Embed Size (px)

DESCRIPTION

COO Insight

Citation preview

myth or reality?

Is there enough oil? Could there be a trade war over rare earths?

How Winfried Seitz, COO at BSH, manages resources

SCarCity

COOinsights

the magazine for Chief operating offiCerS

issUE 02.2013

FIGURE IT OUT

1300

A magnet made from a neodymium compound* can carry

1,300 times its own weight

(*For details of the make-up of neodymium and what it is used for, see pages 28-29)

3COO Insights | 02.2013

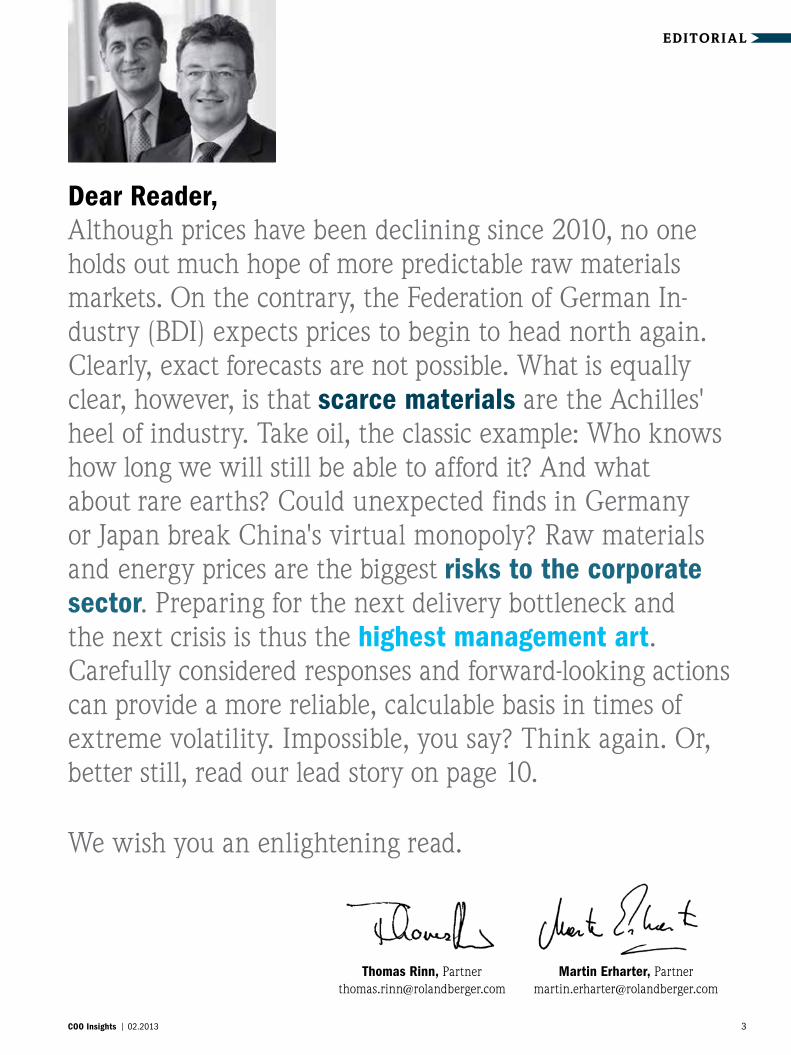

EdITORIal

Thomas Rinn, [email protected]

Martin Erharter, [email protected]

Dear Reader, Although prices have been declining since 2010, no one holds out much hope of more predictable raw materials markets. On the contrary, the Federation of German In-dustry (BDI) expects prices to begin to head north again. Clearly, exact forecasts are not possible. What is equally clear, however, is that scarce materials are the Achilles' heel of industry. Take oil, the classic example: Who knows how long we will still be able to afford it? And what about rare earths? Could unexpected finds in Germany or Japan break China's virtual monopoly? Raw materials and energy prices are the biggest risks to the corporate sector. Preparing for the next delivery bottleneck and the next crisis is thus the highest management art. Carefully considered responses and forward-looking actions can provide a more reliable, calculable basis in times of extreme volatility. Impossible, you say? Think again. Or, better still, read our lead story on page 10.

We wish you an enlightening read.

COO Insights | 02.20134

TITLE6

SNAPSHOTS

Pictures in this edition Digging for coal. Toiling for gold. Our photographic angle on the subject of scarcity

10SCARCITY

A problem recognized is a problem solved. Right?

Financial crisis? Done and dusted. Scarce raw materials are the real challenge to industry. How can we manage scarcity?

20INTERvIEw

"We won't be held to ransom"Winfried Seitz, COO at Bosch und Siemens Hausgeräte, on the daily struggle

against supply-side concentration and turbulent prices

28RARE EARTHS

Will wonders never cease?To date, no one has questioned China's virtual monopoly of rare earths – but

for how much longer? The competition is catching up

wORkSHOP33

wORTH kNOwING

Facts and figures about critical raw materials, product innovations, modularization

and the transformation of business models

37kIOSk

Readers' corner Management and strategy in an uncertain world

387 QUESTIONS FOR...

Peter BuchholzRaw materials are scarce. What assistance can companies expect from outside

instances? Answers from the Head of the German Mineral Resources Agency, DERA

14gloBal

perSpeCtive scarce resources?

so far, the geo- logical perspective

begs to differ

27Copper

Criminal energy as the mother of

invention? Bizarre developments in

a world of affluent thieves

2figUre it oUt

3editorial

39imprint

cOnTEnTs | ISSUE 02.2013

18voiCeSthere is certainly no shortage of views on the subject of scarcity. in case you haven't heard them all, here are a few more

39oUtlooK

Frugal products are playing an ever more

important role on Western markets

TITLE

| MAIN TOPIC | SCARCITY

>noun The quality or state of being scarce; especially: want of provisions for the

support of life; insufficiency of amount or supply; shortage.<

/sker-s -te/

PICTURES IN THIS EDITION germany

dIGGInG FOR cOal

>Measuring more than 110 square kilometers and containing well over a billion tonnes of lignite, RwE's Garz-weiler open-face mine in North Rhine-westphalia is a gaping hole with the feel of a prehistoric meteor crater. The lignite can be traced back to the forests and moors that thrived in the Lower Rhine Basin millions of years ago. Today, gigantic bucket-wheel excavators relentlessly chew their way through up to 240,000 tonnes of this semi-buried treasure a day. Yard for yard, the face of the landscape is changing – and will continue to do so through 2045. villages are being re-settled. Thousands of people are having to leave house and home. Germany's Federal Supreme Court is investigating whether this expropriation violates the owners' fundamental rights.

COO Insights | 02.2013 7

TITlE | SNAPSHOTS

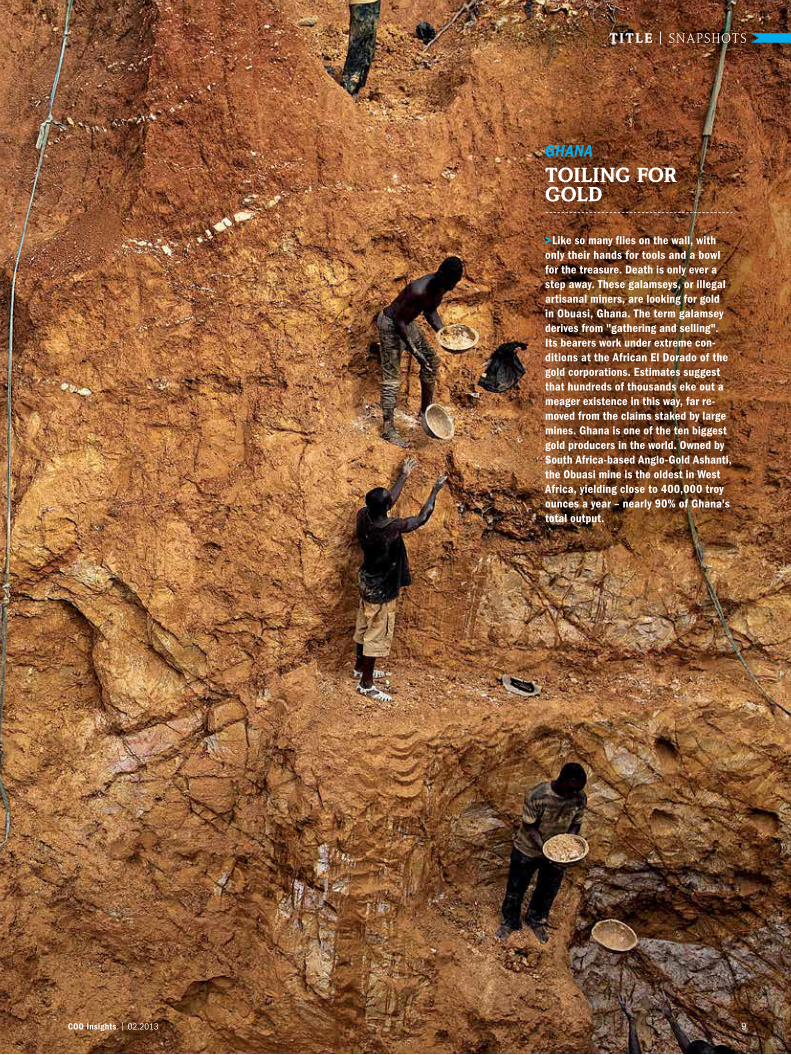

ghana

>Like so many flies on the wall, with only their hands for tools and a bowl for the treasure. Death is only ever a step away. These galamseys, or illegal artisanal miners, are looking for gold in Obuasi, Ghana. The term galamsey derives from "gathering and selling". Its bearers work under extreme con- ditions at the African El Dorado of the gold corporations. Estimates suggest that hundreds of thousands eke out a meager existence in this way, far re-moved from the claims staked by large mines. Ghana is one of the ten biggest gold producers in the world. Owned by South Africa-based Anglo-Gold Ashanti, the Obuasi mine is the oldest in west Africa, yielding close to 400,000 troy ounces a year – nearly 90% of Ghana's total output.

TOIlInG FOR GOld

TITlE | SNAPSHOTS

COO Insights | 02.2013 9

COO Insights | 02.201310

A PROBLEMRECOGNIzED IS

A PROBLEMSOLvED. RIGHT?

When Joachim Hüttemann thinks of the raw materials crisis, he thinks of "Inger". This green- ish brown willow plant stretches toward the heavens, modest and ecologically friendly.

"Inger" needs little in the way of light, nutrients or pesticides. It can be coppiced (cut down to encourage new growth) and grows extremely fast, making it the ideal plant for short-rota-tion forestry with maximum yield. After only three years, this Swedish-Russian hybrid willow is already several meters taller than Hüttemann himself, owner of the large-scale agricultural enterprise in Soltau, Lower Saxony in northern Germany. When turned into wood chips, this biomass helps offset exploding gas and heating oil prices. The use of wood in wood-burning and pellet stoves is becoming increasingly popular. In 2012, Germans burned an estimated 70 million cubic meters of wood, compared to 30 million a decade ago. The University of Hamburg's Institute of Forestry and Timber Management expects this figure to rise by another 10%.

Can agriculture be an answer to the global scarcity of resources? Can "turbotrees" (as reported by German maga-

zine Wirtschaftswoche) take over from rapeseed and coal as a response to the tyranny and unpredictability of energy-producing superpowers? Can imaginative innovation satisfy emerging markets' insatiable hunger for raw materials? One thing is certain: Although Inger may not be able to solve Europe's energy crisis single-handedly, this charming little plant from the German countryside is symbolic of one of the greatest threats to advanced industries: a lack of natural resources.

Entrepreneurs and their leading representatives have long since overcome their reservations. Ulrich Grillo, President of the Federation of German Industry (BDI), sees the develop-ment of energy and raw materials prices as the "biggest risk factor" for 75% of companies. When he served as chair of the BDI's committee for raw materials, Grillo already viewed secure, clean and affordable energy as well as a reliable supply of raw materials at competitive prices as "megatopics for the future".

In a study by Commerzbank's initiative "Unternehmer-Perspektiven" (Entrepreneurial Perspectives), Markus Beumer,

The raw materials markets are going haywire. Scarcity is threatening industry and prices are on a roller-coaster ride. Everyone's

talking about the crisis. But why not talk about opportunities too – for the company and the product portfolio?

TITlE | SCARCITY

w

one of the bank's Managing Directors, was amazed to note that "companies see raw materials as a much more urgent issue than energy". For many companies, the scarcity of raw materials is a question of survival.

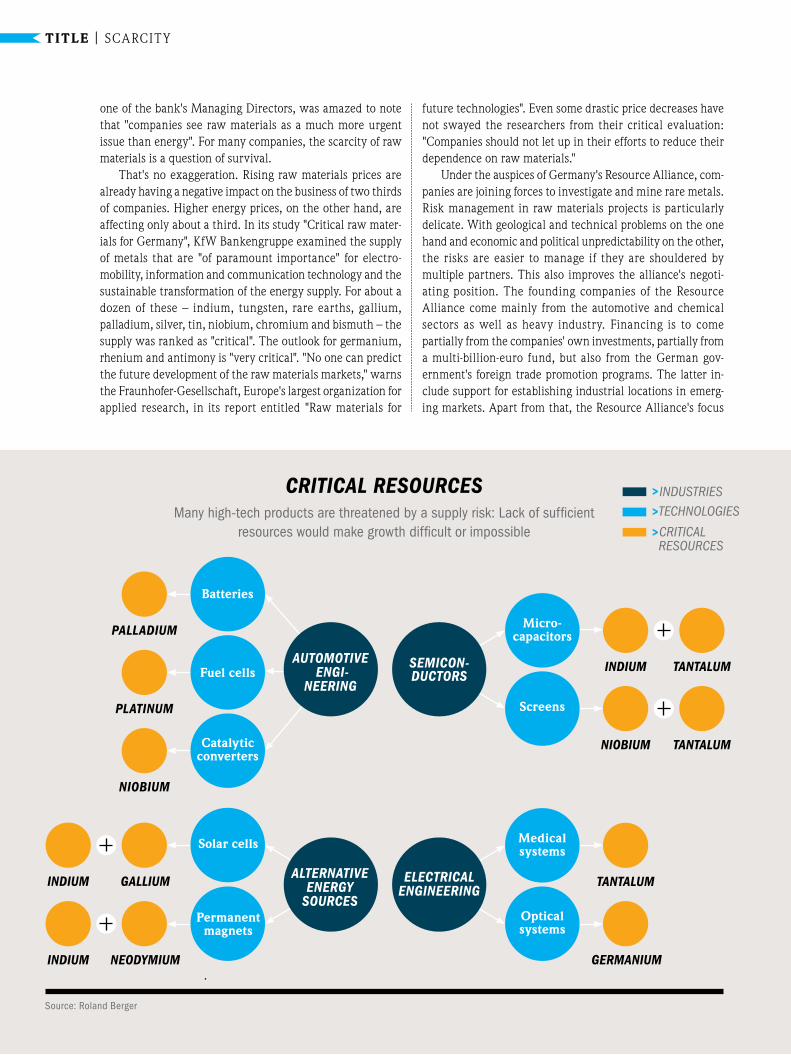

That's no exaggeration. Rising raw materials prices are already having a negative impact on the business of two thirds of companies. Higher energy prices, on the other hand, are affecting only about a third. In its study "Critical raw mater-ials for Germany", KfW Bankengruppe examined the supply of metals that are "of paramount importance" for electro-mobility, information and communication technology and the sustainable transformation of the energy supply. For about a dozen of these – indium, tungsten, rare earths, gallium, palladium, silver, tin, niobium, chromium and bismuth – the supply was ranked as "critical". The outlook for germanium, rhenium and antimony is "very critical". "No one can predict the future development of the raw materials markets," warns the Fraunhofer-Gesellschaft, Europe's largest organization for applied research, in its report entitled "Raw materials for

future technologies". Even some drastic price decreases have not swayed the researchers from their critical evaluation: "Companies should not let up in their efforts to reduce their dependence on raw materials."

Under the auspices of Germany's Resource Alliance, com-panies are joining forces to investigate and mine rare metals. Risk management in raw materials projects is particularly delicate. With geological and technical problems on the one hand and economic and political unpredictability on the other, the risks are easier to manage if they are shouldered by multiple partners. This also improves the alliance's negoti-ating position. The founding companies of the Resource Alliance come mainly from the automotive and chemical sectors as well as heavy industry. Financing is to come partially from the companies' own investments, partially from a multi-billion-euro fund, but also from the German gov-ernment's foreign trade promotion programs. The latter in-clude support for establishing industrial locations in emerg- ing markets. Apart from that, the Resource Alliance's focus

TITlE | SCARCITY

CritiCal reSoUrCeS Many high-tech products are threatened by a supply risk: Lack of sufficient

resources would make growth difficult or impossible

source: Roland Berger

palladiUm

platinUm

nioBiUm

nioBiUm tantalUm

indiUm tantalUm

germaniUm

tantalUmgalliUmindiUm

neodymiUmindiUm

> INDUSTRIES>TECHNOLOGIES

>CRITICALRESOURCES

SemiCon- dUCtorS

eleCtriCal engineering

alternative energy

SoUrCeS

aUtomotive engi-

neering

Batteries

Fuel cells

catalytic converters

solar cells

Permanent magnets

Optical systems

Medical systems

screens

Micro-capacitors

13COO Insights | 02.2013

is on countries such as Canada or Australia, although it also seeks support from the political arena where necessary, for example in countries with trade barriers. This support may take the form of country-to-country partnerships, such as those recently set up with Mongolia and Kazakhstan.

Europe too wants to bundle its resources "to become the world leader in the capabilities related to exploration, extrac-tion, processing, recycling and substitution," says European Commissioner for Industry Antonio Tajani. Beginning in 2014, EUR 90 million is to be invested each year in procuring raw materials. Tajani also calls for the expansion of recycling efforts and better exploitation of domestic resources. He estimates Europe's untapped mineral resources at a depth of 500 to 1,000 meters to be worth about EUR 100 billion.

Global alliances will buttress this strategy. At the EU-Latin America summit in Santiago, Chile, German Chancel-lor Angela Merkel signed an agreement to work with Chile in exploring and developing further deposits, for example of copper, rhenium, lithium and iodine. Chile alone is home to more than 34% of the world's copper. The mining coopera-tion is to be overseen by Germany's Federal Ministry of Economics, which is currently negotiating a similar arrange-ment with Peru.

By turns jubilant and despondent: Ever since the turn of the millennium, the price carousel has been spinning so quickly that even hardened materials purchasers must be getting dizzy. Nickel, for

instance, became five times as expensive in 2006/2007, only to slide back down almost to its low of 2002 over two years. Platinum and copper fared no differently. In 2010, rare earths accounted for an average of 45% of the value added by one tier-3 supplier that manufactures magnets for the automotive industry. This share had climbed to 89% by July 2011. In the same period, skyrocketing prices for rare earths had an even more drastic impact for a tier-2 producer of electric motors: Its share of value added rose from 6% to 41%. For a tier-1 maker of steering systems, the figure shot up tenfold. Pro-ducers of hybrid cars had to cope with a factor of 14.

But according to Roland Berger Strategy Consultants, it's not just the nerve-wracking volatility of the markets that makes raw materials a strategic component of corporate de-velopment. Five other factors also come into play: industrial incidents and natural disasters; the dangerous dependence on high-performance materials that have no substitute; rock-solid supplier monopolies; government regulation; and the increasing difficulty and expense of exploring new deposits.

Regional disasters or local accidents can hit industries anywhere at any time. And when production halts, prices for raw materials shoot up. The tsunami that devastated Japan in May 2011, costing almost 19,000 people their lives and triggering the Fukushima disaster, also pulled 30 semicon-

ductor manufacturers over the brink. As these 30 companies controlled 40% of the global wafer market, this had grave repercussions for the automotive and electronics industry in Japan, Europe and the US. In 2012, an Evonik chemicals plant in the German town of Marl exploded, halting production of Nylon 12. Car manufacturers from around the world quickly met in Detroit to discuss the crisis, as Nylon 12 plays a crucial role in the production of fuel and brake hoses. This reaction demonstrates just how fragile global supply chains can be: Even Evonik's main competitor, French company Arkema, announced last-minute production interruptions, since Evonik normally supplies it with cyclododecatrien, the raw material for Nylon 12 production. For months, 50% of the world's Nylon 12 market was lost.

The dependency on raw materials is nowhere more ap-parent than for rare earths. These 17 metals are the stuff that dreams of future industries are made of (see also page 31). Take europium, for example: Europium accounts for just 0.0002% of the net weight of a cell phone. Combined with palladium, niobium and terbium, that's still not even 3% of the total weight. But these four elements account for 40% of material costs.

China still has a virtual monopoly on rare earths, ac- counting for more than 90% of global production. Russia and South Africa aren't far behind, controlling 83% of the world's palladium. Brazil and Canada control a whopping 99% of niobium production. So trying to change the status quo re-quires tremendous patience – and deep pockets. Tapping new deposits of rare earths usually takes five to ten years. But how can companies plan and intelligently calculate massive in-vestments when market prices experience double-digit swings every day?

It therefore comes as no surprise that studies by Roland Berger put raw materials and energy prices top of the list of the biggest risks facing companies – well ahead of issues such as domestic demand or labor costs. The cost

of raw materials is the biggest single problem. When asked if they had a special task force for, say, purchasing rare earths, nearly one third of the companies Roland Berger surveyed in September 2011 answered "yes". Almost a year later, in June 2012, this was up to half. A problem recognized is a problem solved, right? Not at all. According to Commerzbank, four

I

B

"The dependency on raw materials is nowhere more apparent than for RARE EARTHS. These 17 metals are the stuff that dreams of future industries are made of."

nEOdYMIUM (nd)>neodymium is rated as one of the most important high-tech metals and is valued in particular for its outstanding magnetic properties. By 2030, de-mand for it is expected to be four times current production.

deposits: China, Russia, south Africa, the UsA

applications: Powerful magnets, smart phones, electric motors

GERManIUM (GE)>germanium is one of the rarest metals on Earth and is possessed of an astonishing density anomaly: its density is lower in the solid state than in the liquid state.

deposits: China, Russia, south Africa, the UsA

applications: solar cells, semiconductors, LED manufacture

TanTalUM (Ta)>high corrosion resistance is what makes tantalum so interesting. the element is used in industry and medicine, e.g. in implants and instruments.

deposits: Australia, Brazil

applications: Micro- capacitors, implants

IndIUM (In)>the display industry and photovoltaic manu-facturers are competing for this particularly scarce metal, demand for which will more than triple between now and 2030. indium is a very soft me- tal that can be cut with a knife.

deposits: China, Japan, Canada, Russia, Peru

applications: Conduc-tors for flat screens, touch screens, solar cells

nIOBIUM (nB) >niobium is extremely resistant to numerous chemicals and is also relatively lightweight. Pro-duction of niobium has increased substantially in recent years.

deposits: Australia, Brazil, Canada, nigeria, Democratic Republic of Congo, Russia

applications: Alloys

canada

PERU

TITlE | KNOWLEDGE

GLOBAL PERSPECTIvE

Critical resources can be found in many countries. Yet a small number of effective monopolies exists too

Usa

dR cOnGO

sOUTH aFRIca

cZEcH REPUBlIc

nORWaY

nETHERlands

alGERIa

UK

14

BRaZIl

MExIcOvEnEZUEla

sURInaM nIGERIa

non

-ene

rgy

reso

urce

s

saUdIa aRaBIa

UnITEd aRaB EMIRaTEs

KUWaIT

IRan

COO Insights | 02.2013

15

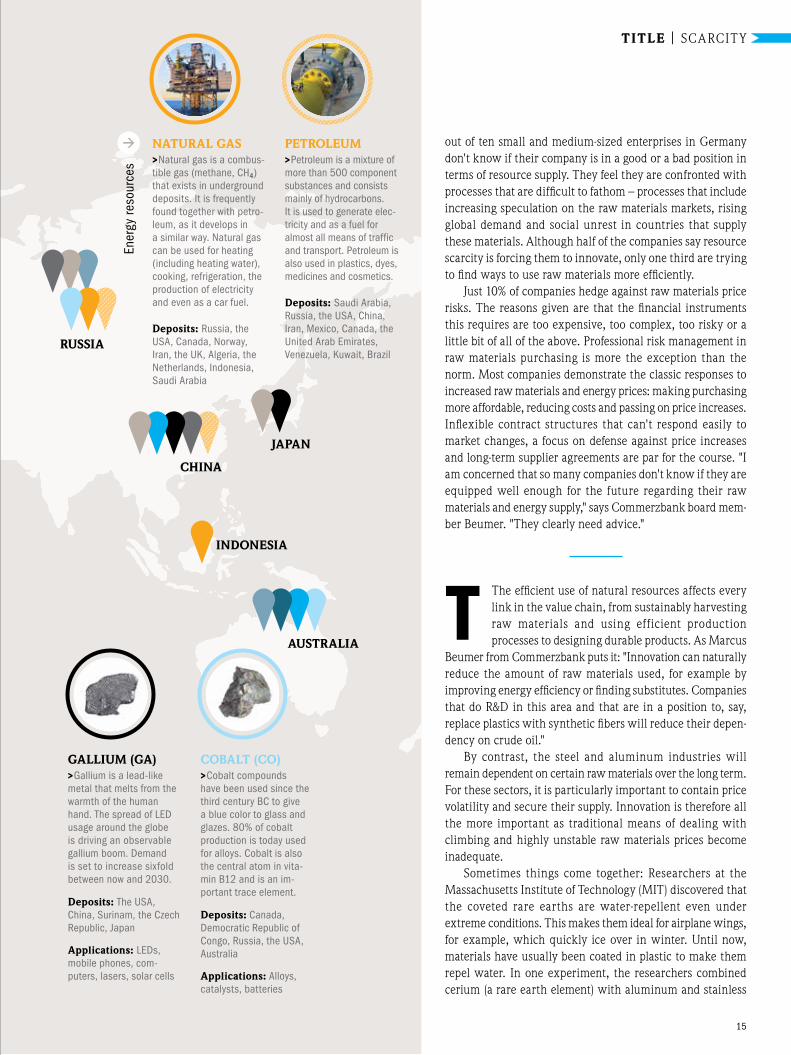

GallIUM (Ga)>gallium is a lead-like metal that melts from the warmth of the human hand. the spread of LED usage around the globe is driving an observable gallium boom. Demand is set to increase sixfold between now and 2030.

deposits: the UsA, China, surinam, the Czech Republic, Japan

applications: LEDs, mobile phones, com- puters, lasers, solar cells

cOBalT (cO)>Cobalt compounds have been used since the third century BC to give a blue color to glass and glazes. 80% of cobalt production is today used for alloys. Cobalt is also the central atom in vita-min B12 and is an im-portant trace element.

deposits: Canada, Democratic Republic of Congo, Russia, the UsA, Australia

applications: Alloys, catalysts, batteries

JaPan

aUsTRalIa

IndOnEsIa

cHIna

out of ten small and medium-sized enterprises in Germany don't know if their company is in a good or a bad position in terms of resource supply. They feel they are confronted with processes that are difficult to fathom – processes that include increasing speculation on the raw materials markets, rising global demand and social unrest in countries that supply these materials. Although half of the companies say resource scarcity is forcing them to innovate, only one third are trying to find ways to use raw materials more efficiently.

Just 10% of companies hedge against raw materials price risks. The reasons given are that the financial instruments this requires are too expensive, too complex, too risky or a little bit of all of the above. Professional risk management in raw materials purchasing is more the exception than the norm. Most companies demonstrate the classic responses to increased raw materials and energy prices: making purchasing more affordable, reducing costs and passing on price increases. Inflexible contract structures that can't respond easily to market changes, a focus on defense against price increases and long-term supplier agreements are par for the course. "I am concerned that so many companies don't know if they are equipped well enough for the future regarding their raw materials and energy supply," says Commerzbank board mem-ber Beumer. "They clearly need advice."

The efficient use of natural resources affects every link in the value chain, from sustainably harvesting raw materials and using efficient production processes to designing durable products. As Marcus

Beumer from Commerzbank puts it: "Innovation can naturally reduce the amount of raw materials used, for example by improving energy efficiency or finding substitutes. Companies that do R&D in this area and that are in a position to, say, replace plastics with synthetic fibers will reduce their depen-dency on crude oil."

By contrast, the steel and aluminum industries will remain dependent on certain raw materials over the long term. For these sectors, it is particularly important to contain price volatility and secure their supply. Innovation is therefore all the more important as traditional means of dealing with climbing and highly unstable raw materials prices become inadequate.

Sometimes things come together: Researchers at the Massachusetts Institute of Technology (MIT) discovered that the coveted rare earths are water-repellent even under extreme conditions. This makes them ideal for airplane wings, for example, which quickly ice over in winter. Until now, materials have usually been coated in plastic to make them repel water. In one experiment, the researchers combined cerium (a rare earth element) with aluminum and stainless

TITlE | SCARCITY

naTURal Gas >natural gas is a combus-tible gas (methane, Ch4) that exists in underground deposits. it is frequently found together with petro-leum, as it develops in a similar way. natural gas can be used for heating (including heating water), cooking, refrigeration, the production of electricity and even as a car fuel.

deposits: Russia, the UsA, Canada, norway, iran, the UK, Algeria, the netherlands, indonesia, saudi Arabia

Ener

gy re

sour

ces

PETROlEUM>Petroleum is a mixture of more than 500 component substances and consists mainly of hydrocarbons. it is used to generate elec-tricity and as a fuel for almost all means of traffic and transport. Petroleum is also used in plastics, dyes, medicines and cosmetics.

deposits: saudi Arabia, Russia, the UsA, China, iran, Mexico, Canada, the United Arab Emirates, Venezuela, Kuwait, Brazil

RUssIa

T

Roland Berger strategy Consultants does not think that compa-nies simply have to "grin and bear" the gyrations of the raw materials markets. there is a way to make planning significantly more reliable. Optimal material management can be achieved in five steps.

PHASE ONE / Transparency and categorization step one of our ap-proach is to systema-tically analyze critical materials in the pro-duction process. What materials are used? in what quantities? For what products? the aim is to precisely identify risks and weaknesses through- out the entire supply

chain. Roland Berger does this by adopting a big-picture, 360° approach that pro- vides insights into the use of materials not only in in-house pro-duction, but also in the components and products provided by suppliers. the use of materials can thus be rendered more trans-parent and catego-rized more precisely.

five StepS to optimal material management

Buyers need a reliable basis for costing and prices – a basis they can plan with for the medium term. Market volatility

makes the price of raw materials unpredictable. Or does it?

1

challenges of the ma-terial markets. some safeguard their supply chains by systemati-cally selecting existing suppliers or cultivating new ones, for example. Others relocate their production to coun-tries such as China, in order to gain preferen-tial status regarding the supply of rare earths. still others pass rising costs on to consumers. hedging – a way of stabilizing prices in the medium term – is another op-tion: it involves guar-ding a position at risk against negative mar-ket price developments by securing adequate counter-positions. however, this can only be done if a contract exists to trade the material on the stock exchange.

PHASE FIvE / Implementationthe last and decisive step is to actually put the defined actions into practice on a day-to-day basis. Only then can material manage-ment be truly success-ful. implementation must therefore be mea- sured and sustained.

5

PHASE TwO / Risk assessment step two involves eva-luating the identified risks. What exactly is driving costs? What are the consequences of real or fictitious delivery bottlenecks? Do they pose a threat to strategic objectives? since not all critical materials have the same impact on pro-duction, the aim is to prioritize or weight them accordingly.

PHASE THREE / scenario development the purpose of step three is to clarify which factors may have an impact on extremely volatile material prices and availability, plus the probability with which they will occur. this is done in order to separate critical uncer-tainties from trends and secondary factors of influence and, on this basis, to be able to make as realistic statements as possib-le about future price developments.

PHASE FOUR / strategic actions step four answers the question what, spe-cifically, the company should now do. Com-panies react in very different ways to the

3

2

4

17COO Insights | 02.2013

steel. They found that cerium's wear rate is much lower than aluminum's and as good as stainless steel's. The best part: Cerium retains its ability to repel water even after abrasion.

For Roland Berger Strategy Consultants, a systematic approach is the best guarantee of professional quality. The foundation for this approach is provided by a precise analysis of mission-critical production materials.

How much of what is needed where and why? Then comes risk assessment: What costs are incurred? Where might supply bottlenecks pose a threat? What strategic risks are involved? Step three involves identifying factors that influence price structures and supply terms. These are used to develop scenarios, which in turn lay the basis for step four: formulating proactive and reactive strategies. The final link in the chain is implementing an action program that anticipates future developments and clearly shows what needs to be done.

What at first appears to be an elegant five-point plan is in reality a highly complex process that puts a figure to probabilities. Raw-material-guzzling companies need to see where they

stand as purchasers of raw materials. However, the difficulties start when one realizes that they are dependent on certain suppliers, who in turn are dependent on other suppliers, whom the purchasers at the consuming companies do not necessarily know about.

It is often very difficult to determine precisely what risks are found where in the supply chain and for which com- ponents. To this end, Roland Berger developed a "Critical Material Cube". This holistic approach makes it possible to identify the consequences of using critical raw materials under certain conditions for each individual product.

Scenario planning likewise takes a methodical approach. The first step is to identify the relevant factors that impact raw materials chains. These are then grouped into trends,

uncertainties and other secondary factors depending on their level of impact and probability of occurrence. Trends form the basis of the scenarios, which differ according to their critical uncertainty. Each scenario is backed up with concrete recom-mendations for action. Let's take rare earths as an example: Some "critical uncertainties" are whether main supplier China will tighten or relax its export restrictions, or if some rare earths can be substituted. Further uncertainties include: how exploration of new deposits in North America, Australia and Germany (see page 30) will play out, how demand will be boosted by the global growth of cutting-edge industries such as communications or renewable energy, and if shutting down illegal mines will further restrict supply.

Secondary factors in this complicated game are political pressure on China to end its monopoly, for instance from the WTO, and crucial successes in recycling. The pricing scenarios developed in scenario planning help size and quantify this problem. This is especially true if the strategies and actions are also supposed to considerably reduce price and supply risks over the long term, e.g. by hedging against high price volatility.

Keeping risks under control improves the opportunities available. Yet scarcity and price increases are not just a threat – they also drive innovation in new industries. Creativity and the ability to innovate are what will make the difference in using shrinking natural resources more efficiently. "A technological edge," according to Germany's Ministry for the Environment, "is an important source of raw materials for a country."

w

TITlE | SCARCITY

31 /Transparency in the supply chain Check and evaluate your direct suppliers' upstream suppliers too to identify any possible supply risks.

2 /Preventive action to avoid supply bottlenecks if you do identify any such risks, all coun-termeasures must be cataloged.

3 /Emergency backup plans for when supply bottlenecks do occurCultivate alternative procurement sources and develop bills of materials that do without the critical assemblies. Contractually agree protective cover in the event of an emergency.

the three rules of thumb at a glance

BUSINESS TIPS

"Although half of the companies say resource scarcity is forcing them to INNOvATE, only one third are trying to find ways to use raw materials more efficiently."

COO Insights | 02.201318

Knowledge is the only raw material of which un-

limited reserves are available on our planet and that isn't consumed but is actually multiplied by use.

7 /HORST köHLER

FORMER GERMAN PRESIDENT

8 /BENjAMIN FRANkLIN

US wRITER AND STATESMAN

Time is money.

6 /THOMAS

LOvE PEACOCk ENGLISH POET

AND PLAYwRIGHT

The waste of plenty is the resource

of scarcity.

4 /ALBERT EINSTEIN

GERMAN PHYSICIST

5 /FRIEDRICH NIETzSCHE

GERMAN PHILOSOPHER

need is regarded as the cause of origin. in truth, it is often only an effect of what has originated.

From William Shakespeare to Milton Friedman, from Albert Einstein to German national soccer coach Joachim Löw, it seems like

everyone has something to say on the subject of scarcity. Their observations are smart to

thought-provoking and witty – and are at times anything but politically correct

wHAT THEY SAY ABOUT SCARCITY

TITlE | vOICES

scarce resources don't put the brake on growth.

On the contrary, if we get ourselves organized properly, they can be

a growth lever.

2 /wILLIAM

SHAkESPEAREENGLISH POET

AND PLAYwRIGHT

When words are scarce, they are seldom

spent in vain.

1 /BURkHARD

SCHwENkER CEO, ROLAND

BERGER STRATEGY CONSULTANTS

3 /jOHN BERGER

ENGLISH wRITER

The poverty of our century is unlike that of any other. It is not, as poverty was before, the result of natural scar-city, but of a set of priorities imposed upon the rest of the world by the rich.

Only two things are infinite, the universe and human stupidity, and I'm not sure about the former.

19COO Insights | 02.2013

13 /DANIEL YERGIN

US AUTHOR

Cycles of shortage and surplus characterize

the entire history of oil.

12 /MARIANNE

GRONEMEYER GERMAN AUTHOR

The first lesson of economics is scarcity: There is never enough of anything to satisfy all those who want it. The first lesson of politics is to disregard the first lesson of economics.

17 /THOMAS SOwELL

US ECONOMIST AND AUTHOR

9 /PETER COYOTE

US ACTOR

11 /MILTON FRIEDMAN

US ECONOMIST AND AUTHOR

if you put the federal government in charge of

the sahara Desert, in five years there'd be a

shortage of sand.

We live in an affluent society. Yet the greater the affluence, the more

needy the people.

14 /DAvID RICARDO

BRITISH ECONOMIC SCIENTIST

gold and silver, like other commodities,

have an intrinsic value, which is not arbitrary,

but is dependent on their scarcity, the quantity of labor be- stowed in procuring them, and the value

of the capital employed in the mines which

produce them.

Money creates scarcity.

10 /HENRIk MüLLER GERMAN EDITOR

Seven scarce resources pose a threat to our future: labor, energy, land, water, time, intel-lect and power. How can we combat this scarcity? By working, saving, being creative, being open, showing solidarity, being original and cooperating.

16 /BURkHARD SCHwENkER CEO, ROLAND BERGER

STRATEGY CONSULTANTS

15 /jOACHIM Löw, GERMAN NATIONAL

SOCCER COACH

I can't just carve them out [of nowhere].

(Background: Difficulties filling the left-back and right- back slots ahead of an international match)

At the risk of sounding like I'm placing a dangerous bet on the future, I will say this: Precisely because resources are running

out, we need growth and, with it, the chance to come up with new inventions that enable us to handle resources in a

completely new way.

COO Insights | 02.201320

The bottleneck manager "Material bottlenecks drive up costs and thus lead to revenue and earnings problems," says Winfried seitz

TITlE | INTERvIEW

21COO Insights | 02.2013

Mr. seitz, can your com- pany be held to ransom? How do you mean?

Because of dependency on materials and the problems that can arise from short-ages and price increases. No, we are too well prepared for that to happen. Sure, we occasionally experience mate-rial bottlenecks that drive up costs and thus lead to revenue or earnings problems. But we can't be held to ransom.

What material bottlenecks are you talking about? Let's define our terminology to start with: When we talk about "material", we don't just mean raw materials, but every kind of part and component that we purchase. The latter usually consist of raw materi-als and their processing. In ei-ther case we face bottleneck and monopoly situations in some areas, and they create dependencies that we have to deal with. All in all, we do so

"wE wON'T BE HELD TO RANSOM"winfried Seitz, COO at Europe's market leader Bosch und Siemens Hausgeräte, talked to COO Insights about the right strategies to prevent bottlenecks from occurring in the first place, about lessons learned from crises such as Fukushima, and about successful business with coffee machines

COO Insights | 02.201322

TITlE | INTERvIEW

very successfully, though in isolated cases we could obvi-ously do better.

To what extent does the material factor affect your earnings? Rare earths, for example, have become as-tronomically expensive. To take an example from the lighting industry: There are some major players for whom the higher prices of europium, yttrium and terbium alone cost around EUR 300 million a year. Rare earths have never had a huge impact for us and are to-day almost entirely negligible. We did build motors that used rare earths for a number of years, but we very quickly switched to ferrite-based solutions when prices went through the roof. We were one of the first companies to use rare earths, but we were also the first to get rid of them again.

so what materials do have a huge impact for you? Mainly metals such as steel and copper, then plastics and foams and a few "little things" like nickel. Incidentally, nickel is a good illustration of the fact that there are at least two important sides to scarcity: cost and availability. You have to draw a distinction between materials that are genuinely in short supply, such as rare earths, and those for which cost is the critical issue. Like steel and plastic granules, nickel is not actually a scarce material. However, its price will tend to increase because production will become more expensive. We have to respond to this situation.

How much does material pur-chasing cost BsH per year?

Around EUR 4.5 billion, of which the materials we just mentioned account for roughly EUR 900 million.

For which materials are market conditions the most difficult right now? For plastics. Here again, that has less to do with availability and more to do with the fact that the most powerful mono-poly situation exists in this context, because many sup-pliers have merged or acquired each other. In many segments there are now only two or three providers. And then there is the fact that BSH pur- chases only 0.5% of their output in some cases, so we are not a major customer for them. In other words, the supply agreements are impor-tant to us but relatively un-important for them. That is not exactly an ideal position from which to negotiate.

What is the situation regarding steel? It is a little easier. There are more competitors, so it is easier for us at least to reduce our dependency on extreme price fluctuations by signing long-term agreements, and because of the competition that exists.

Mr. seitz, if you think back, what developments in recent years have brought the most far-reaching changes to BsH's materials business? I see two things. One is sup-ply-side concentration as sup-pliers have acquired and taken each other over. The other is volatility. Even when you buy semifinished products, you are still dependent on price fluctu-ations for the underlying mate-

rials, such as ore and scrap prices in the steel sector. For some years, volatility has also been made worse by the fact that the prices of input materi-als are no longer determined by supply and demand alone, but increasingly also by financial speculation on the part of institutional investors.

How far does that affect BsH? In the past, prices were more readily calculable because they were more closely linked to the economic cycle. You paid more in the boom years, but you could sell more too. When the economy was faltering and you weren't earning so much money, you were at least able to pay less on the purchasing side. Sadly, that is no longer necessarily the case today, which makes it more difficult to be prepared. There is there-fore a greater risk that business performance will fluctuate more strongly and that, in the worst-case scenario, the bad times could be made even worse by the burden of ex-tremely high material prices.

How can you respond to this situation? We can do so only to a limited extent – via long-term supply agreements or hedging instru-ments and, in the long term, preferably by going the way of substitution. On the latter score, we have done a lot in recent years to make ourselves less dependent. I have already mentioned the example of motors for which we now use ferrites instead of rare earths.

How far ahead do you think when making such plans? Five years? Or is it more like twenty?

The company in figures

9.8

46,000

42

BSH

BILLION EUROSwas the sales figure post- ed in 2012, making Bsh Bosch und siemens haus-geräte gmbh the biggest manufacturer of domestic appliances in Europe. Bsh is also one of the world's leading companies in this industry.

EMPLOYEESwork at around 70 com-panies in 50 countries.

FACTORIESare operated in 13 coun-tries in Europe, the UsA, Latin America and Asia.

23COO Insights | 02.2013

That varies considerably. You can't hedge for more than one or two years, because no one can predict what prices will be in the longer term. When look- ing at ways to make ourselves less dependent on scarce min-eral resources, we are talking about something like five to ten years. We need that kind of period, because developing products accordingly and modifying specifications and material requirements alone takes between one and three years. And then we want to use the new solutions success-fully for at least five years.

What is more important for you when dealing with critical materials: com-mercial solutions such as long-term agreements, or technical solutions such as substitution? Both are equally important, they go hand in hand. Product development tends to have a

more long-term effect, whereas commercial methods usually have a more short-term impact.

Have you ever had the assembly lines come to a standstill because you were out of material at some point? Regrettably, that will always happen from time to time. Fortunately, though, that is a very rare occurrence at BSH, because we have set up very professional purchasing and supply chain processes.

can you recall a recent case? We learned a lot in 2008/2009, when the automobile indus-try was experiencing terrible sales problems. The situation showed us the various de-pendencies, even if it didn't stop the production lines rolling this time around. We had our hands full making sure that didn't happen,

though. Back then, a lot of electronics suppliers were rolling back their production – on a huge scale in some cases – because of the automotive crisis. Since some of them were also our suppliers, we too suddenly found ourselves confronted with supply-side bottlenecks.

so availability problems are due rather to a lack of supplier capacity than to scarce materials? Let me put it like this: On the subject of scarcity, you have to consider very many aspects and their long-term influence. Of course there are the materi-als. But there are also the sup-pliers, machines and tools that could fail. Increasingly, there are also other industries who-se influence would never even have come up on the radar screen in the past. It is usually easy to control one factor. But when you suddenly have sev-

>Born in nuremberg in 1953, seitz completed his apprenticeship as an in-dustrial clerk at siemens before studying business administration at the Friedrich-Alexander-Univer-sität Erlangen-nuremberg.

>he began his career in 1979 as a trainee at Robert Bosch gmbh in nuremberg, where he rose to the position of Deputy head of Accounting.

>A 1983 move saw him appointed as head of Central Plant Controlling at Bsh Bosch und siemens hausgeräte gmbh in Munich.

>Following on from stints as Commercial Executive at the Bsh factory in Dillingen, head of the Dishwashers Product Division and head of the Laundry Care Product Division, seitz became a member of the Board of Management and Chief Operating Officer in 2009.

>Winfried seitz is married and has two children. he has a passion for ball sports and skiing.

about

wINFRIEDSEITz

InterviewRoland Berger Part-ners thomas Rinn and Jochen gleis-berg in conversation with Winfried seitz

COO Insights | 02.201324

TITlE | INTERvIEW

eral factors in combination, it gets difficult. For us, there is also the seasonal issue, which reaches the greatest extremes in our business with Tassimo coffee machines. Here, we have intra-year fluctuations of 10:1.

In terms of volume sales per month? Exactly, in volume sales – and hence in production too. The fourth quarter in general and the December Christmas bu-siness in particular tends to be the strongest period for coffee machines. So that forces us to be very accurate in the way we plan the purchase of materials. However, since we normally do a very good job of that, our coffee machine business is highly successful.

How far ahead do you schedule purchases? Let's take steel as an example. Here, scheduling systemati-cally takes place 12 to 18

months in advance, on a rolling monthly basis. For us, it is very important to reserve sufficient capacity because, if other industries – such as the auto industry – suddenly take off, we can very quickly find ourselves back in second place. That's why we are continually talking to our suppliers about the quantities we expect.

What form do these plan-ning talks take? As a rule, we give our sup-pliers an annual forecast to enable them to do their planning. We naturally then draw on the scheduled quanti-ties at very short notice to keep our inventories low. This rolling planning is incredibly important, because steel has delivery lead times of nine to twelve weeks. So if you get your math wrong and have to order more, it can take two to three months before the material is available. And if the supply chain is long because

materials have to be shipped, say, from Asia to Germany, you can quickly run into short-term bottlenecks.

are there points at which this planning reaches its limits? Yes – in the case of unforesee-able events such as the Fuku-shima nuclear disaster in 2011, for instance. There is nothing all the long-term planning can do about that. What did work well, though, was our crisis management. In a very short time, we had thoroughly screened our entire supply chain, down to the second and third tiers. We wouldn't have been able to do that ten years ago. This exercise quickly showed us where the bottle-necks would be – for special films for electronics applica-tions that are only made in Japan, for example – so we were then able to swiftly find alternative suppliers. Ulti-mately, we came through the crisis with no significant production outages.

as sad as it sounds, such tragic events seem to make you better as a company… Yes. That is perhaps overstat- ing the case, but yes. We had already tried to develop alter-native suppliers before then, including second-tier suppliers. But Fukushima taught us that the tier-3/tier-4 suppliers are in some cases the much more critical ones, in part because you usually don't know them, which makes it more difficult to prepare yourself.

"never miss a good crisis" is a common saying among consultants. are you glad about some crises because they give you, the market

leader, the chance to further consolidate your position – especially with regard to material bottlenecks? We have learned a lot from various crises in the past, but to be glad about them would be cynical. Quite apart from which, times of crisis affect different parts of a company in very different ways. They tend to be generally good times for purchasing depart-ments, but this advantage is bought at the price of a deteriorating sales situation.

Mr. seitz, how do organi-zations such as BsH learn specific lessons from such cases? and how can this knowledge be applied to the issue of material bottlenecks? In the wake of these situa-tions, we have also taken a closer look at other supply chains, such as the one for plastic granules. The rigorous application of dual supplier strategies, close and constant contact with suppliers – my core task in my capacity as COO – and clear priorities are all very important. We need to know where we are particular-ly dependent, because that is where we must take precau-tionary measures. On the other hand – and this is another lesson we have learned – it is certainly neither possible nor financially feasible to engage in preventive monitoring for all chains down to tier x and to stuff every drawer full of emergency back-up plans. To some extent, you have to trust that you will do the right thing in an emergency. Any attempt to try to cover all the bases is doomed tofailure.

"NICkEL IS A GOOD ILLUSTRATION OF THE FACT THAT THERE ARE TwO IMPORTANT SIDES TO SCARCITY: COST AND AvAILABILITY."

25COO Insights | 02.2013

What BsH functions con-cern themselves with the issue of prevention? It seems to us that these pro-cesses are growing ever more complex for cor-porate groups. In the past, the Purchasing department used to take care of the matter, and maybe the R&d unit too if there was a need for substitution… That is nowhere near enough these days, of course. At BSH, prevention is an issue for almost every function, from Development, through Purchasing, Supply Chain Ma-nagement and Production to the Finance Department and Quality Control. Not everyone is involved in everything, clearly. For example, financial audits of suppliers in Spain were recently conducted joint-ly by the Purchasing and Finance Departments – as a prophylactic measure in light of Spain's generally higher risk of insolvency at present.

do you have other strate-gies to combat material bottlenecks? One important one is stan-dardization – for electronic components just as much as for plastic granules. The more suppliers provide comparable input products and the more we use standardized input pro-ducts, the easier it is to switch in the event of a crisis.

We were also thinking of recycling... Obviously, a lot is happening in this area, and we too are heavily involved. Right now, we are discussing how recy-cling targets – more and more of which are coming from the EU – affect product design and development. Key issues

here include ease of repair and material purity. At the same time, we are working on ways to step up the recycling of our own old products. These are both important matters, although they are still in their early days.

How do you view the government's stipulations on recycling? It's time we started thinking about whether our chief regulators in the EU are not perhaps scoring one own goal after the other. To rightly want companies to recycle materi-als, but then also to insist that some ppm targets or other must be met in the materials used is a contradiction in terms. Of course we can com-ply with the European direc-tive to limit certain hazardous substances in our products, for example. However, we can do that only if we purchase new materials. If we use recy-cled materials, which we are supposed to do according to another directive, it is simply impossible. You can't have it both ways.

Is reverse integration an option for you? some groups – in response to price hikes for rare earths, for example – have ac-quired suppliers at the start of the value chain. BsH could treat itself to its own ore mine, for example… (laughs) I don't think we'd go for a mine! But we did acquire at least part of a supplier not long ago.

How did that go? very well, although it was an absolute exception and for want of a better solution, re-ally. The company was in dire

SMART AND CLEAN >Dose the detergent and water correctly when you wash your laundry and you will save money, safeguard the environ-ment and protect your machine. Bsh's i-DOs automatic dosing unit works out exactly what is needed based on water hardness, load volume and how dirty the linen is. Bsh claims the unit can save over 7,000 liters of water a year.

COOL wAY TO SAvE ENERGY >taking the energy transition into the home: the Kg39E-Ai40 refrigerator-freezer now boasts efficiency label A+++, which is awarded only to refrigerators that save 60% more energy than A-class appliances. interior LED lighting is one way the Kg39EAi40 reduces power consumption.

EXTRA MILk AND TwO SUGARS >the fully automated EQ.7 Plus aromasense remembers the preferences of as many as six different coffee drinkers. it records your preferred variety (such as espresso or latte macchiato), size and strength and will make you a cup when you select your name.

HOTPLATES? A THING OF THE PAST >the Freeinduction hob from Bsh brand neff lets you put your pots and pans wherever you like. the technology recognizes the size, shape and position of your cookware. A tFt display shows the relevant area and lets you choose the cooking temperature with a touch-screen function.

EXAMPLES

Products from BsH

Ready for collection Packaged goods ready and

waiting in a warehouse at Bsh's Dillingen facility

COO Insights | 02.201326

TITlE | INTERvIEW

1 /PLANNING

"Planning is an essential topic for me, irrespective of whether you are talking about short-, medium- or long-term processes. Everything gets built on sensible planning."

2 /RELATIONSHIPS

"You should constantly be cultivating your contact with suppliers. that goes as far as financial health checks of suppliers and joint efforts to raise productivity."

3 /COMPETITION

"Competition among sup-pliers makes negotiating vastly easier. You should never make yourself dependent on monopolists – if you have the chance to avoid doing so."

4 /COURAGE

"however far you think ahead and however well you prepare, no one can be ready for all eventualities. that makes it all the more im-portant to trust that you will respond quickly and do the right thing in an emergency."

financial straits and was also extremely important to us – with a monopoly in some ar-eas, in fact. That is why we had to acquire some of its plants, facilities and staff. Generally speaking, though, this kind of acquisition is not the solution we would prefer.

Why not? In other indus-tries – such as automotive engineering – OEMs take over whole rafts of suppliers. You can't compare the two. First, players in the auto market are ten to twenty times bigger and therefore have an entirely different dimension of financial leeway. Second, we attach very great impor-tance to keeping core and non-core competencies sepa-rate. And third, our vertical integration already goes down a very long way. In terms of our core areas, it is undoubt- edly deeper than in the auto industry.

can you give us an example? We produce our own electric motors in-house, for example. You won't find many auto makers who do that.

Our perception is that BsH and your industry as a whole are nevertheless very heavily dependent on individual suppliers. Is that true? Yes, I think that is indeed an industry-specific issue to some extent. One main reason is that we place very exacting demands on suppliers. We expect tremendous precision, quality and reliability at low prices. We have often found that suppliers who manu-facture for both us and the automotive industry either

have to concede significant markdowns when they work for us or are simply unable to compete on price as far as we are concerned.

What strategy do you adopt when selecting sup-pliers with a view to BsH's international growth? There are so many differ-ent approaches. The Ja-panese and Koreans, for instance, often trust the traditional keiretsu struc-tures, i.e. home-grown suppliers whom they tie closely to themselves and then take over – not least to avoid procurement bottlenecks. What is your approach? Historically, we too have tend- ed to come from the keiretsu corner, albeit in a much weaker form than the total economic dependency you see in Japan and Korea. In the past, established suppliers have been our mainstay. However, with a view to low-cost-country sourcing, we have for some time been learning that this is often only the sec- ond-best solution. Technically they may be a little better, but most are unable to compete on cost in the markets in which they operate. For this reason, we are increasingly also looking for suppliers in the "truly local" category – suppliers who are at home in the relevant low-labor-cost market, and who are there-fore more attractively priced. Having said that, you usually end up needing a healthy mix of both groups of suppliers.

To sum up, Mr. seitz: Where do you see potential to improve how scarcity is managed in the future?

Supplier enablement is an important topic for us in this regard. vertical integration is another one, at least in cer-tain areas. And dual or triple sourcing also fall into the same category. Without a doubt, the latter issue is partly a reaction to the various crises we have seen in recent years. Our individual functions already work well together with a strong focus on finding solutions. But I am sure we can step that up a little as well.

and in what areas are you already ahead of the competition? Certainly on reliability and quality of our products, because we pay a great deal of attention to that during procurement and in our mate-rials. In the solid, long-term collaboration we enjoy with suppliers too. And by now we are probably also ahead on the flexibility of our procure-ment. We have learned a lot.

In closing, one question about day-to-day business: When does the issue of scarcity land on your desk – the boss's desk – in the daily business routine? It doesn't "land" on my desk, it is basically always there. It starts with us regularly sitting together to think about how to avoid bottlenecks be-fore they ever materialize. And if anything does happen, I am obviously the one who has to deal with it. After the event, we then sit down again to talk about lessons we can learn for the future. Seen from this angle, the fight against materi-al scarcity is always on the boss's desk at BSH. But it also needs a very good team that works well together.

4 x Winfried seitz

INSIGHTS

2727

TITlE | KNOWLEDGE

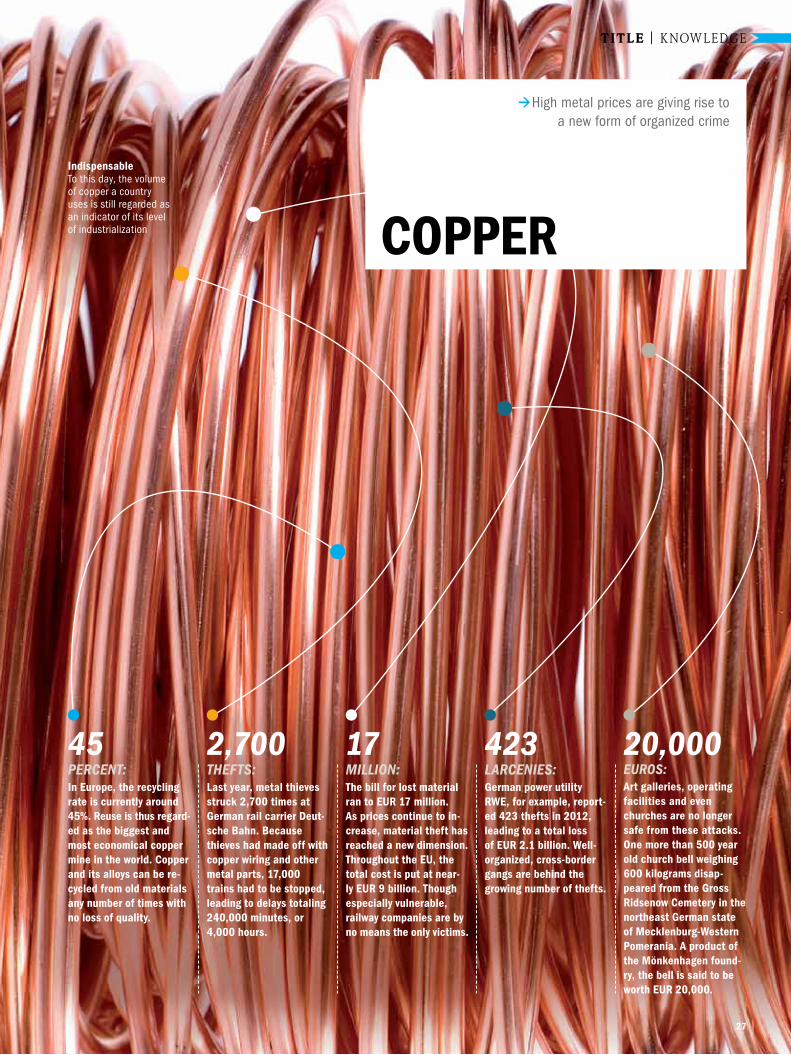

perCent: In Europe, the recycling rate is currently around 45%. Reuse is thus regard- ed as the biggest and most economical copper mine in the world. Copper and its alloys can be re-cycled from old materials any number of times with no loss of quality.

theftS: Last year, metal thieves struck 2,700 times at German rail carrier Deut-sche Bahn. Because thieves had made off with copper wiring and other metal parts, 17,000 trains had to be stopped, leading to delays totaling 240,000 minutes, or 4,000 hours.

million: The bill for lost material ran to EUR 17 million. As prices continue to in-crease, material theft has reached a new dimension. Throughout the EU, the total cost is put at near- ly EUR 9 billion. Though especially vulnerable, railway companies are by no means the only victims.

larCenieS: German power utility RwE, for example, report- ed 423 thefts in 2012, leading to a total loss of EUR 2.1 billion. well-organized, cross-border gangs are behind the growing number of thefts.

eUroS: Art galleries, operating facilities and even churches are no longer safe from these attacks. One more than 500 year old church bell weighing 600 kilograms disap-peared from the Gross Ridsenow Cemetery in the northeast German state of Mecklenburg-western Pomerania. A product of the Mönkenhagen found-ry, the bell is said to be worth EUR 20,000.

Indispensableto this day, the volume of copper a country uses is still regarded as an indicator of its level of industrialization

2,70045 423 20,00017

high metal prices are giving rise to a new form of organized crime

COPPER

COO Insights | 02.201328

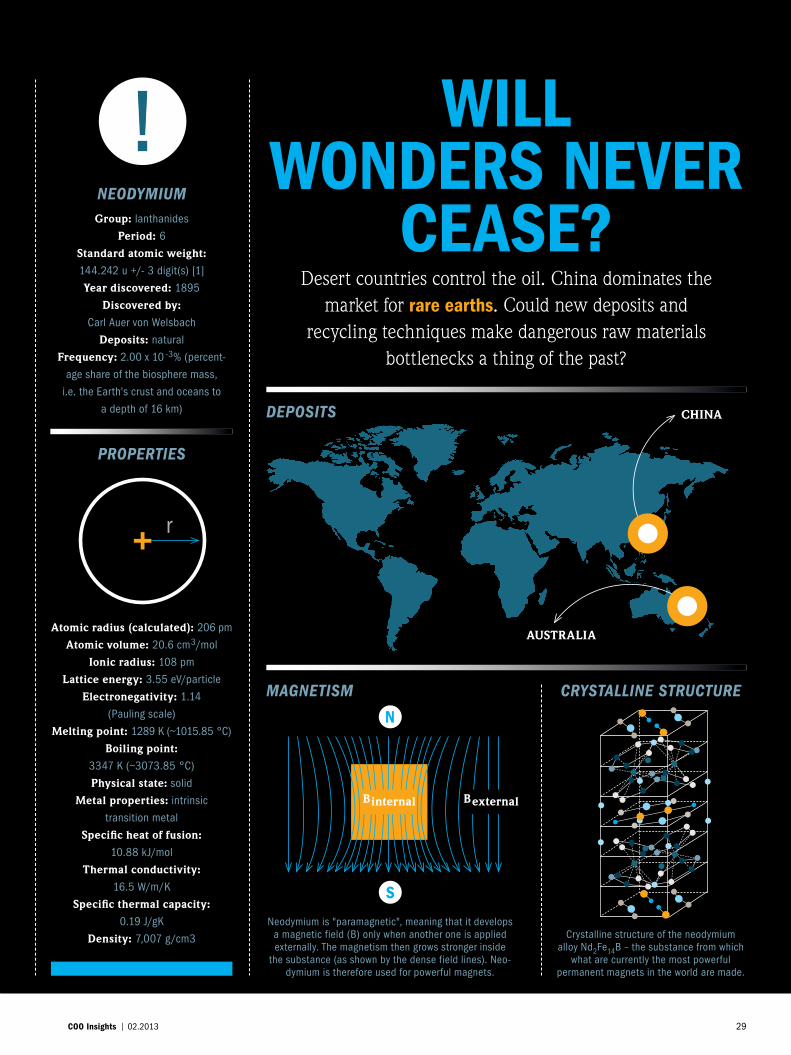

TITlE | R ARE EARTHS

Ndneodymium

60

Chinese gold Roughly 97% of the neody-mium produced in the world comes from China. the country's effective monopoly increases the risk of bottle-necks and price volatility

periodiC SyStem

29COO Insights | 02.2013

neodymium is "paramagnetic", meaning that it develops a magnetic field (B) only when another one is applied externally. the magnetism then grows stronger inside

the substance (as shown by the dense field lines). neo-dymium is therefore used for powerful magnets.

Crystalline structure of the neodymium alloy nd2Fe14B – the substance from which

what are currently the most powerful permanent magnets in the world are made.

Group: lanthanides

Period: 6

standard atomic weight: 144.242 u +/- 3 digit(s) [1]

Year discovered: 1895

discovered by:

Carl Auer von Welsbach

deposits: natural

Frequency: 2.00 x 10 -3% (percent-

age share of the biosphere mass,

i.e. the Earth's crust and oceans to

a depth of 16 km)

atomic radius (calculated): 206 pm

atomic volume: 20.6 cm3/mol

Ionic radius: 108 pm

lattice energy: 3.55 eV/particle

Electronegativity: 1.14

(Pauling scale)

Melting point: 1289 K (~1015.85 °C)

Boiling point:

3347 K (~3073.85 °C)

Physical state: solid

Metal properties: intrinsic

transition metal

specific heat of fusion:

10.88 kJ/mol

Thermal conductivity:

16.5 W/m/K

specific thermal capacity:

0.19 J/gK

density: 7,007 g/cm3

propertieS

neodymiUm

depoSitS

CryStalline StrUCtUre magnetiSm

Desert countries control the oil. China dominates the market for rare earths. Could new deposits and

recycling techniques make dangerous raw materials bottlenecks a thing of the past?

wILL wONDERS NEvER

CEASE?

cHIna

aUsTRalIa

N

S

Binternal Bexternal

r

COO Insights | 02.201330

environmental technologies is also driving demand. Global consumption of rare earths amounted to about 108,000 tonnes in 2006; experts predict this figure will rise dramatically to 240,000 tonnes by 2020. Of this total, 70,000 to 90,000 tonnes will be consumed by countries other than China. This prognosis paints an alarming picture, since countries that have few of these raw materials – like Germany – depend on imports.

The Earth currently has about 114 million tonnes of rare earth elements – in Russia, the US, Australia and India, but above all in China, which is estimated to be home to roughly half the world's reserves. China is also by far the largest producer, accounting for about 90% of the rare earths consumed worldwide. For China's former leader Deng Xiaoping, rare earths are to China "what oil is to Saudi Arabia".

THAT'S wHY ALL EYES ARE TURNING to Storkwitz in the triangle of land between Leipzig, Halle and Dessau in eastern Germany. This area is so far the only known rare earth deposit in Central Europe. Until the 1950s, there was no serious interest in this group of elements. Promethium, the last rare earth element, wasn't even discovered until 1947. Nor did East German geologists searching for uranium ascribe any particular importance to their surprise discovery in Storkwitz. The area first came under closer scrutiny by Seltenerden Storkwitz AG (SES), a subsidiary of Deutsche Rohstoff AG (founded in 2006). SES engaged Australian geo-con-sulting firm Mining One to assess the deposit. Their findings: A good 20,000 tonnes of rare earths lie packed in the gravel and sand under the village, not to mention 4,000 tonnes of niobium. Experts put the value of these raw materials at a minimum of EUR 2 billion.

It could be even more, much more. The ore body where the high-tech metals are found was tested only to a depth of 600 meters. But the report indicates that the body extends 1,200 meters down, perhaps even farther. Estimates therefore tend toward a minimum of 80,000 tonnes of rare earths – more than five times as much as China plans to export in 2013 (15,501 tonnes) and about 60% of global consumption in 2011 (137,000 tonnes). At today's prices, that reflects a value of over EUR 8 billion.

Having said that, any figure based on "today's prices" can only be an approximation, since the prices for rare earths fluctuate wildly. Although price levels are still dangerously high, dramatic plunges in the wake of the global economic crisis are letting

TITlE | R ARE EARTHS

"We used to sell rare earths for the price of salt," says former Chinese Premier Wen Jiabao. "But they are as valuable as gold." If that's true, Storkwitz is sitting on a gold mine worth billions, according to Germany's newspaper Bild: It has the rare

earth elements cerium, praseodymium, neodymium, europium and yttrium plus the heavy metal niobium, which makes steel harder and cars lighter. This makes Storkwitz one of the most important deposits of raw materials for the European high-tech world.

"Rare earths" is a misnomer: These elements are in fact metals, and by no means rare. Even thulium, the rarest of the rare earth elements, occurs more frequently than gold. The difficulty is that extracting and processing these elements is very expensive. Each one is found only in small quantities in rocks and minerals. And yet they have become an indispensable part of our world.

Without these elements there would be no smart phones. No computers, flat screens, DvD players. No batteries, high-perfor-mance magnets, semiconductors or solar units. The largest con-sumers are China, Japan and the US, and the rising importance of

THE CITY wAS FIRST MENTIONED in 1166 AD, as "Dielc". In 1348 it was ravaged by the plague; in 1539, gripped by the Reformation. On April 19, 1795, naturalist and Humboldt follower Christian Gottfried Ehrenberg was born there. Then came the railroad, the gas companies, the Nazi terror, the Americans, the Soviets, the East German Communist Party, the brown coal excavators, the peaceful revolution and the rebirth of the Free State of Saxony. From the 46-meter-high Breiter Turm, built in 1396, with a bit of luck you can see the small town of Storkwitz 1.5 kilometers to the west. That's where the city of Delitzsch in northwest Saxony discovered its El Dorado – an El Dorado for those with an interest in rare earth elements.

w

| What are...? |

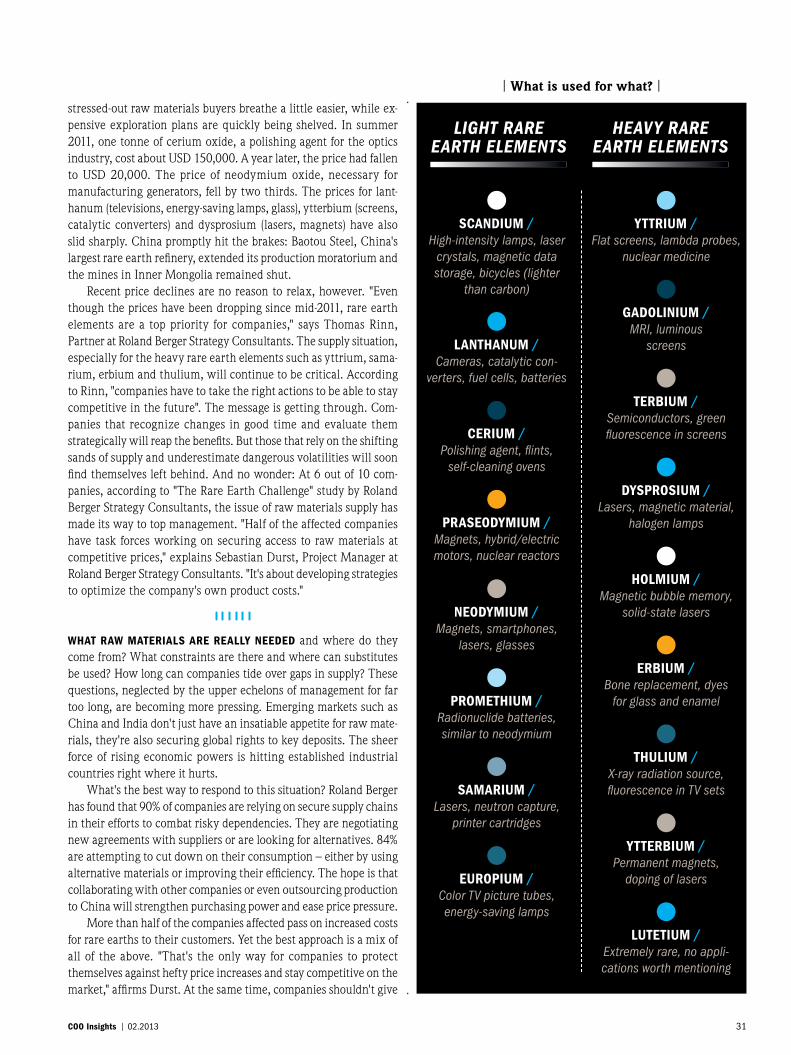

RARE EARTHS

the term "rare earths" is doubly misleading: they are actually metals – and not exactly rare. the first of these elements were discovered toward the end of the 18th century in sweden, the last of them not quite 70 years ago. they were first isolated as oxidized minerals – what

used to be referred to as "earths", hence the phrase "rare earths". they occur relatively frequently, but in such scattered quantities that extracting them is ex-pensive and laborious. the rare earths are comprised of 17 metals: scandium, yttrium and lanthanum plus the 14 metals that follow lanthanum in the periodic table (the lanthanide elements). these include cerium, praseodymium, neodymium, europium and ytterbium.

31COO Insights | 02.2013

stressed-out raw materials buyers breathe a little easier, while ex-pensive exploration plans are quickly being shelved. In summer 2011, one tonne of cerium oxide, a polishing agent for the optics industry, cost about USD 150,000. A year later, the price had fallen to USD 20,000. The price of neodymium oxide, necessary for manufacturing generators, fell by two thirds. The prices for lant-hanum (televisions, energy-saving lamps, glass), ytterbium (screens, catalytic converters) and dysprosium (lasers, magnets) have also slid sharply. China promptly hit the brakes: Baotou Steel, China's largest rare earth refinery, extended its production moratorium and the mines in Inner Mongolia remained shut.

Recent price declines are no reason to relax, however. "Even though the prices have been dropping since mid-2011, rare earth elements are a top priority for companies," says Thomas Rinn, Partner at Roland Berger Strategy Consultants. The supply situation, especially for the heavy rare earth elements such as yttrium, sama-rium, erbium and thulium, will continue to be critical. According to Rinn, "companies have to take the right actions to be able to stay competitive in the future". The message is getting through. Com-panies that recognize changes in good time and evaluate them strategically will reap the benefits. But those that rely on the shifting sands of supply and underestimate dangerous volatilities will soon find themselves left behind. And no wonder: At 6 out of 10 com-panies, according to "The Rare Earth Challenge" study by Roland Berger Strategy Consultants, the issue of raw materials supply has made its way to top management. "Half of the affected companies have task forces working on securing access to raw materials at competitive prices," explains Sebastian Durst, Project Manager at Roland Berger Strategy Consultants. "It's about developing strategies to optimize the company's own product costs."

wHAT RAw MATERIALS ARE REALLY NEEDED and where do they come from? What constraints are there and where can substitutes be used? How long can companies tide over gaps in supply? These questions, neglected by the upper echelons of management for far too long, are becoming more pressing. Emerging markets such as China and India don't just have an insatiable appetite for raw mate-rials, they're also securing global rights to key deposits. The sheer force of rising economic powers is hitting established industrial countries right where it hurts.

What's the best way to respond to this situation? Roland Berger has found that 90% of companies are relying on secure supply chains in their efforts to combat risky dependencies. They are negotiating new agreements with suppliers or are looking for alternatives. 84% are attempting to cut down on their consumption – either by using alternative materials or improving their efficiency. The hope is that collaborating with other companies or even outsourcing production to China will strengthen purchasing power and ease price pressure.

More than half of the companies affected pass on increased costs for rare earths to their customers. Yet the best approach is a mix of all of the above. "That's the only way for companies to protect themselves against hefty price increases and stay competitive on the market," affirms Durst. At the same time, companies shouldn't give

LANTHANUM / Cameras, catalytic con-

verters, fuel cells, batteries

YTTRIUM / Flat screens, lambda probes,

nuclear medicine

SCANDIUM /High-intensity lamps, laser

crystals, magnetic data storage, bicycles (lighter

than carbon)

DYSPROSIUM /Lasers, magnetic material,

halogen lamps

CERIUM /Polishing agent, flints,

self-cleaning ovens

GADOLINIUM /MRI, luminous

screens

PRASEODYMIUM /Magnets, hybrid/electric motors, nuclear reactors

TERBIUM /Semiconductors, green fluorescence in screens

NEODYMIUM / Magnets, smartphones,

lasers, glasses

HOLMIUM /Magnetic bubble memory,

solid-state lasers

PROMETHIUM /Radionuclide batteries, similar to neodymium

ERBIUM /Bone replacement, dyes

for glass and enamel

SAMARIUM /Lasers, neutron capture,

printer cartridges

THULIUM /X-ray radiation source, fluorescence in TV sets

EUROPIUM /Color TV picture tubes, energy-saving lamps

YTTERBIUM /Permanent magnets,

doping of lasers

LUTETIUM /Extremely rare, no appli-cations worth mentioning

light rare earth elementS

heavy rare earth elementS

| What is used for what? |

COO Insights | 02.201332

up the hope that new and, given high price levels, lucrative deposits could yet be found. Companies around the world are working feverishly to crack China's monopoly on rare earths. American, Australian and Canadian outfits have seven major projects in the pipeline through 2015. The focus: restarting production in California's Mountain Pass mine (closed in 2002) and tapping the deposits on Australia's Mount Weld. With a combined production volume of about 64,000 tonnes, experts estimate that both facilities could cover roughly half of the current global annual consumption of rare earths – if only the mines would start producing.

Elsewhere in the Pacific, Japanese researchers have reported a gigantic deposit of rare earths just off the island of Minami-Torishi-ma (Marcus Island), nearly 200 kilometers south of Tokyo. They believe the concentration of rare earth elements there to be 20 to 30 times greater than in China. The bad news is that the deposit lies 5,800 meters below sea level, and no commercial mining ex-pedition to depths of over 5,000 meters has thus far been successful. The good news: If this attempt is successful, Japan would have its demand for rare earths met for the next 230 years – at least in theory. For the moment, Japanese automotive manufacturer Toyota is having to place its hopes in a mining project near the Indian city of Chatrapur.

Steel alone is no longer enough for the troubled ThyssenKrupp, located in Germany's Ruhr region. The group plans to join forces with Tantalus Rare Earths, located near Munich, to embark on one of the largest rare earths projects outside of China, namely in Madagascar. At the beginning of this year, Germany's Federal Ministry of Economics launched a special program to support com-panies (especially SMEs) in exploring possible sources of critical raw materials. Loans granted on favorable terms are intended to make the expensive search process more affordable. About EUR 30 million will be made available over the next three years.

YET OBTAINING THESE MATERIALS may turn out to be not so difficult after all. Ordinary households are proper treasure troves, harboring millions of old cell phones, forgotten computers, monitors and television sets. All of which contain copper, silver, gold – and rare earths. But recycling these materials is still in its infancy. Currently, about 25% of the gold, silver and palladium found in electronics is being recovered, but there is no system in place for the large-scale recycling of rare earths. For a laptop, raw materials account for just 2% to 10% of the production costs – hardly worth the trouble of sifting through electronic waste just for a few milligrams of rare earths. Instead, high-tech metals from, say, old batteries wind up in

slag from furnaces. Lastly, modern electronics contain more than just a rich amount of valuable material: They're also poisonous. To sort and process these various materials is very technologically demanding. That's why most devices never even make it into the recycling loop; instead, they get shipped off to Africa and Asia.

According to the Hamburg University of Technology (TUHH), "industry is finally realizing that raw materials are scarce and costly". In five to ten years, the university says, we could see a mature process for recovering rare earth elements. Efforts by academics and business have increased significantly, they note. Experts at the Öko-Institut Freiburg estimate that about 15 tonnes of neodymium (valued for its magnetic properties) and 2 tonnes of praseodymium were built into the PCs sold in Germany in 2010. Not an overwhelming amount for profitable recycling, but it's a start. Geodis Logistics predicts that "demand for neodymium will become so great over the next few years that it's worth it for investors today to put the necessary millions into developing the recycling process".Under the auspices of Germany's Federal Institute for Materials Research and Testing, the city of Darmdorf (near Hamburg) plans to launch a pilot recycling facility in early 2014. The valuable slag will be provided by the city of Hamburg and by Berlin's municipal cleaning company (BSR).

THE FRENCH HAvE ALREADY gone a step further. At the end of 2012, the world's first rare earths recycling facility went into operation in La Rochelle. The facility uses a patented process that can extract the metals from various types of waste. Mid-sized company Loser Chemie from Hainichen, Germany, is managing a pilot program for recycling magnets that contain rare earths. The German states of Bavaria and Hesse are financing a new institute for materials science as part of Fraunhofer-Gesellschaft's research. This new institute will examine problems associated with recycling and recovery. Re- searchers at the Dresden branch of the Fraunhofer Institute for Manufacturing Technology and Advanced Materials have already developed a way to recover neodymium and samarium from mag-netic materials. This process, a combination of pyrometallurgical and wet-chemical techniques, is of particular interest to manu- facturers of electric motors in the automotive industry. Yield and purity, the researchers state, are reportedly "very high". The metals can easily be transformed into the elements for manufacturing new magnetic materials.

But can they be used in industry? Huge question marks remain. Because even more so than recovery processes, newly discovered deposits like that in Storkwitz are triggering high hopes. Extraction here could begin in 2017 at the earliest, provided the prices for rare earths remain at a level attractive for investment.

And if they don't? The ambitious project has already suffered one setback: The concentration of the sought-after metals in the bastnaesite mineral ore found here is barely 0.5%. That figure is even lower for each individual rare earth element – hardly a good sign for the "Storkwitz miracle" (Bild). Especially as the competition is not standing idly by: Australia's Mount Weld has twenty times as high a concentration of rare earths.

"Companies that recognize CHANGESin good time and evaluate them strategically will reap the benefits."

TITlE | R ARE EARTHS

wORkSHOP

| FACT |

>Companies that combine methods across all their functions are 15% more

successful with their new products. Read on for more on this and

other studies...<

15 %

COO Insights | 02.201334

WORKsHOP

cOO InsightsIssue 02.2013

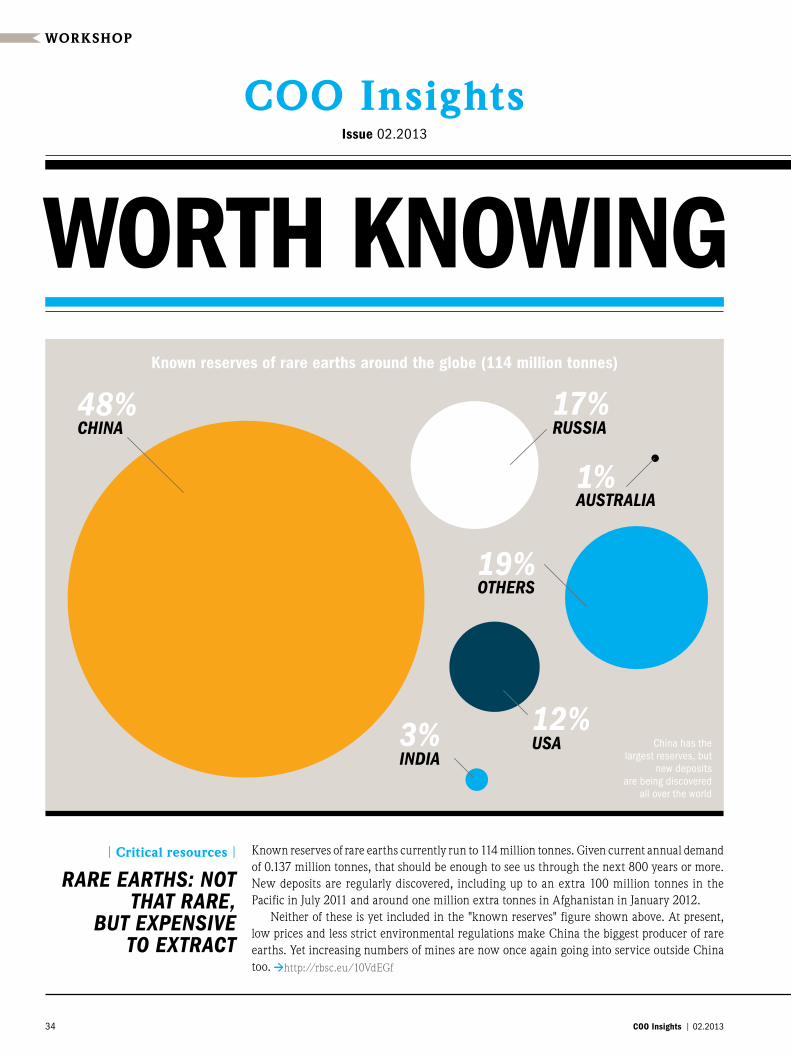

Known reserves of rare earths currently run to 114 million tonnes. Given current annual demand of 0.137 million tonnes, that should be enough to see us through the next 800 years or more. New deposits are regularly discovered, including up to an extra 100 million tonnes in the Pacific in July 2011 and around one million extra tonnes in Afghanistan in January 2012.

Neither of these is yet included in the "known reserves" figure shown above. At present, low prices and less strict environmental regulations make China the biggest producer of rare earths. Yet increasing numbers of mines are now once again going into service outside China too. http://rbsc.eu/10vdEGf

rare earthS: not that rare,

BUt eXpenSive to eXtraCt

| critical resources |

China has the largest reserves, but

new deposits are being discovered

all over the world

19%

17%

12%3%

1%

48%China rUSSia

indiaUSa

otherS

aUStralia

known reserves of rare earths around the globe (114 million tonnes)

wORTH kNOwING

35COO Insights | 02.2013

cOO InsightsIssue 02.2013

Companies that combine methods across all their functions are 15% more successful with their new products. Finding the right com-

| Guidelines for product innovations |

ComBine and SUCCeed

BUSineSS model tranSformation – a

Key iSSUe

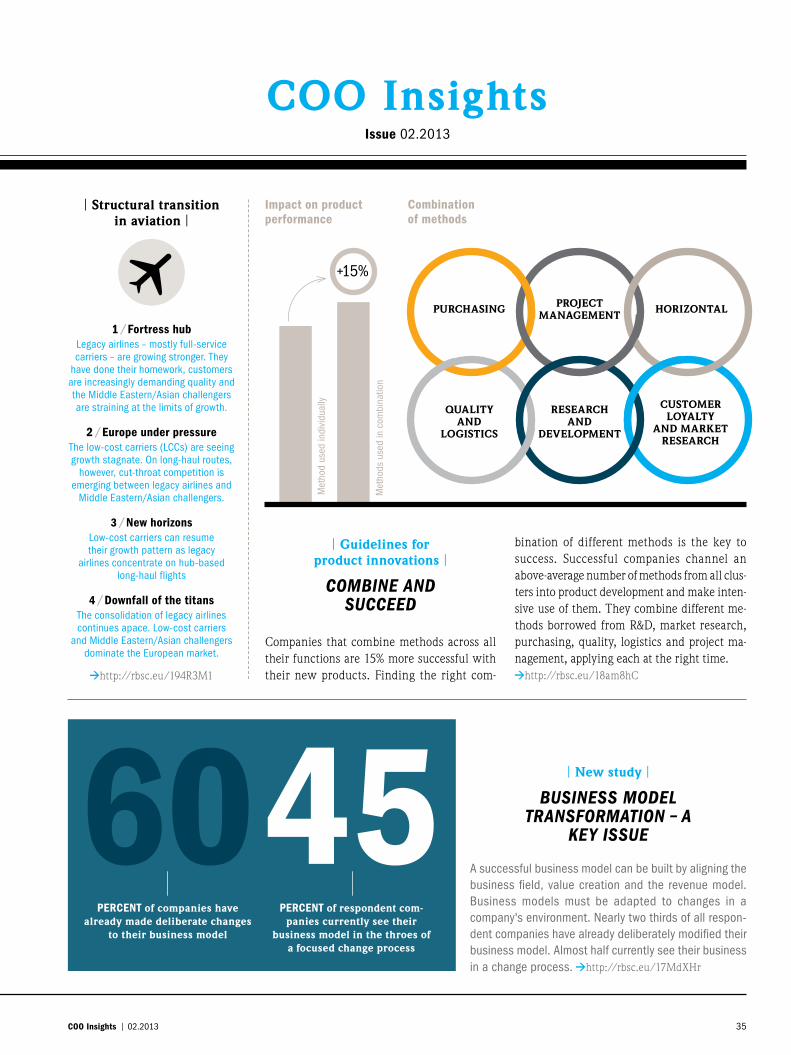

| structural transition in aviation |

1 / Fortress hub Legacy airlines – mostly full-service carriers – are growing stronger. they

have done their homework, customers are increasingly demanding quality and the Middle Eastern/Asian challengers are straining at the limits of growth.

2 / Europe under pressure the low-cost carriers (LCCs) are seeing growth stagnate. On long-haul routes,

however, cut-throat competition is emerging between legacy airlines and

Middle Eastern/Asian challengers.