Embed Size (px)

Citation preview

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 1/40

Convertible Bonds: Best of Both Worlds

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 2/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 2

Contents

Introduction to convertible bonds

Do we have a real stand alone asset class?

• Historical performance

• What are the risk / return characteristics? Measuring convexity

• Is strategic allocation possible?

• Is sustained allocation possible?

Outlook for the convertible bonds market

What investment process to use?

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 3/40

Introduction to Convertible Bonds

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 4/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 4

What is a convertible bond

A convertible bond is a bond which is convertible into the equity of the issuing company. Incase the bond is convertible into the equity of another company it is called anexchangeable bond. The investor can convert the bond at anytime before the maturity and

it is a choice for the investor, not an obligation.

As such, convertible bonds have characteristics of fixed income instruments (a fixedmaturity, an annual coupon rate, a redemption value) and equity instruments (via itspossibility to exchange it for shares)

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 5/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 5

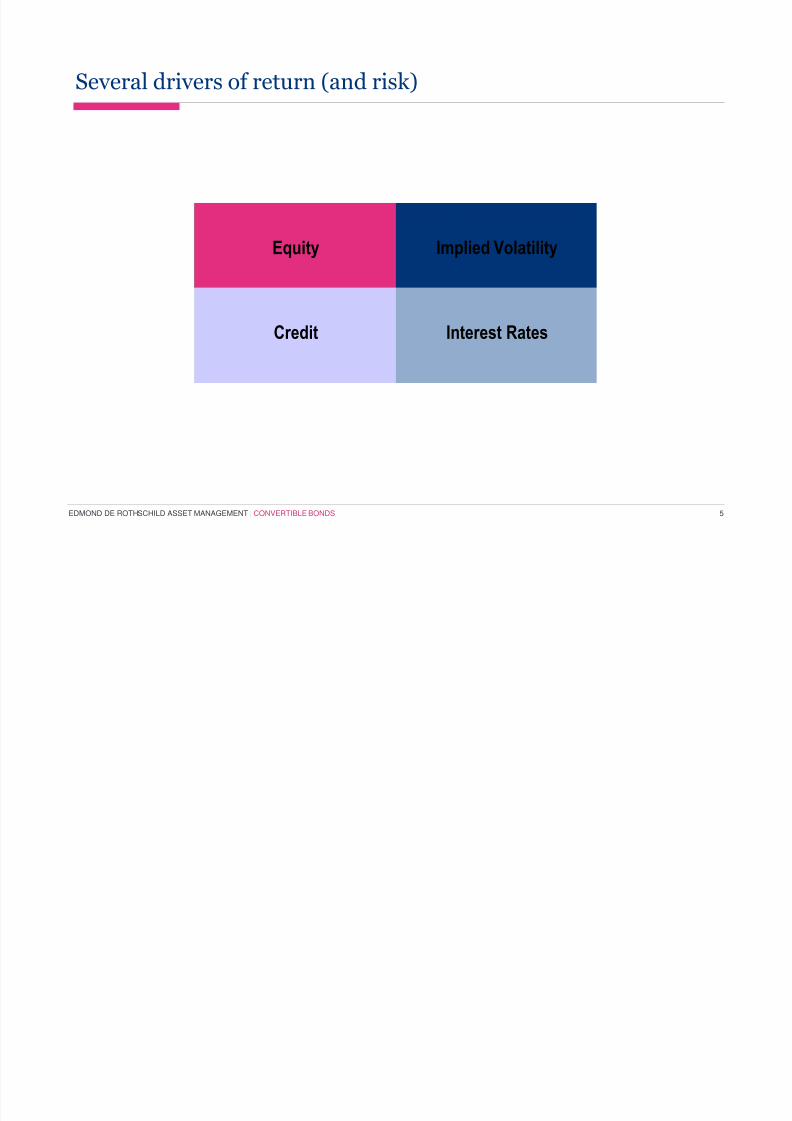

Several drivers of return (and risk)

Equity

Credit

Implied Volatility

Interest Rates

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 6/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 6

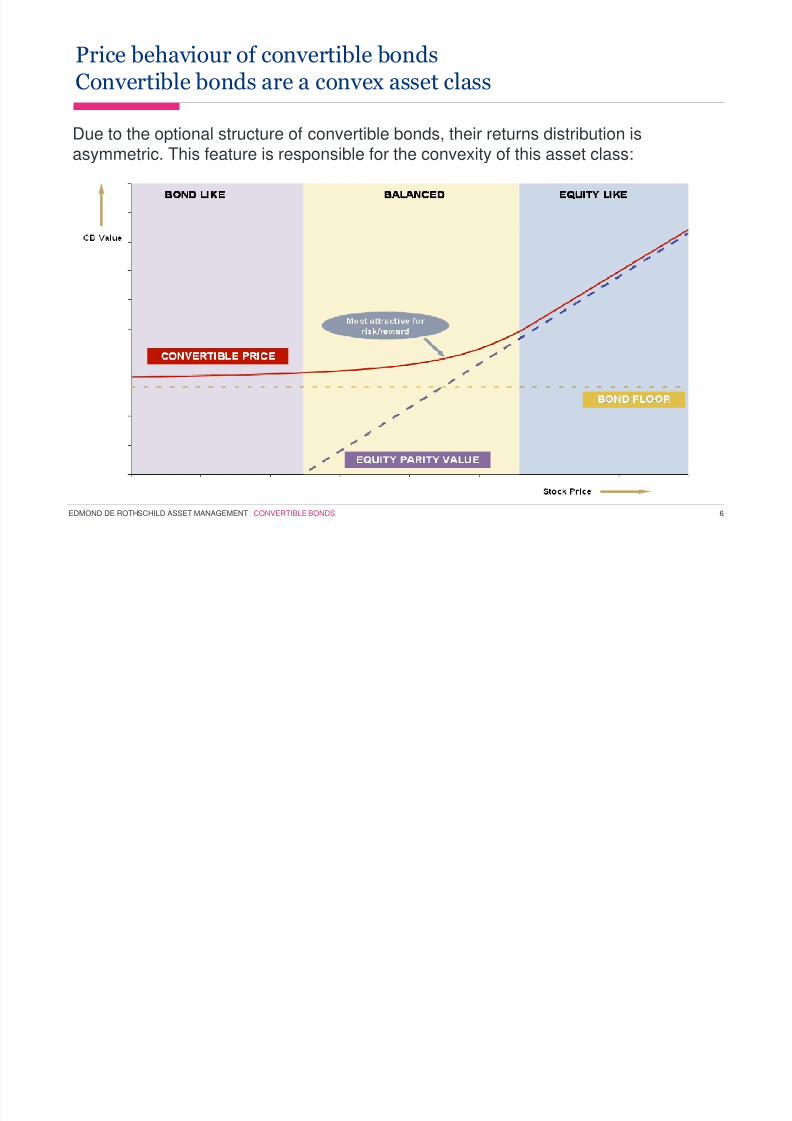

Due to the optional structure of convertible bonds, their returns distribution isasymmetric. This feature is responsible for the convexity of this asset class:

Price behaviour of convertible bondsConvertible bonds are a convex asset class

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 7/40

Do we have a real stand alone asset class?

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 8/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 8

Illustration of the convertible bond convexity: historical analyses

Convexity increases in line with the investment horizon for convertibles, from 4 yearsonwards convertible bonds deliver a positive performance on average when equities

are moving downwards

Convertible bonds* participation to upside and downside equity* movements over various investmenthorizons: average annualized performance given by monthly returns over the last 10 years

-60%

-40%

-20%

0%

20%

40%

60%

80%

1 year 2 years 3 years 4 years 5 years

Average upside participation

Average downside participation

*Convertibles: UBS Global Focus EUR HedgedEquities: MSCI World AC Local Currency Source: EdRAM, data from 31/12/1993 to 31/12/2010

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 9/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 9

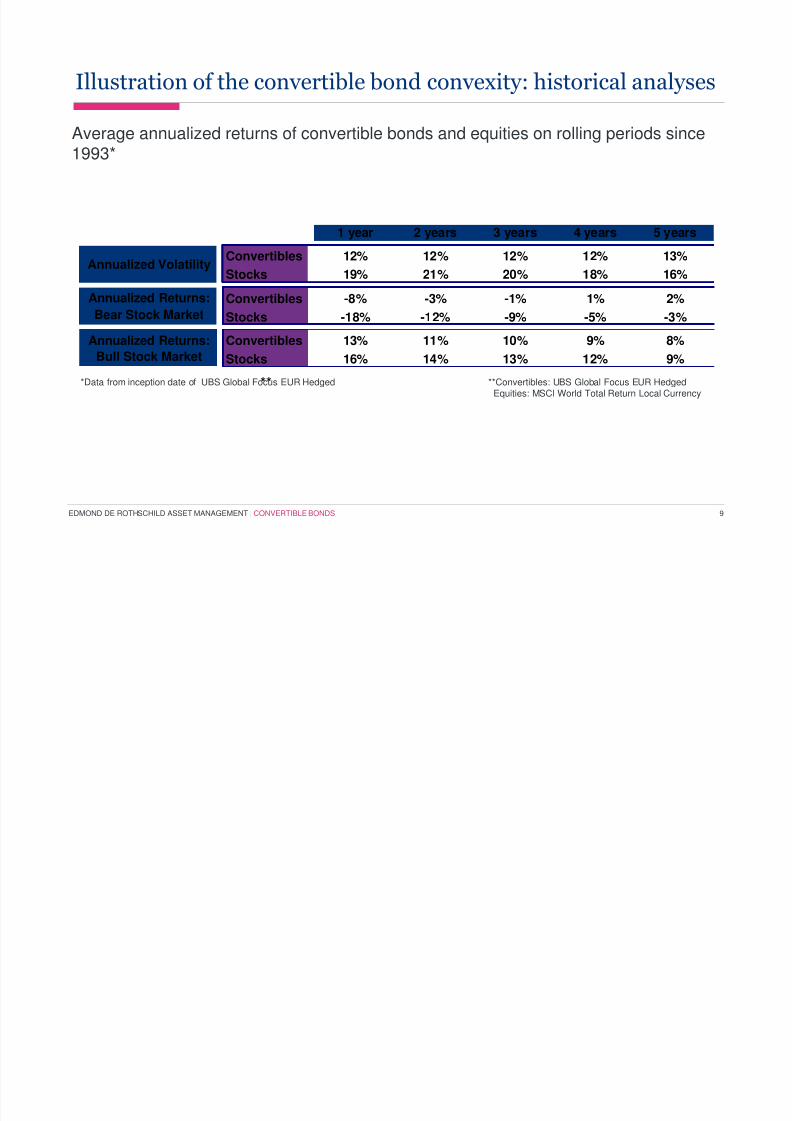

Average annualized returns of convertible bonds and equities on rolling periods since1993*

Illustration of the convertible bond convexity: historical analyses

**Convertibles: UBS Global Focus EUR Hedged

Equities: MSCI World Total Return Local Currency

**

**

**

1 year 2 years 3 years 4 years 5 years

Convertibles 12% 12% 12% 12% 13%

Stocks 19% 21% 20% 18% 16%

Convertibles -8% -3% -1% 1% 2%

Stocks -18% -12% -9% -5% -3%

Convertibles 13% 11% 10% 9% 8%

Stocks 16% 14% 13% 12% 9%

Annualized Returns:Bear Stock Market

Annualized Returns:

Bull Stock Market

Annualized Volatility

*Data from inception date of UBS Global Focus EUR Hedged

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 10/40

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 11/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 11

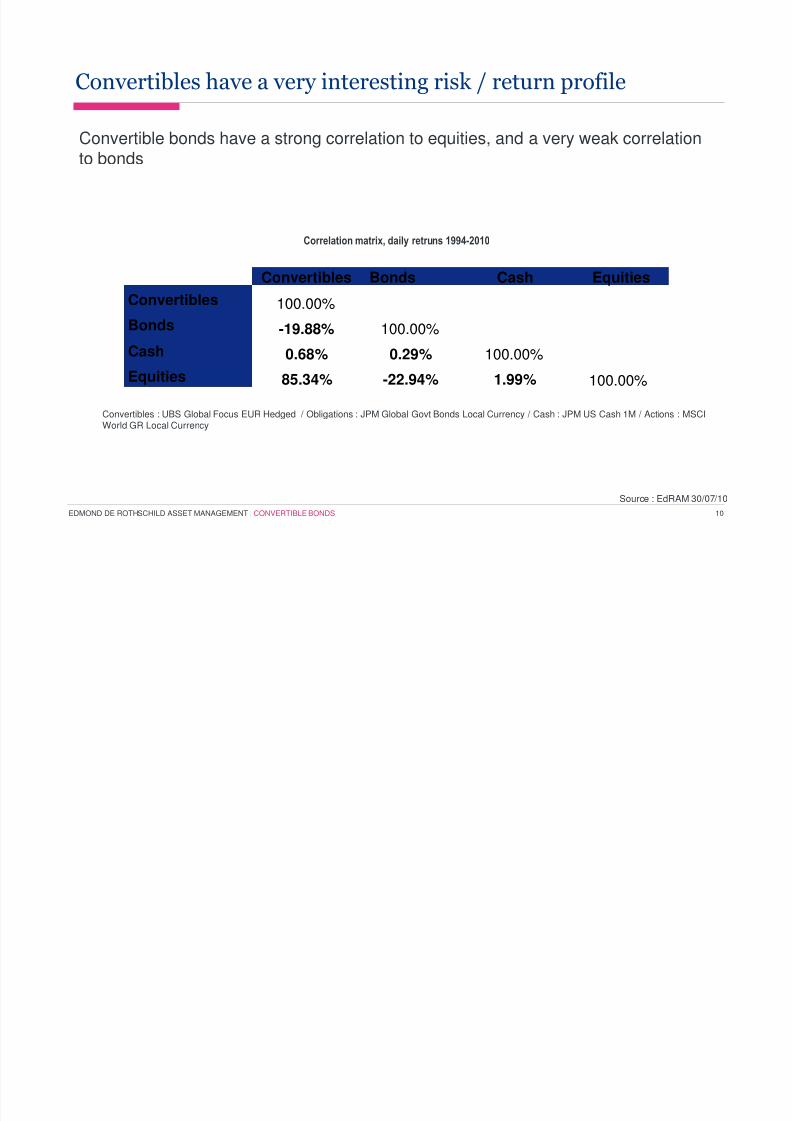

A very low correlation to bonds

A risk / return profile which is superior to the one of equities, stable over differentinvestment horizons

The performance is linked to the convexity of the instrument which benefits from rising

equity markets whilst benefiting from fixed income characteristics : a fixed coupon and aredemtion date

Convertibles have a very interesting risk / return profile

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 12/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 12

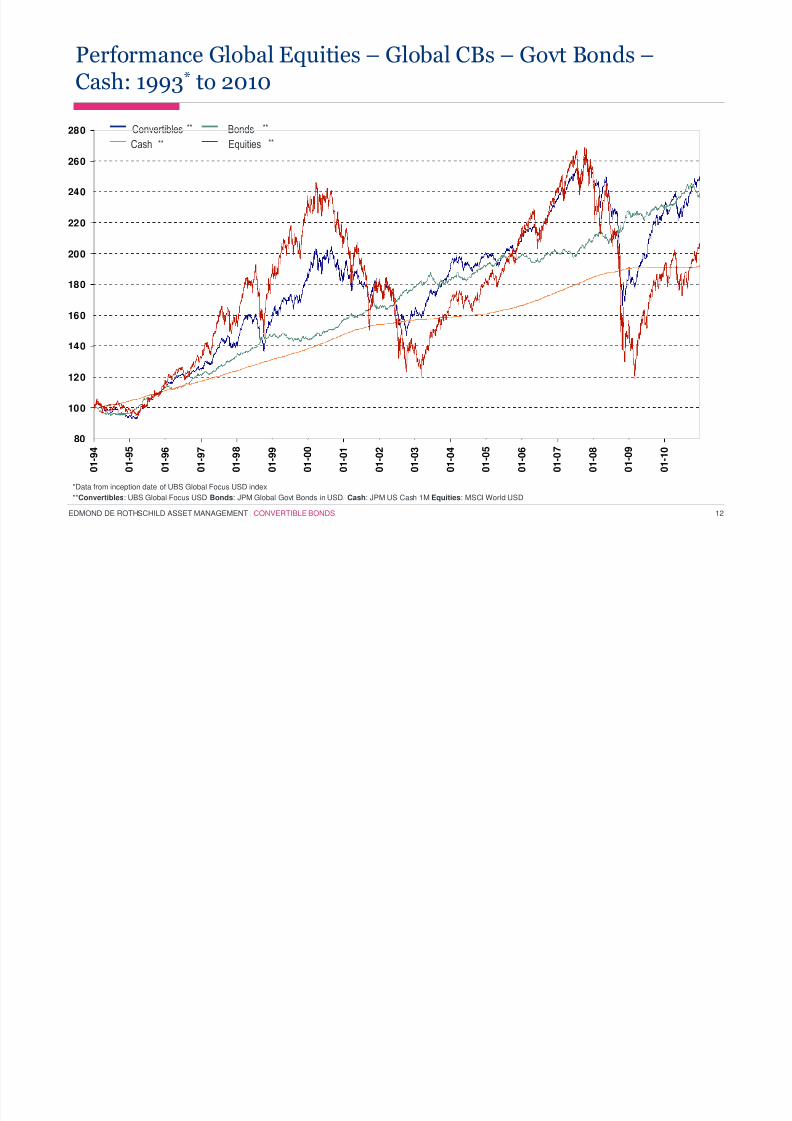

Performance Global Equities – Global CBs – Govt Bonds –Cash: 1993* to 2010

*Data from inception date of UBS Global Focus USD index.**Convertibles: UBS Global Focus USD Bonds: JPM Global Govt Bonds in USD. Cash: JPM US Cash 1M Equities: MSCI World USD

Convertibles Bonds

Cash Equities

**

****

**

80

100

120

140

160

180

200

220

240

260

280

0 1 - 9 4

0 1 - 9 5

0 1 - 9 6

0 1 - 9 7

0 1 - 9 8

0 1 - 9 9

0 1 - 0 0

0 1 - 0 1

0 1 - 0 2

0 1 - 0 3

0 1 - 0 4

0 1 - 0 5

0 1 - 0 6

0 1 - 0 7

0 1 - 0 8

0 1 - 0 9

0 1 - 1 0

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 13/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 13

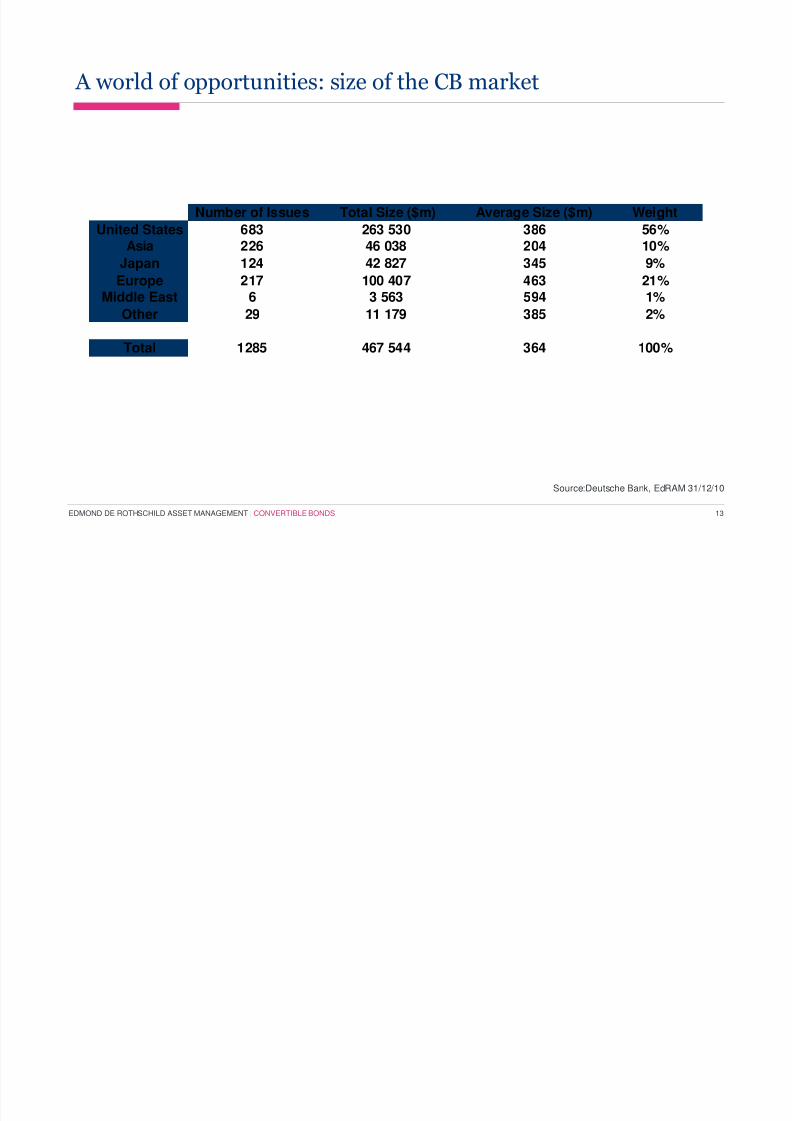

A world of opportunities: size of the CB market

Source:Deutsche Bank, EdRAM 31/12/10

Number of Issues Total Size ($m) Average Size ($m) Weight

United States 683 263 530 386 56%Asia 226 46 038 204 10%

Japan 124 42 827 345 9%

Europe 217 100 407 463 21%

Middle East 6 3 563 594 1%Other 29 11 179 385 2%

Total 1285 467 544 364 100%

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 14/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 14

For an institutional investor who manages USD 100 billion, a 5% allocation to convertiblebonds represents

• About 1% of the universe

• An investment in all geographical zones

• An acces to varied profiles, diversified over all sectors

A strategic allocation is possible

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 15/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 15

According to the paper «Convertible Bonds as an Asset Class : 1957-1992»

• Convertible bonds are a very effective diversification tool for low risk portfolios composed mainly ofbonds and real estate

• In an optimisation without constraints, the minimum variance portfolio contains 5% of convertibles

• In portfolios that are optimised with constraints on the maximum allocation to equities (which is thecase for most institutional investors), we observe that the minimum variance portfolio will allocateout of equities into convertibles

A strategic allocation is possible

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 16/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 16

Convertible bonds have a long history

• The first convertible was issued by an American rail tycoon in 1880

• In Europe France has a legal framework since 1953

• The asset class adapts itself to the needs of the modern investor: ringfence clauses, dividendprotection clauses and takeover protection clauses are common today

An enduring asset class

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 17/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 17

Issuers per geographic zone include

• United States: Microsoft, Intel, EMC, Gilead, Amgen, Medtronic, Ford, Qwest, Goldcorp, NewmontMining

• Europe: KfW/Deutsche Telekom, KfW/Deutsche Post, Artemis/PPR, Alcatel, Publicis, Shire,Eurazeo/Danone, MNV/Gedeon Richter

• Azia: Sinopec, Plus Expressways, Telekom Malaysia, SK Telecom, Capitaland, Olam, Hynix

• Japan: Suzuki Motor, Toshiba, Hitachi, Sharp, Nikon, Nidec, Softbank, Orix

• Others: BES/Bradesco, AngloGold, Cemex, Vedanta

An enduring asset class

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 18/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 18

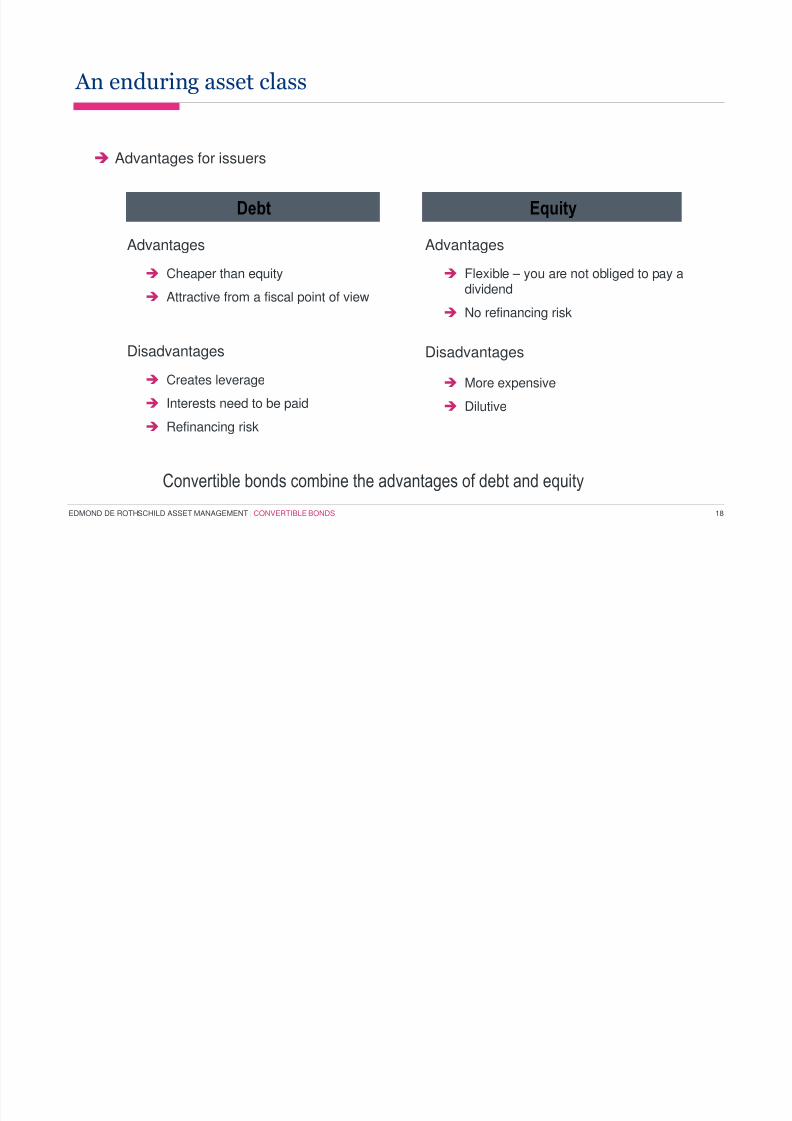

Advantages for issuers

An enduring asset class

Advantages

Cheaper than equity

Attractive from a fiscal point of view

Disadvantages

Creates leverage

Interests need to be paid

Refinancing risk

Advantages

Flexible – you are not obliged to pay adividend

No refinancing risk

Disadvantages

More expensive

Dilutive

Debt Equity

Convertible bonds combine the advantages of debt and equity

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 19/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 19

Various types of issuers will animate the primary market in various stages of the businesscycle

• Diversification and optimisation of company finances

• Delayed equity issuance for growth companies

• Opportunistic issuance (share buybacks) for investment grade companies

• Monetisation of participation when issuing exchangeables

• Refinancing of last recourse

The bonds will adapt various profiles over there lifecycle, bonds that are less interesting at

issue can become so during there life on the secondary market, not everything is worthbuying at issuance

An enduring asset class

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 20/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 20

An stand alone asset class

Convertible bonds are an asset class :

• A very a-typical risk return profile, in combination with a strong correlation to equity markets

• A specialised investor base

• A universe big enough to have a significant allocation for most investors

• A universe that renews itself over time

Various articles have been published on the subject, in particular «Convertible Bonds asan Asset Class : 1957-1992» by Scott L. Lummer et Mark W. Riepe published in theJournal of Fixed Income in 1993

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 21/40

Outlook for the convertible bond market

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 22/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 22

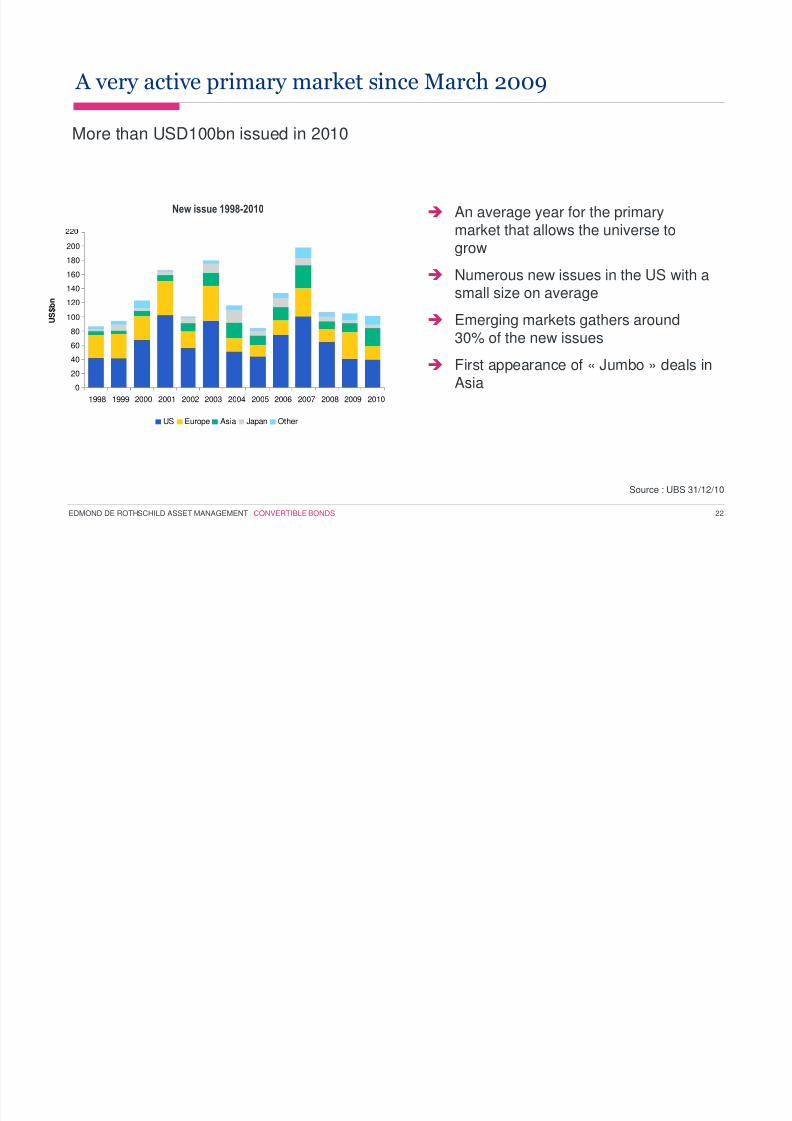

A very active primary market since March 2009

Source : UBS 31/12/10

New issue 1998-2010

0

20

40

60

80

100

120

140

160

180

200

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

U S $ b n

US Europe Asia Japan Other

More than USD100bn issued in 2010

An average year for the primarymarket that allows the universe togrow

Numerous new issues in the US with a

small size on average Emerging markets gathers around

30% of the new issues

First appearance of « Jumbo » deals inAsia

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 23/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 23

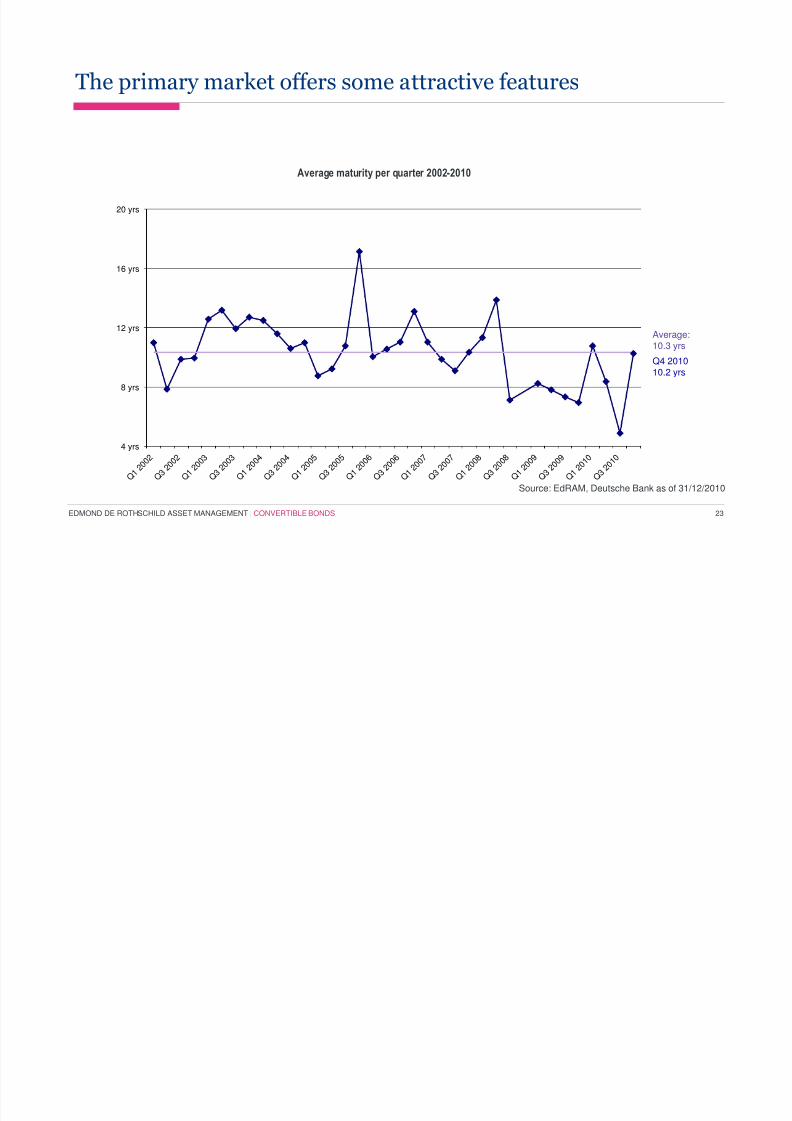

The primary market offers some attractive features

Average maturity per quarter 2002-2010

Average:10.3 yrs

Q4 201010.2 yrs

4 yrs

8 yrs

12 yrs

16 yrs

20 yrs

Q 1 2 0 0 2

Q 3 2 0 0 2

Q 1 2 0

0 3

Q 3 2 0

0 3

Q 1 2 0

0 4

Q 3 2 0

0 4

Q 1 2 0

0 5

Q 3 2 0 0 5

Q 1 2 0 0 6

Q 3 2 0 0 6

Q 1 2 0

0 7

Q 3 2 0

0 7

Q 1 2 0

0 8

Q 3 2 0

0 8

Q 1 2 0 0 9

Q 3 2 0

0 9

Q 1 2 0

1 0

Q 3 2 0

1 0

Source: EdRAM, Deutsche Bank as of 31/12/2010

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 24/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 24

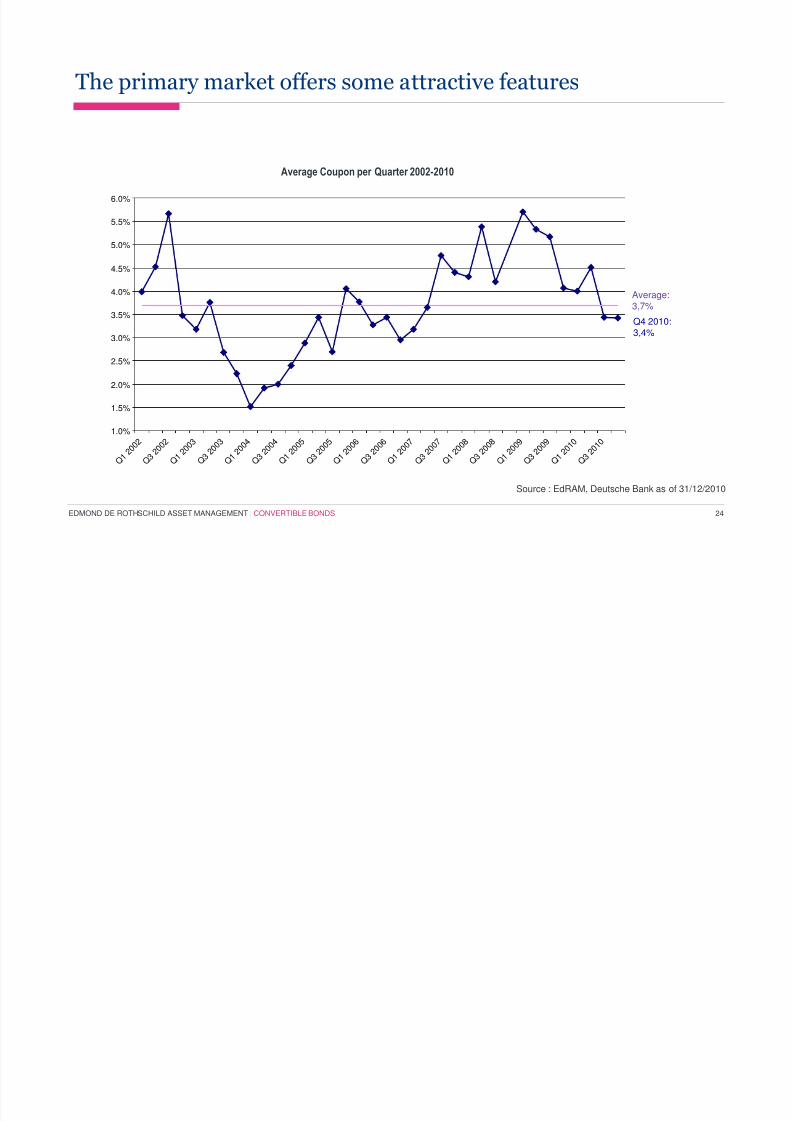

The primary market offers some attractive features

Average Coupon per Quarter 2002-2010

Source : EdRAM, Deutsche Bank as of 31/12/2010

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

Q 1 2 0 0 2

Q 3 2 0 0 2

Q 1 2 0 0 3

Q 3 2 0 0 3

Q 1 2 0 0 4

Q 3 2 0 0 4

Q 1 2 0

0 5

Q 3 2 0 0 5

Q 1 2 0

0 6

Q 3 2 0

0 6

Q 1 2 0

0 7

Q 3 2 0

0 7

Q 1 2 0

0 8

Q 3 2 0

0 8

Q 1 2 0

0 9

Q 3 2 0

0 9

Q 1 2 0

1 0

Q 3 2 0 1 0

Q4 2010:3,4%

Average:3,7%

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 25/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 25

The primary market offers some attractive features

Average Premium by Quarter 2002-2010

Q4 2010:

27,0%

Average:28,3%

Source : EdRAM, Deutsche Bank as of 31/12/10

20%

25%

30%

35%

40%

45%

50%

Q 1 2 0

0 2

Q 3 2 0 0 2

Q 1 2 0

0 3

Q 3 2 0

0 3

Q 1 2 0 0 4

Q 3 2 0

0 4

Q 1 2 0 0 5

Q 3 2 0 0 5

Q 1 2 0

0 6

Q 3 2 0 0 6

Q 1 2 0

0 7

Q 3 2 0 0 7

Q 1 2 0 0 8

Q 3 2 0

0 8

Q 1 2 0 0 9

Q 3 2 0

0 9

Q 1 2 0

1 0

Q 3 2 0

1 0

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 26/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 26

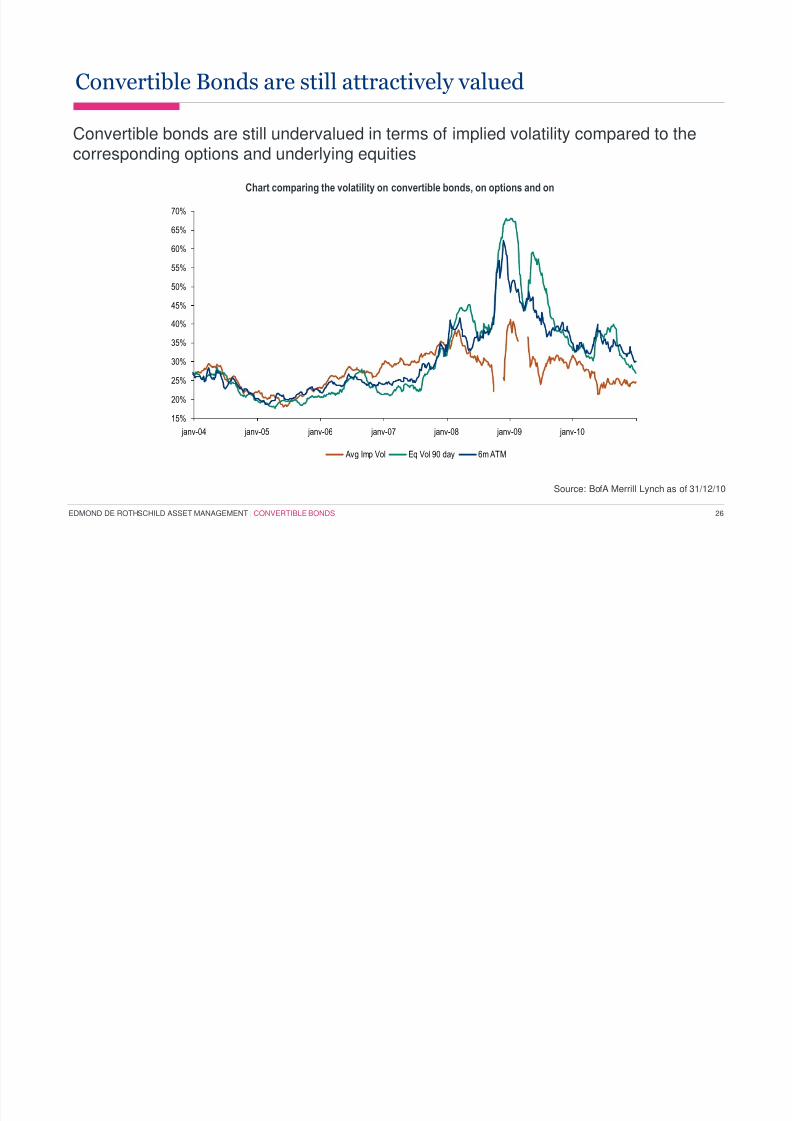

Convertible Bonds are still attractively valued

Convertible bonds are still undervalued in terms of implied volatility compared to thecorresponding options and underlying equities

Chart comparing the volatility on convertible bonds, on options and on

their underlying equities for the European universe

Source: BofA Merrill Lynch as of 31/12/10

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

janv-04 janv-05 janv-06 janv-07 janv-08 janv-09 janv-10

Avg Imp Vol Eq Vol 90 day 6m ATM

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 27/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 27

Several drivers of return (and risk) What to expect?

Equity

Credit

Implied Volatility

Interest Rates

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 28/40

What investment process to use?

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 29/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 29

A global convertible bond fund, targeting a consistent performance over thebusiness cycle

Limited credit risk:

• Minimum 50% of the CBs in the portfolio are investment grade

Focus on balanced convertibles:

• Individual holdings’ equity sensitivity <80%

• Fund equity sensitivity within range of 20 to 60%

Moderate Emerging markets’ risk

• Maximum 40% of exposure to the Emerging markets

Limited currency risk:

• At least 80% of the portfolio is hedged

Active management, independent from benchmarks

Saint-Honoré Global Convertibles: A proven expertise, a world of opportunities

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 30/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 30

A global investment universe 5 times bigger than the European universe

A well diversified global universe on a sector level

An actively managed fund, reflecting Edmond de Rothschild Asset Management’sstrongest global investment convictions, implemented through a CB portfolio

A vehicle to play the global recovery, with a bond floor

Saint-Honoré Global Convertibles: A proven expertise, a world of opportunities

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 31/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 31

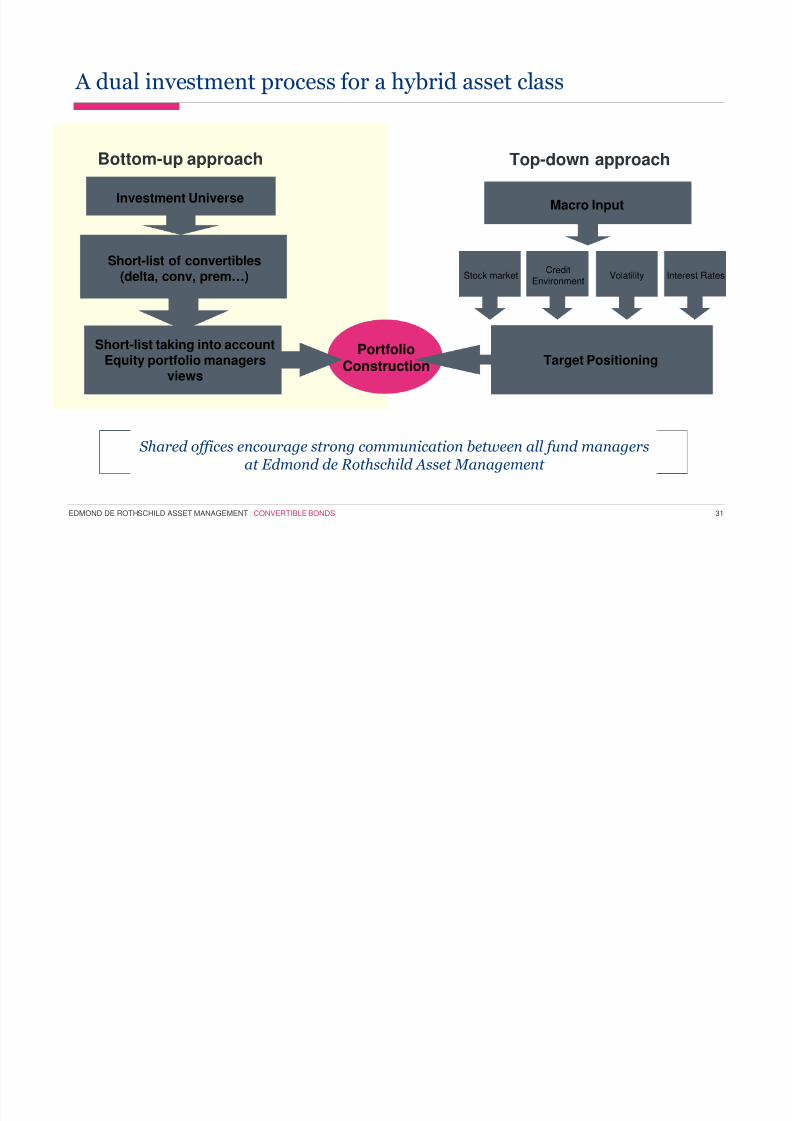

A dual investment process for a hybrid asset class

Investment Universe

Short-list of convertibles(delta, conv, prem…)

Bottom-up approach

PortfolioConstruction

Top-down approach

Target Positioning

Stock marketCredit

EnvironmentVolatility Interest Rates

Macro Input

Short-list taking into accountEquity portfolio managers

views

Shared offices encourage strong communication between all fund managersat Edmond de Rothschild Asset Management

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 32/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 32

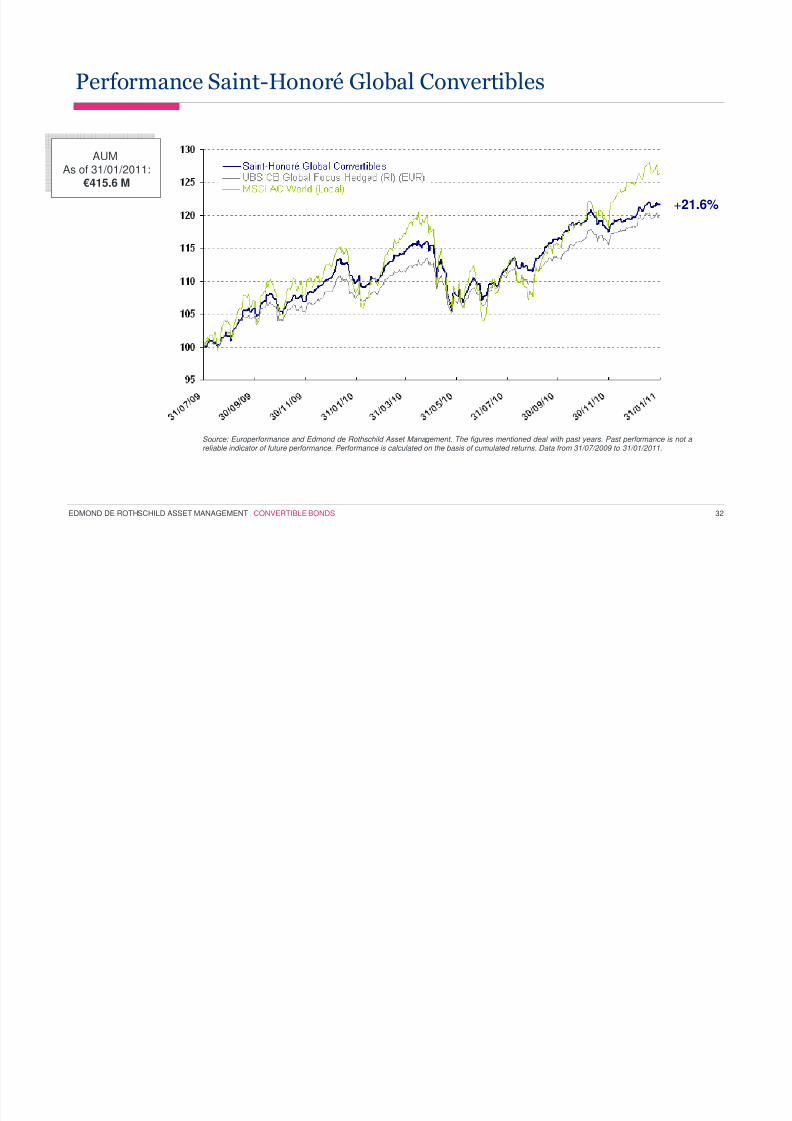

Performance Saint-Honoré Global Convertibles

Source: Europerformance and Edmond de Rothschild Asset Management. The figures mentioned deal with past years. Past performance is not areliable indicator of future performance. Performance is calculated on the basis of cumulated returns. Data from 31/07/2009 to 31/01/2011.

AUMAs of 31/01/2011:

€415.6 M

AUMAs of 31/01/2011:

€415.6 M

+21.6%

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 33/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 33

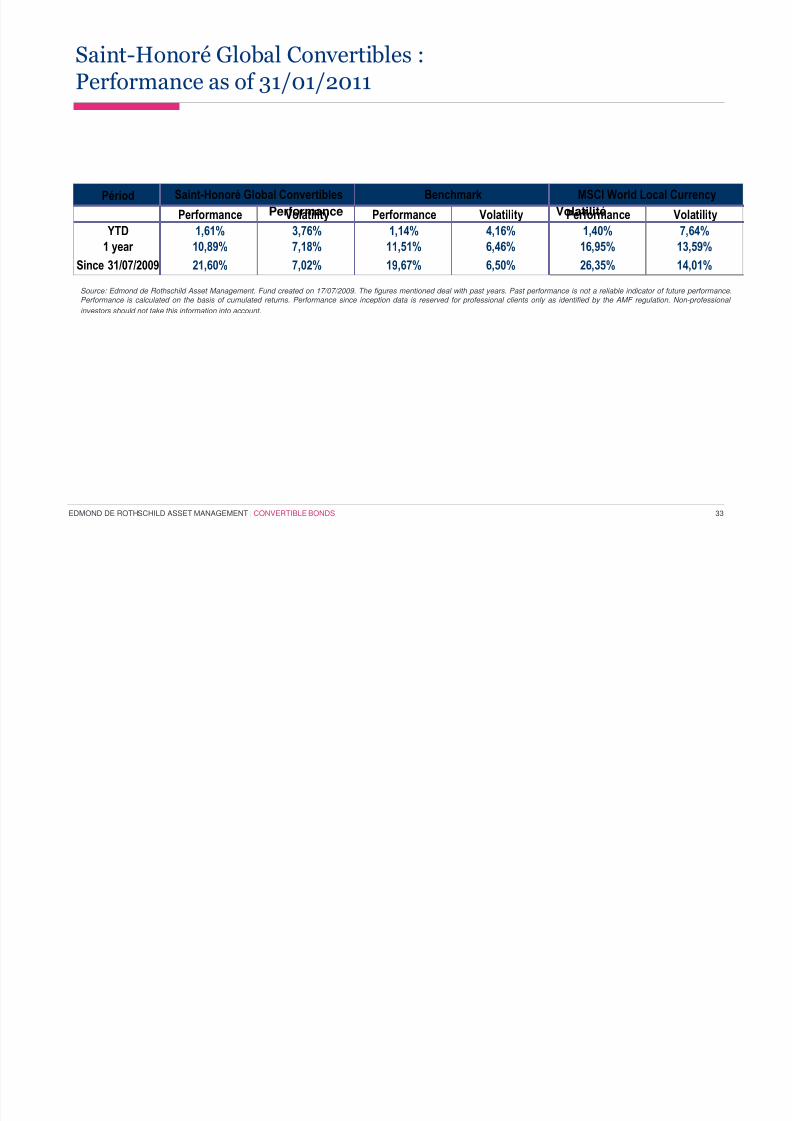

Saint-Honoré Global Convertibles :Performance as of 31/01/2011

VolatilitéPerformance

Source: Edmond de Rothschild Asset Management. Fund created on 17/07/2009. The figures mentioned deal with past years. Past performance is not a reliable indicator of future performance.

Performance is calculated on the basis of cumulated returns. Performance since inception data is reserved for professional clients only as identified by the AMF regulation. Non-professionalinvestors should not take this information into account.

Périod

Performance Volatility Performance Volatility Performance Volatility

YTD 1,61% 3,76% 1,14% 4,16% 1,40% 7,64%

1 year 10,89% 7,18% 11,51% 6,46% 16,95% 13,59%

Since 31/07/2009 21,60% 7,02% 19,67% 6,50% 26,35% 14,01%

MSCI World Local CurrencyBenchmarkSaint-Honoré Global Convertibles

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 34/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 34

Performance Saint-Honoré Global Convertibles

Saint-Honoré Global Convertibles benefited from the following investment themes in 2010:

Gold miners: Newmont Mining, AngloGold, Hochschild Mining

Agricultural commodities: Olam, Marine Harvest

Pharmaceuticals: Gilead Sciences, Onyx Pharmaceuticals

Technologies: EMC, Priceline.com

M&A stories: Sybase, Saks

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 35/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 35

Conclusion

The new cycle that has begun in 2009 should carry on during the next years.

As of today our portfolios are balanced, with equity sensitivity near 35% and yield tomaturity/put around 2.5%. However we have a more defensive sector bias than in 2009and 2010.

Convertible bonds have a low interest rate sensitivity and represent an good alternativeto rates/credit in a low interest rate environment.

An active management of the funds is crucial to avoid a bias on sectors/areas overweightin the indices.

We prefer Saint-Honoré Global Convertibles and Saint-Honoré Emerging Convertibles inorder to benefit from a better geographical diversification and/or benefit from an exposureto Emerging markets

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 36/40

Convertible Bonds

The Team

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 37/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 37

The Investment Team

Kris Deblander Deputy Director - Head of Convertible Bonds

Kris Deblander joined Edmond de Rothschild Asset Management in November 2008 as Head of Convertible Bondsmanagement.Kris Deblander is a graduate of the Solvay Business School.In 1997, after spending a year in research at Brussels University, he joined Fortis Investment Management in Brussels to be in

charge of structured product development and management. In 2002, he joined Fortis Investment Management Paris as co-managerof European Convertible Bonds. For over 6 years he took an active part in developing Convertible Bond funds both geographically – Europe/Asia/World – and in terms of investment techniques (Convertible arbitrage funds). In 2006, he was appointed Deputy CIOConvertible Bonds. He was in charge of convertible arbitrage funds and jointly responsible for fifteen portfolios including mandates forFrench and international institutional clients.The Convertible bond team reports to Philippe Uzan, Director of Research & Global Allocation.

Laurent Le Grin Fund Manager - Convertible Bonds

Laurent Le Grin joined Edmond de Rothschild Asset Management in November 2010 as portfolio manager in theConvertible Bonds team.Laurent Le Grin holds a Master’s in Banking and Finance and a post graduate degree in economics from the University of Paris II.

He first worked as an equity analyst at the Banque Générale du Luxembourg where he covered banks and technology in SouthernEurope. In September 2002, he joined Fortis in Paris to manage European equity funds and micro-caps. In March 2006, he joined theconvertible bond team at Fortis Investments/BNP Paribas Asset Management as a senior manager of European convertible bonds.

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 38/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 38

The Investment Team

Nicolas Schrameck Fund Manager – Convertible Bonds

Nicolas Schrameck joined Edmond de Rothschild Asset Management in April 2009 as an analyst in the Convertible Bondsteam.Nicolas Schrameck graduated from the EDHEC Business School.

In the past, he worked for J.P. Morgan Asset Management as a convertible bonds management assistant.

Cristina JARRIN Fund Manager – Convertible Bonds

Cristina Jarrin joined Edmond de Rothschild Asset Management in December 2010 as portfolio manager in the ConvertibleBonds team.Cristina Jarrin holds an MBA from HEC Paris, a Master’s in Finance from the University of CEMA in Argentina as well as a BA inFinance from the University of San Francisco.She joined Citigroup in 1998 where she first worked as a risk analyst in Quito, Ecuador and subsequently as a financial analyst inBuenos Aires, Argentina. In 2004, as part of her MBA programme at HEC, she worked at Calyon Investment Banking (Paris) whereshe was in charge of a private fund placement. In 2005, she moved to BNP Paribas Investment Partners - Fortis Investments, first asa convertible bond specialist and then as the manager of a US convertible bond fund with EUR 800m under management.

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 39/40

7/21/2019 Edmond de Rothschild AM - Kris Deblander 14h40

http://slidepdf.com/reader/full/edmond-de-rothschild-am-kris-deblander-14h40 40/40

EDMOND DE ROTHSCHILD ASSET MANAGEMENT | CONVERTIBLE BONDS 40

Disclaimer (2/2)

Details of the principal risks in the funds can be found in the pertinent Prospectus. The summary Prospectuses approved by the French market authority andall legal documentation regarding the funds are available upon request and may be found on our website at www.edram.fr (http://www.edram.fr).

The funds mentioned in this document have not been necessarily approved, registered or authorized for public or private offering or distribution to investors inother countries. The funds are not being offered in any particular jurisdiction but in those were they have been registered, authorized or approved for public orprivate offering. The funds should not be marketed to or subscribed by investors except in countries where they are registered, authorized or approved for

public or private offering.

In countries where these funds are not registered, they can be purchased by institutional investors only if local regulations authorize these institutionalinvestors to subscribe to a non registered fund.

Edmond de Rothschild Asset Management therefore recommends that all interested parties ensure that they are legally authorized to subscribe to theproducts and/or services before any investment is made.

This document is distributed on a confidential basis. This document may not be reproduced in any form or transmitted to any person other than the person to

whom it is addressed.