Embed Size (px)

Citation preview

Copyright © 2015 by the Board of Trustees of Stanford and Stanford Technology Ventures Program (STVP).

This document may be reproduced for educational purposes only.

Session 9A: Sources of Capital, VC Fund Economics

E 1 4 5 | F A L L 2 0 1 5

Tom Byers and Chi-Hua Chien

e145.stanford.edu

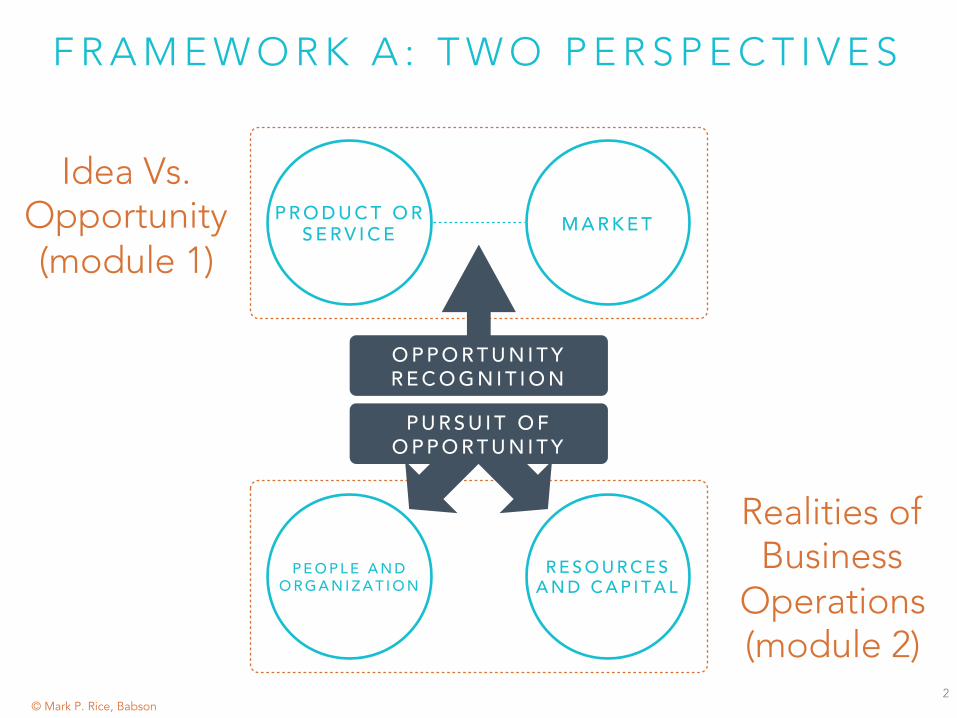

Idea Vs. Opportunity(module 1)

Realities ofBusiness

Operations(module 2)

© Mark P. Rice, Babson

P R O D U C T O R S E R V I C E M A R K E T

P E O P L E A N D O R G A N I Z A T I O N

R E S O U R C E S A N D C A P I T A L

P U R S U I T O F O P P O R T U N I T Y

O P P O R T U N I T Y R E C O G N I T I O N

2

F R A M E W O R K A : T W O P E R S P E C T I V E S

S A M P L E O U T L I N E O F T R A D I T I O N A L B U S I N E S S P L A N

• Executive Summary

• Market Analysis

• Vision and Concept (Including Technology)

• Competitive Positioning and Marketing

• Business Model• Organization• Financial Projections

• Ownership

3

} Amplify inE145 Module 2

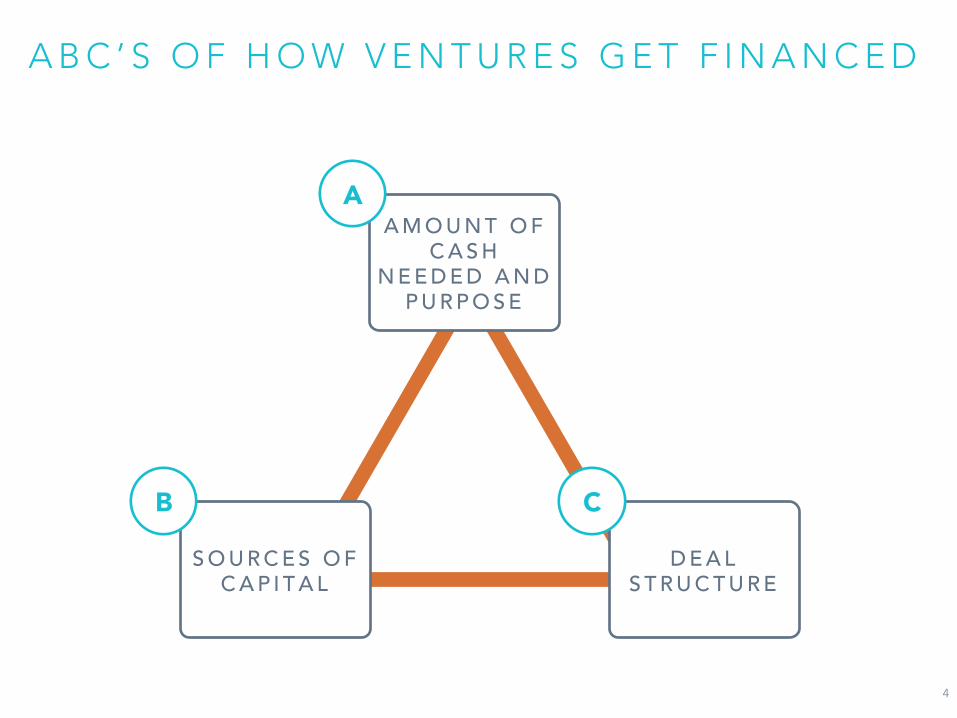

A B C ’ S O F H O W V E N T U R E S G E T F I N A N C E D

4

A M O U N T O F C A S H

N E E D E D A N D P U R P O S E

A

S O U R C E S O F C A P I T A L

B

D E A L S T R U C T U R E

C

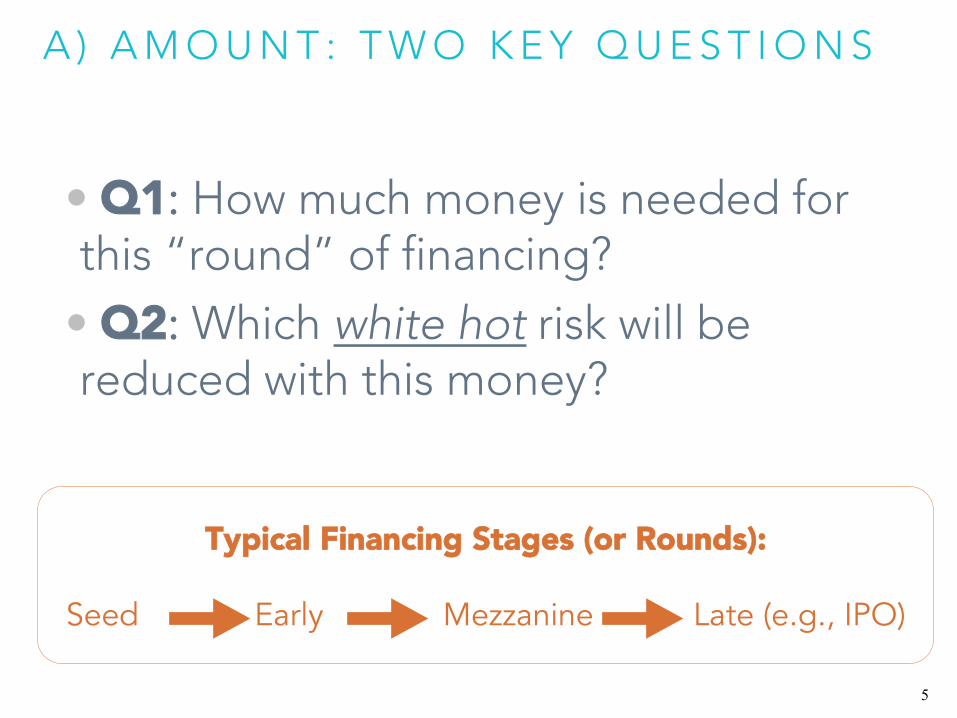

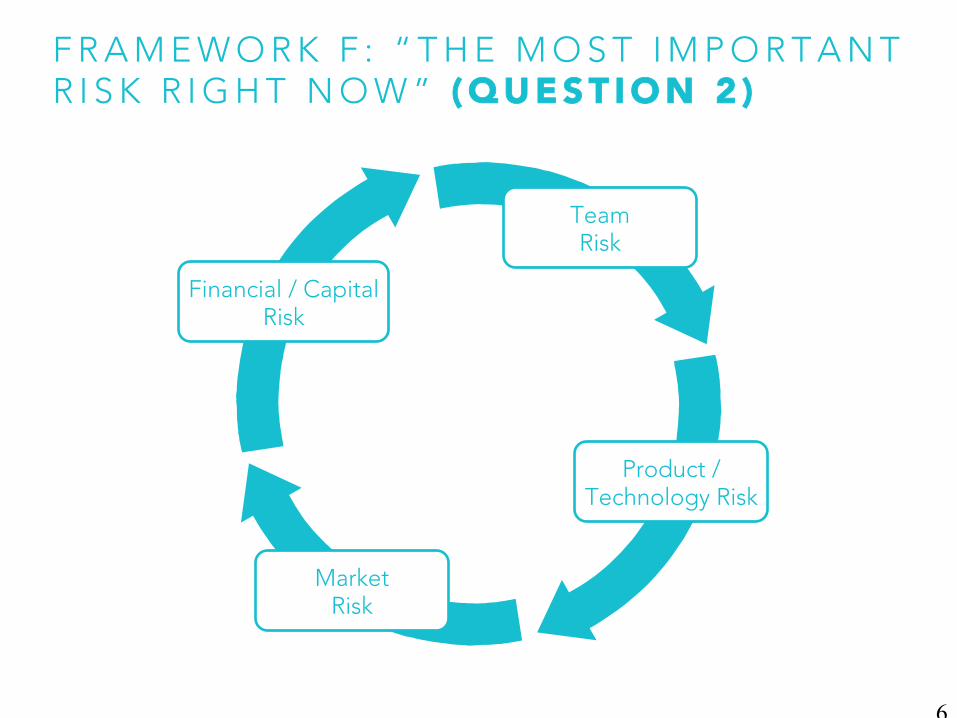

A ) A M O U N T : T W O K E Y Q U E S T I O N S

• Q1: How much money is needed for this “round” of financing?

• Q2: Which white hot risk will be reduced with this money?

Typical Financing Stages (or Rounds):

Seed Early Mezzanine Late (e.g., IPO)

5

F R A M E W O R K F : “ T H E M O S T I M P O R T A N T R I S K R I G H T N O W ” ( Q U E S T I O N 2 )

MarketRisk

Product / Technology Risk

Financial / CapitalRisk

TeamRisk

6

R E C A L L T H E Y A H O O C A S E

• Yahoo: What are the advantages and disadvantages of each of the three major options they could pursue to finance the venture in 1995 (e.g., venture capital, corporate partnerships and sponsorships, and acquisition to become an operating division of an established company)?

• ”I suggest that Jerry and David [accept/do not accept] Sequoia's offer because..."

8

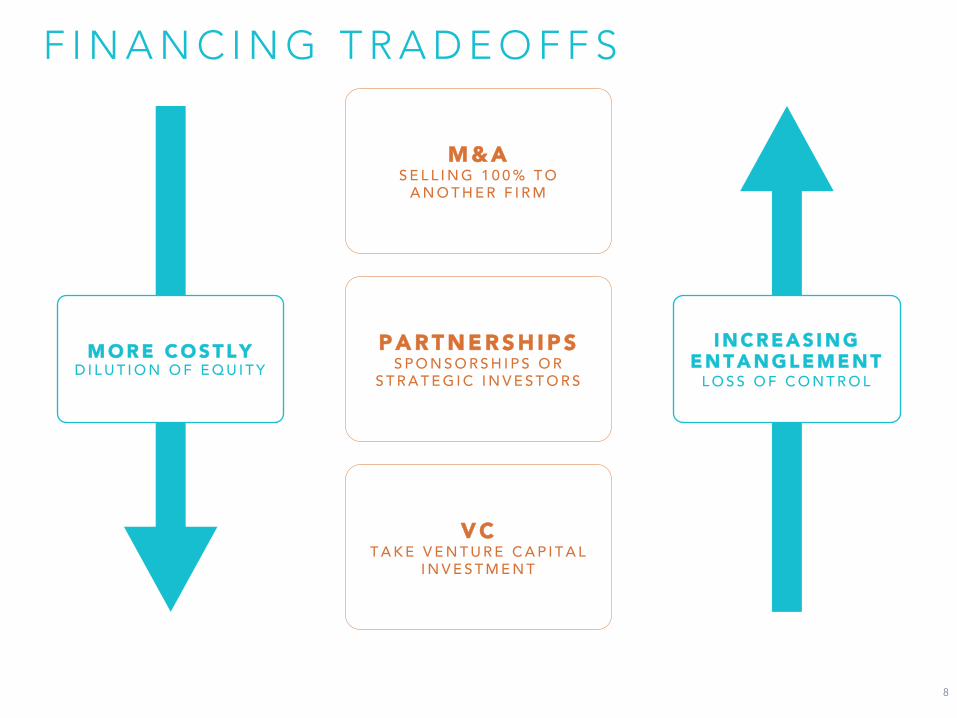

M O R E C O S T L YD I L U T I O N O F E Q U I T Y

M & AS E L L I N G 1 0 0 % T O

A N O T H E R F I R M

P A R T N E R S H I P SS P O N S O R S H I P S O R

S T R A T E G I C I N V E S T O R S

V CT A K E V E N T U R E C A P I T A L

I N V E S T M E N T

I N C R E A S I N G E N T A N G L E M E N T

L O S S O F C O N T R O L

F I N A N C I N G T R A D E O F F S

A N G E L S S E E D O R S E R I E S A

9

New Business

Firm

I N V E S T M E N T B A N K S

I P O & P U B L I C P L A C E M E N T

V E N T U R E C A P I T A L

F I R M S S E R I E S A , B , C

F R I E N D S A N D F A M I L Y

S E E D F U N D S

Table 18.4

P E N S I O N F U N D S P R I V A T E I N V E S T O R S

C O R P O R A T I O N S

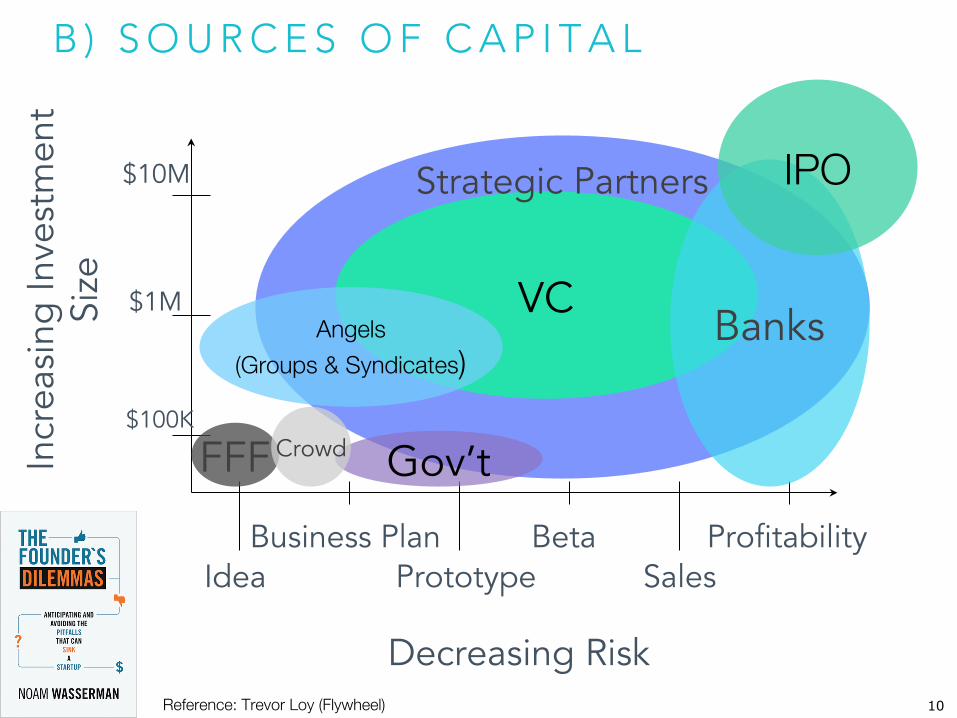

B ) S O U R C E S O F C A P I T A L

10

Idea Business Plan

Prototype Beta

Sales Profitability

Decreasing Risk

$100K

$1M

$10M

Incr

easi

ng In

vest

men

t Si

ze

VC Banks Angels !

(Groups & Syndicates)

FFF Gov’t

IPO Strategic Partners

Reference: Trevor Loy (Flywheel)

Crowd

B ) S O U R C E S O F C A P I T A L

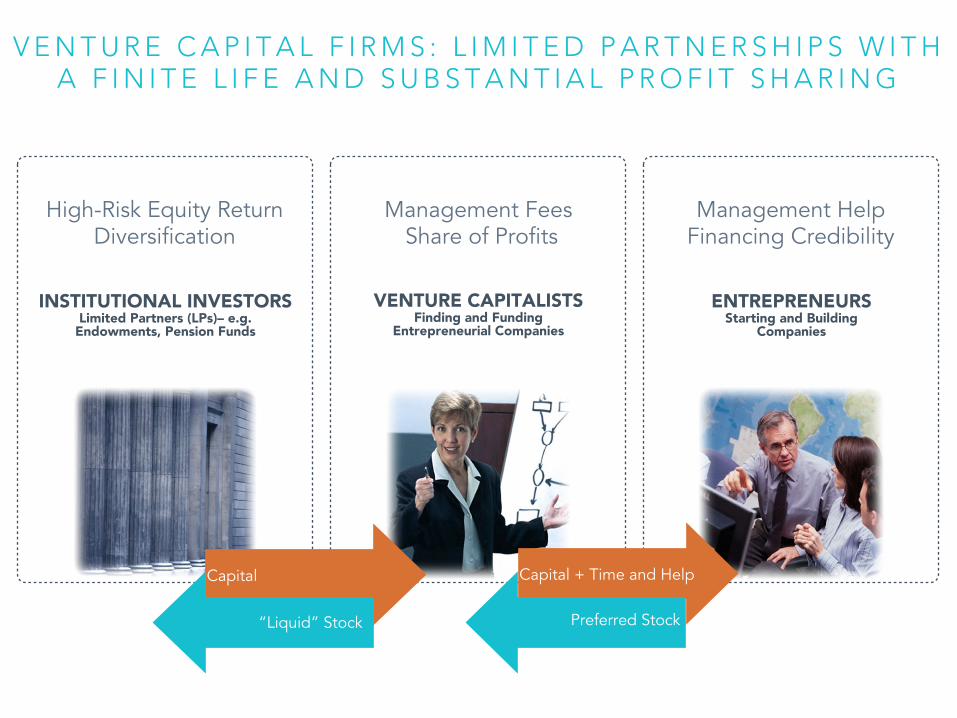

VENTURE CAPITALISTSFinding and Funding

Entrepreneurial Companies

ENTREPRENEURSStarting and Building

Companies

INSTITUTIONAL INVESTORSLimited Partners (LPs)– e.g.

Endowments, Pension Funds

High-Risk Equity Return Diversification

Management Fees Share of Profits

Management Help Financing Credibility

V E N T U R E C A P I T A L F I R M S : L I M I T E D P A R T N E R S H I P S W I T H A F I N I T E L I F E A N D S U B S T A N T I A L P R O F I T S H A R I N G

Capital + Time and Help Capital

Preferred Stock “Liquid” Stock

12

V C B A C K E D C O M P A N I E S > 2 0 % O F U S G D P

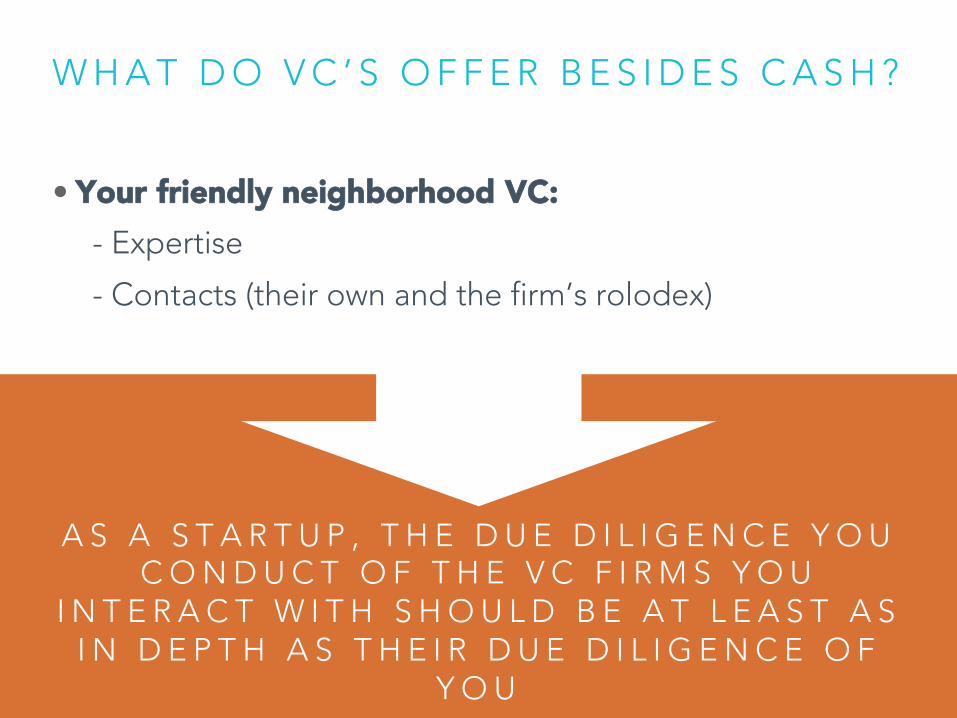

W H A T D O V C ’ S O F F E R B E S I D E S C A S H ?

• Your friendly neighborhood VC:- Expertise

- Contacts (their own and the firm’s rolodex)

13

A S A S T A R T U P , T H E D U E D I L I G E N C E Y O U C O N D U C T O F T H E V C F I R M S Y O U

I N T E R A C T W I T H S H O U L D B E A T L E A S T A S I N D E P T H A S T H E I R D U E D I L I G E N C E O F

Y O U

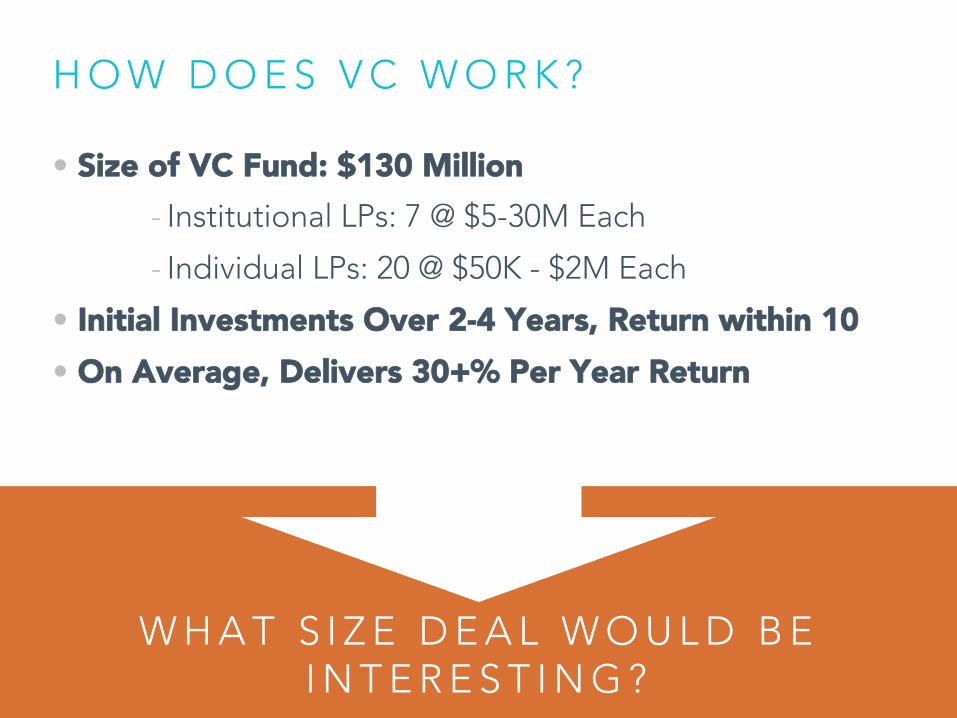

H O W D O E S V C W O R K ?

• Size of VC Fund: $130 Million- Institutional LPs: 7 @ $5-30M Each

- Individual LPs: 20 @ $50K - $2M Each

• Initial Investments Over 2-4 Years, Return within 10• On Average, Delivers 30+% Per Year Return

14

W H A T S I Z E D E A L W O U L D B E I N T E R E S T I N G ?

W H I C H D O Y O U P R E F E R ?

Suppose you were to invest $10 million…• Fund 1:

• 2x return on all 10 $1M investments

• Fund 2:

• Loses all $1M investments in 8 deals

• Wins 20x on the remaining 2 $1M investments

15Source: Andy Rachleff

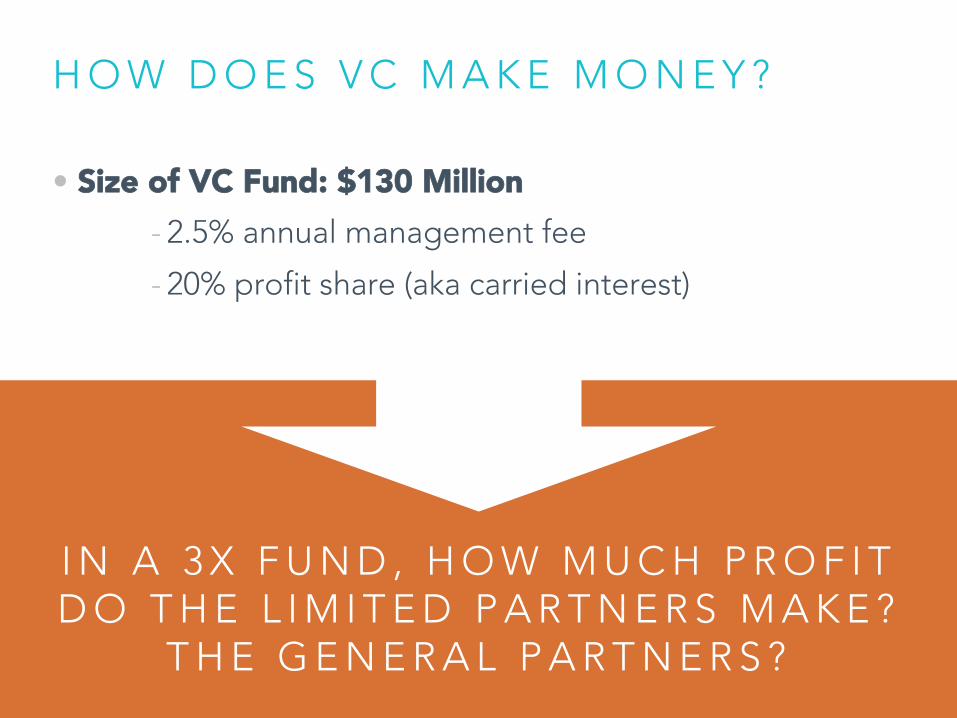

H O W D O E S V C M A K E M O N E Y ?

• Size of VC Fund: $130 Million- 2.5% annual management fee

- 20% profit share (aka carried interest)

16

I N A 3 X F U N D , H O W M U C H P R O F I T D O T H E L I M I T E D P A R T N E R S M A K E ?

T H E G E N E R A L P A R T N E R S ?

Break

e145.stanford.edu