Embed Size (px)

Citation preview

1

Economic Analysis of Solar Power: Achieving Grid Parity

Annie HazlehurstJoint MBA / MS Environment & Resources CandidateStanford Graduate School of Business

2

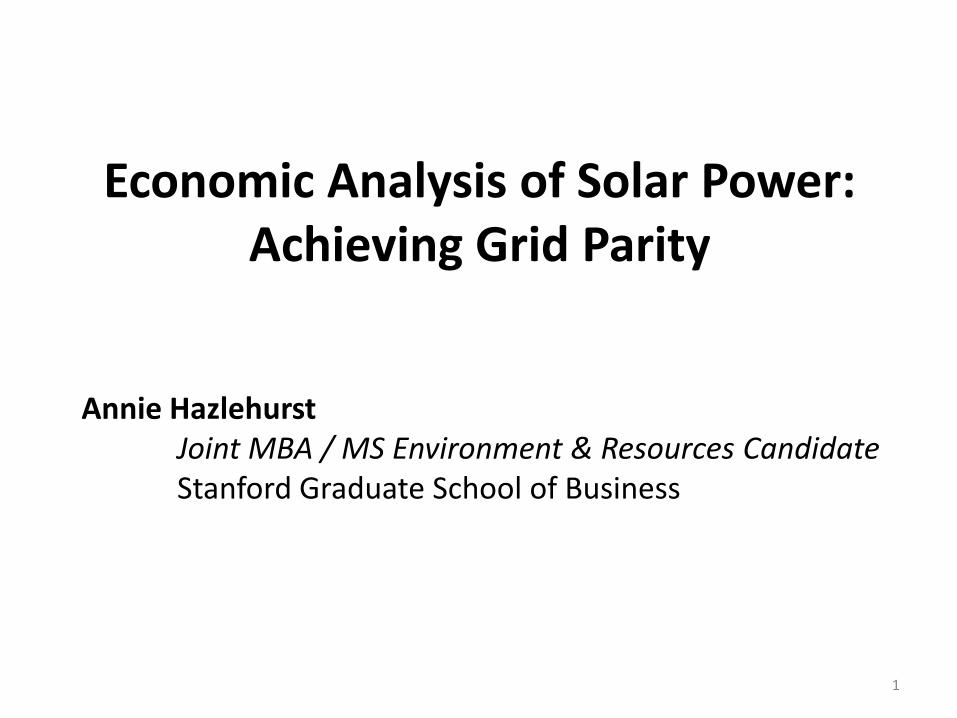

Questions to be Answered

• What are the markets for solar?

• How do we think about the cost of solar relative to other power sources?

• What do cost profiles need to be in order to achieve grid parity?

• Where is the industry today and where is it headed?

3

3 Primary Types of Solar Power

Photovoltaics (PV) Concentrating PV Solar Thermal

4

3 Primary PV Markets TodayResidential Rooftop Commercial Rooftop

Ground-mounted (Usually utility scale)

5

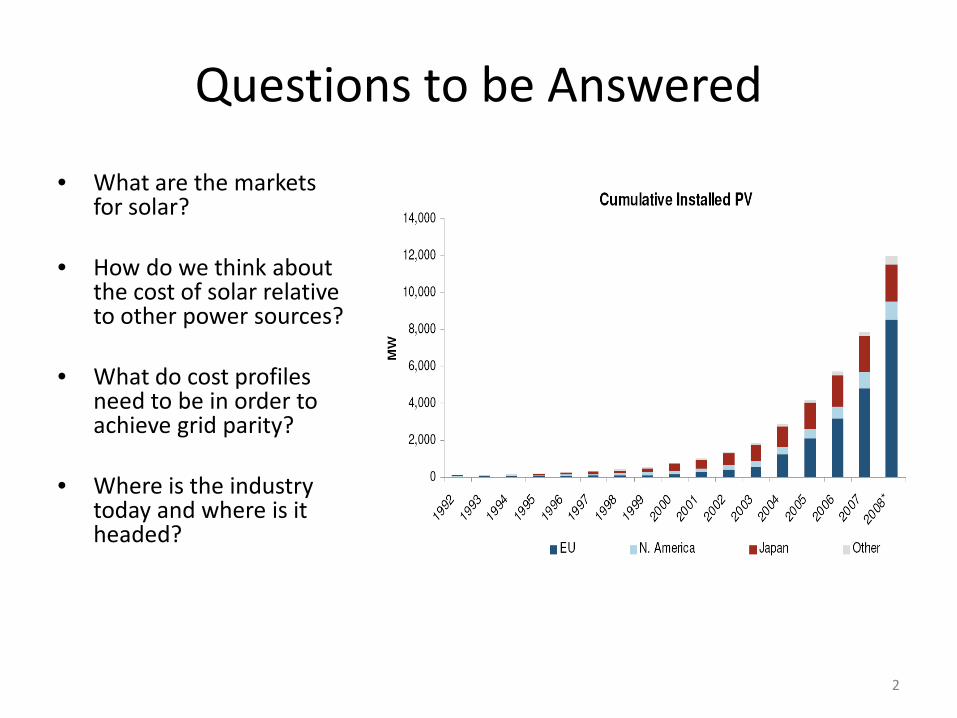

2 Emerging PV Markets

Also niche applications: calculators, satellites, remote power, etc.

Building-Integrated PV (BIPV)

• Enabled by flexible form-factor

Rural Electrification

• Requires cheaper batteries and panels for wide-spread adoption

66

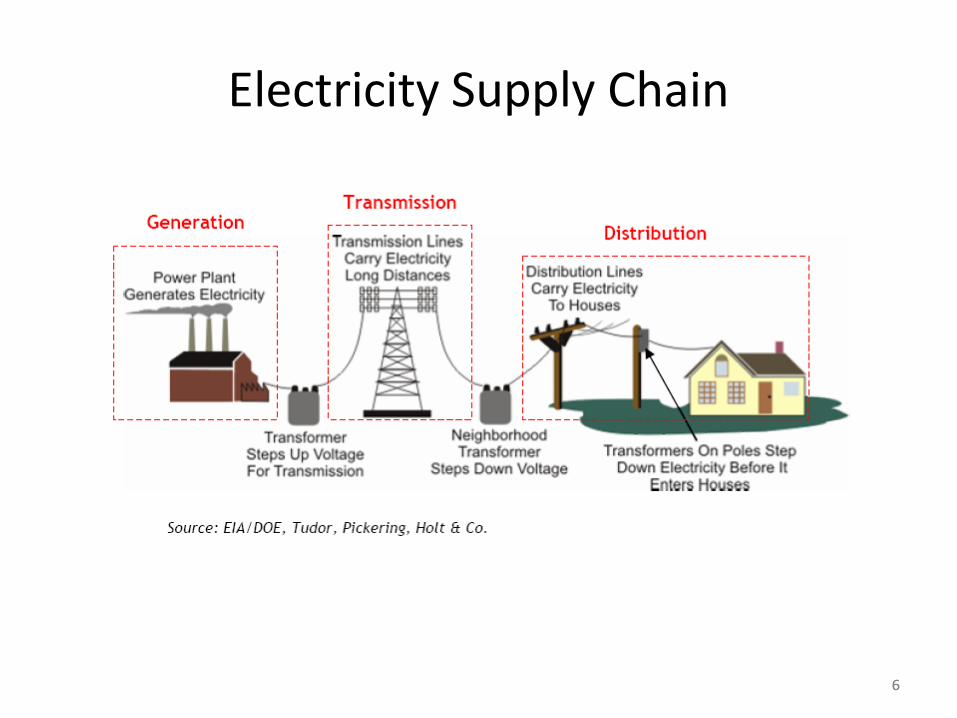

Electricity Supply Chain

7

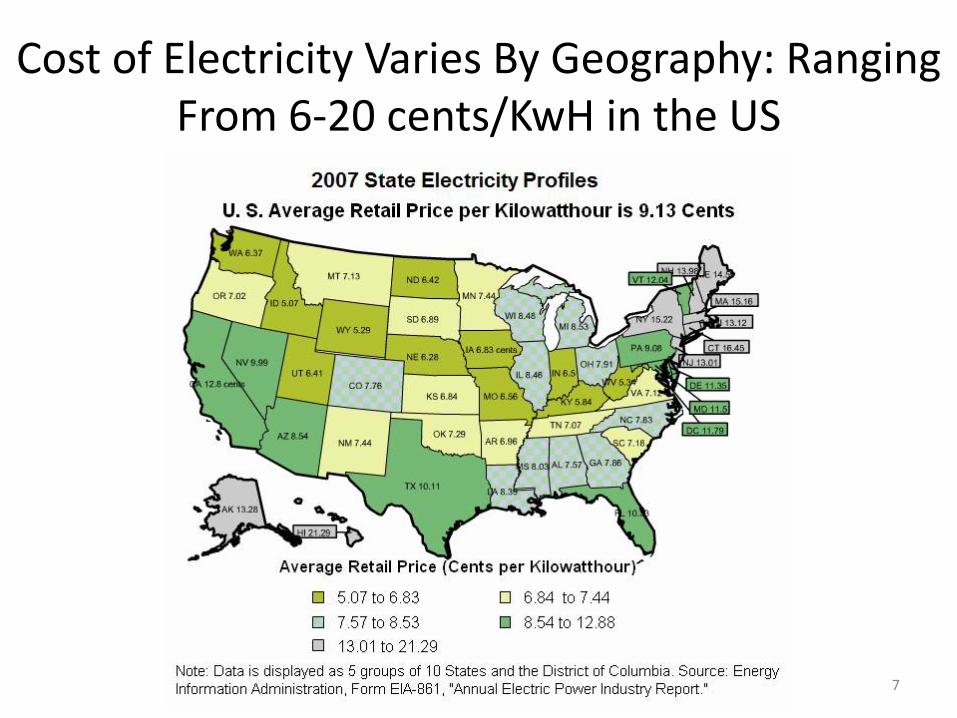

Cost of Electricity Varies By Geography: Ranging From 6-20 cents/KwH in the US

88

Incentives Driving Adoption

Source: www.dsireusa.org

Renewables Portfolio Standards

State renewable portfolio standard

State renewable portfolio goal

Solar water heating eligible *† Extra credit for solar or customer-sited renewables

Includes non-renewable alternative resources

WA: 15% by 2020*

CA: 33% by 2020

☼ NV: 25% by 2025*

☼ AZ: 15% by 2025

☼ NM: 20% by 2020 (IOUs)10% by 2020 (co-ops)

HI: 40% by 2030

☼ Minimum solar or customer-sited requirement

TX: 5,880 MW by 2015

UT: 20% by 2025*

☼ CO: 20% by 2020 (IOUs)10% by 2020 (co-ops & large munis)*

MT: 15% by 2015

ND: 10% by 2015

SD: 10% by 2015

IA: 105 MW

MN: 25% by 2025(Xcel: 30% by 2020)

☼ MO: 15% by 2021

WI: Varies by utility; 10% by 2015 goal

MI: 10% + 1,100 MW by 2015*

☼ OH: 25% by 2025†

ME: 30% by 2000New RE: 10% by 2017

☼ NH: 23.8% by 2025

☼ MA: 15% by 2020+ 1% annual increase(Class I Renewables)

RI: 16% by 2020

CT: 23% by 2020

☼ NY: 24% by 2013

☼ NJ: 22.5% by 2021

☼ PA: 18% by 2020†

☼ MD: 20% by 2022

☼ DE: 20% by 2019*

☼ DC: 20% by 2020

VA: 15% by 2025*

☼ NC: 12.5% by 2021 (IOUs)10% by 2018 (co-ops & munis)

VT: (1) RE meets any increase in retail sales by 2012;

(2) 20% RE & CHP by 2017

29 states & DChave an RPS

6 states have goals

KS: 20% by 2020

☼ OR: 25% by 2025 (large utilities)*5% - 10% by 2025 (smaller utilities)

☼ IL: 25% by 2025WV: 25% by 2025*†

99

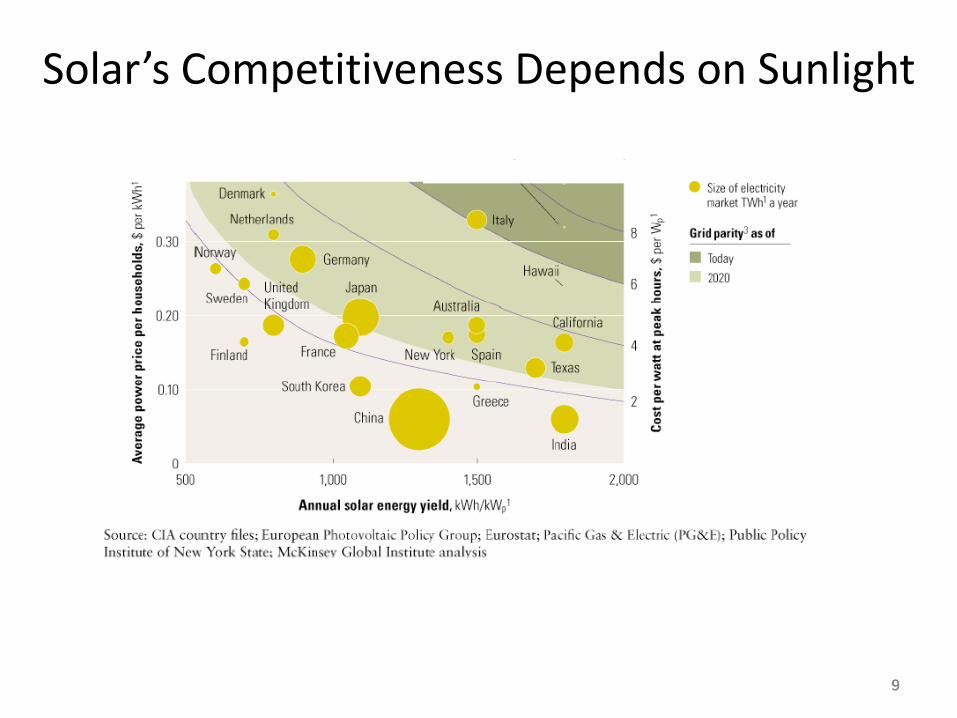

Solar’s Competitiveness Depends on Sunlight

10

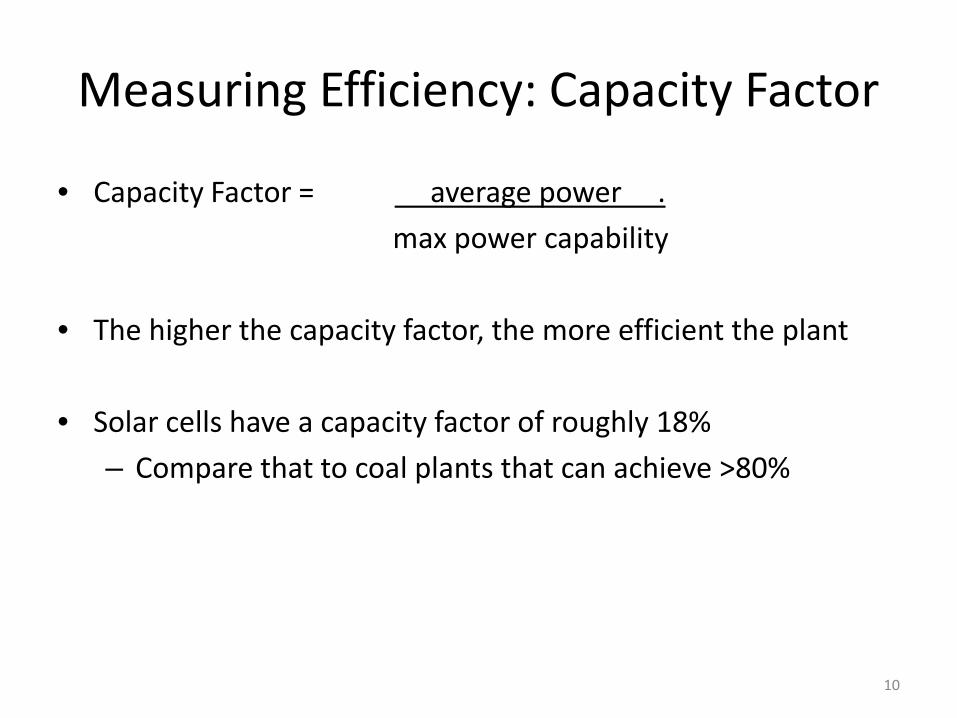

Measuring Efficiency: Capacity Factor

• Capacity Factor = average power .

max power capability

• The higher the capacity factor, the more efficient the plant

• Solar cells have a capacity factor of roughly 18%

– Compare that to coal plants that can achieve >80%

11

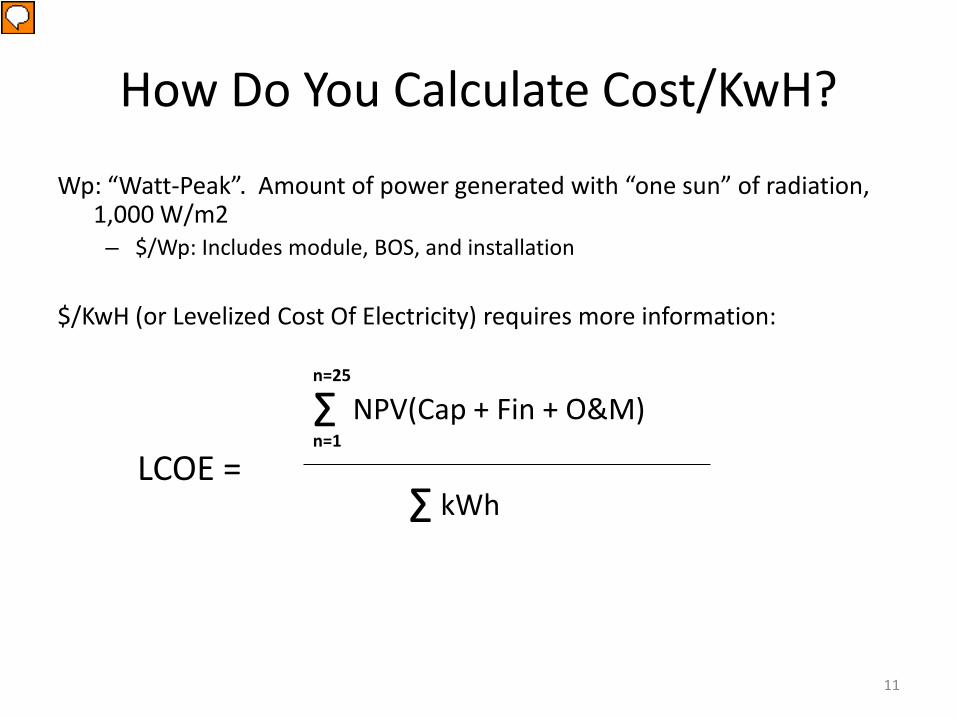

How Do You Calculate Cost/KwH?

Wp: “Watt-Peak”. Amount of power generated with “one sun” of radiation, 1,000 W/m2– $/Wp: Includes module, BOS, and installation

$/KwH (or Levelized Cost Of Electricity) requires more information:

LCOE =

Σ NPV(Cap + Fin + O&M)

kWhΣn=1

n=25

1212

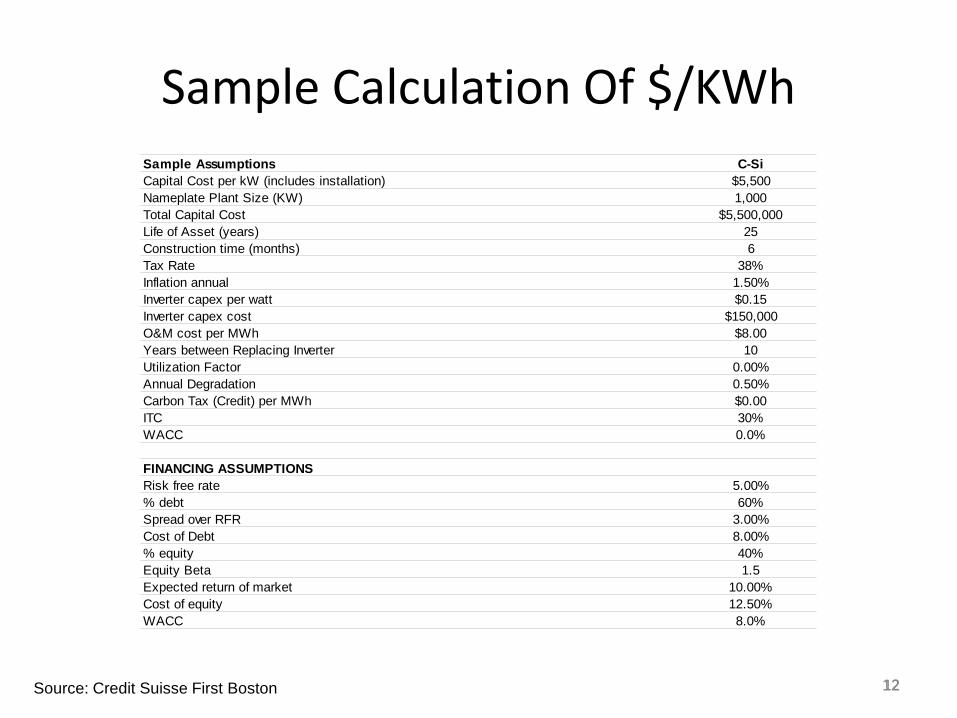

Sample Calculation Of $/KWh

Source: Credit Suisse First Boston

Sample Assumptions C-SiCapital Cost per kW (includes installation) $5,500Nameplate Plant Size (KW) 1,000Total Capital Cost $5,500,000Life of Asset (years) 25Construction time (months) 6Tax Rate 38%Inflation annual 1.50%Inverter capex per watt $0.15Inverter capex cost $150,000O&M cost per MWh $8.00Years between Replacing Inverter 10Utilization Factor 0.00%Annual Degradation 0.50%Carbon Tax (Credit) per MWh $0.00ITC 30%WACC 0.0%

FINANCING ASSUMPTIONSRisk free rate 5.00%% debt 60%Spread over RFR 3.00%Cost of Debt 8.00%% equity 40%Equity Beta 1.5Expected return of market 10.00%Cost of equity 12.50%WACC 8.0%

1313

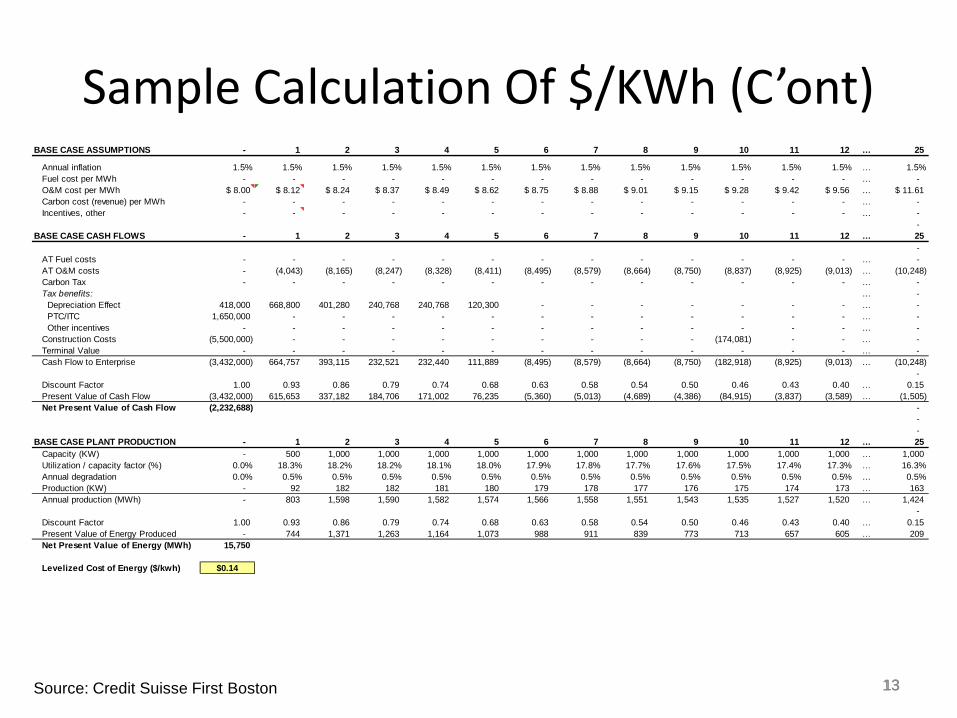

Sample Calculation Of $/KWh (C’ont)

Source: Credit Suisse First Boston

BASE CASE ASSUMPTIONS - 1 2 3 4 5 6 7 8 9 10 11 12 … 25

Annual inflation 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% … 1.5% Fuel cost per MWh - - - - - - - - - - - - - … - O&M cost per MWh $ 8.00 $ 8.12 $ 8.24 $ 8.37 $ 8.49 $ 8.62 $ 8.75 $ 8.88 $ 9.01 $ 9.15 $ 9.28 $ 9.42 $ 9.56 … $ 11.61 Carbon cost (revenue) per MWh - - - - - - - - - - - - - … - Incentives, other - - - - - - - - - - - - - … -

- BASE CASE CASH FLOWS - 1 2 3 4 5 6 7 8 9 10 11 12 … 25

- AT Fuel costs - - - - - - - - - - - - - … - AT O&M costs - (4,043) (8,165) (8,247) (8,328) (8,411) (8,495) (8,579) (8,664) (8,750) (8,837) (8,925) (9,013) … (10,248) Carbon Tax - - - - - - - - - - - - - … - Tax benefits: … - Depreciation Effect 418,000 668,800 401,280 240,768 240,768 120,300 - - - - - - - … - PTC/ITC 1,650,000 - - - - - - - - - - - - … - Other incentives - - - - - - - - - - - - - … - Construction Costs (5,500,000) - - - - - - - - - (174,081) - - … - Terminal Value - - - - - - - - - - - - - … - Cash Flow to Enterprise (3,432,000) 664,757 393,115 232,521 232,440 111,889 (8,495) (8,579) (8,664) (8,750) (182,918) (8,925) (9,013) … (10,248)

- Discount Factor 1.00 0.93 0.86 0.79 0.74 0.68 0.63 0.58 0.54 0.50 0.46 0.43 0.40 … 0.15 Present Value of Cash Flow (3,432,000) 615,653 337,182 184,706 171,002 76,235 (5,360) (5,013) (4,689) (4,386) (84,915) (3,837) (3,589) … (1,505) Net Present Value of Cash Flow (2,232,688) -

- -

BASE CASE PLANT PRODUCTION - 1 2 3 4 5 6 7 8 9 10 11 12 … 25 Capacity (KW) - 500 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 … 1,000 Utilization / capacity factor (%) 0.0% 18.3% 18.2% 18.2% 18.1% 18.0% 17.9% 17.8% 17.7% 17.6% 17.5% 17.4% 17.3% … 16.3% Annual degradation 0.0% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% … 0.5% Production (KW) - 92 182 182 181 180 179 178 177 176 175 174 173 … 163 Annual production (MWh) - 803 1,598 1,590 1,582 1,574 1,566 1,558 1,551 1,543 1,535 1,527 1,520 … 1,424

- Discount Factor 1.00 0.93 0.86 0.79 0.74 0.68 0.63 0.58 0.54 0.50 0.46 0.43 0.40 … 0.15 Present Value of Energy Produced - 744 1,371 1,263 1,164 1,073 988 911 839 773 713 657 605 … 209 Net Present Value of Energy (MWh) 15,750

Levelized Cost of Energy ($/kwh) $0.14

1414

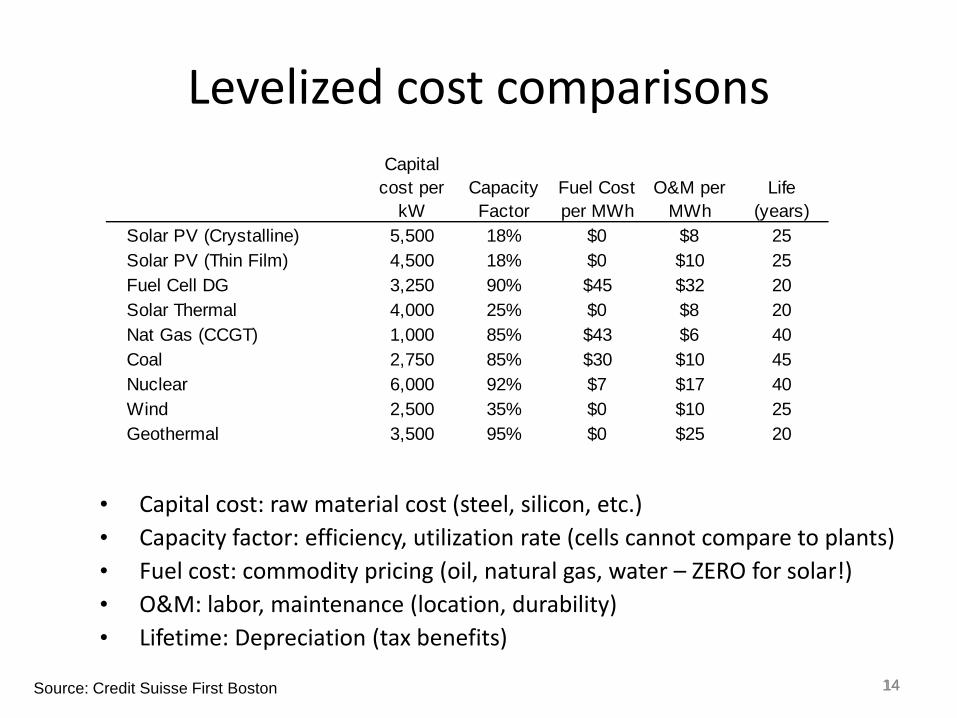

Levelized cost comparisons

• Capital cost: raw material cost (steel, silicon, etc.)• Capacity factor: efficiency, utilization rate (cells cannot compare to plants)• Fuel cost: commodity pricing (oil, natural gas, water – ZERO for solar!)• O&M: labor, maintenance (location, durability)• Lifetime: Depreciation (tax benefits)

Source: Credit Suisse First Boston

Capital cost per

kWCapacity Factor

Fuel Cost per MWh

O&M per MWh

Life (years)

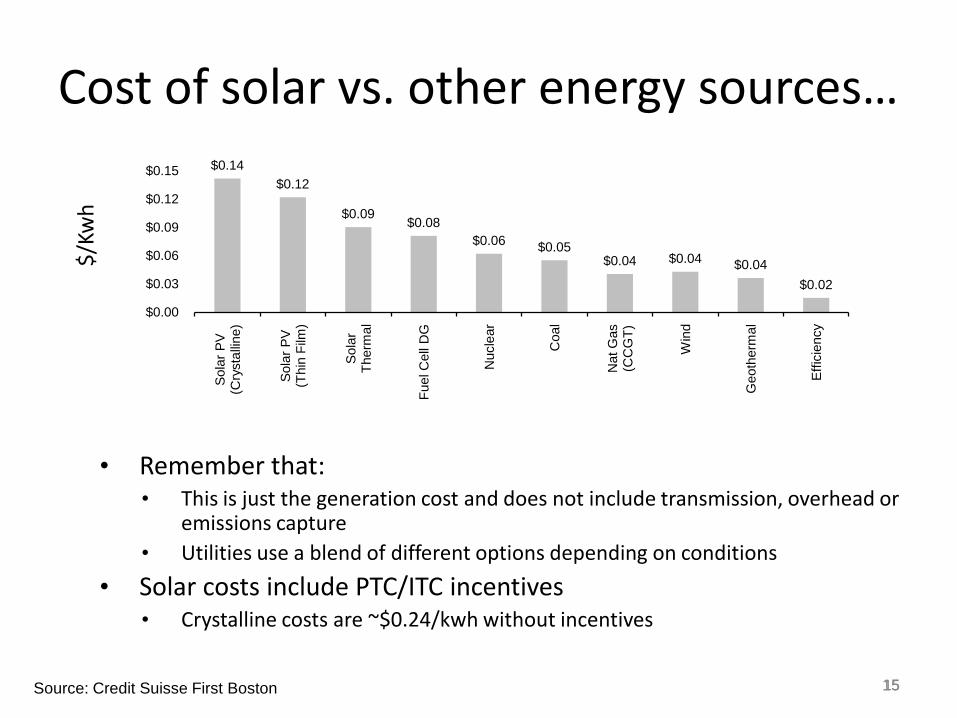

Solar PV (Crystalline) 5,500 18% $0 $8 25Solar PV (Thin Film) 4,500 18% $0 $10 25Fuel Cell DG 3,250 90% $45 $32 20Solar Thermal 4,000 25% $0 $8 20Nat Gas (CCGT) 1,000 85% $43 $6 40Coal 2,750 85% $30 $10 45Nuclear 6,000 92% $7 $17 40Wind 2,500 35% $0 $10 25Geothermal 3,500 95% $0 $25 20

1515

Cost of solar vs. other energy sources…

• Remember that: • This is just the generation cost and does not include transmission, overhead or

emissions capture• Utilities use a blend of different options depending on conditions

• Solar costs include PTC/ITC incentives• Crystalline costs are ~$0.24/kwh without incentives

Source: Credit Suisse First Boston

$/Kw

h

$0.14 $0.12

$0.09 $0.08

$0.06 $0.05 $0.04 $0.04 $0.04

$0.02

$0.00

$0.03

$0.06

$0.09

$0.12

$0.15

Sola

r PV

(Cry

stal

line)

Sola

r PV

(Thi

n Fi

lm)

Sola

r Th

erm

al

Fuel

Cel

l DG

Nuc

lear

Coa

l

Nat

Gas

(C

CG

T)

Win

d

Geo

ther

mal

Effic

ienc

y

1616

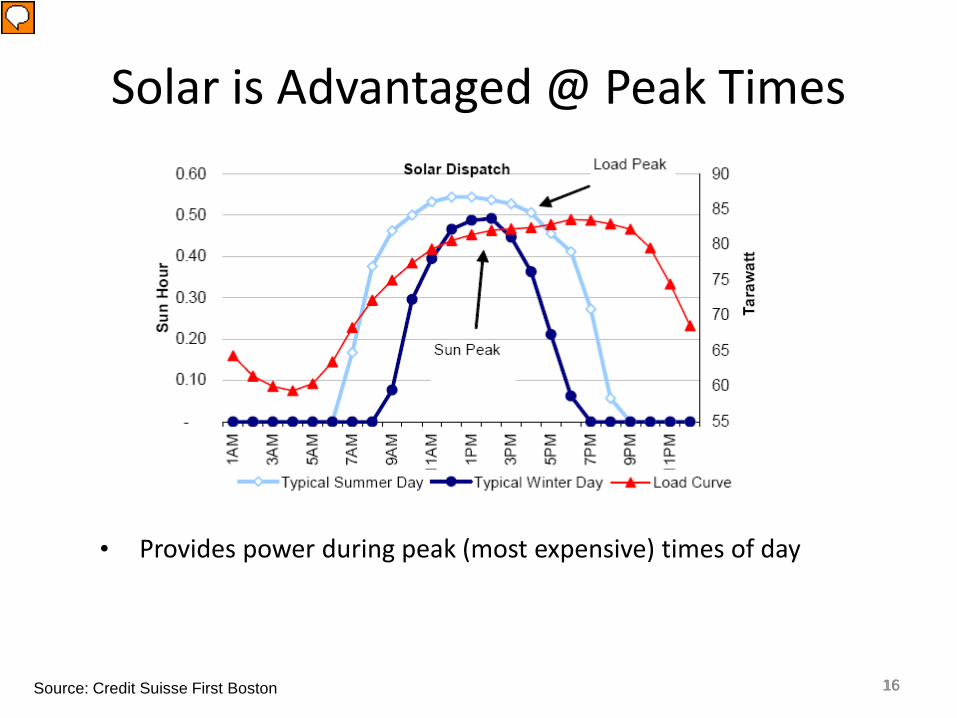

Solar is Advantaged @ Peak Times

• Provides power during peak (most expensive) times of day

Source: Credit Suisse First Boston

1717

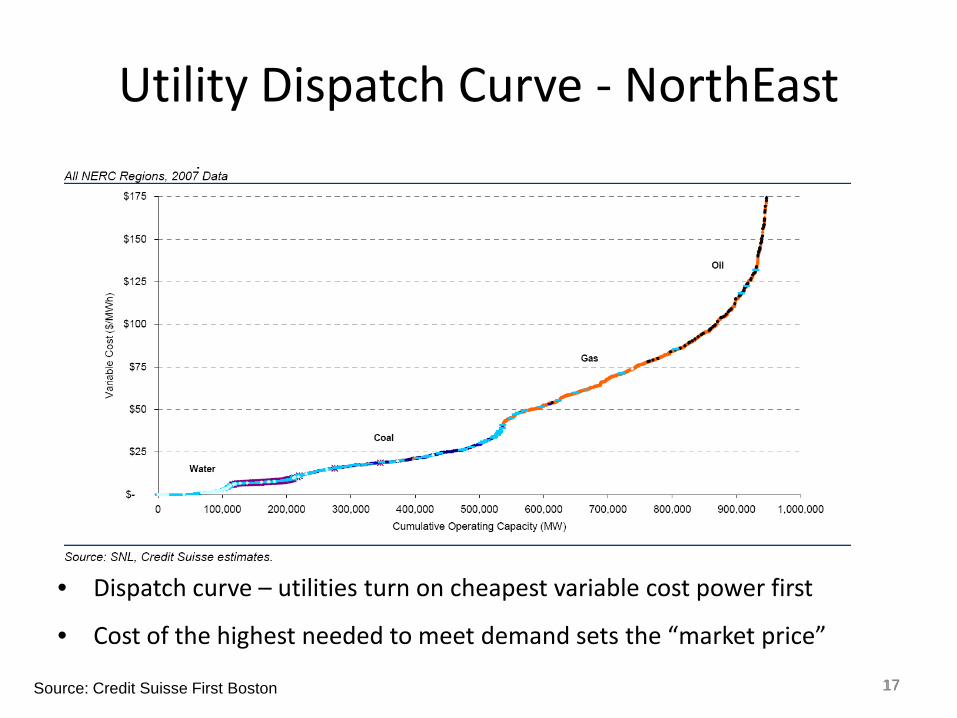

Utility Dispatch Curve - NorthEast

Source: Credit Suisse First Boston

• Dispatch curve – utilities turn on cheapest variable cost power first

• Cost of the highest needed to meet demand sets the “market price”

1818

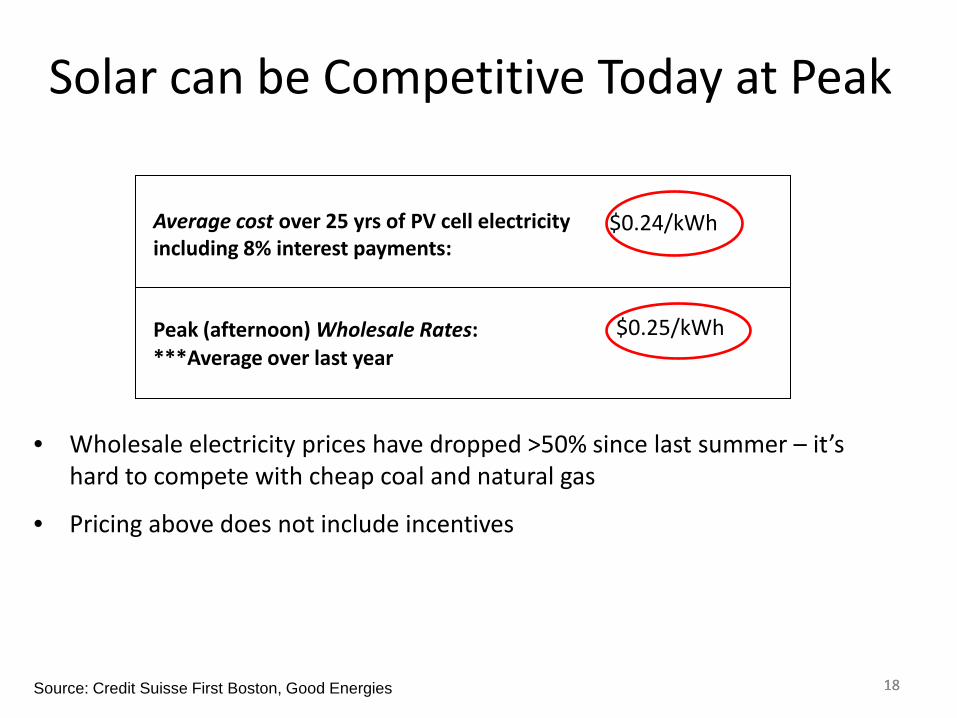

Solar can be Competitive Today at Peak

Average cost over 25 yrs of PV cell electricity including 8% interest payments:

Peak (afternoon) Wholesale Rates:***Average over last year

$0.24/kWh

$0.25/kWh

• Wholesale electricity prices have dropped >50% since last summer – it’s hard to compete with cheap coal and natural gas

• Pricing above does not include incentives

Source: Credit Suisse First Boston, Good Energies

1919

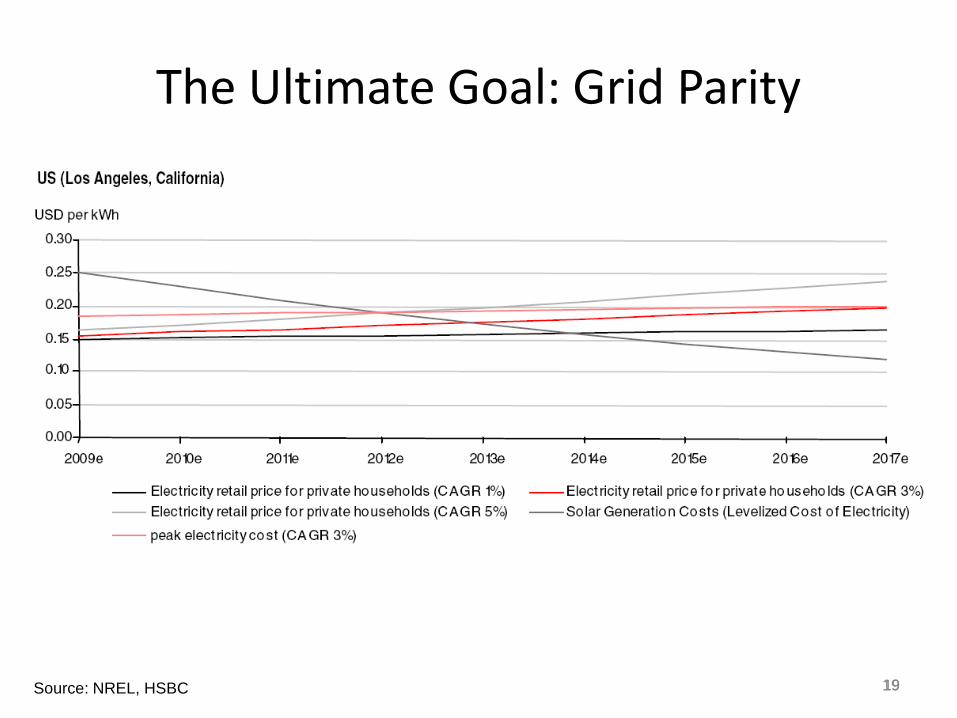

The Ultimate Goal: Grid Parity

Source: NREL, HSBC

2020

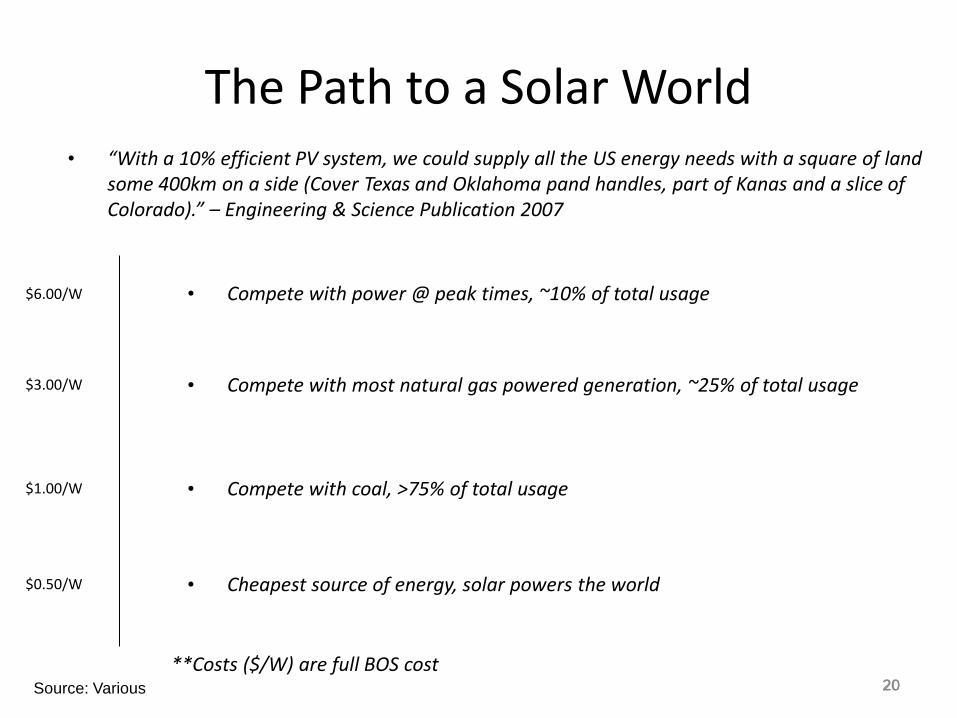

The Path to a Solar World

Source: Various

• “With a 10% efficient PV system, we could supply all the US energy needs with a square of land some 400km on a side (Cover Texas and Oklahoma pand handles, part of Kanas and a slice of Colorado).” – Engineering & Science Publication 2007

$6.00/W

$3.00/W

$1.00/W

$0.50/W

• Compete with power @ peak times, ~10% of total usage

• Compete with most natural gas powered generation, ~25% of total usage

• Compete with coal, >75% of total usage

• Cheapest source of energy, solar powers the world

**Costs ($/W) are full BOS cost

21

$/Wp Ranges From $4-9 Depending On Type Of Installation

Representative Costs, 2008

Source: SAM model, built by DOE and Sandia National Labs. Costs are representative of realistic figures, not average costs from sample installations. Does not include incentives.

Residential Commercial Utility

System size 3.8KW 210KW 10MW

$/Wp, in US $8.98 $6.68 $4.93

¢/kWh - Phoenix, AZ 31.78 22.91 26.09

¢/kWh - Boston, MA 41.89 30.44 36.49

• Costs for 2009 will be even lower, some installations are being done as low as $3 / watt

22

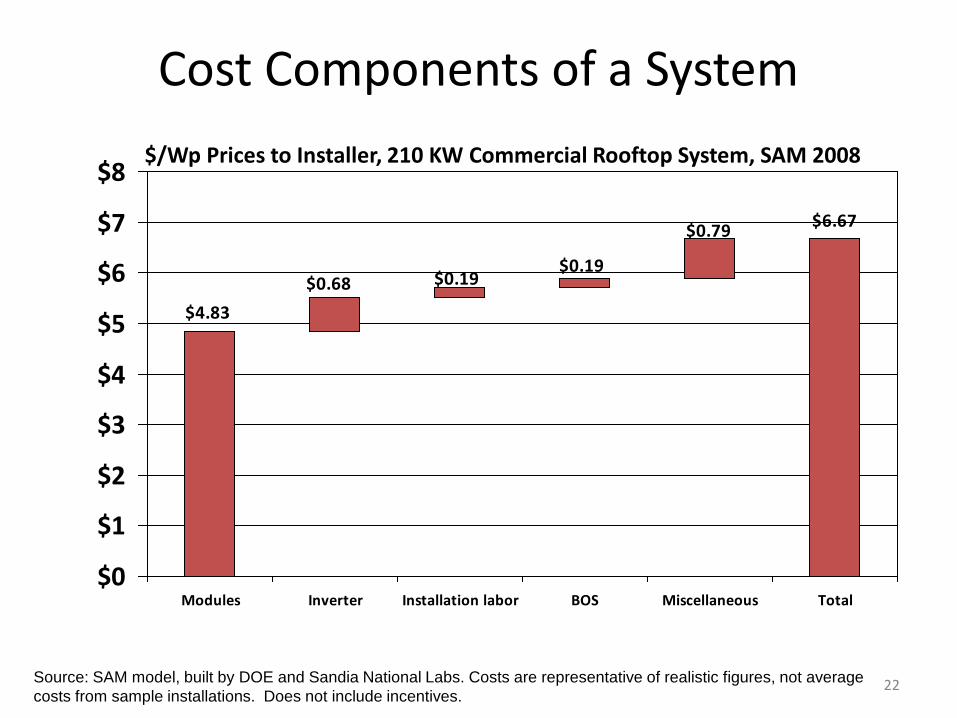

Cost Components of a System

$6.67$0.79

$0.19$0.19$0.68

$4.83

$0

$1

$2

$3

$4

$5

$6

$7

$8

Modules Inverter Installation labor BOS Miscellaneous Total

Source: SAM model, built by DOE and Sandia National Labs. Costs are representative of realistic figures, not average costs from sample installations. Does not include incentives.

$/Wp Prices to Installer, 210 KW Commercial Rooftop System, SAM 2008

2323

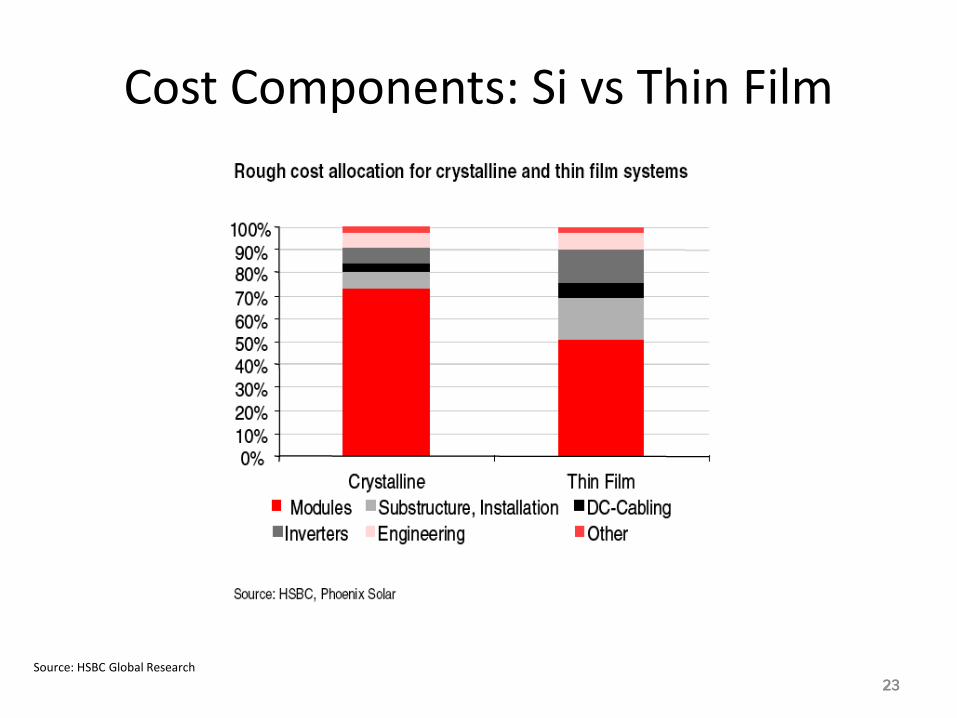

Cost Components: Si vs Thin Film

Source: HSBC Global Research

2424

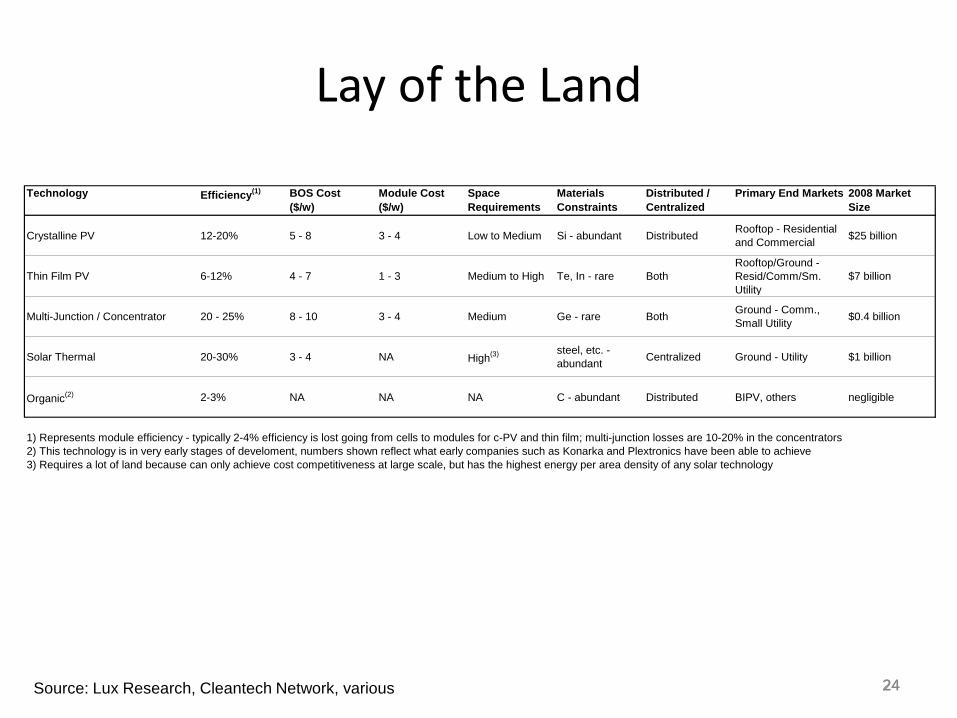

Lay of the Land

Source: Lux Research, Cleantech Network, various

Technology Efficiency(1) BOS Cost ($/w)

Module Cost ($/w)

Space Requirements

Materials Constraints

Distributed / Centralized

Primary End Markets 2008 Market Size

Crystalline PV 12-20% 5 - 8 3 - 4 Low to Medium Si - abundant Distributed Rooftop - Residential and Commercial $25 billion

Thin Film PV 6-12% 4 - 7 1 - 3 Medium to High Te, In - rare BothRooftop/Ground - Resid/Comm/Sm. Utility

$7 billion

Multi-Junction / Concentrator 20 - 25% 8 - 10 3 - 4 Medium Ge - rare Both Ground - Comm., Small Utility $0.4 billion

Solar Thermal 20-30% 3 - 4 NA High(3) steel, etc. - abundant Centralized Ground - Utility $1 billion

Organic(2) 2-3% NA NA NA C - abundant Distributed BIPV, others negligible

1) Represents module efficiency - typically 2-4% efficiency is lost going from cells to modules for c-PV and thin film; multi-junction losses are 10-20% in the concentrators2) This technology is in very early stages of develoment, numbers shown reflect what early companies such as Konarka and Plextronics have been able to achieve3) Requires a lot of land because can only achieve cost competitiveness at large scale, but has the highest energy per area density of any solar technology

2525

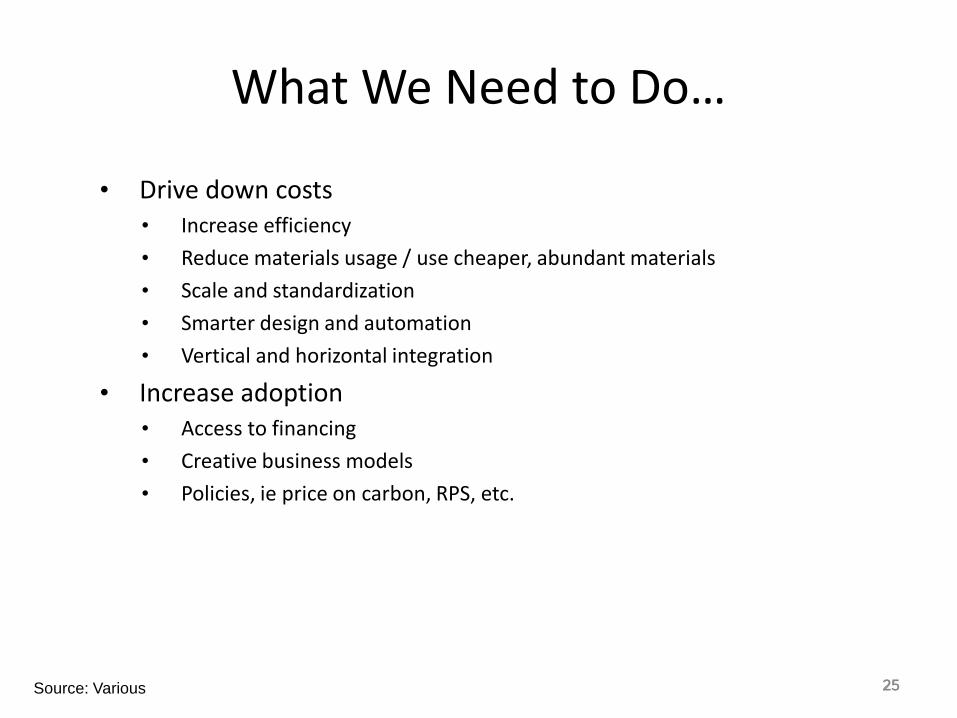

What We Need to Do…

• Drive down costs• Increase efficiency

• Reduce materials usage / use cheaper, abundant materials

• Scale and standardization

• Smarter design and automation

• Vertical and horizontal integration

• Increase adoption• Access to financing

• Creative business models

• Policies, ie price on carbon, RPS, etc.

Source: Various

2626

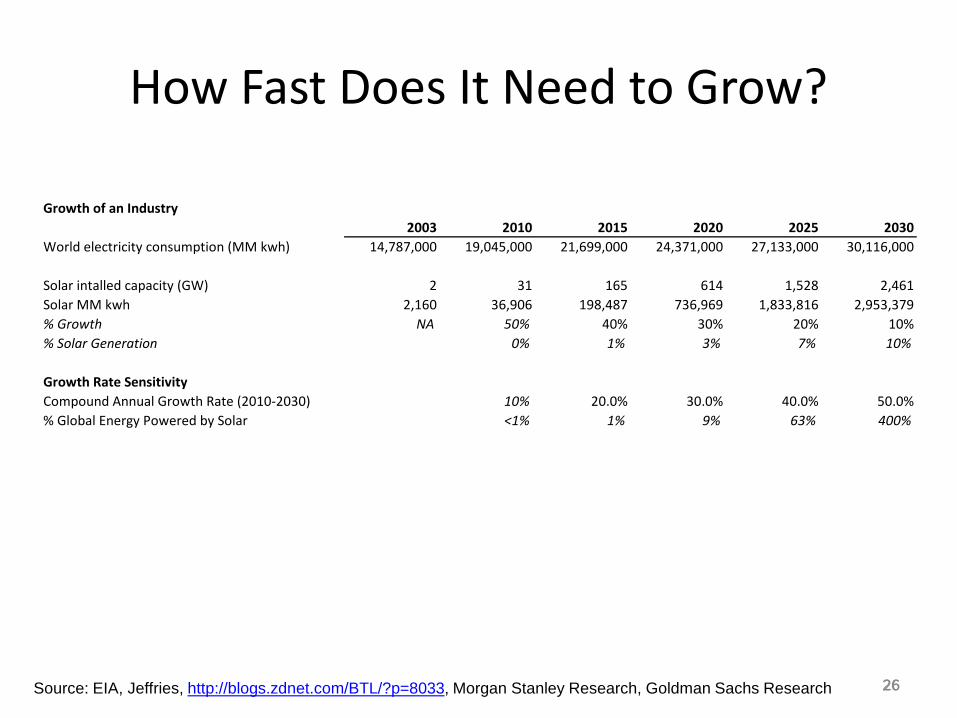

How Fast Does It Need to Grow?

Source: EIA, Jeffries, http://blogs.zdnet.com/BTL/?p=8033, Morgan Stanley Research, Goldman Sachs Research

Growth of an Industry2003 2010 2015 2020 2025 2030

World electricity consumption (MM kwh) 14,787,000 19,045,000 21,699,000 24,371,000 27,133,000 30,116,000

Solar intalled capacity (GW) 2 31 165 614 1,528 2,461Solar MM kwh 2,160 36,906 198,487 736,969 1,833,816 2,953,379% Growth NA 50% 40% 30% 20% 10%% Solar Generation 0% 1% 3% 7% 10%

Growth Rate SensitivityCompound Annual Growth Rate (2010-2030) 10% 20.0% 30.0% 40.0% 50.0%% Global Energy Powered by Solar <1% 1% 9% 63% 400%

2727

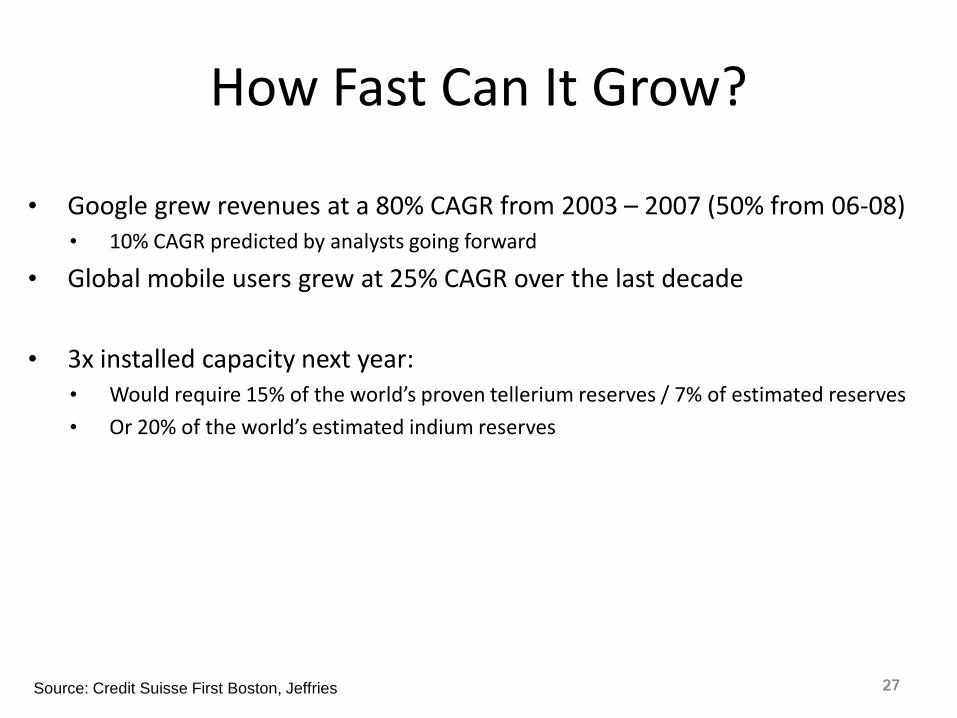

How Fast Can It Grow?

• Google grew revenues at a 80% CAGR from 2003 – 2007 (50% from 06-08)• 10% CAGR predicted by analysts going forward

• Global mobile users grew at 25% CAGR over the last decade

• 3x installed capacity next year: • Would require 15% of the world’s proven tellerium reserves / 7% of estimated reserves

• Or 20% of the world’s estimated indium reserves

Source: Credit Suisse First Boston, Jeffries

2828

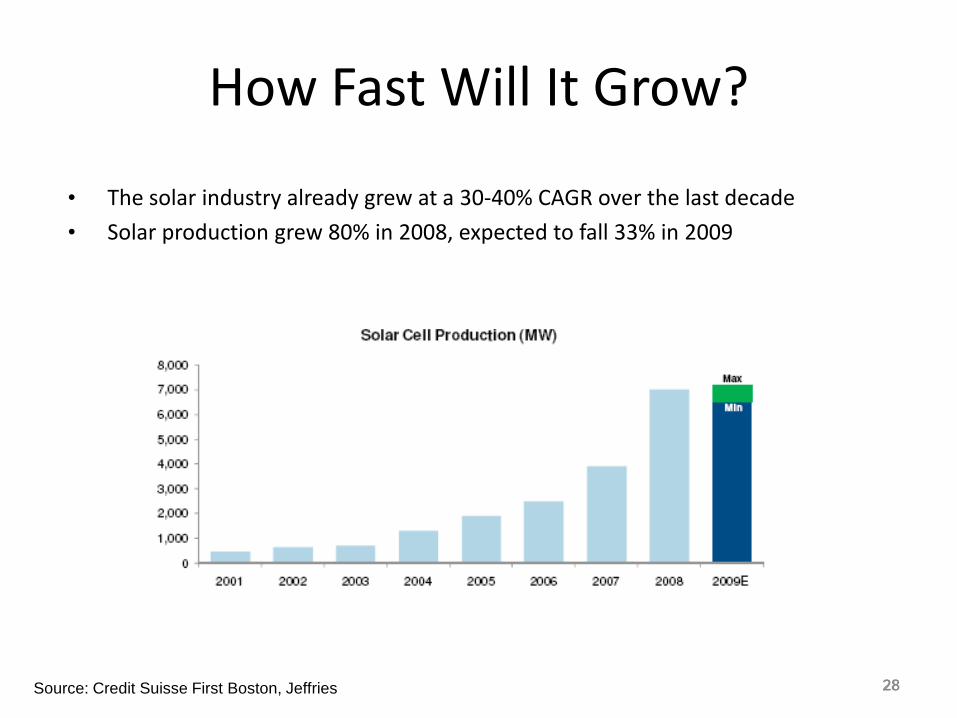

How Fast Will It Grow?

Source: Credit Suisse First Boston, Jeffries

• The solar industry already grew at a 30-40% CAGR over the last decade

• Solar production grew 80% in 2008, expected to fall 33% in 2009

2929

Current State of Solar Industry

Source: Jeffries Clean Tech Primer 2009

3030

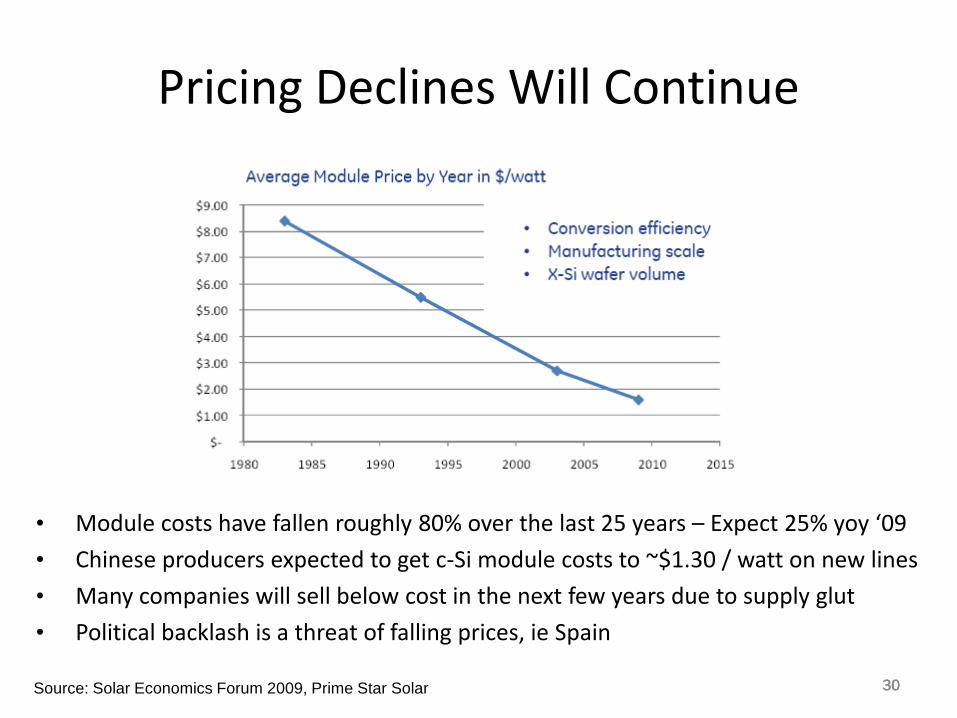

Pricing Declines Will Continue

Source: Solar Economics Forum 2009, Prime Star Solar

• Module costs have fallen roughly 80% over the last 25 years – Expect 25% yoy ‘09

• Chinese producers expected to get c-Si module costs to ~$1.30 / watt on new lines

• Many companies will sell below cost in the next few years due to supply glut

• Political backlash is a threat of falling prices, ie Spain

3131

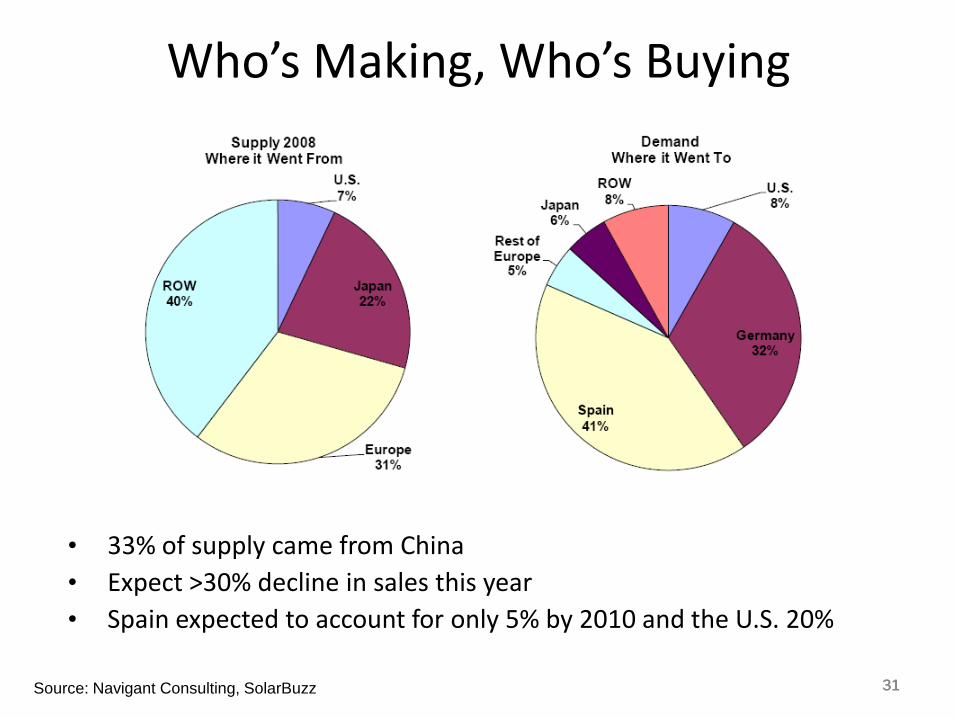

Who’s Making, Who’s Buying

Source: Navigant Consulting, SolarBuzz

• 33% of supply came from China• Expect >30% decline in sales this year• Spain expected to account for only 5% by 2010 and the U.S. 20%

3232

Increase in Utility Scale Systems

Source: Emerging Energy Research

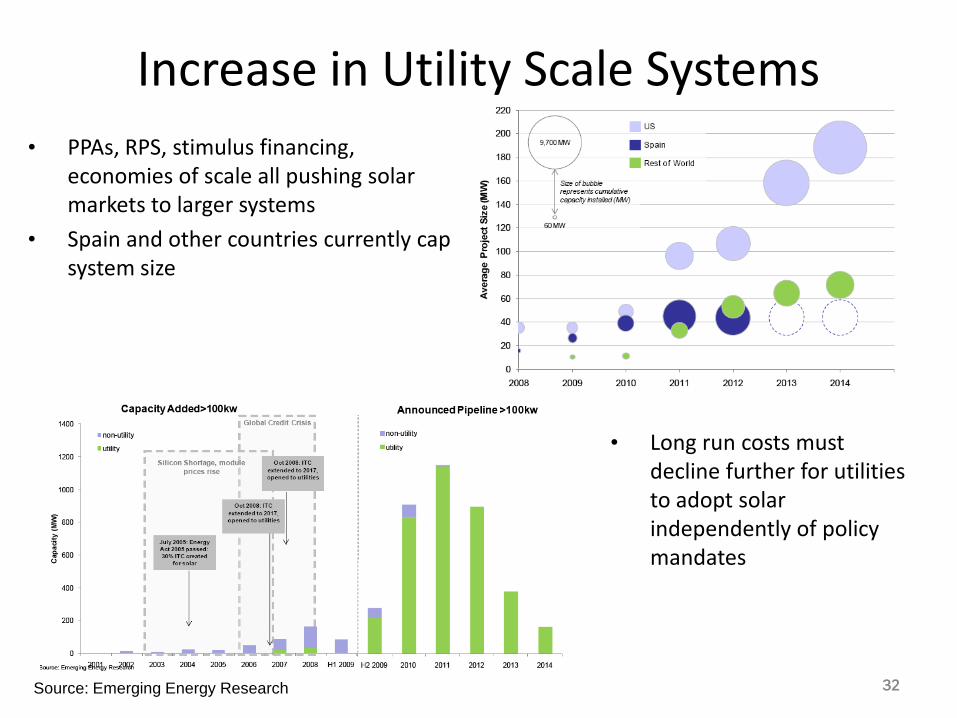

• PPAs, RPS, stimulus financing, economies of scale all pushing solar markets to larger systems

• Spain and other countries currently cap system size

• Long run costs must decline further for utilities to adopt solar independently of policy mandates

3333

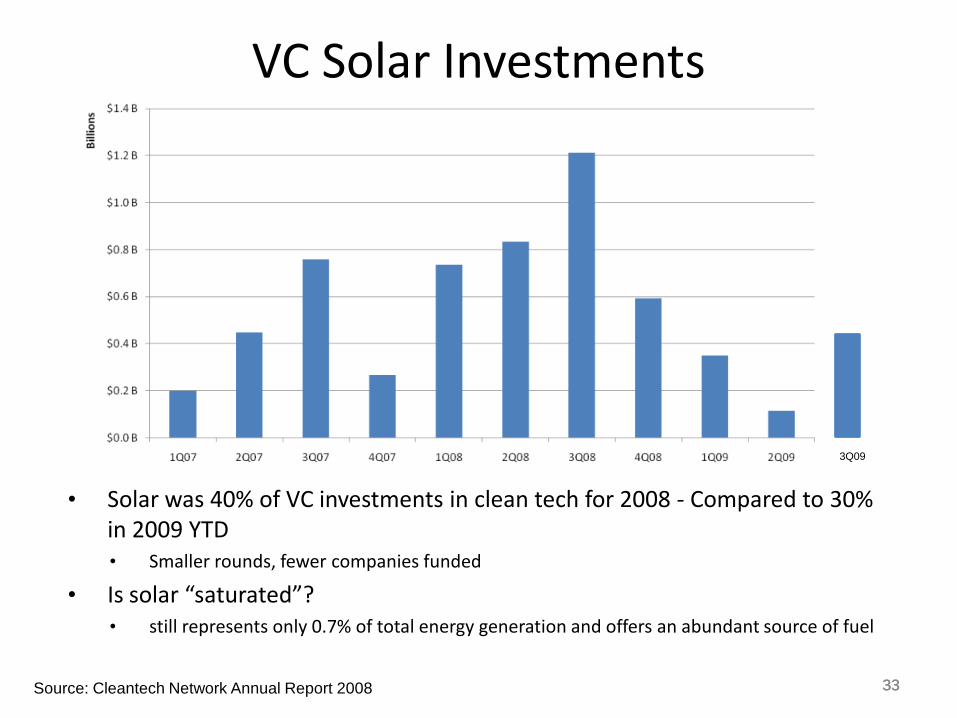

VC Solar Investments

• Solar was 40% of VC investments in clean tech for 2008 - Compared to 30% in 2009 YTD• Smaller rounds, fewer companies funded

• Is solar “saturated”? • still represents only 0.7% of total energy generation and offers an abundant source of fuel

Source: Cleantech Network Annual Report 2008

3Q09

3434

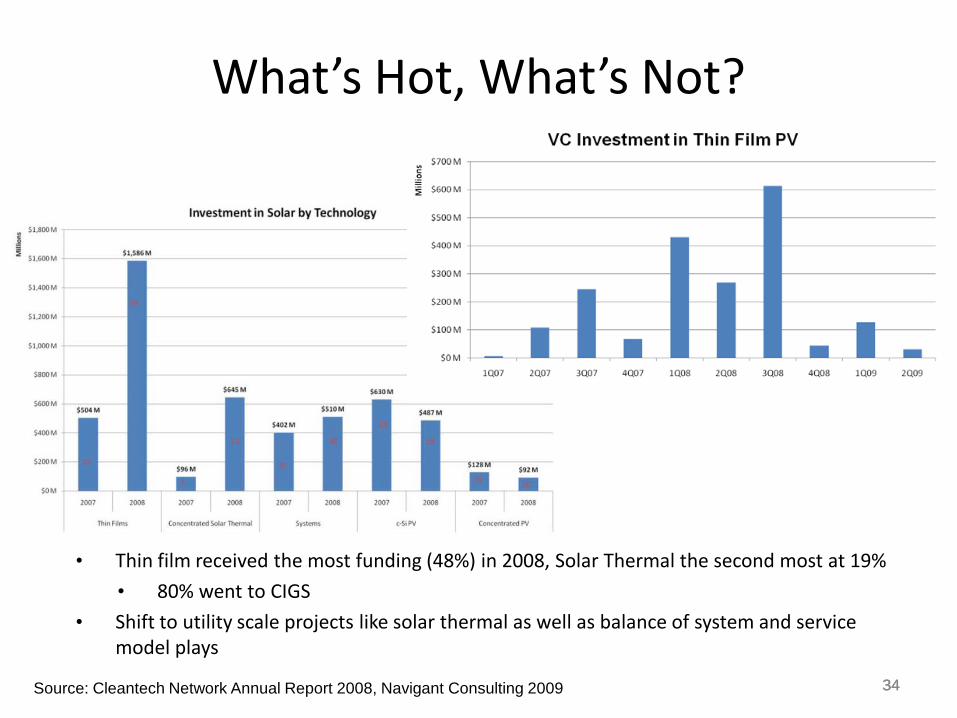

What’s Hot, What’s Not?

• Thin film received the most funding (48%) in 2008, Solar Thermal the second most at 19%

• 80% went to CIGS

• Shift to utility scale projects like solar thermal as well as balance of system and service model plays

Source: Cleantech Network Annual Report 2008, Navigant Consulting 2009

3535

What and Who to Watch• The big players

• First Solar, Sunpower, Suntech, etc.

• Low cost or high quality that will enable them to capture margins

• Emerging technologies• Thin film, solar thermal

• Chinese manufacturing• Access to low cost financing will drive capacity building

• Industry consolidation• First Solar acquired OptiSolar

• MEMC acquiring SunEdison

• Materials access• Tellerium and Indium could be constrained

• Creative business models and financing• SolarCity

• Smart grid integrated plays

• Global policies and incentives• Many European countries are capping subsidies by industry size

• Impact of stimulus funding in the U.S.

3636

“ The way we use energy strengthens our adversaries and threatens our planet” – President Obama 1/20/09