Embed Size (px)

Citation preview

Economic Report 1st Quarter 2009 1/17

CONTENTS

1. Process of Group Strategy and Integration

- Group integration - Information systems - Group strategy

2. Business evolution

- Market situation in Europe - Group positioning - Group financial positioning

3. Analysis by geographical areas 4. Headcount evolution

5. Later events

- Change of members of the Auditing Committee - Approval of the issue of Convertible Bonds

Economic Report 1st Quarter 2009 2/17

1. Process of Group Strategy and Integration

1.1 Group integration

The Group Management considers the period of expansion through takeovers at an end, and will focus its resources on strengthening and intensifying the integration processes of the different businesses taken over, paying special attention to achieving the underlying synergies in the areas of procurement, industrial process optimisation, distribution logistics and general expenditure. In 2008-2012 we can distinguish three stages which have to be developed consecutively to achieve the expected results: a) Restructuring: This basically consists of integrating the business that has been taken over in the past two years. This stage, which started in 2007 and spread throughout 2008, is characterised by: • Establishment of the basic corporate and business structure • Consolidation of the operation of the different sites, both organisationally

and operatively • Reduction of fixed costs • Restructuring and optimisation of the production assets, considering the

possibility of closing some of them which may not be strategically competitive in the short-term

• Continuity in the resin degree rationalisation and homogenisation processes

• Optimisation of the catalogue of products to be commercialised b) Consolidation of the competitive position on the market, approaching the end consumer via joint management of PET and packaging. c) Profitable growth: This is a stage based on innovation, investment for developing new products, and on growth both in volume and profitability of the specialities and on growth in the environmental/ecological side of recycled PET.

Economic Report 1st Quarter 2009 3/17

1.2 Information system The corporate management system of the La Seda Group, SAP R/3, covers the business processes of the following functional areas: Financial Management-Management Control, Logistics-Commercial Management, Production Management-Quality Control and General Service Management. Additionally, part of the management of the logistics and production is carried out with industrial applications totally integrated with the Corporate SAP R/3 management system. The corporate reporting tool is BW of SAP. Today, the companies which use the Corporate SAP R/3 management system are: in Spain, Artenius Prat Pet, La Seda de Barcelona, Artenius San Roque, IQA (Industrias Químicas Asociadas, Tarragona), Inmoseda, Artenius Green (Balaguer) and Biocombustible La Seda (Tarragona), in Italy, Artenius Italia (San Giorgio) and Simpe (Nápoles), in Turkey, Artenius Turkpet, in Portugal, Artenius Sines and in Greece, Artenius Hellas. In addition to the Corporate SAP, the La Seda Group has three additional R/3 management systems, which are: for the Preform Division, the R/3 APPE environment, which gives support to companies (Artenius PET recycling France, Artenius PET packaging Belgium, Artenius PET packaging UK, Artenius PET packaging France, Artenius PET packaging Deutschland, Artenius PET Packaging Europe and Artenius pet packaging Iberia (Toledo), for Artenius UK, the R/3 Wilton environment and for Artenius Selenis (Portalegre, Portugal) the SAP R/3 Selenis environment. The calendar for introducing the SAP R/3 management system in the last quarter of 2008 and first quarter of 2009 has been:

• October, the company Inmoseda was included in the Corporate SAP R/3 management system and the economic-financial processes were started in the Company SIMPE (Italy) in the Corporate SAP.

• November, the Corporate SAP R/3 management system was

introduced in the recycling company Artenius Green. The production processes will be introduced in 2009 following the change of the physical location of the plant.

• The R/3 management system will be introduced in the company SIMPE

(in October, the financial and management control processes were introduced) of the PET Division in Naples. The introduction of the production, logistics and commercial processes has been put off for the final start-up of the plant, which is expected in 2009.

• In January 2009, the Company Artenius Sines PTA in Sines (Portugal)

was introduced in the Corporate SAP R/3 finance, purchasing and plant and equipment maintenance processes.

Economic Report 1st Quarter 2009 4/17

In November, the Corporate Information Systems Project was started in the functional area of human resources, and the SAP R/3 HR-HCM management system is going to be implemented as a back-office solution, and the SAP PORTAL-ESS solution as a corporate portal. In addition to this, among the jobs of the Project, the SAP KM solution is going to be implemented as a corporate tool of Documentary Management. The principal objective lies in having a centralised environment for the Human Resource management (personnel administration, organisational structure, training, benefits and compensation, career plan, etc) and a Portal with corporate tools available to all of the employees of the La Seda Group. In December 2008, four Project Offices were constituted to manage all of the Projects of the Corporate and Operative Management of the SEDA Group (Government Project Office, Finance Project Office, Operations Project Office and Human Resource Project Office). These Project Offices are permanent entities which are going to provide all of the Projects of the SEDA Group with methodology, policies and resources, and will allow the Management to know the priority, sequence and dependency of all of the Projects. In January 2009, the Alternative Backup Centre Project was started, which in the event of disaster in the Primary Centre, will ensure that the daily operation of the SEDA Group is not affected, and information is not lost from applications critical for the business. The project is expected to be complete in July 2009. In recent months different projects have been carried out to cover the reporting needs of different functional areas of the Group (Commercial area, Production area Management Controlled area, credit control area, treasury area etc.) in the SAP BW corporate reporting tool, with individual and aggregate information of all of the management systems of the SEDA Group. January 2009 saw the end of the Analysis and Design phase of the functionality of Organisational Structure and Personnel Administration, and in February 2009, the Analysis and Design phase was completed of Profits, Compensation, Training and Employee Portal.

Economic Report 1st Quarter 2009 5/17

1.3 Group strategy

The strategy of the LA SEDA DE BARCELONA Group (LSB Group) is aimed at integrating its PET and preform businesses. The result will be a single “PET- Packaging” business which will be the central core of the business of the Group and will cover the whole process, from PET production to pack delivery to the end customer, from a global perspective in a European environment. The business management is aimed at geographical control of this single integrated business. Around this central business of the Group, there will be other businesses essentially aimed at providing materials and services for the main PET-Packaging business and in which minority interests with specialised experience in these businesses might be included: - Raw materials: Centralisation of the businesses intended to supply the

raw materials (PTA, MEG, Technology) to the main business. Equally, the business will be controlled from a geographical perspective.

- Energy: Centralisation of the power supply services and creation of new

services based on the needs of the Group, through multigeneration units. In this context, the “Seda Energy” company has been created as a company which centralises and coordinates this activity.

- Management services: Centralisation of the corporate management

services (administrative, financial, legal, tax…) and others of operative management (purchasing, global sales to customers in multinational environments…) for all the companies belonging to the Group.

The LSB Group management considers that this strategy might be able to be consolidated in the near future (in between one and two years), and the first steps have already been taken to start it up.

Economic Report 1st Quarter 2009 6/17

2. Business evolution

2.1 Market situation in Europe

In 2008, PET consumption in Western Europe grew slower than expected, basically due to the growing use of r-PET (recycled PET), to the developments in preform lightweighting and, in the case of European producers, to exchange-rate conditions highly favourable to imports. PET imports in 2008, according to market reports, were exceptionally high with a rise of almost 17% over the previous year due, above all, to the new plants installed in the Middle East. The volume of imports in the first quarter of 2009 has gradually stabilised and dropped to levels which could be considered “normal“ for this part of the year. The fall in imports allowed a slight recovery in the margins of the European producers. The difference between the European PET and the production cost of Asiatic PET plaster cost of transport to European customers increased by around 40-50 euros per tonne, although forecasts point to a fall in this difference in the future. For the moment, this represents support to the position of the European producers and a ceiling on imports in the coming months. Crude oil prices stabilised in the first quarter of 2009, and determined relative stability too in the price of PET. In this quarter, stronger demand was registered than expected, a positive tendency which has appeared since January and has caused a return to normality among the stocks of any customers, which had been severely reduced in the last part of 2008. The offer in general was recorded with a higher plant utilization rate than in the last quarter of 2008, and the stocks were corrected. The seasonal nature of “bottle demand” which leads to an increase in consumption as temperatures rise, would tend to reinforce the market in the coming months. The serious financial crisis and the problems of access to credit indicate that in 2009 there will be an adjustment in the productive capacity to adapt to demand, and no symptoms are appreciated of a sharp fall in this (in fact a certain upturn is seen), the commercial margins currently being higher than usual for this time, a situation which benefits from the scarce current appeal of imports and the lack of interest in the alternative consumption of r-PET not directly linked to crude oil prices.

Economic Report 1st Quarter 2009 7/17

2.2 Group positioning

The LSB Group has 22 production plants in 11 European countries with over 2,300 employees. The Group has become the European leader and the third company in the world in the PET-Packaging sector:

• By manufacturing and supplying PET and recycled PET to its customers

(a material which replies to the needs of the consumers due to its ability to be recycled, its lightness and strength)

• By designing, transforming and commercialising PET and recycled PET

packs to satisfy the needs of end customer/consumers

• By performing R&D to develop new applications and varieties of PET, which contribute to disseminating this material as that preferred by the end customers and consumers

The LSB Group is the first European group capable of supplying and guaranteeing PET packs, from their initial design to the finished product, by gathering all of the production stages of PET packs in a single company. It is able to offer its customers an end product and a service which are distinguished from the rest of the competitors on the market. From the combination of the PET manufacturing experience and the experience brought in by APPE in designing and manufacturing packs, clear synergies are occurring in manufacturing in an ever more demanding market with regard to differentiating its products, and the quality of the materials used. In PET Packaging, the segmentation of the final product and its customers are divided between:

• Carbonated soft drinks and mineral waters (CSDW): In this segment, long-term contracts are established and the customers are large multi-brand multinationals from the water and beverage sectors

• Specific drinks: These are mainly used in natural juices, isotonic drinks,

beers and wines. It is a growing segment where new packs are constantly launched

• Diversified products: Applications for the packing industry in general.

Their main applications are household cleaning products and cosmetic products. It is a segment where the consumption figures remained constant throughout the year. In general, these products are characterised by their great speciality and high added value

Economic Report 1st Quarter 2009 8/17

2.3 Financial position of the group In May 2008, the company management had foreseen possible liquidity tensions, so they asked the banks making up the syndicated loan led by Deutsche Bank for some modifications to the original contract, with the aim, amongst others, of increasing the resource-free factoring limit to €150m, of modifying the “technical covenants” and excluding the Sines project from the financing perimeter. However, the exceptional market conditions registered in the second part of 2008 have had a considerable negative impact on the financial results of the Company, due to:

• Strong fall in crude oil prices to levels of c.$50/bbl from the peaks of c.$150/bbl registered in July 2008.

• Significant contention of PET demand volume (due to lightweighting,

customer stock reductions and the general economic slowdown).

• Dumping of the Asiatic producers

At the end of 2008, the financial position of the company deteriorated rapidly due to the obligations to pay for raw materials purchased at higher prices, to the fall in sales volumes, and to the impossibility of using the whole of the €150m credit line due to the present credit crisis. The company is involved in a negotiation process in order to prevent the financial entity from requiring compliance with certain conditions demanded in the financing agreements of the LSB, S.A syndicated loan for the fourth quarter 2008, and the whole of 2009. As a result of this, the financial entities might require early payment of the syndicated loan. Amongst other measures, the Company is contemplating issuing bonds which may be converted into shares at maturity for 150 million euros. On the date on which this report is issued, the operations have not started for issuing bonds, and negotiation is still underway which is intended to result in agreements on the restructuring of debt times with suppliers and credit entities, to allow the re equilibrium of working capital.

Economic Report 1st Quarter 2009 9/17

3. Analysis by geographical areas

In line with the strategy defined by the LSB Group, in 2008 the LSB Group management defined four large Business Units by geographical areas and markets, according to the origin and predominant nature of the risks, returns, growth opportunities and expectations of the Group. These are:

• United Kingdom: Artenius Uk; Artenius PET- Packaging Uk • Western Europe (Spain and Portugal): Artenius Portugal; Artenius San Roque;

La Seda de Barcelona; Artenius PET- Packaging Iberia; IQA; Selenis Serviços; Biocombustibles; Artenius Green; Inmoseda. This area also includes other less important plants in the Group

• Central Europe (Belgium, Germany, France and Italy): Artenius PET- Packaging Belgium; Artenius PET- Packaging Deutschland; Artenius Pet-Packaging France; Artenius Pet Recycling France; Artenius Italia; Simpe, Erreplast.

• Eastern Europe (Greece, Turkey and Romania): Artenius Turkpet; Artenius Romania; Artenius Hellas

• Others: Artenius PET- Packaging Maroc

Information has also been included for the preform plant that the Group has in Morocco under the caption of “Others”, for its commercial consideration is that of supplying the North African and Near Eastern markets, although it currently depends industrially on Western Europe.

Overall, the group's financial performance was below its internal budget. Despite the upturn in market conditions, the operation and efficiency of both the PET and PTA business divisions were affected by the financial position described in the previous point, which prevented the production plants from operating at a high utilization rate, which has worn down the margins. In some cases, PET production has stopped, and therefore the income statement is negatively affected due to the higher fixed costs. With respect to the PTA plant, there was an early technical stoppage, which was prolonged due to a lack of raw materials. In this quarter, we might highlight the good performance of the preform business unit, which lies above budget both in sales and margins. The stability of this business is largely due to the contracts which guarantee the supply of raw materials and the volume of sales, which allowed the Group to partially mitigate the impact of the losses caused by the other businesses.

Economic Report 1st Quarter 2009 10/17

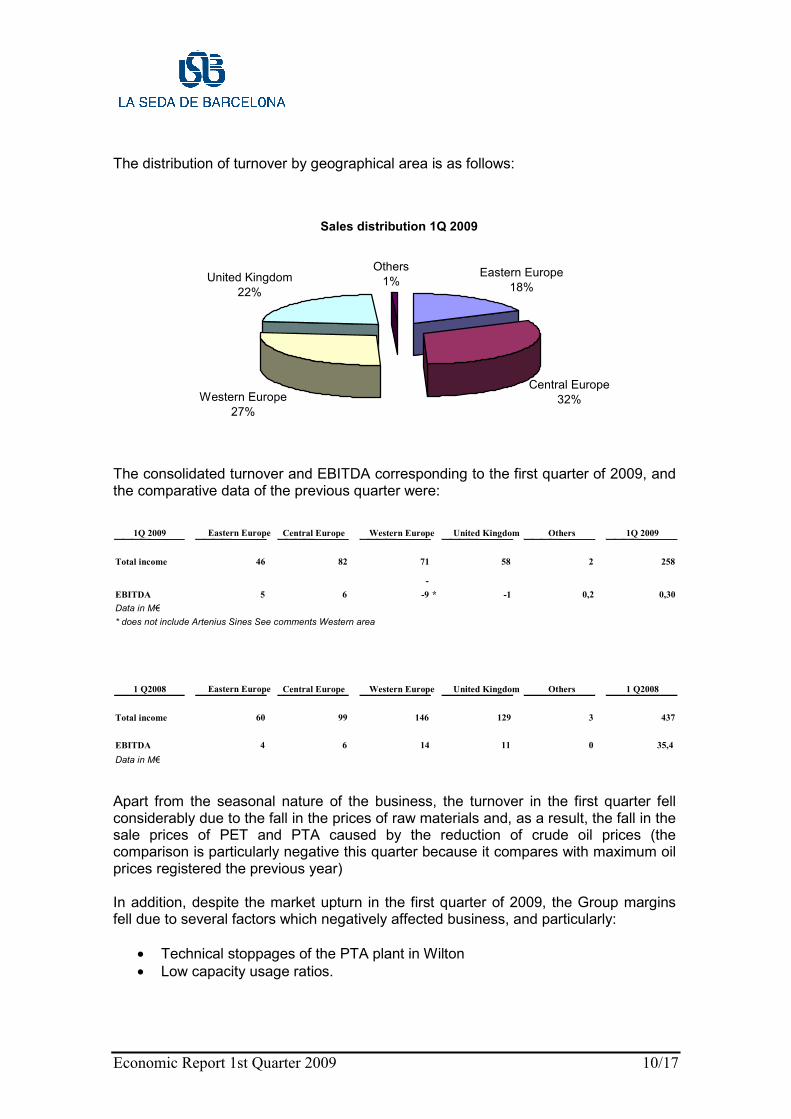

The distribution of turnover by geographical area is as follows:

Sales distribution 1Q 2009

Central Europe32%Western Europe

27%

Eastern Europe18%

Others1%United Kingdom

22%

The consolidated turnover and EBITDA corresponding to the first quarter of 2009, and the comparative data of the previous quarter were:

Apart from the seasonal nature of the business, the turnover in the first quarter fell considerably due to the fall in the prices of raw materials and, as a result, the fall in the sale prices of PET and PTA caused by the reduction of crude oil prices (the comparison is particularly negative this quarter because it compares with maximum oil prices registered the previous year) In addition, despite the market upturn in the first quarter of 2009, the Group margins fell due to several factors which negatively affected business, and particularly:

• Technical stoppages of the PTA plant in Wilton • Low capacity usage ratios.

1Q 2009 Eastern Europe Central Europe Western Europe United Kingdom Others 1Q 2009

Total income 46 82 71 58 2 258

-EBITDA 5 6 -9 * -1 0,2 0,30Data in M€ * does not include Artenius Sines See comments Western area

1 Q2008 Eastern Europe Central Europe Western Europe United Kingdom Others 1 Q2008

Total income 60 99 146 129 3 437

EBITDA 4 6 14 11 0 35,4Data in M€

Economic Report 1st Quarter 2009 11/17

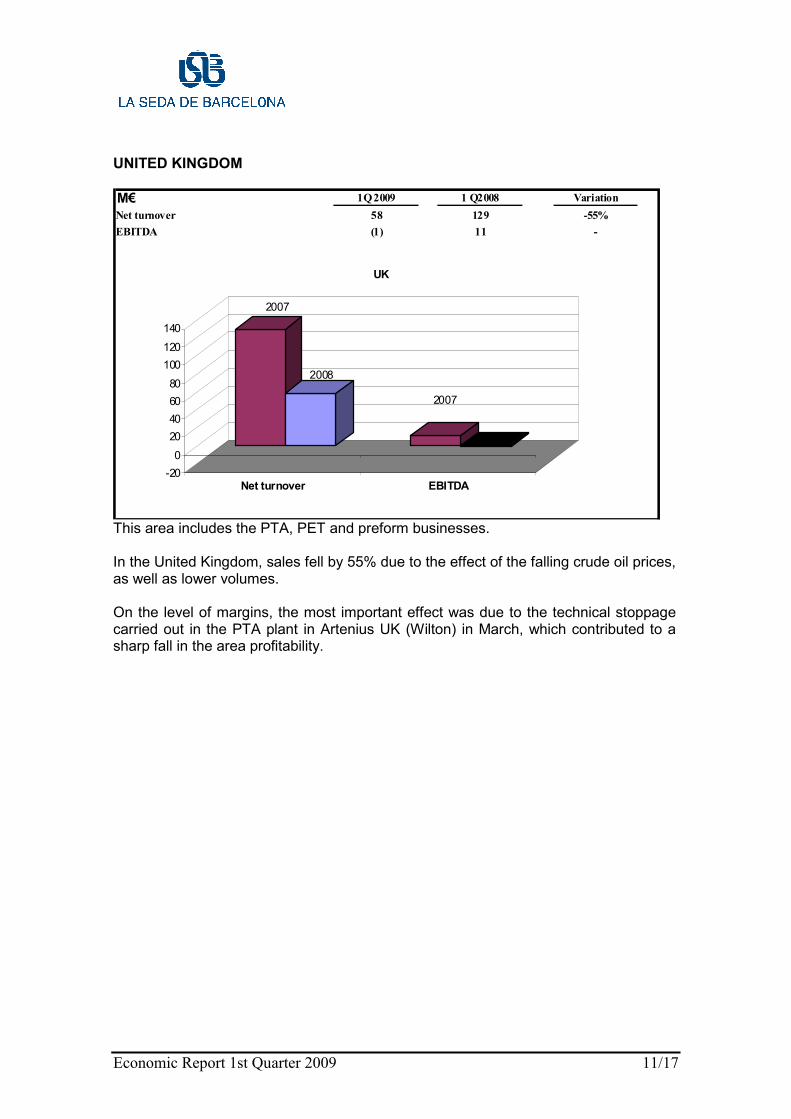

UNITED KINGDOM M€ 1Q 2009 1 Q2008 VariationNet turnover 58 129 -55%EBITDA (1) 11 -

2007

2008

2007

2008

-200

20406080

100120140

Net turnover EBITDA

UK

This area includes the PTA, PET and preform businesses. In the United Kingdom, sales fell by 55% due to the effect of the falling crude oil prices, as well as lower volumes. On the level of margins, the most important effect was due to the technical stoppage carried out in the PTA plant in Artenius UK (Wilton) in March, which contributed to a sharp fall in the area profitability.

Economic Report 1st Quarter 2009 12/17

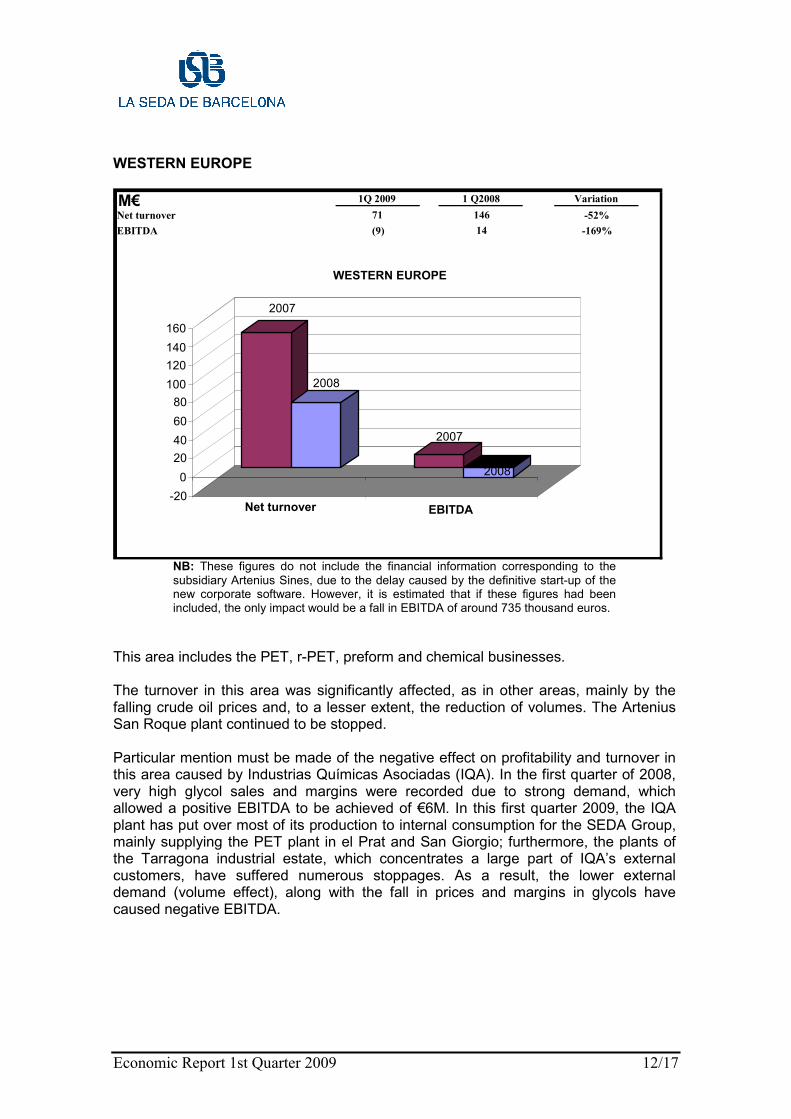

WESTERN EUROPE

NB: These figures do not include the financial information corresponding to the subsidiary Artenius Sines, due to the delay caused by the definitive start-up of the new corporate software. However, it is estimated that if these figures had been included, the only impact would be a fall in EBITDA of around 735 thousand euros.

This area includes the PET, r-PET, preform and chemical businesses. The turnover in this area was significantly affected, as in other areas, mainly by the falling crude oil prices and, to a lesser extent, the reduction of volumes. The Artenius San Roque plant continued to be stopped. Particular mention must be made of the negative effect on profitability and turnover in this area caused by Industrias Químicas Asociadas (IQA). In the first quarter of 2008, very high glycol sales and margins were recorded due to strong demand, which allowed a positive EBITDA to be achieved of €6M. In this first quarter 2009, the IQA plant has put over most of its production to internal consumption for the SEDA Group, mainly supplying the PET plant in el Prat and San Giorgio; furthermore, the plants of the Tarragona industrial estate, which concentrates a large part of IQA’s external customers, have suffered numerous stoppages. As a result, the lower external demand (volume effect), along with the fall in prices and margins in glycols have caused negative EBITDA.

M€ 1Q 2009 1 Q2008 Variation Net turnover 71 146 -52% EBITDA (9) 14 -169%

2007

2008

2007

2008

-20 0

20 40 60 80

100 120 140 160

Net turnover

EBITDA

WESTERN EUROPE

Economic Report 1st Quarter 2009 13/17

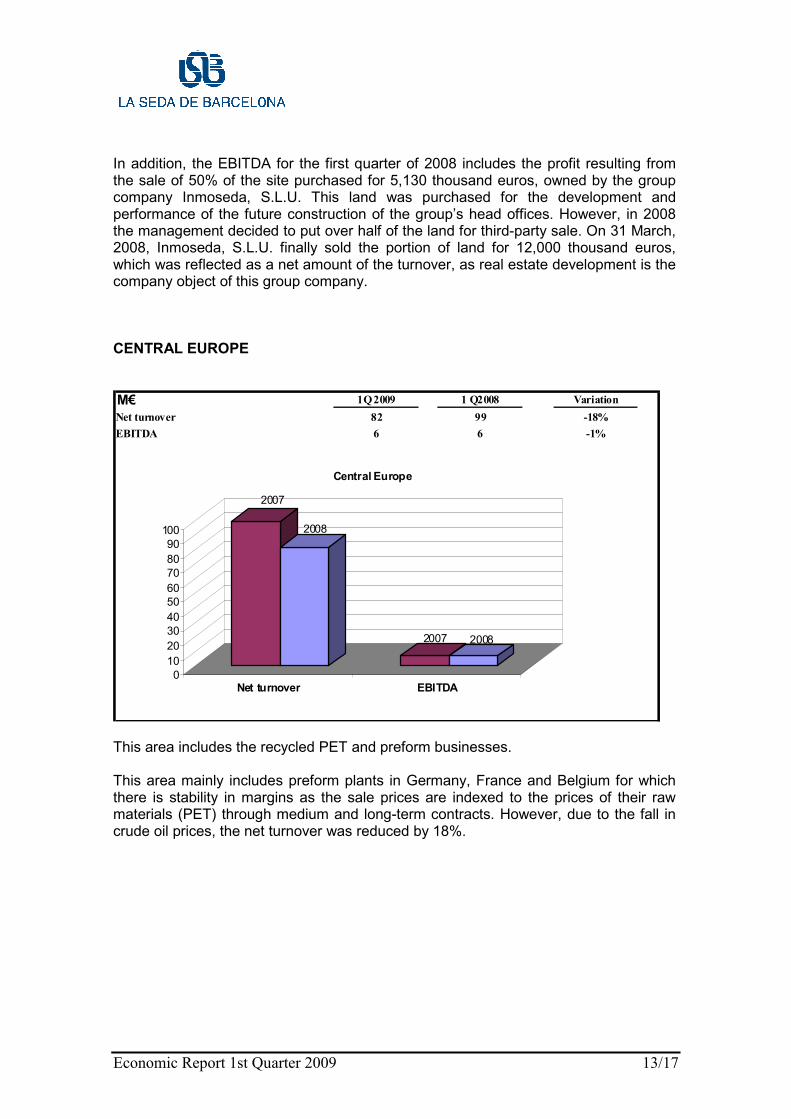

In addition, the EBITDA for the first quarter of 2008 includes the profit resulting from the sale of 50% of the site purchased for 5,130 thousand euros, owned by the group company Inmoseda, S.L.U. This land was purchased for the development and performance of the future construction of the group’s head offices. However, in 2008 the management decided to put over half of the land for third-party sale. On 31 March, 2008, Inmoseda, S.L.U. finally sold the portion of land for 12,000 thousand euros, which was reflected as a net amount of the turnover, as real estate development is the company object of this group company. CENTRAL EUROPE

M€ 1Q 2009 1 Q2008 VariationNet turnover 82 99 -18%EBITDA 6 6 -1%

2007

2008

2007 2008

0

10

20

30

40

50

60

Net turnover EBITDA

EUROPA ESTE

2007

2008

2007 2008

0102030405060708090

100

Net turnover EBITDA

Central Europe

This area includes the recycled PET and preform businesses. This area mainly includes preform plants in Germany, France and Belgium for which there is stability in margins as the sale prices are indexed to the prices of their raw materials (PET) through medium and long-term contracts. However, due to the fall in crude oil prices, the net turnover was reduced by 18%.

Economic Report 1st Quarter 2009 14/17

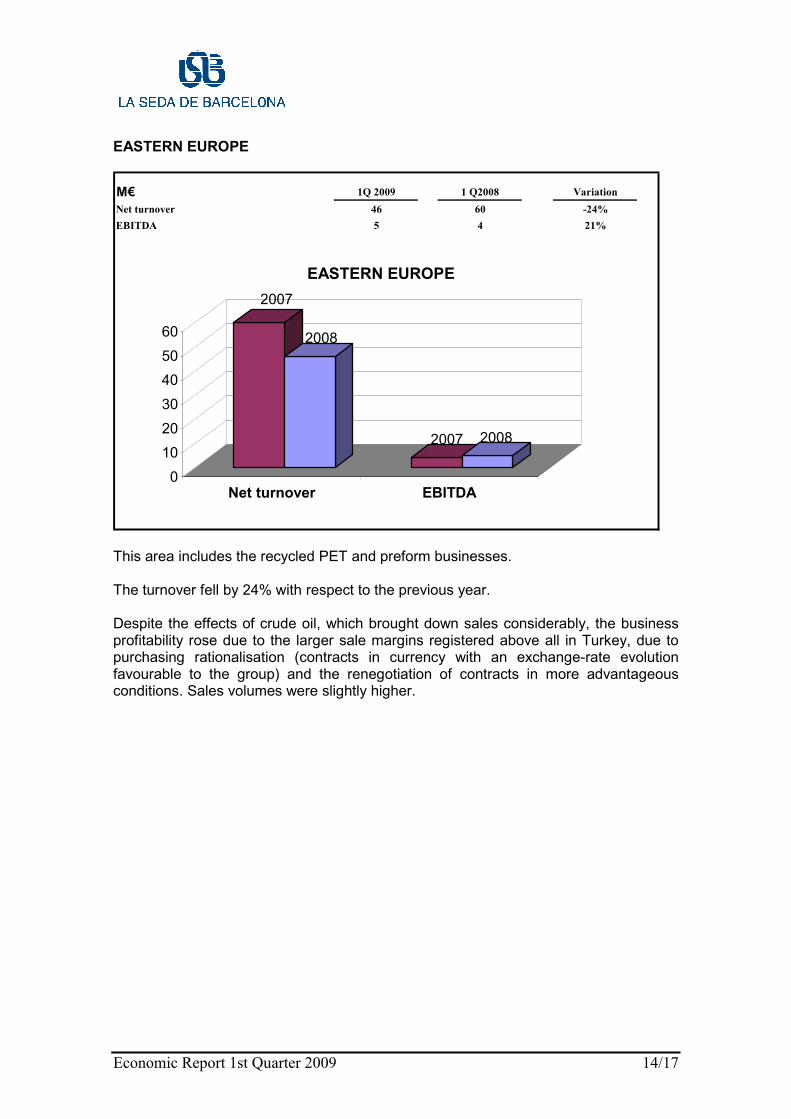

EASTERN EUROPE

M€ 1Q 2009 1 Q2008 VariationNet turnover 46 60 -24%EBITDA 5 4 21%

2007

2008

2007 2008

0102030405060

Net turnover EBITDA

EASTERN EUROPE

This area includes the recycled PET and preform businesses. The turnover fell by 24% with respect to the previous year. Despite the effects of crude oil, which brought down sales considerably, the business profitability rose due to the larger sale margins registered above all in Turkey, due to purchasing rationalisation (contracts in currency with an exchange-rate evolution favourable to the group) and the renegotiation of contracts in more advantageous conditions. Sales volumes were slightly higher.

Economic Report 1st Quarter 2009 15/17

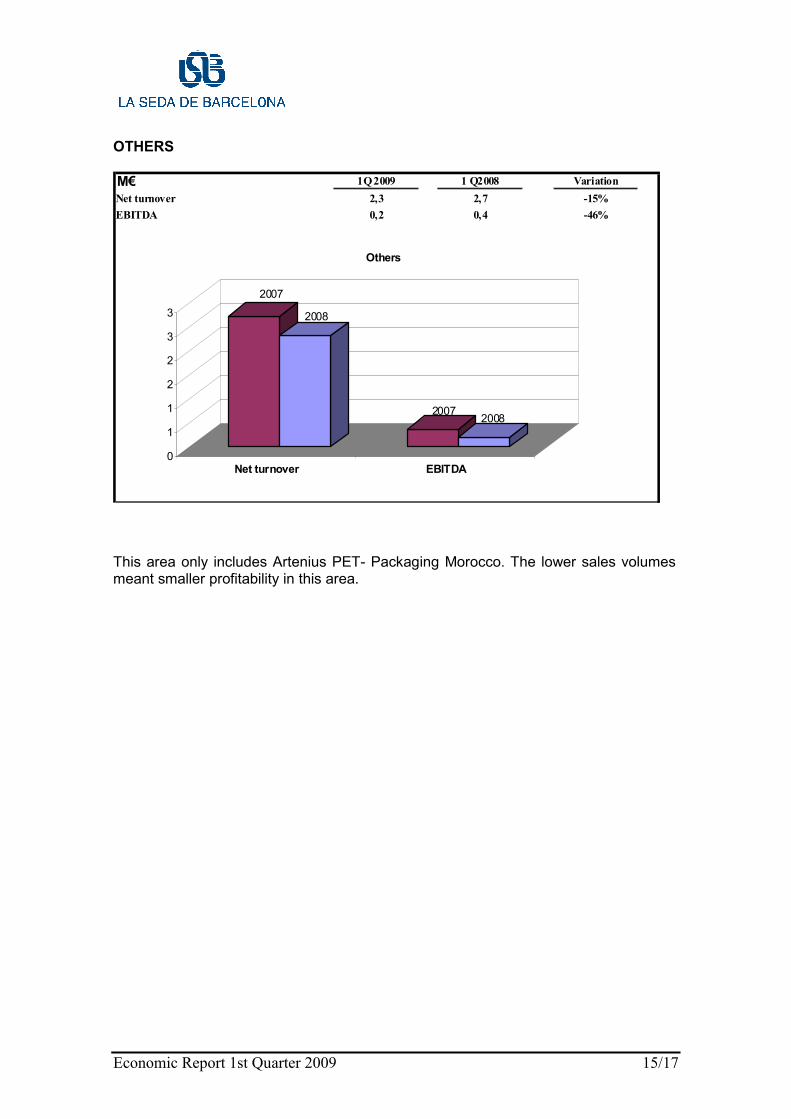

OTHERS M€ 1Q 2009 1 Q2008 VariationNet turnover 2,3 2,7 -15%EBITDA 0,2 0,4 -46%

2007

2008

2007 2008

0

1

1

2

2

3

3

Net turnover EBITDA

Others

This area only includes Artenius PET- Packaging Morocco. The lower sales volumes meant smaller profitability in this area.

Economic Report 1st Quarter 2009 16/17

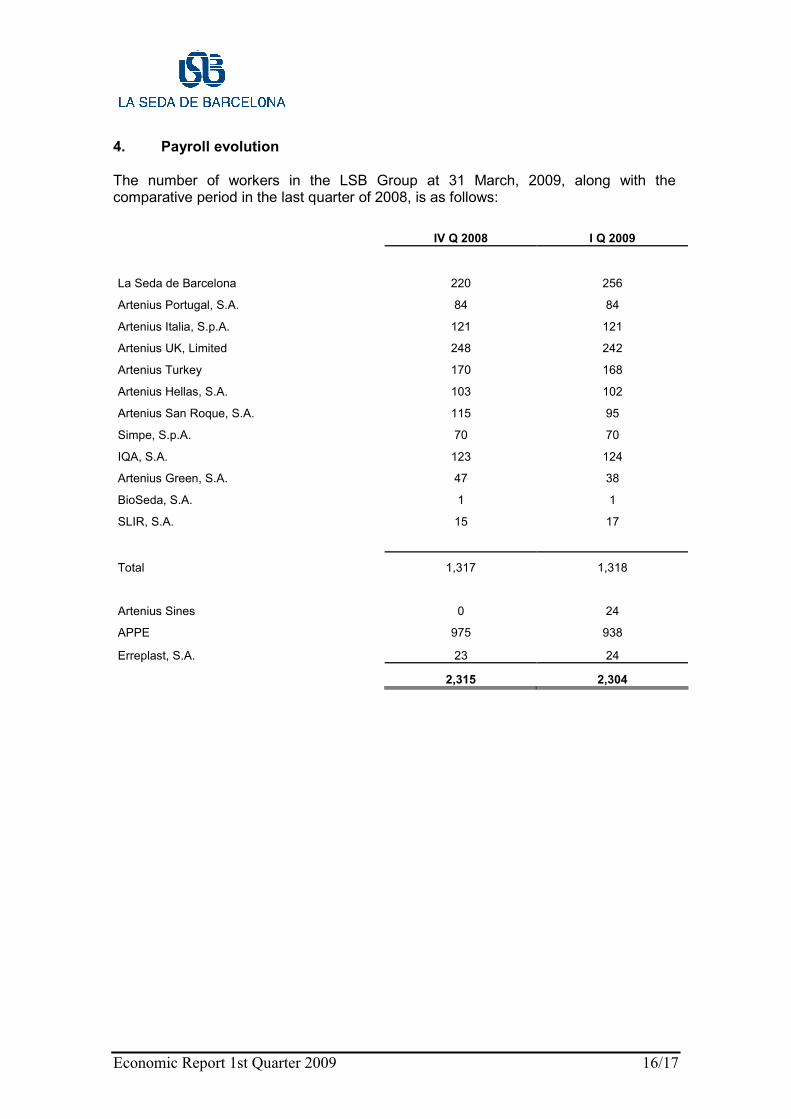

4. Payroll evolution The number of workers in the LSB Group at 31 March, 2009, along with the comparative period in the last quarter of 2008, is as follows: IV Q 2008 I Q 2009

La Seda de Barcelona 220 256

Artenius Portugal, S.A. 84 84

Artenius Italia, S.p.A. 121 121

Artenius UK, Limited 248 242

Artenius Turkey 170 168

Artenius Hellas, S.A. 103 102

Artenius San Roque, S.A. 115 95

Simpe, S.p.A. 70 70

IQA, S.A. 123 124

Artenius Green, S.A. 47 38

BioSeda, S.A. 1 1

SLIR, S.A. 15 17

Total 1,317 1,318

Artenius Sines 0 24

APPE 975 938

Erreplast, S.A. 23 24

2,315 2,304

Economic Report 1st Quarter 2009 17/17

5. Later events 5.1 Changes among the members of the Auditing Committee In the session of the Board of Directors held on 31 March, 2009, the Board Member Mr. José Luis Morlanes Galindo was appointed Chairman and member of the Auditing Committee in the place of the Board Member Ms. Helena Guardans Cambó, who handed in her resignation from the Board. Mr. Morlanes, by becoming a member of the Auditing Committee, was dismissed from the executive Commission.

5.2 Approval of the issue of Convertible Bonds In session on 31 March, 2009, the Board of Directors agreed to carry out an Issue of convertible bond for an amount of 150,000,000,- Euros, as far as they are guaranteed by the Shareholders, Banks or Public Institutions.