Embed Size (px)

Citation preview

EFAMA’s ACTIVITIES

Peter De Proft, Director General

17-18 September 2015, Ljubljana

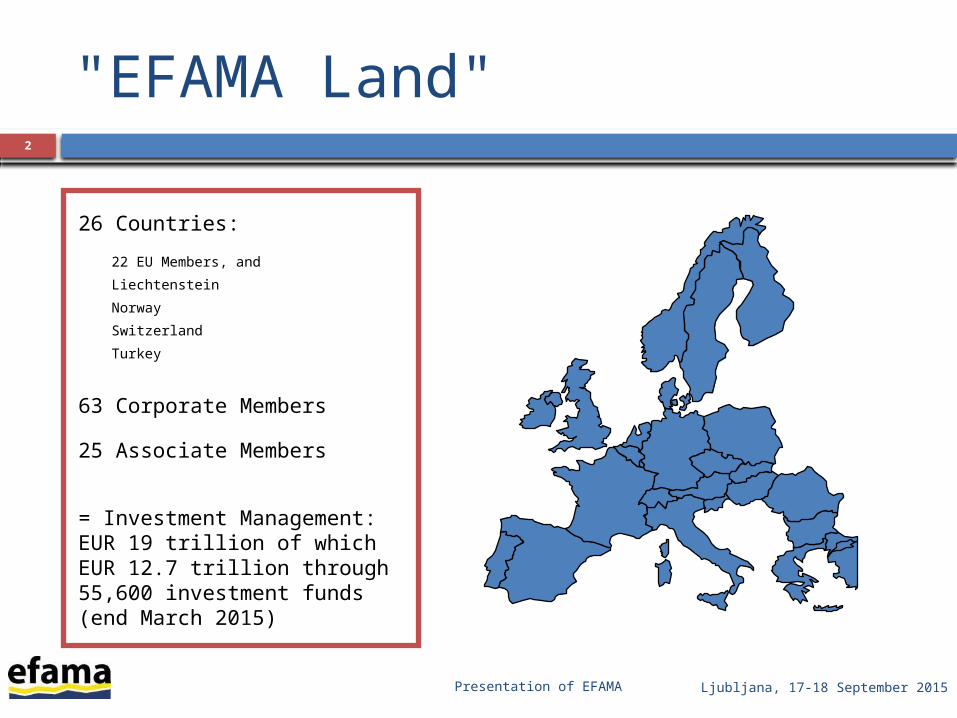

"EFAMA Land"2

26 Countries:

22 EU Members, and

Liechtenstein

Norway

Switzerland

Turkey

63 Corporate Members

25 Associate Members

= Investment Management: EUR 19 trillion of which EUR 12.7 trillion through 55,600 investment funds (end March 2015)

Ljubljana, 17-18 September 2015Presentation of EFAMA

Asset Management in EuropeTotal AuM: EUR 19 trillion at end 2014

3

106% 102%81%

96%101%

98%106%

114%124%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 est.

Investment Funds Discretionary Mandates AuM/GDP

13.6

10.9

12.313.6 13.6

15.116.5

19.0

13.4

Source: EFAMA Asset Management Report 2015

Ljubljana, 17-18 September 2015Presentation of EFAMA

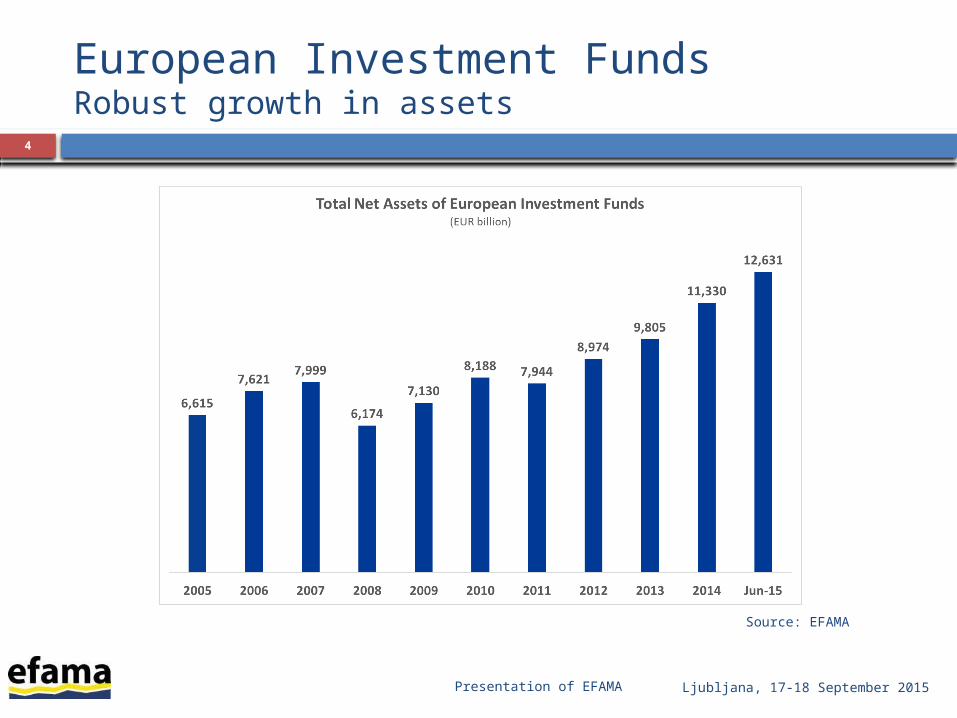

European Investment FundsRobust growth in assets

4

Source: EFAMA

Ljubljana, 17-18 September 2015Presentation of EFAMA

European Investment FundsAssets of UCITS and AIFs

Ljubljana, 17-18 September 2015Presentation of EFAMA

5

Source: EFAMA Funds classified according to regulatory definition of UCITS and AIFs

European Investment FundsNumber of UCITS and AIFs Funds

6

Source: EFAMA Funds classified according to regulatory definition of UCITS and AIFs

Ljubljana, 17-18 September 2015Presentation of EFAMA

European Investment FundsSustained investor demand over the last decade

7

Source: EFAMA

Ljubljana, 17-18 September 2015Presentation of EFAMA

European Investment FundsStrong recovery of net sales after 2008

8

Source: EFAMA

Ljubljana, 17-18 September 2015Presentation of EFAMA

European Investment FundsGrowing importance of cross-border UCITS

9

Source: EFAMA

Ljubljana, 17-18 September 2015Presentation of EFAMA

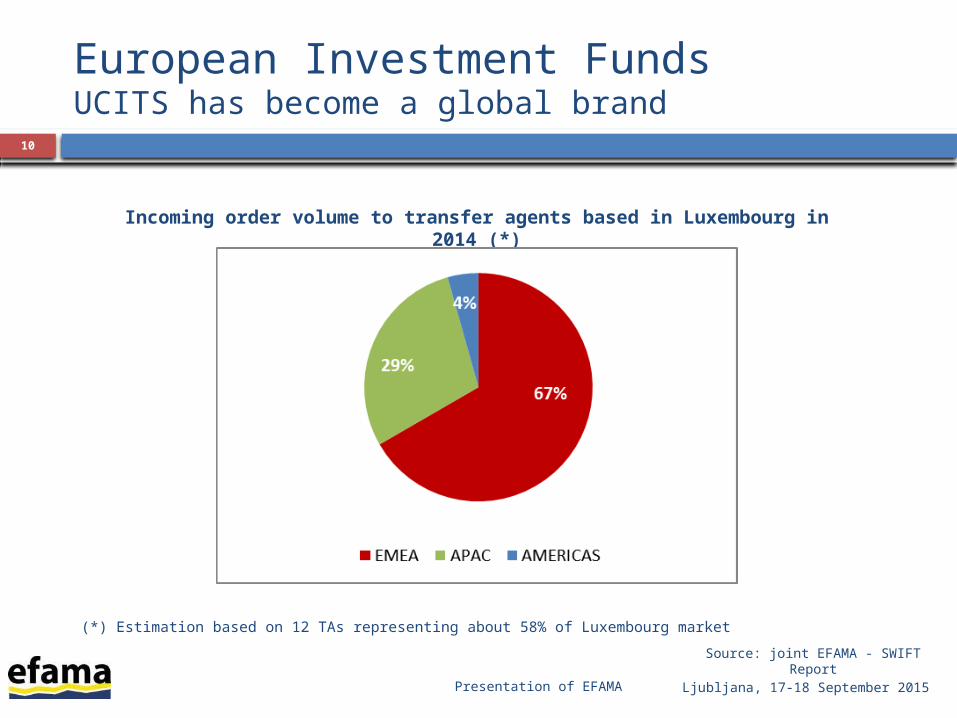

European Investment FundsUCITS has become a global brand

10

Incoming order volume to transfer agents based in Luxembourg in 2014 (*)

(*) Estimation based on 12 TAs representing about 58% of Luxembourg market

Source: joint EFAMA - SWIFT Report

Ljubljana, 17-18 September 2015Presentation of EFAMA

European Investment FundsInternationalisation of sales of UCITS

Ljubljana, 17-18 September 2015Presentation of EFAMA

11

The growth of the UCITS market is driven by the sales of cross-border UCITS

The global financial crisis has strengthened the sales of cross-border UCITS

Different factors can explain the success of cross-border UCITS The move towards guided/open architecture Growing demand for UCITS brand Growing importance of fund platforms in distribution of third-

party funds

There is an unprecedented wave of regulatory initiatives affecting the asset management industry

Ljubljana, 17-18 September 2015

12

Initiatives targeting specifically the European AM industry

▪ UCITS IV▪ UCITS V▪ UCITS VI ▪ ETFs▪ Money Market Funds▪ AIFMD▪ Venture Capital Funds▪ Social Entrepreneurship

Funds▪ Long-term investment funds

Initiatives not targeting the AM industry but having spill-over effects

▪ Banking Union▪ Recovery and resolution▪ Liikanen report▪ Basel III▪ Solvency II▪ IMD review▪ Revision of IORP▪ White Paper on pensions▪ Credit rating agencies ▪ SLD▪ Audit review

▪ PRIPs▪ MiFID review▪ ICSD▪ Shadow banking▪ EMIR▪ EU Supervisory structure▪ Short selling▪ Financial Transaction Tax▪ Corporate Governance

Initiatives targeting financial institutions, comprising the European AM industry

▪ FATCA (US)▪ Dodd Frank (US)▪ Volcker Rule (US)▪ European national initiatives to

– Ban inducements (e.g. UK, NL)– Ban complex products (e.g. Belgium)

Reg

ula

tory

in

itia

tive

s at

Eu

rop

ean

lev

el

Presentation of EFAMA

Dimensions to Regulation

Ljubljana, 17-18 September 2015

13

Presentation of EFAMA

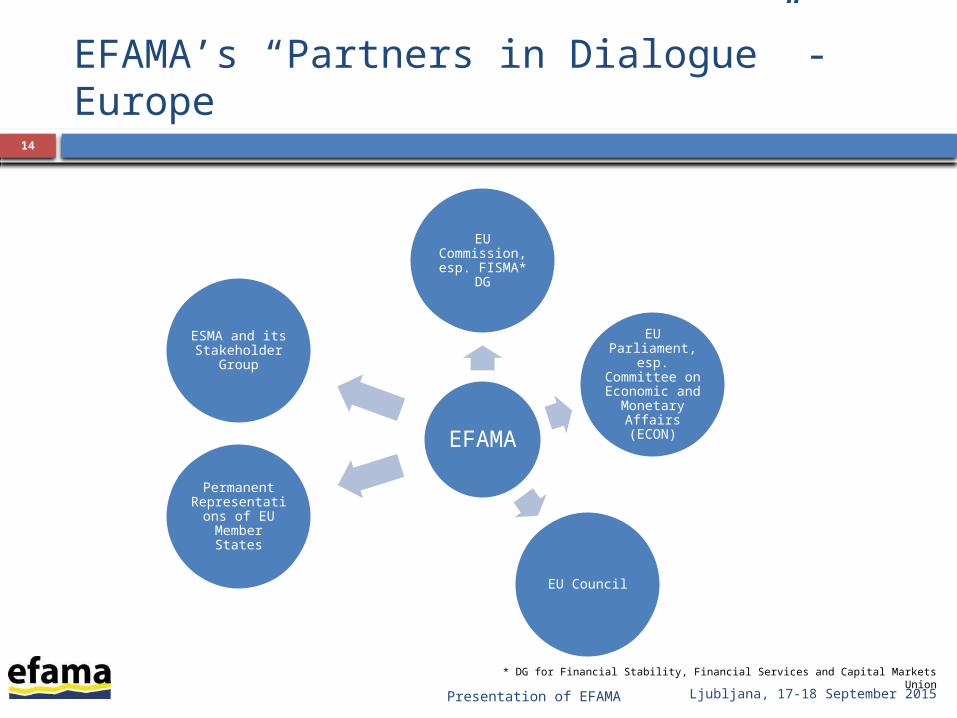

EFAMA’s “Partners in Dialogue” - Europe14

EFAMA

EU Commission, esp. FISMA* DG

EU Parliament, esp. Committee

on Economic and Monetary Affairs (ECON)

EU Council

Permanent Representations of EU Member

States

ESMA and its Stakeholder

Group

* DG for Financial Stability, Financial Services and Capital Markets Union

Presentation of EFAMA Ljubljana, 17-18 September 2015

EFAMA’s International "Partners in Dialogue "

Ljubljana, 17-18 September 2015Presentation of EFAMA

15

AMAC

HK SFC

MAS (Singapore)

IIFA

CFTC

U.S. SEC

U.S. IRS

U.S. Treasury

IOSCO

FSB / ESRB

National EU Regulators

CSRC (China)

EFAMA - top performing association in Financial Services category

Ljubljana, 17-18 September 2015Presentation of EFAMA

On 19 May 2015, APCO and EurActiv announced the top performing trade association in Brussels in the second edition of the TradeMarks Survey 2015. The 2015 survey was conducted between November 2014 and April 2015.EFAMA was ranked the top performing association in the Financial Services category.

16

17

Presentation of EFAMA

Competition

New distribution models Emergence of new actors

Ljubljana, 17-18 September 2015

Increasing demand for transparency and independence

European discussions around the ban on inducements

New technologies and social media increasing connectivity

Driving forces…

1

2

3

Superior technological capabilities

Web giants key advantages…

1

Major traffic on their platforms

Indicators of clients’ interests

2

3

Strong financial capabilities4

Globalisation also accelerates competition

Presentation of EFAMA

18

Competition: Implications

New distribution rules will have an impact – and some unintended consequences – on the future of open architecture models.

Technology firms will be competing with asset managers (possibly) by entering into asset management and (most likely) by changing the ecosystem around asset managers.

Tougher competition means continued pressure on fees.

The best defense is to attack, in particular in the areas of innovation, investment capabilities and costs.

Ljubljana, 17-18 September 2015

Commission Green Paper, 18 February 2015Focus on funding for SMEs and infrastructure, on attracting more investment into the EU and opening up a wider range of funding sources.

Develop proposals to encourage high quality securitisation and free up bank balance sheets to lend

Review the Prospectus Directive to make it easier for (smaller) firms to raise funding and reach investors cross border

Improve the availability of credit information on SMEs so it is easier to invest in them

Work with the industry to put in place a pan-European private placement regime to encourage direct investment into smaller businesses

Support the take-up of European Long-term Investment Funds (ELTIFs) to channel investment in infrastructure and other long-term projects

1

2

3

4

5

Hill addressing ECON, February 2015

…a major upgrade to the financial system, linking those who want investment to those with funds to invest…needs to be faster and more efficient… not just institutional investors - also direct retail investors who want more choice but need confidence to invest cross-border… needs to be bottom up and industry-led to work.. need proper analysis before acting…some cultural barriers but mainly information and confidence - countries have vested interests that need to be overcome

© 2015 KPMG LLP, a UK limited liablility partneship and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Ljubljana, 17-18 September 2015Presentation of EFAMA

19

A change of tone from the Commission

Helping businesses

grow

Banking, investments and

funds

Tax treatments and incentives

Financing, venture capital and private

placements

Validation, assurance and

accounting

Financing and investing in

infrastructure

Data, digital and technology

Corporate governance and

board effectiveness

Risk and regulation

The new Commission’s agenda is a break from the post-crisis ‘regulate everything’ approach. CMU is an opportunity to create a more joined-up vision that brings together a number of important commercial and public policy interests.

EU’s “Better Regulation” approach

© 2015 KPMG LLP, a UK limited liablility partneship and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Ljubljana, 17-18 September 2015Presentation of EFAMA

20

Endorse the Commission’s stated objective to conduct a cumulative impact analysis

The IM industry’s response

Key points from EFAMA’s response to the Green Paper.

A priority is to rebuild confidence in financial markets by putting investors’ interests at the heart of CMU

© 2015 KPMG LLP, a UK limited liablility partneship and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Ljubljana, 17-18 September 2015Presentation of EFAMA

22

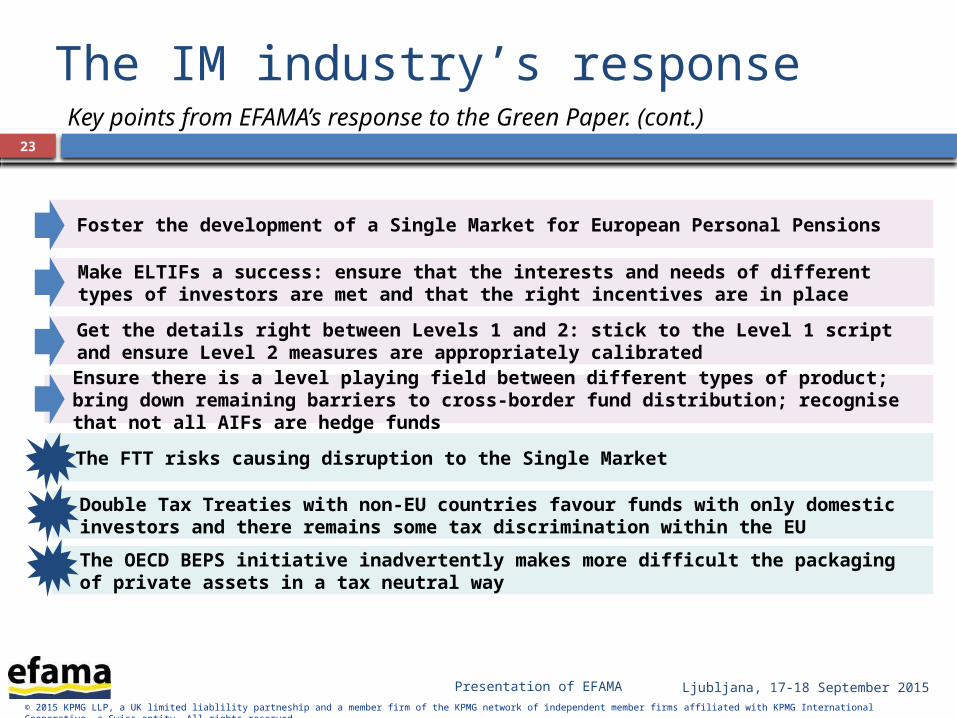

The IM industry’s responseKey points from EFAMA’s response to the Green Paper. (cont.)

Foster the development of a Single Market for European Personal Pensions

Get the details right between Levels 1 and 2: stick to the Level 1 script and ensure Level 2 measures are appropriately calibrated

Make ELTIFs a success: ensure that the interests and needs of different types of investors are met and that the right incentives are in place

The FTT risks causing disruption to the Single Market

Ensure there is a level playing field between different types of product; bring down remaining barriers to cross-border fund distribution; recognise that not all AIFs are hedge funds

Double Tax Treaties with non-EU countries favour funds with only domestic investors and there remains some tax discrimination within the EU

The OECD BEPS initiative inadvertently makes more difficult the packaging of private assets in a tax neutral way

© 2015 KPMG LLP, a UK limited liablility partneship and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

Ljubljana, 17-18 September 2015Presentation of EFAMA

23

EFAMA’s ACTIVITIES

Peter De Proft, Director General

17-18 September 2015, Ljubljana