Embed Size (px)

Citation preview

Brussels Development Briefing n.35

Revolutionising finance

for agri-value chains 5 March 2014

http://brusselsbriefings.net

E-warehouse Initiative.

David RUCHIU, Farm Concern International.

E-warehouse Initiative

Farm Concern International

David Ruchiu

Africa Director, Farm Concern International

Farm Concern International, FCI. GROUP

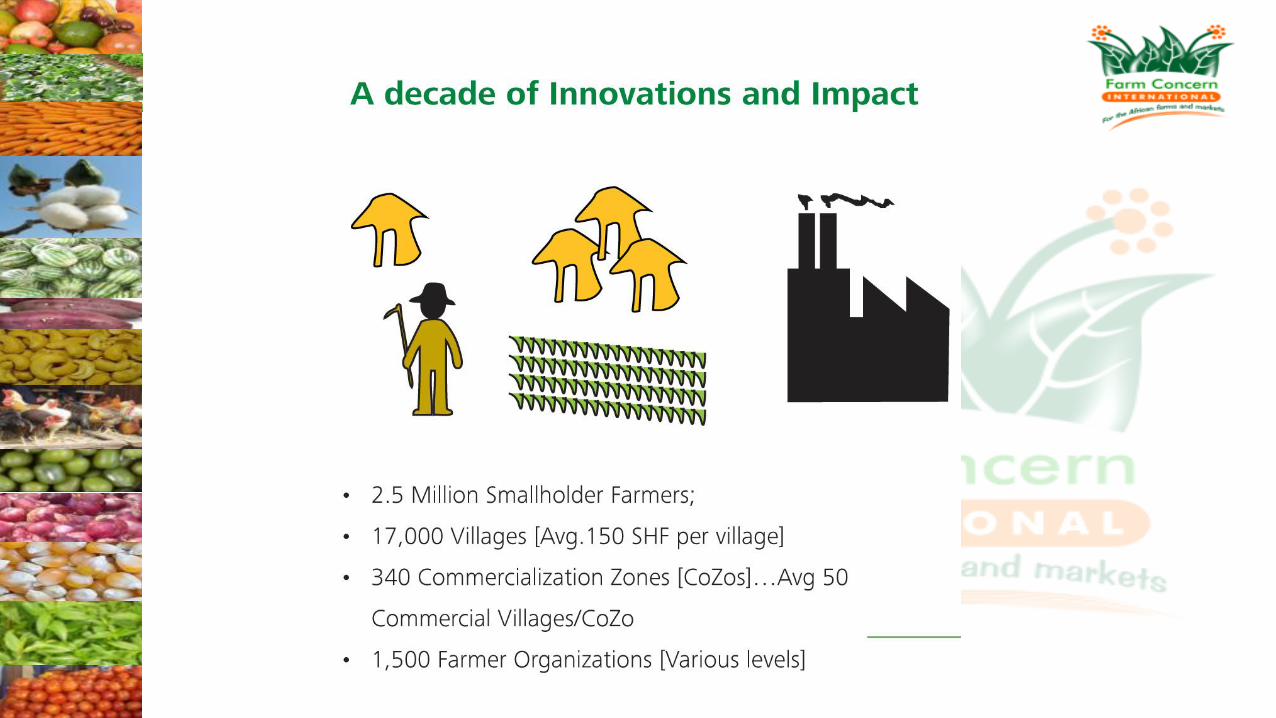

FCI wins markets for Africa for economic development and business partnerships

FCI models are benchmarked to private sector approaches to enhance smallholder competitiveness

FCI models adapted to addressing global dynamics (changing trade patterns, climate change and changing policies)

FCI promotes technologies and innovations that enhance smallholder competitiveness and resilience

FCI is partnership oriented organization

FCI responds to food security, nutrition security and Income growth

FCI Mission & Vision

Our Mission

To build and Implement innovative pro-

poor market and Business Models that

catalyse solutions for smallholder

commercialization and Competitiveness

in the value networks for household

economic growth and Community

empowerment in Africa and Beyond

Our Vision

Commercialized smallholder

Communities with increased

incomes for improved, stabilized

and sustainable livelihoods in Africa

and Beyond

FCI Regions & Countries

FCI Programmes

200 Km

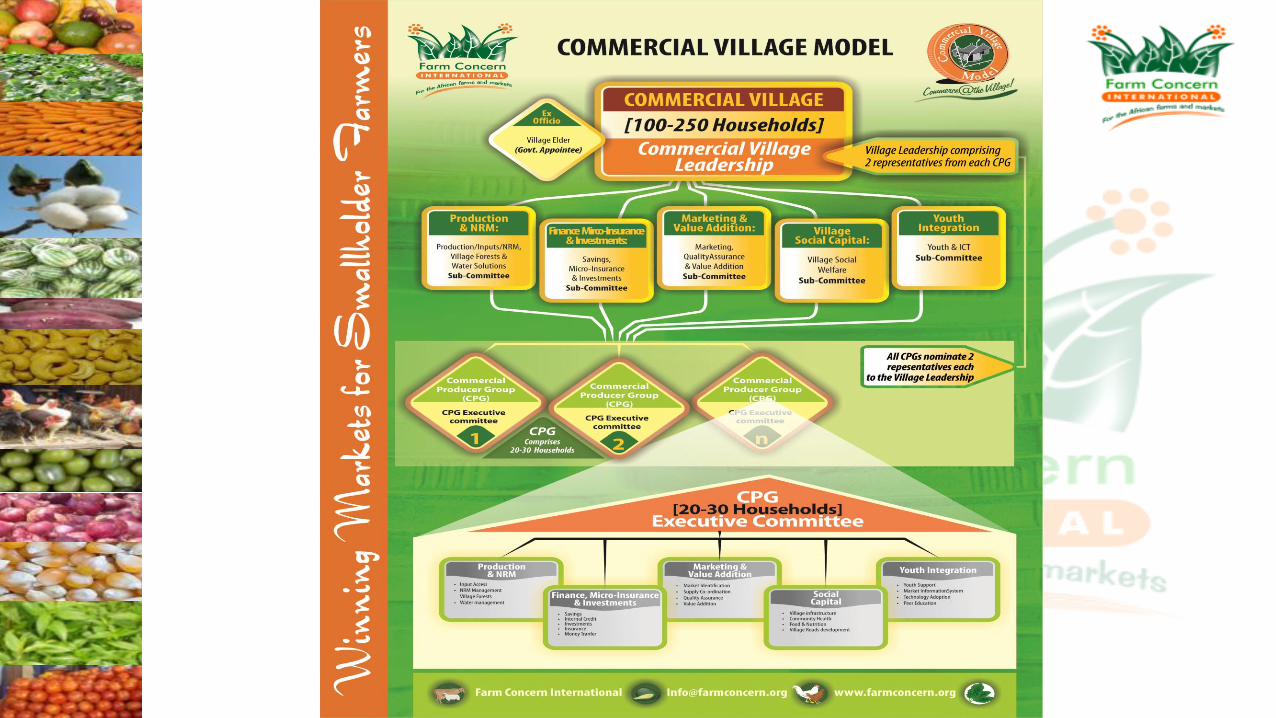

Commercial Producer Groups (CPGs)

within Commercial Villages

• Organized based basket of value chains

• Structured governance

• Business partnership with buyers

• Focus is village collective action

• Information exchange platform

established

Efficiencies in out-sourcing / marketing systems through of CV

model

Wholesale market

E-warehouse Initiative

Why eWarehouse?

• Smallholder farmers are often isolated from markets and lack access

to financial services that would allow them to smooth their income

• Lack of appropriate financing for smallholder farmers. Only 17.6% of

those living in rural areas have access to formal financial services,

and many of the financing options available to farmers are not well-

suited to their needs and farming cycles.

• At harvest time, when prices are lowest due to excess supply, most

smallholder grain farmers cannot afford to wait for optimal prices

before selling to buyers

• Large grain warehouses are not generally available to smallholder

farmers, and many risk losing their entire crop yields by not

following proper storage practices

eWarehouse purpose

eWarehouse intervention seeks to address ;

• Identified market gaps through an integrated and mobile-

enabled system

• Designed to support smallholder farmers to properly store

and manage their grain post-harvest and virtually bulk grain

during harvest time,

• Facilitate linkage to financial services to provide partial

advances against the value of the stored grain

• Link smallholders with markets when prices increase.

e-warehouse Strategic

Objectives • Enable farmers to collectively store and sell grains at higher prices through

use and development of appropriate technology;

• Utilize technology and information as collateral by smallholder farmers.

• Increase the value retained by smallholder farmers for their crop by

facilitating access to mobile financial services

• Enhanced market access for smallholder farmers

• Leverage on technology as the basis of increasing efficiency in payment

processes

• Leverage on technology to provide actionable agronomic and market

information to farmers;

• Build capacity of smallholder farmers in proper post-harvest storage

practices to minimize risk of post-harvest waste

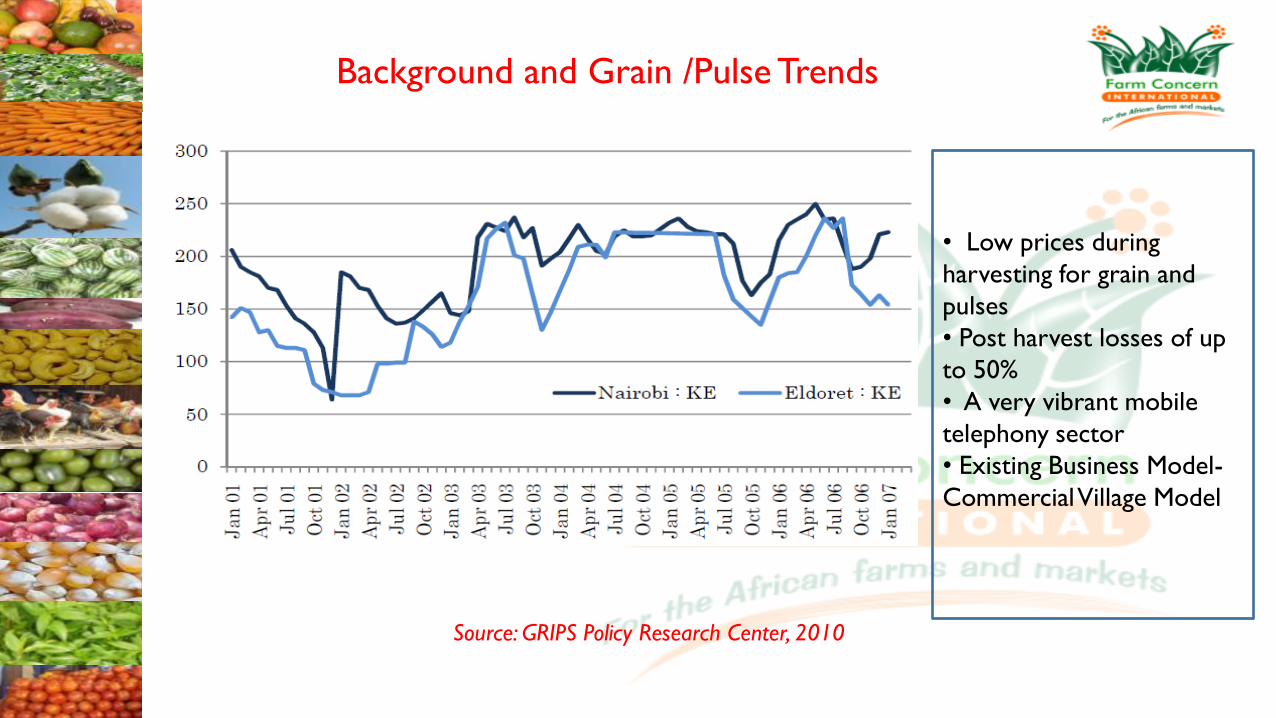

Background and Grain /Pulse Trends

Source: GRIPS Policy Research Center, 2010

• Low prices during

harvesting for grain and

pulses

• Post harvest losses of up

to 50%

• A very vibrant mobile

telephony sector

• Existing Business Model-

Commercial Village Model

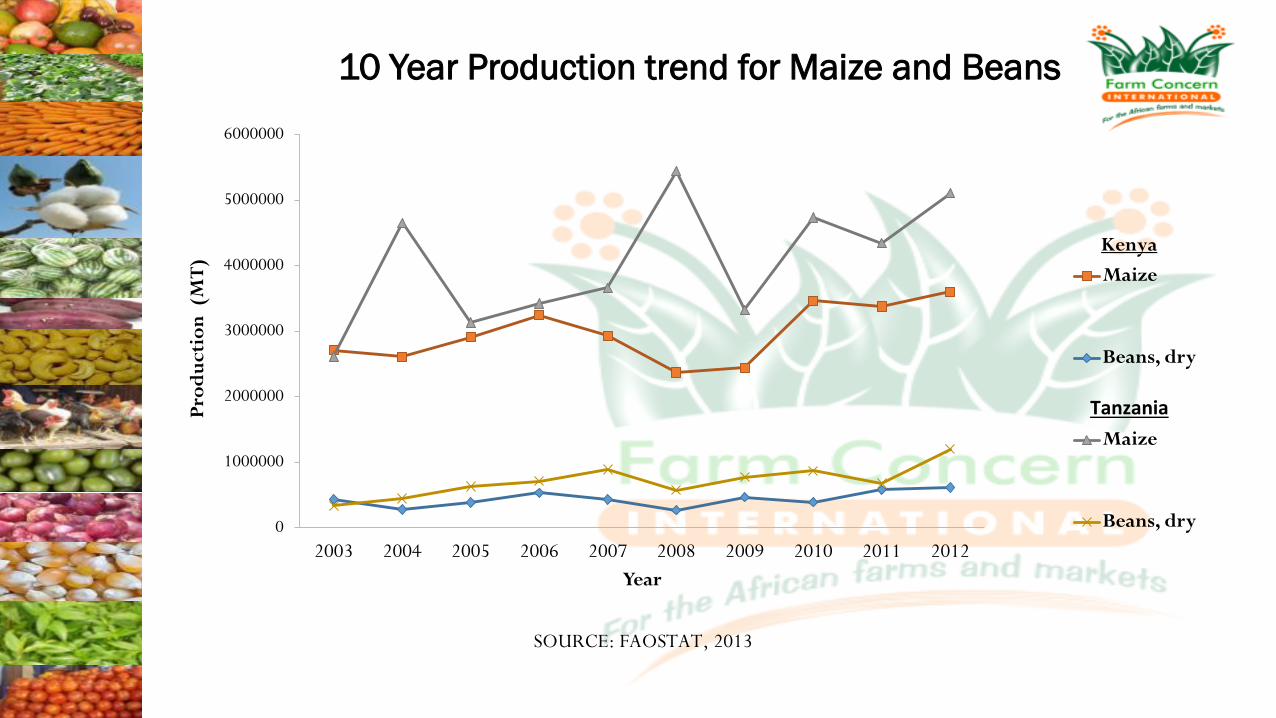

10 Year Production trend for Maize and Beans

0

1000000

2000000

3000000

4000000

5000000

6000000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Pro

du

ctio

n (

MT

)

Year

Maize

Beans, dry

Maize

Beans, dry

Kenya

Tanzania

SOURCE: FAOSTAT, 2013

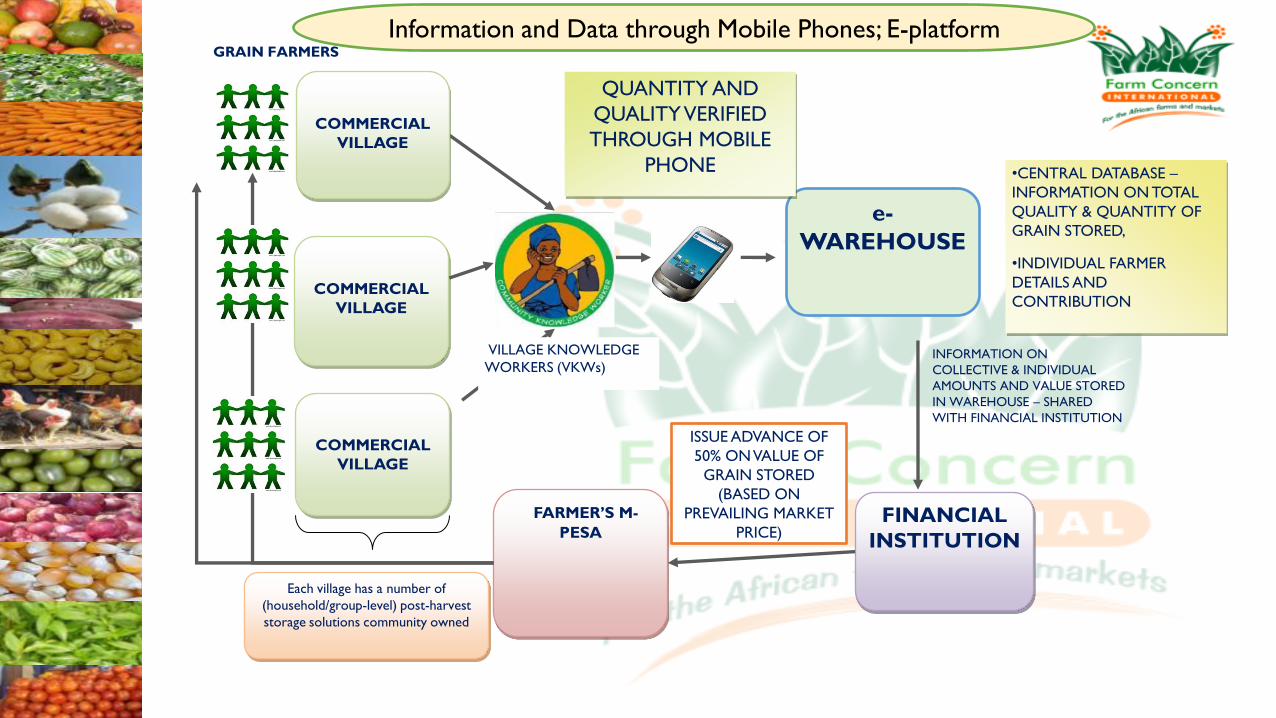

e-

WAREHOUSE

COMMERCIAL

VILLAGE

COMMERCIAL

VILLAGE

FARMER’S M-

PESA

•CENTRAL DATABASE –

INFORMATION ON TOTAL

QUALITY & QUANTITY OF

GRAIN STORED,

•INDIVIDUAL FARMER

DETAILS AND

CONTRIBUTION

FINANCIAL

INSTITUTION

INFORMATION ON

COLLECTIVE & INDIVIDUAL

AMOUNTS AND VALUE STORED

IN WAREHOUSE – SHARED

WITH FINANCIAL INSTITUTION

ISSUE ADVANCE OF

50% ON VALUE OF

GRAIN STORED

(BASED ON

PREVAILING MARKET

PRICE)

VILLAGE KNOWLEDGE

WORKERS (VKWs)

QUANTITY AND

QUALITY VERIFIED

THROUGH MOBILE

PHONE

GRAIN FARMERS

Each village has a number of

(household/group-level) post-harvest

storage solutions community owned

COMMERCIAL

VILLAGE

Information and Data through Mobile Phones; E-platform

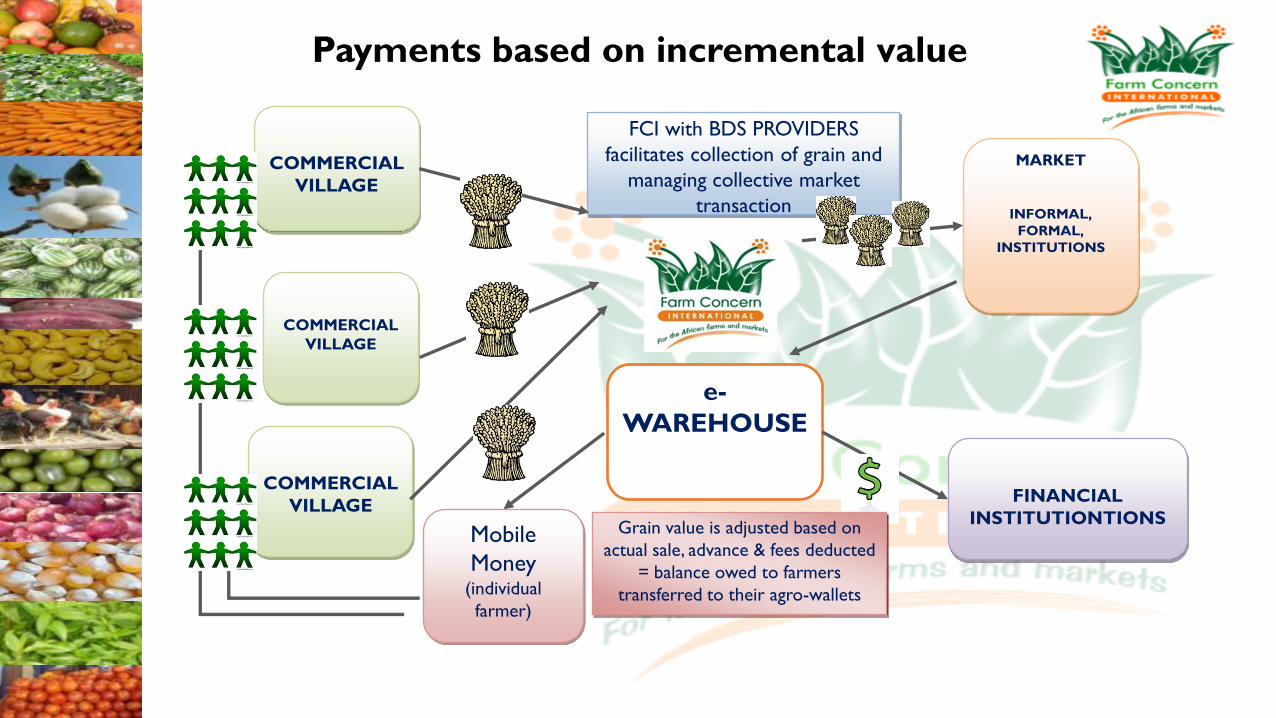

FCI with BDS PROVIDERS

facilitates collection of grain and

managing collective market

transaction

e-

WAREHOUSE

COMMERCIAL

VILLAGE

COMMERCIAL

VILLAGE

COMMERCIAL

VILLAGE

MARKET

INFORMAL,

FORMAL,

INSTITUTIONS

Mobile

Money

(individual

farmer)

FINANCIAL

INSTITUTIONTIONS Grain value is adjusted based on

actual sale, advance & fees deducted

= balance owed to farmers

transferred to their agro-wallets

Payments based on incremental value

19

E-warehouse Financial Access Market Support

Disbursement of credit to farmers

Farmers biodata and Volume of stored

grain

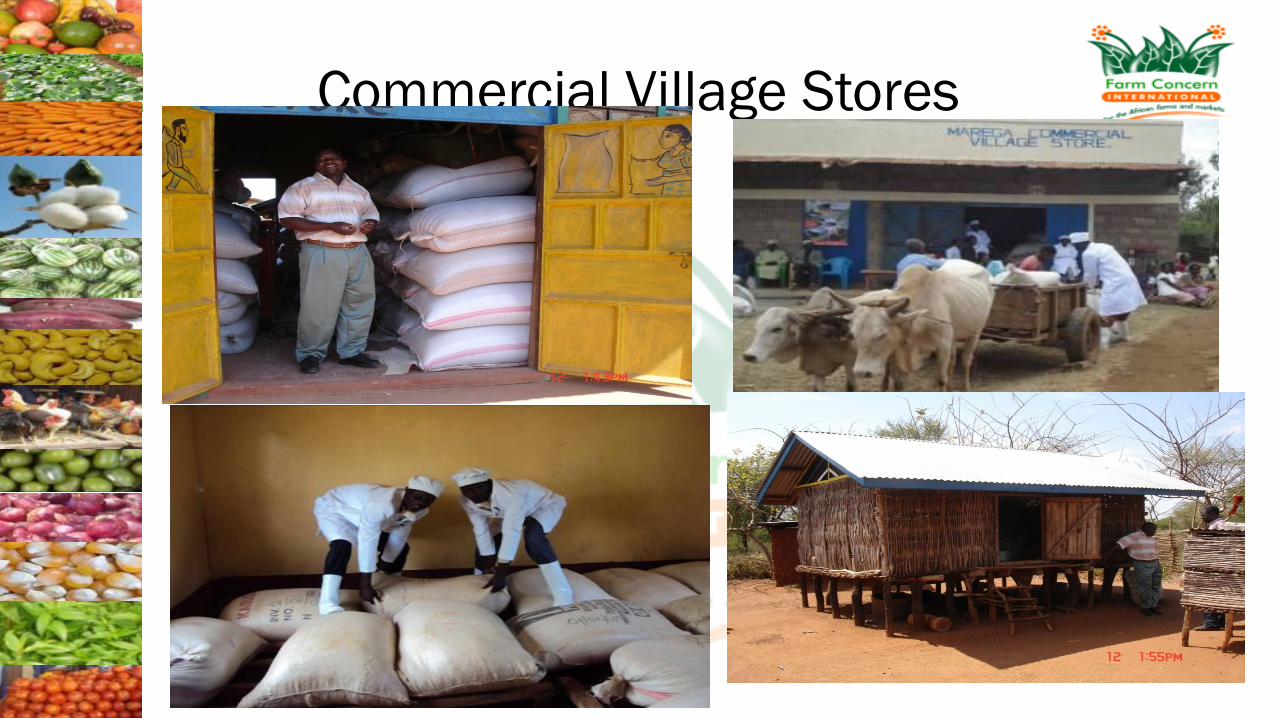

Grain Commercial

Villages Stores

Commercial Villages

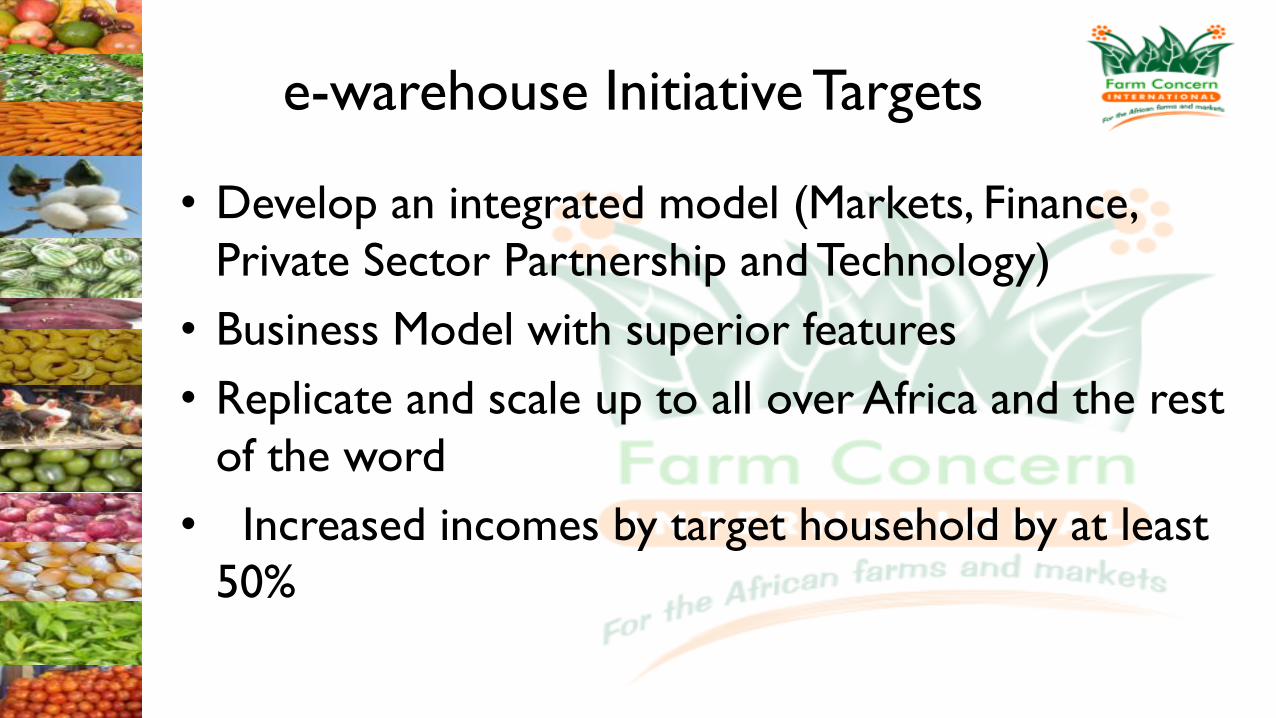

e-warehouse Initiative Targets

• Develop an integrated model (Markets, Finance,

Private Sector Partnership and Technology)

• Business Model with superior features

• Replicate and scale up to all over Africa and the rest

of the word

• Increased incomes by target household by at least

50%

Enhanced

Value delivery

mechanisms

New marketing

Landscapes Higher

investment

levels

Reduced post-

Harvest

losses

Enhanced

efficiency

Technical Service

provision

Increased value

Chain capacity

VALUE PROPOSITIONS

eWarehouse Partners

• Financial Institution

• Government Agencies

• Mobile Communication Service provider

• Grameen Foundation

• Input companies

• Grain buyers

• Commercial Villages

Village Knowledge Workers (VKW)

• Trained on production, commercialization & market development

• Offer onsite Technical support to Commercial Villages

• Equipped with training Kits – Mobile platforms, Moisture metres, Aflatoxin kits etc

Commercial Village Stores

One on One Support!

Winning Markets for the Poor!

FOR MORE INFORMATION VISIT

www.farmconcern.org