Embed Size (px)

Citation preview

Why postal operators need to orchestrate the market and expand along the entire eCommerce value chain

Vol. 2 | Issue 2 | 2014

The Postal Innovation Platform (PIP) is a unique open platform and forum that focuses on innovative postal services and studies the future of the postal industry with a solution oriented approach. It provides a conference, think tank and research platform that is unique in the postal world and shall ease the implementation of new and innovative postal business solutions.

Reflections on the discussions and outcome of the UPU/POC eCommerce Forum in March, the Turkish Post eCommerce Symposium in May as well as the two Postal Inno-vation Platform (PIP) Roundtables in Hong Kong and Turkey in May 2014

eCommerce

c o n t e n t s

Dossier

3 It’s All about the Value ChainBernhard Bukovc

5 Postal Operators as Information Intermediaries?Matthias Finger

7 The Booming eCommerce, What Is ‘PeP’ - and Why Do We Need Each Other?Thomas Baldry, Deutsche Post DHL

9 Want to Be Successful in the eCommerce Gold Rush? Act now!Michaela Hohlwein and Hans G. Landgraf, SAP

10 Big Data’s Two Big MythsArjen Heeres, Quintiq

12 Can the Posts manage individuals as customers?Dave Williams, Blackbay

13 A View on the Posts’ Evolution into Cross-Border ParcelsDavid Spottiswood, Neopost ID

14 Interview with Mr. Gözalan, YandexMatthias Finger

EditorialAn eCommerce eco system is the key to capture business opportunities in the growing eCommerce market. Postal operators are in a difficult position because they are the ones not driving this market, but rather being one element in the entire value chain which is responsible for one task only, i.e. transport and delivery of the goods. This is one of the weakest positions in the entire eCommerce value chain because this is where everyone wants to cut costs.

But what if postal operators shift from being the delivery provider to being the ones driving the market? What if posts create what the market is looking for, which is an entire eCommerce eco system? Indeed, postal operators are ideally positioned because they are as intermediaries close to customers, in particular small and medium sized potential e-retailers and they are also close to the buyers. Moreover, several postal operators have shown that they can expand along the entire eCommerce value chain, thus not only getting into the driver’s seat, but also generating additional turnover. Posts can orchestrate and manage the market and experts from the eCommerce and postal industry discussed at several events during the first half of 2014 how this can be done. In this newsletter you can find some opinions, ideas and answers.

We hope that you enjoy reading our Postal Industry Newsletter and if you have any comments, ideas or suggestions please let us know.

Bernhard Bukovc,General Manager and Chairman of the

Postal Innovation Platform

the Postal Industry | The Postal Industry newsletter provides original analysis, information and opinions on current

issues. The editor establishes caps, headings, sub-headings, introductory abstract and inserts in articles. He also edits

the articles. Opinions are the sole responsibility of the author(s).

Subscription | The subscription is free. Please do register at <http://mir.epfl.ch/newsletter> to be alerted upon

publication.

Letters | We do publish letters from readers. Please include a full postal address and a reference to the article under

discussion. The letter will be published along with the name of the author and country of residence. Send your letter

(maximum 450 words) to the editor-in-chief. Letters may be edited.

Publication director | Matthias Finger

Editor in chief | Bernhard Bukovc

Co-editor | Toni Männistö

Founding editor | Matthias Finger

Publisher | Chair MIR, Matthias Finger, director, EPFL-CDM, Building Odyssea, Station 5, CH-1015 Lausanne,

Switzerland (phone: +41.21.693.00.02; fax: +41.21.693. 00.80)

email: <[email protected]>

Website: <http://postal-innovation.epfl.ch/>

Published in Switzerland

3the Postal Industry | Vol 2 | Issue 2 | 2014

D o s s i e r

eCommerce remains one of the key topics the postal in-dustry talks about. The sheer growth opportunities pro-vide bright perspectives for revenue growth and additional business. This is of course good news in an industry that has been talking for many years about the unstoppable mail volume decline. And it is good to see that after years of talking about eCommerce the postal industry has taken steps to overcome some of the frictions and barriers which should eventually create a seamless cross-border customer experience.

Leaders of the postal industry, eCommerce experts, the big e-retailers and suppliers gathered at different oc-casions during the first half of 2014, including the UPU/POC eCommerce Forum in March, the Turkish Post eCommerce Symposium in May as well as the two Postal Innovation Platform (PIP) Roundtables in Hong Kong and Turkey in May, to see where the latest initiatives and product developments stand and discuss the next steps that need to be taken.

eCommerce customers, either buyers or e-retailers keep repeating what they need most. These needs have not changed over the last years. Instead, more needs were added to the list they put forward. It’s still about seam-less track&trace, lower cross border prices, more flexibility with regard to delivery time, delivery place or re-routing, standardized labeling, return solutions or data sharing.

As stated above, the postal industry started to move and various initiatives try to cope with the challenges and im-plement what the market asks for. Some posts have started to develop bilateral solutions which is a fast way to over-come barriers and remove frictions. Groups of postal op-erators are in the process of developing regional solutions that could be rolled out to other regions. The International Post Corporation develops a cross-border solution among their members and invites other posts and regions to join in a second or third wave. PUMED, the Postal Union for

the Mediterranean started to develop a solution for their region and the Universal Postal Union is in the process of developing a global framework. In the end, postal opera-tors have to take a pragmatic approach and implement existing solutions as quickly as possible - because time is the most crucial factor in this game.

On the domestic level most posts were innovative and have introduced new solutions and services in order to respond to customer needs. However, there is still a big disparity between posts and the service levels vary from one country to another. For example, while some posts have introduced different solutions to make the delivery of the ordered goods more flexible through setting up a dense network of parcel locker delivery stations or eve-ning delivery, other posts still adhere to traditional deliv-ery means and times. Not moving forward and adapting the operations to market needs is the biggest risk posts are facing today. The market will not wait for them to change and respond to customer needs. We can see various exam-ples where customers start to build up delivery networks themselves thus gaining control of the delivery processes and better serving the needs of their buyers. Already today we can see that a huge share of the eCommerce volume by-passes the postal network and if posts don’t leave their traditional paths they might not even play a relevant role in the eCommerce delivery business in the future any-more. When looking at the postal landscape today we can see several posts that decided to adapt and conquer the market, but we can also see postal operators where things don’t move that quickly and who run the risk of missing out on their future.

So what can postal operators do in order to create a robust eCommerce eco-system? The international dimen-sion, as explained above, is one key element. But this is only about the operational infrastructure and framework which would guarantee that there are no cross border fric-

* General Manager and Chairman of the Postal Innovation Platform, <[email protected]>

It’s all about the value chainBernhard Bukovc*

The postal industry is talking about eCommerce as the opportunity to generate turnover, making up for the losses in mail revenues and being the basis for the new and re-invented postal industry, which would be defined by a completely new business model, a different organizational structure and a shift in its core business. The industry is in the process of creating the necessary framework, but will the industry obtain the status as the main eCommerce stakeholder and intermediary or will it merely deliver part of the eCommerce parcel volume?

4 the Postal Industry | Vol 2 | Issue 2 | 2014

do

ssie

r

tions or barriers anymore. A robust eco-system requires posts to not only provide a delivery solution, but to enable eCommerce and orchestrate the market. Several posts are forerunners in this area and have shown that posts don’t need to be only the transport and logistics provider, but could become a partner along the entire eCommerce value chain. This starts with training future e-retailers, providing them with a shop solution through a marketplace platform and offering them all necessary features and services e-re-tailers need, from a reliable and safe payment interface to a warehouse management solution and customer relation-ship management. Some postal operators even go a step further and offer services and solutions for taking pictures of products that will be presented on the postal operators marketplace platform. This does not necessarily mean that postal operators have to hire photographers or website de-velopers. They don’t need to run these businesses them-selves, but they should offer the solution and can thus co-operate with businesses that have an expertise in this area. In essential, postal operators can establish themselves as partners for small and medium sized e-retailers, help them in entering the market, train them in better understanding the business, its opportunities and its risks, and run for them the systems they need to operate their business.

This opens an entirely new perspective for postal opera-tors because they would eventually become the main infor-mation and data hub. Postal operators are already sitting on a huge amount of data that only waits to be monetized. With their new role of managing eCommerce information streams they would acquire an immense amount of data and information - one of the most valuable goods in to-day’s commerce. The partnership between postal operators and e-retailers would thus extend beyond the posts’ role of enablers of eCommerce to supporting the e-retailers to expand and grow by analyzing, translating and interpret-ing the data. This data could provide e-retailers with key information to attract new customers, sell more and find additional revenue streams.

eCommerce is not only important for postal opera-tors. It became one of the main growth areas of commerce in general and regions as well as countries benefit from the economic growth generated through eCommerce. However, frictions and barriers on governmental level turn out to be one of the biggest obstacles to eCommerce growth. Different taxes and tax levels, customs duties, cus-toms processes and procedures or other administrative and bureaucratic hurdles pose a steadily increasing burden on the eCommerce sector. Taxes, duties and customs proce-dures considerably increase the administrative costs, lead to delays and make it impossible to predict the delivery of an item, one of the key requirements of eCommerce customers. This is an area where posts need to cooperate

- with each other, but also with governments - in order to solve the issue and overcome the barriers, involving the support of the Universal Postal Union (UPU) and the World Customs Organization (WCO).

While eCommerce growth is indeed the most promis-ing area where postal operators can potentially generate additional business and turnover, it is not a business op-portunity that will simply fall into their laps. Quite the contrary, there is a huge potential, but posts will have to work hard in order to get their share and realize the benefits from eCommerce growth. If they don’t create the foundation and change some of their business models they will not play a relevant role and will see the market growth by-pass them. So what do postal operators need to do in order to play a relevant and profitable role? The main out-put and findings of the eCommerce initiatives during the first half 2014 lead to the following recommendations:

1. Postal operators need to be enablers and orches-trate the eCommerce market; they must create a robust eCommerce eco-system. They need to extend their service portfolio along the entire eCommerce value chain and be-come the most important partner and stakeholder for the eCommerce sector, thus being the main intermediary for the entire business, including financial and information services and solutions and helping e-retailers to establish and run their business.

2. A seamless cross-border network and service is a must and current activities in the postal sector show that the industry is moving into the right direction. This should lead to a better predictability and should help to establish trust in cross-border eCommerce. However, it is crucial to implement these solutions quickly because the important market players will not wait for the posts and, if necessary, duplicate the postal delivery networks.

3. Posts have to cooperate with the relevant stake-holders in order to remove bureaucratic bottlenecks, in-cluding customs barriers, different regulations or issues like weight limitations. Likewise, governments have to eliminate unnecessary barriers and help to establish easy and unbureaucratic processes and rules for the global eCommerce environment.

4. The postal sector needs to cooperate closely with all market players, such as e-retailers or manufacturers. This cooperation should particularly relate to data exchange. Packaging can be an important element to ease transport and delivery processes. In addition, postal operators need to structure their operations in line with customer needs, thus offering, for example, flexibility and choice for pick-up and delivery.

5. Data itself is an important aspect and posts must become data and information hubs managing the data for their customers and monetize it.

5the Postal Industry | Vol 2 | Issue 2 | 2014

D o s s i e r

Postal operators as information intermediaries?

Matthias Finger*

The recent international postal Symposium organized by Turkish Post (Fethiye, May 26-27, 2014), along with the in-depth discussion held at the PIP Roundables in Turkey and Hong Kong, focusing on e-commerce have all led to very interesting insights. In particular, they have highlighted the fact, that, while Posts are still valuable logistics intermedi-aries, they are in danger of becoming marginalized if they do not managed to also evolve into financial and especially information intermediaries.

Historically, postal operators have been physical inter-mediaries between senders and receivers, even though, generally, the senders have paid for the service. Until not so long ago, they even enjoyed a monopoly position as such physical intermediaries. Traditionally, a distinction was made between letter mail and parcels, but the func-tion of physical intermediary was of course the same. As of recently, letter mail is being substituted by electronic mail, while parcels are actually being boosted because of electronic or e-commerce, to the point that some postal operators have come to think that their growing parcels business could compensate for their declining mail busi-ness. In this short article, I would like to show that this may not be the case. Another element in the equation is the financial dimension : historically, again, many postal operators were also financial intermediaries between send-ers and receivers of money (e.g., giro). While many postal operators have (been forced to) privatize(d) their financial intermediary function, a few others have managed to enter the banking market. No postal operator, however, has re-ally succeeded (or even tried to succeed) in establishing strong synergies between their physical and their financial intermediary functions. Yet, as I want to also show in this article, this would be a competitive advantage in the new e-commerce world.

e-commerce has not been invented by postal operators. Rather, it is the combined result of the revolution of the Information and Communication Technologies (ICTs), the internet and (economic and cultural) globalization. The ones who drive and control such e-commerce have been (and continue to be) online e-commerce platforms, also called e-retailers, such as Alibaba, Amazon, Rakuten, but also e-Bay and many others more. As such, they are neither logistics, nor financial intermediaries, but so-called

information intermediaries, linking sellers of goods and services with (potential) buyers. Of course, they will need financial and physical intermediaries to execute their busi-ness proposition. Their preferred financial intermediaries have come to be credit card companies, such as Visa and Mastercard … but postal financial operators, even though they may be more trustworthy (or perceived to be more trustworthy), are generally left aside. When it comes to the physical delivery of the goods ordered via e-commerce, posts remain in the loop. E-commerce operators do in-deed use postal operators, at times, to execute their on-line orders. But, some of them are developing their own physical delivery options (e.g., Amazon), while most of them have postal operators compete with other physical intermediaries, and by doing so put pressure on postal op-erators and their margins.

The power relationships between all the involved ac-tors in the e-commerce value chain are clear: value is cap-tured primarily by the information intermediaries, i.e., these e-commerce operators that control the information flows between the producer of a good and a service or service and their buyers. Financial intermediaries come second and physical intermediaries, such as postal opera-tors, come last. Not only do they have to compete for the so-called «e-fulfillment business», but moreover are they pressured by the e-retailers because they control all the rel-evant information, including the information about the efficiency and the quality of the deliverers of their goods (among which the postal operators). Consequently, physi-cal intermediaries are entirely substitutable and have no control as to whether they can participate in the e-com-merce value chain. Their only competitive asset is price, which, for a state-owned postal operator, constitutes a serious handicap. This situation is unlikely to improve

* Professor, Chair MIR, EPFL,<[email protected]>

6 the Postal Industry | Vol 2 | Issue 2 | 2014

do

ssie

r

for the physical intermediaries in general and the postal operators in particular. Rather the opposite is likely to be case: the more information the e-retailers accumulate, the bigger the (financial) pressure on the physical (and finan-cial) intermediaries. In other words, while e-commerce is a thing of the future, it is unlikely to become a high-margin business for the postal operators, at least as long as they remain confined to their physical intermediary function.

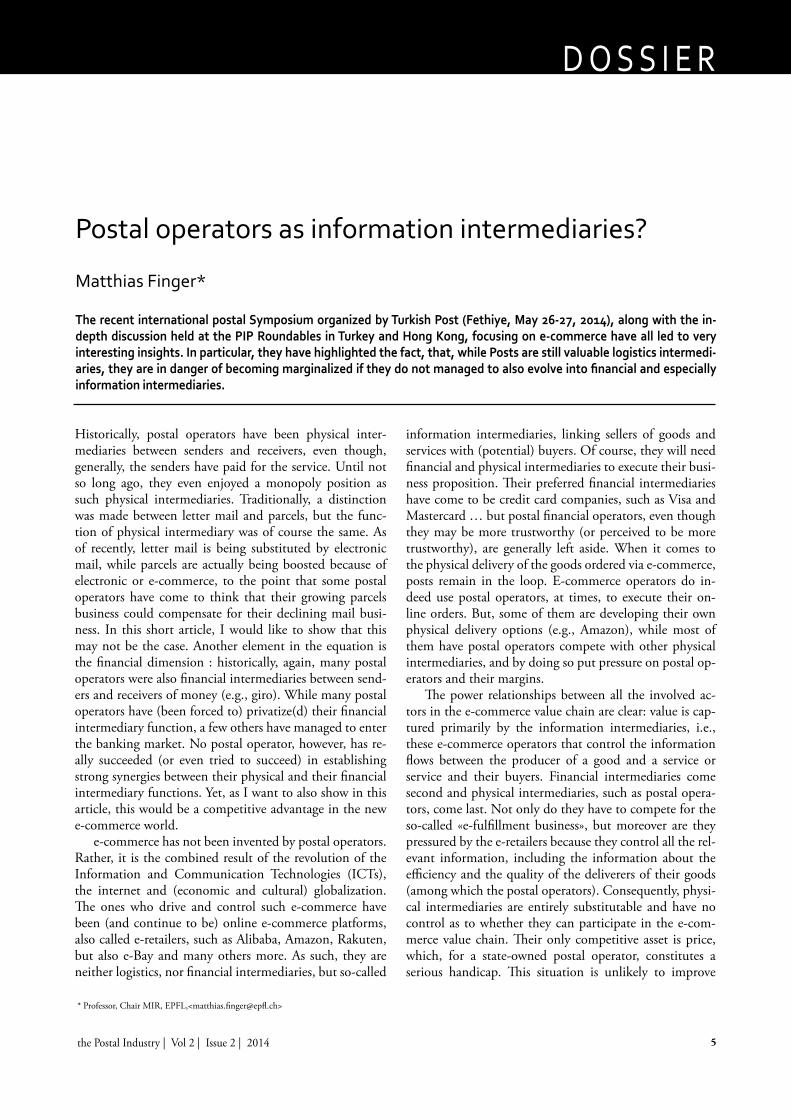

So what is the solution for the postal operators? As il-lustrated in the graphics below, their only strategic option is to also take on the function of information interme-diary and of course uniquely combine this information

intermediary function with their financial intermediary and especially their physical intermediary functions. Post would, indeed, have certain strong assets in order to do so, being, for example, the only ones capable of linking a virtual with a real (physically rooted) consumer. However, e-commerce being by nature a global endeavor, the posts’ main handicap remains the fact that they are nationally organized. Only if they managed to overcome their na-tional limitations by way of international standardization, collaboration and ultimately strong integration, will they be able to successfully capture some of the value currently captured by the information intermediaries.

7the Postal Industry | Vol 2 | Issue 2 | 2014

D o s s i e r

The booming eCommerce, what is ‘PeP’ - and why do we need each other?

Thomas Baldry*

Recently, Frank Appel, CEO Deutsche Post DHL, won the World Mail Award in the category “industry leader”. This reflects his persistent strive for excellence and customer focus. To aspire to be first choice for eTailers and Internet-Shoppers on a global level requires not only massive investments in infrastructure but also a pro-active approach to upgrade global network capabilities.

In other words, we continuously have to deliver value to our customers by doing the right things in the appropriate areas and to co-operate effectively to cover those in which we do not operate ourselves.

Postal business stands for services in communication and delivery but in today’s world the boundaries between these two areas get increasingly blurred. We communicate via our tablets and smart phones, send messages, receive pictures from our friends at the same time as a reminder for the next business review meeting pops up. We also use the same devices for entertainment and online shopping. So, we see our communications behaviour changing rap-idly and that the pace at which new technology enters our day-to-day life accelerates faster and faster.

Despite it seem to be a given fact that we all are actively using these devices and that internet and mobile commu-nication will have an even more profound impact on our future, it helps our understanding to approach this devel-opment also on a more analytical level. To this extend we carried out a comprehensive study on how this develop-ment will shape our way of doing business and how our business and private customers will be affected. We named this study “Global E-Tailing 2025” and you can download the study from our corporate website.

We wanted to understand future shopping behav-iour and the role of cross-border eCommerce in differ-ent regions of the world. We went to Berlin, New York, Shanghai, to Bangalore and Jakarta. We interviewed typi-cal consumers and corporate clients. We analysed internet behaviour in Brazil as well as in Turkey. We also applied different scenarios on the world-wide economic and envi-ronmental development. And of course in the study you will also find all these buzz words such as gamification or hyper-connectivity that you might consider as either being

very trendy or only fuzzy.It’s up to the interested reader what specific scenario he

or she considers to be of importance for his or her busi-ness and personal view on the world. The future is always uncertain (probably one of the top 3 no-brainers) and all investment decisions are a bet on the future. It is worth mentioning one result from the study that could make you think twice: In 2013, world-wide online shopping revenues where roughly at € 500 bn, and global distance shopping revenue is estimated to grow by 10% p.a. for the next years. The top 3 categories of products sold via the internet were apparel and footwear, consumer electron-ics, and media products (like books, CDs and DVDs). Delivery of these products should be the natural business resort of posts as all these products are deliverable via a letter, as a small packet or a parcel.

So, in a nutshell, we all need to adapt our business models accordingly. At Deutsche Post DHL we have done just that. We have launched a comprehensive corporate strategy ‘2020 – Focus.Connect.Grow’ as the logical evo-lutionary step to our current Strategy 2015 – ‘unlocking our potential’. Consequently, we re-named our postal business to PeP: Post – eCommerce – Parcel. With this move, we aim to become the world’s leading ‘eCommerce enabler’ with a broad portfolio of logistics services for eTailers and consumers.

Our new PeP division consists of two main business pillars, the sub-division “Deutsche Post” and the sub-division “DHL eCommerce & Parcel”. Each pillar with the brand power, expertise and resources necessary to meet our ambitious growth targets. Under the brand ‘Deutsche Post’ there are all activities concentrated that are related to the postal business in a broader sense: communication mail, secure email/ E-Post services, dialogue marketing,

* Senior Vice President, Global Mail, Deutsche Post DHL

8 the Postal Industry | Vol 2 | Issue 2 | 2014

do

ssie

r

publications services and international mail services. The sub-division DHL eCommerce & Parcel positions itself as the global eCommerce enabler. We aim to export our German domestic capabilities to other countries and re-gions and tap opportunities in eCommerce services in se-lectively chosen markets. This also implies an even more intensified collaboration with postal delivery networks world-wide, although we consider entering some markets to facilitate parcel delivery by our own networks.

We are one of the keenest supporters of International Post Corporation’s Interconnect Programme (eCIP) which aims to adapt cross-border eCommerce delivery networks to changed customer needs. 33 postal operators are cur-

rently working on ambitious targets and timelines to offer track & trace solutions, access to last mile delivery op-tions, harmonised labelling and better end-to-end service levels to cover the needs we feel consumer and business community alike do have.

‘Co-opetition’ is therefore the name of the game. Deutsche Post DHL continues to stay a faithful ally to those active in international co-operation, although this does not mean that there is no dedicated competition in specific markets. In analogy to the soccer world champi-onships: There is no beautiful game to watch, if nobody wants to score a goal. And being alone on the turf is also no fun.

9the Postal Industry | Vol 2 | Issue 2 | 2014

D o s s i e r

Want to be successful in the eCommerce gold rush? Act now!Michaela Hohlwein* and Hans G. Landgraf**

On May 19, 2014, SAP and the Postal Innovation Platform co-hosted a roundtable on eCommerce in Hong Kong. Market needs and areas of cooperation were discussed; ideas and knowledge were shared, it is now time to act. Some recom-mendations are listed below and we encourage all participants to use Design Thinking Workshops as a starting point or point of validation on the transformation journey.

An example of an innovative service and solution was presented from Germany, where DHL is offering its own marketplace “meinpaket.de” to increase parcel shippings with over 5 Mio. products promoted and sold via their website. Successful postal operators like German Post, Poste Italiane, and Swiss Post diversified their business years ago and are therefore much better prepared to deal with declining revenues in their traditional mail business.

In contrast, there are postal operators who think if they keep going as usual they will stay in business, ignoring the fact that competition is capturing their market share, espe-cially in the parcel business. In addition, customers expect a seamless omni-channel experience, particularly those that are frequent online shoppers, and postal operators are suddenly overwhelmed in making this happen with the multiplication of channels and customer touch points. It is not as simple as buying some drones when some provid-ers have actually figured out how to successfully use them for deliveries. To catch up with them would take three to four years and market share might be lost forever.

Posts need to lead the change and be proactive in changing and adopting technologies and channels – from mobile, social media, to omni-channnel or e-commerce, posts need to be setting the pace for the industry! The changes required today are much more technology-driven and technology dependent than many may realize. bpost is a good example for having a clear innovative vision and a

strategy which they execute. This is one example of a post that is setting the pace and leading change.

What actions can be taken? The first recommendation is to put the customer at the center of the business and with that to establish a central Customer Relationship Management system. This will break down department silos and it will support diversification efforts with cross- and upsell benefits. The next logical step would be to create an omni-channel strategy and introduce a central mobile platform and eCommerce Suite. Once these are in place, analytical tools can be used, for example to help better understand customer buying behavior and optimize email and website marketing campaigns. For example: an US-based retailer moved to automatically created predic-tive models and increased its online sales 8-12 percent in three months.

For postal operators interested in learning about best business practices and how to leapfrog the competition, we offer a variety of tools and workshops, including Design Thinking sessions. Design thinking is a user-cen-tric approach specifically geared towards solving known and unknown problems. In contrast with other problem-solving approaches, design thinking initially focuses on problem definition, instead of analyzing potential solu-tions. It offers a process to find solutions that users will love, and which are technologically feasible and viable for the business.

* Solution Manager Postal Services, SAP, <[email protected]>

** Head of Business Segment - Postal Services, <[email protected]>

10the Postal Industry | Vol 2 | Issue 2 | 2014

D o s s i e r

Big Data’s two big myths

Arjen Heeres*

At current postal conferences, there is much discussion on data, and the ability to take control rather than simply be commoditized as an operational base that provides execution service for e-retailers. Then the challenge is about what data is useful and what to do with it. Understanding your own network better provides opportunities for more efficien-cies, operational agility and greater profitability. Also where possible, understanding the consumer better allows you to take a role as partner than just execute e-retailer’s logistics requirements.

Big Data’s two big myths... you’ve probably heard them already. Most supply chain directors have:

• Myth 1: You have to act really fast – like by yesterday• Myth 2: You never know what might be useful

Taken together, these myths have given rise to the ‘leap before you look’ approach to big data that’s already end-ing in crashes. Or as a December 2013 Harvard Business Review (HBR) article puts it: Companies are investing like crazy in data scientists, data warehouses, and data analytics software. But many of them don’t have much to show for their efforts. It’s possible they never will. The title of that HRB article? You may not need big data after all. Perhaps. What’s more likely is that most supply chains will need big data. The big unanswered questions are:• How supply chain directors should approach big data

initiatives • What they should be focusing on

(1) Start smallBig data is going to have a significant impact on supply chain planning. That said, the facts simply don’t support the idea that there’ll be an abrupt change in the way supply chains are designed and managed.

Instead of jumping on the big data bandwagon, thoughtful supply chain directors are taking small steps towards big wins.

For example, a delivery company might benefit from insight into the relation between the addresses it delivers to and delivery performance. Such a company might then start collecting and analyzing data on how long it takes to deliver packages to various addresses; the number of failed delivery attempts associated with each address; and the ef-fect of weather conditions/drivers/vehicles etc. on delivery

performance. These insights could be fed back into an in-telligent supply chain planning and optimization system to enable more efficient, profitable operations.

Similarly, a manufacturer might be interested in the factors affecting the failure rate of various components, and what this means for certain product categories. What’s the percentage that’s really usable? What’s the quality of inflow? Under which conditions should you allocate more buffer stock?

Once again, an intelligent supply chain planning and optimization system will transform this input into real de-cision making power by helping planners create optimized schedules that minimize disruptions.

(2) Target your efforts and insist on resultsWhile the details will change from company to company, successful applications of big data share a common ap-proach. They focus on areas where high levels of uncer-tainty are having a significant impact on the supply chain. Once you have that figured out, it’s possible to ask intelli-gent questions about how big data and advanced analytics can be used to generate better outcomes.

It’s easy to lose sight of this goal in all the hype. In fact, that HBR article went on to say, The biggest reason that investments in big data fail to pay off, though, is that most companies don’t do a good job with the information they already have. Until a company learns how to use data and analysis to support its operating decisions, it will not be in a position to benefit from big data.

Here at Quintiq, we believe that big data is extremely helpful in developing predictive analytics – those patterns and trends that help you make sense of huge quantities of data.

These patterns then need to be combined with domain knowledge: your own intimate knowledge of your supply

* COO, Quintiq

11

do

ssier

the Postal Industry | Vol 2 | Issue 2 | 2014

chain. But it doesn’t stop there.The final, crucial step lies in transforming that input into better supply chain decisions. And for this, you need to link big data and predictive analytics with the supply

chain planning and optimization systems that will help you make better, more profitable decisions.

Because isn’t that what big data is really all about?

12the Postal Industry | Vol 2 | Issue 2 | 2014

D o s s i e r

Can the Posts manage individuals as customers?Dave Williams*

As Posts around the world try to deal with a reduction in letters, the question as to core business is being addressed. Are they communications organisation with a distributed resource or a transport and logistics organisation? If it’s a commu-nity based communications organisation, then the interaction with the consumer needs to change.

Our business tracks hundreds of millions of parcel per an-num and in the past this tracking information was only ever referred to if something went wrong and then perhaps only days later. I’m very happy to say this is no longer the case. This change is being driven by a number of dif-ferent factors none of which have much to do with ship-per or carriers. The core of this change is the expectation, driven by social media that all information is available, all the time and on any platform (PC, Phone, Table, Watch and Tablet). IMRG’s latest report notes that over 80% of consumers expect to see multiple tracking points and that the tracking points are more important than the PoD.

Alongside this change we are all far too aware of the massive decline in letter volume and its effect on Postal carriers and their ability to maintain a universal service. Conversely the explosive growth of e-commerce and its ef-fect on high street retail has seen a vast increase in small value shipment and has been the saviour of many postal organisation. As such Posts have now been repurposed to look and act like logistics organisation. But in doing this, post has lost its soul and some may say its purpose as a communication and community service organisation.

Combining the mega trends of ecommerce and social media the likes of Amazon and eBay along with many smaller shippers have built strong brand equity by pro-filing consumers via buying patterns and demographics. This has allowed these on-line organisation to know the customers far better than the Post, even though the post visits homes every day. With this knowledge on the online retailers, they are able to make recommendation based on buying profiles that are often acted upon.

In comparison Postal and Logistics organisation know little or nothing about the end customer, still transfixed by the address as the single significant piece of data. The tragedy of this situation is that Postal organisation have the capability to have more knowledge than any other carrier or shipper in the industry based on the daily involvement in the community. Posties see customers on a regular basis, they often know them by name and/or sight, and understand the communities they live in. Many posties (and couriers) will make operational choices about the de-

liveries while on the door step, to leave in a safe place, to hold or give to a neighbour. Currently little if any of this information is captured or used and certainly no attempt is made to build a profile that would enhance the relation-ship with the customer.

While major shippers (and this is not always the case) don’t want to share information about the receiver, as it is seen as proprietary information many smaller shipper would be happy to. This need to share email and mobile phone details with the carrier is driven by the requirement to provide a much higher level of service and far more effective real time information to both the receiver and the delivery person. Once a unique identifier such as an email has been provided, the carrier is able to perform all sorts of magic; a person can be tied to an address, com-municated with as an individual, questions asked about preferences and other services offered.

Picture the following. You are at home expecting a de-livery and the school rings to say a child is sick. You know that no matter when you go out that will be the time that the delivery person turns up, so you call the carriers call centre to ask about the location of the driver. If you are lucky they will answer and may even confirm your pack-age is on board but little more. The alternate is that you have a profile with the carrier and by simply logging onto mobile device you can change your delivery options to a “safe place” as you will only be out for a few minutes or “divert to a neighbour”. This information is passed to the delivery person in real time and the delivery is successful. The outcome is significantly less frustration for you, the carriers cost for the delivery is significantly reduced and the following process is completely avoided; failed carded, return to depot, communication with the receiver, rede-livery, return to sender, loss of business.

The question remains however, can the structure of a Post deal with individuals as customers? If not, the Post as a community based organisation is dead and the change to logistics provider must be completed quickly. If “yes” then the current network could be significantly reinvigo-rated with many different services that are based on rela-tionships rather than just on allow cost a logistics pipe.

* VP North America & Asia Pacific, Blackbay

13the Postal Industry | Vol 2 | Issue 2 | 2014

D o s s i e r

A view on the Posts’ evolution into cross border parcelsDavid Spottiswood*The discussion around the transformation within the postal industry is always an interesting topic. The lead to any dis-cussion is always based on the backdrop of declining mail volumes and the need to morph into “something” else. At the Postal Innovation Platform (PIP) meeting in Hong Kong that discussion moved into what are some of the key priorities that face posts today in that journey of change.

The question was posed: is speed or the ability to provide data with the parcel for clearance the priority?

As a long serving “Express” man, these questions are indeed important but I think do not really address the fun-damental change that the postal companies need to make.

As an observation posts have a unique opportunity to capture and dominate the global e-Commerce parcel vol-umes simply by nature of their perceived position by not only the consumer but also the e-tailers… their trusted position, their geographical coverage and their ability to provide a last and first mile proposition based on an exist-ing infrastructure.

Should the rules of engagement be adapted then there is no doubt that the power of cooperative postal compa-nies would outstrip even the best of the express operators.

What needs to change, “people, data management and contracts?”

Why do I say people, I don’t mean a wholesale change, but if posts want to address the parcel industry, it makes sense to employ expertise from that industry.

As an example the raised question of speed or data with parcel would not be a question in the express industry. In the early eighties the express operators concentrated on how to manage data with parcel through the customs pro-cess. Why?, simple we understood that the barrier to speed was at this point, and if you cracked this process then you could offer speed... simple for those that developed this solution… providing data on a parcel to inbound customs before it had even left the export country allowed smooth customs clearance and therefore provided the ability to of-

fer speed.Data Management. In todays environment the ability

to interconnect all areas of the cross border supply chain is key to any to the survival of any company wanting to operate in this space.

The management of information from point of pur-chase, the checkout, through to pre-notification, line haul, customs clearance, distribution then last mile is cru-cial for the seamless experience across the supply chain, not to mention the reverse flow. Posts need to collaborate to provide standardized date flows on individual packages across multiple networks, simple... if you have the right people!

The power of the information provision creates mul-tiple benefits from customs clearance to route planning and optimization.

With regards to contracts and collaborations the struc-ture and nature will need to evolve ands more and more posts go through IPO changing the nature of existing agreements.

As the worlds of post and retail start to come closer together, the nature of cooperation and competition will change driving different contractual arrangements.

In short, the postal world is and will continue to go through a revolution being challenged on ideals and working practice that has existed for decades.

The opportunity is knocking on the door, those that open it and embrace the change will prosper, those that don’t will quickly disappear.

* Director Asia Pacific, Neopost ID

14the Postal Industry | Vol 2 | Issue 2 | 2014

D o s s i e r

Interview with Mr. Mustafa Gözalan, Member of the Executive Committee, YandexMr. Gözalan was interviewed by Prof. Matthias Finger

Mr. Gözalan, your thoughtful comments on the missed op-portunities of the postal operators in e-commerce drew the at-tention of the audience during the recent Postal Forum in Fethiye, Turkey. Could you please elaborate for our audience?

I simply observed that, from an investor’s perspective it is striking to observe that the e-retailers, i.e., the internet platform providers, draw much higher valuations than the logistics companies. Even the most innovative logistics companies, such as Arvato from the Bertelsmann group, are not as valuable as e-retailers. Yet, without logistics there is no e-commerce. In theory, logistics operators are opti-mally placed between the retailers and their consumers. Somehow, logistics operators in general, and postal opera-tors in particular, do not seem to be able to capitalize on this strategic position in the new e-commerce world.

And why is that, in your opinion?

E-retailers appear to be able to monetize the data, while logistics operators somehow are not able to do so … even though they sit on a lot of very valuable data. As for postal operators, they have a lot of very valuable information, which they derive from their direct contact with and trust from their customers, as well as from their daily logistics

activities (e.g., geo-locational data), but somehow they do not seem to be able to capitalize on these assets. I am sure that, if you had a choice, you would rather entrust your valued personal data to your postal operator, rather than to Amazon or Google.

So what should postal operators do differently?

First of all, they must realize on what invaluable stock of data they are actually sitting (e.g., geo-locational data, transport data, customer related data, etc.). They must realize that by not exploiting these data, they are open-ing the space for the other actors, notably the e-retailers, … only to be pressured by them for efficiency later. Of course, analyzing and exploiting such data is not one of the postal operators’ historical strengths, but if they don’t, they will just see the train pass by and ultimately be left outside of the huge potential of e-commerce. In this mat-ter, it is probably advisable for postal operators to team up with data analytics companies, such as Yandex. Thanks to such a partnership, posts may be able to regain a higher status within the e-commerce value chain.

Thank you, Mr. Gözalan, for your insights.