Embed Size (px)

Citation preview

James Philip Caldwell– Senior Industry Analyst

Economic Insights: COVID-19 and the NZ Economy

Agenda:

- Macroeconomic update- Most exposed industries- International trade- Government response

Macroeconomic Update

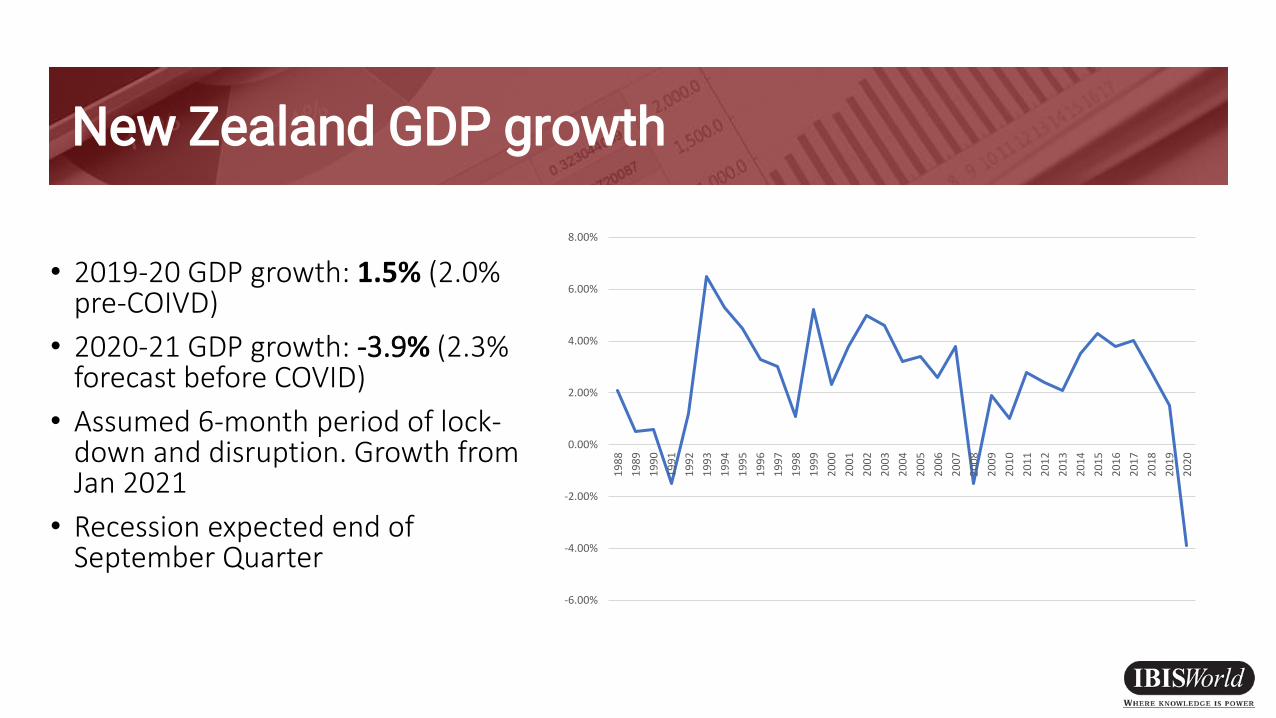

New Zealand GDP growth

• 2019-20 GDP growth: 1.5% (2.0% pre-COIVD)

• 2020-21 GDP growth: -3.9% (2.3% forecast before COVID)

• Assumed 6-month period of lock-down and disruption. Growth from Jan 2021

• Recession expected end of September Quarter

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Unemployment rate

• Rise from 4.1% in 2019-20 to 7.5% in 2020-21.

• Annual average of monthly results, which understates the peak

• Peak unemployment of 9.5% (in June Quarter)

• Partially contained by the Government’s Wage Subsidy

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Household discretionary income

• 2019-20: -0.2% decline

• 2020-21: -8.2% decline

• and insurance costs rising.

• Weak wage growth was already limiting consumer spending power.

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

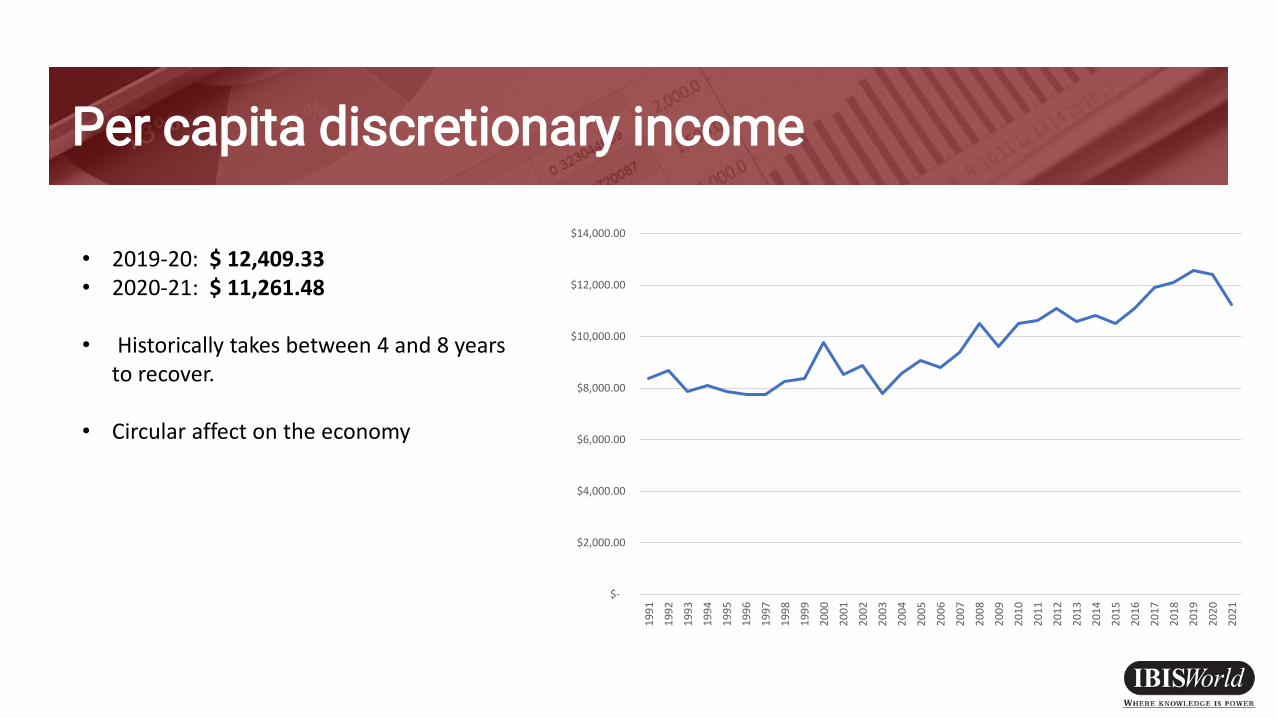

Per capita discretionary income

$-

$2,000.00

$4,000.00

$6,000.00

$8,000.00

$10,000.00

$12,000.00

$14,000.00

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

• 2019-20: $ 12,409.33 • 2020-21: $ 11,261.48

• Historically takes between 4 and 8 years to recover.

• Circular affect on the economy

Tourism & Hospitality

International travel to New Zealand

GFC

COVID-19

• Strongest fall since the GFC outbreak (-4%)

• Factors:

• Border Closures

• Deterioration of Global Economy

• Trans-Tasman Bubble

• International travel by New Zealanders is also expected to fall

• Both inbound and outbound tourism expected to rebound strongly in 2021-22

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

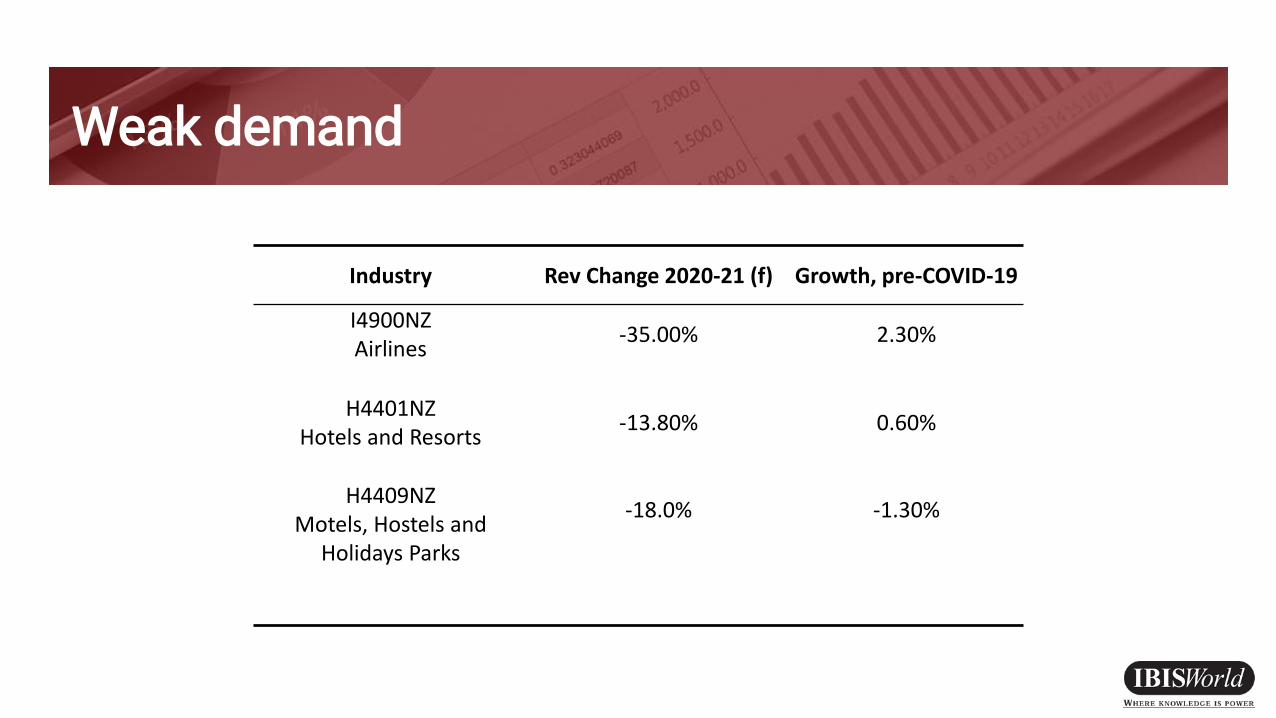

Weak demand

• Australia is the largest market in terms of tourism expenditure

• The travel ban has put pressure on tourism businesses across Australia

• High impact:• Airlines• Accommodation providers• Travel agencies

• IBISWorld expects that rev + profit will fall for all these three industries in 2020-21.

• Moderate impact:• Restaurants/food-service• Recreational and cultural sites• Local transport services

Australia55%

China, People's Republic of

16%

United States of America

13%

United Kingdom8%

Germany4%

Japan4%

Domestic Demand

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

• Domestic tourism worth approximately $23 billion in 2018-19.

• Expected to decline by 14.2% in the current year, recovering in 2023-24.

Weak demand

Industry Rev Change 2020-21 (f) Growth, pre-COVID-19

I4900NZAirlines

-35.00% 2.30%

H4401NZ Hotels and Resorts

-13.80% 0.60%

H4409NZMotels, Hostels and

Holidays Parks

-18.0% -1.30%

Hospitality

• Most severe revenue declines could be similar to airlines in 2020-21 (20%+)• Pubs, bars, nightclubs – 47.8%

• Restaurants and Café’s – 25.1%

• IBISWorld expects that rev + profit will fall for all hospitality industries in 2020-21.

• Delivery services• Double edged sword

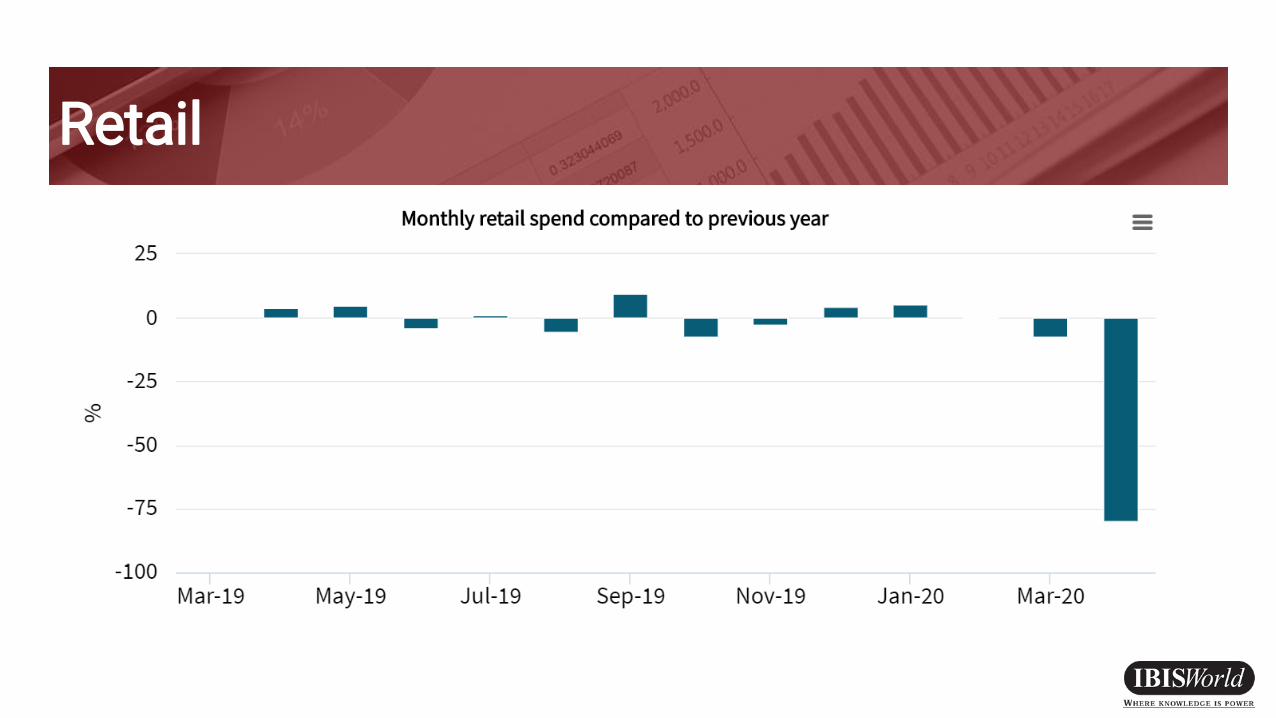

Retail

Supermarkets

• Supermarket store traffic surged during the rush to stockpile (mid-march)• Drove growth in industry

revenue in 2019-20 FY

• Forecast decline of 2.3% in current year

Postal Services

• Growth in online shopping is expected to lead to a surge in parcel’s requiring delivery.

• Forecast growth of 2.4%, revised upwards from -0.3%

International Trade

Exports: Country of Destination

• Highly exposed to China

• Australia has had some success in ‘flattening the curve.’• Tourism expected to limit decline in exports.

• United States and European Union• Struggling to contain the outbreak

• Overall: Highly exposed with a sustained downturn predicted.

Country of final destination2019 (NZ$ Millions) Share

TOTAL 77,961

China, Peoples Republic of 15,329 19.7%

Australia 13,852 17,8%

European Union (including United Kingdom) 8,835 11.3%

United States of America 8,517 10.0%

Japan 4,167 5.3%

Korea, Republic of 2,122 2.7%

India 1,862 2.4%

Singapore 1,615 2.1%

Hong Kong, SAR 1,584 2.0%

Other 20,080 25.8%

Government response

Wage Subsidy Scheme

• Initial cost of $12 billion

• Payment rates• $585.80 (gross) per week for full-time employees,

where full-time is 20 hours or more per week.

• $350.00 (gross) per week for part-time employees, where part-time is less than 20 hours per week.

• Estimated to save 140,00 jobs – limiting the decline in unemployment.

Cash rate

• Currently: 0.25%

• Quantitative Easing

• Factors:• Soft economic growth

• Below-target inflation (potential deflation from 2021)

• Rising unemployment

• Weak wage growth

• Negative consumer sentiment

• COVID-19 0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Thank you!

![Mer for optimum allocation accross investment alternatives [autosaved]-gfc-office-gfc-office-gfc-office-gfc-office](https://img.pdfslide.us/doc/110x75/58e91bcf1a28ab6e0e8b5dbd/mer-for-optimum-allocation-accross-investment-alternatives-autosaved-gfc-office-gfc-office-gfc-office-gfc-office.jpg)