Embed Size (px)

Citation preview

ASX RELEASE 31 May 2011

Perth: Level 2 Aquila Centre, 1 Preston Street, Como WA 6151 Telephone (61) 8 9423 0111Facsimile (61) 8 9423 0133 Brisbane: Level 18, 10 Eagle Street, Brisbane QLD 4000 Telephone (61) 7 3229 5630 Facsimile (61) 7 3229 5631 Thabazimbi: C/O Platina and Lood Avenue, Thabazimbi 0380, South Africa Telephone (27) 14 772 3337 Facsimile (27) 14 772 3337 Northern Cape: Stand 585 Opwag, Groblershoop, Northern Cape, South Africa Telephone (27) 798 816 459 Facsimile (27) 866 838 065

Eagle Downs Hard Coking Coal Project Study Results

Highlights:

� The Manager of the Eagle Downs Hard Coking Coal Project (the “Project”) has released a Study detailing the outcomes of work to date which address the deliverables of the owners’ project delivery requirements.

� The Project has a total JORC compliant resource of 959 million tonnes and a reserve of 254 million tonnes.

� The Mine, once constructed with the longwall installed in the Harrow Creek Upper Seam, will produce on average 4.5Mtpa of hard coking coal.

� The Study confirms the Project’s technical and financial viability which is based on initially securing rail and port capacity at Wiggins Island Coal Export Terminal (WICET) Stage 2.

� The Project has an estimated mine life of approximately 48 years.

� Capital expenditure in the Schedule B option, is estimated at $1,254 million, which includes provisions for EPCM ($39 million) and contingency ($85 million).

� Operating costs in the Schedule B option, of approximately $94 per tonne (excluding State royalties).

Schematic of the proposed surface layout of the Eagle Downs Coal Mine

For

per

sona

l use

onl

y

2

Aquila Resources Limited (ASX:AQA “the Company” or “Aquila”) is pleased to announce that the Manager has released the Study for the Eagle Downs Hard Coking Coal Project (‘Eagle Downs” or the “Project””) (owned 50% Aquila, 50% Bowen Central Coal Pty Ltd a wholly owned subsidiary of Vale (“Vale”)). The Project is located in the Bowen Basin in Central Queensland, adjacent to and immediately down dip from the BHP Billiton Mitsubishi Alliance (“BMA”) operating Peak Downs Coal Mine. The Project involves proposed construction, development and operation of an underground longwall hard coking coal mine in Queensland’s resource-rich Bowen Basin. Eagle Downs Coal Management Pty Ltd (“Manager”) represents owners Aquila and Vale in the development and operation of this Project. The Study proposes an underground multi seam longwall mine, producing initially up to 5.1Mtpa and an average of 4.5Mtpa of hard coking coal from one longwall. The Study specifically addresses the following issues:

• The project deliverables requested by Aquila Resources for a Definitive Feasibility Study; • The project deliverables requested by Vale for a FEL3 study; • An update of the Project development schedule; • A number of schedules for developing the Project; • Technical and engineering reports and costings; • A capital budget for the Project; • An update of the Project economics.

This Study has positively addressed these issues and confirms the Project’s technical and financial viability, based on initially securing rail and port capacity at WICET Stage 2.

Schematic of the proposed Train Load Out at the Eagle Downs Hard Coking Coal Project

The Study

The Study provides detailed work (technical studies, engineering and costings) on the following areas: • Market analysis and business strategy • Project Expenditure • Geology and resource • Surface Infrastructure • Underground Mining • Coal Handling and Preparation Plant • Approvals, Agreements and Arrangements • Risk Management • Operations Management • Marketing and Logistics • Project Sustainability

For

per

sona

l use

onl

y

3

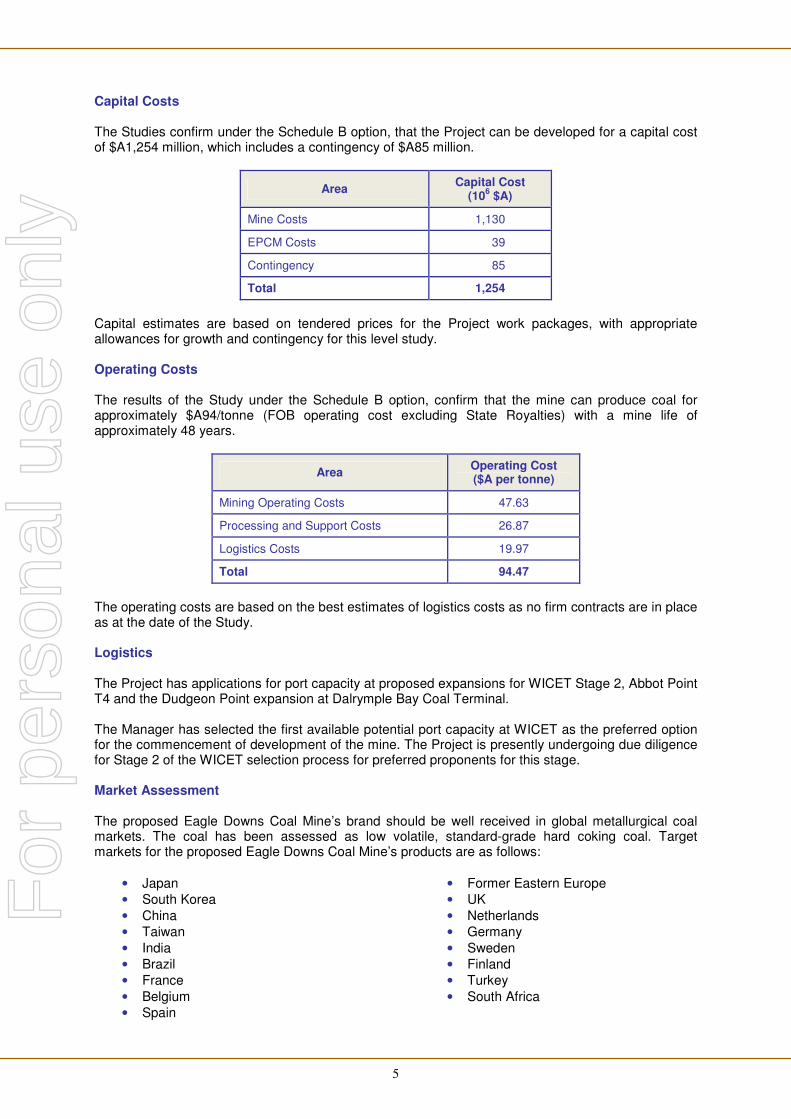

The Study will be the subject of detailed review over the next month by the Company. A summary of the key outcomes are contained in this announcement. Construction Schedule The Manager presented two alternate schedules in the Study (Schedule A and Schedule B). The basis of the schedules was driven by the first available port capacity which the Project was likely to achieve. Whilst both options envisaged the logistics capacity for the Project being satisfied by Stage 2 of WICET, the Schedule B option envisaged that initial development and longwall coal produced from the Project, would be shipped through the terminal. The costs presented in this announcement are based on this schedule. Another option, Schedule A, was presented that assumed that shipping through that terminal would only occur once the longwall commenced production, meaning there was no logistics solution provided for the initial development coal. (Whilst Schedule A provides an earlier start date for the Project, it was not preferred by the Company as it is not practical to store or stockpile coking coal on the surface due to product deterioration). Based on Schedule B, the Project is scheduled to require Sanction by the Owners in April 2012 based on an offer of a Take-or-Pay contract for the WICET Stage 2 expansion. The construction duration is estimated to be 28 months from project commitment. The key dates for construction and production under Schedule B are:

Milestone Scheduled Date

Mining Lease granted June 2011

Potential Project Sanction April 2012

Construction of Surface Infrastructure Complete June 2014

Drifts Complete:

- First Access to Coal

(Aligns with WICET Mechanical Completion)

- CHPP commissioning

October 2015

Practical Completion December 2015

Longwall Starts Production October 2016

For

per

sona

l use

onl

y

4

Schedule B – Net Cash Flows

Coal Handling and Preparation Plant The Coal Handling and Preparation Plant (CHPP) will have a throughput of 1,200tph Run of Mine (ROM) to a standard consistent with a 50-year Life of Mine (LOM). The capital cost estimate for the complete facility was subjected to a high-level risk review to determine the most likely project cost with the average LOM total operating cost estimated at $6.81/ROMt.

Schematic of the proposed Coal Handling and Preparation Plant of the Eagle Downs Hard Coking Coal Project Production Schedule The mine design has been optimised during the studies based on the extensive exploration program including a 3D seismic program over the mining area. Technical studies have been completed including but not limited to ventilation, gas drainage, geotechnical design and hydrogeology. Production schedules have been developed for the mine layout and have been benchmarked against leading Australian longwall mines. The mine plan will involve the systematic recovery of coal from the Harrow Creek Upper (HCU), Harrow Creek Lower (HCL) and Dysart (DY) Seams over a 48 year mine life. The annual average production rate over the initial 10 years following commissioning of the longwall will be 4.5 million tonnes per annum of hard coking coal. The majority of the mine reserves are classified as hard coking coal. F

or p

erso

nal u

se o

nly

5

Capital Costs The Studies confirm under the Schedule B option, that the Project can be developed for a capital cost of $A1,254 million, which includes a contingency of $A85 million.

Area Capital Cost

(106 $A)

Mine Costs 1,130

EPCM Costs 39

Contingency 85

Total 1,254

Capital estimates are based on tendered prices for the Project work packages, with appropriate allowances for growth and contingency for this level study. Operating Costs The results of the Study under the Schedule B option, confirm that the mine can produce coal for approximately $A94/tonne (FOB operating cost excluding State Royalties) with a mine life of approximately 48 years.

Area Operating Cost ($A per tonne)

Mining Operating Costs 47.63

Processing and Support Costs 26.87

Logistics Costs 19.97

Total 94.47

The operating costs are based on the best estimates of logistics costs as no firm contracts are in place as at the date of the Study. Logistics The Project has applications for port capacity at proposed expansions for WICET Stage 2, Abbot Point T4 and the Dudgeon Point expansion at Dalrymple Bay Coal Terminal. The Manager has selected the first available potential port capacity at WICET as the preferred option for the commencement of development of the mine. The Project is presently undergoing due diligence for Stage 2 of the WICET selection process for preferred proponents for this stage. Market Assessment The proposed Eagle Downs Coal Mine’s brand should be well received in global metallurgical coal markets. The coal has been assessed as low volatile, standard-grade hard coking coal. Target markets for the proposed Eagle Downs Coal Mine’s products are as follows:

• Japan • South Korea • China • Taiwan • India • Brazil • France • Belgium • Spain

• Former Eastern Europe • UK • Netherlands • Germany • Sweden • Finland • Turkey • South Africa

For

per

sona

l use

onl

y

6

Resource The revised resource statement has been prepared by Mr Mal Blaik from JB Mining Services, was previously advised to the ASX. The total resource has increased to 959 million tonnes with the JORC classification of the resource improved significantly since the previous assessment. The work in the past 12 months involved:

• Completion of 3D seismic data interpretation • The drilling of 10 cored holes including 4 new sites, 4

redrills and two large diameter holes; • 65 new raw coal quality seam analyses; • 73 new clean coal composite seam analyses

including redrills; • Ongoing large scale coking tests; • Geostatistics completion of the HCU, HCL and DY

seam studies. This has further improved the existing robust geological model for the Project. The outcomes of this work are:

• Total resource to 959Mt. • Measured resource of 648Mt. • Measured and Indicated Resources of 819Mt.

Results are detailed below:

Table 1 – Summary of In situ Resources by Seam (depths from 150m to >600m)

Seam Measured

Tonnes x 106

Indicated

Tonnes x 106

Total Measured &

Indicated Tonnes x 10

6

Inferred Tonnes x 10

6

Total Measured

Indicated & Inferred

Tonnes x 106

Q 73 20 93 15 108

HCU 123 36 158 31 189

HCL 281 70 351 49 400

HCL “PCI” 3 3 8 11

DY 164 13 177 16 193

DY – “PCI” 7 30 37 22 58

Total 648 171 819 141 959

Reserve Statement

A revised reserve statement was developed as part of the studies and was released by the Company to the ASX in April 2011.

The process for the review and audit of the underground Coal Reserves was undertaken by Mr J Steenekamp of Mining Consultancy Services (Australia) Pty Ltd. The objective was to determine whether there is a reasonable prospect of the Resources being economically mined, and to confirm the magnitude and categorisation of the subsequent Coal Reserves. The basic methodology of each stage of the review and audit process comprised the following steps:

• Checking the basis and application of the physical cut-off parameters which qualify the Resources for inclusion in the Reserves.

For

per

sona

l use

onl

y

7

• Reviewing the proposed mining method for the deposit and verifying that adequate mine plans exist and that the mining parameters are appropriate.

• Checking the reasonableness of the assumptions for coal recovery, product quality and market requirements.

• Reviewing the likelihood of any other obvious legal, social and environmental detriments which might prevent the economic mining of the Resource.

• Random auditing of the estimation of the Reserve numbers.

• Confirming the classification of the Reserves with respect to the underlying Resource categories and the risk of actually realising the Reserve.

Results are detailed below:

Table 2 – Summary of In situ Reserves

Category Run of Mine Million Tonnes (Mt)

Harrow Creek Upper Seam (HCU)

Proved 60.1

Probable 13.5

JORC Reserves 73.6

Harrow Creek Lower Seam (HCL)

Proved 91.1

Probable 21.9

JORC Reserves 113.0

Dysart Seam (DY)

Proved 55.4

Probable 12.1

JORC Reserves 67.5

Total

Proved 206.6

Probable 47.5

JORC Reserves 254.1

Progress to Development Decision The Manager of the Project has informed the Participants that the Project “Feasibility Study” cannot be completed to the standard required by the Joint Venture Agreement due to a lack of a logistics solution and firm off take arrangements. Aquila’s preferred option, Schedule B, allows for a Development Decision to be made when Take-or-Pay Contracts are expected to be offered for WICET Stage 2 capacity.

Tony Poli Executive Chairman For further information regarding this announcement, please contact Tony Poli.

Telephone: (08) 9423 0111 Facsimile: (08) 9423 0133 Email address: [email protected] Visit us at: www.aquilaresources.com.au

For

per

sona

l use

onl

y

8

The information in this announcement that relates to the Resource Statement has been based on information compiled by Mr Mal Blaik who is a member of the Australian Institute of Mining and Metallurgy. Mr Blaik is a Principal Consultant of JB Mining Services Pty Ltd. Mr Blaik is a qualified geologist (BSc App Geol (Hons) University of QLD, 1979) and is a member of the Australasian Institute of Mining and Metallurgy and has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person under the JORC Code. Mr Blaik has consented to the inclusion in the announcement of the matters based on their information in the form and context in which it appears. This Reserves Statement presented in this report has been prepared under and in accordance with the Guidelines of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves, prepared by the Joint Ore Reserves Committee, December 2004.

The information in this report to which this Statement is attached that relates to Coal Reserves, is based on information reviewed by Mr J Steenekamp, who is a Fellow of the Australasian Institute of Mining and Metallurgy. Mr Steenekamp has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 edition of the JORC Code.

Mr Steenekamp is a full time employee of Mining Consultancy Services (Australia) Pty Ltd and holds the position of Operations Director. Mr Steenekamp has consented to the inclusion in the announcement of the matters relating to Coal Reserves based on the information he has reviewed, in the form and context in which it appears.

For

per

sona

l use

onl

y