Embed Size (px)

Citation preview

ECA & SAL Conference Sydney, August 2012

TOWAGE & MARINE SERVICES BUILDING COMPETIVENESS

Melbourne

Harbour Towage Operations Terminal Towage Salvage Warehouse

Newcastle

Weipa

Cairns

Mourilyan

Lucinda

Bowen – Abbott Point

Mackay

Brisbane

Bundaberg

Sydney (Port Jackson & Port Botany)

Port Kembla

Westernport

Geelong

Port Adelaide

Whyalla

Port Pirie

Ardrossan

Port Giles

Project Magnet

Port Bonython

Port Lincoln

Thevenard

Albany

Kwinana

Fremantle

Geraldton

Koolan Island

Cockatoo Island

Darwin

Darwin LNG

Eden

Port Moresby

Rabaul

Kimbe

Lae

Madang

Papua New Guinea

Australia

New Zealand

Suva

Lautoka

Fiji

New Caledonia

Gorgon LNG

TOWAGE & MARINE SERVICESSVITZER AUSTRALASIA COVERAGE

TOWAGE & MARINE SERVICESHOW RELEVANT ARE TOWAGE CHARGES

• Towage represents on average 30% of the cost for calling at an Australian Port

• Different ports vary to a significant degree based upon

- Size of vessels- Number of vessels calls- Frequency of individual vessel calls- Tug intensity per ship movement

TOWAGE & MARINE SERVICES CURRENT COST OVERVIEW

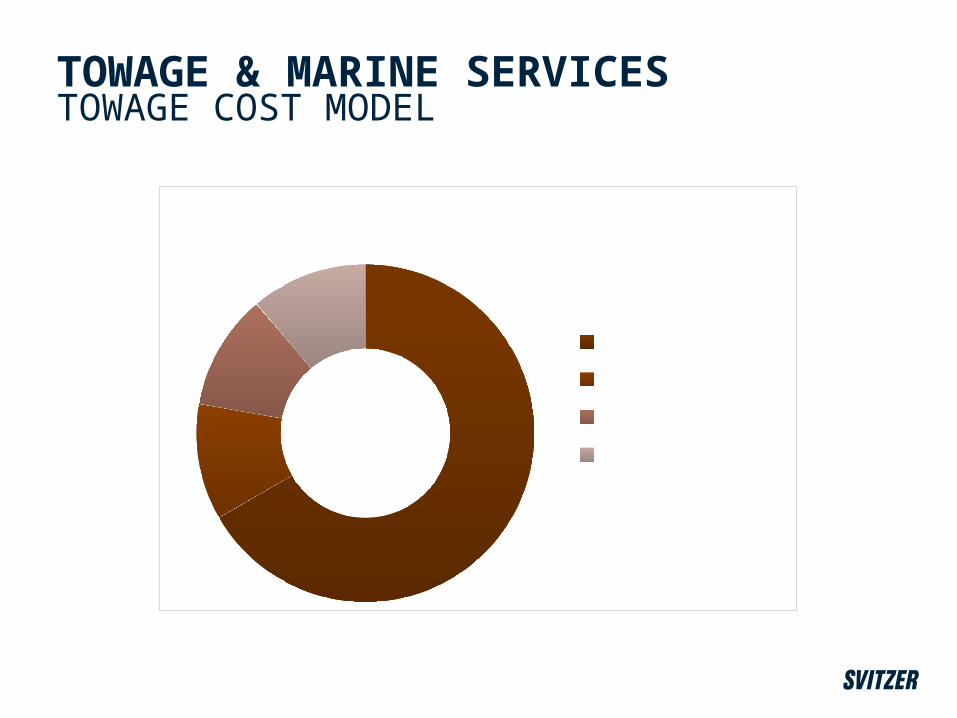

TOWAGE & MARINE SERVICESTOWAGE COST MODEL

OPEX

LabourFuelRunning CostsOverheads

TOWAGE & MARINE SERVICESTARIFF V LABOUR COST TREND

Productivity/Recruitment/Redundancy

2008 2009 2010 2011 2012

Salary TrendLabour Cost TrendTariff TrendHT Activity

Productivity/Recruitment/Redundancy

TOWAGE & MARINE SERVICESSERVICE PROFILE

• Service reliability, as an industry, is extremely high

• Service provision typically covers all eventualities

• Economic impact of >99% service level perhaps not the most efficient, how any lowering of service will not equitably effect all ports users

• Cost of service failures to our customers can be extreme e.g. demurrage, fuel etc

• What is the correct and most efficient level? What would the market accept?

TOWAGE & MARINE SERVICESEXPERIENCE PROFILE

• Towage is a “facilitation” service and is to a large degree insurance

• The skill of the crew is more important than the tug capabilities

• The importance of local knowledge and experience cannot be underestimated

• The retention of skills/experience is a KPI and increasingly challenging

• Finding the correct balance between “fit for purpose” and upgrading fleet capability is key component of cost mitigation

TOWAGE & MARINE SERVICES HOW WE ARE IMPROVING COMPETITIVENESS

TOWAGE & MARINE SERVICESLABOUR COST COMPETIVENESS

• Three factors are driving labour cost trend;

- availability (projects, supply v demand)- “Traditional” waterfront attitudes (reluctance to change)- retention of core skills/experience

• We are taking a number of steps to address the trend;

- Roster certainty and improved work/life balance- TABU, improved empowerment/ownership/job satisfaction- Advisory board concept, both nationally and locally- Increased transparency on cost outcomes/modelling- Annual employee engagement survey- Clarify the delta between salary trend and cost trend

TOWAGE & MARINE SERVICESASSET UTILISATION

• Looking to cover increased work levels with the same tug fleet by;

- Reviewing optimal tug configuration- Greater utilisation of assets via roster enhancements- Utilising scale of operation to mitigate off service periods- Cascading of older tugs to suit commercial and operational requirements

• Review and match our operational capability to the needs of our customers and stakeholders.

• Consider alternative use of HT assets to decrease the financial burden on the customers of a port (where operationally feasible)

TOWAGE & MARINE SERVICESFUEL COSTS AND EMISSIONS REDUCTION

• Circa 10% of our operating costs

• Fuel consumption linked closely to operational behaviour

• Chemical solutions being trialled to reduce fuel burn and emission per litre consumed

• Improved planned maintenance system being rolled out to increase operational efficiency

TOWAGE & MARINE SERVICES FURTHER OPPORTUNITIES

TOWAGE & MARINE SERVICESSHIPPING REFORM PROCESS

• Towage (and offshore) not currently considered as part of initial reform

• Largest trade sectors with regard to existing employment, significant growth profile

• Any workforce initiatives will need and should need to involve towage/offshore sectors

• An opportunity exists to meet both shipping reform ambitions and the future training and employment needs of the country whilst making port services more internationally competitive

• AMTA recently established to consider, alongside ASA, how this can best be achieved

TOWAGE & MARINE SERVICESSTAKEHOLDER DIALOGUE

• Long term views with regard to capability to allow efficient planning

• Port Licensing process to permit a continuous competitive landscape

• A balanced approach to marrying desired marine capability with a competitive “fit for purpose” capability customers can afford

• Flexible labour paths and certification routes to maximise workforce opportunities and efficiency and avoid “boom and bust”

• Weigh up cost/benefit analysis of 100% service level capability 24/7

SUMMARY