Embed Size (px)

Citation preview

EconomicFreedom

James Gwartne y

Robert Lawson

Walter Bloc k

United States

Economic Freedom of the World: 1975-1995 co-publishers

Cato Institute, Washington, D.C., United States of AmericaFounded in 1977, the Cato Institute is a public policy research foundationdedicated to broadening the parameters of policy debate to allow con-sideration of more options that are consistent with the traditional Amer-ican principles of limited government, individual liberty, free markets,and peace. To that end, the Institute strives to achieve greater involve-ment of the intelligent, concerned lay public in questions of policy andthe proper role of government through an extensive program of publica-tions and seminars.

Centro de Investigaciones Economicas Nacionales,Guatemala City, GuatemalaThe Center for Research on the National Economy (CIEN) was estab-lished in Guatemala in 1982. It is a private, non-partisan, not for profitpublic policy institute, funded by the sale of its books and periodicalpublications, income from conferences and seminars, and the support itreceives from its members and the public. The Center's program isdevoted to the technical study of economic and social problems that needto be resolved to promote the stable development of the nation. Itsmembers, staff, research associates, and its supporters share the princi-ples of a social order of free and responsible individuals interactingthrough a market economy functioning within the rule of law.

Centro de Investigaciones Sobre la Libre Empresa, A.C.,Mexico City, MexicoThe Centro de Investigaciones Sobre la Libre Empresa (CISLE) is anonprofit educational and public policy organization founded in 1984.Its aim is to defend and promote the ideals of free trade and free enterprisein all areas of society. CISLE maintains that the fundamental source ofwell being and the wealth of nations is a sound institutional order whichguarantees competition, private ownership, and open markets. CISLE* sactivities are Financed by a select group of generous donors.

The Fraser Institute, Vancouver, CanadaThe Fraser Institute is an independent Canadian economic and socialresearch and educational organization. It has as its objective the redirectionof public attention to the role of competitive markets in providing for thewell-being of Canadians. Where markets work, the Institute's interestlies in trying to discover prospects for improvement. Where markets donot work, its interest lies in finding the reasons. Where competitivemarkets have been replaced by government control, the interest of theInstitute lies in documenting objectively the nature of the improvementor deterioration resulting from government intervention. The work of theInstitute is assisted by an Editorial Advisory Board of internationallyrenowned economists. The Fraser Institute is a national, federally char-tered, non-profit organization financed by the sale of its publications andthe tax-deductible contributions of its members.

The Free Market Foundation of Southern Africa,Johannesburg, South AfricaThe Free Market Foundation of Southern Africa was established in 1975to promote economic freedom. The FMF sponsors and conducts research,publications, conferences, lectures, training programs and lobbyingefforts in support of the free market. Its funding comes from membershipsubscriptions, project sponsorships, and income from sales and fees.

The Hong Kong Centre for Economic Research,Hong KongThe Hong Kong Centre for Economic Research is an independent freemarket policy research institute. The Centre was established in 1987 as

a charitable trust. Untill 992 it was affiliated with the Chinese Universityof Hong Kong, and since then it has been affiliated with the Universityof Hong Kong. The Centre recognizes that the economic success of HongKong is the result of policies that protected private property rights, freeenterprise, and limited the role of the government. It also recognizes thatthe political foundation of these policies is always vulnerable, and thatthe case for preserving these policies and expanding its scope has to becontinuously articulated. The main activities of the Centre are to influ-ence public opinion and policy outcomes through a program of researchand education.

The Institute of Economic Affairs, London, EnglandThe IEA 's mission is to improve public understanding of the foundationsof a free and harmonious society by expounding and analyzing the roleof markets in solving economic and social problems, and bringing theresults of that work to the attention of those who influence thinking, TheIEA achieves its mission by a high quality publishing program; conferen-ces, seminars and lectures on a range of subjects; outreach to school andcollege students; brokering media introductions and appearances; andother related activities. Incorporated in 1955 by the late Sir AnthonyFisher, the IEA is an educational charity, limited by guarantee. It isindependent of any political party or group, and is financed by sales ofpublications, conference fees, and voluntary donations.

The Institute of Economic Affairs, Accra, GhanaThe Institute of Economic Affairs (IEA) Ghana is an independent,non-governmental institution dedicated to the establishment andstrengthening of a market economy and a democratic, free and opensociety. The IEA was founded in October 1989. It considers im-provements in the legal, social and political institutions as necessaryconditions for sustained economic growth and human development. TheIEA supports research, and promotes and publishes studies on importanteconomic socio-political and legal issues i n order to enhance understand-ing of public policy.

Institute of Public Affairs, Jolimont, AustraliaEstablished in 1943, thelPAis Australia's oldest and largest private-sec-tor "think tank." Its aim is to advance the interests of the Australianpeople. Those interests include prosperity and full employment, the ruleof law, democratic freedoms, security from crime and invasion, highstandards in education and family life. To identify and promote the bestmeans of securing these values, the IP A undertakes research, organizesseminars, and publishes widely.

The Israel Center for Social and Economic Progress,Mevasseret Zion, IsraelThe Israel Center for Social and Economic Progress (ICSEP) is anon-partisan public policy think tank advocating free market policies inIsrael. It holds conferences and seminars for Israeli decision makers andpublic opinion moulders. It runs an extensive publications and audiovisual program. It is also engaged in teaching basic economic conceptsto high school students and new immigrants.

Liberales Institut, Bonn, GermanyThe Liberales Institut (Liberty Institute) is the think tank of the Friedrich-Naumann-Foundation. The Bonn-based institute devotes itself to spread-ing ctassical liberal/free market ideas through the publication of classicalliberal literature, the analysis of current political trends and the promo-tion of research. By organizing conferences and workshops, the institutetries to stimulate an intellectual exchange among liberals around theworld.

www.fraserinstitute.org

ECONOMIC FREEDOMOF THE WORLD:1975-1995

www.fraserinstitute.org

www.fraserinstitute.org

ECONOMIC FREEDOMOF THE WORLD:1975-1995

byJames GwartneyRobert LawsonWalter Block

www.fraserinstitute.org

Copyright © 1996 by The Fraser Institute. All rights reserved. No part of thisbook may be reproduced in any manner whatsoever without written permis-sion except in the case of brief quotations embodied in critical articles andreviews.

The authors of this book have worked independently and opinions expressedby them, therefore, are their own, and do not necessarily reflect the opinionsof the members or the trustees of The Fraser Institute.

Printed in Canada.

Canadian Cataloguing in Publication Data

Gwartney, James D.Economic Freedom of the World, 1975-1995

Includes bibliographical references.ISBN 0-88975-157-9

1. Free enterprise. 2. Economic history—1971-1990. 3.Economic history—1900- 4. Economic development—Measurement. I. Lawson, Robert A. (Robert Allen), 1967- II.Block, Walter, 1941- III. Fraser Institute (Vancouver, B.C.) IV.TitleHB95.G92 1995 330.9'045 C95-911182-4

www.fraserinstitute.org

TABLE OF CONTENTS

Foreword vii

List of Exhibits ix

About the Authors xii

Acknowledgments xiii

Executive Summary xv

Graphic Summary of Major Findings xix

Introduction: The Historical Development of The Economic Freedom Indexby Michael A. Walker 1

Chapter 1 Construction of the Economic Freedom Index 11

• The Concept of Economic Freedom / 12• The Components of Our Index of Economic Freedom / 14• Attaching Weights to the Components / 37

Chapter 2 Rating the Economic Freedom of Countries in 1993-1995, 1990, 1985,1980, and 1975 47

• Country Ratings in 1993-1995 / 47• Country Rankings: 1975-1995 / 62• The Persistently High and Persistently

Low Rated Countries: 1975-1995 / 66

Chapter 3 Changes in the Economic Freedom of Countries: 1975 to 1995 71

• Changes in the Economic Freedom of Countries / 71• Changes in the Economic Freedom of the World / 80• Changes in Economic Freedom By Development

Status and Region / 84

www.fraserinstitute.org

Chapter 4 Economic Freedom and Economic Growth 89

• Measurement Problems and the Relationship BetweenEconomic Freedom and Income / 90

• The Level of Economic Freedom, Income, and Growth / 92• Changes in Economic Freedom and the Growth of GDP / 97• Economic Freedom and Economic Growth: Some Reflections / 104• Concluding Remarks / 107

Chapter 5 Country Profiles I l l

Appendix I The Summary Index Ratings for 1975, 1980, 1985, and 1990 . . . . 229

Appendix II The Underlying Data Used to Calculate the Indexes 243

VI

www.fraserinstitute.org

FOREWORD

Freedom is a big word, and economic freedom not much smaller. To talk abouteconomic freedom is easy; to measure it, to make fine distinctions, assign numbers to itsattributes, and combine them into one overall magnitude—that is a very different andmuch more difficult task, as we found out when we started on this quest some thirteenyears ago (see Michael Walker's introduction).

James Gwartney, Robert Lawson, and Walter Block deserve great credit for havingbrought this quest to so satisfactory a temporary conclusion—I say temporary because thisstudy of economic freedom for more than 100 countries provides a cornucopia forstudents of the relation between economic freedom, political freedom, and civil freedom,and for further explorations of the relation between economic freedom and the level andrate of economic growth. The resulting studies will surely make revised editionsnecessary, both to bring the indexes of economic freedom up to date and to incorporatethe additional understanding that will be generated.

For many of us, freedom—economic, political, civil—is an end in itself not a meansto other ends—it is what makes life worthwhile. We would prefer to live in a free countryeven if it did not provide us and our fellow citizens with a higher standard of life thanan alternative regime. But I am firmly persuaded that a free society could never surviveunder such circumstances. A free society is a delicate balance, constantly under attack,even by many who profess to be its partisans. I believe that free societies have arisen andpersisted only because economic freedom is so much more productive economically thanother methods of controlling economic activity.

It did not require the construction of an index of economic freedom for it to bewidely believed that there is a close relation between economic freedom and the level andrate of economic growth. Theoretical considerations gave reason to expect such arelation, and little more than casual observation sufficed to show that what theorysuggested, experience documented. We have not in a sense learned any big thing fromthis book that we did not know before. What we have done is to acquire a set of datathat can be used to explore just how the relation works, and what are the essentialconnections, and that will enable skeptics to test their views objectively.

Vll

www.fraserinstitute.org

To achieve these advantages, it was essential that the measure of economicfreedom not beg any questions by depending on outcomes; it was essential that it dependonly on objective characteristics of an economy. This may seem obvious but I assure youthat it is not. After all, the rate of economic growth or the level of living may be anexcellent proxy for economic freedom, just as an auto's maximum speed may be anexcellent proxy for the power of its motor. But any such connections must bedemonstrated not assumed or taken for granted. There is nothing in the way the indexesare calculated that would prevent them from having no correlation whatsoever with suchcompletely independent numbers as per capita GDP and the rate of growth of GDP. Yetthe actual correlation between the indexes and the level and rate of economic growthdocumented in some of the extraordinarily informative graphs in the book (e.g., ExhibitS-2) is most impressive. No qualitative verbal description can match the power of thatgraph.

Milton FriedmanThe Hoover Institution

Stanford University

via

www.fraserinstitute.org

List of Exhibits

EXHIBIT TITLE PAGE

Exhibit S-1A: The Average of the Three 1993-95 Summary Index Ratings of EconomicFreedom xx

Exhibit S-1B: The 1993-95 Summary Index (Isl) of Economic Freedom xxi

Exhibit S-2: The 1995 Economic Freedom, Grade Level, Per Capita GDP,and Growth xxii

Exhibit S-3: The Income Levels and Growth Rates of Persistently Highand Persistently Low Rated Countries xxiii

Exhibit S-4A: The Economic Freedom Ratings (Isl) During 1975-1995and Growth Rate for High-Rated Non-Industrial Economies . . . . xxiv

Exhibit S-4B: The Economic Freedom Ratings (Isl) During 1975-1995and Growth Rate for Low-Rated Non-Industrial Economies . . . . xxv

Exhibit S-4C: The Economic Freedom Ratings (Isl) and Growth Rates ofLess-Developed Economies That Became More Free During1975-1995 xxvi

Exhibit S-4D: The Economic Freedom Ratings (Isl) and Growth Rates ofLess-Developed Economies That Became Less Free During1975-1995 xxvii

Exhibit S-5: Growth Rates During 1980-1994 of the Ten Countries withthe Largest Increases and Largest Declines in EconomicFreedom During 1975-1990 xxviii

Exhibit S-6: The Growth of Per Capita GDP During 1980-1990 for theCountries That Had a One Unit Increase in the IslEconomic Freedom Rating Between 1975 and 1985 (andMaintained the Increase into the 1990s) Compared tothe Growth of Countries with a One Unit DeclineDuring 1980-1990 xxix

Exhibit S-7: Changes in the Average Country Rating for theSummary Indexes and the Components: 1975-1995 xxx

IX

www.fraserinstitute.org

Exhibit 1-1: Components of the Index of Economic Freedom 16

Exhibit 1-2: The Weights Attached to Each Component in theAlternative Indexes 38

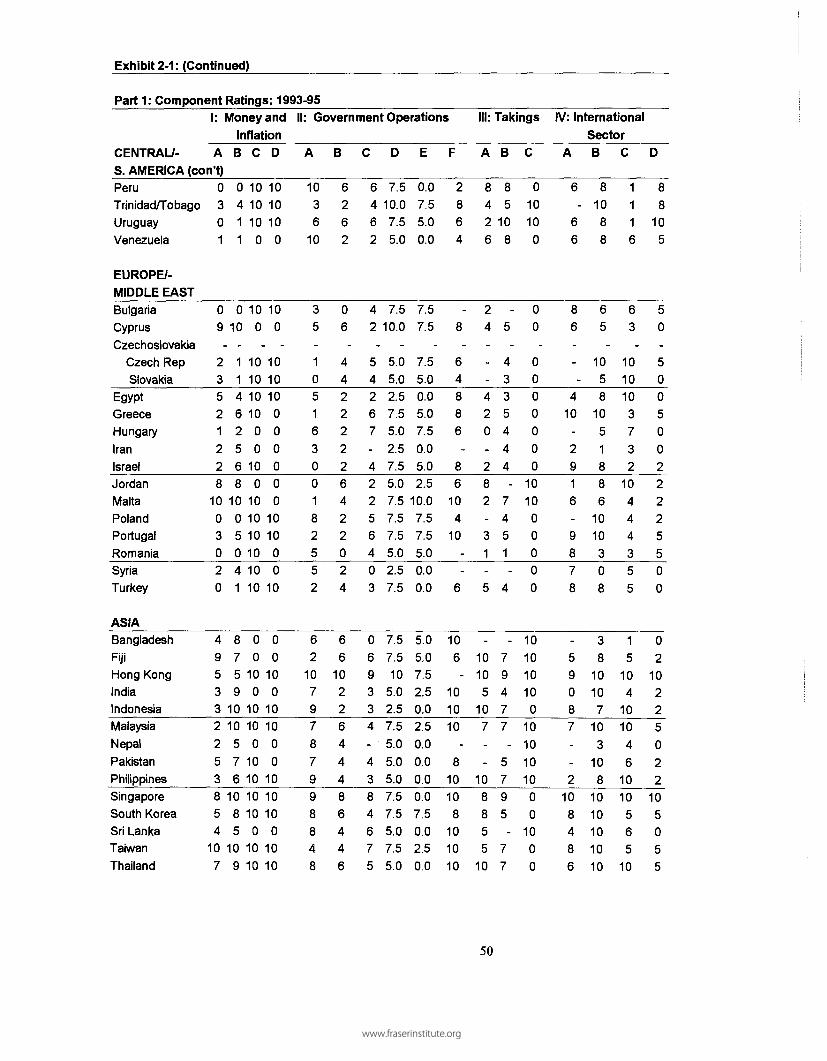

Exhibit 2-1: Component, Area, and Summary Index Ratings: 1993-1995 48

Exhibit 2-2: The Economic Freedom Rating (Isl) of the 15Highest, 15 Lowest and Selected Middle-ratedCountries for 1975, 1980, 1985, 1990, and 1995 64

Exhibit 2-3: Countries with Either Persistently High orPersistently Low Ratings Throughout the1975-1995 Period 67

Exhibit 3-1: The Ratings of the 15 Countries with the LargestIncrease in the Index of Economic Freedom (Isl)During the 1975-1990 Period 72

Exhibit 3-2: The Ratings of the 15 Countries with the LargestDecline in the Index of Economic Freedom (Isl)During the 1975-1990 Period 74

Exhibit 3-3: Countries With at Least a One Unit Increase in theIsl Summary Rating Between 1975 and 1985 and Main-tenance of This Increase Between 1985 and 1995 75

Exhibit 3-4: The Ten Countries With the Largest Increase in theIsl Summary Rating Between 1980 and 1990 and theMaintenance of This Increase Between 1990 and 1995 77

Exhibit 3-5: The Fifteen Most Improved Countries During 1985-1995 and 1990-1995 79

Exhibit 3-6: Changes in the Average Value of the Components ofthe Index of Economic Freedom and the AverageSummary Rating of Countries: 1975-1995 82

Exhibit 3-7: Average Summary Rating (Isl) by Level of Develop-ment and Region: 1975-1995 86

www.fraserinstitute.org

Exhibit 4-1A:

Exhibit 4-1B:

Exhibit 4-2:

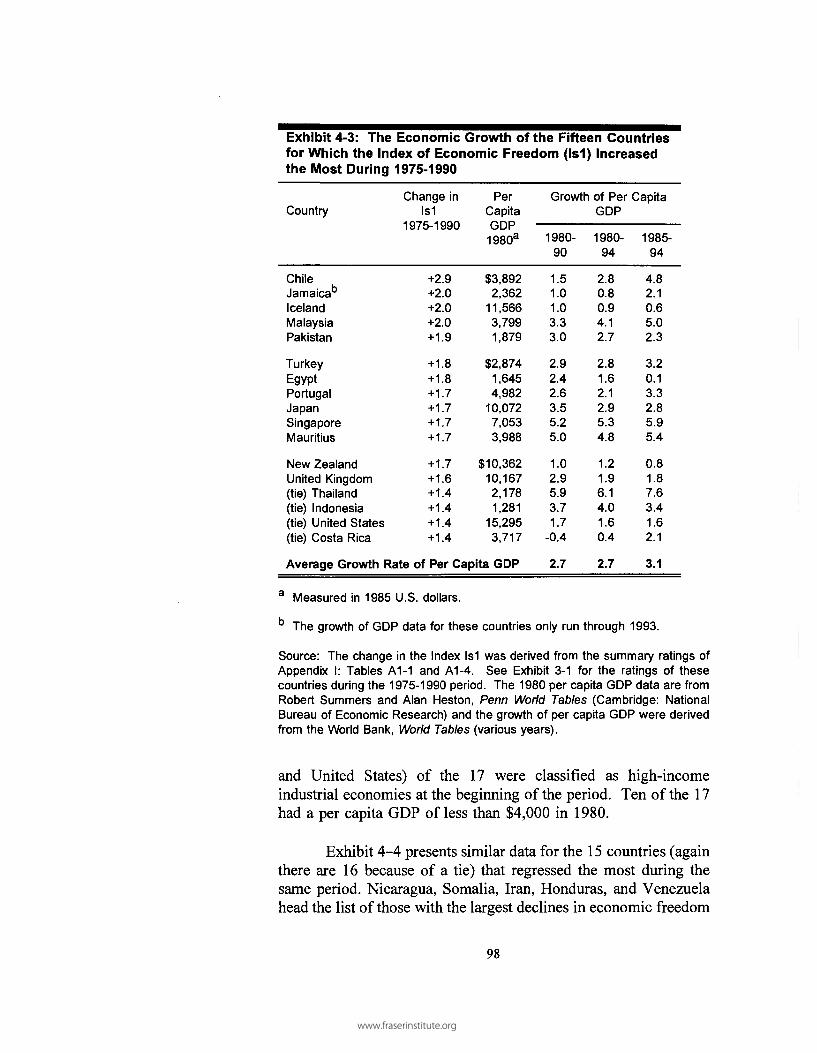

Exhibit 4-3:

Exhibit 4-4:

Exhibit 4-5:

Exhibit 4-6:

Exhibit 4-7:

The Per Capita GDP and the Growth of Per Capita GDPfor the Countries with an Index Rating Grade of Aor B in 1993-1995 93

The Per Capita GDP and the Growth of Per Capita GDPfor the Countries with an Index Grade of F-, 1993-1995 94

The Growth of Per Capita GDP for Countries With aPersistently High and Persistently Low EconomicFreedom Rating During 1975-1995 95

The Economic Growth of the 15 Countries for Whichthe Index of Economic Freedom (Isl) Increased theMost During 1975-1990 98

The Economic Growth of the 15 Countries for Whichthe Index of Economic Freedom (Isl) Declined theMost During 1975-1990 99

The Growth of Per Capita GDP for Countries with atLeast a One Unit Change in the Isl Summary Indexof Economic Freedom Between 1975 and 1985 101

The Growth of Per Capita GDP for the Ten Countrieswith the Largest Change in the Isl Summary RatingBetween 1980 and 1990 102

Selected Comparisons Between Countries with Increasesand Decreases in Economic Freedom During Various Periods . 106

XI

www.fraserinstitute.org

About the Authors

James Gwartney is a Professor of Economics and Policy Sciences at Florida StateUniversity. His Ph.D. in Economics is from the University of Washington (1969). Heis the co-author (with Richard Stroup) of Economics: Private and Public Choice, awidely-used university level text and What Everyone Should Know About Economics andProsperity, a popular book that has already been translated to ten foreign languages. Heis also the author of several other books and articles published in the leading professionaljournals of economics.

Robert Lawson is an Associate Professor of Economics at Shawnee StateUniversity. He received his Ph.D. from Florida State University in 1992. In addition tothe study of economic systems, freedom and growth, his major area of research is publicchoice.

Walter Block is an Associate Professor of Economics at the College of the HolyCross. His Ph.D. in economics is from Columbia University (1972). Senior Economistat The Fraser Institute from 1978 to 1991, he is the author (or co-author) of six books andthe editor (or co-editor) of twelve others. He is currently the co-editor of two journals,The Review of Austrian Economics and The Journal of Libertarian Studies. He has alsoserved as the guest editor of The Journal of Labor Economics and Cultural Dynamics.

Xll

www.fraserinstitute.org

Acknowledgments

This project is the fruition of a team effort. It is an outgrowth of a series of sixconferences jointly sponsored by the Fraser Institute of Vancouver, British Columbia andthe Liberty Fund of Indianapolis, Indiana. We owe an enormous debt to both thesponsors and conference participants. The free wheeling discussions stimulated ourthinking and provided us with several ideas, many of which are incorporated into ourmeasure of economic freedom.

While we benefitted from discussions and papers presented by numerousparticipants, we must mention the specific contributions of three. First, Mike Walkerprovided the entrepreneurial insight for the topic, the energy to organize the conferenceseries, and the persuasiveness to attract several of today's finest intellects to address thetopic. Without his contribution, we would probably have not even thought about themeasurement of economic freedom, much less undertaken the task. His Introduction tothe book presents the historical background that proceeded our work on this topic.

Second, the contribution of Alvin Rabushka was also crucial. His enthusiasm forthe project supported it during the early days. His paper, "Preliminary Definition ofEconomic Freedom" presented at the second conference, outlined the key attributes ofeconomic freedom and provided us with invaluable guidance concerning how they shouldbe measured. More recently as our work developed, he has given us additional directionand encouragement.

Third, we would like to thank Milton Friedman. No words can fully express ourdebt to him. He attended each of the Fraser/Liberty Fund conferences and his ferociouslove for intellectual inquiry was an inspiration to all participants. His pointed and oftenrevealing criticisms challenged us to work harder and think deeper. His directions havehelped us avert at least a few of the treacherous swamps that inevitably accompany aproject of this type.

We would also like to express our appreciation to the Policy Sciences Center ofFlorida State University for providing the research and word processing support that madethe project feasible. Barbara Morgan and Frank Keuchel assisted with data gathering,calculations, and the checking of the figures in the manuscript. Kristin McCahon,Director of Publications at the Fraser Institute, did an excellent job of coordinating thedesign and publication of the book. Finally, no one will be happier to see this projectcompleted than Valerie N. Colvin, Senior Art/Production Specialist. She maintained herpatience during numerous occasions when data were updated, a variable or a countryadded, or an exhibit redesigned. It was a challenging task and she handled it well.

James GwartneyRobert LawsonWalter Block

xm

www.fraserinstitute.org

www.fraserinstitute.org

Executive Summary

1. The central elements of economic freedom are personal choice, protection ofprivate property, and freedom of exchange. The goal of this study is to constructan index that is (a) a good indicator of economic freedom across countries and (b)based on objective components that can be updated regularly and used to trackfuture changes in economic freedom.

2. An index containing 17 components was designed to provide an empirical measurefor economic freedom. The components were grouped into four major areas: I.Money and Inflation, II. Government Operations and Regulations, III. Takingsand Discriminatory Taxation, and IV. Restrictions on International Exchange.Exhibit 1-1 provides a description of the specific components of the index. Datawere assembled and procedures adopted to rate countries on a zero to ten scale foreach of the components. Chapter 1 indicates the data sources used and explainshow the each of the component ratings were derived. See Appendix II for thetables containing the underlying data and the ratings for each of the 17components.

3. Since there is not a single "best way" to weight the components into an aggregatesummary rating, three alternative summary indexes were derived. See Exhibit 1-2for the component weights used to derive each of the three indexes.

4. Exhibit 2-1 presents the 1993-1995 ratings for each of the 17 components in ourindex, as well as area ratings, and the three alternative summary indexes (and theaverage of the three). With the exception of the high-income industrial countries,the three alternative summary ratings yield similar results. In the case of theindustrial countries, the summary index that allocates only a very small weight tothe size of government consumption expenditures and transfers and subsidies asa share of the economy yielded ratings that were approximately one unit higherthan the two other summary ratings.

5. In terms of economic freedom, Hong Kong is the highest rated country in theworld. Since Hong Kong's average for the three alternative ratings in 1993-1995 was significantly higher than any other country, it was given a lettergrade of A+. New Zealand, Singapore, and United States earned a gradeof A. The following ten countries were assigned a grade of B: Switzerland,United Kingdom, Canada, Australia, Ireland, Japan, Netherlands, Germany,Belgium, and Malaysia. Exhibit S-1A (Graphic Summary) indicates theaverage of the three indexes for each country and their ranking. Exhibit S-1Bprovides the same information for the Isl index.

XV

www.fraserinstitute.org

6. At the other end of the spectrum, the following 27 countries earned a grade of F-:Brazil, Haiti, Nicaragua, Venezuela, Hungary, Iran, Romania, Syria, Nepal,Algeria, Benin, Burundi, Central African Republic, Congo, Cote d'lvoire,Madagascar, Morocco, Niger, Nigeria, Rwanda, Sierra Leone, Tanzania, Togo,Uganda, Zaire, Zambia, and Zimbabwe. The policies and institutionalarrangements of these countries were inconsistent with economic freedom inalmost every area.

7. In addition to the mid-1990s ratings, indexes were also derived for 1975, 1980,1985, and 1990. Exhibit 2-2 presents the summary rating Isl for the Top 15,Bottom 15, and selected middle-rated countries for these years as well as for 1995.Some of the top-rated countries were able to maintain their high rating throughoutthe 1975-1995 period, but there was also a great deal of both upward anddownward mobility. Several top-ranked countries in 1975 and 1985 fell welldown the rankings in later years (for example, Honduras and Venezuela).Correspondingly, several economies with low ratings in 1975, 1980, or 1985substantially improved their scores in recent years (for example, New Zealand,Thailand, South Korea, and Costa Rica).

8. The five countries that improved their economic freedom rating the most duringthe 1975-1990 period were: Chile, Jamaica, Iceland, Malaysia, and Pakistan. SeeExhibit 3-1 for more a complete list of countries that improved substantiallyduring the 1975-1990 period. The five countries for which the economic freedomrating declined the most during the 1975-1990 period were: Nicaragua, Somalia,Iran, Honduras, and Venezuela. See Exhibit 3-2 for a more complete list of thesecountries.

9. The summary indexes indicate that there was little change in the average economicfreedom rating for the more than 100 countries of our study during the 1975-1985period. However, since 1985 there is evidence of an increase in economicfreedom. The average summary ratings of both industrial and less developedcountries rose during the last decade. The primary factors contributing to thisimprovement were: greater price level stability, greater freedom to maintainforeign currency bank deposits, improved credit market policies, lower topmarginal tax rates, reductions in taxes (tariffs) on international trade, liberalizationof exchange rate controls, and relaxation of restrictions on the movements ofcapital. See Exhibits 3-6 and 3-7 for details. Also see Exhibit S-7 in the GraphicSummary.

10. Economic theory indicates that economic freedom will enhance the gains fromtrade and entrepreneurship. Therefore, if economic freedom is measured properly,a positive impact on economic growth is the expected result. The data areconsistent with this view. As Exhibit 4-1A shows, the 14 countries that earned asummary rating grade of either A or B in 1993-1995, achieved an average annual

XVI

www.fraserinstitute.org

growth rate in per capita real GDP of 2.4% during 1980-1994 and 2.6% during1985-1994. In contrast, the average annual growth of per capita real GDP for the27 countries with a summary rating of F- in 1993-1995 was minus 1.3 percentduring 1980-1994 and minus 1.6 percent for the 1985-1994 period. Twenty-oneof the 27 experienced declines in real per capita GDP during 1980-1994. SeeExhibits 4-IB for additional details. Also see Exhibit S-2 in the GraphicSummary for evidence that differences in economic freedom (and theaccompanying grade level) exert a positive impact on both income levels andgrowth rates.

11. Since increases in economic freedom and maintenance of a high level of freedomwill positively influence growth, countries that achieve and sustain high levels ofeconomic freedom over a lengthy time period will tend to be high-incomecountries. The six countries (Hong Kong, Switzerland, Singapore, United States,Canada, and Germany) with persistently high ratings throughout the 1975-1995period were all in the Top Ten in terms of 1994 per capita GDP. No countrywith a persistently high economic freedom rating during the two decadesfailed to achieve a high level of income. In contrast, no country with apersistently low rating was able to achieve even middle income status. SeeExhibit 4-2 and Exhibit S-3 in the Graphic Summary for additional details.

12. The countries with the largest increases in economic freedom during the period,achieved impressive growth rates. As Exhibit 4-3 shows, the 15 countries(actually there are 17 because of a tie) with the most improvement in the indexof economic freedom during the 1975-1990 period experienced an average growthrate in per capita GDP of 2.7 percent during 1980-1990 (and 3.1% during 1985-1994). All 17 of the countries in the most improved category experiencedpositive growth rates. In contrast, the average real per capita GDP declined atan annual rate of 0.6% in the 15 countries (there were also 16 in this group dueto a tie) for which the index of economic freedom fell the most during the sameperiod. Eleven of the 16 countries with the largest declines in economic freedomexperienced declines in real per capita GDP during 1980-1994. See Exhibit 4-4and Graphic Exhibit S-5 for additional details.

13. Countries that achieved a one unit increase in the Is 1 economic freedom ratingbetween 1975 and 1985 and maintained that increase during the next decade grewat a average rate of 3.5% during 1985-1994. Mauritius, Pakistan, Japan, Chile,Jamaica, Singapore, Portugal, United Kingdom and Turkey comprised thiscategory. In contrast, the growth rates of the countries where economic freedomdeclined during 1975-1985 were persistently negative. The pattern was similar forthe countries that achieved and sustained increases in economic freedom between1980 and 1990 compared to those experiencing declines in freedom. See Exhibits4-5 and 4-6 for additional details. Also see Exhibits S-4C and S-4D in theGraphics Summary section.

XVll

www.fraserinstitute.org

14. Chapter 5 presents detailed data for both economic freedom ratings and recentindicators of economic performance for many of the countries included in ourstudy.

XVlll

www.fraserinstitute.org

Graphic Summary

of

Major Findings

www.fraserinstitute.org

Exhibit S-1A: The Average of the Three 1993-95 Summary Index Ratings ofEconomic Freedom

Average Rating

0 2 4 6 8 10

Average Rating

2 4 6 8 10

nony r\ony \.New Zealand 2.

Singapore 3.United States 4.

Switzerland 5.United Kingdom 6.

Canada 6.Ireland 8.

Australia 8.Japan 10.

Netherlands 11.Germany 12.Belgium 12.

Malaysia 12.Thailand 15.

Costa Rica 16.Denmark 16.

Taiwan 16.Panama 16.France 20.

South Korea 20.Norway 22.

Spain 23.Austria 23.Belize 23.

Argentina 26.Chile 26.

Finland 26.Uruguay 26.

Guatemala 26.Bolivia 31.

Italy 31.Jamaica 31.Iceland 31.

Mauritius 31.Sweden 31.

El Salvador 36.Philippines 36.

Trinidad/Tob. 36.Paraguay 40.

Fiji 41.Portugal 41.

Malta 41.Indonesia 41.

Mexico 45.Botswana 46.

Peru 47.Honduras 47.

Ecuador 49.Colombia 50.

Czech Rep 51.Pakistan 51.

I I I I I

|^^HH^MH8.5^MHHHI^H8.2• • ^ • ^ ^ • • 8 . 0^^••^^^•7.9^ • •^^• •7 .6^•^••^^7.6^^M^^H7.4•i^^^^H7.4^^^^^••7.3^^•^•••7.2•H^HHH7.1••^^^M7.1•1^HHMH7.1^^M^^H6.9^^•^••6.8• • • ^ • • • 6 . 8^ ^ • • • • 6 . 8• • • •^^ •6 .8^^^^^M6.7• • •^^•6.7•••^^•6.4IHBBHB6.3^^•^^•6.3••^^^•6.3•^^^••6.2• • • • ^ • 6 . 2••^^^•6.2• •^^•6 .2• • • • • • • 1 6 . 2^^•^^6.1• • •^^6 .1•••^^•6.1• • •6 .1^^^H^6.11^HBHH6.1^^••••6.0^ ^ ^ ^ ^ • 6 . 0IB^^^M6.0^§••15.9^^•^M5.8^^•^•15.8^^§^• •15 .8•^•^•••5.8^^• •5 .7^^••••5.6• • • ^ ^ 5 . 5• • • •^•5 .5^• • • •15 .4^1^BHB5.3••^^•5.2^^•^^5.2

Domin. Rep 53 .Greece 54.Cyprus 54.

South Africa 54.Jordan 57.

Sri Lanka 57.Poland 57.Gabon 60.

Chad 61.Bulgaria 62.

Ghana 62.India 62.

Tunisia 65.Turkey 66.

Bangladesh 66.Israel 66.Egypt 69.

Mali 70.Slovakia 70.

Cameroon 72.Malawi 72.Kenya 72.

Senegal 75.C African R 75.Venezuela 75.

Morocco 75.Sierra Leone 79.

Benin 80.Niger 81.

Rwanda 82.Togo 82.

Congo Rep 82.Zimbabwe 85.

Hungary 85.Nepal 85.

Madagascar 88.Nigeria 88.

Cote d' Ivoire 90.Tanzania 90.

Haiti 90.Zambia 93.Uganda 93.

Romania 95.Burundi 96.

Brazil 97.Nicaragua 98.

Syria 99.Algeria 100.

Iran 101.Zaire 101.

Somalia 103.

t i l l

•^•^•15.0MHHM4.9••^^•4.91MMH4.9^••^•14.8HHBM4.8•••1^4.8•IM^H4.7• • •^4.5••^H4.4^HM^.4• • • • 4 . 4• • •^ •4 .3•^••14.2•^•^4.2^M^4.2• •^•4.2l ^ ^ ^ 4 . 1

^•••4.1••H4.0••1^4.0MH1M4.0•^^•3.9• • • • 3 . 9^^IH|3.9^••13.9•^^3.8^••13.7^•••3.6• • • 3 . 5• • • 3 . 5• • • 3 . 5^ ^ ^ 3 . 4^ ^ • 3 4^§••3.4• • •3 .3• • •3 .3^••3.2• • •3.2•^•3.2• • •3.1• M 3 1• • • 3 . 0•^•2.9••12.8• • •271 ^ ^ 2 . 4

^•2.1•11.9^•1.9-N/R

Note: Chapter 1 explains how the three summary indexes (le, Is1, and Is2) are derived. The rating

above is the average of these three. See Exhibit 2-1 for each of the three ratings.

XX

www.fraserinstitute.org

Exhibit S-1B: The 1993-95 Summary Index (Is1) of Economic Freedom

Is1 Rating

2 4 6 8 10

Is1 Rating

2 4 6 8 1 0

Hong Kong 1.Singapore 2.

New Zealand 3.United States 4.

Switzerland 5.Malaysia 6.

Unit. Kingdom 6.Thailand 6.Canada 9.

Japan 9.Australia 11.

South Korea 12.Ireland 12.

Costa Rica 12.Panama 15.Taiwan 15.

Guatemala 17.Bolivia 18.

Netherlands 18.Germany 18.Argentina 21 .

Belgium 21.Mauritius 21 .Jamaica 21.

El Salvador 21 .Belize 21.

Philippines 27.Uruguay 28.

Paraguay 28.Fiji 28.

Indonesia 28.France 32.

Denmark 32.Ecuador 34.

Peru 34.Mexico 36.Spain 36.Chile 36.

Austria 36.Trinidad/ 36.

Norway 41.Dom. Rep. 41.

Iceland 41.Italy 44.

Malta 44.Finland 44.

Honduras 47.Sweden 47.Portugal 47.Pakistan 50.

I I I I I

:::::::::::•:::::::::::::::::::::::::::::::::::::::::::::! 9 .2

"" : 3 8 2: : s so

! 7 6-i 7 5

I 70•;.:.... •;:: 170

I 70• . :.. 1 6 9

I 693685 6 7

-::::... " ::.. : :::.J 6 7-:::::::: ::::: : :::::J 6 7

.1661661653 64

.:: : J6 4:::::::::::::::::::::::::::::::::::::::a6 4

:: : : 16 3" j 6 3

163":::.. 3 63

:::• :..:: : :::J 6 3::::::::::::::::::::::::::::::::::::::3 6 3

! 6 2"•:: "le i

161"' : "16 1

: : : :..ie i:::::::::::::::::::::::::::::::::::] 6 0

3 60559159I 5 8I 5 8

:::::::::::::::::::::::::::::::::::] 5 8. I 58

: 15 8357

:: ::ii 5 7_ " 3 5 6

3 5 63 5 6j 5 5J55

' ! 5 5" " " 15 4

Botswana 50.Colombia 52.

Chad 53.Sri Lanka 53.

Cyprus 53.Greece 56.

Czech Rep. 56.Jordan 56.

S. Africa 56.Poland 60.Ghana 60.Gabon 62.Kenya 63.

Venezuela 63.India 63.

Bangladesh 66.Mali 67.

Malawi 67.Tunisia 67.

Israel 70.Sierra Leone 70.

Bulgaria 70.Cameroon 70.

Turkey 70.C African 70.

Senegal 76.Madagascar 77.

Benin 77.Egypt 77.

Nigeria 80.Morocco 80.Rwanda 82.Uganda 82.

Tanzania 82.Slovakia 82.

Togo 86.Niger 86.

Zambia 86.Nepal 86.

Congo 90 .Zimbabwe 91 .

Hungary 92.Nicaragua 93.

Brazil 93.Burundi 95.

Cote d'lvoire 95.Romania 97.

Haiti 97.Syria 99.Iran 100.

Algeria 100.Zaire 102.

Somalia 103.

. ...

... .

.

• — - . . ,

i i i

HN/R

I 1 1 1 1

% 5.4T : i 5.3:::::::::::::::™;-| b. o

i 5. 0ZIZZZJb.0

1 4.9:::::::::::....::::i 4.9

14.9::: : : i 4.9

•••3 4 8

3 4.8_ J 4 V

14 5_ l 4 . b

I4.b14.4

Z Z _ J 4 334 3

__J43™~~~!42

. ,,! 4 2~"TZZ142'.'."" ! 4 7

1 14 2"™~142

. 14 1Z Z Z D 4 0' .....'" 3 4 0ZZU40

! 3 9i 3 937

l-AfZZD3/

37ZZ336— 1 3 ( 5

3 3 63365

'3 3 b34

~ 13 3.. 133Z Z ] 3 3•^"132ZZ332ZH29~~129Z126121321]1 9

Note: Chapter 1 explains how this rating was derived. Se e Exhibit 2-1 for information on the componentsthat underlay the rating. I n the judgment of the authors, the Is1 index is the most reliable indicator ofdifferences in economic freedom across a wide range of countries.

XXI

www.fraserinstitute.org

Exhibit S-2: The 1995 Economic Freedom, Grade Level Per CapitaGDP, and Growth

A. Averag e Per Capita GDP by1995 Economic Freedom Grade

The graph at the right indicatesthe average per capita GDP ofcountries grouped according totheir 1995 economic freedomgrade. On average, countries withmore economic freedom havea higher per capita GDP. (The GDPfigures are derived by thepurchasing power parity method,Summers and Heston, Penn WorldTables data). They are measuredin 1985 U.S. dollars.

20

3 15

&o 10S 8

o<u 50.

$13,659

F- F D C B A1995 Economic Freedom Grade

B. Th e Average Growth Rate of PerCapita GDP Between 1980 and 1994by 1995 Economic Freedom Grade

Here we illustrate the annualgrowth rate of per capita GDPby economic freedom grade. Notonly do countries with moreeconomic freedom have a higherper capita GDP (see above),they also generally grow morerapidly.

F- F D C B A1995 Economic Freedom Grade

xxn

www.fraserinstitute.org

Exhibit S-3: The Income Levels and Growth Rates of Persistently High and PersistentlyLow Rated Countries

As the graphs below indicate, countries with persistently high economic freedom ratingsduring the last two decades have a very high per capita GDP while those with persistentlylow ratings have extremely low incomes. The growth rates of the persistently high-ratedgroup are also positive, while those for the low-rated group are low and often negative.

Persistently High-rated Countries: 1975-1995

1994 Per Capita GDP0 5 1 0 1 5 2 0 2

Hong Kong

Switzerland

Singapore

United States

Canada

Germany

IHiH^HIHH$1? '832

H H H H | $15,980

H | H | H | H $14,415

l i ^ H H H i l H i $18,850H H H H I i H I $17,510m m m $15,005

Persistently Low-rated Countries: 1975-1995

1994 Per Capita GDP

Somalia

Zimbabwe

Growth of Per Capita GDP 1980-940 3 6

Hong Kong •

Switzerland H

Singapore H

United States •

Canada 1

Germany 1

HHH^HH||^HH| 5.0

Ho.8

HHHHHH53

I ^H 1.6[HI 1.3| H H | 1.8

Growth of Per Capita GDP 1980-94- 6 - 3 0 3

Somalia

Zambia

Hungary

Romania

Brazil

Syria

Uganda

Zaire -

Zimbabwe -

-3.7

-2.0

-2.1

-2.3

-0.7

0.2

0.1

| 0.2

l o . 4

Note: The countries with a grade of A or B in 1995 and a ranking in the top 15 in the other yearscomprise the persistently high-rated group. Countries with a summary economic freedom rating (Isl) ofless than 4.0 for every year throughout the 1975-1995 period comprise the persistently low-rated group.See Exhibits 2-3 and 4-2 for additional details. The GDP per capita figures (measured in 1985 U.S.dollars) are updates of the Summers and Heston data. They were derived by the purchasing power paritymethod.

xxin

www.fraserinstitute.org

Exhibit S-4A: The Economic Freedom Ratings (Is1) During 1975-1995 andGrowth Rate for High-Rated Non-Industrial Economies

Hong Kong

Singapore

Malaysia

Thailand

12

c? 8toa:"w 4

n

12

D) gc 8

••(0

or5 4

n

12

Rat

ing

00

w 4

0

Economic Freedom Rating

9 2 9. 4 9. 5 9. 3 9 1

Hill1975 198 0 198 5 199 0 199 5

Year

S 1 2

o•f 8coO

0 Aa. 4

c

jk 0

Economic Growth

^ ^ ^ 5. 7

O 1975-8 5 1985-9 4Year

8 0 8 5 8. 2•mi1975 198 0 198 5 199 0 199 5

Year

S 1 2n

hg. i

n P

er C

apita

<o

A

co • 1

° 1975-8 5 1985-9 4Year

7.1 7. 1 7. 0_ _ • • ••III!• • • • • i1975 198 0 198 5 199 0 199 5

Year

Q . 1 2

oen

r Cap

itC

O

CU A

a. 4

4.2 5 °

^0LM_MJ° 1975-8 5 1985-9 4

Year

12

Is1 R

atin

g.&

. C

O

U

R , 7. 0

4.9 5.0 5-3 • • ^Mmil1975 198 0 198 5 199 0 199 5

Year

OCO

I. 8CO

O(D 4.EO) o

7.6

M lO 1975-8 5 1985-9 4

Year

XXIV

www.fraserinstitute.org

Exhibit S-4B: The Economic Freedom Ratings (Is1) During 1975-1995 andGrowth Rate for Low-Rated Non-Industrial Economies

Economic Freedom Rating Economic Growth

Brazil

1975 1980 1985 1990 1995

Syria

Algeria

Nigeria

1975 1980 1985 1990 1995 1975-85 1985-94

1975-85 1985-941975 1980 1985 1990 1995

1975 1980 1985 1990 1995 1975-85 1985-94

XXV

www.fraserinstitute.org

Exhibit S-4C: The Economic Freedom Ratings (Is1) and Growth Rates ofLess-Developed Economies That Became More FreeDuring 1975-1995

Economic Freedom Rating

Chile

Portugal

•nil1975 1980 1985 1990 1995

1975 1980 1985 1990 1995

PakistanU)

tin

CO cQL 5

n

2.33.5

13.9

14.2

I5.4•1

1975 1980 1985 1990 1995

Year

Mauritius

Is1 R

atin

g

10

5

0

' 3. 9

11975

3.8

11980

6.0

|

1985Year

5.6

11990

6.3

I1995

Economic Growth

Q- 10QO

Cap

itaU

l

Per

c

_g> 0o

4.8

2.4 ^ ^ |

LJBHL^^BJ1975-85 1985-9 4

Year

Q_ 1 nQ 1 0

Ba.COO 5Q5Q.c

F oo

3.3

1.8 ^^M

_^H_HLJ1975-85 1985-9 4Year

fe10o

Cap

itaU

l

Per

c

°> 0o

5.6

2.8 ^^M

LJHH_^HJ1975-85 1985-9 4

Year

XXVI

www.fraserinstitute.org

Exhibit S-4D: The Economic Freedom Ratings (Is1) and Growth Rates ofLess-Developed Economies That Became Less FreeDuring 1975-1995

Venezuela

Economic Freedom Rating

10

(DQL

-5

6.9 6.65.2 5.5 4.5

1975 1980 1985 1990 1995

Year

Economic Growth

Honduras

Iran

Nicaragua

6.1 6.0 6.0

1975-85 1985-941975 1980 1985 1990 1995

2.5 2.7 3.2

1975-85 1985-9 41975 1980 1985 1990 1995

1975-85 1985-941975 1980 1985 1990 1995

XXV11

www.fraserinstitute.org

Exhibit S-5: Growth Rates During 1980-1994 of the Ten Countries with the LargestIncreases and Largest Declines in Economic Freedom During 1975-1990

Change in Per Capita GDPBetween 1980 and 1994

Ten Countries with Larges tIncrease in Economic Freedo mRatings: 1975-199 0(Change in Is1 rating in parentheses. )

All of these countriesachieved positive growth rates.Their average increase in percapita GDP was 2.7%. (SeeExhibit 4.3 for additionaldetails.)

(2.9) Chile

(2.0) Jamaica

(2.0) Iceland

(2.0) Malaysia

(1.9) Turkey

(1.9) Pakistan

(1.8) Egypt

tie (1.7) Portuga l

tie (1.7) Japan

tie (1.7) Singapore

tie (1.7) Mauritius

tie (1.7) New Zealand

1 1 1

• 0. 8• 0. 9

• 1 1. 2

2.8

•2.8

2.7

1

2.9

••

1

4.1

| 5. 3

| 4. 8

-6 -3

Ten Countries with Larges tDecline in Freedom Ratings:1975-1990(Change in Is1 rating in parentheses.

Nine of the 11 countries withthe largest declines in economicfreedom during 1975-1990 alsoexperienced declines in percapita GDP. On average, theirper capita GDP declinedapproximately 1% annuallyduring 1980-1994. (SeeExhibit 4-4 for additionaldetails.)

tie (-0.7) Panama

tie (-0.7) Morocco

(-0.8) Algeria

(-1.0) Tanzania

(-1.1) Zambia

(-1.2) Congo

(-1.4) Venezuela

(-1.4) Honduras

(-1.8) Iran -

(-1.8) Somalia -

(-4.4) Nicaragua \- -3. 3

-0.6

-0.6

-2.1m

-0.7

-1.2m

-0.7 I

-0.2

-2.0

0.4

I 0.6

XXVlll

www.fraserinstitute.org

Exhibit S-6: The Growth of Per Capita GDP During 1980-1990 for the Countries That Had aOne Unit Increase in the Is1 Economic Freedom Rating Between 1975 and1985 (and Maintained that Increase into the 1990s) Compared to the Growthof Countries with a One Unit Decline During 1980-1990

Growth of Per CapitaGDP 1980-199 0

Countries with a One UnitIncrease in Is1 IndexBetween 198 0 and 1990(Change in Is1 rating in parentheses.)

All nine of the countrieswith a unit increase between1980 and 1990 achieved positivegrowth rates. Their averageincrease in per capita GDP was3.1%. (See Exhibit 4.5 foradditional details.)

-6

Countries with a One UnitDecline in Is1 IndexBetween 1980 and 1990(Change in Is1 rating in parentheses. )

Among the nine countries witha one unit or more decline ineconomic freedom between 1980and 1990, only Tanzania wasable to achieve a positivegrowth rate. The average forthese countries was minus 1.3%.(See Exhibit 4-5 for additionaldetails.)

Note: Se e Exhibits 3-3 and 4-5 for details.

(-1.0) Syria

(-1.1) Algeria

(-1.3) Bolivia

(-1.4) Tanzania

(-1.4) Honduras -

(-1.5) Somalia

(-1.7) Venezuela

(-2.5) Iran

(-4.6) Nicaragua

-1.2

-0.1

-2.4

-0.9

-1.2

-1.8

-1.1

- -3. 7

0.6

XXIX

www.fraserinstitute.org

Exhibit S-7: Changes in the Average Country Rating for the SummaryIndexes and the Components: 1975-1995

A: Average Summary Rating of Countries, 1975-1995

The average country rating increasedby only a small amount (0.3 or less)between 1975 and 1985, but it rose bya larger amount (approximately 1.0)between 1985 and 1995. (Note thateach of our three indexes followed thissame pattern.) This suggests thatthere has been a modest move towardeconomic freedom during the lastdecade.

Summary Index Is1

Average Country Rating2 4 6 8

1975

1980

1985

1990

1995

Summary Index le Summary Index Is2

c

1975

1980

1985

1990

1995

Average Country Rating) 2 4 6

1 | |

^ ^ ^ ^ ^ 4 . 1

^ ^ ^ ^ ^ ^ ^ ^ ^ 4 . 4

^ ^ ^ ^ ^ ^ ^ ^ • 4 . 7

^ ^ ^ ^ ^ ^ ^ ^ ^ 1 5'2

8 1I

Average Country Rating2 4 6

1975

1980

1985

1990

1995

3.9

4.1

10

xxx

www.fraserinstitute.org

B. Averag e Component Rating of Countries:

IA: Money

0

1975 •1985 •1995 •

Expansion

Average2 4

1Country Rating

6 8 1 0

IIH3.6• • 1• • 1

• 5.114.2

| IC:ForeignCurrency Accounts jAverage Country Rating

0 2 4 6 8

ID: Deposits Abroad I

MA.: Government Consumption

IB: Inflation Variability!

0

1975 •1985 •1995 •

Average Country Rating2 4 6 8 1 0

•••3.8•^• •5 .1

10

0

1975 •1985 •1995 Hj

Average2 4

H i 2.5^•2.8

•H

Country Rating6 8 1

(J5.0

Average Country Rating0 2 4 6 8 1 0

1975 flH||

1985 i ^ m1995 H |

^ 5 . 3

^••5.0HH|4.8

IIB: Government Enterprises \

Average Country Rating0 2 4 6 8

1975

IF: Credit Market)

IIIB: Margina l Tax Rates [Average Country Rating

0 2 4 6 8

10

Average Country Rating0 2 4 6 8 1 0

1975 i m1985 p H1 9 9 5 l | ^ |

^••4.8• • •wmmmI7-1

H7'6

IIIA:

0

1975 1

1985 1

1995 1

Transfers & Subsides |Average Country Rating2 4 6 8

•1HM5.9••^••5.0• • • 1 4 . 9

10

10

NIC:

1975

1985

1995

Conscription jAverage Country

0 2 4 6

Hm^i4.9

HUH4-1

IHHH4'3

Rating8 1 0

XXXI

www.fraserinstitute.org

Exhibit S-7: (con't)

IVA:

1975

1985

1995

Trade Taxes |Average

0 2 4

—

^ Bmm

Country6

14.4

I5'1• •

Rating8

6.4

10

|lVC:

1975

1985

1995

Size

0

•i•

of Trade Sector |Average Country2 4 6

HI^Hfl4.9^^^^•5.0

^HHH4'8

Rating8 1 0

IVB

1975

1985

1995

: Exchange Rate Controls |

Average0 2 4

—

Sm

Country Rating6 8 1 0

• I 5.4([5.0

H^HI75

IVD: Capital Mobility Restraints IAverage Country Rating

0 2 4 6 8 1 0

The component ratings indicate that the major areas of improvement during the last 20 years were greaterprice stability (IB), increased freedom to maintain foreign currencies both domestically and abroad (IC andID), more orderly credit markets, lower marginal tax rates (since 1985), lower taxes on international trade(IVA), relaxation of foreign exchange controls (since 1985), and fewer restrictions on capital mobility.Larger government consumption and transfer sectors (IIA and III A) were areas of declining economicfreedom.

Note: See Exhibit 3-6 for additional details.

xxxii

www.fraserinstitute.org

INTRODUCTION:

The Historical Development of TheEconomic Freedom Index

by Michael A. Walker

The current volume is the culmination of a process whichbegan at the 1984 meetings of the Mont Pelerin Society inCambridge, England. In the course of a comment on a paper byPaul Johnson, I made reference to the famous passage in Capitalismand Freedom written by Milton Friedman and Rose Friedman, inwhich the authors note that, "Historical evidence speaks with asingle voice on the relation between political freedom and a freemarket. I know of no example in time or place of a society thathas been marked by a large measure of political freedom, and thathas not also used something comparable to a free market toorganize the bulk of economic activity."

There then ensued a discussion about the relationshipbetween economic and political freedom led by the late Max Thurn,a long time member of the Society. It became clear during thecourse of this discussion that while Milton and Rose Friedman'scomment had been extant for three decades there had been noserious attempt to explore the relationship between economic andpolitical freedoms in a scholarly way. At the meeting I approachedMilton and Rose Friedman to invite them to co-host a symposiumto investigate these relationships. They agreed and subsequentlyDr. Neil McLeod, President of the Liberty Fund, Inc. ofIndianapolis agreed to provide the funding to bring a group ofdistinguished economists from all over the world to the NapaValley, California in 1986.

The proceedings of this first symposium were published ina book which I edited entitled, Freedom, Democracy and EconomicWelfare, published by the Fraser Institute in 1988. Meanwhile,Alvin Rabushka, Milton Friedman's colleague at the HooverInstitution who had been concerned about these issues for nearly adecade because of his direct involvement in the study and

www.fraserinstitute.org

documentation of the economic development of Hong Kong, helda series of Liberty Fund conferences. One, on "Taxation andLiberty" was held in Santa Fe, New Mexico in 1985 and anotheron "Taxation, Democracy, and Threats to Liberty" in Savannah,Georgia in 1987. Alvin Rabushka was also a participant in the1986 Napa Valley Conference and he was to play a central role indeveloping the symposium series.

Milton Friedman had suggested to me that I should inviteto the first meeting in the Napa Valley a representative fromFreedom House because they had expanded their 1982 AnnualReport on political and civil liberties around the world to include,on an experimental basis, ratings for economic freedom. RaymondGastil, then the President of Freedom House and Lindsay Wright,a young economist working for the organization, came andpresented a paper on their findings on economic freedom at thefirst conference.

As Gastil and Wright shared their views on economicliberty, it was obvious that they differed significantly from those ofmost conference participants. The Gastil-Wright approach reflectedthe Freedom House perspective that democratic political proceduresand civil liberties were the most important aspects of freedom.According to this philosophy, highly progressive taxation and largeincome transfers are entirely consistent with individual liberty, ifpolicies in these areas are approved by democratic majorities oflegislative bodies.1 Several of the participants in this firstconference, including myself, Walter Block, and Alvin Rabushka,believed that the Freedom House approach trivialized and distortedeconomic freedom, making it dependent on the political process.We came away even more convinced that development of a soundmeasure of economic freedom was a vitally important project.

My colleague Walter Block and Alvin Rabushka had asubsequent meeting in which they decided to suggest that a seriesof follow up symposia be held in order to explore the weaknessesof the Freedom House approach and to develop an index ofeconomic freedom that was consistent with the history and propermeaning of economic liberty. The long term objective would beto develop a measure of economic freedom that would be publishedon a regular basis just like the Freedom House's annual survey ofpolitical and civil liberties.

www.fraserinstitute.org

It was then left for me to persuade Milton and RoseFriedman to co-host a series of symposia to properly elucidate thesubject and to persuade the Liberty Fund to provide the financing.The new President of Liberty Fund, Inc., Mr. W. W. Hill was quiteexcited by the project, could see its implications, and happilyagreed to fund a further five meetings in which internationalexperts would build up an intellectual base from which the indexmight be formed.

The second conference of the series was held in Vancouverin July of 1988 and centred on a paper presented by AlvinRabushka on how economic freedom should be defined.2 Buildingon the work of John Locke, Adam Smith, Milton Friedman, MurrayRothbard, and his own extensive empirical and theoretical analysis,Rabushka examined the attributes of economic freedom and thenature of policies consistent with that freedom. He argued thatprivate property and rule of law provided the foundation—theinstitutional basis—for economic freedom. Rabushka applied theconcept of economic freedom to five basic areas—taxation, publicspending, economic regulation of business and labour, money, andforeign trade—and outlined some ideas about how it might bemeasured in each of these areas. This work proved to be quiteimportant in focusing subsequent discussion at the other symposia.

Also at the second meeting came the first attempt to provideempirical measures with a paper by Zane Spindler and Laurie Still.In their paper they added to the taxonomy suggested by AlvinRabushka and provided a first-cut try at evaluating the FreedomHouse Index and adding to it a measure of freedom based oninvoluntary military service and freedom of foreign trade andinvestment. One of the consequences of the discussion of thispaper was the suggestion that all of the participants produce a listof factors that they felt should go in to an index of economicfreedom and there resulted a list of indicators which might be usedfor this purpose.

The third meeting was held in 1989 at Banff, Alberta andrepresented the first real attempt to construct both theoretical andempirical measures which were derived from the principlessketched out by Rabushka at the second session. Sectoral papersexplored the construction of indices for labour markets,international trade and money markets. The discussions weremostly interesting for the direction they would provide for the

www.fraserinstitute.org

papers presented at the fourth meeting held at Sea Ranch,California in 1990.

The fourth symposium saw the investigation proceed to amuch higher level of understanding both empirically andtheoretically. A theoretical paper by Ronald Jones and Alan C.Stockman built upon two papers by Stephen Easton to specificallyconsider freedom as part of the standard economic model. Theiranalysis put to rest a confusion which often attends suchdiscussions and that is the difference between wealth and freedom.They showed that there could simultaneously be a reduction infreedom and an increase in wealth.

Also at the fourth symposium there was the beginning of theindex which is presented in this book. James Gwartney workedwith Walter Block and Robert Lawson to produce the firstcomprehensive index which ranked 79 countries in the sectorswhich Rabushka had outlined and which were further discussed atthe third symposium. The fourth symposium also involved, in apaper by Zane Spindler and Joanna Miyake, the consideration ofthe list of indices of freedom which had been devised during thesecond symposium.

One of the most interesting aspects of the fourth symposiumwas a survey of economic freedom conducted by Milton and RoseFriedman. Each of the symposium participants was asked to rank11 countries which would be familiar to all participants. Miltonand Rose then analyzed the ranking during the evening andpresented it the following day. This simple survey and analysis ofit proved to be quite helpful in discovering the dispersion ofestimates of the freedom of countries that were neither very freenor very unfree but somewhere in between. The classic problemof distinguishing amongst things that are similar was also seen toplague the task of measuring freedom.

One of the conclusions that emerged from the Sea Ranchmeeting was that there are two ways in which to construct an indexof freedom. The "low tech," judgmental way in which a numberof individuals are asked to provide their subjective ranking of agroup of countries and the "high tech" way in which a largenumber of criteria, based on a series of measurable quantities, areapplied to produce the rating.

www.fraserinstitute.org

By way of testing further the low tech approach, it wasdecided to have a future meeting consider a group of countries andto have individuals who were familiar with the countries rank themon a freedom scale. The fifth symposium held in 1991 at MontereyCalifornia focused on a series of papers which had been constructedin this way. Essentially, groups of respondents in Asia, LatinAmerica, Africa, Europe and North America were asked to rankcountries in their region as well as countries outside their regionwhich were common to all of the lists. In this way it was hopedthat an integrated picture might emerge of the economic freedomrankings of all countries considered.

While this exercise produced some interesting insights, ingeneral it was found that respondents did not possess enoughinformation about the countries they were asked to rank and it wasquite difficult to find people in a given region who wereknowledgeable about more than one or two countries. While therewere many interesting insights generated from the various regions,it did not prove possible to derive a coherent index from thecomponents.

In a separate survey conducted by Stephen Easton andmyself, members of the Mont Pelerin Society were also asked torank countries in their region and this survey did prove to becoherent. However, it was in general felt that more success mightbe achieved by reverting to the "high tech" method and the use ofmany index series for each country which Gwartney, Block andLawson had begun in the fourth session. This objectification of themeasurement process would overcome the problems of subjectivityand the difficulty of finding knowledgeable people to do the rating.

However, a serious problem remained. Namely, to find theweights that should be attached to the various data series in theGwartney, Block and Lawson index. In partial response to therecognition of this problem, Easton and I undertook another surveyof the Mont Pelerin Society membership in which we asked therespondents to rank each country's performance in a number ofgeneral areas such as international trade, monetary freedom, etc.The sixth symposium focused entirely on the revised Gwartney,Block and Lawson paper and the second paper which Easton andI had constructed.

The sixth symposium was held in Sonoma California in1993 and the focus of discussion was a greatly revised Gwartney,

www.fraserinstitute.org

Block and Lawson paper and the paper Easton and I had written toreport the results of our second survey. Many suggestions forimprovement were advanced and a number of approaches to theproblem of weighting the components of the index were discussed.The Index of Freedom which is presented in this volume reflectsthe valuable contributions of the participants toward resolving thedifficulties which were identified.

All told, 61 people have contributed to the Rating EconomicFreedom program of the Fraser Institute. We feel that it would beappropriate to acknowledge their contribution to the process andthey are therefore named at the end of this introduction. However,it goes without saying that they are not responsible for the resultingindex nor do they necessarily endorse it or its implications.

Recently, the Heritage Foundation of Washington, D.C., haspublished an index of Economic Freedom. There is some question,therefore, as to why we should produce another, seeminglycompeting index. The answer is simple.

First of all, as The Heritage Foundation was careful to notein their publication, the research which has been produced by theRating Economic Freedom Project of the Fraser Institute is of afundamental kind and attempts to deal with the key methodologicalissues involved in the creation of such an index. The HeritageFoundation index reflects some of this research but is not ascomplete or as comprehensive as the index published here. It ishoped that the Heritage Foundation will incorporate the advancesin the state of research which are reflected in this index.

Secondly, this index provides a historical measurement ofeconomic freedom. It is possible therefore to use this index toundertake analysis of the relationship between economic freedomand other variables through time. This is a very importantconsideration.

Finally, we believe that this index represents the "state ofthe art" in the measurement of economic freedom and that itestablishes both a new bench mark for economic freedom and anew starting point for research that will improve our understandingof this vital aspect of the human condition.

www.fraserinstitute.org

Endnote:

1. For the presentation of this view, see Lindsey M. Wright, "A ComparativeSurvey of Economic Freedoms" in Freedom in the World: Political Rights andCivil Liberties, 1982, ed. Raymond D. Gastil (Westport and London: GreenwoodPress, 1982), pp. 51-90 and Raymond D. Gastil and Lindsey M. Wright, "TheState of the World: Political and Economic Freedom," in Freedom, Democracyand Economic Welfare, ed. Michael Walker (Vancouver: The Fraser Institute,1988), pp. 85-119. For a detailed criticism of this view, see Alvin Rabushka"Freedom House Survey of Economic Freedoms," in Economic Freedom: Towarda Theory of Measurement, ed. Walter Block (Vancouver: The Fraser Institute,1991), pp.57-71.

2. For those interested in the papers and a summary of the discussion from theentire Fraser Institute/Liberty Fund series, see Michael A. Walker, ed., Freedom,Democracy, and Economic Welfare, (Vancouver: Fraser Institute, 1988); WalterBlock, ed., Economic Freedom: Toward and Theory of Measurement,(Vancouver: Fraser Institute, 1991); and Stephen T. Easton and Michael A.Walker, eds., Rating Global Economic Freedom, (Vancouver: Fraser Institute,1992).

www.fraserinstitute.org

Participants in Fraser Institute/Liberty Fund Series:

James AhiakporProfessor of EconomicsCalifornia State Universityat Hayward

Armen AlchianProfessor of EconomicsUniversity of Calif.—LosAngeles

Peter BauerProfessor Emeritus ofEconomicsLondon School ofEconomics

Gary S. BeckerProfessor of EconomicsUniversity of Chicago

Juan F. BendfeldtExecutive SecretaryCentro de EstudiosEconomico-SocialesGuatemala

Walter BlockProfessor of EconomicsCollege of the Holy Cross

Jack CarrInstitute for Policy AnalysisUniversity of Toronto

John F. ChantProfessor of EconomicsSimon Fraser University

Edward CranePresident, Cato Institute

William C. DennisLiberty Fund, Inc.

Arthur T. DenzauProfessor of EconomicsWashington University

Governor Ramon P. DiazCentral Bank of Uruguay

Thomas J. DiLorenzoProfessor of EconomicsLoyola College—Baltimore

Stephen EastonProfessor of EconomicsSimon Fraser University

David FriedmanUniversity of Chicago LawSchool

Milton FriedmanThe Hoover InstitutionStanford University

Rose FriedmanThe Hoover InstitutionStanford University

Raymond GastilFreedom House

John C. GoodmanPresident, National Centerfor Policy Analysis

John G. GreenwoodChairman/Chief EconomistG.T. Capital Management

www.fraserinstitute.org

Herbert GrubelProfessor of EconomicsSimon Fraser University

James D. GwartneyProfessor of EconomicsFlorida State University

William HammettManhattan Institute

Arnold HarbergerProfessor of EconomicsUniversity of Chicago

W.W. HillLiberty Fund., Inc.

Edward L. HudginsHeritage Foundation

Ronald W. JonesProfessor of EconomicsUniversity of Rochester

Professor Brian KantorProfessor of EconomicsUniversity of Capetown

Henry KierzkowskiProfessor of EconomicsGrad. Inst. of InternationalStudiesGeneva, Switzerland

Henri LePagePresident, Institut deL' EntrepriseParis, France

Robert LawsonProfessor of EconomicsShawnee State University

Assar LindbeckProfessor of EconomicsInst. for InternationalEconomic StudiesUniversity of Stockholm

Tibor MachanProfessor of PhilosophyAuburn University

Henry MarineDean, School of LawGeorge Mason University

Antonio MartinoProfessor of EconomicsUniversity of Rome

Hugo MaulProfessor of EconomicsCentro de EstudiosEconomico-SocialesGuatemala

Richard B. McKenzieProfessor of EconomicsGraduate School ofManagementUniversity of California,Irvine

Charles MurrayAmerican EnterpriseInstitute

Douglass C. NorthProfessor of EconomicsWashington University

Simon OgusG.T. Management (Asia)LimitedHong Kong

www.fraserinstitute.org

Filip PaldaProfessor of EconomicsEcole nationaled'administration publiqueMontreal, Quebec

Ellen PaulProfessor of PhilosophyBowling Green StateUniversity

Michael ParkinProfessor of EconomicsUniversity of WesternOntario

Gramoz PashkoDeputy Prime MinisterGovernment of Albania

Svetozar PejovichProfessor of EconomicsTexas A & M University

Sally PipesPresident, Pacific ResearchInstitute

Robert PooleEditor, Reason

Alvin RabushkaThe Hoover InstitutionStanford University

Gerald RadnitskyProfessor of PhilosophyUniversity of Trier

Richard W. RahnPresident, Novecon Corp.

Alan ReynoldsHudson Institute

Gerald W. ScullyProfessor of EconomicsSchool of ManagementUniversity of Texas atDallas

Bernard SieganProfessor of LawUniv. of San Diego Schoolof Law

Zane SpindlerProfessor of EconomicsSimon Fraser University

Ingemar StahlProfessor of EconomicsUniversity of LundLund, Sweden

Alan C. StockmanProfessor of EconomicsUniversity of Rochester

Richard L. StroupProfessor of EconomicsMontana State University

Melanie TammenCato Institute

Gordon TullockProfessor of EconomicsUniversity of Arizona

Michael WalkerExecutive DirectorFraser Institute

Sir Alan WaltersThe World Bank

Lindsay WrightFreedom House

10

www.fraserinstitute.org

CHAPTER 1

Construction of theEconomic Freedom Index

Measurement is the making of distinction; precisemeasurement is making sharp distinctions.

-Enrico Fermi

Most people prefer to choose for themselves. This indicatesthat freedom, including economic freedom, has intrinsic value.Adam Smith noted that human beings have a natural inclination to"truck and barter." Restrictions on the freedom to choose andengage in voluntary exchange deny human beings something theyvalue—something that is an integral part of their humanity. Inaddition, economic theory indicates that economic freedom affectsincentives, productive effort, and the effectiveness of resource use.Since the time of Smith, economists have argued that the freedomto choose, supply resources, compete in business, and trade withothers is a central ingredient—perhaps the fundamental element—ofeconomic progress.

If economic freedom is this important, why have weinvested so little time attempting to measure it? The obviousanswer is that economic freedom is multi-dimensional and thereforeits measurement is a difficult—some would say impossible—task.These same arguments were presented prior to the development ofthe national income accounts used to measure gross domesticproduct. Of course, there is a parallel here. Since most thoughtmeasurement of output with any degree of accuracy was animpossible task, it was 150 years after Smith's Wealth of Nationsbefore a comprehensive measure was developed.

If we are unable to measure economic freedom, we are ina poor position to judge its significance as a source of progress.Clearly, the degree of economic freedom present is influenced bynumerous factors. No single statistic will be able to fully captureall of them and their interrelations. However, we believe that it ispossible to devise measures and develop indicators that will capture

www.fraserinstitute.org

the most important elements of economic freedom and provide areasonably good measure of differences in economic freedomacross countries and time periods.2 As the quotation of ProfessorFermi indicates, measurement involves making distinctions. Whensomething is difficult to measure precisely, the distinctions may notbe as refined as we would like. This is the case with economicfreedom. The measures developed in this study might best beviewed as approximations rather than precise measures. Therefore,small differences between countries and across time periods shouldnot be taken very seriously.

This chapter addresses three topics. We begin with adiscussion of the concept of economic freedom. The secondsection describes the various components of our indexes andindicates how the economic freedom ratings for each of thecomponents are derived. The final section considers the problemsthat arise when the components are aggregated into a summaryindex and explains how the three summary indexes of economicfreedom are derived.

An index ofeconomic freedomshould measure theextent to whichrightly acquiredproperty is protect-ed and individualsare free to engagein voluntarytransactions.

THE CONCEPT OF ECONOMIC FREEDOM

The central elements of economic freedom are personalchoice, protection of private property, and freedom of exchange.Individuals have economic freedom when (a) property they acquirewithout the use of force, fraud, or theft is protected from physicalinvasions by others and (b) they are free to use, exchange, or givetheir property to another as long as their actions do not violate theidentical rights of others. Thus, an index of economic freedomshould measure the extent to which rightly acquired property isprotected and individuals are free to engage in voluntarytransactions. In an economically free society, the fundamentalfunction of government is the protection of private property and theenforcement of contracts. When a government fails to protectprivate property, takes property itself without full compensation, orestablishes restrictions that limit voluntary exchange, it violates theeconomic freedom of its citizens.4

This concept of economic freedom reflects the prior workof others. Alvin Rabushka, a pioneer researcher and leadingscholar in this area, highlighted the relationship between privateproperty and economic freedom in the following manner:

12

www.fraserinstitute.org

Private property is the common denominator that underpinsevery liberal philosophical treatment of individual economicfreedom. John Locke regarded the existence of privateproperty as the proper condition of man in a state of nature;the primary function of civil society, to which man granted therights he enjoyed in the state of nature, was to protect andpreserve private property. Most important, the state has noright to take any part of a man's property without his consent.

Lindsey Wright of the Freedom House has also stressed thecentral role of private property. In the 1982 Freedom Houseannual report, she stated:

The freedom to have property and control its use isfundamental to the ability of individuals and groups to makeeconomic choices independent of arbitrary intervention byotherx6

Freedom of exchange and the autonomy of the individualare also integral elements of economic freedom. As AlvinRabushka put it:

The free and voluntary exchange of property titles goes handin hand with the rights of private property. Unless eachindividual controls the use of his property, including his rightto transfer it to another party in exchange for someconsideration, the notion of private ownership and use haslittle meaning. Thus, freedom of contract is inherent in privateproperty.... A free society affords every individual freedom ofcontract in contrast with, say, an aristocratic society in whichonly the nobility can enter into contracts to exchange titles.

It is useful to view economic freedom within the frameworkQ

of protective rights and intrusive rights. Protective rights provideindividuals with a shield against others who would invade and/ortake what does not belong to them. Since they are nonaggressionrights, all citizens can simultaneously possess them. In order tomaintain protective rights, preventing people from initiatingaggression against others is all that is required. In contrast,intrusive rights (or "positive rights" as they are sometimes called),such as a "right" to food, clothing, medical services, housing, or aminimal income level impose "forced labor" requirements on others.If A has a right to housing, for example, this logically implies thathe has a right to force B to provide the housing. But A has noright to the labor of B or any other individual. Thus, A cannotpossibly have a right to housing and other things that can only be

Intrusive rightssuch as a "right"to foody clothing,medical services,housing, or aminimal incomelevel impose"forced labor"requirements onothers. Alleged"rights" of this typeare simply dis-guised demands forthe forced transfersof income andwealth.

13

www.fraserinstitute.org

supplied if they are provided by other people. Intrusive rightstherefore conflict with economic freedom because such "rights"imply that some have a right to the labor and possessions of others.In reality, alleged "rights" of this type are simply disguiseddemands for the forced transfers of income and wealth.

It is important to distinguish economic freedom frompolitical and civil liberties. Political freedom has to do with theprocedures that are used to elect government officials and decidepolitical issues. Political liberty is present when all adult citizensare free to participate in the political process (vote, lobby, andchoose among candidates), elections are fair and competitive, andalternative parties are allowed to participate freely. Civil libertyencompasses the freedom of the press and the rights of individualsto assemble, hold alternative religious views, receive a fair trial,and express their views without fear of physical retaliation. Acountry may have a substantial amount of both political and civilliberty—it may be highly democratic and the major civil libertiesmay be protected—and still adopt policies that conflict witheconomic freedom. Countries like Israel, Sweden, and Indiaillustrate this point. Political and civil liberties are present in suchcountries, but nonetheless, their policies—for example, the levels oftaxation, government spending, and regulations—are often inconflict with economic freedom.

Our goal is toconstruct an indexthat is (a) a goodindicator ofeconomic freedomacross countriesand (b) based onobjectivecomponents thatcan be updatedregularly.

THE COMPONENTS OF OUR INDEXOF ECONOMIC FREEDOM

Our goal is to construct an index that is (a) a good indicatorof economic freedom across a large number of countries and (b)based on objective components that can be updated regularly. Tothe extent possible, we want to avoid having to make "judgmentcalls" when rating the policies, legal structures, and institutions ofa country.

As Exhibit 1-1 indicates, our index has 17 components thatare allocated to four major areas: (1) money and inflation, (2)government operations and regulations, (3) takings anddiscriminatory taxation, and (4) international exchange.9 Since wewant the ratings to be easily comparable across countries and time

14

www.fraserinstitute.org

periods, a zero to ten rating scale was used for each component inthe index. A ten represents the highest possible rating and a zerothe lowest.

Because the structure of the underlying data used to derivethe ratings was not always the same, three alternative methods wereused to derive them. A continuous variable provided the underlyingdata for seven of the components. When this was the case, the datafor 1985—our base year—were arrayed from the highest to thelowest values and divided into eleven groups containing an equalnumber of countries. Nations in those 11 groups were thenassigned ratings ranging from ten to zero. For example, if therewere 99 countries (for which the required data were available), thenthe nine countries that rated best in this category in 1985 wouldreceive a rating often, the next nine would receive a rating of nine,and so on. The cutoff points between groups in the 1985 datawere then used to rate each country in the other years (1975, 1980,1990 and 1995). To determine the interval cutoff points between,say, a ten and a nine rating, we calculated the midpoint in the 1985data between the country with the lowest ten rating and the countrywith the highest nine rating.