Embed Size (px)

Citation preview

Economic Transition andAccounting System Reform inVietnam

NGUYEN CONG PHUONG∗ and JACQUES RICHARD∗∗

∗College of Economics, University of Danang, Vietnam and ∗ ∗University of Paris Dauphine,

France

(Received: November 2009; accepted August 2011)

ABSTRACT Since 1986, Vietnam has been reforming its economic system, moving froma centrally planned economy to a market-oriented economy connected to the rest of theworld. This process has been shaped by the tensions and power relationship betweenmoderate and radical reformers and the interaction of their reform strategies. This paperdemonstrates that, unlike many reforms in former socialist countries, the Vietnameseaccounting reform resulted from both external pressures and internal needs. BecauseVietnam switched from state capitalism to a type of mixed capitalism, the country wasin a position to adapt the former ‘socialist’ accounting system relatively ‘quietly’,moving towards a private capitalist accounting model but preserving many fundamentalpeculiarities of the old system. The maintenance of the old accounting structure can beexplained by the continuity of the political, economic and social environment.However, the transformation has also generated some difficulties due to adapting aprivate capitalist accounting system to work in a state-dominated market economy.

1. Introduction

Since the purpose of an accounting system is to record and disclose useful infor-

mation, accounting systems do not function in an isolated fashion, but incorporate

and reflect the socio-economic and political characteristics of a country (Burchell

et al., 1985; Miller, 1994; Ezzamel et al., 2007). An extensive body of literature

testifies that the accounting system existing in a particular country is a product of

the economic and political environment as well as other factors (Mueller, 1967,

European Accounting Review

Vol. 20, No. 4, 693–725, 2011

Correspondence Address: Nguyen Cong Phuong, College of Economics, University of Danang, 71

Ngu Hanh Son, Danang, Vietnam. Tel.: 84 511 3766862; Fax: 84 511 3836255; Email: phuong.

European Accounting Review

Vol. 20, No. 4, 693–725, 2011

0963-8180 Print/1468-4497 Online/11/040693–33 # 2011 European Accounting Associationhttp://dx.doi.org/10.1080/09638180.2011.623858Published by Routledge Journals, Taylor & Francis Ltd on behalf of the EAA.

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

1968; Richard, 1977, 1980; Choi and Mueller, 1992; Nobes, 1998; Meek and

Saudagaran, 1990; Saudagaran, 2001; Cooper and Sherer, 1984). Thus, the

characteristics of an accounting system can be expected to vary from country

to country (Berry, 1983) as a result of social change (Gilling, 1976; Hopwood,

1983; Nobes, 1992; Potter, 2005).

Vietnam has been moving away from a highly centralised planned economy

towards a market economy since 1986, and its accounting system was modified

in 1995. The aim of our research is to explain this reform in light of its economic,

social and political context. Economic reform is a dynamic process that usually

leads to further change in politics and economic policy. As we demonstrate, the

entire process of reform and opening up in Vietnam has been shaped by the

tensions and power relationship between moderate and radical reformers and

the interaction of their reform strategies. We underline that the accounting trans-

formation has generated some difficulties due to adapting a private capitalist

accounting system to work in a state-dominated market economy.

This paper makes four distinctive contributions to the literature. First, while

there have been several studies on the changes in accounting of countries in

Eastern Europe, no comparable work about the Vietnamese reform has been pub-

lished so far. Second, the dominant literature on former socialist countries such as

the Soviet Union over-emphasises the differences between the former ‘socialist’

or ‘Marxist’ accounting systems and the new ‘capitalist’ ones. We argue that

former ‘socialist’ countries were characterised by a kind of state capitalism, so

that the main features of the two accounting systems are not so different. This

observation enables us to propose a new conceptual framework for studying

the accounting systems of former and present ‘communist’ countries. Third,

we show how the Vietnamese bureaucracy, in a relatively quiet way, transformed

the state-capitalism accounting system into a more privately oriented accounting

system. This transition preserves much fundamental specificity, while at the same

time preserving the political power of the Communist Party. We define and

illustrate the basic principles of accounting for state capitalism. Fourth, looking

towards the future, we suggest that as the International Financial Reporting

Standards (IFRS) have not yet been totally applied and more drastic changes

are to come that will imply a new philosophy of management, it is possible that

the ‘quiet’ change could become a more problematic one, notably with regard to

the fate of the state-capitalist bureaucracy in competition with new kinds of

capitalists.

This paper has six main parts. As the concept of state capitalism and the

discussion on the nature of former or present ‘socialist’ countries play a crucial

role in explaining the similarities and differences of accounting systems before

and after the change to a new kind of economy, Section 2 discusses this issue

at some length. Section 3 explains accounting in Vietnam under the former com-

munist economic system. Section 4 presents the economic reforms, while Section

5 analyses the effects of these reforms on the social environment of accounting.

Section 6 deals with the reform of accounting itself and Section 7 reveals the

694 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

contradictions between the internationalisation of Vietnam and its desire to

remain a state-controlled country.

2. The Concept of State Capitalism and the Nature of Former and

Present ‘Socialist’ Countries

A rich scientific literature devoted to the concept of state capitalism already

exists. Our study is mainly based on the writings of Mattick (1947), Gouldner

(1955) and Buick and Crump (1986). All these authors contest the dominant

thesis according to which so-called ‘real socialist’ countries differ sharply from

capitalist countries, arguing that this division is falsely based on three elements

that are not pertinent for judging the real nature of these economic systems,

namely, the type of ownership, the nature of the market ties between the units

of production and the existence of democracy.

Contrary to Le (2008, p. 17), who emphasises the role of state ownership,

Buick and Crump (1986, p. 15) state that ‘the substitution of state for private

(individual or corporate) ownership does not mean the abolition of capitalism

. . . it merely means that capital has come to be embodied by the state, or

rather, in practice, by several different state-enterprises’. In the same way,

while many studies such as those of Guesnerie (1996) and Le (2008) distinguish

between ‘socialist’ and capitalist regimes on the basis of an opposition between a

totally planned and a market economy, Gouldner (1955, p. 496) deems that the

nature of interrelationships between production units is not a critical factor in dif-

ferentiating between the two economic systems. Concerning democracy, Mattick

(1947) insists that the capitalist system has undergone anti-democratic phases,

notably during the pre-Second World War fascist experiments, which prove

that the existence of democracy is not the point. We could add that the develop-

ment of capitalism largely preceded that of democracy. Obviously, democracy in

the form of free elections cannot be a valid criterion for capitalism.

What then is the main element differentiating a true socialist economic system

from a capitalist one? According to these authors, the main issue is labour

relations inside the units of production: whether workers can dictate firm policies

or are merely wage earners dominated by private employers or state bureaucrats

(see notably, Gouldner, 1955, p. 497; Buick and Crump, 1986, p. 17). Thus, the

true differentiating factor is not ownership but power. According to Gouldner

(1955, p. 496), this focus on labour relations, derived from the work of sociol-

ogists and politicians such as E. Durkheim, B. Russell and M. Weber (who

were much more interested in social problems than economic or legal ones),

explains why Weber (quoted specifically by Gouldner, 1955, p. 497) asks, ‘if

labour relations inside socialist and capitalist factories are fundamentally alike

in that they are both bureaucratic, then does a socialist revolution yield very

much improvement for the capitalist proletarian’?

Accordingly, Buick and Crump (1986, pp. 5–14) show that the key element for

the determination of a capitalist economy is the existence of wage labour and a

Economic Transition and Accounting System Reform in Vietnam 695

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

wage labour market. The existence of wage labour means that there is profit for a

certain dominant class as well as capital, or self-expanding value. This is the

reason why, while characterising capitalism as a system where there is an ‘invest-

ment of capital in production with a view to profit’, they also deem that the fun-

damental basis for all of this is the existence of the ‘exploitation of wage labour’

and the existence of a labour market where labour can sell its ‘labour force’. On

the basis of this reasoning, these authors characterise the so-called socialist

regime of the former USSR as ‘state capitalism’. Buick and Crump (1986,

p. 72) list seven characteristics of a state-capitalist regime: ‘state-ownership of

the principal means of production’, ‘generalized wage labour’, ‘generalized use

of money and monetary calculation’, ‘a free market for consumer goods in the

form of agricultural products and light industrial products’, ‘a market for

means of production which is closely monitored and directed by the state’, ‘a

wide-scale planning activity, although a fully planned economy is not achieved’

and a ‘sizeable black market’.

Since the publication of Buick and Crump’s book in 1986, some features of the

Soviet Union’s state capitalism have become clearer. In 1984, the economist

J. Sapir underlined three main points that contradict the traditional view of the

Soviet Union regime. First, not one but at least four economies existed at the

same time, including a strict state-planned economy for some companies, a

legal private economy, notably for small companies, a non-legal private

economy resulting from bartering for raw materials between the directors of

big officially ‘planned’ companies, and a criminal economy (1984, p. 26).

Second, state planning rapidly ‘disappeared’ (p. 11) because it was difficult

and/or authorities lacked the will to control the division of activities among

the four types of ‘economies’. Proof of this disappearance is the suppression of

the five-year plan in favour of the one-year plan (p. 11). Third, ‘the planning

system was never directly applied to labour’ and there was always a ‘labour

market’ characterised by ‘strong competition to obtain supplements of labour

force’ in times of growth and the possibility of dismissing workers on the

pretext of work errors in times of crisis or ‘zastoj’ (pp. 13–14). One of Sapir’s

conclusions is that it was impossible to manage the economy as a single enter-

prise and that directors had real opportunity to manage their business while

‘being judged on the basis of their ability to obtain production performances’

(p. 16).

All these recent views, especially the existence of a labour market, are totally

at odds with the traditional view of the Soviet economy and clearly support the

thesis of state capitalism. However, who were the ‘capitalists’ in this system?

According to Buick and Crump (1986, p. 56), they were all the people ‘supervis-

ing the extraction of surplus value from the working class’, meaning ‘heads of the

party, the upper level of the state bureaucracy, the senior management in the

economic enterprises and the top ranks of the military and police forces’. All

these people were in a position to reap very high incomes compared to ordinary

workers (Binns, 1987, p. 74).

696 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

Lenin himself had clearly declared that the way to socialism first went through

state capitalism. In early 1918, he stated that ‘our duty is to study the German

school of state capitalism, and do all we can to assimilate it’;

in that country we find the last word in modern techniques of large-scale

capitalism and methodical organisation serving the capitalism of the

middle class and the Junkers. If you . . . replace the military state, the aris-

tocratic State (the Junker’s State), the imperialist middle class State with

another State, a socially different State with a different class content, a

Soviet State, i.e. a proletarian State, you will obtain the entire set of con-

ditions that lead to Socialism. (Lenin, 1962, pp. 712–713)

This extraordinary declaration was probably influenced by Hilferding’s well-

known thesis on finance capital:

the socializing function of finance capital facilitates enormously the task of

overcoming capitalism. Once finance capital has brought the most impor-

tant branches of production under its control, it is enough for society,

through its conscious executive organ – the state conquered by the

working class – to seize finance capital in order to gain immediate

control of these branches of production. (1981, part 5, p. 25)

Thus the Soviet model that Lenin, Stalin and their successors developed, with

different variants, from 1917 to the collapse of the USSR was essentially state

capitalism. We hypothesise that Vietnam also has adopted a certain variant of

state capitalism. If this is the case, the system of accounting that prevailed

before the reform of 1995 should display the main characteristics of capitalist-

style accounting. This 1995 reform, in the context of greater cooperation with

the private capitalist world, should have brought this former state-capitalist

accounting somewhat closer to private capitalist accounting, while preserving

many fundamental features.

3. Vietnamese Accounting under a Centrally Planned Economy

At the end of the Second World War, Vietnam pronounced its independence as a

sovereign state by declaring the establishment of the Democratic Republic of

Vietnam on 2 September 1945. When the Geneva Agreement was signed (in

1954) between the Vietnamese and the French, the country was divided into

two parts, the Democratic Republic of Vietnam in the North and the Republic

of Vietnam, backed by the USA, in the South, with two very different political

and economic systems that lasted 20 years (from 1954 to 1975).

Divided by politics and war, the economies of both the North and the South

developed along two different paths in the two ensuing decades of separation.

While the South, nurtured by the US military presence and the comprador

Economic Transition and Accounting System Reform in Vietnam 697

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

economy, followed the capitalist path, the North sought to adopt the Soviet

approach of political and socio-economic systems for social management and

industrialisation and planning. This approach continued to expand over the

entire country after reunification (1975) but became less influential after the

renewal policy was launched in 1986 (Griffin, 1998a, p. 2). The socio-economic

environment of accounting and the fundamental characteristics of the old

accounting system provide a comparative framework for assessing the original

features of the new accounting system.

3.1. The Political and Economic Systems

Until 1986, the economic system in North Vietnam had all the characteristics of a

Soviet-style ‘command economy’ (Van Arkadie, 2003, p. 39) regulated by the

Party-State (Griffin, 1998; McCormick, 1998b; Leung and Riedel, 2001).

Nearly all facets of economic activity were subject to central planning and

control. All the means of production belonged to the state in the form of state

ownership or collective ownership (Van Arkadie, 2003, p. 4). Agriculture was

made collective, prices were set and administered by the government, state enter-

prises dominated the industrial sector and all foreign trade was controlled by the

state. Interest and exchange rates, strictly managed by the government, bore no

relationship to market prices (Harvie and Hoa, 1997, p. 32). State economic

units were set up in accordance with Soviet managerial concepts. The basis of

this system was the use of state monopoly to concentrate resources as the top pri-

ority task for nation building, and the focus on rapid industrialisation (Harvie and

Hoa, 1997, p. 32).

Vietnam (like China) had previously adopted a Marxist–Leninist ideology and

a Leninist political framework from the Soviet Union. The Communist Party of

Vietnam established a Leninist state that deployed high levels of despotic power

over infrastructure (McCormick, 1998, p. 123). The Communist Party’s influence

over the planning process was reinforced by its control of all-important manage-

rial positions in the economy, from the state planning bureaucracy to individual

enterprises (Bergeret, 2002, p. 16; McCormick, 1998). All major appointments,

promotions and dismissals were decided by various party bodies. Moreover,

for every important sphere of state activity, such as a ministry, there was a cor-

responding group or department within the party apparatus responsible for super-

vising it (Bergeret, 2002, p. 16).

Bergeret (2002, p. 23) observes that under this system enterprises (units) had

very little autonomy in decision-making and took little responsibility for the

effective use of economic resources; the unit was given a regular production

target in terms of quantity, and, to meet this target, the state directly provided

it with capital and inputs. According to many economists including Harvie and

Hoa (1997) and Lavigne (1999), profitability was apparently not a primary objec-

tive for enterprises: the top priority task for nation building was to control

resources. This point will be discussed in detail later. These specific features of

698 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

the socio-economic system generated a demand for appropriate accounting

control and information.

3.2. An Accounting System Oriented towards Strong State Bureaucracy

Control

In 1948, three years after the foundation of the Democratic Republic of Vietnam,

‘Revenue and Expense Rules and General Accounting’ (Decree No. 1535/VP/TDQ, Government of Vietnam, 1948) was promulgated. This regulation was

based on the French cash basis system used by the French colonial authority

(Bui Van Mai, 2001, p. 43). It was intended mainly to control the monetary

flows of the centralised budget system (Dang Van Thanh, 1995, p. 1).

However, after 1956, new accounting rules based on the Soviet accounting

style were gradually promulgated for each economic sector. This accounting

system was used until 1996, when the new accounting system took over.

The Soviet-style accounting system, used as an instrument of control, was

incorporated into the centralised administrative system to supervise the activities

of all state enterprises. This regulation concerned not only various accounting

concepts such as equity, income, return on equity, revenue and expense, but

also the whole activity of planning and budgeting, the valuation system and

the use of charts of accounts.

3.3. The Concept of Equity

In the former Vietnamese economic system, the equity of the enterprise was the

total sum of resources including all kinds of debts, not only the owners’ equity

excluding the debts, as in the case of private capitalist firms familiar to Wester-

ners. This enlarged concept of equity is a logical extension of the viewpoint that

the state is the dispenser and owner of all means of financing (see Richard, 1977,

1980). It was comparable to the ‘entity approach’ debated in Western theory of

accounting and put forward notably by Paton and Littleton to enlarge the

concept of private equity for big entities: ‘to management the bondholder’s

dollars and the money furnished by the stockholders become amalgamated in

the body of resources subject to administration’ (1940, p. 43). There was thus

no Marxist doctrine, as Le (2008, pp. 35–39) emphasised, but merely the use

of a truly capitalist concept!

3.4. The Concept of Income

Nobes (1998) suggests that an economic system is characterised in general by the

domination of a particular financing system. Richard and Collette (2005, p. 38),

on the other hand, consider that the question of power is the most important one

and that power finds its concrete expression in the accounting definition of

income. As in other former ‘socialist’ countries, the net income of Vietnamese

Economic Transition and Accounting System Reform in Vietnam 699

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

socialist enterprises was obtained after the deduction of all traditional expenses

from revenues except for tax and interest on loans, which were not deducted.

Net income thus was determined in a similar way as for private capitalist enter-

prises, except for tax and interest on loans. A proportion of the income was

retained by enterprises to feed a fund for the emulation of workers, and the

rest was paid either to the state as taxes or to the state-owned banks as interest

on loans. These taxes and interest were considered not as expenses but as distri-

butions of income (see Richard, 1980 for the example of Soviet-style treatment of

interest and taxes). This situation can be explained by the fact that income was

considered from the viewpoint of the controller of all assets, the communist

state bureaucracy. The income derived from state enterprises was taken to be a

part of state income. This type of calculation has sometimes been interpreted

as proof of a ‘Marxist’ type of economy based on the recourse to the concept

of ‘surplus value’. However, this concept of ‘surplus value’ as used by Marx

applied not to a communist state but to a capitalist society as seen from a

global viewpoint without differentiating between equity and debts. Paton and Lit-

tleton, not known as Marxist theoreticians, also put forward the idea that ‘from

the point of view of the enterprise as an economic entity . . . treatment of interest

as a charge analogous to operating costs such as labour and materials is objection-

able’ (1940, p. 43). Therefore, surplus value as used by the Soviet and

Vietnamese states was indeed proof of a state-capitalist regime and not of a

Marxist-type economy.

The crucial point in this matter is that employees’ salaries were considered as

an expense to be deducted from profit (surplus), as in every private capitalist

enterprise. Contrary to what was promised by Lenin and Ho Chi Minh before

the revolutions, workers were not the owners of created value but only, like

their counterparts in the West, the recipients of a contractual part of the value

that was defined by the state bureaucracy and was negotiable when conditions

were favourable. As Richard (1983) showed, the only socialist accounting

system in which the workers’ pay was treated as the distribution of added

value and not as expenses was the Yugoslavian accounting system at the time

of the self-management experiment led by Tito. The main conclusions here are

that, contrary to Chiapello and Ding (2004), the notion of profit existed in ‘social-

ist’ countries and that, contrary to both Le (2008, p. 69) and Chiapello and Ding

(2004), it could hardly be said that in the Soviet Union and Vietnam the workers

were (are) ‘collective masters’ of the enterprises.

3.5. The Concept of Return on Equity

Thanks to these two concepts of capital and income, Vietnamese communist

firms, like their Soviet counterparts, were able to determine a ratio of return on

equity that was officially considered as the criterion of efficiency, to be maxi-

mised in accordance with communist doctrine (Richard, 1977, p. 324). This

assertion has been challenged, however. A majority of Soviet Union specialists,

700 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

like Sokolov and Petrachkov, contend that in a communist state, a concept of

return comparable to the return on equity in use in ‘Western countries’ cannot

exist because of the absence of a real market and a real concept of profit.

Other similar studies done by Bailey (1995), Krzywda et al. (1995), Mihaylova

(2000) and Le (2008) suggest that Soviet-type accounting systems are not actu-

ally oriented towards a measure of economic performance, but are merely ‘book-

keeping’. On the contrary, Richard and Collette (2005) asserts that within the

frame of state planning, the goal was to maximise a return on equity in a

manner very similar to that of large Western enterprises, so the Soviet system

could be designated as state capitalism. The fact that this kind of capitalism

was inefficient is a not a reason to refuse to take seriously its attempts to

create its own instruments of ‘rational counting’, to use Weber’s terminology.

This thesis seems to be confirmed by the declarations of retired Vietnamese

accounting specialists. When asked by Le (2008, pp. 560, 670, 634), these ‘veter-

ans’ asserted, surprisingly enough, that the concept of income was important and

that it was used to measure performance. This opinion also seems to be shared by

some Chinese accountants (Ezzamel et al., 2007, pp. 678, 680).

3.6. The Concepts of Revenue and Expense

In the Vietnamese socialist accounting system as well as in the Soviet system, the

revenues of a firm were registered at the time of collection, not at the time of

invoice. Many commentators have deduced from this that these systems were

based on a kind of cash accounting that ignored the benefits of ‘modern’

Western accrual-based accounting, reinforcing the myth that it was mere ‘book-

keeping’. This opinion is not correct. Although revenues corresponded to cash

movements, this was not the case for expenses, because expenses were not

cash expenditures but were calculated on accrual principles so as to reflect, in

an original fashion, not the cost of goods sold, but the cost of products sold

and paid for (Richard, 1977, 1980). Why was it preferable to register revenues

at the collection stage? The reason was connected not to any motive of prudence

but to a question of efficiency: planners struggling with the slowness of firms had

elaborated a device to encourage payments for sales by preventing the distri-

bution of any profits before the termination of the accounting process (Richard,

1980). It also had nothing to do with a Marxist view of the economy, which

focuses on the famous equation MGM (money, goods, money).

3.7. Planning and Budgeting

As in other former socialist countries, the budget was the heart of the state machin-

ery in Vietnam, where there were only state and collective ownerships (Vu Quang

Viet, 1998, p. 129). Enterprises’ funds (capital in the wide sense) were allocated by

the state for specific goals such as investment in fixed assets, production and pay-

ments to suppliers. Each fund allocated could not be used for other ends, and the

Economic Transition and Accounting System Reform in Vietnam 701

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

use of the funds was controlled and supervised, notably through the use of a special

type of balance sheet without any practical counterpart in Western countries,

where financing is generally freely used. Up to the end of 1995, each enterprise

had to list on its balance sheet the funds specified by the government, namely,

the fixed assets fund, the current assets fund and the specific assets fund. Each

fund corresponded to a separate group of assets. The basic accounting equation

underlying the financial statements of all organisations was ‘fund applications

equal fund resources’. Fund application meant the use of funds to acquire property,

goods and materials used in operations, while fund resources represented the

various channels to obtain operational funds. This type of fund accounting, as

invented by Soviet specialists (Richard, 1977, p. 406), allowed the state to check

whether allocated resources were being well used in accordance with the plan. It

was intended not to evaluate the enterprise’s performance (this objective was

achieved by calculating the return on equity), but to facilitate central control and

implementation of the economic policies of the authorities in terms of resource

allowance and use. This was logical because the state possessed all means of pro-

duction and allocated all resources of enterprises. This system, at least in the case

of Soviet enterprises, obviously did not prevent managers from trying to find

non-planned resources by negotiating agreements with their counterparts in

other enterprises. According to Sapir (1984, p. 12), this kind of barter, also to be

found in Vietnam, might well have represented half of the planned flows!

3.8. Rules of Valuation

Both Vietnamese and Soviet enterprises had to evaluate their goods and assets accord-

ing to a kind of ‘true’ historical cost system in line with the precepts of the ‘dynamic’

German school, notably Schmalenbach, who had a strong influence on the founders of

Soviet accounting (Richard, 1980, 1995a, 1998). There was no question of assessing

assets at their market value or even evaluating inventories at the lower of cost or

market. This point was not so strongly ideological as it would appear from the declara-

tions of Soviet or Maoist politicians against private capitalist accounting (Ezzamel

et al., 2007); it was partly due to the absence of failures and above all to the existence

of a shortage economy (Sapir, 1984, p. 21). As in other former socialist countries, the

recourse to the concept of value in use (based on discounted cash flows) was also

unknown since enterprises were not to be sold. The historical evaluation was used

to measure the ‘real’ performance of enterprises, that is, the degree of realisation

of the plan. The use of the historical cost system was also justified by the objective

assigned to accounting, that is, to give the central authority the means to measure

product prices and control manufacturing costs (see Richard, 1980).

3.9. Use of Charts of Accounts

In May 1918, in his paper on left-wing infantilism, Lenin wrote that ‘the predo-

minant feature in Russia at present is petit bourgeois capitalism from which there

702 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

is but one single route to both big state capitalism and Socialism, and that route

goes through the same intermediary stage, which is called “accounting and

control”’ (1962, p. 713). We have already seen that this intermediary stage is,

as a matter of fact, ‘state capitalism’, but the quoted words focus on the main

instrument of the realisation of state capitalism: a certain type of control by

accounting. Where did the Soviet leaders find this type of accounting and

control? The answer, again, is in Germany! It is known that as early as 1918,

Lenin and Soviet specialists were acquainted with the most modern German tech-

niques of management, namely, those recommended by the businessman and

specialist in war economics Rathenau. His book The New State (Der neue

Staat) had been commented on by Lenin himself (1919), and his collaborators

went to Russia in the 1920s (Sapir, 1984, p. 6). It is equally well known that in

1929, Schmalenbach received a visit from a Soviet delegation (Forrester, 1977,

p. 60) and that a year earlier his famous chart of accounts was published in the

USSR (Mazdorov, 1972, p. 85) and became the basis for the construction of all

future Soviet accounting plans (Richard, 1995a).

Much later, in 1970 (Decree No. 425 TC/CDKT), Vietnamese socialist

accountants also adopted a variant of this Soviet model inspired by Schmalen-

bach’s famous Kontenrahmen. The model was characterised by the principle of

‘formal monism’ (unity of cost accounting and financial accounting) and by

the logic of the circuit (classification of accounts according to the order of the

operating cycle in accordance with the three stages of the reproduction process

– purchase, production and sale). As Richard (1995b) remarks, there were two

logical reasons for the choice of a chart of accounts of a monist type. First,

this very standardised accounting plan enabled the state bureaucracy to control

the process of production. Second, it also enabled the state planners to aggregate

macro-economic indicators efficiently, notably concerning the average cost of

production. It has been asserted that circuit logic is related to Marxist ideology,

but in fact all this is correlated not with a Marxist conception but with concrete

needs of management control: this kind of circuit logic had already existed in the

cost accounting systems of the early nineteenth century, well before Marx’s birth.

Thus, the basic concepts and tools of Vietnamese accounting were taken from

the capitalist system, including a concept of return on capital comparable to the

famous return on assets.

4. Economic Transition to a Market Economy and its Consequences

4.1. Reforms at Macro and Micro Levels Led to Important Changes Affecting

the Social Environment of Accounting

The Vietnamese economic reform, in conformity with the slogan of ‘Doi moi’

(renovation) proposed at the Sixth Congress of the Communist Party in 1986,

shifted the Vietnamese economy from a centrally planned economy to a ‘socialist

market economy’. While the majority of Eastern European countries recognised

Economic Transition and Accounting System Reform in Vietnam 703

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

the ‘transition’ as a radical change from a planned economy to a market one,

Vietnamese leaders saw Doi moi as a way to improve the socialist model and

not to abandon it (e.g. see Dixon, 2003). Macro-economic stabilisation, the

restructuring of the economic system and the opening of ‘doors’ to the rest of

the world contributed towards remarkable changes in the socio-economic

environment (Cuong et al., 1998; Leung and Riedel, 2001, p. 3) in which

accounting took place. Since 1987, many reforms have been implemented, and

this process has accelerated since 1989 (Cuong et al., 1998, pp. 37–48; Vu

Quang Viet, 1998; Riedel and Turley, 1999). The changes can be seen in the

reduction of differences between free market and official prices, the abolition

of rationing for many commodities, the removal of the checkpoints on internal

trade, the enactment of a foreign investment code and the establishment of the

State Committee for Co-operation and Investment. The following changes may

also be noted: giving farmers the right to use land for at least 15 years and to

cooperate with their partners in agriculture, reducing restrictions on foreign

trade and separating the role of a central bank from that of commercial banks.

Conspicuously absent were moves to relinquish administered pricing, unify

exchange rates, substitute positive for negative interest rates and harden budget

constraints on state enterprises. Thus, Vietnam managed to secure a successful

macro-economic stabilisation. This stabilisation, once achieved in 1993, has

enabled Vietnam to enjoy a favourable macro-economic environment until

now. This adjustment was carried out without any significant international finan-

cial aid, either from the IMF or from anyone else (Dixon, 2003).

At a micro-economic level, the reform programme between 1986 and 1995

consisted of fundamentally restructuring state-owned enterprises (SOEs). Piece-

meal reforms increased SOE autonomy through 1988 (Decree No. 217/HDBT,

Government of Vietnam, 1988), and then in 1989 the government hardened the

budget constraint, ended direct operating subsidies and easy bank credits, and

shifted to market pricing for both inputs and outputs. Profitability and perform-

ance of SOEs improved. The number of SOEs declined from 12,297 to 6310

by the end of 1995 (Vu Quoc Ngu, 2002, p. 7). In addition to the restructuring

of the SOEs, equitisation was used to increase the effectiveness of the

economy in the future. In early 1992, the government promulgated an experimen-

tal programme of equitisation (Decree No. 388/HDBT, Government of Vietnam,

1992). However, the experience of Russia raises questions about the approach

chosen by the Vietnamese government. In order to maintain the state’s control

over the economy, Vietnam chose a gradualist approach (Le Thanh Ton, 2000,

p. 157), unlike the sudden spontaneous programmes of privatisation in Eastern

Europe and the former USSR (see, for example, Gros and Steinherr, 2005;

Dixon, 2003). Following this approach, the government would retain substantial

ownership, while the bulk of shareholders would be managers and other employ-

ees. The prevalence of ‘insider equitization’ (managers and workers taking the

majority of shares) and the fact that the state could retain a controlling interest

have clearly demonstrated the ability of the Vietnamese government to resist

704 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

external pressures and to maintain a consensus-driven policy approach (Beres-

ford, 2008, p. 232).

The development of the private sector was mentioned in the Document of the

Sixth Party Congress. After many years of discrimination, the government pro-

moted the development of this sector, although its contribution to the GDP is

still relatively small. The Laws on Companies and Private Enterprises, passed in

1991 (No. 47/LCT/HÐNN and No. 48/LCT/HÐNN, National Assembly of

Vietnam, 1991a, 1991b), gave the informal sector official sanction. This was

identified further in the country’s new constitution (in 1992), which clarified the

rights of the private sector by recognising its important role in the economy and

providing explicit protection of private property rights. This policy led to the

emergence of groups of users of accounting information (see below).

4.2. The Role of the State

These developments in Vietnam in the 1980s and the early 1990s clearly show the

key role played by the state in moving away from central planning. By introducing a

series of reforms piecemeal, at both macro and micro levels, the state allowed

parallel markets to flourish. Moreover, the role of the state was re-defined,

moving from that of ‘direct controller’ of the economy to that of an indirect

intervener and ‘partner’ working with the private sector to promote growth, and

from that of company manager to that of owner (see Leung and Riedel, 2001,

p. 34). However, although Vietnam is a country where economic reform and devel-

opments have gone hand in hand with significant changes in political attitude, this

has been achieved within a framework of continuing governmental control, which

remains particularly strong with regard to accounting organisations and decisions.

This approach to reform has resulted in a substantial but somewhat uneven

development of elements of the market economy. The system, labelled with

variations of such terms as ‘market socialism’ or ‘socialist market-oriented

economy’, is officially depicted as being placed under state management

with the key means of production remaining publicly owned (see, for

example, Communist Party of Vietnam, 1986, 1991, 1996, 2001). In

Vietnam it is claimed that the state uses the market mechanism and

applies economic forms and managerial methods of the market economy

to activate production and release productive forces, promoting the positive

aspects of the market mechanism while limiting and overcoming its nega-

tive aspects, and protecting the interests of the working people and the

population as a whole. (Communist Party of Vietnam, 2001, pp. 33–34)

4.3. Resistance to Reforms

As we noted above, accounting reform in Vietnam has been shaped by the tension

between moderate and radical reformers (Guo, 2004, p. 400). In general, the

Economic Transition and Accounting System Reform in Vietnam 705

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

conservative leaders have a strong preference for a ‘socialist market economy’.

They are concerned about the corrosive impact of the pure market economy

and the development of private sectors on the Vietnam Communist Party

(VCP) leadership and the socialist direction of reform. The radical reformers

are more interested in the efficient functioning of the system than in the survival

of ideology and have a strong preference for a comprehensive market reform

and opening of the economy to the world market. They want Vietnam to change

more rapidly and join the global market to enhance its long-term development

prospects (Quan Xuan Dinh, 2000).

Policy debate about the nature of socio-economic development in Vietnam

began during the economic difficulties of 1979–80 (see Guo, 2004, p. 398).

There were two tendencies as regards reform. The conservative leaders (for

example, Nguyen Duy Trinh) disputed the proposal that ‘all sectors, especially

the individual and capitalist ones, should be allowed to expand’, and furthermore

maintained that ‘the scope of relying on markets should be limited by the need to

subordinate them to the plan’. They also added that the basic reason for failure

was the slow pace of change in planning methods and management structure.

In contrast, the liberal leaders (for example, Nguyen Lam) took a stand against

‘planning everything’ and favoured the use of markets and multiple planning

levels, underlining the need to pay attention to the material interests of peasants,

regions and so on (Fford and de Vylder, 1996, p. 131). The reform policy in the

first half of the 1980s was, in general, a compromise between the two groups: the

private sector and free market were to play a more important role but nevertheless

should still be subordinated to the state plan; furthermore, subsidised supply

would continue as part of state central management, with resources allocated

directly to high-priority areas (Fford and de Vylder, 1996, pp. 126–127).

However, at the Sixth Party Congress in December 1986, the policy debate

began to favour reformers, for whom the central economic management of the

state was a key factor inhibiting both economic growth and micro-level

reforms. The earlier policies were rejected, starting with far greater formal decen-

tralisation, allowing markets to play a more important role in the allocation of

resources and encouraging non-public sectors to develop in production and

services. This shift away from long-accepted orthodoxy created opposition

from conservatives, and this, yet again, slowed down the transition pace (Fford

and de Vylder, 1996, pp. 127–149).

In the 1990s, particularly during the 1997 Asian financial crisis, the internal

conflict between conservatives and reformers intensified (Guo, 2004, p. 399).

Conservatives blamed the crisis of capitalism as a whole and believed that Viet-

nam’s lack of economic integration was a blessing. Reformers blamed the crisis

of ‘crony’ capitalism, imperfect markets and too much government intervention.

Since the Eighth Party Congress in 1996, the Politburo has been deadlocked and

unable to implement any bold reforms to stimulate the economy, because it is

divided along ideological lines and unable to come to an agreement on the

direction of the reform programme (Guo, 2004, p. 399).

706 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

The tensions between these two groups have determined not only the policy

choice of economic reform but also the sequence of economic and political

reforms. However, such tensions should not be interpreted as a struggle

between those who favour reform and those who oppose it (Guo, 2004,

p. 400). Reform was made easier in Vietnam by a highly favourable social con-

sensus, which lowered resistance to change and propelled it forward (Riedel and

Turley, 1999, p. 45). Disagreement was over the pace and scope of the reforms,

between those who pushed for more radical or speedy reforms and those who

favoured gradual and steady reforms. Faced with powerful resistance from the

conservatives, the reformists have been careful in their approach to reform and

in finding ways to compromise. The lack of agreement between the conservatives

and the reformists over the direction, extent, pace and depth of reforms has made

the party indecisive over many pressing structural problems faced by the country.

The result is a gradual, partial and piecemeal response to those problems and

challenges (Quan Xuan Dinh, 2000, pp. 360–388).

4.4. Comparison with Other Former Socialist Countries

During the 1990s, the phenomenon of transitional economies in Eastern Europe

and East Asia brought a new dimension to the development debate: the discussion

on the ideal transition paths from a centrally planned to a market economy. Since

1989, the majority of Eastern European states have adopted a neo-liberal

approach, mainly induced by international agencies, major trading partners,

investors and aid donors (see, for example, Dixon, 2003; Guo, 2004, p. 393).

This approach is seen often as ‘shock therapy’. Russia is a specific example of

this approach, with its explicit commitments to the development of a full

Western-style market economy, combined with rapid democratisation. Central

features have been reductions in the centralised direction of the economy and

direct state involvement in production, together with the end of single-party

rule (Dixon, 2003, p. 292). However, the transition in Eastern Europe has

proved to be a complex and problematic process, with recurrent economic and

political crises and a wide range of situations and trajectories (see, for

example, Dunford, 1998).

Vietnam (like China) has adopted a different approach of gradual economic

reform while the single party has stayed in power (Guo, 2004, p. 393). This pro-

gressive approach has been conducive to the continuation of strong governmental

control and of a leading role in economic development for SOEs. The transition

from a centrally planned to a market economy, albeit one with a ‘socialist orien-

tation’, took place without any kind of political revolution or ideological conver-

sion but with significant changes in political attitude on the part of the leadership

within a framework of continuing strong governmental control (Riedel and

Turley, 1999, p. 8). Vietnam, along with China, has, until recently, passed the

transition test relatively well, as concerns the way towards a certain type of

market economy. As Griffin (1998b) has stressed:

Economic Transition and Accounting System Reform in Vietnam 707

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

Vietnam, along with China, stands out as a success story among the transi-

tional economies. All the other transitional economies have run into severe

problems, often a combination of falling output, decline in average

incomes, sharp increases in poverty, rising mortality and falling birth-

rates, rapid inflation and so on. (p. x)

This relative success has taken place in the context of maintaining single-party rule,

high levels of state intervention and significant direct control of production through

SOEs. Economic growth has been heavily concentrated in the state sectors. It is

argued that a significant proportion of the growth has resulted from the ‘party-

state’s’ promotion of growth, establishment of incentives and encouragement of

more localised activity. Dixon (2003, p. 298), however, remarks that the positions

adopted by Vietnam (and China) on state protection of major parts of the domestic

economy, the reluctance to privatise SOEs and the maintenance of central party

rule have attracted increasing criticism from international agencies, main trading

partners, investors and commentators. Reform and development in Vietnam have

been a significant challenge to the Western neo-liberal and democratic model.

It is obvious that the Doi moi that started in 1986 has caused the Vietnamese

economy to become a type of mixed economy with a combination of private and

public ownership of production means. Vietnam is only partly market driven,

retaining non-market capitalist forms of production and ideology. The leading

role of SOEs and strong control of the state-party in the socio-economy make

the Vietnamese economy different from a traditional mixed economy such as

that in France in the 1960s. The Vietnamese economy is officially a ‘market-

oriented socialist economy under state control’ (Communist Party of Vietnam,

1991). While developing countries apply Western policies that consider the gov-

ernment as a ‘market facilitator’, Vietnam has consistently expressed the inten-

tion of controlling the market (Beresford, 2008, p. 222). Dixon (2002) stresses

that, in Vietnam, the development of elements of the market economy and inte-

gration into the global system are taking place under the auspices of a single-party

state that continues to affirm its commitment to state control over the economy.

5. The Effects of Macro and Micro Reforms on the Social Environmentof Accounting

These economic reforms have brought about important changes in the social

environment of accounting, changes relating to social players, administrative

functions, ownership structure, the complexity of operations and relations with

the outside world.

5.1. Change of Social Players

Although public ownership and the role of the state remain dominant, the private

sector has developed quickly (its GDP fluctuates at around 55%, but within this

708 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

percentage, the contribution of the ‘informal’ sector is the largest, at approxi-

mately 97%). This change has led to the emergence of certain accounting interest

groups, such as entrepreneurs, foreign investors and bankers. However, state

bureaucracy still plays a dominant role. Thus, the state sector has continued to

be favoured, with large parts of the economy remaining heavily protected and

reserved for its activities (Guo, 2004, p. 409).

5.2. The Decentralisation of Economic Administration

The restructuring of SOEs and their access to a free market has resulted in greater

autonomy for management decisions and in creating financial incentives for man-

agers (Riedel and Turley, 1999, pp. 32–34; Harvie and Hoa, 1997, p. 57). After

1986, the managers of state enterprises no longer had to achieve centrally determined

production targets. They had greater autonomy in determining where their output

was sold and from where input could be obtained on the basis of market prices.

Greater autonomy for enterprise managers has brought a more important role

for accounting information. Previously, the performance of state enterprises was

measured by comparing the planned indicators with the actual indicators,

whereas the new evaluation of performance is based in theory only on market

profitability.

Obviously, the SOE reform and the emergence of the private sector increased

the decentralisation of state macro-economic management and the autonomy of

enterprises (World Bank, 1993), reflecting a gradual evolution in the style of

governance from ‘rigid state control’ towards ‘state regulation’. However,

Vietnam remains a very strongly bureaucratised and centralised country with

multiple power networks co-habiting, at both central and local levels (see

Riedel and Turley, 1999; Guo, 2004; Leung and Riedel, 2001).

5.3. Change of Ownership Structure

The privatisation of SOEs and the recognition of the private sector have consider-

ably changed the ownership structure in the economy, which in turn has changed

accounting. In addition to SOEs and collectively owned enterprises, there are

now private enterprises, mixed-ownership enterprises (SOEs combined with

collective ownership enterprises) and enterprises with capital owned partially or

completely by foreigners (foreign enterprises located in Vietnam, joint-venture

enterprises and enterprises cooperating with foreign partners). The introduction

of a shareholding system means that the state is no longer the sole user of account-

ing statements.

5.4. The Emergence of New and Complex Business Operations

The new market economy has significantly affected the economic performance

of SOEs and stimulated the development of the national economy. Many new

Economic Transition and Accounting System Reform in Vietnam 709

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

business transactions and financial activities have appeared, such as the transfer

of the right of land use, leasing, instalment sale, purchase of intangible assets, etc.

The old accounting system covered only certain simple transactions and could not

be used in these new activities, so it had to be replaced.

5.5. The Change in Relationships with the Outside World

After the fall of the former USSR and countries of Eastern Europe in 1989, Vietnam

did not receive any economic aid from them. In order to maintain its position and

carry out its ambitious modernisation programme, Vietnam needed international

assistance in capital and technology, and therefore adopted an ‘open-door’ policy

to attract foreign direct investment. The Documents of the Sixth Congress of the

Communist Party mention the mobilisation of external resources for the develop-

ment of the country (Communist Party of Vietnam, 1986). According to the

Seventh Congress, one of the solutions for the development of the country was

‘to mobilize all possibilities of attracting foreign investments’ (Communist Party

of Vietnam, 1991). Since then, the signs of the success of the policy are numerous:

Vietnam is a favourite destination for international investors (from zero in 1987, in

1995 Vietnam attracted 6,530,800,000 USD). Although the law on foreign invest-

ment is appealing to foreign investors, it has come up against many obstacles.

The old regulations and accounting practices constricted the capital flow of direct

foreign investment into Vietnam. Many foreign investors complained that the

old accounting system did not meet their needs. For example, Richard Martin,

Chairman of the ANZ Bank branch in Hanoi said, ‘We hope to better understand

local creditworthiness. Right now, local accounting and audit practices do not

give us the level of comfort we need. But it’s clear they’ll change soon’ (Nguyen

Duc Tho and Eddie, 1995, p. 13). This explains how the accounting reform of

1995 was an immediate response to the economic reform, the ‘open-door’ policy

and the promotion of investment (Yang and Anh Thuc Nguyen, 2003, p. 175).

6. Accounting Changes Following the Economic Transition

The main accounting changes concern the modification of accounting objectives;

the emergence of a new concept of capital and new definitions of assets, income,

revenue and expenses; the modification of valuation principles; the transform-

ation of the chart of accounts; and the reshaping of financial statements.

6.1. The Modification of Accounting Objectives

Modified accounting objectives were incorporated into the new accounting

system introduced in 1995 to take into account the information needs of new

users. The 1995 accounting system stipulates that the objective of the establish-

ment of financial statements is ‘to provide useful economic and financial infor-

mation for evaluating and predicting the financial performance and position of

710 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

the enterprise. Financial information is also useful to owners, managers, inves-

tors, and creditors in decision-making’ (Ministry of Finance, 1995, p. 2).

Identification of the primary group of accounting information users is a funda-

mental requirement for any accounting system. No legal text explicitly identifies

the principal group of users, but identification can be implicit. Clearly, accounting

objectives have been modified because the system now has to satisfy the needs of

emerging economic groups (owners, managers, investors and creditors). This has

been confirmed by Dang Van Thanh, director of the Department of Accounting

Policies (within the Ministry of Finance), whose mandate ran from 1994 to 1998:

Since accounting is a crucial factor in the system of governmental admin-

istration, its instruments play an important role in the management, direc-

tion and control of economic activities. . . . Accounting should provide

useful information to enable users to take economic decisions. Therefore,

the role of accounting is important not only for the State, but also for enter-

prises and others. (Dang Van Thanh, 1995, p. 1)

These objectives are in conformity with the current political and economic situ-

ation in Vietnam, where the state enterprises continue to dominate in the major

sectors of the economy (the share of the state sector is relatively stable: it accounted

for 42.7% in 1986, 43.1% in 1995, 43.8% in 1996 and 44.2% in 2006). Large SOEs

are regarded as a macro-economic regulatory instrument of the state despite the

weak performance of some of them. Although the private sector has developed

quickly since the launching of economic reform, it is still too weak to achieve

economic power in general and accounting power in particular.

6.2. A New Concept of Capital

Changing the financing system from a sole funding source (the state as represented

by the bureaucracy) to a variety of financing sources did away with the old concept

of capital. The old legal division into the fund of fixed assets and the fund of

current assets has been completely abandoned. The new Vietnamese balance

sheet (see below) now has two headings, ‘Equities’ and ‘Liabilities’, and the

‘private capitalist’ accounting equation (Assets 2 Liabilities ¼ Owner’s equity)

has been adopted. However, the ‘funds for social welfare functions’, an element

of the old system, remain (see below) within the heading ‘Equities’, a survival

that testifies that many state enterprises use their market-oriented businesses to

provide a social welfare function.

6.3. A New Definition and New Content for Assets

Within the communist framework, an accounting asset was a fund application;

plots of land were excluded because socialist enterprises were not allowed to

acquire land, and only goods legally acquired were allowed to figure on the

Economic Transition and Accounting System Reform in Vietnam 711

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

assets side. In the 1995 accounting system, an asset corresponds to future econ-

omic benefit, held and used by the enterprise. This new concept differs comple-

tely from the old one. The term good, reflecting a traditionally ‘legal’ concept,

has been replaced by benefit, reflecting the ‘economic’ concept of accounting

in use in many capitalist countries. A property right is not essential to determine

an asset. For example, a financial lease is registered as an asset if the enterprise

controls the benefits generated from its use even if there is no legal claim on its

property. The fact that Vietnamese enterprises can register leased assets under

certain conditions reflects an economic approach to accounting.

6.4. A New Concept of Income

The income concept has evolved since 1989, but gradually, falling into line with

the capital concept (distribution of result according to the interests of the contri-

butors of capital) and taking into account the new economic management rules

that have been applied to enterprises since 1987. Under the old system, the

income of the enterprise was regarded as the income of the state, and thus it

included interest and ‘taxes’. Since 1990, interest on loans has been registered

as an expense, conforming to bank reforms. This new position reflects an align-

ment with the regulations of private capitalist countries and the recognition of the

leadership of equity owners. At the beginning of the reform, taxes, unlike interest,

were registered not as expenses but as an element of the distribution of income, a

situation that reflected the residual bureaucratic power of the state. However,

since the 2006 promulgation of the new accounting standard on income taxes,

income taxes have been recognised as an expense.

6.5. A New Concept of Revenue

The assimilation of revenues with receipts in the old system was removed in

1995. Under the 1995 system, revenues consist of delivered sales and are recog-

nised in conformity with the realisation principle. This fact is not connected to

any theoretical consideration, but testifies that Vietnamese legislation has

adopted a micro-economic definition of income, aligning itself with the dominant

world practice.

6.6. A New Concept of Expenses

The new requirement to register interest on loans as expenses has created a new

problem in a context where two types of firms – state firms and private firms –

can exist. While private firms relying heavily on debts had to reduce their income

by registering interest expenses, their ‘rivals’, the state enterprises, relying on govern-

mental subsidies and capital funds, did not have to register such expenses; thus the

comparison of results was biased. Initially, in 1990–91, the government wanted to

ensure equal competition between the two types of enterprises and so decided that

712 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

SOEs should pay and register a fee on their equities. This logical point of view is not a

novelty in the Western world and has been supported by certain theorists. However, in

spite of this sound theoretical base, in 1997 the Vietnamese government renounced its

original innovation in order to follow world practice; fees on equities financed by the

state were no longer an expense but a deduction from profit, a practice consistent with

the traditional Western recognition of the cost of equity.

6.7. New Principles of Valuation

The new accounting system privileges the viewpoint of historical cost:

in the market economy, all assets and capital must be presented in the

balance sheet as real costs. (Dang Van Thanh, 1995, p. 2)

However, a more prudent evaluation also appears in the 1995 accounting system:

SOEs must maintain the State’s capital by creating provisions for inventory

obsolescence, loss in value of investments and allowance for doubtful debts

which are recognized as expenses. (article 13, Decree No. 59-CP, Ministry

of Finance, 1996)

The emergence of this type of valuation can be explained by the influence of the

‘insiders credit’ financing system, which accounts for 32% of SOE financing.

Inventories are measured at the lower of cost or net realisable value; financial

instruments are measured at the lower of cost or market value; allowance for

doubtful debts is permitted. We know that this traditional conservatism, which

is very different from the one in line with the IFRS (see below), aims to

measure the liquidity value of assets pessimistically to check the capacity of

the enterprise to refund its liability immediately. Historically, traditional conser-

vatism appears when creditors’ interests are influential enough to require specific

protection (Richard and Collette, 2005, p. 15). The appearance of a prudent

valuation in the 1995 accounting system aims at protecting the state banks,

since the latter represent 75% of the assets of the financial sector.

Prudent evaluation also aims at avoiding overly massive and rapid distributions

to owners, employees and the tax office. The Communist Party clearly states that

a market economy and market rules do not belong solely to a private capitalist

system, but must be integrated into Vietnamese ‘socialism’. Since Vietnam

now recognises the diversification of ownership forms (see above), if the conser-

vatism principle is not applied, part of the income of SOEs will be distributed in

advance to stakeholders other than the state, and this risks reducing state capital

in enterprises. In a situation where the state is only one of the contractors and is in

partnership with private capital, the considerations that associate the develop-

ment of conservatism with contracting arguments become meaningful, as

Watts has pointed out (2003, p. 214).

Economic Transition and Accounting System Reform in Vietnam 713

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

Moreover, a tax evaluation category appeared. Under the planned economy

system, as in the former Soviet countries, the problem of tax evaluation did

not arise, because the regulatory instrument was the plan: there was no fiscal

policy as understood in the West. Income tax was conceived as a simple deduc-

tion from a result determined by the planning rules. The tax reform in 1990 was

one of the Vietnamese government’s ambitious moves towards a market

economy. Taxation had become the major source of the state budget and an

important regulatory instrument (Chan et al., 1998, p. 1). Consequently, account-

ing became the essential control tool of the tax office. Tax regulations then

‘entered’ the accounting field to set the evaluation rules and the methods for pre-

senting financial statements. These rules (in particular as regards evaluation at

historical cost) were imposed to determine taxable income. In practice, Vietna-

mese accountants often recognise only tax-deductible expenses, reflecting a

lack of interest in operational management (Nguyen Cong Phuong, 2010,

p. 32). Contrary to Anglo-Saxon practice, but in line with the approach in Con-

tinental Europe, there are no significant differences between accounting income

and taxable income. This reflects the domination of the interest of the state. This

is logical in so far as the majority of enterprises are not joint-stock companies and

are not yet listed on the stock exchange, and so do not take other competitive

objectives into account in the presentation of their financial statements.

6.8. New Charts of Accounts

The reform of 1995 led to the adoption of a chart of accounts (which persisted in

the 2006 version) that constitutes a revolution; it replaced the circuit model inher-

ited from Schmalenbach, through the intermediary of Soviet accounting, with a

model based on the ‘balance-sheet’ principle: arrangement of the classes of

accounts in relation to the financial statements (balance sheet and income state-

ment). Indeed, the new regulation clearly privileges financial accounts to the det-

riment of production cost accounts. This viewpoint appeared in an article by

Dang Van Thanh published in April 1996, four months after the promulgation

of the 1995 accounting system:

The arrangement of accounts is based on the principle of balance between

the assets and the passive (equity and liability), which is in conformity with

the headings of the balance sheet. Moreover, this arrangement relates to

the comparison between income and expense. (p. 4)

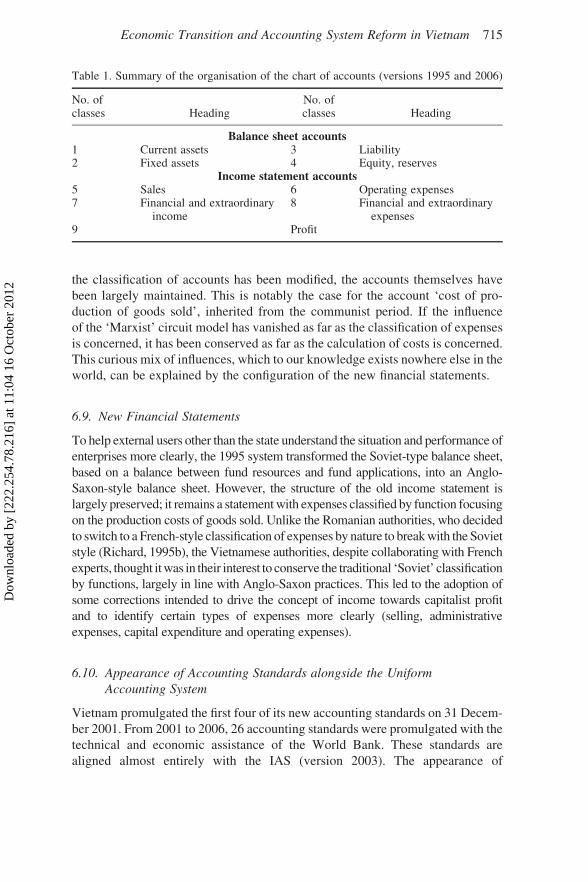

The new chart, summarised in Table 1, arranges the classes of accounts in relation

to the synthetic financial statements in order to improve financial information for

external users, whereas the old model aimed only at satisfying internal users.

Although this change was brought about with the help of French experts (the

EURO-TAPVIET project), the Vietnamese Ministry of Finance decided not to

adopt a purely ‘financial style’ chart of accounts like that in France. Although

714 Nguyen Cong Phuong and J. Richard

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

the classification of accounts has been modified, the accounts themselves have

been largely maintained. This is notably the case for the account ‘cost of pro-

duction of goods sold’, inherited from the communist period. If the influence

of the ‘Marxist’ circuit model has vanished as far as the classification of expenses

is concerned, it has been conserved as far as the calculation of costs is concerned.

This curious mix of influences, which to our knowledge exists nowhere else in the

world, can be explained by the configuration of the new financial statements.

6.9. New Financial Statements

To help external users other than the state understand the situation and performance of

enterprises more clearly, the 1995 system transformed the Soviet-type balance sheet,

based on a balance between fund resources and fund applications, into an Anglo-

Saxon-style balance sheet. However, the structure of the old income statement is

largely preserved; it remains a statement with expenses classified by function focusing

on the production costs of goods sold. Unlike the Romanian authorities, who decided

to switch to a French-style classification of expenses by nature to break with the Soviet

style (Richard, 1995b), the Vietnamese authorities, despite collaborating with French

experts, thought it was in their interest to conserve the traditional ‘Soviet’ classification

by functions, largely in line with Anglo-Saxon practices. This led to the adoption of

some corrections intended to drive the concept of income towards capitalist profit

and to identify certain types of expenses more clearly (selling, administrative

expenses, capital expenditure and operating expenses).

6.10. Appearance of Accounting Standards alongside the Uniform

Accounting System

Vietnam promulgated the first four of its new accounting standards on 31 Decem-

ber 2001. From 2001 to 2006, 26 accounting standards were promulgated with the

technical and economic assistance of the World Bank. These standards are

aligned almost entirely with the IAS (version 2003). The appearance of

Table 1. Summary of the organisation of the chart of accounts (versions 1995 and 2006)

No. ofclasses Heading

No. ofclasses Heading

Balance sheet accounts1 Current assets 3 Liability2 Fixed assets 4 Equity, reserves

Income statement accounts5 Sales 6 Operating expenses7 Financial and extraordinary

income8 Financial and extraordinary

expenses9 Profit

Economic Transition and Accounting System Reform in Vietnam 715

Dow

nloa

ded

by [

222.

254.

78.2

16]

at 1

1:04

16

Oct

ober

201

2

accounting standards testifies to the international harmonisation of Vietnamese

accounting in the context of globalisation. However, the coexistence of account-

ing standards (VAS) and a Uniform Accounting System (UAS) is specific to

Vietnam (see below).

6.11. Accounting Organisations and Decisions

In the Western world, the evolution of accounting cannot be seriously studied

without reference to the interrelationships between the state and private or

public organisations, especially accounting organisations. Many studies have

been devoted to this question, both in a general way (Miller, 1990) and

through case studies, notably concerning the development of cash flow account-

ing (Miller, 1991; Young, 1995). The problem is totally different in the case of

Vietnam because, even in the transition period, the role of accounting and

private organisations was minimal. As Nguyen Cong Phuong has shown, the

Association of Vietnamese Accountants (AVA)

has no power relative to the creation or application of accounting rules, nor

sufficient financial resources, nor independence. Since its creation, the

Department of Accounting Policies in the Ministry of Finance has played

a major role in the majority of functions of the AVA and has financed

the biggest part of its budget (Narayan and Godden, 2000). One of the