Embed Size (px)

Citation preview

ECONOMIC SURVEY OF SINGAPORE2005

Published byMinistry of Trade and IndustryRepublic of SingaporeFebruary 2006

ISSN 0376–8791

Published February 2006

Ministry of Trade and IndustrySingapore

website: http://www.mti.gov.sgemail: [email protected]

All rights reserved. No part of thispublication may be reproduced, storedin a retrieval system or transmitted inany form or by any means, electronic,mechanised, photocopying, recordingor otherwise, without the prior permissionof the copyright holder.

Printed by SNP Security Printing Pte Ltd

CONTENTS

Economic Survey of Singapore 2005

Chapter 1The World Economy 5

Chapter 2Output, Expenditure and National Income 16

Chapter 3Employment, Wages and Productivity 24

Chapter 4Prices 34

Chapter 5Macroeconomic Policies 38

Chapter 6External Trade 48

Chapter 7Balance Of Payments 58

Chapter 8Economic Outlook 61

Chapter 9Manufacturing 65

Chapter 10Construction 77

Chapter 11Wholesale & Retail Trade and Hotels & Restaurants 81

Chapter 12Transport and Communications 85

Chapter 13Financial and Business Services 92

Feature ArticleLearning and Productivity Performance in Singapore

Manufacturing Industries 103

Statistical Appendix 111

Editorial Committee 195

Statistical and Administrative Support 196

1 The World Economy 5

1.1 GDP Growth 5

1.2 GDP Growth 6

1.3 Private Investment Growth 6

1.4 Private Consumption Growth 7

1.5 Inflation 8

1.6 Interest Rate 8

1.7 GDP Growth 9

1.8 Export Growth 9

1.9 Inflation 10

1.10 GDP Growth 12

1.11 Private Consumption Expenditure Growth 13

1.12 Gross Fixed Capital Formation Growth 13

1.13 Export Growth 14

1.14 Inflation 14

2 Output, Expenditure and National Income 16

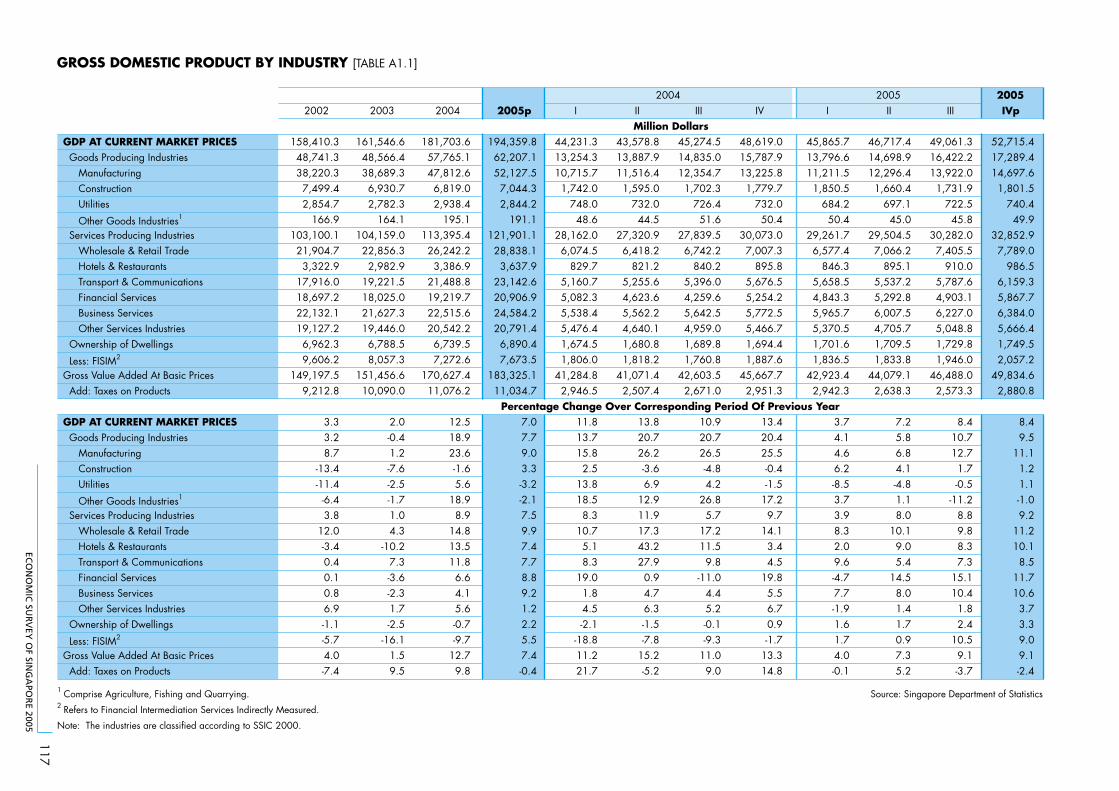

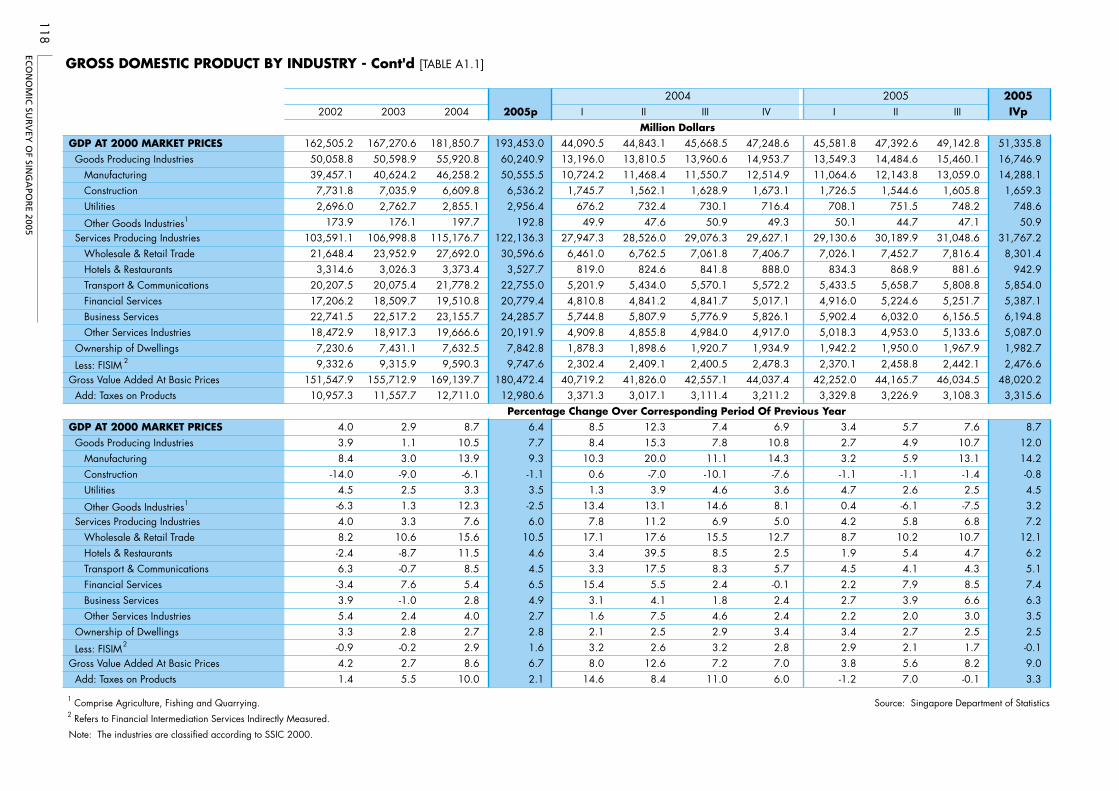

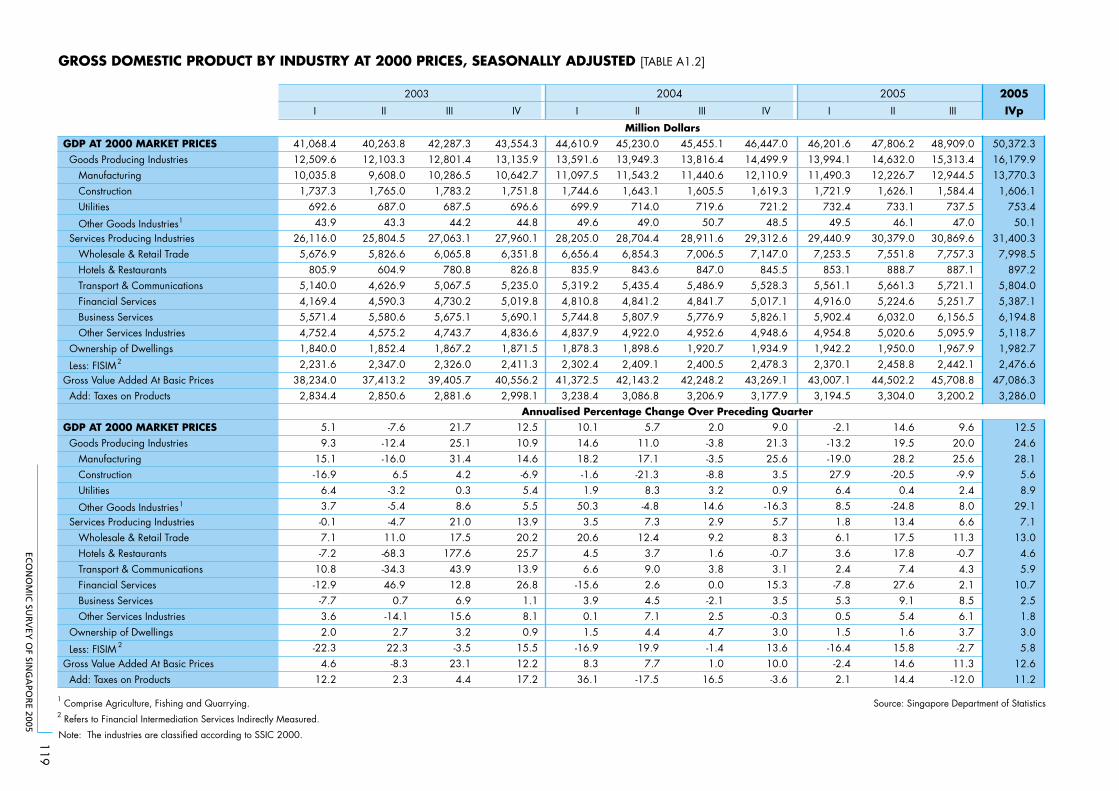

2.1 Gross Domestic Product at Market Prices 16

2.2 Changes in Gross Domestic Product at Market Prices 16

2.3 Changes in Real GDP by Industry 17

2.4 Changes in Total Demand at 2000 Market Prices 20

2.5 Singapore’s Earnings from External Economy as Proportion ofTotal Income 22

3 Employment, Wages and Productivity 243.1 Changes in Total Employment 24

3.2 Changes in Employment by Industry 25

3.3 Unemployment Rate 26

3.4 Retrenchment 27

3.5 Changes in Labour Productivity by Industry 28

3.6 Changes in Real Average Monthly Earnings and Productivity 29

3.7 Wage Share in Nominal GDP 29

3.8 Unit Business Cost Index of Manufacturing 29

3.9 Singapore’s Relative Unit Labour Cost in ManufacturingAgainst Selected 16 Economies 30

CHARTS IN TEXT

4 Prices 34

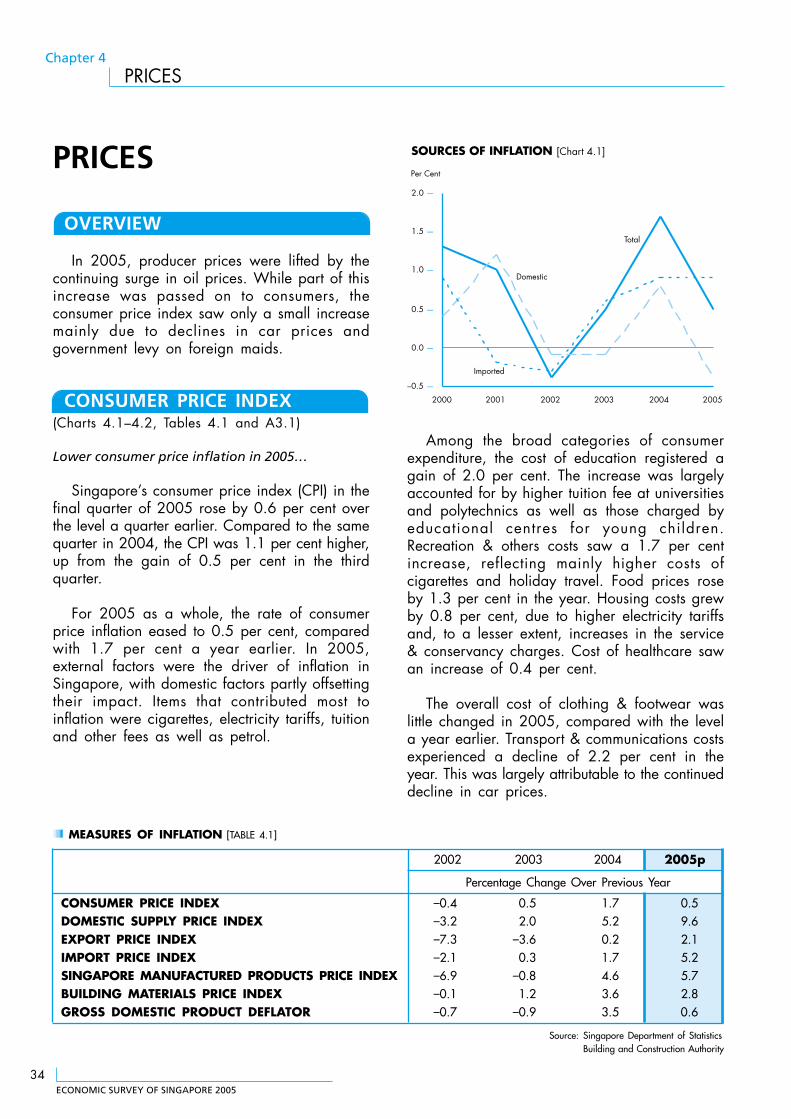

4.1 Sources of Inflation 34

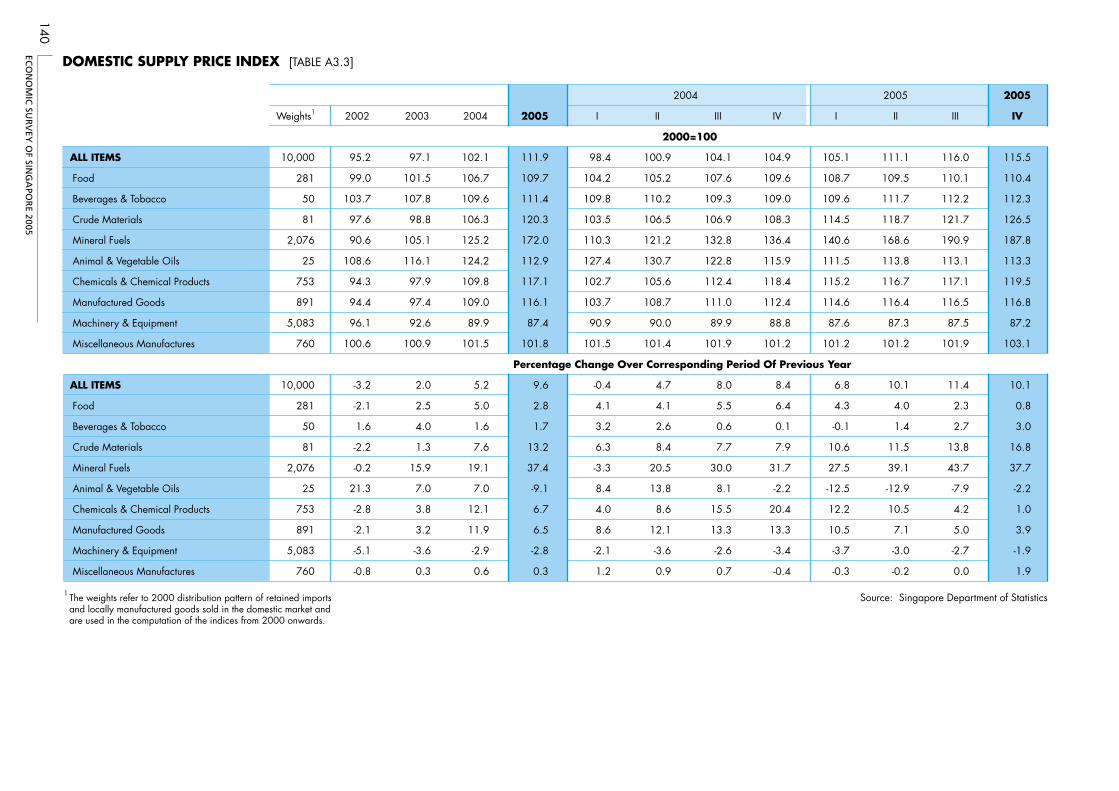

4.2 Changes in Consumer Price Index 35

4.3 Changes in Domestic Supply Price Index 36

4.4 Changes in Price Indices 36

5 Macroeconomic Policies 38

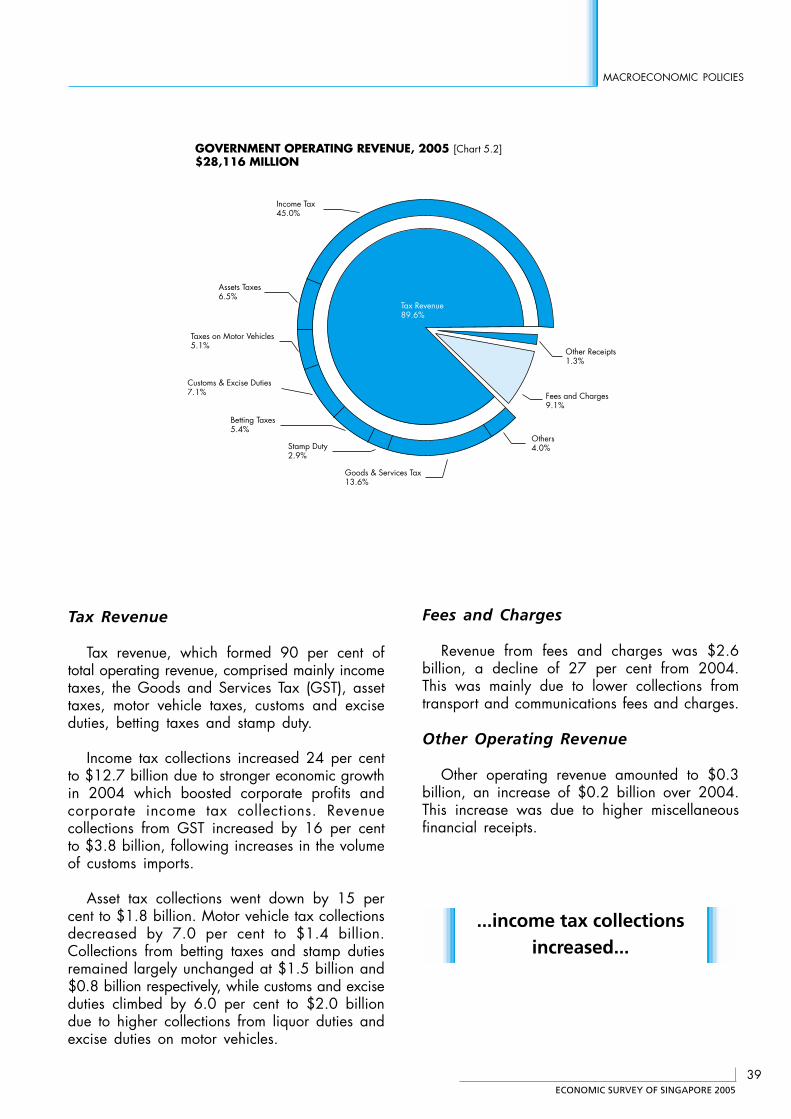

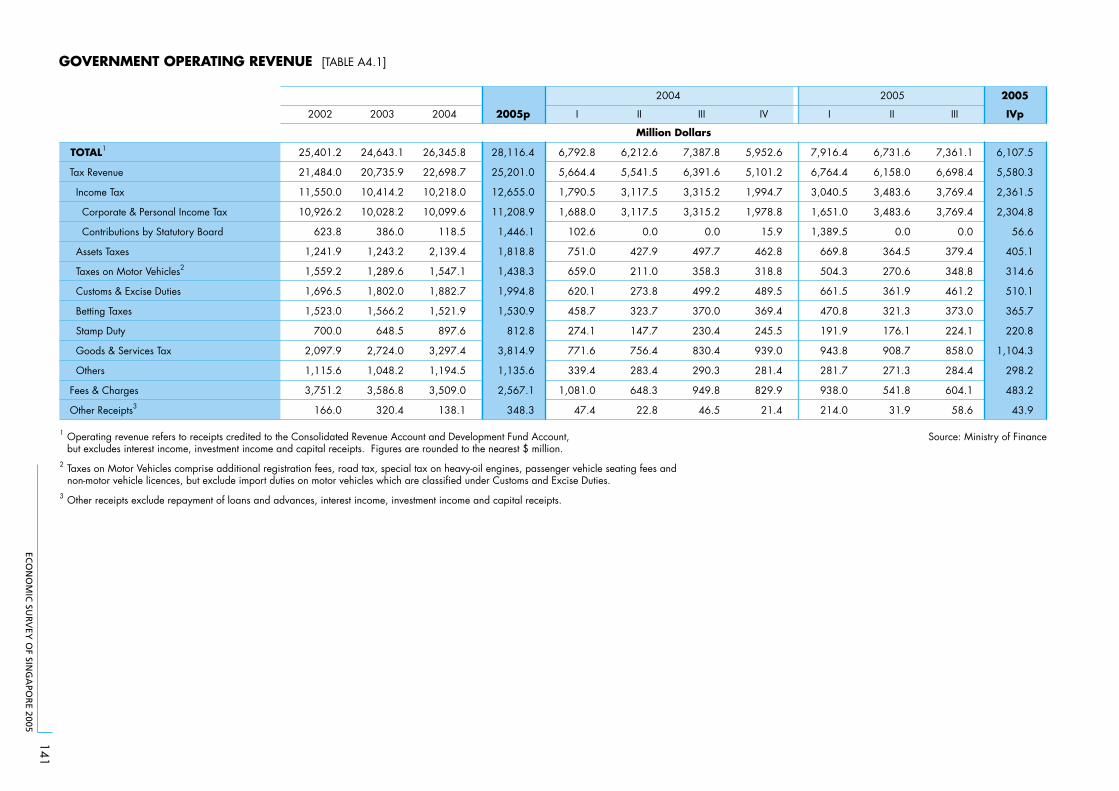

5.1 Government Operating Revenue as a Percentage of GDP 38

5.2 Government Operation Revenue, 2005 39

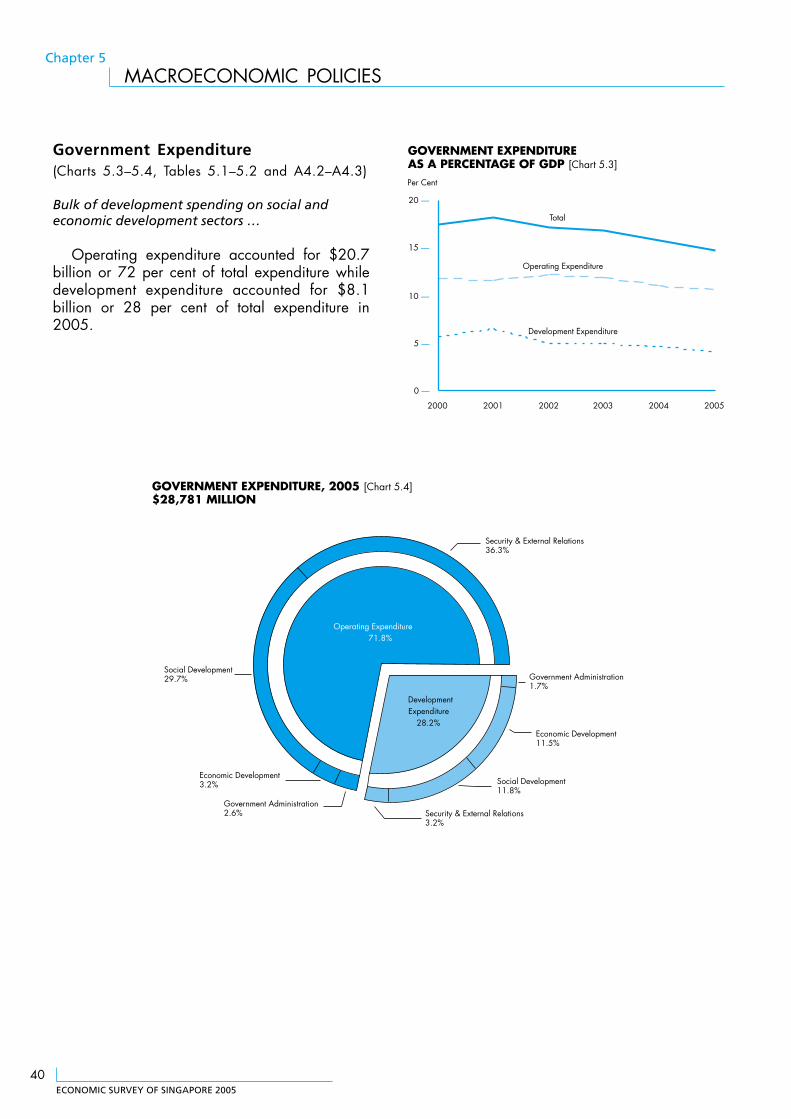

5.3 Government Expenditure as a Percentage of GDP 40

5.4 Government Expenditure, 2005 40

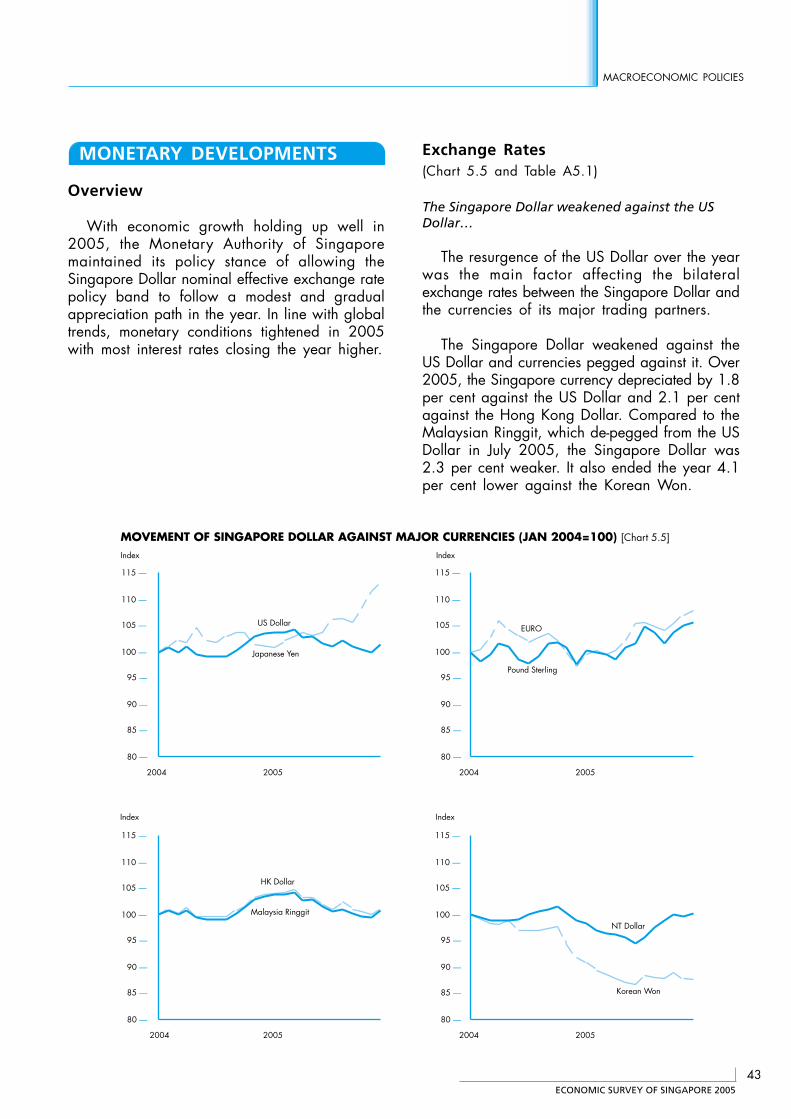

5.5 Movement of Singapore Dollar Against Major Currencies 43

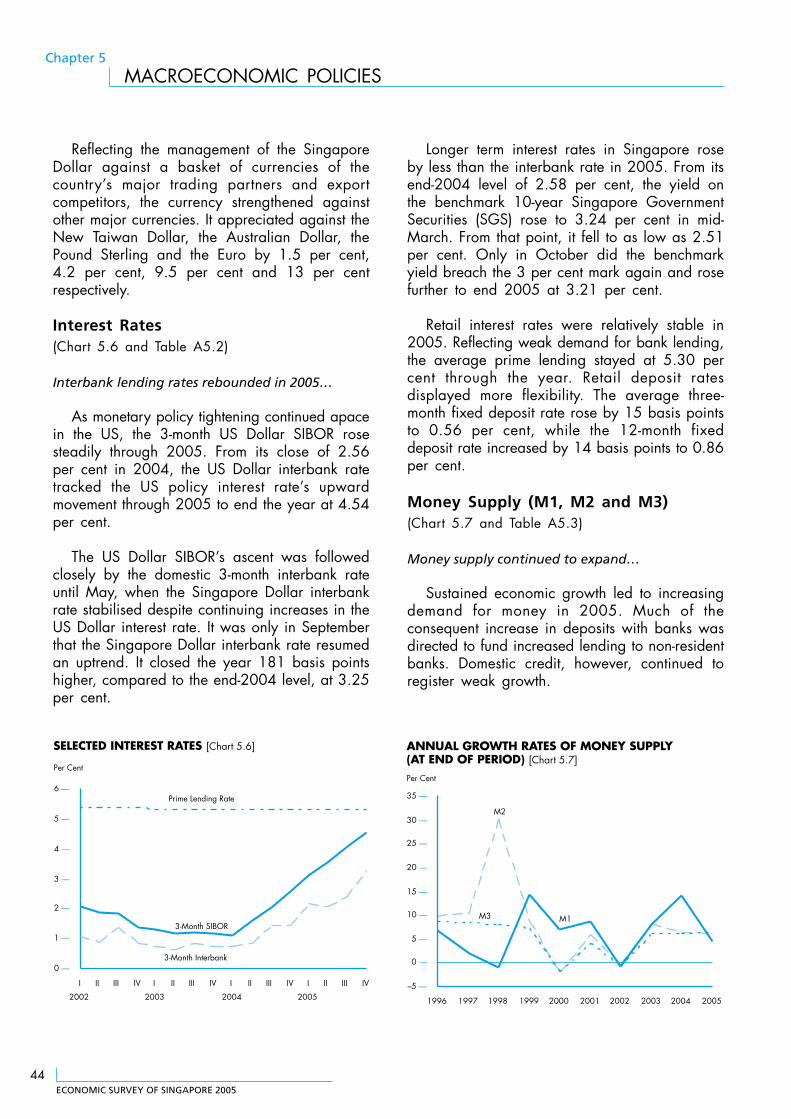

5.6 Selected Interest Rates 44

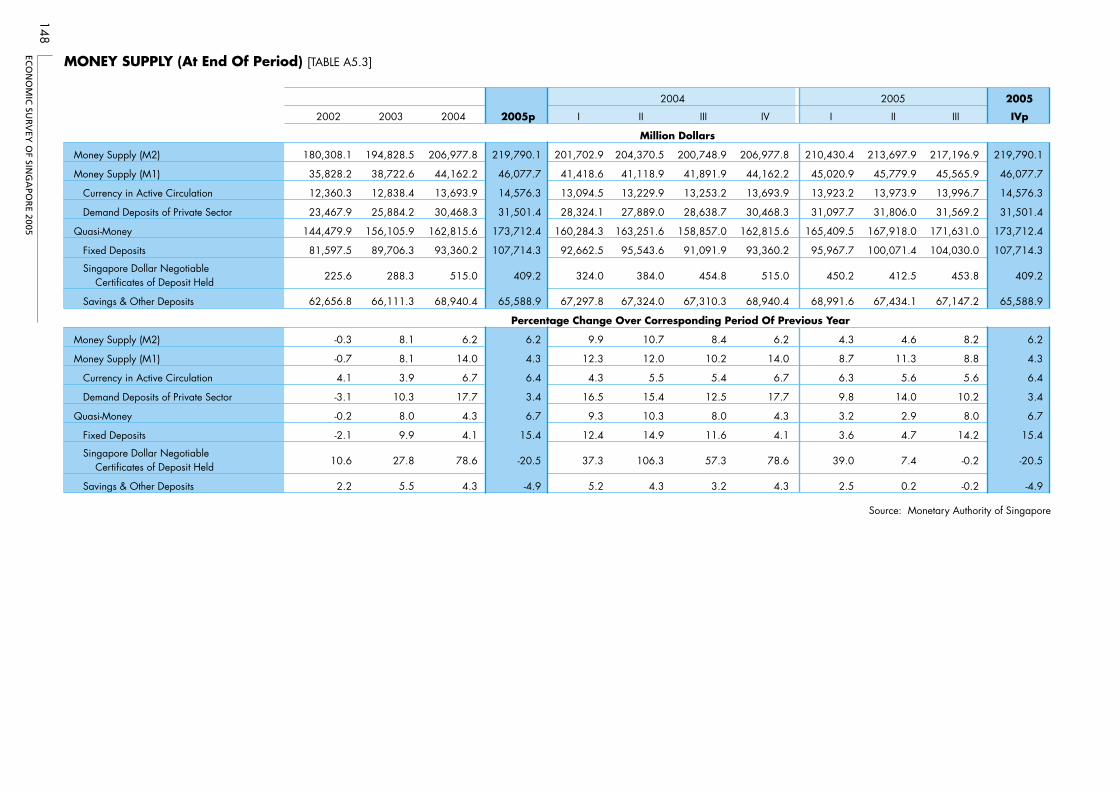

5.7 Annual Growth Rates of Money Supply 44

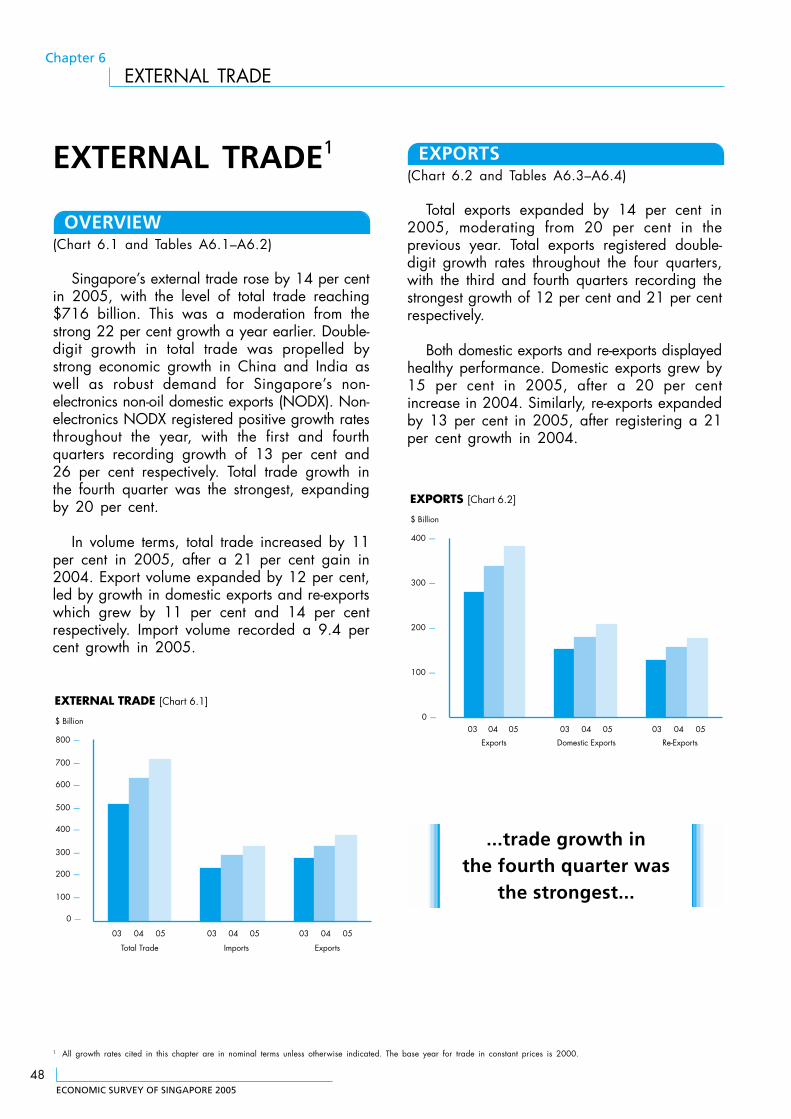

6 External Trade 48

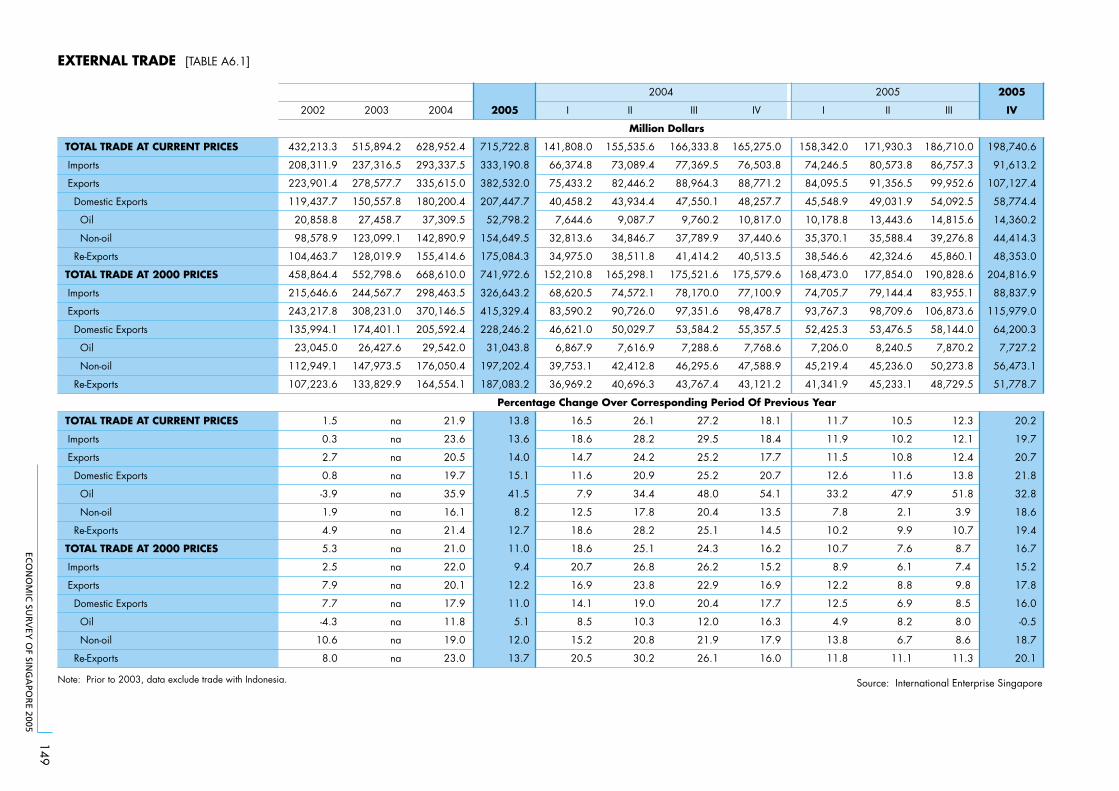

6.1 External Trade 48

6.2 Exports 48

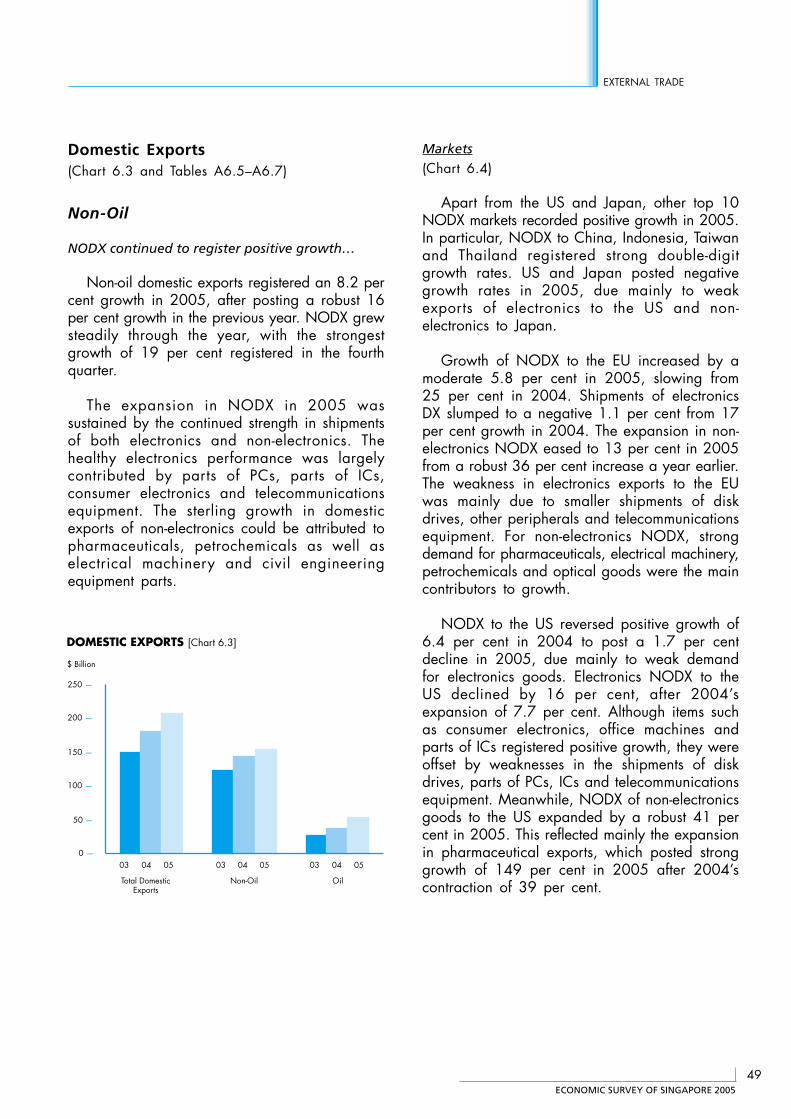

6.3 Domestic Exports 49

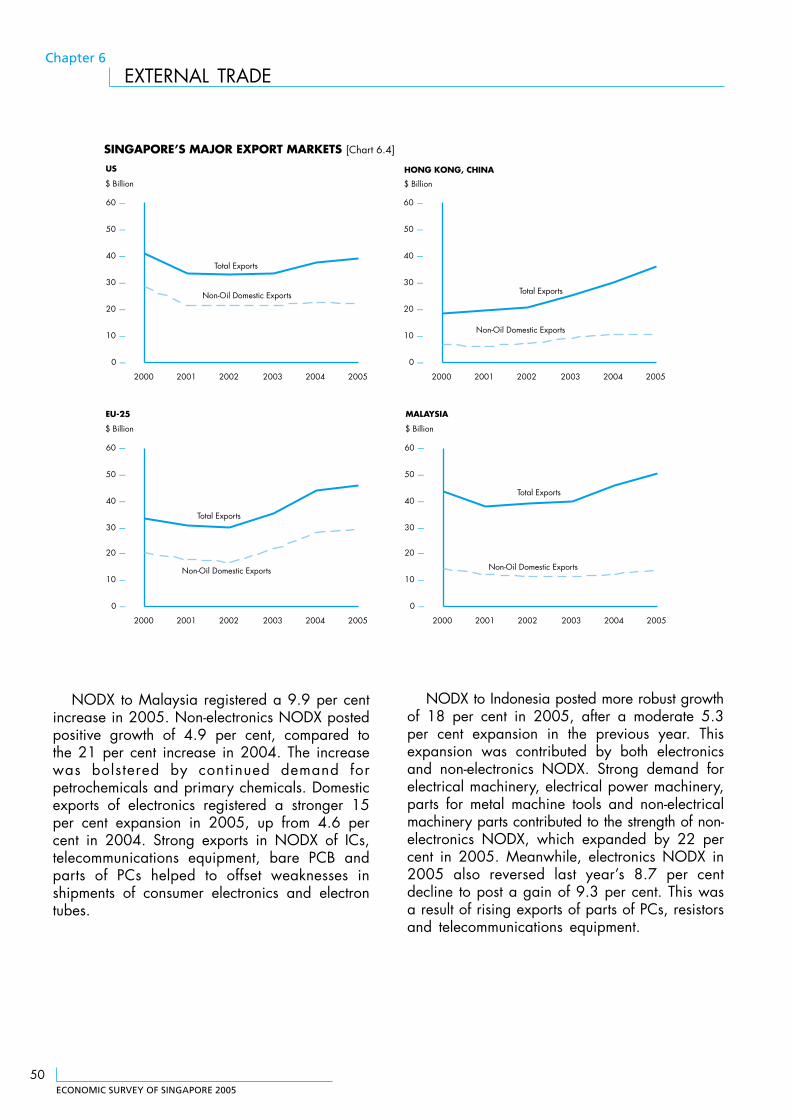

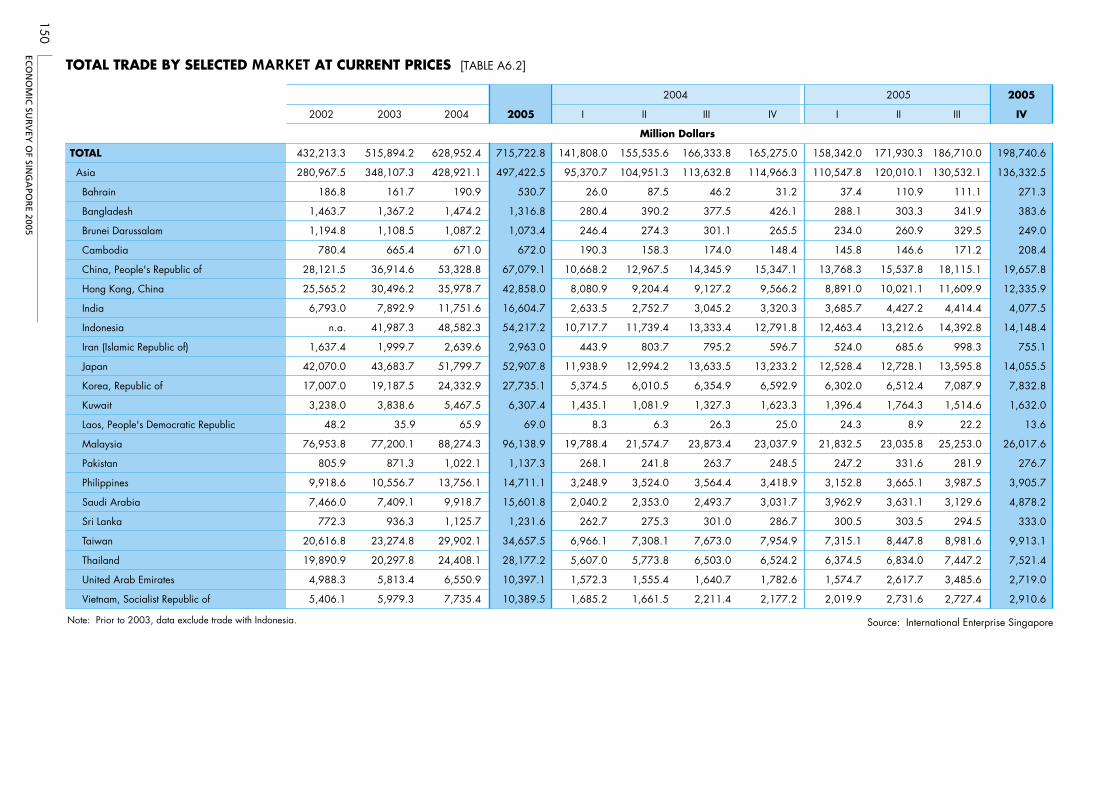

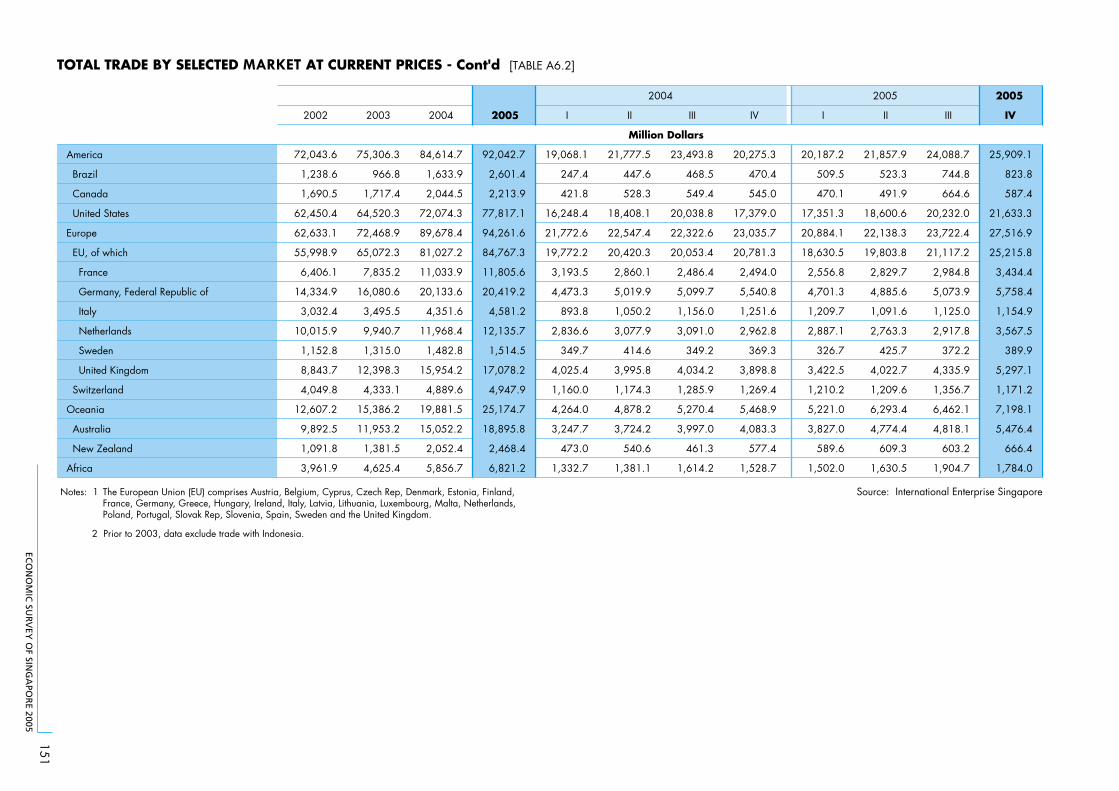

6.4 Singapore’s Major Export Markets 50

7 Balance of Payments 58

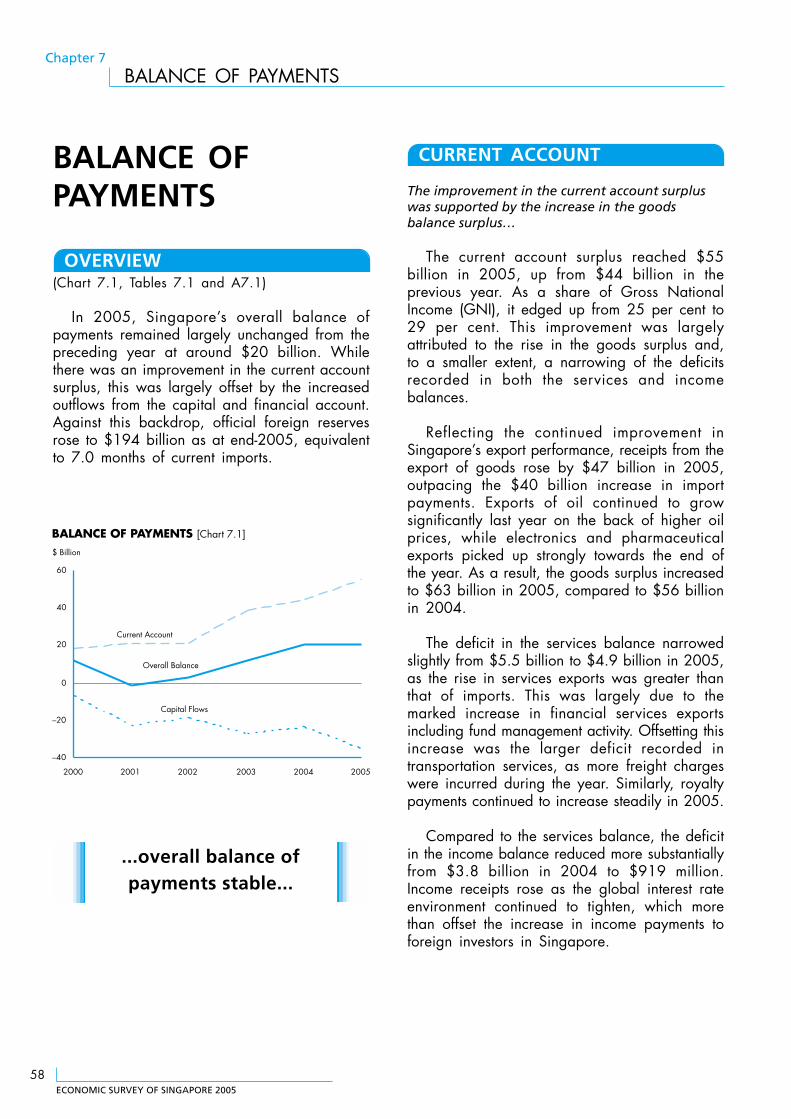

7.1 Balance of Payments 58

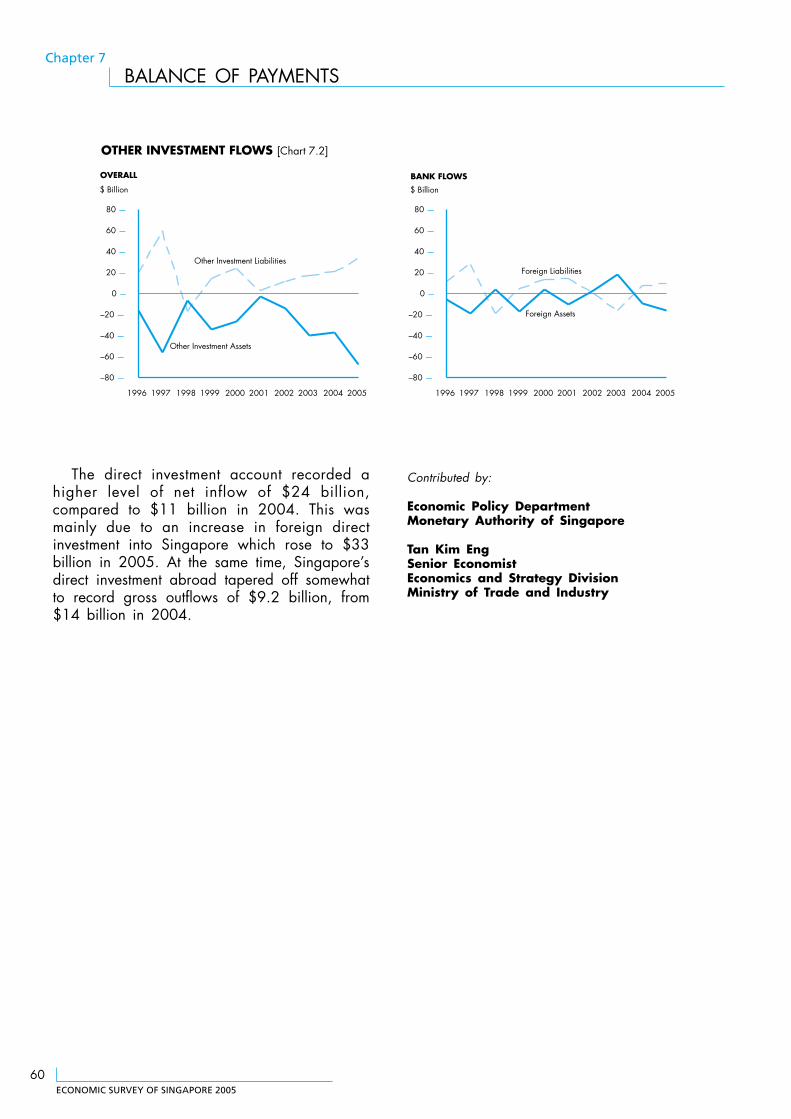

7.2 Other Investment Flows 60

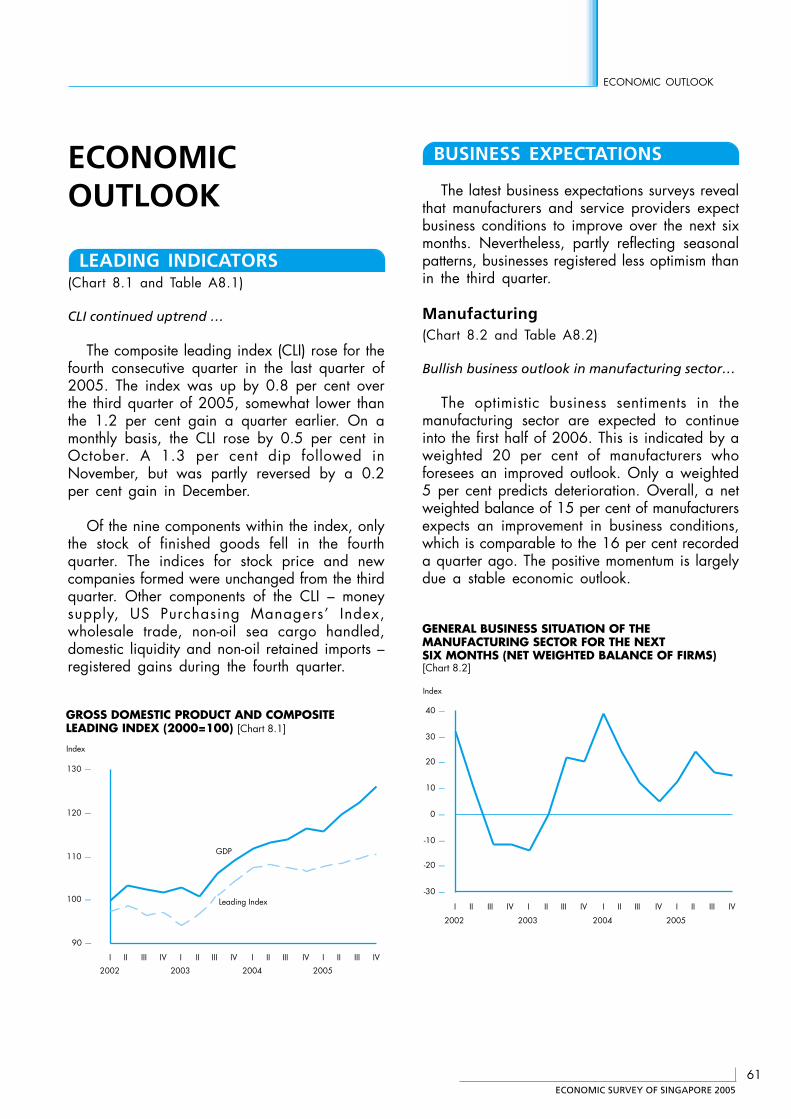

8 Economic Outlook 61

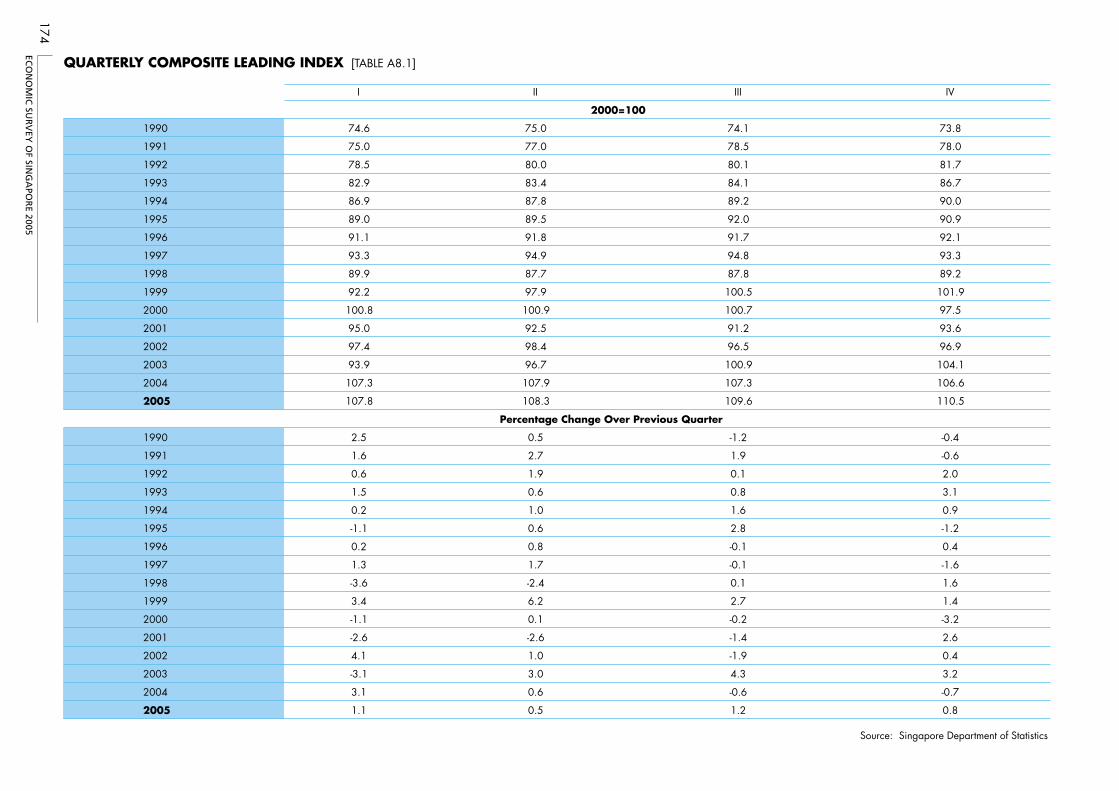

8.1 Gross Domestic Product and Composite Leading Index 61

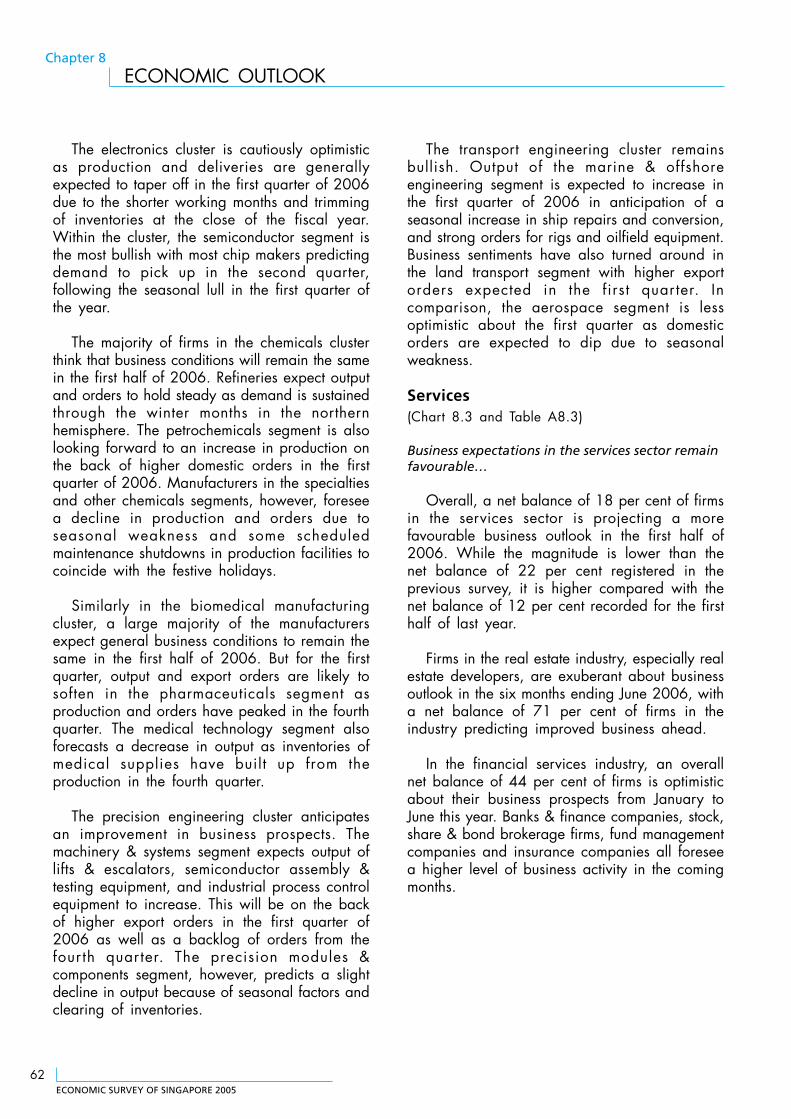

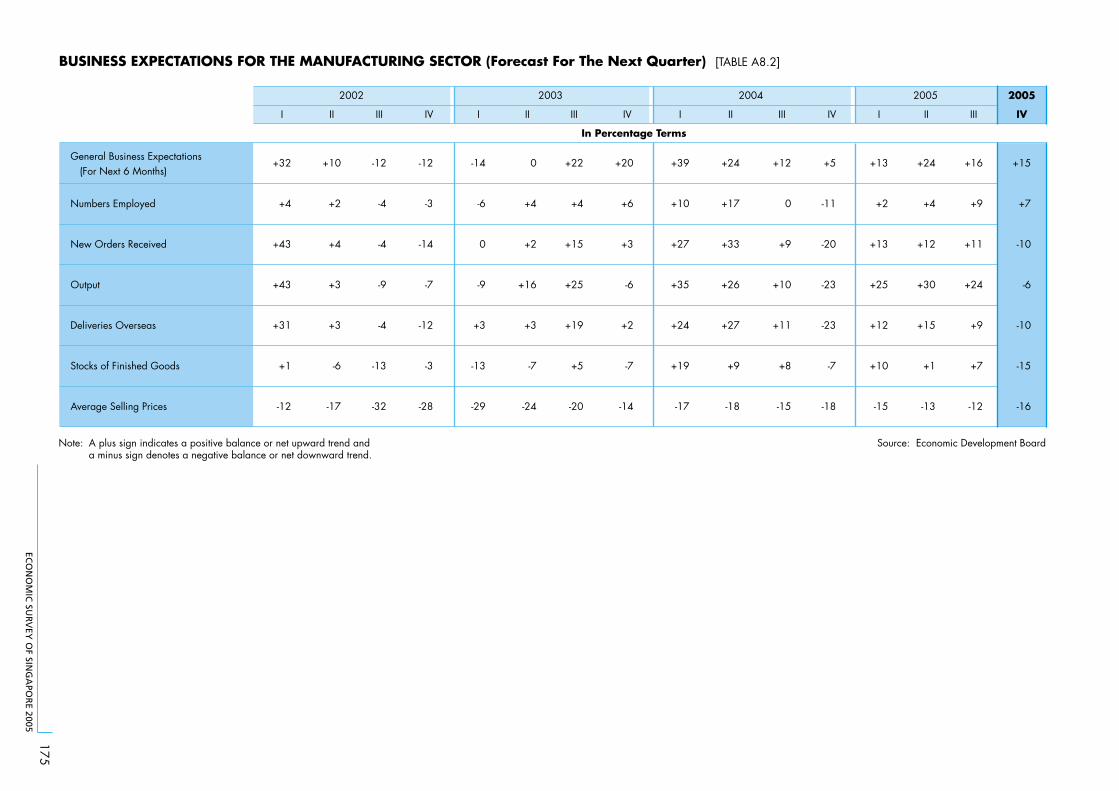

8.2 General Business Situation of the Manufacturing Sector for theNext Six Months 61

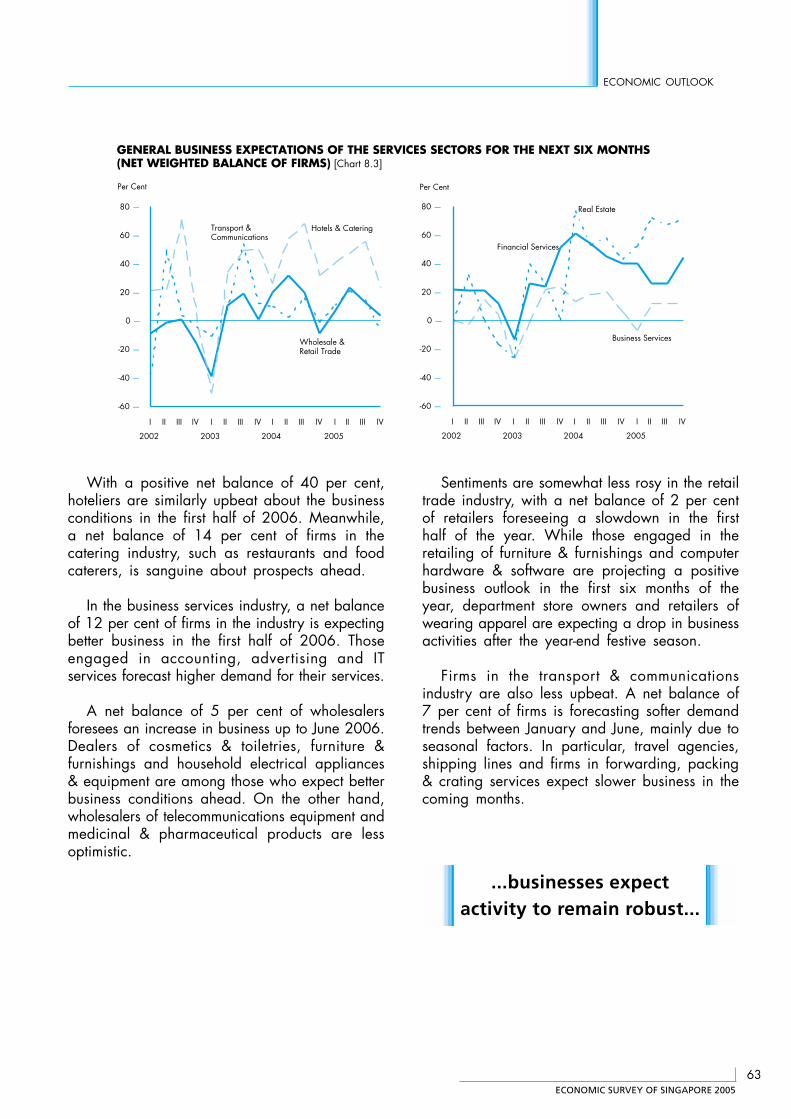

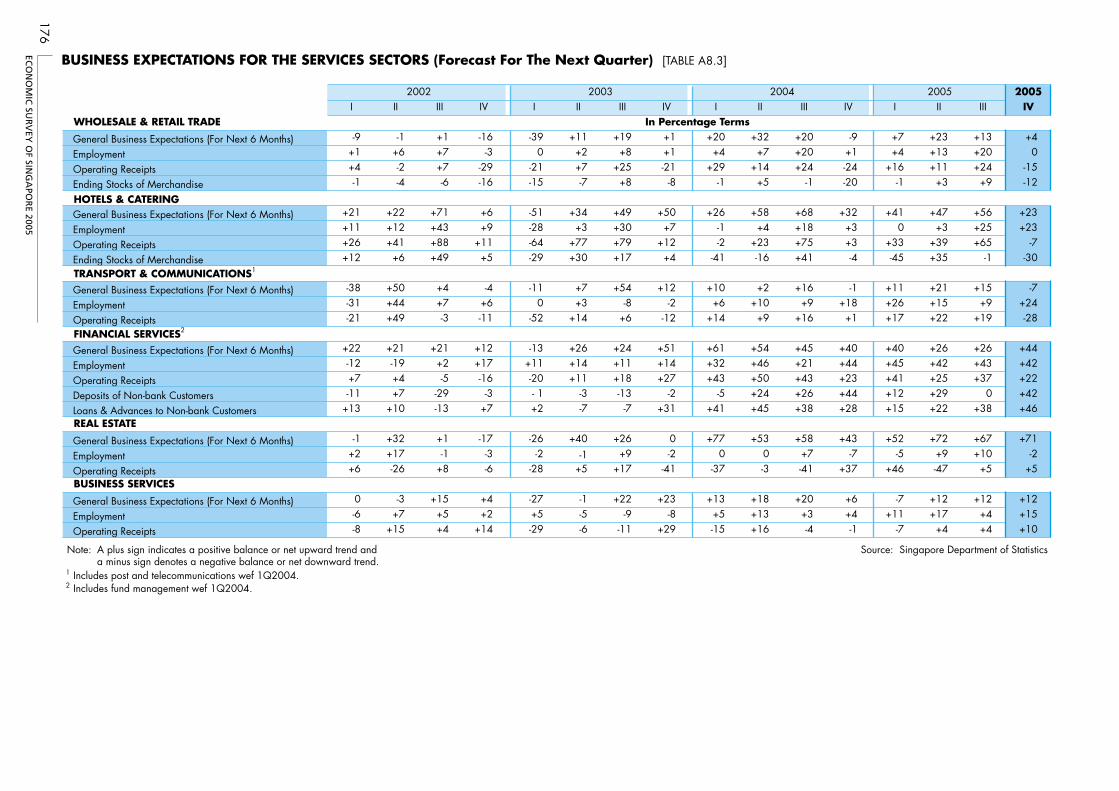

8.3 General Business Expectations of the Services Sectors for theNext Six Months 63

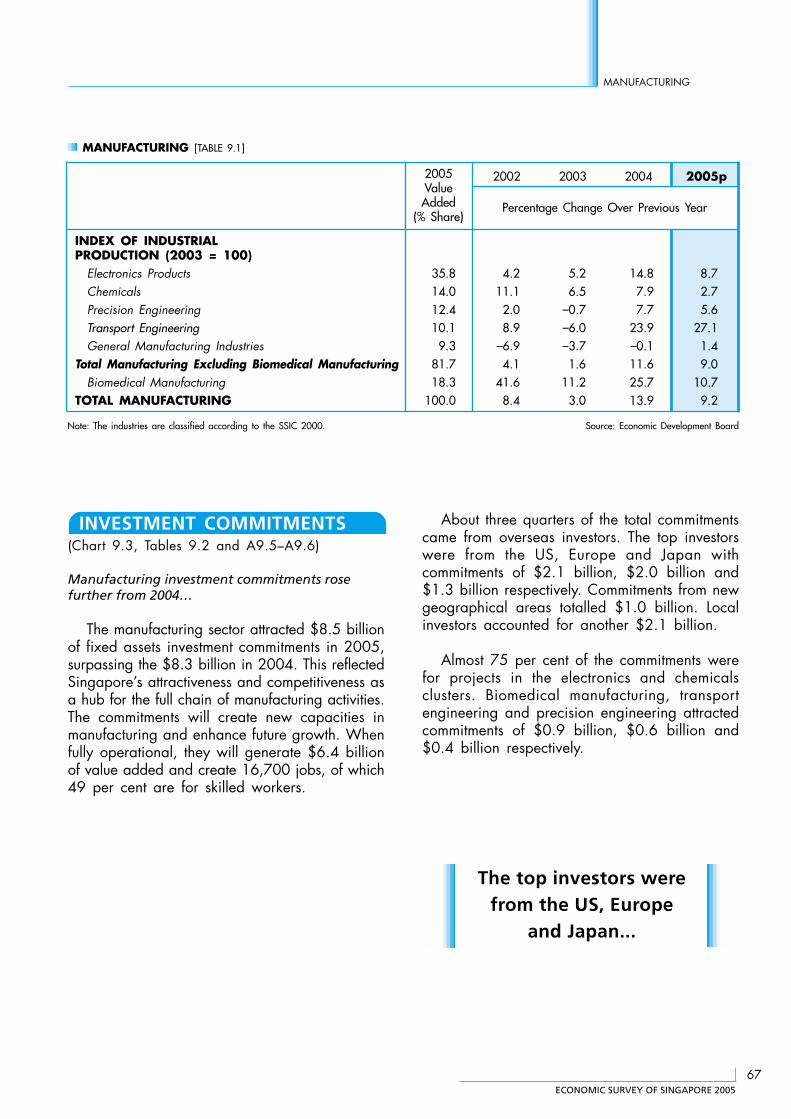

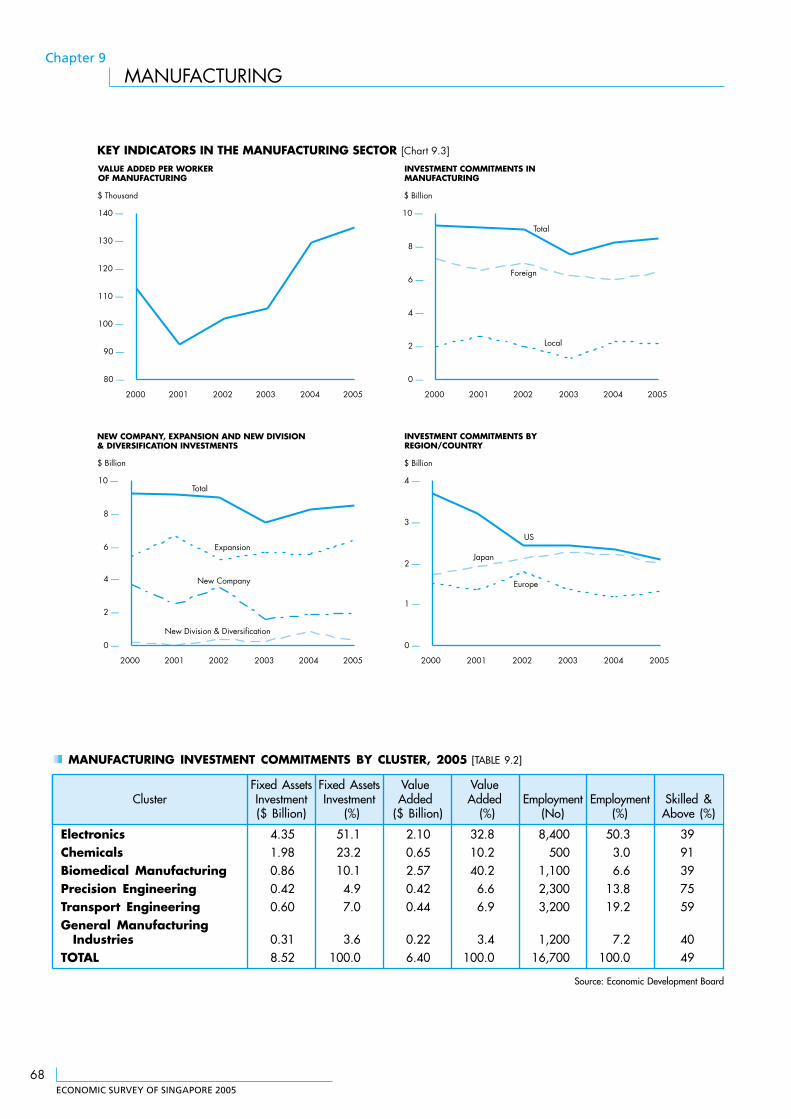

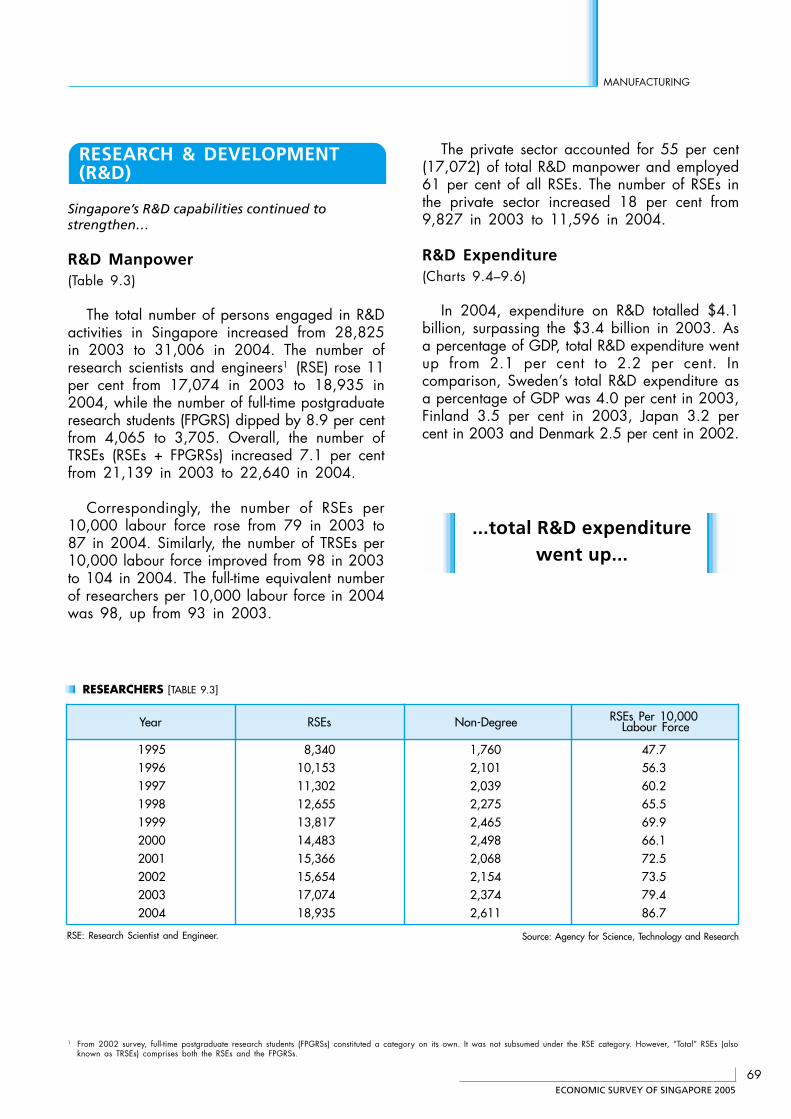

9 Manufacturing 65

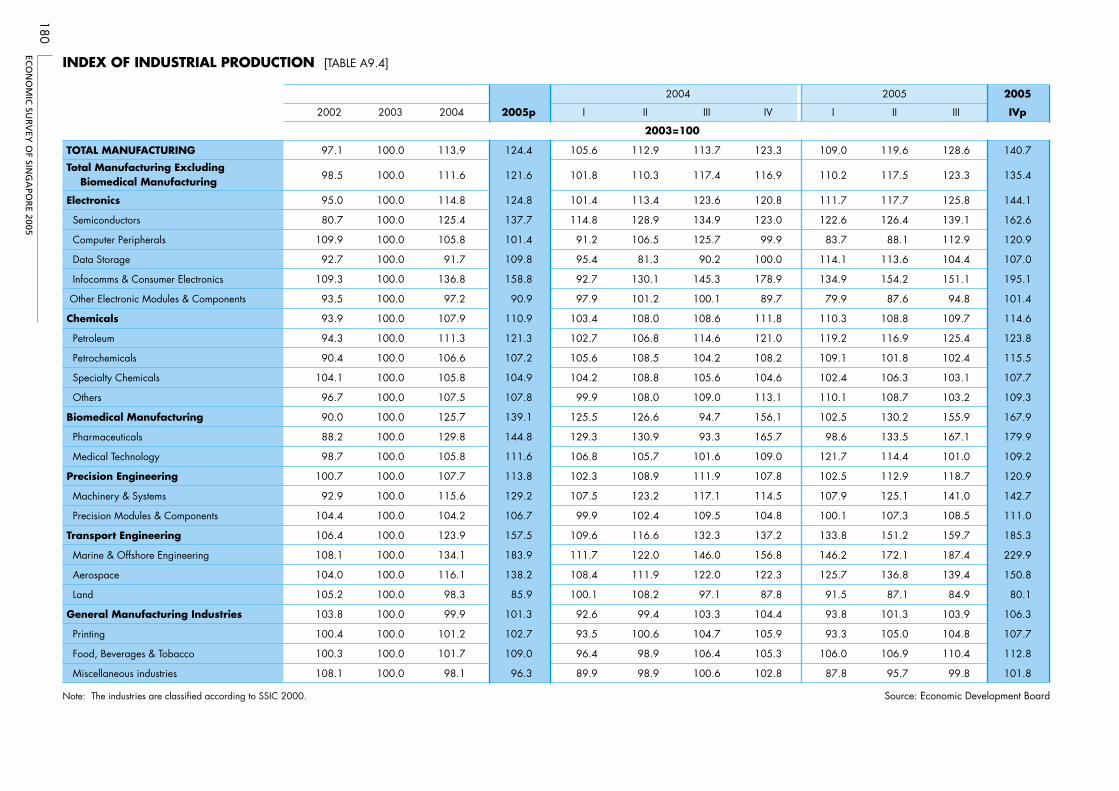

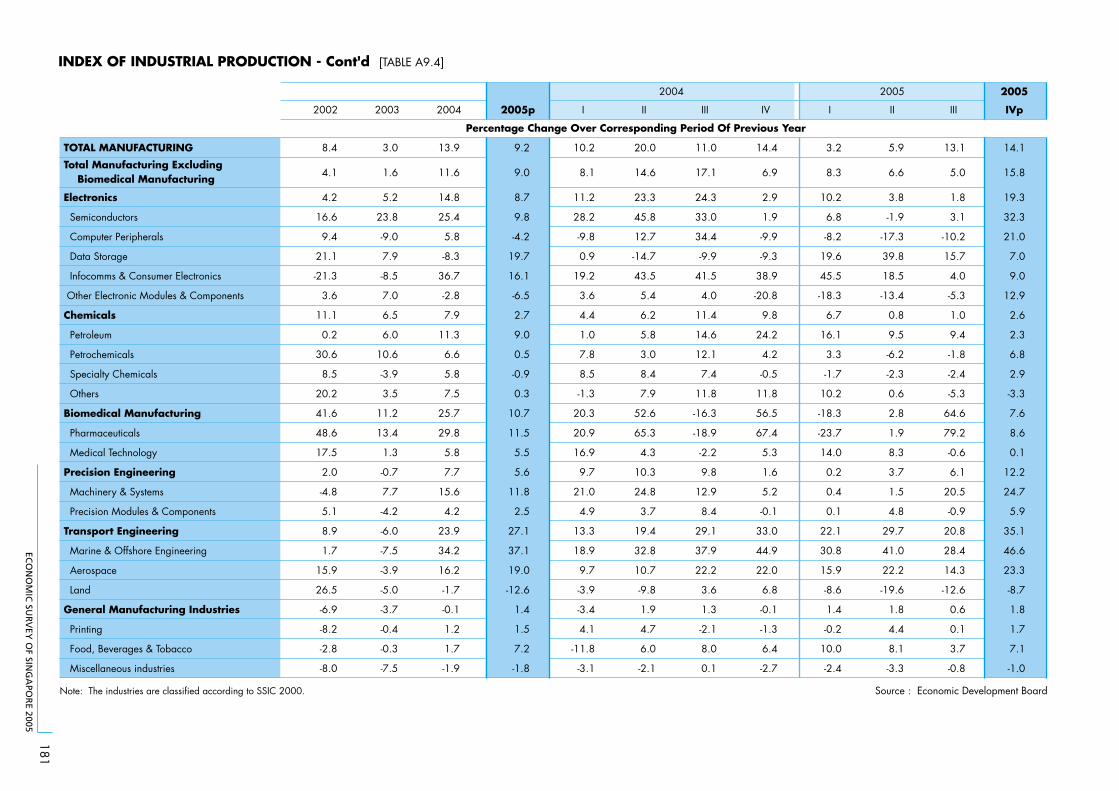

9.1 Quarterly Index of Industrial Production 65

9.2 Changes in Index of Industrial Production 66

9.3 Key Indicators in the Manufacturing Sector 68

9.4 Private Sector R&D Expenditure 70

9.5 Distribution of R&D Expenditure in the Manufacturing Industries in2004 70

9.6 Distribution of R&D Expenditure in the Services Industries in 2004 70

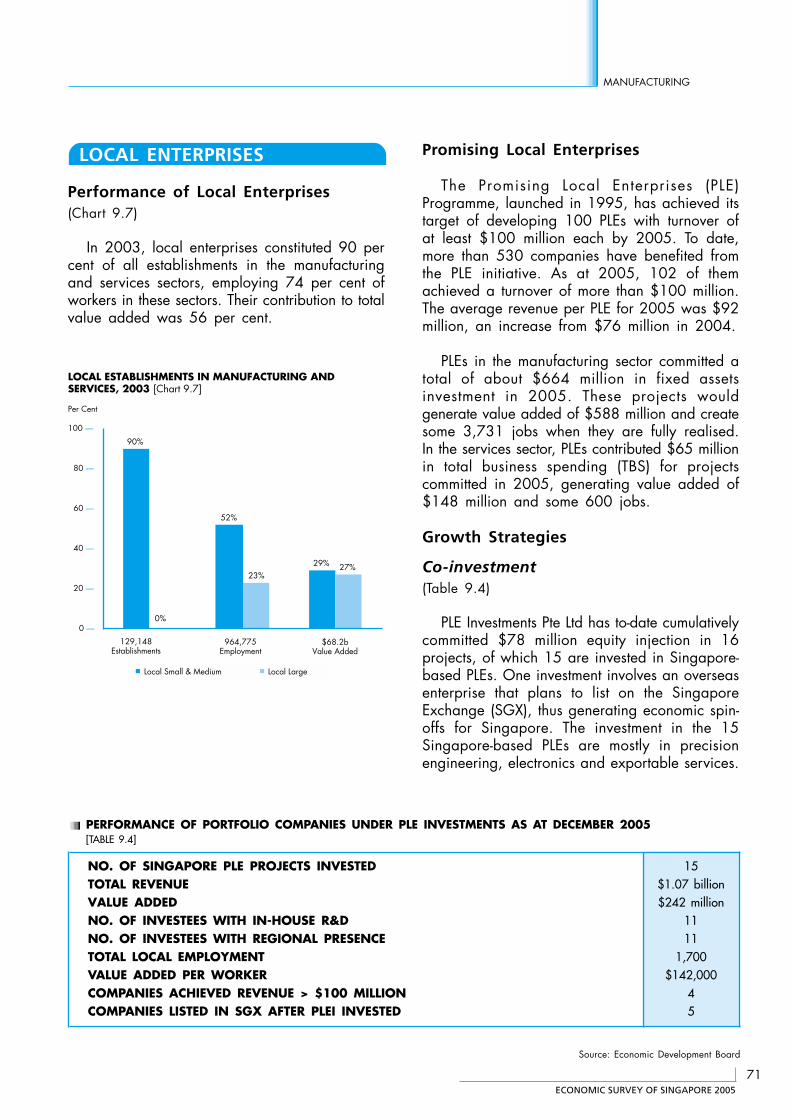

9.7 Local Establishments in Manufacturing and Services, 2003 71

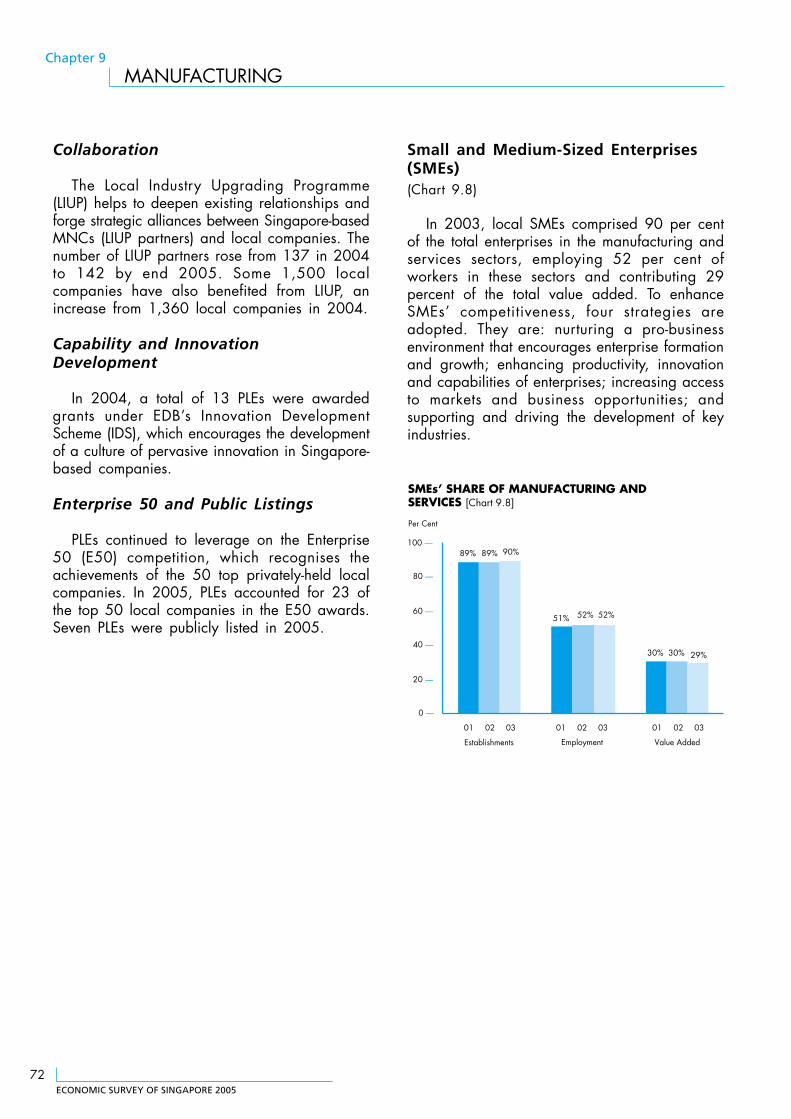

9.8 SMEs’ Share of Manufacturing and Services 72

CHARTS IN TEXT (CONT’D)

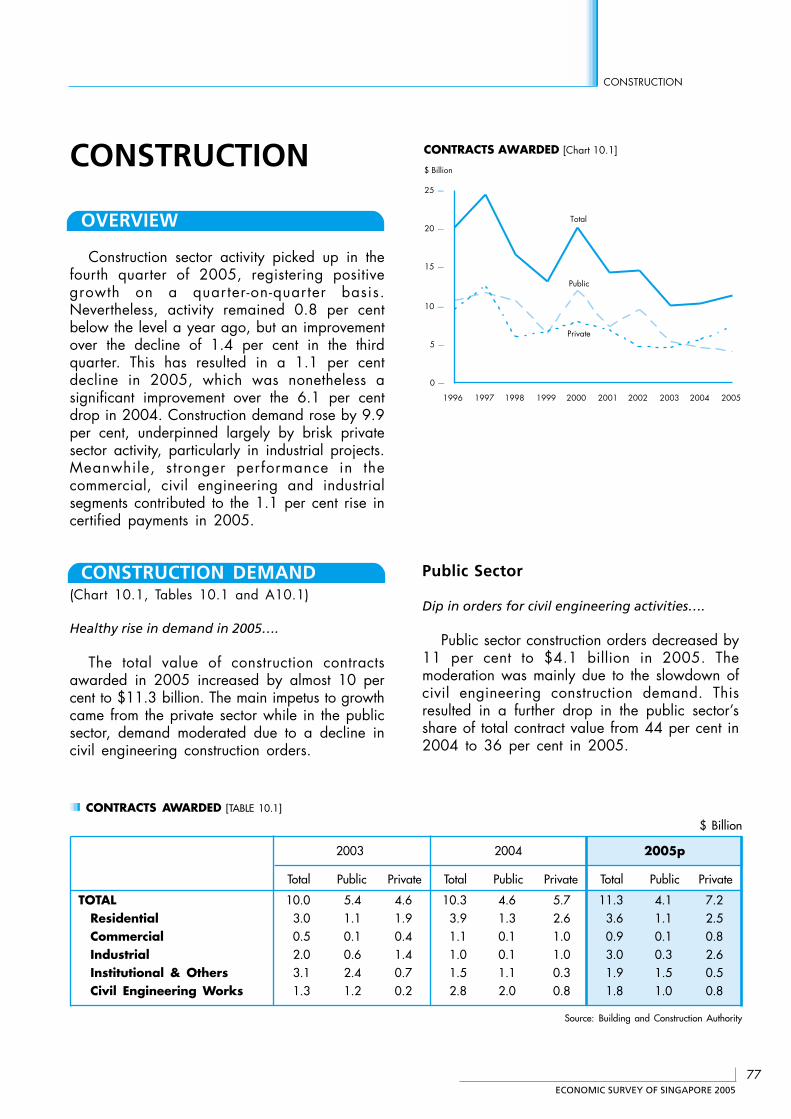

10 Construction 77

10.1 Contracts Awarded 77

11 Wholesale & Retail Trade and Hotels & Restaurants 81

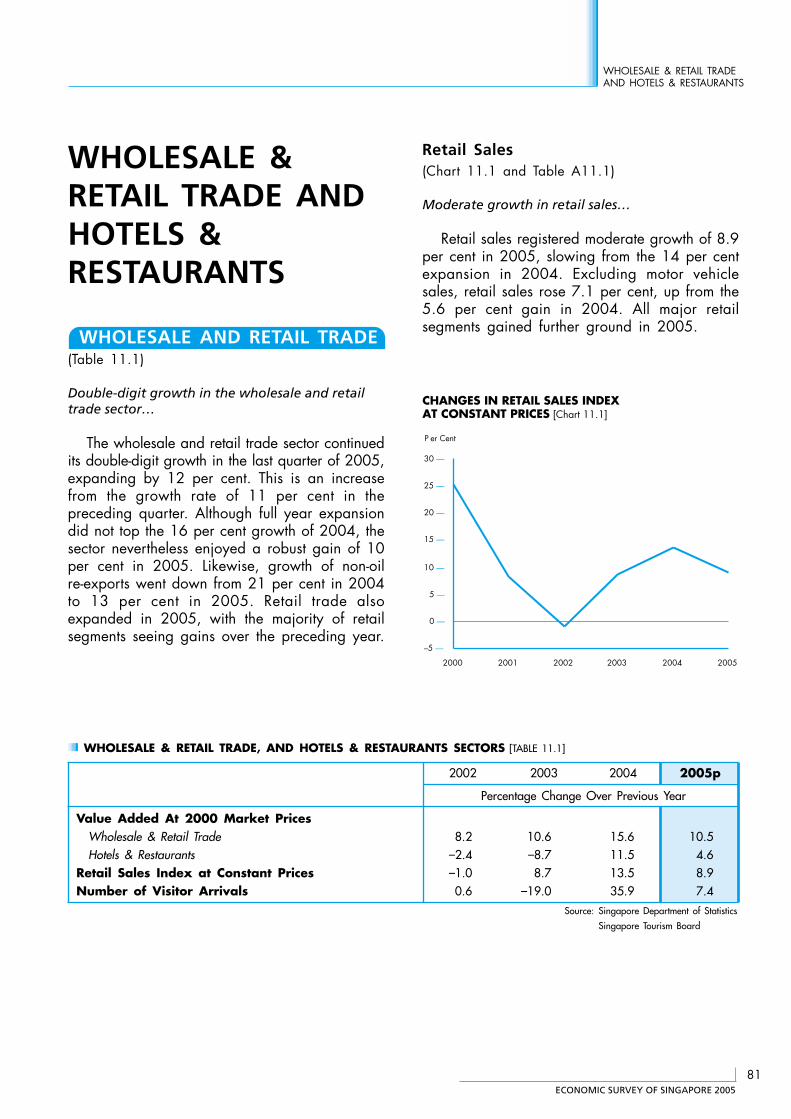

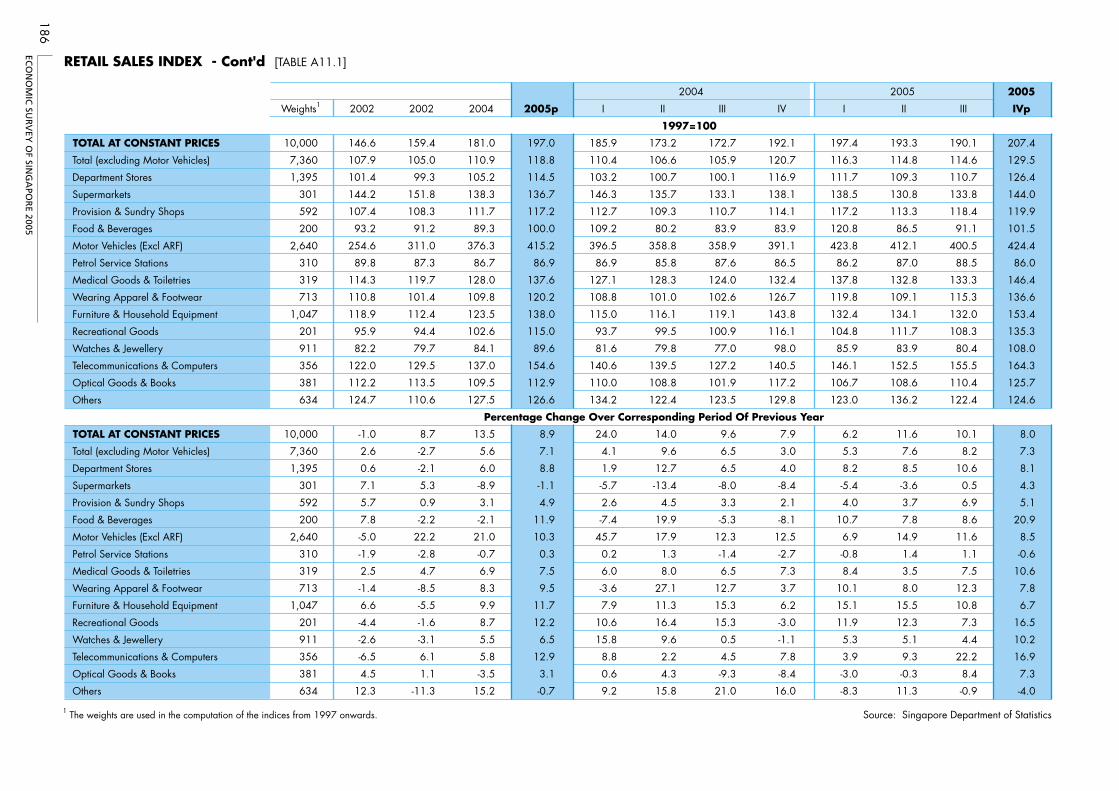

11.1 Changes in Retail Sales Index at Constant Prices 81

11.2 Average Occupancy Rate of Gazetted Hotels 82

11.3 Average Hotel Room Rate 83

11.4 Visitor Arrivals 83

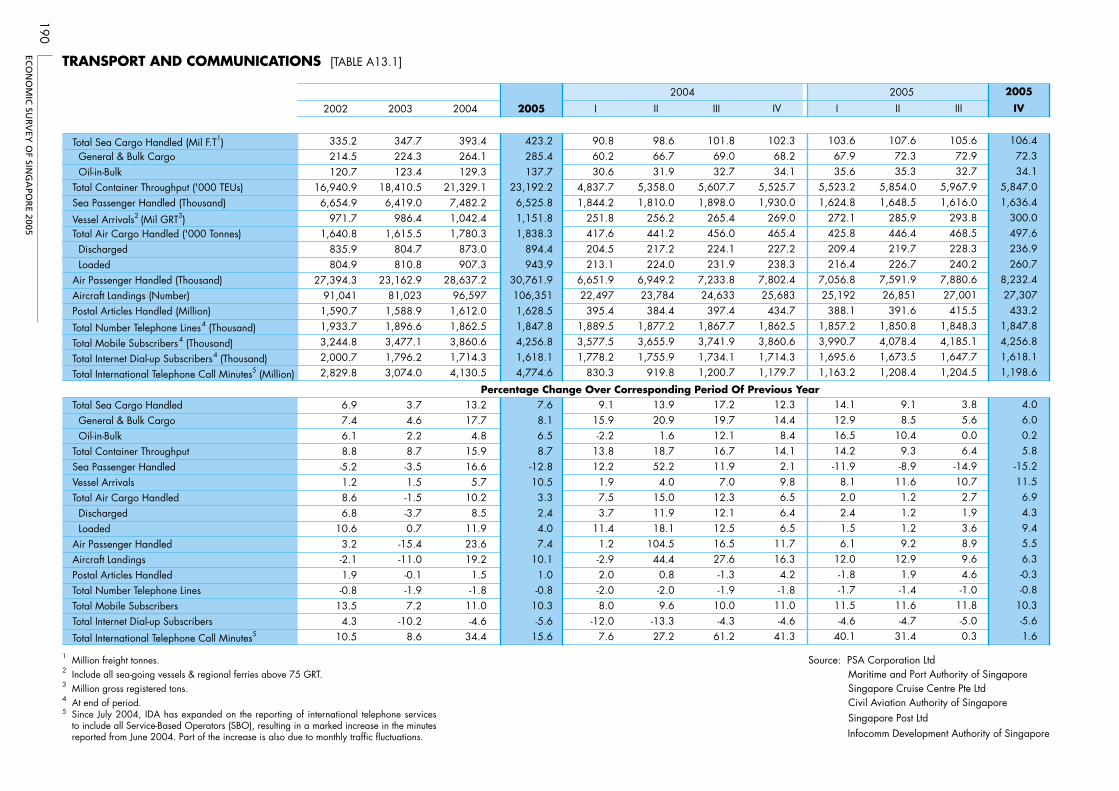

12 Transport and Communications 85

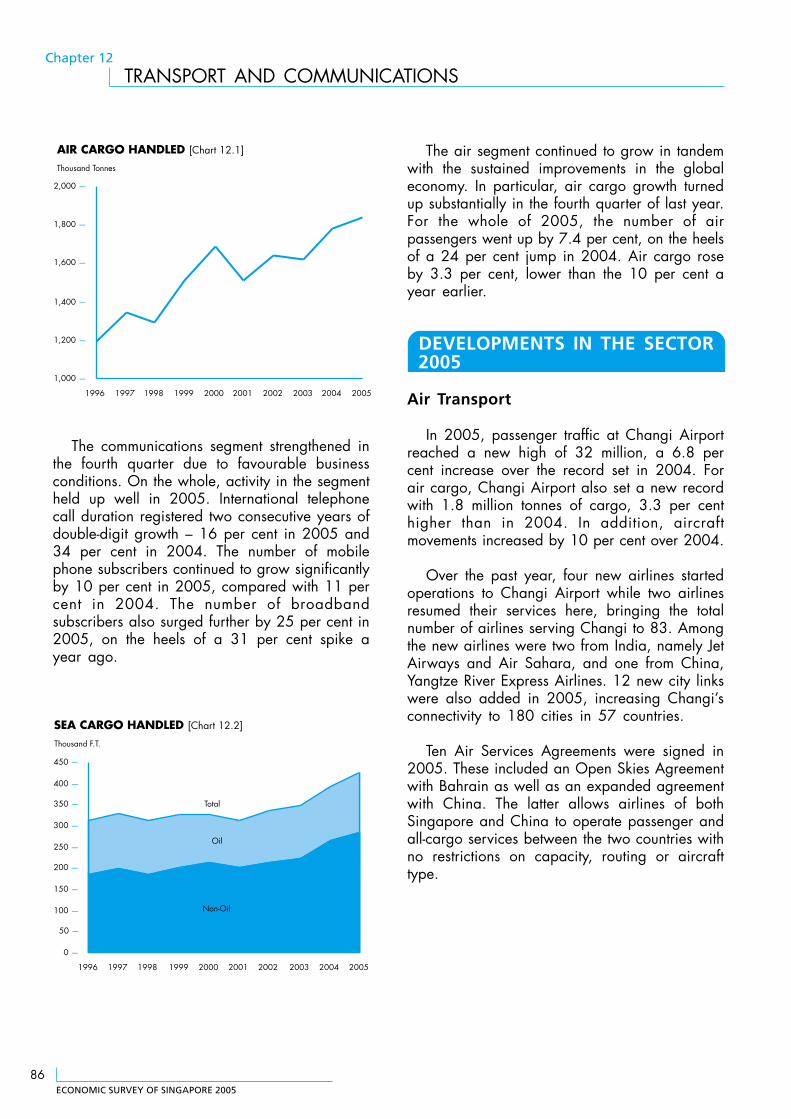

12.1 Air Cargo Handled 86

12.2 Sea Cargo Handled 86

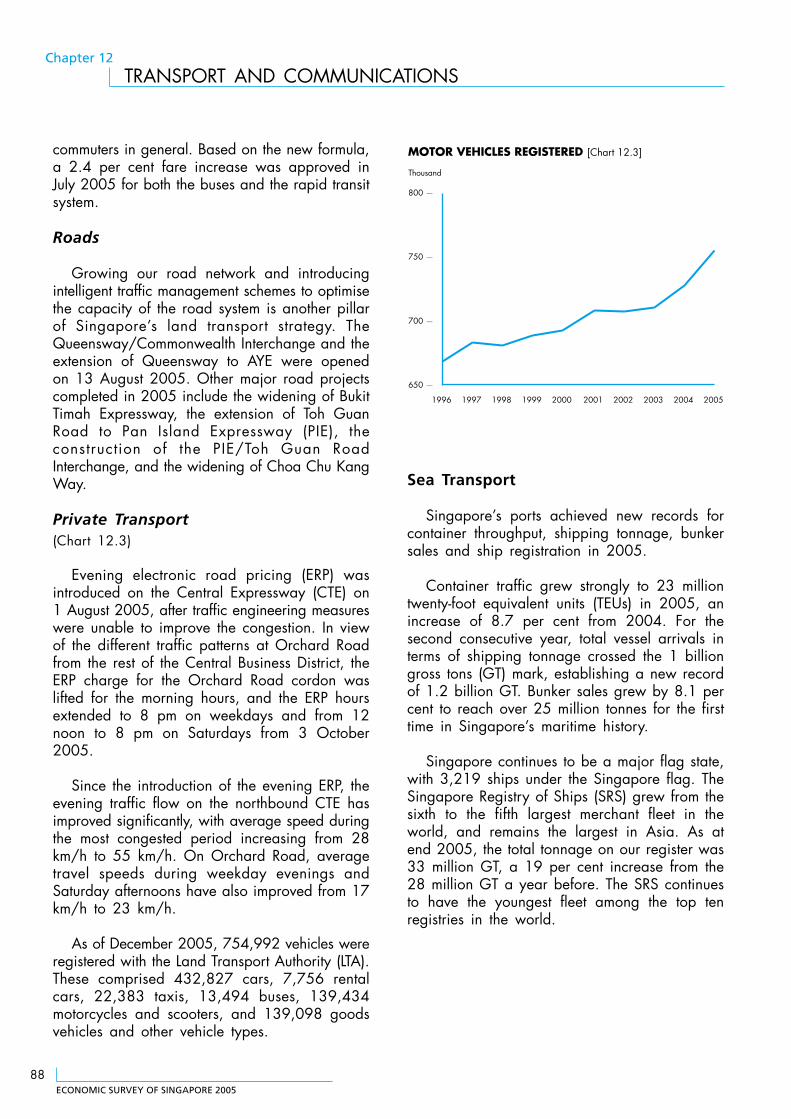

12.3 Motor Vehicles Registered 88

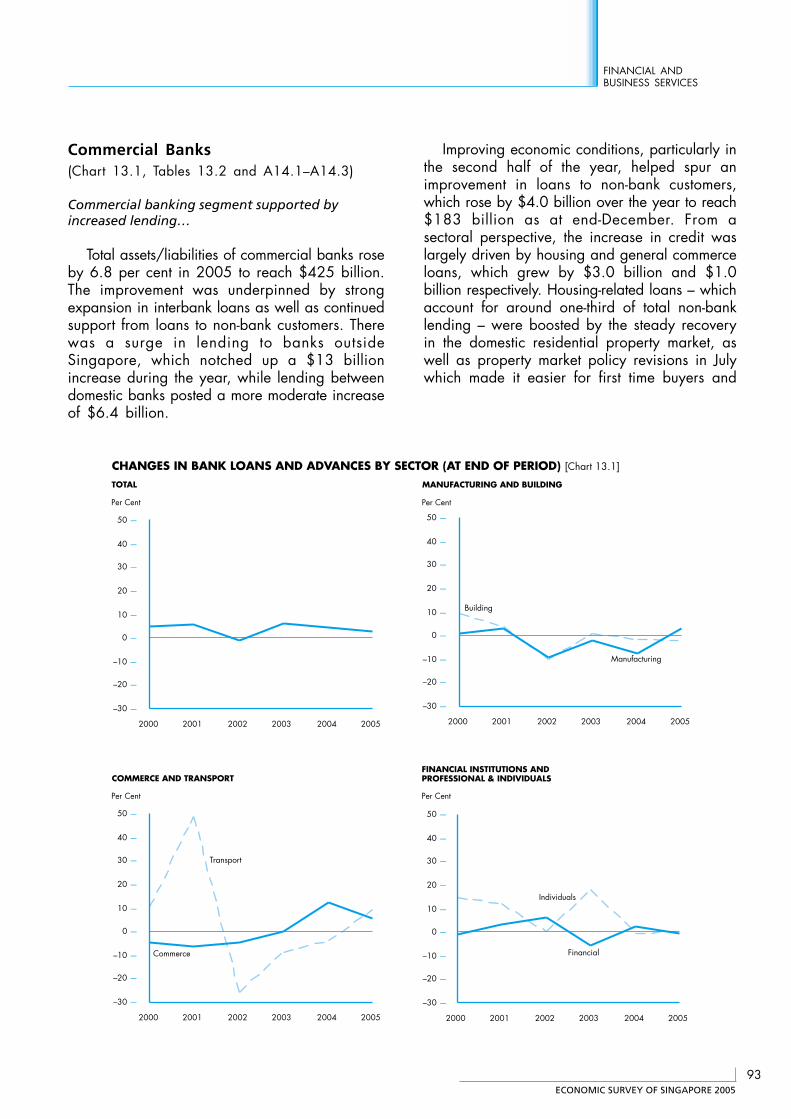

13 Financial and Business Services 92

13.1 Changes in Bank Loans and Advances by Sector 93

CHARTS IN TEXT (CONT’D)

TABLES IN TEXT

2 Output, Expenditure and National Income 16

2.1 Gross Domestic Product at 2000 Market Prices 18

2.2 Percentage Contribution to Growth in Real GDP 19

2.3 Annual Changes and Contribution to Growth in Total Demand at2000 Market Prices 20

2.4 Annual Changes in Gross Fixed Capital Formation at 2000 MarketPrices 21

2.5 Percentage Distribution of Gross Fixed Capital Formation atCurrent Market Prices 21

4 Prices 34

4.1 Measures of Inflation 34

4.2 Changes in Gross Domestic Product Deflator 37

5 Macroeconomic Policies 38

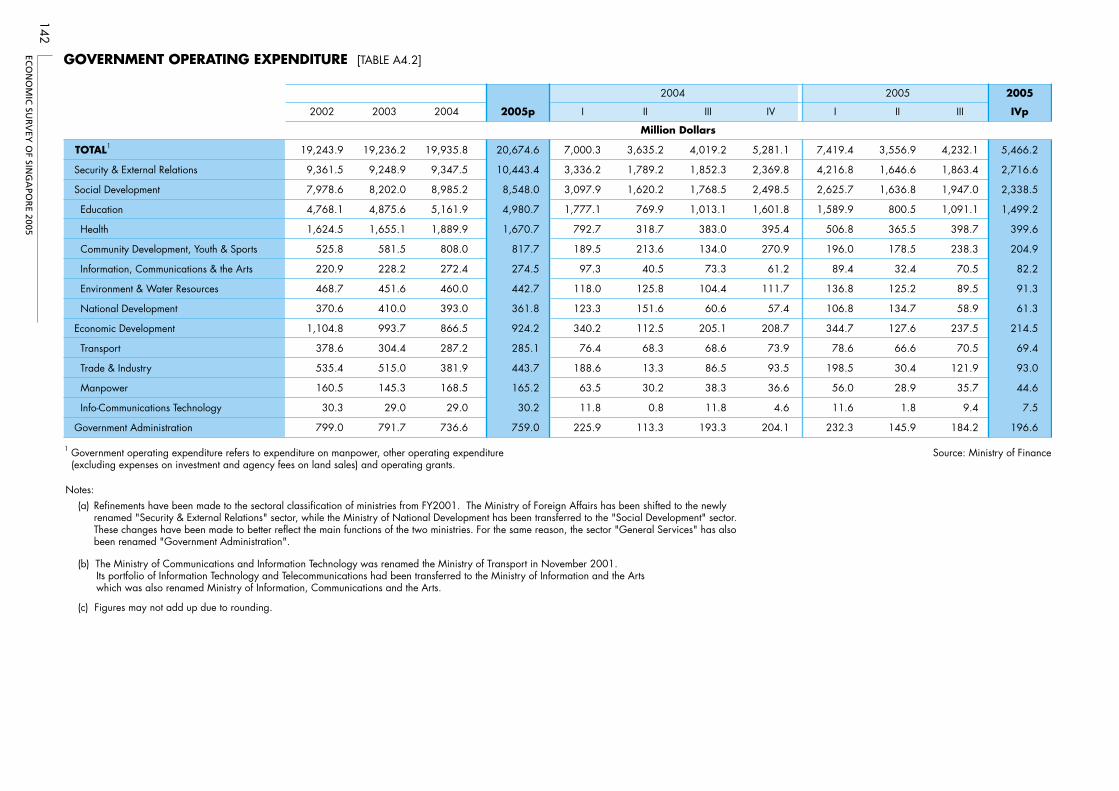

5.1 Government Operating Expenditure 41

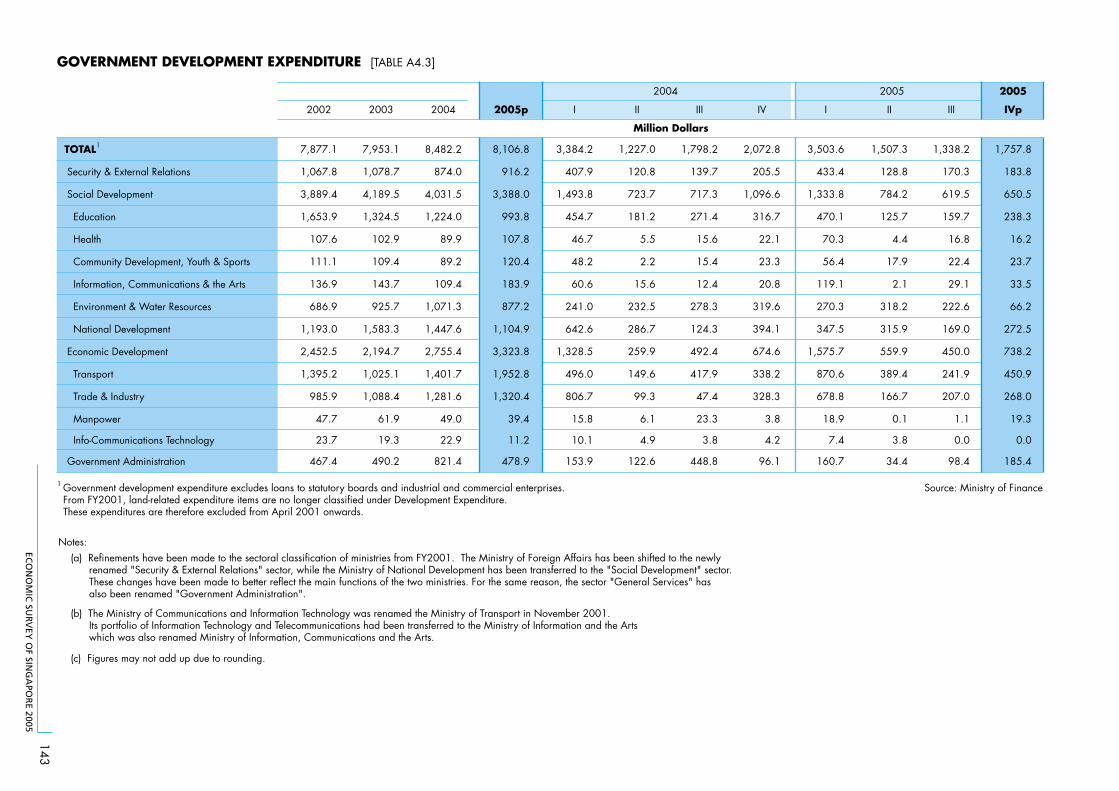

5.2 Government Development Expenditure 42

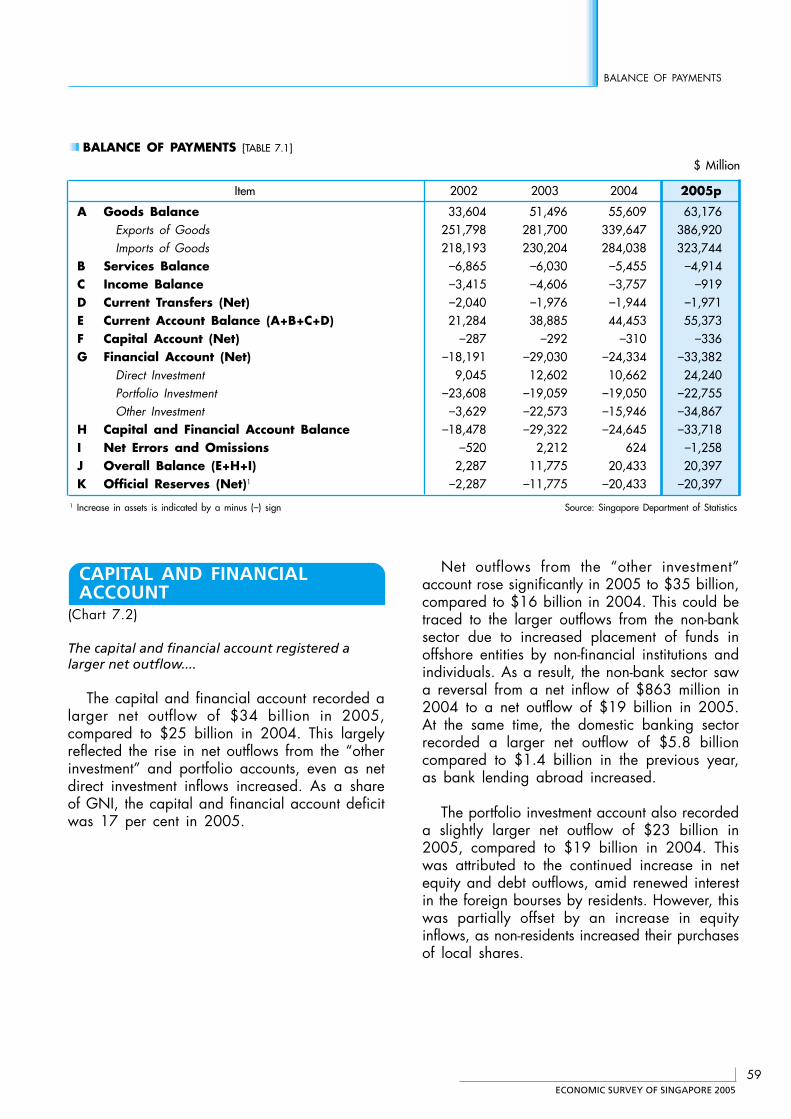

7 Balance of Payments 58

7.1 Balance of Payments 59

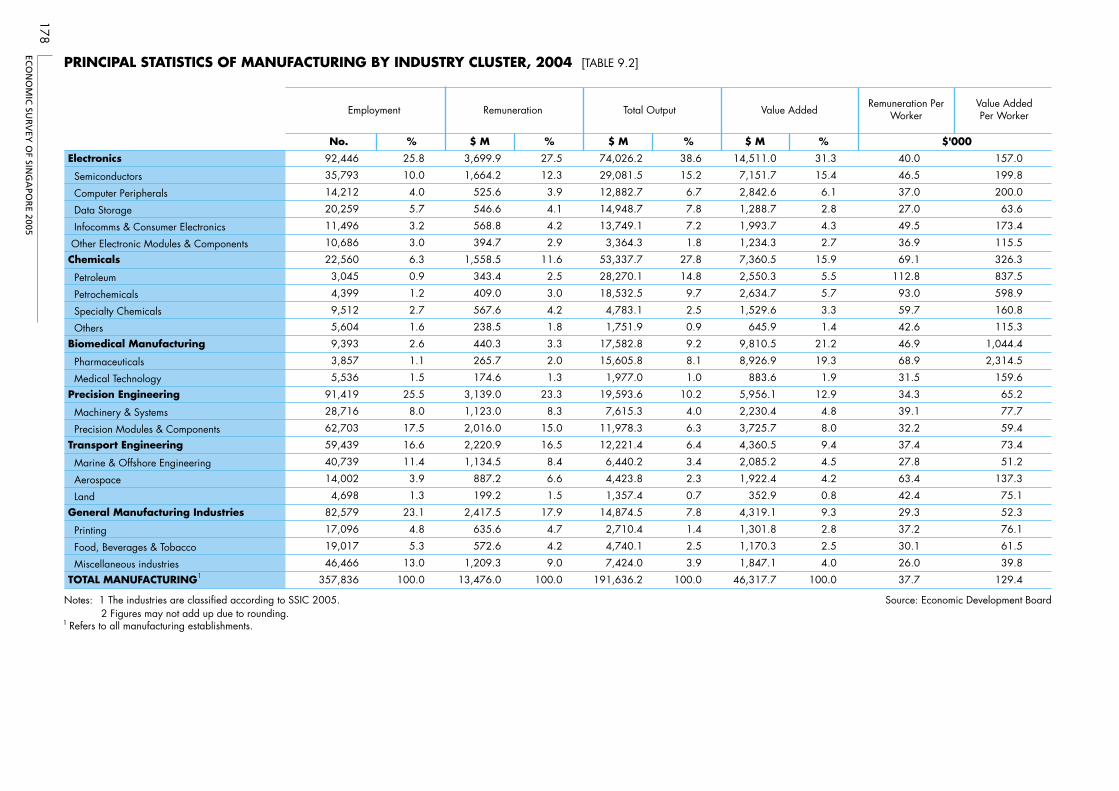

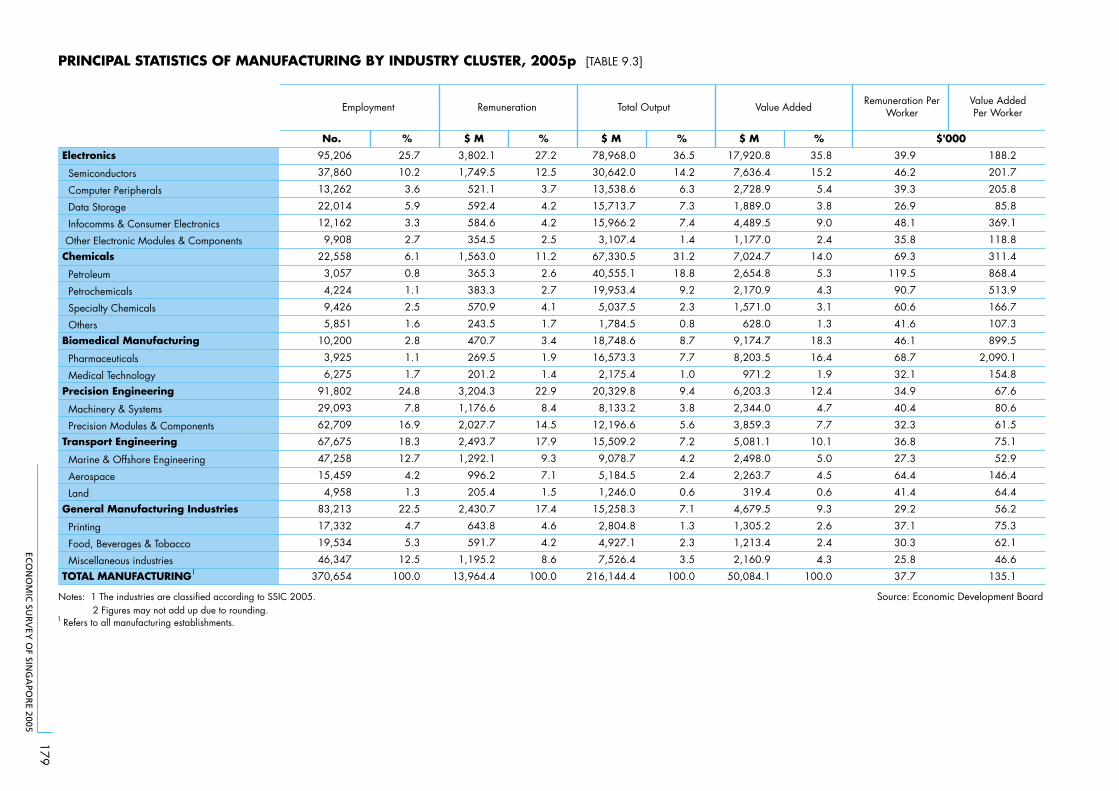

9 Manufacturing 65

9.1 Manufacturing 67

9.2 Manufacturing Investment Commitments by Cluster, 2005 68

9.3 Researchers 69

9.4 Performance of Portfolio Companies under PLE Investmentsas at December 2005 71

10 Construction 77

10.1 Contracts Awarded 77

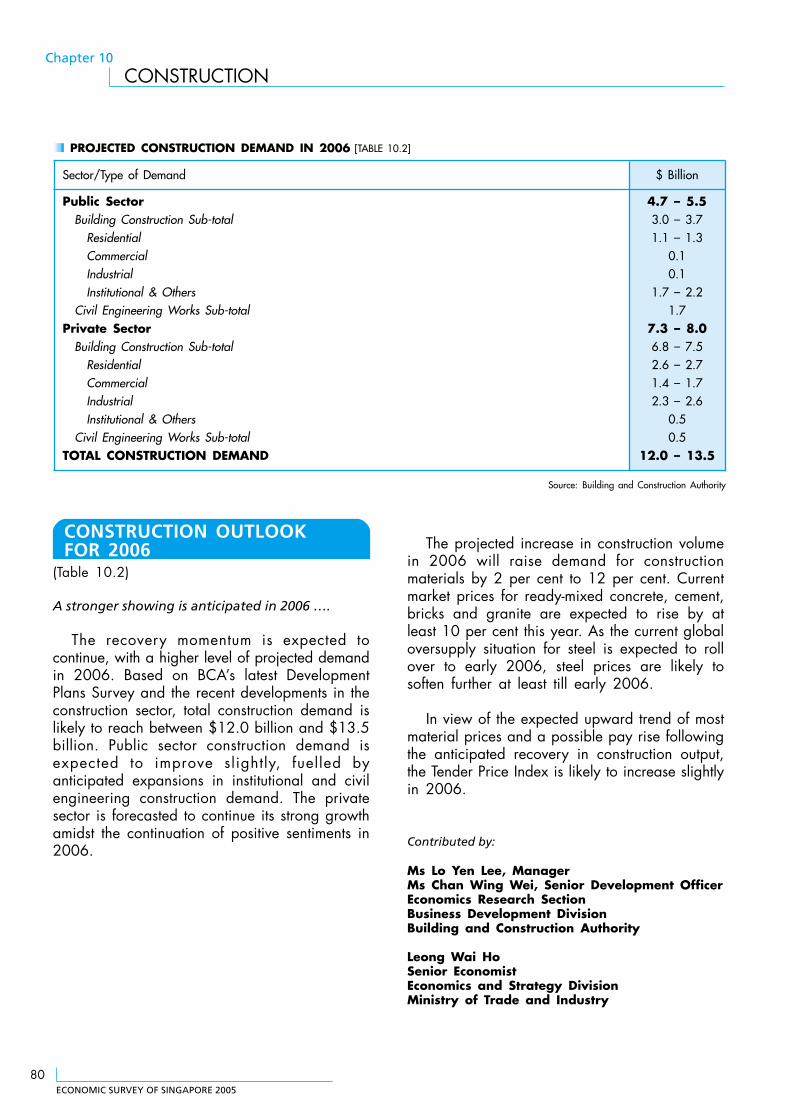

10.2 Projected Construction Demand in 2006 80

11 Wholesale & Retail Trade and Hotels & Restaurants 81

11.1 Wholesale & Retail Trade, and Hotels & Restaurants Sectors 81

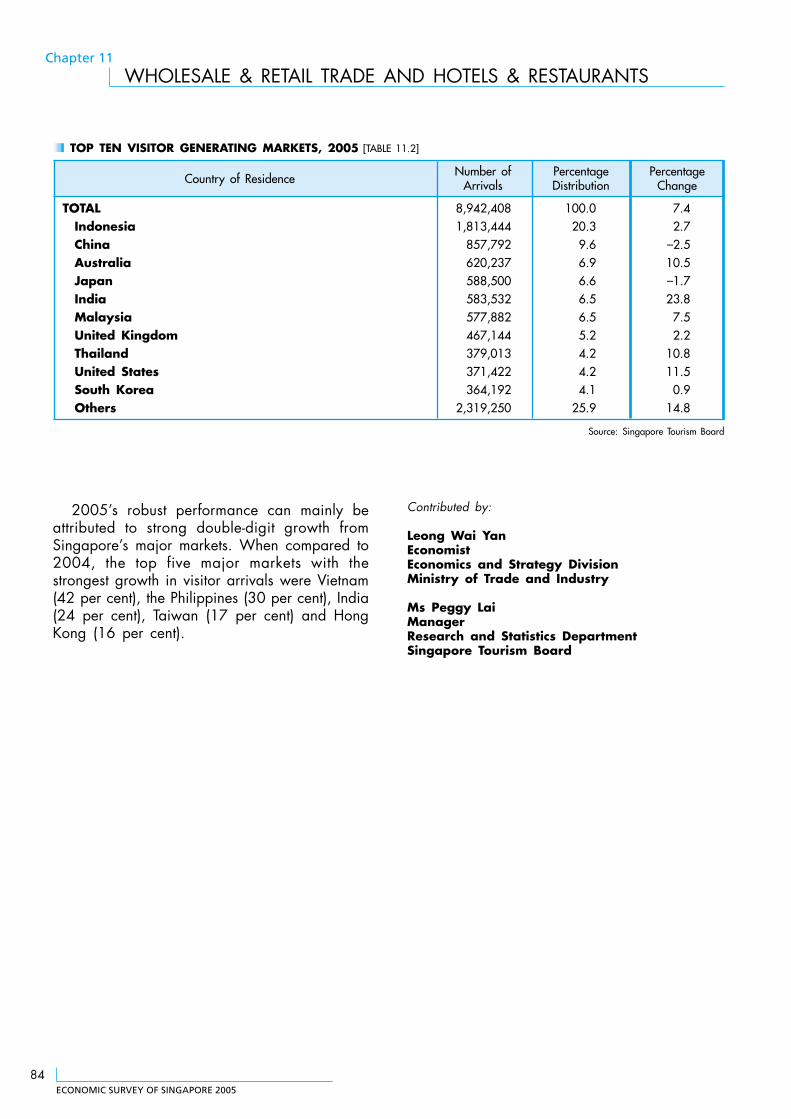

11.2 Top Ten Visitor Generating Markets, 2005 84

12 Transport and Communications 85

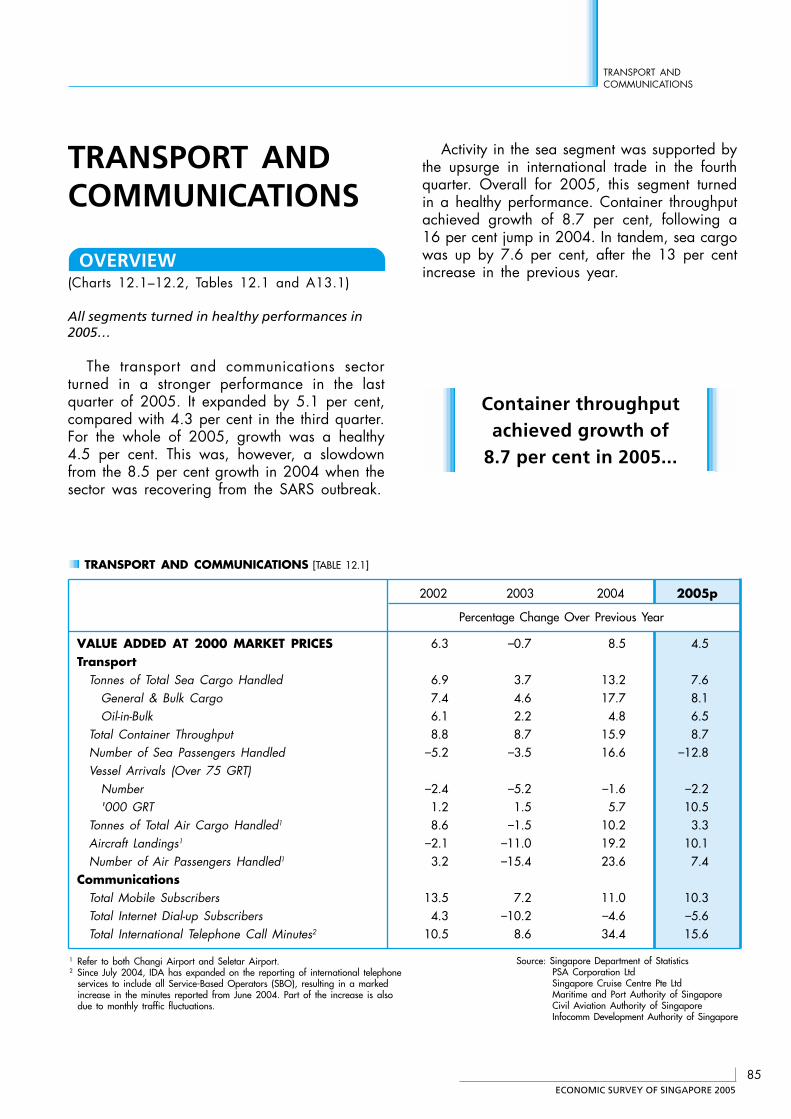

12.1 Transport and Communications 85

13 Financial and Business Services 92

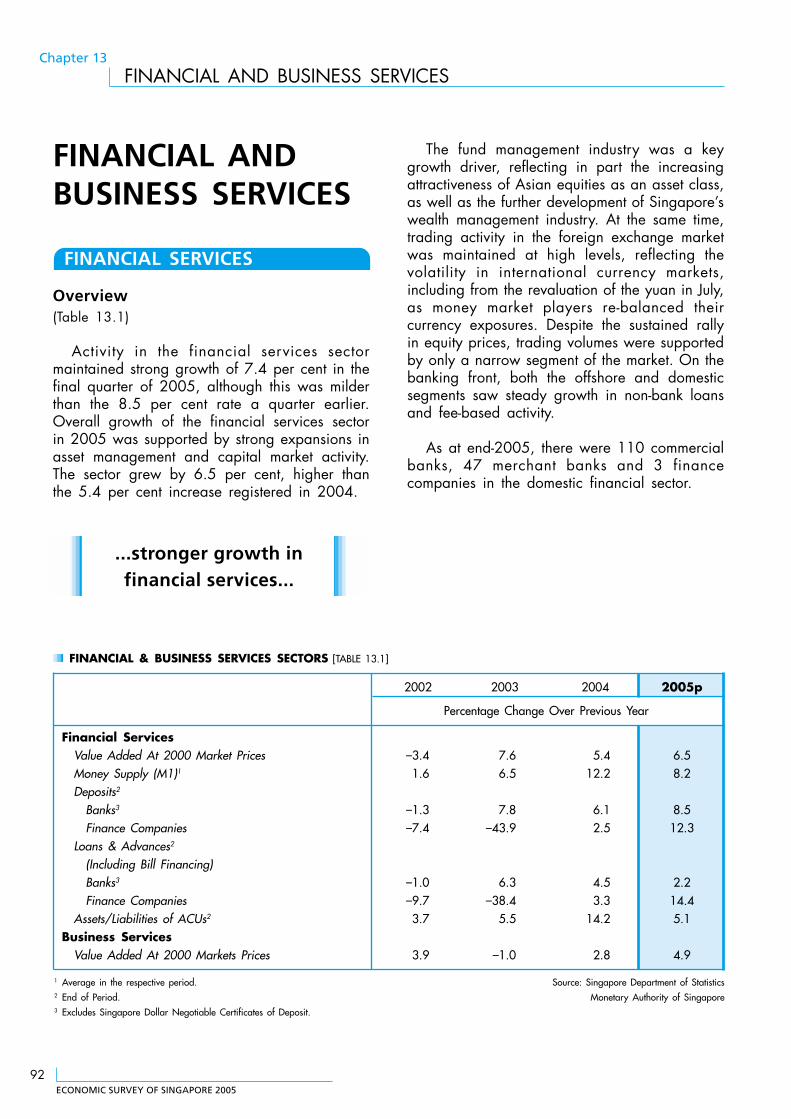

13.1 Financial & Business Services Sectors 92

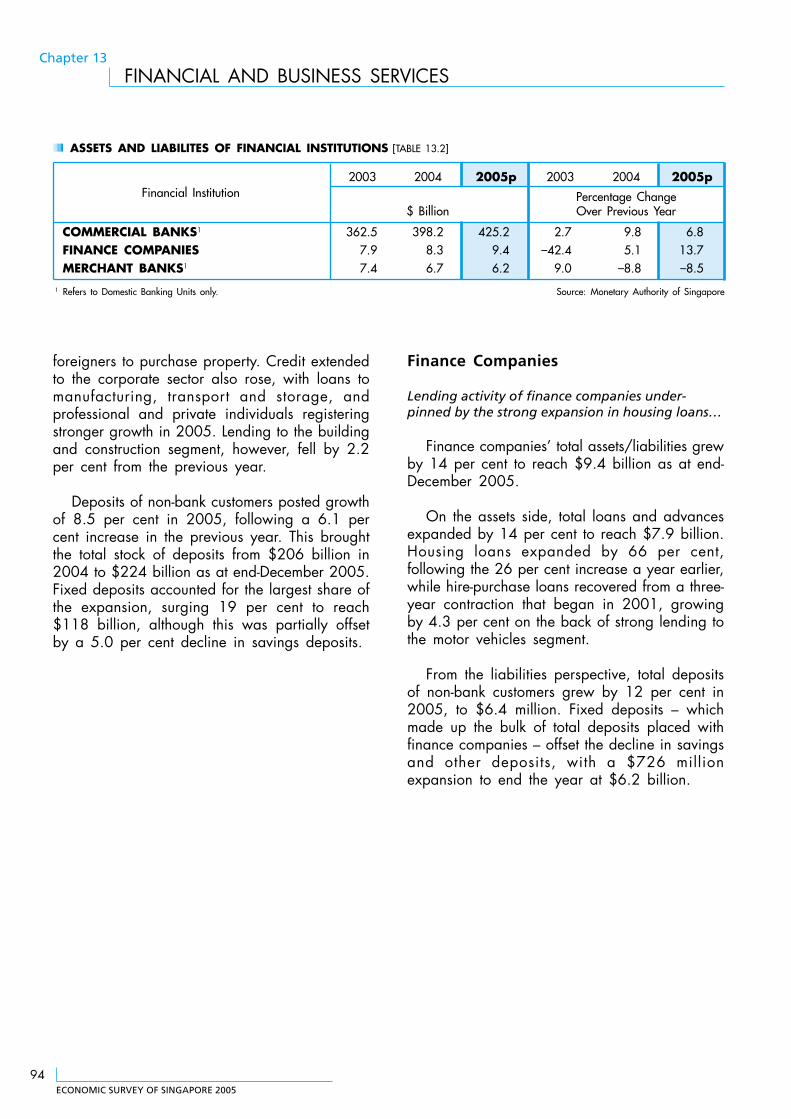

13.2 Assets and Liabilities of Financial Institutions 94

13.3 Services Investment Commitments by Cluster, 2005 99

ECONOMIC SURVEY OF SINGAPORE 2005

1

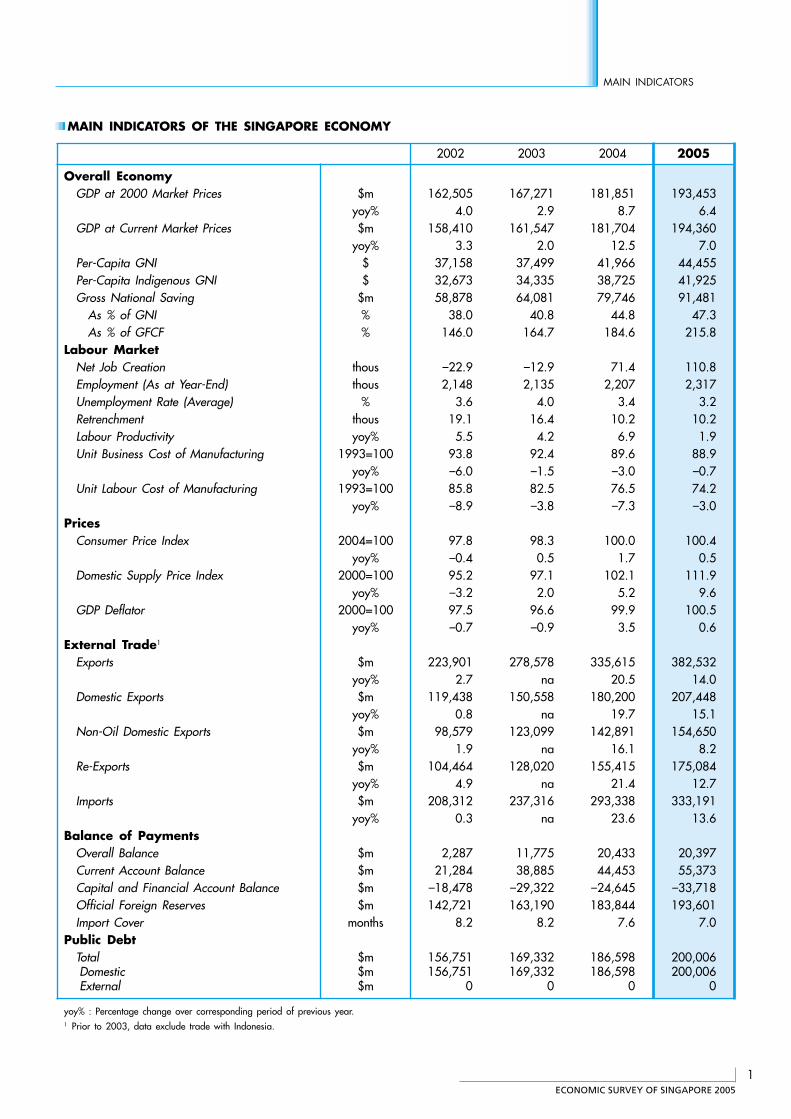

MAIN INDICATORS

2002 2003 2004 2005

Overall EconomyGDP at 2000 Market Prices $m 162,505 167,271 181,851 193,453

yoy% 4.0 2.9 8.7 6.4GDP at Current Market Prices $m 158,410 161,547 181,704 194,360

yoy% 3.3 2.0 12.5 7.0Per-Capita GNI $ 37,158 37,499 41,966 44,455Per-Capita Indigenous GNI $ 32,673 34,335 38,725 41,925Gross National Saving $m 58,878 64,081 79,746 91,481

As % of GNI % 38.0 40.8 44.8 47.3As % of GFCF % 146.0 164.7 184.6 215.8

Labour MarketNet Job Creation thous –22.9 –12.9 71.4 110.8Employment (As at Year-End) thous 2,148 2,135 2,207 2,317Unemployment Rate (Average) % 3.6 4.0 3.4 3.2Retrenchment thous 19.1 16.4 10.2 10.2Labour Productivity yoy% 5.5 4.2 6.9 1.9Unit Business Cost of Manufacturing 1993=100 93.8 92.4 89.6 88.9

yoy% –6.0 –1.5 –3.0 –0.7Unit Labour Cost of Manufacturing 1993=100 85.8 82.5 76.5 74.2

yoy% –8.9 –3.8 –7.3 –3.0Prices

Consumer Price Index 2004=100 97.8 98.3 100.0 100.4yoy% –0.4 0.5 1.7 0.5

Domestic Supply Price Index 2000=100 95.2 97.1 102.1 111.9yoy% –3.2 2.0 5.2 9.6

GDP Deflator 2000=100 97.5 96.6 99.9 100.5yoy% –0.7 –0.9 3.5 0.6

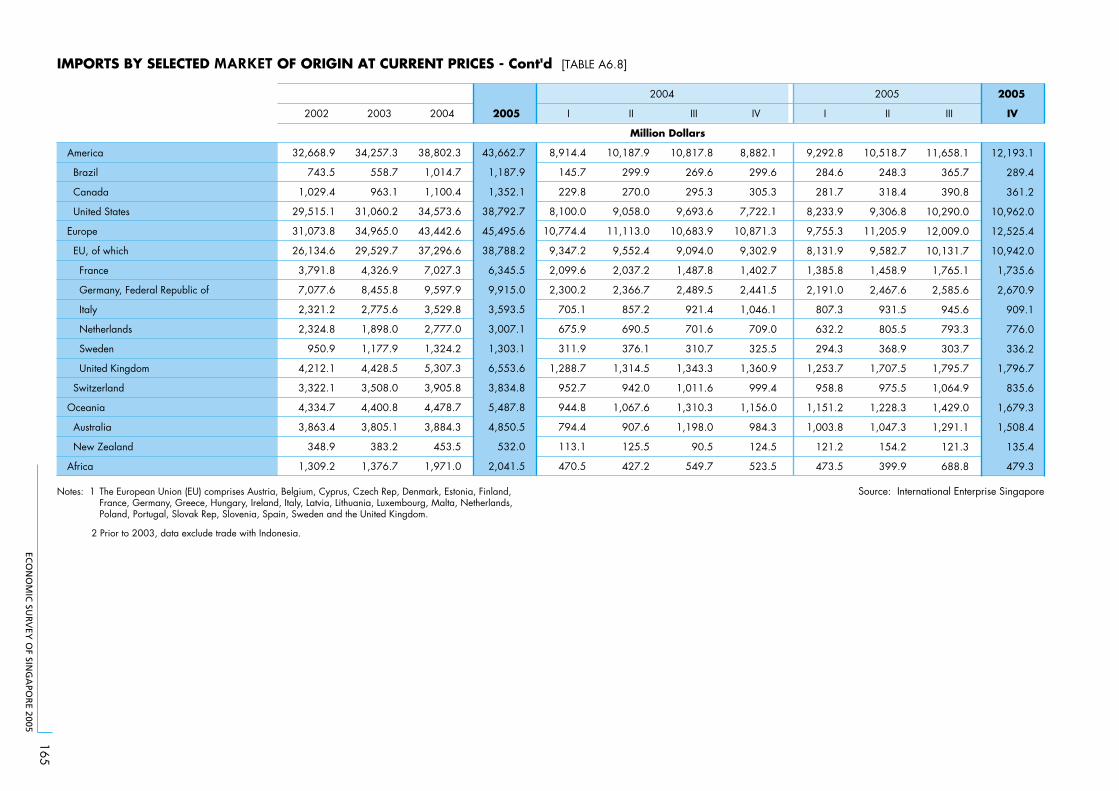

External Trade1

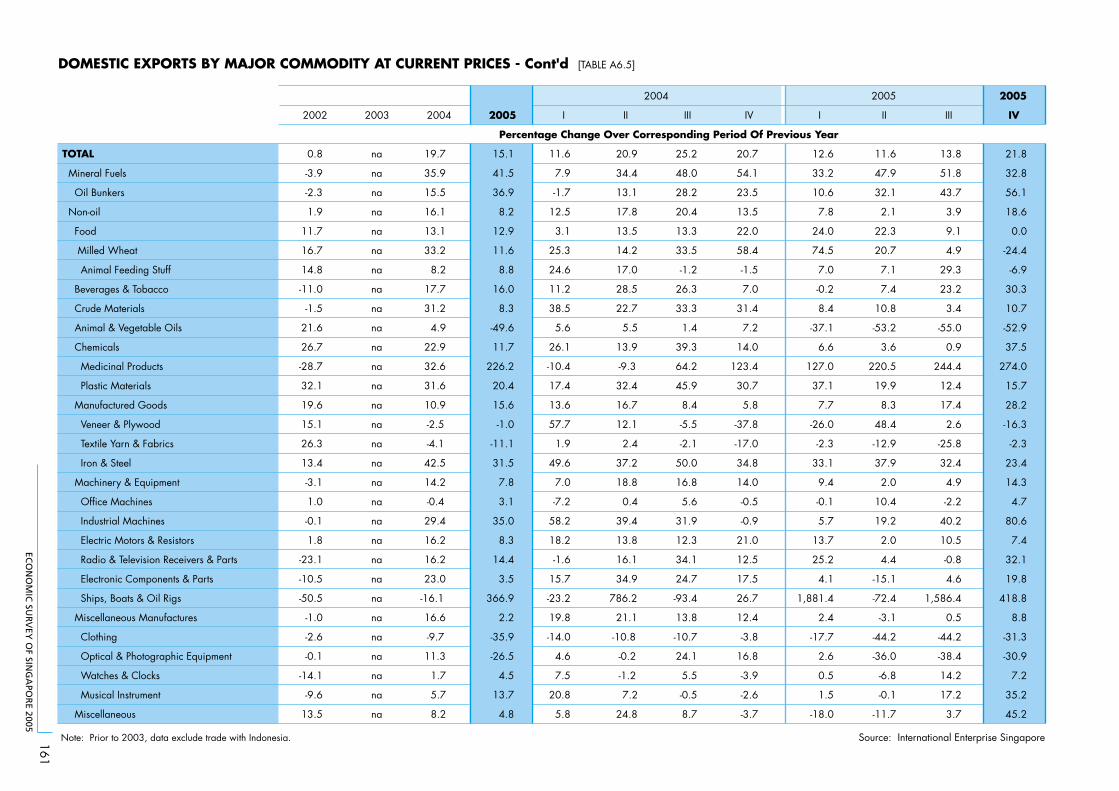

Exports $m 223,901 278,578 335,615 382,532yoy% 2.7 na 20.5 14.0

Domestic Exports $m 119,438 150,558 180,200 207,448yoy% 0.8 na 19.7 15.1

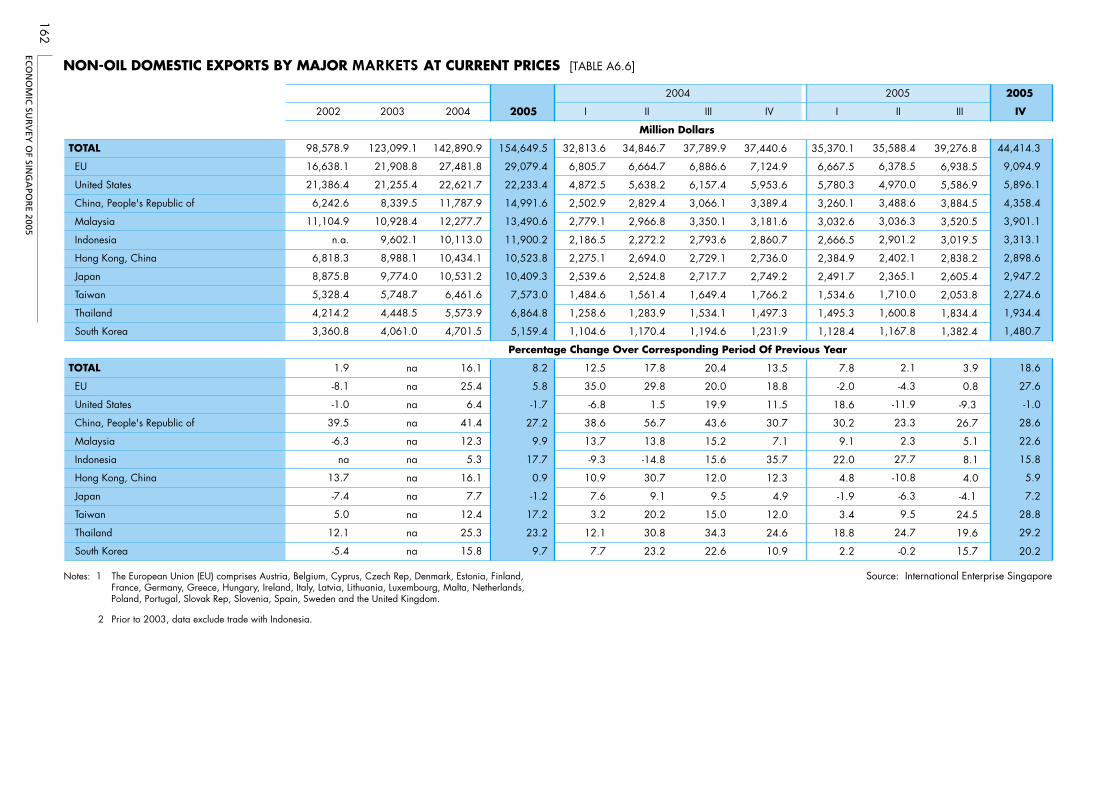

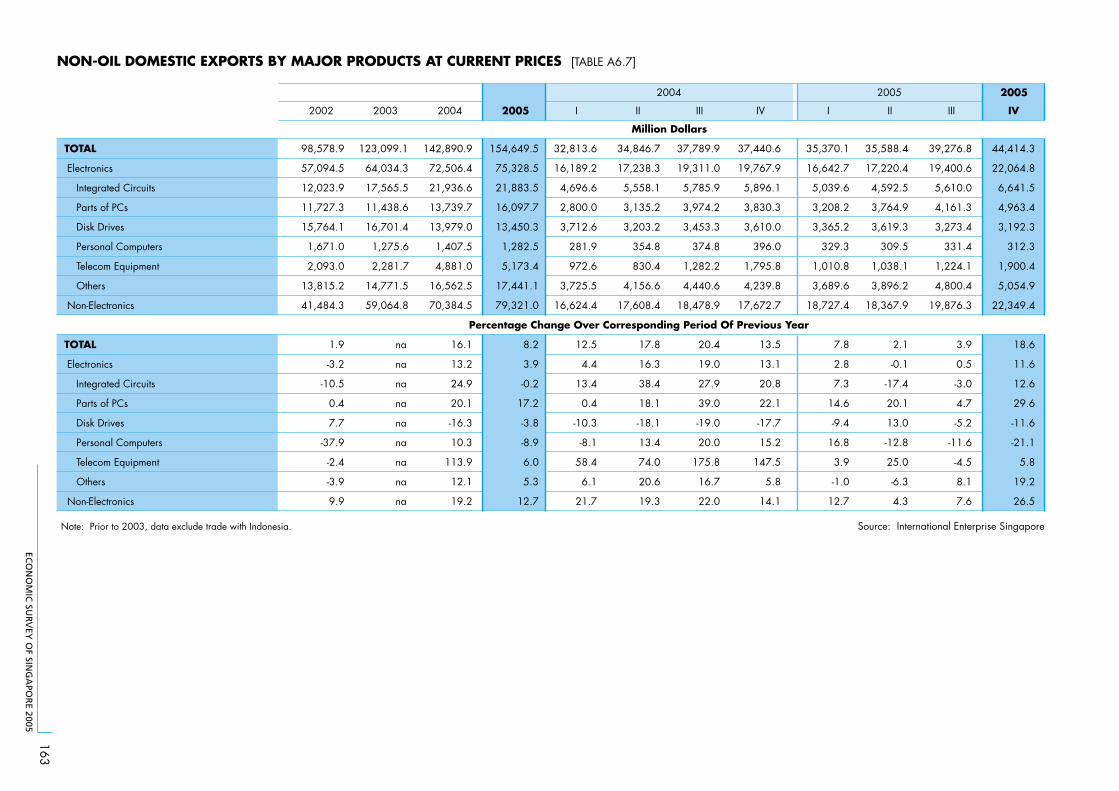

Non-Oil Domestic Exports $m 98,579 123,099 142,891 154,650yoy% 1.9 na 16.1 8.2

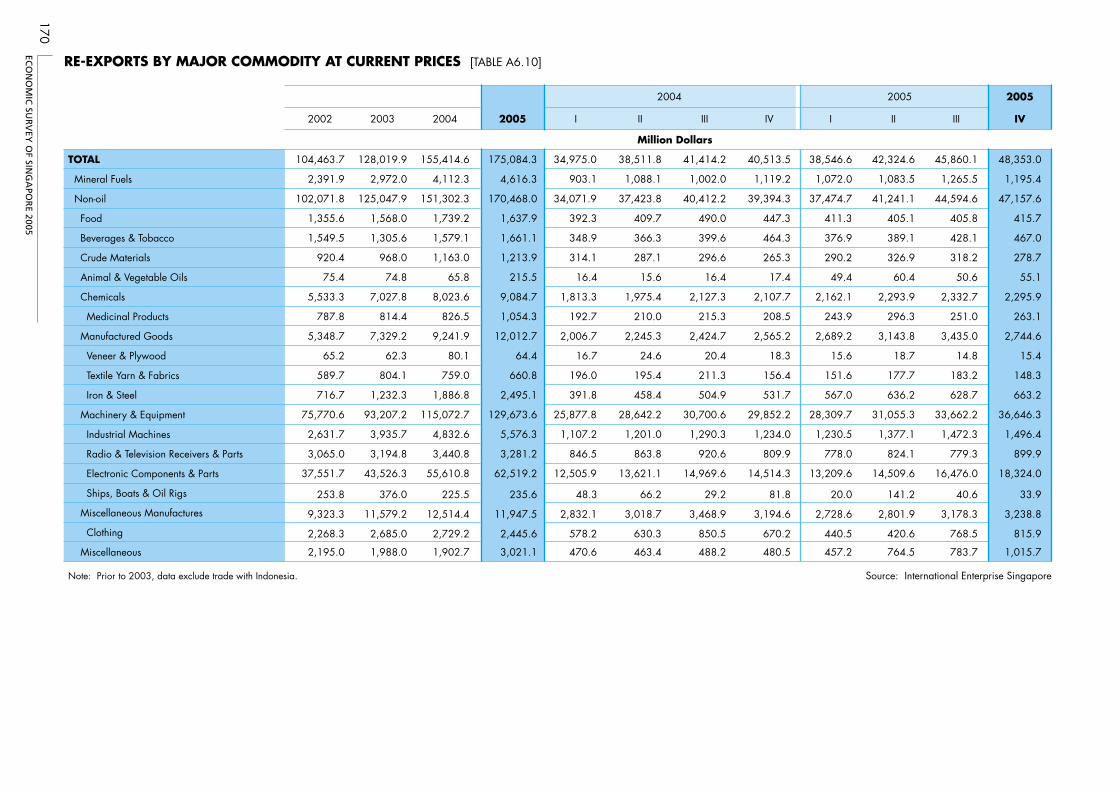

Re-Exports $m 104,464 128,020 155,415 175,084yoy% 4.9 na 21.4 12.7

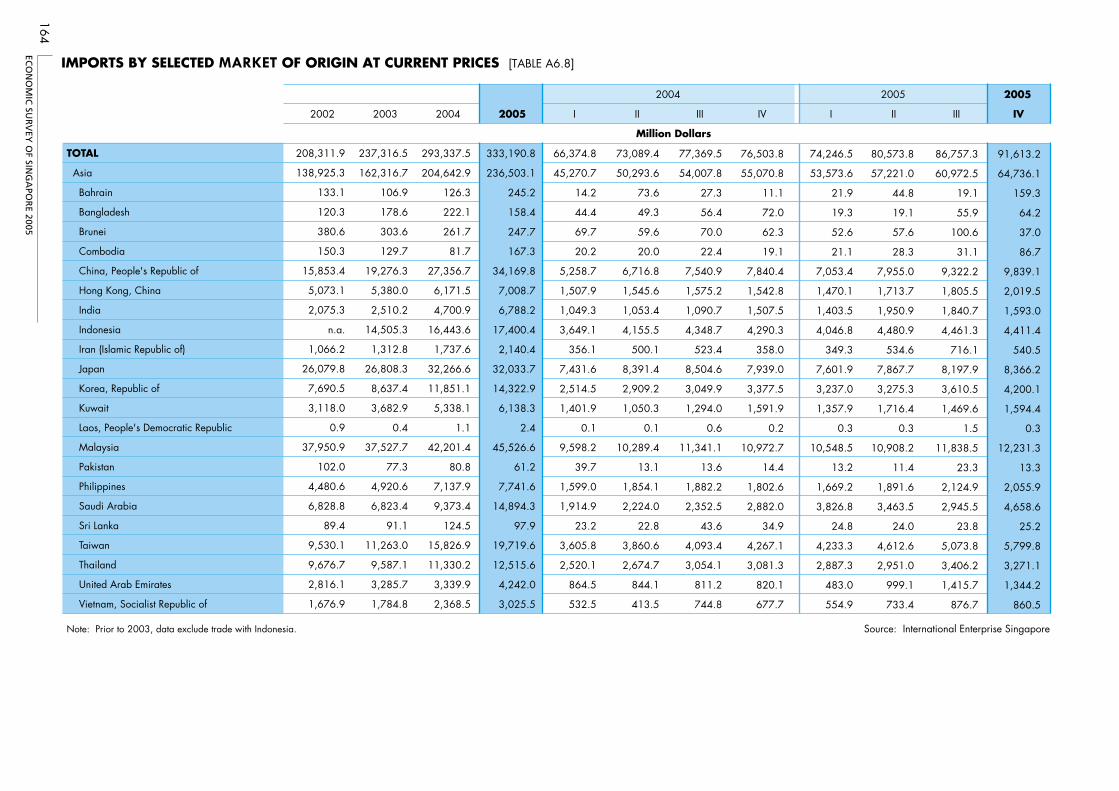

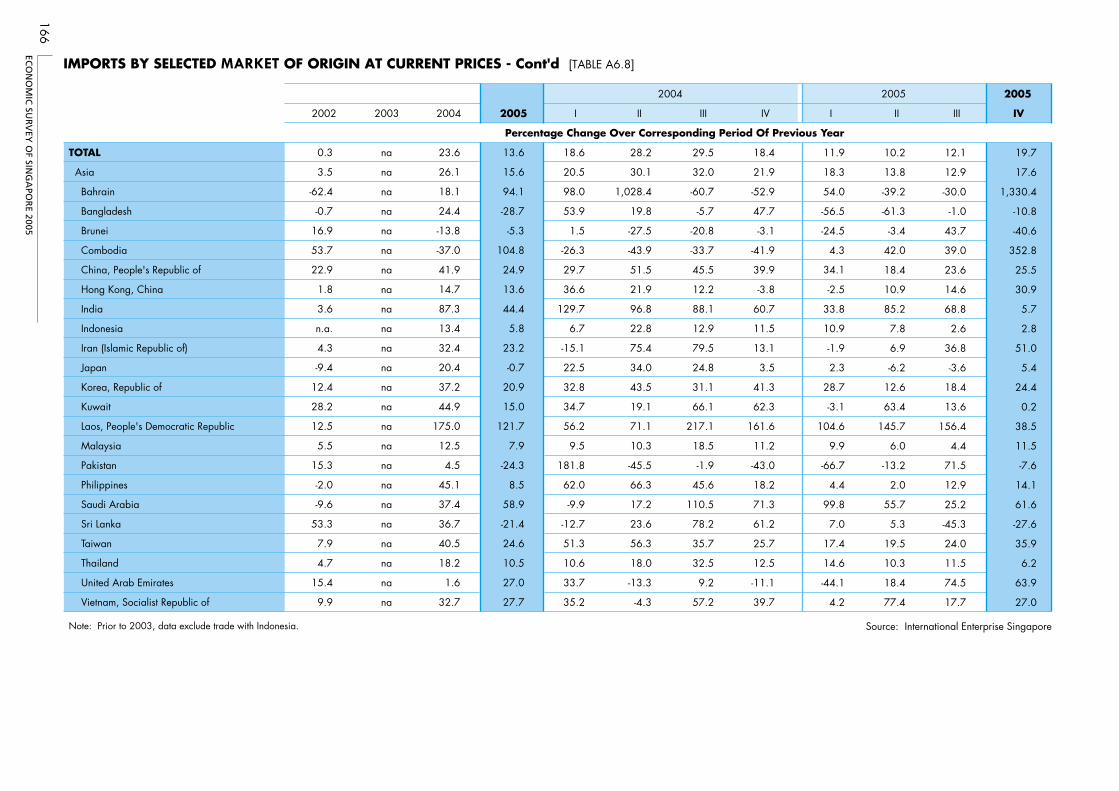

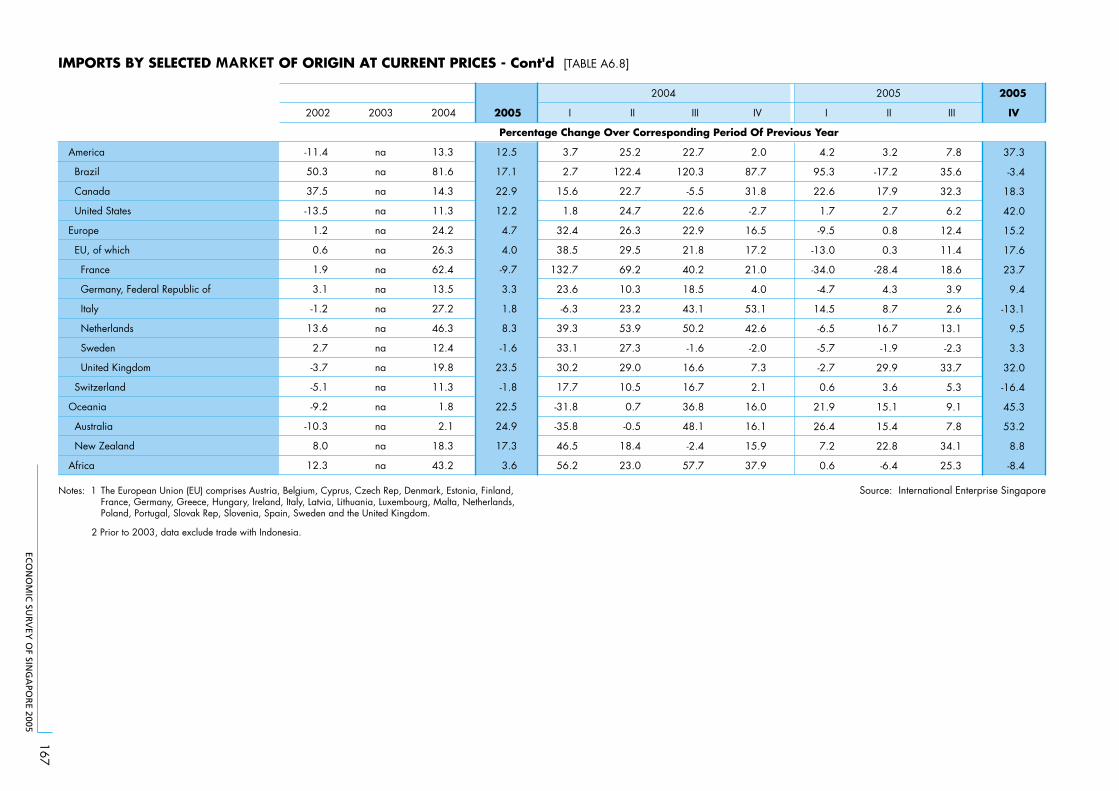

Imports $m 208,312 237,316 293,338 333,191yoy% 0.3 na 23.6 13.6

Balance of PaymentsOverall Balance $m 2,287 11,775 20,433 20,397Current Account Balance $m 21,284 38,885 44,453 55,373Capital and Financial Account Balance $m –18,478 –29,322 –24,645 –33,718Official Foreign Reserves $m 142,721 163,190 183,844 193,601Import Cover months 8.2 8.2 7.6 7.0

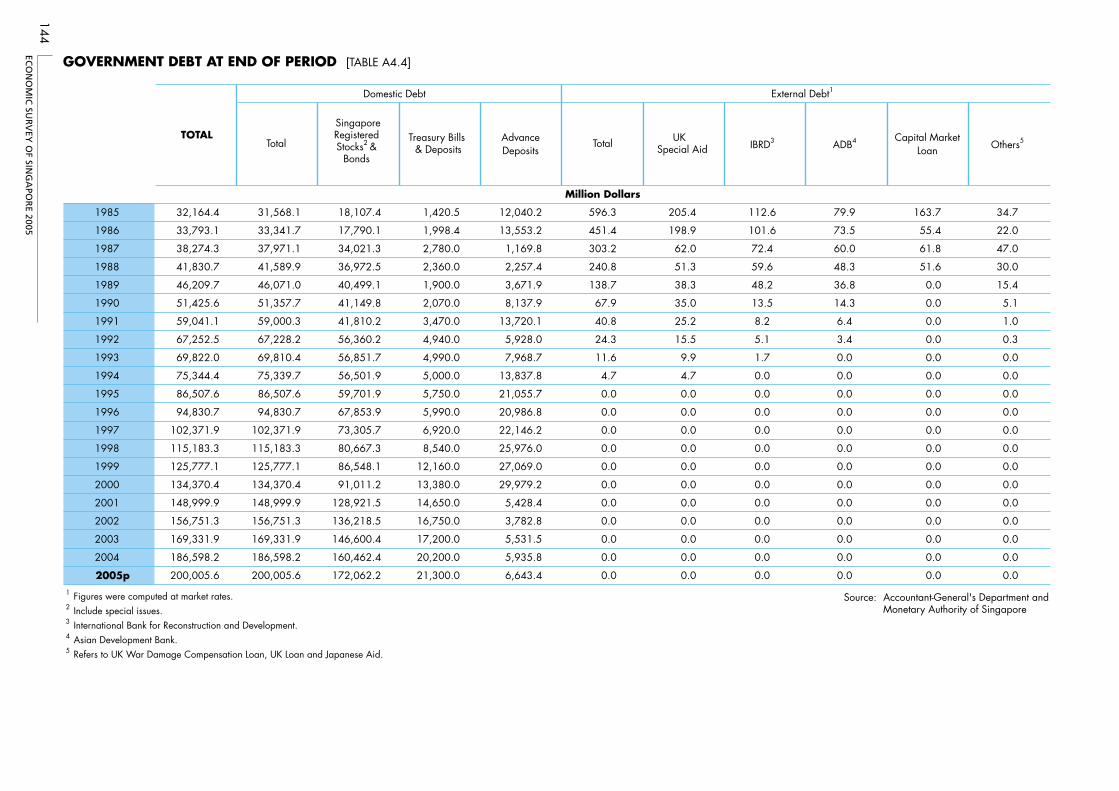

Public DebtTotal $m 156,751 169,332 186,598 200,006

Domestic $m 156,751 169,332 186,598 200,006 External $m 0 0 0 0

yoy% : Percentage change over corresponding period of previous year.1 Prior to 2003, data exclude trade with Indonesia.

MAIN INDICATORS OF THE SINGAPORE ECONOMY

ECONOMIC SURVEY OF SINGAPORE 2005

2

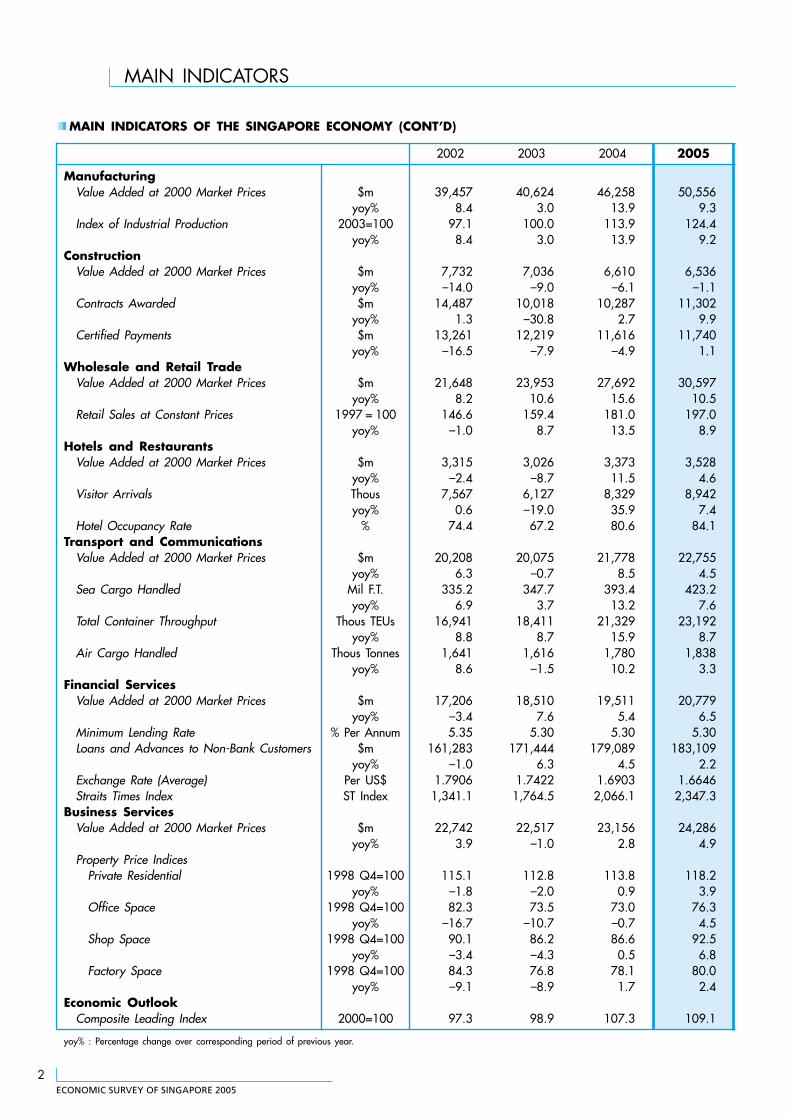

MAIN INDICATORS

MAIN INDICATORS OF THE SINGAPORE ECONOMY (CONT’D)

2002 2003 2004 2005

ManufacturingValue Added at 2000 Market Prices $m 39,457 40,624 46,258 50,556

yoy% 8.4 3.0 13.9 9.3Index of Industrial Production 2003=100 97.1 100.0 113.9 124.4

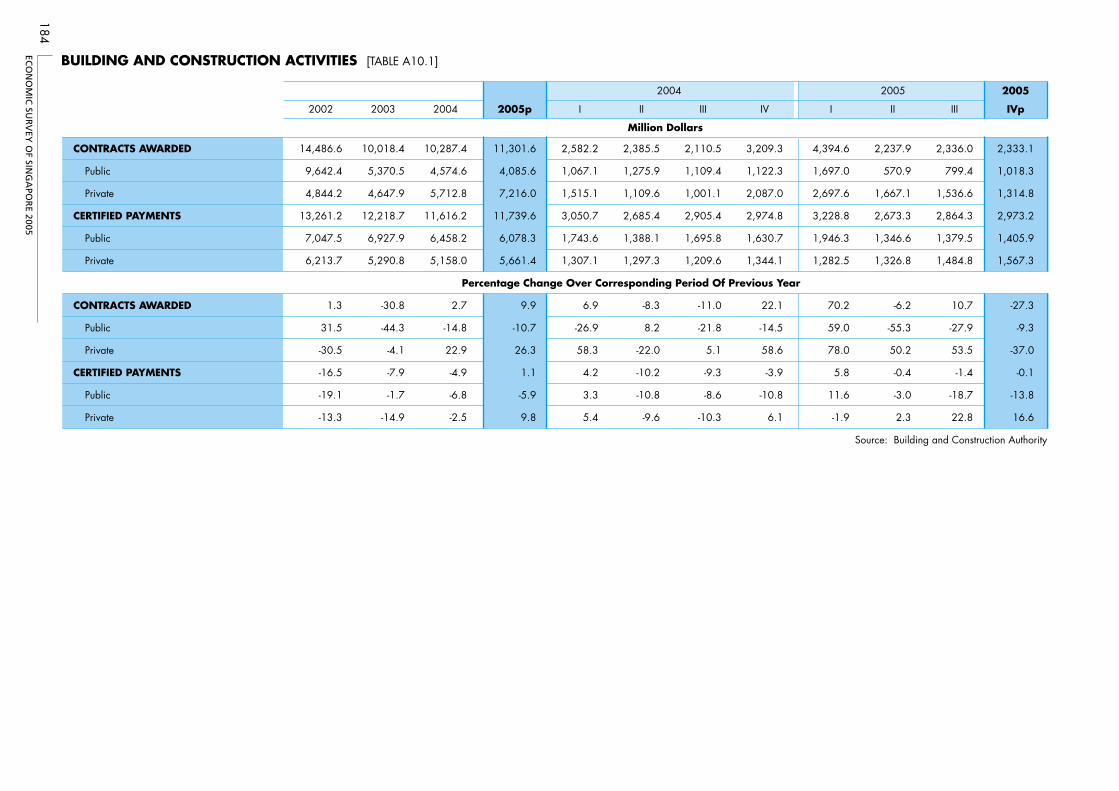

yoy% 8.4 3.0 13.9 9.2Construction

Value Added at 2000 Market Prices $m 7,732 7,036 6,610 6,536yoy% –14.0 –9.0 –6.1 –1.1

Contracts Awarded $m 14,487 10,018 10,287 11,302yoy% 1.3 –30.8 2.7 9.9

Certified Payments $m 13,261 12,219 11,616 11,740yoy% –16.5 –7.9 –4.9 1.1

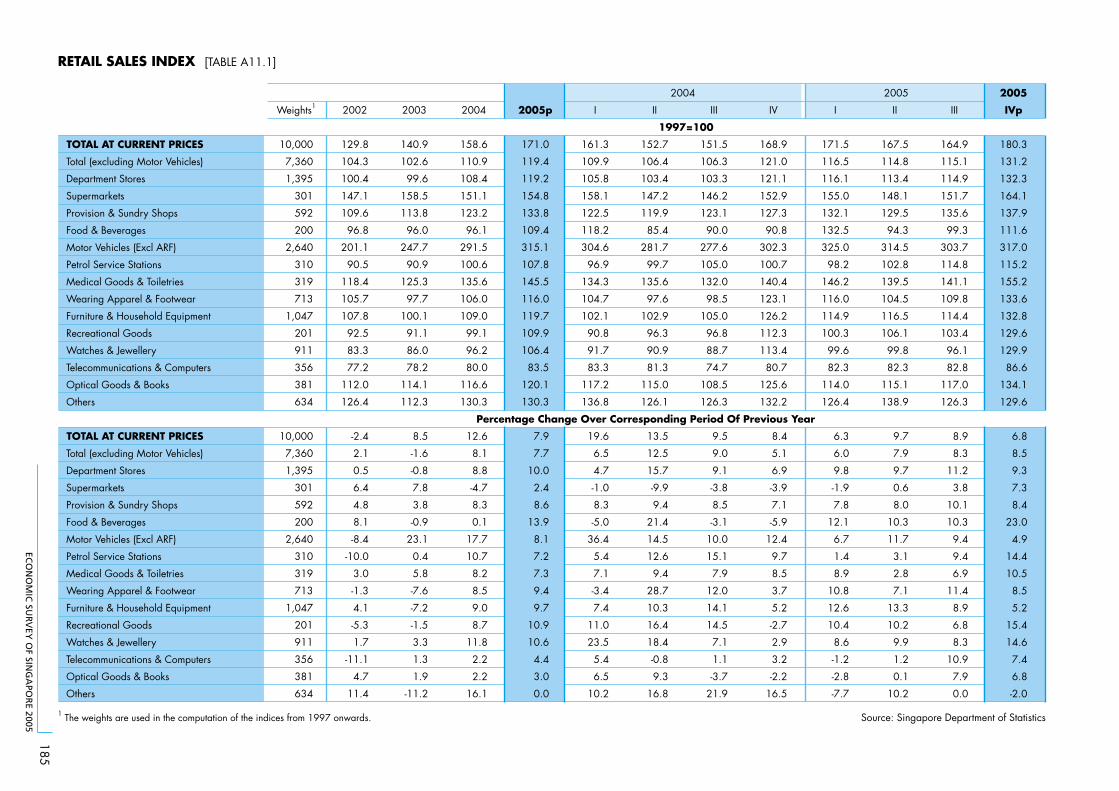

Wholesale and Retail TradeValue Added at 2000 Market Prices $m 21,648 23,953 27,692 30,597

yoy% 8.2 10.6 15.6 10.5Retail Sales at Constant Prices 1997 = 100 146.6 159.4 181.0 197.0

yoy% –1.0 8.7 13.5 8.9Hotels and Restaurants

Value Added at 2000 Market Prices $m 3,315 3,026 3,373 3,528yoy% –2.4 –8.7 11.5 4.6

Visitor Arrivals Thous 7,567 6,127 8,329 8,942yoy% 0.6 –19.0 35.9 7.4

Hotel Occupancy Rate % 74.4 67.2 80.6 84.1Transport and Communications

Value Added at 2000 Market Prices $m 20,208 20,075 21,778 22,755yoy% 6.3 –0.7 8.5 4.5

Sea Cargo Handled Mil F.T. 335.2 347.7 393.4 423.2yoy% 6.9 3.7 13.2 7.6

Total Container Throughput Thous TEUs 16,941 18,411 21,329 23,192yoy% 8.8 8.7 15.9 8.7

Air Cargo Handled Thous Tonnes 1,641 1,616 1,780 1,838yoy% 8.6 –1.5 10.2 3.3

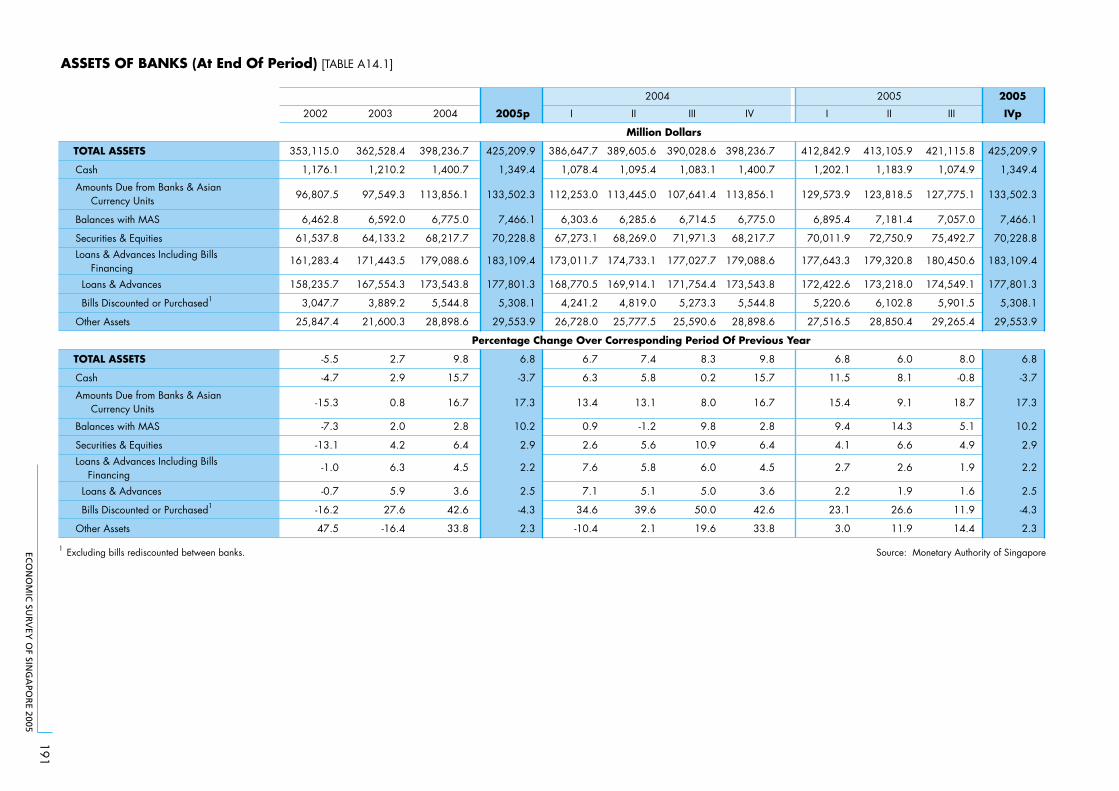

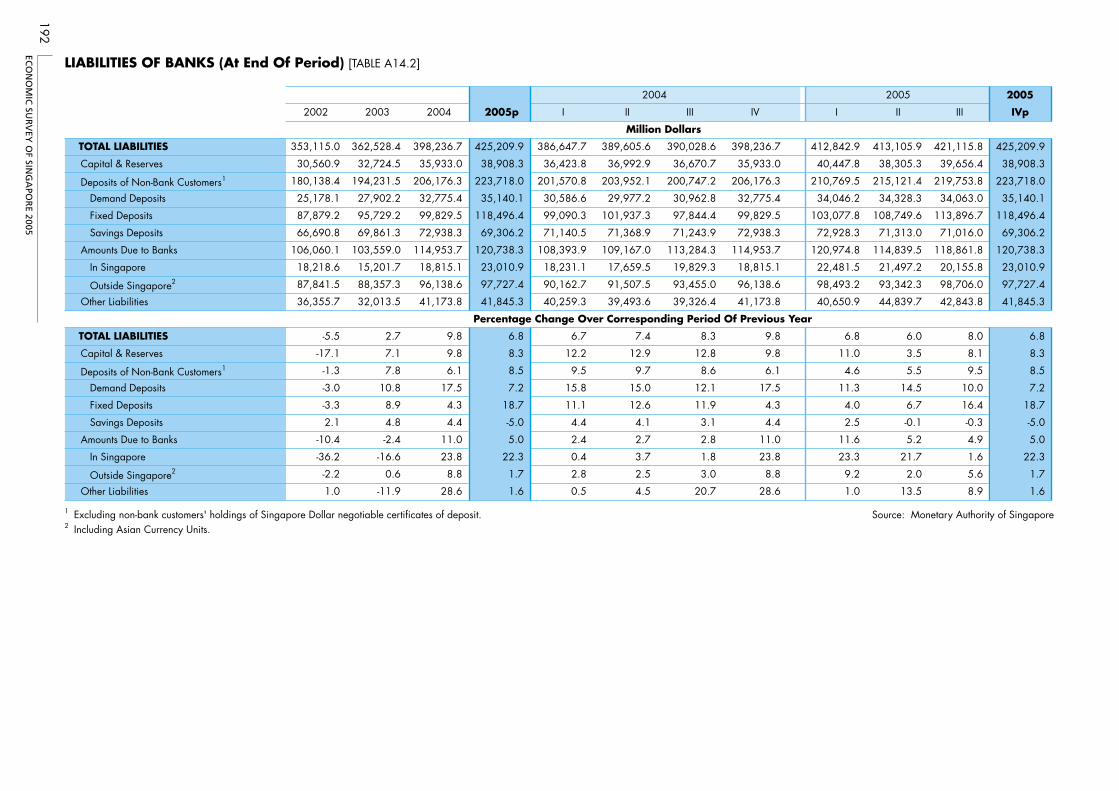

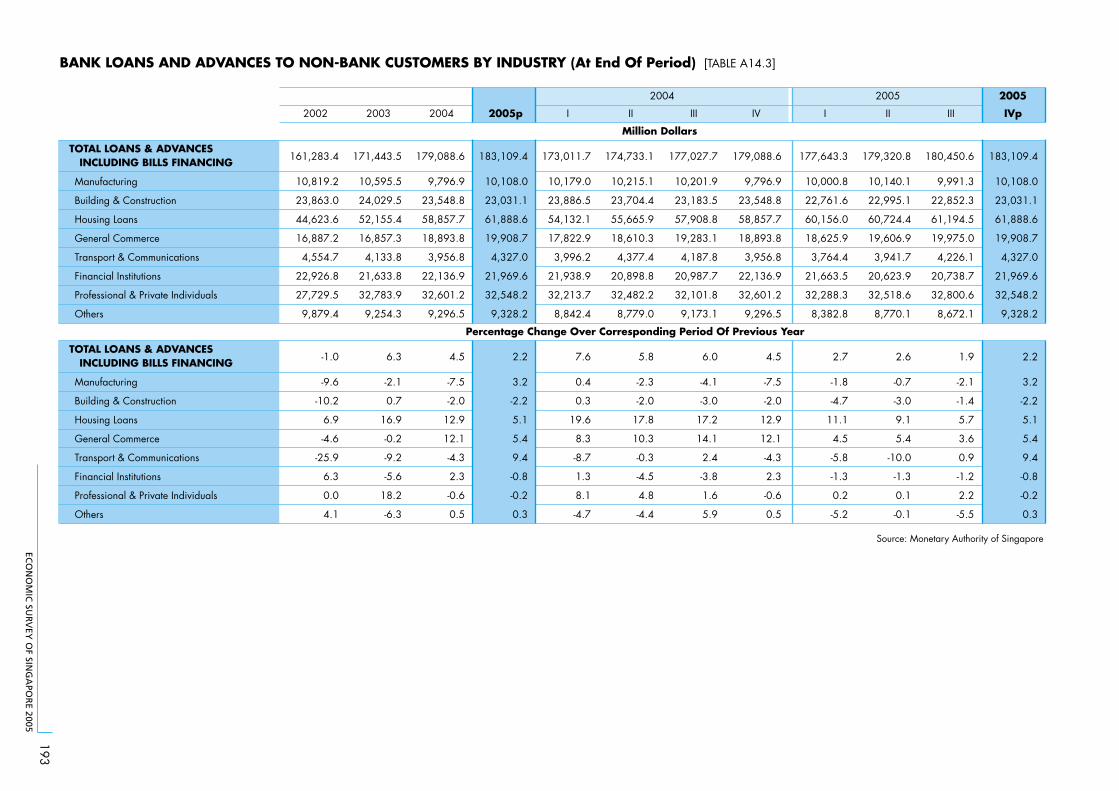

Financial ServicesValue Added at 2000 Market Prices $m 17,206 18,510 19,511 20,779

yoy% –3.4 7.6 5.4 6.5Minimum Lending Rate % Per Annum 5.35 5.30 5.30 5.30Loans and Advances to Non-Bank Customers $m 161,283 171,444 179,089 183,109

yoy% –1.0 6.3 4.5 2.2Exchange Rate (Average) Per US$ 1.7906 1.7422 1.6903 1.6646Straits Times Index ST Index 1,341.1 1,764.5 2,066.1 2,347.3

Business ServicesValue Added at 2000 Market Prices $m 22,742 22,517 23,156 24,286

yoy% 3.9 –1.0 2.8 4.9Property Price Indices

Private Residential 1998 Q4=100 115.1 112.8 113.8 118.2yoy% –1.8 –2.0 0.9 3.9

Office Space 1998 Q4=100 82.3 73.5 73.0 76.3yoy% –16.7 –10.7 –0.7 4.5

Shop Space 1998 Q4=100 90.1 86.2 86.6 92.5yoy% –3.4 –4.3 0.5 6.8

Factory Space 1998 Q4=100 84.3 76.8 78.1 80.0yoy% –9.1 –8.9 1.7 2.4

Economic OutlookComposite Leading Index 2000=100 97.3 98.9 107.3 109.1

yoy% : Percentage change over corresponding period of previous year.

ECONOMIC SURVEY OF SINGAPORE 2005

3

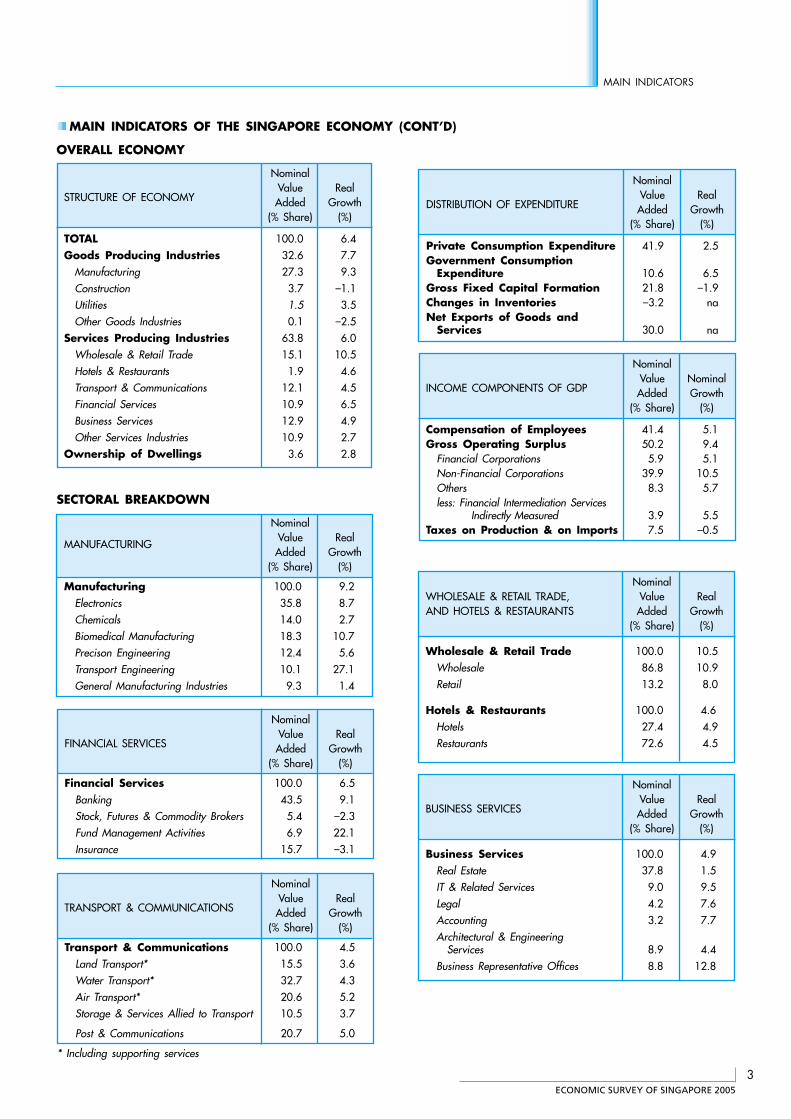

MAIN INDICATORS

MAIN INDICATORS OF THE SINGAPORE ECONOMY (CONT’D)

OVERALL ECONOMY

Nominal

STRUCTURE OF ECONOMYValue RealAdded Growth

(% Share) (%)

TOTAL 100.0 6.4Goods Producing Industries 32.6 7.7

Manufacturing 27.3 9.3Construction 3.7 –1.1Utilities 1.5 3.5Other Goods Industries 0.1 –2.5

Services Producing Industries 63.8 6.0Wholesale & Retail Trade 15.1 10.5Hotels & Restaurants 1.9 4.6Transport & Communications 12.1 4.5Financial Services 10.9 6.5Business Services 12.9 4.9Other Services Industries 10.9 2.7

Ownership of Dwellings 3.6 2.8

Nominal

DISTRIBUTION OF EXPENDITUREValue RealAdded Growth

(% Share) (%)

Private Consumption Expenditure 41.9 2.5Government Consumption

Expenditure 10.6 6.5Gross Fixed Capital Formation 21.8 –1.9Changes in Inventories –3.2 naNet Exports of Goods and

Services 30.0 na

SECTORAL BREAKDOWN

Nominal

MANUFACTURINGValue RealAdded Growth

(% Share) (%)

Manufacturing 100.0 9.2Electronics 35.8 8.7Chemicals 14.0 2.7Biomedical Manufacturing 18.3 10.7Precison Engineering 12.4 5.6Transport Engineering 10.1 27.1General Manufacturing Industries 9.3 1.4

Nominal

INCOME COMPONENTS OF GDPValue NominalAdded Growth

(% Share) (%)

Compensation of Employees 41.4 5.1Gross Operating Surplus 50.2 9.4

Financial Corporations 5.9 5.1Non-Financial Corporations 39.9 10.5Others 8.3 5.7less: Financial Intermediation Services

Indirectly Measured 3.9 5.5Taxes on Production & on Imports 7.5 –0.5

Nominal

BUSINESS SERVICESValue RealAdded Growth

(% Share) (%)

Business Services 100.0 4.9Real Estate 37.8 1.5IT & Related Services 9.0 9.5Legal 4.2 7.6Accounting 3.2 7.7Architectural & Engineering

Services 8.9 4.4Business Representative Offices 8.8 12.8

Nominal

FINANCIAL SERVICESValue RealAdded Growth

(% Share) (%)

Financial Services 100.0 6.5Banking 43.5 9.1Stock, Futures & Commodity Brokers 5.4 –2.3Fund Management Activities 6.9 22.1Insurance 15.7 –3.1

Nominal

TRANSPORT & COMMUNICATIONSValue RealAdded Growth

(% Share) (%)

Transport & Communications 100.0 4.5Land Transport* 15.5 3.6Water Transport* 32.7 4.3Air Transport* 20.6 5.2Storage & Services Allied to Transport 10.5 3.7

Post & Communications 20.7 5.0

* Including supporting services

NominalWHOLESALE & RETAIL TRADE, Value RealAND HOTELS & RESTAURANTS Added Growth

(% Share) (%)

Wholesale & Retail Trade 100.0 10.5Wholesale 86.8 10.9Retail 13.2 8.0

Hotels & Restaurants 100.0 4.6Hotels 27.4 4.9Restaurants 72.6 4.5

ECONOMIC SURVEY OF SINGAPORE 2005

4

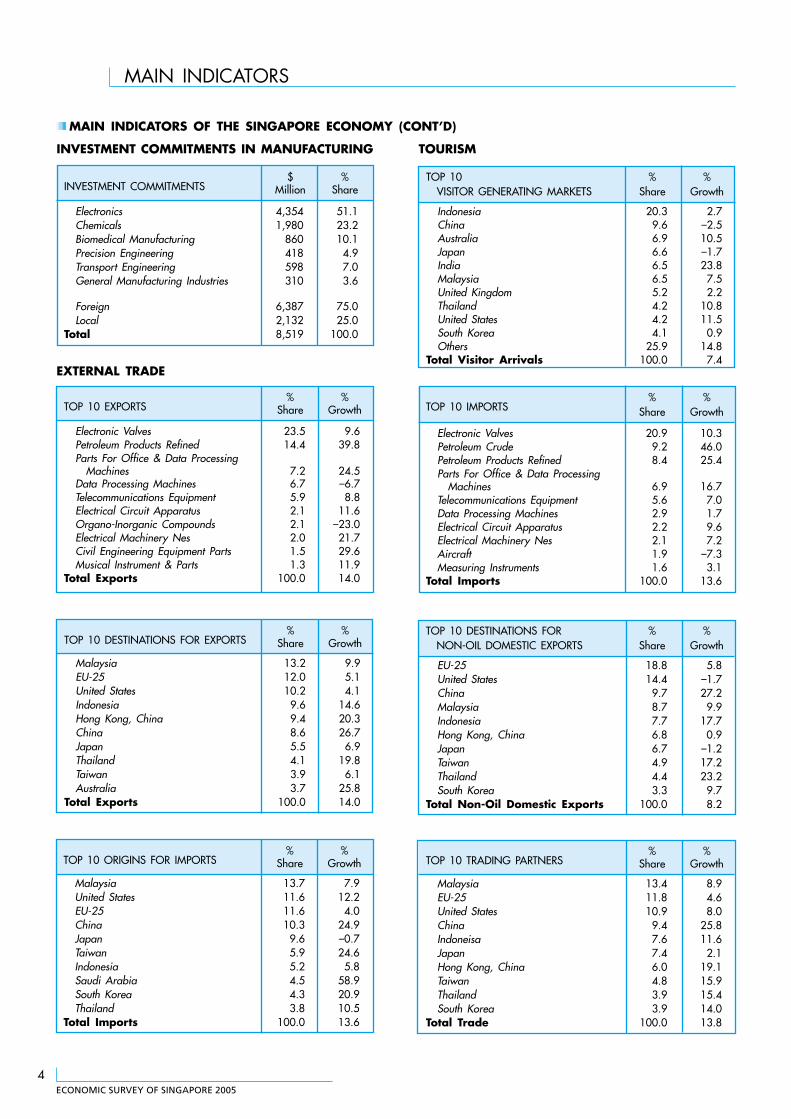

MAIN INDICATORS

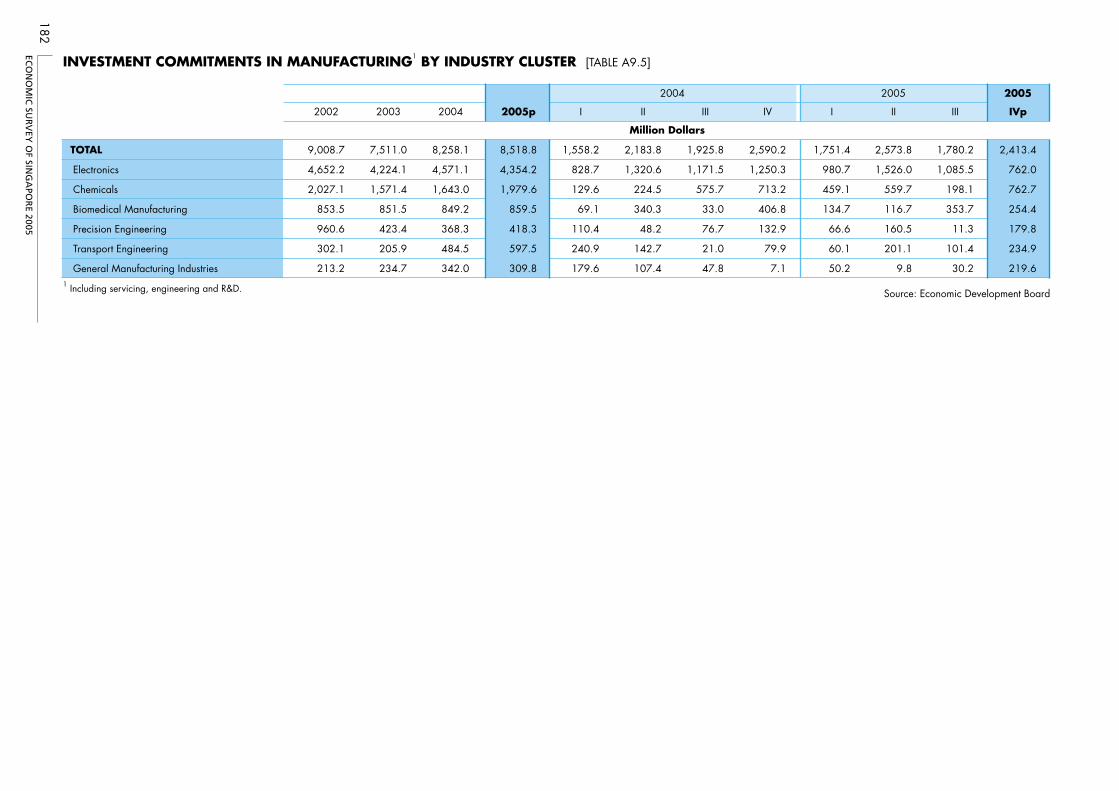

INVESTMENT COMMITMENTS IN MANUFACTURING

INVESTMENT COMMITMENTS$ %

Million Share

Electronics 4,354 51.1Chemicals 1,980 23.2Biomedical Manufacturing 860 10.1Precision Engineering 418 4.9Transport Engineering 598 7.0General Manufacturing Industries 310 3.6

Foreign 6,387 75.0Local 2,132 25.0

Total 8,519 100.0

MAIN INDICATORS OF THE SINGAPORE ECONOMY (CONT’D)

EXTERNAL TRADE

TOP 10 EXPORTS% %

Share Growth

Electronic Valves 23.5 9.6Petroleum Products Refined 14.4 39.8Parts For Office & Data Processing

Machines 7.2 24.5Data Processing Machines 6.7 –6.7Telecommunications Equipment 5.9 8.8Electrical Circuit Apparatus 2.1 11.6Organo-Inorganic Compounds 2.1 –23.0Electrical Machinery Nes 2.0 21.7Civil Engineering Equipment Parts 1.5 29.6Musical Instrument & Parts 1.3 11.9

Total Exports 100.0 14.0

TOP 10 DESTINATIONS FOR EXPORTS% %

Share Growth

Malaysia 13.2 9.9EU-25 12.0 5.1United States 10.2 4.1Indonesia 9.6 14.6Hong Kong, China 9.4 20.3China 8.6 26.7Japan 5.5 6.9Thailand 4.1 19.8Taiwan 3.9 6.1Australia 3.7 25.8

Total Exports 100.0 14.0

TOP 10 ORIGINS FOR IMPORTS% %

Share Growth

Malaysia 13.7 7.9United States 11.6 12.2EU-25 11.6 4.0China 10.3 24.9Japan 9.6 –0.7Taiwan 5.9 24.6Indonesia 5.2 5.8Saudi Arabia 4.5 58.9South Korea 4.3 20.9Thailand 3.8 10.5

Total Imports 100.0 13.6

TOP 10 IMPORTS% %

Share Growth

Electronic Valves 20.9 10.3Petroleum Crude 9.2 46.0Petroleum Products Refined 8.4 25.4Parts For Office & Data Processing

Machines 6.9 16.7Telecommunications Equipment 5.6 7.0Data Processing Machines 2.9 1.7Electrical Circuit Apparatus 2.2 9.6Electrical Machinery Nes 2.1 7.2Aircraft 1.9 –7.3Measuring Instruments 1.6 3.1

Total Imports 100.0 13.6

TOP 10 DESTINATIONS FOR % %NON-OIL DOMESTIC EXPORTS Share Growth

EU-25 18.8 5.8United States 14.4 –1.7China 9.7 27.2Malaysia 8.7 9.9Indonesia 7.7 17.7Hong Kong, China 6.8 0.9Japan 6.7 –1.2Taiwan 4.9 17.2Thailand 4.4 23.2South Korea 3.3 9.7

Total Non-Oil Domestic Exports 100.0 8.2

TOP 10 TRADING PARTNERS% %

Share Growth

Malaysia 13.4 8.9EU-25 11.8 4.6United States 10.9 8.0China 9.4 25.8Indoneisa 7.6 11.6Japan 7.4 2.1Hong Kong, China 6.0 19.1Taiwan 4.8 15.9Thailand 3.9 15.4South Korea 3.9 14.0

Total Trade 100.0 13.8

TOURISM

TOP 10 % %VISITOR GENERATING MARKETS Share Growth

Indonesia 20.3 2.7China 9.6 –2.5Australia 6.9 10.5Japan 6.6 –1.7India 6.5 23.8Malaysia 6.5 7.5United Kingdom 5.2 2.2Thailand 4.2 10.8United States 4.2 11.5South Korea 4.1 0.9Others 25.9 14.8

Total Visitor Arrivals 100.0 7.4

ECONOMIC SURVEY OF SINGAPORE 2005

5

THE WORLD ECONOMY

THE WORLDECONOMY1

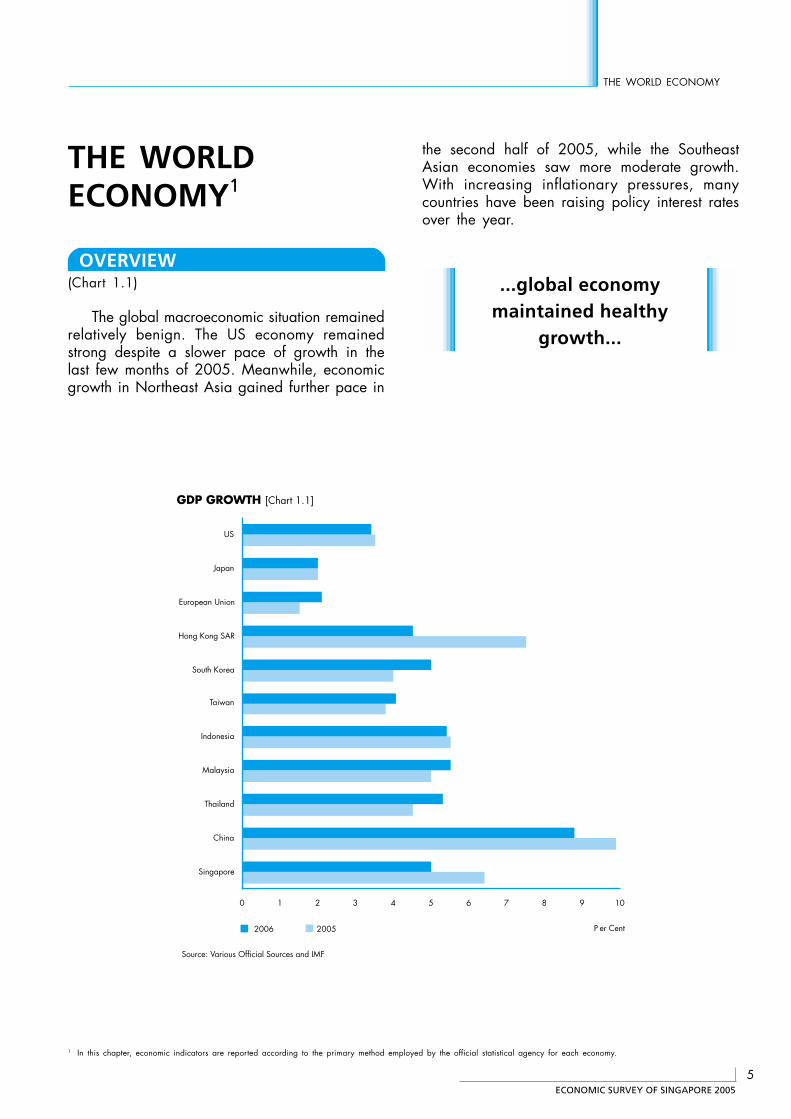

OVERVIEW(Chart 1.1)

The global macroeconomic situation remainedrelatively benign. The US economy remainedstrong despite a slower pace of growth in thelast few months of 2005. Meanwhile, economicgrowth in Northeast Asia gained further pace in

the second half of 2005, while the SoutheastAsian economies saw more moderate growth.With increasing inflationary pressures, manycountries have been raising policy interest ratesover the year.

GDP GROWTH [Chart 1.1]

0 1 2 3 4 5 6 7 8 9 10

Singapore

China

Thailand

Malaysia

Indonesia

Taiwan

South Korea

Hong Kong SAR

European Union

Japan

US

2006 2005 P er Cent

Source: Various Official Sources and IMF

1 In this chapter, economic indicators are reported according to the primary method employed by the official statistical agency for each economy.

...global economymaintained healthy

growth...

ECONOMIC SURVEY OF SINGAPORE 2005

6

Chapter 1

THE WORLD ECONOMY

DEVELOPED ECONOMIES

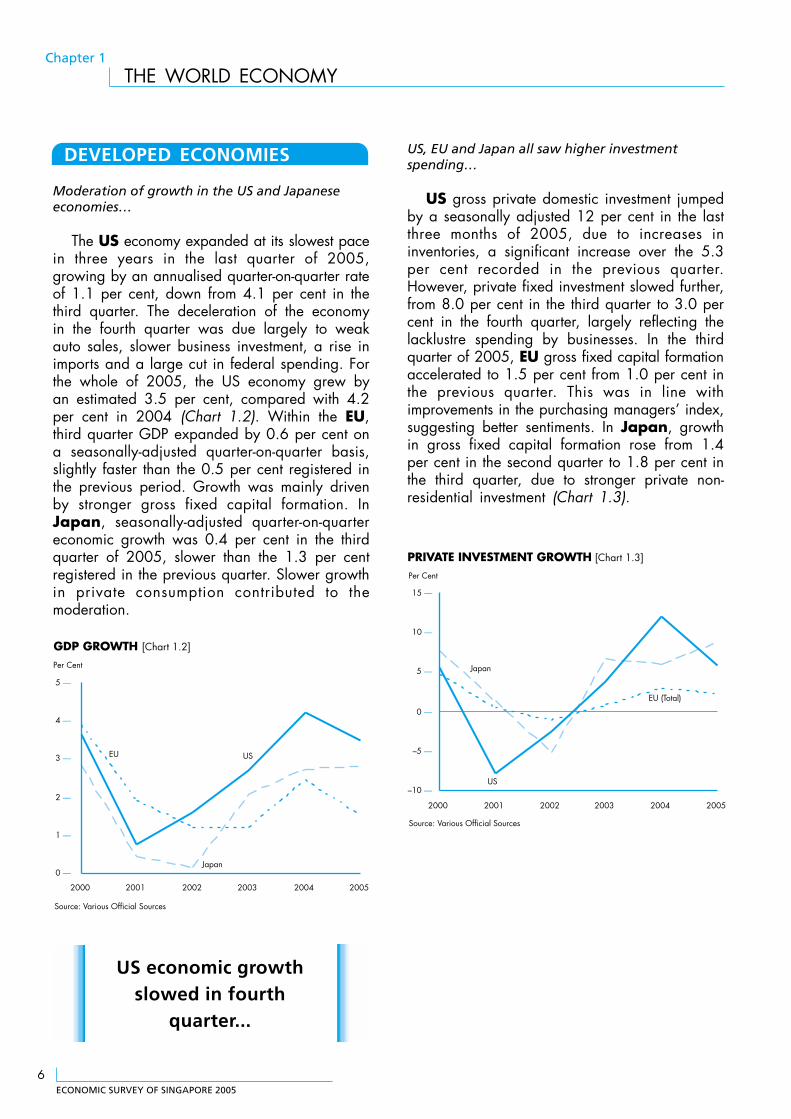

Moderation of growth in the US and Japaneseeconomies…

The US economy expanded at its slowest pacein three years in the last quarter of 2005,growing by an annualised quarter-on-quarter rateof 1.1 per cent, down from 4.1 per cent in thethird quarter. The deceleration of the economyin the fourth quarter was due largely to weakauto sales, slower business investment, a rise inimports and a large cut in federal spending. Forthe whole of 2005, the US economy grew byan estimated 3.5 per cent, compared with 4.2per cent in 2004 (Chart 1.2). Within the EU,third quarter GDP expanded by 0.6 per cent ona seasonally-adjusted quarter-on-quarter basis,slightly faster than the 0.5 per cent registered inthe previous period. Growth was mainly drivenby stronger gross fixed capital formation. InJapan, seasonally-adjusted quarter-on-quartereconomic growth was 0.4 per cent in the thirdquarter of 2005, slower than the 1.3 per centregistered in the previous quarter. Slower growthin private consumption contributed to themoderation.

US, EU and Japan all saw higher investmentspending…

US gross private domestic investment jumpedby a seasonally adjusted 12 per cent in the lastthree months of 2005, due to increases ininventories, a significant increase over the 5.3per cent recorded in the previous quarter.However, private fixed investment slowed further,from 8.0 per cent in the third quarter to 3.0 percent in the fourth quarter, largely reflecting thelacklustre spending by businesses. In the thirdquarter of 2005, EU gross fixed capital formationaccelerated to 1.5 per cent from 1.0 per cent inthe previous quarter. This was in line withimprovements in the purchasing managers’ index,suggesting better sentiments. In Japan, growthin gross fixed capital formation rose from 1.4per cent in the second quarter to 1.8 per cent inthe third quarter, due to stronger private non-residential investment (Chart 1.3).

0 —

1 —

2 —

3 —

4 —

5 —

2000 2001 2002 2003 2004 2005

GDP GROWTH [Chart 1.2]

Per Cent

Source: Various Official Sources

EU

Japan

US

–10 —

0 —

5 —

10 —

15 —

2000 2001 2002 2003 2004 2005

US

Source: Various Official Sources

PRIVATE INVESTMENT GROWTH [Chart 1.3]

Per Cent

EU (Total)

Japan

–5 —

US economic growthslowed in fourth

quarter...

ECONOMIC SURVEY OF SINGAPORE 2005

7

THE WORLD ECONOMY

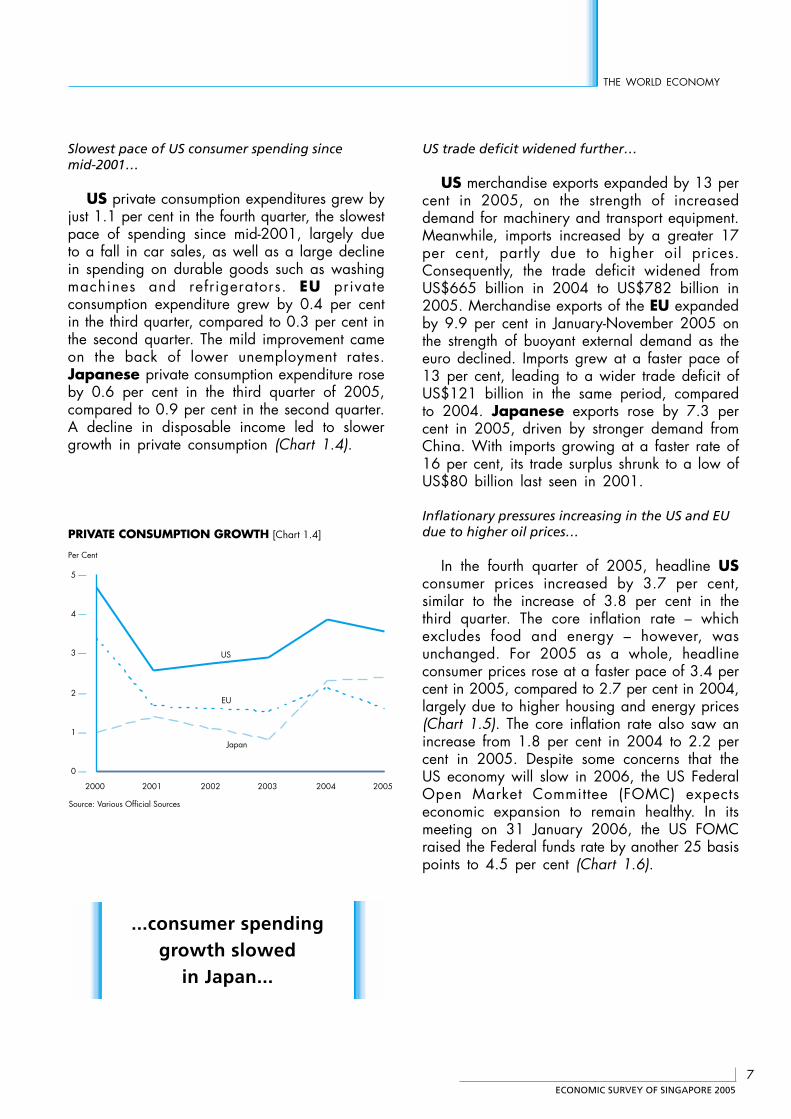

Slowest pace of US consumer spending sincemid-2001…

US private consumption expenditures grew byjust 1.1 per cent in the fourth quarter, the slowestpace of spending since mid-2001, largely dueto a fall in car sales, as well as a large declinein spending on durable goods such as washingmachines and refrigerators. EU privateconsumption expenditure grew by 0.4 per centin the third quarter, compared to 0.3 per cent inthe second quarter. The mild improvement cameon the back of lower unemployment rates.Japanese private consumption expenditure roseby 0.6 per cent in the third quarter of 2005,compared to 0.9 per cent in the second quarter.A decline in disposable income led to slowergrowth in private consumption (Chart 1.4).

US trade deficit widened further…

US merchandise exports expanded by 13 percent in 2005, on the strength of increaseddemand for machinery and transport equipment.Meanwhile, imports increased by a greater 17per cent, partly due to higher oil prices.Consequently, the trade deficit widened fromUS$665 billion in 2004 to US$782 billion in2005. Merchandise exports of the EU expandedby 9.9 per cent in January-November 2005 onthe strength of buoyant external demand as theeuro declined. Imports grew at a faster pace of13 per cent, leading to a wider trade deficit ofUS$121 billion in the same period, comparedto 2004. Japanese exports rose by 7.3 percent in 2005, driven by stronger demand fromChina. With imports growing at a faster rate of16 per cent, its trade surplus shrunk to a low ofUS$80 billion last seen in 2001.

Inflationary pressures increasing in the US and EUdue to higher oil prices…

In the fourth quarter of 2005, headline USconsumer prices increased by 3.7 per cent,similar to the increase of 3.8 per cent in thethird quarter. The core inflation rate – whichexcludes food and energy – however, wasunchanged. For 2005 as a whole, headlineconsumer prices rose at a faster pace of 3.4 percent in 2005, compared to 2.7 per cent in 2004,largely due to higher housing and energy prices(Chart 1.5). The core inflation rate also saw anincrease from 1.8 per cent in 2004 to 2.2 percent in 2005. Despite some concerns that theUS economy will slow in 2006, the US FederalOpen Market Committee (FOMC) expectseconomic expansion to remain healthy. In itsmeeting on 31 January 2006, the US FOMCraised the Federal funds rate by another 25 basispoints to 4.5 per cent (Chart 1.6).

0 —

1 —

2 —

3 —

4 —

5 —

2000 2001 2002 2003 2004 2005

EU

US

PRIVATE CONSUMPTION GROWTH [Chart 1.4]

Per Cent

Source: Various Official Sources

Japan

...consumer spendinggrowth slowed

in Japan...

ECONOMIC SURVEY OF SINGAPORE 2005

8

Chapter 1

THE WORLD ECONOMY

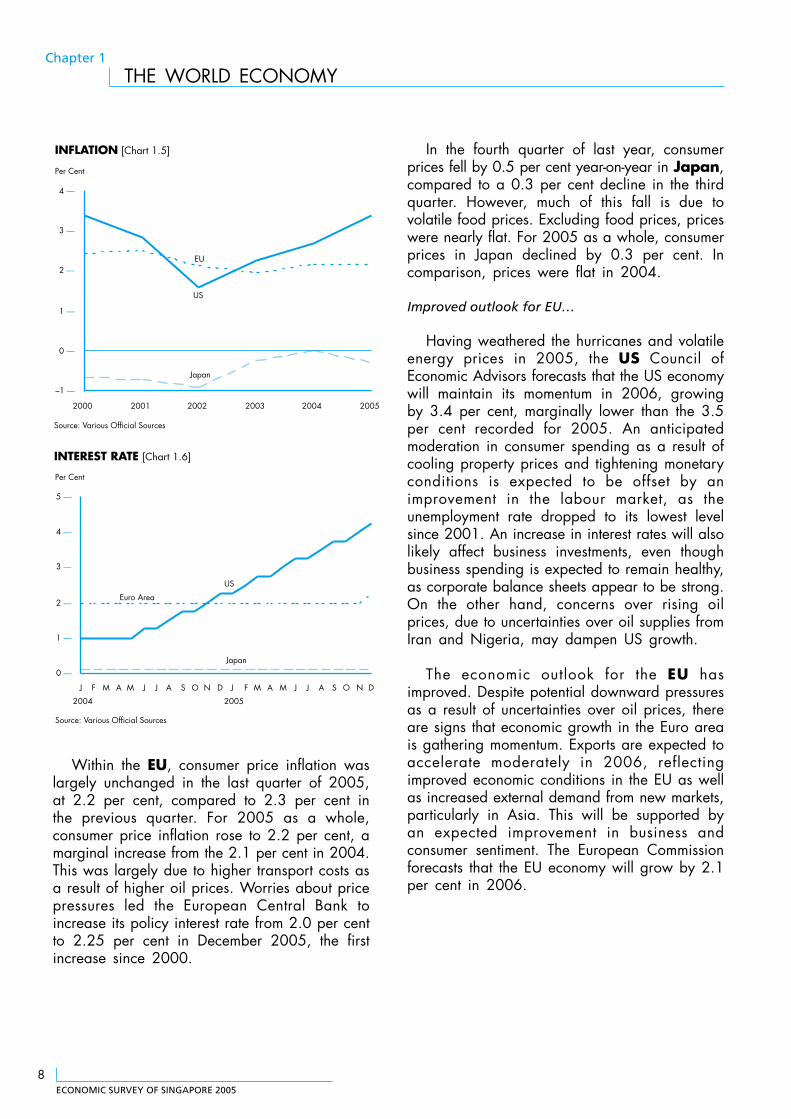

Within the EU, consumer price inflation waslargely unchanged in the last quarter of 2005,at 2.2 per cent, compared to 2.3 per cent inthe previous quarter. For 2005 as a whole,consumer price inflation rose to 2.2 per cent, amarginal increase from the 2.1 per cent in 2004.This was largely due to higher transport costs asa result of higher oil prices. Worries about pricepressures led the European Central Bank toincrease its policy interest rate from 2.0 per centto 2.25 per cent in December 2005, the firstincrease since 2000.

In the fourth quarter of last year, consumerprices fell by 0.5 per cent year-on-year in Japan,compared to a 0.3 per cent decline in the thirdquarter. However, much of this fall is due tovolatile food prices. Excluding food prices, priceswere nearly flat. For 2005 as a whole, consumerprices in Japan declined by 0.3 per cent. Incomparison, prices were flat in 2004.

Improved outlook for EU…

Having weathered the hurricanes and volatileenergy prices in 2005, the US Council ofEconomic Advisors forecasts that the US economywill maintain its momentum in 2006, growingby 3.4 per cent, marginally lower than the 3.5per cent recorded for 2005. An anticipatedmoderation in consumer spending as a result ofcooling property prices and tightening monetaryconditions is expected to be offset by animprovement in the labour market, as theunemployment rate dropped to its lowest levelsince 2001. An increase in interest rates will alsolikely affect business investments, even thoughbusiness spending is expected to remain healthy,as corporate balance sheets appear to be strong.On the other hand, concerns over rising oilprices, due to uncertainties over oil supplies fromIran and Nigeria, may dampen US growth.

The economic outlook for the EU hasimproved. Despite potential downward pressuresas a result of uncertainties over oil prices, thereare signs that economic growth in the Euro areais gathering momentum. Exports are expected toaccelerate moderately in 2006, reflectingimproved economic conditions in the EU as wellas increased external demand from new markets,particularly in Asia. This will be supported byan expected improvement in business andconsumer sentiment. The European Commissionforecasts that the EU economy will grow by 2.1per cent in 2006.

–1 —

0 —

1 —

2 —

3 —

4 —

2000 2001 2002 2003 2004 2005

EU

US

INFLATION [Chart 1.5]

Per Cent

Source: Various Official Sources

Japan

0 —

1 —

2 —

3 —

4 —

5 —

J

2004

F M A M J J A S O N D J

2005

F M A M J J A S O N D

Euro Area

US

INTEREST RATE [Chart 1.6]

Per Cent

Source: Various Official Sources

Japan

ECONOMIC SURVEY OF SINGAPORE 2005

9

THE WORLD ECONOMY

Similarly, the economic outlook for Japan isimproving. According to the Bank of Japan’sTankan survey in December 2005, businessconditions are expected to continue improving.The survey also revealed better profit expectationsand a tightening labour market. In line with theseexpectations, industrial production expanded inthe last quarter of 2005, reversing fiveconsecutive quarters of slower growth. Inaddition, the seasonally adjusted consumerconfidence index excluding one person householdhas risen to a record high, since the last peak inJune 1991. For FY2006, the Bank of Japanexpects GDP growth to be between 1.6 and 2.2per cent.

NORTHEAST ASIA

Economic growth picked up in second half of2005…

Economic activity in Northeast Asia gainedfurther pace in the second half of 2005. For theyear as a whole, the region also consolidatedits economic growth following the strong recoveryof 2004.

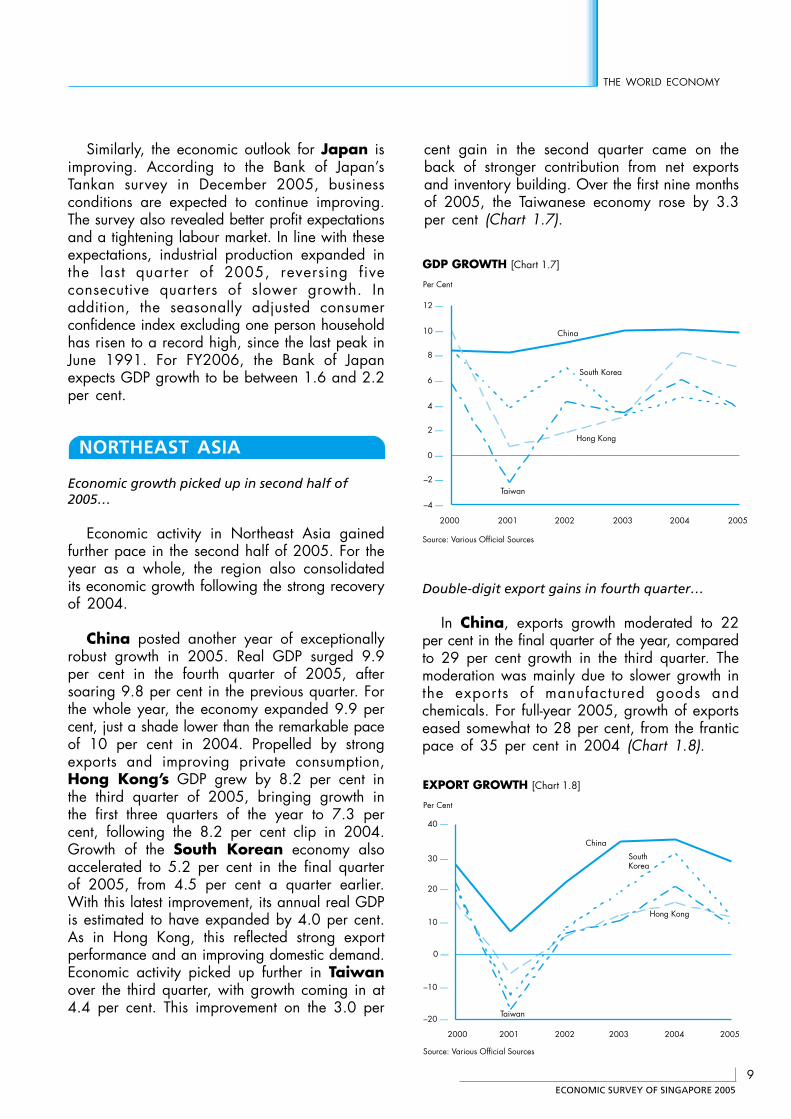

China posted another year of exceptionallyrobust growth in 2005. Real GDP surged 9.9per cent in the fourth quarter of 2005, aftersoaring 9.8 per cent in the previous quarter. Forthe whole year, the economy expanded 9.9 percent, just a shade lower than the remarkable paceof 10 per cent in 2004. Propelled by strongexports and improving private consumption,Hong Kong’s GDP grew by 8.2 per cent inthe third quarter of 2005, bringing growth inthe first three quarters of the year to 7.3 percent, following the 8.2 per cent clip in 2004.Growth of the South Korean economy alsoaccelerated to 5.2 per cent in the final quarterof 2005, from 4.5 per cent a quarter earlier.With this latest improvement, its annual real GDPis estimated to have expanded by 4.0 per cent.As in Hong Kong, this reflected strong exportperformance and an improving domestic demand.Economic activity picked up further in Taiwanover the third quarter, with growth coming in at4.4 per cent. This improvement on the 3.0 per

Double-digit export gains in fourth quarter…

In China, exports growth moderated to 22per cent in the final quarter of the year, comparedto 29 per cent growth in the third quarter. Themoderation was mainly due to slower growth inthe exports of manufactured goods andchemicals. For full-year 2005, growth of exportseased somewhat to 28 per cent, from the franticpace of 35 per cent in 2004 (Chart 1.8).

–4 —

–2 —

0 —

2 —

4 —

6 —

8 —

10 —

12 —

2000 2001 2002 2003 2004 2005

China

GDP GROWTH [Chart 1.7]

Per Cent

Hong Kong

South Korea

Taiwan

Source: Various Official Sources

–20 —

–10 —

0 —

10 —

20 —

30 —

40 —

SouthKorea

Hong Kong

Taiwan

Per Cent

China

EXPORT GROWTH [Chart 1.8]

Source: Various Official Sources

20012000 2002 2003 2004 2005

cent gain in the second quarter came on theback of stronger contribution from net exportsand inventory building. Over the first nine monthsof 2005, the Taiwanese economy rose by 3.3per cent (Chart 1.7).

ECONOMIC SURVEY OF SINGAPORE 2005

10

Chapter 1

THE WORLD ECONOMY

In Hong Kong, growth of domestic exportsimproved to 25 per cent in the final quarter of2005 from 14 per cent in the third quarter,fuelled by a 97 per cent leap in the exports ofelectronics goods. For the whole of 2005,domestic exports expanded 7.9 per cent,compared to 3.6 per cent increase a year ago.On the other hand, in line with the slowdown inChina’s external trade, Hong Kong’s re-exportsgrowth moderated to 9.0 per cent in the fourthquarter from 12 per cent in the third quarter.Full year re-exports growth receded to 12 percent from 17 per cent in 2004.

Taiwan’s exports in the final quarter of 2005rose sharply, compared to the more gradualincrease of the second and third quarters. Exportgrowth in October to December reached 14 percent, following a 7.1 per cent gain in the secondquarter. During this period, increased shipmentsto the mainland and to Hong Kong contributedmost to export growth. For the year as a whole,Taiwanese exports rose by 8.8 per cent afterchalking up a 21 per cent gain a year earlier.

South Korea’s exports increased by 12 percent in the final quarter of 2005, slowing froma 15 per cent gain in the earlier quarter. Thequarter saw lower growth of shipment of industrialinputs –such as metal and chemicals – after along period of double-digit gains. Lower growthof exports to China contributed most to theslowdown although the rate of growth remainedabove 20 per cent. Full year growth of exportsin 2005 remained healthy at 12 per cent,although it slowed from 31 per cent in 2004.

Private consumption continued to grow…

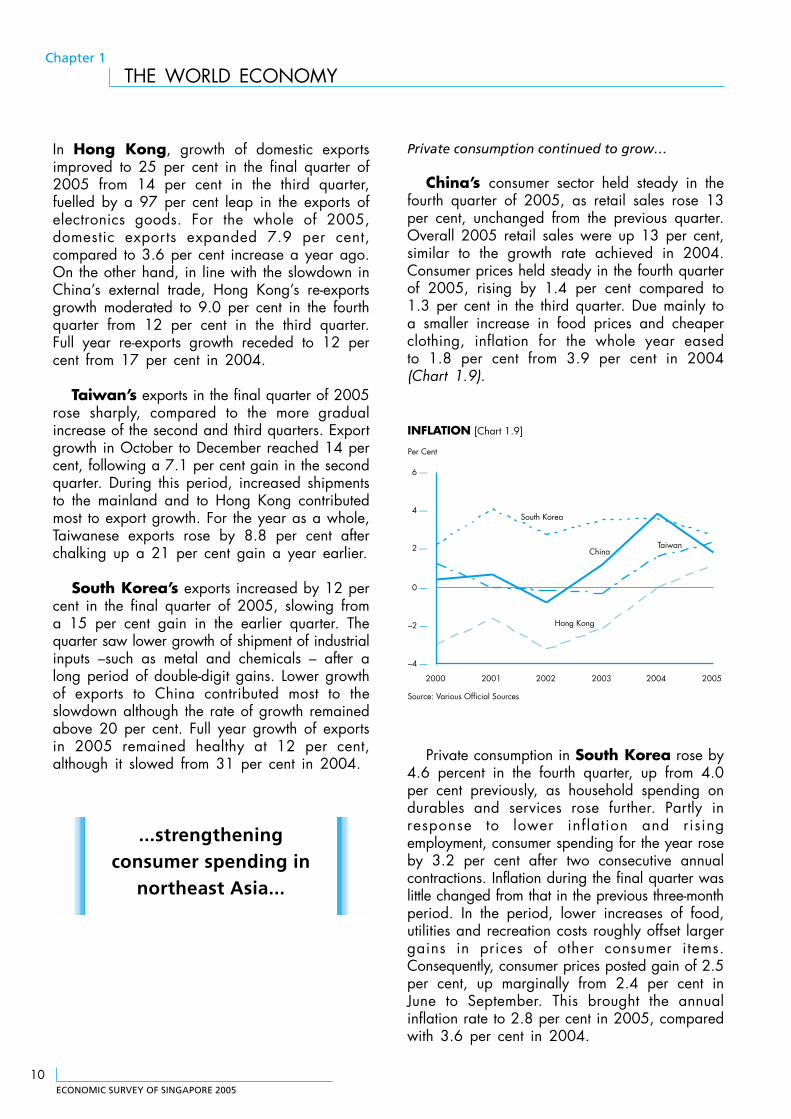

China’s consumer sector held steady in thefourth quarter of 2005, as retail sales rose 13per cent, unchanged from the previous quarter.Overall 2005 retail sales were up 13 per cent,similar to the growth rate achieved in 2004.Consumer prices held steady in the fourth quarterof 2005, rising by 1.4 per cent compared to1.3 per cent in the third quarter. Due mainly toa smaller increase in food prices and cheaperclothing, inflation for the whole year easedto 1.8 per cent from 3.9 per cent in 2004(Chart 1.9).

Private consumption in South Korea rose by4.6 percent in the fourth quarter, up from 4.0per cent previously, as household spending ondurables and services rose further. Partly inresponse to lower inflation and risingemployment, consumer spending for the year roseby 3.2 per cent after two consecutive annualcontractions. Inflation during the final quarter waslittle changed from that in the previous three-monthperiod. In the period, lower increases of food,utilities and recreation costs roughly offset largergains in prices of other consumer items.Consequently, consumer prices posted gain of 2.5per cent, up marginally from 2.4 per cent inJune to September. This brought the annualinflation rate to 2.8 per cent in 2005, comparedwith 3.6 per cent in 2004.

INFLATION [Chart 1.9]

Source: Various Official Sources

–4 —

–2 —

0 —

2 —

4 —

6 —

2000 2001 2002 2003 2004 2005

South Korea

Hong Kong

Taiwan

Per Cent

China

...strengtheningconsumer spending in

northeast Asia...

ECONOMIC SURVEY OF SINGAPORE 2005

11

THE WORLD ECONOMY

Similarly, private consumption in Hong Konggrew 4.6 per cent in the third quarter of 2005,after a 2.7 per cent growth in the second quarter.For the first three quarters of the year, however,consumption growth slowed to 3.9 per centcompared to 6.8 per cent in 2004, as consumersentiments were hit by successive interest ratehikes and a cooling property market. Consumerprices rose 1.7 per cent in the final quarter, upfrom 1.4 per cent in the preceding quarter, drivenby higher prices for housing, utilities andtransport. For 2005, consumer prices rose 1.2per cent, after six consecutive years of deflationthat began in 1999.

Consumer spending in Taiwan rose by 3.7per cent in the third quarter, compared to the3.0 per cent of the second quarter. Althoughprivate spending on medical care and transportand communications eased in the quarter, it wasmore than offset by rising spending on food andhousehold operations. Over the first nine months,overall private consumption expenditure rose by3.1 per cent, compared with 3.9 per cent in2004. Consumer price inflation eased in the finalquarter to 2.5 per cent, from 3.0 per cent in theprevious three-month period. Over the quarter,food prices eased from levels reached in thewake of disruptions to food production causedby typhoon damage. Over 2005, inflation roseto 2.3 per cent from 1.6 per cent in 2004, whenit came out of deflation. The increase camelargely on account of higher food prices.

China continues double-digit gains in investment…

In China, investment in fixed assets jumped26 per cent in 2005, similar to the growth ratein 2004. Reflecting continued strength of stateinvestments in rural infrastructure, fixed assetinvestment in rural areas rose 27 per cent in2005, outpacing the 18 per cent growth in urbanareas. Gross fixed capital formation in SouthKorea increased by 3.7 per cent in the fourthquarter, up substantially from 2.0 per cent in thethird quarter. This reflected mainly a sharpincrease in spending on transport equipment andmachinery investment. Due to weakness inspending early in the year, gross fixed capitalformation grew by just 2.1 per cent in 2005,little changed from 1.9 per cent in 2004.

In Hong Kong, investment slowed asconstruction activities eased following thecompletion of several major projects. Gross fixedcapital formation decelerated to 2.4 per cent inthe third quarter of 2005, from 4.5 per cent inthe previous quarter. For the first three quartersof 2005, investment grew 2.5 per cent, incontrast to 4.1 per cent for 2004. Similarly,Taiwanese gross fixed capital formation slowedsharply in the third quarter to 0.3 per cent, from7.4 per cent in the second quarter. The declinereflected a turnaround in private sector investmentin machinery and equipment. Due to the strengthof investment spending in the first half of theyear, however, gross fixed capital formation inthe first three quarters increased by 5.8 per centcompared to the same period a year earlier.

Steady growth expected in 2006…

Growth prospects in China remain bright thisyear. In December 2005, the National Bureauof Statistics revised 2004 nominal GDP upwardsby a hefty 16.8 per cent, which mostly reflecteda larger services industry than formerly recorded.The revision in national accounts also revealedthat growth has been more balanced betweenconsumption and investment than previouslythought. Looking ahead, the engines ofinvestment, consumption and exports are expectedto remain firm. The National Development andReform Commission expects GDP growth to reach8.5–9.0 per cent this year.

...strong investmentsustained in China...

ECONOMIC SURVEY OF SINGAPORE 2005

12

Chapter 1

THE WORLD ECONOMY

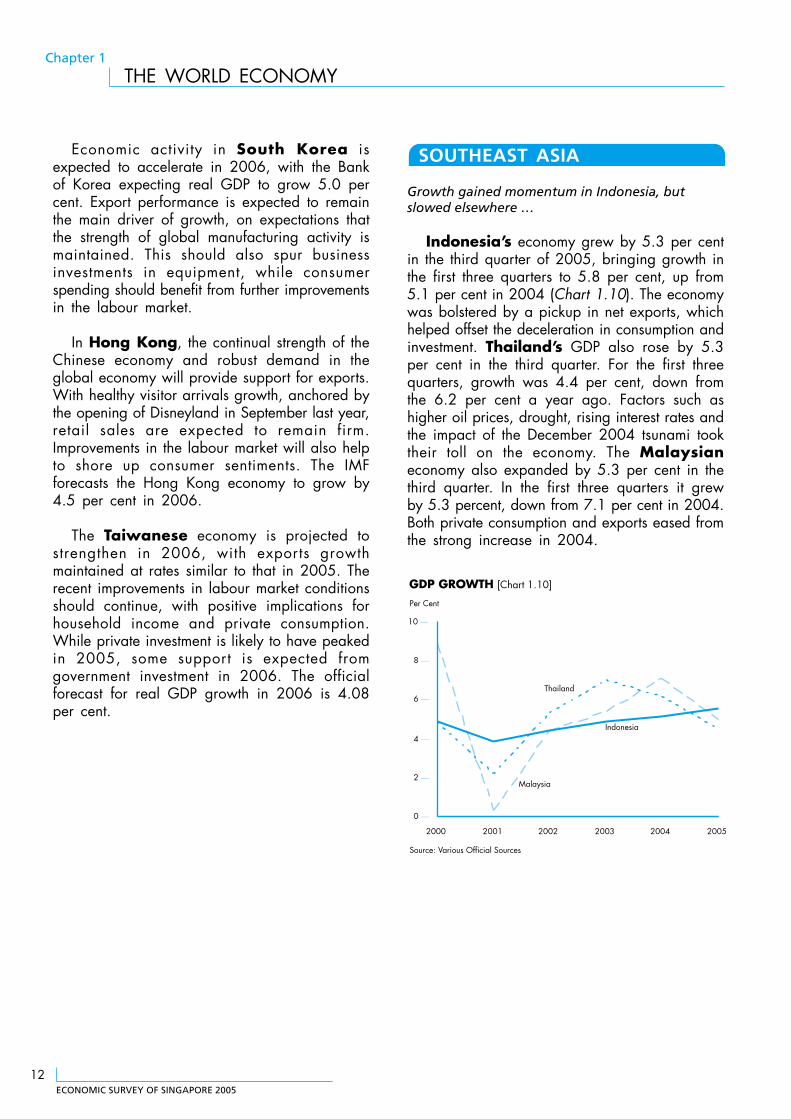

Economic activity in South Korea isexpected to accelerate in 2006, with the Bankof Korea expecting real GDP to grow 5.0 percent. Export performance is expected to remainthe main driver of growth, on expectations thatthe strength of global manufacturing activity ismaintained. This should also spur businessinvestments in equipment, while consumerspending should benefit from further improvementsin the labour market.

In Hong Kong, the continual strength of theChinese economy and robust demand in theglobal economy will provide support for exports.With healthy visitor arrivals growth, anchored bythe opening of Disneyland in September last year,retail sales are expected to remain firm.Improvements in the labour market will also helpto shore up consumer sentiments. The IMFforecasts the Hong Kong economy to grow by4.5 per cent in 2006.

The Taiwanese economy is projected tostrengthen in 2006, with exports growthmaintained at rates similar to that in 2005. Therecent improvements in labour market conditionsshould continue, with positive implications forhousehold income and private consumption.While private investment is likely to have peakedin 2005, some support is expected fromgovernment investment in 2006. The officialforecast for real GDP growth in 2006 is 4.08per cent.

SOUTHEAST ASIA

Growth gained momentum in Indonesia, butslowed elsewhere …

Indonesia’s economy grew by 5.3 per centin the third quarter of 2005, bringing growth inthe first three quarters to 5.8 per cent, up from5.1 per cent in 2004 (Chart 1.10). The economywas bolstered by a pickup in net exports, whichhelped offset the deceleration in consumption andinvestment. Thailand’s GDP also rose by 5.3per cent in the third quarter. For the first threequarters, growth was 4.4 per cent, down fromthe 6.2 per cent a year ago. Factors such ashigher oil prices, drought, rising interest rates andthe impact of the December 2004 tsunami tooktheir toll on the economy. The Malaysianeconomy also expanded by 5.3 per cent in thethird quarter. In the first three quarters it grewby 5.3 percent, down from 7.1 per cent in 2004.Both private consumption and exports eased fromthe strong increase in 2004.

GDP GROWTH [Chart 1.10]

Source: Various Official Sources

0 —

2 —

4 —

6 —

8 —

10 —

2000 2001 2002 2003 2004 2005

Indonesia

Malaysia

Per Cent

Thailand

ECONOMIC SURVEY OF SINGAPORE 2005

13

THE WORLD ECONOMY

Private consumption growth moderated in allthree economies …

In Indonesia, private consumption grew by3.7 per cent in first three quarters, down fromthe 4.9 per cent clip in 2004 (Chart 1.11). Thiswas in part due to the steady rise in interestrates and fuel prices. Similarly, in Thailand,private consumption rose by 4.6 per cent in thefirst nine months of 2005, easing off from 5.9per cent growth in the previous year, due toconcerns over rising interest rates and oil prices.In Malaysia, private consumption growth alsoslowed from 11 per cent in 2004 to 9.3 percent in the first three quarters of 2005. Consumerconfidence was affected partly by the fuel pricehikes arising from high oil prices.

Investment growth cooled in Indonesia andThailand …

Investments in Indonesia rose at a healthyrate of 12 per cent in the first three quarters of2005, albeit easing off from the 16 per centclip in 2004 (Chart 1.12). Higher investmentswere seen in the financial services, transport andcommunications as well as utilities sectors.Similarly, weaker business sentiment in Thailandmoderated investment growth from 14 per centin 2004 to 12 per cent in the first three quartersof 2005. In contrast, investment spending inMalaysia climbed by 6.2 per cent in the firstthree quarters, after rising 3.1 per cent theprevious year.

PRIVATE CONSUMPTION EXPENDITURE GROWTH [Chart 1.11]

Source: Various Official Sources

0 —

5 —

10 —

15 —

2000 2001 2002 2003 2004 2005

Indonesia

Malaysia

Per Cent

Thailand

GROSS FIXED CAPITAL FORMATION GROWTH [Chart 1.12]

Source: Various Official Sources

–10 —

0 —

10 —

20 —

30 —

2000 2001 2002 2003 2004 2005

Indonesia

Malaysia

Per Cent

Thailand

Rising interest rates andenergy costs have

moderatedconsumption...

ECONOMIC SURVEY OF SINGAPORE 2005

14

Chapter 1

THE WORLD ECONOMY

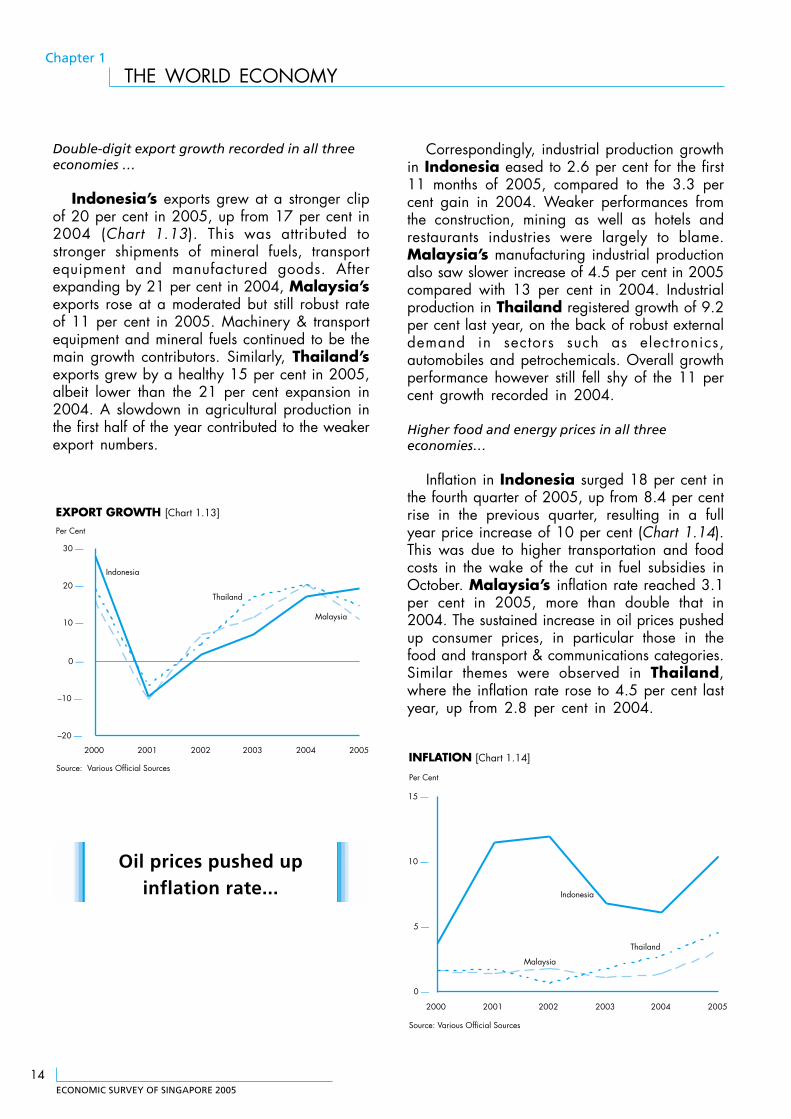

Double-digit export growth recorded in all threeeconomies …

Indonesia’s exports grew at a stronger clipof 20 per cent in 2005, up from 17 per cent in2004 (Chart 1.13). This was attributed tostronger shipments of mineral fuels, transportequipment and manufactured goods. Afterexpanding by 21 per cent in 2004, Malaysia’sexports rose at a moderated but still robust rateof 11 per cent in 2005. Machinery & transportequipment and mineral fuels continued to be themain growth contributors. Similarly, Thailand’sexports grew by a healthy 15 per cent in 2005,albeit lower than the 21 per cent expansion in2004. A slowdown in agricultural production inthe first half of the year contributed to the weakerexport numbers.

Correspondingly, industrial production growthin Indonesia eased to 2.6 per cent for the first11 months of 2005, compared to the 3.3 percent gain in 2004. Weaker performances fromthe construction, mining as well as hotels andrestaurants industries were largely to blame.Malaysia’s manufacturing industrial productionalso saw slower increase of 4.5 per cent in 2005compared with 13 per cent in 2004. Industrialproduction in Thailand registered growth of 9.2per cent last year, on the back of robust externaldemand in sectors such as electronics,automobiles and petrochemicals. Overall growthperformance however still fell shy of the 11 percent growth recorded in 2004.

Higher food and energy prices in all threeeconomies…

Inflation in Indonesia surged 18 per cent inthe fourth quarter of 2005, up from 8.4 per centrise in the previous quarter, resulting in a fullyear price increase of 10 per cent (Chart 1.14).This was due to higher transportation and foodcosts in the wake of the cut in fuel subsidies inOctober. Malaysia’s inflation rate reached 3.1per cent in 2005, more than double that in2004. The sustained increase in oil prices pushedup consumer prices, in particular those in thefood and transport & communications categories.Similar themes were observed in Thailand,where the inflation rate rose to 4.5 per cent lastyear, up from 2.8 per cent in 2004.

EXPORT GROWTH [Chart 1.13]

Source: Various Official Sources

–20 —

–10 —

0 —

10 —

20 —

30 —

2000 2001 2002 2003 2004 2005

Indonesia

Malaysia

Per Cent

Thailand

INFLATION [Chart 1.14]

Source: Various Official Sources

0 —

5 —

10 —

15 —

2000 2001 2002 2003 2004 2005

Indonesia

Malaysia

Per Cent

Thailand

Oil prices pushed upinflation rate...

ECONOMIC SURVEY OF SINGAPORE 2005

15

THE WORLD ECONOMY

Favourable economic growth across the region in2006 …

To curb inflationary tendencies, BankIndonesia raised benchmark interest rates againin December to 12.75 per cent, up from 11 percent in early October. While higher capital costswould cloud domestic consumption and businessspending, the Bank expects the economy to growby between 5.0 and 5.7 per cent in 2006,supported by planned fiscal stimulus packagesand a buoyant export outlook.

Growth momentum has gathered pace in theMalaysian economy after the slowdown in thefirst half of 2005. The continued growth in themajor economies and sustained expansion in theglobal electronics industry will provide impetusto the Malaysian economy this year. TheMalaysian government expects the economy togrow by 5.5 per cent in 2006.

Outlook remainsrosy in 2006...

To keep inflation in check, the Bank ofThailand raised its benchmark interest rate by25 basis points in January 2006, following asimilar increase in December 2005. Thai interestrates now stand at 4.25 per cent. For 2006, theBank of Thailand has narrowed its growthforecast to between 4.75 and 5.75 per cent.Strengthening external demand is expected tolend support to economic growth this year.

Contributed by:

Leong Wai Ho, Senior EconomistMs Soo Cheng Ghee, Senior EconomistTan Kim Eng, Senior EconomistLim Teng Kiat, Senior EconomistPuah Kok Keong, EconomistBenedict Chia, EconomistLee Lay Keng, EconomistLeong Wai Yan, Economist

Economics and Strategy DivisionMinistry of Trade and Industry

ECONOMIC SURVEY OF SINGAPORE 2005

16

Chapter 2

OUTPUT, EXPENDITURE AND NATIONAL INCOME

OUTPUT,EXPENDITURE ANDNATIONAL INCOME

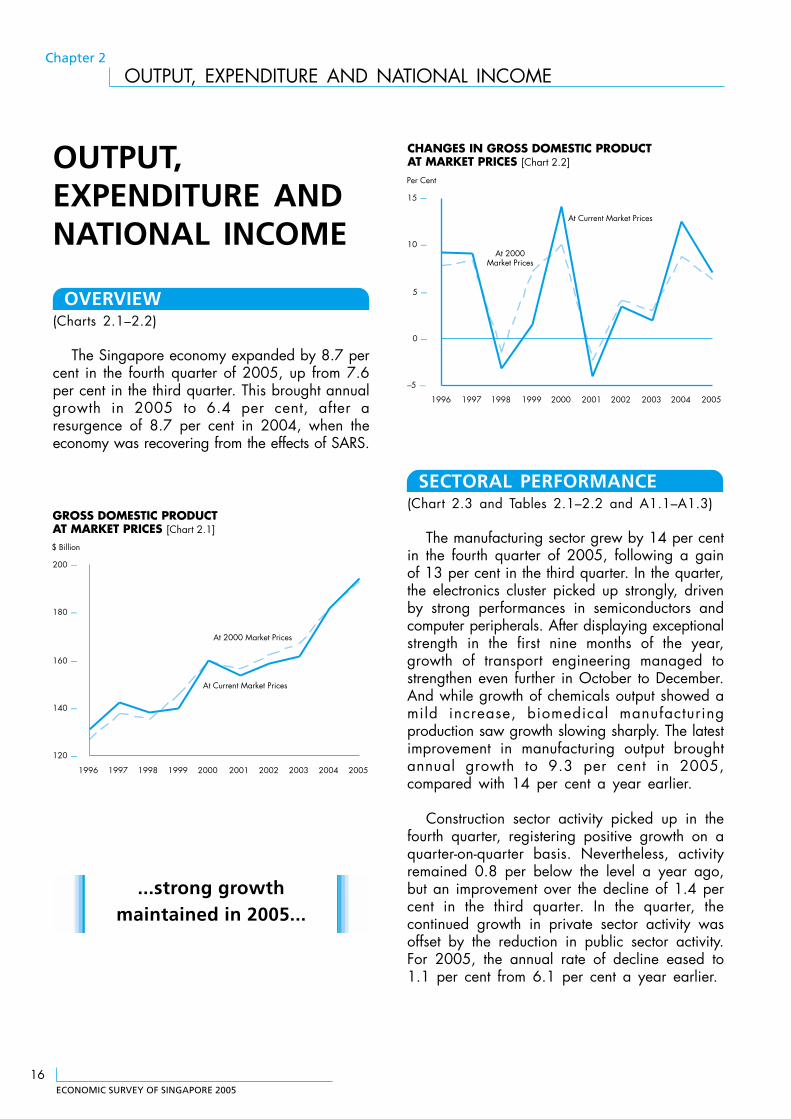

OVERVIEW(Charts 2.1–2.2)

The Singapore economy expanded by 8.7 percent in the fourth quarter of 2005, up from 7.6per cent in the third quarter. This brought annualgrowth in 2005 to 6.4 per cent, after aresurgence of 8.7 per cent in 2004, when theeconomy was recovering from the effects of SARS.

...strong growthmaintained in 2005...

GROSS DOMESTIC PRODUCTAT MARKET PRICES [Chart 2.1]

120 —

140 —

160 —

180 —

200 —

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

At 2000 Market Prices

$ Billion

At Current Market Prices

CHANGES IN GROSS DOMESTIC PRODUCTAT MARKET PRICES [Chart 2.2]

–5 —

0 —

5 —

10 —

15 —

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

At Current Market Prices

Per Cent

At 2000Market Prices

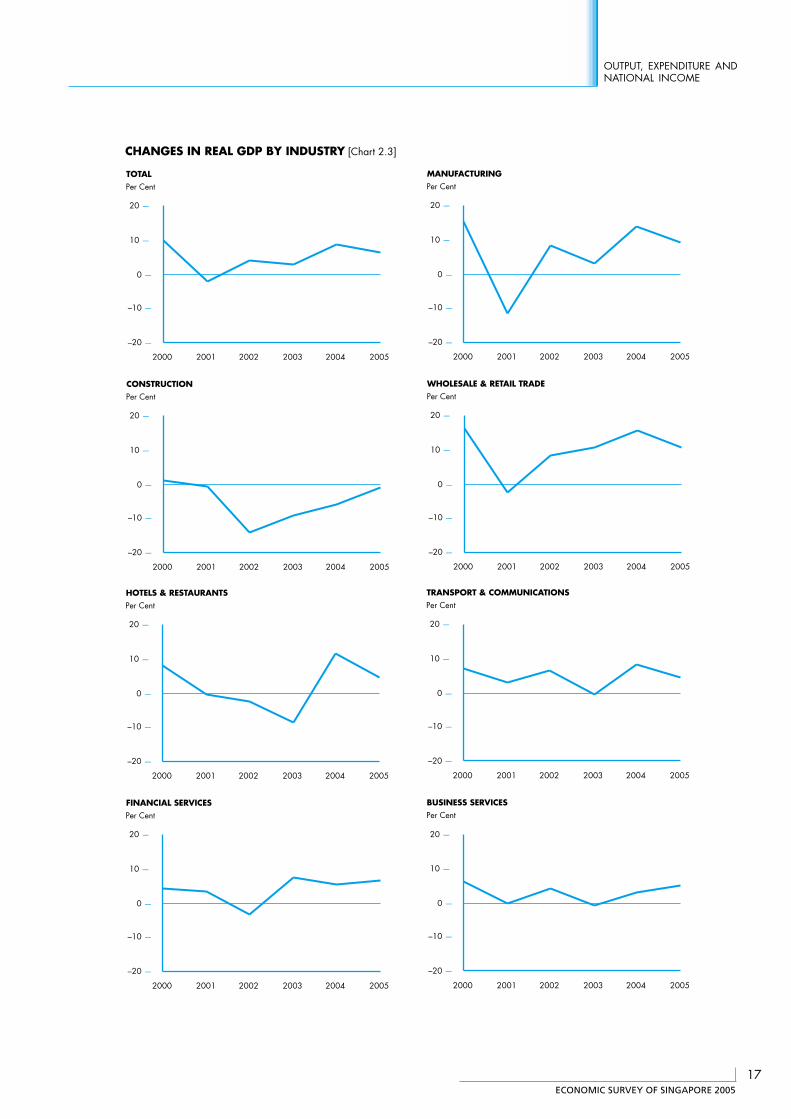

SECTORAL PERFORMANCE(Chart 2.3 and Tables 2.1–2.2 and A1.1–A1.3)

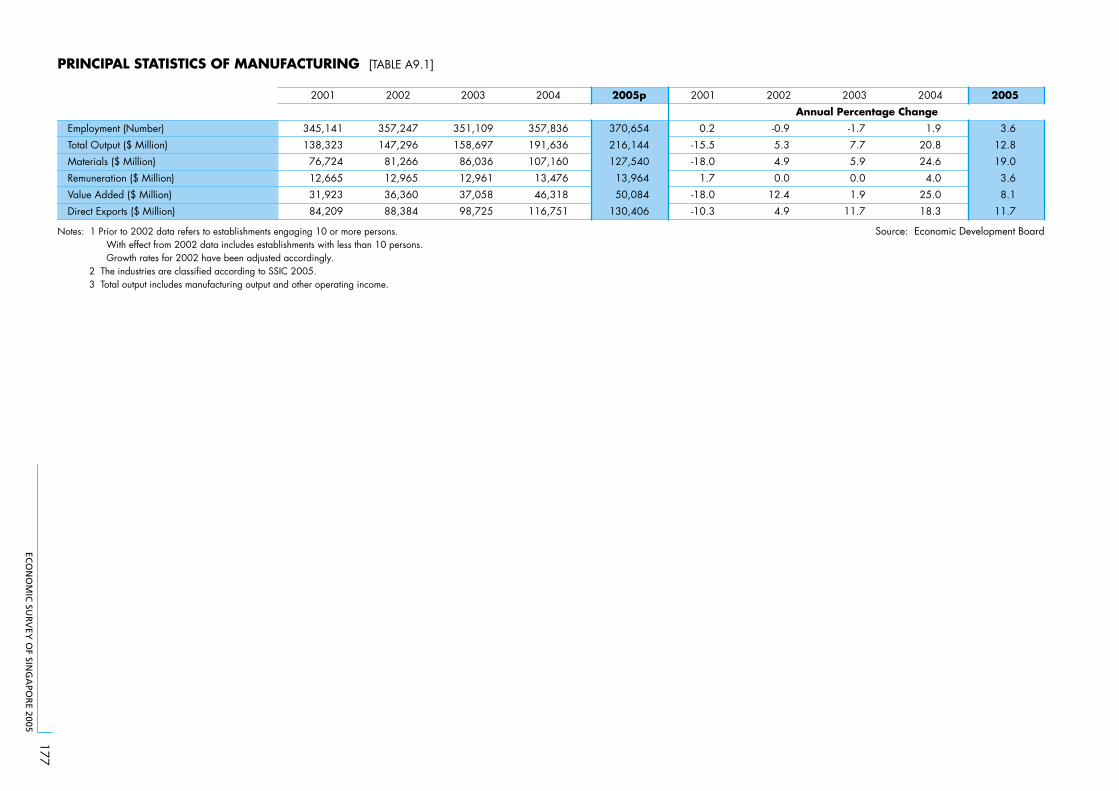

The manufacturing sector grew by 14 per centin the fourth quarter of 2005, following a gainof 13 per cent in the third quarter. In the quarter,the electronics cluster picked up strongly, drivenby strong performances in semiconductors andcomputer peripherals. After displaying exceptionalstrength in the first nine months of the year,growth of transport engineering managed tostrengthen even further in October to December.And while growth of chemicals output showed amild increase, biomedical manufacturingproduction saw growth slowing sharply. The latestimprovement in manufacturing output broughtannual growth to 9.3 per cent in 2005,compared with 14 per cent a year earlier.

Construction sector activity picked up in thefourth quarter, registering positive growth on aquarter-on-quarter basis. Nevertheless, activityremained 0.8 per below the level a year ago,but an improvement over the decline of 1.4 percent in the third quarter. In the quarter, thecontinued growth in private sector activity wasoffset by the reduction in public sector activity.For 2005, the annual rate of decline eased to1.1 per cent from 6.1 per cent a year earlier.

ECONOMIC SURVEY OF SINGAPORE 2005

17

OUTPUT, EXPENDITURE ANDNATIONAL INCOME

CHANGES IN REAL GDP BY INDUSTRY [Chart 2.3]

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

Per CentTOTAL

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

Per CentCONSTRUCTION

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

Per CentHOTELS & RESTAURANTS

–20 —

–10 —

0 —

10 —

20 — 20 —

2000 2001 2002 2003 2004 2005

Per CentFINANCIAL SERVICES

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

Per CentMANUFACTURING

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

Per CentWHOLESALE & RETAIL TRADE

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

Per CentTRANSPORT & COMMUNICATIONS

–20 —

–10 —

0 —

10 —

2000 2001 2002 2003 2004 2005

Per CentBUSINESS SERVICES

ECONOMIC SURVEY OF SINGAPORE 2005

18

Chapter 2

OUTPUT, EXPENDITURE AND NATIONAL INCOME

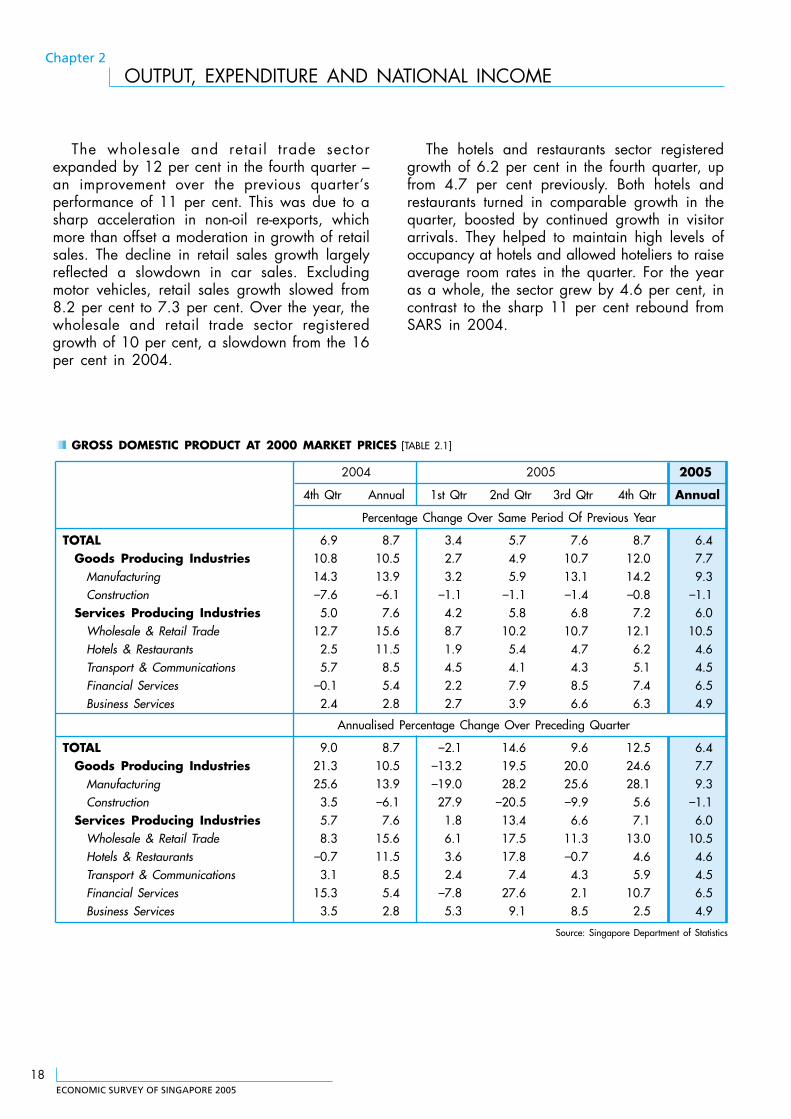

The wholesale and retail trade sectorexpanded by 12 per cent in the fourth quarter –an improvement over the previous quarter’sperformance of 11 per cent. This was due to asharp acceleration in non-oil re-exports, whichmore than offset a moderation in growth of retailsales. The decline in retail sales growth largelyreflected a slowdown in car sales. Excludingmotor vehicles, retail sales growth slowed from8.2 per cent to 7.3 per cent. Over the year, thewholesale and retail trade sector registeredgrowth of 10 per cent, a slowdown from the 16per cent in 2004.

The hotels and restaurants sector registeredgrowth of 6.2 per cent in the fourth quarter, upfrom 4.7 per cent previously. Both hotels andrestaurants turned in comparable growth in thequarter, boosted by continued growth in visitorarrivals. They helped to maintain high levels ofoccupancy at hotels and allowed hoteliers to raiseaverage room rates in the quarter. For the yearas a whole, the sector grew by 4.6 per cent, incontrast to the sharp 11 per cent rebound fromSARS in 2004.

GROSS DOMESTIC PRODUCT AT 2000 MARKET PRICES [TABLE 2.1]

2004 2005 2005

4th Qtr Annual 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Annual

Percentage Change Over Same Period Of Previous Year

TOTAL 6.9 8.7 3.4 5.7 7.6 8.7 6.4Goods Producing Industries 10.8 10.5 2.7 4.9 10.7 12.0 7.7

Manufacturing 14.3 13.9 3.2 5.9 13.1 14.2 9.3Construction –7.6 –6.1 –1.1 –1.1 –1.4 –0.8 –1.1

Services Producing Industries 5.0 7.6 4.2 5.8 6.8 7.2 6.0Wholesale & Retail Trade 12.7 15.6 8.7 10.2 10.7 12.1 10.5Hotels & Restaurants 2.5 11.5 1.9 5.4 4.7 6.2 4.6Transport & Communications 5.7 8.5 4.5 4.1 4.3 5.1 4.5Financial Services –0.1 5.4 2.2 7.9 8.5 7.4 6.5Business Services 2.4 2.8 2.7 3.9 6.6 6.3 4.9

Annualised Percentage Change Over Preceding Quarter

TOTAL 9.0 8.7 –2.1 14.6 9.6 12.5 6.4Goods Producing Industries 21.3 10.5 –13.2 19.5 20.0 24.6 7.7

Manufacturing 25.6 13.9 –19.0 28.2 25.6 28.1 9.3Construction 3.5 –6.1 27.9 –20.5 –9.9 5.6 –1.1

Services Producing Industries 5.7 7.6 1.8 13.4 6.6 7.1 6.0Wholesale & Retail Trade 8.3 15.6 6.1 17.5 11.3 13.0 10.5Hotels & Restaurants –0.7 11.5 3.6 17.8 –0.7 4.6 4.6Transport & Communications 3.1 8.5 2.4 7.4 4.3 5.9 4.5Financial Services 15.3 5.4 –7.8 27.6 2.1 10.7 6.5Business Services 3.5 2.8 5.3 9.1 8.5 2.5 4.9

Source: Singapore Department of Statistics

ECONOMIC SURVEY OF SINGAPORE 2005

19

OUTPUT, EXPENDITURE ANDNATIONAL INCOME

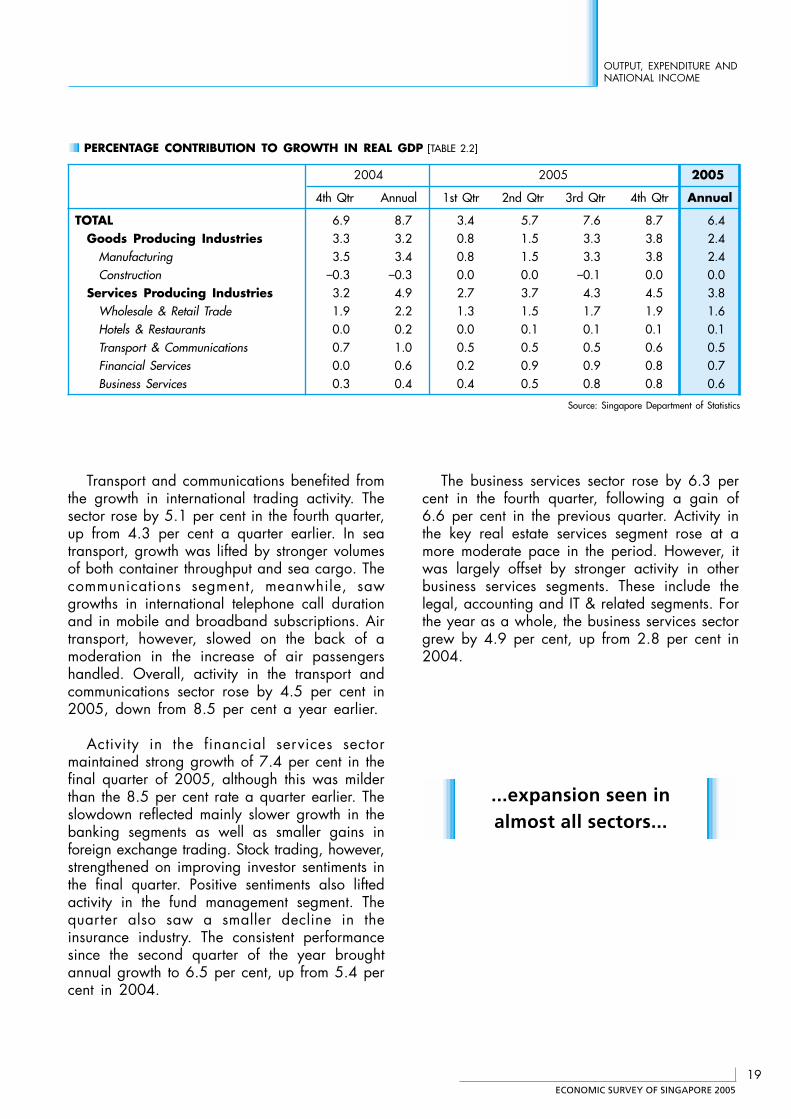

Transport and communications benefited fromthe growth in international trading activity. Thesector rose by 5.1 per cent in the fourth quarter,up from 4.3 per cent a quarter earlier. In seatransport, growth was lifted by stronger volumesof both container throughput and sea cargo. Thecommunications segment, meanwhile, sawgrowths in international telephone call durationand in mobile and broadband subscriptions. Airtransport, however, slowed on the back of amoderation in the increase of air passengershandled. Overall, activity in the transport andcommunications sector rose by 4.5 per cent in2005, down from 8.5 per cent a year earlier.

Activity in the financial services sectormaintained strong growth of 7.4 per cent in thefinal quarter of 2005, although this was milderthan the 8.5 per cent rate a quarter earlier. Theslowdown reflected mainly slower growth in thebanking segments as well as smaller gains inforeign exchange trading. Stock trading, however,strengthened on improving investor sentiments inthe final quarter. Positive sentiments also liftedactivity in the fund management segment. Thequarter also saw a smaller decline in theinsurance industry. The consistent performancesince the second quarter of the year broughtannual growth to 6.5 per cent, up from 5.4 percent in 2004.

The business services sector rose by 6.3 percent in the fourth quarter, following a gain of6.6 per cent in the previous quarter. Activity inthe key real estate services segment rose at amore moderate pace in the period. However, itwas largely offset by stronger activity in otherbusiness services segments. These include thelegal, accounting and IT & related segments. Forthe year as a whole, the business services sectorgrew by 4.9 per cent, up from 2.8 per cent in2004.

PERCENTAGE CONTRIBUTION TO GROWTH IN REAL GDP [TABLE 2.2]

2004 2005 2005

4th Qtr Annual 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr Annual

TOTAL 6.9 8.7 3.4 5.7 7.6 8.7 6.4Goods Producing Industries 3.3 3.2 0.8 1.5 3.3 3.8 2.4

Manufacturing 3.5 3.4 0.8 1.5 3.3 3.8 2.4Construction –0.3 –0.3 0.0 0.0 –0.1 0.0 0.0

Services Producing Industries 3.2 4.9 2.7 3.7 4.3 4.5 3.8Wholesale & Retail Trade 1.9 2.2 1.3 1.5 1.7 1.9 1.6Hotels & Restaurants 0.0 0.2 0.0 0.1 0.1 0.1 0.1Transport & Communications 0.7 1.0 0.5 0.5 0.5 0.6 0.5Financial Services 0.0 0.6 0.2 0.9 0.9 0.8 0.7Business Services 0.3 0.4 0.4 0.5 0.8 0.8 0.6

Source: Singapore Department of Statistics

...expansion seen inalmost all sectors...

ECONOMIC SURVEY OF SINGAPORE 2005

20

Chapter 2

OUTPUT, EXPENDITURE AND NATIONAL INCOME

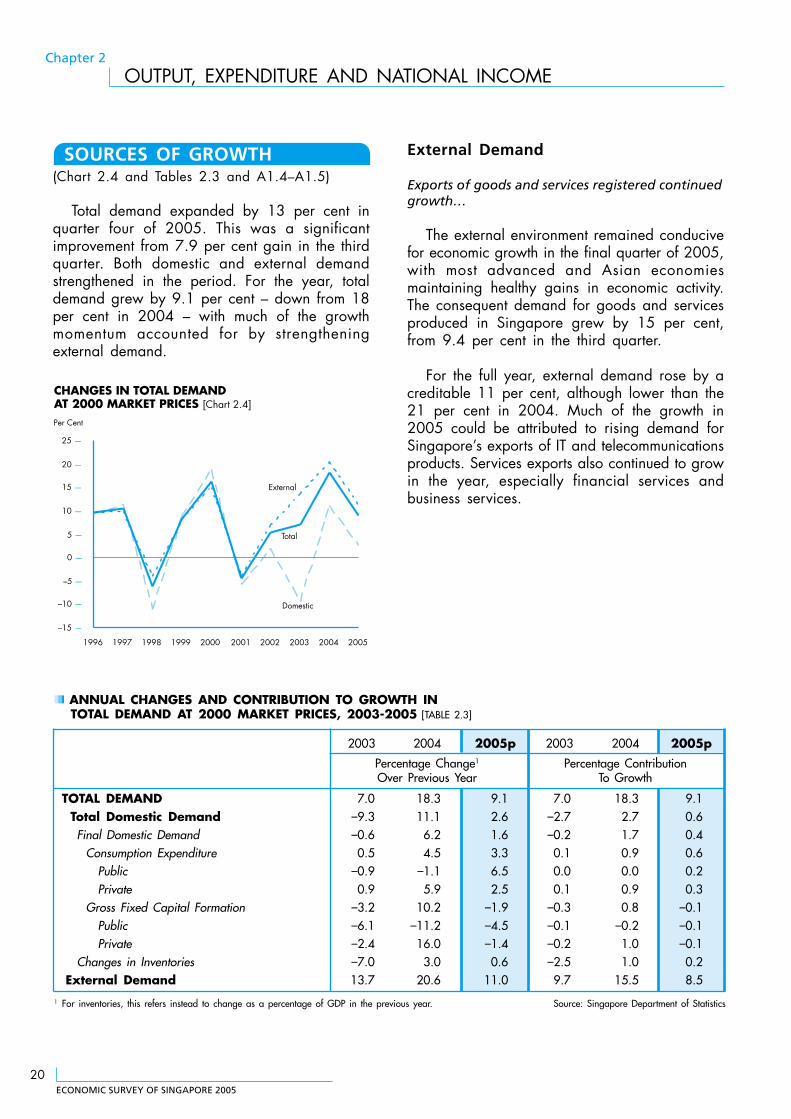

SOURCES OF GROWTH(Chart 2.4 and Tables 2.3 and A1.4–A1.5)

Total demand expanded by 13 per cent inquarter four of 2005. This was a significantimprovement from 7.9 per cent gain in the thirdquarter. Both domestic and external demandstrengthened in the period. For the year, totaldemand grew by 9.1 per cent – down from 18per cent in 2004 – with much of the growthmomentum accounted for by strengtheningexternal demand.

External Demand

Exports of goods and services registered continuedgrowth…

The external environment remained conducivefor economic growth in the final quarter of 2005,with most advanced and Asian economiesmaintaining healthy gains in economic activity.The consequent demand for goods and servicesproduced in Singapore grew by 15 per cent,from 9.4 per cent in the third quarter.

For the full year, external demand rose by acreditable 11 per cent, although lower than the21 per cent in 2004. Much of the growth in2005 could be attributed to rising demand forSingapore’s exports of IT and telecommunicationsproducts. Services exports also continued to growin the year, especially financial services andbusiness services.

CHANGES IN TOTAL DEMANDAT 2000 MARKET PRICES [Chart 2.4]

–15 —

–10 —

–5 —

0 —

5 —

10 —

15 —

20 —

25 —

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

External

Per Cent

Domestic

Total

ANNUAL CHANGES AND CONTRIBUTION TO GROWTH INTOTAL DEMAND AT 2000 MARKET PRICES, 2003-2005 [TABLE 2.3]

2003 2004 2005p 2003 2004 2005p

Percentage Change1 Percentage ContributionOver Previous Year To Growth

TOTAL DEMAND 7.0 18.3 9.1 7.0 18.3 9.1Total Domestic Demand –9.3 11.1 2.6 –2.7 2.7 0.6Final Domestic Demand –0.6 6.2 1.6 –0.2 1.7 0.4

Consumption Expenditure 0.5 4.5 3.3 0.1 0.9 0.6Public –0.9 –1.1 6.5 0.0 0.0 0.2Private 0.9 5.9 2.5 0.1 0.9 0.3

Gross Fixed Capital Formation –3.2 10.2 –1.9 –0.3 0.8 –0.1Public –6.1 –11.2 –4.5 –0.1 –0.2 –0.1Private –2.4 16.0 –1.4 –0.2 1.0 –0.1

Changes in Inventories –7.0 3.0 0.6 –2.5 1.0 0.2External Demand 13.7 20.6 11.0 9.7 15.5 8.5

1 For inventories, this refers instead to change as a percentage of GDP in the previous year. Source: Singapore Department of Statistics

ECONOMIC SURVEY OF SINGAPORE 2005

21

OUTPUT, EXPENDITURE ANDNATIONAL INCOME

Domestic Demand

Domestic demand growth slowed in 2005…

Total domestic demand grew by 3.9 per centin the fourth quarter, up from 2.5 per cent in thethird quarter. Full year growth was 2.6 per cent,down sharply from 11 per cent in 2004.

Consumption Expenditure(Table A1.6)

Consumption expenditure growth eased…

Total consumption expenditure grew at a fasterrate of 5.1 per cent in the fourth quarter, upfrom a gain of 1.8 per cent a quarter earlier.2005 growth reached 3.3 per cent, comparedwith 4.5 per cent in 2004. The moderation couldbe attributable to lower expenditure on vehiclepurchase, audio-visual & photographic equipmentas well as residents’ expenditure abroad.

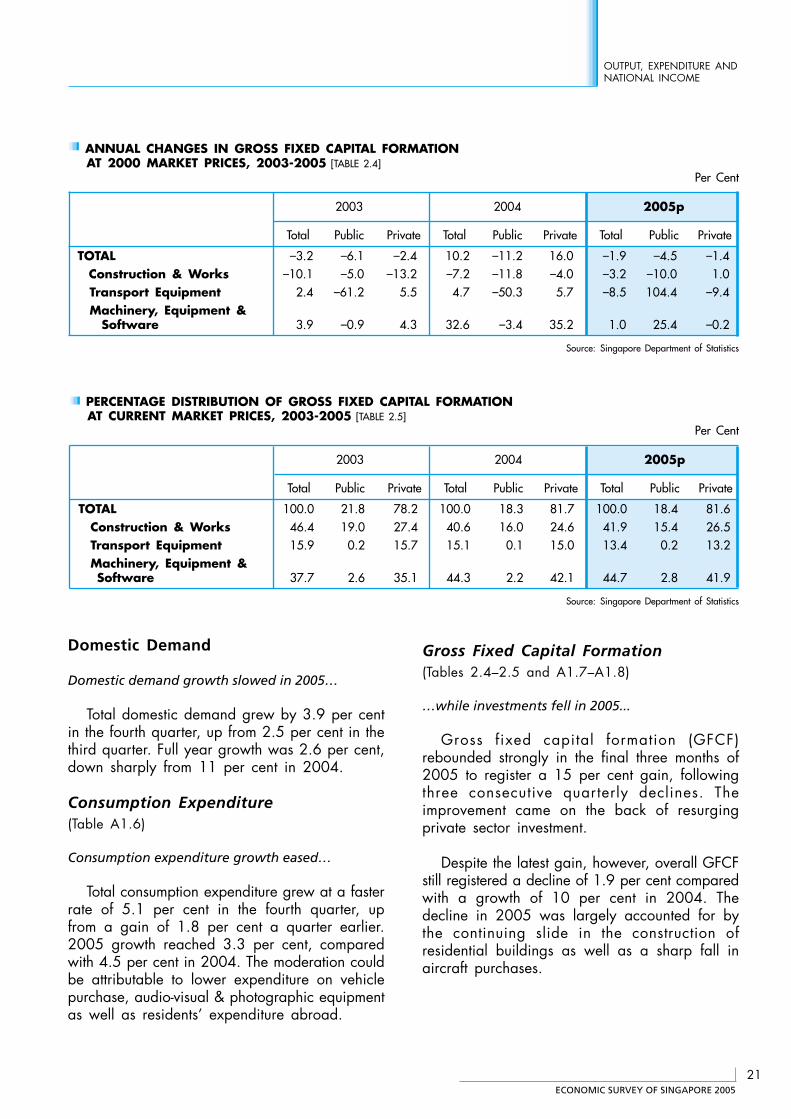

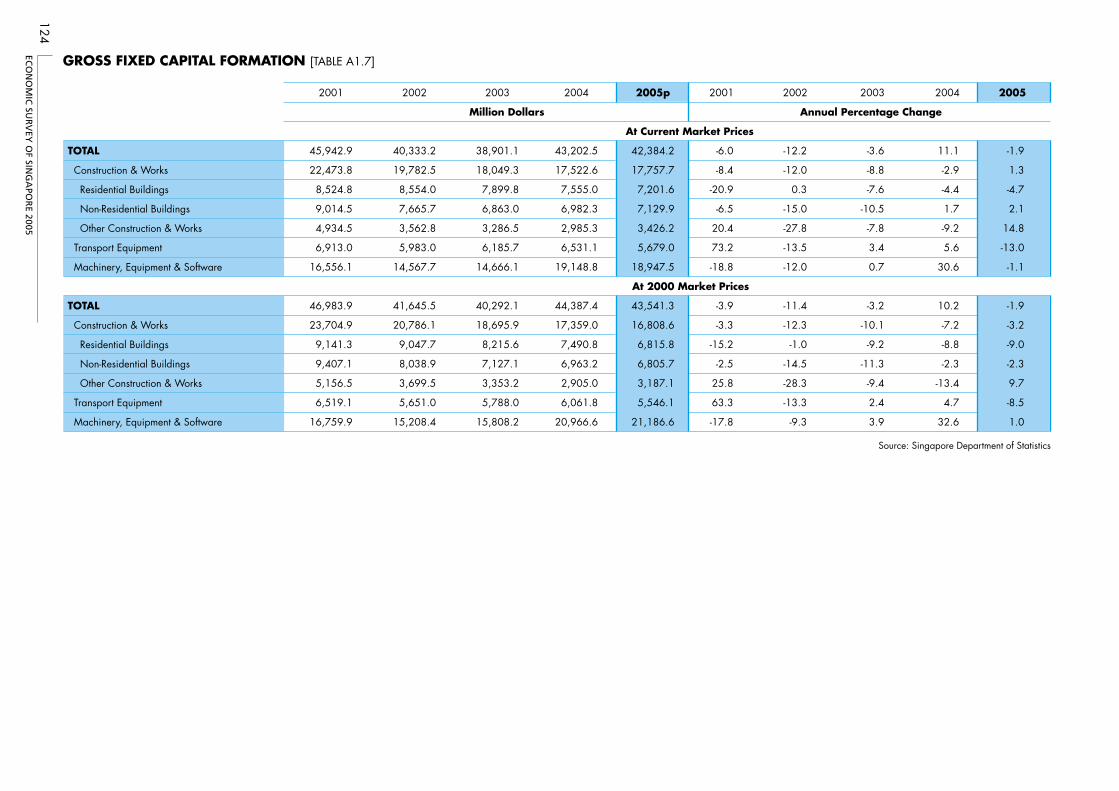

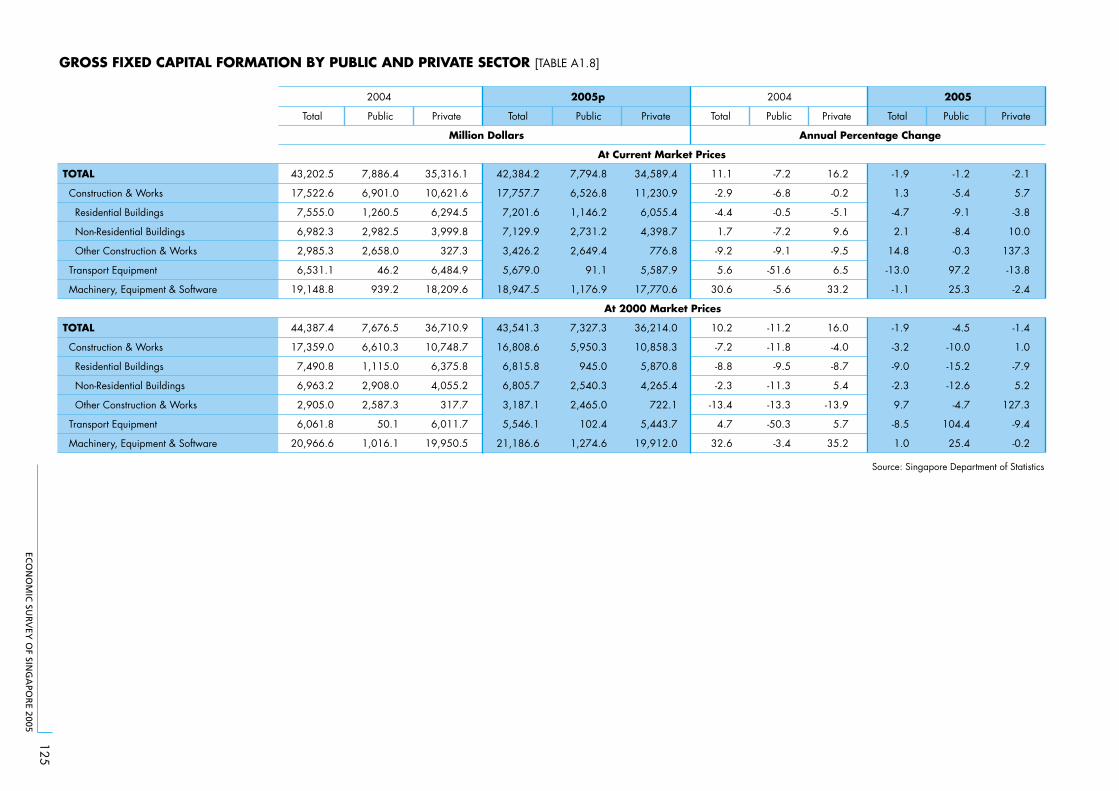

ANNUAL CHANGES IN GROSS FIXED CAPITAL FORMATIONAT 2000 MARKET PRICES, 2003-2005 [TABLE 2.4]

Per Cent

2003 2004 2005p

Total Public Private Total Public Private Total Public Private

TOTAL –3.2 –6.1 –2.4 10.2 –11.2 16.0 –1.9 –4.5 –1.4Construction & Works –10.1 –5.0 –13.2 –7.2 –11.8 –4.0 –3.2 –10.0 1.0Transport Equipment 2.4 –61.2 5.5 4.7 –50.3 5.7 –8.5 104.4 –9.4Machinery, Equipment &

Software 3.9 –0.9 4.3 32.6 –3.4 35.2 1.0 25.4 –0.2

Source: Singapore Department of Statistics

PERCENTAGE DISTRIBUTION OF GROSS FIXED CAPITAL FORMATIONAT CURRENT MARKET PRICES, 2003-2005 [TABLE 2.5]

Per Cent

2003 2004 2005p

Total Public Private Total Public Private Total Public Private

TOTAL 100.0 21.8 78.2 100.0 18.3 81.7 100.0 18.4 81.6Construction & Works 46.4 19.0 27.4 40.6 16.0 24.6 41.9 15.4 26.5Transport Equipment 15.9 0.2 15.7 15.1 0.1 15.0 13.4 0.2 13.2Machinery, Equipment &

Software 37.7 2.6 35.1 44.3 2.2 42.1 44.7 2.8 41.9

Source: Singapore Department of Statistics

Gross Fixed Capital Formation(Tables 2.4–2.5 and A1.7–A1.8)

…while investments fell in 2005...

Gross fixed capital formation (GFCF)rebounded strongly in the final three months of2005 to register a 15 per cent gain, followingthree consecutive quarterly declines. Theimprovement came on the back of resurgingprivate sector investment.

Despite the latest gain, however, overall GFCFstill registered a decline of 1.9 per cent comparedwith a growth of 10 per cent in 2004. Thedecline in 2005 was largely accounted for bythe continuing slide in the construction ofresidential buildings as well as a sharp fall inaircraft purchases.

ECONOMIC SURVEY OF SINGAPORE 2005

22

Chapter 2

OUTPUT, EXPENDITURE AND NATIONAL INCOME

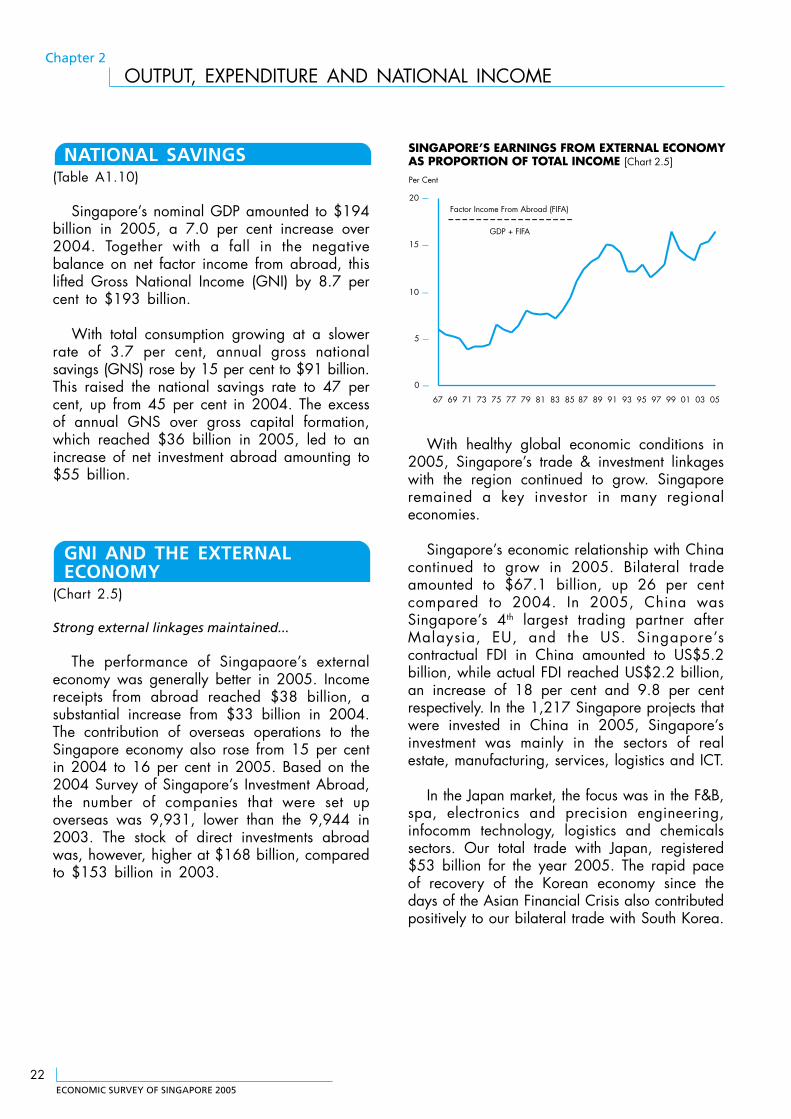

NATIONAL SAVINGS(Table A1.10)

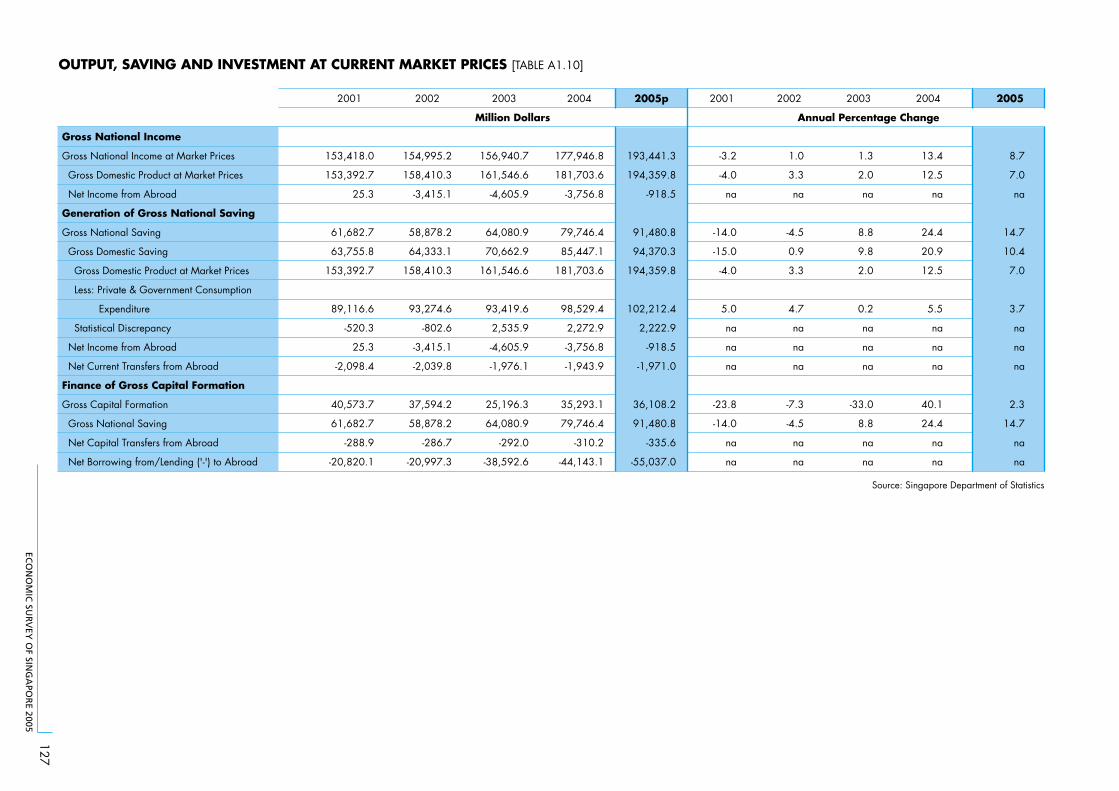

Singapore’s nominal GDP amounted to $194billion in 2005, a 7.0 per cent increase over2004. Together with a fall in the negativebalance on net factor income from abroad, thislifted Gross National Income (GNI) by 8.7 percent to $193 billion.

With total consumption growing at a slowerrate of 3.7 per cent, annual gross nationalsavings (GNS) rose by 15 per cent to $91 billion.This raised the national savings rate to 47 percent, up from 45 per cent in 2004. The excessof annual GNS over gross capital formation,which reached $36 billion in 2005, led to anincrease of net investment abroad amounting to$55 billion.

SINGAPORE’S EARNINGS FROM EXTERNAL ECONOMYAS PROPORTION OF TOTAL INCOME [Chart 2.5]

0 —

5 —

10 —

15 —

20 —

67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05

Per Cent

Factor Income From Abroad (FIFA)

GDP + FIFA

With healthy global economic conditions in2005, Singapore’s trade & investment linkageswith the region continued to grow. Singaporeremained a key investor in many regionaleconomies.

Singapore’s economic relationship with Chinacontinued to grow in 2005. Bilateral tradeamounted to $67.1 billion, up 26 per centcompared to 2004. In 2005, China wasSingapore’s 4th largest trading partner afterMalaysia, EU, and the US. Singapore’scontractual FDI in China amounted to US$5.2billion, while actual FDI reached US$2.2 billion,an increase of 18 per cent and 9.8 per centrespectively. In the 1,217 Singapore projects thatwere invested in China in 2005, Singapore’sinvestment was mainly in the sectors of realestate, manufacturing, services, logistics and ICT.

In the Japan market, the focus was in the F&B,spa, electronics and precision engineering,infocomm technology, logistics and chemicalssectors. Our total trade with Japan, registered$53 billion for the year 2005. The rapid paceof recovery of the Korean economy since thedays of the Asian Financial Crisis also contributedpositively to our bilateral trade with South Korea.

GNI AND THE EXTERNALECONOMY

(Chart 2.5)

Strong external linkages maintained...

The performance of Singapaore’s externaleconomy was generally better in 2005. Incomereceipts from abroad reached $38 billion, asubstantial increase from $33 billion in 2004.The contribution of overseas operations to theSingapore economy also rose from 15 per centin 2004 to 16 per cent in 2005. Based on the2004 Survey of Singapore’s Investment Abroad,the number of companies that were set upoverseas was 9,931, lower than the 9,944 in2003. The stock of direct investments abroadwas, however, higher at $168 billion, comparedto $153 billion in 2003.

ECONOMIC SURVEY OF SINGAPORE 2005

23

OUTPUT, EXPENDITURE ANDNATIONAL INCOME

In the Middle East, there was a markedincrease in the number of Singapore companieskeen to explore business opportunities in thebooming infrastructure sector. Seven infrastructure-related business missions to the Middle East wereorganised in 2005, with particular focus on realestate & construction services, oil & gassupporting infrastructure services, andtransportation & logistics services.

There was increased interest in Russia in2005. Opportunities for Singapore companieswere in the F&B, hospitality and automotivesectors.

In Western Europe, the focus was on tappingthe wave of European outsourcing opportunities.In particular, efforts were made to address theprocurement needs of small and mediumenterprises through an SME survey and marketingplan in Germany. Business linkages with the USand Latin America were also deepened over theyear.

Contributed by:

Tan Kim EngSenior EconomistEconomics and Strategy DivisionMinistry of Trade and Industry

Ms Grace ChuaSenior OfficerResearch and Statistics DivisionInternational Enterprise Singapore

ECONOMIC SURVEY OF SINGAPORE 2005

24

Chapter 3

EMPLOYMENT, WAGES AND PRODUCTIVITY

EMPLOYMENT,WAGES ANDPRODUCTIVITY

OVERVIEW

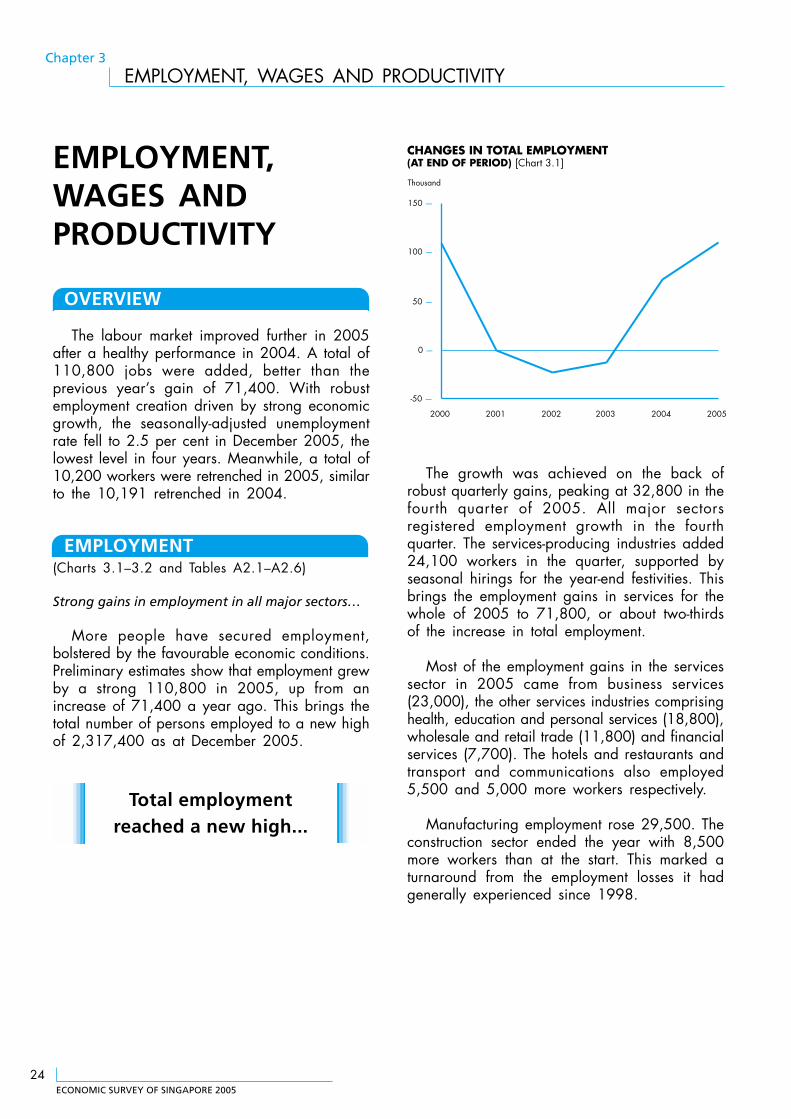

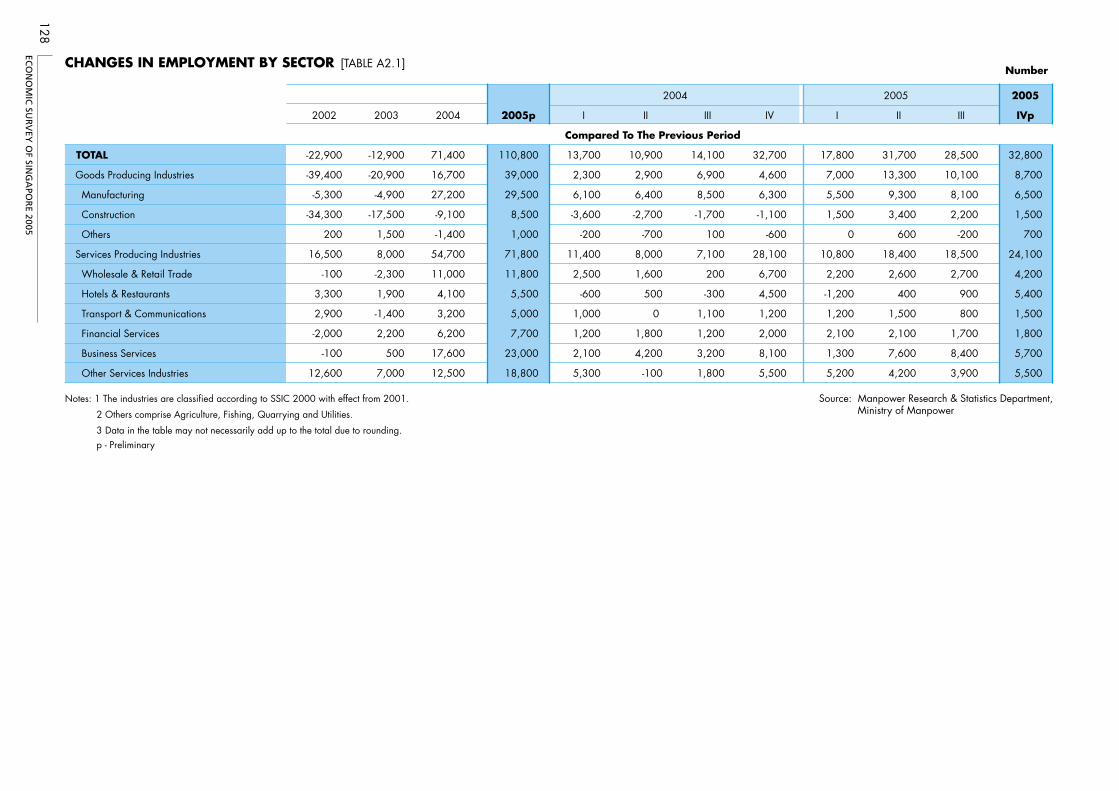

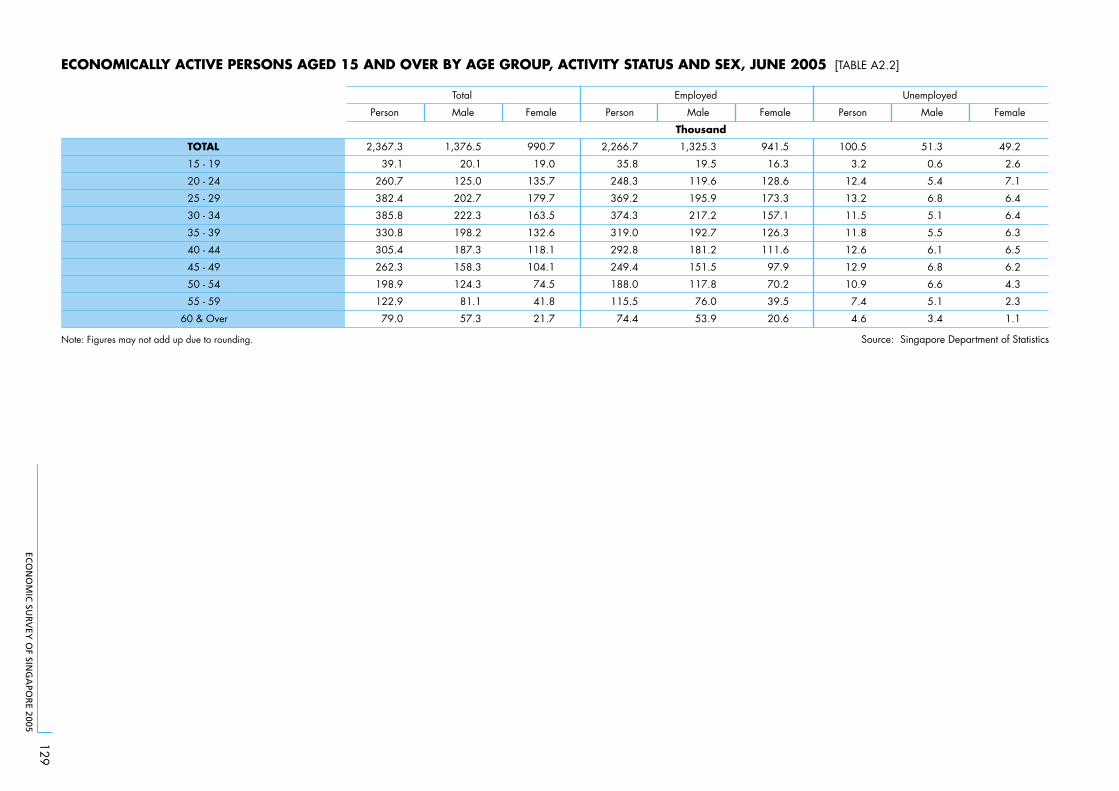

The labour market improved further in 2005after a healthy performance in 2004. A total of110,800 jobs were added, better than theprevious year’s gain of 71,400. With robustemployment creation driven by strong economicgrowth, the seasonally-adjusted unemploymentrate fell to 2.5 per cent in December 2005, thelowest level in four years. Meanwhile, a total of10,200 workers were retrenched in 2005, similarto the 10,191 retrenched in 2004.

EMPLOYMENT(Charts 3.1–3.2 and Tables A2.1–A2.6)

Strong gains in employment in all major sectors…

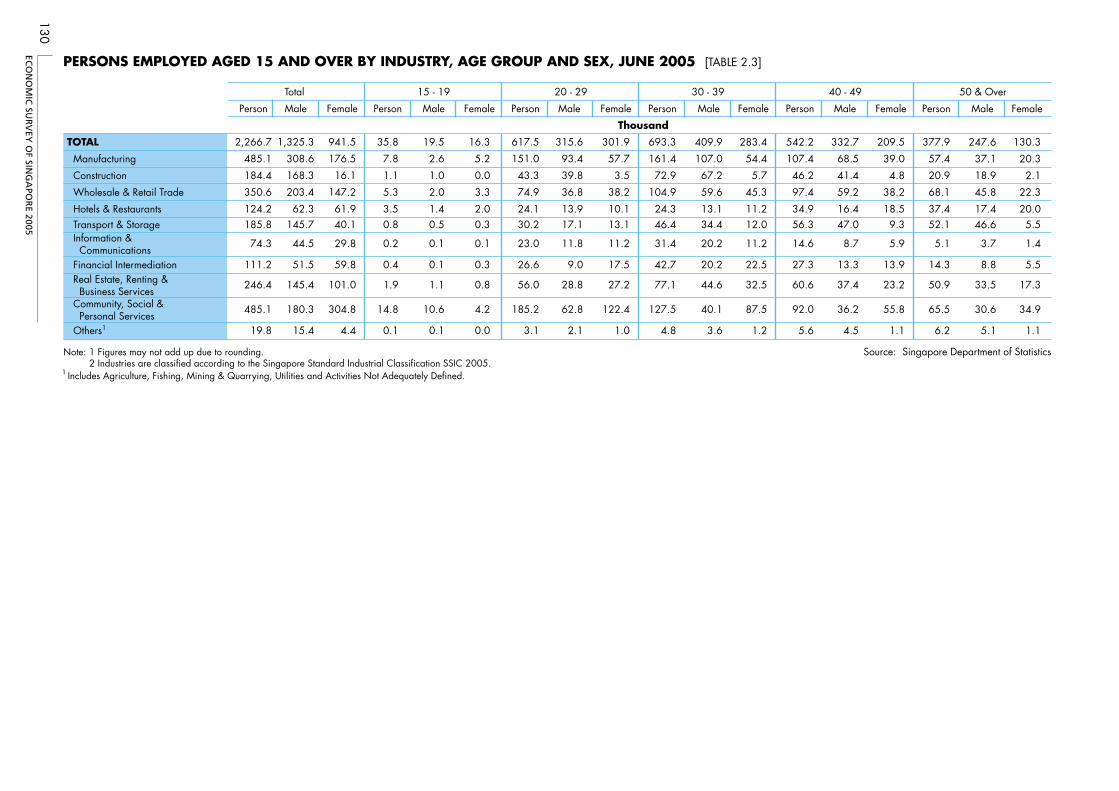

More people have secured employment,bolstered by the favourable economic conditions.Preliminary estimates show that employment grewby a strong 110,800 in 2005, up from anincrease of 71,400 a year ago. This brings thetotal number of persons employed to a new highof 2,317,400 as at December 2005.

-50 —

0 —

50 —

100 —

150 —

2000 2001 2002 2003 2004 2005

Thousand

CHANGES IN TOTAL EMPLOYMENT (AT END OF PERIOD) [Chart 3.1]

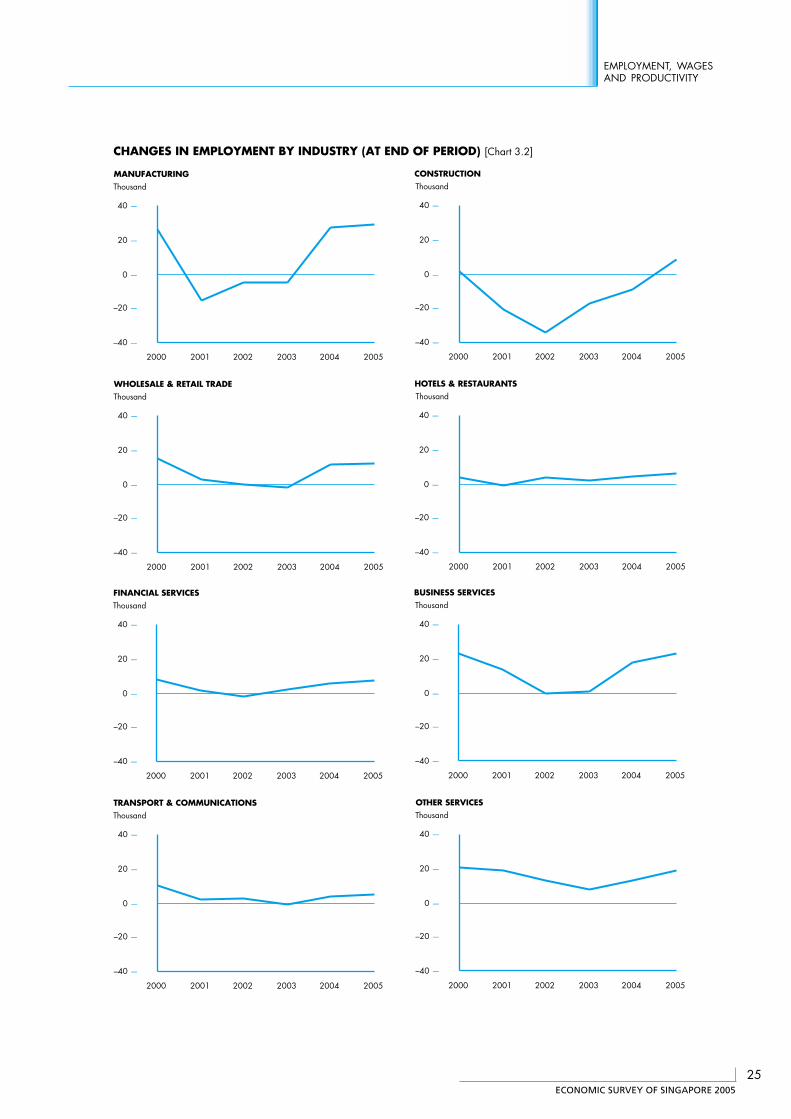

The growth was achieved on the back ofrobust quarterly gains, peaking at 32,800 in thefourth quarter of 2005. All major sectorsregistered employment growth in the fourthquarter. The services-producing industries added24,100 workers in the quarter, supported byseasonal hirings for the year-end festivities. Thisbrings the employment gains in services for thewhole of 2005 to 71,800, or about two-thirdsof the increase in total employment.

Most of the employment gains in the servicessector in 2005 came from business services(23,000), the other services industries comprisinghealth, education and personal services (18,800),wholesale and retail trade (11,800) and financialservices (7,700). The hotels and restaurants andtransport and communications also employed5,500 and 5,000 more workers respectively.

Manufacturing employment rose 29,500. Theconstruction sector ended the year with 8,500more workers than at the start. This marked aturnaround from the employment losses it hadgenerally experienced since 1998.

Total employmentreached a new high...

ECONOMIC SURVEY OF SINGAPORE 2005

25

EMPLOYMENT, WAGESAND PRODUCTIVITY

CHANGES IN EMPLOYMENT BY INDUSTRY (AT END OF PERIOD) [Chart 3.2]

–40 —

–20 —

0 —

20 —

40 —

2000 2001 2002 2003 2004 2005

ThousandMANUFACTURING

–40 —

–20 —

0 —

20 —

40 —

2000 2001 2002 2003 2004 2005

ThousandWHOLESALE & RETAIL TRADE

–40 —

–20 —

0 —

20 —

40 —

2000 2001 2002 2003 2004 2005

ThousandFINANCIAL SERVICES

–40 —

–20 —

0 —

20 —

40 —

2000 2001 2002 2003 2004 2005

ThousandTRANSPORT & COMMUNICATIONS

–40 —

–20 —

0 —

20 —

40 —

2000 2001 2002 2003 2004 2005

ThousandCONSTRUCTION

–40 —

–20 —

0 —

20 —

40 —

2000 2001 2002 2003 2004 2005

ThousandHOTELS & RESTAURANTS

–40 —

–20 —

0 —

20 —

40 —

2000 2001 2002 2003 2004 2005

ThousandBUSINESS SERVICES

–40 —

–20 —

0 —

20 —

40 —

2000 2001 2002 2003 2004 2005

ThousandOTHER SERVICES

ECONOMIC SURVEY OF SINGAPORE 2005

26

Chapter 3

EMPLOYMENT, WAGES AND PRODUCTIVITY

UNEMPLOYMENT(Chart 3.3)

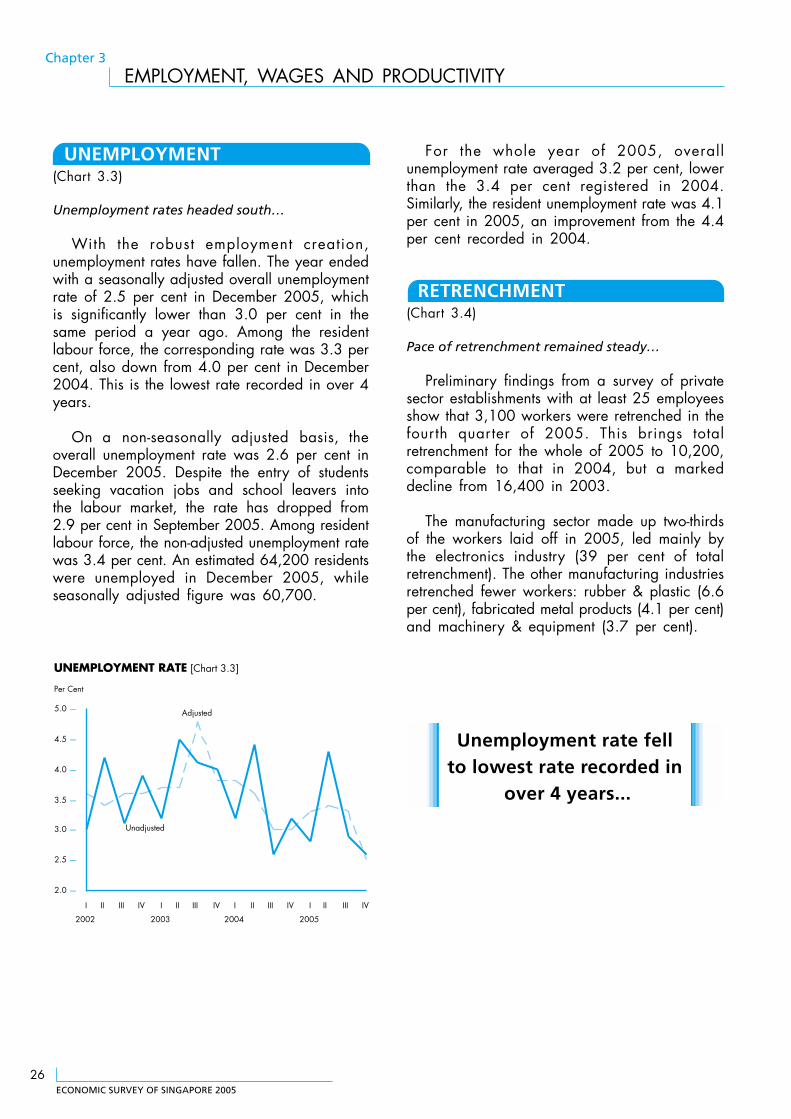

Unemployment rates headed south…

With the robust employment creation,unemployment rates have fallen. The year endedwith a seasonally adjusted overall unemploymentrate of 2.5 per cent in December 2005, whichis significantly lower than 3.0 per cent in thesame period a year ago. Among the residentlabour force, the corresponding rate was 3.3 percent, also down from 4.0 per cent in December2004. This is the lowest rate recorded in over 4years.

On a non-seasonally adjusted basis, theoverall unemployment rate was 2.6 per cent inDecember 2005. Despite the entry of studentsseeking vacation jobs and school leavers intothe labour market, the rate has dropped from2.9 per cent in September 2005. Among residentlabour force, the non-adjusted unemployment ratewas 3.4 per cent. An estimated 64,200 residentswere unemployed in December 2005, whileseasonally adjusted figure was 60,700.

For the whole year of 2005, overallunemployment rate averaged 3.2 per cent, lowerthan the 3.4 per cent registered in 2004.Similarly, the resident unemployment rate was 4.1per cent in 2005, an improvement from the 4.4per cent recorded in 2004.

RETRENCHMENT(Chart 3.4)

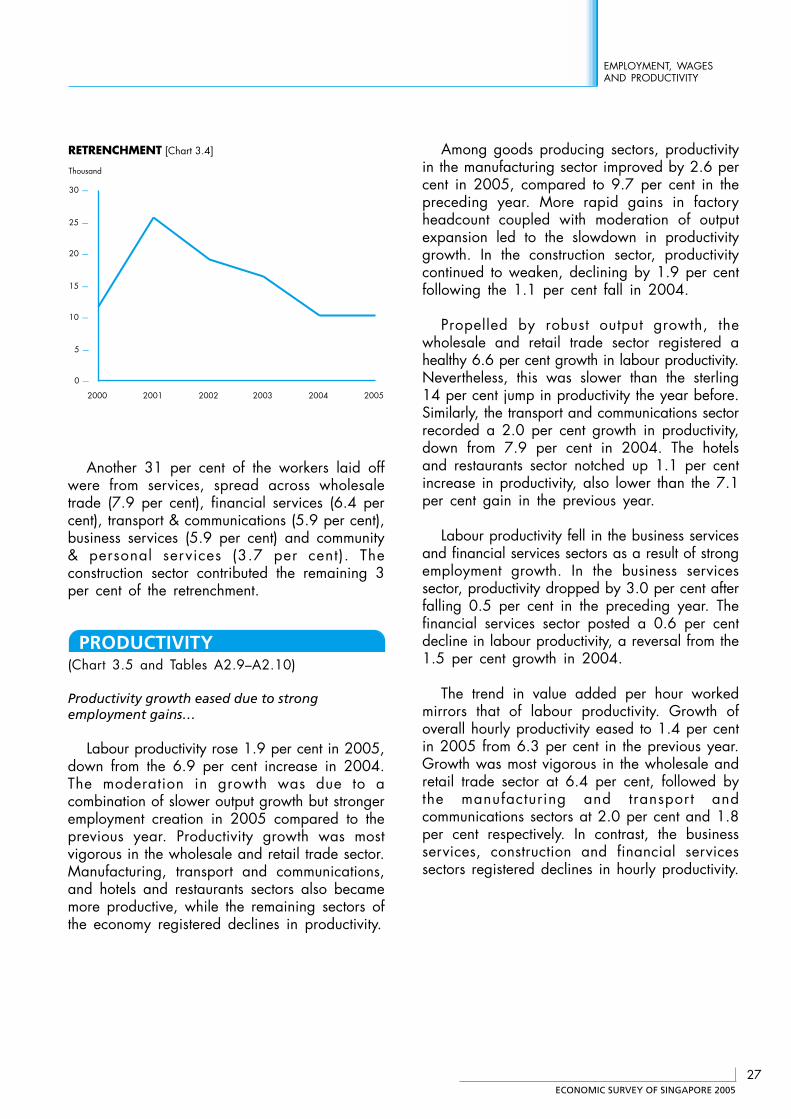

Pace of retrenchment remained steady…

Preliminary findings from a survey of privatesector establishments with at least 25 employeesshow that 3,100 workers were retrenched in thefourth quarter of 2005. This brings totalretrenchment for the whole of 2005 to 10,200,comparable to that in 2004, but a markeddecline from 16,400 in 2003.

The manufacturing sector made up two-thirdsof the workers laid off in 2005, led mainly bythe electronics industry (39 per cent of totalretrenchment). The other manufacturing industriesretrenched fewer workers: rubber & plastic (6.6per cent), fabricated metal products (4.1 per cent)and machinery & equipment (3.7 per cent).

2.0 —

2.5 —

3.0 —

3.5 —

4.0 —

4.5 —

5.0 —

I

2002

II III IV I

2003

II III IV I

2004

II III IV I

2005

II III IV

Unadjusted

Adjusted

Per Cent

UNEMPLOYMENT RATE [Chart 3.3]

Unemployment rate fellto lowest rate recorded in

over 4 years...

ECONOMIC SURVEY OF SINGAPORE 2005

27

EMPLOYMENT, WAGESAND PRODUCTIVITY

Another 31 per cent of the workers laid offwere from services, spread across wholesaletrade (7.9 per cent), financial services (6.4 percent), transport & communications (5.9 per cent),business services (5.9 per cent) and community& personal services (3.7 per cent). Theconstruction sector contributed the remaining 3per cent of the retrenchment.

PRODUCTIVITY(Chart 3.5 and Tables A2.9–A2.10)

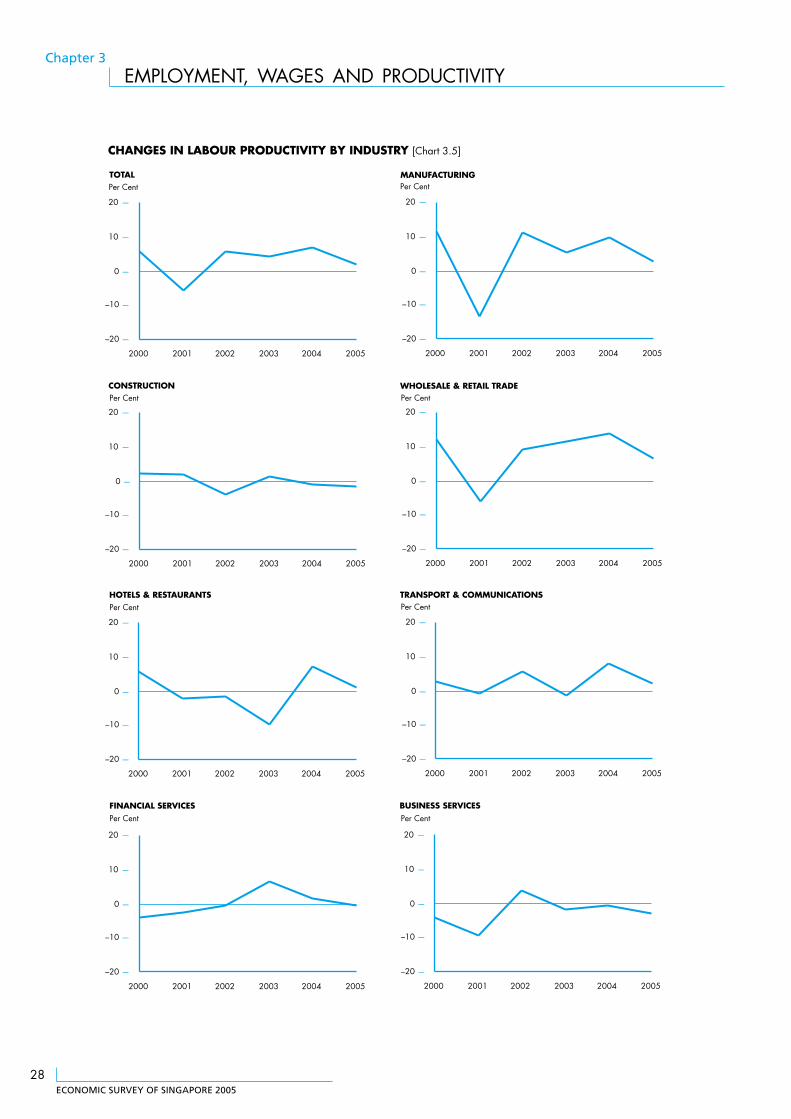

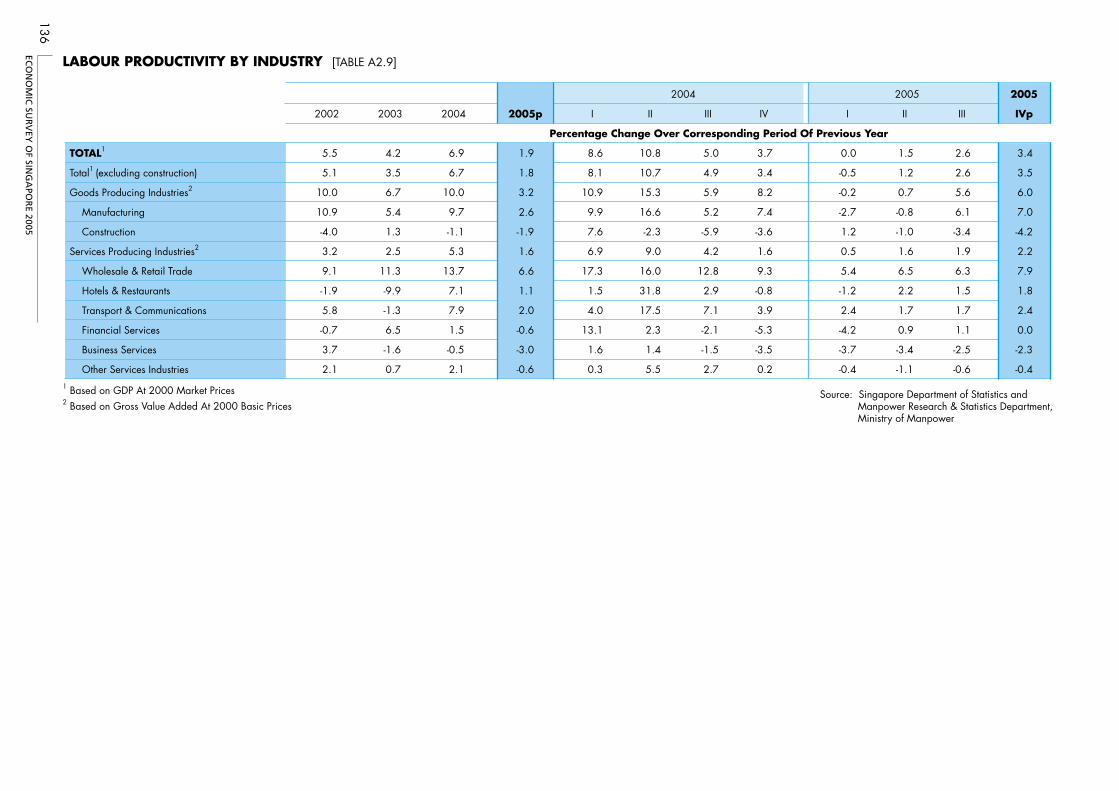

Productivity growth eased due to strongemployment gains…

Labour productivity rose 1.9 per cent in 2005,down from the 6.9 per cent increase in 2004.The moderation in growth was due to acombination of slower output growth but strongeremployment creation in 2005 compared to theprevious year. Productivity growth was mostvigorous in the wholesale and retail trade sector.Manufacturing, transport and communications,and hotels and restaurants sectors also becamemore productive, while the remaining sectors ofthe economy registered declines in productivity.

Among goods producing sectors, productivityin the manufacturing sector improved by 2.6 percent in 2005, compared to 9.7 per cent in thepreceding year. More rapid gains in factoryheadcount coupled with moderation of outputexpansion led to the slowdown in productivitygrowth. In the construction sector, productivitycontinued to weaken, declining by 1.9 per centfollowing the 1.1 per cent fall in 2004.

Propelled by robust output growth, thewholesale and retail trade sector registered ahealthy 6.6 per cent growth in labour productivity.Nevertheless, this was slower than the sterling14 per cent jump in productivity the year before.Similarly, the transport and communications sectorrecorded a 2.0 per cent growth in productivity,down from 7.9 per cent in 2004. The hotelsand restaurants sector notched up 1.1 per centincrease in productivity, also lower than the 7.1per cent gain in the previous year.

Labour productivity fell in the business servicesand financial services sectors as a result of strongemployment growth. In the business servicessector, productivity dropped by 3.0 per cent afterfalling 0.5 per cent in the preceding year. Thefinancial services sector posted a 0.6 per centdecline in labour productivity, a reversal from the1.5 per cent growth in 2004.

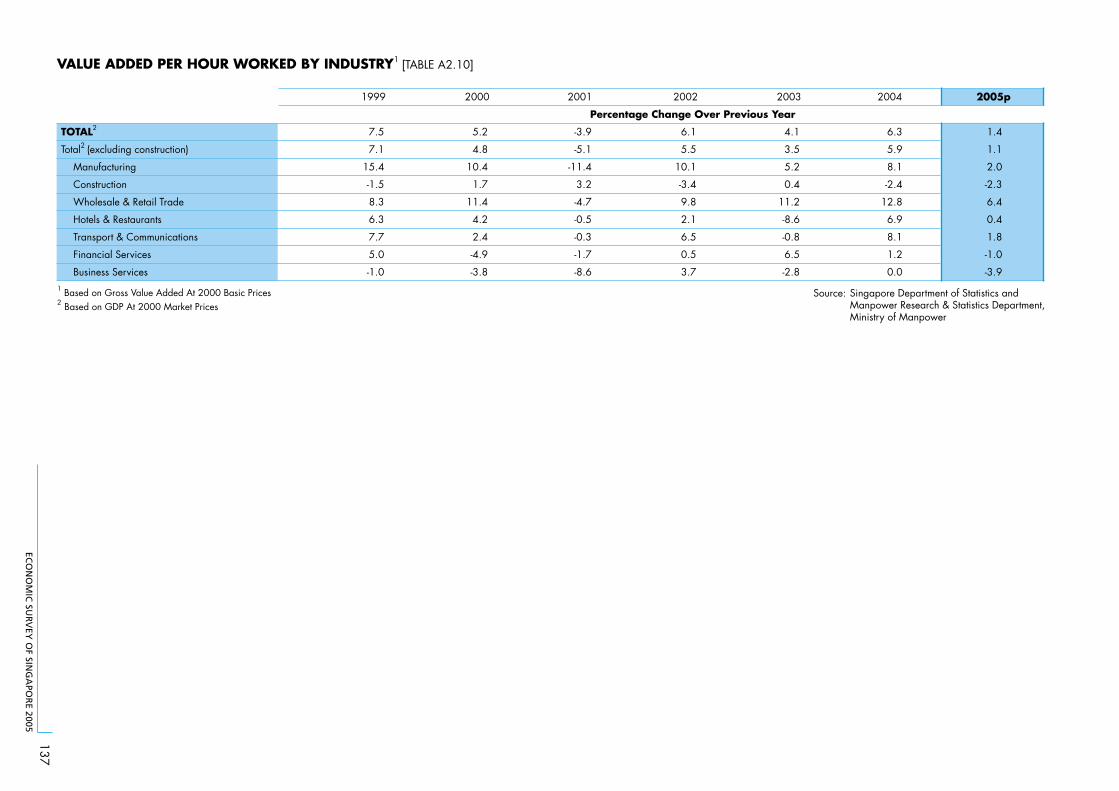

The trend in value added per hour workedmirrors that of labour productivity. Growth ofoverall hourly productivity eased to 1.4 per centin 2005 from 6.3 per cent in the previous year.Growth was most vigorous in the wholesale andretail trade sector at 6.4 per cent, followed bythe manufacturing and transport andcommunications sectors at 2.0 per cent and 1.8per cent respectively. In contrast, the businessservices, construction and financial servicessectors registered declines in hourly productivity.

0 —

5 —

10 —

15 —

20 —

25 —

30 —

2000 2001 2002 2003 2004 2005

Thousand

RETRENCHMENT [Chart 3.4]

ECONOMIC SURVEY OF SINGAPORE 2005

28

Chapter 3

EMPLOYMENT, WAGES AND PRODUCTIVITY

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

–20 —

–10 —

0 —

10 —

20 —

2000 2001 2002 2003 2004 2005

Per CentTOTAL

CHANGES IN LABOUR PRODUCTIVITY BY INDUSTRY [Chart 3.5]

Per CentMANUFACTURING

Per CentCONSTRUCTION

Per CentWHOLESALE & RETAIL TRADE

Per CentHOTELS & RESTAURANTS

Per CentTRANSPORT & COMMUNICATIONS

Per CentFINANCIAL SERVICES

Per CentBUSINESS SERVICES

ECONOMIC SURVEY OF SINGAPORE 2005

29

EMPLOYMENT, WAGESAND PRODUCTIVITY

COSTS(Charts 3.6–3.9 and Tables A2.7–A2.8)

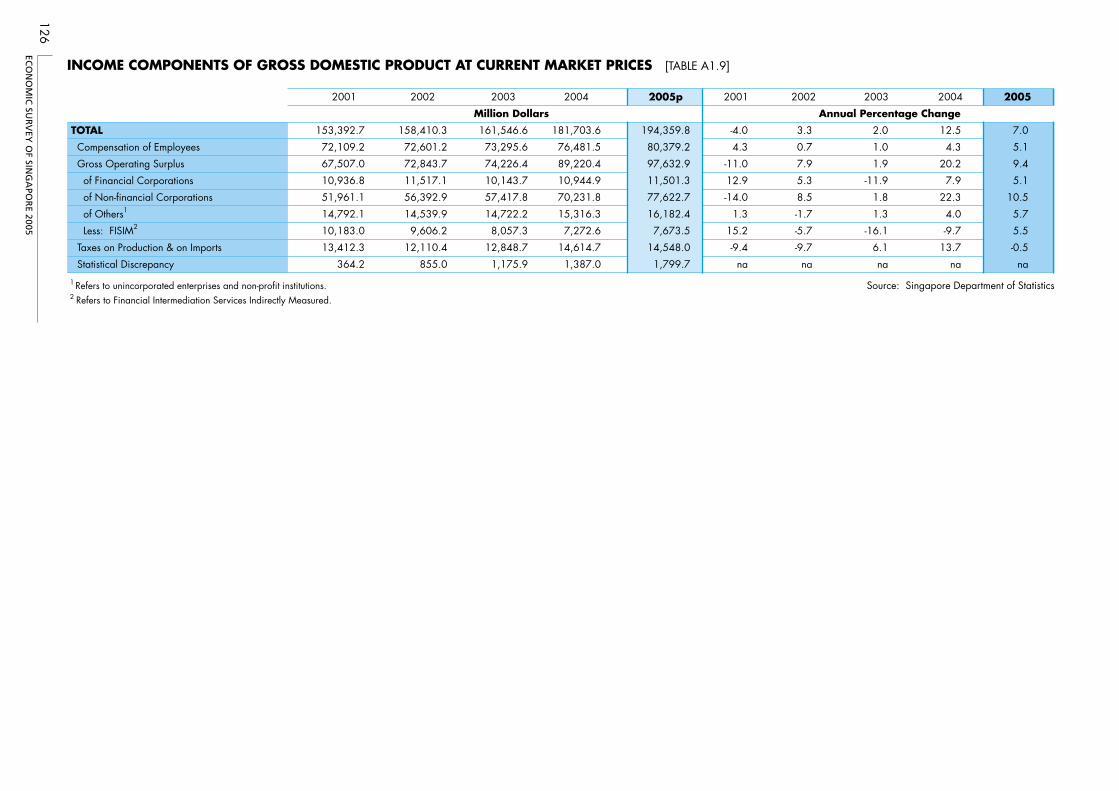

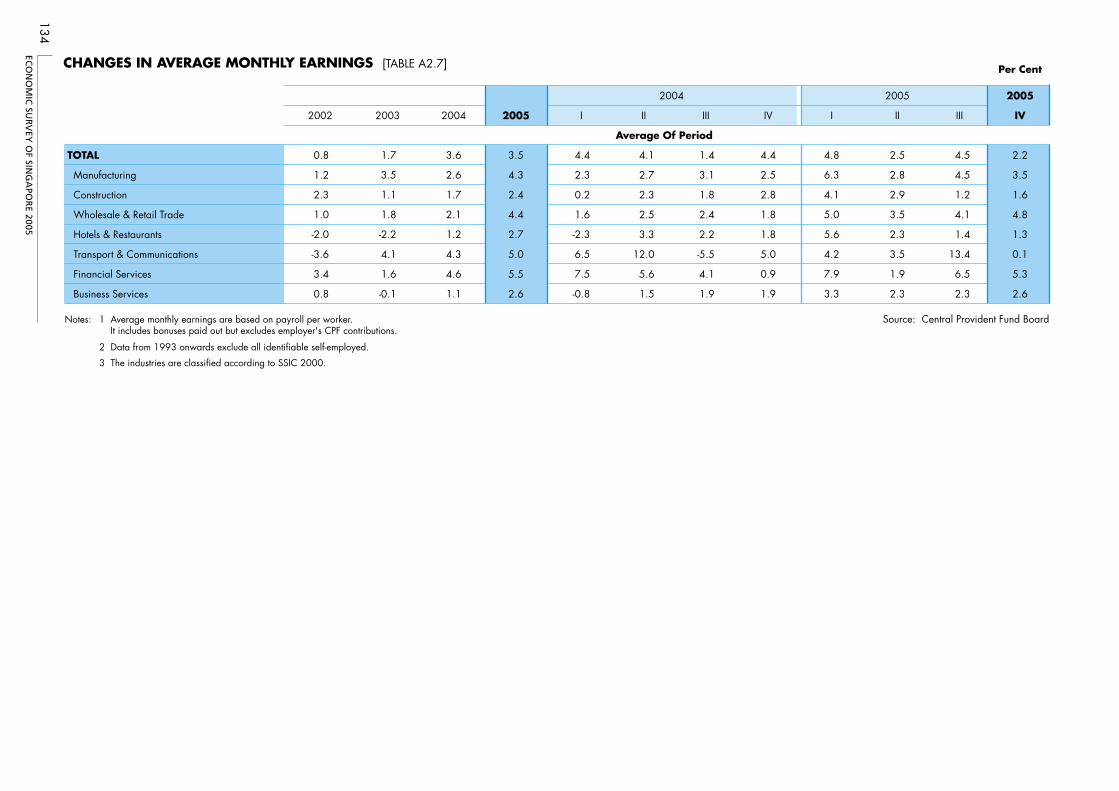

Real wages rose at a faster pace in 2005…

Strong employment growth and fallingunemployment rate have translated into higherwages in 2005. Average monthly earnings rose3.5 per cent, similar to the pace registered in2004. However, the share of wages in nominalGDP slipped to 41 per cent from 42 per centthe year before. In real terms, earnings growthimproved to 2.9 per cent compared to near flatgrowth in the previous year. This was largely onaccount of a decline in GDP deflator growth to0.6 per cent, after hitting 3.5 per cent a yearago.

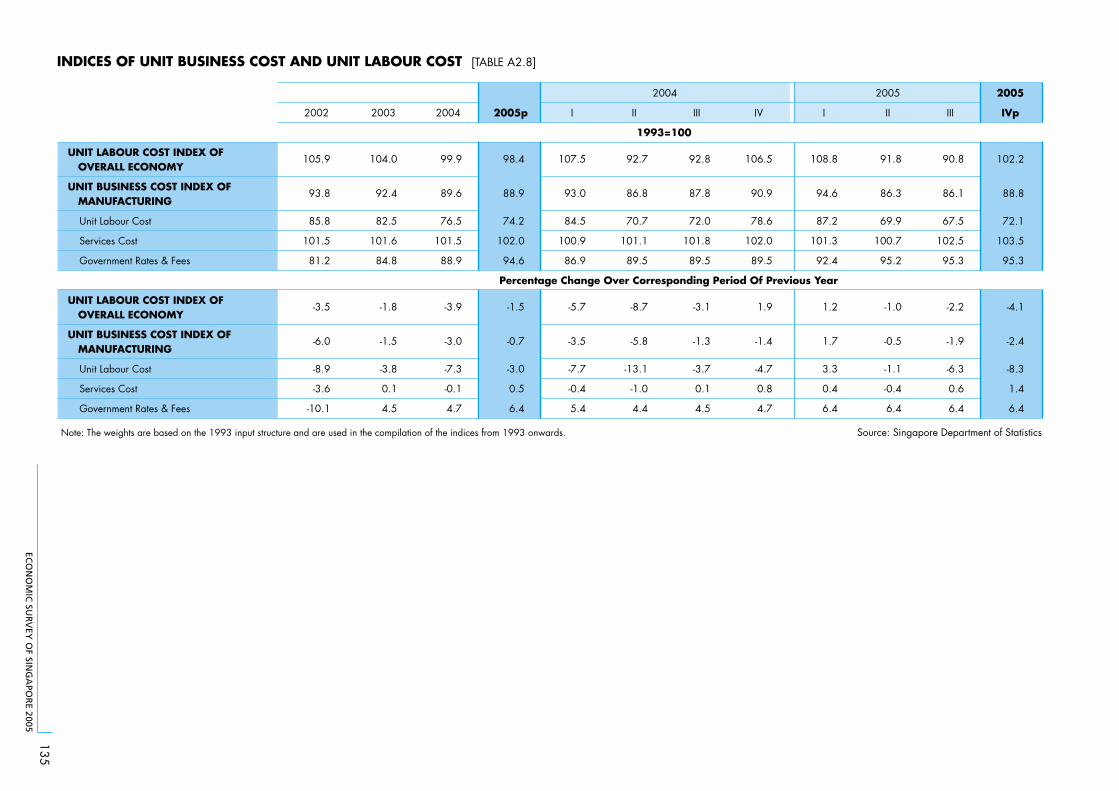

…but business costs remained on a downwardtrend…

Underpinned by improvements in productivity,the overall unit labour cost (ULC) edged downby 1.5 per cent in 2005. However, the rate ofdecline was less than the 3.9 per cent fall in2004.

Similarly, unit business cost (UBC) in themanufacturing sector was down by 0.7 per centin 2005, compared to the larger 3.0 per centdecrease in the preceding year. The decline inUBC was led by a 3.0 per cent fall inmanufacturing ULC, which came on the back ofthe 2.6 per cent growth in manufacturingproductivity.

CHANGES IN REAL AVERAGE MONTHLY EARNINGSAND PRODUCTIVITY [Chart 3.6]

–6 —

–4 —

–2 —

0 —

2 —

4 —

6 —

8 —

10 —

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Per Cent

Productivity

Real Monthly Earnings

WAGE SHARE IN NOMINAL GDP [Chart 3.7]

41 —

42 —

43 —

44 —

45 —

46 —

47 —

48 —

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Per Cent

UNIT BUSINESS COST INDEX OFMANUFACTURING (1993=100) [Chart 3.8]

88 —

90 —

92 —

94 —

96 —

98 —

100 —

102 —

104 —

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Index

In contrast, government rates and fees wentup 6.4 per cent compared to a 4.7 per centrise the year before, largely due to an increasein import duties.

ECONOMIC SURVEY OF SINGAPORE 2005

30

Chapter 3

EMPLOYMENT, WAGES AND PRODUCTIVITY

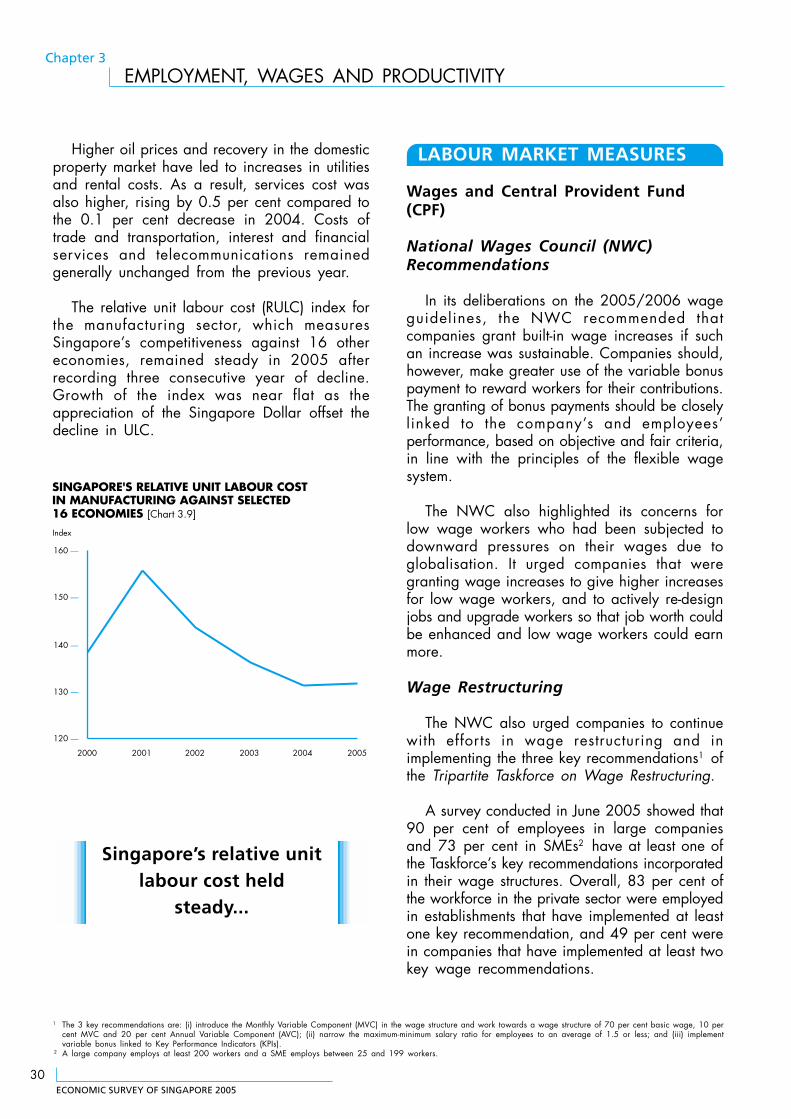

Higher oil prices and recovery in the domesticproperty market have led to increases in utilitiesand rental costs. As a result, services cost wasalso higher, rising by 0.5 per cent compared tothe 0.1 per cent decrease in 2004. Costs oftrade and transportation, interest and financialservices and telecommunications remainedgenerally unchanged from the previous year.

The relative unit labour cost (RULC) index forthe manufacturing sector, which measuresSingapore’s competitiveness against 16 othereconomies, remained steady in 2005 afterrecording three consecutive year of decline.Growth of the index was near flat as theappreciation of the Singapore Dollar offset thedecline in ULC.

LABOUR MARKET MEASURES

Wages and Central Provident Fund(CPF)

National Wages Council (NWC)Recommendations

In its deliberations on the 2005/2006 wageguidelines, the NWC recommended thatcompanies grant built-in wage increases if suchan increase was sustainable. Companies should,however, make greater use of the variable bonuspayment to reward workers for their contributions.The granting of bonus payments should be closelylinked to the company’s and employees’performance, based on objective and fair criteria,in line with the principles of the flexible wagesystem.

The NWC also highlighted its concerns forlow wage workers who had been subjected todownward pressures on their wages due toglobalisation. It urged companies that weregranting wage increases to give higher increasesfor low wage workers, and to actively re-designjobs and upgrade workers so that job worth couldbe enhanced and low wage workers could earnmore.

Wage Restructuring

The NWC also urged companies to continuewith efforts in wage restructuring and inimplementing the three key recommendations1 ofthe Tripartite Taskforce on Wage Restructuring.

A survey conducted in June 2005 showed that90 per cent of employees in large companiesand 73 per cent in SMEs2 have at least one ofthe Taskforce’s key recommendations incorporatedin their wage structures. Overall, 83 per cent ofthe workforce in the private sector were employedin establishments that have implemented at leastone key recommendation, and 49 per cent werein companies that have implemented at least twokey wage recommendations.

SINGAPORE'S RELATIVE UNIT LABOUR COST IN MANUFACTURING AGAINST SELECTED 16 ECONOMIES [Chart 3.9]

120 —

130 —

140 —

150 —

160 —

2000 2001 2002 2003 2004 2005

Index

1 The 3 key recommendations are: (i) introduce the Monthly Variable Component (MVC) in the wage structure and work towards a wage structure of 70 per cent basic wage, 10 percent MVC and 20 per cent Annual Variable Component (AVC); (ii) narrow the maximum-minimum salary ratio for employees to an average of 1.5 or less; and (iii) implementvariable bonus linked to Key Performance Indicators (KPIs).

2 A large company employs at least 200 workers and a SME employs between 25 and 199 workers.

Singapore’s relative unitlabour cost held

steady...

ECONOMIC SURVEY OF SINGAPORE 2005

31

EMPLOYMENT, WAGESAND PRODUCTIVITY

CPF Changes

In 2003, the Government announced changesto the CPF salary ceiling and contribution rates,to be implemented over a 2-year period – 2005to 2006.

The salary ceiling for contributions fromemployees and employers was lowered from$5,500 to $5,000 with effect from 1 January2005. It was further lowered to $4,500 on 1January 2006, bringing the salary ceiling to thetargeted level of income earners at the 80th

percentile.

To help the employability of older workers,the CPF contribution rate for workers agedbetween 50 and 55 was also reduced from 33to 30 per cent on 1 January 2005, and to 27per cent on 1 January 2006.

Labour Market Developments

Workforce Skills Qualifications System(WSQ)

The Workforce Skills Qualifications (WSQ)system was launched in October 2005. It is anational skills and qualifications framework forworkers to upgrade their skills to remainemployable and competitive. The system sets outthe training and certification pathways for workersto enhance their skills. It will also help companiesto plan for the upgrading of their workers.

With WSQ, workers will benefit from betterstructured and competency-based training,industry recognised qualifications and accreditedtraining providers. This will help our workersprogress better in their jobs or to switch to newjobs.

Low Wage Workers

Even as Singapore’s economy continues togrow and provide enough jobs for Singaporeans,workers who do not upgrade their skills will facesignificant challenges. They are vulnerable tostructural unemployment and downward wagepressures from lower-cost workers in emergingeconomies like China, India and Eastern Europe.

The Ministerial Committee on Low WageWorkers was set up in July 2005 to identifysustainable solutions to help low wageSingaporean workers adjust to these challenges.The Committee proposed a $1 billion Workfarepackage to help low wage workers findmeaningful jobs, earn adequate wages to supportthemselves and their families so that they canown their own homes, educate their children andprepare for their medical and retirement needs.The Workfare package included broad measuresin the following areas:

(i) Providing incentives to reward workthrough a Workfare Bonus;