Embed Size (px)

Citation preview

Roland Berger Institute

May 2017

Economic Indicators

2 Roland Berger Economic Indicators May 2017 External version.pptx

Overview

Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic facts and figures. The presentation is updated regularly.

Sources We screen the insights of the most important economic research institutes, think tanks and corporate research units around the world. These include IMF, OECD, WTO, Consensus as well as databases such as Bloomberg and Oxford Economics.

Real economic indicators > Economic indicators promise a brightening outlook, but there

is a multitude of risks

> With GDP growth of 3.5% in 2017 and 3.6% in 2018 global growth is back on track, however below pre-crisis levels

> Due to the uptick of commodity prices an increase in inflation rates is expected for 2017

Financial indicators > Equities all around the world reach new heights

> Fed rate expected to rise to 1.75% by end-2018, while ECB's expected to stay at zero – Euro slightly gaining on the Dollar

> Bond yields still on very low levels – CDS indices with downward trend indicating a decline of implied risk

Other indicators > Sentiment in the world economy and major regions

is recovering

> Especially in China, the economic climate improved

> Consumer sentiment in in the US approaches new heights

1

2

3

Key points

3 Roland Berger Economic Indicators May 2017 External version.pptx

Economic indicators promise a brightening outlook, but there is a multitude of risks potentially destabilizing the global path of growth

Development of the world economy

Potential risk factors for the world economy

> Inward shift in policies towards protectionism

> A faster-than-expected pace of interest rate hikes in the US, possibly triggering a more rapid tightening in global financial conditions

> An aggressive rollback of financial regulation

> Financial tightening in emerging market economies

> Adverse feedback loops among weak demand, low inflation, weak balance sheets, and anemic productivity growth

> Noneconomic factors such as geopolitical factors, political discord or risks from weak governance and corruption

> Average global economic growth is expected to increase to 3.5% in 2017, but longer-term potential growth rates remain subdued in advanced economies

> Prospects are brightening for many countries, but growth for a sizeable number of commodity exporters remains modest

> According to the IMF, the global economy seems to "be gaining momentum" and could be at a turning point. However, IMF advises policymakers to invest in their economies, particularly in people, to build up greater resilience to structural changes, including the changing modalities of globalization

> Among the reforms suggested by the IMF are: "active labor market policies, greater tax progressivity where helpful, more effective investment in education and changes to housing and credit markets that facilitate worker mobility". In addition, growing inequalities within countries should be addressed "to ensure the stability of an open, collaborative trading system"

Source: IMF

4 Roland Berger Economic Indicators May 2017 External version.pptx

Global growth is back on track, however below pre-crisis levels

2008 2010 2012 2014 2016 2018

3.6 3.5

3.1 3.4

5.4

3.5 3.5

4.2

-0.1

3.4

3.0

2017

World

2015

3.4

2016

Advanced economies2) 2.1

US 2.6 1.6

Eurozone 1.7 2.0 1.7 (0.2)

Germany 1.6 1.5 1.8 (0.2)

France 1.4 1.3 1.2 (0.1)

Japan 1.2 1.2 1.0

Emerging/dev. economies

China 6.6 6.9 6.7 (0.4)

Russia 1.4 -2.8 -0.2 (0.3)

Spain 2.6 3.2 3.2 (0.4)

(change in forecast)1)

Italy 0.8 0.8 0.9 (-0.1)

4.2

2018

2.5 (0.4)

1.6 (0.0)

1.5 (0.1)

1.7 (0.0)

6.2 (0.2)

1.4 (0.2)

2.1 (0.2)

0.8 (-0.3)

3.1

1.7

4.1

(change in forecast)1)

2.3 (0.1)

2. Financial indicators 3. Other indicators 1. Real economic indicators

2.0 (0.2)

3.5

2.0 (0.2)

(0.1) 3.6 (0.0)

(0.6) 0.6 (0.1)

4.5 (-0.1) 4.8 (0.0)

World

1) Change related to previous forecast (October 2016) indicates stability of the forecast; All 2017 and 2018 figures on the following slides are forecasts 2) Advanced economies is the term used by IMF to describe developed countries

Real GDP growth [%]

Source: IMF

5 Roland Berger Economic Indicators May 2017 External version.pptx

Brazil, Russia and Nigeria coming out of recession in 2017 – India's GDP growth increases, while China's declines but still above 6%

2016

Brazil

Russia

India

China

2017 2016 2018 2017 2016 2018

Bangladesh

Egypt

Iran

Mexico

Nigeria

Pakistan

6.9

4.3

6.5

2.3

4.7

South Korea

Turkey

2.8

2.9

7.0

4.5

4.3

2.0

5.2

2.8

3.3

6.9

3.5

3.3

1.7

Indonesia

Malaysia

Philippines

Thailand

Vietnam

5.0

4.2

6.8

3.2

6.2

5.3

4.7

6.9

3.3

6.3

5.1

4.5

6.8

3.0

6.5 Weighted avg.3)

Weighted avg.3)

Weighted avg.3)

2017 2016 2018

Weighted avg.3)

Real GDP growth [%]

1.9

BRIC NEXT-112) ASEAN-5

MIST1)

5.0

2.7

2.5

2018

1) The MIST states include Mexico, Indonesia, South Korea and Turkey 2) Except for the Asean-5 countries Indonesia, Philippines and Vietnam. However the weighted average includes all countries of the aggregate Next 11, not only the ones listed 3) Average weighted via GDP in PPP current international dollar

2017

5.7 5.7 5.1

3.6 3.2 3.4

5.2 5.0 4.9

3.9 4.1 3.6

Source: IMF

2. Financial indicators 3. Other indicators 1. Real economic indicators

1.7 0.2

1.4

-3.6

1.4 -0.2

0.8 -1.5

6.8 7.7 7.2

6.7 6.2 6.6

6 Roland Berger Economic Indicators May 2017 External version.pptx

The risk of recession has declined in most regions worldwide in comparison to the October 2016 forecast – Japan is an exception

2. Financial indicators 3. Other indicators 1. Real economic indicators

> Probability of a recession over a four-quarter horizon till Q1 2018 declined in most regions compared to the October 2016 report

> Japan shows the highest recession risk with 44% up until the first quarter of 2018. Within the Eurozone, the risk is estimated at 30% while the United States face only 22%

> Growth outlook in advanced economies is lifted due to a stronger cyclical momentum and the anticipated US fiscal stimulus, external demand and commodity prices boosting growth perspectives in emerging Asia

Comments

22

30

44

2933

10

5

10

15

20

25

30

35

40

45

Emerging Asia

Latin America

Rest of the World

Japan Eurozone United States

October 2016 WEO: Probability of recession within the period 2016 Q4 – 2017 Q3

Probability of recession within the period 2017 Q2 – 2018 Q1 [% ]

Source: IMF

7 Roland Berger Economic Indicators May 2017 External version.pptx

Global investment levels remain constant – Relative to GDP China invests 2.5 times more than the US and the Eurozone

2. Financial indicators 3. Other indicators 1. Real economic indicators

2008 2010 2012 2014 2016 2018

25.2 25.6 25.2 24.3

23.0

25.1 25.6

US

Eurozone

Germany

Italy

Japan

China

Russia

20.6 19.7

20.2 19.9

19.2 19.1

17.6

23.7 23.4

22.9 25.6

Advanced economies 21.4

20.0

20.0

19.1

17.3

23.5

22.2

World 25.6

Spain 20.6 20.5

(0.2)

(-0.1)

(-0.3)

(1.9)

(0.1)

(0.7)

(-0.1)

(-0.4)

(0.5)

(2.0)

(0.4)

(-0.7)

France 21.9 22.2 (-0.2)

Emerging/dev. economies

20.3

19.9

19.2

23.9

25.8

32.0 32.2 32.0 (0.1) (0.0)

22.1

32.9

22.8 (0.0) 22.4

17.0

20.4

(0.6)

(-0.7)

17.3

20.1

21.1 21.1 (0.3) (0.5)

25.2 (0.2) 25.4 (0.3)

World

2017 2015 2016 (change in forecast)1)

2018 (change in forecast)1)

20.8

43.4 44.1 44.0 (0.9) (0.8) 44.7

Total investment [% of GDP]

Source: IMF

1) Change related to previous forecast (October 2016) indicates stability of the forecast

8 Roland Berger Economic Indicators May 2017 External version.pptx

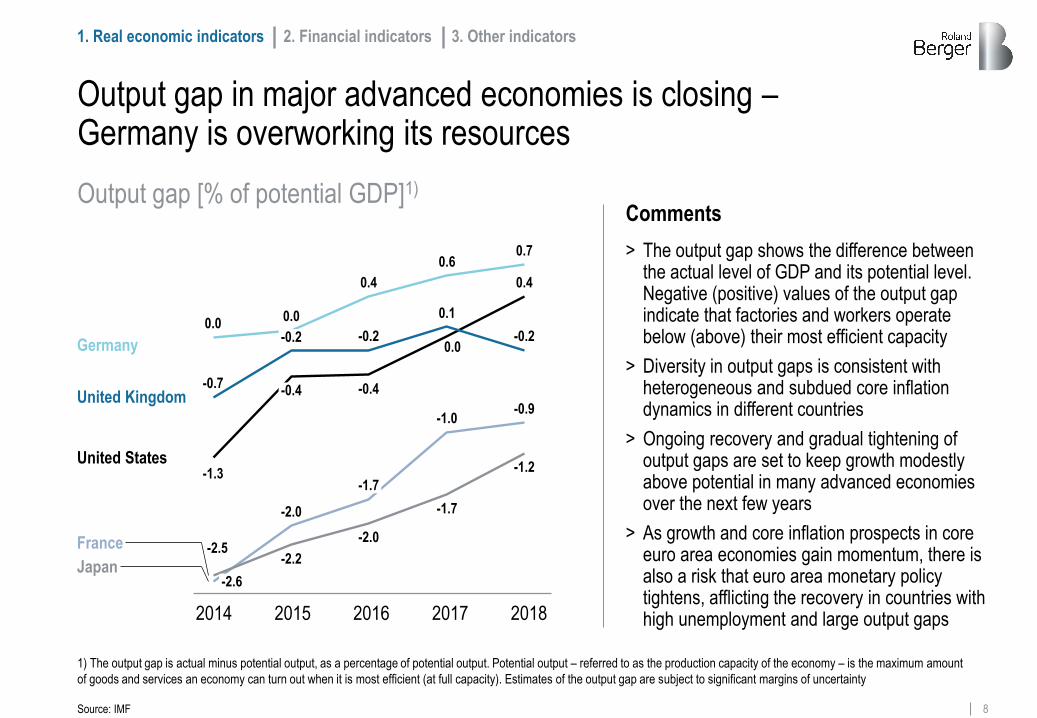

Output gap in major advanced economies is closing – Germany is overworking its resources

-0.2

United Kingdom

France

Japan

Germany

United States

-1.0

0.1

0.4

-1.2

-1.7

0.7

-2.0

-0.9

-0.2 0.0

-1.3

0.0

-2.6

-2.5

-0.7 -0.4

0.0

-2.0

-2.2

-0.2

-0.4

0.4

-1.7

0.6

2. Financial indicators 3. Other indicators 1. Real economic indicators

Source: IMF

1) The output gap is actual minus potential output, as a percentage of potential output. Potential output – referred to as the production capacity of the economy – is the maximum amount

of goods and services an economy can turn out when it is most efficient (at full capacity). Estimates of the output gap are subject to significant margins of uncertainty

Output gap [% of potential GDP]1)

> The output gap shows the difference between the actual level of GDP and its potential level. Negative (positive) values of the output gap indicate that factories and workers operate below (above) their most efficient capacity

> Diversity in output gaps is consistent with heterogeneous and subdued core inflation dynamics in different countries

> Ongoing recovery and gradual tightening of output gaps are set to keep growth modestly above potential in many advanced economies over the next few years

> As growth and core inflation prospects in core euro area economies gain momentum, there is also a risk that euro area monetary policy tightens, afflicting the recovery in countries with high unemployment and large output gaps

Comments

2014 2015 2016 2017 2018

9 Roland Berger Economic Indicators May 2017 External version.pptx

53.9

66.8

53.0

112.4

97.8

122.9 125.9

87.4

45.6

57.4

75.2

Oil price doubled since its low in January 2016, but declined in the first months of 2017 – Forward curve remains flat

Oil price (Brent) [USD/barrel]1) Forward curve and forecast2)

52.1

39.0

76.0

52.2

37.0

80.0

52.4

35.0

75.0

52.5

39.0

70.0

52.3

43.0

66.0

52.2

47.0

66.0

Jan 2006 May 2017 Jan 2008 Jan 2010 Jan 2012

Highest value Jul 2008

147.5 +26.8

Lowest value Jan 2016

-120.4

Jan 2014 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18

1) All values (except highest, lowest and latest) are end-of-month based; highest and lowest values are the max-/minimum on a daily basis, latest value is end-of-day value of May 22nd 2017 2) The blue dashed lines indicate a forecast range of highest and lowest values; the black dashed line is the forward curve

Source: Bloomberg

61.8

2. Financial indicators 3. Other indicators 1. Real economic indicators

27.1

+85.7

10 Roland Berger Economic Indicators May 2017 External version.pptx

1,260.6

1,152.3

1,351.0

724.6

974.2

1,293.0

1,061.4

1,327.3

1,234.6

1,179.6

10

Gold price is volatile around 1,200 USD since mid-2013 – Commodity prices on an upward trend, but still relatively low

Highest value Sep 2011

Lowest value Jan 2006

-660.5 1,921.2

516.9

+121.9

+1,404.3

Highest value Jul 2008

-618.5

Jan 2008 Jan 2006 Jan 2010 May 2017 Jan 2012 Jan 2008 Jan 2006 May 2017

Gold price [USD per ounce]1) S&P GSCI [Index value]1) 2)

Source: Bloomberg

Jan 2014 Jan 2014

271.8

Jan 2010

Lowest value Jan 2016

Jan 2012

890.3

393.7

445.6

703.5

591.0

658.6

758.8

549.9

336.2

599.3

453.9

1) All values (except highest, lowest and latest) are end-of-month based, highest and lowest values are on a daily end-of-day basis, latest value is end-of-day value of May 22nd 2017 2) S&P GSCI (formerly Goldman Sachs Commodity Index): serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time

2. Financial indicators 3. Other indicators 1. Real economic indicators

+436.4

11 Roland Berger Economic Indicators May 2017 External version.pptx

52.8 50.5

53.2

48.6

51.3 52.9

49.1

193.5

181.8

165.6

143.0

148.9 146.6

139.3

180.7

Highest value Jul 2006

In the US, housing market continues its upward trend towards its 2006 high – Global manufacturing index also on a positive trend

-72.4

Lowest value Dec 2008

Highest value April 2010 and Feb 2011

-4.6

34.3

54.6

+23.1

+59.4

Jan 2008 Jan 2006 Jan 2010 Feb 2017 Jan 2012 Jan 2008 Jan 2006 Jan 2010 April 2017 Jan 2012

206.5

Case Shiller Index [Index]1) 3) JPM Global Manufacturing PMI [Index]2) 3)

Jan 2014 Jan 2014

202.0

57.4

1) Measure for the US residential housing market 2) JP Morgan's Purchasing Managers' Index is based on surveys covering purchasing executives in 40 countries accounting for an estimated 95% of global manufacturing output; 50 = neutral mark (no change on prior month) values above 50 indicate rising and below falling values 3) All values are end-of-month based

2. Financial indicators 3. Other indicators 1. Real economic indicators

Lowest value March 2012

134.1

Source: Bloomberg

+4.5

-20.3

12 Roland Berger Economic Indicators May 2017 External version.pptx

With the uptick of commodity prices, an increase in inflation rates is expected for 2017, particularly in advanced economies

2008 2010 2012 2014 2016 2018

3.4 3.5

2.8 2.8

3.2

3.7

4.1

5.0

3.7

2.7

6.3

US

Eurozone

Germany

Italy

Japan

China

Russia

0.1 2.7

0.0 1.7

0.1 2.0

0.1

0.8 1.0

1.4 2.4

15.5 4.5

Advanced economies 0.3

2.4

1.5

1.7

1.3

0.6

2.3

4.2

World 2.8

Spain -0.5 1.4

(0.3)

(0.6)

(0.5)

(0.5)

(0.1)

(-0.6)

(-0.3)

(0.2)

(0.0)

(0.5)

(0.0)

(-0.1)

(-0.3)

(0.4)

France 0.1 1.2 (0.1)

Emerging/dev. economies

1.3

0.2

0.4

-0.1

2.8

4.7 4.7 4.4 (0.2) (0.2)

2.0

7.0

4.4

1.4 (0.4) 0.3

1.3

2.4

(0.8)

(1.4)

-0.1

-0.2

0.8 2.0 1.9 (0.3) (-0.1)

3.5 (0.3) 3.4 (0.1)

2. Financial indicators 3. Other indicators 1. Real economic indicators

World

2017 2015 2016 (change in forecast)1)

2018 (change in forecast)1)

Inflation rate [%]

Source: IMF

1) Annual change in average consumer prices (headline inflation) 2) Change from previous forecast (October 2016) indicates instability of the forecast

13 Roland Berger Economic Indicators May 2017 External version.pptx

2008 2010 2012 2014 2016 2018

4.6

9.1

4.7

9.4

4.9

10.0

5.3

10.9

6.2

11.6

7.4

12.0

8.1

11.4

8.9

10.2

9.6

10.2

9.3

9.7

5.8

7.6

US

Eurozone

Unemployment rates are further decreasing, but still high in Spain, Italy and France and above pre-crisis level in Eurozone

US

Eurozone

Germany

France

Japan

5.3

10.9

4.6

10.4

3.1 3.4 3.1

Advanced economies 6.2 6.7

3.1

Spain 22.1

China

Russia

4.0 4.1 4.0

5.5 5.6 5.5

4.0

5.5

(-0.1)

(0.0)

(-0.4)

(-0.1)

(0.0)

(0.0)

Italy 11.9

4.7 4.6 (-0.1) (-0.1) 4.9

10.0

4.2 4.2 4.2 (-0.3) (-0.4)

10.0

11.7

19.6

9.6 9.3 (0.0) (0.0)

11.4 11.0 (0.2) (0.2)

17.7 16.6 (-0.3) (-0.3)

Source: IMF

1) Change from previous forecast (October 2016) indicates instability of the forecast

2. Financial indicators 3. Other indicators 1. Real economic indicators

2017 2015 2016 (change in forecast)1)

2018 (change in forecast)1)

9.4 9.1 (-0.2) (-0.2)

6.0 5.8 (-0.1) (-0.2)

Unemployment rate [%]

14 Roland Berger Economic Indicators May 2017 External version.pptx

1,871

3,076

4,612

3,235

2,048

3,412

12,811

13,930

10,913

16,285

18,308

20,895

+14,699

US and German equities reach new heights …

Jan 2006 May 2017

Highest value March 2017

Highest value May 2017

Highest value Oct 2007

+9,253

-3,048

May 2017

10,865

Dow Jones [Index value]1) DAX [Index value]1) Shanghai Composite [Index value]1)

-274

6,124 12,842

Lowest value Mar 2009 6,470

Lowest value Jan 2006

-4,395 -2,085

+4,962

Jan 2006

1,162

Jan 2006 May 2017

Lowest value Mar 2009

-223

5,674

12,619

9,495

5,502

7,376

8,067

3,589

1) All values (except highest, lowest and latest) are end-of-month based; highest and lowest values are the max-/minimum on a daily basis, latest value is end-of-day value of May 22nd 2017

Source: Bloomberg

2. Financial indicators 3. Other indicators 1. Real economic indicators

21,169

15 Roland Berger Economic Indicators May 2017 External version.pptx

19,678

15,576

16,291

8,928

11,090

18,262

16,650

3,577

2,865

3,697

2,119

3,013

Highest value Jun 2007

… a positive trend all around the globe

+1,812

+13,958 +2,857

Jan 2006 May 2017 Jan 2006 May 2017

-2,807

Jan 2006

6,168 Highest value Jun 2007

3,692

Highest value June 2015

4,948

-3,703

May 2017

4,573

EURO STOXX [Index value]1) Nikkei [Index value]1) CAC 40 [Index value]1)

Lowest value Mar 2009 1,765

Lowest value Oct 2008

20,953

-1,274

-9,655

+881 5,323

4,110

3,017

5,083

4,237

Lowest value Mar 2009

2,465

2. Financial indicators 3. Other indicators 1. Real economic indicators

+1,220

Source: Bloomberg

1) All values (except highest, lowest and latest) are end-of-month based; highest and lowest values are the max-/minimum on a daily basis, latest value is end-of-day value of May 22nd 2017

6,995

16 Roland Berger Economic Indicators May 2017 External version.pptx

1.12 1.15

1.25

1.39

1.23

1.45

1.50

1.18

0.00

0.50 0.25

1.50

1.00

0.25

2.00

4.25

5.25

4.50

2.25

Fed interest rate expected to rise to 1.75% by end of 2018, while ECB's expected to stay at zero – Euro slightly gaining on the Dollar

Source: Bloomberg, Commerzbank

Highest value Apr 2008

Lowest value Jan 2017 1.03

1.60

Jan 2006 May 2017 Jan 2006 May 2017

Fed

1.75

0.00

Q1 2018

1.12

0.90

1.19

1.11

0.99

1.15

ECB

Q2 2018

Interest rates [%]1) EUR/USD exchange rate [EUR/USD]1) Forecast2) Forecast3)

1.23

1) All values (except highest, lowest and latest) are end-of-month based; highest and lowest values are the max-/minimum on a daily basis, latest value is end-of-day value of May 22nd 2017 2) The forecast shows the medium line "consensus" 3) The blue dashed lines indicate a forecast range of highest and lowest values; the black dashed line is the forward curve

1.00

2. Financial indicators 3. Other indicators 1. Real economic indicators

1.25 1.50

17 Roland Berger Economic Indicators May 2017 External version.pptx

-5

0

5

10

15

20

25

30

35

Bond yields still on very low levels – CDS indices with downward trend indicating a decline of implied risk

May 2017 Jan 2008

0

50

100

150

200

First 36 month LTRO2) announcement 21 Dec 2011

Eurozone 70

US 72

Asia 87

Jan 2010 Jan 2012 Jan 2014

Yields of 10y government bonds [%]1) Credit default swaps [Index 01/11=100]1)

Source: Bloomberg

May 2017 Jan 2011 Jan 2013 Jan 2015

1) All values (except latest) are end-of-month based; latest value is for May 22nd 2017 2) LTRO: Long Term Refinancing Operations. ECB lends money to Eurozone banks at a very low interest rate

2. Financial indicators 3. Other indicators 1. Real economic indicators

LATEST VALUES LATEST VALUES

Greece 5.7

Italy 2.1

France 0.8

Germany 0.4

Spain 1.6

Portugal 3.2

China 3.7

18 Roland Berger Economic Indicators May 2017 External version.pptx

2016 2015 2017 2018

Fiscal balance [% of GDP]1)

-3.9

-2.7

-4.8

-2.9

-1.6

-3.6

-0.9

-6.2

-3.7

-8.6

1.3

-1.4 -1.0

-3.3

Austerity efforts in EU and Eurozone continue, while in developing countries lowering fiscal debt is expected for 2017 and 2018

0.6

-1.5

-0.9

-2.4

-4.0

-1.9

-3.3

-2.8

-4.0

-3.2

-9.1

-3.7

-6.4

-2.9

-2.6

0.7

-3.4

-2.7

-3.5

-4.4

-5.1

-4.4

-3.5

-3.5

-10.3

-2.8

-7.1

-4.0

-3.4

0.8

0.0

-1.9

-2.4

-4.2

-2.3

-4.6

-3.1

-4.4

-3.3

-9.0

-3.7

-6.6

-2.9

-3.7

-2.8

0.6

-1.0

-0.5

-1.4

-3.3

-2.2

-2.7

-2.1

-4.5

-7.5

-3.4

-6.3

-2.5

-1.9

-0.3

Advanced economies2)

Emerging & developing economies2)

1) Fiscal balance is represented by the IMF indicator "general government net lending/borrowing" 2) Average of all advanced and emerging & developing countries in line with the following chart (general government gross debt)

Source: IMF

2. Financial indicators 3. Other indicators 1. Real economic indicators

2004 2006 2008 2010 2012 2014 2016 2018

Selected advanced economies

Selected emerging economies

EU-28

Eurozone

Germany

Greece

Ireland

Italy

Japan

Portugal

Spain

United Kingdom

United States

France

Brazil

China

India

Mexico

Russia

-1.8

-1.5 -2.1

-2.3

-1.7

-1.7

-1.2

-1.3

19 Roland Berger Economic Indicators May 2017 External version.pptx

2016 2015 2017 2018

General government gross debt [% of GDP]1)

5047

403738

3437

47

79

106107105107

98

7477

2004 2006 2008 2010 2012 2014 2016 2018

Government debt in advanced economies set to stay at a high level with total annual GDP not sufficient to pay off

Emerging & developing economies

Advanced economies

180.7

132.8

239.2

90.1

84.7

64.7

74.8

128.6

98.5

89.0

108.3

97.4

92.6

86.7

71.2

179.4

78.7

132.0

238.0

129.0

99.8

89.0

105.6

96.2

91.3

85.8

67.6

181.3

76.4

132.6

239.2

130.3

99.3

89.2

107.4

96.6

81.2

49.3

67.8

57.2

17.1

72.5

42.6

69.6

53.7

15.9

78.3

46.2

69.5

58.1

17.0

97.4

62.0

181.5

73.4

131.6

239.4

127.1

97.9

88.7

108.9

88.6

83.4

82.7

52.0

66.1

56.8

17.3

1) Gross debt consists of all liabilities that require payments of interest and/or principal by the debtor to the creditor in the future. No financial assets of a state, such as gold, currency reserves, loans and other accounts receivables are deducted

2. Financial indicators 3. Other indicators 1. Real economic indicators

EU-28

Eurozone

Germany

Greece

Ireland

Italy

Japan

Portugal

Spain

United Kingdom

United States

France

Brazil

China

India

Mexico

Russia

Advanced economies

Emerging economies

Source: IMF

20 Roland Berger Economic Indicators May 2017 External version.pptx

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160 170 180 190 200 210 220 230 240

Russia Mexico

India

China

Brazil

Eurozone

EU-28

United States

UK

Spain

Portugal

Japan

Italy

Ireland

Greece

Germany

France

Germany is the only big EU country coming within reach of the original Maastricht criteria of 60% government debt

Fiscal balance

General government gross debt

Former Maastricht criteria: max. 60%

Former Maastricht criteria: max. 3%

2. Financial indicators 3. Other indicators 1. Real economic indicators

Public finances 2017 – Fiscal balance and general government gross debt [% of GDP]

Source: IMF

21 Roland Berger Economic Indicators May 2017 External version.pptx

14.9 26.8

-14.7

17.2 13.0

-7.5

Sentiment in the world economy and major regions is recovering …

Q1 2006 Q2 2017 Q1 2006 Q2 2017 Q1 2006 Q2 2017

World economic climate [Balances]1) Economic climate – EU [Balances]1) Economic climate – Asia [Balances]1)

1) Arithmetic mean of judgment about the present and the expected economic situation. As of the first quarter 2017 the Ifo Institute uses "balances" to illustrate the economic climate instead of indices. The balances range between − 100 and + 100 points.

Highest value Q3 2007 30.2

+3.4

Lowest value Q1 2009 -52.7

-82.9

24.8

-28.9

-0.4

-28.9

17.0 10.1

27.8

Highest value Q3 2007 32.4

+15.4

Lowest value Q1 2009 -61.2

-93.6

14.8

22.5

-8.8

17.6

-7.2

33.4 32.2

Highest value Q2 2010 33.4

Lowest value Q1 2009 -47.4

-79.6

2. Financial indicators 3. Other indicators 1. Real economic indicators

+80.8

Source: Ifo Institute

+65.7 -18.6 +86.0

0 0 0

22 Roland Berger Economic Indicators May 2017 External version.pptx

27.8

2.5

30.0

-1.4

-31.3

14.0 19.6

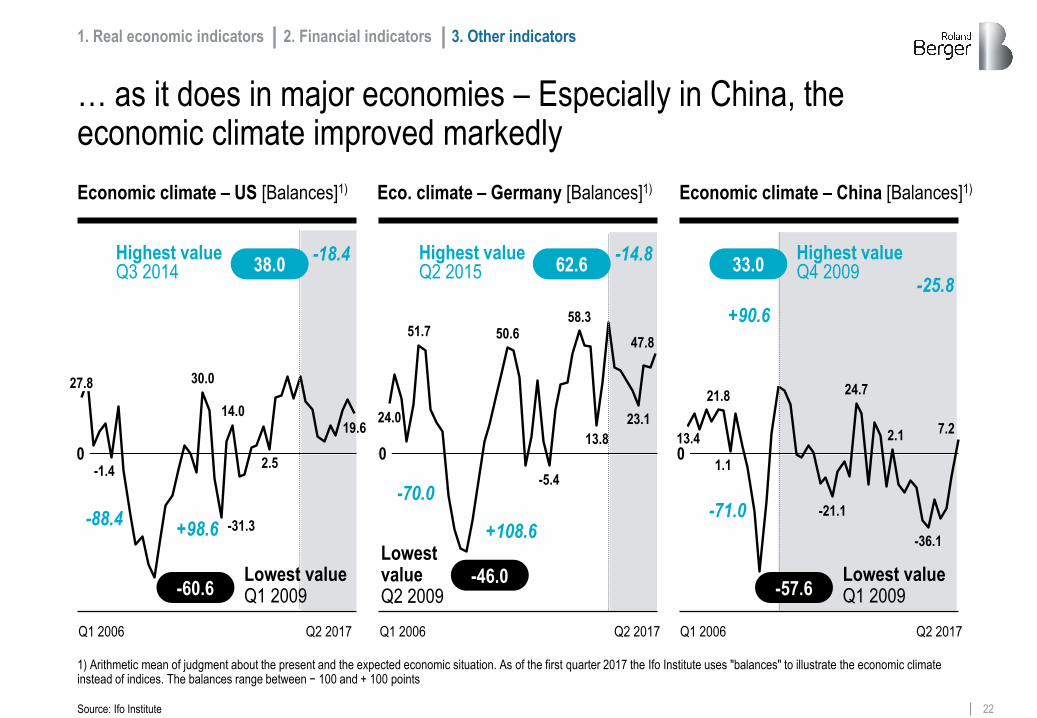

… as it does in major economies – Especially in China, the economic climate improved markedly

Q1 2006 Q2 2017 Q1 2006 Q2 2017 Q1 2006 Q2 2017

Economic climate – US [Balances]1) Eco. climate – Germany [Balances]1) Economic climate – China [Balances]1)

Highest value Q3 2014 38.0

Lowest value Q1 2009 -60.6

-88.4

51.7

24.0 23.1

47.8

13.8

58.3 50.6

-5.4

13.4

21.8

1.1

-21.1

24.7

-36.1

7.2 2.1

Highest value Q4 2009 33.0

+90.6

Lowest value Q1 2009 -57.6

-71.0

2. Financial indicators 3. Other indicators 1. Real economic indicators

Lowest value Q2 2009

Highest value Q2 2015

-46.0

62.6 -14.8

+108.6

-70.0

-18.4

+98.6

Source: Ifo Institute

-25.8

0 0 0

1) Arithmetic mean of judgment about the present and the expected economic situation. As of the first quarter 2017 the Ifo Institute uses "balances" to illustrate the economic climate instead of indices. The balances range between − 100 and + 100 points

23 Roland Berger Economic Indicators May 2017 External version.pptx

10.2

9.8 8.9

5.7

6.0

4.2

4.6

8.4

9.1

97.7

87.2

94.7

73.2

85.1 82.7

55.7

77.5

70.3

90.4

96.9

79.1

91.2

Consumer confidence in Germany again at highest level – US sentiment strongly improved lately, heading to its January 2015 high

Highest value Jan 2015

Lowest value Nov 2008

4.0

Lowest value Sep 2008

Highest value June 2015, Sep. 2016 Feb. 2017 and May 2017

1.5 55.3

98.1

Jan 2006 Jan 2008 May 2017 Jan 2010 Jan 2012

+8.7 +42.8

Consumer index – Germany1) [Indicator] Consumer sentiment – US [Index; 1966=100]

-0.4

Jan 2014 Jan 2006 Jan 2008 May 2017 Jan 2010 Jan 2012 Jan 2014

-2.5

-35.9

1) Indicates change in real private consumption compared to the year before divided by 10; value of 10 indicates consumption growth of 1%

Source: GFK, University of Michigan

2. Financial indicators 3. Other indicators 1. Real economic indicators

10.2

24 Roland Berger Economic Indicators May 2017 External version.pptx

24

Contacts & selected resources for further reading

Klaus Fuest +49 (211) 4389-2231

Christian Krys +49 (211) 4389-2917

Eurostat Data for short term economic analysis (April 2017) Link

OECD Economic outlook and interim economic outlook (March 2017) Link

Contacts Further reading IMF World Economic Outlook (April 2017)

Link