS IN ESTONIA .................................................................................. 371 Table II.18 TRANSITION MATRICES OF INTER-QUARTILE MOVEMENTS IN TFP DISTRIBUTION OF LOCAL FIRMS IN HUNGARY ................................................................................ 372 Table II.19 TRANSITION MATRICES OF INTER-QUARTILE MOVEMENTS IN TFP DISTRIBUTION OF LOCAL FIRMS IN SLOVAKIA ............................................................................... 372 Table II.20 TRANSITION MATRICES OF INTER-QUARTILE MOVEMENTS IN TFP DISTRIBUTION OF LOCAL FIRMS IN SLOVENIA ............................................................................... 373 Table II.21 KOLMOGOROV SMIRNOV TEST PER INDUSTRY AND FOREIGN OWNERSHIP TYPE IN SLOVENIA, PRINTOUT FROM STATA ................................................................................... 374 Table II.22 KOLMOGOROV SMIRNOV TEST PER INDUSTRY AND FOREIGN OWNERSHIP TYPE IN SLOVAKIA, PRINTOUT FROM STATA ................................................................................... 375 Table II.23 KOLMOGOROV SMIRNOV TEST PER INDUSTRY AND FOREIGN OWNERSHIP TYPE IN HUNGARY, PRINTOUT FROM STATA ................................................................................... 376 Table II.24 TABLE 4 18 KOLMOGOROV SMIRNOV TEST PER INDUSTRY AND FOREIGN OWNERSHIP TYPE IN ESTONIA, PRINTOUT FROM STATA .......................................................... 378

ix

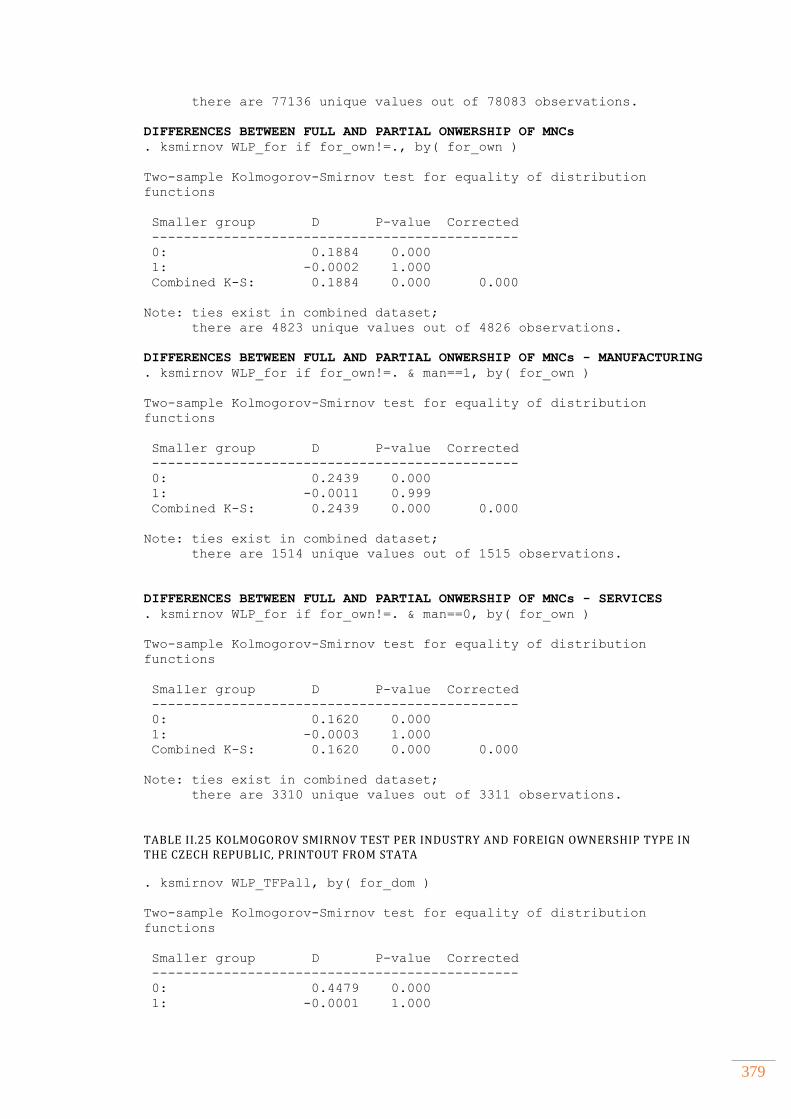

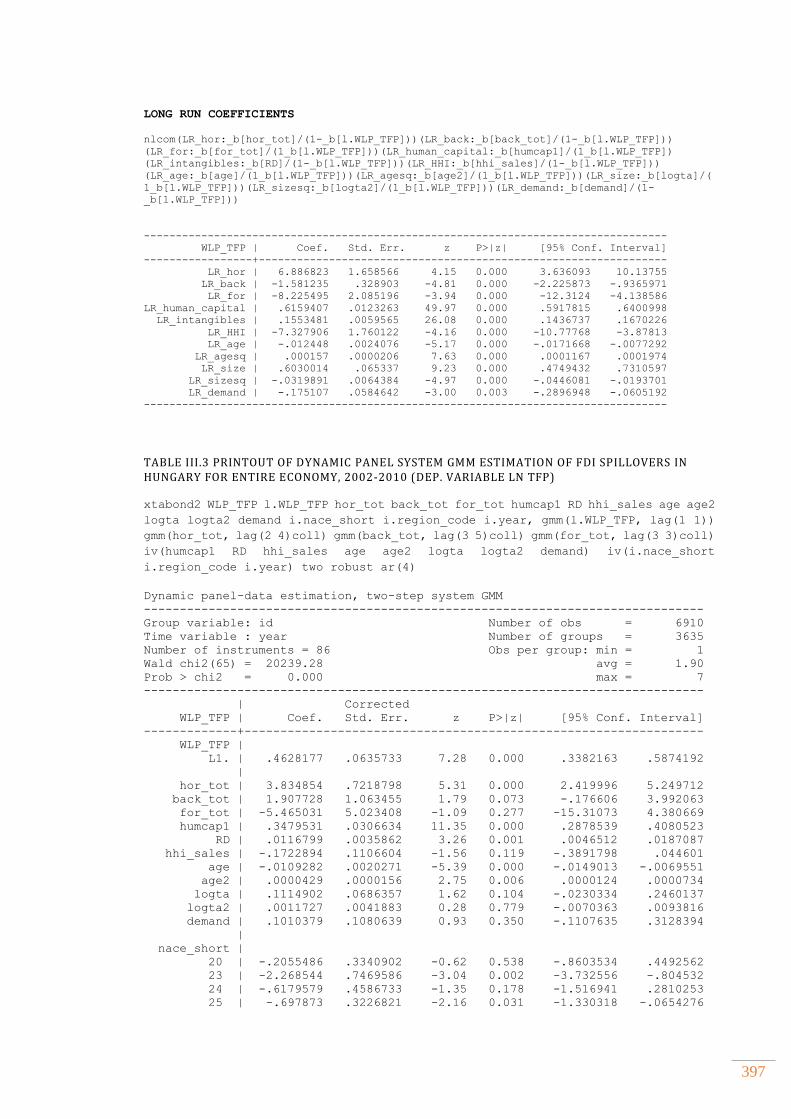

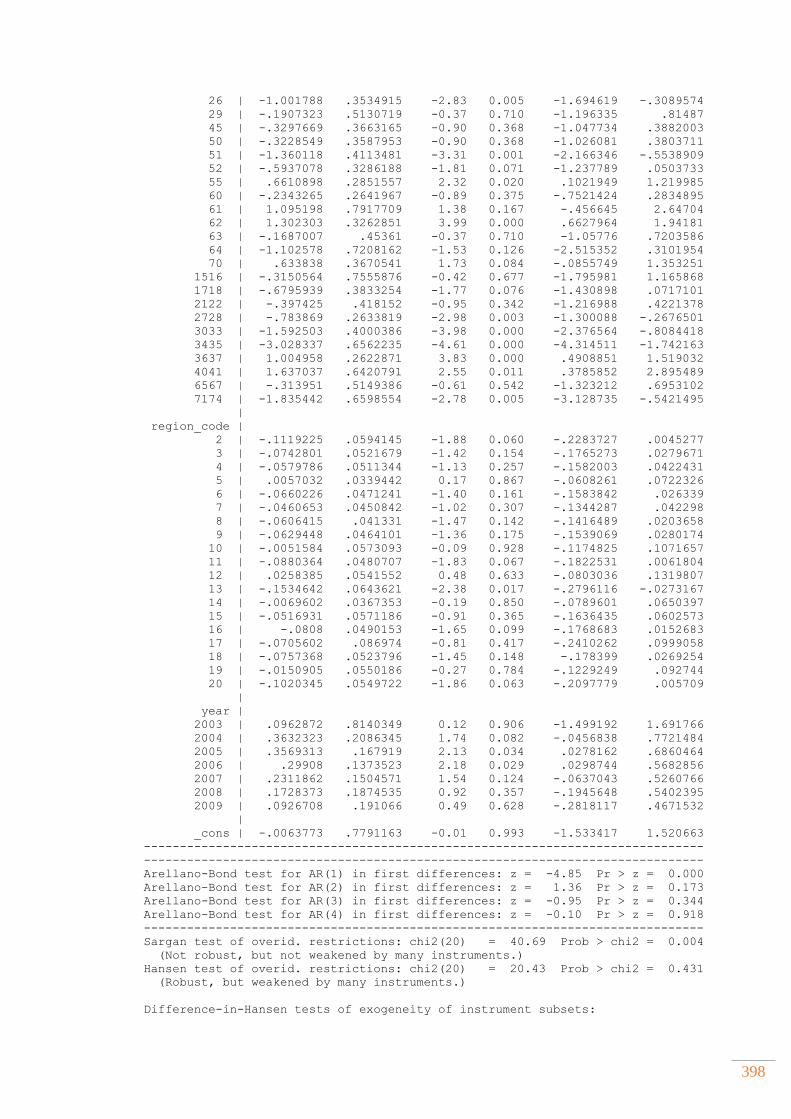

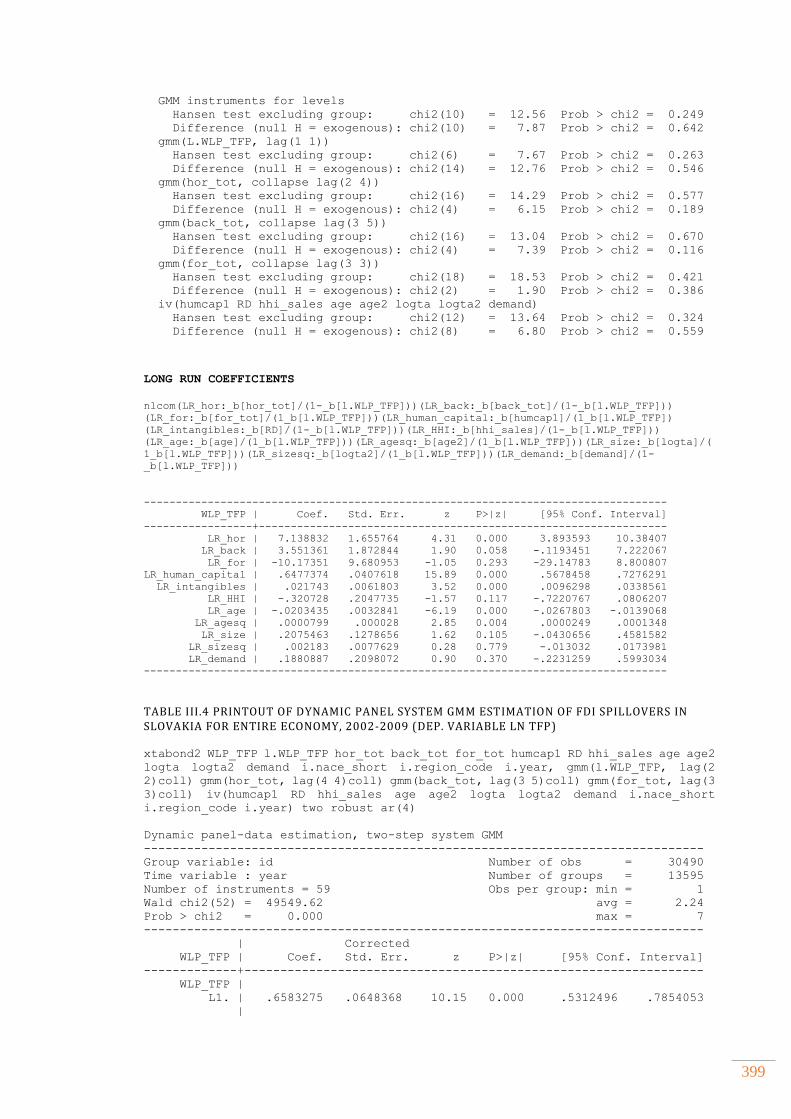

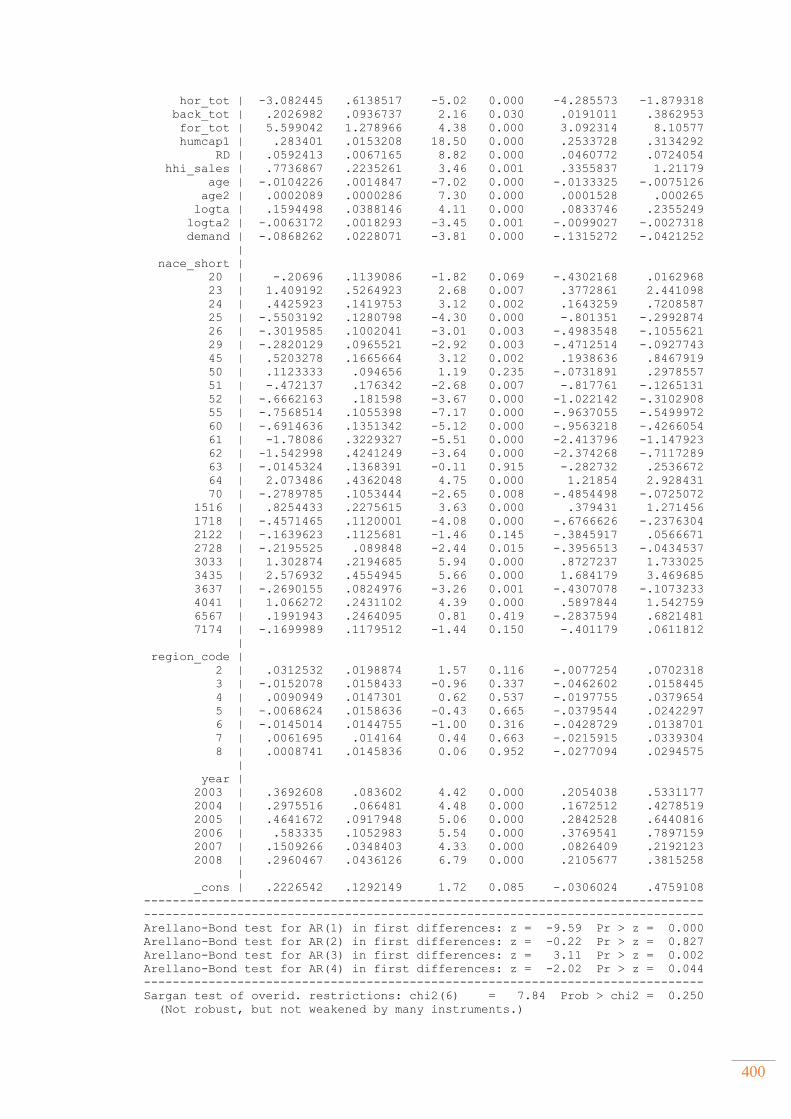

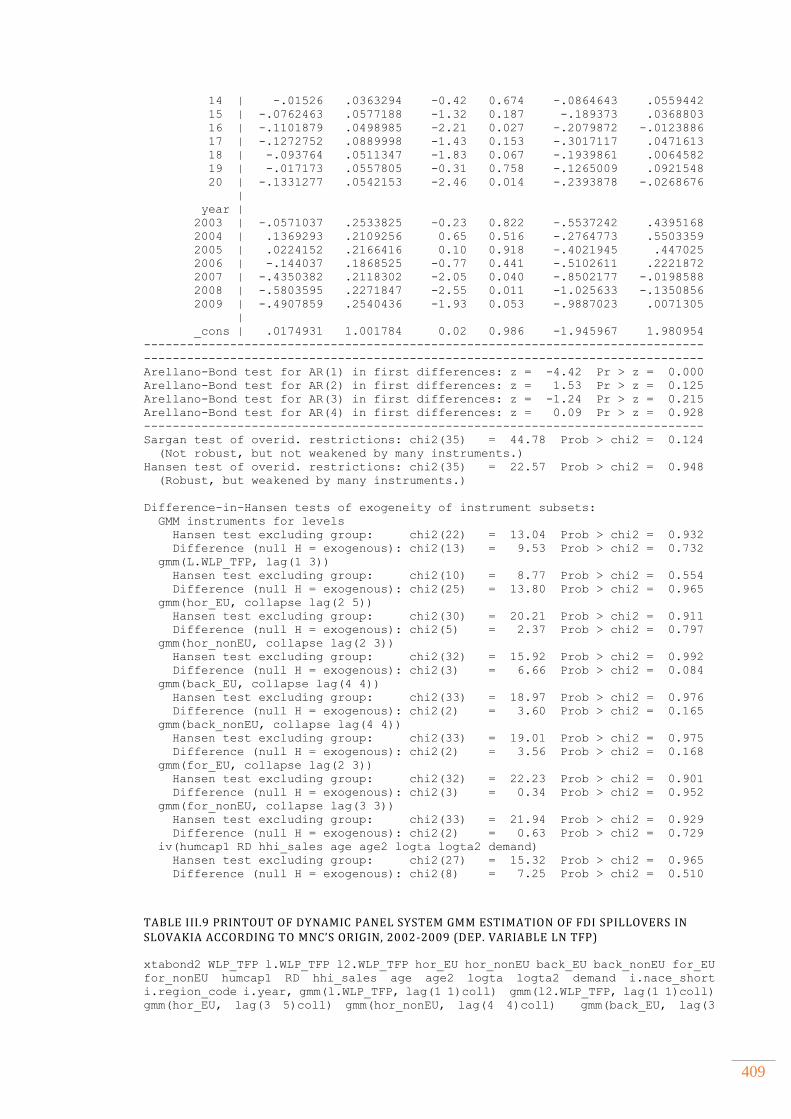

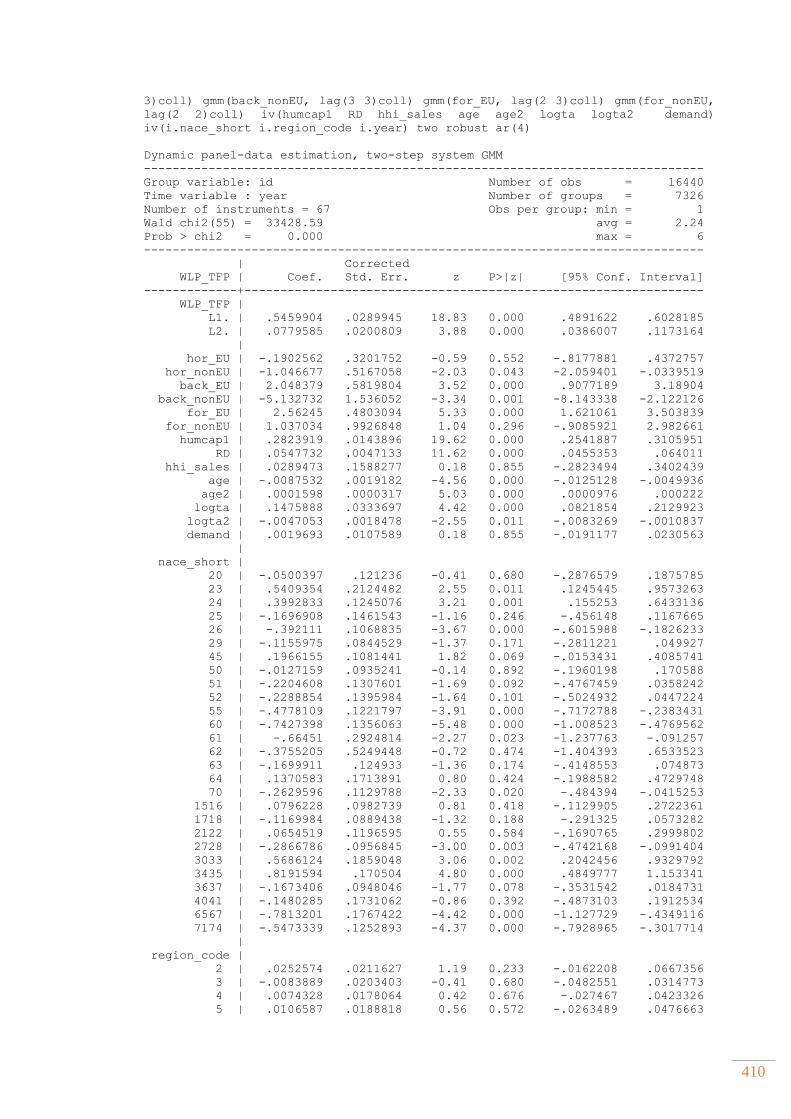

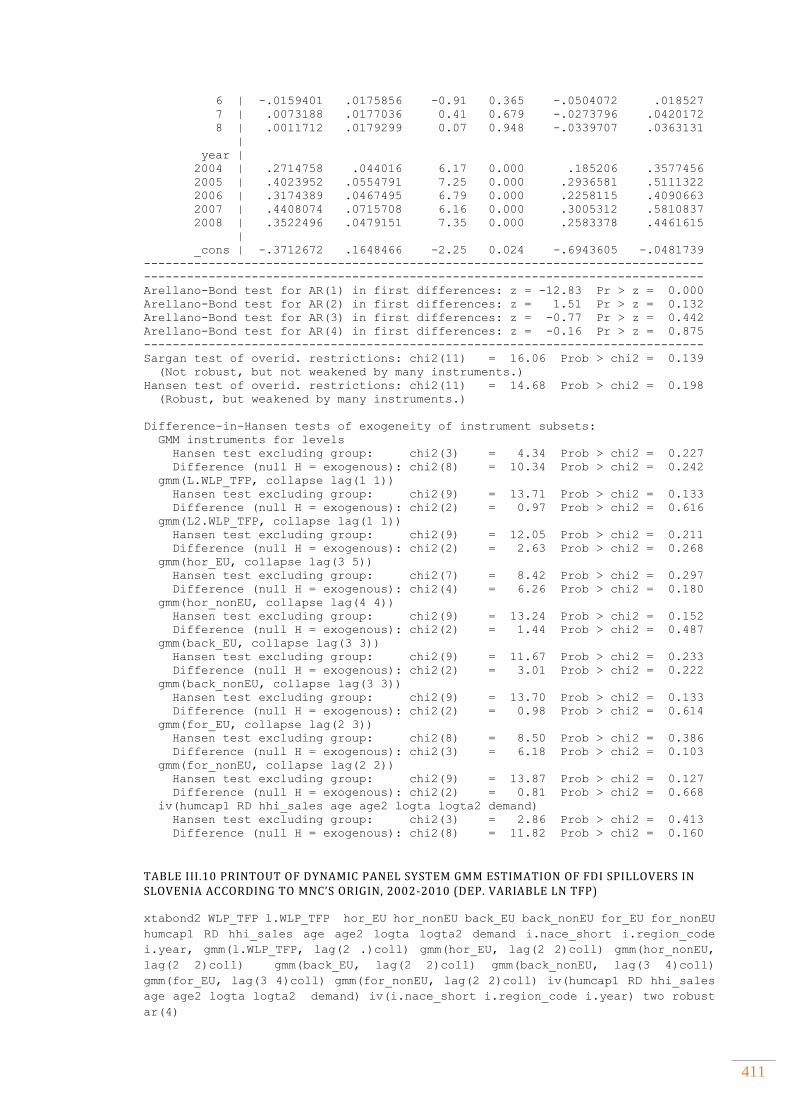

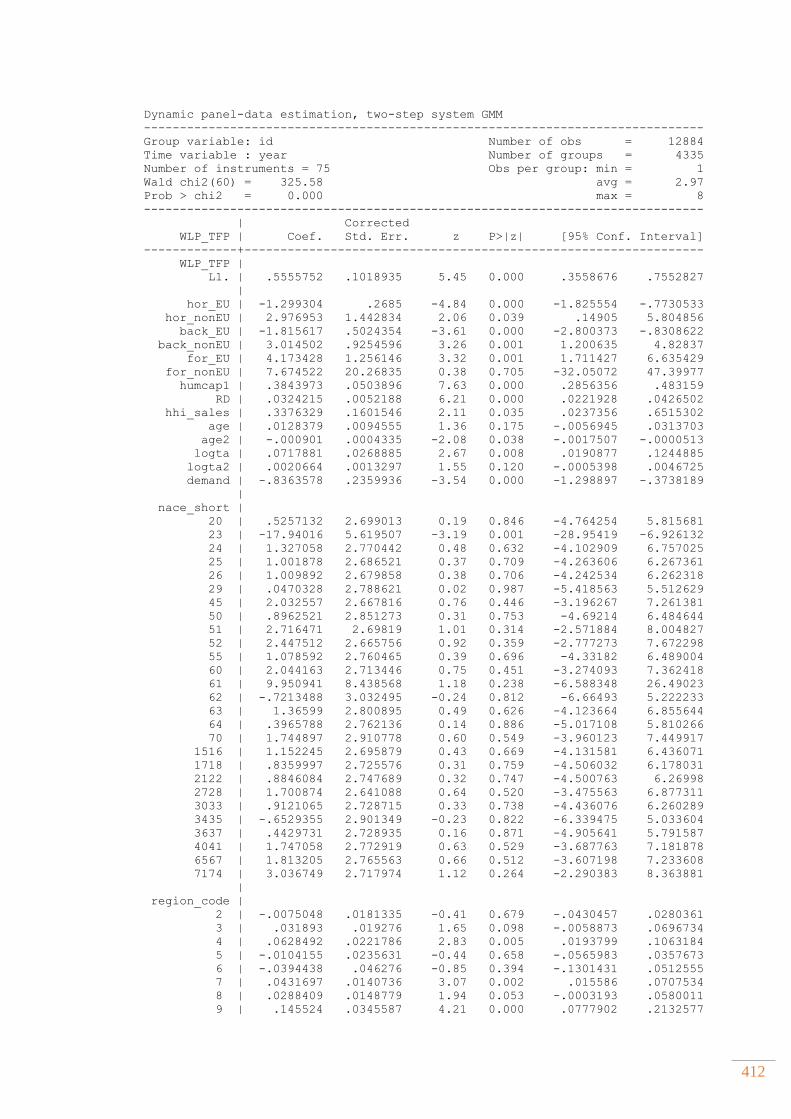

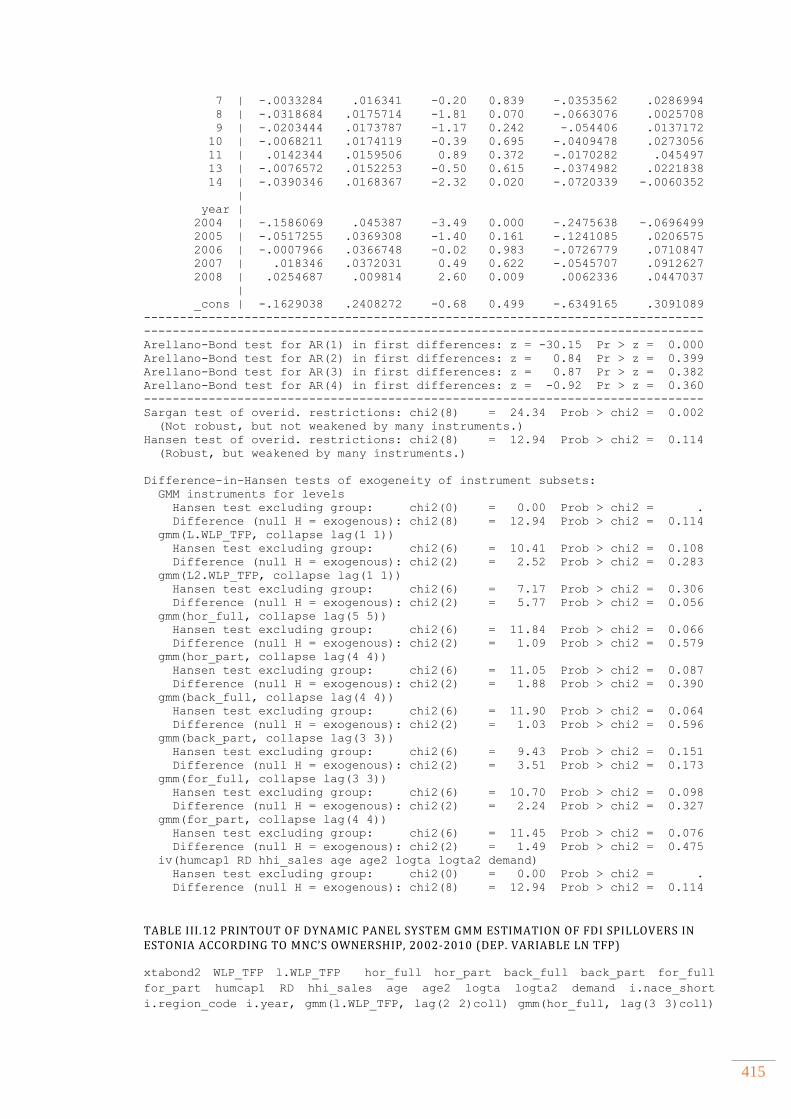

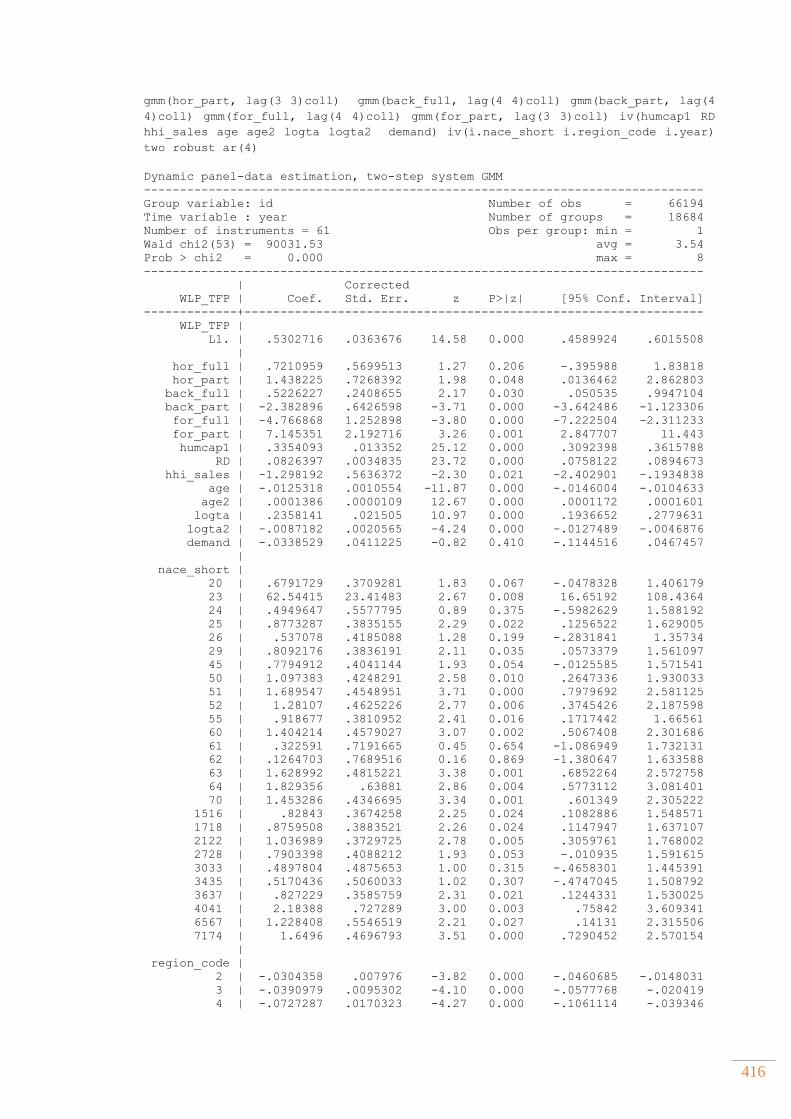

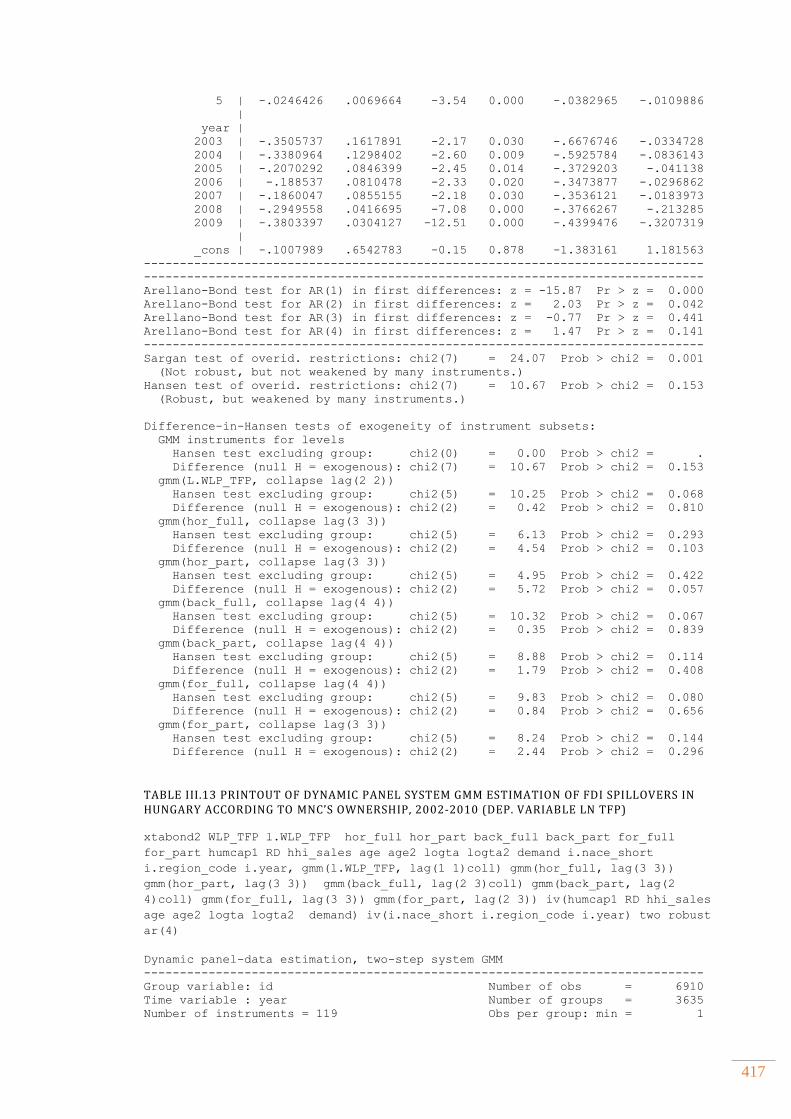

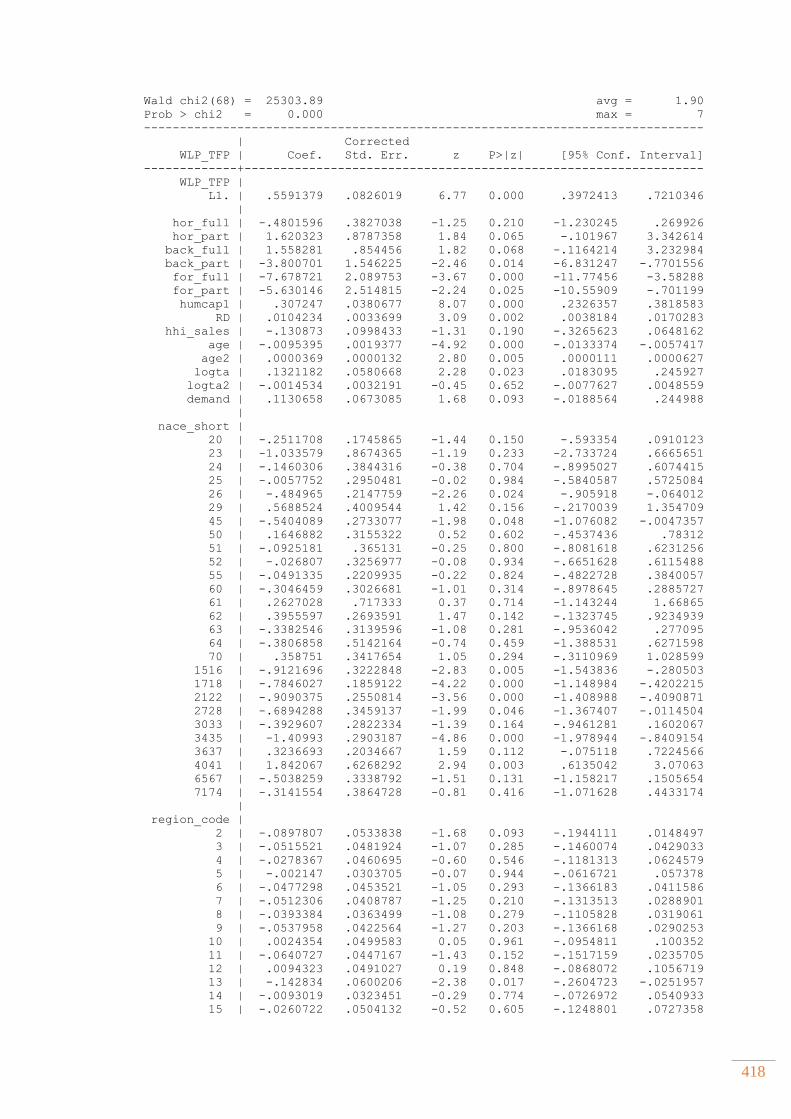

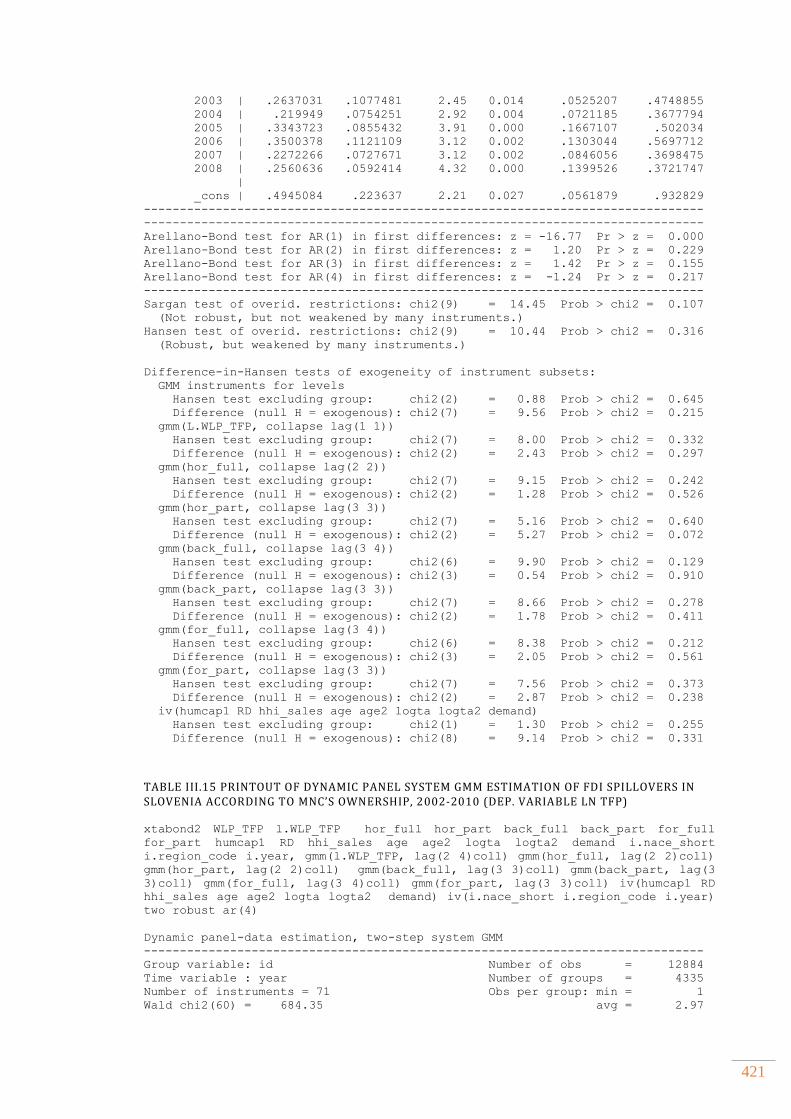

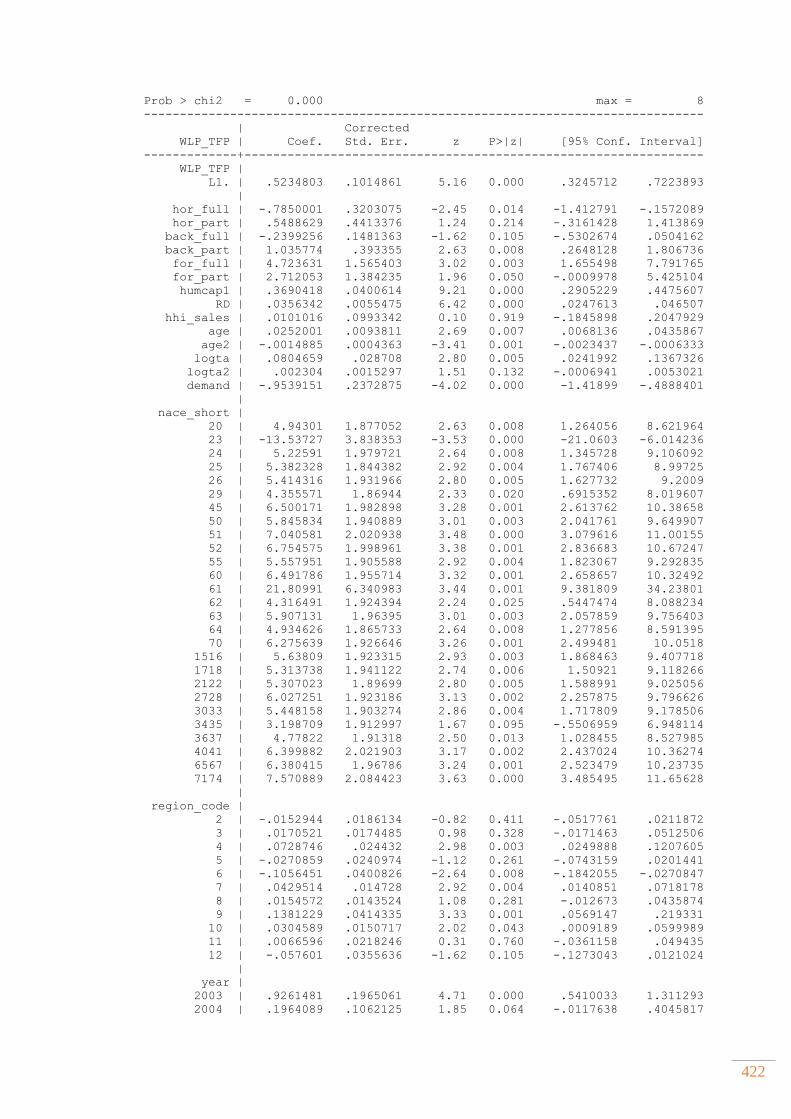

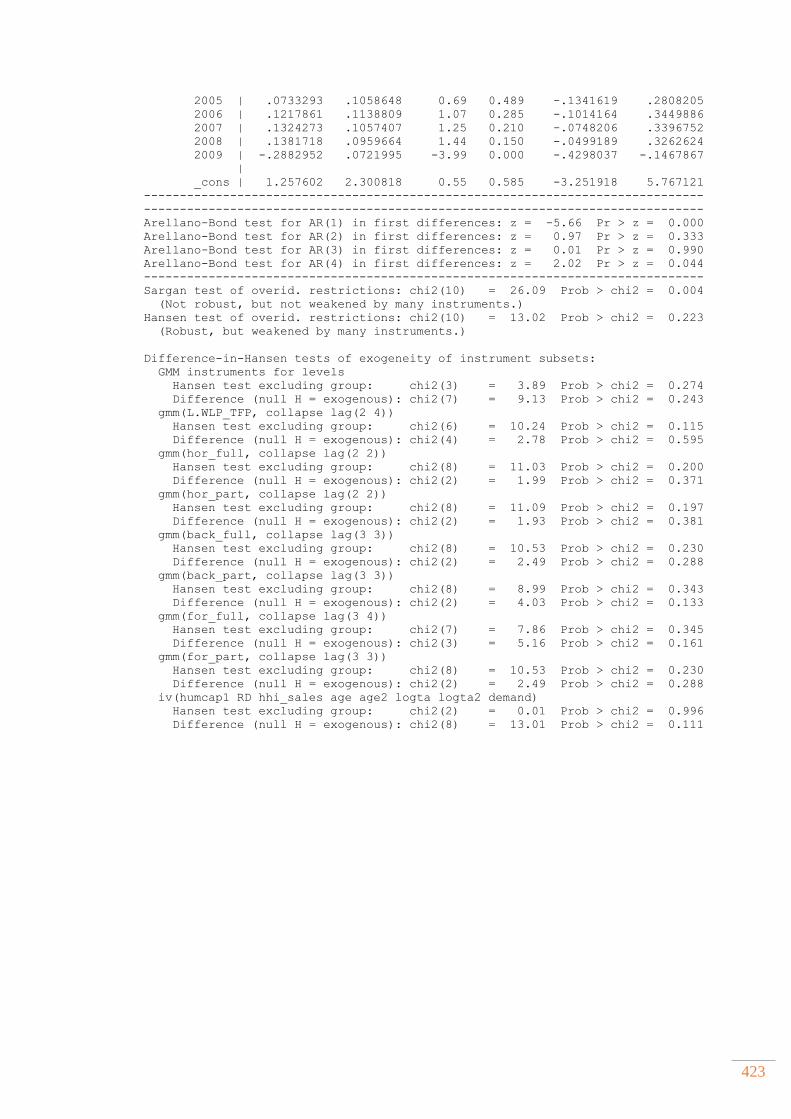

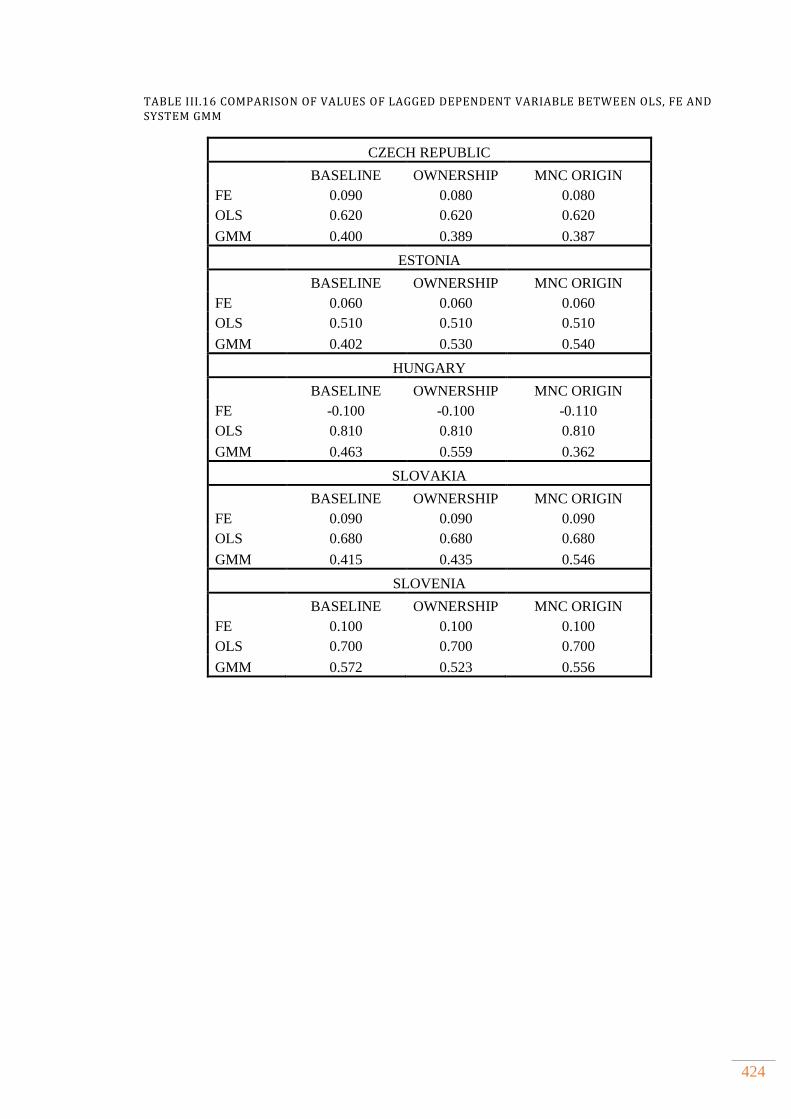

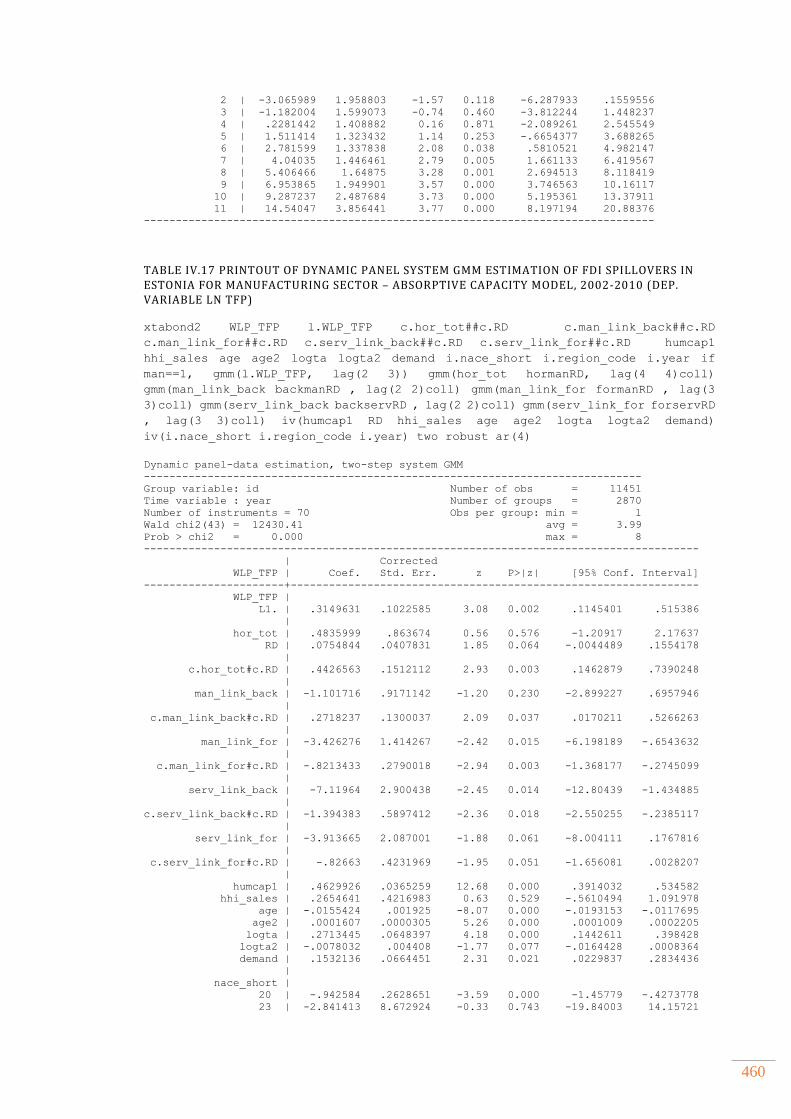

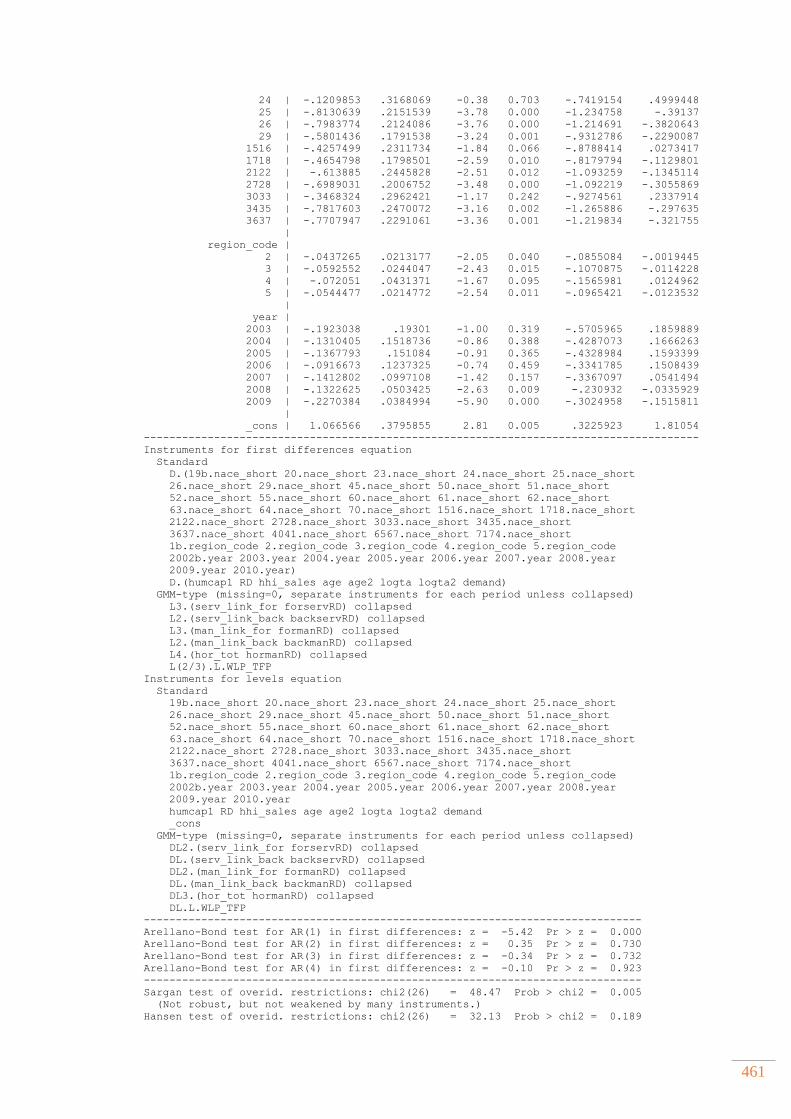

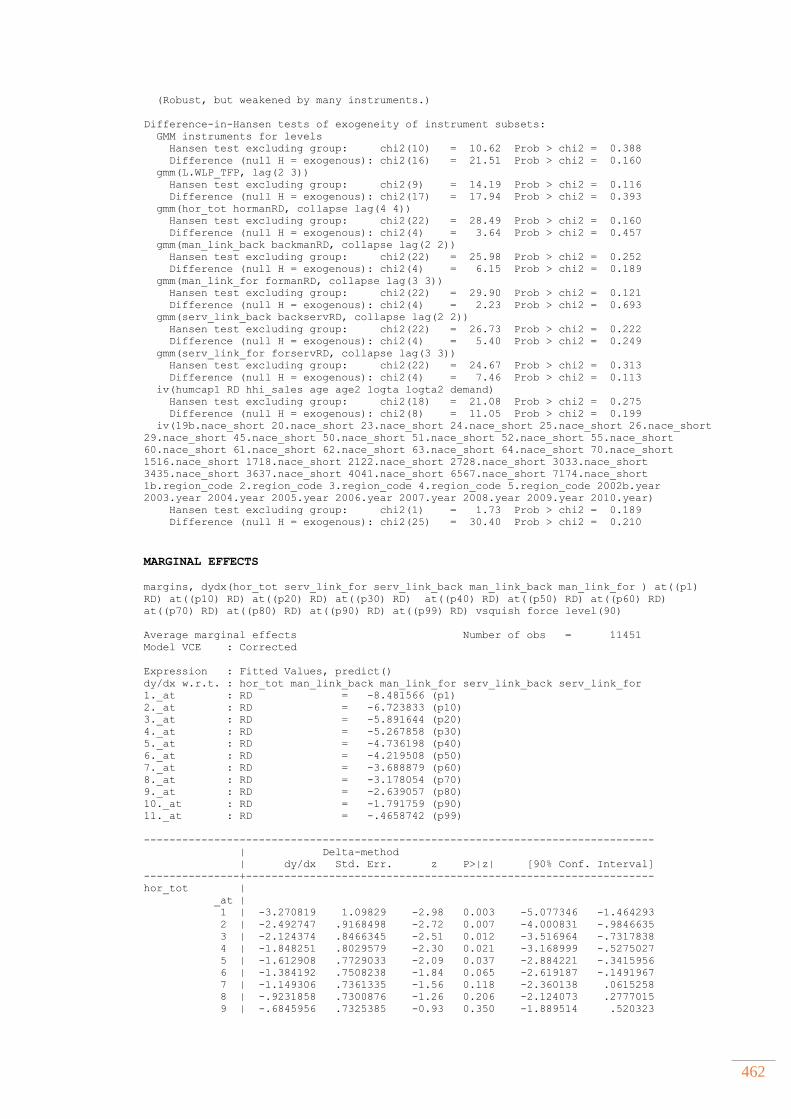

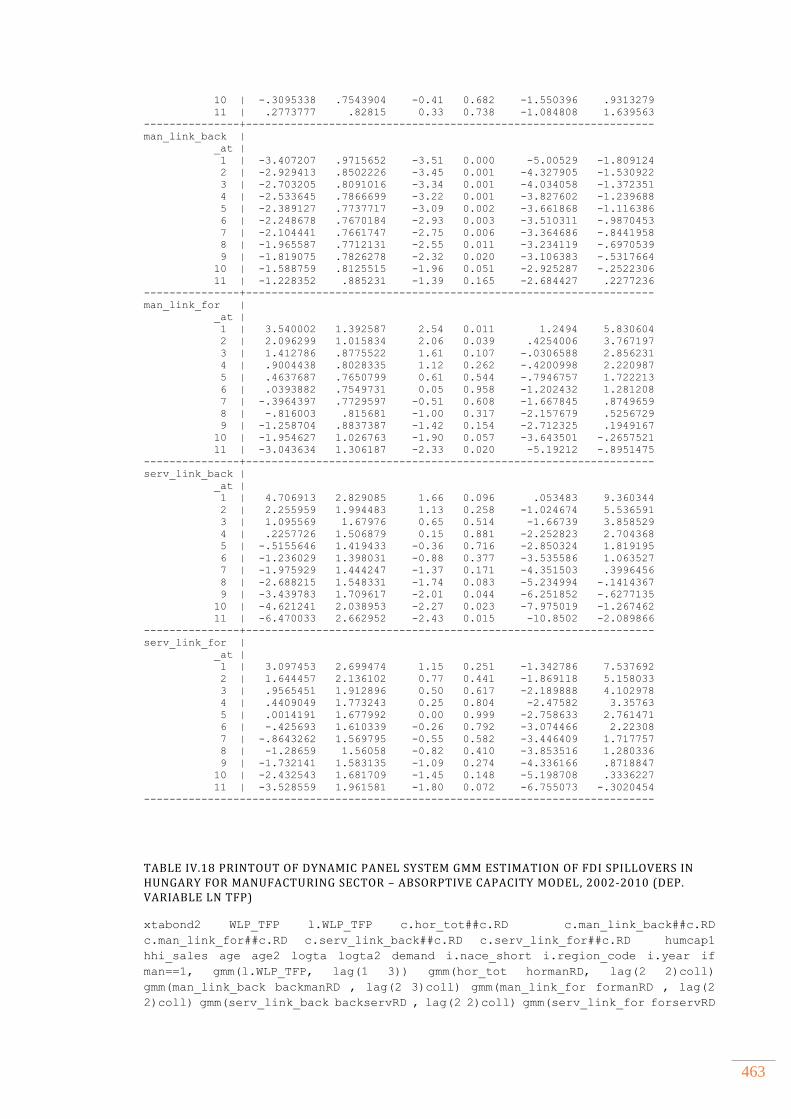

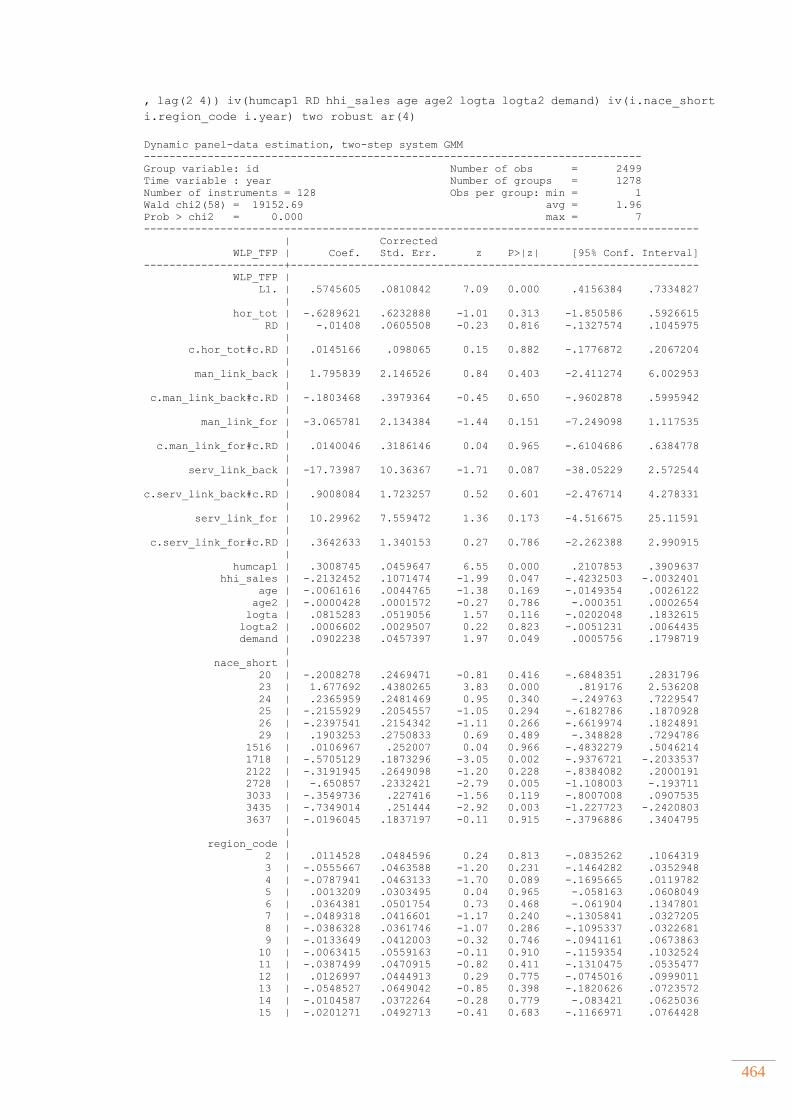

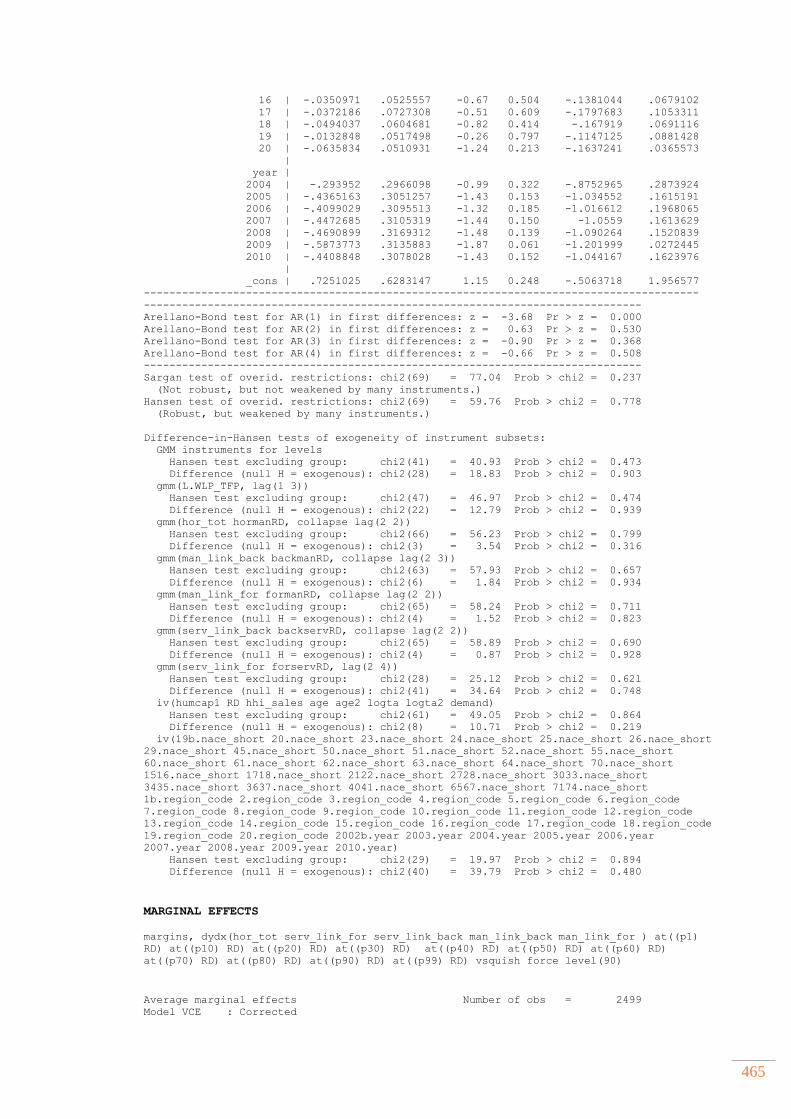

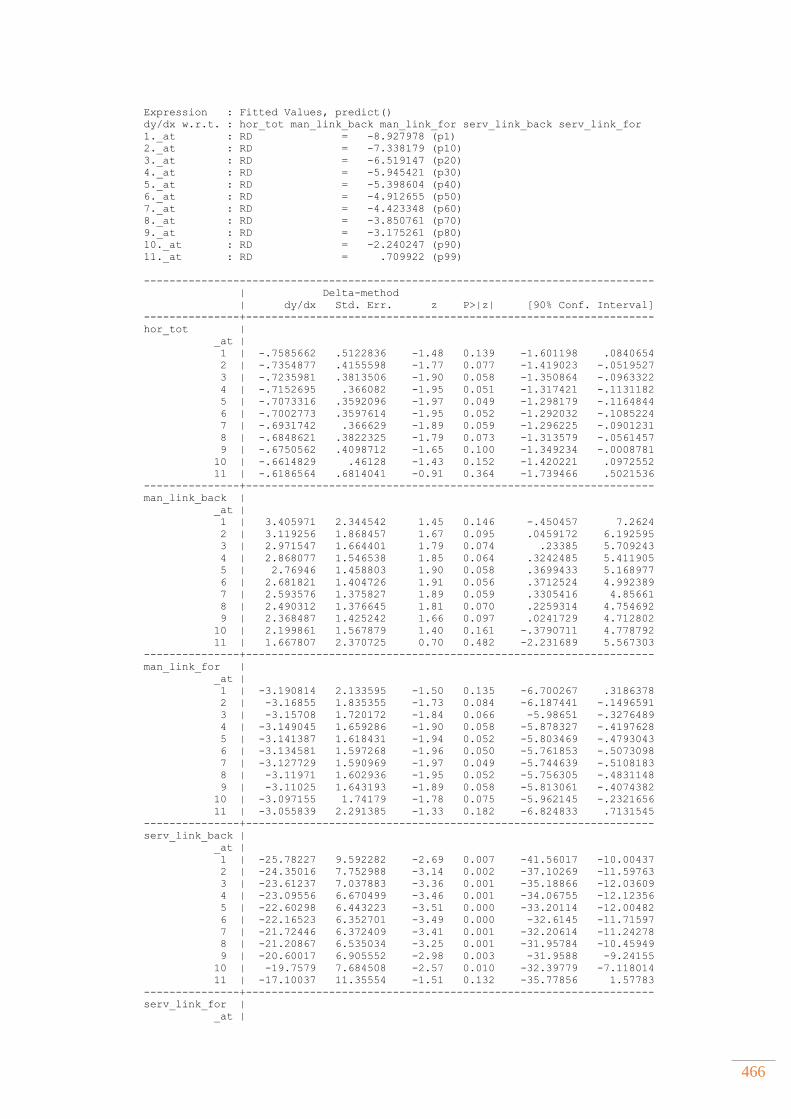

Table II.25 KOLMOGOROV SMIRNOV TEST PER INDUSTRY AND FOREIGN OWNERSHIP TYPE IN THE CZECH REPUBLIC, PRINTOUT FROM STATA .......................................................... 379 Table II.26 KOLMOGOROV SMIRNOV TEST FOR EQUALITY OF DISTRIBUTIONS IN CZECH REPUBLIC USING OLS ESTIMATION OF TFP ...................................................................................... 381 Table II.27 KOLMOGOROV SMIRNOV TEST FOR EQUALITY OF DISTRIBUTIONS IN ESTONIA USING OLS ESTIMATION OF TFP ......................................................................................... 383 Table II.28 KOLMOGOROV SMIRNOV TEST FOR EQUALITY OF DISTRIBUTIONS IN HUNGARY USING OLS ESTIMATION OF TFP....................................................................................... 385 Table II.29 KOLMOGOROV SMIRNOV TEST FOR EQUALITY OF DISTRIBUTIONS IN SLOVAKIA USING OLS ESTIMATION OF TFP ...................................................................................... 386 Table II.30 KOLMOGOROV SMIRNOV TEST FOR EQUALITY OF DISTRIBUTIONS IN SLOVENIA USING OLS ESTIMATION OF TFP ...................................................................................... 388 Table III.1 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN THE CZECH REPUBLIC FOR ENTIRE ECONOMY, 2002-2009 (DEP. VARIABLE LN TFP) ........................................................................................................................................ 392 Table III.2 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN ESTONIA FOR ENTIRE ECONOMY, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................................................................................................................ 394 Table III.3 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN HUNGARY FOR ENTIRE ECONOMY, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................................................................................................................ 397 Table III.4 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVAKIA FOR ENTIRE ECONOMY, 2002-2009 (DEP. VARIABLE LN TFP) ................................................................................................................................................................................ 399 Table III.5 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVENIA FOR ENTIRE ECONOMY, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................................................................................................................ 401 Table III.6 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN THE CZECH REPUBLIC ACCORDING TO MNC’S ORIGIN, 2002-2009 (DEP. VARIABLE TFP) ............................................................................................................................................... 403 Table III.7 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN ESTONIA ACCORDING TO MNC’S ORIGIN, 2002-2010 (DEP. VARIABLE LN TFP) ...................................................................................................................................................................... 405 Table III.8 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN HUNGARY ACCORDING TO MNC’S ORIGIN, 2002-2010 (DEP. VARIABLE LN TFP) ............................................................................................................................................................... 407 Table III.9 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVAKIA ACCORDING TO MNC’S ORIGIN, 2002-2009 (DEP. VARIABLE LN TFP) ............................................................................................................................................................... 409 Table III.10 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVENIA ACCORDING TO MNC’S ORIGIN, 2002-2010 (DEP. VARIABLE LN TFP) ............................................................................................................................................................... 411 Table III.11 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN THE CZECH REPUBLIC ACCORDING TO MNC’S OWNERSHIP, 2002-2009 (DEP. VARIABLE LN TFP) ............................................................................................................................ 413 Table III.12 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN ESTONIA ACCORDING TO MNC’S OWNERSHIP, 2002-2010 (DEP. VARIABLE LN TFP) ........................................................................................................................................ 415 Table III.13 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN HUNGARY ACCORDING TO MNC’S OWNERSHIP, 2002-2010 (DEP. VARIABLE LN TFP) ........................................................................................................................................ 417

x

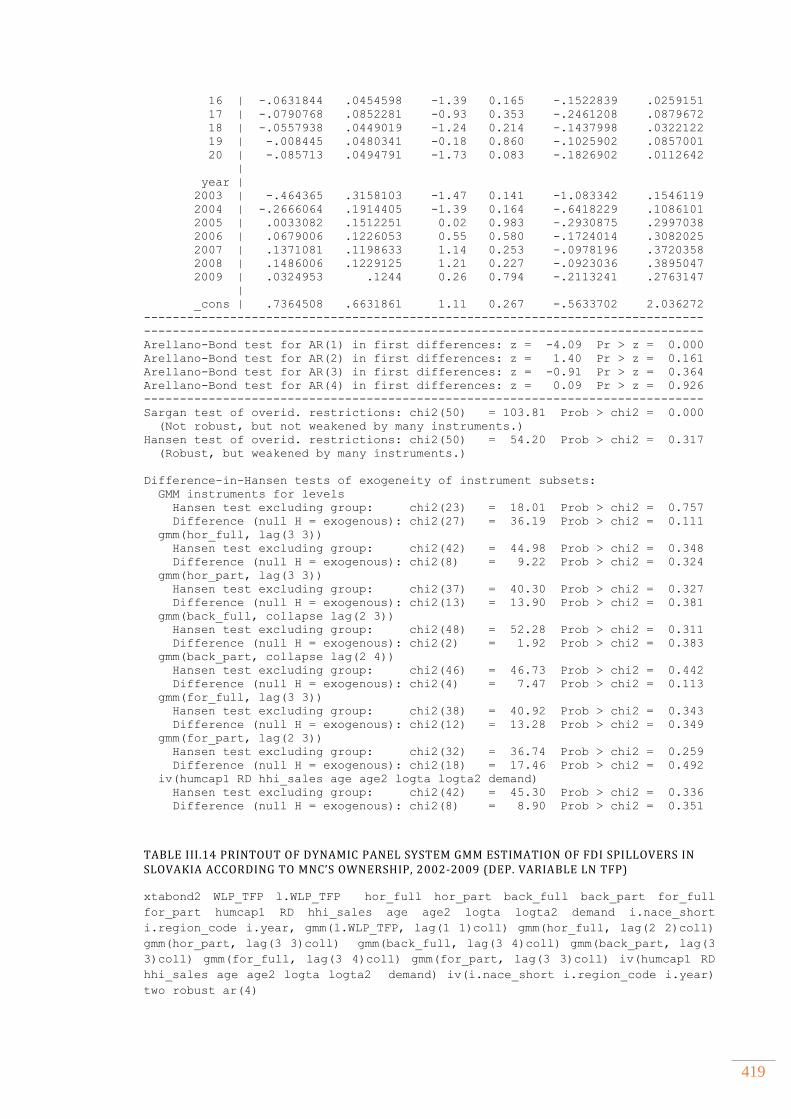

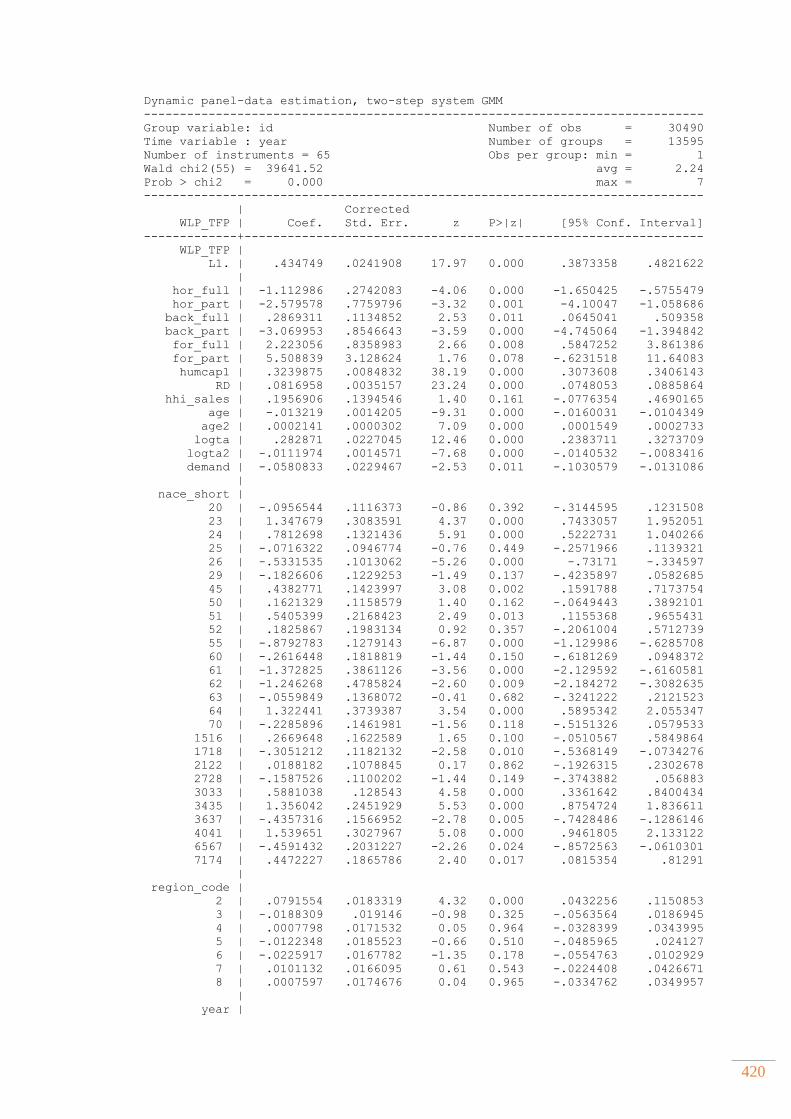

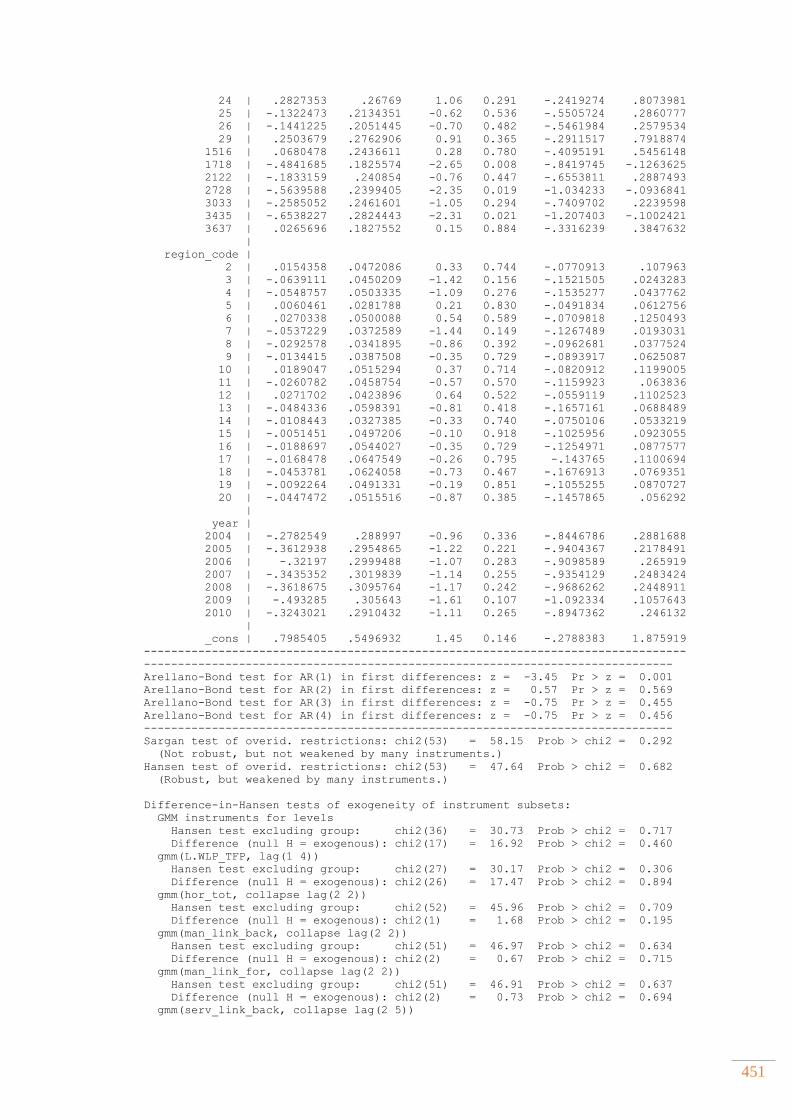

Table III.14 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVAKIA ACCORDING TO MNC’S OWNERSHIP, 2002-2009 (DEP. VARIABLE LN TFP) ........................................................................................................................................ 419 Table III.15 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVENIA ACCORDING TO MNC’S OWNERSHIP, 2002-2010 (DEP. VARIABLE LN TFP) ........................................................................................................................................ 421 Table III.16 COMPARISON OF VALUES OF LAGGED DEPENDENT VARIABLE BETWEEN OLS, FE AND SYSTEM GMM ........................................................................................................................ 424 Table IV.1 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN THE CZECH REPUBLIC FOR MANUFACTURING SECTOR, 2002-2009 (DEP. VARIABLE LN TFP) ........................................................................................................................................ 427 Table IV.2 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN ESTONIA FOR MANUFACTURING SECTOR, 2002-2010 (DEP. VARIABLE LN TFP) ............................................................................................................................................................... 428 Table IV.3 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN HUNGARY FOR MANUFACTURING SECTOR, 2002-2010 (DEP. VARIABLE LN TFP) ............................................................................................................................................................... 430 Table IV.4 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVAKIA FOR MANUFACTURING SECTOR, 2002-2009 (DEP. VARIABLE LN TFP) ............................................................................................................................................................... 432 Table IV.5 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVENIA FOR MANUFACTURING SECTOR, 2002-2010 (DEP. VARIABLE LN TFP) ............................................................................................................................................................... 434 Table IV.6 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN THE CZECH REPUBLIC FOR SERVICES SECTOR, 2002-2009 (DEP. VARIABLE LN TFP) ........................................................................................................................................ 436 Table IV.7 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN ESTONIA FOR SERVICES SECTOR, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................................................................................................................ 438 Table IV.8 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN HUNGARY FOR SERVICES SECTOR, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................................................................................................................ 440 Table IV.9 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVAKIA FOR SERVICES SECTOR, 2002-2009 (DEP. VARIABLE LN TFP) ................................................................................................................................................................................ 442 Table IV.10 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVENIA FOR SERVICES SECTOR, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................................................................................................................ 444 Table IV.11 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN THE CZECH REPUBLIC FOR MANUFACTURING SECTOR ACCORDING TO INDUSTRY SOURCE, 2002-2009 (DEP. VARIABLE LN TFP) ......................................................... 446 Table IV.12 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN ESTONIA FOR MANUFACTURING SECTOR ACCORDING TO INDUSTRY SOURCE, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................ 448 Table IV.13 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN HUNGARY FOR MANUFACTURING SECTOR ACCORDING TO INDUSTRY SOURCE, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................ 450 Table IV.14 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVAKIA FOR MANUFACTURING SECTOR ACCORDING TO INDUSTRY SOURCE, 2002-2009 (DEP. VARIABLE LN TFP) ................................................................................ 452

xi

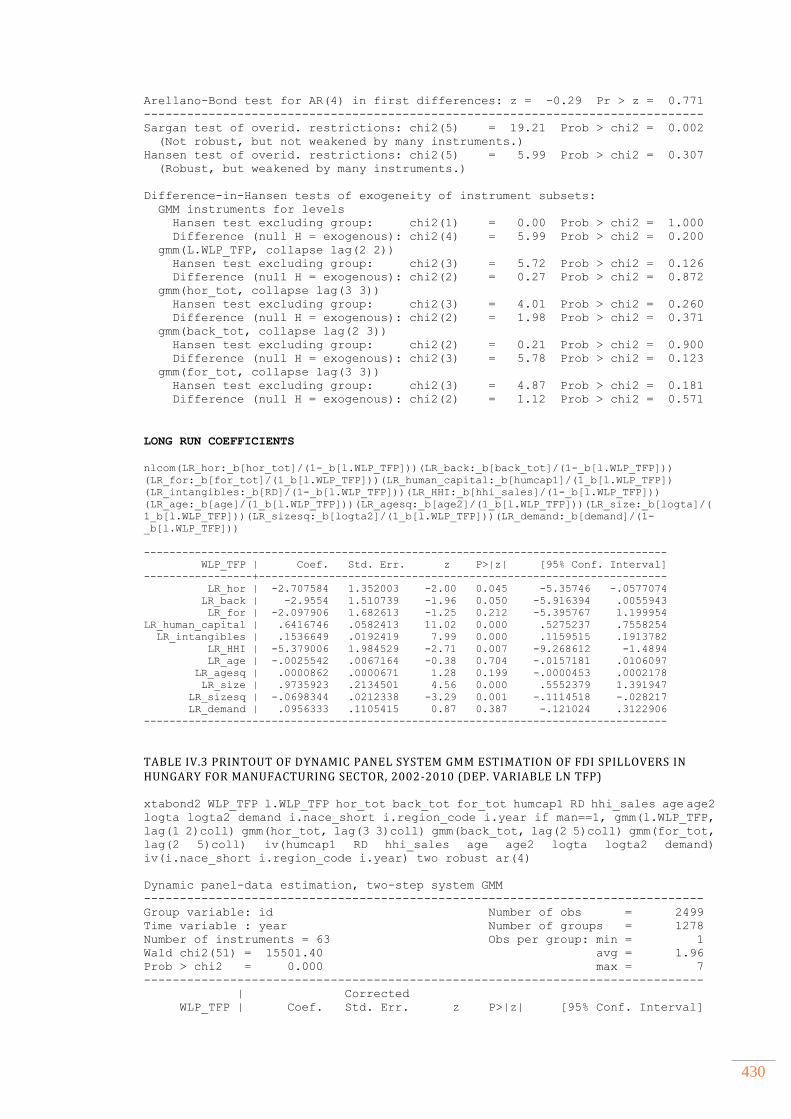

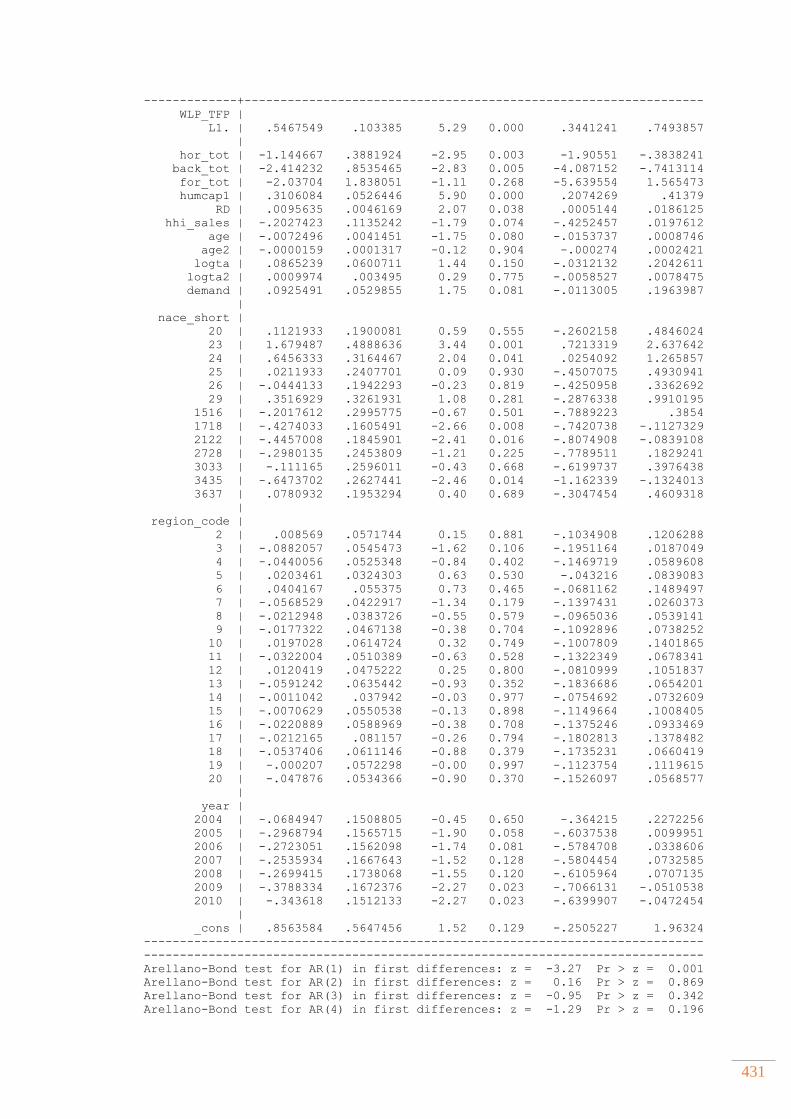

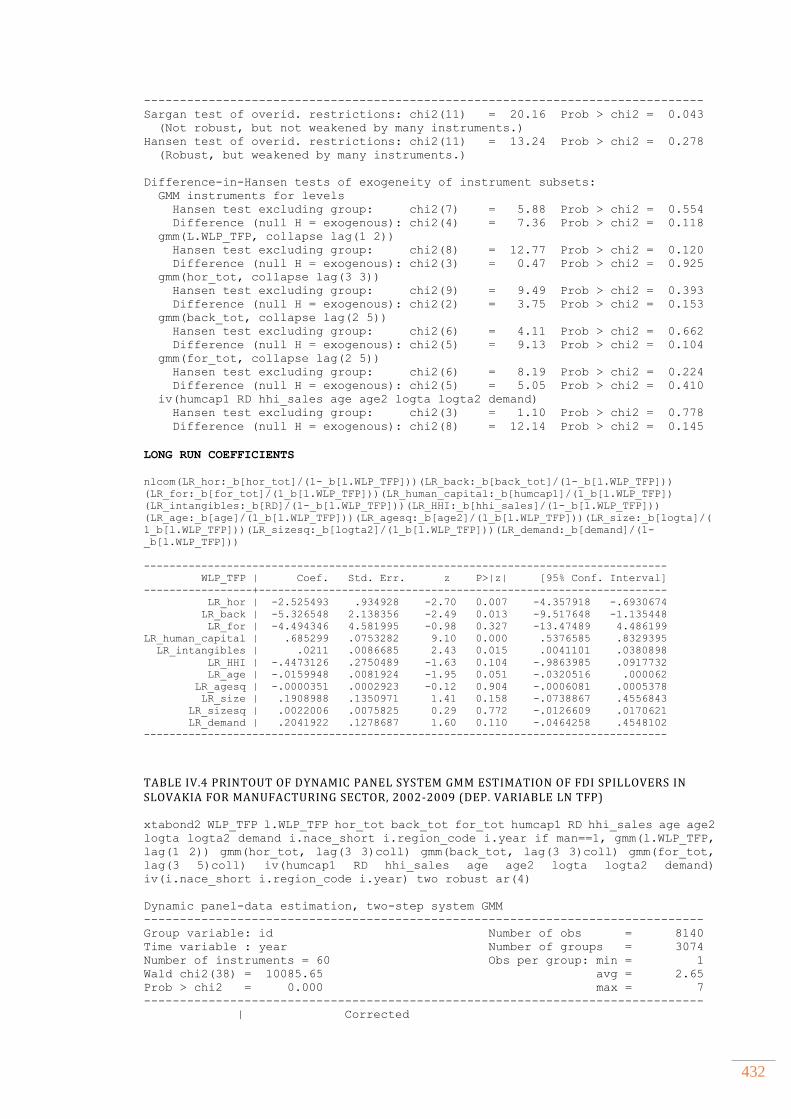

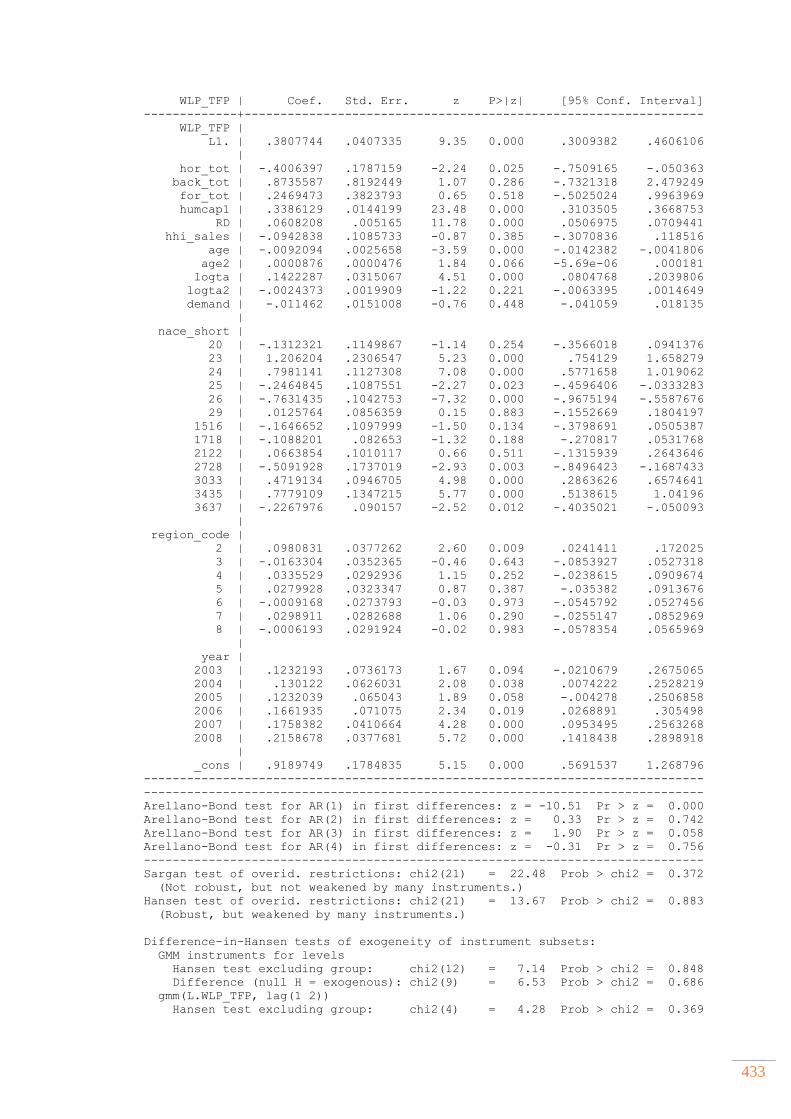

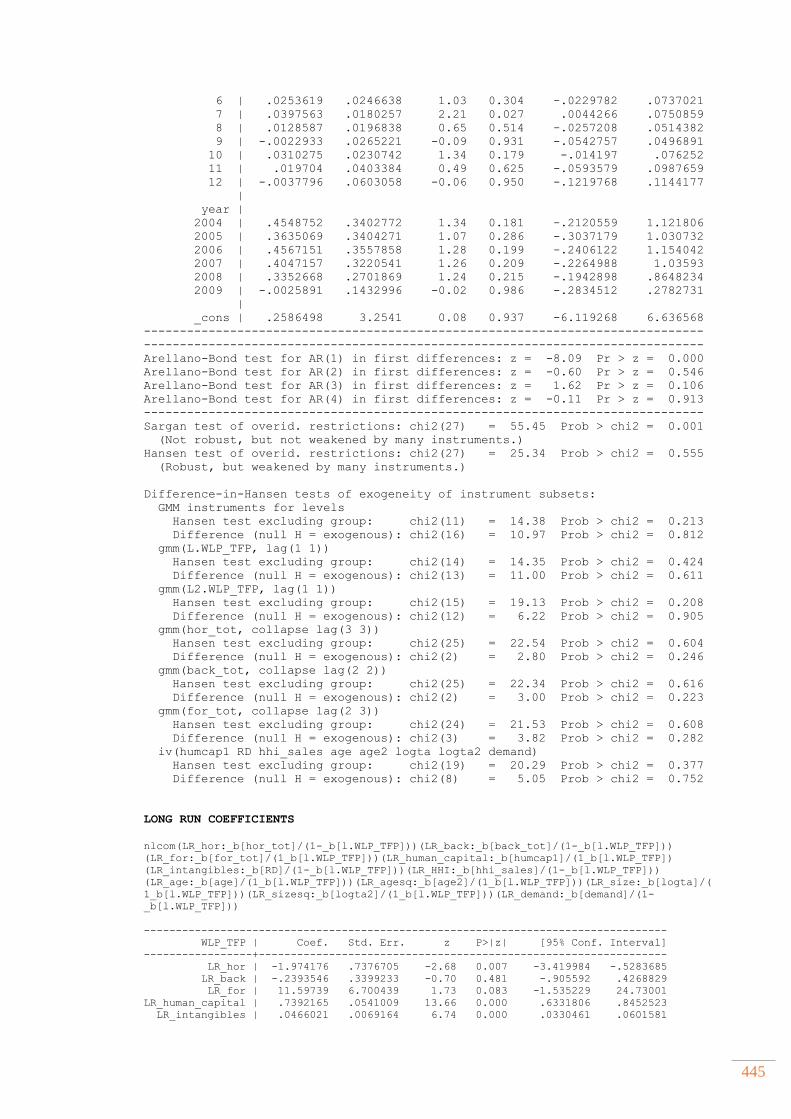

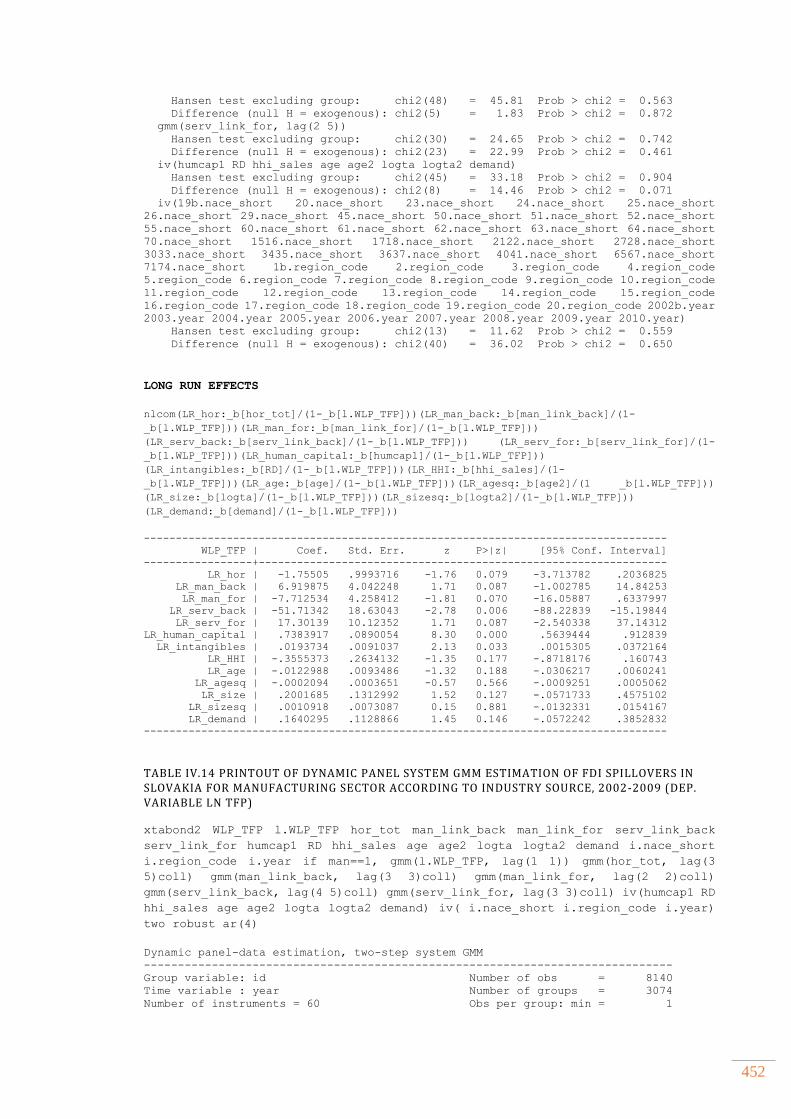

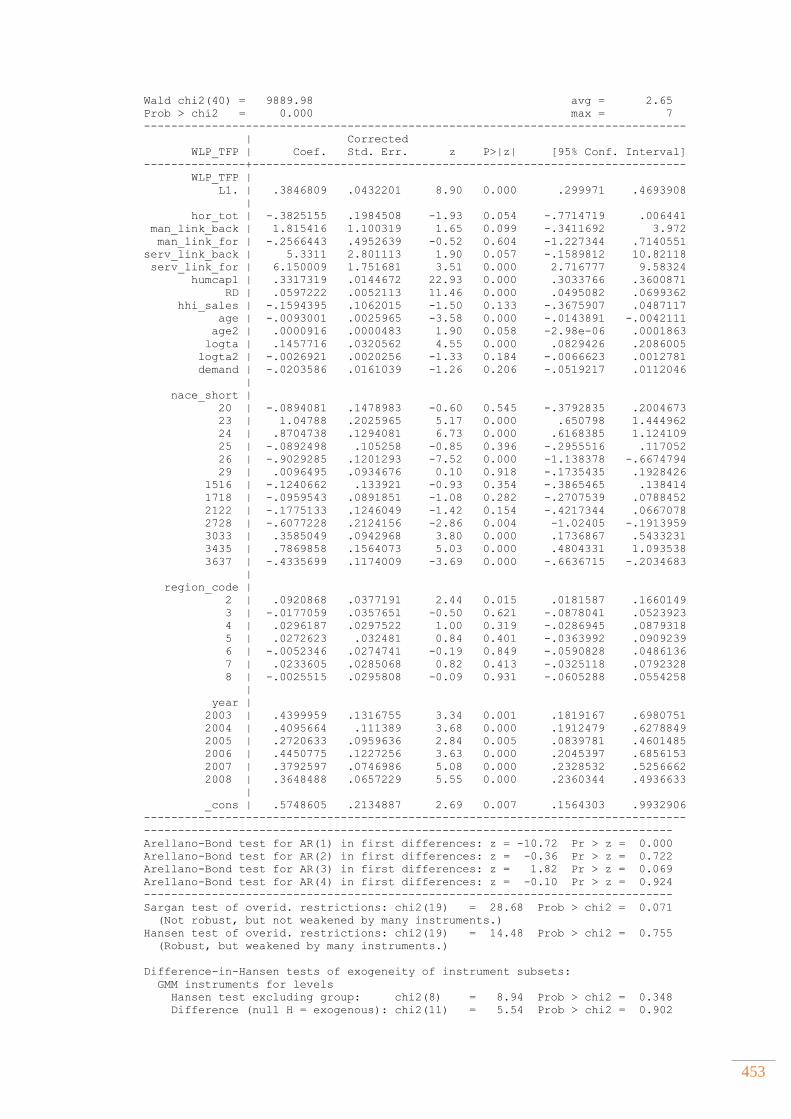

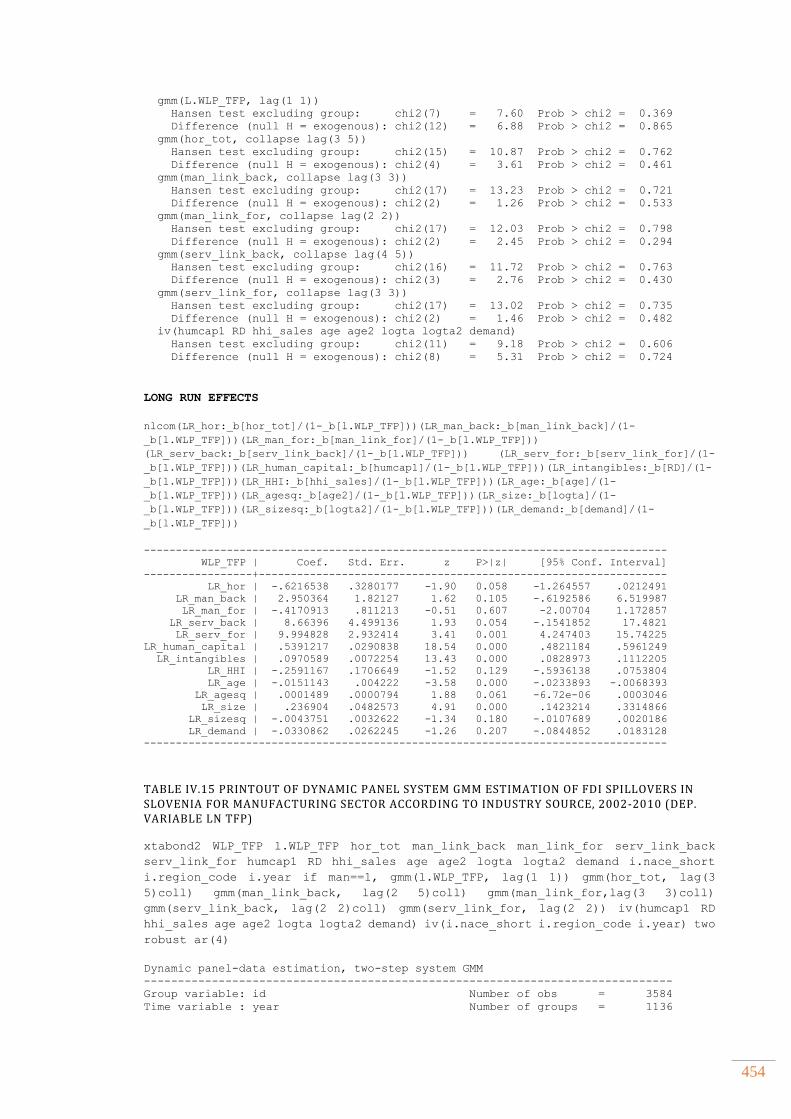

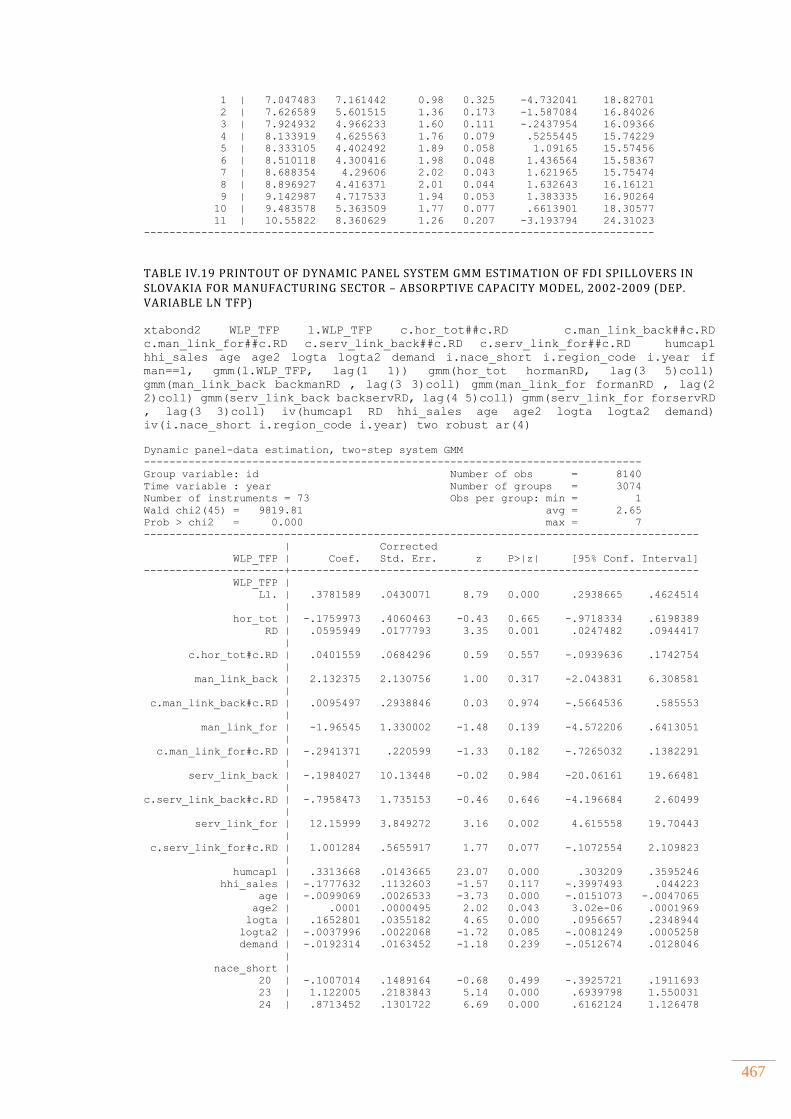

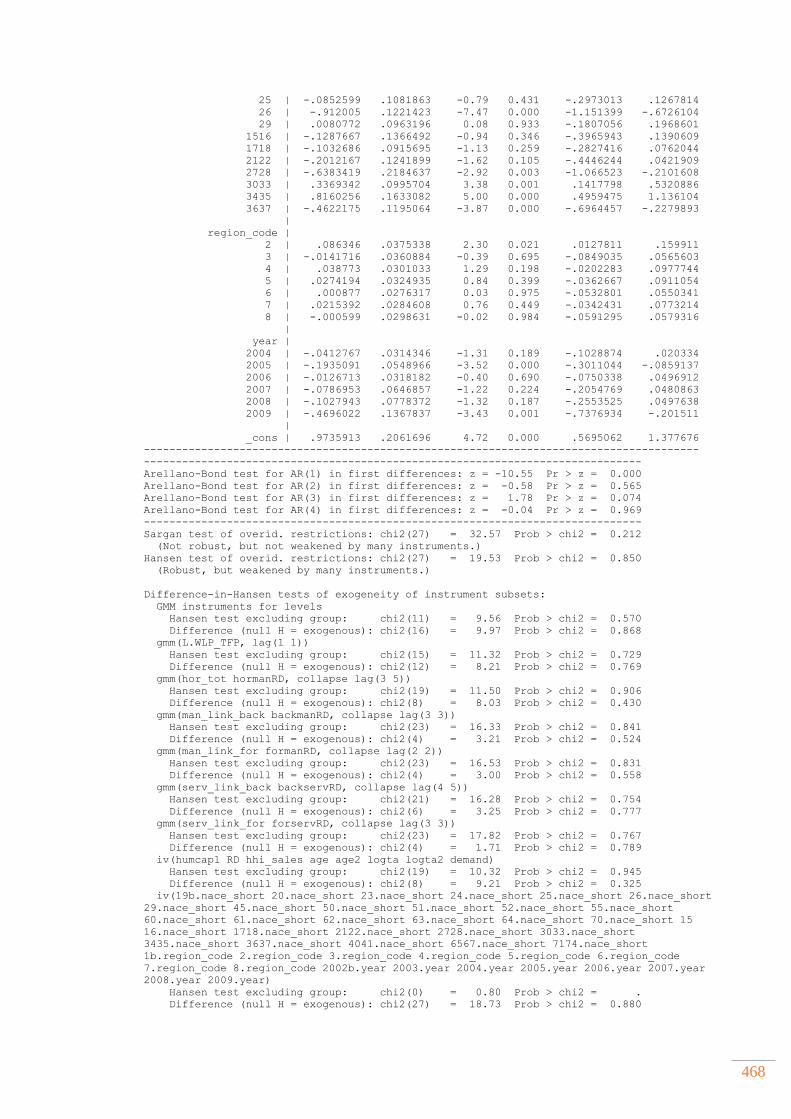

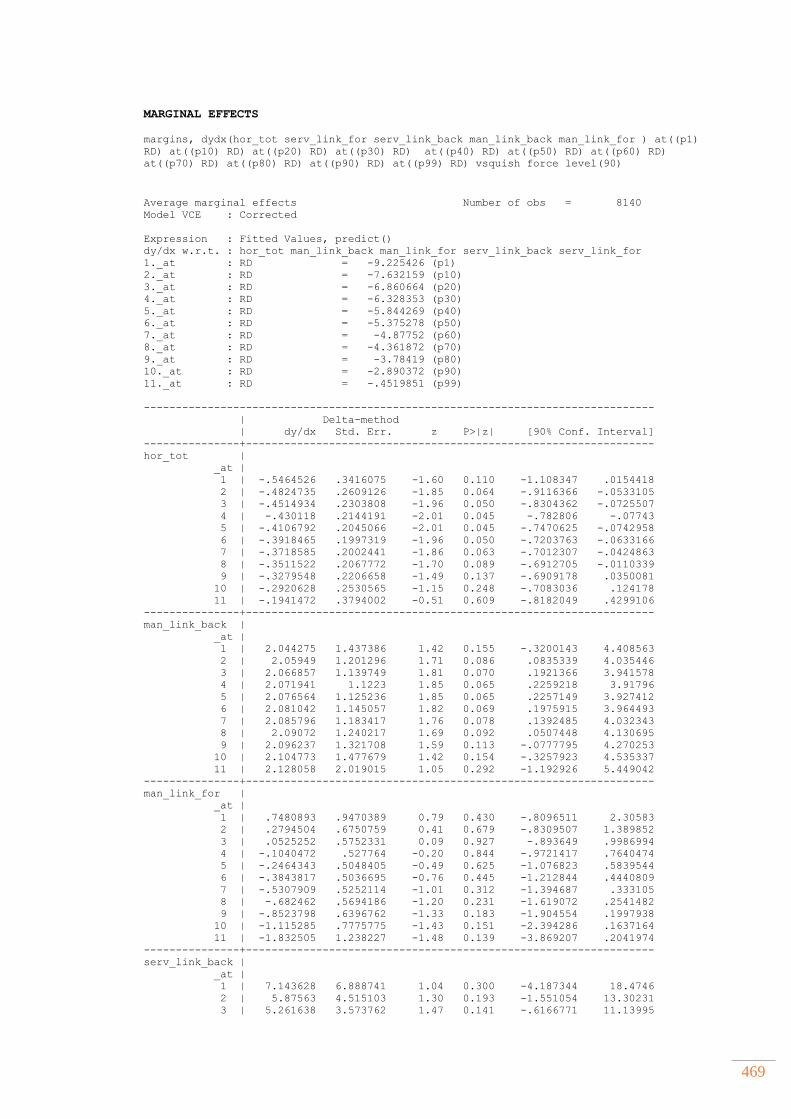

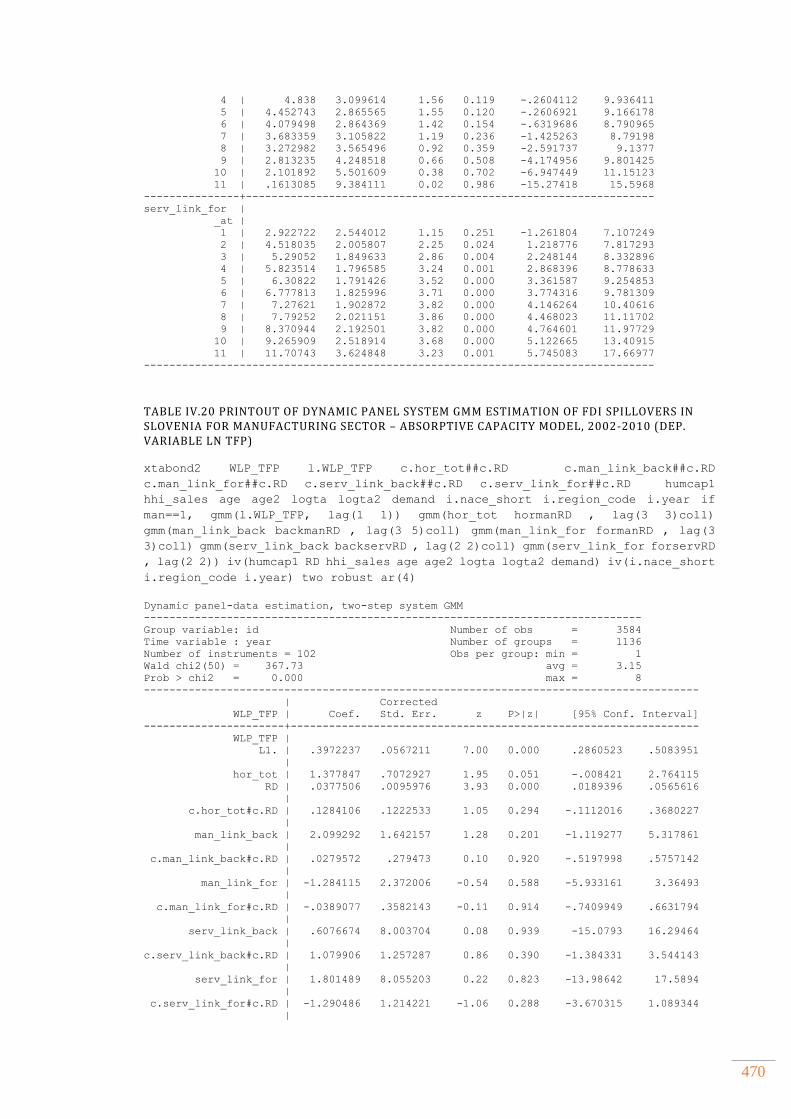

Table IV.15 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVENIA FOR MANUFACTURING SECTOR ACCORDING TO INDUSTRY SOURCE, 2002-2010 (DEP. VARIABLE LN TFP) ................................................................................ 454 Table IV.16 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN THE CZECH REPUBLIC FOR MANUFACTURING SECTOR – ABSORPTIVE CAPACITY MODEL, 2002-2009 (DEP. VARIABLE LN TFP) ........................................................... 457 Table IV.17 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN ESTONIA FOR MANUFACTURING SECTOR – ABSORPTIVE CAPACITY MODEL, 2002-2010 (DEP. VARIABLE LN TFP) .................................................................................. 460 Table IV.18 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN HUNGARY FOR MANUFACTURING SECTOR – ABSORPTIVE CAPACITY MODEL, 2002-2010 (DEP. VARIABLE LN TFP) .................................................................................. 463 Table IV.19 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVAKIA FOR MANUFACTURING SECTOR – ABSORPTIVE CAPACITY MODEL, 2002-2009 (DEP. VARIABLE LN TFP) .................................................................................. 467 Table IV.20 PRINTOUT OF DYNAMIC PANEL SYSTEM GMM ESTIMATION OF FDI SPILLOVERS IN SLOVENIA FOR MANUFACTURING SECTOR – ABSORPTIVE CAPACITY MODEL, 2002-2010 (DEP. VARIABLE LN TFP) .................................................................................. 470

xii

LIST OF FIGURES FIGURE 2.1 A CONCEPTUAL FRAMEWORK FOR FDI SPILLOVER CHANNELS AND MECHANISMS AND THEIR POTENTIAL DETERMINANATS ............................................................ 49 FIGURE 3.1 GDP PER CAPITA (PPP) GROWTH CONVERGENCE, DIFFERENCES TO EU-15 AVERAGE (1995=100) .................................................................................................................................... 82 FIGURE 3.2 ABSOLUTE BETA-CONVERGENCE OF NMS DURING 1995-2013 PERIOD ........ 83 FIGURE 3.3 GDP PER CAPITA (PPP) LEVELS, PERCENT OF EU-15 .................................. 84 FIGURE 3.4 LABOR PRODUCTIVITY PER PERSON EMPLOYED (CONVERTED TO 2013 PRICE LEVEL WITH 2005 PPP, 1995=100) ....................................................................... 85 FIGURE 3.5 TOTAL FACTOR PRODUCTIVITY OF NMS AND EU-15 (1995=100) ...... 85 FIGURE 3.6 ANNUAL FDI INFLOWS PER CAPITA IN GROUPS OF NMS, EUR .............. 88 FIGURE 3.7 ANNUAL FDI INFLOWS TO NMS, MILLIONS USD ............................................. 89 FIGURE 3.8 THE STOCK OF INWARD FDI IN NMS, MILLIONS USD, 2014 .................... 90 FIGURE 3.9 AVERAGE FDI INWARD STOCK (INFLOWS) AS A PERCENTAGE OF GDP (GFCF) IN NMS, 1995-2014 ...................................................................................................................... 91 FIGURE 3.10 AVERAGE VALUE OF GREENFIELD AND M&A PROJECTS, MILLIONS USD (2003-2014) ........................................................................................................................................... 91 FIGURE 3.11 PERCENTAGE CHANGE OF FDI STOCK IN NMS BETWEEN 2004-2007 ................................................................................................................................................................................... 92 FIGURE 3.12 PERCENTAGE CHANGE OF FDI STOCK IN THE NMS BETWEEN 2008-2012 ....................................................................................................................................................................... 93 FIGURE 3.13 GROWTH OF GDP AND RATIO OF FDI STOCK TO GDP(PPP) .................. 97 FIGURE 3.14 SHARE OF FATS IN TOTAL DOMESTIC EMPLOYMENT OF BUSINESS ECONOMY ............................................................................................................................................................ 98 FIGURE 3.15 SHARE OF FATS IN TOTAL VALUE ADDED OF BUSINESS ECONOMY ................................................................................................................................................................................ 100 FIGURE 3.16 SHARE OF FATS IN TOTAL TURNOVER OF BUSINESS ECONOMY ............... 100 FIGURE 3.17 FATS SHARE OF TURNOVER IN TOTAL DOMESTIC ECONOMY IN DIFFERENT TECHNOLOGY GROUPS, 2011 .................................................................................. 104 FIGURE 3.18 FATS SHARE OF VALUE ADDED IN TOTAL DOMESTIC ECONOMY BY TECHNOLOGY INTENSITY, 2011 ........................................................................................................ 105 FIGURE 3.19 FATS SHARE OF EMPLOYMENT IN TOTAL DOMESTIC ECONOMY BY TECHNOLOGY INTENSITY, 2011 ........................................................................................................ 105 FIGURE 3.20 FATS LABOUR PRODUCTIVITY PREMIUM ...................................................... 106 FIGURE 3.21 RATIO OF LABOUR PRODUCTIVITY FOR FOREIGN TO DOMESTIC FIRM BY TECHNOLOGY INTENSITY GROUP OF MANUFACTURING INDUSTRIES, 2011 .................................................................................................................................................................... 107 FIGURE 3.22 SECTORAL CONTRIBUTION TO EXPORT GROWTH IN %, 1995-2010 ................................................................................................................................................................................ 108 FIGURE 3.23 DOMESTIC VALUE ADDED SHARE IN COUNTRY EXPORT, % ............. 110 FIGURE 3.24 PARTICIPATION OF NMS IN GVC ........................................................................ 110 FIGURE 3.25 CORRELATION BETWEEN FDI STOCK AND GVC PARTICPATION OF NMS ...................................................................................................................................................................... 111 FIGURE 3.26 CORRELATION BETWEEN FDI STOCK AND GVC PARTICPATION OF INDUSTRIES, 2009 ...................................................................................................................................... 112 FIGURE 3.27 RELATIVE POSTION OF COUNTRIES IN GVC IN 1995 AND 2009 ..... 113 FIGURE 3.28 CORRELATION BETWEEN FDI STOCK AND BACKWARD PARTICIPATION IN GVC PER INDUSTRY, 2009 ........................................................................ 115

xiii

FIGURE 3.29 CORRELATION BETWEEN FDI STOCK AND FORWARD PARTICIPATION IN GVC PER INDUSTRY, 2009 ........................................................................ 115 FIGURE 4.1 APPROACHES TO TFP MEASUREMENT AT MICRO LEVEL .................................. 123 FIGURE 4.2 WITHIN AND ACROSS INDUSTRY TFP DISPERSION ................................... 160 FIGURE 4.3 TFP DISTRIBUTION OF FOREIGN AND DOMESTIC FIRMS IN MANUFACTURING SECTOR ................................................................................................................... 163 FIGURE 4.4 TFP DISTRIBUTION OF FOREIGN AND DOMESTIC FIRMS IN SERVICE SECTOR .............................................................................................................................................................. 163 FIGURE 5.1 HORIZONTAL SPILLOVERS ACROSS INDUSTRIES AND COUNTRIES .............. 189 FIGURE 5.2 BACKWARD LINKAGES ACROSS INDUSTRIES AND COUNTRIES ...................... 190 FIGURE 5.3 FORWARD LINKAGES ACROSS INDUSTRIES AND COUNTRIES ......................... 191 FIGURE 6.1 MANUFACTURING LINKAGES ACROSS INDUSTRIES AND COUNTRIES ......... 244 FIGURE 6.2 SERVICES LINKAGES ACROSS INDUSTRIES AND COUNTRIES ........................... 245 FIGURE 6.3 AVERAGE MARGINAL EFFECTS OF INTANGIBLE ASSET RATIO AND HORIZONTAL SPILLOVERS WITH 90% CI ........................................................................................... 263 FIGURE 6.4 AVERAGE MARGINAL EFFECTS OF INTANGIBLE ASSET RATIO AND MANUFACTURING LINKAGES WITH 90% CI ...................................................................................... 264 FIGURE 6.5 AVERAGE MARGINAL EFFECTS OF INTANGIBLE ASSET RATIO AND SERVICES LINKAGES WITH 90% CI ............................................................................................................................. 265 Figure I.1 DECOMPOSITION OF GROSS EXPORTS INTO VALUE ADDED COMPONENTS . 347 Figure I.2 VISUALISATION OF VALUE ADDED COMPONENTS OF GROSS EXPORTS ......... 348 Figure I.3 AVERAGE LABOUR PRODUCTIVITY GROWTH IN MANUFACTURING INDUSTRIES OF NMS-8 VS. EU-15, 1995-2009 .................................................................................. 349 Figure I.4 AVERAGE LABOUR PRODUCTIVITY LEVELS IN MANUFACTURING INDUSTRIES OF NMS-8 VS. EU-15, 1995-2009 ............................................................................................................ 350 Figure I.5 AVERAGE LABOUR PRODUCTIVITY GROWTH IN SERVICE INDUSTRIES OF NMS-8 VS. EU-15, 1995-2009 .................................................................................................................... 350 Figure I.6 AVERAGE LABOUR PRODUCTIVITY LEVELS IN SERVICES INDUSTRIES OF NMS-8 VS. EU-15, 1995-2009 ............................................................................................................................... 351 Figure I.7 TOTAL FACTOR PRODUCTIVITY AND INDUSTRY CONTRIBUTIONS TO VALUE ADDED GROWTH, 1996–2009 .................................................................................................................. 351 Figure IV.1 DEVELOPMENT OF FOREIGN FIRMS’ OUTPUT IN SERVICES .............................. 426 Figure IV.2 AVERAGE SHARE OF FOREIGN SERVICES INPUTS IN MANUFACTURING INDUSTRIES ...................................................................................................................................................... 426

xiv

LIST OF ABBREVIATIONS

ACF – Ackerberg, Caves and Frazer

AMADEUS – Analyse MAjor Database from EUropean Sources

BEEPS – Business Environment and Enterprise Survey

CEE – Central and Eastern Europe

CEEC – Central and Eastern European Country

CIS – Commonwealth of Independent States

FATS – Foreign Affiliates Statistics

FDI – Foreign Direct Investment

FE – Fixed Effects

FTA – Free Trade Agreements

GDP – Gross Domestic Product

GFCF – Gross Fixed Capital Formation

GMM – Generalised Method of Moments

GVC – Global Value Chain

ICT – Information and Communication Technology

IV – Instrumental Variable

JV – Joint Venture

LP – Levinsohn and Petrin

LSDV – Least Squares Dummy Variable

MNC – Multinational Corporation

NACE – Nomenclature Générale des Activités Économiques dans les Communautés

Européennes

NMS – New Member States

NUTS - Nomenclature of Territorial Units for Statistics

OECD – Organisation for Economic Co-operation and Development

OLI – Ownership-Location-Internalisation

OLS – Ordinary Least Squares

OP – Olley and Pakes

R&D – Research and Development

SBS – Structural Business Statistics

TFP – Total Factor Productivity

TiVA – Trade in Value Added

UNCTAD – United Nations Conference on Trade and Development

VTT – Vertical Technology Transfer

WIIW – Vienna Institute for International Economic Studies

WIOD – World Input-Output Database

WO – Wholly Owned

xv

ACKNOWLEDGMENTS

I would like to thank Open Society Institute and Staffordshire University Business

School for their generous financial support during my PhD studies. Special gratitude goes

towards prof. Iraj Hashi as my principal supervisor owing to whose encouragement, wide

knowledge and academic guidance helped me to grow as a researcher. Your advice

during write up of the thesis as well as on my academic career is priceless. I would also

like to thank to dr. Mehtap Hisarciklilar and dr. Nebojsa Stojcic whose suggestions,

experience, constructive criticism and advice kept me on track and guided me towards

the completion of this thesis. Dear supervisors, thank you very much for everything you

have done for me.

Writing a thesis is a complex and sometimes frustrating process and the presence of

friends who share the same process and understand problems is of utmost importance for

successful completion. I had a rare opportunity to share this long journey with my partner

Merima whose advice, support and love encouraged me to endure any difficulties

encountered on the way. Having the opportunity to meet new people and share plenty of

loughs made this journey much more relaxed. Some of them became very close friends

whose sense of humour, emotional support and incentive to explore every corner of the

UK made my studies even more pleasant.

Last, but certainly not the least, I would like to thank to my family. I am deeply grateful

to my family for their support, patience and belief in me. Special thanks go to my mother

Ana and father Mirko who is unfortunately not with us anymore for all the love, caring

and simply always being there for me and for teaching me values without which I would

not be able to complete this thesis.

xvi

PREFACE

Since the collapse of the communist system Central and Eastern European Countries

(CEEC) have been characterised by significant structural changes and increased

globalisation amplified by the liberalisation of trade and capital markets. One of the most

pertinent features of CEECs’ integration into global trade and capital flows has been a

surge in FDI. Increased inflow of foreign investment in these countries was primarily

motivated by the opening of new markets. Also increased globalisation of countries

around the world enabled MNCs to become major players in global production of

tangible goods, technology and investment in R&D. The opening of CEECs to

international capital flows was closely followed by the increase in global stock of FDI

from US$ 2.1 trillion in 1990 to US$ 26 trillion in 2015 (UNCTAD, 2015). The increased

internalisation of firms has also had a profound impact on host economies since the share

of foreign firms’ output in global GDP rose from 21 percent in 1990 to 47 percent in

2014. Over the same time period the value added of foreign firms increased eightfold,

exports fourfold and employment twofold (UNCTAD, 2015). As both theoretical

(Helpman et al., 2004) and empirical literature (e.g. Mayer and Ottaviano, 2007) suggest,

MNCs are more productive due to their advanced production technology, management

and organizational know-how, marketing expertise, production networks, access to

finance and codified and tacit knowledge giving them advantage over their domestic

counterparts. In international technology diffusion, MNCs are seen as an important agent

since almost two thirds of all private R&D expenditure is conducted by them (UNCTAD,

2005). With this in mind, an investigation of the role of MNCs on the prospects of

industrial development, increase in exports, competition and technology diffusion that

ultimately determine economic growth is highly relevant for countries which lack

advanced knowledge and technology.

During the process of transition from centrally planned to market economy Central and

East European countries (CEECs) have completely transformed their economic and

institutional framework and relied on internationalisation of their trade and capital

markets. Owing to a number of reasons such as obsolete capital, technological

backwardness, lack of innovation and specialisation in industries with low value added

the performance of these countries was lagging behind those of more advanced Western

xvii

economies. The expectations were that opening to FDI would bring the necessary capital,

technology, know-how, access to new markets and open new jobs resulting in a reduction

in technology gap, enterprise restructuring, modernization of industries and ultimately

economic growth. Therefore, most countries liberalised their FDI regime and started

offering generous investment and tax incentives. The particular aim of these incentives

was the that the entry of foreign firms will increase the productivity of indigenous firms

through technology spillovers or the inclusion of latter in Global Value Chains (GVC).

However, the success of CEECs in attracting FDI has been far from uniform across the

region, depending partially on privatisation policies in early transition period and later

on institutional progress, comparative advantages, macroeconomic policies and

transition specific factors such as regional integration (Seric, 2011). The differences in

determinants were also linked to FDI motives and types. Despite clear theoretical

arguments in favour of positive effects of FDI, empirical results remain inconclusive at

both macro and micro level.

Notwithstanding the importance of the direct effects of FDI in terms of their contribution

to capital accumulation, positive changes in export structure, enterprise restructuring,

improvements in infrastructure and development of the service sector, the emphasis of

this research is on the FDI spillover process. The issue of FDI spillovers has attracted

considerable attention among policy makers as the existence of spillovers may be

regarded as indicator of efficiency of policy measure (Rugraff, 2008). The process of

transition and large influx of FDI has provided a unique opportunity to investigate the

effects of FDI spillovers on domestic firms’ productivity. As CEECs have established

their institutional frameworks and well-functioning market economies, the main question

remains how firms in these countries can become more competitive and productive. The

answer lies in FDI spillovers, occurring horizontally through demonstration, worker

mobility and competition or vertically through buyer-supplier linkages, which have

become the major factors for positioning of CEECs in GVCs and for the development of

knowledge based economy. Since technological spillovers and transfer predominantly

occur between firms, the analysis has to be conducted at firm level using firm level data.

The current empirical research on FDI spillovers has, by and large, neglected foreign

affiliates in the service sector which is somewhat surprising given the large share of FDI

in services. In addition, the existing research has focused on the characteristics of local

firms and industries that could influence the extent and magnitude of knowledge

xviii

spillovers. Notwithstanding their importance, the role of foreign affiliates’ characteristics

has received much less attention. Foreign affiliates may differ in their productivity levels,

knowledge stock, motives, mode of entry, ownership levels, autonomy, functional scope,

technological intensity and embeddedness in the local economy. There is also relatively

little research on the ability of domestic firms to enter GVCs through vertical linkages

with foreign affiliates in the service sector. Although the existing evidence points to

positive effects of backward linkages when domestic firms act as suppliers to foreign

affiliates in the manufacturing sector, little is known about the effects of linkages in the

service sector.

This research aims to fill these gaps in the literature by investigating the relationship

between total factor productivity (TFP) and FDI spillovers differentiating between firms

which are vertically integrated with MNCs and those in direct competition in the same

sector. For this reason, several empirical models are being developed at the firm level

and estimated using a rich firm level database containing firms in manufacturing and

service industries from several CEECs. In this way we aim to address one of the empirical

shortcomings in the FDI spillovers literature related to use of different data,

methodologies and models applied in single country framework. By analysing

theoretically, the reasons for MNCs’ existence and their potential benefits for the host

country economy we are able to gain insight into the possible channels of influence on

indigenous firms as well as their differential impact conditional on firm, sector and

country heterogeneity. This will inform the choice of variables used to construct the

empirical models differentiating between horizontal and vertical FDI spillover channels

and their effects conditional on across differences in MNCs such as the level of

ownership and their origin. It will also enable us to investigate specificities of domestic

firms operating in different sectors, the interrelationship between different sectors, the

moderating role of domestic firm’s absorptive capacity and to examine how these factors

determine domestic firms’ TFP in short and long run. In addition, the investigation will

address several firm specific factors such as the firms’ intangible assets, human capital,

experience and size which are found to be relevant for explaining TFP. We further control

for competition and demand effects at industry level which if not included may provide

an upward bias in FDI spillover variables. The originality of our approach also lies in the

estimation method and checking for robustness of several TFP estimates at industry level

in a multi-country framework which, to the best of our knowledge, has not been

xix

addressed in firm level productivity estimation in transition countries. When estimating

the effects of FDI spillovers we emphasize the dynamic nature of TFP and control for

the potential endogeneity between our variables of interest and TFP using instrumental

variable methods which has rarely been addressed in empirical work on FDI spillovers.

Bearing in mind the context outlined above, the aim of this thesis is to quantify the effects

of FDI spillovers on productivity of domestic firms. For this purpose, several research

objectives have been developed:

To provide a comprehensive and critical review of theories explaining the

emergence of MNCs and sources of their technological advantages and identify

potential benefits to host countries

To critically evaluate the theoretical and empirical literature related to FDI

spillovers with special emphasis on potential channels and determinants of FDI

spillovers from supply and demand sides

To provide a comprehensive analysis of productivity convergence and FDI

performance in the New Member States (NMS) at country and industry level with

special emphasis on the inclusion of NMS in GVC

To critically examine the methods used for the estimation of firm level

productivity and their application in the context of NMS

To develop an empirical model to investigate the effects of FDI spillovers on

domestic firms’ productivity in selected NMS, highlighting the sectoral and

foreign affiliates heterogeneity

To empirically evaluate the interrelationship between FDI in services and

downstream manufacturing productivity and examine the moderating role of

manufacturing firms’ absorptive capacity in selected NMS

To discuss some policy implications and provide policy recommendations to

governments and Investment Promotion Agencies in order to devise effective

policies to improve productivity effects of FDI.

The novelty of this research is reflected in: (i) the critical examination of methods

available for estimating firm level productivity and the application of relatively new

econometric method applied in the context of industry and country heterogeneity

which are theoretically more appropriate than methods employed in existing studies;

(ii) the examination of supply side factors affecting FDI spillover process in the

xx

context of European transition countries; (iii) exploring the effects of FDI in services

and manufacturing on both upstream and downstream manufacturing firms by

examining four possible channels of vertical linkages simultaneously, thus shedding

new light on the importance of supplier-client relationship in manufacturing firms.

The structure of this thesis is as follows. Chapter 1 starts with defining the concept

of FDI and continues with review of theories explaining the emergence and growth

of MNCs. The focus is on a critical examination of different approaches explaining

the motives for FDI. Despite being a relatively old concept, its explanation still

generates considerable debate among scholars in international business and

international economics literature. The purpose is to examine their suitability for the

analysis of FDI spillover process in the context of this thesis as they rest on different

assumptions regarding technology transfer and effects on economic development of

host countries. The second part of this chapter is concerned with explanation of

motives and their potential effects on host countries. In addition, we discuss other

strategically important decisions of MNCs upon their entry into host markets. Finally,

we examine the potential benefits associated with FDI, differentiating between direct

and indirect effects.

Chapter 2 examines the concept of FDI spillovers. We emphasize that term

technology is used in its broadest sense including both codified and tacit knowledge,

management and organizational skills, product and process technology. We also use

the term spillovers in broad sense including pecuniary and pure technological

externalities since it is not possible to empirically disentangle voluntary and

involuntary knowledge transfer. We continue by explaining channels of influence of

MNCs pointing out the differences between horizontal and vertical spillovers as well

as heterogeneous approaches within each main channel. We distinguish between

three strands of literature according to the way in which intra industry spillovers

occur. The earliest neoclassical approach is based on the simple notion that the mere

foreign presence explains the spillover benefits due to the public good nature of

spillovers. The second strand recognizes the costs related to absorbing the spillovers

and argues that they are endogenously determined. The most recent strand

emphasizes worker mobility as the potential channel. Regarding vertical spillovers,

theoretical studies distinguish between backward and forward linkages and discuss

their impact on host country development through increased demand for intermediate

xxi

inputs, assistance in acquisition of new technology, knowledge diffusion and

availability and quality effects.

The second part of this chapter is devoted to the critical examination of factors which

may influence the extent and intensity of spillovers with particular emphasis on

foreign and domestic firms’ heterogeneity and methodological issues pertinent to the

examination of FDI spillovers. The last part of the chapter identifies the shortcomings

of the current empirical literature which, together with insights from Chapter 1, leads

to the conceptual framework used throughout this thesis.

Chapter 3 starts with the investigation of major features of the transition process in

NMS and the role played by FDI. In the first part, we analyse the convergence process

of NMS and the distribution of FDI across countries and industries. We show that

countries which liberalised their trade and capital accounts quickly were the

forerunners in structural and institutional reforms, and succeeded in attracting large

amounts of FDI. In the second part of the chapter, we focus on the effects of FDI on

structural change and the inclusion of NMS in GVCs. We also provide a comparative

analysis of the performance of foreign and domestic firms across industries and

countries and argue that the contribution of foreign firms to structural change in NMS

has been substantial. For the analysis of this chapter we rely on several databases

such as UNCTAD FDI database to gauge the size of FDI stock and its relative

importance for each country. The Total Economy Database and the Eurostat database

are used to gain more insight into the productivity convergence and the structure of

FDI across industries. We also used the Eurostat Foreign Affiliates (FATS database

and Structural Business Statistics (SBS) when measuring performance of foreign and

domestic firms. Finally, the OECD TiVA is used to measure GVC participation of

countries and industries.

Chapter 4 discusses the importance of the correct measurement of productivity

followed by a detailed review of the available methods for the estimation of firm

level productivity. We emphasize that the choice of preferred methods depends on

several assumptions which are critically examined. In addition, we discuss the

potential problems (such as measurement errors in output and inputs, for example)

when estimating TFP in a production function framework. Furthermore, several

methodological problems related to firm level estimation of TFP such as simultaneity

xxii

bias, selection bias, omitted price bias and the presence of multiproduct firms are

discussed together with potential solutions offered by different estimation methods.

We argue that the semiparametric methods which incorporate assumptions on firms’

behaviour and timing of inputs are the most appropriate methods for the estimation

of TFP at firm level. Other issues that are considered in this chapter include a detailed

description of the Amadeus database used in this and the following empirical

chapters, estimation of TFP using several methods in order to test their robustness as

well as the estimation of foreign ownership premium using non-parametric and

parametric methods to gauge the potential for FDI spillovers.

In Chapter 5 we develop an empirical model of FDI spillovers and apply it to firms

from the Czech Republic, Estonia, Hungary, Slovakia and Slovenia. The construction

of FDI spillover variables relies on a combination of firm and industry level data

obtained from Amadeus and World Input Output Database in order to separate intra-

industry and inter-industry spillovers. A dynamic system GMM model is used in

order to capture the dynamic nature of productivity as suggested by semi parametric

techniques described in Chapter 4. Furthermore, by using internal instruments we

control for possible endogeneity of FDI spillover variables. To capture the

heterogeneity of the supply side of the spillover process the baseline model is

augmented in order to take into account different ownership levels and the country

of origin of foreign investors. In addition, the role of knowledge capital, other firms

and industry characteristics are included as potential determinants of firm level

productivity. This chapter is of particular interest as it sheds more light on the supply

side of spillovers process including firms from the service sector which differentiate

our study from previous analysis.

Chapter 6 focuses on the cross-sectoral spillovers. The goal here is to establish

whether the effects of FDI differ between manufacturing and service firms. In

addition, we test the hypothesis that the previous findings of insignificant forward

linkages were related to the fact that the relationship between services and

manufacturing sectors was ignored. It is argued that the liberalisation of services has

important implications for productivity of downstream manufacturing firms as it

provides more variety, better quality and reduced prices of intermediate inputs than

those available in local markets. This question is of interest for both economists and

policy makers because of the far-reaching liberalisation of service industries in the

xxiii

last ten years - since these countries joined the EU. The analysis follows the same

methodological approach as in Chapter 5 and employs the same control variables.

Due to the richness of firm level data we are able to test the moderating effects of

local firms’ absorptive capacity on the occurrence and magnitude of FDI spillovers

in manufacturing sector through five channels of influence, one horizontal and four

vertical. To the best of our knowledge the empirical model based on firm level data

and annual input output tables for NMS is the first study to disentangle vertical

linkages according to industry source and to measure their impact on productivity of

domestic firms in manufacturing industries which are at the same time both suppliers

and customers.

Chapter 7 formulates the conclusions of this thesis. Special emphasis is given to

contributions to knowledge, limitations of the thesis and possible directions for future

research. We also provide some policy recommendations aimed at improving the

effectiveness of policies related to attracting the right type of foreign investor, linkage

promotion, strengthening absorptive capacity and providing incentives in certain

industries which would result in improving the technological competences of local

firms.

1

CHAPTER 1. THEORIES OF FOREIGN DIRECT

INVESTMENT

1.1 Introduction ............................................................................................................................................... 2

1.2 Concept of FDI – definition, measurement and types .............................................................. 4

1.3 Theories of FDI ......................................................................................................................................... 5

1.3.1 The neoclassical theory of capital movement ..................................................................... 6

1.3.2 Industrial organization theory .................................................................................................. 7

1.3.3 Macroeconomic development approach ............................................................................... 9