Embed Size (px)

Citation preview

Effects of Airline Industry Changes on Small- and Non-Hub Airports

This presentation from the AAAE 2015 National Air Service Conference presents findings from ACRP Project 03-29.

Effects of Airline Industry Changes on Small- and Non-Hub Airports

AAAE National Air Service Conference March 9, 2015

GRA, IncorporatedDr. William Spitz

Headquarters: 115 West Avenue • Suite 201 • Jenkintown PA 19046 • USA 215-884-7500 • 215-884-1385 www.gra-inc.com [email protected]

Bowling Green State UniversityDr. Russell W. Mills

225 Troupe Ave • Bowling Green, OH 43403 • USA419-372-7329 [email protected]

GRA, Incorporated

Outline

ACRP Projects Related to Air Service

Industry Trends Related to Studies

Introduction to ACRP 03-29 Project and Research Team

Changes in Air Service at Small and Non-Hub Airports (2001-2013)

Case Studies and Focus Groups

Preliminary Lessons Learned and Strategies

Products and Outcomes

March 9, 20151

GRA, Incorporated

Airport Cooperative Research Projects (ACRP)

ACRP 03-29 “Effects of Airline Industry Changes on Small and Non-Hub Airports”

ACRP Synthesis 56 “Understanding the Value of Social Media at Airports for Customer Engagement” Deals with using Social Media to make

customers more aware of the Airport in theircommunity

ACRP 03-31 “Aligning Community Expectations with Airport Roles”

Available at the TRB website (TRB.org)

2 March 9, 2015

GRA, Incorporated

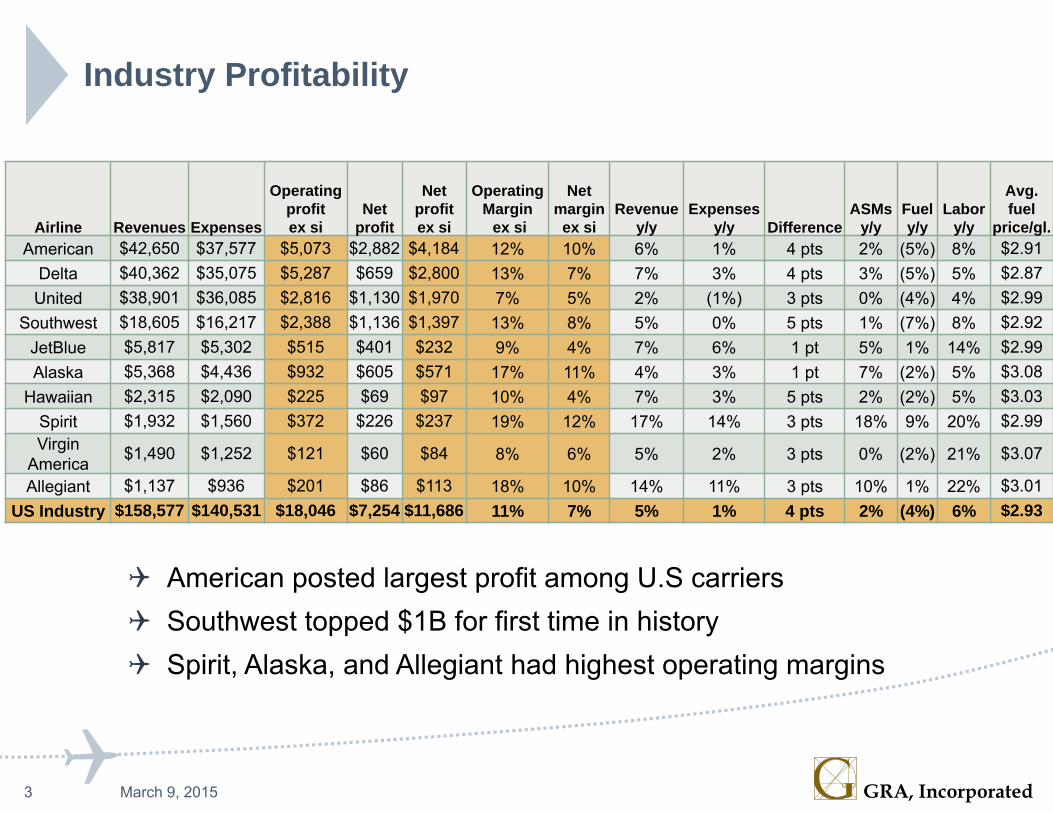

Industry Profitability

3 March 9, 2015

Airline Revenues Expenses

Operating profit ex si

Net profit

Net profit ex si

Operating Margin

ex si

Net margin

ex siRevenue

y/yExpenses

y/y DifferenceASMs

y/yFuel y/y

Labor y/y

Avg. fuel

price/gl.American $42,650 $37,577 $5,073 $2,882 $4,184 12% 10% 6% 1% 4 pts 2% (5%) 8% $2.91

Delta $40,362 $35,075 $5,287 $659 $2,800 13% 7% 7% 3% 4 pts 3% (5%) 5% $2.87 United $38,901 $36,085 $2,816 $1,130 $1,970 7% 5% 2% (1%) 3 pts 0% (4%) 4% $2.99

Southwest $18,605 $16,217 $2,388 $1,136 $1,397 13% 8% 5% 0% 5 pts 1% (7%) 8% $2.92 JetBlue $5,817 $5,302 $515 $401 $232 9% 4% 7% 6% 1 pt 5% 1% 14% $2.99 Alaska $5,368 $4,436 $932 $605 $571 17% 11% 4% 3% 1 pt 7% (2%) 5% $3.08

Hawaiian $2,315 $2,090 $225 $69 $97 10% 4% 7% 3% 5 pts 2% (2%) 5% $3.03 Spirit $1,932 $1,560 $372 $226 $237 19% 12% 17% 14% 3 pts 18% 9% 20% $2.99 Virgin

America $1,490 $1,252 $121 $60 $84 8% 6% 5% 2% 3 pts 0% (2%) 21% $3.07

Allegiant $1,137 $936 $201 $86 $113 18% 10% 14% 11% 3 pts 10% 1% 22% $3.01 US Industry $158,577 $140,531 $18,046 $7,254 $11,686 11% 7% 5% 1% 4 pts 2% (4%) 6% $2.93

American posted largest profit among U.S carriers Southwest topped $1B for first time in history Spirit, Alaska, and Allegiant had highest operating margins

GRA, Incorporated

Capacity Trends

4 March 9, 2015

Small hub and non-hub airports hurt by reduction in “regional hubs” with fewer options and fleet transition

GRA, Incorporated

Introduction to ACRP 03-29

Research Objectives Identify and quantify impacts on small- and non-hub airports

and the communities they serve, of changes in commercialairline service resulting from airline consolidation, fleetrealignment and other factors

Develop strategies for maintaining or achieving desired commercial service at these airports in response to changing market conditions and airline business plans

5 March 9, 2015

GRA, Incorporated

Project Team Leaders

GRA, Incorporated Rich Golaszewski, Project Manager William Spitz, Ph.D., Principal Investigator Primary responsibility for analysis and dissemination of air service changes across all small and

non-hub airports; overall project management

Bowling Green State University Center for Regional Development Russell Mills, Ph.D., Lead Investigator Primary responsibility for conducting case studies and focus groups of selected airports; analysis of

air service development strategies

Strategic Partners and Associates (SPA) Sonjia Murray, Lead Investigator Primary responsibility for conducting on-line surveys of airport managers and airline route planners

6 March 9, 2015

GRA, Incorporated

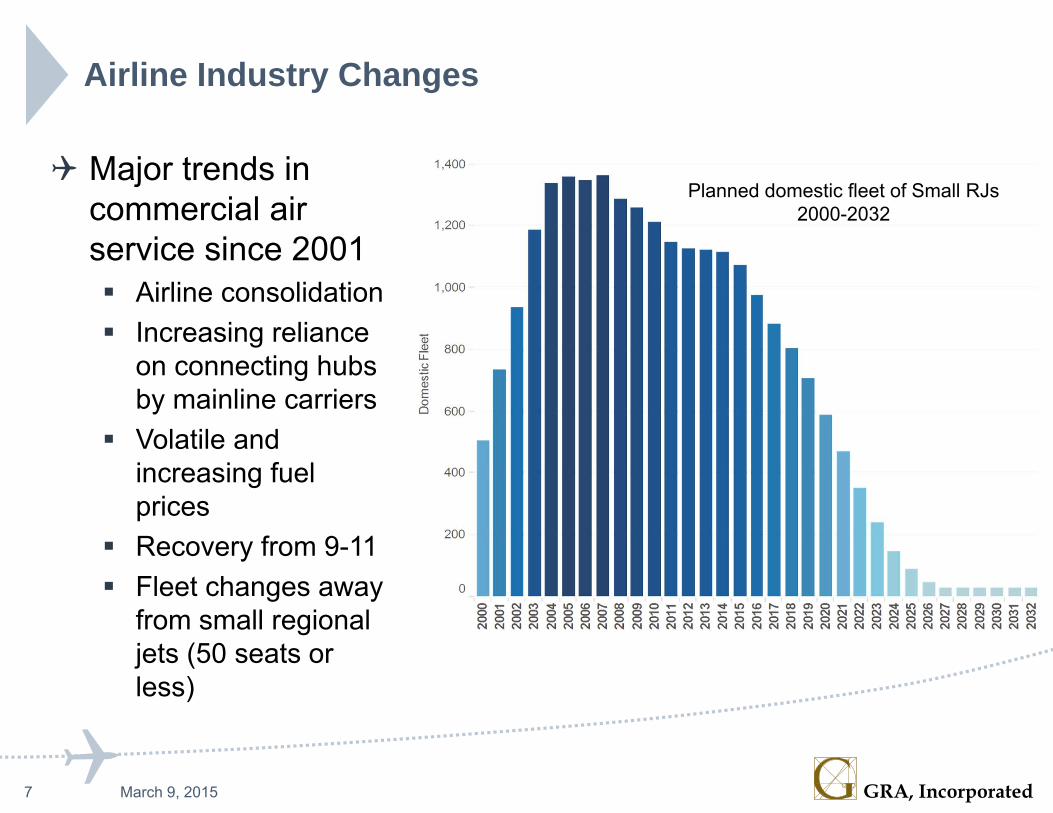

Airline Industry Changes

Major trends in commercial air service since 2001 Airline consolidation Increasing reliance

on connecting hubsby mainline carriers

Volatile andincreasing fuelprices

Recovery from 9-11 Fleet changes away

from small regionaljets (50 seats orless)

7 March 9, 2015

Planned domestic fleet of Small RJs2000-2032

GRA, Incorporated

Change in Small- and Non-Hub Flights, 2001-2013(Lower 48 States)

8 March 9, 2015

GRA, Incorporated

Change in Small- and Non-Hub Seats, 2001-2013(Lower 48 States)

9 March 9, 2015

GRA, Incorporated

Mainline/Regional Seat Shares at Small- and Non-Hubs, 2001-2013 (Lower 48 States)

10 March 9, 2015

GRA, Incorporated

Flight Shares at Small- and Non-Hubs by Aircraft Type, 2001-2013 (Lower 48 States)

11 March 9, 2015

Small Hubs Non-Hubs

GRA, Incorporated

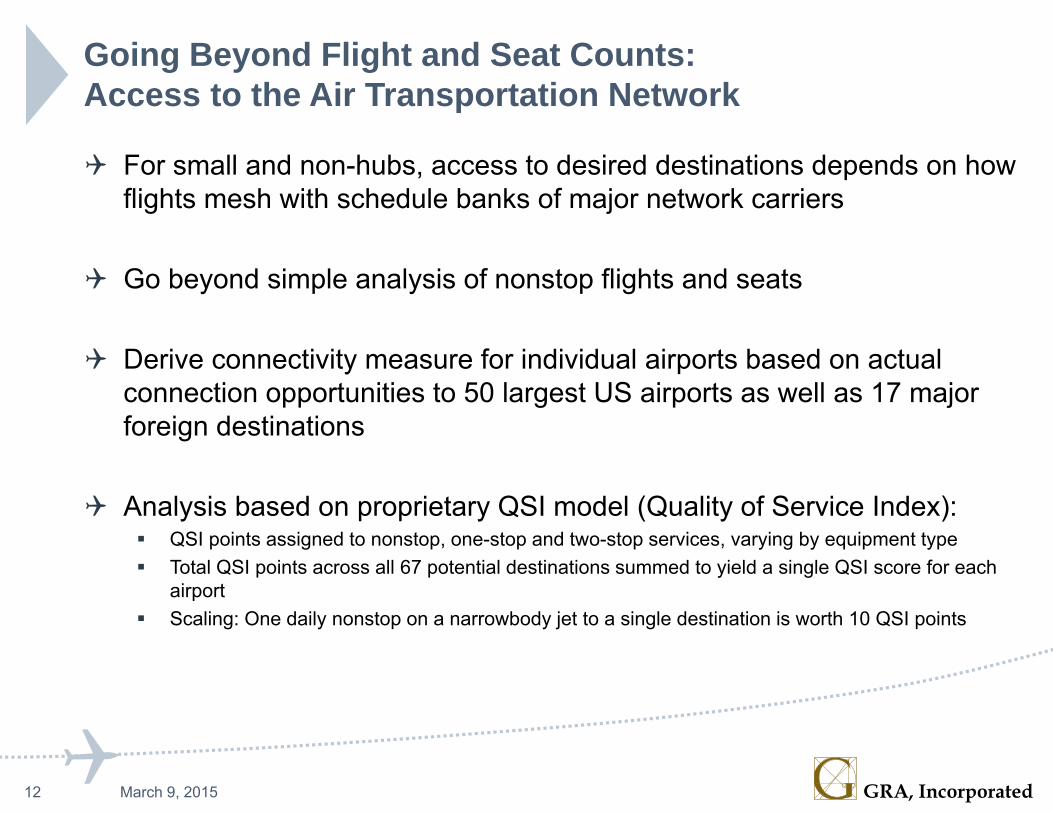

Going Beyond Flight and Seat Counts:Access to the Air Transportation Network

For small and non-hubs, access to desired destinations depends on how flights mesh with schedule banks of major network carriers

Go beyond simple analysis of nonstop flights and seats

Derive connectivity measure for individual airports based on actual connection opportunities to 50 largest US airports as well as 17 major foreign destinations

Analysis based on proprietary QSI model (Quality of Service Index): QSI points assigned to nonstop, one-stop and two-stop services, varying by equipment type Total QSI points across all 67 potential destinations summed to yield a single QSI score for each

airport Scaling: One daily nonstop on a narrowbody jet to a single destination is worth 10 QSI points

12 March 9, 2015

GRA, Incorporated

Change in Nonstop Seats vs. QSI at Small- and Non-Hub Airports, 2006-2013

13 March 9, 2015

TOL

RDD

BTVICT

MRY

FAR

AVL CAKBZN

AGS

‐100%

‐80%

‐60%

‐40%

‐20%

0%

20%

40%

60%

80%

100%

Pct C

hange 20

06 ‐20

13

Small- and Non-Hub Service to Major US and Foreign DestinationsPercent Change Nonstop Seats vs. QSI, 2006-2013

Nonstop Seats QSI ‐ Study Airports QSI ‐ Other

GRA, Incorporated

QSI Estimates by Hub Type, 2006-2013

14 March 9, 2015

9,296 Large Hubs‐6.7%

8,677

4,107Medium Hubs

‐18.7%3,339

1,544Small Hubs‐17.8%

1,270

325Non‐Hubs‐11.6%

2880

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2006 2007 2008 2009 2010 2011 2012 2013

Avg QSI Points p

er Airp

ort

Average Airport QSI by Hub Group

GRA, Incorporated

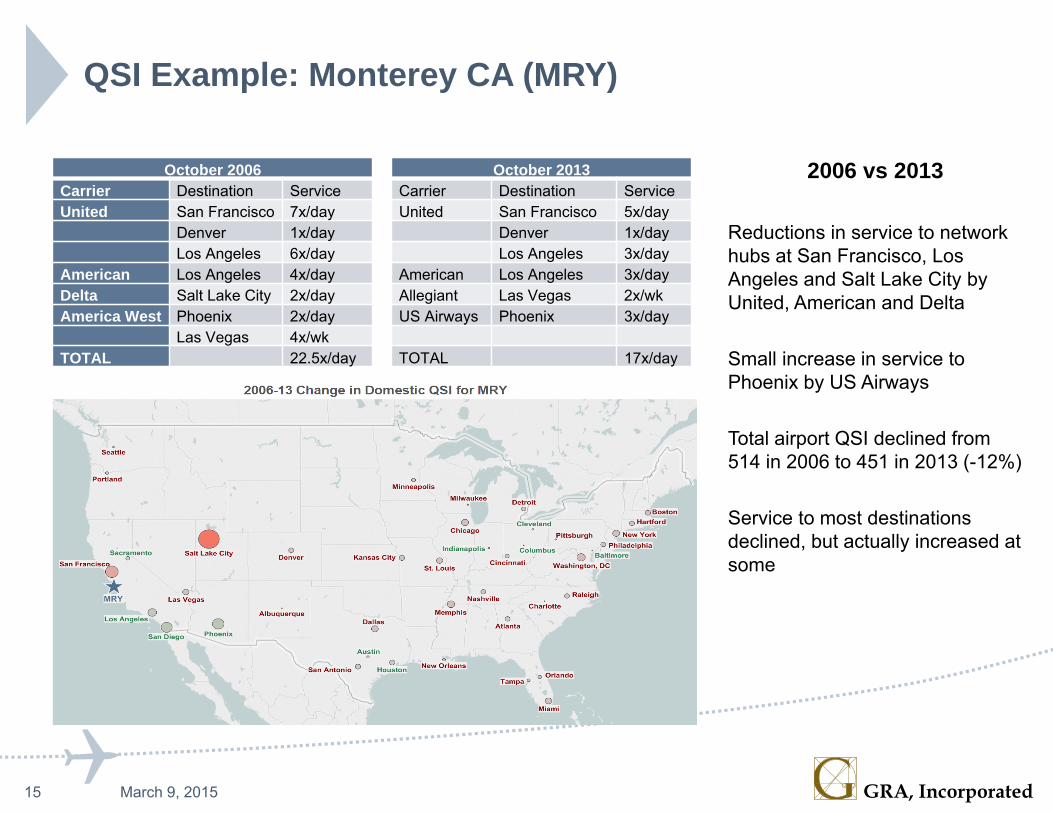

QSI Example: Monterey CA (MRY)

2006 vs 2013

Reductions in service to network hubs at San Francisco, Los Angeles and Salt Lake City by United, American and Delta

Small increase in service to Phoenix by US Airways

Total airport QSI declined from 514 in 2006 to 451 in 2013 (-12%)

Service to most destinations declined, but actually increased at some

15 March 9, 2015

October 2006 October 2013Carrier Destination Service Carrier Destination ServiceUnited San Francisco 7x/day United San Francisco 5x/day

Denver 1x/day Denver 1x/dayLos Angeles 6x/day Los Angeles 3x/day

American Los Angeles 4x/day American Los Angeles 3x/dayDelta Salt Lake City 2x/day Allegiant Las Vegas 2x/wkAmerica West Phoenix 2x/day US Airways Phoenix 3x/day

Las Vegas 4x/wkTOTAL 22.5x/day TOTAL 17x/day

GRA, Incorporated

Ongoing Analysis of Airport Access to the Air Transportation Network

www.gra-inc.com → Areas of Practice → Insights

Adjustments and improvements from current analysis:

Looks at domestic airports of all sizes, not just Small and Non-hubs

Considers economic importance of destinations

16 March 9, 2015

GRA, Incorporated

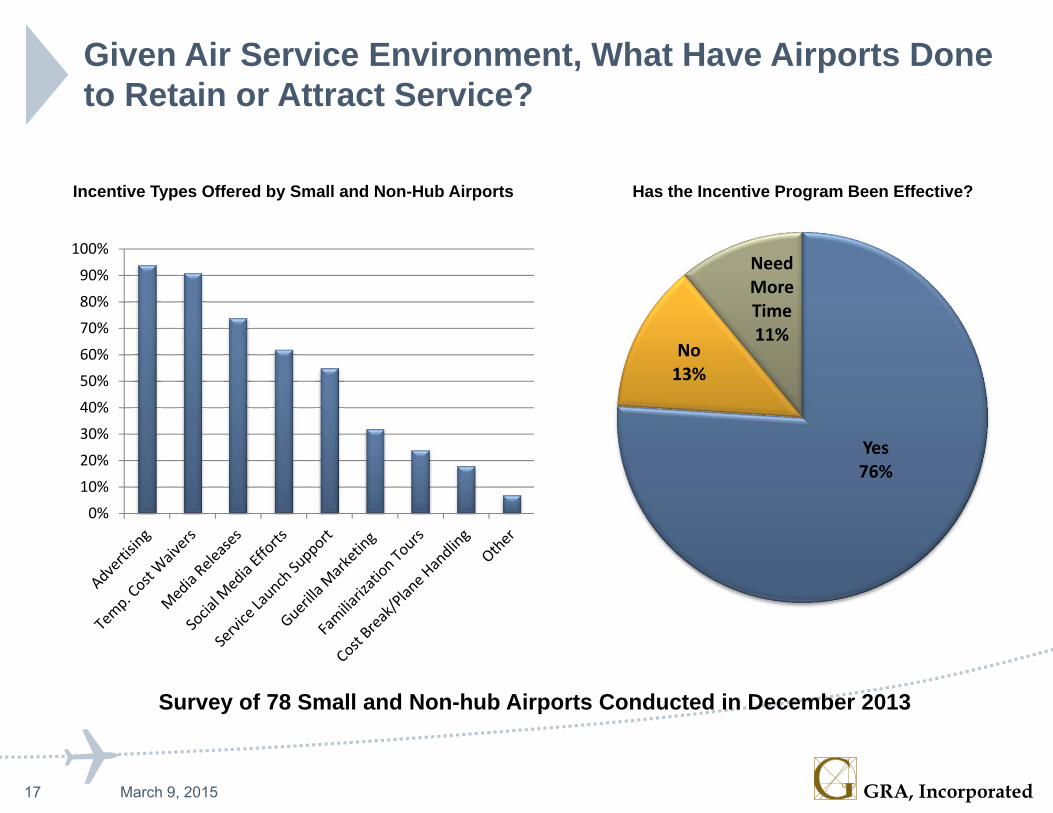

Given Air Service Environment, What Have Airports Done to Retain or Attract Service?

17 March 9, 2015

Yes76%

No13%

Need More Time11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Incentive Types Offered by Small and Non-Hub Airports

Survey of 78 Small and Non-hub Airports Conducted in December 2013

Has the Incentive Program Been Effective?

GRA, Incorporated

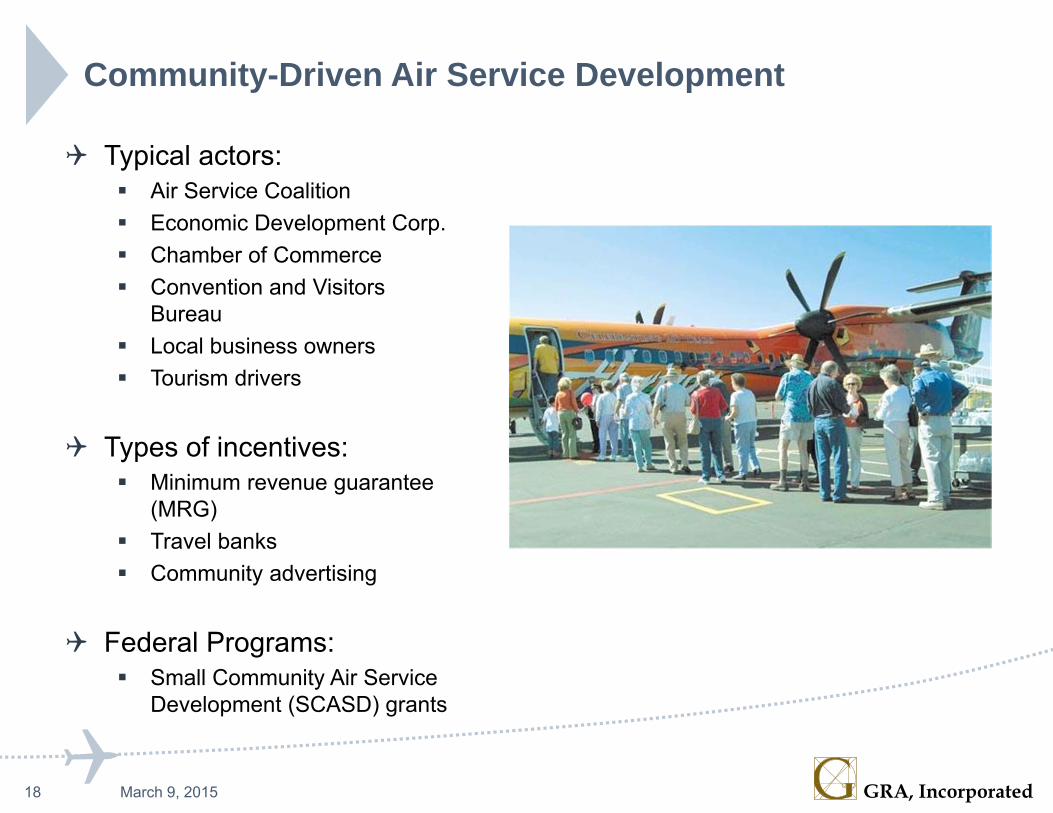

Community-Driven Air Service Development

Typical actors: Air Service Coalition Economic Development Corp. Chamber of Commerce Convention and Visitors

Bureau Local business owners Tourism drivers

Types of incentives: Minimum revenue guarantee

(MRG) Travel banks Community advertising

Federal Programs: Small Community Air Service

Development (SCASD) grants

18 March 9, 2015

GRA, Incorporated

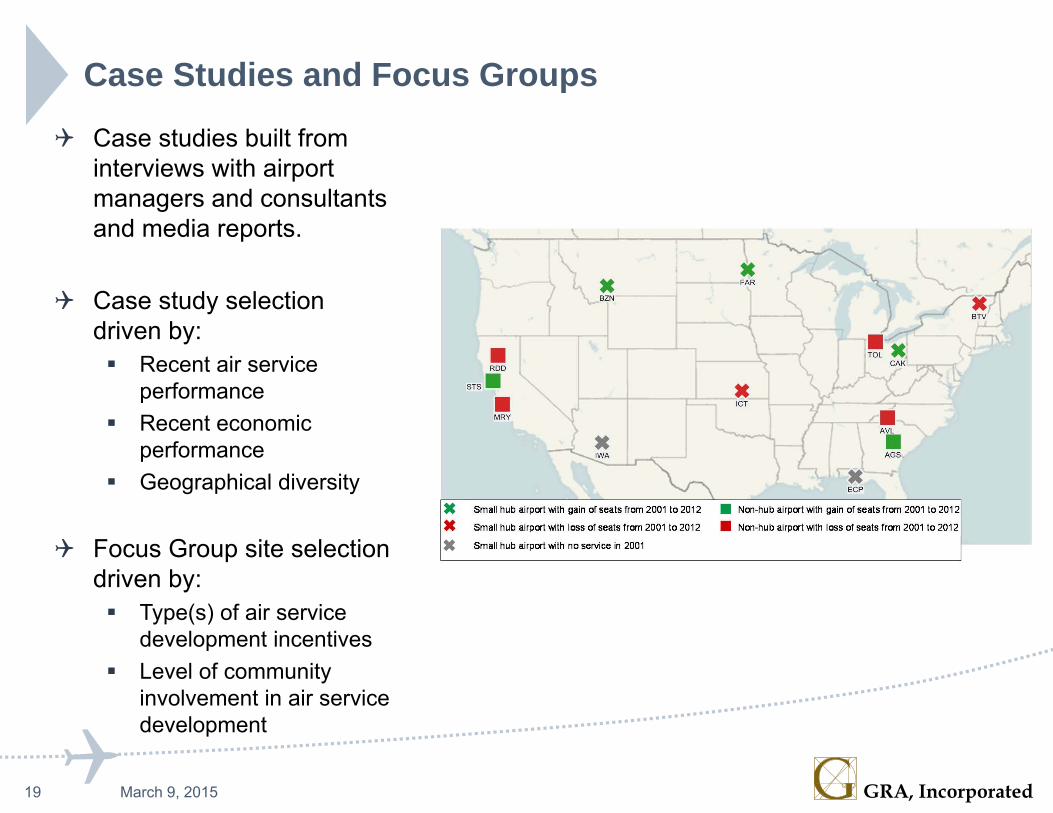

Case Studies and Focus Groups

Case studies built from interviews with airport managers and consultants and media reports.

Case study selection driven by: Recent air service

performance Recent economic

performance Geographical diversity

Focus Group site selection driven by: Type(s) of air service

development incentives Level of community

involvement in air servicedevelopment

19 March 9, 2015

GRA, Incorporated

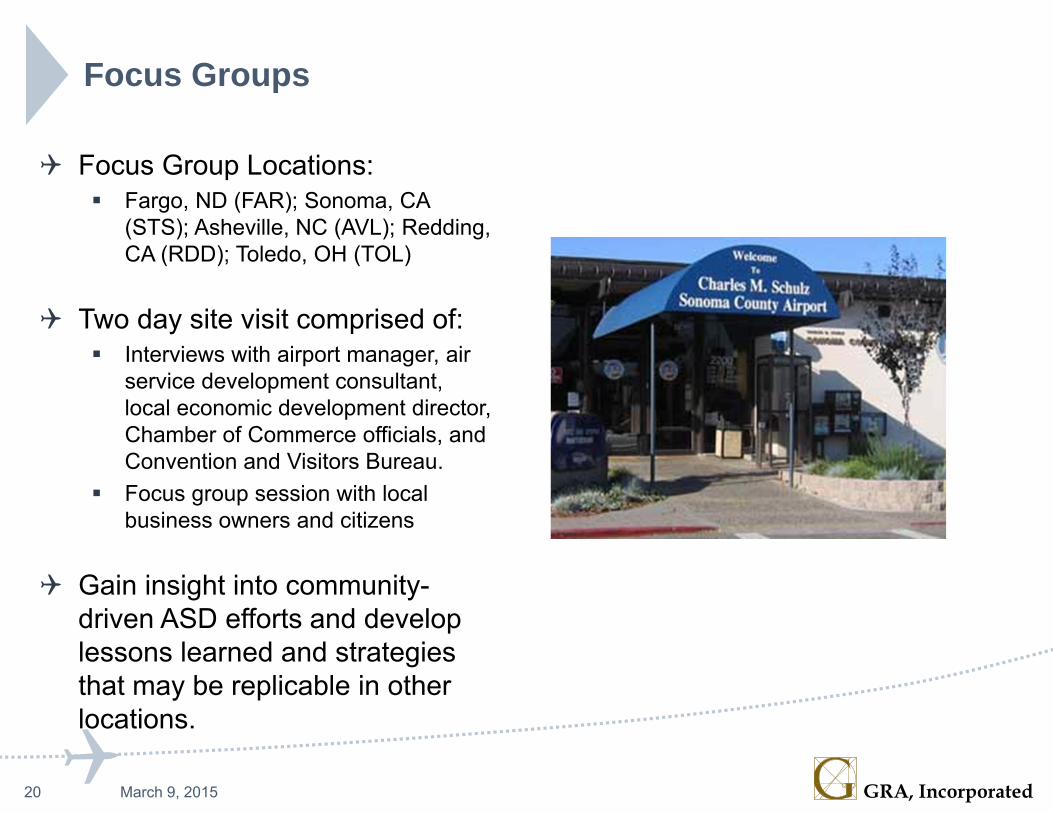

Focus Groups

Focus Group Locations: Fargo, ND (FAR); Sonoma, CA

(STS); Asheville, NC (AVL); Redding,CA (RDD); Toledo, OH (TOL)

Two day site visit comprised of: Interviews with airport manager, air

service development consultant,local economic development director,Chamber of Commerce officials, andConvention and Visitors Bureau.

Focus group session with localbusiness owners and citizens

Gain insight into community-driven ASD efforts and develop lessons learned and strategies that may be replicable in other locations.

20 March 9, 2015

GRA, Incorporated

Seats by Type of Carrier for Small Hub Case Study Airports, 2001 – 2013

21 March 9, 2015

GRA, Incorporated

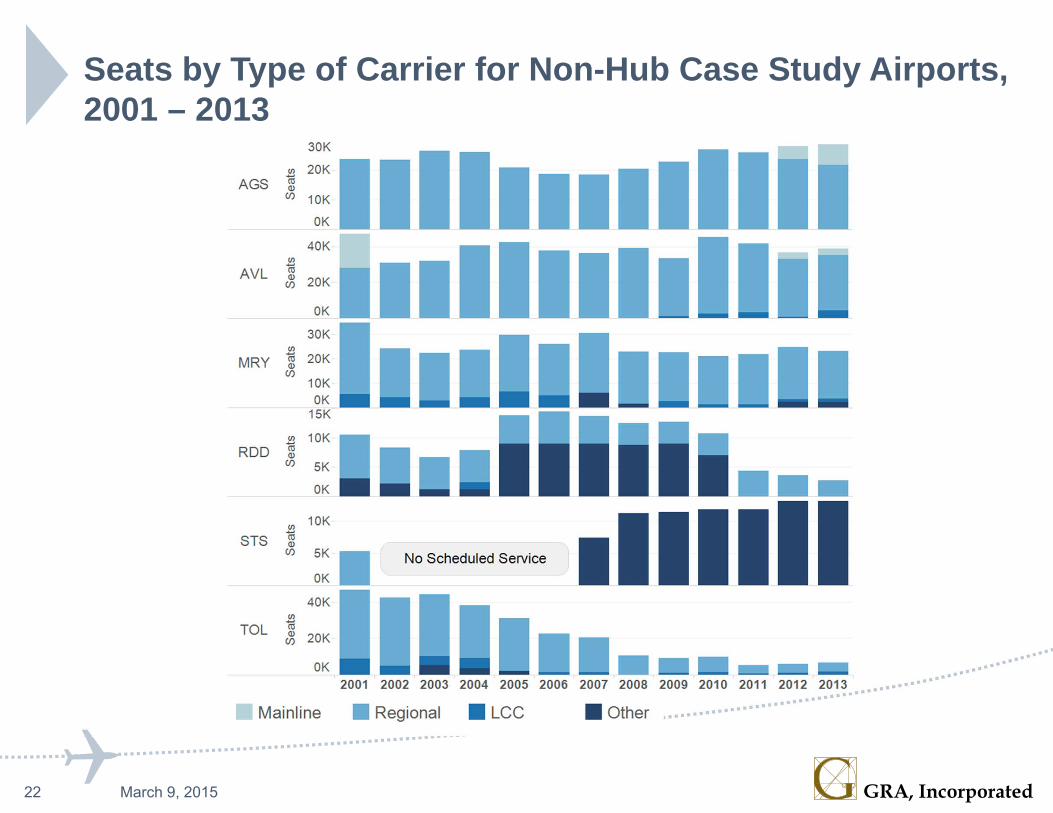

Seats by Type of Carrier for Non-Hub Case Study Airports, 2001 – 2013

22 March 9, 2015

GRA, Incorporated

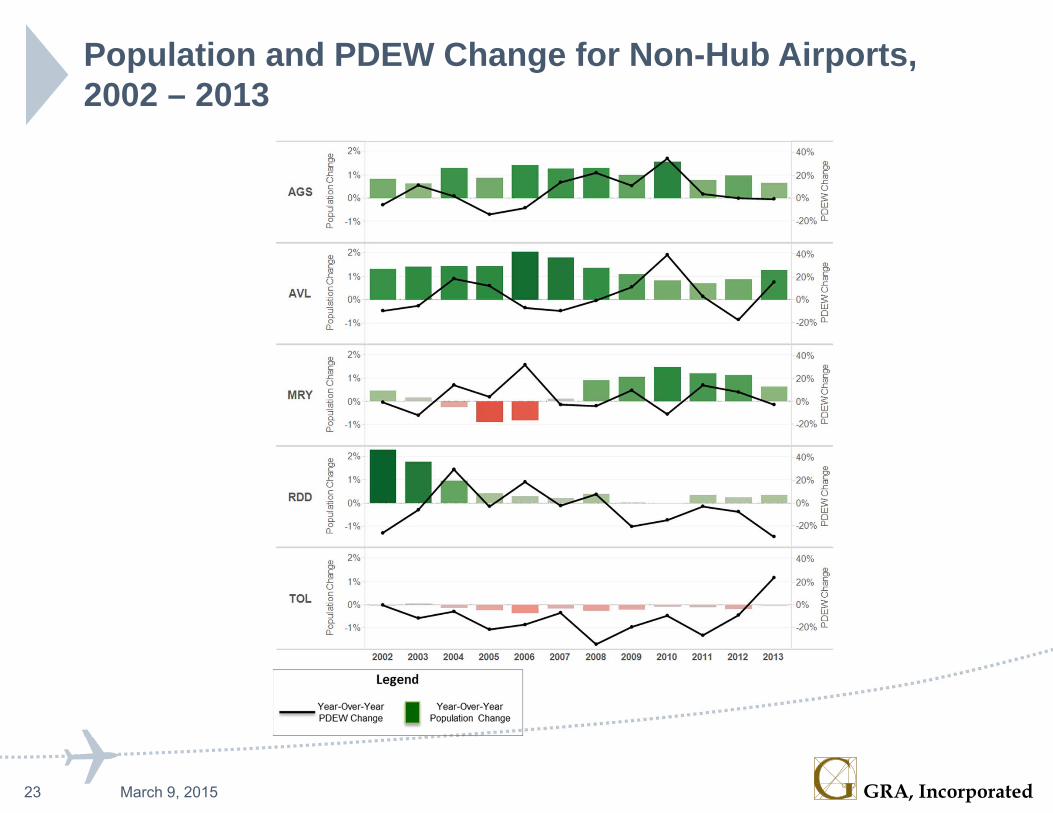

Population and PDEW Change for Non-Hub Airports, 2002 – 2013

23 March 9, 2015

GRA, Incorporated

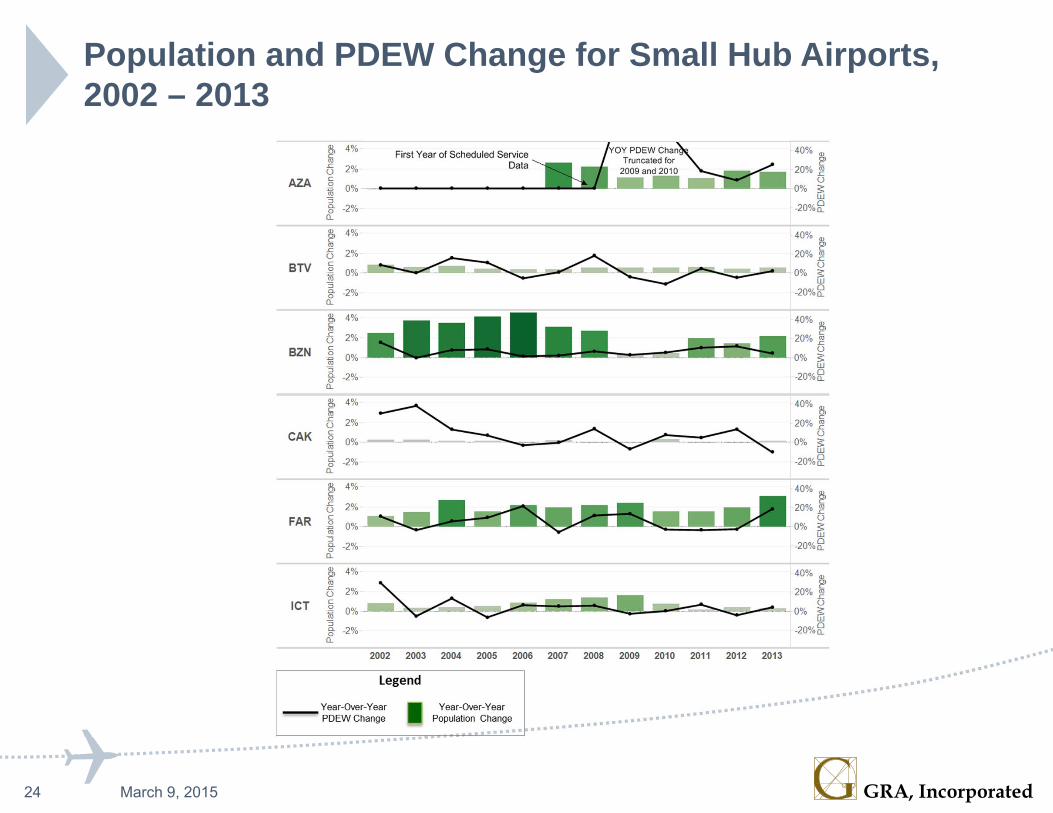

Population and PDEW Change for Small Hub Airports, 2002 – 2013

24 March 9, 2015

GRA, Incorporated

Lessons Learned Air service development is relative. Air carriers do not choose new routes in

a vacuum but through a comparative analysis of profitability across communities.

Many of the factors that determine whether an air carrier will start new service in a community are out of the hands of airport and community leaders.

When deciding whether to initiate an air service development program, communities must weigh the cost of the initial investment in incentives for new air service with the likelihood that their market can sustain the service once the incentives end.

As communities look to organize and develop air service development efforts, alternative modes of transportation that take passengers to larger hub airports are an effective way to build community support for the local airport.

25 March 9, 2015

GRA, Incorporated

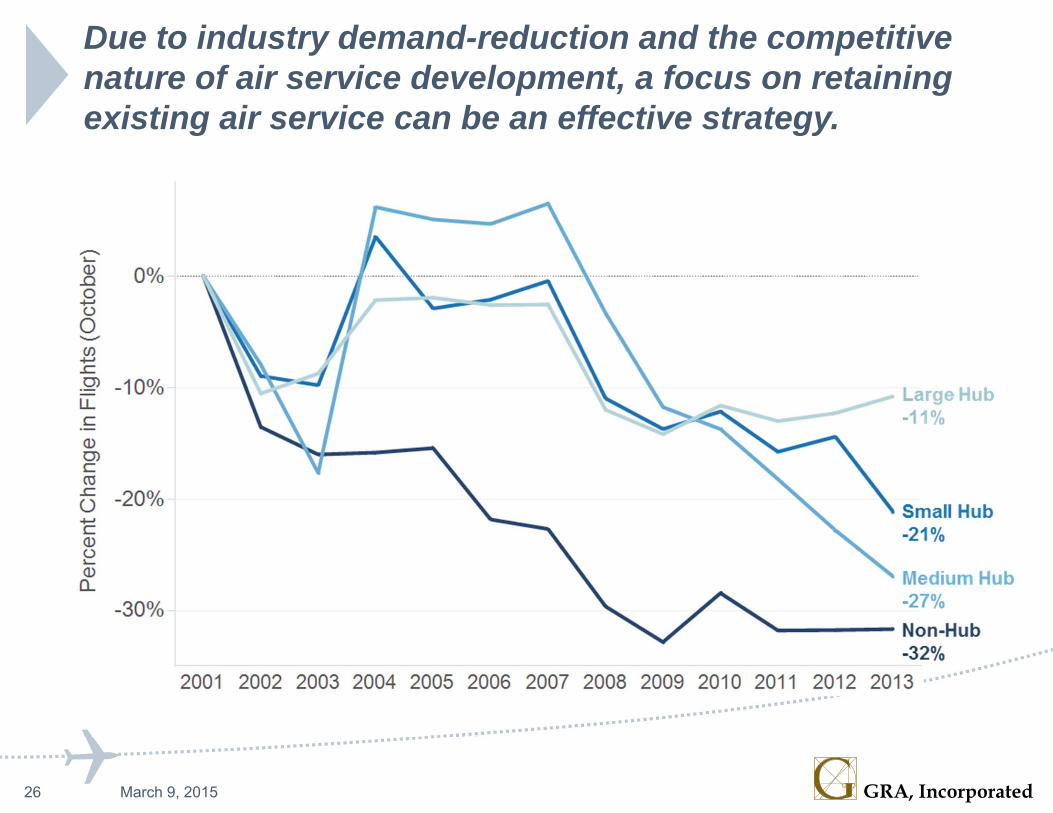

Due to industry demand-reduction and the competitive nature of air service development, a focus on retaining existing air service can be an effective strategy.

26 March 9, 2015

GRA, Incorporated

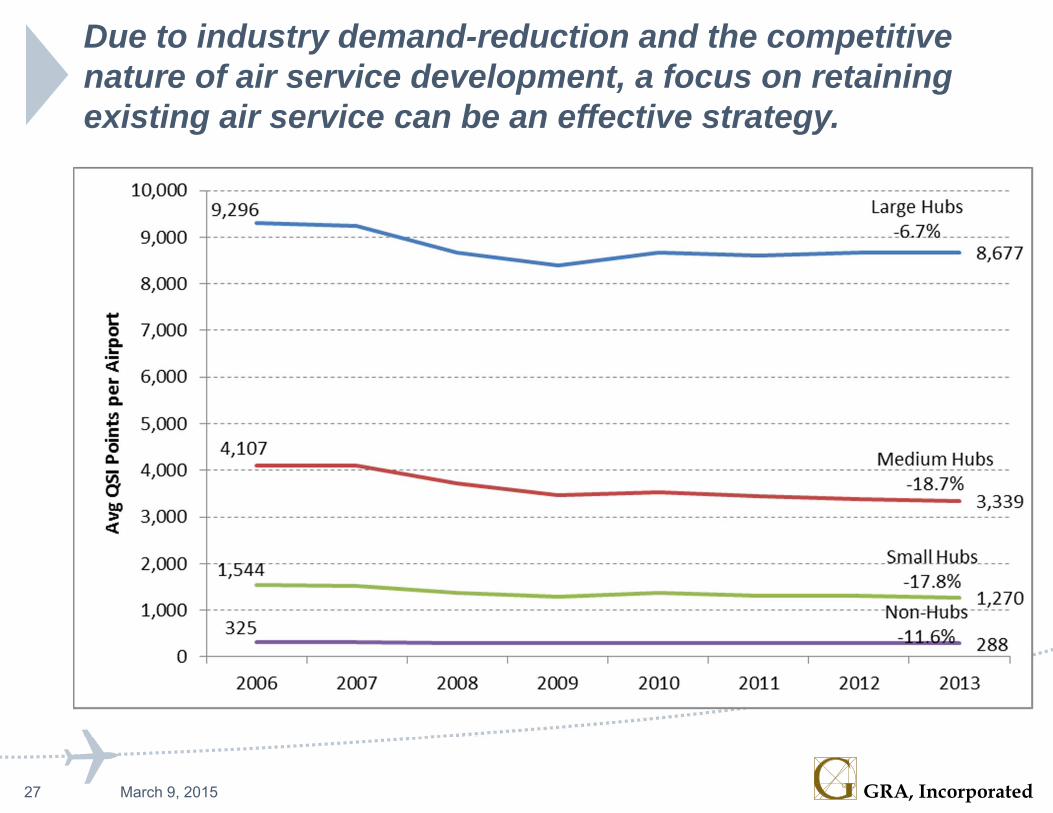

Due to industry demand-reduction and the competitive nature of air service development, a focus on retaining existing air service can be an effective strategy.

27 March 9, 2015

GRA, Incorporated

There is little connection between air service growth and population growth; however, there is a stronger connection between air service growth and regional employment change

28 March 9, 2015

-10% -5% 0% 5% 10% 15% 20% 25%Employment Change 2001-2013

-100%-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

Sea

t Cha

nge

2001

-201

3TOL

RDD

MRY

AVL

ICTBZNAGS

FARCAK

ECP

STS

GRA, Incorporated

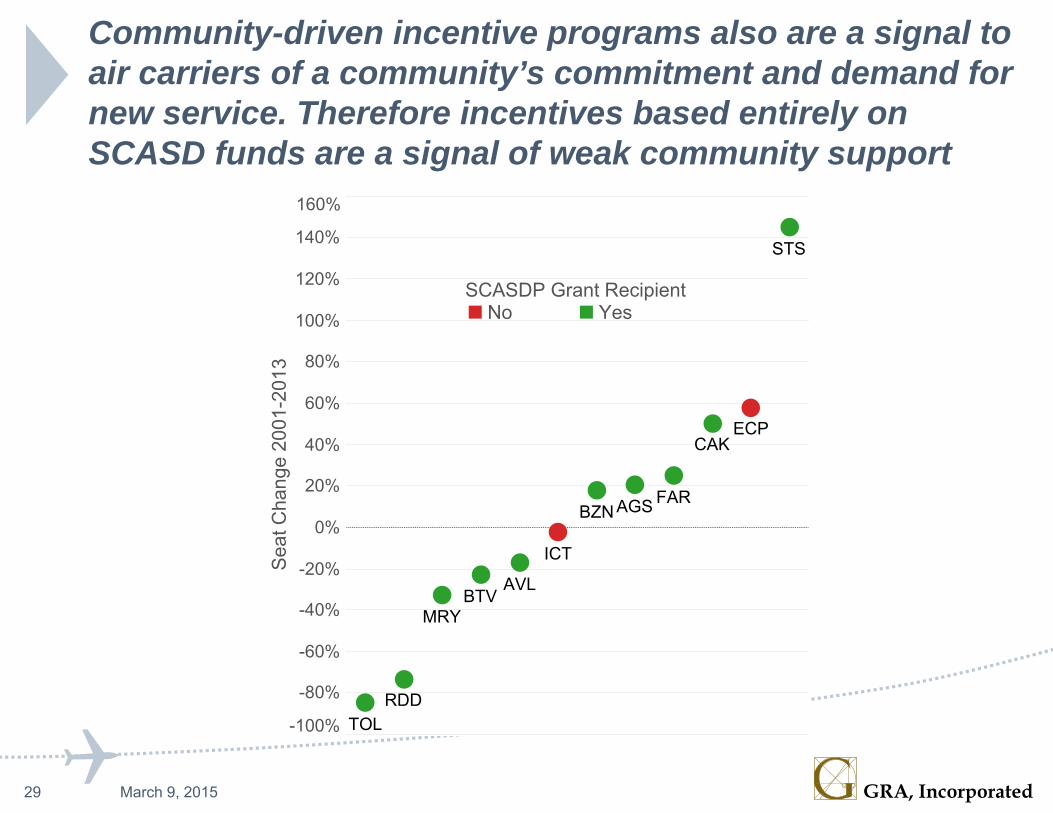

Community-driven incentive programs also are a signal to air carriers of a community’s commitment and demand for new service. Therefore incentives based entirely on SCASD funds are a signal of weak community support

29 March 9, 2015

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

Sea

t Cha

nge

2001

-201

3

MRY

RDD

AGS

CAKECP

FAR

BTV

BZN

TOL

STS

AVL

ICT

SCASDP Grant RecipientNo Yes

GRA, Incorporated

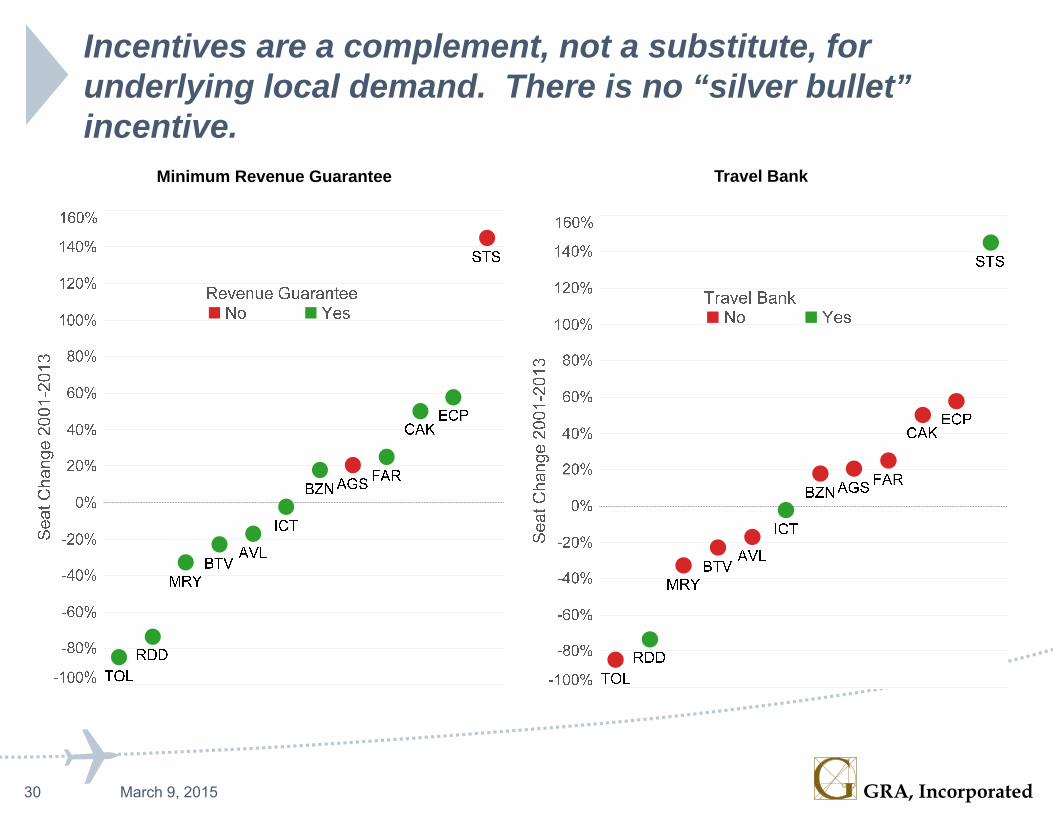

Incentives are a complement, not a substitute, for underlying local demand. There is no “silver bullet” incentive.

30 March 9, 2015

Minimum Revenue Guarantee Travel Bank

GRA, Incorporated

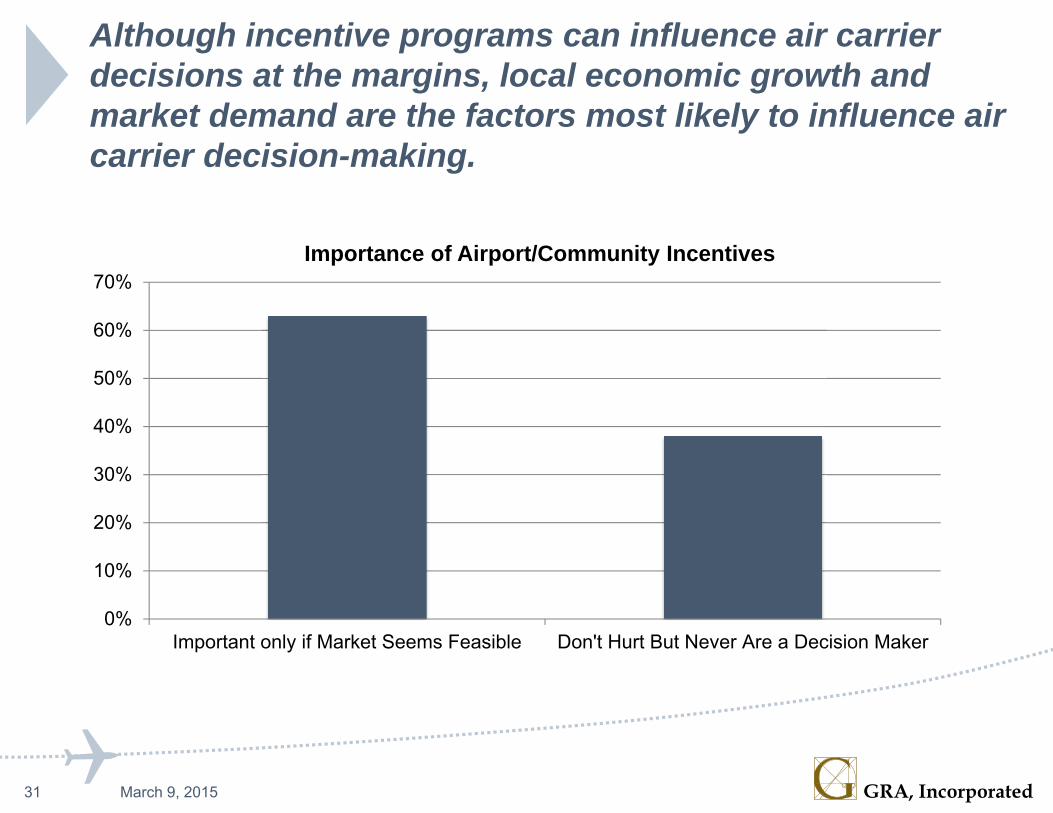

Although incentive programs can influence air carrier decisions at the margins, local economic growth and market demand are the factors most likely to influence air carrier decision-making.

31 March 9, 2015

0%

10%

20%

30%

40%

50%

60%

70%

Important only if Market Seems Feasible Don't Hurt But Never Are a Decision Maker

Importance of Airport/Community Incentives

GRA, Incorporated

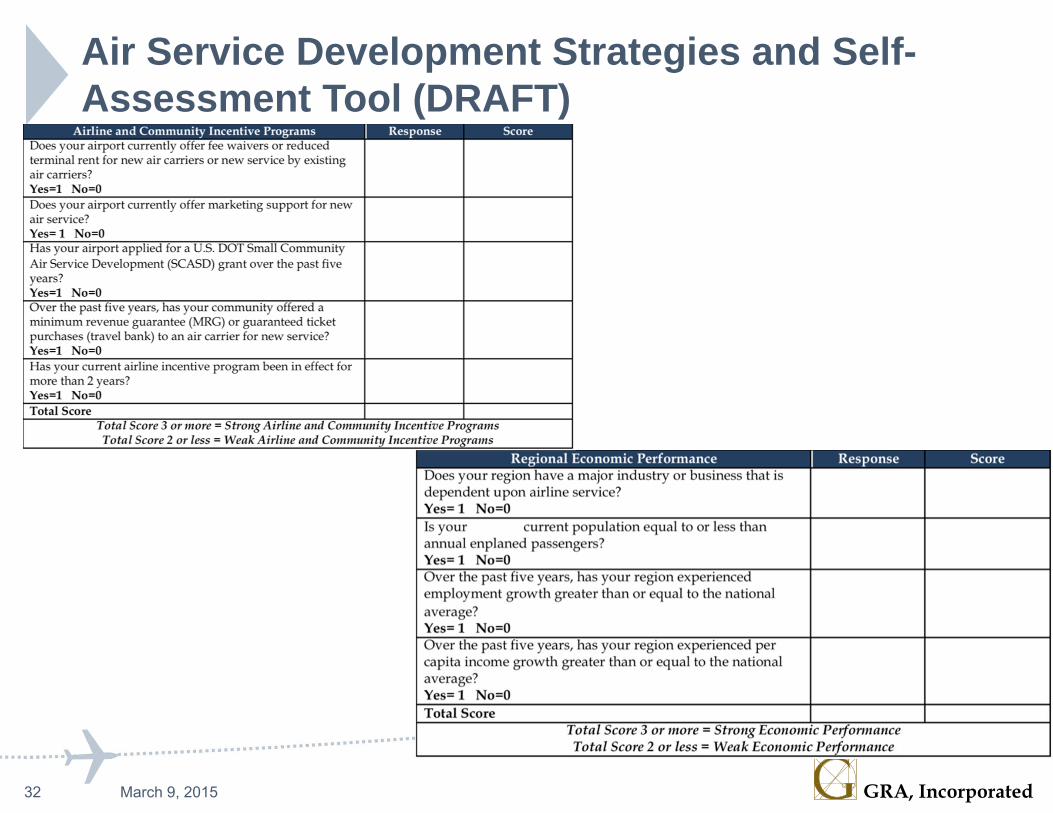

Air Service Development Strategies and Self-Assessment Tool (DRAFT)

32 March 9, 2015

GRA, Incorporated

Air Service Development Strategies and Self-Assessment Tool (DRAFT)Strong Regional Economic Performance

Ensure that Major Businesses that Depend on Air Service are Active Members of Airline Attraction Committees

Officials Should Routinely Meet to Quantify Both Realized and Unrealized Demand for Air Service Generated by Changes in Economic Indicators and Demographic Factors.

Use Indicators of Strong Economic Performance to Expand Existing Service

Weak Regional Economic Performance

Airport Managers Should Be Actively Involved in Local Economic Development Efforts to Attract New Businesses or Industries to a Region

Airport Experience Branding or Tourism Investment Can be an Effective Strategy to Overcome Limited Economic Growth and Generate Demand for New Service

33 March 9, 2015

GRA, Incorporated

Air Service Development Strategies and Self-Assessment Tool (DRAFT)Strong Level of Community Engagement Airport Managers Must Continue to

Educate and Reach Out to Local Businesses and Civic Groups on the Performance of the Airport and the Airline Industry.

Formalize Governance Arrangements to Allow for Nimble Responses to Future Air Service Development Opportunities

Weak Level of Community Engagement Airport Managers Must Establish

Education and Outreach Programs that Communicate the Value of the Airport to the Community

Develop Close Working Relationships with Key Community and Economic Leaders Such as the EDC, CVB, and Chamber of Commerce

34 March 9, 2015

GRA, Incorporated

ACRP 03-29 Materials

Searchable database of airport-specific air service performance data from 2001-2013.

Guidebook that contains case studies, focus groups, lessons learned and strategies for airport managers and community leaders: Linking Economic Performance and Air Service Development Developing an Air Service Development Program Identifying an Air Carrier and a New Destination Developing an Effective Incentive Program Meeting with Air Carriers and Community Leaders Ensuring the Sustainability of New Service

Airport/Community Self-Assessment Tool and Customized Strategies for Air Service Development

35 March 9, 2015